REPUBLICOF KENYA IN THE TAX APPEALSTRIBUNAL ...

30

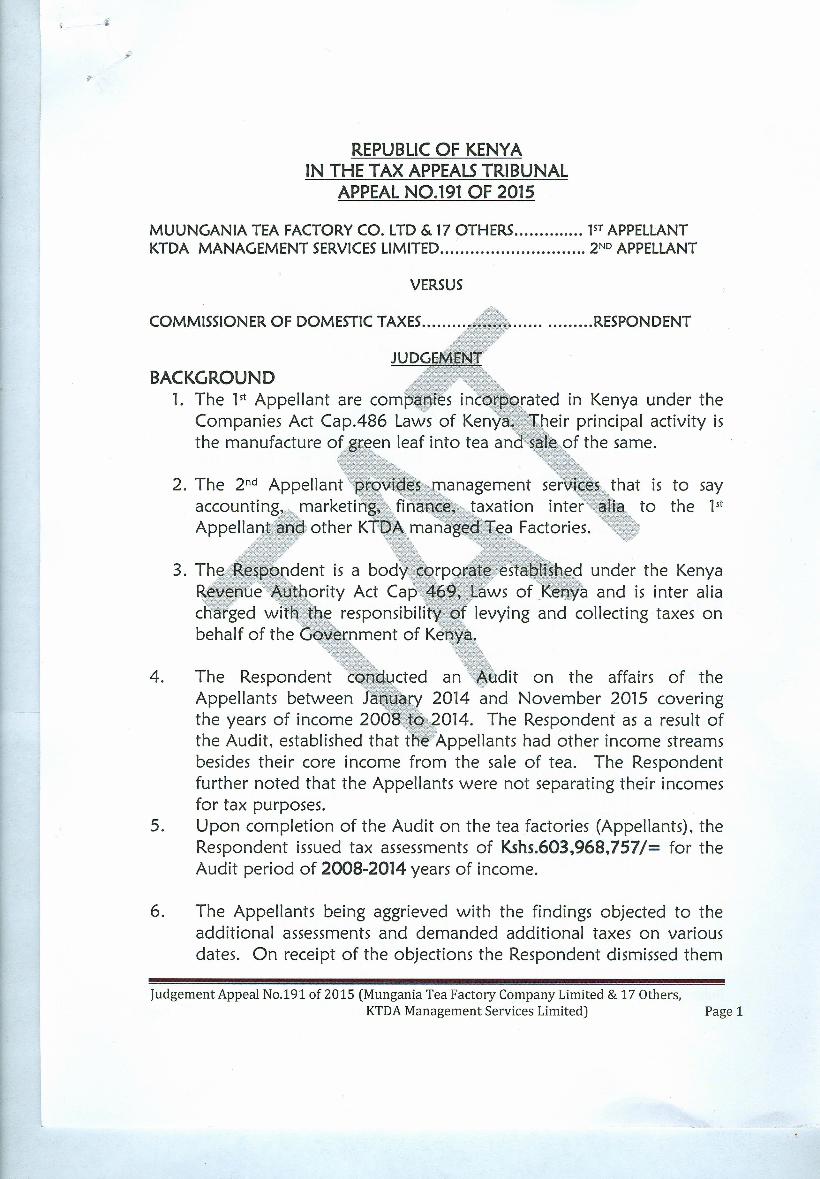

REPUBLICOF KENYA IN THE TAX APPEALSTRIBUNAL APPEALNO.191 OF 2015 MUUNGANIA TEA FACTORY CO. LTD & 17 OTHERS 1 sT APPELLANT KTDA MANAGEMENT SERVICES LIMITED 2ND APPELLANT VERSUS ent is a bod ority Act Ca responsibili nment of K . RESPONDENT COMMISSIONER OF DOMESTIC TAXES . BACKGROUND 1. The 1 st Appellant are com si Companies Act Cap.486 Laws of Ken the manufacture of en leaf into tea an rated in Kenya under the eir principal activity is of the same. 2. The 2 nd Appellant accounting marketi Appella other K anagement se taxation inter a Factories. that is to say to the 1 st 4. The Respondent cted an dit on the affairs of the Appellants between 2014 and November 2015 covering the years of income 20 014. The Respondent as a result of the Audit, established that t Appellants had other income streams besides their core income from the sale of tea. The Respondent further noted that the Appellants were not separating their incomes for tax purposes. 5. Upon completion of the Audit on the tea factories (Appellants), the Respondent issued tax assessments of Kshs.603,968,757/= for the Audit period of 2008-2014 years of income. 6. The Appellants being aggrieved with the findings objected to the additional assessments and demanded additional taxes on various dates. On receipt of the objections the Respondent dismissed them Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others, KTDAManagement Services Limited) Page 1

-

Upload

khangminh22 -

Category

Documents

-

view

6 -

download

0

Transcript of REPUBLICOF KENYA IN THE TAX APPEALSTRIBUNAL ...

REPUBLICOF KENYAIN THE TAX APPEALSTRIBUNAL

APPEALNO.191 OF 2015

MUUNGANIA TEA FACTORY CO. LTD & 17 OTHERS 1sT APPELLANTKTDA MANAGEMENT SERVICES LIMITED 2ND APPELLANT

VERSUS

ent is a bodority Act Ca

responsibilinment of K

. RESPONDENTCOMMISSIONER OF DOMESTIC TAXES .

BACKGROUND1. The 1st Appellant are com s i

Companies Act Cap.486 Laws of Kenthe manufacture of en leaf into tea an

rated in Kenya under theeir principal activity is

of the same.

2. The 2nd Appellantaccounting marketiAppella other K

anagement setaxation inter

a Factories.

that is to sayto the 1st

4. The Respondent cted an dit on the affairs of theAppellants between 2014 and November 2015 coveringthe years of income 20 014. The Respondent as a result ofthe Audit, established that t Appellants had other income streamsbesides their core income from the sale of tea. The Respondentfurther noted that the Appellants were not separating their incomesfor tax purposes.

5. Upon completion of the Audit on the tea factories (Appellants), theRespondent issued tax assessments of Kshs.603,968,757/= for theAudit period of 2008-2014 years of income.

6. The Appellants being aggrieved with the findings objected to theadditional assessments and demanded additional taxes on variousdates. On receipt of the objections the Respondent dismissed them

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 1

and confirmed its assessments. The Appellants being dissatisfiedwith the confirmation decision proceeded to file the Appeals.

