Running business like a government in the new economy: lessons for organizational design and...

25

Running Business Like a Government in the New Economy: Lessons for Organisational Design and Corporate Governance Bryane Michael, Oxford University and Randy Gross, Tempe City Government Table of Contents Introduction .................................................................................................................... 1 Current Trends in “Private Sector Reform” ................................................................... 3 Lessons from Public Sector Reform .............................................................................. 7 Example from Tempe Arizona..................................................................................... 11 Some Lessons for Running Business like a Government ............................................ 16 Bibliography ................................................................................................................ 19 Abstract: Principal-agent problems are largely responsible for poor corporate governance. Much work on private sector corporate governance reform seeks to address transparency, accountability and responsiveness to stakeholder interests under the new category of corporate social responsibility. Yet, these issues are not new. The public sector has been working on these issues for many years – especially in looking at ways of reducing malfeasance and also optimizing use of resources for the benefit of principals. Some lessons from public sector reform include promoting information dissemination, participation, and balancing powers between a corporation's executive and supervisory entities. While firms should not necessarily be administered like governmental bodies, there are many lessons from public sector organisational reform and institutional governance that may be applicable to large-scale public corporations. Keywords: Corporate governance, comparative governance, business organisation, local government. We would like to thank Anna Ossipova of Business Development Consulting for useful comments on an earlier draft of the paper. All faults remain our own.

Transcript of Running business like a government in the new economy: lessons for organizational design and...

Running Business Like a Government in the New Economy: Lessons for Organisational Design and Corporate Governance

Bryane Michael, Oxford University and Randy Gross, Tempe City Government

Table of Contents

Introduction....................................................................................................................1 Current Trends in “Private Sector Reform”...................................................................3 Lessons from Public Sector Reform ..............................................................................7 Example from Tempe Arizona.....................................................................................11 Some Lessons for Running Business like a Government ............................................16 Bibliography ................................................................................................................19

Abstract: Principal-agent problems are largely responsible for poor corporate governance. Much work on private sector corporate governance reform seeks to address transparency, accountability and responsiveness to stakeholder interests under the new category of corporate social responsibility. Yet, these issues are not new. The public sector has been working on these issues for many years – especially in looking at ways of reducing malfeasance and also optimizing use of resources for the benefit of principals. Some lessons from public sector reform include promoting information dissemination, participation, and balancing powers between a corporation's executive and supervisory entities. While firms should not necessarily be administered like governmental bodies, there are many lessons from public sector organisational reform and institutional governance that may be applicable to large-scale public corporations. Keywords: Corporate governance, comparative governance, business organisation, local government. We would like to thank Anna Ossipova of Business Development Consulting for useful comments on an earlier draft of the paper. All faults remain our own.

1

Introduction If the 1980s and 1990s were the era of public sector reform, then the early 2000s is

the era of private sector reform. A wave of reforms -- including the Sarbanes-Oxley Act, the

Commission of the European Communities’ (2002) white paper on corporate social

responsibility, and New York Stock Exchange rules on corporate governance structures of

listed members -- all seek to change the governance of the private sector. Such changes

generally stress increased transparency, accountability, and responsiveness to stakeholder

interests in corporate governance.

In much of the literature about corporate governance reform, reform is treated as

occurring on a tabula rasa. Business relations in the new economy are ostensibly completely

different due to the rise of the network society (Castells, 1996), multi-layered governance

controlled partly by multi-national enterprises (Held et al., 1999), post-Fordian economic

relations (Amin, 1995; Piore and Sabel, 1984 ), new production of knowledge (Gibbons et

al., 1994), and corporate social responsibility (Baukol, 2002; Bendell, 2000; Holme and

Watts, 2000 ). In this new economy, the organisational boundaries between states and firms

become blurry as firms are required to act more like states (Hilton and Gibbons, 2002;

Grayson, 2001) and states act more like firms (Monbiot, 2000; Strange, 1997). Yet,

organisational reform in this supposedly new environment has already been underway for a

decade in the public sector. Such work has aimed at increasing transparency, accountability

and responsiveness to stakeholder interests (Langseth, 1995; Bangura, 2000; World Bank,

1997). Such experience is informative for private sector reform because whether in the public

or private sector, many of the information asymmetries and principal-agents problems which

appear in contractual relationships may be analysed in a similar fashion (Stiglitz, 1995;

Gibbons, 1998; Eggertsson, 1990; Datta-Churadari, 1990). The main issue at stake is not

whether the organisation is technically classified as “public” or “private” but how resources

in the organisation are controlled and how that control is determined.

2

This paper will argue that behind both public and private sector malfeasance lies the

principal-agent problem.1 Such principal-agent problems have been addressed by public

sector reform and there are roughly two important main lessons which we would like to

stress: that participatory organisational structures can yield greater accountability and

transparency and that governance based on open feedback can increase responsiveness to

stakeholders. Section I will present a rough theoretical overview of the negotiation of

interests and politics within the firm. Section II of the paper will put the argument into

context by discussing one of the most salient current approaches to corporate governance

reform, namely corporate social responsibility. Section III will highlight some lessons from

public sector management reform aimed at increasing public sector transparency and

accountability. Section IV will present a case study from Tempe Arizona highlighting how

public sector transparency plays a role in the performance of a city government. Section V

will present some lessons or issues for consideration for corporate governance reformers

whether they be regulators, consultants, stockholders, boardmembers or managers.

There are several caveats to note before we begin. First, we strongly do not suggest

that business should be administered like a public entity (or that private sector bodies should

adopt similar organisational and regulatory principles as public sector organisations).

Organisational performance between national administrations and between sub-national

entities varies greatly and is highly contingent on a wide range of political and historical

variables (Grindle, 1991; Wood and Waterman, 1994). Proposing that firms should run more

like governments may seen counter-intuitive Conventional wisdom states that government

should run more like business and many public management critics seek to install private

sector mechanisms into the public sector.2 Instead, we argue that there are many lessons to be

learned from reform – and mainly from reform aimed at increasing transparency,

accountability and responsiveness to stakeholders. Second, we will not provide an exhaustive

overview of the public sector management reform or corporate governance literatures.

Readers interested in exploring these topics further may consult the references.3 Third, given

that this paper is based on our experience as practitioners, other readers will undoubtedly

1 The principal-agent problem refers to a core issue in institutional and information economics – where managers (as agents) may not act in the best interests of the principals (be they shareholders or stakeholders). Given the extensive coverage of the principal-agent problem, we will not review this literature here (see Williamson, 1985; Eggertsson, 1990; Gibbons, 1998; or Pejovich, 1990). 2 For more on New Public Management or introducing market mechanisms in the public sector, see Barzelay (1992) or Thompson (1997). 3 See Monks and Minow (2001), Harvard Business Review (2000), or Baukol (2002).

