Practice Final – ACCT&203, Spring 2013 Key

33

Practice Final – ACCT&203, Spring 2013 Key 1. The following information summarizes the company's cost structure: Required: Estimate the following costs at the 40,000 unit level of activity: a. Total variable cost. b. Total fixed cost. c. Variable cost per unit. d. Fixed cost per unit. Parts a., b., c., & d. Note: The total fixed cost is 48,000 units $4.50 per unit = $216,000. AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Blooms: Application Garrison - Chapter 02 #157 Learning Objective: 02-03 Understand cost behavior patterns including variable costs; fixed costs; and mixed costs Level: Easy

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of Practice Final – ACCT&203, Spring 2013 Key

Practice Final – ACCT&203, Spring 2013 Key

1. The following information summarizes the company's cost structure:

Required:

Estimate the following costs at the 40,000 unit level of activity:

a. Total variable cost.

b. Total fixed cost.

c. Variable cost per unit.

d. Fixed cost per unit.

Parts a., b., c., & d.

Note: The total fixed cost is 48,000 units $4.50 per unit = $216,000.

AACSB: Analytic

AICPA BB: Critical Thinking AICPA FN: Measurement

Blooms: Application

Garrison - Chapter 02 #157 Learning Objective: 02-03 Understand cost behavior patterns including variable costs; fixed costs; and mixed costs

Level: Easy

2. Corio Corporation reports that at an activity level of 3,800 units, its total variable cost is $221,464 and its

total fixed cost is $94,848.

Required:

For the activity level of 3,900 units, compute: (a) the total variable cost; (b) the total fixed cost; (c) the total

cost; (d) the average variable cost per unit; (e) the average fixed cost per unit; and (f) the average total cost per

unit. Assume that this activity level is within the relevant range.

AACSB: Analytic

AICPA BB: Critical Thinking AICPA FN: Measurement

Blooms: Application

Garrison - Chapter 02 #158 Learning Objective: 02-03 Understand cost behavior patterns including variable costs; fixed costs; and mixed costs

Level: Easy

3. Utility costs at one of Helker Corporation's factories are listed below:

Management believes that utility cost is a mixed cost that depends on machine-hours.

Required:

Estimate the variable cost per machine-hour and the fixed cost per month using the high-low method. Show

your work! Round off all calculations to the nearest whole cent.

Variable cost = Change in cost Change in activity

= ($35,138 - $34,762) (4,780 machine-hours - 4,704 machine-hours)

= $376 76 machine-hours

= $4.95 per machine-hour

Fixed cost element = Total cost - Variable cost element

= $34,762 - ($4.95 per machine-hour 4,704 machine-hours)

= $34,762.00 - $23,284.80

= $11,477.20

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 02 #163

Learning Objective: 02-04 Analyze a mixed cost using a scattergraph plot and the high-low method Level: Easy

4. Whitman Corporation, a merchandising company, reported sales of 7,400 units for May at a selling price of

$677 per unit. The cost of goods sold (all variable) was $441 per unit and the variable selling expense was $54

per unit. The total fixed selling expense was $155,600. The variable administrative expense was $24 per unit

and the total fixed administrative expense was $370,400.

Required:

a. Prepare a contribution format income statement for May.

b. Prepare a traditional format income statement for May.

a. Contribution Format Income Statement

b. Traditional Format Income Statement

AACSB: Analytic

AICPA BB: Critical Thinking AICPA FN: Measurement

Blooms: Application

Garrison - Chapter 02 #166 Learning Objective: 02-05 Prepare income statements for a merchandising company using the traditional and contribution formats

Level: Medium

5. Hartoon Company's quality cost report is to be based on the following data:

Required:

Prepare a Quality Cost Report in good form with separate sections for prevention costs, appraisal costs, internal

failure costs, and external failure costs.

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 02 #41

Learning Objective: 02B-09 Identify the four types of quality costs and explain how they interact Learning Objective: 02B-10 Prepare and interpret a quality cost report

Level: Medium

6. Alam Company is a manufacturing firm that uses job-order costing. At the beginning of the year, the

company's inventory balances were as follows:

The company applies overhead to jobs using a predetermined overhead rate based on machine-hours. At the

beginning of the year, the company estimated that it would work 45,000 machine-hours and incur $180,000 in

manufacturing overhead cost. The following transactions were recorded for the year:

a. Raw materials were purchased, $416,000.

b. Raw materials were requisitioned for use in production, $420,000 ($380,000 direct and $40,000 indirect).

c. The following employee costs were incurred: direct labor, $414,000; indirect labor, $60,000; and

administrative salaries, $212,000.

d. Selling costs, $141,000.

e. Factory utility costs, $20,000.

f. Depreciation for the year was $81,000 of which $73,000 is related to factory operations and $8,000 is related

to selling, general, and administrative activities.

g. Manufacturing overhead was applied to jobs. The actual level of activity for the year was 48,000 machine-

hours.

h. The cost of goods manufactured for the year was $1,004,000.

i. Sales for the year totaled $1,416,000 and the costs on the job cost sheets of the goods that were sold totaled

$989,000.

j. The balance in the Manufacturing Overhead account was closed out to Cost of Goods Sold.

