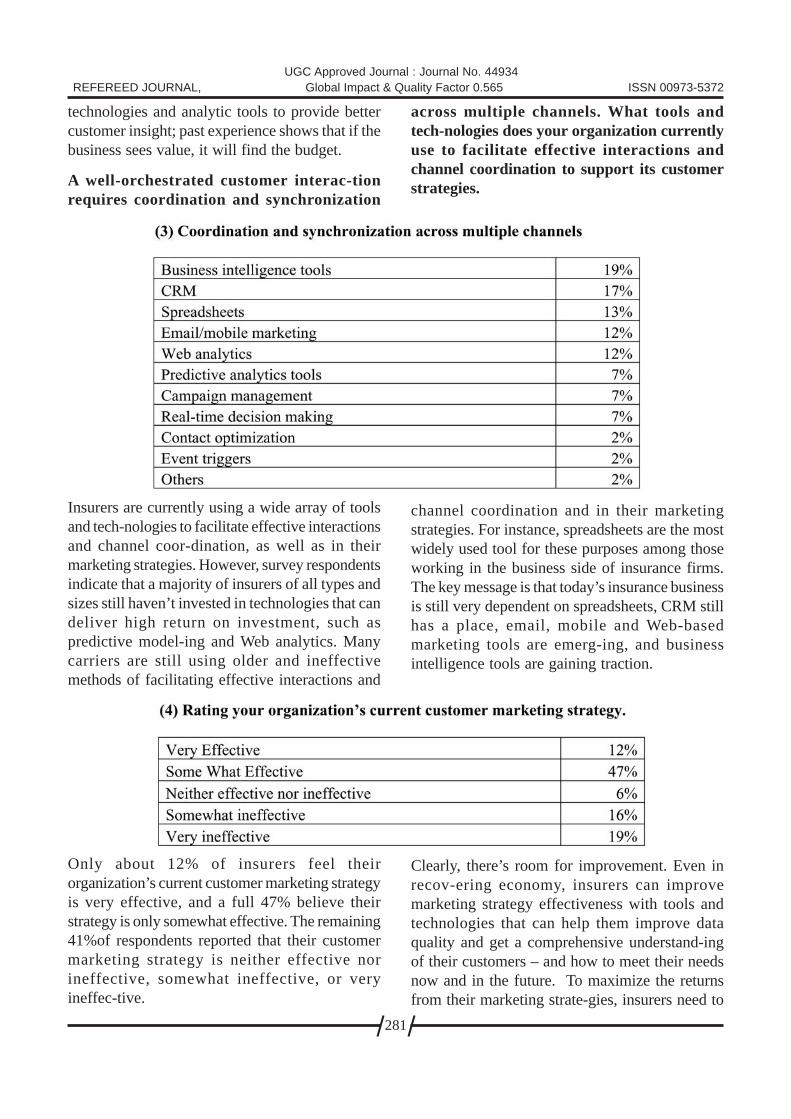

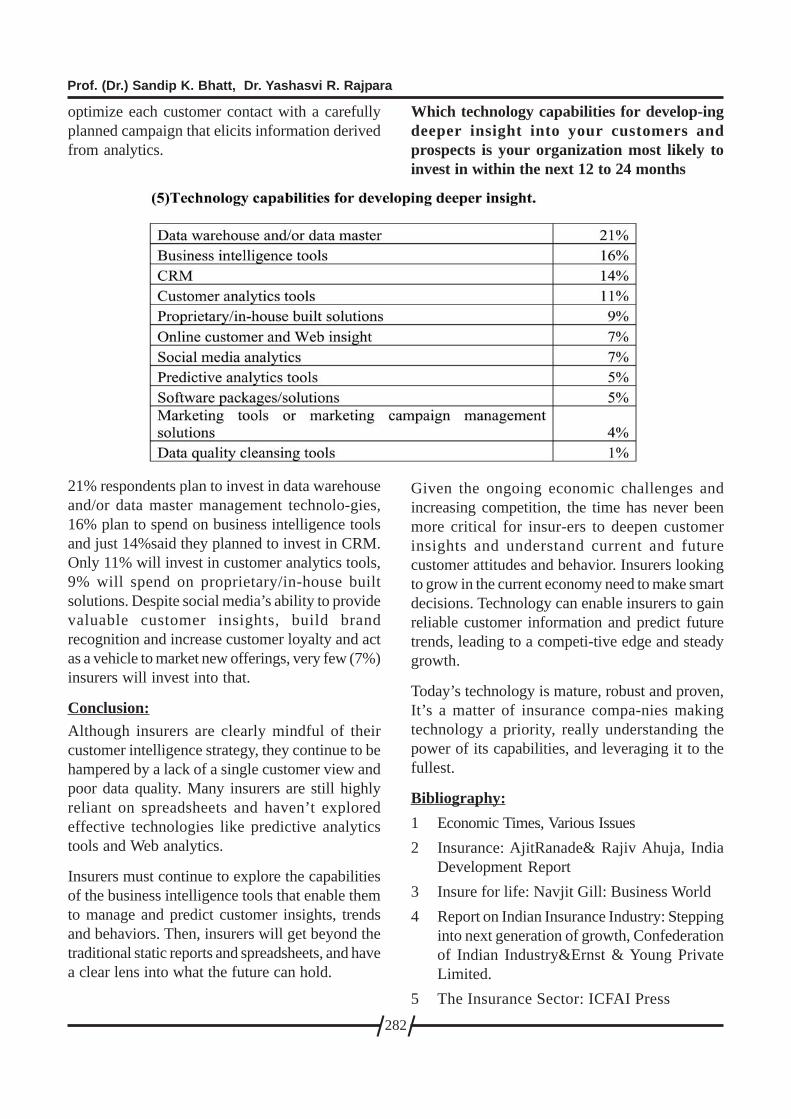

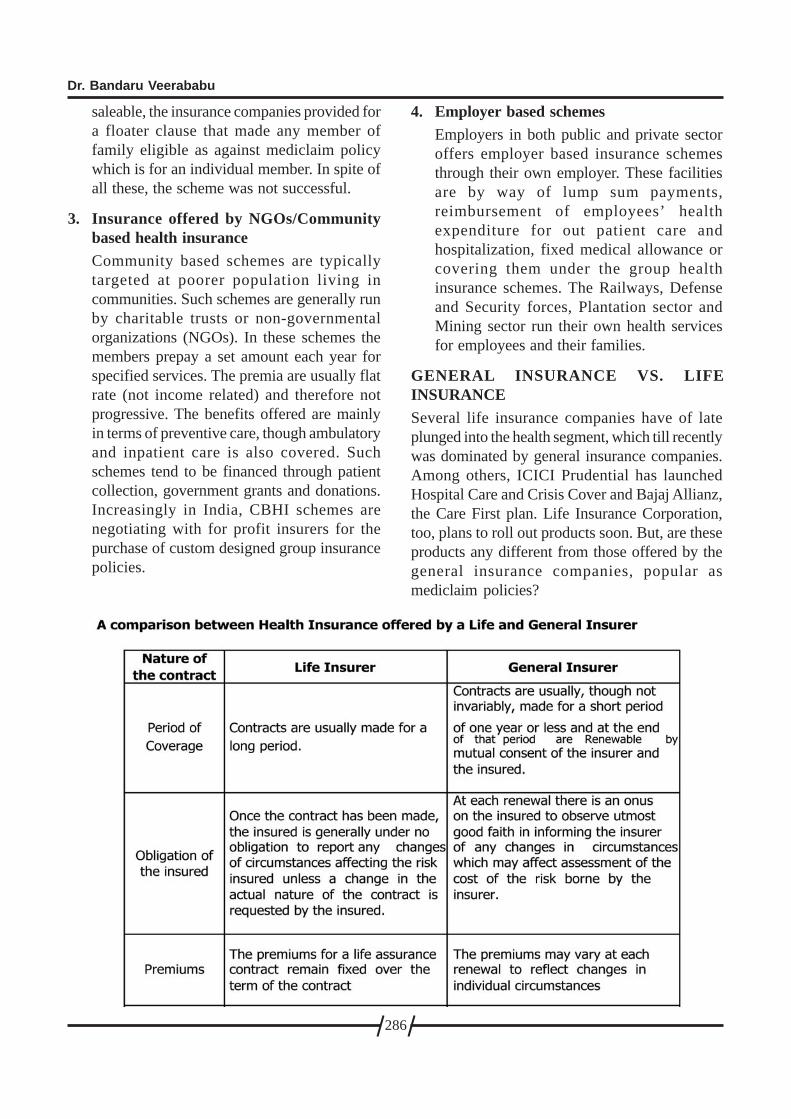

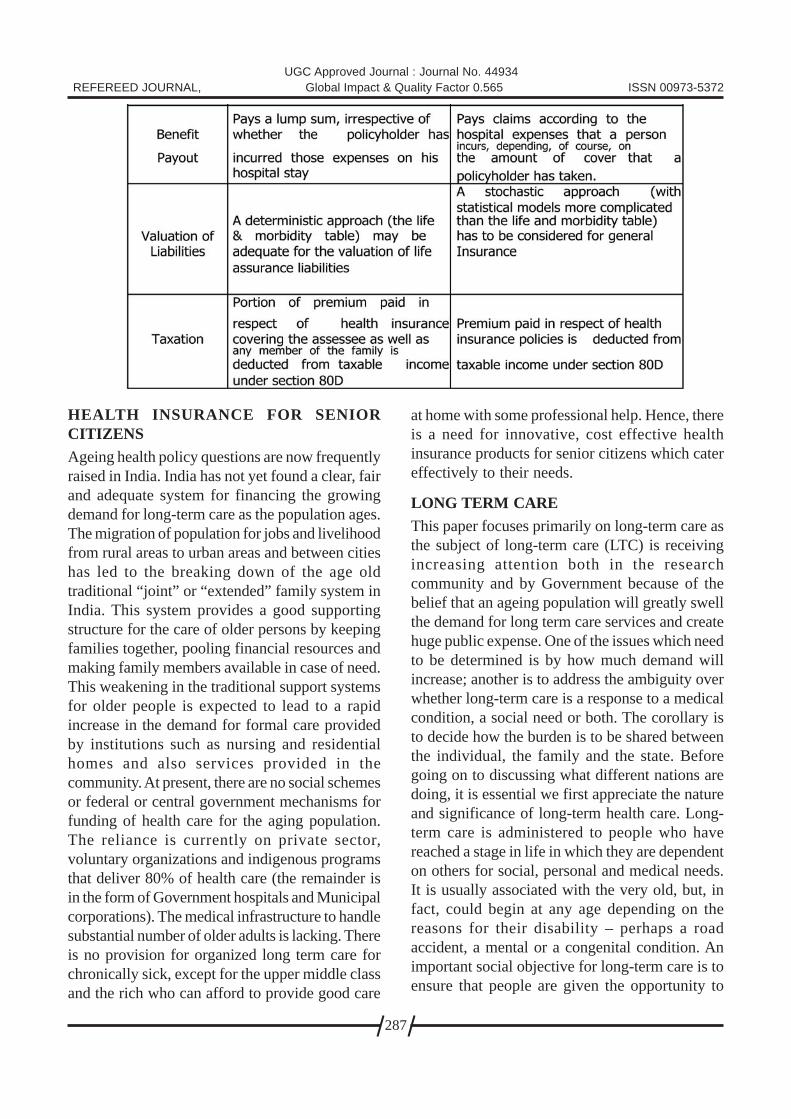

Osmania Journal of International Business Studies

383

Global Impact & Quality Factor 0.565 ISSN 00973-5372 REFEREED JOURNAL Osmania Journal of International Business Studies Vol. XII No.1 Bi – Annual January - June 2017 CONFERENCE ISSUE UGC Approved Journal : Journal No. 44934 Department of Commerce Osmania University Hyderabad, Telangana

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Osmania Journal of International Business Studies

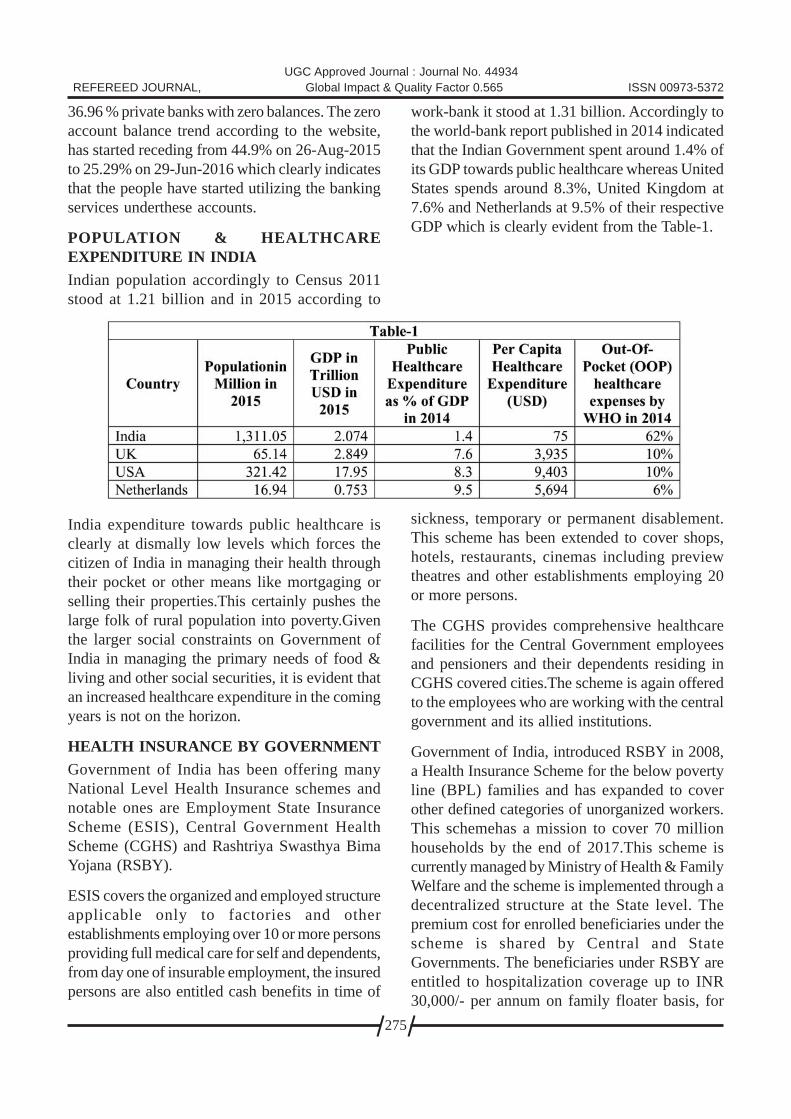

Global Impact & Quality Factor 0.565 ISSN 00973-5372

REFEREED JOURNAL

Osmania Journal of International Business StudiesVol. XII No.1 Bi – Annual January - June 2017

CONFERENCE ISSUE

UGC Approved Journal : Journal No. 44934

Department of CommerceOsmania University

Hyderabad, Telangana

For subscription, the payment can be made by a crossed demand draft in favour of “Osmania Journal

of International Business Studies” and send to Dr.D.Chennappa, Professor and Executive

Editor, Department of Commerce, Osmania University, Hyderabad 500 007, A.P., India. You can

also reach through e-mails : [email protected]; [email protected]; Mobile no:

9440 360 149.

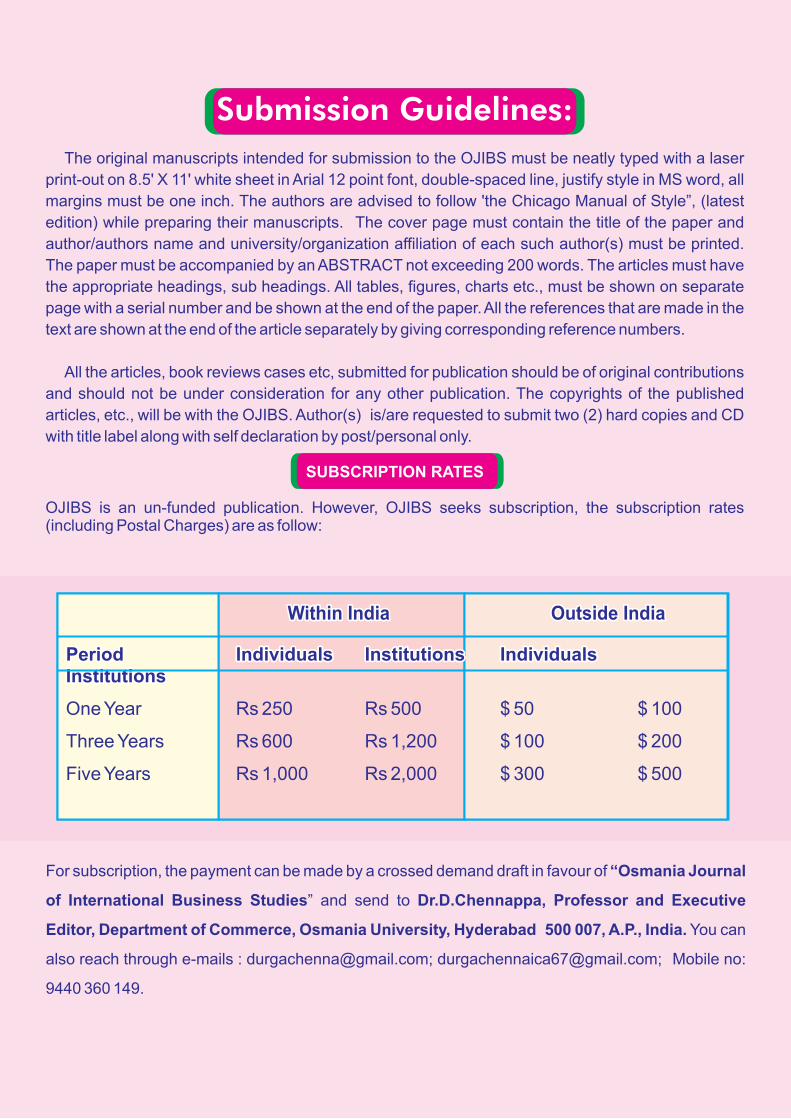

Submission Guidelines:

SUBSCRIPTION RATES

The original manuscripts intended for submission to the OJIBS must be neatly typed with a laser

print-out on 8.5' X 11' white sheet in Arial 12 point font, double-spaced line, justify style in MS word, all

margins must be one inch. The authors are advised to follow 'the Chicago Manual of Style”, (latest

edition) while preparing their manuscripts. The cover page must contain the title of the paper and

author/authors name and university/organization affiliation of each such author(s) must be printed.

