PROCESS GOVERNANCE & SUSTAINABILITY - ABEPRO

15

PROCESS GOVERNANCE & SUSTAINABILITY: THE CASE OF CEMENT INDUSTRY Carlos Eduardo Durange de Carvalho Infante (UFRJ) [email protected] Paula Michelle Purcidonio (UFRJ) [email protected] Rogerio de Aragao Bastos do Valle (UFRJ) [email protected] This article presents a conceptual framework that aligns process governance and sustainability. This study is justified by the absence of literature that interrelates both issues and allows organizations to achieve their sustainable strateggies with focus on stakeholders, through the process governance. To achieve these goals, was summarize an extensive literature on the topics and from the reviews built the conceptual framework of the coupled Process Governance & Sustainability, based also in the study by Braganza (2000). This structure is recommended, as was seen in the example, for the extinction of the paradigm of sustainable use of non-routine processes, whether internal or external organizations. The ELECTRE III method was used in order to obtain the best ranking of the alternatives. Palavras-chaves: Process Governance, Sustainbility, Sustainable Governance, ELECTRE III XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of PROCESS GOVERNANCE & SUSTAINABILITY - ABEPRO

PROCESS GOVERNANCE &

SUSTAINABILITY: THE CASE OF

CEMENT INDUSTRY

Carlos Eduardo Durange de Carvalho Infante (UFRJ)

Paula Michelle Purcidonio (UFRJ)

Rogerio de Aragao Bastos do Valle (UFRJ)

This article presents a conceptual framework that aligns process

governance and sustainability. This study is justified by the absence of

literature that interrelates both issues and allows organizations to

achieve their sustainable strateggies with focus on stakeholders,

through the process governance. To achieve these goals, was

summarize an extensive literature on the topics and from the reviews

built the conceptual framework of the coupled Process Governance &

Sustainability, based also in the study by Braganza (2000). This

structure is recommended, as was seen in the example, for the

extinction of the paradigm of sustainable use of non-routine processes,

whether internal or external organizations. The ELECTRE III method

was used in order to obtain the best ranking of the alternatives.

Palavras-chaves: Process Governance, Sustainbility, Sustainable

Governance, ELECTRE III

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario.

Belo Horizonte, Brazil, 04 to 07 October – 2011

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

2

1. Introdução

In recent years, the importance of generating sustainable business for productive

organizations has become evident. However, despite some initiatives, the viability of

sustainable strategies still constitutes a great organizational challenge.

Organizational sustainability is focused on the future and is attained through the allocation of

current resources, without regard to present decisions and their implications for the reduction

of resources in the long term this requires treating any cost in the present as an investment in

the future (ARAS & CROWTHER, 2008).

Organizations should be seen as a complementary part of social, economic and environmental

systems, as they involve the measurement of financial effects and the creation of values,

increasing the value chain not just for today but also for the long term (HART, 1997).

Just as there has been an increase in interest in and concern for sustainability, there has been a

similar increase in interest in governance, which is evidenced by the various uses of the term

found in the literature, such as: ―corporate governance‖, ―governance of information

technology‖ (IT), ―governance of the global value chain‖ and ―process governance‖.

Jeston and Nelis (2008) say that process governance, which we describe below, is more

important to longevity and long-term success in creating an organization focused on process

and high performance management.

Within this context, the aim of this paper is to propose a conceptual framework for sustainable

governance that integrates process governance with sustainability.

This structure suggests that in order to meet new environmental and social demands,

organizations can use the proposed model to achieve consistent business management, thus

gaining greater external stability and ability to achieve internal goals.

The method used in this paper utilized an extensive literature search, seeking to appropriate

models and concepts already developed and published by other authors regarding process

governance and sustainability. The proposed conceptual framework (Figure 1) was based on

the study by Braganza and Lambert (2000).

To illustrate the conceptual framework was applied in two companies the ELECTRE III

method, which uses the outranking of alternatives. This method appropriates concepts of

qualitative and quantitative solutions, in its origin fuzzy formulations.

2. Perspectives From The Literature

2.1 Current thinking on Process Governance

Over the years, the term governance instituted by Williamson (1985), was being used and

adapted for other subject areas, with emphasis on organizational theory, whenever wishes to

define a structure of power or control and positioning them into a given context.

Adaptations of the governance term emerge from the competitive landscape in which business

leaders are faced with the difficult task of leading their organizations into unknown

environments, where traditional governance mechanisms become insufficient (BRAGANZA

& LAMBERT, 2000; PRAHALAD & OOSTERVELD, 1999).

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

3

While the Corporate Governance and IT Governance have been substantially studied, the

literature focused on Process Governance is still incipient with little research in this area

(KORHONEN, 2007).

Among the papers presented in the literature on Process Governance, this paper was based on

the following authors: Markus and Jacobson (2010); Spanyi (2010); Jeston and Nelis (2008),

Korhonen (2007a), Korhonen (2007b); Rosemann (2006a); Rosemann (2006b) Bruin and

Rosemann (2006); Braganza and Lambert (2000).

