Make in India - assets.kpmg

31

Voices on Reporting 16 December 2015 KPMG.com/in

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Make in India - assets.kpmg

Voices on Reporting

16 December 2015

KPMG.com/in

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 2

Welcome

Series of knowledge sharing calls

Covering current and emerging reporting issues

Scheduled towards the end of each month

Look out for our Accounting and Auditing Update, IFRS Notes and First Notes publications

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 3

Speaker for the call

Nirav PatelDirectorAccounting Advisory ServicesKPMG in India

AgendaUpdates on

• Ind AS road map, IFC and ICDS

• The SEBI matters

• The accounting matters

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 5

Timelines

16 February 20151

Road map for companies

29 September 20152

RBI recommended a road map for banks and NBFCs

20 October 20153

RBI issued a report on implementation

17 November 20154

IRDA recommended a road map forinsurance companies

7 December 20155

IRDA issued a DP on convergence

1 April 20161

Effective date of Ind AS for companies(Phase I)

1 April 20171

Effective date of Ind AS for companies(Phase II)

Ind AS implementation is now just three months away

Others

• Reporting on IFC – countdown begins

• Update on ICDS implementation

Listing regulations have introduced Ind AS specific disclosures:

• Results for period covered by first Ind AS financial statements to include disclosures as per Ind AS 101* (to the extent applicable for interim financial reports)

• Comparatives for quarterly/annual results should be Ind AS compliant

* Ind AS 101, First-time Adoption of Indian Accounting Standards

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 6

RBI recommends a road map for implementation of Ind AS for banks and NBFCs and issues a report of the working group

• On 29 September 2015, the Reserve Bank of India (RBI) informed its stakeholders that it has recommended to the Ministry of Corporate Affairs (MCA) a road map for the implementation of Ind AS for banks and Non-Banking Financial Companies (NBFCs) from 2018-19 onwards2.

• The RBI constituted a working group (under the chairmanship of Shri Sudarshan Sen) for the same.

• Recently, on 20 October 2015, the RBI issued a report of the working group which portrays the potential issues with respect to the implementation of Ind AS (Ind AS 109, Financial Instruments in particular) by banks in India along with its recommendations to ease out the implementation process3.

• The working group structured its recommendations into some key areas with a focus on financial instruments.

• The working group also devised formats for financial statements of banks under Ind AS and application guidance thereon which are comprised in Annexures I to VIII of the RBI circular3.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 7

The IRDA provides an update on the implementation of Ind AS in the insurance sector

• In November 2015, the Insurance Regulatory and Development Authority of India (IRDA) announced that the country’s insurance sector would be converging with IFRS post issuance of the revised standard on insurance contracts i.e. IFRS 4, Insurance Contracts by the International Accounting Standards Board (IASB) 4.

• Currently, IFRS 4 is being deliberated upon by the IASB and a final standard is expected to be issued in 2016.

• The IRDA has constituted an implementation group to discuss and lay down a road map for the convergence.

• The terms of reference of the implementation group comprise-review the applicability of Ind AS notified by the MCA, study the potential impact of Ind AS on the insurance sector, identify issues involved in the implementation of Ind AS, etc.

• The implementation group would be submitting its report in three months.

• On 7 December 2015, the IRDA released a Discussion Paper (DP) on the convergence to Ind AS in the insurance sector5.

• DP covers a recommended draft of the regulations on financial statements and auditor’s report which are compliant with Ind AS.

Agenda

Updates on

• Ind AS road map, IFC and ICDS

• The SEBI matters

• The accounting matters

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 9

Interim relief provided to companies for use of IFRS for consolidated results6

• Submission of consolidated

results is optional

‒ Option to be exercised in

the first quarter

‒ Option to use IFRS for

consolidated results.

Listing Agreement(Pre-revised)

• Option to submit consolidated

results continues.

• Consolidated results are to be

prepared as per Indian GAAP

‒ IFRS results can be submitted

additionally (optional).

Transitional challenges

• Entities may continue to

submit consolidated results

under IFRS for the balance

quarters and for the year

ending March 2016.

