Magic-Fintech roundtable report

55

FINTECH REIMAGINED: POWERED BY:

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Magic-Fintech roundtable report

FINTECHREIMAGINED:

P O W E R E D B Y :

Fintech Roundtable Report 2021

Foreword

Fintech Case Studies

Challenges in Fintech in Malaysia

Overview of the Fintech Ecosystem

What's Next?

Envisioning The Future of Fintech in Malaysia

TABLEOF CONTENTS

01

05

03

02

06

04

DZULEIRA ABU BAKARGROUP CEO OF TECHNOLOGY PARKMALAYSIA

FOREWORD BY MaGIC

Developments in Malaysian Fintech are altering the country’s financial landscape. It israpidly becoming a central part of the country’s financial sector, with considerablepromise for expansion. For years, Fintech has helped countries overcomedevelopment challenges by improving financial inclusion and lifting people out ofpoverty, empowering vulnerable communities, while also boosting jobs, businessesand ultimately, economic growth.

Digital technologies are reshaping payments, lending, insurance and wealthmanagement – a process that the COVID-19 pandemic has accelerated. Many Fintechcompanies have enjoyed significant growth; and businesses and consumers alike arereaping the benefits of improved global money transfers through Fintech innovations.

There are 440,000 more businesses registered for QR code payments in 2020 - a hikeof 164%; and 131% growth in the number of e-wallet transactions in Malaysia in thesame year, amounting to a record US$600 million. Also 106% growth in the value of e-remittance transactions in 2020. Throughout the same calendar year, Malaysia alonerecorded 2.5 billion online banking transactions representing a 50% jump on a base ofabout 20 million consumers.

The MaGIC Fintech Roundtable report aims to give an overview of the MalaysianFintech ecosystem, diving into the adoption across various Fintech verticals, lookingat some key movements and updates within the local Fintech space.

The MyDigital initiatives blueprint launched by the government in late February 2021is indeed vital to propel Fintech and bridging the gap to place Malaysia as the leadingregional digital economy by 2030. This is imperative especially in the space ofelectronic payments and ecommerce.

While Fintech is pervasive and omnipresent, there are barriers that we need to break.The report raised regulatory matters, low financial literacy, low potential and lack ofincumbent support as among the obstacles impacting the industry.

FOREWORD BY MaGIC Nonetheless, the worldwide Fintech sector is predicted to develop strongly in thefuture years, thanks to the expansion of digital payments and growing investments intech-based financial solutions. Along that line, we see a positive upward trend in thefollowing key areas - the value of internet banking transactions in Malaysia, theinternet banking penetration rate and the value of mobile banking transactions.

Visualising the nation’s future Fintech growth, among the recommended actions aresynchronizing the evolution of our regulatory and supervisory policy instrumentsalong with trends, enhancing local talent base and forming industry-wide partnership.

Also explored are the business models of some remarkable Fintech startups, thenumerous problem statements they are ambitiously tackling, the creative solutionsand their collective effort of making Fintech a success in Malaysia. Budding agri-Fintech startup, Kapitani’s noble vision of success for Malaysia is empowering thefinancial literacy of our smallholder farmers by way of open access to knowledge,capital and resources to unlock greater market and investment opportunities. Pod, inthe meantime is offering solutions by way of enabling microfinancing opportunities tobe accessible, encouraging saving behaviour with direct debit. Their app allows usersto track their expenses and transfer their leftover change into savings to progresstowards their saving goals. While the more-established MoneyMatch provides lowcost, simple and transparent international money transfer services, and is redefiningthe way people send money abroad by eliminating hidden fees and vague processes

We seek to establish a pool of companies that allow us to draw greater socioeconomicvalue, which is sustainable and offers shared success for the public, business, andgovernment, by accelerating the journey from innovation to commercialisation. Webelieve that commercialisation will increase the availability, affordability, andaccessibility of inventions.

To achieve this purpose, the Malaysian Research Accelerator for Technology andInnovation (MRANTI) is established to generate higher Return on Ideas (ROI). MRANTIa consolidation of MaGIC and Technology Park Malaysia, two strong agencies underMOSTI, and will operationalise in 2022.

Moving forward, we anticipate a rise of interconnected, inclusive and sustainableplatforms offering a variety of solutions catering to different needs, providing a one-stop, integrated experience. We are optimistic Fintech is poised for further growth,and we hope to grow alongside it.

We are also thankful for the support of 1337 Ventures for helping us make thispossible.

BIKESH LAKHMICHANDFOUNDER AND CEO OF 1337VENTURES

FOREWORD BY 1337 VENTURES

Fintech has long disrupted traditional financial systems, with innovative servicesbenefiting customers, end users and investors across different business sectors andvalue chains. Amidst the COVID-19 pandemic, we have also witnessed great resilienceand growth in Fintech, both globally and within the ASEAN region.

Yet, the financial reality is that the pandemic has been a great challenge for manyMalaysian SMEs and individuals. Making up almost 98% of Malaysian businesses, SMEshave been hit hardest by COVID-19. Further, the previous B40 income group has nowexpanded to include the B50. In this post-pandemic era, there is no doubt that SMEdigitalisation and financial inclusivity are few of the key areas for Fintech stakeholdersto prioritise on and develop. How might we, as a nation, build solutions that prioritiserecovery and financial resilience for businesses and individuals alike?

The Fintech Reimagined: Roundtable Report 2021 looks at Malaysia’s Fintechecosystem and explores 3 broad themes — Fintech Innovation, the FintechRegulatory Landscape and Fintech Funding and Investments. We brought togetherFintech players from different organisations and utilised Design Thinkingmethodologies to identify the different perspectives and insights, dissecting thechallenges faced by each of them, as well as potential solutions that can beimplemented. The report also features notable Malaysian Fintech startups that havemade waves in society in their own unique ways, be it via financial inclusivity, SMEempowerment, or even financial health and literacy.

We encourage more aspiring startups and entrepreneurs to be innovative and stepup to solve pertinent problem statements within the Fintech space. We believe thatcollectively, we can pave the way for greater and more sustainable Fintechdevelopment in Malaysia.

As Malaysia continues to recover from the pandemic, it is hoped that Fintech willcontinue to be one of the key enablers in rebuilding our country’s economy. We hopethat you find this report beneficial and catalysing as we move towards a moredeveloped and inclusive society.

OVERVIEWOF THEFINTECHECOSYSTEMDisruption, Innovation, Inclusion and Transformation — Fintech isundoubtedly a game changer both globally and within Malaysia,with new technology revolutionising the concept of financialservices while disrupting traditional business models. Despite theCOVID-19 pandemic, we have witnessed industry resilience andadaptibility, as well as strong growth in all types of digital financialservices globally.

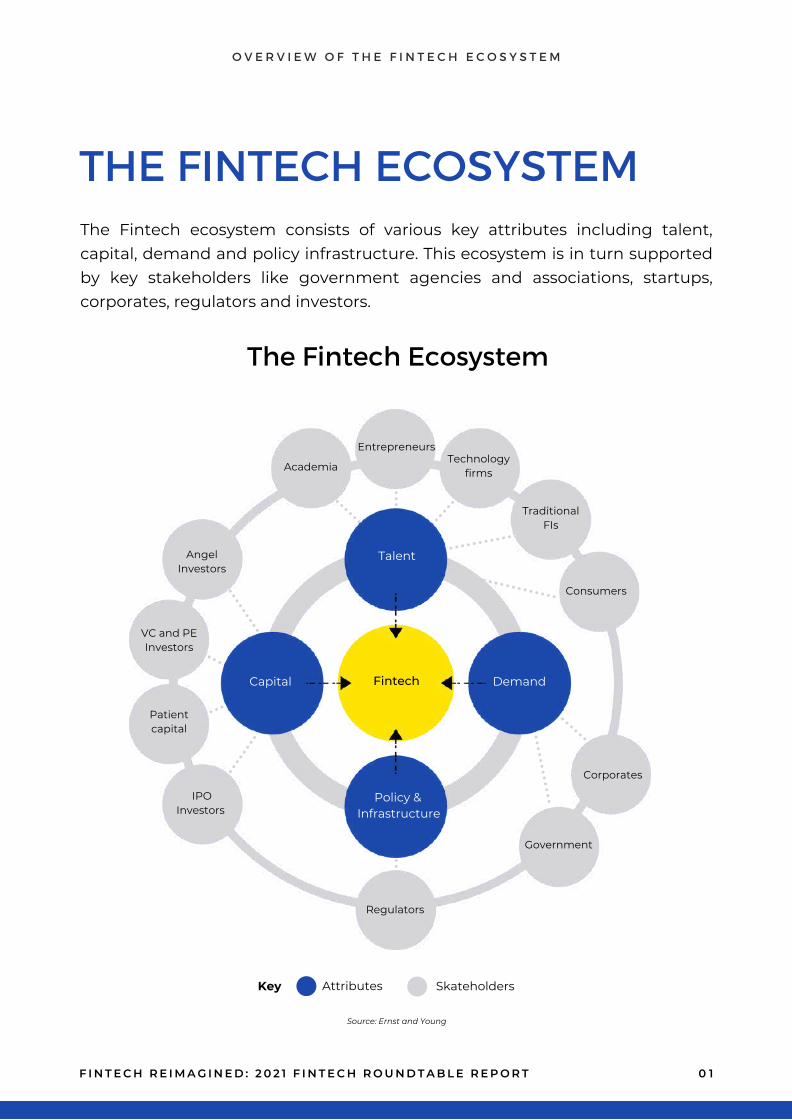

THE FINTECH ECOSYSTEM

Source: Ernst and Young

Key SkateholdersAttributes

Fintech

Talent

Demand

Policy &Infrastructure

Capital

Academia

Entrepreneurs Technology

firms

TraditionalFIs

Consumers

Corporates

Government

Regulators

IPOInvestors

Patientcapital

VC and PEInvestors

AngelInvestors

O V E R V I E W O F T H E F I N T E C H E C O S Y S T E M

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 0 1

The Fintech ecosystem consists of various key attributes including talent,capital, demand and policy infrastructure. This ecosystem is in turn supportedby key stakeholders like government agencies and associations, startups,corporates, regulators and investors.

