Optimizing Guinea-Bissau's natural wealth

68

Optimizing Guinea-Bissau’s natural wealth Helen Edmundson Poverty Reduction and Economic Management Africa Region September 2014 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Optimizing Guinea-Bissau's natural wealth

Optimizing Guinea-Bissau’s

natural wealth

Helen Edmundson

Poverty Reduction and Economic Management

Africa Region

September 2014

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ii

Acronyms and Abbreviations

CAIA Celula de Avalicao de Impacte Ambiental

CBA Cost Benefit Analysis

CER Certified Emission Reduction

CPIA Country Policy and Institutional Assessment

DBT Dulombi-Boé-Tchetche

EIA Environmental Impact assessment

EU European Union

EU ETS European Union Emission Trading Scheme

FAO Food and Agriculture Organization

GDP Gross Domestic Product

GEF Global Environment Fund

GNI Gross national income

MRV Monitoring Reporting and Verification

NTFR Non-timber forest resources

ODA Official Development Assistance

PA Protected areas

REDD Reducing Emissions from Deforestation and Forest Degradation

RER Real exchange rate

SEEA System of Integrated Economic and Environmental Accounts

SNA System of National Accounts

SSA Sub-Saharan Africa

UN United Nations

UNDP United Nations Development Programme

VER Voluntary Emission Reduction

WAEMU West African Economic and Monetary Union

iii

Acknowledgments

This paper was prepared during 2012-2013, with the involvement and advice of several experts in The

World Bank Group and the government and agencies of Guinea-Bissau, as well as local Bissau-Guineans.

Without their support and input this paper would not have been possible.

Esther G. Naikal and Marie Le-Grange from the Wealth Accounting and the Valuation of Ecosystem

Services (WAVES) team provided support and advice on the methodologies and cross-cutting assumptions

needed for the natural wealth and adjusted net savings calculations. Gary Joseph Raymond McMahon and

Martin Lokanc gave useful inputs and suggestions on Guinea-Bissau’s minerals, their prospects, and key

assumptions on how the sectors are likely to evolve. Jingjie Chu’s work and modelling on West Africa’s

Regional Fisheries Trust Fund contributed to the assessment of Guinea-Bissau’s fishing sector, updated

with local data. Tanya Yudelman’s expertise and knowledge of Guinea-Bissau’s biodiversity, in addition

to support and insights from Institute of Biodiversity and Protected Areas (IBAP) helped strengthen this

paper’s overview of protected areas.

The paper also benefited from peer review comments from Sebasstien Dessus, John Virdin, and Glenn-

Marie Lange. Fernando Blanco, Miria Pigato and Vera Songwe provided additional comments, which

further strengthened the overall narrative and focus of the findings. Judite Fernandes helped coordinate the

inputs from the peer reviewers, ensuring their comments were duly addressed.

Finally, this paper could not have been completed without the support and technical expertise of Jose

D'Bettencourt. He conducted all of the interviews and collated on-the-ground information. His knowledge

of the issues, combined with his familiarly of the country made his insights and findings invaluable.

The preparation and analysis in this paper has been a team effort. I apologize to those highlighted above for

any mistakes or misrepresentation of views. The findings are intended to help facilitate a dialogue on

Guinea-Bissau’s natural wealth, both exhaustible and renewable forms. I hope therefore that in this regard,

the paper starts a useful debate on how best Guinea-Bissau can benefit from its natural resources.

iv

Contents

Acronyms and Abbreviations ....................................................................................................................... ii

Acknowledgments ........................................................................................................................................ iii

Executive Summary ...................................................................................................................................... 1

A. Introduction ........................................................................................................................................... 4

B. What does the past tell us: Guinea-Bissau’s current natural wealth estimates ..................................... 5

C. What does the present tell us: new estimates of Guinea-Bissau’s natural wealth ................................. 8

I. Exhaustible resources ........................................................................................................................ 8

Phosphate ............................................................................................................................................ 10

Bauxite ................................................................................................................................................ 12

Exhaustible resource considerations ................................................................................................... 13

II. Non-Exhaustible resources ............................................................................................................. 17

Fishing................................................................................................................................................. 18

Timber and non-timber forest related resources ................................................................................. 25

Mangroves ........................................................................................................................................... 29

Carbon ................................................................................................................................................. 32

Crop and pasture land ......................................................................................................................... 33

Protected areas/Biodiversity ............................................................................................................... 38

III. Total wealth ................................................................................................................................ 42

D. What does the future hold: policy implications for sustainable development .................................... 43

Exhaustible resources .......................................................................................................................... 44

Non-exhaustible resources .................................................................................................................. 44

Fishing................................................................................................................................................. 44

Timber and non-timber forest resource ............................................................................................... 45

Carbon ................................................................................................................................................. 46

Crop and pasture land ......................................................................................................................... 47

Biodiversity/protected areas ................................................................................................................ 47

Appendix A - Methodologies and assumptions .......................................................................................... 49

References ................................................................................................................................................... 62

List of Figures

Figure 1. Current estimates of total wealth in Guinea-Bissau ...................................................................... 6

Figure 2. Current natural wealth per capita estimates for Guinea-Bissau ..................................................... 6

v

Figure 3. Phosphate, Bauxite and Petroleum prices have been increasing ................................................... 8

Figure 4. Guinea-Bissau’s RER has stayed relatively constant over the past decade ................................. 15

Figure 5. Landings of artisanal and industrial fish ...................................................................................... 24

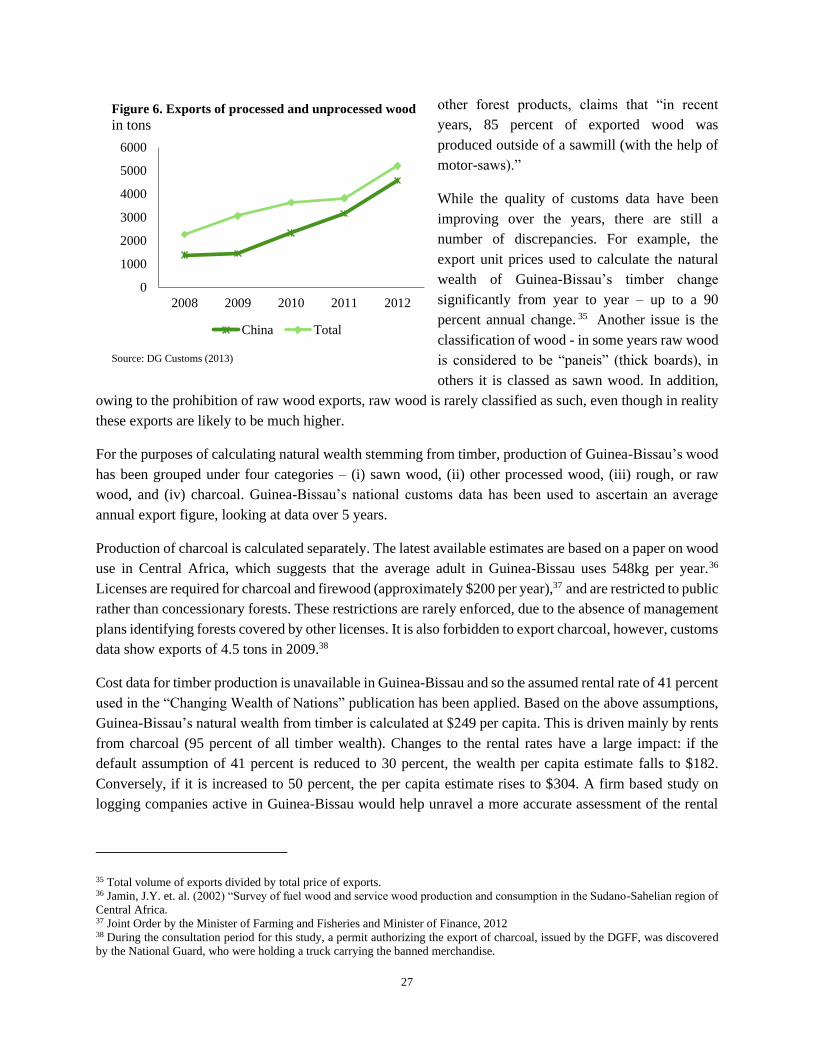

Figure 6. Exports of processed and unprocessed wood .............................................................................. 27

Figure 7. Top five export destinations for Guinea-Bissau’s Exports .......................................................... 35

Figure 8. Top five exported products from Guinea-Bissau......................................................................... 35

Figure 9. Tourism arrivals and receipts of West Africa countries with “pre-emerging” tourism sectors ... 39

Figure 10. Average tourism receipts per tourist arrival .............................................................................. 39

Figure 11. New and old calculations of Guinea-Bissau’s total wealth ....................................................... 42

Figure 12. Gross and adjusted net savings .................................................................................................. 43

Figure 13. Total volume of timber exports ................................................................................................. 55

Figure 14. Export unit values of Guinea-Bissau’s main timber exports .................................................... 55

