Samsung Electronics

87

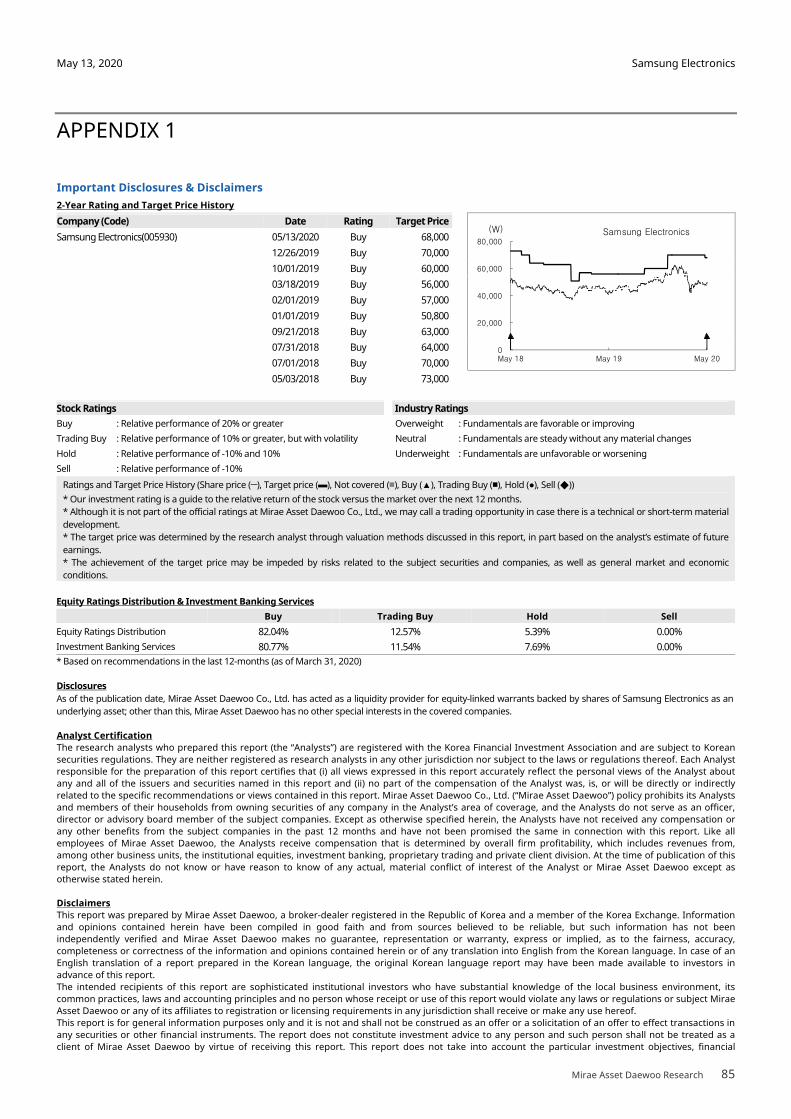

Samsung Electronics ( 005930 KS) Pay attention to potential returns on invested capital Investment points I. Increased visibility on foundry capex to drive up valuation: For 2021, we forecast Samsung Electronics’ (SEC) foundry capex at W9.2tr or higher, which we estimate will translate into a roughly W40tr boost to the company’s value. II. Lower DRAM investments to support structural earnings growth: We believe SEC’s conservative DRAM investments will help keep DRAM prices steady, leading to sequential earnings growth and the opening of a structural growth phase. III. NAND market share expansion to boost earnings: We expect SEC’s NAND capex to far exceed the market average. We believe SEC will continue to execute massive capex and enjoy a dominant earnings share in the NAND market. Earnings outlook For 2Q20, we forecast SEC to post revenue of W48.1tr (-14.3% YoY, -13.1% QoQ) and operating profit of W5.9tr (-10.4% YoY, -8.3% QoQ). By business division, we expect: 1) operating profit of W5.2tr for semiconductor; 2) an operating loss of W0.6tr for display; 3) operating profit of W1.2tr for IT & mobile communications (IM); and 4) operating profit of W0.3tr for consumer electronics (CE). We estimate foundry capacity will expand 43,000 wpm in 2020 and 53,000 wpm in 2021. With a utilization rate at the 90% level, we expect such capacity expansion to lead to revenue growth. For 2020, we forecast system LSI and foundry to see revenue of W17.3tr (+17.3% YoY) and an OP margin of 10.4%. For 2021, we forecast the division to deliver revenue of W21.3tr (+23.3% YoY) and an OP margin of 13.4%, as foundry supplies to Qualcomm (QCOM US/CP: US$78.09) and Nvidia (NVDA US/CP: US$352.22) should gather traction. Initiate coverage with Buy rating and target price of W68,000 We initiate our coverage on SEC with a Buy rating and SOTP-based target price of W68,000. In deriving our target price, we applied a 2020F EV/EBITDA of 5.3x for semiconductors, 4.0x for display, 10.7x for IM, and 5.5x for CE. We believe the broader multiple of roughly 6.0x is highly reasonable, as it represents a premium of just 10.3% to the average 2020F EV/EBITDA of pure memory names Micron (MU US/CP: US$45.12) and SK Hynix (000660 KS/Buy/TP: W110,000/CP: W82,700). FY (12) 12/17 12/18 12/19 12/20F 12/21F 12/22F Revenue (Wbn) 239,575 243,771 230,401 218,366 255,586 299,150 OP (Wbn) 53,645 58,887 27,769 30,807 45,409 53,642 OP Margin (%) 22.4 24.2 12.1 14.1 17.8 17.9 NP (Wbn) 41,345 43,891 21,505 23,903 34,545 40,186 EPS (W) 5,421 6,024 3,166 3,519 5,086 5,916 ROE (%) 21.0 19.6 8.7 9.1 12.2 13.1 P/E (x) 9.4 6.4 17.6 13.8 9.5 8.2 P/B (x) 1.8 1.1 1.5 1.2 1.1 1.0 Dividend Yield (%) 1.7 3.7 2.5 3.3 3.7 3.7 Note: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interests Source: Company data, Mirae Asset Daewoo Research estimates Technology Initiation Report May 13, 2020 (Initiate) Buy Target Price(12M, W) 68,000 Share Price (05/13/20, W) 48,550 Expected Return 40% OP (20F, Wbn) 30,807 Consensus OP (20F, Wbn) 32,813 EPS Growth (20F, %) 11.2 Market EPS Growth (20F, %) 28.5 P/E (20F, x) 13.8 Market P/E (20F, x) 13.0 KOSPI 1,940.42 Market Cap (Wbn) 289,833 Shares Outstanding (mn) 6,793 Free Float (%) 74.8 Foreign Ownership (%) 55.0 Beta (12M) 0.98 52-Week Low 41,200 52-Week High 62,400 (%) 1M 6M 12M Absolute 0.5 -7.5 13.8 Relative -5.4 1.2 22.0 Mirae Asset Daewoo Co., Ltd. [ Semiconductors] Young-gun Kim +822-3774-1448 [email protected] Yumi Cha +822-3774-1770 [email protected] 60 80 100 120 140 160 5.19 9.19 1.20 5.20 Samsung Electronics KOSPI

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Samsung Electronics

Samsung Electronics (005930 KS)

Pay attention to potential returns on invested capital

Investment points

I. Increased visibility on foundry capex to drive up valuation: For 2021, we forecast

Samsung Electronics’ (SEC) foundry capex at W9.2tr or higher, which we estimate will

translate into a roughly W40tr boost to the company’s value.

II. Lower DRAM investments to support structural earnings growth: We believe SEC’s

conservative DRAM investments will help keep DRAM prices steady, leading to

sequential earnings growth and the opening of a structural growth phase.

III. NAND market share expansion to boost earnings: We expect SEC’s NAND capex to

far exceed the market average. We believe SEC will continue to execute massive capex

and enjoy a dominant earnings share in the NAND market.

Earnings outlook

For 2Q20, we forecast SEC to post revenue of W48.1tr (-14.3% YoY, -13.1% QoQ) and

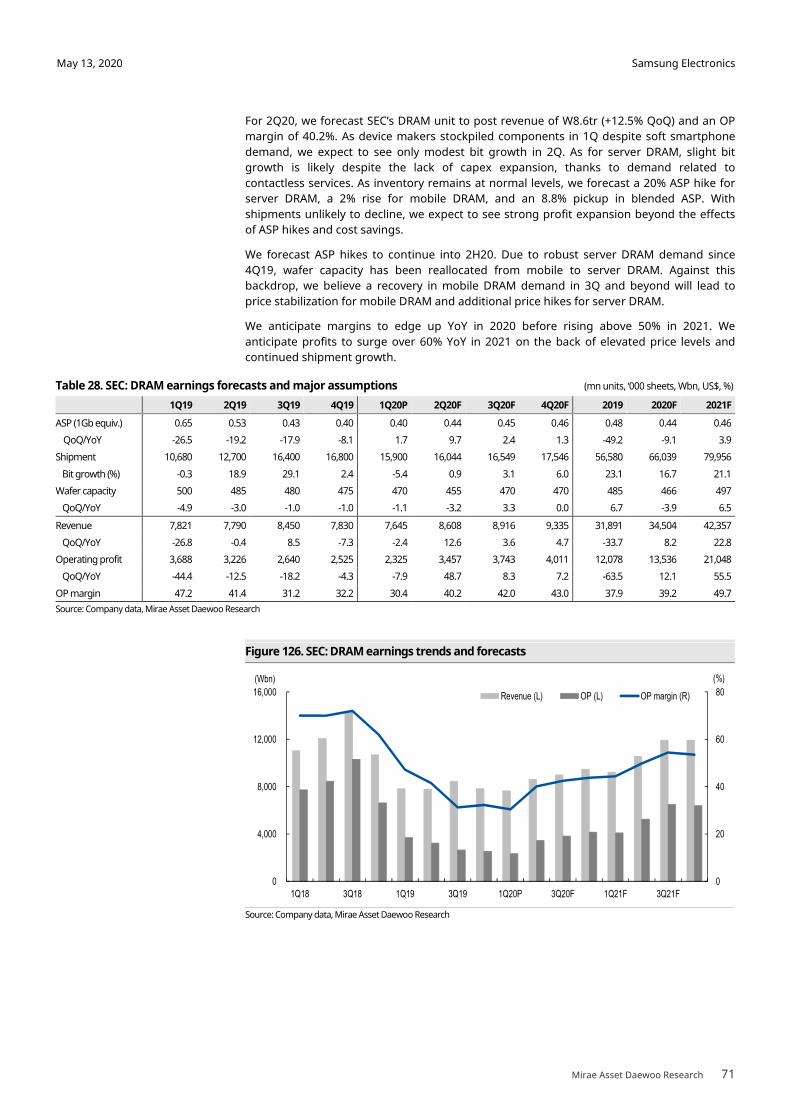

operating profit of W5.9tr (-10.4% YoY, -8.3% QoQ). By business division, we expect: 1)

operating profit of W5.2tr for semiconductor; 2) an operating loss of W0.6tr for display;

3) operating profit of W1.2tr for IT & mobile communications (IM); and 4) operating

profit of W0.3tr for consumer electronics (CE).

We estimate foundry capacity will expand 43,000 wpm in 2020 and 53,000 wpm in

2021. With a utilization rate at the 90% level, we expect such capacity expansion to lead

to revenue growth. For 2020, we forecast system LSI and foundry to see revenue of

W17.3tr (+17.3% YoY) and an OP margin of 10.4%. For 2021, we forecast the division to

deliver revenue of W21.3tr (+23.3% YoY) and an OP margin of 13.4%, as foundry

supplies to Qualcomm (QCOM US/CP: US$78.09) and Nvidia (NVDA US/CP: US$352.22)

should gather traction.

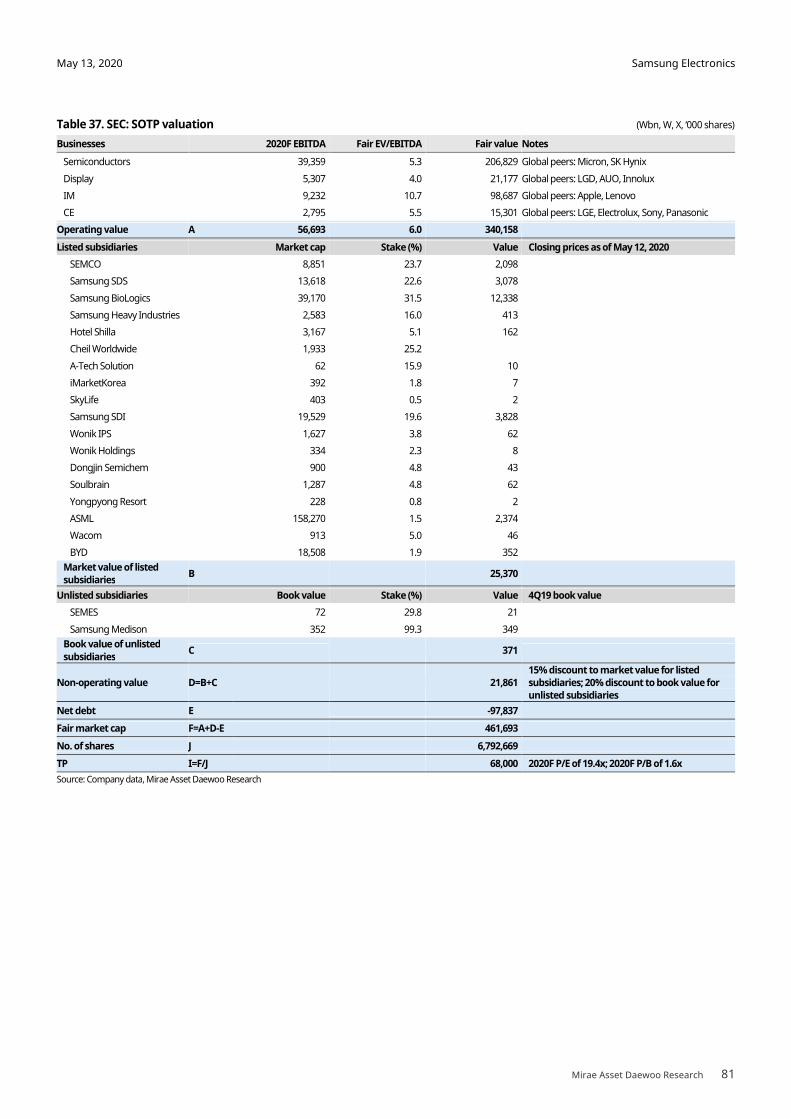

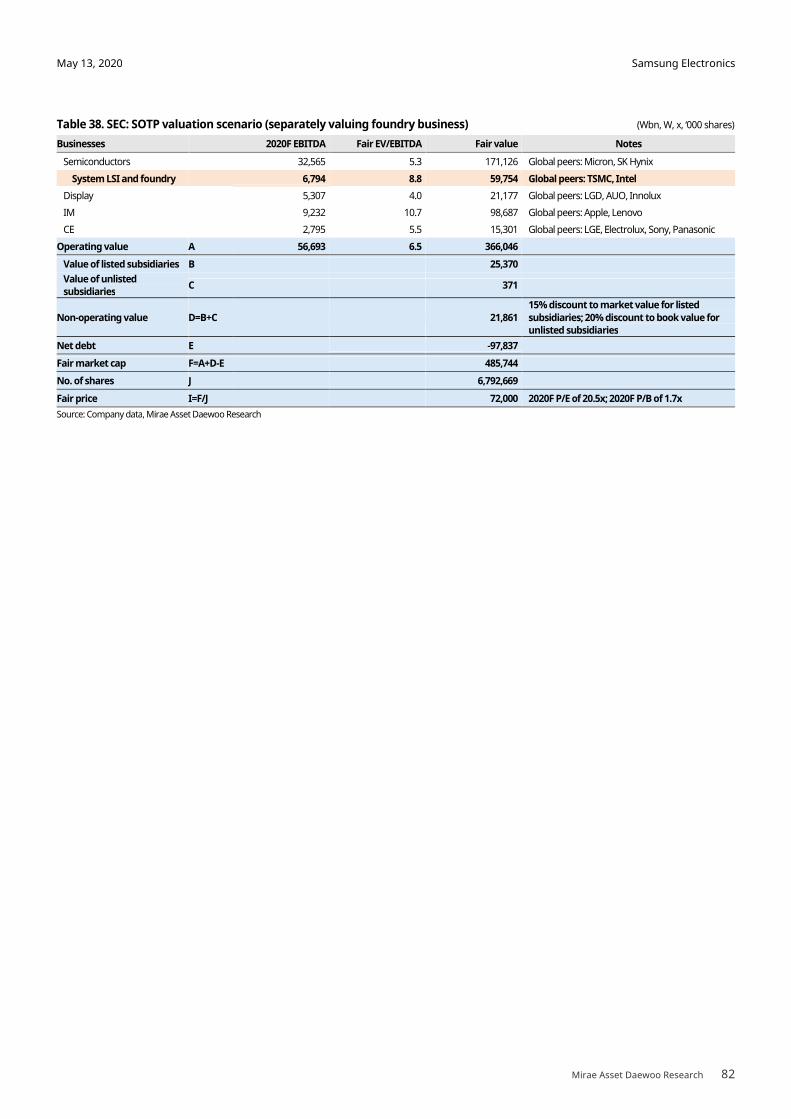

Initiate coverage with Buy rating and target price of W68,000

We initiate our coverage on SEC with a Buy rating and SOTP-based target price of

W68,000. In deriving our target price, we applied a 2020F EV/EBITDA of 5.3x for

semiconductors, 4.0x for display, 10.7x for IM, and 5.5x for CE. We believe the broader

multiple of roughly 6.0x is highly reasonable, as it represents a premium of just 10.3%

to the average 2020F EV/EBITDA of pure memory names Micron (MU US/CP: US$45.12)

and SK Hynix (000660 KS/Buy/TP: W110,000/CP: W82,700).

FY (12) 12/17 12/18 12/19 12/20F 12/21F 12/22F

Revenue (Wbn) 239,575 243,771 230,401 218,366 255,586 299,150

OP (Wbn) 53,645 58,887 27,769 30,807 45,409 53,642

OP Margin (%) 22.4 24.2 12.1 14.1 17.8 17.9

NP (Wbn) 41,345 43,891 21,505 23,903 34,545 40,186

EPS (W) 5,421 6,024 3,166 3,519 5,086 5,916

ROE (%) 21.0 19.6 8.7 9.1 12.2 13.1

P/E (x) 9.4 6.4 17.6 13.8 9.5 8.2

P/B (x) 1.8 1.1 1.5 1.2 1.1 1.0

Dividend Yield (%) 1.7 3.7 2.5 3.3 3.7 3.7

Note: All figures are based on consolidated K-IFRS; NP refers to net profit attributable to controlling interests

Source: Company data, Mirae Asset Daewoo Research estimates

Technology

Initiation Report

May 13, 2020

(Initiate) Buy

Target Price(12M, W) 68,000

Share Price (05/13/20, W) 48,550

Expected Return 40%

OP (20F, Wbn) 30,807

Consensus OP (20F, Wbn) 32,813

EPS Growth (20F, %) 11.2

Market EPS Growth (20F, %) 28.5

P/E (20F, x) 13.8

Market P/E (20F, x) 13.0

KOSPI 1,940.42

Market Cap (Wbn) 289,833

Shares Outstanding (mn) 6,793

Free Float (%) 74.8

Foreign Ownership (%) 55.0

Beta (12M) 0.98

52-Week Low 41,200

52-Week High 62,400

(%) 1M 6M 12M

Absolute 0.5 -7.5 13.8

Relative -5.4 1.2 22.0

Mirae Asset Daewoo Co., Ltd.

