stimulating demand and designing financial literacy campaign ...

43

Shriju Dhakal Rimal DAAYITWA SUMMER FELLOW 2016 WITH NEPAL RASTRA BANK STIMULATING DEMAND AND DESIGNING FINANCIAL LITERACY CAMPAIGN TO INCREASE SUSTAINABLE ACCESS TO FINANCE IN NEPAL

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of stimulating demand and designing financial literacy campaign ...

ShrijuDhakalRimal

DAAYITWASUMMERFELLOW2016WITHNEPALRASTRABANK

STIMULATINGDEMANDANDDESIGNINGFINANCIALLITERACYCAMPAIGNTOINCREASESUSTAINABLEACCESSTOFINANCEINNEPAL

2

Listoffigures………………………………………………………………………………………………………….Pg.

Figure1:GrowthofFinancialInstitutions…………………………………………………………………….4Figure2:FinancialInclusion…………………………………………………………………………………………6Figure3.Financialliteracystrategy…………………………………………………………………………….10

ListofTables

Table1.NumberofBranchesofBanksandFinancialInstitutions………………………………..5

Acknowledgement

IwouldliketoextendmygratitudetoDaayitwaforgivingmeanopportunitytobepartofthefellowshipprogramandNepalRastraBankforallowingmetoworkundertheirguidance.Firstofall, Iwould like to thank theDaayitwa teamandspeciallymymentorsManojandPrakriti who guidedme throughout the research. Besides I would also like to thankMr.TrilochanPangeni,Mr.GunakarBhatta,Mr.BhubaneshPant,Mr.RamHariDahal,Mr.SubodhManShrestha,Mr.DeepakKcandMrs.AsmitaGorkhali.TheirfaithinmeasaDaayitwafellowandwillingnesstohelpwasinstrumentalforconductingthisresearch.Besidesthem,allthewonderfulandsupportivestaffatNRBwhoweresowelcoming.

3

TableofContentsPg.

1.Introduction…………………………………………………………………………………………………………………1

1.1Background………………………………………………………………………………………………………………….1

1.2RationalandSignificanceofthestudy………………………………………………………………………….2

2.Methodology……………………………………………………………………………………………………………….3

3.ScenarioofFinancialInclusioninNepal……………………………………………………………………….4

3.1FinancialSystemataGlance………………………………………………………………………………………..4

3.2UnderstandingdemandforfinancialservicesinNepal…………………………………………………6

4.ReviewofLiterature…………………………………………………………………………………………………….8

5.Analysis………………………………………………………………………………………………………………………10

5.1AstudyofInternationalPractices:CasesofIndia,Mexico,Spain,U.KandIndonesia….10

5.2AnoverviewoffinancialliteracyinitiativesinNepal……………………………………………………18

5.3Excerptsofinteractionwithstakeholders……………………………………………………………………31

6.Findings………………………………………………………………………………………………………………………34

7.Recommendations………………………………………………………………………………………………………35

4

1.Introduction

1.1 BackgroundThe Nepalese financial system has a very recent history that started just from the earlytwentiethcentury.TheformalfinancialsysteminNepalstartedquitelatecomparedtoothercountries.ThedevelopmentoffinanceinNepalcanbedividedintothreedistinctphases.ThefirstphasecorrespondswiththeinitiationofformaldomesticbankingsysteminNepal.Thisphaseofficiallystartedin1880withtheestablishmentofTejarathAdda,aninstitutionthatheldfundsgivenbygovernmenttogivecredittotheirstaffand landlordsonly, itwasnotallowedtotakepublicdepositsandprovidecredittopublic.OnlywhenNepalBanklimitedwasestablishedin1937thatthefinancialservicesweremadeavailabletothegeneralpublic.Theestablishmentofthecentralbanki.e.NepalRastraBankin1956markedthebeginningofthesecondphasethateasedtheprocedureofestablishingbanksandfinancialinstitutionsinthe country. This period saw the set-up of the first joint venture bank inNepal after theadoptionofGovernment’sLiberalizationPolicy.ThisperiodexperiencedasteepriseinthenumberofbanksandfinancialinstitutionsinNepalthussignificantlyenhancingtheaccessoffinancetomanyindividualsandenterprises.ThethirdphasethatiscurrentlygoingonstartedwiththeNRBactof2002.ThisactallowedNRBtobemoreautonomousinexercisingdecisionsrelatingtoformulationofmonetaryandforeignexchangepolicyaswellasmonitoringandregulatingbanksandfinancialinstitutionsacrossthenation.The post liberalization periodwitnessed the growth of BFI’s inNepal thatmade financialservicesavailabletothegeneralpeoplenotjustinmajorcitiesbutalsoinruralareas.Aworldbankreportstatesthatfinancialinclusionorbroadaccesstofinancialservices,isdefinedastheabsenceofpriceornon-pricebarriersintheuseoffinancialservices.Thisreportstressesadifferencebetween“accessto”and“useof”financialservices.“Access”essentiallyreferstothesupplyoravailabilityofserviceswhereastheuseisdeterminedbydemandaswellassupply.(FederationofIndianChambersofCommerceandIndustry,2011)AccessoffinanceinNepalhasbeenrisingsubstantiallyovertheyearswiththe increment inthenumberofBFI’s.Severalpolicieshavebeenintroducedtostrengthenfinancialinclusionbutthepoliciesformulatedhaveyettocreateasubstantialimpactonincreasingaccessiblefinancialservicestotheexcludedpopulation.ThegrowthoftheseinstitutionshasbeensuchthatthereishighconcentrationofBFI’s inurban,semiurbanandprivilegedcitiesandvery lesspresence inruralareas;creatinganunequaldistributionoffinancialservices.(Chaulagain,2015)TheBFI’sare operatingwithin a limitedmarket competing against each other for a small group ofcustomerstheydeemprofitable.Somepoliciesattemptedtoincreaseaccesshavecreatedrequirementsforopeningbranchesinruralareasorlendingtothedeprivedsector.Buttheinstitutionsdon’tseetheserequirementsashavingaprofitableimpactontheirbusinessesandhencetheyjustmeettheminimumrequirementsofthegovernment.Atpresent,61%ofthepeopleinNepalareformallyservedbybanksandfinancialinstitutionsthatareregulatedbyNRBorGON.21%ofthepeopleareinformallyservedbyorganizationslikesavingsgroupsandprivatemoneylendersthatarenotregulated.Therest18%ofthepeopleinNepalarecompletely financially excluded whichmeans that they do not use or have any financial

1

productsor service, they relyon friendsand family toborrowandkeepsavingsathome.(FinMarkTrust,2014)Improvedaccesstofinancecreatesanenvironmentconducivetonewfirmentry,innovationandgrowth.Moderndevelopmenttheoriesemphasizeontheroleofaccessoffinanceontheeconomicdevelopmentofacountry.Accessoffinancetoallcreatesanenvironmentofequalopportunitiesandreducesinequalitieswhereaslackoffinanceisoftenanunderlyingcauseof persistent income inequality and slower growth. (TheWorld Bank, 2008)The access offinanceonNepalisatamodestlevelwithmajorityofthepeopleturningtoinformalsourcesfortheirfinancialneeds.Astheinformalsourcesarenotregulatedthereisgreaterchanceofexploitation of rights of individuals and enterprises by informal lenders.Hence, access toaffordableandappropriatefinancial instrumentsandproductscan improvethewelfareoftheun-servedandunder-servedportionsofthepopulationbyhelpingthemconducttheirfinancial lives more efficiently, create income, manage risk and build wealth over time.(FinMarkTrust,2014)Initiallyeffortstoenhanceaccesstofinancewereconcentratedonsupplysideendeavors.Policy level initiations were taken to encourage a wider availability and accessibility offinancial services. But only an increment in number of financial intermediaries does notguaranteequalitative financialaccess, sustainabilityandsatisfactionofserviceconsumers.(Chaulagain,2015)Financialliteracyisalsousedasaneffectivemechanismtoboostdemandfor financial services ultimately increasing the access of finance. Financial literacy willencouragedesired financialbehaviors suchas saving,budgetingandusing credit thatwillcreateafavorableenvironmentforthedevelopmentofthefinancialsector.Whileitisknownthatfinancialliteracydoesenhanceaccesstofinancebutitisdifficulttosayexactlybyhowmuchaccesstofinancialservicesisaffectedbyfinancialknowledgeandskills.Nonetheless,NRBisworkingoncreatingafinancialliteracystrategy.Ithasemphasizedonthetriangularrelationshipamongfinancialaccess,financialliteracyandfinancialinclusionandaimstousefinancialliteracyasapromotionaltoolforincreasingaccesstofinance.Thisreportaimstorecommendaroadmapforformulatingnationalfinancialliteracystrategyin Nepal by outlining the key variables that need to be taken into consideration forformulation of such a strategy. Thiswould be done by studying international trends andpracticesandstudyingtheexistingstakeholdersandinitiativesalreadytakeninNepal.

1.2RationaleandSignificanceofthestudy

Theglobalcommunityhasalsoacknowledgedtheneedofenhancingfinancialaccesstopoorpeople.Worldbankandabroadgroupofpartners includingmultilateral agencies,banks,credit unions, micro finance institutions and telecommunications have set up a goal ofachievinguniversal financialaccessby theyear2020.Enhancingaccess to financehasalsobeen a major priority of NRB. In Sept 13, 2013 NRB signed the Maya declaration i.e. acommitment tounlock theeconomicandsocialpotentialof the2billionunbanked in theworld through financial inclusion. Under the commitments made by NRB includes thecommitmentstopromotefinancialliteracybydevelopingafinancialliteracystrategy.Ithasalready initiated “NRB with students” program at the school level to enhance financialliteracy,especiallytargetingtheyoungsters.Itaimstoconductruralcreditsurveyfocusingon

2

accessoffinance,creditandinterestratestructure,andfinancialliteracytousetheresulttoframeappropriatepoliciesandstrategiesforruralfinance.Ithasalsoplannedtodevelopafinancialsectordevelopmentstrategybymakinginstitutionalarrangements,strengtheningregulatoryandsupervisorynorms formicrofinance institutions,enhancepublicawarenessandfinancialeducation.Italsomadeacommitmenttoimprovethequalityofexistingmobilemoneyservicesandalsointroducenewonesforimprovingaccessforthepoor.NRBhadalsoformedallianceswithUNDPandUNCDFandinitiatedaprojecttitledEnhancingAccesstoFinancialServices(EAFS)toimprovetheoutreachoffinancialservices.Thisproject’scommitment is towards building a sound microfinance sector in the country to provideservices to theruraland low incomepeople.Similarly,NRBhasalsopartneredwithotheragencies like DFID, UNCDF and initiated UNNATI- Access to Finance(A2F) project forexpandingfinancialservicesforindividualsandmicroandsmallbusiness.AccordingtoNepalRastraBank(NRB),thelongtermobjectivesinNepalistoachieveagreaterdegreeoffinancialinclusion,todeliverfinancialservicesatanaffordablecosttotheunservedandunderservedpopulations,especiallydisadvantagedand low incomegroups.Financial inclusion inNepalcanbestimulatedonlyby imparting financialeducation toourpeopleas largenumberofpeoplearenotevenawareofbasicknowledgeofhowtousebankingservices.Identifyingtheimportanceof financial literacyNRBstarted initiatives like“NRBwithstudents”,published“Paisa ko Bot” and even conducted a survey to assess financial literacy among collegestudents.Around50countriesintheworldhavealreadyadoptedsomesortofnationalfinancialliteracystrategy. This issue is relevant to both developed and developing countries as developedcountriesarehavingincreasingcomplexfinancialmarketwithawiderangeoffinancialtoolsthatcaneasilyconfusea layman.Speciallyaftertheglobalfinancialcrisismanydevelopednationsareformulatingfinancialliteracystrategytohavecapablecitizenswhoknowhowtohandlecreditwiselyandnotmakewrongfinancialdecisions.Intermsofdevelopingcountriesfinancialliteracyisusedasatooltostimulatedemandforfinancialservices.Hencethisstudyishighlyrelevantnowandcanbeofusetodifferentstakeholderswhoareinterestedinthistopic.AsNRBiscurrentlydraftingpolicyforfinancialliteracyinthisreportcouldnotbeundertakenatamoreappropriatetime.Thisreportaimstoaddsomevalueandprovidesomeinsightsontheissueoffinancialliteracy.

