Rama 2014 (1).doc FINAL doc RECTIFIED

88

EXAMINATION OF FACTORS LEADING TO THE GROWTH OF BANKS: THE CASE OF CRDB, STNBIC, BARKLAYS, NMB AND NBC IN THE PERIOD BETWEEN 2006 TO 2012 BY Ramadhan Kisuda Lesso SEPTEMBER 2014 i

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Rama 2014 (1).doc FINAL doc RECTIFIED

EXAMINATION OF FACTORS LEADING TO THE GROWTH OF BANKS: THE

CASE OF CRDB, STNBIC, BARKLAYS, NMB AND NBC IN THE PERIOD

BETWEEN 2006 TO 2012

BY

Ramadhan Kisuda Lesso

SEPTEMBER 2014

i

The work contained within this document has been submittedby the student in partial fulfillment of the requirement

for the Degree of Masters of Science in Finance andInvestment of Coventry University.

Author: Ramadhan Kisuda Lesso

Student ID: MSC-FI/0204/T.2013

Course Title: Masters of Science in Finance and

Investment (MSC-FI)

Module: Dissertation

Date: SEPTEMBER 2014

Thesis submitted in Partial Fulfillment of the Requirement

for the Award of the Degree of Master of Science Finance

ii

and Investment – of the Institute of Accountancy Arusha

(IAA) in collaboration with the Coventry University

iii

CERTIFICATION

I, the undersigned certify that I have read and hereby

recommend for acceptance by Coventry University the

dissertation entitled: the contribution of microfinance

institutions to the development of SMES in fulfillment of

the requirements for the degree of Masters of Science in

finance and investment (MSC-FI) offered in collaboration

between Institute of Accountancy Arusha and Coventry

University.

…………………………………………………….

Boniface Michael

(Supervisor)

Date ………………………………

iv

DECLARATION

I, Ramadhan Kisuda Lesso declare that this dissertation is

my own original work and that it has not been presented and

will not be presented to any university for similar or any

other degree award.

Signature…………………………………………

Date…………………………………..

v

COPYRIGHT

© Copyright

This paper should not be reproduced by any means, in full

or in part, except for short extract in a fair dealing, for

research or private study, critical scholarly review or

discourse with an acknowledgement. No part of this

dissertation may be reproduced, stored in any retrieval

system, or transmitted in any form or by any means without

prior written permission of the author or Coventry

University.

vi

DEDICATION

I dedicate this dissertation to my parents; my dad the late

Mzee Kisuda-Mussa Lesso and my Mum Zena Selemani Mukhandi

who took care of, raised me up and oriented me in

excellence investment.

vii

ACKNOWLEDGEMENT

I am highly grateful to the almighty ‘Allah’ for giving me

the opportunity to attend this precious programme and to

enabled me to successfully complete this great learning

course at Coventry University

I am highly indebted to my supervisor, Mr. Boniface Michael

for his time, guidance and tireless support in research

skills which has contributed a lot in positively changing

my intellect.

I would also like to express my sincere gratitude to my

colleagues, relatives and classmates especially Mr. Edward

and Walter Edgar who assisted me in one way or anotherviii

during the course of my research work, May lord continue to

bless them.

My special thanks to my lovely; family, my wife, Rose-Koku,

and my son Mussa-Kisuda for their kindness, moral support

and patience in my absences during the research, I must

also thank my employer FBME Bank Ltd and co-workers

especially my line manager; the Head of Branch Operations

Mr. Nassor Dachi, the Head of Human Resources Ms. Lucie

Qorro and my Arusha office predecessor Mr. Haidar

Mwinyimvua for their moral and financial support during the

entire course.

ix

LIST OF ABBREVIATIONS

BOT Bank of Tanzania CRDB Cooperative Rural Development Bank ES Efficiency Structure GDP Gross Domestic Product NBC National Bank of Commence NMB National Microfinance Bank NPC Non Performing Loans SAP Structural Adjustment Program SSA Sub Saharan Africa

x

ABSTRACT

The study was about assessment of factors that lead to thegrowth of commercial banks in Tanzania. The study attemptedto find out general trends of growth of commercial banks inTanzania in the period of 2006 to 2012, and identifyfactors positively affecting the upward trend of thebanking industry in Tanzania,

Chapter one is about setting the problem, chapter two isabout literature review, chapter three is about researchmethodology, chapter four is about data analysis andchapter five is about conclusion and recommendations.Qualitative and quantitative methodologies have beenapplied. The qualitative methodology probed feelings andperceptions of respondents on the research theme, and thequantitative approach made the study capable of producingand presenting numerical information in figures.Questionnaire and interview guide were the key tool fordata collection. Data were analyzed using (SPSS)Statistical Packaging for Social Sciences programme,Microsoft office excel and special table as shown in theresearch methodology.

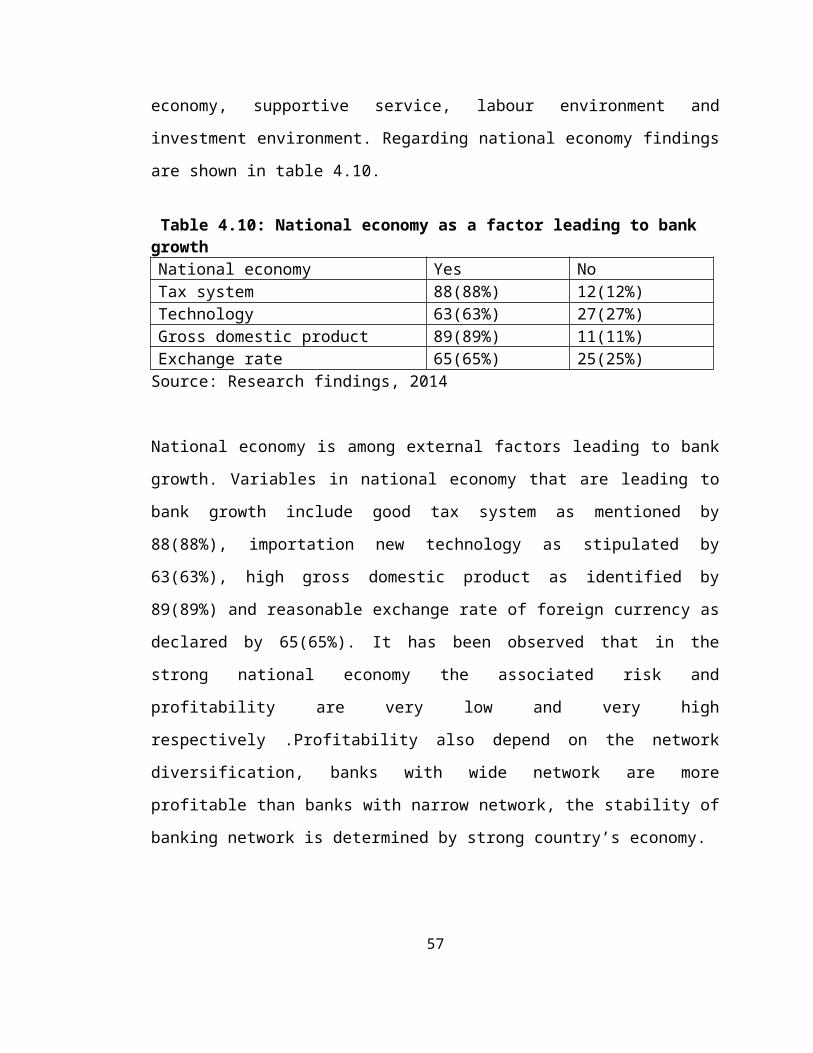

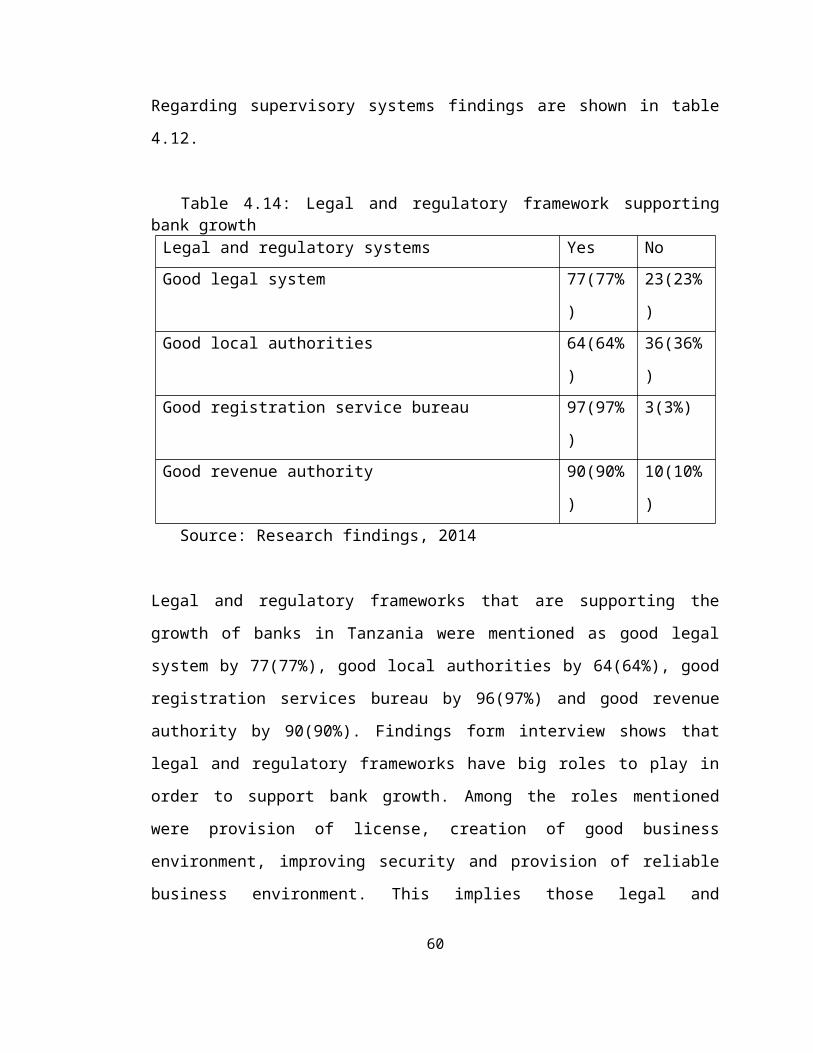

Findings shows from 2006 to 2012 banks have been growing asindicated by increase of operation income, net income,total assets, total deposits, number of customers andnumber of employees. The growth of banks have been partlycontributed by internal and external factors and legal andregulatory environment. Regarding internal factor effectiveinternal operations, reliable human resources, availabilityof facilities and advertisement have been crucial inachieving bank growth. On the other part external factorssuch as fair national economy, availability of supportive

xi

services, reasonable labor environment and attractiveinvestment environment have led to tremendous bank growth.Both external factors could have done nothing if therecould not be good legal and regulatory environment.

Thus the study concluded that generally commercial banks inTanzania are growing drastically. Findings show that theaforementioned internal and external factors together withregulatory authority have contributed a lot on bank growth.Key recommendation given is that since bank need tomaximize profits the following are recommendations;Regarding internal factors leading to bank growth banksneed to improve their performance by shifting its attentionto the current need that forecast challenges rendered byglobalization.

xii

TABLE OF CONTENT

Certification IvDeclaration VCopyright ViAcknowledgement Vii

iDedication IxList of abbreviations XAbstract XiTable of Content XiiList of Tables XivList of Figures Xv

Chapter One: Problem Setting 11.11.2

Introduction Background to the problem

13

1.3 Statement of the problem 31.4 Research question 31.5 Research objectives 31.6 Significance of the study 41.71.81.9

Justification and purpose of the studyLimitations and delimitations of the studyScope of the study

455

1.10

Brief discussion of dissertation 6

Chapter Two: Literature Review 62.1 Introduction 62.2 Foreign direct investment in Tanzania 62.3 Empirical literature review 142.4 Conceptual framework 17

Chapter three: Research Methodology 193.1 Introduction 193.23.3

Research Paradigm Type of the study

1919

3.4 Study Area 193.5 Study population 21

xiii

3.6 Unity of analysis 213.7 Variables and their measurement 213.8 Sample size and sampling techniques 223.9 Type and sources of data 223.10

Data collection methods 22

3.11

Reliability and validity 23

3.12

Ethical consideration 23

3.13

Data analysis methods 23

Chapter Four: Presentation, Analysis and Discussion of Findings

24

4.1 Introduction 244.2 Personal information 244.3 General growth trends of commercial banks in

Tanzania between 2006 to 201226

4.4 Internal factors that led to the growth of commercial banks in Tanzania

30

4.5 External factors that led to the growth of commercial banks in Tanzania

33

4.6 Role of legal and regulatory framework in supporting the growth of banks in Tz.

35

Chapter Five: Conclusion and Recommendations 355.1 Introduction 365.2 Conclusion 365.3 Recommendations 365.4 Policy implications 37

xiv

xv

LIST OF TABLES

Table 3.1 Sample size 22Table 4.1 Operation income from 2006 to 2012 27Table 4.2 Net income from 2006 to 2012 28Table 4.3 Total assets from 2006 to 2012 28Table 4.4 Total deposits from 2006 to 2012 29Table 4.5 Number of employees from 2006 to 2012 30Table 4.6 Operational factors leading to bank

growth

30

Table 4.7 Human resources factors leading to bank

growth

32

Table 4.8 Facilities factors leading to bank

growth

32

Table 4.9 Advertisement factors leading to bank

growth

32

Table 4.10 National economy as a factor leading to

bank growth

33

Table 4.11 Supportive services as a factor leading

to bank growth

33

Table 4.12 Labour environment as a factor leading

to bank growth

34

Table 4.13 Investment environment as a factor

leading to bank growth

34

Table 4.14 Legal and regularity framework

supporting bank growth

35

xvi

LIST OF FIGURES

Figure 2.1 Conceptual map 1

7Figure 4.1 Respondents by gender 2

4Figure 4.2 Respondents by age 2

5Figure 4.3 Respondents by marital status 2

6Figure 4.4 Respondents by level of education 2

6

xvii

CHAPTER ONE

PROBLEM SETTING

1.1 Introduction

The banking industry is facing a number of challenges in

its growth; issues like sovereign debt crises are blocking

the financial markets from its growth trend globally in the

economy

The challenges that banks face today are of the highest

order. Most of the developed countries are facing inactive

growth economically such as growth in unemployment, high

inflation rates, capital and liquidity accessibility are

not easy and manageable. On the other hand, there is the

issue of Politicians and regulators who are imposing and

reviewing financial regulations at a very high frequency.

