Biden launches bid for 2020 presidency - The Indian Panorama

Upload

khangminh22Category

view

0download

0

NOVEMBER 14TH–20TH 2020

The economy Joe Biden will inherit

America’s allies: a long wishlist

The trouble with value investing

Zambia, becoming the next Zimbabwe

Suddenly, hope

DOWNLOAD

Email: [email protected]

The CSS Point, Pakistan’s The Best Online FREE Web source for All CSS

Aspirants.

Download CSS Notes

Download CSS Books

Download CSS Magazines

Download CSS MCQs

Download CSS Past Papers

CSS Notes, Books, MCQs, Magazines

www.thecsspoint.com

BUY CSS / PMS / NTS & GENERAL KNOWLEDGE BOOKS

ONLINE CASH ON DELIVERY ALL OVER PAKISTAN

Visit Now:

WWW.CSSBOOKS.NET

For Oder & Inquiry

Call/SMS/WhatsApp

0333 6042057 – 0726 540141

CSS Solved Compulsory MCQs

From 2000 to 2020

Latest & Updated

Order Now

Call/SMS 03336042057 - 0726540141

PPSC Model Papers

78th Edition (Latest & Updated)

By Imtiaz Shahid

Advanced Publishers For Order Call/WhatsApp 03336042057 - 0726540141

FPSC Model Papers

50th Edition (Latest & Updated)

By Imtiaz Shahid

Advanced Publishers

For Order Call/WhatsApp 03336042057 - 0726540141

The Economist November 14th 2020 5

Contents continues overleaf1

Contents

The world this week8 A summary of political

and business news

Leaders11 Vaccines

Suddenly, hope

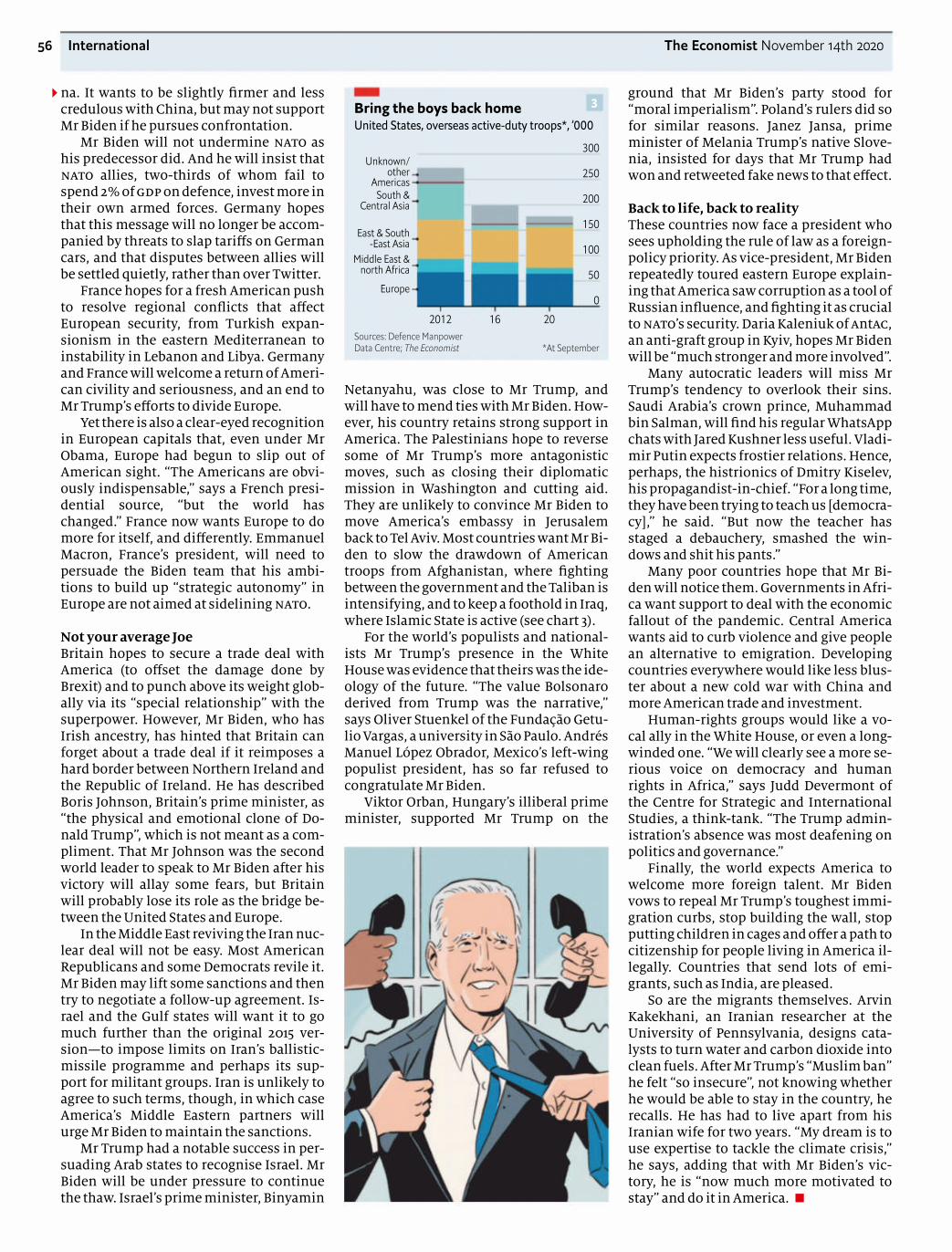

12 America and its alliesGreat expectations

12 America’s next presidentBiden’s economy

13 Asset managementBeyond Buffett

14 Democracy in AfricaZambia’s descent

Letters16 On transgender sports,

diplomacy, Facebook,management, Armenia,avatars, Brazil

Briefing19 Covid-19 vaccines

The technology of hope

Special report:Asset managementThe money doctorsAfter page 42

United States23 Covid-19 and Biden

24 Republicans and the result

25 The Pentagone

26 Fox News

26 Unhappy cowboys

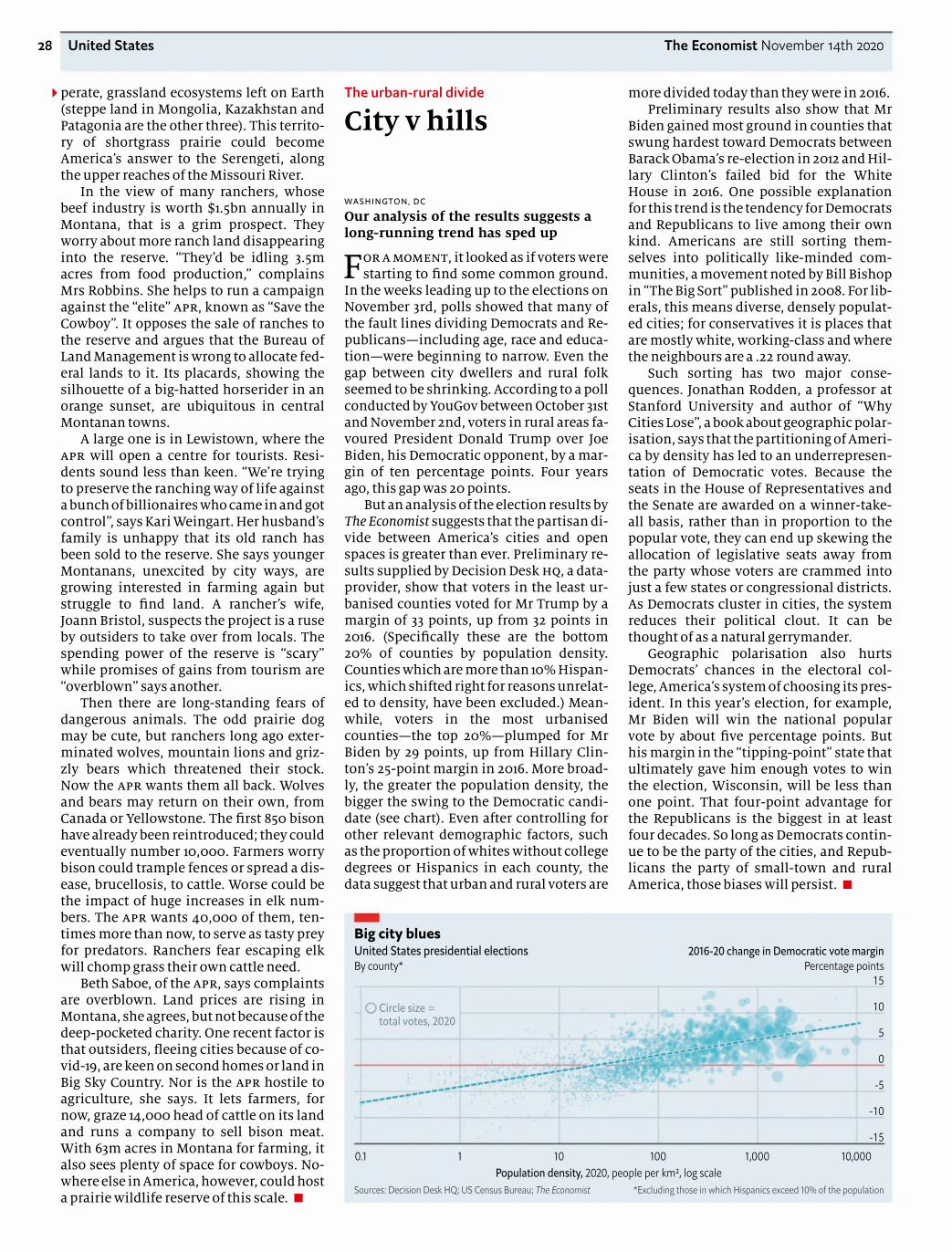

28 The urban-rural divide

30 Lexington A Democraticdefeat in victory

The Americas31 The impeachment of

Martín Vizcarra

32 Hurricane Eta

33 Bello Proxy presidents

Asia35 Kyrgyzstan’s president

36 Sino-Australian trade

37 India’s covid-19-proofruling party

37 Myanmar’s election

38 Banyan Filipinos abroad

China39 Hong Kong’s legislature

40 Self-help books

42 Chaguan Musing over tea about unequal lives

Middle East & Africa43 Corruption in South Africa

44 Why Zambia may default

45 Fed-up feminists in Egypt

46 Saeb Erekat, RIP

Bagehot How PrincessDiana shaped politics,page 53

On the cover

A highly effective vaccineshould transform the fightagainst covid-19. But a lotremains to be done: leader,page 11, and briefing, page 19.Cheap, rapid tests forsars-cov-2 are here. Will theybe the stopgap needed? Page 71

• The economy Joe Biden will inherit He faces twoextraordinary challenges: leader,page 12. What he would dodifferently, and how muchdifference it would make, page 23. A vaccine and theworld’s largest economy, page 65

• America’s allies: a longwishlist What they can do forJoe Biden: leader, page 12. Andwhat the world wants from him,page 54

• The trouble with valueinvesting Made famous byWarren Buffett, it is struggling toremain relevant: leader, page 13,and briefing, page 62. A specialreport on asset managementafter page 42

We are working hard toensure that there is no dis-ruption to print copies of The Economist as a result ofthe coronavirus. But if youhave digital access as part ofyour subscription, then acti-vating it will ensure that youcan always read the digitalversion of the newspaper aswell as all of our daily jour-nalism. To do so, visit economist.com/activate

PEFC certifiedThis copy of The Economistis printed on paper sourcedfrom sustainably managedforests certified to PEFCwww.pefc.orgPEFC/29-31-58

PleaseSubscription serviceFor our full range of subscription offers, includingdigital only or print and digital bundled, visit:Economist.com/offers

If you are experiencing problems when trying tosubscribe, please visit our Help pages at:www.economist.com/help for troubleshootingadvice.

Published since September 1843to take part in “a severe contest betweenintelligence, which presses forward,and an unworthy, timid ignoranceobstructing our progress.”

Editorial offices in London and also:Amsterdam, Beijing, Berlin, Brussels, Cairo,Chicago, Johannesburg, Madrid, Mexico City,Moscow, Mumbai, New Delhi, New York, Paris,San Francisco, São Paulo, Seoul, Shanghai,Singapore, Tokyo, Washington DC

The best way to contact our Customer Serviceteam is via phone or live chat. You can contact uson the below numbers; please check our websitefor up to date opening hours.