The Fintech Ecosystem

O V E R V I E W O F T H E F I N T E C H E C O S Y S T E M

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 0 2

Malaysia Going Digital

WHY IS FINTECHINCREASINGLYRELEVANT TODAY?

Over the years, demand for digital finance and various other forms of financialtechnology products and services has increased tremendously. According tothe 12th Malaysia Plan, the digital economy is expected to contribute 25.55% tothe country's gross domestic product (GDP) by 2025. Further, the government-launched MyDIGITAL or the Malaysia Digital Economy Blueprint aims totransform Malaysia into a digitally-driven nation and a regional leader in digitaleconomy.

Economic and Financial InclusivityFintech, with its scalable accessibility, is an important tool to help alleviatepoverty and enable economic mobility for the underserved community andlow-income individuals who are often financially excluded and sidelined. WhileMalaysia has a total employment of 15.37 million, only half contribute to theEmployees Provident Fund. Further, more Malaysians are slipping into the B50bracket, and Malaysia's absolute poverty rate has spiked to 8.4% in 2020 due tothe effects of COVID-19. Financial inclusion through Fintech is key to tacklingthese economic divisions.

Financial Wellness Through InnovationNew technologies are allowing companies and financial institutions to servecustomers in novel ways. More innovative solutions across different verticalshave emerged in the market and are playing a substantial role in improvingthe day-to-day lives of people, be it in the space of banking and payments,insurance, wealth and more.

O V E R V I E W O F T H E F I N T E C H E C O S Y S T E M

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 0 3

Low Financial Literacy

WHAT IS HOLDINGMALAYSIA’S FINTECHECOSYSTEM BACK?

In general, we notice a lack of financial literacy among Malaysians to navigatethe complicated financial landscape. Bank Negara Malaysia’s FinancialCapability and Inclusion Demand-Side Survey 2018 highlighted few financialliteracy concerns among Malaysians, which includes level of financialknowledge, saving and budgeting, readiness for unexpected life events, andplanning for retirement.

Profit vs. PurposeThere often exists an emphasis on profit rather than purpose in the industry. Aslow-income individuals are not seen as a profitable market segment by manycompanies, they are often excluded from targeted product development.

Lack of Incumbent SupportFintech startups need to collaborate with existing incumbents to gain marketparticipation. Albeit present, there seems to be insufficient incumbentparticipation in Fintech innovation, for instance via the setting up ofaccelerators and incubators or even internal innovation initiatives. A healthyecosystem is one that encourages collaboration and innovation between bothtraditional financial institutions and new startups.

Regulatory ChallengesThe Fintech industry is one of the most highly regulated sectors, justifiably sodue to its scope, scale and dynamism. However, this has led to an array ofchallenges for Fintech companies, such as the speed and pace of regulatoryclarity i.e. turnaround times from regulators, which may impede thegeneration of valuable Fintech innovations and even investments.

Global Fintech Market

USD7301.78 billion in 2020

Global Fintech Market

USD7301.78 billion in 2020

O V E R V I E W O F T H E F I N T E C H E C O S Y S T E M

0 4

The Global Fintech MarketIn 2020, the global Fintech market was valued at $7301.78 billion with aprojected CAGR of 26.87% during the forecast period of 2021 - 2026. With therise of digital payments as well as increased investments in technology-basedfinancial solutions, the global Fintech market is expected to experience healthygrowth in the coming years.

Global Fintech funding in 2021 has surpassed 2020 totals by 96%, reaching atotal funding amount of $94.7 billion in 2021 YTD from a mere $48.4 billion in2020.

Source: CB Insights State of Fintech Q3 2021

2015 2016 2017 2018 2019 2020 2021YTD

$21.8B $23.4B$28.8B

$52.9B$46.5B $48.4B

$94.7BFunding

3,549Deals

1,9942,307

2,868

3,502 3,510 3,443

As for funding in Asia, Fintech funding has gone up by 51% in 2021 YTDcompared to the 2020 total, which is a positive sign for continued Fintechinvestment in the region.

Source: CB Insights State of Fintech Q3 2021

2015 2016 2017 2018 2019 2020 2021YTD

$7.8B

$12.0B $10.9B

$28.6B

$12.7B$10.5B

$15.8BFunding

881Deals

471582

734

1,014

936877

Global FintechMarket

USD7301.78 billionin 2020

CAGR 26.87% from 2021-2026

Source: Global FinTech Market, By Technology, By Service, By Application, By Region, Competition Forecast & Opportunities, 2026

O V E R V I E W O F T H E F I N T E C H E C O S Y S T E M

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 0 5

SUMMARY OF FINTECHADOPTION IN MALAYSIA

Here is a brief overview of Malaysia’s Payment and Digital Payment Statistics:

Source: Bank Negara Malaysia, World Bank Global Financial Inclusion Data, Statista Digital Market Outlook for Fintech Jan 2021

85.3%

(Jan 2021)

Has an Account with aFinancial Institution

140.5%

(Sept 2021)

Debit CardOwnership

29.3%

(Sept 2021)

Credit CardOwnership

119.5%

(Sept 2021)

Internet BankingPenetration

69.7%

(Sept 2021)

Mobile BankingPenetration

38.8%

(Jan 2021)

Makes Online Purchasesand/or Pays Bills Online

13.1 million

(Jan 2021)

Number of PeopleMaking Digitally Enabled

Payment Transactions

$12.3 billion

(Jan 2021)

Total Annual Revenueof Digitally Enabled

Consumer Payments

$940

(Jan 2021)

Digital Payments:Average Value of Annual

Transactions Per User

Global Fintech Market

USD7301.78 billion in 2020

O V E R V I E W O F T H E F I N T E C H E C O S Y S T E M

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 0 6

From 2019 to 2020, we see that the value of internet banking transactions inMalaysia have increased from RM836.8 billion to RM1060.9 billion. The internetbanking penetration rate has also increased from 97.6% in 2019 to 112.5% in2020, and subsequently 119.5% as of September 2021. As for the value of mobilebanking transactions, its value has increased from RM203.8 billion to RM458.9billion in 2020. The mobile banking penetration rate has seen a rise from 52.9%in 2019 to 61.8% in 2020, and 69.7% in 2021.

Source: Bank Negara Malaysia, Statista 2021

2016 2017 2018 2019 2020

494.4

622.1

737.8836.8

Value of internet banking transactions by private persons in Malaysia from 2016 to2020 (in billion Malaysian ringgit)

1060.9

Val

ue

in t

ran

sact

ion

s in

bill

ion

Mal

aysi

anri

ng

git

Global Fintech Market

USD7301.78 billion in 2020

Source: Bank Negara Malaysia, Statista 2021

2016 2017 2018 2019 2020

36.2 50.7

100.1

203.8

Value of mobile banking transactions in Malaysia from 2016 to 2020 (in billionMalaysian ringgit)

458.9

Val

ue

in t

ran

sact

ion

s in

bill

ion

Mal

aysi

an r

ing

git

Global Fintech Market

USD7301.78 billion in 2020

O V E R V I E W O F T H E F I N T E C H E C O S Y S T E M

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 0 7

When it comes to electronic money transactions, the total value has increasedfrom RM18.2 billion in 2019 to RM29.6 billion in 2020, a 63% increase.

Source: Bank Negara Malaysia, Statista 2021

2016 2017 2018 2019 2020

7.79.1

11

18.2

Value of electronic money transactions in Malaysia from 2016 to 2020 (in billion Malaysian ringgit)

29.6

Val

ue

in t

ran

sact

ion

s in

bill

ion

Mal

aysi

anri

ng

git

According to a study conducted by VISA, an average of 85% of consumersacross Southeast Asia embrace an array of cashless payment methods. Whencomparing against the Southeast Asian average as well as other SoutheastAsian countries, it is apparent that Malaysia ranks high in its cashless paymentsadoption rate, coming 2nd behind Singapore at 96%.

