MEASURING THE SUCCESS OF TELECOM REGULATION: A BALANCED SCORECARD APPROACH

56

MEASURING THE SUCCESS OF TELECOM REGULATION: A BALANCED SCORECARD APPROACH Jarkko U. Vesa (corresponding author) Research Fellow Helsinki School of Economics P.O.Box 1210, FIN-00101 Helsinki, Finland [email protected] Matti Kotisaari Director, Business Development Finnet Group [email protected] Aimo Maanavilja Research Fellow Elisa Oyj [email protected] Pekka Rauhala Vice President, Products and Services TeliaSonera Oyj [email protected] Reijo Svento Managing Director Finnish Federation for Communications and Teleinformatics (FiCOM) [email protected] JEL Codes: L16, L22, L96 Keywords: mobile industry, cellular industry, telecom regulation, regulatory authorities, regulatory framework, balanced scorecard, mobile services

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of MEASURING THE SUCCESS OF TELECOM REGULATION: A BALANCED SCORECARD APPROACH

MEASURING THE SUCCESS OF TELECOM REGULATION:

A BALANCED SCORECARD APPROACH

Jarkko U. Vesa (corresponding author)

Research Fellow Helsinki School of Economics

P.O.Box 1210, FIN-00101 Helsinki, Finland [email protected]

Matti Kotisaari

Director, Business Development Finnet Group

Aimo Maanavilja Research Fellow

Elisa Oyj [email protected]

Pekka Rauhala

Vice President, Products and Services TeliaSonera Oyj

Reijo Svento Managing Director

Finnish Federation for Communications and Teleinformatics (FiCOM) [email protected]

JEL Codes: L16, L22, L96

Keywords: mobile industry, cellular industry, telecom regulation, regulatory authorities,

regulatory framework, balanced scorecard, mobile services

2

1 Introduction

One of the most widely debated subjects in the field of telecom business is the role of

regulation in the evolution of the fixed and mobile telecom industry. Strong arguments have

been presented against too aggressive regulation [37, 39,40] but also in favor of an active role

of the government in protecting the interests of consumers and business customers against

potential misuse of monopoly power in the telecom markets. It is easy to see how different

stakeholders (e.g., telecom network and service operators, various government bodies

participating in the process of telecom regulation, consumers, and business customers)

interpret the very same facts and figures in a very different – and sometimes even opposite –

ways. Furthermore, even within a given stakeholder group, such as telecom operators or

regulatory authorities, it is easy to detect strategic behavior depending on factors such as

operators’ market position or growth strategies, or political ambitions of various regulatory

bodies.

Against this background it is easy to understand how big a challenge it is for national

regulatory authorities (NRAs) to find a balance between numerous and often contradictory

interests and goals of various stakeholders.

Governments struggle to get regulation right

So what do we know about the role of telecom regulation. In their recent report “Regulation

that’s good for competition”, consulting company McKinsey described the goal of economic

regulation in the following way:

“The aim of economic regulation should be the same in all sectors: to facilitate fair

competition among players or, where natural monopolies exist, to ensure fair

pricing and service levels. Greater competition means stronger growth, which in

turn means a faster-growing economy and more wealth to share.” [2]

Despite these noble and widely accepted goals, the McKinsey article points out that

governments everywhere “struggle to get regulation right” [2].

3

Regulation costs are high

Although regulation aims at providing us citizens with protection against large telecom

operators and their evil plans to grab an increasing share of our wallets, this kind of service

has its cost. The British “Better Regulation Task Force” (BRTF) emphasizes the fact that

regulation “represents a significant cost for the economy” [26]. They point out that the cost of

regulation “is borne by government, regulators and those being regulated.” Especially the last

item on the list is somewhat peculiar; no wonder you can sometimes hear people from

teleoperators making jokes about how regulatory authorities beat them up with a stick – and

they even pay for it (against their will, of course).

Furthermore, despite the high cost of regulation (BRTF estimates the total cost of regulation

to be around 10-12% of GDP), OECD reports that in today’s business environment

“regulatory costs are the least controlled and least accountable amongst government costs”

[20].

More mature industry requires less regulation

Why is telecom regulation such a topical issue despite the fact the regulations has been

around since the early days of telecommunication? One explanation is that there seems to be

certain realities related to the maturity of technology and technological standards behind the

services we use on a day-to-day basis in order to satisfy our need to communicate and access

content either via wireless or fixed networks. According to a recent article by The Economist,

the telecom industry “has matured and can now standard-setting on its own” [28]. It is argued

that in this new situation regulators can step back and let the competition take care of many

the things that were tightly regulated for instance when the 2nd generation GSM-based mobile

networks were introduced in Europe - very successfully, one might add.

The point the article by the Economist make is that albeit Europe played its cards right when

introducing 2G mobile standards (while the U.S. managed to turn their mobile market into a

real mess by allowing too many critical issues to be solved by the market) the current

situation in the telecom industry, with the roll-out of new 3G networks and the emerging new

technologies such as WLAN/Wi-Fi or Wimax, calls for another kind of approach to the

telecom regulation. According to some experts interviewed by the Economist, Europe could

now use some of the American “laissez-fair” thinking when it comes to regulation existing

and especially the new wireless technologies [28].

Based on his analysis of the evolution of mobile services industry in various geographic

markets, Vesa [38, 39, 40] illustrated the importance of timing of regulative actions by using

4

the Double Helix model [6]. His main argument was that regulatory framework needs to adapt

to the changes in the markets and technologies that are being regulated. Furthermore,

regulatory framework has to be adapted at the same pace as the industry evolves. As the

telecom business represents an industry with a high “clockspeed”, i.e. high speed of change at

various levels of the business, telecom regulation should be adjusted accordingly. However,

this seems to be a major problem especially for Europe as the common legislative work of

European Union has turned out to be so slow that even the general manager of the Finnish

Ministry of Transport and Communication (MINTC), Mr. Harri Pursiainen, has argued that

the built-in inertia of the regulatory process of EU is too high for the converging world of

telecommunications [25].

One of the leading countries in Europe, when it comes to trying to make regulation more

efficient, is the UK where a special body called “Better Regulation Task Force” (BRTF) has

been set up in order to improve the quality of regulation. BRTF emphasizes the importance of

a constant evaluation of the regulatory framework in a given country and the need for

regulatory reform where inefficient or unnecessary regulation is detected:

“Regulations that are demonstrably not working, where the costs significantly

exceed the benefits or where there is no commitment to compliance or enforcement,

should be revised or removed.” [26]

Telecom regulation in Finland

In this article we will build on our experience the Finnish market and the ways in which the

telecom industry is being regulated there as we develop the new framework for the

measurement of the performance of telecom regulations.

During the past 18 months there has been a lively debate about the role of regulation in the

evolution of the Finnish telecom market which has been experiencing something that reminds

the ”creative destruction” as visioned by Schumpeter [27]. Many distinguished parties have

participated in this debate including the top management of local telecom operators and even

the Prime Minister who has expressed his concern about the overheated competition in the

Finnish market [36].

The reason for the current situation is that the Finnish telecom market, and especially the

mobile services industry, have been experiencing an unprecedented turmoil over the past few

years. The Finnish mobile market can be best described as a churn-friendly and price

competitive market. Let’s take a few examples. According to a recent survey by the Ministry

5

of Telecommunications and Transportation (MINTC), in year 2004 the prices of telecom

services declined 6.6 percent. This price reduction was biggest since 1996 when so called

telecom tax was removed [31].

