Public Finance in Rajasthan (Published in Indian Economic Journal)

14

1 Management of Public Finances in Rajasthan Govind Bhattacharjee 1 , Abstract Having long extricated itself out of the so-called BIMARU status, Rajasthan today is marching ahead towards development and progress along with all other states of India. Thanks partly to its FRBM Act, the state’s public finances are today in a healthy sta te though there remains areas of concern. The state has been able to increase its own revenues, both tax and non-tax, appreciably over the last five years, thereby reducing its dependence on Central grants significantly. VAT constitutes the most important source of its revenues followed by state excise, stamps & registration fees and taxes on vehicles, all of which are also highly buoyant and which together account for most of its own tax receipts, while royalty from petroleum is the main source of its non-tax revenues. As regards Central funds, direct off-budget transfers of Central plan funds to state implementing agencies have always far exceeded the Central grants routed through state budgets; this aberration is likely to stop from this year onwards, giving the state more autonomy and control over development expenditure. Though state revenues have grown faster than total expenditure, enabling the state to progressively increase a surplus in the revenue account, the ever-growing committed expenditure on salary, pension, interest and subsidy continue to consume a large of its revenue expenditure, seriously limiting the scope of expenditure on maintenance of assets. Populist subsidies like that on electricity needs to be curtailed, and non-developmental expenditure on running the day to day administration of the State also needs to be controlled. The fiscal deficit of the state is under control, but borrowings, even without posing any immediate danger in view of high growth rate of the state economy, need to be carefully calibrated and controlled as the state is unable to derive any benefit from the debt funds. It has actually been paying far more than what it borrows due to its high debt servicing obligations and cutting down on subsidy and other unproductive expenditure is urgently warranted to bring this problem under control. This would also allow the State to increase its capital outlay. The state compares well with its neighbours in respect of important parameters with regard to management of public finances. 1 The author is Director General, Eastern Region, at the Office of the Comptroller & Auditor General of India, New Delhi. Sources of all data used in this paper are the Finance Accounts of the Government of Rajasthan compiled by the Comptroller & Auditor General of India, unless otherwise stated. Opinions expressed in the paper are strictly personal and do not reflect the view of the Indian Audit & Accounts Department.

-

Upload

independent -

Category

Documents

-

view

5 -

download

0

Transcript of Public Finance in Rajasthan (Published in Indian Economic Journal)

1

Management of Public Finances in Rajasthan

Govind Bhattacharjee1,

Abstract

Having long extricated itself out of the so-called BIMARU status, Rajasthan today is

marching ahead towards development and progress along with all other states of India.

Thanks partly to its FRBM Act, the state’s public finances are today in a healthy state though

there remains areas of concern. The state has been able to increase its own revenues, both

tax and non-tax, appreciably over the last five years, thereby reducing its dependence on

Central grants significantly. VAT constitutes the most important source of its revenues

followed by state excise, stamps & registration fees and taxes on vehicles, all of which are

also highly buoyant and which together account for most of its own tax receipts, while royalty

from petroleum is the main source of its non-tax revenues. As regards Central funds, direct

off-budget transfers of Central plan funds to state implementing agencies have always far

exceeded the Central grants routed through state budgets; this aberration is likely to stop

from this year onwards, giving the state more autonomy and control over development

expenditure.

Though state revenues have grown faster than total expenditure, enabling the state to

progressively increase a surplus in the revenue account, the ever-growing committed

expenditure on salary, pension, interest and subsidy continue to consume a large of its

revenue expenditure, seriously limiting the scope of expenditure on maintenance of assets.

Populist subsidies like that on electricity needs to be curtailed, and non-developmental

expenditure on running the day to day administration of the State also needs to be controlled.

The fiscal deficit of the state is under control, but borrowings, even without posing any

immediate danger in view of high growth rate of the state economy, need to be carefully

calibrated and controlled as the state is unable to derive any benefit from the debt funds. It

has actually been paying far more than what it borrows due to its high debt servicing

obligations and cutting down on subsidy and other unproductive expenditure is urgently

warranted to bring this problem under control. This would also allow the State to increase its

capital outlay.

The state compares well with its neighbours in respect of important parameters with regard

to management of public finances.

1 The author is Director General, Eastern Region, at the Office of the Comptroller & Auditor General of India,

New Delhi. Sources of all data used in this paper are the Finance Accounts of the Government of Rajasthan

compiled by the Comptroller & Auditor General of India, unless otherwise stated. Opinions expressed in the

paper are strictly personal and do not reflect the view of the Indian Audit & Accounts Department.