7. On perusal of the correspondence and the Pleadings by bothparties, the issues for determination can be narrowed to two broadcategories. The two broad issues are;

i) Whether the principle of separation of accounts in law forspecifi.ed sources of income applies to the interest, dividendand rental incomes of the App . lants and; Secondly;

~

ii) Whether in Law the contents of a letter can oust the expressprovisions of a Statute

Prior to the Hearing of these Appeals, during the mention on 18th

May, 2016 an Application for consolldatioa was made and theTribunal granted Ie same. Subsequentl·'· h,e following wereconsolidated with "fAT 191/2015 (MUUNGANIA)i) TAT 19/2016 Kionyo Tea Factory LtdII) TAtOi2016 Ig tr Jea Factory Ltiii) TAT 2V2016 lrnenti-Tea Factory Ltdiv) li T 22/2016 *Kinoro ea ~actGry Ltd

~9. During a fu er mention on 16th August 2016, an application for

consolidation was" made and tbe Tribunal granted the same.Subsequently furthlr~!nsolidation ~£ the following Appeals with theseAppeal was granted na ely;

i) TAT 83/2016ii) TAT 84/2016iii) TAT 85/2016iv) TAT 86/2016v) TAT 87/2016vi) TAT 88/2016vii) TAT 89/2016viii) TAT 90/2016ix) TAT 91/2016x) TAT 92/2016xi) TAT 93/2016xii) TAT 94/2016xiii) TAT95/2016

8.

Chinga Tea Factory LtdGathuthi Tea Factory LtdGitugi Tea Factory LtdGatunguru Tea Factory LtdKangaita Tea Factory LtdMununga Tea Factory LtdNdima Tea Factory LtdRagati Tea Factory LtdThumaita Tea Factory Ltdlriaini Tea Factory LtdKimunye Tea Factory LtdKathangariri Tea Factory LtdRukuriri Tea Factory Ltd

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 2

APPELLANTSCASE

10.The 2nd Appellant is Kenya's premier organisation, providing

management services to the small scale tea sector for effective

production, processing and marketing of high quality teas. Currently, it

manages more than 60 tea factories on a management agreement with

ity of Munge tea is ex

anies. Among the factoriesthe factories which are limited liability

managed is Mungania Tea Facto

appeal as a test case.

11.The 2nd Appellant provides accounting athe management servl rovides to the fac

services among

12. Mungania Tea FactoP00061203 r purp

venue Auth

13.The

tax payeinistration, t

x office.

holds PINctory falls

e manufacture ofthe Mombasa Tea

14.As in any other manufarespect of the raw material.made to the supplier of rawcredit period.

entity, payment has to be made inordinary business, payment will be

aterials within a certain agreed upon

15.However, in the case of the 2nd Appellant, and due to the sensitivity ofthe suppliers of the raw materials, who in this case are farmers, thepayment terms are clearly defined. It pays a monthly rate of KShs 14per Kg of green leaf and a 2nd payment at the end of the year once theaccounts are audited.

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 3

16.The initial payment which acts as a prepayment to the farmers isintended to cater for plucking and other farm maintenance and thefinal payment is based on the final valuation of the green leaf that isbased on the market prices.

17.The surplus funds received from the export of tea which would havebeen payable to the grower in the case of a normal manufacturingscenario are held in Active Deposit Accounts which pay interestpending withdrawal as 2nd payment.

18.This method increases the payments t be received by the farmers asthey are paid both the interest income and the outstanding amountsof the green leaf. In addition, this acts as a cushion to the farmers

"'"when the prices of tea are unstable as ex~~nced in the year 2013and 2014 where the interest income addea'~ the farmers paymentwhen the market prices w~re at their lowest point in two years.

20. Upon the review of the assessment, a response outlining the reasonsfor non -separatiogof incomes for tax purposes as well as errors in thecalculations of theax"l,~ssessed was, ~t to the Respondent on 17th

February 2015. .. J/':

21.ln particular, the letter dated 17th February 2015 highlighted the factthat separation of incomes for ta'X purposes had not been done as theCommissioner of Income Tax ,vide the letter dated 7th February 1979addressed to the Institute of Certified Public Accountants of Kenya(ICPAK) waived the requirements of preparation of separate subaccounts for larger companies. The letter has not been revoked todate.

22. The 1st Appellant falls within the definition of a large manufacturingconcern and therefore is not required to separate incomes for taxpurposes as provided in the letter dated 7th February 1979.

