ST.TERESA'S COLLEGE PG PROGRAMME REGULATIONS ...

126

1Curriculum & Syllabus 2014 Admission onwards ST.TERESA’S COLLEGE PG PROGRAMME REGULATIONS FOR CREDIT AND SEMESTER SYSTEM 1. SHORT TITLE 1.1. These Regulations shall be called The College Regulation governing Post Graduate Programmes under the Credit Semester System 1.2. These Regulations shall come into force from the Academic Year 2014-2015 onwards. 2. SCOPE 2.1. These Regulation provided here in shall apply to M Com Programme conducted by the college with effect from the academic year 2014-2015 admission onwards. 2.2. The provisions here in supersede all the existing regulations for the regular post- graduate programmes02 conducted by the college unless otherwise specified. 3. DEFINITIONS 3.1. ‘Programme’ means the entire course of study and Examinations. 3.2. ‘Duration of Programme’ means the period of time required for the conduct of the programme. The duration of post-graduate programme shall be of 4 semesters. 3.3. ‘Semester’ means a term consisting of a minimum of 90 working days, inclusive of examination, distributed over a minimum of 18 weeks of 5 working days each. 3.4. (a) ‘Academic Week’ is a unit of 5 working days in which distribution of works is organized from day 1 today 5, with 5 contact hours of 1 hour duration in each day. A sequence of 18 such academic week constitutes a semester. (b) ‘Zero semesters’ means a semester in which a student is permitted to opt out due to unforeseen genuine reasons. 3.5. ‘Course’ means a segment of subject matter to be covered in a semester. Each Course is to be designed variously under lectures / tutorials /laboratory or fieldwork / seminar /project/practical training /assignments/evaluation etc., to meet effective teaching and learning needs. 3.6. ‘Credit’ (Cr) of a course is a measure of the weekly unit of work assigned for that course in a semester.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of ST.TERESA'S COLLEGE PG PROGRAMME REGULATIONS ...

1Curriculum & Syllabus 2014 Admission onwards

ST.TERESA’S COLLEGE PG PROGRAMME REGULATIONS

FOR CREDIT AND SEMESTER SYSTEM

1. SHORT TITLE

1.1. These Regulations shall be called The College Regulation governing Post Graduate

Programmes under the Credit Semester System

1.2. These Regulations shall come into force from the Academic Year 2014-2015

onwards.

2. SCOPE

2.1. These Regulation provided here in shall apply to M Com Programme conducted by

the college with effect from the academic year 2014-2015 admission onwards.

2.2. The provisions here in supersede all the existing regulations for the regular post-

graduate programmes02 conducted by the college unless otherwise specified.

3. DEFINITIONS

3.1. ‘Programme’ means the entire course of study and Examinations.

3.2. ‘Duration of Programme’ means the period of time required for the conduct of the

programme. The duration of post-graduate programme shall be of 4 semesters.

3.3. ‘Semester’ means a term consisting of a minimum of 90 working days, inclusive of

examination, distributed over a minimum of 18 weeks of 5 working days each.

3.4. (a) ‘Academic Week’ is a unit of 5 working days in which distribution of works

is organized from day 1 today 5, with 5 contact hours of 1 hour duration in each day.

A sequence of 18 such academic week constitutes a semester.

(b) ‘Zero semesters’ means a semester in which a student is permitted to opt out

due to unforeseen genuine reasons.

3.5. ‘Course’ means a segment of subject matter to be covered in a semester. Each

Course is to be designed variously under lectures / tutorials /laboratory or fieldwork /

seminar /project/practical training /assignments/evaluation etc., to meet effective teaching

and learning needs.

3.6. ‘Credit’ (Cr) of a course is a measure of the weekly unit of work assigned for that

course in a semester.

2Curriculum & Syllabus 2014 Admission onwards

3.7. ‘Course Credit’ One credit of the course is defined as a minimum of one hour

lecture /minimum of 2 hours lab/field work per week for 18 weeks in a Semester. The

course will be considered as completed only by conducting the final examination.No

regular student shall register for more than 24 credits and less than 16 credits per semester.

The total minimum credits, required for completing a PG programme is 80.

3.8. ‘Programme Core course ’Programme Core course means a course that the student

admitted to a particular programme must successfully complete to receive the Degree and

which cannot be substituted by any other course.

3.9. ‘Programme Elective course ’Programme Elective course means a course, which can

be substituted, by equivalent course from the same subject and a minimum number of

courses is required to complete the programme.

3.10. ‘Programme Project’ Programme Project means a regular project work with stated

credits on which the student undergo a project under the supervision of a teacher in the

parent department/any appropriate research center in order to submit a dissertation on the

project work as specified.

3.11. ‘Plagiarism’ Plagiarism is the unreferenced use of other authors ’material in

dissertations and is a serious academic offence.

3.12. ‘Tutorial’ Tutorial means a class to provide an opportunity to interact with

students at their individual level to identify the strength and weakness of individual

students.

3.13. ‘Seminar‘ seminar means a lecture expected to train the student in self-study,

collection of relevant matter from the books and Internet resources, editing, document

writing, typing and presentation.

3.14. ‘Evaluation’ means every student shall be evaluated by 25% internal assessment and

75% external assessment.

3.15. ‘Repeat course’ is a course that is repeated by a student for having failed in that

course in an earlier registration.

3.16. ‘Improvement course’ is a course registered by a student for improving his

performance in that particular course.

3.17. ‘Department’ means any teaching Department offering a course of study approved by

the University in a college as per the Actor Statute of the University.

3.18. ‘Parent Department’ means the Department which offers a particular post graduate

programme.

3Curriculum & Syllabus 2014 Admission onwards

3.19. ‘Department Council’ means the body of all teachers of a Department in a College.

3.20. ‘Faculty Advisor’ is a teacher nominated by a Department Council to coordinate the

continuous evaluation and other academic activities undertaken in the Department.

3.21. ‘Course Teacher’ means the teacher who is taking classes on the course.

3.22. ‘College Co-ordinator’ means a teacher from the college nominated by the College

Council to look into the matters relating to MGU-CSS-PG System

3.23. ‘Letter Grade’ or simply ‘Grade’ in a course is a letter symbol (A,B,C,D, E) which

indicates the broad level of performance of a student in a course.

3.24. Each letter grade is assigned a ‘Grade point’ (G) which is an integer indicating the

numerical equivalent of the broad level of performance of a student in a course.

3.25. (a) ‘Credit point’ (P) of a course is the value obtained by multiplying the grade

point (G) by the Credit (Cr) of the course P=G x Cr.

(b) Extra credits are additional credits awarded to a student over and above the

minimum credits required for a programme for achievements in co-curricular

activities carried out outside the regular class hours, as decided by the university.

3.26. ‘Weight’ is a numerical measure quantifying the comparative range of an answer or

the comparative importance assigned to different components like theory and practical,

internal and external examinations, core and elective subjects, project and viva-voce etc.

3.27. (a) ‘Weighted Grade Point’ is grade points multiplied by weight.

(b) ’Weighted Grade Point Average’ (WGPA) is an index of the performance of

a students in a course. It is obtained by dividing the sum of the weighted Grade

Points by the sum of the weights of the grade points. WGPA shall be obtained for

CE and ESE separately and then the combined WGPA shall be obtained for each

course.

3.28. ‘Grade Point Average’ (GPA) is an index of the performance of a student in a

course. It is obtained by dividing the sum of the weighted grade point obtained in the

course by the sum of the weights of Course.

3.29. ‘Semester Grade point average’ (SGPA) is the value obtained by dividing the sum of

credit points (P)obtained by a student in the various courses taken in a semester by the total

number of credits taken by him/her in that semester . The grade points shall be rounded off

to two decimal places. SGPA determines the overall performance of a student at the end of

a semester.

4Curriculum & Syllabus 2014 Admission onwards

3.30. ‘Cumulative Grade point average’(CGPA) is the value obtained by dividing the sum

of credit points in all the courses taken by the student for the entire programme by the total

number of credits and shall be rounded off to two decimal places.

3.31. ‘Grace Grades Points’ means grade points awarded to course/s, as per the choice of

the student, in recognition of meritorious achievements in NCC/NSS/Sports/Arts and

cultural activities.

4. PROGRAMME STRUCTURE

4.1. Students shall be admitted into postgraduate programme under the faculties.

4.2. The programme shall include two types of courses, Program Core (PC) courses

and Program Elective (PE) Courses. There shall be a Program Project (PP)with

dissertation o be undertaken by all students. The Programme will also include

assignments, seminars /practical viva etc,if they are specified in the Curriculum.

4.3. There shall be various groups of Programme Elective courses for a programme such

as Group A, Group B etc. for the choice of students subject to the availability of facility

and infrastructure in the institution and the selected group shall be the subject of

specialization of the programme.

4.4. Project work

4.4.1. Project work shall be completed by working outside the regular teaching hours.

4.4.2. Project work shall be carried out under the supervision of a teacher in

the concerned department.

4.4.3. A candidate may, however, in certain cases be permitted to work on the

project in an industrial/Research Organization on the recommendation of the

Supervisor.

4.4.4. There should be an internal assessment and external assessment for the

project work.

4.4.5. The external evaluation of the Project work is followed by presentation of

work including dissertation and Viva-Voce.

4.4.6. The title and the credit with grade awarded for the program project should

be entered in the grade card issued by the college.

4.5. Assignments: Every student shall submit one assignment as an internal component for

5Curriculum & Syllabus 2014 Admission onwards

every course with a weightage one. The Topic for the assignment shall be allotted within the

6th week of instruction.

4.6. Seminar Lecture: Every PG student shall deliver one seminar lecture as an internal

component for every course with a weightage two. The seminar lecture is expected to train

the student in self-study, collection of relevant matter from the books and Internet

resources, editing, document writing, typing and presentation.

4.7. Every student shall undergo at least two class tests as an internal component or

every course with a weightage one each.

4.8. The attendance of students for each course shall be another component of internal

assessment as prescribed with weightage one.

4.9. No courses shall have more than 4 credits.

4.10. Comprehensive Viva-voce shall be conducted at the end semester of the program

comprehensive Viva-Voce covers questions from all courses in the programme.