3

have different opinions and experiences related to the value of public sector reform for the

debate on corporate governance reform. Our purpose here is to explore a relatively new area

for ideas about corporate governance reform rather than prove empirically or model-

theoretically conditions under which lessons from public sector reform may enhance public

company stakeholder welfare. Further empirical research should explore these linkages.

Politics and the Firm

Governmental and political organisations are very different from private sector

firms. Government organisations necessarily are designed to incorporate a wide range

of interests reflecting in the voting process for government officials (Shepsle and

Bonchek, 1997), in policy consultation (Weimer and Vining, 1998; Grindle and

Thomas, 1991), and even within the government itself (Wood and Waterman, 1994).

The social obligation of private sector and business organisations has traditionally

been seen to maximise profits (Friedman, 1973). If there are politics within the firm,

these politics are not seen as competition for social policies, values or votes – but the

conflict of one groups interests over another’s that comprises an entire system of

managing “interest politics” (Morgan, 1996).

The firm as a site of political negotiation and resolution extends back to John

Common’s Conflict Resolution School which sees the firm, its rules and procedures

as the result of the resolution of previous conflicts (Rutherford, 1994). March (1962)

stresses the nature of the firm as a political conflict system such that the firm (and its

executive) act to broker settlements between the firm’s various stakeholders. Hatch

(1996) notes that interest conflict can arise due to different groups in the organisation

seeking to capture “strategic contingencies” or develop “resource dependency”. Such

brokerage would favour groups or coalitions of groups which best fit the strategic

environment. In this perspective, the dominance of shareholders reflects the

importance of equity markets in firm capitalisation over bank finance – and the

decreased relative importance of other corporate stakeholders such as suppliers due to

increasingly think competition (Fligstein, 1987). Often the chief executive must act as

a diplomat or statesman – exercising leadership that gives a firm its distinctive

competence (Selznick, 1957).

4

Negotiation can be distributive or integrative bargaining (Walton and McKersie,

1965). Distributive bargaining consists of political settlements between stakeholders

and such theorising was important during the 1960s and 1970s, attendant with

industrial conflict between unions and management that coloured the nature of

business theory. Since the 1980s until today and concomitant with the decrease in

union activity throughout most of the OECD, theories of political settlement have

been more integrative or consensual. The have been a number of management fads –

the most recent being “stakeholder theory” (Walker and Marr, 2001; Argandoña,

1998; Brenner, 1993).4 Corporate Social Responsibility strongly represents an

application of such stakeholder thinking which ignores political factors and principal-

agent problems.

Current Trends in “Private Sector Reform” In the 1990s and early 2000s, the discourse about reforming the private sector and

particularly “Corporate Social Responsibility” (CSR) became increasing prominent within

company, government and civil society writing.5 While there are many definitions of CSR,

Holmes and Watts (2000) of the World Business Council for Sustainable Development

provide a reasonably representative definition as the “continuing commitment by business to

behave ethically and contribute to economic development while improving the quality of life

of the workforce and their families as well as of the local community and society at large."6

Lying behind this definition is the belief that the firm’s main objective as defined in the field

of corporate finance -- maximising shareholder value -- is not sustainable because it ignores a

wide range of other actors (or “stakeholders” such as creditors, customers, debtors,

environmental interests, and future generations). Implicit in this definition is also the

assumption that executives should act – not in their own self-interest, but in the interest of

other actors such as minority shareholders. This encapsulates many of the issues raised in the

corporate governance literature.

4 As will be argued later in the paper, such a consensual view of the firm ignores politics but also ignores principal-agent problems due to unclear accountability (Jensen, 2001). 5 For a fuller treatment of CSR organisations and the failure of CSR, see Michael (2002). 6 A survey based attempt at defining CSR done by Corrado and Hines (2001) in Great Britain shows that “responsibility to customers” was the most important element of CSR (at 20%), followed closely by “responsibility toward the local community” (17%).

5

Yet, the corporation is not seen as altruistically implementing CSR initiatives – but

responds to external pressures aimed at promoting transparency, accountability, and

responsiveness to stakeholder interests. Examples of company programmes include those of

Daimler-Chrysler, Du Pont, Shell, and DHL. Programmes include those such as triple bottom

line initiatives (Elkington, 1997), stakeholder boards (Leam, 2002), and voluntary

compliance with codes such as Caux Principles, the Global Sullivan Principles, and the

Keidanren Charter. Other types of programmes include product certification – such as the

Global Reporting Initiative (GRI) guidelines, the Social Accountability 8000 (SA 8000)

standard, and the AccountAbility 1000 standard. Other authors place stock in business ethics

(Diehart, 2000).

While there are many more examples of CSR and corporate governance programmes,

these programmes in general appear not to address the deep underlying incentive structure

governing the relation between principals and agents. First, CSR-type programmes may

cause resource misallocation and diversion within the firm. Resource misallocation within

the firm includes the diversion of managerial time and resources through the creation of CSR

executive posts and staff time dedicated to activities which are essentially in the marketing

function (Murray, 2002). Second, CSR activity may politicise the organisation or accentuate

interests based on pre-existing relationships include public relations (PR) interests within the

firm (Tomlinson, 2002). The "stakeholder model" politicises the organisation at two levels.7

At the governance level, "stakeholder" boards may introduce a range of politically appointed

or “token” representatives. At the operational level, to the extent that guidelines such as the

GRI appear to politicise the organisation, they may create directly unproductive activity or

generate tournaments rather than promote responsibility. The CSR function just like any

other bureaucratic entity is another “lobby” for budgetary resources and senior managerial

attention – a lesson which many over-sized governments and conglomerate corporations

learned in the US in the 1970s. Even assuming that stakeholder interests could be adequately

identified and priorities established, many CSR initiatives involve significant “transactions

costs” as many of the proposed guidelines entail relatively large costs in time and money for

preparing, interpreting, and using them.

7 See Freeman (1994) for a discussion on the politics of stakeholder theory.

6

Regulation based CSR also does not appear to address principal-agent problems.

First, CSR regulation seems to herald an era of government co-operation in private sector

development and progressive regulation aimed at creating a better kind of capitalism.