• This does not change the

position under the 2013 Act,

whereby consolidated

statements for the year

ending March 2016 would be

as per Indian GAAP.

Relaxation by SEBIListing Regulations (Revised)

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 10

Financial Results under new Listing Regulations – Equity7

Major changes due to Regulations 33 and Part A of Schedule IV of new Listing Regulations along with circular dated 30 November 2015 regarding formats.

• Disclosures no longer required as part of financial results:

– Public/promoter and promoter group shareholding

(However, as earlier, these are to be filed with stock exchanges at least on quarterly basis)

– Investor complaints pending at the beginning and end of the quarter including the movement - to be disclosed to the stock exchange separately from the results.

• Information to be published in the newspaper is now limited to key parameters e.g. total income, PBT*, PAT**, equity share capital, reserves, EPS***. A weblink to be given so that the detailed results can be seen.

• Where both standalone and consolidated financial results are submitted to stock exchange, only key parameters of consolidated financial results to be published in newspaper along with turnover, PBT and PAT on standalone basis.

• Ind AS specific disclosures introduced:

– Results for the period covered by first Ind AS financial statements to include disclosures as per Ind AS 101 (to the extent applicable for interim financial reports)

– Comparatives for quarterly/annual results should be Ind AS compliant.

* Profit before tax** Profit after tax*** Earning per share

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 11

Financial Results under new Listing Regulations – Debt and Preference Shares8

• Listed non-convertible redeemable preference shares brought under the requirement of submission of half yearly financial results

− For both (debt and preference shares), the requirement is to submit results on a half yearly basis.

• In case of debt securities - detailed information relevant for lenders e.g., credit rating, asset cover, debt service coverage ratio, debenture redemption reserve, debt equity ratio, etc. required to be given in the half yearly/annual results

• In the case of listed non-convertible redeemable preference shares - apart from information for lenders (as above), further information relevant for holders/investors required e.g. capital redemption reserve, track record of dividends, free reserves, etc.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 12

SEBI’s new circular prescribes additional regulatory requirements for schemes of arrangement of listed companies9

• Schemes submitted to stock exchange prior to 1 December 2015 would continue to be governed by the erstwhile

requirements.

• Reinstates requirement of the auditor to certify that accounting treatment as per scheme is in compliance with

Accounting Standards(AS) prescribed under the 2013 Act or by respective sectoral authorities.

– Mere disclosure of deviations in scheme’s accounting treatment from aforesaid standards not adequate.

• Requirement of the valuation report from an independent CA or another person (as applicable) continues.

• All valuation reports to be considered by Audit Committee before finalising its report recommending scheme.

• No fixed time limit for giving ‘objection/no objection letter’ by stock exchanges to SEBI.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 13

Penal provisions for non-compliance with certain provisions of the Listing Regulations10

• SEBI issued directions to stock exchanges to monitor compliance by listed entities with the provisions of the Listing Regulations.

• The SEBI’s new circular states that recognised stock exchanges impose fines as an action of first resort in case of non compliance with the provisions of the Listing Regulations and invoke suspension of trading in case of subsequent and consecutive defaults.

• The following procedure has been prescribed in order to maintain consistency and uniformity of approach:

- Uniform structure to implement ‘fines’.

- Depositories may freeze/unfreeze the entire shareholding of the promoter and promoter group on receipt of intimation.

- Two or more consecutive defaults of the prescribed provisions of the Listing Regulations, the scrip of the listed entities could move to ‘Z’ category wherein trades should take place on a ‘Trade for Trade’ basis.

- Specific SOP for suspension of trading and revocation of suspension of trading laid down for stock exchanges.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 14

SEBI’s DP on review of framework for public issuance of convertible securities11

Current requirements Proposals

• No specific provision for tenure except for financing of group companies

• No specific mention about convertible securities regarding selling shares to the public

• An issuance can be made on a fixed price basis or through the book building route. The conversion price may either be pre-fixed at the time of issuance or linked to the market price at the time of conversion.

• Tenure of five years

• Explicitly permit the existing holders of convertible securities as well to sell their securities to the public

• Disclosure should be made upfront in an offer document.