Required:

Prepare the appropriate journal entry for each of the items above (a. through j.). You can assume that all

transactions with employees, customers, and suppliers were conducted in cash.

AACSB: Analytic

AICPA BB: Critical Thinking AICPA FN: Measurement

Blooms: Application

Garrison - Chapter 03 #139 Learning Objective: 03-01 Compute a predetermined overhead rate

Learning Objective: 03-02 Apply overhead cost to jobs using a predetermined overhead rate

Learning Objective: 03-04 Understand the flow of costs in a job-order costing system and prepare appropriate journal entries to record costs Learning Objective: 03-07 Compute underapplied or overapplied overhead cost and prepare the journal entry to close the balance in Manufacturing Overhead to the

appropriate accounts

Level: Medium

7. Babb Company is a manufacturing firm that uses job-order costing. The company's inventory balances were

as follows at the beginning and end of the year:

The company applies overhead to jobs using a predetermined overhead rate based on machine-hours. At the

beginning of the year, the company estimated that it would work 17,000 machine-hours and incur $272,000 in

manufacturing overhead cost. The following transactions were recorded for the year:

Raw materials were purchased, $416,000.

Raw materials were requisitioned for use in production, $412,000 $(376,000 direct and $36,000 indirect).

The following employee costs were incurred: direct labor, $330,000; indirect labor, $69,000; and

administrative salaries, $157,000.

Selling costs, $113,000.

Factory utility costs, $29,000.

Depreciation for the year was $121,000 of which $114,000 is related to factory operations and $7,000 is

related to selling, general, and administrative activities.

Manufacturing overhead was applied to jobs. The actual level of activity for the year was 15,000 machine-

hours.

Sales for the year totaled $1,282,000.

Required:

a. Prepare a schedule of cost of goods manufactured in good form.

b. Was the overhead underapplied or overapplied? By how much?

c. Prepare an income statement for the year in good form. The company closes any underapplied or overapplied

manufacturing overhead to Cost of Goods Sold.

a. Schedule of cost of goods manufactured

b. Overhead underapplied or overapplied

c. Income Statement

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 03 #140

Learning Objective: 03-01 Compute a predetermined overhead rate Learning Objective: 03-02 Apply overhead cost to jobs using a predetermined overhead rate

Learning Objective: 03-06 Prepare schedules of cost of goods manufactured and cost of goods sold and an income statement

Learning Objective: 03-07 Compute underapplied or overapplied overhead cost and prepare the journal entry to close the balance in Manufacturing Overhead to the appropriate accounts

Level: Medium

8. Sandler Corporation bases its predetermined overhead rate on the estimated machine-hours for the upcoming

year. Data for the upcoming year appear below:

Required:

Compute the company's predetermined overhead rate.

Estimated total manufacturing overhead = $838,770 + ($3.49 per machine-hour 73,000 machine-hours) =

$1,093,540

Predetermined overhead rate = Estimated total manufacturing overhead Estimated total amount of the

