KINGDOM OF CAMBODIA The Principal Recipient For The Global Fund to Fight AIDS, TB and Malaria...

124

KINGDOM OF CAMBODIA Nation Religion King MINISTRY OF HEALTH The Principal Recipient For The Global Fund to Fight AIDS, TB and Malaria (GFATM) FINANCIAL GUIDELINES FINANCIAL GUIDELINES Version 4 August 2006 REVISED BY: THE PRINCIPAL RECIPIENT FINANCIAL TEAM Principal Recipient

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of KINGDOM OF CAMBODIA The Principal Recipient For The Global Fund to Fight AIDS, TB and Malaria...

KINGDOM OF CAMBODIA Nation Religion King

MINISTRY OF HEALTH

The Principal Recipient For

The Global Fund to Fight AIDS, TB and Malaria (GFATM)

FINANCIAL GUIDELINES

FIN

AN

CIA

L G

UID

ELIN

ES

VVeerrssiioonn 44

August 2006

REVISED BY: THE PRINCIPAL RECIPIENT FINANCIAL TEAM

Principal Recipient

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MOH/PR Finance Team i

PREFACE

These Financial Guidelines have been developed for use by the office of the Principal Recipient, Ministry of Health, as well as by the approved Sub-recipients, hereinafter referred to as SR), in receipt of grants from the Global Fund, (hereinafter referred to as GF), through the office of the Principal Recipient, (hereinafter referred to as PR), for the purpose of managing their respective financial transactions in the implementation of their approved proposals relating to the GF program to Fight AIDS, Tuberculosis and Malaria.

These Financial Guidelines are intended to assist staff designated to perform finance related functions at the office of the PR as well those working at SRs and sub-sub recipients (hereinafter referred to as SSR).

Adherence to these Financial Guidelines by designated finance staff and managers will facilitate the latter’s tasks, safeguard their accountability, ensure that the correct financial procedures have been applied and that transparency has been demonstrated.

The office of the PR shall distribute these Financial Guidelines to all SRs, and in turn, all SRs dealing with SSRs must ensure that these Financial Guidelines are shared with and used by the SSRs for the implementation of their GF related financial activities for which they have been provided GF funds and delegated authority by the SR to manage such GF financial resources regardless of the amount of money provided to the latter.

Procurement Guidelines have also been developed by the office of the PR that are equally intended to guide the PR, SRs and SSRs in procuring goods and/or services financed from GF grants. Payment for such goods and/or services will therefore have to be made in accordance with these Financial Guidelines noting that when procurement concerns ARVs and/or such types of medicines, these will be purchased by the Ministry of Health as has been determined by the GF. For other types of procurement officials responsible for finance and accounting must ensure that such procurement is processed in strict compliance with the applicable Procurement Guidelines in a rationalized fashion meeting priority targets, effectiveness, transparency leading to an efficient utilization of GF grants.

A number of accounting forms, designed by the office of the PR, have been included in the Financial Guidelines that are intended to facilitate financial reporting by the SRs to PR. Upon receipt and verification of the SRs Quarterly Reports, and/or on more frequent intervals, as may have been agreed upon with specific SRs, the PR will incorporate SRs’ financial data into its own Semi-annual Reports that are required to be sent to the Global Fund in Geneva, Switzerland by the PR.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MOH/PR Finance Team ii

The following is a concise overview on how the GF views the roles and responsibilities of grant recipients and how best it considers fiduciary arrangements can be implemented by the PR, the SR and the SSRs to ascertain overall compliance and accountability and to ensure that minimum standards have been met:

- Assure an efficient flow of funds to all implementing parties with appropriate accountability arrangements to ensure that funds were used for the intended purposes;

- Provide adequate and transparent reporting of programmatic results and financial accountability;

- Ensure transparent, competitive and effective procurement and supply management with appropriate quality assurance mechanisms in accordance with national laws and applicable Procurement Guidelines;

- Ensure effective monitoring and evaluation with appropriate quality control mechanisms;

- Rely on local stakeholders for the implementation of approved programs and management of grant proceeds;

- Promote rapid release of funds to target populations;

- Monitor and evaluate program effectiveness and make decisions for future funding based on programmatic performance and financial accountability;

- As far as possible encourage the use of existing standards and processes in grant recipient entities.

The office of the Principal Recipient has carried-out a financial and procurement management and implementation capacity assessment of approved sub-recipients. The assessment of sub-recipients for future Rounds will also be carried-out to ensure that such sub-recipients fulfill certain minimum requirements before approved proposals are endorsed and first disbursements are released.

Throughout the grant period, the Fund authorizes disbursement of funds to the PR and to the SRs through the PR periodically based on program performance and financial accountability, and arranges for independent external audits, normally on a yearly basis. It is the responsibility of the PR to ensure that effective arrangements are put in place prior to the release of the first disbursement to the stakeholders. The following minimum implementation capacity requirements at the level of the PR and the SRs are:

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MOH/PR Finance Team iii

(a) On Financial Management and Systems: that the PR, SR and SSRs:

(i) Can correctly record all transactions and balances;

(ii) Can disburse funds to legitimate payees and suppliers in a timely, transparent and accountable manner;

(iii) Can support the preparation of regular reliable Financial Statements and Semi-annual Reports;

(iv) Can safeguard the GF assets; and

(v) Are subject to acceptable auditing arrangements.

(b) On Financial Management of Procurement: that the PR, SR and SSRs

(i) Have the accounting and procurement systems that can assure that disbursements for procurement are based upon existing efficient internal control systems;

(ii) Have ensured that the disbursements for supplies and/or services are being processed for services actually received as certified and approved by officially designated officials;

(iii) Have assured that any type of payment for procurement is being processed by the recipient based upon legitimate activities for which budgetary provisions are available;

(iv) That payments for procurements of goods, supplies and/or services are being processed based upon competitive and transparent purchasing practices and that such procurement has been made in compliance with existing Procurement Guidelines.

Results Based Disbursement:

- Results based disbursements means that disbursements of funds is driven by results, and calculated on the PR, SR and SSR’s anticipated expenditure.

- Results based disbursement is a management tool that links programmatic and financial monitoring, and a strategic mechanism to build evidence on results and on a sound utilization of resources.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MOH/PR Finance Team iv

Oversight by Sub-Recipients of Sub-sub-Recipients’ Financial Transactions and SRs’ Periodic Reporting Requirements to the PR:

In preparing their activity and financial Semi-annual Reports for submission to the office of the Principal Recipient, Sub-Recipients dealing with Sub-sub recipients must ensure to incorporate SSRs’ financial transactions into their own Quarterly Reports using the same account codes, component numbers, etc., as appearing in the “Chart of Accounts (Summary)”, (see CHAPTER II), to account for the financial transactions of SSRs.

It is understood that SRs are fully responsible and accountable to the office of the Principal Recipient and to the Global Fund overall for the financial activities and the financial reporting by the approved SSRs they deal with. Independent external audits to be carried-out periodically consistency with the Global Fund guidelines. This requirement is part and partial of the Global Fund prescribed pre-conditionality as stipulated in the “Memoranda of Agreement” signed between the PR and all SRs.

Conclusion:

The detailed guidelines for fiduciary arrangements and disbursement mechanisms are provided to all GF grant Recipients, whose GF program proposals have been approved, as contained in the following pages of the “Financial Guidelines” prepared in July 2003 and the fourth revised in August 2006 by Finance Team, PR/MoH of the Office of the Principal Recipient.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MOH/PR Finance Team

TABLE OF CONTENTS

CHAPTER I: INTRODUCTION

CHAPTER II: BUDGET AND PROCEDURE APROVALII.1 GENERAL PROCEDURE

III.2 BUDGET APPROVAL II.3 BUDGET CONTROL

a) Monthly Budget Control Statements b) Quarterly Fund Status Reports c) Year-end Budget Control Statement

II.4 VARIANCE OF BUDGET II.5 REALLOCATING OF THE BUDGET/PROGRAMME

CHAPTER III: FINANCIAL APPROVAL III.1 GENERAL APPROVAL III.2 TRAINING FOR ACCOUNTANTS III.3 ADVANCE ACCOUNT CEILING

CHAPTER IV: NON-EXPENDABLE ITEMS MANAGEMENTIV.1 NON-EXPENDABLE ITEMS MANAGEMENT IV.2 REGISTER OF NON-EXPENDABLE ITEMS IV.3 PHYSICAL COUNT OF NON-EXPENDABLE ITEMS IV.4 NON-EXPENDABLE ITEMS STICKERS/TAGING SYSTEM IV.5 INVENTORY RECONCILIATION IV.6 MOVEMENT OF NON-EXPENDABLE ITEMS IV.7 NON-EXPENDABLE ITEMS LOGBOOK IV.8 PROJECT AUTOMOBILES IV.9 INSURANCE

CHAPTER V: EXPENDITURE CONTROLV.1 VERIFICATION OF PAYMENT V.2 APPROVING (VERIFYING) OFFICER a) Designation of approving (verifying) office b) Function of the approving (verifying) officer

c) Personal Responsibility of Certifying (Committing) Officer V.3 CERTIFYING (COMMITTING) OFFICER

a) Designation of the Approving (Verifying) Officer b) Functions of the Approving (Verifying) Officer c) Personal Responsibility of the Approving (Verifying) Officer

V.4 LIMIT APPROVAL THRESHOLD FOR PR and SRs V.5 EXPENSE AUTHORIZATION GUIDANCE

CHAPTER VI: PERMISSIBLE RATES FOR PER DIEM, INCENTIVE AND ALLOWANCES VI. 1 PER DIEM FOR IN-COUNTRY TRAVEL (SUPERVISION AND TRAINING) VI. 2 ALLOWANCE FOR TRAINING AND WORKSHOP VI. 3 RATE FOR WORK OR SERVICE VI. 4 INTERNATIONAL TRAVEL

CHAPTER VII: DISBURSEMENTS VII.1 Disbursement of Resources VII.2 Disbursement Policies

Page

1

222223334

5555

6666777788

9999910 10 10 10 11 11 12

1313 13 13 15

1616 16

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MOH/PR Finance Team

VII.3 Disbursement procedures VII.4 Opportunity to Inspect

CHAPTER VIII: ADVANCED PROCEDURES VIII.1 ADVANCED PROCEDURE

a) Initial advanced b) Replenishment

VIII.2 Disbursement of revolving fund VIII.3 Policy for individual cash advanced VIII.4 Advanced Register VIII.5 Individual ledger for cash advanced VIII.6 Personal Cash Advance

CHAPTER IX : CASH AND BANK MANAGEMENT IX.1 CASH MANAGEMENT a) Banking

b) Establishment of the PR and the SRs Bank Accounts) c) Types of Bank Accounts d) Currency of the Bank Account

IX.2 DESIGNATION AND RESPONSIBILITY OF BANK SIGNATORIES a) Bank Signatory Panel

b) Responsibilities of Bank Signatories IX.3 BANK TRANSFERS a) Management of Bank Transfers and Controls

b) Numbering of Bank Transfers c) Signature of Bank Transfers

IX.4 USE OF CHEQUES a) Management of Cheques

b) Numbering of Cheques c) Control of Cheques d) Safekeeping of Cheques e) Mutilated Cheques f) Voided Cheques g) Outstanding Cheques

IX.5 CASH BOOK a) Maintenance of the Cash Book

b) Monthly Closing of the Cash Book IX.6 BANK STATEMENTS a) Timing of Receipt of Bank Statements from the Bank

b) Bank Reconciliations

CHAPTER X: PETTY CASH BOOK X.1 Maintenance of the Monthly Petty Cash Book X.2 Petty Cash Limits X.3 Closing of the Petty Cash Book X.4 Keeping Petty Cash X.5 Cash Reconciliation Statement X.6 Petty Cash Replenishment

CHAPTER XI: ACCOUNTING XI.1 Receipt Vouchers:

i. Form of Receipt Vouchers ii. Provisional Receipts

XI.2 Payment Vouchers or disbursement Vouchers: XI.3 Journal Vouchers XI.4 Supporting document

17 17

1818 18 18 19 19 21 21 21

2222 22 22 22 22 23 23 23 23 23 23 24 24 24 24 24 24 22 25 25 25 25 23 26 26 26

2727 27 27 27 27 28

2929 29 29 29 30 30

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MOH/PR Finance Team

CHAPTCHAPTER XII : PAYROLL PRECEDURES XII.1 Payroll Procedures (General) XII.2 Payroll Deductions

CHAPTER XIII: RETENTION/PROTECTION OF FINANCIAL RECORDS & DOCS. XIII.1 Period of Retention of Financial Records XIII.2 Routine Measures for Safekeeping Financial Documents and Records

CHAPTER XIV: HAND-OVER INSTRUCTIONS FOR FINANCIAL MATTERS a) General Requirements for Hand-over of Financial Matters

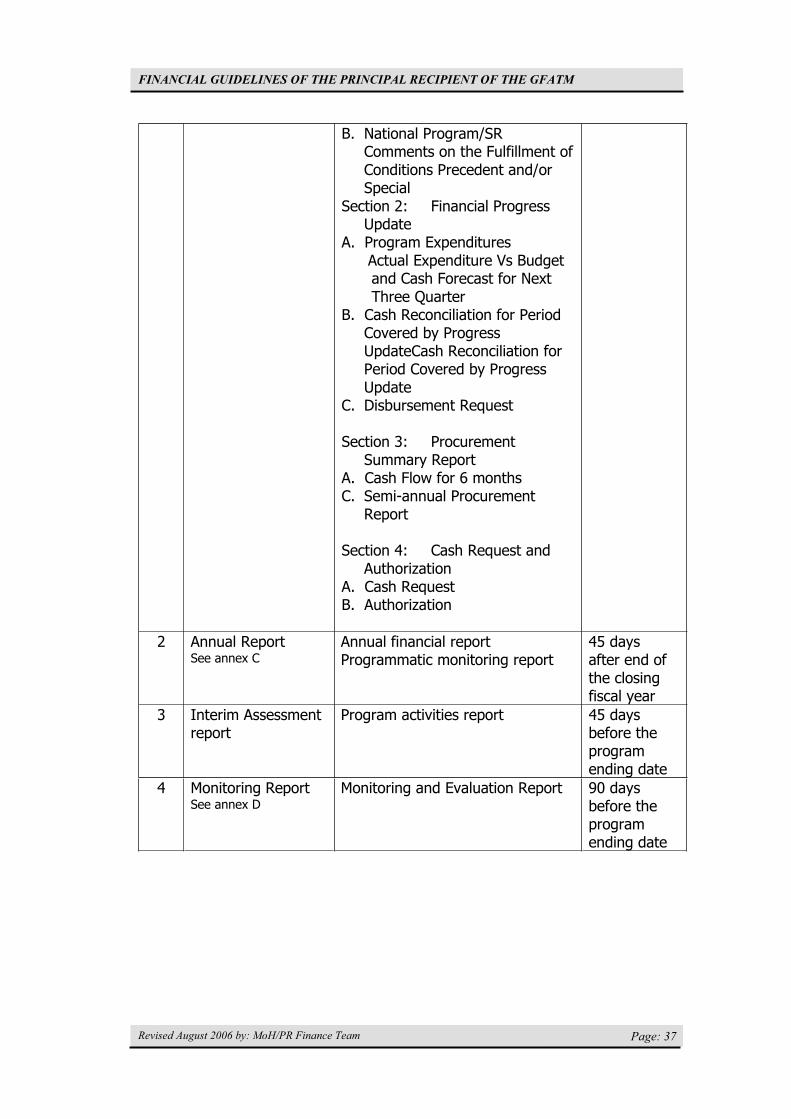

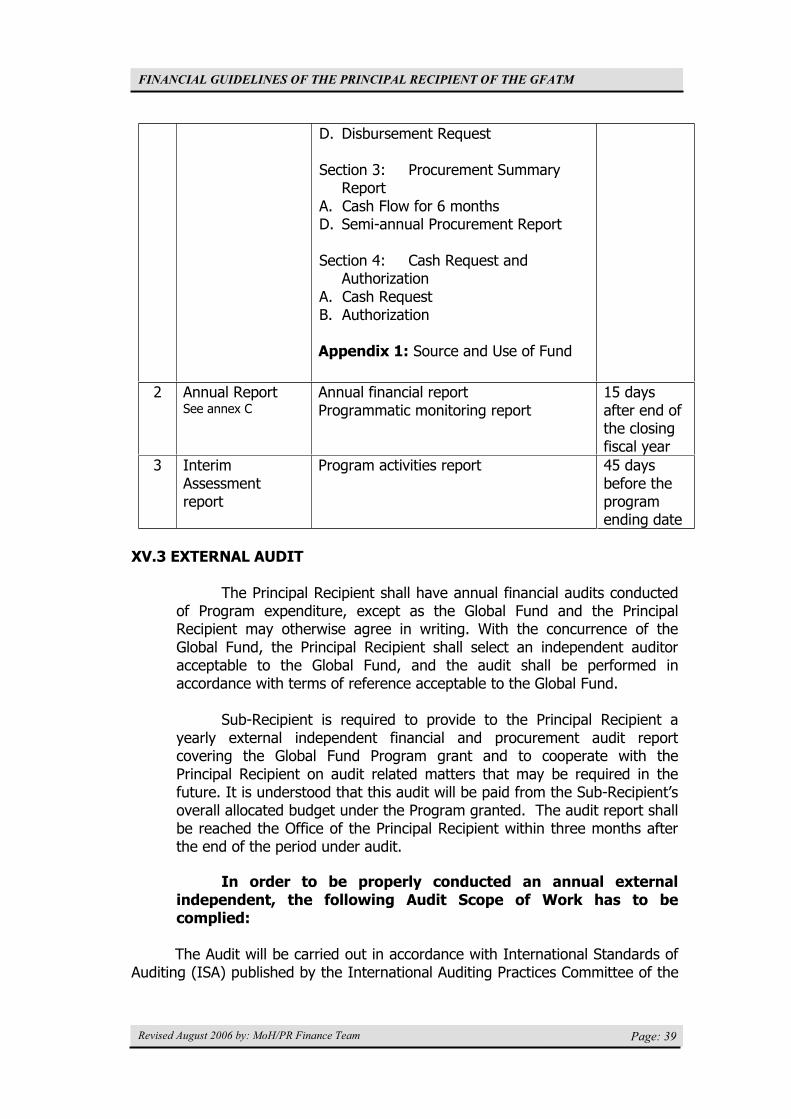

CHAPTER XV: REPORTING REQUIREMENTS XV.1 YEAR END REPORT REQUIREMENT XV.2 FINANCIAL REPORT

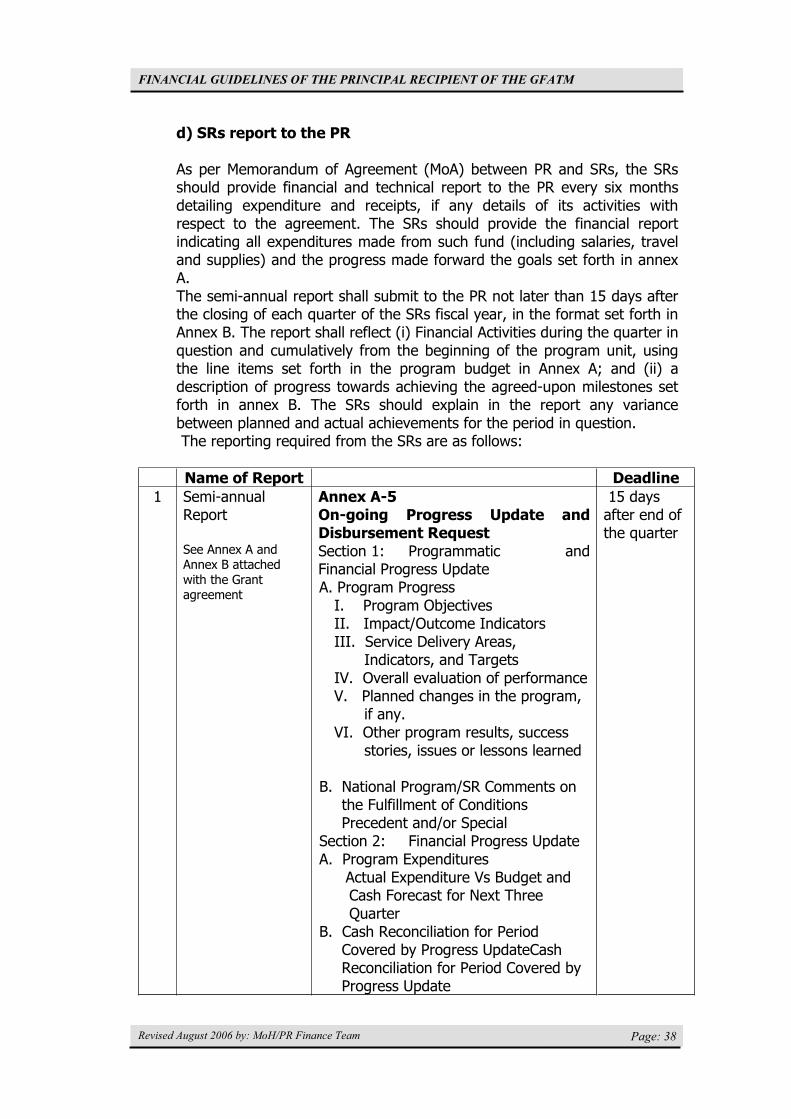

a) Month end procedure b) Monthly financial report format for the PR c) PR reporting to Global Fund d) SRs report to the PR

