maldon district council statement of accounts 2011/12

64

MALDON DISTRICT COUNCIL STATEMENT OF ACCOUNTS 2011/12 APPENDIX 1 1/64

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of maldon district council statement of accounts 2011/12

MALDON DISTRICT COUNCIL

STATEMENT OF ACCOUNTS 2011/12

APPENDIX 1

1/64

MALDON DISTRICT COUNCIL

STATEMENT OF ACCOUNTS 2011/2012

Chairman of Finance and Corporate Services Committee

Councillor D M Sismey

Chief Executive

Ms F Marshall C.P.F.A.

Maldon District CouncilFinancial Services

Council OfficesPrinces Road

MaldonCM9 5DL

APPENDIX 1

2/64

MALDON DISTRICT COUNCIL

STATEMENT OF ACCOUNTS 2011/2012

CONTENTS

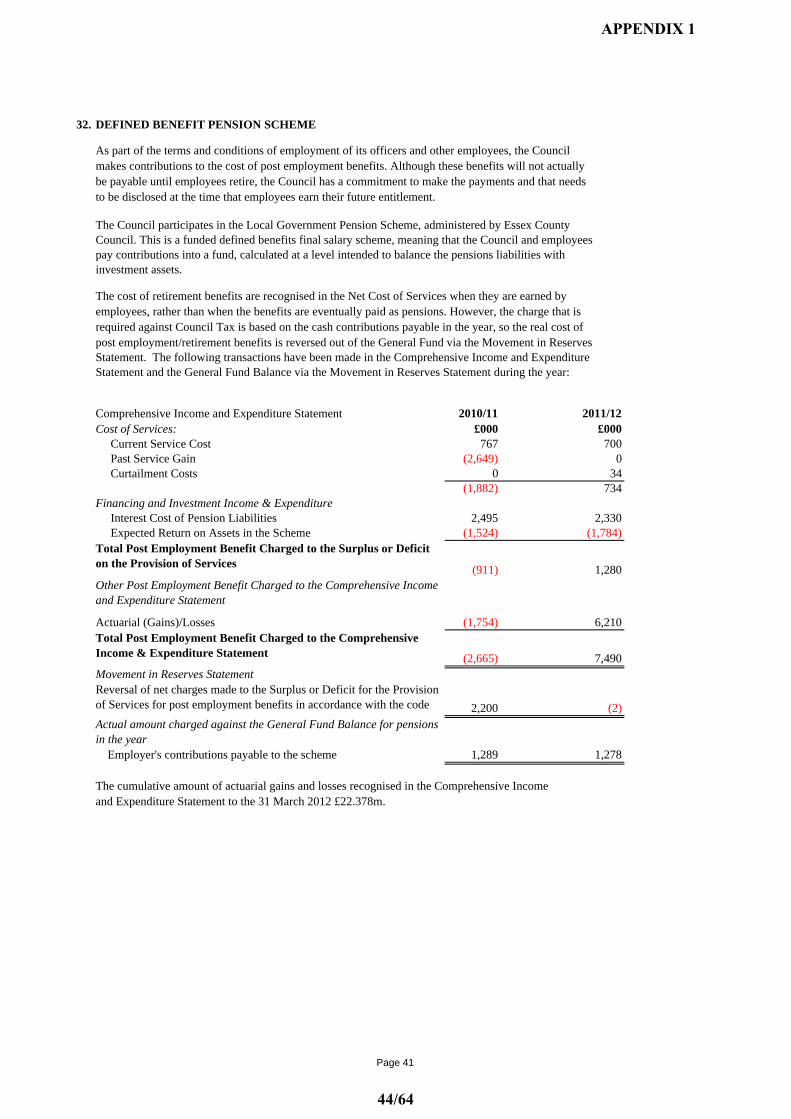

Page(s)Explanatory Foreword 1-4

Statement of Responsibilities for the Statement of Accounts 5

The Core Accounting Statements: Movement In Reserves Statement 6-7

Comprehensive Income and Expenditure Statement 8

Balance Sheet 9

Cash Flow Statement 10- Notes to the Cash Flow Statement 11

The Collection Fund 12Notes to the Collection Fund 13

Notes to the Core Accounting Statements

1 Accounting Policies 14-222 Prior Year Adjustments 233 Accounting Standards issued but not adopted 244 Assumptions about the future 245 Material Items of Income or Expense 256 Events after the Balance Sheet date 257 Transfers to/from Earmarked Reserves 258 Property, Plant & Equipment valuation 259 Property, Plant & Equipment movement on Balances 26

10 Capital Commitments 2711 Investment Properties 2712 Intangible Assets 2713 Financial Instruments 28-3014 Inventories 3015 Debtors 3016 Long Term Debtors 3017 Cash & Cash Equivalents 3118 Creditors 3119 Usable Reserves 3120 Unusable Reserves 3121 Segmental Reporting 32-3322 Trading Accounts 3423 Agency Services 3424 Members Allowances 3425 Remuneration of Senior Staff 35-3626 Audit and Inspection Costs 3627 Grant Income 3728 Related Party Transactions 3729 Capital Expenditure 3830 Capital Financing 3831 Leases 39-4032 Defined Benefit Pension Scheme 41-4433 Capital Disposals 4534 Local Area Agreement 4535 Contingent Liabilities 4636 Contingent Assets 4637 Glossary 47-50

Annual Governance Statement 51-58Independent Auditor's Report 59-61

APPENDIX 1

3/64

The purpose of the Statement of Accounts and the accompanying information is to give electors, those subject to locally levied taxes and charges, members of the Council, employees and other interested parties clear information about the Council’s finances.It provides information on the cost of providing services in the year, where the funding has come from, and the Council’s assets andliabilities at the year-end.The Statement of Accounts is prepared in accordance with the Code of Practice on Local Authority Accounting in the United Kingdom (the Code) which sets out the proper accounting practices for accounting for transactions of the Council and the presentation of the financial statements. The Code is based on International Financial Reporting Standards (IFRS) and International Public Sector Accounting Standards (IPSAS) interpreted for use by local authorities.

Statement of Accounts and accompanying informationThe Statement of Accounts and the accompanying information comprises various sections which are explained below:

Management commentaryThe management commentary section contained within the explanatory foreword is to offer interested parties an easily understandable guide to the most significant matters reported in the accounts. It provides an explanation in overall terms of the Council’s financial position, and assists in the interpretation of the financial statements. It summarises the major influences affecting the Council’s income and expenditure and cash flow, and information on the financial needs and resources of the Council. Although an integral part of this publication, it accompanies this document and is not formally part of the Statement of Accounts.Statement of responsibilities for the Statement of AccountsThis statement sets out the responsibilities of the Council and the chief financial officer in respect of the proper administration of the financial affairs the Council and for the preparation of the Statement of Accounts.Movement in Reserves StatementThis statement shows the movement in the year on the different reserves held by the Council, analysed into ‘usable reserves’ (ie those that can be applied to fund expenditure or reduce local taxation) and other reserves. The surplus or (deficit) on the provision of services line shows the true economic cost of providing the Council’s services, more details of which are shown in the Comprehensive Income and Expenditure Statement. These are different from the statutory amounts required to be charged to the general fund balance for council tax setting purposes. The net increase / decrease before transfers to earmarked reserves line shows the statutory general fund balance before any discretionary transfers to or from earmarked reserves undertaken by the Council.Comprehensive Income and Expenditure StatementThis statement shows the accounting cost in the year of providing services in accordance with generally accepted accounting practices, rather than the amount to be funded from taxation. Councils raise taxation to cover expenditure in accordance with regulations; this may be different from the accounting cost. The taxation position is shown in the Movement in Reserves Statement.Balance SheetThe Balance Sheet shows the value as at the balance sheet date of the assets and liabilities recognised by the Council. The net assets of the Council (assets less liabilities) are matched by the reserves held by the Council. Reserves are reported in two categories. The first category of reserves are usable reserves, ie those reserves that the Council may use to provide services, subject to the need to maintain a prudent level of reserves and any statutory limitations on their use (for example the capital receipts reserve that may only be used to fund capital expenditure or repay debt). The second category of reserves is those that the Council is not able to use to provide services. This category of reserves includes reserves that hold unrealised gains and losses (for example the revaluation reserve), where amounts would only become available to provide services if the assets are sold; and reserves that hold timing differences shown in the Movement in Reserves Statement line ‘adjustments between accounting basis and funding basis under regulations’.Cash Flow StatementThe Cash Flow Statement shows the changes in cash and cash equivalents of the Council during the reporting period. The statement shows how the Council generates and uses cash and cash equivalents by classifying cash flows as operating, investing and financing activities. The amount of net cash flows arising from operating activities is a key indicator of the extent to which the operations of the Council are funded by way of taxation and grant income or from the recipients of services provided by the Council. Investing activities represent the extent to which cash outflows have been made for resources which are intended to contribute to the Council’s future service delivery.Collection FundThe Collection Fund is an agent’s statement that reflects the statutory obligation for billing authorities to maintain a separate Collection Fund. The statement shows the transactions of the billing authority in relation to the collection from taxpayers and distribution to local authorities and the Government of council tax and non-domestic rates.Notes to the core accounting statementsThe notes to the core accounting statements present information about the basis of preparation of the financial statements and the specific accounting policies used, disclose additional information required by the Code that is not presented elsewhere in the financial statements, and provide information that is not presented elsewhere in the financial statements, but is relevant to an understanding of any of them.

EXPLANATORY FOREWORD

Page 1

APPENDIX 1

4/64

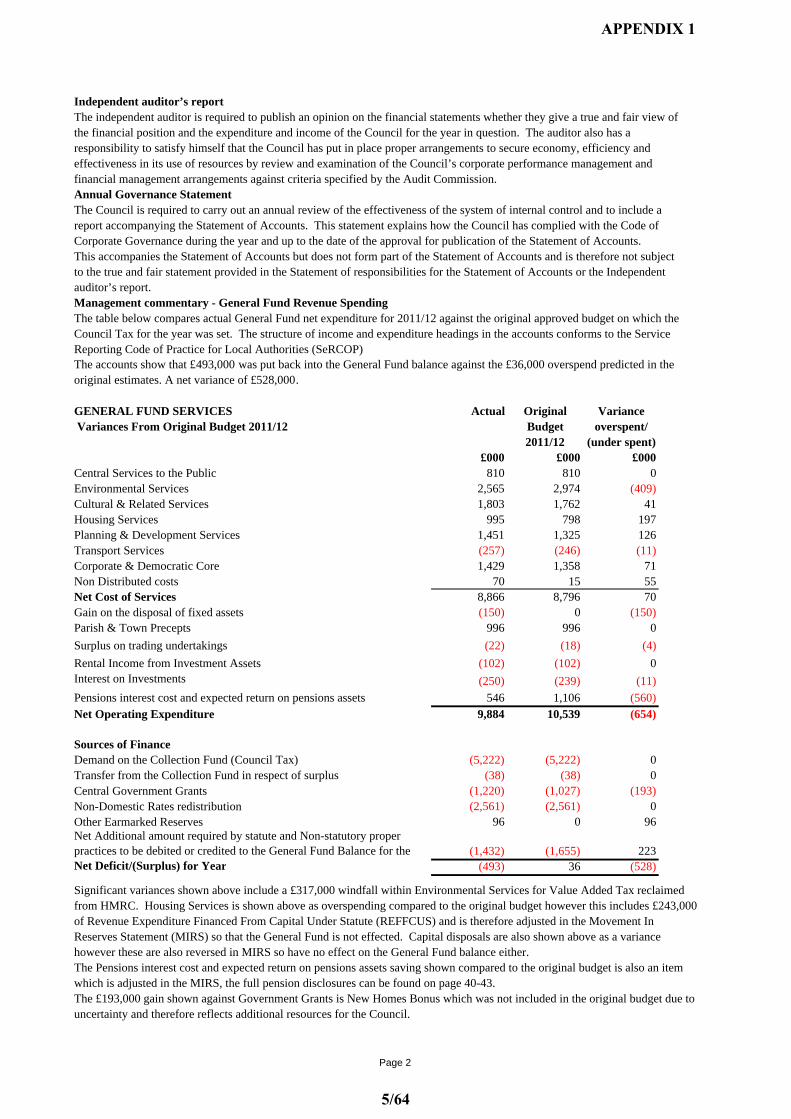

Independent auditor’s reportThe independent auditor is required to publish an opinion on the financial statements whether they give a true and fair view of the financial position and the expenditure and income of the Council for the year in question. The auditor also has a responsibility to satisfy himself that the Council has put in place proper arrangements to secure economy, efficiency and effectiveness in its use of resources by review and examination of the Council’s corporate performance management and financial management arrangements against criteria specified by the Audit Commission.Annual Governance StatementThe Council is required to carry out an annual review of the effectiveness of the system of internal control and to include a report accompanying the Statement of Accounts. This statement explains how the Council has complied with the Code of Corporate Governance during the year and up to the date of the approval for publication of the Statement of Accounts. This accompanies the Statement of Accounts but does not form part of the Statement of Accounts and is therefore not subject to the true and fair statement provided in the Statement of responsibilities for the Statement of Accounts or the Independent auditor’s report.Management commentary - General Fund Revenue Spending The table below compares actual General Fund net expenditure for 2011/12 against the original approved budget on which the Council Tax for the year was set. The structure of income and expenditure headings in the accounts conforms to the Service Reporting Code of Practice for Local Authorities (SeRCOP)The accounts show that £493,000 was put back into the General Fund balance against the £36,000 overspend predicted in the original estimates. A net variance of £528,000.