Other factors facing financial institutions from growth are

competition among themselves which is currently very tough;

clients now have knowledge on the newly developed products,

they are therefore highly arduous and complicated they thus

demand more sophisticated products and a world class

service, the large area of competition nowadays is all

about a banker – customer relationship.

If banks want to maintain growth and overcome the range of

challenges they are facing, they need to ensure that their

business are modernized ,are up to date with technologies

and customers relationship enhanced. Failure to that, they1

are more likely to lag behind. Their failure will not

necessarily be on insolvency or illiquidity but failure to

meet customer demands, revenue collection and profit

maximization, and the most important to meet shareholders

expectation (Oracle Financial Services Thought Leadership

Paper February 2012). I would like to economically discuss

the aspect of issues influencing the growth of Commercial

banks in Tanzania in post trade liberalization and

enactment of banking and financial institution act (1991).

1.2 Background to the Problem

Banking industry can be traced back to the year 1694 with

the establishment of the bank of England. Initially the

bank was established by a few people who in reality were

money lenders with an aim of lending money to get interest

(Lim & Tang, 2000). The banking industry was therefore

traditionally old-fashioned because of its traditional

management methods and legal limits (Lim & Tang, ibid). In

Tanzania the banking system can be traced from colonial era

to the time of socialism regime and now to the market

oriented economy. Banks contribute to economic growth

through their financial intermediation role.

We can gauge the level of banks’ operations by its service

resource supply and demand and in part by legal

restrictions. The main financial capital for bank is2

derived from shareholders contribution and customer

deposits. Bank facing a form outside the region, adding to

their deposits are increasing the supply of loans (Bies,

1971). These additional loans, in turn, help to generate

further economic growth in the area (Bies, 1971). Bank size

is also affected by a number of factors such as bank

structure, laws and regulations governing the banks

operations such as restricting banks operations to certain

location, rates of interests paid on deposits, or rates

interests charges on loans and overdrafts, demands for

banking services. These restrictions may place banks in one

location at a competitive disadvantage with banks in other

areas (Bies, 1971).

For the past 20 years African banks have experienced a

significant changes gearing at improving reforms. Before

going to these reforms it is necessary to note that

initially banks industry in Africa were owned and dominated

by government (Beck and Cull, 2013). Regarding bank reforms

in 1980s which included regulation in interests’ rate

ceilings, credit quotas, financial liberalization,

institutional regulatory upgrades and globalization, the

face of bank systems and other financial institutions

across the region have changed (Beck and Cull, ibid).

3

In Tanzania these reforms have been implemented from mid-

1980s according to Wangwe (2004) This happened during trade

liberalization privatization of state owned led economy.

The industry was again underwent various changes following

the enactment of the Banking and Financial Institutions Act

1991 whereby the state owned banks were restructured,

privatized and foreign private banks were licensed to carry

out banking business. Financial sector reforms according to

Wangwe (2004) caused broader economic reforms which led to

decontrolling of interest rates restructuring and

privatization of government banks and entrance for foreign

private banks into the country.

Despite the above reforms according to ESFR (2009) in

Tanzania the banking industry competition was not

there ,the banking services did not reach the large

population most of whom live in rural areas following this

situation, there was a number of challenges such as banks’

failure to expansion and diversification of their

investment potentials and opportunities, inadequate

resources mobilization reduces lending activities and

accelerates external financing barriers and thus limits

bank growth. However, the banking system in Tanzania,

which dominates the financial system, is liquid, well

capitalized, and resilient to most shock (ESFR, 2009). This

4

study is an attempt to identify factors leading to the

growth of banks in Tanzania.

1.3 Statement of the Problem

Following the enactment of the legislation that allowed the

operations of the private owned banks in Tanzania in 1991,

the BOT has reported an increase of private owned banks

from three to above fifty by 2012.Empirical studies on

growth factors according to De Melo et al.; (1996),

Havrylyshyn (2001), Berg et al. (1999) the differences in

economic growth rather than examining factors that

influence such growth. Most of the studies are on

developed countries and to our knowledge non cover Tanzania

or this region. Therefore studying factors that influence

bank growth in our region and Tanzania in particular is

very pertinent. Interestingly, banks in Tanzania continued

to grow in terms of capital and expansion through opening

up more branches in the country (Ernst & Young, 2010).

1.4 Research Questions

1.4.1 General Question

What are the factors that lead to the growth of

commercial banks in Tanzania?

1.4.2 Specific Question

5

i. What are the general trends of growth of

commercial banks in Tanzania between years 2006

to 2012?

ii. What are the internal factors that led to the

growth of commercial banks in Tanzania?

iii. What are the external factors that led to the

growth of commercial banks in Tanzania?

iv. What is the role of legal and regulatory

framework in supporting the growth of banks in

Tanzania?

1.5 Research Objectives

1.5.1 General Objective

To assess factors that lead to the growth of

commercial banks in Tanzania

1.5.2 Specific Objectives

v. To find out general trends of growth of

commercial banks in Tanzania between 2006 to 2012

vi. To identify internal factors that led to the

growth of commercial banks in Tanzania.

vii. To identify external factors that led to the

growth of commercial banks in Tanzania.

viii. To evaluate the role of legal and regulatory

framework in supporting the growth of banks in

Tanzania.6

1.6 Significance of the Study

The study examined the factors leading to the growth of the

banking industry in Tanzania in the period between 2006 and

2012; what were the internal and external factors, the

regulatory framework that favored the growth of commercial

banks in the country. Study findings are expected to

provide an insight in the banking industry on what to be

done in order to overcome challenges that are likely to

hinder smooth growth of bank industry. The bank industry

will also use these findings to improve bank management. On

the other part the study has strengthened researchers’

skills capacity regarding banking industry. Hence the

research is now more competent regarding banking industry.

Finally the study had made massive contribution to the

existing banking literature especially on the factor and

challenges facing growth of bank sector in Tanzania.

1.7 Justification and Purpose of the Study

Commercial banks play important role in the economic

resource allocation in any countries. They channel funds

from depositors to investors. Nevertheless, this is

possible if banks are generating necessary income to cover

their operational cost they incur in the due course

(Ongore, 2013). Alternatively bank can facilitate financial

services if they are financially growing. Also banks have7

intermediation functions and their performance which is

determined by their level of growth significantly implies

the trend of economic growth of the relative countries. If

bank are not well organized and are retarding rather than

growing can have negative impact to the national economy.

Since bank failure can lead to negative repercussions on

the economic growth the study to analyze growth of bank

industry in the country is justifiable.

1.8 Limitations and delimitation of the Study

The study faced limitations like timeframe, data

accessibility and financial factors. These limitations were

solved as follows. The research accessed published data so

as to minimize time and financial cost. Also the researcher

ignore multiple banks, even though such comparisons could

have been valuable, in order to allow more depth of

understanding regarding the banks because of complexity in

accessing data.

1.9 Scope of the Study

The scope of the study is restricted to the assessment of

the internal and external factors leading to bank growth

from 2006 to 2012 using five commercial bank that are CRDB,

STANBIC, BARCLAYS, NMB and NBC banks.

1.10 Brief of Dissertation8

The study engages in participant-observation over eight-

week period, from 7 July to 31 August for approximately

four hours per week. The study examined the bank’s annual

financial and other important reports. The study examined

the major commercial banks in Tanzania for the period of

2006 to 2012. The study is divided into five chapters as

follows. Chapter one is an introduction chapter. It has

presented the background to the problem. Further an

explanation of the research problem, formulation of the

research objectives and research questions were taken into

consideration. Chapter two discusses conceptual

definitions, reviewed the supporting theories and presented

an empirical analysis of relevant studies. Chapter three

discusses the research methodology to be used on the study.

The discussion covered the following; research paradigm,

research design, research area, population of the study,

sampling techniques, data collection methods and tools and

data analysis. Chapter four present the findings of the

study thus fulfill the objectives. Chapter five present a

summary of the study, conclusion and necessary

recommendations.

9

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

Banking sector has undergone tremendous changes especially

in recent years. This chapter has attempted to show changes

undergone that were gearing at improving the banking sector

globally and in Tanzania. This chapter has reviewed

literature related to general trends of growth of

commercial banks in Tanzania and growth of commercial banks

in sub-Sahara Africa, factors contributing to commercial

bank growth, bans economic environment, bank loans and bank

deposit and assets growth, empirical literature review and

conceptual framework.

2.2 Theoretical literature review

2.2.1 General Trends of Growth of Commercial Banks

Both in the developed and developing world, the Banking

sector acts as a financial intermediary for mobilizing

funds from depositors and lending the same to investors

hence it is a very crucial in facilitation of commercial

transaction and completion of major projects requiring both

small and huge capital in the modern business. This

increasing phenomenon of globalization has made the concept

of efficiency more important both for the non-financial and

financial institutions and banks are the part of them.

Banks largely depends on competitive marketing strategy10

that determines their success and growth. The modalities of

the banking business have changed a lot in the new

millennium compared to the way they used to be in the last

years (Hussain and Bhatti, 2010).

During the 21st century the world economy has been

experiencing bank becoming big and complex financial

industry offering numbers of services to international

markets and in return banks are controlling billions of

currencies and asserts. Technology growth has supported

banks and now it is the banks duty now to work on business

potentials identification and develop products that will

meet customers demand. They must also ensure implementation

of innovative strategies and large market share.

Globalization also plays the role of broadening,

consolidation, deregulation and diversification of the

financial industry, the banking sector will become even

more complex.

Throughout the world, banks operates in terms of

commercial banking whereby they play the role of financial

intermediation by covering crucial services such as cash

transactions, cash management and fund transfers, payment

services, lending in real estate loans and commercial loans

in terms of working capital, account maintenance for

11

savings and current accounts and services of foreign

financial exchange.

Most commercial banking provides commercial lending like

long term loans and overdraft facilities for working

capital purposes. Investment banking on the other hand

deals with provision of services like asset securitization,

coverage of mergers, acquisition and corporate

restructuring to security underwriting, equity private

placement and placement of debt securities with

institutional investors. During the past ten years it has

been experienced that an interaction of the commercial and

investment banking activities in the financial markets and

financial consultancy works contribute highly in the global

economy.

Apart from those functions nowadays banking brought about a

wider business diversification. In developed world banks

are now engaged in insurance, portfolio management and

security underwriting. Due to this development banks have

advanced to the high Importance institutions businesswise

in the world. Many studies have indicated that Commercial

banks play a vital role in the economic resource

allocation. Funds are channeled from depositors to

investors continuously (Flamini et al., 2009). However, for

the banks to be able to do that, they must ensure that they

12

improve income generation, profit maximization and cost

reduction to be sustainable in the market. .

Apart from financial intermediation role, the banks another

critical role positively affecting the country’s economic

growth is that effective and profitable banks provide

provides investment returns to the shareholders and owners

accordingly thus attracting more investment hence adding

value and instigating more sparks in the country’s economic

growth while the non-performing banks prompts financial

crisis which brings about adverse results in the economy.

2.2.2 Characteristics of Banks in Sub-Saharan Africa

An understanding of banking system in Sub-Saharan Africa

will widen the scope of understanding generally bank growth

in Sub-Saharan African and particularly in Tanzania. To

begin with, it has been documented that in Sub-Saharan

Africa financial sectors including banking sector is

generally underdeveloped. Banks in Sub-Sahara Africa have

been expanding geographically and private sector

contribution to GDP have been increasing drastically over

the past decades (Kasekende, 2010). Despite these

tremendous achievements the scale of financial

intermediation and access to financial services is low as

compared with developing countries (Cihak et al 2012).

According to World Bank the World’s developing regions have

13

lowest dimension of financial development such as

efficiency of financial institutions (Cihak et al ibid).