XV.3 EXTERNAL AUDIT

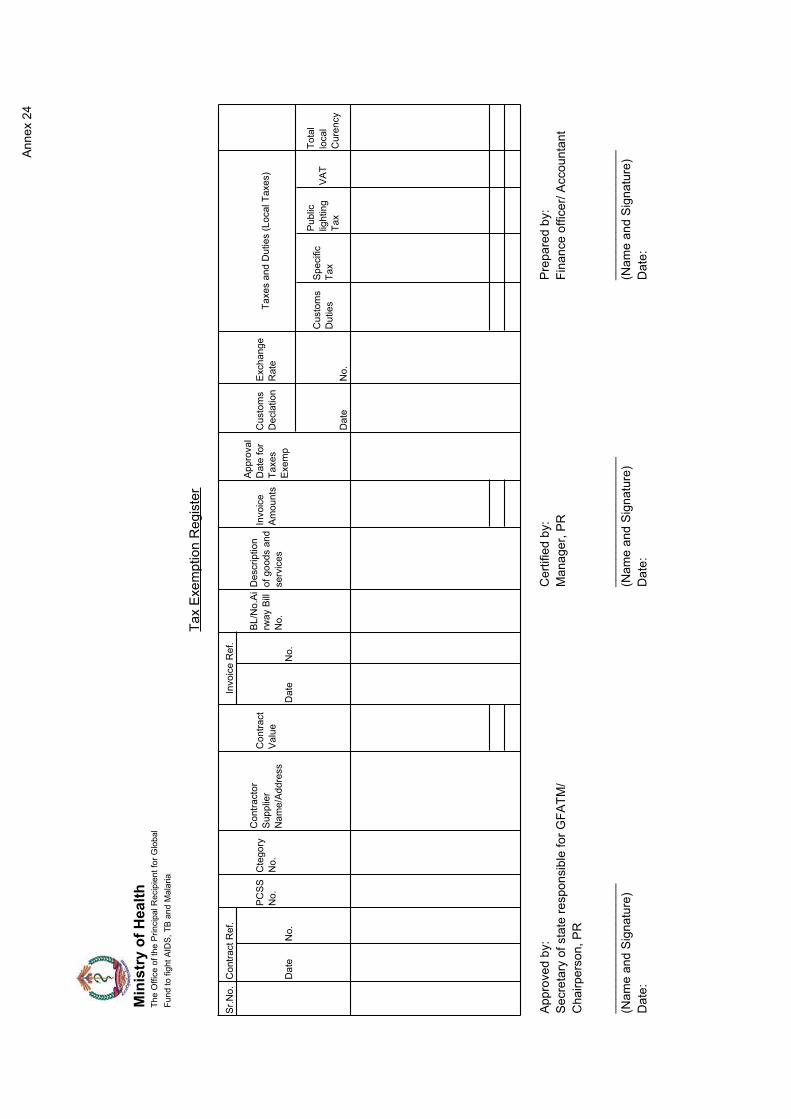

CHAPTER XVI: GOVERNMENT TAXATION AND DUTIES XVI.1 TAXES AND DUTIES XVI.2 TAX EXEMPTING XVI.3 TAX EXEMPTION REGISTERS

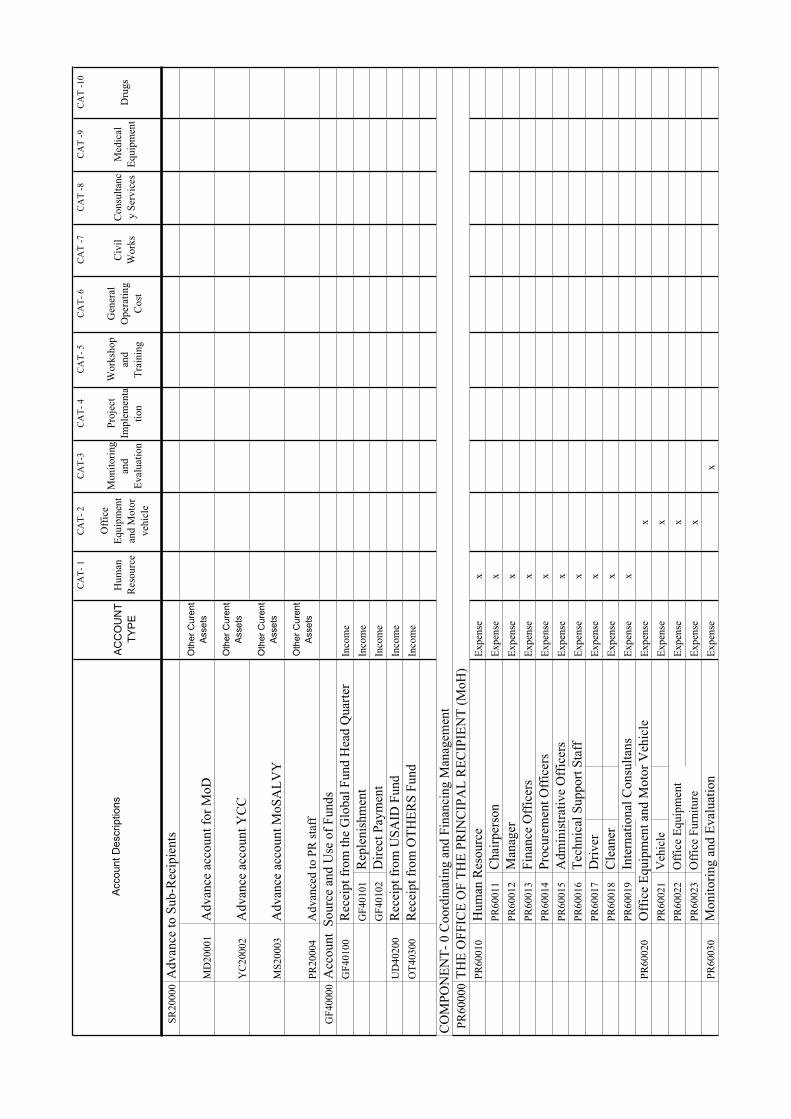

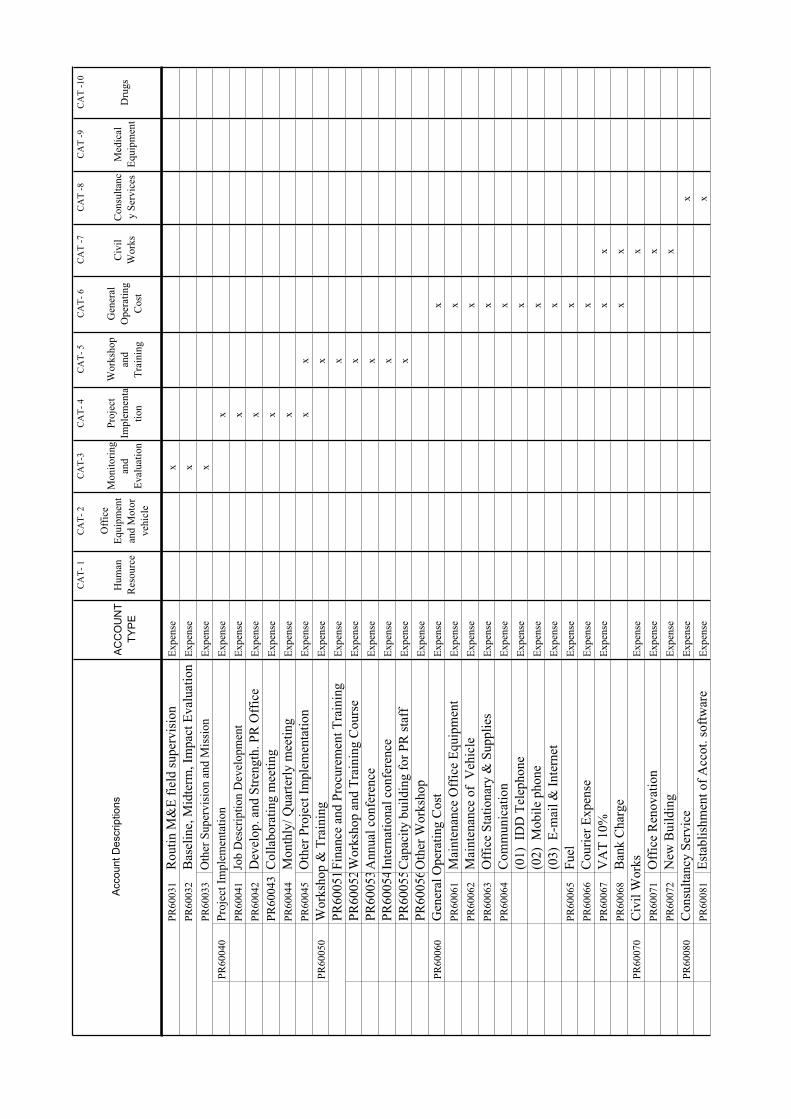

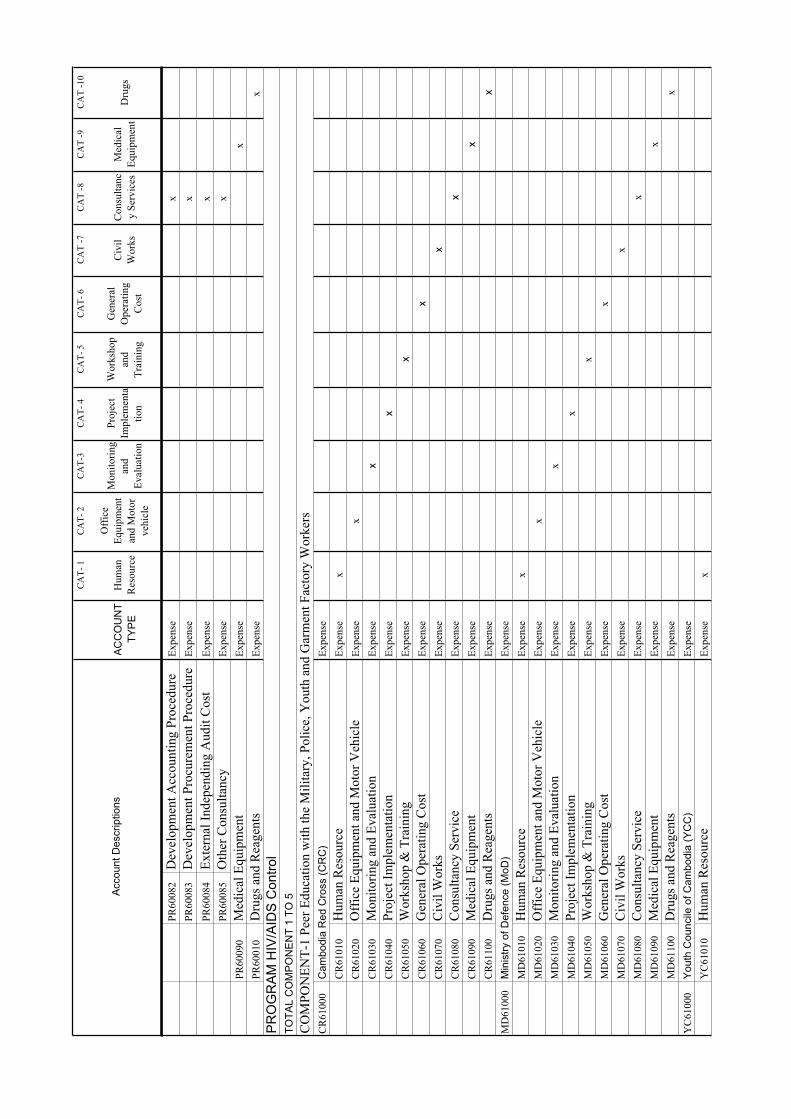

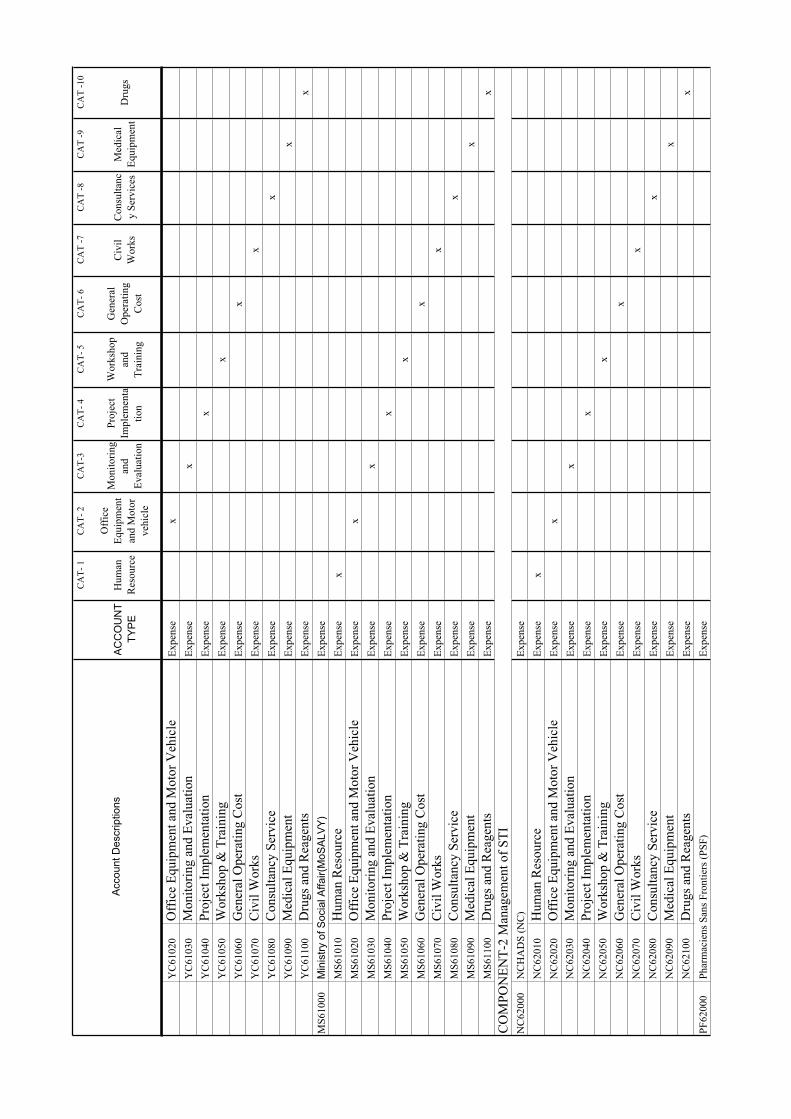

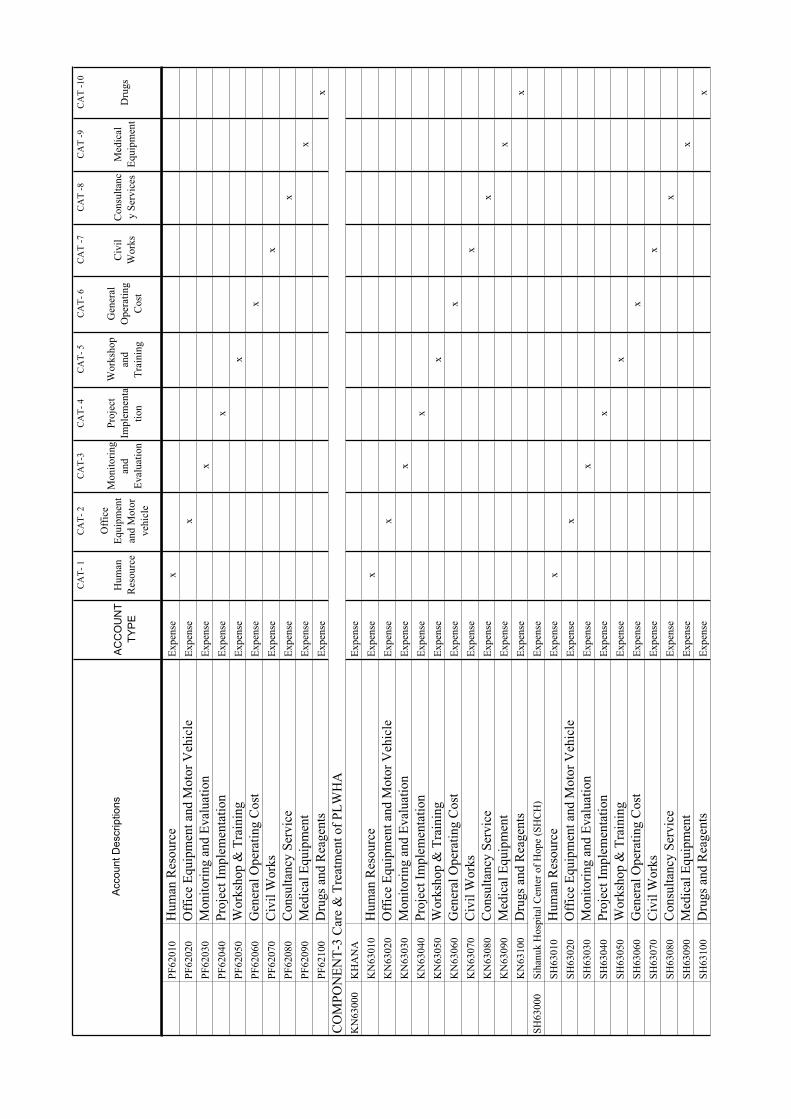

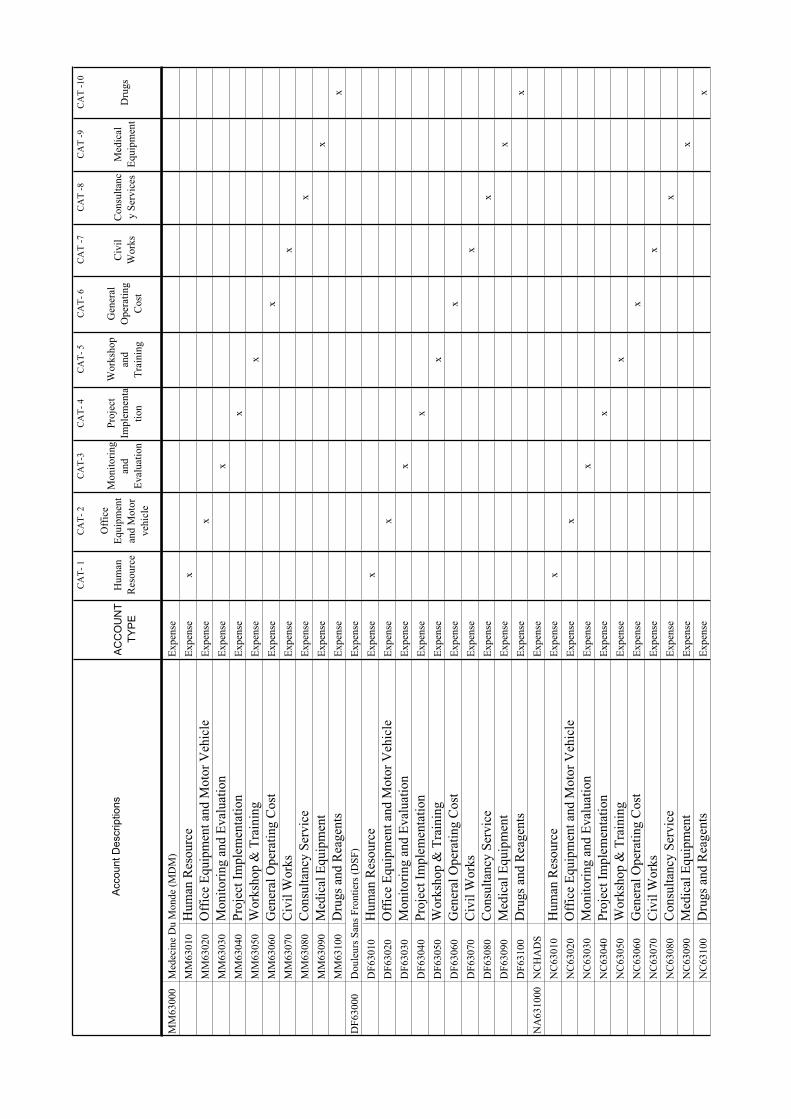

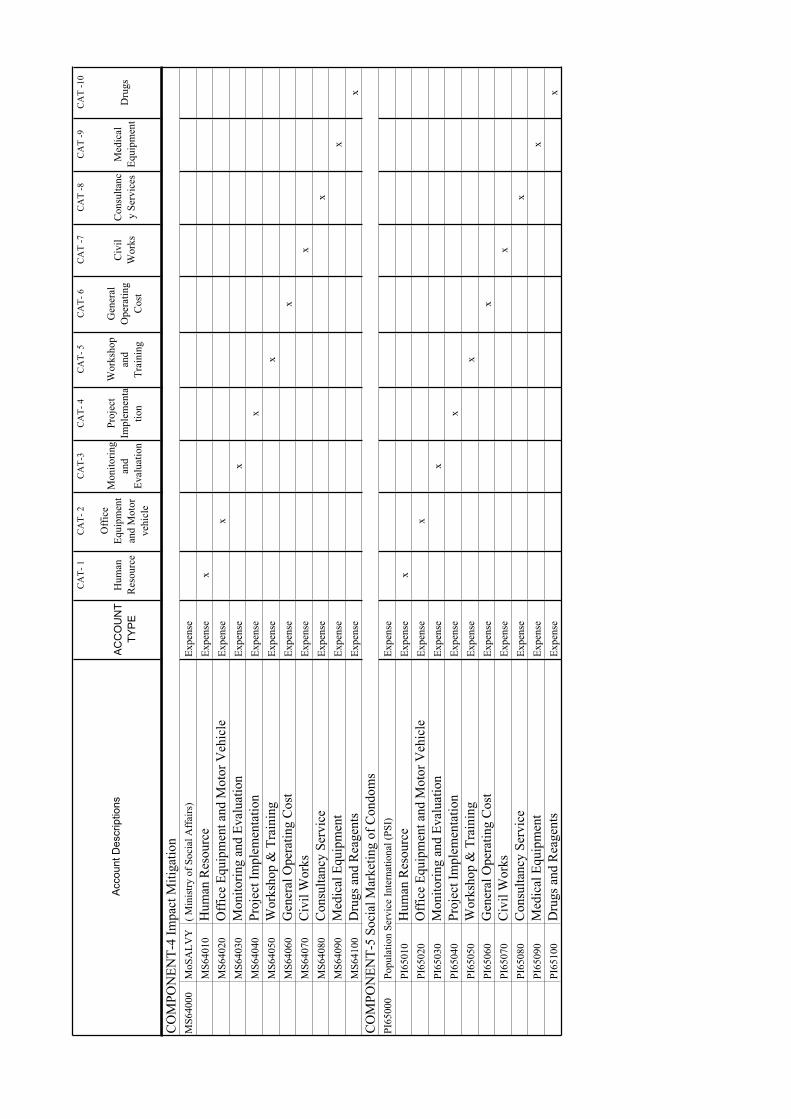

CHAPTER XVII: CHART OF ACCOUNTS XVII.1 GENERAL STRUCTURE XVII.2 CLASSIFICATION OF THE EXPENDITURES

Appendix 1 Chart of Accounts

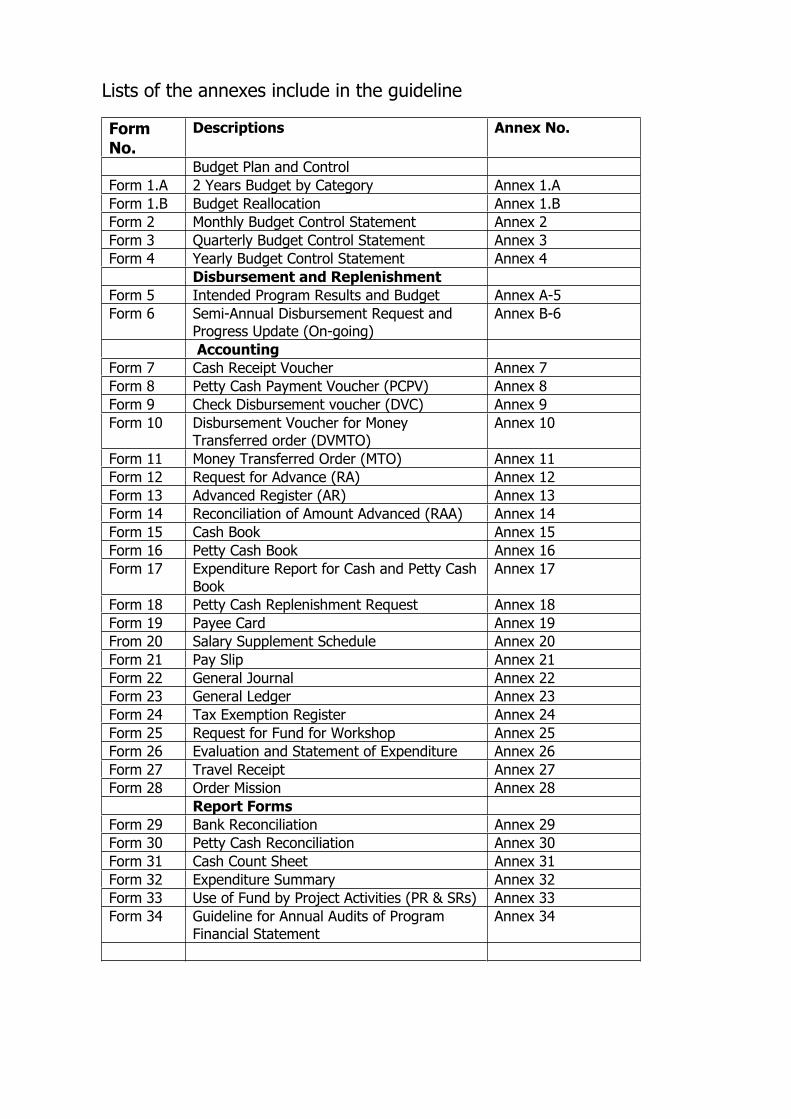

List of the ANNEXES include in the Guideline

3131 31

3232 32

3333

3434 34 34 36 36 38 39

4242 42 42

4344 44

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 1

CHAPTER I: INTRODUCTION

In its capacity as the Principal Recipient (PR) for the Global Fund to Fight AIDS, Tuberculoses and Malaria (GFATM), Ministry of Health assumes responsibility for ensuring the adequacy of the overall supervision and management of the Global Fund. To ensure that the Project achieved its goals and objective, the PR needs to ensure that decision are made in timely fashion, that activities are implemented in an efficient manner, and that disbursements keep up with the planned disbursements for the Project. Therefore, these policies and guidelines will present and describe how to provide more direction to implementers at all levels for the PR and Sub-recipients (SRs) and how fund can be used properly. For accurate recording of advances and or reimbursements, and to facilitate the review and auditing of executed project transactions, the executing agency such as SRs must maintain accounting book and records that clearly identify the project fund and follow the procedure of the PR and the Global Fund.

The purpose of these procedures is to define:

a mechanism for approval of programme activities financial management model, which outlines the approval processes and ceilings for disbursement through check or money transfer order (MTO) and for petty cash a set of procurement procedures for goods, services and civil works (See Procurement Guideline) a monitoring and reporting schedule permissible rates for payment of per diem, incentives, allowances, etc Mechanisms and procedures for decentralization to National Programs (NPs) and SRs.

