MIDLANDS STATE UNIVERSITY FACULTY OF COMMERCE DEPARTMENT OF BANKING AND FINANCE AN EVALUTION OF...

60

i MIDLANDS STATE UNIVERSITY FACULTY OF COMMERCE DEPARTMENT OF BANKING AND FINANCE AN EVALUTION OF PRIVATE EQUITY INVESTMENT IN EMERGING MARKETS (1990-2010). BY MARVELOUS NGUNDU STUDENT NUMBER R0825331V SUPERVISOR: MR CHIGAMBA This dissertation is submitted in partial fulfillment of the requirements of the Bachelor 0f Commerce in Banking and Finance Honours Degree in the Department of Banking and Finance at Midlands State University May 2012 Gweru: Zimbabwe

Transcript of MIDLANDS STATE UNIVERSITY FACULTY OF COMMERCE DEPARTMENT OF BANKING AND FINANCE AN EVALUTION OF...

i

MIDLANDS STATE UNIVERSITY

FACULTY OF COMMERCE

DEPARTMENT OF BANKING AND FINANCE

AN EVALUTION OF PRIVATE EQUITY INVESTMENT IN

EMERGING MARKETS (1990-2010).

BY

MARVELOUS NGUNDU

STUDENT NUMBER R0825331V

SUPERVISOR: MR CHIGAMBA

This dissertation is submitted in partial fulfillment of the requirements of the Bachelor 0f

Commerce in Banking and Finance Honours Degree in the Department of Banking and

Finance at Midlands State University

May 2012

Gweru: Zimbabwe

i

APPROVAL FORM

The undersigned certify that they have supervised the student Marvelous Ngundu’s

dissertation entitled An Evaluation of private equity investment in emerging markets

(1990-2010) submitted in Partial fulfillment of the requirements of the Bachelor of

Commerce in Banking and Finance Honours Degree at Midlands State University.

…………………………………………… ……………………………..

SUPERVISOR DATE

…….……………………………………… ……………………………..

CHAIRPERSON DATE

….………………………………………… ……………………………..

EXTERNAL EXAMINER DATE

ii

RELEASE FORM

NAME OF STUDENT: MARVELOUS NGUNDU

DISSERTATION TITLE: An Evaluation of Private Equity Investment in

Emerging Markets (1990-2010)

DEGREE TITLE: Bachelor of Commerce in Banking and Finance

Honours Degree

YEAR THIS DEGREE GRANTED: 2012

Permission is hereby granted to the Midlands State

University Library to produce single copies of this

dissertation and to lend or sell such copies for private,

scholarly or scientific research purpose only. The

author reserves other publication rights and neither the

dissertation nor extensive extracts from it may be

printed or otherwise reproduced without the author’s

written permission.

SIGNED: …………………………………………………

PERMAMENT ADDRESS: 3 Kudu way

M’shumavale

Kadoma

Zimbabwe

DATE: May 2012

iii

DEDICATIONS

This dissertation is dedicated to my parents, brothers and sisters for their unwavering support,

love and compassion. They beat me to it!

iv

ACKNOWLEGDEMENTS

As with any major building project, it takes a great team to make all the elements come

together in a book. I am grateful for all the support I have received whilst researching and

writing up this dissertation.

I would like to thank Mr Chigamba, my supervisor on this dissertation, for his challenging,

yet always supporting, comments and suggestions, as well as for his guidance in my

academic career. Without his expertise, this study would not have been possible. Thanks for

encouraging me to “put my heart on paper.” I would also like to thank my lectures on the

Department of Banking and Finance especially Mrs Santu for her thorough remarks and

insights as well as her continued suggestions and encouragement. My appreciation also goes

to Mr J Nkomazana, “regression guru”, for always being available to lend a helping hand.

A reserved acknowledgment goes to my immediate family for all the financial and moral

support. You know me the best; you love me the most and have supported me in all my

endeavours. I love you all very much. I also want to thank my life partner Misper for

generously giving me a well-needed boost to complete this work. Last but not least I

acknowledge the contribution of my friends especially Donaldson, Raphael, Clever and

Conilius to whom I owe invaluable inspiration and reassurance.

TO PAPA GOD BE THE GLORY

v

ABSTRACT

Over the twenty year period spanning from 1990 through 2010, private equity investments

have grown exponentially, both globally and in emerging markets, making private equity

investors and funds increasingly important actors in emerging markets necessitating the need

to understand how private equity investments influence economic growth through

entrepreneurship. In this study, the researcher examine the hypothesis that private equity

investors in emerging markets are entrepreneurial i.e., are more focused on creating new

firms or growing and globalizing existing ones, based on a sample of ten emerging countries

namely, Zimbabwe, South Africa, Egypt, Nigeria, China, India, Brazil, Mexico, Russia and

Turkey. Using Ordinary least Squares (OLS) regression, the researcher employed E-views 3.1

to examine the hypothesis outlined above. The study found out that private equity investors in

emerging markets can initiate new ventures and grow or globalise the existing firms. The

findings of this study are highly relevant to emerging markets because of their urgent need

for risk capital to finance all kinds of infrastructures. Hence, policy makers in emerging

countries like Zimbabwe should focus on the creation of an adequate setting for a prospering

Private Equity market to support investments, growth, competitiveness and entrepreneurship

activities. On the whole, private equity investment in emerging markets encourages

entrepreneurship activity, a primary catalyst of economic growth.

vi

TABLE OF CONTENTS

APPROVAL FORM ................................................................................................................... i

RELEASE FORM ...................................................................................................................... ii

DEDICATIONS ....................................................................................................................... iii

ACKNOWLEGDEMENTS ...................................................................................................... iv

ABSTRACT ............................................................................................................................... v

TABLE OF CONTENTS .......................................................................................................... vi

LIST OF FIGURES .................................................................................................................. ix

LIST OF TABLES ..................................................................................................................... x

LIST OF APPENDICES ........................................................................................................... xi

LIST OF ACRONYMS ........................................................................................................... xii

CHAPTER ONE: INTRODUCTION ........................................................................................ 1

1.1 Introduction ...................................................................................................................... 1

1.2 Background of the study .................................................................................................. 1

1.3 Statement of the problem ................................................................................................. 4

1.4 Objectives of the study ..................................................................................................... 4

1.5 Hypotheses of the study ................................................................................................... 4

1.6 Significance of the study .................................................................................................. 4

1.7 Assumptions of the study ................................................................................................. 5

1.8 Scope of the study ............................................................................................................ 5

1.9 Limitations of the study.................................................................................................... 5

1.10 Definition of terms ......................................................................................................... 5

1.11 Organisation of the study ............................................................................................... 6

CHAPTER TWO: LITERATURE REVIEW ............................................................................ 7

2.1 Introduction ...................................................................................................................... 7

2.2 Theoretical literature ........................................................................................................ 7

2.2.1 Private Equity defined ................................................................................................... 7

2.2.2 Structure of Private Equity Industry.............................................................................. 9

2.2.3 Venture Capital ............................................................................................................. 9

2.2.4 Leveraged Buyout ......................................................................................................... 9

2.2.5 Mezzanine Investment................................................................................................. 10

2.2.6 Secondaries / Fund of Funds ....................................................................................... 10

2.3 Structure of Private Equity Market ................................................................................ 11

vii

2.4 Overview of Emerging Markets ..................................................................................... 14

2.5 Empirical literature review ............................................................................................. 15

2.6 Private Equity Investments in Emerging Markets.......................................................... 17

2.6.1 Defining Entrepreneurial ............................................................................................. 18

2.6.2 Initiating new ventures through venture capital .......................................................... 19

2.6.3 Green field investments ............................................................................................... 20

2.6.4 Creating new companies through joint ventures ......................................................... 20

2.6.5 Growing and globalizing portfolio companies ............................................................ 20

2.7 Private Equity activity in Emerging Markets ................................................................. 21

2.8 Summary ........................................................................................................................ 22

CHAPTER THREE: RESEARCH METHODOLOGY .......................................................... 23

3.1 Introduction .................................................................................................................... 23

3.2 Unit root test ................................................................................................................... 23

3.3 Cointergation analysis .................................................................................................... 23

3.4 Specification of model ................................................................................................... 23

