Natural Gas: Designing a Distinctive and Incentive Driven Legal and Regulatory Regime

80

“Designing a Distinct and Incentive Driven Legal and Regulatory Regime as a Means towards Investment Surety: Making the Case for Natural Gas in Developing Economies” A Dissertation by Marcia Ashong, Submitted to the Centre for Energy, Petroleum & Mineral Law and Policy, University of Dundee. 2011

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Natural Gas: Designing a Distinctive and Incentive Driven Legal and Regulatory Regime

“Designing a Distinct and Incentive Driven Legal

and Regulatory Regime as a Means towards

Investment Surety: Making the Case for

Natural Gas in Developing Economies”

A Dissertation by Marcia Ashong, Submitted to the Centre for Energy, Petroleum

& Mineral Law and Policy, University of Dundee.

2011

Contents ABSTRACT……………………………………………………………………………………………………..I

ABBREVIATIONS…………………………………………………………………………………………......II

TABLE OF

FIGURES……………………………………………………………………………………….........................III

CHAPTER 1: INTRODUCTION………………………………………………….................................................1

CHAPTER 2: STATUS OF NATURAL GAS……………....................................................................10

2.1. Gas Worldwide……………....................................................................................................10

2.1.1. Significance of Future Reserves……………..........................................................13

2.2. Natural Gas Specific Issues & Challenges…..........................................................................13

2.2.1. Associated vs. Non-Associated…......................................................................13

2.2.2. Associated…...................................................................................................14

2.2.3. Non-associated…............................................................................................ 16

2.2.4. Volume Risk Allocation…................................................................................17

2.3. Gas Market Considerations: Obstacles for Regulations….......................................................18

2.4. LNG Opportunities and Challenges…...................................................................................20

CHAPTER 3: SECTOR SPECIFIC APPROACH............................................................................22

3.1. Power................................................................................................................................22

3.2. Mining Sector....................................................................................................................23

CHAPTER 4: LEGAL & REGULATORY MEASURES & RISK MITIGATING INCENTIVES........24

4.1. Legal Instruments...............................................................................................................24

4.2. Risks and Legal Arrangements............................................................................................26

4.2.1. Exploration Risks and Legal Arrangements..................................................................26

4.2.2. Development and Production Risks and Arrangements..................................................29

4.3. Nature of Gas Clauses........................................................................................................36

4.3.1. Broad Policy Principles: Ghana Case Study..................................................................38

4.4. Gas Specific Regulation and Government Control.................................................................42

CHAPTER 5: PETROLEUM LICENSING & NATURAL GAS..........................................................47

5.1. Evolution of the Licensing System......................................................................................47

5.2. Petroleum Licensing Today................................................................................................50

5.3. Allocation of Petroleum Prospective Acreage......................................................................52

5.4. Bidding Terms..................................................................................................................55

CHAPTER 6: EVALUATING LICENSING POSSIBILITIES: LESSONS FROM MINING AND

POWER.....................................................................................................................................57

6.1. Designing a Legal Framework for Allocating Natural Gas Rights Lessons from the Mining and

Power Sectors................................................................................................................57

6.1.1. Form of License...............................................................................................61

CHAPTER 7: CONCLUSION.....................................................................................................64

BIBLIOGRAPHY........................................................................................................................66

ACKNOWLEDGEMENT

In life it is often said that “no man is an Island.” Well such a phrase became more glaring

throughout the period of my studies at the CEPMLP (as we have all fondly come to know of

it). It is without a doubt that a Masters degree in Law is turbulent enough but to couple that

with a specialised area (that is, Energy) with all the curve balls life can through at one, it

would have perhaps been suicidal to consider taking such a journey without bearing in mind

that indeed no man is an island.

So it was perhaps my most joyous moment during writing this piece when I discovered that

“aha I will indeed get to thank those that have stuck with me through this vital period of my

life.” First and foremost I want to say a big thank you to my fellow students, without you,

waking up every day would not have been the same – and it is safe to say that through this

short period of our lives we all become brothers and sisters. I am even more excited to know

that no matter where I go in the world I know that I will have a friend just around the corner.

I also want to take this opportunity to thank Mrs Janeth Warden-Fernandez – until I met you,

I was soon forgetting what it really meant to have a teacher; it was translated very eloquently

in English once that “a good teacher is like a candle – it consumes itself to light the way for

others.” This is what you have been to me, and you will continue to hold a very dear place in

my life. I also wish to express my deepest gratitude to Prof. David Cameron and Mr Stephen

Dow, Prof. Cameron, your dedication to your students has been unwavering thank you for

your support through the highest and lowest points, and may you continue to prosper in your

endeavours. Mr Dow, until I attended your lectures, I never knew that years later I would still

be daydreaming about sitting in Mr Dows lecture, you have an uncanny way of delivering

knowledge and most importantly I am eternally grateful for all the humour-filled support you

have given me, and the patient guidance you have afforded me throughout the writing of this

dissertation.

I dedicate this to my mother and my family, most importantly to my beloved grandmother

who recently passed. I pray that I continue to live in her light and go through life with the

same unapologetic vigour she did.

I

ABSTRACT

This research stems from recent developments in the world natural gas markets, exciting

developments that will see surging interests for natural gas in the coming years. In 2009

natural gas reserves were approximately 82% of oil reserves, yet gas consumption was only

approximately one-fifth of oil consumption, moreover, there is a trend showing an increase in

natural gas demand as evidence points to its premium qualities among which is its carbon

emitting benefits.

These trends however, have not necessarily corresponded with sharp increases in natural gas

development projects; the case even more glaring in gas rich emerging economies, some of

whom have commercially recoverable reserves of natural gas, enough to contribute to

national development agendas as well as upstage their importance in the global energy

markets. Even more pressing is the case that the natural gas legal and regulatory frameworks

in these regions remain inefficient for attaining the goals envisaged by policy-makers.

The paper takes stock of the challenges and to rectify the underlying issues, the approach

taken is to attempt addressing them by offering recommendations for the design of regulatory

and licensing regimes, recommendations which attempt to solve these issues from the

perspective of gas rich developing economies- that is, economies where the natural gas

market is either lacking or non-existent. These recommendations it is hoped, would be a

means towards establishing not only a natural gas market but also addressing the concerns of

investors; towards a market which balances both private and public sector concerns.

II

ABBREVIATIONS

AG Associated Gas

BOT Build Operate Transfer

DGO Domestic Gas Obligation

DMO Domestic Market Obligation

E&E Exploration and Exploitation

EGPC Egyptian General Petroleum Corporation

E&P Exploration and Production

ERT Enhanced Recovery Technique

GDE Gas del Estado

GNGC Ghana National Gas Company

GOG Government of Ghana

GSA Gas Sales Agreement

GTP Gas Transfer Price

HC Host Country

HG Host Government

IEA International Energy Agency

IMF International Monetary Fund

IOC International Oil Company

LNG Liquefied Natural Gas

LCV Local Content Vehicle

MIGA Multilateral Insurance Guarantee Agency

NGDT National Gas Development Task Force

NNPC Nigeria National Petroleum Corporation

NOC National Oil Company

OECD Organization for Economic Co-operation and Development

III

OML Oil Mining Lease

OPL Oil Prospecting License

PA Petroleum Agreement

PEMEX Petroleos Mexicanos

PSC Petroleum Sharing Agreement

SA Service Agreement

TOP Take or Pay

US United States of America

UK United Kingdom

YPF Yacimientos Petroliferos Fiscales

IV

TABLE OF FIGURES

Figure 1 Gas Flaring Volume

Figure 2 Nigerian Gas Utilization and Flaring

Figure 3 Nigerian Gas Utilization Forecast

Figure 4 Proven Gas Reserves by Region

Figure 5 Natural Gas Value Chain

Figure 6 Agreements and Risk Distribution Diagram

Figure 7 Commercial Agreement Matrix

1

1. Introduction

Natural gas has become quite the commodity in recent years, it was largely a misunderstood

fuel fighting to find its place as a petroleum commodity but hitherto rarely getting the equal

amount of attention afforded to oil. Nevertheless, it is of little surprise that the demand for

natural gas has increased significantly in the past two decades, particularly now, a time in

history where topical matters such as climate change and the race to find cleaner sources of

energy dominate international agendas.

