Normative barriers to imitation: social complexity of core competences in a mutual fund industry

24

UNCORRECTED PROOFS JOHN WILEY & SONS, LTD., THE ATRIUM, SOUTHERN GATE, CHICHESTER P019 8SQ, UK *** PROOF OF YOUR ARTICLE ATTACHED, PLEASE READ CAREFULLY *** After receipt of your corrections your article will be published initially within the online version of the journal. PLEASE NOTE THAT THE PROMPT RETURN OF YOUR PROOF CORRECTIONS WILL ENSURE THAT THERE ARE NO UNNECESSARY DELAYS IN THE PUBLICATION OF YOUR ARTICLE READ PROOFS CAREFULLY ONCE PUBLISHED ONLINE OR IN PRINT IT IS NOT POSSIBLE TO MAKE ANY FURTHER CORRECTIONS TO YOUR ARTICLE This will be your only chance to correct your proof Please note that the volume and page numbers shown on the proofs are for position only ANSWER ALL QUERIES ON PROOFS (Queries are attached as the last page of your proof.) List all corrections and send back via e-mail to the production contact as detailed in the covering e-mail, or mark all corrections directly on the proofs and send the scanned copy via e-mail. Please do not send corrections by fax or post CHECK FIGURES AND TABLES CAREFULLY Check sizes, numbering, and orientation of figures All images in the PDF are downsampled (reduced to lower resolution and file size) to facilitate Internet delivery. These images will appear at higher resolution and sharpness in the printed article Review figure legends to ensure that they are complete Check all tables. Review layout, titles, and footnotes COMPLETE COPYRIGHT TRANSFER AGREEMENT (CTA) if you have not already signed one Please send a scanned signed copy with your proofs by e-mail. Your article cannot be published unless we have received the signed CTA OFFPRINTS 25 complimentary offprints of your article will be dispatched on publication. Please ensure that the correspondence address on your proofs is correct for dispatch of the offprints. If your delivery address has changed, please inform the production contact for the journal – details in the covering e-mail. Please allow six weeks for delivery. Additional reprint and journal issue purchases Should you wish to purchase a minimum of 100 copies of your article, please visit http://www3.interscience.wiley.com/aboutus/contact_reprint_sales.html To acquire the PDF file of your article or to purchase reprints in smaller quantities, please visit http://www3.interscience.wiley.com/aboutus/ppv-articleselect.html. Restrictions apply to the use of reprints and PDF files – if you have a specific query, please contact [email protected]. Corresponding authors are invited to inform their co-authors of the reprint options available To purchase a copy of the issue in which your article appears, please contact [email protected] upon publication, quoting the article and volume/issue details Please note that regardless of the form in which they are acquired, reprints should not be resold, nor further disseminated in electronic or print form, nor deployed in part or in whole in any marketing, promotional or educational contexts without authorization from Wiley. Permissions requests should be directed to mailto: [email protected]

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of Normative barriers to imitation: social complexity of core competences in a mutual fund industry

UNCORRECTED PROOFS

JOHN WILEY & SONS, LTD., THE ATRIUM, SOUTHERN GATE, CHICHESTER P019 8SQ, UK

*** PROOF OF YOUR ARTICLE ATTACHED, PLEASE READ CAREFULLY ***

After receipt of your corrections your article will be published initially within the online version of the journal.

PLEASE NOTE THAT THE PROMPT RETURN OF YOUR PROOF CORRECTIONS WILLENSURE THAT THERE ARE NO UNNECESSARY DELAYS IN THE PUBLICATION OF

YOUR ARTICLE

READ PROOFS CAREFULLY

ONCE PUBLISHED ONLINE OR IN PRINT IT IS NOT POSSIBLE TO MAKE ANY FURTHERCORRECTIONS TO YOUR ARTICLE

� This will be your only chance to correct your proof� Please note that the volume and page numbers shown on the proofs are for position only

ANSWER ALL QUERIES ON PROOFS (Queries are attached as the last page of your proof.)

� List all corrections and send back via e-mail to the production contact as detailed in the covering e-mail,or mark all corrections directly on the proofs and send the scanned copy via e-mail. Please do not sendcorrections by fax or post

CHECK FIGURES AND TABLES CAREFULLY

� Check sizes, numbering, and orientation of figures� All images in the PDF are downsampled (reduced to lower resolution and file size) to facilitate Internet

delivery. These images will appear at higher resolution and sharpness in the printed article� Review figure legends to ensure that they are complete� Check all tables. Review layout, titles, and footnotes

COMPLETE COPYRIGHT TRANSFER AGREEMENT (CTA) if you have not already signed one

� Please send a scanned signed copy with your proofs by e-mail. Your article cannot be publishedunless we have received the signed CTA

OFFPRINTS

� 25 complimentary offprints of your article will be dispatched on publication. Please ensure that thecorrespondence address on your proofs is correct for dispatch of the offprints. If your delivery addresshas changed, please inform the production contact for the journal – details in the covering e-mail.Please allow six weeks for delivery.

Additional reprint and journal issue purchases

� Should you wish to purchase a minimum of 100 copies of your article, please visithttp://www3.interscience.wiley.com/aboutus/contact_reprint_sales.html

� To acquire the PDF file of your article or to purchase reprints in smaller quantities, please visithttp://www3.interscience.wiley.com/aboutus/ppv-articleselect.html. Restrictions apply to the use ofreprints and PDF files – if you have a specific query, please contact [email protected] authors are invited to inform their co-authors of the reprint options available

� To purchase a copy of the issue in which your article appears, please contact [email protected] publication, quoting the article and volume/issue details

� Please note that regardless of the form in which they are acquired, reprints should not be resold, norfurther disseminated in electronic or print form, nor deployed in part or in whole in any marketing,promotional or educational contexts without authorization from Wiley. Permissions requests should bedirected to mailto: [email protected]

UNCORRECTED PROOFS

SMJ739

Strategic Management JournalStrat. Mgmt. J., 30: 000–000. (2009)

Published online in Wiley InterScience (www.interscience.wiley.com) DOI: 10.1002/smj.739

Received 3 April 2008; Final revision received 30 September 2008

NORMATIVE BARRIERS TO IMITATION: SOCIALCOMPLEXITY OF CORE COMPETENCES IN AMUTUAL FUND INDUSTRY

STEFAN JONSSON1* and PATRICK REGNER2

1 Stockholm School of Economics, Department of Marketing and Strategy, Instituteof International Business Stockholm, Sweden; and Uppsala University, Departmentof Business Studies, Uppsala, Sweden2 Stockholm School of Economics, Department of Marketing and Strategy, Instituteof International Business, Stockholm, Sweden

Imperfectly imitable resources are central in contemporary analysis of sustainable competitiveadvantage. While prior work has focused on limitations on the ability to imitate, we argue that itis only a third step in an imitation procedure that also involves the identification of what to imitateand the willingness to imitate. In this study we focus on this last step of unwillingness to imitatedue to institutionalized professional norms on product appropriateness. Drawing on institutionaltheory, we test hypotheses and discuss the complex relationship between institutionalized norms,core competences, and systematic differences in the willingness to imitate. Copyright 2009John Wiley & Sons, Ltd.

123456789

1011121314151617181920

INTRODUCTION

Imperfectly imitable resources are central in con-temporary discussions concerning sustainable com-petitive advantage (Barney, 1986, 1991; Lippmanand Rumelt, 1982) and the attention to conditionsunder which valuable and rare resources are costlyto imitate have been described as what was mostnew and important about resource-based theory(Barney, 2001). There are, however, significantcomplications in evaluating imitation difficulties.While the ability of firms to imitate have been

Keywords: resource-based view–sustainability; capabil-ity acquisition/strategic factor markets; institutional theory*Correspondence to: Stefan Jonsson, Stockholm School of Eco-nomics, Department of Marketing and Strategy, Institute of Inter-national Business, PO Box 6501, 113 83, Stockholm, Sweden.E-mail: [email protected]

2122232425262728293031323334353637383940

extensively discussed (Barney, 1991; Dierickx andCool, 1989; Peteraf, 1993; Reed and DeFillippi,1990; Wernerfelt, 1984), it only represents a laststep in an imitation process. The imitation processincludes, first, the identification of what to imi-tate, second, the willingness to imitate, and third,the ability to do so. While research on resourceimitability has focused on the last stage, with aconcomitant interest in failures in resource mar-kets (Peteraf, 1993), limits on resource imitabilitythat arise from the two earlier steps in the processare more closely related to behavioral aspects ofstrategy.

