Taxation of Electronic Commerce: A Developing Problem

17

INTERNATIONAL REVIEW OF LAW COMPUTERS &TECHNOLOGY,VOLUME 16, NO. 1, PAGES 35–52, 2002 Taxation of Electronic Commerce: A Developing Problem RICHARD JONES and SUBHAJIT BASU ABSTRACT The rapid growth of e-commerce, especially the sale of goods and services over the internet, has fuelled a debate about the taxation regimes to be used. The shift from a physically oriented commercial environment to a knowl- edge-based electronic environment poses serious and substantial issues in relation to taxation and taxation regimes. Tax administration s throughout the world face the formidable task of protecting their revenue base without hindering either the development of new technologies or the involvement of the business community in the evolving and growing e-market place. Concerns of governments centre on the impact of e-commerce on the state and local revenue. Whereas states can impose a tax on residents’ purchases from out-of-state vendors, they cannot impose an obligation on those vendors to collect the tax unless the vendor has a substantial presence, or nexus, in the state. These problems will be greater for developing countries. The shrinking of the tax base will have a disproportionat e effect and further jeopardize the already fragile economy of the developing world. Introduction Why do we have to pay taxes? A very simple answer could be, that until someone comes up with a better idea, taxation is the only practical means of raising the revenue to nance government spending on the goods and services that most of us demand. Establishing an ef cient and fair tax system is, however, far from simple. The ideal tax system, especially in the developing countries, should raise essential revenue without excessive government borrowing and should do so without discouraging economic activity and without deviating too much from the tax systems of other countries. Any taxation solutions to this problem should be ef cient, simple, exible and have neutral effect. E-commerce and globalizatio n challenge traditional tax regimes. Historically goods were physical, the production, distribution and consumption of these goods was easily traceable and therefore easily taxable. Physical goods were produced at a manufacturing plant, shipped off to wholesalers and boxed on to retailers—the nal consumer walking away Correspondence: Richard Jones and Subhajit Basu, School of Law and Applied Social Studies, Liverpool John Moores University, Liverpool, UK; e-mail: [email protected] and [email protected]. ISSN 1360-0869 print/ISSN 1364-6885 online/02/010035-18 Ó 2002 Taylor & Francis Ltd DOI: 10.1080/ 13600860220136093

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of Taxation of Electronic Commerce: A Developing Problem

INTERNATIONAL REVIEW OF LAW COMPUTERS

amp TECHNOLOGY VOLUME 16 NO 1 PAGES 35ndash52 2002

Taxation of Electronic Commerce ADeveloping Problem

RICHARD JONES and SUBHAJIT BASU

ABSTRACT The rapid growth of e-commerce especially the sale of goods andservices over the internet has fuelled a debate about the taxation regimes to beused The shift from a physically oriented commercial environment to a knowl-edge-based electronic environment poses serious and substantial issues in relationto taxation and taxation regimes Tax administrations throughout the world facethe formidable task of protecting their revenue base without hindering either thedevelopment of new technologies or the involvement of the business communityin the evolving and growing e-market place Concerns of governments centre onthe impact of e-commerce on the state and local revenue Whereas states canimpose a tax on residentsrsquo purchases from out-of-state vendors they cannotimpose an obligation on those vendors to collect the tax unless the vendor has asubstantial presence or nexus in the state These problems will be greater fordeveloping countries The shrinking of the tax base will have a disproportionat eeffect and further jeopardize the already fragile economy of the developing world

Introduction

Why do we have to pay taxes A very simple answer could be that until someone comesup with a better idea taxation is the only practical means of raising the revenue to nancegovernment spending on the goods and services that most of us demand Establishing anef cient and fair tax system is however far from simple The ideal tax system especiallyin the developing countries should raise essential revenue without excessive governmentborrowing and should do so without discouraging economic activity and without deviatingtoo much from the tax systems of other countries Any taxation solutions to this problemshould be ef cient simple exible and have neutral effect

E-commerce and globalization challenge traditional tax regimes Historically goods werephysical the production distribution and consumption of these goods was easily traceableand therefore easily taxable Physical goods were produced at a manufacturing plantshipped off to wholesalers and boxed on to retailersmdashthe nal consumer walking away

Correspondence Richard Jones and Subhajit Basu School of Law and Applied Social Studies LiverpoolJohn Moores University Liverpool UK e-mail rpjoneslivjmacuk and lswsbasulivjmacuk

ISSN 1360-0869 print ISSN 1364-6885 online02010035-18 Oacute 2002 Taylor amp Francis Ltd

DOI 10108013600860220136093

R Jones and S Basu36

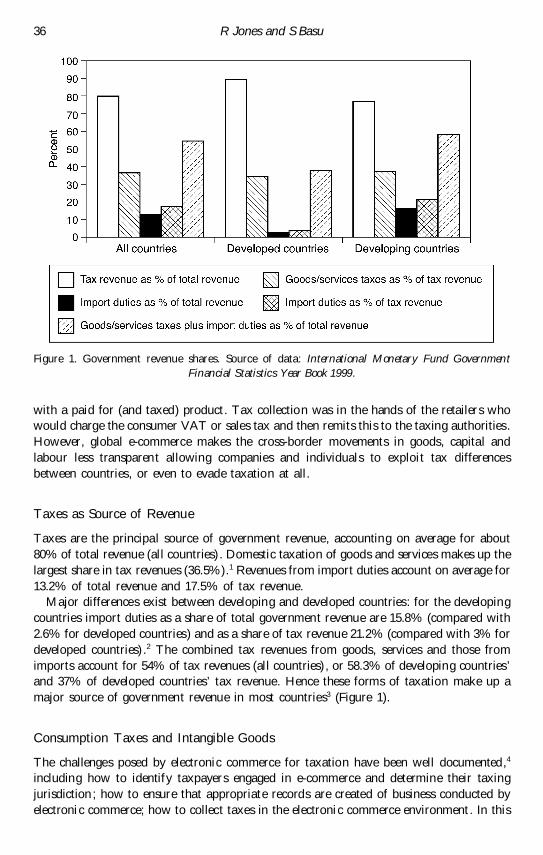

Figure 1 Government revenue shares Source of data International Monetary Fund GovernmentFinancial Statistics Year Book 1999

with a paid for (and taxed) product Tax collection was in the hands of the retailers whowould charge the consumer VAT or sales tax and then remits this to the taxing authorities However global e-commerce makes the cross-border movements in goods capital andlabour less transparent allowing companies and individuals to exploit tax differencesbetween countries or even to evade taxation at all

Taxes as Source of Revenue

Taxes are the principal source of government revenue accounting on average for about80 of total revenue (all countries) Domestic taxation of goods and services makes up thelargest share in tax revenues (365)1 Revenues from import duties account on average for132 of total revenue and 175 of tax revenue

Major differences exist between developing and developed countries for the developingcountries import duties as a share of total government revenue are 158 (compared with26 for developed countries) and as a share of tax revenue 212 (compared with 3 fordeveloped countries) 2 The combined tax revenues from goods services and those fromimports account for 54 of tax revenues (all countries) or 583 of developing countriesrsquoand 37 of developed countriesrsquo tax revenue Hence these forms of taxation make up amajor source of government revenue in most countries3 (Figure 1)

Consumption Taxes and Intangible Goods

The challenges posed by electronic commerce for taxation have been well documented4

including how to identify taxpayers engaged in e-commerce and determine their taxingjurisdiction how to ensure that appropriate records are created of business conducted byelectronic commerce how to collect taxes in the electronic commerce environment In this

Taxation of Electronic Commerce 37

paper we concentrate particularly on the possible decline in the overall tax base which inour view will have a disproportionate effect on the economies of the developing countriesThis decline is even more pronounced where more reliance is placed on consumption taxes

Consumption taxes are intended to be borne by consumers and are dependent uponretailers acting as tax collectors Sellers bear the cost of determining the applicable taxrate5 preparing invoices according to tax rules collecting tax ling and remitting tax andmaintaining tax records If the tax is assessed incorrectly the seller (or its third-party agent)typically will be held responsible for any shortfall and will not be able to reclaim it fromthe customer

