Not To Be Reproduced

24

Published by: Not To Be Reproduced

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Not To Be Reproduced

Published by:Not To B

e Rep

roduc

ed

Book 1.indb 2 3/25/11 11:40:53 AM

Agensi Kaunseling dan Pengurusan Kredit (AKPK)Level 8, Maju Junction Mall1001, Jalan Sultan Ismail50250 Kuala LumpurFax: 03-2616 7601 E-mail: [email protected]

© AKPKSecond Edition 2013

The copyright of this book belongs to Agensi Kaunseling dan Pengurusan Kredit (AKPK). This book or parts thereof, may be reproduced, translated, or transmitted in any form with prior written permission from AKPK only for the sole purpose of education. No monetary gain in any form should be made or derived, whether direct or indirect from such reproduction.

ISBN 978-983-44004-2-2

Disclaimer:

The information contained in this book is solely for educational purpose. It is not intended as a substitute for any advice you may receive from a professional �nancial advisor.

AKPK disclaims all and any liability to any person using the information in this book as a basis for making any �nancial decision or taking an action.

While all e�orts have been made to make the information contained in this book accurate, AKPK seeks your understanding for any errors or omission.

The names and details of individuals in the real life cases have been changed to protect their identities.

Not To B

e Rep

roduc

ed

CHAPTER

1CASH FLOWMANAGEMENT

Book 1.indb 1 3/25/11 11:40:57 AM

Not To B

e Rep

roduc

ed

2

Book 1.indb 2 3/25/11 11:40:58 AM

Managing your cash is important to ensure that you have complete control over your �nances. Since cash is an exchange tool that allows you to buy goods and services, it is important for you to �rst understand your money managing habits.

Do you normally run out of cash before your next pay cheque arrives? Or are you the type who has more than enough balance in your bank account? Regardless of your answer, this �rst step of a realistic assessment will help you analyse how much cash you earn against what you spend. This simple concept is called cash �ow management.

Analysing your cash �ow can tell you a lot about the nature of your income, spending habits and lifestyle requirements. Let us get started by learning about cash �ow management.

Not To B

e Rep

roduc

ed

3

Book 1.indb 3 3/25/11 11:40:58 AM

WHAT IS CASH FLOW MANAGEMENT?Cash �ow management is the process of monitoring, analysing and adjusting your personal cash �ow. Your personal cash �ow is made up of two main components; your income (in�ows) and your expenses (out�ows).

Your income or cash in�ows may consist of active income and passive income.

Activeincome

Passiveincome

Is derived from your employment or business ventures. The moment you stop working or doing business, your active income also stops. Examples of active incomes are salary from employment and pro�ts from businesses

Is derived from your savings or investments. Passive income is received regardless of your employment status. Examples of passive incomes are income from interest or pro�t, rentals, dividends and royalties

Not To B

e Rep

roduc

ed

4

Discretionaryexpenses

Fixedexpenses

Variableexpenses

Book 1.indb 4 3/25/11 11:40:58 AM

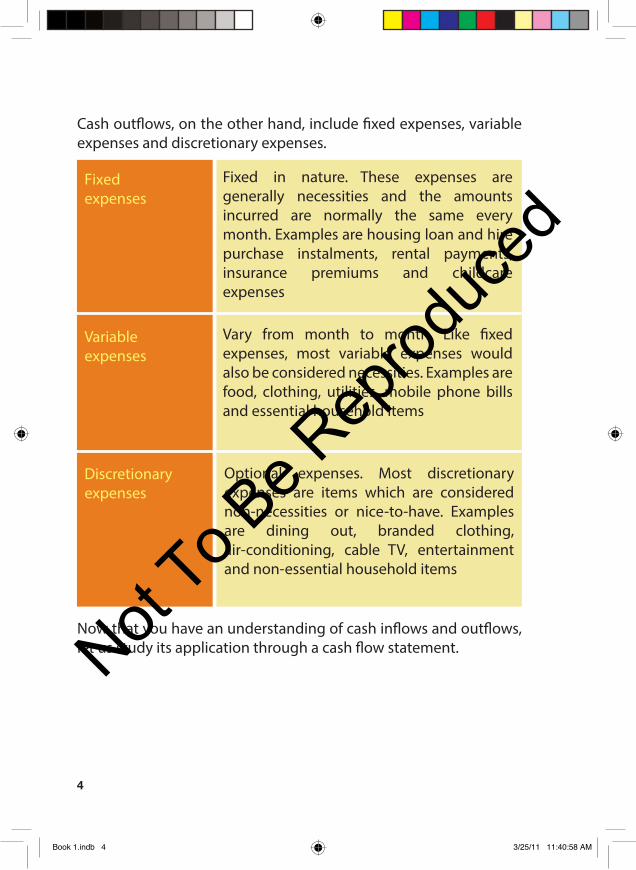

Cash out�ows, on the other hand, include �xed expenses, variable expenses and discretionary expenses.

