NEW APPROACHES IN FINANCIAL REPORTING

27

NEW APPROACHES IN FINANCIAL REPORTING FİNANSAL RAPORLAMA Yrd. Doç. Dr. TÜLAY YEL Abdul Qayum Shafaq Bolu- 2014

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of NEW APPROACHES IN FINANCIAL REPORTING

NEW APPROACHES IN FINANCIAL REPORTING

FİNANSAL RAPORLAMA

Yrd. Doç. Dr. TÜLAY YEL

Abdul Qayum Shafaq

Bolu- 2014

NEW APPROACHES IN FINANCIAL REPORTING Information is the lifeblood of the capital markets. Globalization efforts in capital markets largely change the information

requirements expected from financial statements. Nowadays companies tend to present more reliable, transparent and high

quality financial and non financial information in the frame of corporate transparency.

To restore public trust, every participant in the chain must embrace and practice a spirit of transparency, a culture of accountability and individual integrity.

Good external reporting requires sound internal management, clear articulation of a value proposition and reporting on the measures most relevant to value creation.

The Three-Tier Model of Corporate Transparency, a new vision of corporate reporting, encompasses Global GAAP, industry-based standards and company-specific information.

New Internet technologies will improve the quality and speed of reporting and enhance corporate transparency.

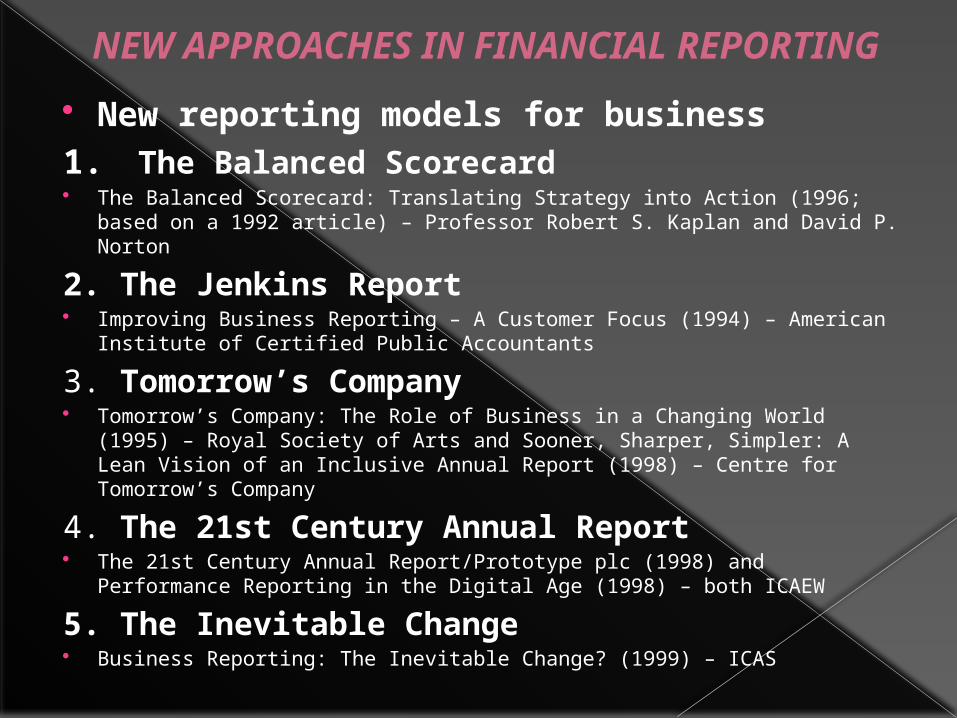

NEW APPROACHES IN FINANCIAL REPORTING New reporting models for business1. The Balanced Scorecard The Balanced Scorecard: Translating Strategy into Action (1996;

based on a 1992 article) – Professor Robert S. Kaplan and David P. Norton

2. The Jenkins Report Improving Business Reporting – A Customer Focus (1994) – American

Institute of Certified Public Accountants

3. Tomorrow’s Company Tomorrow’s Company: The Role of Business in a Changing World

(1995) – Royal Society of Arts and Sooner, Sharper, Simpler: A Lean Vision of an Inclusive Annual Report (1998) – Centre for Tomorrow’s Company

4. The 21st Century Annual Report The 21st Century Annual Report/Prototype plc (1998) and

Performance Reporting in the Digital Age (1998) – both ICAEW

5. The Inevitable Change Business Reporting: The Inevitable Change? (1999) – ICAS

NEW APPROACHES IN FINANCIAL REPORTING6. Inside Out Inside Out: Reporting on Shareholder Value (1999) – ICAEW

7. Value Dynamics Cracking the Value Code: How Successful Businesses are Creating Wealth in the New Economy

(2000) – Arthur Andersen

8. GRI Sustainability Reporting Guidelines (2000; revised 2002) – Global Reporting

Initiative.