A behavioral strategy approach recognizes thedifficulty of identifying particular resources andcapabilities that underlie competitive advantage(cf. Denrell, Fang, and Winter, 2003). Accordingly,cognitive imperfections have been introduced in

Copyright 2009 John Wiley & Sons, Ltd.

UNCORRECTED PROOFS

2 S. Jonsson and P. Regner

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

the discussion of limits to imitability and the cre-ation of sustainable competitive advantage (e.g.,Amit and Schoemaker, 1993; Conner and Prahalad,1996; Zajac and Bazerman, 1991). A three-stageunderstanding of imitation suggests furthermorethat even where competitor competences are iden-tified, imitation can still be hampered by a lackof willingness to imitate. Unwillingness to imitateand its strategic implications have received littleprior attention in strategic management research,and it is the focus of this study. Of particu-lar interest to strategic management theory is thecase where unwillingness to imitate is rooted inadherence to institutionalized sets of practices andnorms, or a logic (cf. Friedland and Alford, 1991).Where unwillingness to imitate emanates frominstitutional practices it is not necessarily uniformacross all organizations (Lounsbury, 2007), but yetsystematic enough to be predictable (Marquis andLounsbury, 2007; Thornton and Ocasio, 1999). Incontrast to earlier studies, we emphasize not onlythe limiting effects of institutionalized norms onthe propensity of firms to imitate, but we alsodiscuss how such limitations on imitability canbe used proactively to achieve competitive advan-tage.

Although there recently has been an interestwithin institutional and sociological perspectiveson strategic management to expand the ambit ofstrategic action (Baum and Dobbin, 2000; Deep-house, 1999; Ingram and Silverman, 2002; Louns-bury and Glynn, 2001; Oliver, 1997), the under-standing of how firms can use institutions strategi-cally to create sustainable competitive advantageremains limited. We focus on how an institutionalcontext influences competitive imitation behaviorof firms and investigate how prior investment ina socially complex core competence—a profes-sional group—interacts with professional norms toproduce ‘institutional barriers to imitation.’ Specif-ically, we show that product niche entry decisionsin the Swedish market for mutual funds dependcrucially on how the product fits with institution-alized professional norms of financial analysts andthe degree to which the individual firm is investedin the financial analysts.

We focus our analysis on two primary questions.First, are there systematic differences at the levelof the product category in the time to imitationfor technically identical product categories thatdiffer only in how they accord with professionalnorms? Second, are there systematic differences at

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

the level of the firm in how such social normsinfluence the speed to imitation? Our results con-firm that some product categories are, due to theirpoor fit with extant professional norms, less likelyto be imitated quickly. Furthermore, we show thatfirms differ with respect to their likelihood andspeed of imitation of these product categories.Because firms differ in their willingness to imi-tate, we suggest and offer preliminary evidencethat some firms see opportunities in relation toinstitutionalized norms and leverage what we labelinstitutional barriers to imitation to delay compet-itive imitation.

We begin with a review of earlier efforts toincorporate social and institutional contexts intoan analysis of strategy and competitive advantage.Where earlier strategic management literature hasconsidered institutions at all, we find that the focushas been on institutional constraints and strate-gic reaction to institutional pressure; the strategicquestion of using institutions as opportunities hasreceived very limited attention. Next we analyze,quantitatively, product niche entries and subse-quent competitive imitation in the Swedish mutualfund market. The Swedish market for mutual fundsis a suitable research setting, because productintroductions are subject to strong competitive andinstitutional forces, but there are no legal or tech-nical limitations on imitation. Finally we concludethat to advance the analysis of sustainable compet-itive advantage we need to incorporate an under-standing of the effects of socially complex com-petences, and one way forward is to pair recentadvances in institutional theory with insights fromthe process school of strategy and the resource-based view. We also offer suggestions for furtherinteresting areas of research.

THEORY

Institutions and imperfect imitability

Resource imitation efforts comprise three parts: theidentification of what to imitate, the willingness toimitate, and finally the ability to imitate. Imperfectimitability, and thereby a longer period of unique-ness of the resource for the early adopter, maystem from either one of these three parts of theimitation process. Previous studies have, however,largely ignored limits to imitability that derivesfrom inaccurate resource identification or a lack of

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

Normative Barriers to Imitation 3

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

willingness to imitate, under the assumption thatfirms always try to imitate quickly anything thatseems profitable. This assumption implies that theprimary sources of inimitability are to be foundin technical complexity and market imperfections(Peteraf, 1993; Rivkin, 2000). Directing attentiontoward the identification and willingness phases ofimitation introduces a host of other possible causesof imitation lags.

An expanded set of conditions for limitedimitability includes factors that are internal as wellas external to individual firms. At an organiza-tional level, the assumption of zero internal resis-tance to imitation has been questioned by severalinfluential strategic thinkers who argue that ‘fric-tions’ and ‘inertia’ can delay imitation efforts overand above technical limitations (Bromiley, 2005;Rumelt, 1995; Schoemaker, 1990). Addressing theissue of resource recognition, Amit and Schoe-maker (1993) suggest that differences in cognitivestructures and beliefs may lead to variations inhow actors identify resources (i.e., the first partof the imitation process). This can, in turn, leadto delays in resource imitation. Apart from inter-nal organizational processes and cognitive biasesof managers, the institutional context of firms alsomatters. Even where cognitive biases are overcomeand valuable resources are identified, firms maystill not be willing to imitate if these do not fit withinstitutionalized norms and logics. In this study wefocus on this second part of the imitation processand ask the question if differences in willingnessto imitate across firms can serve as a barrier toimitation.

Because of its bias toward analysis of individualfirms—a bias that has only increased since Pfef-fer’s (1987) plea for bringing the social contextinto strategy research—current strategic thinkingis unfortunately of limited use in addressing ourquestion of interest. While Barney (1991) recog-nizes ‘social complexity’ as a possible source ofimperfect imitability, it has rarely been empiricallyinvestigated. To address the possible influence ofsocial context on the willingness of individualfirms to imitate, we turn to institutional analysis inorganization theory, where the question of externalinfluences on organizations and their decision mak-ing has been a central research theme for severaldecades (Scott, 2001).

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

Strategic management and institutional theory

There have been several calls to widen the researchon institutional effects outside public agencies,nonprofit organizations, and highly institutional-ized fields (Powell, 1991; Scott, 2001) and strat-egy researchers have begun to explore poten-tial synergies between strategic management andinstitutional theory (Bresser and Millonig, 2003;Ingram and Silverman, 2002; Oliver, 1997). Todate, research that bridges institutional and strate-gic management theory primarily falls into oneof two categories. One set of studies emphasizesinstitutions as a social fact. Institutions are, in thisview, fully internalized rules of the game that ren-der institutional strategic action literally unthink-able (Goodrick and Salancik, 1996). Choice inthe face of institutional pressure thus becomesrestricted to situations of uncertainty where thereare several conflicting institutions (Heimer, 1999).The other set of studies allows for greater strategicflexibility, and institutions are seen as exogenouspressures that actors often comprehend and can,to the extent that their context and capabilitiesallow, react to strategically (Bresser and Millonig,2003; Goodstein, 1994; Ingram and Simons, 1995;Oliver, 1991). Common to both lines of researchis their focus on strategic reaction to institutionalconstraints, and neither streams of research per-ceives institutions as a strategic opportunity and abasis for potential differentiation and strategic pro-action. To further our analysis, we therefore drawon recent developments in institutional theory tonuance the role of institutions in strategic decisionmaking.

Institutions as barriers to imitation

Although most institutional literature emphasizehow institutions can enhance the spread of newthings deal through the process of legitimization(for an overview see Strang and Soule, 1998),institutionalized norms can also limit the spread ofpractices (Davis and Greve, 1997; Jonsson, 2008).Underlying these findings is the insight that, allelse being equal, actors hesitate to adopt practicesthat do not accord with social norms, which slowsdown adoption (Scott, 2001). Similarly, a strategicmove that runs counter to industry norms is lesslikely to be imitated quickly.