At the same time Finnish mobile phone users keep changing their operators at an increasing

rate. During the first half of 2005, more than every fifth subscriber switched cellular operator

which exceeds the total amount of ported numbers in year 2004. According to CEO Markku

Brummer of Numpac Ltd., the company managing the master system required for number

portability in Finland, Finnish mobile operators’ churn rates reaching over 50 percent of the

customer base are exceptionally high. In a “normal” market situation churn is typically

somewhere between 10 to 30 percent [17]. Since the introduction of mobile number

portability (MNP), i.e. from July 2003 to June 2005, close to two and a half million

subscribers have switched operator in the Finnish market – out of a total market of

approximately 4.5 million subscribers (source: www.numpac.fi).

And finally, if we add to these figures the number of services operators which is close to

fifteen in a market of five million people, one could argue that competition in the field of

mobile telephone services has very favorable ground.

The enigma of successful regulation

Although the characteristics of the Finnish mobile market discussed above may well be

described as virtues from the end-users’ and national regulatory authorities’ perspectives in

the short run, the recent development in the market has raised the question whether this kind

of competition will be good news in the longer run. Furthermore, there are also very different

views on the root causes of the current “hyper-competition”. The two camps in this fight are

the operators and the government bodies regulating the market.

The Finnish telecom operators have been putting the blame on the regulatory authorities for

driving the market into the current hullabaloo where the prices, giveaways and free airtime are

the only sales arguments. Recently Matti Vikkula, the CEO of virtual operator Saunalahti

warned that the current price war can’t continue very long because the lower end-user prices

are offered at the expense of profitability [33]. Furthermore, in May 2004 Anni Vepsäläinen,

the former CEO of TeliaSonera Finland, raised the question of the relationship between

regulatory environment and the attractiveness of the Finnish mobile market to foreign

investors: In March 2004 investment bank Credit Suisse – First Boston gave a

recommendation in their analyst report “Euro Telcos Regulation” to avoid investments in

TeliaSonera due to over-zealous regulatory authorities in the Swedish-Finnish telecom

6

operator’s home markets [37]. In other words, the Finnish telecom market is suffering from a

“country risk” due to telecom regulation from investors’ point of view.

The national regulatory authorities, i.e. the Ministry of Transport and Communication

(MINTC), the Finnish Communications Regulatory Authority (FICORA), and various other

government bodies involved in the telecom regulation process – including the Prime Minister

[36], have responded that it is the operators who set their own prices and decide how they

wish to compete. The truth is probably somewhere between these to extremes but the parties

involved in this debate seem to have difficulties in settling their dispute, albeit recently the

discussion has been more productive.

As the discussion earlier in this article demonstrates, the fact that the regulatory environment

in Finland has been very successful in promoting competition and guaranteeing low end-user

prices, there are evidently side effects (e.g., decreasing market, diminishing ability and

willingness to invest, extensive lay-offs, and slow development of new services) in the way in

which the Finnish mobile market has been and currently is regulated. Against this

background it is justified to ask what has been the true cost of achieving the extremely low

end-user prices for mobile phone calls. As the creators of the Balanced Scorecard concept

Kaplan and Norton pointed out in their Harvard Business Review article in 1992, “even the

best objective can be achieved badly” [15]. In other words, it is “important to make sure that

“improvement in one area has not been achieved at the expense of another” (p. 73).

Even if we could agree that the results of telecom regulation are, at least predominantly,

positive and beneficial to the evolution of the telecom services in a given market, one should

also consider what is the cost of regulation, i.e. how much has the whole economy paid for the

design, implementation and control of the national regulatory framework. As discussed earlier

in this paper, regulation represents a major cost for the whole economy. Is it very easy to

share the following view of the “Better Regulation Task Force” of the UK:

“We need to be confident that this level of investment is being well managed, represents

value for money and is delivering the outcomes we want as efficiently as possible” [26].

The British Government has set an example of how to develop regulation both in the national

and the EU level. The goal of BRTF is to assess the quality of existing and proposed

regulation by evaluating whether the regulation is necessary, affordable, effective, and easy

to administer [26]. Likewise, OECD has an ongoing project called “Measuring administrative

burdens: The OECD Red Tape Scorecard” (see www. oecd.org) which aims at developing a

7

methodology to measure and compare administrative burdens across OECD countries. The

methodology will be based on the Standard Cost Model [19] originally developed in the

Netherlands and now used also in other countries.

The objective of the article

In this paper we will introduce a novel approach to the measurement of the success of telecom

regulation. We believe that all stakeholders in the telecom market, i.e. regulators, operators

and customers, would benefit from having a common way of measuring how well regulation

is achieving its goals. In order to achieve this objective, we will adapt the Balanced Scorecard

framework developed by Kaplan and Norton [15] to the measurement of the performance of

national telecom regulation.

This goal is in line with the need to create “a shared commitment between government,

business and other stakeholders to work together to reduce regulatory costs through

simplification” as the British Better Regulation Task Force defines the shortage of a shared

understanding of the telecom regulation (2005, p. 9). Furthermore, BRTF has also identified

the need for “a methodology for assessing the cumulative costs of regulation” [26]. However,

we believe that focusing only the cost side of the equation is not enough: Just as business

organizations realized in the beginning of the 1990s that pure quantitative financial measures

do not give adequate picture of a firm’s performance today and in the future, we argue that

even telecom regulation needs to be measured in a more balanced way taking both qualitative

and quantitative measures into account. Therefore we have chosen to apply the Balanced

Scorecard framework [15] in this context. The Balanced Scorecard concept and its adaptation

to the public service organizations and more specifically to telecom regulation will be

discussed in detail in the following chapter.

The fact that this article is jointly written by a researcher, the chairman of the Finnish

Federation for Communications and Teleinformatics (FiCOM), and representatives of the

three leading telecom operators in Finland shows that the need for new tools and a common

language has been recognized also amongst those being regulated. This is, in fact, what BRTF

has been missing:

”Those being regulated need to participate as full partners, providing accurate

information on regulatory costs and benefits and identifying candidates for simplification

and deregulation.”[26]

8

We believe that the Balanced Scorecard for telecom regulation -framework presented in this

paper demonstrates the willingness of those being regulated to help regulative authorities to

keep improving the efficiency and effectiveness of regulatory work. Furthermore, our goal is

that the new measurement framework would help to overcome the lack of appropriate tools.

According to BRTF, the concept of regulatory budgets has not been adopted anywhere due to

“the lack of agreed methodology and the practical difficulties of measuring the total effects of

regulation” [26]. Although we realize that telecom regulation is only a minor part of the total

regulation of a given market, hopefully the introduction of the new measurement framework

for the fast-evolving telecom industry provides new insight into this matter.

And finally, as Kaplan and Norton put it, “if you can’t measure it, you can’t manage it”. They

note that an effective measurement must be an integral part of the management process [14].

Just as the balanced scorecard provides executives with “a comprehensive framework that

translates a company’s strategic objectives into a coherent set of performance measures” [14],

the Balanced scorecard for telecom regulation –framework translates the vision and objectives

of national telecom regulation in to well-defined performance measures.

We hope that the framework presented in this article will help the industry to have more

fruitful and productive discussions about the future of the telecom industry. Although we are

using the Finnish telecom market as the starting point of this article, we hope this tool will

help other countries to avoid some of the problems the Finnish market has been suffering

from during the past few years. Some analysts have concerns that the kind of price war that

has driven the telecom industry into trouble in Finland may diffuse to other parts of Europe

[30]: It is very difficult to develop business in a longer term when the growth rate of

operators’ revenue is – 12% and the growth of operators’ gross margins is in the range of –

25% (this is what the Q1 2005 looks like for Finnish telecom operators vis-a-vis Q1 2004).