9. The Brookings Institution Unseen Wealth: Report of the Brookings Task Force on Understanding Intangible Sources of

Value (2001) and Professor Baruch Lev’s Intangibles: Management, Measurement, and Reporting (2001) – both Brookings Institution

10. Value Reporting The Value Reporting™ Revolution: Moving Beyond the Earnings Game (2001) and Building

Public Trust: The Future of Corporate Reporting (2002) – both PricewaterhouseCoopers

11.The Hermes Principles The Hermes Principles: What Shareholders Expect of Public Companies – and What

Companies Should Expect of Their Investors (2002) – Hermes Pensions Management Limited

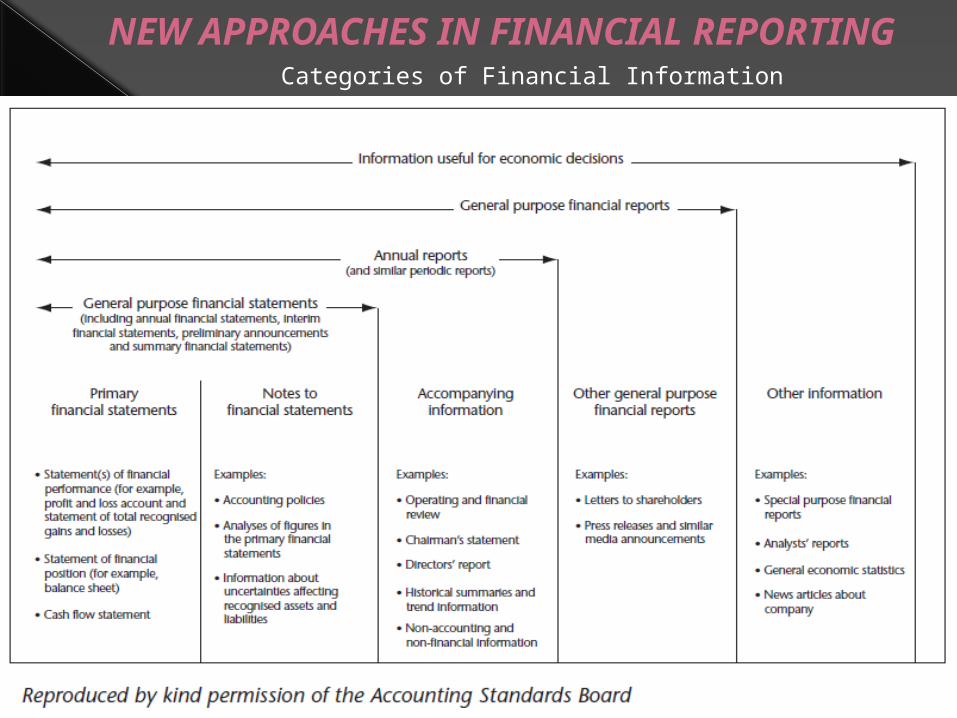

NEW APPROACHES IN FINANCIAL REPORTING Changing in Financial Reporting System General purpose financial statements, which

include annual financial statements, are one type of general purpose financial report. ‘General purpose financial reports’ are negatively defined as ‘financial information that, although prepared by the entity itself, is not in the form of a special purpose financial report.’ ‘Special purpose financial reports’ are defined as ‘financial information prepared by the entity itself at the behest of, and in the form specified by, persons who have the authority to obtain the information they require to meet their needs.’

A figure that shows Categories of Financial Information In 1998 institute of Chartered Accountants in England and Wales.

NEW APPROACHES IN FINANCIAL REPORTINGCategories of Financial Information

NEW APPROACHES IN FINANCIAL REPORTING

According to the ASB’s Statement: ‘The objective of financial statements is to provide

information about the reporting entity’s financial performance and financial position that is useful to a wide range of users for assessing the stewardship of the entity’s management and for making economic decisions.’

That objective can usefully be met by focusing exclusively on the information needs of present and potential investors, the defining class of user.’

‘Present and potential investors need information about the reporting entity’s financial performance and financial position that is useful to them in evaluating the entity’s ability to generate cash (including the timing and certainty of its generation) and in assessing the entity’s financial adaptability.’

NEW APPROACHES IN FINANCIAL REPORTING The 21st Century Annual Report The 21st Century Annual Report proposes that

businesses publish a wider range of leading indicators of financial performance, take a more inclusive view of stakeholders, and harness advances in information technology in their reporting.

NEW APPROACHES IN FINANCIAL REPORTING

The 21st Century Annual Report

The editors provide a summary of the differences between the ‘old’ system of reporting and the ‘new’.

NEW APPROACHES IN FINANCIAL REPORTING

“The future of corporate reporting is inevitably moving toward greater transparency.”

