Sample Pages - Preqin

18

© 2010 Preqin Ltd 1 1. Executive Summary - Sample Pages Private equity fund of funds have always been amongst the most significant and important providers of capital to private equity fund managers. In addition, they have provided a valuable investment opportunity for investors lacking the funds or expertise to construct their own portfolio. Following the onset of the prevailing financial crisis their importance within the industry has grown even further. Growing Importance of Fund of Funds as Investors The importance of fund of funds managers as investors in new funds has grown considerably as other prominent investor types such as pension funds, endowments and foundations have cut back on the number of new commitments they are making, with some institutions ceasing new investment activity altogether. With all their capital invested in one asset class, fund of funds managers have not been affected by any denominator effect or lack of funds, and although many of them hold reservations towards certain areas of the industry, they have retained their ability to invest in new vehicles. Fig. A shows the investor make-up of the average fund closed in 2008 and 2009. Fund of funds managers have become increasingly significant, growing from making up 16% of the average fund in 2008 to 22% in 2009. A number of direct fund managers that were previously able to form a fund based on traditional institutional investors such as pension funds have been increasingly turning to multi-managers when raising new vehicles. Executive Summary Fig. A: Average Capital Contribution to Direct Private Equity Funds: Fund of Funds Managers vs. Other Investors Fig. B: Motivations for Investors Utilising Funds of Funds Fund Final Close Date Proportion of Respondents

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Sample Pages - Preqin

© 2010 Preqin Ltd 1

1. Executive Summary - Sample Pages

Private equity fund of funds have always been amongst the most signifi cant and important providers of capital to private equity fund managers. In addition, they have provided a valuable investment opportunity for investors lacking the funds or expertise to construct their own portfolio. Following the onset of the prevailing fi nancial crisis their importance within the industry has grown even further.

Growing Importance of Fund of Funds as Investors

The importance of fund of funds managers as investors in new funds has grown considerably as other prominent investor types such as pension funds, endowments and foundations have cut back on the number of new commitments they are making, with some institutions ceasing new investment activity altogether. With all their capital invested in one asset class, fund of funds managers have not been affected by any denominator effect or lack of funds, and although many of them hold reservations towards certain areas of the industry, they have retained their ability to invest in new vehicles.

Fig. A shows the investor make-up of the average fund closed in 2008 and 2009. Fund of funds managers have become increasingly signifi cant, growing from making up 16% of the average fund in 2008 to 22% in 2009. A number of direct fund managers that were previously able to form a fund based on traditional institutional investors such as pension funds have been increasingly turning to multi-managers when raising new vehicles.

Executive SummaryFig. A: Average Capital Contribution to Direct Private Equity Funds:

Fund of Funds Managers vs. Other Investors

Fig. B: Motivations for Investors Utilising Funds of FundsFund Final Close Date

Pro

porti

on o

f Res

pond

ents

© 2010 Preqin Ltd 2

1. Executive Summary - Sample Pages

A Compelling Investment Solution

Funds of funds have also grown in importance as investment propositions for institutional investors over the course of 2009. Investors with less capital available to invest have been attracted by the diversifi cation that they can gain through investing in a fund of funds, while the uncertainty that is surrounding the industry at present has led other investors to seek the expert knowledge and experience of fund of funds managers in addition, or as an alternative, to constructing a portfolio of direct fund investments themselves. As Fig. B shows, the most common reason for investors to seek a fund of funds is due to the diversifi cation that vehicles of this type offer. Manager expertise is also a key factor, with the access that such vehicles can provide to leading direct funds also an important consideration, albeit less important than in previous years when many brand name funds were signifi cantly over-subscribed.

Fundraising for new fund of funds vehicles has dropped in capital terms from previous years. However, their size relative to the rest of the market has increased in 2009. As Fig. C shows, capital raised for funds of funds relative to direct funds has grown signifi cantly over the past year, with fund of funds capital equivalent to 11% of capital raised for direct funds in 2009, up from 7% in 2008 – a 57% increase. The fi gures for 2009 do not include December fi gures, and with this month traditionally being a strong month for fund of funds closes, this percentage is likely to increase further.

How do Fund of Funds Managers View the Market?

With fund of funds managers becoming an increasingly important source of capital, understanding their views and concerns towards the industry is a

Fig. C: Fund of Funds Fundraising as a Percentage of Direct Fundraising, 2005 - 2009

Fig. D: Proportion of Fund of Funds Managers Investing in Fewer 2009 Vintage Funds vs. 2008 Vintage Funds

Fund

of F

unds

as

% o

f Dire

ct F

undr

aisi

ng

Year

© 2010 Preqin Ltd 3

1. Executive Summary - Sample Pages

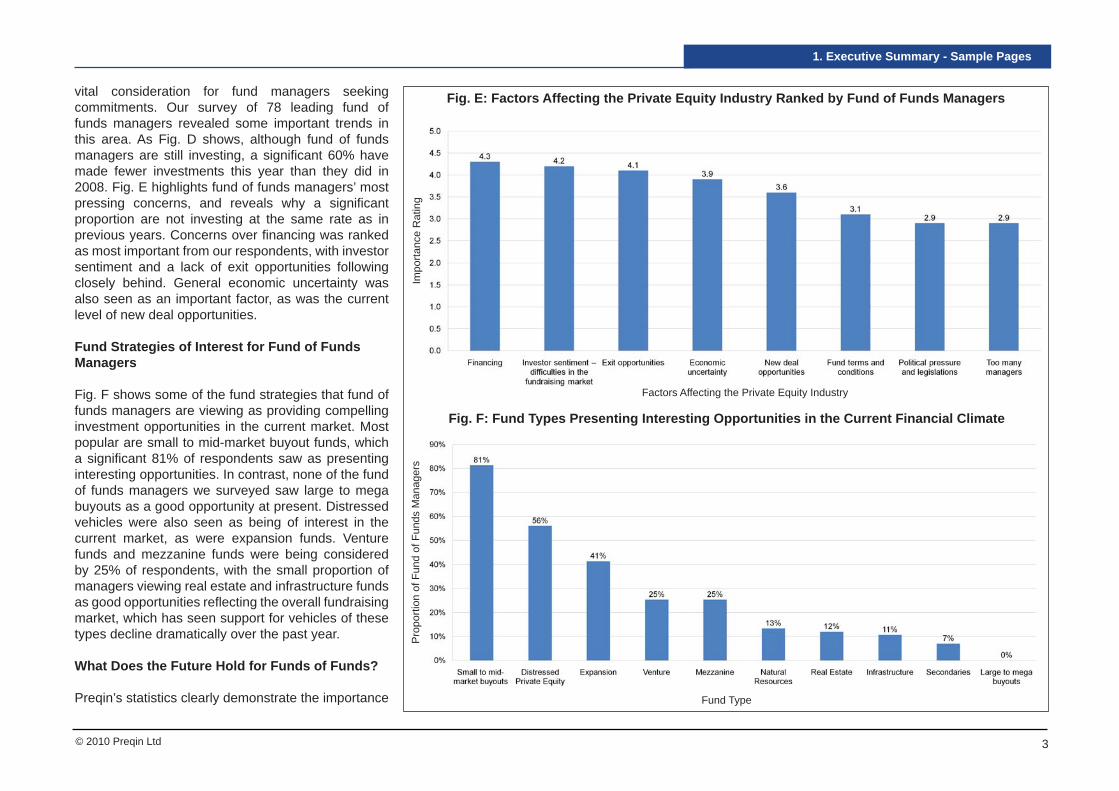

vital consideration for fund managers seeking commitments. Our survey of 78 leading fund of funds managers revealed some important trends in this area. As Fig. D shows, although fund of funds managers are still investing, a signifi cant 60% have made fewer investments this year than they did in 2008. Fig. E highlights fund of funds managers’ most pressing concerns, and reveals why a signifi cant proportion are not investing at the same rate as in previous years. Concerns over fi nancing was ranked as most important from our respondents, with investor sentiment and a lack of exit opportunities following closely behind. General economic uncertainty was also seen as an important factor, as was the current level of new deal opportunities.

