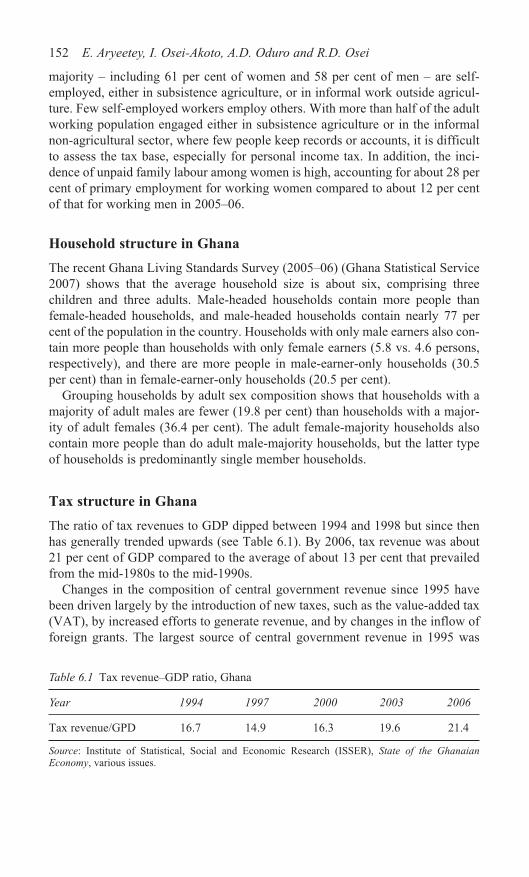

Taxation and Gender Equity - cawtar

348

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Taxation and Gender Equity - cawtar

Researchers, activists and analysts concerned about gender equity have not paidsufficient attention to the taxation system and the manner in which taxes and taxpolicies may impact on the gendered nature of economic and social life.Similarly, tax analysts and policymakers have not paid attention to how tax poli-cies and tax reforms may interact with gendered social norms. Yet, around theworld, there are concerns that tax systems are biased against women, and thatcontemporary tax reforms may increase the incidence of taxation on the poorestwomen while failing to generate enough revenue to fund the programmes neededto improve these women’s lives.

Drawing on a three-year eight-country study Taxation and Gender Equity out-lines why gender equity advocates need to interrogate the revenue side of publicfinances, and why tax analysts and policymakers should carefully consider thegender impacts of tax policies and tax reforms. This book develops a conceptualframework and methodology for examining and evaluating the impacts of directand indirect taxation on different types of households, based on sex compositionand employment status; presents the results of the in-country and cross-countryresearch; and suggests a set of principles and guidelines for gender-equityenhancing tax policies and tax reforms in developing and developed countries.

This is the first book to systematically examine gender and taxation within andacross countries at different levels of development. It presents original researchon the gender equity dimensions of personal income taxes, value-added taxes,excise taxes, and fuel taxes in Argentina, Ghana, India, Mexico, Morocco, SouthAfrica, Uganda and the United Kingdom. This book will be of interest to tax ana-lysts and policymakers, gender analysts and activists, and postgraduate studentsand researchers studying Public Finance, International Economics, DevelopmentStudies, Gender Studies, and International Relations, among other disciplines.

Caren Grown is Economist-In-Residence at American University, WashingtonDC, USA.

Imraan Valodia is Associate Professor in the School of Development Studies atthe University of KwaZulu-Natal, Durban, South Africa.

Taxation and Gender Equity

‘This book shows that taxation is often not neutral between the genders when itshould be, and is sometimes neutral when it should not be. Taking the perspec-tive of horizontal and vertical equity, its case studies illuminate how tax systemsand tax reforms can be inequitable across genders, and much of the time becausethe gendered structure of economy and society is not an integral part of the taxdesign debate. The book represents an important contribution to that debate, andwill be very useful to researchers and practitioners, particularly in developingcountries.’

—Ravi Kanbur, Cornell University, USA

‘As the pendulum swings once again towards greater state economic involvementand therefore an increased need for state resources, there is an urgent need tounderstand whether tax systems are biased against women and if they could bereinforcing gender inequalities. This groundbreaking volume examines thegender dimensions of tax systems in seven developing and one developed countryand is the first systematic treatment of its kind. The conceptual framework that itposes should be part of the toolkit of policy professionals, donor staff, and genderspecialists in years to come.’

—Manuel F. Montes, Development Policy and Analysis Division,UNDESA, USA

‘Equity issues are again attracting attention from academics and policy analystsconcerned with taxation. This book makes a substantial contribution to this newawareness by emphasizing the important role that gender, like other social strati-fications such as race and income, often plays in determining the impact of taxa-tion on well-being. The editors have done a fine job not only in setting out thequestions considered in the volume clearly and in context but also by establish-ing a uniform methodological approach that has been followed in the countrypapers, thus allowing them to present the results in a comparable and compre-hensible form. In turn, the case studies of mainly developing countries are richin detail and make it clear that those concerned with the extent to which taxationperpetuates or alters distributional outcomes in any country need to pay closeattention to how taxes on consumption are structured and administered as well asto such more traditional gender-related income tax issues as the treatment ofhousehold income. This book should be on the shelf of anyone concerned witheither tax policy or gender issues in both developing and developed countries.’

—Richard Bird, University of Toronto, Canada

1 Private Banking in EuropeLynn Bicker

2 Bank Deregulation and MonetaryOrderGeorge Selgin

3 Money in IslamA study in Islamic political economyMasudul Alam Choudhury

4 The Future of European FinancialCentresKirsten Bindemann

5 Payment Systems in GlobalPerspectiveMaxwell J. Fry, Isaak Kilato, SandraRoger, Krzysztof Senderowicz, DavidSheppard, Francisco Solis and JohnTrundle

6 What is Money?John Smithin

7 FinanceA characteristics approachEdited by David Blake

8 Organisational Change and RetailFinanceAn ethnographic perspectiveRichard Harper, Dave Randall andMark Rouncefield

9 The History of the BundesbankLessons for the European CentralBankJakob de Haan

10 The EuroA challenge and opportunity forfinancial marketsPublished on behalf of the SociétéUniversitaire Européenne deRecherches Financières (SUERF)Edited by Michael Artis, Axel Weberand Elizabeth Hennessy

11 Central Banking in Eastern EuropeEdited by Nigel Healey and BarryHarrison

12 Money, Credit and Prices StabilityPaul Dalziel

13 Monetary Policy, Capital Flows andExchange RatesEssays in memory of Maxwell FryEdited by William Allen and DavidDickinson

14 Adapting to Financial GlobalisationPublished on behalf of the SociétéUniversitaire Européenne deRecherches Financières (SUERF)Edited by Morten Balling, Eduard H.Hochreiter and Elizabeth Hennessy

15 Monetary MacroeconomicsA new approachAlvaro Cencini

16 Monetary Stability in EuropeStefan Collignon

17 Technology and FinanceChallenges for financial markets,business strategies and policy makersPublished on behalf of the SociétéUniversitaire Européenne deRecherches Financières (SUERF)Edited by Morten Balling, FrankLierman and Andrew Mullineux

18 Monetary UnionsTheory, history, public choiceEdited by Forrest H. Capie andGeoffrey E. Wood

19 HRM and Occupational Health andSafetyCarol Boyd

Routledge International Studies in Money and Banking

20 Central Banking SystemsComparedThe ECB, the pre-Euro Bundesbankand the Federal Reserve systemEmmanuel Apel

21 A History of Monetary UnionsJohn Chown

22 DollarizationLessons from Europe and theAmericasEdited by Louis-Philippe Rochon andMario Seccareccia

23 Islamic Economics and FinanceA glossary, 2nd EditionMuhammad Akram Khan

24 Financial Market RiskMeasurement and analysisCornelis A. Los

25 Financial GeographyA banker’s viewRisto Laulajainen

26 Money DoctorsThe experience of internationalfinancial advising, 1850–2000Edited by Marc Flandreau

27 Exchange Rate DynamicsA new open economymacroeconomics perspectiveEdited by Jean-Oliver Hairault andThepthida Sopraseuth

28 Fixing Financial Crises in the 21stCenturyEdited by Andrew G. Haldane

29 Monetary Policy andUnemploymentThe U.S., Euro-area and JapanEdited by Willi Semmler

30 Exchange Rates, Capital Flows andPolicyEdited by Peter Sinclair, RebeccaDriver and Christoph Thoenissen

31 Great Architects of InternationalFinanceThe Bretton Woods eraAnthony M. Endres

32 The Means to ProsperityFiscal policy reconsideredEdited by Per Gunnar Berglund andMatias Vernengo

33 Competition and Profitability inEuropean Financial ServicesStrategic, systemic and policy issuesEdited by Morten Balling, FrankLierman and Andy Mullineux