5. ATTENDANCE

5.1. The minimum requirement of aggregate attendance during a semester for appearing

the end semester examination shall be 75%. Condonation of shortage of attendance to a

maximum of 10 days in a semester subject to a maximum of two times during the whole

period of postgraduate programme may be granted by the College

5.2. If a student represents his/her institution, University, State or Nation in Sports, NCC,

NSS or Cultural or any other officially sponsored activities such as college union/university

union activities, he/she shall be eligible to claim the attendance for the actual number of

days participated subject to a maximum of 10 days in a Semester based on the specific

recommendations of the Head of the Department and Principal of the College concerned.

5.3. A student who does not satisfy the requirements of attendance shall not be

permitted to take the end Semester examinations.

6. BOARD OFSTUDIESAND COURSES.

6.1. The PG Board of Studies concerned shall design all the courses offered in the PG

programme. The Boards shall design and introduce new courses, modify or re-design

existing courses and replace any existing courses with new/ modified courses to facilitate

better exposures and training for the students.

6.2. The syllabus of a course shall include the title of the course, contact hours, the

number of credits and reference materials.

6Curriculum & Syllabus 2014 Admission onwards

6.3. Each course shall have an alpha numeric code number which includes abbreviation

of the programme, the semester number, and the code of the course (‘COM’ for Program,

’PD’’ for project/Dissertation and” VV” for viva voce).

6.4. Every Programme conducted under Credit Semester System shall be monitored by

the College Council.

7. REGISTRATION/ DURATION

7.1. The duration of PG programmes shall be 4 semesters.

7.2. The duration of each semester shall be 90 working days. Odd semesters from June to

October and even semesters from December to April. There will be one month semester

breaks each in November and May.

7.3. A student may be permitted to complete the programme, on valid reasons, with ina

period of 8 continuous semesters from the date of commencement of the first semester of

the programmes.

8. ADMISSION

8.1. The admission to all PG programmes shall be as per the rules and regulations of the

College

8.2. The eligibility criteria for admission shall be as announced by the College from time

to time.

8.3. Separate rank lists shall be drawn up for reserved seats as per the existing rules.

8.4. The college shall make available to all students admitted a Prospectus listing all the

courses offered including programme elective during a particular semester. The information

provided shall contain title of the course and credits of the course.

8.5. There shall be a uniform academic and examination calendar prepared by the

College for the conduct of the programmes. The College shall ensure that the calendar

is strictly followed.

8.6. There shall be provision for inter collegiate and inter University transfer in 3rd

semesters within a period of two weeks from the date of commencement of the

semester.

8.7. There shall be provision for credit transfer subject to the conditions specified by the

Board of Studies concerned.

7Curriculum & Syllabus 2014 Admission onwards

9. ADMISSION REQUIREMENTS

9.1. Candidates for admission to the first semester of the PG programme through CSS

shall be required to have passed an appropriate Degree Examination of Mahatma Gandhi

University as specified or any other examination of any recognized University or authority

accepted by the Academic council of College as equivalent thereto.

9.2. The candidate must forward the enrollment form to the Controller of Examinations

of the College through the Head of the Institution, in which he / she is currently studying.

9.3. The candidate has to register all the courses prescribed for the particular

semester. Cancellation of registration is applicable only when the request is made

within two weeks from the time of admission.

9.4. Students admitted under this programme are governed by the Regulations in

force.

10. PROMOTION: A student who registers for the end semester examination shall be

promoted to the next semester

11. EXAMINATIONS

11.1. There shall be examination at the end of each semester.

11.2. Practical examinations shall be conducted by the College at the end of each

semester.

11.3. Project evaluation and Viva -Voce shall be conducted at the end of the programme

only. Practical examination, Project evaluation and Viva-Voce shall be conducted by two

external examiners and one internal examiner.

11.4. End-Semester Examinations: There shall be one end-semester examination of 3 hours

duration in each lecture based course and practical course

11.5. A question paper may contain short answer type/annotation, short essay type

questions/problems and long essay type questions. Different types of questions shall have

different weightage to quantify their range. Weightage can vary from course to course

depending on their comparative importance, but a general pattern may be followed by the

Board of Studies.

12. EVALUATION AND GRADING

12.1. Evaluation: The evaluation scheme for each course shall contain two parts; (a)

internal evaluation and (b) external evaluation. 25% weightage shall be given to internal

evaluation and the remaining 75% to external evaluation and the ratio and weightage

between internal and external is 1:3. Both internal and external evaluation shall be carried

8Curriculum & Syllabus 2014 Admission onwards

out using Direct grading system.

12.2 Internal evaluation: The internal evaluation shall be based on predetermined

transparent system involving periodic written tests, assignments, seminars and

attendance in respect of theory courses and based on written tests, lab

skill/records/viva and attendance in respect of practical courses. The weightage

assigned to various components for internal evaluation is a follows.

13. Components of Evaluation

The evaluation of each course shall contain two parts – Sessional Assessment and

Final Assessment. The Sessional and Final Assessments shall be made using a Direct Grading

System based on a 5 – point scale to evaluate the performance (External and Internal

Examination of students)

Letter grade Performance Grade

points (G)

Grade Range

A Excellent 4 3.5 to 4.00

B Very Good 3 2.5 to 3.49

C Good 2 1.5 to 2.49

D Average 1 0.5 to 1.49

E Poor 0 0.00 to 0.49

13.1. Sessional Assessment

The Sessional evaluation is to be done by continuous assessment of the following

components. The components of the evaluation for theory and practical and their weights are

as below.

A. Distribution of Sessional marks

(a) For courses without practical

Attendance - 1weight

Assignment - 1 weight

Seminar - 2 weight

Test paper - 2 weight

Total - 6 weight

9Curriculum & Syllabus 2014 Admission onwards

B. Attendance Evaluation

A student should have a minimum of 75% attendance. Those who do not have

the minimum requirement for attendance will not be allowed to appear for the Final

Examinations.

Grades for attendance:

90% - 100% - A

85% - 89% - B

80% - 84% - C

75% - 79% - D

<75% - E

C. Assignment

1stto 4th semesters - Assignment

Component Weightage

Punctuality 1

Review 1

Content 2

Conclusion 1

Reference 1

D. Seminar

Component Weightage

Area/Topic 1

Review 1

Content 2

Presentation 2

Conclusion 1

E. Test Paper

Average mark of two sessional examinations shall be taken.

13.2. Final Assessment

The final examination of all semesters shall be conducted by the institution on the

10Curriculum & Syllabus 2014 Admission onwards

close of each semester. For reappearance/ improvement, students may appear along with the

next batch.

Courses such as core courses and elective course do not contain practical courses.

The pattern of questions for these courses without practical are listed below.

(a) Each question paper has four parts A, B & C.

(b) Part A contains 8 questions of 1 weight each out of which the candidate

has to answer 5.

(c) Part B contains 8 questions spanning the entire syllabus and the candidate

has to answer 5 questions. Each question carries 2 weights.

(d) Part C contains 6 questions spanning the entire syllabus and the candidate

has to answer 3 questions. Each question carries 5 weights.

(e) The total weight is 30.

13.3. Project Evaluation

All students have to begin working on the project in the THIRD semester and must

submit it in the FOURTH semester.

The ratio of Sessional to Final component of the project is 1:3. The weightage

distribution for assessment of the various components is shown below.

(a) Sessional Evaluation: 4 weights

Component Weight

Component 1

Experimentation/

Data collection 1

Compilation 1

Content 1

11Curriculum & Syllabus 2014 Admission onwards

(b) External Evaluation of Dissertation: 12weights

(c) Viva –Voce: 4 weights

13.4. To ensure transparency of the evaluation process, the internal assessment grade

awarded to the students in each course in a semester shall be published on the notice

board at least one week before the commencement of external examination. There shall

not be any chance for improvement for internal grade.

13.5. The course teacher and the faculty advisor shall maintain the academic record of

each student registered for the course which shall be forwarded to the college through the

college Principal and a copy should be kept in the college for at least two years for

verification.

13.6. External evaluation: The external Examination in theory courses is to be

conducted by the college with question papers set by external experts. The evaluation of

the answer scripts shall be done by examiners based on a well-defined scheme of

valuation. The external evaluation shall be done immediately after the examination

preferably through Centralized Valuation

13.7. Photocopies of the answer scripts of the external examination shall be made

available to the students for scrutiny on request and revaluation/scrutiny of answer

scripts shall be done as per the existing rules prevailing in the College.

13.8. The question paper should be strictly on the basis of model question paper set by

BOS and there shall be a combined meeting of the question paper setters for scrutiny and

finalisation of question paper. Each set of question should be accompanied by its scheme

of valuation.

13.9. DIRECTGRADING SYSTEM Direct Grading System based on a 5 – point scale is

used to evaluate the performance (External and Internal Examination of students)

Component

Weight

Area/topic selected

1

Objectives 2

Review 1

Materials and methods 2

Analysis 2

Presentation 2

Conclusion 2

12Curriculum & Syllabus 2014 Admission onwards

13.10. The overall grade for a programme for certification shall be based on CGPA

With a 7- point scale given below

CGPA Grade

3.80 to 4.00 A+

3.50 to 3.79 A

3.00 to 3.49 B+

2.50 to 2.99 B

2.00 to 2.49 C+

1.50 to 1.99 C

1.00 to 1.49 D

A separate minimum of C Grade for internal and external are required for a pass for a

course. For a pass in a programme a separate minimum grade C is required for all the

courses and must score a minimum CGPA of 1.50 or an overall grade of C and above.

13.11. Each course is evaluated by assigning a letter grade (A, B, C, D or E) to that

course by the method of direct grading. The internal (weightage =1) and external weightage

=3) components of a course are separately graded and then combined to get the grade of the

course after taking into account of their weightage.

13.12. A separate minimum of C grade is required for a pass for both

internal evaluation and external evaluation for every course.

13.13. A student who fails to secure a minimum grade for a pass in a course will

be permitted to write the examination along with the next batch. There will be no

supplementary examination.