North America: +1 800 456 6086Latin America & Mexico: +1 636 449 5702

© 2020 The Economist Newspaper Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying,recording or otherwise, without the prior permission of The Economist Newspaper Limited. The Economist (ISSN 0013-0613) is published every week, except for a year-end double issue, by The Economist Newspaper Limited, 750 3rdAvenue, 5th Floor, New York, N Y 10017. The Economist is a registered trademark of The Economist Newspaper Limited. Periodicals postage paid at New York, NY and additional mailing offices. Postmaster: Send address changes to TheEconomist, P.O. Box 46978, St. Louis , MO. 63146-6978, USA. Canada Post publications mail (Canadian distribution) sales agreement no. 40012331. Return undeliverable Canadian addresses to The Economist, PO Box 7258 STN A, Toronto,ON M5W 1X9. GST R123236267. Printed by Quad/Graphics, Saratoga Springs, NY 12866

6 Contents The Economist November 14th 2020

Volume 437 Number 9220

Europe47 Nagorno- Karabakh

48 Corruption and Ukraine

49 Europe’s recovery fund

49 France fights jihadistsin Africa

Britain51 Protest in the provinces

52 Foreign-investment rules

53 Bagehot Princess Diana,populist politician

International54 What the world wants

from Biden

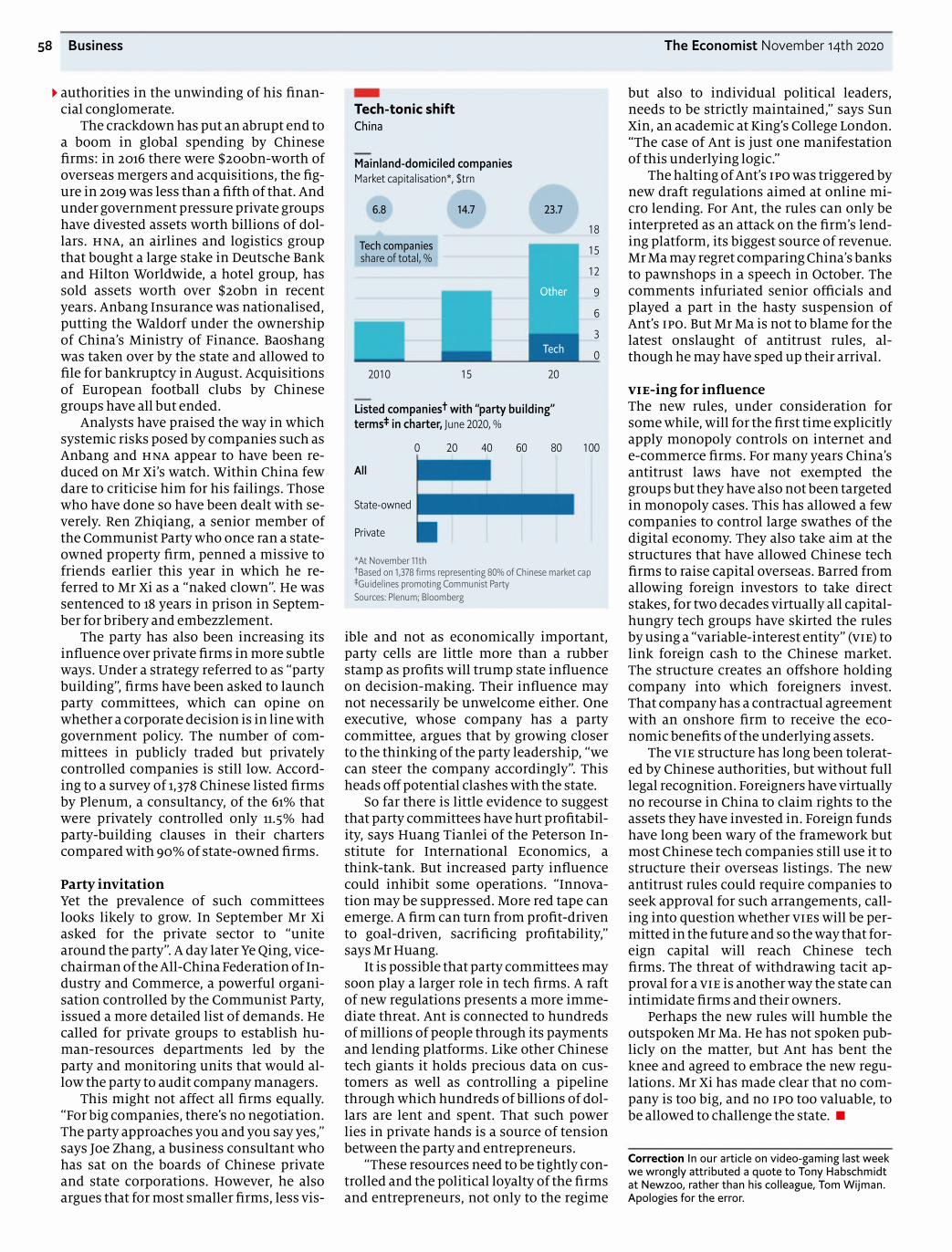

Business57 China’s battered

entrepreneurs

59 Disney’s TV success

59 A growing taste for pasta

60 Royal Enfield revs up

61 Schumpeter McDonald’ssupersized comeback

Briefing62 Value investing struggles

Finance & economics65 America’s rebound

66 The vaccine and investors

67 Buttonwood Emergingmarkets

68 Turkey’s economic policy

68 Grain prices in America

69 A Swedish unicorn

70 Free exchange Workingwith epidemiologists

Science & technology71 Fast tests for covid-19

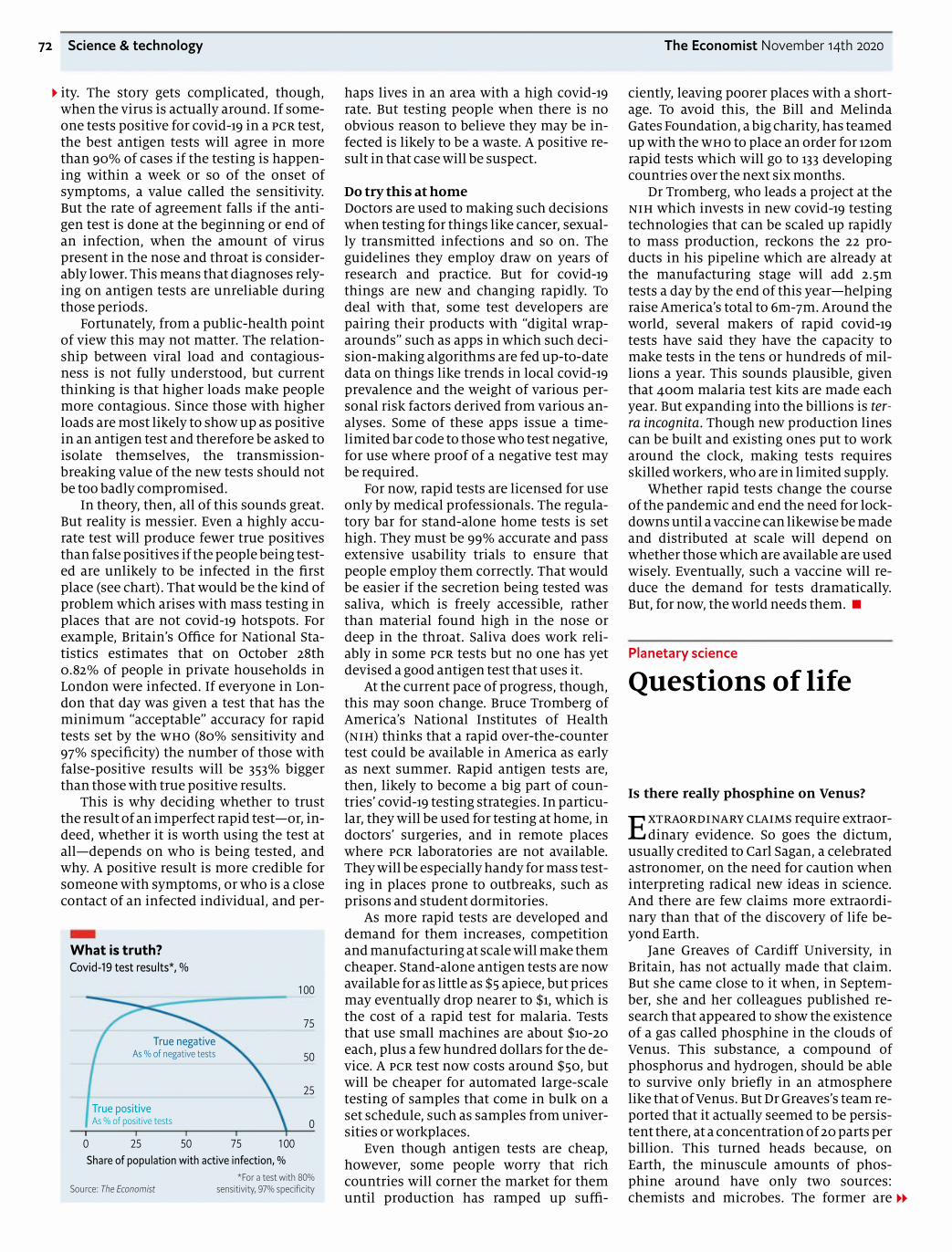

72 Life on Venus, redux

73 Better disposable cups

Books & arts75 Britain and slavery

76 Chinatown chic

77 American society

77 Billy Wilder’s story

78 Johnson Language andevolution

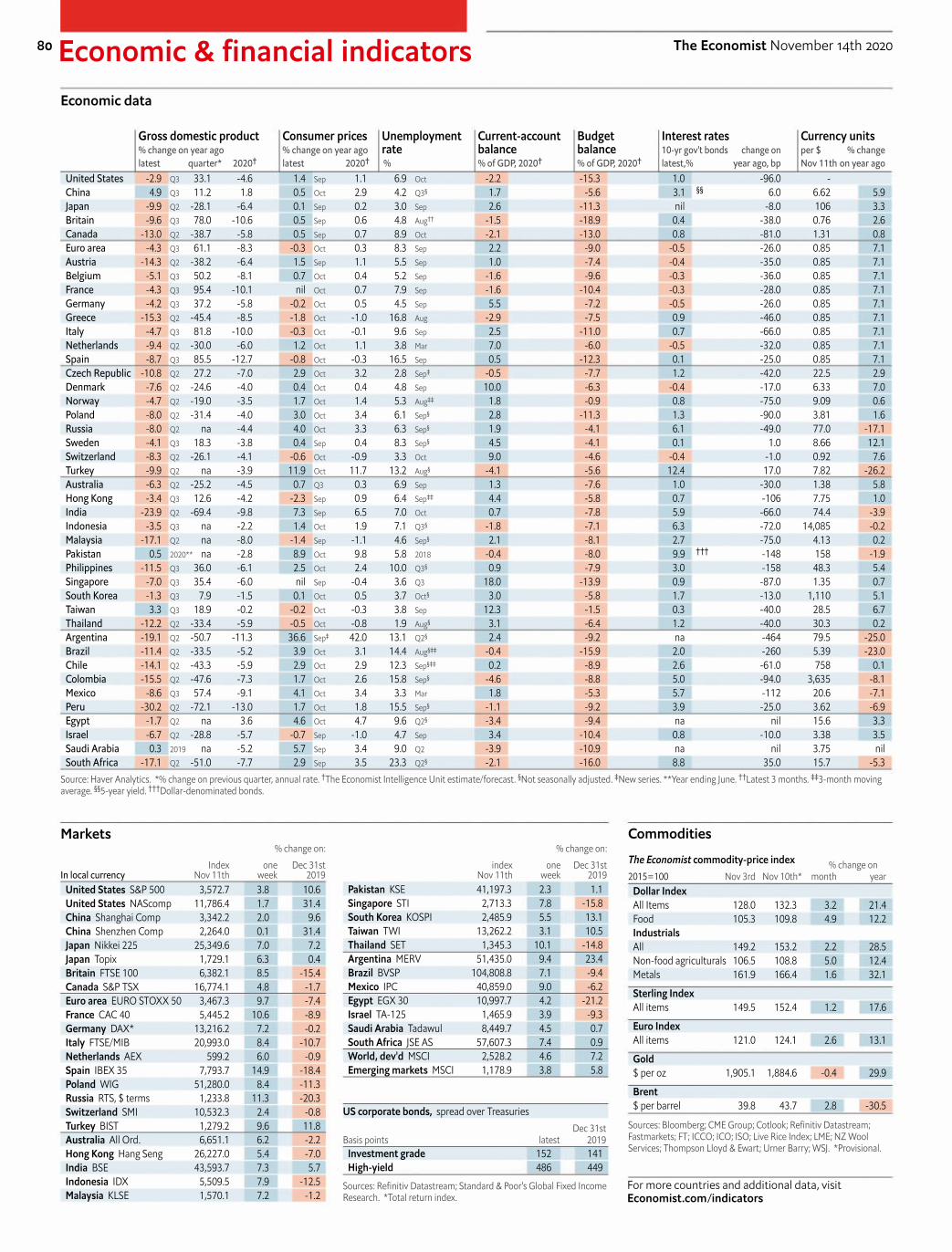

Economic & financial indicators80 Statistics on 42 economies

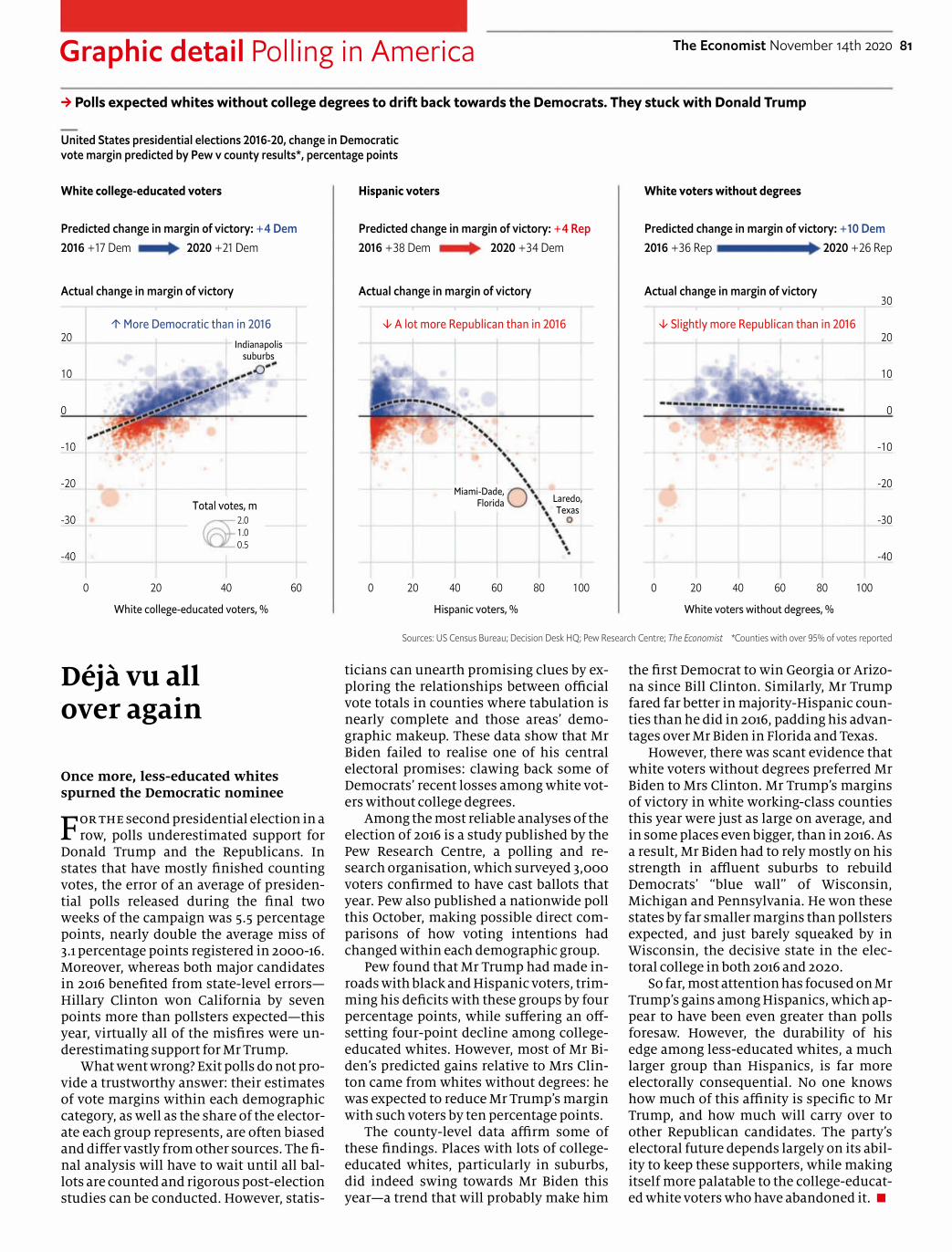

Graphic detail81 How less-educated whites spurn Joe Biden

Obituary82 James Randi, magician and professional sceptic

New consumer accounts only. Approval required. Food and beverages provided by a third party. Cafés available in select locations. Go to locations.capitalone.com for locator.Cafés do not provide the same services as bank branches but do have ATMs and associates who can help you. Off ered by Capital One, N.A., Member FDIC. © 2020 Capital One

Banking in the palm of your hands.

Capital One® checking and savings accounts have no fees or minimums and a top-rated banking app thatlets you manage your money anytime, anywhere.

This is Banking Reimagined.®

8 The Economist November 14th 2020

For our latest coverage of thevirus and its consequencesplease visit economist.com/coronavirus or download theEconomist app.

The world this week Politics

Donald Trump refused toconcede defeat in America’selection, despite Joe Biden’spassing the required 270electoral-college votes. Thepresident is pursuing severallegal challenges to states’results. None is expected tosucceed. Mr Biden’s transitionteam is considering suing toobtain federal funds and infor-mation usually granted toincoming administrations.

World leaders queued up tocongratulate Mr Biden. Amongthe strongmen who have so fardemurred are Vladimir Putinof Russia, Xi Jinping of Chinaand Jair Bolsonaro of Brazil. MrBolsonaro railed against MrBiden’s proposals to punishBrazil for not protecting theAmazon rainforest, saying,“Diplomacy alone won’t work.Once the saliva runs out, youhave to have gunpowder.”

Joe Biden announced acovid-19 advisory board to dealwith the pandemic. He said hisresponse would be led “byscience and by experts”.

Donald Trump tweeted that hehad “terminated” his defencesecretary, Mark Esper. In JuneMr Esper publicly disagreedwith the president about theuse of troops to quash protests.

Peru’s Congress removed fromoffice the president, MartínVizcarra. He has been accusedof taking bribes when he was agovernor, which he denies. Thelegislature’s speaker, ManuelMerino, succeeded Mr Vizcarraas president.

Luis Arce was sworn in asBolivia’s president. He was thecandidate of the Movement toSocialism, founded by EvoMorales, who was forced into

exile last year after protestsagainst his re-election. AfterMr Arce took office Mr Moralesreturned overland to Boliviafrom Argentina.

Eta, this year’s strongesthurricane, killed at least 130people in Central America.Perhaps 300,000 lost theirhomes. Eta broke a record setin 2005 for the number ofnamed storms in a season.

Britain’s House of Lords votedto amend a bill that wouldallow the government to re-write parts of its EuropeanUnion withdrawal treaty,including provisions aboutNorthern Ireland. The govern-ment says it will override thechanges. Joe Biden warnedBoris Johnson, Britain’s primeminister, not to imperil peacein Ireland.

After weeks of fighting overNagorno-Karabakh, Armeniaand Azerbaijan agreed to apeace deal. Armenia surren-dered the districts surround-ing the enclave, though a corri-dor linking Armenia andNagorno-Karabakh will beplaced under Russian control.Protesters demanded theresignation of Armenia’s primeminister, Nikol Pashinyan.

The European Parliamentreached an agreement with eu

member states over the cre-ation of a €1.8trn ($2.1trn)spending package for the nextseven years, including a€750bn recovery fund whichwill be raised on the capitalmarkets by the eu itself, not byindividual countries.

