Review of Policies in the Traditional Energy Sector

110

r S I6OI3 Review of Policies in the Traditional EnergySector Discussion Paper Series FILE Directed by The World Bank, Africa Region Supported by DirectorateGeneralfor IntemationalCooperation The Netherlands Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

9 -

download

0

Transcript of Review of Policies in the Traditional Energy Sector

r S I6OI3

Review of Policies in the Traditional Energy Sector

Discussion Paper Series

FILE Directed byThe World Bank, Africa Region

Supported byDirectorate General for Intemational Cooperation

The Netherlands

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

b

RPTES Program Staff

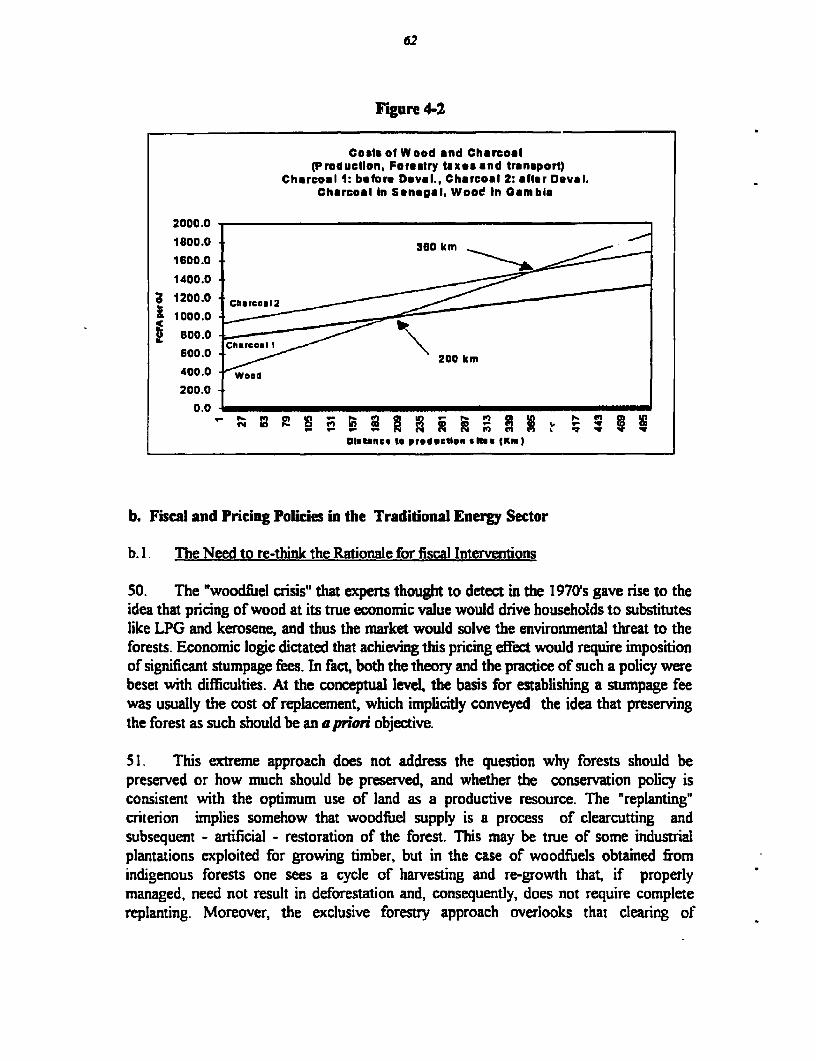

Boris Utria, Task ManagerMax Wilton, Senior Adviser

Azedine Ouerghi, Energy EconomistSuzanne Roddis, Projects Assistant

For additional information on the RPTES program or the Discussion Paper series, please contact:

RPTES ProgramWestern Africa Department

The World Bank1818 H Street, NW

Washington, DC 20433

tel: (202) 473-4488 J 473-0719fax: (202) 473-5143

RE_VEW OF POLICIES IN THE TRADITIONALENERGYSECTOR

RPTES

REGIONAL REPORT

Burkina Faso - Mali - Niger - Senegal - The Gambia

2nd. EditionMay 1996

THIS REPORT IS NOT AN OFFICIAL DOCUMENT OF THE WORLD BANK. IT CONTAINS THERESULTS OF COUNTRY- AND REGIONAL ANALYSES THAT ARE PRESENTED FORDISCUSSION AND COMMENTS. THE FINDINGS, INTERPRETATIONS AND CONCLUSIONSARE ENTIRELY THOSE OF THE AUTHORS.

Review of Policies in the Traional Eneap Sector - RPTESRegional Rqport

TABLE OF CONTENTS

PrefaceExecutive Summary

L Introduction

1.1 Plan of the Report 11.2 Physiography and Population 11.3 The Sub-regional and National Economies 31.4 The Energy Sector 5

H. Profile of the existing Traditional Energy Sector

2.1 General 92.2 A critical Evaluation of the Biomass Resource Base 10

a. Agro-ecological Zones in the RPTES Countries 10b. The Genesis of Action Programs in the traditional

Energy Sector 13c. Overview of the RPTES Data Bases 13d. Key Issues in Data Collection and Management 18e. Key issues in biomass Supply-Demand Balances 23

2.3 Fuelwood Supply and Denand in Rural Areas 262.4 Urban Markets for Fuelwood and Charcoal .. 272.5 Commercial Supply of Urban Markets 292.6 The Role of Institutions 332.7 Main Sector Issues 34

m. The outlook to the year 2020

3.1 The traditional Energy sector from a NEXUS Perspective 373.2 Population Growth, Migration and Urbanization 383.3 Demand for Food, Energy and corresponding Land Use 393.4 Scenarios for Demand for Traditional Energy 413.5 The Supply Potential 423.6 The Implications of economic Growth for Sector Policy 46

Ji

TABLE OF CONTENTS (Continuation)

IV. Towards improved Sector Management

4.1 Options for Interventionsa. Non-price Demand Management 47b. Demand Substitution 48c. Promotion of sutinable Supply 53d. Priorities for Action 55

4.2 Implementation Tools for Supply-side Actionsa Forest Management 56b. Fiscal and Pricing policies in the traditional Energy Sector 62c. Institutional Adaptation and Management of Change 70

4.3 Integration of Fuelwood Management schemes in overallrural development 71

4.4 Human Resources Development 724.5 Orientaion of Extenal Aid 73

V. Country-specific Overviews

5.1 Senegal 775.2 Gambia 805.3 Burkina Faso 835.4 Mali 855.5 Niger 87

Annex

List of the RPTES thematic studies 91

Hi

Tables

1-1 Population and Urbanization 31-2 Selected Economiic Statistics 51-3 Condensed Energy balance 7

2-1 Agroecological Zones in the RPTES Countries (part I) 12Agro-ecological Zones by Country (part II) 12

2-2 Compaison of Results of two regional Inventories 162-3 Main Results of national Inventories 172-4 Summary of Analyses of national RPTES Reports 202-5 Major Urban Woodfuel Markets 282-6 Fuelwood and Charcoal Prices 32

3-1 Population Projection for 2020 383-2 Estimated Evolution of Land Use (Scenario n) 403-3 Comparison of Demand and potentialy sustainable Supply ofWoodfuels 43

4-1 Markets and Price Structure for Petroleum Fuels 544-2 Financial Resources 64

Figures

4-1 Energy Consumption by Fuel Mix: 50- Total energy (part I)- Useful energy (Part II)

4-2 Cost of Wood and Charcoal and distances to production Sites 62

Iv

Acronyms

ASG African Support GroupAVBRR Advanced Very High Resolution RadiometryCIF Cost, insurance and freightCFMA Community Forest Management AgreementCILSS Permanent Inter-State Committee for Drought Control in the SahelCINERGIE Cellule internationale d'itude et de recherches pour la gestion de

l'information sur les echangesCONACILSS Cordination National du CILSSCRES Centre Regional de l'Energie SolaireDGIS Directorate General of International CooperationECU European Currency UnitEEC European Economic CommunityENDA-TM Environnement et d6veloppement du tiers mondeE/DI Energy Development InternationalESMAP Energy Sector Managenent Assistance ProgrammeFAO Food and Agricultural Organization of the United NationsFCFA Franc de la communaute financiere africaineFD (Gambian) Forestry DepartmentGBA Greater Banjul AreaGEAP Gambia Environmental Action ProgramGGFP Gambian-German Forestry ProjectRMF International Monetary FundLPG Liquid petroleum gasMAI Mean Annual IncrementM MinistTy of Trade, Industry and Employment (The Gambia)

NGO Non-governmental OrganizationNOAA (The US) National Oceanic and Atmospheric AdministrationRPTES Review of Policies in the Traditional Energy SectorSAR Societe Africaine de RaffinageSED Strategie Energie DomestiqueSEED Strategie Energie Environnement DeveloppementSIR Societe Ivoirieme de RaffinageSONICHAR Societe Nigerierme de CharbonnageUSAID United States Agency for Intemational DevelopmentUNDP United Nations Development ProgramUNEP United Nations Enviromnent ProgramUNIFSTD United Nations Interim Fund on Science and Technology for

DevelopmentWALTPS West Africa Long Term Perspective Study

v

PREFACE

The search for sustainable development in Sub-Saharan Africa has created agrowing awareness of the multi-sectorial nature of problems in the field of traditionalenergy. This became especially evident in the course of the World Bank research on theso-called NEXUS of population, agriculture and enviromnent, which links populationpressure on natural resources to food security, poverty and environmental degradation.The supply of energy from biomass resources constitutes an important subset of theseissues needing special attention. Rural populations using traditional production methodsmake growing demands on the limited land- and forest resources. In parallel, rapidurbanization creates large concentrated markets for commercialized woodfuels which, inturn, has a significant influence on the exploitation of biomass resources and on thedevelopment of the rural economy.