Fund Strategies of Interest for Fund of Funds Managers

Fig. F shows some of the fund strategies that fund of funds managers are viewing as providing compelling investment opportunities in the current market. Most popular are small to mid-market buyout funds, which a signifi cant 81% of respondents saw as presenting interesting opportunities. In contrast, none of the fund of funds managers we surveyed saw large to mega buyouts as a good opportunity at present. Distressed vehicles were also seen as being of interest in the current market, as were expansion funds. Venture funds and mezzanine funds were being considered by 25% of respondents, with the small proportion of managers viewing real estate and infrastructure funds as good opportunities refl ecting the overall fundraising market, which has seen support for vehicles of these types decline dramatically over the past year.

What Does the Future Hold for Funds of Funds?

Preqin’s statistics clearly demonstrate the importance

Fig. E: Factors Affecting the Private Equity Industry Ranked by Fund of Funds Managers

Fig. F: Fund Types Presenting Interesting Opportunities in the Current Financial ClimateP

ropo

rtion

of F

und

of F

unds

Man

ager

sIm

porta

nce

Rat

ing

Factors Affecting the Private Equity Industry

Fund Type

© 2010 Preqin Ltd 4

1. Executive Summary - Sample Pages

of fund of funds managers in the current environment, but what does the future hold for these fund managers? Performance of the private equity asset class was showing signs of improvement for Q2 2009 (the latest available at time of writing in December 2009), and signs indicate that investor sentiment was beginning to improve. Will investors continue to invest in funds of funds, or will more institutions choose to avoid the dual layer of fees and branch out on their own?

The question can be partly answered by viewing the intentions of current investors in funds of funds. Preqin’s survey of 180 LPs in funds of funds revealed that 42% of current investors would be increasing their fund of funds allocations over the next three years, 28% would maintain, and 30% would be decreasing (Fig. G). These results show the natural churn of institutions through the fund of funds sector, with many choosing to make their earliest investments in private equity via a fund of funds, before reducing their activity in the area, and increasing the direct component of their portfolio. The 42% looking to increase activity is a relatively high proportion, and would suggest that a large proportion of smaller investors do not have enough confi dence in their own abilities to start forming a portfolio of direct interests themselves, instead favouring the expertise of a fund of funds manager.

In addition to smaller and newer investors in private equity, there are also a signifi cant number of larger, more experienced investors that invest in fund of funds in order to gain access to new geographic areas and new types of investment. In recent years there has been a number of funds established to focus on emerging markets, such as Africa and Asia, and also on new areas of the industry, with funds of funds focusing specifi cally on emerging areas such as cleantech.

Fig. G: Investors’ Fund of Funds Allocations Intentions: Next Three Years

Fig. H: Underlying Fund Investments Made by Fund of Funds Managers Split by Quartile Ranking

© 2010 Preqin Ltd 5

1. Executive Summary - Sample Pages

The future for funds of funds therefore looks bright, but much will rely on managers’ ability to live up to their claims of superior fund selection, and this will largely determine the ability of fund of funds managers to attract new investors in such a competitive market. As Fig. H shows, fund of funds managers are enjoying some success when it comes to fund selection, with 56% of underlying investments made by fund of funds managers beating the median, and only 18% of underlying funds appearing in the bottom quartile.

Such performance may not seem overly impressive, but this is taken over the industry as a whole. Within the industry there is a signifi cant difference between the best and worst performing managers, and critically there is strong evidence that the top managers are enjoying a good degree of consistency in terms of performance. As Fig. I shows, managers with a top quartile fund will follow this up with another top fund 43% of the time, and only see their follow-on fund fall into the bottom quartile 6% of the time. In contrast the worst performing fund managers will only see their follow-on fund fall into the top quartile 4% of the time, with the follow-on funds for bottom quartile performers remaining in the bottom segment in 50% of cases. For investors, a diligent analysis of past performance is therefore an essential consideration when selecting a fund of funds. Preqin’s research would suggest that investors can take some comfort in the fact that there are some excellent fund of funds managers that are managing to regularly outperform the benchmark returns for the industry.

The outlook for the sector is encouraging, with fund of funds managers becoming increasingly important for both investors and fund managers alike. It is likely that the recent tumultuous conditions in the market will highlight poor investment decisions made by some multi-managers, and as with other areas of the private

equity industry, it is certain that not all managers will be able to raise new funds in a market where there are fewer investors committing to new vehicles, and those that do have capital available are being increasingly stringent with their due diligence processes. However, in the long run the sector will emerge stronger, and looks set to be an integral part of the private equity landscape for the foreseeable future.

The 2010 Preqin Private Equity Fund of Funds Review

For this year’s publication we have sought to include data, listings, profi les and analysis on every aspect of the private equity fund of funds industry, including fund managers, fundraising, fund terms and conditions, fund performance, institutional investors in funds of

funds and more. We have gone to extreme lengths to ensure that the publication is as accurate as possible, gathering intelligence though a number of different channels, including most importantly from the fund managers and investors themselves. We hope that you fi nd this year’s edition to be a valuable resource, and as ever we welcome and comments and feedback that you may have.

Fig. I: Fund of Funds - Relationship between Predecessor and Successor Fund Quartiles

© 2010 Preqin Ltd 6

The 2010 Preqin PE Fund of Funds Review - Sample Pages

The 2010 Preqin Private Equity Fund of Funds Review

- Sample Pages

© 2010 Preqin Ltd 7

The 2010 Preqin PE Fund of Funds Review - Sample Pages

Contents

1. Executive Summary 7

2. Data Sources 15

3. Review of Historical Fund of Funds Fundraising Market 19- Historic fundraising, market share, funds closed by geography, funds closed by

GP location, average fund size evolution, funds closed by fund size, fi rst-time funds of funds fundraising

4. Listings of Funds of Funds Closed: 2008-2009 27

5. Review of Current Fund of Funds Fundraising Market 43- Growth in fundraising market over time, funds raising by geography, funds raising

by GP location, funds raising by fund size, largest funds on the road, placement agent use, fi rst-time funds raising

6. Listings of Funds of Funds Currently Raising 49

7. Fund of Funds Terms and Conditions Analysis 61- Management fees during investment period, management fees by underlying fund

focus, management fee discounts for large investors, mechanisms for reducing management fees after the investment period, carried interest, basis for charging carried interest, hurdle rates, key-man and no-fault divorce clauses, manager commitments, fund formation costs

8. Fund of Funds Terms Listings 69

9. Review of the Performance of Funds of Funds 81- Net IRR dispersion, median benchmark deviation, private equity horizon IRRs,

DPI, RVPI and TVPI, median net IRRs and quartile boundaries, DPI ratio dispersion, net multiples, net IRR J-curve, fund selection performance, top managers, synthetic IRR benchmarks, relationship of predecessor and successor fund quartiles, risk and return by fund strategy

10. Fund of Funds Managers as Investors 91- Regional breakdown of fund of funds managers, attitudes to fi rst-time funds,

attitudes to emerging markets, allocations to fund types, allocations by primary commitments, secondary purchases and co-investments

11. Fund of Funds Managers as Investment Consultants 103- Overview of investment consulting services offered, proportion of managers

offering investment consulting services, geographic breakdown of fund of funds managers acting as investment consultants

12. Profi les for 230 Active Private Equity Fund of Funds Managers 109

13. Analysis of Investors in Funds of Funds 321- Investors’ motivations for investing in funds of funds, investor experience, investor

sizes, make-up of investors in closed funds, investor base by GP location and fund focus, investor types, returning investors, survey of investor appetite going forwards

14. Investors to Watch 333- Most important 24 institutional investors to watch in 2010

15. Profi les of Investors in Private Equity Funds of Funds 339- Listings of 150 key investors in funds of funds

16. Index 389- Fund of Funds Managers

- Investors in Funds of Funds

- Figure Index

17. Other Publications and Services 397- Other Preqin Products

© 2010 Preqin Ltd 8

3. Review of FoF Fundraising Market - Sample Pages

market worth nearly $172bn in the year to date.