0% 25% 50% 75% 100%

Singapore

Malaysia

Indonesia

Vietnam

Philippines

Thailand

Myanmar

Cambodia

Southeast Asia

Source: Visa Consumer Payments Attitude Study 2021

Cashless payments adoption rate in Southeast Asia in 2020, by country

98%

96%

93%

89%

89%

87%

64%

40%

85%

0% 10% 20% 30%

Bank Transfer

Credit Card

Digital/Mobile Wallet

Cash on Delivery

Direct Debit

Debit Card

Other

Charge & Dererred Debit Card

Pre-paid Card

O V E R V I E W O F T H E F I N T E C H E C O S Y S T E M

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 0 8

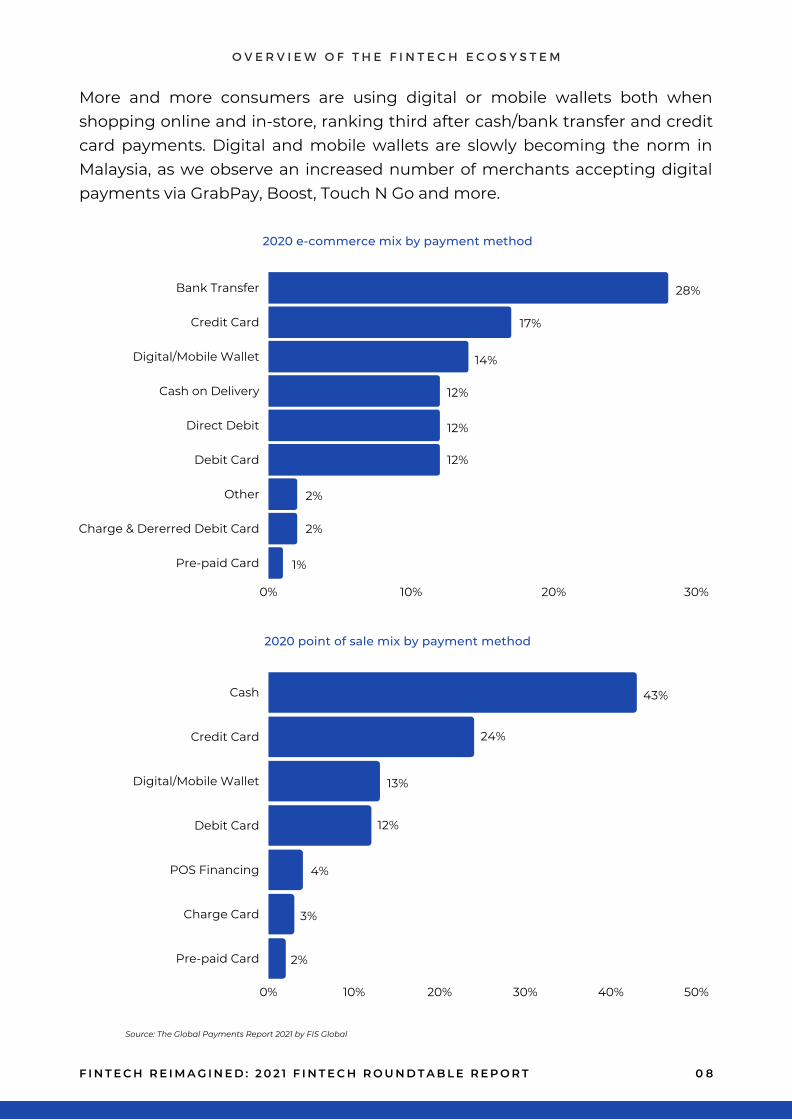

More and more consumers are using digital or mobile wallets both whenshopping online and in-store, ranking third after cash/bank transfer and creditcard payments. Digital and mobile wallets are slowly becoming the norm inMalaysia, as we observe an increased number of merchants accepting digitalpayments via GrabPay, Boost, Touch N Go and more.

0% 10% 20% 30% 40% 50%

Cash

Credit Card

Digital/Mobile Wallet

Debit Card

POS Financing

Charge Card

Pre-paid Card

Source: The Global Payments Report 2021 by FIS Global

2020 e-commerce mix by payment method

28%

17%

14%

12%

12%

12%

2%

2%

1%

2020 point of sale mix by payment method

43%

24%

4%

3%

2%

13%

12%

Digital payments Digital remittance Digital Insurance Digital lending

100%

75%

50%

25%

0%

O V E R V I E W O F T H E F I N T E C H E C O S Y S T E M

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 0 9

Certainly, it is apparent that digital merchants in Malaysia are gettingincreasingly tech-savvy and are expected to become even more so in thefuture in their usage of digital financial services such as digital payments,digital remittance, digital insurance and digital lending.

Source: e-Conomy SEA Report 2021

Digital financial services

73%

92%

72%65%

62%

18%

35%

37%

24%28%

41% 34%

% of digital merchants likely to increase or maintain usage ofdigital financial services in the next 1 to 2 years

Likely to maintain same usage Likely to increase usage

O V E R V I E W O F T H E F I N T E C H E C O S Y S T E M

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 1 0

FINTECH ECOSYSTEM MAPHere are the ecosystem in Malaysia contributing towards the developmentand innovation in Fintech:

Source: 1337 Ventures analysis

Here are the different Fintech offerings in Malaysia, categorised by verticals:

Source: Malaysia Fintech Report 2021 by Fintech News Malaysia, Malaysia Insurtech Opportunity Report 2021/2022 by 1337 Ventures

CHALLENGESIN FINTECH INMALAYSIA During the roundtable discussion, our team of moderators andfacilitators utilised Design Thinking methodologies to pry anddiscuss challenges identified from different perspectives byvarying stakeholders. By having discussions cross-stakeholderswith different perspectives, we are able to generate an exhaustiveand wide perspective, primarily, around the themes of Innovation,Funding and Regulation.

According to most stakeholders, one of the biggest challenges of innovation inFintech is the lack of talent in the space. Unlike most fields, Fintech requiresmore than just a stroke of genius. Since Fintech has matured drastically overthe past few years, newer innovations are getting more technical and, in turn,require much more industry knowledge to identify the problems and needs inthe financial world.

According to the Stockholm Fintech Report in 2018, the average age of Fintechcompany leaders in Stockholm ranges between 36 and 40, while the averageCEO is 40 years old. Due to the industry experience required to betterunderstand the needs within this industry, it is no surprise that the averageFintech founder would require extensive knowledge from work experience.

With that being said, talents required to operate a Fintech startup or venturewould also need to be multifaceted in terms of possessing technical skills andalso industry knowledge.

Lack of Talent

1 1F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

C H A L L E N G E S I N F I N T E C H I N M A L A Y S I A

INNOVATION IN FINTECH

Unlike other less regulated industries, Fintech innovation is much riskier. Dueto the uncertainty of regulations, many corporates may take a “sit-and-observe” approach when it comes to new technologies. Due to thisuncertainty, investors may also take a major risk when investing in newtechnologies.

An example often brought up during the roundtable is the rise of Buy-Now-Pay-Later (BNPL) solutions. With its popularity ballooning in ourneighbourhood in Singapore, according to Finder, over a quarter ofSingaporeans admit to being worse off financially due to a BNPL mistake. Dueto this, regulators in Singapore are reviewing this new business model overconcerns of rising consumer debt. In Malaysia, Bank Negara is also leadingefforts to regulate BNPL schemes in 2022 via the Consumer Credit Act.

With this, new startups, corporates, or even investors may find it hard toengage in new cutting-edge technology or business models.

1 2F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

High Risk

C H A L L E N G E S I N F I N T E C H I N M A L A Y S I A

The high risk inherent in exploring newFintech innovation is attributed to theresponse rates by regulators. Somestakeholders mention that upon seekingadvice from regulators prior to exploringFintech innovation, regulators often taketime to respond to requests or changes.

It is unfair, however, to put the blame solelyon regulators, when such frontiertechnologies may have unforeseenconsequences. For instance, the initial goal ofthe BNPL model is to provide consumerswithout a credit score the opportunity tocredit, and, slowly, build up their own creditvia an alternative credit scoring method. Thisfinancial inclusion dream, however, onlyshowed adverse consequences 5 years afterits initial introduction. It is, therefore, difficultfor regulators to provide quick responses tothese frontier technologies that may requiremonths, or years, to study before providing adefinitive framework or response thatensures the safety of all stakeholdersinvolved.

To potentially accelerate regulatory responserates, industry players, together withregulators, must work together tounderstand and map out the key risks andimplications of new technologies andbusiness models. As regulators become moreinformed earlier, holistic and comprehensiveframeworks may be developed at a morereasonable pace for the market.

1 3F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

Regulatory ResponseRates

C H A L L E N G E S I N F I N T E C H I N M A L A Y S I A

Startups identified a lack of investment opportunities in Malaysia. According toinvestors and government agencies, this is because of the lack of investmentappetite in Malaysia due to limited potential. Fintech solutions typically requiremore funds than ventures in other sectors especially when it comes tolicensing requirements. It is noteworthy that this creates a vicious cycle — dueto lack of investment opportunities in Fintech, entrepreneurs steer away fromFintech innovations. However, this in turn leads to a lack of investmentopportunities in Malaysia.

Corporates, on the contrary, raise an interesting point — how can it be thatinvestors are claiming a lack of potential in Malaysia due to its small populationcompared to its neighbours (Indonesia with 273 million population, Thailandwith 69 million population), when Singapore, with only 20% of Malaysia’s totalpopulation, is able to receive more investment compared to Malaysia?

Lack of Investment Appetite in Malaysia dueto Limited Potential

1 4F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

FINTECH FUNDING ANDINVESTMENTS

C H A L L E N G E S I N F I N T E C H I N M A L A Y S I A

Another main concern raised bystartups is that the funding processis highly complex and time-consuming. An example of this is theSimple Agreement for Future Equity(SAFE) document. This commoninvestment vehicle, utilised by manyinvestors overseas, is a simplemethod to provide earlyinvestments to startups, especiallywhen the valuation of a startup atsuch a stage can be uncertain.Though, this has not been acommon practice in Malaysia untilrecently — Malaysian entrepreneurshad to play keep-up to betterunderstand this new instrumentwhile investors have to furtherunderstand its mechanics beforeutilising the SAFE in their owninvestments.

