The case of LNG as fuel for merchant vessels in the Special Emission Control Areas

15

The case of LNG as fuel for merchant vessels in the Special Emission Control Areas Dr Alkis J. Corres, Dr Andreas Frangos, Yvonne Papachristou City Law School, City University. London, U.K. Email: [email protected] UNICOM Management services (Cyprus) Ltd., Limassol, Cyprus Email:[email protected] PPA Consultant, Piraeus, Greece Email: [email protected] March 2014 Abstract The issues connected to the introduction of the SECAs by January 1 st 2015 are numerous and interconnected constituting a mesh of problems through which ship owners and charterers have to pass. Decisions have to be made amid uncertainty and are bound to influence a much wider number of players than the two aforementioned ones. The European Union, itself confused about incentives and subsidies, is unable to provide assistance to its affected member states which will be left to their own devices. The same applies to ship owners who see the huge amounts of money available under the various schemes go to infrastructure projects rather than the cost of retrofits. There is no doubt there is going to be an impact on the terms of trade and most writers on this subject agree there will be higher freight rate levels in short sea shipping and a significant degree of backshift of cargoes from the sea to the land modes. This summary paper attempts to depict the larger picture in a concise way and suggests that the problem has been approached from the wrong angle ab originem. Keywords: LNG, vessels, sulphur, retrofit, scrubber, EU policy, environmental gain, shortsea shipping 1. Introduction After years of debate the International Maritime Organization (IMO) has approved the creation of Special Emission Control Areas where ships will only be allowed to trade on condition that low levels of sulphur

Transcript of The case of LNG as fuel for merchant vessels in the Special Emission Control Areas

The case of LNG as fuel for merchantvessels in the Special Emission

Control Areas

Dr Alkis J. Corres, Dr Andreas Frangos, Yvonne PapachristouCity Law School, City University. London, U.K.

Email: [email protected] Management services (Cyprus) Ltd., Limassol, Cyprus

Email:[email protected] Consultant, Piraeus, Greece

Email: [email protected]

March 2014

Abstract The issues connected to the introduction of the SECAs by January 1st 2015 arenumerous and interconnected constituting a mesh of problems through which shipowners and charterers have to pass. Decisions have to be made amid uncertaintyand are bound to influence a much wider number of players than the twoaforementioned ones. The European Union, itself confused about incentives andsubsidies, is unable to provide assistance to its affected member states whichwill be left to their own devices. The same applies to ship owners who see thehuge amounts of money available under the various schemes go to infrastructureprojects rather than the cost of retrofits. There is no doubt there is going tobe an impact on the terms of trade and most writers on this subject agree therewill be higher freight rate levels in short sea shipping and a significantdegree of backshift of cargoes from the sea to the land modes. This summarypaper attempts to depict the larger picture in a concise way and suggests thatthe problem has been approached from the wrong angle ab originem.

Keywords: LNG, vessels, sulphur, retrofit, scrubber, EU policy, environmental gain, shortsea shipping

1. Introduction After years of debate theInternational Maritime Organization

(IMO) has approved the creation ofSpecial Emission Control Areas whereships will only be allowed to trade oncondition that low levels of sulphur

A. Corres ET AL.

will be emitted. This regulation hasfollowed the failure to reach ameaningful agreement at IMO in the1990s, so the problem is not new.These areas come officially on streamon January 1st 2015 and for the timebeing are restricted to the EuropeanUnion EU (North Sea and the Baltic)and in North America (US and Canada).The obvious way to comply with the lowsulphur emission obligation is to useLow Sulphur Fuel (LSF) by ships whilesailing in those areas. The oilindustry is in position to providesuch fuels at a cost. The use ofLiquefied Natural Gas (LNG) and thefitting of scrubbers have also beensuggested as possible alternatives tothe use of LSF. Both of these methodsof compliance entail high upfrontinvestment for existing ships as wellas the creation of infrastructureashore in the case of LNG. Presently the debate on methods ofcompliance is at its highest point andone would not exaggerate by sayingthat the entire shipping industry isin a state of anxiety regarding thegeneral issue of compliance. Thereason for this unusual and unpleasantsituation is the non-commercialapproach to the problem adopted byregulators and classificationsocieties alike. The former may begiven the benefit of doubt concerningtheir technical appreciation of theproblem unlike the latter which appearto have seen additional businessopportunities in the emergence of thenew multimillion market in retrofits.The shipping Industry has been usingLNG as fuel in LNG carrying vesselsfor quite long time. On the contrary,its use on the wider merchant fleethas been negligible. LNG consistsmostly of methane (CH4) and contains

the highest amount of energy per unitof carbon of any fossil fuel. It is acolorless and odorless flammable gasignitable by static electricity,although it is an extremely cold andvolatile liquid. Liquefaction makes it possible toincrease density to 4609 kg/m3,although in the form of compressednatural gas (CNG) has a density of 185kg/m3. The gas may be stored anddistributed either as compressednatural gas or liquefied natural gas.The gas composition can vary dependingon the source and the processing ofthe gas. Ship Managers and ship-owners areconfronted with a number of importantinvestment decisions with respect totrading if they want to do businesswithin the limits of Special EmissionControl Areas (SECAs) which startofficially on January 1st 2015. The core issue is the sulphur contentof bunkers used by ships sailing inNorth American and Northern EuropeanECAs which is limited to 1.00% m/muntil 2015. That limit will be loweredto 0.10% m/m after that date. Lowsulphur fuel oil (LSFO) allowed until1st January 2015, is currentlyapproximately USD 15 per mt moreexpensive than HFO, compared to themuch costlier marine gas oil (MGO)representing a current mark-up of USD258 per mt over HFO. These approximatefigures reflect the case as seen todaywith a strong possibility of steepprice hikes on the cost of gasoil oncepast January 1st 2015.LNG is not easy to implement as itrequires heavy investment in way ofcreating a network of bunkeringstations which will allow for thereplenishment of LNG tanks onboardmerchant vessels. It is expected that

2

A. Corres ET AL.

such facilities, some of which alreadyexist, will be located in and aroundSECA ports. Port operators areexpected to sell installation licensesrather than enter in the LNG bunkeringbusiness, a matter that calls forstandards and specifications on onehand and national legislation on theother. LNG bunkering companies will thereforehave to pay substantial amounts ofmoney for the creation of the relevantfacilities, afloat and ashore, plusthe cost of the license. Thisinvestment will have, one way oranother, to be amortized and the onlyway this can happen is through salesto LNG burning ships. Here lies themost difficult aspect of the LNGoption which takes the form of achicken and egg problem: In order tomake sense any investment in LNGfacilities there must be LNG sales toships and these cannot happen withoutan LNG burning fleet. This issue isdiscussed at some length later in thispaper.Back to shipowners’ options, managersand owners instead of paying for theabove mentioned expensive low -sulphur marine fuel, have the option ascrubber; the latter enablescontinuation of the use of cheaper HFOfuel. A conversion of the vessel toLNG calls for an expensive vesselmodification, while scrubbers – bulkyexhaust gas cleaners - could be seenas an alternative. There is a debategoing on however regarding theefficiency of scrubbers.The scrubber also requires asignificant upfront cost as well asslightly elevated OPEX, but thesavings in fuel expenses willeventually amortize installationcosts, depending on the actual time

spent in ECAs and on the cost spreadbetween low sulphur heavy fuel oil andstandard HFO. What exactly is going to happen in theSECAs as of January 2015 is open toanybody’s guess. Due to the overallsize of the regions covered by theSECAs the market disturbance willprobably assume global proportions andit will certainly have an impact on EUshort sea shipping where the absenceof an EU coordinated response will befelt at various levels.