The story of Vanguard and the first U.S. indexfund offers an interesting example of how break-ing with institutionalized industry norms about

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

4 S. Jonsson and P. Regner

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

what constitutes a mutual fund product signifi-cantly delayed competitive imitation and providedcompetitive respite. Because the index fund wasinitially not considered a ‘proper’ mutual fund withother industry actors Vanguard’s pioneering prod-uct introduction was largely ignored by its com-petitors. Marketing an index fund was consideredsuch an apart strategic move within the mutualfund industry that the anticompetition clause inVanguard CEO John Bogle’s contract with his for-mer employers, Wellington never was enforced(Targett, 2001). The significant lag in time to imi-tation allowed Vanguard to build a strong marketposition in this niche.

Although introducing an index fund was a suf-ficiently extreme strategic move to lead to unusu-ally long imitation lag, it was not an ‘illegitimate’move in the sense of a classical reading of institu-tional theory, where such moves would be virtuallyunthinkable. In line with current institutional think-ing we do not use ‘legitimacy’ as a binary concept(Deephouse and Suchman, 2008) but rather as a‘zone of acceptability’ within which an actor canadapt more or less closely and thus be seen as moreor less legitimate as an actor (Zuckerman, 1999).Outside such a zone, however, an actor loses legit-imacy and ceases to be considered a serious actor.Furthermore, recent institutional studies emphasizethat institutional pressures on organizations seldomare unitary but fragmented and often contradictory(D’Aunno, Sutton, and Price, 1991; Lounsbury,Ventresca, and Hirsch, 2003). When there is a dis-crepancy between what is considered legitimate,among for instance finance professionals in theindustry and the rest of society, organizations havea strategic choice of whose legitimacy endorse-ment to seek (Ruef and Scott, 1998).

The introduction of practices with a poor norm-fit such as Vanguard introducing the index fundneed thus not be ‘illegitimate’ in the sense thatVanguard ceases to be considered a legitimateexchange partner by all. Introducing an index fundcan rather be understood as a challenge to a dom-inant, yet not constitutive, set of competitive prac-tices (Rao, Monin, and Durand, 2003). Lounsbury(2007) has shown how geographically boundedsets of such ‘logics’ can influence and yet notdetermine the strategic moves of U.S. mutual fundfirms, leading to variation in organizational adop-tion patterns. As long as the fit with extant normsis not beyond the zone of acceptance of criticalaudiences, such contestation of norms can lead

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

to limited loss of legitimacy with one audience(e.g., the other mutual fund firms) but not withanother (e.g., the consumers who continued pur-chasing Vanguard funds). From a strategic man-agement perspective this suggests that a resourceor competence that does not fit the dominant norm,although not impossible to imitate, can be thoughtof as encompassing a temporary barrier to imi-tation (Bresser and Millonig, 2003) that derivesfrom the unwillingness of a competitor to imitate(cf. MacMillan, McCaffery, and Van Wijk, 1985;Rumelt, 1995) rather than identification difficul-ties or inabilities to imitate. We thus have our firsthypothesis:

Hypothesis 1: Strategic moves of poor fit withdominant norms, all else being equal, havelonger lag times to imitation than other strategicmoves.

Strategic action in relation to institutions

When unwillingness to imitate is based in institu-tionalized norms or logics, imitation lags becomesystematic across firms that adhere to these normsand thereby gain potential strategic importance.As long as adherence to these norms can be pre-dicted, it is also possible to envisage competitivespace where the risk of being imitated is lowerthan for other resources. Introducing norm deviantcompetence or practice however comes at a socialcost, and an important question when strategizingaround norms is the likely sanctions of those whochallenge norms. Institutional theory predicts thatorganizations like Vanguard would be sanctionedby its exchange partners for introducing a productthat deviates from norms (Scott, 2001; Zuckerman,1999). While Vanguard most likely lost some legit-imacy with its peer organizations, consumers didnot react in the same way. An important consider-ation in relation to normative barriers to imitationis thus how different audiences (i.e., other firms,customers, suppliers) react to and are likely tosanction a strategic move that goes against estab-lished norms. The strategic question to ask is:‘whose norms does this action go against?’ Opti-mally a strategic move would be repulsive enoughfor competitors to delay imitation but would notantagonize consumers and customers. History sug-gests that the benefits that Vanguard derived frominitially being ignored by competitors paid off in

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

Normative Barriers to Imitation 5

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

the long run and thus outweighed the sanction itreceived for contesting norms.

Another important issue is to understand whichof the competitors is likely to be limited by norma-tive barriers to imitation. Prior studies of strategicresponse to institutional pressures provide someguidance as to what firms are more or less likelyto be restrained by normative barriers to imitation.Broadly, these studies suggest that it is difficultto introduce practices that are counternormativeto influential stakeholders of the firm (Goodstein,1994; Ingram and Simons, 1995; Jonsson, 2008).For instance, Palmer and Barber (2001) show thatit was primarily CEOs who were not constrainedby memberships in elite networks that introducedand drove the adoption of hostile acquisitions inthe 1980s in the United States.

Top management is, however, only one out ofseveral important stakeholders that influence thedecision-making context of a firm. Among stake-holders, owners play a particularly important rolein encouraging or sanctioning the introductionof new and norm challenging practices (Baron,Dobbin, and Jennings, 1986; Dacin, 1997). Fissand Zajac (2004), for example, show that thespread among German firms of the controversialcorporate practice of shareholder value orientationwas dependent on the shareholder constellationof individual firms, and Davis and Greve (1997)found ownership patterns as important predictorsof what corporations were likely to adopt the con-troversial antitakeover practice of using ‘GoldenParachutes.’ With respect to the introduction of anew practice, owners can for several reasons bemore or less open to their firm adopting challeng-ing new competitive practices. While considera-tions of legitimacy within a network of top man-agement peers may be important in the case ofcorporate practices (Davis and Greve, 1997), it isnot our main consideration here—we are investi-gating barriers to the spread of specific products.What is more pertinent to our case is that ownersare responsible to their constituencies, and somefirms have more varied and activist constituen-cies. This will provide an industry with firms thatare exposed to varying strengths of pressure onwhat is considered appropriate products to intro-duce. Therefore, to further define the scope of anormative barrier within an industry, our secondhypothesis speaks to the role of owners as stake-holders in rendering a firm more or less likely toimitate prior norm challenging strategic moves:

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

Hypothesis 2: Firms with ownership that is neg-ative to challenging norms are, all else beingequal, slower in imitating a norm-challengingstrategic move.

Although stakeholders may influence thepropensity of a firm to challenge norms, the levelof internal resistance to a particular strategic moveis crucial to its implementation. Firms are coali-tions of interests, and firm-level choice is oftenan outcome of the influence of different groupswithin the organization (March, 1961). It is wellrecognized in the strategic decision-making liter-ature that powerful organizational groups have animportant influence over critical strategic choices(Narayan and Fahey, 1982; Pettigrew, 1973, 1985;Wayward and Boeker, 1998). Prior work hasshown the role of professionals as key internal ref-erents of acceptance of a new practice (Ferlie et al.,2005; Jonsson, 2008; Lounsbury and Leblebici,2004). Of further interest to the question of norma-tive barriers to imitation is the role that profession-als often play as a strategic resource that is likely todiffer in strength across organizations (Goodstein,Boeker, and Stephan, 1996; Pfeffer, 1981).

The role of professional groups in strategic deci-sion making is useful to note in the context of ourstudy. Early work on imitation within the com-mercial banking industry suggests that a poor fitbetween a new product and the existing jurisdictionand internal belief systems gives a longer imita-tion response time for new product introductions(MacMillan et al., 1985). In the mutual fund indus-try, the internal belief system concerning what con-stitutes an appropriate product is closely related tothe opinions of finance professionals.