In terms of private equity market share by the number of vehicles raised, funds of funds are again relatively consistent. In each of the years between 2006 and 2009 inclusive, 16-18% of private equity vehicles raised were funds of funds, an increase from the 13% and 15% market share in 2004 and 2005 respectively. Fundraising by Geographic Focus

As of November 2009, $15bn had been raised by 28 funds of funds primarily targeting opportunities in North America, while 18 vehicles with Europe as a key focus secured commitments totalling $4.6bn. As Fig. 3.3 illustrates, 9 Asia and Rest of World focused vehicles achieved fi nal closes totalling $1bn in the year to date. These fi gures are not only lower than those for all three regions in 2008, but they are also lower than the fi gures achieved by November of that year. Fig. 3.4 shows that the fund of funds market has experienced an increasing prevalence of vehicles with a primary focus on North America in recent years. Since 2006, the proportion of capital committed to funds of funds predominantly targeting North American opportunities has increased year-on-year, while the focus on both Europe and Asia and Rest of World has declined in the same period. As of November 2009, nearly three-quarters of the capital committed to funds of funds in the year to date was pledged to North America focused vehicles, while 22% was raised by funds of funds with Europe as the key region of focus with the remaining 5% secured by Asia and Rest of World vehicles. Fig. 3.5 confi rms that the gap between the capital raised by North America and Europe focused funds of

Fig. 3.3: Funds of Funds by Geographic Focus (2009 YTD)

Fig. 3.4: Fundraising Market Share by Fund Focus

© 2010 Preqin Ltd 9

4. Listings of FoFs Closed: 2008-2009 - Sample Pages

Fund Name / Firm Name Target Close(mn)

Final Close(mn)

Close Date

Placement Agent

Strategy Fund Type Preference Geographic Focus Sample Investors

HarbourVest Partners VIII - Mezzanine

500.0 USD 485.0 USD Jan-08 Distressed Debt, Mezzanine

Regions: Global New York State Teachers' Retirement System, Pennsylvania State Employees' Retirement System, West Midlands Pension Fund, Tennessee Valley Authority Retirement System, Tyne and Wear Pension Fund, Australia Post Superannuation Scheme, South Yorkshire Pensions Authority, London Pensions Fund Authority, Army & Airforce Exchange Service Pension Fund (US), Hertfordshire County Council Pension Fund, Staffordshire County Pension Fund, East Sussex County Council Pension Fund, Montgomery County Employees' Retirement System, Metropolitan Government of Nashville & Davidson County Emplo, Shropshire County Council Pension Fund, Cardiff and Vale of Glamorgan Pension Fund, Lewisham Borough Council Pension Fund, Health Care Foundation of Greater Kansas City, University of Houston System Endowment, Kensington Capital Partners, City of Aurora General Employees' Retirement Plan, Brookline Retirement System

HarbourVest Partners Countries: US

Hirtle Callaghan Private Equity Fund VII

250.0 USD 300.0 USD Sep-08 Not Used Primary (90-100%), Secondary (0-10%)

Buyout (30-40%), Distressed Debt (20-25%), Real Estate (15-20%), Venture (20-30%)

Regions: North America (55-65%), Europe (25-35%), Asia (10%), Emerging Markets (5-10%)

Hirtle, Callaghan & Co.H21 Growth Opportunities I 500.0 USD 174.0 USD Dec-08 Not Used Primary (70-100%),

Secondary (0-20%), Direct (0-20%)

Buyout (0-30%), Expansion (60-100%), Venture (0-30%)

Regions: North America (20-40%), Europe (20-40%), Asia (30-60%)

Swiss Re, ASGA Pensionskasse, Feronia

Horizon21 Private EquityHorsley Bridge Fund IX 1,750.0 USD 1,760.0 USD Jun-08 Not Used Primary Venture (100%) Countries: US (100%) North Carolina Department of State Treasurer, PFA Pension,

Railways Pension Trustee Company, Indiana Public Employees' Retirement Fund, Compagnia di San Paolo

Horsley Bridge Partners

Horsley Bridge International V 1,600.0 USD 1,540.0 USD May-09 Primary Buyout, Venture Regions: North America, Europe, Asia

Kentucky Retirement Systems

Horsley Bridge PartnersLittle Hawk Fund of Funds 2006 50.0 USD 30.1 USD Jan-08 Not Used Primary (65-100%),

Secondary (0-35%)Venture (100%) Regions: Global (0-10%)

Industry Little Hawk Countries: US (90-100%)ING Private Equity Fund 4 250.0 AUD 183.0 AUD May-08 Not Used Primary (90%), Direct

(10%)Buyout, Venture Regions: Australasia

(100%)Mercy Super

ING Investment Management (Australia)

Countries: Australia, New Zealand

INVESCO Partnership Fund V 500.0 USD 126.0 USD Jun-09 Primary (95-100%), Secondary (0-5%)

Buyout (65%), Venture (35%)

Regions: North America (70%), Global (30%)

London Borough of Hammersmith & Fulham Pension Fund, Brookline Retirement System

Invesco Private CapitalCalSTRS New and Next Generation Manager Fund II

200.0 USD Mar-08 Buyout, Expansion, Venture

Regions: North America California State Teachers' Retirement System (CalSTRS)

Invesco Private CapitalJade China Value Partners 150.0 USD Aug-09 Not Used Primary (80-100%),

Direct (0-20%)Any (15%), Buyout (50%), Venture (35%)

Regions: Asia (100%) Kuwait Investment Authority, National Investments Company, Kuwait Financial Centre S.A.K.Jade Invest Countries: China (100%)

Kenmont Capital Private Equity Partners II

Feb-08 Not Used Buyout (50-70%), Special Situation (0-25%), Venture (0-25%)

Regions: North America, Global

Kenmont Capital PartnersKensington Private Equity Fund IV

250.0 CAD 84.6 CAD Dec-08 Not Used Primary (50%), Secondary (25%), Direct (25%)

Buyout (75%), Venture (25%)

Countries: Canada (100%) ATB Investment Management

Kensington Capital Partners

© 2010 Preqin Ltd 10

9. Review of the Performance of FoF - Sample Pages

Fund of Funds J-Curve: Annual Median Net IRRs

Fig. 9.8 demonstrates the median net IRR at each year in the investment cycle for funds of funds of vintage years 2000 to 2008, and thus gives us an indication of what the median “J-curve” for funds of funds would look like. It appears that across the vintages displayed, IRRs have dropped since 2008; this is related to the fi nancial crisis and the portfolio devaluation of private equity funds which followed public market price falls.

Vintage 2004 and 2005 funds of funds posted positive IRRs prior to the 2008 fi nancial crisis, but dropped below zero in 2009 due to devaluations of underlying investments. Also to be noted is that the J-curve shows that more recent funds of funds appear to have become quicker in moving their net IRRs up to positive return levels; the median 2005 vintage fund of funds for example posted positive returns in its third investment year whilst median 2000 and 2001 vintage funds of funds did not post positive net IRRs until their sixth and fi fth investment years respectively. As with

most performance data, the most recent vintage fund of funds vehicles have yet to generate positive returns as they are still early in their fund lives

Fund Selection Performance of Funds of Funds

In order to scrutinise the fund selection skills of fund of funds managers, we used our Investor Intelligence online database, containing comprehensive information on private equity investors and their investment activities. Investor Intelligence holds data on 8,350 fund investments made by fund of funds managers. When considering only fund of funds managers for which we have performance data for at least ten funds in their portfolios, this leaves us with 4,159 fund investments across 107 fund of funds managers.

