March 2021 - ValueGuide

77

ValueGuide March 2021 Intelligent Investing Stock Idea Stock Updates Viewpoints Sector Updates Regular Features Report Card Earnings Guide Products & Services PMS MF Picks Advisory Trader’s Edge Technical View Currencies F&O Insights For Private Circulation only www.sharekhan.com

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of March 2021 - ValueGuide

ValueGuideMarch 2021

Intelligent Investing

Stock IdeaStock Updates

ViewpointsSector Updates

Regular Features

Report CardEarnings Guide

Products & Services

PMSMF PicksAdvisory

Trader’s Edge

Technical ViewCurrencies

F&O Insights

For Private Circulation only www.sharekhan.com

Whether you’re a trader, an investor or a complete newbie who has recently opened an account with Sharekhan, there’s a module designed especially for you.

Register today

Take your pickChoose from a variety of courses from customised categories

It’s completely onlineAttend the sessions from anywhere you want, all you need is an internet connection

Learn it liveGet a feel of the markets and how they work by attending the sessions during market hours

3 Reasons to be a Classroom regular

Come one, come allThere’s something for everyone at

Sharekhan Classroom

I am a Beginner I am an Online Trader I am an Investor

Explore the module of your choice

I am a Trader

Registered O�ce: Sharekhan Limited, 10th Floor, Beta Building, Lodha iThink Techno Campus, O�. JVLR, Opp. Kanjurmarg Railway Station, Kanjurmarg (East), Mumbai – 400042, Maharashtra. Tel: 022 - 61150000. Sharekhan Ltd.: SEBI Regn. Nos.: BSE / NSE / MSEI (CASH / F&O / CD) / MCX - Commodity: INZ000171337; DP: NSDL/CD-SL-IN-DP-365-2018; PMS: INP000005786; Mutual Fund: ARN 20669; Research Analyst: INH000006183; Compliance O¤cer: Mr. Joby John Meledan; Tel: 022-61150000; email id: [email protected]; For any queries or grievances kindly email [email protected] or contact: [email protected]: Client should read the Risk Disclosure Document issued by SEBI & relevant exchanges and the T&C on www.sharekhan.com; Investment in securities market are subject to market risks, read all the related documents carefully before investing.

CONTENTS

3MARCH 2021 Sharekhan ValueGuide3

disclaimer

Disclaimer: This document has been prepared by Sharekhan Ltd. (SHAREKHAN) and is intended for use only by the person or entity to which it is addressed to. This Doc-ument may contain confidential and/or privileged material and is not for any type of circulation and any review, retransmission, or any other use is strictly prohibited. This Document is subject to changes without prior notice. This document does not constitute an offer to sell or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Though disseminated to all customers who are due to receive the same, not all customers may receive this report at the same time. SHAREKHAN will not treat recipients as customers by virtue of their receiving this report.

The information contained herein is obtained from publicly available data or other sources believed to be reliable and SHAREKHAN has not independently verified the accuracy and completeness of the said data and hence it should not be relied upon as such. While we would endeavour to update the information herein on reasonable basis, SHAREKHAN, its subsidiaries and associated companies, their directors and employees (“SHAREKHAN and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance, or other reasons that may prevent SHAREKHAN and affiliates from doing so. This document is prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Recipients of this report should also be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The user assumes the entire risk of any use made of this infor-mation. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. We do not undertake to advise you as to any change of our views. Affiliates of Sharekhan may have issued other reports that are inconsistent with and reach different conclusions from the information presented in this report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other ju-risdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject SHAREKHAN and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

The analyst certifies that the analyst has not dealt or traded directly or indirectly in securities of the company and that all of the views expressed in this document accurately reflect his or her personal views about the subject company or companies and its or their securities and do not necessarily reflect those of SHAREKHAN. The analyst further certifies that neither he or its associates or his relatives has any direct or indirect financial interest nor have actual or beneficial ownership of 1% or more in the securities of the company at the end of the month immediately preceding the date of publication of the research report nor have any material conflict of interest nor has served as officer, director or employee or engaged in market making activity of the company. Further, the analyst has also not been a part of the team which has managed or co-managed the public offerings of the company and no part of the analyst’s compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this document. Sharekhan Limited or its associates or analysts have not received any compensation for investment banking, merchant banking, brokerage services or any compensation or other benefits from the subject company or from third party in the past twelve months in connection with the research report.

Either SHAREKHAN or its affiliates or its directors or employees / representatives / clients or their relatives may have position(s), make market, act as principal or engage in transactions of purchase or sell of securities, from time to time or may be materially interested in any of the securities or related securities referred to in this report and they may have used the information set forth herein before publication. SHAREKHAN may from time to time solicit from, or perform investment banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall SHAREKHAN, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind.

Compliance Officer: Mr. Joby John Meledan; Tel: 022-61150000; email id: [email protected];

For any queries or grievances kindly email [email protected] or contact: [email protected]

Registered Office: Sharekhan Limited, 10th Floor, Beta Building, Lodha iThink Techno Campus, Off. JVLR, Opp. Kanjurmarg Railway Station, Kanjurmarg (East), Mumbai – 400042, Maharashtra. Tel: 022 - 61150000. Sharekhan Ltd.: SEBI Regn. Nos.: BSE / NSE / MSEI (CASH / F&O / CD) / MCX - Commodity: INZ000171337; DP: NSDL/CDSL-IN-DP-365-2018; PMS: INP000005786; Mutual Fund: ARN 20669; Research Analyst: INH000006183; For any complaints email at [email protected]. Disclaimer: Client should read the Risk Disclosure Document issued by SEBI & relevant exchanges and the T&C on www.sharekhan.com; Investment in securities market are subject to market risks, read all the related documents carefully before investing.

The policy push given by

a growth-oriented Budget

helped Indian equities rally

for most part of February,

driving them up nearly 1,500

points. It would have been a

happy ending, but for the

From the Editor’s Desk

PMS DESK

Star Moder Portfolio 45

Power Model Portfolio 46

MUTUAL FUND DESK 48

08

EQUITY

FUNDAMENTALS

TECHNICALS DERIVATIVES

Nifty 42 View 43

ADVISORY DESK DERIVATIVES

MID Trades 47 Derivatives Ideas 47

CURRENCY

TECHNICALS

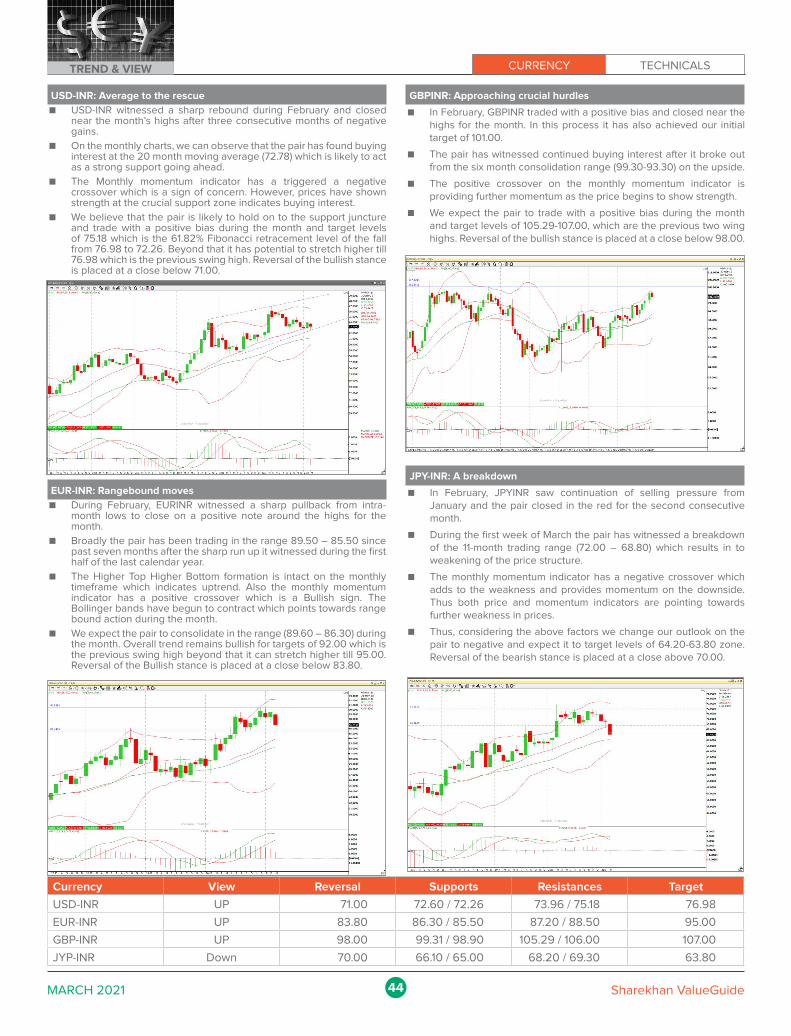

USD-INR 44 GBP-INR 44

EUR-INR 44 JPY-INR 44

3R Stock Idea 09 REGULAR FEATURES

Stock Update 11 Report Card 04

Sector Update 38 Earnings Guide 52

fact that the benchmark indices shed half of what they

gained in the last week....

EQUITY FUNDAMENTALSREPORT CARD

4MARCH 2021 Sharekhan ValueGuide

STOCK IDEAS STANDING (AS ON MARCH 03, 2021)

COMPANYCURRENT

RECOPRICE AS ON

03-MAR-2021PRICE

TARGET 52 WEEK ABSOLUTE PERFORMANCE RELATIVE TO SENSEX

HIGH LOW 1M 3M 6M 12M 1M 3M 6M 12M

Autos

Alicon Castalloy Buy 464 500 490 170 8.2 28.9 29.2 73.7 6.4 13.0 -3.7 29.7

Amara Raja Batteries Buy 914 1146 1025 350 -4.8 0.2 23.1 43.5 -6.3 -12.2 -8.2 7.1

Apollo Tyres Buy 250 290 261 74 2.5 32.9 106.7 78.8 0.9 16.4 54.1 33.5

Ashok Leyland Buy 131 151 139 34 -3.5 38.4 88.0 81.0 -5.1 21.2 40.1 35.1

Bajaj Auto Buy 3900 4589 4361 1793 -7.6 17.7 35.3 43.9 -9.1 3.2 0.9 7.5

Balkrishna Industries Hold 1634 1800 1885 678 -10.6 -1.0 26.4 47.3 -12.1 -13.2 -5.7 10.0

Bosch Buy 15238 18156 16900 7874 -6.7 16.5 18.3 13.2 -8.2 2.1 -11.8 -15.5

Exide Industries Buy 207 229 221 122 2.0 11.0 26.8 28.2 0.3 -2.7 -5.4 -4.3

GNA Axles Buy 393 490 430 132 1.8 48.0 73.2 102.7 0.2 29.7 29.2 51.3

Greaves Cotton Buy 137 170 149 66 53.4 63.3 73.7 5.5 51.0 43.1 29.5 -21.2

Hero MotoCorp Buy 3425 4030 3629 1475 -0.5 7.8 17.5 67.3 -2.1 -5.6 -12.4 24.9

Lumax Auto Technologies Buy 155 ** 168 48 21.5 49.5 58.9 71.3 19.5 31.0 18.5 27.9

M&M Buy 852 1000 952 246 -1.7 13.6 34.8 79.6 -3.2 -0.5 0.5 34.1

Maruti Suzuki Buy 7124 9000 8400 4002 -6.7 -8.7 -0.9 11.6 -8.3 -20.0 -26.1 -16.7

Mayur Uniquoters Buy 418 500 479 118 39.9 43.8 47.0 74.1 37.6 26.0 9.6 30.0

Schaeffler India Buy 5227 5900 5265 3044 13.5 33.3 31.7 19.9 11.6 16.8 -1.8 -10.5