A fuel which just a few decades ago was considered an „inconvenient truth‟1 is now sort after,

primarily for household heating and large-scale power generation. As early as the 1960‟s

there was essentially no international market for gas. The existing markets were

predominantly internal (that is Europe and the United States), this reality further kept gas

development at bay. Algeria led the way with the world's first gas export from Arzew in the

early 1960s. Libya followed suit with the building of the liquefied natural gas plant (its first

attempt to commercialise and export gas) at Marsa Brega. During this period however,

exploration for natural gas was for the most part discouraged, often the phrase “gas prone”

would be used by oil companies to discourage further exploration or capital expense.2

Globally the importance of natural gas has taken a turning point (there is even talk of a future

where the phrase “associated oil” would be the norm). Between the periods of 1971 to 2000,

world gas demand more than tripled from 895 million tonnes of oil equivalent (mtoe) to

2,085 mtoe.3 Moreover, the preference of gas for power generation has been fuelled by highly

technical and economically efficient gas turbines, (namely; the Combined Cycle Gas

Turbine), technologies whose long term efficiency pave way for future reliability of the

power sector, thereby encouraging gas-rich countries to develop their gas resources as

catalyst for national development.

1 Companies in search of oil, were often faced with large fields of gas finds, proving an added burden as oil

development with associated gas involved heavy reliance on capital costs. Moreover, gas was heavily flared in its early year, Michael Bunter for instance recalls his first experience in the Oil Industry in Libya, where at night the sky would be light up, not from street lights but from flared gas, to such an extent that it would navigate across the dessert. Michael Bunter, Interview, January 21, 2011 2 Ibid

3 International Energy Agency, Security of Gas Supply in Open Markets: LNG and Power at a Turning Point, (IEA,

2004)

2

Considering the growing demand for natural gas, the trend therefore has been to increase the

availability of it. The challenge of energy supply security has unveiled the interest of nations

to develop their stranded reserves as a means to increasing their global market importance.

The challenge looking ahead, however, is that the market must clearly be able to sustain the

supply and demand balance. But with the natural gas market the demand and supply balance

rarely meet at a corresponding equilibrium in response to market signals in ways typical of

other commodities. For that reason the natural gas market has become a major source of

frustration for producers and consumers alike.

Though trends have shown marked increases in the demand in the past decade, often times

the corresponding increase in production rates have been inefficient at meeting the demand

assumptions, this in effect has caused low demand for the fuel considering where availability

doesn‟t exist, there can surely not be demand and alternatives are thus utilised.

There are several reasons for this, one being the very nature of the gas market itself; whereas

with other commodities, where supply and demand are typically balanced by the price

mechanisms, and where buyers are usually responsive to price signals, this does not quite

work the same in the gas market, especially where the consumer in that case is unable to

switch to other fuels so easily (the case for majority of natural gas consumers). Gas

production is contemplated across the value-chain, infrastructure and transportation is thus

fixed, this means a project‟s carrying capacity is predetermined, likewise a consumers ability

to switch based on market signals become limited.4 This is the case with core household

consumers- large industrial consumers on the other hand, take for instance combined

electricity generators may switch from using natural gas to cheaper fuels such as coal or fuel

oil. But even where this is possible, the price of crude oil for instance is determined on the

world market, while natural gas markets, tend to be regionally segmented. The domestic

natural gas market is therefore much smaller than the global oil market, and as such, events or

conditions in the United States‟ gas market for example, seems unlikely to be able to

4 Note that though there exists gathering and fixed transportation systems for oil as well as for natural gas, the

above statement would not lead to cost equalisation of the fuels considering the various dynamics of the end user and or sale agreement- natural gas is typically tied to long term sales agreement and therefore prices are typically fixed ahead of sales.

3

influence the global price of oil.5 It therefore becomes a commodity whose price mechanisms

can vary dramatically from region to region depending mostly on the level of maturity of its

market. We therefore tend the see lower gas prices in regions like the United States and

Europe where gas markets are fully established and where sudden increases in volume is

possible.6

To set aside the lack of equilibrium of the gas market as the main concern surrounding

deficiency in natural gas utilization however, would be painting a narrow picture and drawing

on financing issues alone would create a skewed image of this complex sector, especially

considering recent announcements of ambitious LNG projects.7 A more pressing response

would be to look into factors that stall development of natural gas in developing economies

and ascertain the difficulties they face in regards to the creation of gas markets.

The paper correspondingly suggests that gas development projects in these regions have

largely fallen behind increasing demand, and that such lag is related almost entirely not to the

lack of availability of markets (since viewing from such a perspective limits the scope of the

underlying issue), but to the lack of focus in the legal and regulatory structures needed not

only to develop a functional market, but to sustain it over time. Perhaps there lies our starting

point. Effectively, when dealing with issues intrinsic to the natural gas industry one cannot

start with the market, but must begin with the availability of the commodity, and factors that

affects its abundance or lack thereof for consumption, the paper will focus on factors that are

legal and regulatory in nature needed to address these underlying concerns.

Why Developing Economies?

According to the International Energy Agency‟s (IEA) statistics, global gas demand is

anticipated to grow by an average of 1.5% per annum through to 2030, it is estimated that

much of this growth will come from non-OECD countries.8 The principle determinants

5 Villar J.A., et al, The Relationship Between Crude Oil and Natural Gas Prices, pg.2, Energy Information

Administration – Office of Oil and Gas (2006) 6 Gas delivery is essentially capacity-bound, therefore, the supply of the commodity is restricted in the short-

term, coupling this with the seeming price inelasticity of demand can lead to a highly volatile market 7 Australia recently announced the world’s first floating LNG terminal (see:

http://uk.reuters.com/article/2011/05/20/uk-shell-prelude-idUKTRE74J27V20110520 ), Papua New Guinea also saw the financing of a merchant LNG project meaning that with the adequate environment financing can be attained. 8 International Energy Agency, World Energy Outlook 2009

4

however, of the success of the gas market in these regions would be the ability of the

production rates to meet such increases in demand, in ways similar to the crude market.

Figures already indicate that this increase in demand would mostly be coming from much of

the developing world including Asia; as the trends in their national development agendas

stipulate access to cheaper and cleaner burning energy fuels. Western Europe‟s declining

production rate is a case in point, and much of this can be attributed to its depleting gas

reserves, and so Europe too is said to be on trend for increased demand in gas, especially as it

struggles to wean itself of high carbon emitting fuels. 9

For Europe therefore, gas from

developing economies will assume a whole new importance.

The main concern however, is that for majority of non-OECD economies (who are also

developing economies) natural gas projects have not picked up as analyst would predict, there

seems a dearth of incentives for gas development, moreover, the investment environment has

often been characterised by uncertainties as well as institutional and infrastructural

challenges. The fact that rents associated with gas development often do not match that of oil

rents also poses further doubt for investors. The deficit of local markets in many of these

countries also presents increased complexities in developing project descriptions for

financing purposes.

In OECD economies, these challenges may not be as glaring as national budgets can always

be brought to bear to mitigate institutional, infrastructural and development and market risks.