Fund of funds managers assert that they have superior selection and due diligence skills which enable them to create portfolios of top performing funds. They also provide access to well-established top-tier fund

managers that are out of reach for many investors, especially those that are new to the private equity asset class or to certain geographic regions or fund types. For example, smaller investors sometimes fi nd it hard to commit to larger buyout funds due to their large minimum capital commitment requirements; funds of funds are a way for these investors to gain exposure to such funds.

Fig. 9.9 testifi es that over half (56%) of fund of funds managers’ underlying investments beat the median benchmark and only 18% of their portfolio funds post net IRRs in the bottom quartile.

In order to support the fi ndings of Fig. 9.9, we also rated the portfolio held by each fund of funds manager for which we had IRRs for their underlying portfolios, scoring each top quartile direct fund in the manager’s portfolio as 1, each second quartile fund as 2, etc. If the manager’s portfolio of funds were spread equally across all four quartiles then its average ranking would be 2.5, whereas if it is skewed towards the

Fig. 9.8: Fund of Funds J-Curve: Annual Median Net IRRs by Vintage Year

Med

ian

Net

IRR

(%)

Investment Year

Fig. 9.9: Split of Underlying Fund Investments made by Fund of Funds Managers by Quartile Ranking

© 2010 Preqin Ltd T = Fund Target 11

12. Profiles for Fund of Funds Managers - Sample Pages

IDFC Capital (Singapore) Raised (mn): Tel: +65 6499 0700 No Website AvailableOne Finlayson Green, 16-02, Singapore, 049246, Singapore Established: 2008 Fax: +65 6536 3359IDFC Capital (Singapore) is a subsidiary of India’s Infrastructure Development Finance Company (IDFC). It is a fund of funds manager that focuses primarily on investment in Asian funds, although it will also invest in funds in otheremerging markets.Emerging Markets Private Equity Fund I Fund Size (mn): 350 USD T RaisingFund Types: Expansion Emerging Markets Private Equity Fund I is an Asia focused emerging markets private equity fund of funds managed by IDFC Capital (Singapore).

The fund is primarily seeking to make investments in private equity funds that will provide expansion capital to companies in Asia. The fund will alsoallocate capital to co-investments, to enhance its overall portfolio return, and to secondary stakes in existing funds, to achieve a greater degree ofvintage year diversification.

IDFC Capital will seek to build a diversified portfolio focused on locally based GPs investing primarily in emerging Asia. 80% of the fund will beallocated specifically to Asian emerging markets, with the remaining 20% being dedicated to other emerging markets. Limited partners solelyseeking exposure to Asia may opt out of the 20% allocation. In total, Emerging Markets Private Equity Fund I plans to invest in 15-20 funds. Theselected GPs will be required to have a record of accessing high-quality deal flow, executing buy and build value-add strategies and well-timed exits.The manager will work with GPs and its investors to support the execution of environmental, social, and governance performance strategies tomanage risk and maximise returns.

As of November 2009, the fund had recently held a first close of USD 50 million, and was planning to continue fundraising during 2010, when it willstart making commitments to funds with selected GPs.

Regions: Asia (80%), Emerging Markets (20%)Countries: China, IndiaStrategies: Primary, Secondary, DirectInvest First-Time Funds: YesFund Investments (Total): 15 to 20Amount Typically Invested in a Fund: USD 10 to 50 mn

Funds Managed

Fund Vintage Status Size (mn) Called % Distributed (%) DPI

Rem. Value (%) RVPI Multiple (X) Net IRR (%) Benchmark IRR Date

ReportedFOFs SyntheticEmerging Markets Private Equity Fund I 2009 First Close 350 USD T n/m n/m

ContactsName Job Title Tel EmailEvan Gallagher Managing Director, Investor Relations +65 6499 0717 [email protected] John CEO +65 6499 0719 [email protected] Raju Managing Director +65 6499 0700 [email protected]

Portfolio Advisors Raised (mn): 7,700 USD Tel: +1 203 662 3456 www.portad.com9 Old Kings Highway South, Darien, CT, 06820-4505, US Established: 1994 Fax: +1 203 662 0013 [email protected] Advisors (PA) is an investment advisory and portfolio management firm specialising in private equity investments. It was established in 1994 and provides services to clients including public and private sector pension funds,corporations, foundations, endowments, insurance companies, financial institutions and family offices. It offers investment advisory services, fund management, portfolio administration and reporting services. As of November 2009, PA hadraised over USD 4.7 billion in private equity funds of funds since the firm’s inception.Portfolio Advisors Private Equity Fund VI Fund Size (mn): 900 USD T RaisingFund Types: Buyout, Distressed Debt, Special Situations, Venture (General) Portfolio Advisors Private Equity Fund VI (PAPEF VI) will follow a similar strategy to that of its predecessor funds. PAPEF VI provides a “flexible”

structure that offers investors the option to select from among its six sector funds, including diversified buyout, venture, Special Situations, Europe/Rest of World mid-market buyout, US mid-market buyout and distressed. Investors allocate a commitment to one or more of these sectors in anyproportion they desire. Each sector of the fund of funds has a target allocation of 20-30% to secondaries. In total, approximately 70% of the fund'scapital is expected to be allocated to North America and the remaining 30% to Europe and Rest of World.

In November 2009, PAPEF VI was still fundraising but had held interim closes. It had made a number of commitments, and had identified additionalfund managers with which it was likely to invest. It would consider committing to first-time funds.

Regions: Global (100%)Countries: USStrategies: Primary, Secondary (20-30%)Invest First-Time Funds: ConsideringFund Investments (Total): 45Amount Typically Invested in a Fund: USD 10 to 25 mn UOB Portfolio Advisors Asia Select Fund II Fund Size (mn): 300 USD T Second Close: 2008Fund Types: Buyout, Expansion, Special Situations, Venture (General) UOB Portfolio Advisors Asia Select Fund II is a joint venture between Portfolio Advisors and United Overseas Bank (UOB). The core focus of the

vehicle is growth equity, expansion capital, small and mid-market buyout and special situations funds that invest in mid-sized companies. It makessecondary market purchases and co-investments on an opportunistic basis. Typical investment sizes are USD 10-20 million.

As of November 2009, UOB Portfolio Advisors Asia Select Fund II had committed/approved five primary investments and identified an additional sixfunds for consideration.

Regions: Asia (100%)Countries: China, India, JapanStrategies: Primary, Secondary (0-20%), DirectInvest First-Time Funds: ConsideringFund Investments (Total): 15 to 18Commitments Made to Date: 5 FundsAmount Typically Invested in a Fund: USD 10 to 20 mn

© 2010 Preqin Ltd T = Fund Target 12

12. Profiles for Fund of Funds Managers - Sample Pages

Portfolio Advisors Private Equity Fund V Fund Size (mn): 1,045 USD Closed: 2008Fund Types: Buyout (50%), Special Situations, Venture (20%) Portfolio Advisors Private Equity Fund V (PAPEF V) makes primary investments in buyout, venture and special situations funds. Investments in

buyout funds comprise globally diversified funds and two additional options, European/Rest of World and mid-market US buyout funds. The fund offunds also makes secondary purchases for each sector (20-30%) on an opportunistic basis. In total, approximately 80% of the fund's capital isallocated to North America and the remaining 20% to Europe and Rest of World. During its investment period, the fund of funds is aiming to committo approximately 45 private equity funds, with a typical bite size of USD 10-25 million. It makes annual commitments to around 15 funds and has athree year investment period, which runs from mid-2007 through to mid-2010.

As of November 2009, PAPEF V was approximately 80% committed to underlying investments.