allocation base = $1,093,540 73,000 machine-hours = $14.98 per machine-hour

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 03 #141

Learning Objective: 03-01 Compute a predetermined overhead rate Level: Easy

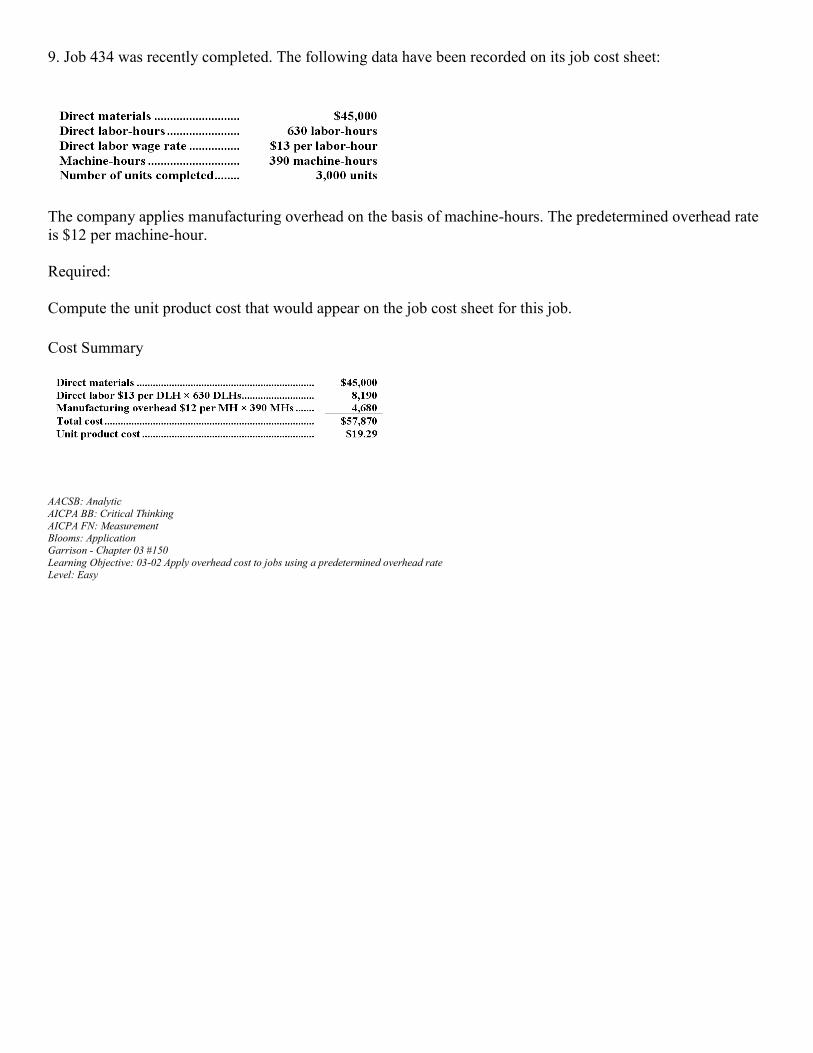

9. Job 434 was recently completed. The following data have been recorded on its job cost sheet:

The company applies manufacturing overhead on the basis of machine-hours. The predetermined overhead rate

is $12 per machine-hour.

Required:

Compute the unit product cost that would appear on the job cost sheet for this job.

Cost Summary

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 03 #150

Learning Objective: 03-02 Apply overhead cost to jobs using a predetermined overhead rate Level: Easy

10. The following monthly data in contribution format are available for the MN Company and its only product,

Product SD:

The company produced and sold 300 units during the month and had no beginning or ending inventories.

Required:

a. Without resorting to calculations, what is the total contribution margin at the break-even point?

b. Management is contemplating the use of plastic gearing rather than metal gearing in Product SD. This change

would reduce variable expenses by $18 per unit. The company's sales manager predicts that this would reduce

the overall quality of the product and thus would result in a decline in sales to a level of 250 units per month.

Should this change be made?

c. Assume that MN Company is currently selling 300 units of Product SD per month. Management wants to

increase sales and feels this can be done by cutting the selling price by $22 per unit and increasing the

advertising budget by $20,000 per month. Management believes that these actions will increase unit sales by 50

percent. Should these changes be made?

d. Assume that MN Company is currently selling 300 units of Product SD. Management wants to automate a

portion of the production process for Product SD. The new equipment would reduce direct labor costs by $20

per unit but would result in a monthly rental cost for the new robotic equipment of $10,000. Management

believes that the new equipment will increase the reliability of Product SD thus resulting in an increase in

monthly sales of 12%. Should these changes be made?

a. The total contribution margin would be $40,000 since it is equal to the fixed expenses at the break-even point.

b. The $18 decrease in variable costs will cause the contribution margin per unit to increase from $170 to $188.

The less costly components should not be used in the manufacture of Product SD. Net operating income will

decrease by $4,000.

c. The decrease in selling price per unit will cause the unit contribution margin to decrease from $170 to $148.

The changes should not be made.

d. The use of the automated process would affect both fixed and variable costs. Fixed expenses will increase by

$10,000 from $40,000 to $50,000. Variable costs will decrease by $20 from $109 to $89, and the unit

contribution margin will increase from $170 to $190.

The changes should be made.

AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Measurement

Blooms: Application Garrison - Chapter 05 #202

Learning Objective: 05-01 Explain how changes in activity affect contribution margin and net operating income

Learning Objective: 05-04 Show the effects on net operating income of changes in variable costs; fixed costs; selling price; and volume Learning Objective: 05-06 Determine the break-even point