GENERAL FUND SERVICES Actual Original Variance Variances From Original Budget 2011/12 Budget overspent/

2011/12 (under spent)£000 £000 £000

Central Services to the Public 810 810 0Environmental Services 2,565 2,974 (409)Cultural & Related Services 1,803 1,762 41Housing Services 995 798 197Planning & Development Services 1,451 1,325 126Transport Services (257) (246) (11)Corporate & Democratic Core 1,429 1,358 71Non Distributed costs 70 15 55Net Cost of Services 8,866 8,796 70Gain on the disposal of fixed assets (150) 0 (150)Parish & Town Precepts 996 996 0

(22) (18) (4)

(102) (102) 0Interest on Investments (250) (239) (11)

546 1,106 (560)Net Operating Expenditure 9,884 10,539 (654)

(5,222) (5,222) 0(38) (38) 0

(1,220) (1,027) (193)(2,561) (2,561) 0

96 0 96

(1,432) (1,655) 223(493) 36 (528)

Significant variances shown above include a £317,000 windfall within Environmental Services for Value Added Tax reclaimed from HMRC. Housing Services is shown above as overspending compared to the original budget however this includes £243,000 of Revenue Expenditure Financed From Capital Under Statute (REFFCUS) and is therefore adjusted in the Movement In Reserves Statement (MIRS) so that the General Fund is not effected. Capital disposals are also shown above as a variance however these are also reversed in MIRS so have no effect on the General Fund balance either.The Pensions interest cost and expected return on pensions assets saving shown compared to the original budget is also an item which is adjusted in the MIRS, the full pension disclosures can be found on page 40-43.The £193,000 gain shown against Government Grants is New Homes Bonus which was not included in the original budget due to uncertainty and therefore reflects additional resources for the Council.

Transfer from the Collection Fund in respect of surplus

Surplus on trading undertakings

Pensions interest cost and expected return on pensions assets

Demand on the Collection Fund (Council Tax)

Rental Income from Investment Assets

Net Deficit/(Surplus) for Year

Non-Domestic Rates redistribution

Sources of Finance

Other Earmarked Reserves

Central Government Grants

Net Additional amount required by statute and Non-statutory proper practices to be debited or credited to the General Fund Balance for the

Page 2

APPENDIX 1

5/64

Financial Activity

The following chart shows proportionately the sources of the Council’s finance.

Services Provided

The following chart shows a breakdown of services provided,by net cost:

Council Tax33%

Non Domestic Rates24%

Revenue Support Grant1%

Investment Interest2%

Fees & Charges21%

Other Income19%

WHERE THE MONEY COMES FROM

Central Services to the Public

9%

Cultural & Related Services

20%

Environmental Services

28%

Housing Services11%

Planning & Development

Services16%

Corporate and Democratic Core

16%

SERVICES PROVIDED

Page 3

APPENDIX 1

6/64

Revenue PositionThe revenue outturn position is better than anticipated in the revised budget. This saving is largely due to reclaimed VAT on Environmental Services provided since April 1973.

Pension Fund PositionThe pension position has deteriorated during the year, mostly due to a fluctuation in the long term discount rate used by the Council's Pension Actuary when estimating the current cost of future liabilities in the scheme. This change in discount rate has meant the current value of future liabilities has increased. Investment returns remain poor in line with the widereconomic situation, this has contributed further to the deterioration. The actuarial deficit and the expenditure required torectify it are a major financial burden although central government is now looking at ways of controlling this in the longerterm and has a number of pension reforms out to consultation.

Capital PositionA small number of projects are incomplete at year end, so expenditure is lower than anticipated in the capital programme with spending of £1,546,000 compared to a revised budget of £1,863,000. Over half of the capital spending has been metfrom grants with only £713,000 of the Council's capital reserves being applied during the year.

Borrowing and Sources of FinanceThe Council’s policy in the year was to fund capital expenditure from grants and capital receipts and not undertake borrowing. As discussed above capital reserves were used to fund £713,000 of spending, £7,900,000 of Usable CapitalReceipts remain at 31st March 2012 and are therefore available to finance future capital expenditure.

InvestmentsInvestment returns are at an historic low, due to the sustained low level of the Bank of England's base rate. Thissituation was anticipated in the budget. Since the banking crisis in 2007/08 the Council has been very risk averse; credit risk was a primary consideration during the year when placing investments.

Impact of Current Economic Climate on the Council and the Services it ProvidesThe Medium Term Financial Strategy (MTFS) anticipates the use of the Council's excess revenue reserves (general fund balance over £1m) over a three year period to help manage the major reduction in formula grant. This together with reductions in on-going expenditure and a programme of boosting income aims to rebalance the budget in the medium term, whilst containing increases in Council Tax.

Page 4

APPENDIX 1

7/64

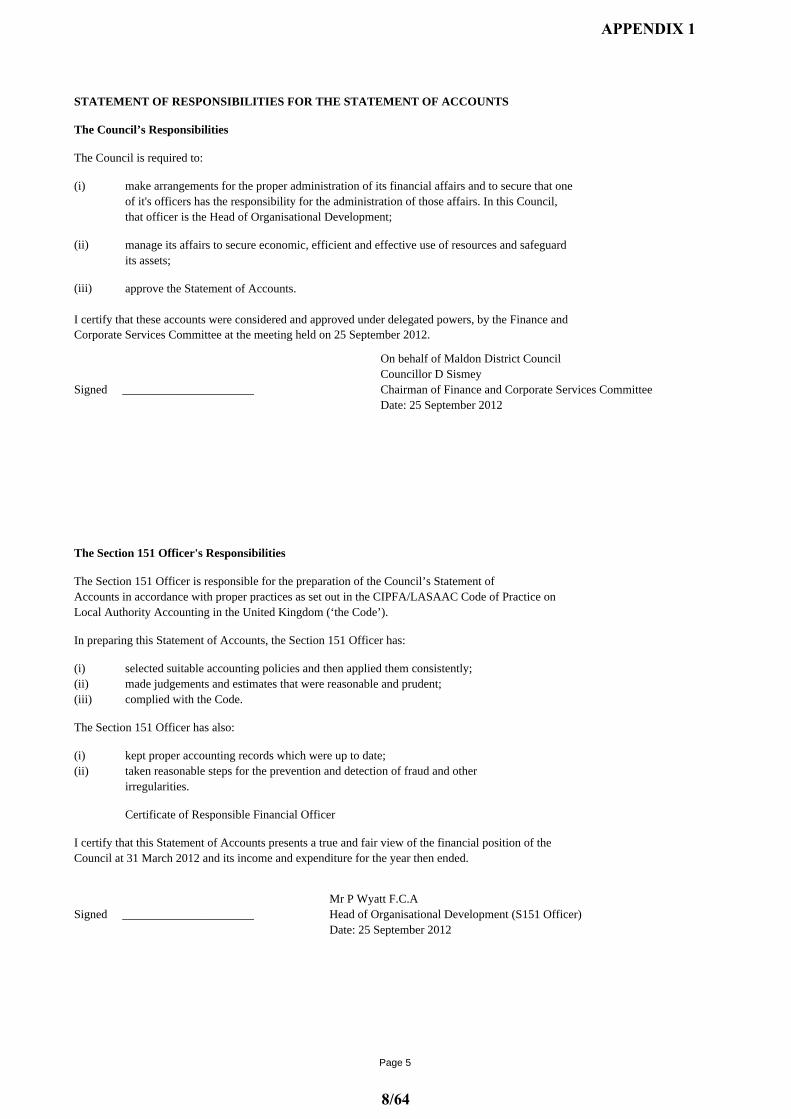

STATEMENT OF RESPONSIBILITIES FOR THE STATEMENT OF ACCOUNTS

The Council’s Responsibilities

The Council is required to:

(i) make arrangements for the proper administration of its financial affairs and to secure that one of it's officers has the responsibility for the administration of those affairs. In this Council, that officer is the Head of Organisational Development;

(ii) manage its affairs to secure economic, efficient and effective use of resources and safeguard its assets;

(iii) approve the Statement of Accounts.

I certify that these accounts were considered and approved under delegated powers, by the Finance and Corporate Services Committee at the meeting held on 25 September 2012.

On behalf of Maldon District CouncilCouncillor D Sismey

Signed ______________________ Chairman of Finance and Corporate Services CommitteeDate: 25 September 2012

The Section 151 Officer's Responsibilities

The Section 151 Officer is responsible for the preparation of the Council’s Statement of Accounts in accordance with proper practices as set out in the CIPFA/LASAAC Code of Practice on Local Authority Accounting in the United Kingdom (‘the Code’).

In preparing this Statement of Accounts, the Section 151 Officer has:

(i) selected suitable accounting policies and then applied them consistently;(ii) made judgements and estimates that were reasonable and prudent;(iii) complied with the Code.

The Section 151 Officer has also:

(i) kept proper accounting records which were up to date;(ii) taken reasonable steps for the prevention and detection of fraud and other

irregularities.

Certificate of Responsible Financial Officer

I certify that this Statement of Accounts presents a true and fair view of the financial position of theCouncil at 31 March 2012 and its income and expenditure for the year then ended.