Even when it comes to typical termsheets and shareholders'agreements, many startups stillstruggle to understand certainterminologies and legal jargons.Furthermore, startups who areraising capital for the first time areunaware of fundraising norms whenit comes to timeline, due diligencerequirements, and more, furtherexacerbating the complexfundraising process for all partiesinvolved.

Complicated FundingProcesses

1 5F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

Another problem noticed, primarilyby government agencies, is thatMalaysia’s funding ecosystem isinherently flawed. Out of the manyfunding means in Malaysia, only ahandful are focused on the early-stage — to make matters worse,only 1-2 are truly of pre-seed stage.Unlike other countries, where mostVCs dwell in the early stages, it isharder to kickstart a Fintech idea inMalaysia through the support ofexternal fundings.

Due to the makeup of this currentVC funnel, later-stage VCsexperience a lack of deal flow asentrepreneurs are deterred fromboth pursuing Fintech ventures inthe first place and subsequentlyraising further capital at a later-stage.

Lack of Funding forEarly-stage Startups

C H A L L E N G E S I N F I N T E C H I N M A L A Y S I A

During the roundtable discussion, many stakeholders were of the opinion thatexisting regulations do not reflect or serve the current technology trends andenvironment. Furthermore, Fintech has evolved and penetrated beyond justthe finance industry, as we see it being applied and utilised in adjacentindustries such as Proptech and Agritech. Instead of providing dedicatedregulatory frameworks for each sector, current regulations are insteadstandardised across all verticals.

This is not a niche problem faced only by startups. With more to lose thanstartups, it is also harder for corporations to experiment with and implementnew technologies. Despite having internal innovation units, they are oftencrippled by slow decision-making processes, multi-layer approvals and longprocessing times. This further hampers potential collaboration betweenstartups and corporates, as startups may not have the liberty of waitingupwards of a year for the corporate’s approval process.

An example of such risk-adversity can be seen with cloud computing — whilemany Fintechs operate with a cloud-first approach for their solutions andstorage management, many corporates shied away from this technology dueto a previous regulation that required data to be stored in Malaysia. While thisregulation has since been amended to accommodate the use of cloudcomputing, it highlights the active role that regulators play in workingtogether with industry players in understanding the risks associated withadoption of new technologies. It is thus imperative that industry players workclosely with regulators in developing frameworks to accommodate the useand mitigate the risks arising from adoption of new technologies.

Regulatory Adaptation is an Iterative Process

1 6F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

REGULATIONS

C H A L L E N G E S I N F I N T E C H I N M A L A Y S I A

For those new to the Fintech scene, navigating through regulatory hurdles canbe a very complex process. Despite this, it is imperative for startups tounderstand these regulations. Founders who do not have the time orexperience to comb through regulation documents will have to outsourcethese professional services to lawyers and shariah advisors. This, however,results in a Catch-22 — early-stage startups that have yet to generate revenueor prove their applicability to investors do not have the funds to hireprofessional services; on the other hand, they require the expertise ofprofessional services prior to launching, generating revenue or testing theirproduct-market fit.

There are support structures currently available for founders, such as the BankNegara Sandbox, which provides startups the opportunity to operate in a“sandbox” environment, and MDEC’s Fintech Booster, which provides startupswith the access to professional services required to navigate through theregulatory environment in Malaysia. Though, it is agreed by participants thatmore can be done to assist founders in overcoming regulatory barriers.

Difficulty in Navigating through RegulatoryHurdles

1 7F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

Several participants from government agencies and associations, however,disagree with the problems stated above. According to them, the purpose ofregulation has never been to hamper innovation — it has always been toprotect stakeholders, especially users of financial services.

Despite the availability of resources for startups, government agencies,regulators, and associations argued that the problem lies in the lack ofunderstanding from the startup founders themselves — when prodded furtherin terms of their business model and value proposition to users, many foundersare said to be unable to elaborate or provide clarifications.

Fintech Startups do not Understand theirValue Proposition clearly

C H A L L E N G E S I N F I N T E C H I N M A L A Y S I A

ENVISIONINGTHE FUTUREOF FINTECHIN MALAYSIAIn response to the various challenges identified in Fintechfunding, regulation, and innovation, ecosystem players haveidentified several wish list items as well as potential opportunitiesthat can be leveraged. Here are some key highlights from theroundtable discussion.

Open Innovation

INNOVATIONIN FINTECH

1 8

Corporates, government agenciesand associations can look intoorganising more innovationbootcamps to facilitate public andprivate sector organisations inchurning out problem statements.There often seems to be a mismatchbetween startups’ offerings andwhat organisations are looking for.Increased clarity in challengestatements will enable startups towork on specific ideas or solutionsthat match the pain points of theseorganisations, while also increasingthe commercialisation rates of thesestartups.

Another way would be to incentivisecorporates to partner with orallocate resources to Fintechstartups. This can be done throughtax rebates, access to matchingfunding and more to enable thempilot certain initiatives.

E N V I S I O N I N G T H E F U T U R E O F F I N T E C H I N M A L A Y S I A

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

Developing Local Talentsin Fintech

1 9

Talent is crucial to innovation. Stakeholderswish to see an increased emphasis in STEMeducation within the country throughpartnerships and collaborations with highereducation institutions. An existing MDECinitiative, #mydigitalmaker, was launched afew years ago to encourage students to adoptdigital skills such as coding, appdevelopment, and data analytics. This isachieved via programmes such as the#mydigitalmaker Champion Schools, DigitalCompetency Scores (DCS), Education FundNetwork and Digital Ninjas. We wish to seemore of such digital initiatives to enhanceMalaysia’s Fintech talentbase.

E N V I S I O N I N G T H E F U T U R E O F F I N T E C H I N M A L A Y S I A

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

CollaborativeEcosystem

Above all, we wish to see the creation of acentralised platform connecting differentstakeholders and industries — for realinteroperability. This would enable theconvenient exchange of information andresources, as well as collaboration to fosterFintech innovation. One local example wouldbe the FWD API Sandbox which exists as anopen facility for innovation communitymembers to experiment and test theirsolutions in a secure, live environment.

Simple Agreement for Future Equity(SAFE) and Keep It Simple Security(KISS) agreements commonly usedby Silicon Valley startups are stillrelatively new in Malaysia. Startupsthat wish to fundraise via thesemethods in Malaysia will still have tocustomise and localise theseagreements. Participants expressedinterest in the introduction ofsimplified fundraising documentsand/or processes to makefundraising easier and moreaccessible. It is hoped thatregulators can work together withthe early-stage fundraisingcommunity to provide greaterregulatory clarity for suchinstruments.

FINTECH FUNDING ANDINVESTMENTSIncreased Clarityon FundraisingInstruments

To close the funding gap that early-stage startups in Malaysia face,Fintech players wish to see moregovernment co-investment intoearly-stage startups, as mostgovernment investments are merelyfocussed on late-stage startups. Onegood example would be the fund-matching initiative under the DanaPenjana Nasional (DPN), where theMalaysian government will matchRM600 million on a 1:1 basis, of thefunds raised by both foreign andprivate domestic venture capitalists.More government partnershipscould also be established withaccelerators that invest into early-stage startups.

More Co-investments by the Government

2 0F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

E N V I S I O N I N G T H E F U T U R E O F F I N T E C H I N M A L A Y S I A

Industry-wide collaborations supporting Fintech offerings will most definitelyspur the Fintech ecosystem, namely collaborations between prominentplayers such as Bank Negara Malaysia, Securities Commission, Employees’Provident Fund, Lembaga Tabung Haji, Kumpulan Wang Persaraan and more.We do observe a couple of initiatives such as the Fintech Booster and FinancialInnovation Lab, though participants are of the consensus that more industrycollaborations can be done to support Fintech startups and foster closerrelations between startups and ecosystem players.

Industry-wide Collaborations

2 1F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

E N V I S I O N I N G T H E F U T U R E O F F I N T E C H I N M A L A Y S I A

More flexible licensing frameworks canallow startups to test out theirconcepts in a controlled setting. Thisincludes conditional licensingframeworks which limit the applicant’sscope and/or size of activities until theymeet the full requirements. MyMyPayments is a Malaysian Fintechstartup that has recently receivedconditional approval for a large schemeElectronic Money License from BankNegara Malaysia.

Licensing based on tiers has also beenadopted by many Regulators incountries like Korea, Singapore, Indiaand Hong Kong. In India, applicantscan select from two tiers of cooperativebank licenses and six tiers ofcommercial bank licenses.

Flexible LicensingFrameworks

FINTECHREGULATIONS

2 2F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

E N V I S I O N I N G T H E F U T U R E O F F I N T E C H I N M A L A Y S I A

Inspired by the Banking-As-A-Service (BAAS) business model,Fintech startups also hope to be ableto leverage on Financial Institutionsfor their existing licenses. Throughthis model, startups can connectwith banks’ systems directly via APIs,build banking offerings on top of theproviders’ regulated infrastructure,while also reducing their lead timeto market. DBS Bank Singapore is anexample of a bank who has adoptedthis model. “Banking is necessary,banks are not” — with the influx ofnew Fintech startups offering faster,cheaper and more personalisedofferings, we anticipate morefinancial institutions exploring theconcept of BAAS.

Banking-As-A-Service

2 3F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

As most startups and innovationshave overlapping regulating bodies,it is proposed that regulators form aspecialised task force to come upwith recommendations and toformulate new and improvedregulatory frameworks. The taskforce can look into the rules andregulations surrounding banking,securities, asset management,insurance and more to discoverways to promote innovation. It isalso hoped that the regulators canfoster more engagement with theFintech startup community forenhanced regulation literacy.