As fund portfolio management became profes-sionalized in the Swedish mutual fund industry andactive asset management was institutionalized asa key organizing principle of the market, finan-cial analysts became elevated in the industry sta-tus structure and became considered the mutualfund firms’ core competences (for similar pro-cesses in a U.S. context see Lounsbury, 2002;Lounsbury and Leblebici, 2004). This increasedtheir organizational power in relation to othergroups within mutual fund firms, and in partic-ular it increased their influence as referents ofthe appropriateness of new product categories.It is not a novel claim that professional groupsinfluence the strategic decision making of firms(Wayward and Boeker, 1998) or that the relative

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

6 S. Jonsson and P. Regner

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

influence of a specific professional group differsacross firms (Baron et al., 1986; Goodstein et al.,1996). Considerations of power and institutions arealso not new to institutional theory (Greenwoodand Hinings, 1996; Hirsch and Lounsbury, 1997;Philips, Lawrence and Hardy, 2004). Nevertheless,we bring together these insights and propose thatnorms held by finance professionals concerningthe social acceptability of specific product cate-gories impact firm-specific willingness to imitatein a manner that is mediated by the relative influ-ence of finance professionals within the firm. Wethus have:

Hypothesis 3: Firms that are more heavily in-vested in a professional group for which thestrategic move is counter to professional normswill, all else being equal, be slower imitators.

The strategic implication of Hypothesis 3 isthat prior strategic investments by some firms ina socially complex resource, such as a profes-sional group, can open up a competitive spacewhere other firms that are less invested in this pro-fessional group—and thereby less constrained bynorms—can acquire contested resources withoutbeing imitated quickly. A scope condition on ourreasoning is that not all institutional logics can bestrategized. When truly internalized and permeat-ing the thinking of all actors, or where there areregulatory limitations, strategizing will be unthink-able or illegal. While a number of institutionsundoubtedly are social facts, we surmise that manyinfluential institutions are not, and are thereby opento strategizing. This reasoning points to the criti-cal importance of an analysis of the institutionalcontext as a part of an analysis of sustainable com-petitive advantage (cf. Oliver, 1997).

RESEARCH METHOD, SETTING ANDDATA

We started out with a claim that current under-standings of barriers to resource imitation miss outon institutional barriers, and thus a dimension inwhich to strategize. Through our theory buildingwe derive three hypotheses that predict how insti-tutionalized norms can limit imitability, and howfirms could use these to strategize. In testing ourhypotheses we recognize two primary concerns.

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

First is the need for a setting with strong institu-tional and economic pressures that influence prod-uct adoption and imitation behavior; an observedlag in imitation must not simply be because thestrategic move in question lacks economic value orthat there are no early mover advantages (Lieber-man and Montgomery, 1988; Schnaars, 1994).Second, we need a setting where strategic movesare clearly identifiable and that imitation is notlimited due to complexity (Rivkin, 2000). Productintroduction and imitation behavior in the Swedishmutual fund industry is a useful setting for ourresearch as it fulfils our primary concerns of anindustry where institutional and economic factorsare important in competition (cf. Khorana and Ser-vaes, 2002; Lounsbury and Leblebici, 2004), thereare advantages to early movers (Makadok, 1998;Tufano, 1989), and product introductions are tech-nically simple but strategically meaningful andobservable moves.

A second layer of complexity in our study designis the need to understand institutionalized norms inthe industry, how norms impact product introduc-tion and imitation behavior, and what is consideredcontrary to these norms. To do this we first adopteda qualitative research approach where we utilizedsecondary documentation in the form of internalcompany documents, documents from the mainindustry association and professional associationin the industry, as well as historical accounts anda large number of interviews with industry actorsand experts. In all, we interviewed 24 executivesand product developers from 15 firms as well as 10industry experts and representatives of the SwedishAssociation of Mutual Fund Firms (SAMFF) andthe Swedish Society of Financial Analysts (SSFA).In our interviews we covered firms that control98 percent of the assets under management andrepresented half of the Swedish firms existing in2000. Most interviews were conducted face to face,lasted between one and three hours, and were tapedand transcribed directly afterward. We were alsogranted access to internal company documents andto the archives of the Swedish Supervisory Author-ity for Financial Markets (SSAFM). This materialenabled a detailed historical understanding of howthe market for mutual funds developed and howinstitutionalized norms developed around productintroductions.

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

Normative Barriers to Imitation 7

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

The development of norms of productintroductions

The professionalization of money management inthe mutual fund industry is one of the most impor-tant factors in shaping norms around new prod-uct introductions (Lounsbury, 2002). The Swedishmutual fund industry was established in the 1960sbut grew to significance only in the mid-1980s andhas since become one of the most advanced mar-kets for mutual funds in Europe. The developmentsin the U.S. market were formative for the develop-ment of the Swedish market, but in contrast to theU.S., where the industry grew out of an alreadystrong cost-minimizing passive fund managementtradition from the Boston area (Lounsbury, 2007),professional fund management in Sweden devel-oped from an almost clean slate with respect tofund management culture, as initial actors camefrom primarily outside the financial sector. Whenfinance sector actors entered in the late 1970s, theywere deeply inspired by the U.S. example of assetmanagement professionalization, and they workedto professionalize Swedish mutual fund managers.This meant the increased importance of financialanalysts in asset management and the establish-ment of a deep-seated belief in the virtues ofactive asset management together with a prolifera-tion of products offered (cf. Lakonishok, Shleifer,and Vishny, 1992; Lounsbury, 2002; Lounsburyand Leblebici, 2004).

Competing on active asset management, withits core belief in analyst prowess, was translatedinto a firm-level industry status structure during the1990s (cf. Podolny, 1993). Firms were identified asmore or less ‘analyst intensive,’ and this related totheir standing within the industry. For instance, thefirms with the highest status within the financialcommunity, the exclusive hedge fund managers,were by far the most analysts intensive. They alsomade the boldest claims to the ability of systemati-cally beating the market. Media and ranking firms,such as Morningstar, took part in constructing thisstatus structure by ranking the analysis capacityand relating this to the success of the firms. Grad-ually, the financial analysts became regarded ascore competences of mutual fund firms. A tellingexample of this shift in the importance of ana-lysts is in how mutual fund firms changed theirannual reports. In the early 1990s there was almostno information about who managed the fund; themutual fund product identity was that of the firm

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

that offered it. By 1999 finance analysts and fundmanagers had taken the center stage in the annualreport that featured lengthy personal biographies;the mutual fund was by now a product producedby a specific fund manager rather than by a mutualfund firm. Part and parcel of this development wasthat analysts and fund managers became impor-tant referents of internal appropriateness of newproduct categories; by judging specific products asmore or less appropriate in conjunction with theirevaluation of product efficiency, they influencedthe willingness of firms to imitate product intro-ductions by competitors.

What is an appropriate mutual product and whatis not?

Our focal question concerns the existence andstrategic use of normative barriers to imitation.We focus on norms on product introductions thatare institutionalized with a professional group. Atthe outset it is important to note that, as in thecase of the U.S. mutual fund industry, there is astrong general pressure on Swedish mutual fundfirms to introduce new product categories in orderto hold a wide product portfolio (cf. Khorana andServaes, 1999). As it is considered expensive toattract a new customer, a wide product portfoliois a commonly used strategy to increase salesper customer. This economic pressure toward abroader product portfolio is reflected in the factthat the average number of product categories thata mutual fund firm markets increased from threein 1985 to eight in 1999. The rapid expansion ofproduct portfolios was facilitated by a high rateof imitation; most of the new product categorieswere imitated within six to eight months of firstintroduction. A product developer we interviewedeven quipped that ‘. . . the most important productdevelopment tool was the Xerox machine.’1

However, this practice of increasing the productportfolio, which meant imitating any new prod-uct as soon as possible, conflicted with deep-seated professional norms of ‘sound asset manage-ment’ among financial analysts in the case of twoproduct categories. Index funds, funds that holdassets in accordance with a prespecified index (forinstance the Standard & Poor’s 500) were often

1 All quotes contained in the article are taken from personalinterviews conducted by the authors with a number of financialprofessionals in the mutual fund industry.

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

8 S. Jonsson and P. Regner

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

contested because their core idea (passive man-agement) questions that professional asset man-agement adds value over the long run (Gruber,1996). When asked about introducing index funds,negating answers were often of an almost ideolog-ical nature. As a CEO of a large mutual fund firmexpressed it:

No, we do not have index funds. And I do notknow if we are going to introduce them either, to behonest. . . somewhere you have to believe in whatyou are doing. If you believe in actively managedfunds, you have to act it.