34 Tax Systems and Tax Reforms inSouth and East AsiaEdited by Luigi Bernardi, AngelaFraschini and Parthasarathi Shome

35 Institutional Change in thePayments System and MonetaryPolicyEdited by Stefan W. Schmitz andGeoffrey E. Wood

36 The Lender of Last ResortEdited by F.H. Capie and G.E. Wood

37 The Structure of FinancialRegulationEdited by David G. Mayes andGeoffrey E. Wood

38 Monetary Policy in Central EuropeMiroslav Beblavý

39 Money and Payments in Theoryand PracticeSergio Rossi

40 Open Market Operations andFinancial MarketsEdited by David G. Mayes and JanToporowski

41 Banking in Central and EasternEurope, 1980–2006Stephan Barisitz

42 Debt, Risk and Liquidity in FuturesMarketsEdited by Barry A. Goss

43 The Future of Payment SystemsEdited by Stephen Millard, Andrew G.Haldane and Victoria Saporta

44 Credit and CollateralVania Sena

45 Tax Systems and Tax Reforms inLatin AmericaEdited by Luigi Bernardi, AlbertoBarreix, Anna Marenzi and PaolaProfeta

46 The Dynamics of OrganizationalCollapseThe case of Barings BankHelga Drummond

47 International Financial Co-operationPolitical economics of compliancewith the 1988 Basel AccordBryce Quillin

48 Bank PerformanceA theoretical and empiricalframework for the analysis ofprofitability, competition andefficiencyJacob Bikker and Jaap W.B. Bos

49 Monetary Growth TheoryMoney, interest, prices, capital,knowledge and economic structureover time and spaceWei-Bin Zhang

50 Money, Uncertainty and TimeGiuseppe Fontana

51 Central Banking, Asset Prices andFinancial FragilityÉric Tymoigne

52 Financial Markets and theMacroeconomyWilli Semmler, Peter Flaschel, CarlChiarella and Reiner Franke

53 Inflation Theory in EconomicsWelfare, velocity, growth andbusiness cyclesMax Gillman

54 Monetary Policy over Fifty YearsHeinz Herrman (DeutscheBundesbank)

55 Designing Central BanksDavid Mayes and Geoffrey Wood

56 Inflation ExpectationsPeter J.N. Sinclair

57 The New International MonetarySystemEssays in honour of AlexanderSwobodaEdited by Charles Wyplosz

58 Taxation and Gender EquityA comparative analysis of direct andindirect taxes in developing anddeveloped countriesEdited by Caren Grown and ImraanValodia

This page intentionally left blank

Taxation and GenderEquityA comparative analysis of direct andindirect taxes in developingand developed countries

Edited byCaren Grown and Imraan Valodia

International Development Research CentreOttawa • Cairo • Dakar • Montevideo • Nairobi • New Delhi • Singapore

First published 2010by Routledge2 Park Square, Milton Park, Abingdon, Oxon, OX14 4RN

Simultaneously published in the USA and Canadaby Routledge270 Madison Avenue, New York, NY 10016

Routledge is an imprint of the Taylor & Francis Group, an informabusiness

Published in association with theInternational Development Research CentrePO Box 8500, Ottawa, ON K1G 3H9, Canadawww.idrc.ca / [email protected] 978–1–55250–469–7 (ebook)

© 2010 selection and editorial matter; Caren Grown and Imraan Valodia,individual chapters; the contributors

Typeset in Times New Roman byBook Now Ltd, LondonPrinted and bound in Great Britain byCPI Antony Rowe, Chippenham, Wiltshire

All rights reserved. No part of this book may be reprinted or reproducedor utilised in any form or by any electronic, mechanical, or other means,now known or hereafter invented, including photocopying and recording,or in any information storage or retrieval system, without permission inwriting from the publishers.

British Library Cataloguing in Publication DataA catalogue record for this book is available from the British Library

Library of Congress Cataloging in Publication DataTaxation and gender equity: a comparative analysis of direct and indirecttaxes in developing and developed countries/edited by Caren Grown andImraan Valodia.

p.cmInlcudes bibliographical references and index.1. Taxation—Developing countires. 2. Taxation—Developed countreis. 3.Fiscal policy—Developing countires 4. Fiscal policy—Developedcountires 5. Women—Government policy—Developing countires 6.Women—Government policy—Developed countires I. Grown, Caren II.Valodia, Imraan.HJ2351.7.T385 2010336.2009172'4—dc22 2009043115

ISBN10: 0–415–56822–6 (pbk)

ISBN13: 978–0–415–56822–7 (pbk)

Contents

List of figures xiList of tables xvNotes on contributors xixAcknowledgements xxiiiList of abbreviations xxvii

1 Taxation and gender equality: A conceptual framework 1CAREN GROWN

2 Methodology and comparative analysis 23CAREN GROWN AND HITOMI KOMATSU

3 Gender equality and taxation in Argentina 64CORINA RODRÍGUEZ ENRÍQUEZ, NATALIA GHERARDI

AND DARÍO ROSSIGNOLO

4 Gender equality and taxation in India: An unequal burden? 94PINAKI CHAKRABORTY, LEKHA CHAKRABORTY,

KRISHANU KARMAKAR AND SHASHI M. KAPILA

5 Gender analysis of taxation in Mexico 119LUCÍA C. PÉREZ FRAGOSO AND FRANCISCO COTA GONZÁLEZ

6 An investigation into the gender dimensions of taxationin Ghana 151ERNEST ARYEETEY, ISAAC OSEI-AKOTO, ABENA D. ODURO

AND ROBERT DARKO OSEI

7 Gender equality and taxation in Morocco 179AHMED EL BOUAZZAOUI, ABDESSALAM FAZOUANE,

HIND JALAL AND SALAMA SAIDI

8 Gender equality and taxation in South Africa 206DEBBIE BUDLENDER, DANIELA CASALE AND IMRAAN VALODIA

9 Gender equality and taxation in Uganda 233SARAH SSEWANYANA, LAWRENCE BATEGEKA,

MADINA GULOBA AND JULIUS KIIZA

10 Gender equality and taxation: A UK case study 261JÉRÔME DE HENAU, SUSAN HIMMELWEIT AND CRISTINA SANTOS

11 Conclusion and policy recommendations 299IMRAAN VALODIA

Index 314

x Contents

Figures

3.1 Argentina: Gross tax burden, 1991–2007 663.2 Argentina: Composition of tax revenue as percentage of

total revenue 673.3 Argentina: Total tax incidence by quintile and household type 773.4 Argentina: VAT incidence by quintile and household type 783.5 Argentina: Excise incidence by quintile and household type 793.6 Argentina: Fuel tax incidence by quintile and household type 803.7 Argentina: Basic food basket incidence by quintile and 81

household type3.8 Argentina: VAT zero rate on food simulation – total incidence –

by quintile and household type 843.9 Argentina: Combined policy simulation – total incidence – by

quintile and household type 874.1 India: Indian labour force by sex: rural and urban differences 954.2 India: Tax to GDP ratio, 1950–51 to 2006–07 994.3 India: Structure of taxes, 1990–91 1004.4 India: Structure of taxes, 2006–07 1004.5 West Bengal: The structure of tax revenues, 2005–06 1054.6 West Bengal: Total VAT incidence, across household type 1134.7 West Bengal: Total tax incidence, across household type 1144.8 West Bengal: Total excise tax incidence, across household type 1144.9 West Bengal: Food tax incidence, across household type 1155.1 Mexico: Incidence on expenditure: total indirect tax incidence by

household type 1325.2 Mexico: Incidence on expenditure: total indirect tax incidence by

household type and location 1325.3 Mexico: Incidence on expenditure: total indirect tax incidence by

occupational status and quintile 1335.4 Mexico: Incidence on income: total indirect tax incidence by

household type 135

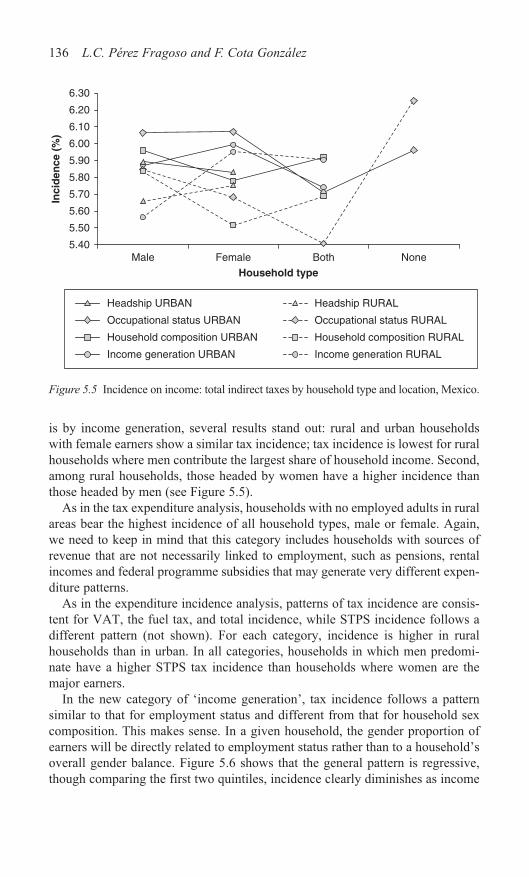

5.5 Mexico: Incidence on income: total indirect taxes by household type and location 136

5.6 Mexico: Incidence on income: total indirect taxes by incomegeneration, number of dependants and quintile 137

5.7 Mexico: Simulations: tax incidence on expenditure 1445.8 Mexico: Simulations: tax incidence on expenditure by quintile 1455.9 Mexico: Simulations: tax incidence on income 147