2. Methodology

Themainobjectiveofthestudyistounderstandthecurrentfinancial literacyinitiativesinNepalandprovidearecommendationonformulatingfinancialliteracystrategy.Thisresearchisqualitativeinnature.Twomethodshavebeenusedforwritingthispaper;deskresearchforavailableliteraturesandinterviewsanddiscussionswithstakeholdersandNRBemployees.Deskresearch:

Identification of stakeholders involved in financial literacy initiatives in Nepal was donethroughdeskresearch.Alsorelevantreviewofliterature,studyofinternationalpracticeswasalldonethroughdeskresearch.

3

Primaryresearch

Interviewsand interactionsare themainsourceofprimarydata for this study. Interviewswereconductedwithstakeholdersoffinancialliteracyinitiatives.Atotaloffiveinstitutionswereinterviewedusingsemistructuredquestionnaires.Also,interactionswithemployeesatNRB,Microfinancedepartmentwasconductedtogainmoreinsightintotheissueoffinancialliteracy.

3.ScenariooffinancialinclusioninNepal

3.1Financialsystemataglance

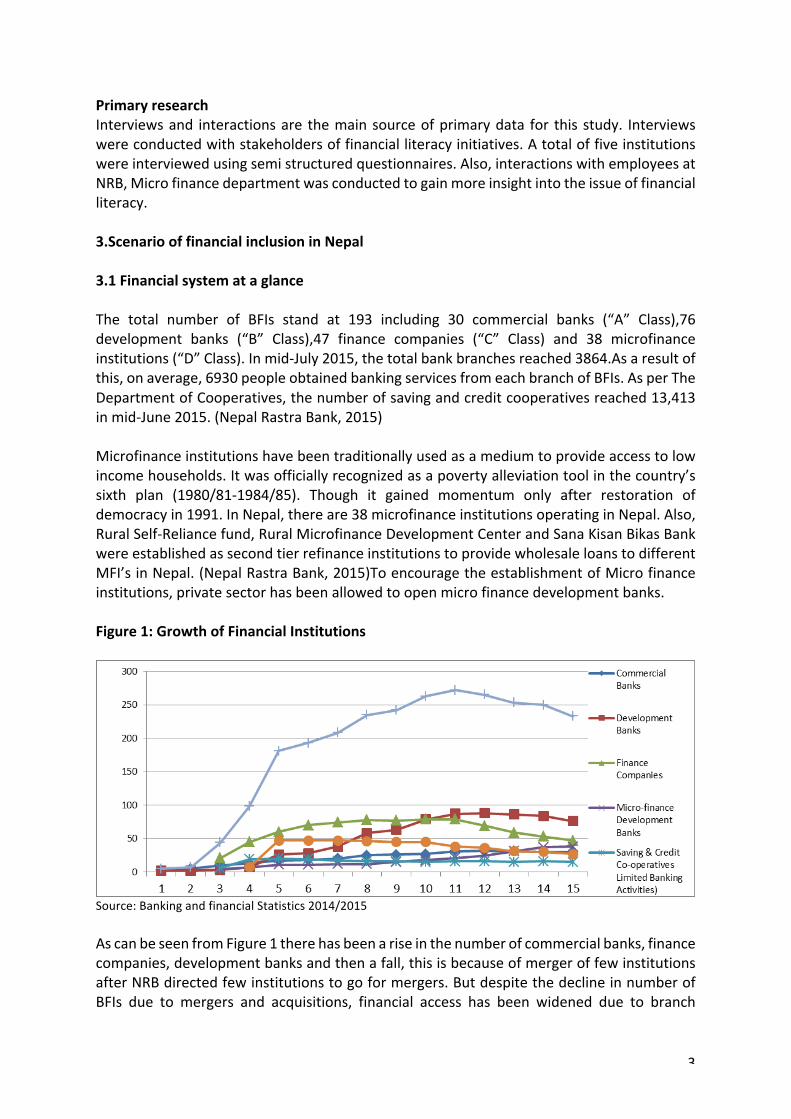

The total number of BFIs stand at 193 including 30 commercial banks (“A” Class),76development banks (“B” Class),47 finance companies (“C” Class) and 38 microfinanceinstitutions(“D”Class).Inmid-July2015,thetotalbankbranchesreached3864.Asaresultofthis,onaverage,6930peopleobtainedbankingservicesfromeachbranchofBFIs.Asper TheDepartmentofCooperatives,thenumberofsavingandcreditcooperativesreached13,413inmid-June2015.(NepalRastraBank,2015)Microfinanceinstitutionshavebeentraditionallyusedasamediumtoprovideaccesstolowincomehouseholds.Itwasofficiallyrecognizedasapovertyalleviationtoolinthecountry’ssixth plan (1980/81-1984/85). Though it gained momentum only after restoration ofdemocracyin1991.InNepal,thereare38microfinanceinstitutionsoperatinginNepal.Also,RuralSelf-Reliancefund,RuralMicrofinanceDevelopmentCenterandSanaKisanBikasBankwereestablishedassecondtierrefinanceinstitutionstoprovidewholesaleloanstodifferentMFI’sinNepal.(NepalRastraBank,2015)ToencouragetheestablishmentofMicrofinanceinstitutions,privatesectorhasbeenallowedtoopenmicrofinancedevelopmentbanks.Figure1:GrowthofFinancialInstitutions

Source:BankingandfinancialStatistics2014/2015

AscanbeseenfromFigure1therehasbeenariseinthenumberofcommercialbanks,financecompanies,developmentbanksandthenafall,thisisbecauseofmergeroffewinstitutionsafterNRBdirectedfewinstitutionstogoformergers.ButdespitethedeclineinnumberofBFIs due to mergers and acquisitions, financial access has been widened due to branch

4

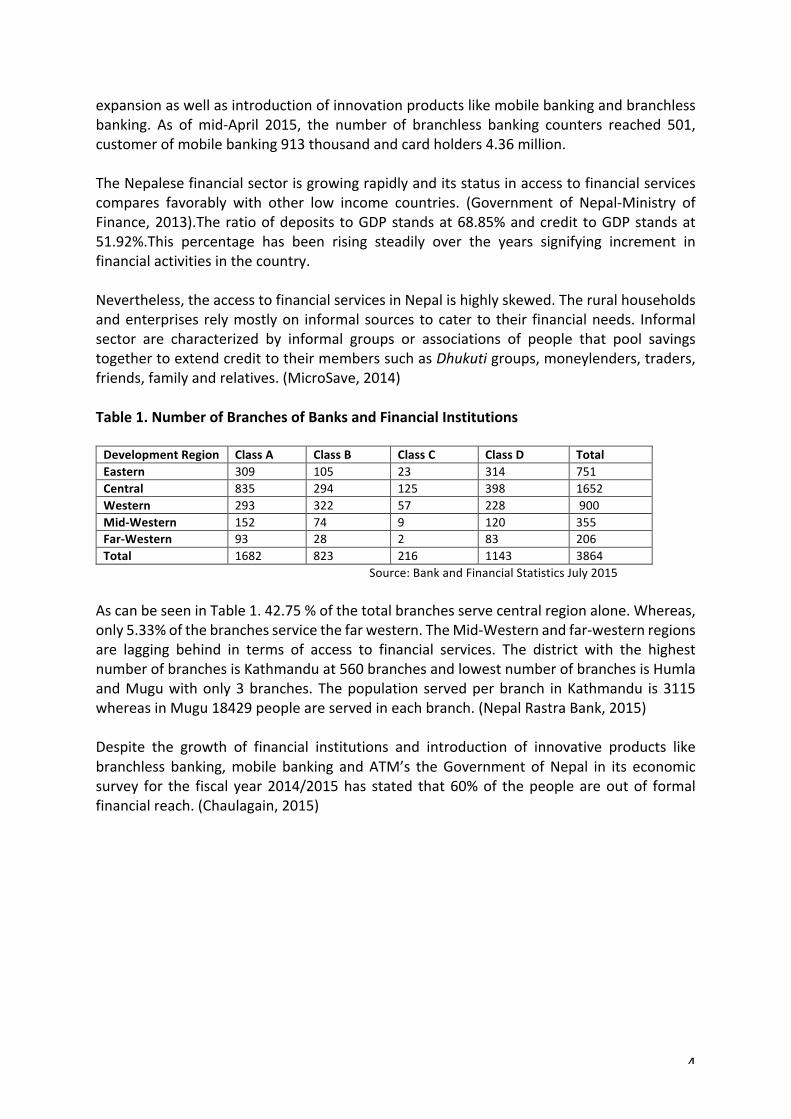

expansionaswellasintroductionofinnovationproductslikemobilebankingandbranchlessbanking. As ofmid-April 2015, the number of branchless banking counters reached 501,customerofmobilebanking913thousandandcardholders4.36million.TheNepalesefinancialsectorisgrowingrapidlyanditsstatusinaccesstofinancialservicescompares favorably with other low income countries. (Government of Nepal-Ministry ofFinance,2013).Theratioofdeposits toGDPstandsat68.85%andcredit toGDPstandsat51.92%.This percentage has been rising steadily over the years signifying increment infinancialactivitiesinthecountry.Nevertheless,theaccesstofinancialservicesinNepalishighlyskewed.Theruralhouseholdsandenterprises relymostlyon informalsources tocater to their financialneeds. Informalsector are characterized by informal groups or associations of people that pool savingstogethertoextendcredittotheirmemberssuchasDhukutigroups,moneylenders,traders,friends,familyandrelatives.(MicroSave,2014)Table1.NumberofBranchesofBanksandFinancialInstitutions

DevelopmentRegion ClassA ClassB ClassC ClassD Total

Eastern 309 105 23 314 751Central 835 294 125 398 1652Western 293 322 57 228 900Mid-Western 152 74 9 120 355Far-Western 93 28 2 83 206Total 1682 823 216 1143 3864