The paper must be accompanied by an ABSTRACT not exceeding 200 words. The articles must have

the appropriate headings, sub headings. All tables, figures, charts etc., must be shown on separate

page with a serial number and be shown at the end of the paper. All the references that are made in the

text are shown at the end of the article separately by giving corresponding reference numbers.

All the articles, book reviews cases etc, submitted for publication should be of original contributions

and should not be under consideration for any other publication. The copyrights of the published

articles, etc., will be with the OJIBS. Author(s) is/are requested to submit two (2) hard copies and CD

with title label along with self declaration by post/personal only.

OJIBS is an un-funded publication. However, OJIBS seeks subscription, the subscription rates (including Postal Charges) are as follow:

Within IndiaWithin India Outside IndiaOutside India

Period Individuals Institutions IndividualsInstitutionsPeriod Individuals Institutions IndividualsInstitutions

One Year Rs 250 Rs 500 $ 50 $ 100

Three Years Rs 600 Rs 1,200 $ 100 $ 200

Five Years Rs 1,000 Rs 2,000 $ 300 $ 500

Osmania Journal of International Business Studies (OJIBS)(ISSN 00973-5372)

Vol. XII No.1 Bi – Annual January-June 2017

DEPARTMENT OF COMMERCEOSMANIA UNIVERSITY

HYDERABAD- 500 007, T. S., INDIA.

UGC Approved Journal : S.No. 714, Journal No. 44934

REFEREED JOURNAL IMPACT FACTOR : 0.565

Prof. S.V. SatyanarayanaHead, Department of Commerce &

Editor-in-Chief

Prof. Gaddam LaxmanDean, Faculty of Commerce &

Associate Editor-in-Chief

Prof. V. Anand KumarChairman, BoS, Department of Commerce &

Associate Editor-in-Chief

Prof. D. ChennappaExecutive Editor

Log on to :www.oucommerce.com

www.osmania.ac.in

@The journal is published twice a year in January-June and July-December1000 Copies

All correspondence concerning contribution, book review, advertisements, orders and otherinformation regarding the journal should be addressed to Executive Editor. The Journal doesnot undertake to return manuscripts unless accompanied by stamped and self-addressedenvelop. The responsibility for statements of facts, quotations given and opinions expressedin the articles and book review published in the journal is borne entirely by the respectiveauthors.

Printed at :

Graphic VisionSecunderabad.Ph : 9032111444

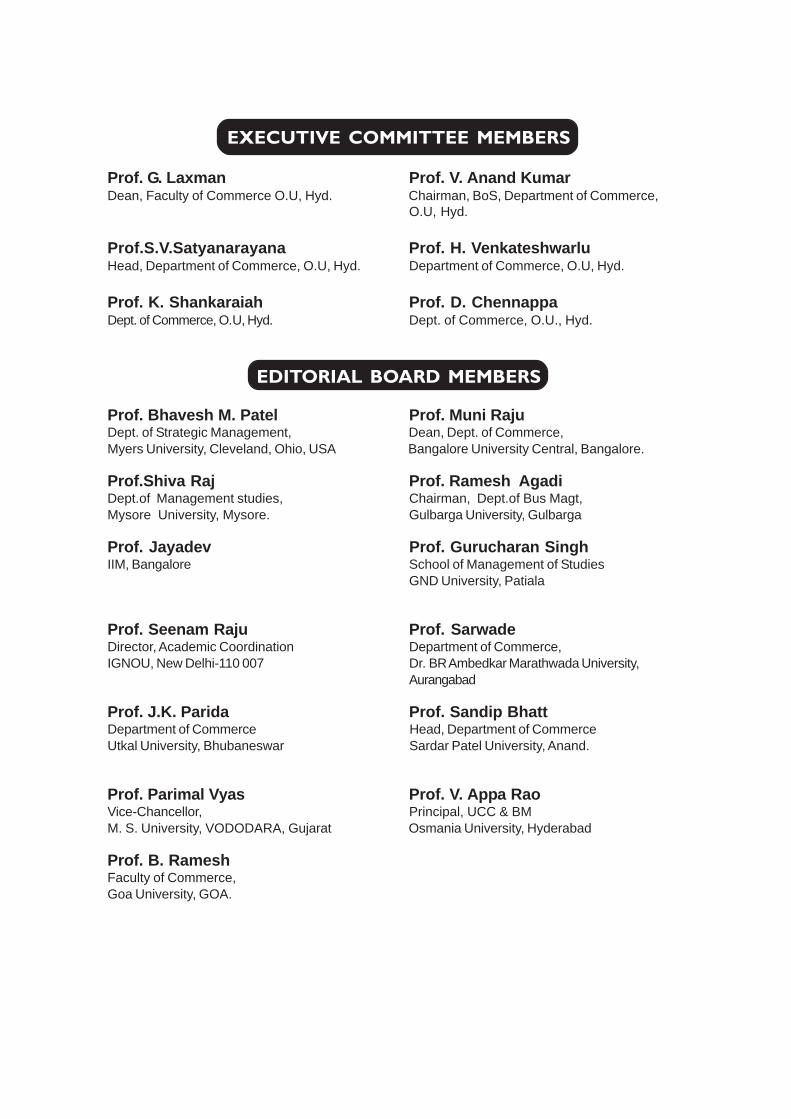

EXECUTIVE COMMITTEE MEMBERS

Prof. G. Laxman Prof. V. Anand KumarDean, Faculty of Commerce O.U, Hyd. Chairman, BoS, Department of Commerce,

O.U, Hyd.

Prof.S.V.Satyanarayana Prof. H. VenkateshwarluHead, Department of Commerce, O.U, Hyd. Department of Commerce, O.U, Hyd.

Prof. K. Shankaraiah Prof. D. ChennappaDept. of Commerce, O.U, Hyd. Dept. of Commerce, O.U., Hyd.

EDITORIAL BOARD MEMBERS

Prof. Bhavesh M. Patel Prof. Muni RajuDept. of Strategic Management, Dean, Dept. of Commerce,Myers University, Cleveland, Ohio, USA Bangalore University Central, Bangalore.

Prof.Shiva Raj Prof. Ramesh AgadiDept.of Management studies, Chairman, Dept.of Bus Magt,Mysore University, Mysore. Gulbarga University, Gulbarga

Prof. Jayadev Prof. Gurucharan SinghIIM, Bangalore School of Management of Studies

GND University, Patiala

Prof. Seenam Raju Prof. SarwadeDirector, Academic Coordination Department of Commerce,IGNOU, New Delhi-110 007 Dr. BR Ambedkar Marathwada University,

Aurangabad

Prof. J.K. Parida Prof. Sandip BhattDepartment of Commerce Head, Department of CommerceUtkal University, Bhubaneswar Sardar Patel University, Anand.

Prof. Parimal Vyas Prof. V. Appa RaoVice-Chancellor, Principal, UCC & BMM. S. University, VODODARA, Gujarat Osmania University, Hyderabad

Prof. B. RameshFaculty of Commerce,Goa University, GOA.

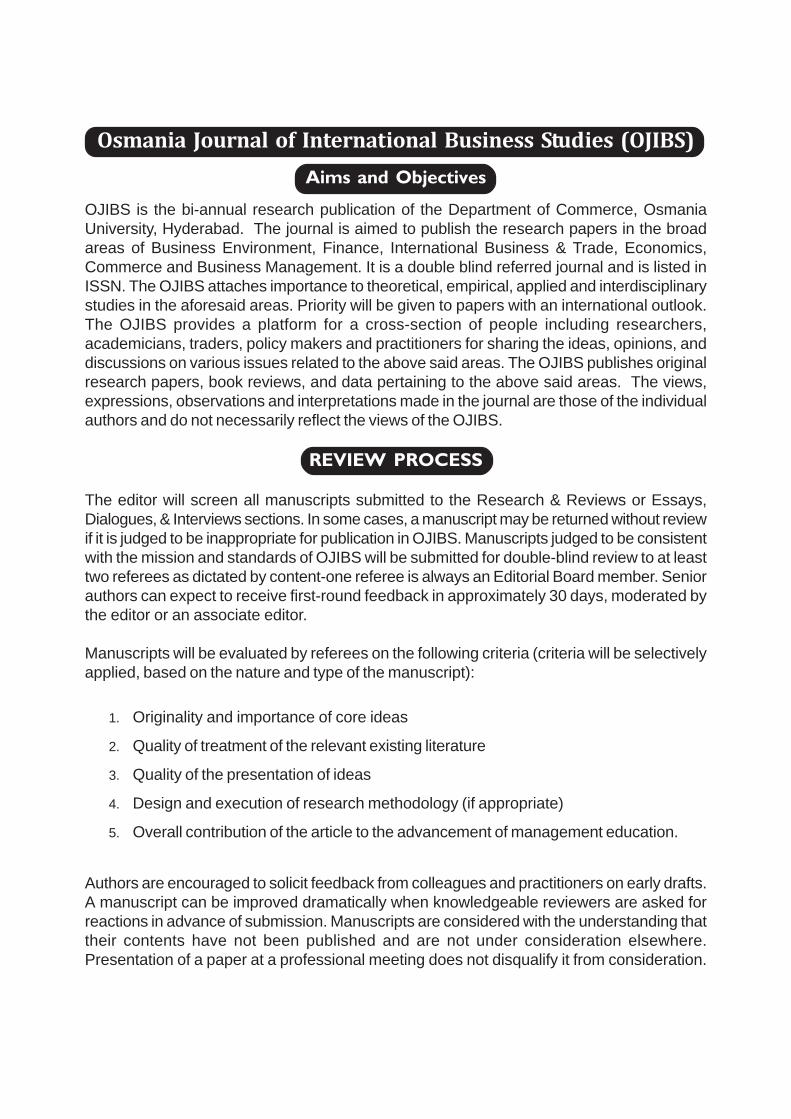

Osmania Journal of International Business Studies (OJIBS)

Aims and Objectives

OJIBS is the bi-annual research publication of the Department of Commerce, OsmaniaUniversity, Hyderabad. The journal is aimed to publish the research papers in the broadareas of Business Environment, Finance, International Business & Trade, Economics,Commerce and Business Management. It is a double blind referred journal and is listed inISSN. The OJIBS attaches importance to theoretical, empirical, applied and interdisciplinarystudies in the aforesaid areas. Priority will be given to papers with an international outlook.The OJIBS provides a platform for a cross-section of people including researchers,academicians, traders, policy makers and practitioners for sharing the ideas, opinions, anddiscussions on various issues related to the above said areas. The OJIBS publishes originalresearch papers, book reviews, and data pertaining to the above said areas. The views,expressions, observations and interpretations made in the journal are those of the individualauthors and do not necessarily reflect the views of the OJIBS.

REVIEW PROCESS

The editor will screen all manuscripts submitted to the Research & Reviews or Essays,Dialogues, & Interviews sections. In some cases, a manuscript may be returned without reviewif it is judged to be inappropriate for publication in OJIBS. Manuscripts judged to be consistentwith the mission and standards of OJIBS will be submitted for double-blind review to at leasttwo referees as dictated by content-one referee is always an Editorial Board member. Seniorauthors can expect to receive first-round feedback in approximately 30 days, moderated bythe editor or an associate editor.

Manuscripts will be evaluated by referees on the following criteria (criteria will be selectivelyapplied, based on the nature and type of the manuscript):

1. Originality and importance of core ideas

2. Quality of treatment of the relevant existing literature

3. Quality of the presentation of ideas

4. Design and execution of research methodology (if appropriate)

5. Overall contribution of the article to the advancement of management education.

Authors are encouraged to solicit feedback from colleagues and practitioners on early drafts.A manuscript can be improved dramatically when knowledgeable reviewers are asked forreactions in advance of submission. Manuscripts are considered with the understanding thattheir contents have not been published and are not under consideration elsewhere.Presentation of a paper at a professional meeting does not disqualify it from consideration.

Osmania Journal of International Business Studies (OJIBS)

(ISSN 00973-5372)

Vol. XII No.1 Bi – Annual January-June 2017

RESEARCH PAPERS Page No

1. IMPACT OF FIRM CHARACTERISTICS ON FINANCIAL PERFORMANCEOF INSURANCE COMPANIES IN NEPAL 1- Jagadish Bist, Rabeena Mali, SabitaPuri, Rajesh Kumar Jha, SachyamKayastha, and Salina Bhattarai

2. CROP INSURANCE: FARMERS PERCEPTIONS AND AWARENESS INSELECT DISTRICT OF TELANGANA STATE 12-Dr Sammaiah Buhukya

3. OPPORTUNITY FOR FDI IN INSURANCE SECTOR IN INDIA 19- Dr. Manisha Bhatt, Jayshree Mandaviya

4. A STUDY ON UNIVERSAL INSURANCE PROGRAM FOR RURAL INSURANCE DEVELOPMENT 30- P. Ajith Kumar, R. Sunil

5. MARKETING STRATEGIES OF SELECT PRIVATE LIFE INSURANCE COMPANIES IN INDIA 37- D. Gnyaneswer

6 .A STUDY ON AWARENESS OF HOUSEHOLDS REGARDING RURALPOSTAL LIFE INSURANCE 45- Mr.B.Santosh Kumar, Dr.Byram Anand