13.14. After the successful completion of a semester, Semester Grade Point Average

(SGPA) of a student in that semester is calculated using the formula given below. For the

successful completion of semester, a student should pass all courses and score a minimum

SGPA of 1.50. However, a student is permitted to move to the next semester irrespective of

her/his SGPA. For instance, if a student has registered for ‘n’ courses of credits C1, C2

…………,Cn in a semester and if she/he has scored credit points P1, P2………….,Pn

respectively in these courses, then SGPA of the student in that

semester is calculated using the formula. SGPA=(P1+P2+…………….+Pn)/(C1+C2+

……………+Cn)

CGPA=[(SGPA)1*S1 +(SGPA)2*S2 +(SGPA)3*S3 +(SGPA)4*S4]/(S1+S2+S3+S4)

Where S1, S2, S3, and S4 are the total credits in semester1, semester2, semester3 and

semester 4

13Curriculum & Syllabus 2014 Admission onwards

13.15. Pattern of questions

Questions shall be set to assess knowledge acquired, standard application of

knowledge, application of knowledge in new situations, critical evaluation of knowledge

and the ability to synthesize knowledge. The question setter shall ensure that question

covering all skills is set. He/she shall also submit a detailed scheme of evaluation along

with the question paper. A question paper shall be a judicious mix of short answer type,

short essay type/ problem solving type and long essay type questions.

Weight: Different types of questions shall be given different weights to quantify

their range as follows.

Sl. No

Type of questions Weight No. of questions

answered

1. Short answer type questions 1 5 out of 8

2. Short essay(problem solving type questions) 2 5 out of 8

3. Long essay type questions 5 3 out of 6

14. GRADE CARD

14.1. The college under its seal shall issue to the students, a grade card

on completion of each semester, which shall contain the following information.

(a) Name of the University.

(b) Name of college

(c) Title of the PG Programme.

(d) Name of Semester

(e) Name and Register Number of students

(f) Code number, Title and Credits of each course opted in the semester,

Title and Credits of the Project Work

(g) Internal, external and Total grade, Grade Point (G), Letter grade and

Credit point (P) in each course opted in the semester.

(h) The total credits, total credit points and SGPA in the semester.

14.2. The Final Grade Card issued at the end of the final semester shall contain

the details of all courses taken during the entire programme including those taken over

and above the prescribed minimum credits for obtaining the degree. The Final Grade

Card shall show the CGPA and the overall letter grade of a student for the entire

programme.

14Curriculum & Syllabus 2014 Admission onwards

15. AWARD OF DEGREE

The successful completion of all the courses with ‘C+’ grade shall be the

minimum requirement for the award of the degree.

16. MONITORING COMMITTEE

There shall be a Monitoring Committee constituted by the principal to monitor the

internal evaluations conducted by institutions. The Course teacher, Faculty Advisor, and

the College Coordinator should keep all the records of the internal evaluation, for at

least a period of two years, for verification.

17. GRIEVENCE REDRESSAL COMMITTEE

17.1. College level: The College shall form a Grievance Redress Committee in each

Department comprising of course teacher and one senior teacher as members and the Head

of the Department as Chairman. The Committee shall address all grievances relating to the

internal assessment grades of the students. There shall be a college level Grievance Redress

Committee comprising of Faculty advisor, two senior teachers and two staff council

members (one shall be an elected member) and the Principal as Chairman.

18. TRANSITORY PROVISION

Notwithstanding anything contained in these regulations, the principal shall, for a

period of three year from the date of coming into force of these regulations, have the power

to provide by order that these regulations shall be applied to any programme with such

modifications as may be necessary

19. REPEAL

The Regulations now in force in so far as they are applicable to programmes offered by

the College and to the extent they are inconsistent with these regulations are hereby repealed.

In the case of any inconsistency between the existing regulations and these regulations relating

to the Choice Based Credit Semester System in their application to any course offered in a

College, the latter shall prevail. Models of distribution of course and credit are given in the

following tables .BOS can make appropriate changes subject to the following conditions.

(a) Total credit of the programme shall be 80

(b) The minimum credit of a course is 2 and maximum credit is 4

(c) Semester-wise total credit can vary from16 to 24

(d) Number of courses per semester can be decided by the BOS concerned.

(e) The credits of Projects, Dissertations and viva-voce can be prescribed by the

BOS

.

15Curriculum & Syllabus 2014 Admission onwards

PG PROGRAMME WITH OUT PRACTICAL-TOTAL CREDITS 80

Semester Course Teaching Hrs credit Total credit

1

PC-1 5 4

20 PC-2 5 4

PC-3 5 4

PC-4 5 4

PC-5 5 4

2

PC-6 5 4

20 PC-7 5 4

PC-8 5 4

PC-9 5 4

PC-10 5 4

3

PC-11 5 4

20 PC-12 5 4

PC-13 5 4

PC-14 5 4

PC-15 5 4

4

PC-16 5 3

20

PC-17 5 3

PE-01 5 3

PC-02 5 3

PC-03 5 3

PROJECT 3

VIVA-VOCE 2

CONSOLIDATION OFGRADES FOR INTERNALEVALUATION (Example)

COMPONENT WEIGHT

(W)

GRADE

AWARDED

GRADE

POINT

(G)

WEIGHTED

GRADE

POINT

(WxG)

Attendance 1 B 3 3

Assignment 1 C 2 2

Seminar 2 B 3 3

Test paper 2 A 4 8

Total 6 16

Grade: Total weighted grade points/Total weights= 16/6=2.66=Grade B

16Curriculum & Syllabus 2014 Admission onwards

CONSOLIDATION OF GRADES FOR EXTERNAL - (ONE ANSWER PAPER-

THEORY) (Example)

The grade of an answer paper (ESE Practical) shall be consolidated by similar

procedure discussed above by assigning weights for the various components. (e.g

procedure, Experiment, Calculation, Accuracy of the reported values, Presentation of

results, Diagrams..etc).The board of studies shall define the components and their weights

and include themin the scheme and syllabus of each practical course.

Type of

question

Question

No

Grade

awarded

Gradepoint Weightage Weighted

grade

points

Short

answer

1 B 3 1 3

2 - - - 0

3 A 4 1 4

4 D 1 1 1

5 - - - 0

6 A 4 1 4

7 B 3 1 3

8 - - - 0

SHORT

ESSAY

9 B 3 2 6

10 C 2 2 4

11 - - - 0

12 - - - 0

13 B 3 2 6

14 A 4 2 8

15 C 2 2 4

16 - - - 0

LONG

ESSAY

17 C 2 5 10

18 - - - 0

19 - - - 0

20 B 3 5 15

21 D 1 5 5

22 - - - 0

TOTAL 30 73

Calculation; overall grade of an answer paper=sum of weighted grade points/sum

of the weightage=73/30=2.43= Grade C

Consolidation of the grade of a course ;The grade for a course is consolidated by

combining the ESE and CE grades taking care of their weights. For a particular rcourse

,if the grades scored by a student is C and B respectively for the external and the

continuous evaluation, as shown in the above examples and then the grade for the

course shallbe consolidated as follows

17Curriculum & Syllabus 2014 Admission onwards

Exam Weight Grade

awarded

Grade

points (G)

Weighted Gradepoint

(WxG)

External 3 C 3 9

Internal 1 B 3 3

Total 4 12

Grade of a

course

(GPA)

Total weighted grade points/Total weights=12/4=3.00

=Grade B

D. Consolidation of SGPA

SGPA is obtained by dividing the sum of credit points (P) obtained in a semester by

the sum of credits ( C ) taken in that semester. After the successful completion of a semester,

semester grade point average (SGPA) of a student in that semester shall be calculated using

the formulae given. Suppose the student has taken three courses each of 4 credits and 2

courses each of 2 credits in a particular semester. After consolidating the grade for each

course as demonstrated above. SGPA has to be consolidated as shown below. Example:

Course code Title of

course

Credit (C) Grade

awarded

Grade

points (G)

Credit

Points

(P=CxG)

1 4 A 4 16

2 4 C 2 8

3 4 B 3 12

4 2 C 2 4

5 2 B 3 6

TOTAL 16 46

SGPA Total credit points/Total credits=46/16=2.87=Grade B

18Curriculum & Syllabus 2014 Admission onwards

E. Consolidation of CGPA If the candidate is awarded two A grades, one B Grade and one C Grade forthe four

semesters and has 80 credits, the CGPA is calculated as follows.

*A Course with practical

*B Course without practical

Semester Credit

taken

Grade Grade

point

Credit points

A* B** A* B**

1 20 19 A 4 80 76

2 20 19 4 80 76

3 20 19 B 3 60 57

4 20 23 C 2 40 55

TOTAL 80 80 260 255

CGPA *Total credit points/Total

credits=260/80=3.25 (Which

is between 3.00 and 3.49 in 7

point scale). The overall

grade awarded is B+

**Total credit points/

Total credits =255/80=3.18 (which is

between 3.00

and 3.49 in 7 point scale). The overall

grade awarded is B+

20Curriculum & Syllabus 2014 Admission onwards

Sl. No Code Title

eee

Instructional Hrs Credit

1

.

COM4ACA Advanced Cost Accounting 90 3

2 COM4DAP Direct Taxes- Assessment and

Procedures

90 3

3

.

COM4IF International Finance 90 3

4

.

COM4FMD Financial Markets and Derivatives 90 3

5 COM4SAPM Security Analysis and Portfolio

Management

90 3

6

.

COM4PD Project/Dissertation 3

7

.

COM4VV Viva-Voce 2

M.COM PROGRAMME

SEMESTER 1

Sl. No Code Title Instructional Hrs Credit

1

.

COM1AFA Advanced Financial Accounting -I 90 4

2 COM1PMOB Principles of Management and

Organizational Behaviour

90 4

3.

COM1FMP Financial Management Principles 90 4

4.

COM1RM Research Methodology 90 4

5.

COM1QT Quantitative Techniques 90 4

SEMESTER 11

Sl. No Code Title Instructional Hrs Credit

1.

COM2AFA Advanced Financial Accounting-II 90 4

2

.

COM2SM Strategic Management 90 4

3

.

COM2FMS Financial Management Strategies 90 4

4.

COM2HRM Human Resource Management 90 4

5.