Let us note here at the outset that there is no ambiguity at present regarding the statusof the goods ordered and paid for on internet but delivered physically in the conventionalmanner The problem is most obvious for intangible products such as music software andservices such as medical or legal consultations that are lsquoproducedrsquo at one location andlsquoconsumedrsquo elsewhere6 It is generally accepted that tax rules for sale of intangible productsand services should be same as those of other goods and that the means of delivery shouldnot govern tax treatment A lsquotechnologicall y neutralrsquo taxation would not treat the sale ofa paperback book any differently than the sale of a digitized book However determiningwhich products are functionally equivalent is less easy Is the text displayed on computerscreen really the same thing as a printed book Is a movie downloaded to computer harddrive really the same thing as a video rental If digitized products are treated as servicesthen further guidance is needed to specify which source of supply rules for services shallgovern because there are many different rules for different types of services Moreover mostof the countries do not have comprehensive taxation to services and few intangibleproducts aside from basic utilities which are subject to special taxes

Existing tax regimes show different and inconsistent rules for different types of servicesand intangible property such as telecommunications broadcast consulting engineeringtraining and education data processing supply of information access to databasesentertainment and content of various types Developing consistent de nitionsclassi cations and tax rates for the many types of services that might be considered to bea part of electronic commerce would provide clarity and certainty reduce double taxationand reduce attempts to manipulate classi cations aimed at tax avoidance Further consist-ent guidelines are also needed for combined or bundled services eg telecommunicationsand internet access which combinations may be dif cult to separate out especially if theyare subject to different rules or tax rates and the apportionment of use of services withinand without a country eg telecommunications services or use of an Intranet network

E-commerce The Challenge

E-commerce provides a qualitively different challenge to tax regimes First it leads to thegradual elimination of intermediaries such as wholesalers or local retailers who in the pasthave been critical for identifying taxpayers especially private consumers Second there willbe discrepancies where foreign suppliers may be tax-exempted whereas local supplierswould be required to charge value added tax (VAT) or sales taxes Third direct ordersfrom foreign suppliers will substantially increase the number of low-value shipments ofphysical goods to individual customers These low-value packages now fall under so-calledde minimis relief from customs duties and taxes in many countries the cost of collectionbeing more that the amount of tax due A substantial increase in these shipments as a resultof e-commerce (where foreign suppliers replace domestic ones) could pose an additional

R Jones and S Basu38

challenge to tax as well as customs authorities who would need to decide whether and howto tax such goods

E-commerce provides threats similar to those posed in the 1980s with the rise of the lsquobigboxrsquo stores their goal was not so much to feed off and feed into indigenous community-based businesses but rather to crush them and be the only retail destination in town Bigbox stores frequently demanded tax abatements from communities in exchange for thepromise of big sales tax windfalls and increased local employment In contrast independentmerchants who have been in main street districts have traditionally done more than sellgoods to local shoppers They have supported the local economies through the buying ofsupplies from other local stores employing the services of local lawyers architectsaccountants and plumbers banking at local banks and employing local builders andcraftsmen

In our view such lsquobig boxrsquo stores are modern day colonialists exploiting local markets bytaking resources out of the community without returning anything in kind There shouldbe a greater level of concern for local businesses who are working to bring economic andcultural enrichment to their communities and who are bearing the burdens of sales tax andproperty tax collection7 E-commerce and internet businesses take the colonialism economicmodel of chain stores one-step further Whereas chain stores collect sales tax pay propertytaxes and hire local workers internet-only businesses evade most of these activities whichare critical to the survival of communities and local economies Whereas states can imposea tax on residentsrsquo purchases from out-of-state vendors they cannot impose an obligationon those vendors to collect the tax unless the vendor has a substantial presence or nexusin the state

Such concerns are however countered by those who argue those tax revenues overall willincrease as productivity enhancements stimulated by the internet and e-commerce willexpand the economy and raise all statesrsquo tax revenues A case has been made that newelectronic technologies are allowing output quality to rise and production costs to fall8

This is certainly true to a degree however9 Goolsbee argued that any tax exemption shouldbe short lived Indeed it may also be argued that non-neutral tax treatment of e-commercetransactions may reduce rather than expand the economy If consumer transactions aretaxed differently on the basis of how commodities are obtained ef ciency losses areprobable Exempting business inputs purchased by e-commerce while taxing many busi-ness inputs obtained in other forms potentially at higher rates could increase thoseef ciency losses in other areas of the economy Further and taking for the moment oneexample it is possible that e-commerce will result in an overall tax loss The taxing ofon-line sales of intangibles is likely to lead to tax loss as the location of customers cannotbe known with certainty Many on-line shoppers do not feel comfortable giving unneces-sary personal information to a web site Consequently they may refuse to type it in shopat a site that does not require it or simply lie The result is an inability to tax and an erosionof the total tax base a matter to which we now turn

Erosion of the Tax BasemdashReduction in Total Tax Income

It is possible that e-commerce will result in an erosion of the consumption tax baseConsumption taxes are borne by the consumer and collected by the seller different taxrules apply depending on the product or service sold the location of consumer and sellerand the type of consumer (business or individual) With e-commerce the number of foreignon-line suppliers who are often subject to different taxation rules has increased consider-ably Goolsbee10 from research in the United States on the impact of taxation on

Taxation of Electronic Commerce 39

e-commerce and consumer on-line purchasing patterns concludes that consumers living inhigh sales tax areas are signi cantly more likely to buy on-line than those living in low salestax areas Hence differentiated internet taxation rules among countries could have asigni cant impact on consumersrsquo purchasing behaviour shifting from domestic to foreignsuppliers 11 Mazerov and Lav12 therefore concludes that a moratorium on taxation ofinternet sales would therefore bene t the af uent consumer able to shop around on theinternet at the expense of those with low and moderate incomes with the resulting loss oftax revenue

The impact of such tax revenue losses will vary according to countriesrsquo reliance onconsumption tax as proportion of their total tax revenue Major differences exist betweenthe EU and the United States the EU countries derive a large proportion of government taxrevenue from consumption taxes on domestic goods and services (mainly VAT)13 Inaddition VAT extra charges contribute 45 to the EU Community budget (in addition tocustoms duties and GNP contributions) 14 The United States government on the otherhand derives most of its tax revenues from personal and corporate income tax and socialsecurity contributions 15 The United States is currently both a net exporter and the mainexporter of e-commerce worldwide Hence it has a great interest in encouraging business(including e-commerce business) to locate in the United States and pay direct taxes toUnited States tax authorities

The EU however has considerable concerns over the increasing import of digital contentand services from outside the EU which would be exempted from VAT payments in theEU It is not surprising therefore that the issue of consumption taxes has received mostattention in the OECD and the EU In particular the EU feels very strongly aboutmaintaining VAT duties and is likely to modify tax rules in a way that will ensure acontinuation of VAT contributions rather than lowering or eliminating them The impactwill be dependent upon the form of e-commerce activity as VAT regulations vary accordingto the trade and the trading partner16 Imported goods from non-EU members are subjectto (import duties and) VAT of the importing country Sales within the EU are subject tothe VAT of the receiving country in the case of business-to-consume r trade Businessesselling to businesses in another Member State are tax-exempted the receiving or importingbusiness is required to pay VAT locally (ie in the country of nal consumption)17 Exportsto non-EU countries are zero-rated Services differ according to the type of services tradedIn the case of information (currently the majority of e-services) imports from non-EUbusinesses to EU consumers are not subject to customs duties and are VAT-exempted(except for Denmark France and Italy) Sales from non-EU businesses to EU businesses aresubject to self-accounted VAT at the local rate (a so-called reverse charge) Intra-EU servicesuppliers are required to charge VAT in the country in which they are established (locationof the seller) if selling to private consumers EU business-to-busines s services trade issubject to VAT in the country of the nal consumer Sales to customers outside the EU aresubject to VAT in the location of the seller18 The challenges to EU tax authorities that arisefrom e-commerce therefore lie in non-EU supplies of e-services to EU customers (and in anincrease in non-EU customers not subject to EU VAT) Under current tax law these areexempted from VAT while at the same time their share is increasing in direct competitionwith EU suppliers who are subject to VAT payments Furthermore the VAT exemptionprovides incentives for suppliers to locate outside the EU a fairly easy undertaking ine-commerce which no longer requires the presence of human and technical resources