3.5 Estimation procedure...................................................................................................... 24

3.6 Justification of the variables ........................................................................................... 25

3.6.1 Venture Capital ........................................................................................................... 25

3.6.2 Green field investments ............................................................................................... 25

3.6.3 Joint Ventures .............................................................................................................. 25

3.6.4 Leveraged Buyout ....................................................................................................... 26

3.6.5 Error term in the function ............................................................................................ 26

3.7 Data types and sources ................................................................................................... 26

3.8 Summary ........................................................................................................................ 26

CHAPTER FOUR: RESULTS PRESENTATION AND ANALYSIS ................................... 27

4.1 Introduction .................................................................................................................... 27

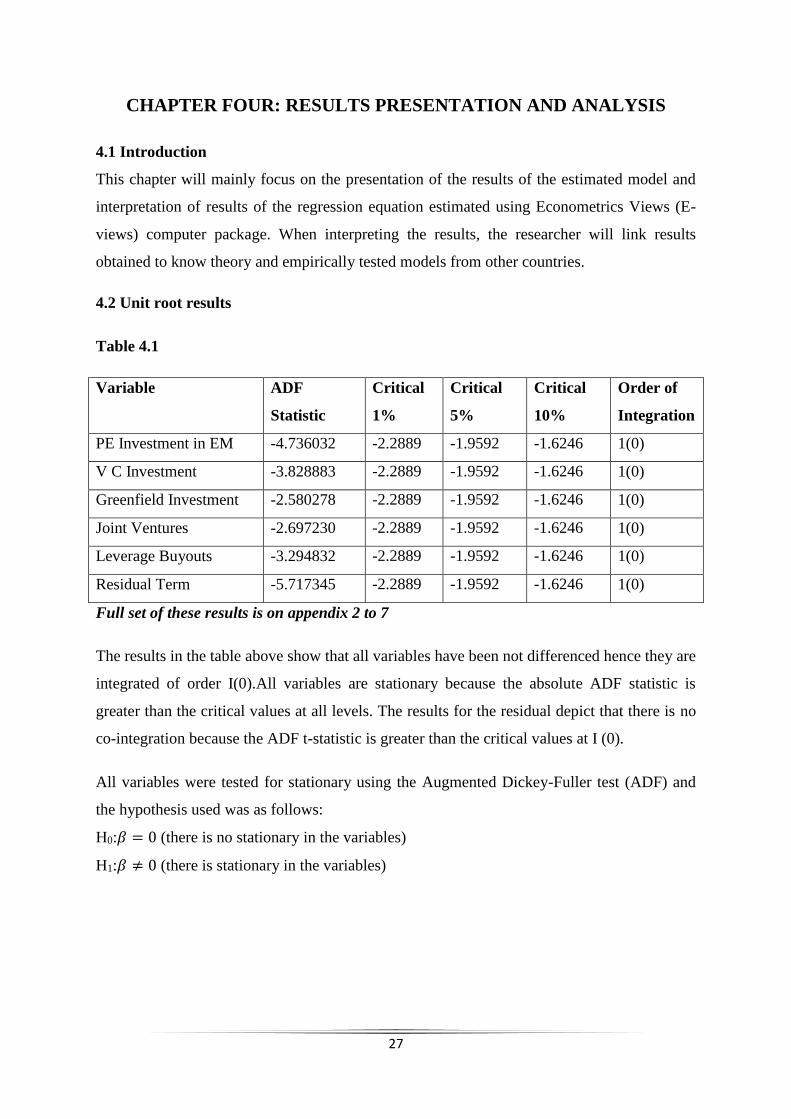

4.2 Unit root results .............................................................................................................. 27

4.3 Econometric model results ............................................................................................. 28

4.4 Interpretation of results .................................................................................................. 29

4.5 Summary ........................................................................................................................ 30

CHAPTER FIVE: SUMMARY, CONCLUSION AND RECOMMENDATIONS................ 31

5.1 Introduction .................................................................................................................... 31

5.2 Summary of the study .................................................................................................... 31

viii

5.3 Conclusion ...................................................................................................................... 32

5.4 Recommendations .......................................................................................................... 32

5.5 Suggestions for further research ..................................................................................... 34

REFERENCES ........................................................................................................................ 35

APPENDICES ....................................................................................................................... xiii

APPENDIX 1 ..................................................................................................................... xiii

APPENDIX 2 ...................................................................................................................... xiv

APPENDIX 3 ....................................................................................................................... xv

APPENDIX 4 ...................................................................................................................... xvi

APPENDIX 5 ..................................................................................................................... xvii

APPENDIX 6 ................................................................................................................... xviii

APPENDIX 7 ...................................................................................................................... xix

APPENDIX 8 ....................................................................................................................... xx

APPENDIX 9 ...................................................................................................................... xxi

ix

LIST OF FIGURES

Figure 2.1: Structure of PE Market.................................................................................12

x

LIST OF TABLES

Table 2.1 Private Equity Investment Stages ..................................................................... 13

Table 4.1 Unit Root Results .............................................................................................. 27

Table 4.2 Correlation Matrix ............................................................................................ 28

Table 4.3 Presentation of Results...................................................................................... 28

xi

LIST OF APPENDICES

Appendix 1 Regression Results ....................................................................................... xiii

Appendix 2 Unit Root Test for PEIEM ........................................................................... xiv

Appendix 3 Unit Root Test for VC ................................................................................... xv

Appendix 4 Unit Root Test for GFI ................................................................................. xvi

Appendix 5 Unit Root Test for JV .................................................................................. xvii

Appendix 6 Unit Root Test for LBO ............................................................................. xviii

Appendix 7 Unit Root Test for Residual ........................................................................ xix

Appendix 8 Correlation Matrix ......................................................................................... xx

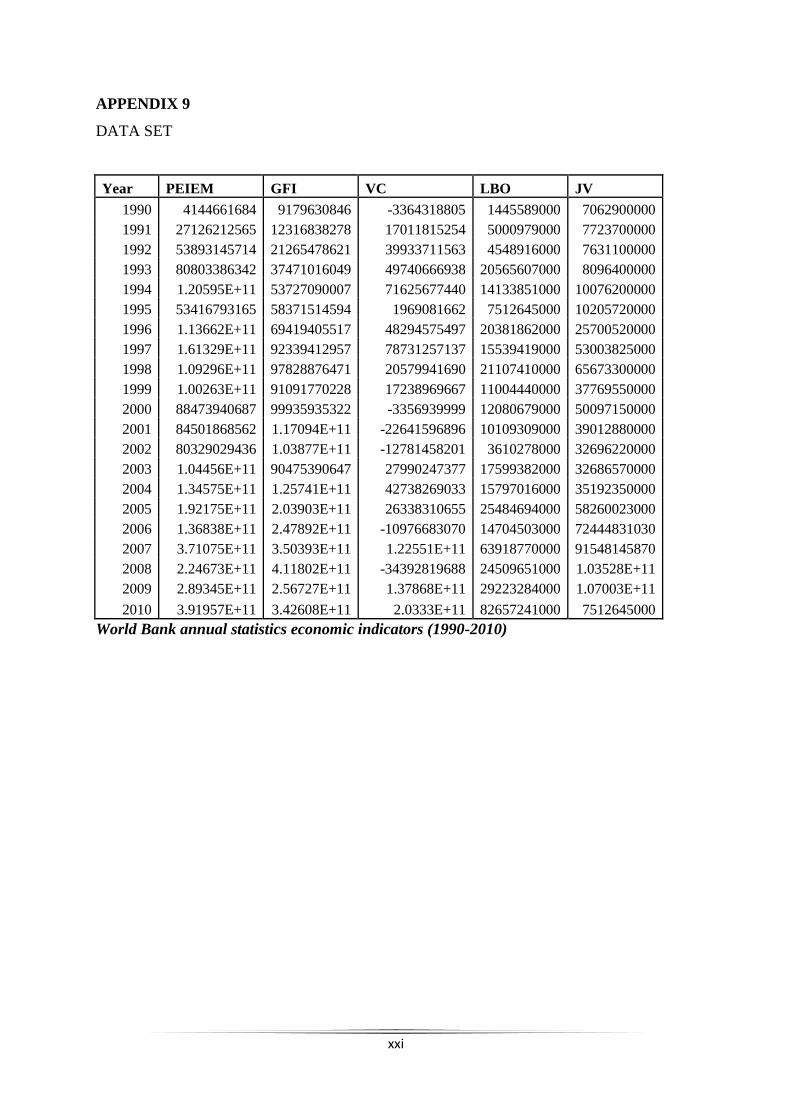

Appendix 9 Data Set ........................................................................................................ xxi