[Semiconductors]

Young-gun Kim +822-3774-1448 [email protected]

Yumi Cha +822-3774-1770 [email protected]

60

80

100

120

140

160

5.19 9.19 1.20 5.20

Samsung Electronics KOSPI

Samsung Electronics

Mirae Asset Daewoo Research 2

May 13, 2020

C O N T E N T S

I. Investment points 4 Point I: Increased visibility on foundry capex to drive up valuation 4 Point II: Lower DRAM investments � Structural earnings growth 14 Point III: NAND market share expansion to boost earnings 19

II. Outlook and earnings forecasts by division 25 Key assumptions for IT product demand forecasts 25 [Semiconductors] NAND outlook 43 [Semiconductors] DRAM outlook 57 [Semiconductors] System LSI and foundry outlook 72 Display outlook 77 IM outlook 79

III. Valuation 80

IV. Shareholder returns 83

Samsung Electronics

Mirae Asset Daewoo Research 3

May 13, 2020

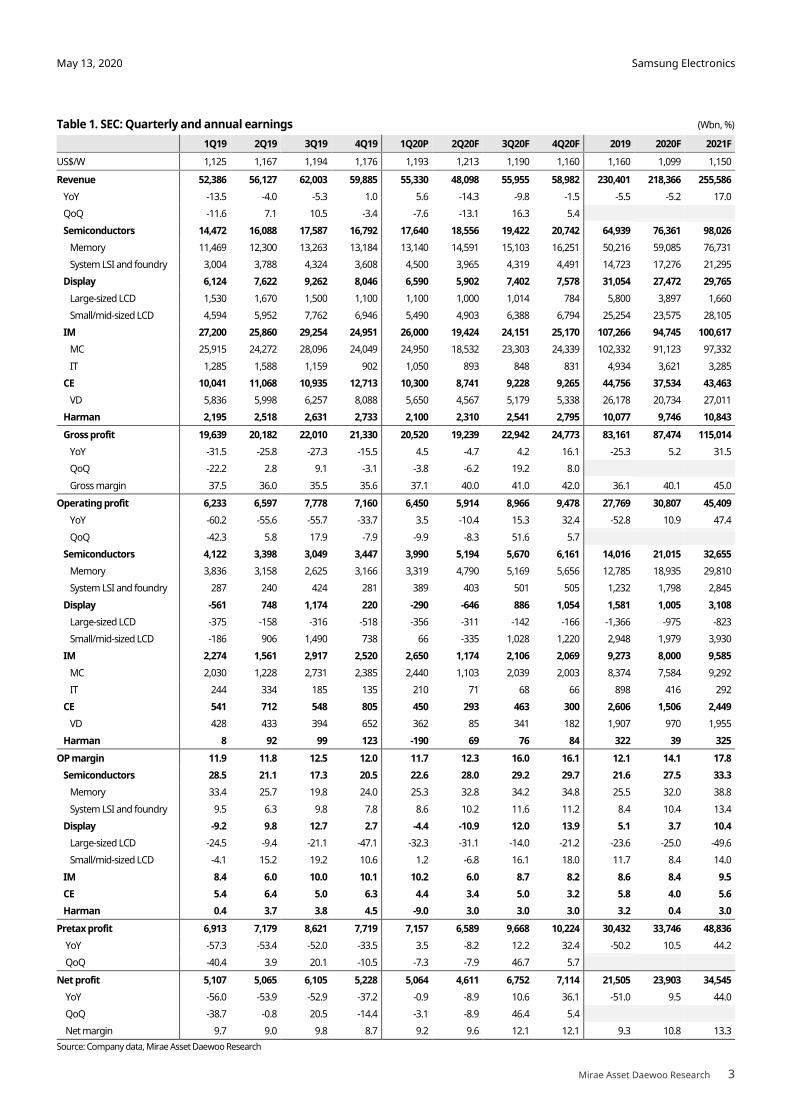

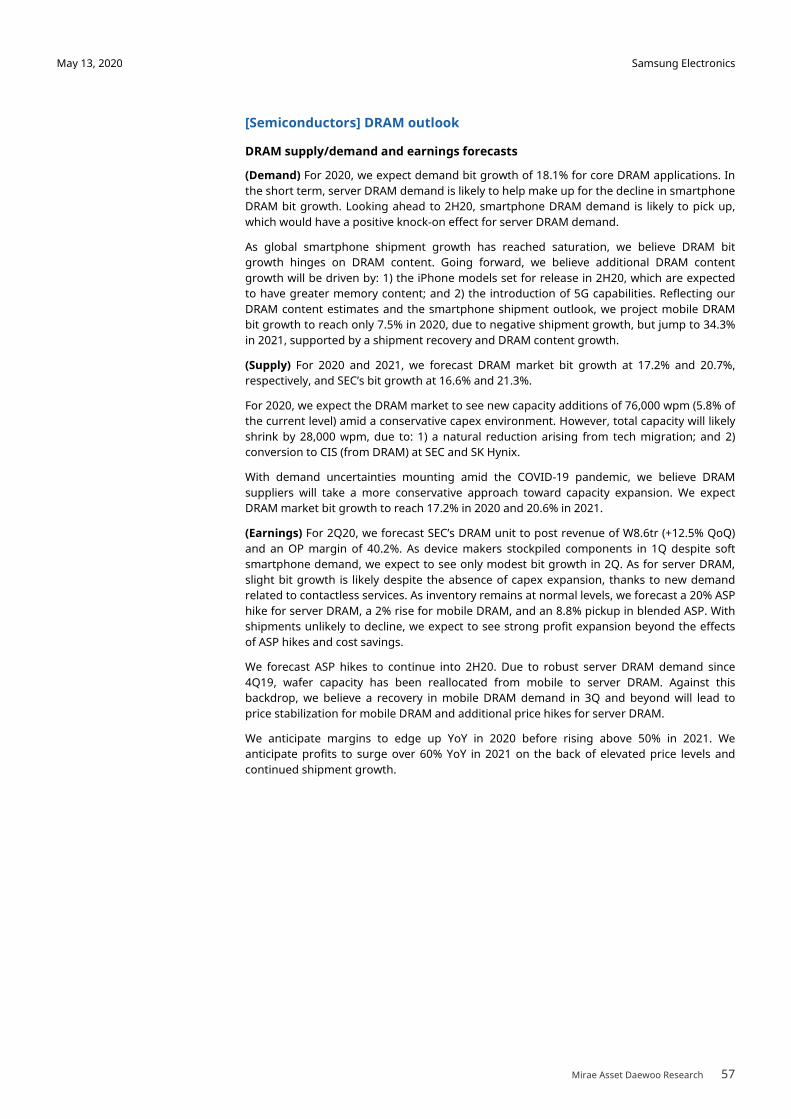

Table 1. SEC: Quarterly and annual earnings (Wbn, %)

1Q19 2Q19 3Q19 4Q19 1Q20P 2Q20F 3Q20F 4Q20F 2019 2020F 2021F

US$/W 1,125 1,167 1,194 1,176 1,193 1,213 1,190 1,160 1,160 1,099 1,150

Revenue 52,386 56,127 62,003 59,885 55,330 48,098 55,955 58,982 230,401 218,366 255,586

YoY -13.5 -4.0 -5.3 1.0 5.6 -14.3 -9.8 -1.5 -5.5 -5.2 17.0

QoQ -11.6 7.1 10.5 -3.4 -7.6 -13.1 16.3 5.4

Semiconductors 14,472 16,088 17,587 16,792 17,640 18,556 19,422 20,742 64,939 76,361 98,026

Memory 11,469 12,300 13,263 13,184 13,140 14,591 15,103 16,251 50,216 59,085 76,731

System LSI and foundry 3,004 3,788 4,324 3,608 4,500 3,965 4,319 4,491 14,723 17,276 21,295

Display 6,124 7,622 9,262 8,046 6,590 5,902 7,402 7,578 31,054 27,472 29,765

Large-sized LCD 1,530 1,670 1,500 1,100 1,100 1,000 1,014 784 5,800 3,897 1,660

Small/mid-sized LCD 4,594 5,952 7,762 6,946 5,490 4,903 6,388 6,794 25,254 23,575 28,105

IM 27,200 25,860 29,254 24,951 26,000 19,424 24,151 25,170 107,266 94,745 100,617

MC 25,915 24,272 28,096 24,049 24,950 18,532 23,303 24,339 102,332 91,123 97,332

IT 1,285 1,588 1,159 902 1,050 893 848 831 4,934 3,621 3,285

CE 10,041 11,068 10,935 12,713 10,300 8,741 9,228 9,265 44,756 37,534 43,463

VD 5,836 5,998 6,257 8,088 5,650 4,567 5,179 5,338 26,178 20,734 27,011

Harman 2,195 2,518 2,631 2,733 2,100 2,310 2,541 2,795 10,077 9,746 10,843

Gross profit 19,639 20,182 22,010 21,330 20,520 19,239 22,942 24,773 83,161 87,474 115,014

YoY -31.5 -25.8 -27.3 -15.5 4.5 -4.7 4.2 16.1 -25.3 5.2 31.5

QoQ -22.2 2.8 9.1 -3.1 -3.8 -6.2 19.2 8.0

Gross margin 37.5 36.0 35.5 35.6 37.1 40.0 41.0 42.0 36.1 40.1 45.0

Operating profit 6,233 6,597 7,778 7,160 6,450 5,914 8,966 9,478 27,769 30,807 45,409

YoY -60.2 -55.6 -55.7 -33.7 3.5 -10.4 15.3 32.4 -52.8 10.9 47.4

QoQ -42.3 5.8 17.9 -7.9 -9.9 -8.3 51.6 5.7

Semiconductors 4,122 3,398 3,049 3,447 3,990 5,194 5,670 6,161 14,016 21,015 32,655

Memory 3,836 3,158 2,625 3,166 3,319 4,790 5,169 5,656 12,785 18,935 29,810

System LSI and foundry 287 240 424 281 389 403 501 505 1,232 1,798 2,845

Display -561 748 1,174 220 -290 -646 886 1,054 1,581 1,005 3,108

Large-sized LCD -375 -158 -316 -518 -356 -311 -142 -166 -1,366 -975 -823

Small/mid-sized LCD -186 906 1,490 738 66 -335 1,028 1,220 2,948 1,979 3,930

IM 2,274 1,561 2,917 2,520 2,650 1,174 2,106 2,069 9,273 8,000 9,585

MC 2,030 1,228 2,731 2,385 2,440 1,103 2,039 2,003 8,374 7,584 9,292

IT 244 334 185 135 210 71 68 66 898 416 292

CE 541 712 548 805 450 293 463 300 2,606 1,506 2,449

VD 428 433 394 652 362 85 341 182 1,907 970 1,955

Harman 8 92 99 123 -190 69 76 84 322 39 325

OP margin 11.9 11.8 12.5 12.0 11.7 12.3 16.0 16.1 12.1 14.1 17.8

Semiconductors 28.5 21.1 17.3 20.5 22.6 28.0 29.2 29.7 21.6 27.5 33.3

Memory 33.4 25.7 19.8 24.0 25.3 32.8 34.2 34.8 25.5 32.0 38.8

System LSI and foundry 9.5 6.3 9.8 7.8 8.6 10.2 11.6 11.2 8.4 10.4 13.4

Display -9.2 9.8 12.7 2.7 -4.4 -10.9 12.0 13.9 5.1 3.7 10.4

Large-sized LCD -24.5 -9.4 -21.1 -47.1 -32.3 -31.1 -14.0 -21.2 -23.6 -25.0 -49.6

Small/mid-sized LCD -4.1 15.2 19.2 10.6 1.2 -6.8 16.1 18.0 11.7 8.4 14.0

IM 8.4 6.0 10.0 10.1 10.2 6.0 8.7 8.2 8.6 8.4 9.5

CE 5.4 6.4 5.0 6.3 4.4 3.4 5.0 3.2 5.8 4.0 5.6

Harman 0.4 3.7 3.8 4.5 -9.0 3.0 3.0 3.0 3.2 0.4 3.0

Pretax profit 6,913 7,179 8,621 7,719 7,157 6,589 9,668 10,224 30,432 33,746 48,836

YoY -57.3 -53.4 -52.0 -33.5 3.5 -8.2 12.2 32.4 -50.2 10.5 44.2

QoQ -40.4 3.9 20.1 -10.5 -7.3 -7.9 46.7 5.7

Net profit 5,107 5,065 6,105 5,228 5,064 4,611 6,752 7,114 21,505 23,903 34,545

YoY -56.0 -53.9 -52.9 -37.2 -0.9 -8.9 10.6 36.1 -51.0 9.5 44.0

QoQ -38.7 -0.8 20.5 -14.4 -3.1 -8.9 46.4 5.4

Net margin 9.7 9.0 9.8 8.7 9.2 9.6 12.1 12.1 9.3 10.8 13.3

Source: Company data, Mirae Asset Daewoo Research

Samsung Electronics

Mirae Asset Daewoo Research 4

May 13, 2020

I. Investment points

Point I: Increased visibility on foundry capex to drive up valuation

SEC’s 2021 foundry capex to reach at least W9.2tr (+77% YoY)

For 2021, we forecast SEC’s foundry capex at W9.2tr or higher, which we estimate will

translate into a roughly W40tr boost to the company’s value (based on TSMC’s [2330 TT/CP:

NT$291.50] average ROIC of 23.5% and P/E of 18x). We believe that capital recovery seems

very likely in the 7nm-or-below segment, in which the company enjoys a duopoly alongside

TSMC.

Technological and capital requirements form high barriers to entry

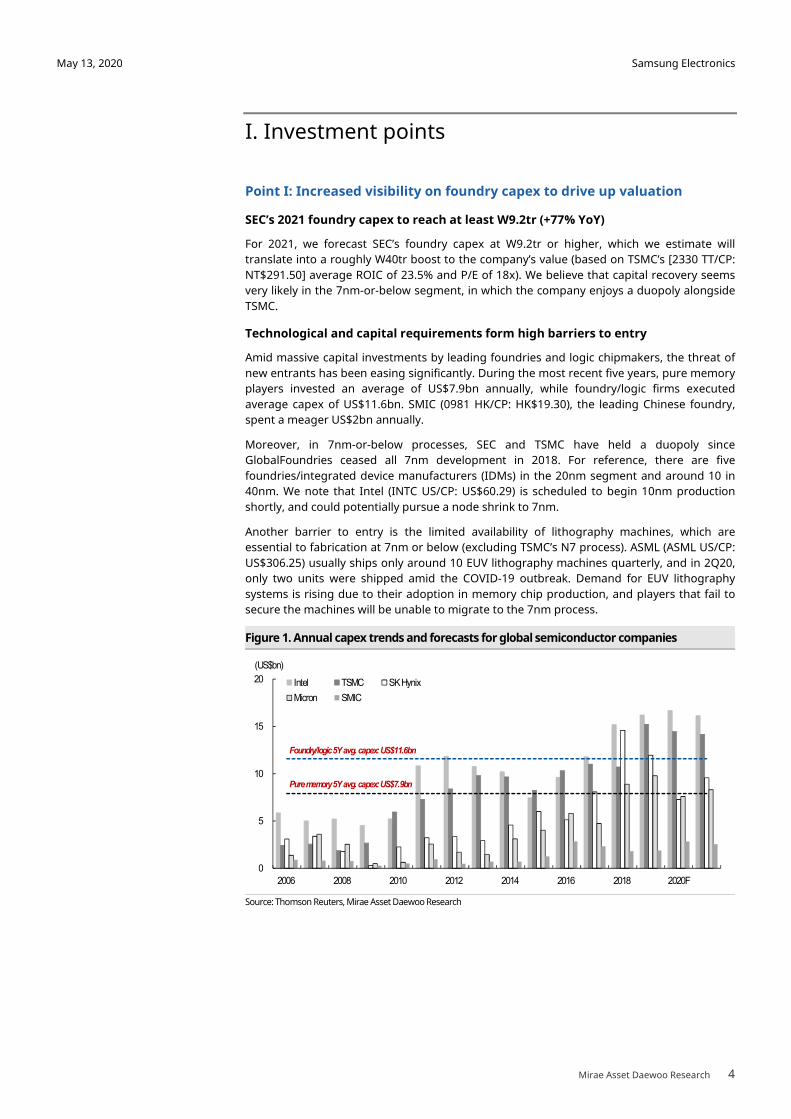

Amid massive capital investments by leading foundries and logic chipmakers, the threat of

new entrants has been easing significantly. During the most recent five years, pure memory

players invested an average of US$7.9bn annually, while foundry/logic firms executed

average capex of US$11.6bn. SMIC (0981 HK/CP: HK$19.30), the leading Chinese foundry,

spent a meager US$2bn annually.

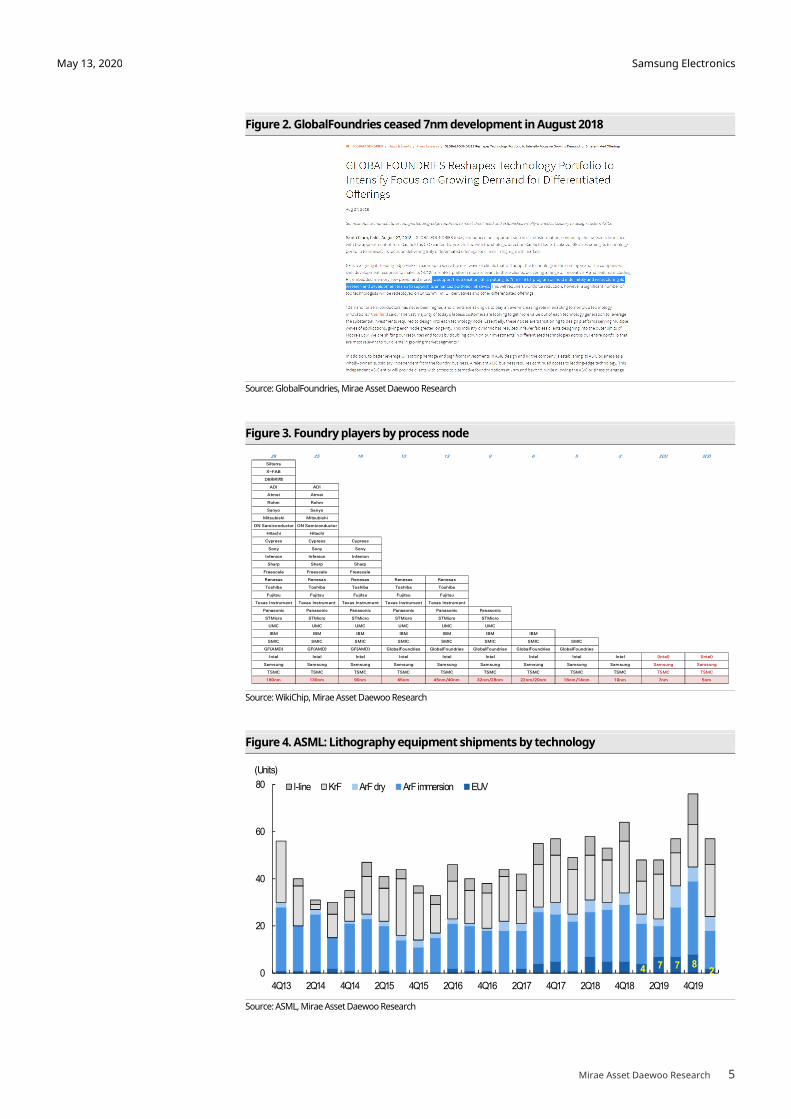

Moreover, in 7nm-or-below processes, SEC and TSMC have held a duopoly since

GlobalFoundries ceased all 7nm development in 2018. For reference, there are five

foundries/integrated device manufacturers (IDMs) in the 20nm segment and around 10 in

40nm. We note that Intel (INTC US/CP: US$60.29) is scheduled to begin 10nm production

shortly, and could potentially pursue a node shrink to 7nm.

Another barrier to entry is the limited availability of lithography machines, which are

essential to fabrication at 7nm or below (excluding TSMC’s N7 process). ASML (ASML US/CP:

US$306.25) usually ships only around 10 EUV lithography machines quarterly, and in 2Q20,

only two units were shipped amid the COVID-19 outbreak. Demand for EUV lithography

systems is rising due to their adoption in memory chip production, and players that fail to

secure the machines will be unable to migrate to the 7nm process.

Figure 1. Annual capex trends and forecasts for global semiconductor companies

Source: Thomson Reuters, Mirae Asset Daewoo Research

0

5

10

15

20

2006 2008 2010 2012 2014 2016 2018 2020F

(US$bn)

Intel TSMC SK Hynix

Micron SMIC

Foundry/logic 5Yavg. capex:US$11.6bn

Pure memory 5Y avg. capex: US$7.9bn

Samsung Electronics

Mirae Asset Daewoo Research 5

May 13, 2020

Figure 2. GlobalFoundries ceased 7nm development in August 2018

Source: GlobalFoundries, Mirae Asset Daewoo Research

Figure 3. Foundry players by process node

Source: WikiChip, Mirae Asset Daewoo Research

Figure 4. ASML: Lithography equipment shipments by technology

Source: ASML, Mirae Asset Daewoo Research

28 25 18 13 13 9 6 5 3 2(3) 2(3)

Silterra

X-FAB

DB하이텍

ADI ADI

Atmei Atmei

Rohm Rohm

Sanyo Sanyo

Mitsubishi Mitsubishi

ON Semiconductor ON Semiconductor

Hitachi Hitachi

Cypress Cypress Cypress

Sony Sony Sony

Infenion Infenion Infenion

Sharp Sharp Sharp

Freescale Freescale Freescale

Renesas Renesas Renesas Renesas Renesas

Toshiba Toshiba Toshiba Toshiba Toshiba

Fujitsu Fujitsu Fujitsu Fujitsu Fujitsu

Texas Instrument Texas Instrument Texas Instrument Texas Instrument Texas Instrument

Panasonic Panasonic Panasonic Panasonic Panasonic Panasonic

STMicro STMicro STMicro STMicro STMicro STMicro

UMC UMC UMC UMC UMC UMC

IBM IBM IBM IBM IBM IBM IBM

SMIC SMIC SMIC SMIC SMIC SMIC SMIC SMIC

GF(AMD) GF(AMD) GF(AMD) GlobalFoundries GlobalFoundries GlobalFoundries GlobalFoundries GlobalFoundries

Intel Intel Intel Intel Intel Intel Intel Intel Intel (Intel) (Intel)

Samsung Samsung Samsung Samsung Samsung Samsung Samsung Samsung Samsung Samsung Samsung

TSMC TSMC TSMC TSMC TSMC TSMC TSMC TSMC TSMC TSMC TSMC

180nm 130nm 90nm 65nm 45nm/40nm 32nm/28nm 22nm/20nm 16nm/14nm 10nm 7nm 5nm

4 7 7 8 2 0

20

40

60

80

4Q13 2Q14 4Q14 2Q15 4Q15 2Q16 4Q16 2Q17 4Q17 2Q18 4Q18 2Q19 4Q19

(Units)

I-line KrF ArF dry ArF immersion EUV

Samsung Electronics

Mirae Asset Daewoo Research 6

May 13, 2020

Demand for SEC’s 7nm-or-below products to expand

� Qualcomm: Mass production of 5nm modem chips to start in 2021

SEC’s foundry unit has won orders for Qualcomm’s Snapdragon X60, the world's first 5nm

5G baseband modem, with mass production scheduled to begin in 2021. We note that,

beginning with the Snapdragon 865 5G platform, Qualcomm has separated its modem and

application processor (AP) orders. While SEC will provide X60 modem chips built on its 5nm

low-power early (LPE) process, TSMC will supply APs built on its N5 process.

Order volumes should be dictated by 5G smartphone demand. Qualcomm is looking for

450mn smartphone sales in 2021 and 750mn units in 2022, and Strategy Analytics forecasts

Qualcomm’s 5G modem shipments at 150mn units. The exact die size of the X60 is not yet

known, but based on the Snapdragon 845’s relatively small die size (91mm2), the production

of 150mn chips annually will require capacity of 30,000 wpm (12”). If mass production

progresses smoothly in 2021, Qualcomm could decide to use SEC’s 4nm LPE process to

manufacture its 5G modems in 2022, in which case additional capex will be needed in 2021.