List of Tables

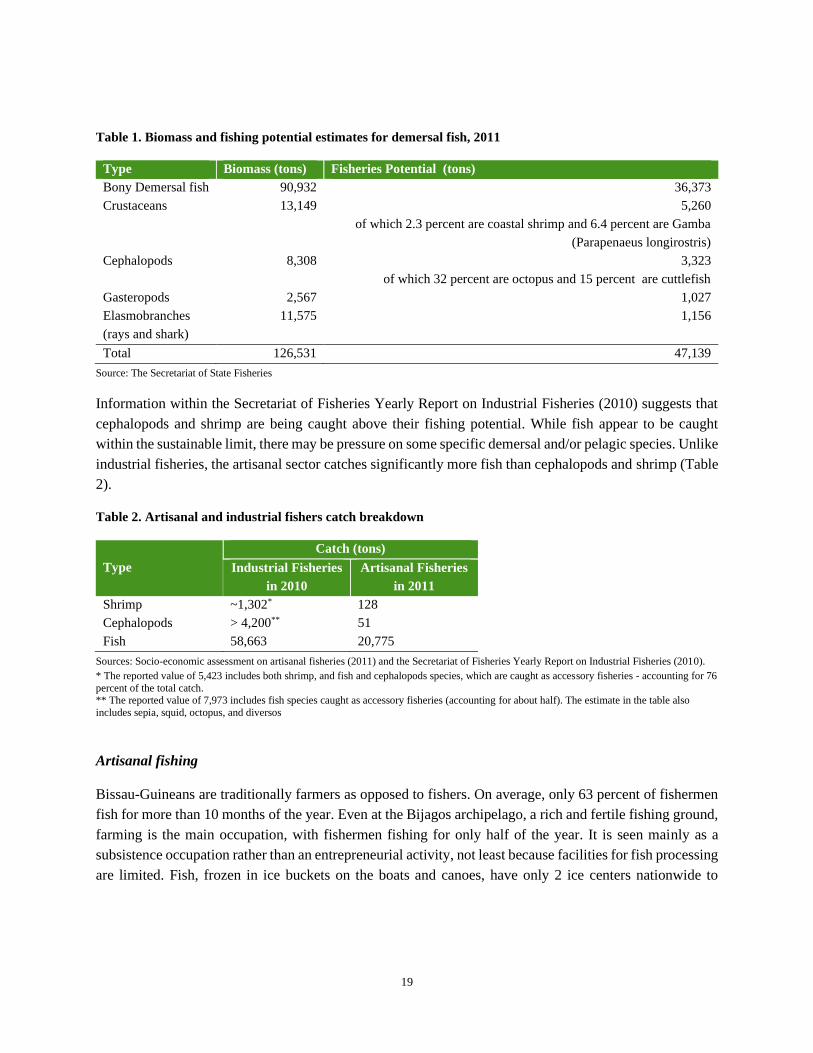

Table 1. Biomass and fishing potential estimates for demersal fish, 2011 ................................................. 19

Table 2. Artisanal and industrial fishers catch breakdown ......................................................................... 19

Table 3. Fishing licenses by vessel type and nationality ............................................................................ 22

Table 4. Industrial fish landings in Guinea-Bissau, 2010 ........................................................................... 24

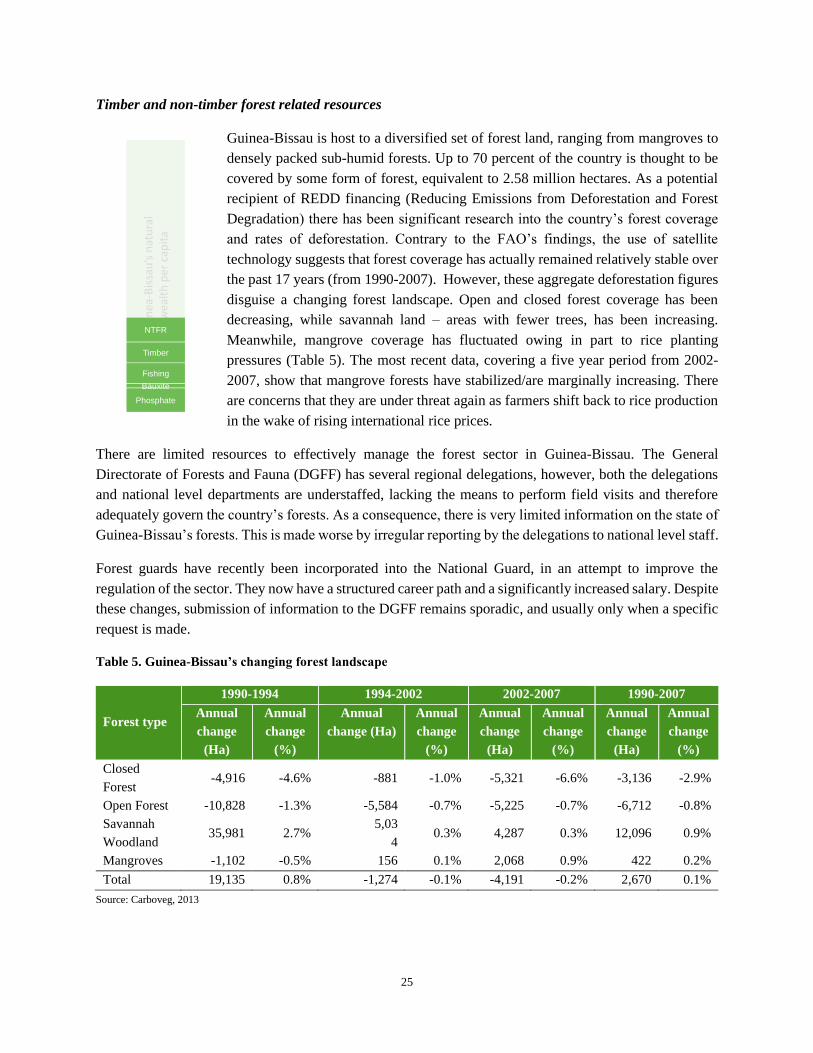

Table 5. Guinea-Bissau’s changing forest landscape .................................................................................. 25

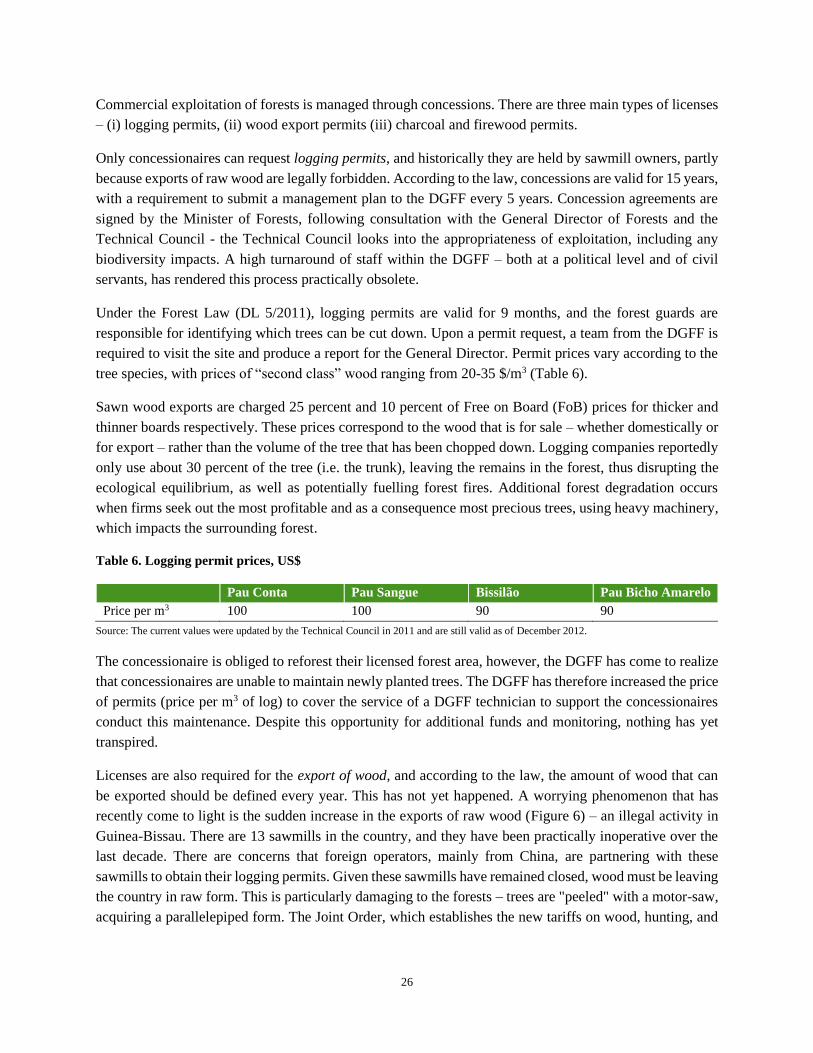

Table 6. Logging permit prices, US$ .......................................................................................................... 26

Table 7. Types and prices of hunting licenses, 2011 .................................................................................. 28