A large part of the active resistance to theintroduction of index funds came from financeprofessionals—as illustrated by a CEO explainingwhy few other firms sell index funds:

. . . because their fund managers are too influential.They do not want it. They [fund managers] areinfluential here [in our firm] too, but I know thatat [a bank name] they would consider it a shameto introduce an index fund and it would directlyinsult their asset managers.

Although an actively managed fund, the sociallyresponsible investment (SRI) fund category wasalso controversial among fund managers andCEOs. SRI funds invest only in assets that havepassed a social responsibility screening, for in-stance no weapon or tobacco firms. In our inter-views, finance professionals often considered SRIfunds with suspicion on the basis that the socialresponsibility restriction would run counter to afocus on maximum return from investment. Asone manager of a medium-sized mutual fund firmexpressed it:

I think that asset management should be doneto earn money. Use a part of the profit anddonate—that is something everybody can do ontheir own. That is my view.

Speculating on why other firms have not intro-duced SRI funds, a manager suggested:

There are some colleagues who have chosen not todevelop ethical products, partly because they do notbelieve in the idea but more importantly because itis. . . something that is not related to ‘sound assetmanagement.’

According to many of the finance profession-als in the industry, there are thus ‘real’ mutual

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

fund products that firms can introduce—those thataccord with the dominant logic of active assetmanagement—and then there are the ‘other’ prod-ucts—those that either are contrary to the corebelief of all active asset managers, or those thatsuggest that there is a ‘softer side’ to firm eval-uation. This has led to a situation where a broadeconomic pressure on firms to quickly imitate anynew product conflicts with professional norms heldby financial analysts, creating a situation wherefirms need to decide to go with the broader pres-sure and risk antagonizing their core competents(financial analysts), or forsake potential economicgains of a broad product portfolio to be sensitiveto professional norms of analysts.

Connecting this insight from our qualitativeresearch into the Swedish market for mutual fundsback into our theoretical discussion about normsas barriers to imitation, these professional normsshould serve as a barrier to imitation that is unre-lated to the technical ability to imitate. We theo-rized that challenging moves, that is, introducingindex or SRI funds, would entail longer imitationlags over all. Furthermore we predicted that basedon the ownership of firms, as well as their invest-ments in the core competence of financial analysts,it should be possible to predict what firms have alonger lag time to imitation of the illegitimate SRIand index funds. In the next section we test thesehypotheses quantitatively.

Quantitative method and data

To test our hypotheses, we use a comprehensiveset of event-history data, detailing the productintroduction pattern for every firm and productin the Swedish mutual fund industry from itsstart in 1959 through 2000. The focus of theanalysis is imitation, so we model the hazard ofadoption, that is, the marginal likelihood of afirm adopting a product for the first time. Thisis a useful way of analyzing longitudinal dataas it deals with the problem of right censoringand offers a convenient way of including time-dependent variables (Blossfeld and Rohwer, 1995).

Sample

The population of potential adopters includes allmutual fund firms that operated in Sweden, from1958 up through the 31st of December 2000.Because imitation is the focus of the analysis,

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

Normative Barriers to Imitation 9

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

firms become at risk of adopting a specific productcategory only after there has been a first industry-pioneering adoption. To allow for different timesthat firms enter into the market, firms enter therisk set only after their entry into the industry.Once a firm has adopted a product category, itis dropped from the risk set for the analysis ofimitation in that category. While we have datafor 11 separate product categories, we utilize thedata from four of these in this analysis: index,SRI, regional, and industry funds. Index and SRIfunds are included as they are considered counterto core analyst norms, and regional and industryfunds are the closest comparable hold-out funds(i.e., fully in line with extant norms of appropri-ate products and introduced into the market aboutthe same time). Both regional and industry fundsare equity funds that build on the idea of activeasset management that draws on the skills of assetmanagement. They differ only in their investmentobjectives. We have also performed the analysis onSwedish equity funds, mixed funds, and a partic-ular ‘tax fund’ that is unique to Sweden. As thoseresults do not differ in a substantial way from theones presented here, we have excluded those fundsfrom the analysis for ease of comparison.

Dependent variable

Day, month, year, and category of product adop-tion per firm were collected from the SSAFM. Allnew products are registered with this authority sothe dataset is a complete inventory detailing theexact timing of all products ever introduced inSweden.

Models

Hypothesis 1 predicts a longer time to imitation forindex and SRI funds than for regional and industryfunds. Earlier studies have tested similar hypothe-ses by simply comparing the difference in averagetime to imitation across the product categories (cf.MacMillan et al., 1985). A simple average timeto imitation is problematic to interpret when firmsenter and exit the industry over the analysis period.More troublesome, it does not take into accountcensored observations, that is, the firms that donot adopt over the observation window (Cleves,Gould, and Gutierrez, 2004). We instead use twodifferent methods to test Hypothesis 1. First we

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

estimate the nonparametrical Kaplan-Meier sur-vival function for firms with respect to the intro-duction of each product category, followed by atest for differences across these survival functions.The usefulness of this method is that it is notdependent on assumptions about the underlyingdata, and it is thus a fairly robust method. Second,we use the estimates from the parametric survivalanalysis model (below) to predict the expectedtime to imitation given our model for each productcategory over time and at the mean values of oursample. We then compare the differences acrossmean survival times predicted by our models.

To analyze what predicts early or late imitationat the firm level (Hypotheses 2 and 3) we usea parametric regression model for survival data.Initial testing indicated that the hazard rates werenot time-independent, and further tests suggested aWeibull distribution as a good fit. As the data con-tains repeated observations over time for a numberof firms, we specified a robust standard error cal-culation to correct for possible interdependenceacross observations from the same firm using thecluster() option in Stata 9.1.

Data

For each of the product categories we fit a base-line model (Model 0) drawing on earlier literatureon product niche entry (e.g., Swaminathan, 1998).Specifically, our base model suggests that the haz-ard of a firm entering into a particular productniche is dependent on the perceived growth poten-tial of the equity market, observed success of theproduct category last year, competition in the prod-uct category, the size and age of the firm, andwhether or not it is before the liberalization of theSwedish financial markets that took place in 1989.We ran initial models that also included the real-ized price (fee) level of the mutual fund category.As this variable proved insignificant for all mod-els—probably because of the limited price com-petition in the Swedish fund industry (Engstrom,2001)—we dropped it from the analysis to con-serve statistical power. The growth potential of themarket is approximated by the lagged savings inmutual funds and the lagged development of themain Swedish stock market index (AFGX). How-ever, preliminary runs showed that lagged savingshad no significant effect on either of the productadoptions, so it was dropped from the model. We