7. ETHIOPIAN INSURANCE CORPORATION – A CASE ANALYSIS 55- Dr. Ravi KanthMakarla, Mr. AshenafiDegefa

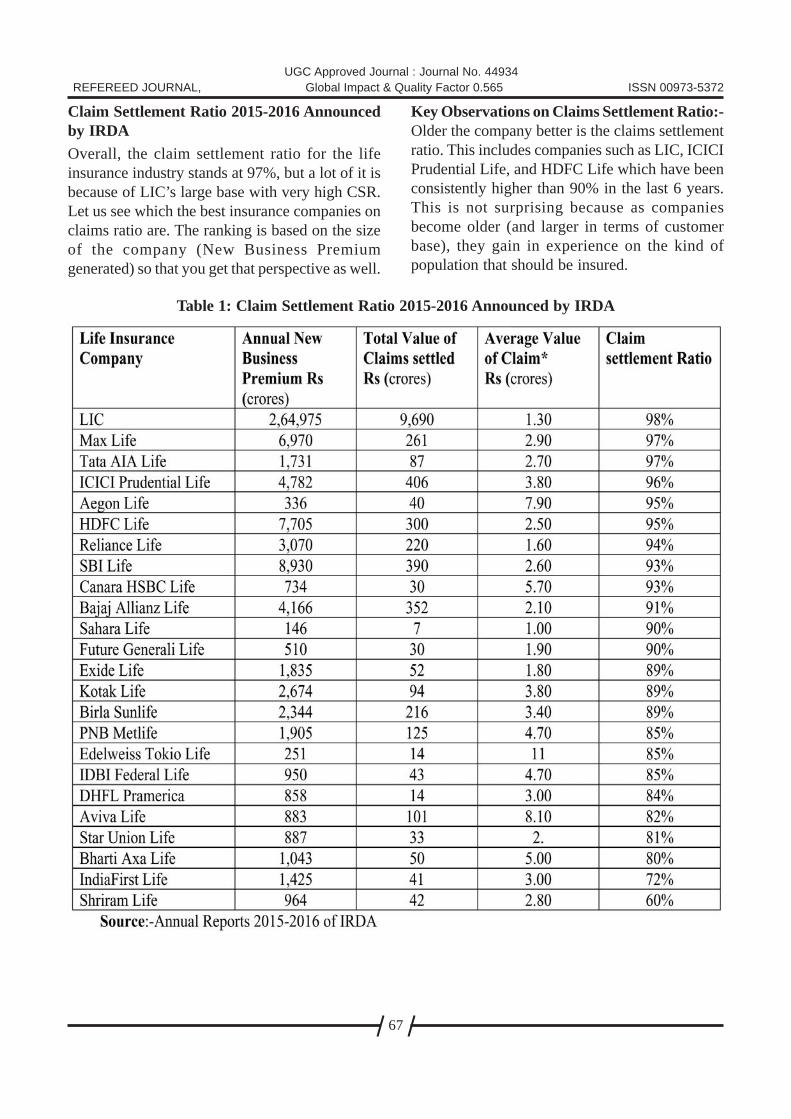

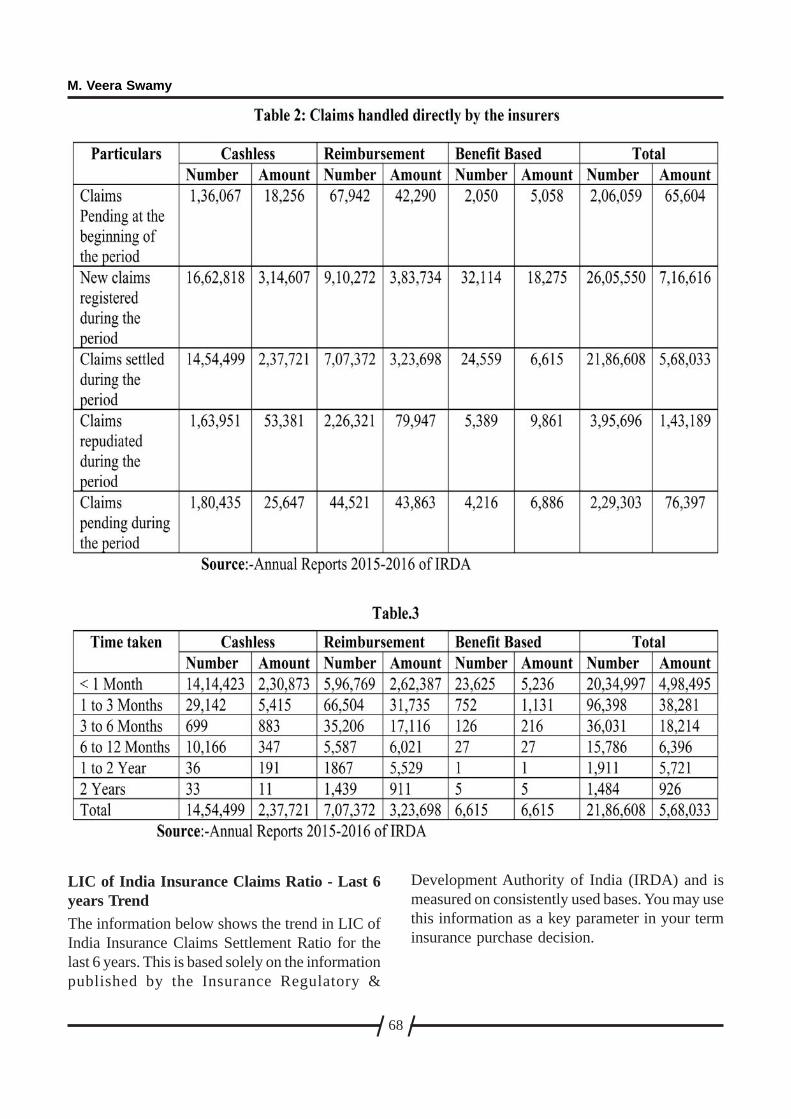

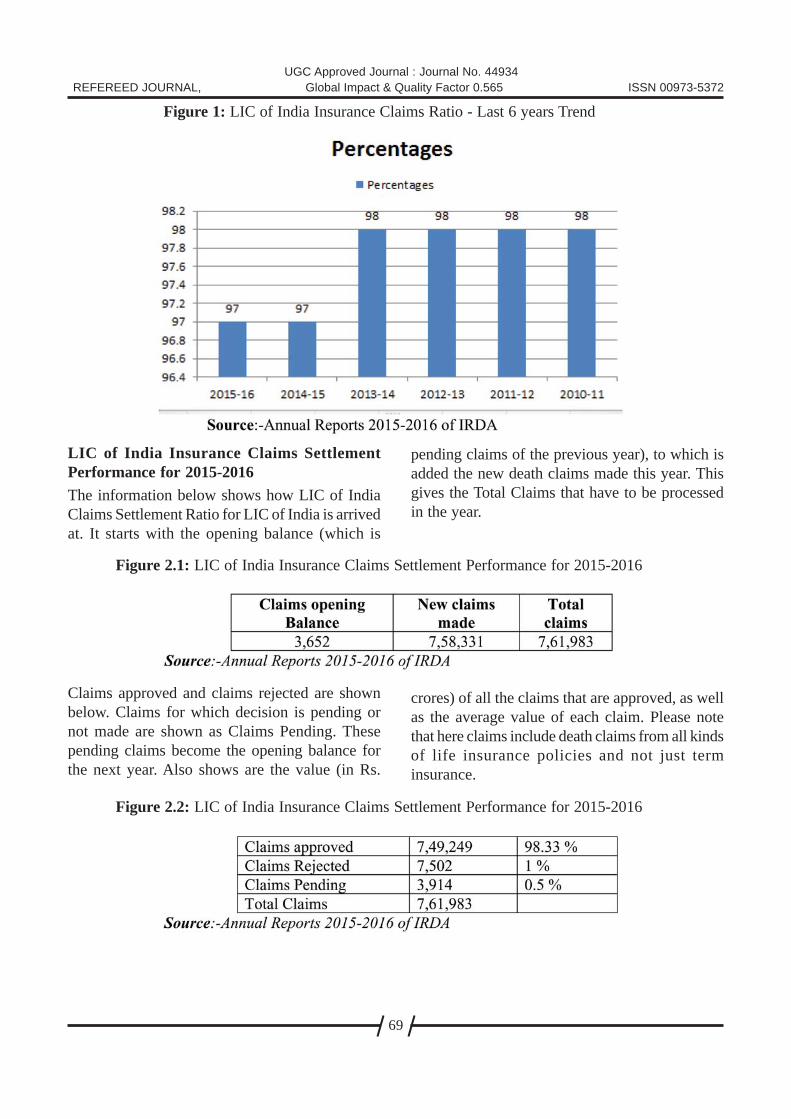

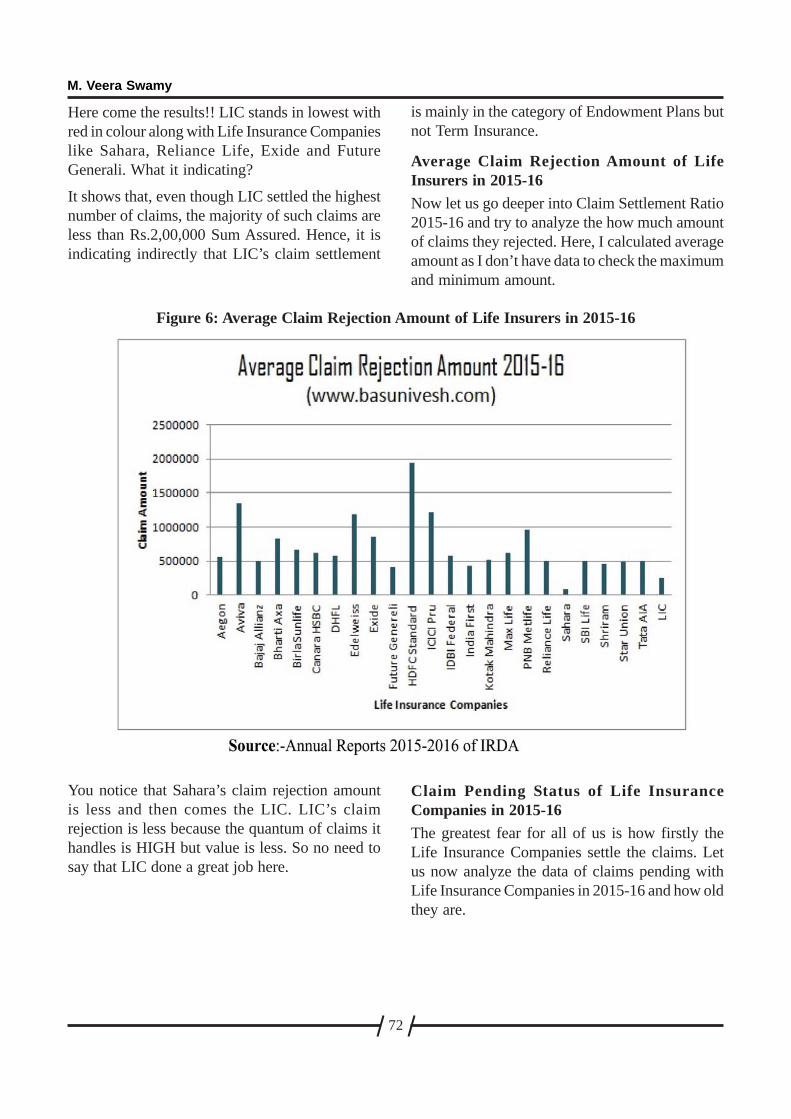

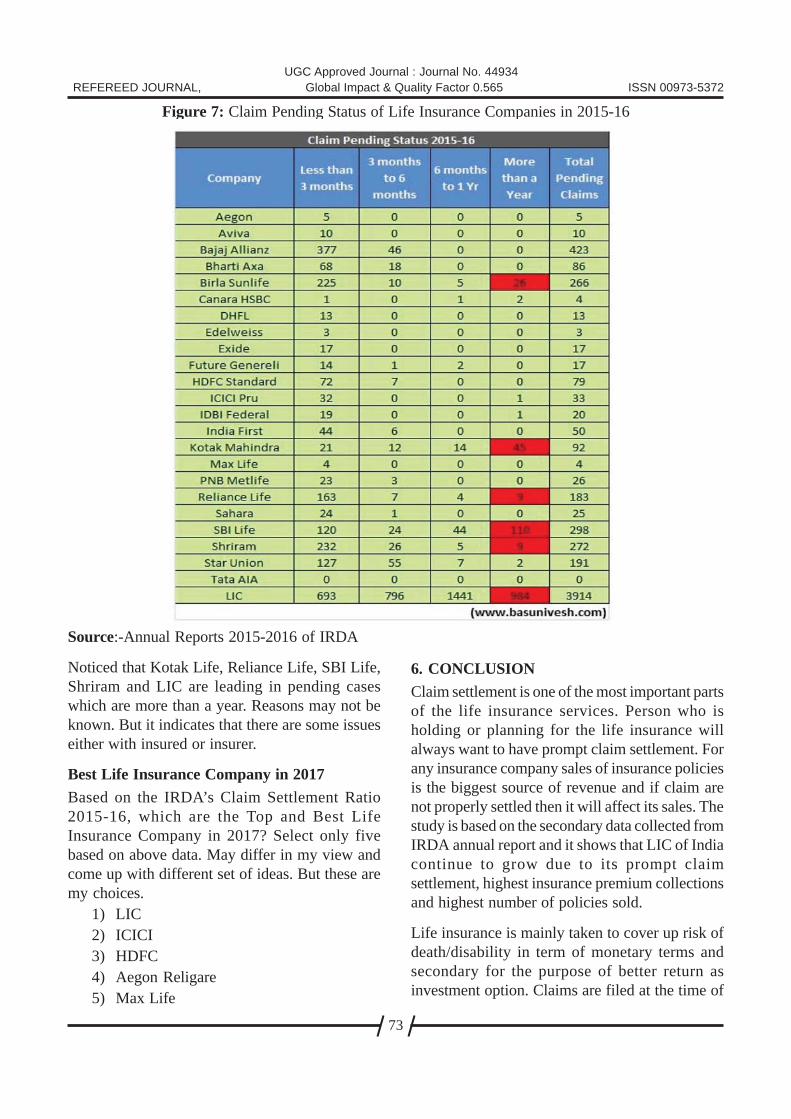

8. ANALYSIS ON CLAIMS SETTLEMENT RATIOS OF LIFE INSURANCE COMPANIESFOR 2015-16 65- M. Veera Swamy

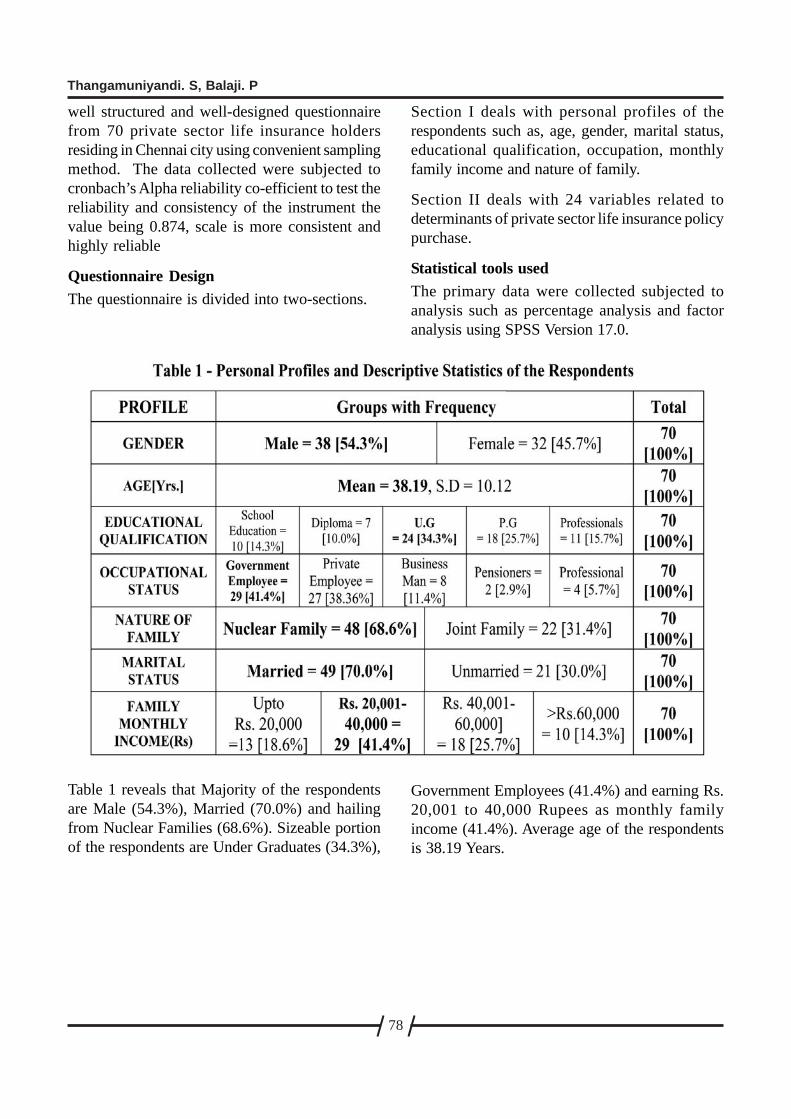

9. DETERMINANTS OF LIFE INSURANCE POLICY PURCHASE – [A STUDY TOEXPLORE NEW MARKETING STRATEGIES FOR PRIVATE LIFE INSURANCE PRODUCTS] 75- Thangamuniyandi. S, Balaji. P

UGC Approved Journal S.No. 714, Journal No. 44934

REFEREED JOURNAL IMPACT FACTOR : 0.565

10. ROLE OF TECHNOLOGY IN INDIAN INSURANCE SECTOR– A SELECT STUDY 81- Oddepalli Sathish, N. Rajendra Prasad

11. FARMERS’ PERCEPTION AND AWARENESS TOWARDS CROP INSURANCE INVILLUPURAM DISTRICT 88- R. Gnanasekaran Dr. L. Pandiyan

12. A STUDY ON CLAIM SETTLEMENT AND POLICYHOLDER’S SATISFACTION OFMOTOR INSURANCE PACKAGE POLICY 95- Mr. Yalama Reddy, Ashok Kumar Reddy, Dr. Byram Anand

13. PERFORMANCE OF PRADHAN MANTRI FASAL BIMA YOJANA (PMFBY) 103- V. Vinay Kumar, M.AnilKumar

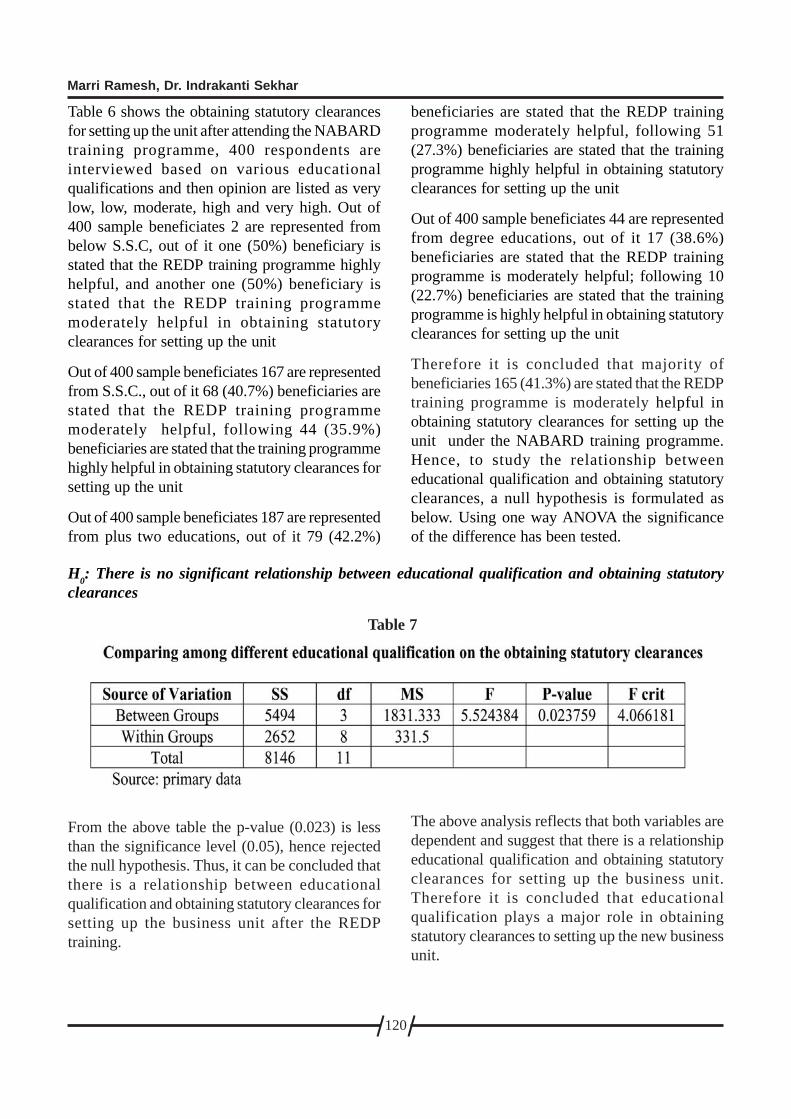

14. IMPACT OF RURAL ENTREPRENEURSHIP DEVELOPMENT PROGRAMME OFNABARD: A STUDY OF SELECT DISTRICTS IN TELANGANA REGION 114- Marri. Ramesh, Dr. Indrakanti Sekhar

15. PERFORMANCE EVALUATION OF NATIONAL PENSION SCHEME– A COMPARATIVEANALYSIS OF SBI AND HDFC 123- Dr. Ravi Kumar Jasti, Mr. B. Arun Kumar