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 4

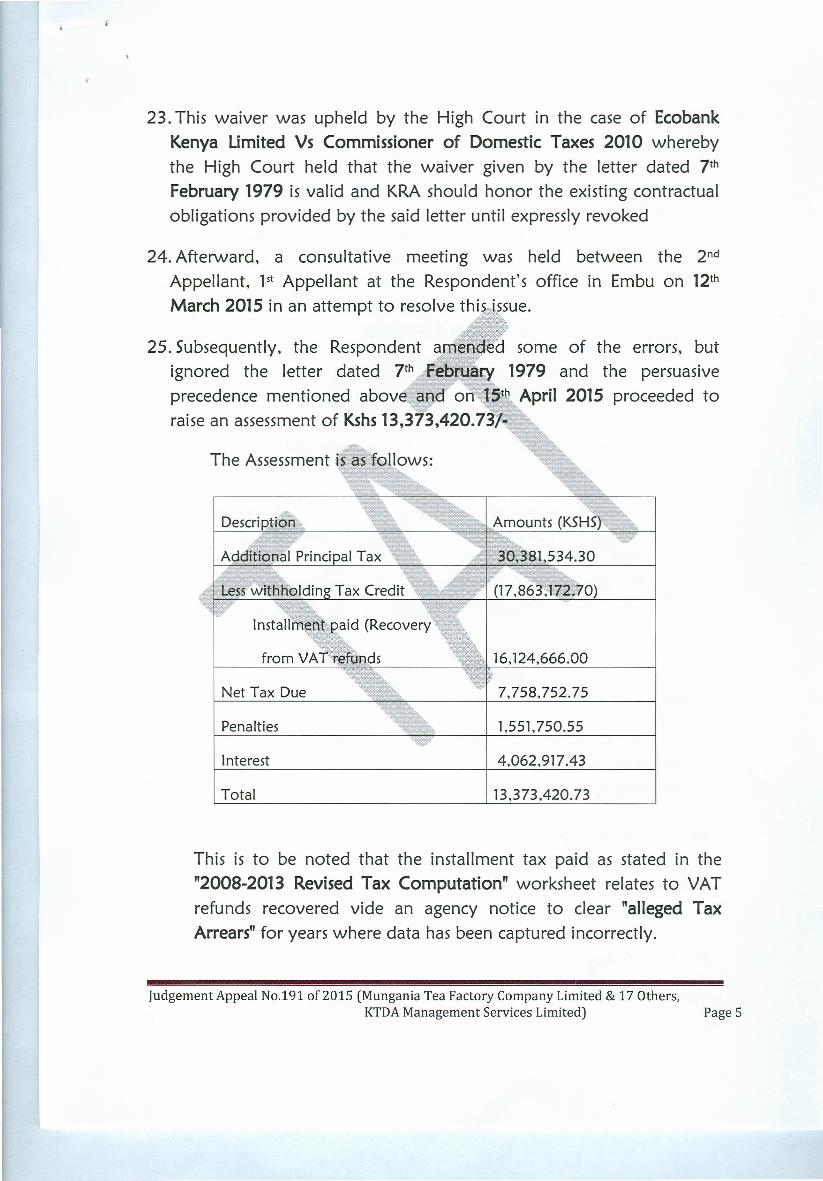

23. This waiver was upheld by the High Court in the case of EcobankKenya Limited Vs Commissioner of Domestic Taxes 2010 wherebythe High Court held that the waiver given by the letter dated 7th

February 1979 is valid and KRA should honor the existing contractualobligations provided by the said letter until expressly revoked

24. Afterward, a consultative meeting was held between the 2nd

Appellant, 1st Appellant at the Respondent's office in Embu on 12th

March 2015 in an attempt to resolve thi

25. Subsequently, the Respondent aignored the letter dated 7th Bprecedence mentioned above and' onraise an assessment of Kshs13,373,420.73

d some of the errors, but1979 and the persuasive

th April 2015 proceeded to

The Assessment is as fellows:

Net Tax Due 7,758,752.75

Penalties 1,551,750.55

Interest 4,062,917.43

Total 13,373,420.73

This is to be noted that the installment tax paid as stated in the"2008-2013 Revised Tax Computation" worksheet relates to VATrefunds recovered vide an agency notice to clear "alleged TaxArrears" for years where data has been captured incorrectly.

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 5

26. On 27th April 2015 the 2nd Appellant on behalf of the 1st Appellantobjected to the assessment. The grounds of the objection are set outbelow:

a) The assessments contain errors which distort the originallydeclared taxable income. In particular, in the year 2013, KRAhas taken the originally taxable income as Kshs 4,245,181instead of taxable loss of Kshs 84,903,629. Additionally, in theyear 2010, withholding tax c1ai has been indicated as Kshs3,341,992 instead of Kshs 3,27

b) The assessment raised by Respondent is erroneous because theseparation of incomes fer tax pueposes for larger companies waswaived by the Commissioner of Income tax vide his letteraddressed to ICPACK dated 7th February 1979. The letter hasnot been revoked to date.

c) A persuasive precedent as been set in case of Ecobank KenyaLimited ys Commissioner of 90mestic Taxes of 20~O, wherebythe High Court held tHat the watver given by the letter dated7th February 1979 is valid and the RespondeDt should honor thecontractual obligation provid d by the letter until expressly

Mrevoked.

27. The Respondent ac epted the obj" on vide the letter dated 15th

May 2015 and stood over the additional tax.

28. The 2nd Appellant acknowledged receipt and requested forobjection worksheets vide the letter dated 20th May 2015 andrequested for objection worksheets which had not been attached.

29. On 23rd June 2015, the Respondent re-confirmed the assessment.These were received by the 2nd Appellant on 29th June 2015. Theconfirmation notice was issued without giving due regard to the factsand law.

30. The 2nd Appellant filed a notice of intention to appeal to the Tax

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 6

Appeals Tribunal on 28th July 2015.

RESPONDENT'S CASE

31.The 1st Appellant is among the tea factories managed by the 2nd

Appellant which, among the management services provided, alsoprovides accounting and taxation services.

dent, the preli

g a specifieurces of inco

ns of sectiointo additio

PIN P000612038K for tax32. The 1st Appellant is registered unpurposes and its principal activity i

33. On 23rd January 2015,Appellant and briefed them he prand (e) of the Income Tax Act. It was agrcommunicated in w

dent's officers visited thes of Section 15(7) (a) (b)

at the issues raised be

dated 11that the App t had not

i.e. "Business income")e") in accordance

of the Inc me Tax Act whichaxes of Kshs 22,050,902.14.

35. Through a letter 17th Feb ry 2015, the 2nd Appellantresponded to the issues . The letter identified errors in the taxcomputation and stated t ' e company had not been treatinginterest income separately because of the following reasons;

a) That the interest earned by the factories is purely incidental,

b) That interest is not specifically mentioned a specified source ofincome in section 15(7) (e) of the Income Tax Act,

c) That the Respondent expressly waived the requirements ofseparation of income for large companies in a letter dated 7thFebruary 1979 issued to lePAK, and

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 7

d) That the Respondent has not raised the issue of separation ofinterest income i previous audits.

36. On 12thMarch 2015, a consultative meeting was held between theRespondent, 1stand 2nd Appellants to discuss the preliminary findings.During the meeting, the Respondent agreed with the Appellant onthe computational corrections to be made but failed to agree ontreatment of Interest Income as a separ - e source of Income for taxpurposes.

37. The Respondent subsequently raised Income Tax additionalassessments Nos. 0445200900027/40;: or 2009, 0445201000024/4for 2010, 0445201100002/4 for 2011, 0445201200002/4 for 2012,and 0445201300001/4 for 2013 demanding additional Principal taxamounting to Kshs J3.~ ~ 20.73 on to- AfIli",-2015 which wascommunicated to the~ o. 0 15thApril 2015.'

, ~ ~ •..