Mr P Wyatt F.C.ASigned ______________________ Head of Organisational Development (S151 Officer)

Date: 25 September 2012

Page 5

APPENDIX 1

8/64

Notes Ge

ne

ral F

un

d B

ala

nce

Ea

rma

rke

d G

en

era

l F

un

d R

ese

rve

s

Ca

pita

l Gra

nts

U

na

pp

lied

Acc

ou

nt

Ca

pita

l Re

ceip

ts

Re

serv

e

To

tal U

sa

ble

R

es

erv

es

Re

valu

atio

n R

ese

rve

Ca

pita

l Ad

just

me

nt

Acc

ou

nt

De

ferr

ed

Ca

pita

l R

ece

ipts

Acc

ou

nt

Pe

nsi

on

s R

ese

rve

Co

llect

ion

Fu

nd

A

dju

stm

en

t Acc

ou

nt

Acc

um

ula

ted

A

bse

nce

s A

cco

un

t

To

tal U

nu

sa

ble

R

es

erv

es

To

tal A

uth

ori

ty

Re

se

rve

s

£000 £000 £000 £000 £000 £000 £000 £000 £000 £000 £000 £000 £000

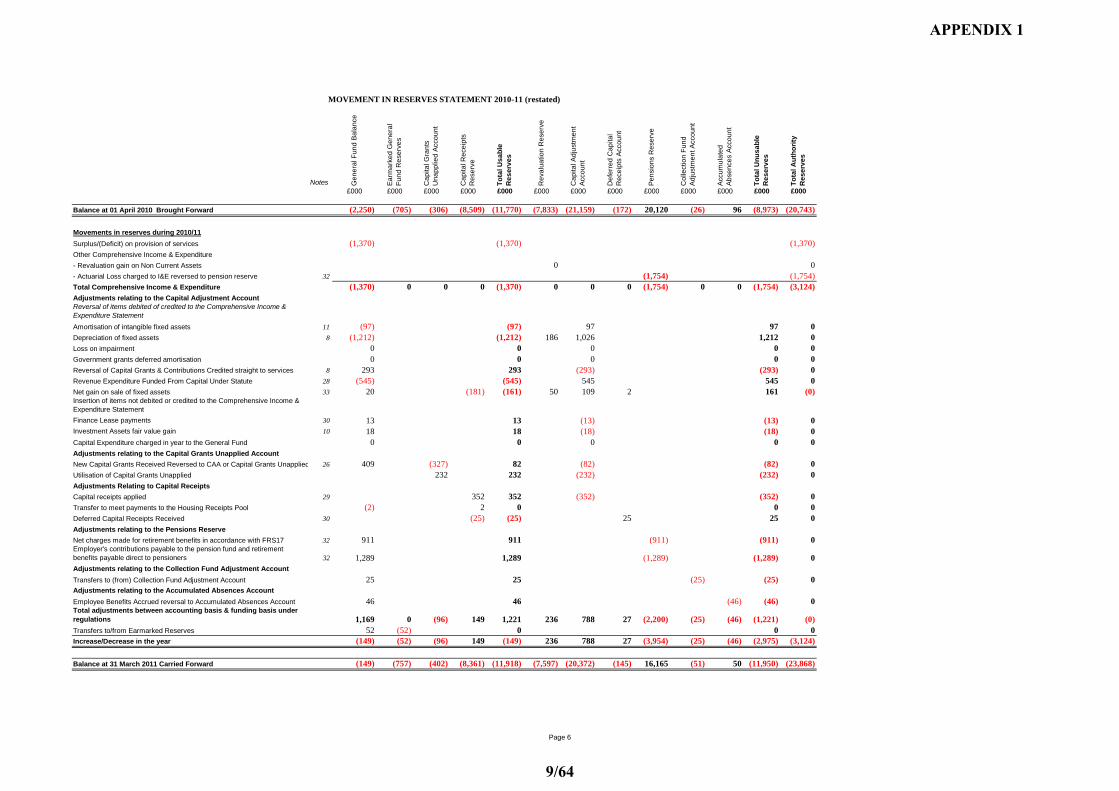

Balance at 01 April 2010 Brought Forward (2,250) (705) (306) (8,509) (11,770) (7,833) (21,159) (172) 20,120 (26) 96 (8,973) (20,743)

Movements in reserves during 2010/11

Surplus/(Deficit) on provision of services (1,370) (1,370) (1,370)Other Comprehensive Income & Expenditure

- Revaluation gain on Non Current Assets 0 0- Actuarial Loss charged to I&E reversed to pension reserve 32 (1,754) (1,754)Total Comprehensive Income & Expenditure (1,370) 0 0 0 (1,370) 0 0 0 (1,754) 0 0 (1,754) (3,124)Adjustments relating to the Capital Adjustment AccountReversal of items debited of credited to the Comprehensive Income & Expenditure StatementAmortisation of intangible fixed assets 11 (97) (97) 97 97 0Depreciation of fixed assets 8 (1,212) (1,212) 186 1,026 1,212 0Loss on impairment 0 0 0 0 0Government grants deferred amortisation 0 0 0 0 0Reversal of Capital Grants & Contributions Credited straight to services 8 293 293 (293) (293) 0Revenue Expenditure Funded From Capital Under Statute 28 (545) (545) 545 545 0Net gain on sale of fixed assets 33 20 (181) (161) 50 109 2 161 (0)Insertion of items not debited or credited to the Comprehensive Income & Expenditure Statement

Finance Lease payments 30 13 13 (13) (13) 0Investment Assets fair value gain 10 18 18 (18) (18) 0Capital Expenditure charged in year to the General Fund 0 0 0 0 0Adjustments relating to the Capital Grants Unapplied Account

New Capital Grants Received Reversed to CAA or Capital Grants Unapplied 26 409 (327) 82 (82) (82) 0Utilisation of Capital Grants Unapplied 232 232 (232) (232) 0Adjustments Relating to Capital Receipts

Capital receipts applied 29 352 352 (352) (352) 0Transfer to meet payments to the Housing Receipts Pool (2) 2 0 0 0Deferred Capital Receipts Received 30 (25) (25) 25 25 0Adjustments relating to the Pensions Reserve

Net charges made for retirement benefits in accordance with FRS17 32 911 911 (911) (911) 0Employer's contributions payable to the pension fund and retirement benefits payable direct to pensioners 32 1,289 1,289 (1,289) (1,289) 0Adjustments relating to the Collection Fund Adjustment Account

Transfers to (from) Collection Fund Adjustment Account 25 25 (25) (25) 0Adjustments relating to the Accumulated Absences Account

Employee Benefits Accrued reversal to Accumulated Absences Account 46 46 (46) (46) 0Total adjustments between accounting basis & funding basis under regulations 1,169 0 (96) 149 1,221 236 788 27 (2,200) (25) (46) (1,221) (0)Transfers to/from Earmarked Reserves 52 (52) 0 0 0Increase/Decrease in the year (149) (52) (96) 149 (149) 236 788 27 (3,954) (25) (46) (2,975) (3,124)

Balance at 31 March 2011 Carried Forward (149) (757) (402) (8,361) (11,918) (7,597) (20,372) (145) 16,165 (51) 50 (11,950) (23,868)

MOVEMENT IN RESERVES STATEMENT 2010-11 (restated)

Page 6

APPENDIX 1

9/64

Notes Ge

ne

ral F

un

d B

ala

nce

Ea

rma

rke

d G

en

era

l F

un

d R

ese

rve

s

Ca

pita

l Gra

nts

U

na

pp

lied

Acc

ou

nt

Ca

pita

l Re

ceip

ts

Re

serv

e

To

tal U

sa

ble

R

es

erv

es

Re

valu

atio

n R

ese

rve

Ca

pita

l Ad

just

me

nt

Acc

ou

nt

De

ferr

ed

Ca

pita

l R

ece

ipts

Acc

ou

nt

Pe

nsi

on

s R

ese

rve

Co

llect

ion

Fu

nd

A

dju

stm

en

t Acc

ou

nt

Acc

um

ula

ted

A

bse

nce

s A

cco

un

t

To

tal U

nu

sa

ble

R

es

erv

es

To

tal A

uth

ori

ty

Re

se

rve

s

£000 £000 £000 £000 £000 £000 £000 £000 £000 £000 £000 £000 £000

Balance at 01 April 2011 Brought Forward (2,399) (757) (402) (8,361) (11,918) (7,597) (20,372) (145) 16,165 (51) 50 (11,950) (23,868)

Movements in reserves during 2011/12

Surplus/(Deficit) on provision of services 514 514 514Other Comprehensive Income & Expenditure

- Revaluation gain on Non Current Assets 0- Actuarial Loss charged to I&E reversed to pension reserve 32 6,210 6,210Total Comprehensive Income & Expenditure 514 0 0 0 514 0 0 0 6,210 0 0 6,210 6,724Adjustments relating to the Capital Adjustment AccountReversal of items debited of credited to the Comprehensive Income & Expenditure StatementAmortisation of intangible fixed assets 11 (83) (83) 83 83 0Depreciation of fixed assets 8 (1,201) (1,201) 184 1,017 1,201 0Reversal of Capital Grants & Contributions Credited straight to services 8 209 209 (209) (209) 0Revenue Expenditure Funded From Capital Under Statute 28 (510) (510) 510 510 0Net gain on sale of fixed assets 33 150 (292) (142) 19 97 26 142 (0)Insertion of items not debited or credited to the Comprehensive Income & Expenditure Statement

Finance Lease payments 30 13 13 (13) (13) 0Investment Assets fair value gain 10 0 0 0 0 0Capital Expenditure charged in year to the General Fund 0 0 0 0 0Adjustments relating to the Capital Grants Unapplied Account

New Capital Grants Received Reversed to CAA or Capital Grants Unapplied 26 350 350 (350) (350) 0Utilisation of Capital Grants Unapplied 275 275 (275) (275) 0Adjustments Relating to Capital Receipts

Capital receipts applied 29 713 713 (713) (713) 0Transfer to meet payments to the Housing Receipts Pool 0 0 0 0 0Deferred Capital Receipts Received 30 0 0 0Adjustments relating to the Pensions Reserve

Net charges made for retirement benefits in accordance with FRS17 32 (1,281) (1,281) 1,281 1,281 0Employer's contributions payable to the pension fund and retirement benefits payable direct to pensioners 32 1,278 1,278 (1,278) (1,278) 0Adjustments relating to the Collection Fund Adjustment Account

Transfers to (from) Collection Fund Adjustment Account (20) (20) 20 20 0Adjustments relating to the Accumulated Absences Account

Employee Benefits Accrued reversal to Accumulated Absences Account (8) (8) 8 8 0Total adjustments between accounting basis & funding basis under regulations (1,103) 0 275 421 (407) 203 147 26 3 20 8 407 0Transfers to/from Earmarked Reserves 96 (96) 0 0 0Increase/Decrease in the year (493) (96) 275 421 107 203 147 26 6,213 20 8 6,617 6,724

Balance at 31 March 2012 Carried Forward (2,892) (853) (127) (7,940) (11,811) (7,394) (20,225) (119) 22,378 (31) 58 (5,333) (17,144)

MOVEMENT IN RESERVES STATEMENT 2011-12

Page 7

APPENDIX 1

10/64

2010/11 2010/11 2010/11 2011/12 2011/12 2011/12

Gross Gross Net Gross Gross Net Expenditure Income Expenditure Expenditure Income Expenditure

£000 £000 £000 Note £000 £000 £000

(As restated)

5,498 (4,799) 699 Central Services to the Public 5,517 (4,707) 8102,668 (783) 1,885 Cultural & Related Services 2,573 (770) 1,8034,501 (1,430) 3,071 Environmental Services 4,363 (1,798) 2,565

16,988 (16,020) 968 Housing Services 17,424 (16,429) 9952,330 (711) 1,619 Planning & Development Services 2,046 (595) 1,451

409 (626) (217) Transport Services 391 (648) (257)571 (143) 428 Concessionary Travel 15 (15) 0

1,419 (6) 1,413 Corporate and Democratic Core 1,439 (10) 1,42914 0 14 Non Distributed Costs 70 0 700 (2,650) (2,650) Change in pension benefits valuation basis (past service gain) 32 0

34,398 (27,168) 7,230 NET COST OF SERVICES 33,838 (24,972) 8,866

993 Parish & Town Precepts 9962 Contribution of housing capital receipts to Government Pool 0

(20) Gains on the disposal of fixed assets (150)* 975 OTHER OPERATING EXPENDITURE 847

1 Interest payable and similar charges 1(293) Interest on investments 13,31 (251)

(8) Surplus on trading undertakings 22 (22)971 Pensions interest cost and expected return on pensions assets 546

(105) Rental Income from Investment Assets 11 (102)(18) Gain on Fair value of Investment Assets 11 0548 FINANCING AND INVESTMENT INCOME & EXPENDITURE 172

* (5,238) Council Tax Icome (5,240)(563) Government Grants (not attributable to specific services) (792)

(35)Area Based Grants (Non ring fenced grants should be treated as general revenue grants - not included in cost of services) (428)

(3,877) Non-Domestic Rates (2,561)(410) Capital Grants and Contributions 27 (350)

(10,123) TAXATION AND NON SPECIFIC GRANT INCOME (9,371)(1,370) (SURPLUS) /DEFICIT ON THE PROVISION OF SERVICES 514

(1,754) ACTUARIAL (GAINS)/LOSSES ON PENSION ASSETS/LIABILITIES 32 6,210(1,754) OTHER COMPREHENSIVE INCOME AND EXPENDITURE (SURPLUS) / DEFICIT 6,210