xii

LIST OF ACRONYMS

PE Private Equity

EM Emerging Markets

PEIEM Private Equity Investment in Emerging Markets

VC Venture Capital

GFI Greenfield Investment

JV Joint Venture

LBO Leveraged Buyout

IPO Initial Public Offering

FDI Foreign Direct Investment

GDP Gross Domestic product

IMF International Monetary Fund

EMPEA Emerging Markets Private Equity Association

MENA Middle East and Central Africa

SMEs Small-Medium Enterprises

1

CHAPTER ONE: INTRODUCTION

1.1 Introduction

Investor interest in emerging market private equity is coming somewhat from the desire for

an absolute return, but it is also part of the growing interest in alternative investment

generally. In this study, the researcher evaluates private equity investment in emerging

markets. A brief background to the study together with the problem statement is provided in

this Chapter. The Chapter also contains the Objectives which were pursued by the study

together with the research hypotheses which the researcher sought to test. The significance of

the study and the main assumptions made in carrying out the investigation are also provided.

The Chapter also contains the delimitations or scope of the study and the major challenges or

limitations which the researcher faced.

1.2 Background of the study

Private equity (PE), which was relatively unknown in the early 1980s, has become an

important asset class in global financial markets. A number of studies have documented the

key role that PE plays in developed countries’ entrepreneurial performance as PE-backed

firms create more innovations, employment and growth than their peers. While the structure

and consequences of private equity investment in the developed countries especially United

States and Great Britain are increasingly well understood, far less is known about the private

equity investments in emerging economies. There now exists a broad consensus that a strong

PE investment is a cornerstone for commercialization and innovation in emerging markets.

In the early 1990s, emerging markets were largely characterized by family-owned companies

with limited access to capital markets and small lines of credit through traditional bank

financing. National savings pools were small, current accounts were typically in deficit and

capital markets tended to be shallow. Given such constraints on capital and equity supply,

emerging market companies were attracted to private equity funds as a source of growth

capital. Moreover, emerging markets seemed like fertile ground for this tested and successful

paradigm. With the unprecedented returns generated from the surge in US equity markets,

institutional investors were on the look-out for new opportunities. They also began to worry

that the enormous increase of capital flowing into U.S. private equity would outpace the

supply of high return investments. The door opened wide, therefore, for those with an

appetite for emerging market risk.

2

Foreign fund investors were equally keen on emerging market companies. Target businesses

were often undervalued in an atmosphere of fierce competition for undersupplied capital,

implying higher rates of return on investment and favourable global economic conditions.

The global economy was in a period of growth and relative macroeconomic stability by the

mid-1990s. Inflation and interest rates were down and policy makers worldwide embraced

the wisdom of open markets without barriers to competition securing investors’ confidence in

emerging markets’ manageable risk (Leeds and Sunderland, 2003).Investors also had a robust

appetite for risk and they were handsomely rewarded in the U.S. venture capital tech boom of

the mid 1990s, having acquired significant gains in industrialized financial markets through

private equity investments. The current of globalization aligned investors with potentially

high return investment opportunities while providing target companies funding and expansion

consultancy to gain competitive prowess in global markets.

From little to no private equity history in previous decades, emerging markets quickly

amassed sizable funds within a short period of time. According to the authors of Private

Equity Investing in Emerging Markets, private equity funds ballooned in emerging markets.

“By the end of 1999, there were more than 100 Latin America funds, where virtually none

had existed earlier in the decade. Between 1992 and 1997, the peak years for fund-raising in

Latin America, the value of new private equity capital grew by 114% annually, from just over

$100 million to over $5 billion. In the emerging markets of Asia, about 500 funds raised more

than $50 billion in new capital between 1992 and 1999. As the transition to market

economies in Eastern Europe took hold in the mid-‘90s, the rapid growth of private equity

told a similar story” (Leeds and Sunderland, 2003).

The spurt in investment was further aided by high-risk stakes taken on by bilateral

international development institutions such as the Overseas Private Investment Corporation,

the U.S. Agency for International Development (USAID), the European Bank for

Reconstruction and Development and the International Finance Corporation (IFC).

Development institutions were often among the first to test emerging markets because of their

primary interest in furthering international development through the private sector. Investors’

confidence was cajoled by the participation of these development institutions, whose

successful early funds hinted at high potential returns in emerging markets.

3

Beginning in the late 1990s and early 2000s, American-style private equity funds in emerging

markets began delivering disappointing results in comparison to expectations and similar

funds in industrialized regions. Explaining this failure, Leeds and Sunderland point to

emerging markets’ low standards of corporate governance, limited legal recourse and

dysfunctional capital markets (2003). It is also worth noting that late 1990s fund returns were

uncharacteristically high in the United States and Europe because of the tech-IPO bubble,

providing a skewed and unrealistic measuring stick for emerging market funds’ performance.

In a 2004 industry survey of 26 investors with an aggregate $108 billion managed funds, the

Emerging Markets Private Equity Association (EMPEA) reported overall investor

dissatisfaction with emerging market return on investment rates. Reasons cited centred on

weak macroeconomic variables such as currency volatility and market liquidity, conflicting

cultural perceptions on entrepreneurial cooperation and market access and managerial issues

such as high turnover in target companies, little general partner operational control of

portfolio companies and insufficient risk mitigation strategies (EMPEA, 2004). But in just

three more years, the same EMPEA annual survey conveyed buoyed investor confidence and

optimistic expectations.

In a nut shell, Private Equity firm’s involvement in emerging markets has increased over the

past years fuelled by a number of factors, including these markets superior growth rates in

GDP and their increasingly high returns in recent years of private equity. According to BCG

November 2010 Research titled “Will emerging markets reshape private equity”, between

2005 and 2009, emerging markets share of the total number of private equity deals more than

doubled from 12% to 30%, while their share of total deal value nearly tripled from 8% to

12%.This jump was broadly in line with growth in emerging markets’ global economic

weight.

Given the above background, is private equity solely an exercise of financial engineering or

is it an ownership model capable of producing sustainable improvement in business? This is

an important question as policy-makers address the question of a new financial architecture

for an emerging market in distress like Zimbabwe.

4

1.3 Statement of the problem

While private equity investment (risk capital finance) has been an important component of

the entrepreneurial process in a number of developed countries, it has not realized its promise

in emerging economies. Rather, the risk capital supply in these economies is small, but the

proportionate need for financing new ventures, underperforming and distressed firms with

risk profiles that are unappealing to banks and security markets is high. However, what is

valid for industrial countries should be even more important for emerging markets and if

private equity has indeed been a stimulus for economic expansion in developed nations then

this alternative investment asset class should be more widely adopted and encouraged as a

vehicle for entrepreneurship and economic growth engine, in non-industrialised nations like

Zimbabwe.

1.4 Objectives of the study

The objectives of this study are to:

Determine if private equity investment in emerging markets can create new firms or

grow and globalize existing ones and,

Identify lessons to improve its effectiveness in order to support private sector

development through the use of private equity instruments.

1.5 Hypotheses of the study

This study was done to test the following hypotheses:

H0: Private equity investors in emerging markets are not entrepreneurial

H1: Private equity investors in emerging markets are entrepreneurial i.e. are more focused on

creating new firms or growing and globalizing the existing ones.

1.6 Significance of the study

To the corporate world, the study may get to have an eye opener on the alternative investment

that emerging markets in financial distress like Zimbabwe can adopt to ensure economic

growth. It may also be very useful to private equity investors in improving their performance

in emerging markets, and on the other dimension to emerging markets in attracting this

alternative class of investment. From a theoretical perspective, it adds to the prevailing

theories on private equity investment in emerging markets.