The decline in the tax base in e-commerce will be caused by the loss of consumption-based taxes resulting from the dif culty in taxing purchases from outside the jurisdiction

R Jones and S Basu40

This will be aggravated by the loss of tax revenue from workers displaced by newinformation technologies To this lsquodouble whammyrsquo will be added the increase in taxavoidance made easier by the lack of paper trails on the internet Countries will beencouraged to move more towards indirect taxation which will impact more on poorerfamilies Between countries there will be considerable differentia l impacts due to thecountries ability to both shift to an indirect taxation system and to participate in thegrowth potential of e-commerce It is our contention developing countries will have greaterdif culty on both these counts

Erosion of the Tax Base The Move from Fair Taxation

Tax regimes should be fair in both their horizontal and vertical dimensions A tax systemviolates horizontal equity if taxpayers in similar situations pay markedly different amountsof tax Vertical equity commonly is framed as ensuring a fair relationship between the taxburdens (usually de ned as a fraction of income paid in tax) on households with differentlevels of income

People who make purchases through the internet are on average more af uent Internetpurchases generally require a personal computer with a modem a connection to theinternet through a service provider and a credit card with which to pay for the purchaseIncome and education are key elements in the ownership of personal computers MediaMetrix19 reports that internet users own the most powerful and expensive computersMoreover the internet is increasingly being used to make purchases of luxury items Theinternet is especially well suited for consumers who want to customize their purchases ofgolf clubs and bicycles from hundreds of possible speci cations20 On the other handlower-income households lack the equipment to access the internet the training to use theequipment andor the nancial stability and credit rating required for maintaining a creditcard

As internet sales become a more signi cant share of consumption states will likely seetaxable salesmdashand consumption tax revenuesmdashdiminish The option would be to raisetheir consumption tax rates to maintain revenues given they are unable to tax internet salesHowever indirect taxes are regressive and they absorb a larger share of the incomes oflower-income households Increase in sales tax rate could set off a vicious cycle leading toever more regressive sales taxes As tax rates rose higher-income households and businesseswith internet access would have an ever greater incentive to make their purchases on-lineto avoid taxes while lower-income households without access to on-line services wouldremain liable for the taxes Sales tax liability would be more and more concentrated amongthe lowest-income segments of the population As already seen in addition to this stateswere forced to reduced state funding programmes to compensate for diminished revenueswhich causes disproportionat e cuts of bene ts for lower-income families and individuals The result is unfairness in both the horizontal and vertical aspects of the tax regime

There is evidence of such patterns of shifting tax liability from the use of mail orderupper-income households tending to use such systems more than low to middle incomehouseholds21 There is no compelling policy reason why the governments should favour thewealthy and well- nanced corporations and their equally wealthy customers at the expenseof other businesses and other consumers Community-based businesses and the cities andtowns they serve are now endangered by unfair and ill-conceived economic distortions dueto the tax breaks e-commerce companies enjoy We accept that governments should be

Taxation of Electronic Commerce 41

encouraging the growth of e-commerce we merely argue that issue of unfairness in the taxregimes be considered in the light of such growth

Developing Countries

Developing Countries The Reduction in the Tax Base

Currently an overwhelming (85) share of electronic commerce is concentrated in theUnited States but diffusion into Europe and Asia followed by Latin America and Africawill be rapid In developing countries internet use and its economic potential are growingexponentially The share of active internet users in AsiaPaci c Rim Latin America andlsquorest of worldrsquo it is estimated could increase from 23 in 1999 to 35 in 2002 In Indiafor example the number of internet users is expected to grow from 05 million in 1998 to9 million in 2003 which translates to a compound annual growth rate of 76 E-commercerevenues could jump from US $28 million in 1998 to US $575 million in 2002 In Chinaa reported 60 of businesses are using the internet and commerce revenues could rise fromUS $43 million in 1999 to US $12 billion in 2004 In Latin America internet usage rosenearly eight-fold between 1995 and 1997 with revenues estimated to US $167 million in1998 and projected to be US $8 billion by 200322

What will be the impacts on the tax incomes of such countries Most rely heavily onconsumption taxes (Figure 1) Data from industrial and developing countries show that theratio of income to consumption taxes in industrial countries has consistently remainedmore than double the ratio in developing countries that is compared with developingcountries industrial countries derive proportionally twice as much revenue from incometax than from consumption tax23 Developing countries are also importing countries thatis its citizens and companies tend to buy from foreign countries more than foreign countriesbuy from its citizens and companies in contrast developed countries consist of relativelywealthy exporting nations While the size of these exportndashimport trade de cits vary fromyear to year and from country to country such de cits nevertheless overwhelmingly existfor developing countries Within the WTO developing countries have raised concerns aboutpossible tariff revenue implications resulting from a ban on customs duties on electronictransmissions However they lack resources to provide evidence which could support theirconcern Many of them are still struggling to keep up with the rapid developments in thearea of e-commerce recognising that e-commerce has two sides and has the potential forsubstantial bene cial effects on their economies

Revenue Loss

The question here is how signi cant is this revenue loss for the developing countries Theanalysis of trade and tariff data given in the UNCTAD study series No 524 shows that themajority of countries most affected by tariff revenue losses come from the developingworld Despite developing countries accounting for only 16 of world import of digitalizedgoods their share for tariff revenue (loss) is almost double that of the developed countriesamounting to 63 of world tariff revenue losses for these products The growth rates forboth exports and imports of digitized products are signi cantly higher than growth ratesfor total merchandise trade Bearing in mind the growth rate of digitized products is relatedto revenue loss it is possible to calculate potential revenue losses resulting from a shift fromphysical to electronic delivery of goods (Figure 2)

R Jones and S Basu42

Figure 2 World trade in digital products 1997

Figures for the United States (to our knowledge no work has been done on this from theperspective of the developing countries) show the scale of the problem Based one-commerce sales drawn from the annual forecasts of Forrester Research Inc for the years1999ndash2003 for 24 categories of business to consumer (B2C) sales and 13 categories ofbusiness to business (B2B) sales forecasts of the incremental revenue loss from e-commercesales is estimated to be US $1080 billion in 2003 The incremental loss is the amount thatwould not have occurred without e-commerce after recognizing the substitution ofe-commerce sales for other remote sales The dominant role that B2B is expected to playin e-commerce sales means that the ability to collect revenues on B2B transactions is veryimportant to the revenue loss for state and local governments B2B is responsible for 701of the expected incremental revenue loss in 2003 with the other 299 coming from B2Csales The total revenue loss from e-commerce equals total taxes due on internet sales anda new or incremental loss from e-commerce occurs only to the extent that taxes on thetransactions would have been collected without e-commerce A recent study25 shows that

Figure 3 Estimated revenue loss based on the study by Bruce and Fox (see note 26)

Taxation of Electronic Commerce 43

by 2011 the revenue losses could equal between 26 and 992 of total state tax collections(Figure 3)26

This loss of revenue could signi cantly impair the ability of some states to provide basicservices to its population Numerous studies project hundreds of billions of dollars inannual purchases by consumers and businesses over the internet just three to four yearsfrom now Not all such purchases represent lost sales tax revenues to state and localgovernments of course some will be goods and services that are not taxed and othersrepresent purchases upon which the tax will be remitted by the seller or the purchaser27