Jeston and Nelis (2008) say that Process Governance is necessary to ensure that the strategy

and project execution/processes have good performance and must be aligned. A few

organizations have a fragmented approach to processes governance, generating little in the

strategy and governance link between strategy and execution of the project and processes.

Korhonen (2007) complements the Process Governance is needed to address the coordination

between organizational units and eliminate the gap between organizational strategies and

work processes. In the context of this paper, the Process Governance is concerned with the

alignment of strategy with organizational processes.

Process governance should be adopted by organizations as a tool to understand the needs of

an increasingly competitive market and to identify sudden changes which require rapid

adaptation to achieve strategic business objectives.

The starting point for the discussion of sustainability must be the Brundtland Report, which

has characterized the main concept of sustainable development (WCED, 1987), which for

Baumgartner & Ebner (2010) is the internalization of external activity which causes

economic, social and environmental issues, and prioritizing the search for long-term

investments in order to create a long corporate value chain. The economic dimension of

corporate sustainability is often referred to as the "generic dimension" (Baedeker et al., 2002),

and covers general organizational conditions that must be met in order to remain in the market

in the long term. A country's productive base--which is the source of its well-being and

includes more than just its capital assets--should last for generations and not be allowed to

decay (AGLIARDI, 2011).

An increasing number of governmental sectors are evaluating the impact of key policies. A

strategic environmental assessment is done to mitigate the impacts of major organizations on

their stakeholders (PETIT & FREDERIKSEN, 2011). Organizations must implement action

plans committed to developing sustainably and combatting system disintegration (TABBUSH

et al., 2008), ultimately achieving the three pillars of sustainability.

Nowadays, sustainable innovation has become a focal point for organizations seeking to

realize activities and commitments—along with the bottom line. Recent literature on

sustainable enterprise development points to the importance of integrating corporate and

social responsibility (BOS-BROUWERS, 2010). By creating business value, organizations,

NGOs and governments have achieved promising results in this field and new concepts have

emerged, although they are still in their initial stages of development (GREENWOOD, 2007).

The challenge of systems integration, according to Holdren (2007), includes the sustainable

improvement of operations and activities. Sustainability is a basis for the improvement of

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

4

practices and services, and therefore unsustainable practices should be eliminated.

2.2 Current thinking on Sustainability

Sustainability, in this paper, has the importance of directs the organizational responsibilities,

guiding them to relevant activities to the decision making.

The starting point for the discussion of sustainability must be the Brundtland Report, which

has characterized the main concept of sustainable development (WCED, 1987), which for

Baumgartner & Ebner (2010) is the internalization of external activity which causes

economic, social and environmental issues, and prioritizing the search for long-term

investments in order to create a long corporate value chain. The economic dimension of

corporate sustainability is often referred to as the "generic dimension" (Baedeker, 2002), and

covers general organizational conditions that must be met in order to remain in the market in

the long term. A country's productive base--which is the source of its well-being and includes

more than just its capital assets--should last for generations and not be allowed to decay

(AGLIARDI, 2011).

An increasing number of governmental sectors are evaluating the impact of key policies. A

strategic environmental assessment is done to mitigate the impacts of major organizations on

their stakeholders (PETIT AND FREDERIKSEN, 2011). Organizations must implement

action plans committed to developing sustainably and combatting system disintegration

(Tabbush et al., 2008), ultimately achieving the three pillars of sustainability.

Nowadays, sustainable innovation has become a focal point for organizations seeking to

realize activities and commitments—along with the bottom line. Recent literature on

sustainable enterprise development points to the importance of integrating corporate and

social responsibility (BOS-Brouwers, 2010). By creating business value, organizations, NGOs

and governments have achieved promising results in this field and new concepts have

emerged, although they are still in their initial stages of development (GREENWOOD, 2007).

The challenge of systems integration, according to Holdren (2007), includes the sustainable

improvement of operations and activities. Sustainability is a basis for the improvement of

practices and services, and therefore unsustainable practices should be eliminated.

3. Conceptual Framework

The conceptual framework presented in Figure 1 is an analysis of the integration of process

governance and sustainability. The structure is explained below.

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

5

Figure 1: The Integration of Process Governance & Sustainability

3.1 Impacting Factors

Over the past several decades, the critical importance of environmental and socioeconomic

problems facing societies and nations around the world has been well-established.

Environmental and natural resource issues have grown in scope and urgency. Impacting

factors have been intensively studied in order to promote a reduction in negative actions by

the systems involved in the entire production chain (HARRIS, 2006). As shown in Figure 1,

these are classified into three systems: economic, environmental and social.

Economic System: In order to assist governments in making important

decisions, all economic phases are considered as major sources of analysis and interpretation

(DOWNS, 1957). The negative impacts caused by this system are fear-provoking and can

cause a cascade of events known as a "negative chain of development". Unemployment, lack

of consumption, low expectations and rising prices are consequences of an economic crisis.