Furthermore, producers in the OECD operate often in mature provinces with years of

technical and production experience.10

For non-OECD developing economies in particular,

(where majority of future predicted rise in demand lies) they find that inadequate national

budgets forces heavy reliance on international oil and gas companies, these companies

however, have as a main objective to find crude oil so where institutional capacity or

mitigated investment risks are eliminated the discovery of gas often leads to stranded gas

fields due to the perceived risks involved. These economies are also paradoxically burdened

9 In early 2011 it was recorded that Norway may lose close to $186 billion as shortfall of Norwegian gas is

estimated to take place as soon as 2015, slashing its estimates and paving way for supply of natural gas from non-European sources. Bloomberg, ‘Norway $186 billion Gas Loss to Cement Russian Grip on Supply’, at http://bloom.bg/ic1UuE, last visited 17, January 2012 10

It was the discovery of gas at Groningen in the Netherlands that changed the European natural gas market because the European countries had hard currencies to buy and sell first Netherlands natural gas and the gas from the UK and Norway. Further, the existence of long-established and mature gas markets also adds an extra value to estimating risks and understanding pricing constraints

5

with severe developmental concerns; at the heart of which lies in-house availability of the

fuel needed to spearhead growth and private sector development.11

Still, the reliance on

external or private capital for infrastructure development requires significant levels of private

sector incentives and regulatory control measures; the combination of these guarantees, also,

poses increased burden on weaker economies. A delicate predicament, considering the bulk

of the world‟s gas reserves are located in non-OECD countries at 90.9 percent (OECD

reserves were at 9.1 percent of the world‟s total as of 2010 statistics).12

Current Approach

In developing petroleum fields a trend has therefore emerged. Within the past few decades

there has been an increase in regulatory intervention, host governments have seen non-gas

flaring policies as necessary for mandating the simultaneous utilisation of natural gas reserves

found in association with crude oil, incentive driven oil and gas contracts (designed in favour

of gas development as well as oil), Petroleum legislation where provisions are cited for the

abatement of gas development and so on. Many of the methods alluded to here have had little

resolve in curbing the issues of natural gas development in these regions, nor the

development of sustainable gas markets.

Take for instance the non-gas flaring agenda (especially in developing economies), which

though have made some progress in discouraging the flaring of associated gas and

encouraged the development of new technologies to abate gas flaring,13

is not and cannot in

effect be a panacea for the development of non-associated natural gas fields.

Moreover, between the periods of 1994 to 2008, a period of which majority of the non-gas

flaring incentives began, globally, there was a decrease in gas-flaring of 7 percent, (less of

this number can be attributed to the developing economies) 2003 marking the highest rate at

172.067819 billion cubic metres (bcm‟s), up from 150.646706 bcm‟s in 1994 (see figure 1).

Furthermore, it is estimated that over 150 bcm‟s of natural gas are flared or vented annually,

in terms of current market value, gas dissipated annually is worth close to 31.6 billion dollars,

11

For instance considering the importance of access to power as a catalyst for industrialisation, it still remains that case that developing countries remain predominantly short in power capacity, as it is estimated that three-quarters of people living within these regions lack access to power, majority of these countries, however, are known to also have large gas reserves. 12

BP, Statistical Review of World Energy, June 2011, pg. 22 13

See for instance the use of natural gas as a reinjection tool for the enhancement of oil recover

6

equivalent to 25 percent of the United States‟ gas consumption, and 30 percent of the

European Union‟s gas consumption per year.14

It is little surprise that the bulk of flaring is

concentrated in developing economies.

Figure 1

United States Gov. National Geographical Data Center, National Oceanic and Atmospheric Administration

In addition, legislative and contractual incentives have shown some development, but most

improvement has been scanty in these regions. Take for instance Nigeria, whose many policy

attempts have failed at escalating its domestic gas production and utilisations rates to industry

changing levels. In most instances Nigeria‟s flaring levels have come close to matching gas

produced (see figure 2).

Figure 2

14

The World Bank, Global Gas Flaring Reduction Partners Unlock Value of Wasted Gas, 2009, at http://bit.ly/x2NKsX , last visited, 17 January, 2012

7

The Nigerian gas reserves account for the 7th

largest in the world, yet out of a total proven

reserve estimate of 186.9 trillion cubic feet (tcf) with upside potential of up to 300 tcf, only

4.5 bcf is produced daily Non-flaring policies have not worked either, it is estimated that

approximately 40 percent of associated natural gas is flared.15

Since it has been noted that

majority of the oil and gas companies prefer to pay costs associated with flaring violations

than invest in adequate infrastructure for gas processing and delivery, the issue of wasted gas

through flaring it seems has become a long-term challenge. It is also evident that the Nigerian

authorities see this as a regular income stream (N530.48 million as (N530.48 million as

penalty collected from oil companies for gas flaring), income they are reluctant to part with.

Associated gas alone in Nigeria can provide a host of opportunities for developing the

country‟s domestic needs. One of the options for utilisation include converting the gas flared

to cooking energy sources, as well as a viable potential for power generation,16

in relation to

the need to augment the export orientation of the sector, but these opportunities requires a

detailed analysis of the future opportunities available for converting the abundance of gas

resources to practically addressing the regulatory challenges of bringing gas to the internal

market.

The attempts in doing so came in its recent „Gas Masterplan‟, aimed at tackling the issue of

investment in gas development, but the Masterplan has provided little resolve on the issue.

Oil Companies are increasingly unsatisfied with the too little too late incentives created in the

policy plan, and price mechanisms introduced, especially in view of the added risks they are

expected to bear. The result being that, 50 years since Nigeria started crude oil production the

country has utilized barely 30 percent of its natural gas capabilities,17

but even with such

results the potential for natural gas utilization in Nigeria remain optimal with the a focused

framework (see figure 3).

15

“Gas Flaring in Nigeria: An overview of the Associated Gas Re-Injection (Amendment) Bill 2010 (the “Bill”)” Aina Blankson LP, 2011 16

Int. J. of Thermal & Environmental Engineering, “Gas Flaring in Nigeria: Opportunity for Household Cooking Utilization” Volume 2, No. 2 (2011) 17

Malumfashi G. I., ‘Phase Out of Gas Flaring in Nigeria by 2008: The Prospect of a Multi Win Project,’ (Petroleum Training Journal, Vol. 4 No. 2. July, 2007)

8

Figure 3

Potential Demand

forecast for Nigeria’s

Gas Sector - Graph

provided by Abel Nsa

(Gas Division),

Nigerian Department

of Petroleum

Resources (2011-

DPR)

Challenges to Regulation

The problems associated with some of the regulatory measures mentioned, are that they have

either not directly targeted the issues, thereby producing meagre results, or on another level,

they have proved rather to be disincentives for potential investors. Such solutions as will be

demonstrated in the later parts of this research have failed to ascertain the key features of

natural gas which is that gas development in these regions require specific risk mitigation

mechanisms; such that those bearing the brunt of the capital expenses are recompensed by

long-term risk mitigating off-take agreements, it is therefore necessary that any legal or

licensing objectives tries to tie the broken link between the legal and regulatory framework

with the end sales agreement, a framework which addresses the entire value chain.

Furthermore, it is argued that such solutions have ignored the nature of natural gas as a

unique fuel deserving of a unique mechanisms and solutions and also within its unique

jurisdictional context.

Justification for a Legal/Regulatory Approach

In the energy world, any plan to promote an energy sub-sector requires a comprehensive,

detailed legal and licensing regime. Governments in developing economies especially must

rely on Oil companies to effectively and efficiently exploit their natural resources due to the

limitations of national budgets, whether they choose to invest directly or allow private

investors to do so their primary concern remains heavy state control and full maximization of

the benefits associated with natural resource exploitation. Legal and regulatory regimes are

9

thus, utilised to address the relationship structure between the government and the private

concessionaire – to a larger extent they mainly address the level of State control over the

resource in question, the level of state control for the creation of a gas market however, must

also be balanced with the main priority for the government, which is the promotion of

development projects, hence state control and policy orientation must be juxtaposed when

defining rules of participation.

At the core of Petroleum licensing literature has been the primary focus on utilization of oil

reserves; hitherto, little attention was paid to the issues associated with gas development in

light of its inclusion as a petroleum commodity. This is understandable, but can also be

considered a contributory factor to the current status of natural gas utilization particularly in

the developing world. Exploration and production (E&P) agreements entered into between

governments and international oil companies (IOC‟s) have as a common assumption a target

for oil discovery. For this reason, they have been habitually vague as to the terms governing

the discovery of natural gas. One reason might be the difficulties that exist in defining the

contractual limits for natural gas development, therefore a rush to conclude E&P agreements

(often with the primary goal of finding oil) results in very few examples in the world of

adequate gas clauses.