Source:BankandFinancialStatisticsJuly2015

AscanbeseeninTable1.42.75%ofthetotalbranchesservecentralregionalone.Whereas,only5.33%ofthebranchesservicethefarwestern.TheMid-Westernandfar-westernregionsare lagging behind in terms of access to financial services. The district with the highestnumberofbranchesisKathmanduat560branchesandlowestnumberofbranchesisHumlaandMuguwithonly3branches.Thepopulationservedperbranch inKathmandu is3115whereasinMugu18429peopleareservedineachbranch.(NepalRastraBank,2015)Despite the growth of financial institutions and introduction of innovative products likebranchless banking,mobile banking andATM’s theGovernment ofNepal in its economicsurvey for the fiscal year2014/2015has stated that60%of thepeopleareoutof formalfinancialreach.(Chaulagain,2015)

5

3.2UnderstandingdemandforfinancialservicesinNepal

Figure2:FinancialInclusion

Source:FinScopeConsumerSurvey2014

Financial inclusion as shown in Figure 1 refers to adultswho have/use financial productsand/orservices-formaland/or informal.According to thesurveydonebyFinMark trustaspartofasurveyforMakingAccessPossible(MAP)programthatoperatesundertheoverallumbrellaofUNNATI-Accesstofinance(A2F)projectimplementedbyNepalRastraBank,only40%ofpeople,claimtobebankedi.e.adultswhohave/usefinancialproductsand/orservicesprovidedbyA,B,C,DclassinstitutionsofNepal,21%claimtouseotherformalfinancialservicelike cooperatives, insurance companies, remittance service providers while another 21%claimtouseinformalsourceslikemoneylendersthatarenotregulatedwhereas18%oftheadultsdonotuseanyformalorinformalfinancialproducts.(FinMarkTrust,2014)Reasonsfornotusingformalfinancialservicescanbedividedbroadlyintolackofknowledgeaboutfinancialinstitutionsandsupplysideconstraints.Mostcommonlycitedreasonsfornotusingbankservicesare:donotneed(33%),donotunderstandhowitworks(9%),financialaccountsarenotforme(8%),donotknow(7%),donotknowhowtoapply(4%)andcanobtain these serviceselsewhere (4%).All these reasons come froma lackofawarenessorlimitedknowledgehowbanksworks.Thesecorrespondtoalackofknowledgeaboutfinancialservices.Supplysideissuesarecannotmaintainminimumbalance(42%),toofaraway(16%)andservicechargetoohigh(4%)thatpresentanopportunityforBFIstomaletheirbranchesaccessible,chargelowerinterestratesandopenzeroorlessbalanceaccountstostimulatedemand.(FinMarkTrust,2014)AccordingtoaresearchdonebyMicroSaveaspartofMM4P,aUNCDFprogramtounderstandthedemandof financialservices inNepal, therehasbeenbehavioralchanges inpeople intheirusageoffinancialservicesinthelast10years.Theuseofformalservicesgivenbybanks,MFIs, finance companies, co-operatives and remittance and insurance companies haveincreased in the period. Because of this, the use of most informal services, such as

40

21

21

18

FinancialInclusionin%

Banked Otherformal(non-bank) Informalonly Excluded

6

moneylenders,friendsandrelativeshavedecreased.Nonetheless,peoplestilluseinformalgroups(women’sgroupsetc.)tomeettheirfinancialneedsbutalsoincreasedtheiruseofformal services. This change can be attributed to the improvement of financial servicedeliverymechanismsinNepal.WhenformalBFIsbegantospreadtheiroperations,peoplemoved away from traditional informal lenders. However, factors such as accessibilitychallenges,costconsiderationsandtrustissueshavemeantthatpeoplestilltendtoresorttoinformalgroupsformanyoftheirfinancialneeds.(MicroSave,2014)60%ofthepeoplewhoarecurrentlyunbankedaretheuntappedconsumersoftheBFIs.In the context of Nepal, the main problems about access to finance are for the ruralhouseholdsandentrepreneurs.People living inurbanareasandcitieshavehighaccesstofinancialservicesandcanbeseenusingcomplexfinancialproducts.Forexample,theNEPSEstockexchangehasdailytransactionsofalmost2billion.TheIPOofcompaniesareusuallyinhighdemandandareoversubscribed.Peoplearekeenoninvestinginthestockmarketandtakecreditforinvestinginshares,realestateandotherproperties.Importantpurchaseslikehouses and cars are bought on EqualMonthly Installments(EMI). Youngsters canbe seenusingATMcards, credit cards forquick cashand shoppingpurposes.Mobile and internetbanking are growing popular. Most of the departmental stores and restaurants acceptdebit/creditcardsandmanycustomersusethisfacility.Butthispictureislimitedtofewbigcities.Thestoryiscompletelydifferentinruralareaswherepeoplehavetowalkforhourstoreachabank.ManyentrepreneursdonotgetcredittoexpandtheirsmallenterprisesasBFIsdonotseethemasprofitable.Thereisuntappedmarketintheruralareasandentrepreneurs.Financial literacy can be used to stimulate demand for financial services. For example,Consumerswhoarefinanciallyliteratearemorelikelytounderstandtheimportanceofsavingandopenasavingsaccount inabank. (Miller,Godfrey,Levesque,&Stark,2009).Financialliteracy benefits consumers but also benefits banks and financial institutions providingfinancialservices.Financiallyeducatedcustomersaremorelikelytousetheseserviceswiselyandpayinterests/loansontime.Hence,institutionsshouldnotseethisissueasanaspectofcorporate social responsibility or expenditure but an investment for betterment of thecompanyitself.

7

4.Reviewofliterature

Organization for Economic Cooperation and Development defines financial literacy as acombinationoffinancialawareness,knowledge,skills,attitudeandbehaviorsnecessarytomakesoundfinancialdecisionsandultimatelyachieveindividualfinancialwell-being.Itisaconcept thathasdifferentmeaning fordifferentpeoplebut theendgoal isattainmentoffinancialwell-being.Indevelopedeconomies,beingfinanciallyliteratemightinvolvehavingknowledgeabouttaxcodes,insurancerequirementsandcreditcards.Ontheotherhandindevelopingcountrieswheremajorityofthepeopleare“unbanked”financialliteracyismorelikelydefinedbybasicconceptsofsafeandsecuresavings,budgetingandwiseborrowing.(Cohen&Nelson,2011)Financial literacy is a broad concept that includes both information and behavior and isrelevantforeverybodyregardlessoftheirwealth.Itincludestechnicalaspectslikeknowingaboutdifferencesbetweensimpleandcompoundinterest,realandnominalinflationratesandalsobehavioralchangeslikeestablishingafamilybudget,payingbillsandloansintime.It is about empowering and educating individuals so that they are knowledgeable aboutfinance inawaythat is relevant to their livesandenables themtouse thisknowledgetoevaluate products and make informed decisions. (Miller, Godfrey, Levesque, & Stark,2009).ThisdefinitionanswersthequestionofwhyfinancialliteracyisofanyimportancetoacountrylikeNepal.It’saboutmakingindividualsknowledgeableaboutfinanceinawaythatisrelevanttothem.InNepalesecontext,wheremajorityofthepeoplearefinanciallyexcluded;financialliteracywouldmeangeneratingawarenessaboutexistenceofdifferenttypesofBFIs,theirproductsoffered, application procedures, pros/cons of services provided, importance of savingbudgetingetc.Thesearebasicelementsoffinancialeducationbutthesearemostrelevanttopeopleresidinginruralareaswhodonotunderstandhowfinancialinstitutionswork.Hence,this is financial literacy to them. In contrast, for university students living in city likeKathmandu,FinancialliteracysessionsongeneratingawarenessaboutexistenceoftypesofBFIsandproductsofferedwillnotmakeanysense.Forthemimpartingknowledgeonstockmarketoperations,mutualfunds,diversificationofriskswouldbemoreappropriate.Sotheissueofrelevancyisanimportantconceptforunderstandingfinancialliteracy.Financialliteracyplaysanespeciallyimportantroleinthecaseofdevelopingcountries.Morefinanciallyliterateconsumersincreasethedemandandresponsibleuseoffinancialservices,help tounderpin financialmarket stability, andcontribute towidereconomicgrowthanddevelopment.Forexample,consumerswhoaremorefinancially literatearemorelikelytounderstandtheimportanceofsavingandtotakeactioninthatrespect.(WorldBank,2009)Financialliteracytrainingsarethemostpopulartoolsofimpartingfinancialeducation.Thesetrainingshavealsoshowntoenhancedemandforfinancialservices.IntheUnitedStates,anevaluation of the American Dream Demonstration’s Financial Education Program foundhighersavingratescorrelatedwiththenumberofhoursoftrainingreceived,upto12hours.Anotherstudyshowedthatworkplacefinancialeducationwascorrelatedwithhigherratesofsaving,especially for consumerswhowerepreviously saving littleornothing. Such savingbehaviorwillencouragepeopletouseservicesofformalfinancial institutions.Manyother

8

programsandpolicieshavebeenevaluatedandshowntobeeffectiveatimpartingfinancialknowledgeandchangingbehavior.(WorldBank,2009)A2010surveyoffinancialregulatorsfrom142economiesshowedthat88%hadsomeaspectoffinancialinclusion,financialeducationorfinancialconsumerprotectionintheirmandate(CGAP/World Bank, 2010). In total 45% of economies had a strategy document for thepromotionoffinancialinclusion,58%hadsomeresponsibilityforfinancialliteracy,whilst68%wereresponsibleforconsumerprotection.Theimpactoffinancialeducationprogramsindevelopingcountriesislimited.Fewfinancialliteracy initiatives exist in developingmarkets and evenwhere they exist rigorous impactevaluation has not been conducted. The research in this area is fairly limited to haveconclusive results on the impact of these programs. In Uganda, two massive savingscampaignswereconductedthatusedradio,posters,tokengifts,communityevents,coupledwithoutreachbymorethanadozensavingsinstitutions.Inathree-yearperiod,300000newbankaccountswereestablished.Butitisnotknownhowmuchthesenewaccountshavebeenusedovertime.(WorldBank,2009)

9

5.Analysis

This section presents analysis of financial literacy initiatives in international and nationalcontexttogainabetterunderstandingoftheissue.5.1AstudyofInternationalPractices:CasesofIndia,Mexico,Spain,UnitedKingdomand

Indonesia

TheanalysisdrawninthissectionforfinancialliteracystrategyhasinformationdrawnheavilyfromthepublicationofOECDandRussia’sG20presidency:AdvancingNationalStrategiesforFinancialeducation.Thisreportwaspreparedtoassistcountriesconsideringformulationofanational strategy toprovidea frameof reference.Manyof thecountrieshave followedOECDrecommendationsandareintheprocessofdesigningfinancialliteracystrategies.DuetothisreasonIhaveconsideredthisstudyasabaseofanalysis.Five of these countries have designed or are designing financial literacy campaign. Theanalysisofthenationalstrategiesofallthesecountriespointsoutsomecommonthingsthatare in each country’s strategy. These things have been explained below as variables thatshouldbeessentialcomponentsofeverynationalfinancialliteracystrategy.Thesevariablesarenotanexhaustivelisttherearemanyotherthingsthatneedtobeincorporatedinthenational strategy but these are some common points that most of the countries havefollowed.Figure3:FinancialLiteracyStrategy

