Raising productivity and reducing risks of informal businesses in Africa, expand access to...

73

Raising productivity and Reducing Risks of Informal Businesses Expanding Access to Microfinance for Household (Micro) Enterprises in Africa? [Wednesday 3 September 2008] Aleke Dondo with Henry Oketch

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of Raising productivity and reducing risks of informal businesses in Africa, expand access to...

Raising

productivity and

Reducing Risks of

Informal

Businesses Expanding Access to Microfinance for

Household (Micro) Enterprises in Africa?

[Wednesday 3 September 2008]

Aleke Dondo with Henry Oketch

P

age2

ABSTRACT

In many African countries, the informal economy provides jobs to millions of the labor

force and contributes from 25 percent to 30 percent of domestic output. Yet, despite

holding much promise for growth and poverty reduction, microfinance is still accessible

to just a handful of small-scale firms and smallholdings in rural parts of Africa. This paper

seeks to answer the question:” what is happening (or not happening) in microfinance to

increase the productivity and reduce the risks of informal businesses of the working poor

in individual African countries, and the impact of such measures." It lays out the current

limitations of the African microfinance system that undermines its potential contribution

to building a more competitive informal economy that can survive in fast globalizing

world.

P

age3

Table of Contents

I. Introduction 5

Table 1. Landscape of African Microfinance Sector at July 2007 6

The importance of microfinance for Africa 7

Application of microfinance by nano enterprises 7

Table 2.2. Typical Investment of Microfinance Loans 8

Table 2.3. Use of Loan by Purpose and Level of Income 9

Obstacles to growth and poverty reduction 10

Table 3. Distribution of MIVs (USD, millions) As At End-2006 13

II. The African Microfinance system 15

Roots and evolution of the system 15

Regional and worldwide distribution of MFIs 17

Table 2.1 Country Distribution of MFIs in Africa, 2007 17

Table 4. Relative Increase in the Number of MFIs 1996-2006 19

Institutional diversity and transformation 20

Table 5. Sample Distribution of MFIs Analyzed by the World Bank in 1995 20

Table 6. Global Landscape of Microfinance Institutions as at End-2005 21

Regional Diversity 22

Gender reach by type of MFI 24

financial products Diversity 24

Table 9. Current Financial Profile of Microfinance Institutions 27

III. Current Limitations, nano firms view 31

P

age4

Institutional perspective 31

Table 3.1. MFIs 3 Top Obstacles to Immediate Priority Goals 34

client satisfaction and perspective of services and Products 35

IV. Improving access and service quality 37

it all begins with the Formulation of a Creative or Innovative Policy 38

The second solution in expanding and deepening access is the mobilization of

adequate resources 41

Role of Standards and Benchmarks 43

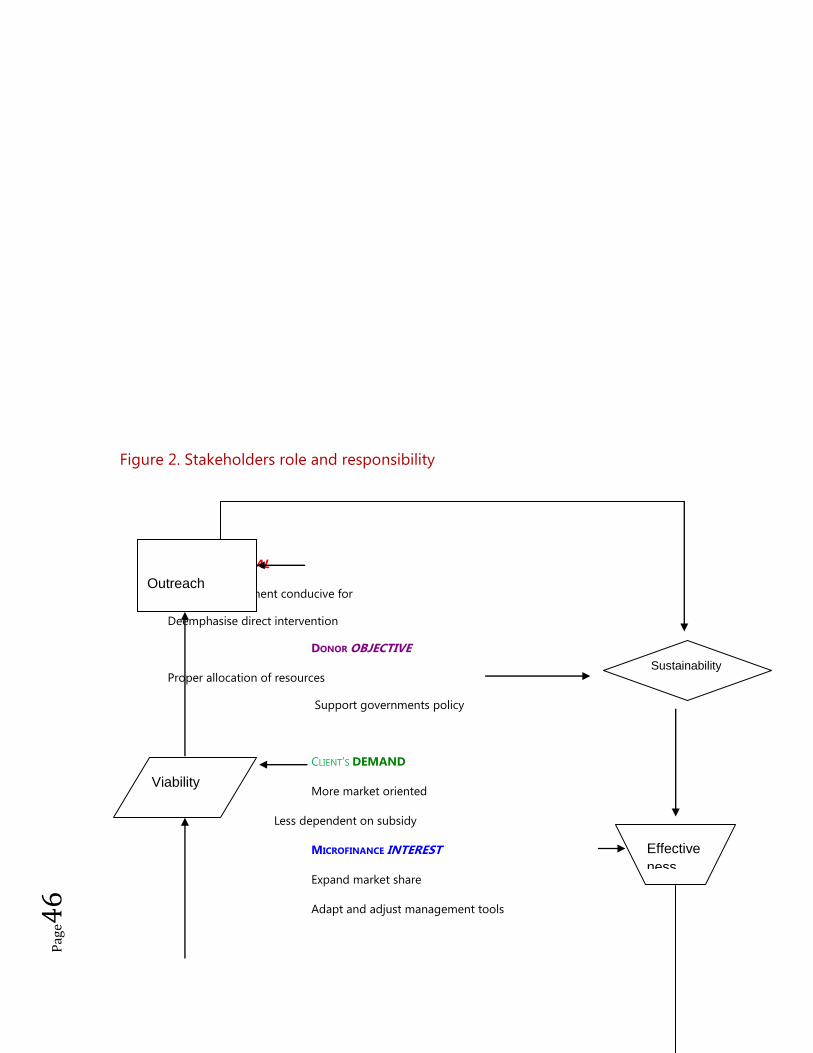

The Government has a Role to Play, but it has to be clearly defined 44

Figure 2. Stakeholders role and responsibility 46

Role of Local Authorities 50

Role of Banks 50

Role of Regional Economic Communities 51

Local ownership and participation 52

Key Principles 52

V. Conclusion and Summary 56

5.1 Creating a conducive environment 56

5.2 Improving Coordination and Cooperation 61

5.3 Introducing industry standards and Ratings 62

5.4 Increasing the supply of capital 64

5.5 Lowering cost and Improving Efficiency 65

5.6 Building and Enhancing Capacity 65

5.7 Integration and Regional Cooperation 66

5.8 Establishment of a Regional Capacity Building Facility 72

5.9 Establishment of Regional Wholesale Fund(s)/Venture Capital 68

5.10 Establishment of a Regional/Sub-Regional Rating Fund 69

References & End Notes 70

P

age5

I. Introduction

Although it took roots in Africa almost at the same time as in Asia and Latin

America (in the mid 1970s), microfinance in its modern form evolved more

steadily in the region only after 1993. Now, just some 15 years later, it has

become such an important and critical component of the region’s formal financial

system that the development of all-inclusive financial system is a palpable dream

for Africa.

From South Africa (the region’s most developed economy), to Sierra Leone and

Liberia in West Africa (two of the least developed and war-ravaged economies

just recovering from years of destruction), microfinance is today a system that

provides structures for people previously excluded to save and take loans, in

addition to smoothing consumption and managing various shocks. On this,

Sodokin notes:

“… MFIs provide the only means of tapping resources on both sides of the financial

divide—they are a new class of customer to banks. Between 1999 and end-2005 in the

UEMOA zone, public deposits with MFIs increased seven-fold within the period of 10 years;

rising from CFAF 38 billion to CFAF 250 billion. In the same period, MFIs’ deposits with

banks increased in turn by almost four-fold, rising from CFAF 13 billion in 1996 to CFAF 59

billion in 2003… As long as MFIs lend from an existing capital base; and not just a portion

of deposits held, reserves held by MFIs with banks are unencumbered and can be

leveraged, thus creating new money income…”1

A recently completed study (African Union, 2008) show that Africa’s microfinance

system presently involve more than 8,532 active microfinance institutions of

diverse institutional forms, and presently serves more than 26.5 million people as

of year-end 2006 (Table 1). The size of the industry, as measured by assets, is

roughly $10 billion and employing as many as 100,000 people, which is certainly

far more people than the number engaged by the regions 670 commercial banks.

P

age6

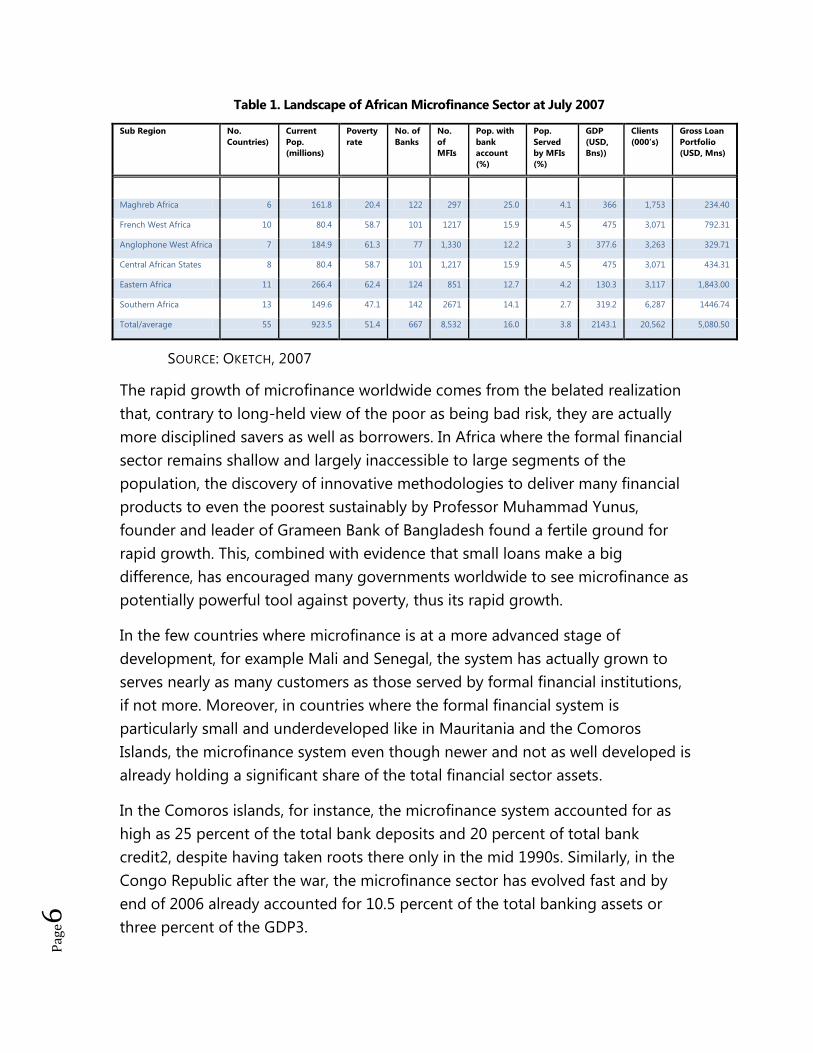

Table 1. Landscape of African Microfinance Sector at July 2007

Sub Region No.

Countries)

Current

Pop.

(millions)

Poverty

rate

No. of

Banks

No.

of

MFIs

Pop. with

bank

account

(%)

Pop.

Served

by MFIs

(%)

GDP

(USD,

Bns))

Clients

(000’s)

Gross Loan

Portfolio

(USD, Mns)

Maghreb Africa 6 161.8 20.4 122 297 25.0 4.1 366 1,753 234.40

French West Africa 10 80.4 58.7 101 1217 15.9 4.5 475 3,071 792.31

Anglophone West Africa 7 184.9 61.3 77 1,330 12.2 3 377.6 3,263 329.71

Central African States 8 80.4 58.7 101 1,217 15.9 4.5 475 3,071 434.31

Eastern Africa 11 266.4 62.4 124 851 12.7 4.2 130.3 3,117 1,843.00

Southern Africa 13 149.6 47.1 142 2671 14.1 2.7 319.2 6,287 1446.74

Total/average 55 923.5 51.4 667 8,532 16.0 3.8 2143.1 20,562 5,080.50

SOURCE: OKETCH, 2007

The rapid growth of microfinance worldwide comes from the belated realization

that, contrary to long-held view of the poor as being bad risk, they are actually

more disciplined savers as well as borrowers. In Africa where the formal financial

sector remains shallow and largely inaccessible to large segments of the

population, the discovery of innovative methodologies to deliver many financial

products to even the poorest sustainably by Professor Muhammad Yunus,

founder and leader of Grameen Bank of Bangladesh found a fertile ground for

rapid growth. This, combined with evidence that small loans make a big

difference, has encouraged many governments worldwide to see microfinance as

potentially powerful tool against poverty, thus its rapid growth.

In the few countries where microfinance is at a more advanced stage of

development, for example Mali and Senegal, the system has actually grown to

serves nearly as many customers as those served by formal financial institutions,

if not more. Moreover, in countries where the formal financial system is

particularly small and underdeveloped like in Mauritania and the Comoros

Islands, the microfinance system even though newer and not as well developed is

already holding a significant share of the total financial sector assets.

In the Comoros islands, for instance, the microfinance system accounted for as

high as 25 percent of the total bank deposits and 20 percent of total bank

credit2, despite having taken roots there only in the mid 1990s. Similarly, in the

Congo Republic after the war, the microfinance sector has evolved fast and by

end of 2006 already accounted for 10.5 percent of the total banking assets or

three percent of the GDP3.

P

age7

The importance of microfinance for Africa

For Africa, where thousands of capital-starved informal enterprises and

smallholder agriculture provide the bulk of total employment4, in addition to

contributing about a fifth to a third of the Gross Domestic Product (GDP), an

improved access to finance through the expansion and further development of

the microfinance system could make a big difference in poverty reduction.

Because of financial exclusion for the greater part of the last 50 years, small firms

in Africa and rural smallholder farmers have been unable to take advantage of

their ingenuity, labor, or knowledge to exploit productive opportunities. Hence,

the evolution and successful development of microfinance in Africa is important

as it holds much promise for accelerated and broad-based economic growth.