Sample Investments: OCM Opportunities Fund VIIB, Battery Ventures VIII, InSight Capital Partners VI, MatlinPatterson Global Opportunities III,Vector Fund IV, Globespan Capital Partners V

Regions: North America (80%), Other (20%)Strategies: Primary, Secondary (20-30%)Invest First-Time Funds: ConsideringFund Investments (Total): 45Commitments Made to Date: 80%Amount Typically Invested in a Fund: USD 10 to 25 mn

Sample Buyout Fund InvestmentsBridgepoint Europe IV (2009), ABRY VI (2008), Apollo Investment Fund VII (2008), Accent Equity 2008 (2007), Apax Europe VII (2007), Bain Capital Asia (2007), Doughty Hanson & Co V (2007), Graphite Capital Partners VII (2007), NewMountain Partners III (2007), Platinum Equity Capital Partners Fund II (2007), Reiten & Co Capital Partners VII (2007), Silver Lake Partners III (2007), Sun Capital Partners V (2007), Wingate Partners IV (2007), Bain Capital Fund IX(2006), Blackstone Capital Partners V (2006), Charterhouse Capital Partners VIII (2006), Clearview Capital Fund II (2006), Golder Thoma Cressey Rauner IX (2006), Lightyear Capital Fund II (2006), Permira IV (2006), RJD Private EquityFund II (2006), STAR II (2006), TA X (2006), Texas Pacific Group Partners V (2006), Apax Europe VI (2005), New Mountain Partners II (2005), PAI Europe IV (2005), Close Brothers Growth Capital Fund II (2004), Close Brothers PE FundVII (2004), Cinven III (2002), Candover 2001 (2001), TA IX (2000), Willis Stein & Partners III (2000), Candover 1997 (1998)Sample Venture Fund InvestmentsCarmel Ventures III (2008), Advanced Technology Ventures VIII (2007), Battery Ventures VIII (2007), Doll Capital V (2007), InSight Capital Partners VI (2007), Vector Fund IV (2007), Vivo Ventures Fund VI (2007), Bay Partners XI (2006),Capital Today China Growth Fund (2006), Globespan Capital Partners V (2006), Hupomone Capital Fund (2006), New Enterprise Associates XII (2006), Oak Investment Partners XII (2006), OpenView Venture Partners (2006), OpusCapital I (2006), True Ventures (2006), Athenian Venture Partners III (2005), Columbia Capital Equity Partners IV (2005), Triathlon Medical Ventures (2004)Other Fund InvestmentsOCM Opportunities Fund VIII (2009), Apollo European Principal Finance Fund (2008), Baring Asia Private Equity Fund IV (2008), Caltius Partners Fund IV (2008), OCM Opportunities Fund VIIB (2008), Avenue Special Situations V (2007),Capital International Private Equity Fund V (2007), Centerfield Capital Partners II (2007), MatlinPatterson Global Opportunities III (2007), OCM Opportunities Fund VII (2007), Sankaty Credit Opportunities Fund III (2007), ABRY SeniorEquity II (2006), Cerberus Institutional Partners (Series Four) (2006), TA Subordinated Debt II (2006), Windjammer Senior Equity Fund III (2006), Escalate Capital (2005), BDCM Opportunity Fund (2003), Lehman Brothers EuropeanMezzanine 2003 (2003), Centerfield Capital Partners (2000)Funds Managed

Fund Vintage Status Size (mn) Called % Distributed (%) DPI

Rem. Value (%) RVPI Multiple (X) Net IRR (%) Benchmark IRR Date

ReportedFOFs SyntheticPortfolio Advisors Private Equity Fund VI 2009 Raising 900 USD T n/m n/mUOB Portfolio Advisors Asia Select Fund II 2008 Second Close 300 USD T n/m n/m n/mPortfolio Advisors Private Equity Fund V 2007 Closed 1,045 USD 30.0 1.9 88.3 0.90 n/m n/m n/m 30-Jun-09UOB Portfolio Advisors Asia Select Fund 2006 Closed 189 USD 51.1 16.1 77.1 0.93 -11.0 -10.9 -12.8 30-Jun-09Portfolio Advisors Private Equity Fund IV 2006 Closed 982 USD 68.9 10.7 76.3 0.87 -9.2 -11.1 -12.7 30-Jun-09Portfolio Advisors Private Equity Fund III 2004 Closed 661 USD 85.3 21.6 73.9 0.93 -2.3 -0.1 4.0 30-Jun-09Portfolio Advisors Private Equity Fund II 2002 Closed 179 USD 89.7 66.2 67.1 1.32 11.1 11.1 14.7 30-Jun-09Portfolio Advisors Private Equity Fund I 2000 Closed 75 USD 94.2 65.3 64.3 1.30 6.2 5.5 30-Jun-09

ContactsName Job Title Tel EmailPaul R. Crotty Managing Director +1 203 662 3464 [email protected] J. Indelicato Managing Director +1 203 662 3460 [email protected] P. Murphy Managing Director +1 203 662 3459 [email protected] Perloff Managing Director +1 203 662 3463 [email protected] Wisdom Managing Director +1 203 662 3467 [email protected]

Robeco Private Equity Raised (mn): 1,831 USD Tel: +31 (0)10 224 7136 www.robeco.com/alternativesCoolsingel 120, Rotterdam, 3011 AG, Netherlands Established: 2000 Fax: +31 (0)10 224 2141 [email protected] Private Equity is the private equity division of Robeco Alternative & Sustainable Investments (RASI). Established in 2000, RASI is an alternative investments platform based in Rotterdam, Netherlands. It offers structured products,funds of hedge funds, single-strategy hedge funds and private equity funds of funds. RASI uses the distribution channel offered by the Robeco Group, as well as partnerships with external distributors.

© 2010 Preqin Ltd T = Fund Target 13

12. Profiles for Fund of Funds Managers - Sample Pages

Robeco SAM Clean Tech Private Equity III Fund Size (mn): 500 USD T AnnouncedRegions: West Europe, Emerging Markets Robeco SAM Clean Tech Private Equity III is expected to follow a similar strategy to Robeco Clean Tech Private Equity II and invest in cleantech

private equity funds.

The fund is expected to launch sometime during 2010.

Strategies: Primary, Direct

Robeco Responsible Private Equity II Fund Size (mn): 250 EUR T First Close: 2009Fund Types: Buyout (70-95%), Venture (5-30%) Robeco Responsible Private Equity II invests in funds with investment plans that adhere to a set of environmental, social and governance principles.

It invests in North America and Europe, as well as in emerging markets. The vehicle is diversified by fund type, region, industry sector and vintageyear. For its North American investments, the fund of funds allocates 5-20% to venture funds, 20-35% to mid-market buyout funds and 5-20% tolarge buyout funds. For its European investments, it allocates 0-20% to venture funds, 20-35% to mid-market buyout funds and 5-20% to largebuyout funds. For emerging markets investments, it allocates 0-10% to venture funds, 15-35% to mid-market buyout funds and 0-15% to largebuyout funds. Across all regions, the split by fund type is 5-30% to venture funds, 55-70% to mid-market buyout funds and 20-40% to large buyoutfunds.

Regions: North America (30-55%), Europe (30-55%), Emerging Markets (15-35%)Countries: Strategies: Primary, SecondaryFund Investments (Total): 20 to 30

Robeco Clean Tech Private Equity II (US) Fund Size (mn): 230 USD Closed: 2009Fund Types: Venture (100%) Robeco Clean Tech Private Equity II (US) focuses on making investments in private equity funds focusing on the cleantech industry. The fund is

open to commitments from US-based investors and is a side-car vehicle to Robeco Clean Tech Private Equity II, which closed in November 2008,having secured USD 320 million in commitments from investors in Europe and Asia. It follows a similar strategy to its twin vehicle, whereby it willmake between 15 and 20 fund commitments, investing up to USD 35 million per fund. Robeco Clean Tech Private Equity II (US) will invest in first-time funds.