2

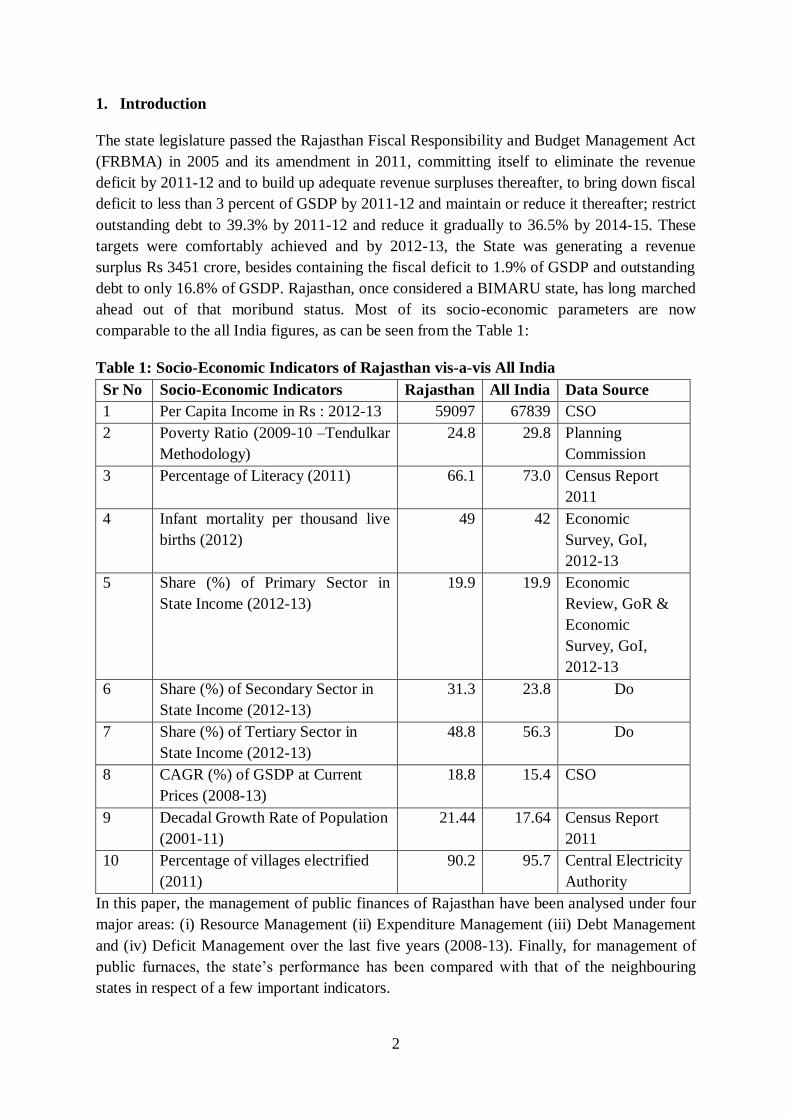

1. Introduction

The state legislature passed the Rajasthan Fiscal Responsibility and Budget Management Act

(FRBMA) in 2005 and its amendment in 2011, committing itself to eliminate the revenue

deficit by 2011-12 and to build up adequate revenue surpluses thereafter, to bring down fiscal

deficit to less than 3 percent of GSDP by 2011-12 and maintain or reduce it thereafter; restrict

outstanding debt to 39.3% by 2011-12 and reduce it gradually to 36.5% by 2014-15. These

targets were comfortably achieved and by 2012-13, the State was generating a revenue

surplus Rs 3451 crore, besides containing the fiscal deficit to 1.9% of GSDP and outstanding

debt to only 16.8% of GSDP. Rajasthan, once considered a BIMARU state, has long marched

ahead out of that moribund status. Most of its socio-economic parameters are now

comparable to the all India figures, as can be seen from the Table 1:

Table 1: Socio-Economic Indicators of Rajasthan vis-a-vis All India

Sr No Socio-Economic Indicators Rajasthan All India Data Source

1 Per Capita Income in Rs : 2012-13 59097 67839 CSO

2 Poverty Ratio (2009-10 –Tendulkar

Methodology)

24.8 29.8 Planning

Commission

3 Percentage of Literacy (2011) 66.1 73.0 Census Report

2011

4 Infant mortality per thousand live

births (2012)

49 42 Economic

Survey, GoI,

2012-13

5 Share (%) of Primary Sector in

State Income (2012-13)

19.9 19.9 Economic

Review, GoR &

Economic

Survey, GoI,

2012-13

6 Share (%) of Secondary Sector in

State Income (2012-13)

31.3 23.8 Do

7 Share (%) of Tertiary Sector in

State Income (2012-13)

48.8 56.3 Do

8 CAGR (%) of GSDP at Current

Prices (2008-13)

18.8 15.4 CSO

9 Decadal Growth Rate of Population

(2001-11)

21.44 17.64 Census Report

2011

10 Percentage of villages electrified

(2011)

90.2 95.7 Central Electricity

Authority

In this paper, the management of public finances of Rajasthan have been analysed under four

major areas: (i) Resource Management (ii) Expenditure Management (iii) Debt Management

and (iv) Deficit Management over the last five years (2008-13). Finally, for management of

public furnaces, the state’s performance has been compared with that of the neighbouring

states in respect of a few important indicators.