Positive impacts can bring transformation along with new activities in organizations as well as

better social prospects. Economic growth is the principal objective for any country (WORLD

BANK 1992). Historically, this goal has not been simple nor easy to achieve. This is the result

of a number of factors—including interactions and changes in production structures,

technology and the social economy (Kuznets, 1974)--and may negatively impact a company‘s

strategic decisions if they are not sustainably analyzed;

Social System: Structures of greater complexity such as social systems cannot

be explained merely by aggregating their constituent elements or analyzing the typology of

their structures. Rather, it is necessary to analyze the relationship between the system and its

environment and of the elements that constitute them (NICOLESCU, 2009). Social systems

have core activities related to the differential and initial expectations of each stakeholder.

Impacts--both positive and negative--affect those decisions, creating a new form or cycle of

organizational orientation. Membership features direct consumption and determines the

degree to which services and activities build the organizations;

Environmental System: Naturally, humans participate in the environmental

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

6

system as they do in any subsidiary. However, human society is designed to exploit the

environment to produce wealth. Its paradoxical role is to use natural wealth in order to

produce capitalist wealth (COMMONER, 1971). Organizations, along with the stakeholders

who take part in them, are directly impacted by these systems, thus making their actions more

strategic and targeted. Therefore, impacting factors are integrated into systems that make use

of current dynamics (economic, social and environmental) to allocate their respective interests

and responsibilities. Impacts are generated, but they are directing real expectations, resulting

in the functional activity of organizations.

3.2 Organization

For-profit organizations face the difficult task of reviewing their essential goal of maximizing

profits. Organizational leaders are subject to a reality that demands a comprehensive

understanding of the role of the organization in society--not only as an agent of the financial

market. Organizations are increasingly required by society to consider the consequences of

their environmental, social and economic activities.

A social dialogue with stakeholders allows the organization to manage its risks and

opportunities before they are rendered moot. Risk management is probably one of the most

significant reasons for organizations to develop sustainability reporting (BRANDÃO &

SANTOS, 2007).

Environmentally, organizations should go beyond compliance and base their activities on the

use of tools such as Eco-efficiency, Life Cycle Management (LCM) and the Global Reporting

Initiative (GRI), which are fundamental to making their business models compatible with

sustainable strategies.

Regarding the creation of economic value in the long term, companies should seek "good

profit" instead of "maximum profit", determined by how results are obtained (BRANDÃO &

SANTOS, 2007).

For organizations responding to this challenge, it has become essential to include the Triple

Bottom Line model (TBL) in their strategies. This model--originated by Elkington (1998)--is

based not only on a company‘s results in the economic system, but also on its social and

environmental impacts. All of these factors are considered together in a seamless manner.

The conceptual framework for sustainable governance (Figure 1) proposes that the alignment

of organizational strategy, stakeholder expectations, activities and processes is essential in

creating sustainable businesses. Thus, sustainability is embraced by the organization and

becomes part of its strategic and operational decisions.

3.3 Stakeholders

Stakeholders are individuals or groups that participate in a decision-making process. Freeman

(1984) notes that they are essential participants in strategic business planning. They can exert

power over the actions of organizations, as well as define the line strategy that the company

will adopt. Stakeholders are external agents to the organization (as are customers, suppliers

and regulatory agencies) as well as external agents (as are employees and affiliates).

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

7

In order to further the integration of stakeholders with the organization, it is essential to better

manage the engagement between the two parties.

Many organizations place a low priority on their stakeholders, resulting in a failure to comply

with their wishes. Engagement creates on impression of corporate responsibility

(GREENWOOD, 2007). The act of engagement benefits both parties. In the Conceptual

Framework (Figure 1), a parallelism can be observed between expectations and motivations,

and this can be used to ensure better integration between stakeholders--whether internal or

external--and organizations.

• Motivations: Stakeholders have motivations--such as the business‘s internal situation, new

sources of negotiation, the need for new technologies, new sources of production, etc.--which

are absorbed by private organizations These motivations lead to new corporate strategies, and

are internalized by a new organizational culture, as the prioritization of these motivations

fosters innovative courses in businesses and organizations (BRAGANZA & LAMBERT,

2000).

• Expectations: Stakeholders have expectations, which include needs, desires, legal

obligations, specifications and requirements (Braganza & Lambert, 2000). These expectations

largely promote motivation within an organization. From the standpoint of process

governance, stakeholders are concerned with the changes inherent to the factors impacting

and contributing to a new application as well as the front organization of the structural model

appropriate to their demands and expectations. It is hoped that there will be a debate regarding

the important theme of 'engagement', because this theme justifies the importance of

stakeholder involvement with organizations, aiming to facilitate an understanding of each

party and their views and demands (NOLAND & PHILLIPS, 2010).

3.4 Process Governance

To better understand the topic of process governance, it is important to make a distinction

between the terms ―management‖ and ―governance‖. Management refers to tasks performed

to ensure regulation of labor and the governance refers to management‘s organization—its

goals and principles. Governance is an organizational structure with defined responsibilities,

decision rights, and policies as well as rules that define managers‘ performance limits

(HARMON, 2008).

Process governance is simply seen as a necessary element to ensure the coordination of

initiatives between processes and functional units in order to eliminate non-alignment

between strategy and organizational efforts of processes (KORHONEN, 2007). In summary,

although some distinctions exist, the definitions have some common ground--that is,

governance acts by the processes‘ orientation being aided by a higher purpose. Roles and

tools are then aligned with this objective.