Bihar, one of the poorest partsof India, voted for an allianceled by the party of NarendraModi, the prime minister, instate elections. It was the firstbig state poll since covid-19swept the country and induceda deep recession. Voters inBihar, at least, do not seem toblame Mr Modi.

The National League for De-mocracy, led by Aung San SuuKyi, retained power in Myan-mar’s election. Despite failingto end the country’s simmering

civil wars, Ms Suu Kyi remainspopular, especially among theethnic-Bamar majority.

China authorised Hong Kong’sgovernment to disbar legisla-tors deemed to oppose Chineserule in the territory or tothreaten national security. Thelocal government promptlydismissed four pro-democracylawmakers. Fifteen others saidthey would resign.

America removed the EastTurkestan Islamic Movementfrom its list of terrorist organi-sations. It said there was nocredible evidence that thegroup, allegedly founded byUyghur separatists, still exist-ed. China reacted angrily,saying the organisation was athreat not only to China but tothe world.

Several people were injured bya bomb at an Armistice Dayceremony in Jeddah, in SaudiArabia. The event was attendedby representatives of foreignconsulates, including that ofFrance. Emmanuel Macron,France’s president, has angeredsome Muslims by defendingthe right to publish caricaturesof religious figures, includingthe Prophet Muhammad.

Saeb Erekat, a veteran Pales-tinian diplomat who wasinvolved in three decades ofnegotiations with Israel, diedafter contracting covid-19. Hewas 65.

Prince Khalifa bin Salmanal-Khalifa, the hardline primeminister of Bahrain, also died.He had held the post sinceindependence in 1971. PrinceKhalifa was 84.

Hundreds of people were killedin fighting between Ethiopiangovernment troops and forcesloyal to the province of Tigray.Abiy Ahmed, the prime min-ister, ordered the army intoTigray after its leaders heldregional elections in defianceof the federal government.

Police in Mozambique saidjihadists had beheaded morethan 50 people in Cabo Delga-do, a province in the north.

Coronavirus briefs

The European Commissionagreed to buy up to 300m dosesof the vaccine developed byPfizer and BioNTech.

Russia’s claims that its home-grown “Sputnik V” vaccine is92% effective in preventinginfection, a similar successrate to Pfizer’s, were met withscepticism.

The number of people in hos-pital with covid-19 in Americareached 65,000, a new record.Europe’s death toll from thevirus passed 300,000.

Lebanon announced a newlockdown that will last untilthe end of November. Authori-ties in Tehran ordered restau-rants and shops to close earlyamid rising cases.

Denmark’s government ad-mitted it could not force minkfarmers to cull livestock butrecommended they do so, afternew strains of covid-19 jumpedfrom the animals to people.

Weekly confirmed cases by area, m

To 6am GMT November 12th 2020

Confirmed deaths* Per 100k Total This week

Sources: Johns Hopkins University CSSE; UN; The Economist *Definitions differ by country

Belgium 118.7 13,758 1,427Peru 106.1 34,992 321Spain 85.8 40,105 1,987Brazil 76.9 163,368 2,262Chile 76.5 14,633 293Argentina 76.4 34,531 2,011Bolivia 75.5 8,818 60Mexico 74.8 96,430 3,202Britain 74.2 50,365 2,623Ecuador 73.2 12,920 216United States 72.7 240,783 7,785

2.0

1.5

1.0

0.5

0

NOSAJJMAM

Europe

US

Latin America

Other

The Economist November 14th 2020 9The world this week Business

Pfizer and BioNTech, twopharmaceutical firms, an-nounced that their vaccineagainst covid-19 is more than90% effective, according toearly results from trials. Thehigh success rate raised hopesof a quicker return to nor-mality than previously expect-ed. Other pharmaceutical firmsare also working on vaccinesand are expected to makeannouncements in the comingweeks. Current projectionssuggest 50m doses of thePfizer-BioNTech vaccine willbe available in 2020, rising to1.3bn the following year. On theday of the announcement,Pfizer’s and BioNTech’s shareprices surged 8% and 14%,respectively.

The news excited stockmark-ets. In America the Dow JonesIndustrial Average jumped by2.9% on Monday. The s&p 500rose sharply when it opened,before ending the day up 1.2%.The stoxx Europe 600 climbed4%. Oil prices increased to $45per barrel. By contrast, manytechnology firms that havebeen buoyed by the pandemicfaced a sell-off, includingZoom, a video-conferencingfirm, Ocado, a grocery deliverycompany, and Peloton, a makerof exercise bikes.

Regulators continued to takeaim at technology firms onantitrust grounds. The Euro-pean Union brought chargesagainst Amazon. After aninvestigation, the EuropeanCommission claimed that thetech giant uses data gatheredfrom vendors to give its ownproducts and services an un-fair advantage. Amazon saidthat it disagrees with the com-mission’s findings.

Meanwhile, India’s competi-tion watchdog has ordered aprobe into Google’s app store.It fears that a requirement thatconsumers buy apps using thefirm’s payment service smoth-ers competition. In Chinaregulators have drafted newantitrust rules aimed at tech-nology firms. They will target arange of practices, includingtreating customers differentlybased on their spending behav-

iour and data. The move fol-lows the suspension of theinitial public offering of AntGroup, a fintech firm, daysbefore its flotation in HongKong and Shanghai.

Out with the old

In a surprise shakeup RecepTayyip Erdogan, Turkey’spresident, fired the country’scentral-bank governor, only 16months after sacking his pre-decessor. One day later theTurkish finance minister, MrErdogan’s son-in-law, resignedsupposedly because of a feudwith the new central-bankgovernor. After the reshuffle,the banking regulator said itwould curb restrictions onforeigners trading the Turkishlira, which were imposed lastyear. Investors seemed towelcome the changes. The lirarose by more than 7% againstthe dollar in the past week,reversing a long decline.

