Research Journal of Commerce & Business Management

244

Research Journal of Commerce & Business Management Published by VICHAYA EDUCATIONAL TRUST Ranchi, Jharkhand, India www.anusandhanika.co.in ISSN 0974 - 200X Special Issue on FDI in India June 2017

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Research Journal of Commerce & Business Management

Research Journal of Commerce & Business ManagementPublished by

VICHAYA EDUCATIONAL TRUSTRanchi, Jharkhand, Indiawww.anusandhanika.co.in

ISSN 0974 - 200X

Special Issue on FDI in India June 2017

Special Issue on FDI in India

June 2017A

NU

SAN

DH

AN

IKA

ANUSANDHANIKARefereed Research Journal of Commerce & Business Management

ISSN 0974-200X

Dr. R.P. Verma

Dr. Navin Kumar

Dr. Jyoti Shekhar

Dr. S.N.L. Das

Dr. Vijay B Singh

Dr. P. K. Pani

Dr. Vijay Kumar Mishra

Dr. M.K. Singh

Dr. Amar Kumar Chaudhary

Special Issue on FDI in India

Editor Madhukar Shyam

Managing Editor Dr. A.K. Chattoraj

Guest Editor Dr Arun Kumar Sinha

Published byVichaya Educational Trust Ranchi, Jharkhand (India)

Printed, published, owned and edited by Madhukar Shyam on behalf of Vichaya Educational Trust, C-1, Shanti Enclave, Kusum Bihar, Road No. - 4, Morabadi, Ranchi - 8 Jharkhand, INDIA

Advisory Board

October 2017

Dr. S.K. Ambashtha

Dr. Shrikant Kumar Sinha

Dr. M.N. Zubairi

Dr. Vishwa Ranjan

Dr. Vikas Kumar

Dr. Vijay Prakash

Dr. Shahid Akhter

Dr. Sandeep Kumar

Impact Factor - 2.118

Office:C-1, Shanti Enclave, Kusum Bihar, Road No. - 4, Morabadi, Ranchi - 8

Website: www.anusandhanika.co.inE-mail : [email protected]

Ph : 09835536035 Published in January and July

� The 'Anusandhanika' is a half yearly Refereed Research Journal published in January and July. It contains articles, useful for professionals, scholars, students as well as for those generally interested in the subject.

� The 'Anusandhanika' desires to bring to the notice of the contributors that The Articles should not normally exceed 5000 words.

� Manuscripts should be composed in (MS - Word or Adobe Page Maker) double spaced typed on one side only of A-4 size paper in font size 12 pts. with margins of 1.25" in left/right/top & bottom and Arial fonts for English and Kruti Dev 010 fonts for Hindi is preferred. The Proposed article should be submitted in original along with a C.D.

� The Editor and Advisory Board is fully empowered to edit, trim and adjust articles in order to conform to Anusandhanika's format.

� While sending an Article to 'Anusandhanika', the author/s should certify that the article is his/her own/original and has not been published elsewhere and would not again be submitted for publication. In case of any litigation regarding any published article, the concerned author(s) would be held responsible. Editor/Editorial Board would not be responsible in the matter

� Normally,articles should be arranged under the heads : (i) Title (ii) An Abstract of the paper not exceeding 200 words (iii) Keywords - maximum five keywords may be placed after the abstract (iv) Introduction (v) Materials and Methods (vi) Results and Discussions (vii) Conclusion and (viii) References.

� References should be arranged in this order- Author's name, name of the book/article/journal, name of Publisher, place of publication, year of publication and page nos.

� Editor and Advisory Board will not be responsible for the views expressed by the author/s in the Anusandhanika.

� Foot notes should be avoided.

� Units of measurement should be in the International (metric) system only.

� Oxford English Dictionary should be followed for disputed spellings.