Figure 5. Snapdragon X60 modem chip to be produced on SEC’s 5nm process (2021)

Source: Qualcomm, Mirae Asset Daewoo Research

Figure 6. 5G smartphone shipment estimates

Source: Gartner, Mirae Asset Daewoo Research

70

190

400

600

950

0

20

40

60

80

0

250

500

750

1,000

2019 2020F 2021F 2022F 2023F

(%)(mn units)

5G smartphone shipments

5G smartphone penetration

Qualcommest.:450mn

Qualcommest.:750mn

Samsung Electronics

Mirae Asset Daewoo Research 7

May 13, 2020

Figure 7. Qualcomm: 5G baseband shipment forecasts

Source: Strategy Analytics, Mirae Asset Daewoo Research

Figure 8. Snapdragon 845 die

Source: TechInsights, Mirae Asset Daewoo Research

Figure 9. Snapdragon 845 production: 540 dies per wafer (12”)

Source: Company materials, Mirae Asset Daewoo Research

9.5mm

632

113

180

248

16

27

63

110

0

100

200

300

400

2019 2020F 2021F 2022F 2023F

(mn units)

SEC

Qualcomm

140

243

Samsung Electronics

Mirae Asset Daewoo Research 8

May 13, 2020

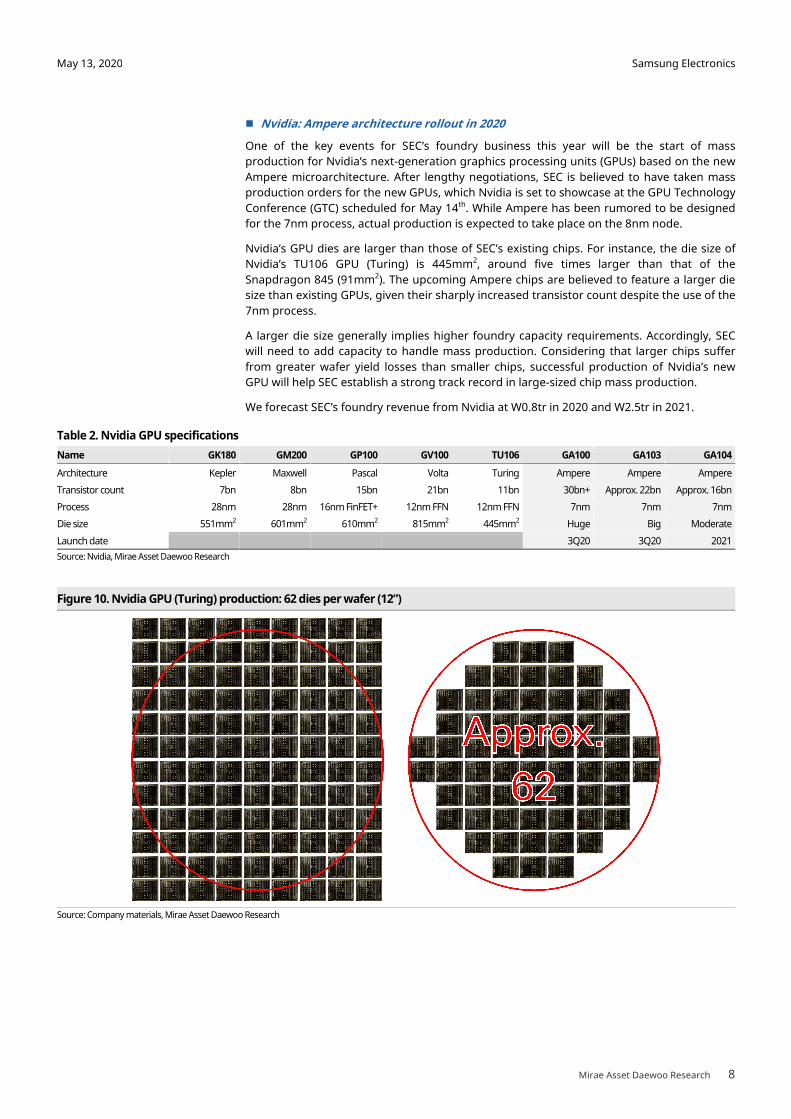

� Nvidia: Ampere architecture rollout in 2020

One of the key events for SEC’s foundry business this year will be the start of mass

production for Nvidia’s next-generation graphics processing units (GPUs) based on the new

Ampere microarchitecture. After lengthy negotiations, SEC is believed to have taken mass

production orders for the new GPUs, which Nvidia is set to showcase at the GPU Technology

Conference (GTC) scheduled for May 14th. While Ampere has been rumored to be designed

for the 7nm process, actual production is expected to take place on the 8nm node.

Nvidia’s GPU dies are larger than those of SEC’s existing chips. For instance, the die size of

Nvidia’s TU106 GPU (Turing) is 445mm2, around five times larger than that of the

Snapdragon 845 (91mm2). The upcoming Ampere chips are believed to feature a larger die

size than existing GPUs, given their sharply increased transistor count despite the use of the

7nm process.

A larger die size generally implies higher foundry capacity requirements. Accordingly, SEC

will need to add capacity to handle mass production. Considering that larger chips suffer

from greater wafer yield losses than smaller chips, successful production of Nvidia’s new

GPU will help SEC establish a strong track record in large-sized chip mass production.

We forecast SEC’s foundry revenue from Nvidia at W0.8tr in 2020 and W2.5tr in 2021.

Table 2. Nvidia GPU specifications

Name GK180 GM200 GP100 GV100 TU106 GA100 GA103 GA104

Architecture Kepler Maxwell Pascal Volta Turing Ampere Ampere Ampere

Transistor count 7bn 8bn 15bn 21bn 11bn 30bn+ Approx. 22bn Approx. 16bn

Process 28nm 28nm 16nm FinFET+ 12nm FFN 12nm FFN 7nm 7nm 7nm

Die size 551mm2 601mm2 610mm2 815mm2 445mm2 Huge Big Moderate

Launch date 3Q20 3Q20 2021

Source: Nvidia, Mirae Asset Daewoo Research

Figure 10. Nvidia GPU (Turing) production: 62 dies per wafer (12”)

Source: Company materials, Mirae Asset Daewoo Research

Samsung Electronics

Mirae Asset Daewoo Research 9

May 13, 2020

� AMD vs. Intel rivalry in 2022 and beyond

The CPU rivalry between Intel and AMD (AMD US/CP: US$55.47) is intensifying. In recent

years, AMD has gained ground with its 7nm technology, while Intel has been held back by

delays to the launch of its 10mn process and poor yields. The primary foundries with which

AMD does business are TSMC (7nm) and GlobalFoundries (14nm+). With Intel already

planning to migrate to 7nm due to poor 10nm yields, AMD will likely have to adopt 5nm to

maintain competitiveness. According to recent press releases, AMD is aiming to kick off 5nm

mass production in 2021, with TSMC handling manufacturing. Meanwhile, the company is

likely to gradually replace its 14nm CPUs with 7nm CPUs, but this migration should prove

complicated given GlobalFoundries’ abandonment of 7nm development. As such, in 2021,

we believe that AMD will decide between: 1) relying solely on TSMC for chip manufacturing;

or 2) choosing to partner with SEC. We believe that both options will be beneficial to SEC.

Indeed, even though the first scenario will not directly benefit the Korean giant, it should be

positive to overall supply/demand dynamics given the likely increase in capacity utilization

on 7nm-or-below processes.

Figure 11. Intel’s manufacturing road map: 7nm CPUs in 2021

Source: Intel, Mirae Asset Daewoo Research

Figure 12. AMD’s CPU and GPU manufacturing road map: 7nm already in place

Source: AMD, Mirae Asset Daewoo Research

Samsung Electronics

Mirae Asset Daewoo Research 10

May 13, 2020

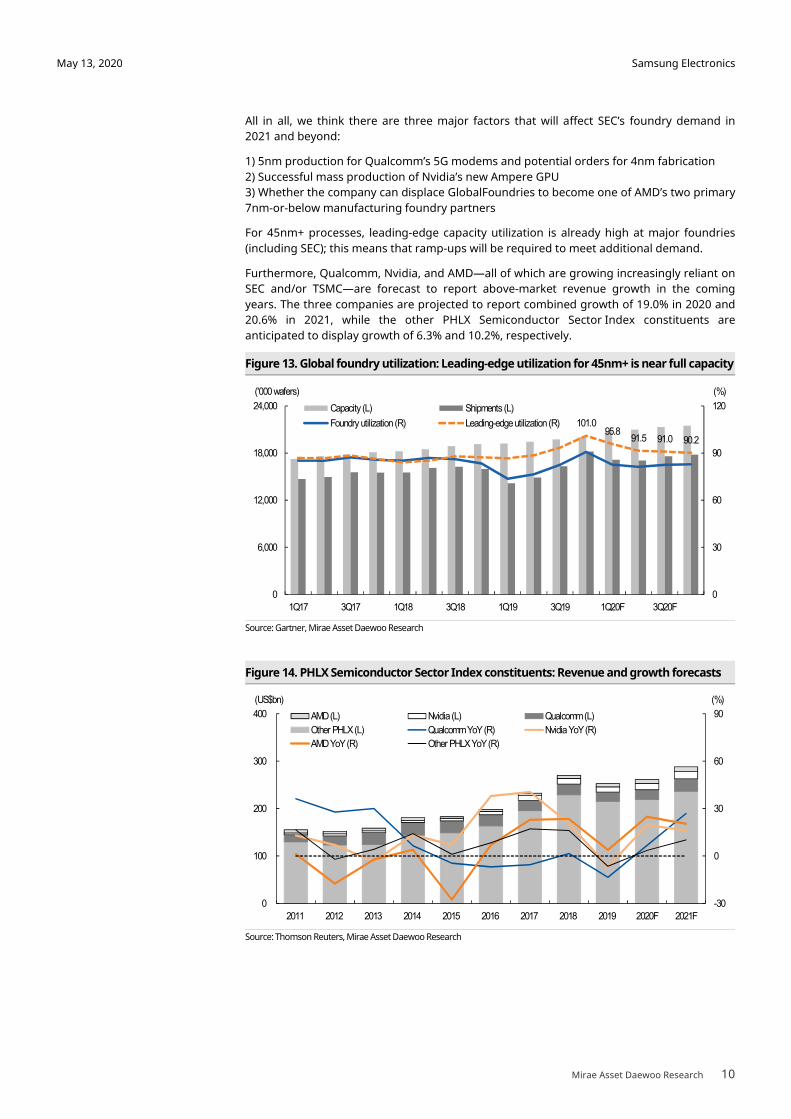

All in all, we think there are three major factors that will affect SEC’s foundry demand in

2021 and beyond:

1) 5nm production for Qualcomm’s 5G modems and potential orders for 4nm fabrication

2) Successful mass production of Nvidia’s new Ampere GPU

3) Whether the company can displace GlobalFoundries to become one of AMD’s two primary

7nm-or-below manufacturing foundry partners

For 45nm+ processes, leading-edge capacity utilization is already high at major foundries

(including SEC); this means that ramp-ups will be required to meet additional demand.

Furthermore, Qualcomm, Nvidia, and AMD—all of which are growing increasingly reliant on

SEC and/or TSMC—are forecast to report above-market revenue growth in the coming

years. The three companies are projected to report combined growth of 19.0% in 2020 and

20.6% in 2021, while the other PHLX Semiconductor Sector Index constituents are

anticipated to display growth of 6.3% and 10.2%, respectively.

Figure 13. Global foundry utilization: Leading-edge utilization for 45nm+ is near full capacity

Source: Gartner, Mirae Asset Daewoo Research

Figure 14. PHLX Semiconductor Sector Index constituents: Revenue and growth forecasts

Source: Thomson Reuters, Mirae Asset Daewoo Research

101.0 95.8

91.5 91.0 90.2

0

30

60

90

120

0

6,000

12,000

18,000

24,000

1Q17 3Q17 1Q18 3Q18 1Q19 3Q19 1Q20F 3Q20F

(%)('000 wafers)

Capacity (L) Shipments (L)

Foundry utilization (R) Leading-edge utilization (R)

-30

0

30

60

90

0

100

200

300

400

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020F 2021F

(%)(US$bn)

AMD (L) Nvidia (L) Qualcomm (L)

Other PHLX (L) Qualcomm YoY (R) Nvidia YoY (R)

AMD YoY (R) Other PHLX YoY (R)

Samsung Electronics

Mirae Asset Daewoo Research 11

May 13, 2020

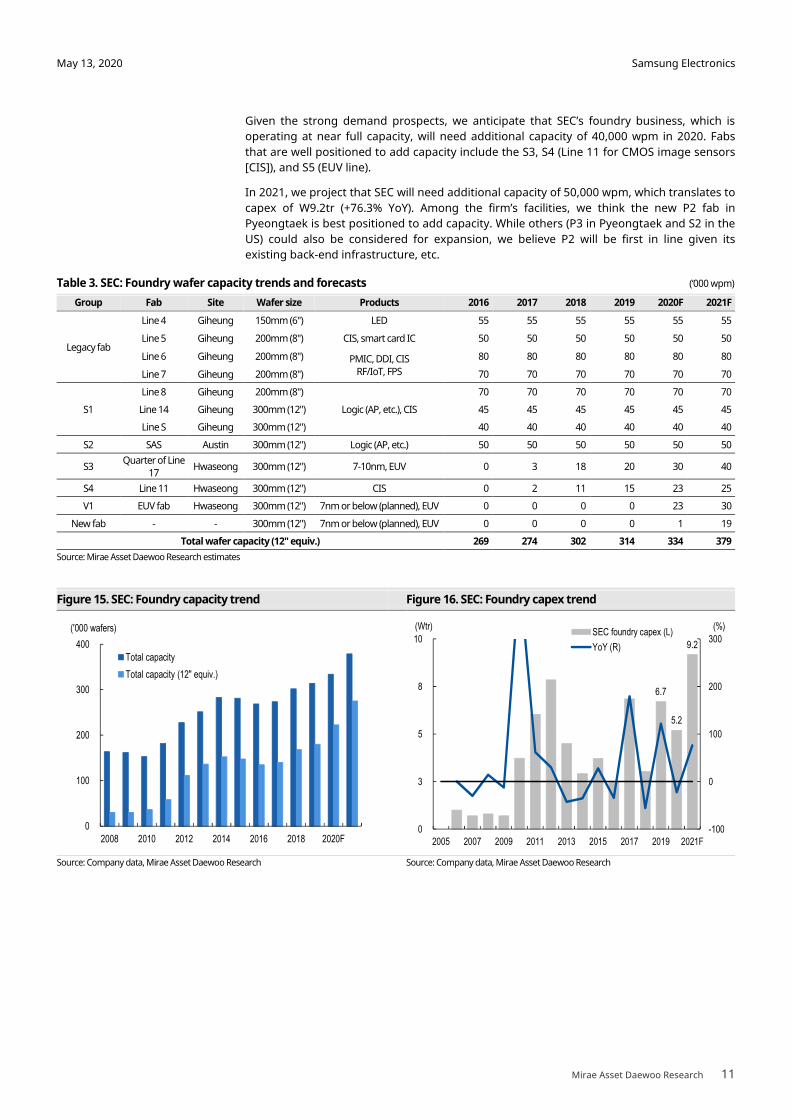

Given the strong demand prospects, we anticipate that SEC’s foundry business, which is

operating at near full capacity, will need additional capacity of 40,000 wpm in 2020. Fabs

that are well positioned to add capacity include the S3, S4 (Line 11 for CMOS image sensors

[CIS]), and S5 (EUV line).

In 2021, we project that SEC will need additional capacity of 50,000 wpm, which translates to

capex of W9.2tr (+76.3% YoY). Among the firm’s facilities, we think the new P2 fab in

Pyeongtaek is best positioned to add capacity. While others (P3 in Pyeongtaek and S2 in the

US) could also be considered for expansion, we believe P2 will be first in line given its

existing back-end infrastructure, etc.

Table 3. SEC: Foundry wafer capacity trends and forecasts (‘000 wpm)

Group Fab Site Wafer size Products 2016 2017 2018 2019 2020F 2021F

Legacy fab

Line 4 Giheung 150mm (6") LED 55 55 55 55 55 55

Line 5 Giheung 200mm (8") CIS, smart card IC 50 50 50 50 50 50

Line 6 Giheung 200mm (8") PMIC, DDI, CIS RF/IoT, FPS

80 80 80 80 80 80

Line 7 Giheung 200mm (8") 70 70 70 70 70 70

S1

Line 8 Giheung 200mm (8")

Logic (AP, etc.), CIS

70 70 70 70 70 70

Line 14 Giheung 300mm (12") 45 45 45 45 45 45

Line S Giheung 300mm (12") 40 40 40 40 40 40

S2 SAS Austin 300mm (12") Logic (AP, etc.) 50 50 50 50 50 50

S3 Quarter of Line

17 Hwaseong 300mm (12") 7-10nm, EUV 0 3 18 20 30 40

S4 Line 11 Hwaseong 300mm (12") CIS 0 2 11 15 23 25

V1 EUV fab Hwaseong 300mm (12") 7nm or below (planned), EUV 0 0 0 0 23 30

New fab - - 300mm (12") 7nm or below (planned), EUV 0 0 0 0 1 19

Total wafer capacity (12" equiv.) 269 274 302 314 334 379

Source: Mirae Asset Daewoo Research estimates

Figure 15. SEC: Foundry capacity trend Figure 16. SEC: Foundry capex trend

Source: Company data, Mirae Asset Daewoo Research Source: Company data, Mirae Asset Daewoo Research

6.7

5.2

9.2

-100

0

100

200

300

0

3

5

8

10

2005 2007 2009 2011 2013 2015 2017 2019 2021F

(%)(Wtr)SEC foundry capex (L)

YoY (R)

0

100

200

300

400

2008 2010 2012 2014 2016 2018 2020F

Total capacity

Total capacity (12" equiv.)

('000 wafers)

Samsung Electronics

Mirae Asset Daewoo Research 12

May 13, 2020

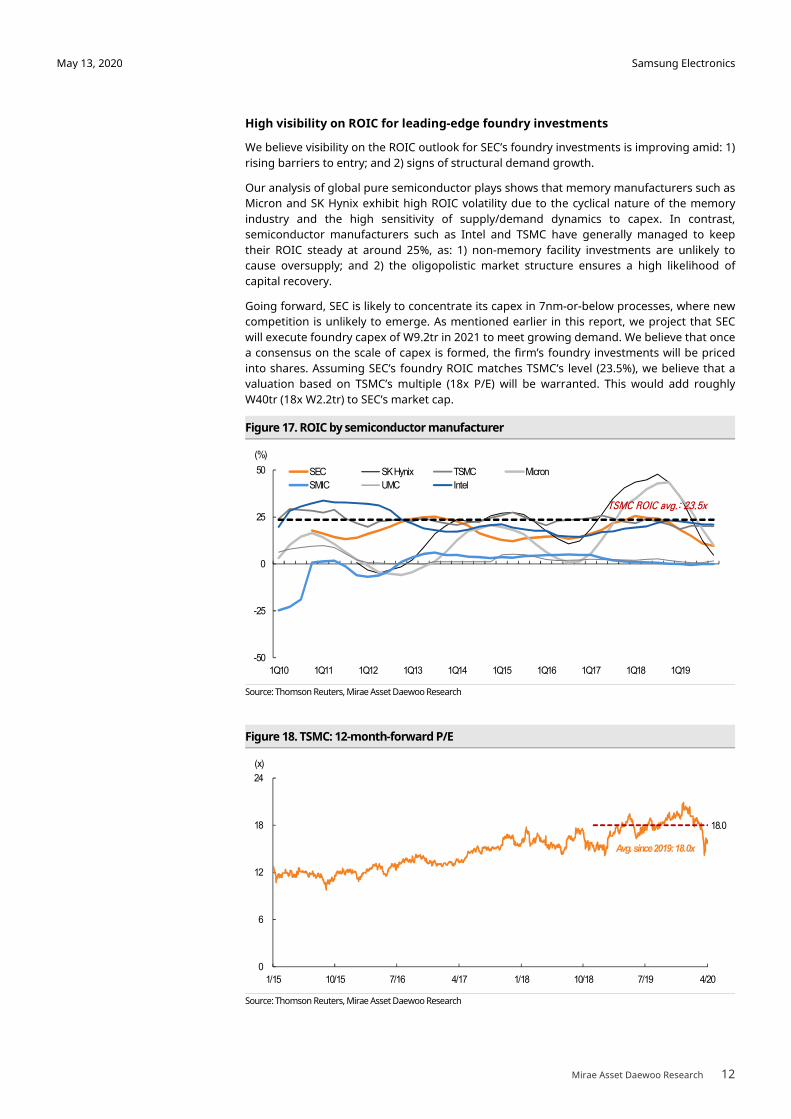

High visibility on ROIC for leading-edge foundry investments

We believe visibility on the ROIC outlook for SEC’s foundry investments is improving amid: 1)

rising barriers to entry; and 2) signs of structural demand growth.

Our analysis of global pure semiconductor plays shows that memory manufacturers such as

Micron and SK Hynix exhibit high ROIC volatility due to the cyclical nature of the memory

industry and the high sensitivity of supply/demand dynamics to capex. In contrast,

semiconductor manufacturers such as Intel and TSMC have generally managed to keep

their ROIC steady at around 25%, as: 1) non-memory facility investments are unlikely to

cause oversupply; and 2) the oligopolistic market structure ensures a high likelihood of

capital recovery.

Going forward, SEC is likely to concentrate its capex in 7nm-or-below processes, where new

competition is unlikely to emerge. As mentioned earlier in this report, we project that SEC

will execute foundry capex of W9.2tr in 2021 to meet growing demand. We believe that once

a consensus on the scale of capex is formed, the firm’s foundry investments will be priced

into shares. Assuming SEC’s foundry ROIC matches TSMC’s level (23.5%), we believe that a

valuation based on TSMC’s multiple (18x P/E) will be warranted. This would add roughly

W40tr (18x W2.2tr) to SEC’s market cap.

Figure 17. ROIC by semiconductor manufacturer

Source: Thomson Reuters, Mirae Asset Daewoo Research

Figure 18. TSMC: 12-month-forward P/E

Source: Thomson Reuters, Mirae Asset Daewoo Research

18.0

0

6

12

18

24

1/15 10/15 7/16 4/17 1/18 10/18 7/19 4/20

(x)

Avg. since 2019:18.0x

-50

-25

0

25

50

1Q10 1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17 1Q18 1Q19

(%)

SEC SK Hynix TSMC Micron

SMIC UMC Intel

TSMC ROIC avg.: 23.5x

Samsung Electronics

Mirae Asset Daewoo Research 13

May 13, 2020

We believe the case of TSMC illustrates how the market reflects capex into share price. The

foundry player’s 12-month-forward P/E—which gradually rose from an average of 13x in

2016 to 15x in 2017 and 16x in 2018—displayed its sharpest rise ever in 2019. Indeed, while

2020-21 earnings forecasts were left virtually unchanged last year, the stock’s valuation

increased by 20%.

We believe the re-rating was driven by capex outlook upgrades rather than by earnings

forecasts. While earnings projections stayed flat, market expectations for TSMC’s 2020

capex were revised upward by 30% in the second half of 2019. As a consensus formed that

the firm’s investments would translate safely into earnings, upward revisions to capex

projections were accompanied by market value expansion. Like TSMC, we expect SEC to see

a valuation re-rating driven by a promising foundry investment outlook.