Most of financial institutions in Sub-Saharan African are

totally small in size and are characterized by low deposit

ration and most of larger shares of assets are held in the

form of government securities and liquid assets

(Milachilaet al 2013).

In Sub Saharan Africa, financial institutions, banking in

particular are found in the cities and townships, local

banks are outnumbered by foreign banks, bank charges and

borrowing costs are relatively on the high level. having

recovered market share as banking systems were restructured

and state banks privatized under reform programs in the

1980s and 1990s (Milachila et al 2013). An important aspect

is that banking systems in Sub-Saharan Africa are

characterized by modest reach in terms of providing

financial services to the population which is very large

with small and medium enterprises which is constrained in

their access to any form of credit. The banking system is

characterized by small size, low income levels, large

informal sectors, and low levels of financial literacy;

weak contractual frameworks for banking activities,

including weak creditor rights and judicial enforcement

mechanisms; and political risk (Beck et al., 2011). Other

characteristics of bank in Sub-Saharan Africa according to

Milachla et al (2013) include excess liquidity, ineffective14

monetary policy, the system rely on the domestic economy

for their funding base and funding from non residents have

a very minor sources of funds in almost all cases.

2.2.3 Growth of Commercial Banks in Sub Sahara Africa

Africa has experienced tremendous financial sector changes

of the past two decades, from state owned banks since

colonial era to the late 19 century during trade

liberalization underwent through by a number of African

countries Tanzania being among them. The state owned banks

were subject to restrictive regulations such as control on

interest rates and credit quotas. This phenomenon was

changed by globalization and financial liberalization

whereby new institutional regulation were upgraded in the

region

(Honohan and Beck, 2007 and Beck et al., 2011).Today, most

countries have deeper and more stable financial systems,

though challenges of concentration and limited competition,

high costs, short maturities, and limited inclusion

persist.

Following the introduction of Structural Adjustment

Programs (SAP) in the late 1980’s, the banking sector

worldwide has experienced major transformations in its

operating environment. Countries have eased controls on

interest rates, reduced government involvement and opened15

their doors to international banks (Ismi, 2004). Due to

this reform, firms of the developed nations have become

more visible in developing countries through their

subsidiaries and branches or by acquisition of foreign

firms. More specifically, foreign banks’ presence in other

countries across the globe has been increasing

tremendously. Since 1980’s, many foreign banks have

established their branches or subsidiaries in different

parts of the world.

In the last two decades or so, the number of foreign banks

in Africa in general and Sub-Saharan Africa in particular

has been increasing significantly (Claessens and Hore,

2012.). These have attracted the interests of researchers

to examine bank performance in relation to these reforms.

There has been noticed a significant change in the

financial configuration of countries in general and its

effect on the profitability of commercial banks in

particular. It is obvious that a sound and profitable

banking sector is able to withstand negative shocks and

contribute to the stability of the financial system

(Athanasoglou et al. 2005.).

In the modern business economic activities cannot be

sustainable without the presence of banks due to its

financial intermediation function for allocation and

facilitation of financial transaction for economic16

production and facilitation of resources movement from

depositors to investors thus enabling productive economic

activities to take place hence prompting economic

development in the respective countries. Financial

intermediation role played by the banks facilitates

movement of funds from those who have to those who don’t

have by way of cash deposits and loans provisions to those

who need to invest or working capital requirements for

regeneration of more funds through business and or projects

like industries . In return the banks earns income on

lending and services provided, the depositors also earn

interest on their deposits mean while the investors also

generate profits from investments, ultimately the

shareholders also receive returns from their investments.

On the other hand non-performing banks, most likely due to

reckless lending and poor cash management causes crisis due

to failure. Banking crisis could entail financial crisis

which in turn brings the economic meltdown as happened in

USA in 2007(Marshall, 2009.) Thus the central banks on

behalf of the relative sovereignty regulates the banking

sector to safeguard customers deposits and ensure solvency

condition of the banks for the country’s economic

protection and prevention of crises. (Heffernan, 1996;

Shekhar and Shekhar, 2007.) Thus, to avoid the crisis due

attention was given to banking performance.

17

2.2.4 Factors contributing to commercial banks growth

The 2008 Credit crunch showed how influential the banking

sector can be in determining investment and growth. If the

banks lose money and no longer want to lend, it can make it

very difficult for firms and consumers leading to a decline

in investment. Therefore banks need to be healthy and

sustainable so as to be able to play the financial

intermediation role. Factors that led to revolution of the

banking sector are among other factors; deregulation, that

is revising prevailed regulations and allowing the presence

of multibank operations in the economy and removal of

monopoly of the state owned banks, this brought about

competition among the banks. Technology advancement brought

about improved and innovative process through computerized

system that moved from old fashioned data process and

analysis and enhanced the banks capability of timely

service provision in increased volume and efficiency.

In addition, financial engineering and risk management,

coupled with the growth of new and broader derivatives

markets were believed to have improved banks’ risk

management capabilities( Barth et al. (2004, 2006, 2008).

Up until the middle of 2007, the general consensus appeared

to be that high performing banking systems, supported by

excess capital and state-of-the-art risk management

capabilities, bolstered by appropriate market-based

18

regulation would continue to finance investment and

stimulate economic growth at recent historical levels.

A more organized study of bank performance started in the

late 1980’s (Olweny and Shipho,2011) with the application

of Market Power (MP) and Efficiency Structure (ES) theories

(Athanasoglou et al., 2005.) The MP theory states that

increased external market forces results into profit.

Moreover, the hypothesis suggest that only firms with large

market share and well differentiated portfolio (product)

can win their competitors and earn monopolistic profit. On

the other hand, the ES theory suggests that enhanced

managerial and scale efficiency leads to higher

concentration and then to higher profitability. According

to Nzongang and Atemnkeng in Olweny and Shipho (2011)

balanced portfolio theory also added additional dimension

into the study of bank performance. It states that the

portfolio composition of the bank, its profit and the

return to the shareholders is the result of the decisions

made by the management and the overall policy decisions.

Basing on the above, it is possible to conclude that bank

performance is influenced by both internal and external

factors. According to Athanasoglou et al., (2005) the

internal factors include bank size, capital, management

efficiency and risk management capacity. The same scholars19

contend that the major external factors that influence bank

performance are macroeconomic variables such as interest

rate, inflation, economic growth and other factors like

ownership.

Commercial banks in Tanzania have gone into significant

changes after the linearization of the banking system. The

reforms removed barriers to entry of commercial banks and

supported the improvement of institutional framework and

more efficiently the performance of commercial banks, with

this it has affected the profitability of commercial banks

and increased banking competition. Profitability of

commercial banks is pro foundation for product innovation,

diversification and efficiency of the commercial banks

(Hempell, 2002). The stability of commercial banks as whole

in the economy depends on profitability level. More

profitability level has tendency to absorb risks and shocks

that commercial banks can face. Moreover profitability is

the perquisite condition for the efficiency of commercial

banks. Empirical evidence from Detriguache (1999) has

showed that the soundness of commercial banks performance

depends on profitability. Francis (2006) has indicated that

markets reforms in the sub-Saharan Africa has worsen the

profitability of commercial banks due to high level of non-

performing loans. This is contradictory to the early study

of Chijoriga (1997) who indicated that market20

liberalization is essential for high level profitability of

commercial banks. Profitability of commercial banks is

important for the efficiency of commercial banks.

According to the bank of Tanzania (2010), the commercial

banks profitability has improved to the greatest extent and

most of them are above the regulatory requirements, the

greatest profitability earned by these commercial banks

indicates that the internal factors has played a great role

toward this profitability. The banking industry in Tanzania

provides an insight into the development of commercial

banks industry. This was activated by the changed policies

from state owned (centralized) economy to more liberalized

economy under the banner of liberalization. Moreover, the

Bank of Tanzania Act of 1991 made a profound impact in

commercial banks investment that cropped up more than forty

three banking institutions.

The changing economic climate in Tanzania has meant

multiple opportunities for international commercial banks.

The banking sector constitutes the largest part of the

financial system in Tanzania, and the sector has been

increasing in size and scope of services over the past few

years, as more and more numbers of international banks move

in to the country.

In an effort to liberalize the banking sector, the Banking

21

and Financial Institution Act, 1991 was introduced to

provide the legal framework for banking operations in

Tanzania that will grant authorization of financial

institutions to receive money on current account subject to

withdraw by cheque. As a result of the Act, the entry of

new banks has enhanced financial competition resulting into

some improvement of the quality and quantity of the

financial services offered.

2.2.5 Banks Economic Environment

It is worth to note that that currently the economic

environment in which most commercial banks operate is

highly volatile and uncertain. The main cause of volatile

and uncertain is due to the high increase of financial risk

to commercial banks (Hillier, 2003). Financial risks has

been caused by increased market globalization which is seen

in increased exchange, interest, inflation rates

fluctuations as well as in high competition, demand levels

to mention few. Exchange rates are among financial risks

whereby the increased volatility is reflected to the

greatest extent and commercial banks are particularly

exposed to exchange rate fluctuation.

2.2.6 Bank loans and Bank Growth

Commercial banks are the dominant financial institutions in

most economies as they accelerate economic growth (Richard,

22

2011). The traditional role of a bank is lending and loans

make up the bulk of their assets (Njanike, 2009). Loans

therefore represent the majority of a banks’ asserts

(Saunders and Cornett, 2005). However, lending is not an

easy task for banks because it creates a big problem which

is called non-performing loans (Upal, 2009). Due to the

nature of their business, commercial banks expose

themselves to the risks of default from borrowers (Waweru

and Kalami, 2009). Following that over the years, there

have been an increased number of significant bank problems

in both, matured as well as emerging economies (Richard

(2011).

According to Alton and Hazen (2001) non-performing loans

are those loans which are ninety days or more past due or

no longer accruing interest. Hennie (2003) agrees arguing

that non-performing loans are those loans which are not

generating income. This is further supported by Fofack

(2005), who define non-performing loans as those loans

which for a relatively long period of time do not generate

income that is, the principal and or interest on these

loans have been left unpaid for at least ninety days. Non-

performing loans are also commonly described as loans in

arrears for at least ninety days (Guy, 2011).

23

According to Kroszner (2002) in Waweru and Kalami (2009),

non-performing loans are closely associated with banking

crises. Greenidge and Grosvenor (2010), argue that the

magnitude of non-performing loans is a key element in the

initiation and progression of financial and banking crises.

Guy (2011) agrees arguing that non-performing loans have

been widely used as a measure of asset quality among

lending institutions and are often associated with failures

and financial crises in both the developed and developing

world. Reinhart and Rogoff (2010) as cited in Louzis et al

(2011) point out that non-performing loan can be used to

mark the onset of a banking crisis. Despite on-going

efforts to control bank lending activities, non-performing

loans are still a major concern for both international and

local regulators (Boudriga et al, 2009).

For example borrowers from the commercial banks and other

financial institutions in Tanzania are already finding it

more expensive to indulge in the habit of borrowing

following a rapidly rising inflation rate, as well as

increased and irregular interest rates mainly on financial

instruments (BoT, 2011). According to Bank of Tanzania

(BoT) reports (2011), the weighted average interest rates

on money market instruments trended upwards. The three

major banks in Tanzania – National Micro-Finance Bank

(NMB), NBC limited and CRDB Bank – which together claim

24

49.4 per cent of the banking market share, were the major

contributors of higher profits and deposits in the banking

sub-sector.

However, the issue of Non-Performing Loans (NPLs) had

remained a big challenge to banking in the country.

Currently, the overall industrial rate has remained at nine

per cent, though some banks have recorded ten per cent of

gross NPL. This has been a wide problem banks have had been

indulged to take the requisite approach to mitigate the

situation. According to selected financial results, most of

the banks, both large and small recorded profit-after-tax

increases compared with the same quarter in 2011. The major

drivers of the relatively good performance were loans and

advances, followed by foreign exchange dealings and

transactions, as well as investments in government

securities.

Studies in other countries show that most of bank failures

have been caused by non-performing loans. Ahmad (2002), in

analyzing the Malaysian financial system, reported a

significant relationship between credit risk and financial

crises and concluded that credit risk had already started

to build up before the onset of the 1997 Asian financial

crisis, and became more serious as non-performing loans

25

increased. Li (2003) also found this relationship to be

significant. There is evidence that the level of non -

performing loans in the US started to increase

substantially in early 2006 in all sectors before the

collapse of the sub-prime mortgage market in August 2007.

In this regard, the institutions are urged to enhance their

credit risk management systems with special emphasis on

credit assessment, origination, administration, monitoring

and control standards (MPS, 2012). Fofack (2005) argues

that when left unsolved, nonperforming loans can compound

into financial crisis, the moment these loans exceed bank

capital in a relatively large number of banks.

2.3 Empirical literature review

Benito (2008) carried study of size, growth and bank

dynamics in Spanish the study had investigated the coverage

of financial services providers such as banks from a

dynamic perspective over the 1970-2006 periods. The study

observed that there was no strong relationship on the size-

growth. Changes depend on the competitive environment of

banks (liberalization, deregulation and integration). For

example the study identified that when Spanish banking was

highly regulated, smaller banks were growing faster than

their larger counterparts. Nevertheless the study pointed

out that larger banks grow at the same rate or faster than

smaller banks.