FinancialLiteracyStrategy

Institutionalization

Stakeholders

Vision,Mission&Goals

Segmentation

NationalcapabilitySurvey

Monitoring&Evaluation

10

1.InstitutionalizationIt can be observed from all these countries that every country has institutionalized theformulationofnationalfinancial literacystrategybyformingacommitteeoraninstitutionwiththesoletaskofoverseeingfinancialinclusionandliteracy.India:AtoplevelinstitutionalstructurewascreatedinIndiain2011asatechnicalgrouptofocus on financial inclusion and literacy under the name of Financial Stability anddevelopmentCouncil(FSDC).Chairedbytheministryoffinanceandincludingheadsfromallfinancialsectorregulatorsasmembers.TheimplementationpartofthepolicywillbethroughtheTechnicalGroupoftheSub-CommitteeoftheFSDC.Also,anationallevelinstitutenamedtheNationalCentre for Financial Educationwasestablishedas a specialized institute thatwouldreporttothetechnicalgroup.Mexico:National council for financial inclusion(CONAIF)andCommittee forFinancial(CEF)education were formed as coordination entities for a better communication betweenstakeholders. CONAIF was formed by presidential agreement and consists only financialauthoritiestoactasanadvisoryandconsultationbodywhereCEFwassetupbyministryoffinanceandpubliccreditandconsistsoffinancialauthorities,developmentbanks,financialpublicinstitutionsandotherpublic/privateandsocialsectorinstitutions.Spain:InitiallyanagreementwassignedbetweenBancodeEspana(CentralBankofSpain)ANDCNMV(ComisionNacionaldelMercadodeValores,TheSpanishsecuritiessupervisorinMay2008.Theseorganizationswereresponsiblefordesign,development,executionoftheplan,coordinationandfinancialsupport.Aworkinggroupwasformedwithrepresentativesoftheseinstitutions.Representativesfromotherorganizationscanattendthemeetingswhentheagendajustifiesit.UnitedKingdom:FinancialServicesauthority(FSA)wasabodywithstatutoryresponsibilityunder the Financial services and Markets Act 2000 for consumer protection in financialmarkets.ItoversawthefirstUKstrategy“FinancialCapabilityintheUK:DeliveringChange”.Lateronresearchidentifiedthatabodyindependentofgovernmentandregulatorswouldhavemoreimpactbydeliveringfreeandimpartialfinancialfinancialadviceandcoordinatefinancialcapabilityatanationallevel.Subsequently,UKparliamentintroducedalegislation(theFinancialServicesAct2010)toestablishanindependentbodytoassumeresponsibilityfrom the FSA for financial capability, paving theway for the launchof theMoneyAdviceServicein2011.Indonesia:TheIndonesianBankingArchitecture(API)waslaunchedonJanuary9th,2004forthe implementation of public education. API has different pillars dedicated to differentaspectsofbankingoutofwhichthesixthpillarisconsumerprotectionunderwhichimprovedprotectionandempowermentofconsumersthatprovidesaplatformforpubliceducation.Bank Indonesia functionsas the leaderof thenationalcampaignunderwhich it formedAworkinggrouphavingrepresentativesfromBankIndonesia,banks(commercialbanks,ruralbanks,Islamicbankstocarryoutthetaskofpubliceducation.BankIndonesiaregularlyholdsmeetingswiththeworkinggroupandreceivesinformationwhichisusedtoformulatepoliciestoincreasethepublic’sfinancialinclusioninparticularforfinancialliteracy. NationalStrategyforFinancialEducationundertheNationalStrategyforFinancial Inclusionwaslaunchedin

11

June2012.Thisstatesthatfinancialeducationwillfocusonincreasingthelevelofknowledgeamong communities regarding financial products and services and financialmanagement,andprovideinformationonconsumerprotection.

2.Vision,MissionandGoal

Allofthesecountrieshaveaclearvision,missionandgoalsthattheyhopetoattainwithinaspecificperiodoftimethatguidestheiraction.India:Thevisionof India’sstrategy is“toprovidefinancialeducationtoall Indianssothatindividuals,attheirlevelofneed,willunderstandtheroleofmoneyintheirlife,theneedandofsavings,theadvantagesofusingtheformalfinancialsector,variouswaystoconverttheirsavings into investments, protection through insurance and a realistic recognition of theattributes of these options.” The mission is “to conduct a massive financial educationcampaigninordertohelppeoplemanagemoneymoreeffectivelyandachievefinancialwell-being.” The goal is “to create awareness and educate consumers on access to financialservices.”Mexico:ThereisgeneralagreementamongNSEFandCEFthatthevisionshouldbethatthepopulation inMexico,accordingtotheirageandneedsunderstandandknowhowtousefinancialproductsinaninformedandresponsiblewaylikesavings,creditandinsuranceaswellastransactionchannelsinordertooptimizethemanagementoftheirresources,improvewell-being and increase their development potential. The mission is to develop thepopulationknowledge,skillsandattitudesthatallowthemtomanagetheirresources.Someoftheobjectivesareknowandunderstandbasiceconomicandfinancialconcepts,rightsandobligations as users of financial services, understand anduse information available aboutfinancialproductsandrisksandcostassociatedwiththem.

Spain:ThemainobjectiveoftheSpanishNationalStrategyis“toimprovethepublic’sfinancialliteracysocitizenscanconfidentlynegotiate financialdecisions.”Theplanhas threemaindefiningcharacteristicsofinclusiveness,co-operationandcontinuity.

UnitedKingdom:Thefirstnationalstrategythatranfrom2006-11hadanobjectiveofhelpingpeoplebecomemoreinformed,confidentconsumerswhoarebetterabletotakecontroloftheirfinances.

Indonesia:Thevisionoftheblueprintforpubliceducationinbankingistocreateasocietywhohaveadequateknowledgeandinformation,understandthefunctionsandrolesaswellasthebenefitandrisksofbankserviceproductsinordertomanagetheirfinancewiselyandeventually enhance their quality of life.” Themain goals are bringing about bankmindedawareness,financialliteracy,riskawarenessandconsumerprotection.

3.Mobilizingtheexistingstakeholders

Therearechances thatvariouspublicandprivatebodiesalreadyhavesomesort financialliteracyinitiativesinplaceandwhenanationallevelstrategyistobeinitiatedmobilizingtheexistingstakeholderscanbeveryhelpfulinimplementationprocess.Itisseenthatmostofthecountriescollaboratewiththeexistingstakeholders.

12

India: The national strategy anticipated active involvement from all stakeholders thatincluded NGOs and civil society, individuals, financial sector regulators, educationalinstitutions,multilateralinternationalplayersandgovernmentsbothatthecentralandstatelevel.Therolesandresponsibilitiesofthestakeholdershasclearlybeendefined.RegulatorswouldhelpNCFEdesigncontentofbasicfinancialliteracyprogrammes,commercialfinancialinstitutionswouldspreadprofessional levelproducteducation ,self-helpandothergroupswouldalsoparticipateinimpartingbasicandsectorspecificeducation,industryassociationswoulddevelopsectorspecificcontentandsharethroughawebsite,otherauthoritiessuchaseducation authorities, agricultural and health services can participate and extend theirinfrastructureforfinancialeducation.AlltheeducationinitiativestakenbythesestakeholderswillbebasedoncontentdevelopedbyNCFEandtheyhavetoregularlyreportonactivitiestheytookaspartoffinancialeducation.Mexico:Mappingofexistingstakeholderswasdonepriortoformulationofnationalstrategy.Recognizingtheeffortsdonebydiverseplayersinthefieldoffinancialeducation,CONAIFandCEF were formed as coordination entities to align everyone’s efforts. CONAIF had onlyfinancial authorities whereas CEF had members from public, private and social sectors.Financialsectorassociations,Academicexperts,financialserviceinstitutionsetc.couldalsobemembersofCEFasinvitees,theycouldsharetheiropinionsbutcouldnotvote.ToensureCONAIFandCEFcollaborationaworkinggroupdedicatedtofinancialeducationwasformedwithemphasisonremittances,savings,microinsuranceandelectronictransfersofwelfareandsubsidiesprograms.ThisworkinggroupwaschairedbyBansefi that isadevelopmentbankdedicatedtopromotingfinancialservicesamongstthebaseofthepyramid.Similarly,twootherworkinggroupsaremappingandidentifyingfinancialeducationinitiativesandbestpractices.Anothergroupcollaborateswiththeworldbanktomeasureandevaluatetheworkdone.Anothermappinggroupwhich is chairedby theministryof finance is conductingastakeholder mapping exercise that will be used to create a webpage containing all thefinancial education materials from the members of the CEF so that all materials andinformationisaccessiblefromoneplace.Spain:Mappingofexistingstakeholderswasdonepriortoformulationofnationalstrategy.TherolesandresponsibilitiesofmainstakeholdersinthenationalStrategyisdeterminedbythefunctionsassignedtoeachonebylaworstatutes.Fore.g.accordingtotheRoyalDecree,G.SofthetreasuryandFinancialpolicy isresponsibleforthecoordinationoftheactivitiesaimedatfinancialeducationandforrepresentationofSpaininOECD/InternationalNetworkon Financial Education. Also, as SpanishNational Strategy has segmented the nation intodifferent target groups, different cooperating agents are used to impart education to aspecifictargetgroup.Fore.g.foreducationaimedatemployees’,tradeunionsareusedascooperatingagents.Hence,TheSpanishstrategyhasmobilizeddifferentagentsforcartingoutthestrategy.

United Kingdom: Mapping of existing stakeholders was done with a Call for Evidencecommunicatedtoacomprehensiverangeofstakeholders.Thisactivityaimedtoidentifyallactivities and interventions that demonstrated a clear, positive and successful effect onindividual’sfinancialcapability.Anonlinehubwascreatedtohosttheresultsofthemappingworkandprovideacentrallibrarythatwouldmakeavailableinsightsintothebestwaystoaffect financial capability. The Money Advice Service i.e. the national strategy of UK

13

collaboratedwithinterestedpartiesinthepubicandvoluntarysectorsinEngland,Scotland,WalesandNorthernIreland.

Indonesia: Bank of Indonesia collaborates with potential stakeholders to enlarge theoutreach of financial education. Policies are issued by Bank Indonesia to build people’sinterestinbankingandraisepublicawareness.Thesepoliciesaremandatorilyimplementedbythestakeholders.Sincetheyaredirectlyinvolvedintheimplementationthesuccessofthepolicydependsonthestakeholders.