Even assuming no growth in traditional direct marketing sales between now and 2003the combined annual revenue loss from untaxed internet and mail order sales in 2003 forthe United States could be US $15 billion (US $5 billion in lost revenue from untaxedmail-order sales plus US $10 billion from internet sales) That should be regarded assigni cant by any objective standard it is for example more than two and one-half timeswhat state and local US governments currently spend on public libraries28 It is theequivalent of US $50000 salaries for 300000 teachers The economic opportunities avail-able to the poor could be reduced if tax base erosion impairs the ability of states andlocalities to nance public services such as education job training library childcarehealth and similar services29 It is obvious that if similar effects are transposed ontodeveloping countries the effect will be devastating

As yet however there appears to be little evidence that major tax basesmdashhouseholdincome taxes corporation income taxes and consumption taxesmdashhave collapsed in thisway Overall taxes have risen not fallen over the past several years and although tax rateshave tended to converge over time there remains substantial variation across countries andwithin countries where there are few formal barriers to geographical mobility differential sof major taxes also seem to be signi cant and stable over time Similarly there is threat ofgeographical tax-base eroding public nances It could be argued that the ability to choosethe location of economic activity offsets shortcomings in government budgeting processeslimiting a tendency to spend and tax excessively

Developing Countries The Move from Fair Tax Systems

We have already alluded to the fact that the digital divide shows that the rich and educatedhave the best access to computers and internet (for more detail see Marsh30) Morehigh-income consumers shop on-line than low-income consumers This is intuitive becausethey have a higher willingness to pay the xed cost to shop on-line and their time is worthmore to them (which makes the conventional shopping less attractive) Therefore if theon-line tax rate is lower than conventional tax rate the average af uent person will payrelatively less of their income in consumption taxes than the average poor person Givena suf cient decrease in the cost xed cost of shopping on-line the electronic region canlsquoenterrsquo and attract a tax base if they set relatively low tax rates As the xed cost ofshopping on-line continues to decrease increase usage of the e-commerce as a way ofshopping is expected to rise Conventional regions will see both lower tax bases and taxrates which will lead to lower tax revenues and this will make the developing countriesmore vulnerable because of their greater dependence on tariffs and taxes as revenue sourcesfor their national budgets In order to raise the lost revenue the situation ideally calls forthe rich to be taxed more heavily than the poor but the economic and political power ofrich tax payers often allows them to prevent tax reforms that would increase their taxburdens This practically explains why developing countries are more dependent on indirect

R Jones and S Basu44

taxes In developing countries tax policy is often the art of the possible rather than thepursuit of the optimal

Developing Countries and Tax Policies

Tax exemption is at present a consistent policy justi ed to encourage the growth ofe-commerce Our previous discussion clearly indicates that e-commerce has achievedunparalleled growth not only in the developed countries but also in a large number ofdeveloping countries It would appear that the success of e-commerce will depend not ontax exemption but on internet access education levels the propensity to consume importedproducts traded on the internet domestic alternatives and prices

The overall impact on developing countriesrsquo taxation revenue and balance of trade willbe dependent on a number of factors such as the value of e-commerce transactions howdomestic taxation laws handle these transactions and the effectiveness of their collectionmechanisms More signi cant will be the international taxation regimes that will ofnecessity be implemented Traditionally tax collection has been based on the belief thatindividual countries have the right to set their own tax rules and little internationalcooperation and few multilateral agreements have been put in place taxation has been evenwithin the OECD a tool to achieve a competitive edge31 (there has been a signi cant lackof co-operation in relation to attempts to have VAT collected from the country of thesupplier32) Unless this approach changes and countries agree to enter into multilateral taxagreements tax competition will intensify with e-commerce This is also why it is unlikelythat countries will collect taxes for other countries for example in the case of VAT whereit has been suggested that VAT be collected from the country of the supplier33

The concern is of increasing numbers of small and medium-sized enterprises (SMEs) thatwill be drawn in by e-commerce from the developing countries which have little experiencein international taxation issues Any solutions must have the con dence of the developingworld lsquoAbove all what is needed is a recognition that globalization is not merely a matterof unrestricted market forces It requires a strengthening of international standards andcooperative arrangements to provide a basis of mutual con dencersquo34

With a few exceptions developing countries will not be part of any OECD agreement oninternet taxation Nevertheless they can use the principles and rules agreed upon as a basisfor adjusting their own legislation In addition developing countries will attempt to use taxlegislation as they have in the past to attract private foreign direct investment (FDI)Multinationals increasingly operate in countries that have low taxes or are willing tonegotiate favourable tax regimes to attract foreign business35 In fact scal incentives arethe most widely used type of FDI incentives36 Depending on the agreements adopted in theOECD developing countries could negotiate speci c bilateral treaties for e-commercetaxation which would give them a competitive edge For example the transaction costs ofsetting up or moving a web server are low hence e-commerce allows companies to respondquickly to tax incentives by governments and move their web servers to a developingcountry

Any decisions which developing countries may take on modifying their tax legislation toaccommodate e-commerce however will have to take into account the signi cant role oftax and tariff revenues in their national budgets Until new international agreements one-commerce taxation have been de ned an increasing number of goods and services will betraded on-line largely tax-free This will have an effect on government revenue especiallyif the goods and services have been subject to import duties in the past

Taxation of Electronic Commerce 45

Global Initiatives for Addressing Tax-Related Issues in E-commerce

OECD Response

The OECD has prescribed certain guidelines that they feel governments should adhere towhile formulating new provisions regulating taxation of e-commerce transactions It ishelpful to revisit these guidelines which are summarized as follows37

middot The technologies underlying electronic commerce offer governments signi cant newopportunities to improve taxpayer service and that those opportunities should bepursued

middot The taxation principles that guide governments in relation to conventional commerceshould quite properly guide governments in relation to e-commerce those principlesbeing neutrality ef ciency certainty and simplicity effectiveness and fairness and exibility

middot Those principles can be implemented for e-commerce through existing tax rules albeitwith some adaptation of the latter

middot There should be no discriminatory tax treatment of e-commercemiddot Application of these principles should maintain scal sovereignty of countries ensure

a fair sharing of the tax base between countries and avoid double and unintentionalnon-taxation

middot The process of putting esh on these principles should involve intensi ed co-operationand consultation with economies outside of the OECD area with business and withnon-business taxpayer groups and

middot When required government intervention should be proportionate transparent con-sistent and predictable as well as technologically neutral

At the time of the 1998 OECD Ministerial meeting on electronic commerce it wasproposed that the OECD form Technical Advisory Groups (TAGs) to assist in takingforward the work on taxation and electronic commerce Five TAGs were established inJanuary 1999 for two years to allow them time for a thorough consideration of all theissues The Consumption Tax TAG is examining consumption taxes and electroniccommerce in the following areas

middot Rules for the consumption taxation of cross-border trade should result in taxation inthe jurisdiction where consumption takes place and an international consensus shouldbe sought on the circumstances under which supplies are held to be consumed in ajurisdiction

middot For the purpose of consumption taxes the supply of digitized products should not betreated as a supply of goods

Where business and other organizations within a country acquire services and intangibleproperty from suppliers outside the country countries should examine the use of reversecharge self-assessment or other equivalent mechanisms where this would give immediateprotection of their revenue base and of the competitiveness of domestic suppliers andcountries should ensure that appropriate systems are developed in co-operation with theWorld Customs Organization and in consultation with carriers and other interested partiesto collect tax on the importation of physical goods and that such systems do not undulyimpede revenue collection and the ef cient delivery of products to consumers The OECDproposal to treat digitized products as services corresponds to a EU proposal that for VATpurposes trade in digital goods be treated as a supply of services The EU also proposes that

R Jones and S Basu46

VAT rates on all e-services be harmonized into a single rate This could result in tax lossessince consumption taxes are lower on services than on goods It could also lead to losseson tariffs and import duties on digital goods that were shipped physically in the past andwhich would now be subject to much lower duties This would impact in particular on thedeveloping countries whose reliance on import duties as a government revenue source ismuch higher than in the developed countries