16. EMOTIONS & CUSTOMER PURCHASE DECISION-WITH REFERENCE TO INSURANCE PRODUCTS 130

- Namratha Sharma, Dr.A.Patrick Anthony

17. IMPACT OF TECHNOLOGY ON LIFE INSURANCE CORPORATION OF INDIA 141- Dr. B. Sandhya Rani,

18. ISSUES AND CHALLENGES OF HEALTH INSURANCE IN LIFE INSURANCECORPORATION OF INDIA - A SELECT STUDY 148- Bojja Sampath

19. FARMERS PERCEPTION AND AWARENESS ABOUT CROP INSURANCE IN ADILABAD 154- Dr. Shubangee L. Diwe, J.Anitha

20. IRCTC – INSURANCE SCHEME FOR E – TICKET PASSENGERS 160- S. Anitha Jyothi

21. CONCEPT, GROWTH, CHALLENGES AND PROSPECTS OF TAKAFUL INSURANCE IN INDIA– A STUDY 165- Sabiha Shareef

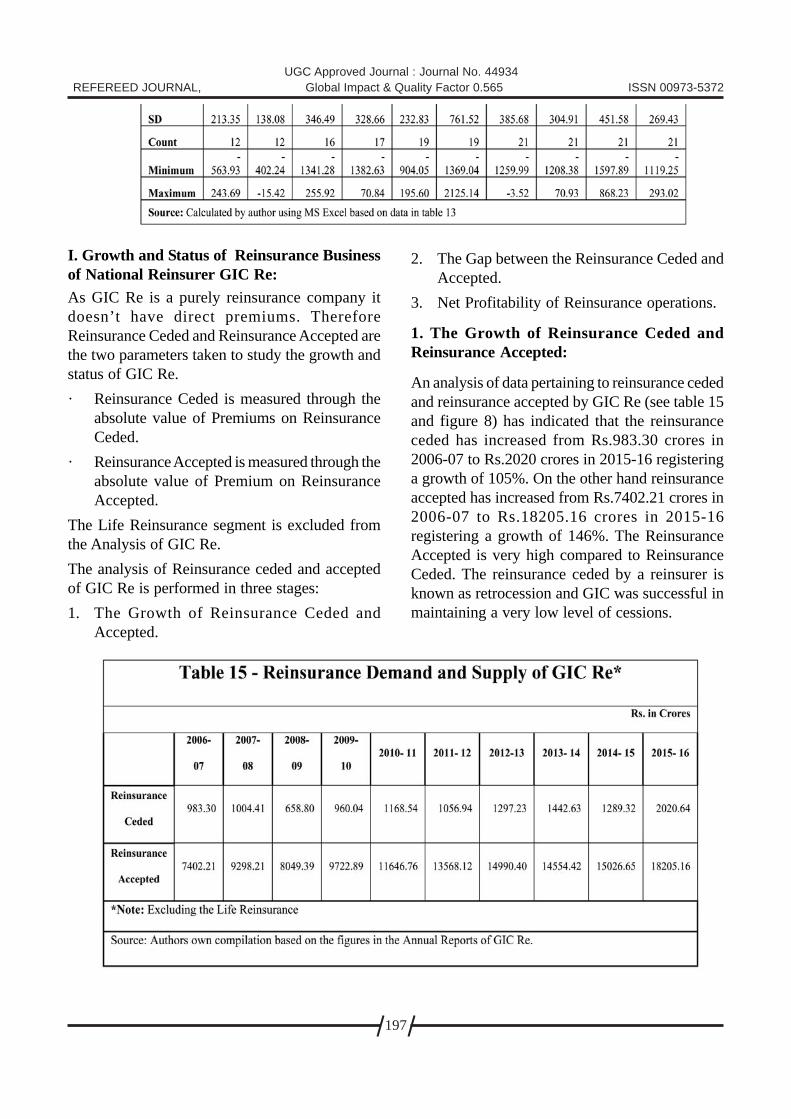

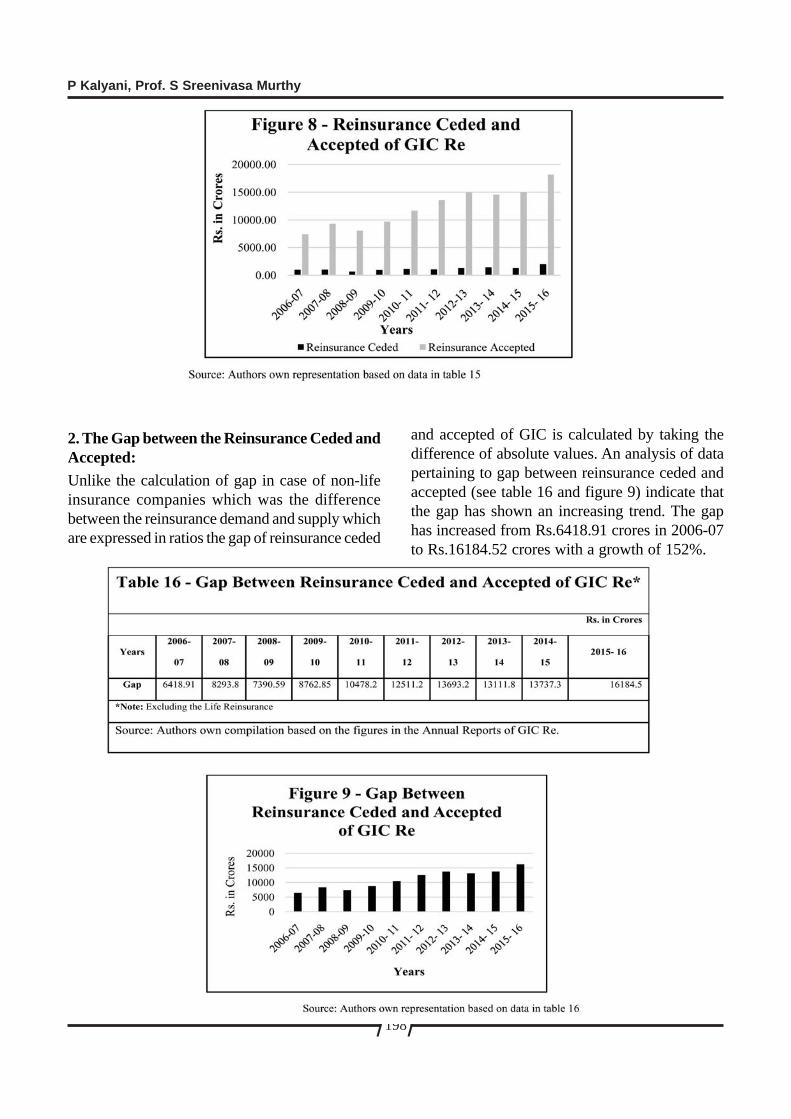

22. GROWTH AND STATUS OF REINSURANCE BUSINESS IN INDIA: A STUDY 175- P Kalyani, Prof. S Sreenivasa Murthy

23. AN EVALUATIVE STUDY OF RAJIV AAROGYASRI HEALTH INSURANCE SCHEME INWARANGAL DISTRICT OF PRE-BIFURCATION OF TELANGANA STATE 202- A. Raveendar Naik

24. EVALUATIVE STUDY OF RAJIV AAROGYASRI HEALTH INSURANCE SCHEME INTELANGANA STATE 211- Ramavath Ravi

25. POLICYHOLDER’S PERCEPTION TOWARDS ONLINE INSURANCE - A PILOT STUDYIN HYDERABAD 219- Mr. D. Mahipal

26. THIRD PARTY ADMINISTRATORS IN HEALTH INSURANCE BUSINESS- A STUDY 226- Dr.E.Shanker

27. HEALTH INSURANCE IN INDIA- A STUDY OF PUBLIC AND PRIVATE SECTOR 231- Dr.D.Satish, P.Shyam Sunder Goud

28. AN EMPIRICAL STUDY ON THE BEHAVIOUR OF LIFEINSURANCE POLICYHOLDERS 237- Bharla Anand

29. EVALUATION OF PERFORMANCE OF AAROGYASRI SCHEME 247- Ramesh.Vavilala

30. A STUDY ON CUSTOMER PERCEPTION AND SATISFACTION TOWARDS MOBILEINSURANCE PRODUCTS IN INDIA 258- Dr. Sakru Ketavath, V.V.Ramana Murthy

31. HEALTH INSURANCE SCHEMES OPERATIONAL POLICIES ISSUES AND DETERMINGPHENOMENON VARIABLES-A STUDY IN TIRUCHIRAPPALLI DISTRICT, TAMIL NADU 265- Dr. R. Ramachandran

32. A CRITICAL ANALYSIS OF PRADHAN MANTRI JAN-DHAN YOJANA (PMJDY) ANDHEALTH INSURANCE- A WIN-WIN COMBINATION FOR BANKS TO OFFERHEALTH INSURANCE TOPMJDY ACCOUNT HOLDERS 273- Dr. Smitha Sambrani, Balaji Prasad Dantu,

33. CUSTOMER INTELLIGENCE STRATEGY IN INDIA: WITH SPECIAL REFERENCE TOINSURANCE SECTOR 279- Prof. (Dr.) Sandip K. Bhatt, Dr. Yashasvi R. Rajpara

34. EVOLUTION OF HEALTH INSURANCE IN INDIA – AN OVERVIEW 283- Dr. Bandaru Veerababu

35 IMPACT OF DIGITALIZATION OF INSURANCE SECTOR (E-INSURANCE) – A STUDY 291- Dr.P.Yadaiah

36. NEPALESE INSURANCE MARKET, ROLE OF REGULATOR AND FINANCIAL SOUNDNESS 295- Sharda Pandey Lohani

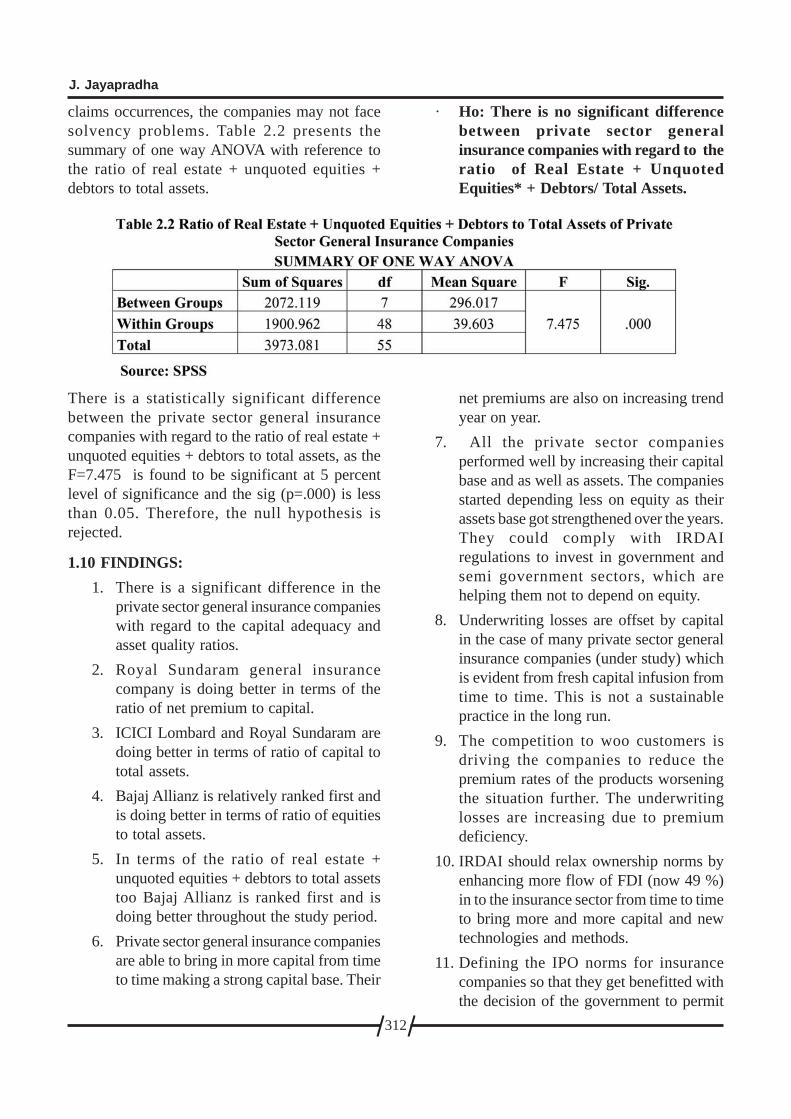

37. A STUDY ON CAPITAL ADEQUACY AND ASSET QUALITY OF SELECT INDIANPRIVATE SECTOR GENERAL INSURANCE COMPANIES 304- J. Jayapradha