5

1.7 Assumptions of the study

In order to make this research possible, the student has found it necessary to assume that:

All emerging markets share similar common economic attributes

The results attained from the study can also be applicable to Zimbabwe since it is also

an emerging market.

The sample chosen is a true representative for entire emerging markets.

1.8 Scope of the study

The study was conducted in Zimbabwe and it incorporates a sample of ten emerging markets

two from each of the following five regions; Southern Africa, MENA, Emerging Asia, East

and Central Europe and Latin America. The data set used in this research is purely secondary

annual data for the period spanning 1990 through 2010.

1.9 Limitations of the study

In conducting this study, the researcher faced the following challenges:

Most of these studies focus on private equity transactions in developed countries using

empirical studies of completed and exited transactions. Similar empirical studies are hard

to replicate in emerging markets due to data limitations, nascent level of private equity

transactions and the fact that most transactions are recent and have not exited yet.

Lack of rigorous studies focused on successful entrepreneurs in emerging markets. At

present, such work is limited to a handful of case studies. Are there common features of

successful entrepreneurship in developing countries, and to what extent are they different

from features of successful entrepreneurship in places such as the United States?

1.10 Definition of terms

The researcher use the term “portfolio companies” to refer to companies that receive

private equity investments, and are hence part of the portfolio of companies owned

(fully or partially) by the private equity firm or fund.

The total value of a company acquired by private equity, sometimes referred to the

enterprise value, includes both equity and debt.

6

1.11 Organisation of the study

This Chapter aimed at introducing the study by providing all relevant information and

orienting the reader with the contents of the research. The Chapter outlined among others the

Statement of the Problem, the Objectives of the study and the Research hypotheses to be

tested by this study. The study is organised into five chapters. Following this introductory

chapter is chapter two in which the theoretical framework is presented basing on previous

emerging markets private equity literature. Based on this theoretical background, a private

equity model is proposed, including hypotheses to be tested. Chapter three describes the

research methodology and also discusses the methodology of spanning tests. The research

methodology for this dissertation is predominantly quantitative. Hence, the research is

derived from industry-related books, journals and articles. Chapter four reports the findings

of the study, it presents and interprets test results and finally chapter five will summarise all

work done in the study and provide conclusions and recommendations pertaining to the

findings in chapter four.

7

CHAPTER TWO: LITERATURE REVIEW

2.1 Introduction

This chapter discusses theoretical and empirical literature concerning private equity

investment in emerging markets. Literature has not yet produced a fully-fledged model of

private equity investment applicable to the context of emerging economies as compared to

other disciplines such as developed markets especially USA and UK. Thus there is a need for

empirical studies that test the validity of private equity investment theory in emerging

countries.

2.2 Theoretical literature

The impact of private equity investment has been studied in the literature from several angles,

but most of these studies focus on private equity transactions in developed countries, using

empirical studies of completed and exited transactions. Similar empirical studies are hard to

replicate in emerging markets due to data limitations and the fact that most transactions are

recent and have not exited yet. However, since 1990s, there has been a ray of sunshine for the

hard-pressed private equity industry in emerging markets because of their secular and

assumed economic growth story. Hence, many private equity investors are looking to the

worlds emerging economies in private equity instruments and strategies to seek optimal

returns in opaque or inefficient markets although these investments carry increased risk.

2.2.1 Private Equity defined

Over the past few decades, financial investors in developed countries have increasingly

diversified their portfolios with a view to broadening their exposure to different sectors and

regions within an ever changing global financial arena, while still seeking higher returns on

invested capital. This phenomenon was a main driver behind the formation of alternative and

innovative asset classes such as private equity.

According to David Snow (2007) in his primer,” Private Equity: A Brief Overview”, private

equity, in a nut shell, is the investment of equity capital in private companies. In other words

private equity refers to medium to long-term shareholder capital investment in private

companies as opposed to publicly listed companies. In broadest sense, it is an alternative

asset class investment that can be used as a means of FDI and provides investors (both

individual and institutional) with professionally managed investment vehicles for equity

investing in unregistered securities of private and publicly-traded companies (Fenn, Liang

8

and Prowse 1995). Sami explained private equity and its function at a 2002 Massachusetts

Institute of Technology (MIT) Entrepreneurship Centre conference, “Venture Capital in

Turkey.” Private equity is “capital to enterprises not quoted on a stock market. Private equity

can be used to develop new products and technologies, to expand working capital, to make

acquisitions, to strengthen balance sheets and to resolve ownership- management issues”

(Sami, 2002).

Moreover, (Leeds and Sunderland 2003) proposed that whether in developed or developing

countries, a broad range of companies have a risk profile that inhibits their ability to raise

capital through conventional channels, such as borrowing from banks or issuing public

securities. Some are too new to have a convincing track record, others are over-burdened with

debt, and still others have opaque financial reporting standards that discourage investors. At a

certain stage of growth, however, these firms can no longer compete effectively without

making new investments that are too large and costly to be financed from within. Private

equity fills this gap between self-financing and conventional capital market activity. Target

firms may be entrepreneurial start-ups, more established small and medium size firms, or

troubled companies that investors perceive as undervalued (i.e. buy-outs).

According to Fischbein (2005), private equity firms invest in new or existing enterprises with

the purpose of increasing their value over the short or medium term. Private equity funds

invest in different situations, including buyouts, where the fund invests in existing (often

distressed) companies through the acquisition of a significant or controlling stake; venture

capital, where they invest in start-up ventures, often based on technological innovations; or

growth capital, where they provide capital to fast-growing companies (Learner and leamon

2008).

Private equity funds maintain their investments for a limited period of time, typically five to

ten years (Fourie, 2008). Fenn et al (1995) suggest that during this period, the portfolio

company, in the case of buyouts, undergoes financial and operational restructuring or

achieves its growth targets, or in the case of new ventures, the start-up matures. At the end of

this period the private equity fund exits the investment by selling the company through an

initial public offering (IPO) in the stock market, to other companies (trade sale), or to other

financial investors (secondary buyout). Private equity funds usually capture significant profits

that exceed the performance of publicly-traded companies; however, these returns reflect

9

higher risks and volatility, along with the illiquid nature of the investments during the

investment period. Further details of all private equity investors are described below.

2.2.2 Structure of Private Equity Industry

According to Jonathan Rotolo (2003), in his document entitled, “Centre for private equity and

entrepreneurship”, private equity industry is generally composed of four major types of

investors: Venture Capital, Leveraged Buyout, Mezzanine, and Secondaries / Funds of Funds

investors. He explained each of the variables as follows:

2.2.3 Venture Capital

A venture capital fund invests in early stage companies in need of capital for growth. Such an

equity investment is often structured as a preferred stock security. It is rare for a venture

capitalist to structure an investment in an early stage company as a straight debt instrument,

as the start-up with unproven products and cash flow constraints would be unable to make the

interest payments. Venture capitalists will usually take a minority, non-controlling stake in

the company and may often syndicate the risk of the investment among a number of firms.

Venture capital investments typically proceed according to a number of different stages. A

pure start-up company will obtain its initial financing through a “seed round.” This round

may not even be sourced from a venture capitalist but rather from an angel investor. An angel

investor is a wealthy individual, acting alone or in a group, that makes small investments of

his or her own personal capital in early stage companies. If the seed round is successful, the

company will often require several rounds of venture financing before the investors are able

to exit their investment through an initial public offering (IPO) or, more commonly, a sale to

a strategic investor.

2.2.4 Leveraged Buyout

A company entering into an LBO is typically a mature but underperforming entity with a

proven product and stable cash flows. Often, an LBO candidate is a subsidiary of a larger

company that has been underperforming or has become non-essential to the parent company’s

operations. An LBO fund is unlikely to undertake a transaction with a high growth

technology company due to its unpredictable cash flows. Cash flow is essential to make

interest payments on debt. Unlike a venture capitalist, an LBO investor will typically take a

control position in the company, investing equity and structuring a combination of loans from

various lending sources.

10

In analysing a transaction, the LBO investor will typically value a business based on a certain

multiple of its EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization).