Methodology

This article is based on desktop research and four roundtable sessions which took place in

February-June 2005. The participants of the roundtable, who are also the authors of this

paper, represent academic world, the Finnish Federation for Communications and

Teleinformatics (FiCOM), and all the three network operators owning 2G and 3G license

spectrum in Finland. In two of the four roundtable sessions a guest speaker was invited: the

first guest speaker represented the Ministry of Transport and Communication, and the second

guest speaker came from the banking industry where he played a key role when the Finnish

9

banking industry created common platform and processes that laid the foundations of the

national online transaction clearing and cooperation for instance in Automated Teller Machine

(ATM) networks.

The creation of the Balanced scorecard for telecom regulation –framework was a very

iterative process where the experience of the key players and information from desktop

research was used in the creation of a shared view of perspectives, goals, constructs, and

measures to be included into the measurement framework. We recognize that this article is

only the first step in promoting fruitful discussions and rewarding dialog between the parties

involved in the telecom regulation process in one way or another.

2 Theoretical background

In this chapter we will learn more about the role of regulation in the telecom industry and the

problems that are typically related to the regulations. We will also review some of the

guidelines for getting the regulation right.

2.1 The role of regulation in the mobile industry

The telecom services industry has been experiencing major changes during the recent years.

There is a broad consensus that these changes need to be reflected also in the regulations of

the industry. But let’s take a look what kind of changes have been identified.

2.1.1 Transformation of the communications market

According to Ms. Rauni Hagman, the General Manager of the Finnish Communications

Regulatory Authority (FICORA), several forces are currently transforming the telecom

market [9]:

traditional telecom business will be challenged by the next generation networks

instead of having monopolistic players in a given sector there will true competitive

markets with new players

moving away from the dominance of communications networks towards a situation

where services drive customers’ choices

from local or national telecom business towards global communications markets.

10

Another set of structural changes in telecommunications industry was identified by professor

Hidenori Fuke of Kansai University based on his analysis of the regulatory framework in

Japan [7]:

development of competition

growth of mobile services and the Internet as cellular is becoming a “significant tool

for high-speed access to the Internet” and broadband access has grown rapidly

decline of POTS as the wide deployment of broadband and IP telephony is starting to

erode the revenues from traditional fixed line telephone services (at an annual rate of

about 20% in Japan): according to Fuke, “the diffusion of cellular and broadband

Internet has changed the structure of telecommunications industry and has hurt the

traditional carriers” (p. 12).

development of media convergence, as “the diffusion of broadband Internet and 3G

cellular blurs the boundary between telecommunications and broadcasting”. [7]

Perhaps the most earth-shaking change in the telecom industry is the gradual erosion of the

traditional “cent per minute” earnings logic – first in the fixed-line business and later in

mobile services. Operators are becoming providers of flat rate –based access and services will

be offered globally through an open IP network. This raises the question of what are the

critical and monopolistic bottlenecks that need to be regulated.

Fuke argues that in the Japanese telecommunications market “it is necessary to design and

introduce a new regulatory framework to accommodate changes in industry structure” [7].

Similar pressures to re-evaluate telecom regulations in the light of the transformation of the

telecom industry exists also in Europe and in the U.S.

There is a plethora of similar lists of forces transforming the telecom industry. The forces

identified by Hagman [9] and Fuke [7] lead us to the following proposition:

P1: As the telecom industry is facing major changes both in technology and the

competitive landscape, it is essential to re-evaluate on a regular basis whether the

existing regulatory framework is still up to date and provides expected results.

11

2.1.2 Is telecom regulation necessary?

One could, of course, raise the question whether telecom regulation is at all necessary –

especially as getting regulation right is not a simple exercise, as we have discussed in the

introduction of this article.

Consulting company McKinsey [2] has listed some of the reasons why regulations is

considered to be necessary. Their first argument is that “market economies can’t function

properly without rules.” The second reason to have regulation is that it is “necessary to

mitigate broader market failures.” And third, “regulatory intervention is vital in supporting

competition and so promoting the welfare of consumers” particularly in so called “network

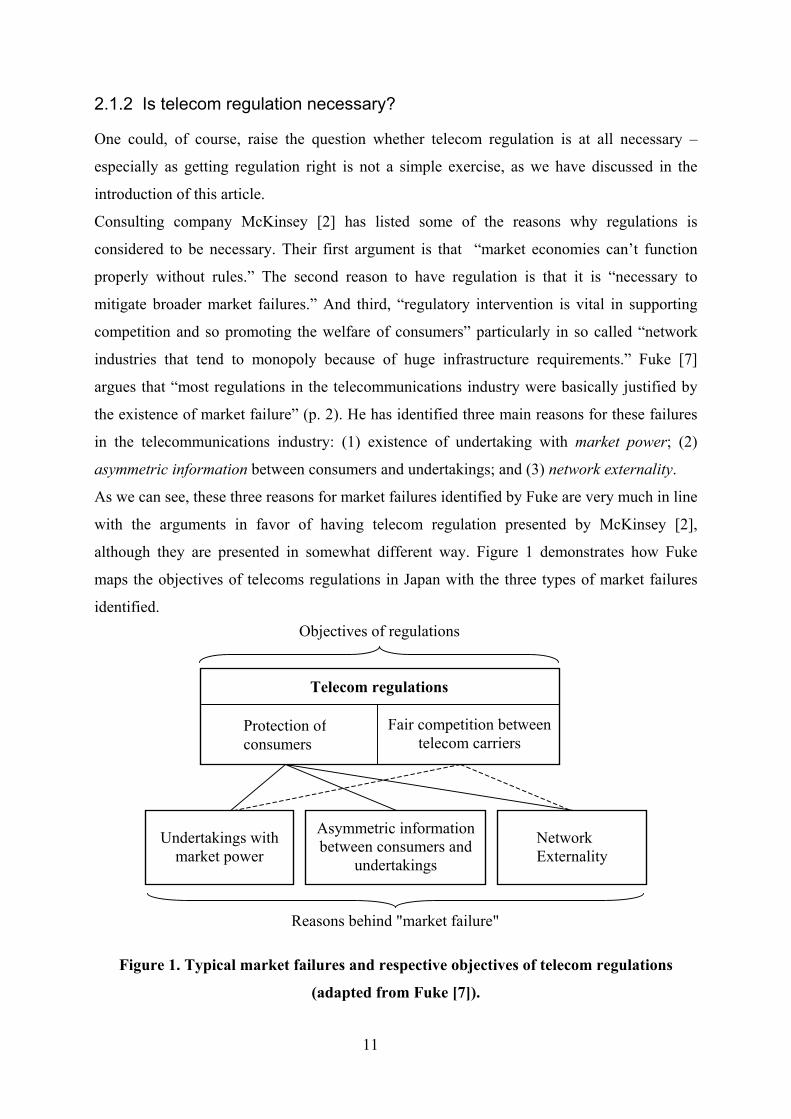

industries that tend to monopoly because of huge infrastructure requirements.” Fuke [7]

argues that “most regulations in the telecommunications industry were basically justified by

the existence of market failure” (p. 2). He has identified three main reasons for these failures

in the telecommunications industry: (1) existence of undertaking with market power; (2)

asymmetric information between consumers and undertakings; and (3) network externality.

As we can see, these three reasons for market failures identified by Fuke are very much in line

with the arguments in favor of having telecom regulation presented by McKinsey [2],

although they are presented in somewhat different way. Figure 1 demonstrates how Fuke

maps the objectives of telecoms regulations in Japan with the three types of market failures

identified.

