Leveraging the new organisation: Personal Care - Unilever

41

Unilever 2011 Investor Seminar Istanbul, Turkey 30 th November – 2 nd December 2011

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Leveraging the new organisation: Personal Care - Unilever

Unilever 2011 Investor Seminar

Istanbul, Turkey

30th November – 2nd December 2011

• First Impressions

• Opportunities

• Acquisitions

• Capabilities

What I want to talk about

First Impressions – Personal Care

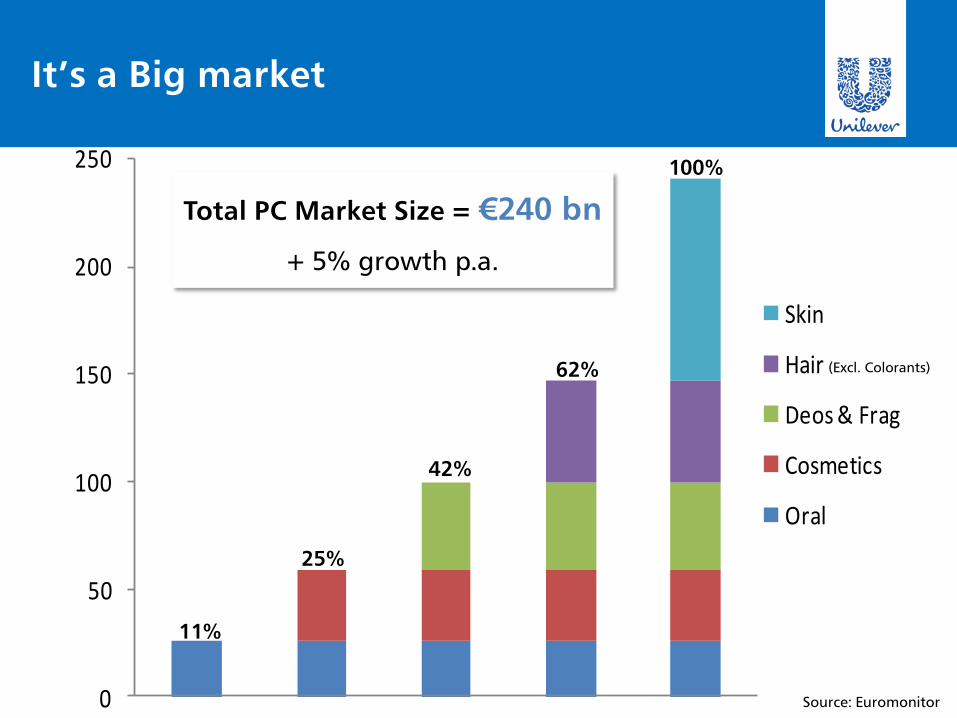

• It’s a BIG market

• We play in only a part

• Our momentum is improving

• We have strong plans for 2012

• And even bigger aspirations for the future.

0

50

100

150

200

250

Skin

Hair

Deos & Frag

Cosmetics

Oral

Total PC Market Size = €240 bn

+ 5% growth p.a.

11%

25%

42%

62%

100%

It’s a Big market

(Excl. Colorants)

Source: Euromonitor

0

5

10

15

20

25

2010 2015

Global Market is Consolidated

55% 54%

% Country Contribution to total PC Market Size (Unilever Categories)