Against this backdrop, the perception arose that a "Review of Policies, Strategiesand Programs in the Traditional Energy Sector" (RPTES) would be essential to orient in amore systematic manner the actions of governments, of external aid donors and of othereconomic agents. With the agreement of the respective national authorities, a group of fiveSahelian countries was chosen to implemnent a first phase ofthe RPTES Program.

Given the nature of a policy review, country ownership of the conclusions isindispensable to a credible follow-up effort that should translate broad outlines intoconcrete action on the ground. It is with this perspective in mind that the RPTES optedfor maximizing the African contribution through an intensive inter-active process ofAfrican and expatriate experts working together. Multi-disciplinary national teams wereset up in each courtry under the leadership of a national coordinator. National teamstypically include officials from the different ministries in charge of energy, environment,forestry and water resources, social and women affiirs, the national CILSS comnmission(CONACELSS) and, in some cases, NGO's. An ad hoc "African Support Group (ASG)",composed by the five national coordinators and a representative from CILSS, was alsoestablished to assure regional communication and the coordination of cross-countrysupport activities. The review progressed in stages marked by three workshops (Bamakio.May 1993; Ouagadougou, February 1994; and Dakar, November 1994) where participantsevaluated each other's contributions, comprising African country reports and specializedstudies, thematic study reports by external consultants, and regional synthesis reportsprepared by the World Bank Team that coordinated the work.

It should be emphasized that the participatory approach has resulted in dualoutputs comprising on the one hand five national reports by teams of counterparts in eachcountry, and on the other hand a regional report by the RPTES coordinating teamThroughout the study it was clearly understood that the views of the national teams andthose of the coordinating team need not converge in every respect. Although the Reviewwas instrumental in forging a consensus on major policy issues, any differences notedamong the end products should be accepted as consistent with the spirit of the RPTES

vi

The regional report and the five national assessments by the African teams werepresented for discussion and evaluation to a meeting with donor experts held from May15-17, 1995 in Maastricht, and sponsored by the Govermment of The Netherlands. Thisvolume is a re-issue of the final regional report as an RPTES Discuion Paper. It takesinto account the valuable comments, received after the Maastricht meeting, from manyexperts inside and outside the World Bank Group, including the contributions by YoubaSokona and Souleymane Diallo of ENDA-Dakar, Miguel Trossero and Mori Keita ofFAO, John Hall of the Agriculture and Environment Division of the Westem AfiicaDepartment, Simon Rietbergen and Christian Taupiac of the Africa Technical Department,and the collective contnbution of colleagues in the Industry and Energy Department.

Following the Maastricht conference, the RPTES has continued to evolve. Withinthe original five-country group, preparation of new investments in the traditional energysector totaling US $40 million is well advanced, and elsewhere the Program has beeninstrumental in accelerating the implementation of projects totaling US $15 million. So far,at least six new countries in various regions of Africa have indicated their interest inpursuing a similar activity with assistance from RPTES staff These developments willgenerate new information to be included in future publications. At present, the report aspresented in Maastricht constitutes a benchmark that, hopefilly, will stimulate reflectionand action throughout the Africa Region.

The World Bank Team gratefully acknowledges the cooperation and support oftheir many African counterparts and the steady encouragement and guidance of theSteering Committee. Finally, sincere thanks are due to the Government of TheNetherlands which, through the Directorate General of International Cooperation (DGIS),provided the trust fund financing that made the original RPTES Program and its currentextension possible, and to the Danish Government for its support to several forestry sectorstudies undertaken by Program with funding from the Danish Consultant Trust Fund at theWorld Bank.

Sihvia B. SagariChief

Industry and Energy DivisionWestern Africa Department

vIl

R P T E S PROGRAM

Steering Committee

Dennis Anderson, Senior Energy Advisor, The World Bankllama Arba Dialo, Executive Director, Interim Secretariat of the Convention to Combat

DesertificationFranvois FaBoux, Environmental Advisor, The World Bank

Eric Ferguson, Consultant, Directorate General for International Cooperation - DGIS,The Netherlands

Youba Sokona, Coordonnateur du Progranime Energie, ENDA TM, Dakar

World Bank Team

Boris Utria, Task ManagerMax Wilton, Senior AdviserAzedine Ouerghi, Economist

Suzanne Roddis, Project Assistant

African Support Group

Saidou Ouiminga, Directeur Gtn6ral de l'Energie, Burkina FasoIsmail Toure, Coordonnateur de la Strategie Energie Domestique, Mali

Kiri Tounao, Directeur Adjoint du Projet Energie IU, NigerOmar Sallah, Director of Energy, The GambiaAlioune Fall, Directeur de l'Energie, Senegal

Ide Bana, Conseiller, Gestion des Ressources Naturelles, CILSS

Jx

EXECUTIVE SUMMARY

General Characteristics of the Region

1. The study region comprises S6n6gal, The Gambia, Burkina Faso, Mali and Niger.The total territory measures almost three nillion square kilometers, of which two-thirds ismade up by the vast desert areas of Mali and Niger. The inhabited parts form a band ofland stretching 3300 km from the Atlantic Ocean in the West to the border of Chad in theheart of Africa. Within this zone, average annual rainfalls vary widely as a function oflatitude. The total population in 1992 was about 35 million, of which 25 % urban. Theeconomies of all five countries are classified as low-income, with Sendgal having abouttwice as much GNP per capita as the other four countries. Agriculture contributes from 20% to 50 % to GDP but as much as 80 % in terms of employment.

2. Per capita final energy demand (of the order of 200 kg of petroleum equivalent) isamong the lowest by world standards. The structure of energy end use is markedlydifferent for the coastal and the land-locked countries. In Senegal and The Gambia theshare of household energy consumption is about 60 % and the transport component(hydrocarbons) ranges from 20 to 24 %. In the interior, the household share rises to 88 %.In al five countries, traditional fuels account for about 90 % or more of all householdenergy consumption.

Profile of the Traditional Energy Sector

3. The analyses of the traditional energy sector developed in the last 20-25 yearswere pattemed after the methods used in the modern sector. Biomass supply and demandwere projected, the role of prices and institutions examrnned, and forecasts (in manycountries of impending shortages) induced action by governments and the donorcommnunity. Although an impressive volume of research at the microeconomic level hasbecome available, the results are less satisfactory for planning and policy making. At themacro level, much information must be inferred from a weak database and extrapolation ofsurvey data, and unwarranted aggregation can undermine the credibility of conclusions atthe national level.

4. The standing stock of forest resources and the annual productivity of the areaunder vegetative cover varies strongly with climatic zone and rainfall. From the NorthernSahelo-Saharan zones to the Sudano-Guinean areas in the extreme South, the averagestanding stock ranges from 4-30 in3 /hectare, and the estimated productivity from 0.1-1.5m3/hectare/year. These orders of magnitude hide considerable uncertainties. Theexamination of available data revealed important differences in the diagnoses and results.Generally speaking it appears that the unit productivity of the land has beenunderestimated and that the biomass stock was not completely assessed. As a result, somepessimistic predictions of the 1980s concerning deforestation have not materialized.

x

5. In 1990, the estimated total demand in the five countries was about 15 milliontons, of which 11 million tons in rural areas. Out of the four million tons of urban demand,about three rnillion was concentrated in the capital cities and major secondary centers witha total population of about six million in 1990. At that time, the best estimate of theavailable aggregate supply was 37 million tons.

6. Urban interests dorninate the commercial forest exploitation and the woodfudlstrade. Since the fuelwood at source is practically a free good, partial or complete verticalintegration of woodcutting, charcoaling and trnsportation can bring large profits to theoperators. The system was sanctioned by forestry codes and enforced by the forestryservices, much to the detriment of ecological protection of the land and of the socialwelfare of the rural population.

7, Taxation of fuelwood and charcoal dates back to colonial days. The economicrationale in later years was based on the perception that private exploitation and pricing donot recognize the replacement value of the resource. The imposition of a stumpage feewas supposed to rectify the price signal to the consumer and also induce a shift tosubstitute fuels like butane and kerosene. However, actual taxation levels, equivalent to 3to 11 % of the retail price, are too small to make much difference in consumer behavior.Because of the poor tax collection record the effect is even more diluted, and the totalsums collected are insignificant relative to total national tax revenues.

S. In contrast with the long standing national preferences for State-ownedenterprises, the production and trade of traditional fuels is essentially a private businessstraddling the border of the formal and informal sectors. Intervention in the traditionalenergy sector is the preoccupation of many government agencies active in forestry,agriculture and environment, energy, commerce and finance. Each interested group bringsits own perspective, inter-agency cooperation is poor and the regulation imposed has notbeen highly effective.