Level: Hard

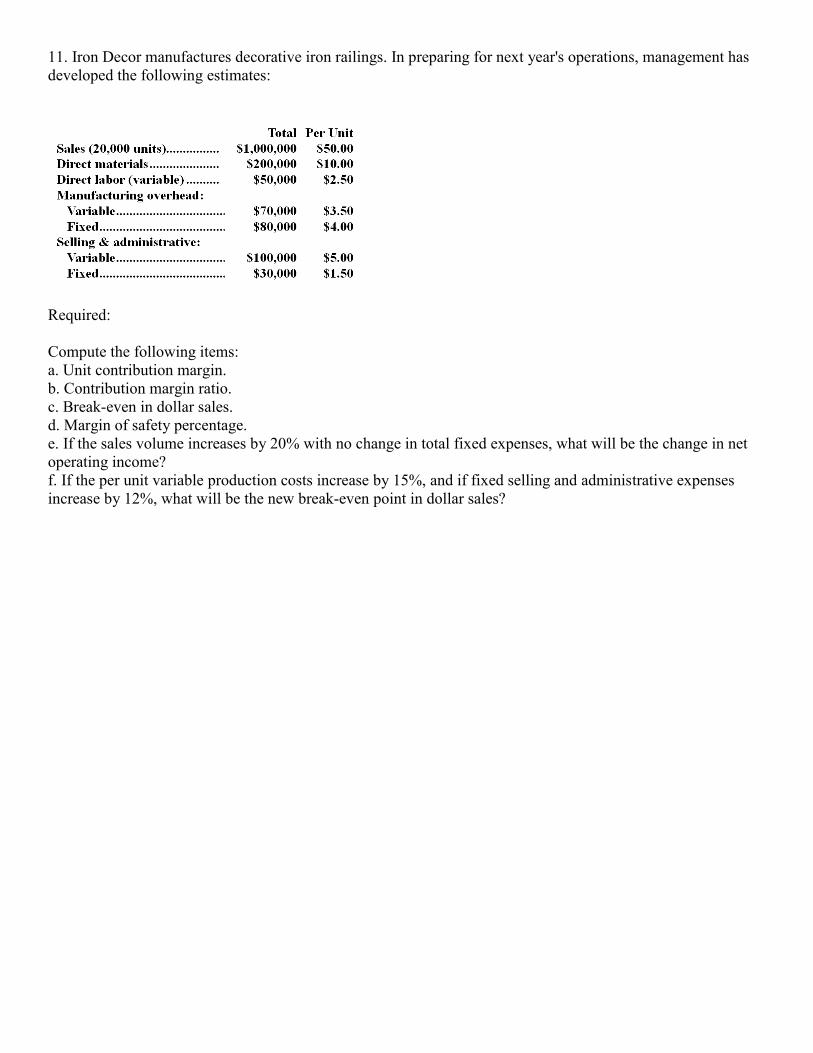

11. Iron Decor manufactures decorative iron railings. In preparing for next year's operations, management has

developed the following estimates:

Required:

Compute the following items:

a. Unit contribution margin.

b. Contribution margin ratio.

c. Break-even in dollar sales.

d. Margin of safety percentage.

e. If the sales volume increases by 20% with no change in total fixed expenses, what will be the change in net

operating income?

f. If the per unit variable production costs increase by 15%, and if fixed selling and administrative expenses

increase by 12%, what will be the new break-even point in dollar sales?

b. CM ratio = Unit CM Selling price = $29.00 per unit $50.00 per unit = 58%

Dollar sales to break even = Fixed expenses CM ratio = $110,000 0.58 = $189,655 (rounded)

Margin of safety percentage = Margin of safety in dollars Current sales

= $810,345 $1,000,000 = 81.03%

CM ratio = $26.60 $50.00 = 53.2%

New break-even in dollars = $113,600 0.532 = $213,534 (rounded)

AACSB: Analytic

AICPA BB: Critical Thinking AICPA FN: Measurement

Blooms: Application

Garrison - Chapter 05 #207 Learning Objective: 05-03 Use the contribution margin ratio (cm ratio) to compute changes in contribution margin and net operating income resulting from changes in

sales volume

Learning Objective: 05-04 Show the effects on net operating income of changes in variable costs; fixed costs; selling price; and volume Learning Objective: 05-06 Determine the break-even point

Learning Objective: 05-07 Compute the margin of safety and explain its significance

Level: Medium

12. Randall Company is a merchandising company that sells a single product. The company's inventories,

production, and sales in units for the next three months have been forecasted as follows:

Units are sold for $12 each. One fourth of all sales are paid for in the month of sale and the balance are paid for

in the following month. Accounts receivable at September 30 totaled $450,000.

Merchandise is purchased for $7 per unit. Half of the purchases are paid for in the month of the purchase and

the remainder are paid for in the month following purchase. Selling and administrative expenses are expected to

total $120,000 each month. One half of these expenses will be paid in the month in which they are incurred and

the balance will be paid in the following month. There is no depreciation. Accounts payable at September 30

totaled $290,000.