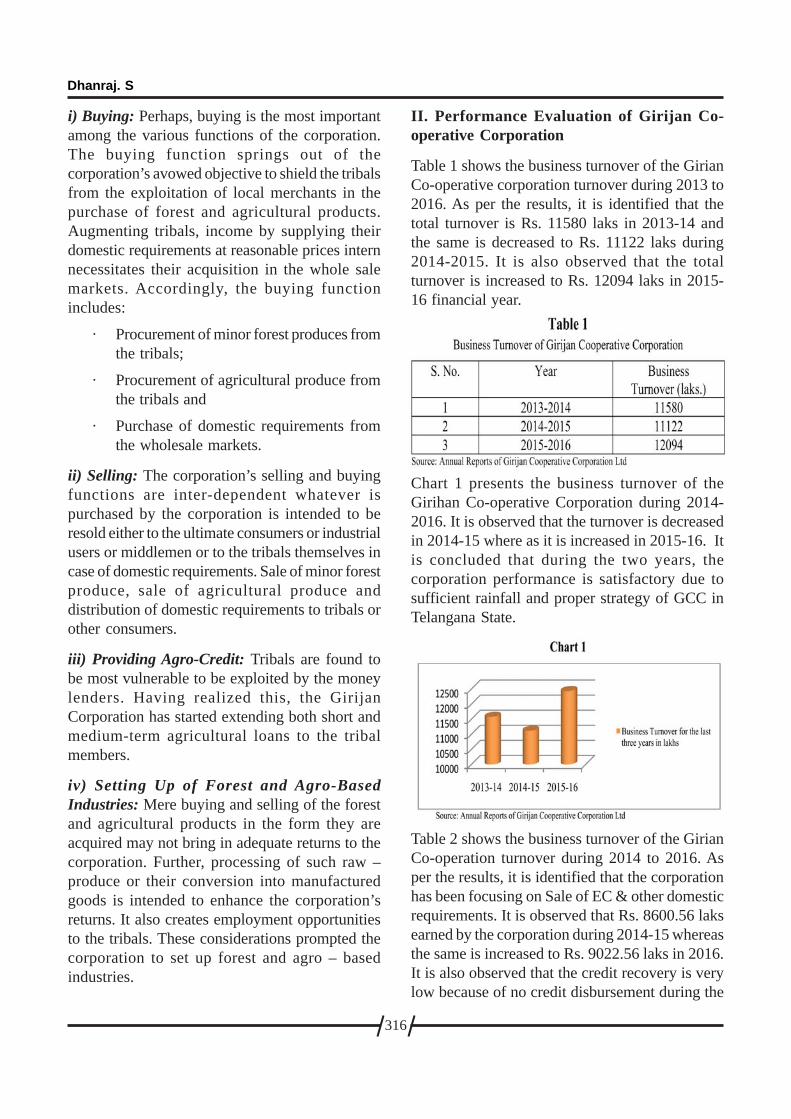

38. PERFORMANCE EVALUATION OF GIRIJAN CO-OPERATIVE CORPORATION LTD.IN TELANGANA STATE 314- Dhanraj. S

39 A STUDY ON THE GROWTH OF INDIAN INSURANCE INDUSTRY 319- Dr. L. Srinivas Reddy

40. AN OPPORTUNITY TO EXPAND ACCESS: EVOLUTION OF HEALTH INSURANCE IN INDIA 325- Ramesh. N

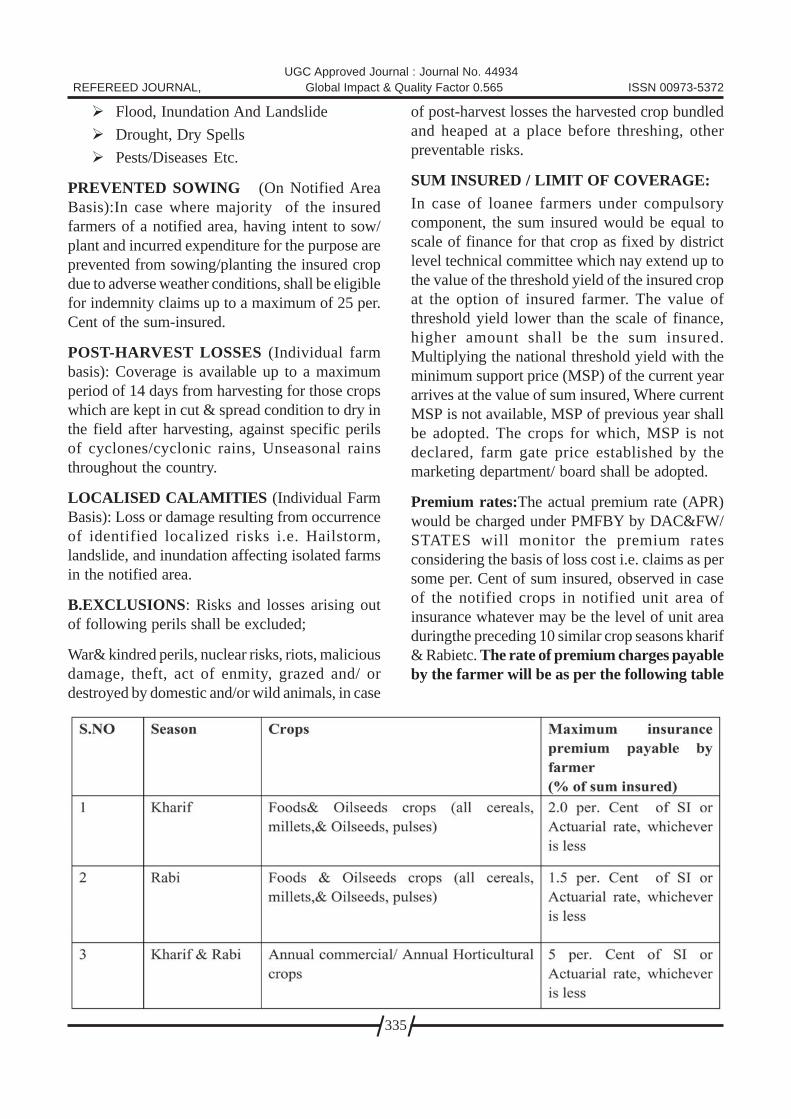

41. PRADHAN MANTRI FASAL BIMA YOJANA - A STEP TOWARDS ERADICATION OFCROP INSURANCE PROBLEMS IN INDIA 331- M. Vamshidhar

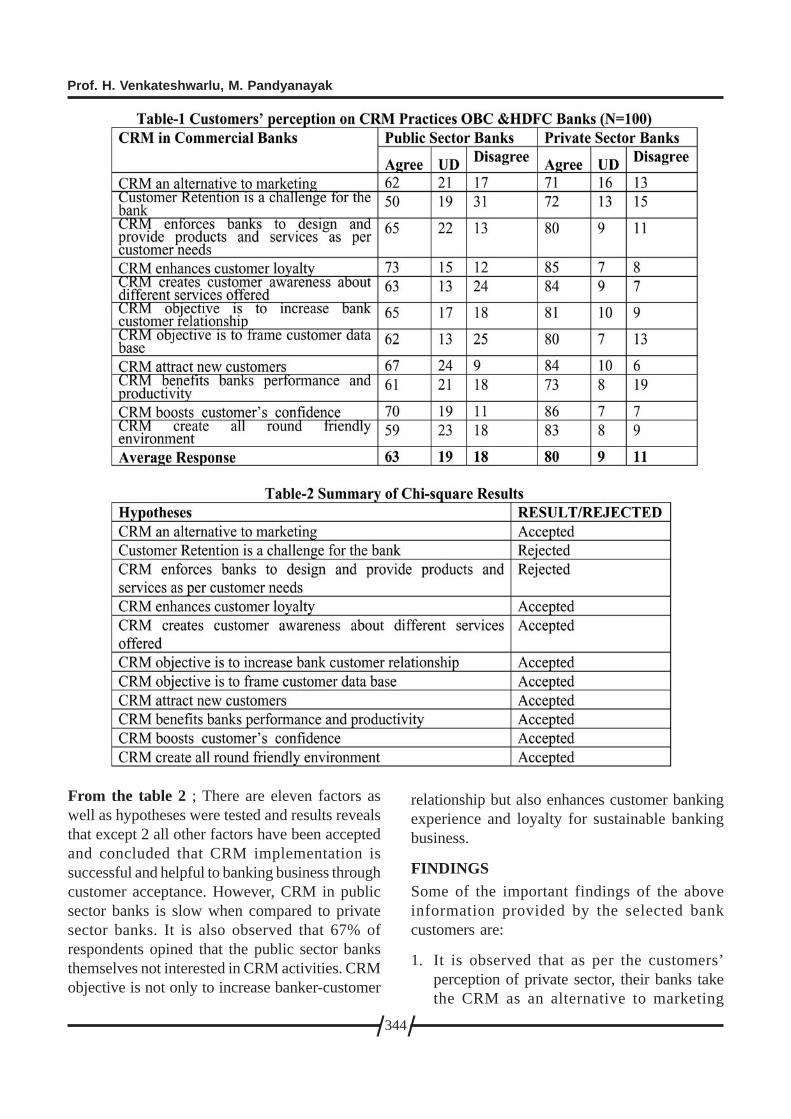

42 CUSTOMER RELATIONSHIP MANAGEMENT (CRM) PRACTICES IN BANKING SECTOR– A STUDY OF SELECT COMMERCIAL BANKS IN HYDERABAD CITY 339- Prof. H. Venkateshwarlu, M. Pandyanayak

43. FACTORS AFFECTING EMPLOYEE MOTIVATION:(WITH REFERENCE TO ACC CEMENTS , WADI) 347- Tabassum Fatima

44. QUALITY OF WORK LIFE IN BPO SERVICE SECTOR 358- Challa Madhavi, Dr.Bhavannarayana.K, Dr.J.Venugopal,

45. TOURISM IN INDIA - A STUDY 364- Dr. J. Seenaiah.

.

For subscription, the payment can be made by a crossed demand draft in favour of “Osmania

Journal of International Business Studies” and send to Dr. D. Chennappa, Associate

Professor and Executive Editor, Department of Commerce, Osmania University,

Hyderabad 500 007, Telangana, India. You can also log on to www.indianjournals.com

for online subscription. You can also reach through e-mails : [email protected],

[email protected], Mobile No. : 9440 360 149.

.

1

UGC Approved Journal : Journal No. 44934REFEREED JOURNAL, Global Impact & Quality Factor 0.565 ISSN 00973-5372

IMPACT OF FIRM CHARACTERISTICS ON FINANCIALPERFORMANCE OF INSURANCE COMPANIES IN NEPAL

Jagadish Bist, Rabeena Mali, SabitaPuri, Rajesh Kumar Jha,SachyamKayastha, and Salina BhattaraiUniglobe College (Pokhara University), Kathmandu, Nepal

ABSTRACT

This study examines the impact of firm specific characteristics on the performance of Nepalese insurancecompanies. The return on asset (ROA) is the dependent variable. The independent variables are theleverage, diversification, size, liquidity, age, claim payment and premium growth. This study is based onthe secondary sources of data that are collected from 18 Nepalese insurance companies leading to atotal of 105 observations. The data were collected from annual reports of the selected Nepalese insurancecompanies. The regression models are estimated to test the significance and impact offirm specificcharacteristics onfinancial performance of insurance companies in Nepal. The regression models areestimated to test the significance and impact offirm specific characteristics on financial performance ofinsurance companies in Nepal.

The study reveals that leverage is positively correlated to return on assets. This shows that higher theleverage, higher would be the return on asset.Similarly, premium growth rate is positively correlated toreturn on assets.This indicates that higher the premium growth rate, higher would be the return onassets. However, diversification is negatively correlated to return on assets. This indicates that higherthe number of branches, lower would be the return on assets. Similarly, size is negatively correlated toreturn on assets. This indicates that higher the size of firm, lower would be the return on assets.Theresult also shows that liquidity is negatively correlated to return on assets. This means that higher theliquidity of firm, lower would be return on assets. However, age of firm is positively correlated to thereturn on assets, which shows that higher the age of firm, higher would be return on assets. The studyalso shows that there is negative relation between claim payment and return on assets. This indicatesthat higher the claim payment incurred, lower would be the return on assets.The result of the regressionanalysis shows that beta coefficients are positive for leverage and premium growth. However, thecoefficients are negative and insignificant for the diversification, size, liquidity and claim payments. Thecoefficients are significant for leverage and premium growth at 1% level.

Keywords:Return on assets, leverage, diversification, size, liquidity, age, claim payment, premiumgrowthand insurance companies.

1. IntroductionThe past decade has seen a dramatic rise in thenumber of insolvent insurers. The perceive causesof these insolvencies were myriad. Some of theinsolvencies were precipitated by rapidly risingor declining interest rates, mispricing of insurancepolicies, natural catastrophes, and changes in legalinterpretations of liability and the filing of falseclaims, poor credit policies among others. Thechurning of polices by unscrupulous sales agents,insolvencies among the re-insurers backing the

policies issued, non-compliance with insuranceregulation, and malfeasance on the part of officersand directors of insurance companies affected aswell (Baldoni, 2008). As a result of globalization,deregulation and terrorist attacks, the insuranceindustry has gone through a tremendoustransformation over the past decade (Sanchez,2006).

The insurance industry plays a major role in thesociety as they stimulate the economy at large. Thisis because the sector is part of immune and repair

2

system of an economy and successful operationof the industry can set energy for other industriesand development of an economy (Abate, 2012).Indeed, a well-developed and evolved insuranceindustry is critical to conditions for economicdevelopment as it provides long term funds forlong term investment and at the same timestrengthens the risk taking ability of the country.

The performance of any business firm not onlyplays the role to increase the market value of thatspecific firm but also leads toward the growth ofthe whole sector and the overall success of theeconomy (Ahmed, 2011). In this regards, a soundfinancial management should be consistent withthe drives to improve and increase profitability soas to meet the goal of individual firm owners. Theprimary desire of any firm is to earn more profitand enhance the wealth of its stakeholders(Gitman, 2007). However due to challenges ininternal and external environment, most firms areunable to meet their goals. In other words,performance is a function of the ability of anorganization to gain and manage its resources inseveral different ways so as to develop competitiveadvantages (Iswatia&Anshoria, 2007).

The performance of the businesses is veryimportant because it leads towards the growth ofthe whole sector where it is involved and of theoverall prosperity of the economy. Profitability,defined as proxy of financial performance, is oneof the main objectives of insurance companies’management (Burca&Batrinca, 2014). Discussingand analyzing the determinants of performance ofinsurance companies, is considered important inthe corporate finance literature because of theirrole as intermediaries. These companies providethe mechanism of risk transfer and also theseinstitutions channelize the funds to support thebusiness activities in the economy. However, it hasreceived little attention particularly in Albania.There are studies on insurance schemes in Albania(Sinaj et al., 2014), role and evolution of insuranceindustry (Sharku et al., 2011), management oninsurance companies (Kume&Xhuka, 2010), butthere isn’t any prior research on the factors thatdetermine insurance profitability.

Insurance companies provide unique financialservices to the growth and development of everyeconomy. Such specialized financial services rangefrom the underwriting of risks inherent ineconomic entities and the mobilization of largeamount of funds through premiums for long terminvestments. The risk absorption role of insurerspromotes financial stability in the financial marketsand provides a “sense of peace” to economicentities. The business world without insurance isunsustainable since risky business may not havethe capacity to retain all kinds of risks in this everchanging and uncertain global economy (Ahmedet al., 2010). Insurance companies’ ability tocontinue to cover risk in the economy hinges ontheir capacity to create profit or value for theirshareholders.

Indeed, a well-developed and evolved insuranceindustry is a boon for economic development as itprovides long- term funds for infrastructuredevelopment of every economy (Charumathi,2012). The majority of research on life insurerperformance has been in terms of identifying thoseinsurer-specific variables that aid in identifyinginsurers that are more likely to become insolvent.BarNiv and Hershbarger (1990) andDeakin(2005)examined the run on the bank risk, and found thatprior to 1992 rating organizations generally didnot appreciate the risks inherent in liabilities suchas guaranteed investment contracts. Cummins etal (1999) showed that cash flow simulationvariables add explanatory power to solvencyprediction models.

While insurance companies hold billions ofshillings belonging to the general public, includingbuyers of their products, retirement benefitschemes and fund’s managers, information onthese companies is scanty. For large consumers ofinsurance products, this group usually relies onthe expertise of qualified risk managementconsultants to offer advice on where to place theirinsurance covers (Kumba, 2011).

Financial performance is a measure of anorganization’s earnings, profits, appreciations invalue as evidenced by the rise in the entity’s share

Jagadish Bist, Rabeena Mali, SabitaPuri, Rajesh Kumar Jha, SachyamKayastha, and Salina Bhattarai

3

UGC Approved Journal : Journal No. 44934REFEREED JOURNAL, Global Impact & Quality Factor 0.565 ISSN 00973-5372

price. In insurance, performance is normallyexpressed in net premiums earned, profitabilityfrom underwriting activities, annual turnover,returns on investment and return on equity. Thesemeasures can be classified as profit performancemeasures and investment performance measures.Profit performance includes the profits measuredin monetary terms. Simply, it is the differencebetween the revenues and expenses. These twofactors, revenue and expenditure are in turninfluenced by firm-specific characteristics,industry features and macroeconomic variables.Investment performance can take two differentforms. One the return on assets employed in thebusiness other than cash, and two, the return onthe investment operations of the surplus of cash atvarious levels earned on operations (Chen andWong, 2004).

In the insurance business, capital is referred to assurplus. Surplus is required for insurancecompanies to have collateral for outstandingpolicies. Without it, insurance companies cannotfulfil their obligations towards the customers.Legislation requires insurance companies to holdcertain levels of surplus to cover default risks(Myers & Read, 2001).

The subject of financial performance has receivedsignificant attention from scholars in the variousareas of business and strategic management. It hasalso been the primary concern of businesspractitioners in all types of organizations sincefinancial performance has implications toorganization’s health and ultimately its survival.High performance reflects managementeffectiveness and efficiency in making use ofcompany’s resources and this in turn contributestothe country’s economy at large (Naser, andMokhtar, 2004).

Financial distress relates to a broad concept withseveral situations in which a firm faces financialdifficulty. These common situations definingfinancial distress include bankruptcy, insolvencyand failure (Maina and Sakwa, 2012). Accordingto Outechever (2007), financial distress is a gradualdynamic process where a firm moves in and outof financial trouble as it passes out through various

stages. These stages have specific attributes andconsequences as they contribute differently tobusiness failure. Financial distress varies withtime. Therefore as a firm enters one state, it doesnot stay in the same state until it recovers or isliquidated. The change in financial conditiontriggers the transition from one state of financialdistress to another. If these conditions are notaggravated, this may lead the firm into bankruptcyproblems.

Owing to an apparent lack of uniform financialreporting formats, a number of insurancecompanies have not published their profit and lossaccounts, making it difficult for the general publicto gauge their profitability, overall writtenpremiums or even their net incomes. Companiesusing this format simply give a skeleton balancesheet, providing little or no information to thepublic. The scanty financial statements, releasedto the public by some companies, create a lot ofgrey areas and room for such unprofessionalactivities as tax evasion and concealing of criticalratios and figures. Based on available credit ratingmethods, profit combined with other ratios andcomputations can provide useful indicators toanyone looking for a stable and financially soundinsurance company (Kumba, 2011).

Other financial ratios, includes current ratio whichsimply shows how fast an insurance company cansettle a claim. These ratios are critical indetermining the financial strength and ability ofany insurance company to settle claims and stayin business. For those wishing to determine if theirinsurance company is failing, risk managementexperts’ advice that one needs to calculate theDebt/Equity ratio, which is total liabilities dividedby shareholders equity. This ratio is also knownas risk gearing and shows the extent to which acompany is financed by borrowed funds. Otherratios include acid test ratios, which is liquid assetsdivided by current assets and the current ratio. Allthe above ratios can determine whether it is safeto place a cover with the insurance company(Kumba 2011). Carson and Hoyt (1995) found thatsurplus and leverage measures are strongindicators of insurer financial strength, and also

4

found a slightly higher risk of failure among stockinsurers than mutual insurers.

In Nepal, banking industries have been sufferedfrom the various anomalies and in insurance sectormay happen at any time if we are not aware onsuch a vulnerable situation. Insurance industriesget momentum after adopting liberalization policyin financial sector which is become moreorganized, Systematized and well regulated afterestablishment of Insurance Board.

Therefore management of insurance company andthe evaluation of their work are very complex. Asinsurance sector is currently facing manychallenges such as increased competition,consolidation, solvency risks and a changingregulatory environment, maintaining the soundfinancial health of insurance industry is mostchallenging job for regulatory agencies while itscontribution to the economy and society isnoteworthy (Ghimire, 2013).

The main objective of this study is to examine therelationship of financial performance in theinsurance companies in Nepal. Specifically, it

examines the claim experience, premium growth,size of companies, liquidity, Age of companies (no.of years since establishment), and diversification(no. Of branch across the region) and leverage onfinancial performance of Nepalese InsuranceCompanies and motivates for best practice andvalued the benefits of good financial performancein Nepal.

The remainder of this study is organized as follows.Section two describes the sample, data, andmethodology. Section three presents the empiricalresults. Section four draws conclusions anddiscusses the implications of the study.

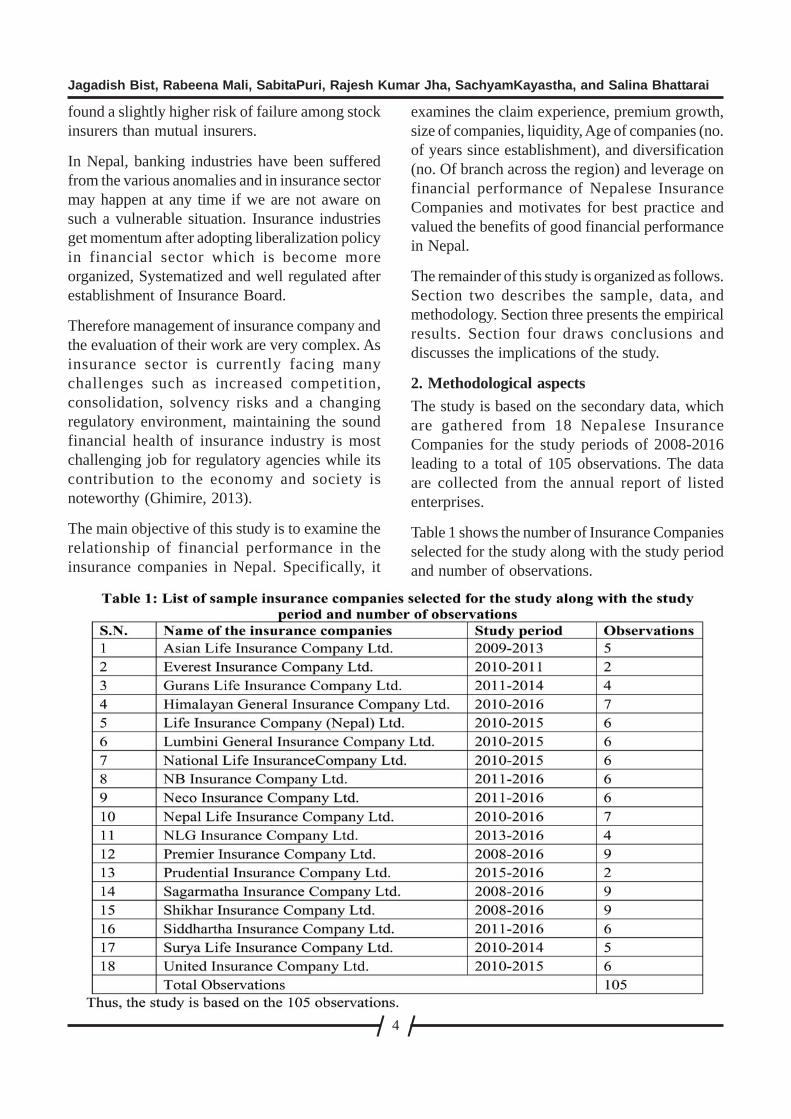

2. Methodological aspectsThe study is based on the secondary data, whichare gathered from 18 Nepalese InsuranceCompanies for the study periods of 2008-2016leading to a total of 105 observations. The dataare collected from the annual report of listedenterprises.