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

10 S. Jonsson and P. Regner

123456789

10111213141516171819202122232425262728293031323334353637383940414243

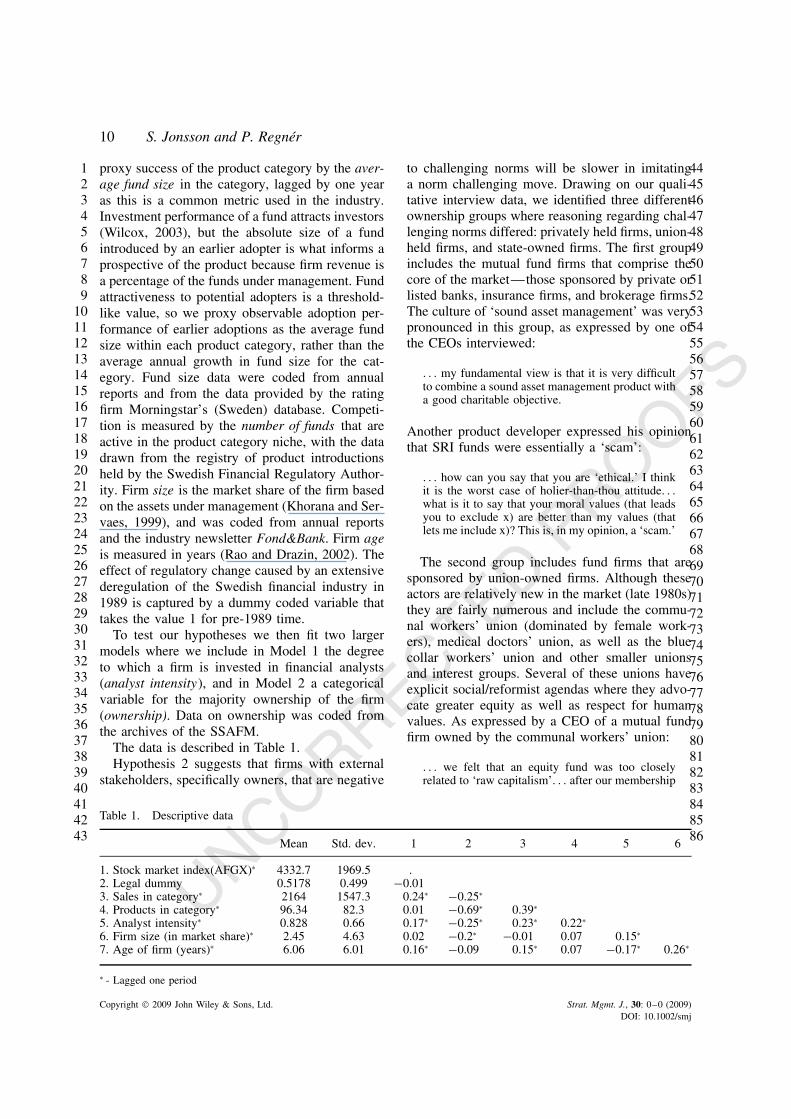

proxy success of the product category by the aver-age fund size in the category, lagged by one yearas this is a common metric used in the industry.Investment performance of a fund attracts investors(Wilcox, 2003), but the absolute size of a fundintroduced by an earlier adopter is what informs aprospective of the product because firm revenue isa percentage of the funds under management. Fundattractiveness to potential adopters is a threshold-like value, so we proxy observable adoption per-formance of earlier adoptions as the average fundsize within each product category, rather than theaverage annual growth in fund size for the cat-egory. Fund size data were coded from annualreports and from the data provided by the ratingfirm Morningstar’s (Sweden) database. Competi-tion is measured by the number of funds that areactive in the product category niche, with the datadrawn from the registry of product introductionsheld by the Swedish Financial Regulatory Author-ity. Firm size is the market share of the firm basedon the assets under management (Khorana and Ser-vaes, 1999), and was coded from annual reportsand the industry newsletter Fond&Bank. Firm ageis measured in years (Rao and Drazin, 2002). Theeffect of regulatory change caused by an extensivederegulation of the Swedish financial industry in1989 is captured by a dummy coded variable thattakes the value 1 for pre-1989 time.

To test our hypotheses we then fit two largermodels where we include in Model 1 the degreeto which a firm is invested in financial analysts(analyst intensity), and in Model 2 a categoricalvariable for the majority ownership of the firm(ownership). Data on ownership was coded fromthe archives of the SSAFM.

The data is described in Table 1.Hypothesis 2 suggests that firms with external

stakeholders, specifically owners, that are negative

44454647484950515253545556575859606162636465666768697071727374757677787980818283848586

to challenging norms will be slower in imitatinga norm challenging move. Drawing on our quali-tative interview data, we identified three differentownership groups where reasoning regarding chal-lenging norms differed: privately held firms, union-held firms, and state-owned firms. The first groupincludes the mutual fund firms that comprise thecore of the market—those sponsored by private orlisted banks, insurance firms, and brokerage firms.The culture of ‘sound asset management’ was verypronounced in this group, as expressed by one ofthe CEOs interviewed:

. . . my fundamental view is that it is very difficultto combine a sound asset management product witha good charitable objective.

Another product developer expressed his opinionthat SRI funds were essentially a ‘scam’:

. . . how can you say that you are ‘ethical.’ I thinkit is the worst case of holier-than-thou attitude. . .what is it to say that your moral values (that leadsyou to exclude x) are better than my values (thatlets me include x)? This is, in my opinion, a ‘scam.’

The second group includes fund firms that aresponsored by union-owned firms. Although theseactors are relatively new in the market (late 1980s)they are fairly numerous and include the commu-nal workers’ union (dominated by female work-ers), medical doctors’ union, as well as the bluecollar workers’ union and other smaller unionsand interest groups. Several of these unions haveexplicit social/reformist agendas where they advo-cate greater equity as well as respect for humanvalues. As expressed by a CEO of a mutual fundfirm owned by the communal workers’ union:

. . . we felt that an equity fund was too closelyrelated to ‘raw capitalism’. . . after our membership

Table 1. Descriptive data

Mean Std. dev. 1 2 3 4 5 6

1. Stock market index(AFGX)∗ 4332.7 1969.5 .2. Legal dummy 0.5178 0.499 −0.013. Sales in category∗ 2164 1547.3 0.24∗ −0.25∗

4. Products in category∗ 96.34 82.3 0.01 −0.69∗ 0.39∗

5. Analyst intensity∗ 0.828 0.66 0.17∗ −0.25∗ 0.23∗ 0.22∗

6. Firm size (in market share)∗ 2.45 4.63 0.02 −0.2∗ −0.01 0.07 0.15∗

7. Age of firm (years)∗ 6.06 6.01 0.16∗ −0.09 0.15∗ 0.07 −0.17∗ 0.26∗

∗ - Lagged one period

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

Normative Barriers to Imitation 11

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

survey we decided that we wanted to provide fundswith a more ‘humane’ face as well as give ourshareholders an option to invest their money whereit would not lead to exploitation of other humanbeings. . .after all, it is not money that is evil, it iswhat you do with it. . .

The third group of state-owned sponsors in-cludes banks, insurance firms, and brokeragehouses. While state-owned actors should, accord-ing to earlier research (Baron et. al., 1986), bemore sensitive to new practices with a claim tosocial justice, we found that representatives of theowners of fund firms did not seem very different intheir attitudes than those that were privately heldor listed.

Out of the three groups, we expect that union-owned mutual fund firms would be the mostlikely to introduce index and SRI funds. Swedishunions view themselves as progressive, in partic-ular with respect to social responsibility, but alsoin challenging the power of financial professionalsin society (Waldenstrom, 2002). Furthermore, theunions represent the newest owners in the fundindustry, and are thereby possibly less involvedin industry-wide norms. We expect privately heldfirms to be the least likely to imitate index and SRIfunds because they are the oldest actors in the field(cf. Fligstein, 1996) and the strongest promoters ofactive asset management. We have no clear predic-tions about how government ownership influencesadoption; on the one hand the government may besensitive to issues of social responsibility, but onthe other hand there is a strong tradition of try-ing to act like private actors to ‘professionalize’government.

While firm ownership may be a useful approx-imation of how likely a firm is to abide by insti-tutionalized ideas of what products to introduceand what not to introduce, our qualitative under-standing of the industry allows us to be even morespecific in our hypotheses (Hypothesis 3). Inde-pendent mutual fund firms, as well as brokeragehouses, are not a homogeneous group of firms.Some are larger and some are smaller and whilemany attempt to market themselves as analyticalpowerhouses, others do not. Drawing on our rea-soning around the role of security analysts andfund managers as core competences defined underthe extant institutionalized competitive logic, weexpect firms that are heavily invested in the corecompetence of analysts to be particularly slow in

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

responding to new products that are seen as con-trary to analysts’ ideas of product appropriateness.

Thus, a more specific prediction is that therewill be a negative influence of financial analystson the keenness of a firm to imitate a competi-tor that adopts index or SRI products. To gaugethe influence of analysts on the speed to imita-tion of the focal firm relative to other firms inthe industry, we use the relative strength of theanalyst collective. Some of the smaller investmentboutiques, for instance hedge fund managers, areanalyst powerhouses, whereas one of the largestbank-owned mutual fund firms is known within theindustry to have a low standing in terms of analystcapacity. Therefore we calculate the analyst inten-sity of a firm as the ratio of equity analysts andfund managers to the number of equity funds mar-keted by a firm at a given point in time. Data wascoded primarily from the annual member direc-tory of the SSFA. Where necessary, this data wassupplemented by information from annual reports,interviews, and visits to the archives of the RoyalSwedish Banking Inspection, the earlier regula-tory authority for the market. This data collectionhas resulted in a reasonably complete dataset forall security analysts and mutual fund managers inthe industry. Unless otherwise specified, all time-varying covariates are updated annually and laggedone period.