5.10 Mexico: Simulations: tax incidence on income by quintile 1486.1 Ghana: Composition of central government revenue 1536.2 Ghana: Incidence of indirect tax on fuel for transport by

household type and expenditure quintile 1716.3 Ghana: Incidence of indirect tax on household fuel by

household type and expenditure quintile 1716.4 Ghana: Incidence of indirect tax on clothing and footwear by

household type and expenditure quintile 1726.5 Ghana: Incidence of indirect tax on tobacco by household

type and expenditure quintile 1736.6 Ghana: Incidence of indirect tax on alcoholic beverages by

household type and expenditure quintile 1736.7 Ghana: Incidence of indirect tax on communication by

household type and expenditure quintile 1747.1 Morocco: Economically active rate by sex and residence area in 2007 1807.2 Morocco: Evolution of tax revenue, 1996–2007 1827.3 Morocco: Structure of tax revenue in 2007 1837.4 Morocco: Evolution of tax revenue structure, 1996–2007 1847.5 Morocco: Tax incidence by gender, employment status and quintile 1937.6 Morocco: Excise tax incidence by gender, employment status

and quintile 1948.1 South Africa: Tax/GDP ratio: 1994–2010 2088.2 South Africa: Total tax incidence by employment status, quintile and

presence of children 2218.3 South Africa: VAT incidence by employment status, quintile

and presence of children 2218.4 South Africa: Excise incidence by employment status, quintile and

presence of children 2228.5 South Africa: Fuel levy incidence by employment status, quintile

and presence of children 2228.6 South Africa: Food tax incidence by employment category and

quintile 2278.7 South Africa: Alcohol tax incidence by employment category

and quintile 2278.8 South Africa: Tobacco tax incidence by employment category

and quintile 2289.1 Uganda: Workforce composition, persons aged over 18 years

by sex 234

xii Figures

Figures xiii

9.2 Uganda: Patterns and trends of tax type in total centralgovernment revenue 238

9.3 Uganda: Incidence of indirect tax by type of tax and householdtypology 244

9.4 Uganda: Incidence of tax by sex of head and expenditure quintile 2479.5 Uganda: Tax incidence by employment status and expenditure

quintile 2489.6 Uganda: Incidence of non-zero expenses on taxable consumption

of categories by sex of head 2509.7 Uganda: Percentage change in VAT incidence with salt zero-rated 2579.8 Uganda: Percentage change in indirect tax incidence with paraffin

levy halved 25810.1 United Kingdom: Total government receipts and taxes (incl.

national insurance contributions) as a percentage of GDP,1978–79 to 2007–08 plus projections to 2013–14 264

10.2 United Kingdom: Composition of government current receipts 2007–08, 1996–97 and 1978–79 265

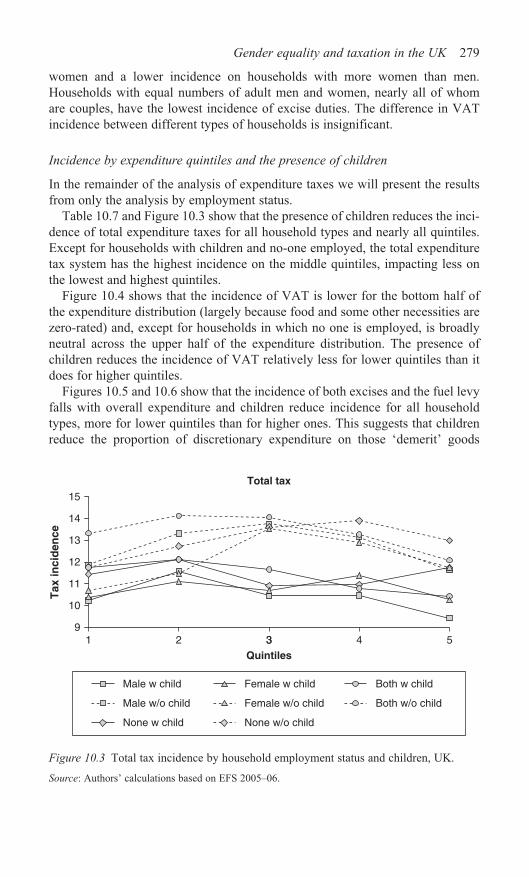

10.3 United Kingdom: Total tax incidence by household employment status and children 279

10.4 United Kingdom: VAT incidence by household employment status and children 281

10.5 United Kingdom: Excise duty incidence by household employmentstatus and children 281

10.6 United Kingdom: Fuel levy incidence by household employmentstatus and children 282

10.7 United Kingdom: Commodity incidence by employment status across quintiles – fuel for transport 286

10.8 United Kingdom: Commodity incidence by employment status across quintiles – alcohol 286

10.9 United Kingdom: Commodity incidence by employment status across quintiles – tobacco 287

10.10 United Kingdom: Commodity incidence by employmentstatus across quintiles – adult clothing 288

10.11 United Kingdom: Commodity incidence by employment status across quintiles – domestic services 288

10.12 United Kingdom: Commodity incidence by employment status across quintiles – meals out 289

10.13 United Kingdom: Policy simulation: percentage change from base scenario – increasing fuel excise duty 289

10.14 United Kingdom: Policy simulation: percentage change from base scenario – standard rating all food 291

10.15 United Kingdom: Policy simulation: percentage change from base scenario – full stimulus package 293

This page intentionally left blank

Tables

1.1 Types of explicit and implicit bias in PIT 122.1 Key deductions and exemptions in PIT (excluding those

for non-earning spouses and dependant children) 262.2 Tax relief for non-earning spouses and dependant children 292.3 On which type of household does the PIT incidence fall at each

income level? 312.4 Zero rating and exemptions 382.5 Which quintile bears the highest incidence of each type of tax? 402.6 Incidence of indirect taxes by household type 412.7 Which household type, by quintile, bears the highest tax

incidence on selected commodity items? 433.1 Argentina: Income tax applicable by income bracket 703.2 Argentina: Annual individual personal allowances 703.3 Argentina: Monthly Monotributo payments: activities related

to the hiring and/or performance of services 713.4 Argentina: Monthly Monotributo payments: other activities 713.5 Argentina: Household composition and income by type 723.6 Argentina: Income tax by type of household and income source 723.7 Argentina: Excise tax rates 743.8 Argentina: Tax rates on fuels 753.9 Argentina: Overall incidence by household type: tax as

percentage of expenditure 763.10 Argentina: Incidence by quintile: tax as percentage of expenditure 773.11 Argentina: Tax incidence by type of tax: base estimates and

simulation of zero tax on food products 833.12 Argentina: Excise tax rates 853.13 Argentina: Estimated revenue comparison 863.14 Argentina: Tax incidence by type of tax: base estimates and

overall tax simulation 86A.1 Estimate of PIT by household type and contribution category 914.1 India: Gender disparities in Indian labour force participation

rates, 2004–05 95

4.2 India: Employment structure of the labour force, 2004–05 964.3 India: Employment by sector, 2004–05 964.4 India: Employment in organized sectors 974.5 India: Ratio of female to male wages 984.6 India: Wage/salary per day received by regular salaried

employees, 2004–05 984.7 India: Income tax rates and brackets, 2008–09 1024.8 India: Income tax paid by dual- and single-income household categories 1044.9 India: Number of effective taxpayers 104

4.10 West Bengal: Nature of commodities and the applicable VAT rate 1054.11 West Bengal: Tax rate on commodities outside the VAT 1064.12 West Bengal: Incidence of consumption tax in households 1074.13 West Bengal: Overall incidence by household type 1084.14 West Bengal: Rural and urban tax incidence by household type 1094.15 West Bengal: Incidence of sex composition, presence of children,

and quintile 1104.16 West Bengal: Tax incidence for each consumption category by sex

composition and quintile 1114.17 India: Policy simulation 1: tax on all food = 0 1174.18 India: Policy simulation 2: tax on tobacco doubled 117

5.1 Mexico: Economically active population by job position, 2006 1205.2 Mexico: Economically active population by income level, 2006 1215.3 Mexico: Federal revenue by source, 2005–08 1225.4 Mexico: Percentage structure of federal government revenues, 2005–08 1235.5 Mexico: Rates for calculating monthly annual income tax, 2001

and 2006 1265.6 Mexico: Earnings schedule for wage credit, 2006 1275.7 Mexico: Tax calculation and application of wage credit 1275.8 Mexico: VAT rates, 2006 1295.9 Mexico: Revenue from indirect taxes 130