The lack of such focus in natural gas E&P agreements has several effects, an obvious one

being the limitation of the scope for identifying sector specific concerns; this status quo has

most certainly lead to difficulties for many policy makers in identifying the area‟s where

natural gas clearly needs to be separated from it oil counterpart. Herewith, lies the scope of

this research. This work is intended to be a detailed treatment of natural gas within its

geographical limits, be it with regards to its value chain and contracts matrix, its

transportation requirements, its place within the fuel market and its energy usage. It is an

attempt to address challenges faced by developing nations as they look to establish natural

gas markets by offering recommendations for the design of legal and regulatory regimes.

10

2. Status of Natural Gas

2.1. Gas Worldwide

Currently, the world boasts total proven gas reserves of approximately 187.1 trillion cubic

metres (tcm‟s), (note, that is number is estimated to grow by at least 1.5% per annum through

to 2030) of this total, 106.7 tcm‟s are located in the Middle-East, Asia and Africa alone, with

the majority of Europe and Eurasia‟s reserves of 44.8 tcm‟s found in Russia. 18

These

numbers obviously do not include those recently discovered reserves that are yet to be

appraised, thus, the prospects of further gas discoveries in these regions alone and including

the America‟s are surmountable as more and more countries revamp their legal regimes to

accommodate for oil exploration.

The Sub-Saharan African region in particular is considered the next frontier as oil and gas

companies compete to secure prime acreage; recent activities in Ghana, Uganda, Sierra

Leone, and Tanzania and even Kenya to name a few, illustrate this urgency.19

But as oil

companies discover more oil, associated are the discoveries of commercially viable natural

gas fields. In just under two decades the continent‟s proven natural gas reserves has more

than tripled, whereas in the 1980‟s only 5 countries had commercially viable reserves

(namely; Algeria, Egypt, Nigeria, Tanzania, Tunisia)20

, today more than 20 African nations

have proven reserves,21

meaning that after careful geological and financial appraisal, all

conservative indications show with a high degree of certainty that their natural gas resources

are commercially recoverable (see: figure 3 below).

Of the proven gas reserves in Africa, close to 78 percent are located in Nigeria, with the

balance concentrated in a few other countries, namely; Algeria, Egypt, Libya, Angola,

Mozambique, Namibia and Tanzania.22

Total natural gas reserves (proven and probable) are

estimated at 4,765 bcm‟s, with present recoverable reserves at an estimated 870 bcm‟s. The

Kudu fields in Namibia are a case in point, recent drilling results in Namibia by the Shell-

18

Supra, note 12, Natural Gas 19

Mozambique for instance one of the lowest income economies in the world with little industrial activity looks set to take advantage of its recent abundant discoveries of natural gas, Tanzania likewise has found vast reserves of the resource in its Songo Songo and Minazi Bay regions. 20

Supra, note 11, pg.4 21

Gas reserves on the continent could possibly exceed oil reserves. 22

Gas Extraction in Africa, read more at, http://bit.ly/zGiJKF last visited 04 January, 2012

11

Engen-Texaco consortium indicated that the field may have enough natural gas to meet the

needs of the entire Southern Africa region.23

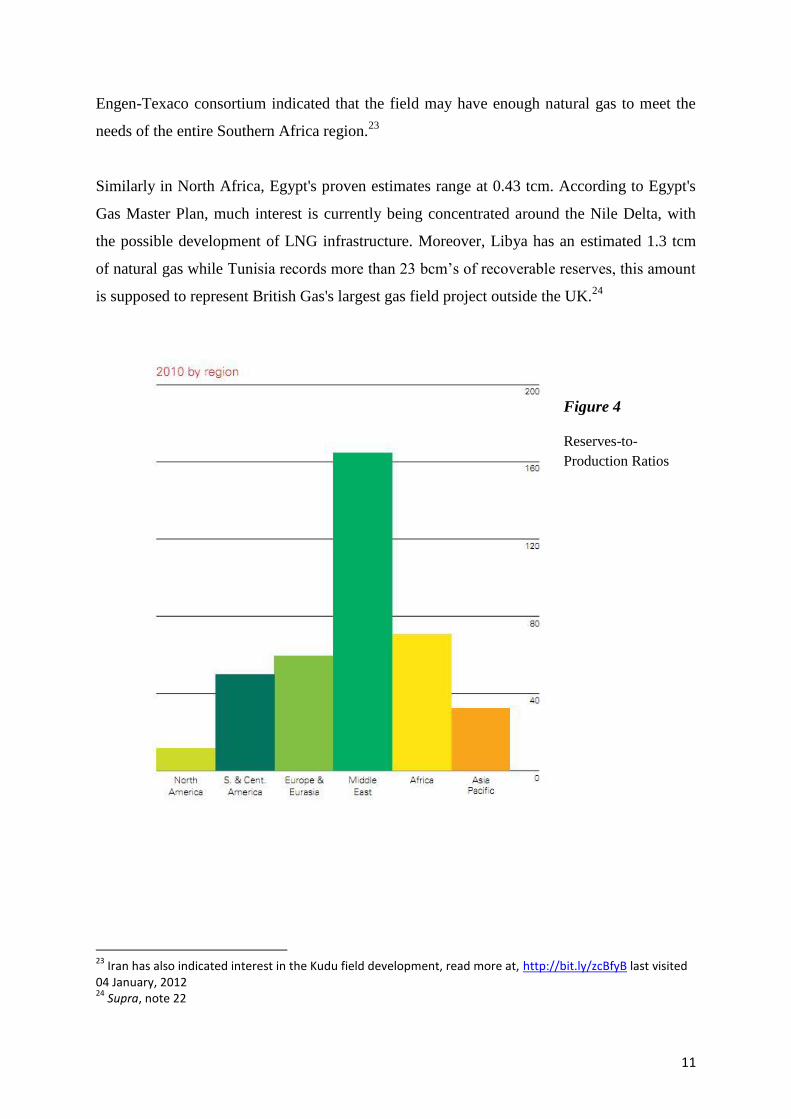

Similarly in North Africa, Egypt's proven estimates range at 0.43 tcm. According to Egypt's

Gas Master Plan, much interest is currently being concentrated around the Nile Delta, with

the possible development of LNG infrastructure. Moreover, Libya has an estimated 1.3 tcm

of natural gas while Tunisia records more than 23 bcm‟s of recoverable reserves, this amount

is supposed to represent British Gas's largest gas field project outside the UK.24

Figure 4

Reserves-to-

Production Ratios

23

Iran has also indicated interest in the Kudu field development, read more at, http://bit.ly/zcBfyB last visited 04 January, 2012 24

Supra, note 22

12

The opportunities for gas development it seems for the most part are extremely diverse and

widespread across Africa. A majority of these Countries are however grossly underutilizing

their proven resources. As of recent data, the total natural gas production rate on the continent

stands at 203.84 billion cubic metres, out of a possible 14.76tcm‟s25

meaning that the

continent is currently utilizing much less than half of its natural gas potential.

The challenges associated with gas development on the Continent cannot solely be assigned

to the difficulties in dealing with associated gas alone, for at most 50 percent of the gas on the

African continent is non-associated gas (the same true for many countries in the Asia Pacific

who among them have total gas reserves of 14.76 tcm‟s).26

Nor can these mostly stranded

resources be a result of their lack of market accessibility, or the lack of demand for natural

gas goods or resources. As is evidenced in Egypt and until most recently Libya, the enabling

legal and regulatory environment often paves way for access to the market as was seen with

Egyptian supply to its Middle Eastern neighbours as well as Libyan export markets to Europe

and other parts of North Africa.