The Outlook to the Year 2020

9. Within the context of the policy study objectives, the RPTES undertook ananalysis of potential future developments that integrated the so-called NEXUS ofpopulation growth, agriculture and environment with the traditional energy sector. Theanalytical approach consisted of examining first the possible settlement pattems ofpopulation, the spatial development of agriculture, and the demand for food and energy.Based on the needs for staple foods, future land use was estimated and next thecorresponding capacity of the land to supply woodfiuels. The accessibility of the resourceswas also considered, taking into account road infrastructure, transportation costs,distribution of resources and market size. The results depend on many assumptions,including the advance of agricultural technology. At this stage, the operational value lies inthe definition of a multi-disciplinary framework for thinking about policy, in the

xl

development of at least some orders of magnitude for the expected changes, and inidentifying priorities for research to firm up the data bases.

10. The underlying population projection was based on a regional study of 19countries in West Africa, of which the RPTES group is a subset. Two scenarios of highand low economic growth were postulated, and each case was associated with acontinuation of inter-regional population movements observed since 1930, generally fromthe countries in the interior to the coast. The greater mobility and more urbanization areexpected to occur under the higher economic growth scenario. In that case the totalpopulation in the RPTES countries would reach 63 million by 2020, of which 43 % urban,compared to 25 % in 1990.

11. The needs for domestically grown staple foods and the accompanying agriculturalexpansion would result in land use shifting from forestry to cultivation, but withoutleading to total loss of forest land. In terms of annual rates of deforestation, the strongestpressure would occur in The Gambia, with Niger a close second.

12. The long-term projection of demand for traditional energy was made separately forrural and urban populations. For rural areas where fuelwood is mostly collected bywomen and children on a subsistence basis rather than traded, the quantities were based onobserved per capita uses that appear to be strongly related to relative availability. Evenwithout price signals, more wood is used where supply is stil plentiful (e.g. SouthernMali), on the other hand, in areas where walking distances for collection become everlarger, per capita use tends to decrease eventually to the minimum physical needs (e.g.Niger). Projections of urban household energy use suggest that a gradual changeoverfrom faelwood to charcoal will take place but that a large-scale substitution of petroleumfuels for woodfuels is not likely to happen.

13. The most striking challenge in the 30-year period would occur in urban demand forwoodfuels. For the five countries taken together, the urban share in the total consumptionrises from about 25 % in 1990 to over 50 % at the end of the period. The change is mostpronounced in the .ountries with the highest urbanization and - presumably - the fastestTransition to charcoal use. In rough numbers, the projected trend is towards a quadrsplingof urban woodfiels consumption while rural consumption increases by only one half overthe period.

14. Any scenario looking 25 to 30 years ahead is full of uncertainties on both thedemand - and the supply side. Macro-economic growth and its effect on householdincomes is a major factor in the development of substitution of modem fuels in the cities.To the extent that they can be influenced by policy, there is nothing deterministic about theprojections However, the fact that many pessimistic predictions of the 1970s have notcome true should not lead to complacency. What was predicted for 1990 may well happenin the next century unless a clear policy direction emerges now and corresponding actions-e taken with reference to two time frames:

xii

* Over the intermediate term (say a horizon to 2005), a more thorough analysisof future land use should be made, folowing the general principles outlinedabove. Since a projection for a shorter period is subject to fewer uncertainties,the results can be more readily interpreted against the existing knownoperational environment.

* With respect to the short term, reforms are clearly necessary regardless of thephysical dimensions of fuitre developments, and they should be undertakennow. They cover a broad spectrum of traditional energy activities that havebeen explored as part of the RPTES Program.

A Review of past Interventions

Demand Intervention through Efficiency Improvement.

15. The use of traditional energy for cooking, the major component of energy demandin the RPTES countries, is inefficient. Efforts to improve the process by promotion ofimproved woodstoves have met miced success. The projects in the Sahel have had animportant social impact in terms of improving household cooking environments,improving health conditions and introducng technical change at the household level.Furthermore, improved stove programs have played a most useful role in the identificationof critical gender issues and in the mobilization of grass-roots women's groups. However,energy savings have been mediocre or poor in relation to the resources expended. Thedisappointing record can be largely traced to a narrow, technology-based approach datingback to the l970s. Projects of more recent date combine socio-economic and earliertechnical experience. On balance, the RPTES review concluded that (i) improved stovesperform a valuable function and should be continued, while incorporating the lessonslearned; (i) since the demonstrated net energy savings are small, stove promotion cannotbe a high priority of energy entities with their limited resources; and (iii) given theimportance of the social dimensions, non-energy organizations are best placed to take alead role, bearing in mind that ultimately the sustainability depends on a full commitmentof the private sector. In summnary, future demand managernent should reflect, at bothtechnical and institutional levels, the evolution from a strongly technological, efficiency-oriented approach to welfare improvement in the broader sense.

Demand Substitution

16. Governments in the RPTES countries are all active in attempting to replaceligneous fuels (fuelwood and charcoal) by petroleum products (Liquid Petroleum Gas -LPG - and kerosene)- However, success basically depends on economic growth and thecorresponding increase of personal incomes that would permit consumers to switch fuels.LPG penetration is farthest advanced in S6negal and to a lesser extent in The Gambia. Thedissemination in the land-locked RPTES countries is hampered by high import costscaused by inefficient procurement of small quantities, and large transportation distances.

xiii

17. The experience with a regional LPG Promotion Program, now discontinued,shows that the means utilized to accelerate the substitution process have not beeneffective. The woodfuel savings are well below the values suggested by straightforwardfuelswitching because consumers tend to change first to multiple fiuel use. Kerosene,already widely used for lighting in non-electrified households, is ordy in Niger beingactively promoted as a cooking fuel but the rate of penetration is still low. The merits ofgovernment subsidies to accelerate substitution are debatable. Whether intended are not,part of the public sector funds tends to benefit higher income strata and commercialestab'shments. Stn6gal operates a cross-subsidy program that clearly has had an impacton consumer demand, but the economic costs are not negligible, and they may be even lesssupportable for countries having only half of Senegal's GDP per capita. These conclusionsapply mainly to fuel subsidies. There may be cases where temporary subsidies of newapplances are desirable to overcome initial marketing problems.

Promotion of Sustainable upply

18. Like woodstove programs targeting the demand side of the market, efforts toimprove supply in the Sahel have gone through a history of trial and error before viablesolutions began to emerge. Three courses of action may be distinguished:

* Large-scale woodfuel plantations have been least successfil, and they seem tomerit consideration only if woodfuels are a byproduct of growing trees fortimber, subject to marketing opportunies.

D Most farming systems in the Sahel are agroforestry systems where trees andannual crops grow together. However, in most cases development has notreached the stage that trees are planted intentionally. This has proven to be aviable option in other parts of Africa and there is a growing body ofencouraging infornation on its potental, provided that constrants related toland- and tree tenure are lifted.

* Meanwhile, better management of the existing forests with participation of therural population appears to offer the best near-term prospects of increasing thesustainable supply of fuelwood. Coincidentally, many experimental projectsstarted up in all RPTES countries at the same time as a drive fordecentralization of the public sector. In its most elementary form, participationmeans that subsistence farmers can earn cash from controlled exploitation ofnearby forests, which would mean the beginning of monetization of theeconomy in the impoverished rural areas and thus provide some financialresources for further developments. This option is strategically closely linkedto agroforestry, because bringing open-access resources under conmnuritymanagement is a precondition for more intensive tree-planting activities.

xiv

It should be recognized that, whatever the option chosen, teir long-run viability, dependson the opportnity cost of land as detemined by its optimum use.

Priorities for Action

19. Priorities for action should flow from a clear defi&ihion of the desired objectivesand targets. The desired developmental objective is the establishmnent of economicallystable, socially equitable and ecologically sustainable traditional energy markets. Therecommendatons for action, without negatng the validity of previous interventions,shoud take into account the existing hman, financial and instittional resourceconstaints in the RPlES counties. Furthermore, any one of the three options outlinedabove (demand-side-, substituton- and supply-side interventions) requires closecooperation of public- and private sector agents In weighing the merits of each potentialaction, the limitations of the public sector need to be clearly recognized. Public sectorresources are scarce; therefore, unless policy is focused, much human effort and resourcescan be dissipated on legislation, fiscal measures, reorganization of institutions and lawenforcement serving different or even contradictory objectives.

20. Viewed from these perspectives, the priorities for government action in theRPTES countries become clearer As discussed, non-price demand interventions(essentially improved stoves) are helpfiul, but are not likely to reduce the pressure onnatural biomass resources significantly in the face of the rapidly growing demand.Substitution is driven essentially by growth of household incomes, and the existing weakeconomies do not have the fiscal means to accelerate this process by subsidizing fi.els(although temporary equipment subsidies may be appropriate in specific situations). Thethird option, pmmotion of sustainable supply through participatory management of thenatural forests and - by extension - agroforestry. has emerged as offerng the best prospectto attain, if not a solution, at least a rapid improvement.

Implementation Instruments

Forestry Management

21. Legislative reforms are necessary to redefine the rights of rural populations byletting them participate in the commercial exploitation of the forests and share the benefits.Senegal and Mali have enacted legislation to that effect, while in the other RPTEScountries new laws are being drafted Regardless of the state of advancement oflegislation, the subject is being examined everywhere in the light of experience alreadygained with pilot projects. Within the legislative framework, the basic implementationinstrument is a management contract between the authorities and villagers spelling out theconditions of sustainable exploitation. the mutual obligations and the sharing of thebenefits. Significant issues remain to be resolved with regard to the security of the rightsgranted, the representation of villate populations, the role of traditional authorities and the

xv

links of village-based production with transportation and marketing operations. It isimportant to foresee the organization of charcoal production in these schemes to avoid thedevelopment of uncontrolled and new ecologically danaging forest exploitation practices.