Notes for Contributors

1. Need of FDI in India- Its impact on Economic Development

ShuchiDr Arun Kumar Sinha

1

2. Foreign Direct Investment (FDI) in India & its impact on Indian Economy

Dr. I. J. Khalkho 6

3. FDI in India: An Analysis Dr. Vijay Prakash 11

4. Problems and Prospects of Foreign Direct Investment in India

Darshana Gopa Minz 16

5. Opportunities and Challenges of FDI in the Indian Telecommunication Sector

Tanuj KhatriDr. S.N.L. Das

21

6. FDI in Broadcasting Sector Dr. Shravan Kumar 26

7. Recent Challenges and Issues of FDI in Retail Trade for Sustainable Development of Business

Dr. Sandeep Kumar 30

8. Impact of Multinational Corporation on Labour Practices in the Era of Liberalisation, Privatisation and Globalisation

Dr. Abha Kumari 38

9. Foreign Direct Investment in India – Retail Sector Aditi SinghaniaPriyanka Chaturvedi

46

10. An Overview of FDI in India and Measures to Increase its Infl ow

Amit Kumar Gupta 52

11. Present Scenario of Foreign Direct Investment in India

Anamika KumariSneha Toppo

60

12. Foreign Direct Investment in Aviation Anand Kumar Chitlangia 67

13. Foreign Direct Investment in Infrastructure Sector and its Impact on Economic Growth in India

Avinash KumarFouzia Tabassum

71

14. Growth of Indian Economy in Foreign Direct Investment

Badal Rakshit 77

15. Impact of FDI in Socio-economic Development of India

Binita KumariDr. Sanjiv Chaturvedi

84

16. Foreign Direct Investment in India : An outline of Develpoment Since 1991

Christina Deogam Dr Arun Kumar Sinha

90

17 A Socio-Economic Analysis of FDI in India Prof. (Dr.) Himadri Ranjan Mishra

95

18 Foreign Direct Investment in Retail Sector Jayshree Gangunly 103

19 Impact of FDI in the Socio- Economic Development in India

Dr. Aditendra Nath ShahdeoKhaleda Rehman

106

Impact Factor - 2.118

ANUSANDHANIKARefereed Research Journal of Commerce & Business Management

ISSN 0974-200X

Special Issue on FDI in India October 2017Contents

1. Need of FDI in India- Its impact on Economic Development

ShuchiDr Arun Kumar Sinha

1

2. Foreign Direct Investment (FDI) in India & its impact on Indian Economy

Dr. I. J. Khalkho 6

3. FDI in India: An Analysis Dr. Vijay Prakash 11

4. Problems and Prospects of Foreign Direct Investment in India

Darshana Gopa Minz 16

5. Opportunities and Challenges of FDI in the Indian Telecommunication Sector

Tanuj KhatriDr. S.N.L. Das

21

6. FDI in Broadcasting Sector Dr. Shravan Kumar 26

7. Recent Challenges and Issues of FDI in Retail Trade for Sustainable Development of Business

Dr. Sandeep Kumar 30

8. Impact of Multinational Corporation on Labour Practices in the Era of Liberalisation, Privatisation and Globalisation

Dr. Abha Kumari 38

9. Foreign Direct Investment in India – Retail Sector Aditi SinghaniaPriyanka Chaturvedi

46

10. An Overview of FDI in India and Measures to Increase its Infl ow

Amit Kumar Gupta 52

11. Present Scenario of Foreign Direct Investment in India

Anamika KumariSneha Toppo

60

12. Foreign Direct Investment in Aviation Anand Kumar Chitlangia 67

13. Foreign Direct Investment in Infrastructure Sector and its Impact on Economic Growth in India

Avinash KumarFouzia Tabassum

71

14. Growth of Indian Economy in Foreign Direct Investment

Badal Rakshit 77

15. Impact of FDI in Socio-economic Development of India

Binita KumariDr. Sanjiv Chaturvedi

84

16. Foreign Direct Investment in India : An outline of Develpoment Since 1991

Christina Deogam Dr Arun Kumar Sinha

90

17 A Socio-Economic Analysis of FDI in India Prof. (Dr.) Himadri Ranjan Mishra

95

18 Foreign Direct Investment in Retail Sector Jayshree Gangunly 103

19 Impact of FDI in the Socio- Economic Development in India

Dr. Aditendra Nath ShahdeoKhaleda Rehman

106

Impact Factor - 2.118

ANUSANDHANIKARefereed Research Journal of Commerce & Business Management

ISSN 0974-200X

Special Issue on FDI in India October 2017Contents

20 Impact of FDI in the Socio-Economic Development of India

Khushboo RaiDr. B.M. Sahu

114

21 Bottleneks in Ariving Foreign Direct Investment in India and Suggestions to Overcome them

CS. Mala Kumari Upadhyay

118

22 Challenges and Future Prospects of FDI in Automobile Industry in India

Gaurav Srivastava 127

23 FDI and Its Impact on Jharkhand’s Socio-Economic Development

Nirmala KhessDr Sanjeev Chaturvedi

131

24 Problems and Prospects of FDI in Indian Retail Sector

Binay Kumar PanjiyarDr. Shravan Kumar

136

25 FDI in Insurance Sector Pervez WahabDr Nayeem Akhatar

142

26 Foreign Direct Investment in India Priyanka ChaturvediDr. H.B Singh

148

27 FDI in Indian Retail Sector Opportunities and Challenges

Priyanka Pandey Dr. D.L Maurya

154

28 Present Scenario of FDI in India Rachana Kumari 161

29 The Opportunities and Challenges for FDI in Retail in India

Ruchi Kumari 166

30 Growth of FDI in Indian Telecom Sector Sagorika RakshitDr. Subhas Kumar

174

31 FDI - An Opportunity to Indian Economy Shradha VermaAnamika Kumari

184

32 Impact of Demonetization on Foreign Portfolio Investment & Return in Stock Market

Sitaram PandeyDr. Amitava Samanta

188

33 Effect of Foreign Direct Investment and Human Capital Formation on Labour Markets in India

Dr. Abha Kumari Sheela Kumari Gupta

197

34 The Impact of FDI & FPI on Human Welfare AmarnathDr. Amitava Samanta

202

35 FDI in Energy Infrastructure – Power Generation & Distribution

Dr. Madan Kumar Singh 207

36 Role of FDI in Economic Growth of India Mantosh Kumar Singh 212

37 FDI in Retail Sector: Opportunities and Challenges Ahead

Dr. Bijay Kumar SinhaMritunjay Kumar Mishra

215

38 Foreign Direct Investment (FDI) in Indian Service Sector

Rajiv Ranjan Sinha 219

39 Role of FDI in Indian Economy and its Problems Dr. Sanjay PrasadProf. Srinath Koley

223

40 Present Scenario of FDI in India Sheela Kumari Gupta 229

-1-

Anusandhanika /Special Issue on FDI in India/ October 2017/ pp 1 - 5 ISSN 0974 - 200X

Need of FDI in India- Its impact on Economic Development

Abstract

As India is a developing country, capital has been one of the scare resources that are usually required for economic development. Capital is limited and there are many issues such as Health, poverty, employment, education, research and development, technology obsolesce, global competition. The flow of FDI in India from across the world will help in acquiring the funds at cheaper cost, better technology, employment generation, and upgraded technology transfer, scope for more trade, linkages to domestic firms. The following arguments are advanced in favour of foreign capital. FDI is an important vehicle of technology transfer from developed countries to developing countries. India is the second fastest growing economy in the world with a GDP growth rate of 7.6% in the FY16. To maintain this growth rate and rank India requires huge foreign investment. Government of India has taken many initiatives to attract foreign investment into India. One of such initiative is “Make in India”, programme to make India a ‘Manufacturing Hub’ of the world. A Foreign Direct Investment is an investment made by a company or entity based in one country, into a company or entity based in another country. A foreign direct investment is a controlling ownership in a business enterprise in one country by an entity based in another country. Foreign Direct Investment has played a crucial role in the economic development of the country.

Keywords : domestic capital, business enterprise, economic growth

ShuchiResearch Scholar

University Department of Commerce & Business ManagementRanchi University, Ranchi

Dr Arun Kumar SinhaP G Head & Dean, Department of Commerce

St Xavier’s College, Ranchi

Introduction

Foreign Direct Investment (FDI) is a type of investment in to an enterprises in a country by another enterprises located in another country by buying a company in the target country or by expanding operations of an existing business in that country. In the era of globalization FDI takes vital part in the development of both developing and developed countries.

If country is interested in rapid economic development, they will have to import machinery, technical know-how, entrepreneurship, and foreign investment. One of the methods of paying for the imports is to set up exports or second alternative is getting foreign technology and equipment and it also depends upon foreign assistance in some forms or the other.

Most countries of the world which embarked on the road to economic development had to depend on foreign capital to some extent. The fact cannot be denied that the foreign capital contributed in many important ways to the process of economic growth and industrialization.

As India is a developing country, capital has been one of the scare resources that are usually required for economic development. Capital is limited and there are many issues such as Health, poverty, employment, education, research and development, technology obsolesce, global competition. The flow of FDI in India from across the world will help in acquiring the funds at cheaper cost, better technology, employment generation,

20 Impact of FDI in the Socio-Economic Development of India

Khushboo RaiDr. B.M. Sahu

114

21 Bottleneks in Ariving Foreign Direct Investment in India and Suggestions to Overcome them

CS. Mala Kumari Upadhyay

118

22 Challenges and Future Prospects of FDI in Automobile Industry in India

Gaurav Srivastava 127

23 FDI and Its Impact on Jharkhand’s Socio-Economic Development

Nirmala KhessDr Sanjeev Chaturvedi

131

24 Problems and Prospects of FDI in Indian Retail Sector

Binay Kumar PanjiyarDr. Shravan Kumar

136

25 FDI in Insurance Sector Pervez WahabDr Nayeem Akhatar

142

26 Foreign Direct Investment in India Priyanka ChaturvediDr. H.B Singh

148

27 FDI in Indian Retail Sector Opportunities and Challenges

Priyanka Pandey Dr. D.L Maurya

154

28 Present Scenario of FDI in India Rachana Kumari 161

29 The Opportunities and Challenges for FDI in Retail in India

Ruchi Kumari 166

30 Growth of FDI in Indian Telecom Sector Sagorika RakshitDr. Subhas Kumar

174

31 FDI - An Opportunity to Indian Economy Shradha VermaAnamika Kumari

184

32 Impact of Demonetization on Foreign Portfolio Investment & Return in Stock Market

Sitaram PandeyDr. Amitava Samanta

188

33 Effect of Foreign Direct Investment and Human Capital Formation on Labour Markets in India

Dr. Abha Kumari Sheela Kumari Gupta

197

34 The Impact of FDI & FPI on Human Welfare AmarnathDr. Amitava Samanta

202

35 FDI in Energy Infrastructure – Power Generation & Distribution

Dr. Madan Kumar Singh 207

36 Role of FDI in Economic Growth of India Mantosh Kumar Singh 212

37 FDI in Retail Sector: Opportunities and Challenges Ahead

Dr. Bijay Kumar SinhaMritunjay Kumar Mishra

215

38 Foreign Direct Investment (FDI) in Indian Service Sector

Rajiv Ranjan Sinha 219

39 Role of FDI in Indian Economy and its Problems Dr. Sanjay PrasadProf. Srinath Koley

223

40 Present Scenario of FDI in India Sheela Kumari Gupta 229

-2- Anusandhanika /Special Issue on FDI in India/ October 2017

and upgraded technology transfer, scope for more trade, linkages and spill over to domestic firms.

The need for Foreign Direct Investment for a developing country like India can arise on account of the following reasons:

i. Sustaining a high level of investment: As all the under-developed and the developing countries want to industrialize and develop themselves, therefore it becomes necessary to raise the level to investment substantially. Due to poverty and low GDP the saving are low. Therefore there is a need to fill the gap between income and savings through foreign direct investments.

ii. Technological gap: In Indian scenario we need technical assistance from foreign source for provision if expert services, training of Indian personnel and educational, research and training institutions in the industry. It only comes through private foreign investment or foreign collaborations.

iii. Exploitation of natural resources: In India we have abundant natural resources such as coal, iron and steel but to extract the resources we require foreign collaboration.

iv. Understanding the initial risk: In developing countries as capital is a scare resource, the risk of investments in new ventures or projects for industrialization is high. Therefore foreign capital helps in these investments which require high risk.

v. Development of basic economic infrastructure: In the recent years foreign financial institutions and government of advanced countries have made substantial capital available to the under developed countries. FDI will help in developing the infrastructure by establishing firm’s different parts of the country. There are special economic zones which have been developed by government for improvising the industrial growth.

vi. Improvement in the balance of payments position: The inflow FDI will help in improving the balance of payment. Firms which feel that the goods produced in India will have a low cost, will produce the goods and export the same to other country. This helps in increasing the exports.

vii. Foreign firm’s helps in increasing the competition: Foreign firms have always come up with better technology, process, and innovations comparing with the domestic firms. They develop a completion in which the domestic firms will perform better it survive in the market.