Regulatory TaskForce

E N V I S I O N I N G T H E F U T U R E O F F I N T E C H I N M A L A Y S I A

FINTECHCASESTUDIESDiscover some notable Fintech startups in Malaysia and exploretheir business models, the industry problem statements they aretackling, their Fintech solution, as well as their founding team’scollective vision of success for Fintech in Malaysia.

FINTECH STARTUPS INMALAYSIA

2 4F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

S t a r t u p D e s c r i p t i o n W h a t p r o b l e m sa r e t h e y s o l v i n g ?

W h a t i s t h e i rs o l u t i o n ?

V i s i o n o f s u c c e s sf o r F i n t e c h i n

M a l a y s i a

D i r e c t L e n d i n gi s a n o n l i n el e n d i n gp l a t f o r m s e t u pt o o f f e r ab e t t e r l e n d i n ge x p e r i e n c e t oc o n s u m e r s i nM a l a y s i a i n af a s t , e a s y ,s e c u r e a n da f f o r d a b l e w a y .

T o i n c r e a s e t h eo p p o r t u n i t y o ff i n a n c i n g f o re v e r y o n e ,e s p e c i a l l y t h eu n d e r s e r v e d ,D i r e c t L e n d i n ga i m s t o m a k ef i n a n c i n g m o r et r a n s p a r e n t a n da f f o r d a b l e t oe v e r y o n e a t a n yt i m e a n da n y w h e r e .

D i r e c t L e n d i n gp r o v i d e s a n e n d -t o - e n d f i n a n c i n gs o l u t i o n w h e r eb o r r o w e r s c a nf i n d , c o m p a r e ,a p p l y a n dr e c e i v e t h ef i n a n c i n g t h a ts u i t s t h e m .

“ A n o p e nb a n k i n g r e g i m et h a t a l l o w sc o n s u m e r s ,e s p e c i a l l y t h eb a n ku n d e r s e r v e d , t oh a v e b e t t e ra c c e s s t o u s e f u la n d a f f o r d a b l ef i n a n c i a lp r o d u c t s &s e r v i c e s . ”

M o n e y M a t c h i sa m u l t i -n a t i o n a lf i n a n c i a lt e c h n o l o g yf i r m f o c u s i n go ni n t e r n a t i o n a lp a y m e n t s ,c o v e r i n g c r o s s -b o r d e r t r a d ep a y m e n t s a n di n d i v i d u a lr e m i t t a n c e s .

M o n e y M a t c hp r o v i d e s l o w -c o s t , s i m p l e a n dt r a n s p a r e n ti n t e r n a t i o n a lm o n e y t r a n s f e rs e r v i c e s , a n d i sr e d e f i n i n g t h ew a y p e o p l e s e n dm o n e y a b r o a d b ye l i m i n a t i n gh i d d e n f e e s a n dv a g u e p r o c e s s e s .

M o n e y M a t c h h a so p t i m i s e d i t st r e a s u r yo p e r a t i o n s w i t hm a c h i n el e a r n i n ga l g o r i t h m s a n di n t e g r a t i o n w i t hb l o c k c h a i ns o l u t i o n s f o rS w i f f e rd i s b u r s e m e n t .T h e y h a v es u c c e s s f u l l ye x e c u t e d o v e rM Y R 2 . 5 b i l l i o n i nt r a n s a c t i o n s .

C o F u n d r i s aP e e r - t o - P e e rf i n a n c i n gp l a t f o r m f o rb u s i n e s si n s u r a n c ep r e m i u mf i n a n c i n g ( I P F )a n d w o r k i n gc a p i t a lf i n a n c i n g( W C F ) . I t i s as a f e r , s m a r t e ra n d m o r er e w a r d i n go p t i o n f o rP e e r - t o - P e e ri n v e s t o r s .

C o f u n d r b r i d g e st h e g a p b e t w e e nr e t a i l i n v e s t o r ss e e k i n g t o i n v e s tw i t h i n l o c a lb u s i n e s s e s a n dt h e b u s i n e s s e st h a t r e q u i r ec a p i t a l . C o f u n d ra i m s t o r e d u c et h e f i n a n c i a lb u r d e n o f S M E sa s t h e y g e t t h en e c e s s a r yp r o t e c t i o n .

W i t h C o f u n d r ,n o t o n l y c a nS M E s c r o w df i n a n c e t h e i rw o r k i n g c a p i t a l ,b u t t h e y c a n a l s oc r o w d f i n a n c e u pt o 7 5 % o f t h e i rb u s i n e s si n s u r a n c ep r e m i u m s .C o f u n d r a c t s a si n t e r m e d i a r yc o n n e c t i n g r e t a i li n v e s t o r s a n db u s i n e s s e s .

“ C o f u n d r b e i n gt h e F i n t e c h ,e n v i s i o n t h ec o n v e r g e n c ew i t h I n s u r t e c h ,w h e r e S M E s c a np r o c u r e g e n e r a li n s u r a n c e a n ds e c u r e f i n a n c i n gf o r t h e i r p o l i c yd i g i t a l l y w i t h i n as i n g l e p l a t f o r m . ”

“ P u t t i n g s a v i n g sb a c k i n t oc u s t o m e r s ’p o c k e t s t h r o u g ht h ed e m o c r a t i s a t i o no f f i n a n c e . ”

2 5F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

S t a r t u p D e s c r i p t i o n W h a t p r o b l e m sa r e t h e y s o l v i n g ?

W h a t i s t h e i rs o l u t i o n ?

V i s i o n o f s u c c e s sf o r F i n t e c h i n

M a l a y s i a

B i l l p l z i s ap a y m e n tp l a t f o r m f o ro r g a n i z a t i o n st o p a y a n d g e tp a i d f a s t a t t h el o w e s t p o s s i b l ec o s t .

F o r g e t a b o u tp r i n t i n g b i l l s o rw a i t i n g f o r t h e mt o g e t d e l i v e r e d .B i l l p l z a i m s t oo v e r c o m e t h ec o s t l y , s l o w a n dn o n -e n v i r o n m e n t a lf r i e n d l y p a p e r -b a s e d b i l l i n gm e c h a n i s m w i t ha d i g i t a l b i l l i n gs o l u t i o n .

B i l l p l z p r o v i d e sa n a r r a y o fs e r v i c e s ,i n c l u d i n g A P I ,B i l l i n g , P a y m e n tF o r m , M a s sP a y m e n t s a n dR e a l T i m eS e t t l e m e n t .

F i n o l o g y i s a ni n n o v a t i v eF i n t e c hc o m p a n y t h a ts p e c i a l i s e s i nl e n d i n g a n di n s u r a n c e t od r i v e c h a n g ew i t h i n t h eb a n k i n g ,p r o p e r t y , a n di n s u r a n c ei n d u s t r i e s .

F i n o l o g y a i m s t os i m p l i f y l e n d i n ga n d i n s u r a n c e ,m a k i n g a c c e s s t of i n a n c i a lp r o d u c t ss e a m l e s s f o re v e r y o n e .

F i n o l o g y o f f e r st w om a r k e t p l a c e s -L o a n s t r e e t w h i c hi s a p e r s o n a lf i n a n c e w e b s i t ea n d p r o d u c ta g g r e g a t o r t h a ta l l o w s u s e r s t oa p p l y f o r l o a n sa n d p u r c h a s ei n s u r a n c et h r o u g h t h ep o r t a l ; L o a n p l u sw h i c h i s am o r t g a g e p r e -a p p r o v a l a n dt r a c k i n gp l a t f o r m f o rp r o p e r t yd e v e l o p e r s .

“ A m o r ec u s t o m e r c e n t r i ci n f r a s t r u c t u r ea n d p r o c e s s e s i nt h e b a n k i n g a n di n s u r a n c e s e c t o r ;a s c e n e w h e r et h e F i n t e c hc o m p a n i e s c a na l s o f i n a l l yo p e r a t e ,i n n o v a t e a n dg r o w w i t hs u s t a i n a b l em a r g i n s .

P o d i s a m i c r o -s a v i n g s a p pt h a t h e l p sy o u n gM a l a y s i a n s a n dg i g w o r k e r sa r o u n dS o u t h e a s t A s i at o l e a d b e t t e rf i n a n c i a l l i v e s .

P o d p r o v i d e sa c c e s s i b l eb a n k i n g t o g i gw o r k e r s a n d t h eu n d e r s e r v e dc o m m u n i t y t oe n c o u r a g es a v i n g b e h a v i o u rf o r b e t t e rf i n a n c i a l s . I ta i m s t o m a k es a v i n g f u n b ye n a b l i n g u s e r st o s a v e m o n e yf o r t h e i rp e r s o n a l i s e dg o a l s , w i t hr e w a r d s a s t h e yr e a c h t h e i rs a v i n gm i l e s t o n e s .

P o d e n a b l e sm i c r o f i n a n c i n go p p o r t u n i t i e s t ob e a c c e s s i b l e ,e n c o u r a g e ss a v i n g b e h a v i o u rw i t h d i r e c t d e b i ta n d a l l o w s u s e r st o t r a c k t h e i re x p e n s e s a n dt r a n s f e r t h e i rl e f t o v e r c h a n g ei n t o s a v i n g s t op r o g r e s s t o w a r d st h e i r s a v i n gg o a l s .