Fiscal- and Pricing Policies

22. Fiscal policy has lacked clear objectives and coherence and, on balance, theimplementation has been ineffective or worse, counterproductive. A re-orientation alongthe following lines is recommended:

d Supporting sustainable woodfuel supply and evironmental protection, by localcommunities managing the existing natural forests and woodlands undercontracts;

* Providing adequate incentives to secure the cooperation of the local ruralpopulations by exempting village-based production from all centrally imposedcommodity taxes (to be distinguished from levies that financially support themanagement schemes and that are collected and spent under local control);

* Protecting the new producers against unfair competition from existingcommercial interests by establishing nimum producer prices until such timethat the woodfuels trade has been successfully restructured;

= Penalizing non-sustainable exploitation by levymg a significant tax on non-managed production; and

a Transforming the forestry services from law-enforcement to ectensionagencies, financed out of general governent revenue rather than earmarkedwoodfuel taxes.

Institutional Adaation and Ma-nanement of Change

23. Public sector regulation of activities in the traditional energy sector has beenlargely ineffective because of uncoordinated interventions of many interested agencies.Central to a solution is the close cooperation of forestry and energy departments. It wasfound that forestry departments are generally better organized and equipped than energydepartments to deal with the crucial traditional energy issues on the supply side. Theacceleration of iitiatives in this area (through development of community-basedmanagement of forests) is creating a dichotomy between ministries with the nsk thatenergy depanments focusing on the demand side will fall more and more behind unlessthey are strengthened in the process. They need no large increases in staff, but rather thecreation of a small core of experts in traditional energy who are capable of working acrossdepartmental boundaries. Regional cooperation is also seen as an important aspect of theneeded capacity building tasks, through exchange of experiences in interdepartmentalcooperation and by peer reviews of project preparation work.

xv

Integation in Overall Rural Development

24. Fuelwood management schemes should be integrated in overall rural development.Future projects could consider as comple cmponents the introduction ofphotovoltaic solar power (for village water pumps, clinics, telecommunications,community TV and distance education), maintenance of feeder roads, schoolsimprovement, etc. A strong case should be made for an explicit recognition of the role ofwomen through their own organizations in the drawing up of local management plans, inthe approval process and in the subsequent implementation, including the use by thecommunity of net profits of fiaeiwood sales.

Development of Human Resources

25. The ongoing experimental work shows already that the re-orientation of thewoodfiuel supply industry requies training and re-training of virtually all economic agentsVillagers need to learn techniques of sustainable production, elementary management skillsand at a later stage marketing. Special attention should be given to ensure an adequateaccess for women in all capacity building activities. The training requirements for theforestry services are no less demanding. Agents need to change their approach frompolice-oriented protection of the forests to support services for the rural populationFinally, where urban oligopolies dominate the markets, the controlling interests, asconcerned elemnents of civic society, should be implicated in the dialogue.

)rientation of External Aid

26. Past external aid has been driven mostly by the project approach which may yieldonly localized results with lite impact on the sector as a whole. Without a well-articulatedpolicy, goverments lacked a screening device to judge where donor aid would be mostappropriate. The relative availability of aid gave rise to the search for projects toperpetuate local structures, thus dispersing scarce African human resources. In the contextof communmty-managed woodfuel production schemes, the RPlES review makes thefollowing recommendations:

* Reach a clear understanding between recipients and donors on the principles.processes and fiscal incentives for forestry management by rural communities.

* Identify local solutions that are considered replicable and that establish anfastructure of human and material resources sufficient to create a multiplier

effect;

* Determine a phased implementation plan, if opportune combined with theintroduction of other forms of renewable energy; and

xvii

Plan for advance training of ecmonoic agents at all levels (including training ofinstructors), in anticipation of long-term needs.

Recapitulation of Country-Specific Recommendations

Sinial

(1) The Govenmment should conmmission a comprehensive inventory of forestry- andother biomass resources, in conjunctic with a survy of land use; this work shouldbe set up with a view to periodic updating that will permit monitoring of standingstocks. (RPTES has been supporting some initial efforts by the Centre de SuiviEcologique in Dakar).

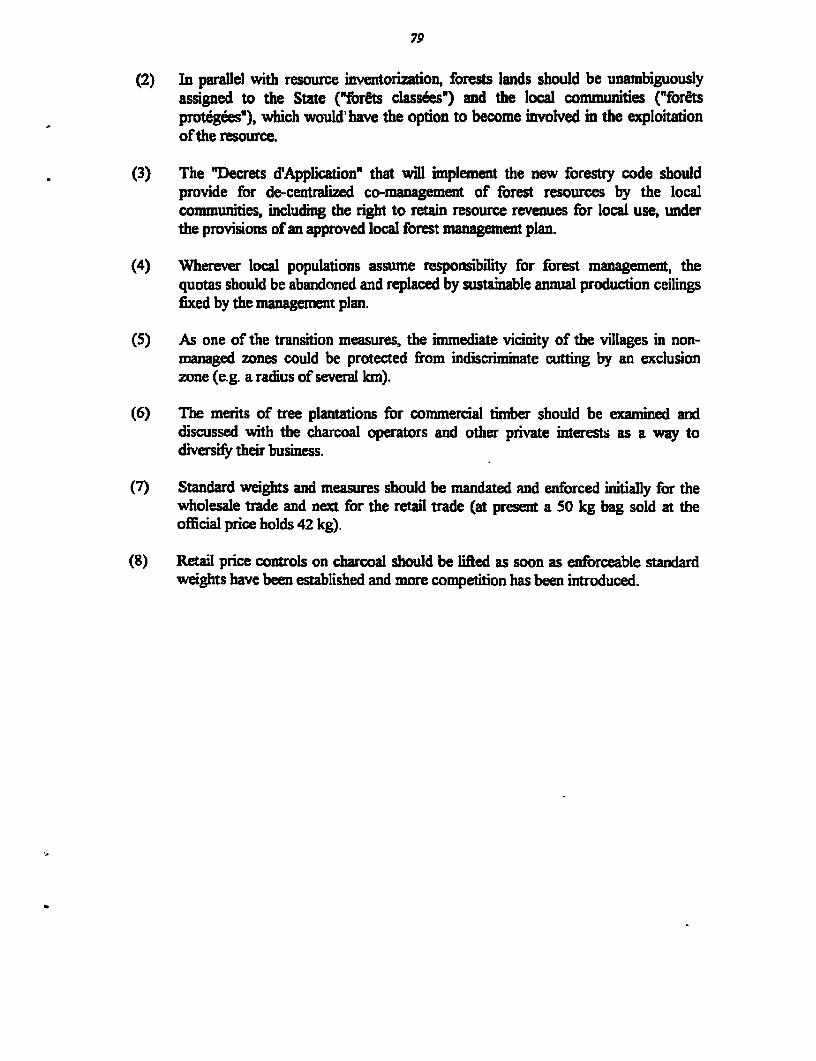

(2) In paralel with resource inventorization, forest lands should be unambiguouslyassigned to the State (forits class6es) and the local communities (foretsprotegees), which would have the option to participate in the exploitation of theresource.

(3) The "Decrets d'Application" that will implement the new forestry code shouldprovide for de-cenraized co-management of forest resources by the localcommunities, including the right to retain resource revenues for local use, underthe provisions of an approved local forest mnangement plan

(4) Whereer local populations assume responsibility for forest management, thequotas should be abandoned and replaced by sustinable annual production ceilingsfixed by the management plan.

(5) As one of the tansition measures, the immediate vicinity of the villages in non-managed zones could be protected from indiscriminate cutting by an exclusionzone (e.g. a radius of several Icm).

(6) The merits of tree plantations for commercial timber should be examined anddiscussed wih the charcoal operators and other prvate interests as a way todiversify their business.

(7) Standard weights and measures should be mandated and enforced initially for thewholesale trade and next for the retail trade (at present a 50 kg bag sold at theofficial price holds 42 kg).

(8) Retail price controls on charcoal should be lifted as soon as enforceable standardweights have been established and more competition has been introduced.

xviii

The Gambia

(1) Without revoking the ban on domestic production of charcoal, the legalization ofthe import and trade of charcoal should be examined, in conjunction with themeans needed to exercise effective monitoring.

(2) There is no official restriction on fiuelwood imports. However, statistics should bekept at border entry points.

(3) Government should legalize the transfer of management responsibility for foreststo local population, thus permitting the multiplication of the present demonstrationprojects.

(4) Harvesting of green trees for woodfuel should be permitted in zones that havebeen brought under community management, under the provisions of agreedmanagement plans between the communities and the Forestry Department.

(5) It is recommended to make a second biomass inventory, which will permit theanalysis of land use change since 1980, and the establishment of permanent sampleplots to measure productivity regularly.

(6) To maintain a broad spectrum of consumer choice of fuels, every effort should bemade by the private sector to reduce the cost of hydrocarbon fuels as substitutes,in particular by attempting to lower the cost of importing, storing and bottlingLPG. The prospects of kerosene should be further examined.

(7) The Energy Division in MTE should be adequately staffed and trained to takecare of minimwn requirements for coordination and liaison, and to supervise theestablishment of a central energy documentation center.

Burkina Faso

(1) The available elements of a master plan (at present focused on supplyingOuagadougou) should be updated and integrated as quickly as possible to define amulti-year program that would assure a virtually 100 % supply of the nationalcapital region and other major urban centers from rural woodfuel productioncenters in community managed forests.