5.10 Mexico: Household categories 1315.11 Mexico: Total indirect tax incidence by consumption categories

and employment status 1405.12 Mexico: Estimate of additional tax revenue through the application

of standard VAT rate to exempt or zero-rated products 1436.1 Ghana: Tax revenue–GDP ratio 1526.2 Ghana: Personal income tax rates, 2000–06 1566.3 Ghana: Hypothetical annual income and tax paid by household

with three children in school 1596.4 Ghana: Excise tax rates 1616.5 Ghana: Tax as a percentage of ex-pump price, January 2006 1616.6 Ghana: Overall indirect tax incidence by household type 163

xvi Tables

Tables xvii

6.7 Ghana: Tax incidence, by employment status, presence of childrenand quintile 164

6.8 Ghana: Tax incidence for main commodity groups by employmentstatus and quintile 166

6.9 Ghana: Tax incidence for main commodity groups by HH adultsex composition and quintile 169

6.10 Ghana: Effects of changes in indirect tax rates on tax incidenceby household type and expenditure quintile 176

7.1 Morocco: Women’s payroll share by sector and year 1817.2 Morocco: Household classification 1817.3 Morocco: Cross-tabulation of household categories by employment

status and sex composition 1827.4 Morocco: Normal PIT rates on salary revenues in 2009 1877.5 Morocco: Distribution of employed people across tax brackets

by sex, 2007 1887.6 Morocco: Comparison of effective average individual tax rates 1897.7 Morocco: Overall incidence by household type 1937.8 Morocco: Tax incidence by gender and employment status,

presence of children and quintile 1957.9 Morocco: Expenditure on basic services and commodities by

household type 1967.10 Morocco: Tax incidence of commodities, by household

employment status and quintile 1977.11 Morocco: Simulation 1: Tax incidence using 2009 tax rates

applied to yr 2000 expenditure (by quintile, household employment category and children) 201

7.12 Morocco: Simulation 2: Tax incidence with selective rate increasesand decreases applied to yr 2000 expenditure (by quintile,presence of children and employment category) 202

8.1 South Africa: Tax structure, 1988–2008 2088.2 South Africa: Distribution of employed people across tax

brackets by sex (September 2005) 2108.3 South Africa: Personal income tax rates, 2007–08 2108.4 South Africa: Hypothetical tax burden of PIT for households,

2007–08 2158.5 South Africa: Indirect tax rates and specific duties 2178.6 South Africa: Overall indirect tax incidence by household type 2198.7 South Africa: Indirect tax incidence by employment status,

presence of children and quintile 2208.8 South Africa: Indirect tax incidence for main commodity groups by

employment status and quintile 224

8.9 South Africa: Indirect tax incidence and government revenueeffect of Vat and zero-rating (selected items) 229

9.1 Uganda: Median employment earnings per person per year,2005–06 235

9.2 Uganda: Distribution of household typology by income 2369.3 Uganda: Share of type of tax to GDP and total tax revenue,

2002–07 2379.4 Uganda: Share of PAYE by income tax bracket 2399.5 Uganda: Tax impact on households by earner 2429.6 Uganda: Distribution of household type by PAYE income tax

bracket and gender 2439.7 Uganda: Incidence of indirect tax by tax type and household

typology 2449.8 Uganda: Incidence of tax by employment status and presence

of children 2469.9 Uganda: Incidence of indirect tax for consumption categories

by employment status, presence of children and quintile 25110.1 United Kingdom: PIT brackets and rates by source of

income, 2008–09 26710.2 United Kingdom: Main taxable personal income, exemptions

and reductions, 2008–09 26910.3 United Kingdom: Tax incidence (income tax + NICs – tax credits)

as percentage of gross household income, couple with two children 273

10.4 United Kingdom: VAT rates and liable goods, April 2005 27510.5 United Kingdom: Excisable goods: incidence of duty and

tax for typical items, April 2005 27710.6 United Kingdom: Overall incidence by household type 27810.7 United Kingdom: Incidence by employment status, presence

of children and quintile 28010.8 United Kingdom: Tax incidence for main commodity groups

by employment status and quintile 28310.9 United Kingdom: Effects of changes in indirect tax rates on

tax incidence by employment status and expenditure quintile 29010.10 United Kingdom: Effects of government’s 2008 stimulus

package on tax incidence by employment status andexpenditure quintile 292

xviii Tables

Contributors

Ernest Aryeetey is the Director of the Institute of Statistical, Social andEconomic Research (ISSER) of the University of Ghana, Legon, Accra. He isa current member of the Boards of the United Nations University WorldInstitute for Development Economics Research (UNU-WIDER) and theGlobal Development Network. He studied Economics at the University ofGhana and holds a PhD from the University of Dortmund, Germany.

Lawrence Bategeka is a Senior Research Fellow with the Economic PolicyResearch Centre at Makerere University in Kampala. His main areas ofresearch are public sector policy, vulnerability, and institutional performance.Mr Bategeka holds a Master’s Degree in Economic Policy and Planning fromMakerere University, and a Master’s Degree in Education from the Universityof Bristol, UK.

Debbie Budlender is a specialist researcher with the Community Agency forSocial Enquiry (CASE), a non-governmental organization working in the areaof social policy research. Previous employment includes administrative andresearch work for trade unions, and research for the Cape Town University-based Southern African Labour and Development Research Unit at the time ofthe Second Carnegie Enquiry into Poverty.

Daniela Casale is a Senior Research Fellow in the School of DevelopmentStudies at the University of KwaZulu-Natal, Durban, South Africa. She worksmainly in the fields of labour and household economics, and is particularlyinterested in the gender aspects of development. She completed her PhD inEconomics at the University of Natal in 2003.

Lekha Chakraborty is a Fellow at the National Institute of Public Finance andPolicy (NIPFP), New Delhi, India. Her research areas are macroeconomicissues in public finance, fiscal decentralization, gender budgeting, and humandevelopment. She holds an MPhil in Applied Economics and a PhD inEconomics from the Centre for Development Studies at Jawaharlal NehruUniversity, New Delhi.

Pinaki Chakraborty is a Professor at the National Institute of Public Financeand Policy (NIPFP), New Delhi, India. His main research areas are macroeco-

nomics and public finance. He was a consultant for the Eleventh FinanceCommission of India, and holds both a PhD in Economics and an MPhil inApplied Economics from the Centre for Development Studies, JawaharlalNehru University, New Delhi.

Jérôme De Henau is a Lecturer in Economics at the Open University. His cur-rent research areas include gender, intra-household inequalities and social poli-cies across Europe. He holds a PhD in Economics and Management from theFree University of Brussels (ULB), Belgium.

Ahmed El Bouazzaoui works in the Moroccan Ministry of Finance. His researchfields include taxation, gender, personnel wages and human resource manage-ment. He holds a Master’s Degree in Information Sciences from the Instituteof Information Sciences, Rabat, Morocco, along with a Certificate ofManagement from the Business School of Al Akhawayn University, Ifrane,Morocco, and a Certificate of Management from the Institute of Managementand Business Administration ISCAE, Rabat, Morocco.

Corina Rodríguez Enríquez is a researcher at the National Council ofScientific Research (Consejo Nacional de Investigaciones Científicas yTécnicas) and the Interdisciplinary Centre for the Study of Public Policies(Centro Interdisciplinario para el Estudio de Políticas Públicas), Argentina.She works on issues related to labour markets, the care economy, poverty andincome distribution, and social and fiscal policies. She holds a Master’sDegree in Public Policy and Administration from the Institute of SocialStudies, The Hague, The Netherlands and a PhD in Social Sciences fromFacultad Latinoamericana de Ciencias Sociales (FLACSO), Argentina.

Abdessalam Fazouane is a statistician demographer. He is Professor of HigherEducation at the National Institute of Statistics and Applied Economics(INSEA). He is a specialist in the areas of population, gender and development,and statistical sampling.

Lucía C. Pérez Fragoso is an economist. She has been working for the past nineyears on gender budget analysis and formulation in the non-governmentalorganization, Equidad de Género: Ciudadanía, Trabajo y Familia (GenderEquity: Citizenship, Work and Family), located in Mexico City. She holds aMaster’s Degree in Economics from the University of Manchester, England.

Natalia Gherardi received an LLM with honours from the London School ofEconomics and Political Sciences (LSE). She is also the Executive Director ofEquipo Latinoamericano de Justicia y Género (ELA) in Argentina.

Francisco Cota González is an independent consultant dealing in strategic plan-ning, economic analysis and forecasting, and part-time professor in the eco-nomics departments of Universidad Anahuac and Universidad del Valle deMéxico. He holds a Bachelor’s Degree in Economics from the UniversidadAnahuac, Mexico City, and a Master’s Degree in Development Banking fromAmerican University, Washington, DC.

xx Contributors

Caren Grown is Economist-In-Residence at American University, Washington,DC. Her current research focuses on assets and women’s well-being, genderequality and public finance, and international trade and gender. She is anAssociate Editor of Feminist Economics and holds a PhD in Economics fromthe New School for Social Research in New York City.

Madina Guloba is an Assistant Research Fellow at the Economic Policy ResearchCentre at Makerere University, Uganda. She holds a Master’s Degree inEconomics from the University of Dar Es Salaam under the CollaborativeMasters Programme of the African Economic Research Consortium.

Susan Himmelweit is Professor of Economics at the Open University. Herresearch is on gender issues in economics. She is an Associate Editor of FeministEconomics, past president of the International Association for FeministEconomics (IAFFE), and the first chair of the UK Women’s Budget Group.