Cash at September 30 totaled $80,000. A payment of $300,000 for purchase of equipment is scheduled for

November, and a dividend of $200,000 is to be paid in December.

Required:

a. Prepare a schedule of expected cash collections for each of the months of October, November, and

December.

b. Prepare a schedule showing expected cash disbursements for merchandise purchases and selling and

administrative expenses for each of the months October, November, and December.

c. Prepare a cash budget for each of the months October, November, and December. There is no minimum

required ending cash balance.

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 08 #96

Learning Objective: 08-02 Prepare a sales budget; including a schedule of expected cash collections Learning Objective: 08-03 Prepare a production budget

Learning Objective: 08-07 Prepare a selling and administrative expense budget

Learning Objective: 08-08 Prepare a cash budget Level: Medium

13. Capp Corporation is a wholesaler of industrial goods. Data regarding the store's operations follow:

Sales are budgeted at $350,000 for November, $360,000 for December, and $340,000 for January.

Collections are expected to be 60% in the month of sale, 39% in the month following the sale, and 1%

uncollectible.

The cost of goods sold is 75% of sales.

The company desires an ending merchandise inventory equal to 40% of the following month's cost of goods

sold. Payment for merchandise is made in the month following the purchase.

The November beginning balance in the accounts receivable account is $70,000.

The November beginning balance in the accounts payable account is $257,000.

Required:

a. Prepare a Schedule of Expected Cash Collections for November and December.

b. Prepare a Merchandise Purchases Budget for November and December.

AACSB: Analytic

AICPA BB: Critical Thinking AICPA FN: Measurement

Blooms: Application

Garrison - Chapter 08 #98 Learning Objective: 08-02 Prepare a sales budget; including a schedule of expected cash collections

Learning Objective: 08-03 Prepare a production budget

Level: Medium

14. Diamond Company produces a single product. The company has set the following standards for materials

and labor:

During the past month, the company purchased 7,000 pounds of direct materials at a cost of $17,500. All of this

material was used in the production of 1,300 units of product. Direct labor cost totaled $36,750 for the month.

The following variances have been computed:

Required:

1. For direct materials:

a. Compute the standard price per pound of materials.

b. Compute the standard quantity allowed for materials for the month's production.

c. Compute the standard quantity of materials allowed per unit of product.

2. For direct labor:

a. Compute the actual direct labor cost per hour for the month.

b. Compute the labor rate variance.

1. a. Materials price variance = AQ (AP - SP)

$1,750 F* = 7,000 pounds ($2.50 per pound** - SP)

-$1,750 = $17,500 - 7,000 pounds SP

7,000 pounds SP = $19,250

SP = $2.75 per pound

* $1,375 U + $375 F = $1,750 F

** 17,500 7,000 pounds = $2.50 per pound

b. Materials quantity variance = (AQ - SQ) SP

$1,375 U = (7,000 pounds - SQ) $2.75 per pound

$1,375 = $19,250 - SQ $2.75 per pound

SQ $2.75 per pound = $17,875

SQ = $17,875 $2.75 per pound

SQ = 6,500 pounds

c. 6,500 pounds 1,300 units = 5 pounds per unit.

2. a. Labor efficiency variance = (AH - SH) SR

$4,000 F = (AH - 3,900 hours*)$10 per hour

-$4,000 = AH $10 per hour- $39,000

AH $10 per hour = $35,000

AH = $35,000 $10 per hour

AH = 3,500

Therefore, $36,750 total labor cost 3,500 hours = $10.50 per hour.

* 1,300 units 3 hours per unit = 3,900 hours.

b. Labor rate variance = AH(AR - SR)

= 3,500 hours ($10.50 per hour - $10.00 per hour)

= 3,500 hours ($0.50 per hour) = $1,750 U

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 10 #167

Learning Objective: 10-01 Compute the direct materials quantity and price variances and explain their significance Learning Objective: 10-02 Compute the direct labor efficiency and rate variances and explain their significance

Level: Hard

15. The following materials standards have been established for a particular product:

The following data pertain to operations concerning the product for the last month:

Required:

a. What is the materials price variance for the month?

b. What is the materials quantity variance for the month?

a. Materials price variance = (AQ AP) - (AQ SP)

= $34,155 - (2,700 pounds $13 per pound)

= $34,155 - $35,100 = $945 F

b. SQ = 500 units 3.8 pounds per unit = 1,900 pounds

Materials quantity variance = (AQ - SQ) SP

= (2,000 pounds - 1,900 pounds) $13 per pound

= (100 pounds) $13 per pound = $1,300 U

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 10 #168

Learning Objective: 10-01 Compute the direct materials quantity and price variances and explain their significance Level: Easy