The main principles for procurement and disbursement are based on procedures derived from experience implementing World Bank (WB), Asian Development Bank and other donor projects in the Ministry of Health.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 2

CHAPTER II: BUDGET PROCEDURE AND APPROVAL

II. 1 General Procedure

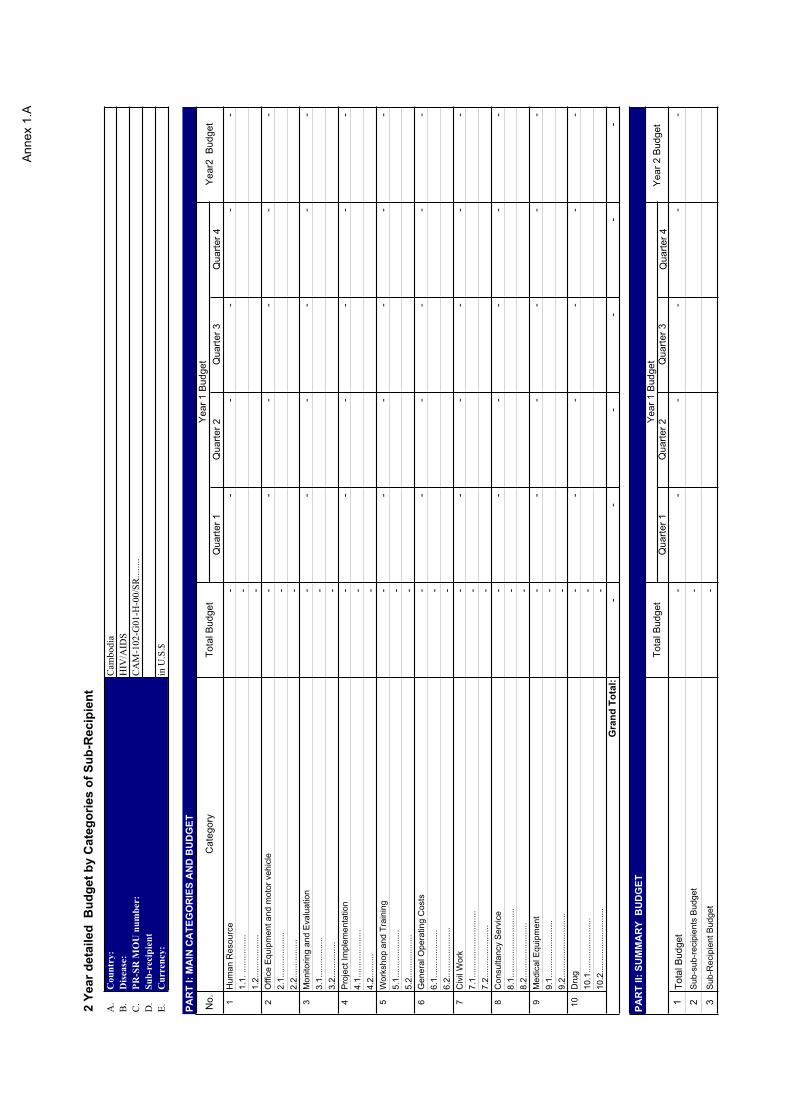

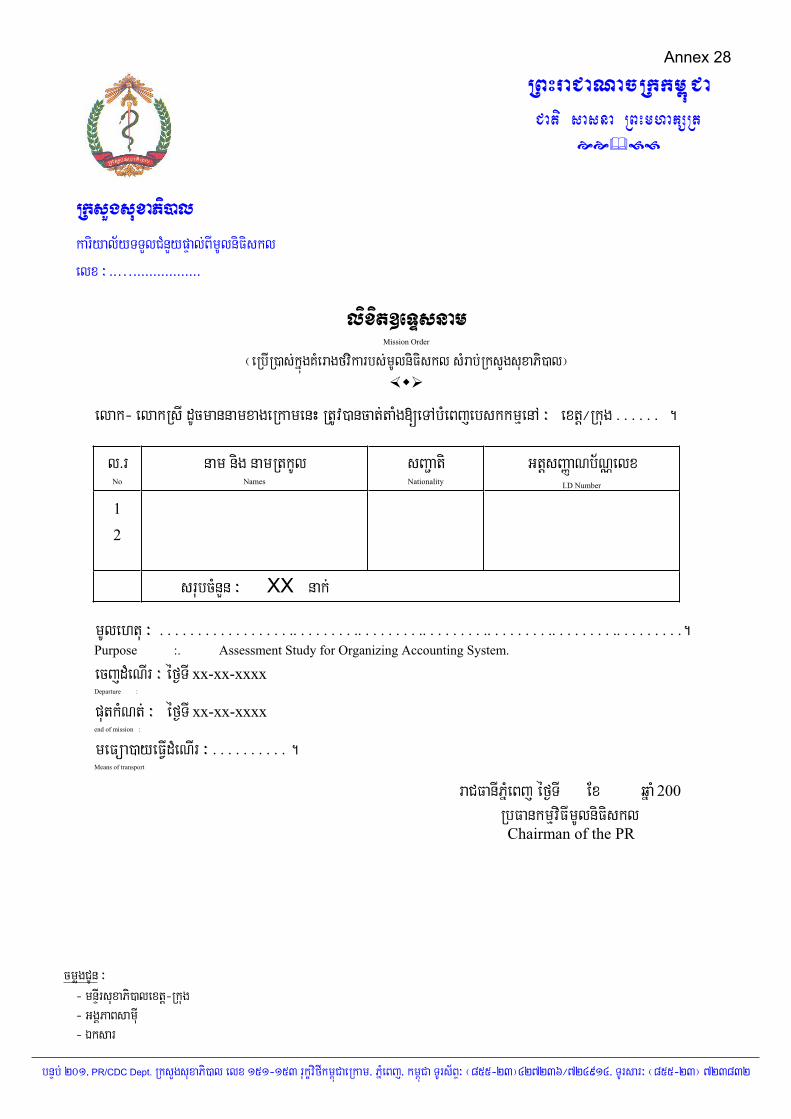

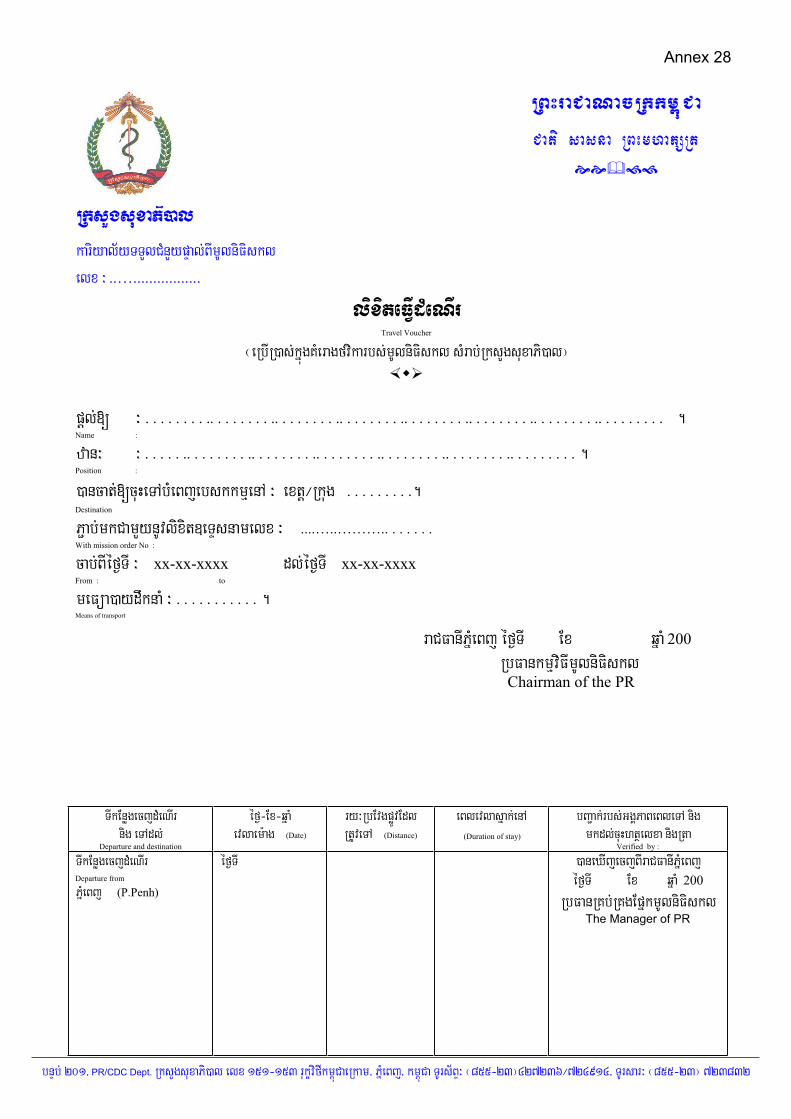

a. The Principal Recipient from the Ministry of Health will be responsible for providing over all guidance in the implementation of the Project, including reviewing and approving of the Annual Operational Plans (AOPs) (Annex 1).

b. The PR is responsible for preparation of the AOP and cash forecast to submit to the Secretary of State responsible for GFATM grants, Ministry of Health and further forwarded to the Global Fund.

c. The annual budget plan agreed by the PR as part of the final program document is called the "Approved Budget". It should be noted that the initial budget submitted to the GF or as part of the program proposal is not necessarily the final approved budget as the original budget may be amended in negotiations with the GF. In any case, if needed of announcement the budget, the MoH will submit to the GF with detail budget and justification.

d. The approved budget shall be entered into the financial management system and also recorded using the Program Budget Drafting Form.

e. Subsequent increase of funds by the Global Fund will require budget revisions to incorporate the additional loans or grant.

II. 2 Budget Approval

After the budget is approved, the PR and Implementing Unit (SRs) will enter into the agreement. The PR will then disburse funds within 10 working days after signing the agreement. Any individual procurement of goods or services held by the Procurement Group or PR Secretariat shall be pre-approved by the Secretary of State, responsible for GFATM grant, Ministry of Health / Project Chairman.