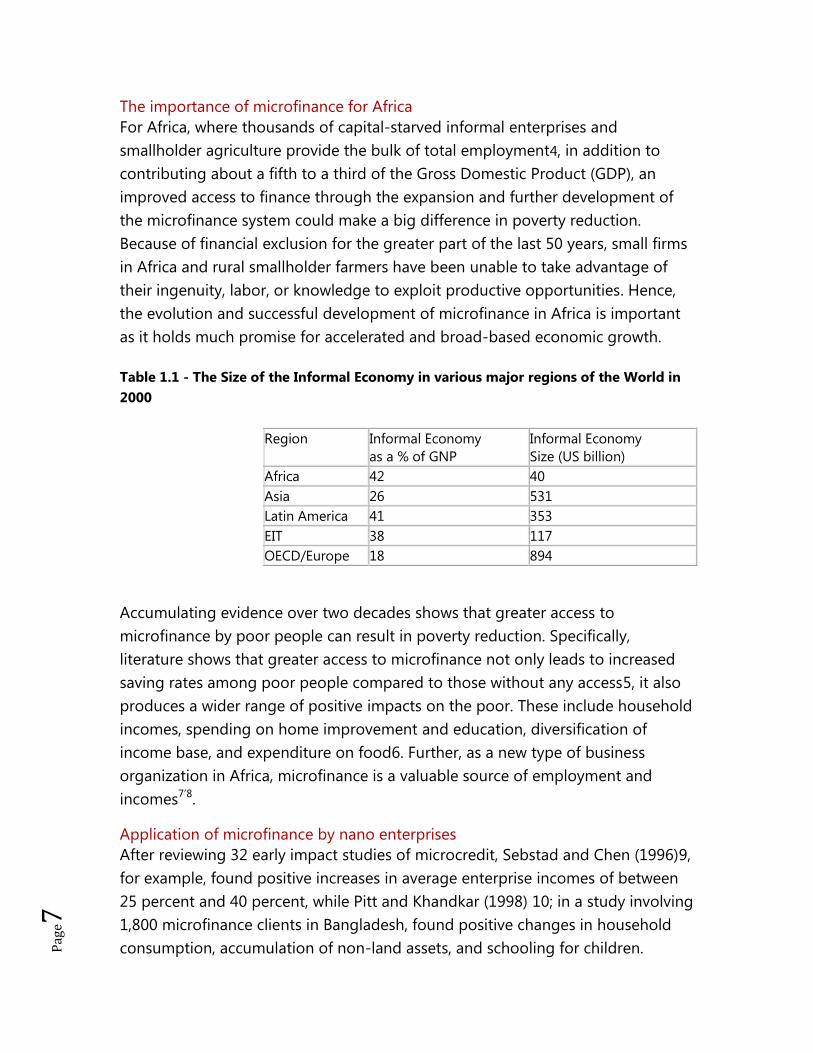

Table 1.1 - The Size of the Informal Economy in various major regions of the World in

2000

Region Informal Economy

as a % of GNP

Informal Economy

Size (US billion)

Africa 42 40

Asia 26 531

Latin America 41 353

EIT 38 117

OECD/Europe 18 894

Accumulating evidence over two decades shows that greater access to

microfinance by poor people can result in poverty reduction. Specifically,

literature shows that greater access to microfinance not only leads to increased

saving rates among poor people compared to those without any access5, it also

produces a wider range of positive impacts on the poor. These include household

incomes, spending on home improvement and education, diversification of

income base, and expenditure on food6. Further, as a new type of business

organization in Africa, microfinance is a valuable source of employment and

incomes7’8.

Application of microfinance by nano enterprises

After reviewing 32 early impact studies of microcredit, Sebstad and Chen (1996)9,

for example, found positive increases in average enterprise incomes of between

25 percent and 40 percent, while Pitt and Khandkar (1998) 10; in a study involving

1,800 microfinance clients in Bangladesh, found positive changes in household

consumption, accumulation of non-land assets, and schooling for children.

P

age8

Remarkably, the latter study showed that 5 percent of the clients studied had

crossed the poverty line each year due to impact of microcredit on their incomes

and household consumption. In disaster situations and post conflict areas, too,

studies of impact show that access to microcredit by affected families enabled

them to rebuild their economic activities and livelihoods if designed

appropriately and conveniently delivered11.

Moreover, in addition to being able to expand and diversify their economic base

or meeting needs for which resources were previously scarce, the clients can

become empowered economic agents with improved and more reliable access to

finance, as explained by Prahalad12:

“… Poverty exists not just, because those affected by it lack the means to improve their

wellbeing. Also, because they have limited income, the poor often buy in small quantities;

hence end up paying more for the same goods and services. Because they do not have their

own means of transport, the poor often do most of their shopping locally in smaller stores

that charge more. If they are able to secure a loan at all, it is often at a much higher price

because of limited supply...”

Yet, if they get access to financial services that are more reliable, the poor would

overcome all of their disadvantages, as Prahalad further aptly notes:

“…When the poor are treated as consumers, they can reap the benefits of respect, choice

and self-esteem, besides an opportunity for them to climb out of the poverty trap”.

The more scientific impact studies completed just in the last five years show

exactly how the poor take advantage of financial services provided by

microfinance institutions to protect themselves from economic and social shocks,

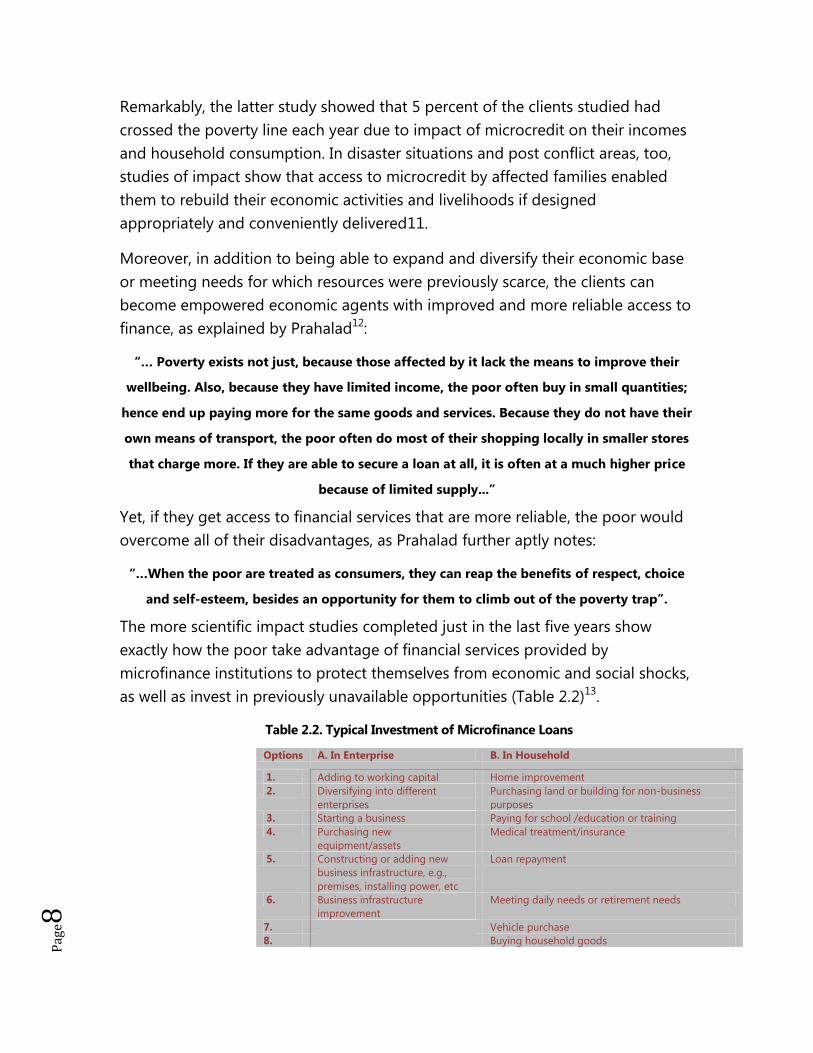

as well as invest in previously unavailable opportunities (Table 2.2)13.

Table 2.2. Typical Investment of Microfinance Loans

Options A. In Enterprise B. In Household

1. Adding to working capital Home improvement

2. Diversifying into different

enterprises

Purchasing land or building for non-business

purposes

3. Starting a business Paying for school /education or training

4. Purchasing new

equipment/assets

Medical treatment/insurance

5. Constructing or adding new

business infrastructure, e.g.,

premises, installing power, etc

Loan repayment

6. Business infrastructure

improvement

Meeting daily needs or retirement needs

7. Vehicle purchase

8. Buying household goods

P

age9

9. Ceremony or social expenditure

10. Holiday/leisure expenditure

11. Jewelry purchase

SOURCE: JOHNSTON AND MURDOCH, 2007

As shown in the table, the population at the lower end of the income spectrum

indeed does apply finance to expand or diversify their economic activities or

finance their immediate household or individual consumption needs in case

resources are either inadequate or totally lacking. In this regard, the people at

lower end of the income spectrum apply access to finance remarkably almost

exactly in the same way as the aristocrats (Table 2.3)14. Therefore, given proper

motivation and the means to do so, the people living on less than US$ 1 a day

can easily take advantage of microfinance to improve their lives.

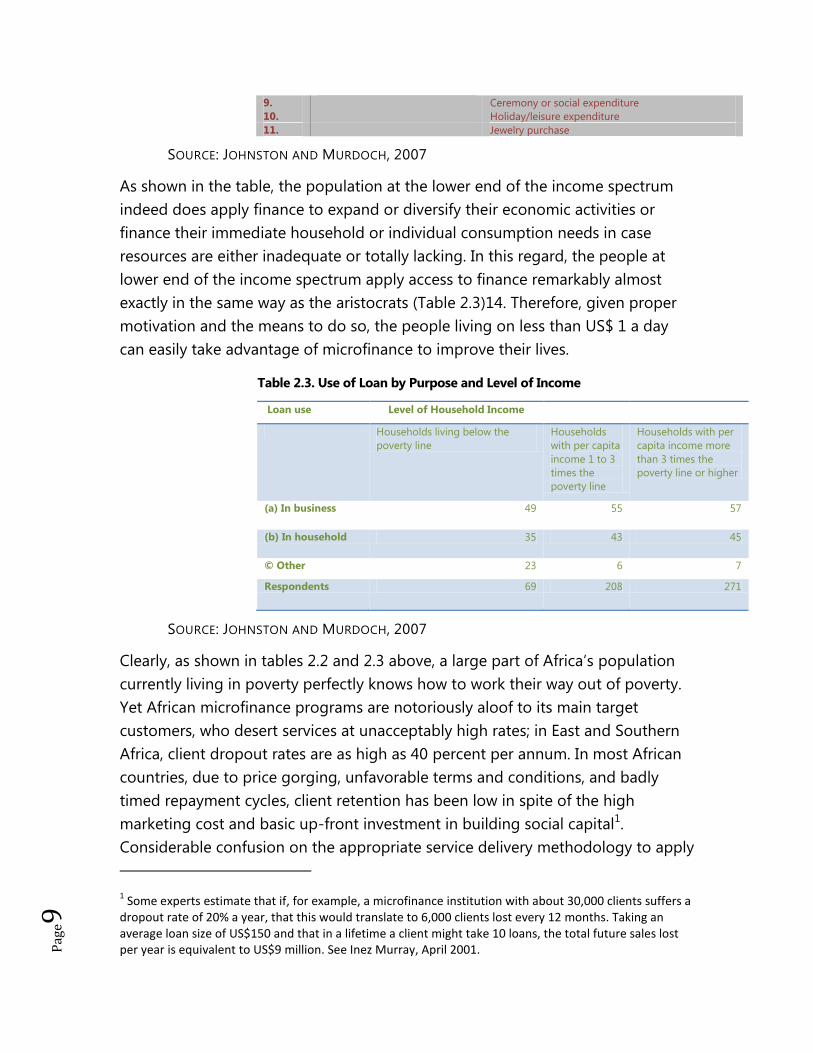

Table 2.3. Use of Loan by Purpose and Level of Income

Loan use Level of Household Income

Households living below the

poverty line

Households

with per capita

income 1 to 3

times the

poverty line

Households with per

capita income more

than 3 times the

poverty line or higher

(a) In business 49 55 57

(b) In household 35 43 45

© Other 23 6 7

Respondents 69 208 271

SOURCE: JOHNSTON AND MURDOCH, 2007

Clearly, as shown in tables 2.2 and 2.3 above, a large part of Africa’s population

currently living in poverty perfectly knows how to work their way out of poverty.

Yet African microfinance programs are notoriously aloof to its main target

customers, who desert services at unacceptably high rates; in East and Southern

Africa, client dropout rates are as high as 40 percent per annum. In most African

countries, due to price gorging, unfavorable terms and conditions, and badly

timed repayment cycles, client retention has been low in spite of the high

marketing cost and basic up-front investment in building social capital1.

Considerable confusion on the appropriate service delivery methodology to apply

1 Some experts estimate that if, for example, a microfinance institution with about 30,000 clients suffers a

dropout rate of 20% a year, that this would translate to 6,000 clients lost every 12 months. Taking an average loan size of US$150 and that in a lifetime a client might take 10 loans, the total future sales lost per year is equivalent to US$9 million. See Inez Murray, April 2001.

P

age1

0

with different segments of the poor, for example the microfinance institutions

overreliance on solidarity group methodology, which requires potential clients to

having a regular (usually household business) source of income, has often

discouraged some potential clients from taking loans and savings facilities.

Occasionally, lack of proper planning, late disbursement of loans or inadequate

assessment of needs has not infrequently encouraged situations where the

proceeds do not necessarily go for business activities.

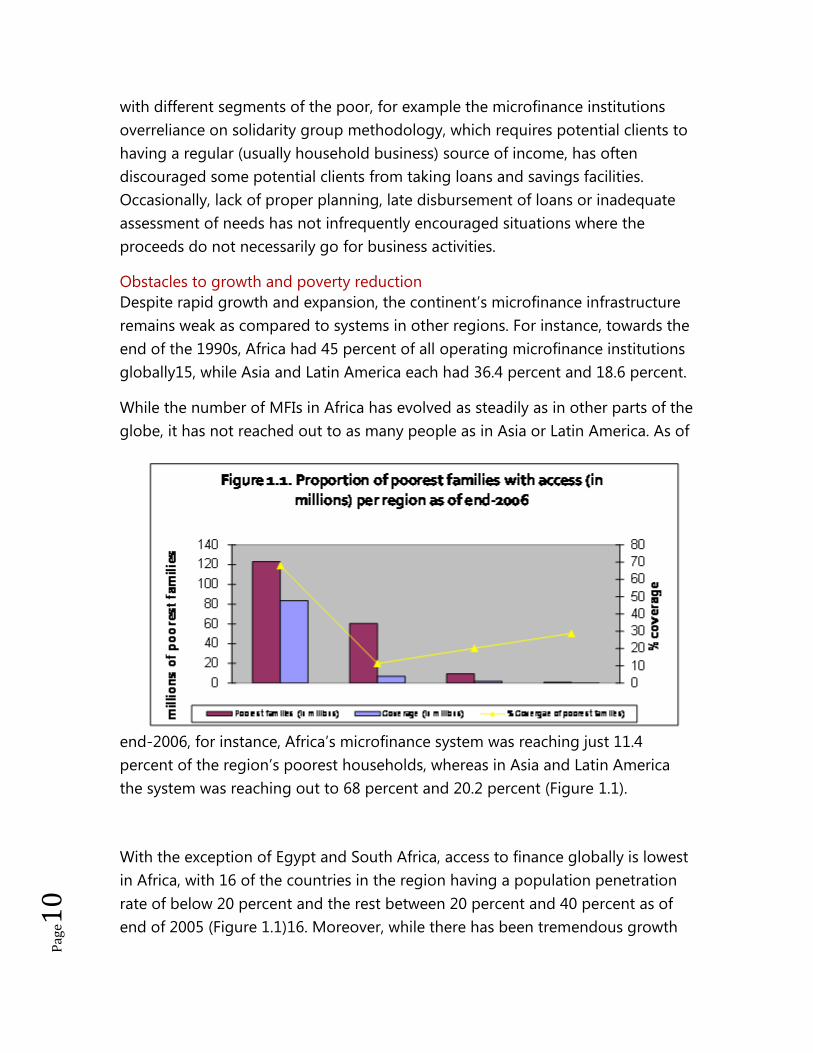

Obstacles to growth and poverty reduction

Despite rapid growth and expansion, the continent’s microfinance infrastructure

remains weak as compared to systems in other regions. For instance, towards the

end of the 1990s, Africa had 45 percent of all operating microfinance institutions

globally15, while Asia and Latin America each had 36.4 percent and 18.6 percent.