Figure 1. Typical market failures and respective objectives of telecom regulations

(adapted from Fuke [7]).

Asymmetric informationbetween consumers and

undertakings

Telecom regulations

Protection ofconsumers

Fair competition betweentelecom carriers

Undertakings withmarket power

Network Externality

Reasons behind "market failure"

Objectives of regulations

12

The concepts of network industries and network externalities is well documented in the

economic literature. Shapiro and Varian [35] note that “when the value of a product to one

user depends on how many other users there are, economists say that this product exhibits

network externalities, or network effects” (p. 13). In other words, “large networks are more

attractive to users than small ones” (p. 183). According to Shapiro and Varian, “the

competitive process can lead to a concentrated industry structure, with one or a few firms

dominating the market” (p. 301). This kind of development is “especially common in

information industries, because the economies of scale involved in creating information and

because of the positive feedback and network externalities” (p. 301). Ironically, this leads to a

situation “our cherished free market economy spawns a powerful monopolist” (p. 301). What

the government often does in this kind of situation is that it starts to directly regulate the

monopoly, as has been the case in the local telephone business for decades. Shapiro and

Varian [35] conclude that “in theory, the regulation will wither away when no longer needed”

(p. 302). However, in practice “regulatory agencies create their own constituencies and often

outlive their usefulness” (p. 302). This last statement is particularly interesting for the

purposes of this article, as our goal is to provide a tool for evaluating the usefulness of

prevailing regulations – in order to identify and remove obsolete regulations if they exist.

Shapiro and Varian note that “regulation makes the most sense when the monopoly is unlikely

to be eroded by entry or technological change” [35]. As we have discussed earlier in this

paper, the telecom industry is facing both extensive entry of new players and a disruptive

technological change. Against this background it justified to assume that the need for strict

telecom regulation should be diminishing. Furthermore, even the shift from traditional fixed-

line telephone calls towards more advanced value-added services changes the competitive

landscape: According to Vickers [41], “in telecommunications, natural monopoly is more a

feature of local network operations than of long-distance operations, and is not present in

apparatus manufacture and supply or in the provision of value added services.”

The observations discussed suggests the following proposition:

P2: Albeit the telecom industry represents a typical network industry with a tendency to

monopoly, the traditional telecom monopolies of local telephone networks will be

eroded by entry or technological changes. Therefore one should expect the total amount

of telecom regulations to decrease in the coming years.

13

2.1.3 What should be regulated?

As discussed earlier in this article, there are numerous arguments in favor of telecom

regulation. However, even if we agree that it makes sense for governments to regulate the

telecom industry the question is what exactly should they regulate.

As Table 1 shows (see the next page), telecom regulation comes in all shapes and sizes.

However, in our analysis of different forms of regulation we have identified four main

categories of telecom regulations: (1) Price regulation of end-user prices and tariffs of

services offered to other players in the market; (2) Conduct regulation defining how different

players (and in particular the ones with monopoly power) in the market show behave in

relation to other players and the customers; (3) Structure regulation giving guidelines how

the dominant players should organize their operations; and (4) Market entry/exit regulation

defining under what kind of terms new players can enter the market or old players can exit the

market or cease to offer certain product and service categories (for instance due to low or

nonexistent profits). Next we will go through these four main categories in order to provide

some background information about them.

(1) Price regulation

The first form of price regulation was described as “fixed price” by Shapira [34], and it refers

to a situation where the prices of certain telecom services are frozen and cannot be changed

by firms. Another form of regulation defined here as “tariff regulation” was presented by

Fuke [7] who listed various policies regarding the tariffs of telecom services in Japan. For

instance, the tariff of the value added POTS services can be set by an operator simply by

giving a notification to the Minister. The same policy applies also to cellular services.

However, for local telephone services and local leased line services of NTT, so called price

cap regulation is applied, while tariffs of other services of NTT and those offered by new

entrants are subject only to a notification [7]. The third form of price regulation is called

“UNE-P pricing” (unbundled network elements pricing) which, according to Shapira [34],

refers to an obligation to offer various service elements at cost or at a reasonable margin also

to competitors. The fourth and final form of price regulation is related to “interconnection

charges”. According to Vickers [41], the UK regulatory body Oftel took major efforts in

order to make sure that BT wouldn’t “use its monopoly in one activity to distort competition

in its own favour in others”. Typically this kind of issues are related to interconnection

between an incumbent’s and rivals’ networks. A common approach to manage the issue

14

related to the level of interconnection charges is a method called “long-run incremental cost”

(LRIC). The Japanese MPT (1999) defines LRIC as a method where “the cost calculated on

the basis of the network model that is built on the most efficient and modern technologies”.

Despite the wide use of LRIC, Fuke argues that it “accompanies a somewhat theoretical

nuances” and that LRIC method is “a kind of pro-competitive policy and its simple and pure

application may accompany harmful effects to development of the telecommunications

industry” [7].

Table 1. Various forms of telecom regulation

Form of regulation Description Author(s) 1. Price regulation Fixed price Prices are frozen and cannot be

changed by firms. Shapira (2004)

Interconnection charges

Based e.g. on the Long-run incremental cost (LRIC) method.

Fuke [7]

Tariff regulation, end-user prices

Notification to the Minister or price cap regulation depending on service.

Fuke [7]

UNE-P pricing Unbundled network elements pricing, i.e. obligation to offer various service elements at cost / with reasonable margin.

Shapira [34]

2. Conduct regulation Regulation of conduct British Telecom (BT) privatized as a

vertically integrated dominant firm. European style “conduct regulation”.

Vickers [41] Fuke [7]

Cross transfer of innovations

Any innovations of the monopoly firm are transferred, at cost, to competing firms.

Shapira [34]

Universal service obligation

Certain services (e.g. basic fixed line services) must be provided throughout the geographic market.

Ofcom [21]

Handset subsidy Mobile operators not allowed to subsidize handset prices.

Vesa [39]

3. Structure regulation Structural separation AT&T was required to divest of its

local network operations. American style “structural separation”.

Vickers [41] Fuke [7]

Interconnection rules Unbundling of network functions. Fuke [7] 4. Market entry/exit New entry New firms are not allowed to enter the

product line Permitted if it would not cause excess

capacity for the market.

Furchgott-Roth [8] Shapira [34] Fuke [7] Fan [5]

No exit The monopoly firm may not exit the product line.

Furchgott-Roth [8] Shapira [34]

15

(2) Conduct regulation

In the case of “conduct regulation” the regulator sets guidelines for the behavior incumbent

monopolising e.g. local network that is essential to other carriers’ new entry [7] as opposed to

structure regulation that requires the incumbent to divest certain parts of the operations.

Vickers (1995:1) uses the case of British Telecom (BT) as an example of conduct regulation.

Fuke [7] argues that conduct regulation is more typical of Europe, whereas the U.S. has used

the structure regulation approach. One form of conduct regulation can be described as “cross

transfer of innovations” [34] which obliges the monopoly firm to transfer any innovations, at

cost, to competing firms. Another form of conduct regulation is so called “universal service

obligation” which obliges an incumbent, and possibly also other players in the market, to

provide certain basic telecom services at an affordable price to all citizen and customers

across the geographic market [21]. The British regulatory authority Ofcom admits that

universal service obligation (“USO”) is somewhat contradictory as it calls for regulator’s

intervention in the market and thereby can create “a need for slightly more detailed regulation

in order to ensure the effective targeting of limited resources” [21]. The final example of

conduct regulation is the case of “handset subsidy” which refers to a situation where the

regulation prohibits operators from subsidizing the purchase price of mobile telephones.