Sundram Fasteners Buy 715 850 755 249 18.4 32.8 63.4 77.0 16.5 16.3 21.9 32.2

Suprajit Engineering Buy 286 300 301 100 33.3 41.9 60.7 49.3 31.1 24.3 19.8 11.4

Tata Motors Buy 349 365 357 64 6.9 89.2 135.9 175.9 5.1 65.8 75.9 106.0

TVS Motor Buy 627 688 660 240 -4.1 25.8 44.5 52.8 -5.6 10.3 7.8 14.1

BSE Auto Index 24066 25073 10141 -1.9 14.5 33.3 53.8 -3.5 0.3 -0.6 14.9

Agri/Specialy Chemical

Aarti Industries Buy 1301 1355 1364 662 8.8 7.9 21.6 34.6 7.0 -5.4 -9.3 0.5

Atul Limited Buy 6649 7540 7021 3257 3.1 8.1 8.8 32.0 1.4 -5.3 -18.9 -1.5

Coromandel International Buy 778 1000 880 444 1.3 -1.6 4.6 26.0 -0.3 -13.8 -22.0 -5.9

Insecticides (India) Buy 459 590 557 207 -10.1 0.4 -7.6 4.0 -11.6 -12.0 -31.1 -22.4

PI Industries Buy 2280 2740 2544 974 1.4 -3.8 21.1 44.6 -0.3 -15.7 -9.7 8.0

SRF Limited Buy 5688 6760 6075 2492 -0.4 6.7 35.3 42.8 -2.0 -6.5 0.9 6.6

Sudarshan Chemicals Buy 574 615 600 286 14.3 12.8 27.5 25.4 12.5 -1.1 -4.9 -6.4

UPL Buy 613 632 631 240 11.9 34.7 20.6 19.9 10.1 18.0 -10.1 -10.5

Vinati Organics Buy 1425 1750 1527 651 14.6 25.1 42.0 41.9 12.7 9.6 5.9 5.9

Banks and Financial Services

AU Small Finance Bank Buy 1199 1500 1294 366 24.4 36.5 81.7 4.0 22.4 19.6 35.5 -22.4

Axis Bank Buy 754 900 800 285 1.3 22.6 65.5 10.5 -0.3 7.5 23.4 -17.5

Bajaj Finance Buy 5545 6000 5922 1783 0.8 13.7 54.2 29.3 -0.8 -0.3 15.0 -3.4

Bajaj Finserv Buy 10387 10860 10586 3986 6.9 14.8 65.5 18.1 5.2 0.6 23.4 -11.8

Bank of Baroda Hold 86 ** 100 36 4.3 45.0 86.5 16.8 2.6 27.0 39.0 -12.8

Bank of India Hold 81 ** 101 30 40.5 67.5 66.1 67.2 38.2 46.8 23.9 24.8

Cholamandalam Investment and Finance Company

Buy 541 580 558 117 16.4 46.2 130.8 83.0 14.5 28.1 72.1 36.6

City Union Bank Buy 181 225 216 110 3.1 0.9 28.5 -16.4 1.5 -11.6 -4.2 -37.6

Federal Bank Buy 88 95 92 36 3.0 33.4 63.7 5.5 1.3 16.9 22.0 -21.2

HDFC Buy 2653 3100 2895 1473 -2.0 18.1 49.9 20.3 -3.6 3.5 11.7 -10.2

HDFC Bank Buy 1586 1810 1650 739 0.5 14.5 41.7 38.1 -1.1 0.4 5.6 3.1

ICICI Bank Buy 632 770 679 269 0.7 25.8 69.5 24.3 -0.9 10.3 26.4 -7.2

Indusind Bank Buy 1100 1340 1119 236 6.6 20.4 78.7 3.2 4.9 5.5 33.2 -23.0

Kotak Mahindra Bank Buy 1899 2130 2049 1000 -0.7 2.9 37.7 18.1 -2.3 -9.9 2.7 -11.8

LIC Housing Finance Buy 464 610 488 186 2.6 33.3 57.1 44.7 1.0 16.8 17.2 8.1

LT FINANCE HOLDING Buy 112 118 113 43 20.4 27.2 70.5 6.4 18.5 11.4 27.1 -20.6

Nippon Life India AMC Buy 361 418 399 201 9.3 22.3 31.3 -8.4 7.5 7.2 -2.1 -31.6

Punjab National Bank Hold 44 ** 46 26 7.5 22.2 29.6 -2.0 5.8 7.0 -3.4 -26.8

EQUITY FUNDAMENTALS REPORT CARD

5MARCH 2021 Sharekhan ValueGuide

STOCK IDEAS STANDING (AS ON MARCH 03, 2021)

COMPANYCURRENT

RECOPRICE AS ON

03-MAR-2021PRICE

TARGET 52 WEEK ABSOLUTE PERFORMANCE RELATIVE TO SENSEX

HIGH LOW 1M 3M 6M 12M 1M 3M 6M 12M

RBL Bank Buy 249 ** 308 102 -3.3 4.9 31.7 -15.9 -4.8 -8.0 -1.8 -37.2

Repco Home Finance Buy 324 400 377 91 23.1 23.8 87.1 15.0 21.1 8.5 39.5 -14.1

SBI Buy 405 460 426 150 14.1 53.7 96.0 42.0 12.2 34.7 46.1 6.0

Spandana Buy 611 850 1098 404 -18.5 -17.7 2.7 -42.8 -19.9 -27.9 -23.4 -57.3

BSE Bank Index 40831 42655 18430 2.2 18.8 56.2 24.0 0.6 4.1 16.5 -7.4

Insurance

HDFC Life Buy 727 850 744 339 6.8 13.0 26.5 27.9 5.1 -1.0 -5.7 -4.5

ICICI Pru Life Buy 490 584 538 222 2.9 3.0 16.4 10.1 1.2 -9.8 -13.2 -17.8

ICICI Lombard Buy 1498 1750 1625 806 2.1 3.3 16.1 23.1 0.5 -9.5 -13.4 -8.1

Max Financial Buy 924 1000 943 280 28.4 45.0 55.6 56.2 26.3 27.0 16.0 16.6

Consumer Goods

Asian Paints Buy 2402 3000 2871 1432 0.0 -1.5 22.8 29.9 -1.6 -13.7 -8.4 -3.0

Britannia Buy 3481 4200 4015 2101 -2.8 -4.6 -6.1 13.6 -4.3 -16.4 -30.0 -15.2

Colgate-Palmolive (India) Buy 1617 1850 1676 1065 -0.2 4.9 18.7 23.2 -1.8 -8.1 -11.5 -8.0

Dabur India Buy 518 605 552 385 -1.5 3.1 7.1 0.6 -3.1 -9.7 -20.2 -24.9

Emami Buy 451 570 520 141 -10.1 8.0 22.0 80.5 -11.6 -5.3 -9.0 34.8

Godrej Consumer Products Buy 699 850 808 425 -9.0 -1.5 6.7 10.7 -10.5 -13.7 -20.4 -17.4

Hindustan Unilever Buy 2194 2790 2614 1756 -2.4 0.3 3.3 0.8 -3.9 -12.1 -23.0 -24.8

ITC Buy 210 265 239 135 -8.7 5.9 12.5 12.0 -10.2 -7.2 -16.2 -16.4

Jyothy Laboratories Buy 150 188 166 86 -4.9 2.8 7.4 21.8 -6.5 -9.9 -19.9 -9.0

Marico Buy 409 477 439 234 -1.5 3.5 9.3 38.4 -3.1 -9.3 -18.5 3.3

Nestle India Buy 16695 19055 18821 12589 -2.2 -6.3 2.9 0.9 -3.8 -17.9 -23.3 -24.6

Tata Consumer Products Ltd Buy 637 740 653 214 8.3 13.0 12.5 82.5 6.6 -1.0 -16.1 36.2

Zydus Wellness Buy 1901 2300 2218 1070 0.7 4.0 19.2 31.0 -0.9 -8.8 -11.1 -2.2

BSE FMCG Index 12325 12895 8491 -3.1 3.1 8.3 12.9 -4.7 -9.7 -19.3 -15.7

IT / IT services

Birlasoft Buy 242 320 284 48 -10.0 28.9 44.4 153.1 -11.5 12.9 7.7 89.0

HCL Technologies Buy 965 1250 1074 376 0.7 12.3 37.6 71.4 -0.9 -1.6 2.6 28.0

Infosys Buy 1344 1650 1393 511 5.0 18.4 46.2 77.1 3.3 3.8 9.0 32.2

Intellect Design Buy 460 500 502 44 15.3 58.3 145.7 322.8 13.5 38.7 83.2 215.6

L&T Infotech Buy 3912 4800 4500 1208 -9.0 19.8 57.9 105.9 -10.5 5.0 17.7 53.8

L&T Technology services Buy 2708 3100 2805 995 3.5 50.2 73.3 64.5 1.8 31.6 29.2 22.8

Mastek Limited Buy 1229 1400 1460 170 4.1 25.3 73.1 199.3 2.4 9.8 29.0 123.5

Persistent Systems Buy 1690 1770 1850 420 0.0 38.6 70.7 139.4 -1.6 21.5 27.3 78.7

Tata Consultancy Services Buy 3059 3590 3345 1504 -4.0 12.2 33.6 46.8 -5.6 -1.7 -0.4 9.6

Tata Elxsi Buy 2564 2850 3050 501 -9.3 53.7 122.8 160.9 -10.8 34.7 66.1 94.8

Tech Mahindra Buy 976 1100 1081 470 0.7 5.8 30.4 26.6 -0.9 -7.3 -2.8 -5.5

Wipro Buy 435 510 467 160 1.3 20.7 57.8 90.4 -0.3 5.8 17.6 42.1

BSE IT Index 25943 27074 10937 1.1 16.5 43.1 67.0 -0.5 2.1 6.7 24.7

Telecom and New Media

Affle (India) Limited Buy 5760 ** 6287 909 51.8 49.4 110.8 233.6 49.4 30.9 57.2 149.1

Bharti Airtel Buy 546 750 623 381 -9.0 10.6 4.4 5.7 -10.5 -3.1 -22.1 -21.1

Info Edge (India) Buy 5048 6100 5876 1580 5.4 19.2 51.3 90.0 3.7 4.5 12.8 41.9

Capital goods / Power

Amber Technologies Buy 3312 3716 3668 922 22.2 42.4 80.4 141.2 20.2 24.8 34.5 80.1

Bharat Electronics Buy 153 190 155 56 8.6 32.3 43.8 104.3 6.8 15.9 7.2 52.6

Carborundum Universal Buy 515 611 571 175 14.8 37.0 101.0 62.5 12.9 20.0 49.9 21.3

CESC Buy 625 825 730 366 1.4 -0.7 2.8 2.4 -0.2 -13.0 -23.3 -23.6

Coal India Buy 155 160 180 110 7.9 16.2 17.0 -13.1 6.1 1.8 -12.8 -35.1

Cummins India Buy 864 1030 899 282 10.0 52.4 85.7 73.8 8.2 33.5 38.5 29.8

Dixon Technologies Buy 19240 ** 20440 2900 19.6 68.9 124.3 392.8 17.7 48.0 67.3 267.9

Finolex Cable Buy 401 475 426 165 8.0 16.9 39.4 23.7 6.2 2.4 3.9 -7.6

New Idea

New Idea

EQUITY FUNDAMENTALSREPORT CARD

6MARCH 2021 Sharekhan ValueGuide

STOCK IDEAS STANDING (AS ON MARCH 03, 2021)

COMPANYCURRENT

RECOPRICE AS ON

03-MAR-2021PRICE

TARGET 52 WEEK ABSOLUTE PERFORMANCE RELATIVE TO SENSEX

HIGH LOW 1M 3M 6M 12M 1M 3M 6M 12M

Honeywell Automation Buy 46945 48200 49596 20142 10.3 52.1 45.6 44.2 8.5 33.2 8.5 7.7