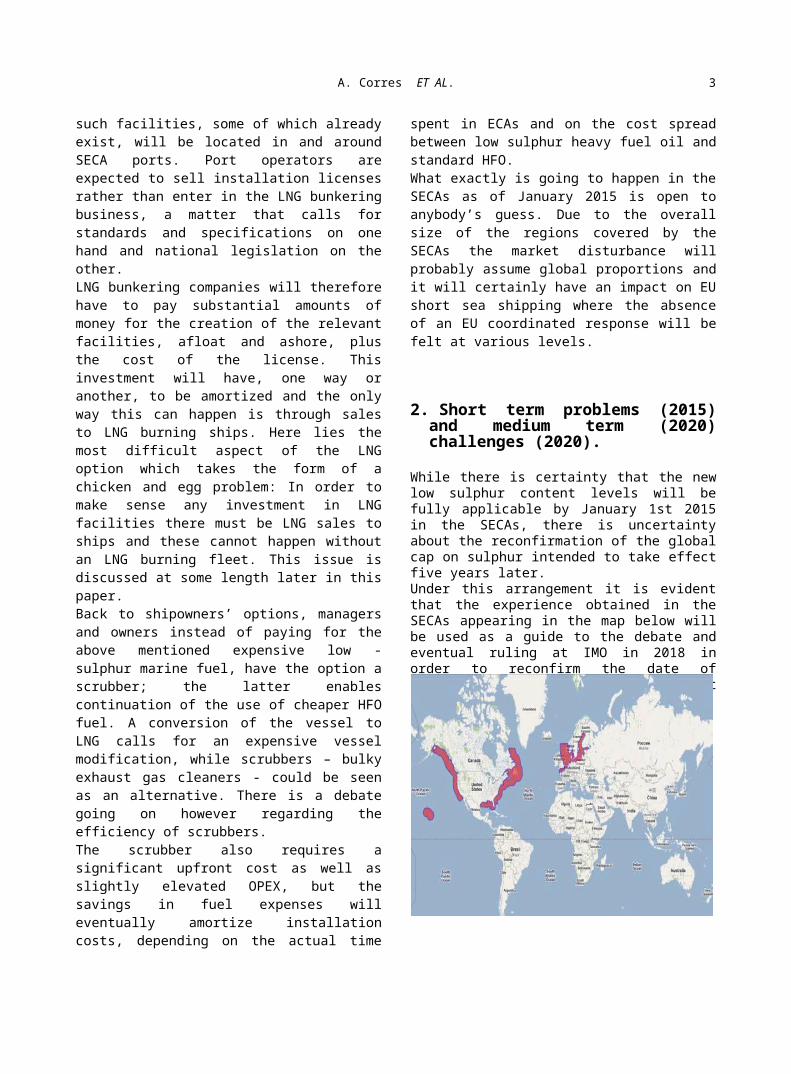

2. Short term problems (2015)and medium term (2020)challenges (2020).

While there is certainty that the newlow sulphur content levels will befully applicable by January 1st 2015in the SECAs, there is uncertaintyabout the reconfirmation of the globalcap on sulphur intended to take effectfive years later. Under this arrangement it is evidentthat the experience obtained in theSECAs appearing in the map below willbe used as a guide to the debate andeventual ruling at IMO in 2018 inorder to reconfirm the date ofapplication presently standing at2020.

3

A. Corres ET AL.

Emission controlled Areas (ECA)

Nitrogen emissions from diesel enginesare also targeted in the context ofSECAs. As far as the limitation of NOxemissions in MARPOL Annex VI,Regulation 13, the IMO effective datesare as follows:

Tier 1 (current limits for newengines): For main engines on ships constructedfrom 01.01.2000 until 31.12.2010, thetarget for retrofit engines (powerover 5 MW) and displacement percylinder over 90 dm3 Tier 2 (level about 20% below tier 1)only in ECA’s:Engines on board vessels constructedfrom 01.01.2011.Tier 3 (Level 80% below Tier 1) onlyin ECA’s: Engines on board vessels constructedfrom 01.01.2016, if combinedpropulsion power is over 750

The implementation schedule for MARPOLAnnex VI is presented on the followinggraph:

Graph.1 Implementation schedule forRevised MARPOL Annex VI (Figure fromMAN Diesel 2009 magazine, Towards IMOTier III)

As one can see Tier 3 NOx limits forvessels trading in SECAs kick-in oneyear after the introduction of the lowsulphur content limits in these areas,attacking the atmospheric pollutionproblem in two fronts.1

The following International and localair quality regulations mandatestringent limits on emission of SO2and other pollutants to protect publichealth and ensure conformity withnational standards:

MARPOL Annex VI European Union (EU) Directive1999/33/EC, amended 2005/33/EC. State of California Air ResourcesBoard (ARB) requirements

The availability of compliant low-sulphur fuel oil must be consideredwhen planning the intended voyage and,if compliant fuel oil is not availablewhere planned, all attempts to locatealternative sources for such fuel oilmust be taken, including attempts toobtain ECA-compliant fuel oil at eachport on the intended voyage. However,it is not required to deviate from the

1 The environmental impact of sulphur oxide (SOX= SO2 + SO3) emissions has gained muchattention over the past ten years. As far asthe Sulphur dioxide (SO2) is concerned, it isproduced during combustion of fossil fuels andcoal; it is one of the primary pollutants,along with nitrogen oxides (NOx) andparticulates, which must be controlled whileSulphur dioxide, or SO2, belongs to the familyof sulphur oxide gases (SOx). SOx gases areformed when fuel containing sulphur, such ascoal and oil, is burned, and when gasoline isextracted from oil or metals are extracted fromore. SO2 dissolves in water vapour to formacid, and interacts with other gases andparticles in the air to form sulphates andother products that can be harmful to peopleand their environment. These gases dissolveeasily in water. Sulphur is prevalent in allraw materials, including crude oil, coal, andore that contains common metals like aluminium,copper, zinc, lead, and iron.