The conceptual framework for process governance proposed by Braganza & Lambert (2000)

provides specific links between strategy, business processes, operational activities and

governance problems that business leaders need to address in order to integrate their

organizations at the strategic and operational levels. The table also highlights the implications

that business leaders face when it comes to governance. As a result, this structure becomes an

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

8

important tool for organizations in an environment in which the implementation of sustainable

strategies still presents great challenges for them.

3.5 Sustainability

In addition to the efforts made by NGOs and governments, organizations are also beginning to

attach importance to sustainable activities. The conceptual framework presented in Figure 1

demonstrates exactly this principle: sustainable activities resulting from the better integration

of stakeholders and organizations. The concept of sustainable development (BRUNDTLAND,

1987), gave rise to what is now called ―sustainable organizational development‖.

Organizations focusing their activities on sustainable results integrate the three main pillars of

sustainability: economic, social and environmental (EBNER & BAUMGARTNER, 2006).

Business strategies focusing on these three pillars are prime examples of direction and

intention. Leaders identify business objectives and make plans to achieve them (BRAGANZA

& LAMBERT, 2000). Some strategies are diagnosed according to the following dimensions,

in terms of organizations, as defined by Dyllick, (2000); Hardtke and Prehn, (2001),

Schaltegger et al. (2002), Baumgartner (2005):

Introverted: Risk Mitigation;

Spills: Legitimating Strategy;

Registrar: Efficiency;

Visionary: Global Sustainability.

Organizations defined by these four strategic dimensions reach the optimal threshold of

sustainability, in accordance with their sizes and profiles. The main goal of organizational

leaders is to establish a specific and effective strategy, resulting in sustainable process value.

The points of focus are integration (as shown in Figure 1), the development of services, the

motivations of stakeholders and the organization‘s scope. Sustainability is directly linked to

process, and both together contribute to the emergence of a so-called ―governance of

sustainability‖.

Organizational sustainability is a priority in establishing a better understanding of the

strategies and the relationships of established processes. Sustainable governance is the best

concept available for developing an integrated approach toward service organizations and

stakeholders.

3.6 Sustainable Governance

The importance of generating sustainable business for productive organizations has become

evident. However, Brandão (2009) says that there is a clear gap in the discourse regarding the

effective alignment of organizations and sustainability, and most of the time the actions taken

are much smaller than reported. In this context, the conceptual framework proposed in this

paper can help organizations to eliminate gaps between the sustainability objectives set out in

strategic planning and the organization‘s activities, thereby allowing for the dissemination of

effectively implemented sustainable actions and creating greater transparency in

organizational operations.

In Figure 1, this paper presents a conceptual framework called sustainable governance that

combines two concepts: process governance and sustainability. It is therefore understood that

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

9

the promotion of sustainability governance of organizational sustainability through process

governance is very significant. Process governance enables the organization's strategy to

focus on dialogue with stakeholders--whose demands and expectations are transformed. In

doing so, organizational activities are internalized, resulting in a sustainable business. Thus,

sustainability is prioritized and absorbed into the activities of organizations.

4. Sustainable Governance Example

To illustrate the conceptual framework presented in this paper, we analyzed the 2009

Sustainability Report of two cement companies. Such companies will be featured in this

paper, as Alpha and Beta, to preserve their identities.

Alpha Company, founded in 1906 in Mexico, has 47,000 employees around the world to

produce, distribute and sell building materials such as cement, aggregates and concrete. It has

branches in America, Europe, Africa and Asia.

Beta Company, founded in 1918 and belongs to a family business group in Brazil, which has

a portfolio of products, like cement, aggregates, cement, lime and agricultural lime. With

11,700 employees in America and Europe.

The multicriteria method used in this analysis was the ELECTRE III, whose main result is the

ranking of the main alternatives.

4.1 Overview of ELECTRE III

ELECTRE III first distinguishes between indifference and strict preference and then extends

this by introducing a ‗‗zone of hesitation‘‘ or weak preference as a buffer between preference

and indifference. The resulting double threshold model is

aPb (a is strongly preferred to b), ↔ g(a) – g(b) > p;

aQb (a is weakly preferred to b), ↔ q < g(a) – g(b) ≤ p; (1)

aIb (a is indifferent to b; and b to a), ↔ │g(a) – g(b) │ ≤ q.

Using thresholds, ELECTRE builds an outranking relation S. To say aSb means that ‗‗a is at

least as good as b‘‘ or ‗‗a is not worse than b‘‘. The assertion aSb is accepted if two

conditions hold:

A concordance condition: a majority of criteria are concordant with aSb

(majority principle), and

A non-discordance condition: none of the non-concordant (discordant) criteria

strongly refute aSb (respect of minorities principle).

aSjb means that ‗‗a is at least as good as b with respect to the jth criterion‘‘, j = 1, . . . , r. The

jth criterion is in concordance with the assertion aSb if and only if aSjb. That is, if gj(a) ≥

gj(b) - qj. Thus, even if gj(a) is < gj(b) by an amount up to qj, it does not contravene the

assertion aSjb and therefore is in concordance. When gj(b) > gj(a) + pj, i.e. when b is strictly

preferred to a for criterion j, then criterion j is clearly not concordant with the assertion aSb.

