Status of Mobile Money Services in Uganda - An Exploratory Study BOUWP0811

36

1 BOUWP/08/11 STATUS OF MOBILE MONEY SERVICES IN UGANDA: AN EXPLORATORY STUDY 1 George Wilson SSONKO 2 ABSTRACT Mobile Money Services were perceived as low-value low-volume payment systems intended to link the bottom of the pyramid clientele to the national payment system. Buoyed by the success of mobile money services in Kenya, mobile network operators set up these services in Uganda. A study to assess the current status of these services in Uganda was undertaken. About 1.74 million clients use mobile money with offerings such as air time purchase, person to person and person to business money transfers. Money transfers are dominated by urban to rural remittances and transaction charges as a proportion of amount sent and received are high on small volumes indicating a potential hindrance of adoption for the poor. On average, 1.64 million transactions worth Shs. 58.2 billion are executed per month. Balances on customers‟ mobile accounts ranged from Shs. 0.6 billion to Shs. 18.0 billion per month, suggesting a use of these accounts as saving vehicles. The mobile network operators are the dominant stakeholders in the mobile money services and utilise the operator-centric business model that locks out competitors and limits interoperability. Commercial banks partnering with mobile operators in the model are mandated by law to maintain an account for the „cash float‟ ensuring that a regulated financial institution holds the physical cash backing the issued e-money. Reduction of costs would necessitate an open business model that encompasses all stakeholders, promotes interoperability and increases the potential customer base. To achieve this there is a need to cultivate institutional relationships that will tap into the synergy of cooperation as well as establishment of a legal framework that does not stifle innovation but ensures safety for customers‟ e-money. Key Words: Mobile Money Services; Mobile Network Operators; Bottom of Pyramid 1 Comments received from colleagues in the Research Department, Bank of Uganda are gratefully acknowledged. All remaining errors are on the part of the author. 2 Research Department, Bank of Uganda. Author‟s e-mail address: [email protected]

Transcript of Status of Mobile Money Services in Uganda - An Exploratory Study BOUWP0811

1

BOUWP/08/11

STATUS OF MOBILE MONEY SERVICES IN UGANDA: AN EXPLORATORY

STUDY1

George Wilson SSONKO2

ABSTRACT

Mobile Money Services were perceived as low-value low-volume payment systems intended to

link the bottom of the pyramid clientele to the national payment system. Buoyed by the success

of mobile money services in Kenya, mobile network operators set up these services in Uganda. A

study to assess the current status of these services in Uganda was undertaken. About 1.74 million

clients use mobile money with offerings such as air time purchase, person to person and person

to business money transfers. Money transfers are dominated by urban to rural remittances and

transaction charges as a proportion of amount sent and received are high on small volumes

indicating a potential hindrance of adoption for the poor. On average, 1.64 million transactions

worth Shs. 58.2 billion are executed per month. Balances on customers‟ mobile accounts ranged

from Shs. 0.6 billion to Shs. 18.0 billion per month, suggesting a use of these accounts as saving

vehicles. The mobile network operators are the dominant stakeholders in the mobile money

services and utilise the operator-centric business model that locks out competitors and limits

interoperability. Commercial banks partnering with mobile operators in the model are mandated

by law to maintain an account for the „cash float‟ ensuring that a regulated financial institution

holds the physical cash backing the issued e-money. Reduction of costs would necessitate an

open business model that encompasses all stakeholders, promotes interoperability and increases

the potential customer base. To achieve this there is a need to cultivate institutional relationships

that will tap into the synergy of cooperation as well as establishment of a legal framework that

does not stifle innovation but ensures safety for customers‟ e-money.

Key Words: Mobile Money Services; Mobile Network Operators; Bottom of Pyramid

1 Comments received from colleagues in the Research Department, Bank of Uganda are gratefully acknowledged.

All remaining errors are on the part of the author.

2 Research Department, Bank of Uganda. Author‟s e-mail address: [email protected]

2

1.0 BACKGROUND AND CONTEXTUALISATION

The success of Mobile Money Services (MMS) in Kenya led many Mobile Network Operators

(MNOs) to venture into offering similar products around the world. In East Africa, the dwindling

revenues in the mobile telephone voice business (Nyabiage, 2011; Musazi, 2010), job market

characterised by migrant workers (Muwanguzi & Musambira, 2009), as well as the proliferation

of mobile phone handsets among the masses (Medhi, Ratan, & Toyama, 2009; Alampay & Bala,

2010; Ivatury & Pickens, 2006; Ndiwalana & Popov, 2008) further enticed the MNOs to

undertake the provision of mobile money.

According to (Ndiwalana, Morawczynski, & Popov, 2010), mobile money is a term used to

loosely refer to money stored using the Subscriber Identity Module (SIM) as an identifier as

opposed to an account number in the conventional banking sense. The authors state that a

notational equivalent in value is kept on the SIM within the mobile phone, which is also used to

transmit payment instructions. Tobbin, (2010) defines mobile money based on its functionality,

uses, and ultimate envisioned purpose by observing that it includes all the various initiatives

(long-distance remittance, micro-payments, and informal air-time battering schemes) aimed at

bringing financial services to the unbanked using mobile technology. By focusing on the gadget

utilised, Jenkins, (2008) described mobile money as money that can be accessed and used via

mobile phone. Depending on the business model employed by the stakeholders (Donner &

Tellez, 2008; Porteus, 2006), the corresponding value is physically held by the MNO such as G-

Cash in the Philippines (Ndiwalana & Popov, 2008), a bank such as MTN mobile money, Airtel

Zap and Uganda Telecom M-Sente in Uganda (MTN, 2010; ZAIN, 2009; UTL, 2010), or

another third party.

Mallat, (2007) argues that it is important to differentiate between mobile payments and mobile

banking services. He opines that mobile banking services are based on the bank‟s own legacy

systems and offered for the bank‟s own customers. Mobile banking services utilise the mobile

device such as mobile phone or Personal Digital Assistant (PDA) as a delivery channel /

3

intermediary between the conventional banking account and the final beneficiary of the financial

transaction such as a merchant (with electronic Point of Sales – POS). It is an evolution of the

bank‟s legacy from (i) „traditional brick and mortar, (physical branches where most interactions

are face to face), to (ii) „click and mortar‟ (multichannel delivery approach involving use of

physical branches and ICT/electronic commerce), and finally to (iii) „click‟ (most transactions

are driven by ICT/electronic commerce) (Hernando & Nieto, 2006).

Mallat, (2007) notes that mobile payments are offered as new payment services to a retail market

which is characterised by 1) a multitude of competing providers such as banks and telecom

operators, 2) two different and demanding groups of adopters – consumers and merchants whose

critical mass in terms of adopting the system is essential for the success of the service, and 3)

challenges regarding standardisation and compatibility of different payment systems. Ernst &

Young, (2010) state that mobile money has various synonyms such as „mobile wallet‟, „mobile

financial service‟ and „mobile payment‟ and can be defined as a term that describes the services

that allow electronic money transactions over a mobile phone that allow applications such as

account access, money transfer, and mobile commerce. The various definitions underscore the

diversity of the usage of the term across the industry and in literature (Ernst & Young, 2010;

Mallat, 2007; Tobbin, 2010).

Despite the diversity in nomenclature, mobile money is increasingly becoming both a marketing

success for MNOs and policy implementers interested in boosting revenue and bringing more

people into the formal financial sector, respectively. A number of scholars, business leaders,

economic development gurus, and opinion leaders have hypothesised that the mobile phone with

its antecedent accessories such as mobile money has the potential to transform the developing

world most especially Africa in ways that the green and industrial revolutions failed. Their

conviction stems from the fact that the mobile phone has been able to short cut the infrastructural

limitations (Aker & Mbiti, 2010; Ajakaiye & Ncube, 2010) that hindered the developing world‟s

agenda.

4

Irrespective of this potential, there is a paucity of research regarding mobile money services.

Earlier studies done thus far are qualitative in nature (Mallat, 2007; Chipchase, 2010) and based

on anecdotal evidence (Bangens & Soderberg, 2011). Using the regulators‟ administratively

collected data about the entire industry, the study presents evidence of the sector‟s sustainable

increase in customers since inception in March 2009. Furthermore, (Ndiwalana, Morawczynski,

& Popov, 2010) point out that only a small proportion of the growing number of studies

discussing mobile money implementations around the globe depend on data from actual adoption

and usage of various m-payments / m-banking systems. As a result, scholars decry the lack of

scholarly research that explores the adoption and use of m-banking / m-payments systems

(Donner & Tellez, 2008; Medhi, Ratan, & Toyama, 2009). The study remedies that by using

population wide statistics to assess the status quo.

Unlike earlier studies that concentrated at the individual and / or firm level, this one will look at

the industry level. Specifically, it examines services provided, transaction charges, number of

registered customers, number and volume of transactions, stakeholders, user interfaces and

security, institutional relationships, policy and regulation, as well as the business model used. By

using the industry level as the unit of analysis, the study would provide the macro level input to

the MMS discussion in Uganda. Given the proliferation of mobile phone ownership and the

increasing clientele of MMS, such information is useful in the assessment of the status of

financial access in the country and devising appropriate policies regarding e-money and its

potential impacts on monetary policy.