3

2. Resource Management

2.1 Tax Revenues

The resource position of Rajasthan during the period 2008-13 is shown in Table 2. Total

Revenue receipts of Rajasthan have doubled over the period growing at a CAGR of about 19

percent. Among the state taxes, stamp & registration fees registered the highest CAGR of

25% during the period, followed by taxes on sales (VAT) which grew at an average rate of

20%. Non-tax revenue grew at a very high CAGR of nearly 33% during this period, growing

more than three folds. Central grants registered a modest average growth of 6% while State’s

share of divisible pool of taxes grew at a CAGR of about 17% during this 5 year period.

Table 2: Resource Mobilisation: 2008-09 through 2012-13 (Rs Crore)

2008-

09

2009-

10

2010-

11

2011-

12

2012-

13

CAGR

2008-13

1. Revenue Receipts 33469 35385 45928 57011 66913 18.9

(i) Own Tax Revenue 14943 16414 20758 25377 30503 19.5

Taxes on Sales, Trade, etc 8904 10163 12630 15767 18575 20.2

State Excise 2170 2300 2861 3287 3988 16.4

Taxes on Vehicles 1214 1373 1612 1927 2283 17.1

Stamps & Registration fees 1357 1363 1941 2651 3335 25.2

Land Revenue 163 148 222 209 304 16.9

Taxes on Goods and

Passengers

190 176 231 220 249

7.0

Other Taxes 945 891 1261 1316 1769 17.0

(ii) Non Tax Revenue 3889 4558 6294 9175 12133 32.9

(iii)State's Share of Union Taxes

& Duties

8999 9258 12856 14977 17103

17.4

(iv) Grants-in-Aid from

Government of India

5638 5155 6020 7482 7174

6.2

2. Miscellaneous Capital Receipts 4 9 13 16 8 18.9

3. Recoveries of Loans and

Advances

89 112 319 1229 1102

87.6

4. Totals Revenue and Non debt

Capital Receipts (1+2+3)

33562 35506 46260 58256 68023

19.3

Charts 1 and 2 depict the growth and composition of state’s resources. State’s own resources

comprised by its own revenues and non-tax revenues has increased its share in total revenue

receipts of the State from 56% to 64% over this period, while the share of Central transfers

comprised by the State’s share of divisible pool of taxes and Central grants, plan and non-

plan combined, declined from 64% to 46%. The growth of all these components accelerated

from 2010-11 onwards, which is understandable in the aftermath of the global economic

meltdown in 2008-09 which affected the finances of all Indian states along with that of the

Union, but recovery did not take long in the case of Rajasthan.

4

From Table 3, it can be seen that among the State taxes, VAT constitutes the most important

source accounting for than 60% of total taxes, followed by State Excise, Stamps &

Registration Fees and Taxes on Vehicles. Together these four taxes constitute more than 90%

of the State’s own tax receipts. Their buoyancies are also high, indicating their continued

potential to higher yields, especially the taxes on vehicles. Total tax revenue also shows high

buoyancy.

0

10000

20000

30000

40000

50000

60000

70000

80000

2008-09 2009-10 2010-11 2011-12 2012-13

Chart 1: Revenue Receipts of Rajasthan: 2008-13 (Rs

Crore)

Grants in Aid and

Contributions

Share of Divisible Pool

Non Tax Revenue

Own Tax Revenue

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008-09 2009-10 2010-11 2011-12 2012-13

Chart 2: Composition of Revenue Receipts (%)

Grants in Aid and

Contributions

Share of Divisible Pool

Non Tax Revenue

Own Tax Revenue

5

Table 3: Composition of Tax Revenues (%)

2008-

09

2009-

10

2010-

11

2011-

12

2012-

13

Buoyancy

(2012-13)

Sales Tax/ VAT 59.6 61.9 60.8 62.1 60.9 1.3

State Excise 14.5 14.0 13.8 13.0 13.1 1.5

Stamps & Registration Fees 9.1 8.3 9.4 10.4 10.9 1.3

Taxes on Vehicles 8.1 8.4 7.8 7.6 7.5 1.9

Subtotal 91.3 92.6 91.7 93.1 92.4 ---

Land Revenue 1.1 0.9 1.1 0.8 1.0 3.3

Taxes on Goods and

Passengers

1.3 1.1 1.1 0.9 0.8

1.0

Other Taxes 6.3 5.4 6.1 5.2 5.8 ---

Tax Revenue 14943 16414 20758 25377 30503 1.5

2.2 Non-Tax Revenues

Major sources of non-tax revenues of the state are Interest receipts and receipts from

petroleum and non-ferrous mining and metallurgical industries (Table 4). Receipts from

petroleum sector have shown astounding growth during the last five years, growing from only

Rs 9 crore to Rs 5070 crore during this period. This growth is a result of higher royalty from

the production of crude oil from Mangala, Bhagyam, Aishwariya and other oilfields in the

State.