• SEBI also seeks suggestions relating to public issuance of optionally convertible securities by a listed entity and public issuance of compulsorily convertible securities by an unlisted entity.

• Time period for receiving comments by SEBI ends on 23 December 2015.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 15

SEBI’s DP on exit offer to dissenting shareholders12

2013 Act requirements

• The 2013 Act requires that dissenting shareholders should be given an exit opportunity by promoters and shareholders having control over the company in accordance with the regulations to be specified by SEBI.

SEBI’s proposal

• SEBI issued a DP on 1 December 2015 which proposes that every company should provide an option to shareholders to exit as required by 2013 Act.

• Some other issues for discussion are as follows:

– Applicability of the provision– Eligibility of the shareholder for availing an exit offer– Offer price for the exit offer– Carveouts for companies with no identifiable promoters or shareholders having control– Exit offer in cases where a high percentage of amount raised for the issue has already been utilised– Manner of providing an exit opportunity to dissenting shareholders.

• Time period for receiving comments by SEBI ends on 23 December 2015.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 16

FAQ on SEBI (Share Based Employee Benefits) Regulations, 2014 (SEBI ESOP) 13

Clarification on grant of ESOP to independent directors

• SEBI recently clarified that the restriction on grant of ESOPs to independent directors in terms of the provisions, SEBI ESOP and the 2013 Act applies only on fresh grants of ESOPs after commencement of the aforesaid provisions.

• Grants made prior to commencement of SEBI ESOP provisions would remain valid i.e. an independent director can exercise such ESOPs, subject to fulfillment of the terms and conditions of the ESOP schemes framed by the companies in terms of the relevant regulations.

On 20 November 2015, SEBI issued two clarifications :

Classification of un-appropriated inventory of shares

Current guidance• SEBI ESOP regulations require the un-appropriated inventory of shares which is not backed by grants but has been

acquired through secondary acquisition by a trust has to be sold on the recognised stock exchange within a period of five years from the date of notification of ESOP Regulations.

Clarifications• SEBI clarified that appropriation towards ESPS/ESOP/SAR/General Employee Benefits Scheme/Retirement Benefit

Schemes would be considered as compliance with the SEBI ESOP Regulations if done by 27 October 2015.• The company may appropriate towards individual employees or sell in the market during the next four years so

that no un-appropriated inventory remains thereafter.

AgendaUpdates on

• Ind AS road map, IFC and ICDS

• The SEBI matters

• The accounting matters

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 18

Depreciation – ICAI’s exposure draft (ED) of the draft Guidance Note (GN) on Schedule II of the 2013 Act 14

Background

• The 2013 Act lays down Schedule II which enshrines within itself the principle for recognising depreciation on the assets over their useful lives.

• The ICAI issued an Application Guide (AG) on 10 April 2015 which addresses certain practical issues in the implementation of Schedule II to the 2013 Act.

New development

• The ICAI issued an ED on the GN on Schedule II on 10 November 2015.

• The ICAI withdrew certain Guidance Notes on Accounting relating to the guidance on accounting for depreciation in accordance with the Companies Act, 1956

• In comparison to the AG, the ED on GN provides

– Classification of useful life/residual value when the management estimate is different from Schedule II – Provides guidance when the residual value of an asset is higher/lower than five per cent of the original

cost of the asset– Provides a step by step approach to multiple shift depreciation– Explains the concept of Continuous Process Plant (CPP) and defines the principle of useful lives for CPP– Clarification is provided on the adoption of different methods of depreciation for similar assets at

different geographical locations– Disclosures.

• Comments period closed on 25 November 2015.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 19

Important Expert Advisory Committee (EAC) opinions issued by the ICAI

Provisioning for doubtful receivables15

• The amount to be provided for in respect of doubtful receivables should be determined after applying judgement by the management of an enterprise.

• This judgement is based on consideration of information available up to the date on which the financial statements are approved and will include a review of events occurring after the balance sheet date, supplemented by experience of similar transactions and, in some cases, reports from independent experts.

• If the uncertainties which created a contingency in respect of an individual transaction are common to a large number of similar transactions, then the amount of the contingency need not be individually determined, but may be based on the group of similar transactions.