Figure 19. TSMC: Quarterly capex Figure 20. TSMC: Quarterly OP

Source: Thomson Reuters, Mirae Asset Daewoo Research Source: Thomson Reuters, Mirae Asset Daewoo Research

Figure 21. TSMC: 12-month-forward P/E Figure 22. TSMC: OP and capex consensus throughout 2019

Source: Thomson Reuters, Mirae Asset Daewoo Research Source: Thomson Reuters, Mirae Asset Daewoo Research

0.0

1.5

3.0

4.5

6.0

1Q15 1Q16 1Q17 1Q18 1Q19 1Q20F 1Q21F

(US$bn)

0.0

1.5

3.0

4.5

6.0

1Q15 1Q16 1Q17 1Q18 1Q19 1Q20F 1Q21F

(US$bn)

9

12

15

18

21

1/19 3/19 5/19 7/19 9/19 11/19

(US$bn)

2020F OP

2021F OP

2020F capex

16.3

20.8

12.9

14.6

15.9

18.0

10

13

16

19

22

1/16 7/16 1/17 7/17 1/18 7/18 1/19 7/19

(x)

Samsung Electronics

Mirae Asset Daewoo Research 14

May 13, 2020

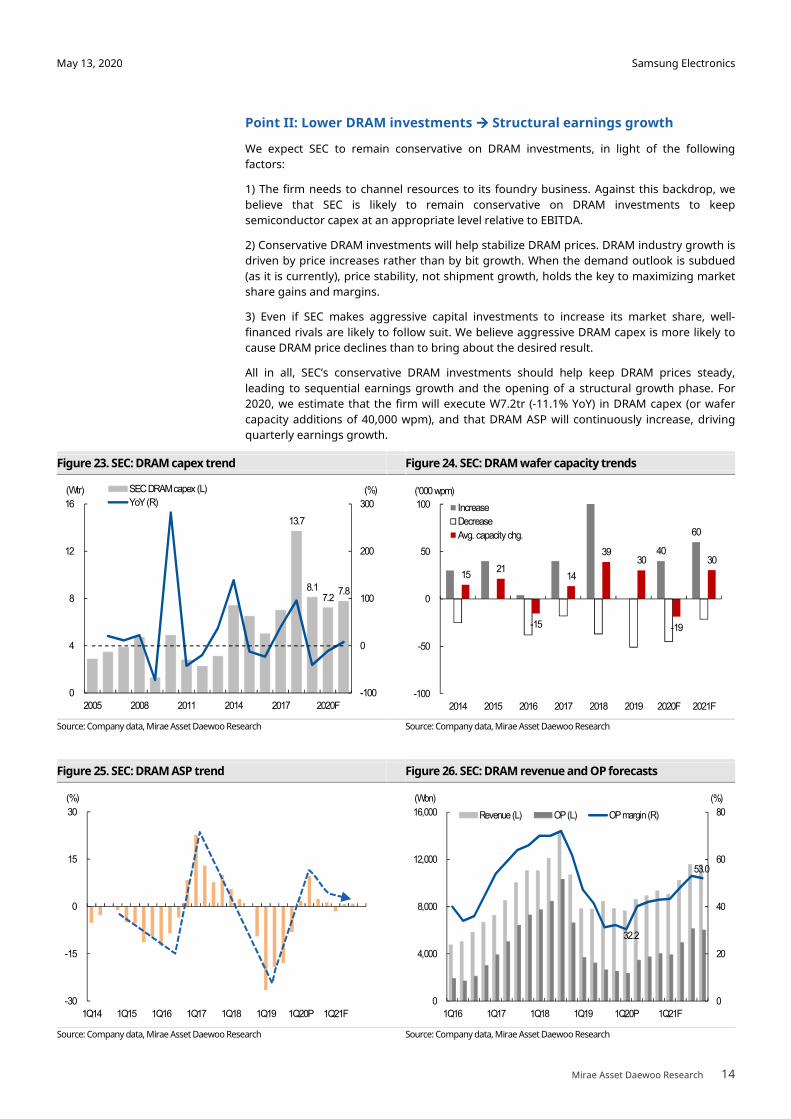

Point II: Lower DRAM investments ���� Structural earnings growth

We expect SEC to remain conservative on DRAM investments, in light of the following

factors:

1) The firm needs to channel resources to its foundry business. Against this backdrop, we

believe that SEC is likely to remain conservative on DRAM investments to keep

semiconductor capex at an appropriate level relative to EBITDA.

2) Conservative DRAM investments will help stabilize DRAM prices. DRAM industry growth is

driven by price increases rather than by bit growth. When the demand outlook is subdued

(as it is currently), price stability, not shipment growth, holds the key to maximizing market

share gains and margins.

3) Even if SEC makes aggressive capital investments to increase its market share, well-

financed rivals are likely to follow suit. We believe aggressive DRAM capex is more likely to

cause DRAM price declines than to bring about the desired result.

All in all, SEC’s conservative DRAM investments should help keep DRAM prices steady,

leading to sequential earnings growth and the opening of a structural growth phase. For

2020, we estimate that the firm will execute W7.2tr (-11.1% YoY) in DRAM capex (or wafer

capacity additions of 40,000 wpm), and that DRAM ASP will continuously increase, driving

quarterly earnings growth.

Figure 23. SEC: DRAM capex trend Figure 24. SEC: DRAM wafer capacity trends

Source: Company data, Mirae Asset Daewoo Research Source: Company data, Mirae Asset Daewoo Research

Figure 25. SEC: DRAM ASP trend Figure 26. SEC: DRAM revenue and OP forecasts

Source: Company data, Mirae Asset Daewoo Research Source: Company data, Mirae Asset Daewoo Research

13.7

8.1 7.2

7.8

-100

0

100

200

300

0

4

8

12

16

2005 2008 2011 2014 2017 2020F

(%)(Wtr) SEC DRAM capex (L)

YoY (R)

-30

-15

0

15

30

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20P 1Q21F

(%)

32.2

53.0

0

20

40

60

80

0

4,000

8,000

12,000

16,000

1Q16 1Q17 1Q18 1Q19 1Q20P 1Q21F

(%)(Wbn)

Revenue (L) OP (L) OP margin (R)

40

60

15 21

-15

14

39 30

-19

30

-100

-50

0

50

100

2014 2015 2016 2017 2018 2019 2020F 2021F

Increase

Decrease

Avg. capacity chg.

('000 wpm)

Samsung Electronics

Mirae Asset Daewoo Research 15

May 13, 2020

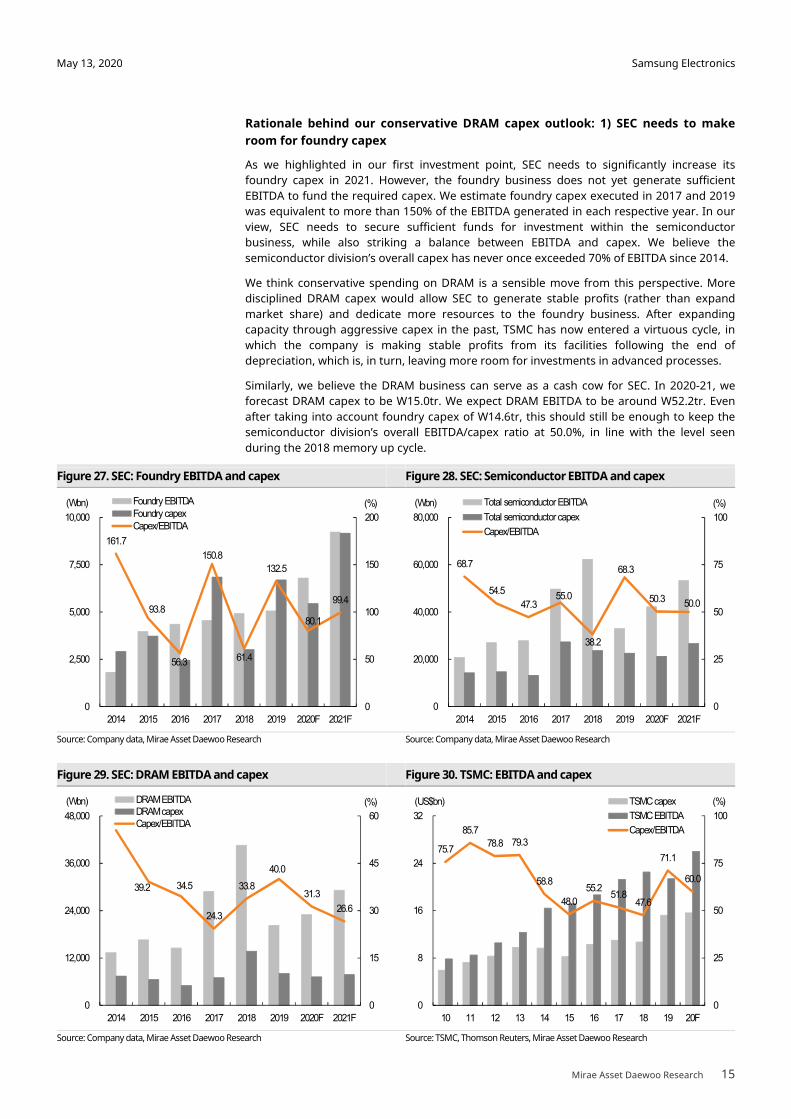

Rationale behind our conservative DRAM capex outlook: 1) SEC needs to make

room for foundry capex

As we highlighted in our first investment point, SEC needs to significantly increase its

foundry capex in 2021. However, the foundry business does not yet generate sufficient

EBITDA to fund the required capex. We estimate foundry capex executed in 2017 and 2019

was equivalent to more than 150% of the EBITDA generated in each respective year. In our

view, SEC needs to secure sufficient funds for investment within the semiconductor

business, while also striking a balance between EBITDA and capex. We believe the

semiconductor division’s overall capex has never once exceeded 70% of EBITDA since 2014.

We think conservative spending on DRAM is a sensible move from this perspective. More

disciplined DRAM capex would allow SEC to generate stable profits (rather than expand

market share) and dedicate more resources to the foundry business. After expanding

capacity through aggressive capex in the past, TSMC has now entered a virtuous cycle, in

which the company is making stable profits from its facilities following the end of

depreciation, which is, in turn, leaving more room for investments in advanced processes.

Similarly, we believe the DRAM business can serve as a cash cow for SEC. In 2020-21, we

forecast DRAM capex to be W15.0tr. We expect DRAM EBITDA to be around W52.2tr. Even

after taking into account foundry capex of W14.6tr, this should still be enough to keep the

semiconductor division’s overall EBITDA/capex ratio at 50.0%, in line with the level seen

during the 2018 memory up cycle.

Figure 27. SEC: Foundry EBITDA and capex Figure 28. SEC: Semiconductor EBITDA and capex

Source: Company data, Mirae Asset Daewoo Research Source: Company data, Mirae Asset Daewoo Research

Figure 29. SEC: DRAM EBITDA and capex Figure 30. TSMC: EBITDA and capex

Source: Company data, Mirae Asset Daewoo Research Source: TSMC, Thomson Reuters, Mirae Asset Daewoo Research

161.7

93.8

56.3

150.8

61.4

132.5

80.1

99.4

0

50

100

150

200

0

2,500

5,000

7,500

10,000

2014 2015 2016 2017 2018 2019 2020F 2021F

(%)(Wbn) Foundry EBITDAFoundry capexCapex/EBITDA

68.7

54.5

47.3 55.0

38.2

68.3

50.3 50.0

0

25

50

75

100

0

20,000

40,000

60,000

80,000

2014 2015 2016 2017 2018 2019 2020F 2021F

(%)(Wbn) Total semiconductor EBITDA

Total semiconductor capex

Capex/EBITDA

39.2 34.5

24.3

33.8

40.0

31.3

26.6

0

15

30

45

60

0

12,000

24,000

36,000

48,000

2014 2015 2016 2017 2018 2019 2020F 2021F

(%)(Wbn) DRAM EBITDADRAM capexCapex/EBITDA

75.7

85.7

78.8 79.3

58.8

48.0

55.2 51.8

47.6

71.1

60.0

0

25

50

75

100

0

8

16

24

32

10 11 12 13 14 15 16 17 18 19 20F

(%)(US$bn) TSMC capex

TSMC EBITDA

Capex/EBITDA

Samsung Electronics

Mirae Asset Daewoo Research 16

May 13, 2020

Rationale behind our conservative DRAM capex outlook: 2) SEC needs to keep

DRAM prices stable

DRAM revenue and profit growth move in line with price changes. It is safe to say that

during the past decade, DRAM revenue and profits have never increased during periods of

price decline. Unlike the NAND market, whether DRAM revenue and profits grow is

determined by whether ASP is rising or falling (not by the price elasticity of shipments), with

bit growth largely fixed.

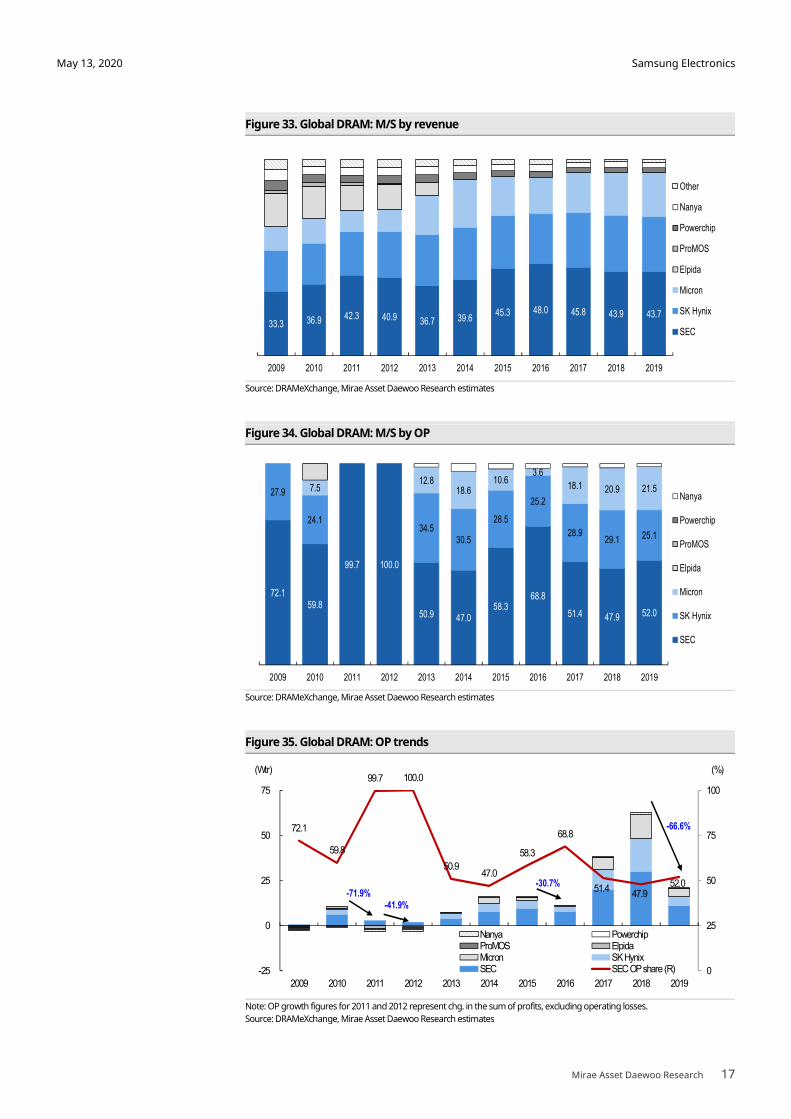

That said, aggressive pricing strategies do work during down cycles. In 2016 and 2019, SEC

was able to either expand or maintain its market share (45.3% � 48.0% in 2016; 43.9% �

43.7% in 2019) by employing an aggressive bit growth strategy. During these years,

operating profit across the DRAM industry declined 30.7% and 66.6%, respectively, but SEC’s

share of overall profits increased from 58.3% to 68.8% and from 47.9% to 52.0%,

respectively. In other words, the company’s strategy of overcoming market downturns

through preemptive inventory depletion has worked well.

However, the DRAM cycle is set to undergo a recovery from 2020. In this case, maintaining

stable prices is likely to take priority over aggressive spending or shipments. Due to SEC’s

conservative capex stance, we expect quarterly ASP to move up in 2020. The uptrend in ASP

should continue through 2021, driving strong profit growth. We forecast SEC’s DRAM

operating profit to grow 12.1% to W13.5tr in 2020 and 55.1% to W21.0tr in 2021.

Figure 31. Global DRAM ASP, bit, revenue, and OP growth

Source: DRAMeXchange, Mirae Asset Daewoo Research estimates

Figure 32. SEC: DRAM ASP, bit, revenue, and OP growth

Source: Company data, Mirae Asset Daewoo Research estimates

-49.9 -29.8

2.3

-0.9 -20.0 -27.0

47.1

14.8

-46.7

50.4

28.6 26.6 34.1 22.8 23.7 19.9 21.0 19.0

-80

0

80

160

240

2011 2012 2013 2014 2015 2016 2017 2018 2019

(%) ASP chg. Bit growth Sales growth OP growth

2011-12Industry-wide losses

-45.8 -29.3

-6.3 -5.0 -17.5

-29.7

48.2

19.5

-49.2

-9.1

3.9

49.8

27.1 25.8

54.1

30.1 35.8

14.7 12.3 23.1 16.7 21.1

-80

0

80

160

240

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020F 2021F

(%)

ASP chg. Bit growth Sales growth OP growth

Samsung Electronics

Mirae Asset Daewoo Research 17

May 13, 2020

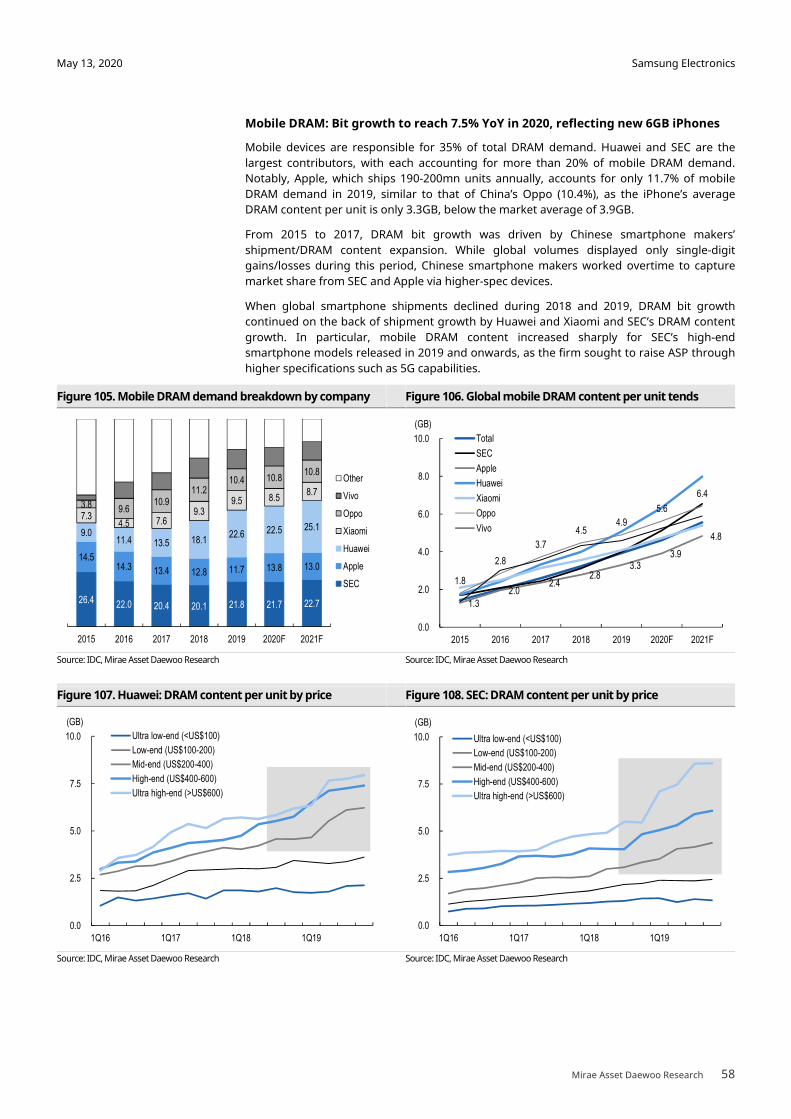

Figure 33. Global DRAM: M/S by revenue

Source: DRAMeXchange, Mirae Asset Daewoo Research estimates

Figure 34. Global DRAM: M/S by OP

Source: DRAMeXchange, Mirae Asset Daewoo Research estimates

Figure 35. Global DRAM: OP trends

Note: OP growth figures for 2011 and 2012 represent chg. in the sum of profits, excluding operating losses.

Source: DRAMeXchange, Mirae Asset Daewoo Research estimates

72.1 59.8

99.7 100.0

50.9 47.0 58.3

68.8

51.4 47.9 52.0

27.9

24.1 34.5

30.5

28.5

25.2

28.9 29.1 25.1

7.5 12.8

18.6 10.6

3.6

18.1 20.9 21.5

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Nanya

Powerchip

ProMOS

Elpida

Micron

SK Hynix

SEC

72.1

59.8

99.7 100.0

50.9 47.0

58.3

68.8

51.4 47.9

52.0

0

25

50

75

100

-25

0

25

50

75

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

(%)(Wtr)

Nanya PowerchipProMOS ElpidaMicron SK HynixSEC SEC OP share (R)

-30.7%

-66.6%

-71.9%-41.9%

33.3 36.9 42.3 40.9 36.7 39.6 45.3 48.0 45.8 43.9 43.7

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Other

Nanya

Powerchip

ProMOS

Elpida

Micron

SK Hynix

SEC

Samsung Electronics

Mirae Asset Daewoo Research 18

May 13, 2020

Rationale behind our conservative DRAM capex outlook: 3) Competitors to follow

suit

If SEC were to execute capex exceeding demand in order to expand its market share, its

competitors would most likely follow suit. SK Hynix has room for an additional 20,000 wpm

at its C2E fab in Wuxi, China, and is set to complete construction of its M16 fab (designed

capacity of around 100,000 wpm). Micron is also likely to complete expansion of its Taichung

fab in Taiwan and its Hiroshima fab in Japan by the end of the year. As such, DRAM makers

are well-positioned to increase capacity swiftly if necessary. And considering that they differ

very little in terms of cost competitiveness, any competition to expand capacity would likely

only lead to price declines, rather than market share gains. As such, we expect SEC to focus

its investments on bolstering its cost competitiveness.

Until early this year, many expected SEC to pursue aggressive DRAM capex as part of its

efforts to widen its lead over rivals. During past periods of rapid growth, all DRAM makers

vied for market share gains via capacity additions. But with the market now stable and

controlled by a handful of players, aggressive capex would be a recipe for losses rather than

market share gains. As such, we believe mega-fabs represent the best strategy, and one

that is already adopted by all DRAM makers. By maintaining sufficient room in such facilities

for potential lines and clean rooms, companies can expand capacity flexibly depending on

market conditions, thus preventing unnecessary capex spending based on excessive

projections.