2.0 REVIEW OF RELATED LITERATURE

2.1 Theoretical Framework

2.1.1 Overview

The high rate of mobile phone adoption and usage has attracted attention from many researchers

world over. Sey, (2008) for instance, studied mobile phone appropriation in Ghana using a mix

5

of three perspectives, that is, Information and Communication Technologies for Development

(ICT4D), Sustainable Livelihoods Approach to Poverty Reduction, as well as Innovation,

Adoption, and Technology Appropriation. Tobbin, (2010) modeled adoption of mobile money

transfer using the Technology Acceptance Model (TAM) and Innovation Diffusion Theory

(IDT). Similarly, Mallat, (2007) explored consumer adoption of mobile payments using the

diffusion of innovations theory (Rogers, 1995) which he described as a powerful tool in

explaining the adoption of a variety of financial and mobile technologies including electronic

payments (Szmigin & Bourne, 1999), mobile commerce (Teo & Pok, 2003), and mobile banking

(Lee, McGoldrick, Keeling, & Doherty, 2003).

The theoretical framework of this study was drawn from the Information and Communication

Technologies for Development (ICT4D) because mobile money perse without its applications of

money transfer / remittance, mobile commerce, and mobile banking would not be a viable field

of exploration. It is the functionality of the mobile money that enables it to bridge the

infrastructure (financial institutions) gap to development. McNamara, (2003) cited in Sey (2008)

posits that „the history of development assistance is riddled with “gaps” (the infrastructure gap,

the financing gap, etc), the “filling” of which was seen as key to solving the conundrum of

sustainable development‟.

2.1.2 The ICT4D-Development Informatics Theory

The ICT4D is a subfield of Information Systems (IS) research that emerged in the late 1980s

(Avgerou, 2008). It is also known as development informatics (Heeks, 2007), and Information

Systems in Developing Countries (ISDC) (Avgerou, 2008). Despite more than two decades of

existence, the epistemology and ontology of this sub-discipline is poorly understood beyond a

circle of specialists (Avgerou, 2008; Best, 2010; Raiti, 2007) observes that the sub-discipline

contains few grand theories compared to other areas of social science partly on account of its

multidisciplinary nature yet its researchers are not multidisciplinary.

6

Brown & Grant, (2008) evaluated 185 journals in leading journals of ICT for development, IS,

and development and concluded that there are two distinct research streams / domains in what is

termed as ICT4D sub-discipline namely, (i) those studies that focus on understanding technology

“for development” and (ii) those studies that focus on understanding technology “in developing

countries”. The latter employ sociological and technological theories used elsewhere and test to

see if they hold in developing countries socio-economic, cultural, and political contexts. These

studies usually deal with issues of ICT diffusion and adoption. The former stream seeks to

establish a link (usually assumed to be causal) between ICT and any socio-economic

development construct.

Avgerou, (2008) posits that there are three discernible discourses in which a number of ISDC

research may be fitted namely, (1) IS innovation in terms of transferring ICT and organizational

practices from advanced economies and adapting them to the context of particular developing

countries, (2) IS innovation as a process embedded in the local conditions of a developing

country, and (3) IS innovation as a transformative intervention and associates it with aspirations

and policies for socio-economic development. Based on Brown & Grant, (2008)‟s dichotomy of

research domains in ICT4D, the latter is an ICT „for development‟ problem area while the former

two issues fall under ICT „in developing countries‟.

Avgerou, (2008) points out that the third discourse is the least developed perspective yet it is the

one that most appropriately deals with the technological, sociological, and socio-economic

development theoretical nexus that should be the gist of ICT4D. It is the third thread that would

provide sufficient rigor to make ICT4D research developments credible and have a substantial

shelf life (Heeks, 2007). Brown & Grant, (2008) concur and observe that most of the work

undertaken in the ICT4D sub-discipline thus far has concentrated on ICT „in developing

countries‟ compared to ICT „for development‟. Consequently, there is a dearth of literature

dealing with the latter research domain.

7

Despite the short comings of the first two ISDC discourses, this study employed the second

discourse that assumes that IS innovation (Mobile Money) in developing countries is about

constructing new techno-organisational structures within a given local social context and places

research emphasis on exploring local meanings and working out locally appropriate techno-

organisational change (Avgerou, 2008). Indeed, the advent of mobile money in Uganda was

sparked by the success of M-PESA in Kenya (DeWaal, 2010), technology appropriation of

mobile users where sending of money to relatives in the shape of air time was already in place

prior to launch of mobile money services (Comninos, Esselaar, Ndiwalana, & Stork, 2009), use

of mobile phones as conduits by donor agencies to transmit agricultural, health, and education

information (Masuki, et al., 2010; Ferris, Engoru, & Kaganzi, 2008), structure of East African

job market that separated breadwinners from their families and created urban-rural money

remittance corridors (Muwanguzi & Musambira, 2009; Mas & Morawczynski, 2009), poor

alternatives for making domestic money transfers (Mas & Morawczynski, 2009), development of

airtime sharing software such as MTN‟s Me2U (Microsoft.NET, 2008; Hellstrom, 2008; Mulira,

Kyeyune, & Ndiwalana, 2010), and the lack of a low cost low volume payment system that could

sufficiently meet the needs of the Bottom of Pyramid (BoP) users left out by the high cost high

volume national payment system (Ndiwalana & Popov, 2008).

Indeed, the mobile money has redefined the relationships between commercial banks and

telecommunication companies (Saxena, 2010), familial relationships between urban remitters

and rural recipients (Morawczynski, 2008), relationships between individuals and their cell

phones (Sey, 2008), relationships between intermediaries (agents) and telecommunication

companies (Davidson & Leishman, 2010), as well as commercial banks, telecommunication

companies, and their regulators (Njiraini, 2011). The context in which this happens is the social

embeddedness alluded to by Avgerou, (2008) and which mobile money scholars such as

Morawczynski, (2007) refer to as context and have used on several occasions to justify

replication of studies across different political/administrative jurisdictions.

8

2.2 Research Questions

2.2.1 Services provided by Mobile Money

The primary objective of setting up mobile money services such as M-PESA was to tap into the

bulk of the people who were not served by the formal financial services system (Hughes &

Lonie, 2007) with a view of augmenting the MNO‟s revenue that was at that time primarily from

voice calls (Nyabiage, 2011). The underlying strategy was for the mobile money providers to

create a link in the payment systems between the high value high volume national payment

setups and the innovative low value low volume MMS (Ndiwalana & Popov, 2008). As a result,

the first successful African MMS (M-PESA) was piloted as a microfinance repayment platform

(DeWaal, 2010; Hughes & Lonie, 2007). All in all, the target clientele were the poor people. The

services provided and the commensurate pricing strategy were indicative of the nature of the

clientele, even though later on individuals who are relatively well off and are banked (Omwansa,

2009) also took up the services on account of convenience, speed, and low transaction charges.

The services offered include cash deposits, cash withdrawals, purchase of airtime, remittance of

funds, and payment of bills amongst others (Mas & Morawczynski, 2009).

2.2.2 Transaction Charges

Mobile Money is usually presented as a low value low volume payment system intended for the

bottom of the pyramid clientele (Ndiwalana & Popov, 2008). However, price alone is not the

only consideration poor people have in mind before adopting a particular payment system (Bold,

2010). Collins, Morduch, Rutherford, & Ruthven, (2009) illustrate this using a South Indian lady

entrepreneur Jyothi who spends her days walking around her slum village collecting very small

deposits from her clients who are low income housewives. The clients are committed to saving in

equal and regular installments and upon achieving 220 deposits; Jyothi returns the value of the

savings less 20 deposits as a fee for her service. The implication is that Jyothi offers her clients a

negative rate of return on their savings. Despite this, the demand for the service increases. The

example indicates that in addition to price, an assortment of other factors such as safety,

reliability, convenience, and quality of service are taken into account by clients (Bold, 2010)

9

prior to adopting a particular payment alternative. Hence, there is a need for MMS to consider

these aspects raised by Bold, (2010) as well as generic issues of pricing such as positioning, cost,

environmental factors, demand curve, market control / share, psychological factors, and value

(Allen, 2010) when setting a price for services provided.

Nevertheless, the practice in African MMS providers is different depending on the objective the

MNO would like to achieve. Gross, (2010)explored four mobile operators namely, Safaricom in

Kenya, Orange in Cote D‟Ivoire, Telma in Madagascar, and MTN in Uganda and found that

MNOs use the “walled garden” commercial approach to pricing where a service such as sending

money to a non-registered user is more expensive than to a registered user. The essence is for the

registered user to encourage the non-registered user to get on board (Morawczynski, 2008) but

the reality is that it locks out other network users as well (Ndiwalana & Popov, 2008).

Furthermore, a GSMA, (2010) case study of Zap in East Africa reveals that Zap‟s pricing

strategy is targeted at encouraging electronic transactions while those of MTN Mobile Money

and M-PESA envision cash as a long term mainstay of the region‟s economies and hence

encourage cash usage. Consequently, in Zap‟s pricing model, the price of cash-out is higher than

cash-in while MTN Mobile Money and M-PESA do not charge cash-in transactions. Another

peculiar difference with Zap is that it does not set uniform transaction charges across its agent

network (GSMA, 2010).

2.2.3 Clientele

Mobile Money does reach substantial numbers of banked as well as unbanked consumers

(McKay & Pickens, 2010). For instance in Kenya, 45 percent of the adult population is registered

for M-PESA (FSD-Kenya, 2009). Apart from Kenya and Brazil, the uptake of mobile money

services in other developing countries is not that outstanding (McKay & Pickens, 2010).