The debt used in the transaction will be raised from the public and/or private markets through

the issuance of high yield bonds and the commitments of commercial banks and other

institutional lenders. The percentage of equity used in a transaction will vary depending on

the investment climate and the projected cash flow of the company compared to its debt

payments. Once the transaction has closed, the LBO firm will seek to improve the company’s

internal processes and structure so as to maximize its free cash flow available for interest

payments and investments in growth projects. Once value has been created, typical exits

include IPO, sale to a strategic buyer or sale to another LBO fund.

2.2.5 Mezzanine Investment

A mezzanine investor is somewhat different from other direct private equity financiers due to

its preference for investments in debt-like securities. A mezzanine investor receives securities

which have greater seniority than equity in a company’s capital structure, typically at the

subordinated debt level. Such securities may feature an accumulating or current pay dividend

and will often include equity warrants. Due to its lower risk tolerance and investment in less

risky securities, the mezzanine investor typically receives a lower return than other private

equity investors. These funds’ ability to generate returns are somewhat dependent on the IPO

market since mezzanine financing is typically used to bridge the financing gap from the time

a firm decides to issue public securities to when it is actually able to execute the sale of these

securities. Recently, mezzanine funds have gained popularity and multi-billion funds have

been raised.

2.2.6 Secondaries / Fund of Funds

A secondaries fund is different from other private equity vehicles in that it does not invest

directly in operating companies. Rather, it purchases interests in existing private equity funds,

often at deep discounts, from limited partners who choose to monetize their investment

before the typical 10-year period of a partnership has been completed. Similarly, a fund of

funds investor is an asset manager that allocates capital among a number of private equity

funds, including both venture and LBO funds. Through this approach, the fund of funds

manager offers diversification and expertise to certain types of limited partners, such as small

11

endowments and foundations that do not have the staff to manage the investment process

effectively.

2.3 Structure of Private Equity Market

According to Prowse (1998), the growth in private equity is a very good example of how

organisational innovation coupled with regulatory and tax structures can lead to increased

interest and activity in a specific market. The primary purpose of private equity was initially

to fund risky start-ups and provide management support for such start-ups. The private equity

market has seen significant growth since the early 1980s and has become an important

mechanism for channelling capital through national and international markets, and funding

business activities at various stages of development. In general, however, the private equity

market has received relatively little attention in academic literature compared with other

financial innovations. This may partly be due to the nature of private equity transactions;

information about which is not always easily accessible.

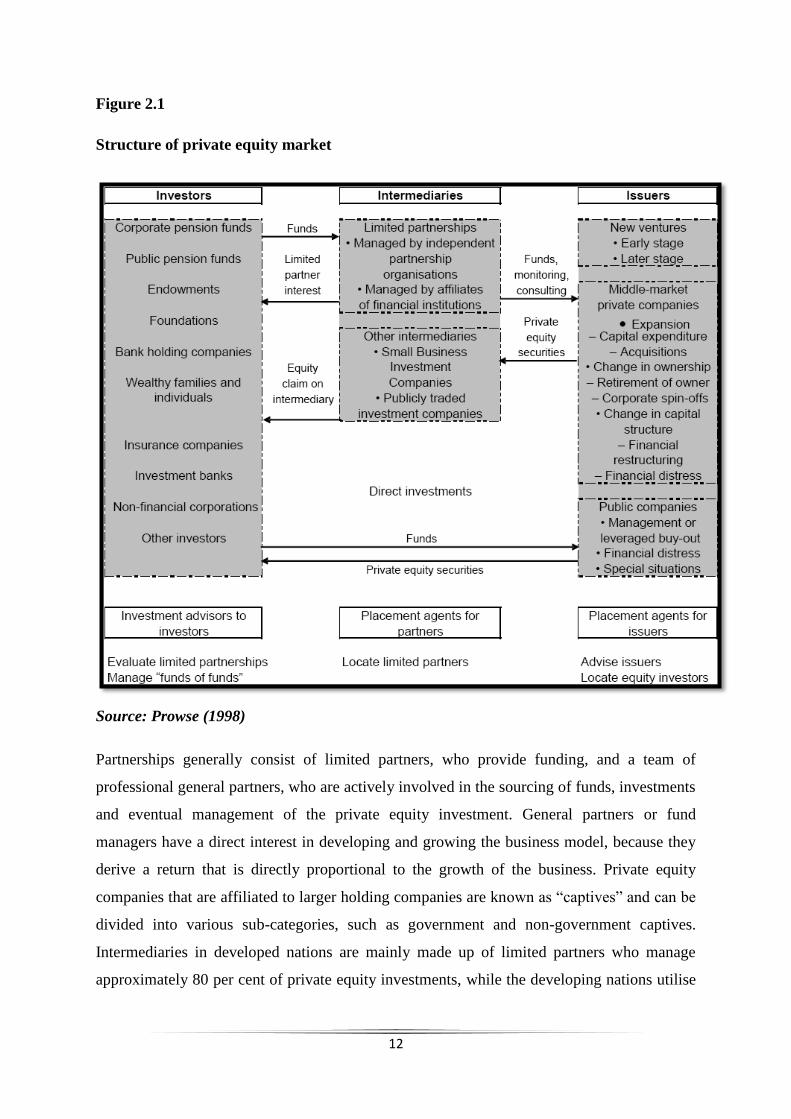

The basic structure of the private equity market is explained in Figure 2.1. The organised

private equity market has three main role-players, namely (1) investors, (2) intermediaries

and (3) issuers of private equity. The arrows in Figure 2.1 indicate the activity and the flow of

that activity between the role-players. Pension funds, insurers and other investment

companies are the main contributors on the investment side. The main reasons institutional

investors may choose to invest via a private equity model is the expectation that risk adjusted

returns will be higher than on other investments, as well as the implied benefits that

diversification into private equity brings into their overall portfolio. The relationship between

the investors and intermediaries often takes the form of a partnership.

12

Figure 2.1

Structure of private equity market

Source: Prowse (1998)

Partnerships generally consist of limited partners, who provide funding, and a team of

professional general partners, who are actively involved in the sourcing of funds, investments

and eventual management of the private equity investment. General partners or fund

managers have a direct interest in developing and growing the business model, because they

derive a return that is directly proportional to the growth of the business. Private equity

companies that are affiliated to larger holding companies are known as “captives” and can be

divided into various sub-categories, such as government and non-government captives.

Intermediaries in developed nations are mainly made up of limited partners who manage

approximately 80 per cent of private equity investments, while the developing nations utilise

13

various other mechanisms for fund structuring due to a lack of legal structures that allow the

establishment of limited partnerships (Lerner and Schoar, 2004).

The issuers (targeted investments) of private equity vary considerably in their size and

motivation for raising funds through this channel. One of the common characteristics shared

by smaller issuers is the difficulty they have in raising financing from debt or public equity

markets, and they thus opt for the more expensive private equity market (Prowse, 1998). The

last set of role-players in the private equity industry is the “information producers” or agents

and advisors who advise on possible target companies, identify sources of funds for private