4

A. Corres ET AL.

intended voyage in order to purchasecompliant fuel oil (change of berth oranchor within a port in order toreceive compliant fuel oil is notconsidered to be a deviation).According to MARPOL Annex VI, if aship cannot purchase compliant fueloil and intends entering the ECA, itshall notify its Administration andthe competent authority of therelevant Port of destination.Although major upsets in internationalshipping are not expected until theglobal cap on sulphur content isimplemented it is fair to say that theentire shipping community is alreadydeeply engaged in discussing optionsfor SECA trading. Concerns areparticularly strong in Scandinaviancountries.

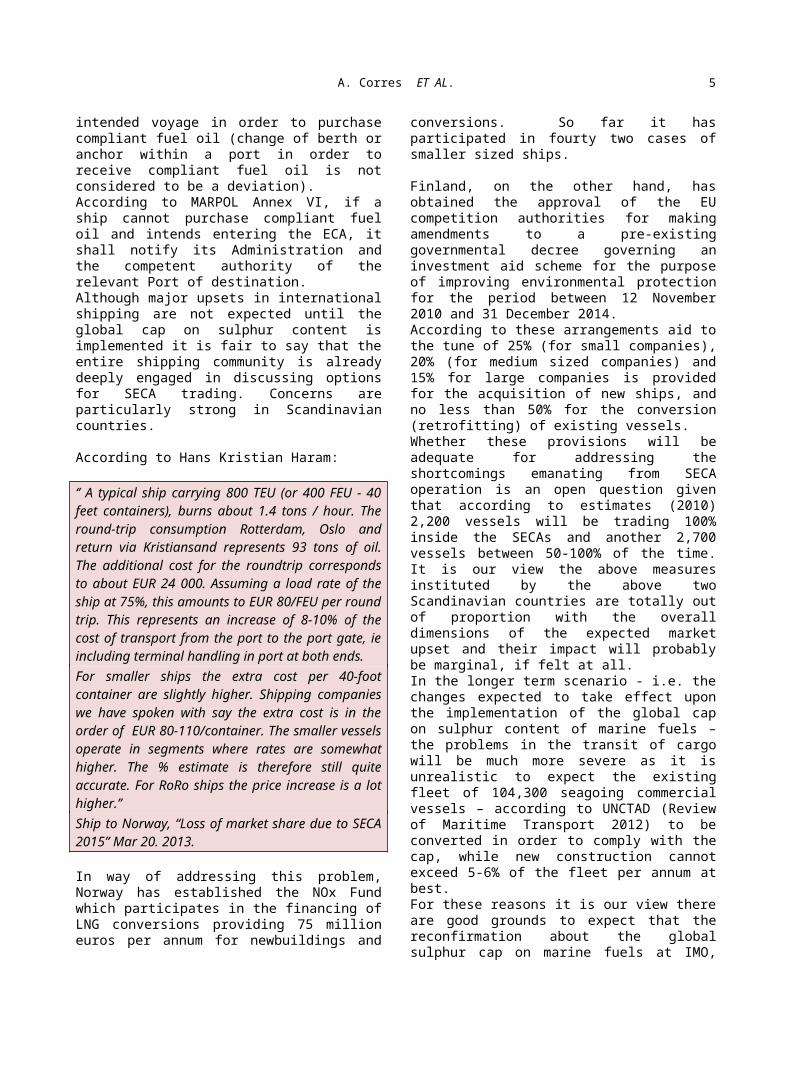

According to Hans Kristian Haram:

‘’ A typical ship carrying 800 TEU (or 400 FEU - 40feet containers), burns about 1.4 tons / hour. Theround-trip consumption Rotterdam, Oslo andreturn via Kristiansand represents 93 tons of oil.The additional cost for the roundtrip correspondsto about EUR 24 000. Assuming a load rate of theship at 75%, this amounts to EUR 80/FEU per roundtrip. This represents an increase of 8-10% of thecost of transport from the port to the port gate, ieincluding terminal handling in port at both ends.For smaller ships the extra cost per 40-footcontainer are slightly higher. Shipping companieswe have spoken with say the extra cost is in theorder of EUR 80-110/container. The smaller vesselsoperate in segments where rates are somewhathigher. The % estimate is therefore still quiteaccurate. For RoRo ships the price increase is a lothigher.’’Ship to Norway, “Loss of market share due to SECA2015” Mar 20. 2013.

In way of addressing this problem,Norway has established the NOx Fundwhich participates in the financing ofLNG conversions providing 75 millioneuros per annum for newbuildings and

conversions. So far it hasparticipated in fourty two cases ofsmaller sized ships.

Finland, on the other hand, hasobtained the approval of the EUcompetition authorities for makingamendments to a pre-existinggovernmental decree governing aninvestment aid scheme for the purposeof improving environmental protectionfor the period between 12 November2010 and 31 December 2014. According to these arrangements aid tothe tune of 25% (for small companies),20% (for medium sized companies) and15% for large companies is providedfor the acquisition of new ships, andno less than 50% for the conversion(retrofitting) of existing vessels. Whether these provisions will beadequate for addressing theshortcomings emanating from SECAoperation is an open question giventhat according to estimates (2010)2,200 vessels will be trading 100%inside the SECAs and another 2,700vessels between 50-100% of the time.It is our view the above measuresinstituted by the above twoScandinavian countries are totally outof proportion with the overalldimensions of the expected marketupset and their impact will probablybe marginal, if felt at all. In the longer term scenario - i.e. thechanges expected to take effect uponthe implementation of the global capon sulphur content of marine fuels –the problems in the transit of cargowill be much more severe as it isunrealistic to expect the existingfleet of 104,300 seagoing commercialvessels – according to UNCTAD (Reviewof Maritime Transport 2012) to beconverted in order to comply with thecap, while new construction cannotexceed 5-6% of the fleet per annum atbest. For these reasons it is our view thereare good grounds to expect that thereconfirmation about the globalsulphur cap on marine fuels at IMO,

5

A. Corres ET AL.

scheduled for 2018 regarding universalapplication by 2020, will be postponedfor a future date when one canrealistically expect it will befeasible. This in essence will meanthat the impact from the transition ofshipping to more environmentallyfriendly fuels will remain localizedin the areas where it becomesapplicable in January 2015 and thatthere will be no wider implicationsfor the mainstream internationalroutes. In case however – which in our view israther unlikely – the vote in 2018gives the green light for a global capin 2020 the implications on trade willassume a universal dimension as thetime horizon for such a measure willbe too short for the world fleet toadapt in the ways discussed so fari.e. through retrofits and newconstruction. The only solution to thegeneral problem of compliance with theglobal low sulphur cap of 0.1% insight at this time is the reschedulingof oil refinery production, with allwhat that entails, to large scaleproduction of suitable gasoil.Such a move would by definition callfor fundamental changes in the oilrefining industry with immediateimplications on commercial andenvironmental costs which would needto be contained and managed. Whilethere can be little doubt about theformer – these would predictably bepassed on to the users of the fuel –there is uncertainty about the way inwhich additional environmentalimpacts emanating from the refiningprocess would be handled from aneconomic point of view.