38. On 27th April 2015, the Appellan bjected the decision of theRespondent on the basis of the followir:1wgrounds of objection;

a) That the assessments contai ed~rrors which distort the originallydeclared tar-e' income as foll . s;

1. In the year 2013, the Resp dent had taken the originallydeclared income as Kshs. 4.245.181 instead of a taxableloss of Kshs. 84.903.629,

ii. In the year 2010, withholding tax claimed had beenindicated as Kshs. 3.341,992 instead of Kshs. 3.270.742.

b. That the Respondent waived the requirement for preparation ofsub accounts for large companies, which include largemanufacturing concerns, through a letter dated 7th February 1979written by the Commissioner of Income Tax to (ICPAK),

Judgement Appeal No,191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 8

c. That 1st Appellant falls within the definition of a largemanufacturing concern,

d. In order to comply with the provision of Section 15(7) of theIncome Tax Act, the company was required to prepare separatesub accounts. This is further supported by section 54 of theIncome Tax Act which provides that return of income should beaccompanied by accounts, and

e. That the precedent created byKenya vs Commissionerguidance that confirmed He7th February 1979 was still valid as I

gh Court ruling of Eco Bankestic Taxes case gave clear

waiver by the letter datednot been revoked.

39. The Respondent, hawng examined the Notice of objection, agreed toamend the assessment in light of the Appella t's first ground ofobjection and disagreed with the ether grounds objection andproceedeyto amend the assessrnen der section SS{I) (b) of theInczax Act on 23,dJune 20B.

40. The" ppellan " 3;, d a notice of in! 'Tribunal against decision ofwhich was received e Respond

Ion to appeal to the Tax AppealsRespondent on 2Sth July 2015

n the same day.

41.0n 11th August 2015, the no Appellant filed with the Clerk of theTribunal Memorandum of ApReal and Statement of Facts and a copyof the same was received by the Respondent on 13th August 2015.

42. The 2nd Appellant's argument that interest income earned by thefactories is purely incidental is incorrect because of the followingreasons:

a. There was no direct correlation between the amounts depositedin the Active Deposit Accounts (ADA) with the 2nd paymentsmade to farmers by the 2nd Appellant.

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 9

b. Regardless of the use of the amounts deposited, interest incomewas earned and it should have been treated separately frombusiness income for tax purposes as is required by the law.

43. Although income from manufacture of tea is not specificallymentioned as a specified source in the Income Tax Act, the incomefrom the manufacture of tea is a specified source under sub paragraph(e) (v) of section 15(7) of the Inc0gf' Tax Act and income fromInterest falls under any other income (tinder Sec 15(7) (a) of the ITA)since it is not one of the specified sources of income. In this regard, thetwo sources of income shouls b cornl~~ted separately and any lossfrom manufacture should NOT be offset against gains from interestincome.

44. Manufacturing income is a speeified source because section 15(7HeHv)of the Income Tax Act Iks~ae- any other sou ~ s of incomechargeable to~ax under ection - ( a) i.e. business income, andmanufacturing income is included in the definition of business incomeunde~ect+Qn,,~f the Income \~R -<8

45. Section 15(7) (a) f the Income tojlXAct is clear with regard to thetreatment of interest i ome as a s~ tate source. It states in part that"the gains or profits of a person derived from one of the six sources ofincome respectively speciff In paragraph (e) of this subsection ...shall be computed separately m the gains or profits of that personderived from any other of the specified sources and separately fromany other income of that person".

46. Income from manufacture of tea is one of the specified sources statedin section 15(7) (eHv) of the Income Tax Act because under section 2of the Income Tax Act. definition of "business" includes everymanufacture. This qualifies the income from manufacture as part ofbusiness income chargeable under section 3(2) (a) (i) of the IncomeTax Act.

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 10

47. Individual discretion by the Commissioner at the time cannot replacethe express provisions of the law. The then Commissioner used thewords "...1 have decided to waive .... " in Paragraph 9 of the letterdated 7th February 1979.

48. Subsequent legislative amendments superseded thisdiscretion by the then Commissioner of Domestic Taxes.these legislative amendments include;

individualExamples of

a. Dividend and interest beca able in 1994 under section3(2)(b) of the ITA through Finan ct for the year 1993. Thiswas more than fourteen years afte then Commissioner ofDomestic taxes gave his guidance on the issue to ICPAK, and

b. Following an amendment to t e Income tax Actt rough FinanceAct Oyt e year 1991, requireme for every taxpayer to furnishthe ornrnlssioner with Self As ' t return was introduced(Sec. 52B of ITA). Tilts ark end of the era where

ss

El\ssessors were determinin t e chargeable income and~'ascertain! se amount a payable by each taxpayer theyassess. The only giving administrativeinstruction rega a the Tax e sors which were then actingunder his instructio e.g. paragraph 8 of the letter dated 7th

February 1979 where it was state that "...Any doubtful case willbe given full and detailed examination by my assessors".

49. The waiver on large companies from filing "sub accounts'" did notaddress a legal issue but an accounting procedure. Accountingprocedures and Tax treatment are quite distinct. This distinction haseven been recognized by the Accounting standards which provides forthis distinction under ISA12.

50. The decision on the Eco Bank vs CDT case was appealed in October2012 and a ruling on the appeal is yet to be delivered. The taxpayer

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 11

cannot rely on a ruling where the judicial process is ongoing and hasnot yet been exhausted.

51. With regards to the taxpayer's argument on legitimate expectation,this is not acceptable because any person cannot rely on a legitimateexpectation when there is an express provision of the law to becomplied with.

It is therefore the Respondent's observatio

a) Interest income falls under the category of "other income" undersection 15(7)(a) ITA and should th&fore be treated separately fortax purposes from business income which is a specified sourceunder section 15(7)(e)(v) of the ITA.

source becauseneorne Tax Act

ana 2l;;l$inessincome is chargeable

c) Losses from sRecified sources of income cannot be deducted from"other incom provided in section 15(7) (b).

d)The Appellants hav not been s ~·arating interest income frombusiness income which re~ulted in the deduction of business lossesfrom interest income in SG e years. This is against the provisions ofsection 15(7) of the Income tax Act.

e) The Appellants cannot rely on the contents of the letter dated 7th

February 1979 from the then Commissioner to ICPAK as a reasonfor not complying with an express provision of the law which issuperior to the letter.

f) The Appellant cannot rely on the precedent of the decision madeby the High Court in Eco Bank vs Commissioner of Domestic

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 12

where the judicial process has not yet been completed because theruling of the case was appealed and is yet to be determined.

52. The Respondent therefore prays that the Tribunal affirms theCommissioner's decision and dismisses the Appeal.

53. The Appeal came up before the Tribunal in the first instant on the7th October 2016 when it was agreed that the Appeal would bedisposed off by way of Writt Submissions which weresubsequently highlighted on the 9th ber 2016.