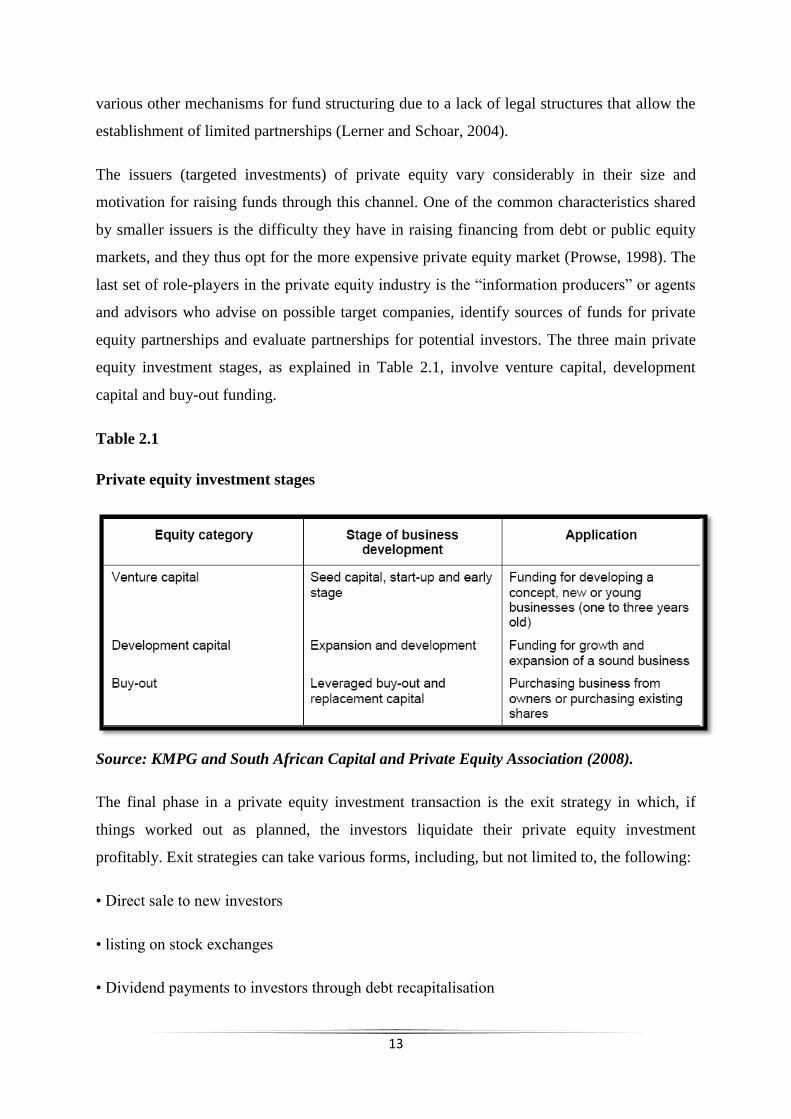

equity partnerships and evaluate partnerships for potential investors. The three main private

equity investment stages, as explained in Table 2.1, involve venture capital, development

capital and buy-out funding.

Table 2.1

Private equity investment stages

Source: KMPG and South African Capital and Private Equity Association (2008).

The final phase in a private equity investment transaction is the exit strategy in which, if

things worked out as planned, the investors liquidate their private equity investment

profitably. Exit strategies can take various forms, including, but not limited to, the following:

• Direct sale to new investors

• listing on stock exchanges

• Dividend payments to investors through debt recapitalisation

14

• Secondary buy-out by another private equity firm.

In short, private equity is both an asset class and an investment strategy. Distinguishing

between the private equity asset class and the private equity investment strategy can be

confusing and creates challenges for asset allocators (Tom Idzorek and Ibboston Associations

2007). Ideally, one could invest in a basket of all private corporations in which the weights of

the companies in the basket are based on their true values. Such a basket would be a true

representation of the private equity asset class. When investors make an allocation to private

equity, it is not a passive investment in the basket of all private companies that form the

private equity asset class. Rather, for most investors, the allocation to private equity is an

investment in a skill-based strategy in which the two primary sub-strategies are leveraged

buyouts and venture capital. The fragmented structure of the private equity market is such

that private equity investors cannot fully-diversify away from private company specific risk;

thus, all private equity investments are a mixture of systematic risk exposure to the private

equity asset class and to private company specific risk.

2.4 Overview of Emerging Markets

The Emerging Markets was a term coined by World Bank economist Antoine W. van

Agtmael in 1981 in reference to nations undergoing rapid economic growth and

industrialization. The term is often used interchangeably with 'emerging and developing

economies'. The IMF classifies 150 countries as Emerging Markets based on the composition

of countries' export earnings and other income from abroad; a distinction between net creditor

and net debtor countries; and, for the net debtor countries, financial criteria based on external

financing sources and experience with external debt servicing.

In addition, the term “emerging market” is used to describe the economies of high-risk

countries with nascent financial markets. In an International Monetary Fund (IMF) working

paper entitled What is an Emerging Market?, Mody argues that emerging market economies

are characterized by “high levels of risk, higher volatility than advanced industrialized

economies, the absence of a history of foreign investment and their transition to market

economies.” (Mody, 2004).

Moreover, the term emerging market, coined by a World Bank Economist in the 1980s, refers

to the market activity in countries that are considered to be in a transitional phase between

developing and developed status. Emerging markets are countries that are working to

15

restructure their economies to interface with market-oriented globalisation, providing

opportunities in trade, technology transfers, and FDI via open door policies. These countries

typically have large population and resources base, and are abandoning traditional state

interventionist policies to seek sustainable economic growth. Emerging markets are the

globe’s fastest growing economies and play a part in contributing to the world’s explosive

trade growth; in time they are projected to become more significant buyers of goods and

services than their industrial counterparts. Among others, Zimbabwe is one of these

economies.

2.5 Empirical literature review

The impact of private equity on the portfolio companies that they acquire has been studied in

the literature from several angles, including impact on labor, wages and employment

(Kearney 2007), productivity (Litchtenberg and Siegel 1987), performance and growth

(Taylor and Bryant 2007), innovation, in the form of investments in research and

development (litchtenberg etal 1990), and governance (Jensen 1989).

Hellmann and Puri (2002), and Kortum and Lerner (2000) show that private equity backed

companies are more efficient innovators. Belke et al. (2003) and Fehn and Fuchs (2003)

prove that they create more employment and growth than their peers. Levine (1997)

documents well the role of PE funds in fostering innovation and competitive firms, and

indeed, there now exists a broad consensus that a strong PE market is a cornerstone for

commercialisation and innovation in emerging economies.

The overarching hypothesis in this type of research is that private ownership of companies by

private equity funds affects their behaviour and performance, compared with public

ownership in the form of publicly-traded corporations. Historically, this research has been

motivated by a vigorous debate in developed countries with a long history of private equity

transactions on whether private equity ownership, especially in leveraged buyout (LBO)

situations, has a positive or negative impact on the portfolio companies. On the one hand,

proponents argue that private equity ownership improves the governance and increases the

productivity and profitability of otherwise distressed or low-performing companies.

(Rappaport 1990) argues that private equity ownership provides a short-term “shock therapy”

that improves the performance and governance of distressed or low-performing companies.

(Jensen1989) argues that the concentrated ownership of private equity firms in LBO

16

situations provides a superior ownership and governance structure over the long term,

compared to the public corporation model. On the other hand, opponents argue that private

equity firms capture significant financial profits by taking a short-term approach by

aggressively cutting costs, reducing employment through layoffs, and reducing investments

in the future of the company (for example in research and development).

The most comprehensive look at the impact of private equity on portfolio companies came in

a recent set of working papers on the globalization of alternative investments and the global

economic impact of private equity, published by the World Economic Forum 2008, which

examined these effects through several large-scale econometric studies using a data set of

global private equity transactions executed over the past three decades, and through six case

studies of private equity transactions in Europe, China and India. In addition to the literature

covering the LBO model, there is an extensive literature covering venture capital in

developed countries, and its role in supporting entrepreneurial ventures (Hellman etal 2002;

Gompers and lerner 2004); however, there is limited literature covering venture capital in

emerging markets.

Even though, the urgent need for capital in emerging markets is evident. The growth potential

is enormous and deserves capital to be exploited. This capital can be provided by financial

institutions that specialise in risk capital investments in SMEs or young firms. Hence, Da

Rin,M Nicodano and Sembelli (2006) argue that policymakers should focus on the creation of

an adequate setting for a prospering PE market to support investment, growth,

competitiveness, and entrepreneurial activities, especially in emerging countries . However,

the risk capital supply is rather small in emerging markets, even if institutional investors are

increasingly looking internationally for new investment opportunities. Armour and Cumming

(2006) confirm this rationale and show that government programms often hinder rather than

develop of PE markets.

One would expect emerging regions to attract PE investors due to the assumed economic

growth rates, and the proportionate need for financing, especially for non-quoted

corporations. Gompers et al (1998) examines the forces that affect independent PE

fundraising in the US. They conclude that regulatory changes affect pension funds and

overall economic growth, while fund specific performance and reputation affect fundraising.

They point out that there are more attractive opportunities for entrepreneurs if the economy is

large and growing. Wilken (1997) argues that economic development facilitates

17

entrepreneurship, as it provides greater accumulation of capital for investment. Romain and

Van Potterlsberghe de la Potterie (2004) find that PE activity is related to GDP growth.

2.6 Private Equity Investments in Emerging Markets

While this body of empirical literature provides an understanding of the impact of private

equity on portfolio companies, some of the findings are primarily based on transactions data

from developed countries, and it is not clear if they can be extended to emerging markets.