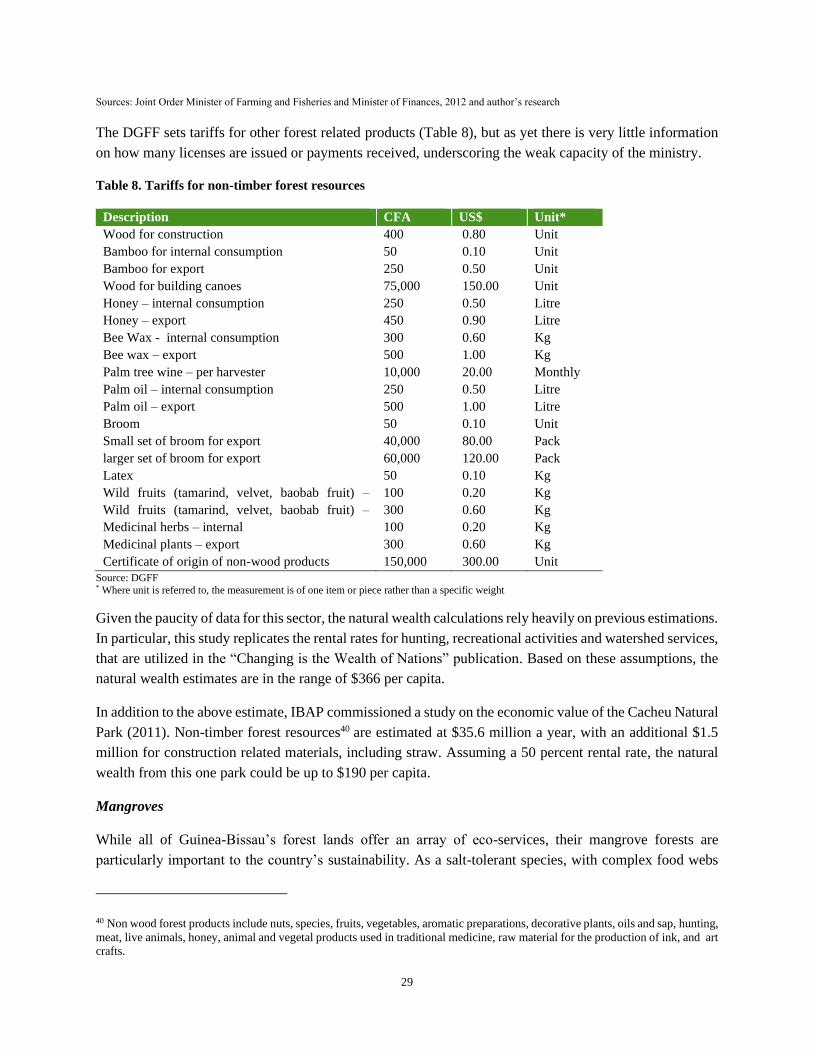

Table 8. Tariffs for non-timber forest resources ......................................................................................... 29

Table 9. Changes in mangrove coverage (1990-2007) ............................................................................... 30

Table 10. Guinea-Bissau’s Carbon Stocks .................................................................................................. 33

Table 11. Average and recent net crop production ..................................................................................... 34

Table 12. Total food surplus/deficit projected for 2012/13 ........................................................................ 36

Table 13. Main livestock production and prices ......................................................................................... 37

Table 14. Guinea-Bissau’s key laws and strategies relating to environmental protection .......................... 38

Table 15. Common assumptions across all natural wealth estimates ......................................................... 50

Table 16. Main assumptions used for the wealth calculations of phosphate and bauxite deposits ............. 51

Table 17. Landings by the artisanal sector, 2010 ........................................................................................ 52

Table 18. Prices for main categories of seafood landed by the artisanal sector .......................................... 53

Table 19. Main assumptions used for the wealth calculations of artisanal fishing ..................................... 53

Table 20. Non forest timber resource estimates .......................................................................................... 56

Table 21. Carbon Stocks (Mtons) in protected areas .................................................................................. 57

Table 22. Crop Unit Price (US$ 2010/ton) ................................................................................................. 59

Table 23. Product Export Unit Values (US$ 2010/ton) .............................................................................. 60

List of Boxes

Box 1. Definition of a mineral resource ........................................................................................................ 9

Box 2. Artisanal fishing assumptions ......................................................................................................... 21

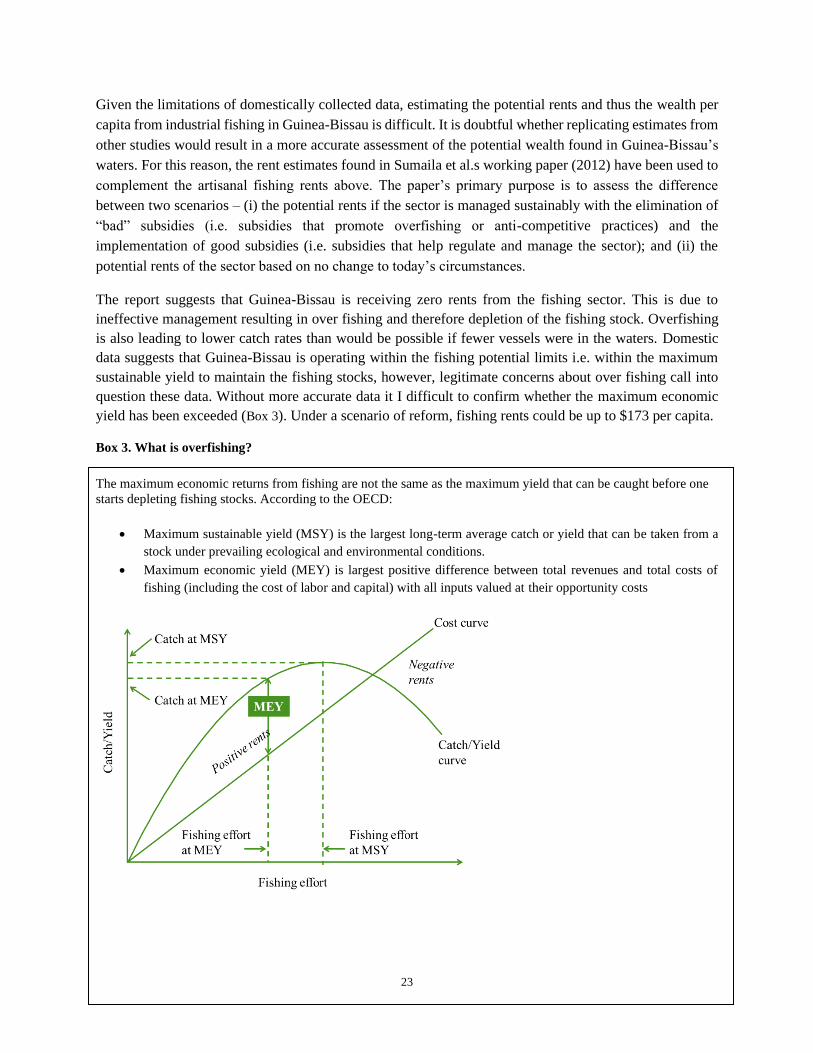

Box 3. What is overfishing? ........................................................................................................................ 23

1

Executive Summary

With a GNI per capita of $5901, and over 70 percent of the population living on less than $2 a day, Guinea-

Bissau is one of the poorest countries in the world. Since independence in 1974, the country has had four

coup d’états, with additional coup attempts and other forms of political violence, and a short but intense

civil war. While democratic rule has been in place between 2000 and 2012, short

lived alliances have resulted in governments that have not survived beyond 18

months. Despite this rather dismal picture the country is not lacking in potential.

Guinea-Bissau’s natural wealth could be up to $3,8742 per capita, including

minerals such as bauxite and phosphate, fisheries, timber and rich fertile lands

and ecosystems (see left). These resources, if sustainably managed, could help

Guinea-Bissau overcome the low-income trap the country appears to be stuck in.

Transforming this potential into poverty reduction will not happen overnight. It

requires concerted action in areas of governance; macroeconomic management

to ensure economic rents are captured and turned into meaningful government

programs; and investment climate reform, to facilitate sustainable and inclusive

business practices. Following Parliamentary and Presidential elections in April

and May, 2014, Guinea Bissau’s new government has started the long journey

towards these goals. Budgets for 2014 and 2015 were quickly prepared and

presented in Parliament; funding for the country’s Foundation for the national parks was secured, and active

negotiations with mining companies have commenced. There is a feeling of renewal and vigor with this

new government, and a hope that patterns of the past do not unveil themselves in the future.

One area the new government could focus on is optimizing its natural assets. This paper provides an

assessment of Guinea-Bissau’s main sources of natural wealth, building on the World Bank’s work on

Wealth Accounting and the Valuation of Ecosystems (http://www.wavespartnership.org/). Previous

estimates of Guinea-Bissau’s wealth are based on data from international databases, and assumptions,

aggregated from cross-country assessments. This has helped provide a global overview of natural wealth.

It has not, however, provided country specific estimates. In-country reports and surveys, alongside on-the-

ground interviews with local fishermen, farmers, government agencies and residents of Bissau provide a

more detailed insight into Guinea-Bissau’s natural wealth. Using this information, this paper confirms the

findings of previous studies: the country is richly endowed with natural resources.

Agricultural land is by far the largest source of natural wealth ($1,734 per capita for crop lands and $591

per capita for pasture land). Given the low productivity levels currently pervading the agriculture sector,

and the array of currently unexploited horticultural products, the natural wealth of this sector deserves more

attention. In particular, productivity improvements could vastly improve the livelihood of the poorest

members of society.

1 2013 data, GNI, Atlas method. Countries with a GNI per capita below $1,035 in 2012 fall under the World Bank’s “low income”

country classification. All $ figures in this report refer to US$. 2 All natural wealth estimates are in US$, 2010 prices.

2

The next largest component lies in Guinea-Bissau’s forests. In addition to timber ($304 per capita), forest

lands provide a multitude of goods and services – non-timber forest resources (NTFR) ($366 per capita).

Recent illegal logging practices could however be adversely affecting the sustainability of the forests, as

well as reducing the amount of economic rent the government is able to capture. The wealth per capita

estimates are also affected by the omission of Guinea-Bissau’s mangrove forests, which act as a nursery

ground for fisheries (especially shrimp), benefiting a large swathe of the West African coast. Mangroves

also act as a natural flood-defense against storm surges, which is extremely valuable for the low-lying

floodplains making up much of Guinea-Bissau. While mangroves have not been quantified in this paper,

anecdotal evidence and research from other countries suggests the economic value of these forests is

significant.

In preparation for a more buoyant carbon market, Guinea-Bissau is working on a Reducing Emissions from

Deforestation and Forest Degradation (REDD) project. While the carbon price is not currently high enough

to warrant investment in essential Monitoring Reporting and Verification (MRV) of forestry activities, the

country has started to set up the infrastructure and institutional framework required to access the carbon

market (potential wealth per capita of $89 should the carbon price rise to $25 per ton of CO2).3 In the

meantime, additional resources are needed to ensure the forestry sector is properly managed.