Table 4: Non-Tax Revenues (Rs Crore)

Revenue Head

2008-

09

2009-

10

2010-

11

2011-

12

2012-

13

CAGR

2008-13

Interest receipts 1,196 1,185 1,277 1,715 2,067 14.7

Dividends & profits 43 37 21 58 57 7.3

Royalty from petroleum 9 111 1,630 3,436 5,070 387.2

Royalty from non-ferrous mining

and metallurgical industries 1,276 1,612 1,930 2,366 2,839 22.1

Other non-tax receipts 1,365 1,613 1,436 1,600 2,100 11.4

Total 3,889 4,558 6,294 9,175 12,133 32.9

2.3 Central Grants

Share of Central grants in the total revenue receipts of Rajasthan has gradually come down

from 16.8% to only 10.7% (Table 5). Most of the grants have come under the plan grants, of

which Grants for Centrally Sponsored Schemes constituted 46% in 2012-13. It is known that

most of these grants were passed directly to the State implementing agencies in respect of the

flagship welfare schemes of the then Central Government bypassing the State budget. Such

direct transfers have now been abolished w.e.f. the current budget and the State government

can now control the use of such funds. It is a well known fact that these schemes were ill-

conceived and badly implemented and were designed more for electoral rather than

developmental purposes, and were at best an aberration in the federal financial relations

between the Union and the states in India. Total amount of such direct transfers in 2012-13

6

was Rs 7826 crore for Rajasthan, which is much higher than the plan funds of Rs 4499 crore

routed through the State budget during the year.

Table 5: Central Grants (Rs Crore)

Particulars 2008-

09

2009-

10

2010-

11

2011-

12

2012-

13

Non-Plan Grants 1,272 1,715 1,716 2,901 2,675

Plan Grants 4,366 3,440 4,304 4,581 4,499

(i) Grants for State Plan Schemes 2,077 1,606 2,488 2,416 2,316

(ii) Grants for Central Plan Schemes 67 128 165 166 92

(iii) Grants for Centrally Sponsored

Schemes 2,222 1,706 1,651 1,999 2,091

Total 5,638 5,155 6,020 7,482 7,174

Percentage of Growth over previous year 14.5 8.6 16.8 24.3 4.1

Share of Grants in Revenue Receipts 16.8 14.6 13.1 13.1 10.7

3. Expenditure Management

The disbursements of the State government during the last 5 years are shown in Table 6 and

Charts 3, 4 and 5. Government expenditure has grown at a lesser rate than revenues after

2009-10, leading to a progressive build up of revenue surplus as we shall see. Though

developmental expenditure constituted around two thirds of the total disbursements made by

the Government during the period, of the total revenue expenditure, the committed

expenditure on salaries, pension, interest and subsidy consumed more than 60% of the

revenue expenditure, leaving very little for the operation and maintenance of the capital

assets. In respect of merit goods like education, public health, water supply and sanitation, the

actual; expenditure on operation and maintenance constituted a negligible percentage of total

expenditure (~ 1 percent). Committed expenditure on subsidy had increased steeply in 2012-

13 due to subsidy on account of electricity which was increased from Rs 2800 crore in 2011-

12 to Rs 4861 crore in 2012-13, and half of it for providing relief to consumers against

increase in tariff, which was an exercise in populism. More than 40% of the non-

developmental expenditure was on account of interest payments alone. The non-

developmental expenditure incurred on running the day-to-day administration of the state has

been rising at an annual compounded rate of more than 12 percent over this period, limiting

the state’s ability to spend more on development.

Plan expenditure constituted about a third of total expenditure in 2012-13. Capital outlays

were made mostly in respect of economic services for creation of physical infrastructure like

road, power and irrigation works. Capital expenditure grew at a CAGR of 16% during this

period financed partly by revenue surpluses and partly by borrowings.