3. Technical and systemic barriersto implementation

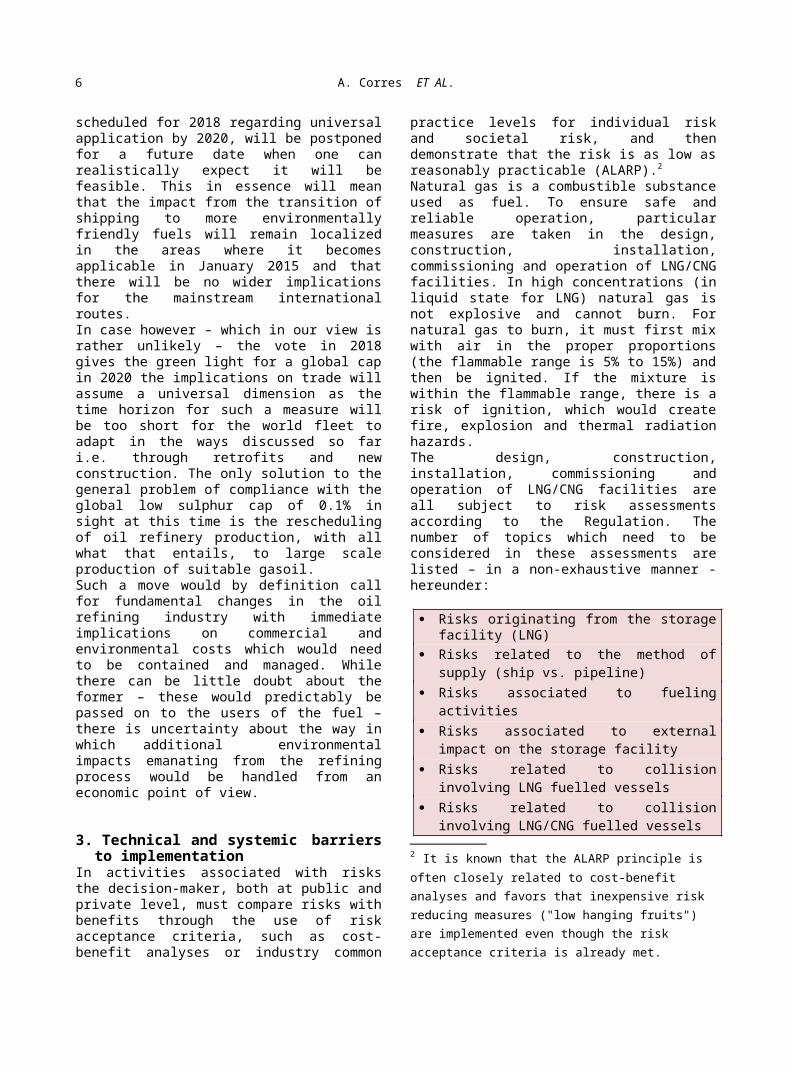

In activities associated with risksthe decision-maker, both at public andprivate level, must compare risks withbenefits through the use of riskacceptance criteria, such as cost-benefit analyses or industry common

practice levels for individual riskand societal risk, and thendemonstrate that the risk is as low asreasonably practicable (ALARP).2

Natural gas is a combustible substanceused as fuel. To ensure safe andreliable operation, particularmeasures are taken in the design,construction, installation,commissioning and operation of LNG/CNGfacilities. In high concentrations (inliquid state for LNG) natural gas isnot explosive and cannot burn. Fornatural gas to burn, it must first mixwith air in the proper proportions(the flammable range is 5% to 15%) andthen be ignited. If the mixture iswithin the flammable range, there is arisk of ignition, which would createfire, explosion and thermal radiationhazards.The design, construction,installation, commissioning andoperation of LNG/CNG facilities areall subject to risk assessmentsaccording to the Regulation. Thenumber of topics which need to beconsidered in these assessments arelisted – in a non-exhaustive manner -hereunder:

Risks originating from the storagefacility (LNG)

Risks related to the method ofsupply (ship vs. pipeline)

Risks associated to fuelingactivities

Risks associated to externalimpact on the storage facility

Risks related to collisioninvolving LNG fuelled vessels

Risks related to collisioninvolving LNG/CNG fuelled vessels

2 It is known that the ALARP principle is often closely related to cost-benefit analyses and favors that inexpensive risk reducing measures ("low hanging fruits") are implemented even though the risk acceptance criteria is already met.

6

A. Corres ET AL.

Regarding previous accidents andlessons learned, there are only a fewaccidents involving LNG on record ofwhich several are only of minorrelevance today as they date back 30-70 years and many of them on recordhave been in production plants, not inships.As far general risks, theimplementation of LNG facilities willbe subject to various risk reducingmeasures of general nature.3 Giventhat the technology to be applied iswell developed, safety standards canbe met in accordance with regulatoryrequirements and best practices forsafety such as those contained in theGas Code. Detailed risk assessmentsand ALARP demonstrations willnevertheless be required.LNG has gained considerable momentumin shipping during the last decade.The Danish Maritime Authority iscurrently heading an internationaleffort seeking to further promote theuse of LNG in shipping by conducting afeasibility study on LNGinfrastructure for short sea shipping.Still, there are considerable barriersrestricting the wider use of LNG incommercial shipping. We need toaddress these briefly before reachinga conclusion regarding the possible

3 Quality management systems in the supply chainare also introduced, includinginspections and audits in the respective phasesof development,implementation and operation;

Procedures for operation and maintenance

Inspection programs Emergency shut-down systems for

sectioning of the installation Fire and gas detection systems Special programs for shut-down,

maintenance and replacement ofinstallation parts;

Safety instructions and work permits; Collision barriers, fencing and access

control.