(3,124) TOTAL COMPREHENSIVE INCOME AND EXPENDITURE (SURPLUS) / DEFICIT 6,724

COMPREHENSIVE INCOME AND EXPENDITURE STATEMENT

Page 8

APPENDIX 1

11/64

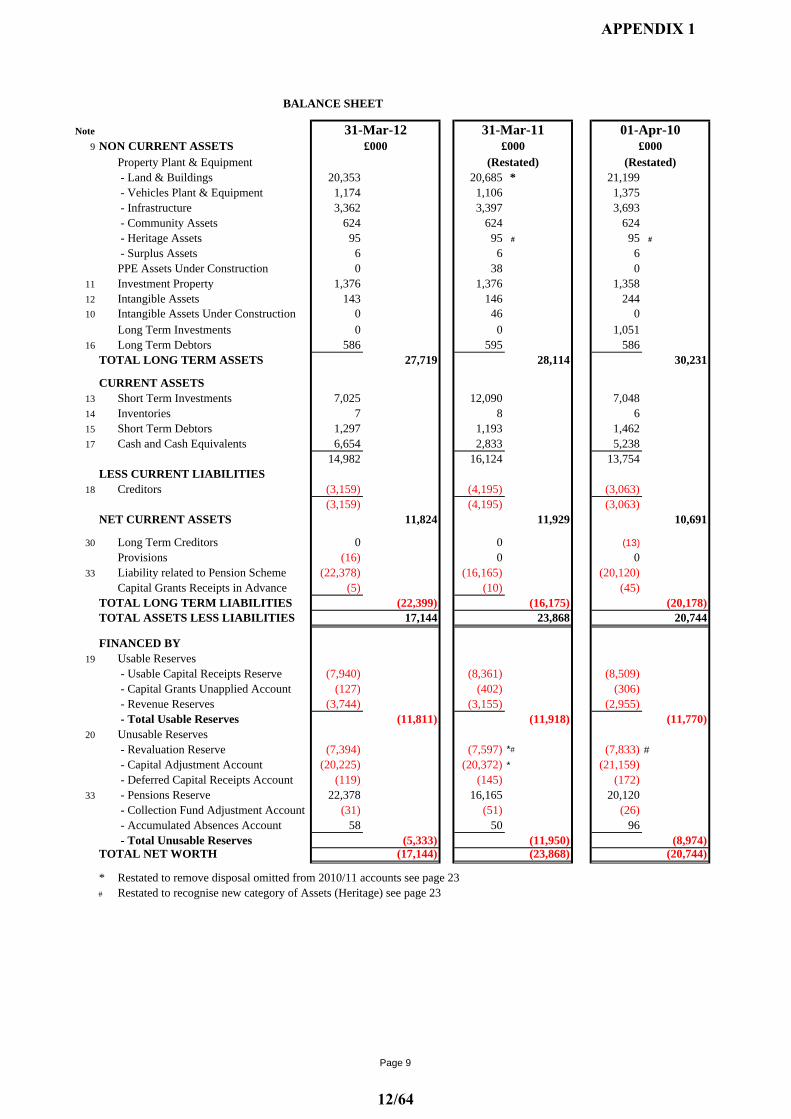

Note 31-Mar-12 31-Mar-11 01-Apr-109 NON CURRENT ASSETS £000 £000

Property Plant & Equipment - Land & Buildings 20,353 20,685 * 21,199 - Vehicles Plant & Equipment 1,174 1,106 1,375 - Infrastructure 3,362 3,397 3,693 - Community Assets 624 624 624 - Heritage Assets 95 95 # 95 #

- Surplus Assets 6 6 6PPE Assets Under Construction 0 38 0

11 Investment Property 1,376 1,376 1,35812 Intangible Assets 143 146 24410 Intangible Assets Under Construction 0 46 0

Long Term Investments 0 0 1,05116 Long Term Debtors 586 595 586

TOTAL LONG TERM ASSETS 27,719 28,114 30,231

CURRENT ASSETS13 Short Term Investments 7,025 12,090 7,04814 Inventories 7 8 615 Short Term Debtors 1,297 1,193 1,46217 Cash and Cash Equivalents 6,654 2,833 5,238

14,982 16,124 13,754LESS CURRENT LIABILITIES

18 Creditors (3,159) (4,195) (3,063)(3,159) (4,195) (3,063)

NET CURRENT ASSETS 11,824 11,929 10,691

30 Long Term Creditors 0 0 (13)

Provisions (16) 0 033 Liability related to Pension Scheme (22,378) (16,165) (20,120)

Capital Grants Receipts in Advance (5) (10) (45)TOTAL LONG TERM LIABILITIES (22,399) (16,175) (20,178)TOTAL ASSETS LESS LIABILITIES 17,144 23,868 20,744

FINANCED BY19 Usable Reserves

- Usable Capital Receipts Reserve (7,940) (8,361) (8,509) - Capital Grants Unapplied Account (127) (402) (306) - Revenue Reserves (3,744) (3,155) (2,955) - Total Usable Reserves (11,811) (11,918) (11,770)

20 Unusable Reserves - Revaluation Reserve (7,394) (7,597) *# (7,833) #

- Capital Adjustment Account (20,225) (20,372) * (21,159) - Deferred Capital Receipts Account (119) (145) (172)

33 - Pensions Reserve 22,378 16,165 20,120 - Collection Fund Adjustment Account (31) (51) (26) - Accumulated Absences Account 58 50 96 - Total Unusable Reserves (5,333) (11,950) (8,974)

TOTAL NET WORTH (17,144) (23,868) (20,744)

* Restated to remove disposal omitted from 2010/11 accounts see page 23# Restated to recognise new category of Assets (Heritage) see page 23

BALANCE SHEET

£000(Restated) (Restated)

Page 9

APPENDIX 1

12/64

£000 £000(restated)

Net (surplus) or deficit on the provision of services (1,451) 514

Adjustments to net (surplus) or deficit for non-cash movements (note A) (103) (548)

Adjustments for items that are financing or investing activities (note B) 549 582

Net cash (inflows)/outflows from operating activities (1,005) 548

Investing activities

Purchase of property, plant and equipment, investment property and intangibles 345 1,025Purchase of short and long term investments 19,500 20,000Other payments made for investing activities 38 55Proceeds of sale of property, plant and equipment, investment property and intangibles (13) (9)Proceeds of sale of short and long term investments (15,500) (25,000)Other receipts from investing activities (600) (630)

Net cash (inflow)/Ouflows from investing activities 3,770 (4,559)

Financing activities

Repayment of finance lease and on-balance sheet PFI contracts 13 13Repayment of short and long term borrowing 0 0Other payments for financing activities 0 177Cash receipts of short and long term borrowing 0 0Other receipts from financing activities (373) 0

Net cash (inflow)/Ouflows from financing activities (360) 190

Net (increase) or decrease in cash and cash equivalents (note C) 2,405 (3,821)

Cash and cash equivalents at the beginning of the year 5,238 2,833

Cash and cash equivalents at the end of the year 2,833 6,654

2011-12 2010-11

The Cash Flow Statement shows the changes in cash and cash equivalents of the authority during the reporting period. The statement shows how the authority generates and uses cash and cash equivalents by classifying cash flows as operating, investing and financing activities. The amount of net cash flows arising from operating activities is a key indicator of the extent to which the operations of the authority are funded by way of taxation and grant income or from the recipients of services provided by the authority. Investing activities represent the extent to which cash flows have been made from resources which are intended to contribute to the authority's future service delivery.

CASH FLOW STATEMENT

Page 10

APPENDIX 1

13/64

Note A: adjustments to net (surplus) or deficit for non-cash movements£000 £000 £000 £000

Depreciation, impairments and amortisation (1,309) (1,283)Amounts credited to CIES in respect of donated assets 0 0Carrying amount of non-current assets sold (80) (86)Increase/(decrease) in inventories 1 0Increase/(decrease) in debtors (251) 103(Increase)/decrease in creditors (715) 807(Increase)/decrease in provisions (7) (89)Pension costs 911 (1,281)Pension charges 1,289 1,278Grants applied to the financing of capital expenditure 40 3Revaluation gains on the value of investment properties 18 0

(103) (548)

Note B: adjustments for items that are financing or investing activities£000 £000 £000 £000

Proceeds of sale of property, plant and equipment, investment property and intangibles 179 236Capital grants received 370 346

549 582

Note C: cash & cash equivalent components TOTAL CashCash floats

£000 £000 £000 £000As at 31 Mar 11 2,494 2,494 338 1As at 31 Mar 12 6,104 6,104 549 1Movement in year 3,610 3,610 211 0

Note D: interest paid & received£000 £000 £000 £000

Interest received (298) (316)Interest paid 1 1Net cash (inflow) / outflow (297) (315)

Restated

2011-122010-11

2011-12

2011-12

2010-11

2010-11

Page 11

APPENDIX 1

14/64

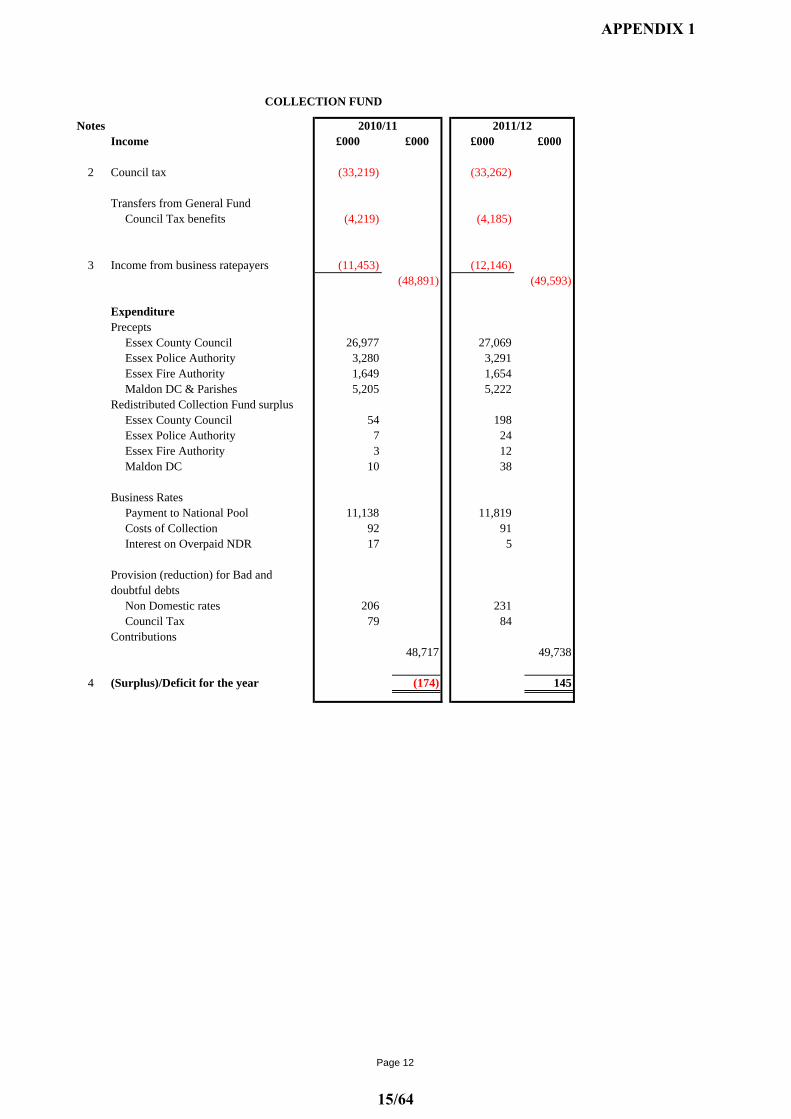

Notes 2010/11 2011/12Income £000 £000 £000 £000

2 Council tax (33,219) (33,262)

Transfers from General FundCouncil Tax benefits (4,219) (4,185)

3 Income from business ratepayers (11,453) (12,146)(48,891) (49,593)

ExpenditurePrecepts

Essex County Council 26,977 27,069Essex Police Authority 3,280 3,291Essex Fire Authority 1,649 1,654Maldon DC & Parishes 5,205 5,222

Redistributed Collection Fund surplusEssex County Council 54 198Essex Police Authority 7 24Essex Fire Authority 3 12Maldon DC 10 38

Business RatesPayment to National Pool 11,138 11,819Costs of Collection 92 91Interest on Overpaid NDR 17 5