Furthermore, the statistics to track developments in the sector are scarce as most stakeholders are

not obliged to file clientele data with their regulators (Ndiwalana, Morawczynski, & Popov,

2010).

10

2.2.4 Transactions

The global value of mobile transactions is projected to increase by more than 500 percent from

US$ 162 billion in 2010 to US$ 984 billion in 2014 (Holland, 2011). Holland, (2011) observes

that the leading adopter is the Asia-Pacific region which will overtake Europe, Middle East, and

Africa (EMEA) as the zone with the largest share of mobile transactions in the world. The active

mobile banking users as a percentage of global usage for EMEA, Asia-Pacific, North America,

and Latin America were 42, 38, 16, and 4 percent respectively in 2010 and are anticipated to be

32, 54, 10, and 4 percent in 2014. Despite a constant ratio in the proportion of Latin America‟s

contribution to global mobile money usage, with 80 percent of Latin Americans carrying a cell

phone but only 30 percent having access to financial services, it is forecast that there will be 75.3

million mobile payment users performing US$ 51.8 billion worth of transactions

(MMTAmericas, 2011). Zelezny-Green & Sonia, (2011) note that by 2015, revenue generated

from mobile money services could represent around 5 percent of total operator revenue on the

African continent and transactions made through MMS would account for nearly 7 percent of

total continental GDP.

In the East African Region, Kenya which is the leader in mobile money had four providers who

have so far registered 15.4 million customers and recruited over 39,000 agents with transactions

having reached KShs. 2.45 billion a day and KShs. 29 billion to KShs. 76 billion per month

(Ndiwalana F. , 2010; Ratemo, 2011). In Uganda, there are three providers with a combined total

of registered users of about 2 million of which 1.6 million are for MTN (80 percent market

share) (Tentena, 2011a; Tentena, 2011b) and MTN transfers up to UShs. 216.00 billion per

month. Despite these milestones in mobile money, Holland, (2011) notes that less than 10

percent of consumers would be willing to pay any additional fees for services making it

necessary for MNOs to devise more creative schemes than per transaction fees modes of pricing.

11

2.2.5 Stakeholders

Freeman, (1999) defines a stakeholder as a group or an individual being affected by the

achievement of the organization‟s objectives or a group or an individual who can affect them. It

is crucial to understand the stakeholders of the mobile money because they are crucial in the

formation of partnerships that are vital for enhancing the relationships upon which the

sustainable development of the mobile money ecosystem will be based (Jenkins, 2008). These

relationships vary across countries as case studies of Uganda, Kenya, Tanzania, and Rwanda in

Muwanguzi & Musambira, (2009) show but stakeholders generally include end users, MNOs,

commercial banks, other Non-bank financial institutions, utility companies, employers,

international financial institutions, donors, civil society organizations, financial platform

providers, regulatory agencies, and governments amongst others (Jenkins, 2008). Napoleon

Nazareno, President, Smart Communications of the Philippines cited in Jenkins, (2008) observes

that stakeholder partnerships are crucial if mobile money services are to take root, proliferate,

and go to scale.

2.2.6 User Interfaces and Security

The security of the mobile phone channel is possibly the greatest impediment to the exponential

growth of mobile money services worldwide on account of consumer perception that the mobile

channel is not safe for personal financial services (Karvonen, 2000). In an online survey of 1,100

respondents in 11 countries (Brazil, China, France, Germany, India, Italy, Japan, Korea, Spain,

UK, and US) showed that nearly half (45 percent) of the most active mobile device users would

welcome the opportunity to pay for goods and services using their mobile phone, despite the fact

that 73 percent expressed significant privacy and identity theft concerns (Accenture, 2011).

Earlier studies such as Karvonen, (1999) and Eremeev, (1999) indicate that users seem to prefer

simplicity when making electronic money transactions (Karvonen, 2000). Irrespective of the

sophistication involved in an electronic medium such as a website, users appreciate a very simple

12

design that allows them to better see the progress of the transaction at each stage (Karvonen,

Cardholm, & Karlsson, 2000). Karvonen, (2000) points out that this kind of transparency

apparently impacts customers‟ gaining trust and willingness to transact.

There are three mobile delivery options namely SMS, mobile internet, and downloadable

applications (Abodeely, 2010). Two interfaces are usually employed with the SMS based

transactions namely, SIM Application Toolkit (STK/SAT) (Schmidt, Pfahler, Kastens, &

Fischer, 2010) and USSD (Unstructured Supplementary Service Data) (Gonzalez, 2002).

Security is an important prerequisite for any type of monetary exchange (Saji & Agrawal, 2008)

because it touches the very heart of the new economy given the proliferation of electronic

systems in global and emerging markets (Glaessner, Kellerman, & McNevin, 2002).

Traditionally, a secure environment requires addressing four elements namely, confidentiality,

integrity, availability, authentication, as well as non-repudiation (Saji & Agrawal, 2008). In

addition to these four elements, the mobile networks security should consider issues relating to

device limitations and network immaturity.

Despite the advances in biometric security systems (Fox, 2011), many mobile money service

providers such as Smart Money of the Philippines (Ndiwalana & Popov, 2008) still utilize low

cost security approaches on account of low value low volume transactions. The focus is to find a

balance between the cost of the security technology and customer satisfaction. In most mobile

money deployments such as M-NAIRA in Nigeria (E-Soft Solutions, 2010), MTN Mobile

Money across 21 African countries (Fundamo, 2009) and Zap (Leishman, 2010), security is

reliant on the use of a Personal Identification Number (PIN) for transaction authentication

(Ndiwalana & Popov, 2008). In addition, certain other aspects like nick names are used in

transaction authentication in mobile money services like Zap (Ghananation.com, 2010).

13

2.2.7 Institutional Relationships

Mobile payment systems require multi-institutional cooperation and interplay between different

stakeholders (Ndiwalana & Popov, 2008). There are three main requirements for operators to

offer MMS namely, enabling technology, enabling regulatory environment, and subsequent

financial institution partner (Daly, 2010). Each participant in the mobile money ecosystem

accrues a variety of benefits (Citigroup, 2010) but for stakeholders working with non-traditional

partners dealing with non-traditional functions requires honing new skills to survive.

Nevertheless, the possibility of unlocking new revenue streams (Mi-Pay, 2009) is luring to most

participants. Ndiwalana & Popov, (2008) observe that the most dominant partner in the

relationship determines the nature of the business model. The authors illustrate the issue by

citing examples of G-Cash and Smart Money in the Philippines where the former started a

subsidiary called G-Xchange regulated by the financial regulator to deal with the financial

aspects of the MMS while the latter cooperates with a commercial bank.

2.2.8 Policy and Regulation

The success of mobile phone payments is dependent upon the cooperation of multiple

stakeholders from different industries with different ethos, interests, and strategies (Ndiwalana &

Popov, 2008). These may include end users, intermediaries (airtime sellers, and agents etc)

MNOs, commercial banks, other Non-bank financial institutions, utility companies, employers,

international financial institutions, donors, civil society organizations, financial platform

providers, regulatory agencies, and governments amongst others (Jenkins, 2008). Because of the

diversity involved in the sector, there is a need for an over reaching national strategy that taps

into the synergy created by the diversity but at the same time encourages competition. Despite

this need, the sectoral formulation of policies that has been a mainstay in government

transactions for a long time provides challenges for different government agencies charged with

regulating the different sectors cooperating. Such a fit requires relationship management amongst

the stakeholders which is not common amongst government regulatory agencies eager to protect

their sectoral turf. Kakooza, (2008) argues that the e-commerce regulatory problem in Uganda is

14

significant and calls for a lot of political and socio-economic innovation commonly termed as an

„e-government strategy‟. The author emphasizes the need for government to take a leading role

in regulating e-commerce because of the Low Developing Country (LDC) status of Uganda.

2.2.9 Business Model

A business model is a business configuration – a design of a business operation (its products,

financing, and revenues) (Osterwalder, 2004) and describes the rationale of how an organization

creates, delivers, and captures value – economic, social, or other forms of value (Zott, Amit, &

Massa, 2010). Malone, et al., 2006 define a business model as what a business does and how a

business makes money doing these things. It spells out how a company makes money and

sustains itself by specifying where it is positioned in the value chain (Rappa, 2010). Osterwalder,

(2004) observes that in the era of internet, World Wide Web, e-commerce, and e-business,

companies can increasingly work in partnerships, offer joint value propositions, build-up

multichannel and multi-owned distribution networks and profit from diversified and shared

revenue streams. The author notes that as a result of these possibilities, a company‟s business has

more stakeholders, becomes more complex and is harder to understand and communicate.

Indeed, mobile money is a unique industry in that its success depends upon developing cross-

industry partnerships across a less-than-well-defined value chain (Jimenez & Vanguri, 2010).

The authors observe that, for the most part, this involves a single bank or MNO attempting to

manage all components of the value chain, partnering reluctantly when required by regulation.

For some providers with significant market share, like Safaricom in Kenya (M-Pesa), this

approach works. For most providers, developing these partnerships will be critical to offering a

compelling mobile money service.