4.NationalFinancialcapabilitysurvey

It is essential that a country gauges the level of financial literacy of its people beforeformulatinganationallevelstrategy.Allthecountrieshaveconductedsomeformofnationalsurveytomeasuretheliteracylevelofitspeople.Itisalsoneededlaterforevaluationwhenthe strategy is complete to compare the before and after results and check how muchprogresswasmadeaftertheimplementationofthestrategy.India: NCFE appointed Mott MacDonald India, a global management and developmentconsultancy organization, to carry out a nationwide baseline survey i.e. NCFR-Financialliteracy and Inclusion Survey(NCFE-FLIS) for assessing the state of financial literacy andfinancialinclusion.Thestudywouldcover75000peopleacross35states.Itwassupposedtoassess the present state of financial literacy and also yield benchmarks of core financialliteracy and financial inclusion art various socio economic groups andmeasure its rateofchange on a continual basis to assess the efficiency of carious financial educationinterventions.Anothertestwasalsolaunchedintheyear2013-2014byNCFEtargetingschoolstudents called national Financial Literacy Assessment Test (NCFE-NFLAT) under whichknowledge of school students on topics such as Money, Savings, Banking, Budgeting,Insurance,InvestmentandRetirementPlanning.ThroughthistestNCFEaimstoencourageschoolstudentstoobtainbasicfinancialskills.(NationalCentreforFinancialEducation,2015)

Mexico: In 2008, Banco Nacional de Mexico(Banamex) and the National AutonomousUniversityofMexico (UNAM)conductedaFinancialCultureSurveyto identify the levelofknowledgeandperceptionofthepopulationaboutdifferentsavingsandcreditproducts,tohaveabetter ideaof theuseornon-useof formaland informal financial services,and tomeasurehabitsandidentifyattitudestowardssavings,expensesandcredit.In2009MinistryofFinanceandPublicCreditalsoconductedaNationalSurveyoftheUseofFinancialServices.Againin2011,theMexicanAssociationofAdministratorsofRetirementSavings(AMAFORE)conductedthesurvey“SavingsandFuture:HowMexicansThink?”toknowthecurrentstateofretirementsavingsculture.TheCNBVandtheNationalInstituteofStatisticsandGeographyconductedthefirstNationalsurveyoffinancialinclusion(ENIF)wasconductedtochecktheusageoffinancialservices.Theobjectiveofthesurveywastoknowthecharacteristicsoftheusers and non-users of formal and informal financial services, to identify population thatkeepstrackofitsexpenses,toprovideinformationabouttheuseofsavings,credit,insuranceandretirementsavingsandtheiraccesschannelsandidentifybarriersthatlimittheaccessanduseofformalfinancialservices.ENIFisthemostcompleteexercisedonetounderstandtherealityoffinancialinclusioninMexico.

14

Spain:Tounderstandthemanpolicyareastoaddressandmoregenerallygaugethelevelsoffinancial literacy of the Spanish Population, the survey of Household Finances (EncuestaFinancieradelasFamilias)wasconducted.Inaddition,reportsoftheCNMVandBancodeEspanaon consultations and claimshighlighted themainproblemareas facedby Spanishpopulationthatbecameabaselineindraftingfinancialeducationstrategy.UnitedKingdom:Thefirstnationalstrategyforfinancialcapabilitywasbasedonthefindingsfrom “Financial Capability in theUK: Establishing a Baseline” thatmeasured the financialcapabilityofadultsacrossthecountryaccordingtofiveelementsofcapability:makingendsmeet, keeping track of personalmoney, planning ahead, choosing financial products andstayinginformedaboutfinancialmatters.MoneyAdviceServicecommissionedIpsosMORI,UK’s largest independent researchagencyand its academicpartners to conducta groundbreakingandinnovativeproject–“Moneylives”-intopeople’srelationshipwithmoney.TheMoneyLivesresearchstudiedhowfinancialcapabilityisdependentonopportunity,attitudesandmotivationofpeople.Itlookedintothebehavioralaspectofmanagingmoneyandhowitisaffectedbycontext,environment,cultureandaspirations.Indonesia:FinancialliteracysurveywasinitiatedbyBankIndonesiain2006toassessthelevelofliteracyofIndonesia’sgeneralpublic.Thesurveywasusedtoassesscustomer’sknowledgeandunderstandingoffinancialeducation,theirleveloftrusttowardsproductsandservicesprovidedbybanks,willingnesstobecomeabankcustomeretc.Thesurveyidentifiedthegapspresent in the country and on the basis of this knowledge Bank Indonesia established aworkinggrouptoimpartfinancialeducationtogeneralpeople.Againin2012,BankIndonesiacollaboratedwithDemographicInstitutetoconductafinancialliteracysurvey.ItwasbasedonOECDrecommendationmakingadjustmentstoreflectthecharacteristicsofIndonesia.Thesurvey indicatedthatwomenhavebetterbehavior towards financebut lackedknowledgecomparedtomen.ThefindingalsoindicatedthatfinancialeducationneedstobetargetedtowomenandSMEs.5.SegmentationAllthepeople inthecountryarenotgoingtobeinthesameleveloffinancialawareness.Somegroupsmaybemoreadvancedwhereassomemay lackbasicawareness.This is thereasonmanycountriessegment thepopulation intodifferent targetgroupsand tailor theeducationinitiativesaccordingtotheneedsofthegroups.India:Indiausedatieredapproachunderthenationalstrategybecauseitspopulationconsistof two type of people, one who are financially included and use sophisticated financialproductsandtheothergroupwhoiscompletelyfinanciallyexcluded.Therefore,thestrategywas to spread awareness about basic products to integrate non users into the financialsystem, educate existing users about making informed financial decisions and to ensureconsumerprotectionforalltheusers.Itclearlymadeadistinctionbetweenusersandnon-users.Alsoithasdividedthecomponentsofnationalstrategyasbasicfinancialeducation,sector focused financial education and product education. It had tailored its content anddelivery channels depending on the target group. Children were reached through schoolcurriculum, employees through employers, homemakers through NGOs. Also, it hasrecognizedtwoothergroupsforimpartingfinancialeducation;illiterateanddifferentlyabled.

15

Mexico:TheMexicanstrategyhasnotdirecteditsfinancialeducationtoparticulargroupsbuthaslistedcertainprioritygroupsthatincludechildrenandyouth.Therationalebehindthisisthatfinancialknowledgeneedstobepresentrightfromchildhoodaschildrenneedtoknowtheimportanceoffinancialplanning.ThepopulationtobetargetedwillbedefinedbyCONAIFthatwouldincludebeneficiariesofwelfareprogrammes,peoplelivinginmarginalizedruralareas etc. Also programmes and policies were formed on the basis of the needs of thepopulation. The strategy recognized understanding the characteristics of their targetpopulation when designing financial education programmes. For instance, in the case ofchildren the school’s curriculum would be redesigned to ensure that children developcompetenciesnecessary for themtobecomecapableofmanaging financesandbecomingresponsibleconsumersoffinancialservices.Spain:SpanishNationalStrategyhassegmentedthetargetaudienceintoeducationsystemand adult population. The education system is divided into secondary education anduniversitywhereasadultpopulationisdividedintoemployees,parentswithyoungchildren,retireesandothers(immigrants,disabled,homemakers,otheryoungpeopleetc.)Theneedsofthetargetgroup,specificactionthatneedstobetakentoeducateeachgroupandthecooperating agents for delivery has been separately identified. The Spanish strategyrecognizes thateachgroupneedsaredifferentandhence requiredifferentapproach.Forinstance,financialliteracycontentwouldbeembeddedintheschoolcurriculumtoeducateschool and university students, the cooperating agents would be national and regionaleducationauthorities.United Kingdom: UK is a developed country with higher financial inclusion that othercounties. It was one of the first countries to introduce a strategy for improving financialcapability. Though theUK strategy did not explicit segment the target population it doesrecognizedifferent segmentsof the society andhas focused its effortson schools, youngadults,workingpeople,newparentsetc.Thestrategyindicatedthatinterventionsmustbedeeplyrootedwithanunderstandingofconsumerneeds.Italsohighlightedthattargetingpeoplefacingkeylifestages,suchasstartingafamily,retirementoftenresultedinsuccessfulinterventions.Indonesia:IndonesianNationalStrategyhassegmentedthepopulationintotargetgroupsoffivenamelyschoolchildren,collegestudents,professionals,financialsupportinginstitutionsandothers(households,informalsectors).Forstudents,financialeducationwasincludedinthe school curriculum, for migrant workers several seminars on financial education formigrants were held, collaboration with ministry of manpower and transmigration of theRepublicofIndonesiawasseenasanoptiontoextendtheoutreachtomigrantworkers,forSMEsfinancialplanningconceptsusingbankingproductsweretaught.Thecontentofeachgroupweredecidedbyadjustingtotheneedsofthegroup.6.MeasurementandEvaluation

Everyactionplanneedstohaveamechanismoftestingwhetheritworkedornotortocheckprogressonwhatishappening.Mostofthenationalstrategiesdevelopedhaveameasuringandevaluationmechanismtotrackprogress.

16

India:Timeframeoffiveyearswasallocatedforimplementationofthestrategy.Anactionplanhasbeenoutlinedregardingthetaskstobeundertaken.Theplanmentionsthatitsinitialgoal is toestablishcontactwith500millionadultsandeducatethenonkeysavings.Suchquantificationmakesmeasurementandevaluationpossible.Mexico:TheMexicanstrategyrecognizestheimportanceofhavinganevaluationmechanisminplacetodeterminewhetherthedesiredimpactoffinancialeducationisbeingcreated.Onwaytotrackprogressisbygivingcontinuitytothesurveyonfinancialcapability.Spain:Spanishplanalsohadatimeframeof5yearsfrom2008-2012.Evaluationandreviewwas allocated time of 2011-2012.Several evaluation mechanisms were used to monitordifferent aspectsof theplan.Oneof themethodsof imparting financial education in theSpanishstrategywas launchingawebsitecontainingpractical financialeducationcontent.Thiswebsitewasextensivelymonitored.Thenumberofvisitswereused toevaluatehowusefulandrelevantthecontentswere.Otherfinancialeducationcourseswereevaluatedwithonlinesurveys.Theresults indicatethat95%oftheparticipantsfeltmoreconfidentaboutfinancialmattersafterreceivingthetraining.Thepilotprogramforfinancialeducationwasevaluated by an independent expert in order to assess possible behavioral and attitudechangeswithrespecttofinancialmattersandsuitability,appropriatenessandeaseofuseofthe materials and resources provided. The results of the evaluation led to the secondprogrammeofFinancialEducationinschoolsduring2012-2013.Asurveywastobedonetotrackprogressonfinancialliteracyinadults.Curriculumreviewwasalsodonetocheckthefeasibilityofintroducingfinancialliteracyasanewsubjectormergingintoexistingsubjects.UnitedKingdom:Theprincipalmethodofevaluatingthestrategywasconductingafinancialcapabilitytrackingsurveytoevaluatetheprogressesmade.Thesamplingwouldbedoneonaquarterlybasis.AstheUKstrategyalsohadanimplementationperiodof5years’reviewwouldbedoneafter18monthsand3years.

Indonesia: The progress of the financial education program is checked throughout theimplementationphase(2007-2013).Thetaskstobeconductedeachyeararedefinedclearly.ThechartonprogressoftheprojectisincludedinAppendix2.