At the Ottawa Conference the United States took a different position on this issuedigital products should be characterized on the basis of the lsquorights transferredrsquo in eachparticular case It argued that some goods that are now zero-rated (such as books ornewspapers) would be subject to VAT if treated as a service Customers may thereforeprefer to buy local zero-rated books rather than digitally imported (and taxed) servicesmany of which could be supplied by US on-line providers

As an alternative the United States has proposed an origin-based consumption tax forintangibles (e-services) which would be collected from the supplier and not from theconsumer It argues that it is easier to identify the supplier than the customer on the basisof permanent establishment rule and since businesses are subject to audit The United Statesas a net exporter of e-commerce would bene t from an origin-based tax while it mayfurther erode the tax base in e-commerce-importing countries

There is a growing environment of trust and co-operation between tax authorities andthe business community which will prove useful in the drive to reach satisfactory taxsolutions in electronic commerce

Development within the EU

In June 1999 The European Commission issued a Working Paper concerning a revision ofthe current tax rules of the 6th VAT Directive for both goods and services regardless ofthe medium through which these items are sold38 The paper also recognizes the need toapply existing taxation rules effectively It acknowledges that VAT procedures tend to beoverly complex and the delays in obtaining refunds of VAT paid in other Member Statesare a major disincentive to cross-border trade The Commission has already made pro-posals to simplify these issues in the short term via abolition of tax representative s andreplacement of VAT reimbursement by a right of deduction Existing VAT rules will alsobe modernized to take into account the evolution of business and particularly e-commerce

On 7 June 2000 the European Commission presented a proposal for a Directive39 tomodify the rules for applying value added tax (VAT) to certain services supplied byelectronic means as well as subscription-base d and pay-per-view radio and televisionbroadcasting The objective of the proposal is to create a level playing eld for the taxationof digital e-commerce in accordance with the principles agreed to at the 1998 OECDMinisterial Conference and to make compliance as easy and straightforward as possibleThe proposal mainly concerns the supply over electronic networks (ie digital delivery) ofsoftware and computer services generally plus information and cultural artistic sportingscienti c educational entertainment or similar services The proposal would ensure thatwhen these services were supplied for consumption within the EU they were subject to EUVAT and that when these services were supplied for consumption outside the EU theywere exempt from VAT The changes modernize the existing VAT rules to accommodatethe emerging electronic business environment and to provide a clear and certain regulatoryenvironment for all suppliers located within or outside the EU

Taxation of Electronic Commerce 47

The proposal also contains a number of facilitation and simpli cation measuresaimed at easing the compliance burden of business According to the EU the currentVAT rules do not however adequately address the supply of services delivered on-lineby digital means notably as regards such services traded between EU and non-EUcountries Such supplies were simply not envisaged at the time the current VAT legis-lation was established As a result application of the current VAT rules to electronicall ydelivered services produces discriminatory results At the moment electronicall y deliveredservices originating within the EU are always subject to VAT irrespective of the placeof consumption whilst those from outside the EU are not subject to VAT evenwhen delivered within the EU Under the proposal the application of VAT woulddepend on the tax status and location of the recipient Electronic services deliveredfrom one Member State to businesses located in another Member State within theEU would be generally supplied without VAT with the VAT paid by the business customeron a self-assessment basis with his regular VAT returns (the so-called lsquoreverse chargemechanismrsquo) Where electronic services were delivered from one Member State toconsumers in another Member State within the EU the supplier would continue tocharge VAT at the applicable rate in the Member State where the supplier was registeredUnder the proposal non-EU operators would only have to register for VAT purposeswhere they undertook business to consumer transactions They would not have to registerif they undertook only business-to-busines s transactions because business customers paythe VAT themselves on a self-assessment basis under the so-called lsquoreverse charge mechan-ismrsquo Where their annual sales to consumers in the EU exceeded a minimum turnoverthreshold of 100 000 non-EU operators would be required to register for VAT purposesbut only in a single Member State (they could choose any Member State where theysupplied services) They would then charge VAT at the rate applicable in the Member Statethey have chosen and only have to deal with a single tax administration within theEU

However the Proposal was eventually rejected and in late November 2000 the ECOFINcouncil recommended to the Commission to rework the proposals and present an amendedversion In practice this has the effect that the proposal was blocked and although notformally withdrawn shelved for the moment lsquoWe assume European Commission staffershave gone back to the drafting table to come up with something that will pleaseeveryonersquo 40 Although the ministers at November meeting could not approve the proposalthey did agree on principles and a draft was prepared for the June 2001 meeting ofECOFIN based on the certain understandings that were reached in the November 2000meeting However the June 2001 meeting once again failed to generate support among allthe Member States The British Finance Minister made known that his country would notsupport the proposal despite the fact that the other 14 Member States expressed theirwillingness for plans to implement the proposal to proceed The UK is opposed to theproposal as long as discussions over indirect taxation of e-commerce are still going onwithin the OECD41

lsquoDespite the opposition to the proposed VAT Directive the European Commission doesnot seem willing to give in In fact the EU Commission has already made plans ahead forthe acceptance of the aforementioned proposalrsquo42 At the time of writing (January 2002)ECOFIN has recently agreed on the broad outlines of a plan to impose VAT one-commerce and scheduled a vote on detailed rules in the very near future Under the planapproved by the Council non-EU sellers would register in one of the 15 Member States ofthe EU but collect tax based on the actual locations of customers

R Jones and S Basu48

Development within the United States

On 12 April 2000 the Advisory Commission on Electronic Commerce presented toCongress the results of its 10-month study of the issues of taxes and the internet43 Althoughthe commission was unable to generate the two-thirds majority vote required by the act tosend a lsquoformalrsquo recommendation to Congress on the subject of taxing electronic commercea simple majority of its 19 members did agree on a fairly comprehensive plan that addressesmany internet and telecommunications tax policy issues The proposal includes

middot Extending the current moratorium on internet taxes for ve yearsmiddot Prohibiting the taxation of digitized goods and products and their non-digitized

counterpartsmiddot Banning all taxes on internet accessmiddot Abolishing the federal excise tax of 3 on telephone callsmiddot Encouraging state and local governments to reform industry-speci c telecommunica-

tions taxesmiddot Establishing rm lsquonexusrsquo rules for electronic commerce to make it clear when state and

local governments could levy taxes on vendors of interstate commercemiddot Encouraging state and local of cials to work together to simplify their sales tax

collection systems and make them more uniform andmiddot Establishing a new Advisory Commission to monitor these ongoing efforts and to

determine whether states and localities should be allowed to collect taxes on out-of-state internet vendors once tax code simpli cation is complete

One of the most fundamental issues before the Commission concerned the application ofstate and local sales and use taxes to internet and other remote retail sales Sales taxes arelsquoconsumption-type rsquo taxes designed to generate revenue In general these taxes are calcu-lated and collected by businesses at the point of sale and remitted to the appropriate taxingauthorities While the exact impact of e-commerce on sales tax revenues may be uncertainclearly the need for substantial sales tax simpli cation is necessary in this emerging digitaleconomy In the course of the Commissionrsquos examination of the impact of e-commerce onsales and use tax collections there was general agreement among the Commissioners thatthe current sales and use tax system is complex and burdensome Most if not all of theCommissioners expressed the view that fundamental uniformity and simpli cation of theexisting system are essential The need for nationwide consistency and certainty for sellersas well as the need to alleviate the nancial and logistical tax collection burdens andliability of sellers were common themes throughout discussions Commissioners alsoidenti ed issues raised by sales of digitized goods over the internet They discussed thechallenge of determining the identity and location of the consumer of digitized goods andthe need to protect consumer privacy rights

The Commissionrsquos proceedings helped widen public awareness of the issue and providedan exceptional framework for debating complex tax issues The US Congress recentlyapproved the extension of the moratorium on the taxation of electronic services at leastuntil 2006 with a high probability of the moratorium being extended even after this date

Conclusion

An increasing amount of commerce is done in digital (ie non-physical ) form where theexistence of customers and payments methods are not traceable E-commerce increases the