Supporters of private foreign investment argue that, the foreign investment brings with it new technology, better management and organization, superior marketing and sometimes cheaper finance. The arguments in favour of private foreign investment are the following:

i. Foreign investment constitutes a net addition to investible resources in host countries and as such raises their rates of growth;

ii. Foreign investment results in a pattern of growth which is desirable from the point of view of underdeveloped countries since new products are introduced and marketed, new tastes are created and specific needs of the host country are met; and

iii. Free flow of capital is conducive for the welfare of both the individual country and the world at large. The operations of foreign firms, especially of modern multinational firms, knit countries together and closer into the web of international commerce, both by(vertical and horizontal) economic integration and by the transmission of tastes, designs, ideas and technology.

Industrial studies have revealed that as foreign investors’ confidence in the Indian government will increase, their levels of investment in India will also go up. In the 2015-2016 fiscal years,

-3- Anusandhanika /Special Issue on FDI in India/ October 2017

it is expected that FDI will exceed 60 billion US dollars. In the 2013-14 fiscal years, the aggregate foreign investment amounted to 29 billion dollars. This increase owes a lot to the high expectations that foreign investors. It has been estimated that in the ongoing Twelfth Five Year Plan, which continues till 2017, India will need almost a trillion US dollars in FDI. This money will be used to develop infrastructure such as highways, airways and ports.

Materials and Methods

For the purpose of in depth study the contents have been taken from interview, relevant books and articles from journals and websites. The method used is analytical and descriptive. Both primary as well as secondary source of Information have been taken.

Results and Discussions

FDI incorporates an important role within the economic progression and development of India. FDI in India in numerous sectors will attain sustained economic growth and development through creation of jobs, growth of existing producing industries. There are various economic factors which affect the inflows of FDI. Even despite the fact that of many factors Indian economy has succeeded to attract FDI inflows. India due to variability and many FDI caps provided by the government and other factors hoard and providing opportunities to many foreign investor countries. India is the second fastest growing economy in the world with a GDP growth rate of 7.6% in the FY16. In terms of GDP it is the 10th largest economy in the world and in terms PPP (Purchasing Power Parity) it is the 3rd largest economy in the world. To maintain this growth rate and rank India requires huge foreign investment. Government of India has taken many initiatives to attract foreign investment into India. One of such initiative is “Make in India”, programme to make India a ‘Manufacturing Hub’ of the world.

A Foreign Direct Investment (FDI) is an investment made by a company or entity based in one country, into a company or entity based in another country. A foreign direct investment is a controlling ownership

in a business enterprise in one country by an entity based in another country. Foreign Direct Investment (FDI) has played a crucial role in the economic growth and development of the country. FDI inflows not only bring capital in the country but also bring technological know-how and managerial skills.

It has been witnessed that with the increase in FDI inflows in India from $0.13 billion to $30.3 billion in 2010-11, the GDP growth rate of the country has accelerated from 1.43 percent in 1990-91 to 7.6 percent in 2015-16. It shows that India’s GDP has increased four times since 1990-91. FDI act as a catalyst in various sectors mainly in manufacturing and service sectors. With the new government in power, there are many reforms to attract FDI inflows in the country. FDI inflows in 2015-16 are more in the areas of service sectors (18%), construction development (10%), telecommunication (7%), computer software and hardware (6%) etc. While the share of industry in GDP remained stagnant, noteworthy over the period there was structural transformation in manufacturing sector. With FDI inflows there are development in many areas like infrastructure, per capita income and standard of living of the people has increased, poverty has declined in absolute terms, unemployment has reduced by 3 times since 1990-91 to 2013-14, clean technology has installed, roads, dams, bridges, schools, colleges, hospitals has been built with new technology. Thereby, overall development has shown in all over India.

For the economic growth and development of the country India requires huge capital. To compensate this domestic capital requirement, FDI inflows are one of the important pre-requisite. FDI is helping developing countries in capital formation by bringing fresh capitals.

Developing countries are lacking technological know-how. With the opening up of their economies for FDI, they will get the access to sophisticated technology from the foreign firms which will enhance their productivity and quality of the products.

FDI inflows are not only helping in capital formation but also help in developing

-4- Anusandhanika /Special Issue on FDI in India/ October 2017

managerial skills. FDI inflows have increased the competitive environment for the domestic firms consequently benefitting the consumers by accessing with better quality products at a lesser price.

With the transfer of technology and enhancement of production techniques, marketing expertise and modern managerial techniques possibilities of export promotion has also been opened up in new areas. With better quality product at a lower price the demand increased for Indian goods and services abroad consequently there is increase in exports. Therefore, exports have increased from $18 billion to $245 billion. With the enhancement in exports BOP deficits has declined. Government of India has also taken many measures to attract FDI to boost exports.

With FDI inflows into the country new job opportunities has been created in various sectors. As more employment opportunities are generated mainly in metropolitan cities where FDI inflows are maximum i.e., Delhi and Mumbai. Therefore more rural-urban migrations are in these cities. India is the second largest populated country in the world. With increase in employment opportunities there is reduction in absolute poverty in India. But as the population base is very high in actual terms poverty has increased. So government has to take measures to attract more FDI and create more employment opportunities to reduce poverty from the country.

With the new reforms to boost FDI inflows in India, the PSU’s reserved areas i.e, where the state have exclusive rights to produce are opened up for Foreign Direct Investments. Earlier Railways and Defence were reserved for PSU’s and now FDI is allowed in these sectors. 100 percent FDI is allowed under automatic route in most of the areas of Indian Railways such as in bullet train, passenger terminal, railway electrification, mass rapid transport systems and IRCTC. 49 percent FDI is allowed in Defence sector but Atomic energy are still under PSU’s reserved areas. To get access to more sophisticated technology in Defence area we have to increase the FDI limit.

In India, the primary sector is in dire needs of foreign investment especially in the areas of agricultural, livestock farming, forestry, fishing etc. FDI inflows into agricultural and allied sectors are still negative despite that 58 percent of Indians are still dependent on agricultural and allied sectors for their livelihood and their contributions to country’s GDP has also declined from 56.5 percent in 1950-51 to 16 percent in 2015-16. To attract FDI’s into this sector government has to make land reforms and ease in the entry of FDI into this area. Therefore, it has been witnessed that FDI inflows are not even in terms of various sectors and regions.

FDI in India has a significant impact on development of India. FDI in India to various sectors can attain sustained economic growth and development through creation of jobs, expansion of existing manufacturing industries. The inflow of FDI in service sectors and construction and development sector, from April, 2000 to March, 2016 attained substantial sustained economic growth and development through creation of jobs in India. Computer, Software & Hardware and Drugs & Pharmaceuticals sector were the other sectors to which attention was shown by Foreign Direct Investors (FDI).

FDI plays a crucial role in enhancing the economic growth and development of the country. Moreover, FDI as a strategic component of investment is needed by India for achieving the objectives of its second generation of economic reforms and maintaining this pace of growth and development of the economy. Hence FDI is a significant factor which influences the level of economic growth in India. It provides a sound base for economic growth and development by enhancing the financial position of the country. It also contributes to the GDP and foreign exchange reserves of the country. India attracted FDI worth US$ 22.42 billion. Tourism, pharmaceuticals services, chemicals and construction were among the biggest beneficiaries. For Indian economy which has tremendous potential, FDI has had a positive impact. FDI inflow supplements domestic

-5- Anusandhanika /Special Issue on FDI in India/ October 2017

capital, as well as technology and skills of existing companies. It also helps to establish new companies. All of these contribute to economic growth of the Indian Economy. India’s Foreign Direct Investment (FDI) policy has been gradually liberalised to make the market more investor friendly. The results have been encouraging. These days, the country is consistently ranked among the top three global investment destinations by all international bodies, including the World Bank.