While the number of MFIs in Africa has evolved as steadily as in other parts of the

globe, it has not reached out to as many people as in Asia or Latin America. As of

end-2006, for instance, Africa’s microfinance system was reaching just 11.4

percent of the region’s poorest households, whereas in Asia and Latin America

the system was reaching out to 68 percent and 20.2 percent (Figure 1.1).

With the exception of Egypt and South Africa, access to finance globally is lowest

in Africa, with 16 of the countries in the region having a population penetration

rate of below 20 percent and the rest between 20 percent and 40 percent as of

end of 2005 (Figure 1.1)16. Moreover, while there has been tremendous growth

P

age1

1

in outreach, the recent ratings indicate that on average the region is moving

away from serving the poor. The estimated average loan size relative to income

per person has increased up to 77 percent, from 71 percent in 2002 and even

further up to 89% by 2003. Average loan size per borrower is also on the

increase—now standing slightly above $346.

A few of the transformed or inspiring to transform are clearly drifting from clients

at or below the poverty line. One institution in Senegal now has the highest

average loan sizes in the region; now standing at $ 1,321 per borrower. In

contrast, the MFI serving the poorest clients, with a depth of reach at 20% and

loan size of 50%, exists in Uganda. Generally, East Africa has some of the deepest

reaching MFIs in the region.

In spite of its potential for poverty reduction and enterprise development, and

widespread acceptance and recognition, access to finance in general and

microfinance in particular remains severely limited in Africa. Altogether, just

about 4 percent of the estimated 560 million low-income populations in the

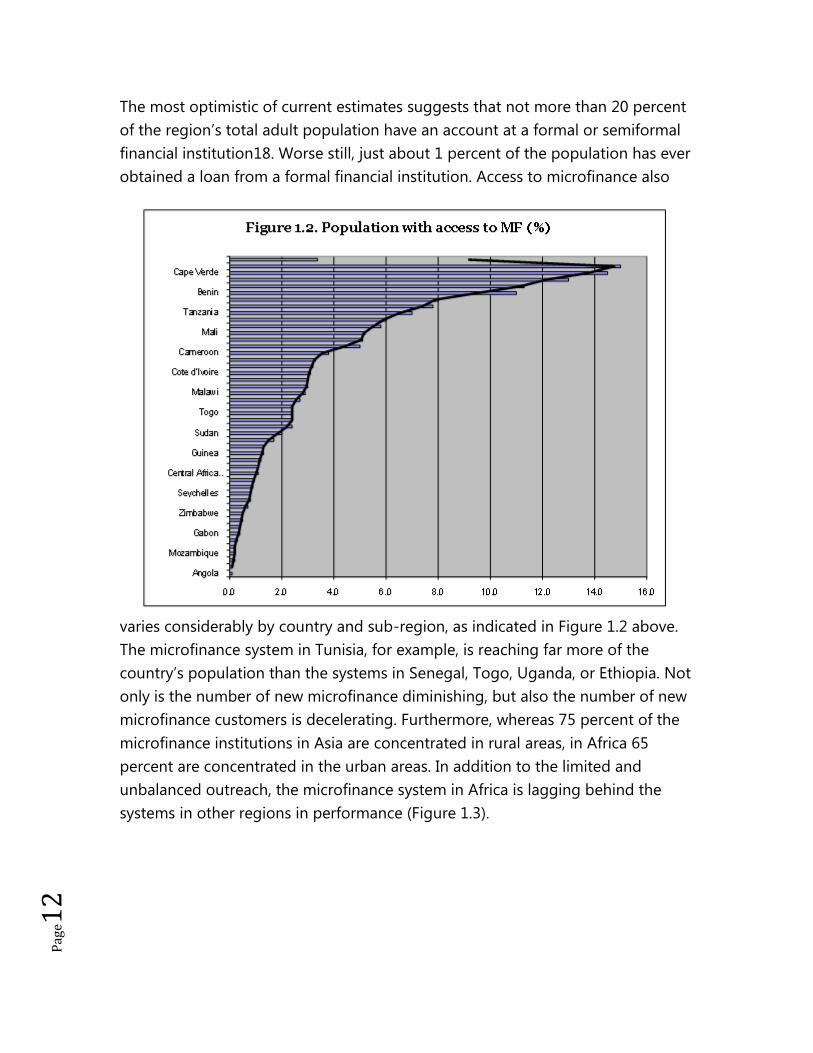

region have any access to finance (Figure 1.2)17.

P

age1

2

The most optimistic of current estimates suggests that not more than 20 percent

of the region’s total adult population have an account at a formal or semiformal

financial institution18. Worse still, just about 1 percent of the population has ever

obtained a loan from a formal financial institution. Access to microfinance also

varies considerably by country and sub-region, as indicated in Figure 1.2 above.

The microfinance system in Tunisia, for example, is reaching far more of the

country’s population than the systems in Senegal, Togo, Uganda, or Ethiopia. Not

only is the number of new microfinance diminishing, but also the number of new

microfinance customers is decelerating. Furthermore, whereas 75 percent of the

microfinance institutions in Asia are concentrated in rural areas, in Africa 65

percent are concentrated in the urban areas. In addition to the limited and

unbalanced outreach, the microfinance system in Africa is lagging behind the

systems in other regions in performance (Figure 1.3).

P

age1

3

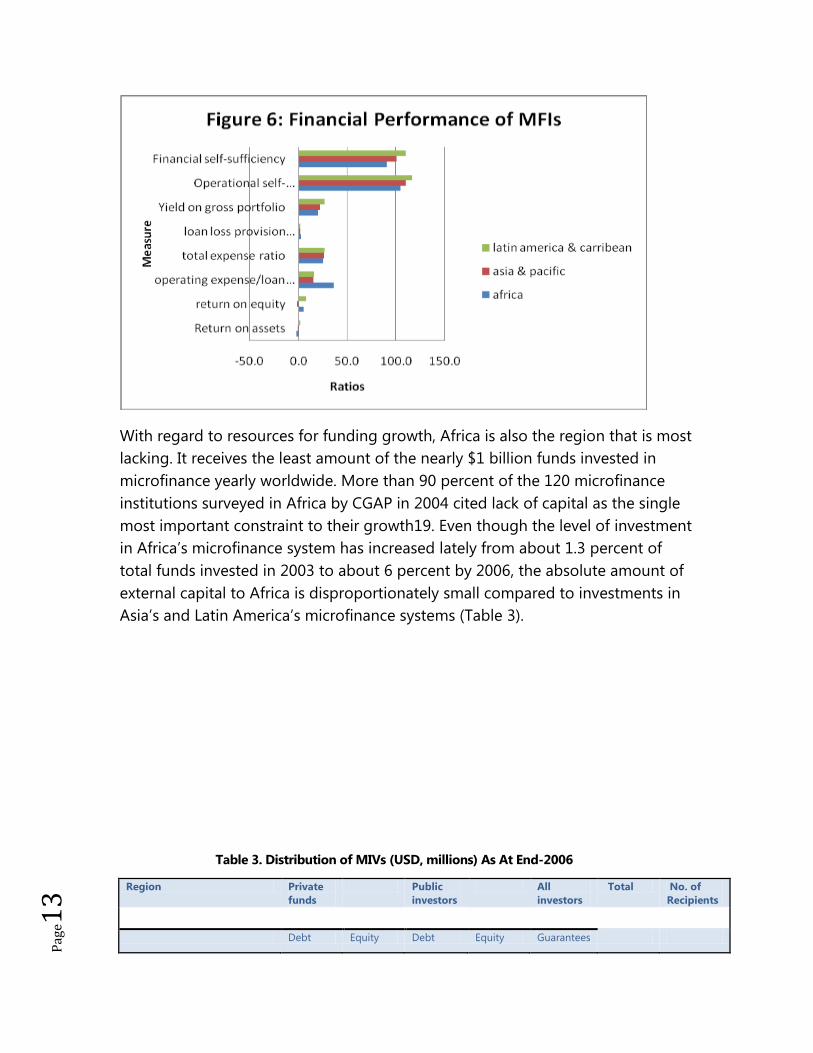

With regard to resources for funding growth, Africa is also the region that is most

lacking. It receives the least amount of the nearly $1 billion funds invested in

microfinance yearly worldwide. More than 90 percent of the 120 microfinance

institutions surveyed in Africa by CGAP in 2004 cited lack of capital as the single

most important constraint to their growth19. Even though the level of investment

in Africa’s microfinance system has increased lately from about 1.3 percent of

total funds invested in 2003 to about 6 percent by 2006, the absolute amount of

external capital to Africa is disproportionately small compared to investments in

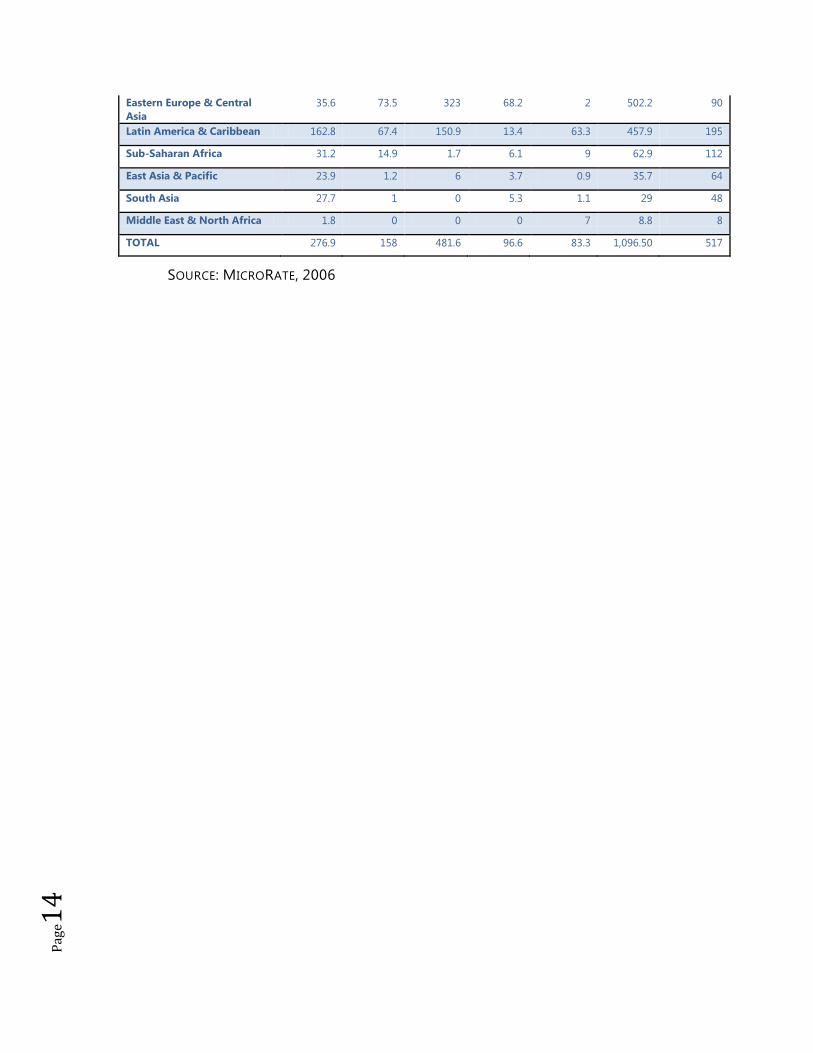

Asia’s and Latin America’s microfinance systems (Table 3).

Table 3. Distribution of MIVs (USD, millions) As At End-2006

Region Private

funds

Public

investors

All

investors

Total No. of

Recipients

Debt Equity Debt Equity Guarantees

P

age1

4

Eastern Europe & Central

Asia

35.6 73.5 323 68.2 2 502.2 90

Latin America & Caribbean 162.8 67.4 150.9 13.4 63.3 457.9 195

Sub-Saharan Africa 31.2 14.9 1.7 6.1 9 62.9 112

East Asia & Pacific 23.9 1.2 6 3.7 0.9 35.7 64

South Asia 27.7 1 0 5.3 1.1 29 48

Middle East & North Africa 1.8 0 0 0 7 8.8 8

TOTAL 276.9 158 481.6 96.6 83.3 1,096.50 517

SOURCE: MICRORATE, 2006

P

age1

5

II. The African Microfinance system

Roots and evolution of the system

The term microfinance refers to the unique technology that enables the delivery

of sustainable financial services to the world’s low-income populations

conveniently and affordably20. Alternatively, the term refers collectively to the

group of self-sustaining financial services designed and targeted at the socially

and economically disadvantaged populations traditionally excluded by

conventional financial institutions.

What sets microfinance apart from conventional financial systems is its high

degree of flexibility21 and unorthodox approach to credit risk analysis and

management, while still serving a customer class that typically lacks assets22 or

records, and is neither well educated nor informed about financial services

generally. As observed by the 2007 Nobel Peace Prize Laureate Prof. Muhammad

Yunus, the Bangladeshi economist and founder and managing director of

Grameen Bank:

“… Microfinance is a revolution in banking that has succeeded in turning the field upside

down. It has opened doors that for years denied financial services to the poor; when banks

lent to the rich, the microfinance institutions lent to the poor. When banks lent to men,

they lent to women. When banks made large loans, they made small ones. When banks

required collateral, their loans were collateral free. When banks required endless

paperwork, their loans were illiterate-friendly. When clients had to come to the bank, the

microlenders instead went to the clients…”23

The microfinance revolution essentially consists of a set of institutional

innovations aimed at resolving information constraints without relying on wealth

as signal of creditworthiness and ability to pay, e.g. the substitution of collateral

lending with group lending with joint liability or village banking. In addition,

where individual lending methodology is applicable, risk assessment dwells on

the analysis of client character and projected cash flow from targeted investment

project instead of the value of collateral or credit history as important proxy for

ability and willingness to pay. Furthermore, the fact that loan disbursement in

solidarity group lending is staggered among group members, and that

incrementally bigger loan sizes are absolutely dependent on past good loan

repayment, introduces dynamic incentives into the basic model. Other dynamic

P

age1

6

incentives, for instance with individual loans, includes graduated interest rate

rebates or more flexible terms that are conditional to timely weekly or monthly

installments throughout a loan repayment cycle. Yet still other MFIs, depending

on clients’ record, exempt good borrowers from certain standard requirements

when they take future loans.