As a consequence, a partial concordance index cj(a, b) is defined as follows for each criterion

j:

1, if gj(a) + qj ≥ gj(b);

cj(a,b) = 0, if gj(a) + pj ≤ gj(b); j = 1; . . . ; r; (2)

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

10

Let kj be the importance coefficient for criterion j. An overall concordance index C(a,b),

which measures the extent to which we are in harmony with the assertion that ‗‗a is at least as

good as b‘‘, is then defined as

(3)

But what disconfirming or ‗‗disharmonious‘‘ evidence is there? How can a minority view be

respected? In other words, is there any discordance associated with the assertion aSb? To

calculate discordance, a further threshold called the veto threshold is defined. The veto

threshold, vj, allows for the possibility of aSb to be refused totally if, for any one criterion j,

gj(b) > gj(a) + vj. Clearly, we should have vj ≥ pj. The discordance index Roger (2000);

Roger & Bruen (1998) for each criterion j, dj(a,b) is calculated as

0, if gj(a) + pj ≥ gj(b)

dj(a,b) = 1, if gj(a) + vj ≤ gj(b); j = 1; . . . ; r (4)

A discordance matrix is produced for each criterion. Unlike concordance, which results from

a cumulative aggregation of partial concordances, one discordant criterion is sufficient to

discard outranking. For each pair of projects (a,b) ∈ AxA, we have a concordance and a

discordance measure. The final step in the model building phase is to combine these measures

and produce a measure of the degree of outranking; that is, a credibility matrix which assesses

the strength of the assertion that ‗‗a is at least as good as b‘‘. The credibility degree for each

pair (a, b) ∈ AxA is defined as

C(a,b), if dj(a,b) ≤ C(a,b) for all j where J(a,b) is the set of

S(a,b) = criteria

C(a,b) , such that dj(a,b) > C(a,b) (5)

This formula assumes that if the strength of the concordance exceeds that of the discordance,

then the concordance value should not be modified. Otherwise, the assertion that aSb must be

questioned and C(a,b) modified according to the above equation. If the discordance is 1.00 for

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

11

any criterion j, then we have no confidence that aSb; therefore, S(a,b) = 0.00. This concludes

the construction of the outranking model. ‗‗Objective‘‘ data are captured in the performance

matrix (ROSS, 2004; ROY, 1996; ROY, 1993; ROY, 1990). ‗‗Subjective‘‘ preference data

are gathered from decision makers in the form of veto thresholds and weights (BUCHAMAN

& VANDERPOOTEN, 2007).

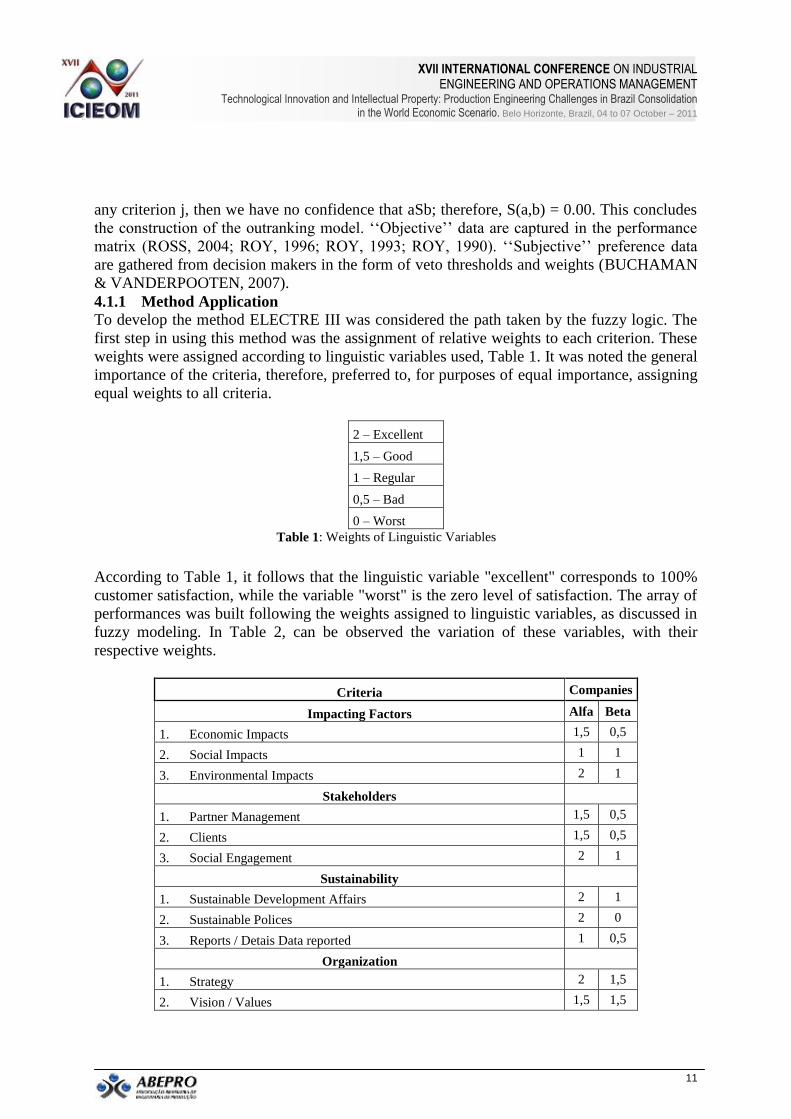

4.1.1 Method Application

To develop the method ELECTRE III was considered the path taken by the fuzzy logic. The

first step in using this method was the assignment of relative weights to each criterion. These

weights were assigned according to linguistic variables used, Table 1. It was noted the general

importance of the criteria, therefore, preferred to, for purposes of equal importance, assigning

equal weights to all criteria.