It is important to note, however, that the analysis here should not preclude a countries

inherent right to decide not to develop its natural gas reserves since such a decision can also

be made in the national interest. Furthermore, it must be noted at the outset that though gas

reserves may be initially deemed as commercially recoverable, the dynamics associated with

delivering the commodity to the market including fiscal policies and incentives (as would be

demonstrated) may in fact make the project non-commercial and gas must in fact be stranded

until such issues are resolved. In cases like these, however, a legal/regulatory framework

must also look into balancing the long-term effect of producing the commodity which might

include tax incentives and or subsidizing for policy purposes. To all these issues the question

derived is; to what extent are legal and regulatory measures stalling the progress of natural

gas development in these regions?

25

Africa's proven gas reserves have grown immensely over the past two decades and in 1995 totalled about 6.3 tcm’s with potential reserves estimated at 17.65 tcm’s in 2010. 26

Supra, note 24

13

2.1.1. Significance of Development of Future Reserves

The above potential demonstrated has several underlying effects for the development of

future natural gas reserves in those regions. The availability of in-house reserves (and thereby

no import dependence), for a developing economy immediately implies the ability for that

country to focus almost entirely on taking advantage of the opportunities in addressing power

sector deficits – a major cause of which is high cost of imported fuels which make power

generation projects especially expensive. With in-house gas policy-makers can address this

deficit from several angles, one being setting various parameters in preference for domestic

consumption (for example a domestic gas obligation), conveniently aided by the lack of

exposure to world prices, a domestic gas obligation (DGO) however, must be designed in

such a manner that guarantees a constant and predictable supply of DGO gas, the producers

exposure to DGO gas must be rewarded in a contractual relationship, then comes designing a

DGO to make it either producer specific or field specific (see later discussions of potential

structures available for DGO gas).

In recent years and as energy security continuously plays centre stage in international

relations supply security alone can elevate a nation‟s relevance on a global scale, and address

the risk of relying on external sources of Energy. For these economies, it is essential that the

development link is not broken by frequent shortages of the fuels needed to spearhead

economic growth. But for nations with reserves enough to surpass domestic use, the right

framework can be implemented to support an export market in order for a producer to exploit

the availability of competitive natural gas markets (see later discussions on this topic).

2.2. Natural Gas Specific Issues & Challenges

2.2.1. Associated versus Non- Associated

There are two main classifications for natural gas. Often a distinction is made between

associated gas (AG) and non-associated gas (non-AG), with non-AG being touted as the

lesser of the evils. This distinction is important in the gas world for several reasons, and could

spell the difference between billions of wasted gas and gas simply just left in the ground.

Looking at the data provided earlier, however, it seems at times, and practically, the

14

difference stipulate that non-associated is more heavily produced (or utilized) than associated

gas.

In view of the fact that associated gas is a by-product of oil-extraction and to add a caveat,

where it is discovered in conjunction with an oil discovery (i.e., the same field) the problem

of the utility of AG arises soon after crude oil is produced from the same well. On the other

hand non-AG, which may also be discovered when the intent is to discover oil, but is

discovered not as a by-product but on its own, has only the added burden of “to produce or

not produce.”

The differences in associated and non-associated become even more glaring when

determining the party who will most bear the market volume risks, or if this risk would be

shared by the producer and buyer.

2.2.2. Associated Gas

There are several problems linked with associated gas (AG) that further adds to the difficulty

of assessing its economic value. One key challenge is the inability to predict to a certain

amount of accuracy production rates from AG fields; this seemingly minor challenge comes

with it a host of problems. External factors such as that governing the extraction of the crude

it is associated with, ultimately determine the rate at which AG is produced. For this reason a

sale agreement between a buyer and seller of such a commodity will take into account this

debilitating factor, and as a result grossly lower the price it would be offered were it non-AG.

Even where financing is secured for those purposes, the payback would be negligible

compared that of a non-AG field. The seller enters a long-term “depletion contract” with the

buyer, and in exchange for volume risk protection the seller promises to sell to the buyer all

the gas that can be commercially produced from the field (see later discussions on volume

allocation). Furthermore for AG the higher costs correlating with the separation of crude and

gas as well as the de-contamination process could mean flaring as a cheaper alternative for

the producer.

15

Low AG premiums, thus, makes it difficult to justify capital expenditure on gathering

systems, gas burning technologies, long-distance pipelines, all of which depend on a constant

and dependable supply of gas.27

Moreover, these low premiums makes AG almost always a

locally consumed commodity, as transportation to international buyers would prove

economically difficult to justify. And where there lacks infrastructure bringing in the gas to

the in-house buyer, flaring would in that case becomes a must. So for developing economies

whose natural gas resources are predominantly AG, a careful assessment must be made as to

the importance of producing such gas and to what extent State aid would be utilised to

develop the gas for local consumption.

The trend in producing countries, especially those in the developing economies, have been

not just to prohibit flaring, but also to require oil companies to hand over gas produced from

these fields to the government for utilisation in the domestic realm. Without further analysis,

however, this may seem to be a solution, but not quite. The issue often arises where policy

very rarely corresponds with implementation or reality. The inclination has been towards

Governments opting to pay much less for AG than they would for non-AG (capital costs are

also rarely compensated fully), creating a great disincentive for oil companies to invest in the

necessary infrastructure to deliver the gas to the government.28

Though in recent years there

have been inclinations towards a flare-free world, the truth is that majority of the Countries

that rely on these policies do not in themselves have the adequate infrastructure to bring gas

to bear, so in actuality although the gas can be handed over to the Government or its national

oil company (NOC), there exists no avenue for its utilisation. In the Nigerian example, a

resulting effect was the development of its LNG export market, but considering that Nigeria

boasts a large percentage of the Continents natural gas reserves, its LNG export business is

relatively un-matured, moreover, its short capacity power sector could desperately do with

gas input.29

In areas with large associated gas volumes, gas can be transported into gathering systems to

supply liquefied natural gas (LNG), methanol, or ammonia, or even power generation plants.

However, for this to be possible several scenarios must be possible:

27

Supra, note 15, pg. 5 28

This pricing of natural gas has been a major issue in Nigeria’s natural gas market 29 As well as other issues the lack of incentive to deal with redundant capacity might also be a contributory

factor in the development of the LNG market in Nigeria.

16

1. High volumes of gas must be dedicated in advance to rationalize the substantial

capital costs. This will prove difficult, considering the uncertainty of volumes coming

from associated fields30

2. The above may be rectified where there exists associated gas fields, supplementary

non associated gas can also offset supply fluctuations, as well as the eventual

depletion of field production.31

3. Where pipelines and gathering systems are not optional the possibility of floating

processing and transportation technologies can meet the demand, however, such

vessels are also capital intensive,32

in addition, a facility would need a steady non

declining gas stream, which often can only be achieved by combining associated

gas with non associated gas from other fields.

2.2.3. Non-Associated Gas

Non-associated gas (non-AG) on the other hand may not be produced at all where there lacks

the necessary infrastructure or market conditions to bring commercial reasoning to the

project. There are situations where exploration is specifically aimed at finding gas, such as in

the North Sea or in the Russian case where, a market is available with the necessary pipeline

facilities for delivery, however, in the developing economies this trend is rare (though

increasing). The advantages therefore of non-AG is that unlike AG it can be left underground

till it is deemed economically viable to continue with development and subsequent

production. Furthermore, non-AG production rates are rarely determined by external factors,

except where Government policy is designed to stipulate the rate of production, but even so a

certain amount of predictability can be assured thereby increasing its the end value of the gas

produced from these fields.

The issue of market imbalance and unpredictability can still be a dissuading factor for

investing in such capital intensive infrastructure for gas delivery. Where there are no essential

export opportunities or persuasive fiscal incentives, non-AG are stranded, that is, left in the

ground waiting in anticipation for a market to develop in its favour. This is the case in Africa

30

Hopper, C., Modular Syncrude Conversion Drives: Oilfield GTL Solution for Associated Gas, SPE Journal of Petroleum Technology, February 2009 31

In this regard government can control depletion rates to maximise the potential of these fields 32

For example, a facility capable of consuming 100 to 150Mmscf/D would cost approximately USD 1 billion

17

where although 50 percent of the natural gas on the continent is non-AG, there still remains

relatively low production rates, and utilization.

