The Effect of Holding Company Affiliation on Bank Risk and the 2008 Financial Crisis

37

Electronic copy available at: http://ssrn.com/abstract=1664105 Electronic copy available at: http://ssrn.com/abstract=1664105 The Effect of Holding Company Affiliation on Bank Risk and the 2008 Financial Crisis Edward R. Lawrence RB 207A, Department of Finance College of Business Administration Florida International University, Miami FL 33199, Tel: (305)348-0082 Email: [email protected] Fernando M. Patterson RB 208, Department of Finance College of Business Administration Florida International University, Miami FL 33199, Tel: (305)348-2680 Email: [email protected] Arun J. Prakash RB 202A, Department of Finance College of Business Administration Florida International University, Miami FL 33199, Tel: (305)348-2680 Email: [email protected]

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of The Effect of Holding Company Affiliation on Bank Risk and the 2008 Financial Crisis

Electronic copy available at: http://ssrn.com/abstract=1664105Electronic copy available at: http://ssrn.com/abstract=1664105

The Effect of Holding Company Affiliation on Bank Risk and the 2008 Financial Crisis

Edward R. Lawrence RB 207A, Department of Finance

College of Business Administration Florida International University, Miami FL 33199, Tel: (305)348-0082

Email: [email protected]

Fernando M. Patterson RB 208, Department of Finance

College of Business Administration Florida International University, Miami FL 33199, Tel: (305)348-2680

Email: [email protected]

Arun J. Prakash RB 202A, Department of Finance

College of Business Administration Florida International University, Miami FL 33199, Tel: (305)348-2680

Email: [email protected]

Electronic copy available at: http://ssrn.com/abstract=1664105Electronic copy available at: http://ssrn.com/abstract=1664105

The Effect of Holding Company Affiliation on Bank Risk and the 2008 Financial Crisis

Abstract

The 2008 financial crisis originated at banking institutions with a specific combination of high leverage, low liquidity, low capitalization and high exposure to subprime mortgage loans. We perform a comparative analysis of independent banks and holding company affiliated banks, and find that during the crisis holding company affiliation was related to a higher risk position in banks, characterized by riskier mortgage loans, higher leverage and lower liquidity and capitalization. Market measures of risk during this period, however, were not different for the different structures, indicating that the market did not price the additional risk contribution of affiliated banks to the main causes of the contagion.

JEL category: G20 G21

Keywords: Bank Risk, Bank Holding Company, Financial Crisis of 2008, Independent Banks, Holding Company Affiliation.

Electronic copy available at: http://ssrn.com/abstract=1664105Electronic copy available at: http://ssrn.com/abstract=1664105

The Effect of Holding Company Affiliation on Bank Risk and the 2008 Financial Crisis

1. Introduction

The financial crisis that erupted in September of 2008 had epic proportions, and led the

world economy into deep recession. In his testimony before The Financial Crisis Inquiry

Commission on April 7, 2010, former Chairman of the Federal Reserve Alan Greenspan

identified the global proliferation of securitized U.S. subprime mortgages as the immediate

trigger of the 2008 financial crisis1. He further attributed the root causes to financial institutions

that held a precarious combination of high leverage and low liquidity and capitalization.

Contagion arose when debt obligations arising from the high leveraged positions could not be

serviced by the low levels of capital in these institutions, which at the same time did not have

enough liquid assets to meet the capital deficiency. In this paper we focus on these central causes

of the financial crisis of 2008, and explore how bank structure contributed to the contagion.

Specifically, we isolate the effect of holding company affiliation on the overall risk position of

banks, as determined by the risk in the loan and security portfolios as well as the leverage,

liquidity and capital adequacy at these institutions.

We compare the holding company affiliated banks and unaffiliated (independent) banks

and find that the holding company affiliated banks have higher leverage than unaffiliated banks,

they take more risk in their lending and investments, hold lower liquidity, and have lower capital

adequacy ratios. In order to determine if the risk effect of holding company affiliation is priced

in the market, we further examine the publically traded institutions within our sample. First, we

1 www.fcic.gov/hearings/pdfs/2010-0407-Greenspan.pdf

ascertain that public banks demonstrate the same pattern of holding company risk effect found

for the entire sample. Then, we examine the stock behavior during the financial crisis period to

determine whether or not this effect was conveyed from the financial statements on to market

measures of risk, namely, the equity and asset betas, the stock volatility and the systematic and

unsystematic risks. We do not find any difference in the market measures of risk between the

public holding company of affiliated banks and public unaffiliated banks. It seems that the

market was both unaware of the higher risk and lower liquidity positions of holding company

affiliated banks, therefore, did not price these risks.

In a recent study Demyanyk and Van Hemert (2009) find that in the years leading to the

crisis, home mortgage loans deteriorated significantly in quality. Notably loans originated in

2006 show a higher delinquency rate and a higher foreclosure rate than loans originated in earlier

years. They also find that the poor quality of these loans was not confined to any particular

segment of the subprime mortgage market, such as adjustable-rate or low-documentation

mortgages. Brunnermeier (2009) attributes this decline in lending standards to the pre-crisis

trend towards an “originate and distribute” model, in which banks pooled and trenched their

loans, and then resold them via securitization. Additionally, Blanchard (2008) reports that

financial institutions financed their portfolios with less and less capital in the years before the

crisis in order to increase the return on that capital. Effectively banks found ways to reduce their

required capital and increase leverage, for example by moving assets off their balance sheets

through structured investment vehicles.

Some banks, however, are naturally more leveraged than others simply due to their

organizational structure. Holding company affiliated banks normally operate like independent

banks, except their interest must be reconciled with the parent company objectives, as well as the

interest of any sister subsidiary company. Because holding company affiliated banks tend to have

higher leverage than individual banks, we hypothesize that they generally take more risk in their

lending and investments, and hold lower liquidity and capital adequacy ratios. For public

companies, we anticipate this additional risk to reflect in a more volatile stock behavior. Hence,

we expect holding company affiliated banks to have had a greater contribution to the 2008

financial crisis. We are able to isolate the risk effect of holding company affiliation by

considering one-bank holding companies (OBHCs) in which the sole subsidiary is a commercial

bank. After controlling for other explanatory factors, such as firm size, geography and

regulation, we are able to attribute any resulting difference in the risk position of banks to their

association with a holding company.

The growing literature on the 2008 financial crisis focuses almost entirely on economy-

wide interpretations to the crisis. Cecchetti (2009) and Goodhart (2008) emphasize the effect of

government agencies response, with particular attention to the Federal Reserve actions.

Cardarelli, Elekdag and Lall (2009) compare and contrast the behavior of global financial

markets. Murphy (2008) and Chari, Lawrence, and Kehoe (2008) discuss the nature of the causes

of the crisis. Ivashina and Scharfstein (2010) provide a forensic analysis of bank lending

activities during the crisis. Our study adds to the developing literature in this topic by focusing

rather on firm-specific characteristics that justify the economic interpretations to the crisis given

in previous studies. Specifically we study whether holding company affiliation put commercial

banks at higher risk during the financial turmoil of 2008, and whether the market was receptive

to the effect of affiliation. Previous studies that have focused exclusively on bank holding

companies analyze the diversification and size effects at these institutions. Demsetz and Strahan

(1997), for example, decompose the stock return volatility of 150 bank holding companies

(BHCs) to measure holding company diversification. They find that the larger the BHC, the

better diversified it tends to be. By identifying several measures of firm-specific risk from the

BHCs financial statements they then find that the larger more diversified BHCs have similar

leverage, capital adequacy ratios, and asset composition as smaller less diversified BHCs. Their

findings suggest that whatever risk reduction benefits BHCs may obtain from diversification they

trade for a higher risk position. In their study, however, it is impossible to attribute the findings

to the effect of any particular institution within the conglomerate. To our knowledge, we are the

first to isolate the effect of bank holding company affiliation on the risk position of commercial

banks.