Underneath this rhetoric though lies conflictual forces which still pit government against

business and visa-versa. Rather than simply representing an area of possible regulation, CSR

represents a site of contestation for the right to determine social objectives and the funding of

these objectives. CSR offers policymaking powers to businesses because it allows them to

determine the CSR agenda. To the extent that companies determine social policy in conflict

with democratically elected and monitored governments, this represents a “democratic

deficit” and lack of democratic accountability. Second, while a certain amount of

“stakeholder” participation may be beneficial, the involvement of business in policymaking

in the CSR context reflects wider trends of changing power between business and

government – resulting in some cases either the “capture” or “retreat” of the state (Monbiot,

2000; Strange, 1997). The effort of the EU to shape the CSR agenda is suggestive of the

political nature of CSR. Third, the increasing elaboration of policies (including CSR at the

international level) represents a type of multi-layered government where power shifts to

international organisations and multi-national corporations – adding another layer of

governance (Held et al., 1999). Such activity represents a type of “mandate creep” (Einhorn,

2001). By appropriating CSR agenda-setting, these institutions arrogate the relatively non-

transparent and non-accountable moral and even legal rights to regulate business and

government relations at the international level.

All these issues suggest that the experience of public sector reform may be important.

First, if the organisation is politicised, then few organisations have more experience dealing

with the balance of political and operational objectives than public sectors. Second, current

reforms fundamentally are about the regulation of the private sector – often by the private

sector itself. States have a long track-record in regulating the private sector, an experience

which the private sector and its advisors can draw upon. Third, the division of regulatory

functions between public and private sectors occurs as the result of a political decision.Yet

the politics behind corporate governance reform is rarely discussed. Such a “silent

revolution” is non-transparent and unaccountable to the stakeholders. Fourth, some public

sector entities are the same size as firms – thus comparison is possible.8

8 For example, Wal-Mart is roughly the size of the Russian Federation.

7

Lessons from Public Sector Reform

In the mid-1990s, the issue of anti-corruption and the attendant values of

transparency and accountability gained prominence. From China to Argentina,

countries, sub-national regions, municipalities have started to pursue “governance”

programmes. According to an anti-corruption donor co-ordination meeting held in

Vienna on May 15th, the distribution of such “governance” programmes varies

geographically and functionally.9 Geographically, listing countries by the number of

anti-corruption focused governance programmes, Russian Federation ranks first with

13 programmes, followed by Romania (8),Ukraine (6), Albania (6), Armenia (6), and

Indonesia (5). Conspicuously absent is greater technical assistance to China (3

projects) due to its size, and Afghanistan due to its global strategic importance.

However, these numbers do not include programmes which were labelled as “global,”

or “regional” programmes. Regarding the global distribution of functions,

programmes (as classified by the UN) are as follows: “law enforcement” (82),

programmes which might be labelled as “capacity building” because they are

primarily focused on “training”, “institution building”, or “capacity building” (38),

“financial sector/financial management” (37), “ awareness raising” (34), legislation

(32), public sector management (23), “judiciary” programmes (16), and private sector

management (11).10

While public sector reform is a much larger area than anti-corruption, the anti-

corruption component of public sector reform is interesting for a number of reasons.

First, it explicitly aims at directly or indirectly changing the incentives which cause

the “use of public power for private gain.”11 Second, it has been tied close with the

Berlin-based NGO Transparency International and as such has recognised the

international dimensions and multi-stakeholder issues tied with governance much

more than the broader public sector reform literature. Within much of the governance

literature, private sector governance is closely tied to the governance of other

stakeholders such as public sector organisations.

9 These data are based on projects reported by the meeting’s participants, of which USAID and World Bank were absent. A complete reference will be provided once these data are finalised and published. 10 Due to reporting of several types of programmes under one heading, these values are approximate. 11 For more information on the elaboration of anti-corruption strategies (see Riley 1993, Langseth 1997, World Bank 2000, or Klitgaard et al., 2000).

8

Based on these experiences, a number of “best practices” and analytical

monographs were published. World Bank (1997) notes the role of several elements of

public sector reform for reducing corruption and increasing transparency. In civil

service reform, “recruitment, promotion, and pay, is clearly a vital issue” for creating

an incentive structure less prone to malfeasance and responding to stakeholder

interests. “Ethics codes and institutional values, once established, help protect a civil

service's integrity and professionalism” as a way of fostering personal incentives.

Even if incentive structures are in place, accountability still needs to be in place as

“financial management systems are powerful instruments for preventing, discovering,

or facilitating the punishment of fraud and corruption. They allocate clear

responsibility for managing resources, reveal improper action and unauthorized

expenditures, facilitate audit by creating audit ‘trails’ and protect honest staff.” While

decentralisation is a contentious area for transparency, the Bank found that

“decentralization can help reduce corruption if it improves government's ability to

handle tasks while increasing transparency and accountability to local beneficiaries.

But decentralization can also increase corruption if local and regional governments

have stronger incentives (because of lower formal pay levels, for example) or more

opportunities to carry out fraudulent activities and are less constrained by financial

management and auditing systems (which are often in even shorter supply in regions

than in the center).”

Underlying these actions to promote transparency, accountability, and

responsiveness to stakeholder interests, the Bank finds that civil society and media

oversight are vital in discouraging corruption. “More participatory approaches” as

well as “coalitions” act to promote this oversight. Finally, regulation plays a role –

especially in information disclosure such as “publication of government budgets and

their availability in easy-to-read summary form, frequent reports to the legislature on

budget implementation that enable comparisons to be made between budgeted and

actual revenues and expenditures, and timely preparation of public accounts and audit

reports and their scrutiny by the legislature

and the media are some of the foundations

of open and accountable government.”

Integrated Strategy for Governance Reform

Economic/Fin. Reform:(tax reform, deregulation,Liberalisation)

LegislativeReform

Citizen Empowerment

RULE OF LAW

Executive Reform/Modernization

Responsible Media

Political Reform

“Watchdog Agencies”

Judicial Reform

Source: adapted from Langseth (1998)

Build multi-stakeholderethics

Integrated governance reform to promote integrated good governance

9

Citing further, “in some countries "sunshine" laws (which require agencies to hold

public hearings before making policy or program decisions) and freedom of

information laws (which require governments to make information surrounding

decisions available unless there are supervening public policy reasons for secrecy)

may be appropriate.” Finally regarding the role of consultation, “the regular

publication of consultative documents when new policy is contemplated is good

practice everywhere.”

Based on the experience of numerous programmes, Langseth et al. (1995) provide a

general strategy for public sector reform (Figure 1) and four key areas of activity.

Langseth and other authors such as Rider (2001) Rose-Ackerman 1996) note the

importance of “integrated strategy.” Such an integrated strategy consists of reform

in several stakeholder groups including executive, legislative and judicial as well as

private sector and media.