Following two quarters ofcontraction, Britain’s gdp

grew by 15.5% between July andSeptember. The economy isstill 8.2% smaller than it wasbefore the virus struck and islikely to shrink again in the lastthree months of the year be-cause of a second lockdown.Unemployment over the sameperiod rose to 4.8%, up from4.5%. Redundancies surged toa record high, as firms wereforced to contribute more tothe cost of furloughed workers.

Unemployment figures fromAmerica were better thanexpected. Non-farm employ-ment rose by 638,000 in Octo-ber. The unemployment ratefell by one percentage point to6.9% in the same month.

China’s consumer-price indexdropped to 0.5% in October, itslowest level in over a decade.That reflects low food prices,particularly of pork, suppliesof which were hit by Africanswine fever but are now recov-ering thanks to record imports.Sluggish consumer demand isanother factor.

SoftBank Group announcedprofits of $6.1bn in the threemonths to the end of Septem-ber. The Japanese firm bookedlosses of $3.7bn with its forayinto investing in publicly listed

technology companies inAmerica. But that was offset byan improved performance byits Vision Fund, which is nowworth $1.4bn more than thecosts of it 83 investments.SoftBank also removed severalexecutives from its board,following investors’ concernsabout governance.

McDonald’s reported revenuesof $5.4bn in the latest quarter,down 2% from the same periodlast year but beating analysts’expectations. It performed wellin America where same-storesales grew by 4.6% from theprevious quarter.

Beyond Meat, an alternativeprotein provider, reportedlosses of $19.3m in the thirdquarter, compared with profitsof $4.1m in the same periodlast year. An easing of covid-induced consumer stockpilingand falling sales to restaurantswere blamed.

What goes aroundSingaporean holiday-makersitching for escape can now takea “cruise to nowhere”. Pas-sengers undergo covid-19 testsbefore boarding and are re-quired to carry contact-tracingdevices. The ship idles in thewaters off the city state for twodays before returning to port.

Banking is going hybrid.How can you create innovative customer experiences and keep regulators happy? With a smarter hybrid cloud approach. Get the tools, platform and expertise your business needs from IBM. The world is going hybrid with IBM.

ibm.com/hybridcloud

IBM and the IBM logo are trademarks of International Business Machines Corporation, registered in many jurisdictions worldwide. Other product and service names might be trademarks ofIBM or other companies. A current list of IBM trademarks is available at ibm.com/trademark. ©International Business Machines Corp. 2020.

Leaders 11

Nine long years elapsed between the isolation of the measlesvirus in 1954 and the licensing of a vaccine. The world waited

for 20 years between early trials of a polio vaccine and the firstAmerican licence in 1955. Marvel, then, at how the world’s scien-tists are on course to produce a working vaccine against sars-cov-2, the virus that causes covid-19, within a single year.

And not just any vaccine. The early data from a final-stagetrial unveiled this week by Pfizer and BioNTech, two pharmacompanies, suggests that vaccination cuts your chances of suf-fering symptoms by more than 90%. That is almost as good as formeasles and better than the flu jab, with an efficacy of just40-60% (see Briefing). Suddenly, in a dark winter, there is hope.

Not surprisingly, Pfizer’s news on November 9th roused themarkets’ bulls. Investors dumped shares in Clorox, Peloton andtech firms, which have all benefited from the coronavirus, andinstead switched into firms like Disney, Carnival and Interna-tional Consolidated Airlines Group, which will do well when thesun shines again (see Finance section). The oecd, a club of main-ly rich countries, reckons that global growth in 2021with an earlyvaccine will be 7%, two percentage points higher than without.

There is indeed much to celebrate. Pfizer’s result suggests thatother vaccines will work, too. Over 320 are in development, sev-eral in advanced trials. Most, like Pfizer’s, focus on the spike pro-tein with which sars-cov-2 gains entry to cells.If one vaccine has used this strategy to stimulateimmunity, others probably can, too.

Pfizer’s vaccine is also the first using a pro-mising new technology. Many vaccines primethe immune system by introducing inert frag-ments of viral protein. This one gets the body tomake the viral protein itself by inserting geneticinstructions contained in a form of rna. Be-cause you can edit rna, the vaccine can be tweaked should thespike protein mutate, as it may have recently in mink. This plat-form can be used with other viruses and other diseases, possiblyincluding cancer, BioNTech’s original focus.

So celebrate how far biology has come and how fruitfully itcan manipulate biochemical machinery for the good of human-ity (there will be time later to worry about how that power mightalso be abused). And celebrate the potency of science as a globalendeavour. Drawing on contributions from across the world, asmall German firm founded by first-generation Turkish immi-grants has successfully worked with an American multinationalcompany headed by a Greek chief executive.

Yet despite the good news, two big questions stand out, aboutthe characteristics of the vaccine and how fast it can be distri-buted. These are early results, based on 94 symptomatic cases ofcovid-19 from among the 44,000 volunteers. Further answersmust wait until the trial has gathered more data. It is, therefore,not clear whether the vaccine stops severe cases or mild ones, orwhether it protects the elderly, whose immune systems areweaker. Nor is it known whether inoculated people can stillcause potentially fatal infections in those yet to receive jabs. Andit is too soon to be sure how long the beneficial effects will last.

Clarity will take time. In the next few weeks the trial should be

declared safe, though further monitoring of the vaccine will beneeded. The companies predict that immunity will last for atleast a year. The 90%-plus efficacy is so high that this vaccinemay offer at least some protection to all age groups.

While the world waits for data, it will have to grapple with dis-tribution. Vaccine will be in short supply for most of next year.Although rna jabs may prove easier to make at scale than thosebased on proteins, Pfizer’s requires two doses. The company hassaid that it will be able to produce up to 50m doses in 2020 and1.3bn next year. That sounds a lot, but America alone has over20m first responders, medical staff, care-home workers and ac-tive-duty troops. Perhaps a fifth of the world’s 7.8bn people, in-cluding two-thirds of those over 70, risk severe covid-19. Nobodyhas ever tried to vaccinate an entire planet at once. As the effortmounts, syringes, medical glass and staff could run short.

Worse, Pfizer’s shots need to be stored at temperatures of-70°C or even colder, far beyond the scope of your local chemist.The company is building an ultra-cold chain, but the logisticswill still be hard. The vaccine comes in batches of at least 975doses, so you need to assemble that many people for their firstshot, and the same crowd again 21 days later for a booster. No-body knows how many doses will be wasted.

So long as there is too little vaccine to go around, prioritiesmust be set by governments. A lot depends onthem getting it right, within countries and be-tween them. Modelling suggests that if 50 richcountries were to administer 2bn doses of a vac-cine that is 80% effective, they would prevent athird of deaths globally; if the vaccine were sup-plied according to rich and poor countries’ pop-ulation, that share would almost double. Thedetails will depend on the vaccine. Poor coun-

tries may find ultra-cold chains too costly. The domestic answer to these problems is national commit-

tees to allocate vaccine optimally. The global answer is covax, aninitiative to encourage countries’ equal access to supplies. Ulti-mately, though, the solution will be continued work on morevaccines. Some might survive in commercial refrigerators, oth-ers will work better on the elderly, still others might confer lon-ger protection, require a single shot, or stop infections as well assymptoms. All those that work will help increase supply.

Only when there is enough to go around will anti-vaxxers be-come an obstacle. Early reports suggest the jab causes fevers andaches, which may also put some people off. The good news is thatan efficacy of 90% makes vaccination more attractive.

The tunnel aheadThe next few months will be hard. Global recorded death rateshave surged past their April peak. Governments will strugglewith the logistics of vaccination. America is rich and it hasworld-class medicine. But it risks falling short because the virusis raging there and because the transition between administra-tions could lead to needless chaos and delays. Squandering liveswhen a vaccine is at hand would be especially cruel. Science hasdone its bit to see off the virus. Now comes the test for society. 7

Suddenly, hope

Scientists have managed to create a vaccine for covid-19. Getting enough people vaccinated will be even harder

Leaders

12 Leaders The Economist November 14th 2020

1

In much of the world, and nowhere more so than amongAmerica’s allies, Joe Biden’s victory has come as a great relief.

Under his presidency there will be no more bullying and threatsto leave nato. America will stop treating the European Union as a“foe” on trade, or its own forces stationed in South Korea as a pro-tection racket. In place of Donald Trump’s wrecking ball, Mr Bi-den will offer an outstretched hand, working co-operatively onglobal crises, from coronavirus to climate change. Under MrTrump, America’s favourability ratings in many allied countriessank to new lows. Mr Biden promises to make America a beaconagain, a champion of lofty values and a defender of humanrights, leading (as he put it in his acceptance speech) “not only bythe example of our power but by the power of our example”.

Allies are central to Mr Biden’s vision. Herightly sees them as a multiplier of American in-fluence, turning a country with a quarter of glo-bal gdp into a force with more than double that.He is also a multilateralist by instinct. On hisfirst day in office he will rejoin the Paris agree-ment on climate change, which America for-mally left on November 4th. Unlike Mr Trumphe believes it is better to lead the World HealthOrganisation than to leave it. He will reinvigorate arms control, apriority being to ensure that New start, the last remaining nuc-lear pact with Russia, is extended beyond February 5th. He wouldlike to rejoin the nuclear deal with Iran that Mr Trump dumped,if he can persuade the Iranians to go back into compliance.

Inevitably, America’s friends have a long list of things theyhope it will do as it re-embraces global leadership (see Interna-tional section). The demands stretch from places and organisa-tions Mr Trump has abused, such as the un and allies like Ger-many, to parts of the world he has ignored, such as much ofAfrica. Yet it will not all be smooth travelling. Not all countriesare nostalgic for a return to Obama-era policies, when America“led from behind” and blurred its red lines. Several countries on

nato’s front line with Russia like the way defences have beenbeefed up under Mr Trump. And Asian allies like how Mr Trumphas confronted China, talked of a “free and open Indo-Pacific”and worked on the “Quad” with Australia, India and Japan. Mr Bi-den needs to prove that he will not turn soft.

His priorities will be to quell the virus and improve the econ-omy. On both counts he can count on little support, and muchpushback, if the Senate is under Republican control, as is likely.Such troubles at home have probably also exacerbated the coun-try’s reluctance to take on more foreign burdens. Who can besure that world-wary Jacksonians won’t come galloping back in2024, perhaps even with Mr Trump in the saddle?

So rather than pile demand upon needy demand, America’sallies should go out of their way to show thatthey have learned to pull their weight. nato

partners, for example, should not relax defencespending just because Mr Trump is no longerbullying them. Germany should pay heed toFrench efforts to build European defence capa-city—there is scope to do so without undermin-ing nato. Europeans could lend a bigger hand toFrance in the Sahel (see Europe section). In Asia

the Quad could keep deepening naval and other co-operation. Ja-pan and South Korea should restrain their feuding. Taiwan oughtto make a more serious contribution to its own defence.

Allies should also work with America to repair the interna-tional order. They can support efforts to resist Chinese or Rus-sian rule-bending. Many countries will want to join Mr Biden’sefforts at concerted carbon-cutting.

Mr Biden will face a world full of problems, but he will alsostart with strengths. Thanks to Mr Trump, he has sanctions onadversaries including Iran and Venezuela that he can use as bar-gaining chips. And among friends, he can seek to convert relief atrenewed American engagement into stronger burden-sharing.His allies would be wise to answer that call with enthusiasm. 7

Great expectations

America’s allies need to show that they have learned to pull their weight

The world and Joe Biden

America’s voters did not elect Joe Biden because theythought he would be the best steward of the economy. The

economy may well define his presidency nonetheless. Mr Bidenwill take office in January amid a crisis brought about by the pan-demic, which is capable of causing immensely more economicharm before vaccination is widespread. He will also inherit abusiness landscape in the throes of a once-in-a-generation shift,as technology becomes more embedded in everyday life and inmore industries—a shift that has been simultaneously hastenedand overshadowed by the disease. Whether Mr Biden succeeds orfails depends on how he manages these twin sources of change.

The good news is that gdp has rebounded impressively fromits collapse in the spring. The unemployment rate has droppedmuch faster than most forecasters expected, from 14.7% in Aprilto 6.9% in October. Were private-sector employment to keepgrowing at the pace of September and October it would return toits pre-pandemic level in less than a year. On most forecastsAmerica’s economy will shrink by less than any other big richcountry’s in 2020—the euro zone will take almost twice the hit,for example. So far there is little sign of the economic scarringthat was feared at the onset of the crisis (see Finance section).