Conclusion

FDI in India has a significant role in the economic growth and development of India. FDI in India to various sectors can attain sustained economic growth and development through creation of jobs, expansion of existing manufacturing industries. The inflow of FDI in service sectors and construction and development sector attained substantial sustained economic growth and development through creation of jobs in India. Computer, Software & Hardware and Drugs & Pharmaceuticals sector were the other sectors to which attention was shown by Foreign Direct Investors (FDI). The other sectors in Indian economy the Foreign Direct Investors interest was, in fact has been quite poor.

FDI has helped to raise the output, productivity and employment in some sectors especially in service sector. Indian service sector is generating the proper employment options for skilled worker with high perks. On the other side banking and insurance sector help in providing the strength to the Indian economic condition and develop the foreign exchange system in country. FDI is always helps to create employment in the country and also support the small scale industries also and helps country to put an impression on the world wide level through liberalization and globalization.

References

1. Kumar Nagesh, Globalization and the Quality of FDI, Oxford University Press, New Delhi, 2015

2. Khan A.Q., Strategy for Foreign Investment Management in 21st century, Kitab Mahal Publication, New Delhi, 2015

3. Shandilya T.K., Thakur A.K., Foreign Direct Investment in India: Problems and Prospects, Deep and Deep Publication, New Delhi, 2014

4. Narayanana M. R., Inflow of Foreign Direct Investment in India- Patterns, Performance, Implications, Foreign Trade Review, Vol. XXXIV, 2015, p 3

5. Grubaugh S.J., Determinants of Direct Foreign Investment, Review of Economics & Statistics, November, 2015

6. Grubaugh S.J., Determinants of Direct Foreign Investment, Review of Economics & Statistics, November, 2015

7. Roy Tirthankar, The Economy of India, Oxford University Press, New Delhi, 2015

8. Srivastava Sadhana, What Is the True Level of FDI Flows to India?, Economic and Political Weekly February 15, 2003

9. Kumar Raj Kapila, A Decade of Economic Reforms in India, published by Academic Foundation, Delhi, 1998

10. Mello Junior Luiz, R., Foreign Direct Investment led growth, Evidence from Time Series and Panel Data, Oxford Economic Papers, 1999

11. Bailliu Jeanine N, Foreign Capital Flows, Financial Development and Economic Growth in Developing Countries, Working Paper Bank of Canada, 2000

-6-

ISSN 0974 - 200XAnusandhanika /Special Issue on FDI in India/ October 2017/ pp 6-10

Foreign Direct Investment (FDI) in India & its impact on Indian Economy

Abstract

Nations’ progress and prosperity is reflected by the pace of its sustained economic growth and development. Investment provides the base and pre-requisite for economic growth and development. Developed economies consider FDI as an engine of market access in developing and less developed countries vis-à-vis for their own technological progress and in maintaining their own economic growth and development. Developing nations looks at FDI as a source of filling the savings, foreign exchange reserves, revenue, trade deficit, management and technological gaps. FDI is considered as an instrument of international economic integration as it brings a package of assets including capital, technology, managerial skills and capacity and access to foreign markets. The impact of FDI depends on the country’s domestic policy and foreign policy. As a result FDI has a wide range of impact on the country’s economic policy. In order to study the impact of foreign direct investment on economic growth, two models were framed and fitted. The foreign direct investment model shows the factors influencing the foreign direct investment in India. The economic growth model depicts the contribution of foreign direct investment to economic growth.

Keywords : vital component, development strategy, managerial skills

Dr. I. J. KhalkhoAssociate Professor

Department of CommerceGossner College, Ranchi

Introduction

One of the most striking developments during the last two decades is the spectacular growth of FDI in the global economic landscape. This unprecedented growth of global FDI in 1990 around the world make FDI an important and vital component of development strategy in both developed and developing nations and policies are designed in order to stimulate inward flows. In fact, FDI provides a win – win situation to the host and the home countries. Both countries are directly interested in inviting FDI, because they benefit a lot from such type of investment. The ‘home’ countries want to take the advantage of the vast markets opened by industrial growth. On the other hand the ‘host’ countries want to acquire technological and managerial skills and supplement domestic savings and foreign exchange. Moreover, the paucity of all types of resources viz. financial, capital, entrepreneurship, technological know- how, skills and practices, access to markets- abroad- in their economic development, developing nations accepted FDI as a sole

visible panacea for all their scarcities. Further, the integration of global financial markets paves ways to this explosive growth of FDI around the globe.

Apart from being a critical driver of economic growth, Foreign Direct Investment (FDI) is a major source of non-debt financial resource for the economic development of India. Foreign companies invest in India to take advantage of relatively lower wages, special investment privileges such as tax exemptions, etc. For a country where foreign investments are being made, it also means achieving technical know-how and generating employment. The Indian Government’s favourable policy regime and robust business environment have ensured that foreign capital keeps flowing into the country. The government has taken many initiatives in recent years such as relaxing FDI norms across sectors such as defence, PSU oil refineries, telecom, power exchanges, and stock exchanges, among others. According to Department of Industrial Policy and Promotion (DIPP), the total FDI investments India

-7- Anusandhanika /Special Issue on FDI in India/ October 2017

received in FY 2015-16 was US$ 40 billion, indicating that government’s effort to improve ease of doing business and relaxation in FDI norms is yielding results

FDI has been associated with improved economic growth and development in the host countries which has led to the emergence of global competition to attract FDI.

Foreign Direct Investment (FDI) is considered as an engine of economic growth. Before the Economic reforms the flow of foreign direct investment to India has been comparatively limited because of the type of industrial development strategy and the various foreign investment policy followed by the nation Not only India but much heralded FDI boom worldwide constitutes a major element of economic globalization Foreign investment was normally permitted only in high technology industries in priority areas and in export oriented areas. So the inflow of FDI before 1990’s was very low. To fully utilize the country’s immense economic potential, the government launched Economic reforms in 1991. The new Government policies are simple, transparent and promote domestic and foreign investment. India’s abundant and diversified natural resources, its sound economic policy, good market condition and high skilled human resources make it a proper destination for FDI. After long years of journey FDI was also introduced in various sectors and states in India. The Investment of FDI in various states and sectors leads to rapid growth of Indian economy Foreign Direct Investment in India is allowed through four basic routes namely financial collaborations, technical collaborations & joint ventures, capital markets via Euro issues, and private placement or preferential allotments. India has opened up its economy & allowed MNEs in core sectors such as Power & Fuels, Electrical Equipments, Transport, Chemicals, Food Processing, Drugs & Pharmaceuticals, Textiles, Industrial Machinery, insurance as well as telecommunication.

India has already marked its presence as one of the fastest growing economies of the world. It has been ranked among the top 3 attractive

destinations for inbound investments. Since 1991, the regulatory environment in terms of foreign investment has been consistently eased to make it investor-friendly.

In the critical face of Indian economy the government of India with the help of World Bank and IMF introduced the macro-economic stabilization and structural adjustment program. As a result of these reforms India open its door to FDI inflows and adopted a more liberal foreign policy in order to restore the confidence of foreign investors. Further, under the new foreign investment policy Government of India constituted FIPB (Foreign Investment Promotion Board) whose main function was to invite and facilitate foreign investment Starting from a baseline of less than USD 1 billion in 1990, a recent UNCTAD survey projected India as the second most important FDI destination (after China) for transnational corporations. As per the data, the sectors which attracted higher inflows were services, telecommunication, construction activities and computer software and hardware. Mauritius, Singapore, the US and the UK were among the leading sources of FDI to the country.

India attracted FDI worth US$ 22.42 billion. Tourism, pharmaceuticals, services, chemicals and construction were among the biggest beneficiaries. For Indian economy which has tremendous potential, FDI has had a positive impact. FDI inflow supplements domestic capital, as well as technology and skills of existing companies. It also helps to establish new companies. All of these contribute to economic growth of the Indian Economy. India’s Foreign Direct Investment (FDI) policy has been gradually liberalised to make the market more investor friendly. The results have been encouraging. These days, the country is consistently ranked among the top three global investment destinations by all international bodies, including the World Bank.

Materials and Methods

For the purpose of in depth study the contents have been taken from interview, relevant books and articles from journals and websites. The method used is analytical and descriptive.