It was in the mid 1980s, following the World Bank-sponsored Structural

Adjustments (SAPs) for African economies, when the drive for self-employment

through the provision of microcredit and technical support led to the discovery

and later the development of microfinance in the region. This early connection

between micro/small-enterprise development, poverty reduction, and access to

finance remains surprisingly strong to the present time, when the new focus on

how to apply an improved access to finance to enhance the competitiveness of

informal enterprises in a globalizing system of production and commerce.

The period between 1993 and 1997, following the launch of the first-ever

worldwide campaign to scale up outreach in Washington DC, USA, was the critical

point in time. From then on, the idea of providing microfinance on sustainable

terms became a goal in its own right. The period also witnessed the most intense

debate on how best to support enterprise development.

The year 1997 became a major turning point for microfinance when those

advocating for a financial system approach to microfinance development seemed

vindicated by the overwhelming success achieved by specialized, minimalist

microfinance institutions, notably Bangladeshi’s Grameen Bank, as compared to

that of organizations that continued providing other services alongside

microfinance. By 2000, the idea of a financial systems approach to microfinance

development had changed completely to a philosophy and movement that

advocated for commercialization and transformation of microfinance as the only

sure way of meeting the huge unsatisfied demand for services among low-

income populations24. Industry leaders now believe that any further

development of the microfinance system depends primarily on the provision of

market-driven financial products and massive participation of the private sector.

As of March 2006, some 43 microfinance intermediaries, seven of them in Africa,

had transformed and commercialized their operations25. Yet, with the notable

exception of Equity Bank in Kenya26, none of these intermediaries exhibits the

scale, growth, or efficiency promised in the commercialization and transformation

model27. Worse still, not only do these pioneers achieve just modest

P

age1

7

improvement in scale, growth, or efficiency, the results are at a prohibitively high

cost28. Furthermore, there is accumulating evidence of mission drift in these

institutions, a fact that is also slowly dampening expectations about the financial

systems approach29.

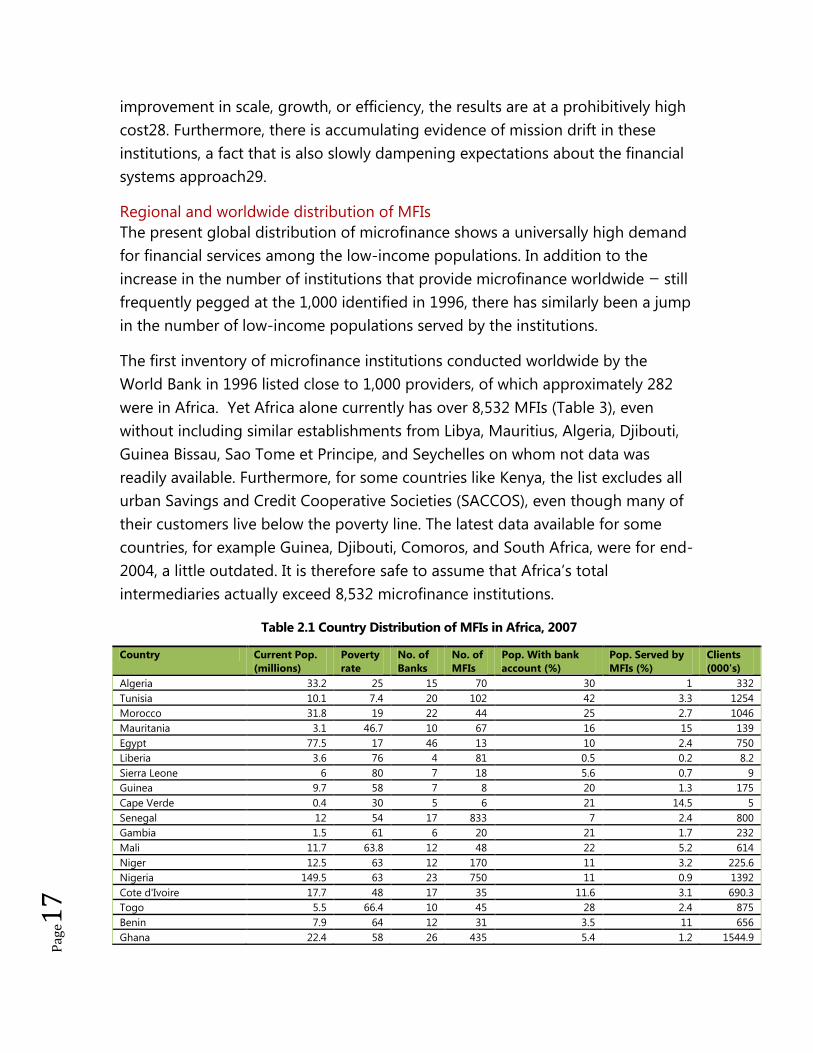

Regional and worldwide distribution of MFIs

The present global distribution of microfinance shows a universally high demand

for financial services among the low-income populations. In addition to the

increase in the number of institutions that provide microfinance worldwide — still

frequently pegged at the 1,000 identified in 1996, there has similarly been a jump

in the number of low-income populations served by the institutions.

The first inventory of microfinance institutions conducted worldwide by the

World Bank in 1996 listed close to 1,000 providers, of which approximately 282

were in Africa. Yet Africa alone currently has over 8,532 MFIs (Table 3), even

without including similar establishments from Libya, Mauritius, Algeria, Djibouti,

Guinea Bissau, Sao Tome et Principe, and Seychelles on whom not data was

readily available. Furthermore, for some countries like Kenya, the list excludes all

urban Savings and Credit Cooperative Societies (SACCOS), even though many of

their customers live below the poverty line. The latest data available for some

countries, for example Guinea, Djibouti, Comoros, and South Africa, were for end-

2004, a little outdated. It is therefore safe to assume that Africa’s total

intermediaries actually exceed 8,532 microfinance institutions.

Table 2.1 Country Distribution of MFIs in Africa, 2007

Country Current Pop.

(millions)

Poverty

rate

No. of

Banks

No. of

MFIs

Pop. With bank

account (%)

Pop. Served by

MFIs (%)

Clients

(000's)

Algeria 33.2 25 15 70 30 1 332

Tunisia 10.1 7.4 20 102 42 3.3 1254

Morocco 31.8 19 22 44 25 2.7 1046

Mauritania 3.1 46.7 10 67 16 15 139

Egypt 77.5 17 46 13 10 2.4 750

Liberia 3.6 76 4 81 0.5 0.2 8.2

Sierra Leone 6 80 7 18 5.6 0.7 9

Guinea 9.7 58 7 8 20 1.3 175

Cape Verde 0.4 30 5 6 21 14.5 5

Senegal 12 54 17 833 7 2.4 800

Gambia 1.5 61 6 20 21 1.7 232

Mali 11.7 63.8 12 48 22 5.2 614

Niger 12.5 63 12 170 11 3.2 225.6

Nigeria 149.5 63 23 750 11 0.9 1392

Cote d'Ivoire 17.7 48 17 35 11.6 3.1 690.3

Togo 5.5 66.4 10 45 28 2.4 875

Benin 7.9 64 12 31 3.5 11 656

Ghana 22.4 58 26 435 5.4 1.2 1544.9

P

age1

8

Burkina Faso 13.9 59 11 424 5.1 5.8 1000

Gabon 1.4 6 13 16 0.4 4.78

Central Africa Republic 3.5 81.5 3 36 1.5 1.1 40

Congo, Brazzaville 4.4 52 4 86 4.1 5.1 12

Chad 10.1 81.7 7 214 0.9 0.5 100

Congo, Democratic Rep. 62.7 92.4 3 70 2.7 0.3 54.5

Cameroon 19 48 11 714 5 3.8 476

Sudan 35.1 41.2 23 70 13 2 842.4

Burundi 8.4 81 7 22 34 2.4 200

Rwanda 8.6 59.4 5 230 12 13 375

Uganda 32 65 6 756 7 3 1300

Ethiopia 85.1 46 9 23 1.3 1700

Eritrea 4.9 53 2 9 0.4 25

Somalia 12 43 0 8 0.1 12

Kenya 38.5 56 41 365 10 7.8 2000

Tanzania 40.4 51.1 25 43 6.4 7 653

Comoros Island 0.7 60 3 2 20 5 57.9

Angola 17.3 70 12 9 5 0.1 11

Mozambique 19.7 54 12 50 0.3 0.2 130.8

Malawi 13 70 9 29 3 2.9 380

Zambia 11.5 72.9 17 95 4.5 0.2 50

Zimbabwe 13.2 52 11 257 17.8 0.5 13

Namibia 1.8 34.9 8 223 28.4 3 300

Lesotho 2.4 49 5 43 18 0.8 19.2

Botswana 1.8 31 7 47 24 6 10.8

Swaziland 1.1 69 5 150 35.3 11.3 121.3

South Africa 47.8 50 28 1,354 31.7 8 5514

Madagascar 18.6 50 10 411 2 1.1 307

Seychelles 0.1 6 3 1.8 0.8 80

Africa wide 945 51.5 667 8,532 12 3.4 26,532

SOURCE: OKETCH, 2007

Altogether, these institutions already serve more than 26.5 million people, or

roughly 3.4 percent of Africa’s total population. In terms of numbers, there are

presently 15.2 times more microfinance institutions in Africa than commercial

banks, although banks serve more people, i.e., 12 percent.

The largest number of MFIs is in South Africa, Nigeria, Uganda, Kenya, Cameroon,

Ghana, Senegal, and Burkina Faso. Yet, depending on the total population, the

countries with greater outreach are not necessarily the countries with the largest

number of MFIs. Although South Africa has the most number of MFIs and

microfinance clients; at approximately 6 million people, its coverage is just eight

percent of the population. Similarly, Nigeria, which has about 1.3 million

microfinance clients, has population coverage below 1 percent.

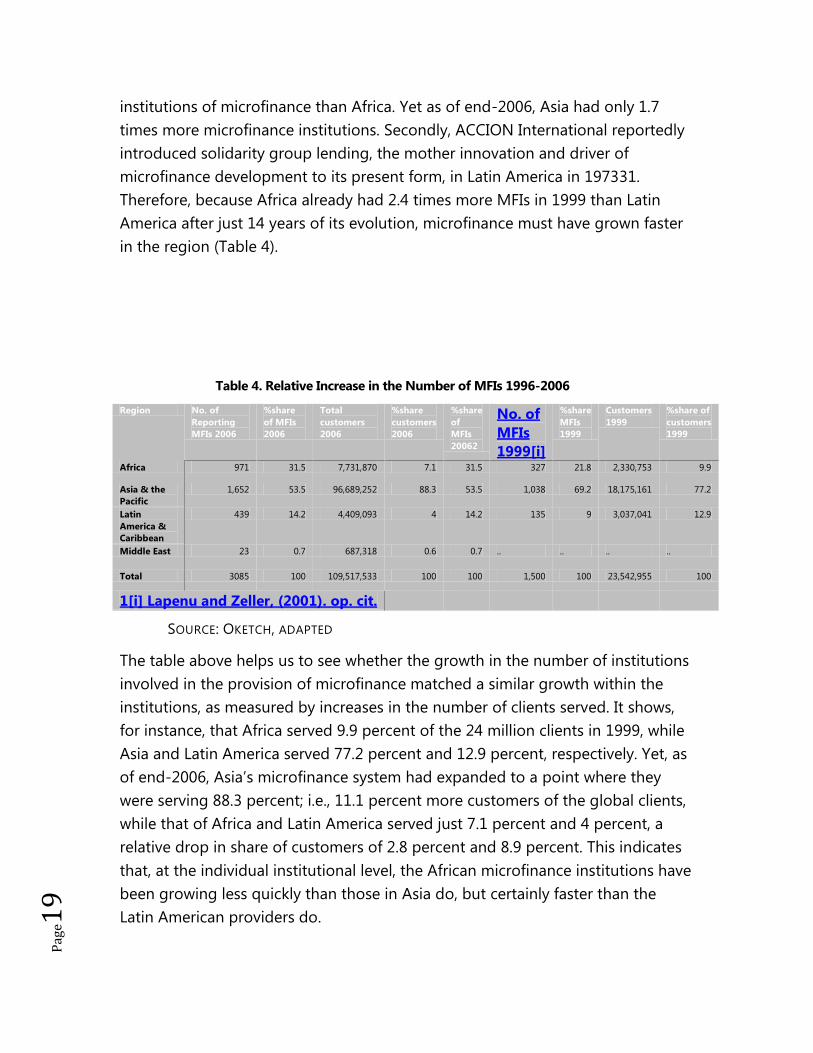

Holding other things constant, for example, randomness and fair representation

of the samples used, microfinance (as measured by the change in number of

institutions involved in its provision) has been more dynamic in Africa than in the

other two regions. According to the 1999 IFPRI Survey30, Asia had 3.7 times more

P

age1

9

institutions of microfinance than Africa. Yet as of end-2006, Asia had only 1.7

times more microfinance institutions. Secondly, ACCION International reportedly

introduced solidarity group lending, the mother innovation and driver of

microfinance development to its present form, in Latin America in 197331.

Therefore, because Africa already had 2.4 times more MFIs in 1999 than Latin

America after just 14 years of its evolution, microfinance must have grown faster

in the region (Table 4).

Table 4. Relative Increase in the Number of MFIs 1996-2006

Region No. of

Reporting

MFIs 2006

%share

of MFIs

2006

Total

customers

2006

%share

customers

2006

%share

of

MFIs

20062

No. of

MFIs

1999[i]

%share

MFIs

1999

Customers

1999

%share of

customers

1999

Africa 971 31.5 7,731,870 7.1 31.5 327 21.8 2,330,753 9.9

Asia & the

Pacific

1,652 53.5 96,689,252 88.3 53.5 1,038 69.2 18,175,161 77.2

Latin

America &

Caribbean

439 14.2 4,409,093 4 14.2 135 9 3,037,041 12.9

Middle East 23 0.7 687,318 0.6 0.7 .. .. .. ..

Total 3085 100 109,517,533 100 100 1,500 100 23,542,955 100

1[i] Lapenu and Zeller, (2001). op. cit.

SOURCE: OKETCH, ADAPTED

The table above helps us to see whether the growth in the number of institutions

involved in the provision of microfinance matched a similar growth within the

institutions, as measured by increases in the number of clients served. It shows,

for instance, that Africa served 9.9 percent of the 24 million clients in 1999, while

Asia and Latin America served 77.2 percent and 12.9 percent, respectively. Yet, as

of end-2006, Asia’s microfinance system had expanded to a point where they

were serving 88.3 percent; i.e., 11.1 percent more customers of the global clients,

while that of Africa and Latin America served just 7.1 percent and 4 percent, a

relative drop in share of customers of 2.8 percent and 8.9 percent. This indicates

that, at the individual institutional level, the African microfinance institutions have

been growing less quickly than those in Asia do, but certainly faster than the

Latin American providers do.