Provision (reduction) for Bad and doubtful debts

Non Domestic rates 206 231Council Tax 79 84

Contributions 48,717 49,738

4 (Surplus)/Deficit for the year (174) 145

COLLECTION FUND

Page 12

APPENDIX 1

15/64

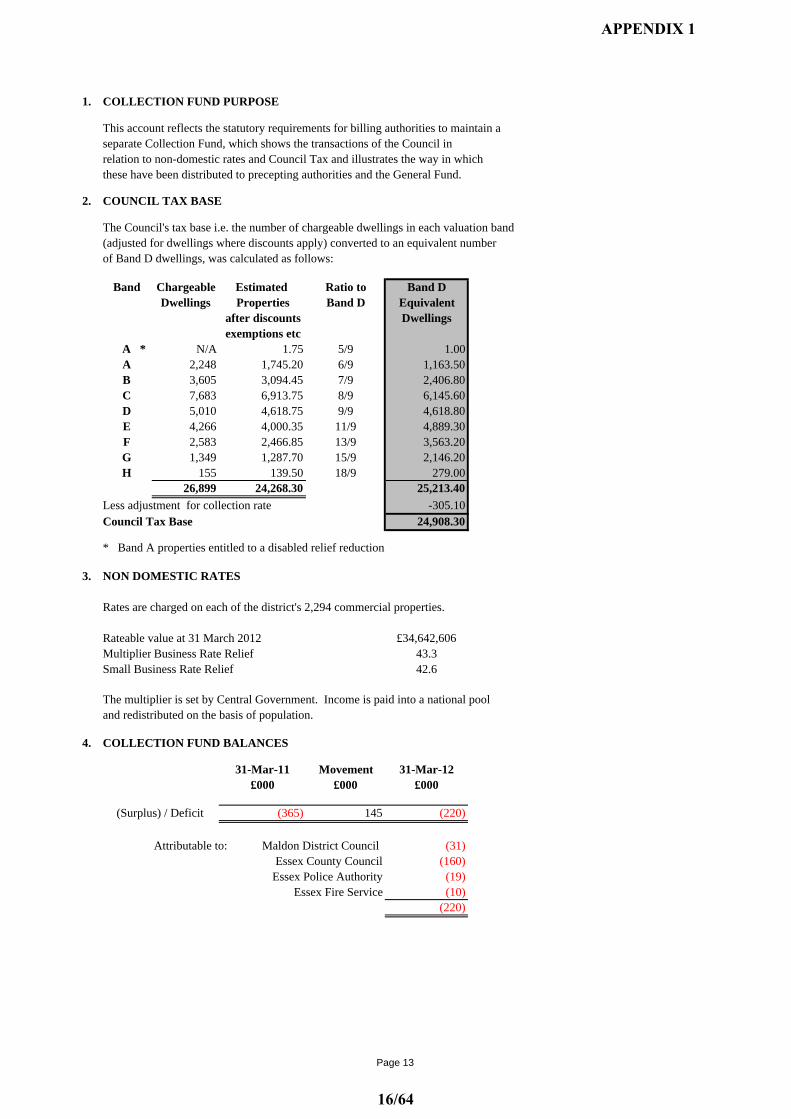

1. COLLECTION FUND PURPOSE

This account reflects the statutory requirements for billing authorities to maintain aseparate Collection Fund, which shows the transactions of the Council inrelation to non-domestic rates and Council Tax and illustrates the way in whichthese have been distributed to precepting authorities and the General Fund.

2. COUNCIL TAX BASE

The Council's tax base i.e. the number of chargeable dwellings in each valuation band(adjusted for dwellings where discounts apply) converted to an equivalent numberof Band D dwellings, was calculated as follows:

Band Chargeable Estimated Ratio to Band DDwellings Properties Band D Equivalent

after discounts Dwellingsexemptions etc

A * N/A 1.75 5/9 1.00A 2,248 1,745.20 6/9 1,163.50B 3,605 3,094.45 7/9 2,406.80C 7,683 6,913.75 8/9 6,145.60D 5,010 4,618.75 9/9 4,618.80E 4,266 4,000.35 11/9 4,889.30F 2,583 2,466.85 13/9 3,563.20G 1,349 1,287.70 15/9 2,146.20H 155 139.50 18/9 279.00

26,899 24,268.30 25,213.40

Less adjustment for collection rate -305.10Council Tax Base 24,908.30

* Band A properties entitled to a disabled relief reduction

3. NON DOMESTIC RATES

Rates are charged on each of the district's 2,294 commercial properties.

Rateable value at 31 March 2012 £34,642,606Multiplier Business Rate Relief 43.3Small Business Rate Relief 42.6

The multiplier is set by Central Government. Income is paid into a national pool and redistributed on the basis of population.

4. COLLECTION FUND BALANCES

31-Mar-11 Movement 31-Mar-12£000 £000 £000

(Surplus) / Deficit (365) 145 (220)

Attributable to: Maldon District Council (31)Essex County Council (160)

Essex Police Authority (19)Essex Fire Service (10)

(220)

Page 13

APPENDIX 1

16/64

NOTES TO THE CORE ACCOUNTING STATEMENTS

1. ACCOUNTING POLICIESGeneral PrinciplesThe Accounts are drawn up to comply with the Accounts and Audit Regulations 2011 in accordance with properaccounting practices. These practices primarily comprise the Code of Practice on Local Authority Accounting in the United Kingdom 2011/12 and the Best Value Accounting Code of Practice 2011/12, supported by International Financial Reporting Standards (IFRS) and statutory guidance issued under section 12 of the 2011 Act.

The accounting convention adopted in the Statement of Accounts is principally historical cost, modified by the revaluation of certain categories of non-current assets and financial instruments.

Income and ExpenditureBoth revenue and capital accounts are prepared on an income and expenditure basis, which is in accordance with the accruals concept as defined in FRS18.

Cash and Cash EquivalentsCash is represented by cash in hand and deposits with financial institutions repayable without penalty on notice of not more than 24 hours. Cash equivalents are investments repayable without penalty on notice of not more than 24 hours i.e.that are readily convertible to known amounts of cash with insignificant risk of change in value. They are held primarily for the purpose of meeting short term cash commitments.In the Cash Flow Statement, cash and cash equivalents are shown net of bank overdrafts that arerepayable on demand and form an integral part of the Council’s cash management.

Exceptional itemsWhen items of income and expense are material, their nature and amount is disclosed separately, either on the face of the Comprehensive Income and Expenditure Statement or in the notes to the accounts, depending on how significant the items are to an understanding of the Council’s financial performance.

Prior Period Adjustments, Changes in Accounting Policies Estimates and Material ErrorsPrior period adjustments may arise as a result of a change in accounting policies or to correct a material error.Changes in accounting policies are only made when required by proper accounting practices or the change provides more reliable or relevant information about the effect of transactions, other events and conditions on the Council’s financial position or financial performance. Where a change is made, it is applied retrospectively (unless stated otherwise) by adjusting opening balances and comparative amounts for the prior period as if the new policy had always been applied.Changes in accounting estimates are accounted for prospectively, i.e. in the current and future years affected by the changeand do not give rise to a prior period adjustment.Material errors discovered in prior period figures are corrected retrospectively by amending opening balances and comparative amounts for the prior period.

Charges to Revenue for Non-Current AssetsServices, support services and trading accounts are debited with the following amounts to record the cost of holding non current assets during the year:

• depreciation attributable to the assets used by the relevant service• revaluation and impairment losses on assets used by the service where there are no accumulated gains in the Revaluation Reserve against which the losses can be written off against• amortisation of intangible assets attributable to the relevant service.

The Council is not required to raise council tax to fund depreciation, revaluation and impairment losses or amortisation. Depreciation, revaluation and impairment losses and amortisation are replaced by the contribution in the General Fund Balance, by way of an adjusting transaction with the Capital Adjustment Account in the Movement in Reserves Statement for the difference between the two.

Page 14

APPENDIX 1

17/64

Employee Benefits-Benefits Payable During EmploymentShort-term employee benefits are those due to be settled within 12 months of the year-end. They include such benefits as wages and salaries, paid annual leave and paid sick leave and non-monetary benefits for current employees and are recognised as an expense for services in the year in which employees render their services to the Council.

An accrual is made for the cost of holiday entitlements, flexi time and time off in lieu earned by employees but not taken before the year-end, which employees can carry forward into the next financial year. The accrual is made at the wage and salary rates applicable in the following accounting year, being the period in which the employee takes the benefit. The accrual is charged to Surplus/Deficit on the Provision of Services in the financial year in which the absences are accrued and it is then reversed out through the Movement in Reserves Statement so there is no charge against Council Tax.

-Termination BenefitsTermination benefits are amounts payable as a result of a decision by the Council to terminate an officer’s employment before the normal retirement date or an officer’s decision to accept voluntary redundancy. They are charged on an accrualsbasis to the relevant service line in the Comprehensive Income and Expenditure Statement when the Council is demonstrably committed to the termination of the employment of an officer or group of officers or making an offer to encourage voluntary redundancy. Where termination benefits involve the enhancement of pensions, statutory provisions require the General Fund balance to be charged with the amount payable by the Council to the pension fund or pensioner in the year, not the amount calculated according to the relevant accounting standards. In the Movement in Reserves Statement, appropriations are required to and from the Pensions Reserve to remove the notional debits and credits for pension enhancement termination benefits and replace them with debits for the cash paid to the pension fund and butpensioners and any such amounts payable unpaid at the year end.

-Post Employment BenefitsEmployees of the Council are members of the Local Government Pension Scheme, administered by Essex County Council.The Local Government Pension Scheme is accounted for as a defined benefits scheme:• The liabilities of the Essex pension fund attributable to the Council are included in the Balance Sheet on an actuarial basis using the projected unit method – i.e. an assessment of the future payments that will be made in relation to retirement benefits earned to date by employees, based on assumptions about mortality rates, employee turnover rates, etc. and earnings for current employees.• Liabilities are discounted to their value at current prices, using a discount rate of 4.6% (based on the indicative rate of return on high quality corporate bond.)• The assets of Essex pension fund attributable to the Council are included in the Balance Sheet at their fair value:

- quoted securities – current bid price- unquoted securities – professional estimate- unitised securities – current bid price- property – market value.

• The change in the net pensions liability is analysed into seven components:i) current service cost - The increase in liabilities as a result of years of service earned this year. This is allocated in the Comprehensive Income and Expenditure Statement to the services for which the Council employees worked.ii) past service costs - the increase in liabilities arising from current year decisions whose effect relates to years of service earned in earlier years. These are debited to the Surplus/Deficit on the Provision of Services in the Comprehensive Income and Expenditure Statement as part of Non Distributed Costs.iii) interest cost – the expected increase in the present value of liabilities during the year as they move one year closer to being paid. This is debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statementiv) expected return on assets – the annual investment return on the fund assets attributable to the Council, based on an average of the expected long-term return. This is credited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement.v) gains or losses on settlements and curtailments – the result of actions to relieve the Council of liabilities or events that reduce the expected future service or accrual of benefits of employees. These are debited/credited to the Surplus/Deficit on the Provision of Services in the Comprehensive Income and Expenditure Statement as part of Non Distributed Costs.vi) actuarial gains and losses – changes in the net pensions liability that arise because events have not coincided with assumptions made at the last actuarial valuation or the assumptions have been updated by the actuary. These are credited/debited to the Pensions Reservevii) contributions paid to the Essex pension fund – cash paid as employer’s contributions to the pension fund in settlement of liabilities; not accounted for as an expense for the Council.

Page 15

APPENDIX 1

18/64

-Post Employment Benefits cont.In relation to retirement benefits, statutory provisions require the General Fund balance to be charged with the amount payable by the Council to the pension fund or directly to pensioners in the year, not the amount calculated according to the relevant accounting standard. This means that there are appropriations to and from the Pensions Reserve to remove the notional debits and credits for retirement benefits and replace them with debits for the cash paid to theThe Pension fund. The negative balance that arises on the Pensions Reserve thereby measures the beneficial impact to the General Fund of being required to account for retirement benefits on the basis of cash flows rather than as benefits areearned by employees.

-Discretionary BenefitsThe Council also has restricted powers to make discretionary awards of retirement benefits in the event of early retirements.Any liabilities estimated to arise as a result of an award to any member of staff are accrued in the year of the decision to make the award and accounted for using the same policies as are applied to the Local Government Pension Scheme.