speed of adaptation of the industry tothe use of Natural Gas in ships.Technical barriers: There are stilltechnical challenges associated withLNG installations onboardparticularly regarding retrofitinstallations. The extent ofexperience is still limited in theindustry. However, considering theinformation provided on the technicalissues here there are no "showstopping" technical barriers to theuse of natural gas for propulsion inshipping.Natural gas cannot utilise existingfuel tanks and piping. Newinstallations have to be fittedalongside the existing ones for HFOand diesel fuel. CNG has twice thespatial requirements of LNG for thesame energy content. Both systemsrequire significant structuralmodifications to accommodate the tankswhen refitting vessels.Supply chain and bunkering barriers:These barriers make reference largelyto sourcing and infrastructure. Bothof these groups of barriers areparticular in every applicationconsidered. The country with the mostLNG distribution points in Europe isclearly Norway where LNG for use asfuel is liquefied in small scaleplants. This approach is apparentlyquite costly given that the retailprice is about 3 times the natural gasspot price.The supply of natural gas in the formof LNG is therefore anticipated as animport to Northern Europe and SouthMediterranean countries from LNGterminals or other suitable suppliersby shuttle tankers. Although nationalregulations and IMO guidance regardingthese activities still need to bedeveloped it is important to permitLNG bunkering in a manner consistentwith the commercial operation ofvessels. Of particular interest in this regardis the location of the shore tank, thepermission from the port authoritiesto perform bunkering operations while

7

A. Corres ET AL.

alongside and the approval ofbunkering procedures while there arepassengers onboard. Political and administrative barriers:During a workshop on "Tomorrow's Fuels- Challenges and Possibilities" heldin May 2010 several representativesfrom the ferry industry mentioned thefollowing barriers of political-administrative nature:• Short time span for concessions

(often five years) disallowsufficient payback time to justifythe investments needed for storagefacilities, filling stations andinstallations onboard ships.

• Tender documents presently do notbenefit - through their selectioncriteria -bidders willing to invest in naturalgas operation or other technologythat reduces emissions.

• Local authorities are reluctant toaccept the storage facilities due toperceived risks.

Another barrier in this category forboth LNG and CNG is that the rules andregulations for ship classificationsocieties have not yet been developed,and that the IMO is still in theprocess of drafting such rules. It isevident that this generates a certainuneasiness regarding the viability ofmulti million euro investments invessels, ports and supply facilities. Economic barriers: LNG conversions onexisting ships as mentioned earlierare quite expensive. Regrettably, thebest hopes of the EU Commission for asmooth introduction of the 2015 SECArules rely on retrofits. There issimply no time for new buildings. LNGtanks with required gas systems so farcost typically 1.2-1.9 Mio Euros andthe engine conversions to run on gascost 0.6-1.2 Mio Euro compared tocorresponding diesel burning engines.In addition, some hullmodifications/reinforcements are

unavoidable including double hulledpiping, pumping, monitoring, and so onincluding ship time in the yard andclassification expenses. These costsare however representative of "pioneerwork" till now, and could drop in thefuture as volume picks up and thetechnology proves to be capable.Unofficial cost estimates for LNGretrofits are in the region of USD 7million compared to 5.7 for a scrubberinstallation. The costs are such thatrender the conversion of vessels overthe age of ten years questionable, asthese represent a very largeproportion of the vessel’s marketvalue, often in excess of 50%. As longas sulphur abatement measures remainon a regional level it is questionableif these additional expenses on thevessel will be recoverable upon sale.Let us consider a couple of examplesas seen from the side of a ship owner.The owners will need to establish: a) What percentage the retrofit represents to the ship’s value. b) What part of it is recoverable if the ship sold. c) If it makes sense to stay on gasoilfor SECA operation, try and sell ‘’as is’’ and (if necessary) buy another already converted vessel.

In connection with (a) using UNCTADfigures we can observe the followingin the short sea.

•Example 1: For a 10 years old 12,000dwt short sea chemical tanker worthUSD 13 m: LNG conversion wouldrepresent 57.6% of its current value,a Scrubber conversion 44.6%.

•Example 2: For a 10 years old geared500 TEU containership worth USD 6m :LNG 125%, Scrubber 96%. Question: Would it make any sense toconvert and sell? Answer: No, as the retrofit costswould not be recoverable.

8

A. Corres ET AL.

For most medium and high age short seaships the conversion will not beconsidered worthwhile. (Secondhandprices today are even lower).

The example ships are too young toscrap therefore will have to trade onGasoil or Low Sulphur Fuel Oil inSECAs.

Surprisingly, a similar pictureappears in the deep sea:

Example A: 10 years old Panamax valuedUSD 12.5m: LNG 60%, Scrubber 46%. Example B: 10 years old Aframax tankervalued 17m: LNG 44%, Scrubber 34%.Secondhand ship values are presentlyat an all time low as earnings havebeen squeezed. Surprisingly, thepicture in these large ships is notvery different from the short seaexample previously. However, there canbe no comparison between them on fuelconsumption; therefore the penalty ofrunning on gasoil will be more severeon large ships.

Question (b) cannot receive a genericanswer as it depends on the tradingpattern envisaged by the buyer. If thebuyer intends to operate the vesseloutside SECAs one would expect thatthe cost of the conversion would notbe recoverable to any significantextent. On the contrary, if the vesselis destined to operate exclusivelywithin SECAs, one would expect that asignificant proportion of the costs ofthe conversion would be recoverable,or even add to the secondhand value ofthe vessel if freight rates withinSECAs rise disproportionally as aresult of capacity shortages.Finally, we shall not attempt todiscuss (c) due to the complexity ofthe outcomes.The main details of the barriersdiscussed are grouped in the following