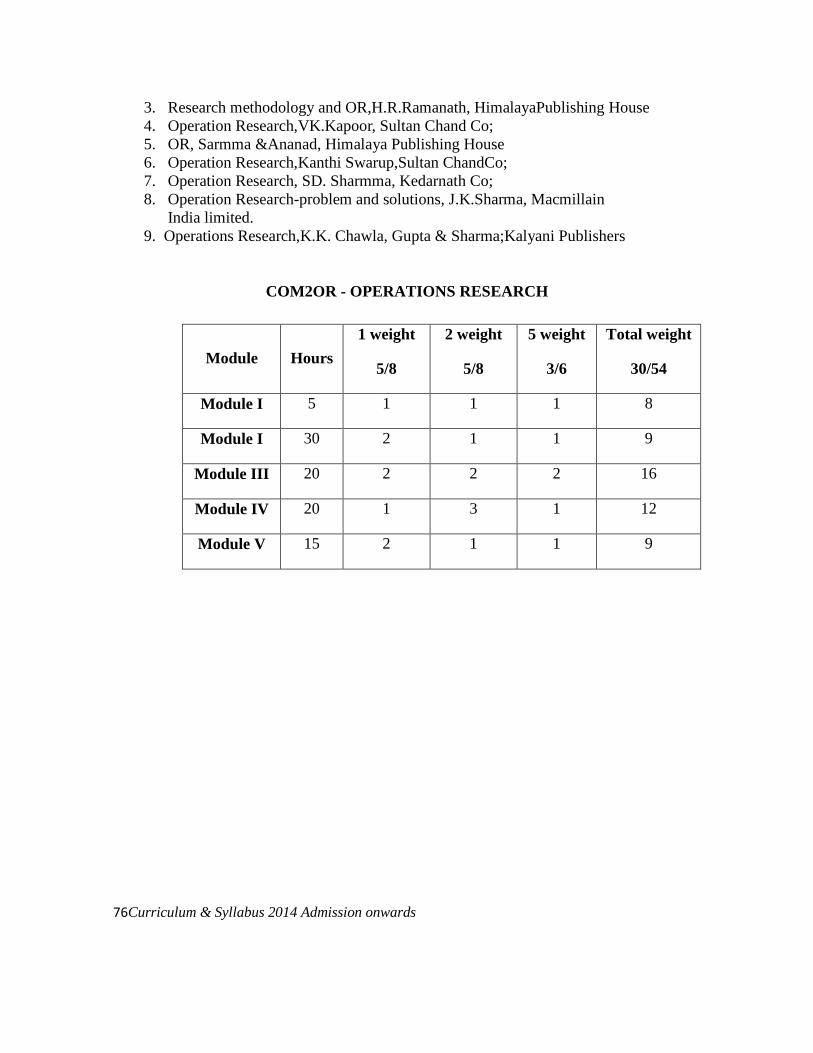

COM2OR Operations Research 90 4

SEMESTER 111

Sl. No Code Title Instructional Hrs Credit

1.

COM3MA Management Accounting 90 4

2.

COM3DLP Direct Taxes- Law and Practice 90 4

3

.

COM3IB International Business 90 4

4

.

COM3CG Corporate Governance 90 4

5.

COM3BE Business Environment 90 4

SEMESTER IV (Elective –Finance)

21Curriculum & Syllabus 2014 Admission onwards

M .COM PROGRAMME- CORE COURSES

SEMESTER I Credit-4

Code : COM1AFA -Hrs90

ADVANCED FINANCIAL ACCOUNTING-1

Objectives

(a) To know the methods of valuation of good will and share

(b) To acquaint with the amalgamation and reconstruction procedures of

companies

(c) To learn the proceedings of insolvency of an individual and international

reporting standards.

MODULE – I : Valuation of Goodwill and shares

(a) Goodwill- meaning and definition, Factors affecting goodwill,- Methods of

valuing goodwill- Average profit method- Super profit method, Annuity method

and capitalization method.

(b) Valuation of share-Need for valuation-Methods of valuation-Net asset

method or intrinsic value method-yield method-earning capacity method-fair value.

(15 Hrs)

MODULE – II : Amalgamation, Absorption and External Reconstruction-

Amalgamation in the nature of merger and Amalgamation in the nature of purchase-

Purchase consideration-Net payment method-Net Asset method- share exchange method-

Entries in the books of purchasing company- entries in the book of vendor company-

consolidated balance sheet- Inter- company Owings and holdings- Advanced problems.

(25 Hrs)

MODULE – III : Alteration of share capital and Internal reconstruction-

Procedure for reducing share capital- Re-organization- Scheme of reconstruction-

Accounting entries on Internal reconstruction. (15 Hrs)

MODULE – IV : Insolvency accounts of an Individual- Statement of

affairs and deficiency account. (20 Hrs)

MODULE – V :

(a) Human Resource accounting- Meaning- Objectives- Valuation of

Human Resource- Advanced and limitations of HRA.

(b) International Financial Reporting Standards (IFRS)

(15 Hrs)

22Curriculum & Syllabus 2014 Admission onwards

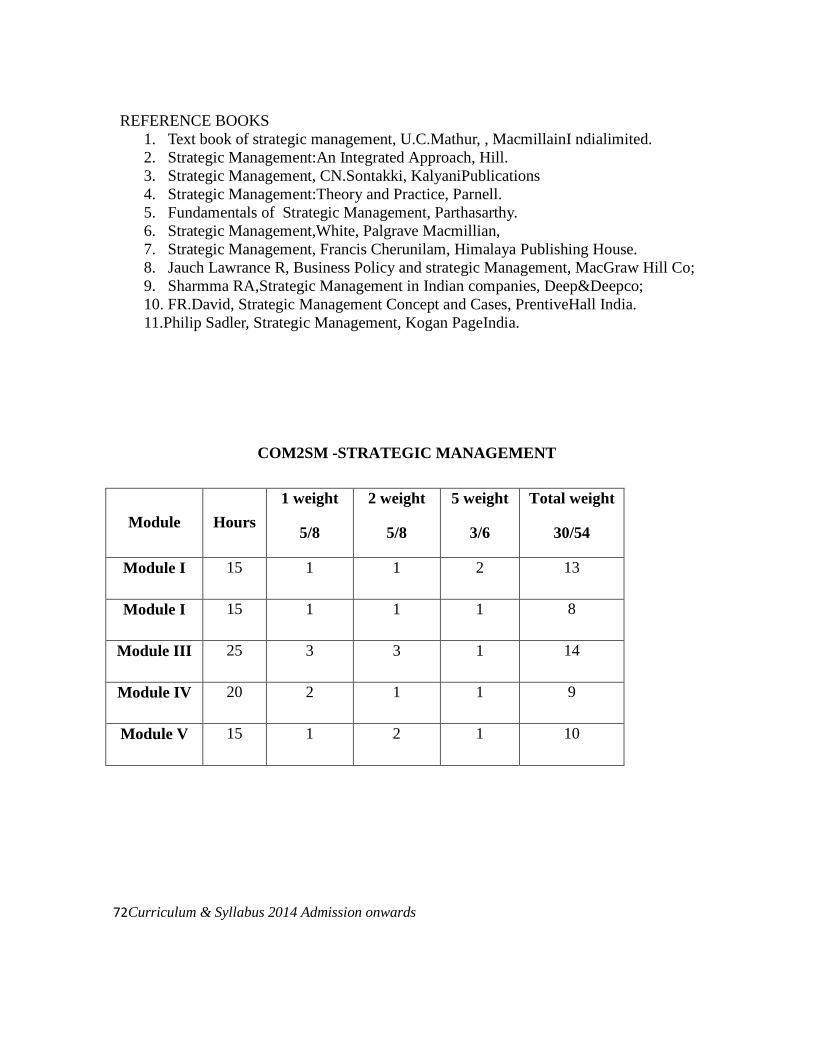

REFERENCE BOOKS

1. Advanced Financial Accounting, M.C.Shukla & T. S. Grewal, S.Chand & Co;

2. Advanced accountancy, Arulanandam & Raman, Himalya Publishing House

3. Fundamentals of Financial accounting, Nassem Ahmed, AnebooksPvt, Limited

4. Advanced Financial Accounting, R.L.Gupta & Radhaswami, Sultan ChandCO; 5. Advanced Financial Accounting, S.N.Maheswari

6. Advanced Financial Accounting, Paul & Kaur

7. Advanced Financial Accounting, B.D.Agarwal

8. Advanced Financial Accounting, S.P.Jain & K.L.Narang; Kalyani Publishers

COM1AFA -ADVANCED FINANCIAL ACCOUNTING

Module Hours 1 weight

5/8

2 weight

5/8

5 weight

3/6

Total weight

30/54

Module I 15 2 2 1 11

Module II 25 3 3 2 19

Module III 15 1 1 1 8

Module IV 20 1 1 1 8

Module V 15 1 1 1 8

23Curriculum & Syllabus 2014 Admission onwards

Reg. No…………...

Name :……………….

M.Com DEGREE (C.S.S) EXAMINATION

First Semester

Faculty of commerce

COM1AFA - ADVANCED FINANCIAL ACCOUNTING – I

Time: Three Hours Maximum weight: 30

Part A

Answer any five questions

Each question carries 1 weight

1. What do you mean by dissenting shareholders?

2. Define Goodwill.

3. What is Amalgamation?

4. What is Internal Reconstruction?

5. What is Deficiency Account?

6. What is Human Resource Accounting?

7. What is Inter-Company Owings?

8. What is External Reconstruction? (5x1=5)

Part B

Answer any five questions

Each question carries 2 weights

9. What are the conditions when Internal Reconstruction is possible?

10. What are the circumstances in which there may be a need for valuation of Shares?

11. Distinguish between Amalgamation by merger and by purchase as per AS14?

12. Explain the meaning of reconstruction of a company. What are its types?

13. What is Statement of Affairs? How does it differ from Balance Sheet?

14. From the following information calculate value of goodwill on the basis of three

years purchase of super profit of the business.

24Curriculum & Syllabus 2014 Admission onwards

a. Sundry assets of the firm are Rs. 22,50,800 and current liabilities are

Rs.93,625.

b. Average Capital employed in the business is Rs.18,00,000

c. Rate of interest expected from the capital having regard to the risk involved

is 10%.

d. Net Trading profits of the firm of the past three years were Rs.322,800.

Rs.2,72,100 and Rs.3,37,500.

e. Fair remuneration to the partners for their services is Rs.36,000 per annum.

15. The Assets of a firm is Rs.27,20,000. The Purchase consideration being the taking

over of the assets and Liabilities at book value were subjected to revaluation of fixed

assets which were reduced by Rs.3,00,000. Payment creditors were Rs.5,70,000.