Most of these studies are based on transactions in the United States and the United Kingdom,

and even when the data set includes global transactions, the majority of these transactions are

still in developed countries.

These large-scale empirical studies cannot be replicated for emerging countries’ private

equity in the near future because of the limited number of transactions, and the fact that most

of these transactions were initiated over the past few years and have not yet been exited

(Lerner, Stromberg and Sorensen 2008). From a theoretical point of view, the researcher

expects the outcomes of these studies to differ between developed countries and emerging

countries due to several factors. Among these factors are the different market conditions and

stages of development; the different value creation strategies used by the private equity firms;

and, the difference in the companies acquired in terms of their size, business challenges,

governance, and management capabilities.

For example, the typical business model for private equity funds in developed countries,

especially in leveraged buyout transactions, is to acquire companies that are suffering from

financial, operational or management problems, and to restructure them to become more

profitable and hence, increase their value. The restructuring process, more often than not, is

associated with replacing management, changing the financial structure to include higher

leverage, aggressively cutting costs and reducing labour, downsizing or closing less

profitable business units and, sometimes, breaking up the company into smaller entities that

may be more valuable separately, or divestment of some assets, especially real estate assets

that maybe of high cash value on their own.

However, analysts observe that private equity transactions in emerging markets show

different value creation strategies, with a greater emphasis on growth. For example, changes

in management are focused on strengthening and professionalizing the management team;

changes in governance are focused on establishing a board where it did not yet exist

18

(especially in recently privatized state-owned enterprises, or family-owned businesses) or

adding stronger members to existing boards; changes in financial structure, while still

benefiting from high leverage, are focused on providing capital for new investments in new

facilities or on regional/global growth. For example, Fang and Leeds (2008d) cite a similar

trend in India and extend this argument to other emerging economies at similar stages of

development.

Like most private equity transactions in India, as well as other emerging markets, it is

noteworthy that these cases do not fit the profile of US and European buyouts both involved

minority investments rather than control, leverage was not a factor, and although major

financial and operational restructuring was extremely important, neither transaction involved

disruptive layoffs, management changes or other features that have been targeted by critics of

Western buyouts. On the contrary, the cases illustrate that for economies like India that are in

the midst of major structural changes, there are ample opportunities for more traditional

“growth capital” investments in companies that are expanding rapidly, especially in sectors

like retail and telecoms that are undergoing consolidation. By contrasting the differences

between the private equity value creation strategies in developed countries versus emerging

markets, this study hypothesize that the impact on the portfolio companies is substantially

different, and likely to be positive and entrepreneurial.

2.6.1 Defining Entrepreneurial

Schumpeter (1961) puts the entrepreneur at the core of economic growth, as the innovator of

new ideas, the risk taker, the agent of change, and the creator of new businesses. In this study,

the research approach focuses on understanding these entrepreneurial value creation

strategies used by private equity firms in emerging markets and how they impact the portfolio

companies. Specifically, the study hypothesize that private equity firms have a positive

impact on the companies that they acquire in emerging economies because they act as

catalysts for initiating, growing and globalizing portfolio companies. In other words, when

private equity firms adopt these growth-oriented value creation strategies, they are likely to

create positive outcomes for their portfolio companies as well as the broader economic

development. Private equity funds initiate new companies through “green field” investments,

venture capital investments, or by financing new joint ventures; they grow these companies

by investing in new operations, manufacturing facilities, or systems; and they expand their

scope of operations from domestic markets to regional and global markets. By doing so, they

19

contribute to economic competitiveness in emerging markets. In this context, private equity

firms play the role of a Schumpeterian entrepreneur.

While initiating new ventures has often been in the realm of individual entrepreneurs; an

analysis of the model used by Ayman Ismali (2010) to investigate the entrepreneurial impact

of private equity investment in Egypt from 2003 to 2008 shows that private equity firms are

actively engaged in initiating new companies as well as in supporting local entrepreneurs. He

suggested that there are three different business models used by private equity firms to

initiate new companies: venture capital, green field investments, and joint ventures. Ismali

(2010) expressed his model to fit the econometric function as follows:

PEIEM = f (VC,JV,GFI) where PEIEM is private equity investment in emerging markets, VC

is venture capital, JV is joint venture and GFI is greenfield investment. His results showed

that the above mentioned variables are significant to be used by private equity firms for

initiating new ventures, growing and globalising the existing firms.

2.6.2 Initiating new ventures through venture capital

Just to add to what have been discussed about this variable, Ismali (2010) define venture

capital (VC) as the typical business model used in developed countries to invest in start-up

companies. Venture capital firms undertake risky investments in unlisted start-ups or

companies with high growth potential. Venture capital can be broadly classified based on the

stage of development of the venture: Seed capital is used by start-ups to finance the early

stages of product innovation and company building; second round financing is used by young

companies to further develop or expand the range of products; and development financing is

used by established companies to develop alternative products or expand through

acquisitions. The venture capital business model is based on a portfolio approach, where the

fund invests small amounts of money in a large number of start-ups, with the expectation that

many of them would fail or have limited success, and the hope that one of them would

become a blockbuster success that would provide significant profits on exit. Start-ups

supported by venture capital are usually based on innovative business models or new

technologies, where the market potential has not been proven or sized yet. They are usually

risky and carry a high potential for failure. Large private equity buyout funds rarely invest in

early-stage ventures that have not yet proven their success.

20

2.6.3 Green field investments

Another business model that some of the large private equity firms in emerging markets have

adopted is initiating large “green field” companies in capital-intensive industries. These are

industries where the private equity firm identifies an attractive opportunity; however, there

are no existing companies operating in this area that they can acquire and grow, so they

proceed to initiate a new business.

2.6.4 Creating new companies through joint ventures

Another business model used by private equity firms to initiate new companies is through

joint ventures (JV), which are partnership agreements between two or more companies to

embark on a new business. In many situations, one of the companies is a multinational

corporation that brings a specific product or manufacturing knowledge to the venture and the

other partner is a local partner with market knowledge, distribution network, or privileged

market access. Private equity firms join this venture as a provider of capital and business

knowledge.

These three business models venture capital, green field investments, and joint ventures

highlight how private equity is initiating new companies in emerging economies, where

private equity funds act as both the financier and risk taker. Throughout the past years, where

the private equity model showed rapid growth, these funds were part of the creation of scores

of new businesses in technology, infrastructure and other industries, with clear contribution to

employment and economic growth. Absent the private equity model, it is unclear which, if

any, of these ventures would have been initiated.

2.6.5 Growing and globalizing portfolio companies

Growing a business seems like an intuitive goal that all companies would aspire toward, but

that is not always the case. There are three reasons why companies do not always try to grow

their business: (i) lack of will to grow, (ii) lack of skill to grow, or (iii) lack of capital to

grow. The first is a matter of risk aversion, especially in many small and medium family

businesses, where the owners may be satisfied with the profits generated, and may not be

willing to take additional risk to grow the business. For example, Donckels and Fröhlich

(1991) compare objectives, values and strategic behaviour of family and nonfamily

businesses using observations of 1,132 small and medium enterprises in eight European

countries. They find that family businesses are typically risk averse, inwardly-focused, and

demonstrate a conservative strategic behaviour. “Risk aversion and fear of losing control of

21

the business lead many family businesses to seriously limit their growth potential by not

adopting generally accepted financial management policies.” This risk averse behaviour is

often compounded by the limited skills and human capital, especially in technical, marketing,

or product design areas, and the limited access to capital to finance the growth opportunities.

2.7 Private Equity activity in Emerging Markets

So why is there such a strong market for PE in the United States, or the United Kingdom, and

why is activity zero or close to zero in many emerging countries for example Zimbabwe?

Spatial variations in PE activity result from numerous factors. Partly, they can be explained

by built-in bias mechanism. The whole investment process from institutional investors (the

Limited Partners or LPs) to the finally-backed corporations is geographically biased: the

largest, most prominent and most active institutional investors in the PE asset class are

located in the United State PE market. However, and not only in the US, institutional

investors allocate their capital via chains of agents and networks in certain regions, and

among countries. These allocations follow, in principle, a simple rationale: First, there is a

professional community required to support transactions and to establish the capital supply

side. Second, there must be expectation for demand of the committed capital.