54. The Written Submissionsessentially expanded the po on takabove and also served to provide furtheand what the parti ht would rendererespective Submissio

arties and their highlightsboth parties as detailed

i1son those positionster clarity to their

55. In obesubrnith .

al the Appe filed theirthe Respondent filing

56. The Appellants co bmission by describing thebusiness model adopt Appellant vis a vis the 1st

Appellant. This model wa ribed as a two tier business model.The 1st Appellants' principal activity is the processing of green leavesmade tea and the sale of the same.

57. The income of the made tea accounts for approximately 94% ofthe Appellants total income while the other streams such as interest,dividends and Rent account for only 6% thereto.

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 13

58. The 2nd Appellant pays the 2nd Appellant's farmer an initialpayment of Kshs 14 per kilogram of green leaf delivered and thesecond payment is paid in October each year.

59. This model is adopted because the final payment for the tea isbased on the Mombasa tea auctions which are conducted weekly.

60. Under this model, the earned dollars (sales proceeds) areconverted to shillings at the prevai ·""'c exchange rate. Thereafter,immediate obligations such as th Ifial monthly payment, loanobligations, electricity, salaries and other bills are settled. Thebalance is then placed in Atlvance' eRosit Accounts (ADA) whichare call deposit accounts.

depending on theprevailing interest rate ' ount of funds a ale. In a month,the receipts from the sa e of rnade tea are approximated at Kshs 4.5billion for all "the 54 te factory tsmpanies managed by the 1st

Appellant. ~

62. The amount ~yable to farmers as second payment (commonlyreferred to as' .{Js)is dependent n the price realized, volume ofmade tea sold as as the intere rnings from the ADA'S.

63. Accordingly according te this model, receipts from sale of madetea are not synchronized with the monthly and final payments.Therefore as a result, the 2nd Appellant on behalf of the 1st Appellantthrough a management service agreement manages these fundspayable to farmers pending payment.

64. The 2nd Appellant manages these funds by placing them in ADA'sfor periods of 7 to 120 days.

65. An ADA is a call deposit account which pays interest depending onthe number of days and amount of funds placed. The funds are

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 14

available for withdrawal to pay for 1st Appellants obligations as andwhen they fall due e.g. initial payment and loan obligation.

66. The difference between an ADA and a fixed/term deposit accountis that the funds can be withdrawn at any time without notice. TheADA also earned interest daily unlike a fixed deposit account wherefunds are placed for a fixed period of time and earn interest only atthe end of the period. It is through this process that interest incomearises.

67. In in computing corporation he Appellants treat interestincome as a business income ~ the model above, while theRespondent alleges that interest inco alJs under other sources ofincome for tax purposes. This is the basis of tfre tax dispute.

68. It is the Appellant ease that under Section 3 (2~ (b) of the ITA asread together with section 3(21 (a) (i) of the ITA the tnterest incomeearned by the Appellants is the "I;) Income" anq not passiveincome which can be brought to tax

. ion also appl]me they are

ITA and n

o Dividends and these incomescified sources of Income under

come from other sources.

70. To fortify its view the-;t(ppellants cited the Indian cases of elT vsRajasthan Land Development ~orporation (1995) as authorities forthe legal proposition that business income and interest incomeearned from the made tea fall under the said seventh schedule andshould be taxed as one stream of income and not two. In any eventthe Appellants argued that it has always computed and paid incometaxes for the 2 streams of income.

71.The Appellants further argues that in bringing to tax the interestincome the Respondent has erroneously assessed the Interest incomeexcessively as it has failed to take into account the expenses incurred

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 15

in earning the said income as per the provisions of section 15 (1) ofthe ITA.

72. Both the Appellants and the Respondent are in agreement that theDividend income earned by the Appellants as a shareholder of the 1st

Appellant's Tea Factory Company is income taxable under section3(2) (b) of the ITA. However, the Respondent should not chargeany further tax after the Appellants have remitted Withholding Tax(WHT) on the Dividend Income at t oint of payment by KTDAH(which is the holding company of t ,r,lO Appellant).

73. This Dividend income is therefore a qualifying Dividend and suchWHT deducted at source is final tax in terms of the provisions ofsection 2 of the ITA and therefore that income should not besubjected to further tax. tion in the mann~ proposed by theRespondent.

74. Some of the Appellan~' Rental irfrome from letting houses tomembers of the staff bot the AepeJlants and the Respondentconcur that the rental income is a separate source of income undersecijen 15 (7,J{~) (i) of the ITA and that the Respondent was at faultin assessing ren kincome excessiVely as the gross income beforetaking into acco the expense acurred in earning the rentalincome under section 15 (1) of the ~A and therefore argue that inthis instant the rental ineel11e should be deducted by 40 010 of thegross rental income under the provisions of section of 123(C) (3) ofthe ITA.

75. In its argument the Appellants maintain that a letter dated the 7th

February 1979 written to ICPAK purportedly giving advice to theAccountants professional body on the treatment of tax losses whencomputing profit amounted to a waiver for the preparation ofseparate sub-accounts which in its view meant that as their businessis of the manufacturing nature they would not be required tomaintain separate sub-accounts and that once they earned income

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 16

from separate sources of income they could offset profit and lossesfrom any source.

76. The Appellants further submitted that the letter of the 7th February1979 which created the said waiver was not revoked by the letter26th October 2002 as alleged by the Respondent and that theAppellants having received both letters have been applying theguidance contained therein in their computation of taxes for all itsTea Factory Companies under its ma ment for the last 37 years.

purposes.

Eco Bank vs Commissioner of. 8 of 2008 and an English

inister for Civil Servicecreated a legitimate

ation of Tax, theyreams for Tax

77. The Appellant also cited theDomestic Taxes, Income Tccase of Council of Civil Se es Unio1985 for the proposition that the saidexpectation upon ellants that the cowould not be requ arate the differ

c Ywitmake sound incommunication a'communication wascreated confusion whicH

ed since the ulatory body it owedto the Tax pa g the Appellants to

ommunicatio lor guidance as these tax payersents decisio the basis of such guidance and

at by argui hat the said guidance and lorntraventi of the law the Respondent

Id be resolved against it.