Figure 36. SEC: DRAM breakdown by tech node (%) Figure 37. SK Hynix: DRAM breakdown by tech node (%)

Source: DRAMeXchange, Mirae Asset Daewoo Research Source: DRAMeXchange, Mirae Asset Daewoo Research

Figure 38. Micron: DRAM breakdown by tech node (%) Figure 39. Avg. tech node factors of major DRAM makers

Source: DRAMeXchange, Mirae Asset Daewoo Research Source: DRAMeXchange, Mirae Asset Daewoo Research

15

20

25

30

35

0

25

50

75

100

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20

Average tech node factor (R)1Znm

1Ynm

1Xnm

20nm

23nm

25nm

35nm

15

20

25

30

35

0

25

50

75

100

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20

Average tech node factor (R) 1Znm

1Ynm

1Xnm

21nm

25m

29nm

38nm

15

20

25

30

35

0

25

50

75

100

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20

Average tech node factor (R)

1Znm

1Ynm

1Xnm

20nm

25m

30nm

15

20

25

30

35

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20

(nm)

SEC

SK Hynix

Micron

Samsung Electronics

Mirae Asset Daewoo Research 19

May 13, 2020

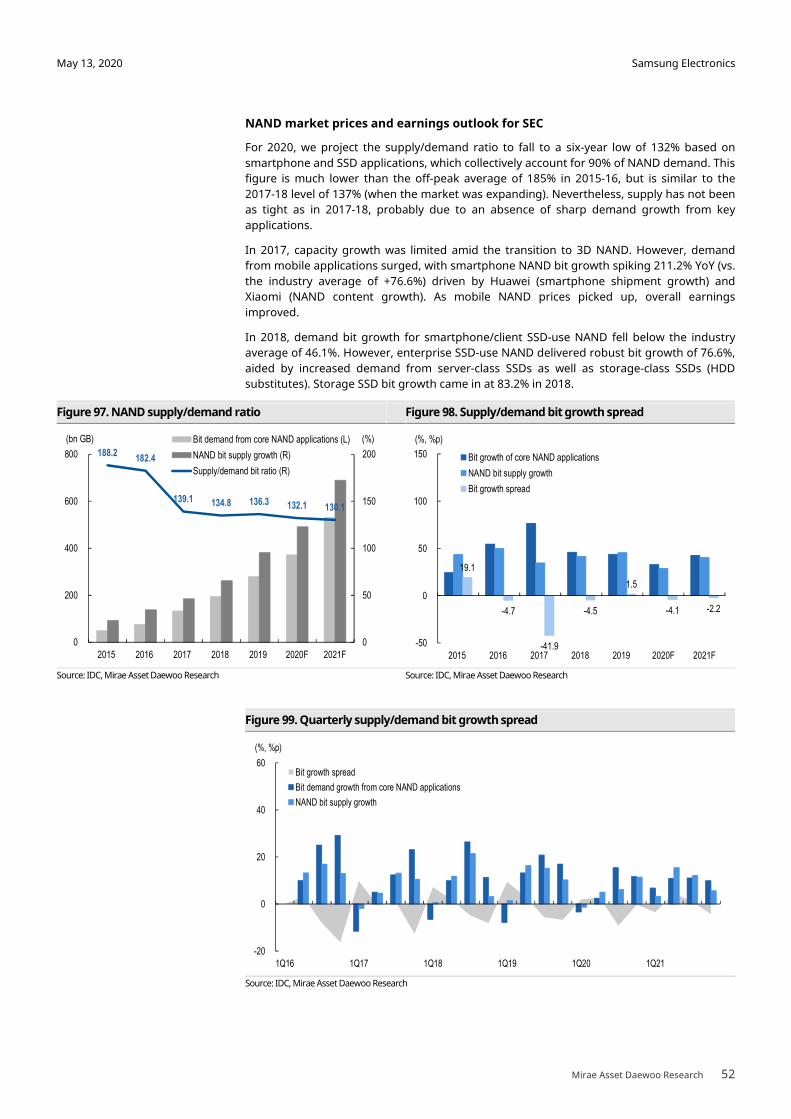

Point III: NAND market share expansion to boost earnings

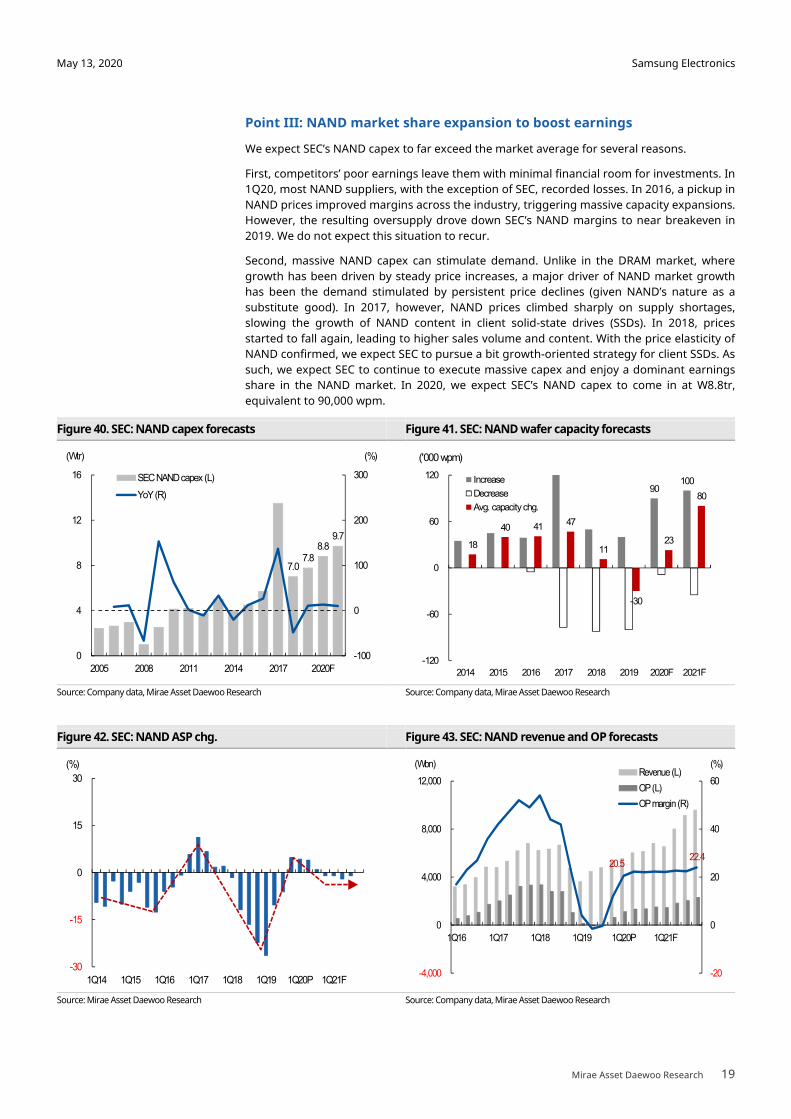

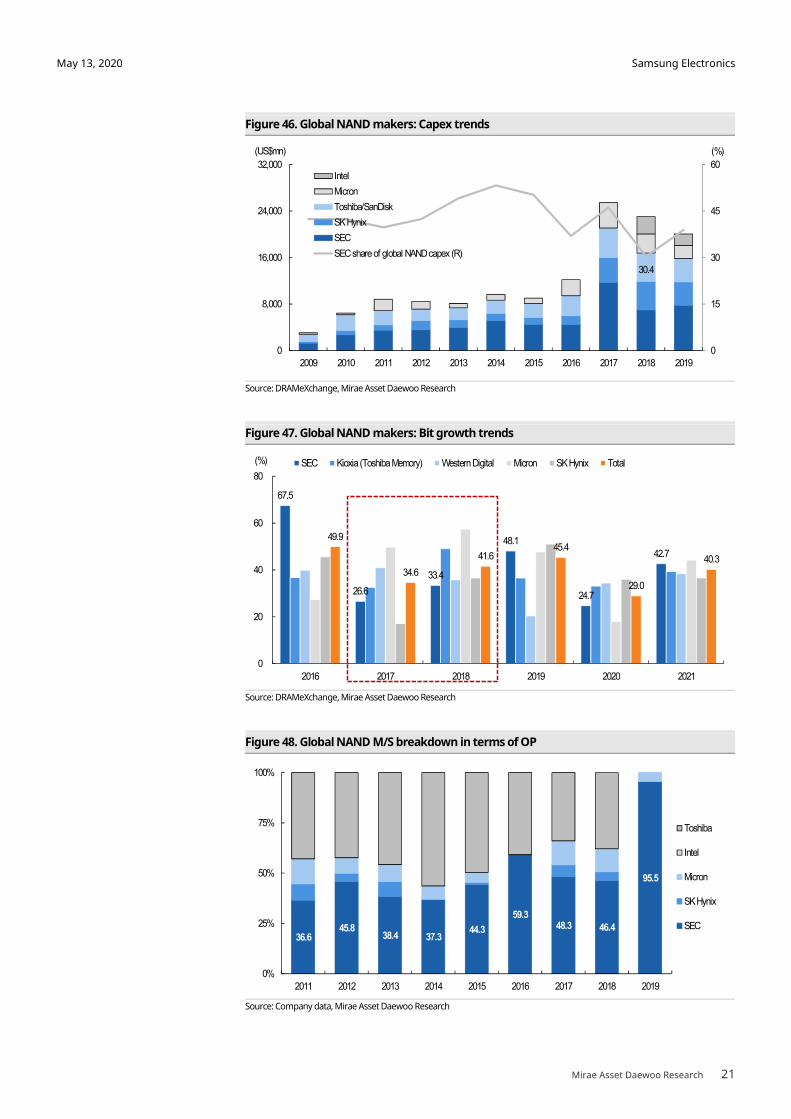

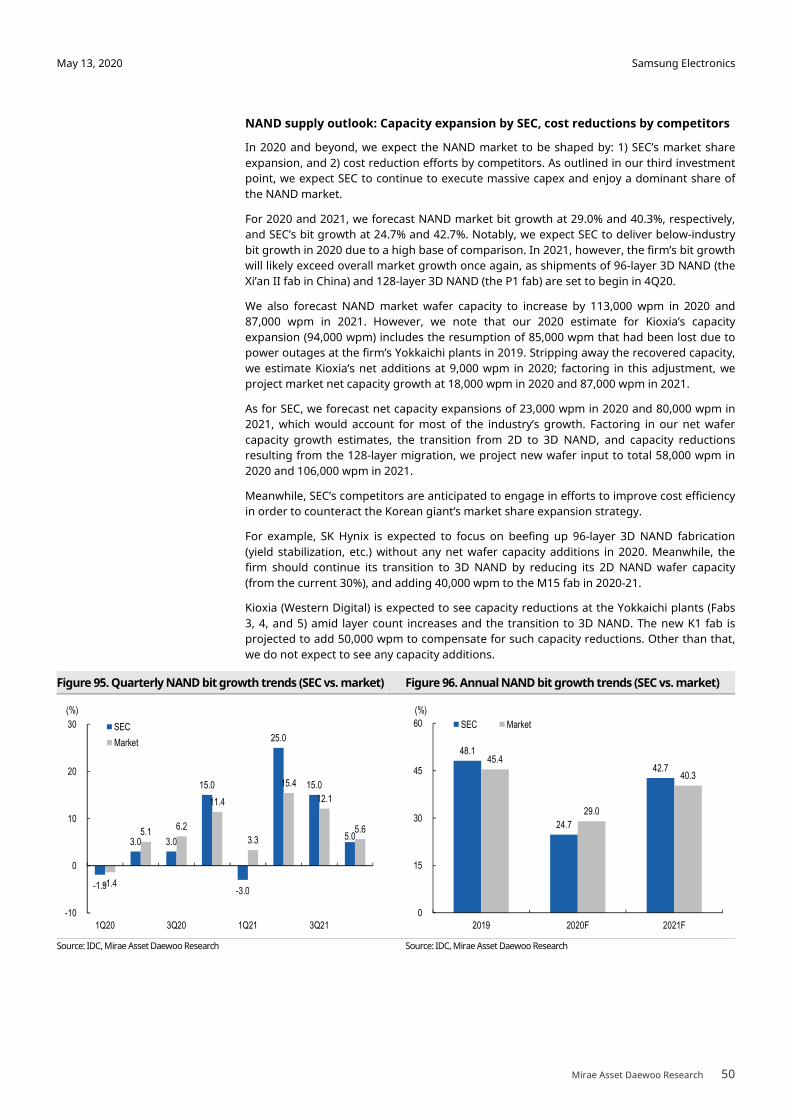

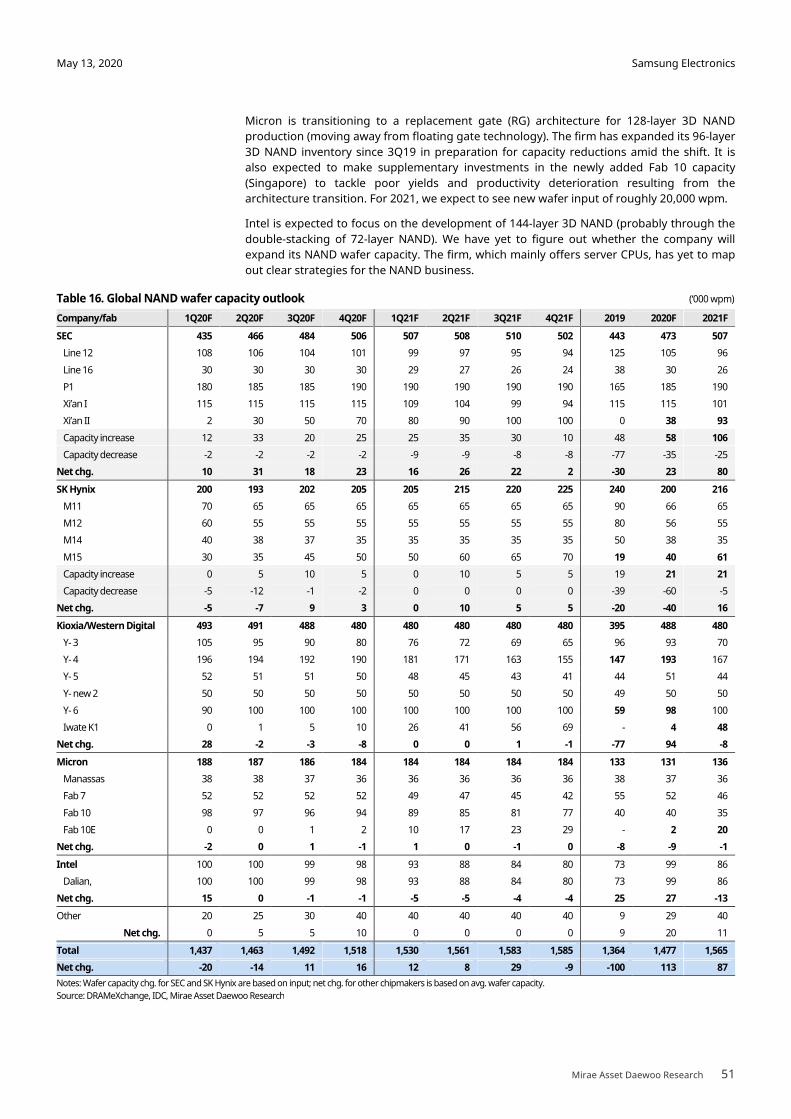

We expect SEC’s NAND capex to far exceed the market average for several reasons.

First, competitors’ poor earnings leave them with minimal financial room for investments. In

1Q20, most NAND suppliers, with the exception of SEC, recorded losses. In 2016, a pickup in

NAND prices improved margins across the industry, triggering massive capacity expansions.

However, the resulting oversupply drove down SEC’s NAND margins to near breakeven in

2019. We do not expect this situation to recur.

Second, massive NAND capex can stimulate demand. Unlike in the DRAM market, where

growth has been driven by steady price increases, a major driver of NAND market growth

has been the demand stimulated by persistent price declines (given NAND’s nature as a

substitute good). In 2017, however, NAND prices climbed sharply on supply shortages,

slowing the growth of NAND content in client solid-state drives (SSDs). In 2018, prices

started to fall again, leading to higher sales volume and content. With the price elasticity of

NAND confirmed, we expect SEC to pursue a bit growth-oriented strategy for client SSDs. As

such, we expect SEC to continue to execute massive capex and enjoy a dominant earnings

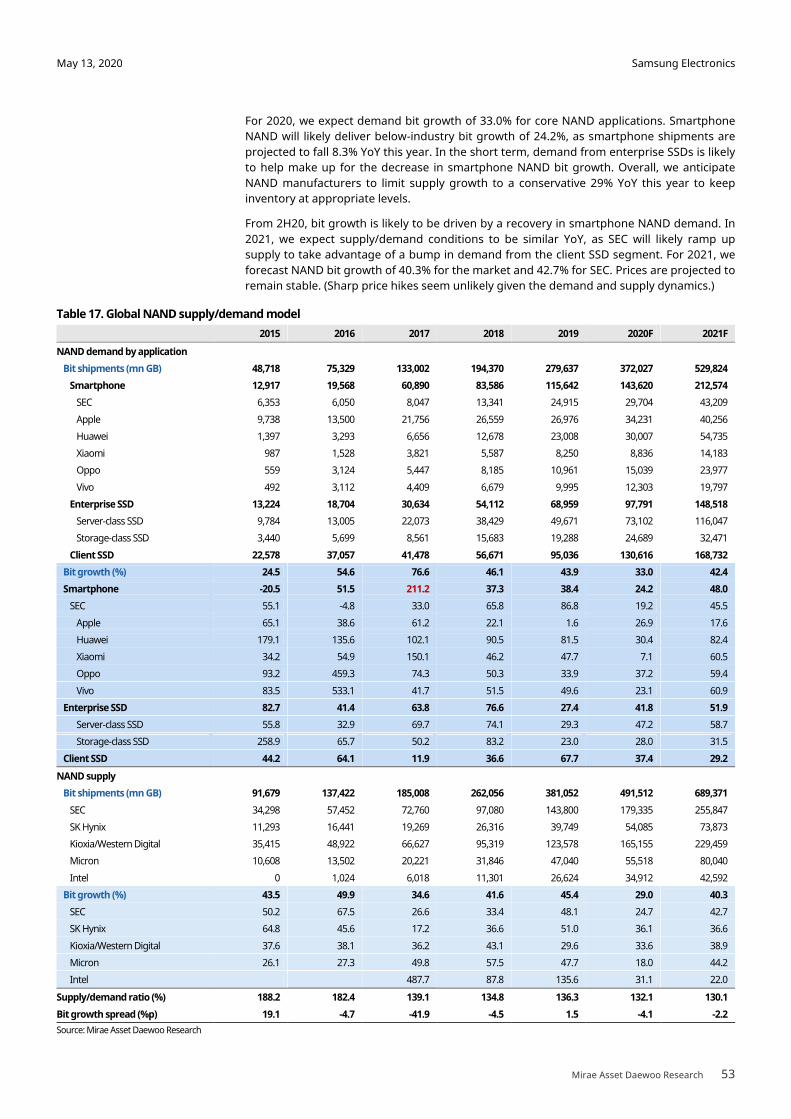

share in the NAND market. In 2020, we expect SEC’s NAND capex to come in at W8.8tr,

equivalent to 90,000 wpm.

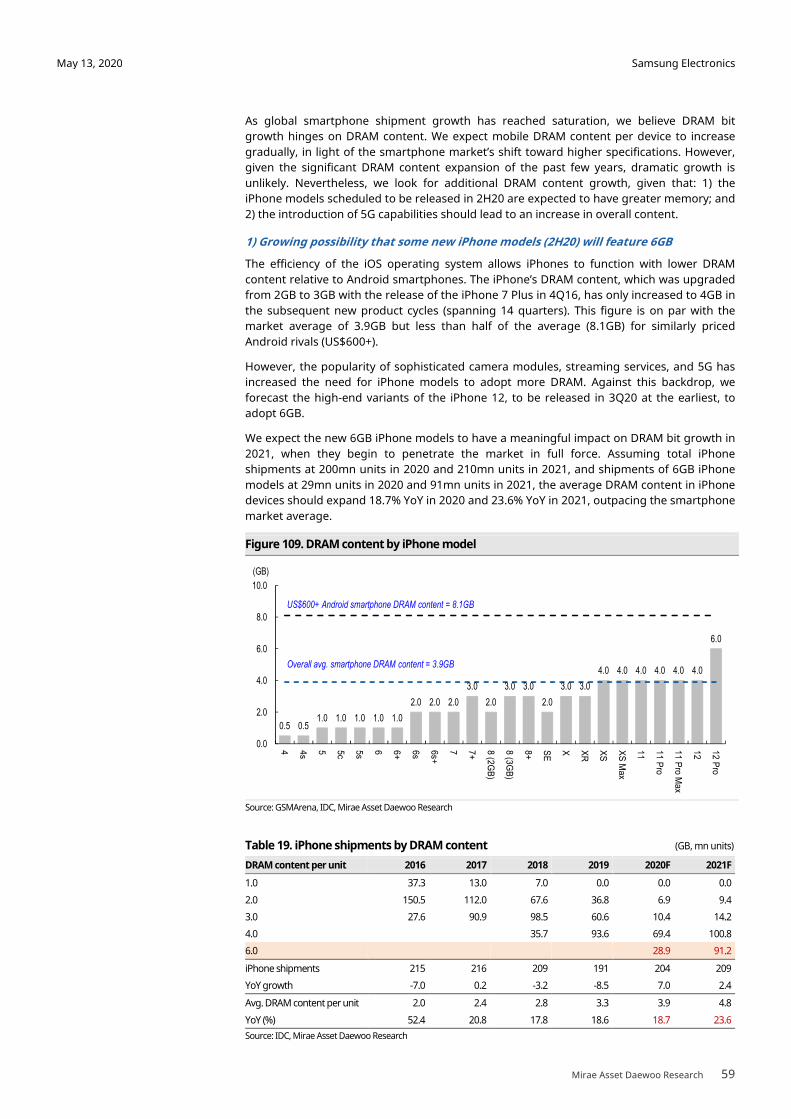

Figure 40. SEC: NAND capex forecasts Figure 41. SEC: NAND wafer capacity forecasts

Source: Company data, Mirae Asset Daewoo Research Source: Company data, Mirae Asset Daewoo Research

Figure 42. SEC: NAND ASP chg. Figure 43. SEC: NAND revenue and OP forecasts

Source: Mirae Asset Daewoo Research Source: Company data, Mirae Asset Daewoo Research

7.0 7.8

8.8 9.7

-100

0

100

200

300

0

4

8

12

16

2005 2008 2011 2014 2017 2020F

(%)(Wtr)

SEC NAND capex (L)

YoY (R)

-30

-15

0

15

30

1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 1Q20P 1Q21F

(%)

20.5 22.4

-20

0

20

40

60

-4,000

0

4,000

8,000

12,000

1Q16 1Q17 1Q18 1Q19 1Q20P 1Q21F

(%)(Wbn)Revenue (L)

OP (L)

OP margin (R)

90 100

18

40 41 47

11

-30

23

80

-120

-60

0

60

120

2014 2015 2016 2017 2018 2019 2020F 2021F

Increase

Decrease

Avg. capacity chg.