The variables mentioned above are not an exhaustive list of elements that need to beconsidered in every national strategy but an outline of common patterns identified indifferentstrategies.Everycountryisdifferentwithdifferenttypesofindividualsandhenceastrategythatworkedinonemightnotnecessarilyworkinothers.Thereareotherthingsthatcould play a very important role inNepaleseNational strategy. For example, Inclusion offinancialliteracycontentinschoolcurriculum.NoteverycountryhasdonethisbutsomelikeIndiahaveincludedfinancialliteracycontentinschoolcurriculum.ThiselementcouldbeveryrelevantinNepal’scasebuthasnotbeenmentionedabove.Thelistprovidedaboveisjustasetofcommonvariablesthatmanycountriesfollowedandhencecanbeusedasareferencepoint.

17

4.2AnoverviewoffinancialliteracyinitiativestakeninNepalInitiatingBody Projecttitle/Initiative Target

GroupDetails Progress

GovernmentofNepal

• Policies andProgrammes ofGovernment 2071-2072

• Policies andProgrammes ofGovernment 2073-2074

• Budget speech

2016/2017

WholeNepal

“Savinghabitswillbeencouragedamongthepeoplewithaviewtospeedingupeconomicdevelopment.Financial inclusion and financial literacy programswillbeexpandedwithhighpriorityforincreasingtheaccess of the masses to financial services.”(GovernmentofNepal,2071)“Inordertoensureaccessofalltofinancialservices,provisionwillbemade,withtheencouragementofthe Government, for all Nepalese to have bankaccounts.Financialliteracyprogrammewillbemadeeffective.”(GovernmentofNepal,2073)“Financial literacy program will effectively beexpedited.”(MinistryofFinance,2015)

Despite the gap of threeyears in thesetwoprogramsof government, significantprogresscannotbeseen.Theissueoffinancial literacyhasnotbeenincludedinpoliciesand programmes for2072/2073probablybecausemore focus was given onprojects related toearthquake affected victims.Both policies and programsmention that financialliteracy programs will beconducted signifying noprogress was made in twoyears. Financial literacy hasbeenmentionedinthisyear’sbudgetwhichisaprogressasit was not mentioned inpreviousyear’sbudget.

Ministry ofFinance

Financial literacy Policy2016

Nepal “Necessaryinfrastructurewillbemadeavailabletosupport the financial literacy campaign such asaccesstotheinternet,roads,markets,powersupplyand capable human resources.

The draft financial literacypolicywas forwarded to theministryoffinanceforreviewand amendments byNRB. It

18

The financial literacy campaign will focus onspreading awareness about banking and non-banking institutions such as the EmployeesProvidentFund,CitizenInvestmentTrust,insurancecompanies, cooperatives, capital market andinfrastructurerelatedtocapitalmarketsuchastheCredit Information Bureau and Clearing House.ThecampaignwillalsoeducatecommunitiesabouttheinformalfinancialsectorsuchasDhukuti,hundiand networking business. The policy also aims topromotethe inflowofremittancethroughbankingsectorandusethemoneyintheproductivesector”(Kathmandu Post, 2016)

hasagainbeenforwardedtonational planningcommissionforreview.1Thistypeofcommunicationisoneway that has made theprocess lengthy andineffective. Theministry hasproposed two types ofstructures, a High LevelNational Financial LiteracyCouncil headed by thefinance minister and aFinancialLiteracyCommitteeheaded by the deputygovernor of Nepal RastraBank, to implement thepolicy. (Kathmandu Post,2016)

Ministry ofEducation

Pilotprogramforincludingfinancial education inschoolcurriculum2014

Schoolchildren

MinistryofEducationhasalreadypreparedapilotproject to introducefinancial literacy intheschoolcurriculum. StudentsingradesVI,VIIandVIIIwillbetaughtaseparatetopiccalled‘Profession,BusinessandTechnology’tofamiliarizethemwithrealworldjobs and options available, and more specificfinancial literacy courses will be introduced forhigherclasses.2(NabilInvest,2014)

Financial literacy has yet tobeincorporatedintheschoolcurriculum.

1BasedondiscussionwithNRBofficial.2StatementbyDrRojnathPande,MinistryofEducation;Undersecretary

19

Ministry ofLabour andEmployment

Migrantworkersandtheirfamilies

TheNationallabourpolicy1999includesinformingmigrants and returnedmigrants regarding optionsfor investing their earnings and providing skillstrainingandfinancialliteracytrainingtopursuesuchopportunities. (Ministry of Labour andEmployment:Department of foreign employment,2013)Ministry in collaboration with InternationalOrganizationforMigration(IOM)conductedasix-daytrainingforgovernmentofficials, NGO trainers, officials of financialcooperativesandprivatebanktohelpthembettereducate families dependent on remittances. Thistraining was based on “financial literacy” manualdeveloped by IOM, Ministry of labour andEmployment and Central Bank of Nepal.(InternationalOrganizationforMigration,2014)

Thetrainedinstitutionsweresupposed to train up to 200householdsonissuessuchasmanaging remittances,setting up a small business,savingsplansandbudgeting,use of formal financialinstitution. A one-day pilottest of the manual wascarried out with 30remittance-receivinghouseholds in the village ofChaimale,ontheoutskirtsofthe Kathmandu Valley.(International OrganizationforMigration,2014)

Nepal RastraBank

NRB strategic plan 2012-2016NRB Maya declaration2013NRBwithstudents2013

NepalNepal

Financial literacy would be enhanced focusing onwomen, victims of conflict, ethnic minorities,deprived and marginalized section of population.This issue was mentioned under strategic priority2.8:Enhancefinancialinclusion.(NepalRastraBank,2012)NRBhassignedtheMayadeclarationunderwhichithad committed to bring about national levelfinancialliteracystrategybymid2014.(NepalBastraBank,2014)

It has been several yearssincetheMayacommitment;andfinancialliteracypolicyisyettobefinalized.Butithasbeen submitted so there ishope for a finalized strategyto come out soon. Financialliteracy has been a topic ofinterest of NRB since pastfour years which is a goodsign. NRB has dedicated asection on its website tofinancial literacy.Thejingles,storybook(PaisakoBot)can

20

Monetary Policy for2014/2015Monetary Policy for2015/2016NRBdirective22/2072National Financial LiteracyStrategy

YoungstersandChildrenNepalNepalNepal

NRBhasstartedaprojecttitled“NRBwithstudents”under which it has published books and recordedaudiojinglesformassawarenessMonetary policy has also focused on extendingcredittotheproductivesectorbyencouragingBFIsandstrengtheningbothdemandaswellasutilizationof loans by promoting financial literacy programs.(NepalRastraBank,2014)NationalFinancialliteracypolicyistobeformulatedto protect right of financial customers and widenfinancial inclusion. Necessary coordination withGON to be done to include content of financialliteracy in informal education, vocational trainingand school level curriculum. (Nepal Rastra Bank ,2014)ConsumerProtectionandFinancialliteracyNRBhasformulatedadraftfinancialliteracystrategyandsubmittedtoministryoffinance.

be found on the windowdedicated to financialliteracy. Also, messagesimparting financialknowledge can be seen inNRB website. NRB incooperationwithUNICEFhascelebrated Global MoneyWeeksince2013forchildandyouth focused financialliteracy that included a rallyhavingstudents,scouts,BFIs,cooperatives, NGOs, donoragenciesandalsointeractionprograms, trainings,publicationreleasesetc.

Otherstakeholders

21

UNDP&UNCDF3

Enhancing access tofinancial services 2008-2012(Joint initiative of UNDPand UNCDF, implementedbyNepalRastraBank)UNNATI-A2F(JointlyImplemented with NepalRastraBankandfundedbytheDanishGovernment.

Poor ruralpeoplethroughoutNepalEasternDevelopment regionmainlyIIam,Panchthar,Dhankuta,Sankhuwasabha,Tehrathum,TaplejungandBhojpur.

The project’s focus was on poverty reduction by expanding outreach of financial services. In this process it worked to strengthen the micro finance institutions to enable them to the lead the growth of inclusive finance across Nepal. The project had initiatives focused on financial literacy, education and capability as a method to promote financial inclusion.

EnhancingAccesstoFinancialServices project providedtechnical assistance to FSPsto conduct trainings onfinancial literacy. Fund forinclusive finance wasallocated which involvedcarryingoutfinancialliteracycampaign targeting urbanMSMEs and rural and urbanhouseholds.Theprojectalsoconductedafinancialliteracystudy on the basis of whichNRBwastoconductfinancialliteracy campaign. Theresearch to launch thefinancial literacy campaignand client protectionguidelinewiththesupportofEAFS began in late 2011(UNCDF, 2012)Financialliteracy trainingmanual wasformulatedunderthisprojectincollaborationwithNRB.Technical Assistancepartnership agreement hasbeen signed with 13 banks

UNCDFlaunchedaninitiativeunderprojectUNNATIthat aimed to empower poor people by teachingthemthebasicsofpersonal finance.Workingwithfinancial service providers and the Central Bank,UNCDF conducted a training course on how todeliverfinancialeducationforspecifictargetgroups.Asaresult,theseorganizationsarenowequippedtobroadentheirclients’knowledgeoffinancialoptionsand promote effective money management. Thecoursecoveredallaspectsoffinancialliteracyfromidentifying the needs and demands for financialeducationtomonitoringandoutcomeevaluation.

3ThetwoUNwingshaveworkedonmostoftheprojectsasajointinitiative.Therefore,thereworkispresenttogetherforsimplicityandtoavoidredundancy.

22

and financial institutionsunderprojectUNNATI.Theseinstitutions will get TA invarious areas includingfinancial literacy to forbuildingcapabilitiesofclientsand potential clients. (NepalRastraBankandUNCDFstartparternship with banks andfinancialinstitutions,2015)

UNICEF

Child Social and FinancialEducation(CSFE)

Childrenaged 6-15years

NepalwasoneofthefournationsworldwiderollingoutaninitiativetointegrateaspectsofChildSocialand Financial Education (CSFE) in the nationalcurriculum. Developed jointly by UNICEF andtechnical partner Aflatoun, CSFE enables childrenand adolescents to become socially andeconomicallyempoweredandencouragesthemtoleadresponsiblelivesandbecomeagentsofchange.Aspartoftheinitialphaseoftherollout,Nepalwilltest components of CSFE curriculumat 15 schoolsandfivealternativeeducationcentersacrossthefivedevelopmentregions.This initiative isalsoexpectedtocontributetotheMinistryofEducation'sresponsibilities,asstatedintheNationalPlanofAction,onHolisticAdolescentDevelopmentinNepal.TheNPAhasa10-yearvisionof an empowered and competent new generationforabetterNepal.(UnitedNations,2014)

Ministry of Education (MoE)organized a two-dayworkshop in Kathmandu tocreateaplanofactionfortherolloutofCSFEinNepal.Since2012,UNICEFNepalhasbeen implementing financialliteracy for adolescents inout-of-school settings underits adolescent developmentand participation programand advocating for CSFE inschools. Through this newinitiative, that work is beingextended to include primaryand secondary schoolchildren and adolescents.UNICEF will be providing afinancial support of USD

23

100,000fortherolloutofthetwo-year initiative in Nepal,whichisexpectedtolastuntil2016.(UnitedNations,2014)

Aflatoun AflatounModel Children Aflatounisasocialandfinancialeducationprogramaimed at training children to “reach theirentrepreneurialpotential”,byencouragingthemto“believe in themselves, know their rights, practicesaving,andstartenterprises”Three partner organizations are currentlyimplementing Aflatoun in the country: JuniorAchievementNepal(JAN),ChildWorkersinNepalConcerned Centre (CWIN) and KapilvastuInformationCenter(KAPINCE).(Marian,Shanker,&Swimmer,2008)

Aflatoun has developed astandardized approach toimplementation, involving asix-stepprocesssupportedbyits program managers. Thesixphasesofimplementationare: initial preparation,planning, materialdevelopment,training,liveinschools and review &reflection. (Marian, Shanker,&Swimmer,2008)

MercyCorps Sustainable Access toFinance And Livelihoods(SAFAL)

Eastern,Mid-Westernand FarWesternregionswithfocus onwomen.