Langseth et al. (1995) categorise organisational reforms around the four principles of

awareness raising, institution building, prevention, and enforcement. In general each

of these principles advocates increasing participation and institutional checks and

balances. Specifically, “awareness raising” includes the involvement of all

stakeholders, access to information, broad-based perceptions surveys, and mass media

campaigns. For example, the Independent Commission Against Corruption (ICAC) in

Hong Kong used awareness raising conferences with almost 1% of the population

every year to signal institutional change (Langseth, 2001). “Prevention activities”

include the implementation of Codes of Conduct, Integrated Financial Management

Systems, “Islands of Integrity/Integrity Pacts” (which seek to create a cordon

sanitaire around a part of the organisation and promote integrity from there), promote

transparent procurement practices. Results-oriented Management include “Citizen’s

Charters” which outline expectations by service users as well as declaration and

monitoring of assets. Finally, “institution building” includes undertaking activities in

other stakeholder institutions which can oversee the probity of the executive. Some of

these bodies include Supreme Audit Institutions, Judiciary, Ombudsman, Media, and

Legislature.

10

The early experience suggests that increasing regulations alone will not

improve accountability or transparency. Looking first at accountability, one

seemingly useful activity for increasing accountability is the audit. Yet, audits have

been found to have a number of drawbacks -- including the acceleration of the lack of

trust, institutionalisation of accountability, replacement of substantive rationality for

instrumental rationality, and the increasing politicisation of the organisation (Power,

1997). Looking at transparency, again the public sector reform literature suggests that

“adding transparency” may not achieve the deeper objectives of eliminating principal-

agent problems. Due to increased politicisation of the public sector and simply

because many voices speaking together creates a ruckus, “transparency” may be

onerous if it hinders the accomplishment of group objectives or even unethical if it

violates the individual’s right to privacy rights of individuals. “Transparency” may

also become a type of fetish, devoid of meaning – as the rise of so many ill-organised

and vague conferences on transparency indicate. Ethics dilemmas arise in the real

world precisely because it is difficult to know if group welfare is being compromised

by a particular action. More transparency by itself probably will not help resolve these

dilemmas. Instead, the “transparency” discourse may cover up the political and ethical

issues resting behind the language of transparency. Geraats (2002) notes, transparency

can reduce hidden action by civil servants. Posen (2002) takes the analysis further by

talking about the objectives of transparency. “Transparency” is not an end in itself but

is usually used in political and social discourse as a means to another end. The

objectives he cites are increased predictability, trust, oversight, credibility and

politicisation. Each of these objectives though is heavily value-laden and assumes

very different judgements about “good” and “bad.”

Instead of a “regulatory approach” to increasing transparency and

accountability, governance structures in both the public and private sectors are

converging upon a system of checks and balanced designed to promote the self-

monitoring necessary to over come principal-agent problems.12 An organisational

approach to governance also combines different types of knowledge, ability,

independence and willingness to act (Gibbons et al., 1994). The analogy of similarity

between the board of directors and the executive in the private sector and the

12 For an example of “self-enforcing” type arrangements, see Coate and Ravallion (1993).

11

legislature and the executive in the public sector is flawed in many respects – being

only an analogy. However, the point that organisational design which promotes

checks and balances and the combination of different types of competencies remains

valid.

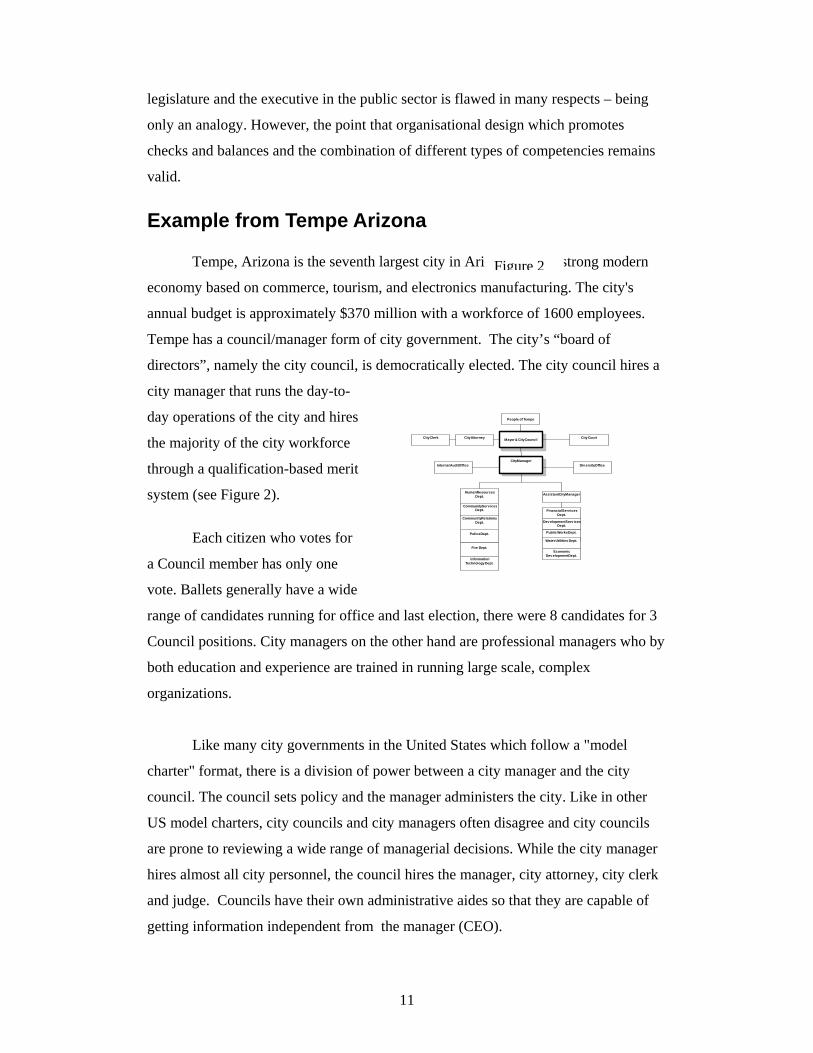

Example from Tempe Arizona

Tempe, Arizona is the seventh largest city in Arizona, with a strong modern

economy based on commerce, tourism, and electronics manufacturing. The city's

annual budget is approximately $370 million with a workforce of 1600 employees.

Tempe has a council/manager form of city government. The city’s “board of

directors”, namely the city council, is democratically elected. The city council hires a

city manager that runs the day-to-

day operations of the city and hires

the majority of the city workforce

through a qualification-based merit

system (see Figure 2).

Each citizen who votes for

a Council member has only one

vote. Ballets generally have a wide

range of candidates running for office and last election, there were 8 candidates for 3

Council positions. City managers on the other hand are professional managers who by

both education and experience are trained in running large scale, complex

organizations.