-8- Anusandhanika /Special Issue on FDI in India/ October 2017

Both primary as well as secondary source of Information have been taken.

Results and Discussions

Foreign investment plays a significant role in development of any economy as like India. Many countries provide many incentives for attracting the Foreign Direct Investment (FDI). Need of FDI depends on saving and investment rate in any country. Foreign Direct investment acts as a bridge to fulfill the gap between investment and saving. In the process of economic development foreign capital helps to cover the domestic saving constraint and provide access to the superior technology that promote efficiency and productivity of the existing production capacity and generate new production opportunity.

India’s recorded GDP growth throughout the last decade has lifted millions out of poverty & made the country a favoured destination for foreign direct investment. A recent UNCTAD survey projected India as the second most important FDI destination after China for transnational corporations during 2010-2015. Services, telecommunication, construction activities, computer software & hardware and automobile are major sectors which attracted higher inflows of FDI in India. Countries like Mauritius, Singapore, US & UK were among the leading sources of FDI in India.

The Economy of India is the seventh-largest economy in the world measured by nominal GDP and the third-largest by purchasing (PPP). The country is classified as a newly industrialized country, one of the G-20 major economies, a member of BRICS and a developing economy with an average growth rate of approximately 7% over the last two decades. Maharashtra is the wealthiest Indian state and has an annual GDP of US$220 billion, nearly equal to that of Portugal, and accounts for 12% of the Indian GDP followed by the states of Tamil Nadu (US$140 billion) and Uttar Pradesh (US$130 billion). India’s economy became the world’s fastest growing major economy from the last quarter of 2014, replacing the People’s Republic of China.

The long-term growth prospective of the Indian economy is positive due to its young population, corresponding low dependency ratio, healthy savings and investment rates, and increasing integration into the global economy. The Indian economy has the potential to become the world’s 3rd largest economy by the next decade, and one of the largest economies by mid-century. And the outlook for short-term growth is also good as according to the IMF, the Indian economy is the “bright spot” in the global landscape. India also topped the World Bank’s growth outlook for 2015-16 for the first time with the economy having grown 7.6% in 2015-16 and expected to grow 8.0 % + in 2016-17.

India has the one of fastest growing service sectors in the world with annual growth rate of above 9% since 2001, which contributed to 57% of GDP in 2012-13. India has become a major exporter of IT services, BPO services, and software services with $167.0 billion worth of service exports in 2013-14. It is also the fastest-growing part of the economy. The IT industry continues to be the largest private sector employer in India. India is also the fourth largest start-up hub in the world with over 3,100 technology start-ups in 2014-15. The agricultural sector is the largest employer in India’s economy but contributes to a declining share of its GDP (17% in 2013-14). India ranks second worldwide in farm output. The Industry sector has held a constant share of its economic contribution (26% of GDP in 2013-14). The Indian auto mobile industry is one of the largest in the world with an annual production of 21.48 million vehicles (mostly two and three wheelers) in FY 2013-14. India has $600 billion worth of retail market in 2015 and one of world’s fastest growing E-Commerce markets.

India’s two major stock exchanges, Bombay Stock Exchange and National Stock Exchange of India, had a market capitalization of US$1.71 trillion and US$1.68 trillion respectively as of Feb 2015, which ranks 11th & 12 largest in the world respectively according to the World Federation of Exchanges. India is a member of the Commonwealth of Nations, the South

-9- Anusandhanika /Special Issue on FDI in India/ October 2017

Asian Association for Regional Cooperation, the Non Aligned Movement, the G20, the G8+5, the International Monetary Fund, the World Bank, the World Trade Organisation, the United Nations, the Shanghai Cooperation Organisation, the New Development BRICS Bank the Asian Infrastructure Investment Bank and Missile Technology Control Regime.

Impact of FDI on Indian Economy

India is the second fastest growing economy in the world with a GDP growth rate of 7.6% in the FY16. In terms of GDP it is the 10th largest economy in the world and in terms PPP (Purchasing Power Parity) it is the 3rd largest economy in the world. To maintain this growth rate and rank India requires huge foreign investment. Government of India has taken many initiatives to attract foreign investment into India. One of such initiative is “Make in India”, programme to make India a ‘Manufacturing Hub’ of the world.

A Foreign Direct Investment (FDI) is an investment made by a company or entity based in one country, into a company or entity based in another country. A foreign direct investment is a controlling ownership in a business enterprise in one country by an entity based in another country. Foreign Direct Investment (FDI) has played a crucial role in the economic growth and development of the country. FDI inflows not only bring capital in the country but also bring technological know-how and managerial skills.

Accelerated Economic Growth

It has been witnessed that with the increase in FDI inflows in India from $0.13 billion to $30.3 billion in 2010-11, the GDP growth rate of the country has accelerated from 1.43 percent in 1990-91 to 7.6 percent in 2015-16. It shows that India’s GDP has increased four times since 1990-91.

Accelerated Economic Development

FDI act as a catalyst in various sectors mainly in manufacturing and service sectors. With the new government in power, there are many reforms to attract FDI inflows in the

country. FDI inflows in 2015-16 are more in the areas of service sectors (18%), construction development (10%), telecommunication (7%), computer software and hardware (6%) etc. While the share of industry in GDP remained stagnant, noteworthy over the period there was structural transformation in manufacturing sector. With FDI inflows there are development in many areas like infrastructure, per capita income and standard of living of the people has increased, poverty has declined in absolute terms, unemployment has reduced by 3 times since 1990-91 to 2013-14, clean technology has installed, roads, dams, bridges, schools, colleges, hospitals has been built with new technology. Thereby, overall development has shown in all over India.

Capital

For the economic growth and development of the country India requires huge capital. To compensate this domestic capital requirement, FDI inflows are one of the important pre-requisite. FDI is helping developing countries in capital formation by bringing fresh capitals.

Technology

Developing countries are lacking technological know-how. With the opening up of their economies for FDI, they will get the access to sophisticated technology from the foreign firms which will enhance their productivity and quality of the products.Managerial SkillsFDI inflows are not only helping in capital formation but also help in developing managerial skills.Competitive EnvironmentFDI inflows have increased the competitive environment for the domestic firms consequently benefitting the consumers by accessing with better quality products at a lesser price.Reduction in Balance of Payment DeficitWith the transfer of technology and enhancement of production techniques, marketing expertise and modern managerial techniques possibilities of export promotion

-10- Anusandhanika /Special Issue on FDI in India/ October 2017

has also been opened up in new areas. With better quality product at a lower price the demand increased for Indian goods and services abroad consequently there is increase in exports. Therefore, exports have increased from $18 billion to $245 billion. With the enhancement in exports BOP deficits has declined. Government of India has also taken many measures to attract FDI to boost exports.Employment GenerationWith FDI inflows into the country new job opportunities has been created in various sectors. As more employment opportunities are generated mainly in metropolitan cities where FDI inflows are maximum i.e., Delhi and Mumbai. Therefore more rural-urban migrations are in these cities.Poverty AlleviationIndia is the second largest populated country in the world. With increase in employment opportunities there is reduction in absolute poverty in India. But as the population base is very high in actual terms poverty has increased. So government has to take measures to attract more FDI and create more employment opportunities to reduce poverty from the country.Opened up Reserved AreaWith the new reforms to boost FDI inflows in India, the PSU’s reserved areas i.e, where the state have exclusive rights to produce are opened up for Foreign Direct Investments. Earlier Railways and Defence were reserved for PSU’s and now FDI is allowed in these sectors. 100 percent FDI is allowed under automatic route in most of the areas of Indian Railways such as in bullet train, passenger terminal, railway electrification, mass rapid transport systems and IRCTC. 49 percent FDI is allowed in Defence sector but Atomic energy are still under PSU’s reserved areas. To get access to more sophisticated technology in Defence area we have to increase the FDI limit.Conclusion

FDI incorporates an important role within the economic progression and development of

India. FDI in India in numerous sectors will attain sustained economic growth and development through creation of jobs, growth of existing producing industries. There are various economic factors which affect the inflows of FDI. Even despite the fact that of many factors Indian economy has succeeded to attract FDI inflows. India due to variability and many FDI caps provided by the government and other factors hoard and providing opportunities to many foreign investor countries. The invasion of FDI in service sectors and construction and development sector earned substantial, sustained economic progression through creation of jobs in Indian economy. FDI has helped to raise the output, productivity and employment in some sectors especially in service sector. Indian service sector is generating the proper employment options for skilled worker with high perks.