Hind Jalal works in the Moroccan Ministry of Economy and Finance. Her areasof research include gender and macroeconomics, gender-responsive budgeting,and international trade and investment. She holds a PhD in Law and Economyof Development from Nice Sophia Antipolis University, France, a Certificateof Management from the Business School of Al Akhawayn University, Ifrane,Morocco, and a Management Degree from the Institute of Management andBusiness Administration ISCAE, Rabat, Morocco.

Shashi M. Kapila is currently practising as an advocate and tax consultant ondirect taxes. From 1992–2001, she was Head, Taxation Unit of ANZ GrindlaysBank and from 1976–92 worked as an Officer of the Indian Revenue Service-Direct Taxes and in the Indian Income Tax Department in various capacities.She is a member of the International Fiscal Association.

Krishanu Karmakar is currently a graduate student at the Andrew YoungSchool of Policy Studies, Georgia State University, USA. He holds a Master’sDegree in Economics from the Delhi School of Economics and worked at theNational Institute of Public Finance and Policy, New Delhi, India.

Julius Kiiza teaches political economy of development and public policy analy-sis in the Department of Political Science and Public Administration atMakerere University. He holds a Bachelor’s (Honours) Degree from MakerereUniversity, and received both a First Class Master of Public Policy and a PhDin economics from the University of Sydney, Australia.

Hitomi Komatsu is a doctoral candidate in Economics at the AmericanUniversity, Washington, DC. Her research interests include labour, fertilityand time use. She holds a Bachelor’s Degree in Economics from UniversityCollege London and a Master’s Degree in Development Economics from theSchool of Oriental and African Studies at the University of London, UK.

Abena D. Oduro is a Senior Lecturer in the Department of Economics at theUniversity of Ghana, Legon, Accra. During 2003, she was a Visiting Lecturer,Council on African Studies, Yale University, New Haven, USA. She holds a

Contributors xxi

Master’s (Honours) Degree in Political Economy and Geography and an MLittin Political Economy from the University of Glasgow, Scotland.

Robert Darko Osei is a Research Fellow in the Economics division of theInstitute of Statistical, Social and Economic Research (ISSER), of theUniversity of Ghana, Legon, Accra. He is currently involved in the develop-ment of a micro-simulation model for Ghana and was part of the Ghana teamthat developed the MCA-Ghana programme, in the capacity as lead economist.

Isaac Osei-Akoto has been working with the Institute of Statistical, Social andEconomic Research (ISSER), University of Ghana, Legon, as a ResearchFellow since 1999. His main research areas relate to household economics,poverty and the provision of public goods and services. He holds a PhD inDevelopment Economics.

Darío Rossignolo has been working as a consultant for various internationalorganizations and is currently a Professor of Macroeconomics and PublicFinance at the University of Buenos Aires, Argentina. His main research areasare public sector economics and the extra fiscal effects of fiscal policy. He is adoctoral candidate in Economics at the University of La Plata in Argentina, andholds a Bachelor’s Degree in Economics from the University of Buenos Airesand a Master’s Degree in Economics from the University Di Tella in Argentina.

Salama Saidi is a former United Nations Regional Advisor on Gender, Populationand Development, and currently President of the Rawabit Association, Morocco,and an international consultant on gender and development. She has conductedresearch in the social sciences with a focus on gender, population and reproduc-tive health, and programme development, monitoring and evaluation. She holds aPhD and a Master’s Degree in Demography from the University of Pennsylvania,and a Master’s Degree in Economics from Temple University, USA.

Cristina Santos is a Lecturer in Economics at the Open University and a researchfellow at the Center for Advanced Studies in Management and Economics ofthe University of Évora (CEFAGE-UE). Her research interests focus ongender, individual and intrahousehold decision-making, poverty, human devel-opment, and domestic violence. She holds a Master’s Degree in Economicsfrom University College London, UK, where she is studying for a PhD.

Sarah Ssewanyana is Senior Research Fellow at the Economic Policy ResearchCentre, Makerere University, Kampala, Uganda. She has carried out appliedpolicy-relevant research in the areas of income poverty, food security, health,education, labour-related issues and on issues related to social service deliveryand has published widely on these topics. She holds a PhD in AgriculturalEconomics from the University of Sydney, Australia.

Imraan Valodia is Associate Professor in the School of Development Studies at theUniversity of KwaZulu-Natal, South Africa. His current research interests includegender and economic policy, the informal economy, and industrial policy. Heholds a doctorate in Economics from the University of KwaZulu-Natal.

xxii Contributors

Acknowledgements

This book is the result of a two-and-a-half-year project which examined thegender dimensions of tax policies and tax reforms in eight countries: Argentina,Ghana, India, Mexico, Morocco, South Africa, Uganda and the United Kingdom.The project emerged from discussions at the workshops and international confer-ences of the Gender and Macroeconomics International Working Group (GEM-IWG), organized at the University of Utah, Salt Lake City, in 2004 and 2005, ofwhich several authors are members. It grew to include individuals and institutionsfrom several countries and policy and academic networks.

The project had three goals: (1) to advance understanding of the genderimpacts of tax policies and tax reforms in countries at various levels of develop-ment; (2) to engender and improve current tools and techniques for analysing taxpolicies and reforms; and (3) to influence tax policy-makers in the focus coun-tries and internationally. Undertaking the work involved multiple expertise andexperiences; within each country, a project team was constituted, comprised ofpublic finance or development economists, feminist economists, lawyers, andpolitical scientists. The institutional partners in each country are:

Argentina Centro Interdisplinario para el Estudio de PolíticasPublicas (CIEPP – Interdisciplinary Centre for the Studyof Public Policies)

Ghana Institute for Statistical, Social and Economic Research(ISSER), University of Ghana

India National Institute for Public Finance Policy (NIPFP)Mexico Equidad de Género: Ciudadana, Trabajo y Familia A.C.

(Equidad)Morocco Rawabit AssociationSouth Africa School of Development Studies, University of

KwaZulu-NatalUganda Economic Policy Research Centre (EPRC), Makerere

UniversityUnited Kingdom Open University

In addition to chapters in this book, each of the country teams also produced threeother outputs in their local languages: (1) a country report on personal incometaxes; (2) a country report on the incidence of indirect taxes; (3) and a policybrief. The chapters in this book synthesize those longer country papers and thereader may wish to consult those papers for more details on methodology andadditional findings not discussed herein.

The project was made possible through the generous financial assistance pro-vided by the International Development Research Centre (Canada), the FordFoundation, the Government of Japan through the United Nations DevelopmentProgramme/Japan Women in Development Fund (UNDP/JWIDF) and the UnitedNations Development Programme (UNDP) Gender Team.

The policy focus of this project cannot be overstated. Over the duration of theproject we have consistently engaged policy-makers at both national and interna-tional levels. Each of the country teams engaged with the relevant tax and treasuryauthorities in their countries, sharing the research findings and pointing to the needto consider adequately the gender implications of tax policies and reforms. At theinternational level, we have had close engagement with a number of key actorsincluding the United Nations, the United Nations Development Programme(UNDP), the World Bank and the International Monetary Fund (IMF).

Participants at the international conference on Gender and Taxation:Improving Equity and Revenue Generation, organized by the UNDP, theAmerican University and the University of KwaZulu-Natal, and hosted by theWorld Bank in December 2008, gave excellent comments on the interim countrypapers, which improved them considerably. The UNDP and the World Bank pro-vided both financial and in-kind support for that conference. The InternationalAssociation of Feminist Economics (IAFFE) also granted us a podium for pre-senting, discussing and disseminating this research on gender equity and taxationduring two annual conferences in 2008 and 2009. The United Nations ResearchInstitute for Social Development (UNRISD) provided support to Imraan Valodia,where he was based on a visiting fellowship, during the final editing states of thisbook and gave him a platform for presenting and discussing this work.

We owe thanks to many people who gave us both guidance and personal andprofessional support during the various stages of the project. We would especiallylike to thank Martha Melesse, Brent Herbert-Copley and Andres Rius fromIDRC, and Winnie Byanyima and Anna Falth from UNDP for their unwaveringinterest in, enthusiasm for and commitment to this project. Shaianne Osterreichprovided useful feedback and ideas to the teams at two project meetings. DebbieBudlender, Diane Elson, Susan Himmelweit, Janet Stotsky and Stephen Youngerserved as members of the project’s Technical Advisory Group. They each con-tributed generous amounts of time and provided words of wisdom, critical intel-lectual guidance and constructive feedback. We owe them our deepest gratitudeand absolve them of any mistakes, for which we are entirely responsible!

The project would also like to recognize Hitomi Komatsu, who provided excel-lent research support throughout the project. We are looking forward to contin-ued collaboration with her on issues of gender and taxation. We received

xxiv Acknowledgements

Acknowledgements xxv

substantial administrative support from our colleagues. At American University,Marie-Ellen Ehounou kept the project focused and on track. At the University ofKwaZulu-Natal, Kanagie Naidoo assisted with the financial administration, andPriya Gayadeen assisted with logistics for various project meetings. We thank allof these colleagues for their diligence and hard work.