Unfortunately this rebound is threatened by the winter wave

The economy Biden inherits

The incoming administration faces two extraordinary economic challenges

America’s new president

The Economist November 14th 2020 Leaders 13

1

2 of the virus. The logistics of rolling out a vaccine are dauntingand at first only emergency workers and the most vulnerable willreceive it. The spread of the disease will worsen before a mass in-oculation can take place. Already more Americans are in hospitalwith covid-19 than at the peak of the outbreak in the spring,though many fewer are dying. Some parts of the country couldsoon face more restrictions and lockdowns. Others might ex-periment with letting the virus rip—an approach which couldstill bring about a sharp drop in consumer spending if peoplechoose to stay at home in order to stay safe.

If the virus again puts the economy to the sword, it might notbenefit from the life support it got in March in the form of lavishunemployment insurance and emergency loans for small busi-nesses. Republicans in the Senate will probablysupport a limited second round of fiscal stimu-lus, but are in no mood for another blowout. Adebate is raging about whether the Federal Re-serve should extend its emergency lending intothe new year. Job cuts by state and local govern-ments, whose budgets have been hit by the pan-demic, are already weighing down the labourmarket. They need a bail-out that Republicansdo not want to give. Mr Biden’s first challenge will be to persuadeCongress to keep the purse strings loose until the vaccine hasbrought about a full reopening.

At the same time the new president will need to grapple withthe post-vaccine economy, which will look different from theone that entered the pandemic. The crisis has hastened the dig-itisation that was already poised to define business and invest-ing in the 2020s. That trend will not fully reverse, even after thepandemic has subsided. Investors are still struggling to makesense of an economy in which intangible capital replaces thebricks-and-mortar kind, and in which network effects make in-cumbents more dominant and profits more enduring.

As technology permeates business, the nature of investment

is changing. After the global financial crisis of 2007-09, the shareof private non-residential investment flowing to intellectualproperty hit 30%. Soon it may breach the 40% threshold (seenext leader). In this world, Walmart must become an e-com-merce giant, Ford must compete with Tesla to make electric cars,and computers must allocate capital. Even McDonald’s has beenworking on its digital strategy (see Schumpeter). The tech re-volution will change the economy as much as the globalisationwave that defined Bill Clinton’s presidency in the 1990s. As it re-shapes the labour market—blue- and white-collar jobs alike—itcould tear at the social fabric, much as the automation of manu-facturing jobs did.

America’s epidemic could be fading by the end of 2021. Thetech surge will outlive Mr Biden’s presidency.Yet the same principle should guide him onboth: that government must not resist eco-nomic change, but should instead help peopleadapt to it. One reason America’s economy isoutperforming Europe’s is that its stimulus hasdone more to prop up household incomes thanit has to preserve redundant jobs. Similarly, gov-ernments that respond to technological change

by remaking safety-nets and rewriting social contracts for thenew era will do better than those which seek to preserve obsoletemodels of capitalism and government.

There are thus reasons to worry that Mr Biden’s platform has aprotectionist streak, a nostalgia for manufacturing jobs and animpulse to load firms with worthy social goals. One of his new-economy policies already looks like a flop: he wants to extendnationwide the regulations for gig-economy work that Califor-nia voters rejected last week. To succeed, Mr Biden will need toshow competent crisis management. But he also needs to recog-nise the deeper changes taking place in the economy, and to helpAmericans profit from them. That is the way to raise living stan-dards—and, as it happens, to succeed as president. 7

GDP forecasts2020, % decrease on a year earlier

United StatesJapanCanadaEuro areaBritain

0-2-4-6-8-10

For a moment this week investors could afford to ignorestockmarket superstars like Amazon and Alibaba. As news of

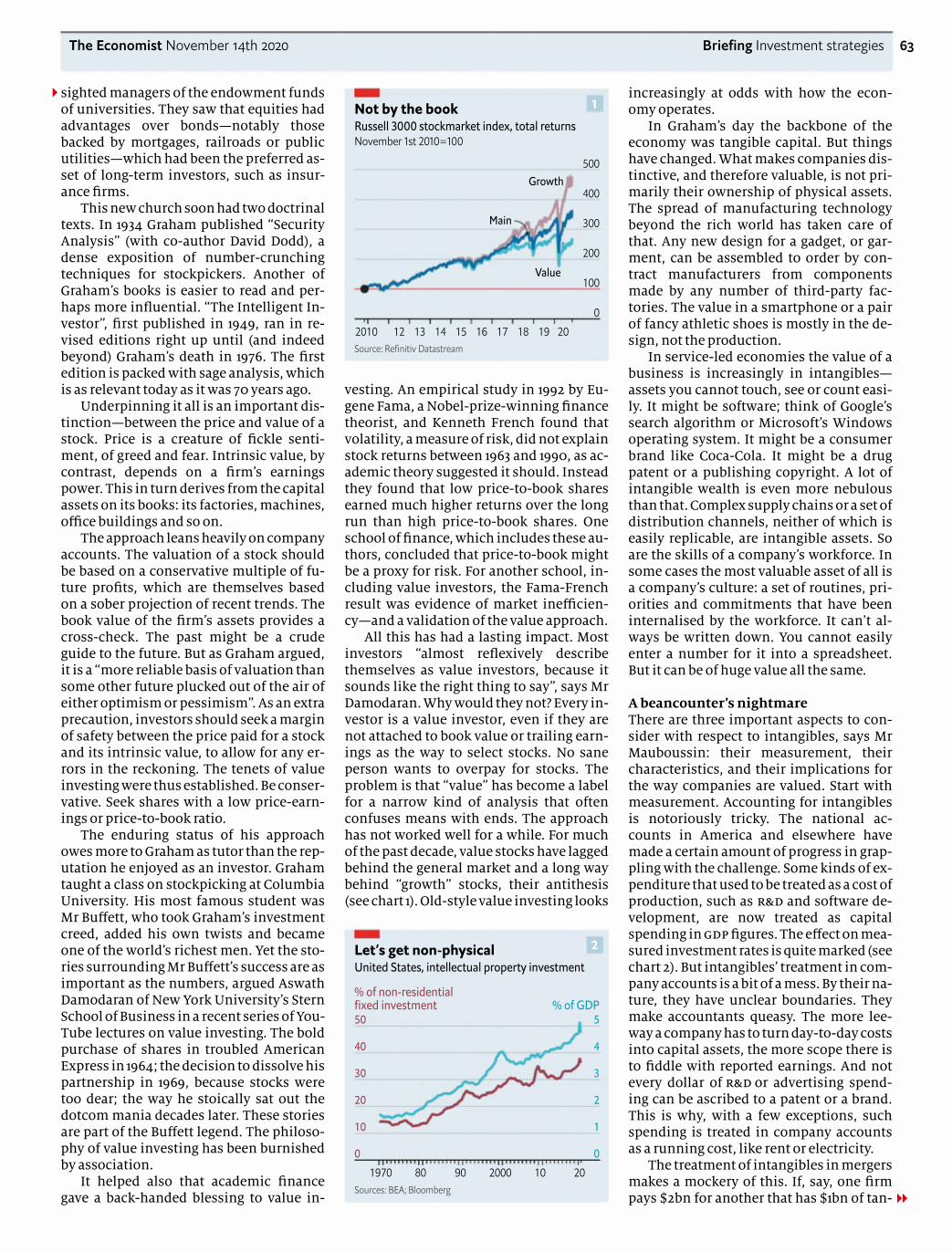

a vaccine broke, a motley crew of more jaded firms led Wall Streethigher, with the shares of airlines, banks and oil firms soaring onhopes of a recovery. The bounce has been a long time coming. So-called value stocks, typically asset-heavy firms in stodgy indus-tries, have had a decade from hell, lagging behind America’sstockmarket by over 90 percentage points. This has led to a crisisof confidence among some fund managers, who wonder if theirframework for assessing firms works in the digital age (see Brief-ing). They are right to worry: it needs upgrading to reflect aneconomy in which intangibles and externalities count for more.

For almost a century the dominant ideology in finance hasbeen value investing. It has evolved over time but typically takesa conservative view of firms, placing more weight on their as-sets, cashflows and record, and less on their investment plans ortrajectory. The creed has its roots in the 1930s and 1940s, whenBenjamin Graham argued that investors needed to move on from

the pre-1914 era, during which capital markets were dominatedby railway bonds and insider-dealing. Instead he proposed a sci-entific approach of evaluating firms’ balance-sheets and identi-fying mispriced securities. His disciple, Warren Buffett, popular-ised and updated these ideas as the economy shifted towardsconsumer firms and finance in the late 20th century. Today mea-sures of value are plugged into computers which hunt for “fac-tors” that boost returns and there are investors in Shanghailoosely inspired by a doctrine born in Depression-era New York.

The trouble is that value investing has led to poor results. Ifyou had bought value shares worth $1 a decade ago, they wouldfetch $2.50 today, compared with $3.45 for the stockmarket as awhole and $4.65 for the market excluding value stocks. Mr Buf-fett’s Berkshire Hathaway has lagged behind badly. Despite its ef-forts to modernise, value investing often produces backward-looking portfolios and as a result has largely missed the rise oftech. The asset-management industry’s business model is understrain, as our special report this week explains. Now one of its

Beyond Buffett

The agonies of traditional value investing are a sign of frothy stockmarkets—and a changing economy

Asset management

14 Leaders The Economist November 14th 2020

2 most long-standing philosophies is under siege, too.Value investors might argue that they are the victims of a

stockmarket bubble and that they will thus be proved right even-tually. The last time value strategies did badly was in 1998-2000,before the dotcom crash. Today stockmarkets do indeed look ex-pensive. But alongside this are two deeper changes to the econ-omy that the value framework is still struggling to grapple with.

The first is the rise of intangible assets, which now accountfor over a third of all American business investment—think ofdata, or research. Firms treat these costs as an expense, ratherthan an investment that creates an asset. Some sophisticated in-stitutional investors try to adjust for this but it is still easy to mis-calculate how much firms are reinvesting—and firms’ ability toreinvest heavily at high rates of return is crucial for their long runperformance. On a traditional definition, America’s top ten list-ed firms have invested $700bn since 2010. On a broad one, the

figure is $1.5trn or more. Intangible firms can also often scale upquickly and exploit network effects to sustain high profits.

The second change is the rising importance of externalities,costs that firms are responsible for but avoid paying. Today thevalue doctrine suggests you should load up on car firms and oilproducers. But these firms’ prospects depend on the potential li-ability from their carbon footprint, the cost of which may rise asemissions rules tighten and carbon taxes spread.

Value investing’s rigour and scepticism are as relevant asever—especially given how frothy markets look. But many inves-tors are still only just beginning to get their heads round how toassess firms’ intangible assets and externalities. It is a laborioustask, but getting it right could give asset management a newlease of life and help ensure that capital is allocated efficiently.In the 1930s and 1940s Graham described how the old investingframework had become obsolete. Time for another upgrade. 7