The increased leverage2 for OBHCs has the effect of increasing interest rate risk since

creditors demand higher interest rates to compensate for the higher default risk. It enables the

company, however, to multiply the profitability of subsidized debt proportional to the degree of

leverage. According to the moral hazard hypothesis associated with equity holders' limited

liability, equity holders have a strong incentive to increase risk because limited liability allows

them to capture all upside gains while sharing their losses with debt holders. Leverage has the

effect of raising this incentive, since debt holder’s stake in the company is directly proportional

to the debt to equity ratio. Equity holders use the capital and liquidity available to hold overall

riskier positions with the hope of achieving a higher return. In particular to our sampled period

this means that OBHCs are expected not only to engage in higher levels of home mortgage loans,

but also to have a higher percentage of them fall in the riskier, more lucrative subprime category.

They are at the same time expected to have higher levels of junior home liens, mortgage backed

2 In Appendix A, we explain the concept of higher leverage in affiliated banks through a simple balance sheet example.

securities (MBSs), and lower liquidity and capital adequacy ratios than unaffiliated banks, where

equity holders have higher stakes.

Our results confirm that OBHCs have indeed higher debt to equity ratios than unaffiliated

banks, and that during the financial crisis they held an overall riskier position marked by higher

levels of home mortgage lending as well as riskier mortgage loans, and lower liquidity and

capital adequacy ratios. The data on investment in securities show that OBHCs engaged in less

MBSs. Though unaffiliated banks had higher levels of MBSs, they also engaged to a greater

extent on the safer US Treasury securities. On the profitability side, the higher risk position of

OBHCs was in fact accompanied by significantly higher returns on assets and returns on equity.

This comes to no surprise; riskier loans have higher interest rates, which lead to higher profits.

During times of crisis, however, riskier loans can also lead to higher losses. We observed that

prior to the economic crisis OBHCs had low liquidity and capital ratios as well as higher total

loans to assets, implying that they were sacrificing their capital and liquidity to engage in more

lending. Though they experienced higher profits as a result, during the crisis their position

became more precarious.

We further analyze the risk positions of the public subsample of affiliated and

unaffiliated banks, and find that public OBHCs underwrite higher amounts of first and junior

home liens than public unaffiliated banks, and have a higher nonperforming percentage of them.

This difference, not seen in the full sample, comes as no surprise. There are many more owners

in stockholder controlled banks than in private equity holder banks.. A larger amount of owners

(shareholders) translates into a smaller stake for the owner manager of the bank. Thus in the

public subsample, the incentive to use the higher leverage in OBHCs to engage in riskier lending

is stronger than in the non public OBHCs. Our results confirm that OBHCs are less liquid and

less capitalized, and higher leveraged (debt to equity) and more profitable structures than

unaffiliated banks in the public subsample.

A consequential matter arises of whether or not the market captures the differences in risk

position between affiliated and unaffiliated banks. Beyond the clear evidence indicating that

public OBHCs have an overall riskier stance than public unaffiliated banks, the usual measures

of market risk fail to account for this difference. No measure of market risk, not even the asset

beta which is most influenced by the debt to equity ratio, show any significant difference

between the banking structures. We find that whether private or public, the effect of holding

company affiliation means a higher risk stance for banks, at least as measured through the

balance sheet. In the context of the financial crisis it means that holding company affiliation

significantly increased the contribution of banks to the root causes of the crisis. This effect,

however, did not translate into more volatile stocks for public OBHCs. The market’s

‘unawareness’ of their higher risk taking combined with higher profits provides a positive

feedback mechanism by which OBHCs actions were rewarded during the financial crisis. Our

study suggests that holding company affiliation is not properly priced by the market.

The remainder of the paper is organized as follows. In section 2 we discuss the relevant

literature. Details about the sample construction and variables of interest are in section 3. In

section 4 we present the methodology. Section 5 has the results. . We conclude with a discussion

in section 6 and a brief conclusion in section 7.

2. Literature Review and Hypothesis Formation

Structural changes in the financial industry during the last few decades reveal why it is

important to study the effect of holding company affiliation on banks. Amel (1996), reports that

in the year 1984 independent banks represented 19.1% of all banking organizations and held

$209.9 billion in deposits. In just ten years these numbers fell to 12.0% and $170.0 billion in

deposits. During the same period the number of one-bank holding companies grew from 16.5%

to 20.4% of all banking organizations, and their deposits from $467.7 to $523.0 billion. Similarly

multibank holding companies grew from 2.4% to 3.7% of all banking organizations, and their

deposits from $936.1 to $1689.6 billion. Janicki and Prescott (2006) study the changes in the size

distribution of banks from 1960 to 2005, and find that while the ten largest banks held 21% of

the banking industry’s assets in 1960, their share grew to nearly 60% by 2005. During this period

the number of independent banks fell sharply from 13,000 to less than 6,500. There has been a

steady change in the financial industry over time towards consolidation and larger size. It is clear

that the larger banking organizations have more of an impact on the financial markets. The

failure of any one of the ten largest depository institutions in the US during the financial crisis

would have bankrupted the FDIC. It would have taken several hundred small banks to do the

same. The effect of holding company affiliation on the financial markets is a less obvious matter,

however. In this study we are concerned with how affiliation influenced the risk position of

banks during the financial crisis, and how this influence specifically contributed to its root

causes.

The literature that explores differences in affiliated and unaffiliated banks is scanty and

outdated. Mayne (1977) compares selected measures of the performance of the banking affiliates

of multibank holding companies with nonaffiliated banks competing in the same local markets.

She studies a sample of 656 banks divided equally between independent banks and holding

company subsidiaries during 1969-1972. Her findings indicate that independent institutions

exhibit greater holdings of cash and low risk securities, and smaller percentage of residential

mortgage loans than affiliated banks. At the same time, independent banks appear to be less

profitable, presumably due to the assumption of lower risk, and commensurate lower return. We

build on Mayne’s multivariate approach in order to isolate the effect of the holding company

from that of other specified factors which influence bank risk position. Our study, however,

differs from Mayne’s in several important ways. For one thing, we restrict our sample to one-

bank holding companies with a commercial bank as its single subsidiary (OBHC). In this way we

are able to attribute the findings specifically to the effect of holding company affiliation, unlike

in Mayne’s study where other subsidiary companies make it impossible to isolate this effect.

Additionally the sheer sample size employed in our study constitutes almost the entire population

of OBHCs and nearly half of individual banks in the USA. Of the 3,097 affiliated banks and the

11,073 independent banks that existed in 1973, Mayne’s sample represents 10.6% of affiliated

banks and 2.9% of independent banks. Our sample, on the other hand, considers 91.6% of OBHC

and 48.5% of unaffiliated banks in existence at yearend 2008. Finally we consider, in addition to

financial statements measures of risk, market measures of risk by examining the stock behavior

of publically traded organizations within our sample.