Ahmed Elbouazzaoui, Hind Jalal and Salama Saidi, from Rawabit in Morocco,and Corina Rodríguez-Enríquez and Agustina Fornasier, from CIEPP inArgentina, hosted valuable meetings for the project teams to develop the concep-tual and methodological issues and to work through earlier drafts of the countrypapers. We thank them for their warm hospitality and generous contributions oftime and help.

Karen Judd edited all the chapters of this book. Her unique talents improvedthe manuscript immeasurably, and we could not have finished this book withouther assistance.

Finally, we would like to acknowledge the members of the country teams, truepartners who also became good friends. We thank each of them for their adven-turous intellectual spirits, collegiality, timeliness, and good humour. We look for-ward to future opportunities for partnership in a second phase of the project.

Caren Grown, Washington, DCImraan Valodia, Durban

July 2009

This page intentionally left blank

Abbreviations

CASE Community Agency for Social Enquiry (South Africa)CEDAW Convention on the Elimination of All Forms of Discrimination

Against WomenCIT corporate income taxCOICOP Classification of Individual Consumption by PurposeCONAPO National Population Council (Mexico)CTL Commercial Transaction LevyEFS Expenditure and Food SurveyENIGH National Household Income and Expenditure Survey (Mexico)ENOE National Occupational Employment Survey (Mexico)FISIM Financial intermediation services indirectly measuredGDP Gross Domestic ProductGEM-IWG Gender and Macroeconomics International Working GroupGLSS 5 Ghana Living Standards Survey 5GNP Gross National ProductHH HouseholdHUF Hindu Undivided Family (India)IAFFE International Association for Feminist EconomicsIDE Tax on Cash Deposits (Mexico)IETU Corporate Flat Rate Tax (Mexico)IMF International Monetary FundINEGI Instituto Nacional de Estadística y Geográfia (National Institute

of Statistics) (Mexico)INSEA National Institute of Statistics and Applied EconomicsISSER Institute of Statistical, Social and Economic Research (Ghana)LST Local Service Tax (Uganda)MDGs Millennium Development GoalsNHIL National Health Insurance Levy (United Kingdom)NICs National Insurance Contributions (United Kingdom)NIPFP National Institute of Public Finance and Policy (India)PEAP Poverty Eradication Action PlanPIT Personal Income TaxRPI Retail Price Index (Uganda)

SARS South African Revenue ServicesSHCP Secretaría de Hacienda y Crédito Público (Mexico)SITE Standard Income Tax on Employees (South Africa)SSNIT Social Security and National Insurance TrustSTPS Secretaría del Trabajo Prévision Social (Mexico)STPS Special Tax on Production and Services (Mexico)UNDP United Nations Development ProgrammeUNRISD United Nations Research Institute for Social DevelopmentURA Uganda Revenue AuthorityVAT Value-Added TaxWFTC Working Families Tax Credit (United Kingdom)

xxviii Introduction

1 Taxation and gender equalityA conceptual framework

Caren Grown

Introduction

Governments everywhere grapple with the problem of generating enough resourcesto reduce poverty and fund essential public services. Fiscal policy, including tax-ation, is at the heart of the debate on which services government should provideand who should pay for them, including the share paid by men and women asconsumers, workers, and employers. The global financial crisis of 2008–09 hasthrown millions of people into poverty worldwide, highlighting the need forstronger, more equitable and efficient tax systems that can ensure a stable flow ofpublic services, even during periods of downturn.

Over the decades, many countries have embarked on extensive reforms of theirtax systems, with some achieving lasting improvements and others managing onlyshort-term or transitional improvements that are gradually undone. Since the1990s, several trends have been seen worldwide. These include reforms to personalincome tax systems to broaden their bases and reduce the highest marginal tax rates,reduction of the highest corporate income tax rates, increasing reliance on broad-based value-added taxes (VATs), and reduced reliance on trade taxes through a flat-tening of the tax structure and removal of discrimination against imported goods inboth indirect and trade taxes (Bahl and Bird 2008). Countries have sought to makeup revenue losses from declining trade taxes, in particular, through a shift to indi-rect taxes, especially the VAT. More than 125 countries now have some form of aVAT, and it is the mainstay of revenue systems in much of the world (Bird 2005).

One of the cornerstones of tax policy, and central to tax reform efforts, is theissue of equity, along with issues of efficiency and ease of administration. A keychallenge facing developing countries is to be able to generate sufficient publicresources in a way that does not place an undue burden on the poor and marginal-ized. Since women are particularly vulnerable to poverty, systematic and robustassessments of the manner in which developing countries are attempting to increasetheir revenue pool and the impact of this on poor women are urgently needed.

To date, however, neither the tax literature nor public debates have adequatelyaddressed how gender-based differences in behaviour affect tax equity consider-ations and outcomes. For example, an assessment of the effect of consumption

taxes on patterns of regressivity, which ignore the fact that men and women havesystematically different expenditure patterns, will fail to capture the differentialeffect of these reforms on different types of households – single parent versusdual-earner parent – across the income distribution.

This book is the result of a two-and-a-half-year project which examined thegender dimensions of tax policies and tax reforms in eight countries: Argentina,Mexico, South Africa, Ghana, Uganda, Morocco, India and the United Kingdom.Like other studies, this volume is concerned with who contributes the greatestshare of their income in taxes. But the work in this volume broadens the under-standing of equity in taxation to include gender differences as a core element indefining notions of tax equity and outcomes. Because women are more likelythan men to be poor, understanding where gender inequities are of greatest con-cern necessarily involves analysis by income and hence a specific focus ongender inequalities among the poor.

The book makes several unique contributions. To evaluate gender equality intaxation, we first develop a conceptual framework based on the Convention for theElimination of All Forms of Discrimination Against Women (CEDAW) and prin-ciples used in the economics literature on taxation. Second, we develop a consistentempirical methodology to analyse on which households – categorized by selectedgender attributes – the incidence of selected indirect taxes is highest. We apply thismethodology to recent household-level data from the eight countries. Third, thefocus on developing countries (seven out of eight countries in our sample) isunique, as virtually nothing has been written on the gender impacts of taxation inthese countries. Finally, based on our conceptual framework and our empirical find-ings, we develop a set of principles for evaluating the gender equity aspects of taxpolicy that we hope will influence real-world tax policy design and implementation.

Tax concepts and issues: a brief summary

A frequently used summary measure of taxation, for purposes of internationalcomparison, is the ratio of total tax revenue to Gross Domestic Product (GDP). Ahigh tax/GDP ratio has also been used by feminist economists as an indicator ofresources that are available for expenditure that promotes poverty reduction andgender equality. This ratio varies widely among both developed and developingcountries. Overall, as countries develop, they tend to be able to generate greaterrevenue relative to GDP. Fox and Gurley (2005) use data from 165 countries andreport that tax ratios range from well under 10 per cent in several countries, mostof which are small and low-income (such as Myanmar, Nepal, Guatemala, Haiti,Niger, Chad and the Central African Republic), to well over 40 per cent in manycountries, mostly in Western Europe (The Netherlands, Denmark, Italy, Franceand Sweden). But these patterns are not uniform, and even among countries at asimilar level of income, there can be considerable variation in revenue yields. Forinstance, some lower-income countries, such as the Democratic Republic of Congo,Sudan, Ukraine, and Belarus, also had high tax ratios. Similarly, some higher-income countries, such as the United States, had notably lower tax ratios than others

2 C. Grown

in that group. A low tax/GDP ratio may reflect an inadequate tax system and/orweak tax administration, or there may be other substantial non-tax sources ofincome, such as petroleum in Nigeria. Alternatively, it may be the result of con-scious policy such as in South Africa where a national tax/GDP target was set in1996 at no more than 25 per cent, or the United States, where it reflects a con-scious effort in recent decades to reduce taxes on high-income earners.

The countries in this volume also have widely varying tax revenue to GDPratios, from 9–15 per cent in Mexico, Uganda and India, to 20 per cent in Ghana,and Morocco, to 27–28 per cent in Argentina and South Africa, and, finally, to36 per cent in the United Kingdom.

All tax systems – in both developed and developing countries – include thesame basic tax categories: direct taxes on income and wealth; indirect taxes onconsumption; property taxes; and trade taxes. The most common direct taxes arethe personal income tax, the corporate income tax, and wealth or inheritancetaxes. The most common indirect taxes are the value-added tax (VAT) andselected sales and excise taxes (e.g., taxes on alcohol and cigarettes). Propertytaxes tend to be imposed on real estate such as land and housing, or on personalproperty such as cars and boats. Trade taxes often take the form of import orexport duties. This volume, rather than focusing on all types of taxes, concen-trates on personal income tax, the VAT, selected excises and fuel levies, whichcan together be considered the basic ‘pillars’ of taxation in most countries(Barreix and Roca 2007).

