Situational Influences on Management Control ... - Canvas

21

Slide 10.1 Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3 rd and Fourth Edition © Pearson Education Limited 2012, 2017 F14a Val av finansiella mått och risk för myopia (dvs kortsiktigt beteende) Merchant; chapter 10: Financial Performance Measures and Their Effects Dessa bilder kan fungera som inläsningsstöd – inte säkert att de behandlas på föreläsning. Jag har kompletterat med något exempel, skrivit en del kommentarer, allt i syfte att öka förståelsen för resonemangen i boken /Johan Å

-

Upload

khangminh22 -

Category

Documents

-

view

6 -

download

0

Transcript of Situational Influences on Management Control ... - Canvas

Slide 10.1

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

F14a Val av finansiella mått och risk för

myopia (dvs kortsiktigt beteende)

Merchant; chapter 10:

Financial Performance Measures and

Their Effects

Dessa bilder kan fungera som inläsningsstöd – inte säkert att

de behandlas på föreläsning. Jag har kompletterat med något

exempel, skrivit en del kommentarer, allt i syfte att öka

förståelsen för resonemangen i boken /Johan Å

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.2

Summary measures

Summary, single-number, aggregate, bottom-line financial measures of performance.

Reflect the aggregate or bottom-line impacts of multiple performance areas.

– e.g., accounting profits reflect the aggregate effects of bothrevenue- and cost-related decisions.

Two types:

– Market measures

» Reflect changes in stock prices or shareholder returns.

– Accounting measures

» Defined in either residual terms (net income after taxes, operating profit, residual income, economic value added) or ratio terms (return on investment, return on equity, or return on net assets).

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

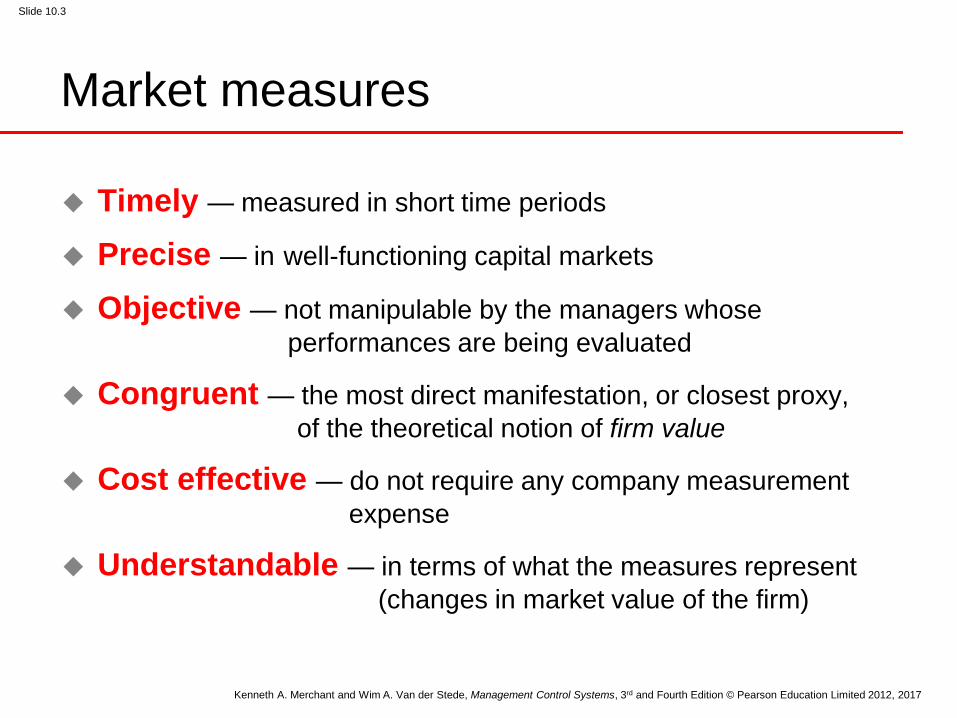

Slide 10.3

Market measures

Timely — measured in short time periods

Precise — in well-functioning capital markets

Objective — not manipulable by the managers whose

performances are being evaluated

Congruent — the most direct manifestation, or closest proxy,

of the theoretical notion of firm value

Cost effective — do not require any company measurement

expense

Understandable — in terms of what the measures represent

(changes in market value of the firm)

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.4

Limitations

Feasibility

– Market measures are not available either for privately-held

firms or wholly-owned subsidiaries or divisions, and they are

not applicable to non-profit organizations.

Controllability

– Market measures can generally be influenced to a significant

extent only by the top few managers in the organization, those

who have the power to make decisions of major importance.

Realized performance

– Market measures are heavily influenced by future expectations,

but these expectations might not be realized.

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.5

Limitations (Continued)

Congruence?