2.2.4. Volume Risk Allocation:

A major risk factor to be taken in consideration before the development gas fields is the

assessment of who along the value chain will bear the resulting volume risk where it arises

(that is, the possibility of failure in delivery of the commodity). In a competitive natural gas

market, take for instance mature markets in the US and the UK, the upstream section, that is,

the seller and or producer will usually assume such a risk. Essentially, a mature market is

perceived as a less risky environment, where buyers are available and as such producers need

fewer guarantees to ensure project cash-flow, and so price as stated earlier, becomes the basis

for competition.

Even in a mature gas market, the distinction between associated versus non-associated gas

can also lead to discussions of volume risk allocation, for the mere fact that a producer in an

associated gas field is unable to any degree of certainty determine the depth of gas resources,

nor a proven production rate, he would, as stated earlier take the price hit (because the buyer

is unable to nominate volume ahead of delivery) and sell at below competitive rates. Most

associated gas fields are therefore monetised through „Depletion Contracts‟ (or Seller‟s

Option Contract). This type of arrangement typically signifies the nature of the field in

question, that is, associated. In a depletion contract the buyer contracts to purchase all the gas

that can be economically produced from a particular reservoir, such that he is not able to

nominate a certain volume ahead of time unless the field has produced what it can.33

The volume risk is thereby moved to the buyer, in this regard to gain value or increase the

selling price, a producer can take the volume risk, this can be achieved by managing

production from several fields.34

However, such a method would only make sense where the

possibility exists for linking fields, not to forget the added infrastructure cost implications for

connecting several fields to one delivery point. In an environment that lacks a gas market, the

33

Competition Commission, UK., Types of Contracts for Gas Supply, 2003 at http://bit.ly/zti2cV 34

See for instance North Sea gas example. Shell and Exxon have monetised associated gas through this method for years. Source “Stephen Dow (CEPMLP)”

18

direction is towards encouraging investors, that is, producers necessarily results to the need to

shift that volume risk away from producer and onto the buyer. The later parts of this paper

will discuss how this can be achieved.

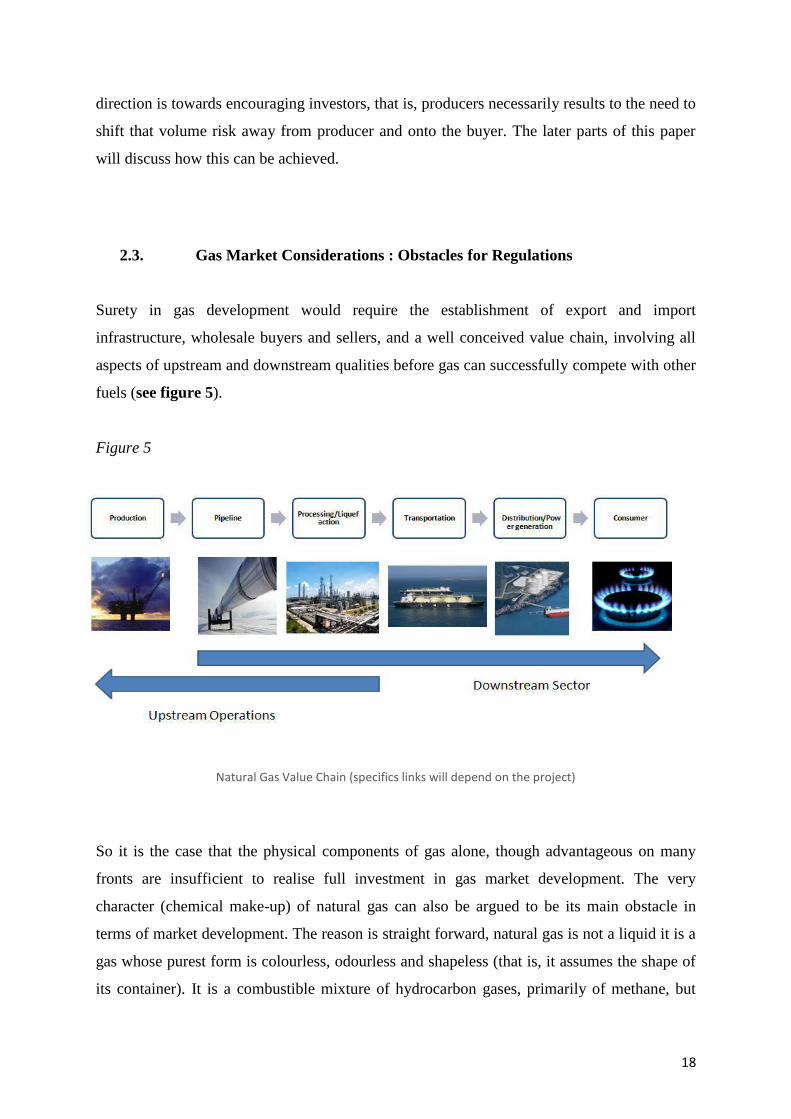

2.3. Gas Market Considerations : Obstacles for Regulations

Surety in gas development would require the establishment of export and import

infrastructure, wholesale buyers and sellers, and a well conceived value chain, involving all

aspects of upstream and downstream qualities before gas can successfully compete with other

fuels (see figure 5).

Figure 5

Natural Gas Value Chain (specifics links will depend on the project)

So it is the case that the physical components of gas alone, though advantageous on many

fronts are insufficient to realise full investment in gas market development. The very

character (chemical make-up) of natural gas can also be argued to be its main obstacle in

terms of market development. The reason is straight forward, natural gas is not a liquid it is a

gas whose purest form is colourless, odourless and shapeless (that is, it assumes the shape of

its container). It is a combustible mixture of hydrocarbon gases, primarily of methane, but

19

can also include ethane, propane, butane and pentane, classified as either „dry‟ or „wet‟. It is

dry when almost purely methane, having removed almost all other associated hydrocarbons.

On the other hand, it is wet when other commonly associated hydrocarbons are present. Its

composition, thus, can vary widely spelling a host of complications for transportation and

storage, as well as create definitional challenges for downstream refinery and pipeline

allocation agreements, especially where different gas fields comingle into a single pipeline

prior to final delivery.35

On the other hand, much can be said for its environmental premium making it a preferred fuel

mainly because of its low emitting rates. Gas burns relatively cleanly, flexible and easier to

concentrate and direct than other fuels. Its premium qualities give it major advantages in

certain industries such as the glass and ceramics industry,36

offering important environmental

benefits. Furthermore the superiority of its environmental qualities over coal or oil provides a

sure bet in environmental assessment and project appraisal for project financing purposes.37

Its non-polluting characteristics therefore, becomes extremely essential, for countries like

China and other emerging markets whose rapid industrial development need to also be

countered with sound environmental standards.

A policy priority in China‟s current power sector is the diversification of its fuel supply,

mainly away from coal (a fuel which is in abundance in the Country) to less polluting fuels

like gas. The security of supply of coal is therefore not the issue but rather the recent trend is

to wean the country off its largest polluter. A gas premium market as a result, would involve

the replacement of fuels producing these high emissions in favour of gas.38

In China‟s case,

however, several obstacles stand in the way of bringing gas to market as the preferred fuel, at

the heart of this is the lack of incentives needed to develop in-house gas fields.39

On the other

side of the spectrum are measures needed to realise the fullest potential of the gas premium,

35

Picton-Turberville, G., ed., Oil and Gas: A Practical Handbook, pg. 187, (London: Globe Business Publishing, 2009) 36

Hurst, C., Davison, A., Mabro, R., Natural Gas: Governments and Oil Companies in the Third World, pg 14 (Oxford, UK: Oxford University Press, 1988) 37

Although on the same token, external factors such as infrastructure development and environmental costs associated with pipeline development might also counter such benefits 38

International Energy Agency, Developing China’s Natural Gas Market: The Energy Policy Challenges, (OECD/IEA 2002) 39

Though realistically speaking the estimated gas reserves in the country are not enough to meet the demand assumptions

20

including the creation adequate market conditions for the competitor „coal‟ as a less desirable

alternative.