Now that you have an understanding of cash in�ows and out�ows, let us study its application through a cash �ow statement.

Fixed in nature. These expenses are generally necessities and the amounts incurred are normally the same every month. Examples are housing loan and hire purchase instalments, rental payments, insurance premiums and childcare expenses

Vary from month to month. Like �xed expenses, most variable expenses would also be considered necessities. Examples are food, clothing, utilities, mobile phone bills and essential household items

Optional expenses. Most discretionary expenses are items which are considered non-necessities or nice-to-have. Examples are dining out, branded clothing, air-conditioning, cable TV, entertainment and non-essential household items

Not To B

e Rep

roduc

ed

5

What is a cash �ow statement?

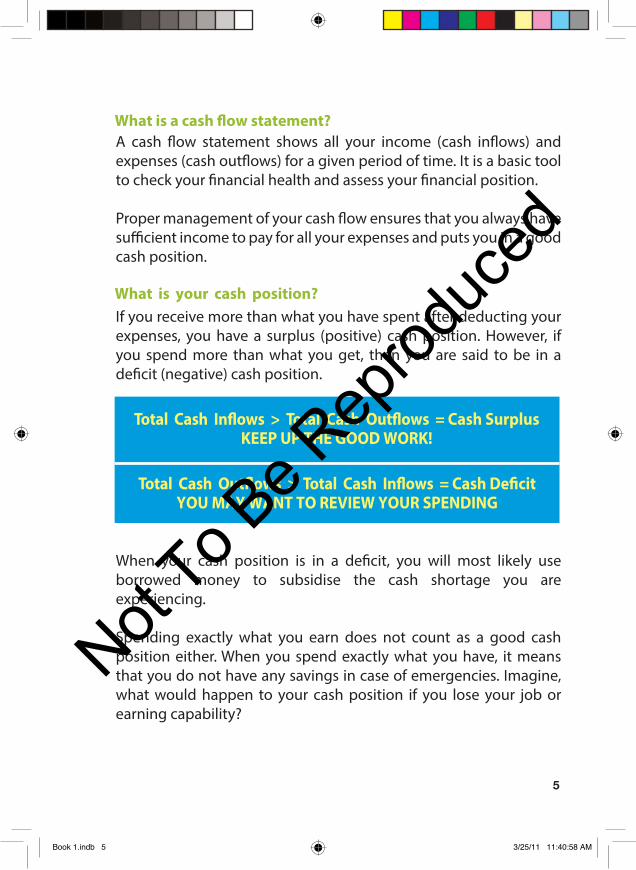

What is your cash position?

Total Cash Inflows > Total Cash Outflows = Cash SurplusKEEP UP THE GOOD WORK!

Total Cash Outflows > Total Cash Inflows = Cash De�citYOU MAY WANT TO REVIEW YOUR SPENDING

Book 1.indb 5 3/25/11 11:40:58 AM

A cash �ow statement shows all your income (cash in�ows) and expenses (cash out�ows) for a given period of time. It is a basic tool to check your �nancial health and assess your �nancial position.

Proper management of your cash �ow ensures that you always have su�cient income to pay for all your expenses and puts you in a good cash position.

When your cash position is in a de�cit, you will most likely use borrowed money to subsidise the cash shortage you are experiencing.

Spending exactly what you earn does not count as a good cash position either. When you spend exactly what you have, it means that you do not have any savings in case of emergencies. Imagine, what would happen to your cash position if you lose your job or earning capability?

If you receive more than what you have spent after deducting your expenses, you have a surplus (positive) cash position. However, if you spend more than what you get, then you are said to be in a de�cit (negative) cash position.

Not To B

e Rep

roduc

ed

6

WHAT IS A BUDGET?

Why do I need a budget?