– For competitive reasons, markets are not always fully

informed about a company’s plans and prospects,

and hence, its future cash flows and risks

– Market valuations can be affected by “carefully timed”

or “managed” disclosures which are not always in

the company’s long-term interest

– Other “anomalies”

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.6

Limitations (Continued)

These limitations of market measures cause

organizations to look for surrogate measures

of performance.

– Accounting measures are the most important

surrogates used, particularly at management

levels below the very top management team.

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.7

Accounting measures

Timely — measured in short time periods

Precise — subject to extensive accounting rules

Objective — audited by independent auditors

Congruent» In for-profit firms, accounting profits or returns are relatively

congruent with the true firm goal of maximizing shareholder value.

» Positive correlations between accounting profits and changes in

stock prices.

Cost effective — already required for financial reporting

Understandable

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

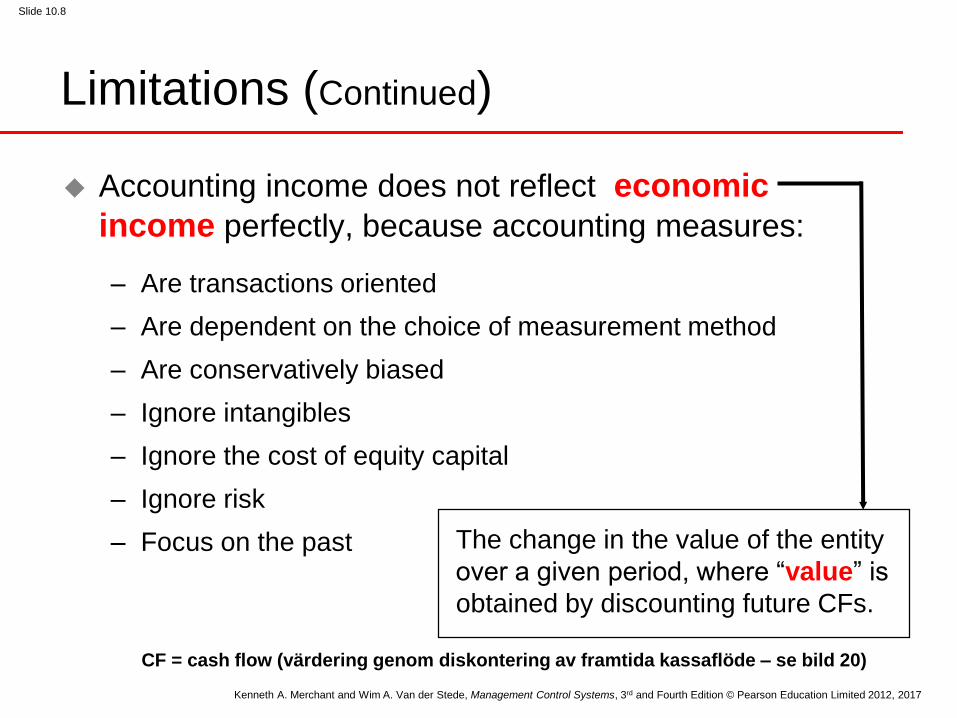

Slide 10.8

Limitations (Continued)

Accounting income does not reflect economic

income perfectly, because accounting measures:

– Are transactions oriented

– Are dependent on the choice of measurement method

– Are conservatively biased

– Ignore intangibles

– Ignore the cost of equity capital

– Ignore risk

– Focus on the past The change in the value of the entity

over a given period, where “value” is

obtained by discounting future CFs.

CF = cash flow (värdering genom diskontering av framtida kassaflöde – se bild 20)

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.9

Myopia

The motivational effect of these measurement limitations

can be perverse because managers who are motivated

to produce accounting profits or returns can (in the

short-term) do so by:

– Not making investments, even worthwhile ones

» Investment myopia

– Making operational decisions to shift income

across periods, even when harmful long-term

» Operational myopia

Exempel: RT kontra RI!

Exempel:

Inslag av redovisnings-

manipulering

Redovisningskreativitet styr operativa beslut….

Vad hände i Eltel inför börsnoteringen?

A. I stora projekt gjordes resultat-

avräkningen på ett ”djärvt” sätt….

B. Vinst i en tvist ”smetades ut” som

rörelsevinst i andra projekt.

A

B

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.11

Redovisningskreativitet styr operativa beslut…

Ur SvD september 2014

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.12

ROI performance measures

Return on Investment

» ROI is a ratio of the accounting profits earned by

the business unit divided by the investment

assigned to it.

» ROI = profits ÷ investment base

Residual Income

» RI is a dollar amount obtained by subtracting a

capital charge from the reported accounting profits.

» RI = profits - capital charge

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.13

Problems caused by ROI-measures

Numerator

» Accounting profits, hence,

» ROI contains all problems associated with these profit

measures.

Denominator

» How to measure the fixed assets portion?