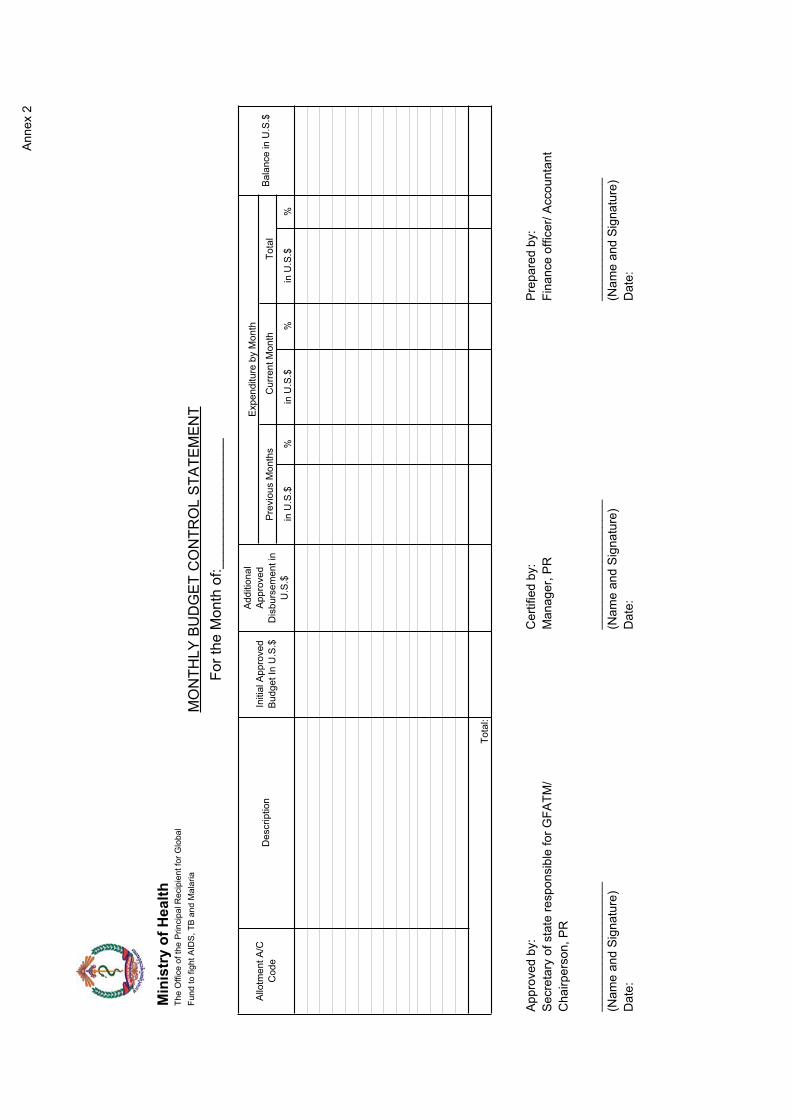

II. 3 Budget Control a) Monthly Budget Control Statements:

A Monthly Budget Control Statement specimen is provided in the accounting forms (Annex 2) and is included in these Financial Guidelines of the office of the principal Recipient (PR) of the MoH. The utilization and completion of the form is advisable and is intended for the accurate control of the budgets of the PR as well as Sub-recipient. The specimen is self explanatory and simple in design and it assist management to maintain continuous control over funds received versus funds available on a monthly basis.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 3

b) Semi-Annual Reports (Annex 3)

This enumerates the progress of the planned (budgeted) project activities for the three consecutive months. The progress of the activities is being explained in quantitative manner as per budget lines. The amount is extracted from the books of the accounts maintained by the SR. This is submitted by the SR of the project outlet to PR on the agreed date.

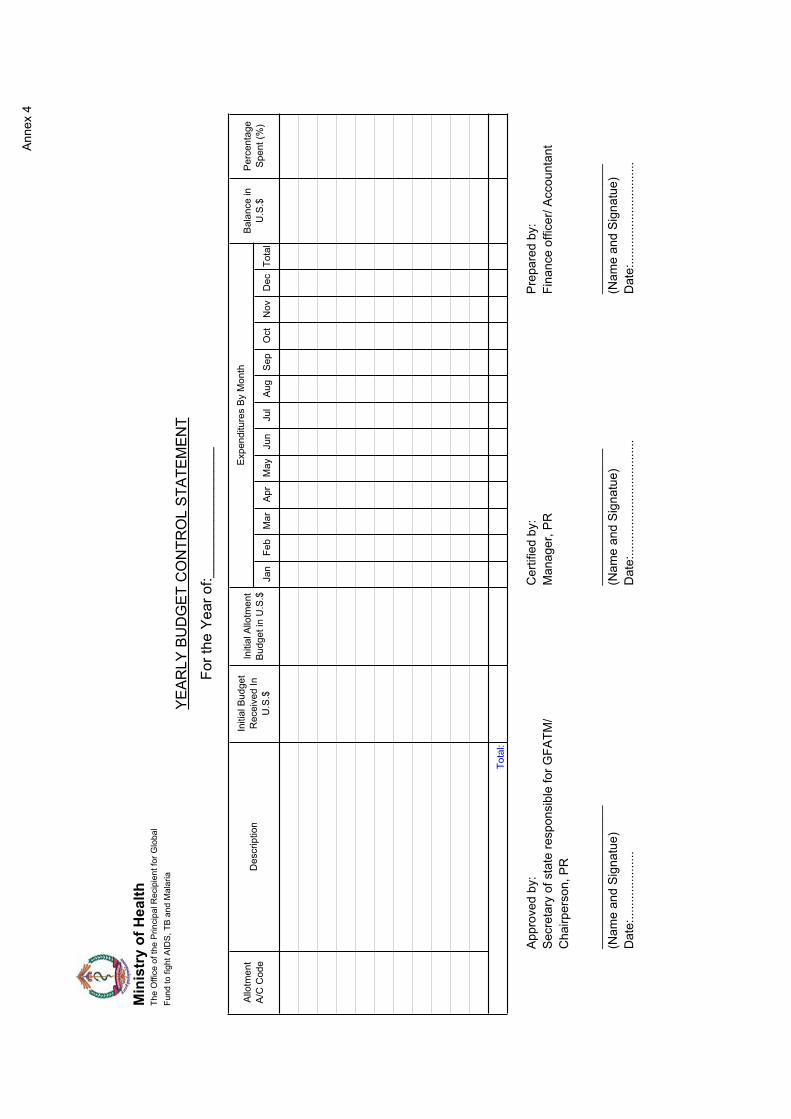

c) Year-end Budget Control Statements:

A Year-end Budget Control Statement is equally provided in these guidelines, i.e., (Annex 4), that is meant for the year-end control of the allocated budget for the purpose of carrying over budget balances to the following year. The Yearly Budget Control Statement is structured in such a manner that it provides budget information by a) Allotment Account code, b) by description of activity, c) amount of initial grant allocation by component, d) by month of expenditure, e) balance of allotment and f) percentage of total expenditure versus actual percentage of initial budget allocation. This form is designed in such a manner that it is self explanatory and easy to use.

II. 4 Variance of Budget

Any significant variance as a result of budget and actual expenditures should be explained in detailed manner. Any remedies or solution to the variance shall be described and properly explained. The SR may allowed to modify the agree activities to reach the objective of the program during the course of the implementation by requesting in writing to the PR. Budget variation from one budget category to another; SR is able to reallocate the fund within 10% without any additional approval, however, the change between 10% and 20% would require the approval from the PR. The budget variation above 20% would require prior acceptance from PR and subsequent approval from CCC.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 4

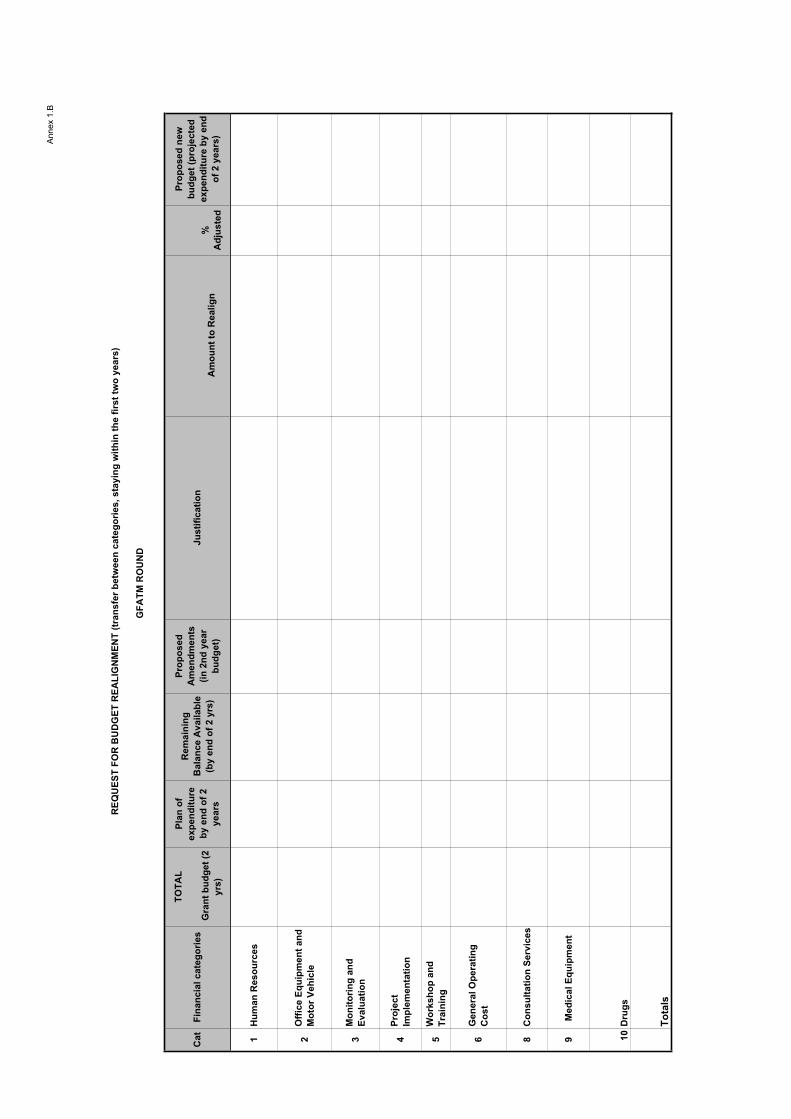

II. 5 Reallocating of the Budget/Programme

During the Training Workshop in Phnom Penh Hotel from May 31st to June 2nd

2006, all Sub-Recipients and Principle Recipient agreed on the reallocating of the Budget/Programme as follow:

In case that the SRs/NPs need to make changes to the existing signed grant, for Procurement/Budget, Monitoring and Evaluation programs, then they would have to conduct a formal “Reprogramming/Budgetary Re-allocation”, using standard form available with PR on request.

The following guidelines should apply:

1. Timeframes:

Reallocation budget can be allowed once a year.

2. Changes to the Procurement/Financial Program(categories): (reallocation of procurement/budget between categories)

a. up to 10% - SRs/NPs are authorized, but should inform PR; b. 10-20% - PR’s approval required;

SRs must submit formal request to the PR (format is available on request)

c. over 20% - formal approval of the CCC-SC required; SRs must submit formal request to the PR, to be submitted to the CCC-SC (format provided)

3. Changes to the Monitoring Evaluation program;

a. It is assumed that the above requests do not produce any changes in the program results (indicators and targets), or

b. there maybe only small changes to the activities, without affecting the overall results negatively.

c. If however, the coverage of services is decreased by 30% as a result of the reprogramming, the GFATM’s approval is required;

SRs must submit formal request to the PR, to be submitted to the CCC-SC, LFA and GFATM.

It is important to bring to the attention of NPs and SRs’ reprogramming of the procurement/budget or monitoring and evaluation program should be done after careful planning.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 5

CHAPTER III: FINANCIAL APPROVAL

III.1 General Approval

The office of Principal Recipient Ministry of Health (PR/MoH) must receive the Budget Plan in a timely manner from the SRs. After receiving the budget plan, the PR/MoH shall compile it in the PR format and submitted to the PR Technical Review Team (PRTRT), CCCSC, CCC, and to Global Fund through LFA for approval. After that the PR/MoH will instruct SRs on the implementation of the approved workplan. Then, SRs can start the procurement process according to the threshold and procurement guidelines privileged by the office of the PR. PR/MoH will disburse fund, after the approval of the Secretary of State of the MoH responsible of the GFATM program, within ten working days.

III.2 Training of Accountant

From time to time The PR/MoH may try to improve financial management through the training, accounting monitoring and supervision, and computerized accounting report format to SRs which need to be improved. In order to provide effective accounting assistance to all SRs with weak financial management the PR should provide the monitoring and/or refresher training in a quarterly basic or more frequent as needed.

III.3 Advanced Accounting Ceiling

The PR/MoH channels fund to SRs. The ceiling amount must set based on analysis of expenditures to be financed through the mechanism (Annual Budget divided by quarter). The approved amount indicated in the workplan/budget plan will be released to the SRs, except some SRs with weak financial management identified by PR for subsequent round the fund will be provided through cash basis advance (Revolving Fund), and ongoing process of liquidation and replenishment upon the satisfaction of the PR for the previous advance.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 6

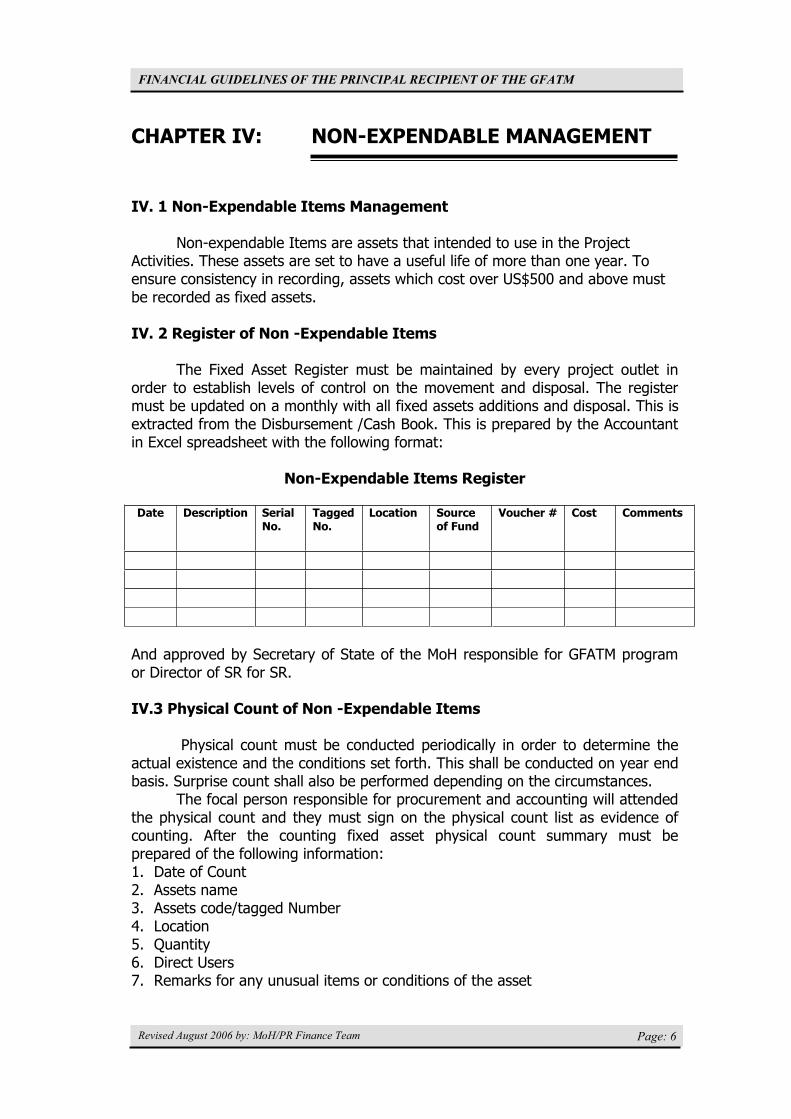

CHAPTER IV: NON-EXPENDABLE MANAGEMENT

IV. 1 Non-Expendable Items Management

Non-expendable Items are assets that intended to use in the Project Activities. These assets are set to have a useful life of more than one year. To ensure consistency in recording, assets which cost over US$500 and above must be recorded as fixed assets.

IV. 2 Register of Non -Expendable Items

The Fixed Asset Register must be maintained by every project outlet in order to establish levels of control on the movement and disposal. The register must be updated on a monthly with all fixed assets additions and disposal. This is extracted from the Disbursement /Cash Book. This is prepared by the Accountant in Excel spreadsheet with the following format:

Non-Expendable Items Register

Date Description Serial No.

Tagged No.

Location Source of Fund

Voucher # Cost Comments

And approved by Secretary of State of the MoH responsible for GFATM program or Director of SR for SR.

IV.3 Physical Count of Non -Expendable Items

Physical count must be conducted periodically in order to determine the actual existence and the conditions set forth. This shall be conducted on year end basis. Surprise count shall also be performed depending on the circumstances.

The focal person responsible for procurement and accounting will attended the physical count and they must sign on the physical count list as evidence of counting. After the counting fixed asset physical count summary must be prepared of the following information: 1. Date of Count 2. Assets name 3. Assets code/tagged Number 4. Location 5. Quantity6. Direct Users 7. Remarks for any unusual items or conditions of the asset

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 7

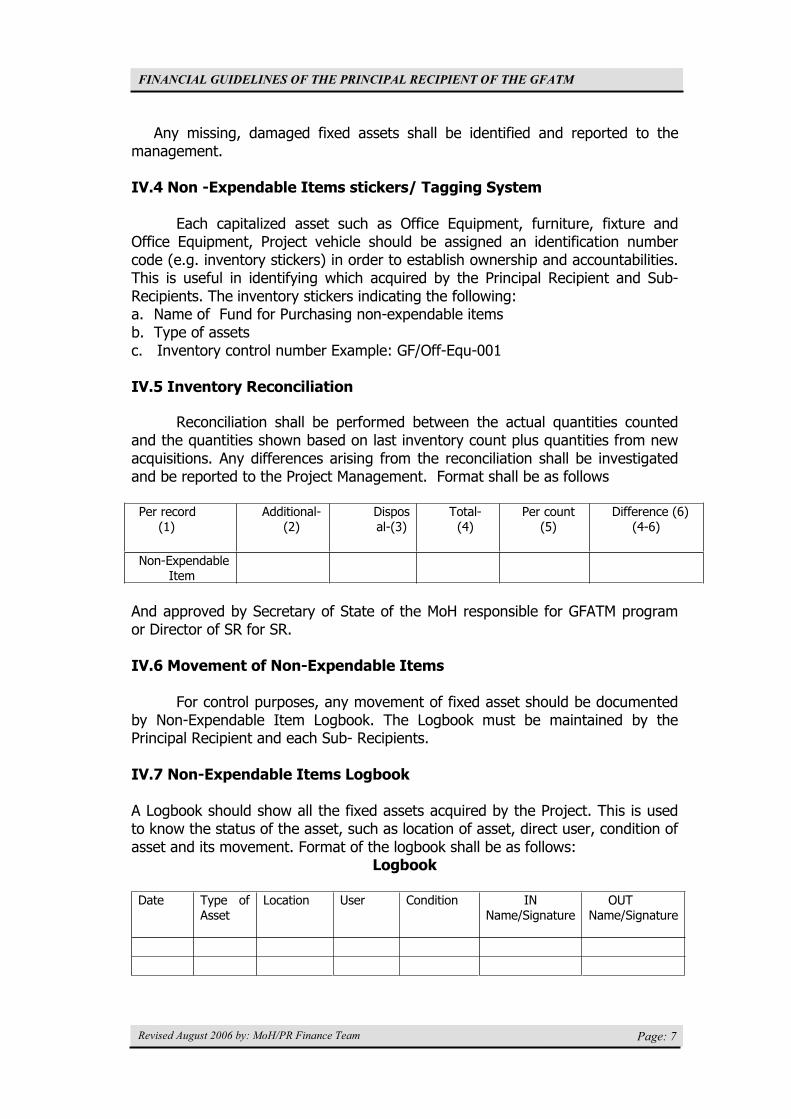

Any missing, damaged fixed assets shall be identified and reported to the management.