We define our measures of risk appropriate for the time period studied. Demyanyk and

Van Hemert (2009) find that risk in financial institutions in the years leading to the financial

crisis was increasingly defined by the degree of low quality home mortgage loans. Hence our

objective becomes uncovering the relevant measures of low quality mortgage loans available in

the financial statements. While banks do not readily report the amount of ‘subprime’ mortgage

loans on their balance sheets, we measure risk in their mortgage loan portfolio through the

amount of nonperforming loans, and of junior home liens. Though an indirect measure of

‘subprime’, nonperforming home mortgage loans provide the best proxy of bad quality loans in

the financial statements. Junior home liens, on the other hand, are not presumed to reflect

‘subprime’ lending; however during times of crisis they can represent significantly riskier loans

over first liens. First home liens have payment priority over junior home liens in the event of

mortgage default. During a booming real estate market, banks can sell a foreclosed property at a

high enough price to cover both first and junior liens. However, during extreme real estate and

credit market contractions, like those experienced during 2008, a foreclosed property may barely

cover the first lien, and almost certainly not be sufficient to honor a junior lien. Hence, we use

junior home liens as a measure of risk in the loan portfolio. Consistent with the higher leverage

available to affiliated banks, and Blanchard (2008) findings that banks came into the financial

crisis with lower capital ratios than they had in years past, we formulate our first two research

hypotheses:

Hypothesis 1: Affiliated banks have higher amounts of nonperforming and junior mortgage loans

than unaffiliated banks.

Hypothesis 2: Affiliated banks have lower percentages of capital and liquid assets than

unaffiliated banks

We test these hypotheses by performing univariate and multivariate tests to compare the ratios of

nonperforming home mortgage loans and junior home liens to total loans, as well as the tier1 and

liquid assets to total assets ratios for the affiliated and nonaffiliated banks.

Our third hypothesis relates to the public institutions in our sample, and measures of

market risk used in a similar manner in previous literature. Maher (1997), for example, employs

a two-factor model of security returns to assess the inter-temporal risk position of bank holding

companies from 1976 to 1989. His primary measure of firm risk is the stock return variance,

which he finds to have gradually increased over time during the sampled period. We use the

stock variance as a measure of total firm risk, but further decompose it into the systematic and

unsystematic components. Additionally we employ the stock beta in order to measure the beta of

the assets in the balance sheet. Our third hypothesis describes our expectations on the market

measures of risk.

Hypothesis 3: Market measures of risk are higher for affiliated banks than for unaffiliated banks.

We test this hypothesis by performing the univariate as well as multivariate tests to compare the

stock and asset betas, as well as total, systematic and unsystematic risks between affiliated and

unaffiliated banks.

3. Sample and Data

In this study we use the Highline Financial3 database to obtain the financial statements of

all the banks is our sample. We identify 2649 OBHCs as having no nonbank, thrift or foreign

subsidiaries at yearend 2008. Entire investment (100%) of the holding companies’ investment is

in subsidiaries and is confirmed to be in a single commercial bank. We identify 2233

independent commercial banks.. The final total sample consists of 2426 OBHCs and 1085

unaffiliated banks, after banks with missing, unreported or otherwise unavailable dependent and

independent variables are removed. In the final sample 259 OBHCs have public holding

companies and private banks. Furthermore, 186 unaffiliated banks in the final sample are public.

Stock and market data is compiled using Bloomberg LP. Companies whose stock traded

continuously for at least 100 of the 104 weeks in the two year sample period are selected into the

final public sample set. Thus, in final sample we have 153 OBHCs and 116 unaffiliated banks.

3Highline Financial can be access at www.highlinefi.com. It provides financial statement data for US financial institutions.

We collect the 2008 end of year financial statements from Highline Financial for each

commercial bank in the sample. The dependent variables selected encompass the breakdown of

loans secured by real estate and their nonperformance, the security investments, and the liquidity,

leverage and capital adequacy of the banks. The independent variables selected control for firm

size, number of branches, local economic market (geography), and bank regulatory authority.

Additionally, weekly stock returns for 2007-2008 is collected from Bloomberg LP for the public

sample set. Betas are calculated through matched weekly S&P 500 index (SPX) returns. Total

stock risk is decomposed into systematic and unsystematic risks using the standard finance

equations.

4. Methodology

Univariate Analysis:

Our goal is to test if the ratios in the unaffiliated bank structure ( 1μ ) are different from

the ratios in the banks of OBHCs ( 2μ ). Hence we test the following null-hypothesis:

0: 210 =− μμH

To select the appropriate test we first test whether the population variances are

statistically equal or not using the Snedecor’s F-test. If the variances are found to be statistically

equal, we use the standard two independent sample t-test to test the equality of population

means4. If the variances are found to be statistically not equal, we use the two independent

sample t- test for equality of population means as proposed by Satterthwaite (1946). The test

4 For the test statistics and procedures to test the equality of two population variances and the equality of two population means when population variances are unknown but equal see any basic standard statistics textbook. Furthermore, the parametric tests require that the populations from which the samples are taken are normally distributed as well. However, we refrain from testing for normality as the sample sizes in our study are very large.

assumes that the two underlying populations are normally distributed with unequal but unknown

population variances, the appropriate two independent sample t-test requires the computation of

the t-statistic given by

21

2

22

1

21

2121

)(

)()(

ns

nsXXt

+

−−−=

μμ

If the null hypothesis is true, the t- statistic will have Student’s t-distribution with

Welch’s (1947) “modified” degrees of freedom given by

df =

2

22

22

1

21

21

2

2

22

1

21

)/()/(nns

nns

ns

ns

+

⎟⎟⎠

⎞⎜⎜⎝

⎛+

Where i and Si ( i = 1,2) respectively are the sample means and standard deviations of

the ith sample.

Multivariate Analysis:

Our multivariate analysis is inspired by Mayne’s (1977) study. Like Mayne, we also use

multiple linear regressions but improve upon by providing better control of the local economy in

which the banks compete, namely the county unemployment rate, the percent change in per-

capita income from 2007 to 2008, and whether or not the organization is in a metropolitan area

(See Thomson (1991)). Additionally, since our sample considers an important number of small

organizations, we also control for the number of branches. Essentially, we perform a cross

sectional multivariate regression analysis with selected variables of interest, which influences the

loan and security investment exposure to the real estate market as well as the leverage, liquidity,

capitalization and profitability. For each of the dependent variables, we run the following

regression model:

Dependent variable = α + β1*UR + β2*%ΔPCI + β3*MSA + β4*LogTA + β5*Charter

+ β6*Branches + β7*HC + ε (1)

The dependent variables are: home mortgage loans per total loans, first home liens per

total loans, junior home liens per total loans, total loans per total assets, nonperforming home

mortgage loans per total loans, nonperforming first home liens per total loans, nonperforming

junior home liens per total loans, nonperforming loans per total loans, US Treasury securities per

total securities, municipal securities per total securities, mortgage backed securities per total

securities, municipal securities per total securities, held to maturity securities per total securities,

total securities per total assets, liquid assets per total assets, tier 1 capital ratio, debt to equity

ratio, return on average asset, and return on average equity. Additionally for the public sample

we include the stock beta, stock return variance, systematic risk, unsystematic risk, and asset

beta.