Fisheries represent the third largest element of natural wealth ($305 per capita). Domestic data suggests

that sustainability levels are not being breeched i.e. the maximum sustainable yield has not been met.

However, there are two important caveats: first, as with the forest sector, management resources are

inadequate. At the artisanal level, public bodies are unable to keep track of foreign vessels (mainly from

Senegal and Guinea-Conakry) accessing Guinea-Bissau waters. At an industrial level, they are unable to

check the catch levels of boats with license fees, and it is believed that there are significant losses of fish

from illegal fishing. Second, aggregate levels mask fishing trends of individual species, which may be under

threat. It is likely therefore that domestic level data is underestimating the landing rates, and thus the

question of sustainability still remains.

The fourth largest component of natural wealth is the country’s protected areas (PA) and biodiversity that

lies within. The data required to fully quantify the “worth” of the country’s rich eco-systems, including

global existence values, is beyond the scope of this paper. The opportunity cost of protected lands is

therefore used as a proxy for its natural wealth value ($305 per capita).

Rents from biodiversity could be generated by fostering eco-tourism. Such an approach has been

successfully adopted in countries such as Costa Rica and Dominica. This is an area Guinea-Bissau could

explore, given the large endowment of biodiversity in the country. Ecotourism could simultaneously ensure

the protection of the environment and social structures needed to implement this protection, as well as create

economic benefits to local communities and the economy at large. Significant investment in tourism related

infrastructure, as well as political stability, is needed before this could become a reality.

Finally, minerals could provide Guinea-Bissau with an important revenue stream ($126 per capita for

phosphate and $55 per capita for bauxite). Rising mineral prices are making Guinea-Bissau an economically

3 A discussion on the chosen carbon price is presented in the Appendix.

3

viable place to engage in extraction activities. However, poor infrastructure and a potentially difficult

regulatory environment limit the rents from minerals, at least in the short term, owing to the large up-front

costs required to start operations. In addition to sustainability issues – i.e. converting natural wealth into

another form of wealth, it is recommended that the government considers how to manage the funds from

mineral extraction so growth is spread over the short and medium term. International experience also

suggests a strong macroeconomic framework is needed to avoid Dutch disease and macro volatility, which

can be particularly damaging for public investment management programs.

The natural wealth estimates in this study are cumulative. It is worth noting however that there are important

trade-offs between the different components of natural wealth, namely:

• Minerals vs. protected areas: extraction of minerals, in particular bauxite, will require access to the

port – both the port and a road, which are yet to be built, lie in Cufada national park

• Mangroves vs. rice: policies to promote rice-production, may lead to the erosion of mangrove

forests

• Timber products vs. REDD: reducing deforestation and degradation in PA may impact the local

communities that use the country’s forests for goods and services and/or slash and burn farming.

Timber rents would also be affected.

Finally, while this paper shows the importance of natural wealth in Guinea-Bissau, it also highlights the

poor state of physical wealth – capital investment. Natural wealth makes up a significant proportion of

Guinea-Bissau’s total wealth (a third), larger than the low-income average. Meanwhile, physical, or

produced capital is less than 10 percent of total wealth. Guinea-Bissau has been dis-saving as the country’s

infrastructure has been left to depreciate, adversely affected by fighting and disruption. Rents from the

exploitation of the country’s natural wealth could be usefully channeled to other forms of wealth, such as

infrastructure and social capital (health and education) to ensure the next generation of Bissau-Guineans is

not worse off than today’s. Given the poor state of public investment management, and the high levels of

poverty, the country may also want to consider channeling a proportion of rents directly towards current

poverty reducing measures.

This paper concludes with some policy recommendations across the areas of Guinea-Bissau’s natural

wealth. The recommendations fall under two categories: governance and investment. Strong governance

is essential, across all areas of natural wealth, if this potential is to be transformed into shared prosperity.

To sustainably manage the country’s mineral resources, the Ministry of Finance needs strengthening to

ensure rents are optimally channeled to other forms of investment, including investment in people. The

State Secretariat of Environment needs to be part of the dialogue so that mining activities are not to the

detriment of surrounding areas and people’s livelihoods. For the countries renewable resources (fishing,

forests, biodiversity) these sectors need stronger management and regulation to attract responsible private

sector investment while ensuring sustainably limits are not breech. On investment, priority sectors include

mining, ecotourism and agriculture – all currently lacking in the infrastructure needed to bring about

productivity improvements. Encouragingly, these recommendations appear to be aligned with emergent

government thinking.

4

A. Introduction

“Adam Smith’s classic was an inquiry into the wealth of nations, not the GNP or NNP of nations, nor the

United Nations Development Programme’s Human Development Index of nations”4

Using the internationally agreed System of National Accounts (SNA), the production and output of

economies is often used as a proxy for overall social welfare. The main indicator of the SNA – Gross

Domestic Product (GDP) - is not designed to provide a measure of wellbeing, welfare, or indeed wealth.

More significantly, it does not set out to capture the sustainability of any one growth path; it does not show

whether an individual’s consumption today, results in a lower level of consumption by an individual in the

future. Governments have a responsibility to ensure social welfare is maximized for people across different

segments of society, as well as across generations. Relying exclusively on GDP as measure of success at

achieving this goal is not therefore sufficient.

One of the main drawbacks is the static nature of GDP, which looks at value added at a single point in time.

GDP does not provide policy makers with a sense of whether government spending is conducive to

medium-term growth, the perennial question of when the business cycle starts and finishes, nor does it

provide an assessment of how natural wealth is being utilized. This issue is extremely pertinent for a number

of countries in Sub-Saharan Africa (SSA). Rising commodity prices and flows of foreign direct investment

into mineral and other natural resource sectors have helped bolster SSA’s growth prospects. Growth was

estimated at 4.7 percent in 2012 – 5.8 if South Africa is excluded, and over a quarter of countries had growth

rates at over 7 percent. The question of how sustainable this growth is remains. Can countries continue

growing at these high rates and is this growth supporting the welfare of citizens both today and tomorrow?

Guinea-Bissau has not had the stellar growth rates seen in other SSA countries. After the 1998-99 civil war,

economic growth has been anemic, averaging 2.1 percent, lower than population growth at 2.3 percent. The

coup d’état of 2012 further damped the country’s prospects, with a transitional government still in place at

the end of 2013. GDP contracted by 4.4 percent and 1.9 percent in 2012 and 2013 respectively. The

economy was essentially crippled for close to two months during the military’s overthrow of the

government in 2012, due to border closures and an exodus of development support. Stability appears to

have been restored following the Parliamentary and Presidential elections in 2014. Budgets were quickly

drawn up and granted Parliamentary approval not long after the new Ministers took office. Donors are keen

to support this fresh start and are convening a meeting in early 2015 to discuss the country’s new growth

strategy.

The cashew nut remains the country’s most important source of income, both for national income as a result

of vast cashew exports, and at a local level with much of the rural population employed in cashew

plantations. There are prospects to diversify, especially given the country’s rich natural resources:

phosphate and bauxite reserves are relatively unexplored; fisheries could generate significantly more

income; sustainably managed forests would ensure both timber and non-timber forest resources contribute

towards Guinea-Bissau’s growth for years to come; and the country’s rich bio-diversity offers a unique

4 P. Dasgupta, Human Well-Being and the Natural Environment OUP, Oxford, 2001 p30

5

opportunity for eco-tourism. All of these sectors could help bolster the country’s country poor rate of

revenue collection as well as provide much needed jobs

At present, most of Guinea-Bissau’s resources are not excessively exploited.5 The country is still at the

beginning of a journey towards ensuring resources are sustainably managed. The leaders of Guinea-Bissau

are in the fortunate position of being able to learn from other countries’ experiences, thus avoiding

sustainability traps many nations have fallen into. This does not imply that the journey will be easy or that

they have time to implement bad practice. Indeed, severe capacity constraints could limit the country’s

ability to implement sustainable policies.

This paper is organized as follows: first, the paper provides a brief overview of current natural wealth

estimates and information on Guinea-Bissau’s natural resources. The paper is then divided into three

sections – the first looks at the natural wealth of the country’s exhaustible resources, namely phosphate and

bauxite, and the second provides an overview of the country’s non-exhaustible, or renewable resources,

including: fishing, timber and non-timber forest resources (NTFR), carbon, crop and pasture land, and

protected areas (PA). The third part ties the results together by summarizing the different components of

Guinea-Bissau’s total wealth. The paper concludes with some recommendations and next steps.

B. What does the past tell us: Guinea-Bissau’s current natural wealth estimates

“Guinea-Bissau houses a wealth of biodiversity that is of local, national, and global significance,

particularly its vibrant coastal zone.”6

The World Bank, alongside the United Nations (UN), has been proactive in developing methodologies to

quantify the natural wealth of countries. Without some form of measurement not only is it is difficult to

gain traction with policy makers, but it is also difficult to assess the impact of social and economic policy.

The various approaches to measuring natural wealth have been heavily criticized, with suggestions that

they fall more under the category of art rather than science.7 While it is true that there is still a degree of

subjectivity involved in creating natural wealth estimates, there is international agreement on most of the

methodologies for these calculations.