RESULTS

We argue that because of long-held beliefs of whatconstitutes appropriate competitive action, productintroductions that fall outside norms will be imi-tated at a slower rate. Testing our Hypothesis 1that index and SRI funds are imitated more slowly,a nonparametric estimation of survival functionsfor imitation of index, SRI, regional, and industryfunds shows a significant longer time to imitationfor index and SRI compared to regional and indus-try funds. The difference is significant at the onepercent level using a log-rank test. To obtain a sim-ilar test of differences across survival functions,but controlling for variables of theoretical interest,we use our parametric model to derive predictionsof the expected survival functions at mean samplevalues using the predict post estimation commandin Stata 9.1 (Jenkins, 2005). For illustrative pur-poses we include Figure 1, which shows the hazard

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

12 S. Jonsson and P. Regner

Regional

Industry

Index & SRI

0

.2

.4

.6

.8

1

Pre

dict

ed s

urvi

val (

non-

adop

tion)

0 2000 4000 6000 8000 10000Analysis time in days

Survival functions at mean values

Figure 1. Survival functions at sample means

123456789

1011121314151617181920212223242526272829303132333435363738394041424344

of adopting the four different fund categories atmean sample values.

Figure 1 shows expected survival (part of sam-ple population that has not imitated) at differentpoints in time and at mean sample values, andillustrates the stark difference in time to expectedimitation across, on the one hand, index and SRIfunds and, on the other hand, regional and indus-try funds. Index and SRI funds look entirely flat-lined in comparison to the faster spreading regionaland industry funds. A test of equality for time toexpected imitation across the four fund categoriesshows, as in the nonparametric estimation, thatindex and SRI funds have a significantly longertime to expected imitation. We thus find strongsupport for our first hypothesis that index and SRIfunds are less likely to be imitated.

To investigate these differences more closely,and to test Hypotheses 2 and 3, we ran hazardrate analyses of product adoption for each of thefour categories. The results are shown in Table 2.

Table 2 details the analysis of the risk of a firmentering any of the four product category fundniches: index, SRI, regional, and industry. Model0 is the baseline model. In Model 1 we add theanalyst intensity variable, and in Model 2 the own-ership variable. The difference in the number ofobservations across the different product categoriesis a reflection of when the first product introduc-tion came: the first index fund was introducedalready in 1975, whereas the first industry fundintroduction came only in 1983. For our analy-sis this means that we have 25 years of observingpossible index imitations per firm, which providesmore observations than the 17 years per firm we

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

have for observing possible industry fund imita-tions. Counting adoptions, on the other hand, wehave more than double the number of industry imi-tations as compared to index imitations.

The strongest finding in our analyses is theclear negative effect that having a strong analystcollective (analyst intensity) has on the chancesthat a firm will imitate either an index or an SRIfund adoption by a competitor. Analyst intensityhad no influence on the risk of imitating entryinto one of the ‘normal’ product categories, butit strongly reduced the risk of imitating an indexor SRI product—across all model specifications.This finding provides clear support for our thirdhypothesis, the degree to which the firm is investedin professionals with opinions concerning the focalproduct impacts its speed to imitation. With respectto Hypothesis 2, where we predict that firms thatare owned by unions would be more likely than aprivately held firm to challenge norms and imitateindex or SRI funds quickly, we obtain partialsupport. Ownership had no significant effect onthe likelihood of a firm imitating an index fund,in the same way that it did not matter to theimitation of regional or industry funds. For SRIfunds, however, union-owned firms were muchmore likely to imitate quickly than privately orgovernmentally held firms. While the increasedlikelihood of unions to introduce SRI funds wasexpected, the lower likelihood of governmentallyowned firms to imitate SRI fund adoptions wassurprising and would be an interesting avenue offurther research.

The non-hypothesis testing variables work moreor less as expected. The product category salesof the previous year strongly predict entry in theregional and industry product categories. The num-ber of funds already in the category (competitivecrowding) is nonsignificant for all categories butindex funds, where it is positive. This is under-standable given the diffusion curve of the indexfunds; it is still in the initial legitimacy buildingphase of adoptions, so another adopter increasesthe likelihood of further imitation. Larger firmswere, all else being equal, more likely to intro-duce industry and regional funds, but the coeffi-cients were not significant for index and SRI funds.Young firms were more likely to imitate indexfunds quickly, whereas age did not significantlyaffect the imitation of other product categories.

While we interpret our results as largely sup-portive of our hypotheses that normative barriers

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

Normative Barriers to Imitation 13

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

Tabl

e2.

Surv

ival

anal

ysis

ofen

try

into

prod

uct

cate

gory

Inde

xfu

nds

SRI

fund

sR

egio

nal

fund

sIn

dust

ryfu

nds

Mod

el0

Mod

el1

Mod

el2

Mod

el0

Mod

el1

Mod

el2

Mod

el0

Mod

el1

Mod

el2

Mod

el0

Mod

el1

Mod

el2

Stoc

km

arke

tin

dex∗

0.00

009

0.00

015

0.00

018

0.00

011

0.00

012

0.00

015

−0.0

0007

8−0

.000

01−0

.000

090.

0006

5∗∗∗

0.00

064∗∗

∗0.

0006

5∗∗∗

(0.0

0036

)(0

.000

37)

(0.0

004)

(0.0

0018

)(0

.000

2)(0

.000

2)(0

.000

1)(0

.000

1)(0

.000

1)(0

.000

24)

(0.0

0024

)(0

.000

2)L

egal

dum

my

−9.1

91∗∗

∗−8

.880

∗∗∗

−9.6

04∗∗

∗−1

7.87

∗∗∗

−17.

95∗∗

∗−1

6.25

∗∗∗

−0.4

4−0

.383

−0.4

50.

081

0.08

860.

099

(2.4

9)(3

.42)

(3.3

5)(0

.63)

(0.6

8)(0

.88)

(0.6

7)(0

.66)

(0.6

8)(1

.06)

(1.0

6)(1

.05)

Sale

sin

cate

gory

∗−0

.000

5∗∗∗

−0.0

005∗∗

∗−0

.000

5∗∗∗

0.00

0035

0.00

009

0.00

013

0.00

025∗∗

0.00

024∗∗

0.00

023∗∗

0.00

029∗∗

0.00

029∗∗

0.00

028∗∗

(0.0

0018

)(0

.000

14)

(0.0

0015

)(0

.000

12)

(0.0

001)

(0.0

001)

(0.0

001)

(0.0

001)

(0.0

001)

(0.0

001)

(0.0

001)

(0.0

001)

Prod

ucts

inca

tego

ry∗

0.05

86∗∗

∗0.

0796

∗∗∗

0.08

02∗∗

∗0.

0004

90.

0003

90.

0029

0.00

40.

0038

0.00

420.

0053

0.00

530.

0053

(0.0

16)

(0.0

23)

(0.0

23)

(0.0

039)

(0.0

037)

(0.0

045)

(0.0

04)

(0.0

039)

(0.0

04)

(0.0

055)

(0.0

056)

(0.0

056)

Firm

size

∗−0

.815

∗−0

.626

−0.6

140.

0587

0.07

17∗

0.16

6∗∗∗

−0.3

32−0

.401

−0.3

60.

174∗∗

∗0.

173∗∗

∗0.

173∗∗

∗

(0.4

7)(0

.43)

(0.5

4)(0

.042

)(0

.039

)(0

.036

)(0

.32)

(0.3

4)(0

.37)

(0.0

42)

(0.0

43)

(0.0

43)

Age

offir

m(y

ears

)∗−.

107∗∗

−0.2

43∗∗

∗−0

.269

∗∗0.