The independent variables are: county unemployment rate (UR), percent change in per-

capita income from 2007 to 2008 (%ΔPCI), area type dummy variable (MSA = 1 for metro, 0 for

non-metro), log of total assets (logTA), regulatory authority (Charter = 1 for federal, 0 for state),

number of branches (Branches), holding company dummy variable (HC = 1 for OBHC, 0 for

independent bank).

The county unemployment rate, the percent change in per-capita income, and the MSA

dummy control for the local economic conditions. These measures have been widely used in

standard banking literature, (for example see Thomson (1991) and Mayne (1977)). In our study

these variables are key factors that affect the real estate market, and in turn the health of banks.

Higher unemployment and lower percent change in per-capita income can translate into higher

mortgage defaults. MSA type area, on the other hand, can make it easier (metropolitan areas) or

harder (micropolitan areas) for banks to increase the size of their home mortgage loan portfolios.

The size of a bank and the number of branches are other variables widely used to capture any

scale effects. They are particularly important in our study since typically independent banks tend

to be smaller than OBHC. Finally the regulatory authority controls for differences in the ‘ease’

by which banks are allowed to operate, given different stringency in the regulatory policy of

federal versus state regulators (Mayne (1977)). The HC dummy represents bank structure, and is

the primary variable of interest in this study.

An identical procedure of univariate and multivariate analysis is conducted for the public

subsample. In addition to comparing financial statement measures, however, we also test for

differences in the various market measures of risk. In principle, the risk embedded in the balance

sheet is captured by the beta of the assets. The asset beta corresponds to the weighted average of

the beta of the debt and the beta of the equity, as enumerated in equation 2 below. Though debt is

not risk-free, for simplicity we assume that it is insured or otherwise backed in its entirety by the

company assets. This assumption makes the debt beta equal zero, and allows us to measure the

asset beta through reduced equation 3. We obtain the equity beta for our public subsample of

unaffiliated banks and OBHCs, where the holding company is the public entity, through equation

4. Additional market measures of risk, such as stock total risk, systematic and unsystematic risk

are measured through equations 5, 6 and 7 respectively.

βassets = βdebt + βequity (2)

βassets = βequity (3)

βequity = (4)

Total stock risk = σi2 (5)

Systematic risk = (βequity)2 * σm2 (6)

Unsystematic risk = Total risk – Systematic risk (7)

Where σi2 is the variance of the stocks’ rates of return, and σm

2 is the variance of the market rates

of return.

5. Empirical Results

In Table 1 we present the univariate statistical tests for the full sample. In Panel A we

show the loan mix at unaffiliated and affiliated banks. We find that for both, total loans are more

than half of the total assets, and real estate loans are more than half of all loans, with OBHCs

offering more total loans to assets, but less real estate loans to total loans. OBHCs offer

significantly more first and junior home liens than unaffiliated banks. Panel B of Table 1 shows

that total nonperforming loans are a relatively small percentage of total loans, with unaffiliated

banks having significantly higher amounts of them. However, nonperforming loan differences

are mainly for construction and land development loans, home equity lines and loans secured by

nonfarm and nonresidential assets. Panel C of Table1 reveals that both OBHCs and unaffiliated

banks engage in security investments to a similar extent; for each, total securities represent about

a quarter of the total assets. OBHCs engage in significantly higher levels of municipal securities,

and have more total securities available for sale. Unaffiliated banks engage more in US Treasury,

MBSs and other debt securities, and also hold more of their total securities to maturity. Panel D

of Table 1 shows that OBHCs are larger in size and are more profitable; however they also hold

higher debt to equity ratios and lower liquid assets and tier 1 capital to total assets than

unaffiliated banks.

In Table 2 we present the full sample regression analysis on the variables of interest we

reported in Table 1. The HC Dummy coefficient indicates differences emanating from the type

of structure, either holding company affiliated or unaffiliated bank. In Panel A of Table 2 we find

positive and significant coefficients for home mortgage loans, first and junior liens and total

loans to assets, indicating that OBHCs engage in higher levels of these loans after controlling for

firm specific, geographical and regulatory differences. In Panel B we report the cross sectional

regression for the non performing loans and find a moderately significant and positive

coefficient for nonperforming home mortgage loans, indicating that the combined first and junior

lien loans are relatively worse in OBHCs. Total loans, however, generally underperform more at

unaffiliated banks, as indicated by the negative and moderately significant HC dummy

coefficient. In Panel C we notice significant differences across all security investment measures.

The negative HC dummy coefficient indicates higher levels of MBS, US Treasury securities,

securities held to maturity and total securities for unaffiliated banks, while OBHCs engage in

higher amounts of municipal securities. The cross sectional regression results in Panel D show

that OBHCs have significantly higher debt to equity ratios, higher return on assets (ROA), higher

return on equity (ROE), lower liquid asset and lower tier1 ratios. The results in Table 1 and 2

support our hypothesis 1 and 2 that affiliated banks have higher amounts of nonperforming and

junior mortgage loans than unaffiliated banks, and that affiliated banks have lower percentages

of capital and liquid assets than unaffiliated banks.

In Table 3 we present the univariate analysis of the public subsample of the unaffiliated

and the affiliated banks of OBHCs. Panel A shows that unaffiliated banks report moderately

higher levels of loans than OBHCs. Real estate loans constitute close to eighty percent of total

loans for both structures. Unaffiliated banks have higher levels of construction and land

development loans, while OBHCs report higher levels of home mortgage loans, both at the first

and junior levels. In Panel B we find higher construction and land development nonperforming

loans for the unaffiliated banks, while nonperforming first and junior home mortgage loans are

significantly higher at OBHCs. In Panel C we show that unaffiliated and the affiliated bank of

OBHCs have similar security mix; the only significant difference is in the municipal securities

where the bank affiliated to OBHCs hold more municipal securities. Lastly the results presented

in Panel D of Table 3 show that public OBHCs are larger and more profitable than public

unaffiliated banks. They also report lower liquid assets and tier 1 to total assets ratios, and higher

debt to equity ratios.

In Table 4 we present the similar regressions as Table 2 for the public subsample. In

Panel A we observe that while both structures engage in similar amounts of total loans, the

mortgage loan composition is substantially higher at OBHCs. Results in Panel B show that

affiliated banks of OBHCs experience higher amounts of nonperforming first and junior home

liens than their unaffiliated counterparts. Consistent with Mayne (1977), in Panel C we find that

public OBHCs engage in higher levels of municipal securities. Our results, however, show no

difference in the levels of MBS or total securities between affiliated and unaffiliated banks. In

Panel D, public OBHCs show the same pattern observed in the full sample regressions reported

in Panel D of Table 2, with lower liquid asset and tier 1 ratios and higher debt to equity, return

on average asset and return on average equity ratios than unaffiliated banks. Finally in Panel E

we find that none of the market measures of risk show any statistical difference between the two

banking structures.