2.4. LNG Opportunities and Challenges

Unlike oil, gas must be transported primarily through pipelines. It is also possible to transport

large quantities in containers for shipment, but this process requires either compression or

liquefaction in the form of liquefied natural gas (LNG). The LNG market is rapidly

expanding; there are currently 337 LNG ships in operation. For governments LNG is still

desirable; the growth of LNG, in this regard has emerged as a result of not its costs

effectiveness but more frequently as a flexible and dependable mechanism for nations

(especially those importing) who wish to access the premium qualities of natural gas.40

For a country developing its natural gas market, LNG is a viable option for the main fact that

it provides a producer with additional avenues for monetising his gas fields, that is, it

provides a further incentive, so whereas the decision for a Government to keep a

predetermined amount in-house for local consumption may become a deterrent, such a policy

can be augmented with allowance for export in which case guaranteeing an investor an

avenue for attaining a competitive price elsewhere. The creation of an LNG export terminal

would achieve this, but the question would be who invests in such infrastructure, the answer

would ideally depend on the type of control the Government would want to assume. An

import terminal for LNG could also serve as a possibility for addressing possible shortfall.41

Though LNG provides further monetising opportunities, worldwide the LNG market share

still remains predominately low (LNG is approximately 8 percent of global gas consumption,

with total gas consumption being 24 percent of total energy consumption, so essentially LNG

is 1.9 percent of global energy consumption) this is due in part to its high upfront costs, such

that without a buyer who in turn has the infrastructure to re-gasify as well as pipeline

capabilities for local consumption, the LNG market in practice, and for that reason, does not

seem to be that more advantageous than conventional methods. Typically, only contracted

40

Politically sensitive cross-border pipelines have played an important role in surging up the need for such a flexible transportation option. The Japanese LNG market was borne out of this need. 41

Note, Africa currently has no import terminals

21

LNG ships would attract financing. As a result, LNG carriers are ordered after long term

contracts have been signed between buyers and sellers tying the gas project with appraised

credit-worthy off-takers. Just like a pipeline, the LNG ship is seldom brought to bear on a

merchant basis, considering that the high upfront costs associated would prevent any lender

from financing without careful assessment of an assignable cash-flow.

Often the appropriate means of addressing the high upfront costs of LNG projects has been

through the design of the fiscal policy to ensure risks are balanced by rewards along the value

chain. LNG projects are typically integrated; for financing reasons it usually makes sense for

lenders to consider the entirety of the project as opposed to a segment of it which might

expose the project to further risk. For regulators integrated projects are also highly attractive

with regards to the ability for the projects to also be fiscally „ring-fenced,‟ in that they

essentially remove concerns associated with unfair transfer pricing. 42

On the other hand bold

fiscal moves might prove to be burdensome administratively, as they require a wholly new

administrative practice, such a process might be a challenge for weaker economies.

Another major stumbling block for investors in developing nations has been that the gas

reserves remain largely under state control in many of these countries. “The inability of

domestic consumers to pay anything like the gas prices received in developed countries has

traditionally meant that local gas projects have been developed by governments.” The LNG

market is therefore desirable as governments are keen to increase export revenues. They also

remain equally dedicated to increasing local gas supply and often these two objectives must

be balanced when designing gas specific regulations.

42

Kellas, G., Natural Gas: Experience and Issues, in The Taxation of petroleum and Minerals: Principles, Problems and Practice , pg.169 ( Daniel, P., Keen, M., McPherson, C., (eds.) Oxon, United Kingdom: Routledge, 2010)

22

3. Sector Specific and Similar Sector Approach

As mentioned earlier, at the outset the limitations in developing natural gas markets was often

associated with the perception that as a petroleum commodity, any legal framework must

essentially be similar to traditional (existing) petroleum legal system. Such an oversight is

now predominantly viewed as wrong and in the author‟s view has often barred the realisation

that lessons can be gained from sectors that function similarly to the natural gas sector.

Understanding these similarities it is presumed, would provide alternative avenues for

addressing the challenges that present themselves when developing a natural gas market, on

the other hand, being aware of their key differences might also provide an avenue for

estimating areas where certain results must be avoided.

3.1. Power Sector

Due to the transportation requirements a proportion of natural gas must typically be

consumed in the country where it is produced, in many respects this makes certain aspects of

the gas market similar to the electricity market. Both requiring complex infrastructure

systems to deliver their various qualities to the market, meaning that essentially where a local

market cannot be established investment would ultimately be stalled until necessary

frameworks are designed to meet expectations. Gas utilization is only possible when

production from reserves finds outlets; so just like electricity, each individual field creates its

own unique market space. For this same reason there is no global price for natural gas or

electricity, as there is for oil or coal respectively.

The similarities between the power and gas sectors do not only correspond in terms of market

similarities, they are also complimentary to each other. For many countries especially those

in emerging markets the power and industrial sectors represent the largest (or potentially

largest) consumers of gas. Almost all developing economies have at their core a huge demand

for power, and in most this demand continues to grow at alarming rates. The potential, thus,

for gas in fuelling this demand is grossly untapped. The early realisation of this can spell

growth for both the power and gas sectors. This complimentary relationship also introduces

to policy makers the opportunity to merge the market risks of both sectors providing an

avenue for their simultaneous development.

23

To achieve this end, a regulatory framework must draw on policy intentions and several

considerations must be made, including:

Assessing the importance of gas fired power generation for local consumption

Assessing the regulatory implications of an integrated power project with natural gas

as feedstock

Addressing ways to merge gas and power sector volume and price risks

Determining the domestic obligation (DGO) for gas in power generation and or

assessing any potential subsidies and the effect they may have on the associated gas

investment

Alternatively, the role DGO can play in merging the price and volume risks

Where gas is to be utilised for local electricity generation, it is important such

measures are in place to relate the power agreement with the gas development and

sales agreement to the extent that gas development efforts are not hindered

Addressing the off-take obligations for both the power and the natural gas sector,

involves careful consideration of the contractual matrix needed to deliver the

obligations and careful assessment of risk allocation.

3.2. Mining Sector

The buck doesn‟t stop there, the lessons that can be borrowed from the mining sector is also

very rarely stated or even deeply analysed. One area of correlation between the two sectors is

the very nature of associated minerals that are extracted in relation to the principle mineral

(for our purposes, the associated minerals). The existence of this possibility has given rise to

a number of policy decisions in relation to how mineral rights are allocated. The design of a

mineral rights allocation system in different jurisdictions have at their core the determination

of whether such mineral rights should be allocated for individual minerals, separately, in

conjunction with other minerals that may be found or sometimes what are known as parallel

licenses.

In the petroleum world, the question would be whether or not to separate a gas PSC for

instance, from the oil PSC and the associated consequences, (see more discussion on this

topic in Chapter 6).

24

4. Legal and Regulatory Measures and Risk Mitigating Incentives

Although there have been marked increases in the demand and uses of natural gas, the

obstacles eluded to in the previous chapter still hinder natural gas development in several

regions as the focus on oil is still foremost on the agenda of hydrocarbon exploration, or that

even though there may be interest in exploiting natural gas resources, often the right

frameworks are not in place to realise those goals. Increasingly however, some governments

have entered into contracts with IOC‟s that are solely dedicated to gas utilisation; Saudi

Arabia, Egypt, Peru and Venezuela to name a few are some of those countries. This chapter

intends to examine some of these structures, the idea is to offer an analytical spectrum of

legal measures governments in developing economies with natural gas reserves or intend to

create natural gas markets can adopt. To add a caveat, it is important to note that the

recommendations are not one-size fits solutions each project must be designed taking into

consideration country specific challenges.

Overview:

The basic underpinning of a petroleum legal framework is drawn in the form of a

hydrocarbon law. The law normally sets out the general principles surrounding the nature of

hydrocarbons and provides broad statements and policy principles surrounding their use.