(2) In conjunction with this master plan, the transportation infrastructure in the CentralPlateau should be examined for potential bottlenecks in the road network thatwould impede woodfuel supplies. The trucking industry should be closelyassociated with this aspect of the planning.

(3) Selection of new forest areas for village management should take into account thepossibility of introducing other forms of renewable energy in rural areas (e.g.

x)x

photovoltaic solar energy for water pumping, health centers, distance education,etc.).

(4) The threat of mushroonming inefficient charcoal production should be contained byorganizing and mobilizing private sector operators, and by promoting energy-efficient charcoaling practices.

(5) For the longer tern, existing biomass inventories and land use mapping datashould be reviewed and a systematic information basis for the future established.

(6) The present, more or less improvised Direction de l'Energie should be reinforced,made permanent and given well-defined responsibilities in the traditional energysector, in conjunction with a clear delineation of the functions of other entities.

Mali

(1) Govermment and donors should reflect on the incentive structure to be associatedwith villagers' responsibility for resource management.

(2) The role of woodfuel taxation merits re-exaniination in relation to budgetallocations for the traditional energy sector.

(3) Based on the existing inventory data, master plans for woodflzel supply to all majorurban centers should be developed

(4) A survey of the possibility to exploit stocks of deadwood in the Niger Delta tosupply remote markets like Mopti, Gao and Timbouctou.

(5) Extension of the forest inventory to biomass stocks on cultivated land.

(6) An assessment of the capacities or the Forestry Services to deliver extensionactivities, and of the associated needs for retraining, in conjunction with areflection on the future responsibilities and organization of law enforcementagencies.

Niier

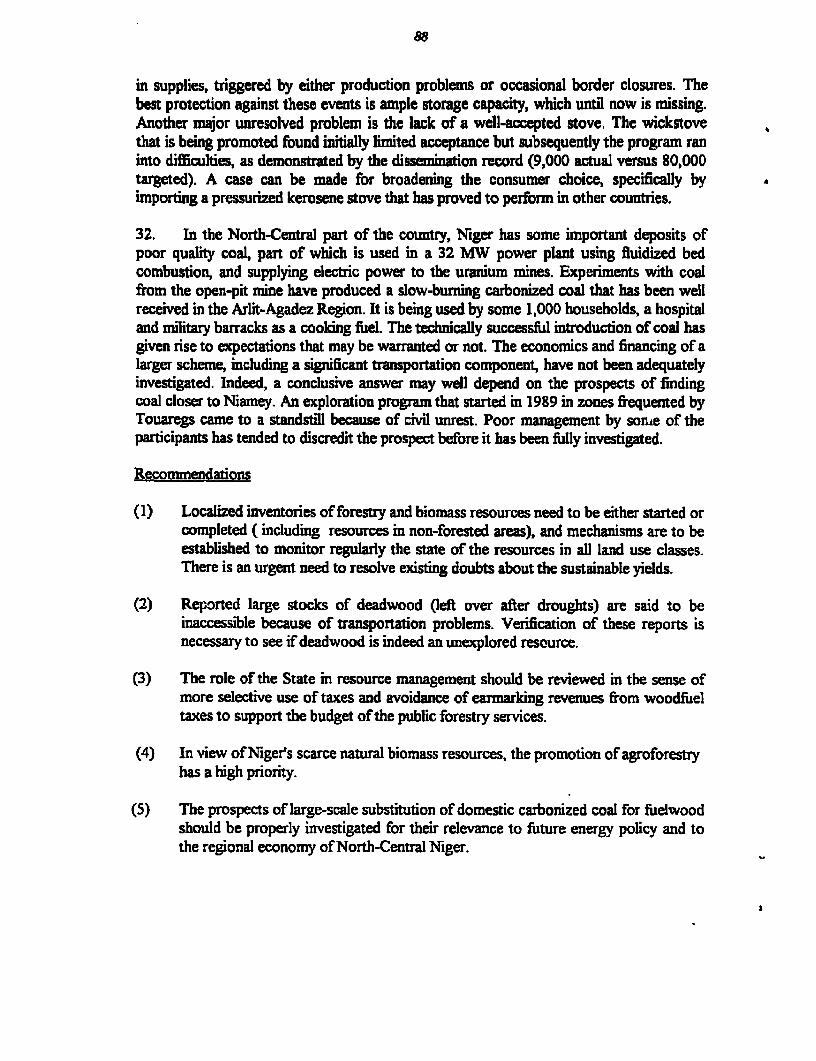

(1) Localized inventories of forestry and biomass resources need to be either started orcompleted (including resources in non-forested areas), and mechanisms are to beestablished to monitor regularly the slate of the resources in all land use classes.There is an urgent need to resolve existing doubts about the sustainable yields.

(2) Reported large stocks of deadwood (left over after droughts) are said to beinaccessible because of transponation problems. Verification of these reports isnecessary to see if deadwood is indeed an unexplored resource.

(3) The role of the State in resource management should be reviewed in the sense ofmore selective use of taxes and avoidance of earmarking revenues from woodfueltaxes to support the budget of the public forestry services.

(4) In view of Niger's scarce natural biomass resources, the promotion of plannedagroforestry has a high priority.

(5) The prospects of large-scale substitution of domestic carbonized coal for fuelwoodshould be properly investigated for their relevance to fiuture energy policy and tothe regional economy of North-Central Niger.

(6) The policies with respect to replacement of fuelwood by petroleum fuels should ber-ammined. After the abandonment of LPG subsidies, fiuther LPG promotion atmarket prices may be left to the private sector. With respect to kerosene, twoaspects need attention: (1) The consumer's choice of stoves should be broadenedand the stove suppl'y secured; and (2) Kerosene storage facilities may be needed tosupport the activities of private traders and to ensure a reasonably reliable fuelsupply at a stable price.

I

L INTRODUCTION

1.I Plan ofthe Report

1. This report begins with a broad outline of the main characteristics of the samplegroup of five RPTES countries. It provides background information on their physiographyand population, and on their position within the larger West Afiica Region. After a briefoverview of the structure of the national economies, the focus shifts to the energy sector.

2. The topic of traditional energy sector policies is presented in two parts:

* Chapters l-IV provide a regional overview of study results that is based on the fivedraft reports prepared by the country teams and on draft reports by consultants thatare concerned with specific policy themes. After a sketch of the traditional energysector as it exists today (Chapter 1I), the report discusses future supply-demandscenarios in the context of the population-agriculture-environment NEXUS (ChapterIII). Against this background, Chapter IV examines Government policies, the role ofother economic agents in the sector, donor responses and options for future action.

* Chapter V gives for each country an overview of the most significant characteristicsthat have a bearing on the functioning of the traditional energy sector; each generalsection is followed by tentative policy recommendations for the specific countrysituation.

1.2 Phvsiography and Population

3 The reasons for choosing the RPTES sample group of countries to launch a policyreview have been explained in previous project documents: (1) A reasonablyhomogeneous group of countries with regard to resource base, state of development,climate and structure of the economy; (2) a significant volume of previous sector workwith complementing data bases; and (3) geographic continuity facilitating communicationsamong African team members. Most of these expectations have been confirmed in thecourse of study implementation. Moreover, the inclusion of Gambia as part of a spatiallycontinuous countny group also added Anglo-Saxon elements to a diversity of institutionaltraditions that is of considerable interest to the study.

4 The RPTES group comprises a more or less horizontal band that stretches roughlySouth of the Sahara over a distance of about 3300 kan and occupies a land area of almostthree mnillion square kilometers. The climatic zones, going from North to South, arebroadly Saharan, Sahelian and Soudano-Guinean. Annual rainfalls range from 200 mm inthe Northern Sahelian zone to 1000-1200 mm in the Southern Regions.

5 It is already evident from this description that any countTy group selection has itslimitations, and this is also true of the RPTES group when its position in the West AfTica

2

Sub-Region is considered. A glance at .the map suffices to see that the mostly land-lockedbelt stretching East-West cannot be considered in isolation from the coastal countries tothe South. The CINERGIE Group in the African Development Bank', looldng at the Sub-Region as a whole, divides the area in three economic-geographic spaces: (1) The Westernspace comprising broadly Sn6gal, Guinea and Western Mali; (2) A central space made upby CMte d'Ivoire, Ghana, Togo, Burkina Faso and Southeastern Mali; and (3) The Easternspace of Nigeria, Beniin and Southern Niger.

6. These distinctions are useful for the RPTES from three angles:

* The economic interdependence of the coastal countries and the Sahelian hinterlandhas resulted, among others, in a strong migratory movement of the populations fromthe interior to the coast. The population prognosis for the RPTES countries takesthis factor into account;

* Migratory movements have an important effect on urbanization and hence on thesize of concentrated woodfulel markets; they also influence the development of maintransportation networks and thus the accessibility of biomass resources; and

* The land-locked RPTES countries are totally dependent on their neighbors on thecoast for petroleum products. From a sub-regional standpoint, the main sources arethe refineries of SAR (Dakar), Tema (Ghana), SIR (Abidjan), Port Harcourt(Nigeria) and Kaduna (Nigeria). The patterns of sub-regional product trade are animportant factor in the import costs incurred by Burkina Faso, Mali and Niger.