6. Discussion

Our results indicate that OBHCs have higher debt to equity ratios than unaffiliated banks,

both in the overall sample and in the public subsample. High leverage is postulated by

economists like Alan Greenspan as having had a pivotal role in the aggregate risk of financial

markets during the 2008 crisis. , increased risk for banks meant engaging in subprime home

mortgage loans or in securities derived from them. These subprime mortgage loans had higher

probability of default, but higher interest, and therefore higher profits than their safer prime loan

counterparts. Our results clearly indicate that at OBHCs, where the leverage is higher, there were

many more home mortgage loans underwritten and underperforming than at unaffiliated banks,

where the leverage is lower.

We find that higher leverage for OBHCs was accompanied by lower liquid assets to total

assets and lower tier 1 to total assets ratios. This suggests that OBHCs did not manage their

higher loan portfolio risk by being better capitalized and liquid than unaffiliated banks. From

table 2 we can determine that they directed their attention instead to safer security investments,

particularly municipal securities. This is likely to explain why we find lower levels of MBS in

the banks of OBHCs. This particular combination of riskier home mortgage loans and safer

security investment proved profitable for OBHCs, as they experienced higher ROA and higher

ROE than unaffiliated banks, who preferentially engaged in more MBSs and managed their risk

through higher liquidity and capitalization.

The public subsample of OBHCs and unaffiliated banks show higher levels of leverage

and even sharper risk differences than the full sample of equivalents. Whereas for the full sample

there is a moderately significant difference in combined nonperforming home liens, public

OBHCs have higher levels of nonperforming first and junior liens than unaffiliated banks.

Furthermore there are no differences in MBSs investment. We observe significantly lower

liquidity and capital adequacy ratios for OBHCs. This suggests that the relative riskiness of

public OBHCs over public unaffiliated banks is larger than the difference in risk stance between

the non public structures. Nevertheless, the higher risk position of public OBHCs proved more

profitable than the relatively safer stance of unaffiliated banks, as measured by higher ROA and

ROE ratios. The market measures of risk did not incorporate the clearly defined risk and

profitability differences between the structures embedded in the balance sheet. The stock of

publically traded OBHCs is no more volatile than the stock of public unaffiliated banks. There

are no differences in the stock betas, and what is more surprising, no differences in the asset beta.

This is surprising indeed given the markedly different debt to equity ratios between the

structures, which is used to compute the asset beta. This asset beta is a proxy for the risk in the

assets that is ‘noticed’ by the market. Yet the market proved totally blind to the sharp differences

noted on the loan portfolios.

7. Conclusion

In this study we isolate the effect of holding company affiliation through sample

selection, and demonstrate that this effect translated into higher contribution of banks to the root

causes of the 2008 financial crisis. Affiliated banks used their higher leveraged positions to

engage in riskier home mortgage lending, sacrificing both liquidity and capital adequacy, the

combined effect of which were the primary reasons of the contagion. Besides this clear higher

contribution, the market did not deem OBHCs any riskier than unaffiliated banks.

In the context of the financial crisis it is important to determine if holding company

affiliation impacted the amounts of subprime mortgage loans underwritten at affiliated institution

versus unaffiliated ones. In this study we did not directly measure this amount, due to the general

unavailability of the specific nature of the home mortgage loans reported on the balance sheets.

Instead we use the percentage of nonperforming loans as a proxy for bad quality loans, though

we are careful not to refer to them as ‘subprime’. Instead, we identify ‘risky’ loans as being

either the nonperforming loans or the junior home liens. Our study could be taken further by

measuring subprime mortgage loans directly, though for our sample this data is not publically (or

freely) available yet. This, however, is a minor point rather than a limitation, considering that our

analysis enraptures more than risky loans and provides a general picture of the risk position of

OBHCs and unaffiliated banks.

REFERENCES

Amel, D., 1996. Trends in the structure of federally insured depository institutions: 1984-94.

Federal Reserve Bulletin January.

Blanchard, O., 2009. The crisis: basic mechanisms, and appropriate policies. International

Monetary Fund, Washington DC, Working Paper 80.

Brunnermeier, M., 2008. Deciphering the liquidity and credit crunch 2007-2008. Journal of

Economic Perspectives Forthcoming.

Cardarelli, R., Selim E., Subir L., 2009. Financial stress, downturns, and Recoveries.

Washington: International Monetary Fund forthcoming.

Cecchetti, S.G., 2009. Crisis and responses: the federal reserve in the early stages of the financial

crisis. Journal of Economic Perspectives 23, 51-75.

Chari, V.V., Lawrence J.C., Patrick J.K., 2008. Facts and myths about the financial crisis of

2008. Federal Reserve Bank of Minneapolis Working Paper no. 666.

Demsetz, R., Strahan, P., 1997. Diversification, size, and risk at bank holding companies. Journal

of Money Credit and Banking 29(3), 303-313.

Demyanyk, Y., Van Hemert, O., 2007. Understanding the subprime mortgage crisis. Stern

School of Business, New York University, Working Paper December 10.

Goodhart, C., 2008. The regulatory response to the financial crisis. LSE Financial Markets

Group Paper Series February.

Greenspan, A., 2010. Testimony before the financial crisis inquiry commission. April 7.

Ivashina, V., Scharfstein, D., 2010. Bank lending during the financial crisis of 2008. Harvard

Business School Working Paper.

Janicki, H., Prescott, E., 2006. Changes in the size distribution of U.S. banks: 1960-

2005.”Federal Reserve Bank of Richmond Economic Quarterly 92:4, 291-316.

Maher, M., 1997. Bank holding company risk from 1976-1989 with a two-factor model. The

Financial Review 32(2), 357-371.

Mayne, L.S., 1977. A comparative study of bank holding company affiliates and independent

banks, 1969-1972. Journal of Finance 32, 147-158.

Murphy, A., 2008. An analysis of the financial crisis of 2008: causes and solutions. Social

Science Research Network.

Thomson, J.B., 1991. Predicting bank failures in the 1980s. Federal Reserve Bank of Cleveland

Economic Review First Quarter, 9-20.

Appendix A: Leverage and Holding Company Affiliation

The concept of higher leverage in affiliated banks can be easily demonstrated through a

simple balance sheet example. Bank A shown below has $100 in assets. On the liability side the

assets are matched with $80 of debt and $20 of equity, which represents a debt to equity ratio of

4. A holding company owning bank A will report on their balance sheet $20 of assets,

corresponding to the equity of bank A. We assume that it has $5 of equity and that it has taken

$15 of debt to purchase the bank. The consolidated balance sheet of the one-bank holding

company consists of $95 of debt and $5 of equity, the equivalent of a debt to equity ratio of 19.

In this example we have assumed that the bank existed prior to the formation of the one-bank

holding company, in which case the minimum equity and debt assumed by the holding company

is the equity of the bank. Holding companies, however, are free to choose additional amounts of

debt, and do so regularly as the cost of capital is usually lower for them than for unaffiliated

banks.

Balance Sheet of Bank A:

Assets Liabilities + Equity

$100 Debt $80

Equity $20

Total $100 Total $100

Balance Sheet of Holding Company:

Assets Liabilities + Equity

$20 This is their investment in the Bank Debt $15

Equity $5

Total $20 Total $20

Consolidated Balance sheet of OBHC:

Assets Liabilities + Equity

$100 Debt $95

Equity $5

Total $100 Total $100

TABLE 1

Comparison of Affiliated Banks and Independent Banks: Univariate Analysis

The table shows the mean and standard deviation of selected balance sheet variables at yearend 2008 for the complete sample of unaffiliated and affiliated banks. Student’s t-test results are indicated by the asterisks; *, ** and *** denote significant differences between the samples means at the 10%, 5% and 1% level respectively. Panel A shows the real estate loan mix. Panel B describes the corresponding nonperforming amounts for the loans shown in Panel A. All loan variables are expressed as a percentage of gross loans and leases. Panel C shows selected security variables expressed as a percentage of total securities. Finally Panel D shows selected ratios that describe sample differences in size, liquidity, capitalization and profitability.