Benefits of having a budget

• Live within your means

• Cultivate a savings habit

Save for �nancial emergencies•

• Enhance your net worth

Book 1.indb 6 3/25/11 11:40:59 AM

How many times have you made ATM withdrawals only to realise that you have spent all your money within a couple of days? Often it becomes extremely di�cult to remember where that money was spent. A lot of people do not keep track of their �nances and end up spending more than they mean to. This is why a budget is important.

A budget is a plan for managing your cash �ow and is used to estimate your future income and expenses. To put it simply, a budget lists all your expected cash in�ows and out�ows to assist you in making prudent �nancial decisions.

To be in a good �nancial position, it is advisable to have cash surplus at all times. A cash surplus not only allows you to keep money aside for unexpected expenses but also gives you an opportunity to build your investment. This will bring you closer towards achieving your �nancial goals.

So, how can you manage cash �ow to achieve cash surplus?One of the most e�ective ways is through the use of a budget.

Not To B

e Rep

roduc

ed

7

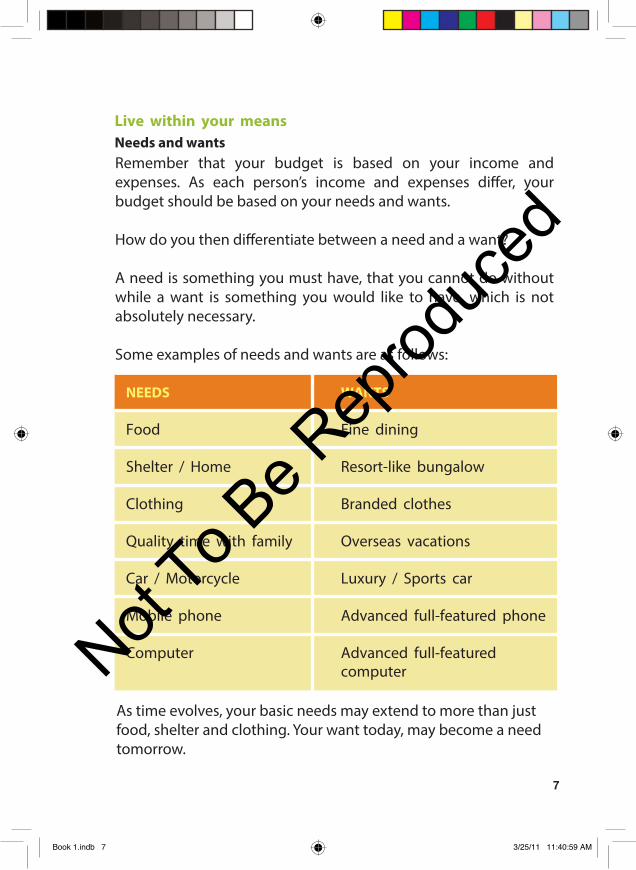

Live within your meansNeeds and wants

NEEDS WANTS

Food Fine dining

Shelter / Home Resort-like bungalow

Clothing Branded clothes

Quality time with family Overseas vacations

Car / Motorcycle Luxury / Sports car

Mobile phone Advanced full-featured phone

Computer Advanced full-featured computer

Book 1.indb 7 3/25/11 11:40:59 AM

Remember that your budget is based on your income and expenses. As each person’s income and expenses di�er, your budget should be based on your needs and wants.

How do you then di�erentiate between a need and a want?

A need is something you must have, that you cannot do without while a want is something you would like to have, which is not absolutely necessary.

Some examples of needs and wants are as follows:

As time evolves, your basic needs may extend to more than just food, shelter and clothing. Your want today, may become a need tomorrow.

Not To B

e Rep

roduc

ed

8

•

•

•

•

Take this example. An individual 20 years ago did not view a mobile phone as a need. Conversely, in today’s modern world, a mobile phone is considered a necessity which makes it a need instead of a want. However, when you choose a mobile phone that is expensive and has all the latest features, you are shifting this need into a want.

The decision you make with regard to what you need or want will directly a�ect your spending.

Delay PurchasesWhenever you intend to make a purchase, especially when it is a want item, take time to think whether it is within your budget.

Living within your means requires you to learn how to say no to unnecessary spending. Look into substitutes for your needs and wants especially if it does not �t your budget.

Ask yourself these questions before you spend:

Instead of buying a car, why not use public transportation?

If you really need a car, can you consider getting a second-hand one?