('000 wpm)

Samsung Electronics

Mirae Asset Daewoo Research 20

May 13, 2020

Rationale behind our aggressive NAND capex outlook: 1) Revisit previous cycle

In 1Q20, margins dipped below breakeven for all NAND makers except SEC, which recorded

an OP margin at the low-20% level. The firm accounted for more than 90% of overall NAND

market profits in the quarter. As SEC will likely strive to maintain its current profit share and

margin levels, we believe it will continue to execute capex in line with demand growth.

We believe NAND makers’ 2016-18 capex strategy is worth revisiting. NAND ASP/GB, which

had declined continuously from 1Q10, picked up in 2H16 on wafer capacity shortages

arising from the conversion to 3D NAND. At that time, both first-tier (including SEC) and

second-tier NAND suppliers enjoyed high margins. Amid high margins and optimistic

demand forecasts, NAND makers executed aggressive capex.

Although SEC’s NAND capex spending in 2017 was the largest in the industry, its 2018 capex

accounted for only 30% of overall market spending. Thus, the firm displayed below-industry

NAND wafer capacity growth and bit growth in 2017-18. In 2018, prices plunged due to

oversupply stemming from aggressive shipments by chipmakers, driving down NAND

makers’ profits to near or below break-even levels. Of note, the easing of the oversupply

seen in 2019 was mainly driven not by demand growth, but by reduced supply caused by

Toshiba Memory’s power outage.

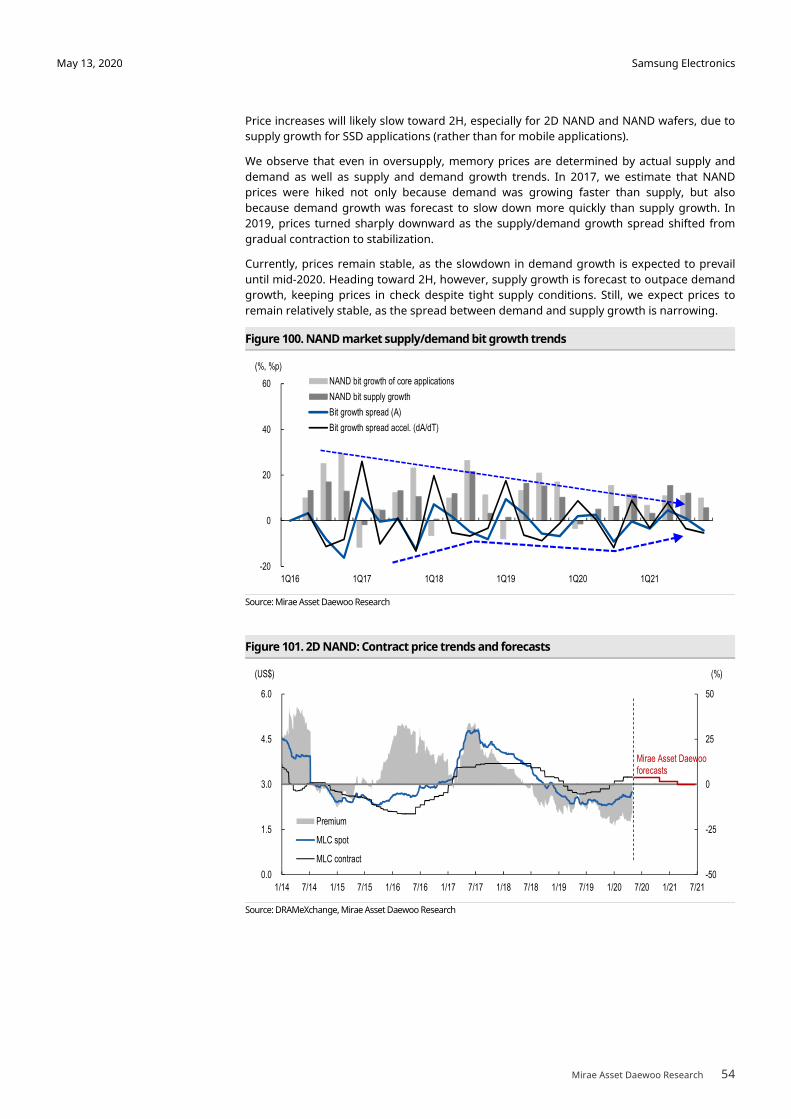

As the NAND market is still not fully concentrated, we think SEC is highly likely to

aggressively ramp up its NAND capex going forward, setting the stage for another game of

chicken among NAND makers. We see NAND prices stabilizing from 2H20 amid a slowdown

in price growth. With upside to NAND prices likely limited, we believe only players capable of

reducing costs will benefit. All in all, we expect SEC to maintain its leading position in the

NAND space (in terms of capex and operating profit) for some time.

Figure 44. Global NAND makers: OP margin trends Figure 45. SEC: NAND capex trend

Source: Company data, Thomson Reuters, Mirae Asset Daewoo Research Source: Company data, Mirae Asset Daewoo Research

-80

-40

0

40

80

1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17 1Q18 1Q19

(%) SEC SK Hynix

Micron Intel

Toshiba

7.0 7.8

8.8 9.7

-100

0

100

200

300

0

4

8

12

16

2005 2008 2011 2014 2017 2020F

(%)(Wtr)

SEC NAND capex (L)

YoY (R)

Samsung Electronics

Mirae Asset Daewoo Research 21

May 13, 2020

Figure 46. Global NAND makers: Capex trends

Source: DRAMeXchange, Mirae Asset Daewoo Research

Figure 47. Global NAND makers: Bit growth trends

Source: DRAMeXchange, Mirae Asset Daewoo Research

Figure 48. Global NAND M/S breakdown in terms of OP

Source: Company data, Mirae Asset Daewoo Research

36.6 45.8

38.4 37.3 44.3

59.3 48.3 46.4

95.5

0%

25%

50%

75%

100%

2011 2012 2013 2014 2015 2016 2017 2018 2019

Toshiba

Intel

Micron

SK Hynix

SEC

67.5

26.6

33.4

48.1

24.7

42.7

49.9

34.6

41.6 45.4

29.0

40.3

0

20

40

60

80

2016 2017 2018 2019 2020 2021

(%) SEC Kioxia (Toshiba Memory) Western Digital Micron SK Hynix Total

30.4

0

15

30

45

60

0

8,000

16,000

24,000

32,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

(%)(US$mn)

Intel

Micron

Toshiba/SanDisk

SK Hynix

SEC

SEC share of global NAND capex (R)

Samsung Electronics

Mirae Asset Daewoo Research 22

May 13, 2020

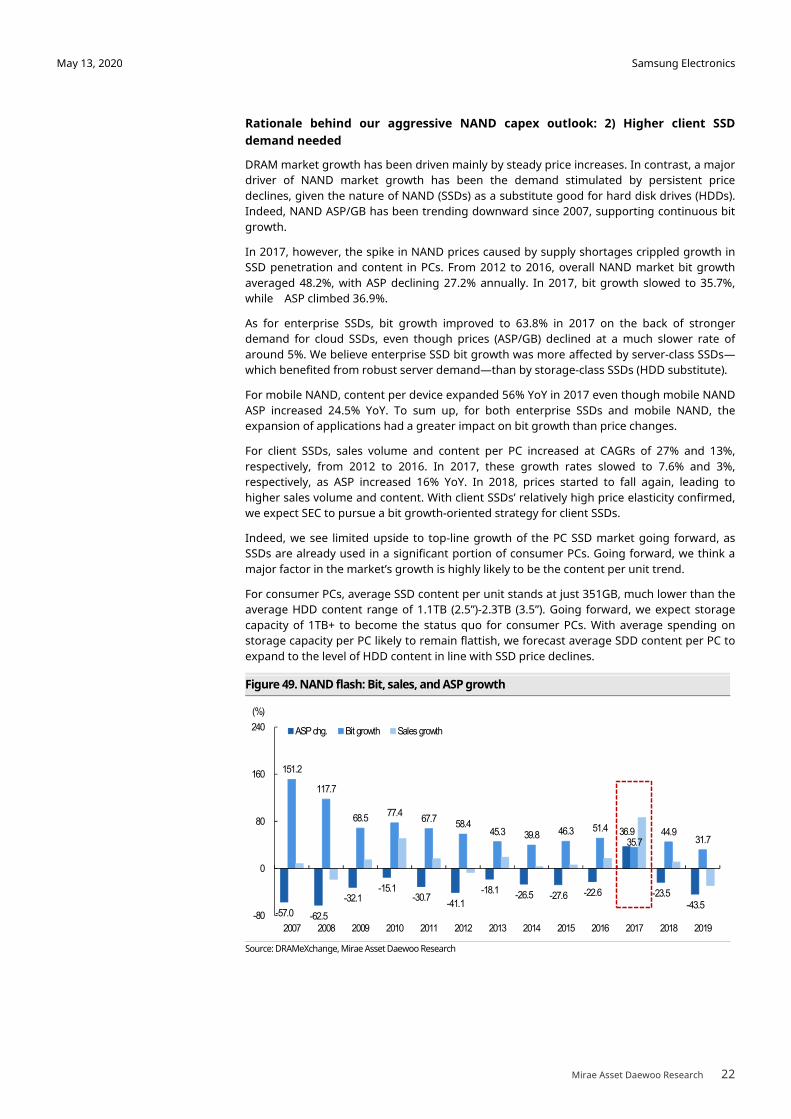

Rationale behind our aggressive NAND capex outlook: 2) Higher client SSD

demand needed

DRAM market growth has been driven mainly by steady price increases. In contrast, a major

driver of NAND market growth has been the demand stimulated by persistent price

declines, given the nature of NAND (SSDs) as a substitute good for hard disk drives (HDDs).

Indeed, NAND ASP/GB has been trending downward since 2007, supporting continuous bit

growth.

In 2017, however, the spike in NAND prices caused by supply shortages crippled growth in

SSD penetration and content in PCs. From 2012 to 2016, overall NAND market bit growth

averaged 48.2%, with ASP declining 27.2% annually. In 2017, bit growth slowed to 35.7%,

while ASP climbed 36.9%.

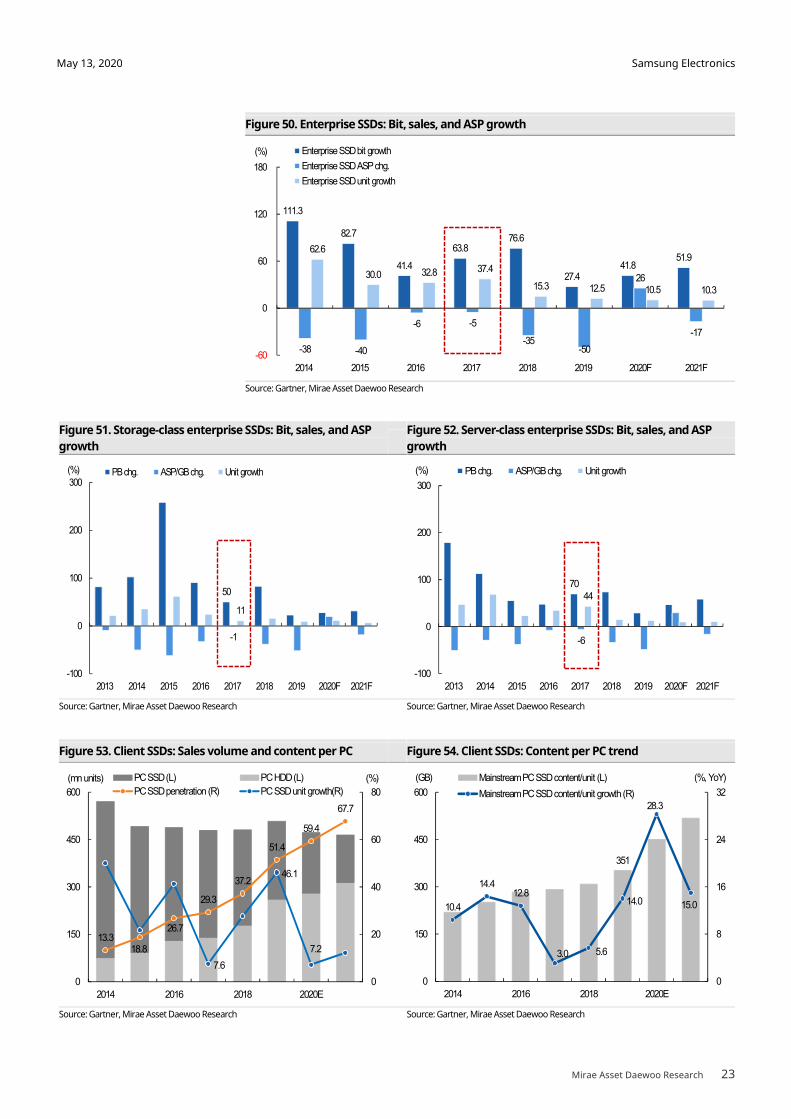

As for enterprise SSDs, bit growth improved to 63.8% in 2017 on the back of stronger

demand for cloud SSDs, even though prices (ASP/GB) declined at a much slower rate of

around 5%. We believe enterprise SSD bit growth was more affected by server-class SSDs—

which benefited from robust server demand—than by storage-class SSDs (HDD substitute).

For mobile NAND, content per device expanded 56% YoY in 2017 even though mobile NAND

ASP increased 24.5% YoY. To sum up, for both enterprise SSDs and mobile NAND, the

expansion of applications had a greater impact on bit growth than price changes.

For client SSDs, sales volume and content per PC increased at CAGRs of 27% and 13%,

respectively, from 2012 to 2016. In 2017, these growth rates slowed to 7.6% and 3%,

respectively, as ASP increased 16% YoY. In 2018, prices started to fall again, leading to

higher sales volume and content. With client SSDs’ relatively high price elasticity confirmed,

we expect SEC to pursue a bit growth-oriented strategy for client SSDs.

Indeed, we see limited upside to top-line growth of the PC SSD market going forward, as

SSDs are already used in a significant portion of consumer PCs. Going forward, we think a

major factor in the market’s growth is highly likely to be the content per unit trend.

For consumer PCs, average SSD content per unit stands at just 351GB, much lower than the

average HDD content range of 1.1TB (2.5”)-2.3TB (3.5”). Going forward, we expect storage

capacity of 1TB+ to become the status quo for consumer PCs. With average spending on

storage capacity per PC likely to remain flattish, we forecast average SDD content per PC to

expand to the level of HDD content in line with SSD price declines.

Figure 49. NAND flash: Bit, sales, and ASP growth

Source: DRAMeXchange, Mirae Asset Daewoo Research

-57.0 -62.5

-32.1 -15.1

-30.7 -41.1

-18.1 -26.5 -27.6 -22.6

36.9

-23.5 -43.5

151.2

117.7

68.5 77.4

67.7 58.4

45.3 39.8 46.3 51.4

35.7 44.9

31.7

-80

0

80

160

240

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

(%)

ASP chg. Bit growth Sales growth

Samsung Electronics

Mirae Asset Daewoo Research 23

May 13, 2020

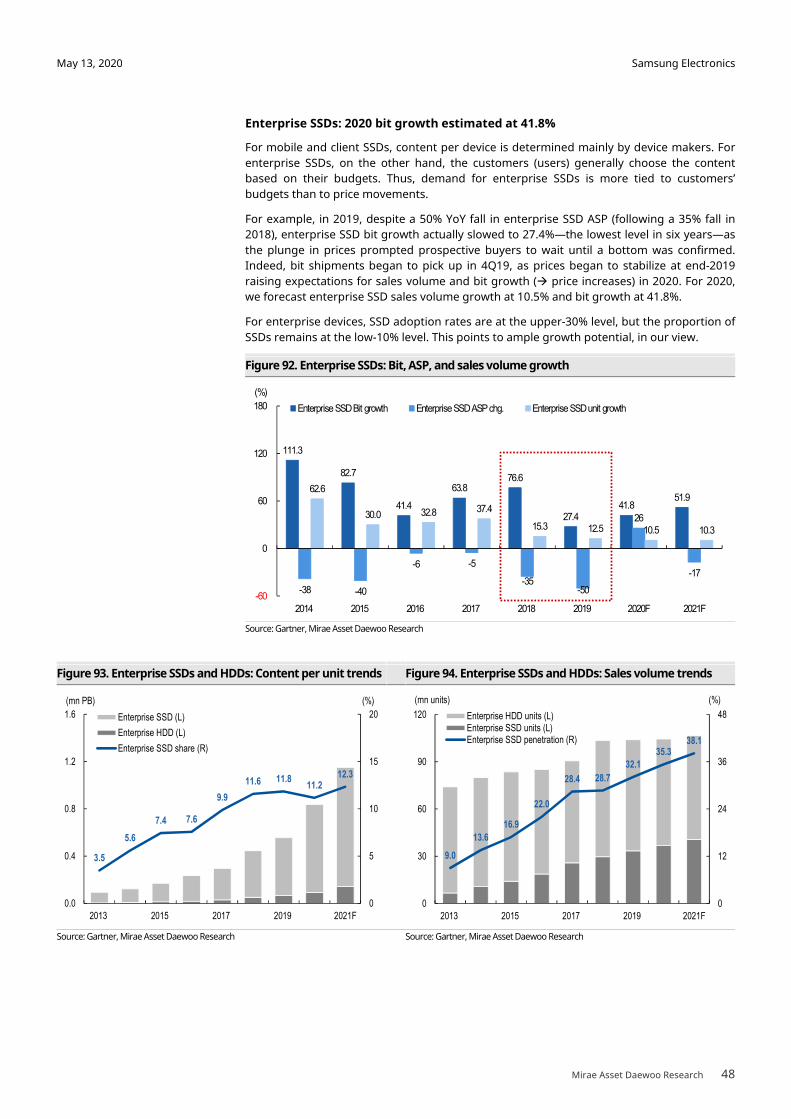

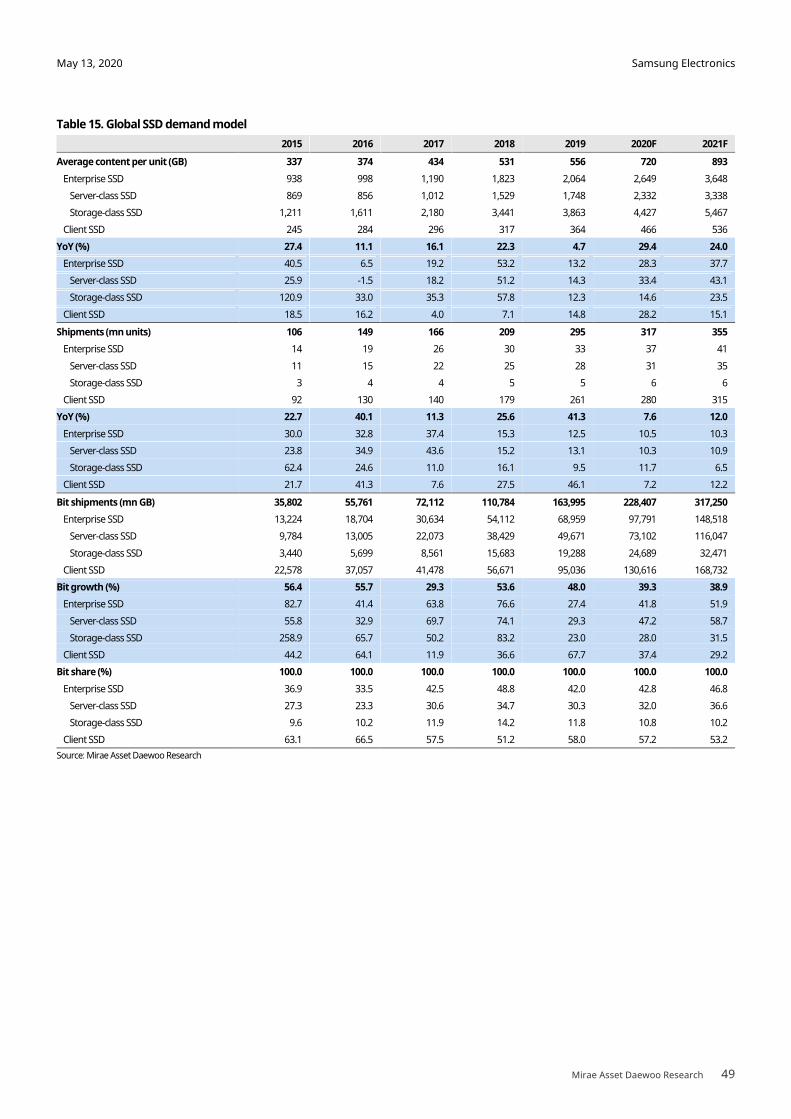

Figure 50. Enterprise SSDs: Bit, sales, and ASP growth

Source: Gartner, Mirae Asset Daewoo Research

Figure 51. Storage-class enterprise SSDs: Bit, sales, and ASP

growth

Figure 52. Server-class enterprise SSDs: Bit, sales, and ASP

growth

Source: Gartner, Mirae Asset Daewoo Research Source: Gartner, Mirae Asset Daewoo Research

Figure 53. Client SSDs: Sales volume and content per PC Figure 54. Client SSDs: Content per PC trend

Source: Gartner, Mirae Asset Daewoo Research Source: Gartner, Mirae Asset Daewoo Research

111.3

82.7

41.4

63.8 76.6

27.4 41.8

51.9

-38 -40

-6 -5

-35-50

26

-17

62.6

30.0 32.8 37.4

15.3 12.5 10.5 10.3

-60

0

60

120

180

2014 2015 2016 2017 2018 2019 2020F 2021F

(%) Enterprise SSD bit growth

Enterprise SSD ASP chg.