Taxation of Electronic Commerce 49

gap between the technology exporting developed country and technology importing devel-oping countries and between those countries whose primary tax base is direct taxation andthose which raise substantial amounts of revenue by consumption taxes The threat is ofdeepening the developing countries disadvantage in competing with developed nations

The effect is that the opportunities and threats brought by e-commerce are quantitativelyand qualitatively different as between developing and developed countries Internationalstrategies and methodologies derive from organizations such the OECD organizationsdominated by the US and the developed world The result is solutions devised for andbene cial to the developed world Developed countries have the nancial strength towithstand the probable revenue loss whereas most developing countries have huge bud-getary de cit and any change in the revenue base will jeopardize the already fragileeconomy

The present initiatives appear to ignore or side step these differences Developingcountries have see the prospective of economic growth due to e-commerce and followed theUNCITRAL Model Law on Electronic Commerce44 yet so far have ignored the probablerevenue loss Industrialized countries have in turn reviewed options including zero taxoptions to boost e-commerce ignoring the fact that developing countries are already shortof resources and a zero tax on e-commerce will result in a huge potential loss of revenuefor them Practically all the bene ts of a zero tax policy will go to industrialized countriesThe multinational corporations of the developed countries will therefore have a strategicweapon to gain competitive advantage in this digital age over the local companies of thedeveloped world increasing the gap between the developed and developing world

Notes and References

1 Mainly sales and value added taxes2 In the case of the European Union individual member countries do not report revenues from

import duties (some report very low values) This is because EU import duties are directly passedon to the EU common budget as a traditional own resources payment and only 10 is retainedby the importing country (this share will be increased to 25 as of 2001) Therefore thecalculations of EU Member Statesrsquo import revenues are based on their individual contributions tothe EU budget (European Commission lsquoFinancing the European Union Commission Report on theoperation of the own resources systemrsquo DG XIX October 1998 Brussels wwweuropaeuintcommdg19agenda2000ownresourceshtmlindexhtm)

3 Other important sources not considered here are income taxes and social security contributions4 The OECD has taken the international leadership in co-ordinating the work on electronic

commerce and taxation working closely with the European Union on the consumption tax issuesThis mandate was proposed in November 1997 and con rmed in Ottawa at the October 1998OECD Ministerial Conference lsquoA Borderless WorldndashRealising the Potential of Electronic Com-mercersquo This meeting also called upon the World Trade Organization (WTO) to concentrate ontariff issues and the World Customs Organisation (WCO) to work on customs issueswwwoecdorgdafFSMtaxationandecommerceprogressreport OECD Discussion Paper lsquoElec-tronic commerce a discussion paper on taxation issuesrsquo 19 September 1998 wwwoecdorg

5 The rate depends on the type of product the location and the type of customer6 A Lukas lsquoTax bytes a primer on the taxation of electronic commercersquo Cato Institute for Trade

Policy Studies Trade Policy Analysis No 9 p 10 17 December 1999 wwwfreetradeorgpubspastpa-009eshtml

7 A Ross lsquoWarning e-commerce may be dangerous to the health of your communityrsquo 1999wwwcodybookcom This is extract of an article written by Andy Ross available at wwwnclorg

R Jones and S Basu50

8 DJ Johnston Secretary-General of the OECD lsquoTaxation and social progressrsquo Editorial The OECDObserver No 215 January 1999 wwwoecdorgpublicationsobserver215etochtm

9 A Goolsbee lsquoIn a world without borders the impact of taxes on internet commercersquo NationalBureau of Economic Research (NBER) Working Paper No 6863 Cambridge MA 1999

10 Ibid11 Although there are also barriers that could prevent this shift such as other regulatory obstacles

(besides taxation) delivery problems or cultural and linguistic barriers To circumvent these someUnited States suppliers have started to buy local competitors in Europe (Economist lsquoA survey ofE-commercersquo 26 February 2000)

12 M Mazerov and IJ Lav lsquoA federal ldquomoratoriumrdquo on internet commerce taxes would erode stateand local revenues and shift burdens to lower-income householdsrsquo Center on Budget and PolicyPriorities 11 May 1998 wwwcbpporg512webtaxhtmIII

13 This equates to 2914 The 45 contribution in 1997 was reduced to 35 in 1999 (projection) European Commission

lsquoFinancing the European Unionrsquo Commission Report on the operation of the Own ResourcesSystem DGXIX October 1988 Brussels wwweuropaeuintcomdg19agenda2000ownre-sourceshtmlindepth

15 Within the United States individual states and local governments have autonomy over determiningand collecting state and local sales tax often their biggest source of revenue Sales taxes differsubstantially among states ranging from 0 to 7 United States-based on-line suppliers selling toout-of-state (including foreign) customers currently do not have to charge local sales tax States aretherefore becoming increasingly worried about how to secure their sales tax revenues in the lightof internet commerce

16 For details and facts on EU VAT rules see European Commission lsquoVAT in the EuropeanCommunityrsquo XXI54197 EC DG XXI January 1997 Brussels The complexity of the existing EUVAT system is considered by business a major barrier to developing e-commerce in Europe

17 This regulation was put in place in 1993 under the lsquotransitional VAT arrangementsrsquo with theobjective of removing border controls for tax purposes inside the European Community

18 A Kerrigan lsquoTaxation of e-commerce Recent developments from a European perspectiversquoWirtschaftspolitische Blatter Vol 5 pp 439ndash447 1999

19 Media Metrix lsquoInternet users spend more time money on PCsrsquo 31 March 1998 Internet NewscomStaff Available at http wwwInternetNewscombus-news1998033102-mediametrixhtml

20 Internet World lsquoBuild it yourselfrsquo is motto of sites selling everything from golf clubs to CDs tobicyclesrsquo Internet World 2 March 1998 at http wwwinternetworldcomprintcurrentecomm19980302-buildhtml

21 Statistics form Direct Marketing 199722 CL Mann lsquoElectronic commerce in developing countries issues for domestic policy and WTO

negotiationsrsquo Institute for International Economics Working paper No00ndash3 March 200023 V Tanzi and H Zee lsquoTax policy for developing countriesrsquo March 2001 International Monetary

Fund Economic Issue No 27 http wwwimforgexternal indexhtm24 S Teltscher lsquoTariffs taxes and electronic commerce revenue implications for developing countriesrsquo

Working paper series UNCTAD 200025 D Bruce and WE Fox lsquoState and local sales tax revenue losses from e-commerce updated estimatesrsquo

September 200126 The US Advisory Commission on Intergovernmental Relations estimated the nationwide state

and local government revenue loss from untaxed mail order sales in 1994 at US $33 billion(Taxation of Interstate Mail Order Sales 1994 Revenue Estimates) According to the DirectMarketing Association catalogue sales grew 86 annually between 1994 and 1999 If all formsof direct marketing matched the growth in catalogue sales during the 1994ndash1999 periods and theshare of all such sales going untaxed remained constant a rough estimate of untaxed mail ordersales in 1999 would be US $5 billion

27 Forrester expects business-to-business sales over the internet to remain many times larger than

Taxation of Electronic Commerce 51

consumer purchases Forrester currently projects US $13 trillion in US business-to-businessinternet sales in 2003 (See lsquoThe online revolutionrsquo Wall Street Journal p R6 12 July 1999) If justone-third of these sales represent items that would be subject to state and local sales taxes and ifit is assumed that just one-third of the taxes due on this one-third of sales would go uncollectedthen the 2003 revenue loss from untaxed business-to-business internet sales (at the average 65tax rate used by Duncan) would be US $96 billion (Assuming that one-third of the US $13 trillionwould be subject to sales tax seems reasonable Computers industrial equipment of ce suppliesand shipping supplies alone account for 40 of the total such items generally do not qualify forsales tax exemptions) Combining the US $96 billion in lost revenues on business-to-business saleswith the US $4 billion in lost revenues on consumer purchases estimated by Duncan yields US $136billion Thus an estimated US $10 billion total revenue loss from untaxed internet sales in 2003appears reasonable if not conservative