Table 1 shows the number of Insurance Companiesselected for the study along with the study periodand number of observations.

Jagadish Bist, Rabeena Mali, SabitaPuri, Rajesh Kumar Jha, SachyamKayastha, and Salina Bhattarai

5

UGC Approved Journal : Journal No. 44934REFEREED JOURNAL, Global Impact & Quality Factor 0.565 ISSN 00973-5372

The modelThe model estimated in this study assumes thatthe performance of insurance companies dependson several firm specific characteristics Therefore,the model takes the following form:

Performance = ƒ (leverage, diversification, sizeof companies, liquidity, age of companies, claimexperience and premium growth).

More specifically, the given model has beensegmented into following models:

lnROAit = â

0+ â

1 LEV

it + â

2 DV

it + â

3SZ

it + â

4LQ

it

+ â5AG

it + â

6CP

it +â

7PG

it + e

it

Where,

ROA = Return on total assets; net profit beforetax/ total assets

LEV = Leverage; total liabilities/ total assets

DV = Diversification; no. of branches acrossthe region

SZ = Size of companies; natural log of totalassets

LQ = Liquidity; current assets/ currentliabilities

AG = Age of companies; no. of years sinceestablishment

CP = Claim payment; net claims incurred/ netearned premiums

PG = Premium growth; PG (t)-PG (t-1)/ PG(t-1) and

e = errors.

LeverageLeverage is the ratio of a company’s total liabilitiesto total assets. Insurance leverage is defined asreserves to surplus by (Chen and Wong, 2004).This ratio demonstrates the potential impact ofdeficiencies in technical reserves due to occurrenceof unexpected losses on the equity (Adams andBuckle, 2003). In this study, insurance leverageratio is calculated by dividing the net technicalreserves to the equity. Capital structure literaturesuggests that as the leverage increases up to anoptimum point, so will the firm value and aftersurpassing this optimum level, the firm value will

decline and the likelihood of insolvency willincrease depending on the increased leverage(Carson and Hoyt, 1995). Therefore, it is expectedthat excessive insurance leverage may have anegative impact on profitability. Based on theabove arguments, the following hypothesis isproposed:

H1: There is a positive relationship between theleverage and ROA.

DiversificationFirm diversification is a corporate strategy toincrease sales volume from new products and newmarkets. Diversification is the ratio of the squaredfraction of sales in a segment to total sales andfinancial performance was measured by ROA(Kaguri, 2012). Diversification is the number ofbranches and subbranches of a firm across theregion or country. If large number of branches andsub branches are established by an insurancecompany, the performance of thefirmdecreases.Ramanujam and Varadarajan(1990)found that there are no consistent or conclusivefindings between firm diversification andperformance. Based on the above arguments, thefollowing hypothesis is proposed:

H2: There is a negative relationship between thediversification and ROA.

SizeSize of companies represents the natural log oftotal assets. Company size is positively related tofinancial performance as large insurancecompanies have greater capacity for dealing withadverse market fluctuations than smaller insurancecompanies. Large insurance companies can easilyrecruit capable and skilled employees withprofessional knowledge compared to smallerinsurance companies, which is the most significantproduction factor for delivering insuranceservices.Beard &Dess(1981) has shownempirically that company size is positively relatedto the financial performance. (Beard &Dess, 1981)revealed that firm size has positive impact on firmperformance. Likewise, Ahmed et al. (2011)indicated that firm size is positively related to firm

6

performance. Additionally, Malik (2011) found apositive relationship between firm size andfinancial performance. Based on above discussion,following hypothesis has been developed.

H3: There is positive relationship between firmsize and ROA.

LiquidityLiquidity is the degree to which an asset or securitycan be quickly bought or sold in the market withoutaffecting the asset’s price. A firm can meet theirshort-term financial obligations with the liquidassets available to them. . Liquidity allowsfinancial institutions to seize opportunities byconverting cash easily and quickly. Liquidityposition of a firm can be determined by using ratioanalysis. It is calculated by dividing the totalcurrent assets by the total currentliabilities.Amihud and Mendelson (2008) found apositive association between liquidity and firmperformance. Fang et. al. (2009) indicated thatliquidity is positively related to firm performance.Similarly,Arabsalehi et al. (2014) identified aconsistent positive relationship between liquidityand firm performance. The firm with good liquidityposition shows that the firm is able to maintainemergency situation and the firm has low chanceof solvency. Chen and Wong (2004) explained thatliquidity is the important determinant of financialhealth of insurance companies. Based on abovediscussion, following hypothesis has beendeveloped.

H4: There is positive relationship betweenliquidity and ROA.

AgeCompany’s age measured as the number of yearsa company is operating in the market since it wasfounded. Firm age is an important determinant offinancial performance. Past research shows thatthe probability of firm growth, firm failure, andthe variability of firm growth decreases as firm’sage. Maturity brings stability in growth as firmslearn more precisely their market positioning, coststructures and efficiency levels. Malik (2011)found that there is no relationship between

profitability and age of the company. Similarly,Loderer and Waelchli (2013) stated that there isnegative relationship between the age ofcompanies and firm performance. Firm age is animportant determinant of financial performance.Past research shows that the probability of firmgrowth, firm failure, and the variability of firmgrowth decreases as firm’s age.

H5: There is negative relationship between age ofcompanies and ROA.

Claim paymentClaim payment is apayment made by an insurancecompany in case of loss or accidents incurred bytheir client. The insurance companies review theclaim for its validity and then pay out to theinsured.Claim payment is measured as the ratioof incurred claims to earned premiums. Thesmaller insurance companies have less profitabilityas a result of very high claims as compared to thepremiums earned whereas thelarger insurancecompanies have larger reserves for claimspayment. Kaguri, (2012) found that there isnegative but significant relationship between claimpayment and firm performance. Denuit (2006)stated that amount of premium depends upon theinsured risk profile and claim history. On the basisof premium earned from the client, the companypaid back claim amount.Lemaire(1995)alsoexplained that claim payment is positivelycorrelated to pure premium earned from thecustomer.

H6: There is positive relationship between claimpayment and ROA.

Premium growthPremium growth is an important financial variablethat influences the financial performance ofinsurance companies. It is measured by percentagechange in total assets or sometimes as percentagechanges in premium of insurance companies andalso measures the rate of market penetration. Somestudies view that premium growth has positive andsignificant influence on the performance ofinsurance companies Ahmed et al (2011) andAyele,(2012). Based on their outcome, they argued

Jagadish Bist, Rabeena Mali, SabitaPuri, Rajesh Kumar Jha, SachyamKayastha, and Salina Bhattarai

7

UGC Approved Journal : Journal No. 44934REFEREED JOURNAL, Global Impact & Quality Factor 0.565 ISSN 00973-5372

further that growth in premium improves theprofitability of the core operations of insurers andtheir overall performance. Contrary to the viewCharumathi (2012) states an inverse relationshipbetween premium growth and firm performance.The first reason according to them is theoverwhelming focus of most insurance companieson various marketing activities to generate morepremiums to the detriment of their investmentactivities, that is, if more resources, especiallyhuman and capital, are directed towards theunderwriting of more policies to grow premiumwith a proportionate concentration of suchresources on the management of their assets 28and liabilities, the investment income will declinedespite an increase in net written premiums. Theyfurther argued that much of premiums written areoutstanding which sometimes turn out as bad debt.

H7: There is positive relationship betweenpremium growth and ROA.

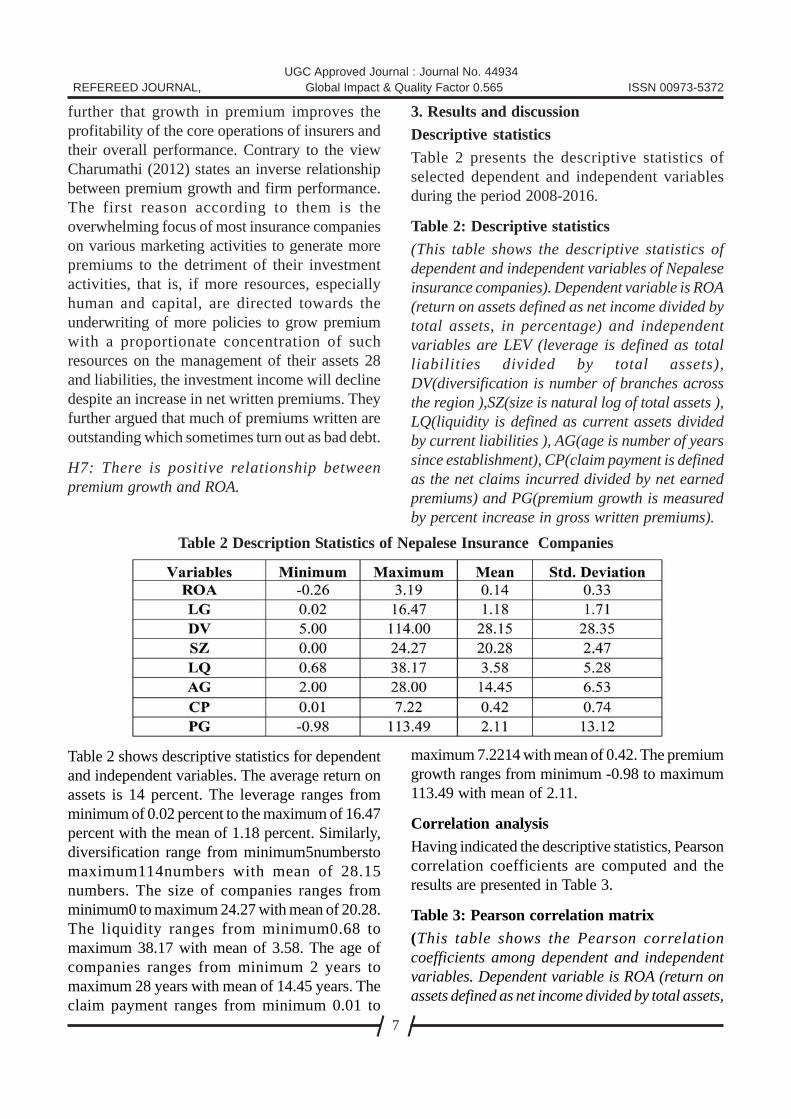

3. Results and discussionDescriptive statisticsTable 2 presents the descriptive statistics ofselected dependent and independent variablesduring the period 2008-2016.

Table 2: Descriptive statistics(This table shows the descriptive statistics ofdependent and independent variables of Nepaleseinsurance companies). Dependent variable is ROA(return on assets defined as net income divided bytotal assets, in percentage) and independentvariables are LEV (leverage is defined as totalliabilities divided by total assets),DV(diversification is number of branches acrossthe region ),SZ(size is natural log of total assets ),LQ(liquidity is defined as current assets dividedby current liabilities ), AG(age is number of yearssince establishment), CP(claim payment is definedas the net claims incurred divided by net earnedpremiums) and PG(premium growth is measuredby percent increase in gross written premiums).

Table 2 shows descriptive statistics for dependentand independent variables. The average return onassets is 14 percent. The leverage ranges fromminimum of 0.02 percent to the maximum of 16.47percent with the mean of 1.18 percent. Similarly,diversification range from minimum5numberstomaximum114numbers with mean of 28.15numbers. The size of companies ranges fromminimum0 to maximum 24.27 with mean of 20.28.The liquidity ranges from minimum0.68 tomaximum 38.17 with mean of 3.58. The age ofcompanies ranges from minimum 2 years tomaximum 28 years with mean of 14.45 years. Theclaim payment ranges from minimum 0.01 to

maximum 7.2214 with mean of 0.42. The premiumgrowth ranges from minimum -0.98 to maximum113.49 with mean of 2.11.

Correlation analysisHaving indicated the descriptive statistics, Pearsoncorrelation coefficients are computed and theresults are presented in Table 3.

Table 3: Pearson correlation matrix(This table shows the Pearson correlationcoefficients among dependent and independentvariables. Dependent variable is ROA (return onassets defined as net income divided by total assets,

Table 2 Description Statistics of Nepalese Insurance Companies

8

in percentage) and independent variables are LEV(leverage is defined as total liabilities divided bytotal assets), DV(diversification is number ofbranches across the region ),SZ(size of companiesis natural log of total assets ), LQ(liquidity isdefined as current assets divided by current

liabilities ), AG(age of companies is number ofyears since establishment), CP(claim payment isdefined as the net claims incurred divided by netearned premiums) and PG(premium growth ismeasured by percent increase in gross writtenpremiums).

The result also shows that there is positive relationbetween leverage andreturn on assets indicates thathigher the leverage, higher would be the return onassets. Similarly, age is positively correlated to thereturn on assets. This means that higher the age ofthe company, higher would be return on assets.Likewise, premium growth rate is positivelycorrelated to return on assets, which indicates thathigher the premium growth rate, higher would bereturn on assets. However, diversification isnegatively correlated to return on assets, whichindicates that higher the number of branches andsub branches, lower would be the return on assets.Similarly, size is negatively correlated to returnon assets. It indicates that larger the size of firm,lower would be the return on assets. Likewise,liquidity is negatively correlated to return onassets. This means that higher the liquidity, lowerwould be return on assets. There is negativerelation between claim payment and return onassets. This means that higher the claim payment,lower would be the return on assets.

Regression analysisHaving indicated the Pearson correlationcoefficients, the regression analysis has been

carried out and the results are presented in Table4.

Table 4: Regression of firm characteristics onReturn on Assets(The results are based on pooled cross-sectionaldata of 18 insurance companies with 105observations by using linear regression model. Themodel is, lnROA

it = â

0+ â

1 LEV

it + â

2 DV

it + â

3SZ

it

+ â4LQ

it + â

5AG

it + â

6CP

it +â

7PG

it + e

it, where,

dependent variables is ROA (Return on assetsdefined as net income divided by total assets), andindependent variables are LEV (leverage is definedas total liabilities divided by total assets),DV(diversification is number of branches acrossthe region ),SZ(size of companies is natural log oftotal assets ), LQ(liquidity is defined as currentassets divided by current liabilities ), AG(age ofcompanies is number of years sinceestablishment), CE(claim payment is defined asthe net claims incurred divided by net earnedpremiums) and PG(premium growth is measuredby percent increase in gross written premiums).

Table 3 Pearson Correlation Matrix

Jagadish Bist, Rabeena Mali, SabitaPuri, Rajesh Kumar Jha, SachyamKayastha, and Salina Bhattarai

9

UGC Approved Journal : Journal No. 44934REFEREED JOURNAL, Global Impact & Quality Factor 0.565 ISSN 00973-5372

The table 4 shows that the beta coefficient for theleverage has positive and significant impact onROA at 1% significance level. This indicates thathigher the leverage, higher would be the value offirm. This finding is consistent with the findingsof Carson and Hoyt (1995). Similarly, premiumgrowth has positive and significant impact onROA. This indicates that as the premium ofinsurance company’s increases then the firmperformance also increases. This finding isconsistent with the findings of Ahmed et al (2011)and Ayele, (2012) but inconsistent with thefindings of Charumathi (2012). However, the betacoefficients for diversification, size, and liquidityand claim payments have negative and

insignificant impact on ROA. This indicates thatincrement in the value of these specificcharacteristics leads to the lower ROA. The betacoefficient for age has positive but insignificantimpact on ROA. This indicates that as the age ofcompanies increases, the performance of firmdecreases. This finding is consistent with thefindings of Loderer and Waelchli (2013).

4. Summary and ConclusionThe performance of insurance companies plays animportant role in any economy and Nepal is noexception. The insurance companies collect largeamount of money from general people in terms ofpremium and shares. So the performance ofinsurance companies must be better to protect the

Table 4 Regression Co-efficient Matrix

10

interest of shareholders, buyer of insurancepolicies and employees. The insurance companieshas significant role in development of Nepalesebusiness and economy. Therefore, it needs to beregulated properly to enhance the Nepalesebusiness environment. Insurance companiesprovide the cushion for business to grow andcompete in the market. It gives variety of financialservices range from the underwriting of risksinherent in economic entities and the mobilizationof large amount of funds through premiums forlong term investments.

This study attempts to examine the impact ofleverage, diversification, size of companies,liquidity, age of companies, claim payment andpremium growth on financial performance ofNepalese insurance companies. The study is basedon the secondary data gathered for 18 Insurancecompanies of Nepal with 105 observations of 2008to 2016.