IV.4 Non -Expendable Items stickers/ Tagging System

Each capitalized asset such as Office Equipment, furniture, fixture and Office Equipment, Project vehicle should be assigned an identification number code (e.g. inventory stickers) in order to establish ownership and accountabilities. This is useful in identifying which acquired by the Principal Recipient and Sub-Recipients. The inventory stickers indicating the following: a. Name of Fund for Purchasing non-expendable items b. Type of assets c. Inventory control number Example: GF/Off-Equ-001

IV.5 Inventory Reconciliation

Reconciliation shall be performed between the actual quantities counted and the quantities shown based on last inventory count plus quantities from new acquisitions. Any differences arising from the reconciliation shall be investigated and be reported to the Project Management. Format shall be as follows

Per record (1)

Additional-(2)

Disposal-(3)

Total- (4)

Per count (5)

Difference (6) (4-6)

Non-Expendable Item

And approved by Secretary of State of the MoH responsible for GFATM program or Director of SR for SR.

IV.6 Movement of Non-Expendable Items

For control purposes, any movement of fixed asset should be documented by Non-Expendable Item Logbook. The Logbook must be maintained by the Principal Recipient and each Sub- Recipients.

IV.7 Non-Expendable Items Logbook

A Logbook should show all the fixed assets acquired by the Project. This is used to know the status of the asset, such as location of asset, direct user, condition of asset and its movement. Format of the logbook shall be as follows:

Logbook

Date Type of Asset

Location User Condition IN Name/Signature

OUT Name/Signature

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 8

And approved by Secretary of State of the MoH responsible for GFATM program or Director of SR for SR.

This format can be used also for controlling of the movement of the Project automobiles.

IV.8 Project automobiles

Automobile logbooks must be used for all Project automobile. The logbooks must be updated every travel. They must be used for Project purposes and must be checked and sign by authorized person.

IV.9 Insurance

Insurance is one of the mechanisms that are to be used in compliance in one of the Principle of Internal Control that is safeguarding of the assets. The Program should provide the following type of insurance.

1. Vehicle Insurance

The Program should provide vehicle insurance for all vehicles used in the implementation of the Program. This insurance should cover the Vehicles from being lost and damaged, passenger's liability, strike riot & civil commotion.

2. Cargo insurance

Cargo insurance is the responsibility of the Supplier during the transportation of Goods. It protects of various risks, such as damage, pilferage and theft, breakage. Cargo insurance provides protection against financial losses resulting from this risk. The PR and SRs should mention this insurance in the request for quotation from the suppliers or bidding document.

IV.10 Report of Non -Expendable Items

The SRs shall submit the Report of Non-Expendable Items to the PR every semi-annually with the other semi-annual financial report. The Report of Non-Expendable Items should includes Non-Expendable Items Register Worksheet, Physical Count Report, Inventory Reconciliation Report, Non-Expendable Items Logbook.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 9

CHAPTER V: EXPENDITURE CONTROL

V.1 VERIFICATION OF PAYMENTS:

Designation and functions of the Approving (verifying) Officers is decided by the Secretary of State of the MoH responsible for GFATM program and by the respective Directors of the Sub-recipients. Accordingly, designated staff will receive a formal letter of designation from the respective Directors. The criteria to be considered when delegating this authority are the ability of the designated staff to minimize the risks articulated in the corresponding paragraphs provided below (by virtue of his/her hierarchical position). In this respect, Approving (verifying) Officers are directly accountable to their respective Directors. In the case of the office of the Principal Recipient (PR), the Approving (verifying) Officer is the Chairperson of the PR and in his absence the designated Manager is the alternate approving (verifying) Officer. In the case of the Sub-recipients, the existing arrangements, as already documented at the SRs offices, will prevail for the financial management of GF allocated grants.

V.2 APPROVING (VERIFYING) OFFICER:

a) Designation of Approving (Verifying) Officer: The Approving (verifying) Officers are designated as main Approving (verifying) Officers in consideration of their ranks and actual functions and any exceptions to such designation must be documented in writing by the respective Directors.

b) Functions of the Approving (Verifying) Officers: The functions of the approving (verifying) Officers include the following:

i. Ensure that the payment is made against a recorded commitment entered into by an appropriate Certifying (committing) Officer;

ii. Ascertain that all the goods or services for which payment is claimed have been delivered, according to the terms outlined in the commitment documents;

iii. Avoid duplicate payments for the said goods and services;

iv. Refuse the payment if there is any reason he/she knows that should bar the payment.

v. The authority assigned to the Approving (Verifying) Officer cannot be delegated.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 10

vi. Officers-in-charge automatically receive the signature authorities of the staff member they are acting for but not the authority to further delegate.

vii. Change in the designation of Approving (Verifying) Officers must be effected in written form and approved by the Secretary of State of the MoH responsible for GFATM program for the office of the Principal Recipient (PR) and by the Directors of the respective sub-recipients.

c) Personal Responsibility of the Approving (Verifying) Officer:

i. Approving (Verifying) Officers should not verify for payments to themselves unless it is documented and placed on record at the concerned office level certifying that there are no other Approving (Verifying) Officers available at the time payment is required.

ii. All personnel of the Ministry of Health and all personnel of sub-recipients are responsible to their respective designated Directors for the regularity of actions taken by them in the course of their official duties. Any personnel who take any action contrary to these Guidelines, and instructions that may be issued in therewith, may be held personally responsible and financially liable for the consequences of such action.

V.3 CERTIFYING (COMMITTING) OFFICER

a) Designation of Certifying (Committing) Officer:

The Certifying (Committing) Officers are designated as main Certifying (Committing) Officers in consideration of their ranks and functions and any exception to such designations must be documented in writing by the respective Directors.

b) Functions of the Certifying (Committing) Officer:

The functions of the Certifying (Committing) Officer include the following:

i. Ensure that the payment is genuine and that the payee is the legitimate beneficiary.

ii. Ascertain that the supporting documents attached to the Payment Voucher are a) complete and b) originals.

iii. Ensure that all Payment Vouchers and/or other accounting documents certified have been correctly entered into the accounting system.

iv. Ascertain that all Payment, Receipt, Journal Voucher and all other accounting documents given to the Approving (Verifying) Officer for signatures have been verified for completeness and correctness.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 11

c) Personal Responsibility of Certifying (Committing) Officer:

i. Certifying (Committing) Officers should not certify payments for themselves unless it is documented and placed on record at concerned offices certifying that there are no other Certifying (Committing) Officers available at the time payment is required. They should ensure that the Approving (Verifying) Officer is not misled by receiving unjustified payments for approval.

ii. All personnel of the Ministry of Health and all personnel of sub-recipient are responsible to their designated Directors for the regularity of actions taken by them in the course of their official duties. Any personnel who take any action contrary to these Guidelines and instructions that may be issued in therewith, may be held personally responsible and financially liable for the consequences of such action.

V. 4 LIMIT APPROVAL THRESHOLD FOR THE PR

FUND LEVEL LIMITS CERTIFYING OFFICER

APPROVAL

On Petty Cash Fund Below $500 Project Manager Chairperson Check, Money Transfer Order disbursements

Below $50,000 Project Manager Chairperson

Check, Money Transfer Order disbursements

Above $50,000 Project Manager and Chairperson

Secretary of State responsible for GFATM program

Note: Approval threshold for SRs should follow their existing procedure, but it shall not exceed the threshold above.

V. 5 EXPENSE AUTHORIZATION GUIDANCE

Approval/recommendations are required from the Heads Before a trip is made/assignment undertaken Before purchasing goods or services For liquidation of expenses In order to obtain cash advance

Head who signed on the Cash Request is responsible for establishing and confirming that the expenditures are:

For official business, not personal Necessary for the operation/activities Reasonable in amount Within the budget line Supported by liquidation forms, where necessary receipts are attached

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 12

Based on standard procedures

No employee has the authority to approve his own expenses/claims. Senior management may permit to authorize his or her employee advances and expenses. For more information see procurement guideline chapter V and VII (The threshold for the procurement of goods, medical equipment, civil works and services).

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 13

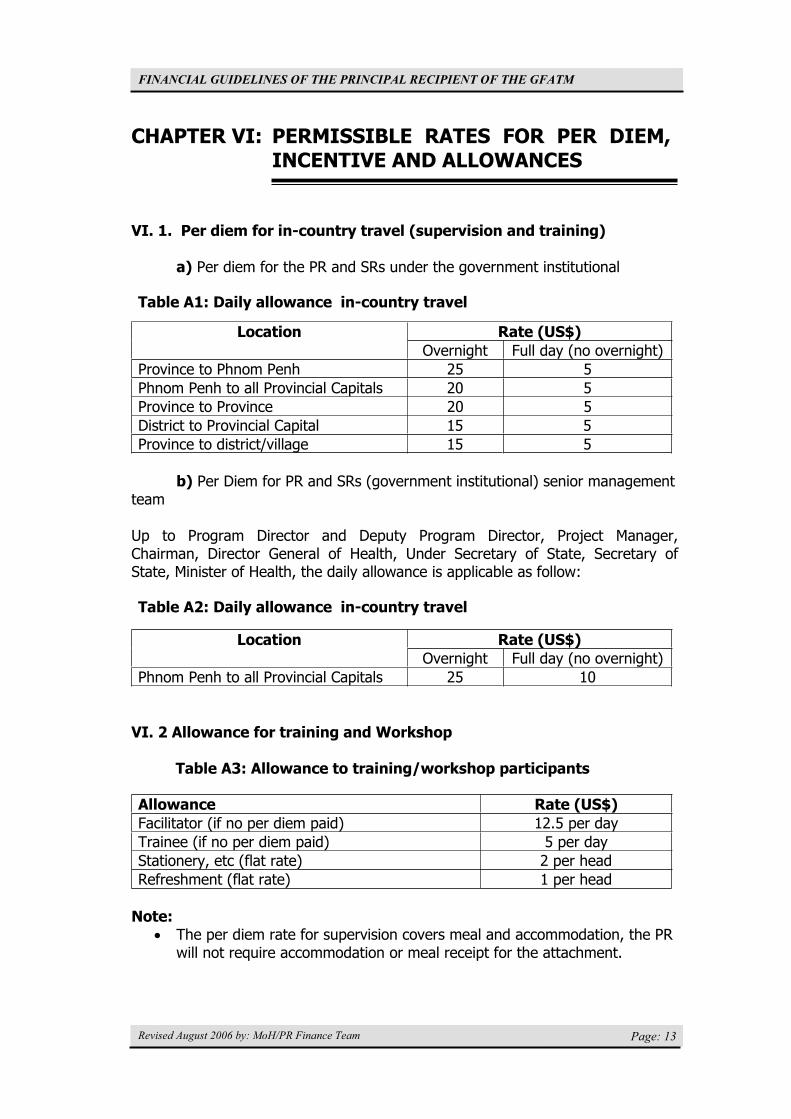

CHAPTER VI: PERMISSIBLE RATES FOR PER DIEM, INCENTIVE AND ALLOWANCES

VI. 1. Per diem for in-country travel (supervision and training)

a) Per diem for the PR and SRs under the government institutional

Table A1: Daily allowance in-country travel

Rate (US$) Location Overnight Full day (no overnight)

Province to Phnom Penh 25 5 Phnom Penh to all Provincial Capitals 20 5 Province to Province 20 5 District to Provincial Capital 15 5 Province to district/village 15 5

b) Per Diem for PR and SRs (government institutional) senior management team

Up to Program Director and Deputy Program Director, Project Manager, Chairman, Director General of Health, Under Secretary of State, Secretary of State, Minister of Health, the daily allowance is applicable as follow:

Table A2: Daily allowance in-country travel

Rate (US$) Location Overnight Full day (no overnight)

Phnom Penh to all Provincial Capitals 25 10

VI. 2 Allowance for training and Workshop

Table A3: Allowance to training/workshop participants

Allowance Rate (US$)Facilitator (if no per diem paid) 12.5 per day Trainee (if no per diem paid) 5 per day Stationery, etc (flat rate) 2 per head Refreshment (flat rate) 1 per head

Note: The per diem rate for supervision covers meal and accommodation, the PR will not require accommodation or meal receipt for the attachment.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 14

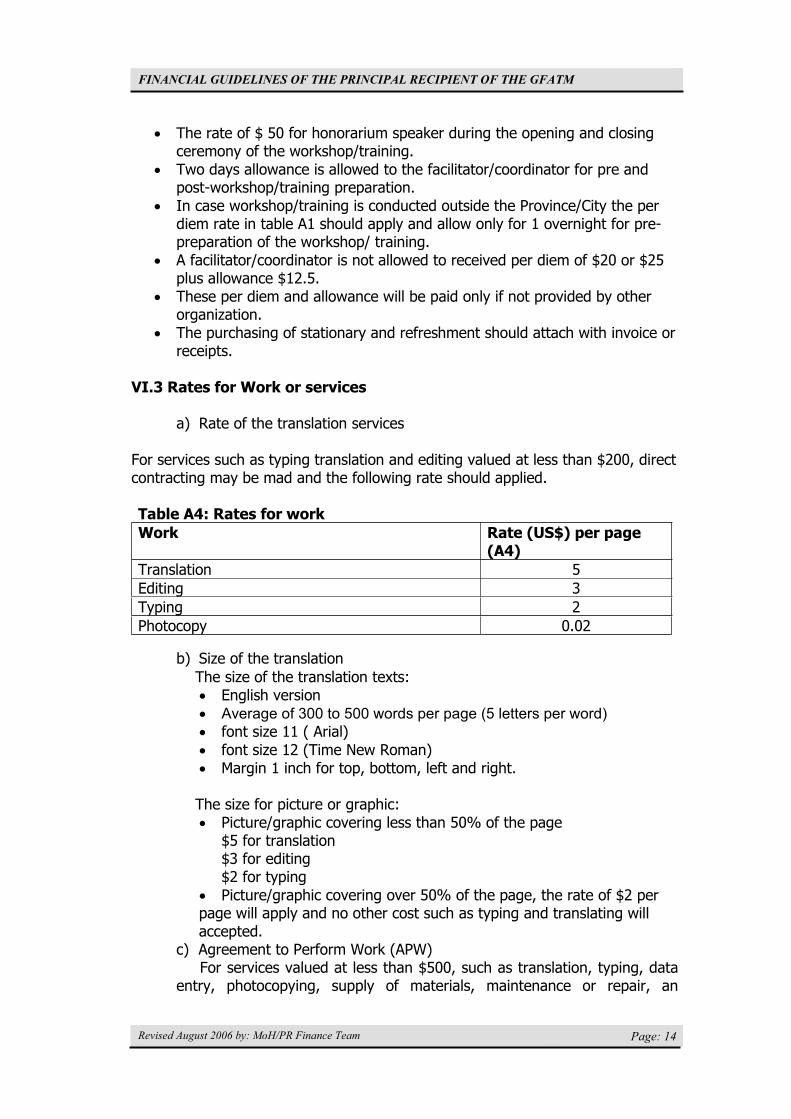

The rate of $ 50 for honorarium speaker during the opening and closing ceremony of the workshop/training. Two days allowance is allowed to the facilitator/coordinator for pre and post-workshop/training preparation. In case workshop/training is conducted outside the Province/City the per diem rate in table A1 should apply and allow only for 1 overnight for pre-preparation of the workshop/ training. A facilitator/coordinator is not allowed to received per diem of $20 or $25 plus allowance $12.5. These per diem and allowance will be paid only if not provided by other organization. The purchasing of stationary and refreshment should attach with invoice or receipts.

VI.3 Rates for Work or services

a) Rate of the translation services

For services such as typing translation and editing valued at less than $200, direct contracting may be mad and the following rate should applied.

Table A4: Rates for work Work Rate (US$) per page

(A4)Translation 5 Editing 3 Typing 2 Photocopy 0.02

b) Size of the translation The size of the translation texts:

English version Average of 300 to 500 words per page (5 letters per word)

font size 11 ( Arial) font size 12 (Time New Roman) Margin 1 inch for top, bottom, left and right.

The size for picture or graphic: Picture/graphic covering less than 50% of the page $5 for translation $3 for editing $2 for typing Picture/graphic covering over 50% of the page, the rate of $2 per

page will apply and no other cost such as typing and translating will accepted.

c) Agreement to Perform Work (APW) For services valued at less than $500, such as translation, typing, data entry, photocopying, supply of materials, maintenance or repair, an

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 15

Agreement to perform Work (APW) may be used (see format APW in Procurement Guideline).

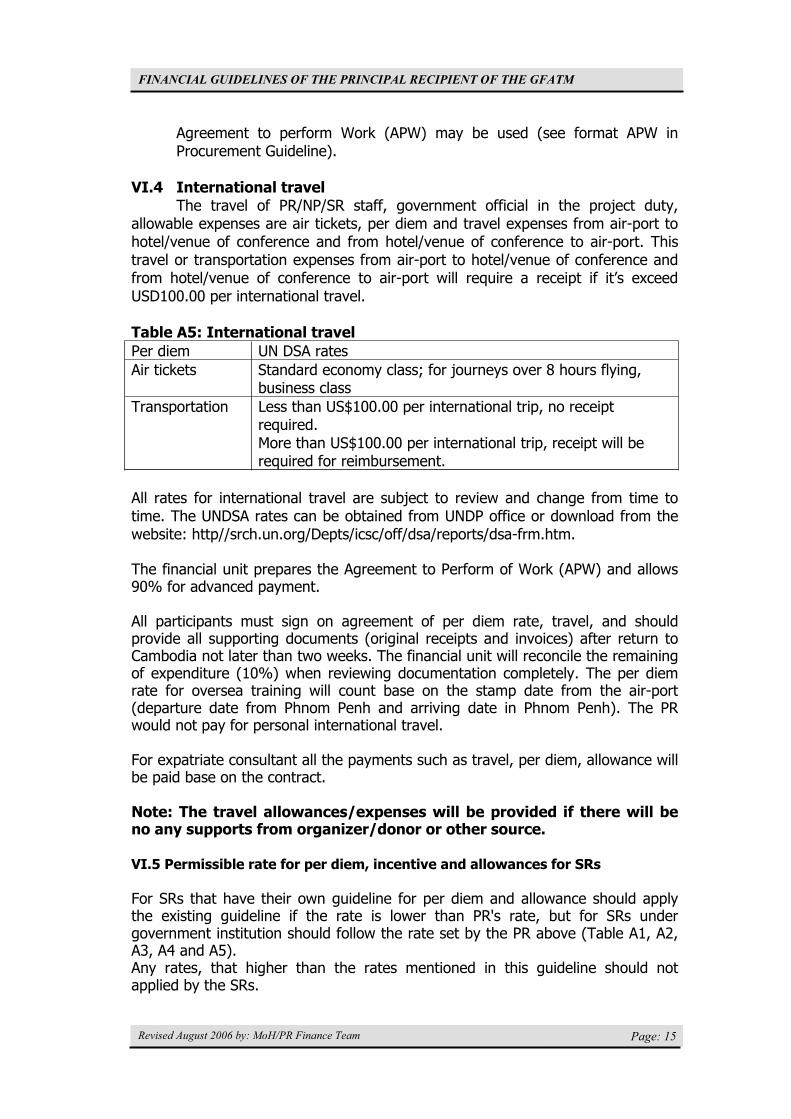

VI.4 International travel The travel of PR/NP/SR staff, government official in the project duty, allowable expenses are air tickets, per diem and travel expenses from air-port to hotel/venue of conference and from hotel/venue of conference to air-port. This travel or transportation expenses from air-port to hotel/venue of conference and from hotel/venue of conference to air-port will require a receipt if it’s exceed USD100.00 per international travel.

Table A5: International travel Per diem UN DSA rates Air tickets Standard economy class; for journeys over 8 hours flying,

business class Transportation Less than US$100.00 per international trip, no receipt

required. More than US$100.00 per international trip, receipt will be required for reimbursement.

All rates for international travel are subject to review and change from time to time. The UNDSA rates can be obtained from UNDP office or download from the website: http//srch.un.org/Depts/icsc/off/dsa/reports/dsa-frm.htm.

The financial unit prepares the Agreement to Perform of Work (APW) and allows 90% for advanced payment.