Top 5 50%Next 10 30%

--------------------Top 15 80%

Source: Euromonitor

Premiumisation:Reaching up – Market Premiumisation

MARKET GROWTH OF GLOBAL PERSONAL CARE

P

RIC

E P

RE

MIU

MIS

AT

ION

% of Market2010

38%

22%

21%

18%

Unilever

28%

24%

21%

27%1.5%

2.7%

4.3%

5.9%

<80

80-100

100-120

>120

Source: UL GMI, Q1 2011

Premiumisation:Reaching up – Under Trade in Premium

% Retail Sales by Price Point

% o

f R

eta

il S

ale

s

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

>120

100-120

80-100

<80

Competitor A Competitor BSource: UL GMI, Q1 2011

We are stepping up our Performance

7.9% 7.8%

4.5%

5.6% 5.3%5.8%

11.3%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011

Personal Care

% USG

Source: UL Internal Data

Dove – €3Bn

0

1

2

3

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Launched in USA 1957

€ Bn

World Wide Roll out 1990+

2010 Dove Men+Care & Dove Hair Therapy

2000-2002 Dove Hair Launch & Roll out

2005 DoveGo Fresh Launch

1997-1999 Dove Deos Launch &

Roll out

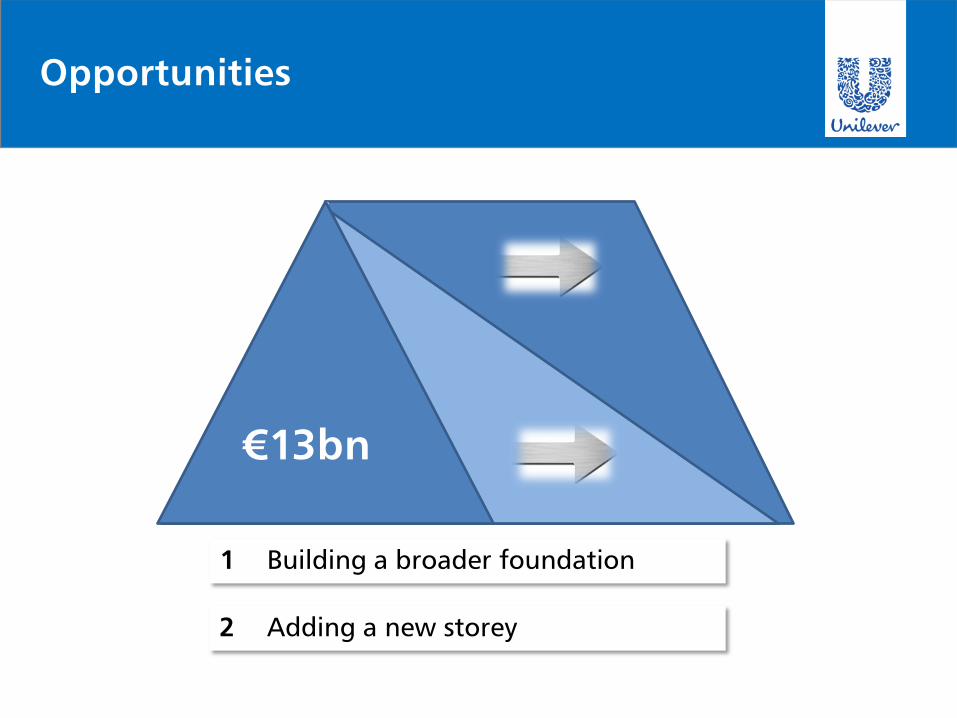

1 Building a broader foundation

Opportunities

2 Adding a new storey

LSM <5

LSM 14+

€13bn

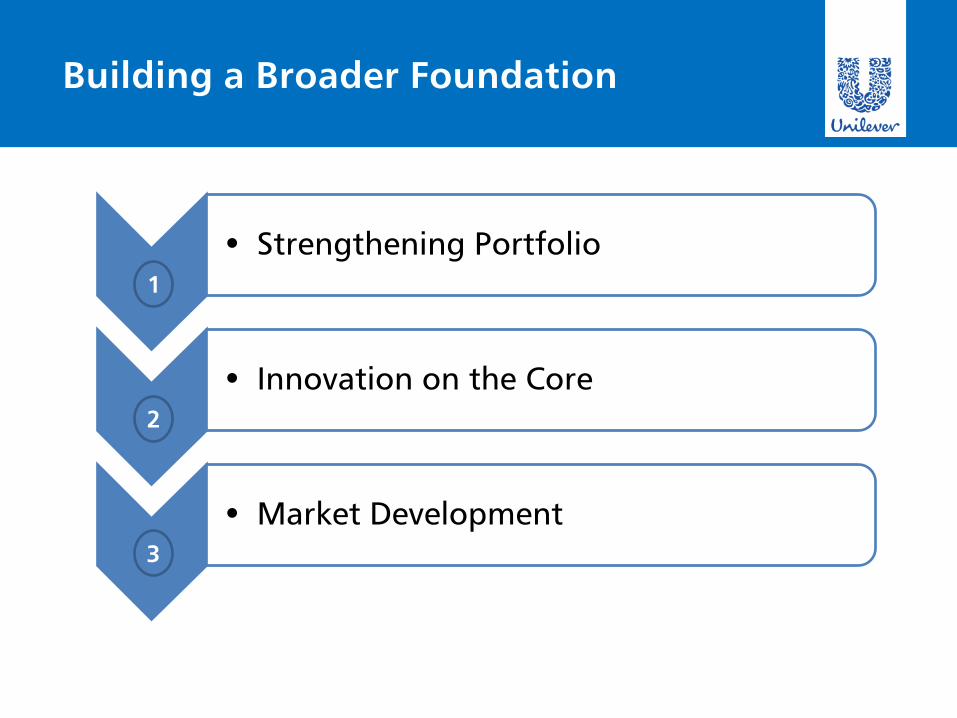

Building a Broader Foundation

• Strengthening Portfolio

• Innovation on the Core

• Market Development

1

2

3

Innovate on the Core: Axe Excite2

Innovate on the Core: Lux2

Innovate on the Core: Dove Hair Damage Therapy

2

Innovate on the Core: White Now2

Innovate on the Core : Radox SPA

2010 NEW 2011

2

Market Development

• More Users

• More Usage

• More Benefits

3

Market Development: Signal Toothpaste

50% of the world’s population do not brush twice a day

3

Market Development: Lifebuoy

70 M people in rural India impacted by the largest private Hygiene Education Programme in the world

3

9.0

11.0

13.0

15.0

17.0

19.0

21.0

23.0

25.0

27.0

29.0

19.4%

18.7%

9.8%

29.0%

Results: Winning in Body Wash China

Develop market via strong portfolio

100

140

Leading Competitor

Leading Competitor

Source: Nielsen Flash Report, Oct’11, UL incl. AC, Dove total (Female + Male), P&G incl. Zest.