Enterprise SSD unit growth

50

-1

11

-100

0

100

200

300

2013 2014 2015 2016 2017 2018 2019 2020F 2021F

(%) PB chg. ASP/GB chg. Unit growth

70

-6

44

-100

0

100

200

300

2013 2014 2015 2016 2017 2018 2019 2020F 2021F

(%) PB chg. ASP/GB chg. Unit growth

13.318.8

26.7

29.3

37.2

51.4

59.4

67.7

7.6

46.1

7.2

0

20

40

60

80

0

150

300

450

600

2014 2016 2018 2020E

(%)(mn units) PC SSD (L) PC HDD (L)

PC SSD penetration (R) PC SSD unit growth(R)

351

10.4

14.412.8

3.0 5.6

14.0

28.3

15.0

0

8

16

24

32

0

150

300

450

600

2014 2016 2018 2020E

(%, YoY)(GB) Mainstream PC SSD content/unit (L)

Mainstream PC SSD content/unit growth (R)

Samsung Electronics

Mirae Asset Daewoo Research 24

May 13, 2020

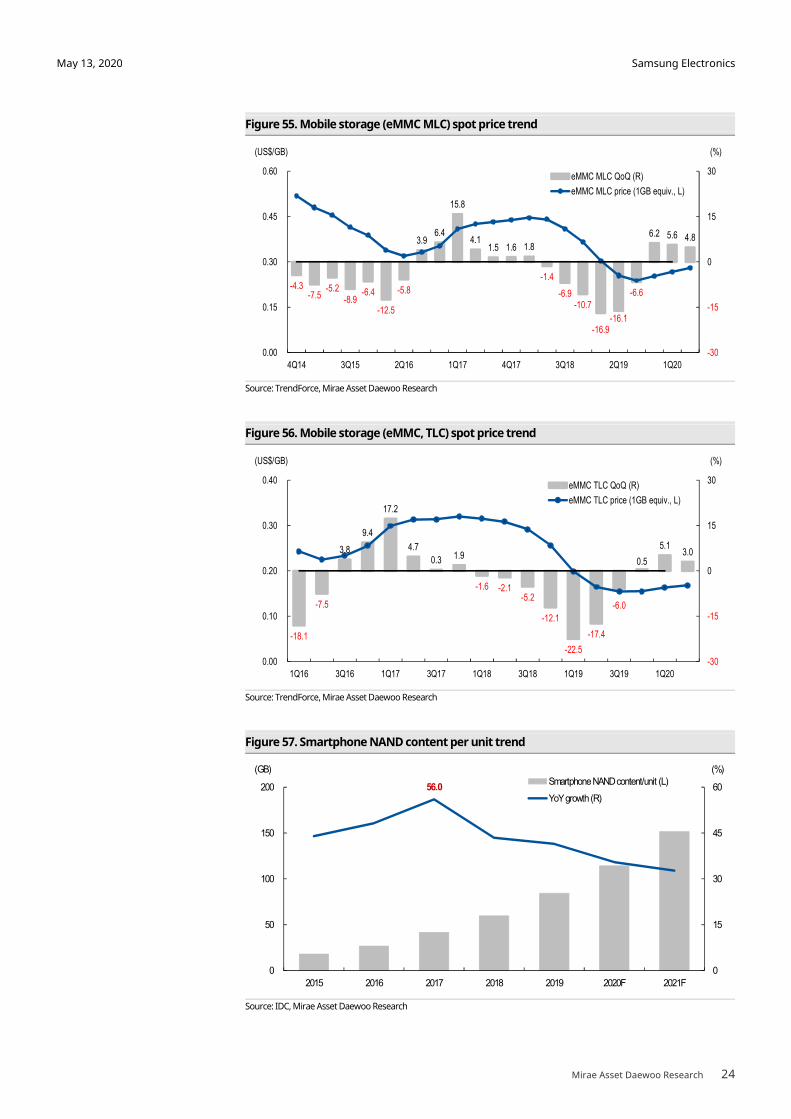

Figure 55. Mobile storage (eMMC MLC) spot price trend

Source: TrendForce, Mirae Asset Daewoo Research

Figure 56. Mobile storage (eMMC, TLC) spot price trend

Source: TrendForce, Mirae Asset Daewoo Research

Figure 57. Smartphone NAND content per unit trend

Source: IDC, Mirae Asset Daewoo Research

56.0

0

15

30

45

60

0

50

100

150

200

2015 2016 2017 2018 2019 2020F 2021F

(%)(GB)Smartphone NAND content/unit (L)

YoY growth (R)

-4.3 -7.5

-5.2 -8.9

-6.4

-12.5

-5.8

3.9 6.4

15.8

4.1 1.5 1.6 1.8

-1.4

-6.9 -10.7

-16.9 -16.1

-6.6

6.2 5.6 4.8

-30

-15

0

15

30

0.00

0.15

0.30

0.45

0.60

4Q14 3Q15 2Q16 1Q17 4Q17 3Q18 2Q19 1Q20

(%)(US$/GB)

eMMC MLC QoQ (R)

eMMC MLC price (1GB equiv., L)

-18.1

-7.5

3.8

9.4

17.2

4.7

0.3 1.9

-1.6 -2.1 -5.2

-12.1

-22.5

-17.4

-6.0

0.5

5.1 3.0

-30

-15

0

15

30

0.00

0.10

0.20

0.30

0.40

1Q16 3Q16 1Q17 3Q17 1Q18 3Q18 1Q19 3Q19 1Q20

(%)(US$/GB)

eMMC TLC QoQ (R)

eMMC TLC price (1GB equiv., L)

Samsung Electronics

Mirae Asset Daewoo Research 25

May 13, 2020

II. Outlook and earnings forecasts by division

Key assumptions for IT product demand forecasts

Given the pace of the COVID-19 spread and the growth of new cases by country, we expect

China to be the first market to see a recovery in IT product demand, followed by the

US/Europe and then India. All in all, our base-case scenario assumes an 8.3% YoY decline in

global smartphone demand and a 15.8% increase in global server demand in 2020.

For smartphone shipment volume, we formulated three scenarios according to the severity

of negative growth in 2Q20 and the extent of demand recovery in 2H20. Our base-case

scenario has smartphone demand: 1) declining at a slower pace QoQ in 2Q20; 2) making a

full-fledged QoQ recovery in 3Q20; 3) and return to the previous year’s levels in 4Q20. Under

our worst-case scenario, which assumes sharper-than-expected contraction in the US and

Europe in 2Q20, demand would continue to decline YoY and fail to recover to the previous

year’s levels in 4Q20.

Table 4. Smartphone shipment scenario analysis (mn units, %)

1Q20F 2Q20F 3Q20F 4Q20F 2019 2020F 2021F

Base case 278 272 336 372 1,372 1,258 1,403

Bear case 278 265 322 370 1,372 1,235 1,287

Worst case 278 255 305 351 1,372 1,189 1,254

YoY

Base case -11.0 -18.1 -6.2 0.7 -2.2 -8.3 11.6

Bear case -11.0 -20.0 -10.0 0.0 -2.2 -10.0 4.2

Worst case -11.0 -23.0 -15.0 -5.0 -2.2 -13.3 5.5

QoQ

Base case -24.9 -2.3 23.7 10.8

Bear case -24.9 -4.6 21.6 14.7

Worst case -24.9 -8.1 19.3 15.3

Source: Mirae Asset Daewoo Research

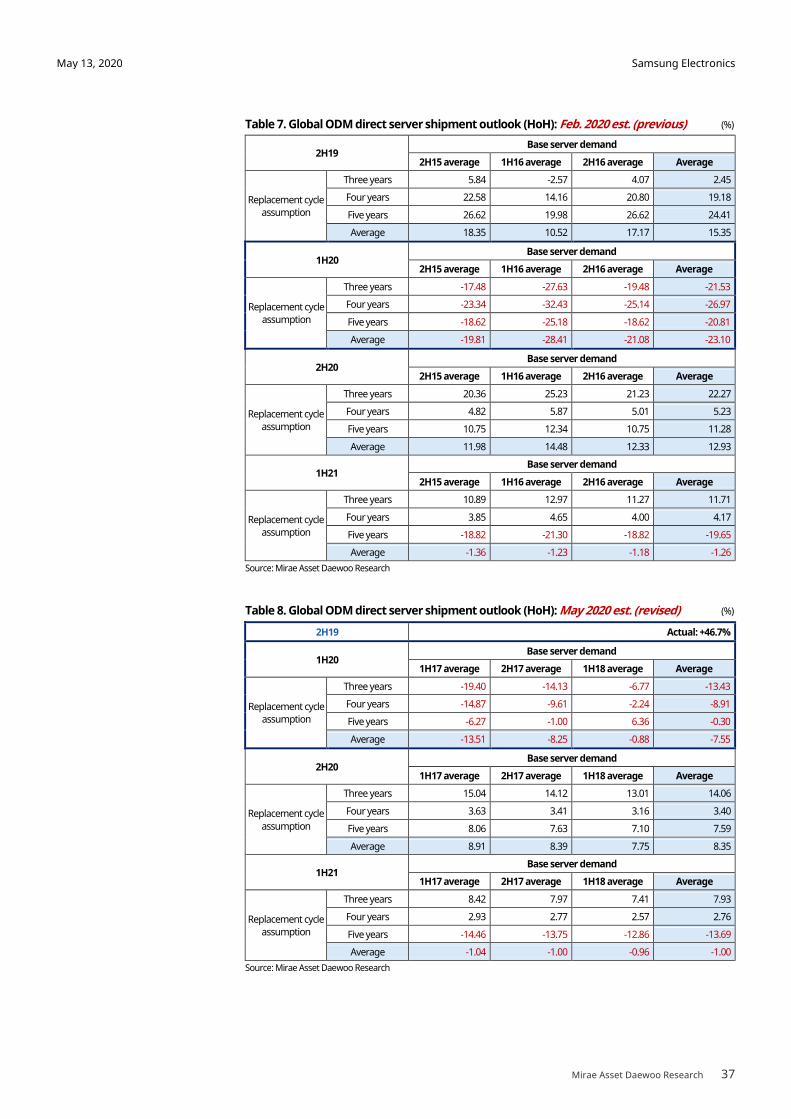

For server shipment volume, we created two scenarios based on server replacement cycle

length and regional COVID-19 impact. In our analysis, we assumed ODM direct servers to be

more sensitive to changes in the replacement cycle due to their high exposure to cloud

infrastructure. That said, given that ODM direct servers account for just a small slice of the

total pie, we believe structural growth of the server market hinges on hyperscale capex. We

note that our bear-case scenario reflects the possibility of disruptions in server

shipments/installations in the US and Europe.

Table 5. Server shipment scenario analysis (mn units, %)

1Q20F 2Q20F 3Q20F 4Q20F 2019 2020F 2021F

Base case 2,980 3,131 3,165 3,262 10,827 12,538 12,704

Bear case 2,980 2,952 2,985 3,076 10,827 11,993 12,704

YoY

Base case 25.1 27.2 11.6 3.7 -1.5 15.8 1.3

Bear case 25.1 19.9 5.2 -2.2 -1.5 10.8 5.9

QoQ

Base case -5.3 5.1 1.1 3.1

Bear case -5.3 -0.9 1.1 3.1

Source: Mirae Asset Daewoo Research

Samsung Electronics

Mirae Asset Daewoo Research 26

May 13, 2020

1) Smartphone shipment outlook and key assumptions

No consensus has formed among market researchers regarding the real impact of COVID-

19 on IT demand. While it appears clear that smartphone shipments posted a quarterly

decline in the mid-20% range in 1Q20, there are diverging views on: 1) the pace of shipment

declines in 2Q20; and 2) the likelihood of a release of pent-up demand in 2H20.

The spread of COVID-19 began to accelerate around the world (beyond China) in March, and

social distancing has been implemented globally since April, dampening consumer

sentiment. Given the cases of China and Korea, where infections peaked two months after

the first cases emerged, we project that smartphone demand will fall off a cliff during the

first two months of 2Q20 before beginning to stabilize..

Our projections also assume that smartphone shipment volume will decline only 6.2% YoY

and expand more than 20% QoQ, supported by the release of pent-up demand, in 3Q20.

Accordingly, our base-case scenario projects full-year shipment volume to decline 8.3% YoY

(or 110mn units) to 1.26bn units in 2020 and increase 11.6% YoY to 1.4bn units in 2021,

matching 2019 levels.

Figure 58. Global smartphone shipment scenario (quarterly)

Source: IDC, Counterpoint, Mirae Asset Daewoo Research

Figure 59. Global smartphone shipment scenario (annual)

Source: IDC, Counterpoint, Mirae Asset Daewoo Research

-40

-20

0

20

40

0

120

240

360

480

1Q19 2Q19 3Q19 4Q19 1Q20F 2Q20F 3Q20F 4Q20F 1Q21F 2Q21F 3Q21F 4Q21F

(%)(mn units) Base case (U-shaped recovery, L) Bear case (L)Worst case (L) Base case YoY (R)Bear case YoY (R) Worst case YoY (R)

12.6

14.0 13.7

12.4

12.9

11.9

12.5

-20

-10

0

10

20

8

10

12

14

16

2016 2017 2018 2019 2020F 2021F

(%)(mn units) Base case (U-shaped recovery, L) Bear case (L)

Worst case (L) Base case YoY (R)

Bear case YoY (R) Worst case YoY (R)

Samsung Electronics

Mirae Asset Daewoo Research 27

May 13, 2020

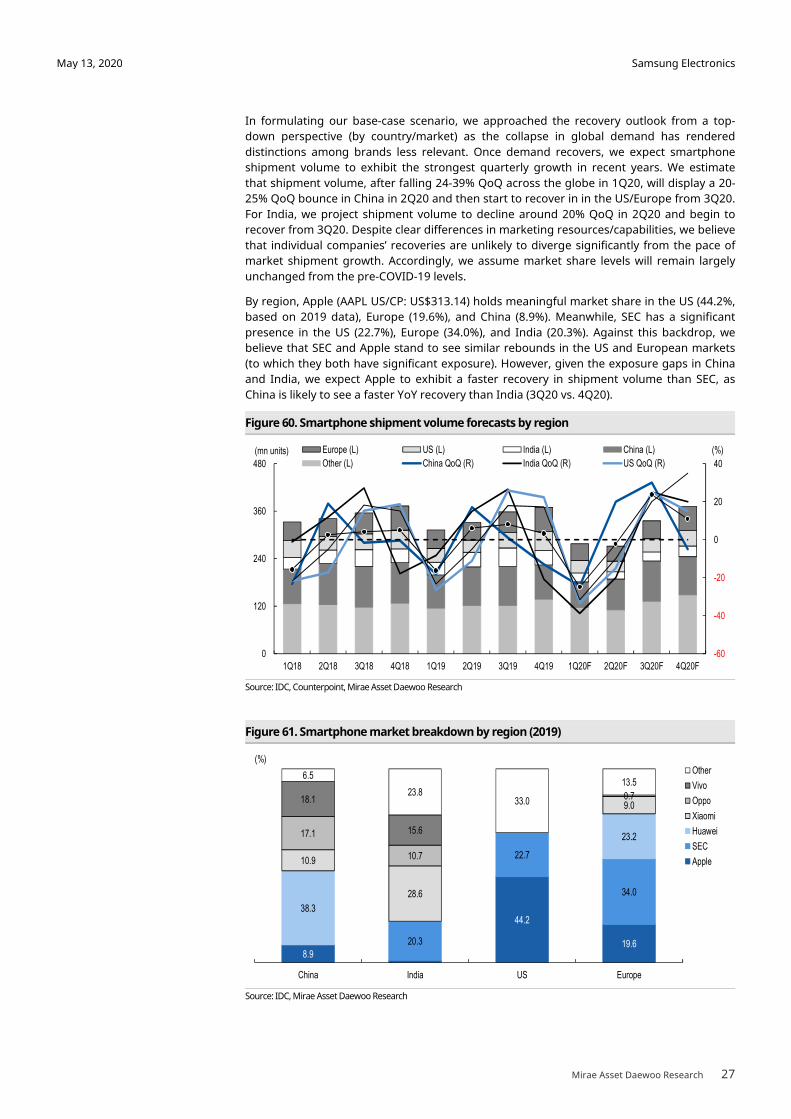

In formulating our base-case scenario, we approached the recovery outlook from a top-

down perspective (by country/market) as the collapse in global demand has rendered

distinctions among brands less relevant. Once demand recovers, we expect smartphone

shipment volume to exhibit the strongest quarterly growth in recent years. We estimate

that shipment volume, after falling 24-39% QoQ across the globe in 1Q20, will display a 20-

25% QoQ bounce in China in 2Q20 and then start to recover in in the US/Europe from 3Q20.

For India, we project shipment volume to decline around 20% QoQ in 2Q20 and begin to

recover from 3Q20. Despite clear differences in marketing resources/capabilities, we believe

that individual companies’ recoveries are unlikely to diverge significantly from the pace of

market shipment growth. Accordingly, we assume market share levels will remain largely

unchanged from the pre-COVID-19 levels.

By region, Apple (AAPL US/CP: US$313.14) holds meaningful market share in the US (44.2%,

based on 2019 data), Europe (19.6%), and China (8.9%). Meanwhile, SEC has a significant

presence in the US (22.7%), Europe (34.0%), and India (20.3%). Against this backdrop, we

believe that SEC and Apple stand to see similar rebounds in the US and European markets

(to which they both have significant exposure). However, given the exposure gaps in China

and India, we expect Apple to exhibit a faster recovery in shipment volume than SEC, as

China is likely to see a faster YoY recovery than India (3Q20 vs. 4Q20).

Figure 60. Smartphone shipment volume forecasts by region

Source: IDC, Counterpoint, Mirae Asset Daewoo Research

Figure 61. Smartphone market breakdown by region (2019)

Source: IDC, Mirae Asset Daewoo Research

-60

-40

-20

0

20

40

0

120

240

360

480

1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20F 2Q20F 3Q20F 4Q20F

(%)(mn units) Europe (L) US (L) India (L) China (L)

Other (L) China QoQ (R) India QoQ (R) US QoQ (R)

8.9

44.2

19.6 20.3

22.7

34.0

38.3

23.2

10.9

28.6

9.0

17.1

10.7

0.7 18.1

15.6

6.5

23.8 33.0

13.5

China India US Europe

(%)Other

Vivo

Oppo

Xiaomi

Huawei

SEC

Apple

Samsung Electronics

Mirae Asset Daewoo Research 28

May 13, 2020

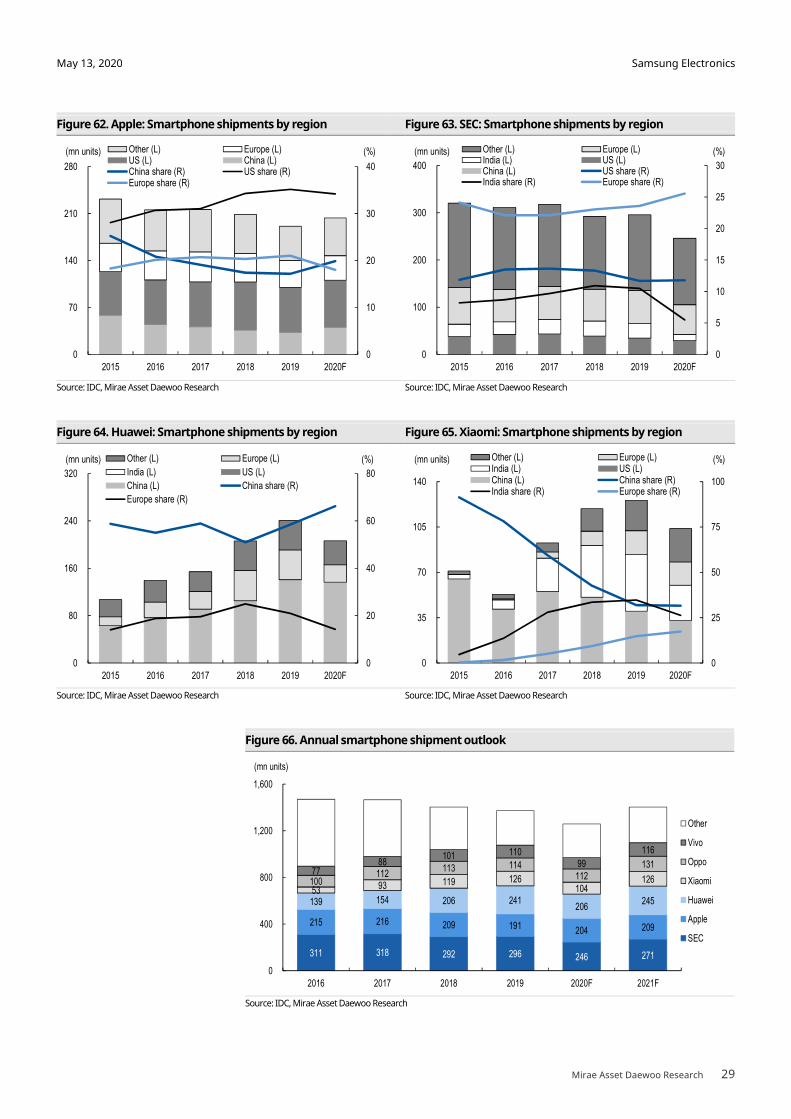

According to Counterpoint Research, SEC’s global smartphone sales volume contracted

20.8% QoQ in March 2020 (based on cumulative sell-through), worsening from a 9.9%

decline one year prior. We estimate that the firm’s sales volume did not decline sharply YoY

until March, when the impact of COVID-19 began to be felt in earnest.

In the US, SEC’s sales volume fell 16.4% QoQ, outperforming the overall market (-33.3%

QoQ). We believe the firm fared similarly well in Europe. However, the firm’s sales volume

plunged 42.2% QoQ in India, one of its key markets, faring worse compared to the same

period last year (-27.2% QoQ in 1Q19) and the overall Indian market (-38.8% QoQ).

By region, Europe accounts for 23.6% (as of 2019) of SEC’s sales volume, the US 12.1%, and

India 7.4% We estimate the firm’s smartphone shipment volume in Europe dropped 31.6%

QoQ in 1Q20, with negative growth likely to continue in 2Q20, albeit at a slower pace (aided

by the absence of the weak seasonality seen in 1Q20). We expect the firm’s shipment

volume to recover QoQ in 3Q20 and achieve positive YoY growth in 4Q20. Accordingly, we

estimate SEC’s annual smartphone shipment volume will reach 246mn units (-16.9% YoY) in

2020 and 271 mn units (+10.1% YoY) in 2021.

By region, the US accounts for 44.2% (as of 2019) of Apple’s sales, Europe 19.6%, and China

8.9%. We estimate that Apple’s US smartphone shipment volume declined 33.3% QoQ in

1Q20, with negative growth likely to continue in in 2Q20. However, given the likelihood of a

slowdown in negative shipment growth in the US and high exposure to China, which is

ahead of the pandemic curve, we project that Apple’s global smartphone shipment volume

will expand 6.8% QoQ in 2Q20 and 7.0% YoY in 2020.