Events after the Balance Sheet DateEvents after the Balance Sheet date are those events, both favourable and unfavourable, that occur between the end of the reporting period (on 31 March) and the date when the Statement of Accounts are authorised for issue.Two types of post Balance Sheet events can be identified:

• Adjusting events are those that provide evidence of conditions that existed at the Balance SheetDate. Where material, the Statement of Accounts is adjusted to reflect the impact of such events.• Non-adjusting events are those that are indicative of conditions that arose after the Balance SheetDate. The Statement of Accounts is not adjusted to reflect such events, but where a category ofevents would have a material effect, additional disclosure is made in the notes of the nature of theevents and their estimated financial effect.

Events taking place after the date the Statement of Accounts is authorised for issue are not reflected in the Statement of Accounts

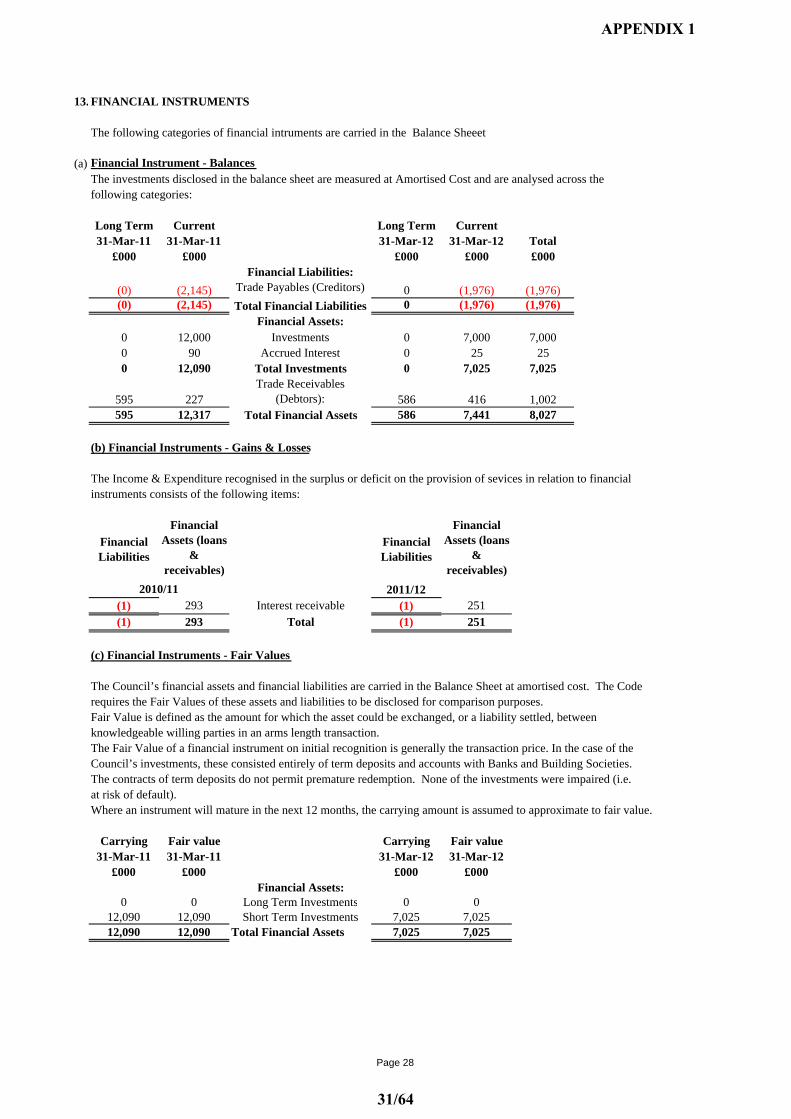

Financial Instruments-Financial LiabilitiesThe Council does not have any borrowing. Trade payables (creditors) are disclosed at face value.

-Financial AssetsThe Council’s portfolio of investments consists of fixed term deposits and call accounts. These are classed as Loans and Receivables and are measured at amortised cost. Trade Receivables (Debtors) are classified as Loans & Receivables and aremeasured at cost on the Balance Sheet. The Council does not enter into investments required to be measured at Fair Value through the Comprehensive Income & Expenditure Statement or classified as Available for Sale.

Soft LoansThe de minimis level for soft loans is £20,000 any loans made at below market rate which are de minimis are disclosed in the accounts as long term debtors.

Page 16

APPENDIX 1

19/64

Government Grants and ContributionsWhether paid on account, by instalments or in arrears, government grants and third party contributions and donations arerecognised as due to the Council when there is reasonable assurance that:

• the Council will comply with the conditions attached to the payments, and• the grants or contributions will be received.

Amounts recognised as due to the Council are not credited to the Comprehensive Income and Expenditure Statement untilconditions attached to the grant or contribution have been satisfied. Monies advanced as grants and contributions for which conditions have not been satisfied are carried in the Balance Sheet as creditors. When conditions are satisfied, the grant or contribution is credited to the relevant service line or Taxation and Non-Specific Grant Income in the Comprehensive Income and Expenditure Statement. Where capital grants are credited to the Comprehensive Income and Expenditure Statement, they are reversed out of the General Fund Balance in the Movement in Reserves Statement. Where the grant has yet to be used to finance capital expenditure, it is posted to the Capital Grants Unapplied reserve. Where it has been applied, it is posted to the Capital Adjustment Account. Amounts in the Capital Grants Unapplied reserve are transferred to the Capital Adjustment Account when they have been applied to fund capital expenditure.

Intangible AssetsExpenditure on non-monetary assets that do not have physical substance but are controlled by the Council as a result of past events (e.g. software licences) are capitalised when it is expected that future economic benefits or service potential will flowfrom the intangible asset to the Council. Intangible assets are measured initially at cost. Amounts are only revalued where the fair value of the assets held by the Council can be determined by reference to an active market. In practice, no intangibleassets are held by the Council which meets this criterion, and they are therefore carried at amortised cost.The depreciable amount of an intangible asset is amortised over its useful life to the relevant service lines in the ComprehensiveIncome and Expenditure Statement. An intangible asset is tested for impairment whenever there is an indication that the asset might be impaired, any losses recognised are posted to the relevant service lines in the Comprehensive Income and ExpenditureStatement. Any gain or loss arising on the disposal or abandonment of an intangible asset is posted to the Other Operating Expenditure line in the Comprehensive Income and Expenditure Statement. Where expenditure on intangible assets qualifies as capital expenditure for statutory purposes, amortisation, impairment losses and disposal gains and losses are not permitted to have an impact on the General Fund Balance. The gains and losses are therefore reversed out of the General Fund Balance in the Movement in Reserves Statement and posted to the Capital Adjustment Account and the Capital Receipts Reserve.

Interests in Companies and Other EntitiesThe Council does not have any material interests in companies and other entities that have the nature of the subsidiaries and does not prepare group accounts

InventoriesInventories are included in the Balance Sheet at cost.

Investment PropertyInvestment properties are those that are used solely to earn rentals and/or for capital appreciation. The definition is not met if the property is used in any way to facilitate the delivery of services or production of goods or if the asset is held for sale.Investment properties are measured initially at cost and subsequently at fair value, based on the amount at which the assetcould be exchanged between knowledgeable parties at arm’s length. Properties are not depreciated but are revalued annuallyaccording to market conditions at the year-end. Gains and losses on revaluation are posted to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. The same treatment is applied to gainsand losses on disposal.All the councils investment assets are currently leased and fair value estimates are therefore based on the rentals received.If the income from investment property does not change materially during the year the fair value is assumed to remain the same and revaluation considered un-necessary. As a minimum, investment properties, regardless of leases, will be revaluedevery 5 years along with other classes of assets.Rentals received in relation to investment properties are credited to the Financing and Investment Income line. Directly attributable operating expenses related to investment properties are debited to the Financing and Investment Income line.Revaluation and disposal gains and losses are not permitted by statutory arrangements to have an impact on the General FundBalance. The gains and losses are therefore reversed out of the General Fund Balance in the Movement in Reserves Statementand posted to the Capital Adjustment Account and the Capital Receipts Reserve (for the sale proceeds).

Page 17

APPENDIX 1

20/64

LeasesLeases are classified as finance leases where the terms of the lease transfer substantially all the risks and rewards incidental toownership of the property, plant or equipment from the lessor to the lessee. All other leases are classified as operating leases.Where a lease covers both land and buildings, the land and buildings elements are considered separately for classification.Arrangements that do not have the legal status of a lease but convey a right to use an asset in return for payment are accountedfor under this policy where fulfilment of the arrangement is dependent on the use of specific assets.

Finance Leases - LesseeProperty, Plant and Equipment held under finance leases is recognised on the Balance Sheet at the commencement of the leaseat the lower of its fair value measured at the lease inception and the present value of the minimum lease payments. The assetrecognised is matched by a liability for the obligation to pay the lessor. Initial direct costs of the Council are added to thecarrying amount of the asset. Premiums paid on entry into a lease are applied to writing down the lease liability. Contingentrents are charged as expenses in the periods in which they are incurred.Finance lease payments are apportioned between:

• a charge for the acquisition of the interest in the property, plant or equipment which is applied to write down the lease liability, and• a finance charge which is debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement.

Property, Plant and Equipment recognised under finance leases is accounted for using the policies applied generally to suchassets, subject to depreciation being charged over the lease term if this is shorter than the asset’s estimated useful life and where ownership of the asset does not transfer to the Council at the end of the lease period.

Operating Leases - LesseeRentals paid under operating leases are charged to the Comprehensive Income and Expenditure Statement as an expense of theservices benefiting from use of the leased property, plant or equipment.

Finance Leases - LessorWhere the Council grants a finance lease over a property or an item of plant or equipment, the relevant asset is written out ofthe Balance Sheet as a disposal. At the commencement of the lease, the carrying amount of the asset in the Balance Sheet (whether Property, Plant and Equipment or Assets Held for Sale) is written off to the Other Operating Expenditure line in theComprehensive Income and Expenditure Statement as part of the gain or loss on disposal. The written-off value is not considered to be a charge against council tax and as such is appropriated to the Capital Adjustment Account from the GeneralFund Balance in the Movement in Reserves Statement.A gain on disposal, representing the Council’s net investment in the lease, is credited to the Other Operating Expenditure line in the Comprehensive Income and Expenditure Statement, matched by a long-term debtor asset in the Balance Sheet. The gainis not permitted by statute to increase the General Fund Balance and is required to be treated as a capital receipt. Where a premium has been received, this is posted out of the General Fund Balance to the Capital Receipts Reserve in the Movement inReserves Statement. Finance lease rentals receivable are apportioned between:

• a charge for the acquisition of the interest in the property which is applied to write down the lease debtor including any premiums received, and• finance income which is credited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement.

Where the amount due in relation to the lease asset is to be settled by the payment of rentals in future financial years, this is posted out of the General Fund Balance to the Deferred Capital Receipts Reserve in the Movement in Reserves Statement. When the future rentals are received, the element for the capital receipt for the disposal of the asset is used to write down the lease debtor. At this point, the deferred capital receipts are transferred to the Usable Capital Receipts Reserve.

Operating Leases - LessorWhere the Council grants an operating lease over a property or an item of plant or equipment, the asset is retained in the Balance Sheet. Rental income is credited to the Comprehensive Income and Expenditure Statement on a straight-line basis over the life of the lease.

Overheads and Support ServicesThe costs of overheads and support services are charged to those that benefit from the supply or service. The total absorption costing principle is used i.e. the full costs are shared between users in proportion to the benefits received, with the exception of:

- Corporate and Democratic Core – costs relating to the Council’s status as a multi-functional democratic organisation such as reporting to elected members;- Non Distributed costs – the cost of discretionary benefits awarded to employees retiring early plus depreciation on non-operational assets and the impairment of assets in accordance with the Best Value Accounting Code of Practice.

These two cost categories are accounted for as separate headings in the Comprehensive Income & Expenditure Statement.

Page 18

APPENDIX 1

21/64

Property Plant and Equipment (PPE)Expenditure on the acquisition, creation and enhancement of fixed assets is capitalised in accordance with the accruals concept.The Council's de minimis level for capital expenditure is £10,000. Expenditure on PPE is capitalised, provided that the fixed asset yields benefit to the Council and the services it provides for a period of more than one year. This excludes expenditure on routine repairs and maintenance on PPE, which does not enhance the asset and is charged direct to service revenue accounts.Assets are initially measured at cost, comprising:

• the purchase price• any costs attributable to bringing the asset to the location and condition necessary for it to be capable of operating in the manner intended by management• the initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located.