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2008 2009 2010 YTD 2010 YTD 2011 L12 wks (Oct'11)

Value Share PW AOC

Unilever Dove Leading Competitor

Va

lue S

ha

re %

Results: Record Shares in US Body Wash

Leading Competitor

Results: South Africa Hair # 3 to # 1

15.3 14.8 15.3

33.2 32.935.0

33.6

38.139.7

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

Q1 Q2 Q3

Unilever Caucasian Hair Value Shares (2011)

UNILEVER PROCTER & GAMBLE L'OREAL COLGATE PALMOLIVE JOHNSON & JOHNSON

12

31

2

3

Acquisition of

Launch of Dove Hair

Launch6 mths early

How?

Leading Competitor

Leading Competitor

Competitor # 2

Competitor # 3

Competitor # 4

Source: Nielsen

Building another storey

• Portfolio & Route to Market

• Premium Innovation

• New Business Development

1

2

3

Premium Innovation

Hair Reborn

2

Premium Innovation2

Premium Innovation2

New Business Development

(1) SALONS: e.g. TIGI, Ponds Institute & Dove Spa

(2) DEVICES: e.g. Dove Hair & Clear Scalp Diagnostic Tools, Pond’s Skin Diagnostics

3

And then there is Men….

€20 Bn Market Opportunity

Acquisitions

•

•

Much more than TRESemmé

3 KPI’s

Over half of our

expected cost synergies achieved

in ‘11

We will exceed 10% synergies in

2012

33

Synergies

Growth

Talent

70%of leaders

accepted key roles

Growing Hair

ShareUS +30 bps

Canada > +100 bps

UK +20 bps

Mexico +10 bps

1

3

2

Market Share Leadership in US

Nielsen All outlet Oct 29, 2011 US

Unilever/AC MFR INCL Tigi, excl VO5, excl Rave

Unilever

Leading

Competitior

Daily Hair Care Value Share

31.6%

28.7%

Leading Competitor

35

Expanding Brands into new markets…TRESemme now in Brazil

On shelf November 1… 175 days from close

36

Expanding Brands into new markets…And into Thailand

Leveraging US Heritage withMotions relaunched in South Africa

37

On shelf November 15… 188 days from close

Kalina Deal to close before year-end

38

Pure Line Black Pearl Silky Hands 100 Recipesof Beauty

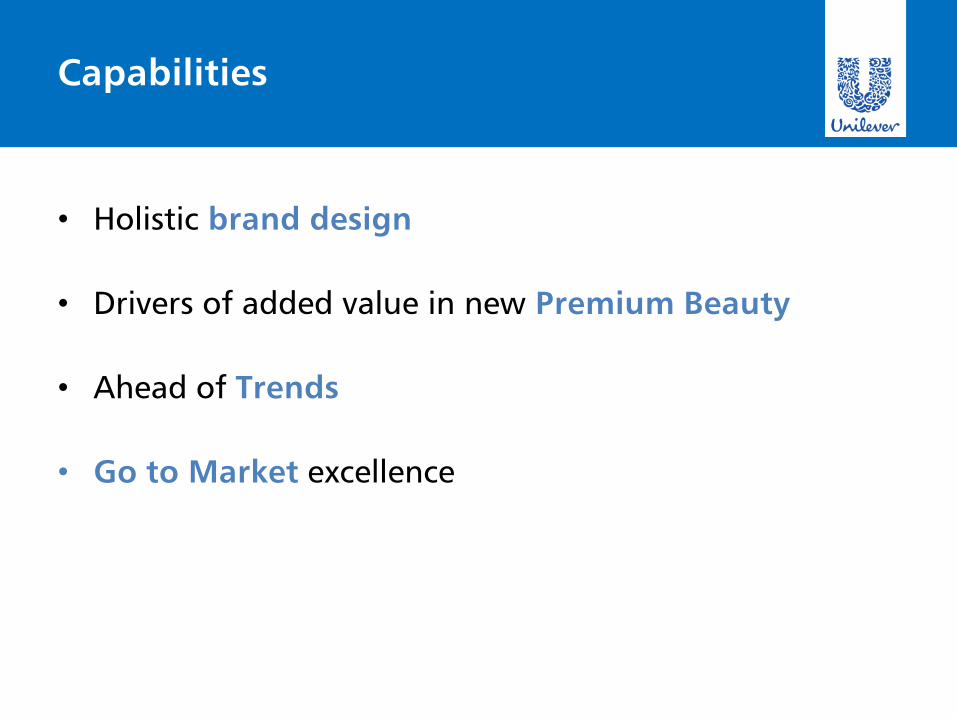

Capabilities

• Holistic brand design

• Drivers of added value in new Premium Beauty

• Ahead of Trends

• Go to Market excellence

First Impressions – Personal Care

• It’s a BIG market

• We play in only a part

• Our momentum is improving

• We have strong plans for 2012

• And even bigger aspirations for the future.

4. Personal Care & Brands VT