According to Vesa [39], the ban of handset subsidies has created interesting side-effects for

instance in the Finnish market. In Finland, the Ministry of Transport and Telecommunication

(MINTC) is currently in the process of adjusting the telecom legislation in order to allow

subsidies of 3G handsets for a period of two years.

(3) Structure regulation

As discussed above, sometimes the regulator requires an incumbent to divest of parts of its

business, as was the case with AT&T in the 1980’s [41]. According to Fuke, this kind of

“structural separation” has been more typical of the U.S. market than Europe [7].

Less radical structural reform in the telecom industry takes place when “interconnection

rules” expects an incumbent to unbundle its network functions and to offer interconnection

services at a reasonable price as discussed earlier in this paper. This happened, for instance, to

NTT in Japan where special obligations were set on NTT’s intra-prefecture

telecommunications facilities.

16

(4) Market entry / exit

One form of regulation deals with market entry and exit policies. Sometimes “new entry” to

the telecom market, or at least to certain product lines, is prohibited for new firms [8, 34].

There are differences between various markets in how strict the market entry rules are: In

Finland, for instance, new mobile service operators need only to notify the authorities about

their plans to enter the market [40], whereas in Japan new entry is “permitted if it would not

cause excess capacity for the market” [7].

One of the peculiarities of the telecom market is that sometimes there is “no exit” from the

market: the monopoly firm may not exit a given product line [34].

This concludes our brief overview of different forms of telecom regulation. We want to point

out that this list is by no means exhaustive – these are only examples of the different

approaches to telecom regulations. The review of forms of telecom regulation leads us to the

following proposition:

P5: While evaluating the success of telecom regulation, one should consider the four main

perspectives of regulation: (1) price regulation; (2) conduct regulation; (3) structure

regulation, and (4) Market entry/exit. However, the importance of these perspectives may

vary according to the maturity of the regulated market and the evolution of technologies

involved.

2.2 Challenges of telecom regulation

Telecom regulation is not an easy job. According to a recent report by McKinsey [2], finding

a balance between multiple and often conflicting goals of regulation is tricky. The report

notes that albeit it is important to protect consumers, the cost of doing so should not be so

high that it would “discourage innovation and halt progress” [2]. This view reflects very well

the concern of the telecom industry in Finland when it comes to defining the goals for

regulatory actions. Next we will go through some of the difficulties – or challenges – of

getting regulations right.

One of the challenges in regulation is to understand the drivers and the goals of new rules and

regulations. The McKinsey report argues that governments are “too inclined to frame policy

17

through trial and error” which leads to situations where the new rules “hamper competition

and create long-term drags on growth” [2]. A representative of the Finnish Ministry of

Transport and Communication is known for his comment that a regulator “needs only a pen,

paper and the Parliament” to impose new regulations. Although this comment was meant as a

joke and it refers to the times when the EU was not dictating such a big part of telecom

regulation, it reflects how the “trial and error” approach the McKinsey report cautions about

may become an acceptable way of creating new regulations. The report warns that poor

regulation and overregulation are important threats to businesses “limiting productivity and

growth in economies throughout the world”. In their research, McKinsey has noticed that an

“inappropriate and unevenly enforced regulations” is limiting growth in naturally competitive

manufacturing and services sectors in many countries [2].

As we have discussed earlier in this paper, the telecom industry is a good example of so called

network industries with a high tendency to monopoly. The McKinsey report points out that in

this kind of industries “regulators often try to lessen the market power of incumbent former

monopolists” [2]. A typical way of achieving this goal is to let new retailers use incumbent’s

networks “at a favorable wholesales prices (e.g. based on the LRIC method) while still

insisting that they provide universal coverage for profitable and unprofitable customers alike”

[2] as discussed in section 2.1.3 of this paper. According to McKinsey, in consequence of this

kind of regulation, “the transfer of profits away from the incumbents has been substantial”

[2]. Furthermore, the McKinsey report pays also attention the market entry regulation by

stating that “the granting of licenses to a host of new mobile-telephony operators has also

increased competition and demand, improved the infrastructure, and cut prices” [2]. However,

this last point may be a problem for telecom operators but probably not for regulatory

authorities or consumers. This kind of development is visible in competitive mobile markets

such as Finland, with 15 service operators in a country of five million people [40], and Hong

Kong, with eleven 2G mobile networks and six mobile operators in a country of less than

seven million people [42].

Another challenge related to telecom regulation is how to deal with emerging new

technologies that are changing the balance of power between incumbents and new arrivals.

The McKinsey report [2] argues that although these new alternative technologies (e.g., cable,

wireless and VoIP) can be seen as substitutes for traditional fixed-line telephony, they “tend

to be regulated separately and, in some cases, circumvent regulation altogether” (p. 3). This

18

leads to another problem related to the regulation of a fast evolving industry such as

telecommunications – regulatory asymmetries. According to McKinsey, if not adjusted to the

new reality, regulatory asymmetries will severely reduce the incumbent’s fixed-line business

which eventually will “undermine the incumbent’s ability to invest in new infrastructure and

technologies (such as a national broadband network) that would benefit consumers and the

overall economy in the long term” [2]. We will return to the question of telecom operators’

willingness and ability to invest later in this article as we discuss the strategic objectives of

regulatory policy.

As we can see, the McKinsey report on telecom regulation [2] has identified difficulties in

many of the forms of regulation described in the previous section: the questions of

interconnection charges, universal service obligation, market entry, and regulatory

asymmetries are all typical sources of dispute when it comes to finding a balance between

consumers’ and the industry’s interest.

It is important to keep in mind that different markets are facing different kinds of regulative

challenges depending on factors such as the maturity of the market and technologies used, and

the prevailing regulatory framework. Furchgott-Roth [8] points out that the telecom regulation

in the U.S. market was characterized by “No entry, No exit, Serve everyone in geographically

protected market, Charge artificially high rates to businesses and urban customers and long

distance services” –type competition until the 1996 Telecommunications Act made

competition possible. Likewise, Fuke [7] argues that the sector-specific regulation of Japan

“has caused over-regulation and has led to failure of regulation”. According to Fuke, a “total

restructuring of regulatory framework is required” in Japan to solve the existing problems in

the regulatory environment. And finally, Fan [5] found in his comparison between the

diffusion of Internet access in China and Australia that “government policies governing the

telecommunications service market and promoting information infrastructure have a

significant impact on the affordability and availability of Internet access” while the most

significant factor was “the level of competition permitted in the telecommunication sector”

[5]. Once again we run into the question of market entry as discussed earlier in this paper.

19

The discussion about the challenges of telecom regulation leads us to the following

proposition:

P4a: The objective of telecom regulation should be to find a balance between the welfare of

consumers and interests of the industry in order not to discourage innovation and halt

progress in the telecom sector.

P4b: When it comes to new technologies and players that are currently not regulated, it is

important to avoid potential regulatory asymmetries in order to make sure that the

incumbents have the ability to invest in new technologies and services.

How much regulation?

Another challenge related to telecom regulation – and in economic regulation in general – is

the question of how much regulation is needed. In the UK, the Better Regulation Task Force

(BRTF) campaigns for a “One in, One out” approach to new regulation, which would force

the government “to prioritise between new regulations and to simplify and remove existing

regulations” [26]. According to BRTF, “every government department should use a

standardised approach to measure the existing administrative burden which it imposes on

business through its regulatory activities” (p. 4) taking into account both national and

European legislation (we will discuss more the relationship between national and the EU

regulations later in this paper).