The study shows that leverage and premiumgrowth rate is positively correlated to return onassets. This indicates that higher the leverage andpremium growth rate, higher would be return onassets. However, diversification is negativelycorrelated to return on assets. This indicates thathigher the number of branches, lower would bethe return on assets. Similarly, size is negativelycorrelated to return on assets. This indicates thatlarger the size of firm, lower would be the returnon assets. The result also shows that liquidity isnegatively correlated to return on assets. Thismeans when the liquidity increases, return onassets will decrease. However, age is positivelycorrelated to the return on assets, which shows thathigher the age of firm, higher would be return onassets. The study also shows that there is negativerelation between claim payment and return onassets. This indicates that higher the claimpayment, lower would be the return on assets. Theresult of the regression analysis shows that betacoefficients are positive for leverage and premiumgrowth. However, the coefficients are negative andinsignificant for the diversification, size, liquidityand claim payments. The coefficients are

significant for leverage and premium growth rateat 1% level.

References

Adams, Mike, and Mike Buckle.”Thedeterminants of corporate financial performancein the Bermuda insurance market.” AppliedFinancial Economics 13.2 (2003): 133-143.

Ahmed, Junaid, Khalid Zaman, and Iqtidar AliShah. “An empirical analysis of remittances-growth nexus in Pakistan using bounds testingapproach.” Journal of Economics andInternational Finance 3.3 (2011): 176.

Ahmed, Naveed, Zulfqar Ahmed, and IshfaqAhmed. “Determinants of capital structure: A caseof life insurance sector of Pakistan.” EuropeanJournal of Economics, Finance and AdministrativeSciences 24 (2010): 7-12.

Ahmed, Naveed, Zulfqar Ahmed, and AhmadUsman. “Determinants of performance: A case oflife insurance sector of Pakistan.” InternationalResearch Journal of Finance and Economics 61.1(2011): 123-128.

Amihud, Yakov, and HaimMendelson.”Liquidity,the value of the firm, and corporatefinance.” Journal of Applied CorporateFinance 24.1 (2012): 17-32.

Arabsalehi, M., M. Beedel, and A. Moradi.“Economic performance and stock marketliquidity: Evidence from Iranian ListedCompanies.” International Journal of Economy,Management and Social Sciences 3.9 (2014): 496-499.

Ayele, Abate Gashaw. Factors AffectingProfitability of Insurance Companies in Ethiopia:Panel Evidence. Diss. Addis Ababa UniversityAddis Ababa, Ethiopia, 2012.

Baldoni, R. “A best practices approach to riskmanagement.” TMA JOURNAL 18 (1998): 30-34.

BarNiv, Ran, and Robert A.Hershbarger.”Classifying financial distress in thelife insurance industry.” Journal of Risk andInsurance (1990): 110-136.

Jagadish Bist, Rabeena Mali, SabitaPuri, Rajesh Kumar Jha, SachyamKayastha, and Salina Bhattarai

11

UGC Approved Journal : Journal No. 44934REFEREED JOURNAL, Global Impact & Quality Factor 0.565 ISSN 00973-5372

Beard, Donald W., and Gregory G.Dess.”Corporate-level strategy, business-levelstrategy, and firm performance.” Academy ofmanagement Journal 24.4 (1981): 663-688.

Burca, Ana-Maria, and GhiorgheBatrinca.”Thedeterminants of financial performance in theRomanian insurance market.” InternationalJournal of Academic Research in Accounting,Finance and Management Sciences 4.1 (2014):299-308.

Carson, James M., and Robert E. Hoyt. “Lifeinsurer financial distress: classification models andempirical evidence.” Journal of Risk andInsurance (1995): 764-775.

Charumathi, B. “On the Determinants ofProfitability of Indian life insurers–an EmpiricalStudy.” Proceedings of the World Congress onEngineering.Vol. 1.No. 2. 2012.

Chen, Renbao, and Kie Ann Wong.”Thedeterminants of financial health of Asian insurancecompanies.” Journal of Risk and Insurance 71.3(2004): 469-499.

Cummins, J. David, Martin F. Grace, and RichardD. Phillips. “Regulatory solvency prediction inproperty-liability insurance: Risk-based capital,audit ratios, and cash flow simulation.” Journalof Risk and Insurance (1999): 417-458.

Deakin, Simon. “The coming transformation ofshareholder value.” Corporate Governance: AnInternational Review 13.1 (2005): 11-18.

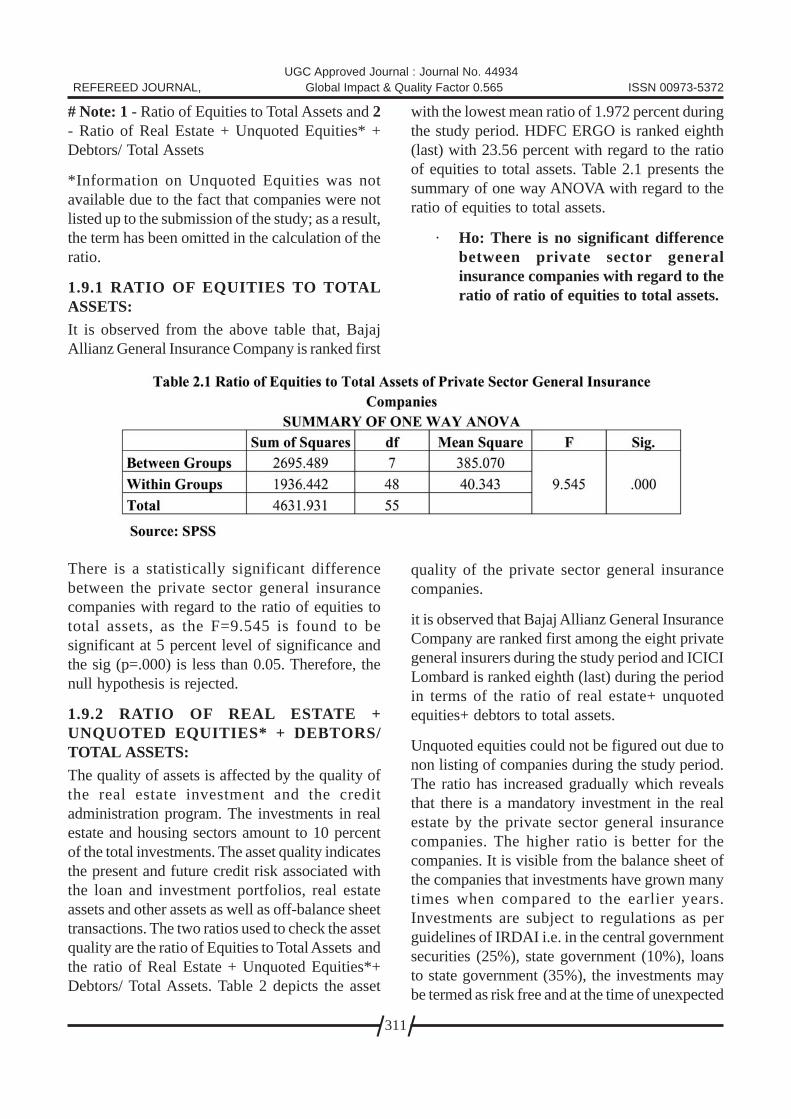

Ghimire, Rabindra. “Financial Efficiency of NonLife Insurance Industries in Nepal.” (2013).

Gitman, Lawrence J. “Principles of ManagerialFinance (2007).”

Iswati, Sri, and MuslichAnshori.”The influence ofintellectual capital to financial performance atinsurance companies in Jakarta Stock Exchange(JSE).” Proceedings of the 13th Asia PacificManagement Conference, Melbourne, Australia.2007.

Kaguri, A. Relationship between firmcharacteristics and financial performance of lifeinsurance companies in Kenya.Diss. Doctoraldissertation, University of Nairobi, 2013.

Kumba, S. “How to determine whether yourfinancier is financially sound.” The FinancialPost 2 (2011): 16.

Kume, Vasilika, ZanaXhuka, and ZvMinister.”Innovation management in the insurancesector in Albania.” Journal of Entrepreneurshipand Innovation 2 (2010): 94-107.

Lemaire, J. “Bonus-malus systems in automobileinsurance.” Insurance Mathematics andEconomics 3.16 (1995): 277.

Loderer, Claudio F., and UrsWaelchli.”Firm ageand performance.” (2010).

Maina, F. G., and M. M. Sakwa.”Understandingfinancial distress among listed firms in Nairobistock exchange: A quantitative approach using theZ-score multi-discriminant financial analysismodel.” Scientific Conference Proceedings. 2012.

Malik, Ali, Jonathan Liu, andOrthodoxiaKyriacou. “Creative accountingpractice and business performance: evidence fromPakistan.” International Journal of BusinessPerformance Management 12.3 (2011): 228-241.

Myers, Stewart C., and James A. Read Jr. “Capitalallocation for insurance companies.” Journal ofRisk and Insurance (2001): 545-580.

Naser, K., and M. Z. Mokhtar.”Firm Performance,Macro-economic Variables and FirmSize.” Journal of Finance (2004): 543-679.

Outecheva, Natalia. Corporate financial distress:An empirical analysis of distress risk. Diss.University of St. Gallen, 2007.

Pitrebois, Sandra, Michel Denuit, and Jean-François Walhin.”An actuarial analysis of theFrench bonus-malus system.” ScandinavianActuarial Journal 2006.5 (2006): 247-264.

Sanchez, Jorge. “Calculating insurance claimreserves with fuzzy regression.” Fuzzy sets andsystems 157.23 (2006): 3091-3108.

Sharku, Gentiana, BrikenaLeka, andEtlevaBajrami.”Considerations on Albanian LifeInsurance Market.” Romanian EconomicJournal 14.39 (2011).

12

CROP INSURANCE: FARMERS PERCEPTIONS ANDAWARENESS IN SELECT DISTRICT OF

TELANGANA STATEDr Sammaiah BuhukyaAssistant Professor, MBA Department,Siddhartha Institute of Engineering & Technology,Vinobha Nagar, Imbrahimpthnam, R.R.DistEmail Id: [email protected],Contact No: 9963225482

ABSTRACT

Agriculture classified as a primary sector and its playing pivotal role in providing employment, incomeand fulfilment of hunger needs and prime source of livelihood for more than 60% of the population. Itsdefect on vagaries of Nature such as flood, drought, tornado, and lightning. In the face of uncertaintyand risk faced by the farming community, various schemes and programmes have evolved over time indifferent countries to protect farmers against risks, such as guaranteed prices, subsidised credit, andcrop insurance. This paper discusses the farmer’s perceptions and awareness of crop insurance, Firstlyit measures the awareness level and source of awareness, secondly examines the farmers’ perception,towards crop insurance. The study was conducted in selected districts of Telangana state. 100 convenientrespondents were chosen and been carried out in the month of March, 2016. From the analysis farmersawareness level about crop insurance was medium with lack of advertisement, Most of the farmers werenot willing to pay for crop insurance because of insecurity, instable income level, premium rate, no orlow compensation, problems with lack of financial knowledge.

Key words: Awareness, Perception, Crop Insurance.

Introduction :Agriculture is a prime sector for rural India andIndian economy and this sector faces differenttypes of uncertain as natural disaster (drought,flood etc.) and delay monsoon which are beyondthe control of the farmers. Due to the naturalcalamities the agricultural production, grossnational product and also the income of the farmersdecrease. Agriculture in India includes with riskand uncertainty all over the world becauseagriculture is subject to vagaries of nature likeflood, drought and cyclone. Agriculture contributesto 24 per cent of the GDP and any change has amultiplier effect on the economy as a whole.Economic growth and agricultural growth areinextricably linked to each other. Crop insurancehelps in stabilization of farm production andincome of the farming community. It helps in

optimal allocation of resources in the productionprocess. Indian Government has been concernedabout the risk and uncertainty prevalent inagriculture. As all of us are aware about theunfortunate deaths of farmers in Maharashtra whogot caught in a debt trap and the devastating effectit had on their families. In the face of uncertaintyand risk faced by the farming community, variousschemes have evolved over time in differentcountries to protect farmers against risks, such asguaranteed prices, subsidised credit, and cropinsurance. Agriculture is an primary economicactivity for the rural population in India more than60 percept of population directly and indirectlydepends on Agriculture sector. People in TelanganaState about 60% of the total population dependson it. The soil and natural conditions of state ofTelangana and select districts allows multiple

13

UGC Approved Journal : Journal No. 44934REFEREED JOURNAL, Global Impact & Quality Factor 0.565 ISSN 00973-5372

cropping pattern and high cropping intensity, butpaddy is being the predominant crop.

Agriculture in sample area is shrinking in termsof arable land and crop net production due toincreasing demand for land from other economicsectors, insufficient labour, frequently affected bynatural calamities, and the increasing cost ofagricultural inputs such as seeds, fertilizers,pesticide and low market price. It is here that cropinsurance plays a vital role in anchoring a stablegrowth of agricultural sector. Crop insurance isan insurance arrangement aiming at mitigating thefinancial losses suffered by the farmers due todamage and destruction of their crops as a resultof various production risks (A.I.C of India). In thisview of this, the need for protecting farmers fromthe various risks and hazards was recognized bythe government and introduce NationalAgricultural Insurance scheme in the state ofTelangana. The crop insurance scheme is deliveredas compulsory along with crop loan from thefinancial institutions like primary agriculturalbanks, regional rural banks and commercial banksand voluntary basis for non crop loaners. But thereis need to study how farmers perceive cropinsurance, are they fully aware about it andwhether the non crop loaners are willing to joinand pay for crop insurance schemes. The presentstudy examines the farmers’ awareness andperception level and source of awareness, finallyidentify the farmers willingness in paying for cropinsurance in the State of Telangana select districts.

Historical Overview of Crop Insurance :The policy makers in India are concerned aboutthe risk and uncertainty prevalent in agriculture.Work on crop insurance received much attentionafter India’s independence in 1947. However, cropinsurance was conceptualized and J.S.Chakravarthi presented a practical scheme suitedto Indian conditions as early as in 1920. A bookentitled “Agricultural Insurance: A practicalScheme Suited to Indian Conditions” waspublished in 1920. In this book he proposed a raininsurance scheme for the Mysore state to protectfarmers against vagaries of monsoon culminatingin drought. The subject of crop insurance was

discussed in the Parliament (Central Legislature)the 1947 and then minister of Food andAgriculture, gave an assurance that the feasibilityof introducing crop and livestock insurance shouldbe considered by government. Two pilot schemeson crop insurance, prepared by Mr. G.S. Priolkar,an officer on special duty, were circulated to thestates for adoption. However, none of the statesagreed to implement the schemes, mainly due topaucity of funds. The interest in the subject wasrekindled during the third five year plan (1961-1966). However, the working group on agriculturewas averse to included crop insurance in the plan.At the same time the government of Punjabproposed the inclination

Mr.Pandaraiah. G & Dr.KV.Sashidar of cropinsurance in its state plan and sort financialassistance from the central government. The stategovernment could not introduce crop insurance asthe power to pass the Legislation related toinsurance was vested with central government.Following these developments and increasingdemand for crop insurance, in 1965, thegovernment of India decided to have a CropInsurance Bill and Model Scheme of CropInsurance. It and it was formulated so that theinterested states could introduce crop insurancein the area under their jurisdiction. A Draft Billand Model Scheme were prepared and circulatedto states to elicit their views and comments on thesame. Further, incorporating the comments and theviews of the states, the government of India inMarch 1970 considered the Draft Bill and ModelScheme. The Draft Bill and Model Scheme werethen referred to the expert committee (Under theChairmanship of Dharm Naraian) in July 1970 forfuller examination of the economic, administrative,financial, actuarial implications. The committeereported that in the conditions obtaining in thecountry, it was not advisable to introduce cropinsurance in the near future on pilot orexperimental basis. Despite the unfavorable reportof the Dharm Naraian Committee, politicalcompulsions forced the government to introducecrop insurance in the country on experimental basisunder the General Insurance Department

14

(Danadekar 1976). The following schemes havebeen implemented by government of India.

Crop Insurance Scheme (CIS) 1972- 1978:-Based on “Individual Approach” the GeneralInsurance Corporation of India introduced thisprogramme and this covered H-4 cotton in Gujaratand it extended to Paddy, Groundnut. Later thisCIS was extended to other States.

Pilot Crop Insurance Scheme (PCIS) 1979-1984:-In the history of Crop Insurance in India thisscheme was introduced based on ‘HomogeneousArea Approach’ by General Insurance Corporationof India. This scheme covered the crops likecereals, millets, oil seeds, cotton, potato, and gramspread across the 13 states but the programme wasrestricted to loanee farmers.

Comprehensive Crop Insurance Scheme(CCIS) 1985-1998:-It had also introduced by GIC based on‘Homogeneous Area Approach’. This schemecovered cereals, millets, oilseeds and pulses spreadcross the 15 states and 2 union territories in India,latter it spill over to five more states in later fewyears. Scheme was restricted to loanee farmers upto of the crop loan or maximum of 10,000 perfarmers.

National Agriculture Crop Insurance Scheme(NAIS) 1999-2000:-India’s modified crop insurance program which iscalled as National Agricultural Insurance Schemeis implemented since Rabi 1999-2000.Unionbudget 2002-03 proposed set up of AgriculturalInsurance Corporation (AIC) with capitalparticipation from General Insurance Corporationof India (GIC), four public sector general insurancecompanies viz. 1. National Insurance Co Ltd., 2.New India Assurance Co. Ltd., 3.OrientalInsurance Co. Ltd and 4. United Insurance Co. Ltd.and NABARD. The promoter’s subscription to thepaid up capital will be: 35 by GIC, by NABARDand each by the four public sector generalinsurance companies. The authorized capital of thenew organization will be Rs.1500 crore, while the

initial paid-up capital will be Rs.200 crore.National Agricultural Insurance Scheme (NAIS)shall be transferred to the new organization andshall form the core of business to begin with.Transition to actuarial regime will be made over aperiod of time. The new organization will, in duecourse of time covers other allied rural/agriculturalrisk along with crop insurance. The specificobjectives of the program are to provide insurancecoverage and financial support to the farmers inthe event of failure of any of the notified crop as aresult of natural calamities; pests and diseases. Toencourage the farmers to adopt progressivefarming practices, high value inputs and improvedtechnology in agriculture.