Information is the lifeblood of the capital markets. Investors risk their hard-earned capital in the markets, and they rely on information they receive from companies in making their investment decisions. They need reliable information on a timely basis. They want it in language they can understand, and they should receive it in formats they can easily use for analysis. Investors have the right to expect that the benefits or consequences they experience will result from the decisions they make, not from fl awed information.

NEW APPROACHES IN FINANCIAL REPORTING Restoring public trust will require that every participant in the

Corporate Reporting Supply Chain embrace and live by three core concepts:

1. A spirit of transparency — All members of the Corporate Reporting Supply Chain must embrace a spirit of transparency.

2. A culture of accountability — Every member of the supply chain must hold itself accountable: management for producing relevant and reliable information; boards of directors for ensuring that management lives up to this obligation; independent auditors for ensuring the objectivity and independence of their audit opinions; and analystsfor producing high quality.

3. People of integrity — Rules, standards and frameworks can only go so far. Transparency and accountability will be achieved only by people committed to individual integrity

NEW APPROACHES IN FINANCIAL REPORTING

The financial reporting supply chain refers to the people and processes involved in the preparation, approval, audit, analysis and use of financial reports. All links in the chain need to be of high quality and closely connected to supply high quality financial reporting.

The cycle both starts and ends with the investors and other stakeholders, who want to make informed economic decisions about a company and, therefore, require financial information to do so.

NEW APPROACHES IN FINANCIAL REPORTING

Potential Effects from Value-Oriented Business Reporting

NEW APPROACHES IN FINANCIAL REPORTING

The Corporate Reporting Supply Chain

NEW APPROACHES IN FINANCIAL REPORTINGAccording to Building Public Trust, the overriding need is for ‘a spirit of transparency. Corporations have an obligation to provide willingly to shareholders the information needed to make decisions.’

Building Public Trust

NEW APPROACHES IN FINANCIAL REPORTING The book sets out a three-tier pyramid of corporate

transparency:1. ‘ A set of globally generally accepted accounting

principles.’

2. ‘Standards for measuring and reporting information that are industry-specific, consistently applied, and developed by the industries themselves.’

3. ‘Guidelines for company-specific information such as strategy, plans, risk management practices, compensation policies, corporate governance, and performance measures unique to the company.’

The allocation of responsibilities in Building Public Trust is consistent with the earlier book, although the responsibilities of analysts are emphasized and all the responsible parties are presented as playing roles in the ‘corporate reporting supply chain’.

NEW APPROACHES IN FINANCIAL REPORTING

Can business reporting achieve transparency? No, according to the established view. Transparency in

business reporting is significantly constrained by considerations of cost, competition, confidentiality and litigation.

Yes, say many reformers. There should be almost no limits on transparency.

NEW APPROACHES IN FINANCIAL REPORTING

The Balanced Scorecard The Balanced Scorecard reports performance not just

from a financial perspective, but also from a customer perspective, a business process perspective and a learning-and-growth perspective.

NEW APPROACHES IN FINANCIAL REPORTING

The Balanced Scorecard

NEW APPROACHES IN FINANCIAL REPORTING

This model explain the following things :

Financial and non-financial data Management’s analysis of financial and non-financial

data Information about management and shareholders Background about the company

NEW APPROACHES IN FINANCIAL REPORTING Tomorrow’s Company Tomorrow’s Company puts forward an inclusive approach

to business and business reporting, in which there would be a broader focus on stakeholder relationships and less emphasis on financial measures.