• If all the above mentioned factors have been considered in the policy for provision of doubtful receivables, then the same would be in compliance of various accounting standards and would also depict true and fair view of the accounts.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20

Important EAC opinions issued by the ICAI

Requirement of preparation of complete/condensed set of financial statements for interim financial reporting15

Amortisation of SAP licence and accounting for annual renewal fee15

• AS 25, Interim Financial Reporting does not mandate which enterprises should be required to present interim financial reports.

• As per the requirements of the standard, an interim financial report means a financial report containing either a complete set of financial statements or a set of condensed financial statements for an interim period.

• Only the preparation of a condensed statement of profit and loss cannot be considered as preparation of an ‘interim financial report’ as per the requirements of AS 25.

• The requirements of AS 25 to prepare either a complete set of financial statements or a set of condensed financial statements for each quarter after delisting of the company are not applicable to the company.

• SAP licence can be considered to be ‘available for use’ only when non-SAP applications and facilities are also ready. Therefore, till the time a SAP licence is not ‘available for use’, the same should be classified as an ‘intangible asset under development’ and thereafter it should be recognised as part of the ‘intangible asset’.

• Such a SAP licence should be tested for impairment and written down for technological obsolescence.

• The expenditure incurred towards the annual renewal fee to continue to retain the licenceand does not generate future economic benefits in excess of originally assessed standard of performance of the licence. Thus, it cannot be capitalised and should be expensed in the statement of profit and loss.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 21

Important EAC opinions issued by the ICAI

Accounting treatment of pension liability post- seperation15

• Although the pension liability to the employee when it becomes due will be met by the support fund, which is fully reinsured, the company continues to be liable for fulfilment of the pension promise, in contingent events such as, if the insurance company goes bankrupt or in the event of underfunding.

• The company will have to pay the part of the benefit due, which cannot be paid by the support fund (because of underfunding) out of its own means.

• In addition to the pension promise, the company is also liable for pension adjustments to the guaranteed vested amount due to inflation.

• Since in case of underfunding with the support fund and in case of contingency of insolvency of the insurer, a deficit is to be met by the employer and the pension scheme cannot be treated as defined contribution accordingly, it is not appropriate to consider the periodic contribution only as its expense for a given period in the financial statements of the company.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 22

Links to previous recordings of VOR

Month/Year Topics Link

January 2015

• Ind AS implementation road map• Revised drafts on Income Computation and Disclosure Standards (ICDS)• Exposure Draft (ED) on Guidance Note (GN) on Accounting for Derivative

Contracts

Click here

February 2015• Overview of Income Computation and Disclosure Standards (ICDS)• Significant impact areas of ICDS• Next steps for ICDS implementation

Click here

March 2015

• Overview of Section 143(12) of the Companies Act, 2013• Persons covered for reporting under Section 143(12) of the Companies Act,

2013• Reporting on frauds in various scenarios

Click here

April 2015

• Overview of key changes and implementation challenges for companies that adopt ICDS from this year

• Overview of the financial reporting and regulatory developments introduced under Indian GAAP during the year ended 31 March 2015

Click here

May 2015

• Salient features of Ind AS 16, Property, Plant and Equipment and Ind AS 38, Intangible Assets

• Key differences between AS 10, AS 26, Ind AS 16 and Ind AS 38• Key aspects of the application guide issued by the Institute of Chartered

Accountants of India (ICAI)

Click here

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 23

Links to previous recordings of VOR

Month/Year Topics Link

June 2015

• Overview of Ind AS 103, Business Combinations• Key differences between AS 14 and Ind AS 103• Overview of key amendments introduced by the Companies (Amendment) Act,

2015

Click here

July 2015

• Overview of Ind AS 110, Consolidated Financial Statements and Ind AS 27, Separate Financial Statements

• Key differences between AS 21, Consolidated Financial Statements and Ind AS 110

• Overview of key relaxations for private companies from certain provisions of the Companies Act, 2013

Click here

August 2015

• Overview of Ind AS 28, Investment in Associates and Joint Ventures, Ind AS 111, Joint Arrangements and Ind AS 112, Disclosure of Interests in Other Entities