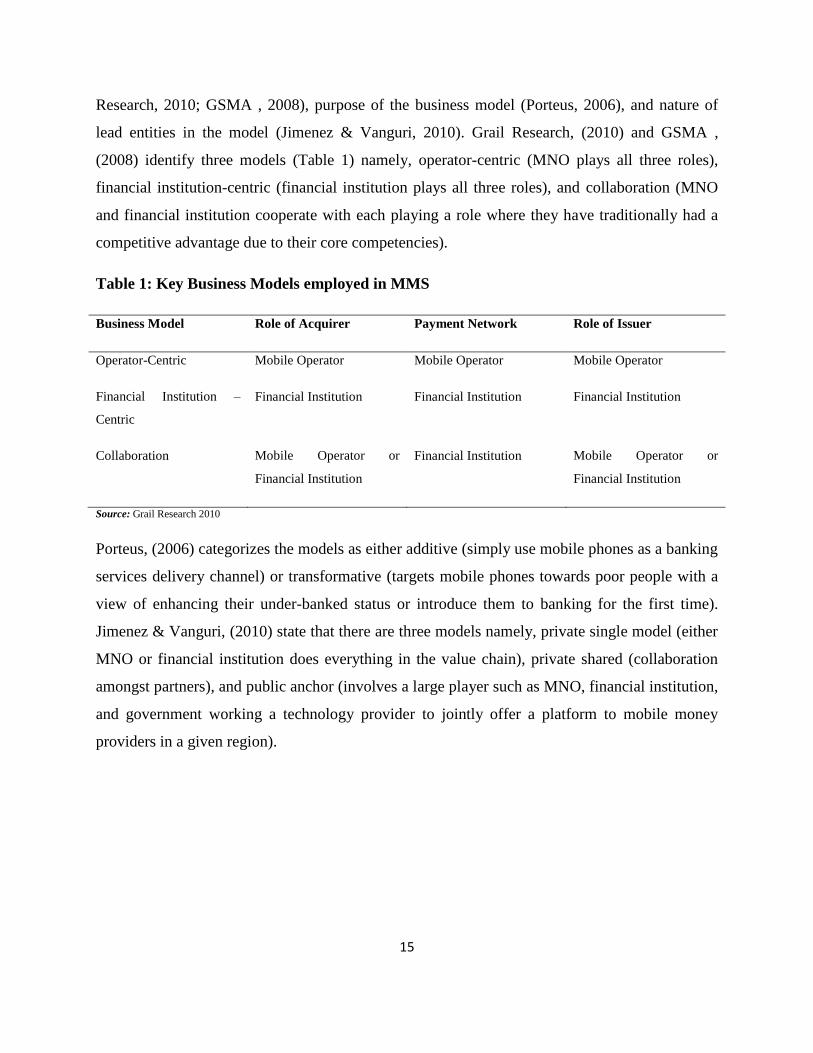

Different methods have been used to categorise the business models used in mobile money

namely, type of organization that plays the role of issuer, acquirer, and payment network (Grail

15

Research, 2010; GSMA , 2008), purpose of the business model (Porteus, 2006), and nature of

lead entities in the model (Jimenez & Vanguri, 2010). Grail Research, (2010) and GSMA ,

(2008) identify three models (Table 1) namely, operator-centric (MNO plays all three roles),

financial institution-centric (financial institution plays all three roles), and collaboration (MNO

and financial institution cooperate with each playing a role where they have traditionally had a

competitive advantage due to their core competencies).

Table 1: Key Business Models employed in MMS

Business Model Role of Acquirer Payment Network Role of Issuer

Operator-Centric Mobile Operator Mobile Operator Mobile Operator

Financial Institution –

Centric

Financial Institution Financial Institution Financial Institution

Collaboration Mobile Operator or

Financial Institution

Financial Institution Mobile Operator or

Financial Institution

Source: Grail Research 2010

Porteus, (2006) categorizes the models as either additive (simply use mobile phones as a banking

services delivery channel) or transformative (targets mobile phones towards poor people with a

view of enhancing their under-banked status or introduce them to banking for the first time).

Jimenez & Vanguri, (2010) state that there are three models namely, private single model (either

MNO or financial institution does everything in the value chain), private shared (collaboration

amongst partners), and public anchor (involves a large player such as MNO, financial institution,

and government working a technology provider to jointly offer a platform to mobile money

providers in a given region).

16

3.0 METHODOLOGY

Out of the five (5) operational mobile network operators in Uganda, three namely MTN, ZAIN

(now Airtel after the purchase by an Indian company Bhati Airtel), and UTL have launched and

implemented mobile money services. The respective names in order of launch of the schemes are

MTN Mobile Money Transfer, Zap, and M-Sente. To study how the various services operate,

content regarding the mobile money service on their websites was scrutinized. The content

scrutinized included how to pay bills, transaction costs, and benefits of the services amongst

others. In addition, publically available information like fliers, brochures, and newspaper pull

outs were analysed. Furthermore, administratively collected quantitative information by Bank of

Uganda was also utilized. Since the study was exploratory in nature, descriptive statistics were

used to present the findings.

4.0 FINDINGS AND DISCUSSION

The paper set out to analyse the state of MMS in Uganda. The advent of MMS in Uganda could

be attributed to both technology appropriation and the success of M-PESA in Kenya. It should be

noted that the launch of the various mobile money schemes simply consolidated the role of

cellular phones in commerce because information and monetary value delivery across the

cellular phones had been in place for a while ever since the mobile network operators put in

place the short messaging service (sms).

4.1 Services provided by the Mobile Money Services

The services provided by the MMS include deposit of funds (cash in), withdraw of funds (cash

out), purchase of airtime, money transfer (person-to-person and person-to-business), mobile

accounts enquiry, and bills payment. The MMS services thus far are in the categories of payment

and remittance services. The MMS are useful for moving cash around the economy and

minimising the dangers associated with carrying cash but not bringing more individuals into the

formal banking system. In addition to the services indicated, mechanisms are being put in place

17

to expand the range of services being provided, for instance, Zain Uganda Limited was

considering introducing school fees payment using MMS by May 2010. These endeavours are

useful for enhancing use of cashless means of payment in the economy and consequently

pushing the frontiers of mobile commerce adoption in Uganda.

4.2 Transaction Charges

According to information on the mobile network operators‟ websites, differences exist in the way

the MMS charge as shown in Table 2. While the variation in MMS charges could be attributed to

competition, there is an element of competitive advantage factored into the pricing. For instance

MTN Mobile Money Service does not charge customers for depositing funds (cash in) while

ZAP charges for the same service based on the amount of money deposited. In addition, an

element of risk appears to be a consideration in the design of the pricing. For example ZAP

charges a slightly higher amount for withdrawing funds (cash out) compared to depositing funds

(cash in). Generally, the rates for services are relatively lower for low volume transactions when

compared to those charged by commercial banks or any other money transfer operator but

increase significantly as the transaction volumes rise. Furthermore, ZAP‟s approach of giving

agents latitude to charge fees based on forces of supply and demand is unique and needs further

investigation as far as its effects on product standardization and customer satisfaction among

other attributes are concerned. As a proportion of the transaction value, the charges are relatively

higher for low volumes compared to high volumes.

In a commercial bank, withdrawing cash worth Shs. 1,000,000 (US$ 384.62) across the counter

costs between Shs. 1,000 (US$ 0.38) and Shs. 10,000 (US$ 3.85) (See Table 3) while MTN

mobile money and Airtel Zap charge Shs. 9,000 (US$ 3.46) and Shs. 5,000 (US$ 1.92),

respectively for cashing out Shs. 1,000,000 (US$ 384.62). The high charges for high volume

transactions could be on account of diseconomies of scale. Since large volumes are normally

few, they incur a high cost whenever they are executed.

18

Table 2: MTN mobile money and Airtel Zap transaction charges as at May 10, 2011

Activity Transaction Tiers (Ushs) Local Charges Transaction Tiers (%)

Minimum Maximum

Minimum Maximum MTN Zap MTN Zap MTN Zap

Pay in Cash 1 5,000 N/A 250 N/A 25,000.00 N/A 5.00

5,001 30,000 0.00 200 0.00 4.00 0.00 0.67

30,001 60,000 0.00 300 0.00 1.00 0.00 0.50

60,001 125,000 0.00 400 0.00 0.67 0.00 0.32

125,001 250,000 0.00 500 0.00 0.40 0.00 0.20

250,001 500,000 0.00 1,000 0.00 0.40 0.00 0.20

500,001 1,000,000 0.00 2,000 0.00 0.40 0.00 0.20

Send Money 1 5,000 N/A 250 N/A 25,000.00 N/A 5.00

(To registered user) 5,001 1,000,000 800 250 16.00 5.00 0.08 0.03

Send Money 1 5,000 N/A n.a N/A n.a N/A n.a

(To non-registered user) 5,001 30,000 1,600 n.a 31.99 n.a 5.33 n.a

30,001 60,000 2,000 n.a 6.67 n.a 3.33 n.a

60,001 125,000 3,700 n.a 6.17 n.a 2.96 n.a

125,001 250,000 7,200 n.a 5.76 n.a 2.88 n.a

250,001 500,000 10,000 n.a 4.00 n.a 2.00 n.a

500,001 1,000,000 19,000 n.a 3.80 n.a 1.90 n.a

Withdraw Money 1 5,000 N/A 250 N/A 25000.00 N/A 5.00

(To registered user) 5,001 30,000 700 1,000 14.00 20.00 2.33 3.33

30,001 60,000 1,000 1,200 3.33 4.00 1.67 2.00

60,001 125,000 1,600 1,600 2.67 2.67 1.28 1.28

125,001 250,000 3,000 2,500 2.40 2.00 1.20 1.00

250,001 500,000 5,000 3,000 2.00 1.20 1.00 0.60

500,001 1,000,000 9,000 5,000 1.80 1.00 0.90 0.50

Withdraw Money 1 5,000 N/A n.a N/A n.a N/A n.a

(To non-registered user) 5,001 100,000 0.00 n.a 0.00 n.a 0.00 n.a

Payment for goods & services

Airtime 1 5,000 0.00 0.00 0.00 0.00 0.00 0.00

5,001 100,000 0.00 0.00 0.00 0.00 0.00 0.00

DSTV, Water etc 1 5,000 N/A n.a N/A n.a N/A n.a

5,000 125,000 400 n.a 8.00 n.a 0.32 n.a

125,001 250,000 700 n.a 0.56 n.a 0.28 n.a

250,001 500,000 1,000 n.a 0.40 n.a 0.20 n.a

Source: MTN Uganda Limited and Airtel Uganda Limited websites NB: (i) ZAP fees are recommended rates which an agent