References1. Prasanna N, FDI in India: Issues and

Challenges, Regal Publications, New Delhi, 2014

2. Chaudhuri Sarbajit, Mukhopadhyay Ujjaini, Foreign Direct Investment in Developing Countries, Springer India, New Delhi, 2015

3. Roy Tirthankar, The Economy of India, Oxford University Press, New Delhi, 2015

4. Kumar Raj Kapila, A Decade of Economic Reforms in India, Academic Foundation, Delhi, 2015

5. Chakraborty S. and Basu P., Foreign Direct Investment and Growth in India: A Co integration Approach, Applied Economics, Vol. 34, 2014

6. https://en.wikipedia.org/wiki/Economy_of_India

7. Narayanana M. R., Inflow of Foreign Direct Investment in India- Patterns, Performance, Implications, Foreign Trade Review, Vol. XXXIV, 2015, p 3

8. Bhasin Nitin, Foreign Direct Investment (FDI) in India, New Century Publications, New Delhi, 2012

-11-

Anusandhanika /Special Issue on FDI in India/ October 2017/ pp 11-15 ISSN 0974 - 200X

FDI in India: An Analysis

Abstract

The economic development witnessed during the past two decades in India rests to a great extent on Foreign Direct Investment (FDI). FDI has been a vital non-debt financial force behind the economic upsurge in India. Special investment vantages like cheap cost wages and tax exemptions on the amount being invested attract foreign companies to invest in India. FDI in India is done across a wide range of industries and its relentless influx reflects the tremendous scope, faith and trust that foreign investors have in the Indian economy. To ensure an uninterrupted inflow of FDI in India, the Indian government has created conducive trade atmosphere and effective business policy measures in place. This strategy is reflected in the steps taken by the government, such as easing out the restrictions levied on sectors like stock exchanges, power exchanges, defence and telecommunications.

Keywords : tax exemptions, trade policies, financial stability

Dr. Vijay PrakashDepartment of Commerce

Gyan Chand Jain Commerce College, Chaibasa

Introduction

FDI have helped India to attain a financial stability and economic growth with the help of investments in different sectors. FDI has boosted the economic life of India and on the other hand there are critics who have blamed the government for ousting the domestic inflows. After liberalization of Trade policies in India, there has been a positive GDP growth rate in Indian economy. Foreign direct investments helps in developing the economy by generating employment to the unemployed, Generating revenues in the form of tax and incomes, Financial stability to the government, development of infrastructure, backward and forward linkages to the domestic firms for the requirements of raw materials, tools, business infrastructure, and act as support for financial system. Forward and back ward linkages are developed to support the foreign firm with supply of raw and other requirements. It helps in generation of employment and also helps poverty eradication. There are many businesses or individuals who would earn their lively hood through the foreign investments. There are legal and financial consultants who also guide in the early stage of establishment of firm.

Foreign investments mean both foreign portfolio investments and foreign direct

investments (FDI). FDI brings better technology and management, marketing networks and offers competition, the latter helping Indian companies improve, quite apart from being good for consumers. Alongside opening up of the FDI regime, steps were taken to allow foreign portfolio investments into the Indian stock market through the mechanism of foreign institutional investors. The objective was not only to facilitate non-debt creating foreign capital inflows but also to develop the stock market in India, lower the cost of capital for Indian enterprises and indirectly improve corporate governance structures. On their part, large Indian companies have been allowed to raise capital directly from international capital markets through commercial borrowings and depository receipts having underlying Indian equity. Thus the country adopted a two-pronged strategy: one to attract FDI which is associated with multiple attendant benefits of technology, access to export markets, skills, management techniques, etc. and two to encourage portfolio capital flows which ease the financing constraints of Indian enterprises.

FDI Policy Framework in India

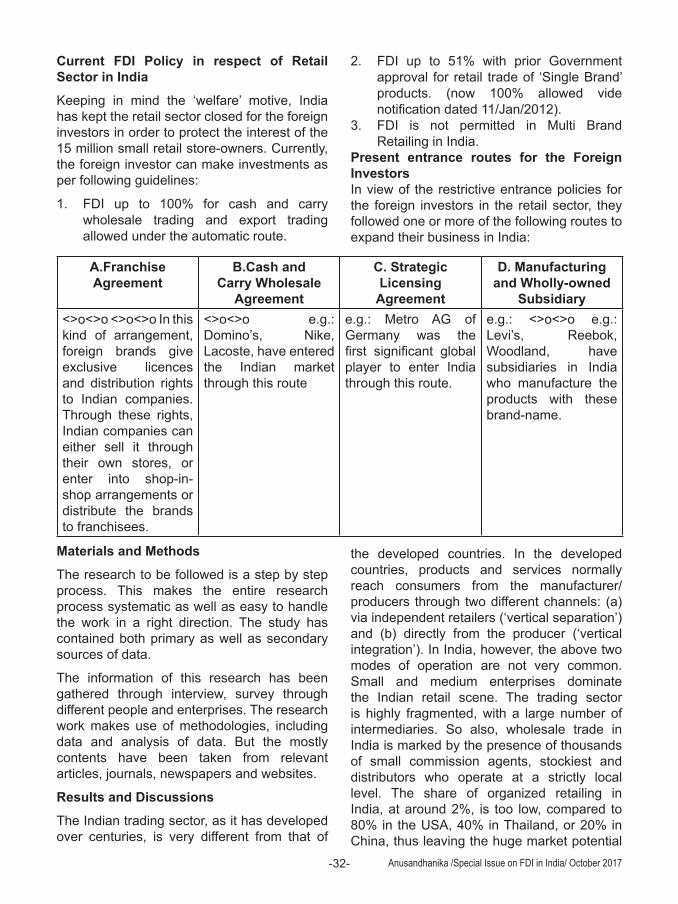

Policy regime is one of the key factors driving investment flows to a country. Apart from underlying overall fundamentals, ability of a nation to attract foreign investment essentially

-12- Anusandhanika /Special Issue on FDI in India/ October 2017

depends upon its policy regime - whether it promotes or restrains the foreign investment flows. This section undertakes a review of India’s FDI policy framework. There has been a sea change in India’s approach to foreign investment from the early 1990s when it began structural economic reforms about almost all the sectors of the economy.

Historically, India had followed an extremely careful and selective approach while formulating FDI policy in view of the governance of „import-substitution strategy‟ of industrialisation. The regulatory framework was consolidated through the enactment of Foreign Exchange Regulation Act (FERA), 1973 wherein foreign equity holding in a joint venture was allowed only up to 40 per cent. Subsequently, various exemptions were extended to foreign companies engaged in export oriented businesses and high technology and high priority areas including allowing equity holdings of over 40 per cent. Moreover, drawing from successes of other country experiences in Asia, Government not only established Special Economic Zones (SEZs) but also designed liberal policy and provided incentives for promoting FDI in these zones with a view to promote exports. The announcements of Industrial Policy (1980 and 1982) and Technology Policy (1983) provided for a liberal attitude towards foreign investments in terms of changes in policy directions. The policy was characterised by de-licensing of some of the industrial rules and promotion of Indian manufacturing exports as well as emphasising on modernisation of industries through liberalised imports of capital goods and technology. This was supported by trade liberalisation measures in the form of tariff reduction and shifting of large number of items from import licensing to Open General Licensing (OGL).

A major shift occurred when India embarked upon economic liberalisation and reforms program in 1991 aiming to raise its growth potential and integrating with the world economy. Industrial policy reforms slowly but surely removed restrictions on investment projects and business expansion on the one

hand and allowed increased access to foreign technology and funding on the other. A series of measures that were directed towards liberalizing foreign investment included:

� Introduction of dual route of approval of FDI– RBI’s automatic route and Government’s approval (SIA/FIPB) route.

� Automatic permission for technology agreements in high priority industries and removal of restriction of FDI in low technology areas as well as liberalisation of technology imports.