The resilient outlook for Apple is due to the fact that 1Q, which marked the peak of the

COVID-19 outbreak, is an off-peak period for Apple in terms of shipments. Indeed, while

Apple’s smartphone shipment volume declined 37.5% QoQ (sell-through basis) in 1Q20, this

figure is largely in line with the average 1Q decline of 34.3% QoQ (sell-in basis) between

2017 and 2019. Even after accounting for the sell-through/sell-in difference, we believe

there remains a possibility that Apple could achieve YoY shipment growth in 2020.

For reference, our base-case scenario is premised on: 1) a significant slowdown in negative

QoQ growth in 2Q20; and 2) a swing to positive QoQ growth in 3Q20 onward, which should

lead to flattish YoY growth in 4Q20.

However, if the decline in shipment growth is sharper than expected in 2Q20, there is a

possibility of demand failing to recover to the previous year’s level in 4Q20. Under this

worst-case scenario, we assume smartphone shipment volume will decline 13.3% YoY (or

180mn units) in 2020 and increase only 5.5% YoY in 2021, failing to reach the 2019 level for

two consecutive years.

Samsung Electronics

Mirae Asset Daewoo Research 29

May 13, 2020

Figure 62. Apple: Smartphone shipments by region Figure 63. SEC: Smartphone shipments by region

Source: IDC, Mirae Asset Daewoo Research Source: IDC, Mirae Asset Daewoo Research

Figure 64. Huawei: Smartphone shipments by region Figure 65. Xiaomi: Smartphone shipments by region

Source: IDC, Mirae Asset Daewoo Research Source: IDC, Mirae Asset Daewoo Research

Figure 66. Annual smartphone shipment outlook

Source: IDC, Mirae Asset Daewoo Research

0

10

20

30

40

0

70

140

210

280

2015 2016 2017 2018 2019 2020F

(%)(mn units) Other (L) Europe (L)US (L) China (L)China share (R) US share (R)Europe share (R)

0

5

10

15

20

25

30

0

100

200

300

400

2015 2016 2017 2018 2019 2020F

(%)(mn units) Other (L) Europe (L)India (L) US (L)China (L) US share (R)India share (R) Europe share (R)

0

20

40

60

80

0

80

160

240

320

2015 2016 2017 2018 2019 2020F

(%)(mn units) Other (L) Europe (L)

India (L) US (L)

China (L) China share (R)

Europe share (R)

0

25

50

75

100

0

35

70

105

140

2015 2016 2017 2018 2019 2020F

(%)(mn units) Other (L) Europe (L)India (L) US (L)China (L) China share (R)India share (R) Europe share (R)

311 318 292 296 246 271

215 216 209 191 204 209

139 154 206 241 206

245 53 93 119 126

104 126 100

112 113 114

112 131

77 88

101 110 99

116

0

400

800

1,200

1,600

2016 2017 2018 2019 2020F 2021F

(mn units)

Other

Vivo

Oppo

Xiaomi

Huawei

Apple

SEC

Samsung Electronics

Mirae Asset Daewoo Research 30

May 13, 2020

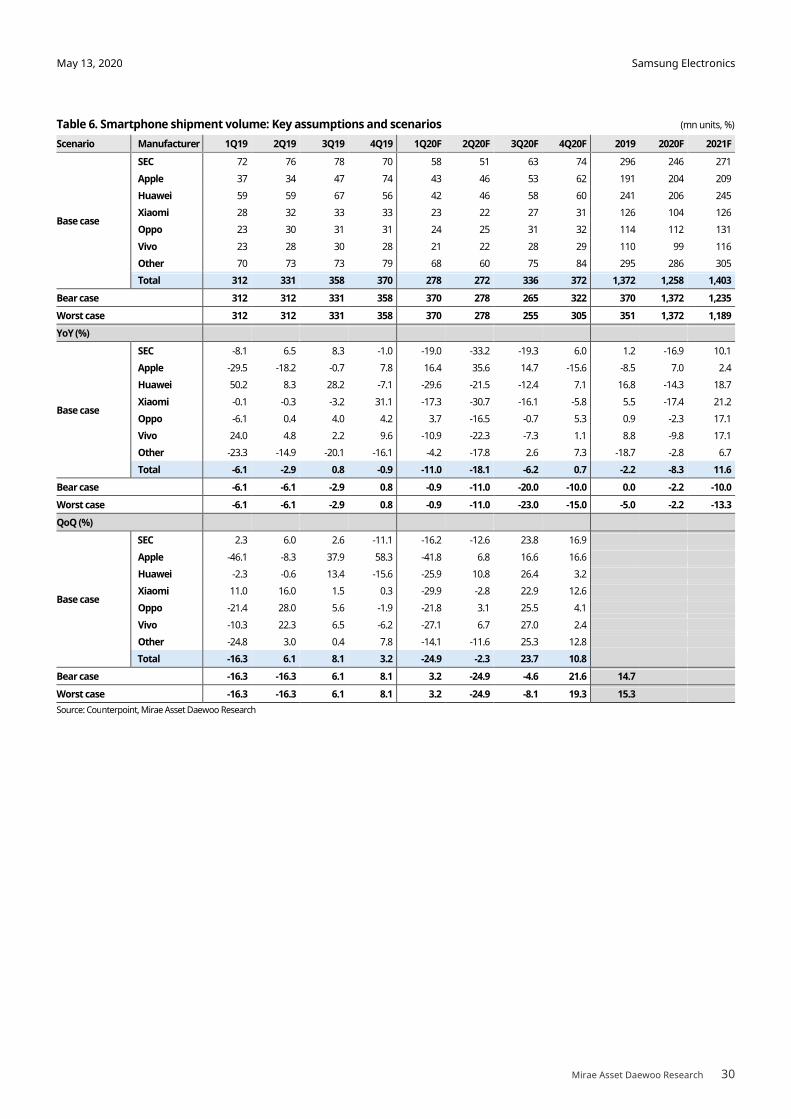

Table 6. Smartphone shipment volume: Key assumptions and scenarios (mn units, %)

Scenario Manufacturer 1Q19 2Q19 3Q19 4Q19 1Q20F 2Q20F 3Q20F 4Q20F 2019 2020F 2021F

Base case

SEC 72 76 78 70 58 51 63 74 296 246 271

Apple 37 34 47 74 43 46 53 62 191 204 209

Huawei 59 59 67 56 42 46 58 60 241 206 245

Xiaomi 28 32 33 33 23 22 27 31 126 104 126

Oppo 23 30 31 31 24 25 31 32 114 112 131

Vivo 23 28 30 28 21 22 28 29 110 99 116

Other 70 73 73 79 68 60 75 84 295 286 305

Total 312 331 358 370 278 272 336 372 1,372 1,258 1,403

Bear case 312 312 331 358 370 278 265 322 370 1,372 1,235

Worst case 312 312 331 358 370 278 255 305 351 1,372 1,189

YoY (%)

Base case

SEC -8.1 6.5 8.3 -1.0 -19.0 -33.2 -19.3 6.0 1.2 -16.9 10.1

Apple -29.5 -18.2 -0.7 7.8 16.4 35.6 14.7 -15.6 -8.5 7.0 2.4

Huawei 50.2 8.3 28.2 -7.1 -29.6 -21.5 -12.4 7.1 16.8 -14.3 18.7

Xiaomi -0.1 -0.3 -3.2 31.1 -17.3 -30.7 -16.1 -5.8 5.5 -17.4 21.2

Oppo -6.1 0.4 4.0 4.2 3.7 -16.5 -0.7 5.3 0.9 -2.3 17.1

Vivo 24.0 4.8 2.2 9.6 -10.9 -22.3 -7.3 1.1 8.8 -9.8 17.1

Other -23.3 -14.9 -20.1 -16.1 -4.2 -17.8 2.6 7.3 -18.7 -2.8 6.7

Total -6.1 -2.9 0.8 -0.9 -11.0 -18.1 -6.2 0.7 -2.2 -8.3 11.6

Bear case -6.1 -6.1 -2.9 0.8 -0.9 -11.0 -20.0 -10.0 0.0 -2.2 -10.0

Worst case -6.1 -6.1 -2.9 0.8 -0.9 -11.0 -23.0 -15.0 -5.0 -2.2 -13.3

QoQ (%)

Base case

SEC 2.3 6.0 2.6 -11.1 -16.2 -12.6 23.8 16.9

Apple -46.1 -8.3 37.9 58.3 -41.8 6.8 16.6 16.6

Huawei -2.3 -0.6 13.4 -15.6 -25.9 10.8 26.4 3.2

Xiaomi 11.0 16.0 1.5 0.3 -29.9 -2.8 22.9 12.6

Oppo -21.4 28.0 5.6 -1.9 -21.8 3.1 25.5 4.1

Vivo -10.3 22.3 6.5 -6.2 -27.1 6.7 27.0 2.4

Other -24.8 3.0 0.4 7.8 -14.1 -11.6 25.3 12.8

Total -16.3 6.1 8.1 3.2 -24.9 -2.3 23.7 10.8

Bear case -16.3 -16.3 6.1 8.1 3.2 -24.9 -4.6 21.6 14.7

Worst case -16.3 -16.3 6.1 8.1 3.2 -24.9 -8.1 19.3 15.3

Source: Counterpoint, Mirae Asset Daewoo Research

Samsung Electronics

Mirae Asset Daewoo Research 31

May 13, 2020

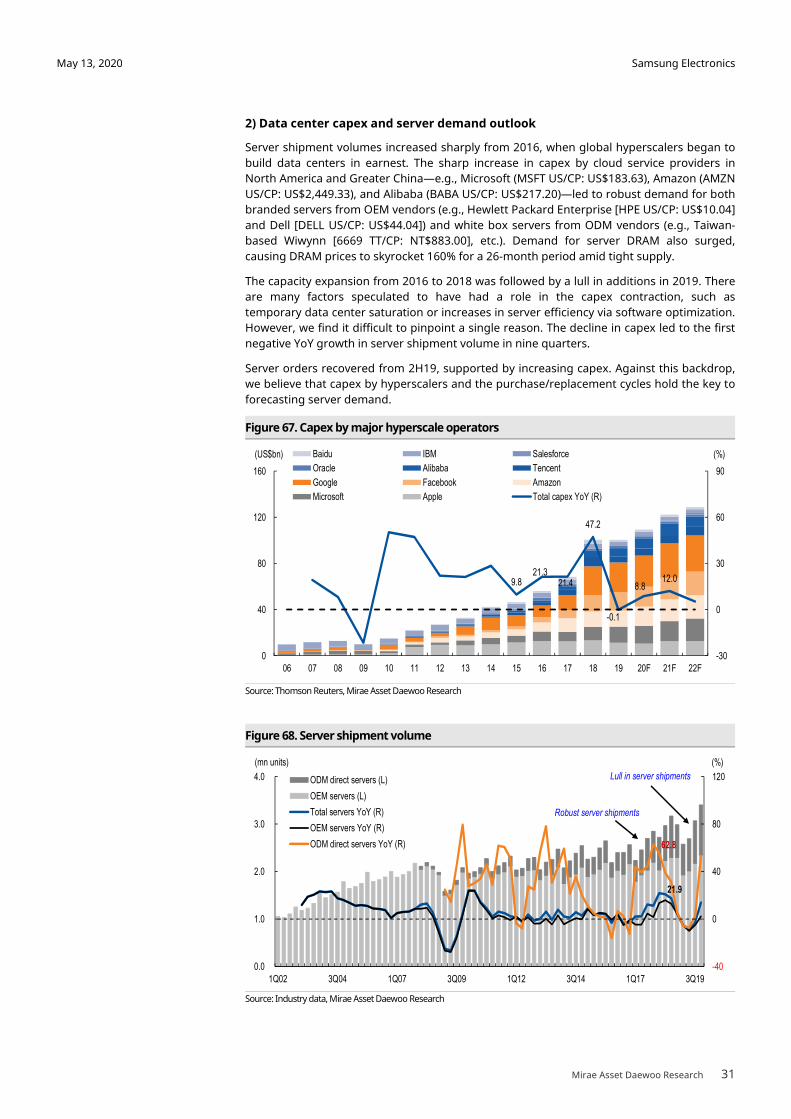

2) Data center capex and server demand outlook

Server shipment volumes increased sharply from 2016, when global hyperscalers began to

build data centers in earnest. The sharp increase in capex by cloud service providers in

North America and Greater China—e.g., Microsoft (MSFT US/CP: US$183.63), Amazon (AMZN

US/CP: US$2,449.33), and Alibaba (BABA US/CP: US$217.20)—led to robust demand for both

branded servers from OEM vendors (e.g., Hewlett Packard Enterprise [HPE US/CP: US$10.04]

and Dell [DELL US/CP: US$44.04]) and white box servers from ODM vendors (e.g., Taiwan-

based Wiwynn [6669 TT/CP: NT$883.00], etc.). Demand for server DRAM also surged,

causing DRAM prices to skyrocket 160% for a 26-month period amid tight supply.

The capacity expansion from 2016 to 2018 was followed by a lull in additions in 2019. There

are many factors speculated to have had a role in the capex contraction, such as

temporary data center saturation or increases in server efficiency via software optimization.

However, we find it difficult to pinpoint a single reason. The decline in capex led to the first

negative YoY growth in server shipment volume in nine quarters.

Server orders recovered from 2H19, supported by increasing capex. Against this backdrop,

we believe that capex by hyperscalers and the purchase/replacement cycles hold the key to

forecasting server demand.

Figure 67. Capex by major hyperscale operators

Source: Thomson Reuters, Mirae Asset Daewoo Research

Figure 68. Server shipment volume

Source: Industry data, Mirae Asset Daewoo Research

9.821.3

21.4

47.2

-0.1

8.812.0

-30

0

30

60

90

0

40

80

120

160

06 07 08 09 10 11 12 13 14 15 16 17 18 19 20F 21F 22F

(%)(US$bn) Baidu IBM Salesforce

Oracle Alibaba Tencent

Google Facebook Amazon

Microsoft Apple Total capex YoY (R)

21.9

62.8

-40

0

40

80

120

0.0

1.0

2.0

3.0

4.0

1Q02 3Q04 1Q07 3Q09 1Q12 3Q14 1Q17 3Q19

(%)(mn units)

ODM direct servers (L)

OEM servers (L)

Total servers YoY (R)

OEM servers YoY (R)

ODM direct servers YoY (R)

Robust server shipments

Lull in server shipments

Samsung Electronics

Mirae Asset Daewoo Research 32

May 13, 2020

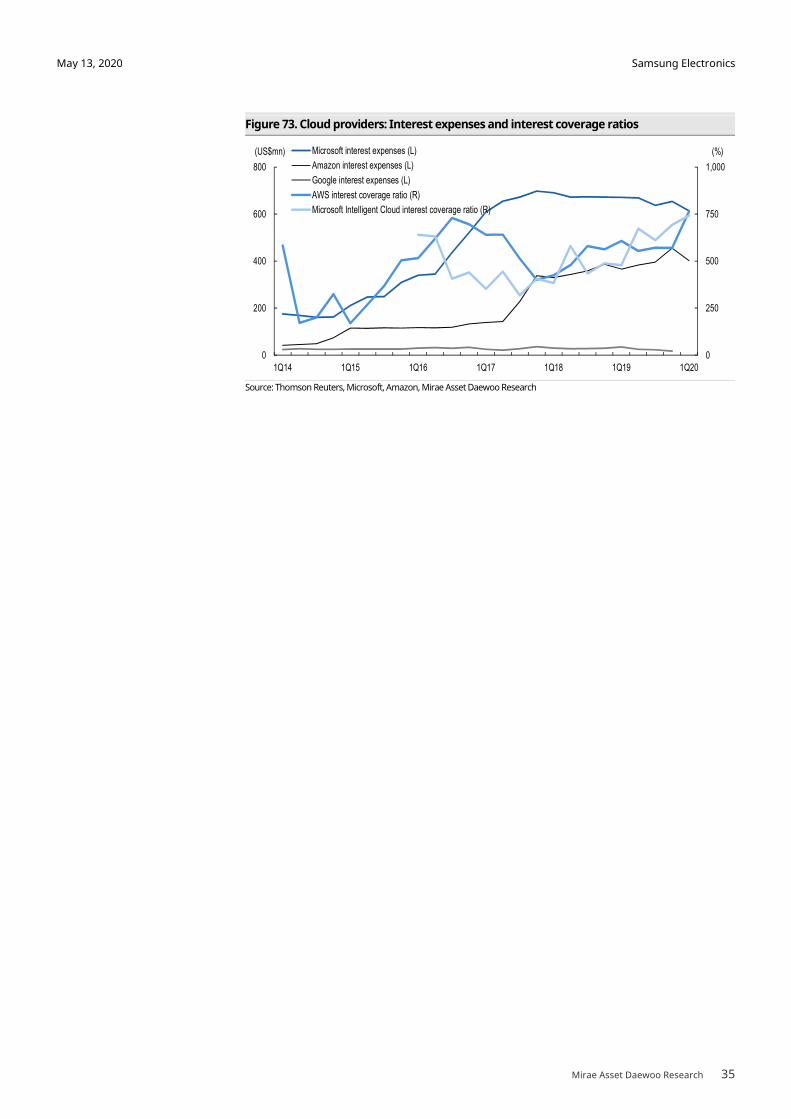

Looking ahead, we expect memory chip demand from data centers to remain stable, in light

of the following: 1) capex trends at cloud service providers suggest that the most recent

memory down cycle (end-2018 to early-2019) was triggered by customers’ inventory

reductions, rather than by fundamental demand contraction; 2) the server replacement

cycle is arriving for hyperscalers; and 3) cloud service providers continue to possess strong

growth potential and profitability. (Their interest coverage ratios have reached peak levels.)

With demand from hyperscalers very likely to remain strong, we believe that the timing of

server memory purchases will depend on the direction of mobile market demand. And we

think supply management at DRAM makers will hasten the timing of purchases.

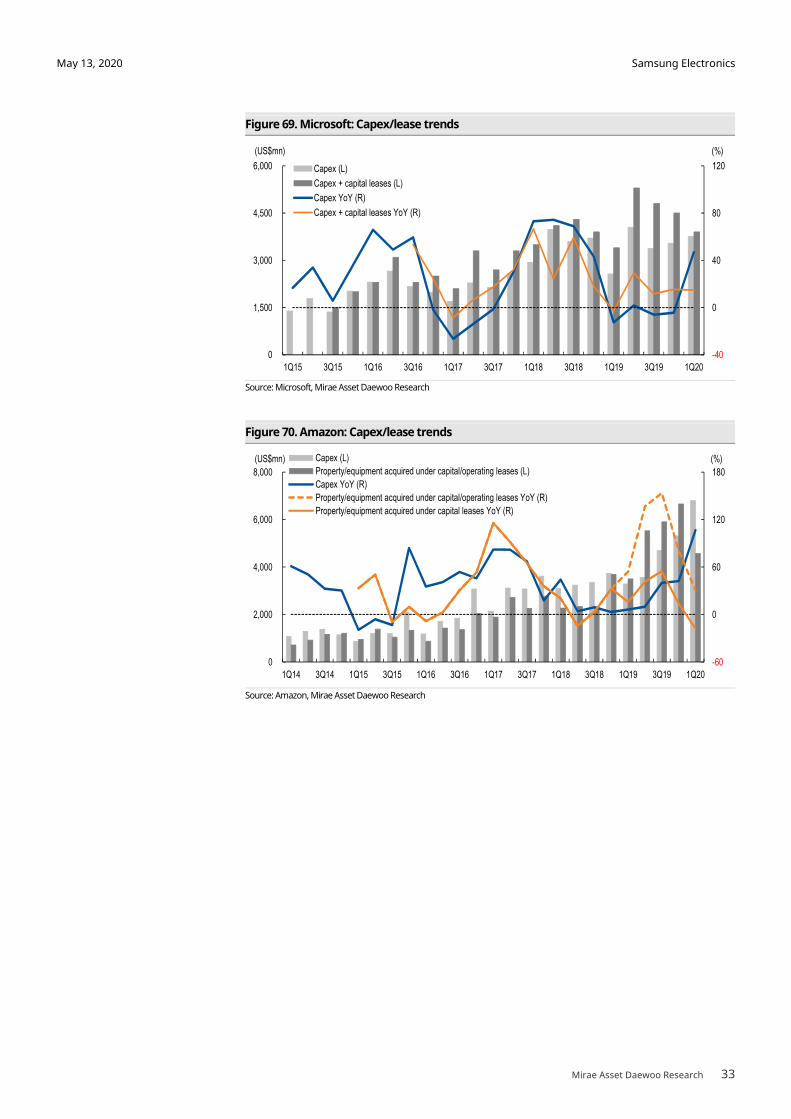

(1) Microsoft and Amazon (cloud service providers): Capex and capital lease trends

Cloud investments at Microsoft and Amazon have shown an oscillating pattern, with

company-wide capex growth and the combined growth of capex and capital leases taking

turns outpacing one another.

At Microsoft, the combined growth of capex and capital leases outstripped capex growth in

4Q16-4Q17. In the subsequent four quarters (1Q18-4Q18), capex displayed faster growth

than capex and capital leases combined. The growth structure reversed in 1Q19-4Q19 (with

capex and capital lease growth prevailing) and again in 1Q20 (with capex growth picking up

more rapidly). Amazon has exhibited a similar, albeit not as pronounced, pattern.

As some servers/network equipment used in data centers are leased assets, we can assume

that new server installations took place during periods in which the combined growth of

capex and capital leases was higher. Accordingly, we estimate that in 1Q20, more

investments were made in infrastructure than in servers. Nevertheless, server DRAM sales

have picked up recently, likely driven by stockpiling demand.

While some market watchers are fretting over the possibility of another server DRAM down

cycle, we note several differences in market conditions compared to in 1Q19. Back before

the onset of the last down cycle, inventory stockpiling continued for over four quarters at

hyperscalers, with capital leases remaining at low levels since 1Q18. With this in mind, we

do not believe that a pickup in stockpiling demand during a single quarter (1Q20) is enough

to give buyers strong bargaining power.

In addition, we believe that DRAM suppliers will no longer just sit on their hands in the face

of a down cycle triggered by stockpiling demand, especially given their oligopolistic market

positioning.

We also note that capital leases continued to expand even during the 2019 memory down

cycle (when capex growth slowed or even turned negative). Microsoft reported zero capex

growth throughout the year, and Amazon posted single-digit capex growth for five

quarters, from 2Q18 to 2Q19. During the same period, however, both companies reported

double-digit growth in capex and capital leases combined. This suggests that investments in

network equipment and servers continued despite the overall fall in investments.

Nevertheless, server DRAM demand stagnated at extremely low levels from end-2018 to