Like many city governments in the United States which follow a "model

charter" format, there is a division of power between a city manager and the city

council. The council sets policy and the manager administers the city. Like in other

US model charters, city councils and city managers often disagree and city councils

are prone to reviewing a wide range of managerial decisions. While the city manager

hires almost all city personnel, the council hires the manager, city attorney, city clerk

and judge. Councils have their own administrative aides so that they are capable of

getting information independent from the manager (CEO).

City Manager

Human ResourcesDept.

Community Serv icesDept.

Community RelationsDept.

Financial Serv icesDept.

Public Works Dept.

Water Utilities Dept.

Mayor & City Council

Dev elopment Serv icesDept.

Police Dept.

People of Tempe

City AttorneyCity Clerk City Court

Fire Dept.Economic

Development Dept.

Assistant City Manager

InformationTechnology Dept.

Internal Audit Office Div ersity Office

Figure 2

12

As elected officials City Council members belong to an extended information

network comprised of citizens, businesses, city employees and other elected officials

who provide information, viewpoints and analysis on city issues. While by charter a

Council's most important duties may be to set the city budget and hire the city

manager, their day-to-day duties include investigation and analysis of a wide-range of

stakeholder issues. A Councilmember's day might begin with breakfast with the local

Chamber of Commerce, followed by a review and site-visit of a multi-million dollar

capitol improvement proposal, followed by a meeting with a neighbourhood

committee facing renewal challenges and ending with a late-night phone conversation

from a disgruntled citizen. This stylised daily meeting schedule illustrates the degree

to which citizens often have access to their local city council. Any of Tempe's

160,000 citizens, thousands of businesses or 1600 employees can contact a

Councilmember by phone, e-mail and/or personal visit. Communication to city policy

makers is both voluminous and diverse.

All city government decisions are made in public and city governments have

to abide by both open meeting and public records laws that are mandated by the State

government. For example, Arizona State Revised Statutes (article 38-431.01) state

that meetings shall be open to the public, require written minutes or a recording of the

meeting, and that that minutes or a recording of the meeting shall be open to public

inspection three working days after the meeting. Significantly, this open public

meeting law states that “a public body may make an open call to the public during a

public meeting, subject to reasonable time, place and manner restrictions, to allow

individuals to address the public body on any issue within the jurisdiction of the

public body.” Every Tempe City Council meeting has an agenda item that allows a

citizen to address the Council on any subject.

Council activities are also monitorable through mass media channels. Council

meetings are public and they are televised and the television broadcast can be

accessed through the City's Internet site (in streaming video) allowing anyone in the

world with Internet access to watch the Tempe City Council decision making process

as it occurs. All of the city's meeting agendas and staff reports for the meetings are

available on the City's Internet site (www.tempe.gov). An example of the type of

detail that is available for public inspection and required Council review is an agenda

13

item called "Report of Claims Paid." Every meeting the Council approves

disbursements paid by the city since the last Council meeting, including such items as

utilities and postage.

When Council members run for office they must abide by a comprehensive set

of financial reporting laws that are defined by Arizona State Statutes (ARS Title 16

Chapter 6). These laws require candidates for office to show from whom they raise

money. In addition, candidates also have to report their sources of personal income,

and any significant stock or ownership interests in a business. This information helps

disclose potential conflicts of interest.

Tempe city government acts according to the principles of sound financial

management. Tempe City government has a AAA bond rating from Fitch, an Aa1

bond rating from Moody's, an AA+ bond rating from Standard and Poor's and places

a premium on securing the lowest possible cost for debt placements. Much finance

theory and public administration theory assumes the good credit ratings are due to the

legal force of violence (to use Max Weber’s term) to collect tax revenue necessary to

repay debt or the ability to call upon national government finance. However, the

ability to raise taxes freely to increase revenue is limited. Tempe's major revenue

source is sales tax collection. All sales tax increases have to be approved by a vote

and the electorate also can vote to decrease or eliminate taxes through the initiative

process. Recourse to exceptional national government finance is also limited. At

annual elections, or special elections that are triggered through the recall process

(given the collection of a required number of signatures), elected officials can be

voted out of office if citizens disagree with city financial (or any other) policy. This

public pressure to be fiscally prudent results in compliance with several good

principles of public finance including integrated and independently verified systems

of commitment, disbursement and audit which keep liabilities “on the books.”

The City's financial management plan is comprehensive and establishes

benchmarks for financial capacity. The financial management plan also generates

long and short term financial forecasts. The debt management plan keeps debt per

capita at around $700-$800, debt to full cash value at between 1.10-1.25% and debt to

14

general government revenue at 10%-15% (within generally accepted financial

parameters).

Tempe manages a $370 million budget comprised of $240 million in current

expenditures and $130 million in capital expenditures. Bi-annually a strategic plan is

generated along with a 6 year capital improvement project plan. These plans help

forecast future needs and allow budget planning in anticipation of current and

forecasted revenues. The monthly monitoring of both revenues and expenditures

allows for mid-budget year spending adjustments in the event of unforeseen economic

changes. City programs have performance measurements that are compared to

industry standards to ensure citizens are receiving “value for money.” The public can

track the city's financial management through the budget document and monthly

revenue and expense reports-- all of which are public documents.

Executive compensation is another area where accountability in the public

sector plays a role. In Tempe, the lowest salary for a city employee is approximately

$25,000 for a custodian. The highest salary is approximately $150,000 for the City

Manager-- a ratio of 6:1. Tempe city council members earn $16,942 annually. As a

comparison, in 1973 the “typical” CEO earned approximately 45 times the wage of

the average worker – in 2000 this ratio exceeded almost 500. The boards of directors

of many major corporations earn over $100,000 in salary and stock options.

Some cities have district systems where representatives are elected from areas

of the city. Cities also have numerous citizen committees -- Tempe has 29 -- that often

have a different viewpoint than either the council or manager. The result of this

democratic governance/professional management dyad is a high degree of satisfaction

amongst residents. In a 1998 citizen satisfaction survey conducted by Dr. Bruce

Merrill of Arizona State University it was found that 96% of Tempe residents were

satisfied or highly satisfied with city services. The survey also showed that 80% of

those expressing an opinion were satisfied or highly satisfied with how city money

was spent.

There are over 80,000 local governments in the United States such as cities,

school boards, and counties. All these governments are in competition with their

15

peers throughout the country to attract business and residents. Yet they all function

with open government and democratic processes. Local governments are an excellent

example of how an organization can govern in a democratic manner, operate

efficiently and be responsive to the needs of stakeholders. Such a trend suggest that

there is not necessary any need for compromise between democracy and

competitiveness.