“ E n a b l i n g g i gw o r k e r s t oa c c e s s f i n a n c i a lp r o d u c t s i n af r i c t i o n l e s s ,d y n a m i c a n dp e r s o n a l i s e dm a n n e r ; a l le m b e d d e dw i t h i n t h e i r d a i l ya c t i v i t i e s . ”

" T h e t o p t h r e ee x p o r t s f o rM a l a y s i a s h o u l db e c o m m o d i t i e s ,s e m i c o n d u c t o r s ,a n d l o c a lF i n t e c h . "

2 6F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

S t a r t u p D e s c r i p t i o n W h a t p r o b l e m sa r e t h e y s o l v i n g ?

W h a t i s t h e i rs o l u t i o n ?

V i s i o n o f s u c c e s sf o r F i n t e c h i n

M a l a y s i a

V i r c l e i sM a l a y s i a ' s f i r s tp a r e n t a lc o n t r o l l e dc a s h l e s sn u r t u r i n gs o l u t i o n f o rc h i l d r e n . I ta l l o w s p a r e n t st o g i v e t h e i rc h i l d r e np o c k e t m o n e y ,t e a c h k i d s t os a v e a n d s p e n dr e s p o n s i b l y .

V i r c l e a i m s t ot u r n e v e r yp a r e n t i n t o ad i g i t a l b a n k f o rk i d s a n d e q u i pe v e r y k i d w i t hf i n a n c i a l l i t e r a c yt o l e a r n h o w t os p e n d , s a v e a n de a r n m o n e yr e s p o n s i b i l i t yu n d e r p a r e n t a lg u i d a n c e .

V i r c l e E - w a l l e te n a b l e s p a r e n t st o p r o v i d ed i g i t a l p o c k e tm o n e y t o t h e i rc h i l d r e n w i t hs p e n d i n g r u l e st o f o l l o w .P a r e n t s g e t t ok n o w h o w t h em o n e y i s s p e n t ,a n d i t a l s o g i v e sp a r e n t s p e a c e o fm i n d o n t h e i rc h i l d ’ s n u t r i t i o nc o n s u m p t i o n .

j o m S E T T L E ™ e m p o w e r sb u s i n e s s e s ,e s p e c i a l l yM i c r oB u s i n e s s e s a n di n d i v i d u a l s , t op a ya n d r e c e i v ec r e d i t c a r dp a y m e n t sv i r t u a l l y f r o mc u s t o m e r s o rt e n a n t sw i t h o u tn e e d i n g aw e b s i t e ,p a y m e n tg a t e w a y , o rc r e d i t c a r dt e r m i n a l .

j o m S E T T L E ™ h a s b e e n s e t u pa s a b r i d g e t oc o n n e c t t h ec r e d i t c a r d u s e r st o g o o d u s eb y a l l o w i n gt h e m t o p a y f o re s s e n t i a lb u s i n e s sp a y m e n t s , w h i c hw a s i m p o s s i b l eb e f o r e .C o n s e q u e n t l y ,t h i s p r o v i d e s ac o m p e t i t i v ee d g e f o r m i c r o -b u s i n e s s e s .

W i t h j u s t ap a y m e n t l i n ks e n t t o t h ec u s t o m e r s v i ae m a i l a n d S M S ,c u s t o m e r s c a ns u b m i t t h e i rp a y m e n t s u s i n ga c r e d i t c a r d .E v e r y t h i n g i sd o n e a t t h e t i po f t h e i r f i n g e r sa n d p a y m e n t sw i l l b e r e c e i v e dw i t h i n 3w o r k i n g d a y s .

“ A n e c o s y s t e mw h e r e F i n t e c hp l a y e r s s h o u l db e m o r e o p e n t oc o l l a b o r a t i n gt h a n t o c o m p e t e .T h e B i g B o y ss h o u l d n u r t u r eo r i g i n a li n n o v a t i v es t a r t u pc o m p a n i e sr a t h e r t h a nc o n t i n u es p i n n i n g o f f i t ss t a r t u p . ”

K a p i t a n i i s a na g r i t e c hs t a r t u p t h a ta i m s t oi m p r o v e t h ep r o d u c t i v i t ya n d l i v e l i h o o do f s m a l l h o l d e rf a r m e r s i nM a l a y s i at h r o u g hf i n a n c i a li n c l u s i o n a n dt e c h n o l o g y -b a s e ds o l u t i o n s .

S m a l l f a r m e r sh a v e p o o r a c c e s st o t e c h n o l o g y ,i n n o v a t i o n , a n df i n a n c i a ls u p p o r t . T h e yh a v e n o p r o p e rr e c o r d k e e p i n go f p a s t b u s i n e s sp e r f o r m a n c e ,h i n d e r i n g t h e mf r o m m a k i n gi n f o r m e dd e c i s i o n s t oi n n o v a t e a n do b t a i n f i n a n c i a ls u p p o r t .

K a p i t a n i ’ sb o o k k e e p i n ga p p l i c a t i o na u t o m a t e s t h eb o o k k e e p i n gp r o c e s s ,p r o v i d i n gf a r m e r s w i t h as o l i d t r a c kr e c o r d t o p r o v et h e i rc r e d i t w o r t h i n e s sa n d g a i n a c c e s st o f u n d i n g f o ri n n o v a t i v es o l u t i o n s t oi n c r e a s e y i e l dp r o d u c t i v i t y .

“ E m p o w e r i n gf i n a n c i a l l i t e r a c yo f M a l a y s i a ns m a l l h o l d e rf a r m e r s t ou n l o c k g r e a t e rm a r k e t a n di n v e s t m e n to p p o r t u n i t i e s . ”

" A r e g u l a t o r yi n n o v a t i o n f l o ww h i c h a l l o w sn e w F i n t e c h s t ol a u n c h w i t h o u tl i c e n s er e s t r i c t i o n s ( s a f em a r k e t t e s tp e r i o d ) a n d t h er e m o v a l o fr e s t r i c t i v e c o s t &a c c e s s b a r r i e r sf o r i n s t r u m e n t sl i k e d u i t n o w Q Ro r M y d e b i t w h i c hs e e m s t o b ee x c l u s i v e l yc r a f t e d f o r t h eb i g p l a y e r s . "

2 7F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

S t a r t u p D e s c r i p t i o n W h a t p r o b l e m sa r e t h e y s o l v i n g ?

W h a t i s t h e i rs o l u t i o n ?

V i s i o n o f s u c c e s sf o r F i n t e c h i n

M a l a y s i a

S e n a n g i s a ni n s u r t e c ho r g a n i s a t i o nt h a t e n a b l e sl o w t o m i d d l e -i n c o m ec u s t o m e r s t op u r c h a s ei n s u r a n c e f o rt h e f i r s t t i m ev i a b i t e - s i z e dm i c r o i n s u r a n c e. I t e n a b l e sM S M E s a n di n d i v i d u a l s t oo b t a i n o n e - o f fi n s u r a n c ec o v e r a g e .

T h e m a r k e t f o rm i c r o a n d s m a l le n t r e p r e n e u r s i nM a l a y s i a i sc u r r e n t l y b e i n gn e g l e c t e d b y t h ei n s u r a n c ed i s t r i b u t i o nc h a n n e l . S e n a n ga i m s t o h a v e a l ll i n e s d e t e r r i n gp e o p l e f r o mh a v i n g a c c e s s t oi n s u r a n c e t h a t i sh a s s l e - f r e e ,b l u r r e d , i f n o tc o m p l e t e l ye r a s e d .

S e n a n g p l a y s ab r o k e r r o l eb e t w e e n t h el a r g e i n s u r a n c ep r o v i d e r s a n dt h o s e w h o n e e dm i c r o - c o v e r a g ea n d l e v e r a g e st e c h n o l o g y t om a k e i t w o r kb e t w e e n t h et h r e e p a r t i e s .

" T r a n s f o r m i n g at e d i o u s , s t a i dp r o c e s s o fp u r c h a s i n g a n dc l a i m i n gi n s u r a n c e i n t o am o r e e f f i c i e n ta n d s e a m l e s se x p e r i e n c e f o rf u t u r ep o l i c y h o l d e r s . "

2 8F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

Determined to reshape the negativeperception of credit cards associatedwith irresponsible spending, MazerFintech Sdn. Bhd. has successfullydeveloped jomSETTLE™ andlaunched it in February 2021 toconnect credit card users to gooduse by allowing them to pay foressential business payments, whichwas impossible before.

jomSETTLE™ empowers businesses,especially micro-businesses andindividuals, to pay and receive creditcard payments virtually fromcustomers or tenants withoutneeding a website, paymentgateway, or credit card terminal.With jomSETTLE™, paymentreceiving methods are nowbroadened, especially for SMEs,micro businesses and freelancers.

DEEP DIVE:

Innovative Servicesfor the Underserved

jomSETTLE™ Make Payment— Pay Bills Virtually with aCredit Card

With the jomSETTLE™ MakePayment solution, the underservedSMEs and micro-businesses cannow make Credit Card payments fortheir business expenses to payee orpayment recipients who do not havecredit card receiving facilities. Thiscan include rental, staff salary,property maintenance fee, legal feesand more.

SMEs and micro-businesses will nowhave immediate access to newworking capital through their creditcard without the hassle of goingthrough the conventional route ofapplying for business loans or high-interest cash advances.

The reason why I use the jomSETTLE™ Make Payment solution is because itallows me to use my credit card to settle my payment to the Payee who doesnot accept credit card payments, which helps me to relieve cash flowconstraints. From there, I can manage my cash flow even better.