Calculate Purchase Consideration.

16. On 31st March 2012, Balance Sheet of Menon Ltd was as follows

Liabilities Amount(Rs) Assets Amount(Rs)

Share Capital

Authorized &Issued:

5000 Equity shares of Rs.

100 each fully paid

500000

Land& Buildings 220000

P&L a/c 103000 Plant&

Machinery

95000

Bank OD 20000 Stock 350000

Creditors 77000 Sundry Debtors 155000

Provision for taxation 45000

Proposed dividend 75000

820000 820000

25Curriculum & Syllabus 2014 Admission onwards

Net profits of the company after deducting all working charges & providing for

depreciation & taxation, were as follows

Year ended 31st March Rs.

2008 85000

2009 96000

2010 90000

2011 100000

2012 95000

On 31st March 2012, Land & Building were valued at Rs. 250000 and Plant &

Machinery at Rs. 150000.

In view of the nature of the business, it is considered that 10% is a reasonable

return on tangible capital.

Prepare a valuation of the company’s shares after taking into account the revised

values of fixed assets & your own valuation of goodwill based on 5 years’

purchase of the super profits based on the average profit of the last 5 year.

(5x2=10)

26Curriculum & Syllabus 2014 Admission onwards

Part C

Answer any 3 question.

Each question carries 5 weights

17. The following are the Balance sheet of Major & Minor Ltd as on 31st December

2003

Liabilities Major

Ltd

Rs

Minor

Ltd

Rs

Assets Major Ltd

Rs

Minor

Ltd

Rs

Issued, Subscribed And

Paid up Capital

Equity shares of Rs 100

each fully paid

Reserves & Surplus

P&LA/C

Current liabilities &

provisions

Sundry Creditors

200000

60000

40000

100000

30000

70000

Fixed Assets:

Machinery

Furniture

Investments:

Shares in Minor

Ltd

Shares in Major

Ltd

Current Assets

Stock

Debtors

Cash at bank

100000

20000

25000

50000

5000

12000

75000

60000

45000

68000

20000 20000

300000 200000 300000 200000

Major Ltd holds 200 shares in Minor Ltd and Minor Ltd holds 100 shares in Major

Ltd.

The two companies agree on amalgamation on the following basis:

27Curriculum & Syllabus 2014 Admission onwards

1. A new company is to be formed called Hind Ltd.

2. The goodwill is valued for Major Ltd Rs. 50000 and for Minor Ltd Rs. 25000.

3. The shares of Hind Ltd are of nominal value of Rs. 10 each.

Prepare

I. Balance Sheet of Hind Ltd resulting from the merger.

II. Schedule showing fully the shareholders there in attributable to -

+shareholdings of Major Ltd & Minor Ltd. All the costs of

amalgamation are to be ignored.

18. On 31st March 2012 the Balance Sheet of a limited company disclosed the following

position:

Liabilities Amount(Rs) Assets Amount(Rs)

Issued capital in Rs10

shares

400000 Fixed Assets 500000

Reserves 90000 Current Assets 200000

P&L a/c 20000 Goodwill 40000

5% Debentures 100000

Current Liabilities 130000

740000 740000

On 31st March, 2012 the fixed assets were independently valued at Rs350000 & the

goodwill at Rs50000. The net profit for the 3 years was:

28Curriculum & Syllabus 2014 Admission onwards

2009-10 Rs 51600; 2010-11 Rs 52000; 2011-12 Rs 51650.

Of which 20% was placed to reserve this proportion being considered reasonable in

the industry in which the company is engaged & where a fair investment return may

be taken at 10%.

Compute the value of the company’s shares by

a. The assets method

b. The yield method

19. The Balance Sheet of R Ltd as at 31st March 2012 was as follows

Liabilities Amount(Rs)

Assets Amount(Rs)

Share Capital:

Authorised

1400000

Intangibles 68000

Issued

Freehold premises

at cost

140000

64000 , 8%

cumulative

preference shares

of Rs 10 each,

fully paid

640000

Plant and

equipment at cost

less depreciation

240000

64000 equity

shares of Rs 10

each, Rs 7.5 Paid

480000

Investment in

shares in Q Ltd at

cost

324000

Loans from

directors

60000

Stocks 248000

Sundry creditors 440000

Debtors 320000

Bank Overdraft

208000

Deferred Revenue

Expenditure

48000

Surplus a/c

29Curriculum & Syllabus 2014 Admission onwards

(Balance) 440000

1828000

1828000

Note: The arrear preference dividends amount to Rs 51200.

A scheme of reconstruction was duly approved with effect from 1st April 2012

under the conditions stated below:

a. The unpaid on the equity shares would be called up

b. The preference shareholders would forgo their arrear dividends. In addition,

they would accept a reduction of Rs 2.5 per share. The dividend rate would be

enhanced to 10%.

c. The equity shareholders would accept a reduction of Rs7.5 per share.

d. R Ltd holds 21600 shares in Q Ltd. This represents 15% of the share capital of

that company. Q Ltd is not a quoted company. The average net profits (after tax

) of the company is Rs 250000. The shares would be valued based on 12%

capitalization rate.

e. A bad debt provision at 2% would be created.

f. The other assets would be valued as under : Intangibles Rs48000; Plant

Rs140000; Freehold premises Rs380000; stocks Rs250000.

g. The P&L A/C debit balance & the balance standing to the debit of the deferred

revenue expenditure a/c would be eliminated.

h. The directors would have to take equity shares at the new face value of Rs 2.5

per share in settlement of their loan.

i. The equity shareholders including the directors, who would receive equity

shares in settlement of their loans, would be would be taken up two new equity

share for every one held

j. The preference shareholders would take up one new preference share for every

four held.

30Curriculum & Syllabus 2014 Admission onwards

k. The authorized share capital would be restated to Rs 1400000.

l. The new face value of the shares – Preference shares and equity shares will be

eliminated at their reduced levels.

You are required to

1. Prepare the necessary ledger accounts to effect the above.

Prepare the Balance sheet of the company after reconstruction.

20. A Merchant became insolvent on 1-1-2012 on which date his total asset value were

Rs 75000 and liabilities Rs 65000 and he estimated a deficiency of Rs 20000 before

taking the following items into consideration which were not passed through his

account books:

1. Interest on his capital of Rs 25000 @ 6% for one year.

2. A Contingent liability for Rs 3000 on bills discounted by him for Rs

8000.

3. Amount due was wages Rs 300; as salaries Rs 600; as rent Rs 500: as

rates and taxes Rs 1000.

4. A Loan of Rs 5000 taken from a friend for the marriage of his daughter

and Rs2000 from his wife.

Prepare a statement of affairs and a deficiency account.

21. Give the need and trace briefly the development of human resource accounting.

22. Distinguish between Statement of Affairs and Balance Sheet. (3x5=15)

31Curriculum & Syllabus 2014 Admission onwards

SEMESTER I Credit-4

Code: COM1PMOB - Hrs90

PRINCIPLES OF MANAGEMENT AND ORGANISATIONAL BEHAVIOUR

Objectives

(a) To help the students to understand the Conceptual framework of

management and organizational behavior

(b) To understand the managerial applicability of the concepts.

MODULE - I : Introduction, The management concept-Different schools of

management thoughts-Nature and functions of management- principles of management-

MBE-Corporate Social Responsibility. (15 Hrs)

MODULE – II : Planning and Organizing-planning process- premises-

forecasting- forecasting techniques- components of planning- MBO-Organisation- Design

and structure- committees- Task force- Matrix Organisation- project organization-

delegation of authority-span of control (15 Hrs)

MODULE – III : Organizational behaviour- concepts and significance-

relationship between management and OB-Models of OB- Contributing disciplines to

OB-Challenges and opportunities- Transaction analysis-Johari window-Organisational

development- concepts- OD Intervention- Change management-Need for change-

resistance to change-Theories of change-Organisational Diagnosis. (20 Hrs)

MODULE – IV : Groups in organization- nature- theories of group formation-

stages of group development- types of groups-formal and informal groups- conflict-

definition-functional and dysfunctional aspect of conflict- types of conflict- conflict

process- intra individual conflict- goal conflict- interpersonal conflict- strategies of

interpersonal conflict-lose lose, win lose, win win-inter group conflict-strategies to

handle inter group conflict-organizational conflict- conflict handling mechanisms.

(25 Hrs)

MODULE – V : Modern techniques in management- quality circle- TQM-

BPR- Six sigma- kaizen- bench marking- MDP-Steps in MDP. (15 Hrs)

32Curriculum & Syllabus 2014 Admission onwards

REFERENCE BOOKS

1. Human relations and organizational behaviour, RS.Dwivedi, Macmillain publishers

India limited.

2. Management Process and OB, Sharmma & Gupta; Kalyani Publishers

3. Principles of management, T Ramaswami, Himalya Publishing House.

4. Management and Organizational Behaviour Essentials,Schermerhorn 5. Organisational behaviour, Aswathappa, Himalaya Publishing House

6. Organisational behaviour, Sujanair, HimalayaPublishingHouse

7. Principles of management, BS.Moshal, Anebooks private limited.

8. Management theory and practice, J.P. Mahajan,Anebooks private limited.

9. Organizational theory and behaviour, B S.Moshal, Ane books private limited.

10. Organisational Behaviour, BS.Moshal,Ane books private imited.

11.Principles and practice of management, PF. Drucker.

12. Principles of management, LM. Prasad, Sultan ChandCo;

COM1PMOB- PRINCIPLES OF MANAGEMENT AND ORGANISATIONAL

BEHAVIOUR

Module Hours 1 weight

5/8

2 weight

5/8

5 weight

3/6

Total weight

30/54

Module I 15 2 1 1 9

Module II 15 2 2 1 11

Module III 20 1 1 1 8

Module IV 25 2 2 2 16

Module V 15 1 2 1 10

33Curriculum & Syllabus 2014 Admission onwards

Reg. No:.......................

Name………………….