These principles essentially emphasis the States‟ ultimate control of hydrocarbons, broad

statements of aspirations, and basic provisions that are designed to be non-changeable. Those

provisions that may need periodic adjustment, for instance, administrative procedures and

technical requirements, are stipulated in secondary legislation pursuant to the basic law, also

referred to as regulations. These basic structures subsequently pave way for a wide array of

legal arrangements made between the government and the private party.

4.1. Legal Instruments

A number of legal and fiscal instruments exist that address the rights and obligations of the

title, (or right to perform is certain action) granted by government to the contractor. These

legal instruments usually provide express statements of the relationship structure between the

State and the contractor and the extent of contractual entitlement given to the contractor.

Today there are arrangements to explore, develop or produce petroleum between the host

country (HC) and the contractor (or IOC), namely; Concessions (also known as royalty tax

25

Concession/ Explorations

License

Sales Agreement

Production Sharing

Agreement

systems), Production Sharing Contracts (PSC‟s), Service Agreements (SA‟s), and

Participation Agreements (PA‟s). While each of these arrangements can be used to

accomplish the same purpose, they are conceptually different from each other. Each grants

different levels of access or control to the IOC, provides for different compensation

arrangements, and permits different levels of government and or National Oil Company

(NOC) involvement.43

Even with that said a Service Agreement can very often be similar to a

PSC depending on its provisions; it is also the case that many governments exercise a hybrid

system; that contains aspects of two or more types of arrangements, for instance, a PSC with

elements of a concession, such as royalty structures. At the heart of the conceptual

differences lie key risks within each.44

Unlike earlier petroleum agreements, most of today‟s existing arrangements recognize that

rights and obligations of parties in relation to crude oil exploration and exploitation (E&E)

need to be modified for rights and obligations associated with natural gas E&E. However, it

still remains an oversight, in that the risks associated with natural gas exploration all the way

from production to sales arrangements need to be adequately allocated if a gas market is

envisaged. The natural gas risk structure must therefore be reflected in any legal or regulatory

arrangement (see figure 6).

Figure 6

43

Smith E. E., et al, International Petroleum Transactions, 3rd

Edn, page 429, (Rocky Mountain Mineral Law Foundation, 2010) 44

Ibid

Transportation

26

4.2. Risks and Legal Arrangements

4.2.1 Exploration Risks and Legal Arrangements

Exploration projects in the petroleum world involve a complex set of decision making,

encompassing both technical and financial analysis. Unlike oil exploration projects, projects

to source for natural gas alone are infrequent, and are found mostly in regions with mature

natural gas markets.45

This is due in part to the initial motivation to go exploring for oil and

not gas. In developing economies, the prospecting stage often commences with the desire to

explore for oil, since the discovery of oil provides often easier access to its rents, it is on this

premise therefore, that any analysis of exploration risks takes stock of the risks structures

associated not only with natural gas exploration but also within the context of oil exploration

in these regions.

Geological risks – that is, the risk of not finding the resource one explores for, in this case

natural gas. Where the intention is to solely explore for oil, natural gas geological risks are

often merged with that of oil exploration risks. Generally with oil, “reducing the geological

risks or rather the perception of risks will reduce the exploration and development threshold,

and the risk premium required by investors,”46

however, the same cannot be said for natural

gas, for the most part even where the risks of finding gas is merged with of oil, the

corresponding increase in investment interest is not realised mainly because of the level of

perceived risks at the other stages of the gas value chain – this is especially one reason why

considerations of developing natural gas markets has to be viewed with the perceived risks

along the whole value chain.

Financing risks – Considering most petroleum exploration projects are rarely financed

through complex financial loans or instruments,47

it is typically the case that the project

company or consortium pull in their resources to fund the high capital costs. Once again this

risked may be merged with oil if the goal is the find oil, in which case gas financing risks will

be assumed almost entirely by the oil risks. But once again considerations of the risks not

45

Recently heightened by the discovery of the potential abundance of Shale gas 46

Tordo, S., Petroleum Exploration and Production Rights: Allocation Strategies and Design Issues, pg. 4, working paper no. 179, (Washington D.C., World Bank, 2009) 47

Considering banks will rarely take the risk of financing projects without assignable cash flow

27

just upstream but downstream must be kept in mind when designing arrangements for

allocating natural gas exploration risks (if at all).

Where the project entity, chooses to prospect for natural gas alone, the financing risks

involved for natural gas would be considerably more onerous that that of oil financial risks.

Securing structured financed instruments for exploration projects are extremely rare, if at all.

Therefore the Project Company or consortium typically assumes the entire financial burden

through equity participation. Such a risk is taken after complex financial analysis and

forecasting taking into consideration technical data and geological knowledge, this

information is further weighed with the risks involved at the development and production

stages, that is, the flexibility of the arrangements in lieu of the financial commitments made

by each entity involved.48

HC‟s usually represented by their NOC especially in developing

economies are typically carried through the exploration stages.49

The project companies or

partners then work out a complex set of agreements that share the financial burden and risk

among themselves, with cash calls as payment arrangements.

There are a number of ways natural gas exploration risks may be mitigated, one avenue is for

the HC to participate in its share of exploration not on a carried basis but as a paying

participant, thereby all parties in the project funds to facilitate exploration activities in

relation to their participatory interest relieving the project partners from the added financial

burden of a carried partner, a clear risk sharing incentive. Where the HC lacks these financial

resources, a possible avenue to access the funds needed is through sovereign loan facilities,

such as World Bank guaranteed loans, or through alternative financing means. Financings

provided by international lenders will be necessary and in most cases they will need country

risk support facilities provided by multilateral agencies like the World Bank.50

Often country specific or political risks may also play a role especially where project partners

might fear the risk of the HC not meeting it “cash call” obligations. Private sector participants

have often relied on political or country risk insurance from multilateral agencies like the

Multilateral Investment Guarantee Agency (MIGA) to insure them against these risks.

However, insurances of this kind are typical especially for foreign investors entering into

48

Where the company involved is purely participating for the exploratory stages, it would ideally wish to have an arrangement which gives it the flexibility to transfer its portion of the assets upon discovery. 49

Usually as a recognition of their inability or lack of financial resources to take on such capital intensive work 50

Smith, V., Project Finance Review, pg.27, University of Dundee, 2007

28

developing countries. But due to the cash strapped nature of national budgets the risk of

default by the HC is heightened, it is therefore necessary that direct government guarantees

are secured to ensure the ability of the government participant in meeting cash call

obligations. In a country which is in production stages of oil development, the HC can choose

to meet it cash call obligations by allowing its partners in the natural gas exploration phase to

lift a percentage of its crude as additional security.51

Where this is not possible, another

means of further assurances can be through the establishment of offshore or escrow accounts,

a third party mechanism where funds can be pre-allocated by all project partners prior to the

commencement of exploration activities, the third party escrow trustee would then be in

charge of disbursing the fund needed as per the cash calls.

Another method of encouraging gas exploration would be to go the route of non-risk SA‟s,

that is, similar to Egypt‟s approach in the 1980‟s where explorers for natural gas were

guaranteed fair compensation upon the discovery of the resource, and to the extent that most

or all of such gas was surrendered to the Egyptian government as a contribution to its national

reserves.52

Not only is this method supported by sound guarantees to mitigate the later

development and production risks, it also secures some future financial reward, that is, if the

compensation is designed favourably. However, it would be difficult for developing

economies to assess this reward especially where there lacks the financial capabilities at the

onset, moreover, where the gas is associated the difficulty in assessing the reward structure

for an undeterminable amount of gas would prove difficult.

In most cases for natural gas, the risk at the exploration stages has to be linked with the risks

foreseeable also at the development and production phase of the value chain. The intention of

participants would most likely be to be involved in the whole value chain, and also for

lending reasons it makes for lenders to consider the whole value chain, for this reason

security of title is especially vital for the investor in natural gas projects. The right to transfer

the title to an eligible third party if the title holder so feels, the right to assign the title to raise