2 9F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

W h a t i s t h e i rs o l u t i o n ?

Many businesses are still unable toaccept credit card payments due tolow credit card payment volumes,high maintenance costs, andtechnical skills needed.

To encourage the adoption ofpayment receiving methods viacredit cards, jomSETTLE™ hasintroduced the jomSETTLE™Request Payment solution. With thissolution, users can request for creditcard payments by simply sending asecure payment link via SMS oremail to their customers.

jomSETTLE™ RequestPayment — First VirtualCredit Card Terminal

Customers can pay businesses fromanywhere at any time via thepayment link issued. This willinstantly broaden the paymentreceiving methods for manybusinesses.

This eventually enables businessesto secure their payments faster andgain a competitive advantage overtheir competitors solely dependenton cash terms.

When my customer wanted to pay me with a credit card, and Ididn't have a credit card payment receiving facility, jomSETTLE™Request Payment solution came to my rescue.

Image Credit: jomSETTLE

3 0F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

jomSETTLE™ was the firstFintech startup to be approvedunder the Malaysia NationalTechnology and InnovationSandbox (NTIS).

jomSETTLE™ aspires to build aFintech ecosystem surroundingcredit facilities via credit cardswith SMEs, micro businesses,and the gig economy in mind. Inline with this, jomSETTLE™ hasalso been the first Fintechsolution to collaborate with theHalal Development Corporationvia the Halal Integrated Platformto empower the growth of theHalal Industry.

jomSETTLE™ has empoweredproperty transactions byenabling the payment ofproperty-related transactions viacredit card. It is the firstMalaysian Fintech company tooffer such services.

Key Results What’s Next forjomSETTLE™?

Settle Now Pay LaterScheme

jomSETTLE™ is currently engagingin a Proof Of Concept (POC) with abank to offer a first of its kind “SettleNow Pay Later” scheme thatprovides jomSETTLE™ users with aninterest-free instalment plan for alltransactions made on the platform.

jomSETTLE™ Virtual Credit Card forSMEs and Gig Workers

In the long run, jomSETTLE™aspires to launch their very ownSME and Gig Workers VirtualCredit Card. This Virtual CreditCard will give absolute control tothe users by allowing them to setthe category of usage and creditlimit. It also allows the users tomonitor their real-time spendingpattern analysis to avoidoverspending.

3 1F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

Advice to Fintech Startups

To Ask: Approach regulators and government agencies to find out moreabout the different types of support available to you.

To Share: Share your ideas with like-minded individuals and gather valuablefeedback.

Of Rejections: Take every rejection as a lesson to nurture and grow your ideas.

Do not be afraid:

Children at the Heartof its Intervention

3 2F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

S t a r t u p D e s c r i p t i o n

Vircle is established in July 2020 as acloud based SaaS solution that allowsparents to provide digital pocketmoney to their children. The team hadbuilt their own card rails with parentaloversight, allowing children to pay formeals at school using the Virclecashless card.

Vircle helps parents raise financiallysmart and responsible children in anincreasingly cashless and digital world.Their aim is to turn every parent into adigital bank for children and equipevery child with financial literacy tolearn how to spend, save and earnmoney responsibly under parentalguidance.

DEEP DIVE:

Leveraging Technologyto Raise a Financially-Smart Child

to the financial and physicalwellness of their children. If a childreceives money, there are chancesthat they could have spent it onchocolates, sugary drinks, or maybenot on food and not in school at all.On top of that, parents are unsurehow to take on the discussion aboutmoney with their kids. As longchildren are transacting in theanalogue world (cash), there isn’tmuch intervention one can do tonurture kids to be moreresponsible.

With that realisation, Gokula andthe Vircle team figured theyneeded to build a child safetechnology which is legal, does notrequire a parent to walk into a bankto set up an account, and at thesame time, give parents sufficientoversight to make sure theirchildren can be safely introduced tothe cashless world.

For every feature built, the team atVircle looks at its impact on childrenand their parents. Vircle’s founder,Gokula Krishnan first realised somemajor concerns among parents,schools and educators when it comes Image Credit: Vircle

Key Results

3 3F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

W h a t i s t h e i rs o l u t i o n ?

Vircle gives a peace of mind to parentsby enabling parental supervision notonly on their child’s spending, but alsoon their child’s food intake.

Malaysia has one of the highestchildren obesity rates in the region.The Vircle app enables parents to pre-oder their child’s meals from theschool canteen on a weekly, monthlyor on term-basis, providing healthierfood choices for their children. Virclehas also gamified food consumptionwith nutrition scores so that childrenare motivated to make healthier andwiser food choices.

Delving into areas beyond the usualFintech solutions, Vircle aims to be theleading parental control payment andnurturing platform for children aged 5to 18, with measurable impact acrosshealth, financial literacy and characterdevelopment.

Not Your TypicalFintech Solution

Vircle is ready to turn parentsinto digital banks with its up andcoming Malaysia’s first and trulyChild Safe Visa Debit Cardthrough the partnership withFasspay™ and the worldpayments leader VISA™.

In just a year, Vircle hassuccessfully partnered with 21schools in Kuala Lumpur,Selangor, Johor Bahru, Ipoh andPenang.

A year back, Vircle launched the 1stfamily wallet in Malaysia, a feat noone else had attempted — 1 ParenteWallet, multiple dependents,shared balance with super securecontrols to safeguard both theparent’s wallet and child’s usage allrunning on Vircle’s proprietary cardnetwork.

Understand your Play in Fintech —Volume or Value. Volume addressesthe mass market while value play isniche.

Give regulators the benefit of doubt.If something can bring real value,regulators will listen.

Build a rock solid product customerswant and to do that right, find your“why”. There are no shortcuts or half-baked approaches in Fintech.

Advice to Fintech startups

Targeting Gig Workersin South East Asia

3 4F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

S t a r t u p D e s c r i p t i o n W h a t p r o b l e m sa r e t h e y s o l v i n g ?

W h a t i s t h e i rs o l u t i o n ?

Co-Founder and CEO of Pod, NadiaIsmadi saw a gap in creating anddistributing financial products for theunderserved. Inspired by the existingFintech solutions in the UnitedKingdom, United States and China,Nadia was determined to makefinancial services more accessible tothe underserved in the South EastAsian region.

With that purpose in mind, Pod wasestablished as a micro-saving app tohelp young Malaysians, gig workersand the underserved society to leadbetter financial lives.

DEEP DIVE:

Accessible FinancialServices for theUnderserved

Enabling them to get the rightfinancial products at the right timewill help them build financialresilience. Pod’s vision is to help atleast 100 million users across theregion to save, have access tofinancing and build their wealth inthe next 5 years.

Gig workers struggle to get accessto the right products at the righttime, particularly credit due to thelack of credit trail within theexisting financial institutions.However, with Pod, they can nowsave and get access tomicrofinancing as well as otherfinancial products.

To further expand Pod’s offering tothe underserved and gig workers,Pod has teamed up with BankIslam and the United NationsCapital Development Fund(UNCDF) to provide accessiblebanking to gig workers and the B40community. The partnership withBank Islam has benefited users byallowing them to build their credittrail using Pod ShariahMicrofinancing and gain access tomore sophisticated financing fromBank Islam.

Pod aims to level the playing field forthe underserved, particularly gigworkers — a segment World Bankpredicts to make up 70% of theworkforce in Southeast Asia.

Making Saving Funand Rewarding

3 5F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

W h a t i s t h e i rs o l u t i o n ?

Saving as an obligation can be toughbut saving with a purpose can berewarding. Pod allows users to save forspecific reasons or goals, such asmortgage payments, vacations,marriage, and so on. What’s morerewarding is that users will berewarded with discounts and cashbonuses when they reach their savingmilestones. Saving without feeling thepinch is also made possible with Pod’sfeature that allows users to save theirleftover change, at as low as 10 cents,into big goals.

We love it when the gig workersshare with us what goals they havemanaged to save for via Pod. Wehave seen so many goals saved foron Pod from emergency fund todownpayment for a car andmarriage fund.

-Nadia Ismadi, Co-Founder and CEO of Pod

Key Results

Pod has successfully whitelistedover 10,000 borrowers for theShariah microfinancing product byleveraging its alternative creditscoring algorithm.

Saving habits have been reinforcedamong Pod’s users as 85% of itsusers are saving consistently for atleast 7 months towards their savinggoals. Gig workers who were livingpaycheck to paycheck are nowsaving on average RM482 permonth.

Financial literacy among womenusers has also improved asindicated by their savings tractionon Pod (up 32% YTD).

Pod was among the 3 startupswhich were selected by UNCDFduring the MyFintech Week ’19 B40Challenge to develop solutions toimprove the financial health of thelow and moderate-incomeMalaysians.

Building a Fintech venture is slightlytrickier and costlier, both in time andcapital resources, than other techventures due to licensingrequirements and other regulatorysafeguards. So if you can worktogether with other stakeholderssuch as the existing financialinstitutions or other digital platformsto test your core hypothesis orassumptions of your problemstatement, it will help cut your time tomarket and validate your ideas earlybefore losing valuable time applyingfor the licenses to make legalproducts that the market might notwant or is ready for.