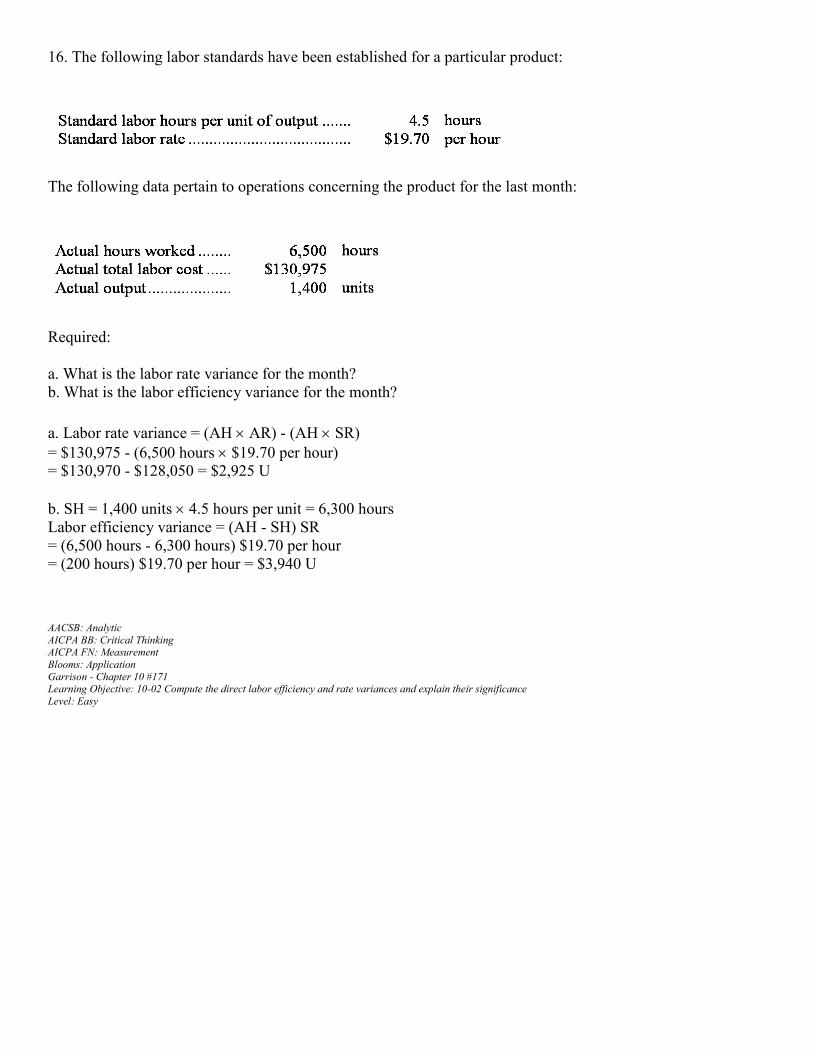

16. The following labor standards have been established for a particular product:

The following data pertain to operations concerning the product for the last month:

Required:

a. What is the labor rate variance for the month?

b. What is the labor efficiency variance for the month?

a. Labor rate variance = (AH AR) - (AH SR)

= $130,975 - (6,500 hours $19.70 per hour)

= $130,970 - $128,050 = $2,925 U

b. SH = 1,400 units 4.5 hours per unit = 6,300 hours

Labor efficiency variance = (AH - SH) SR

= (6,500 hours - 6,300 hours) $19.70 per hour

= (200 hours) $19.70 per hour = $3,940 U

AACSB: Analytic

AICPA BB: Critical Thinking AICPA FN: Measurement

Blooms: Application

Garrison - Chapter 10 #171 Learning Objective: 10-02 Compute the direct labor efficiency and rate variances and explain their significance

Level: Easy

17. Marcell Corporation is considering two alternatives that are code-named M and N. Costs associated with the

alternatives are listed below:

Required:

a. Which costs are relevant and which are not relevant in the choice between these two alternatives?

b. What is the differential cost between the two alternatives?

AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Measurement

Blooms: Application Garrison - Chapter 12 #127

Learning Objective: 12-01 Identify relevant and irrelevant costs and benefits in a decision

Level: Easy

18. The management of Therriault Corporation is considering dropping product U51Y. Data from the

company's accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company's accounting system. Further

investigation has revealed that $280,000 of the fixed manufacturing expenses and $140,000 of the fixed selling

and administrative expenses are avoidable if product U51Y is discontinued.

Required:

What would be the effect on the company's overall net operating income if product U51Y were dropped?

Should the product be dropped? Show your work!

Net operating income would increase by $8,000 if product U51Y were dropped. Therefore, the product should

be dropped.