The Council does not have any borrowing costs. The cost of assets acquired other than by purchase is deemed to be its fairvalue, unless the acquisition does not have commercial substance (i.e. it will not lead to a variation in the cash flows of the Council). In the latter case, where an asset is acquired via an exchange, the cost of the acquisition is the carrying amount of theasset given up by the Council.Large assets are divided into their component parts only if the components have materially different useful lives compared to the rest of the asset. This allows depreciation charges for assets to more accurately reflect the consumption of economic benefit which takes place at different rates for each component.Assets are subsequently carried in the Balance Sheet using the following measurement bases:

• Plant, Vehicles, Furniture and Equipment assets, Infrastructure assets and Community assets – Depreciated Historic Cost• Other land and buildings and Surplus Assets – Fair Value, determined as the amount that would bepaid for the asset in its Existing Use (EUV).• Components of buildings - Depreciated Historic Cost

Where there is no market-based evidence of fair value because of the specialist nature of an asset, depreciated replacementcost (DRC) is used as an estimate of Fair Value. Where non-property assets (Plant, Vehicles, Furniture and Equipment assets) that have short useful lives or low values (or both), depreciated historical cost basis is used as a proxy for Fair Value.

Assets included in the Balance Sheet at fair value are revalued sufficiently regularly to ensure that their carrying amount is notmaterially different from their Fair Value at the financial year end, but as a minimum every five years.Increases in valuations are matched by credits to the Revaluation Reserve to recognise unrealised gains. Exceptionally, gains might be credited to the Comprehensive Income and Expenditure Statement where they arise from the reversal of a loss previously charged to a service. Where decreases in value are identified, they are accounted for as follows:

• where there is a balance of revaluation gains for the asset in the Revaluation Reserve, the carryingamount of the asset is written down against that balance (up to the amount of the accumulated gains)• where there is no balance in the Revaluation Reserve or an insufficient balance, the carrying amountof the asset is written down against the relevant service line(s) in the Comprehensive Income andExpenditure Statement.

The Revaluation Reserve contains revaluation gains recognised since 1 April 2007 only, the date of its formal implementation.Gains arising before that date have been consolidated into the Capital Adjustment Account.

ImpairmentAssets are assessed at each financial year end as to whether there is any indication that an asset may be impaired. Where indications exist and any possible differences are estimated to be material, the recoverable amount of the asset is estimated and,where this is less than the carrying amount of the asset, an impairment loss is recognised for the shortfall.Where impairment losses are identified, they are accounted for as follows:

• where there is a balance of revaluation gains for the asset in the Revaluation Reserve, the carrying amount of the asset is written down against that balance (up to the amount of the accumulated gains)• where there is no balance in the Revaluation Reserve or an insufficient balance, the carrying amount of the asset is written down against the relevant service line(s) in the Comprehensive Income and Expenditure Statement.

Where an impairment loss is reversed subsequently, the reversal is credited to the relevant service line(s) in the ComprehensiveIncome and Expenditure Statement, up to the amount of the original loss, adjusted for depreciation that would have been charged if the loss had not been recognised.

Page 19

APPENDIX 1

22/64

DepreciationDepreciation is provided for on assets with a finite useful life (which can be determined at the time of acquisition orrevaluation) according to the following policy:

- Newly acquired assets are depreciated from the mid-point of the year except for assets in the course of construction which are not depreciated until they are brought into use.

- Where depreciation is provided for, assets are depreciated using the straight line method over the following periods:

• Buildings (where appropriate) 5 - 60 years• Infrastructure 5 - 30 years• Vehicles, Plant & Equipment 3 –10 years• Intangible assets 3 - 7 years

- Land, including car parks, is not depreciated

Assets Held for SaleWhen it becomes probable that the carrying amount of an asset will be recovered principally through a sale transaction rather than through its continuing use, it is reclassified as an Asset Held for Sale. The asset is revalued immediately before reclassification and then carried at the lower of this amount and fair value less costs to sell. Where there is a subsequent decrease to fair value less costs to sell, the loss is posted to the Non Distributed costs line of the Surplus/Deficit on the Provision of Services in the Comprehensive Income and Expenditure Statement. Gains in fair value are recognised only up to the amount of any previous losses recognised in the Surplus/Deficit on Provision of Services. Depreciation is not charged on Assets Held for Sale. If assets no longer meet the criteria to be classified as Assets Held for Sale, they are reclassified back tonon-current assets and valued at the lower of their carrying amount before they were classified as held for sale; adjusted for depreciation, amortisation or revaluations that would have been recognised had they not been classified as Held for Sale, and their recoverable amount at the date of the decision not to sell.Assets that are to be abandoned or scrapped are not reclassified as Assets Held for Sale.

Disposals of Plant, Property and Equipment, Investment Properties and Assets held for SaleWhen an asset is disposed of or decommissioned, the carrying amount of the asset in the Balance Sheet (whether Property, Plant and Equipment or Assets Held for Sale) is written off to the Other Operating Expenditure line in the Comprehensive Income and Expenditure statement as part of the gain or loss on disposal. Receipts from disposals are credited to the same line in the Comprehensive Income and Expenditure Statement also as part of the gain or loss on disposal (i.e. netted off against the carrying value of the asset at the time of disposal). Any revaluation gains accumulated for the asset in the Revaluation Reserve are transferred to the Capital Adjustment Account.All amounts for disposal of assets currently recognised on the balance sheet are categorised as capital receipts. Amounts for other asset disposals in excess of £10,000 are categorised as capital receipts.

Contingent LiabilitiesA contingent liability arises where an event has taken place that gives the Council a possible obligation whose existence will only be confirmed by the occurrence or otherwise or uncertain future events not wholly within the control of the Council. Contingent liabilities also arise in circumstances where a provision would otherwise be made but either it is not probable that an outflow of resources will be required or the amount of the obligation cannot be measured reliably.Contingent liabilities are not recognised in the Balance Sheet but disclosed in a note to the accounts.

Contingent AssetsA contingent asset arises where an event has taken place that gives the Council a possible asset whose existence will only be confirmed by the occurrence or otherwise of uncertain future events not wholly within the control of the Council. Contingent assets are not recognised in the Balance Sheet but disclosed in a note to the accounts where it is probable that there will be an inflow of economic benefits or service potential.

Page 20

APPENDIX 1

23/64

ReservesThe Council has the power to keep reserves for certain purposes by setting aside specific amounts as reserves for future policypurposes or to cover contingencies. Reserves are created by appropriating amounts out of the General Fund Balance in the Movement in Reserves Statement. When expenditure is incurred that is to be financed from a reserve, it is charged to the appropriate service in that year to be included as expenditure in the Surplus / Deficit on the Provision of Services in the Comprehensive Income and Expenditure Statement. The reserve is then appropriated back into the General Fund Balance in the Movement in Reserves Statement so there is no charge against Council Tax for the expenditure incurred. Separate earmarked reserves are held by the Council as follows:

• Efficiency Fund The purpose of this fund is to support future "invest to save initiatives", where existing budgets are insufficient to support the additional spending that maybe required to unlock on-going revenue savings.• Community Grants and Parish Projects Fund This reserve is used when the time limits for payment of grants exceed the financial year in which budget provision is made, necessitating a reserve to be set aside to cover the outstanding liabilities.• Heritage Projects The Council gives grants in support of environmental initiatives and historic buildings. The time limits for payment of these grants exceed the financial year in which budget provision is made, necessitating a reserve to be set aside to cover the outstanding liabilities.• Insurance The Council maintains external insurance policies to cover major risks. In many cases the policies have excess clauses that require the Council to meet the first part of each claim. The Council has established this reserve to cover its liabilities under policy excesses, finance any claims for small risks not insured externally and cover any future liability that may arise from the winding up of Municipal Mutual Insurance.• Repairs & Renewals Fund This reserve is operated to meet major expenditure incurred in maintaining, replacing and renewing the Council’s buildings and facilities.• Revenue Commitments This reserve exists to smooth out the timing differences between monies being earmarked to fund expenditure from the annual revenue budget and the expenditure actually occurring.• Local Plan Development The Council has budgeted for large costs associated with developing what was known as a Local Development Plan. This requirement has been superseded by the developing localism agenda of the new Government and spending has been halted, but the Council will still need a Local Plan for Policy Planning purposes. The Council has decided to set aside the money already budgeted, but unspent, to support the creation of a new plan which is scheduled for completion and introduction in 2014.• Land Charges A grant was received from the Government in 2010/11 to support the possible loss of income on personal search fees that local authorities have been levying under legislation that is now considered to be unsound. Any possible refund liability remains to be resolved, therefore a reserve was set up to hold this money pending a final solution.• Preventing Repossessions A grant was received from the Government in 2011/12 to support work to prevent homes being repossessed this is x expected to be spent in 2012/13• Community Sports Network A grant was received from the Government in 2011/12 to support sports networks this is expected to be spent in 2012/13

Certain reserves are kept by the Council to manage the accounting processes for non-current assets (e.g. Revaluation Reserve and Capital Adjustment Account), retirement benefits (e.g. Pensions Reserve) and employee benefits (e.g. Accumulated Absences Account) and do not represent usable resources for the Council.

Revenue Expenditure Funded from Capital under StatuteExpenditure incurred during the year that may be capitalised under statutory provisions but that does not result in the creation of a non-current asset has been charged as expenditure to the relevant service in the Comprehensive Income and Expenditure Statement in the year. Where the Council has determined to meet the cost of this expenditure from existing capital resources orgovernment Grant, a transfer in the Movement in Reserves Statement from the General Fund Balance to the Capital Adjustment Account then reverses out the amounts charged so that there is no impact on the level of Council Tax.

Page 21

APPENDIX 1

24/64

Provision for Bad and Doubtful DebtsProvision has been made in the accounts for potential bad and doubtful debts in accordance with thefollowing policy. Known uncollectible debts have been written off against provisions made.

Council TaxYears 1 to 6 based on the previous year’s collection profileModification for any unusual circumstances 100% coverage is provided for debts over 6 years old

Non Domestic Rates Years 1 & 2 based on the previous year’s collection profile 100% coverage is provided for debts over 2 years old

Overpaid Housing Benefit Years 1 to 2 based on previous year’s collection profile 100% coverage is provided for debts over 2 years old

Car Park Penalty NoticesAs there is still no collection profile to base the provision on, prudence dictates the following:

50% provision for 2011/12 debts 100% provision for previous years

Miscellaneous Debts 100% of debts outstanding beyond 255 days

VariationThe above methodologies are the basis of calculating the bad debt provisions. From time to time figures are distorted and un-representative of the true debt position. Finance officers will always apply prudent judgement in arrivingat final bad debt figures. Where there is a departure from the above methodology the reasons will be clearly documented.

Heritage AssetsThe IFRS Code of Practice on Local Authority Accounting in the United Kingdom 2011/12 (the Code) has introduced a changein accounting policy in relation to the treatment of heritage assets held by the Council.Heritage assets are assets that are held by the Council principally for their contribution to knowledge or culture. The Council does not own any historic buildings, however, where items such as statues or museum artefacts are owned these areincluded in the balance sheet based on insurance valuations. Heritage assets are not depreciated as they are considered to have an indeterminable useful life.