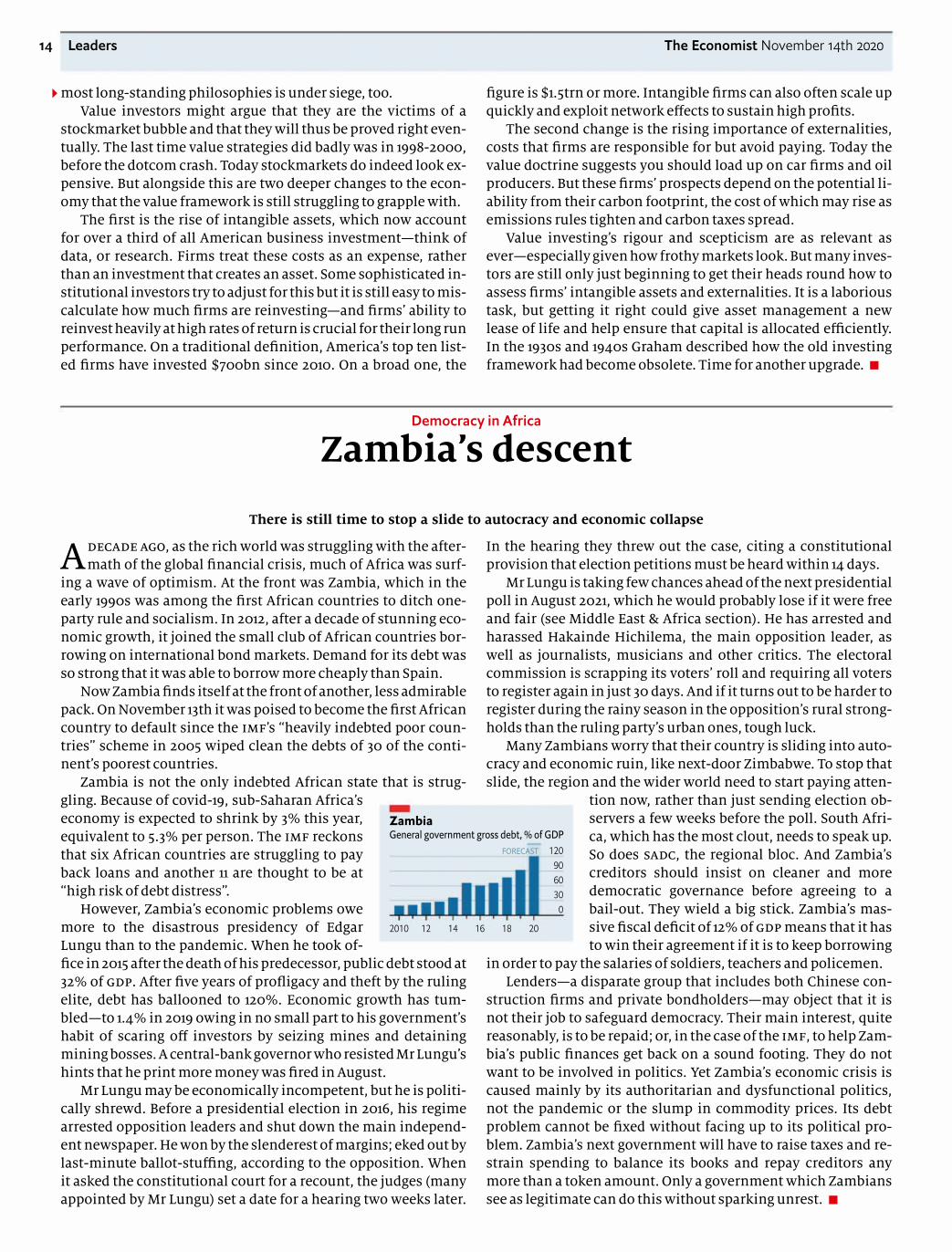

Adecade ago, as the rich world was struggling with the after-math of the global financial crisis, much of Africa was surf-

ing a wave of optimism. At the front was Zambia, which in theearly 1990s was among the first African countries to ditch one-party rule and socialism. In 2012, after a decade of stunning eco-nomic growth, it joined the small club of African countries bor-rowing on international bond markets. Demand for its debt wasso strong that it was able to borrow more cheaply than Spain.

Now Zambia finds itself at the front of another, less admirablepack. On November 13th it was poised to become the first Africancountry to default since the imf’s “heavily indebted poor coun-tries” scheme in 2005 wiped clean the debts of 30 of the conti-nent’s poorest countries.

Zambia is not the only indebted African state that is strug-gling. Because of covid-19, sub-Saharan Africa’seconomy is expected to shrink by 3% this year,equivalent to 5.3% per person. The imf reckonsthat six African countries are struggling to payback loans and another 11 are thought to be at“high risk of debt distress”.

However, Zambia’s economic problems owemore to the disastrous presidency of EdgarLungu than to the pandemic. When he took of-fice in 2015 after the death of his predecessor, public debt stood at32% of gdp. After five years of profligacy and theft by the rulingelite, debt has ballooned to 120%. Economic growth has tum-bled—to 1.4% in 2019 owing in no small part to his government’shabit of scaring off investors by seizing mines and detainingmining bosses. A central-bank governor who resisted Mr Lungu’shints that he print more money was fired in August.

Mr Lungu may be economically incompetent, but he is politi-cally shrewd. Before a presidential election in 2016, his regimearrested opposition leaders and shut down the main independ-ent newspaper. He won by the slenderest of margins; eked out bylast-minute ballot-stuffing, according to the opposition. Whenit asked the constitutional court for a recount, the judges (manyappointed by Mr Lungu) set a date for a hearing two weeks later.

In the hearing they threw out the case, citing a constitutionalprovision that election petitions must be heard within 14 days.

Mr Lungu is taking few chances ahead of the next presidentialpoll in August 2021, which he would probably lose if it were freeand fair (see Middle East & Africa section). He has arrested andharassed Hakainde Hichilema, the main opposition leader, aswell as journalists, musicians and other critics. The electoralcommission is scrapping its voters’ roll and requiring all votersto register again in just 30 days. And if it turns out to be harder toregister during the rainy season in the opposition’s rural strong-holds than the ruling party’s urban ones, tough luck.

Many Zambians worry that their country is sliding into auto-cracy and economic ruin, like next-door Zimbabwe. To stop thatslide, the region and the wider world need to start paying atten-

tion now, rather than just sending election ob-servers a few weeks before the poll. South Afri-ca, which has the most clout, needs to speak up.So does sadc, the regional bloc. And Zambia’screditors should insist on cleaner and moredemocratic governance before agreeing to abail-out. They wield a big stick. Zambia’s mas-sive fiscal deficit of 12% of gdp means that it hasto win their agreement if it is to keep borrowing

in order to pay the salaries of soldiers, teachers and policemen. Lenders—a disparate group that includes both Chinese con-

struction firms and private bondholders—may object that it isnot their job to safeguard democracy. Their main interest, quitereasonably, is to be repaid; or, in the case of the imf, to help Zam-bia’s public finances get back on a sound footing. They do notwant to be involved in politics. Yet Zambia’s economic crisis iscaused mainly by its authoritarian and dysfunctional politics,not the pandemic or the slump in commodity prices. Its debtproblem cannot be fixed without facing up to its political pro-blem. Zambia’s next government will have to raise taxes and re-strain spending to balance its books and repay creditors anymore than a token amount. Only a government which Zambianssee as legitimate can do this without sparking unrest. 7

Zambia’s descent

There is still time to stop a slide to autocracy and economic collapse

Democracy in Africa

ZambiaGeneral government gross debt, % of GDP

120906030

0

20181614122010

FORECAST

16 The Economist November 14th 2020

Letters are welcome and should beaddressed to the Editor atThe Economist, The Adelphi Building,1-11 John Adam Street, London WC2N 6HT

Email: [email protected] letters are available at:Economist.com/letters

Letters

The sporting lifeThe problem of ensuring faircompetition in women’s sportgoes wider and deeper than thequestion of whether transwomen should compete asfemales (“Scrum down”, Octo-ber 17th). There really are bigdifferences between men andwomen in genes and geneactivity, size and strength,although there is a lot of varia-tion and some overlap in anytrait you can measure. Thesedifferences are largely, but notentirely, the result of androgenaction during development,and are not obviated by anti-androgen treatment.

It is clear that athletes whowere born and developed asmales have the advantage ofhigher stature, more leanmuscle and a bigger heart andlungs. But so, too, do femaleathletes with naturally hightestosterone levels. It seemsnonsensical to apply arbitrarylimits to testosterone levels insport, unless you were to banathletes with unusually longlegs, big hearts or lungs as well.Elite athletes are usually on thevery edge of distributions of allsorts of qualities that enhanceperformance.jenny graves

Melbourne

Few aspiring trans athletes willbe tempted to compete aswomen, given the massivedisadvantages they face. In theUnited States, trans women aretwice as likely to live below thepoverty line. Trans women ofcolour face higher risks ofmurder and other violence.That’s a poor swap for a leg upin the 100-metre sprint.peter johnston

San Francisco

A bizarre fixation on sportdominates the conversation ontrans rights. The only realadvantage possessed by a transwoman would be that of testos-terone if she has not begunhormone treatment. The Inter-national Olympic Committeesuggests changing resultsbased on testosterone levels.Given that these levels can varyamong cis women, should thisbe imposed on them also? Or

on men with different testos-terone levels?

The supposed risk thatwomen face from trans rightsis as much a mirage as was thefear of homosexual indoctrina-tion in the 1980s, which led tooppressive legislation, such asBritain’s Section 28.thomas robertson

Oxford

Diplomatic dispatchesThank you for introducing anew black humour section inyour edition of October 24th. Itis regrettable, though, that youhad to sacrifice over twocolumns of your Letters page toa response from the Chineseembassy to your articles on theUyghurs to do so.ian cartwright

Isle of Lewis, Outer Hebrides

Filter out the noiseSchumpeter missed a trickwith regard to annoyingadvertisements and newsfeeds on Facebook (October24th). Not only are ad blockersavailable, many other anti-spyware and tracker-blockingapps can easily be installed. Inparticular, an app known as fb

Purity integrates with Face-book and enables me to blockout not just annoying news-feeds and adverts, but alsoirritating spam thanks tokeyword-based text filtering.nicholas coote

Devizes, Wiltshire

Army trainingBartleby’s column on what thearmed forces can teach busi-ness scratched the surface ofmuch deeper opportunities(October 24th). In the 1980s thestrategy for the defence ofwestern Europe was changedfrom positional defence tofighting a mobile defensivebattle. This meant a highdegree of uncertainty with theneed for increased agility, alatter-day buzzword in busi-ness. As a battlefield com-mander I pushed the decisionsI would normally take down tothe lowest possible level. Somethings that would take 30minutes to accomplish could

be done in an astonishing 30seconds. The key is for leader-ship to move beyond being arole, position or competence(which are typically static) to avibrant dynamic. This achievesagile self-organisation that cannavigate uncertainty better,faster and with less stress.

Various companies aroundthe world have since used thisapproach to good effect. InChina, a team at Dow Chemicalachieved a 25% increase inproject productivity. In Ameri-ca two senior leaders of Nokiaachieved six times in a fewweeks what had taken a previ-ous team many months.

Sadly, many see the armedforces in light of the movies,strictly “command and con-trol”. The truth is far from that.major (ret’d) prince

nicholas obolensky

FounderComplex Adaptive LeadershipBath

Armenia respondsYour article on the fighting inNagorno-Karabakh provided adistorted picture of the conflict(“The wheel turns, this time”,October 31st). The reality is thatArtsakh (Nagorno-Karabakh)has always been populatedoverwhelmingly by Armeniansand it has never been a part ofindependent Azerbaijan. In1991 Nagorno-Karabakh votedfor its independence based onthe same legal framework asAzerbaijan.

Armenia has been consis-tent in its intentions for peace,by pushing for a compromiseacceptable to the people of allparties: Artsakh, Armenia andAzerbaijan. This message hasnever been reciprocated, thusmaking it clear that Azerbai-jan’s intention is neither nego-tiations nor peace, but war.

In the month of this latestconflict Azerbaijan, compre-hensively backed by Turkeyand with the use of interna-tional terrorist fighters, hasconsistently shelled Artsakh’stowns and villages. Civilianinfrastructure, hospitals,schools and even kinder-gartens have been bombed andwar crimes committed by theAzerbaijani armed forces.

The only alternative is apeaceful resolution, in whichthe security of Armenians ofArtsakh finds its expressionand their legitimate right forself-determination will bedelivered.aram araratyan

Press officerEmbassy of ArmeniaLondon

How might you feel?Technology Quarterly reportedon virtual realities (October3rd), noting that in virtualworlds “users will often co-optthe avatars as almost real ex-tensions of their own bodies”.One interesting experimentwould be to use avatars toimplement the veil of igno-rance as set out by John Rawlsin his “A Theory of Justice”. Letthe subjects of the experimentsmake decisions about fairnessand equity while inhabitingavatars with characteristicsother than their own.

How might evangelicalChristians feel about abortionif their avatars were rape vic-tims? How might supporters ofBlack Lives Matter feel aboutpolice intervening in riots iftheir avatars were Koreangrocery-store owners? Howmight rich people feel abouttax reform if their avatars werepoorer citizens?christopher bruce

Calgary, Canada

Reaching the bottom of a caseI was intrigued to read in Theworld this week (October 24th)that Brazilian police had raideda senator’s home and discov-ered about $5,000 wedgedbetween his buttocks. He hasdenied diverting funds thatwere meant for the pandemic.If he is innocent then this is amost unfortunate case of abum rap.david roessler

Hazel Park, Michigan

COVID-19 has aff ected billions of lives. Some call it a ‘black swan event’. But it isn’t, pandemics have always existed.

Many of the eff ects of a pandemic of this scale have been known for years, knowledge to which Swiss Re’s analysis has contributed. As the world’s leading provider of reinsurance and risk transfer, we specialise in modelling and underwriting risk.

Swiss Re and the re/insurance industry have set aside billions to help shoulder the fi nancial impact of the pandemic. And across the world, countries have made emergency aid programmes available. Still, the suff ering and the uncertainty for those aff ected is enormous.

To do better next time, we as a society need to be better prepared. One solution is to partner in public-private risk-sharing arrangements to cover pandemic-related losses.

Swiss Re is committed to helping society become more resilient and progress.

swissre.com

18 Executive focus

The Economist November 14th 2020 19

1

Deliverance, when it arrives, willcome in a small glass vial. First there

will be a cool sensation on the upper arm asan alcohol wipe is rubbed across the skin.Then there will be a sharp prick from a nee-dle. Twenty-one days later, the same again.As the nurse drops the used syringe intothe bin with a clatter, it will be hard not towonder how something so small can solvea problem so large.