P

age2

0

It is instructive that, whereas Asia’s microfinance system served 12.5 times more

clients in 1999 than Africa’s as of end-2006, the gap in outreach between the two

regions had narrowed to a difference of just 7.8 times more clients. Strikingly,

Latin America’s microfinance system, which is reportedly older and presently the

most developed as a market, has been less dynamic than Africa’s.

The global microfinance system has expanded almost five-hold (4.6 times more

institutions within 14 years) between 1999 when IFPRI conducted the second

global inventory and year-end 2006.

Institutional diversity and transformation

Not only has the microfinance system in Africa expanded in terms of institutions

globally, there is greater diversity in the types of institutions that have emerged

or entered the market. From the pool of institutions identified in 1996, the bank

picked a random sample of 205 institutions for more detailed analysis of their

legal profile, service delivery methodology, gender distribution of clients, financial

products offered, and the depth and breadth of outreach. All the institutions

studied came into existence in either 1992 or later and had expanded their

outreach to the point where they were each serving at least 1,000 people.

Of the many MFIs identified by the World Bank in 1995, just 870 qualified for

further analysis, based on these criteria, and thus provided the universal sampling

frame for further analysis of structure and profile of the microfinance system

then. According to this inventory, and assuming that the sample was

representative of the prevailing situation in East, Central, and Southern Africa,

non-governmental organizations (NGOs) were the dominant type of service

providers (Table 5), accounting for 81.3 percent of all the institutions surveyed.

Table 5. Sample Distribution of MFIs Analyzed by the World Bank in 1995

Region Number of MFIs %Share

East, Central, and Southern Africa 134 17.6

East Asia & Pacific 122 16.1

Western & Central Africa 124 16.3

Middle East & North Africa 30 3.9

Europe & Central Asia 24 3.2

South Asia 98 12.9

Latin America & Caribbean 362 47.6

P

age2

1

Total 760 100

SOURCE: ADAPTED BY AUTHOR

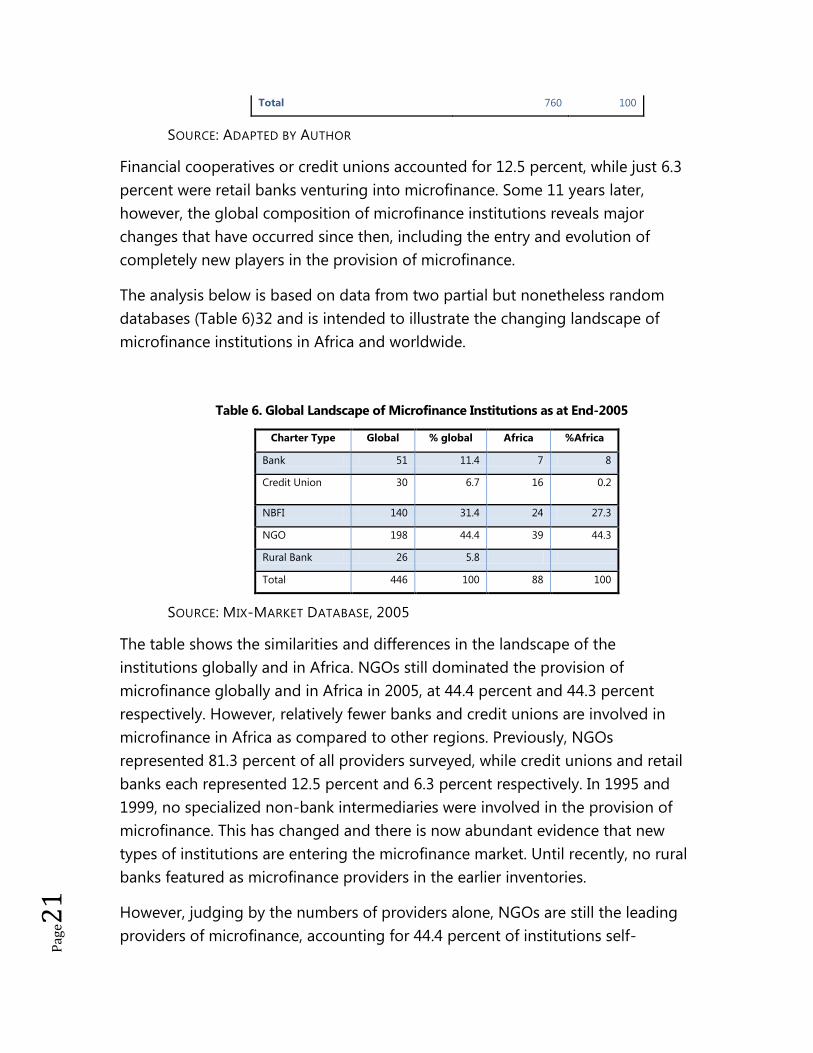

Financial cooperatives or credit unions accounted for 12.5 percent, while just 6.3

percent were retail banks venturing into microfinance. Some 11 years later,

however, the global composition of microfinance institutions reveals major

changes that have occurred since then, including the entry and evolution of

completely new players in the provision of microfinance.

The analysis below is based on data from two partial but nonetheless random

databases (Table 6)32 and is intended to illustrate the changing landscape of

microfinance institutions in Africa and worldwide.

Table 6. Global Landscape of Microfinance Institutions as at End-2005

Charter Type Global % global Africa %Africa

Bank 51 11.4 7 8

Credit Union 30 6.7 16 0.2

NBFI 140 31.4 24 27.3

NGO 198 44.4 39 44.3

Rural Bank 26 5.8

Total 446 100 88 100

SOURCE: MIX-MARKET DATABASE, 2005

The table shows the similarities and differences in the landscape of the

institutions globally and in Africa. NGOs still dominated the provision of

microfinance globally and in Africa in 2005, at 44.4 percent and 44.3 percent

respectively. However, relatively fewer banks and credit unions are involved in

microfinance in Africa as compared to other regions. Previously, NGOs

represented 81.3 percent of all providers surveyed, while credit unions and retail

banks each represented 12.5 percent and 6.3 percent respectively. In 1995 and

1999, no specialized non-bank intermediaries were involved in the provision of

microfinance. This has changed and there is now abundant evidence that new

types of institutions are entering the microfinance market. Until recently, no rural

banks featured as microfinance providers in the earlier inventories.

However, judging by the numbers of providers alone, NGOs are still the leading

providers of microfinance, accounting for 44.4 percent of institutions self-

P

age2

2

reporting to the Micro Banking Bulletin even though there seems to have been a

more rapid growth in the category of financial cooperatives and non-bank

financial intermediaries. With the exception of BancoSol in Bolivia, which was

established in 1992 as the first-ever NGO to transform into a regulated bank, 44

other NGOs have since followed suit, as of March 2006.

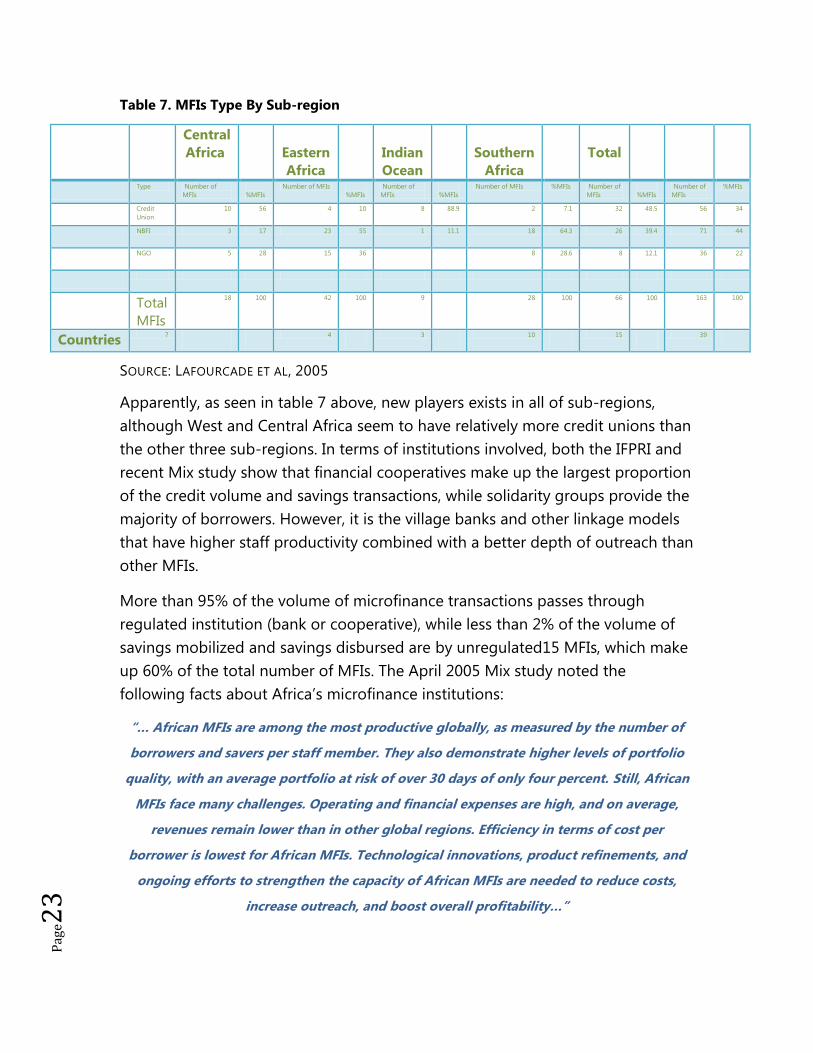

Regional Diversity

In addition to rural banks, savings and loan companies, and community banks —

mostly found in Ghana, Nigeria, Sierra Leone, and Tanzania, — Africa is fast

becoming home to varied types of regulated microfinance institutions.

Presently, close to a third of all institutions involved in microfinance in Africa are

non-bank financial intermediaries. In 2005, CGAP conducted a detailed analysis of

300 microfinance institutions in Africa33, which confirmed the changing

landscape (Table 7).

P

age2

3

Table 7. MFIs Type By Sub-region

Central

Africa

Eastern

Africa

Indian

Ocean

Southern

Africa

Total

Type Number of

MFIs

%MFIs

Number of MFIs

%MFIs

Number of

MFIs

%MFIs

Number of MFIs %MFIs Number of

MFIs

%MFIs

Number of

MFIs

%MFIs

Credit

Union

10 56 4 10 8 88.9 2 7.1 32 48.5 56 34

NBFI 3 17 23 55 1 11.1 18 64.3 26 39.4 71 44

NGO 5 28 15 36 8 28.6 8 12.1 36 22

Total

MFIs

18 100 42 100 9 28 100 66 100 163 100

Countries 7

4

3

10

15

39

SOURCE: LAFOURCADE ET AL, 2005

Apparently, as seen in table 7 above, new players exists in all of sub-regions,

although West and Central Africa seem to have relatively more credit unions than

the other three sub-regions. In terms of institutions involved, both the IFPRI and

recent Mix study show that financial cooperatives make up the largest proportion

of the credit volume and savings transactions, while solidarity groups provide the

majority of borrowers. However, it is the village banks and other linkage models

that have higher staff productivity combined with a better depth of outreach than

other MFIs.

More than 95% of the volume of microfinance transactions passes through

regulated institution (bank or cooperative), while less than 2% of the volume of

savings mobilized and savings disbursed are by unregulated15 MFIs, which make

up 60% of the total number of MFIs. The April 2005 Mix study noted the

following facts about Africa’s microfinance institutions:

“… African MFIs are among the most productive globally, as measured by the number of

borrowers and savers per staff member. They also demonstrate higher levels of portfolio

quality, with an average portfolio at risk of over 30 days of only four percent. Still, African

MFIs face many challenges. Operating and financial expenses are high, and on average,

revenues remain lower than in other global regions. Efficiency in terms of cost per

borrower is lowest for African MFIs. Technological innovations, product refinements, and

ongoing efforts to strengthen the capacity of African MFIs are needed to reduce costs,

increase outreach, and boost overall profitability…”

P

age2

4

Gender reach by type of MFI

Regional studies of outreach show significant gender differences among the

clients served by regulated and non-regulated microfinance institutions, and by

poverty profile. For instance, the unregulated MFIs reportedly serve the highest

percentage of women borrowers (at 69%) compared to the regulated (63%), with

the cooperatives serving the least percentage of women at just 50% of total

borrowers. Secondly, using the average outstanding savings and loans as proxy

for clients’ socio-economic profile, the Mix study shows that the unregulated

MFIs are reaching relatively poorer clients than the regulated ones.

Finally, Sergio et al (1998) analyzed the depth of outreach for five MFIs in Bolivia

and the findings from their study suggest that both the design of financial

products and service delivery used by a particular institution have a bearing on

relative impact of microcredit. MFIs using group-lending technology especially

reach poorer clients than those using individual lending methodology.

In spite of these remarkable results, there has been a general decline in growth

and expansion, with clients growing at below 50 percent and the loan portfolio

even less; from 58 percent in 2002 to around 32 percent in 2003.

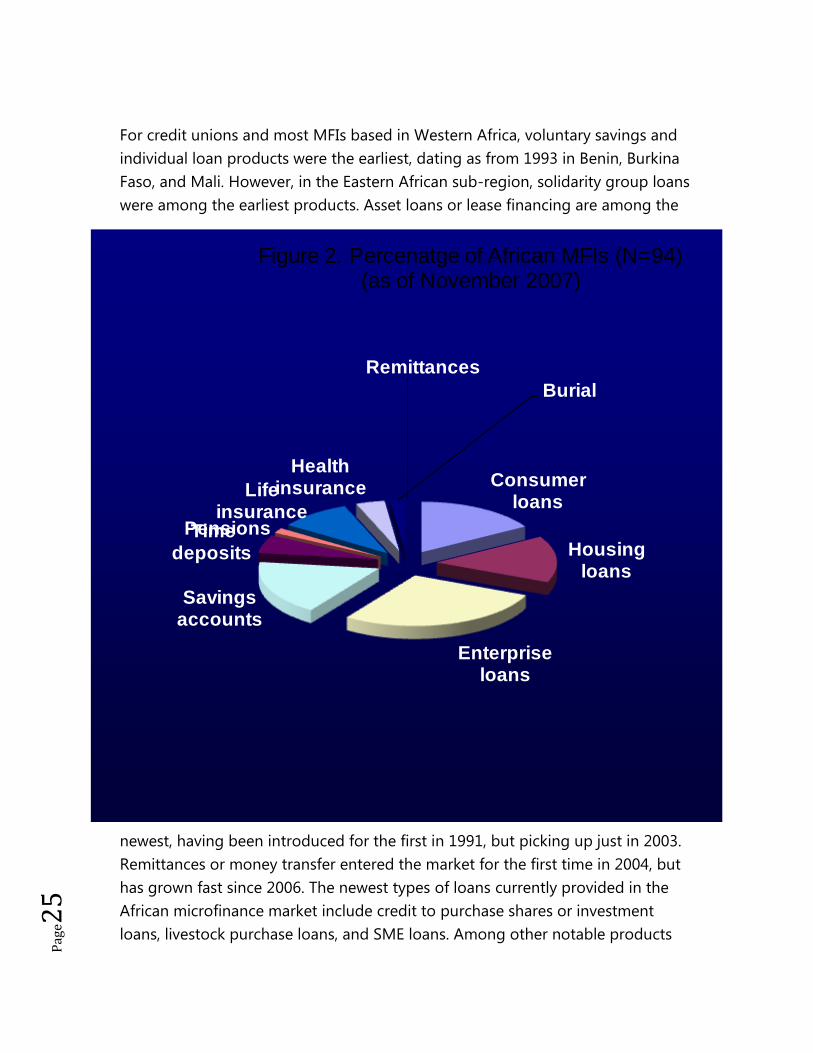

financial products Diversity

Microfinance institutions worldwide initially offered just one product —

microcredit — thereby leading some commentators to refer to savings as the

“forgotten half of financial services to the low-income populations”. However,

along with the changing landscape of microfinance service providers discussed

above, there are now more products on offer to these populations. These include

savings and micro-insurance financial products (Figure 2). Yet, by far, microcredit,

or simply enterprise loans, remains the oldest and flagship of microfinance

institutions worldwide.