Regions: North America (40-70%), Europe (20-50%), Asia (10-20%)Strategies: Primary (30-40%), Secondary (10-20%), Direct (50%)Invest First-Time Funds: YesFund Investments (Total): 15 to 20Amount Typically Invested in a Fund: Up to USD 35 mnRobeco Clean Tech Private Equity II Fund Size (mn): 320 USD Closed: 2008Fund Types: Venture (100%) Robeco Clean Tech Private Equity II (RCTPE II) focuses on making investments in cleantech funds. It aims to make between 15 and 20 fund

commitments in total, investing up to USD 35 million per fund. Robeco Clean Tech Private Equity II considers investing with first-time fundmanagers. Robeco Clean Tech Private Equity II closed in November 2008 with commitments from European and Asian investors.

Sample Investments: Altira Technology Fund V, China Environment Fund III, Environmental Technologies Fund, Global Environment EmergingMarkets Fund III, Israel Cleantech Ventures Fund I, Technology Partners Fund VIII, Nth Power IV

Regions: Global (100%)Strategies: Primary, SecondaryInvest First-Time Funds: ConsideringFund Investments (Total): 15 to 25Commitments Made to Date: 10 FundsAmount Typically Invested in a Fund: USD 20 to 35 mnRobeco European Private Equity III Fund Size (mn): 54 EUR Closed: 2007Fund Types: Buyout (100%) Robeco European Private Equity III (REPE III) focuses on investments in European funds, with up to 15% dedicated to private equity funds targeting

new EU accession countries. The vehicle invests up to EUR 15 million per underlying fund. Robeco European Private Equity III considers investingin first-time funds with teams that have a track record of previously working together.

Sample Investments: Investindustrial Fund IV, PAI Europe V

Regions: Europe (100%)Strategies: Primary (95%), Secondary (5%)Invest First-Time Funds: Spin-OffsFund Investments (Total): 15 to 20Commitments Made to Date: 68%, 12 FundsAmount Typically Invested in a Fund: EUR 5 to 15 mnRobeco Global Private Equity III Fund Size (mn): 135 USD Closed: 2007Fund Types: Buyout (70-90%), Venture (10-30%) Robeco Global Private Equity III (RGPE III) primarily focuses on funds that take advantage of mid-market opportunities. 40-70% of capital is to be

invested in mid-market buyout funds, 25-55% in large buyout funds and 10-30% in venture funds. About 10-30% of committed capital is allocated toNorth American funds and 30-50% to European funds, of which up to 15% is represented by new EU accession countries. The remaining 10-30% ofcapital is allocated to funds targeting emerging markets. RGPE III considers investing with first-time fund managers. The vehicle invests up to USD15 million per fund and plans to make commitments to approximately 30 funds in total.

Sample Investments: Investindustrial Fund IV, PAI Europe V, Investindustrial Fund III

Regions: North America (10-30%), Europe (30-50%), Emerging Markets (10-30%)Strategies: Primary (100%), SecondaryInvest First-Time Funds: ConsideringFund Investments (Total): 30Amount Typically Invested in a Fund: 5 to 15 mn USD

© 2010 Preqin Ltd T = Fund Target 14

12. Profiles for Fund of Funds Managers - Sample Pages

Sample Buyout Fund InvestmentsExponent Private Equity Partners II (2008), Investindustrial Fund IV (2008), Accent Equity 2008 (2007), Baring Vostok Private Equity Fund IV (2007), Brait IV (2007), Cinven IV (2007), Gresham IV Fund (2007), Terra Firma Capital PartnersIII (2007), 21 Centrale Partners III (2006), 3i Europe Partners V (2006), Argan Capital I (2006), Bain Capital Fund IX (2006), Charterhouse Capital Partners VIII (2006), Court Square Capital Partners II (2006), EdgeStone Capital EquityFund III (2006), EQT V (2006), Green Equity Investors V (2006), Lightyear Capital Fund II (2006), Lindsay Goldberg - Fund II (2006), Nordic Capital Fund VI (2006), Permira IV (2006), Quadriga Capital Private Equity Fund III (2006), AdventGlobal Private Equity V (2005), Apax Europe VI (2005), Apollo Investment Fund VI (2005), Barclays Private Equity European Fund II (2005), BC European Cap VIII (2005), Brazos Equity Fund II (2005), CVC European Equity Partners IV(2005), Emerging Europe Convergence Fund II (2005), Investindustrial Fund III (2005), PAI Europe IV (2005), Sovereign Capital II (2005), Sterling Capital Partners II (2005), TA Atlantic & Pacific V (2005), Wellspring Capital Partners IV(2005), EQT IV (2004), Exponent Private Equity Fund (2004), Friedman Fleischer & Lowe Capital Partners II (2004), Kelso Investment Associates VII (2004), Permira Europe III (2004), Swander Pace Capital Fund III (2004), Accent Equity2003 (2003), Bencis Buyout Fund II (2003), FS Equity Partners V (2003), Green Equity Investors IV (2003), Nordic Capital Fund V (2003), 3i Europe Partners IV (2002), Barclays Private Equity European Fund (2002), Charterhouse CapitalPartners VII (2002), Cinven III (2002), Lindsay Goldberg - Fund I (2002), Wellspring Capital Partners III (2002), Advent Global Private Equity IV-D (2001), JP Morgan Partners Global Investors (2001), Lightyear Capital Fund I (2001),Heartland Industrial Partners (2000), Willis Stein & Partners III (2000), Deutsche European Partners IV (1999), Industri Kapital 2000 Fund (1999), Green Equity Investors III (1998), Stonebridge Partners Equity Fund II (1997)Sample Venture Fund InvestmentsAltira Technology Fund V (2008), Demeter FCPR 2 (2008), Element Partners II (2008), Braemar Energy Ventures II (2007), China Environment Fund III (2007), Environmental Technologies Fund (2007), Global Environment EmergingMarkets Fund III (2007), Israel Cleantech Ventures Fund I (2007), SV Life Sciences Fund IV (2007), Technology Partners Fund VIII (2007), Blue River Capital I (2006), Nth Power IV (2006), VantagePoint Venture Partners V (2006),Chrysalix Energy II (2005), Institutional Venture Partners XI (2005), Forward Ventures V (2003), Atlas Ventures VI (2001), Crimson@Velocity (2001), Index Ventures II (2001), AIG Brazil Special Situations Fund (2000), Taiwan SpecialOpportunity Fund III (1999), Environmental Private Equity Fund II (1998), Excelsior V (1998), Apax UK VI (1997), Taiwan Special Opportunity Fund II (1997)Other Fund InvestmentsClimate Change Capital Private Equity Fund (2007), Capital International Private Equity Fund IV (2004), Apax Europe V (2001), Knightsbridge Integrated Holdings V (2001), Grotech Partners VI (2000), Warburg Pincus InternationalPartners (2000), Knightsbridge Integrated Holdings IV (1999), Bain Capital Fund VI Coinvestment Fund (1998), Knightsbridge Integrated Holdings III (1996), Knightsbridge Integrated Holdings II (1992)Funds Managed