Page 22

APPENDIX 1

25/64

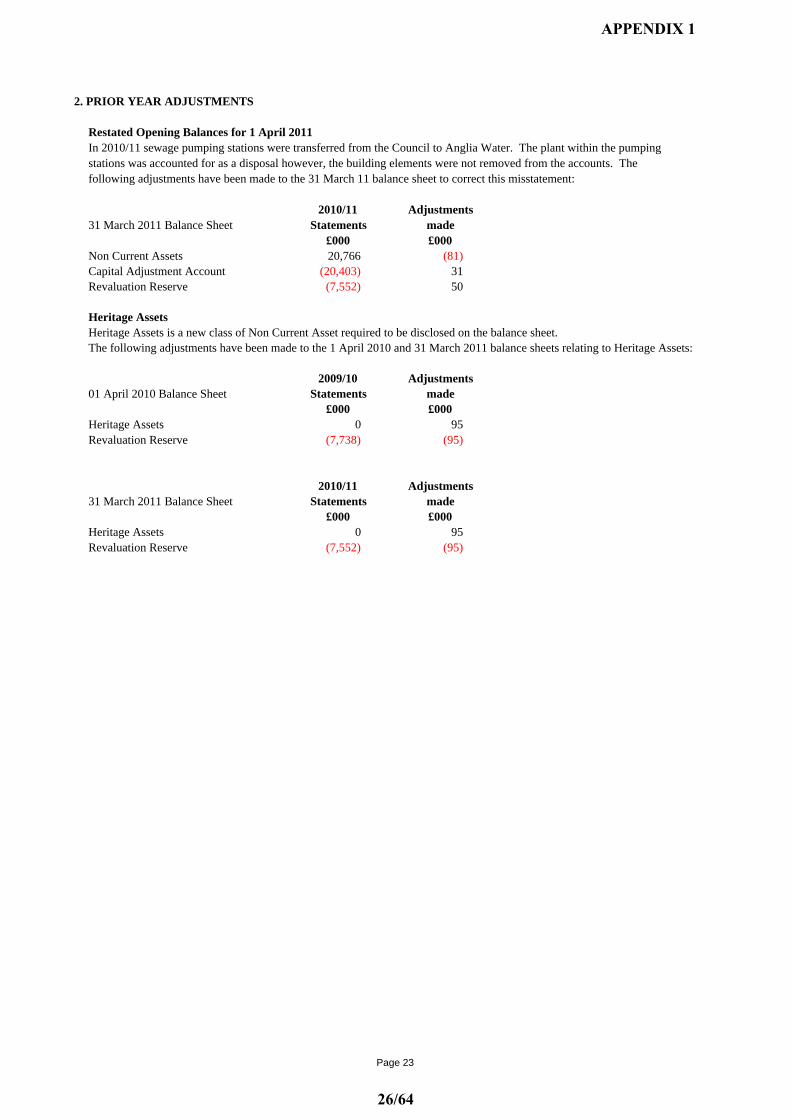

2. PRIOR YEAR ADJUSTMENTS

Restated Opening Balances for 1 April 2011In 2010/11 sewage pumping stations were transferred from the Council to Anglia Water. The plant within the pumping stations was accounted for as a disposal however, the building elements were not removed from the accounts. The following adjustments have been made to the 31 March 11 balance sheet to correct this misstatement:

2010/11 Adjustments31 March 2011 Balance Sheet Statements made

£000 £000Non Current Assets 20,766 (81)Capital Adjustment Account (20,403) 31Revaluation Reserve (7,552) 50

Heritage AssetsHeritage Assets is a new class of Non Current Asset required to be disclosed on the balance sheet.The following adjustments have been made to the 1 April 2010 and 31 March 2011 balance sheets relating to Heritage Assets:

2009/10 Adjustments01 April 2010 Balance Sheet Statements made

£000 £000Heritage Assets 0 95Revaluation Reserve (7,738) (95)

2010/11 Adjustments31 March 2011 Balance Sheet Statements made

£000 £000Heritage Assets 0 95Revaluation Reserve (7,552) (95)

Page 23

APPENDIX 1

26/64

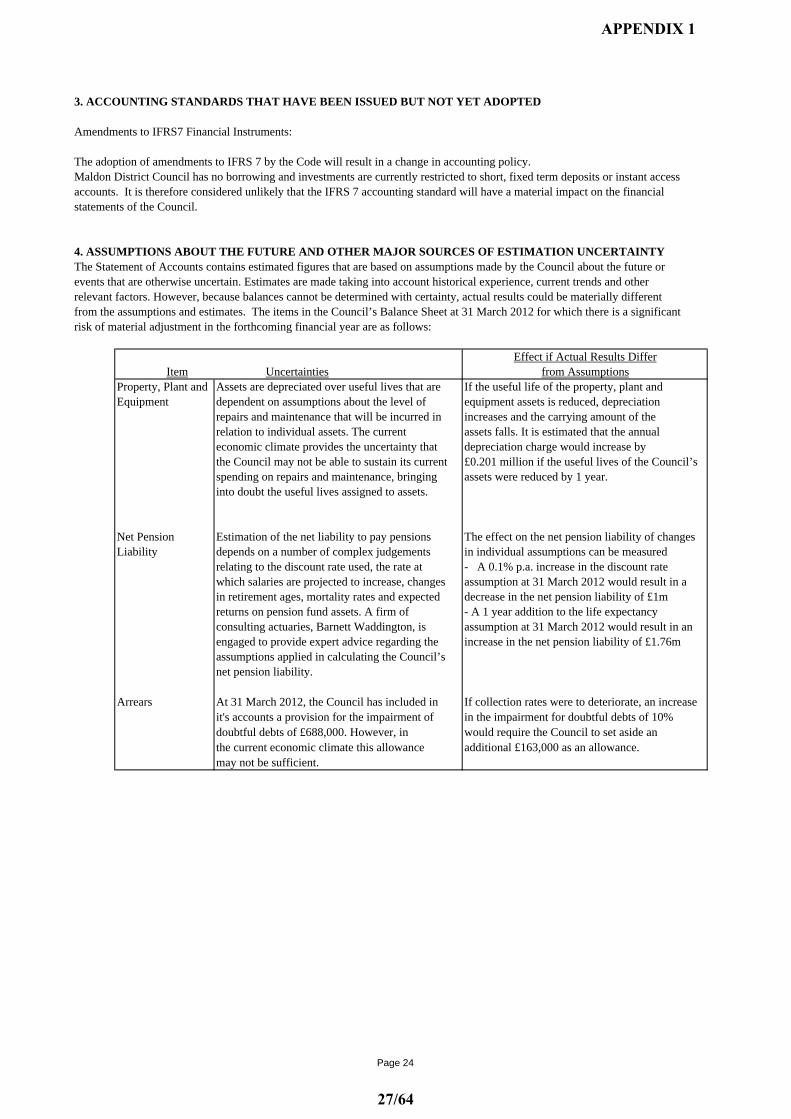

3. ACCOUNTING STANDARDS THAT HAVE BEEN ISSUED BUT NOT YET ADOPTED

Amendments to IFRS7 Financial Instruments:

The adoption of amendments to IFRS 7 by the Code will result in a change in accounting policy.Maldon District Council has no borrowing and investments are currently restricted to short, fixed term deposits or instant access accounts. It is therefore considered unlikely that the IFRS 7 accounting standard will have a material impact on the financial statements of the Council.

4. ASSUMPTIONS ABOUT THE FUTURE AND OTHER MAJOR SOURCES OF ESTIMATION UNCERTAINTYThe Statement of Accounts contains estimated figures that are based on assumptions made by the Council about the future or events that are otherwise uncertain. Estimates are made taking into account historical experience, current trends and other relevant factors. However, because balances cannot be determined with certainty, actual results could be materially different from the assumptions and estimates. The items in the Council’s Balance Sheet at 31 March 2012 for which there is a significant risk of material adjustment in the forthcoming financial year are as follows:

Effect if Actual Results DifferItem Uncertainties from Assumptions

Property, Plant and Assets are depreciated over useful lives that are If the useful life of the property, plant and Equipment dependent on assumptions about the level of equipment assets is reduced, depreciation

repairs and maintenance that will be incurred in increases and the carrying amount of therelation to individual assets. The current assets falls. It is estimated that the annual economic climate provides the uncertainty that depreciation charge would increase by the Council may not be able to sustain its current £0.201 million if the useful lives of the Council’s spending on repairs and maintenance, bringing assets were reduced by 1 year.into doubt the useful lives assigned to assets.

Net Pension Estimation of the net liability to pay pensions The effect on the net pension liability of changesLiability depends on a number of complex judgements in individual assumptions can be measured

relating to the discount rate used, the rate at - A 0.1% p.a. increase in the discount rate which salaries are projected to increase, changes assumption at 31 March 2012 would result in a in retirement ages, mortality rates and expected decrease in the net pension liability of £1mreturns on pension fund assets. A firm of - A 1 year addition to the life expectancy consulting actuaries, Barnett Waddington, is assumption at 31 March 2012 would result in anengaged to provide expert advice regarding the increase in the net pension liability of £1.76massumptions applied in calculating the Council’snet pension liability.

Arrears At 31 March 2012, the Council has included in If collection rates were to deteriorate, an increaseit's accounts a provision for the impairment of in the impairment for doubtful debts of 10% doubtful debts of £688,000. However, in would require the Council to set aside an the current economic climate this allowance additional £163,000 as an allowance.may not be sufficient.

Page 24

APPENDIX 1

27/64

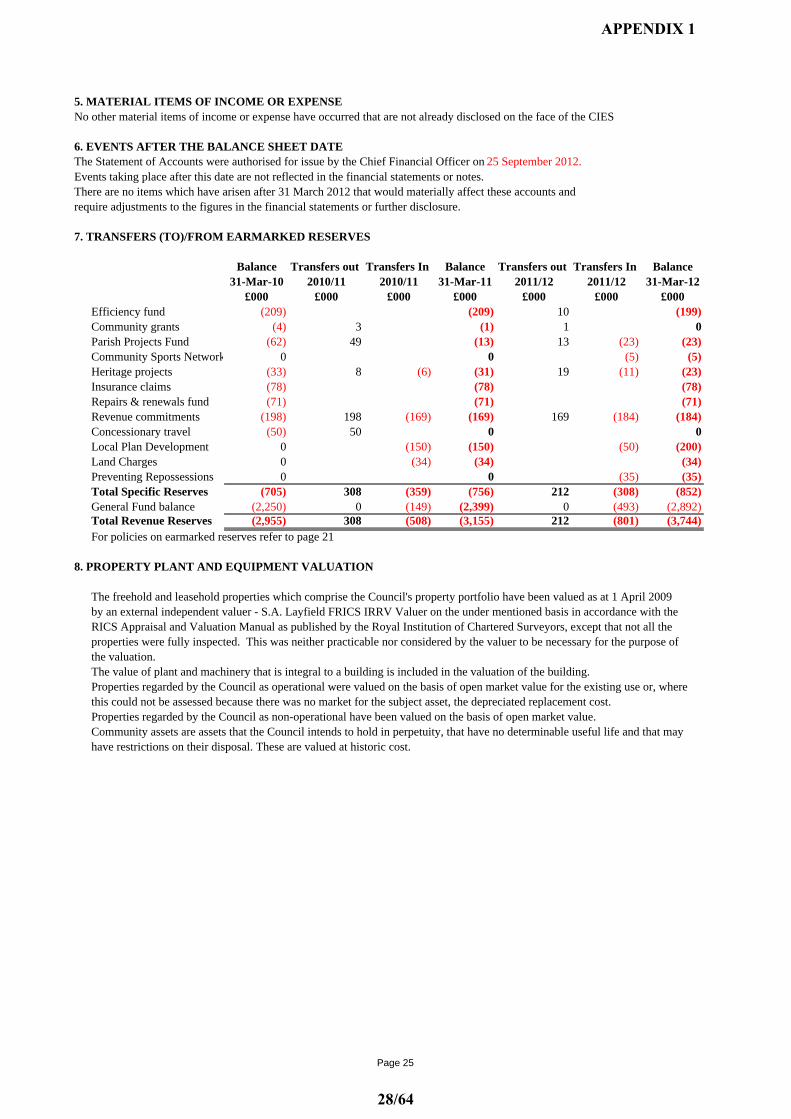

5. MATERIAL ITEMS OF INCOME OR EXPENSENo other material items of income or expense have occurred that are not already disclosed on the face of the CIES

6. EVENTS AFTER THE BALANCE SHEET DATEThe Statement of Accounts were authorised for issue by the Chief Financial Officer on 25 September 2012.Events taking place after this date are not reflected in the financial statements or notes.There are no items which have arisen after 31 March 2012 that would materially affect these accounts andrequire adjustments to the figures in the financial statements or further disclosure.

7. TRANSFERS (TO)/FROM EARMARKED RESERVES

Balance Transfers out Transfers In Balance Transfers out Transfers In Balance31-Mar-10 2010/11 2010/11 31-Mar-11 2011/12 2011/12 31-Mar-12