All participants must sign on agreement of per diem rate, travel, and should provide all supporting documents (original receipts and invoices) after return to Cambodia not later than two weeks. The financial unit will reconcile the remaining of expenditure (10%) when reviewing documentation completely. The per diem rate for oversea training will count base on the stamp date from the air-port (departure date from Phnom Penh and arriving date in Phnom Penh). The PR would not pay for personal international travel.

For expatriate consultant all the payments such as travel, per diem, allowance will be paid base on the contract.

Note: The travel allowances/expenses will be provided if there will be no any supports from organizer/donor or other source.

VI.5 Permissible rate for per diem, incentive and allowances for SRs

For SRs that have their own guideline for per diem and allowance should apply the existing guideline if the rate is lower than PR's rate, but for SRs under government institution should follow the rate set by the PR above (Table A1, A2, A3, A4 and A5). Any rates, that higher than the rates mentioned in this guideline should not applied by the SRs.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 16

CHAPTER VII: DISBURSEMENTS

VII.1 Disbursement of Resources

i. Payments to vendors, staff members must be supported by an official Payment Voucher.

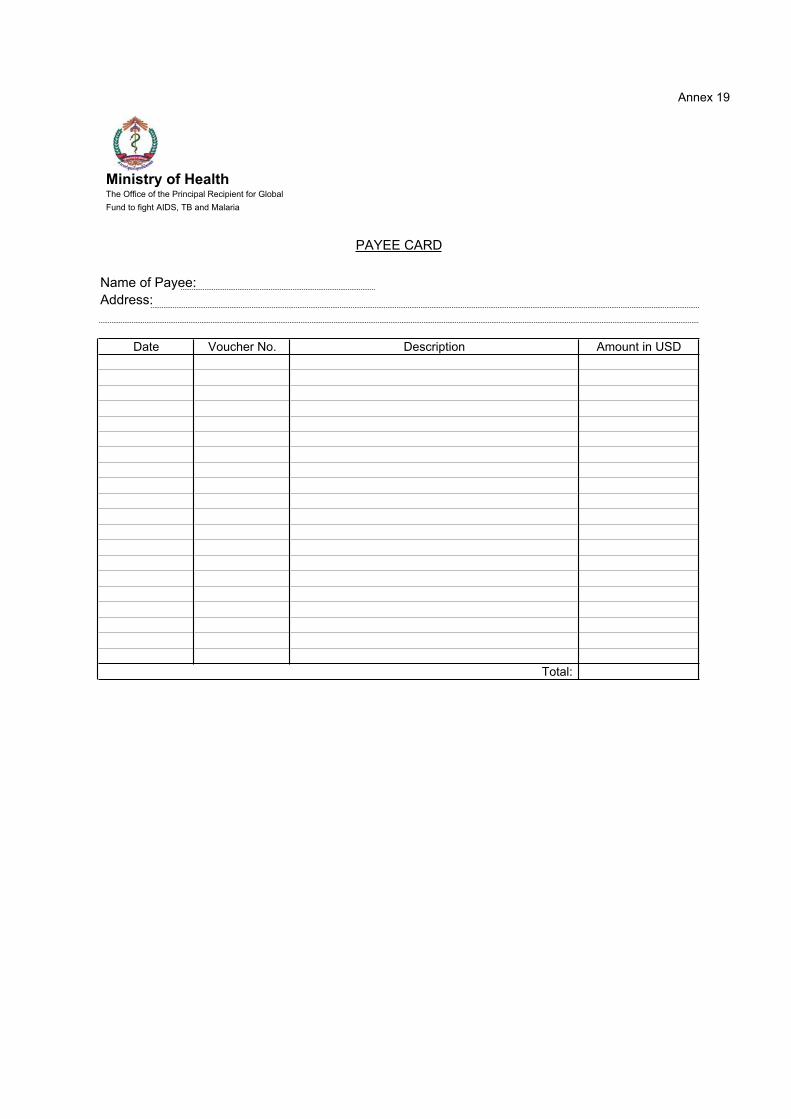

ii. To avoid duplication of payments, the Payee Card annex 19 must be consulted prior to preparation of each payment.

iii. Each payee must be assigned only one Payee Card. iv. Payments made for deposits to obtain services of telephone,

electricity, water, telex, etc. must be charge directly to an appropriate account. The original receipt for these deposits with a copy of the Payment Voucher must be retained in a refundable deposits file. The original receipt will be used for future recovery of the deposit on termination of contract or on discontinuation of service.

VII.2 Disbursement policies

a. Eligible expenditures shall be utilized based on the approved budget and annual operating plans.

b. All payments should be made by cheque or money transferred order (MTO) and cash transactions should be minimized, except for petty cash fund expenditures

c. Voucher system shall be used in the utilization of fund, where all payments of expenditures must be documented properly by appropriate controlled Vouchers, properly signed and approved by the authorized signatory.

d. Expenditures are controlled through formally established expense authorization and approval limits.

e. A person handling asset custodianship should not have access in recording of the disbursement; this is in order to discourage fraud.

f. Before making payment to supplier for purchasing of goods or office supplies, the financial person must verify on the receiving of goods or completion of the services.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 17

VII.3 Disbursement Procedures

Voucher System

A method of controlling payment of expenditures through the use of a Voucher. A voucher is a document prepared to authorize and describe expenditure. Once paid, a voucher as well as the supporting documents must be controlled to eliminate the possibility of presenting again for another payment. This control is affected by the proper stamping, as ‘PAID with the Logo of the PR or SR’. Voucher must also be sequentially numbered to controls its use. Any break in the sequential number series may mean a discrepancy. This system provides assurance that every expenditure is systematically reviewed and verified before payment will be made.

Utilization of Fund will be disbursed in three ways

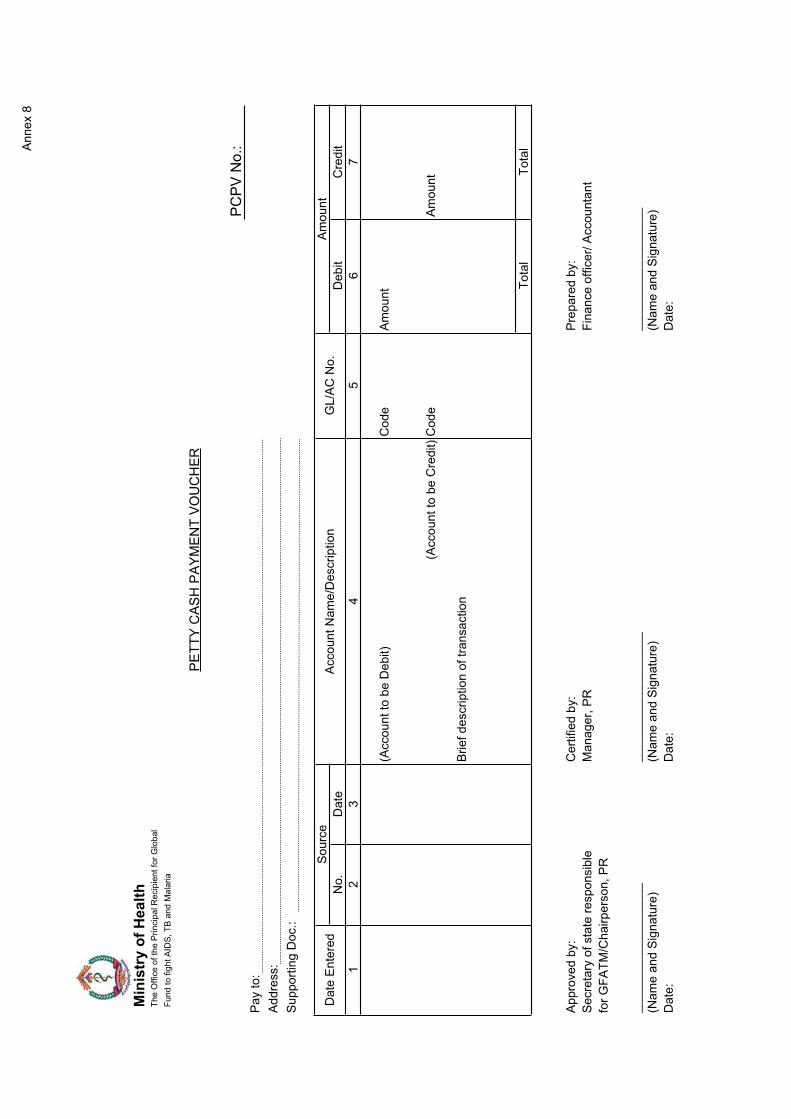

1. Disbursement through Petty Cash (Petty Cash Payment Voucher) PCPV We use PCPV for expenditure less than $500 (Annex 8)

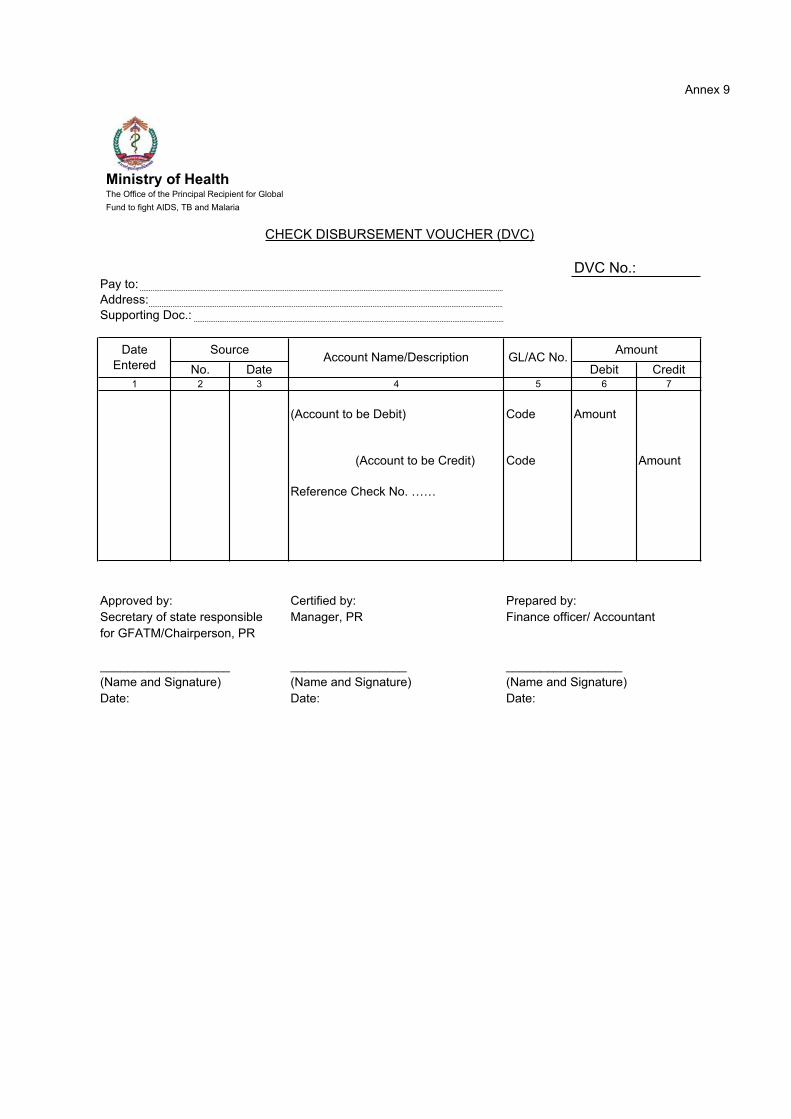

2. Disbursement through cheque (Cheque Disbursement Voucher) DVC We use DVC for expenditure over $500 (Annex 9)

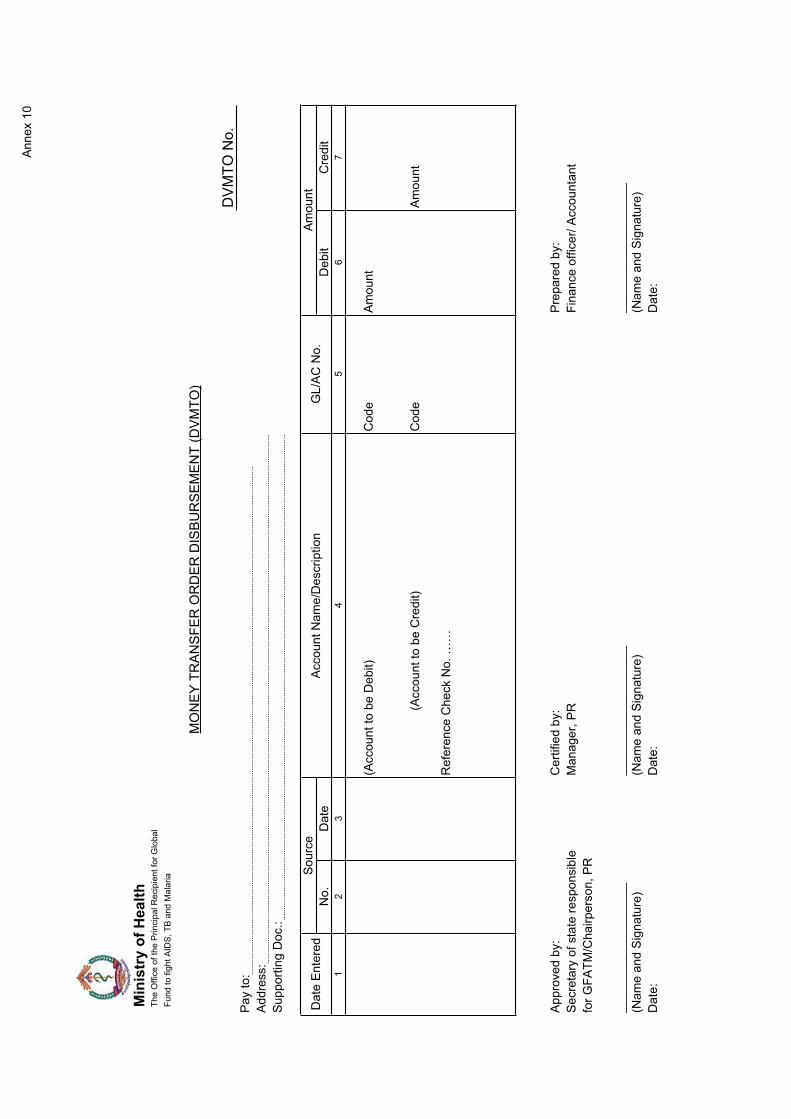

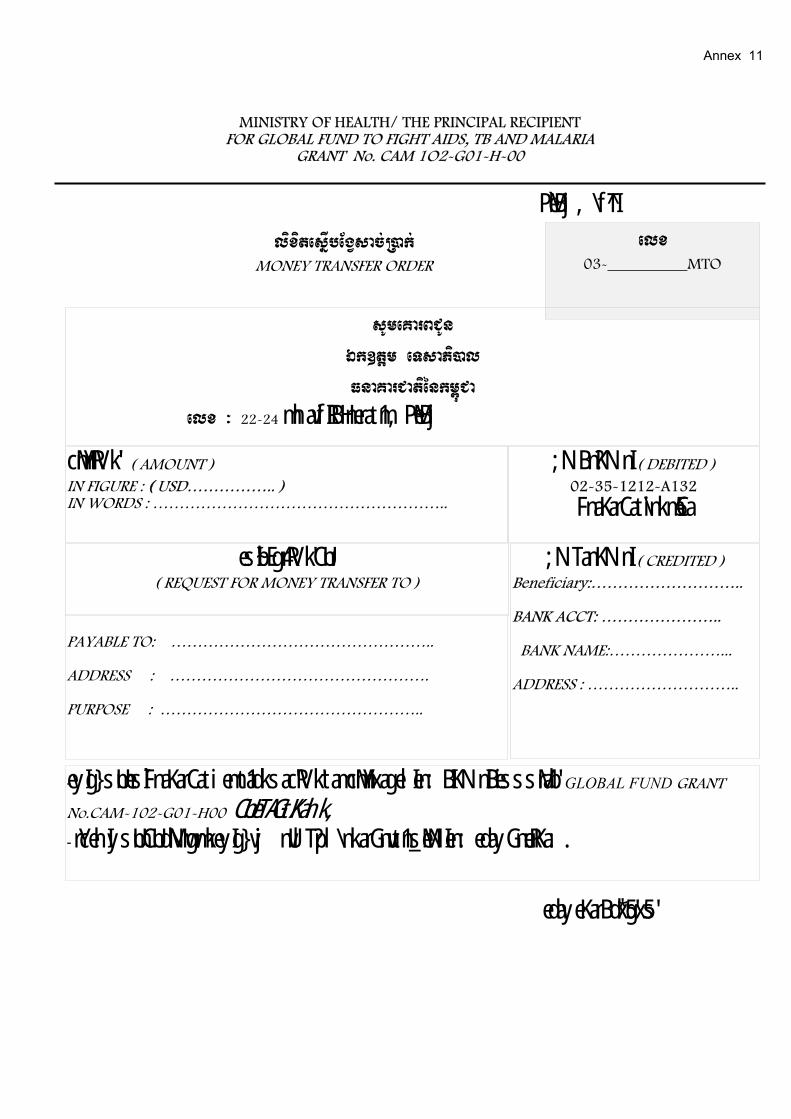

3. Disbursement through Money Transferred Order (DVMTO) (Annex 10 and Annex 11) We use DVMTO for expenditure in large amount and transfer the money to international Bank.

Note: SRs can use their existing disbursement forms. Some SRs with weak financial management identified by PR for subsequent round should follow the form mentioned above.

d) Opportunity to Inspect

The Principal Recipient shall afford authorized representative of the Global Fund and its agents or third party of which the Global Fund notified the opportunity at all reasonable times to inspect activities financed by the Grant, the utilization of goods or service financed by the grant, and agreement books and record.

The SRs shall afford authorized representative of the PR and its agents or third party of which the PR notified the opportunity at all reasonable times to inspect activities financed by the Grant, the utilization of goods or service financed by the grant, and agreement books and record.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 18

CHAPTER VIII: ADVANCED PROCEDURES

VIII. 1. Advanced Procedure

a) Initial advanced

The Principal Recipient channels funds to Sub-Recipients through the advanced system. The ceiling balance is setting base on an analysis of expenditures to be financed through the mechanism of approved quarterly or annual budget divided by quarters. The periodic of advance is quarterly basic. These amounts have been released to their respective programs and Sub-Recipients Bank Accounts, and on going process of liquidation of advanced.

b) Replenishment

1. Requirement On semi-annual basis, Sub-Recipients should prepare a disbursement

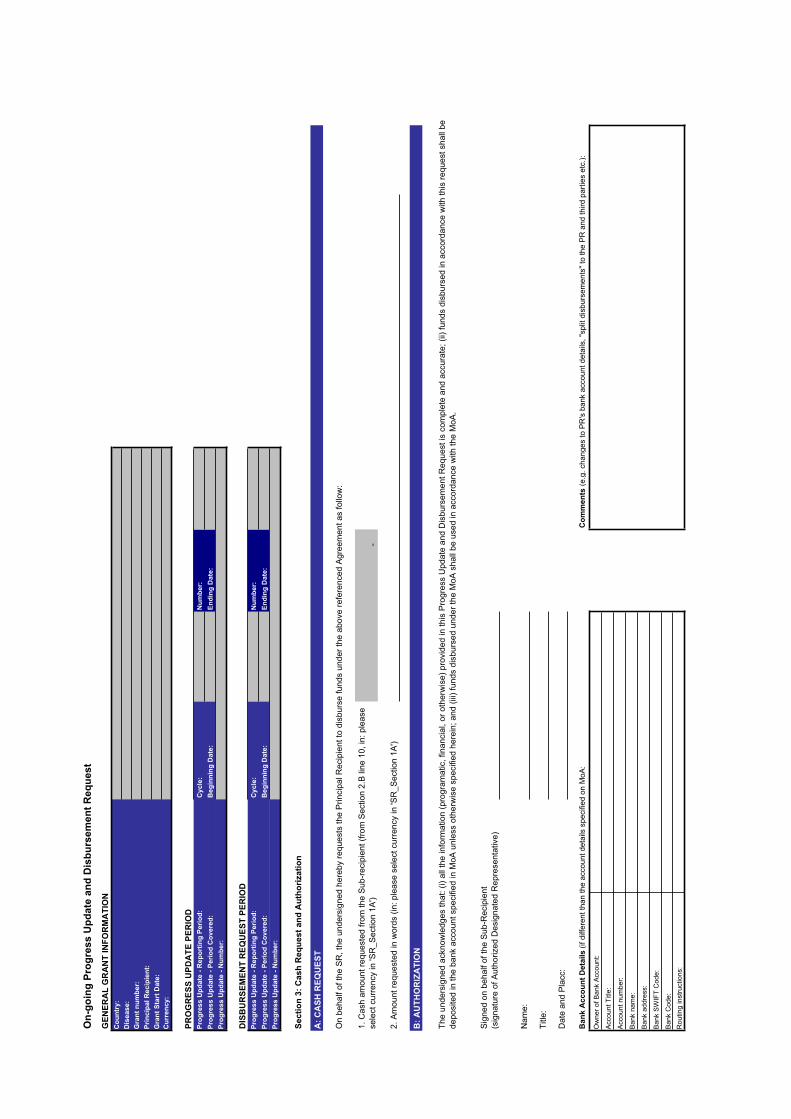

requested and progress update to PR for replenishment of fund, along with necessary supporting documentation, such as annex A, annex B and statement of source and uses of funds. The SRs should follow the format provided by the PRs attached with the Memorandum of Agreement (MoA) and other additional formatted as required by GF and LFA. The PR expects that the SRs could clearly show its disbursements to sub-sub recipients, if it is applicable.