Kalpataru Power Transmission Buy 399 485 406 170 9.9 18.0 57.4 20.7 8.1 3.4 17.4 -9.9

KEC International Buy 461 505 486 155 11.4 27.3 41.2 47.2 9.6 11.6 5.3 9.9

KEI Industries Buy 500 540 530 208 3.7 16.2 28.7 -1.9 2.1 1.8 -4.0 -26.8

NTPC Buy 113 140 115 74 13.7 14.3 18.8 4.3 11.8 0.1 -11.4 -22.2

Polycab India Buy 1355 1530 1387 572 2.6 35.1 56.6 30.0 0.9 18.4 16.7 -3.0

Power Grid Corporation Buy 227 245 239 130 10.8 17.0 29.9 15.4 9.0 2.6 -3.1 -13.8

Ratnamani Metals and Tubes Buy 1965 ** 2050 716 20.1 19.3 67.3 47.7 18.1 4.5 24.8 10.2

Thermax Hold 1374 ** 1459 644 13.5 49.5 78.5 52.6 11.7 31.0 33.1 14.0

Triveni Turbine Buy 111 ** 118 46 22.0 32.1 50.2 21.6 20.0 15.8 12.0 -9.2

V-Guard Industries Buy 223 311 255 149 -11.5 17.7 32.3 10.4 -12.9 3.1 -1.3 -17.6

BSE Power Index 2546 2583 1275 14.4 22.2 50.1 44.0 12.5 7.0 11.9 7.5

BSE Capital Goods Index 22312 22435 9499 2.3 27.0 59.5 45.0 0.6 11.3 18.9 8.2

Infrastructure

Ashoka Buildcon Buy 112 125 119 37 9.6 29.8 62.3 30.9 7.8 13.7 21.0 -2.3

JMC Projects Buy 77 95 82 30 3.1 2.7 47.9 13.5 1.5 -10.0 10.3 -15.3

KNR Constructions Buy 209 270 242 86 -8.1 -33.5 -14.8 -21.4 -9.5 -41.7 -36.5 -41.3

Larsen & Toubro Buy 1497 1795 1593 661 -2.1 30.2 58.7 27.1 -3.7 14.1 18.4 -5.1

PNC Infratech Buy 262 300 291 81 14.3 43.2 61.6 44.6 12.4 25.5 20.5 8.0

Sadbhav Engineering Buy 73 100 85 23 12.2 9.5 40.4 13.4 10.4 -4.1 4.7 -15.3

CNX Infra Index 4282 4316 2073 5.8 20.1 35.0 41.6 4.1 5.2 0.7 5.7

BSE Real estate Index 2888 2910 1259 7.4 29.0 66.7 35.3 5.7 13.0 24.3 1.1

Metal & mining

JSW Steel Buy 428 432 435 133 6.9 15.5 51.6 74.4 5.2 1.2 13.0 30.2

NMDC Buy 137 165 140 62 17.3 28.0 45.7 44.9 15.4 12.1 8.6 8.2

MOIL Buy 169 170 178 87 19.0 22.7 13.8 33.5 17.1 7.5 -15.2 -0.3

Oil & gas

Bharat Petroleum Corporation Buy 466 520 482 252 11.3 18.9 15.6 11.6 9.5 4.2 -13.8 -16.6

Castrol India Buy 135 150 141 90 3.4 3.3 12.7 -4.2 1.7 -9.5 -16.0 -28.5

GAIL (India) Buy 147 175 153 66 12.4 22.7 49.9 38.6 10.6 7.5 11.7 3.5

Gujarat Gas Buy 550 ** 568 191 44.4 58.1 78.9 89.7 42.0 38.6 33.4 41.6

Gujarat State Petronet Limited Buy 276 300 311 146 34.7 25.0 38.9 22.2 32.5 9.5 3.6 -8.8

Hindustan Petroleum Corporation

Buy 249 275 259 155 8.6 15.0 26.3 21.0 6.8 0.8 -5.8 -9.7

Indian Oil Corporation Buy 103 115 108 71 -1.0 13.5 22.2 -3.8 -2.6 -0.5 -8.9 -28.2

Indraprastha Gas Limited Buy 517 650 595 285 -5.1 8.1 29.1 18.9 -6.6 -5.2 -3.7 -11.2

Mahanagar Gas Buy 1182 1380 1257 666 7.4 14.0 29.5 16.7 5.6 -0.1 -3.5 -12.9

Oil India Ltd Hold 128 130 139 66 8.4 19.7 35.6 16.0 6.6 4.9 1.1 -13.4

Petronet LNG Buy 256 300 280 171 2.2 -2.4 8.8 4.2 0.5 -14.5 -18.9 -22.2

Reliance Ind Buy 2201 2400 2369 868 14.4 13.1 6.0 64.4 12.6 -0.9 -21.0 22.7

BSE Oil and gas Index 16159 16588 8724 9.5 15.3 24.9 27.7 7.7 1.0 -6.9 -4.6

Pharmaceuticals

Abbott India Buy 14609 19425 18569 12500 0.8 -4.2 -11.7 -2.6 -0.8 -16.0 -34.2 -27.3

Aurobindo Pharma Buy 881 1100 1023 281 -4.9 -2.2 9.0 69.1 -6.5 -14.3 -18.7 26.3

Biocon Buy 403 470 488 236 -1.7 -9.0 -4.3 32.7 -3.3 -20.3 -28.6 -1.0

Cadila Healthcare Buy 446 560 509 213 -7.0 -5.4 18.2 74.0 -8.5 -17.1 -11.9 29.9

Cipla Buy 812 950 879 357 -2.7 6.0 12.1 81.4 -4.2 -7.1 -16.4 35.5

Divi's Labs Buy 3565 4500 3913 1633 -3.1 -3.9 10.5 63.9 -4.7 -15.8 -17.6 22.3

DR Reddy's Buy 4501 6500 5515 2498 -3.5 -8.3 4.1 41.8 -5.1 -19.6 -22.4 5.9

Gland Pharma Buy 2433 3040 2692 1701 13.8 11.7 - - 11.9 -2.1 - -

Granules Buy 364 475 438 115 4.9 -13.6 5.3 111.0 3.2 -24.3 -21.5 57.5

IPCA Lab Buy 1961 2560 2456 1162 -2.0 -12.8 -2.9 37.4 -3.6 -23.6 -27.6 2.6

New Idea

EQUITY FUNDAMENTALS REPORT CARD

7MARCH 2021 Sharekhan ValueGuide

** Price under review @ Reco price adjusted for demerger # Reco price adjusted for bonus ^ Reco price adjusted for stock split* Price targets will be reviewed after we get further clarity on operations from companies post Q4FY2020 result announcements.

STOCK IDEAS STANDING (AS ON MARCH 03, 2021)

COMPANYCURRENT

RECOPRICE AS ON

03-MAR-2021PRICE

TARGET 52 WEEK ABSOLUTE PERFORMANCE RELATIVE TO SENSEX

HIGH LOW 1M 3M 6M 12M 1M 3M 6M 12M

Laurus Labs Buy 365 450 386 62 5.1 9.9 -69.2 -13.0 3.4 -3.7 -77.0 -35.1

Lupin Hold 1061 1350 1122 505 0.9 13.7 12.3 59.8 -0.7 -0.3 -16.3 19.3

Sanofi India* Buy 8294 9249 8999 5900 6.3 5.0 -1.5 11.4 4.6 -8.0 -26.6 -16.8

Shilpa Medicare Buy 369 520 692 240 -16.4 -19.2 -27.7 -18.4 -17.8 -29.2 -46.1 -39.1

Solara Active Pharma Sciences Buy 1300 1700 1625 367 -8.6 1.7 36.6 104.4 -10.0 -10.8 1.9 52.6

Strides Pharma Sciences Buy 890 1020 1000 271 0.3 11.8 48.7 91.4 -1.3 -2.0 10.8 42.9

Sun Pharmaceutical Industries Buy 624 700 654 315 -1.2 9.7 21.8 53.8 -2.8 -3.9 -9.2 14.9

Torrent Pharma Hold 2497 3100 3040 1619 -6.9 -6.3 -9.9 14.1 -8.4 -17.9 -32.8 -14.8

BSE Health Care Index 21560 22464 10948 -0.3 2.8 15.1 53.1 -1.9 -9.9 -14.2 14.3

Building materials

APL Apollo Tubes^ Buy 1243 1330 1379 205 33.8 -66.6 -48.2 -35.3 31.6 -70.7 -61.3 -51.7

Astral Poly Technik Hold 2207 ** 2332 748 7.0 45.6 81.2 95.7 5.2 27.6 35.1 46.1

Century Plyboards (India) Buy 319 340 340 95 17.8 40.6 96.4 106.2 15.9 23.2 46.4 53.9

Dalmia Bharat Buy 1502 1900 1570 406 18.7 33.6 101.8 105.9 16.8 17.1 50.5 53.7

Grasim Buy 1318 1430 1372 380 11.1 41.7 86.6 91.2 9.3 24.2 39.2 42.8

Greenlam Industries Buy 944 1100 976 450 4.5 8.2 31.3 4.0 2.8 -5.2 -2.1 -22.4

JK Lakshmi Cement Buy 421 525 448 180 17.7 16.1 59.6 40.2 15.8 1.7 19.0 4.7

Kajaria Ceramics Buy 972 1200 1016 295 8.4 44.6 119.0 78.7 6.6 26.7 63.3 33.4

Pidilite Industries Buy 1765 1875 1850 1186 0.3 9.9 22.9 11.5 -1.3 -3.7 -8.4 -16.8

Shree Cement Buy 27686 31610 29098 15500 1.8 11.1 39.0 19.0 0.2 -2.6 3.6 -11.2

Supreme Industries Limited Buy 2110 2330 2131 791 6.8 26.9 52.9 70.4 5.1 11.2 14.0 27.2

The Ramco Cements Buy 1017 1150 1043 457 17.2 14.4 41.9 35.5 15.3 0.2 5.8 1.2

UltraTech Cement Buy 6500 8000 6946 2913 5.1 27.7 65.5 55.7 3.4 11.9 23.4 16.2

Logistics

Gateway Distriparks Buy 176 210 189 71 7.4 57.6 82.5 40.6 5.6 38.1 36.1 5.0

Mahindra Logistics Buy 481 562 544 199 -0.9 20.8 36.4 34.7 -2.5 5.8 1.7 0.6

TCI Express Buy 910 1150 1024 491 -5.1 4.5 17.4 18.0 -6.7 -8.4 -12.4 -11.9

Discretionary

ABFRL Buy 209 255 248 96 31.6 31.0 52.9 -16.3 29.5 14.8 14.0 -37.5

Arvind@ Buy 76 95 84 19 46.9 83.3 125.0 107.8 44.5 60.6 67.7 55.1

Bata India Buy 1525 1765 1705 1017 -4.1 -2.5 13.0 -4.0 -5.7 -14.6 -15.8 -28.4

Inox Leisure Buy 322 400 394 158 -2.4 14.9 10.9 -15.6 -4.0 0.7 -17.3 -37.0

Jubilant Foodworks Buy 3142 3380 3215 1142 11.1 22.6 40.0 89.9 9.3 7.5 4.4 41.8

KPR Mill Buy 960 1100 1019 317 3.6 19.3 73.9 65.7 1.9 4.5 29.7 23.7

Relaxo Footwear Buy 839 1005 928 493 -0.1 15.5 27.8 21.3 -1.7 1.2 -4.7 -9.4

The Indian Hotels Company Buy 125 155 139 62 4.3 -2.3 22.8 1.0 2.6 -14.4 -8.5 -24.6