7. The existing data on population and urbanization of the five countries are compiledin Table 1-1. Their estimated total population in 1992 was about 35 nillion, of which 25% was urbanized. It should be noted that urbanization figures are often based on differentnational census definitions, which can produce inconsistent statistics. The tabulated dataare obtained from the data base of the West Africa Long Term Perspectives Studv(WALTPS)2 , which employs a uniform definition of urban settlements (over 5000). Acrosscountries, Sbn6gal leads with the highest urbanization (43%) and Niger is at the otherextreme (16%).

8. The projected natural growth rates of the population vary little from country tocountry. On the other hand, the net growth rates after migration diverge considerably Therange shown in the table represents two scenarios: (1) Economic recovery after years ofstagnation and continuation of the present migration trends with fairly open borders, and(2) Relative economic stagnation and tightening imnigration controls. The projected netgrowth rates show that under the optimistic, high-migration scenario (1), Senegal andGambia are the net winners with growth of 2.9 and 3.3 %, while the other three countries

'¶Intgrauion Rfgionale cn Afriquc de l'Oucsr. CINERGIE. mars 1993.

2 "Elemcints t'conomie spacialc des cncrgies raditiormelleeC. RPTES- Benoit Nmmn. janvier 1995

3

would see growti at only 1.9 %. Under the pessimistic, low-migration scenario (2), themigration effect on Senegal becomes zero, Gambia still would show a significant net gain;the land-locked countries would continue to lose population by migration but at a muchlower rate.

9. The thematic study of demographic development assumes that most migration isessentially directed towards urban areas. Therefore, the range of net growth rates for thetotal population carries over into a range of urban growth rates. It should be noted thatthese projections cover the entire urban population rather than the existing largemetropolitan centers. Within the five-country group, the land-locked countries losemigrants to Sendgal and Gambia. Therefore, in the lines for net growth and urban growth,the high end of the range for the coastal countries corresponds to the low end of the rangefor the land-locked countries.

Table 1-1Population and Urbanization (1992)

Category Unit SE)gal Gambia Burkina Mali Niger Total

Area hm2 x 103 197 12 274 1241 1267 2991Population

Total millions 7.8 0.9 9.5 9.0 8.2 35.4Urban millions 3.4 0.3 2.1 2.0 1.3 9.1Urban share % 43 32 22 22 16 25

Growth ratesTotal natural OM=ea 2.5 2.4 2.5 2.5 2.6 2.5Total net °l/yu 2.9-2.5 3.3-3.0 1.9-2.3 1.9-2.3 1.9-2A 2.2-2.4Urban Va/year 4.2-3.0 4.7-3.7 3.1-3.8 2.9-3.7 3.3-4.0 3.1-4.0

Density Inha.lan 2 40 75 35 7.2 6.5 12

Sources:Area: Countzy reports.Total population (1992): 1993 Annua Rport Global Coalition forAfiicaUrbanization: West Afica Long Term Perspectives Study (WALTPS).Grwth Rates: WALTPS Scenarios.

1.3 The Sub-regional and National Economies

10. Table 1-2 shows some selected economic statistics of the five countries; in the caseof the FCFA countries they pre-date the January 1994 devaluation. In terms of registeredGNP per capita, all countries except Senegal fall in the category of the poorest in theworld. The infonnal sector may cany considerable weight but is not likely to change therelative ranking among the group of five.

11. Economic growth from 1988 to 1992 lagged definitely behind population increasesin Senegal, Burkina and Niger. The heavy dependence on external financing shows up in

4

the gap between savings and investments, especially in Gambia, Burldna Paso and Mali. Inview of the close relationship of the traditional energy sector with issues of land use andfood security, the table includes some specifics on the agricultural sector. The importanceof agricultre is evident from its contribution to GDP, varying from 20 % for S6n6gal to50 % for Mali. The social significance of the agricultural sector is much more pronounced:Agricultural employment as a percentage of the total economically active population is ata high and fairly unifornm level in all five countries, ranging from 78 to 87 %.

12. The external trade data also include a large contribution of agriculture: Onaverage, agricultural products in 1990 accounted for 30 % of imports (with Senegal andGambia showing the largest proportions) and 45 % of exports (with Burkina Faso andMali in the lead). All countries have a negative overall trade balance; relative to GNP,GCambia had the largest deficit and Mali and Niger the smallest. Imports of petroleumproducts are in part estimated; in 1990 they represented on average about 18 % of exportearnings but for Gambia this proportion rises to 45 %.

13. In view of the known large business tumover of woodfiuel sales, it would be ofinterest to know the contribution of this sector to GDP and, in that context, in the relativecontributions of traditional and modem energy. This review has attempted to producesome data with inconclusive results. Two major problems arise:

* The macro aggregates do not isolate energy subsectors. The electricity componentof the modern energy sector is included in utilities (power, water, gas). A large partof the traditional energy activity fills under the forestry sector, which also includesmany non-energy outputs.

* Almost by definition, the real traditional energy contribution to GDP includes a largeunrecorded component.

14. It was noted that the contribution of forests and fisheries in the national accounts isof the order of four to five percent in all RPTES countries. As a broad judgment aneconomic study concluded that the traditional energy contribution may be in the 1.5 to 2.0percent range. This would indicate a contnbution of the same order of magnitude as themodem energy sector in a non-oil producing country.

S

Table 1-2Sdected Economic Statistics

Category Unit S6nagaI Gambia Burlina Mali Niger Total

Popuation 1992 nillion 7.8 0.9 9.5 9.0 8.2 35.4GDP Growth '88-!92 % per year 2,2 3.2 2.5 3.0 1.2Av. GNP '90-' 92 S x 106 5,062 269 2,356 2,043 2,435 1.2165GNP/Cap.'90-'92 1987 S 649 299 248 227 297 344

Gros Domestic lnvett % GDP 13.1 19.1 21.8 22.1 13.01988-92Gross Domestic Savings % GDP 8.2 8.6 2.2 5.1 10.81988-'92GDP in Agricult. % 20 30 31 50 36Labor Force % 78 81 84 B0 87Agricultue

Trade Balance 1990 S x 106 - 551 -159 - 384 .94 - 106 - 1294imports

Total 1.292 199 536 432 389 2848Agricultual 454 68 102 116 129 869Petr. Products 120 18 59 53 33 283

ExportsTotal 741 40 152 338 283 1554Agricultur 219 14 142 254 74 703

Source:Population and national accouit items: 1993 Annual Rcport Global Coalition for AfricaApicultural Sector and Trade figures: World Agiculture. Trends and Indicators 1977-91, US Dpt of Agnculture

1 4 The Eners Sector

15. The national country teams have analyzed the more recent performance of theentire energy sector (i.e. traditional and modem) in their respective countnres The salientstatistical information is found in energy balances for the year 1992, which are presentedin an abbreviated forn in Table 1-3 Although some numbers need further verification(mostly for Gambia), the overall pattern confirms findings for earlier years

16. Energy end use per capita (in kg of oil equivalent) is about the same for Senegal,Burkina Faso and Mali, i.e. in the 180-200 kg range, the average for Gambia (280 kg) ismuch higher, possibly because petroleum products for re-export are included in thenational consumption; Niger is lowest (137 kg). which may be attributable to the low rateof urbanization and to unrecorded supplies from Nigeria.

6

17. With regard to the structure of end use, within the five countries there is a cleardivide between the two maritime and the three land-locked countries. The former have amuch higher transport component (20-24 %) and a corresponding lower share ofhouseholds (62-68%). Only Senegal has a significant industrial component (18%),although in this category the numbers are probably influenced by differences inclassification.

18. The share of traditional energy in total end use shows again a marked differencebetween coastal countries (56-60 %) and the others (all 88 %/6). The ratios of traditionalenergy to all household energy are indicative of the lovw percentage of the populationhaving access to electricity and petroleum fuels: The shares of traditional energy rangefrom 88-91 % for Gambia and Sen6gal to 98-99 % in the interior.

19. Finally, the total losses, expressed as a percentage of all primary energy supplied,provide an interesting insight in the nature of the energy sector. Seinigal, with 35 % losses,leads the group of five and the reasons are obvious from the breakdown of losses bycategory: It has the highest charcoal consumption per capita and also the highest rate ofelectrification, both energy forms having very high transformation losses. Niger, with II%, holds second place, clearly because of the cvonversion losses associated with theSONICHAR power generation in the uranium district (Arlit-Agadez). The losses in Mali,(7 %), although not far ahead of Burlina Faso and Gambia, show the effect of growingcharcoal consmption. The loss percentages should not be interpreted as measures ofenergy efficiency. The countnes having the lowest losses are the heaviest users offuelwood. This component is recorded as "End Use" in the energy balance but it should benoted that it is in reality pimary input for cooking devices with efficiencies of only 15-20%.

7

Table 1-3Condensed Energy Balances

Cm thousands of Tons of Oil Equivalent)- 1992 -

Country Singal Gambia Burkina Mali Niger

1. Primary Energ

Woodfuels 1446 179 1605 1754 946Petoleum Fuels 860 87 202 198 128Other 2 - 2 23 153

Total 2308 266 1809 1975 1267

2. Lomes

Charcoal Conversion 559 - 30 127Electricity Thermal) 224 lOc 53 15 145Other 20 3 2 2 -

Total 803 13 85 144 145

3. End Uses

Households 931 172 1538 1638 1005(ofwhich traditional) (847) (152) (1512) (1617) (986)

Transport 310 62 117 132 79Industry 264 10 28 47 33Other - 9 41 14 5Total 1505 253 1724 1831 1122

4. Shares of End Uses

Households 62 68 89 89 89Transport 20 24 7 7 7Industry '8 4 2 3 3Other - 4 2 1 1

5. Ratios

Population (millions) 7.8 0.9 9.5 9.0 8.2End use pcr capita (kg) 193 280 181 203 137Trad./total (0%e) 56 60 88 88 88Traditotal household use 91 88 98 99 98Loss as % of Primary 35 5 5 7 11

9

IL PROFIE OF THE EXISTING TRADMONAL ENERGY SECTOR

2.1 General

1. Woodfiuel problems became promient especially after eruption of the petroleumpricing crises in the 1970's. This section begins with some comments on the analyticalapproach to the sector that developed, because it has important implications for futureaction.