P

age2

5

Consumer loans

Housing loans

Enterprise loans

Savings accounts

Time deposits

Pensions

Life insurance

Health insurance

Burial

Remittances

Figure 2. Percenatge of African MFIs (N=94)(as of November 2007)

For credit unions and most MFIs based in Western Africa, voluntary savings and

individual loan products were the earliest, dating as from 1993 in Benin, Burkina

Faso, and Mali. However, in the Eastern African sub-region, solidarity group loans

were among the earliest products. Asset loans or lease financing are among the

newest, having been introduced for the first in 1991, but picking up just in 2003.

Remittances or money transfer entered the market for the first time in 2004, but

has grown fast since 2006. The newest types of loans currently provided in the

African microfinance market include credit to purchase shares or investment

loans, livestock purchase loans, and SME loans. Among other notable products

P

age2

6

making a debut in the African market are village phone loans (so far found only

in Uganda), food/security farming loans in Ethiopia, Kenya, and many parts of

Western Africa, education loans, and emergency loans. So far, credit life insurance

and funeral or burial insurance cover financial products are available only in the

Southern part of Africa. In Western and Eastern Africa, particularly in Kenya, the

microfinance institutions also provide varied types of savings accounts.

The strong demand, hence relevance of the financial products, explains the rapid

growth of the microfinance sector in Africa. As an example, the number of

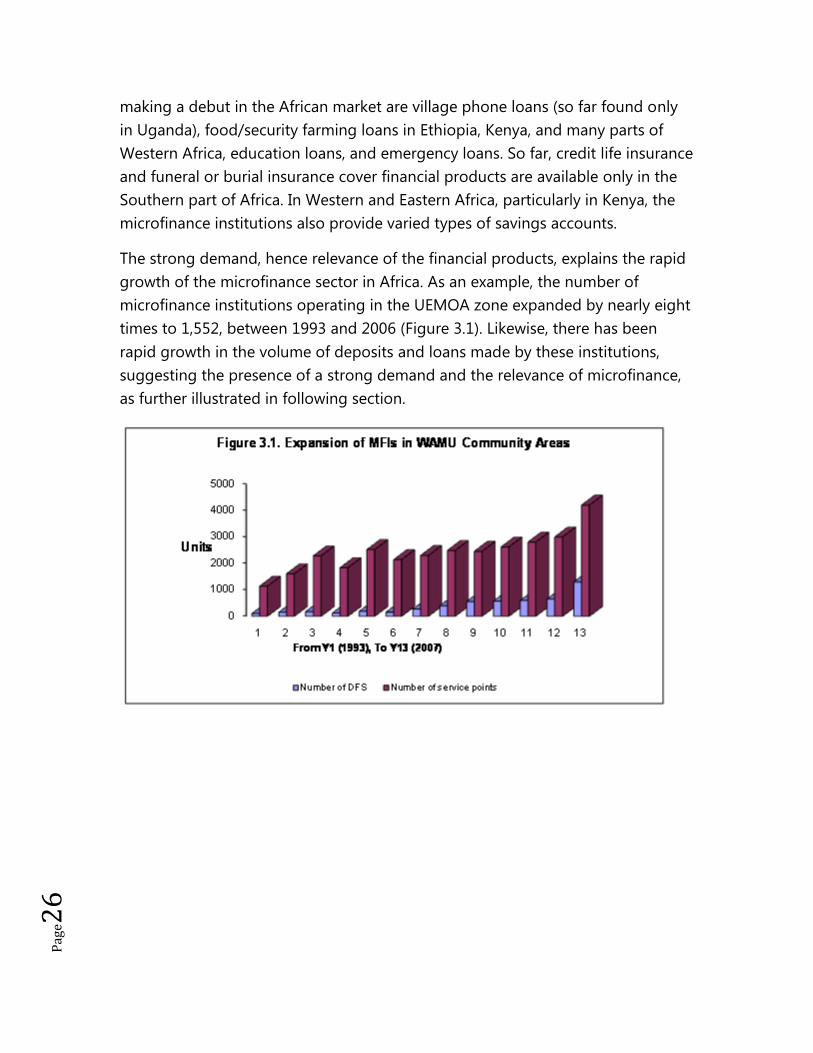

microfinance institutions operating in the UEMOA zone expanded by nearly eight

times to 1,552, between 1993 and 2006 (Figure 3.1). Likewise, there has been

rapid growth in the volume of deposits and loans made by these institutions,

suggesting the presence of a strong demand and the relevance of microfinance,

as further illustrated in following section.

P

age2

7

Lastly, while there were hardly any microfinance intermediaries in Africa that had

an outreach above 50,000 clients a decade ago, 38.1 percent of the

intermediaries currently have an outreach that exceeds 100,000 customers

each34.

Outreach and Financial Performance

This section draws from 89 ratings of African microfinance institutions between

2001 and 2007 and several new and old surveys of the sector (Table 9). Because

they are more objective, rating reports provide reliable benchmarks for

comparative analysis between institutions. Ratings are also good in revealing

important industry trends.

In the past three years, the African microfinance system has scored significant

results in several areas, for example, declining average expense ratio, which

suggests an increasing operational efficiency. Cost per loan has also dropped

significantly to within 30 percent of outstanding loan portfolio balances, while the

average operating self-sufficiency has improved from 110 percent as of

December 2002 to 117 percent a year later. In addition to the rapid growth and

expansion of microfinance in Africa since the mid 1990s in terms of institutions

and products, there has also been an impressive growth in volume at the

individual provider level (Figure 3.3), as earlier discussed.

Table 9. Current Financial Profile of Microfinance Institutions

P

age2

8

Region Total outlets Rural outlets Age Lending portfolio (US$)

Africa

Average 42 31 1993 22,890,491

Median 21 14 1995 7,694,700

Sum 1,250 893 709,605,233

Americas

Average 14 13 1993 115,662,750

Median 10 8 1996 7,000,000

Sum 307 286 2,660,243,250

Asia

Average 279 286 1991 154,426,210

Median 15 12 1992 3,384,565

Sum 9,776 8,873 41,015,081,458

All INAFI,

sample

Average 130 123 1992 92,311,624

Median 16 11 1994 7,236,510

Sum 11,33

3

10,05

2

7,384,929,941

Global 17,62

9

15,63

6

1993 11,487,668,797

SOURCE: INAFI AFRICA, NOVEMBER 2007

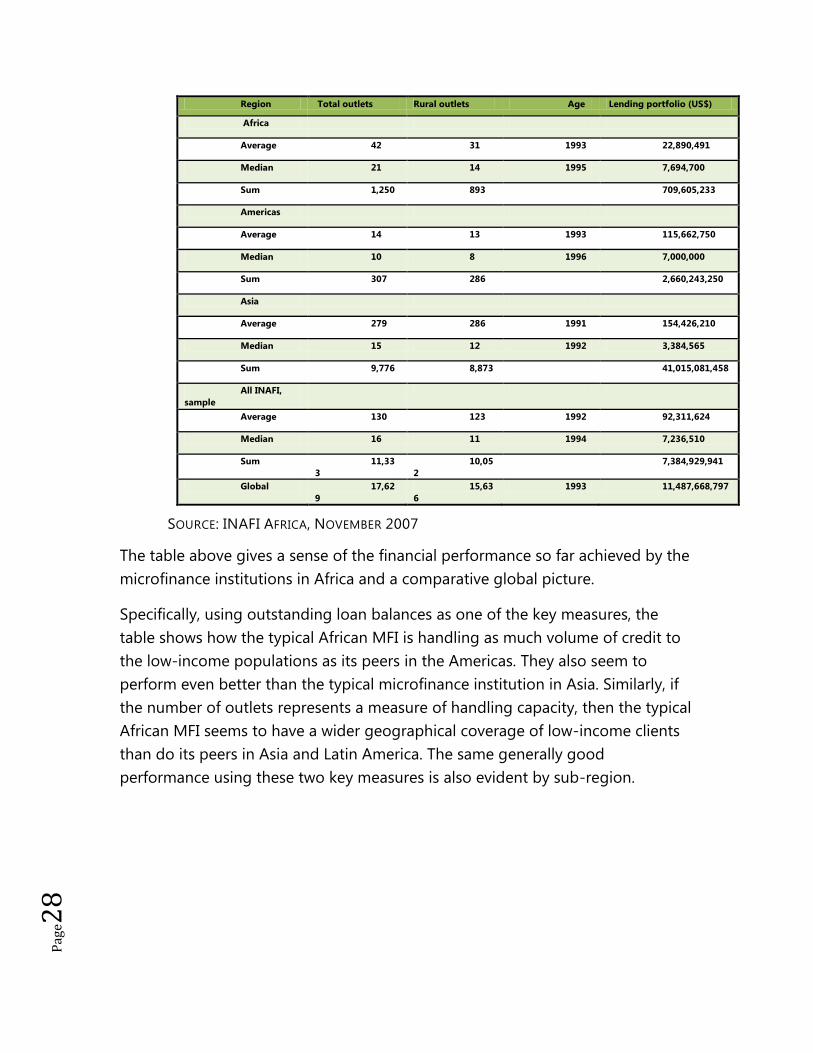

The table above gives a sense of the financial performance so far achieved by the

microfinance institutions in Africa and a comparative global picture.

Specifically, using outstanding loan balances as one of the key measures, the

table shows how the typical African MFI is handling as much volume of credit to

the low-income populations as its peers in the Americas. They also seem to

perform even better than the typical microfinance institution in Asia. Similarly, if

the number of outlets represents a measure of handling capacity, then the typical

African MFI seems to have a wider geographical coverage of low-income clients

than do its peers in Asia and Latin America. The same generally good

performance using these two key measures is also evident by sub-region.

P

age2

9

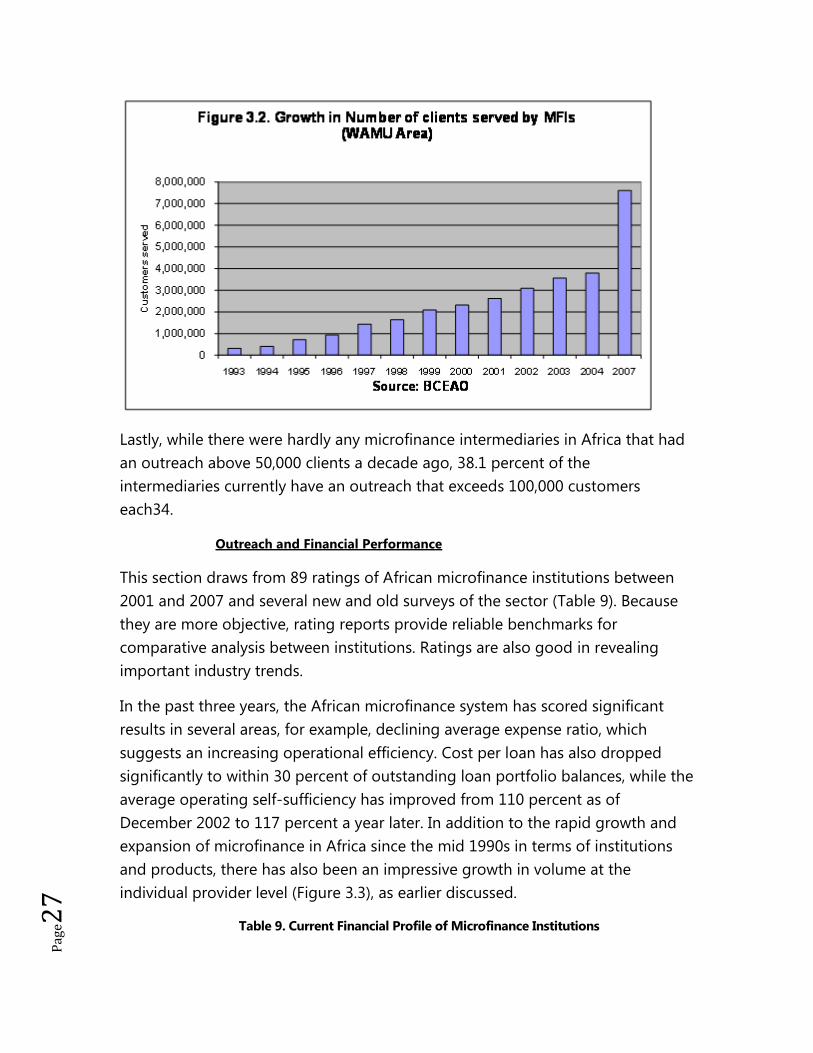

Take the case of the West Africa sub-region where we have decade-long time

series data at the country level (Figures 3.1 and 3.2, above), for example. In 1993,

when microfinance came under financial systems regulation in the UEMOA zone,

the system served under half a million clients. However, 14 years later, it now

serves 7.8 million low-income households and individuals in the eight countries.