26

In the study carried out by Ngoc (2008) on financial

markets liberalization and the role of banks, the

researcher examined the development of financial

institutions trend following financial sector reforms and

deregulation that allowed entrance of foreign banks in the

Czech Republic, Hungary, and Poland. The study ultimately

found out dates on which bank liberalization occurred in

each country that allowed foreign banks operations.

According to Timoth et al (2006). The short-term and long-

term impact of bank supervision on different categories of

loan growth that is commercial and industrial loans,

consumer loans, and real estate loans. The study finds

little evidence suggesting the effects of changes in any of

the components of ratings differ systematically from the

effects of changes in the composite.

David (2010) carried study on whether political connection

help firms gain access to bank credits in Vietnam. The

study established that one of the major contributing

factors to Vietnam’s macroeconomic instability has been the

massive growth of credit inflows and its often inefficient

allocations. Vietnam is in a state of economic transition

from state-planned to open market based. The private sector

has grown very rapidly but private firms’ demand for credit

is still largely crowded out by the state sector. The study

27

specifically focuses on the use and impact of political

connections by private firms to gain access to bank loans.

Ogilo (2012) carried study on the impact of credit risk

management on financial performance of commercial bank in

Kenya. The study analyzed the impact of credit risk

management on the financial performance of commercial banks

and also attempted to establish if there exists any

relationship between the credit risk management

determinants by use of CAMEL indicators and financial

performance of commercial banks in Kenya. A causal research

design was undertaken in this study and this was

facilitated by the use of secondary data which was obtained

from the Central Bank of Kenya publications on banking

sector survey. Furthermore bank performance is reflected by

accounting measures of profitability, net interest margin,

and operating costs. The results show a very limited effect

of the entry of Greenfield banks on domestic banking market

in the early transition period. In contrast, the foreign

entry by mergers and acquisitions of domestic banks exerts

significant impacts on bank performance.

Abera (2012) carried study on factors affecting

profitability on Ethiopa banking industry. The study

examined the bank-specific, industry-specific and macro-

economic factors affecting bank profitability for a total28

of eight commercial banks in Ethiopia, covering the period

of 2000-2011. Findings had shown a relationship between

capital strength, income diversification, bank size, gross

domestic product and bank profitability. Also the study had

shown close ling between liquidity risk, concentration and

inflation to be statistically insignificant. The study

recommends the focus of bank on key internal drivers that

would enhance the profitability as well as the performance

of the commercial banks in Ethiopia as well as

consideration of internal environment and the macroeconomic

environment that will improve growth or profit.

Javaid et al (2011) carried study on determinants of bank

profitability in Pakistan. The study had found that

financial sector plays a pivotal role in the economic

development. Furthermore the study had generally agreed

that a strong and healthy banking system is a prerequisite

for sustainable economic growth. The study had established

that banks in Pakistan have been undergoing major

challenges in the dynamic environment over the past few

years. However in order to resist negative shocks and

maintain financial stability, it is important to identify

the factors that mostly cause the general performance of

banks in Pakistan. The study used case of top 10 banks’

profitability in Pakistan over the period 2004-2008. The

empirical results have found strong evidence that mentioned29

parameters have a strong influence on the profitability.

However, the results show that higher total assets may not

necessarily influence higher profits due to diseconomies of

scales.

Athanasoghou et al (2008) assessed output and productivity

growth in banking industry in Greece. The study has

assessed the evolution of output and productivity in the

Greek banking industry for the period 1990-2006. Three main

categories of bank output were estimated based on modern

theoretical approaches. The results show that bank output

and labor productivity has increased significantly

throughout the period under examination, outpacing the

respective GDP growth and labor productivity of the Greek

economy. Capital output of the Greek banking industry have

also improved extremely mostly since 1999, as a result of

the structural changes that took place within the industry,

capital investments as well as improvement in the quality

of human capital.

Cornett et al (2005) carried out a study on long

performance of rival banks around bank failures in USA. The

study reveals that bank failures are associated with

changes in long-term performance at rival banks.

Nevertheless, the change in performance is not the same for

all banks. Additionally the study noted that if the bank 30

failure was the result of a problem that was similar to

other banks, rival banks performance increase after failure

and if bank failure was due to problem that is unique to

the failing bank rival bank performance decreases after the

bank failure.

Thi N. A. V (2009) carried out a study on banking market

liberalization and bank performance in Czech Republic. The

study considered two modes of foreign bank entry that were

entry by Greenfield investments and by foreign mergers and

acquisitions of domestic banks. The study measured bank

performance through accounting measures of profitability,

net interest margin, and operating costs. The results show

that minimal effect on entry of Greenfield banks on

domestic banking market in the early transition period.

Contrarily the foreign entry by mergers and acquisitions of

domestic banks exerts significant impacts on bank

performance. More importantly the study observed

significant declines in banks’ profits and net interest

margins, and a significant increase in operating costs.

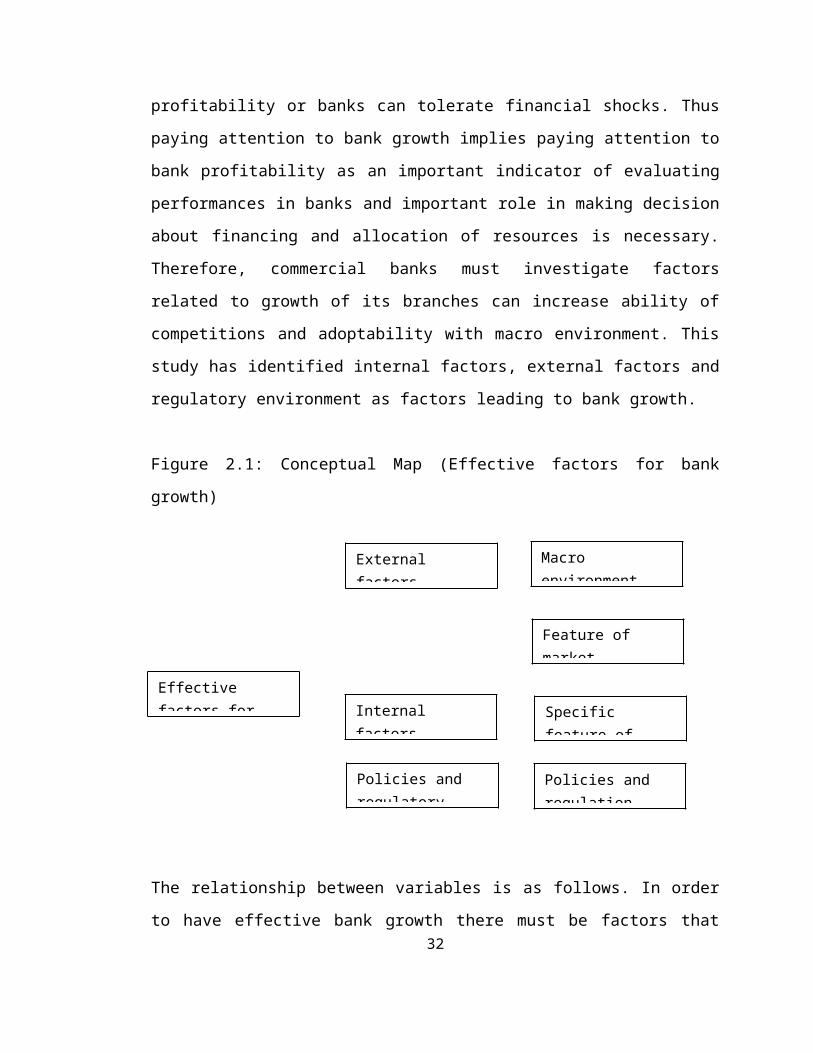

2.4 Conceptual Framework

Expanding global markets and increasing competition in

financial services markets has affected the bank growth and

profitability of the banking industry. Bank growth is an

important function of banks as financial intermediately and31

profitability or banks can tolerate financial shocks. Thus

paying attention to bank growth implies paying attention to

bank profitability as an important indicator of evaluating

performances in banks and important role in making decision

about financing and allocation of resources is necessary.

Therefore, commercial banks must investigate factors

related to growth of its branches can increase ability of

competitions and adoptability with macro environment. This

study has identified internal factors, external factors and

regulatory environment as factors leading to bank growth.

Figure 2.1: Conceptual Map (Effective factors for bank

growth)

The relationship between variables is as follows. In order

to have effective bank growth there must be factors that32

Effective factors for

External factors

Internal factors

Macro environment

Feature of market

Policies and regulatory

Specific feature of

Policies and regulation

are influencing that growth. These factors are external

factors, internal factors and policies and regulatory

environment. While external factors are influenced by both

macro environment and feature of markets; internal factors

are influenced by specific feature of bank and policies and

regulatory environment is influenced by good policies and

regulations.

33

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Introduction

The study explores factors that lead to growth of

commercial banks in Tanzania. The research design covered

the reasons for selecting respondents, data sources, data

analysis and a brief note on assumptions and weaknesses.

This chapter covers the following issues. Research

paradigms, type of the study, study area, study population,

units of analysis, variable and their measurement, sample

size and sampling techniques and types and sources of data.

Other things covered include data collection methods,

reliability and validity of data and data analysis methods.

3.2 Research Paradigms

This study has considered views held by Balling et al

(2012) that there is a need for a paradigm shift in the

area of financial supervision. The paradigm need to

containing what was prevailing before financial crisis and

actions taken such as national concerns. The paradigm also

portray financial supervision by concluding that integrated

and stable financial markets can go hand in hand, and even

though it is quite a challenging task to make sure that

this is the case, it is nevertheless possible, and you do

not need a trail between integration and stability as long

as you have adequate cross border financial stability34

arrangements in place. This is what Tanzania banking sector

could try to build. Balling et al (2012) argues that we

cannot have integration and stability financial sector at

regional level if national supervisors remain fully in

charge and if their only mandate is to cater for the

protection of national consumers and for financial

stability at national level. We now all agree that there is

no such thing as national financial stability anymore.

Financial stability which determines bank growth has to be

international or it has to be at least regional.

3.3 Type of Study

The study used both qualitative and quantitative research

design.This explains types of Academic research of which

its results are based on documents analysis, literature

reviews and past research findings in drawing up

conclusions. The explanatory research design, adopted the

steps such as review of the related literature to know the

work already done by others, Survey of people who had

practical experience with the problems to be studied and

the analysis of insight stimulating examples.

3.4 Study Area

The study was carried out in five banks that are CRDB bank,

STANBIC bank, Barclays bank, NMB bank and NBC bank. CRDB

Bank Plc is a leading, wholly-owned private commercial bank35

in Tanzania. The Bank was established in 1996 and has grown

and prospered over the years to become the most innovative,

first choice, and trusted bank in the country. CRDB Bank

offers a comprehensive range of Corporate, Retail,

Business, Treasury, Premier, and wholesale microfinance

services through a network of 60 branches, ATMs, Depository

ATMs, Mobile branches, Point of Sales (POS) terminals and

scores of Microfinance partners institutions. The Bank also

operates through internet and Mobile banking services

Stanbic Bank in Tanzania came into being in May 1995 when

Standard Bank Group acquired the operations of Meridien

Biao Bank Tanzania Limited. They have nine branches and two

service centers in the country. Standard Bank Group is a

global bank with African roots. It is South Africa's

largest bank, distinguished by its extensive operations in

17 African countries. Outside the African continent,

Standard Bank Group's operations span to 15 countries, with

an emerging market focus

Barclays is a global financial services provider, engaged

in retail and commercial banking, credit cards, investment

banking, wealth management and investment management

services all over the world. With a vast, international

reach, Barclays offers innovative products and services to

meet the needs of its diverse base of customers and clients36

NMB is the largest bank in Tanzania, both when ranked by

customer base and branch network. With over 139 branches we

are located in more than 80% of Tanzania's districts. This

broad branch network distinguishes NMB from other financial

institutions in Tanzania. With our 139 branches we are

located in more than 80% of Tanzania's districts. This

broad branch network distinguishes NMB from other financial

institutions in Tanzania. We are committed to sustaining

and enhancing our branch network in order to provide access

to capital to citizens in all areas of Tanzania, including

the most remote

NBC Ltd. was formed on 1st April 2000 when NBC (1997) Ltd.

was privatized and sold to ABSA Group Ltd. of South Africa.

NBC (1997) Ltd. was itself born out of the nationalization

of banks and financial institutions in Tanzania in 1967.

NBC Ltd. is one of the largest commercial banks in

Tanzania, with a network of 53 branches and 6 business

centers strategically located in retail centers and other

major towns across the country. Having joined forces with

Africa's largest banking group, South African based Absa

Group Ltd, NBC Ltd. has given its clients access to a

global banking environment. Wherever you may be, NBC Ltd is

the solution to all your banking requirements

37

3.5 Study population

The population of this study includes all workers,

regularity boards, board of trustees and customer of the

selected five major commercial banks in Tanzania for the

period of 2006 to 2012.