The last elements along the chain of agents are private equity funds (the General Funds or

GPs). They prefer spatial proximity in their investments to facilitate the transaction processes,

monitoring and active involvement. It is popular for GPs to focus on a particular region, or

just on one single country when searching for ideal opportunities. Hence, the geographical

source of PE is generally not very distant from the demand. This built-in bias mechanism is

intensified by the institutional investors’ international allocation approaches. Diversification

needs urge the LPs to commit capital of funds that cover a particular country or region.

Therefore, LPs make a geographical selection of promising spots. The selection follows in

principle their expectations of the demand for PE, and their evaluation of the host country’s

professional finance community.

22

2.8 Summary

Private equity ownership of portfolio companies affects companies in many ways. This has

been demonstrated by many empirical studies using data sets of completed private

transactions in developed countries. Changes are often made to employment, wages,

productivity, performance, growth, innovation and governance. However, regardless of the

country or culture, successful entrepreneurs share numerous traits, particularly during the

critical start-up phase of launching a new business. They tend to have an uncompromising,

single-minded persistence, a fierce determination to overcome adversity, and unbridled

optimism, regardless of the odds. Private equity investing in emerging markets is akin to a

start-up company, and successful practitioners must be endowed with a similar arsenal of

personal characteristics not unlike the U.S. venture capital pioneers in the sixties. They too

were hard pressed to convince skeptical investors to commit capital in high-risk companies

with no track records; they also complained about ill-prepared and secretive entrepreneurs;

and, long before the NASDAQ emerged as an IPO outlet for small companies, they had

difficulty planning profitable exit opportunities.

23

CHAPTER THREE: RESEARCH METHODOLOGY

3.1 Introduction

This chapter seeks to explore the research methodology used by the researcher. A linear

regression model will be used to present the relationship that exists between private equity

investment in emerging markets and the explanatory variables in question. The variables

under consideration are PEIEM, LBO, VC, GFI and JV. A statistical E-views package is used

to fit a regression model for the data and an econometric investigation will be carried out to

obtain the final results.

3.2 Unit root test

Before estimating the model, it is necessary to examine the order of the integration series. By

so doing, the researcher avoids the existence of spurious correlation between variables in a

regression equation. The Augmented Dickey Fuller (ADF) test is employed to test for

stationarity. Non stationary variables are made stationary by differencing and if the time

series is differenced once to become stationary, then the original time series integrated to

order one, that is 1(1).

3.3 Cointergation analysis

Co-integration is relevant to the problem of determining the long run or equilibrium

relationships. It allows the researcher to describe the existence of long run relationship among

variables. The method to be used in this study is testing the stationarity of the residual. If the

residual term is stationary at level that is 1(0), it implies that there is co-integration among

variables.

3.4 Specification of model

In modeling a PE investment function for EM, a linear econometric function was used on the

basis of yearly data covering period 1990-2010 and a sample of ten emerging countries from

Southern Africa (Zimbabwe and South Africa), Emerging-Asia (China and India), MENA

(Egypt and Nigeria), latin-America (Brazil and Mexico), East and Central Europe (Russia and

Tuckey). Two countries were randomly selected from each region just as shown on the

preceding statement. The data for all the above listed countries was aggregated accordingly

with relevant variables to form a solid value that will represent emerging markets.

24

The researcher is going to adopt one model used by Ayman Ismail (2010) who investigated

the entrepreneurial impact of private equity investment in Egypt from 2003 to 2008. The

model can be specified as follows:

PEIEM = f (VC, GFI, JV, LBO)

Where : PEIEM - Private equity investment in emerging markets

VC - Venture capital

GFI - Greenfield investment

JV - Joint Venture

LBO - Leveraged Buyout

The error term is included to capture the effects of other variables omitted from this model.

Therefore the functional econometric model in this study is:

𝑷𝑬𝑰𝑬𝑴 =∝ +𝜷𝟏𝑽𝑪 + 𝜷𝟐𝑮𝑭𝑰 + 𝜷𝟑𝑱𝑽 + 𝜷𝟒𝑳𝑩𝑶 + 𝝁

Where = autonomous level of investment and 1, 2, 3 and 4 are coefficients, which

measure the changes in investment per unit change of the explanatory variable.

3.5 Estimation procedure

The researcher adopted Ordinary Least Square (OLS) method in estimating the equation

parameters. To justify the OLS, estimators are expressed solely in terms of observable

quantities such that they can be easily computed. The strength of OLS method lies in its

properties of best, linear, unbiased estimator (BLUE).The fact that it stresses linearity among

variables; such variables are usually linearly related. Estimation of parameters using the

linear specification form makes the parameters unbiased and significant. OLS is the best

estimator for the research model because it minimises the sum of squared residuals and it

maximises the coefficient of determination (R2).The model used is also a time series analysis

and all the regressions or estimation of the model will be done using E-views.

25

3.6 Justification of the variables

While initiating new ventures has often been in the realm of individual entrepreneurs; an

analysis of private equity transactions in emerging markets shows that private equity

investors are actively engaged in initiating new companies as well as in supporting local

entrepreneurs. There are four different business models used by private equity investors to

initiate new companies: venture capital, green field investments, joint ventures and leverage

buyouts.

3.6.1 Venture Capital

In VC, the emphasis is on providing capital and management support to start-up

firms/ventures and small businesses which do not have access to capital markets and cannot

raise funds by issuing debt due to their limited operating history. As a result, VC should be

considered as a variable because it does not only initiate new ventures but also grow and

globalize the existing ones.

3.6.2 Green field investments

In GFI, private equity firms act as the entrepreneur and initiate new capital-intensive

companies. GFI constructs new operational facilities from the ground up. It occurs when

multinational corporations enter into the country in form of FDI to start new ventures. Hence,

there is a need to consider GFI as a variable because creation of more firms could result from

an increase in FDI inflows.

3.6.3 Joint Ventures

In JV, the emphasis is on supporting existing underperforming companies that have reached

financial closure, (be it a private or public firm) as they start a new line of business through a

joint venture. By so doing, the private equity investors commit their investment facilities in

new facilities or expansion and modernisation of existing companies. As a result, forming a

joint venture is a good way for growing existing firms and initiating new ventures so it must

be considered as a variable.

26

3.6.4 Leveraged Buyout

This is a source of capital for underperforming entity with a proven product and stable cash

flow. LBO investor seeks to improve the company’s internal processes, structure and

investments in growth projects. Hence, increase of high yield portfolio investment bonds may

result to growth and globalisation of firms so LBO should be considered as a variable.

3.6.5 Error term in the function

The error term is important for it captures the influence of all independent or exogenous

variables that are excluded in the model. This is due to factors such as data unavailability,

inaccuracy in estimation of the data and more just to mention a few. In this case the error

term captures all the macro-economic factors that influence entrepreneurship activities of

private equity investment in emerging markets.

3.7 Data types and sources

The data set used in this research is purely secondary annual data obtained from various

sources, which include publications and internet facilities. The study uses aggregate time

series data for the following emerging markets; Zimbabwe, South Africa, Egypt, Nigeria,

China, India, Brazil, Mexico, Russia and Turkey and other macro-economic variables for the

period spanning 1990 through 2010. Most of the data used in this research are from World

Bank, EMPEA publications and IMF.

3.8 Summary

This chapter has given the methodological outline to be adopted in this study. The analysis

set out the route for modeling specification and econometric procedures used in the study.

The nature of this study provokes the use of comparative analysis thus the series of equations

to consolidate the different aspect of determining the choice of currency into our

comprehensive study. The estimation of the model and other tests were carried out using

econometric views (E-views version 3.1).

27

CHAPTER FOUR: RESULTS PRESENTATION AND ANALYSIS

4.1 Introduction

This chapter will mainly focus on the presentation of the results of the estimated model and

interpretation of results of the regression equation estimated using Econometrics Views (E-

views) computer package. When interpreting the results, the researcher will link results

obtained to know theory and empirically tested models from other countries.

4.2 Unit root results

Table 4.1

Variable ADF

Statistic

Critical

1%

Critical

5%

Critical

10%

Order of

Integration