While all countries generate tax revenue from broadly the same sources, the taxsystem of each country reflects its specific history, legal tradition, political structureand economic base (Bahl and Bird 2008). The structure of tax revenue also varieswith the level of national income. Across low-income countries, about two-thirds oftax revenue is raised through indirect taxes. In contrast, across high-income coun-tries, indirect taxes account for only about one-third of tax revenue, with the remain-ing two-thirds coming from direct taxes. In low-income countries, personal incometax accounts for just over a quarter of tax revenue, while in high-income countries,it accounts for over a third of tax revenue.

The countries in this volume generally reflect this pattern but with some indi-vidual variation. In 2006–08, as a share of total tax revenue, personal income tax(PIT) represented between 14 and 21 per cent in Argentina, India, Morocco andUganda. The percentage was substantially higher in the United Kingdom at 27per cent, although Mexico and South Africa, much poorer countries, had a highshare of PIT in total tax revenue, at 56.4 and 30 per cent, respectively, in 2007.1

The share of VAT in total tax revenue varied from 15 to 18 per cent in Uganda,Ghana,2 and the United Kingdom, and was about ten percentage points higher inArgentina, Morocco and South Africa, and 46 per cent for Mexico.3

Gender differences that affect taxation

It is important to clarify upfront our use of the term ‘gender’ throughout this volume.Average differences between men and women observed in economic, social and

Taxation and gender equality 3

political life are not the result of sex (e.g., biology) but rather are the result of socialrelations that ascribe different roles, rights, responsibilities and obligations to malesand females.4 The structures that govern gendered social relations have basic com-monalities across different societies, although how they are manifest in specificbeliefs, norms, organizations, behaviours and practices can and do vary.

Gender analysis involves examining the inequalities between women and menthat result from social power relations in households, markets, and organizations.Social power relations are based not only on gender but also arise from class,race, ethnicity, caste, and location (e.g., urban or rural), which again vary acrosssocieties. Gender is a social stratifier that interacts with these other powerfulsocial stratifiers. When analyzing the distributional impact of tax systems, it istherefore important to go beyond a mere focus on women as a distinct group inrelation to men as a distinct group and to incorporate all relevant social stratifiers.Several of the chapters in this volume therefore include income, race and locationas stratifiers in the gender analysis of taxation.

Barnett and Grown (2004) note four ‘stylized facts’ about gender differencesin economic activity that should be used to understand the impact of taxation onmen and women. These are:

1 gender differences in paid employment – including formal/informal employ-ment, wages and occupational segregation;

2 women’s work in the unpaid care economy;3 gender differences in consumption expenditure;4 gender differences in property rights and asset ownership.

Gender differences in employment

In all countries, women’s labour force participation rates are lower than men’s,although women contribute more time in total to paid and unpaid work (UnitedNations Development Programme 1995; United Nations Development Fund forWomen 2000; United Nations 2009). Within paid employment, several gender dif-ferences are important to note in a gender analysis of taxation. First, women enterand exit the labour force more frequently than do men, which means their partici-pation is more discontinuous than is men’s, and they are more likely to be in part-time and seasonal jobs, while men are concentrated more than women in full-timepositions (International Labour Organization 2009b). Second, women earn lessthan men, even after controlling for standard human capital variables (age, educa-tion, job experience), though the gap has narrowed in some countries, over the lastdecade (Tzannatos 1999; Artecona and Cunningham 2002; Oostendorp 2004;International Labour Organization 2009a). Third, in many countires, especiallydeveloping countries, women work predominately in informal employment whichin many cases puts them outside the income tax net either because they earn toolittle to file returns or choose not to do so knowing that the tax system has fewways to track their income, which may not otherwise be reported. Informal employ-ment includes market-oriented employment in small workshops, family busi-nesses, contract or subcontract work often undertaken in the home, and domestic

4 C. Grown

work for others. Informal employment represents about 80 per cent of women’semployment in Sub-Saharan Africa, Southern Asia and the Pacific, compared toabout 74 per cent of men’s, although for developing countries as a whole, it rep-resents 67 per cent of women’s employment and 60 per cent of men’s employment(United Nations 2009).

The result of women’s employment profile – their discontinuous employment,lower relative earnings and predominance in the poorly paid forms of informalemployment – means that they are unlikely to bear a large share of the personalincome or direct tax burden in many countries. However, their inferior employ-ment status may also prevent them from accessing certain benefits affordedthrough the tax system to employees.

Unpaid work and care

Taxes are generally assessed on income. But as the recent literature on povertynotes, there are different concepts of income, depending on what is included, e.g.,market income, non-market income from household production, the value ofleisure, or other factors (Martinez-Vazquez 2001). Most countries do not includenon-market production in income that is liable to tax.

In every country around the world, women do most of the unpaid care work,that is, tasks such as housework, cooking and caring for children, the elderly, andsick people, where the person doing this work is not paid (Budlender 2002).Unpaid care work also includes volunteer work, where individuals assist otherhouseholds or the community more generally. As Elson (1995) points out, these areall vital services that enable the paid economy to function. In many developingcountries, unpaid work that goes beyond care includes subsistence production –production for home use of goods and services such as food, clothing, and otheritems – and unpaid work in family businesses.5

The issue of whether and how to value unpaid work is a subject of debate inthe feminist economics and feminist legal communities. It affects the notion ofincome and consequently the interpretation of who bears the burden of taxes. Thisis discussed further below.

Gender differences in expenditure

Not only do women allocate their time differently than do men – between paidwork, unpaid work and leisure – but there is also evidence that gender relationsand bargaining power among household members affect the types of expenditureshouseholds make, the amount and type of savings and other allocation decisions,which is especially important for understanding the incidence of consumptiontaxes, that is, value-added, excise and fuel taxes.

Across a wide range of cultures, empirical studies have revealed gender dif-ferentials in expenditure (Haddad et al. 1997; Lundberg et al. 1997; Browningand Bonke 2006; Doss 2006). Women, compared to men, tend to spend a higherproportion of income under their control on goods such as food, education andhealth care that enhance the well-being and capabilities of children (Thomas

Taxation and gender equality 5

1993; Haddad et al. 1997; Quisumbing and Maluccio 2000). Indeed, gender dif-ferences in expenditure emerge across all countries in this project, as will be dis-cussed further below and in subsequent chapters. It is therefore important toanalyse how changes in the relative prices of various commodities will affectwomen’s and men’s expenditure patterns and household welfare.

Gender differences in property rights

In many developing countries, women are frequently denied the right to own andinherit property. In many regions of Africa and Asia, men hold formal land titlewhen land is private. Social norms may dictate that businesses are owned by malefamily members although women may supply labour to them. In light of this sit-uation, some countries (e.g., India, see Chapter 4) are using the tax system to pro-vide incentives to increase female property ownership.

Nonetheless, in recent decades, women have made strides in some areas ofproperty ownership, most notably in entrepreneurship and business development.Yet tax systems may not recognize female business ownership even when itexists. Stotsky (1997) found that family business income is attributed in manycountries (e.g., Tanzania) to the husband regardless of the spouse’s role in thebusiness and that in some countries, limitations are placed on the allocation ofincome from a family business to an unpaid family member because when thespouses are taxed separately, shifting the income to the spouse who pays tax at alower marginal tax rate is one form of tax avoidance. Gender differences in busi-ness and other forms of property ownership are becoming relatively more impor-tant but have not yet systematically been addressed in the tax literature.

Gender equality and tax equity: conceptual framework

Although there are gender issues in all facets of tax policy, including efficiencyand ease of administration, this volume concentrates on equity. Gender equalityin tax policy can be examined from several perspectives. Our framework buildson the work of two scholars: Janet Stotsky and Diane Elson. Stotsky (1997) pio-neered one of the first assessments of the gender implications of taxation systemsin developing countries and her work provides a useful framework for assessingthe notion of gender ‘bias’ in taxation systems.

Stotsky distinguishes between explicit and implicit bias. Explicit forms ofgender bias refer to specific regulations or provisions in tax law that treat men andwomen differently. They are more common in personal income tax arrangementsthan in other forms of taxation in both developed and developing countries.Implicit forms of gender bias, on the other hand, relate to provisions in tax sys-tems that, because of systematically gendered social and economic customs andarrangements, have different impacts on men and women. These may be found inpersonal income tax systems if they have joint filing requirements that tax secondary-earner income (primarily women’s) at a higher marginal tax rate than primary-earner income, thus affecting women’s labour supply and other decisions.

6 C. Grown

Implicit bias may also be found in consumption taxes as a result of gender dif-ferences in spending behaviour.

There is much that is useful in Stotsky’s framework, but Elson (2006) pointsout that it has some limitations. She argues that the term ‘bias’ is a normative andpejorative term, implying an unjustified asymmetry that stems from treating menand women differently. By contrast, a non-biased system would treat them thesame. Yet, Elson argues that a gender analysis of taxation must go beyond theprinciple of sameness to recognize that discrimination and bias take differentforms, and that, in order to achieve substantive equality, different groups insociety may require different treatment. Different treatment is, therefore, not nec-essarily biased treatment.