001

−0.0

16−0

.028

7−0

.049

−0.0

46−0

.045

−0.0

55−0

.053

−0.0

53

(0.0

53)

(0.0

87)

(0.1

1)(0

.046

)(0

.046

)(0

.054

)(0

.043

)(0

.044

)(0

.045

)(0

.042

)(0

.04)

(0.0

4)A

naly

stin

tens

ity∗

−2.9

36∗∗

∗−2

.934

∗∗∗

−1.5

2∗∗∗

−1.6

04∗∗

∗0.

262

0.25

00.

051

0.05

5(1

.03)

(0.9

9)(0

.42)

(0.4

7)(0

.26)

(0.2

6)(0

.27)

(0.2

6)

Ow

ners

hip

(Pri

vate

owne

rshi

pre

fere

nce

cate

gory

)U

nion

−0.4

91.

621∗∗

∗−0

.33

0.10

3(0

.61)

(0.6

0)(0

.51)

(0.5

3)G

over

nmen

t0.

446

−2.7

25∗∗

∗0.

160.

075

(1.2

9)(0

.95)

(0.4

)(0

.61)

Con

stan

t−2

3.13

∗∗∗

−30.

03∗∗

∗−3

0.75

∗∗∗

−8.4

01∗∗

∗−7

.51∗∗

∗−1

0.06

∗∗∗

−10.

3∗∗∗

−10.

73∗∗

∗−1

0.7∗∗

∗−1

3.87

∗∗∗

−13.

89∗∗

∗−1

3.91

∗∗∗

(4.5

9)(7

.10)

(7.4

4)(2

.66)

(2.8

1)(3

.47)

(1.6

3)(1

.73)

(1.7

4)(2

.02)

(2.0

5)(2

.02)

Obs

erva

tion

s15

947

1594

715

947

1374

013

740

1374

010

114

1011

410

114

9610

9610

9610

Ado

ptio

ns10

1010

1313

1332

3232

2222

22

∗∗∗

p<

0.01

,∗∗

p<

0.05

,∗

p<

0.1

∗L

agge

don

eye

ar

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

14 S. Jonsson and P. Regner

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

to imitation limit the imitability of specific prod-ucts, there may of course be alternative explana-tions for our findings. The first explanation thatoften comes up in discussions of these results withpractitioners is the question of the efficiency ofadoption; the explanation is that index and SRIfunds were not adopted as quickly because theywere inferior products. Inferior products are heretaken to mean three things. First, index funds areoften managed at a lower fee than actively man-aged funds and thereby may seem less profitableto market. Second. it is argued that adopting indexfunds is suboptimal use of a core competence (i.e.,analysts) as no analyst competence is required torun an index fund. If this was the only explana-tion for the lower degree of imitation it, is curiousas to why the actively managed fund categoryof SRI funds also is imitated at a slower pace,and SRI funds are also primarily shunned by thefirms with strongest analyst collectives. Third, andpotentially more troublesome to our interpretation,is the argument that neither index nor SRI fundsperformed well in the market. Market performancefor a mutual fund is not the same as performancein terms of yield. Although it is always preferablefor a mutual fund firm to be the sponsor of a well-performing fund, it is the size of the fund thatmatters most to the revenue generation, becausethe management fee is a percentage of the totalassets under management. The relevant adoptionperformance dimension of mutual funds is thus itstotal asset size—a fund that performs well fromthe fund management firm’s point of view is large,while a poor performer is small. What casts doubton this explanation is that the average fund size,measured four years after adoption, was very simi-lar across all mutual fund categories. Average fundsize ranges from a low of Swedish kronor (SEK)45 million for mixed-asset funds to a high of SEK190 million for global equity funds, with index andSRI funds squarely in the middle of the perfor-mance distribution with SEK 120 and 130 million.The average fund size for index and SRI funds isthe same as for the regional and industry funds;it was thus not more efficient on average to adoptindustry or regional funds, and yet index and SRIfunds were shunned.

From a strategic theory interpretation, it canalso be questioned as to whether delaying entryis perhaps a useful strategy in itself, becausea delayed response may be desirable dependingon the firm’s resource base and complementary

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114

assets (Lieberman and Montgomery, 1988, 1998;Mitchell, 1989; Schoenecker and Cooper, 1998;Shamsie, Phelps, and Kuperman, 2004; Shankar,Carpenter, and Krishnamurthi, 1998). Slow imi-tation may thus be a deliberate response basedon first-mover disadvantages and follower advan-tages (Lieberman and Montgomery, 1998). Thisalso follows from research that has demonstratedthat strategic change and response (and imitation)may be more or less desirable depending on var-ious environmental and organizational factors andthe gains of strategic fit between them vs. the costsconnected with the realization of this fit (Zajac,Kraatz, and Bresser, 2000). However, earlier stud-ies from the U.S. fund market show discernablefirst-mover advantages that are not eroded veryquickly (Makadok, 1998; Tufano, 1989), indicat-ing limited scope for late-mover advantages. Fur-thermore, there are few technological uncertain-ties coupled with new product introductions in themutual fund market, which further limits strate-gic motivations for late imitation (Lieberman andMontgomery, 1998; Schnaars, 1994).

Another question that often comes up is whether‘institutional barriers’ is just shorthand for a poweranalysis. It is natural that financial analysts arenonplussed about index funds as they representa deskilling, and thereby loss of power, of theirprofessional role. Similarly it can be argued thatchoosing SRI funds means handing over part of theresponsibility of selecting assets to an SRI screen-ing firm. To our minds there is not a contradictionbetween an analysis of the power consequenceson a professional group and an institutional anal-ysis. It is not contradictory to argue that analystsresist index funds because they feel their power-base threatened and they feel it is contrary to theirprofessional identity (cf. Hirsch and Lounsbury,1997). Furthermore it is crucial to understand thatthe reason why active asset management is a dom-inant logic is closely bound up in the profession-alization project of analysts (Lounsbury, 2002),which is also a quest for intraorganizational power(Abbott, 1988). Institutions, norms, and powerstructures are thus inexorably bound together, andas recent theorists inform us an institutional anal-ysis is also an analysis of power (Clemens andCook, 1999; Fligstein, 1996; Lounsbury and Rao,2003; Schneiberg and Soule, 2004).

Copyright 2009 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 0–0 (2009)DOI: 10.1002/smj

UNCORRECTED PROOFS

Normative Barriers to Imitation 15

123456789

101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354555657

DISCUSSION AND CONCLUSION

Departing from the common assumption thatimperfect resource imitability solely depends onthe techno-legal ability of firms to imitate, we shiftthe focus to question what causes unwillingnessamong firms to imitate. We thereby address thesecond step in a resource imitation process thatcomprises the identification of what to imitate, thewillingness to imitate and, last and most commonlyevaluated, the ability to imitate. To address theorigins of unwillingness to imitate, we draw oninstitutional theory, where the role of institutional-ized norms of appropriate actions has long been aresearch focus. While prior institutional-strategicintegrative work have broadly emphasized insti-tutional constraints on economic action (Ingramand Silverman, 2002) and advantages of comply-ing with institutional pressures (Deephouse, 1999;Oliver, 1997), we further this discussion throughan investigation of the opportunities of strategicmoves in relation to institutions and norms. Inresponse to DiMaggio’s (1988) plea for more inter-est and agency inclusion in institutional studies andOliver’s (1991) call for examining effects of insti-tutions on strategies, we examined product imi-tation behavior as affected by norms concerningproduct legitimacy and possible proactive strate-gies in relation to such institutions.

Our results show that among technically iden-tical products with comparable economic con-sequences of adoption, product categories thatfinancial professionals consider less professionallyappropriate are imitated with significantly longertime lags. Our results pertain to the mutual fundindustry with low barriers to imitation, early-mover advantages, and intense competition (cf.Makadok, 1998). Our results show further that theownership of firms also influences the firm-levelpropensity to imitate norm-challenging strategicmoves. At the firm level, our strongest result isthat a strong presence of financial analysts signifi-cantly delays firm imitation of both index and SRIfunds.

Product inimitability thus differs across firms,depending on how heavily invested they are inthe industry core competence of security analysts,which leads us to conclude that normative institu-tionalization can be a significant factor in sociallycomplex competences (Barney, 1991), and thatsome firms can bring this fact into play and in

585960616263646566676869707172737475767778798081828384858687888990919293949596979899

100101102103104105106107108109110111112113114