M.Com DEGREE (C.S.S) EXAMINATION

First Semester

Faculty of commerce

COMIPMOB - PRINCIPLES OF MANAGEMENT AND ORGANIZATIONAL

BEHAVIOUR

Time: Three Hours Maximum weight:30

Part A

Answer any five questions

Each question carries 1weight each

1. Define management.

2. What is meant by TQM?

3. Define conflict.

4. Define group.

5. What are organization charts?

6. Explain span of control.

7. Explain 6 P’s of planning.

8. Explain the functions of top management?

(5x1=5)

Part B

Answer any 5 questions

Each question carries 2 weights each

9. What is meant by quality circles? What are their characteristics?

10. Explain the steps in planning

11. Explain the various stages in conflict in an organization

12. Describe forecasting techniques

13. What are the sources of group cohesiveness?

14. Explain the characteristics of organization behavior

34Curriculum & Syllabus 2014 Admission onwards

15. State the need for principles of management

16. Distinguish between line and staff organization

(5x2=10)

Part C

Answer any 3 questions.

Each question carries 5 weights each

17. What is meant by MBO? What are its features?

18. Elaborate the meaning and theories of business forecasting

19. What is organisational behaviour? Explain different approaches to the study of

organisational behaviour

20. Explain the various types of groups

21. Briefly explain the functions of management.

22. Explain the principles of scientific management.

(3x5=15)

35Curriculum & Syllabus 2014 Admission onwards

SEMESTER I Credit-4

Code: COM1FMP - Hrs90

FINANCIAL MANAGEMENT PRINCIPLES

Objectives

(a) To introduce the subject of financial management

(b) To acquaint the student with various methods and techniques of financial

management.

MODULE – I : Financial management- meaning- goals and objectives-

Functions of a financial manager- financial decision making- financial planning- concept

and relevance of time value of money- compounding technique-discounting

technique. (15 Hrs)

MODULE – II : Cost of capital- concepts-importance- computation- cost of

debt-cost of preference capital-cost of equity-cost of retained earnings-weighted average

cost of capital-book value and market value weights-marginal cost of capital. (15 Hrs)

MODULE – III : Financing decision and capital structure- finance structure-

pattern of capital structure-concept of balanced capital structure- determinants of capital

structure- optimum capital structure-theories of capital structure-net income approach-net

operating income approach- traditional approach-MM approach. (20 Hrs)

MODULE – IV : Long term investment decisions- capital budgeting- nature

features and significance of capital budgeting- traditional methods-payback period- ARR-

Discounted cash flow methods- Bailout payback period-NPV-IRR- Profitability index-

Risk analysis in capital budgeting- techniques of risk analysis. (25 Hrs)

MODULE – V : Leverage analysis- concept- meaning and measurement of

financial leverage. Operating leverage- Financial risk and operating isk-EBIT- EPS-

Indifference point. (15 Hrs)

36Curriculum & Syllabus 2014 Admission onwards

REFERENCE BOOKS

1. Contemporary financial management, Rajeshkothari, Macmillain India limited.

2. Financial management,PV.Kulkarni, Himalya Publishing House.

3. Financial management, Srivastava, Himalya PublishingHouse

4. Fundamentals of financial management, Preetisingh,Anebooks private limited.

5. Financial management, Dhagat,kogent. 6. Financial management, Shah.

7. Financial management, Knott, Palgrave Macmillian.

8. Financial management, S.N.Maheswari, SultanChandCo;

9. Financial management, VanHorn, James C, Prentice HallIndia, Limited.

10. Financial Management, Khan MY, JainPK,Tata MacgrawHill publishingCo;

11.Financial Management, PandeyIM, Vikas publishinghouse.

COM1FMP -FINANCIAL MANAGEMENT PRINCIPLES

Module Hours 1 weight

5/8

2 weight

5/8

5 weight

3/6

Total weight

30/54

Module I 15 2 0 2 12

Module II 15 1 3 0 7

Module III 20 2 3 1 13

Module IV 25 2 1 2 14

Module V 15 1 1 1 8

37Curriculum & Syllabus 2014 Admission onwards

Reg. No…………...…

Name :……………….

M.Com DEGREE (C.S.S) EXAMINATION

First Semester

Faculty of commerce

COM1FMP- FINANCIAL MANAGEMENT PRINCIPLES

Time: Three Hours Maximum Weight: 30

Part A

Answer any five questions

Each question carries 1 weight each

1. Define capital budgeting.

2. What do you understand by business finance?

3. What is trading on equity?

4. What is implicit cost of capital?

5. What are the limitations of financial planning?

6. What is sweat equity?

7. What is factoring?

8. What is Net operating income approach?

(5x1=5)

Part B

Answer any 5 questions

Each question carries 2 weights each

9. What are the assumptions upon which cost of capital is computed?

10. Discuss the relation between debt financing and financial leverage.

11. What are the assumptions of MM hypothesis?

12. What is capitalization? Explain the cost theory and earnings theory of

capitalization.

38Curriculum & Syllabus 2014 Admission onwards

13. What are the different methods of ranking investment proposals?Briefly discuss.

14. What is weighted average cost of capital? How is it computed.

15. X Ltd. Is expecting an annual EBIT of Rs1,00,000.The company has Rs4,00,000 in

10%debentures.The cost of equity capital is 12.5%.Calculate the total value of the

firm according to NI approach.

16. The market price of equity shares of a company is Rs150.The company had paid a

dividend of Rs30 last year. The investors expect a growth of 5%in dividend every

year. Calculate the cost of equity capital. If the expected growth rate is 10%per

annum, calculate market price per share. (5x2=10)

Part C

Answer any 3 questions.

Each question carries 5 weights each

17. Critically evaluate the Net Income theory

18. Explain the methods of capital budgeting.

19. Discuss the determinants of financial plan.

20. Discuss the role of a finance manager in a modern business enterprise.

21. A firm has sales of Rs.75,00,000; Variable cost of Rs.42,00,000 and fixed cost of

Rs.6,00,000.It has a debt of Rs.45,00,000 at 9%equity of Rs.55,00,000.

What is the firm’s ROI?

Does it have a favourable financial leverage?

What are the operating ,financial and combined leverage of the firm?

If the sales drop to Rs.50,00,000 what will be the new EBIT?

22. Rose Ltd. Is considering a new project for which the investment data are as

follows:

Capital outlay Rs.2,00,000

Depreciation 20%p.a.

Annual income before charging depreciation, but after all other charges are follows:

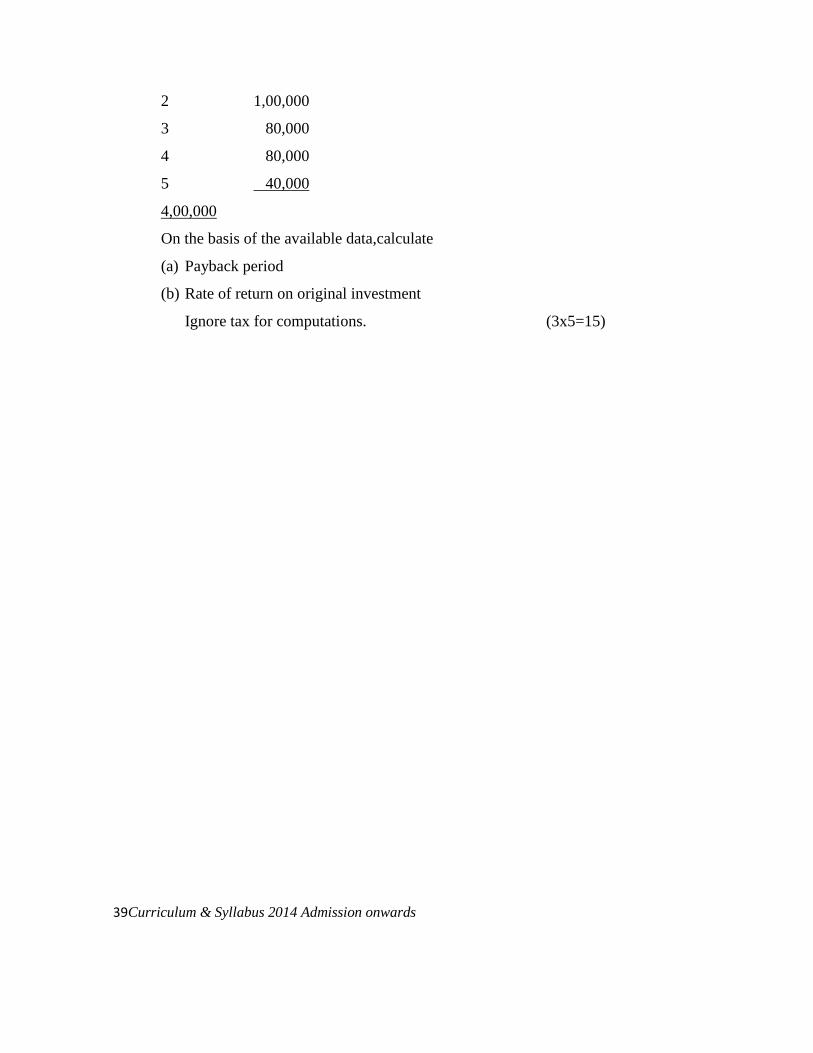

Year Amount

1 1,00,000

39Curriculum & Syllabus 2014 Admission onwards

2 1,00,000

3 80,000

4 80,000

5 40,000

4,00,000

On the basis of the available data,calculate

(a) Payback period

(b) Rate of return on original investment

Ignore tax for computations. (3x5=15)

40Curriculum & Syllabus 2014 Admission onwards

SEMESTER I Credit-4

Code: COM1RM - Hrs90

RESEARCHMETHODOLOGY

Objectives

(a) To help the students to understand how to do research in the area of

commerce and management.