The main message by BRTF regarding the amount of regulation is that regulatory bodies must

prioritise regulations: which are the most important regulations, which are nice to have but

not vital, and which ones could be removed. BRTF’s solution to the challenge of regulation is

simplification which results from deregulation, consolidation and rationalisation of

regulations.

This leads us to the following proposition regarding the total amount of telecom regulation:

P5: Regulatory authorities should follow carefully how the total administrative burden

resulting from telecom regulation develops over time. Government departments need to

prioritize regulations in order not to increase the total amount of regulation, for instance by

following the “One in, One out” policy.

20

The cost of regulation

Yet another issue related to regulations is the cost of regulation. According to BRTF,

regulatory costs can be divided into policy costs and administrative costs. Policy costs are the

“costs directly attributable to the policy goal”, and administrative costs are all those “costs

associated with familiarisation, record keeping and reporting, including inspection and

enforcement” [26]. Another perspective to the cost of regulation is administrative burden

which refers to “the costs imposed on businesses, when complying with information

obligations stemming from government regulation” [19].

The point is that if we wish to evaluate whether certain regulation makes sense from various

stakeholders’ point of view we need to know – in addition to the potential or realized benefits

– also the costs of achieving the results. Another dimension of the cost issue is whether the

same results could be achieved with lower costs, i.e. the efficiency of regulatory work. We

will return to this question as we develop the balanced scorecard framework for the

measurement of the success of telecom regulations. This leads us to the following proposition:

P6: Governments should follow carefully what are regulatory costs of achieving the results,

and if the same results could be achieved at lower costs – or perhaps even without sector-

specific regulation.

Regulation and investments

The amount and type of regulation plays an increasing role when investors evaluate the

attractiveness of a given telecom services market. A good example of this was the

recommendation by the investment bank Credit Suisse – First Boston to avoid investments in

TeliaSonera due to over-zealous regulator in telecom operator’s home markets in Sweden and

Finland [37]. The regulatory authorities in Finland seem to have a different view of the

relationship between investments and the regulation favoring strong competition. Recently the

General Manager of the Ministry of Transport and Telecommunications Harri Pursiainen

argued that the reason why investors from Iceland wanted to invest in the Finnish MVNO

Saunalahti was because they consider the Finnish market “the most advanced and toughest in

the world” [24]. In the same column Pursiainen noted also that “communications policy looks

after primarily the interests of end users and thereby the interests of the government – and not

the interests of the owners of telecom companies” [24]. We will return to the question of

regulation’s role in the ability and willingness of the industry to invest in new technologies

and services later in this paper.

21

The observations discussed suggest the following proposition:

P7: One element of the measurement of the success of telecom regulation should be the

interplay between regulations and investments in new technology and services in order to

ensure investors interest in maintaining or increasing the level of investment in the market.

2.3 Getting regulation right – guidelines for regulators

As we have discussed earlier in this paper, there are lots of issues related to telecom

regulation. However, earlier research has identified also useful guidelines for how to get

regulation right. Next we will go through some of these recommendations.

Make regulation fact based and transparent

In their recent report called “Regulation that is good for competition”, consulting company

McKinsey [2] emphasize the importance of understanding how various regulations affect the

economics of competition in a given market but also their broader social and political

implications. It is important that decisions about regulation are based on facts, not “trial and

error” type approach. According to Beardsley and Farrell, “detailed modeling and analysis

are required to clarify the trade-offs and to judge whether the goals of regulation will be met”

[2]. They recommend also that levels of regulation should be measured against international

benchmarks. Governments should carry through proper impact assessments, i.e. “systematic

examinations of the advantages and disadvantages of ways to achieve an objective” by the

means of regulation [2]. Some governments have established independent consultative bodies

to achieve this goal, such as the Better Regulation Task Force (BRTF) in the UK. What is also

important is the role of post-implementation reviews. The United Kingdom’s Better

Regulation Task Force gives the following recommendation regarding reviews:

“Post-implementation review has an important role in identifying proposals for

simplification. There is often a high degree of uncertainty surrounding the impact of

new regulation. It is therefore sensible to review how regulations are working to make

sure they are hitting the mark and do not have significant unforeseen costs or

unintended consequences.” [26]

22

This leads us to the following proposition:

P8: Regulation should be based on detailed modeling and analysis instead of “trial and

error” type approach. Furthermore, it is important to evaluate the impact of new regulations

both prior (“impact assessment”) and after (“post-implementation reviews”).

Make regulation dynamic

Another perspective to successful regulation is understanding the dynamic nature of

regulation. Beardsley and Farrell [2] recommend that regulators should continually assess the

kind of rules different regulatory bodies require but also “if competition is already

established, whether fewer rules might make sense” (p. 4). They note that “regulations are

hard to remove or reduce, but doing so may be necessary to stimulate growth and innovation.”

One way to make regulations more dynamic is to adopt so called “sunset clause” to new

regulations. BRTF defines a sunset clause as “a legal instrument that requires a piece of

legislation to lapse after a specified period of time, usually after a review has been carried

out” [26]. According to Beardsley and Farrell, adopting a sunset clause forces governments to

review on a regular basis “how well regulations fulfill their purpose” [2]. BRTF notes that

introducing sunset clauses may be appropriate where “technological advances are likely to

outstrip the regulation”, or when there is “a high degree of uncertainty surrounding the

implementation and likely effect of the proposal” [26]. Needless to say that these two

characteristics are very typical of the telecom industry. Despite the benefits of using sunset

clauses, BRTF concludes that sunsetting is rarely used. The observations discussed suggest

the following proposition:

P9: Regulators should continually assess the kind of regulation they impose but also if

competition already exists making sector-specific regulation unnecessary, or if fewer rules

might be sufficient. Adopting sunset clauses is recommended in order to ensure regular

reviews of telecom regulation.

23

2.4 European Regulations and Directives vs. national regulation

At this point we would like to raise the question of the relationship between European

regulations and national regulation of EU member states. According to BRTF, roughly half of

the British regulations come today from the European Union which makes it harder to reduce

the burden of regulation. However, it is important to make a distinction between two different

acts of law within the European Union: Piepenbrock and Schuster [23] note that European

regulations are “directly applicable with little national discretion” whereas European

directives “must first be adopted into national law” (p. 4). In other words, European

directives “give countries flexibility on how they are transposed into domestic law” [26].

According to Piepenbrock and Schuster [23], European telecom regulation is in the process of

shifting from “sector-specific regulation to the application of general competition law” (p. 3).

However, they point out that the amount of regulation has been increasing during the past few

years, although the EU Commission’s original goal was “to reduce the density of regulations”

(p. 38). Piepenbrock and Schuster [23] note that Europe has not succeeded very well in

reducing the amount of regulation:

“The trends towards a greater role for general competition law and towards the

relaxation of sector-specific regulations are clearly apparent, but the repeatedly

stressed goal of a “reduction” in the volume of regulation has not been achieved.”

Piepenbrock and Schuter point out that not only has regulation become much more complex

but national regulatory authorities have also been given “considerable freedom to make

market-regulating intervention” (p. 38) as it is the national regulatory authorities who

determine whether effective competition exists in the market, or whether it is characterized by

significant market power. According to Piepenbrock and Schuter, the responsibility for

conducting such an analysis lies with the national regulatory authorities: “Whenever a

national regulatory authority comes to the conclusion that the market is not effectively

competitive, it shall define those companies having significant market power and impose

specific obligations on the same” [23].