could alter based on supply and demand; (ii) MTN‟s lowest amount is Shs. 5,000/=; (iii) M-Sente‟s website does not show the

service charges; (iv) Services such as balance check and change of password are free; (v) N/A means Not Applicable while n..a

means not accessed

The mobile network operators must find a balance between breaking even / making a profit and

charging relatively lower transaction costs compared to the traditional money remittance and

payment systems. Without such an approach, the clients are likely to perceive MMS as any other

money remittance business say the post office or international remittance companies like Money

Gram and Western Union.

19

Table 3: Select Commercial Bank Charges as at March 31, 2011

Activity No. of banks charging Range of Charges Mean (Shs)

for service (Shs.)

SAVINGS ACCOUNTS

Statement 3 500-3000 2,000.00

Interim Statement 19 1500-10000 3,000.00

Duplicate Statement 20 100-10000 3,850.00

Additional Statement 13 500-5000 2,807.69

Customised Statement 7 2500-20000 9,071.43

Drawings / Withdrawals 14 300-25000 2,378.57

Withdrawals without Identity 4 300-5000 2,325.00

Cash Deposit Charge 3 300-2500 1,766.70

CURRENT ACCOUNTS

Statement 3 500-3000 2,000.00

Interim Statement 22 500-10000 2,886.36

Duplicate Statement 22 100-10000 4,136.36

Additional Statement 17 500-10000 3,117.65

Customised Statement 7 2500-20000 10,071.43

Cash Withdrawal at counter 13 1000-10000 2,923.08

Cash Deposit Charge 5 1000-10000 4,500.00

ATMs

ATM Card Issued 13 2000-15000 6,807.69

ATM Withdrawal 22 250-800 531.82

ATM Deposits 3 300-2000 933.33 Source: Bank of Uganda; NB: (i) Citibank and NBC do not issue ATM cards; (ii) There are 24 commercial banks in Uganda

4.3 Number of registered customers

By February 2011, MTN mobile money transfer, a service launched in March 2009 had

registered 1,553,770 users (See Table 4). This translates into an adoption rate of 64,740 persons

per month. In contrast, M-PESA Kenya registered 7,000,000 users by August 2009 since its

inception in March 2007. The rate of adoption for M-PESA in Kenya as at August 2009 was

233,333 persons per month which is much higher than that of MTN mobile money in Uganda.

Despite the differences in the duration since inception, the different adoption rates could also be

explained by the differences in underlying contextual / environmental factors such as demand for

domestic remittances, quality of existing financial services, and regulatory framework amongst

others. About 60 percent of the transfer recipients are located in rural areas for MTN MMS.

20

Table 4: Number of MMS registered customers in Uganda March 2009 to February 2011

Month Number of Registered Customers Market Share of MMS

MTN Airtel Zap UTL M-Sente TOTAL MTN Airtel Zap UTL M-Sente

Mar-09 10,011.00 N/A N/A 10,011.00 100.00 N/A N/A

Apr-09 26,247.00 N/A N/A 26,247.00 100.00 N/A N/A

May-09 49,369.00 N/A N/A 49,369.00 100.00 N/A N/A

Jun-09 80,786.00 2,146.00 N/A 82,932.00 97.41 2.59 N/A

Jul-09 118,026.00 15,321.00 N/A 133,347.00 88.51 11.49 N/A

Aug-09 155,842.00 26,212.00 N/A 182,054.00 85.60 14.40 N/A

Sep-09 219,713.00 35,140.00 N/A 254,853.00 86.21 13.79 N/A

Oct-09 304,405.00 49,494.00 N/A 353,899.00 86.01 13.99 N/A

Nov-09 383,670.00 69,460.00 N/A 453,130.00 84.67 15.33 N/A

Dec-09 472,663.00 79,384.00 N/A 552,047.00 85.62 14.38 N/A

Jan-10 565,705.00 84,710.00 N/A 650,415.00 86.98 13.02 N/A

Feb-10 684,604.00 88,105.00 N/A 772,709.00 88.60 11.40 N/A

Mar-10 791,293.00 92,640.00 3,566.00 887,499.00 89.16 10.44 0.40

Apr-10 856,320.00 96,047.00 12,912.00 965,279.00 88.71 9.95 1.34

May-10 919,110.00 101,584.00 18,912.00 1,039,606.00 88.41 9.77 1.82

Jun-10 973,467.00 109,883.00 22,931.00 1,106,281.00 87.99 9.93 2.07

Jul-10 1,028,214.00 114,319.00 26,827.00 1,169,360.00 87.93 9.78 2.29

Aug-10 1,094,888.00 116,728.00 32,033.00 1,243,649.00 88.04 9.39 2.58

Sep-10 1,180,773.00 119,199.00 52,998.00 1,352,970.00 87.27 8.81 3.92

Oct-10 1,263,670.00 122,430.00 52,998.00 1,439,098.00 87.81 8.51 3.68

Nov-10 1,336,940.00 124,520.00 52,998.00 1,514,458.00 88.28 8.22 3.50

Dec-10 1,403,425.00 126,837.00 52,998.00 1,583,260.00 88.64 8.01 3.35

Jan-11 1,481,874.00 129,114.00 52,998.00 1,663,986.00 89.06 7.76 3.19

Feb-11 1,553,770.00 131,136.00 52,998.00 1,737,904.00 89.40 7.55 3.05

Source: Bank of Uganda data; NB: N/A means Not Applicable because the service had not yet been launched

On average the relative market shares of MTN Mobile Money, ZAP, and M-Sente between

March 2009 and February 2010 was 89.6 percent, 9.1 percent, and 1.3 percent, respectively.

MTN Mobile Money has the largest share of the MMS market in Uganda. In this aspect, MTN

Uganda is similar to Safaricom in Kenya which is the dominant player in the market and has the

largest MMS adoption rate.

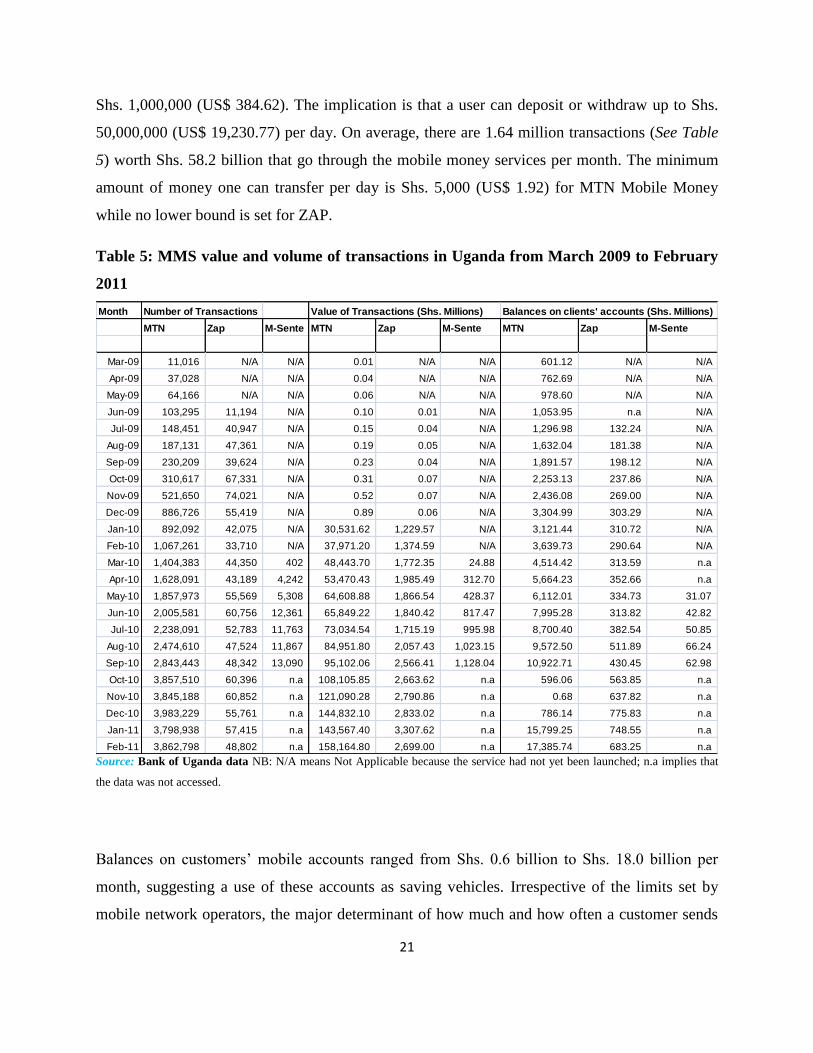

4.4 Number and volume of transactions and balances on customers’ accounts

The maximum number of transactions for either depositing or withdrawing cash for ZAP and

MTN mobile money is 50 per day per user with a maximum transfer amount per transaction of

21

Shs. 1,000,000 (US$ 384.62). The implication is that a user can deposit or withdraw up to Shs.