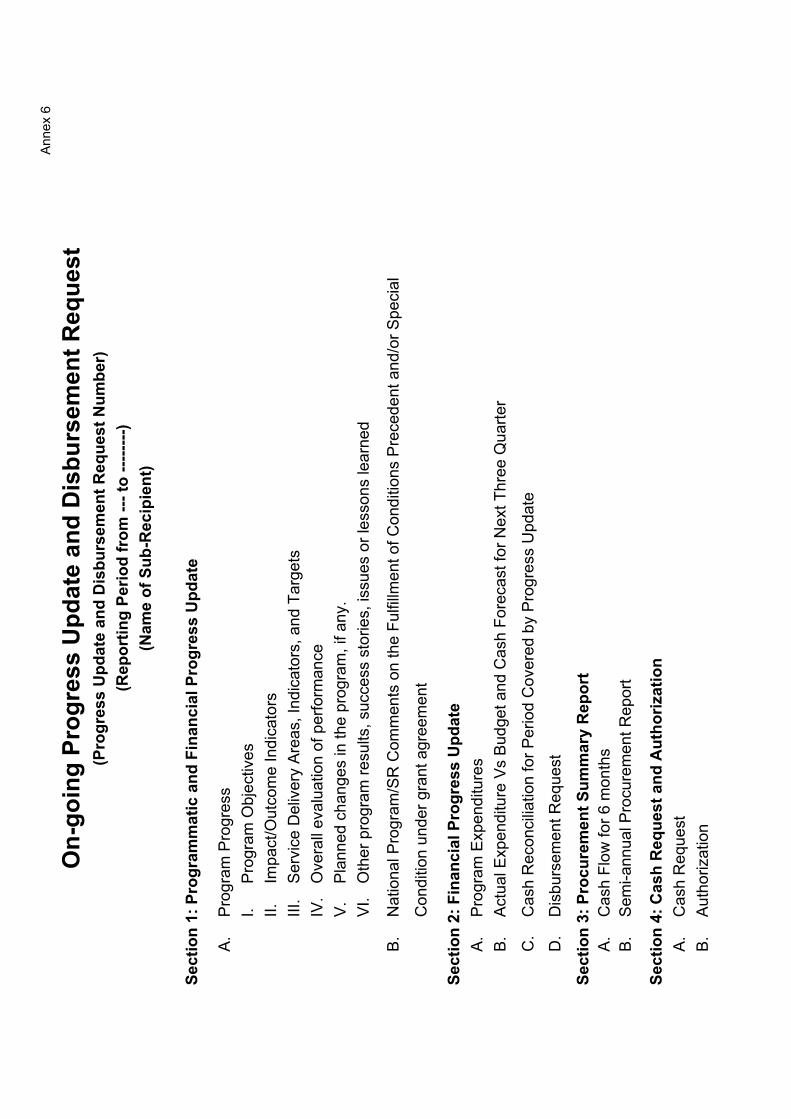

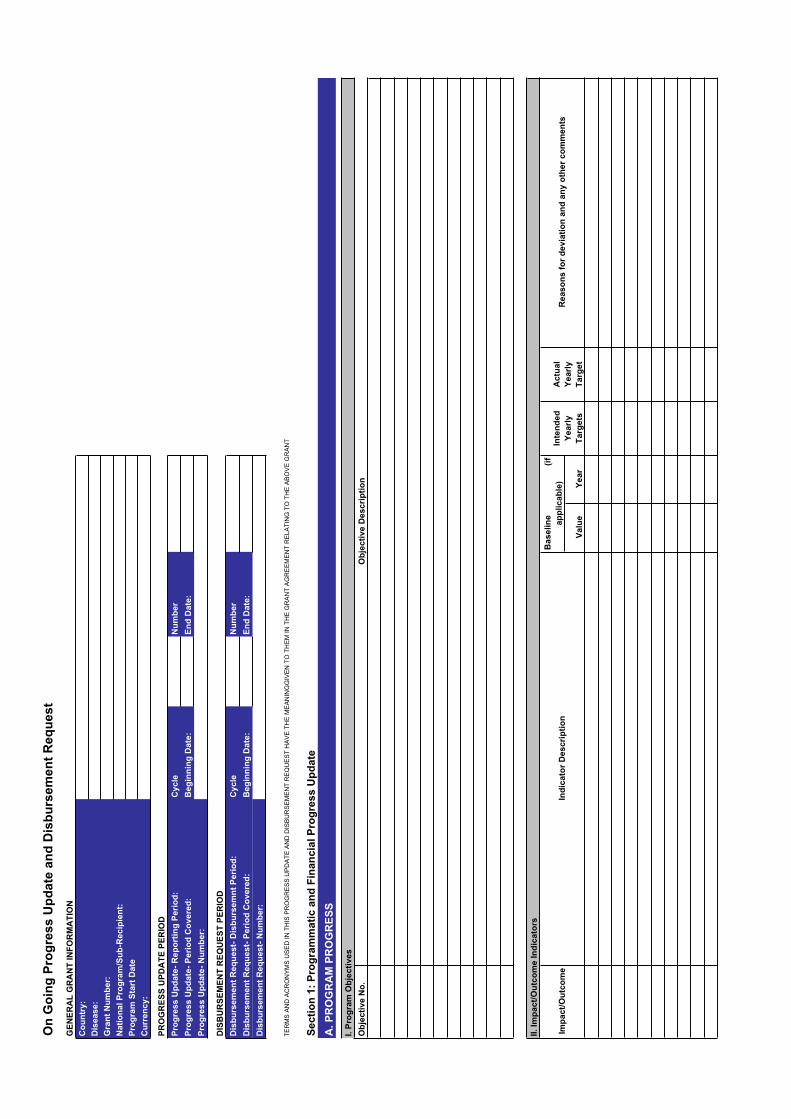

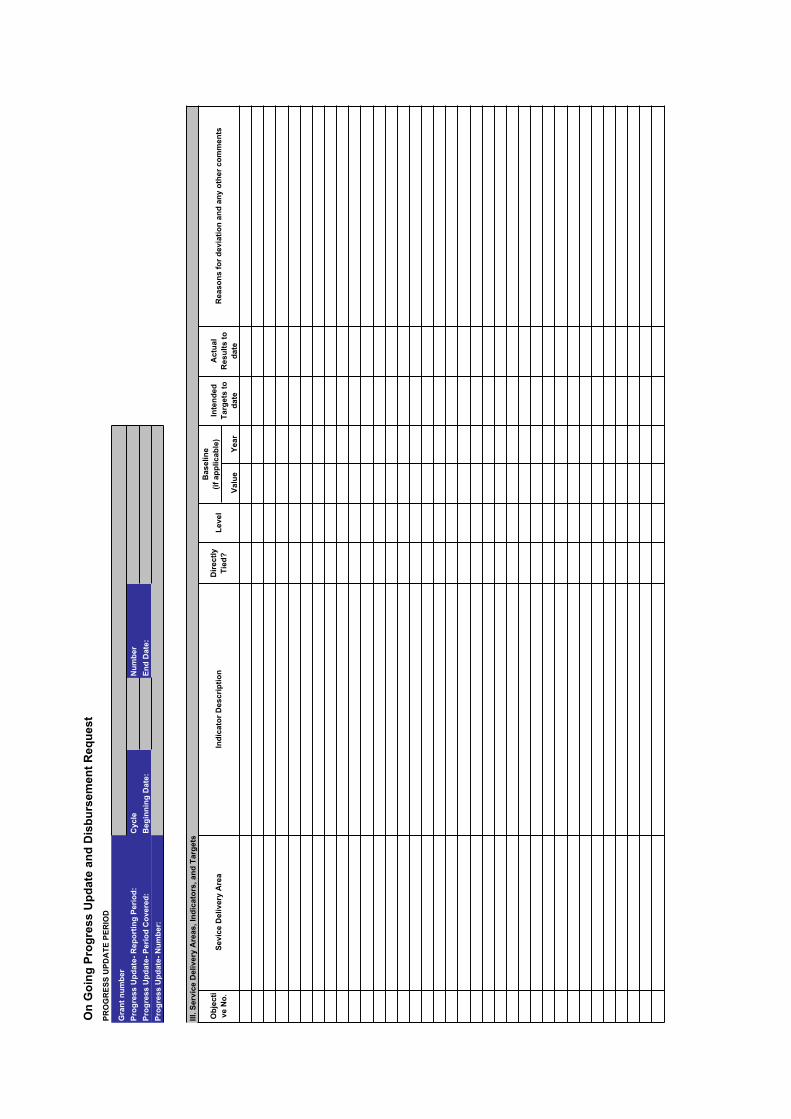

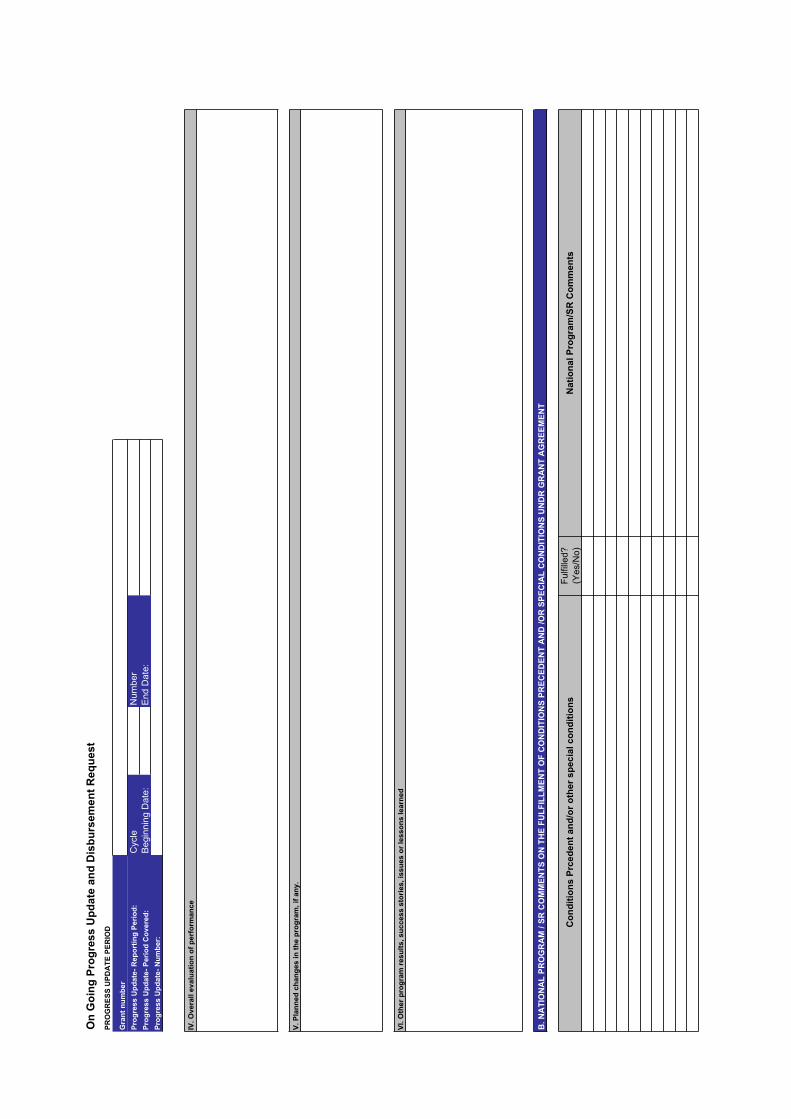

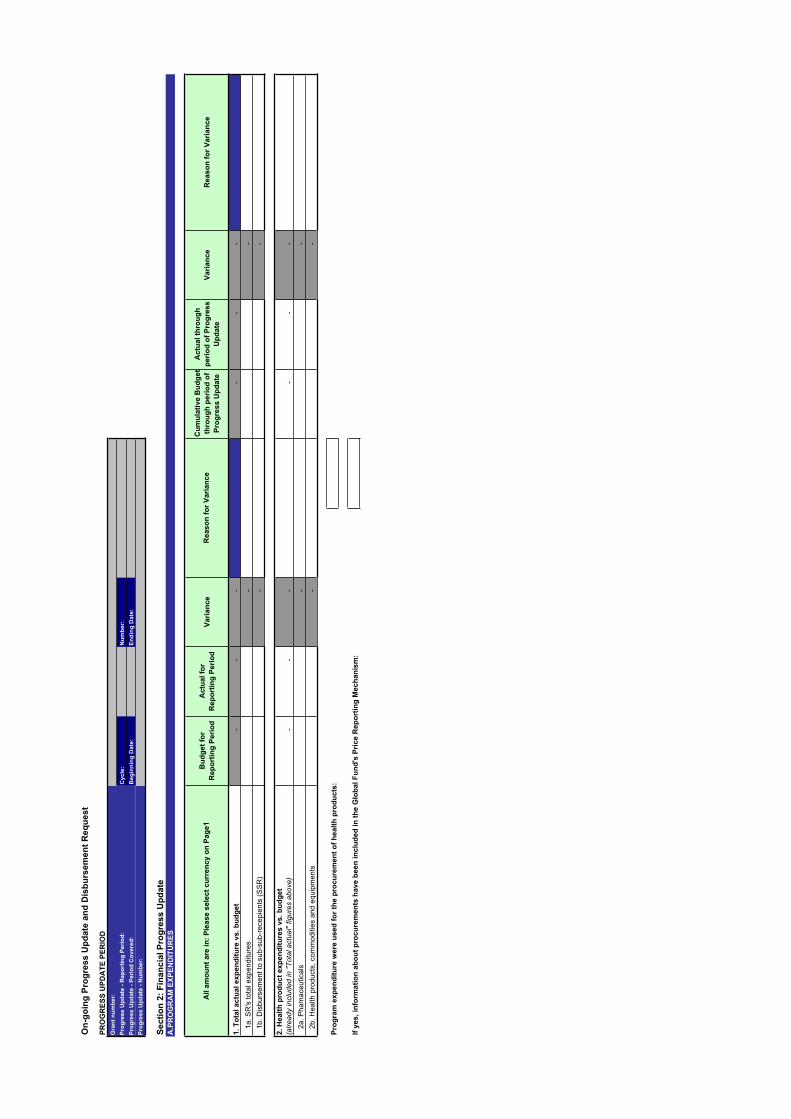

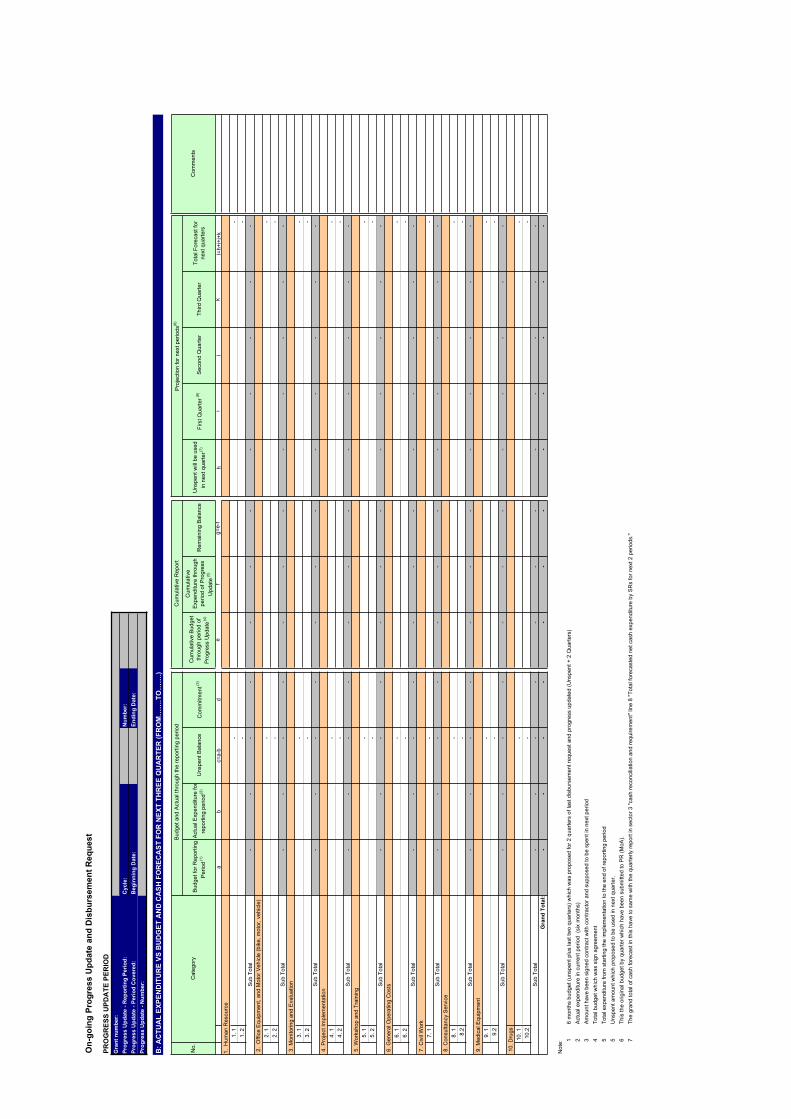

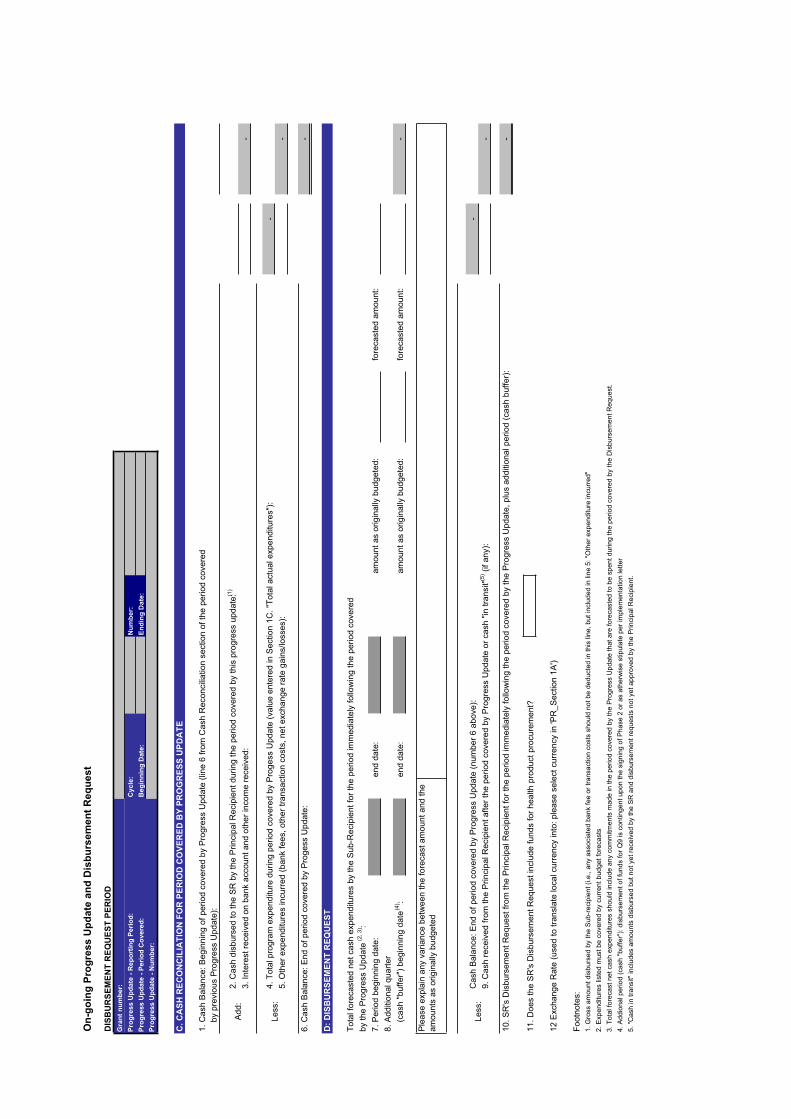

2. Supporting DocumentsOn-going Progress Update and Disbursement Request Section 1: Programmatic and Financial Progress Update