2 – Excellent

1,5 – Good

1 – Regular

0,5 – Bad

0 – Worst

Table 1: Weights of Linguistic Variables

According to Table 1, it follows that the linguistic variable "excellent" corresponds to 100%

customer satisfaction, while the variable "worst" is the zero level of satisfaction. The array of

performances was built following the weights assigned to linguistic variables, as discussed in

fuzzy modeling. In Table 2, can be observed the variation of these variables, with their

respective weights.

Criteria Companies

Impacting Factors Alfa Beta

1. Economic Impacts 1,5 0,5

2. Social Impacts 1 1

3. Environmental Impacts 2 1

Stakeholders

1. Partner Management 1,5 0,5

2. Clients 1,5 0,5

3. Social Engagement 2 1

Sustainability

1. Sustainable Development Affairs 2 1

2. Sustainable Polices 2 0

3. Reports / Detais Data reported 1 0,5

Organization

1. Strategy 2 1,5

2. Vision / Values 1,5 1,5

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

12

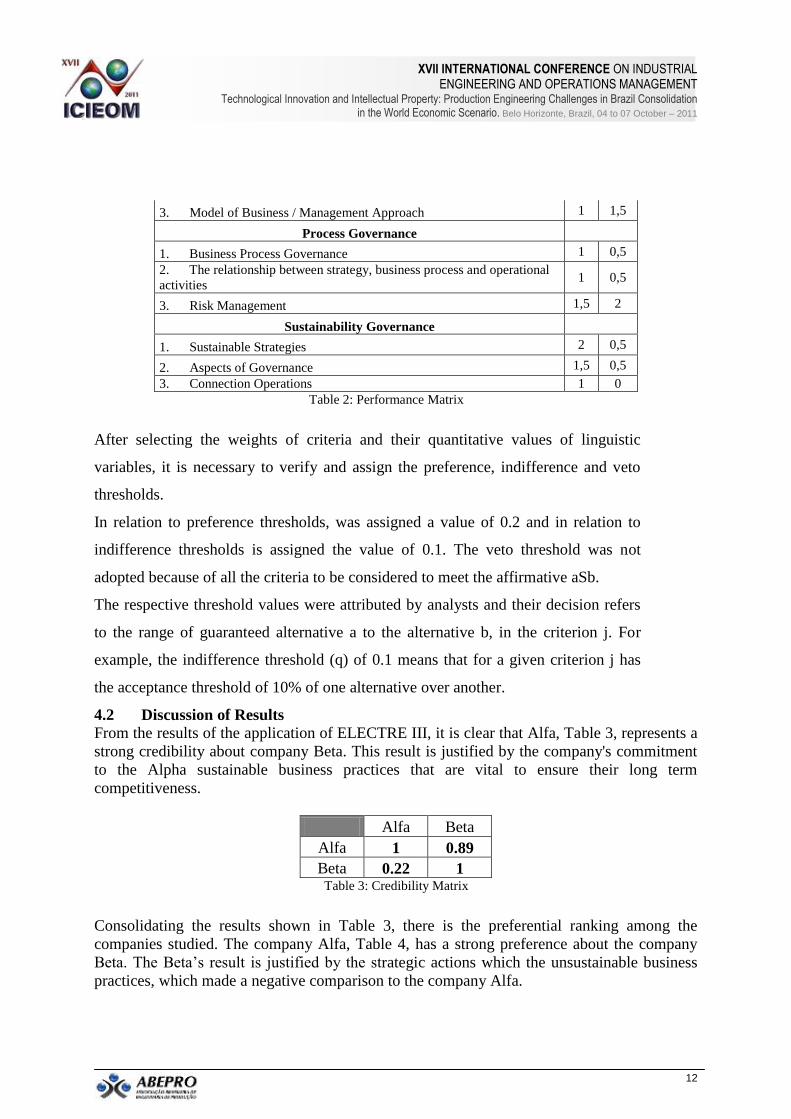

3. Model of Business / Management Approach 1 1,5

Process Governance

1. Business Process Governance 1 0,5

2. The relationship between strategy, business process and operational

activities 1 0,5

3. Risk Management 1,5 2

Sustainability Governance

1. Sustainable Strategies 2 0,5

2. Aspects of Governance 1,5 0,5

3. Connection Operations 1 0

Table 2: Performance Matrix

After selecting the weights of criteria and their quantitative values of linguistic

variables, it is necessary to verify and assign the preference, indifference and veto

thresholds.