On November 9th Pfizer and BioNTech,two firms working as partners on a vaccineagainst covid-19, announced somethingextraordinary about the first 94 people ontheir trial to develop symptoms of the dis-ease. At least 86 of them—more than nine

out of ten—had been given the placebo, notthe vaccine. A bare handful of those vacci-nated fell ill. The vaccine appeared to bemore than 90% effective.

Within a few weeks the firms couldhave the data needed to apply for emergen-cy authorisation to put the vaccine to use.The British and American governmentshave said that vaccinations could start inDecember. The countries of the eu havealso been told it will be distributed quickly.

The news lifted spirits around theworld, not to mention stockmarkets (seeFinance). The end of the pandemic seemedin sight; scientific insight and industrialknow-how had, in a bravura display of their

power, provided an exit strategy. Pfizer andBioNTech have not just developed a vaccineagainst a previously unknown disease in ascant ten months. They have done so on thebasis of an approach to vaccination neverbefore used in people. And their novel vac-cine has shown an unanticipated efficacy.Most in the field thought 70% efficacy wasgood as could be hoped for first time out;just 50% could have been good enough forregulatory approval. Exceeding 90% hitsthe virus for six.

Russia and China have been vaccinatingsome citizens against covid-19 for sometime outside the scope of clinical trials. OnNovember 11th the Russian Direct Invest-ment Fund announced that data showedRussia’s vaccine, known as Sputnik V, to be92% effective. Before the Pfizer announce-ment this would have seemed highly im-plausible. Now it may seem less so, thoughthe evidence is weak compared withPfizer’s. And neither Sputnik V nor the Chi-nese vaccines have yet had their safety andefficacy addressed by the stringent regula-tors at the Food and Drug Administration(fda) in America and the European Medi-cines Agency (ema).

Pfizer’s vaccine is now headed into thatregulatory gamut with a small posse of fol-lowers hot on its heels (see table on nextpage). Two other vaccines which are inphase-three trials—the sort of large, rando-mised trials designed to show the efficacyof a treatment—could submit data to theregulators fairly soon. Moderna, an Ameri-can biotech firm, is expected to deliver in-terim findings about the efficacy of its vac-cine in the next few weeks. AstraZeneca, apharmaceuticals company working inpartnership with the University of Oxford,should deliver results from its trial beforethe end of the year.

Challenges remain. Though the regula-tors will want to move quickly, they willstill have to do their job. Missteps coulderode confidence in the vaccine, as well asvaccination more generally. Plans for scal-ing up manufacture and for distribution onan unprecedented scale have been beingmade around the world for months, but it ishard to imagine that they will not requirerevision on the hoof. Even if the news con-tinues to be good, the numbers vaccinatedwill remain small for months to come. Buta fateful corner has been turned.

The technology of hopeGreat speed has come from great efforts.Cath Green, the boss of the clinical bioma-nufacturing facility at the University of Ox-ford, remembers the pressure to get thefirst candidate-vaccine vials filled in April.Everyone was doing double shifts andworking on weekends. “We knew it had tobe this fast if we were to get a vaccine topeople this year,” she says.

Bullseye

A highly effective vaccine will transform the fight against covid-19. But a lotremains to be done

Briefing Covid-19 vaccines

20 Briefing Covid-19 vaccines The Economist November 14th 2020

2

1

But it was not just hard work. New tech-nology, a lack of financial constraint and acommitment to speeding up regulatoryprocesses without sacrificing standardsmattered, too.

Technology first. Vaccines against vi-ruses used to be based on the virus parti-cles they were meant to stymie. Some werestrains of the virus “attenuated” so as not tocause disease; some were normal virus par-ticles inactivated so that they could not re-produce at all. Design was somewhat hitand miss. Today vaccine development isbased on viral genomes. Researchers lookfor a gene which describes a protein the im-mune system seems likely to recognise.Then they put that gene into a new context.

In the case of sars-cov-2, the virus thatcauses covid-19, the genome was publishedon January 10th. Understanding its struc-ture on the basis of their experience withother coronaviruses, would-be vaccine-makers immediately homed in on the genefor the distinctive spike protein withwhich the virus’s membrane is studded:just the sort of thing, they reckoned, to pro-voke a response from the immune system.

At BioNTech, a German biotechnologycompany that specialises in the use ofmrnas—sequences of genetic materialthat provide cells with recipes for makingproteins—the spike-protein gene wasmore or less all it took. The company’s re-searchers made an mrna version of it thatcould be injected into the body in tiny cap-sules made of lipids. There it would leadcells to produce the spike protein, and theimmune system would then take note. Orso they hoped: no mrna vaccine had beenused in humans before. Moderna, too, hasas its name suggests taken the mrna route.

In Oxford a version of the spike genewas instead put into the genome of a harm-less adenovirus originally found in mon-keys; when the resultant virus infects cellsit, too, makes them produce spike proteinsthat attract the immune system’s atten-tion. The vaccine developed by J&J alsouses the adenovirus approach, as doesSputnik V.

It is no accident that the vaccines thathave come along fastest are based on thesenovel strategies. Before the coronavirusstruck these technologies were already be-ing developed as platforms on which a rap-id response to a new viral disease could bebuilt, work supported in part by the Co-alition for Epidemic Preparedness Innova-tions (cepi). Vaccines which are built onsuch platforms are quick to engineer andcomparatively easy to make.

The correct egg-to-basket ratioThat said, the work still requires money,which in the vaccine world is usually inshort supply. With covid-19, though, gov-ernments have been willing to shovel cashat vaccine developers even though therewas a risk they would get nothing in return.“We persuaded the uk government to fundus before they had any idea whether itwould work,” says Dr Green. It was thisready cash, sometimes provided in theform of a commitment to buy the end pro-duct, which sped the process up, ratherthan any loosening of normal rules andprocedures. “We haven’t cut any corners,”Dr Green continues. “And we haven’t takenany risks with our product.”

Rather than standing back, regulatorsin many countries have worked closelywith companies to make sure their trialsprovide all the data needed for approvalwhen the time is right. When it was safe todo so, the different phases of trials were al-lowed to overlap, with larger, later trialsstarting before smaller preliminary oneshad produced all their data. At Oxford theywere able to start human trials the day afteranimal safety data had been published.

Richard Hatchett, the head of cepi, saysPfizer’s positive results increase the proba-bility that other covid vaccines will be suc-cessful, too. They show that an mrna vac-cine can work, which is good news forModerna; they also show that targeting thespike protein pays off. And the success goesbeyond the current pandemic. Work cepi

expected to take five or ten years has beenmanaged in less than one; if the various

platforms in play all pay off, Dr Hatchettsays, it will “transform vaccinology”.

The fact that there are more vaccines onthe way matters for a number of reasons.One is that, despite this week’s good news,the Pfizer vaccine is not yet guaranteed ap-proval. For one thing, its safety needs to bemore fully ascertained. The firm says thatno serious safety concerns have arisen dur-ing the trial. But the vaccine will come withside-effects, at least for some, and the com-pany will only be in a position to requestapproval for the vaccine on an “emergencyuse” basis after it has two months of safetydata showing such effects to be manage-able. That requirement looks likely to bemet in time for an application in the thirdweek of November.

Then comes the question of what exact-ly the vaccine does: is it stopping infec-tions completely—providing “sterilisingimmunity”—or simply amping up thebody’s response so that infections do notcause disease? The latter attribute is un-doubtedly a useful one for the individualconcerned; all the better if, as well as lower-ing the chance of infection leading to dis-ease, it also makes the disease less severe inthose who succumb (there is as yet noavailable data on this). But it is a lot less de-sirable in public-health terms. If the vac-cine stops disease but not infection, vacci-nated people may be able to infect otherswhile staying safe themselves.

If the Pfizer vaccine does not providesterilising immunity there will be a needfor one that does. And there are other waysthat subsequent vaccines might provepreferable. Different vaccines can workbetter or worse with different populations,and for covid-19 it is important to find avaccine which works well in old people.Their immune systems can often be unre-sponsive to vaccination, and they may dobetter with vaccines which, in the generalpopulation, do not look as effective. Thereis no guarantee that the best vaccine overallwill be the best for the elderly.

And the Pfizer vaccine has some incon-venient characteristics. It needs to be keptat -70°C or even colder as it is moved fromwhere it is made to where it is used, whichrequires a lot of equipment that other vac-cines do not need. Seth Berkley, head of thevaccine finance group gavi, warns thatmany countries do not currently have thewherewithal to meet that challenge. But healso notes that the lack is not insuperable.The Democratic Republic of Congo suc-cessfully deployed an Ebola vaccine thatrequired similarly special care. “It’s a painin the ass, it’s expensive, but it’s doable.”

Still, a vaccine which, if not liking it hot,at least liked it less cold would be a boon. Sowould one that only needed to be givenonce. The Pfizer, AstraZeneca and Modernavaccines all require two jabs weeks apart. Aone-and-done vaccine, which is what J&J

A full field

Sources: PLOS; VFA; ClinicalTrials.gov; press reports *Estimated number of enrolees in phase three †US trial ‡Announcement of phase 2/3

Selected covid-19 vaccines in phase-three clinical trials, 2020

Developer Participants*Type Doses Study locationPhase-3start date

Johnson & Johnson

AstraZeneca/Oxford University

Moderna

Sinovac

Gamaleya (Sputnik V)

Novavax

International Sep 7th

Aug 28th†

Jul 27th‡

Sep 7th

Jul 27th

Jul 21st

Sep 28th

Viral vector

Viral vector

Inactivated

mRNA

Inactivated

Viral vector

International

United States

Britain, US, Mexico

International

International

1

2

2

2

2

2

Pfizer/BioNTech

60,000

45,000

50,000

30,000

27,980

43,600

43,998mRNA International2

The Economist November 14th 2020 Briefing Covid-19 vaccines 21

2 hopes for, makes setting up a vaccinationprogramme far simpler. It also means a giv-en number of doses will go a lot further.

On top of all this, the long-term efficacyof the vaccine will matter a lot. The Pfizer/BioNTech collaboration says that protec-tion should last at least a year. But that willnot be known for sure before they apply toregulators for full authorisation on the ba-sis of final trial results, which they are ex-pected to do in the first quarter of next year(as are the makers of the other front-run-ners). A vaccine that provides protectiononly briefly might well not be able to dis-rupt the virus’s transmission, instead feed-ing a constant stream of newly susceptiblepeople back into the population at large.Marcus Schabacker, the boss of the Emer-gency Care Research Institute, an Ameri-can organisation focused on the qualityand safety of medical practices, thinks sixmonths of follow-up data ought to be scru-tinised, not just two, before final decisionsare made on deploying the vaccine.

Such questions will be on the minds ofregulators at the fda and ema when theyare asked to consider the Pfizer vaccine foremergency use later this month and whenPfizer and the makers of other vaccinessubmit all the data from their trials nextyear. Their opinions will have worldwideeffects, as the World Health Organisation(who) will use the analytical capabilities ofthose authorities to accelerate the reviewof vaccines for use in low- and middle-in-come countries.

If emergency authorisation is granted itis likely the agencies will restrict the use ofthese vaccines, initially, to those at highestrisk of death or serious disease. If after see-ing the full data the regulators still haveworries they may continue to limit the vac-cines’ use. Whatever they decide they arevery likely to insist on years of follow up.

Andrew Pollard, director of the OxfordVaccine Group, says it is important that all

developers carry on with trials as long aspossible. But this may be hard unless earlyuse is restricted to specific groups. If a vac-cine is approved for use in the general pop-ulation, few will volunteer to take part in atrial for another vaccine that uses a placeboas a control (if Pfizer and BioNTech receivean emergency authorisation they plan tooffer all the volunteers who were given aplacebo the active vaccine). A trial thatcompares an experimental vaccine withone that is already approved needs to bevery large to get results, since both wingscan be expected to show comparatively fewinfections. Such trials are under discus-sion, but they will take a long time.

If vaccines are approved for widespreaduse, the world will face what some havecalled the largest supply-chain challengein history. There is normally little sparevaccine-manufacturing capacity to repur-pose. And production is not the only limit-ing factor. Analysts at ubs, a bank, warnthat “fill and finish”, where the vaccine isput into vials and packaged, could be one ofthe most significant bottlenecks.

Pfizer says it will only be able to makeenough vaccine to inoculate 25m people in2020. Up to 1.3bn doses are possible, in the-ory, next year—enough for another 650mpeople. If other vaccines are approved thenthe supply will increase. In even the mostoptimistic scenarios, though, Dr Hatchettexpects demand to exceed supply through-out 2021.