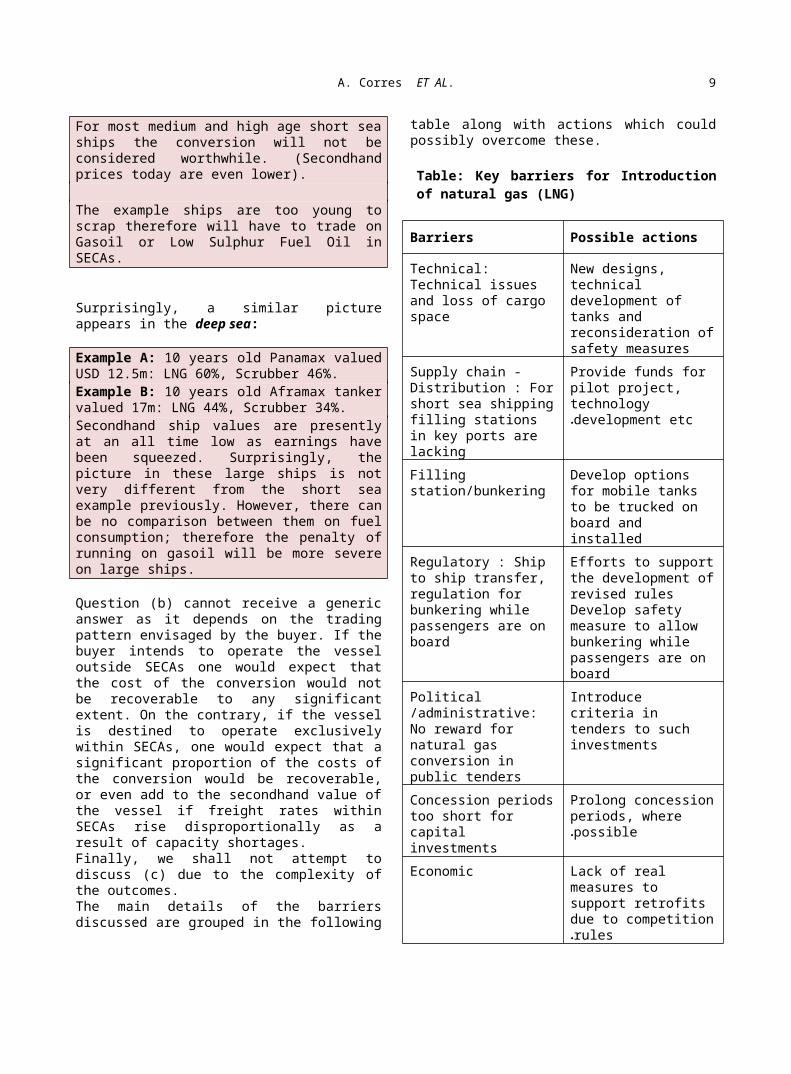

table along with actions which couldpossibly overcome these.

Table: Key barriers for Introductionof natural gas (LNG)

Barriers Possible actions

Technical: Technical issues and loss of cargo space

New designs, technical development of tanks and reconsideration ofsafety measures

Supply chain -Distribution : Forshort sea shippingfilling stations in key ports are lacking

Provide funds for pilot project, technology development etc.

Filling station/bunkering

Develop options for mobile tanks to be trucked on board and installed

Regulatory : Ship to ship transfer, regulation for bunkering while passengers are on board

Efforts to supportthe development ofrevised rules Develop safety measure to allow bunkering while passengers are on board

Political /administrative: No reward for natural gas conversion in public tenders

Introduce criteria in tenders to such investments

Concession periodstoo short for capital investments

Prolong concessionperiods, where possible.

Economic Lack of real measures to support retrofits due to competitionrules.

9

A. Corres ET AL.

(Table originally retrieved fromDanish Ministry of the environment,Natural gas for ship propulsion inDenmark, Sytuer et al, 2005).

4. The options open to shipowners.

Classification societies argue thereare presently only three options opento existing ship owners and managersin order to comply with the 2015requirements when the sulphur contentfalls to 0.1% within the emissionscontrol areas (ECA):

use of low sulphur fuels

installation of a scrubber forexhaust gas purification, and

LNG retrofit

According to the ‘’ECA RetrofitTechnology’’ project -whose partnerswere blue chip shipping companies,ship suppliers and a classificationsociety - funded by Danish Maritimefund, one can comment as follows: The fuel switch to MGO only requiressmall modifications; Generallyspeaking, the installation of a fuelcooling system to increase theviscosity of the MGO would be needed,and some extra attention should bepaid to the lubrication of the Mainengine.1. Alfa Laval has designed a scrubber

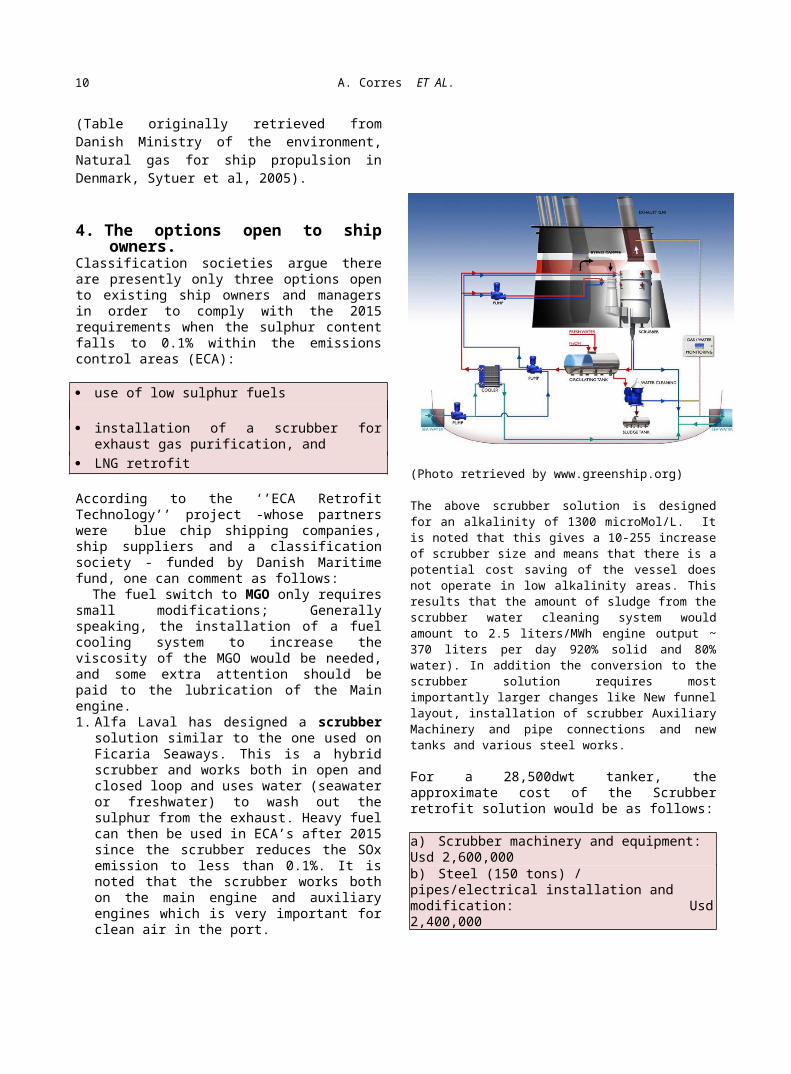

solution similar to the one used onFicaria Seaways. This is a hybridscrubber and works both in open andclosed loop and uses water (seawateror freshwater) to wash out thesulphur from the exhaust. Heavy fuelcan then be used in ECA’s after 2015since the scrubber reduces the SOxemission to less than 0.1%. It isnoted that the scrubber works bothon the main engine and auxiliaryengines which is very important forclean air in the port.

(Photo retrieved by www.greenship.org)

The above scrubber solution is designedfor an alkalinity of 1300 microMol/L. Itis noted that this gives a 10-255 increaseof scrubber size and means that there is apotential cost saving of the vessel doesnot operate in low alkalinity areas. Thisresults that the amount of sludge from thescrubber water cleaning system wouldamount to 2.5 liters/MWh engine output ~370 liters per day 920% solid and 80%water). In addition the conversion to thescrubber solution requires mostimportantly larger changes like New funnellayout, installation of scrubber AuxiliaryMachinery and pipe connections and newtanks and various steel works.