RESPONDENT'S WRITTEN SUBMISSIONS

79. In its Written Submission and highlights the Respondent argued thatthe rationale informing the concept of separation of Accounts forspecified sources of income as provided for by section 15 (7) of theITA is to guard against lumping up of income and thus allowing fora loss from one source eating into the other source that way eatinginto the profit of the other source eventually depriving theGovernment off the taxation.

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 17

80. The Respondent argued that interest income is a separate source ofincome for the Appellants and is to be accounted for separatelyunder section 15 (7) (a) as read together with section 15 (7) (e) partV as the Appellants earn the interest income separately from its gainsand profit and this has to be accounted for.

81.The Respondent further argued that the Appellants in any event inthe audited books of accounts and " line with the InternationalFinancial Reporting Standards (Iii ccounted and reported theinterest, rent and dividend as other income other than their mainincome and in the Appellants m~nCi these were different andseparate streams of income which requires separate sub-accounts incompliance with section17 (7) of the ITA.

82. It is the Appellantsa business income as it ifrom funds it deposits at

83. As regards the issue of the taxatio 4 th Bividend income theResg,ondent c01;ltend that whilst conducting the audit WHT wasdeducted at th, .•..urce but the a "', ition assessment arose from theremainder of the ameunt since the ellants being corporation aresubject to charge tax at the corpo q: Ion rate set out in the thirdschedule of Paragraph 2 {~ as 6 shillingsgot for every 20 thereforethe allegation by the Appellants that that the 5% WHT is a final taxcannot be sustained as is not correct.

84. The Respondent moreover argues that the Appellants complaint asregards the issue of Dividend was wrongfully and unlawfullyintroduced by the Appellants during the preliminary hearing. Thisissue was not subject of objection nor was it one of the grounds ofAppeal therefore it violates the provisions of Section 22 of the TaxAppeals Tribunal Act (TATA).

Judgement Appeal No,191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 18

85. As regards the rental income earned by the 1st Appellant theRespondent insist that such income is required by law to beseparately accounted for.

86. According to the Respondent the Appellants reliance on theprovisions of Section 123 (C) of the ITA is without any basis as thisprovision was in respect to rental Income Amnesty. In any event theAppellants were not applying nor were they qualified for thatamnesty which was not in force duri e time of such audit.

pondent did not account fore said rental income, the

ction 15 (1) of ITA a taxo as to make such

him to establishents to rental

sion of theccordance

87.ln regard to the argument ththe expenses incurred inRespondent argued that undpayer should provide such documentaexpense ascertaina the Commissionwhether those exp , for structural apremises or aintena e or for therental pr which w able expensewith 15 (2) (f) of t

88. espothe Appellantsof Appeal whichTATA and should no

complainedot one of

offended tntertaine

e issue on t e rental income byround of objection or a ground. rovisions of section 22 of the

this juncture

89. In response to the issue whether the letters dated the 7th

February 1979 and of the 10th and 11thDecember 2015 can oust thespecific provisions of the statute which created legitimateexpectations in their mind it argued firstly that the said letters didnot relate to the Appellants and therefore it could not remotely beconsidered creating any legitimate expectations to their detriment.

90. The Respondent's clear reading of the contents of the letter datedthe 7th February 1979 meant that it was clear that the contentsthereto did not relate to the Appellants whose activities include

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 19

those of Agriculture which did not bring the Appellants within thepurview of the waiver contained therein as the Agriculture act (Cap318 laws of Kenya) defined Agricultural activities as:-

a) Horticultural, fruit growing and seed growingb) .e) The use of land as grazing meadow land, market gardens or

nursery grounds

91.lt was the Respondent's position a card the letters dated the 10thand 11th December 2015 these we1r'sneaked in after some of theAppeals herein had been filed and were not part of the Appellants'grounds of Appeal and are therefore an afterthought.

92. The reliance on tile 5' id letters having r Tssued after the~objections had bee,ould never be .. ~to create any

legitimate expectation 0 ucn expectation can be created afterthe facts. These letters we e in any euent addressed to 3 companieswhich" are not part to these, proceeding and their effect was tosuspend assessment of the said actories subject to furtherinfer ation be.eoming available.

93. The Respondent ok the posit]",

letters which made reference to e Eco Bank case had noconnection with the Appe~Lants' case as the Eco Bank case dealt withthe rental income of a financial institution which could have said tobe covered by the contents of the said letters.

94. It was the Respondent further Submission that the said letters couldnot create and estoppel against the Respondent in contravention ofthe specific provisions of section 15 (7) (a) and (e) of the ITA whichrequired the Respondent to enforce such provisions of the statuteand which the Respondent could not countermand by a mere letter.

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 20

95. The Respondent proceeded to cite the case of Maritime ElectricCompany Ltd Vs General Dairies Ltd (1937 (ALL ER 748 where itwas held that a dairy company which sought an estoppel from andelectric utility company to recover the arrears of eclectic supplywhich arose due to a mistake of the electric company the said dairyfactory could not rely on an estoppel which would have an effect ofdefeating unconditional statutory obligation imposed bythe Public Utility Act.

96. In the case of Tarmal Industries Commissioner of Customsand Excise it was held" It wout e duty of the Commissioner toclassify the substance under- 105 which attracts duty,rather than under tariff 108(1<)whk: es not. The fact that hefailed to do so, on the authorities above 'tte'd. cannot estoppel himfrom carrying out ts. duty when he discofl..ers the original error.Indeed his earlier claJ"Silicationunder item 108 (k) 'asin breach of s.105 of the East African Customs Mpnagement Act. t 'as in breachof a statute ."duty, and io that sen was not lawfut and estoppelcannot be raised against 'him to p Jim from correcting thatact.

97. There was a Sl case of Nrb. H.C Misc . CivilApplication No. f 2004 blic - Vs - KRA, Ex-parteAberdare Freights seroic Lts & Anor where it was held "in thecircumstance of the case I fin(J..that any legitimate expectation not tobe charged more than what was accepted by the Respondent hasclearly been taken away firstly by the conduct of the applicant andthe provisions of the Statute Act and for this reason I cannotproperly hold the respondent to their bargain in accepting paymentin advance. In this matter the respondent has a clear Statutory dutyunder s 127(3) to charge duty. It is not a discretion and thereforethis is clearly distinguishable from the cited case o/Congreve v HomeOfficer IQB 629 which was a case touching on the Minister'sdiscretion and in which the licensee was placed in double jeopardy. "

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 21

98. The Respondent further argued that the said letters amounted to astatutory instrument which by dint of section 21 of the StatutoryInstruments Act No. 23 of 2013 expired within 10 years after theirpublication pursuant to the provisions of section 12 of the said Act.