3.6 Units of analysis

The unit of analysis is the core unity analyzed from the

population. The unity of analysis implies exactly thing to

be studied. In this study unity of analysis were bank

managers and bank officials at all rank.

3.7 Variable and their measurement

The study was about evaluation of factor leading to the

growth of banks in Tanzania. Bank growth is determined by

both external and internal factors. The growth trend from

2006 to 2012 will determine whether banks are growing or

not growing. Variables to be measured include size of

capital, increment of services, geographical coverage,

number of customers, improvement of technology, profits and

regulatory environment.

3.8 Sample size and sampling techniques

This study used purposely for sampling method by selecting

5 commercial banks operating in Tanzania in studying the

growth trends of commercial banks in the country. The38

sample for the study included 100 respondents from five

banks and one regulatory board as shown in table 3.1.

Simple random probability sampling and purposeful

techniques were used to draw a suitable sample of the study

for the purpose of providing equal chance for every

respondents of being selected and reduce selection bias.

Table 3.1 Sample Size (N=100)Category

SAMPLE SIZE AND SAMPLING METHOD

CRDB STANBIC

BARCLAYS

NMB NBC Total

Samplingmethod

Manager 1 1 1 1 1 5 Purposeful Bank officers

19 19 19 19 19 95 Random

Total 20 20 20 20 20 100Source: Survey data, 2014

3.9 Types and sources of data

Two types of data were collected from this study. Types of

data collected include secondary and primary data. Primary

data form first –form information that the researcher

collects for his/her particular study (Saunders, 2000).

Secondary data are normally data collected earlier for

different uses, and which are equally used in a current

study (Saunders, 2000).

3.10 Data collection methods

39

Data were collected from published reports, inquiries and

questionnaires form the various stake holders. Secondary

data were gathered from published banks reports. Primary

data were collected through the use of structured

questionnaire, physical interviews with the respondents and

self observation.

3.10.1 Interview

The research used open ended question in order to allow

respondents to be open and to express themselves freely.

The researcher had opportunities to discover new view and

perception regarding factors regarding growth of bank

sector. It was a face to face interview and prior to that

researcher met respondents introduced them the study and

seek appointment. Key areas expected to be coved were

discussed in the first meeting.

3.10.2 Questionnaire

An open ended and closed questionnaire was used in this

study. Questionnaires were expected to bring quantitative

information that enabled the researcher to come up with

frequencies, percentages and cross tabulated answers. The

researcher requested respondent to fill questionnaire in

his presence to avoid delays. In each bank all respondents

were gathered together after immediately after working

hours. In each bank the exercise took two days.40

3.11 Reliability and validity

Since interviews and questionnaires were used as the data

collection methods, it important to establish adequate

level of validity and reliability to the respondents. This

was done by using appropriate data collection methods

designed in the way that would measure an attitudes and

opinions of the participants on a subject matter related

with bank growth

3.12 Ethical Consideration

The study considered the following ethical issues. The

researcher has research permit and prior doing anything he

disclosed the permit to bank managers and was allowed to

continue with the research. The researcher considered

privacy of respondents and that is why research was done

after working hours. Data gathered are discussed and

interpreted in the manner that they bring relevant and

accurate conclusions. Moreover, the researcher protected

his work against plagiarism by make sure that all ideas

taken from diverse authors are accurately agreed with its

source citation and mentioned on list of references. In

other way around, a researcher reduced the extent of

plagiarism by using their own words that relate with the

borrowed ideas without losing the primary idea.

41

3.13 Data analysis methods.

The main tool which will be used for data analysis will

beStata, data analysis and statistical software such as

SPSS to calculate of percentages, Measures of central

tendency like Arithmetic mean, Mode, Median, Range and

Regression analysis where applicable.

CHAPTER FOUR

PRESENTATION, ANALYSIS AND DISCUSSION OF FINDINGS

4.1 Introduction

Chapter four present, analyze and discuss quantitative and

qualitative data. This chapter addresses four sub-sections

that are general trends of growth of commercial banks in

Tanzania from 2006 to 2012, internal factors that led to

the growth of commercial banks in Tanzania, external

factors that led to the growth of commercial banks in

Tanzania and role of legal and regulatory framework in

supporting the growth of banks in Tanzania.

4.2 Personal Information

Personal information is an important aspect in research as

it determines accuracy of data provided. It is worth

noting that respondent’s gender, education and age

42

determines type of data. Determined by their gender women

and men might have different opinions on similar matter due

to their differences in feelings, perceptions and social

responsibilities. Age and education determines peoples’

wisdom and thinking capacity. Along this reflection age and

education of respondents might determine accuracy and

reliability of data. Therefore it is crucial to balance

respondents while conducting a research. Within this

framework personal information taken into consideration in

this study were gender, age, level of education and both

working department and experience for bank officers. Gender

is my point of departure as stipulated hereunder.

Figure 4.1: Respondents by gender

Source: Research findings, 2014.

Gender inequality generates wasted opportunities and

cognitive errors in knowledge. Research has shown that

43

gender bias has important implications for the content of

research itself. The integration of sex and gender analysis

in the research content increases the quality of research

and improves the acceptance of data. Thus in this study

gender balance was considered as there were 55(55%) male

and 45(45%) female. In some cases gender biasness in

working places has been reported and it is still an issue.

This means if we treat respondents with biasness to one

gender the possibility of getting biased data is higher.

Thus gender balancing is very important in order to get

unbiased data. That is why respondents for this study are

gender balanced. Gender balances were followed by

determining age of respondents which were as hereunder.

Respondents by age were as follows.

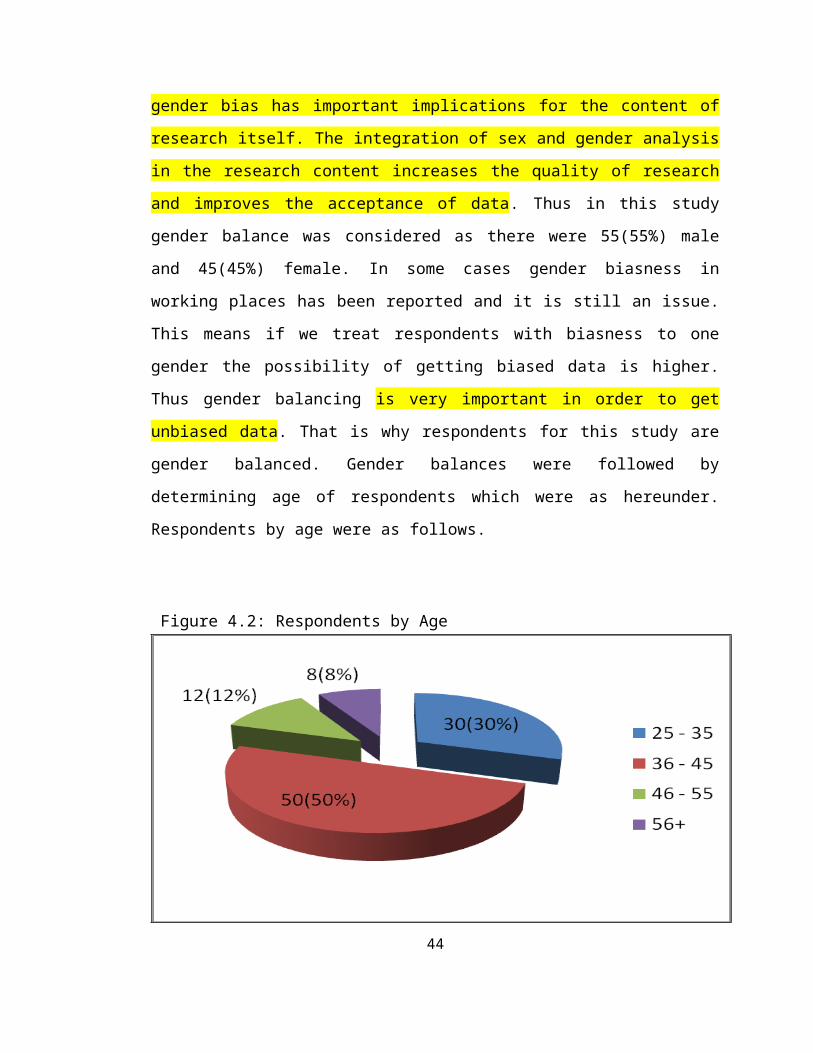

Figure 4.2: Respondents by Age

44

Source: Research Findings, 2014

The study assumed twenty years to be minimum year a person

could start working. Categorically, 30(30%) respondent

were between 25 to 35 years, 50(50%) respondent were

between 36 to 45 years, 12(12%) respondent were between 46

to 55 years and 8(8%) respondent were 56 and above years.

As seen in data, most of respondents are young and

energetic implying that bank workers are young people

probably capable of maneuvering with globalization

challenges. Level of education was another characteristic

considered and the distribution was as follows.

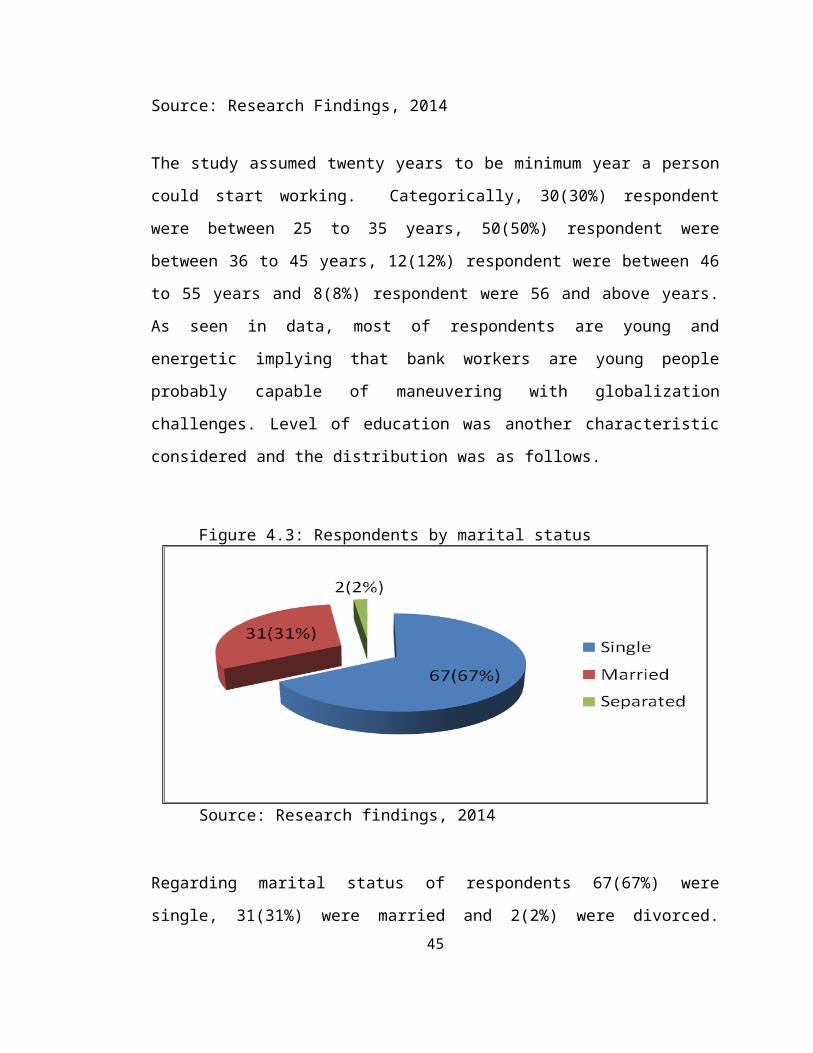

Figure 4.3: Respondents by marital status

Source: Research findings, 2014

Regarding marital status of respondents 67(67%) were

single, 31(31%) were married and 2(2%) were divorced.45

Regarding education level of respondents findings were as

hereunder.