50,000,000 (US$ 19,230.77) per day. On average, there are 1.64 million transactions (See Table

5) worth Shs. 58.2 billion that go through the mobile money services per month. The minimum

amount of money one can transfer per day is Shs. 5,000 (US$ 1.92) for MTN Mobile Money

while no lower bound is set for ZAP.

Table 5: MMS value and volume of transactions in Uganda from March 2009 to February

2011

Month Number of Transactions Value of Transactions (Shs. Millions) Balances on clients' accounts (Shs. Millions)

MTN Zap M-Sente MTN Zap M-Sente MTN Zap M-Sente

Mar-09 11,016 N/A N/A 0.01 N/A N/A 601.12 N/A N/A

Apr-09 37,028 N/A N/A 0.04 N/A N/A 762.69 N/A N/A

May-09 64,166 N/A N/A 0.06 N/A N/A 978.60 N/A N/A

Jun-09 103,295 11,194 N/A 0.10 0.01 N/A 1,053.95 n.a N/A

Jul-09 148,451 40,947 N/A 0.15 0.04 N/A 1,296.98 132.24 N/A

Aug-09 187,131 47,361 N/A 0.19 0.05 N/A 1,632.04 181.38 N/A

Sep-09 230,209 39,624 N/A 0.23 0.04 N/A 1,891.57 198.12 N/A

Oct-09 310,617 67,331 N/A 0.31 0.07 N/A 2,253.13 237.86 N/A

Nov-09 521,650 74,021 N/A 0.52 0.07 N/A 2,436.08 269.00 N/A

Dec-09 886,726 55,419 N/A 0.89 0.06 N/A 3,304.99 303.29 N/A

Jan-10 892,092 42,075 N/A 30,531.62 1,229.57 N/A 3,121.44 310.72 N/A

Feb-10 1,067,261 33,710 N/A 37,971.20 1,374.59 N/A 3,639.73 290.64 N/A

Mar-10 1,404,383 44,350 402 48,443.70 1,772.35 24.88 4,514.42 313.59 n.a

Apr-10 1,628,091 43,189 4,242 53,470.43 1,985.49 312.70 5,664.23 352.66 n.a

May-10 1,857,973 55,569 5,308 64,608.88 1,866.54 428.37 6,112.01 334.73 31.07

Jun-10 2,005,581 60,756 12,361 65,849.22 1,840.42 817.47 7,995.28 313.82 42.82

Jul-10 2,238,091 52,783 11,763 73,034.54 1,715.19 995.98 8,700.40 382.54 50.85

Aug-10 2,474,610 47,524 11,867 84,951.80 2,057.43 1,023.15 9,572.50 511.89 66.24

Sep-10 2,843,443 48,342 13,090 95,102.06 2,566.41 1,128.04 10,922.71 430.45 62.98

Oct-10 3,857,510 60,396 n.a 108,105.85 2,663.62 n.a 596.06 563.85 n.a

Nov-10 3,845,188 60,852 n.a 121,090.28 2,790.86 n.a 0.68 637.82 n.a

Dec-10 3,983,229 55,761 n.a 144,832.10 2,833.02 n.a 786.14 775.83 n.a

Jan-11 3,798,938 57,415 n.a 143,567.40 3,307.62 n.a 15,799.25 748.55 n.a

Feb-11 3,862,798 48,802 n.a 158,164.80 2,699.00 n.a 17,385.74 683.25 n.a

Source: Bank of Uganda data NB: N/A means Not Applicable because the service had not yet been launched; n.a implies that

the data was not accessed.

Balances on customers‟ mobile accounts ranged from Shs. 0.6 billion to Shs. 18.0 billion per

month, suggesting a use of these accounts as saving vehicles. Irrespective of the limits set by

mobile network operators, the major determinant of how much and how often a customer sends

22

money is the price structure. The price structure is designed in such a way that it is cheaper for a

registered user to send money or execute other transactions. This price structure is similar to that

employed by M-PESA in Kenya.

4.5 Stakeholders

The focus of the MMS in Uganda is the MNO (s). The roles of the commercial banks are

secondary in nature. Table 6 shows the stakeholders involved in the various MMS in the country.

Table 3: Stakeholders in the various MMS in Uganda

Name of MMS Mobile Operator Commercial Bank Electronic Platform

MTN MTN Uganda Ltd Stanbic Bank -

ZAP ZAIN Standard Chartered Bank -

M-Sente Uganda Telecom DFCU Bank MAP Switch

The business models in Uganda follow the Smart Money of Smart Communications of the

Philippines where a MNO collaborates with a commercial bank to offer MMS. This arrangement

allows each partner to focus on an area where they have distinctive competences and

comparative advantage. In Uganda, this business model is dominated by the MNOs that do most

of the marketing as well as opening up and maintaining accounts for the subscribers. However,

such a model lacks interoperability amongst MNOs in the industry and thus limits

standardization of the service provision across networks. In the current arrangement, accounts

opened are merely conduits for money transfer and have managed to reduce the cost of small

volume transfers when compared to traditional money remittance providers such as Postal

Services, Western Union, Money Gram, and Courier Services of various bus companies in the

country.

23

The opening of accounts by the MNOs does not require any money nor does a client have to

maintain a minimum balance on the account. Like bank accounts, there are efforts by mobile

operators through their MMS agents to ensure that the Know Your Customer (KYC) guidelines

are adhered to avoid exposure to risk due to information asymmetry. As a result of the KYC

guidelines, agents may require all or any of the following information and documentation prior

to opening up an account:- (i) full name; (ii) physical address; (iii) date of birth; (iv) gender; (v)

mobile number (which serves as the account number as well); (vi) identity card (voter‟s card,

military ID, and passport etc); and (vii) source of income amongst others.

The relationship between the agents and MNOs exposes customers to a risk of financial loss

without appropriate insurance and / or coverage save for the initial deposit of Shs. 1,000,000

(US$ 384.62) placed in a bank account by the agent upon applying for permission to run an

outlet of the MMS. The terms and conditions of use stipulate that the mobile operator would not

be liable to the customers for any losses suffered on account of the agent. Given the

responsibilities of agents, this aspect of customer safety ought to be addressed if the MMS are to

become reliable mechanisms of storing and transferring monetary value. The roles of agents

include:- (i) registration of mobile money clients; (ii) depositing cash into registered customers‟

accounts; and (iii) processing of cash withdrawals for both registered and non-registered clients.

Country wide, the number of agents registered by the MMS providers range from 400 to 3000

per company. The requirements for registration as an agent vary across the telecommunications

companies. The basic necessities for operating an MMS outlet are: - (a) certificate of registration

/ incorporation; (b) copies of memorandum and articles of association; (c) completed agent

agreement; (d) list of outlets; (e) deposit of at least Shs. 1,000,000 (US$ 384.62) per outlet in a

specified partner commercial bank; and (f) maintenance of a cash float of Shs. 1,000,000 (US$

384.62) per outlet. In addition, there are basic office requirements such as personnel for handling

day-to-day operations, photocopying machines for duplicating the identity cards of customers,

furniture, telephone, and e-mail contacts.

24

Cash shortages in rural areas as well as theft of cash from agents are challenges that have been

reported so far in Uganda. As a means of risk mitigation and / or control, mechanisms should be

put in place to beef up security at the premises of agents. Installation of safes in the short to

medium term could help minimize the risk of cash theft. In the long term, the solution lies in

leveraging ICT such that mobile money can be used at the Point of Sale (POS). The implication

is that merchants would have to invest in the hardware and software necessary to establish POS.

With the existence of the financial infrastructure for debit/credit cards and mobile money in

countries such as the Philippines and Turkey, such an endeavour would not be technologically

demanding to set up in Uganda apart from the high initial costs required for the equipment. The

other risk posed by the MMS is the money laundering and financing of terrorism (ML/FT). This

ML/FT risk is always present even in traditional financial systems. However, adherence to KYC

guidelines recommended by the regulator ought to minimize this challenge.

The issue of a client sending money to a wrong mobile account number is a challenge that could

affect the trust of individuals who have adopted the MMS. Without a system of registering SIM

cards in Uganda coupled with the low cost of cards as well as phones and easy accessibility on

street corners, sending money to a wrong mobile account would certainly result in the loss of

those funds by the sender. The mobile money agents have no way of helping the clients re-route

the funds or track the individual if they are not registered MMS users. The only way of retrieving

such funds would be to launch a criminal investigation that is usually expensive and out of reach

for the Bottom of Pyramid (BoP) clients. Such an investigation could entail the use of a special

electronic serial number known as the IMEI (International Mobile Equipment Identity) to track

the owner of the phone to which the money was sent. It is a tedious and expensive process that

can be overcome by registration of SIM Cards / mobile phone numbers as is done in countries

like South Africa. Clients need to be sure that they can trust the system to help them against such

systemic risks.