� Permission to Non-resident Indians (NRIs) and Overseas Corporate Bodies (OCBs) to invest up to 100 per cent in high priorities sectors.

� Hike in the foreign equity participation limits to 51 per cent for existing companies and liberalisation of the use of foreign ‘brands name’.

� Signing the Convention of Multilateral Investment Guarantee Agency (MIGA) for protection of foreign Investments.

These efforts were boosted by the enactment of Foreign Exchange Management Act (FEMA), 1999 [that replaced the Foreign Exchange Regulation Act (FERA), 1973] which was less stringent. In 1997, Indian Government allowed 100% FDI in cash and carry wholesale and FDI in single brand retailing was allowed 51% in June, 2006. After a long debate, further amendment was made in December, 2012 which led FDI to 100% in single brand retailing and 51% in multiple brand retailing.

Materials and Methods

For the purpose of in depth study the contents have been taken from interview, relevant books and articles from journals and websites. The method used is analytical and descriptive. Both primary as well as secondary source of Information have been taken.

Results and Discussions

India is a developing country; capital has been one of the scare resources that are usually required for economic development. Capital

-13- Anusandhanika /Special Issue on FDI in India/ October 2017

is limited and there are many issues such as Health, poverty, employment, education, research and development, technology obsolesce, global competition. The flow of FDI in India from across the world will help in acquiring the funds at cheaper cost, better technology, employment generation, and upgraded technology transfer, scope for more trade, linkages to domestic firms. The following arguments are advanced in favour of foreign capital.

As per the International Monetary Fund (IMF), Foreign Direct Investment, commonly referred to as FDI is an investment made to acquire lasting or long-term interest in enterprises operating outside of the economy of the investor. It is not ‘portfolio foreign investment (supine investment in another country’s securities like bonds and stocks)’. Inorganically or organically done investment in another country is not FDI. To understand the difference better, a British daily, the Financial Times puts it this way: “Standard definitions of control use the internationally agreed 10 percent threshold of voting shares, but this is a grey area as often a smaller block of shares will give control in widely held companies. Moreover, control of technology, management, even crucial inputs can confer de facto control. Ever since coming to power, the NDA government has taken a number of steps to bolster the FDI scenario in India. It has enabled international entities like Carrefour and Walmart to come and invest in the multi-brand retail market in India. The retail market in India has been growing at a substantial rate and at present, it is worth somewhere around 28 billion dollars. It is expected that in 2020, this value will reach approximately 260 billion dollars. However, there are certain conditions that need to be fulfilled by international entities that are thinking of coming and investing in the retail market in India. The minimum amount that needs to be invested by a foreign entity to gain entry in India’s retail market is 100 million dollars. There are also some restrictions in choosing the place where their stores can be opened. They can only start stores in cities where the population is at least 1 million. At

least half of their investment should be for back-end infrastructure such as warehouses. They will also need to get permission from the state government where they wish to open their stores.

The last fiscal (2014-15) year saw a considerable increase in the FDI made in India. India’s pro-growth business policies have contributed a great deal in making this possible. The first five months of the 2014-15 fiscal year noticed a net inflow of US$ 14.1 million FDI in India, amounting to a good 33.5 percent rise in the FDI influx registered for the corresponding period during the previous fiscal year. With an aggregate investment of US$ 353,963 million between April 2000 and November 2014, neighbouring country Mauritius has become the country with the largest Foreign Direct Investment (FDI) inflow into India.

There are several benefits of increasing foreign direct investment in India. First of all, with more FDI, consumers will be able to save 5 to 10 percent on their expenses because products will be available at much less rates and to top it all, the quality will be better as well. In short, it will be a win-win situation for the buyers. It is also expected that the farmers who face a lot of economic problems will also get better payment for their produce. This is a major benefit considering how many farmers have been giving up their lives lately. It is expected that their earnings will increase by 10 to 30 percent. FDI is also supposed to have a positive effect on the employment scenario by generating approximately 4 million job opportunities. Areas like logistics will be benefited as well because of FDI and it is assumed that 6 million jobs will be created. The governments – both central and state – will be benefited because of FDI. An addition of 25-30 billion dollars to the national treasury is also expected. This is a substantial amount and can really play a major role in the development of Indian economy in the long term.

Steps Taken by Government to Promote FDI

The Indian Government has taken a number of steps to show its willingness to allow more

-14- Anusandhanika /Special Issue on FDI in India/ October 2017

foreign direct investment in the country. In the infrastructure development sector, it has relaxed the norms pertaining to area restriction, the laws regarding gaining a comfortable exit from a particular project and the requirements relating to minimum capitalization. If companies are ready to commit 30 percent of their investments for affordable housing, then the rules for minimum capitalization and area restriction will be waived off. It is expected that this will benefit the construction sector a lot, especially in the form of greater investment inflow. The situation will only get better once sectoral conditions are further relaxed and the terms that have been used in the policy are clarified up to a greater extent. This is likely to get more investment especially in the newer areas. This will also act as a fillip for entities eagerly interested in developing plots for serviced housing. This is going to be a major development considering the fact that the land in the urban areas is inadequate. One also needs to factor in the high costs of land in this regard. It will also lead to the creation of cost-beneficial, affordable houses. It will help with the ‘Smart Cities’ programme as well. In the insurance sector too, the government has increased the upper limit of FDI from 26 percent to 49 percent. It is an amalgamation of different areas of investment such as:

� Foreign portfolio investment

� Foreign venture capital investment

� Foreign institutional investment

� Non-resident investment

� Qualified foreign investment

The Indian Ministry of Finance has also proposed that 100 percent FDI will be allowed in railways-related infrastructure. However, this does not include the operational aspects. While it is true that the foreign investors will not be allowed to intervene in railway operations, they will be able to provide for high-speed trains, such as bullet train, and enhance the overall network in the process.

Investments in India during 2015-16

The Government in the centre has announced

a lot of relaxations for FDI and the business done under the FDI umbrella in India. The Union Budget presented in the Lok Sabha mentioned that the procedures through which the corporate houses attract foreign investment into India will be simplified and made uncomplicated. From now onwards, there will hardly be any difference between ‘Portfolio Foreign Investment’ and ‘Foreign Direct Investment’. The composite cap has replaced the concept of individual cap; for instance, there is now a composite cap of 49 percent foreign investors allowed in the insurance sector. The Indian government, during the 2014-15 fiscal year, announced that it would allow FDI worth US$ 14.65 billion into the railways infrastructure. Some of the most expensive and largest railway projects will be carried out under these investments. During the next three years, ADAMA Agrochemicals, an Israeli firm, has set its targets to spend US$ 50 million in India. The company plans to enhance R&D and manufacturing facilities in India to grow at a better rate than the current industry growth rate. Hundred percent FDI into the health sector will be allowed by the Department of Industrial Policy and Promotion (DIPP) to enable indigenous manufacturing and reduce imports of medical devices. By the next fiscal year, the value of medical devices in the world market will be worth US$ 400 billion. The equity investment in the real estate is expected to go twofold as the Indian government has allowed 100 percent FDI into the construction sector. As per the real estate experts’ beliefs, the demand from foreign property buyers will rise. Currently valued at US$ 1.5 billion, the real estate equity will reach a value of US$ 3 billion in a few years, the experts and analysts opine.

Conclusion

The sectoral level of the Indian economy, FDI has helped to raise the output, productivity and employment in some sectors especially in service sector. Indian service sector is generating the proper employment options for skilled worker with high perks. On the other side banking and insurance sector help in providing the strength to the Indian economic

-15- Anusandhanika /Special Issue on FDI in India/ October 2017

condition and develop the foreign exchange system in country. FDI is always helps to create employment in the country and also support the small scale industries also and helps country to put an impression on the world wide level through liberalization and globalization.