Panel A Unaffiliated Bank Bank of OBHC Loan Mix Mean S. Dev Mean S. Dev Loans Secured by Real Estate: 67.33% 0.2278 66.67% 0.1847 Construction & Land Development *** 10.88% 0.1213 7.98% 0.0920 Secured by Farmland *** 5.48% 0.0900 8.62% 0.0954 Secured by 1-4 Family Residential: *** 23.02% 0.1704 27.30% 0.1564 Home Equity Loans *** 2.82% 0.0461 2.38% 0.0378 Home Mortgage Loans: *** 20.20% 0.1680 24.92% 0.1523 Secured by First Liens *** 18.92% 0.1624 23.28% 0.1464 Secured by Junior Liens *** 1.28% 0.0218 1.63% 0.0217 Secured by 5+ Residential *** 2.36% 0.0542 1.56% 0.0305 Secured by Nonfarm, Nonresidential *** 25.59% 0.1853 21.20% 0.1394 Gross Domestic Loans & Leases/TA *** 62.96% 0.1904 65.40% 0.1515 #banks: 1085 2426

Panel B Unaffiliated Bank Bank of OBHC Nonperforming Loan Mix Mean S. Dev Mean S. Dev Loans Secured by Real Estate: ** 1.64% 0.0314 1.44% 0.0220 Construction & Land Development *** 0.79% 0.0241 0.53% 0.0149 Secured by Farmland 0.06% 0.0041 0.07% 0.0031 Secured by 1-4 Family Residential: 0.37% 0.0099 0.38% 0.0069 Home Equity Loans *** 0.04% 0.0023 0.02% 0.0008 Home Mortgage Loans: 0.34% 0.0095 0.36% 0.0068 Secured by First Liens 0.31% 0.0091 0.34% 0.0061 Secured by Junior Liens 0.02% 0.0012 0.03% 0.0016 Secured by 5+ Residential * 0.05% 0.0032 0.03% 0.0026 Secured by Nonfarm, Nonresidential *** 0.35% 0.0089 0.44% 0.0089 Gross Domestic Office Loans & Leases *** 2.17% 0.0451 1.86% 0.0240 #banks: 1085 2426

Panel C Unaffiliated Bank Bank of OBHC Security Investment Mix Mean S. Dev Mean S. Dev US Treasury Secs *** 3.73% 0.1489 2.01% 0.1062US Govt Agency Secs 42.59% 0.3410 41.75% 0.3190Municipal Secs *** 14.22% 0.2175 24.01% 0.2278Mortgage Backed Secs: *** 33.76% 0.3404 29.28% 0.2923 Secs Issue FNMA & FHLMC 6.19% 0.1563 7.04% 0.1468 Pass Through Secs *** 27.57% 0.3121 22.24% 0.2516Other Debt Secs ** 2.99% 0.0999 2.31% 0.0805Held-to-Maturity Secs *** 20.55% 0.3603 13.93% 0.2869Avail-for-Sale Secs *** 79.45% 0.3603 86.07% 0.2869 Securities/TA 22.14% 0.1709 22.02% 0.1409 #banks: 1085 2426

Panel D Unaffiliated Bank Bank of OBHC Selected Measures Mean S. Dev Mean S. Dev Log (TA) *** 4.93 0.4600 5.00 0.4014Liquid Assets/Total Assets *** 14.85% 0.1274 11.42% 0.0887Tier 1 Ratio *** 14.90% 0.1140 10.70% 0.0412Debt/Equity *** 36.63% 0.6567 45.76% 0.6436Return on Average Assets (ROA) *** -0.30% 0.0302 0.59% 0.0129Return on Average Equity (ROE) *** 0.06% 0.1704 5.90% 0.1178 #banks: 1085 2426

TABLE 2

Comparison of Affiliated Banks and Independent Banks: Cross Sectional Regression

The table presents the regression coefficients on selected variables as well as their significance on regressions ran on the entire sample of affiliated and unaffiliated banks. The independent variables are used to control for firm size, geography and regulatory authority. Panel A shows the breakdown of home mortgage loans into first and junior liens, and the total loans to total assets. Panel B describes the corresponding nonperforming amounts for the loans shown in Panel A. Panel C shows selected security investment variables. Finally Panel D shows regression results for variables that describe liquidity, capitalization and profitability. The variable of interest is the HC dummy, which takes value of 1 for affiliated banks, and of 0 for unaffiliated banks. *, ** and *** denote significant differences between the samples means at the 10%, 5% and 1% level respectively. The following acronyms are used: Mortgage (Mtg), Loans (Lns), Total Assets (TA), Nonperforming (NP), Securities (Secs), Mortgage backed securities (MBS), Held to maturity securities (HTM), Return on assets (ROA), and Return on equity (ROE).

Panel A Regression Coefficient Home Mtg

Lns First Liens Junior Liens Total Lns/TA

Independent Variable Intercept ***0.3335 ***0.3368 -0.0033 ***0.1556HC Dummy ***0.0453 ***0.0409 ***0.0044 ***0.0336Log (TA) ***-0.0452 ***-0.0478 **0.0025 ***0.0896MSA Type ***-0.0322 ***-0.0376 ***0.0053 ***0.0468%ΔPCI ***-0.2812 ***-0.2481 ***-0.0331 ***-0.17272008 UR ***1.9277 ***1.9277 3.69E-05 **0.3212Authority Charter ***0.0330 ***0.0307 **0.0022 ***-0.0586No Branches ***0.0026 ***0.0023 ***0.0003 -0.0003 R2 0.0976 0.1049 0.0523 0.1263

#Unaffiliated banks: 1085#OBHC banks: 2426

Panel B Regression Coefficient NP Home Mtg

Lns NP First Lns NP Junior

Lns NP Lns/Total

Lns Independent Variable Intercept 0.0002 0.0002 -4.9E-05 ***-0.0256HC Dummy *0.0005 0.0004 9.2E-05 *-0.0020Log (TA) 2.04E-05 -7.9E-06 2.83E-05 ***0.0090MSA Type 0.0004 0.0002 **0.0001 ***0.0040%ΔPCI **-0.0065 **-0.0057 -0.0008 **-0.02642008 UR ***0.0532 ***0.0513 0.0018 0.0373Authority Charter 0.0002 0.0002 -5.1E-05 *-0.0025No Branches -2E-05 -1.5E-05 -4.6E-06 **-0.0003 R2 0.0201 0.0209 0.0042 0.0274