Various countries have already set uppurchase agreements with vaccine devel-opers (see chart). The covax facility set upby cepi, gavi and the who will buy vac-cines for 150 countries, and aims to procureenough for them to get 20% of their popu-lations vaccinated over the course of 2021.unicef, the un’s children’s agency, willtake a leading role in distribution. It nor-mally procures 600m-800m syringes forroutine childhood immunisations every

year. The demands of covid are likely to tre-ble or quadruple that number.

There is clearly a risk that nations willhoard some vaccine for their own use rath-er than that of the most needy, but it is noteasy to say how large the problem will be.Pharma firms have cleverly placed manu-facturing sites around the world, includingin small countries such as Belgium andSwitzerland which can quickly producemore vaccine than these countries couldever want. And the covax framework haswide international support.

That framework follows advice from thewho in identifying three priority groupsfor early vaccination: front-line health-and social-care workers; the over 65s; andthose under 65 who have underlying healthconditions, such as diabetes, which putthem at particular risk. Countries settingtheir own priorities are by and large priori-tising the same groups. This means thatyoung and middle-aged people not in anyrisk categories are unlikely to be vaccinat-ed until well into next year. Social distanc-ing and mask wearing will stay importantfor some time to come even after vaccina-tion becomes widespread. But a more nor-mal form of life looks unlikely to be toolong delayed.

For vaccination to work as well as it canrequires a widespread willingness to bevaccinated—something that cannot be tak-en for granted in a world where anti-vac-cine disinformation has a strong foothold.The data on this front, though, are broadlyencouraging. A survey of 20,000 adults in27 countries undertaken for the World Eco-nomic Forum this August found that 74%would get a vaccine if it were available. InChina the figure was 97%, in India 87%, inAmerica 67%. Countries with low rates ofacceptance were Russia (54%), Poland andHungary (both 56%) and France (59%).

A cold comingBetter testing, new antibody treatmentsand improvements in care will continue todrive down the death rate for coronavirusboth before widespread vaccination andafter it. Vaccination will instead change thefundamentals. Its advent marks the begin-ning of the end of covid-19 as a pandemic.

But for all the hope that diligence andscience have kindled, there are hard wintermonths to face before that spring. The offi-cial tally of daily deaths round the world isnow for the first time higher than it was inthe pandemic’s first peak, and the spread ofthe virus in America appears to be out ofcontrol (see United States). In the nextthree months hundreds of thousands ofpeople look likely to die. Not only will theirloved ones have to come to terms with thisloss, they will also have to live with theknowledge that a vaccine that could havesaved them, even though developed atbreakneck speed, arrived just too late. 7

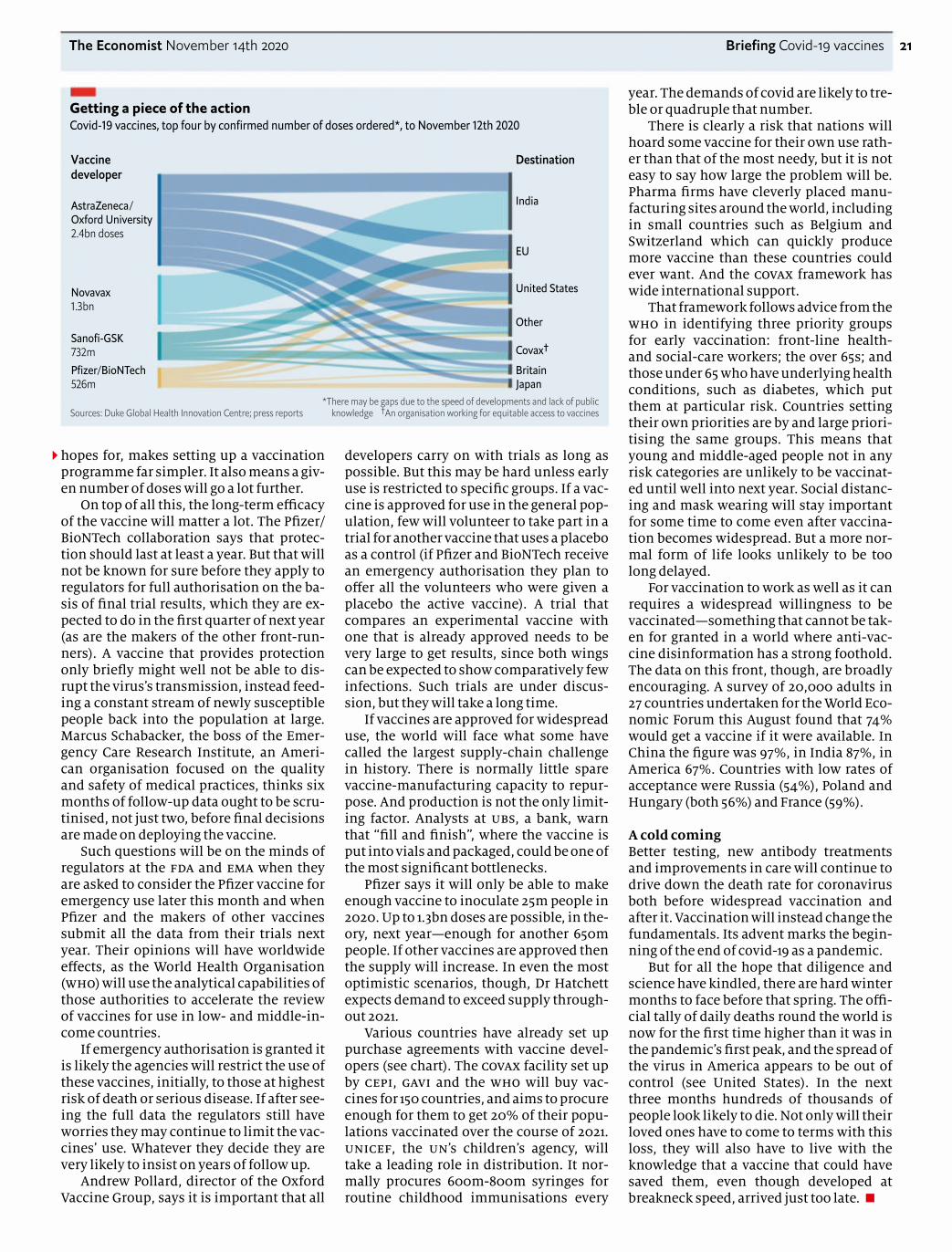

AstraZeneca/Oxford University2.4bn doses

Novavax1.3bn

Sanofi-GSK732mPfizer/BioNTech526m

Covax†

EU

JapanBritain

Other

United States

India

Vaccinedeveloper

Destination

Getting a piece of the action

Sources: Duke Global Health Innovation Centre; press reports*There may be gaps due to the speed of developments and lack of public

knowledge †An organisation working for equitable access to vaccines

Covid-19 vaccines, top four by confirmed number of doses ordered*, to November 12th 2020

Get started with our free toolsor talk to an advisor today at:

personalcapital.com/econ

1-"Corporate Sustainability: First Evidence on Materiality,” Harvard Business School, 2015, https://dash.harvard.edu 2-Advisory services are offered for a fee by PCAC, a wholly owned subsidiary of Personal Capital Corporation, an Empower company. Personal Capital Advisors Corporation (“PCAC”) is a registered investment adviser with the Securities and Exchange Commission (“SEC”). SEC registration does not imply a certain level of skill or training. Investing involves risk. Past performance is not a guarantee nor indicative of future returns. The value of your investment will fluctuate, and you may lose money. All charts, figures, and graphs are for illustrative purposes only and do not represent an actual client experience. Featured individuals are actors and not clients of PCAC. Personal Capital Corporation is a wholly owned subsidiary of Empower Holdings, LLC. © 2020 Personal Capital Corporation, an Empower Company. All rights reserved.

Do you want your investments to align with your values? Our Socially Responsible Personal Strategy® is a wayfor you to support companies that proactively manage ESG-related issues. Studies show that investing in higher-rated ESG (Environmental, Social, Governance) companies could also lead to better returns over time.1Ready to start? Talk to an advisor about buildinga personalized plan.2

Socially Responsible InvestingPut new energy in your portfolio.

FREE FINANCIAL TOOLS AVAILABLE ON WEB & MOBILE

The Economist November 14th 2020 23

1

Partisanship has long coloured Ameri-can perceptions of covid-19. Even so, the

contrast between the top echelons of themain parties was striking on November9th, the day the country passed 10m record-ed cases of the disease. On that day theWhite House of outgoing President DonaldTrump was dealing with reports that it mayhave hosted a second superspreadingevent in the span of a month—this one foran election-night party that may have sick-ened Ben Carson, the housing secretary,among others. The same day, President-elect Joe Biden announced the members ofthe coronavirus advisory board for histransition, staffed by the sort of public-health experts the president likes to mock.

While national attention was otherwisediverted, an extraordinary third surge incovid-19 infections began in the weeks be-fore the presidential election. There arenow 1,000 new deaths reported each dayalong with 120,000 new infections. Eventhough testing has been ramped up to near-ly 1.5m per day, the test-positivity rate is ap-

proaching 10%—suggesting that even now,many infections are being missed. In allbut a handful of states, there seems to beuncontrolled transmission, limiting theefficacy of contact-tracing. Hospitalisa-tions had been declining up until the endof September, when they bottomed out un-der 30,000. Now they have doubled to over60,000—higher than the previous peak inApril. In North Dakota, the location of theworst outbreak in the country, nearly everyintensive-care bed is occupied.

The argument that Mr Trump has han-dled the epidemic uniquely terribly mayjust have cost him the election. However,this most recent surge is not an AmericaFirst phenomenon. It has roughly coincid-ed with a second wave in Europe which,measured both by deaths and by cases perperson, is even more severe. Europeancountries have reimposed harsh lockdownmeasures, whereas the president andAmerica’s governors have been less draco-nian. France’s intensive-care wards look al-most as strained as those of North Dakota.

But whereas President Emmanuel Macronhas declared a second national lockdown,Governor Doug Burgum, a Republican, re-cently declined to impose even a maskmandate in his state.

Forecasting the course of the diseasehas proved supremely difficult. It is there-fore unclear how bad a situation a newlyinaugurated President Biden would inheriton January 20th 2021. But current signs donot augur well. Ashish Jha, dean of theBrown University School of Public Health,reckons that there may be 100,000 newdeaths between now and then. The Econo-mist’s best estimate of total deaths in Amer-ica, including those we think are missed byofficial reporting, is nearly 300,000. Afternine long months of living with the virus,Americans and their elected officials seemtired of restrictions on movement andbusinesses. With no new curbs, exponen-tial growth could continue for weeks. Coldweather may push more people to movetheir gatherings indoors, where transmis-sion is much more likely. Many Americanswill travel for Thanksgiving and Christmas;no politicians will want to take the blamefor cancelling the holidays.

Federal action on the economy does notseem imminent either. Democrats and Re-publicans in Congress have been dead-locked over a new economic stimulussince many supports expired in July. Thestalemate has not yet been broken. NancyPelosi, the Democratic leader in the House

Covid-19 and the next president

Transmission and the transition

WA S H I N GTO N , D C

What the Biden administration would do differently, and howmuch difference it would make

United States

24 Digesting the election

25 Firings and hirings

26 Fox News and Donald Trump

26 Rewilding the prairie

28 The urban-rural divide

30 Lexington: A Democratic defeat inthe midst of victory

Also in this section

24 United States The Economist November 14th 2020

2

1

of Representatives, may with to hold outfor the larger package her party couldachieve if Democrats win two run-off Sen-ate elections in Georgia, thus flipping con-trol of the chamber. Mitch McConnell, theRepublican leader in the Senate, may notwant to concede a pre-emptive victory tothe Biden administration.

A virus spreading fast with no compen-sating stimulus would be a brutal startingposition for a Biden administration. Evenwith expedited approval and distribution,getting a vaccine to every American whoneeds it would take months (see Briefing).Mr Biden has announced plans to takemore serious federal action. He has namedRon Klain, who co-ordinated Obama WhiteHouse’s response to an Ebola outbreak in2014, as chief-of-staff. Mr Biden would usehis executive authority to create a Roose-veltian Pandemic Testing Board to compelcompanies to produce more tests, labora-tory materials and personal protectiveequipment. He probably lacks the author-ity to impose a mask mandate nationwide,but would push states to do so.

Most Republican governors are alreadywary about implementing public-healthmeasures. They might see the chance todefy Mr Biden’s recommendations as anadditional incentive to stay that course.Democratic ones seem averse to a Euro-pean-style response too. The ban an-nounced by Phil Murphy, the Democraticgovernor of New Jersey, on indoor diningin restaurants between 10pm and 5am,typifies the urge to do something, but nottoo much.