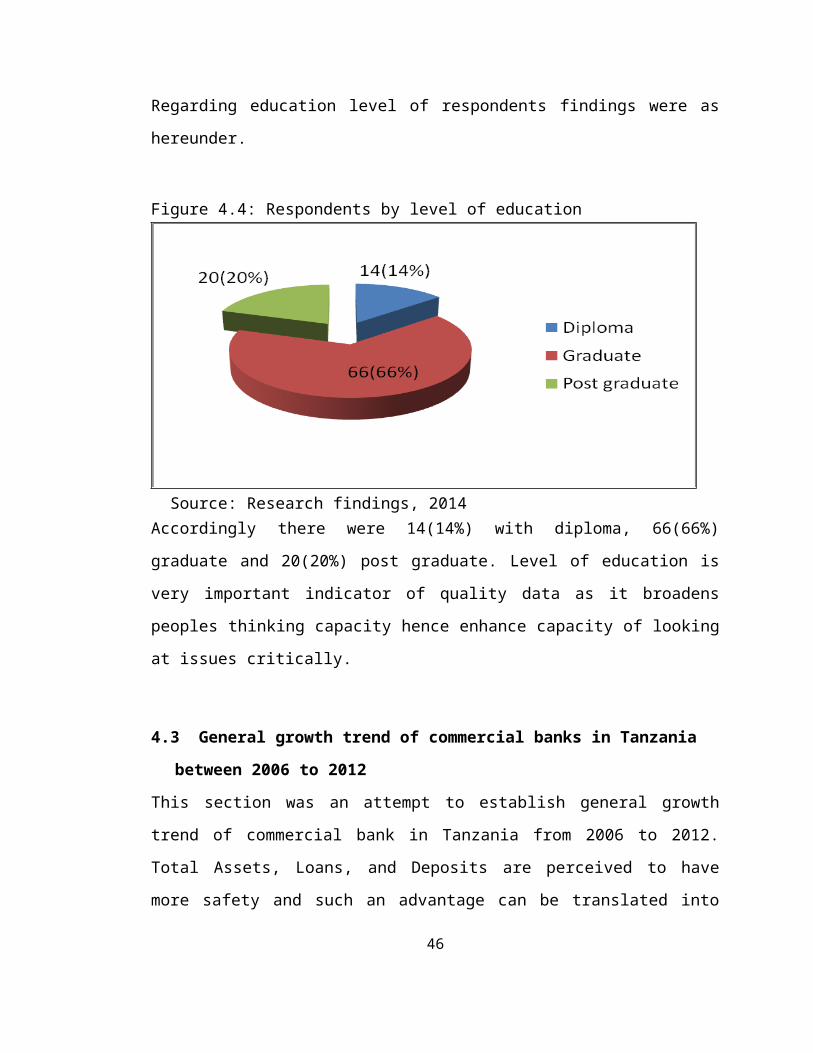

Figure 4.4: Respondents by level of education

Source: Research findings, 2014Accordingly there were 14(14%) with diploma, 66(66%)

graduate and 20(20%) post graduate. Level of education is

very important indicator of quality data as it broadens

peoples thinking capacity hence enhance capacity of looking

at issues critically.

4.3 General growth trend of commercial banks in Tanzania

between 2006 to 2012

This section was an attempt to establish general growth

trend of commercial bank in Tanzania from 2006 to 2012.

Total Assets, Loans, and Deposits are perceived to have

more safety and such an advantage can be translated into

46

higher profitability and hence bank growth. This section is

the review of different bank document related to annual

financial reports. Factors considered in the section are

trends in operation income, net income, total assets, total

deposits and number of employees. It is important to note

that some data were not available as seen in below table.

However, accessed data were enough to determine the trend.

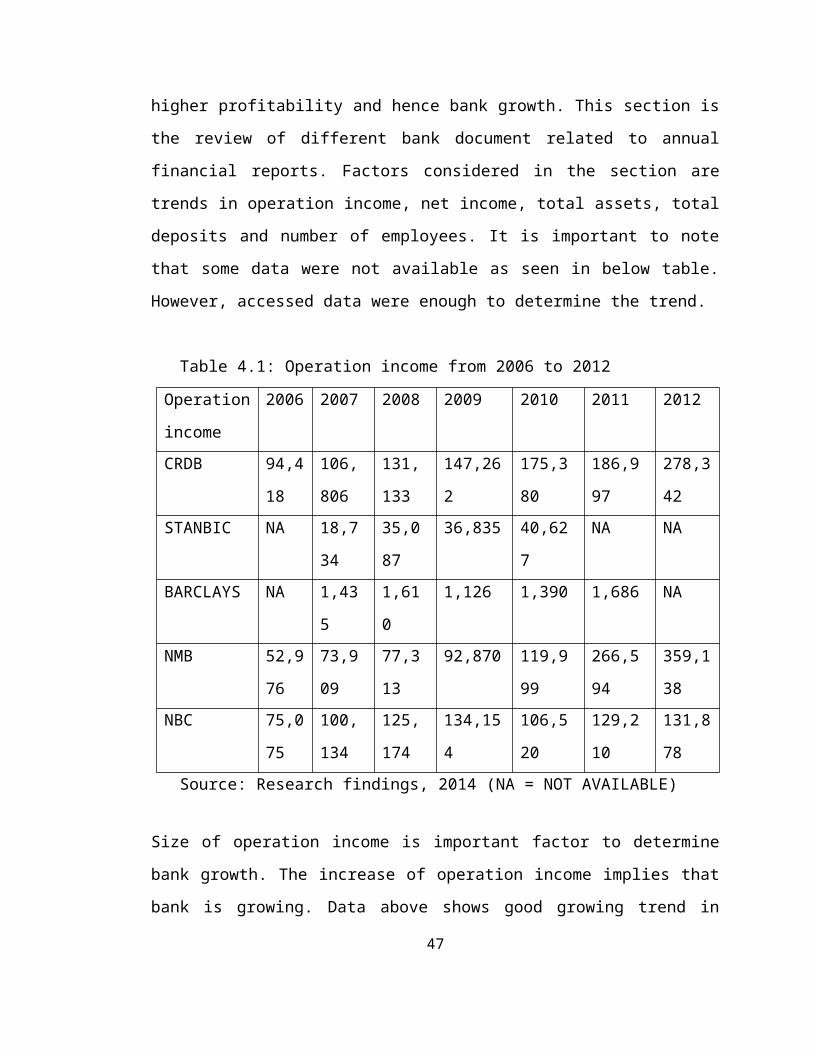

Table 4.1: Operation income from 2006 to 2012

Operation

income

2006 2007 2008 2009 2010 2011 2012

CRDB 94,4

18

106,

806

131,

133

147,26

2

175,3

80

186,9

97

278,3

42STANBIC NA 18,7

34

35,0

87

36,835 40,62

7

NA NA

BARCLAYS NA 1,43

5

1,61

0

1,126 1,390 1,686 NA

NMB 52,9

76

73,9

09

77,3

13

92,870 119,9

99

266,5

94

359,1

38NBC 75,0

75

100,

134

125,

174

134,15

4

106,5

20

129,2

10

131,8

78 Source: Research findings, 2014 (NA = NOT AVAILABLE)

Size of operation income is important factor to determine

bank growth. The increase of operation income implies that

bank is growing. Data above shows good growing trend in

47

operation income as there is annual increment for all banks

except Barclays bank in 2009 and NBC bank in 2010 where

there was a decline. The growth of operational income

implies that bank can perform its core function that is

providing loans to many customers factor suggesting its

growth. This is similar to Richard (2011) and Njanike

(2009) that commercial banks are the dominant financial

institutions in most economies as they accelerate economic

growth and the traditional role of a bank is lending and

loans make up the bulk of their assets (Njanike, 2009).

Regarding bank net income data are shown in table 4.2.

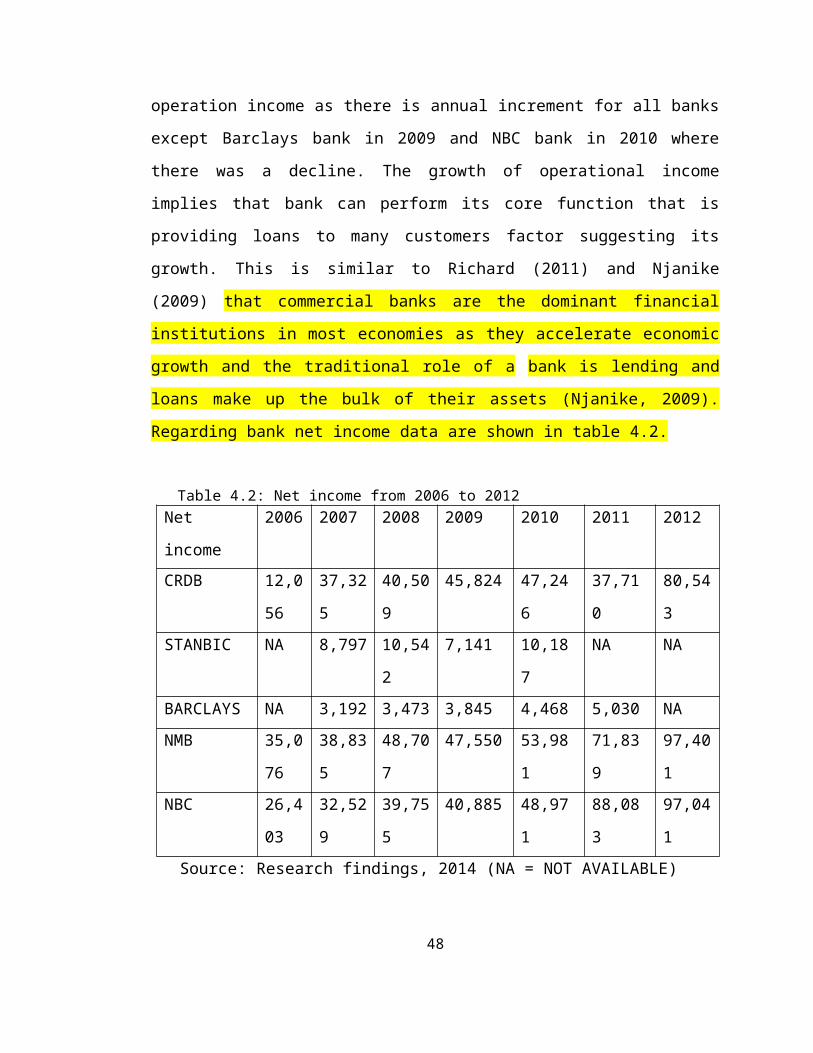

Table 4.2: Net income from 2006 to 2012Net

income

2006 2007 2008 2009 2010 2011 2012

CRDB 12,0

56

37,32

5

40,50

9

45,824 47,24

6

37,71

0

80,54

3STANBIC NA 8,797 10,54

2

7,141 10,18

7

NA NA

BARCLAYS NA 3,192 3,473 3,845 4,468 5,030 NANMB 35,0

76

38,83

5

48,70

7

47,550 53,98

1

71,83

9

97,40

1NBC 26,4

03

32,52

9

39,75

5

40,885 48,97

1

88,08

3

97,04

1 Source: Research findings, 2014 (NA = NOT AVAILABLE)

48

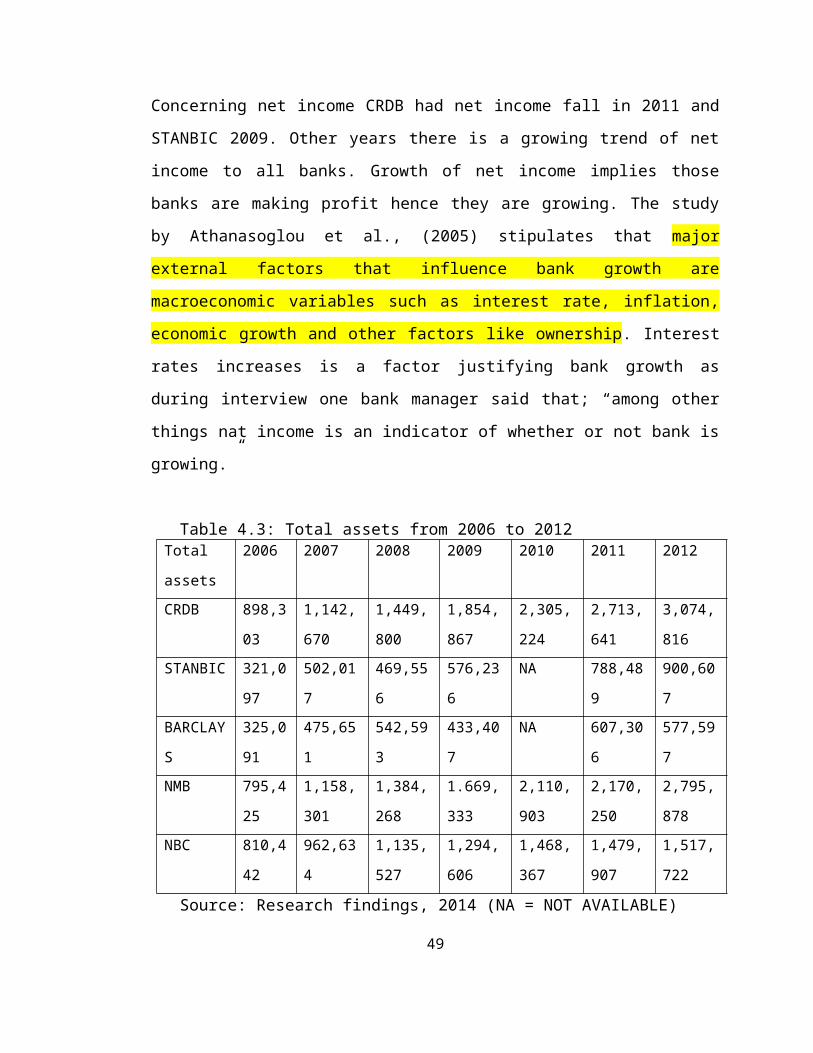

Concerning net income CRDB had net income fall in 2011 and

STANBIC 2009. Other years there is a growing trend of net

income to all banks. Growth of net income implies those

banks are making profit hence they are growing. The study

by Athanasoglou et al., (2005) stipulates that major

external factors that influence bank growth are

macroeconomic variables such as interest rate, inflation,

economic growth and other factors like ownership. Interest

rates increases is a factor justifying bank growth as

during interview one bank manager said that; “among other

things nat income is an indicator of whether or not bank is

growing.”