Titan Company Limited Buy 1474 1710 1621 720 -2.6 2.6 27.2 17.9 -4.2 -10.1 -5.1 -12.0

Trent Ltd Buy 911 1015 944 368 36.2 34.4 40.3 32.1 34.0 17.7 4.6 -1.4

Welspun India Buy 71 90 79 18 -2.8 6.7 24.9 80.4 -4.4 -6.5 -6.9 34.7

Wonderla Holidays Hold 208 227 227 105 -0.7 0.0 12.4 3.2 -2.3 -12.4 -16.2 -23.0

ZEE Entertainment Buy 222 275 261 114 -11.0 7.3 0.7 -11.8 -12.4 -6.0 -24.9 -34.1

Diversified / Miscellaneous

Bajaj Holdings Buy 3663 4312 3785 1472 7.1 16.6 41.4 10.2 5.3 2.2 5.4 -17.7

Mahindra Lifespace Buy 529 655 561 171 29.8 60.7 118.5 55.9 27.7 40.8 62.9 16.4

JSW Steel Buy 428 432 435 133 6.9 15.5 51.6 74.4 5.2 1.2 13.0 30.2

Polyplex Corporation Hold 870 950 945 283 16.4 11.0 21.8 83.6 14.6 -2.7 -9.2 37.0

Quess Corp Buy 736 ** 807 165 15.9 47.8 92.4 46.1 14.1 29.5 43.4 9.1

Triveni Engineering & Industries Buy 94 ** 98 29 25.3 30.3 24.6 54.1 23.2 14.2 -7.1 15.0

BSE500 Index 20306 20329 9758 3.9 16.5 36.3 38.4 2.3 2.1 1.6 3.3

CNX500 Index 12765 12782 6152 3.9 16.3 36.1 37.9 2.2 1.9 1.5 2.9

CNXMCAP Index 24488 24740 10750 8.0 21.2 44.7 46.2 6.3 6.2 7.9 9.2

New Idea

New Idea

New Idea

8MARCH 2021 Sharekhan ValueGuide

Look beyond bond blues

The policy push given by a growth-oriented Budget helped Indian equities rally for most part of

February, driving them up nearly 1,500 points. It would have been a happy ending, but for the

fact that the benchmark indices shed half of what they gained in the last week. The sharp fall in

the last trading session was significant – with the Sensex and Nifty dropping nearly 3.8% each,

ending the month on a negative note.

What led to the sudden rout? A sudden spike in bond yields has created a flutter in financial

markets globally. For the first time since the meltdown in March 2020, the 30-year and 10-year

bond yields crossed physiologically important level of 2% and 1.5% respectively, sparking fears

that the US Federal Reserve may now start tightening policy rates, sooner than expected. The

Indian bond market too mirrored trends in the US, with the yield on the 10-year government

bond soaring to 6.2% -- up 35 bps in one month.

However, given that it is hope of a strong economic bounceback that is driving up bond yields,

the event is only likely to be a temporary blip for equities. What’s more, liquidity in the global

markets is still gushing as interest rates haven’t climbed back to their pre-COVID levels. The

liquidity gush amid a weak US Dollar will ensure that India will see steady foreign inflows, what

with the economic and earnings recovery also looking more promising.

For Q3FY21, India’s GDP managed to beat the COVID blues, rising by 0.4%, which means that

the nation is technically out of a recession. Q2FY21 growth too was revised upwards to -7.3%.

But all is not well. The full fiscal FY2021 estimates for GDP has been revised to -8% from -7.5%

earlier. This implies weakness in Q4 with expectations of a marginally negative growth in GDP

for Q4FY2021.

On the brighter side, the easing of the COVID-led lockdowns and strong progress in the

country’s vaccination program offer hope that the economic recovery will only strengthen

through the next fiscal. Key macro indicators such as the Manufacturing PMI, automobile sales,

GST collections and industrial output also showed a steady improvement.

Complementing the pick-up in macros is the continued momentum in corporate earnings.

Q3FY21 proved to be a strong quarter yet again, with the pace increasing from Q2FY2021.

Earnings were better than expected across sectors and companies management commentary

also added to the positivity. For Nifty companies, aggregate sales and net profits grew 2.7% and

22%, respectively, in what was one of the best earnings growth in the past five years.

To sum it up, there is a lot of steam left in the equities rally, despite blips such as rising bond

yields, new waves of COVID cases and other developments across the globe. Thus, one must

stay invested for the long haul to reap the benefits well.

Happy investing!

Fro

m t

he

Ed

ito

r’s

De

skFrom the Editor’s Desk

9MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALS STOCK IDEA

Intellect Design Arena LimitedDate: February 03, 2021 Designing the Future

Reco Price

Buy PT : Rs. 500 Rs. 361

Summary

• We initiate coverage on Intellect Design with a Buy rating, with a PT of Rs. 500 as it is well-poised to gain market share given its future-ready products with flexible

modules.

• Stock trades at reasonable valuation of 16x/12x its FY2022E/FY2023E earnings. Favorable industry tailwinds, anticipated improving financial metrics to aid re-rating

of stock.

• The company focuses on increasing license-linked revenues, which is expected to improve profitability. Company turned net cash positive of Rs. 124 crore in Q3FY2021

from net debt of Rs. 102 crore in Q3FY2020.

• Huge addressable market, strong traction for mature products, rising annuity revenue, and improving margins would help company to clock revenue and earnings

CAGR of 14% and 27% respectively over FY2021-23E.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Intellect-Feb03_2021_3R_StockIdea.pdf

Greenlam Industries LimitedDate: February 03, 2021 A perfect fit

Reco Price

Buy PT : Rs. 1,100 Rs. 842

Summary

• We initiate coverage on Greenlam Industries Limited (GRLM) with a Buy rating and price target of Rs. 1100.

• Greenlam is expected to ride on a strong growth trajectory led by its leadership positioning, strong domestic growth outlook and rising export opportunities.

• Brownfield capacity expansions would be the next leg of growth. Despite capex, balance sheet and return ratios would improve further.

• Structural growth drivers such as rising incomes, urbanisation, real estate construction, Atmanirbhar Bharat, etc, would provide long-term sustainable growth trajectory.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Greenlam-Feb03_2021_3R_Stock%20Idea.pdf

Gland Pharma LimitedDate: February 26, 2021 A giant in the making

Reco Price

Buy PT : Rs. 3,040 Rs. 2,412

Summary

• We Initiate coverage on Gland Pharma Limited (Gland) with a Buy recommendation and a price target of Rs. 3,040.

• Gland is an established player in Injectables space and is well-placed to harness the growth opportunities in this space. It has a strong compliance record with nil

observations from the USFDA across all its plants.

• Gland has a unique B2B business model, which enables it grow its market share while maintaining cost leadership.

• Strong domain expertise, robust growth prospects, sturdy & consistent earnings track record, and healthy return ratios make Gland an ideal long-term investment pick.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Gland_Pharma-Feb26_2021_3R_StockIdea.pdf

10MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALSSTOCK IDEA

Sharekhan Limited, its analyst or dependant(s) of the analyst might be holding or having a position in the companies mentioned in the article.

Dalmia Bharat LimitedDate: March 02, 2021 Rising through the ranks

Reco Price

Buy PT : Rs. 1,900 Rs. 1,467

Summary

• We initiate coverage on Dalmia Bharat (Dalmia) with a Buy rating and price target of Rs. 1,900. Multiples to expand from 8.5x EV/EBITDA FY23E currently as it gains

size, geographical diversification and higher operational profitability.

• Dalmia is on an expansion spree in the medium to long term and aims to double its capacity and become a larger pan-India player.

• Despite aggressive expansions, it is likely to achieve net cash position by FY2023E led by free cash flows of almost Rs. 1,200 crore p.a. during FY2021-FY2023E.

• The government’s infrastructure investment plan over the next five years, impetus on affordable housing and India’s structural growth drivers for cement consumption

present strong growth tailwinds.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Dalmia-Mar01_2021_3R_Stock_Idea.pdf

Stock Update

11MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation

Reco Price (Rs.)Price Target/ Upside (%)