NEW APPROACHES IN FINANCIAL REPORTING

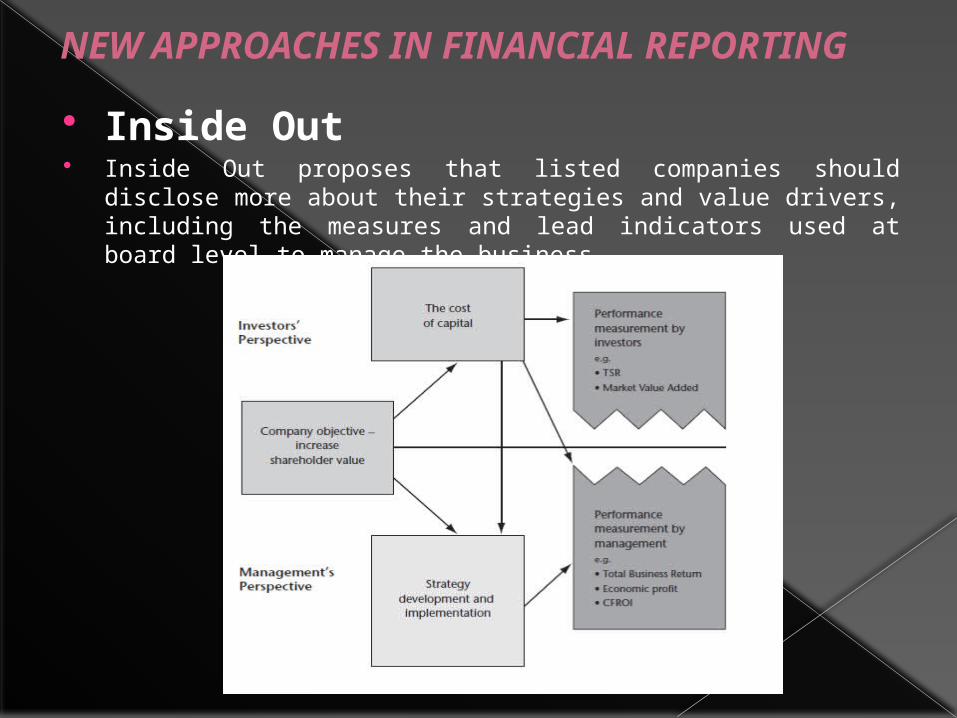

Inside Out Inside Out proposes that listed companies should

disclose more about their strategies and value drivers, including the measures and lead indicators used at board level to manage the business.

NEW APPROACHES IN FINANCIAL REPORTING

The desired result Inside Out disclosures are intended to bridge the

gap between managers’ perceptions of their companies’ potential and the market’s. Also, by allowing investors to value companies more accurately, the proposed disclosures ‘may reduce capital market volatility’.

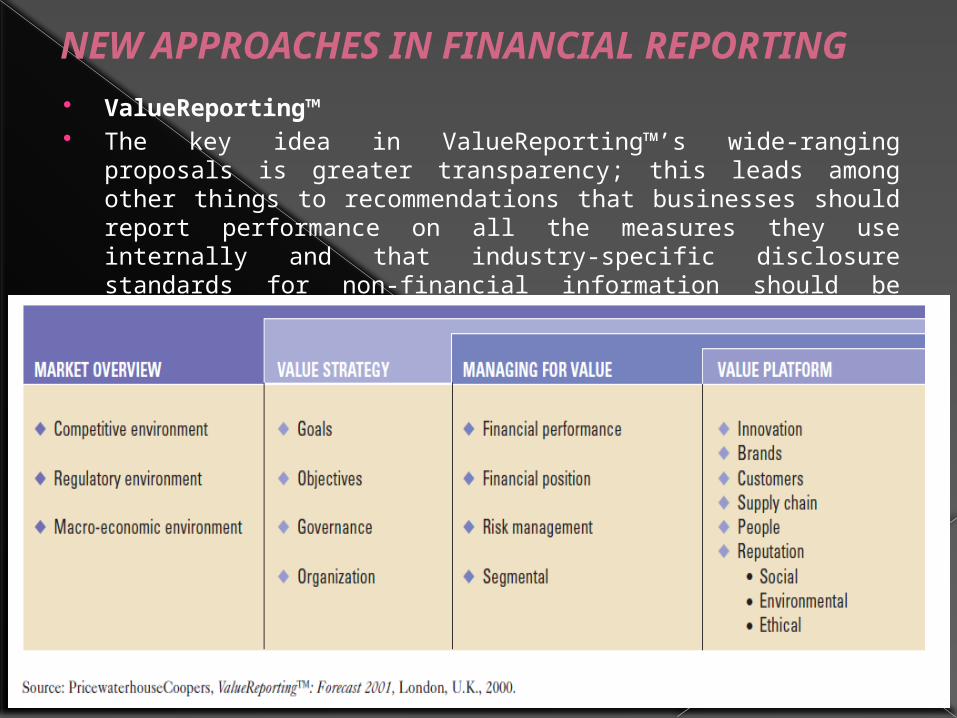

NEW APPROACHES IN FINANCIAL REPORTING ValueReporting™ The key idea in ValueReporting™’s wide-ranging

proposals is greater transparency; this leads among other things to recommendations that businesses should report performance on all the measures they use internally and that industry-specific disclosure standards for non-financial information should be developed on a voluntary basis.

NEW APPROACHES IN FINANCIAL REPORTING

“Stakeholders are not data miners. They require and deserve clear, logically presented information.”

NEW APPROACHES IN FINANCIAL REPORTING

References DiPiazza and Eccles, 2002, “Building Public Trust”,

“The Future of Corporate Reporting”.

NEW REPORTING MODELS FOR BUSINESS, Information for Better Markets initiative, 2003, reprinted, 2010.

S C H U S T E R and C O N N E L L, The Trend Toward Voluntary

Corporate Disclosures.

Lyle, 2005 FINANCIAL REPORTING SUPPLY CHAIN

![[Charles H. Gibson] Financial Reporting and Analys](https://static.fdokumen.com/doc/165x107/6319729465e4a6af370fcfc8/charles-h-gibson-financial-reporting-and-analys.jpg)