In 1993, the System of National Accounts (SNA) added subsoil assets to the national balance sheet, making

mineral accounts a core component of the internationally agreed methodology for national accounts. The

System of Integrated Economic and Environmental Accounts (SEEA) Central Framework, which was

adopted as an international statistical standard by the UN Statistics Commission in 2012, provides further

discussion of issues related to calculating the asset value of minerals and energy stocks, and provides a

methodology for calculating depletion costs. The SEEA also includes guidance on calculating rents from

5 That is not to say that the natural resources are not being utilized, or that current practices are sustainable, rather that there is still

time to reverse activities that have the potential of making Guinea-Bissau’s non-exhaustible resources exhaustible. 6 “Maintaining coastal biodiversity and natural resources as mainstays of Guinea Bissau’s economy”, The Global Environment

Facility, 2010 7 See for example Solow’s comments on Arrow et al.s recent paper (2012) “ Sustainability and the measurement of wealth”

6

renewable natural resources, although apart from methodologies for calculating rents of timber, this is less

well developed.

The process of collecting relevant data and surveying natural resource sectors can often be more useful than

the final natural wealth estimate itself. This is particularly relevant for low income countries like Guinea-

Bissau where data are not always available or of variable quality. Interviews with local communities and

government agencies can shed light on the operation of sectors and the governance of natural resources,

which if acted upon can help strength sustainability and boost incomes.

To date, the most comprehensive assessment of Guinea-Bissau’s natural wealth is covered under the World

Bank’s Wealth of Nations publications.8 These wealth estimates use international databases to calculate

comparable natural wealth per capita estimates for more than 120 countries. In low income countries,

natural wealth estimates, on average, account for over a quarter of all wealth, while 16 percent is attributed

to physical capital and the remaining 58 percent to intangible (e.g. human and social) capital.9 For Guinea-

Bissau, “The Changing Wealth of Nations” estimates show that natural wealth represents close to 50 percent

of all capital, demonstrating simultaneously the importance of the natural environment for the country,

while at the same time the poor state of public infrastructure (Figure 2).

It is likely that these natural wealth estimates are significantly underestimated. On the one hand the

calculations omit key elements such as fishing, carbon credits, and biodiversity, and on the other, the data

and assumptions have been aggregated to allow for cross county comparisons; country specificities are

ignored. Furthermore, the potential wealth of sub-soil assets in Guinea-Bissau (phosphate and bauxite) has

not been included, owing to the relatively nascent prospects for extraction (Figure 2).

Figure 1. Current estimates of total wealth in

Guinea-Bissau

Figure 2. Current natural wealth per capita estimates

for Guinea-Bissau

Source: The Changing Wealth of Nations, 2011

8 “Where is the Wealth of Nations?: Measuring Capital for the 21st Century”, (2006) World Bank, Washington, D.C., and “The

Changing Wealth of Nations: Measuring Sustainable Development in the New Millennium” (2011), World Bank, Washington,

D.C. 9 Intangible capital is not specifically calculated, rather it is the residual of the total, physical and natural wealth estimates. This

paper does not attempt to calculate more specific intangible capital estimates for Guinea-Bissau, This is an area where future

research would be helpful.

Produced

Capital

Natural

capital

Intangible

capital

Net foreign

assets

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

7

This paper builds on the methodologies and estimates calculated under the publication series mentioned

above by including country specific assumptions, where available, as well as estimates for the potential

wealth per capita from phosphate, bauxite, fisheries, and carbon. The estimates have been updated using a

combination of desk based research and on the ground field work, where local communities and

organizations have been interviewed to determine the costs, and production levels associated with various

natural resource based sectors. This paper draws on analysis conducted by three main sources: (i) the World

Bank’s Country Economic Memorandum for Guinea-Bissau (2011, mimeo), which provides a helpful

overview of the country’s main sectors including agriculture, fishing and eco-tourism; (ii) “CarboVeg”, an

analysis on deforestation rates and the state of Guinea-Bissau’s forests – a much needed update on the Food

and Agriculture Organization’s (FAO) 1990 based assessment and (iii) World Bank analysis prepared to

assess the benefit of investing in the management of West Africa’s fisheries. The underlying methodologies

are based on quantifying economic rents from different resources. The main assumptions and calculations

are set out in the Appendix, with the high level results summarized in the body of this paper.

For phosphate and bauxite, the wealth calculations illustrate the potential wealth, given commercial mining

has yet to commence. Deposits of both minerals are thought to be substantial, and so while sustainability

issues may not therefore be an issue for the next generation, there are certain macroeconomic factors that

need to be considered, e.g. how to spend and manage the volatility of mineral rents, while maintaining

environmental and social considerations.

For most of the renewable or non-exhaustible resources the wealth calculations are based on rents if existing

practices were to continue. Contrary to previous studies, the fishing and forest sector do not appear to be

exceeding sustainability levels. However, there are two important caveats to this statement. First, an

aggregate overview of the sectors masks impacts on certain species, which may in fact be threatened, and

second, official data and monitoring of these sectors is not particularly strong, suggesting the rents could

be much higher if sustainability measures were put in place. Despite these two caveats, the use of national

data and qualitative information is preferred to using earlier studies that are either based on outdated data,

or extrapolations from neighboring countries.

There are two main areas that have not been quantified: water and mangroves. These resources are

particularly important to Guinea-Bissau, but without more research and data collection, estimates at this

stage would be purely speculative. There have been some attempts to quantify the economic value of the

country’s mangrove forests but this is still at an early stage and would need to be developed further to be

useful for policy making.

8

C. What does the present tell us: new estimates of Guinea-Bissau’s natural wealth

I. Exhaustible resources

“…income from these sources [phosphate mining, bauxite and possibly oil] could amount to as much as

30% of GDP”10

While mining in Guinea-Bissau is currently limited to small scale production of construction materials (e.g.

granite, limestone, and clays), rich mineral reserves of phosphate, bauxite and petroleum could see this

landscape change (Box 1 provides an overview of mineral reserve definitions). Poor infrastructure,

relatively low mineral prices, and political instability have prevented investment in this sector to date.

However, increasing commodity prices may be able to circumvent Guinea-Bissau’s weak institutional

environment and dilapidated infrastructure (Figure 3).

Interest in Guinea-Bissau’s minerals is not

a new phenomenon. International

organizations and companies have been

exploring the country’s lands for the past

forty years, and more recently, there have

been several offshore discoveries of heavy

oil deposits. What is new is a more

realistic outlook for mining sector

investment. The last decade has witnessed

a number of long term exploration leases

signed between the government and

interested investors. While a number of

companies are investigating the potential

of offshore oil in Guinea-Bissau, progress

is slow and extraction is still far off.

Bauxite, and in particular phosphate,

however, are closer to viability.

Calculations of Guinea-Bissau’s potential natural wealth from sub-soil assets have therefore been limited

to rents from phosphate and bauxite reserves.

This section provides an overview of the mining potential of phosphate and bauxite, as well as an indicative

wealth per capita estimate for the two minerals. These estimates are based on a number of assumptions,

which could easily change, not least because mining activity has not yet started in either of the bauxite or

phosphate sites.

10 S. Kyle, 2009, “The Macroeconomic Context for Trade in Guinea-Bissau”, Working Paper No.26, p8

Figure 3. Phosphate, Bauxite and Petroleum prices have been

increasing

US$, 2005 prices

Sources: World Bank commodities database and Bauxite prices from USGS

0

50

100

150

200

250

300

Phosphate ($/Mt) Bauxite ($/Mt)

Petroleum (crude) ($/bbl)

9

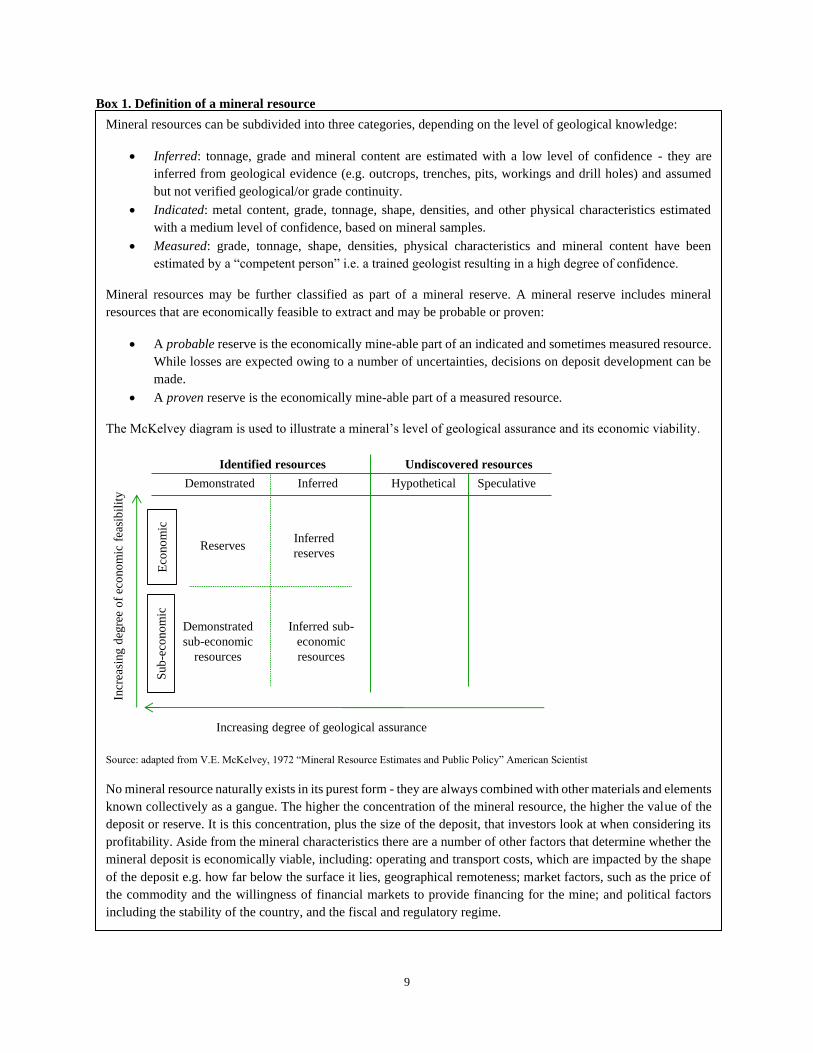

Box 1. Definition of a mineral resource

Mineral resources can be subdivided into three categories, depending on the level of geological knowledge:

• Inferred: tonnage, grade and mineral content are estimated with a low level of confidence - they are

inferred from geological evidence (e.g. outcrops, trenches, pits, workings and drill holes) and assumed

but not verified geological/or grade continuity.