Latest Chg Latest Chg

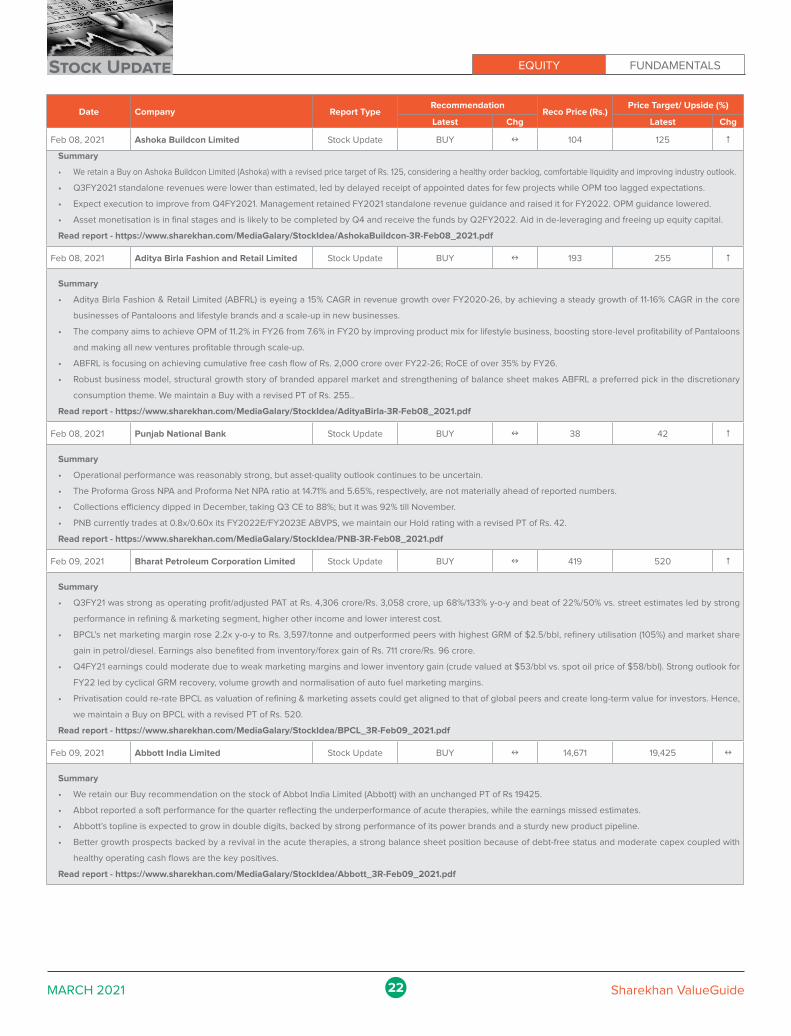

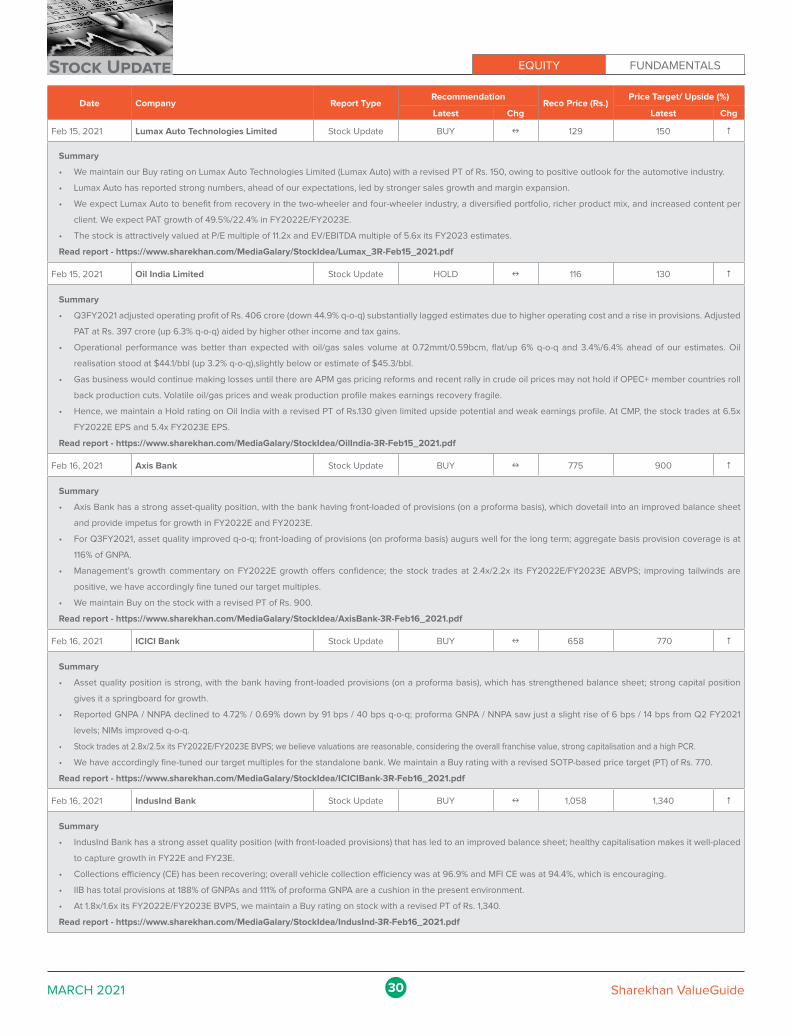

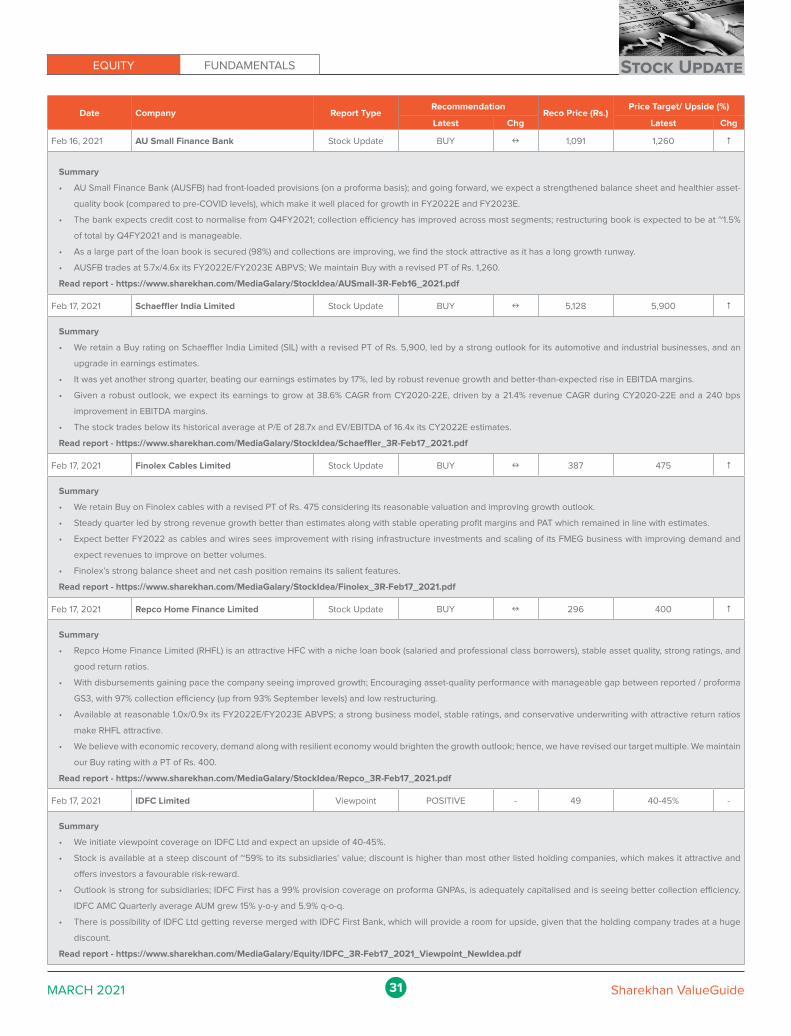

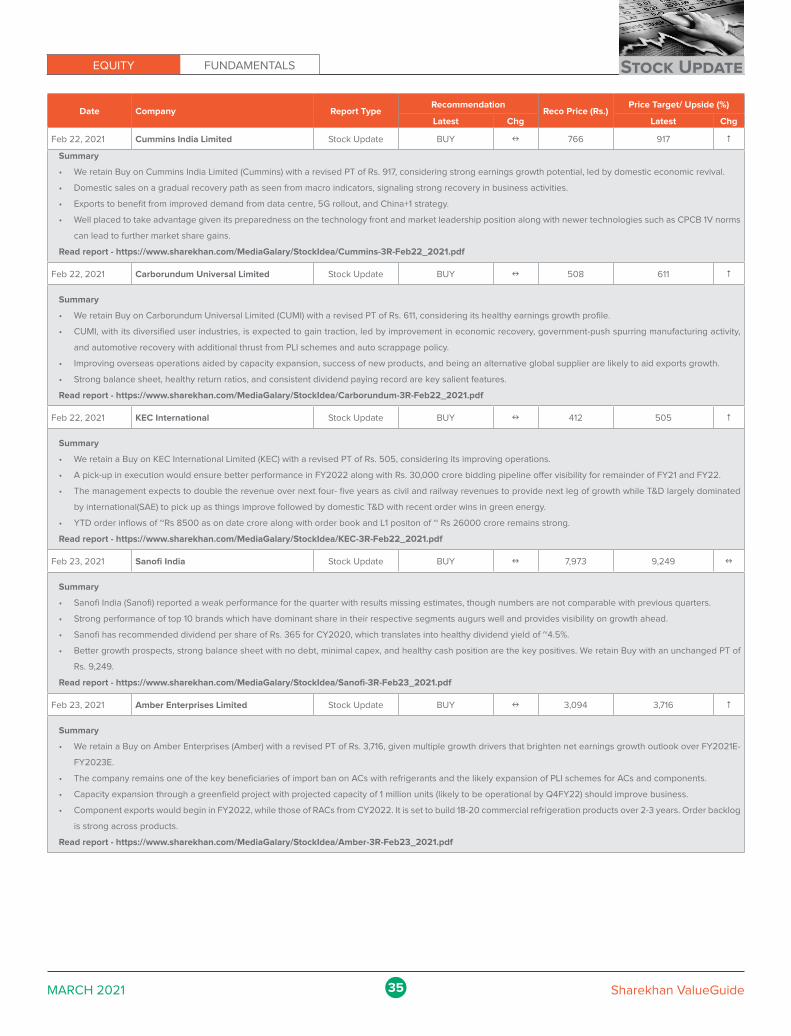

Feb 01, 2021 Cholamandalam Investment and Finance Company Stock Update BUY x 520

Summary

• CIFC posted mixed results with a rise in proforma GNPA against reported GNPA levels, but improvement in margins was the bright spot.

• Healthy business traction seen with total AUM rising 15% y-o-y to Rs 75,813 crore; reported asset quality improved with Stage 3 assets at 2.57% (improved from 2.75%

in Q2 FY2021).

• Buoyancy in rural markets augurs well, a well-capitalised balance sheet, and rigorous risk management practices provides long-term visibility; the stock is available

at 4.1x/3.4x its FY2022E/FY2023E ABVPS.

• Healthy traction in automobile demand, resilient rural economy brighten growth outlook; we maintain Buy rating with an unchanged price target (PT) of Rs. 520.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Cholamandalam_3R-Feb01_2021.pdf

Feb 01, 2021 Zydus Wellness Limited Stock Update BUY 1,949 2,300

Summary

• Zydus Wellness Limited (ZWL) posted strong performance in Q3FY2021 with revenue and operating profit growing by ~15% and ~33%, respectively (OPM expanding

by 176 bps); lower interest cost led to PAT standing at Rs. 29 crore versus Rs. 9 crore in Q2FY2020.

• Excluding Nutralite, all brands reported strong double-digit revenue growth in Q3. Nutralite business recovered to 90% of pre-COVID level and will reach 100% in Q4.

• Improving penetration of Complan, higher traction for Sugarfree and Glucon D along with new products performing well and improved growth of Everyuth brand

coupled with distribution enhancement will be key revenue drivers in the near term.

• With improving growth prospects in key brands and deleveraged balance sheet, ZWL is well poised to achieve earnings CAGR of 28% over FY2020-FY2023. We

maintain our Buy recommendation on the stock with an unchanged PT of Rs. 2,300.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Zydus_3R-Feb01_2021.pdf

Feb 01, 2021 Amber Enterprises Limited Stock Update BUY 2,621 3,170

Summary

• We retain Buy on Amber Enterprises Limited (Amber) with an unchanged PT of Rs. 3,170, given a strong net earnings growth outlook over FY2021E-FY2023E.

• Q3FY21 was an operationally strong quarter leading to better-than-expected net profit, while normalised inventory levels led to muted revenues.

• Management expects Q4FY21 to be much better as inventory normalises and hopes of a strong summer. Company would be one of the key beneficiaries from import

ban on ACs with refrigerants and likely expansion of PLI schemes for AC and components.

• Management remains optimistic about export prospects for both fully built-up units and components that can potentially emerge over the next 3-4 years.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Amber_3R-Feb01_2021.pdf

Feb 02, 2021 Housing Development Finance Corporation Stock Update BUY 2,658 3,100

Summary

• Q3FY2021 results were strong as operational numbers beat expectations; asset quality improved sequentially and growth traction improved.

• Overall collection efficiency for individual loans stood at 97.6 in December (from 96.3% in September) which is encouraging.

• Asset quality improved with reported NPA ratio declining, proforma NPA well-contained, company is better capitalised (Tier-I at 19.9%) which demonstrates balance

sheet strength.

• Stock trades at reasonable valuations of 4.8x / 4.4x its FY2022E / FY2023E ABV; we maintain a Buy with a revised SOTP based price target (PT) of Rs. 3,100.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/HDFC_3R-Feb02_2021.pdf

Feb 02, 2021 Dixon Technologies Limited Stock Update BUY 15,716 18,700

Summary

• We retain a Buy rating on Dixon Technologies with a revised PT of Rs. 18700 considering its strong net earnings growth outlook for FY2021E-FY2023E and its strong

compounding structural growth story.

• Strong performance during Q3FY21 led by strong beat in revenues along with stable margins leading to strong PAT beat. It continued to add new clients and scale

up wallet share from existing clients.

• Macro tailwinds and sharp rise in new business volumes, scaling-up of mobile vertical with approval of PLI scheme and capacity expansions brightens core business’

growth outlook.

• Capacity expansion in LED TVs, batons, down lighters, and washing machines on track. Upbeat on increasing overall ODM share as the mobile vertical achieves scale.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Dixon-3R-Feb02_2021.pdf

� Upgrade � No change � Downgrade

� Note: The arrow indicates change in call and price target, if any, vis-à-vis the previous report

Stock Update

12MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation

Reco Price (Rs.)Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 02, 2021 Tata Consumer Products Limited Stock Update BUY 576 685

Summary

• Tata Consumer Products Ltd (TCPL) Q3FY2021 was a mixed bag, as revenues grew by ~23%, but gross margins declined by 574 bps, synergistic benefits and

efficiencies resulted in just a 99 bps decline in OPM to 11.8%.

• India beverages business grew by 46%; India foods revenues rose by 19%, US Coffee by 11% and International tea by 14%.

• Acquisition of Soulfull will add value to India foods business with ‘better for you’ products. Out-of-home businesses NourishCo and Tata Starbucks have seen

substantial improvement and will add-on to growth in the coming quarters.