16

Some Lessons for Running Business like a Government

Behind both public and private sector non-optimal use of funds and resources

lies the principal-agent problem. In the 1970s and 1980s, public sector organisations

tried to figure out how to have civil servants as agents act in accordance with the

wishes of the principals (their voting constituencies and public service users). In the

early 2000s, firms and especially large, diversified multinational enterprises face

similar decisions about how managers should act as agents of a wide range of

principals which include shareholders and bondholders but now also environmental

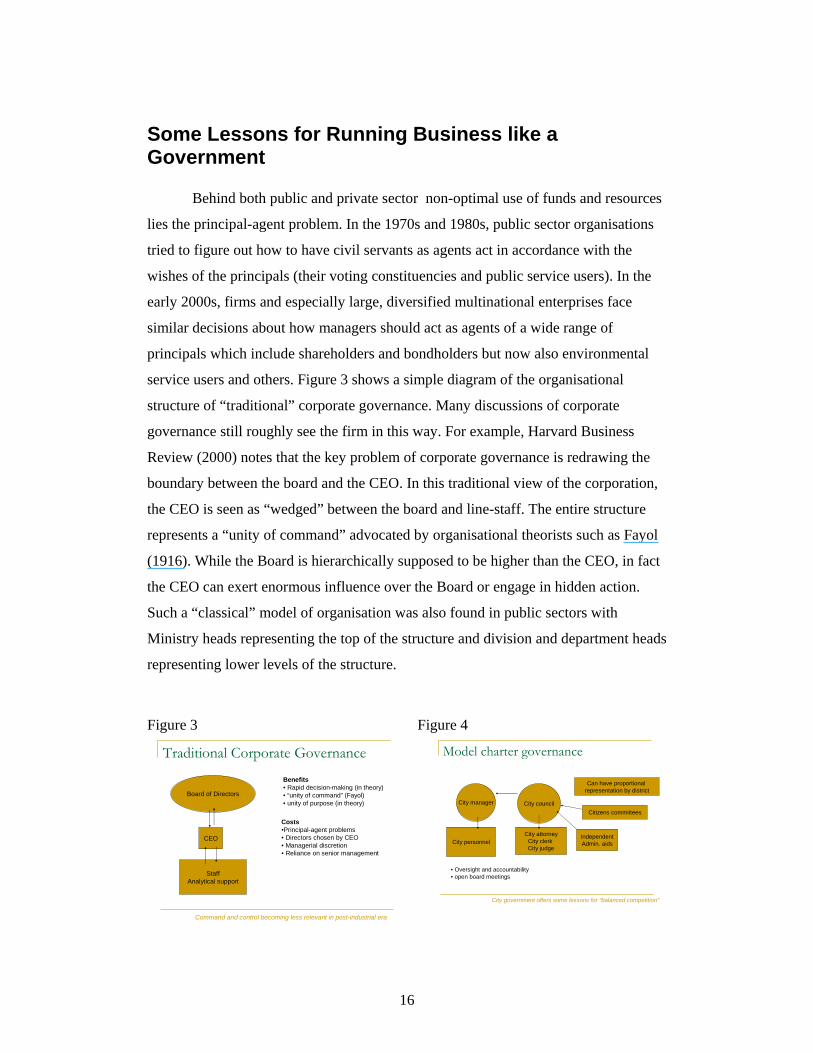

service users and others. Figure 3 shows a simple diagram of the organisational

structure of “traditional” corporate governance. Many discussions of corporate

governance still roughly see the firm in this way. For example, Harvard Business

Review (2000) notes that the key problem of corporate governance is redrawing the

boundary between the board and the CEO. In this traditional view of the corporation,

the CEO is seen as “wedged” between the board and line-staff. The entire structure

represents a “unity of command” advocated by organisational theorists such as Fayol

(1916). While the Board is hierarchically supposed to be higher than the CEO, in fact

the CEO can exert enormous influence over the Board or engage in hidden action.

Such a “classical” model of organisation was also found in public sectors with

Ministry heads representing the top of the structure and division and department heads

representing lower levels of the structure.

Figure 3 Figure 4

Traditional Corporate Governance

Board of Directors

CEO

Costs•Principal-agent problems• Directors chosen by CEO• Managerial discretion• Reliance on senior management

StaffAnalytical support

Benefits• Rapid decision-making (in theory)• “unity of command” (Fayol)• unity of purpose (in theory)

Command and control becoming less relevant in post-industrial era

Model charter governance

City manager City council

• Oversight and accountability• open board meetings

City personnelCity attorney

City clerk City judge

IndependentAdmin. aids

Can have proportional representation by district

Citizens committees

City government offers some lessons for “balanced competition”

17

Figure 4 however shows how the public sector has dealt with some of these

issues. Rather than a simple machine structure, public sectors have moved to

structures based on checks-and-balances. In the charter model, the city manager (as

the executive in charge of executing policy) shares responsibility with the city

council. In their relationship, both entities have clearly defined responsibilities and

authority.

The experience of public sector reform suggests a number of lessons for

organisational reform. First, public corporations should have an “integrated strategy”

rather than piece-meal approach to reform. Rather than simply adopting Triple

Bottom Line initiatives or accounting recommendations, the entire governance

structure should be discussed by stakeholders who should have greater say in

governance structures. Second, scandals and newspaper articles have raised awareness

about corporate malfeasance. But as practitioners learned from anti-corruption work,

more awareness raising about “solutions” rather than “problems” needs to be

undertaken. Especially important is the role of data collection to raise awareness and

collect preferences.13 Third, corporations should increase the involvement of other

stakeholders in basic documents such as their mission statement (and the experience

of Citizen’s Charters may be relevant here). Fourth, corporations should resist the

trend toward increasing regulation. The public sector has created regulations, codes of

conduct, and numerous reporting requirements. Often, their impact on transparency

and accountability is unclear.14 Rather than regulating, organisational reform and

information dissemination should be undertaken to balance interests where

appropriate.15

The Tempe case study also suggests some lessons for transparency,

accountability and responsiveness to stakeholders. Regarding transparency,

information disclosure and access to information may be increased. Private sector

13 The role of data collection in marketing had been well established. However, the role of data collecting in establishing social preferences is much less commented on and corporations may benefit from the experience of “social marketing” (Kotler, 1989). 14 Power (1997) refers to the growing frequency of the use of audits and the growth of audit bodies as the “audit explosion.” For Power and other commentators the effects of audit on public service delivery have been far from clear. 15 Much of the literature suggests that incentive-based contracts are a more effective way of regulating than adding bureaucracy.