Fund Vintage Status Size (mn) Called % Distributed (%) DPI

Rem. Value (%) RVPI Multiple (X) Net IRR (%) Benchmark IRR Date

ReportedFOFs SyntheticRobeco SAM Clean Tech Private Equity III 2010 Announced 500 USD T n/m n/mRobeco Responsible Private Equity II 2009 First Close 250 EUR T 0.0 0.0 0.0 0.00 n/m n/m 0.0 30-Jun-09Robeco Clean Tech Private Equity II (US) 2008 Closed 230 USD 16.9 0.0 58.2 0.58 n/m n/m 30-Jun-09Robeco Clean Tech Private Equity II 2007 Closed 320 USD 48.9 0.0 83.5 0.84 n/m n/m -15.7 30-Jun-09Robeco European Private Equity III 2007 Closed 54 EUR 29.4 0.0 73.0 0.73 n/m n/m -27.0 30-Jun-09Robeco Global Private Equity III 2007 Closed 135 USD 33.7 0.0 68.7 0.69 n/m n/m -24.9 30-Jun-09Robeco European Private Equity II 2005 Closed 102 EUR 80.6 0.0 78.6 0.79 -11.4 -9.0 -5.4 30-Jun-09Robeco Global Private Equity II 2005 Closed 236 USD 83.3 0.0 80.3 0.80 -10.4 -9.0 -5.4 30-Jun-09Robeco Sustainable Private Equity 2004 Closed 303 USD 85.4 0.0 89.1 0.89 -7.7 -0.1 -1.5 30-Jun-09Robeco Global Private Equity I 2001 Closed 197 USD 64.0 63.4 117.3 1.81 12.2 12.6 20.1 30-Jun-09Robeco European Private Equity I 2001 Closed 80 EUR 55.7 66.1 111.1 1.77 14.8 12.6 22.9 30-Jun-09Robeco Private Equity Opportunities 2001 Listed 15 EUR 20.3

ContactsName Job Title Tel EmailJesse De Klerk Senior Investment Manager +31 (0)10 224 2242 [email protected] Musters Head of Private Equity +41 (0)44 653 1502 [email protected] Quartel Senior Investment Manager +31 (0)10 224 3066 [email protected] van den Ouweland Managing Partner +31 (0)10 224 7231 [email protected] van Zanten Partner +1 212 908 0124 [email protected]

© 2010 Preqin Ltd 15

13. Analysis of Investors in Funds of Funds - Sample Pages

investing in funds of funds can allow them to achieve an additional layer of diversity in their portfolios. Merseyside Pension Fund allocates approximately half of its private equity portfolio to funds of funds and uses these vehicles for diversifi cation purposes, as well as to access specifi c funds and to benefi t from manager expertise. Other investors solely use funds of funds to gain exposure to the private equity market, and consequently look to invest in vehicles that can provide them with exposure to funds of a range of types and geographies. Ann Arbor Area Community Foundation, which solely invests in private equity via funds of funds, feels that these vehicles help it to maximise diversifi cation in its portfolio.

Funds of funds are frequently used by new investors in private equity as a method of gaining their initial exposure to the asset class. Highland County Council Pension Fund, for example, is considering making its maiden investments in private equity and expects to make a decision in March 2010. Should it decide to invest, it has identifi ed funds of funds as the means

of gaining its initial exposure. One respondent to our survey, a North American endowment, told us, “a couple of years ago, we were heavily weighted to funds of funds relative to our total private equity portfolio as a ‘start-up program’,” though the proportion has since fallen as the endowment has gained in knowledge and experience of investing in the asset class. In fact, in our survey, just over a third of respondents, 35%, told us that the expertise of fund of funds managers in building portfolios of private equity funds made these attractive prospects for investment and 11% of investors felt that they lacked a suffi cient degree of experience to effectively form and maintain a private equity portfolio and that this had prompted them to utilise funds of funds.

Further evidence of the considerable number of LPs that use funds of funds as a result of a lack of experience in investing in private equity can be seen in Fig. 13.3, which shows investors in funds of funds split by the number of portfolio investments they hold. A considerable 57% have between one and

ten funds currently in their portfolios, demonstrating their relative lack of experience of investing in private equity. However, it is also worth noting that 17% of investors with an interest in funds of funds have over 50 funds in their portfolios, and these LPs frequently use funds of funds to access specifi c markets or fund managers. California State Teachers’ Retirement System (CalSTRS), for example, has used funds of funds to make socially responsible and community focused investments within California.

Smaller investors can also fi nd it more diffi cult to access the private equity market; large minimum commitment sizes can frequently prevent small LPs from being able to commit to larger vehicles and investors with small allocations to the asset class might fi nd it diffi cult to achieve a suitable degree of diversifi cation in their portfolios if they were to invest in funds directly. 20% of respondents to our survey felt that they lacked suffi cient resources to invest in funds directly and that they prefer to utilise funds of funds to invest in private equity. Such investors may not feel

Fig. 13.2: Split of Investors in Funds of Funds by Assets under Management

Pro

porti

on o

f LP

s w

ith a

Pre

fere

nce

for F

unds

of F

unds

Assets under Management ($bn)

Fig. 13.3: Split of Investors in Funds of Funds by Previous Private Equity Investment Experience

Pro

porti

on o

f LP

s w

ith a

Pre

fere

nce

for F

unds

of F

unds

No. of Fund Investments

© 2010 Preqin Ltd 16

15. Profiles of Investors in Funds of Funds - Sample Pages

Bank Leumi Group Bank

34 Yehuda Halevi St., Tel Aviv, 65546, IsraelTel: +972 (0)3 5148 111 www.bankleumi.comFax: +972 (0)3 5148 656 [email protected] Leumi Group uses funds of funds as a means of gaining exposure to private equity vehicles targeting marketsoutside Israel. The bank tends to invest with fund of funds managers that can provide it with globally diverseexposure to funds of different types and strategies. At the end of 2009, the bank was considering when next to makeinvestments in private equity but will look to continue its strategy of investing in global funds of funds over the nextfew years. It is due to have a budget meeting in Q1 2010 in which it will set its allocation to private equity for the year.On recommencing investment in funds of funds, the bank will look to forge new relationships with managers as wellas investing with existing managers in its portfolio. It is unlikely to consider first-time fund of funds managers,preferring to invest with experienced managers with proven track records.Total Assets (mn): 319,346 ILSAllocation to Private Equity (mn): 7,183 ILS (2.2%)Geographic Preferences for Funds of Funds Investments

N.America Europe Asia Rest of World• • • •

Underlying Fund Type Preferences for Funds of Funds InvestmentsBuyout Venture Distressed PE Other

• • • •Sample Fund InvestmentsContact Name Position Telephone EmailElad Dubrovsky Investment Manager +972 (0)3 5411 259 [email protected]

Croydon Council Pension Fund Public Pension Fund

Taberner House, Croydon, CR9 1JL, UKTel: +44 (0)20 8760 5768 www.croydon.gov.ukCroydon Council Pension Fund gains exposure to the private equity market entirely through fund of funds vehicles. Itbelieves these vehicles offer access to underlying funds diversified across type, regional focus and managementstyle. It places great importance on fund manager experience and will therefore not invest in first-time funds of funds.The pension fund is currently invested with three private equity fund of funds managers: Pantheon Ventures,Hermes Private Equity and UBS Alternative Portfolio. It has reached its target allocation to the asset class, having4% of its total assets allocated to private equity as of Q4 2009. In 2010, Croydon Council Pension Fund expects tocommit between GBP 10 million and GBP 20 million to up to three funds of funds. These would be mostly re-upinvestments with existing managers in its portfolio, but it will consider forging new relationships with managers. It isadvised by Mercer Investment Consulting, which has partial discretion over investment decisions.Total Assets (mn): 461 GBPTarget Allocation to Private Equity (mn): 18 GBP (4.0%)Allocation to Private Equity (mn): 18 GBP (4.0%)Plans - Next 12 Months: GBP 10 to 20 mn (up to 3 funds)Geographic Preferences for Funds of Funds Investments

N.America Europe Asia Rest of World• • •

Underlying Fund Type Preferences for Funds of Funds InvestmentsBuyout Venture Distressed PE Other

• • • •

Sample Fund Investments Pantheon Europe Fund III (2001), Pantheon Asia Fund III (2000), Pantheon USA FundIV (2000)

Contact Name Position Telephone Email

Nigel Cook Assistant Treasurer +44 (0)20 8760 5768 Ext 62552 [email protected]