2. In many reports of an earlier date one recognizes that the methods to analyze themodem sector were adopted for traditional energy. Assessments of the resource base,demand projections, nationwide aggregation of supply and demand, and energy balancesused as indicators of "crisis" years. Often, the conclusions carried over into predictions ofprogressive deforestation, and the recommended solutions tended to focus on the demandside with a strong technological bias. In brieC the result was the now widely discredited"Gap Theory" in woodfuel analysis.

3. The reservatons about the value of this work arose in part from the practicalobservation that certain pessimistic predictions simply have not come true, in part from thegrowing awareness of data problems. On the demand side, consumer behavior, unitconsumption of fuelwood and retail prices can only be studied by sample surveys, andaggregate consumption depends basically on population census data of variable qualityand uncertain extrapolations thereof. A better indication of demand could be obtained bymeasuring transport flows at major entry points of urban markets, but the results aredistorted if this work is also done on a sample basis, and without coordination withdemand surveys. Continuous records are rarely reliable because tax evasion distorts thestatistics. On the suRply side, the inventorization of the resource base leaves much to bedesired, not because good work canot be found but rather because it is not managed insuch a manner as to provide consistent methodology and time series giving an insight inthe changing use of land over time. Common to all activities in the sector is the difficultyof capturing seasonal variation and the lack of standardization and control of weights andmeasures.

4. Nevertheless, the defects of the "Gap Theory" should not be exaggerated. Themain problems are unwarranted aggregation (which is a pitfall in any market in whichtransportation distances are large) and data (which also must be dealt with in anymethodology). After all, econonmics is about scarcity and hence about "Gaps". It wouldseem that in disaggregated markets it is quite appropriate to use the conventional tools ofmicroeconomic analysis which trace the factors behind supply- and demand schedules andintroduce the behavior of economic agents in the fiuelwood chain as an essential input(examples: monopolies, oligopolies, vertical integration, taxation effects, regulation).Better a priori theoretical analysis will probably lead to better planning andimplementation of data collection.

10

5. Notwithstanding cerain reservations about the applicability of methods borrowedfrom the modem sectors of the economy, the subject of traditional energy is no different inthat it can be grouped under the headings of supply, demand, pricing and the worldngs ofinstitutions. This presentation contains the same fbur elements, but the approach has beenadapted to some special characteristics of the traditional energy sector.

6. It should be noted that the sector covers both the modern, monetized and mostlyurban sector of the economy and the essentially mral subsistence sector, with someexceptions such as the groundnut basin in Central-Eastern Senigal and the cotton growingareas of Southern Mali. The biomass supply is of rural origin, but demand is foundeverywhere: (1) concentrated in urban markets where the traded commodity is obviouslymonetized; and (2) dispersed throughout the rural areas. Therefore, it is convenient tolook at the supply potential of ural areas in conjunction with subsistence demand, and toevaluate the excess supply that will be available for urban markets, and the role that suchexcess supply could play in the monetization ofthe rural economy.

7. Despite some severe data limitations, the urban markets for fuelwood and charcoalcan be evaluated with more or less elaborate surveys. However, the seemingly simple nextstep of balancing demand and supply over time, and inferring the evolution of prices,becomes much more complex in the traditional energy sector. Rural excess supply andurban markets are linked by a variety of means of transportation and trading channels thatare difficult to analyze adequately, and this weakness carries over into the understandingof the price formation process.

8. Based on these perceptions, the presentation begins with an overview of thebiomass resource base, an assessment of the quality of available information and of itsusefiilness for energy studies. Summaries of rural and urban markets and of factorsinfluencing consumer behavior follow. The next section combines a discussion of thecommercial chain (filiere) Lnldng nural production areas with the cities, and the relatedpricing issues. After discussion of the role of the - mostly public - sector institutions, thechapter concludes with a sumning up of the main issues.

2-2 A critical Evaluation of the Biomass Resource Base

a. Agro-ecological Zones in the RPTES Countries

9. The total area of the five RPTES countries amounts to almost-3 million km2, witha population estimated at 35.4 million in 1992. The agro-ecological zones fall into fourbroad categories:

The scarcely populated Saharan/Sahelo-Saharan zone which receives less than 300mm of rain per year. Most of the biomass in the Saharan part is in the root systemsof drought-resistant plants. ln the Sahelo-Saharan areas, the vegetation is mainly

II

composed of grassland with bushes and small bushy trees. The grassland isephemeral except where shaded by large trees (Millington et a]. 94). This zoneincludes over three quarters of Mali and Niger, the largest Sahelian countries.

* The Sahel and the Sudano-Sahelian areas receive up to 600 mm of rainfall a yearand provide the habitat for a large proportion of the population. The landscape isdomninated by wooded bushland and a herbaceous layer of mainly anmal grass(Millington et al. 1994). Processes such as agricultural and pastoral intensificationand overgrazing around tube wells have destroyed a great deal of woody biomass(Graham, 1969). Over three quarters of Burkina Faso, half of The Gambia andabout one quarter of Niger fall in this zone.

* The Sudanian zone receives up to 900 mm of rainfal a year. The vegetation ismainly an open tree savanna of 15 to 25 meters high, or shrub savanna Perennialand annual grasses at the ground layer are subject to easy burning during the dryseason (Mfllington et al., 94). It covers the southern half of SenegaL half of TheGambia and southern areas of Mali and Burkina Faso.

D Finally, the Sudano-Guinean zone receives rainfall of over 900 mm per year. Muchof the area may be described as derived savanna, ranging from closed canopysavanna woodlands to thicket savanna (MlLington et al. 1994). The zone coversGuinea-Bissau, Guinea and Cote dIvoire, and extends only in the southemmostareas of Mali and Sdn6gal.

10. Table 2-1 summarizes in Part I the geographic distnbution of the RPTES studyarea of 2.8 million km2 according to the four agro-ecological zones descnbed above, withsome very approximate indications of standing stock and annual productivity of woodybiomnass. It should be noted that the more productive areas (excluding the Sahelo-Saharanzone) cover only 38 % of the total territory. Standing stock and productivity increaserapidly with the annual rainfalls. Part II of the Table provides a more detailed breakdownof climatic zones, rainfalls and the corresponding areas in each RPTES country.

12

Table 2-1Agro-ecological Zones in the RITES Countries

Part I: Main Features of the RPTES Study Area

Climatic Zone RainfaZ Area Distribution Standing Stock Productivitynon $ (*) m3 hbctare m3lha/year

1- Sahelo-Sahaan <300 62 - 3.9 0.13

2-SahclSudano/Sahelian <600 21 56 8.0 0.4

3- Sudanian <900 11 32 15.0 0.9

4- Sudano-Guincan >900 6 12 30.0 1.5

Tolal - 100 100

Source: Zone (1) ESMAP. Mali 1992Zone (2), (3) and (4) extrapolated fomtbeNational Forestynvcw of Mali 1987

Note: () Sabelo- aea discounted for illustation pwos due to low pmductivty and standg volune.

Part [I Agro-ecological Zones by CountryCm thousands of square kilometers)

Rainfan Senegl Gambia Bmina Mali Niger TOrALMMNzm Faso RPTES

(1) (2) (3)AGRO-ECOLOGICAL ZONES

SahanmSaelo-Sahan <300 894 975 1,869

Sahel 300400 39 69 152 260

Sudano-Sahel 40 00 6 136 87 127 359

Sidanian 600-900 119 6 69 111 13 318

Sudano-Guinean >0 39 149 188

Total Area (DkmZ) 197 12 274 1.241 1.267 2,991

Source: - Compiled from RPTES National rpons- (1) S. Amous: UNEP Greenhouse Gas Abatement Costing Studies- (2) RPTES estUnate- (3) Les Atlas Jecue Afriquc: Burkina Faso

13

b. The Genesis of Action Programs in the traditional Energy Sector

11. The importance of establishing a reliable data base fbr biomass is illustrated by thepolicy experience in the Sahel. In the eighties, policies in the traditional energy andforestry sectors were very much influenced by the conclusions of an FAO reportpublished in 19823. The study examined the outlook by the year 2000 for fiuelwood supplyand demand in seven countries (the five RPTES countries plus Mauritania and Chad). Thebalance of sustainable biomass supply and demand, as developed in the study, indicatedthat only Chad would still have a surplus by the year 2000. According to the report, theestimated total annual demand of 22.4 million m3 of fuelwood in 1980 had already causeda deficit of 4.2 milion m3, and the shorffail was predicted to reach 18 million m3 by theyear 2000, Although the report is silent regarding the total resource base, theextrapolation of these figures to another decade or so could have led to the prediction ofthe total disappearance of the forest area in the RPTES countTies. Put in the context ofdesertification, especially with vivid memories of the severe droughts of the seventies, thisapparentl alarming situation prompted govrerments to take actions and it also generatedsignificant donor attention. The declared main objective was to stop and reverse thedesertification process through, among others, filling the perceived gap between demandand sustainable supply of fuelwood. This has resulted in the implementation of a largenumber of projects to control the demand (improved cooking stoves, inter-fuelsubstitution) and to enhance the supply (afforestation and industrial plantations). Pricingm-echanisms were also used to influence consumer behavior and to motivate producers

12. In parallel with the execution of specific projects, several forest inventories wereundertaken. This work, intended to firm up the data base, has revealed new contradictions,thus creating more confusion among potential users (e.g. energy planners). The causes canbe traced to different approaches used to conduct the inventories, the complexity of forestdynamics, and lack of knowledge of the practical behavior of producers and consumersin the woodfuels sector. Given the persistence of so much uncertainty and the risk ofcommitting costly policy mistakes, the upgrading of the information base remains a highpriority. The remainder of this Section 2.2 assesses the available supply data and identifieshow the situation could be improved quickly and at the least cost.

c. Overview of the R1PTES Data Bases

c.l Information Sources

13. The inforrnation sources available at present fai in four major categories:

* Regional assessments covering a number of countries or parts of countries;* National inventories extending to the entire country;

3 Les disponibilites de bois de feu ca region Saheliennc de f'Aikique Occidentalc Siwauton et perspectives".M.N. Kcata, consultant FAO. 1982.