This is about twice as many clients served by the decentralized financial system in

2004, up from the 4.3 million customers in 2000 and nearly eight times the

number of clients served as of year-end 2006. The total volume of deposits and

credits channeled through the system stood at $750 million and $645 million,

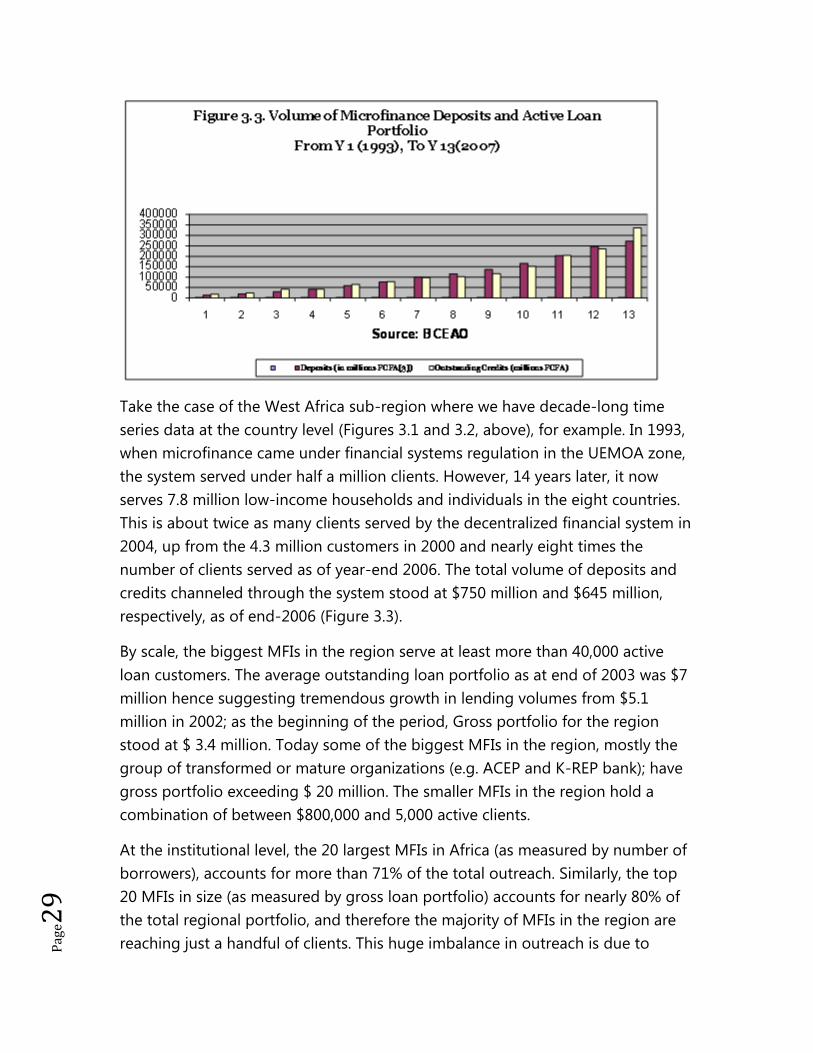

respectively, as of end-2006 (Figure 3.3).

By scale, the biggest MFIs in the region serve at least more than 40,000 active

loan customers. The average outstanding loan portfolio as at end of 2003 was $7

million hence suggesting tremendous growth in lending volumes from $5.1

million in 2002; as the beginning of the period, Gross portfolio for the region

stood at $ 3.4 million. Today some of the biggest MFIs in the region, mostly the

group of transformed or mature organizations (e.g. ACEP and K-REP bank); have

gross portfolio exceeding $ 20 million. The smaller MFIs in the region hold a

combination of between $800,000 and 5,000 active clients.

At the institutional level, the 20 largest MFIs in Africa (as measured by number of

borrowers), accounts for more than 71% of the total outreach. Similarly, the top

20 MFIs in size (as measured by gross loan portfolio) accounts for nearly 80% of

the total regional portfolio, and therefore the majority of MFIs in the region are

reaching just a handful of clients. This huge imbalance in outreach is due to

P

age3

0

differences in the MFIs access to resources and legal status. The biggest of the

MFIs happens to be savings-led and member-owned institutions, for example

FCPB in Burkina Faso, DECSI in Ethiopia, and Kafo Jiginew in Mali.

According to the IFPRI survey, Asia accounts for the largest volume of savings

and loans and employs the largest number of staff. Asia’s MFIs also reportedly

had lower personnel costs than those in Africa and Latin America.

Due to poor infrastructure, undiversified economies, high transaction costs, and

because of poor and illiterate microfinance clients, African MFIs have low staff

productivity. However, as a percentage of GNP per capita, African MFIs still

handle relatively larger loan sizes than Asia, but not Latin America.

The IFPRI report attributes the relatively high rural outreach in Asia to the densely

populated irrigated or fertile areas widely available in the region.

P

age3

1

III. Current Limitations, nano firms view

Institutional perspective Despite the outlined developments, the microfinance system in Africa has yet to

realize its full potential. Even after growing rapidly and extensively throughout

the region since the mid 1990s, access remains limited.

As of December 2006, for instance, just about four percent of the region’s

potentially eligible population had services. Secondly, the market is highly

concentrated in a small number of leading institutions and countries. In the entire

region, the top 10 providers cater to nearly two thirds of the entire market35. The

imbalance is evident even among the countries, with Ethiopia alone accounting

for six of the top 10 biggest microfinance institutions in Africa in 2007. Next in

line is Senegal and Burkina Faso.

In the CEMAC zone covering seven Central African states, almost two thirds of all

microfinance institutions and volumes of credit and deposits are concentrated in

Cameroon36. In many of the 53 AU member states, often just two to three

players control a high share of the total national markets; of between 60 percent

and 80 percent. In Malawi, for instance, a single microfinance institution (the

MRFC) controlled as much as 80 percent of the national market in 2006. In Mali,

during the same period37, three of the biggest microfinance institutions —

Nyesigiso, Kafo Jiginew, and Kondo Jigime — controlled 60 percent of the entire

national market, taking up 75 percent of deposits and 50 percent of the total

outstanding loan portfolio.

By volume and sub-region, the microfinance system in the AU member states is

least developed in the CEMAC zone. More than 340 microfinance institutions

closed shop38 after failing to meet newly introduced licensing requirements by

the deadline of February 200539.

The inevitable conclusion from this analysis is that, while Africa’s microfinance

system has acquired a considerable level of professionalism over the past two

decades, it still lags behind other regions in several fundamental areas.

First, the total outreach remains insignificant and a largely urban phenomenon.

Second, although some linkages are starting to emerge between conventional

banking and non-banking financial institutions and microfinance institutions —

P

age3

2

especially in a few countries like Mali, South Africa, Kenya, and Tanzania — the

market as a whole remains fragmented and uncoordinated while access to funds

for intermediation is still a major problem40. In many parts of Africa,

microfinance institutions rely on domestic commercial loans to grow their loan

portfolios. This is short-term, expensive, and largely dependent on continued

good personal relations between managers.

Equity and debt capital remain elusive, probably because many microfinance

institutions are not financially self-sustainable. The cost of access to finance

provided by microfinance institutions, at upwards of between 30 percent per

annum to as high as 86 percent, is too high for the low-income populations. In

many of the AU member states, interest rates on borrowed funds roughly

average 43 percent a year, with a median interest rate of around 29 percent.

P

age3

3

Other pressing problems among African MFIs include high client dropout rates,

typically ranging between 20 percent and 25 percent annually. In Mozambique,

for example, annual client dropout rates of between 30 percent and 40 percent

are common41, while in the Eastern Africa region, annual client exit rates of as

high as 60 percent occur widely. African microfinance institutions exhibit highly

uneven levels of performance, even those of the same age, size, or legal form.

This underscores the lack of generally accepte90- operational standards for

practitioners within the region. In addition to this baffling wide variance in

performance — and in spite of progress made in developing people and systems

over

the

past

three

decades—the microfinance system in Africa has failed to attract foreign and local

investment capital to finance growth and expansion.

Not surprisingly, most African microfinance institutions have failed to develop

institutionally or expand outreach significantly, primarily because of lack of

adequate capital (Table 3). Lack of adequate capital is the single most important

P

age3

4

factor why so few African microfinance institutions have become both

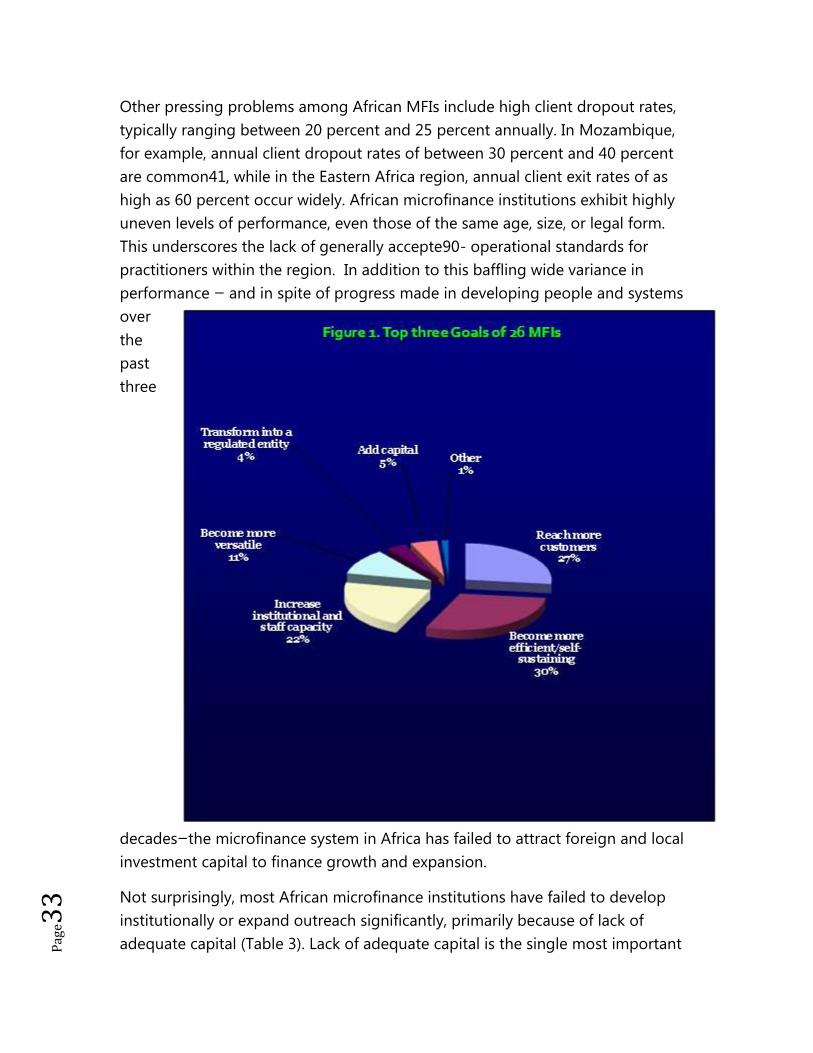

operationally and financially self-sustaining (Figure 1).

Without adequate resources to finance their growth and satisfactorily meet

customer needs for services on demand, many African microfinance institutions

have traded off essential investments for upgrading management systems and

enhancing human and institutional capacity with loan funding. Because of this,

the institutions have failed to match current expansion with greater capability,

thus facing the risk of higher loan delinquency and default.

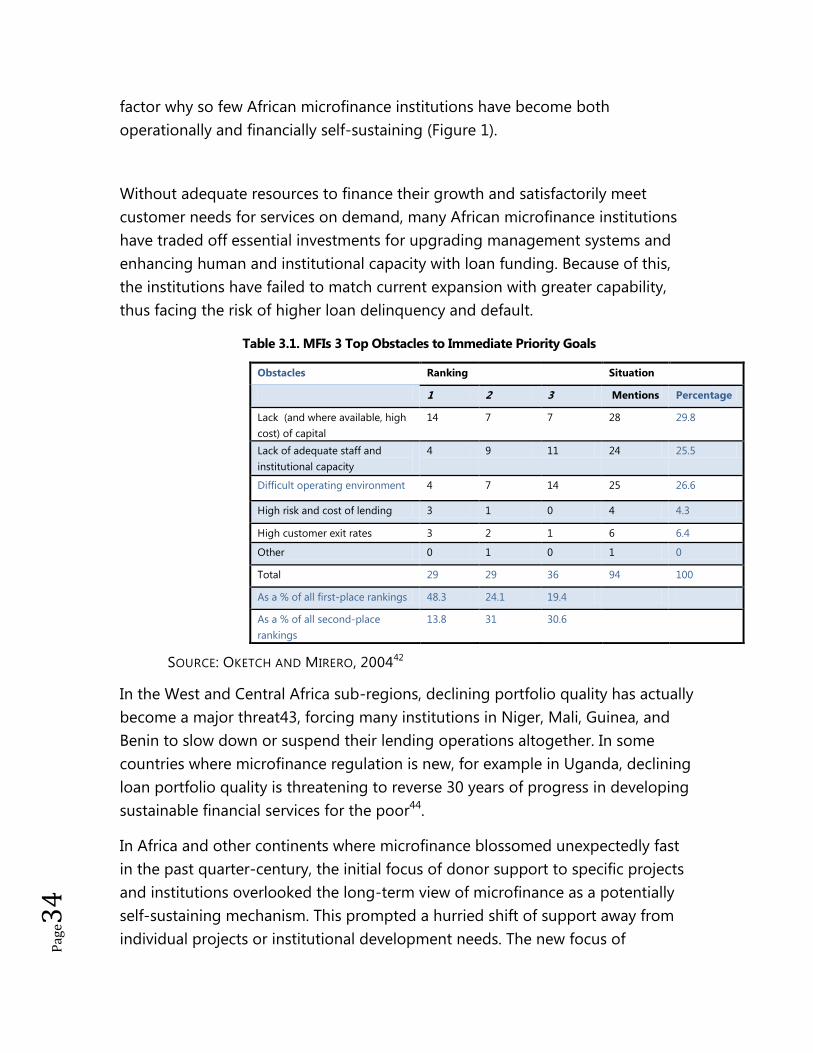

Table 3.1. MFIs 3 Top Obstacles to Immediate Priority Goals

Obstacles Ranking Situation

1 2 3 Mentions Percentage

Lack (and where available, high

cost) of capital

14 7 7 28 29.8

Lack of adequate staff and

institutional capacity

4 9 11 24 25.5

Difficult operating environment 4 7 14 25 26.6

High risk and cost of lending 3 1 0 4 4.3

High customer exit rates 3 2 1 6 6.4

Other 0 1 0 1 0

Total 29 29 36 94 100

As a % of all first-place rankings 48.3 24.1 19.4

As a % of all second-place

rankings

13.8 31 30.6

SOURCE: OKETCH AND MIRERO, 200442

In the West and Central Africa sub-regions, declining portfolio quality has actually

become a major threat43, forcing many institutions in Niger, Mali, Guinea, and

Benin to slow down or suspend their lending operations altogether. In some

countries where microfinance regulation is new, for example in Uganda, declining

loan portfolio quality is threatening to reverse 30 years of progress in developing

sustainable financial services for the poor44.

In Africa and other continents where microfinance blossomed unexpectedly fast

in the past quarter-century, the initial focus of donor support to specific projects

and institutions overlooked the long-term view of microfinance as a potentially

self-sustaining mechanism. This prompted a hurried shift of support away from

individual projects or institutional development needs. The new focus of

P

age3

5

microfinance development then became the urgent need to build the prospective

industry’s infrastructure. This achieved less than satisfactory results because the

strategy failed to address the missing retail and institutional capacities45.