25

Apart from the M-Sente MMS, the other two services, that is, ZAP and MTN Mobile Money are

not in collaboration with a financial platform provider such as MAP switch. The financial

platform provider‟s role is to create a link amongst other stakeholders. With a switch like that of

MAP, other telecommunication companies as well as commercial banks can be incorporated in

the MMS without necessarily creating new arrangements. Such an arrangement would allow

more individuals to benefit from the MMS.

4.6 User interfaces and security

All the three MMS rely on Short Messaging System (SMS) to deliver the service to their clients.

By following the prompts of the mobile operator‟s menu, a client can craft a message for a given

transaction. For security purposes all the MMS providers rely on the use of Personal

Identification Numbers (PINs) for transaction authentication. In addition, the physical safety of

the cellular phone which is the customer‟s responsibility must be undertaken. In case of cellular

phone loss, the client ought to file a police case and report to the MNO to block the SIM card

immediately. A lot remains to be done to enhance the security of client transactions. For

instance, the integration of the mobile money account with a commercial bank account to enable

the holder withdraw money from an ATM machine would greatly reduce the reliance on the

agents for all money withdrawals, minimize cash shortages, and reduce the risk exposure for the

agent. Furthermore, there is a need for all stakeholders to undertake a thorough review of the

biometric identification systems employed in India and cellular phone security measures used in

Turkey with an intention of adapting them to Ugandan circumstances. However, a balance must

be struck between convenience and security given the cost of the biometric security equipment

and level of literacy in the country.

4.7 Institutional relationships

The current institutional arrangement in Uganda is skewed in favour of MNOs who undertake

marketing, customer care, mobile account opening and regulation as well as the ultimate

clientele safety. As a result, a substantial portion of the proceeds accrue to the MNOs in the

26

shape of user fees. Financial Institutions on the other hand get to increase their deposits through

maintenance of the MNO „cash float‟ account, in addition to those of the outlets run by agents.

The maintenance of mobile money accounts by MNOs prevents the holders from directly

accessing the financial system. As a result the benefits that could accrue from the increasing

number of individuals accessing the formal financial system such as lowering interest rates on

account of increased clientele (market size) are stifled. The mechanisms of transforming the

mobile money accounts into bank accounts should be the focus of the regulatory agencies (BOU

and UCC).

The economic potential provided by MMS to the various stakeholders such as merchants, agents,

cellular phone kiosk owners, mobile operators, and financial institutions is immense. In order to

harness the potential, collaborative arrangements ought to be undertaken that allow an open

system that can be accessed by both commercial banks and MNOs more easily. Apart from

encouraging more subscribers to join the MMS, collaborative arrangements would allow for

standardization of product / service offerings, better coverage, and efficiency. The current

business models in Uganda do not encourage synergy and may not be in position to achieve the

economic potential.

4.8 Policy and Regulation

There is no clear cut regulatory framework governing MMS in Uganda. Little progress has been

made in regulating electronic transactions ever since the adoption of the National ICT

(Information Communication & Technology) Policy in 2003 (Kakooza, 2008). Kakooza (2008)

observes that the status of regulatory provisions concerning electronic transactions in Uganda is

wanting in many respects.

27

The sectoral laws that govern the various areas that straddle MMS include:- (i) The Bank of

Uganda Act 2000 Cap 51 of the Laws of Uganda 2000 that mandates the central bank to

supervise, regulate, control and discipline all entities that receive money from the public; (ii) The

Financial Institutions Act 2004 that provides for the regulation, control, and discipline of

financial institutions by the Central Bank; (iii) The Micro-Finance Deposit-taking Institutions

Act 2003 that provides for the licensing, regulation and supervision of microfinance business;

(iv) The Uganda Communications Act 1997 Cap 106 of the Laws of Uganda 2000 that created

Uganda Communication Commission (UCC) and liberalized the telecommunications sector; (v)

The Bills of Exchange Act Cap 68 of the Laws of Uganda 2000 which deals with the bill of

exchange transactions; (vi) The Electronic Transactions Act of 2004 that provides for the use,

security, facilitation and regulation of electronic communications and transactions and the

encouragement of the use of e-government services; and (vii) The Electronic Signatures Act of

2004 that provides for and regulates the use of electronic signatures.

In terms of regulating MMS, the major challenge is with regard to the definition, nature, and

scope of MMS. If the MMS is perceived as a delivery channel of banking products, then the onus

would be to regulate the banking sector in light of the new technology. If it is perceived as a

payment system, mechanisms must be devised to liberalise the payment systems such that laws

regulating private providers are formulated. In the current state, only BOU with its Uganda

National Interbank Settlement System (UNISS) are handling national payments.

In order to achieve this, there is a need for cooperation and strategic alliances among

stakeholders such as Bank of Uganda, Uganda Communications Commission, and Uganda

Bankers Association to mention a few. These strategic alliances would be aimed at streamlining

various laws and regulations that relate to financial institutions, mobile network operators,

electronic commerce, and contracting. The overall aim would be to synchronize the requisite

laws and regulations to enable successful implementation of MMS in the Ugandan context.

28

Other areas that ought to be addressed include registration of SIM cards, Anti-Money

Laundering and Combating Financing of Terrorism (AML/CFT), and electronic crimes.

4.9 Appropriateness of the Current Business Model

In Uganda, all the three MMS are operator-centric. The challenge with such a model is the

interoperability. Since, they are dominated by Mobile Network Operators (MNOs), multiple

financial institutions but not other MNOs could theoretically be involved in the MMS. The

implication is that subscribers of the other networks may not be in position to exploit such a

service.

5.0 CONCLUSIONS AND RECOMMENDATIONS

5.1 Conclusions

The primary aim of the study was to establish the status of MMS in Uganda. The findings

indicate that MMS provide critical services to both the banked and un-banked population of

Uganda. These services have greatly improved money remittance across the country. However,

the operator centric business model used by all the MMS providers thus far limits the creation of

the ideal open system that could facilitate participation of various stakeholders. Furthermore, low

volumes attract a substantial proportion of transaction charges when expressed as a percentage of

the total amount transferred / received. With regular users increasingly sending smaller amounts

of money, there is a need for evaluating the pricing mechanism with a view of establishing an

optimal cost structure to guide policy and ensure sustainability of the MMS providers.

Otherwise, if the cost structure were to remain burdensome on low volume users, then the MMS

would be like the high value – high volume national payment system (UNISS) and this could

lead to its demise. Irrespective of the milestones achieved thus far, challenges related to the

security of the MMS services, regulations, and trust still remain.

29

5.2 Recommendations

The liberalization of the economy following the Washington Consensus policy prescription of

the late 1980‟s has been instrumental in Uganda‟s economic prosperity as it ushered in an era of

privatization that spurred innovativeness and productivity. The telecommunications sector

revolution and its now world famous „financial inclusion panacea‟ mobile money is a result of

that liberalization. Mobile Money Services are not new perse but their rapid adoption in the

emerging economies of the world has spurred a scholarly revolution about them. Though a lot

remains to be studied in order to consolidate the contribution of MMS to the ICT4D literature,

the qualitative studies undertaken thus far reveal a lot about its potential in a multitude of

development related endeavours. In Uganda‟s case, the past 26 months since the first MMS in

Uganda launched in March 2009 indicate substantial milestones achieved so far. In order to

consolidate those milestones, the following recommendations ought to be adopted.

i) There is a need to establish an open business model that allows all stakeholders to participate

more freely and competitively.

ii) Stakeholders need to work collaboratively in the review of the appropriate biometric

identification system that could enhance the existing PIN security system.

iii) There is a need for enhancing the role of financial institutions in the opening of mobile

accounts. The involvement of financial institutions more closely would allow the expertise they

possess in KYC guidelines implementation to be exploited to ensure that challenges associated

with Money Laundering / Financing of Terrorism are kept to a minimum. Furthermore, it would

introduce the clientele to the financial institutions and open up the possibilities of these clients

opening up bank accounts or upgrading mobile accounts into bank accounts.

iv) Bank of Uganda, Uganda Communications Commission and Uganda Bankers‟ Association

should work together to establish an appropriate regulatory framework. This working partnership

should take a holistic re-evaluation of all potential laws governing transactions in the financial

sector as well as the communications sector. The laws could also provide reporting mechanisms

for MMS so as the regulatory bodies could collect useful data administratively to enhance

research in the field to foster development.

30

5.3 Future Research

Mobile Money Services and mobile phone usage in general promise to contribute immensely to

the literature in the Information Systems (IS) sub-discipline of ICT4D, shortcomings such as

repetitive qualitative studies notwithstanding. Ndiwalana et al., (2010a) argue that as far as

research concerning MMS in Uganda is concerned, they have barely scratched the surface.

Hence, the following research areas are worth studying further. These are: i) Efficacy of the three

business models under Ugandan circumstances; ii) State of Mobile Phone Industry; iii) Impact of

current regulatory framework on MMS; and iv) Cost benefit analysis of the available biometric

and / or security systems amongst others.

References

Abodeely, J. (2010). How will your enterprise go mobile? Evaluating three mobile delivery

options for customer care. Tampa, Florida, USA.