• We have fine-tuned earnings estimates for FY21/22/23 to factor in higher-than-expected revenue growth and lower OPM. We maintain a Buy with unchanged PT of Rs. 685.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/TCPL_3R-Feb02_2021.pdf

Feb 02, 2021 Coromandel International Limited Stock Update BUY 789 1,000

Summary

• Q3FY2021 operating profit at Rs. 499 crore (up 15.6% y-o-y) was ahead of our estimate, led by 95 bps beat in OPM at 14.1%, given strong gross margin at 32.7% (up 118

bps y-o-y) and operating efficiencies. PAT at Rs. 333 crore (up 25.8% y-o-y) further benefited from lower interest cost.

• Good agronomics, new product launch and capex of Rs. 750 crore-900 crore over FY2021E-FY2022E is expected to drive 18% PAT CAGR over FY2020-FY2023E

along with high RoE of 25%.

• Likely clearance of past subsidy dues given additional allocation of Rs. 65,000 crore for fertiliser subsidy would reduce working capital and further strengthen the

balance sheet (Coromandel received Rs. 1,366 crore in January as against outstanding subsidy of Rs. 2,853 crore as of December 2020).

• We maintain our Buy rating on Coromandel International with unchanged PT of Rs. 1,000. At the CMP, the stock trades at 15.1x its FY2022E EPS and 13.3x its FY2023E

EPS (at a discount of 18% to its historical average one-year forward PE multiple of 16.3x).

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Coromandel-3R-Feb02_2021.pdf

Feb 02, 2021 Mastek Limited Stock Update BUY 1,194 1,400

Summary

• We recommend a Buy with a price target (PT) of Rs. 1,400 as risk-reward balance remains favourable.

• Strong beat on all fronts, led by strong growth in the UK public sector, accelerated growth in Evosys business and recovery in US business; EBITDA margin rose 233

bps q-o-q to 23.5%; added 57 new customers

• The management remains confident on delivering strong growth in the UK public and Evosys businesses in FY2022, led improving demand, strong deal wins and

addition of new logos. US recovery likely to aid growth

• Stock trades at a reasonable valuation of 13x its FY2023E EPS; cash & cash equivalents represent 26% of its current market capitalisation.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Mastek_3R-Feb02_2021.pdf

Feb 02, 2021 Relaxo Footwears Limited Stock Update BUY 841 1,005

Summary

• Relaxo Footwears (Relaxo’s) Q3FY2021 revenue was exactly in-line with our expectation at Rs. 672 crore (grew by 12%y-o-y), led by improving demand across

categories and geographies.

• Better product mix, benign input prices led to 107 bps expansion in gross margin; saving in selling and administrative expenses resulted in OPM expanding by 519 bps to 22%.

• Going ahead, demand is likely to improve due to reducing COVID-19 cases leading to increased mobility and improvement in economic activities.

• We have increased our estimates for FY2021/FY2022/FY2023 by 11%/9%/8% to factor higher margin trajectory. We maintain our Buy recommendation on the stock

with a PT of Rs. 1,005.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Relaxo-3R-Feb02_2021.pdf

Feb 02, 2021 JK Lakshmi Cement Limited Stock Update BUY 350 525

Summary

• We retain a Buy rating on JK Lakshmi Cement with an unchanged PT of Rs. 410 given attractive valuations and healthy net earnings CAGR over FY2021E-FY2023E.

• JKL reported better-than-expected performance for Q3FY2021 led by a beat in volume offtake, higher other income, fall in interest costs and lower ETR. EBITDA/

tonne rose 9% to Rs. 712.

• We expect strong demand environment to sustain during Q4 along with increase in prices expected during February 2020 in its region of operations. Impact of higher

petcoke prices to be felt from Q1FY2022.

• Company to raise equity at UCW level through rights issue for its Rs. 1,500 crore expansion plan, which is expected to ease clinker and capacity constraints.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/JK_Lakshmi_3R-Feb02_2021.pdf

Stock Update

13MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation

Reco Price (Rs.)Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 02, 2021 Indian Oil Corporation Limited Stock Update BUY 99 115

Summary

• Q3FY21 adjusted PAT at Rs. 6,505 crore (up 178% y-o-y) was above consensus estimates led by robust petchem EBITDA (up 2.6x y-o-y) and higher inventory gain of

Rs. 2,630 crore (versus 1,804 crore in Q3FY20).

• Volume recovery was strong with refinery utilization reverting to 103% versus 80% in Q2FY21 and petrol/diesel sales volume up 13%/36% q-o-q. Robust petchem

EBITDA/tonne of $335/tonne (up 2x y-o-y) but core GRM remained weak at $1.26/bbl.

• Potential monetisation of pipeline assets and BPCL privatisation would be key re-ratings catalyst. Strong earnings momentum to sustain in Q4FY21 on likely inventory

gain despite recent weakness in auto fuel marketing margin (likely to normalise with gradual price hikes).

• IOCL’s steep valuation discount of 57% to that of BPCL likely to narrow down amid strong earnings visibility, RoE of 15.4%, and high dividend yield of ~9-10%. Hence,

we maintain a Buy with an unchanged PT of Rs. 115.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/IOCL-3R-Feb02_2021.pdf

Feb 02, 2021 Alicon Castalloy Stock Update BUY - 424 500 -

Summary

• We recommend Buy rating on Alicon Castalloy Limited (Alicon) with a PT of Rs. 500, factoring its long-term average multiple on a strong traction in business outlook

and an upgrade in earnings estimates.

• Alicon reported better-than-expected Q3FY2021 results consolidated net profit growing by 35.7% y-o-y and 116.8% q-o-q driven by solid demand growth.

• We expect Alicon’s business to turnaround in FY2022E by registering PAT of Rs 24 crore versus a loss of Rs 8 crore in FY2021E. We expect a solid growth of 114% in

FY23E, driven by revenue CAGR of 29% during FY2021E-23E and a 370 bps EBITDA margin expansion.

• The stock trades attractively at P/E multiple of 10.9x and EV/EBITDA multiple of 5.5x its FY2023E estimates.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Alicon-3R-Feb02_2021.pdf

Feb 02, 2021 Triveni Turbine Limited Stock Update BUY 87 105

Summary

• We retain a Buy on Triveni Turbine Limited (TT) with a revised PT of Rs.105, rolling forward our valuation multiples to FY2023E

• Q3FY21 results lagged estimates wherein revenues declined due to order deferrals and an almost flat OPM led to muted PAT.

• The management largely maintained its earlier stance the company is likely to see a decline in revenue by 10% to 15%, margins of 20-22%. Expect better revenues

from FY2022 as large order deliveries expected.

• Balance sheet remains strong with strong cash position and current order book remain healthy providing revenue visibility of 1x its TTM consolidated revenue.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Triveni_Turbine_3R-Feb02_2021.pdf

Feb 03, 2021 Jubilant FoodWorks Limited Stock Update BUY 2,644 3,145

Summary

• Jubilant Foodworks Limited’s (JFL) revenue stood flat at Rs. 1,057.2 crore; Delivery and takeaway revenue grew by ~19% and 64%, respectively.

• Benign input prices, delivery charges of Rs. 30 per order, and wastage saving led to 340 bps improvement in gross margin to ~78%. Higher ticket price per customer

and improving volumes would help gross margin to remain high despite inflation in input prices.

• JFL added 57 new stores (including 50 Domino’s store) in Q3 and would maintain the run rate of adding around 50 stores every quarter, considering strong growth

prospects in the QSR space.

• With business recovering to 100%, management is focusing on improving revenue growth trajectory through strengths of its distribution model and varied offerings.

We recommend Buy with a PT of Rs. 3,145.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Jubilant-3R-Feb03_2021.pdf

Stock Update

14MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation

Reco Price (Rs.)Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 03, 2021 PI Industries Stock Update BUY 2,251 2,740

Summary

• Q3FY2021 results were strong with revenues/operating profit of Rs. 1,162 crore/Rs. 276 crore, up by 36.7%/47.7% y-o-y and 9%/14.8% above our estimate of Rs. 1,066

crore/Rs. 240 crore.

• Revenue beat was driven by a strong outperformance of the CSM business (40.1% y-o-y growth) and domestic business (26.2% y-o-y growth). Strong gross margins

and efficient capacity utilisation drove up OPM by 176 bps y-o-y to 23.7%.

• The management expects strong growth momentum to sustain and guided for revenue growth of 20% each in FY2021 and FY2022. Outlook for CSM business is

robust with the likely start of a new MPP in Q4FY21 and launch of 5-6 new molecules in FY22 while strong demand for branded products to drive growth for domestic

business.

• Likely successful deployment of QIP money of Rs. 2,000 crore in high-margin, high-return pharma and specialty chemicals could act as a key re-rating catalyst. Hence,

we maintain a Buy on PI Industries with an unchanged PT of Rs. 2,740.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/PI_Industries_3R-Feb03_2021.pdf

Feb 03, 2021 Astral Poly Technik Limited Stock Update HOLD 1,944 2,100

Summary

• We downgrade Astral Poly Technik (Astral) to hold with a revised price target of Rs. 2,100 owing to unfavourable risk-reward ratio awaiting a better entry point.

• In Q3, the company reported better-than-expected performance along with sharp expansion in operating margins. Demand momentum accelerated in Q3 for both

pipes and adhesives.

• Long term outlook for pipes and adhesives remains healthy. A sharp increase in PVC price a concern. Expansion plans on track to maintain growth.

• Board recommends bonus issue of 1:3.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Astral-3R-Feb03_2021.pdf

Feb 03, 2021 Indian Hotels Company Limited Stock Update BUY 123 155

Summary

• Indian hotel Company Limited’s (IHCL’s) Q3FY2021 performance improved q-o-q as revenues rose to Rs. 559.9 crore from Rs. 256.7 crore in Q2FY2021.

• Standalone occupancy ratio improved to 47.4% in Q3FY2021 from 32.3% in Q2FY2021 and 20.5% in Q1FY2021; average room rentals (ARR) rose by 53% to Rs. 8,300

versus Q2.

• Prudent asset management helped fixed costs decline by Rs. 64 crore and corporate overheads to decrease by 28% to Rs. 67crore in 9MFY2021.

• Hotel industry set for a strong revival in FY2022/23 as foreign tourist arrivals regain momentum. As IHCL has a strong room inventory and stable balance sheet among

peers, we recommend a Buy with a PT of Rs. 155.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/IndianHotel-3R-Feb03_2021.pdf

Feb 03, 2021 City Union Bank Stock Update BUY 186 225

Summary

• Q3FY21 numbers were mixed; Reported asset quality improved sequentially; elevated provisions cause PAT to marginally miss estimates.

• Total SMA accounts constituted 0.85% of total advances; improving over the last nine months. Restructured standard advances to gross advances ratio stood at 2.21%.

• Stock trades at 2.0x/1.7x its FY2022E/FY2023E BVPS. Factors such as increasing retail focus, being adequately capitalised (Tier-1 at ~16.3%), and incremental lending

to better-rated borrower(s) are positives; secured loans 99% of total loans.

• We maintain a Buy rating on the stock with an unchanged price target (PT) of Rs. 225.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/CityUnionBank-3R-Feb03_2021.pdf

Feb 03, 2021 Castrol India Limited Stock Update BUY 129 150

Summary

• Q4CY20 results lagged our expectations as revenue/adjusted operating profit at Rs. 935 crore/Rs. 274 crore, down 7.6%/19.6% y-o-y, missing our estimate by 9%/11%.

• The miss in operating performance was due to lower-than-expected OPM at 29.3% (down 438 bps y-o-y), volumes of 52 million litre (down 3.7% y-o-y) and weak

realisations (down 4% y-o-y). However, gross margins improved by 172 bps y-o-y to 59.4%.