Review of Literature :Ali, Jabir and Sanjeev Kapoor (2008), this paperprovides an assessment of agriculturaldiversification trends towards fruits and vegetablesproduction in the state of Uttar Pradesh. In the firstpart, food consumption, crop production patternsand value of output in the region during the pasttwo decades are reviewed. Next, the farmers’perceived risks on a variety of sources and the useof different risk management strategies arediscussed. The principal contribution of this paperis to draw of attention towards some neglectedaspects of diversification, especially the biophysical and economic constraints to the processof fruits and vegetables production system. Thedata were collected using a pre tested structuredquestionnaire and data was also collected from theAgricultural Statistics at a glance. The study hasrevealed that the annual growth in production ofhigh value crops has increased to augment incomeand manage risks and uncertainties. Cultivationof high value crops involves risk and uncertaintydue to high resource requirement and high perishesability. Thus, farmers’ adoption of cropdiversification practices requires a favorableenvironment that fulfills resourceRequirements and effective policy support forReducing their risk. Public intervention scanfacilitate better risk management throughimproved information system, development offinancial markets and promotion of market based

Dr Sammaiah Buhukya

15

UGC Approved Journal : Journal No. 44934REFEREED JOURNAL, Global Impact & Quality Factor 0.565 ISSN 00973-5372

price and yield insurance schemes, thus ensuringthat the marginal farmers are able to benefit fromthese interventions as well as participate in theemerging system.

Mamata Swain, (2008) The paper attempts toexamine the need for crop insurance in anagriculturally backward state like Orissa in EasternIndia and to what extent the crop insurance schemeas implemented in the state has helped the farmersin managing risk in agricultural production. A cropinsurance scheme was introduced in Orissa on pilotbasis from Kharif 1981 to Rabi 1984-85, but itshowed a high and unfavorable claim- premiumratio. The Comprehensive Crop Insurance Scheme(CCIS) was launched in Orissa in 1985 and itsmajor drawback was that its coverage was verylow. As it was accredit linked insurance scheme,only the farmers taking loans from institutionalcredit agencies (typically the medium and largefarmers) could insure their crops. Further, it wasfound to be financially unsustainable due to highclaim- premium ratio. To overcome the aboveproblems, the improved National AgricultureInsurance Scheme (NAIS) was implemented inOrissa since 1999. This scheme was extended tonon-loanee farmers, as a result of which area andnumber of farmers under the scheme increasedenormously. The claim-premium ration was alsofound to be favorable in most seasons. However,it was also suggested in this scheme that alongwith crop insurance other risk reducing measureslike income generating activities in non-farmsector and food for work programme should beundertaken to lower income variability. In

Mr.Pandaraiah. G & Dr.KV.Sashidar (2010) afrequently disaster affected state like Orissa, alongwith the public sector, private sector participationin agricultural insurance needs to be encouragedby providing subsidy, guarantee and reinsurancefacility. Credible long-term statistical informationshould be made available for formulation ofpolicies. Vulnerability maps of different regionsshould be prepared which will help in setting theprice of risk (premium). Education and training tofarmers on the benefits of crop insurance anddifferent insurance products should be imparted.

Insurance is a contract made for financialarrangement between two parties when fewsuffered losses are met from the funds accumulatedthrough small contributions made by many whoare exposed to similar risks.

Crop Insurance : Crop insurance has been oneof the most reliable and longest running programsfor stabilization and risk management for farmersin many countries. This has been particularly truein parts of North America, where crop insurancebecame more common and commercially availablearound 1960. Multi-peril crop insurance, the mostpopular type of crop insurance, usually insuresfarmers against yield losses from natural causessuch as weather (e.g. drought, excessive moisture,wind, snow, and frost), insects, and disease. Aproperly designed and implemented crop insuranceprogramme will protect the numerous vulnerablesmall and marginal farmers from hardship, bringin stability in the farm incomes and increase thefarm production (Bhende 2002).

The farmer is likely to allocate resources in profitmaximizing way if he is sure that he will becompensated when his income is catastrophicallylow for reasons beyond his control. A farmer maygrow more profitable crops even though they arerisky. Similarly, farmer may adopt improved butuncertain technology when he is assured ofcompensation in case of failure (Hazell 1992). Thiswill increase value added from agriculture, andincome of the farm family. Bhende (2005) foundthat income of the farm households from semi-arid tropics engaged predominantly in rain-fedfarming was positively associated with the levelof risk. Hence, the availability of formal instrumentfor diffusion of risk like crop insurance willfacilitate farmers to adopt risky but remunerativetechnology and farm activities, resulting inincreased income. It is observed that insuredhouseholds invest more on agricultural inputsleading to higher output and income per unit ofland. Interestingly, percentage increase in outputand income is more for small farms. Based on 1991data, CCIS was found to contribute 23, 15, and 29per cent increase in income of insured farmers in

16

Gujarat, Orissa and Tamil Nadu, respectively(Mishra 1996)

Objectives of the Study :1. To assess the farmers awareness and perception

towards crop insurance.

2. To identify the non insured farmers willingnessin join for crop insurance.

Study Area :Warangal district was selected purposively. Totalnumber of 100 respondents was selected throughrandom sampling from five villages. Thestructured schedule was developed keeping in viewthe objectives and variable to be studied. Therespondents were contacted personally for datacollection. For the purpose of the study, knowledgewas defined as the perception and awareness,extent and manner of the use of the Crop insurancescheme was measured by knowledge test used inthis study. Knowledge about the scientific Crop

insurance scheme using the knowledge testdeveloped by the investigator and used. Themodifications in the existing knowledge test werein relation to item regarding scientific Cropinsurance Scheme. All the question for knowledgewas dichotomized having two dimension yes/no,if the answer was yes the respondents wereassigned 1 score and if answer was no, therespondents were assigned 0 score. The study wascarried on knowledge and adoption of Cropinsurance scheme among farmers. The range ofscores obtained by the respondents might vary inlow, medium and high range in the knowledge testwhich indicated the knowledge level of therespondents.

Results and discussionResult and discussion of crop insurance schemein select districts of Telangana state aboutknowledge and awareness about the crop insurancescheme.

12

3

4

56789

10

11

12

13

14

Dr Sammaiah Buhukya

17

UGC Approved Journal : Journal No. 44934REFEREED JOURNAL, Global Impact & Quality Factor 0.565 ISSN 00973-5372

InterpretationFrom the Table 1 That among all 24 StatementCrop insurance scheme, Have you heard of cropinsurance and do you know about of crop insuranceawareness and kisahan credit cards (98%) was rankat 1st as far as knowledge possessed by therespondents was concerned. Do you know aboutthe crop insurance period? rank at 2nd (96%),

followed by Do you know about allied agricultureinsurance? at rank 3rd (91%), Do you know aboutcrop insurance scheme at rank 4th (85%),and Itprovides the loan for the Rabi and Kharif cropproduction not for Zayad crop at rank 5th (82%),The overall adoption index was calculated to be68.41 %. Knowledge level of farmers in Cropinsurance scheme

1516

17

18

19

202122

23

24

18

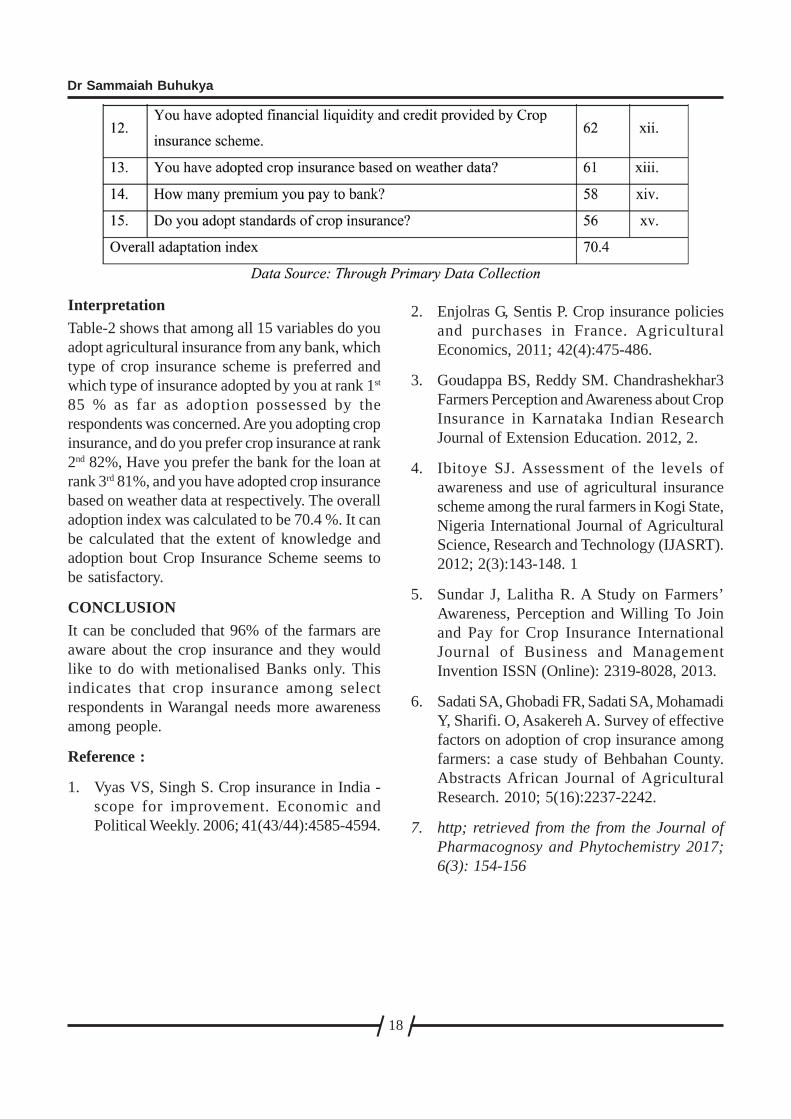

InterpretationTable-2 shows that among all 15 variables do youadopt agricultural insurance from any bank, whichtype of crop insurance scheme is preferred andwhich type of insurance adopted by you at rank 1st

85 % as far as adoption possessed by therespondents was concerned. Are you adopting cropinsurance, and do you prefer crop insurance at rank2nd 82%, Have you prefer the bank for the loan atrank 3rd 81%, and you have adopted crop insurancebased on weather data at respectively. The overalladoption index was calculated to be 70.4 %. It canbe calculated that the extent of knowledge andadoption bout Crop Insurance Scheme seems tobe satisfactory.

CONCLUSIONIt can be concluded that 96% of the farmars areaware about the crop insurance and they wouldlike to do with metionalised Banks only. Thisindicates that crop insurance among selectrespondents in Warangal needs more awarenessamong people.

Reference :

1. Vyas VS, Singh S. Crop insurance in India -scope for improvement. Economic andPolitical Weekly. 2006; 41(43/44):4585-4594.

2. Enjolras G, Sentis P. Crop insurance policiesand purchases in France. AgriculturalEconomics, 2011; 42(4):475-486.

3. Goudappa BS, Reddy SM. Chandrashekhar3Farmers Perception and Awareness about CropInsurance in Karnataka Indian ResearchJournal of Extension Education. 2012, 2.

4. Ibitoye SJ. Assessment of the levels ofawareness and use of agricultural insurancescheme among the rural farmers in Kogi State,Nigeria International Journal of AgriculturalScience, Research and Technology (IJASRT).2012; 2(3):143-148. 1

5. Sundar J, Lalitha R. A Study on Farmers’Awareness, Perception and Willing To Joinand Pay for Crop Insurance InternationalJournal of Business and ManagementInvention ISSN (Online): 2319-8028, 2013.

6. Sadati SA, Ghobadi FR, Sadati SA, MohamadiY, Sharifi. O, Asakereh A. Survey of effectivefactors on adoption of crop insurance amongfarmers: a case study of Behbahan County.Abstracts African Journal of AgriculturalResearch. 2010; 5(16):2237-2242.

7. http; retrieved from the from the Journal ofPharmacognosy and Phytochemistry 2017;6(3): 154-156

Dr Sammaiah Buhukya

19

UGC Approved Journal : Journal No. 44934REFEREED JOURNAL, Global Impact & Quality Factor 0.565 ISSN 00973-5372

OPPORTUNITY FOR FDI IN INSURANCESECTOR IN INDIA

Dr. Manisha Bhatt Jayshree MandaviyaAssistant Professor Assistant Professor C. Z. Patel College S. R. Luthra Institute of Managementof Business &Management, Surat, Anand, Gujarat, IndiaNear Vallabh Vidhyanagar, [email protected],Anand, Gujarat, India Mo: [email protected] 09427457271

ABSTRACT

Parliament has passed Insurance Laws (Amendment) Bill, 2015. It was first passed in Lok Sabha on 4March 2015 and later in Rajya Sabha on 12 March 2015, which will become an Act when the Presidentsigns it. The amendment bill aims to bring improvements and revisions in the existing laws relating toinsurance business in India. The bill also seeks to remove archaic provisions in previous laws andincorporate modern day practices of insurance business that are emerging in a changing dynamicenvironment, which also includes private participation. It is expected that the foreign investment wouldbring about 20,000-25,000 crore in short funds. The amendment bill hikes Foreign Direct Investment(FDI) cap in the insurance sector to 49 percent from present 26 percent. The foreign investment ininsurance would be routed under foreign direct investment, foreign portfolio investment, foreign venturecapital investment, depository receipts, and non resident Indians. Insurance companies are permitted toraise capital through instruments other than equity shares. Instruments would be specified throughseparate regulations by the Insurance Regulatory and Development Authority of India (IRDA). However,the voting rights of shareholders are restricted only to equity shares. Sale of shares over 1% of the totalequity share capital and purchase of shares resulting in total equity share capital of more than 5%,requires the prior approval of the IRDA. It also adds provision for the establishment of Life InsuranceCouncil and the General Insurance Council. These councils will act as self-regulating bodies for theinsurance sector. The bill also grants permission to PSU general insurers to raise funds from the capitalmarket and increases the penalty to deter multilevel marketing of insurance products. There is a strongrelationship between foreign investment and economic growth. Larger inflows of foreign investmentsare needed for the country to achieve a sustainable high trajectory of economic growth. A major roleplayed by the insurance sector is to mobilize national savings and channelize them into investments indifferent sectors of the economy. FDI in insurance would increase the penetration of insurance in India;FDI can meet India’s long term capital requirements to fund the building of infrastructures. The presentpaper focuses on the overview of the Indian insurance sector along with the opportunities due to expansionof FDI in insurance in India and the major challenges that it faces.

Keywords: Insurance; FDI; Insurance Laws (Amendment) Bill

IntroductionThe insurance industry of India consists of 53insurance companies of which 24 are in lifeinsurance business and 28 are non-life insurers.Among the life insurers, Life InsuranceCorporation (LIC) is the sole public sector

company. Apart from that, among the non-lifeinsurers there are six public sector insurers. Inaddition to these, there is sole national re-insurer,namely, General Insurance Corporation of India.Other stakeholders in Indian Insurance marketinclude agents (individual and corporate), brokers,

20

surveyors and third party administrators servicinghealth insurance claims1.

Out of 28 non-life insurance companies, fiveprivate sector insurers are registered to underwritepolicies exclusively in health, personal accidentand travel insurance segments. They are StarHealth and Allied Insurance Company Ltd, ApolloMunich Health Insurance Company Ltd, MaxBupa Health Insurance Company Ltd, ReligareHealth Insurance Company Ltd and Cigna TTKHealth Insurance Company Ltd. There are twomore specialized insurers belonging to publicsector, namely, Export Credit GuaranteeCorporation of India for Credit Insurance andAgriculture Insurance Company Ltd for cropinsurance.

Insurance in India is a flourishing industry in Indiawith both national and international playerscompeting and growing at rapid rate. Together withbanking and real estate it constitutes 12.9% of GDPin India. However the penetration of insurancecoverage for both life and non life insurance isstill very less and was 3.9% in 2013.

Indian insurance sector was liberalized in 2001.Liberalization has led to the entry of the largestinsurance companies in the world, who have takena strategic view on India being one of the toppriority emerging markets. The Insurance industryin India has undergone transformational changesover the last 14 years. With raising the cap on FDIinto Indian insurance companies to 49% from the26% would allow global reinsurance companiesto set up branches in India 2.

According to the insurance amendment bill (2015),the section 24 of the Pension Fund Regulatory andDevelopment Authority ( PFRDA) Act providesthat the foreign investment limit in the pensionsector will be linked with the ceiling in theinsurance sector, which has gone up to 49% from26%. Under the legislation, while up to 26 per centforeign capital will be under the automatic route,the balance 23 per cent has to secure approval fromthe Foreign Investment Promotion Board (FIPB).According to the General Insurance Business(Nationalization) Act, 1972 (GIBNA, 1972) the

four general insurance companies (GICs) had tobe 100% government owned, however TheInsurance Laws (Amendment) Bill, 2015 —passed by the Rajya Sabha on March 12 and bythe Lok Sabha on March 4 — will change that.The GICs “are now allowed to raise capital,keeping in view the need for expansion of thebusiness in the rural and social sectors, meetingthe solvency margin for this purpose and achievingenhanced competitiveness subject to thegovernment equity not being less than 51% at anypoint of time. The amendment also clearly defineshealth insurance business to include travel andpersonal accident cover. It is also expected thatthe proposed increase in the FDI limit will have afollow on impact on other sectors, including thepension industry creating further momentum.

Objectives of the StudyThe present paper focuses on

• The overview of the Indian insurancesector

• To know opportunities and expansion ofFDI in insurance in India

• To know major challenges that it faces.