If you need a mobile phone or a computer, will a basic model serve your purpose?

If you want branded clothing, can you substitute for reasonably priced and good quality clothing instead?

Book 1.indb 8 3/25/11 11:40:59 AM

Not To B

e Rep

roduc

ed

9

• Can I a�ord to buy it?

• Do I really need it?

• Is there something cheaper?

• Can I delay buying it?

A budget needs to be realistic and tailored to meet your earning capacity and spending needs. Living on a budget does not mean sacri�cing all your luxuries. It simply means that you will have to plan and at times, change your perceptions and spending habits.

Spending wiselyThe key to a successful budget is to spend less than what you earn. When you have the urge to buy something, pause and ask yourself the following questions:

Book 1.indb 9 3/25/11 11:41:00 AM

Not To B

e Rep

roduc

ed

10

TIME

•

•

•

•

LIST

•

•

•

COMPARE

•

•

Plan your purchases to avoid making multiple trips to the store

Optimise the use of your resources, including petrol and time

Avoid getting caught in last minute shopping frenzies

Stock up household items in advance to avoid festive rush

Always have a shopping list to avoid unnecessary buying

Avoid buying things you do not need

Always keep to your budget

Compare prices at various outlets before buying

Keep a ‘price book’ to track prices on frequent purchases

TIPS ON SPENDING WISELY

Book 1.indb 10 3/25/11 11:41:00 AM

Not To B

e Rep

roduc

ed

11

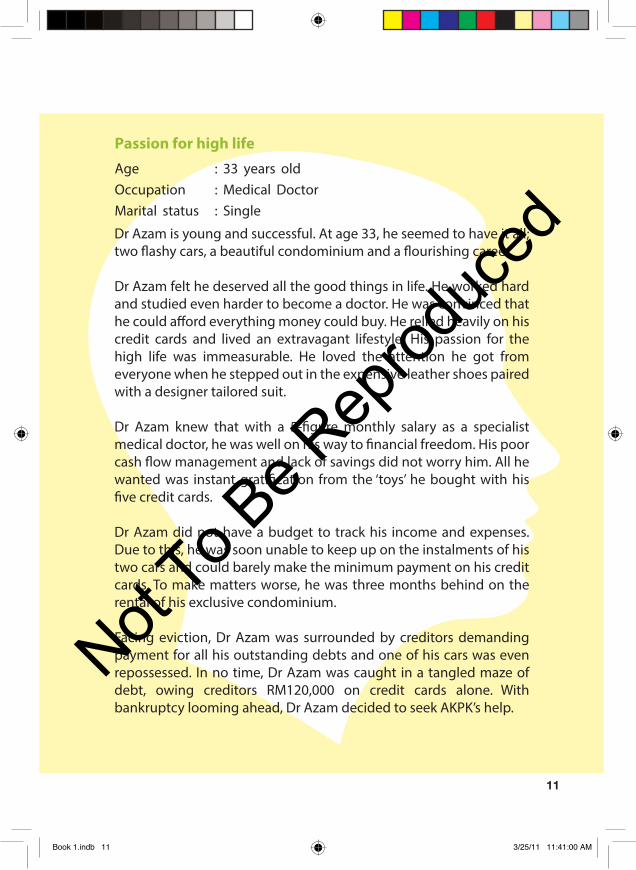

Passion for high life

Age : 33 years oldOccupation : Medical DoctorMarital status : Single

Dr Azam is young and successful. At age 33, he seemed to have it all; two �ashy cars, a beautiful condominium and a �ourishing career.

Dr Azam felt he deserved all the good things in life. He worked hard and studied even harder to become a doctor. He was convinced that he could a�ord everything money could buy. He relied heavily on his credit cards and lived an extravagant lifestyle. His passion for the high life was immeasurable. He loved the attention he got from everyone when he stepped out in the expensive leather shoes paired with a designer tailored suit.

Dr Azam knew that with a 5-�gure monthly salary as a specialist medical doctor, he was well on his way to �nancial freedom. His poor cash �ow management and lack of savings did not worry him. All he wanted was instant grati�cation from the ‘toys’ he bought with his �ve credit cards.

Dr Azam did not have a budget to track his income and expenses. Due to this, he was soon unable to keep up on the instalments of his two cars and could barely make the minimum payment on his credit cards. To make matters worse, he was three months behind on the rental of his exclusive condominium.