TRIBUNAL ANALYSISAND FINDINGS

99. At the onset of this Judgment two issues for determination hadbeen narrowed down especially the perspective of theAppellants at paragraph 7 hereof.

100.Subsequent to the Appeal having I'l filed the hearing concludedand both oral and written Submission'S delivered by the parties itwas agreed and the Tribunal concurs that in order to address all theissues in dispute in hls Appeal the issues for determination should beexpanded to four as hereunder stated:-

i. Whether the Principle of Separ:ation of Accounts fer specifiedsources of income applies t e Interest Income of theApp-ellant.

ss

'"

aration of Income for Specifiedae Dividend Income earned by

ii. Whethe principle of .Sources of e Appliesthe Appellants.

iii. Whether the Principle of Separation of Account for SpecifiedSources of Income applies to the Rental Income of theAppellants.

iv. Whether the contents of a letter can oust the expressprovisions of a Statute.

101. The 2nd Appellant was served with the Tax Assessment dated 11thFebruary 2105 which is a tax decision in terms of section 12 of theTax Appeals Tribunal Act [rATA). The said assessment is set out at

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 22

Annexure 1 of the Appellant's Statement of Facts. The saidAssessment merely required the 2nd Appellant to separate the incomefrom the manufacture of tea (Business Income) from income interestas in the said Assessment the 2nd Appellant had combined theseincomes in contravention of section 15 (7) (e)(5) of ITA.

102. The Respondent in issuing the said assessment had established thatthe 2nd Appellant was utilizing interest income to offset the lossesincurred by the 1stAppellant by way usiness income.

103. On the 17th February 2015 th ppellant filed their objectionwhich specifically dealt with the I s interest income and businessincome and the separation of-accounts yed on the various streamsof income earned and by the Appellants. ®n the 23rd June 2015 theRespondent reconftdned its assessment and on tfie 28th July 2017 the2nd Appellant filed its Notice of Appeal and proceeded to file itsMemorandu of Appeal on the 11thAugust 2015.

104.ln their said Memorandum of AR ~ be Appellants' grounds ofAppeal ;$ at ttie ~Respondent did not

y the Respondent dated the 7threquirement of preparation of

mpanies and described theAppellant as a large ~ ufacturing ...~. pany. Secondly that the saidAssessment contravened .tHe precedent set forth in the case of EcoBank Kenya Limited set out earlier in the Judgment and thirdly thatthe Respondent had conducted various audits on the records of theAppellant but never raised the issue of separation of account therebycreating a legitimate expectation that the Respondent would notrequire then to prepare separate sub accounts for their variousdifferent accounts.

105. The Respondent has argued that the Appellants' subsequentarguments on the issues of Dividend and rental income were not

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 23

part of the Appellants' objection and neither were these issues raisedin the appellants' Memorandum of Appeal.

106.We have carefully perused the Respondent's Assessment, theAppellants' objection and the Appellants' Memorandum of Appealand agree that these issues were neither the subject of theappellant's' objection nor their grounds of Appeal, Section 13 (3) ofthe TATA states "The Appellant shall. unless the Tribunal ordersotherwise. be limited to the groundated in the Appeal to whichthe decision relates"

107.The Appellants did not befo e the mmencement of the hearingof the Appeal seek leave of t e Tribunal t urge it on both the issueof rental income and Dividend and sine aese issues were neverpart of the RespoAaen~s assessment (Tax ecision) they were notAppealable without the leave - f the Tribunal.

108.Conse ~-ry,on this s, -~the Tr~hal finds that tne Appellantsarguments in support of its ~ peal ~ the ~ih issues of the Rentalin:~me and Dividend were not part of Grounds stated in theirMemorandum Appeal and since they were not part of the TaxDecision these a, ents have no ' is and cannot be sustained.

109. There is no dispute between the parties that when the Respondentcarried out an audit of the A,epellants' Accounts, the Appellants hadprepared sub-accounts specifically for their business income, rentalincome, interest income and Dividend income. In short theAppellants in obedience to the principles of the IFRS had compliedwith the provisions of section 15 (7) of the ITA by maintaining sub-accounts for the said streams of Rental Income.

110. The Appellant's have not advanced any reason or grounddemonstrating that they suffered any prejudice by the separation ofthe Accounts, which they had already effected and which was the

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 24

••

basis of the audit carried out by the Respondent. Their Appealtherefore on the issue of the non- separation of accounts to reflectthe difference streams of income from their various businesses is tosay the least hollow.

111. is not in dispute that in its business the Appellant earned Businessincome from the sale of green tea leaf, Rental Income, DividendIncome and Interest Income.

112. The Tribunal has no hesitatio aking the finding that therationale for the requlrernentsg on 15 (7) of the ITA which isto guard the lumping of inc n' s allowing for the loss fromone source eating into other sources tll y depleting the profit ofthe other is sound in principle as it is aT eGi at ensuring that theGovernment earns revenue which it could be deprived off werethese different streams of lncorne lumped togetner and applied tooffset losses from some of those income streams.

114. Even though the Tribuna has already established that no Appeallies on both the issue of Rental and Business Income as earlier statedthe Tribunal has after due consideration made a finding to the effectthat the Appellants' argument on these two issues cannot bemaintained even where these issued are examined in substance andon merit.

115. It is quite clear from all the pleadings, the oral and writtenSubmissions that interest income is a separate source of income asthis income is earned separately from the gains and profits of the

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 25

Appellants' "Business Income" which arises from the manufactureand sale of green tea. It therefore follows that the interest incomeshould be treated separately as expressly provided for by theprovisions of section 15 (7) (a) of the ITA as read with section 15 (7)(e) part 5 of ITA.

116. Both the Appellants and the Respondent agree that DividendIncome is a separate income which attracts a separate sub -accountunder Section 17 (7) of the ITA. The departure between them ariseswhen the Appellants argue that WHT having been brought tocharge at source no additional assessment should be levied for theremainder of the amount of the Dividend Income and that the saidWHT is a final tax. It characterises the said Dividend as a "QualifyingDividend."

117. The Appellants' arguments cannot be sustained siAce the Appellantsas corporations are subject ~t~poration tax as provided for underthe third scheduled of paragraph 2 (ej-whlch works out at 6 shillingsfor every 20 shillings earned and therefore since corporation taxapplies WHT cannot be treated or considered as the final tax.Consequently, arguments on this core cannot therefore be sustained.