7

Table 6: Disbursements of Rajasthan Government, 2008-13 (Rs Crore)

2008-

09

2009-

10

2010-

11

2011-

12

2012-

13

CAGR

2008-

13

(i) Revenue Expenditure 34296 40132 44873 53654 63462 16.6

Plan 5771 6287 8752 12416 14235 25.3

Non-Plan 28525 33845 36121 41238 49227 14.6

Committed Expenditure 22684 27179 29317 32859 38257 14.0

Committed Expenditure % of

Revenue Expenditure 66.1 67.7 65.3 61.2 60.3 ----

General Services, of which 12950 15647 16737 18709 20496 12.2

Interest payments 6224 6769 7369 7892 8340 7.6

Social Services 14053 16494 17895 21928 25293 15.8

Economic Services 7267 7972 10220 12744 17408 24.4

Grants-in-aid-and

Contributions

26 19 21 273 265 78.7

(ii) Capital Expenditure 5900 5175 5251 7119 10683 16.0

Plan 5704 4530 5231 7103 10682 15.1

Non-Plan 196 645 20 16 1 -73.3

General Services -145 -577 155 204 249 14.5

Social Services 3088 2506 1836 1997 2840 -2.1

Economic Services 2957 3246 3260 4918 7594 26.6

(iii) Disbursement of

Loans and Advances

340 498 262 1109 2412 63.2

Total Expenditure 40536 45805 50386 61882 76557 17.2

Composition of Expenditure

Developmental Expenditure

(%)

67.7 64.6 66.5 69.4 72.9 -----

Non- Developmental

Expenditure (%)

32.3 35.4 33.5 30.6 27.1 -----

Plan Expenditure (%) 29.2 26.4 27.8 31.5 32.5 -----

Non-Plan Expenditure (%) 70.8 75.3 71.7 66.7 64.3 -----

8

0 10000 20000 30000 40000 50000 60000 70000 80000 90000

Chart 3: Expenditure of Rajasthan

Government by Type of Expenditure (Rs

Crore)

Disbursement of

Loans and Advances

Capital Expenditure

Revenue Expenditure

0

10000

20000

30000

40000

50000

60000

70000

Chart 4: Revenue Expenditure by Services

(Rs Crore)

Grants-in-aid-and

contributions

Economic

Services

Social Services

General Services

11703 14030 14570 15847 17595

6224 6769 7369

7892 8340

3322

4887 5151 5920

6858

1435

1493 2227

3200

5464

2008-09 2009-10 2010-11 2011-12 2012-13

Chart 5: Committed Expenditure (Rs Crore)

Salary Interest Pension Subsidy

9

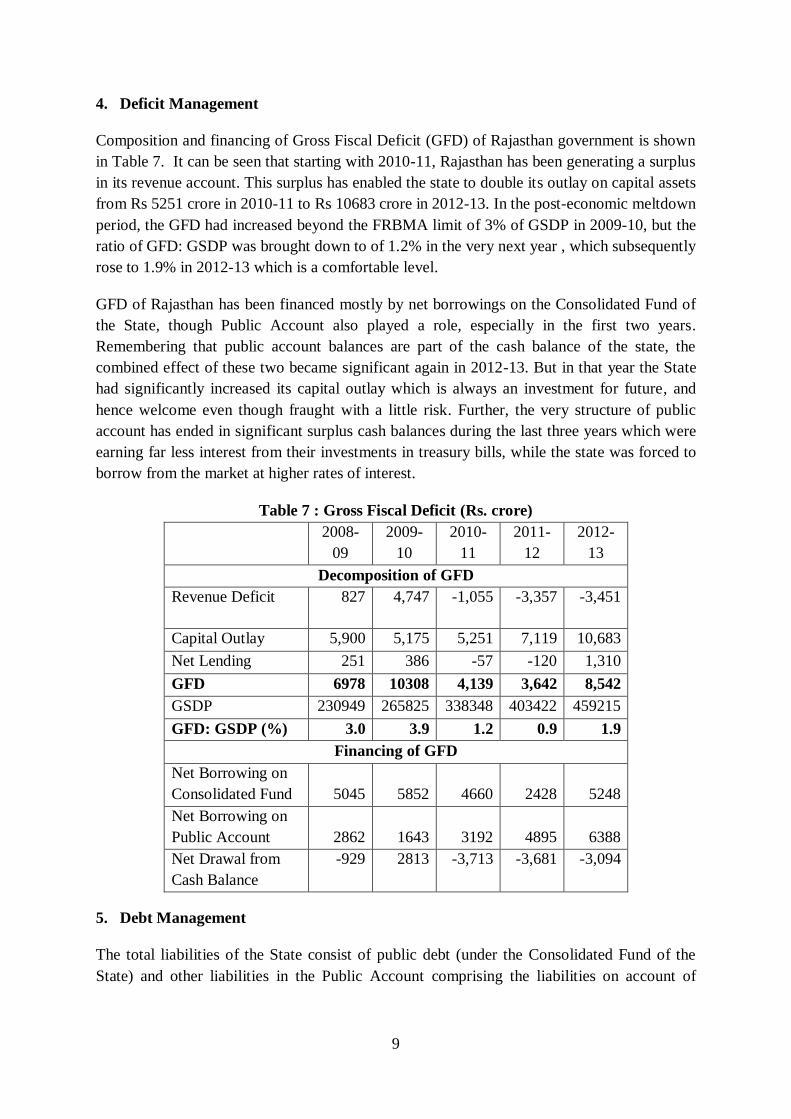

4. Deficit Management

Composition and financing of Gross Fiscal Deficit (GFD) of Rajasthan government is shown