Facing eviction, Dr Azam was surrounded by creditors demanding payment for all his outstanding debts and one of his cars was even repossessed. In no time, Dr Azam was caught in a tangled maze of debt, owing creditors RM120,000 on credit cards alone. With bankruptcy looming ahead, Dr Azam decided to seek AKPK’s help.

Book 1.indb 11 3/25/11 11:41:00 AM

Not To B

e Rep

roduc

ed

12

•

•

•

•

123

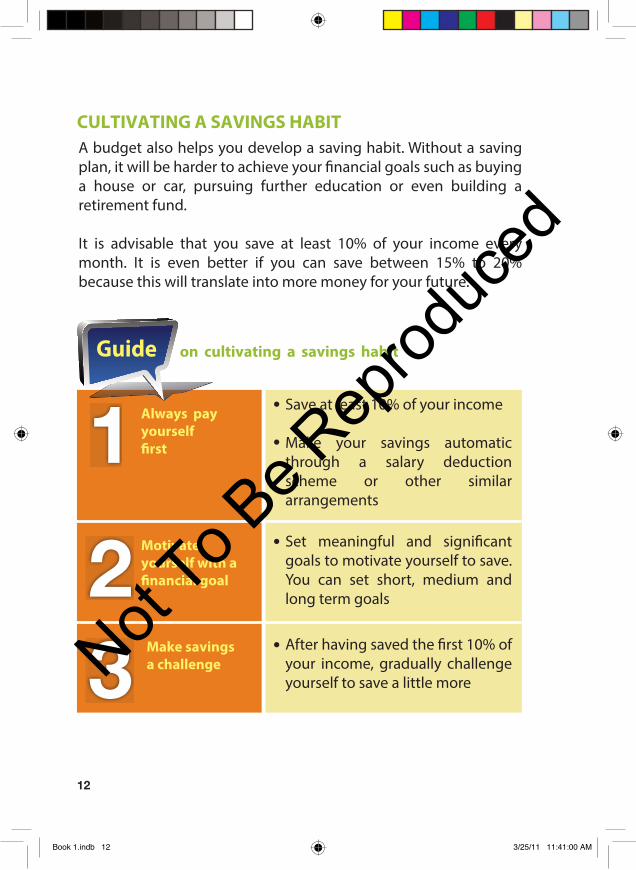

Save at least 10% of your income

Make your savings automatic through a salary deduction scheme or other similar arrangements

Set meaningful and signi�cant goals to motivate yourself to save. You can set short, medium and long term goals

After having saved the �rst 10% of your income, gradually challenge yourself to save a little more

CULTIVATING A SAVINGS HABIT

on cultivating a savings habit

Always payyourself�rst

Motivateyourself with a�nancial goal

Make savingsa challenge

Guide

A budget also helps you develop a saving habit. Without a saving plan, it will be harder to achieve your �nancial goals such as buying a house or car, pursuing further education or even building a retirement fund.

It is advisable that you save at least 10% of your income every month. It is even better if you can save between 15% to 20% because this will translate into more money for your future.

Book 1.indb 12 3/25/11 11:41:00 AM

Not To B

e Rep

roduc

ed

13

•

•

4 Wind falls

Save for �nancial emergencies - emergency bu�erIn life, there are many �nancial emergencies which may limit or take away your earning capacity; some even require you to come up with substantial amounts of money urgently.

The most common need for an emergency fund includes sudden loss of income through unemployment and unexpected medical, home and car repair expenses. If you lose your job, you will still have to continue paying your bills!

To cope with these uncertain situations, it is important to have an emergency fund that will help you deal with such events. As a guide, you should have an equivalent of at least three to six months’ worth of your basic living expenses. The last thing that you want is to be forced to rely on a loan which could simply compound the problem.

Apart from saving for �nancial emergencies, a budget can also help you save for other big ticket items or special events while enhancing your net worth.

Every time you get an extraordinary income – such as a bonus or cash gift – put part of it into your savings account Immediately

If you get a pay rise, keep to your current standard of living and put the additional money towards your savings

Book 1.indb 13 3/25/11 11:41:01 AM

Not To B

e Rep

roduc

ed

14

ENHANCE YOUR NET WORTHA net worth statement is your �nancial scorecard which can be used regularly to assess your �nancial standing. It serves as a reference point in making money-related decisions and reports on what you own (assets) and what you owe (liabilities).