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 12 #129

Learning Objective: 12-02 Prepare an analysis showing whether a product line or other business segment should be added or dropped Level: Easy

19. Mr. Earl Pearl, accountant for Margie Knall Co., Inc., has prepared the following product-line income data:

The following additional information is available:

* The factory rent of $1,500 assigned to Product C is avoidable if the product were dropped.

* The company's total depreciation would not be affected by dropping C.

* Eliminating Product C will reduce the monthly utility bill from $1,500 to $800.

* All supervisors' salaries are avoidable.

* If Product C is discontinued, the maintenance department will be able to reduce monthly expenses from

$3,000 to $2,000.

* Elimination of Product C will make it possible to cut two persons from the administrative staff; their

combined salaries total $3,000.

Required:

Prepare an analysis showing whether Product C should be eliminated.

Since there is a net $800 disadvantage to dropping Product C, it should not be dropped.

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 12 #132

Learning Objective: 12-02 Prepare an analysis showing whether a product line or other business segment should be added or dropped Level: Medium

20. The Hayes Company manufactures and sells several products, one of which is called a slip differential. The

company normally sells 30,000 units of the slip differential each month. At this activity level, unit costs are:

An outside supplier has offered to produce the slip differentials for the Hayes Company, and to ship them

directly to the Hayes Company's customers. This arrangement would permit the Hayes Company to reduce its

variable selling expenses by one third (due to elimination of freight costs). The facilities now being used to

produce the slip differentials would be idle and fixed manufacturing overhead would continue at 60 percent of

its present level. The total fixed selling expenses of the company would be unaffected by this decision.

Required:

What is the maximum acceptable price quotation for the slip differentials from the outside supplier?

The total cost savings from purchasing the slip differentials is $420,000 as computed below:

Therefore, the company would be willing to pay no more than $14 for each unit since the total purchase price

would then be $420,000 ($14 30,000 = $420,000), which is exactly the cost savings.

$14 is the relevant cost figure. To be acceptable, the quotation received from the outside supplier must be less

than $14.

AACSB: Analytic

AICPA BB: Critical Thinking AICPA FN: Measurement

Blooms: Application

Garrison - Chapter 12 #133 Learning Objective: 12-03 Prepare a make or buy analysis

Level: Medium

21. Kramer Company makes 4,000 units per year of a part called an axial tap for use in one of its products. Data

concerning the unit production costs of the axial tap follow:

An outside supplier has offered to sell Kramer Company all of the axial taps it requires. If Kramer Company

decided to discontinue making the axial taps, 40% of the above fixed manufacturing overhead costs could be

avoided. Assume that direct labor is a variable cost.

Required:

a. Assume Kramer Company has no alternative use for the facilities presently devoted to production of the axial

taps. If the outside supplier offers to sell the axial taps for $65 each, should Kramer Company accept the offer?

Fully support your answer with appropriate calculations.

b. Assume that Kramer Company could use the facilities presently devoted to production of the axial taps to

expand production of another product that would yield an additional contribution margin of $80,000 annually.

What is the maximum price Kramer Company should be willing to pay the outside supplier for axial taps?

a. The analysis of the alternatives follows below:

The company should make the part rather than buy it from the outside supplier since it costs $4 less under that

alternative.

b. The maximum acceptable price is $81 since that is the cost to the company of making the part itself when the

opportunity cost is included:

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 12 #135

Learning Objective: 12-03 Prepare a make or buy analysis Level: Hard

22. Jerston Company has an annual plant capacity of 3,000 units. Data concerning this product are given below:

The company has received a special order for 500 units at a selling price of $45 each. Regular sales would not

be affected, and sales commissions on the 500 units would be reduced by one-third. This special order would

have no impact on total fixed costs.

Required:

Determine whether the company should accept the special order. Show all computations.

AACSB: Analytic

AICPA BB: Critical Thinking AICPA FN: Measurement

Blooms: Application

Garrison - Chapter 12 #139 Learning Objective: 12-04 Prepare an analysis showing whether a special order should be accepted

Level: Medium

23. Block Corporation makes three products that use the current constraint, which is a particular type of

machine. Data concerning those products appear below:

Required:

a. Rank the products in order of their current profitability from the most profitable to the least profitable. In

other words, rank the products in the order in which they should be emphasized. Show your work!

b. Assume that sufficient constraint time is available to satisfy demand for all but the least profitable product.

Up to how much should the company be willing to pay to acquire more of the constrained resource?

Resulting ranking of products: FX, JR, ZZ

b. The company should be willing to pay up to $13.80 per minute to obtain more of the constrained resource

since this is the value to the company of using this constrained resource to make more of product ZZ. By

assumption, the other products will already have been produced up to demand.

AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Measurement

Blooms: Application Garrison - Chapter 12 #146

Learning Objective: 12-05 Determine the most profitable use of a constrained resource

Learning Objective: 12-06 Determine the value of obtaining more of the constrained resource Level: Easy

24. (Ignore income taxes in this problem.) Jim Bingham is considering starting a small catering business. He

would need to purchase a delivery van and various equipment costing $125,000 to equip the business and

another $60,000 for inventories and other working capital needs. Rent for the building used by the business will

be $35,000 per year. Jim's marketing studies indicate that the annual cash inflow from the business will amount

to $120,000. In addition to the building rent, annual cash outflow for operating costs will amount to $40,000.

Jim wants to operate the catering business for only six years. He estimates that the equipment could be sold at

that time for 4% of its original cost. Jim uses a 16% discount rate.

Required:

Would you advise Jim to make this investment?

Bingham should make this investment because the NPV is positive.

AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Measurement

Blooms: Application Garrison - Chapter 13 #125

Learning Objective: 13-01 Evaluate the acceptability of an investment project using the net present value method

Level: Medium

25. (Ignore income taxes in this problem.) The management of Peregoy Corporation is considering the purchase

of an automated molding machine that would cost $255,552, would have a useful life of 5 years, and would

have no salvage value. The automated molding machine would result in cash savings of $64,000 per year due to

lower labor and other costs.

Required:

Determine the internal rate of return on the investment in the new automated molding machine. Show your

work!

Factor of the internal rate of return = Investment required Annual net cash inflow

= $255,552 $64,000 = 3.993

The factor of 3.993 for 5 years represents an internal rate of return of 8%.

AACSB: Analytic

AICPA BB: Critical Thinking

AICPA FN: Measurement Blooms: Application

Garrison - Chapter 13 #131

Learning Objective: 13-02 Evaluate the acceptability of an investment project using the internal rate of return method Level: Easy

26. (Ignore income taxes in this problem.) Rosenholm Corporation uses a discount rate of 18% in its capital

budgeting. Partial analysis of an investment in automated equipment with a useful life of 5 years has thus far

yielded a net present value of -$327,960. This analysis did not include any estimates of the intangible benefits

of automating this process nor did it include any estimate of the salvage value of the equipment.

Required:

a. Ignoring any salvage value, how large would the additional cash flow per year from the intangible benefits

have to be to make the investment in the automated equipment financially attractive?

b. Ignoring any cash flows from intangible benefits, how large would the salvage value of the automated

equipment have to be to make the investment in the automated equipment financially attractive?

a. Minimum annual cash flows from the intangible benefits

= Negative net present value to be offset Present value factor

= $327,960 3.127 = $104,880

b. Minimum salvage value

= Negative net present value to the offset Present value factor

= $327,960 0.437 = $750,481

AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Measurement

Blooms: Application Garrison - Chapter 13 #134

Learning Objective: 13-03 Evaluate an investment project that has uncertain cash flows

Level: Easy

27. (Ignore income taxes in this problem.) Limon Corporation is considering a project that would require an

initial investment of $204,000 and would last for 6 years. The incremental annual revenues and expenses for

each of the 6 years would be as follows:

At the end of the project, the scrap value of the project's assets would be $12,000.

Required:

Determine the payback period of the project. Show your work!

Payback period = Investment required Annual net cash inflow

= $204,000 $111,000 = 1.84 years

AACSB: Analytic AICPA BB: Critical Thinking

AICPA FN: Measurement

Blooms: Application Garrison - Chapter 13 #142

Learning Objective: 13-05 Determine the payback period for an investment

Level: Easy

Diorio Corporation keeps careful track of the time required to fill orders. The times recorded for a particular

order appear below:

28. The delivery cycle time was:

A. 29.1 hours

B. 30.6 hours

C. 8 hours

D. 2.7 hours

Throughput time = Process time + Inspection time + Move time + Queue time

= 1.4 hours + 0.1 hours + 2.7 hours + 5.3 hours = 9.5 hours

Delivery cycle time = Wait time + Throughput time

= 21.1 hours + 9.5 hours = 30.6 hours

29. The throughput time was:

A. 4.2 hours

B. 9.5 hours

C. 30.6 hours

D. 26.4 hours

Throughput time = Process time + Inspection time + Move time + Queue time

= 1.4 hours + 0.1 hours + 2.7 hours + 5.3 hours = 9.5 hours

30. The manufacturing cycle efficiency (MCE) was closest to:

A. 0.15

B. 0.05

C. 0.45

D. 0.18

Throughput time = Process time + Inspection time + Move time + Queue time

= 1.4 hours + 0.1 hours + 2.7 hours + 5.3 hours = 9.5 hours

MCE = Value-added time (Process time) Throughput (manufacturing cycle) time

= 1.4 hours 9.5 hours = 0.15