Evangelical Lutheran Church of America Pension Board

Public Pension Fund

800 Marquette Avenue, Suite 1050, Minneapolis, MN, 55402-2892, USTel: +1 612 333 7651 www.elcabop.orgFax: +1 612 334 5399 [email protected] Lutheran Church of America Pension Board (ELCA Board of Pensions) is an active investor in privateequity and typically allocates about 70% of its private equity portfolio to fund of funds vehicles. The pension fund hasa long-standing relationship with Adams Street Partners. It is looking to make one or two new commitments to fundsof funds in 2010 and expects one of these to be with a manager it has invested with previously, while the other couldsee it invest with a manager that it has not invested with in the past. The pension fund requires managers to have anestablished track record of investing in the asset class, so it will not invest with first-time fund of funds managers;however, it does consider investing with spin-off firms. ELCA Board of Pensions will continue to use funds of funds togain exposure to venture and buyout opportunities that are focused on markets outside North America, as it feelscomfortable enough to make its own direct fund investments domestically. The pension fund will look to maintain itsallocation to private equity over the next few years.Total Assets (mn): 6,000 USDTarget Allocation to Private Equity (mn): 294 USD (4.9%)Allocation to Private Equity (mn): 180 USD (3.0%)Plans - Next 12 Months: USD 20 to 50 mn (1 - 2 funds)Geographic Preferences for Funds of Funds Investments

N.America Europe Asia Rest of World• • •

Underlying Fund Type Preferences for Funds of Funds InvestmentsBuyout Venture Distressed PE Other

• •

Sample Fund Investments

Wilshire Private Markets Fund VI US (2005), Adams Street Non-US Partnership 2003(2003), Adams Street US Partnership 2003 (2003), Adams Street Non-US Partnership2002 (2002), Adams Street US Partnership 2002 (2002), Wilshire Private MarketsFund III (2000), Wilshire Private Markets Fund II (1999), Brinson Partnership Fund -1998 Primary (1998), Wilshire Private Markets Fund I (1998), Progress Fund I (1995)

Contact Name Position Telephone Email

Mike Clancey Associate Alternative Investment Analyst +1 612 752 4205 [email protected]

David Quello Alternative Investment Manager +1 612 752 4249 [email protected]

This 450 page publication shows you:

• Manager Profi les: Detailed profi les for over 230 fund of funds managers from around the globe, including fi rm and individual contact details.

• Fund Profi les: Vehicle-specifi c details for each manager’s most recent funds, with a breakdown of investments by fund type, location and investment type (primary, secondary and direct).

• Performance: Key fund performance metrics for over 500 individual fund of funds vehicles.

• LP Investors: Detailed profi les for 150 LP investors investing in funds of funds. Information on specifi c plans for fund of funds investing, sample investments and key contact details. Who are the top 20 investors to watch in 2010?

• Fundraising: In depth listings of all fund of funds closed during 2008 and 2009, funds currently raising and funds predicted to be raising in the near future. Shows sample investors, fund preferences, placement agents used.

• Fund Terms: Data on typical fund terms - management fees, carry, hurdles, fee rebates, key man provisions, etc. Full key terms listings for 159 fund of funds.

• Analysis: Detailed analysis on all aspects of funds of funds, including fundraising trends, current fundraising conditions, fund of funds terms and conditions, fund of funds managers as investors, performance, investors in fund of funds including composition of investors in closed funds, fund of funds as investment advisors.

• Survey Results: Includes the results of a survey of 78 leading fund of funds managers, covering their views of the market and the effect of the current fi nancial climate on their investments. Also includes a survey of 180 institutional investors in funds of funds, covering their motivations for investing in funds of funds and their future plans for investment in these vehicles.

2010 Preqin Private Equity Fund of Funds Review - Chapters

01............................................................................................. EXECUTIVE SUMMARY

02.......................................................................................................... DATA SOURCES

03................................................................................ REVIEW OF HISTORICAL FUND OF FUNDS FUNDRAISING MARKET

04........................................... LISTINGS OF FUNDS OF FUNDS CLOSED: 2008-2009

05.................................................................REVIEW OF CURRENT FUND OF FUNDS FUNDRAISING MARKET

06.............................................................................. LISTINGS OF FUNDS OF FUNDS CURRENTLY RAISING

07........................................ FUND OF FUNDS TERMS AND CONDITIONS ANALYSIS

08...............................................................................FUND OF FUNDS TERMS LISTINGS

09.......................................... REVIEW OF THE PERFORMANCE OF FUNDS OF FUNDS

10.............................................................FUND OF FUNDS MANAGERS AS INVESTORS

11.............................. FUND OF FUNDS MANAGERS AS INVESTMENT CONSULTANTS

12..............................................................PROFILES FOR 230 ACTIVE PRIVATE EQUITY FUND OF FUNDS MANAGERS

13........................................................ANALYSIS OF INVESTORS IN FUNDS OF FUNDS

14...................................................................................................INVESTORS TO WATCH

15..........................PROFILES OF INVESTORS IN PRIVATE EQUITY FUNDS OF FUNDS

Maintaining intelligence on the fund of funds sector is essential for all fund of fund managers, private equity fi rms seeking capital, investment advisors, institutional investors, placement agents, law fi rms, consultants and other private equity professionals. Now into its fourth edition, the 2010 Preqin Fund of Funds Review has been completely updated to provide the most comprehensive and up to date guide available yet.

2010 Preqin Private Equity Fund of FundsReview

© 2010 Preqin Ltd. / www.preqin.com

Purchase online: www.preqin.com/pefof or see following page for order form

2010 Preqin Private EquityFund of Funds Review:Order Form

2010 Preqin PE Fund of Funds Review Order Form - Please complete and return via fax, email or post

Name:

Firm: Job Title:

Address:

City: Post / Zip Code: Country:

Telephone: Email:

I would like to purchase the Preqin PE Fund of Funds Review:£885 + £10 Shipping $1,495 + $40 Shipping €950 + €25 Shipping

Additional Copies£110 + £5 Shipping $180 + $20 Shipping €115 + €12 Shipping

(Shipping costs will not exceed a maximum of £15 / $60 / €37 per order when all shipped to same address. If shipped to multiple addresses then full postage rates apply for additional copies)

The 2010 Preqin Private Equity Fund of Funds Review

I would like to purchase the Preqin PE Fund of Funds Review Graphs & Charts Data Pack in MS Excel Format:

$300 / £175 / €185

Payment Options:

Credit Card Visa AmexMastercard

Cheque enclosed (please make cheque payable to ‘Preqin’)

Please invoice me

Card Number:

Expiration Date:

Name on Card:

Security Code*:

Visa / Mastercard: the last 3 digits printed on the back of the card.

American Express: the 4 digit code is printed on the front of the card.

*Security Code:

(contains all underlying data for charts and graphs contained in the publication. Only available alongside purchase of the publication).

Now into its fourth edition, the 2010 Preqin Private Equity Fund of Funds Review has been completely updated to provide the most comprehensive and up to date guide available yet. Full contents include:

• Profi les for over 230 fund of funds managers from around the globe, including individual contact details and vehicle-specifi c details for each manager’s most recent funds.

• Key fund performance metrics for over 500 individual fund of funds vehicles.• Detailed profi les for 150 LP investors investing in funds of funds. Information on specifi c

investment plans.• Detailed analysis on all aspects of funds of funds, including fundraising, terms and

conditions, fund of funds managers as investors, performance, investors in fund of funds, fund of funds as investment advisors.

• Includes the results of a survey of 78 leading fund of funds managers, covering their views of the market and the effect of the current fi nancial climate on their investments.

• Includes a survey of 180 institutional investors in funds of funds, covering their motivations for investing in funds of funds and their future investment plans.

Purchase online: www.preqin.com/pefof

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

Equitable House, 47 King William Street, London, EC4R 9AF230 Park Avenue, 10th fl oor, New York, NY 10169

Samsung Hub, 3 Church Street, Level 8, Singapore 049483,

w: www.preqin.com / e: [email protected] / t: +44 (0)20 7645 8888 or +1 212 808 3008 / f: +44 (0)87 0330 5892 or +1 440 445 9595