#Unaffiliated banks: 1085#OBHC banks: 2426

Panel C Regression Coefficient US Treasury

Secs Municipal

Secs MBS HTM Total

Secs/TA Independent Variable

Intercept ***0.1149 0.0068 ***-0.3932 ***0.9705 ***0.2982HC Dummy ***-0.0151 ***0.0776 ***-0.0457 ***-0.0659 ***-0.0165Log (TA) **-0.0153 ***0.0363 ***0.1386 ***-0.1413 -0.0090MSA Type 0.0068 ***-0.0659 ***0.0426 ***-0.0358 ***-0.0516%ΔPCI -0.0093 0.1320 0.1744 ***-0.3897 ***0.27792008 UR -0.1332 -0.1822 0.3576 ***-0.8795 -0.2328Authority Charter -0.0002 -0.0065 -0.0056 -0.0136 ***0.0489No Branches 0.0004 0.0016 -0.0019 ***0.0073 *-0.0012 R2 0.0069 0.0627 0.0436 0.0404 0.0737

#Unaffiliated banks: 1085#OBHC banks: 2426

Panel D Regression Coefficient Liquid

Assets/TA Tier 1 Debt/Equity ROA ROE

Independent Variable

Intercept ***0.5980 ***0.3478 ***-1.8422 ***-0.0411 ***-0.1453HC Dummy ***-0.0297 ***-0.0349 ***0.0840 ***0.0055 ***0.0363Log (TA) ***-0.0888 ***-0.0425 ***0.4642 ***0.0096 ***0.0448MSA Type -0.0010 ***0.0133 *0.0415 ***-0.0090 ***-0.0647%ΔPCI -0.0298 ***-0.1165 -0.0454 ***0.0545 ***0.30362008 UR ***-0.2616 0.0797 -0.9957 ***-0.0944 ***-0.7867Authority Charter ***0.0176 *0.0058 ***-0.1141 0.0011 0.0067No Branches **0.0009 0.0003 ***-0.0117 **-0.0002 -0.0004 R2 0.1440 0.1154 0.0823 0.1280 0.1213

#Unaffiliated banks: 1085#OBHC banks: 2426

TABLE 3

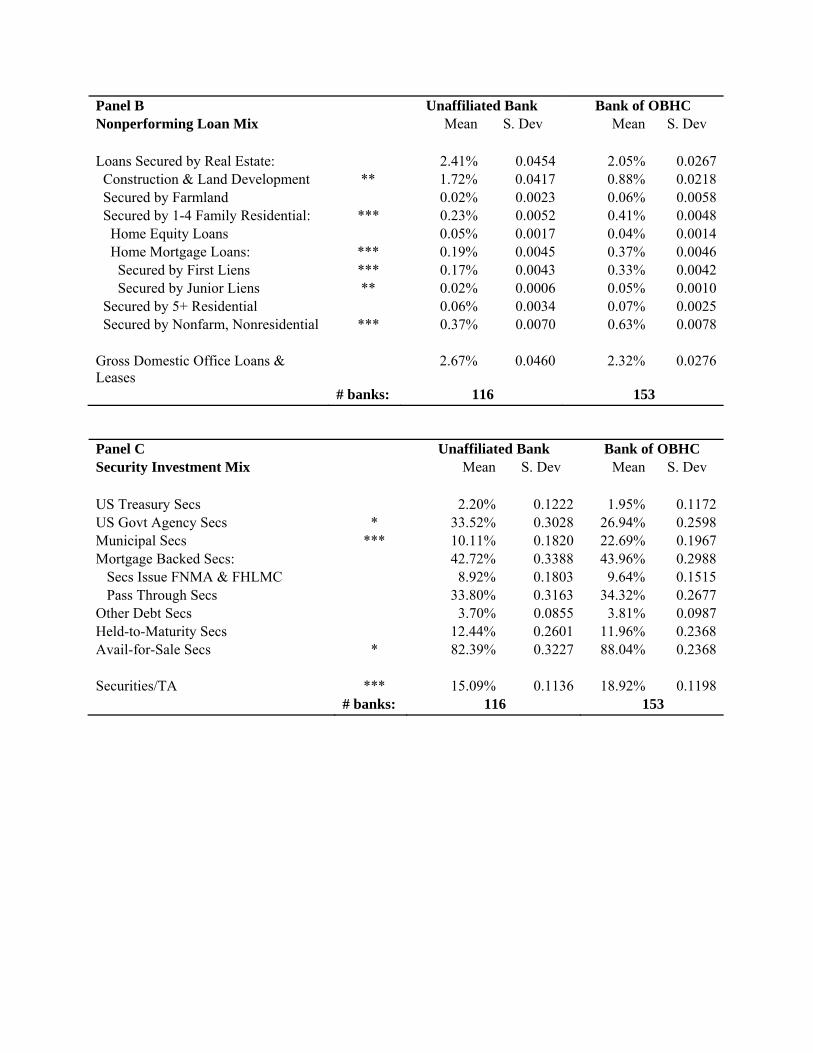

Comparison of Public OBHCs and Public Independent Banks: Univariate Analysis

The table shows the mean and standard deviation of selected balance sheet variables at yearend 2008 for the public subsample of unaffiliated and affiliated banks, which are composed of a private bank and a public holding company. Student’s t-test results are indicated by the asterisks; *, ** and *** denote significant differences between the samples means at the 10%, 5% and 1% level respectively. Panel A shows the real estate loan mix. Panel B shows the nonperforming loan mix presented in Panel A. All loan variables are expressed as a percentage of gross loans and leases. Panel C shows selected security variables expressed as a percentage of total securities. Finally Panel D shows selected variables that describe sample differences in size, liquidity, capitalization and profitability.

Panel A Unaffiliated Bank Bank of OBHC Loan Mix Mean S. Dev Mean S. Dev Loans Secured by Real Estate: *** 75.58% 0.1256 79.71% 0.1111 Construction & Land Development *** 16.95% 0.1210 10.76% 0.1048 Secured by Farmland *** 0.87% 0.0187 1.99% 0.0362 Secured by 1-4 Family Residential: *** 17.72% 0.1375 32.71% 0.1859 Home Equity Loans 5.18% 0.0454 5.19% 0.0381 Home Mortgage Loans: *** 12.78% 0.1307 27.52% 0.1841 Secured by First Liens *** 10.88% 0.1218 24.32% 0.1665 Secured by Junior Liens *** 1.66% 0.0224 3.20% 0.0379 Secured by 5+ Residential 2.98% 0.0344 2.37% 0.0264 Secured by Nonfarm, Nonresidential *** 37.06% 0.1387 31.90% 0.1292 Gross Domestic Loans & Leases/TA * 73.87% 0.1208 71.18% 0.1215 # banks: 116 153

Panel B Unaffiliated Bank Bank of OBHC Nonperforming Loan Mix Mean S. Dev Mean S. Dev Loans Secured by Real Estate: 2.41% 0.0454 2.05% 0.0267 Construction & Land Development ** 1.72% 0.0417 0.88% 0.0218 Secured by Farmland 0.02% 0.0023 0.06% 0.0058 Secured by 1-4 Family Residential: *** 0.23% 0.0052 0.41% 0.0048 Home Equity Loans 0.05% 0.0017 0.04% 0.0014 Home Mortgage Loans: *** 0.19% 0.0045 0.37% 0.0046 Secured by First Liens *** 0.17% 0.0043 0.33% 0.0042 Secured by Junior Liens ** 0.02% 0.0006 0.05% 0.0010 Secured by 5+ Residential 0.06% 0.0034 0.07% 0.0025 Secured by Nonfarm, Nonresidential *** 0.37% 0.0070 0.63% 0.0078 Gross Domestic Office Loans & Leases