18

decisions are often made in private and in secret. Government has the open public

meeting and public records requirements. Except for legal, personnel and real estate

matters, all business is conducted in full view of the public and media. Governments

concerned about the negative impacts of information disclosure on policymaking have

found these fears to be largely unsubstantiated.

Second, boards should consider more democratic methods of appointing

members of the Board. One possibility would be to have some limited form of

election based on a qualified pool of candidates. In the modern corporation, the CEO

often handpicks Board members. A third and related lesson is that perhaps the voting

arrangements for directors should not simply be based on the number of shares owned

but on a “non-linear” voting arrangement. In the public choice literature, they find

that weighted voting may overcome “impossibility paradoxes” and lead to better

decisions. Such voting rules may stem from seats on the board reserved for

specifically stakeholder groups. The specific weighting of votes (or even if the

optimality of such an arrangement) would need to be explored with limited

experiments or theoretical work.

Third, in line with the recommendations of the Harvard Business Review

(2000) the line does need to be redrawn between the CEO and the Board. At present,

the CEO of a corporation wields tremendous clout as most of the decision making

power is concentrated in the hands of one person. In a city government, administrative

and policy making powers are split between the Mayor, Council and City Manager .

While some city governments may have a reputation for indecision and inflexibility

due to such balances-of-power, other cities perform well and it has not been

empirically proven that city administrations always are less efficient than the private

sector in making equivalent decisions.

Fourth, private sector organisations may promote a policy of prudential

investment. Public finance is based on husbandry of public resources with low risk.

Private sector organisations may resort to the use of “junk bond” finance and paying

high rates to raise capital. Even in the private sector corporate finance literature, a

lower risk strategy of value investing (buy and hold) may provide higher long-run

returns. Fifth, corporate board members and executives are encouraged to engage in

19

activities that increase their net worth, even though in the long run these activities

may be injurious to the organization and stockholders.

Sixth, like the council-manager form of government, perhaps there should be

some permanent positions that report to the board, not the CEO. Positions that report

to the board, not the CEO, may provide the independence necessary to take long-run

based decisions and reduce self-dealing of senior executives. Seventh, the committee

system may be revised so that shareholder or consumer committees that report

directly to the board and have full independence in their advisory capacity. Such a

system would also act as an effective form of marketing. Eighth, City Councils meet

almost every week of the year. Boards of Directors meet about once a month. Cities

are subject to initiatives and referenda that force the Council to change policy. So-

called public companies infrequently, if ever, bring policy questions to the

shareholders and boards have been known to ignore shareholder resolutions.

Government has a long history of dealing with principal-agent problems.

Some governments at certain times have been successful in bringing the concerns of

the principals to the agents and controlling agent “hidden action” through mechanisms

of democratic governance. The challenge for public corporations will be to devise

increasing transparent and accountable (if even democratic) mechanisms of policy

formulation and implementation. In the short-term, corporate executives may see this

type of process as being counterproductive for profits or even impinging upon their

own vested interests. However, as the experience of public sector reform shows,

increased transparency and accountability does not have to negatively affect

performance – even if it does necessarily have to reduce managerial self-seeking.

Bibliography Amin, A. (1995). (ed) Post-Fordism: A Reader. Oxford: Blackwell Arnold, N. (1994). The Philosophy and Economics of Market Socialism: A Critical Study. New York: Oxford University Press. Banerjee, A. (1997). A Theory of Misgovernance. Quarterly Journal of Economics. November: 1289-1332

20

Bangura, Y. (2000). Public Sector Restructuring, The Institutional and Social Effects of Fiscal, Managerial and Capacity-Building Reforms", UNRISD Occasional Paper. No. 3. Geneva. Barry A.K. Rider (2001). Corruption: The Enemy Within Barzelay, M. (1992). Breaking Through Bureaucracy. University of California Press. Baukol, R. (2002). Corporate Governance and Social Responsibility. Presentation at the Caux Round Table. April 19th. Tokyo Stock Exchange. Bendell, J. (2000). Terms for Endearment - Business, NGOs and Sustainable Development. Greenleaf Publishing. Castells, M. (1996). The Rise of the Network Society, The Information Age: Economy, Society and Culture, Vol. I. Cambridge, MA. Clarson, M. A Stakeholder Framework for Analyzing and Evaluation Corporations. The Academy of Business Review, 20 (1): 92-117 Clegg, S., C. Hardy and W. Nord. Eds. (1996). Handbook of Organization Studies. Sage. Coate, S. and M. Ravallion. (1993). Reciprocity without Commitment: Characterisation and Performance of Informal Insurance Arrangements. Journal of Development Economics 40(1). Corrado, M. and C. Hines. (2001). Business Ethics-Making The World a Better Place. Available at: http://www.mori.com/pubinfo/pdf/business_ethics.pdf Commission Of The European Communities (2002). Corporate Social Responsibility: A business contribution to Sustainable Development. COM(2002) 347 final. Brussels, 2nd July. Davis, G. K. Diekmann, and C. Tinsley. (1994). The decline and fall of the conglomerate firm in the 1980s: the deinstitutionalization of an organizational form. American Sociological Review, v. 59 (4), pp. 547-570. Datta-Chauduri, M. (1990). Market Failure or Government Failure? Journal of Economic Perspectives 4(3). Department of Trade and Industry (2001). Developing corporate social responsibility in the UK Business and Society Eggertsson, T. (1990). Economic behavior and institutions. Cambridge: Cambridge University Press. Einhorn, J. (2001). The World Bank's Mission Creep. Foreign Affairs. September / October 2001

21

Elkington, J. (1997). Cannibals With Forks - The Triple Bottom Line of the 21st Century Business. Fayol, H. (1916). Administration Industrielle et Generale. Geraats, P. (2002). Central Bank Transparency. Economics Journal. Gibbons, M., C. Limoges, H. Nowotny, S. Schwartzman, P. Scott, and M. Trow. (1994). The New Production of Knowledge: The Dynamics of Science and Research in Contemporary Societies. Sage Publications. Gibbons, R. (1998). Incentives in Organizations. Journal of Economic Perspectives 12(4). Fall. Giddens, A. (1998). The Third Way: The Renewal of Social Democracy (Cambridge, Eng.: Polity Press. Grayson, D., A. Hodges, D. Kindersley and the Financial Times. (2001). Everybody's Business: managing risks and opportunties in today's global society. Grindle, M. (1991). Public Choices and Policy Change. Harmon, M. (1995). Responsibility as Paradox: A Critique of Rational Discourse on Government. Held, D. and A. McGrew, D. Goldblatt, and J. Perraton. (1999). Global Transformations: Politics, Economics and Culture. Polity. Henderson, D. (2001). Misguided Virtue: False Notions of Corporate Social Responsibility. Hilton, S. and G. Gibbons. (2002). Good Business: Your World Needs You. Textere. Holme, L. and R. Watts. (2000).Corporate Social Responsibility: Making Good Business Sense. The World Business Council for Sustainable Development Hopkins, M. (1998). The Planetary Bargain: Corporate Social Responsibility Comes of Age Klitgaard, R., R. MacLean-Abaroa, and Parris, H. L. (2000). Corrupt Cities. A Practical Guide to Cure and Prevention. Klein. N. (2000). No Logo. HarperCollins. Kotler, P. (1989). Social Marketing: Strategies for Changing Public Behavior. Free Press. Langseth, P. and Stolpe, O. (2001) The United Nations Approach to Helping Countries Help Themselves by Strengthening Judicial Integrity:

Langseth, P (2001) Value Added of Partnership in the Fight against Corruption. OECD’s Third Annual Meeting of the Anti-Corruption Network of Transition Economies in Europe, Istanbul, March 20-22

22

Langseth, Petter. (2000). Integrated vs. Quantitative Approach. Lessons Learned. Corruption: Critical Assessments of Contemporary Research. A workshop hosted by Chr. Michelsen Institute and Norwegian Institute for Foreign Affairs in collaboration with NORAD in Oslo 19-21 Oct. 2000 Langseth, P and R. Stapenhurst. (1997). The Role of the National Integrity System in Fighting Corruption. EDI Staff Working Paper. Washington, D.C.: World Bank. Leam, D. (2002). All Aboard: Improving Public Service Accountability. McIntosh, M, D. Leipziger, K. Jones and G. Coleman. (1998) Corporate Citizenship: Successful strategies for responsible companies. London: Financial Times Management. Monbiot, G. (2000). Captive State: The Corporate Takeover of Britain. Macmillan. Monks, R. and N. Minow. (2001). Corporate Governance. Blackwell Business. MORI. (2000). Corporate Social Responsibility Update. Issue 2 / Autumn 2000 Munro, R. and J. Mouritsen, J. Eds. (1995). Accountability: power, ethos and the technologies of managing. International Thomson Business Press. National Policy Association. (2002). The Government's Role in CSR and Governmental Activities. Available at: http://www.multinationalguidelines.org/csr/government's_role.htm OECD. (2000). OECD Guidelines for Multinational Enterprises: Ministerial Booklet. Pejovich, S. (1990). The Economics of Property Rights: Towards a Theory of Comparative Economic Systems, Kluwer Academic Publishers Piore, M. and C. Sabel (1984), The Second Industrial Divide: Possibilities for Prosperity. New York: Basic Books Posen, A. (2002). Six Practical Views of Central Bank Transparency. Institute for International Economics. Power, M. (1997). The Audit Society: rituals of verification. Reyes, I. (2002). Nation-Building and Good Governance: CSR contributes to national development. Business World. June 12. Rose-Ackerman, Susan. (1996). "Redesigning the State to Fight Corruption: Transparency, Competition, and Privatization." Viewpoint 75 (April). Schwartz, Peter & Gibb, Blair (1999), When Good Companies Do Bad Things: Responsibility and Risk in an Age of Globalization, Wiley, New York. Stiglitz, J. (1995). Whither Socialism? MIT Press. Cambridge, MA.

23

Social Investment Forum. (2001). Report on Socially Responsible Investing 2001. Steiner and Steiner. (2000). Business, Government and Society. McGraw Hill. Strange, S. (1997). The Retreat of the State. Cambridge: Cambridge University Press. Strathern, M. Ed. (2000). Audit Cultures. Routledge. Tomlinson, H. (2002). Ethics Treated As Pr Exercise. Independent on Sunday (London). July 21. Thompson, F. (1997). The New Public Management. Journal of Policy Analysis and Management 16(1). United Nations. (1999). The Global Compact: The Nine Principles. Walker, J. (1998). Socially responsible business. Department for International Development. Social Development Division. Williamson, O. (1985). The Economic Institutions of Capitalism. Wood, D., K. Davenport, L. Blockson, and H. Van Buren III. (2002). Corporate involvement in community economic development. Business and Society 41(2). Chicago; Jun 2002: 208-241 Wood, B. and R. Waterman. (1994). Bureaucratic Dynamics. Woods, N (1988) "Editorial’ Introduction Globalisation, Definitions Debates and implications" Oxford Development Studies 26(10): 8-23 World Bank. (1997). Helping Countries Curb Corruption. Washington: The World Bank. World Business Council for Sustainable Development (1999). Corporate Social Responsibility, Geneva, Switzerland. 1994 Institutions in Economics: the Old and the New Institutionalism. Cambridge University Press:

* March, J.G. (1962) ‘The Business Firm as a Political Coalition’, Journal of Politics, vol. 24(4): 662-78.

Selznick, A. (1957) Leadership in Administration (Evanston, Ill: Row Peterson). Walton, R. E., & McKersie, R. B. (1965). A behavioral theory of labor negotiations. New York: McGraw-Hill Weimer, D. and Adrian Vining. (1998). Policy Analysis: Concepts and Practice. Prentice Hall.

24

Wood, B. and R. Waterman. (1994). Bureaucratic Dynamics. Merilee Grindle and John Thomas, Public Choices and Policy Change: The Political Economy of Reform in Developing Countries. Baltimore, MD: Johns Hopkins University Press, 1991, pp. 1-42. Shepsle, Kenneth A. and Mark S. Bonchek. 1997. Analyzing Politics: Rationality, Behavior, and Institutions. New York: W.W. Norton. Milton Friedman, “The Social Responsibility of Business Is to Increase Its Profits,” The New York Times Sunday Magazine, September 13, 1973 Fligstein, Neil (1987) - "The intra-organizational power struggle: The rise of finance presidents in large corporations" 1919-1979," American Sociological Review, 1987: 44-58. Steven F. Walker and Jeffrey W. Marr in Stakeholder Power: A Winning Plan for Building Stakeholder Commitment and Driving Corporate Growth (2001). MICHAEL C. JENSEN. (2001). Value Maximization, Stakeholder Theory, and the Corporate Objective Function. Journal of Applied Corporate Finance, Vol. 14, No 3, Fall 2001. Brenner, Steven N. 1993. "The Stakeholder Theory of the Firm and Organizational Decision Making: Some Propositions and a Model." International Association for Business and Society Proceedings : 205-210. Argandoña, Antonio. 1998. "The Stakeholder Theory and the Common Good." Journal of Business Ethics 17 (9-10) (July): 1093-1102. Freeman, R. Edward. 1994. "The Politics of Stakeholder Theory: Some Future Directions." Business Ethics Quarterly 4 (4): 409-421