So even though the EU regulatory framework is extensive, it still leaves an important role to

NRAs. In addition to making decisions about effective competition, or rather lack thereof,

national authorities still have their say in how certain EU regulations and directives are

24

implemented. The introduction of mobile number portability (MNP) in Finland is a good

example of this: According to a representative of Ministry of Transport and Communication

(MINTC), Finland was initially reluctant to introduce in Finland but once it could not be

avoided, the Finnish authorities decided to implement MNP is such a manner that the porting

of mobile number is totally free for end-users. However, the EU Directive defined that the

interconnection rates charged for number portability must be cost oriented, and that “rates

possibly billed directly to customers may not act as a disincentive for the use of the facilities”

[23]. The introduction of MNP in Finland led to a situation where Finnish mobile operators’

churn rates are over 50 percent of the customer base, and where over half of the subscribers

have switched operator in two years time since the introduction of MNP (source:

www.numpac.fi). The point we wish to make here is that the question is not only what kinds

of directives or regulations the EU imposes but also how much to the letter they are followed

and how fast they are implemented. It is a well-known fact that different EU member states

implement new directives and regulations at a very different pace – within the tolerance

permitted by the legislation process of the EU.

Even the national regulatory authorities are not always very pleased with the way the

communications sector is being regulated in the EU. The general manager of Ministry of

Transport and Communication (MINTC) Harri Pursiainen expressed in a recent column [25]

his concern that the speed of legislative work in the EU is too slow for the Digital Age.

Pursiainen noted that although it is good to prepare things thoroughly one can always question

who has the wisdom to know what kinds of paragraphs are needed for the European

communications market in year 2015. More important than detailed legislation is to make sure

that regulation that was meant to improve competition does not turn out to be a burden for the

European market. What is even more alarming, according to Pursiainen [25], is that the FCC

in the U.S. and the regulatory authorities in Japan seem to manage adjust the regulatory

framework much faster than Europe – and this has direct implications for the competitiveness

of Europe in the global telecom race. The observations about the relationship between the EU

directives and regulations vs. national telecom regulation discussed suggest the following

proposition:

P10: When evaluating the success of telecom regulations in a given market, it is important to

analyze how the EU Directives and Regulations are implemented in the national market, i.e.

are the national interests taken care of.

25

2.5 Technology neutrality

One dimension of telecom regulation is the question of technology neutrality, i.e. should

regulators tell telecom operators which technologies to use or should the market decide what

are the winning technologies. According to a recent article by The Economist (2005), Europe

has traditionally been more specific about which technologies operators should use, whereas

the regulatory authorities in the U.S. have favored a more neutral approach to technologies.

Even though GSM, which was strictly coordinated in the European level, turned out to be a

huge success for Europe the technical evolution in the telecom industry may have come to a

point very the industry should made decisions about which technologies to use.

This leads us to the following proposition:

P11: The guiding principle for the European and national regulations of the telecom industry

should be “technology neutrality”.

2.6 Summary of propositions

This concludes our brief overview of topical issues and theoretical background of telecom

regulation. We have formulated the findings of literature review in the form of propositions

which are summarized in Table 2. These propositions will guide in their part the development

of the balanced scorecard for telecom regulation later in this article.

26

Table 2. Summary of propositions based on literature review

Nr Description P1 As the telecom industry is facing major changes both in technology and in the

competitive landscape, it is essential to re-evaluate on a regular basis whether the existing regulatory framework is still up to date and provides expected results.

P2 The traditional telecom monopolies of local telephone networks will be eroded by entry or technological changes. Therefore one should expect the total amount of telecom regulations to decrease in the coming years.

P3 While evaluating the success of telecom regulation, it is important to pay attention to the four main perspectives of regulation: (1) price regulation; (2) conduct regulation; (3) structure regulation, and (4) market entry/exit. However, the importance of these perspectives may vary according to the maturity of the regulated market and the evolution of technologies involved.

P4a The objective of telecom regulation should be to find a balance between the welfare of consumers and interests of the industry in order not to discourage innovation and halt progress in the telecom sector.

P4b When it comes to new technologies and players that are currently not regulated, it is important to avoid potential regulatory asymmetries in order to make sure that the incumbents have the ability to invest in new technologies and services.

P5 Regulatory authorities should follow carefully how the total administrative burden resulting from telecom regulation develops over time. Government departments need to prioritize regulations in order not to increase the total amount of regulation, for instance by following the “One in, One out” policy.

P6 Governments should follow carefully what are regulatory costs of achieving the results, and if the same results could be achieved at lower costs – or perhaps even without sector-specific regulation.

P7 One element of the measurement of the success of telecom regulation should be the interplay between regulations and investments in new technology and services in order to ensure investors interest in maintaining or increasing the level of investment in the market.

P8 Regulation should be based on detailed modeling and analysis instead of “trial and error” type approach. Furthermore, it is important to evaluate the impact of new regulations both before (“impact assessment”) and after (“post-implementation reviews”) the implementation.

P9 Regulators should continually assess if competition already exists making sector-specific regulation unnecessary, or if fewer rules might be sufficient. Adopting sunset clauses is recommended in order to ensure regular reviews of telecom regulation.

P10 It is important to analyze how the EU Directives and EU Regulations are implemented in the national market, i.e. are the national interests taken care of.

P11 The guiding principle for the European and national regulations of the telecom industry should be “technology neutrality”.

27

3 Telecom regulation in Finland In this article we will use the regulatory environment of Finland as the “empirical foundation”

when developing the balanced scorecard for regulatory authorities. Next we will go briefly

through what are the strategic objectives of telecom regulation in Finland, and how telecom

regulation is organized in Finland.

3.1 The Finnish Communications Legislation

According to the Ministry of Transport and Telecommunications [18], a comprehensive

reform of communications legislation was started in Finland in autumn 2000. The purpose of

the reform was to ensure that telecom operators and other players in the communications

market could operate in a modern legislative environment that takes the technological

development into account.

The reform was carried out in two stages. In the first stage (in 2000-2001), the most urgent

amendments were made to the Telecommunications Market Act (Viestintämarkkinalaki,

VML, 396/1997) which is the foundation of the Finnish telecom regulations. The most

significant amendment concerned the technology-neutral approach to networks, the

application of uniform legislative to television and radio networks as well as conventional

telecommunication networks. For example, the Act made it possible to divide the licences for

terrestrial digital television into network and programme licences.

The first state of the Communications Market Act entered into force in July 2002. In the

second stage of the comprehensive reform in 2001-2002, a completely new legislative

framework – the new Communications Market act – was created. It supports network

business, television and radio operations and content production. According to the Ministry of

Transport and Telecommunications, the aim of the new Communications Market Act is “to

improve the legislative environment for competing businesses, development of

communications technology and innovations” [18]. In addition, the Act implemented four

new EU Directives on electronic communications.

According to the Communications Market Act, telecom operators’ obligations mainly concern

operators with significant market power. The Finnish Communications Regulatory Authority

(FICORA) performs market analyses of relevant wholesale and retail markets. If there is not

enough competition, special obligations will be imposed on individual operators with

significant market power within that particular market. FICORA is using 18 different market

28

categories to be analyzed (see www.ficora.fi, “Huomattava markkinavoima”, HMV). As

discussed earlier in this article, decisions on these obligations are made by the

Communications Regulatory Authority (FICORA). According to MINTC, “the objective is to

impose only those obligations that are absolutely necessary in order to ensure competition”

[18]. This objective is in line with the principle of avoiding unnecessary regulations as

discussed earlier in this paper (see “How much regulation?”, p. 19). Should telecom operators

be discontented with the decisions made by FICORA, they can appeal to the Supreme

Administrative Court. Typical obligations imposed on operators with significant market

power include various obligations to provide access to their networks. In special

circumstances, a telecom operator is obliged “to relinquish to another telecom operator, at

cost-oriented price, for example an access right to mobile subscription (SIM card) capacity or

some equivalent capacity” [18].