MODULE – I : Research-meaning-significance-objectives-types of

research-research methods Vs methodology-steps in research. (15 Hrs)

MODULE – II : Research problem- definition –nature- formulation

techniques of defining the problem – research design - meaning- needs types of research

design- variables- dependent and independent variables- extraneous variables- intervening

variable-dichotomous variable- research proposal and its preparation-Research

hypothesis-types of hypotheses. (20 Hrs)

MODULE – III : Sampling design-census and sample survey-sample frame-

sample size- methods of sampling. (15 Hrs)

MODULE – IV : Collection and analysis of data- Data types of data- methods

of data collection-preparation of questionnaire or interview schedule- measurement and

scaling techniques- nominal data- interval data- ordinal data –ratio data- Reliability

analysis and its need- analysis of data- uni-variate analysis-bi- variate analysis- multi-

variate analysis- cross tabulation. (30 Hrs)

MODULE – V : Research reporting- relevance- characteristics of a good

research reports-contents of are port-citing references using APA style- MLA style-

Chicago style- plagiarism (10 Hrs)

45Curriculum & Syllabus 2014 Admission onwards

REFERENCE BOOKS

1. Statistical methods for research, Prf.K.Kalyanaraman, Prentice Hall Pvt.Limited

2. Business research,Collis, Palgrave Macmillian.

3. Research Methods for Business:ASkill Building Approach, Sekaran.

4. Management Research Methods, Velde.

5. Business Research Methodology, Dwivedi.

6. Research methodology,Ramamoorthi.

7. Research methodology,CR.Kothari,Wishwaprakasan.

8. Research methodology,R.Paneerselvam, Prentice HallofIndia.

9. Research Methodology, OR.Krishna Swami, Himalaya Publishinghouse

10. Methodology and techniques of social research, Himalya Publishing House.

11.Goodewj and Hatt, Social research methods,Magraw Hill,Newyork.

12. Bajpai,SR, Methods of Social Survey and Resaerch, Kitab Ghar,Kanpur.

COMIRM - RESEARCH METHODOLOGY

Module Hours

1 weight

5/8

2 weight

5/8

5 weight

3/6

Total weight

30/54

Module I 15 1 2 1 10

Module II 20 1 3 1 12

Module III 15 1 1 1 8

Module IV 30 3 2 2 17

Module V 10 2 0 1 7

46Curriculum & Syllabus 2014 Admission onwards

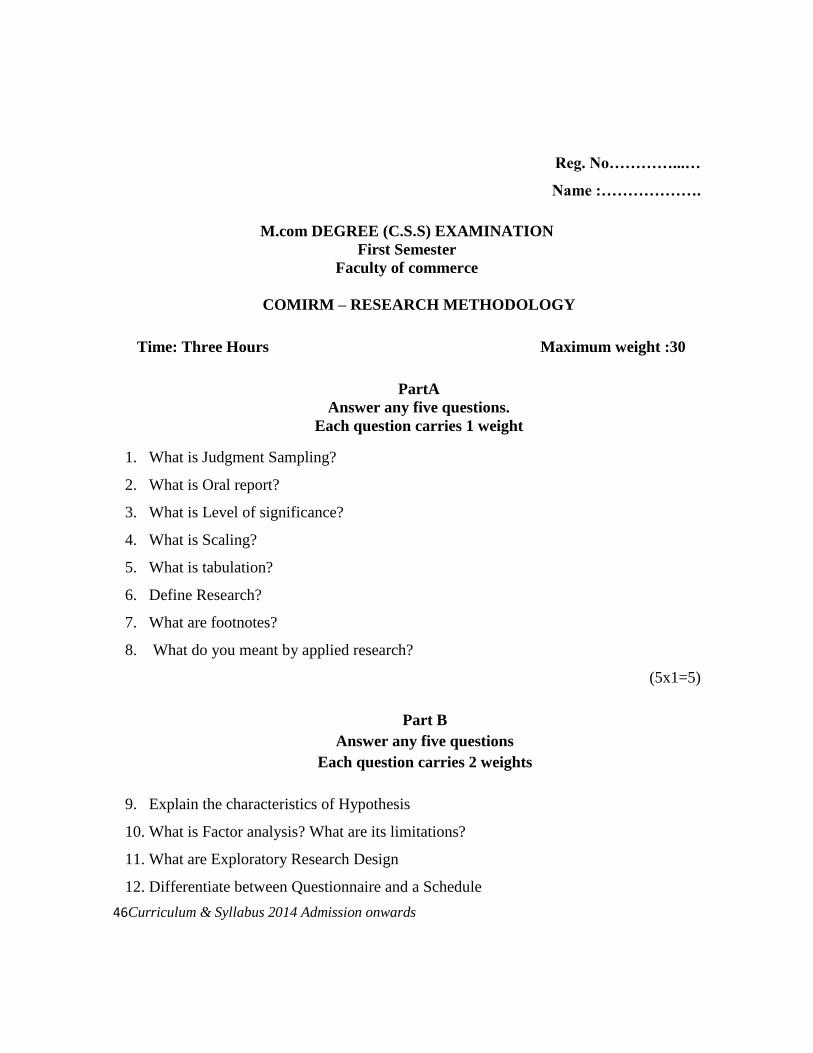

Reg. No…………...…

Name :……………….

M.com DEGREE (C.S.S) EXAMINATION

First Semester

Faculty of commerce

COMIRM – RESEARCH METHODOLOGY

Time: Three Hours Maximum weight :30

PartA

Answer any five questions.

Each question carries 1 weight

1. What is Judgment Sampling?

2. What is Oral report?

3. What is Level of significance?

4. What is Scaling?

5. What is tabulation?

6. Define Research?

7. What are footnotes?

8. What do you meant by applied research?

(5x1=5)

Part B

Answer any five questions

Each question carries 2 weights

9. Explain the characteristics of Hypothesis

10. What is Factor analysis? What are its limitations?

11. What are Exploratory Research Design

12. Differentiate between Questionnaire and a Schedule

47Curriculum & Syllabus 2014 Admission onwards

13. What are the attributes of a good research?

14. Explain Stratified Sampling

15. Explain the significance of research?

16. Explain the sources of research problem? (5x2=10)

Part C

Answer any three questions

Each question carries 5weights

17. What are the advantages and disadvantages of secondary data?

18. Explain the Layout of a Research Report?

19. Explain the different types of interview method

20. What are steps involved in constructing a questionnaire?

21. Explain the types of sampling techniques.

22. Explain Research Process in detail.

(5x3=15)

48Curriculum & Syllabus 2014 Admission onwards

SEMESTER I Credit-4

Code: COM1QT- Hrs90

QUANTITATIVE TECHNIQUES

Objectives

(a) To understand statistical tools for quantitative analysis

(b) To understand the statistical tools for research and business decision making.

MODULE – I : Meaning of quantitative techniques, Classification of QT-

application of QT in business, Industry and management-merits and limitations of QT.

(05Hrs)

MODULE – II : Continuous probability distribution- Normal distribution-

characteristics- construction of normal curves- Standard normal curves-properties of

standard normal curves- measurement of probability based on area under normal curve-

Normal approximation to binomial distribution and Poisson. (10 Hrs) MODULE – III : Sampling theory and statistical inference- sampling and non

sampling errors-statistic and parameter- sampling distribution-standard error- point

estimate-interval estimate-statistical inference-test of hypotheses-procedure-type1error-

type11error- ZTest, t Test- features-application- Z/ttest for population mean and sample

mean- interpretation with hypothesis-confidence limit for population mean- two sample

mean-test for sample proportion and population proportion-confidence limit for population

proportion-two sample proportion-paired t test-testing difference between observed value

and expected value and expected value of X-two sample proportion of heterogeneous

population-combined mean test-test for population standard deviation and sample standard

deviation-test for two sample standard deviation-testing significance of difference between

two sample means when samples are correlated-testing significance of correlation

coefficient- z transformation. (40 Hrs)

MODULE - IV

(a) Ftest- ANOVA- one way, two way-Latin square technique

(b) Non- parametric test-Chi-square test-Sign test-Run test-Mann

Whitney U test-Kruskalwallis Htest-

(c) Association of attributes-consistency of data-association and disassociation-

methods to study association-comparison of actual and observed frequency-

comparison of actual and observed frequency-comparison of proportion and

products-Yule’s co-efficient of association-coefficient of Colligation-co-efficient of

contingency. (25 Hrs)

49Curriculum & Syllabus 2014 Admission onwards

MODULE – V : Statistical Quality Control– Techniques of SQC–

Control charts– Control charts for variables–Xchart, Rchart–Control chart for attributes p

chart, np – chart and c chart. (10 Hrs)

REFERENCE BOOKS

1. Quantitative techniques for statistical decision making, Digambar Patri &

Priyambada Patr

2. Statistics for Management, Richard Levin, Printice Hall, India.

3. Quantitative methods and OR, Reddy& Appanayya, Himalaya Publishing House

4. Statistical methods for Research, Prof. K. Kalyanaraman, Printice Hall, India.

5. Statistical Methods, SP, Gupta

6. Fundamentals of statistics, D.N. Elhance.

7. Quantitative Techniques, CR. Kothari

8. Quantitative methods, D.R. Agarwal.

COM1QT - QUANTITATIVE TECHNIQUE

Module Hours

1 weight

5/8

2 weight

5/8

5 weight

3/6

Total weight

30/54

Module I 5 2 2 1 11

Module II 10 1 1 1 8

Module III 40 4 4 1 17

Module IV 25 1 1 2 13

Module V 10 0 0 1 5

50Curriculum & Syllabus 2014 Admission onwards

Reg. No…………...…

Name :……………….

M.com DEGREE (C.S.S) EXAMINATION

First Semester

Faculty of commerce

COM1QT -QUANTITATIVE TECHNIQUES

Time: Three Hours Maximum Weight :30

Part A

Answer any five questions.

Each question carries 1 weight

1. What is Normal Distribution? Explain its properties?

2. What is type 1 and type 11 errors?

3. Distinguish between statistics and a parameter.

4. Explain briefly Students‘t’ test pointing out its salient features.

5. A soap manufacturing company was distributing a particular brand of soap through

a number of retail shops. Before a heavy advertisement campaign, the mean sales

per week per shop were 140 dozens. After the campaign a sample of 20 shops was

taken and mean sales was found to be 147 dozen with standard deviation of 16. Can

you consider the advertisement to be effective?

6. What do you mean by one and two-tailed test?

7. Explain judgment sampling and quota sampling.

8. Explain Level of significance.

(5x1 =5)

Part B

Answer any five questions

Each question carries 2 weights

9. What are estimators and parameters?

51Curriculum & Syllabus 2014 Admission onwards

10. Explain the procedure for testing hypothesis.

11. What do you mean by sampling and non sampling error?

12. Explain (a) stratified sampling; (b) systematic sampling.

13. Three varieties of wheat(A,B,C) were sown in four plots and the following yields

were obtained (varieties)

14.

Two chemical solutions, A and B were tested for their pH values i.e., the degree of

acidity of the solutions. Six observations on each chemical solution for their pH

values were taken as:

A 7 6 8 9 5 8

B 6 8 5 7 7 6

Can we say that two types of solutions have different mean pH values of 5 per cent

level of significance?