14

* Local inventories; and* Updates and syntheses in the RPTES reports of the national teams, mainly based on

the data bases listed above.

14. The following subsections c.2 through c.5 recapitulate the information provided ineach category. As will be seen, many unexplained discrepancies exist and they are notlikey to be resolved until the systematic collection of field data is further advanced.Subsection c.6 provides a - mostly qualitative - evaluation of the field work already done,with recommendations on priorities for confinuation.

c.2 Regional Assessments

15. During the 19B0's, two experts made comprehensive assessments of the resowucesin the Sahel at the regional level, including parts of the five RPTES countries: Keita forFAO in 1980 and Mfllington et al. for the ESMAP program of UNDP/World Bank in19864.

16. Keita used the FAO general map of the distnbution of forestry resources inAfrica5 . As noted above, his study addressed the supply-demand balance in the fiveRPTES countries plus Mauritania and Chad. However, the assessment covered only partsof these countries, basically excluc2ing the non-productive desert areas. The total areacoverage was about one miilion kIn . The assessment focused on sustainable productivityof forestry resources and corrected the results for physical accessibility of fuelwood toestimate the utiizable supply. Given the scope of the study, it provides no estimates ofstanding stock. Because of the lack of field data in the countries covered, the productivitywas estimated using the "Clement" formula that is based on empirical data in othercountries having similar agro-ecological conditions. In this formula, productivity is afunction of rainfall, and an adjustment factor is used to reflect the conditions of resourcemanagement. ApaiL from the fact that the estimated productivities have proven to beunderesimated, the assessment excluded nearly all the cultivated land with trees andcovered only trees with diameters larger than 10 cm at 1.3 meter of height (DBH).Although this kind of measurement is useful for assessing the potential for timberproducts, it is certainly too restrictive in an estimation of the natural stock of fiuelwood.Therefore, the assessment is likely to have underestimated the available resources.

17. Millington et al. conducted a biomass resource assessment in Sub-Saharan Africabased on the interpretation of AVHRR satellite imagery from NOAA His study coveredall territory, which for the seven countries of the Keita study adds up to 5.3 million km2.The initial resolution of the imagery is 1.1 km. However, the final resolution used forinterpretation after re-sampling was 8 km (6,400 ha.). Apart from this limitation, thereport acknowledges that for West Africa it was not possible to "distinguish between

4 "Esimating Woody Biomass in Sub-Sabaran Africa ", A. Millington et al., thc World Bank. 1994

S"Les ressources foresiiercs de rAfnique Tropicalc'- Part I and Pan D (citcd m Jensen. RPn-S 94)

I5

herbaceous and woody biomass. In a region like the Sahel, which includes areas ofseasonal grassland, this is obviously significant" (llington et al. page 30). The difficultyin discriminating between seasonal crops and natural wooded grassland requiredaggregation of these two land use classes. Because the estimated productivity was derivedfrom forested land, it is likely that the 1986 assessment has yielded an overestimation ofthe resources available in the five RPTES countries. As was the case in the Keitaassessment, this study had also to resort to productivity estimates based on data compiledfrom other countries.

18. Table 2-2 below compares the results of the two assessments in the sevencountries. The interpretation of the results should take into account that the Keita studycovered only parts of the seven countries (19%) whereas Mllington provided fullcoverage. If the desert areas in each study are excluded, the Keita study covered 37 % ofthe area in the Millington study. Since the study resuts do not permit their segregation bycounty, the comparson in Table 2-2 applies to various land use classes'. Theproductivities estimated by the 1980 assessment were invariably lower than those used inthe 1986 study, except for the sylvo-pastoral bush land. The largest discrepancies (over100 %) are seen in the categories of wooded savanna and wooded land. On average,Keita's sustainable yield was 31 % below Mlllington's, if desert areas are excluded fromboth studies; even so, the comparison of the total areas surveyed is biased by the differentweights of each land category.

c.3 National Inventories

19. All RPTES countries, except Niger have national irventories7, of which the mainresults are presented in Table 2-3. They all relied on satellite imagery of variousresolutions to conduct the initial mapping and land cover classification. The volumes ofstanding stocks were assessed through sample measurements in Burldna Faso, Gambiaand Mali. In Senegal the standing volume was estimated by multiplying the areas ofidentified land use classes by corresponding stocldng units (m3/ha.) derived from theliterature. In some cases (Mali and Senegal-1978), the inventories excluded the biomassresources on cultivated land9 and focused on standing trees with certain minimumdiameters. Only the Mali inventory took into consideration all trees taller than one meterregardless of their diameters. The Gambian assessment counted the small trees andconsidered them as part of the regeneration process but did not include their biomasscontent. All these elements suggest that as far as fiuelwood is concerned the available

6 The way the results wer preseted doe not permit to islatc the five RPIES countrics.

7 TIM national inventory of Mali coven:d only the pmovnces orKayes, KIoulikom, Sikasso, Sgou and Mopti. Theseprovinces cover about 47% of the total area ofthe country and housc about 75% of the population (RPTES.Mali 94). The excluded areas ae mainlv the desert puts of the Eastern and Northen areas of the countrv.

E In Burkina Faso, the estimate of ihe standing stock has a significant and high statistical mar.

9 The National Forest Inventory of Mali mav have included cultivated areas. However, the resources were notmcluded m the reported available biomass.

16

resources have certainly been underestimated. The investigation also illustrates thedivergence in method that hamper cross-country comparisons.

Table 2-2Comparison of Results of two regional Inventories

1936 ASSESSMENT 190 ASSESSMENT COMPARATIVE(Millington et Rl) (Keita) PRODUCTIlTY

Area Volume Total Area Total 19R6 1980'000 ha OOOm3 Productivity WDO ha Productivity m3/hfyear

00Om3/year WOm3/yearLAND USE

Desert 259,034 0 0 4,700 412 0.00 0.09

Sylvo-Pastoral 102,208 556,227 17,069 20,840 3,809 0.17 0.138Bush land

Wooded Savanna 87,996 213,520 51,307 16,600 4290 0.58 026

Wooded land 74,138 3,396,910 98,183 59,310 33,458 1.32 0.56

TOTAL 534,426 4,171,727 166,559 101,450 41.969

Total Admin area 530,000

Total ss desert) 264,392 4,171,727 166.559 96,750 41,557 0.62 0.43

Source: Jense, RPTES 94.

20. The productivity, or sustainable yicld. is the most crucial element in natural forestmanagement in general and traditional energy issues in particular. The values in thenational inventories are based on assumptions derived from research undertakenelsewhere, using the Clement formula alreadv employed by Keita. The RPTES evaluationof available information on biomass resources (Jensen 1994) gathered - still anecdotal -evidence suggesting that the productVit has been underestimated. Apart fromdeficiencies in terms of coverage. there is no logical explanation for the fact that theunitary productivity in Burkina Faso and Gambia is about half of the productivityestimated in Mali as shown in Table 2-3

21. The comparison of national inventories u-th regional assessments for similar yearscasts more doubt on the reliability of information on the resource base. The results of thethree inventories conducted around the same time (Burkina Faso -1980, Gambia -1980and Senegal -1978) showed that the Keita study underestimated the sustainable yield byabout 50%. On the other hand, the results of the later assessments conducted for Senegal(1985) and Mali (1987) showed that, compared to the national inventories, the Millingtonstudy overestimated the standing stock by about two thirds and the sustainable yield byabout one-third

17

Table 2-3Main Results of national Inventories

YEAR AREA VOLUME PRODUCTIVITY COVERAGEAdmin Covered ToWa Unimuy Famland Size

COUNTRY vOO ha '0D0m3 m3fha )00m3/yea m3halyear (1) (2)

Senegal 197B 19,700 13,845 194,845 14.0 8.297 0.6 Excl. d>10crn1985 18,915 31S,779 16.9 13,353 0.7 lncl. dt40cm

Gambia 1980 1,200 846 16,542 19.6 407 0.5 Inci. d>l10cm

Buritna 1980 27,400 24,190 502,199 20.8 10,279 OA bncl. d>7.5cm