References

1. Singh Rampal, FDI in India: Issues and Challenges, Regal Publications, New Delhi, 2014

2. Thakur Pooja and Burange L.G., An Analysis of Productivity Spillovers from FDI in India’s Services Sector, Foreign Trade Review, SAGE Publications, New Delhi, 2014

3. Consolidated FDI Policy, Department of Industrial Policy and Promotion, Ministry of Commerce and Industry, Government of India, 2015

4. http://en.wikipedia.org/wiki/Foreign_direct_investment_in_India

5. Ghosh, Rajarshi, Foreign Direct Investment – Policies and Experiences, ICFAI University Press, Hyderabad, 2015

6. Pradhan Rudra and Prakash P, ICFAI Journal of Financial Economics, Vol. 6, Issue 2, 2014

-16-

ISSN 0974 - 200XAnusandhanika /Special Issue on FDI in India/ October 2017/ pp 16-20

Problems and Prospects of Foreign Direct Investment in India

Abstract

Foreign Direct Investment (FDI) in India has played an important role in the development of the Indian economy. It has in lot of ways facilitated India to achieve a certain degree of financial stability, growth and development. It is the objective of the Government of India to attract and promote foreign direct investment in order to supplement domestic capital, technology and skills, for accelerated economic growth. Foreign Direct Investment (FDI) and trade are often seen as important catalysts for economic growth in the developing countries. FDI is an important vehicle of technology transfer from developed countries to developing countries. FDI is one example of international factor movement. An investment abroad, usually where the company being invested in is controlled by the foreign corporation. The simplest explanation of FDI would be a direct investment by a corporation in a commercial venture in another country. A key to separating this action from involvement in other venture in foreign country is that the business enterprise operates completely outside the economy of the corporation’s home country.

Keywords : domestic investment, emerging economies, privatization of markets

Darshana Gopa MinzResearch Scholar

University Department of Commerce & Business ManagementRanchi University, Ranchi

Introduction

The rapid expansion in FDI by multinational enterprises since the mid-eighties may be attributed to significant changes in technologies, greater liberalization of trade and investment regimes, and deregulation and privatization of markets in many countries including developing countries like India. FDI is not permitted in the arms, nuclear, railway, coal or mining industries. The objective behind allowing FDI is to harmonize and complement domestic investment, for achieving a higher level of economic development and providing more opportunities for up gradation of technologies as well as to have an access to global managerial skills and practices.

FDI is as an engine of capital, technology, managerial skills, technological progress & capacity, access to foreign markets and in maintaining economic growth and development for developing countries, where as for developed countries it is considered as a tool for accessing the market of emerging economies. Foreign investors showed keen

interest in Indian economy because of liberalized regime pursued and followed by Indian economy. This may be due to the low flow of FDI into India both at the macro level as well as at the sartorial level. It implies that the spirit in which the economy has been liberalized and exposed to the world economy at the late eighties and early nineties has not been achieved after so many years. This calls for a judicious policy decision towards FDI at the sartorial level. A large number of changes that were introduced in the country`s regulatory economic policies heralded the liberalization era of the FDI policy regime in India and brought about a structural breakthrough in the volume of the FDI inflows into the economy maintained a fluctuating and unsteady trend during the study period. It might be interest to note that more than 50 per cent of the total FDI inflows received in India come from Mauritius, Singapore and the USA. The main reason for higher levels of investment from Mauritius was that the fact that India entered into a Double Taxation Avoidance Agreement (DTAA) with Mauritius were protected from taxation in India.

-17- Anusandhanika /Special Issue on FDI in India/ October 2017

Among the different sectors, the service sector had received the larger proportion followed by computer software and hardware sector and then telecommunication sector. The process of economic reforms which was initiated in July 1991 to liberalize and globalize the economy had gradually opened up many sectors of its economy for the foreign investors.

Foreign Direct Investment (FDI) is a type of investment in to an enterprises in a country by another enterprises located in another country by buying a company in the target country or by expanding operations of an existing business in that country. In the era of globalization FDI takes vital part in the development of both developing and developed countries. FDI has been associated with improved economic growth and development in the host countries which has led to the emergence of global competition to attract FDI.

Foreign Direct Investment (FDI) is considered as an engine of economic growth. Before the Economic reforms the flow of foreign direct investment to India has been comparatively limited because of the type of industrial development strategy and the various foreign investment policy followed by the nation Not only India but much heralded FDI boom worldwide constitutes a major element of economic globalization Foreign investment was normally permitted only in high technology industries in priority areas and in export oriented areas. So the inflow of FDI before 1990’s was very low. To fully utilize the country’s immense economic potential, the government launched Economic reforms in 1991. The new Government policies are simple, transparent and promote domestic and foreign investment. India’s abundant and diversified natural resources, its sound economic policy, good market condition and high skilled human resources make it a proper destination for FDI. After long years of journey FDI was also introduced in various sectors and states in India. The Investment of FDI in various states and sectors leads to rapid growth of Indian economy Foreign Direct Investment in India is allowed through four basic routes namely financial collaborations,

technical collaborations & joint ventures, capital markets via Euro issues, and private placement or preferential allotments. India has opened up its economy & allowed MNEs in core sectors such as Power & Fuels, Electrical Equipments, Transport, Chemicals, Food Processing, Drugs & Pharmaceuticals, Textiles, Industrial Machinery, insurance as well as telecommunication.

Materials and Methods

For the purpose of in depth study the contents have been taken from interview, relevant books and articles from journals and websites. The method used is analytical and descriptive. Both primary as well as secondary source of Information have been taken.

Results and Discussions

Foreign direct investment refers to the investment in a business from another country for which the foreign investor has control over the company purchased According to Organization of Economic Cooperation & Development (OECD) for an FDI control should be 10 % or more of business A parent business enterprise & its foreign affiliates are the two sides of the FDI relationship Together they comprise an MNC or MNEs The parent enterprise through its foreign direct investment effort seeks to exercise substantial control over the foreign affiliate company Control as defined by UN is ownership of greater than or equal to 10% of the ordinary shares or access to voting rights in an incorporated firm Ownership share amounting to less than that stated above is termed as portfolio investment & is not categorized as FDI

India has already marked its presence as one of the fastest growing economies of the world. It has been ranked among the top 3 attractive destinations for inbound investments. Since 1991, the regulatory environment in terms of foreign investment has been consistently eased to make it investor-friendly.

The historical background of FDI in India can be traced back with the establishment of East India Company of Britain. British capital came to India during the colonial era of Britain in India.

-18- Anusandhanika /Special Issue on FDI in India/ October 2017

The industrial policy of 1965, allowed MNCs to venture through technical collaboration in India. Therefore, the government adopted a liberal attitude by allowing more frequent equity.

In the critical face of Indian economy the government of India with the help of World Bank and IMF introduced the macro-economic stabilization and structural adjustment program. As a result of these reforms India open its door to FDI inflows and adopted a more liberal foreign policy in order to restore the confidence of foreign investors. Further, under the new foreign investment policy Government of India constituted FIPB (Foreign Investment Promotion Board) whose main function was to invite and facilitate foreign investment Starting from a baseline of less than USD 1 billion in 1990, a recent UNCTAD survey projected India as the second most important FDI destination (after China) for transnational corporations. As per the data, the sectors which attracted higher inflows were services, telecommunication, construction activities and computer software and hardware. Mauritius, Singapore, the US and the UK were among the leading sources of FDI to the country.

India attracted FDI worth US$ 22.42 billion. Tourism, pharmaceuticals, services, chemicals and construction were among the biggest beneficiaries. For Indian economy which has tremendous potential, FDI has had a positive impact. FDI inflow supplements domestic capital, as well as technology and skills of existing companies. It also helps to establish new companies. All of these contribute to economic growth of the Indian Economy. India’s Foreign Direct Investment (FDI) policy has been gradually liberalised to make the market more investor friendly. The results have been encouraging. These days, the country is consistently ranked among the top three global investment destinations by all international bodies, including the World Bank.

Problems of FDI in India

India, the largest democratic country with the second largest population in the world, with rule of law and a highly educated English

speaking work force, the country is considered as a safe haven for foreign investors.

Yet, India seems to be suffering from a host of self-imposed restrictions and problems regarding opening its markets completely too global investors by implementing full scale economic reforms. Some of the major impediments for India’s poor performance in the area of FDI are: political instability, poor infrastructure, confusing tax and tariff policies, Draconian labour laws, well entrenched corruption and governmental regulations.

Lack of adequate infrastructure: It is cited as a major hurdle for FDI inflows into India. This bottleneck in the form of poor infrastructure discourages foreign investors in investing in India. India’s age old and biggest infrastructure problem is the supply of electricity. Power cuts are considered as a common problem and many industries are forced to close their business.