• Key differences between AS 23, Accounting for Investment in Associates in Consolidated Financial Statements and Ind AS 28 and between AS 27, Financial Reporting of Interests in Joint Ventures and Ind AS 111

• Overview of key clarifications to IFRS 15, Revenue from Contracts with Customers proposed by the IASB

Click here

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 24

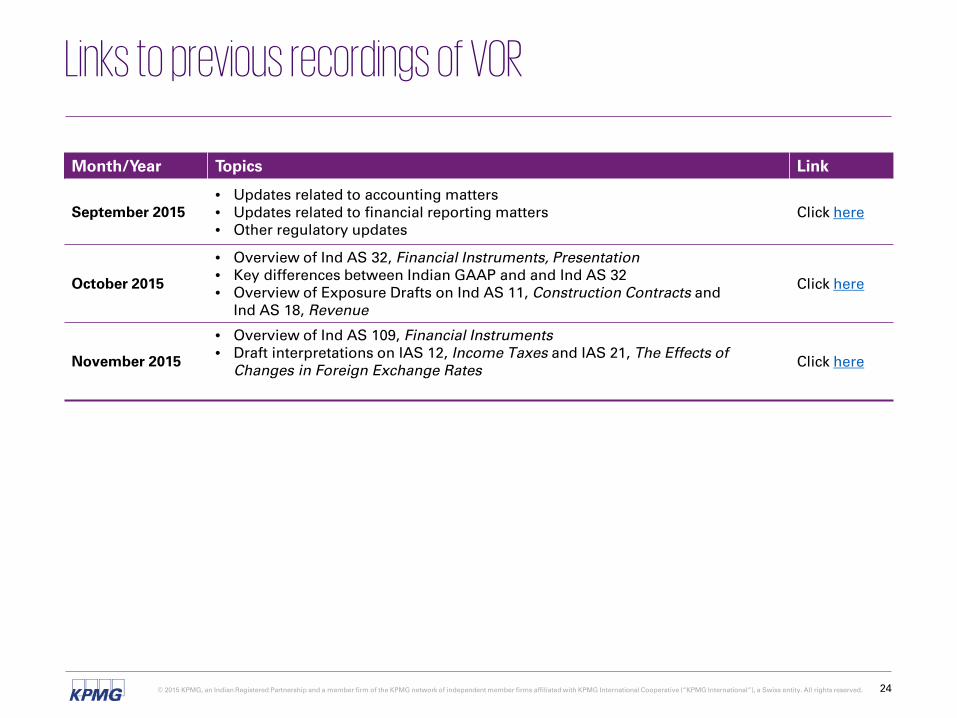

Links to previous recordings of VOR

Month/Year Topics Link

September 2015• Updates related to accounting matters• Updates related to financial reporting matters• Other regulatory updates

Click here

October 2015

• Overview of Ind AS 32, Financial Instruments, Presentation• Key differences between Indian GAAP and and Ind AS 32• Overview of Exposure Drafts on Ind AS 11, Construction Contracts and

Ind AS 18, Revenue

Click here

November 2015

• Overview of Ind AS 109, Financial Instruments• Draft interpretations on IAS 12, Income Taxes and IAS 21, The Effects of

Changes in Foreign Exchange Rates Click here

Q&A

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26

KPMG in India’s IFRS institute

KPMG in India is pleased to re-launch IFRS Institute - a web-based platform, which seeks to act as a wide-ranging site for information and updates on IFRS implementation in India.

The website provides information and resources to help board and audit committee members, executives, management, stakeholders and government representatives gain insight and access to thought leadership publications on the evolving global financial reporting framework.

In addition to proprietary KPMG content, the website provides links to several other sources of information related to IFRS and its implementation. The site can be accessed by all interested parties at no cost. Additionally, the site provides the facility of registering as a member by providing certain minimal information.

To download KPMG content, become registered members of the website by following a few easy steps.

https://www.in.kpmg.com/IFRS

You can reach us for feedback and questions at: [email protected]

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 27

Sources1. MCA notification dated 16 February 2015.