MercycorpsaimstoreducepovertyinremoteandruralareasinNepalbyexpandingsustainableaccessto financeby strengtheningandenhancingmoneymanagement skills with financial literacy ofcommunity based cooperatives that create betterlivelihood opportunities for the beneficiaries. It isexpectedthat35,500householdwouldbenefitfromthis project out which 60% are expected to bewomen.Theprojectwillalsoassist11.000financiallyexcluded people in getting responsible loans.(MercyCorps,2015)

The project is workingdirectly with clients,providing technical supporttoMFIsandassistingtheminprovidingfinancialliteracytotheir clients. The financialliteracy training model hasbeen developed specificallyforthecontextofruralNepalbuilding on Mercy corpsfinancial literacy trainingexperience globally andincluding a comprehensivepackage comprised of

24

financialgoalsetting;savings,credit management; riskmanagement;safemigrationand remittances; wants,needs and asset creation;financial services andproviders and financialmanagement. The approachisexpectedtoensuregreaterinvolvement ofdisadvantaged and excludedgroups in the mainstreamdevelopment process.25,000clients(8000menand17000women)willbetrainedusingthis methodology.(MercyCorps,2015)

EntrepreneursNepal

FinancialLiteracy2016 Remittanceworkersandfamilies

Provide financial education to Nepalese workersgoing abroad, or those about to go abroad,remittancebasedfamiliesandstudents.Theaimoffinancial education is to cut unnecessaryexpenditure of the emittance based workers andfamilies, promote saving culture and make themawareaboutsavingtoolsandeducatethemaboutneed of investment and financial planning. Theirtargetgroupareremittanceworkers,theirfamiliesand students in the age group of 18-24.(EntrepreneursNepal,2016)

Their intervention will beimplementedincoordinationwith consultancies thatprovide orientations tomigrants’ workers, NRNorganizations, differentgroups and unions, studentunions, Nepal government,Local Government and NRB.media such as Facebook,Twitter, Pictographic,cartoons, audio VisualPresentationsarebeingused

25

to educate those alreadyabroad. They also organizeworkshops and give face toface trainings.(EntrepreneursNepal,2016)

Bank ofKathmandu

GharDailoSaptaha The awareness campaign was initiated with anobjective of creating awareness about financialliteracy and mobilizing deposit collection. ThecampaignhasbeendoneaspartofitsCSRactivities.(BankofKathmandu,2014)

“Ghar Dailo Week” wasconductedinvariouspartsofthe country. Till date thebankhasorganizedprogramsinAmlekhganj,Baglung,Balaju,Beni,Bhaktapur,Biratnagar,Butwal,Chabahil,Pokhara,Ithari,Birtamod,Dharan,Narayangadh,Sankhu,Dhangadi,Diktel,Gongabu,Gyaneshwor,Hetauda,Janakpur,Jumla,Khairenitar,Lhan,Mahargunj,New/OldBaneshwor,Panauti,Thamel,Urlabari. (Bank ofKathmandu,2014)

SEBAC Nepal Girl PowerProject(GPP)(April2013-March2016)

Adolescentgirls’inSunsari

GPPwas initiatedwithan intentiontoensurethatgirls and youngwomen have sufficient knowledgeandskillstoshapetheirownlives.Self-reliantgroupswere formed in which poor marginalized womenbelow25yearsparticipated,thegroupmetonceinamonthandcollectedRs.100each.Memberscouldobtainloanfromthisfundatinterestratesdecidedbythegroups.Thesegroupsweretrainedinfinancialliteracybutalsosupportedthemtobeginvegetable

GPP trained the groups onfinancial literacy and bookkeeping. A total of 207women were trained onfinancial literacy and 331women were acquaintedwith different techniques ofmanaging groups. (SEBACNepal,2014)

26

farming with training ,improved seeds, fertilizersandbio-pesticidesaspartofanefforttomaketheactivitiessustainable.(SEBACNepal,2014)

Sakchyam AccesstoFinance ThisprogrammeisaninitiativefundedwithUKaidfrom the British government as part of a bilateralagreementbetweengovernmentofNepaland theUK.Increasingfinancialcapabilityisoneofthethreemajor components of the Sakchyam Access toFinance.Theybelieveitisnecessarytoworkonbothdemand and the supply side of access to finance.Theirobjectiveistomakepeoplefinanciallycapableso that they can take informed decisions onobtainingfinancialservicesfromformalinstitutions.Designingandlaunchingfinancialliteracyinitiativesis a part of sakchyam’s integrated approach tosustainable interventions for enhancing access tofinance.(Sakchyam:AccesstoFinance,n.d.)

Firstly, they are developingthe service they provide byupdating and/or creatingcurriculum to better coverimportant concepts likesavings, loans,household/enterprise,budgeting. Second, they arealso developing alternativedelivery channels to betteraccommodate rural client’sneeds. They are introducingmobile based financialliteracyknownas interactiveVoice Response (IVR) topartner’s clients. They havealready worked with 5different partners andreached10,000clients.ShortVideo films on six differentthemesoffinancialeducationlike savings, credit,remittance,familybudgetingand micro enterprise werebroadcasted in every centermeeting. They are creating“jingles” or short

27

advertisements that areadvertised on radio ortelevision to communicatefinancial concepts andproduct offerings. Leaflets,brochure and other paperbasedpromotionalmaterialsalso printed. Third, they areworkingforclientprotection.They are working withpartners to establishgrievance redressalmechanismswherebyclientscanformallyfileandmediateany concerns. They areworking with partners toundertake and receiveSMART certification for thefirst time in Nepal. Smartcertification provides anindependent, objective sealofconfidencethatafinancialinstitutionisdoingeverythingit can to treat its clientwellandprotectthemfromharm.(Sakchyam:Access toFinance,n.d.)

VijayaLaghubittaBittiyaSanstha

Financial literacy throughmobilevoicemessage

Rapti zone(Dang,Salyan,

Financial literacy campaign by sending mobile voice message (Interactive Voice Response – IVR) imparting financial education to Dalit women. VLBS

The IVR technology alonereaches out messages onfinancial literacy to 6000

28

Pyuthan,Rolpa andRukum)

is working with Sakchyam: Access to finance program on other areas like capacity enhancement, enforcement of technology based financial literacy curriculum and educating target groups through community radio, tablet and interactive voice recording message. (Adhikari, 2015)

people.13000 membersaffiliated to the partnerinstitute sakchyam arereceiving messaged onfinancial literacy throughvarious media. VLBS targetwas to enable 4200 familiesto get into the habit ofmaking savings in threeyears.(Adhikari,2015)

NationalBankingInstitute

FinancialliteracyTraining Backwardsections ofsociety

National Banking Institute has been conductingprograms on creating awareness on access tofinance. The initiativewas startedwith a vision ofhelping people at the base of the pyramidsunderstandtheimportanceofsavingsandfinancialplanning.Theyidentifiedthatyoungstudents,ruralhousewives, remittance dependent families,membersofcooperatives,disadvantagedandunderprivileged need financial education to enhanceaccess to a formal financial channel. FinancialliteracyprogramsweretobeconductedaspartofitsCSRactivities.The initiativewastargetedatyoungstudents, rural housewives, remittance dependentfamilies, members of cooperatives, anddisadvantagedandunderprivilegedgroupsamongstothersatthebaseofthepyramidtounderstandtheimportanceofsavinghabitsandfinancialplanning.(NationalBankingInstitute,n.d.)

NBI has successfullyconductedprogramsatgrassrootlevelofdifferentareasofKathmandu, Chitwan,Makwanpur, Dhading, Dang,Dolakha, Ramechhap,Sindhupalchowk districts.their programs includeawareness program onfinancial literacy, training onfinancialliteracyandtrainthetrainer on financial literacy.They have also concludedprograms in various parts ofTehrathum and Sunsaridistrictsintheeasternregion.Apartfromthat,NBIhasalsobeen conducting exposurevisits, seminars, trainings,etc. on Access to

29

Finance. (National BankingInstitute,n.d.)Theyhavealsopublished a training bookname “Financial Literacy”.NBI also collaborates withbanks to conduct financialliteracytrainings.Recently,itcollaborated with NIC ASIAbank and conducted theseprograms at 11 locationsoutsideKathmanduvalleyatan initial phase. There areplans to reach out to moredistricts in the next phase.(SPOTLIGHT,2014)

*Thelistisnotanexhaustivelistoforganizationsconductingfinancialliteracyinitiatives.TheabovelistisjusttoprovideapictureonwhatworkiscurrentlybeingdoneinNepalinthisregards.