For a 28,500dwt tanker, theapproximate cost of the Scrubberretrofit solution would be as follows:

a) Scrubber machinery and equipment: Usd 2,600,000b) Steel (150 tons) / pipes/electrical installation and modification: Usd2,400,000

10

A. Corres ET AL.

c) Design and classification cost:Usd 500,000

d) Off-hire (about 20 days) at rate Usd 11,000 per day:

Usd 220,000 Total approximate cost: Usd5,720,000

It is interesting to note that in thecase of a newbuilding cost items (b)and (d) would be zeroed and item (c)would probably be halved, or less,bringing the cost of the scrubberinstallation down by 50%. Unlike the case of the scrubber theretrofit of a ship to run on LNG doesnot require new technology. LNGtankers have been using the boil-offfrom the LNG tanks as fuel.Nevertheless, the use of LNG as fuelin the main engines still raises sometechnical issues which the shippingindustry needs to resolve. In order to make an existing ship touse LNG one has to retrofit the mainengine and the fuel system. The MainEngine should converted to a ME-typeengine (electronic fuel injection andalso converted to ME-GI dual fuelengine). The conversion shouldpreferably also include the auxiliaryengines so that the vessel can burnclean and cheap LNG while in ports. By using LNG as fuel, the vessel showsconsiderably cleaner exhaustemissions:

a) 30% lower CO2 (thanks to low carbonto hydrogen ratio of fuel).b) 85% lower NOx (due to lean burningconcept i.e.high air-fuel ratio)c) Zero SOx emissions (as sulphur wasremoved from fuel when liquefied).d) Very low Volatile Organic Compounds(i.e.no visible smoke or sludgedeposits).

LNG vapour is lighter than air, it isvery safe and non toxic, so if LNGspills on the ground or on water andthe resulting flammable mixture of vapour and

air does not encounter an ignition source,then it will warm up, rise anddecapitate into the atmosphere. For a 28,500 dwt tanker, theapproximate cost of an LNG retrofit isas follows:

LNG machinery,tanks and equipment, MEconversion:

Usd4,380,000Steel (300 tons): Usd2,000,000Design and classification cost:

Usd 500,000Off-hire (about 40 days) at rate Usd 11,000 per day:

Usd440,000Total approximate cost:Usd 7,320,000

Again, the cost to include LNG in thespecification of a newbuilding isconsiderably lower ( 36%) whencompared to the cost of a retrofit,yet this remains an expensive option. The scrubber and LNG alternatives havebeen evaluated on basis of investmentcosts (CAPEX) and operational costs(OPEX). The NPV and payback period arecalculated for a 10-year period (2015-2024) assuming an interest rate of 9%.The outcome of the estimates is afunction of the fuel cost on one hand,and of the percentage of vessel’soperation inside ECA’s. One can have an approximate idea aboutpayback times in the various scenariosfrom the table that follows:

Scrubber versus LNG Payback Times

11

A. Corres ET AL.

(based on USD 400 cost spread betweenMGO/HFO and MGO/LNG

SCRUBBER RETROFIT LNG RETROFIT100% time in SECA 3.0 years

2.7 years50% time in SECA 5.5 “ 6.0 “25% time in SECA 7.5 “ 12.0“Source: P. G., Zacharioudakis, "Thefinancials of LNG as fuel", 2013We take this opportunity to stressthat the above estimates areapproximate and subject to assumptionsregarding the fuel cost spread and thediscount rate chosen (9%).Nevertheless, the cost of retrofittingis substantial and also substantial isthe time needed to amortize theinvestment needed. On the other hand,there should be no doubt that themajority of ship owners locatedoutside SECAs will probably go for the‘’do nothing’’ option waiting to seein which direction the 2018 IMO votewill go. Recent evidence from Norwayindicates that the ‘’do nothing’’option is presently the most favouredaccounting for approximately 70% ofthe answers received.During informal discussions with theGreek Shortsea Promotion Center andthe Hellenic Shortsea Shipowners’Association we have been able toestablish two important things.Firstly, there is keen interest fromthe side of shipowners to knoweverything about retrofits, costs,times etc. Secondly, the majority ofship owners outside SECAs appear totemporise in hope that the situationwill become clearer and thatconversion costs come down.We take this opportunity to stressthat the above estimates areapproximate and subject to assumptionsregarding the fuel cost spread and thediscount rate chosen (9%).Nevertheless, the cost of retrofittingis substantial and also substantial isthe time needed to amortize theinvestment needed. On the other hand,

there should be no doubt that themajority of ship owners locatedoutside SECAs will probably go for the‘’do nothing’’ option waiting to seein which direction the 2018 IMO votewill go. Recent evidence from Norwayindicates that the ‘’do nothing’’option is presently the most favouredaccounting for approximately 70% ofthe answers received.During informal discussions with theGreek Shortsea Promotion Center andthe Hellenic Shortsea Shipowners’Association we have been able toestablish two important things.Firstly, there is keen interest fromthe side of shipowners to knoweverything about retrofits, costs,times etc. Secondly, the majority ofship owners outside SECAs appear totemporise in hope that the situationwill become clearer and thatconversion costs come down.

5. A brief assessment of therepercussions on trade

The fundamental premise that largesections of the world merchant fleetwill have to be retrofitted to meetthe post 2020 requirements for lowersulphur in the atmosphere is at leastdebatable. One must not lose sight of thefundamental requirement which is lesssulphur from shipping in theatmosphere to conserve air quality andsave many regions from the nightmareof acid rain. If ships will need to burn low sulphurfuel this is an issue for the oilindustry rather than the ship owners.If low sulphur fuel is available inabundance at reasonable cost we see noneed to spend any more time on adiscussion about retrofits.