~118. Both the Appe1181:}tsand the, Respondent concur that Rental~

Income earned by the 1st Appellant i~ a separate source of incomewhich should be accorded its sub-account in conformity with thesaid provisions of the ITA. The appellants argue that the Respondentassessed this form of income excessively as it did not take intoaccount "the expenses incurred in earning" the said Rental Incomeunder the provisions of section 15 (1) of the ITA. It therefore urgesthe Tribunal to deduct rental income by 40 % of the gross incomeunder the provisions of section 123 C (3) of the ITA.

119. The Appellants arguments in this respect is fundamentally flawedfirstly because it was incumbent upon the Appellants to documentthe said expenses which were incurred in earning the rental incomefor the Responded to establish whether those expenses were for

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 26

structural adjustments to rental premises or maintenance of the sameor expansion of the said premises which would be allowableexpenses under section 15 (5) (f) of the ITA,

120.Since and as we have seen the Appellants' argument on the issue ofrental income was an afterthought as it did not canvass it at theonset or at the Appeal and as it did not and never produced thedocumented expenses which could have assisted the Respondent toascertain whether to allow them ot in order to reduce thetaxable income and by way Qi 7 al expenses it cannot besustained.

I~,,,,,,,,of the ITA in furtheranceof its argument is misplaced and cannc vall it since the saidprovision is in res~ect to Rental Income Amnesty, which does notarise in the present Iii. peal.

both parties s ,0 whetherth February 1979 and the

st fRe specific Provisions ofe ITA which according to thepectation" that the Respondent

are separate sub- accounts forrally because that section didas they constituted large

123.lt was the Appellants' argument that this letter specifically created a"waiver" in this respect and that in any effect that waiver had beensanctioned by the High Court decision in the Eco Bank Limited case.The Respondent in its case argued that the said letter could notcreate any legitimate expectation to the appellants since it was ageneral letter addressed to ICPAK and was not specifically addressedto the appellants.

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 27

124.lt was the Respondent's further argument that in any event thecontents of the said letter could not apply to the Appellant whowere involved in Agricultural Activities as defined in the Agricultur4il.Act and who were specifically excluded from the alleged waivercontained in the said letter by the Respondent

125. Both the Appellants and the Respondent cited various authoritiesin support of their arguments in this respect for the principle oflegitimate expectation and the pri2liR!e of estoppel in respect oftheir respective arguments. We fiofl the following definition of"Legitimate Expectation" instructive in this Appeal "De Smith Woolf& Jowell in Judicial Review of Admi istrative Action 6th and Sweet& Maxwell, page 609 A defi#res it as ~~leg.·imate expectation ariseswhere a person responsible for taking "ecisionhas induced insomeone a reasonabJ expectation that he will receive or retain acertain benefit of advantage. It is a basic principle of fairness thatlegitimate espectstion 'tJughFfrpt to be thwarted. 7iheRrotection oflegitimafjectation /!e the roo 'nstttuttonet pnl;rcipleof therule 0 w, which requires pn, teta ulity and certainty ingovernment's dealings with the'pubIIC}'.

126. We have similarly had recourse,.t~he Court's decisions in the EcoBank Limited Cas , ill e Maritime\&l . tric case, the case of TarmalIndustries and other cases and the pr~\7isions of the Agriculture Acttogether with the said letter and accorded them due regard,consideration and thought. :;;

127.We find the contents of the letter dated the 7th February 1979 bythe Respondent could not amount to a waiver or an estoppelousting the specific prov.isions of section 15 of the ITA. In the letterthe Respondent clearly states that "this piece of legislationintroduces a completely new concept in computing profit and I feelthat a general appraisal of a situation from me might be helpful". Inother words the Respondent was not substituting the expressprovisions of section 15 of ITA with its letter but ':'Vas as stated

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 28

communicating his understanding of the said provisions which hadbeen recently introduced by the Finance Act of 1978 and which hetermed as introducing "a new concept in computing profits".

128. We have not come across any contents of that letter where theRespondent can be said to have substituted its view andunderstanding of the provisions of Section 15 of ITA. We alsobelieve that the Appellants as taxpayers were entitled in the sameway as the Respondent to im t the interpretation andunderstanding of the said section 7 could not be influenced bythe contents of the said letter Iu ay.

129. We have no hesitation in making th 'ding that the principle oflegitimate expectation as defined could net 5e invoked in aid of theAppellants on the asis of the contents of t e said letter since thecontents of the said lette were not conclusive and expressly referredto a specific statutory provision as being the basis for the accountingin respect10 the different •.streams; 0 • come of an organisation .

.(.; "

The grovision did not itself ~f;eafe,.~ ectation.

Oth and 11th December 2015 theAppellants as they were issued, ssessment in this Appeal had

been filed and wer erefore an ;terthought as no "legitimateexpectation" could have been created after the event.

131. In our reading of the Agriculture Act we have no hesitation infinding that the 1st Appellant engaged mainly in Agricultural activitiesand were therefore exempt from the contents of the said letter.

132.ln the course of hearing this Appeal, the Tribunal was informed bythe Respondent that an Appeal has been filed against the Eco Banklimited decision but we have not been informed of the fate of thesaid Appeal. We are however, satisfied that the ratio decidendi ofthat case revolved on the rental income of a financial institution

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 29

which is one of the institutions envisaged in the contents of the saidletter and is therefore not applicable to the 1st and 2nd Appellantswhose business is different.

133.The Tribunal further fails to comprehend how a general appraisalof an accounting method can be stretched to apply to the principlesof Legitimate Expectation and Estoppel which are substantivedoctrines of the law of Equity.

134. The upshot is therefore that the 1st and 2nd Appellants' Appeal hasno merit, is dismissed and the Re~~ondent's Assessment is dulysustained.

Each party shall bear its own costs.

OMAR J. MOHAMMED ....................• ,. . MEMBER

PONANGIP ALLI V. R. RAO ....•••.....•• ~~~~ ••...........•..••....•.. MEMBER

r.

JOSEPIDNE K. MAAN I. ..~,~, MEMBER

WILFRED GJCHUKI •.... ~ .2 :: MEMBER

Judgement Appeal No.191 of 2015 (Mungania Tea Factory Company Limited & 17 Others,KTDAManagement Services Limited) Page 30