28 According to the US Census Bureau state and local governments combined spent US $57 billionon libraries in for year 1995ndash1996 the most current scal year for which data are available Seewwwcensusgovftppubgovs estimate96stlustxt

29 United Nations Conference on Trade and Development Policy Issues in International Trade andCommodities Study Series No 5 lsquoTariffs taxes and electronic commerce revenue implications fordeveloping countriesrsquo UNCTAD Geneva Switzerland November 2000

30 lsquoElectronic commerce and tax competition when consumers can shop across borders and on-linersquoDepartment to Economics University of Colorado Working paper No00ndash13 November 2000

31 Even within the EU VAT differs among Member States32 The Economist lsquoA survey of e-commercersquo 26 February 200033 Ibid34 S Picciotto lsquoLessons of the MAI towards a new regulatory framework for international invest-

mentrsquo Law Social Justice and Global Development No 1 2000 http eljwarwickacukglobal is-sue2000ndash1picciottohtml

35 Op cit note 3336 UNCTAD lsquoIncentives and foreign direct investmentrsquo UNCTADDTCI28 Current Studies Series

A No 30 1996 Geneva37 OECD op cit note 438 European Commission Directorate General XXI Working Paper No 1 lsquoHarmonization of

turnover taxesrsquo Working Paper 8 June 1999 wweuropaeuint 39 European Commission lsquoProposal for a regulation of the European Parliament and of the Council

amending regulation (EEC) No 21892 on administrative co-operation in the eld of indirecttaxation (VAT) and proposal for a Council Directive amending Directive 77388EEC as regardsthe value added tax arrangements applicable to certain services supplied by electronic meanrsquo COM(2000) 349 nal 7 June 2000 Brussels

40 D Hardesty lsquoEU withdraws proposals for VAT on digital salesrsquo 4 February 2001 E-Commerce TaxNews

41 Heise online News 6 June 200142 JLN Snel lsquoEuropean Union reaches out across borders EU proposes to tax US-based e-commerce

companies with value added tax in the EUrsquo Baker amp McKenzie Palo Alto San Francisco 200043 Advisory Commission on Electronic Commerce lsquoReport to Congressrsquo April 2000 wwwecommerce

commissionorgreporthtm44 Such as Republic Act No 8792 or E-Commerce Act 1999 of the Philippines Information Technol-

ogy Act 2000 of India Digital Signature Act 1997of Malaysia Singapore Electronic TransactionAct 1998

R Jones and S Basu36

Figure 1 Government revenue shares Source of data International Monetary Fund GovernmentFinancial Statistics Year Book 1999

with a paid for (and taxed) product Tax collection was in the hands of the retailers whowould charge the consumer VAT or sales tax and then remits this to the taxing authorities However global e-commerce makes the cross-border movements in goods capital andlabour less transparent allowing companies and individuals to exploit tax differencesbetween countries or even to evade taxation at all

Taxes as Source of Revenue

Taxes are the principal source of government revenue accounting on average for about80 of total revenue (all countries) Domestic taxation of goods and services makes up thelargest share in tax revenues (365)1 Revenues from import duties account on average for132 of total revenue and 175 of tax revenue

Major differences exist between developing and developed countries for the developingcountries import duties as a share of total government revenue are 158 (compared with26 for developed countries) and as a share of tax revenue 212 (compared with 3 fordeveloped countries) 2 The combined tax revenues from goods services and those fromimports account for 54 of tax revenues (all countries) or 583 of developing countriesrsquoand 37 of developed countriesrsquo tax revenue Hence these forms of taxation make up amajor source of government revenue in most countries3 (Figure 1)

Consumption Taxes and Intangible Goods

The challenges posed by electronic commerce for taxation have been well documented4

including how to identify taxpayers engaged in e-commerce and determine their taxingjurisdiction how to ensure that appropriate records are created of business conducted byelectronic commerce how to collect taxes in the electronic commerce environment In this

Taxation of Electronic Commerce 37

paper we concentrate particularly on the possible decline in the overall tax base which inour view will have a disproportionate effect on the economies of the developing countriesThis decline is even more pronounced where more reliance is placed on consumption taxes

Consumption taxes are intended to be borne by consumers and are dependent uponretailers acting as tax collectors Sellers bear the cost of determining the applicable taxrate5 preparing invoices according to tax rules collecting tax ling and remitting tax andmaintaining tax records If the tax is assessed incorrectly the seller (or its third-party agent)typically will be held responsible for any shortfall and will not be able to reclaim it fromthe customer

Let us note here at the outset that there is no ambiguity at present regarding the statusof the goods ordered and paid for on internet but delivered physically in the conventionalmanner The problem is most obvious for intangible products such as music software andservices such as medical or legal consultations that are lsquoproducedrsquo at one location andlsquoconsumedrsquo elsewhere6 It is generally accepted that tax rules for sale of intangible productsand services should be same as those of other goods and that the means of delivery shouldnot govern tax treatment A lsquotechnologicall y neutralrsquo taxation would not treat the sale ofa paperback book any differently than the sale of a digitized book However determiningwhich products are functionally equivalent is less easy Is the text displayed on computerscreen really the same thing as a printed book Is a movie downloaded to computer harddrive really the same thing as a video rental If digitized products are treated as servicesthen further guidance is needed to specify which source of supply rules for services shallgovern because there are many different rules for different types of services Moreover mostof the countries do not have comprehensive taxation to services and few intangibleproducts aside from basic utilities which are subject to special taxes

Existing tax regimes show different and inconsistent rules for different types of servicesand intangible property such as telecommunications broadcast consulting engineeringtraining and education data processing supply of information access to databasesentertainment and content of various types Developing consistent de nitionsclassi cations and tax rates for the many types of services that might be considered to bea part of electronic commerce would provide clarity and certainty reduce double taxationand reduce attempts to manipulate classi cations aimed at tax avoidance Further consist-ent guidelines are also needed for combined or bundled services eg telecommunicationsand internet access which combinations may be dif cult to separate out especially if theyare subject to different rules or tax rates and the apportionment of use of services withinand without a country eg telecommunications services or use of an Intranet network

E-commerce The Challenge

E-commerce provides a qualitively different challenge to tax regimes First it leads to thegradual elimination of intermediaries such as wholesalers or local retailers who in the pasthave been critical for identifying taxpayers especially private consumers Second there willbe discrepancies where foreign suppliers may be tax-exempted whereas local supplierswould be required to charge value added tax (VAT) or sales taxes Third direct ordersfrom foreign suppliers will substantially increase the number of low-value shipments ofphysical goods to individual customers These low-value packages now fall under so-calledde minimis relief from customs duties and taxes in many countries the cost of collectionbeing more that the amount of tax due A substantial increase in these shipments as a resultof e-commerce (where foreign suppliers replace domestic ones) could pose an additional

R Jones and S Basu38

challenge to tax as well as customs authorities who would need to decide whether and howto tax such goods

E-commerce provides threats similar to those posed in the 1980s with the rise of the lsquobigboxrsquo stores their goal was not so much to feed off and feed into indigenous community-based businesses but rather to crush them and be the only retail destination in town Bigbox stores frequently demanded tax abatements from communities in exchange for thepromise of big sales tax windfalls and increased local employment In contrast independentmerchants who have been in main street districts have traditionally done more than sellgoods to local shoppers They have supported the local economies through the buying ofsupplies from other local stores employing the services of local lawyers architectsaccountants and plumbers banking at local banks and employing local builders andcraftsmen

In our view such lsquobig boxrsquo stores are modern day colonialists exploiting local markets bytaking resources out of the community without returning anything in kind There shouldbe a greater level of concern for local businesses who are working to bring economic andcultural enrichment to their communities and who are bearing the burdens of sales tax andproperty tax collection7 E-commerce and internet businesses take the colonialism economicmodel of chain stores one-step further Whereas chain stores collect sales tax pay propertytaxes and hire local workers internet-only businesses evade most of these activities whichare critical to the survival of communities and local economies Whereas states can imposea tax on residentsrsquo purchases from out-of-state vendors they cannot impose an obligationon those vendors to collect the tax unless the vendor has a substantial presence or nexusin the state