3 6F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

F I N T E C H C A S E S T U D I E S

S t a r t u p D e s c r i p t i o n W h a t p r o b l e m sa r e t h e y s o l v i n g ?Advice to Fintech Startups

Image Credit: Pod

WHAT'SNEXT?As the 2022 budget brings forth a “Keluarga Malaysia” approach, itis hoped that the Fintech ecosystem in Malaysia can continue todrive socio-economic development, inclusivity, resilience andrecovery for our nation.

VISION OF SUCCESS FORFINTECH IN MALAYSIA

W H A T ' S N E X T ?

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 3 7

At the Fintech Reimagined: Virtual Roundtable Discussion, we asked Fintechleaders and players all over Malaysia about their vision of success for the futureof Fintech in Malaysia. They revolve around three common themes, mainlyInclusion and Sustainability, Digital and Collaboration.

Inclusionand

Sustainability

“Everyone in Malaysiahaving a credit trailenabling them access tobasic financial services”

“Malaysia as a high-incomenation covering all stratas”

“Purpose-driven Fintechs”

Digital

“Digital servicesenabling betterhuman experience”

“Smart Country”

“Everything connectedand accessible via acommon digital identity”

Collaboration

“Collaboration between banking &Fintech players locally”

“An inclusive ecosystem forregulatory support, talents andfunding”

“Open banking APIs”

“Corporate involvement in funding ecosystem”Here are some key trends and opportunitiesthat will drive Malaysia’s Fintech sector.

TRENDS AND OPPORTUNITIESDRIVING THE SECTORFORWARD

W H A T ' S N E X T ?

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 3 8

Where do we go from here? Moving forward, here are the key focus areas thatwill continue to drive Malaysia’s Fintech sector forward.

The Digital Consumer

MoreFinancial

Inclusivity

The Futureis Digital

The Rise ofEcosystems

ContinuedGovernment &RegulatorySupport

With 81% of all internet users nowconsuming digital services, we havewitnessed the growth of onlineservices such as online shopping,ride-hailing and food deliveries,coupled with the move towardscashless and contactless payments.Fintech is present anywhere andeverywhere as consumersmanoeuvre into a digital way of life.

The DigitalConsumer

3 9F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

As most startups and innovationshave overlapping regulating bodies,it is proposed that regulators form aspecialised task force to come upwith recommendations and toformulate new and improvedregulatory frameworks. The taskforce can look into the rules andregulations surrounding banking,securities, asset management,insurance and more to discoverways to promote innovation. It isalso hoped that the regulators canfoster more engagement with theFintech startup community forenhanced regulation literacy.

More FinancialInclusivity

W H A T ' S N E X T ?

Bank Negara is set to issue digital banking licenses in 2022, making Malaysiathe second country in ASEAN to do so after Singapore. It has received 29applications for a maximum of 5 licenses. Further, with VSure.life becoming thefirst insurtech company in the country to have secured approval from BankNegara to introduce lifestyle digital insurance, we anticipate Malaysia toemerge as one of the regional leaders in Fintech.

The Future is Digital

4 0F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T

W H A T ' S N E X T ?

For years, Fintech companies have struggled with balancing betweeninnovation and regulation. Governments and regulators have also recognisedthe need to build a framework to foster innovation while ensuring complianceto regulations. The Bank Negara Regulatory Sandbox and National TechnologyInnovation Sandbox (NTIS) are examples of platforms providing Fintechstartups with the opportunity to test their products and services in a regulatedmanner.

Continued Government and RegulatorySupport

The Rise of Ecosystems We expect to see more and more local and regional tech companiesexpanding into the Fintech space, as well as increased participation fromtraditional incumbents. These models will be a critical means for companieslooking to expand their service offerings or transform their business models.We also anticipate a rise of interconnected platforms offering a variety ofproducts and services catering to different needs, providing a one-stop,integrated experience.

APPENDIX

REFERENCES

A P P E N D I X

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 4 1

Bank Negara Malaysia. (2021). Payment Statistics: Internet Banking and Mobile Banking Subscribers.https://www.bnm.gov.my/documents/20124/57659/04_Internet+%26+Mobile+banking.pdf

Bank Negara Malaysia. (2021). Payment Statistics: Number of Cards and Users of PaymentInstruments. https://www.bnm.gov.my/documents/20124/57659/03_cards.pdf

CB Insights. (2021). State of Fintech Global Q3 2021. https://www.cbinsights.com/reports/CB-Insights_Fintech-Report-Q3-2021.pdf

DataReportal by Kepios. (2021). Digital 2021: Malaysia. https://datareportal.com/reports/digital-2021-malaysia

Financial Education Network. (2019). Malaysia National Strategy for Financial Literacy 2019 - 2023.https://www.sc.com.my/api/documentms/download.ashx?id=6385977c-bd2c-4612-bda8-9ce6a5961720

Fintech News Malaysia. (2021). Malaysia Fintech Report 2021. https://fintechnews.my/wp-content/uploads/2021/05/Fintech-Report-Malaysia-2021-Fintech-News-Malaysia-x-BigPay.pdf

FIS Global. (2021). The Global Payments Report. https://offers.worldpayglobal.com/rs/850-JOA-856/images/1297411%20GPR%20DIGITAL%20ENGLISH%20SINGLES%20RGB%20FNL11.pdf

Google, Temasek, Bain & Company. (2021). e-Conomy SEA Report 2021 Malaysia.https://services.google.com/fh/files/misc/malaysia_e_conomy_sea_2021_report.pdf

KPMG. (2021). Pulse of Fintech H1 '21. https://assets.kpmg/content/dam/kpmg/xx/pdf/2021/08/pulse-of-fintech-h1.pdf

TechSci Research. (2021). Global FinTech Market, By Technology, By Service, By Application, ByRegion, Competition Forecast & Opportunities, 2026.https://www.researchandmarkets.com/reports/5031390/global-fintech-market-by-technology-by-service

The Star. (2021). Bank Negara to enact Consumer Credit Act in 2022.https://www.thestar.com.my/business/business-news/2021/11/12/bank-negara-to-enact-consumer-credit-act-in-2022

UOB Group. (2021). Fintech in ASEAN 2021: Digital Takes Flight.https://www.uobgroup.com/techecosystem/pdf/fintech-in-asean-2021.pdf

Visa. (2021). Visa Consumer Payment Attitudes Study 2021: Powering The Acceleration of Digital-FirstExperiences. https://www.visa.com.my/dam/VCOM/regional/ap/documents/visa-cpa-report-2021-smt.pdf

LIST OF PARTICIPANTS

A P P E N D I X

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 4 2

AirAsia BerhadAlfie Tech Sdn BhdASEAN Fintech GroupBank Islam Malaysia BerhadBank Pembangunan MalaysiaBerhadBillplzBlocklime Technologies Sdn BhdBoostorder Sdn BhdBursa Malaysia BerhadDigital PenangDirect Lending Sdn BhdFicus Venture CapitalFinologyFintech Association of MalaysiaGrab Financial GroupHariGajiHive SEAHomeCrowd Sdn BhdHong Leong Bank BerhadIzwan & PartnersKapitani Sdn BhdkipleXLAKSANA - Ministry of FinanceMalaysia Digital EconomyCorporation (MDEC)Malaysian Global Innovation &Creativity Centre (MaGIC)Masryef Academy Sdn BhdMBSB BankmicroLEAPMIGHTMr Pay Later

Pay Direct TechnologyPayments Network MalaysiaPodProsper by CGS-CIMBRHB Banking GroupSecurities CommissionSingularSME Bank Malaysia BerhadTune Protect Group BerhadUnited Nations CapitalDevelopment FundUnited Overseas BankUniversiti Teknologi MARAXeraya CapitalZaidIbrahim & Co

ABOUT US

We work with corporations on bespoke accelerators, corporate innovation, anddigital transformation to help individuals and organisations become more resilient.Among our clients are FWD, NTIS, Bank Negara Malaysia, Khazanah Nasional,Telekom, Digi, MDEC, MaGIC, CIMB, RHB, and Maybank, to name a few.

To democratise fundraising, Leet Capital is an Equity Crowdfunding (EFC) platformlicensed by the Securities Commission (SC) that connects firms with angels andregular investors. We created Muru-ku.com, a one-stop portal with 730+ MalaysiaStartups Listed, VC, Grants, Events & Problem Statements to bridge the gapbetween startups, corporations, and the government.

Visit www.1337.ventures to learn more about 1337 Ventures and our ecosystem.

Since its inception in 2014, MaGIC has provided its community of start-ups, investorsand ecosystem players with capacity building programmes, funding opportunitiesand regulatory assistance that impacted more than 100,000 aspiring and seasonedentrepreneurs with an overall value creation of RM1.9 billion.

As an agency under the Ministry of Science, Technology and Innovation (MOSTI),MaGIC facilitates, navigates and enables the ecosystem with the mission ofstrengthening Malaysia’s position as an emerging innovation nation. For moreinformation on MaGIC, please visit mymagic.my.

ABOUT MaGIC

A B O U T U S

F I N T E C H R E I M A G I N E D : 2 0 2 1 F I N T E C H R O U N D T A B L E R E P O R T 4 3

ABOUT 1337 VENTURES

MaGIC discovers and empowers technology startupsand social innovators through creativity, innovationand technology adoption, and develops a vibrantand sustainable entrepreneurship ecosystem inMalaysia.

1337 Ventures is a Malaysian early-stage venture capital (VC)firm. We are Malaysia's first accelerator programme, havingstarted in 2012. Through Leet Academy, we've accelerated thegrowth of over 1,000+ startups from 5 different countries bypioneering the Design Thinking Methodology and DesignSprints in Malaysia.