However, the country-level networks or associations of microfinance service

providers emerging in most of the 53 AU member countries are trying to address

the institutional- and industry-level capacity constraints. These professional

membership practitioner associations only acquired a serious institutional

outlook in the past six to seven years and are themselves still weak,

notwithstanding efforts by the World Bank and Women’s World Banking 199841

initiative to strengthen them. In the absence of such strong networks, therefore,

much of Africa’s microfinance industry grew in the past without any proper

coordination or cooperation among the market players. In fact, the industry still

lacks a common vision for the future. This also explains much of the current

confusion and disagreements about what should be the proper role of the state

and some considerable confusion about suitable legal and regulatory settings for

microfinance development in Africa.

client satisfaction and perspective of services and Products

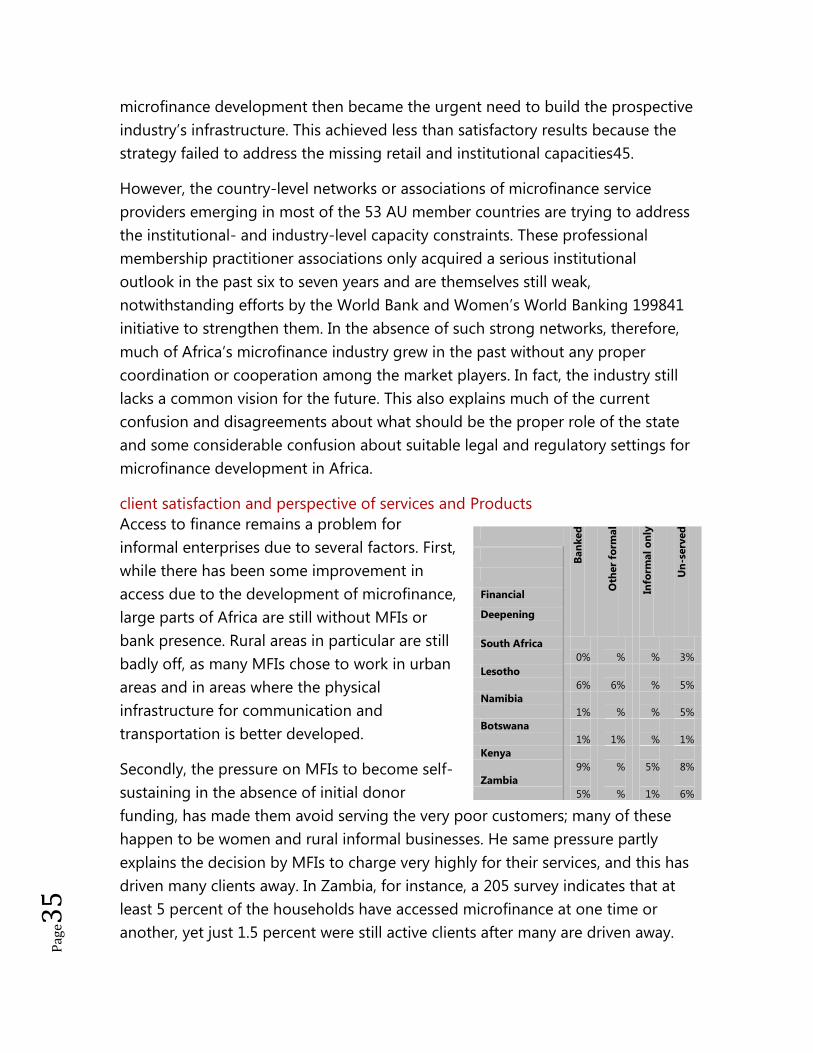

Access to finance remains a problem for

informal enterprises due to several factors. First,

while there has been some improvement in

access due to the development of microfinance,

large parts of Africa are still without MFIs or

bank presence. Rural areas in particular are still

badly off, as many MFIs chose to work in urban

areas and in areas where the physical

infrastructure for communication and

transportation is better developed.

Secondly, the pressure on MFIs to become self-

sustaining in the absence of initial donor

funding, has made them avoid serving the very poor customers; many of these

happen to be women and rural informal businesses. He same pressure partly

explains the decision by MFIs to charge very highly for their services, and this has

driven many clients away. In Zambia, for instance, a 205 survey indicates that at

least 5 percent of the households have accessed microfinance at one time or

another, yet just 1.5 percent were still active clients after many are driven away.

Ban

ked

Oth

er

form

al

Info

rmal

on

ly

Un

-serv

ed

Financial

Deepening

South Africa 5

0%

7

%

9

%

3

3%

Lesotho 4

6%

1

6%

4

%

3

5%

Namibia 5

1%

3

%

1

%

4

5%

Botswana 4

1%

1

1%

5

%

4

1%

Kenya 1

9%

8

%

3

5%

3

8%

Zambia 1

5%

8

%

1

1%

6

6%

P

age3

6

In addition to the high cost of services, many dropouts and even some active

clients find the available services not appropriate enough; loans are typically

group-based, require regular weekly or monthly repayments, and have very short

tenor that at times are at great odds with needs and abilities of the clients.

P

age3

7

IV. Improving access and service quality

The primary concern in trying to develop a microfinance system in any part of the

world is how to reach millions of people financially excluded on sustainable

terms. The second concern is ensuring that those who get access to finance

actually invests it wisely and effectively to resolve both their short term and long-

term needs, for instance the desire of self employed entrepreneurs to expand

and/or improve their businesses and, thus, improve their incomes.

Ultimately the success of a nation in developing a microfinance system for its

poor and financially excluded population must be judged on the basis of

sustainable improvements to their welfare/ standards of living. Inevitably, this is

only achievable by increasing outreach, resource mobilization, cost coverage, and

dynamic growth. In this connection, therefore, this section tries to deal with the

following issues:

What does it take to build a successful microfinance

market in Africa that fulfils its role as desired by

society?

What role should the governments play in expanding

and deepening outreach?

What values should guide investors, on the one hand,

and microfinance institutions, on the other hand, as

they seek to increase outreach and become long-

lasting and self-sustaining alternative financial

institutions for the currently excluded rural and urban

poor?

Firstly, in seeking to advance the development of microfinance in Africa, each

country should pursue the following five priority goals:

1. To increase the number of poor families and

individuals with access to finance.

2. To improve and increase the distribution of

microfinance to rural areas, especially to smallholder

P

age3

8

farmers and the more disadvantaged social groups,

e.g., women and the youth.

3. To improve and enhance the social and economic

impact of microfinance, especially maximizing its

potential contribution towards achieving the MDGs by

also providing complementary services.

4. To increase the share of local savings invested in

financial assets by the rural and urban poor, and

increase the share of local deposits mobilized and

invested towards expanding and diversifying the rural

economy.

5. To increase backward and forward linkages between

formal and informal financial systems, thereby help

increase and improve the supply of various financial

services to the poor, and enabling job creation, trade,

and investment to flourish.

it all begins with the Formulation of a Creative or Innovative Policy

Among the measures to achieve these five priority goals include encouraging

(through policy and other incentives) the provision of suitable financial products,

i.e., products that meet the needs of poor people.

Microfinance clients not only want permanent or reliable services, they also care

about price and want quality services at reasonable prices. Furthermore, in

addition to access to finance, the poor in their endeavor to improve livelihoods

and well-being may require other equally important non-financial services, e.g.

access to reliable markets for their goods/produce and services or getting fair

price for their output, etc. Therefore, an improved access to microcredit, for

instance, needs to be accompanied with appropriate non-financial services; these

need not to be provided by the same agency, but can be arranged between

different specialized agencies. In this regard, therefore, policy geared towards

advancing the development of microfinance in a particular country ought to

outline areas where such strategic alliances or partnerships would make a

difference in lifting people out of poverty.

Similarly, the absence of linkages between formal financial system and

microfinance institutions can thwart growth of a dynamic and vibrant sector.

P

age3

9

Where government has developed national microfinance policy and regulatory

environment—and also established strong agencies to coordinate and supervise

the development—it has been relatively easy to mobilize local and external

resources for the development of the microfinance sector. The presence of strong

national microfinance practitioner’s associations or networks, for example the

ones existing in Ethiopia and Senegal, can also encourage many microfinance

institutions to aim for higher standards and superior performance, through

exchange of ideas, collaboration in training, and self-monitoring. Actually, it is in

countries such as the two mentioned above where many practitioners face

relatively few hurdles in tracking and regularly reporting their performance, and

where more MFIs are engaging ratings services, thereby improving transparency

and wining the confidence of more investors to enter their market. Thus,

cooperation, coordination, and dialogue among various market players are

essential elements of good sector development practice, which policy can

promote and influence.

However, in the process of policy making and regulation of microfinance,

governments must engage closely with the providers in dialogue and discussion

of market requirements/rules. Similarly, at another different level, governments

must also effectively engage donors, other development partners, and the private

sector to succeed in mobilizing the resources needed to expand and build the

industry. In this regard, it is necessary for government to coordinate and

encourage cooperation and partnerships among different stakeholders through

appropriate public policy and clear definition of roles for each group.

Furthermore, to ensure that providers are market-driven, it is necessary to have

policy that encourages and permits a wide range of financial products demanded

by customers at the right price, so that access to services is sustainable in the

long-term. Yet this also means that providers must remain dynamic to evolve in

tandem with changing customer needs and the market in general. In this regard,

considering that lack of adequate, reasonably-priced, and appropriately

structured capital is currently a major constraint to microfinance market

development, policy should make or encourage the provision of savings as one

of the priority services, besides creating adequate measures to protect

depositors.

Accordingly, financial sector policy should encourage and allow institutions

involved in microfinance to mobilize liquidity right from the grassroots. Similarly,

P

age4

0

because the microfinance clients themselves have vested interest and capacity to

save and invest, both policy and corresponding regulatory framework should

encourage and provide room for the poor to invest in microfinance institutions,

as well as promoting and encouraging their participation in domestic and

regional capital markets.

Yet, the fact that financial intermediation is a risky business means that

microfinance institutions must be professionally managed; by people with high

integrity, knowledge, and skills in serving the poor sustainably. However, to guide

and ensure that microfinance institutions are managed professionally, standards

and benchmarks to inspire excellence are also required, and these should be

incorporated in policy and regulatory framework. A confident and well trained

human resource base is the ultimate solution to building market-driven

microfinance institutions that grow and evolve with their customers’ needs.

Hence, in the area of human resource development, policy must push for strong

management and leadership, which invariably determines the success of any

enterprise; and an MFI, is in every sense, an enterprise. Secondly, at the level of

staff who provide the primary contact between customers and MFI, there is a

continuous need for credit officers and operations staff especially to constantly

upgrade their skills and knowledge-base just to keep pace with developments in

the field. On this matter one specialist organization notes46:

“… Recent trends in microfinance—fast growth, change, stiff competition—have made

achieving the mission more challenging than ever. Given these circumstances, MFIs need to

reinforce their strategic management practices: more systematic planning and

management of strategy will enhance their success. Thus effective management should be

(a) inspired and guided by the mission, the most vital aspect of any organization; (b) be on-

going and integrated into every level of the organization, informing and strengthening all

management practices. A continuous assessment of the strategy’s implementation, and sue

of results, will help managers to prioritize and improve decision-making, (c) involve

everyone; strategy is the result of hundreds of activities. Therefore, an MFIs’ strategy

cannot be left to only a few people at the top o the organization; it should be both

understood and executed by all the employees, and (d) lastly, facilitate change

management: because change is inevitable during pursuit of the mission, it is important to

have set of tools and practices to facilitate smooth transitions…”

P

age4

1

Regrettably, many transformed MFIs have tended to place too faith in newly

introduced banking technology and knowledge—even retrenching and replacing

seasoned microfinance staff with traditional bankers—only to discover significant

client exists because of inevitable differences in organizational culture and service

orientation. Several such MFIs have rushed to serve new markets, e.g., individual

SME loans, with disastrous results because they were unprepared. Equally

important is the challenge on management to keep refining, updating, or

developing more appropriate management systems in tandem with changes in

demand and market conditions; at any one time, management systems should

enable the workforce to identify and manage risks effectively. In fact these

systems should enable the workforce to also assess their institutional

performance and continued relevance in the market place, thus it is important to

have these continuously improved and upgraded in tandem with growth and

market dynamics.

The second solution in expanding and deepening access is the mobilization of

adequate resources

So far, the opportunities in modern microfinance are just unfolding. So there is a

general lack of investors or capital for market development. In addition, lack of or

insufficient promotion of the sector –combined with lack of suitable policy—has

contributed to poor resource mobilization.

Most of the existing MFIs in Africa were established at a time when there were no

standards or benchmarks to inspire excellence. In spite of recent improvements in

policy environment and greater awareness of the potential gains from

microfinance, lack of basic standards or benchmarks means that providers have

not felt the pressure to excel. Hence, creating and promoting industry standards

and benchmarks is an important intervention that could drive up performance to

a higher level of efficiency and professionalism, as mentioned before.

In many countries where microfinance has developed relatively well, there has

been a broadening of partnerships between governments and the private sector.

Moreover, the role of subsidies in facilitating institutional and market

development is widely appreciated. However, dependence on subsidies can

undermine the emergence of strong, long-lasting institutions if not well-

coordinated and managed. As a matter of good practice, subsidies should be

selective and should be provided only when they are high-value adding, or when

they have a clear chance of changing attitudes and behavior. In considering

P

age4

2

subsidies, it is important for private-public sector partnerships to include both

institutional and market development priorities, since balanced growth is possible

only when there is a good match between capacity and the demand for services.

In this regard, African can learn much from South Africa, where the government-

promoted Black Economic Empowerment (BEE) Financial Sector Charter47, has

inspired the private sector to innovate and seek ways of reaching the still

financially and economically excluded population with new products and delivery

systems—including wide scale application of technology.

For Africa, where the market is relatively young, it would be good practice if more

of the resources mobilized through public-private sector are channeled as

subsidies into building industry standards, national microfinance networks, and

management/leadership. As observed by one Jean-Luc, Camilleri (2005):

“… It is only the well managed MFIs that are likely to meet the needs of the huge, currently

financially excluded population. At the stage of experimentation, the role of some NGOs

has been crucial. But today, MFIs must be more professional so that they can increase their

impact and reach more of those still without access. It is more efficient 9and cost-effective

for poverty alleviation) so use subsidies in strengthening the MFIs whose capacities for

intervention is high enough to respond to the needs of the most dynamic micro/small-scale

enterprises…” 48

The role of the public sector in developing the market, encouraging competition,

and attracting investors to serve neglected or difficult to reach areas cannot be

ignored. Yet government involvement is more effective through public-private

partnerships. Where the public sector finds it necessary to get involved in the

provision of microfinance, it is more effective if it does so by sub-contracting or

outsourcing the responsibility to specialized and experienced firms.

In conclusion, best practice in the provision of microfinance means full cost

coverage, market-driven approach to service provision, scaling up operation (or

being able to expand outreach at low marginal cost, and making rational

economic decisions. It requires competent, committed managers and workforce

that also have high levels of integrity and ability to relate to ordinary people.

In making difficult choices, managers must consider risk and cost, as well as the

long-term survival of their enterprises, i.e. choices must be made on sound

business principles, while keeping in mind poverty reduction as the ultimate goal.

Subsidies will continue to be relevant, but these should be allocated wisely only

P

age4

3

to high-value adding initiatives, such as new product development or