In relation to preference thresholds, was assigned a value of 0.2 and in relation to

indifference thresholds is assigned the value of 0.1. The veto threshold was not

adopted because of all the criteria to be considered to meet the affirmative aSb.

The respective threshold values were attributed by analysts and their decision refers

to the range of guaranteed alternative a to the alternative b, in the criterion j. For

example, the indifference threshold (q) of 0.1 means that for a given criterion j has

the acceptance threshold of 10% of one alternative over another.

4.2 Discussion of Results

From the results of the application of ELECTRE III, it is clear that Alfa, Table 3, represents a

strong credibility about company Beta. This result is justified by the company's commitment

to the Alpha sustainable business practices that are vital to ensure their long term

competitiveness.

Alfa Beta

Alfa 1 0.89

Beta 0.22 1 Table 3: Credibility Matrix

Consolidating the results shown in Table 3, there is the preferential ranking among the

companies studied. The company Alfa, Table 4, has a strong preference about the company

Beta. The Beta‘s result is justified by the strategic actions which the unsustainable business

practices, which made a negative comparison to the company Alfa.

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

13

Alfa Beta

Alfa I P

Beta P- I

Tabela 4: Preferencial Ranking

5. Conclusion

This research paper has developed a conceptual framework called ―sustainable governance‖

that combines two concepts: process governance and sustainability. This integration enables

organizations to eliminate the gap between sustainable strategies and organizational activities

by interacting with their stakeholders.

The example studied, described the importance of effective implementation of sustainable

strategies, as can be seen in the of company Alfa success.

Overall, we conclude that the Sustainable Governance involves aligning of the three levels:

strategic, tactical and operational by organizations. Is also important that the stakeholders

engagement is fundamental to ensure the longevity of business. Likewise, the maintenance of

long-term business cannot be based only on economic results, but also in social and

environmental aspects, all of them seamlessly.

Referências

AGILARDI, E. Sustainability in Uncertain Economies. Environ Resource Econ, Vol. 48 No. 1, pp. 71 – 82,

2011.

ARAS, G. & CROWTHER, D. Governance and Sustainability. An investigation into the relationship between

corporate governance and corporate sustainability. Management Decision. Vol. 46 No. 3, pp. 433 – 448, 2008.

BAEDEKER, C. & HAEUER, P. & KLEMISCH, H. & ROHN, H. Handbuch zur Anwendung von SAFE –

Sustainability Assessment for Enterprises. Institut für Klima, Umwelt, Energie GmbH: Wuppertal, 2002.

BAUMGARTNER, R.J. & EBNER, D. Corporate Sustainability Strategies: Sustainability Profiles and

Maturity Levels. Sustainable Development, Vol. 18, pp. 76 – 89, 2010.

BOS-BROUWERS, H. E. J. Corporate Sustainability and Innovation in SMEs: Evidence of Themes and

Activities in Practice. Business Strategy and the Environment, Vol. 19, pp. 417 – 435, 2010.

BRAGANZA, A. & LAMBERT, R. Strategic Integration: Developing Process Governance Framework.

Knowledge and Process Management, Vol. 7 No. 3, pp. 177 – 186, 2000.

BRANDÃO, C. E. L. Sustentabilidade e Empresas: Uma Reflexão Crítica. Tese de Doutorado – UFRJ/ Instituto

de Química/ Programa de Pósgraduação em História das Ciências das Técnicas e Epistemologia, 2009.

BRANDÃO, C. E. L. & SANTOS, H. L. Prefácio Mervyn E. King. Guia de Sustentabilidade para as

Empresas. Instituto Brasileiro de Governança Corporativa, São Paulo, SP: IBGC, 2007.

BRUIN, T. & ROSEMANN, M. Towards Understanding Strategic Alignment of Business Process

Management, paper presented at 17th Australasian Conference on Information Systems. Australia, 2006.

BRUNDTLAND REPORTING. available at: www.globalreporting.org. 1997. (Accessed in 20 January 2011).

BUCHANAN, J. & VANDERPOOTEN, D. Ranking projects for an electricity utility using ELECTRE III.

International Transactions in Operational Research, Vol. 14, pp. 309-323, 2007.

COMMONER, B. The Costing Circle. Nature, Man, and Technology. New York, 1971.

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

14

DOWNS, A. An Economic Theory of Political Action in a Democracy. The Journal of Political Economy, Vol.

65, No. 2, pp. 135-150, 1957.

DYLLICK, T. Strategischer Einsatz von Umweltmanagementsystemen. Umweltwirtschaftsforum. Vol. 8, pp. 64

– 68, 2000.

EBNER, D. & BAUMGARTNER, R.J. The Relationship Between Sustainable Development and Corporate

Social Responsibility. available at: www.crrconference.org (accessed in 17 September 2010), 2006.

ELKINGTON, J. Cannibals with forks: the triple bottom line of the 21st century. Gabriola Island: New Society

Publishers, 1998.

FREEMAN, R. E. Strategic Management: A Stakeholder Approach, Pitman, Boston, 1984.