3.2 Regulatory regime in Finland

Next we will familiarize ourselves with the key players of the Finnish telecom regulations. As

discussed earlier in this paper (see 2.4 European regulations and directives vs. national

regulation), a large part of telecom regulation in EU member states comes from the EU

legislation. However, numerous government bodies are involved in the process of national

telecom regulation. These include, for instance, the Parliament of Finland, the Government,

various ministries such as Ministry of Transport and Communications (MINTC), Ministry of

Trade and Industry (MTI), and Ministry of Justice. Once the communications laws and

regulations have been passed, regulatory agencies such as Finnish Communications

Regulatory Authority (FICORA), Finnish Competition Authority, and the Consumer Agency

& Ombudsman are in charge of the execution of the laws and regulations. Figure 2

demonstrates the organization of the Finnish regulative regime.

The two most important players from this article’s point of view are Ministry of Transport

and Communications (MINTC) which prepares the bills for the Parliament, and Finnish

Communications Regulatory Authority (FICORA) which executes the telecom laws and

regulations as the national regulatory authority (NRA). Next we will go through the role and

responsibilities of FICORA in the Finnish telecom market.

29

Figure 2. Policy and regulatory authority in Finland.

The objectives of FICORA as the regulatory authority in Finland are the following [9]:

to promote competition in the telecommunications market in Finland

to supervise the use of communications networks, and to ensure their functionality

to coordinate the use of the limited resources available, such as radio frequencies and

numbering

to warn about security threats in communications networks

to supervise the quality of communications services.

According to Rauni Hagman, General Manager of FICORA, as the regulator of the Finnish

communications market, her organization tries to anticipate industry development and

potential changes in market conditions. Further, FICORA generates appropriate rules for the

industry and supervises that they are adhered to - and if the rules are broken, FICORA takes

appropriate action. Finally, FICORA‘s goal is to adjust rules and regulations if the changes in

the environment call for it.

The Parliament of

The Government

Ministry of Transport and Communications (MTC)

Ministry of Tradeand Industry (MTI)

Finnish CompetitionAuthority

Consumer Agency &Ombudsman

Ministry ofJustice

Finnish Communications Regulatory Authority

(FICORA)

The EU Commission

30

In her presentation at FiCOM’s (Finnish Federation for Communications and Teleinformatics)

seminar on the future ICT industry in Finland in June 2005, Hagman [9] listed the following

roles and responsibilities for FICORA: To steer, supervise and regulate the telecom market, to

promote national and international cooperation; and to act as a catalyst and facilitator for the

telecom industry. The objective of this article is to provide a tool for measuring to what extent

this role has materialized and to what extent these goals have been achieved from telecom

operators’ point of view.

3.3 Strategic objectives of telecom regulations in Finland

Ministry of Transport and Communications (MINTC) defined the goal of telecom regulation

as “the long-run benefit of the users” [16]. Interestingly, the European Commission has

defined their goal as “the benefit of the users”. Albeit this may sound like a minor nuance, or

hair-splitting, there is often major differences between an optimal solution in the short term

and in the long term.

Table 3. Mission and strategic objectives of NRAs (FICORA, MINTC 2005)

Ministry of Transport and

Telecommunications (MINTC)

Finnish Communications Regulatory

Authority (FICORA)

Mission:

”High-quality, secure and inexpensive

communications networks”

Mission:

”Well-functioning, secure and inexpensive

communications networks and services for all”

Strategic objectives (”impact”):

”High-quality communications services

are universally available, they are

inexpensive and they are offered by

efficient communications markets.”

“Citizens and businesses trust the

services offered by the information

society.”

”Innovative services are promoted.”

“Information and communications

technology is used efficiently to increase

productivity and competitiveness.”

Strategic objectives (”impact”):

”To promote competition in the

communications markets.”

“Efficient communications markets: Businesses

strive to produce advanced and inexpensive

communications services to the market.”

“The number of services offered, and the use of

services increases.”

“The economy grows, boosting new

investments and production.”

31

According to a representative of MINTC [16], the role of regulation is to ensure fair play

between operators and other players in the telecom market. However, the environment

changes fast and the old rules can easily become an obstacle for the evolution of the telecom

competition.

The vision of MINTC is that Finland would be one of the global leaders in the quality,

efficiency and know-how in transport and communications. Furthermore, the mission of

MINTC states that the ministry promotes the functionality of the society and the welfare of

the population by ensuring that citizens and the economic institutions have high quality,

secure and inexpensive transport and communications services at their disposal – offering

them to be competitive in their businesses.

An interesting question from telecom regulation’s point of view is of course, how well

MINTC and FICORA have aligned their strategic goals. In Table 3 we present a comparison

of mission and strategic objectives of the two regulatory bodies. As the comparison shows,

the objectives seem to be well aligned despite some minor differences in the wordings.

This concludes our brief overview of existing literature of telecom regulation internationally

and particularly in Europe, and the review of the regulatory framework of Finland which will

be used as a reference point in our efforts to develop a new tool for the measurement of the

success of telecom regulation in various markets.

In the previous two chapters we have identified quite a few characteristics of successful

regulation. Interestingly, many of these ideals, such as technology neutrality, separation of

various layers of business (i.e., networks and services), and the attempt to reduce the amount

of regulation, were taken into account when the Finnish government reformed the

Telecommunications Market Act. However, simply including these noble objectives into the

visions and missions of regulatory authorities does not mean that they will become reality.

Therefore, in the remaining chapters we will focus on developing a toolkit for measuring how

well the goals have been achieved.

32

4 Methodology

The objective of this paper is to develop a new tool to measure the success of telecom

regulation in a given market based on the concept of Balance Scorecard [15]. The new

framework called “Balanced Scorecard for Telecom Regulation”, or “BASTER”, was

developed in an inductive manner in a series of roundtable meetings during the first half of

2005. The participants of the roundtable are also the authors of this article. They represent the

three leading telecom operators in Finland, the Finnish Federation for Communications and

Teleinformatics (FiCOM), and Helsinki School of Economics – each participant with at least

20 years of experience in the ICT industry.

Each roundtable session started with an introduction which consisted of a brief presentation

on a topical subject, and a summary of the previous meeting’s discussion. The representative

of the academic world acted as a facilitator. To some extent, albeit unintentionally, this

approach reminds the action research method as described by Checkland [3]. During the

roundtable sessions, participants shared their views of the critical measures of the success of

mobile industry today and in the future. Furthermore, guest speakers from the Ministry of

Transport and Telecommunications and from the banking industry were invited to bring their

views of how the mobile industry should be developed and measured.

The introductions in the roundtable sessions and the analysis of discussions during those

session were based on a review of earlier research and topical issues covered in the business

press and academic journals. A series of propositions were developed based on the literature

review, to be used in the development of the new framework. However, the guiding principle

in the development of the BASTER model was to built on the experience of the participants

of the roundtable, i.e. the authors of this paper.

And finally, what we believe is special about this article is that it represents rarely seen co-

operation between all three mobile network operators in Finland: despite the fact that the

companies are competing extremely hard in the telecom market, by this article the

representatives of Finnet, Elisa, and TeliaSonera wish to bring new insights into to the

discussion about the success of telecom regulations in the Finnish and other national telecom

markets.

33