in Table 7. It can be seen that starting with 2010-11, Rajasthan has been generating a surplus

in its revenue account. This surplus has enabled the state to double its outlay on capital assets

from Rs 5251 crore in 2010-11 to Rs 10683 crore in 2012-13. In the post-economic meltdown

period, the GFD had increased beyond the FRBMA limit of 3% of GSDP in 2009-10, but the

ratio of GFD: GSDP was brought down to of 1.2% in the very next year , which subsequently

rose to 1.9% in 2012-13 which is a comfortable level.

GFD of Rajasthan has been financed mostly by net borrowings on the Consolidated Fund of

the State, though Public Account also played a role, especially in the first two years.

Remembering that public account balances are part of the cash balance of the state, the

combined effect of these two became significant again in 2012-13. But in that year the State

had significantly increased its capital outlay which is always an investment for future, and

hence welcome even though fraught with a little risk. Further, the very structure of public

account has ended in significant surplus cash balances during the last three years which were

earning far less interest from their investments in treasury bills, while the state was forced to

borrow from the market at higher rates of interest.

Table 7 : Gross Fiscal Deficit (Rs. crore)

2008-

09

2009-

10

2010-

11

2011-

12

2012-

13

Decomposition of GFD

Revenue Deficit 827 4,747 -1,055 -3,357 -3,451

Capital Outlay 5,900 5,175 5,251 7,119 10,683

Net Lending 251 386 -57 -120 1,310

GFD 6978 10308 4,139 3,642 8,542

GSDP 230949 265825 338348 403422 459215

GFD: GSDP (%) 3.0 3.9 1.2 0.9 1.9

Financing of GFD

Net Borrowing on

Consolidated Fund 5045 5852 4660 2428 5248

Net Borrowing on

Public Account 2862 1643 3192 4895 6388

Net Drawal from

Cash Balance

-929 2813 -3,713 -3,681 -3,094

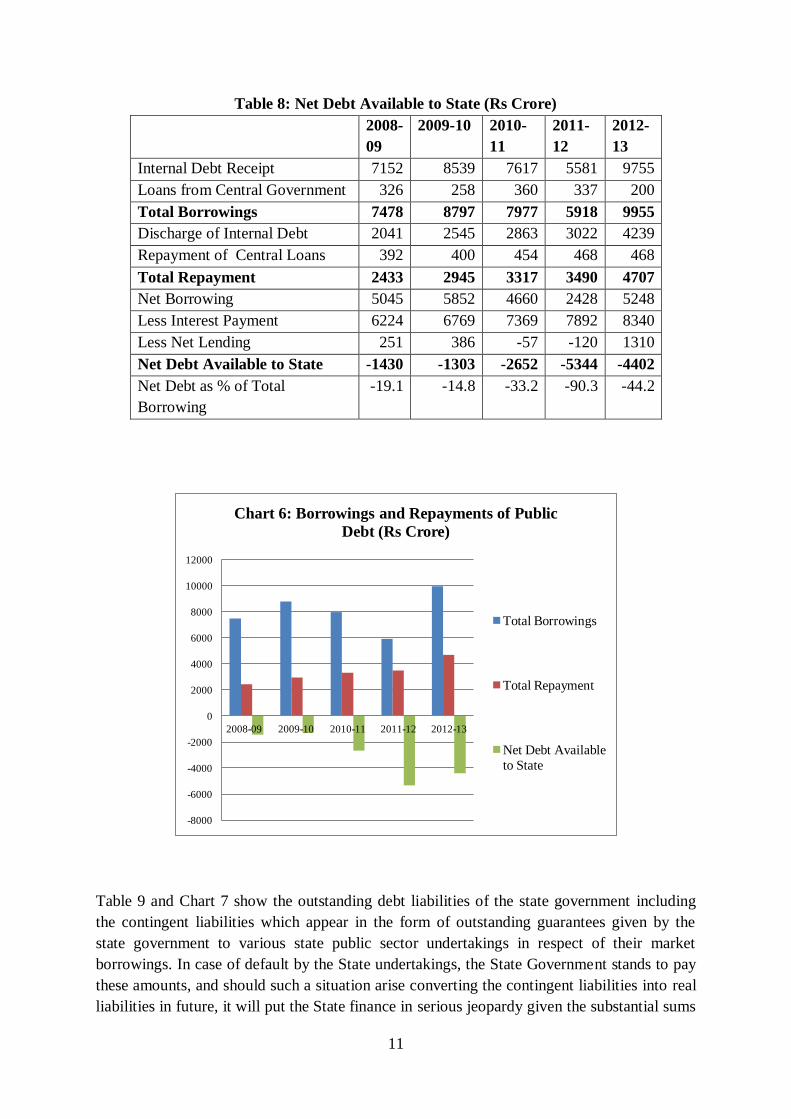

5. Debt Management

The total liabilities of the State consist of public debt (under the Consolidated Fund of the