Elson (2006) develops the implications of the Convention on the Eliminationof All Forms of Discrimination Against Women (CEDAW) for tax systems.Although there is no specific mention in CEDAW of taxation, CEDAW requiresthat families be based on ‘principles of equity, justice and individual fulfilmentfor each member’ (General Recommendation 21, para. 4). It implies that womenbe treated as equal to men in tax laws: as individual, autonomous citizens, ratherthan as dependants of men. Article 1, for instance, specifies that marital status isnot an acceptable basis for any ‘distinctions, exclusions or restrictions’ whichimpair women’s equality with men in the enjoyment of human rights.6

CEDAW also recognizes that to achieve substantive (as opposed to formal)equality, different treatment of males and females may be permissible when thattreatment is aimed at overcoming discrimination. Article 5 ‘requires State partiesto modify social and cultural patterns of men and women to eliminate practicesbased on the idea of sex role stereotyping or the inferiority or superiority of eitherof the sexes’ (Inter-Parliamentary Union 2003). Thus, one could argue (as Elsondoes) that taxation systems should seek to help transform the traditional genderedroles in society that are inequitable. In other words, personal income tax systems(e.g., the structure of rates, exemptions, deductions, allowances, credits, etc.)should be designed to actively promote an equal sharing of both paid and unpaidwork between women and men as well as eliminate incentives for the perpetua-tion of gender inequitable roles. This is quite a different interpretation from thatprovided by standard welfare economics, which takes individual utility as thebasis of a social evaluation function to assess whether a policy reform improvessocial welfare and which adheres to the principle that reforms that make onegroup better off while making other groups worse off are undesirable.

Re-interpreting horizontal and vertical equity from aCEDAW perspective

The ideas put forth by Elson and Stotsky can be used to re-examine the notion ofequity in tax theory and policy. Public finance theory and practice have long dis-tinguished ‘equity’ or fairness as one pillar of taxation (Musgrave and Musgrave1989). Equity in taxation expresses the idea that taxes should be ‘fair’ and is aconcept used in all tax policy analysis. However, it should be noted that

Taxation and gender equality 7

equity/fairness is a normative, value-based concept and its interpretation differsacross individuals, countries, cultures and time, making it difficult to apply in anyconsistent and meaningful way to facilitate comparisons across countries.

Tax equity is commonly discussed according to two definitions of ‘fairness’.These definitions are also normative, and sometimes conflict, so they too are dif-ficult to apply in practice. However, they are a common reference point for dis-cussion. Horizontal equity posits that taxpayers who are equally situated ineconomic terms should be treated equally for tax purposes. Vertical equity positsthat taxpayers who are not identical from an economic standpoint, but are differ-ently situated, should be treated appropriately differently for tax purposes.7 Inpractice, it is difficult to come to any definite consensus as to what counts asequivalent and what counts as different. And, even if there is rough agreement onwhat count as equivalent and what counts as different, it can be very difficult toapply these concepts in tax policy. Many countries do achieve some degree ofvertical equity, but horizontal equity is nearly impossible to achieve for reasonsthat are discussed below.

Horizontal equity in personal income taxes

As noted above, horizontal equity is defined as the requirement that equals betreated equally. From a gender perspective, there are a number of problemswith this concept. The first is that horizontal equity is equivalent to whatCEDAW considers to be formal equality. Yet, as noted above, formal equalityis not necessarily sufficient to change the underlying conditions that producegender (and other forms of) inequality. As Claire Young (2000: 7) notes, agender analysis must

encompass the concept of substantive equality. An approach based on for-mal equality would treat all individuals the same regardless of the differ-ences between them. This approach is inadequate to the task of creatingreal equality because it does not encompass or even acknowledge inequal-ity of condition.

Julie Nelson (1996: 97) raises another problem with the traditional notion ofhorizontal equity:

The conception of horizontal equity not only requires that one answer thequestion of what ‘the same situation’ means across units, but also, morefundamentally, that one determine a proper unit across which to make thecomparison. The notion of horizontal equity requires a belief in a funda-mental similarity among the units being compared, something that is mucheasier envisioned in the abstract, than in concrete cases.

She goes on to note that the translation of the ideal of horizontal equity into actual taxpolicy has been strongly influenced by ‘patriarchal’ interpretations of what constitutes

8 C. Grown

the same situation and what constitutes the appropriate unit of taxation, e.g., the indi-vidual, the family, or the household. This is taken up in the next section.

The proper unit of taxation: individuals or households?

An important question for all countries is whether the proper unit of taxation isthe household or the individual. Every country in this study has adopted individ-uals as the filing unit for personal income taxes.8 Under an individual filing sys-tem, all persons are responsible for filing a tax return if they have taxable income.Married individuals file a separate return based on their own labour earnings,and non-labour earnings and exemptions or deductions for children and otherpurposes are allocated in some way determined by the tax law (Stotsky 1997).Systems that use joint filing assess tax liability on the combined income of bothpartners and the couple is the filing unit.

An individual filing structure is considered by many feminist economists to bemore gender-equitable than joint or family taxation.9 As Sue Himmelweit (2002:16) states:

[S]eparate taxation means men and women are taxed on and therefore faceincentives based on their own income alone. This can be seen as a steptowards gender equality in employment, since it favours a household withtwo earners over a single-earner household with the same income. Separatetaxation also improves women’s bargaining power within their households;as women usually earn less than their husbands, wives will generally gainfrom being taxed at an individual, rather than a joint, rate.

Because individual filing systems avoids incentives to have male-breadwinnerfamilies with female dependants, they are more gender-equitable.

Although individual filing systems are more gender-equitable than joint orfamily taxation systems, most analyses of horizontal tax equity take the house-hold as the unit of analysis. Assessing equity on a household (as opposed to indi-vidual) basis shows that many individual filing systems are not horizontallyequitable. First, individualization of personal income tax results in an overall sys-tem that is less well targeted on household income, and, therefore, for the sameoverall tax take, can be less progressive in terms of the distribution of after-taxincome between households as compared to systems of joint taxation (ibid.).

Second, as the chapters on Argentina, Ghana, India, South Africa, Ugandaand the United Kingdom illustrate, individual filing systems also introduceinequities between households with two earners and those with one earner anda financially dependent spouse, both of which have the same number ofchildren and the same total household income.10 Households with the singleearner and financially dependent spouse generally pay higher tax on theirincome than dual-earner households. Some have argued that this constituteshorizontal inequity, although others counter that it may not because thesehouseholds are not ‘the same’.

Taxation and gender equality 9

If financially dependent spouses provide unpaid work in male-breadwinnerhouseholds, this household ‘production’ creates in-kind income which should befactored into total household income (Pechman 1987). As Young (1999: 4) states:

The issue is that the value of women’s labour in the home is earned incomein kind, a form of imputed income, and one that gives a personal benefiteither to the person who performs it or to other members of the family.Ignoring its value for tax purposes is problematic.

Nelson (1996) echoes this view, arguing that horizontal equity requires that taxsystems should take into account the value of the output of unpaid work done inthe home, as well as the value of income earned outside the home. If this is notdone, she concludes, there will be unfair treatment of households in which bothhusband and wife do paid work, as compared to those with a male breadwinnerand a financially dependent female homemaker who provides a significantamount of unpaid work (see also Staudt 1996).

The idea that unpaid domestic work should be quantified and included in totalhousehold income for tax purposes is, however, controversial. Some are con-cerned that the tax burden of low-income households would increase more thanthe tax burden of high-income households. Phillips (2002: 65) notes that manytax analysts agree that it is appropriate for one-earner couples with a breadwin-ner and stay-at-home spouse to pay somewhat more tax on their market incomein order to offset the substantial tax-free economic benefits (goods and services)generated by the stay-at-home spouse’s unpaid work. Moreover, as Elson (2006:82) points out, taxes have to be paid in money, and cannot be paid through unpaiddomestic work (one cannot bake a cake and take it to the tax office as part of thepayment of the tax bill). She suggests that the value of unpaid work can beaddressed in other ways, for instance, through the provision of tax allowances towomen who participate in paid employment in order to offset some of the costsof buying substitutes for the unpaid domestic work they would otherwise do, orthrough the expenditure side of the budget in the provision of subsidized depend-ent care and other services.

Households with one earner, a stay-at-home spouse and children should alsobe compared to households with one earner, no stay-at-home spouse and children.In Argentina, Ghana and Morocco, the availability of a deduction for a depend-ent spouse causes single-parent households to bear a larger burden than male-breadwinner households with financially dependent spouses.

If household services are counted as income, the ability to pay of a householdwith one earner and a stay-at-home spouse will be higher than a household withtwo earners and the same money income because the two-earner couple needsmore income to purchase market goods to replace home production. The abilityto pay of a household with one earner and a stay-at-home spouse will also behigher in single-parent households. Although older children in both householdsare likely to provide some household production, the level will probably notapproach that provided by a full-time adult homemaker. Young children are

10 C. Grown

likely to provide even fewer services and may in fact require more attention fromthe adult earner. As Nelson (1996: 104) asks, why, with less household production,should the single parent have to often pay more in taxes than the dual-earner cou-ple with the same money income? This is clearly a relevant issue for several coun-tries in this study. In Ghana, for instance, a substantial minority, and in SouthAfrica, a majority of single-earner households with children are headed by women,and they bear a heavier burden of income tax than other types of households.