2. Press release by the RBI dated 29 September 2015.

3. Press release by the RBI dated 20 October 2015.

4. Order no. IRDA/F&A/ORD/ACTS/201/11/2015 by the IRDA dated 17 November 2015

5. Discussion Paper (DP) on Convergence to Ind AS in Insurance Sector by the IRDA dated 7 December 2015.

6. Circular no. CFD/CMD/HB/MT/31333/2015 by the SEBI dated 6 November 2015.

7. Circular no. CIR/CFD/CMD/15/2015 by the SEBI dated 30 November 2015

8. Circular no. CIR/IMD/DF1/9/2015 dated 27 November 2015.

9. Circular no. CIR/CFD/CMD/16/2015 by the SEBI dated 30 November 2015.

10. Circular no. CIR/CFD/CMD/12/2015 by the SEBI dated 30 November 2015.

11. Discussion Paper on ‘Review of framework for public issuance of Convertible Securities’ by the SEBI dated 1 December 2015.

12. Discussion Paper on “Exit Offer to Dissenting Shareholders” by the SEBI dated 1 December 2015.

13. Frequently Asked Questions (FAQ) on SEBI (Share Based Employee Benefits) Regulations, 2014 dated 20 November 2015.

14. Exposure Draft of Draft Guidance Note on Some Important Issues Arising from Schedule II to the Companies Act, 2013 by the ICAI dated 9 November 2015.

15. ICAI Journal: The Chartered Accountant for the months September 2015, October 2015, November 2015 and December 2015.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 28

IFRS Notes

Issue 2015/11

The IRDA issues a discussion paper on convergence to Ind AS in the insurance sector

14 December 2015

The Insurance Regulatory and Development Authority of India (IRDA) on 7 December 2015 issued a Discussion Paper (DP) on the convergence to Ind AS in the insurance sector. The Standing Committee on Accounting Issues (SCAI) of the IRDA has recommended a draft of the regulations on financial statements and auditors’ report which are compliant to Ind AS. The DP is open for comments.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 29

Topics discussed in AAU and First Notes

Issue no. 4/2015 | Pharmaceutical

• Revenue recognition in the pharmaceutical sector – Key considerations

• Potential impact of Ind AS on pharmaceutical sector

• Survey analysis

• Ind AS 108, Operating Segments and its impact on the pharmaceutical sector

• Business combinations and accounting for intangibles

• ICDS – Potential impact on the pharmaceutical sector

• Export benefits to pharmaceutical sector

• GST – A sweet pill for the Indian pharmaceutical sector

• Tax deductibility of business promotion expenses

• Regulatory updates

SEBI provides relaxation to listed entities for filing financial results under IFRS

1 December 2015

Under Section 143(3)(i) of the Companies Act, 2013 (2013 Act), an auditor is required to state in their audit report whether the company has an adequate Internal Financial Controls (IFC) system in place and the operating effectiveness of such controls. Explanation to Section 134(5)(e) of the 2013 Act defines IFC to include policies and procedures adopted by the company for ensuring orderly and efficient conduct of its business, accuracy and completeness of the accounting records, and timely preparation of reliable financial information. The ICAI issued a Guidance Note in November 2014. This guidance note was revised subsequently and the ICAI issued a revised ‘Guidance Note on Audit of Internal Financial Controls Over Financial Reporting’ (Guidance Note) on 14 September 2015. Our issue of First Notes provides an overview of the Guidance Note issued by the ICAI.

Accounting and

Auditing Update(AAU)

First Notes

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 30

Others

Coming up next

January 2016

New issue of:

• Accounting and Auditing Update

• First Notes

• IFRS Notes

Missed an issue of Accounting and

Auditing Update?

Missed an issue of First Notes?

Download from www.kpmg.com/in

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 31

Thank You

The views and opinions expressed herein are those of the presenters to the topics covered in today’s ‘Voices on Reporting’ knowledge sharing call and do not necessarily represent the views and opinions of KPMG in India. The information contained in the slide pack is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Nirav PatelDirectorAccounting Advisory ServicesKPMG in IndiaE-mail: [email protected]

KPMG in India contacts:

Feedback/queries can be sent to: [email protected]