• However, the highlight was the strong operating cashflow of Rs. 893 crore (153% of CY20 reported PAT) due to strong working capital management and maintained

DPS of Rs. 5.5 (payout of 93%). Alliance with Jio-BP retail network and focus on gaining market share bodes well for volume growth.

• Attractive valuation of 13.5x CY22E EPS (close to decade-low valuations) despite strong cash positions, FCF/dividend yields of 6%/9% and RoE of ~56-60%. Hence,

we recommend a Buy on Castrol with PT of Rs. 150.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Castrol_3R-Feb03_2021.pdf

Stock Update

15MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation

Reco Price (Rs.)Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 03, 2021 Carborundum Universal Limited Stock Update BUY 427 540

Summary

• We retain Buy on Carborundum Universal Limited (CUMI) with a revised PT of Rs. 540, considering its reasonable valuations and healthy earnings growth profile.

• Q3FY2021 performance remained strong on all parameters (better than estimates), led by improving business sentiment and strong demand across segments.

• Strong domestic operations led by core user industries along with improving overseas operations aided by capacity expansion, success of new products, and being

an alternative global supplier are likely to aid domestic and exports growth.

• Strong balance sheet, healthy return ratios and consistent dividend paying record are key salient features.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Carborundum-3R-Feb03_2021.pdf

Feb 03, 2021 Ratnamani Metals & Tubes Limited Stock Update BUY 1,574 1,790

Summary

• We maintain Buy on Ratnamani Metals & Tubes Limited (RMTL) with a PT of Rs. 1,790.

• Soft quarter, EBITDA margin expanded by 379 bps y-o-y to 18.1%, led by change in product mix; order book increased by 15% q-o-q to Rs. 1,359 crore.

• Management remains confident on pick-up in order intake from Q4FY2021E because of anticipated normalisation of steel prices, strong order inflows during QTD of

Q4FY2021, and improving demand environment.

• We expect strong revenue growth of 35% y-o-y in FY2022E, led by availability of expanded capacities, improvement in capex cycle, and return of spending on

infrastructure projects.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Ratnamani-3R-Feb03_2021.pdf

Feb 03, 2021 Solara Active Pharma Sciences Stock Update BUY 1,458 1,700

Summary

• We retain our Buy recommendation on Solara Active Pharma Sciences (Solara) with a revised PT of Rs. 1700.

• Solara delivered its best-ever quarterly performance for Q3FY2021 with revenues and earnings staging an impressive 24% and 59% y-o-y, growth respectively.

• Given the strong demand traction and ramp up of the Vizag plant (Phase I), strong new product launches, especially in the limited competition space augur well from

a growth perspective.

• The company’s strong growth prospects, better earnings visibility, healthy balance sheet, and improving return ratios would support multiple expansion.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Solara_Active_3R-Feb03_2021.pdf

Feb 03, 2021 Wonderla Holidays Limited Stock Update HOLD 203 227

Summary

• Wonderla Holidays (WHL) posted revenues of Rs. 5 crore in Q3FY2021 for minimal days of operations in Bangalore (from November 9) and Kochi Park (from December

20) with permitted capacity of 50% only on weekends.

• Initial response was good with average visitors to the Bangalore Park standing at 1500 per day and 1,227 for the Kochi Park (some days saw 4,000-5000 visitors).

• With higher pent-up demand, the company expects footfalls to improve hugely in FY2022, reaching close to FY2020 levels by FY2023.

• With a strong balance sheet and cash of ~Rs. 90 crore as of December, WHL is well-placed to exploit opportunities in the entertainment industry. We maintain a Hold

with a revised PT of Rs. 227.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Wonderla_3R-Feb03_2021.pdf

Feb 04, 2021 State Bank of India Stock Update BUY 355 460

Summary

• SBI posted strong results with mixed operational numbers, but asset quality performance improved; loan growth too outperformed system growth, indicating market share gains.

• Strong asset quality performance, GNPA declined 217 bps y-o-y and 51 bps q-o-q to 4.77%. NNPA ratio at 1.23% is down 142 bps y-o-y and 36 bps q-o-q; Proforma

GNPA / NNPA too were well contained.

• Asset quality is finally emerging from the shadows; we believe that a strong balance sheet, market-share gains can drive re-rating of stock.

• Stock trades at 1.6x / 1.3x its FY2022E / FY2023E ABVPS, which we believe are reasonable. We maintain a Buy on the stock with a revised SOTP-based price target

(PT) of Rs. 460.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/SBI_3R-Feb04_2021.pdf

Stock Update

16MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation

Reco Price (Rs.)Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 04, 2021 Bharti Airtel Stock Update BUY 600 750

Summary

• We maintain a Buy on Bharti Airtel with a revised PT of Rs. 750, given favourable market structure, reasonable valuations and strength in core business.

• Stellar performance; ARPU improvement led by strong net 4G subscriber additions; company gained revenue market share in its India wireless business and sees

strong traction in broadband & enterprise businesses.

• Strong 4G subscriber addition creates platform for healthy growth of India wireless business; Bharti optimistic that digital services through the partnership-led model

would help drive growth.

• Bharti is well-positioned to capitalise opportunities from weakness in competitors and tariff hikes. We expect company to register a 14%/23% growth in revenue/

EBITDA over FY2020-FY2023E.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Bharti_Airtel_3R-Feb04_2021.pdf

Feb 04, 2021 NTPC Limited Stock Update BUY 99 140

Summary

• Q3FY2021 performance was steady with a 24% y-o-y increase in adjusted PAT to Rs. 3,308 crore (in line with consensus estimates). Earnings growth was driven by a 14.5% y-o-y increase

in regulated equity base, 35% rise in surcharge income to Rs. 565 crore and higher PLF incentive income of Rs. 76 crore (versus just Rs. 9 crore in Q3FY20).

• The management has guided for strong commercialisation of 5,074 MW for FY2021E and 6,000 MW for FY2022E and eyes lower fixed cost under-recoveries of Rs.

350-400 crore by March-2021. Board declared interim dividend of Rs3/share.

• A risk averse regulated business model provides earnings visibility (19% PAT CAGR over FY2021E-FY2023E) as a robust commercialisation target would drive strong

growth in regulated equity base.

• We maintain a Buy on NTPC with an unchanged PT of Rs. 140, as valuation remains attractive at 0.7x its FY2023E P/BV (48% discount to historical multiple) despite

strong earnings visibility, decent RoE of 13% and dividend yield of 6-7%.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/NTPC_3R-Feb04_2021.pdf

Feb 04, 2021 Apollo Tyres Limited Stock Update BUY 244 290

Summary

• We maintain Buy rating on Apollo Tyres Limited (ATL) with a PT of Rs. 290, factoring strong traction in business outlook and an upgrade in earnings estimates.

• Q3FY2021 results were better than expected as EBITDA margins rose sharply.

• On back of strong operational performance, we have upgraded our earnings estimates by 55%/49% for FY22E/FY23E, largely driven by a 220 bps/280 bps EBITDA

margin expansion to 16.4%/17.4%, respectively, to reflect a sharp increase in operational improvements in the company.

• The stock trades attractively at P/E multiple of 10.2x and EV/EBITDA multiple of 5x its FY2023E estimates.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Apollo_3R-Feb04_2021.pdf

Feb 04, 2021 Thermax Stock Update HOLD 1,210 1,350

Summary

• We retain our Hold rating on Thermax with a revised PT of Rs. 1350.

• In Q3FY2021, Thermax’s overall performance remained mixed where revenues remained muted along with strong operational performance led by cost rationalization

and higher gross margins. However exceptional loss led to PAT decline.

• Weak order inflow, which was largely on expected lines, and lower execution during the same period led to lower depletion of the exit order backlog to 1.2x TTM

consolidated revenue.

• Expect order booking in FY2021 to be lower compared to last year due to expectation of lower large ticket-size orders from segments such as steel, fertiliser, and

cement; enquiry pipeline remains positive in food processing, steel, cement, chemical and pharma.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Thermax_3R-Feb04_2021.pdf

Stock Update

17MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation

Reco Price (Rs.)Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 04, 2021 Vinati Organics Limited Stock Update BUY 1,244 1,550

Summary

• Q3FY2021 results were weak with 6% miss in operating profit at Rs. 72 crore (down 13.1% y-o-y) due to higher cost (given commissioning of Butyl Phenol plant) and

weak revenue mix (ATBS share at 38% versus 56% in Q3FY2020 and specialty products at 6% versus 17% in Q3FY2020).

• Management has guided for strong revenue growth of 20% each in FY2022 and FY2023 as its key ATBS segment has recovered to pre-COVID level and likely ramp-

up of utilisation at Butyl Phenol plant. Thus, we expect a strong 29% PAT CAGR over FY2021E-FY2023E.

• Amalgamation of Veeral Additives Private Limited (subject to NCLT approval) seems in right direction as it provides entry into antioxidants (AO – forward integration

for Vinati Organics) with incremental revenue opportunity of Rs. 300 crore.

• We like Vinati Organics’ business (global market share of 65% each in IBB and ATBS), debt-free status, and solid return profile (RoE/RoCE of 23%/30%). Hence, we

maintain our Buy rating on Vinati Organics with an unchanged PT of Rs. 1,550.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Vinati_Organics_3R-Feb04_2021.pdf

Feb 04, 2021 Sundram Fasteners Limited Stock Update BUY 602 700

Summary

• We maintain our Buy rating on Sundram Fasteners Limited (SFL) with a revised PT of Rs. 700, on a strong traction in business outlook and an upgrade in earnings

estimates. Q3FY2021 results beat expectation on higher-than-expected demand and margin expansion.

• We expect SFL to benefit from strong growth traction in the automotive industry with its clients well diversified across segments. Export and non-automotive segments

continue to be the focus area with a strategy to de-risk business from cyclicality.

• We expect SFL’s earnings to grow by 86.8% in FY2022E and 42.8% in FY2023E, driven by a 25.2% revenue CAGR during FY2021E-23E and a 350-bps improvement

in EBITDA margin.

• Stock trades at P/E multiple of 22.2x and EV/EBITDA multiple of 13.2x its FY2023E estimates.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Sundram_3R-Feb04_2021.pdf

Feb 04, 2021 V-Guard Industries Limited Stock Update BUY 252 311

Summary

• We retain Buy on V-Guard Industries Limited (V-Guard) with a revised PT of Rs. 311, considering its improving business operations.

• V-Guard reported strong revenues and operating margins leading to 79.6% y-o-y growth in net profit which remained better than estimates.

• Management expects to get back on to the growth path with a rebound in business environment and highlighted that demand drivers remain healthy across

businesses. Expect summer products to come back strongly with some pent-up demand.

• The company’s strong balance sheet, cash flow and reputed brand along with strong business fundamentals provide comfort in the present environment.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/V-Guard_3R-Feb04_2021.pdf

Feb 04, 2021 Strides Pharma Science Limited Stock Update BUY 887 1,020

Summary

• We retain Buy recommendation on Strides Pharma Sciences (Strides) with a revised PT of Rs 1,020.

• Q3FY2021 was a weak quarter for Strides on the back of weak flu season, & price erosion in US markets and one off expenses. The results missed estimates.

• Healthy growth in the base business and strong product launch pipeline provides ample visibility for growth of the US business. Growth prospects in other regulated

markets are also likely to get better, led by new product launches, increased market share, and portfolio optimization efforts.

• Strong growth prospects and earnings visibility, improving balance sheet strength, and healthy return ratios would support multiple re-ratings.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Strides_3R-Feb04_2021.pdf

Feb 04, 2021 Triveni Engineering & Industries Limited Stock Update BUY 75 90

Summary

• Triveni Engineering & Industries (TEIL) Q3FY21 results were better than expectations mainly led by a sharp expansion of 609 bps in OPM to 14.3%, resulting in a 3.5x

growth in PAT to Rs. 139 crore; revenue grew by 5%.