State) and other liabilities in the Public Account comprising the liabilities on account of

10

Small Savings and Provident Fund, Deposits and Advances and Reserve Funds – some of

these are interest bearing and some are not.

Table 8 shows the debt receipts and repayment liabilities of the state government during the

period 2008-13 and the net debt available to the State after discharging the debt servicing

obligations. In 2012-13, the total repayment of principal by the state government amounted to

Rs. 4707 crore, while the interest payment was much higher at Rs 8340 crore. In each of the

previous years the interest payments were more than double the total repayment of principal

amounts of the outstanding loans. The annual interest burden has increased from Rs 6224

crore to Rs 8340 crore over the past 5 years, at an annual compounded rate of 7.6%, almost in

tandem with the rate of growth of total outstanding liability on which the interest is paid,

which has grown at an annual compounded rate of 8.8%. Most of these repayments were due

to the internal loans from the market as in the case of other states in the post 12th Finance

Commission era; Central loans no longer play any significant role in the borrowing portfolio

of the State. It is also to be noted that interest on Pubic Account balances, which are not

really Government money but are held in trust by the Government on behalf of the

depositors, are paid from the Consolidated Fund of the State, sometimes even when the State

did not need those balances to borrow from. It was rather a question of availability rather than

of need and that introduces some distortion in the whole scheme of borrowing, the basic

purpose behind which is to create income generating capital assets for the State.

Public debt can be a powerful agent of economic growth, if it is utilised for the creation of

productive assets. But as can be seen from Table 8, the State could never utilise the debt

resources for creating productive assets. They were completely used up to discharge the

existing debt servicing obligations including payment of interests on outstanding loans and

were not even adequate for that purpose. In none of the years, anything accrued to the state

out of its borrowed funds; rather the state had to spend its own precious resources for

discharging some of its existing debt obligations. Even though the borrowings have been

growing steeply, this draining of the state’s own resources also continues at an increasing

pace as easily seen from Chart 6, shrinking the fiscal space available to the State. Only in

2012-13, the situation appears to have improved marginally.

If unchecked this has the potential of upsetting the gains made by the State in managing its

finances; fiscal consolidation cannot be achieved if this state of affairs is allowed to continue.

The government must find a way to reduce its borrowings by curtailing unproductive

expenditure and expenditure on administration, which constitutes a significant part of its total

expenditure as we have seen earlier.

11

Table 8: Net Debt Available to State (Rs Crore)

2008-

09

2009-10 2010-

11

2011-

12

2012-

13

Internal Debt Receipt 7152 8539 7617 5581 9755

Loans from Central Government 326 258 360 337 200

Total Borrowings 7478 8797 7977 5918 9955

Discharge of Internal Debt 2041 2545 2863 3022 4239

Repayment of Central Loans 392 400 454 468 468

Total Repayment 2433 2945 3317 3490 4707

Net Borrowing 5045 5852 4660 2428 5248

Less Interest Payment 6224 6769 7369 7892 8340

Less Net Lending 251 386 -57 -120 1310

Net Debt Available to State -1430 -1303 -2652 -5344 -4402

Net Debt as % of Total

Borrowing

-19.1 -14.8 -33.2 -90.3 -44.2

Table 9 and Chart 7 show the outstanding debt liabilities of the state government including

the contingent liabilities which appear in the form of outstanding guarantees given by the

state government to various state public sector undertakings in respect of their market

borrowings. In case of default by the State undertakings, the State Government stands to pay

these amounts, and should such a situation arise converting the contingent liabilities into real

liabilities in future, it will put the State finance in serious jeopardy given the substantial sums

-8000

-6000

-4000

-2000

0

2000

4000

6000

8000

10000

12000

2008-09 2009-10 2010-11 2011-12 2012-13

Chart 6: Borrowings and Repayments of Public

Debt (Rs Crore)

Total Borrowings

Total Repayment

Net Debt Available

to State

12

involved. This carries a risk for the State and the repayment of loans by these undertakings

needs to monitored by the State government to minimise this risk.