• Indicated: metal content, grade, tonnage, shape, densities, and other physical characteristics estimated

with a medium level of confidence, based on mineral samples.

• Measured: grade, tonnage, shape, densities, physical characteristics and mineral content have been

estimated by a “competent person” i.e. a trained geologist resulting in a high degree of confidence.

Mineral resources may be further classified as part of a mineral reserve. A mineral reserve includes mineral

resources that are economically feasible to extract and may be probable or proven:

• A probable reserve is the economically mine-able part of an indicated and sometimes measured resource.

While losses are expected owing to a number of uncertainties, decisions on deposit development can be

made.

• A proven reserve is the economically mine-able part of a measured resource.

The McKelvey diagram is used to illustrate a mineral’s level of geological assurance and its economic viability.

Source: adapted from V.E. McKelvey, 1972 “Mineral Resource Estimates and Public Policy” American Scientist

No mineral resource naturally exists in its purest form - they are always combined with other materials and elements

known collectively as a gangue. The higher the concentration of the mineral resource, the higher the value of the

deposit or reserve. It is this concentration, plus the size of the deposit, that investors look at when considering its

profitability. Aside from the mineral characteristics there are a number of other factors that determine whether the

mineral deposit is economically viable, including: operating and transport costs, which are impacted by the shape

of the deposit e.g. how far below the surface it lies, geographical remoteness; market factors, such as the price of

the commodity and the willingness of financial markets to provide financing for the mine; and political factors

including the stability of the country, and the fiscal and regulatory regime.

Identified resources Undiscovered resources

Demonstrated Inferred Hypothetical Speculative

Reserves

Increasing degree of geological assurance

Incr

easi

ng d

egre

e o

f ec

ono

mic

fea

sib

ilit

y

Demonstrated

sub-economic

resources

Inferred sub-

economic

resources

Inferred

reserves

Eco

no

mic

S

ub

-eco

no

mic

10

Phosphate

Phosphate rock is found in the north of the country, just 5 kilometers from the small

town of Farim (population 7,000). The main deposit site is close to the Cacheu River,

25 kilometers from the border with Senegal, and approximately 100 kilometers

northeast of the capital city, Bissau. The Cacheu River has direct access to the

Atlantic and is navigable by boat (175 kilometers). At present, there are no tarred

roads to the coast. Any mining would therefore need to use river transport, or invest

in an 80 kilometer road to export the mined phosphate.

The United Nations Development Programme (UNDP) was the first international

organization to investigate the phosphate deposits, in 1978, shortly after

independence. Subsequently, in 1981-85, the Bureau de Recherches Géologiques et

Minières of France built upon these initial findings, and in 1986, Sofremines

conducted a prefeasibility study.

Despite promising findings, the infrastructure in Guinea-Bissau was deemed too

weak to warrant mining investment and the site was left untouched for over 10 years,

before Champion Resources Inc. of Canada acquired a 2 year exploration permit in 1997. Their findings

confirmed the results of previous assessments: Guinea-Bissau is rich in phosphate rock – close to 100

million tons of high quality clay bounded ore, with 30.1% raw phosphate rock (approximately 40 years’

worth of mining), plus an additional 400 million tons of lower quality calcium bounded rock (up to 200

years of mining potential). However, in addition to existing concerns of poor infrastructure, the onset of a

civil war in 1998 once again put mining prospects to bed for another decade.

After some deliberations with the government, GB Minerals (formerly GB Phosphate Mining Limited) was

granted an exploration license in 2009. More recently (February 2013), Plains Creek Phosphate Corporation

bought out GB Minerals, including its license in Guinea-Bissau.11 While the coup d’état in April 2012

delayed progress towards the construction of a functioning mine yet again, Plains Creek are trying to move

forward with positive pre-feasibility assessments paving the way.12 Negotiations between Plains Creek and

the government of Guinea-Bissau (on royalties, taxes, project areas) are moving ahead with the new

Ministers in place and the Company keen to start developing the mine as soon as possible.

Guinea-Bissau’s phosphate wealth estimates are based on the assessments made by Plains Creek. The

feasibility study outlines two proposals: (i) a 1.3 million ton per year Direct Shipping Option (DSO) product

production and (ii) a 1 million ton per year Beneficiated Phosphate Rock Concentrate (BPRC) product

production.13 Both proposals are for 25 year mines and rely on barges to transport phosphate down the river

11 Plains Creek Phosphate Corporation has subsequently changed its name to GB Minerals. 12 Refer to www.plainscreek.com for more information. The November 23rd 2012 news release provides details on their pre-

feasibility study. 13 The difference lies in the level of processing. The BPRC option involves additional refinement of the phosphate rock to a higher

grade, attracting a higher price and a higher variable cost.

Gu

inea

-Bis

sau

’s n

atu

ral

wea

lth

per

cap

ita

Phosphate

11

Cacheu, rather than include a road investment linking the mine with the coast. In both cases, phosphate

rock will be made available to the domestic market for use in fertilizers.

Owing to the poor electrification rates and reliability of electricity supply in Guinea-Bissau, both proposals

will rely on diesel generators for the operations of the mine. Poor transport links and expensive energy

supplies make Guinea-Bissau an expensive place to invest. High phosphate rock prices have helped offset

these challenges and have made the Farium deposit increasingly attractive to investors. The persistently

high demand for phosphate in recent years suggests that prices will remain high,14 however, as with all

commodity forecasts, there remains a large degree of uncertainty associated with this outlook.

The natural wealth estimates are extremely sensitive to fluctuations in the price of phosphate. A central

price of $125 per ton gives a natural wealth per capita figure of $126.15 However an increase in the price to

levels seen in 2012 ($185 per ton), increases the wealth per capita estimates to $682. Conversely, a $60

shift in the other direction would put the rents into negative territory.16

There are a number of positive spillover effects from phosphate mining, which extend beyond essential

fiscal revenues.17 The mine could directly employ a number of people living in the neighboring town Farim.

There could also be significant multiplier effects with jobs created in the services industry to cater for

people’s new found wealth. All of these avenues could create important poverty reducing opportunities for

the country’s poorest. Initial consultations with local communities in 2010 suggested that there is support

for the mining project, although people are frustrated by the lack of progress. An Association of the Young

People of Farim for Phosphate Development has been set up to ensure that any benefits from the mining

project spillover to the local area.

There are also a number of potentially negative consequences from the development of a phosphate mine,

both in terms of environmental and health impacts, and socio-economic effects. Phosphate mining,

especially when beneficiation takes place, requires a substantial amount of water to help with the processing

of the mineral. Once the phosphate has been separated from other components such as clays and sands, it

may be disposed of via rivers, or in a pre-identified waste disposal area. There is therefore a risk that the

local river, River Cacheu, is polluted and possibly drained. This could have a direct impact on the local

communities that use the river for washing and income generating activities such as fishing. Furthermore,

a large mining project is likely to attract migrants, which could undermine the social fabric of the local area

if service provision does not match increasing demand. Strong governance and institutional reform are

therefore essential if Guinea-Bissau’s phosphate reserves are to be transformed into poverty reduction and

economic growth.

14 There are concerns that the world’s phosphate resources are running low, and that we will reach “peak phosphate” in early 2030s.

Given its importance for agriculture, as a key ingredient in fertilizers, efficient use of the resource will be essential for sustainable

agricultural practices. 15 All estimates have been calculated in 2010 prices. A $150 per ton price of phosphate in today’s prices is equivalent to $146 in

2010 prices. 16 A full description of the calculations and assumption are included in the Appendix. The price of phosphate is assumed to stay

constant over the duration of the mine. 17 Calculations in the World Bank’s Country Economic Memorandum for Guinea-Bissau estimate fiscal revenues of between10-

15 percent of current revenues.

12

Bauxite

At the opposite end of the country, in the southeast, there are five neighboring

bauxite deposits in the Boe region. Boe, 100 kilometers from the port of Buba and

near the border with Guinea-Conakry, was formally the capital of Guinea-Bissau,

until the country declared independence from Portugal in 1974. Up until recently,

the area was infiltrated by landmines put in place during three periods of conflict:

the War of Liberation in the 1970s, the civil war in the late 1990s and the

Casamance rebellion in 2006.

The Dutch were the first to conduct a geological survey of the area in the 1950s,

concluding that the bauxite deposits amounted to over 100 Mt, with average

alumina and silica content of 46.5 and 3.5 per cent respectively.18 Twenty years

later, the Soviets returned to the site and in 1983 the first feasibility study took

place. Historical bauxite prices (US$10-15 per ton) have not been high enough to

attract mining investment in Guinea-Bissau, not least because the Boe region is not

connected to the shallow and under-developed Buba port, driving up the costs of

shipping and transport. Any investment therefore needs to factor in additional up-

front capital costs for roads and port rehabilitation.19

Recent bauxite prices have, along with other minerals, increased substantially, and are now in the range of

$30-50 per ton (as opposed to $15-20 per ton at the turn of the century).20 This has made Guinea-Bissau’s

bauxite deposits look significantly more attractive, and in 2007, Bauxite Angola entered into a contract with

the government to start exploring the region. While prospects looked promising, little investment has

actually taken place. The Minster of Natural Resources in the transitional government recently announced

(March 2013) that no investment had taken place, neither had there been any environmental impact

assessments or economic viability reports since the signing of the lease. It has also been suggested that the

lease is not in line with current legislation and could therefore be revoked.