The analysis so far has shown that themission can be accomplished without a

12

A. Corres ET AL.

need to resort to retrofittingexercises. If that happened howeverthe lucrative- for many players in theshipping community - pie of retrofitswould be reduced to nothing. Being that as it may, it is our viewthat the new low-sulphur oil canguarantee an immediate and distortion-free compliance both at SECA and laterat world level without any need foradditional infrastructure. Under thispoint of view, the IMO is not theappropriate forum to handle thismatter.Short sea shipping primarily in theEU, but also in North America andCanada, will feel the brunt of therepercussions once SECAs officiallystart to operate. For internationalshipping the problem will becomparatively less pressing as thoseships typically spend only a fractionof their trading time within SECAs.The big question is how the localeconomies will be impacted.Local economies in SECAs are expectedto experience a number of directeffects as a result of SECAregulations. Let us list a few ofthese:

a) Rise in the cost of importsb) Rise in the cost of exportsc) Rise in the cost of domestic

sea/river/lake transportd) Backshift of cargoes from the

sea to the landThe rise in the cost of internationaltrade (categories a and b) followingSECA operation is likely to bemoderate insofar as ships will have touse the more expensive fuel for afraction of their voyage and duringport operations. It must be stressedhere that cost rises in key importssuch as oil and its products,agriprods, feedstocks, fertilizers andso on – limited as these may be - canimpact across the board a widespectrum of activities and ultimatelycontribute to the rise of thecountry’s inflation rate.Imports from and exports to otherports within the SECA will

proportionally become more expensiveas these will mandate the vessels tooperate on expensive fuel for theentirety of the voyage. In the lattercategory will also fall all domesticshipping volume, i.e. cargo andpassenger movements by sea or byriver. The cost of living in regionsdepending on shipping fortransportation as for example the caseis in islands, will show higher risesthan in the mainland, something thatmay necessitate adjustments to theapplicable taxes to restore anequitable apportionment of the SECAburden among the various citizengroups.Whenever possible shippers willrediscover the joys of roadtransportation as short sea shippingwill become less attractive as aresult of cost rises. In Norway it hasbeen estimated that the backshift willbe to the tune of 10%, the figure inFinland may be even higher.Important as the consequences may bein the field of imports and in thedomestic market, the consequences onexports may potentially be even moresevere. While the cost of importedgoods is spread across the economyafter international competition hasplayed its part, export sales are wideopen to competition from otherinternational players, from the EU, orfrom abroad. SECAs by definitionintroduce an element of distortionpressing against the interests of SECA– based exporters. Already negativelyimpacted SECA-based exporters willhave to compete against other EU basedexporters who are outside SECAs aswell as exporters from, say, the FarEast. In a world economy running itsfifth year of economic crisis theeffects of a higher production costdue to SECA could become catastrophicfor exporters unable to place theirproducts in the international market.

6. Summary of main findings andconclusions

13

A. Corres ET AL.

1) The operation of Special Emission

Control Areas coincides with theintroduction of Tier 3 limits onship engine NOx emissions and theimplementation of the EU Directiveon Sulphur. These regulatorychanges are expected to give riseto market distortions within theSECAs for the next few years.

2) Shortsea shipping is expected tosuffer losses in market share as aresult and the main beneficiarywill be road transport. This willreverse the short sea initiativewhich has been observed for thelast two decades in the EU.

3) The measures taken by Scandinavianstates to address thesedistortions are totally out ofproportion with the size of theproblem.

4) There have been suggestions toship owners and operators butthese entail risks which have yetto be addressed at internationaland national levels.

5) Other than risks, specificbarriers to implementation havebeen identified which – togetherwith the high cost of retrofits –raise doubts about theeffectiveness of the solutionssuggested.

6) The majority of ship ownerssurveyed have indicated theirintention not to retrofit and useexpensive gasoil while tradinginside SECAs.

7) The EU does not have a specificplan to assist country-memberswithin SECAs at the moment and itis unlikely to put something inplace before January 1st 2015.

8) As a result of the above thecountries in question are bound toexperience cost rises inconnection with sea transportcosts impacting imports, exportsand domestic trading.

9) The approach presently adopted byall parties i.e. via retrofits isflawed as it puts excessive costs

on ship owners which will becarried over to cargo receivers,while at the same time it distortsthe market.

10) An alternative approach vianegotiations with the oil refiningsector to provide reasonablypriced low sulphur fuel oil wouldallow full access of ships tothese markets without any freightmarket distortions owed to shipscarcity in the SECAs.

REFERENCES[1] M. Bagniewski,: “LNG fuel for ships. A

Chance or a Must? ’’ DNV (2009). [2] E. Bardram: “Integrating Maritime Transport

emissions in the EU’s Greenhouse Gas ReductionPolicies’’ Council WP Environment , Brussels,05/07/201.

[3] A. J. Corres: LNG: ‘’The fuel for the GreenCorridors of Europe?‘’ Proccedings of the COSTAConference, Lisbon, April 2012.

[4] A. J. Corres, A. Frangos, Y.Papachristou: ‘’The case of LNG asfuel for merchant vessels in theSpecial Emission Control Areas’’unpublished article, Piraeus,20.02.2014.

[5] Danish Maritime Authority: “North Euro-pean LNG Infrastructure Project: A feasibility studyfor an LNG filling station infrastructure and test ofrecommendations’’ Full Report, Copenhagen,May 2012.

[6] European Commission: “Report from theCommission to the Council: “Pollutantemission reduction from maritime transport and theSustainable Waterborne Transport Toolbox” COM(2013) 475 Final, 4th June 2013.

[7] European Shortsea Network: “Short SeaShipping:The Way Forward” Market Regional Report,Atlantic Arc, November 2013.

[8] Gas LNG Europe: “Development of small LNG:The view of EU LNG terminal opera-tors’’ Small-Scale LNG Forum, Istanbul, 24.10.2012(Presentation).

[9] H. K. Haram: Ship to Norway, “Loss ofmarket share due to SECA 2015” Mar 20.2013.

[10] A. Harsema - Mensonides: “Scale LNG-Going beyond base load LNG applications”

14

A. Corres ET AL.

Proccedings of the Marine Service GmbH, SmallScale LNG Forum 22-24.10.2012, Istanbul.

[11] J. Herdzik: ‘’Consequences ofusing LNG as a marine fuel’’ Journalof Kones, ISSN 1231-4005, 2013.

[12] IMO Resolution MSC.285 (86).“Interim Guidelines on safety fornatural Gas-Fuelled engineinstallation in ships”. London

[13] MAN Diesel Magazine, “Towards IMOTier III”, 2009

[14] A. McArthur: “LNG as fuel for theshipping Industry- Opportunities andChallenges”, 2011, DNV Managing Risk,Helsinki)

[15] M. Chennoufi: “Analysing the dynamics ofLNG supply and how small-mid scale LNG fits intothe picture” Proccedings of the Royal Dutch Shell,Small Scale LNG Forum 22-24.10.2012, Istanbul.

[16] North Sea Consultation Group: “The

impact on short sea shipping and the risk of amodal shift from the establishment of a NOxemission control area” INCENTIVE, Final Draft, 14July 2013.

[17] K. Pihlajaniemi: “Short SeaShipping and Motorway of the Sea FocalPoints Meeting” Presentation, EuropeanCommission, Brussels 04.06.2013

[18] TNO Report: ‘’Environmental andEconomic Aspects of using LNG as fuelfor shipping in the Netherlands’’ TNORpt 2011-00166.

[19] P. G. Zacharioudakis, “The financials ofLNG as fuel”, Proceedings of the International workshop in the framework of COSTA project, Lisbon-Portugal, 20 February 2013.

15