Table 4.3: Total assets from 2006 to 2012Total

assets

2006 2007 2008 2009 2010 2011 2012

CRDB 898,3

03

1,142,

670

1,449,

800

1,854,

867

2,305,

224

2,713,

641

3,074,

816STANBIC 321,0

97

502,01

7

469,55

6

576,23

6

NA 788,48

9

900,60

7BARCLAY

S

325,0

91

475,65

1

542,59

3

433,40

7

NA 607,30

6

577,59

7NMB 795,4

25

1,158,

301

1,384,

268

1.669,

333

2,110,

903

2,170,

250

2,795,

878NBC 810,4

42

962,63

4

1,135,

527

1,294,

606

1,468,

367

1,479,

907

1,517,

722

Source: Research findings, 2014 (NA = NOT AVAILABLE)

49

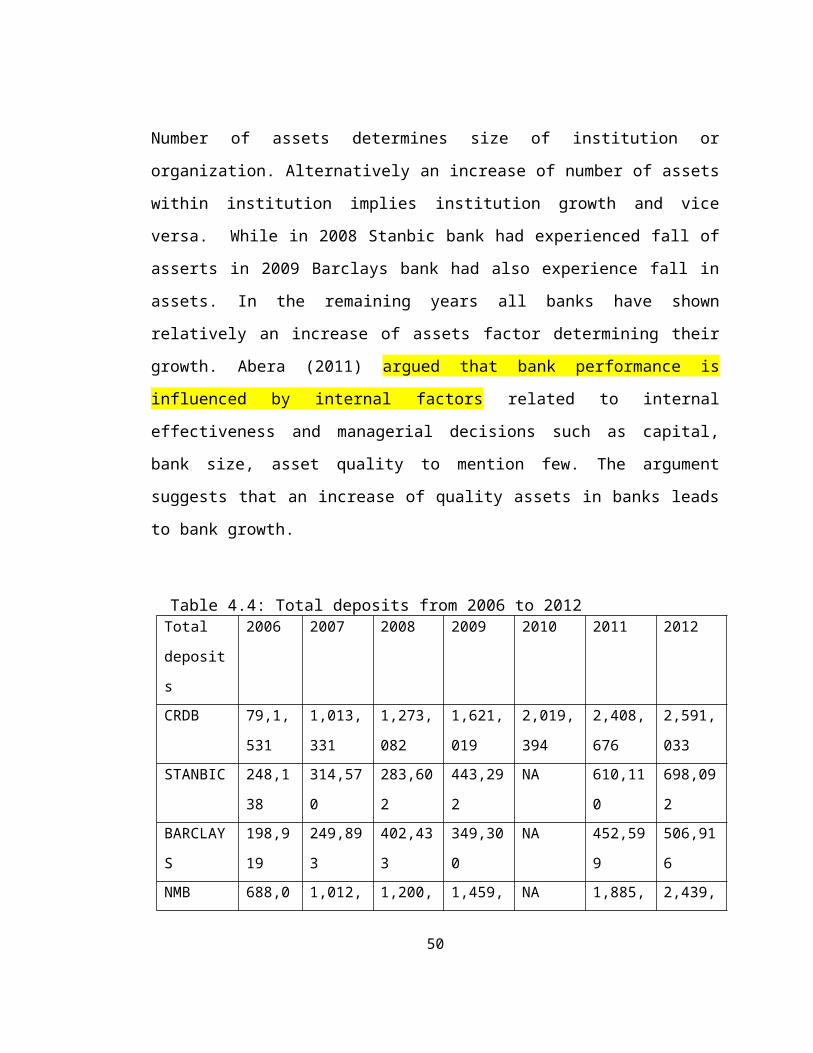

Number of assets determines size of institution or

organization. Alternatively an increase of number of assets

within institution implies institution growth and vice

versa. While in 2008 Stanbic bank had experienced fall of

asserts in 2009 Barclays bank had also experience fall in

assets. In the remaining years all banks have shown

relatively an increase of assets factor determining their

growth. Abera (2011) argued that bank performance is

influenced by internal factors related to internal

effectiveness and managerial decisions such as capital,

bank size, asset quality to mention few. The argument

suggests that an increase of quality assets in banks leads

to bank growth.

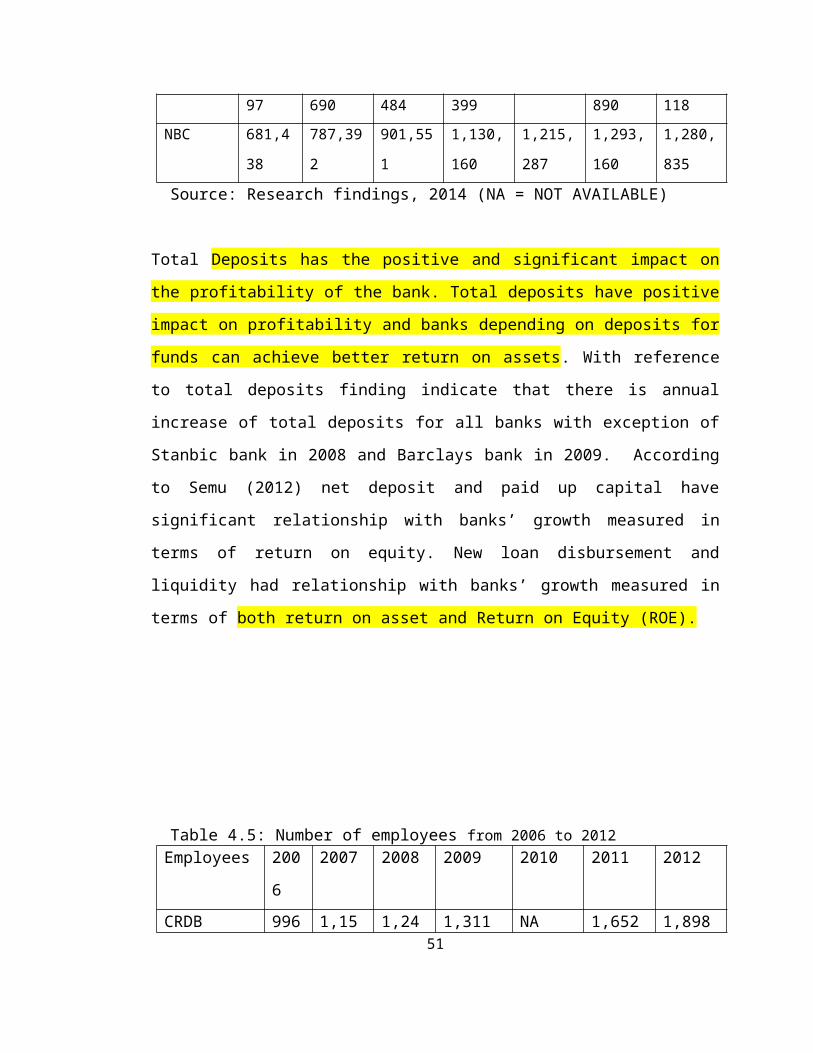

Table 4.4: Total deposits from 2006 to 2012Total

deposit

s

2006 2007 2008 2009 2010 2011 2012

CRDB 79,1,

531

1,013,

331

1,273,

082

1,621,

019

2,019,

394

2,408,

676

2,591,

033STANBIC 248,1

38

314,57

0

283,60

2

443,29

2

NA 610,11

0

698,09

2BARCLAY

S

198,9

19

249,89

3

402,43

3

349,30

0

NA 452,59

9

506,91

6NMB 688,0 1,012, 1,200, 1,459, NA 1,885, 2,439,

50

97 690 484 399 890 118NBC 681,4

38

787,39

2

901,55

1

1,130,

160

1,215,

287

1,293,

160

1,280,

835

Source: Research findings, 2014 (NA = NOT AVAILABLE)

Total Deposits has the positive and significant impact on

the profitability of the bank. Total deposits have positive

impact on profitability and banks depending on deposits for

funds can achieve better return on assets. With reference

to total deposits finding indicate that there is annual

increase of total deposits for all banks with exception of

Stanbic bank in 2008 and Barclays bank in 2009. According

to Semu (2012) net deposit and paid up capital have

significant relationship with banks’ growth measured in

terms of return on equity. New loan disbursement and

liquidity had relationship with banks’ growth measured in

terms of both return on asset and Return on Equity (ROE).

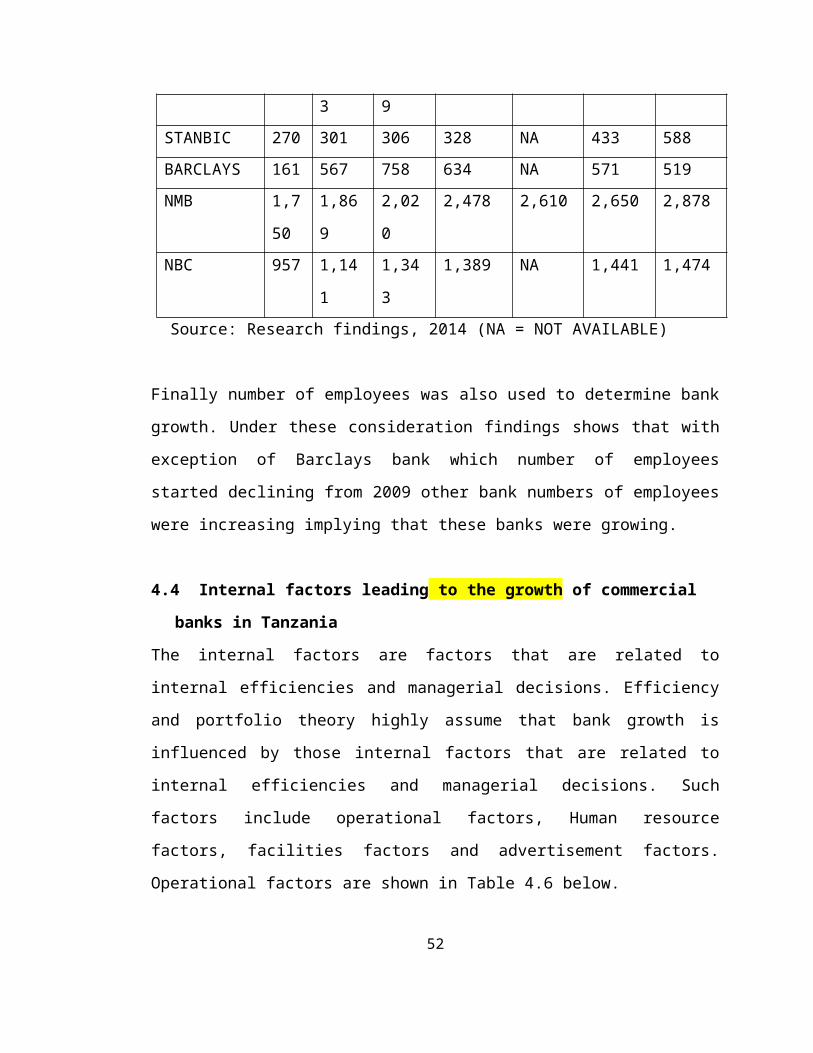

Table 4.5: Number of employees from 2006 to 2012Employees 200

6

2007 2008 2009 2010 2011 2012

CRDB 996 1,15 1,24 1,311 NA 1,652 1,89851

3 9STANBIC 270 301 306 328 NA 433 588BARCLAYS 161 567 758 634 NA 571 519NMB 1,7

50

1,86

9

2,02

0

2,478 2,610 2,650 2,878

NBC 957 1,14

1

1,34

3

1,389 NA 1,441 1,474

Source: Research findings, 2014 (NA = NOT AVAILABLE)

Finally number of employees was also used to determine bank

growth. Under these consideration findings shows that with

exception of Barclays bank which number of employees

started declining from 2009 other bank numbers of employees

were increasing implying that these banks were growing.