Despite these set-backs, Bauxite Angola still maintains an interest in the region and has indicated that it

would invest in the road and the port, as well as the mining infrastructure.21 Unlike the phosphate deposits

however, there are still a number of outstanding issues and analysis that needs to be conducted before

commercial activity can take place. One of the major issues to be resolved, in addition to the legal standing

of Bauxite Angola and their relationship with the government of Guinea-Bissau, is the potential

environmental impact. While impacts on the environment from the Bauxite mine, if properly regulated, are

containable, it is the adverse effects on protected areas (PA) that need to be taken account of. The proposed

18 Bauxite can be refined into aluminum, attracting a much higher price, but at a much greater cost. The higher the alumina content

the more aluminum available for extraction. Conversely, the lower the silica content the better, as silica is difficult and costly to

remove. 19 Alternatively, the bauxite could be transported to the recently expanded port at Kamsar in Guinea. While farther than Buba, it

would only be necessary to build a new road or rail line to the Boke bauxite area of Guinea and use existing infrastructure. 20 Real prices. 21 The United Arab Emirates has recently announced an interest in Guinea-Bissau’s bauxite reserves, offering to build a large port

at Kamsar to export both bauxite and aluminum.

Gu

inea

-Bis

sau

’s n

atu

ral

wea

lth

per

cap

ita

Phosphate

Bauxite

13

road to the port would transverse directly through the soon to be established Boe national park, which is to

be part of the Dulombi-Boé-Tchetche (DBT) complex. Once at the port, there would be further

environmental impacts, both at the ocean access point and the Cufada protected area, impacting fishing,

terrestrial areas (Cufada), the riverine (rio buba) and marine biodiversity at the site and neighboring lagoons.

In 2008, Bauxite Angola upgraded part of an existing road through the Cufada national park (widening and

improving), in addition to clearing 113 hectares of land to make room for a larger port. There were no

environment impact assessments accompanying the construction, and calls to end the developments by the

Institute of Biodiversity and Protected Areas (IBAP) were ineffective. Local communities and NGOs are

acutely aware of the environmental and subsequent socio-economic damages a mine could bring to the area

and are actively rallying the government to prevent these sorts of incidences. It does not have to be one

project verses another. A bauxite mine and a national park could work together side by side, providing

environmental impacts are managed. Indeed, there could be several benefits, including direct and indirect

employment opportunities. Improved access to the region could also improve access to health and education

facilities as well as stimulate other income generating activities.

Owing to the uncertainties linked to the potential timing and project specification of a bauxite mine, the

natural wealth estimates for Guinea-Bissau’s bauxite reserves are indicative. However, they do at least

provide an indication of the scale of potential mineral rents. A number of the assumptions have been taken

from reports and studies on bauxite mines in Guinea-Conakry.22 A recent mine investment proposal in

Guinea-Conakry assumes a US$37 per ton price for bauxite and a variable cost of US$12 per ton. Bauxite

Angola have previously suggested the up-front capital costs for the mine and related infrastructure could

be up to $500 million, with some of the financing provided by the government given the public good nature

of the road and port. Assuming Bauxite Angola funds $400 million, with a mining start date of 2018, the

natural wealth estimate comes to $55 per capita. However, if the company pays for the full $500 million

this would drop to negative $86, suggesting that the mine is bordering on commercial viability.

Exhaustible resource considerations

There are three main issues that are worth considering when assessing potential rents from mineral

resources in Guinea-Bissau: (i) trade-offs between consumption and investment spending; (ii) managing

volatility and ensuring macroeconomic stability; and (iii) environmental and socio economic impacts. All

three issues underscore the need for stronger governance.

Consumption vs. investment

One of the main decisions facing governments with newly acquired resource rents, or even just the prospect

of resource rents, is whether to spend the resources on consumption, thus benefiting the population today,

or on investment, with some benefits accrued today, but with the lion’s share arriving in the future. As a

poor, capital scarce developing country, this decision is even more pronounced for Guinea-Bissau, as both

avenues represent worthwhile endeavors.

22 Bauxite in Guinea-Conakry is what cashew is to Guinea-Bissau, accounting for close to 85 percent of external revenues.

14

Freidman’s permanent income hypothesis can provide governments with a framework to help address this

dilemma – borrowing against potential future rents to invest and promote consumption today, and then

using the interest and increased productivity of investments to pay for the borrowing in the future. The

approach is appealing because of its apparent equality across time. However, Collier et. al. (2010) argue

against this approach for capital scarce developing countries, not least because access to finance, especially

international finance, is not always possible. This is definitely the case in low income Guinea-Bissau. With

over 70 percent of the population living on less than $2 a day, one could easily argue that resource rents

should be used to help alleviate poverty in the immediate term.

Social cost-benefit-analysis (CBA) (which utilizes a social discount rate), can help governments determine

whether revenues are used to support consumption today verses consumption tomorrow. The Guinea-

Bissau government is faced with a choice of spending money on consumption related activities, with a

social discount rate of 3.5-7.5, or investment in medium to long term wealth creation, such as capital

infrastructure or health and education systems.23

Domestic investment and in particular public investment in essential public goods is historically low in

Guinea-Bissau. The investment rate over the past 5 years has hovered around 10 percent of GDP, and

national savings closer to 4 percent of GDP. At the same time, health and education indicators are

depressing: child and infant mortality rates have been increasing since 2000, with a high proportion of

recorded deaths as a result of preventable diseases (malaria, diarrhea, respiratory infections); and just over

a quarter of children of primary school age are enrolled in school – only 12 percent of girls actually finish

(UNICEF). Given the poor state of existing infrastructure, as well as the abysmal performance of health

and education provision, there are a number of domestic investments that could potentially generate a high

rate of return, as well as improve the country’s Human Development Index (currently 177 out of 187,

(2013)). When this rate of return is greater than the social discount rate, CBA suggests the government

should invest in such wealth creating activities.24 The quality of public investment, including the ability to

maintain and ensure operating costs are factored into budgetary frameworks needs to be included in this

CBA assessment. In some cases it might worth investing in the investment process before channeling

money into poorly managed areas.

Volatility and stability

The causes and symptoms of Dutch disease are well documented as is the infamous resource curse.25 The

average poverty headcount in the 41 established and prospective natural resource rich developing countries

identified by the IMF is as high as 60 percent.26 Many of these countries struggle to raise non-resource

related revenues and public infrastructure remains weak and fragmented. An influx of foreign exchange

revenues can put pressure on the exchange rate in these countries, leading to an appreciation of the domestic

23 A derivation of the discount rate for Guinea-Bissau is presented in the Appendix. 24 Ideally, an institutional framework for resources rents and an associated communications strategy should be devised before the

revenues started flowing to help manage citizen’s expectations on expenditures, as well as internal public finance capacity. This

requires sufficient foresight and internal capacity – both elements are difficult to come by in a fragile state. 25 See for example Gelb (1988), Sachs and Warner (1999), Sachs and Warner (2001), and van der Ploeg (2011) 26 See Berg et al., 2012, “Public investment in resource rich developing countries”, IMF working paper. The average poverty

headcount is based on the proportion of the population living at or below $2 a day.

15

currency, thus hindering the tradables

sector. While Guinea-Bissau is unlikely to

witness an appreciation of their nominal

exchange rate, given it is part of the West

African Economic and Monetary Union

(WAEMU), which pegs its currency to the

Euro, an appreciation of the real exchange

rate (RER) seems almost inevitable, at

least in the short term.27

The RER in Guinea-Bissau has stayed

relatively constant during the past 10

years, especially as their trading partners

are subject to the same supply shocks and

inflationary pressures (Figure 4). Inflation

has generally been low over the past

decade, apart from in 2008 when soaring

international food prices adversely

affected the price of the country’s

consumer basket – in particular rice. Huge inflows of Official Development Assistance (ODA) since the

year 2000 do not appear to have affected the country’s inflation rate either. This may be due to aid money

filling an output gap rather than generating excess demand, and the use of the funds, which were mainly

used for imported products rather than stimulating domestic consumption.

Mining rents and economic activity from mining, could however, lead to an appreciation of the RER. It

would come from two main avenues: first, from increased government spending on both consumption and

capital related activities; and second, directly from mining activities.

Aside from inflationary pressures and effects on the RER, resource rents require strong macro oversight, to

manage the volatility of flows. Phosphate prices have fluctuated dramatically in recent years, in part because

of the concentration of phosphate production in one country: Morocco, and also because of “peak

phosphate” speculation – concerns that reserves are running out and the effect this will have on the

agriculture sector. As a core component of aluminum, bauxite prices are also likely to fluctuate, albeit in a

general upward trajectory.

The uncertainty caused by these fluctuations will make it difficult for the authorities to plan, and can

adversely affect welfare.28 Public investment is usually the area of spending that is cut first, adversely

affecting the quality and quantity of public infrastructure and thus long-term growth prospects. This is even

more marked in countries in a monetary union where other tools such as interest rates and allowing

27 With an estimated 30 percent contribution to GDP, it is impossible for there not to be some effect on the real economy, at least

in the short run. 28 Hnatkovska and Loayza (2005) estimate that a one-standard-deviation increase in macroeconomic volatility can lower average

annual GDP per capita growth by 1.28 percent. For more details on the model, and for an overview of links between macroeconomic

volatility and growth in developing countries, refer to N. V. Loayez, 2007.