Such concerns are however countered by those who argue those tax revenues overall willincrease as productivity enhancements stimulated by the internet and e-commerce willexpand the economy and raise all statesrsquo tax revenues A case has been made that newelectronic technologies are allowing output quality to rise and production costs to fall8

This is certainly true to a degree however9 Goolsbee argued that any tax exemption shouldbe short lived Indeed it may also be argued that non-neutral tax treatment of e-commercetransactions may reduce rather than expand the economy If consumer transactions aretaxed differently on the basis of how commodities are obtained ef ciency losses areprobable Exempting business inputs purchased by e-commerce while taxing many busi-ness inputs obtained in other forms potentially at higher rates could increase thoseef ciency losses in other areas of the economy Further and taking for the moment oneexample it is possible that e-commerce will result in an overall tax loss The taxing ofon-line sales of intangibles is likely to lead to tax loss as the location of customers cannotbe known with certainty Many on-line shoppers do not feel comfortable giving unneces-sary personal information to a web site Consequently they may refuse to type it in shopat a site that does not require it or simply lie The result is an inability to tax and an erosionof the total tax base a matter to which we now turn

Erosion of the Tax BasemdashReduction in Total Tax Income

It is possible that e-commerce will result in an erosion of the consumption tax baseConsumption taxes are borne by the consumer and collected by the seller different taxrules apply depending on the product or service sold the location of consumer and sellerand the type of consumer (business or individual) With e-commerce the number of foreignon-line suppliers who are often subject to different taxation rules has increased consider-ably Goolsbee10 from research in the United States on the impact of taxation on

Taxation of Electronic Commerce 39

e-commerce and consumer on-line purchasing patterns concludes that consumers living inhigh sales tax areas are signi cantly more likely to buy on-line than those living in low salestax areas Hence differentiated internet taxation rules among countries could have asigni cant impact on consumersrsquo purchasing behaviour shifting from domestic to foreignsuppliers 11 Mazerov and Lav12 therefore concludes that a moratorium on taxation ofinternet sales would therefore bene t the af uent consumer able to shop around on theinternet at the expense of those with low and moderate incomes with the resulting loss oftax revenue

The impact of such tax revenue losses will vary according to countriesrsquo reliance onconsumption tax as proportion of their total tax revenue Major differences exist betweenthe EU and the United States the EU countries derive a large proportion of government taxrevenue from consumption taxes on domestic goods and services (mainly VAT)13 Inaddition VAT extra charges contribute 45 to the EU Community budget (in addition tocustoms duties and GNP contributions) 14 The United States government on the otherhand derives most of its tax revenues from personal and corporate income tax and socialsecurity contributions 15 The United States is currently both a net exporter and the mainexporter of e-commerce worldwide Hence it has a great interest in encouraging business(including e-commerce business) to locate in the United States and pay direct taxes toUnited States tax authorities

The EU however has considerable concerns over the increasing import of digital contentand services from outside the EU which would be exempted from VAT payments in theEU It is not surprising therefore that the issue of consumption taxes has received mostattention in the OECD and the EU In particular the EU feels very strongly aboutmaintaining VAT duties and is likely to modify tax rules in a way that will ensure acontinuation of VAT contributions rather than lowering or eliminating them The impactwill be dependent upon the form of e-commerce activity as VAT regulations vary accordingto the trade and the trading partner16 Imported goods from non-EU members are subjectto (import duties and) VAT of the importing country Sales within the EU are subject tothe VAT of the receiving country in the case of business-to-consume r trade Businessesselling to businesses in another Member State are tax-exempted the receiving or importingbusiness is required to pay VAT locally (ie in the country of nal consumption)17 Exportsto non-EU countries are zero-rated Services differ according to the type of services tradedIn the case of information (currently the majority of e-services) imports from non-EUbusinesses to EU consumers are not subject to customs duties and are VAT-exempted(except for Denmark France and Italy) Sales from non-EU businesses to EU businesses aresubject to self-accounted VAT at the local rate (a so-called reverse charge) Intra-EU servicesuppliers are required to charge VAT in the country in which they are established (locationof the seller) if selling to private consumers EU business-to-busines s services trade issubject to VAT in the country of the nal consumer Sales to customers outside the EU aresubject to VAT in the location of the seller18 The challenges to EU tax authorities that arisefrom e-commerce therefore lie in non-EU supplies of e-services to EU customers (and in anincrease in non-EU customers not subject to EU VAT) Under current tax law these areexempted from VAT while at the same time their share is increasing in direct competitionwith EU suppliers who are subject to VAT payments Furthermore the VAT exemptionprovides incentives for suppliers to locate outside the EU a fairly easy undertaking ine-commerce which no longer requires the presence of human and technical resources

The decline in the tax base in e-commerce will be caused by the loss of consumption-based taxes resulting from the dif culty in taxing purchases from outside the jurisdiction

R Jones and S Basu40

This will be aggravated by the loss of tax revenue from workers displaced by newinformation technologies To this lsquodouble whammyrsquo will be added the increase in taxavoidance made easier by the lack of paper trails on the internet Countries will beencouraged to move more towards indirect taxation which will impact more on poorerfamilies Between countries there will be considerable differentia l impacts due to thecountries ability to both shift to an indirect taxation system and to participate in thegrowth potential of e-commerce It is our contention developing countries will have greaterdif culty on both these counts

Erosion of the Tax Base The Move from Fair Taxation

Tax regimes should be fair in both their horizontal and vertical dimensions A tax systemviolates horizontal equity if taxpayers in similar situations pay markedly different amountsof tax Vertical equity commonly is framed as ensuring a fair relationship between the taxburdens (usually de ned as a fraction of income paid in tax) on households with differentlevels of income

People who make purchases through the internet are on average more af uent Internetpurchases generally require a personal computer with a modem a connection to theinternet through a service provider and a credit card with which to pay for the purchaseIncome and education are key elements in the ownership of personal computers MediaMetrix19 reports that internet users own the most powerful and expensive computersMoreover the internet is increasingly being used to make purchases of luxury items Theinternet is especially well suited for consumers who want to customize their purchases ofgolf clubs and bicycles from hundreds of possible speci cations20 On the other handlower-income households lack the equipment to access the internet the training to use theequipment andor the nancial stability and credit rating required for maintaining a creditcard

As internet sales become a more signi cant share of consumption states will likely seetaxable salesmdashand consumption tax revenuesmdashdiminish The option would be to raisetheir consumption tax rates to maintain revenues given they are unable to tax internet salesHowever indirect taxes are regressive and they absorb a larger share of the incomes oflower-income households Increase in sales tax rate could set off a vicious cycle leading toever more regressive sales taxes As tax rates rose higher-income households and businesseswith internet access would have an ever greater incentive to make their purchases on-lineto avoid taxes while lower-income households without access to on-line services wouldremain liable for the taxes Sales tax liability would be more and more concentrated amongthe lowest-income segments of the population As already seen in addition to this stateswere forced to reduced state funding programmes to compensate for diminished revenueswhich causes disproportionat e cuts of bene ts for lower-income families and individuals The result is unfairness in both the horizontal and vertical aspects of the tax regime

There is evidence of such patterns of shifting tax liability from the use of mail orderupper-income households tending to use such systems more than low to middle incomehouseholds21 There is no compelling policy reason why the governments should favour thewealthy and well- nanced corporations and their equally wealthy customers at the expenseof other businesses and other consumers Community-based businesses and the cities andtowns they serve are now endangered by unfair and ill-conceived economic distortions dueto the tax breaks e-commerce companies enjoy We accept that governments should be

Taxation of Electronic Commerce 41

encouraging the growth of e-commerce we merely argue that issue of unfairness in the taxregimes be considered in the light of such growth

Developing Countries

Developing Countries The Reduction in the Tax Base