GREENWOOD, M. Stakeholder Engagement: Beyond the Myth of Corporate Responsibility. Journal of

Business Ethics, Vol. 74, pp. 315 – 327, 2007.

Hardtke, A, & Prehn, M. Perspektiven der Nachhaltigkeit 1. Gabler: Wiesbaden, 2001.

HARMON, P. Process Governance. available at: www.bptrends.com (accessed in 10 February 2011), 2008.

HARRIS, J. M. Environmental And Natural Resource Economics: A Contemporary Approach. Second Edition,

2006.

HART, S. L. Beyond Greening: strategies for a sustainable world. Harvard Business Review, Vol. 75 No. 1, pp.

67 – 76, 1997.

HOLDREN, J.P. Energy and Sustainability. Editorial Science, 2007.

JESTON, J. & NELIS, J. Management by Process: A roadmap to sustainable Business Process Management.

Oxford: Butterworth-Heinemann, 2008.

KORHONEN, J. J. Agile Organizational Governance and Streering: HolacracyTM and BPM, 2007a.

KORHONEN, J. J. On the Lookout for Organizational Effectiveness – Requisite Control Structure in BPM

Governance, paper presented in 1th Business Process Governance - WoGO‘2007, 2007b.

KUZNETS, S. S. Teoria do Crescimento Econômico Moderno. Rio de Janeiro, Zahar, 1974.

MARKUS, M. L. & JACOBSON, D. D. Business Process Governance, in Brocke, J. V. and Rosemann, M.

(Ed.), Handbooh on Business Process Management 2, Springer, New York, pp. 201 – 222., 2010.

NICOLESCU, C. E. The Unity Of The Social System - Emergence Of Diversity. National School of Political

Studies and Public Administration, Romania, 1974.

NOLLAND, J. & PHILLIPS, R. Stakeholder Engagement, Discourse Ethics and Strategic Management.

International Journal of management Reviews. DOI: 10.1111/j.1468-2370.2009.00279.x, 2010.

PETIT, S. & FREDERIKSEN, P. Modelling land use change impacts for sustainability assessment. Ecological

Indicators, Vol. 11, pp. 1 – 3, 2011.

PRAHALAD, C. K. & OOSTERVELD, J. P. Transforming Internal Governance: The challenge for

multinationals. Sloan Management Review, Vol. 40 No. 3, pp. 31, 1999.

RELATÓRIO DE SUSTENTABILIDADE. Votorantim. available at: www.votorantim.com.br (acessed in 10

March 2011), 2009.

ROGER, M. & BRUEN, M. Choosing realistic values of indifference, preference and veto thresholds for use

with environment criteria with ELECTRE. European Journal of Operational Research, 107, pp. 542-551, 1998.

ROGER, M. & BRUEN, M. & MAYSTRE, L. Electre and decision support, Kluwer, Academic Publishers,

2000.

XVII INTERNATIONAL CONFERENCE ON INDUSTRIAL ENGINEERING AND OPERATIONS MANAGEMENT

Technological Innovation and Intellectual Property: Production Engineering Challenges in Brazil Consolidation in the World Economic Scenario. Belo Horizonte, Brazil, 04 to 07 October – 2011

15

ROSEMANN, M. Potential pitfalls of process modeling: part A. Business Process Management Journal –

BPMJ, Vol.12, pp. 249 – 254, 2006a.

ROSEMANN, M. Potential pitfalls of process modeling: part B. Business Process Management Journal –

BPMJ, Vol.12, pp. 377 – 384, 2006b.

ROSS, T J. Fuzzy Logic with Engineering Applications. England: John Wiley and Sons LTD, pp. 308-357,

2004.

ROY, B. & BOUYSSOU, D. Aide multicritère à la décision: Méthodes et ca, Paris, Economica, 1993.

ROY, B. The outranking approach and the foundations of ELECTRE methods. In: Reading in Multiple Criteria

Decision Aid [edited by C.A. Bana e Costa], Springer Verlag, Berlin, 155-183, 1990.

ROY, B. Multicriteria Methodology for Decision Aiding, Kluwer, 1996.

SCHALTEGGER, S. & DYLLICK, T. Nachhaltig managen mit der Balanced Scorecard. Gabler: Wiesbaden,

2002.

SPANYI, A. Business Process Management Governance. in Brocke, J. V. & Rosemann, M. (Ed.), Handbooh on

Business Process Management 2. Springer, New York, pp. 223 – 238, 2010.

SUSTAINABILITY REPORT. Cemex. available at: www.cemex.com (acessed in 10 March 2011), 2009.

TABBUSH, P. & FREDERIKSEN, P. & EDWARDS, D. Impact Assessment in the European Commission in

relation to multifunctional land use. Sustainability Impact Assessment of land use policies. Springer, 2008.

WCED (World Commission on Environment and Development), Our Common Future (The Brundtland Report),

Oxford University Press, Oxford, 1987.

WILLIAMSON, O. E. The Economic Institutions of Capitalism. USA: Free Press, 1985.

WORLD BANK. World development report. Washington: Oxford University Press – RJ – FGV.

WORLD BANK. www.worldbankgroup.com. (accessed in 20 January 2011).