Assets include items such as cash, savings, real estate, unit trusts and shares while liabilities include all types of loans including borrowings from family and friends, credit card debts, payments for rental and utility bills.

Your net worth can be enhanced by monitoring your expenses through the use of a budget.

A budget helps you to control your expenditure. This, in turn, enhances your net worth by assisting you to invest and accumulate assets.

Therefore, the key to enhancing your net worth is simply to spend less and save more for your investment.

Book 1.indb 14 3/25/11 11:41:01 AM

Not To B

e Rep

roduc

ed

15

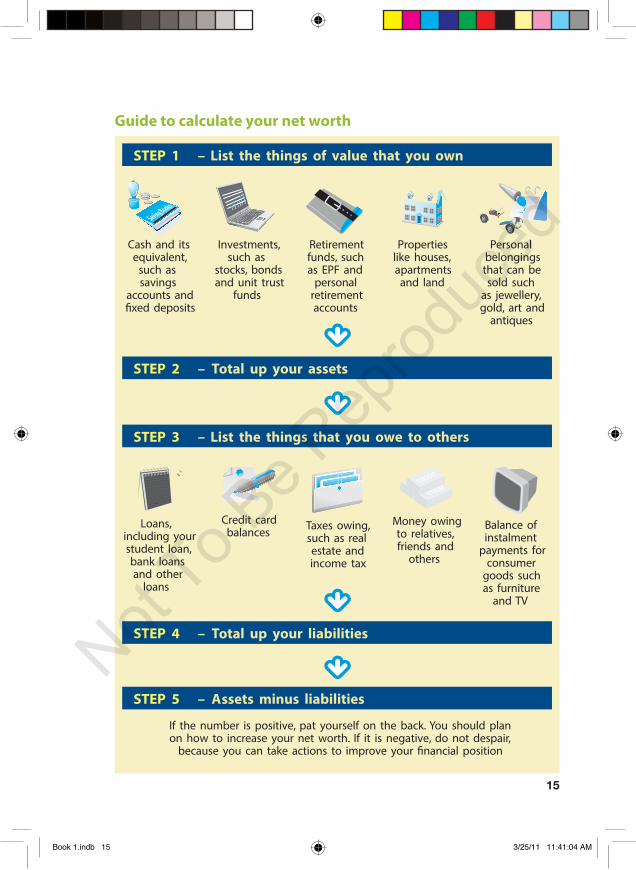

Guide to calculate your net worth

STEP 1 – List the things of value that you own

STEP 2 – Total up your assets

STEP 4 – Total up your liabilities

STEP 3 – List the things that you owe to others

STEP 5 – Assets minus liabilities

If the number is positive, pat yourself on the back. You should plan on how to increase your net worth. If it is negative, do not despair,

because you can take actions to improve your financial position

Cash and its equivalent,

such as savings

accounts and fixed deposits

Investments, such as

stocks, bonds and unit trust

funds

Retirement funds, such as EPF and

personal retirement accounts

Properties like houses, apartments

and land

Loans, including your student loan, bank loans and other

loans

Personal belongings that can be sold such

as jewellery, gold, art and

antiques

Money owing to relatives, friends and

others

Balance of instalment

payments for consumer

goods such as furniture

and TV

Taxes owing, such as real estate and income tax

Credit card balances

Book 1.indb 15 3/25/11 11:41:04 AM

Not To B

e Rep

roduc

ed

16

After knowing the benefits of having a budget, you are now ready to create your own. All it takes are three simple steps:

1. List down all your sources of income

• Your salary should be net of EPF, tax and SOCSO deductions

2. List down your expenses

• Your expenses should include �xed expenses, var iable expenses and discretionary expenses

• Here, you need to ‘pay yourself �rst’ as savings (minimum 10% of your total income)

3. Determine your net cash �ow position

• If it is a surplus, well done! Try to keep to that budget of yours in your actual spending

• If it is a de�cit, revise your budget by cutting back on discretionary expenses until you get a positive net cash flow position

• Ideally, you want a surplus to be able to build up your emergency funds

Preparinga budget

Book 1.indb 16 3/25/11 11:41:05 AM

Not To B

e Rep

roduc

ed

17

•

•

•

FINANCIAL SCAMS

As you can see, it is not di�cult to create a budget. However, successfully maintaining and sticking to one requires a little more time and e�ort.