30

4.3ExcerptsofinteractionwithStakeholdersThe government, central bank, commercial bank, microfinance institutions, NGOs/INGOshavebeeninvolvedinfinancialliteracyinitiativesinNepal.Interviewswereconductedwithfewofthesestakeholderstobetterunderstandtheirinitiatives.Atotaloffivestakeholderswereinterviewed.Aformofsemi-structuredinterviewwasusedforinteraction.The interactionswith these stakeholders lead to the conclusion that all these institutionsstartedeffortsinfinancialliteracyonavoluntaryorself-interestbasis.Alltheseinstitutionswere working directly or indirectly for enhancing access to finance. Mercy corps hadconductedastudyforassessmentofthegapinfinancialservicethatledtotheconclusionthatpeoplehadverylimitedknowledgewithregardstomanagingmoney.Theintentionwasto increase awareness about financial issues. Vijaya Laghubitta also started working onfinancialliteracyastheybelievededucationcouldincreasethecapabilityofthepeopleandthecompanywouldalsobefulfilling itssocialdutyorcorporatesocialresponsibility.NBI’sCEO;SanjibSubbaaddedthathestartedtheworkonfinancialliteracyasaresultofhisownpassionandinterest.NBIsoughttoserveallstrataofthepyramidandascommercialbankswould not be interested in rural finance they started the work in rural part of Nepal.EntrepreneursNepalperceivesfinancialliteracyasanecessarysteptobetakenforpromotingentrepreneurship.CWINNepalisworkingforchildreninNepalandconsidersfinancialliteracyasanimportantdimensionforoverallchilddevelopment.ThetargetareaformostofthesestakeholderswereruralpartsofNepal.Theselectionofareaswasbasedonfeasibilityfortheorganization.Mostoftheorganizationsselectedareaswhere theywerealreadyworkingorwhere theirothersprojectswerebeingdone.MercyCorpswasworkingforoveralldevelopmentofadhuwaandalaichifarmersandprovidedthemfinancialliteracytraininginadditiontoothertechnicalsupport.ThefirstprojectonfinancialliteracybyMercyCorpswasfundedbyWesternUnionFoundationasaresultofwhichtheytargeted eastern part of Nepal where there is more remittance flow. Rai, Limbu, BritishGorkha, Hong Kong Laure, Indian army families were targeted as they were remittancegeneratingfamilies.1682womenreceivedfinancialliteracytraininginBhojpurandPanchthardistricts.Thesewomenweremembersofcooperativesinthosedistricts.AnotherprojectwasthenfundedbyDFIDandMercyCorpscontinuedthefinancialliteracycampaign.Thetargetgroupwereusuallymembersoflocalcooperativesandmicrofinanceinstitutionsattheearlierstages.Butlatertheparticipationwasopentonon-membersaswell.VijayaLaghubittaalsoconducted these trainingson their areasofoperation.The targetaudience selectedweretheirownclientsandotherpeopleintheirareasofoperation.AstheaimofNBIwastoreachout to rural Nepal; areas were randomly selected for trainings. Clients of cooperatives,schools,youth,womengroups,remittancedependentfamilieswereusuallythebeneficiariesof financial literacy. EntrepreneursNepal has beenworking inside KathmanduValley andoutside Nepal mainly gulf countries. It has been targeting school, college children andremittance sending and receiving communities. CWIN is focused on enhancing children’scapability and is implementing Aflatoun model in schools in Nepal. Hence their targetaudienceareschools,orphanagehomes,droppingcenters,clubsetc.MercyCorpswasalreadyworkingonfinancialliteracyprojectsinothercountriessotheyusedtheexistingcurriculumandlocalizedittobeappropriateforNepal.Theydevelopedtrainer’s

31

manualaswellasbooksforparticipants.Thebooksrelyheavilyonpictorialdescription,flipcharts,stories,poems,songsareusedtomake learning interesting.VijayaLaghubittaalsodevelopedtheircontentinternallytogivelecturebasedtrainingtoitsclients.Theyalsoreliedheavilyonpictures,flipcharts,storiesasmostofthepeopleareilliterate.Theyalsousedaninnovativesystemforfinanciallyeducatingitsclients.Ituseditsclientdatabasetosendshortvoice messages in their mobile phones about relevant concepts of financial literacy forexample;importanceofsaving,insurancetoitsclients.NBIalsopublishedtheirownbookonfinancial literacy that is in Nepali language. Entrepreneurs Nepal had different format oftrainingtobegiventodifferentgroups.Inschools,theyusedgamestoeducatechildreninaninterestingfashion.Fore.g.Inonegamechildrenwouldbegivenfakecashthattheywouldhave to invest in different alternatives like banks, insurance and whoever had earnedmaximummoneyattheendofthegamewouldbethewinner.Theyalsogiveonlinecoachingto remittanceworkers in gulf countries. CWIN isworking to incorporate financial literacycontentintheschoolcurriculumitselfaspartofthetheAflatounproject.Thecontentof financial literacy trainingwasmostlysimilarof theall thestakeholders.Asmostof them targeted rural areasandpeoplewhowerenotmuch familiarwith financialsystem it included importanceofhavinga financial target, identificationanddifferenceoffinancial service providers, how to select services, savings importance, how to take loan,importanceofpayinginterestandloanontime,importanceofsendingremittancethroughformal channels, micro insurance, animal insurance, prioritizing needs and wants,expendituretracking,budgetcreation,financialplanning,enterprisedevelopment,risktakingbehavioretc.Mostofthemagreedthattherationaleofimpartingfinancialliteracytotheseindividualsistoencourageentrepreneurialbehavior.Mercycorpspartneredwiththelocalcooperativesandmicrofinanceinstitutionstoconductthesetrainings.The institutionsusedtonominateacapabletrainerwhowouldbefurthertrainedfor6daysafterwhichthetrainingwouldbegivenfor46daysonfinancialliteracy.The participants were given the flexibility of choosing the time and place of training toencourage participation. Later the training was reduced to 26 days to encourage moreparticipation.VijayaLaghubittahiredconsultantstogivetrainingsonfinancialliteracy.Thetrainingwasfor1to2hourseachdayfor2to3days.Theentiresessionwasa5to6hours’module.Thevoicemessagessendwasshortandfocusedononetopicatatime.Thesemessagesweresendtoclientseachdaycontinuouslyforamonthandafterabreakforfewmonthsagaintheyusedtobe send.These institutionsalso released jingles,PSAon the local radiobenefitting thewholeregion.NBI’sfinancialliteracytrainingwasfortwodayswithtwohourseachday.Theymentionedthattheparticipantsexpectedmoneytobegivenforattendanceandwerenotenthusiasticto takethetraining.Butafterconvincingandproviding lunch/Tea/Coffeethetrainingwasmadefeasible.EntrepreneursNepalorganizedifferentsessionsfordifferenttargetgroups.Theyhave180minssessions,360minssessions.Theyalsoconductgamesforschoolchildrenasamechanism

32

forgivingfinancialknowledge.Theyconductsessionsforindividualsgoingtogulfcountriesforworkandprovideonlinecoachingtothosealreadyabroad.CWINgivestrainingstoteachersforaweekandtheygivefinancialeducationtochildreninschoolsthroughouttheyear.Thebasictopicsincludedaresavingsimportanceforwhichtheyholdkhutrukeyprograms,balbachatkosh,sikshyakosh,encouragingaccountopeningetc.Financial literacy is supposed tobringchanges inbehaviorof thepeoplewhich ishard tomeasure.Allof the institutionsexceptMercyCorpshasnotconductedany formal impactassessment/monitoringandevaluation.MercyCorpsconductedanimpactassessmentafterits initial financial literacy project funded by western union foundation. To measure theimpactandoutcomes,variablessuchasknowledge,skills,attitudeandbehavioroffinancialliteracy participants were compared with a control group. The overall conclusion of theevaluationwasthatfinancialliteracytrainingwasviewedfavorablybytheparticipantsandwasexpectedtoinstillpositivemoneymanagementbehaviorsinthem.Butasthisstudywasdone immediately after the trainings were over it is hard to say how much long termbehavioralchangewasactuallyinduced.Otherinstitutionshavenotbeenabletoconductanymonitoringandevaluationbecauseofseveralreasons.Themostcommonlycitedreasonwaslackofbudget.Asmanyofthemwereconductingthesetrainingsonavoluntaryandcomplimentarybasistheydonothaveenoughbudgetallocatedtoconductimpactassessment.Buttheyallstatedthattheresponseoftheindividualstakingtrainingwaspositivebasedontheirinformalconversationswiththem.Forexample,CEOofVijayaLaghubittastatedthatthepublicresponseofthecampaignwasgoodbasedonhisinteractionswithpeoplepostthetraining.Mostof thesestakeholdersperceive financial literacyasanecessarystep forencouragingentrepreneurshipinpeople.Thelogicbehindthisisthatwhenpeoplewillsavemoneytheywouldinvestitsomewhereoruseitforstartingtheirownbusinessthatcouldbeassmallasbuyingacoworagoatthatcouldbeusedasasourceofincome.Also,financialliteracywouldbe of utmost importance to entrepreneurs tomanage their business. Financial literacy isconsideredasmoreofaskillthatneedstobepossessedtoenhanceone’seconomicsituation.AlloftheseinstitutionsshowwillingnesstocontributeinsomewayifNRBdevelopsafinancialliteracystrategy.Somebelievethat theycanbevaluable ingivingsuggestionsonstrategyformulationandotherswere ready tobe implementing agents. The common feeling thattheseinstitutionsshowedwerethattheinitiativestakenbythemwillnotbesustainable.Theybelieve thework they are doing is temporary and imparting financial literacy is not theirprimaryjob.Mostoftheinitiativescurrentlytakenareprojectfundedorareoncostsharingbasissowhentheprojectendsthereisnosuretythatthetrainingswillcontinue.TheyfeelthatthereisagapwiththegovernmentandNRBalsohasnotbeenabletoacknowledgetheworkthattheyaredoingandtakethisissueseriously.TheyfeelthereisalackofsupportfromNRBtoconducttheseactivities.SomeopinedthatevenifNRBactsjustasacoordinatingbodyand comes up with policies that necessitate spending and reporting of financial literacyinitiativesbyBFIsthenahugeimpactwouldbecreated.SotheoverallexpectationfromNRBisjusttocreateanenablingenvironmentthrougheffectivepolicyinterventionsthatwouldencouragefurtherfinancialliteracyinitiatives.

33

6.FindingsThemajorfindingsthatwasderivedafteranalyzinginternationaltrends,nationalinitiativesanddiscussionwithlocalstakeholdersarelistedbelow.International

• Institutionalization,Mobilizingtheexistingstakeholders,Vision/Mission/Goals,Segmentation,NationalCapabilitySurveyandMonitoringandEvaluationarethecommonelementsfoundinstrategiesofothercountries(India,Mexico,Indonesia,UnitedKingdom,Spain)

National

• Governmentalpoliciesintroducedforimplementingfinancialliteracyhavenotyetmaterialized.

• Non-governmentalagencieshavebeenworkingonfinancialliteracyonavoluntarybasis.

• The campaigns are conducted in areas where their other existing projects arerunning.

• Mostofthesecampaignsaredonorfundedandwillnotcontinueoncethefundingstops.

• ManystakeholdersconductedfinancialliteracytrainingsaspartoftheirCSR.• The content was designed in- house and covers basic financial topics such as

savings,budgeting,basicknowledgeofbanksandfinancialinstitutions,insuranceetc.

• Nominimumstandardhasbeenset,theno.ofdaysoftrainingrangesfromafewhourstoupwardsof46days.

• Nomonitoringandevaluationsysteminplacesoitishardtoassesstheimpactofthesetrainings.

34

7.RecommendationsOnthebasisofstudyof internationalpracticesandunderstandingthe initiatives takenbyvariousstakeholdersinNepalIhavepresentedfewrecommendationsthatcouldbeusedforformulationofnationalfinancialliteracystrategy.a) Forpolicyintervention

• Thenationalfinancialliteracypolicythatisunderwayneedstobepublishedasfast

aspossibletopavethewayforfinancialliteracyactionswithoutitworkhasnotbeenabletoprogress.

• CSRconductedbyBFIsneedstohaveacomponentoffinancialliteracyinthem.Itshould bemandatory for BFIs to spend a certain percentage of their profit onconducting financial literacy campaignsand report the same toNRB.ApossibleoptioncouldbetoallocatefundtoaninterestedNGO,microfinanceinstitutions,cooperativesorotherinstitutionstoconductthesecampaignsifcommercialbankscan’t do it themselves. But reporting and monitoring and evaluation of thesecampaignsshouldbemandatory.