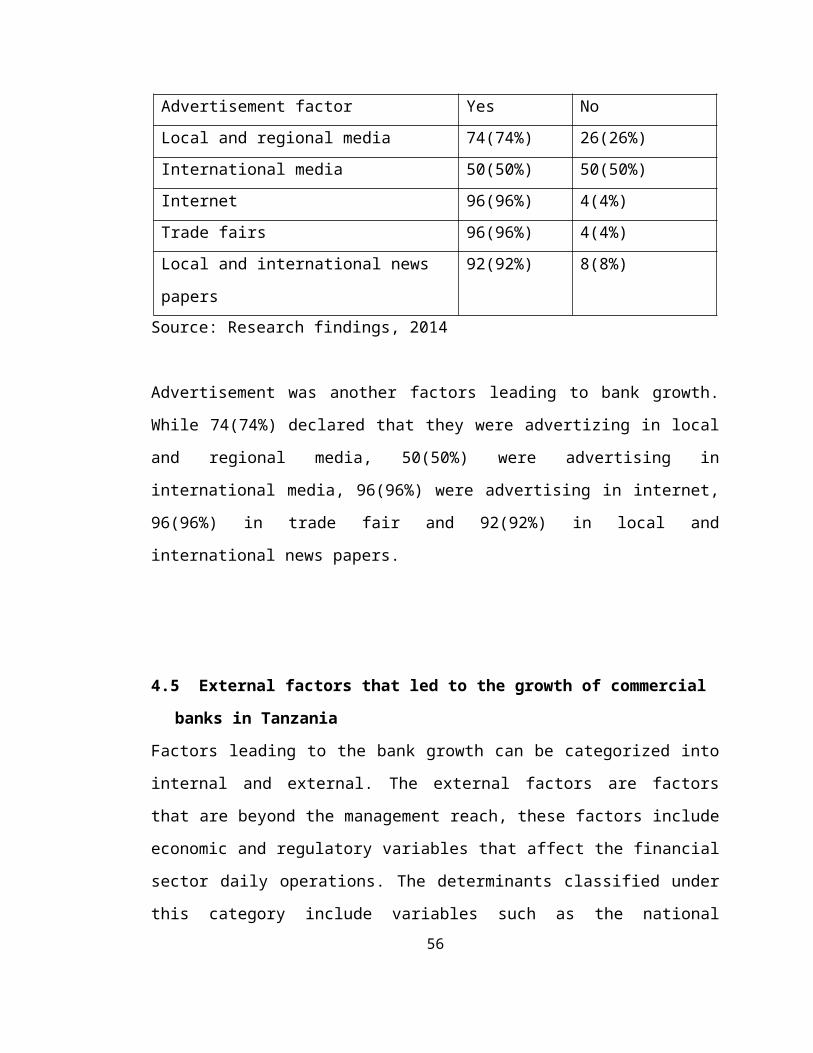

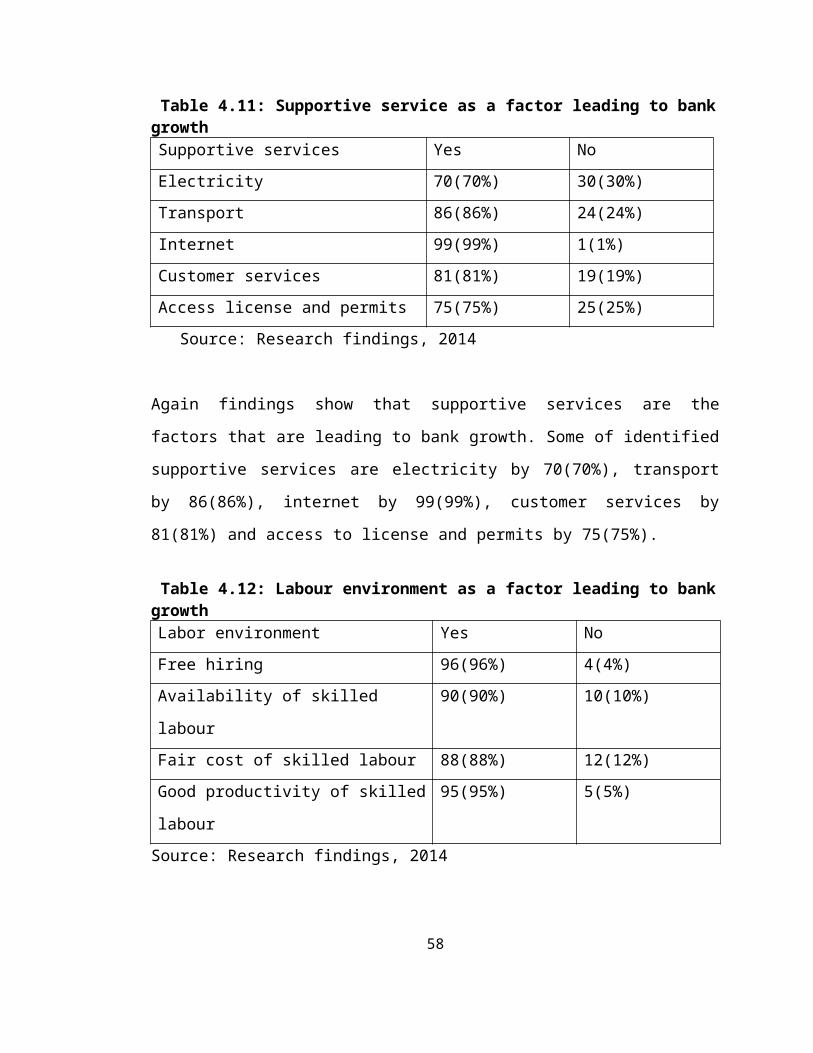

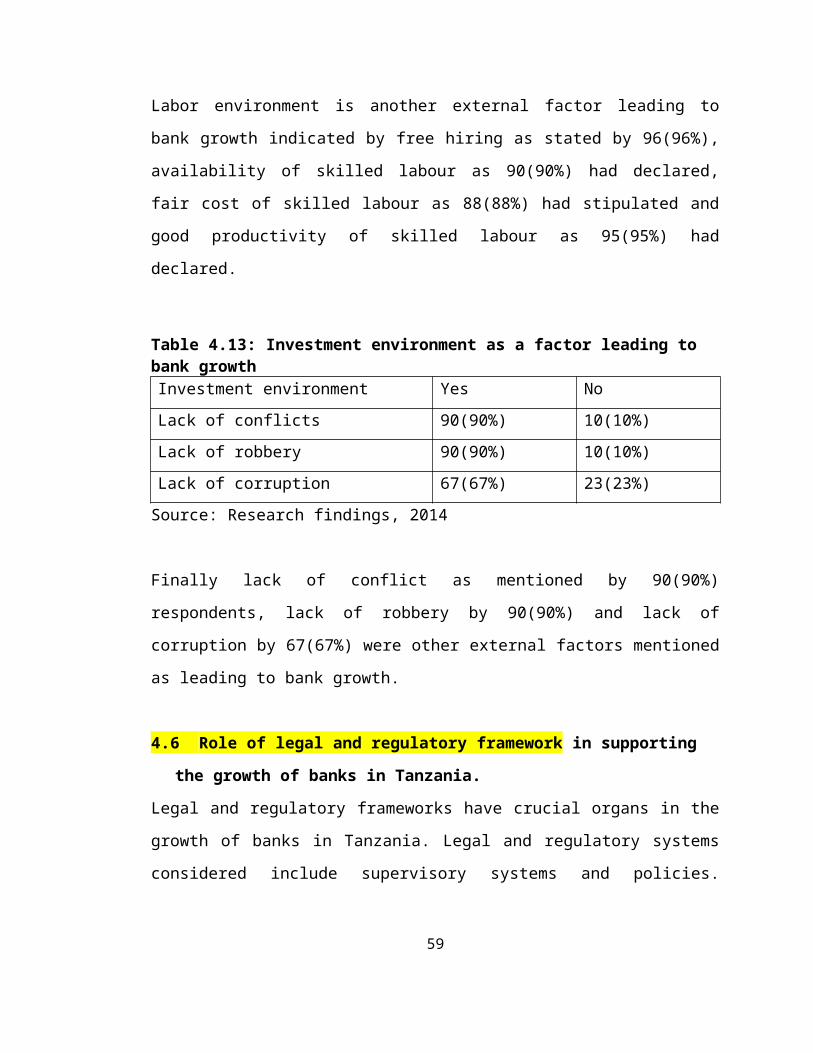

4.4 Internal factors leading to the growth of commercial

banks in Tanzania

The internal factors are factors that are related to

internal efficiencies and managerial decisions. Efficiency

and portfolio theory highly assume that bank growth is

influenced by those internal factors that are related to

internal efficiencies and managerial decisions. Such

factors include operational factors, Human resource

factors, facilities factors and advertisement factors.

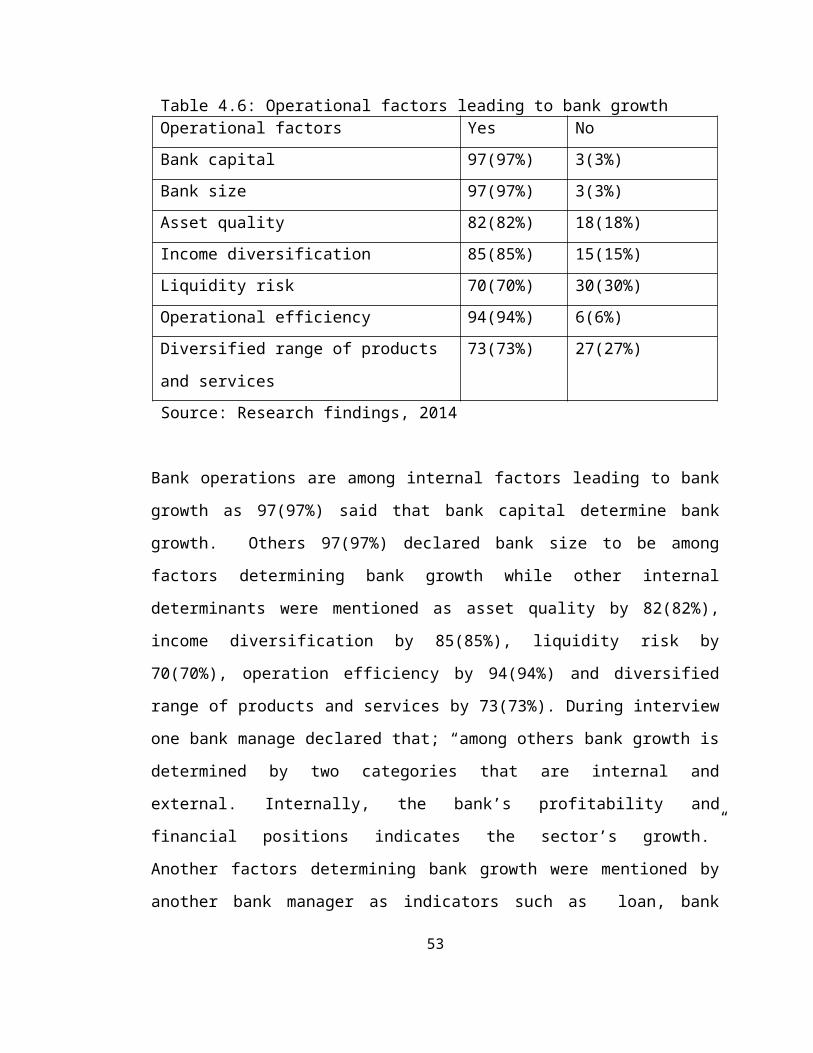

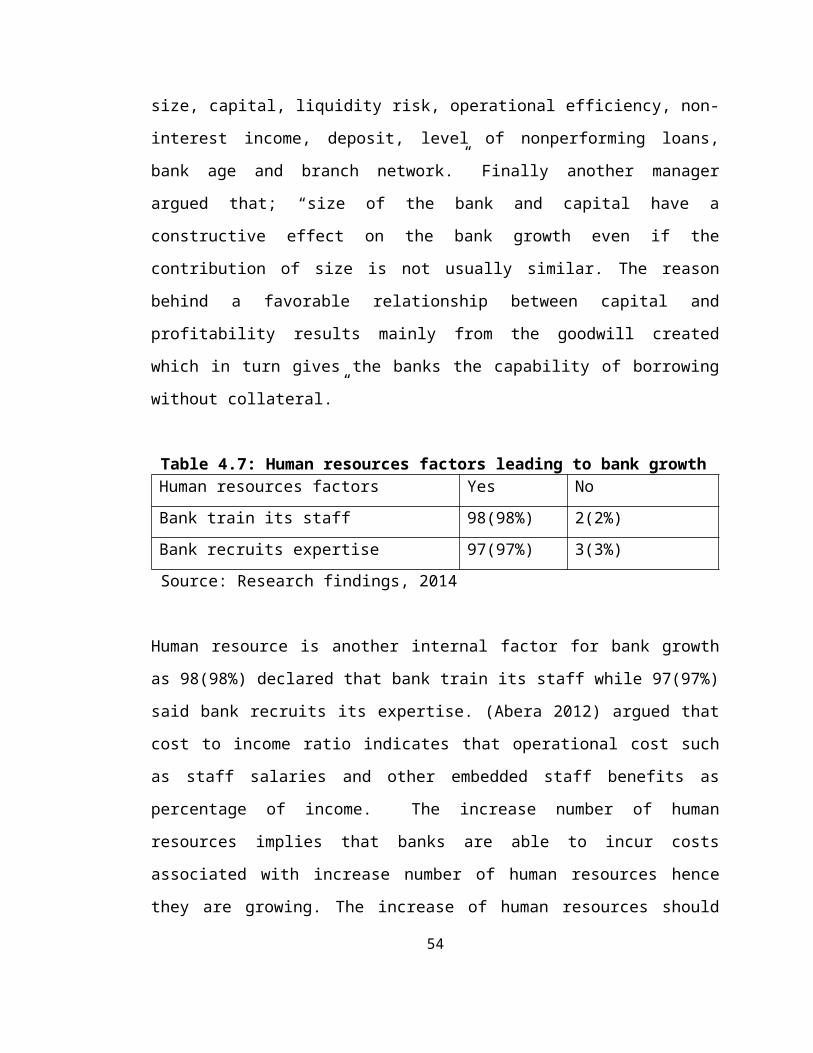

Operational factors are shown in Table 4.6 below.

52