2.67% 0.0460 2.32% 0.0276

# banks: 116 153

Panel C Unaffiliated Bank Bank of OBHC Security Investment Mix Mean S. Dev Mean S. Dev US Treasury Secs 2.20% 0.1222 1.95% 0.1172US Govt Agency Secs * 33.52% 0.3028 26.94% 0.2598Municipal Secs *** 10.11% 0.1820 22.69% 0.1967Mortgage Backed Secs: 42.72% 0.3388 43.96% 0.2988 Secs Issue FNMA & FHLMC 8.92% 0.1803 9.64% 0.1515 Pass Through Secs 33.80% 0.3163 34.32% 0.2677Other Debt Secs 3.70% 0.0855 3.81% 0.0987Held-to-Maturity Secs 12.44% 0.2601 11.96% 0.2368Avail-for-Sale Secs * 82.39% 0.3227 88.04% 0.2368 Securities/TA *** 15.09% 0.1136 18.92% 0.1198 # banks: 116 153

Panel D Unaffiliated Bank Bank of OBHC Selected Measures Mean S. Dev Mean S. Dev Log (TA) *** 5.28 0.4070 5.50 0.3221Liquid Assets/Total Assets *** 9.81% 0.0687 7.41% 0.0519Tier 1 Ratio *** 12.74% 0.0530 9.20% 0.0215Debt/Equity *** 54.64% 0.5452 83.16% 0.7920Return on Average Assets (ROA) *** -0.65% 0.0182 0.16% 0.0121Return on Average Equity (ROE) *** -3.94% 0.1202 1.85% 0.1255 # banks: 116 153

TABLE 4

Comparison of Public OBHCs and Public Independent Banks: Cross Sectional Regression

The table shows the regression coefficients on variables of interest as well as their significance on regressions ran on the public subsample of affiliated and unaffiliated banks. The independent variables are used to control for firm size, geography and regulatory authority. Panel A shows the breakdown of home mortgage loans into first and junior liens, and the total loans to total assets. Panel B describes the corresponding nonperforming amounts for the loans shown in Panel A. Panel C shows selected security investments. Panel D shows regression results for variables that describe liquidity, capitalization and profitability. Panel E shows the regression results for variables describing market measures of risk. In all regressions the variable of interest is the HC dummy, which takes value of 1 for affiliated banks, and of 0 for unaffiliated banks. *, ** and *** denote significant differences between the samples means at the 10%, 5% and 1% level respectively. The following acronyms are used: Mortgage (Mtg), Loans (Lns), Total Assets (TA), Nonperforming (NP), Securities (Secs), Mortgage backed securities (MBS), Held to maturity securities (HTM), Return on assets (ROA), and Return on equity (ROE).

Panel A Regression Coefficient Home Mtg

Lns First Liens Junior Liens Total Lns/TA

Independent Variable Intercept 0.2778 0.2014 0.0495 ***1.1155HC Dummy ***0.0884 ***0.0777 ***0.0124 0.0129Log (TA) -0.0043 0.0052 -0.0055 ***-0.0717MSA Type ***-0.1008 ***-0.1057 0.0043 0.0273%ΔPCI ***1.8010 ***1.4261 ***0.3570 **-1.01412008 UR *-1.1183 -0.8162 *-0.2307 -0.1100Authority Charter **0.0500 **0.0452 0.0057 ***-0.0658No Branches 0.0007 0.0005 0.0002 0.0011 R2 0.3173 0.3212 0.1119 0.1392

#Unaffiliated banks: 116#OBHC banks: 153

Panel B Regression Coefficient NP Home Mtg

Lns NP First Lns NP Junior

Lns NP Lns/Total

Lns Independent Variable Intercept -0.0019 -0.0018 -8.7E-05 -0.0035HC Dummy **0.0015 **0.0013 *2.3E-04 -0.0018Log (TA) 0.0006 0.0005 6.6E-05 0.0042MSA Type -0.0005 -0.0006 1.3E-04 0.0003%ΔPCI 0.0021 -0.0032 *5.3E-03 -0.16582008 UR 0.0157 0.0200 -4.3E-03 0.1757Authority Charter -0.0005 -0.0006 7.6E-05 -0.0040No Branches 0.0000 0.0000 -3.3E-06 0.0000 R2 0.0574 0.0572 0.0427 0.0185

#Unaffiliated banks: 116#OBHC banks: 153

Panel C Regression Coefficient US Treasury

Secs Municipal

Secs MBS HTM Total

Secs/TA Independent Variable

Intercept -0.0609 **-0.5217 0.1702 0.2657 ***-0.3706HC Dummy 0.0005 ***0.0787 0.0184 0.0203 -0.0049Log (TA) 0.0184 ***0.1191 0.0436 -0.0246 ***0.0982MSA Type 0.0129 -0.0496 0.0083 0.0570 -0.0125%ΔPCI 0.1082 0.3614 -0.3258 *-1.4240 ***1.24392008 UR -0.3947 0.5462 0.5443 -0.9297 -0.0770Authority Charter -0.0196 0.0298 -0.0140 0.0296 ***0.0680No Branches -0.0003 -0.0004 -0.0016 0.0016 -0.0013 R2 0.0122 0.1567 0.0040 0.0344 0.1949

#Unaffiliated banks: 116#OBHC banks: 153

Panel D Regression Coefficient Liquid

Assets/TA Tier 1 Debt/Equity ROA ROE

Independent Variable

Intercept ***0.2280 ***0.3058 **-1.8636 ***-0.0575 ***-0.3872HC Dummy **-0.0210 ***-0.0291 **0.2235 **0.0042 *0.0286Log (TA) **-0.0272 ***-0.0355 ***0.5131 ***0.0110 ***0.0767MSA Type 0.0004 0.0101 -0.1290 -0.0026 -0.0186%ΔPCI -0.1156 -0.0065 -0.4645 *0.0961 *0.74882008 UR 0.1859 -0.0769 -1.5264 -0.0941 -0.8011Authority Charter **0.0195 **0.0113 *-0.1949 -0.0002 0.0061No Branches 0.0003 *0.0006 **-0.0112 -0.0001 -0.0004 R2 0.0794 0.2531 0.0990 0.1559 0.1235

#Unaffiliated banks: 116#OBHC banks: 153

Panel E Regression Coefficient Beta Var (Tot Risk) SYS Risk UNSYS Risk Asset Beta Independent Variable Intercept **-0.87247 ***0.012453 ***-0.00161 ***0.014066 -0.26328HC Dummy -0.0526 2.09E-05 -5.4E-05 7.49E-05 -0.02945Log (TA) ***0.203474 **-0.00189 ***0.000308 ***-0.0022 *0.075892MSA Type 0.006033 *0.001189 0.000115 *0.001075 0.014612%ΔPCI -1.3876 -0.01525 0.000603 -0.01585 -0.632922008 UR 0.119263 0.009215 0.000802 0.008412 -0.26138Authority Charter -0.07433 -0.00046 *-0.00012 -0.00034 *-0.05405No Branches *0.004002 4.56E-05 4.97E-06 4.07E-05 **0.003365 R2 0.122556 0.054334 0.136684 0.064849 0.083935

# Individual banks: 116 #One-bank shell HCs: 153