15. Given is the following information:-

Brand A Brand B

Sample size n 1 = 21 n 2 = 16

Standard deviation S1 = 2.5 S1 = 1.5

Mean X1 = 100 X2 = 95

Apply F-test at 5% level to know if the variances of the two makes are significantly

different.

Plots A B C

1 10 9 4

2 6 7 7

3 7 7 7

4 9 5 6

52Curriculum & Syllabus 2014 Admission onwards

16. In a factory producing 50000 pairs of shoes daily for a sample of 500 pairs, 2%

were found to be of sub standard quality. Estimate the number of pairs that can be

reasonably expected to be spoiled in the daily production and assigned limits at 95%

level of confidence.

A soap manufacturing company was distributing a particular brand of soap through a

number of retail shops. Before a heavy advertisement campaign, the main sales per

week per shop were 140 dozens. After the campaign, a sample of 20 shops was taken

and mean sales was found to be 147 dozen with SD 16. Can you consider the

advertisement affected? (5 x 2=10)

Part C

Answer any three questions

Each question carries 5 weights

17. The following data relate to literacy and unemployment in group of 500 persons.

You are required to calculate Yule’s coefficient of association between literacy and

unemployment and interpret it

Illiterate unemployed 220

Literate employed 20

Illiterate employed 180

18. The following table gives the number of refrigerators sold by 4 salesmen in three

months March ,April and may:

Month Salesman

March 50 40 48 39

April 46 48 50 45

53Curriculum & Syllabus 2014 Admission onwards

May 39 44 40 39

Is there a significant difference in the sales made by the four salesmen? Test also

whether there is any difference in the sales during different months. Take = 0.05

19. A company appoints four salesmen P, Q,R,S and observes their sales in 3 seasons

summer, winter ,monsoon. The figures (in lacks) are given as:

Season Salesmen

P Q R S

Summer 13 16 16 14

Winter 17 16 17 16

Monsoon 13 14 15 15

Carry out the analysis of variance. What conclusions do you draw from the

analysis?

20. Two sample polls of votes 2 candidates A & B for a public office are taken, one

from among residence of rural areas and other from among residence of urban areas.

The results are given below:

Examine whether the nature of the area is related to voting preference in this

election.

AREA CANDIDATES TOTAL

A B

Rural 620 480 1100

Urban 380 520 900

TOTAL 1000 1000 2000

21. What is meant by sampling? What are the essentials qualities of a good sample?

Why sampling necessary in many statistical enquiries?

22. Define Quantitative Techniques. Discuss the scope and limitations of Quantitative

Techniques. Explain the uses of QT.

54Curriculum & Syllabus 2014 Admission onwards

SEMESTER II Credit-4

Code: COM2AFA- Hrs90

ADVANCED FINANCIAL ACCOUNTING- PAPER II

Objectives

(a) To understand the proceedings of the preparation of consolidated balance

sheet.

(b) To get an idea about Green accounting, Double accounts, Farm accounts,

voyage accounts, and liquidation proceedings of companies.

MODULE-I : Accounts of holding companies, consolidated balance sheet-

minority interest-cost of control- pre- acquisition and post-acquisition profit- elimination

of common transaction-contingent liabilities-unrealized profit-bonus issue-revaluation of

assets and liabilities-treatment of dividend-debentures and preference shares of subsidiary

companies- (30 Hrs)

MODULE-II : Accounts of public utility undertakings –double

account system- accounts of electricity concerns- computation of reasonable return and

clear profit-replacement of asset. (20 Hrs)

MODULE-III : Liquidation accounts- statement of affairs-

deficiency accounts- liquidators final statement of accounts. (15 Hrs)

MODULE-IV : Accounting for specialized type of business-voyage

accounts-farm account-accounts of underwriters. (15 Hrs)

MODULE-V : Green accounting- meaning- scope and importance- green

accounting concepts- advantages and limitations (10 Hrs)

REFERENCE BOOKS

1. Financial Accounting, Nirmal gupta,Anebooksprivatelimited.

2. Advanced Financial Accounting, M.C. Shukla &T.S.Grewal, S.Chand&Co;

3. Advanced accountancy, Arulanandam & Raman,HimalayaPublishing House.

4. Fundamentals of Financialaccounting, Nassem Ahmed,Anebooks Pvt,Limited

5. Advanced Financial Accounting, R.L.Gupta& Radhaswami, Sultan ChandCO;

6. Advanced Financial Accounting, S.N.Maheswari

55Curriculum & Syllabus 2014 Admission onwards

7. Advanced Financial Accounting, Paul&Kaur

8. Advanced FinancialAccounting, B.D.Agarwal

9. Advanced FinancialAccounting, S.P.Jain&K.L.Narang; Kalyani Publishers

ADVANCED FINANCIAL ACCOUNTING II

Module Hours 1 wt

5/8

2 wt

5/8

5 wt

3/6

Total weight

30/54

Module I 30 3 2 2 17

Module I 20 1 2 1 10

Module III 15 1 1 2 13

Module IV 15 2 2 1 11

Module V 10 1 1 0 3

56Curriculum & Syllabus 2014 Admission onwards

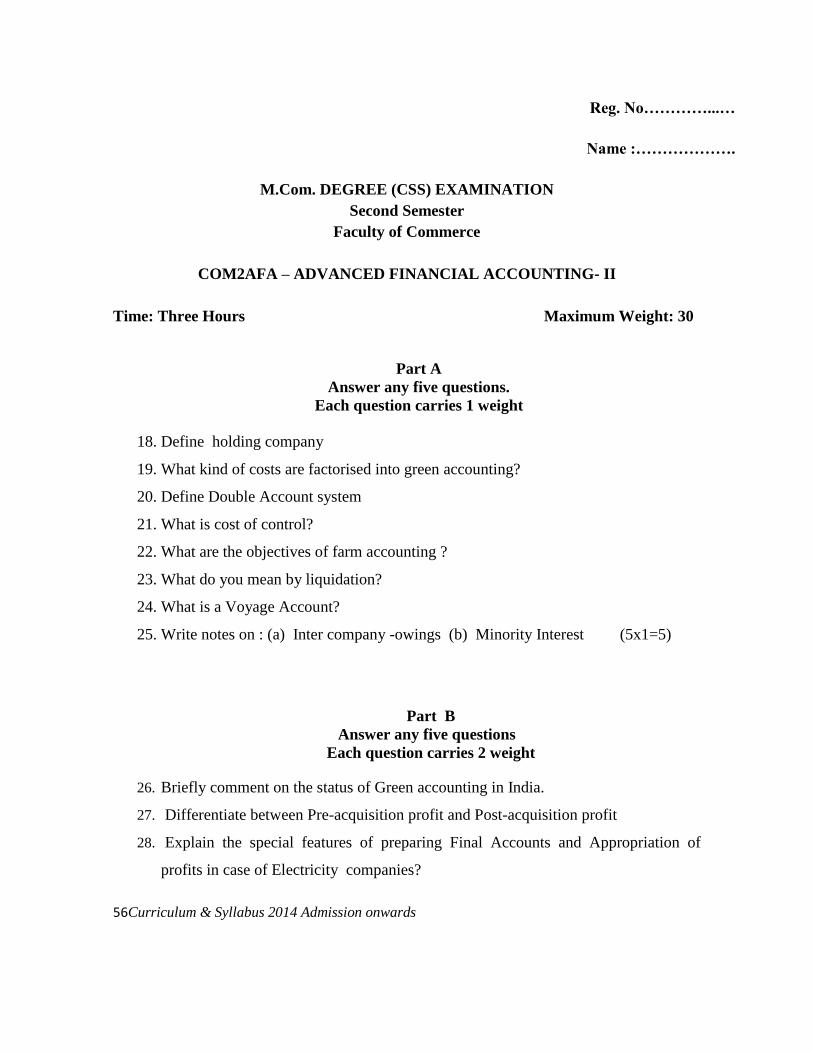

Reg. No…………...…

Name :……………….

M.Com. DEGREE (CSS) EXAMINATION

Second Semester

Faculty of Commerce

COM2AFA – ADVANCED FINANCIAL ACCOUNTING- II

Time: Three Hours Maximum Weight: 30

Part A

Answer any five questions.

Each question carries 1 weight

18. Define holding company

19. What kind of costs are factorised into green accounting?

20. Define Double Account system

21. What is cost of control?

22. What are the objectives of farm accounting ?

23. What do you mean by liquidation?

24. What is a Voyage Account?

25. Write notes on : (a) Inter company -owings (b) Minority Interest (5x1=5)

Part B

Answer any five questions

Each question carries 2 weight

26. Briefly comment on the status of Green accounting in India.

27. Differentiate between Pre-acquisition profit and Post-acquisition profit

28. Explain the special features of preparing Final Accounts and Appropriation of

profits in case of Electricity companies?

57Curriculum & Syllabus 2014 Admission onwards

29. Bring out clearly the distinction between a winding up by the court and a

members’ voluntary winding up.

30. Mr X enter in to a contract with B Ltd, to underwrite its 8,000 shares of Rs 10 each

in consideration of 5%commission. He also enters into an agreement with C to sub

underwrite 2,000 shares of B Ltd at a commission on 3%.The public subscribes for

3,000 shares only and subsequently the shares were taken up by x who sold his

shares @ Rs 9 per share. The share taken up by C were sold @ Rs 10 per share.

Expenses of underwriting amounts to Rs600.Prepare underwriting account in the

books of X

31. From the following information, prepare Cattle account to ascertain the profit made

by the cattle division

No. Value

Opening stock of livestock 100 2,00,000

Closing stock of livestock 118 2,42,000

Opening stock of cattle food 4,000

Closing stock of cattle food 5,000

Purchase of cattle during the year 180 3,70,000

Sales of cattle during the year 175 4,38,000

Sale of carcasses 5 1,000

Purchase of cattle food 40,000

Wages for rearing cattle 10,000

Crop worth Rs 11,100 grown in the farm was used for feeding the cattle. Out of the

calves born 4 died and their carcasses realized Rs 100

32. On April1,2011 S Ltd. issued 10% preference shares of Rs 1,00,000 at par. on this

date, S, Ltd’s General reserve and surplus account showed balances of Rs 80,000