Accenture. (2011). Interest in Mobile Phone payments strong among most active mobile users.

Retrieved May 02, 2011, from http://newsroom.accenture.com/article-

display.cfm?article_id=5149

Ajakaiye, O., & Ncube, M. (2010). Infrastructure and Economic Development in Africa: An

Overview. Journal of African Economies , 19 (1), i3-i12.

Aker, C. J., & Mbiti, M. I. (2010). Mobile Phones and Economic Development in Africa.

Journal of Economic Perspectives , 207-232.

Alampay, E., & Bala, G. (2010). Mobile 2.0: M-Money for the BoP in the Philippines.

Information Technologies & International Development , 6 (4), 77-92.

Allen, S. (2010). Factors to consider in your pricing strategy . Retrieved April 27, 2011, from

http://www.openforum.com/idea-hub/topics/money/article/factors-to-consider-in-your-pricing-

strategy-scott-allen

Avgerou, C. (2008). Information Systems in Developing Countries: a Critical Research Review.

London, London, UK.

Bangens, L., & Soderberg, B. (2011). Mobile Money Transfers and usage among micro-and

small businesses in Tanzania: Implications for policy and practice. Stockholm: SouthCliff, AB.

Best, M. (2010). Understanding our knowledge gaps: Or do we have an ICT4D field? And do we

want one?

31

Bold, C. (2010). A mobile wallet and the price of money. Retrieved April 27, 2011, from

http://technology.cgap.org/2010/02/04/a-mobile-wallet-and-the-price-of-money

Brown, A., & Grant, G. (2008). Is it ICT "for development" or "in developing countries"?

Exposing the duality of the ICT and development research agenda. Retrieved April 24, 2011,

from http://www.globedev.org

Chipchase, J. (2010). Mobile Phone Practices & the design of mobile money services for

emerging markets. California, California, USA.

Citigroup. (2010, November/December). Mobile money policy forum: partnerships for financial

inclusion in Africa. Nairobi, Kenya.

Collins, D., Morduch, J., Rutherford, S., & Ruthven, O. (2009). Portfolios of the Poor: How the

World's Poor live on $2 a day. Princeton, NJ, USA: Princeton University Press.

Comninos, A., Esselaar, S., Ndiwalana, A., & Stork, C. (2009). Airtime to Cash: Unlocking the

potential of Africa's mobile phones for banking the unbanked. Kampala, Uganda.

Daly, N. (2010). Mobile money transfer international remittance service providers. An overview

of mobile international remittance service provider service offerings . London, UK: Global

System for Mobile Communications Association (GSMA).

Davidson, N., & Leishman, P. (2010). Mobile Money for the unbanked: Building, Incentivizing,

and Managing a Network of Mobile Money Agents- A Handbok for Mobile Network Operators.

DeWaal, M. (2010, September 02). M-PESA arrives in SA hoping to repeat its Kenyan success.

Daily Maverick . South Africa: Daily Maverick.

Donner, J., & Tellez, C. (2008). Mobile Banking and Economic Development: Linking adoption,

impact, and use. Asian Journal of Communication , 18 (4), 318-322.

Eremeev, A. (1999). e-commerce trust study. Materials of Dagstuhl Seminar , 6061.

Ernst, & Young. (2010). Mobile Money: an overview of global telecommunications operators.

E-Soft Solutions. (2010). M-NAIRA mobile money solution converts any mobile phone to a

micro bank for the unbanked. Lagos, Nigeria.

Ferris, S., Engoru, P., & Kaganzi, E. (2008). Making market information services work better for

the poor in Uganda. Kampala, Uganda.

Fox, D. (2011, April 14). Villages leap frog the grid with biometrics and mobile money. The

Christian Science Monitor . San Francisco , California, USA.

32

Freeman, E. R. (1999). Response: Divergent Stakeholder Theory . The Academy of Management

Review , 24 (2), 233-236.

FSD-Kenya. (2009). Fin Access 2009. Retrieved April 27, 2011, from Financial Sector

Deepening : http://www.fsdkenya.org/finaccess/documents/09-06-10-FinAccess-FA09-

Report.pdf

Fundamo. (2009). MTN mobile money case study. Cape Town, Western Cape, South Africa.

Ghananation.com. (2010, March 17). Zain introduces enhanced payment product. Accra, Ghana.

Glaessner, T., Kellerman, T., & McNevin, V. (2002). Electronic Security: Risk Mitigation in

Financial Transactions. Washington, D.C: World Bank.

Gonzalez, E. (2002). USSD (Unstructured Supplementary Service Data). Retrieved May 04,

2011, from http://searchnetworking.techtarget.com/definition/USSD

Grail Research. (2010, February). Mobile payment opportunity in the Middle East and Africa

(MEA) region. Retrieved May 02, 2011, from

http://grailresearch.com/pdf/ContenPodsPdf/Mobile_Payment_Opportunity_in_MEA_Region.pd

f

Gross, I. (2010). Mobile payment structure: a two speed service with most African mobile

operators. Retrieved April 27, 2011, from http://mobilemoneyafrica.com/?p=3247

GSMA . (2008). Mobile money transfer regulatory impact on business model choice. Retrieved

May 05, 2011, from http://www.gsmworld.com/documents/GSMA_-

_Regulatory_Impact_on_Business_Model_0908.pdf

GSMA. (2010). What makes a successful mobile money implementation? Learnings from M-

PESA in Kenya and Tanzania.

Heeks, R. (2007). Theorizing ICT4D Research. Information Technologies and International

Development , 3 (3), 1-4.

Hellstrom, J. (2008). The use and possibilities of m-applications in East Africa.

Hernando, I., & Nieto, M. J. (2006). Is the internet delivery channel changing banks'

performance? The Case of Spanish Banks. Madrid, Madrid, Spain: BancodeEspana.

Holland, N. (2011). A view from the trenches: what consumers think of mobile transactions.

Yankee Group.

33

Hughes, N., & Lonie, S. (2007). M-PESA: Mobile money for the "unbanked" turning cell phones

into 24-hour tellers in Kenya. Innovations: Technology, Governance, Globalisation , 2 (1-2), 63-

81.

Ivatury, G., & Pickens, M. (2006). Mobile Phone banking and low-income customers: evidence

from South Africa. Washington, D.C: Consultative Group to Assist the Poor / The World Bank

and United Nations Foundation.

Jenkins, B. (2008). Developing Mobile Money Ecosystems . Washington, D.C, Washington,

D.C, USA: IFC and Harvard Kennedy School of Government.

Jimenez, A., & Vanguri, P. (2010). Deconstructing the mobile money value chain through cloud

to create new business opportunities. Somers, USA.

Kakooza, A. C. (2008, August 06). Embracing E-Commerce in Uganda: Prospects and

Challenges. Kampala, Uganda.

Karvonen, K. (1999). Enhancing Trust Online. . 2nd International Workshop on Philosophy of

Design and Information Technology Proceedings of PhD IT99: Ethics in Information

Technology Design. Saint-Ferreol, Toulouse, France.

Karvonen, K. (2000). Experimenting with Metaphors for all: a user interface for a mobile

electronic payment device . 6th ERCIM Workshop "User Interfaces for All". Espoo, Finland.

Karvonen, K., Cardholm, L., & Karlsson, S. (2000). Cultures of Trust: A Cross-cultural study on

the formation of trust in an electronic environment. Helsinki, Finland.

Lee, M. S., McGoldrick, P. F., Keeling, K. A., & Doherty, J. (2003). Using ZMET to explore

barriers to adoption of 3G mobile banking services . International Journal of Retail &

Distribution Management , 31 (6), 340-348.

Leishman, P. (2010). A closer look at ZAP in East Africa. Retrieved May 06, 2011, from

http://mmublog.org/wp-content/files-mf/zaineastafrica.pdf

Mallat, N. (2007). Exploring Consumer Adoption of Mobile Payments. A Qualitative Study . The

Journal of Strategic Information Systems , 16 (4), 413-432.

Malone, T. W., Peter, W., Lai, R. K., D'Urso, V. T., Herman, G., Apel, T. G., et al. (2006, May

18). Do some business models perform better than others? Working Paper 4615-06 . Cambridge,

Massachusetts, USA: MIT Sloan School of Management .

Mas, I., & Morawczynski, O. (2009). Designing Mobile Money Services: Lessons from M-

PESA. Boston, Massechusetts, USA.

34

Masuki, K. F., Kamugisha, R., Mowo, J. G., Tanui, J., Tukahirwa, J., Mogoi, J., et al. (2010).

Role of mobile phones in improving communication and information delivery for agricultural

development: Lessons from South Western Uganda. Kampala, Uganda.

McKay, C., & Pickens, M. (2010). Branchless Banking 2010: Who's served? At what price?

What's Next? Focus Note No. 66 . CGAP - Consultative Group to Assist the Poor .

McNamara, K. C. (2003). Information and Communication Technologies, Poverty and

Development: Learning from Experience. Washington, D.C: InfoDev, World Bank .

Medhi, I., Ratan, A., & Toyama, K. (2009). Mobile Banking Adoption and Usage by low-

literate, low-income users in the developing world. Internationalisation, Design and Global

Development , 5623/2009, 485-494.

Microsoft.NET. (2008). Cost Effective Development System makes mobile telephony more

accessible in Uganda. Kampala, Uganda.