Table 9 also shows the sustainability of the public debt of the State Government. A state can

afford of a higher level of debt if its income is high enough to enable the state to service its

debt without putting its finances into unnecessary strain. The determinants of sustainability

are therefore the relative rates of growth between the State income (GSDP of the State) and

the cost of additional borrowings for which the average interest on outstanding debt can serve

as a proxy. The condition for debt stabilisation implies that the State income should grow

faster than the cost of borrowings. In addition, the primary balance of the state is important;

the state should not have a large negative balance in its primary account. If these two

conditions are satisfied, the debt to GSDP ratio should stabilise or fall.

In the case of Rajasthan, we see that both these conditions are satisfied, even if we take the

total outstanding liabilities including those on public account into consideration, given the

healthy growth of GSDP of the State. Primary account of the State also started showing

substantial surpluses since 2010-11 and even though it has turned into a small deficit in 2012-

13, the smallness of this deficit is unlikely to alter the inherent strength of economic

fundamentals of the State. But there is no alternative to limit the borrowing as we have

pointed out earlier so as to contain the debt servicing obligations of the state.

Table 9: Sustainability of Public Debt (Rs Crore)

2008-

09

2009-

10

2010-

11

2011-

12

2012-

13

Public Debt Outstanding 58766 64618 69278 71706 76954

Outstanding Liability in

Public Account2 25257 26915 30007 34854 40855

Total Outstanding

Liabilities including Net

Public Account Liabilities 84023 91533 99285 106560 117809

Outstanding Guarantees 27765 39069 50692 60711 75546

Debt : GSDP Ratio 25.4 24.3 20.5 17.8 16.8

Primary Deficit 1146 4829 -3230 -4250 202

Growth Rate of GDSP (%) 18.5 15.1 28.6 21.9 14.7

Average Interest Rate on

Borrowings 11.1 11.0 11.0 11.2 11.2

Growth Rate of

Outstanding Public Debt

(%) 9.4 10.0 7.2 3.5 7.3

Growth Rate of

Outstanding Liabilities

(%) 9.2 8.9 8.5 7.3 10.6

2 This excludes balances in the adjustment-nature accounts under Suspense and Remittance transactions.

13

6. Comparative Fiscal Performance

Lastly, we compare the fiscal parameters of Rajasthan with other members of the so-called

unceremonious BIMARU group of states as well as with the neighbouring states of Gujrat,

Punjab and Haryana. The parameters considered are shown in Table 10, from which we can

see mixed results in respect of Rajasthan’s performance vis-à-vis the other states. Overall,

Rajasthan’s performance lies somewhere in the middle within this group of states.

Table 10 : Comparison of Major Fiscal Ratios (2012-13)

Ratio of

Figures in percent

(i)

Revenue

Deficit

(ii)

Capital

Outlay

(iii)

Non-Dev.

Rev. Exp

(iv)

Interest

Payment

(v)

Own

Revenue

(vi)

Gross

Transfers

(vii)

State’s

Own Tax

(viii)

Debt

State to

GFD GFD Agg. Dis Rev. Exp Rev. Exp. Agg. Dis. GSDP GSDP

Bihar -77.9 146.4 28.2 8.6 31.9 63.8 6.0 19.4

Madhya Pradesh -79.2 122.8 22.2 7.4 61.3 42.2 8.2 17.9

Rajasthan -40.4 125.2 26.8 13.1 67.2 31.4 6.6 16.8

Uttar Pradesh -26.9 123.9 36.2 12.0 50.5 44.5 7.4 21.1

Gujarat -31.2 119.0 26.3 17.5 86.0 25.7 8.0 20.4

Punjab -79.3 20.5 44.7 17.3 63.9 16.3 7.9 25.0

Haryana 42.8 55.6 26.8 13.0 74.2 12.0 6.9 14.9

7. Conclusion

Rajasthan today is a state marching towards development and progress along with the other

states of India. Its public finances are in a healthy state though there are areas of concern. Its

own revenues have registered appreciable growth over the period of this study and the

0

20000

40000

60000

80000

100000

120000

140000

2008-09 2009-10 2010-11 2011-12 2012-13

Chart 7: Outstanding Liabilites (Rs Crore)

Public Debt Outstanding Total Outstanding Liabilities

Outstanding Guarantees

14

dependence of Central grants has consequently been much reduced. But the ever-growing

committed expenditure on salary, pension, interest and subsidy restricts the scope of

developmental expenditure. The state has kept its fiscal deficit under control, but borrowings,

even though these do not pose any immediate danger in view of the high growth of its

economy, need to be carefully calibrated and controlled as the state is repaying far more than

what it borrows. It needs to cut down on subsidy and other unproductive expenditure to bring

this problem under control, which would also allow the State more leeway to increase its

capital outlay.