• Sugar division and distillery division revenues grew by 9% and 7% each; engineering business has almost reached to 7 0% of pre-COVID levels.

• Higher sugar under ethanol blending and export quota of 6 million tonnes would lead to better performance in FY2022 despite higher sugar production. Engineering

business is expected to recover strongly with strong order book.

• We have broadly maintained our earnings estimates for FY2022/23. We recommend Buy on the stock with the price target of Rs. 90.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Triveni_Engineering_3R-Feb04_2021.pdf

Stock Update

18MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation

Reco Price (Rs.)Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 04, 2021 Arvind Limited Stock Update BUY 52 68

Summary

• Q3FY2021 revenue recovered to ~80% led by a strong recovery in Denim and garments segment, which stood at 81% and 89%, of pre-COVID levels.

• Textile business’ EBIDTA margins reverted to FY2020 levels of 12.5%, while advanced material prices stood at 14%, resulting in a 79 bps improvement in the OPM to

10.7%.

• Better operating leverage and higher margins from AMD would mitigate impact of a sharp increase in input prices in the near term. Debt reduced by Rs. 300 crore

in last nine months.

• We broadly maintained our earnings estimates for FY2022/23. We maintain our Buy recommendation with PT of Rs. 68.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Arvind_3R-Feb04_2021.pdf

Feb 05, 2021 Mahindra & Mahindra Stock Update BUY 865 1,000

Summary

• We retain our Buy rating on Mahindra and Mahindra (M&M) with revised price target of Rs. 1,000 factoring earnings upgrade owing to its robust outlook of its core

businesses and improving fortunes of key subsidiary companies

• M&M’s Q3FY21 results were broadly in-line with our estimates and it reported another quarter of strong operating performance.

• We expect M&M to benefit from its leadership status in tractor space, strengthened position in LCV segment and steady market share gains in UV segment.

• Stock is attractively valued at a P/E multiple of 17x and EV/EBITDA multiple of 9.6x its FY2023E estimates.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/MnM-Feb05_2021.pdf

Feb 05, 2021 Divis Laboratories Limited Stock Update BUY 3,820 4,500

Summary

• We retain Buy recommendation on Divis Laboratories (Divis) with a revised PT of Rs 4,500.

• Divis reported yet another impressive performance for the quarter with results ahead of estimates. The sales at Rs 1,701 cr grew 22% y-o-y while PAT at Rs 471 cr was

up 31% y-o-y.

• Robust demand traction, incremental capacities coming on stream, plans to enter the high value space of Contrast Media Manufacturing would be the key growth

drivers.

• Strong earnings visibility, almost zero debt, and strong return ratios bode well and could support P/E multiple expansion.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/DivisLab-3R-Feb05_2021.pdf

Feb 05, 2021 Hero MotoCorp Limited Stock Update BUY 3,428 4,030

Summary

• We reiterate our Buy rating on Hero MotoCorp Limited (HERO) with a PT of Rs. 4,030, factoring better multiples owing to business outlook and earnings upgrade.

• HERO’s Q3FY21 results were slightly ahead of expectations due to improvement in EBITDA margin expansion.

• We believe structural growth traction in the two-wheeler (2W) industry remains intact and HERO continues to benefit from premiumization of its products, its strong

hold in the economy and executive motorcycle segments, and aggressive products offerings in the premium bike and scooters segments.

• The stock is valued at P/E multiple of 16.2x and EV/EBITDA multiple of 9.5x its FY2023E estimates. We retain our Buy rating on the stock.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/HeroMoto-3R-Feb05_2021.pdf

Feb 05, 2021 Cadila Healthcare Limited Stock Update BUY 475 560

Summary

• We retain Buy recommendation on Cadila Healthcare Limited (Cadila) with a revised PT of Rs 560.

• Q3FY2021 was a healthy quarter for Cadila with revenues and PAT reporting a growth of 4% and 40% YoY respectively.

• Traction across all the three segment – Human Health, Animal Health and Consumer wellness to drive the India business growth. Sturdy new product pipeline and

growth in the existing products basket to fuel the growth for US.

• Strong growth prospects and earnings visibility, a sturdy balance sheet, and healthy return ratios, coupled with multiple growth triggers are the key positives for Cadila.

Covid Vaccine, up on approval can open up substantial growth opportunities.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Cadila-3R-Feb05_2021.pdf

Stock Update

19MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation

Reco Price (Rs.)Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 05, 2021 Honeywell Automation India Limited Stock Update BUY 41,949 48,200

Summary

• We retain a Buy on Honeywell Automation India with a revised price target of Rs. 48,200.

• Q3 results lagged estimates. OPM matched estimates, led by rationalisation in employee and other expenses.

• Honeywell is expected to benefit from domestic growth driven by increasing technological capabilities with large opportunities in the oil & gas space, smart cities,

upcoming airports and building solutions.

• Exports may stay muted in near term owing to subsequent waves of the COVID-19 pandemic.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Honeywell_3R-Feb05_2021.pdf

Feb 05, 2021 Hindustan Petroleum Corporation Limited Stock Update BUY 225 275

Summary

• Q3FY21 operating profit at Rs. 3,002 crore (up 91.8% y-o-y) lagged ours and the street’s estimates as derived blended marketing margin missed expectations, at Rs.

2,489/tonne (down 8.8% q-o-q). PAT at Rs. 2,355 crore (up 215% y-o-y) was led by inventory gain of Rs. 1,343 crore, forex gain of Rs. 297 crore, higher other income

and lower interest costs.

• HPCL gained market share gain in petrol (volumes rose by 6.6% y-o-y versus industry growth of 6.3% y-o-y) and diesel (volume up by 1.3% y-o-y versus industry decline

of 1.1% y-o-y). Reported GRM was in line at $1.9/bbl, but core GRMs were negative at $1/bbl.

• Gradual auto fuel price hikes would bring back marketing margins to normal; expect strong Q4FY21 on volume growth and potential inventory gain. A cyclical recovery

in refining margins in CY2021 would aid to earnings growth.

• Valuation of 5x FY2023E EPS is attractive given strong earnings visibility, high dividend yield of 8% and RoE of ~18%. BPCL’s privatisation could re-rate marketing

business. We maintain a Buy on HPCL with an unchanged PT of Rs275.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/HPCL-3R-Feb05_2021.pdf

Feb 05, 2021 Gujarat Gas Limited Stock Update BUY 380 500

Summary

• Q3FY21 operating profit/PAT at Rs. 615 crore/Rs. 392 crore, up 66%/99.5% y-o-y strongly beat estimates due to a 39% and 5.8% beat in EBITDA margin at Rs. 5.8/scm

(up 35% y-o-y) and volume at 11.4 mmscmd (up 22.9% y-o-y), respectively.

• Stellar growth of 29% y-o-y for Industrial PNG (I-PNG) volume at 9.2 mmscmd due to improved demand from Morbi and Pharma/Chemicals belt. CNG volume of 1.5

mmscmd (up 2.2% y-o-y) recovered above pre-COVID levels.

• Management guided for strong 25% volume growth for FY22E and 10% annual growth for next 2-3 years on a high base of FY22. Price hike of Rs. 9/scm for I-PNG

indicates pricing power and would help sustain margin. We raise FY21E/FY22E/FY23E EPS by 16%/10%/9% to factor higher volumes.

• GGAS is one of the best bets in the CGD space as consistent high-volume growth and potential to become net cash positive makes valuation of 15.4x its FY23E EPS

attractive. Hence, we maintain a Buy rating on GGAS with a revised PT of Rs. 500.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Gujarat_Gas_3R-Feb05_2021.pdf

Feb 05, 2021 Ipca Laboratories Limited Stock Update BUY 1,936 2,560

Summary

• We retain a Buy recommendation on IPCA Laboratories (IPCA) with an unchanged PT of Rs. 2,560.

• Ipca Laboratories Limited (Ipca) reported a strong performance in Q3FY2021, with earnings coming slightly ahead of estimates.

• Ipca’s API business is witnessing strong demand traction, which is expected to sustain going ahead, while the formulations is business is also expected grow at a

healthy pace.

• Strong earnings prospects, a sturdy balance sheet, and healthy return ratios augur well for Ipca.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/IPCA-3R-Feb05_2021.pdf

Feb 05, 2021 Trent Limited Stock Update BUY 906 1,015

Summary

• Trent witnessed ~83% recovery in Q3FY2021,boosted by higher sales during the festive season and all stores were operational at optimum levels. Recovery improved

from 55% in Q2.

• Online sales grew by 80%, while strong traction was seen inthe EOSS in January with salescoming back to pre-COVIDlevels.

• Trent prioritised cost-saving measures of cutting discretionary spends and renegotiating rental expenses, which aided in486 bps expansion in OPM to 24.8% in Q3.

• We have increased our estimates for FY2022/FY2023 to factor in faster recovery in performance. We maintain Buy with a revised PT of Rs. 825.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Trent_3R-Feb05_2021.pdf

Stock Update

20MARCH 2021 Sharekhan ValueGuide

EQUITY FUNDAMENTALS

Date Company Report TypeRecommendation

Reco Price (Rs.)Price Target/ Upside (%)

Latest Chg Latest Chg

Feb 05, 2021 Zee Entertainment Enterprises Limited Stock Update BUY - 215 275 -

Summary

• We re-initiate coverage on Zee Entertainment Enterprises Limited (ZEEL) with a Buy rating with a PT of Rs. 275, considering better ad growth outlook and reducing

balance sheet concerns.

• Q3FY21 numbers were strong; expect ZEEL to clock revenue/net profit growth of 18%/22% over FY21-FY23E.

• Management is focusing on rebuilding investor confidence by 1) improving disclosures, 2) introducing polices and 3) strengthening board composition.

• We believe ZEE5 is one of the leading digital platforms, centered on regional content and would continue to leverage its reach further led by hyperlocal content.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Zeel-3R-Feb05_2021.pdf

Feb 05, 2021 Birlasoft Limited Stock Update BUY 272 320

Summary

• We recommend a Buy on Birlasoft Ltd with a price target (PT) of Rs. 320 as risk-reward ratio remains favourable.

• Stock trades at 16x of FY2023E earnings, implying reasonable valuations given strong earnings growth expectations. Cash & cash equivalents account for 13% of

market capitalisation. FCF generation remains strong.

• Management is confident of delivering double-digit growth in FY2022 led by higher contribution of annuity revenue, healthy deal pipeline and higher spends on

transformational initiatives.

• We expect revenue to clock a 14% CAGR over FY2021-23E, while earnings are likely to record a 24% CAGR as profitability improves and tax provisions stay low

(adopted new tax regime in Q3).

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/Birlasoft_3R-Feb05_2021.pdf

Feb 05, 2021 KPR Mill Limited Stock Update BUY 922 1,100

Summary

• KPR Mill (KPR) registered strong performance in Q3FY2021 with revenues and PAT growing by 21% and 66% respectively (OPM expanded by 917BPS to 27.0%); interest

cost down by 36% y-o-y.

• Textile business revenues grew by ~19% driven by a strong 20% growth in garment segment sales; garmenting production grew by 22% y-o-y to 27.9million garments.

• Balance sheet strengths visible with cash balance improving from Rs. 250 crore in Q2 to Rs. 356 crore in Q3 and debt standing at Rs. 556 crore (including working

capital requirements); debt:equity of 0.3x.

• We have increased our earnings estimates for FY2021/22/23 and maintain a Buy on the stock with a revised PT of Rs. 1,100.

Read report - https://www.sharekhan.com/MediaGalary/StockIdea/KPR-3R-Feb05_2021.pdf

Feb 05, 2021 PNC Infratech Limited Stock Update BUY 245 300

Summary

• We retain Buy on PNC Infratech Limited(PNC) with a revised price target of Rs. 300, as we factor in upwardly revised estimates for FY2021-FY2023E.