Figure 4. Guinea-Bissau’s RER has stayed relatively

constant over the past decade

Annual percentage change CFAF per US$

Source: International Monetary Fund

-250-150-5050150250350450550650

-6

-4

-2

0

2

4

6

8

10

12

CPI (annual average) (LHS)

RER (LHS)

Nominal exchange rate (average) (RHS)

16

fluctuations in exchange rate are unavailable. Since the introduction of fiscal convergence criteria in

WAEMU, fiscal policy has been found to be pro-cyclical, with capital spending bearing the brunt of

government’s need to cut spending (World Bank, 2013).

In terms of taxation, setting the optimal rate requires an assessment of the uncertainty of commodity prices.

The larger the unit price, the larger the resource rents (assuming the marginal cost of production remains

constant). Governments also need a good appreciation of costs and reserves, as well as strong audit capacity

to ensure contract enforcement. Without this, the majority of the mineral rents will leave the country via

the international investor, rather than being channeled back into the country. Several Sub-Saharan African

(SSA) countries have fallen foul to international firms’ claims of limited profitability, subsequently wooing

them by significant tax holidays and royalty free periods (e.g. Zambia’s privatization of the copper mines

in the 1990s). While Guinea-Bissau’s environment – investment, governance, and general infrastructure -

is weak, careful consideration will be needed when assessing potential benefits to interested mining

companies, to ensure the country’s interests are safeguarded. This is a daunting challenge, with countries

such as Ghana, which has one of the highest Country Policy and Institutional Assessment (CPIA) ratings

in SSA (3.4, where 6 is the highest possible score) still struggling to capture mineral rents and transform

them into development assets (World Bank 2012). Prospects for Guinea-Bissau, with a CPIA rating of 2.6

are somewhat daunting.

Environmental and socio economic externalities

The rent calculations used to estimate phosphate and bauxite natural wealth are based on market prices and

as such have not taken into account any negative externalities that may arise from mining activity (e.g.

carbon emission, air and water pollution, environmental degradation), or any positive externalities such as

improved access to public services. This would require a much more detailed assessment and yet would

still be relatively high level, given mining activities have not started. As such, they have been excluded

from this analysis, however, it should be noted that they could have a significant impact on the above

estimates.

Unfortunately, given the country’s historical record – Bauxite Angola’s unauthorized construction through

the park – the likelihood of strong environmental regulation seems distant. Capacity within the government

to conduct environmental impact assessments is weak, and enforcement of environmental regulation

remains significantly under-resourced. Enacting laws to ensure companies abide by environmental

standards will only be as successful as the country’s ability to monitor and enforce them. The country’s

environment law includes a requirement of extractive industries to undertake an Environmental Impact

Assessment (EIA). A body has been set up to oversee and implement this new regulation - Celula de

Avalicao de Impacte Ambiental (CAIA). While this is a positive development, the issue of capacity, both

financial and human, is still a constraint.

Socio-economic considerations are a compulsory part of any EIA for projects (not for plans or programs)

in Guinea-Bissau however the implementation of these assessments remains fragmented and weak. Mining

activities could bring significant positive externalities – employment, training, and development of local

infrastructure, providing socio-economic considerations are factored into project planning. If regulations

are not strictly enforced, the alternative scenario is one of limited investment into local infrastructure and

17

slow growth in non-mining income generating activities.29 EIAs help highlight where potential tensions

may arise and mitigating factors to help ameliorate these negative side-effects. Stronger governance and

enforcement of the outcomes of an EIA is needed in Guinea-Bissau to ensure the recommendations are

followed through.

II. Non-Exhaustible resources

“The historical record shows that biological over- exploitation is almost universal at some point in the

development of a resource, and even when biological overexploitation is avoided, economic

overexploitation is the norm.”30

Unlike the mineral reserves described above, non-exhaustible resources are a form of wealth that if

maintained, can continue producing income for many years. This requires sustainable management as if

sustainability yields are breached the once non-exhaustible resources develop the characteristics of a finite

material.

Guinea-Bissau is rich in natural resources with many areas still left untouched and unexploited. However,

this is changing, and at a relatively fast pace. Weak institutional capacity has limited the country’s ability

to monitor and regulate key sectors such as fisheries and forestry. Weak administration also means local

data for these sectors are limited and of variable quality. Previous studies have relied on data collected

many years ago and extrapolated forward – e.g. FAO information on forests was collected in 1990 - or

alternatively, studies have used assumptions from neighboring countries. Recent analysis on Guinea-

Bissau’s forests, as well as interviews with local authorities and communities, has helped fill in the gaps

and paint a more accurate picture, although further work is needed to improve the quality of domestically

collected data.

This paper makes two key assumptions when estimating the value of per capita wealth of Guinea-Bissau’s

non-exhaustible resources: first, that current practices continue and second, that the estimates are

cumulative. By assuming that the status quo is maintained, the natural wealth estimates may be lower than

their potential. Recorded exports of fish, timber and agricultural goods are relatively small – although there

are genuine concerns that unofficial exports of these goods are much larger. The estimates are based on the

historical growth of these exports and domestic production levels. No step changes in production or rental

values due to improved infrastructure or training is introduced into the calculations. Given Guinea-Bissau

is starting from such a low base in terms of productivity, the potential could be significantly larger than

what is currently practiced.

The second assumption may overestimate natural wealth. Maximizing rents from all sectors is not

necessarily possible or optimal. There are important trade-offs between the different sectors. For example,

limiting forest degradation and/or deforestation to attract rents from carbon credits may adversely impact

29 Take for example the village of Mambia in Guinea-Conakry. Local infrastructure and housing are run down and land-owners are

not receiving the tax owed to them by the mining companies for use of their land. In the meantime, environment degradation by

the mines has adversely impacted the fertility of the soil and thus agriculture output 30 R. Hilburn et al, 1995, “Sustainable Exploitation of Renewable Resources”, Annual Review of Ecology and Systematics, Vol.

26 p.61.

18

the timber rents as well as the rents local communities get from non-timber forest resources. Similarly,

encouraging greater rice production could negatively affect mangrove forests and their associated co-

benefits. While this paper does not attempt to answer the question of how these trade-offs should be

answered, it does suggest how they should be approached.

This section provides an overview and natural wealth estimates of the following areas: fishing; timber and

non-timber forest resources, including mangroves; carbon; crop and pasture lands; and biodiversity/PAs.

Fishing

Despite having a coastline of only 274 km, Guinea-Bissau is situated next to a 45,000

Km2 continental shelf – one of the largest in West Africa. Seven river systems indent

the coast, adding fresh, nutrient rich, cold water to the warm shallow waters of the

continental shelf. These conditions create a favorable ecosystem for marine fish and

other species. In addition to the mainland coastline, the country’s geography is

defined by the 88 islands and islets of the Arquipélago dos Bijagós, creating

additional opportunities for artisanal fishing.

There are two main types of fish in Guinea-Bissau’s waters: pelagic (living in water

columns e.g. sardines, jacks, tuna), and demersal (bottom-dwelling e.g. cuttlefish,

breams), as well as crustaceans, cephalopods and others (e.g. shrimp, lobster,

octopus). While fisheries data in Guinea-Bissau are of variable quality, there have

been a number of scientific campaigns undertaken by international research centers

to assess the biomass and fishing potential of Guinea-Bissau’s coast. The latest review

took place during September-October 2011 (IMROP-CIPA, 2011) and confirms the

biomass and production rates of previous campaigns (2004 and 2008).

Demersal fish biomass is estimated at 126,531 tons, while fishing potential for demersal fish, cephalopod

and crustaceans is 47,139 tons (Table 1). 31 The pelagic fish biomass and small pelagic biomass is estimated

at 163,000 tons and 200,000 tons, respectively. The Secretariat of State Fisheries estimates the fishing

potential of pelagic fish to be approximately 73,000 tons, bringing the total fishing potential to just over

120,000 tons.

31 Biodynamic models are used to calculate fishing potential estimates. These models are based on a set of assumptions relating to

the ability of different fish species to reproduce, for example, a ratio of less than 40 percent of biomass for all types of fish is

assumed, except for elasmobranches, where a ratio of less than 10 percent is assumed, due to their longevity, tardy reproduction,

week fecundity and slow growth rate. The model used to calculate Guinea-Bissau’s fishing potential is based on Diop, M.,

Abdallahi, I., Bouzouma, M., Sidina, E., Hamady, B., Meissa, B. and N. Abdoulaye, 2004. Rapport du la Campagne D’evaluation

des Resources Demersales de la ZEE de la Guinee- Bissau. pp90

Fishing

Phosphate

Bauxite

Gu

inea

-Bis

sau

’s n

atu

ral

wea

lth

per

cap

ita

19

Table 1. Biomass and fishing potential estimates for demersal fish, 2011

Type Biomass (tons) Fisheries Potential (tons)

Bony Demersal fish 90,932 36,373

Crustaceans 13,149 5,260

of which 2.3 percent are coastal shrimp and 6.4 percent are Gamba

(Parapenaeus longirostris)

Cephalopods 8,308 3,323

of which 32 percent are octopus and 15 percent are cuttlefish

Gasteropods 2,567 1,027

Elasmobranches

(rays and shark)

11,575 1,156

Total 126,531 47,139

Source: The Secretariat of State Fisheries

Information within the Secretariat of Fisheries Yearly Report on Industrial Fisheries (2010) suggests that

cephalopods and shrimp are being caught above their fishing potential. While fish appear to be caught

within the sustainable limit, there may be pressure on some specific demersal and/or pelagic species. Unlike

industrial fisheries, the artisanal sector catches significantly more fish than cephalopods and shrimp (Table

2).

Table 2. Artisanal and industrial fishers catch breakdown

Type

Catch (tons)