Suboptimization

» ROI-measures can lead division managers to make

decisions that improve division ROI even though the

decisions are not in the corporation's best interest.

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.14

Suboptimization is not an issue with residual income (RI)

measures when the capital charge is set at or above the cost

of capital.

ROE measures induce managers to use debt financing

(if they have financing authority).

» This is not the case with RI if the capital charge is equal

to the weighted average cost of debt and equity.

ROA measures induce managers to lease assets (again, if

they have authority over such decisions).

Other issues

Mkt sällsynt att finansiering är

decentraliserat i koncerner

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.15

The fixed assets portion (se mitt exempel sid 17)

Net Book Value

» Both ROI and RI get better merely to passage of time

» Both ROI and RI are usually overstated if the division

includes a relatively large number of older assets

» Example

Invest $100; Cash flow $27 per year; Depreciation $20 (5 years)

Yr

1

2

3

4

5

NBV

100

80

60

40

20

Incremental

Income

7

7

7

7

7

Capital

Charge

10

8

6

4

2

RI

-3

-1

1

3

5

ROI

7%

9%

12%

18%

35%

(=27-20)10 %

Kenneth A. Merchant and Wim A. Van der Stede, Management Control Systems, 3rd and Fourth Edition © Pearson Education Limited 2012, 2017

Slide 10.16

Division managers are encouraged to retain assets beyond

their optimal life and not to invest in new assets.

Corporate managers may be induced to over-allocate

resources to divisions with older assets.

Combined with the suboptimization issue, managers of

entities with older assets, and hence a higher ROI, are

likely to be more reluctant to invest in “desirable” projects

with an IRR higher than the corporate cost of capital.

Misleading performance signals

Johan Åkesson

Handelshögskolan vid Göteborgs UniversitetRedovisningen kontra kassaflöde

Exempel:

Anläggningsinvestering; 150 Mkr

Årliga inbetalningsöverskott; 20 Mkr/år

Ekonomisk livslängd; 15 år

Kalkylränta; 10%

Exempel för att illustrera….

….Misleading performance signals…….

Johan Åkesson

Handelshögskolan vid Göteborgs Universitet

Bör investeringen genomföras?

Hur bedömer vi det?

Redovisnings-

mässigt?

Kalkyl-

mässigt?

Investeringskalkylering - redovisningen?

Balansräkning

+150?

Risk? Tid?

NPV – nuvärde idag?Räntabilitet över tiden?

Exempel:

Anläggningsinvestering; 150 Mkr

Årliga inbetalningsöversk; 20 Mkr/år

Ekonomisk livslängd; 15 år

Kalkylränta; 10%

20 20 20 osv

År

150 Mkr

Diskontering, ränta = 10%

L

O

G

I

K

?

Exempel - fortsättning:

Johan Åkesson

Handelshögskolan vid Göteborgs Universitet

Exempel - fortsättning:

Kalkylmässig lönsamhet (NPV-nuvärde) = + 2,1 Mkr

Logiskt beslut = investera!

Räntabilitetseffekt med linjär avskrivning:

Räntabilitet år 1 = 6,7 %

Räntabilitet år 2 = 7,1 %

Räntabilitet år 3 = 7,7 %

Räntabilitet år 4 = 8,3 % osv..

Praxis är att investeringsutvärdering sker med NPV-kalkyl

och löpande verksamhetsutvärdering med räntabilitet, ex.

ROCE, eller något residualmått som RI, EVA m.fl.

Beräkningar / resultat

Bokfört

värde

År15

150

Logiskt beslut = investera ej!

Johan Åkesson

Handelshögskolan vid Göteborgs UniversitetEffekt ’externredovisningsstörning’ & reflektion

Exempel - fortsättning:

Effekten blir att en godkänd investering blir

en kvarnsten för räntabiliteten de första åren!

Obs!

Detta problem identifierades redan på 1960-talet men

någon åtgärd har sällan gjorts i praxis. Skälet till det kan

vara att många företag historiskt investerat ungefär lika

mycket varje år och då har den synliga störningen blivit

liten. Idag är investeringstakten i många företag

ojämnare och beräkningsproblemen därför större.

Inte ens möjligheten att ersätta linjär avskrivning har

blivit populärt…..

Johan Åkesson

Handelshögskolan vid Göteborgs Universitet

Kritiken av redovisningen har utmynnat i många

s.k. värdebaserade modeller för styrning(”shareholder value” – debatten under 1990 och tidigt 2000-tal)

Diskontering (%)

Värdet på verksamhetens delar och helhet utgörs av det

framtida kassaflödet diskonterat till idag!

Finansiellt mål blir att ’maximera’ nuvärdet vilket leder

till andra finansiella mål – nedbrytning av ingående

faktorer! (tid, kassaflöde och kalkylränta)

År 1 År 2 År 3 År 4 År 5 År 6 osv.

Nuvärde

Tid