You also need to be realistic and �exible in your approach. If you have a moderate income, do not expect to save a lot of money in a short period of time. Also, there may be times when you need to revise your budget to cater for unexpected expenses.

When you are in a good �nancial position with cash �ow surplus, then you are ready to invest. There are many types of investments, including real estate, stocks and bonds in the market. Returns on these investments vary in tandem with the risks associated. If you plan on being an investor, be mindful of your risk appetite levels before investing.

When investing your hard earned money, be extra careful of get-rich-quick schemes. Such schemes promise high returns with little or no risk. These get-rich-quick schemes are frequently promoted through various channels, with the Internet and short message service (SMS) being the more common platforms. The next time you come across these get-rich-quick schemes, be vigilant and remember that if it sounds too good to be true, it probably is!

Invest only on products that are familiar to you

Do your homework and make sure you understand the risks involved

Do not put all your eggs in one basket. Remember, spreading your money across a variety of investments is the key to spreading your risks

Book 1.indb 17 3/25/11 11:41:05 AM

Not To B

e Rep

roduc

ed

18

Tell-tale signs of �nancial scams:

•

•

•

•

•

Browse websites ofBNM (www.bnm.gov.my) and SC (www.sc.com.my)for further information

The golden rule is not to be greedy. Always check with friends, family and professionals whether such investment opportunities are genuine or otherwise, even if it is recommended by someone close to you.

Find out more about the o�er. Be particularly suspicious of an investment that o�ers high returns, low risk and is free of investment costs, as it is unlikely that a business venture can provide all these.

Promise of high returns of between 5% to 20% a month with little or no risk

The o�er is for a limited period only and you are asked to sign up immediately

The scheme is in another country and you cannot check on its o�ce or con�rm its status

You are asked to give con�dential information such as your bank account number

You are asked to deposit a small sum of money to meet the processing and administrative fees

Book 1.indb 18 3/25/11 11:41:06 AM

Not To B

e Rep

roduc

ed

19

takeaways

•

•

•

•

•

A cash �ow statement shows you where your money is coming from and where it is going over a period of time

A budget is simply a tool to help you manage and track your cash �ow more e�ectively

A budget is the best tool to ensure you spend and live within your means

Having savings is very important as it will help with emergencies

A net worth statement gives you a snapshot of your �nancial position at any given time and serves as a tool to help you track your progress

Book 1.indb 19 3/25/11 11:41:07 AM

Not To B

e Rep

roduc

ed

20

Checklist

Appendix 1.1: Sample of Budget and Cash Flow StatementAppendix 1.2: Template of Budget and Cash Flow StatementAppendix 1.3: Sample of Net Worth StatementAppendix 1.4: Template of Net Worth Statement

Book 1.indb 20 3/25/11 11:41:07 AM

Draw up your monthly cash �ow statement showing all in�ows and out�ows

Set aside at least 10% of your income as savings in your budget

Prepare your net worth statement to see how much you are worth now

Not To B

e Rep

roduc

ed

21

SELF ASSESSMENT

1. Which of the following are the main components ofcash �ow management?

a. Income and expenses

b. Assets and liabilities

c. Debtors and creditors

d. Profit and loss account and balance sheet

2. A budget helps you to _________

a. live within your means

b. achieve financial goals

c. set aside money for savings

d. all of the above

3. Why is savings important?

a. To plan for your retirement

b. To prepare for emergencies

c. Down payment to buy your first house / car

d. All of the above

4. How many months of living expenses are recommended for your emergency fund?

a. One to two months

b. Three to six months

c. Eight to nine months

d. 12 to 24 months

Book 1.indb 21 3/25/11 11:41:07 AM

Not To B

e Rep

roduc

ed

22

5. What is your net worth?

What is a good �nancial habit?

a. My total liabilities plus total assets

b. My total income plus total expenses

c. My total assets minus total liabilities

d. My total income minus total expenses

6. What is the minimum monthly recommended percentage of your income to be set aside as savings (apart from EPF contribution)?

a. As and when you have it

b. At least 50% each month

c. At least 10% each month

d. None of the above

7.

a. Having monthly repayments of more than 40% of your net monthly income

b. Tracking your expenses and cash flow

c. Living lavishly

d. Paying the minimum amount on your credit cards

Check your answers at the end of this book

Book 1.indb 22 3/25/11 11:41:08 AM

Not To B

e Rep

roduc

ed