A. Program Progress I. Program Objectives II. Impact/Outcome Indicators III. Service Delivery Areas, Indicators, and Targets IV. Overall evaluation of performance V. Planned changes in the program, if any. VI. Other program results, success stories, issues or lessons

learned B. National Program/SR Comments on the Fulfillment of

Conditions Precedent and/or Special Section 2: Financial Progress Update

A. Program Expenditures B. Actual Expenditure Vs Budget and Cash Forecast for Next

Three Quarter C. Cash Reconciliation for Period Covered by Progress Update

Cash Reconciliation for Period Covered by Progress Update D. Disbursement Request

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 19

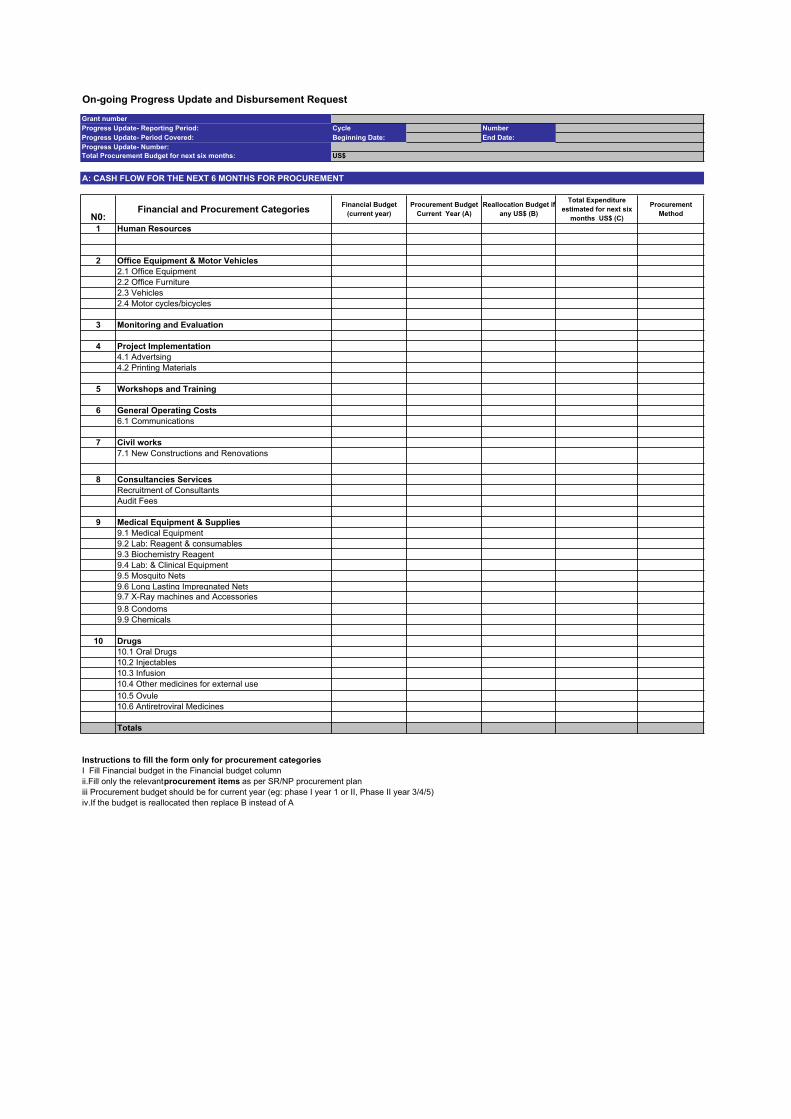

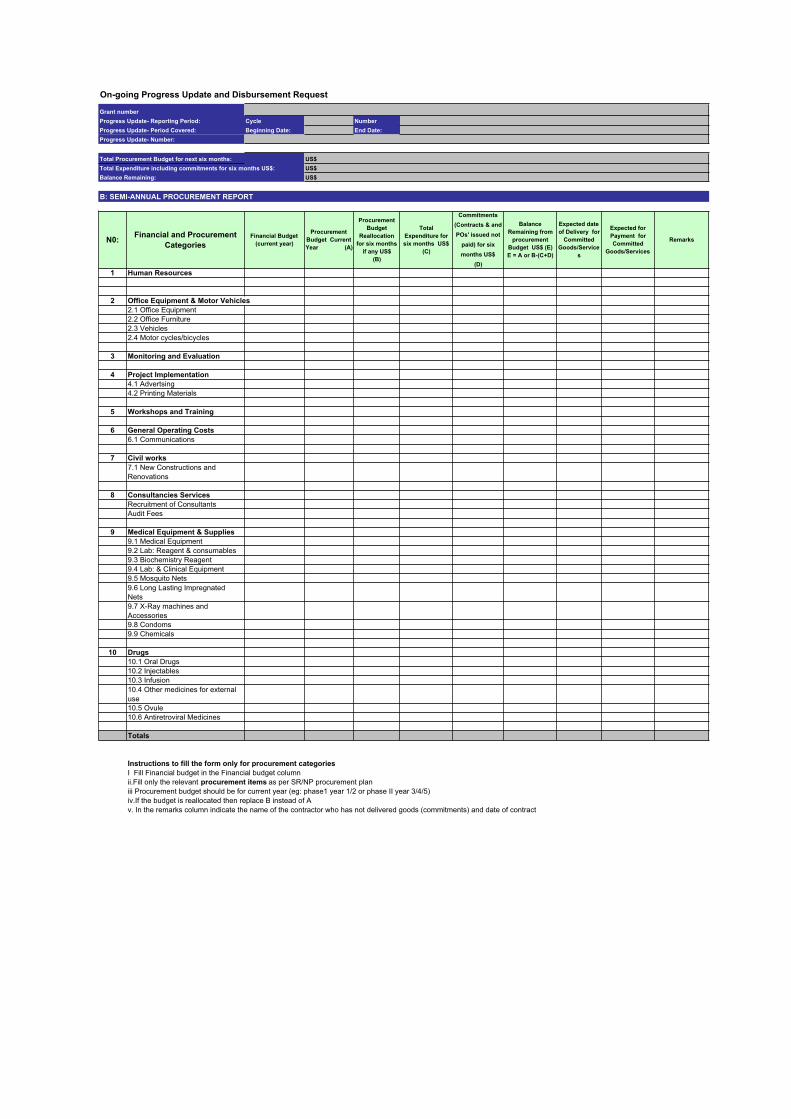

Section 3: Procurement Summary Report A. Cash Flow for 6 months B. Semi-annual Procurement Report

Section 4: Cash Request and Authorization A. Cash Request B. Authorization

3. Submission PR reviews/verifies document and when satisfied, submit for approval. The PR will not replenish any unjustified or ineligible expenditure.

VIII.2 Disbursement of Revolving Fund

This procedure applies for sub-recipient with weak financial system and has no separate Bank Account. It may be necessary to advanced cash amount to sub-recipient or Project Implementation Unit staff for required of expenditure such as conducting workshop or need to supervise in provincial level. The amount of revolving fund that should be set up will depend upon on their average monthly needs. In this case the PR decided to establish $5,000 as revolving fund. The SRs may request two times or three times a month according to their need of activities, but the disbursement of revolving fund should not exceed from $20,000 per disbursement request. This idea came from the Implementation letter on 29 August 2003 of the Global Fund in Geneva.

VIII.3 Policy for individual cash advanced

Individual cash advanced could be an advanced to staff for supervision or advanced for purchase of the supplies.1. Cash advances are only allowed for official project transactions, not for personal use. 2. Cash advances must be authorized by PR, SR senior management (Project Manager, chairperson or Secretary of State of the MoH responsible for GFATM program) based on the expense authorization and approval limits. 3. No cash advance should be approved for PR, SR or any PIU staff, who has previously unliquidated or unsettled cash advances. 4. Cash advance should be settled or liquidated at once, or in the following time frame

Inside Cambodia: within two weeks from the date of ending activities advance Outside Cambodia: within two weeks from the date of ending activities advance

5. Any violation on this aspect shall be subject for disciplinary actions under the sanctions by not providing cash advanced any more or request for refunding of the previous advanced amount.

6. Settlement of Cash Advances by the use of Liquidation Form

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 20

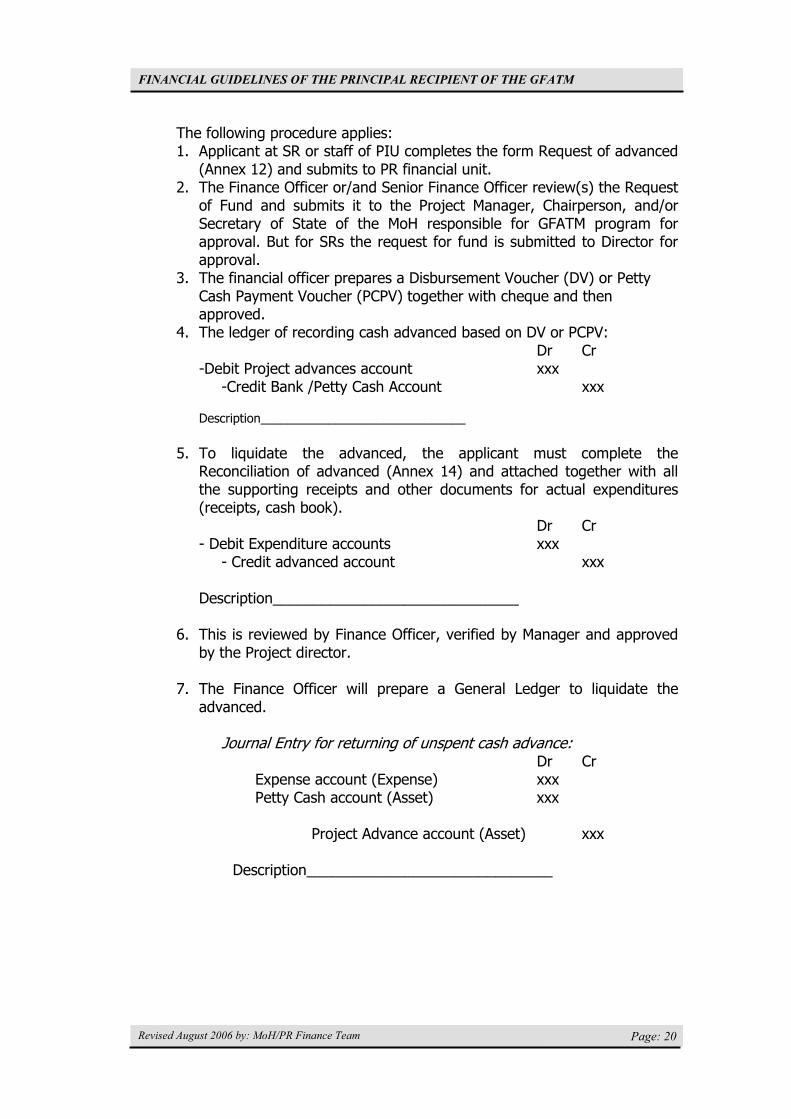

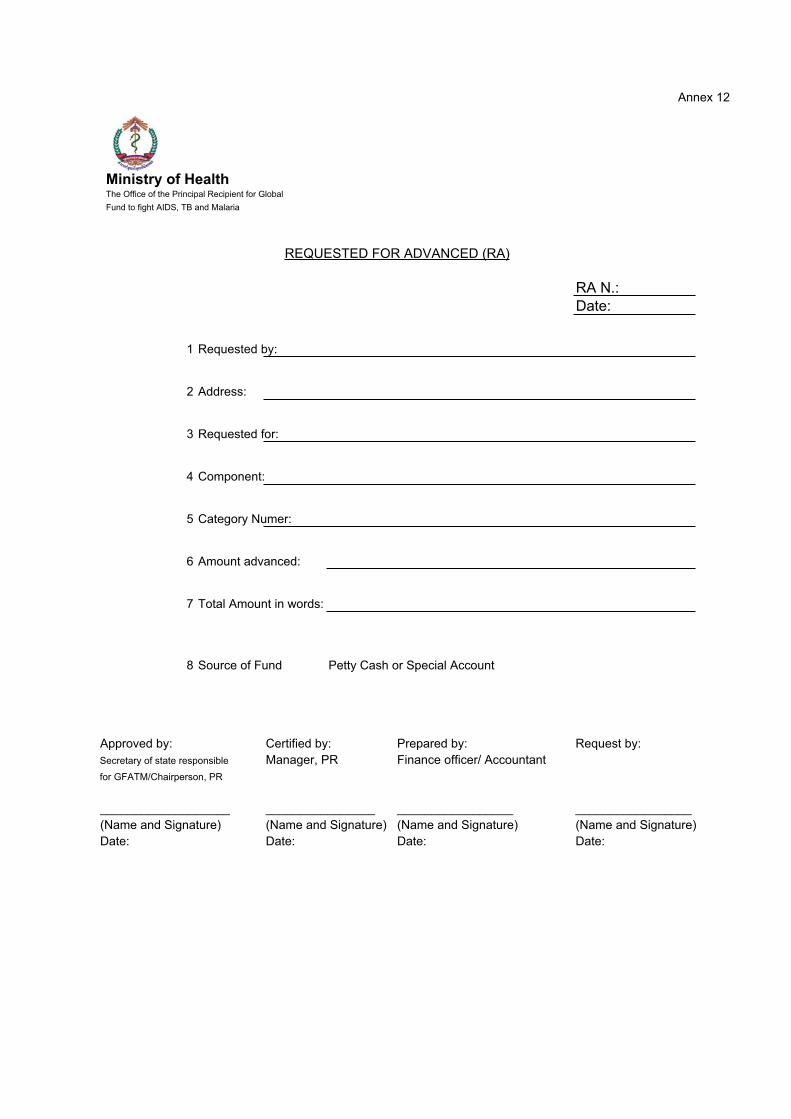

The following procedure applies: 1. Applicant at SR or staff of PIU completes the form Request of advanced

(Annex 12) and submits to PR financial unit. 2. The Finance Officer or/and Senior Finance Officer review(s) the Request

of Fund and submits it to the Project Manager, Chairperson, and/or Secretary of State of the MoH responsible for GFATM program for approval. But for SRs the request for fund is submitted to Director for approval.

3. The financial officer prepares a Disbursement Voucher (DV) or Petty Cash Payment Voucher (PCPV) together with cheque and then approved.

4. The ledger of recording cash advanced based on DV or PCPV: Dr Cr

-Debit Project advances account xxx -Credit Bank /Petty Cash Account xxx

Description______________________________

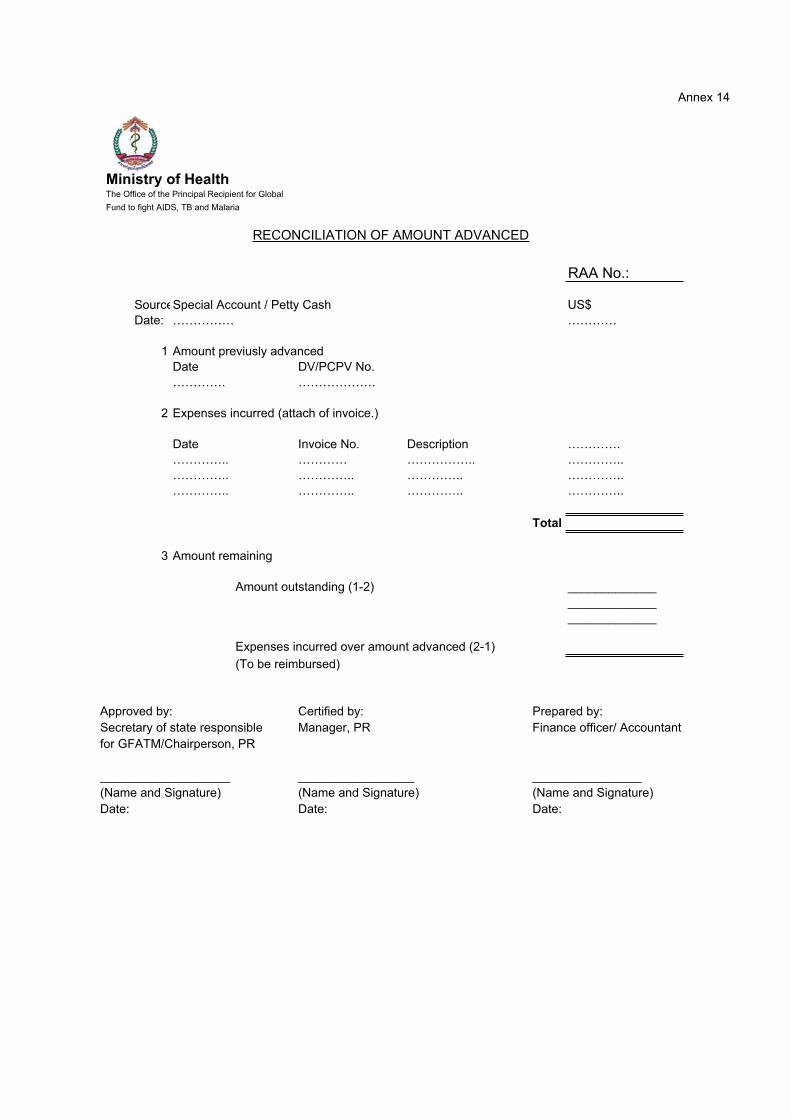

5. To liquidate the advanced, the applicant must complete the Reconciliation of advanced (Annex 14) and attached together with all the supporting receipts and other documents for actual expenditures (receipts, cash book).

Dr Cr - Debit Expenditure accounts xxx - Credit advanced account xxx

Description______________________________

6. This is reviewed by Finance Officer, verified by Manager and approved by the Project director.

7. The Finance Officer will prepare a General Ledger to liquidate the advanced.

Journal Entry for returning of unspent cash advance: Dr Cr

Expense account (Expense) xxx Petty Cash account (Asset) xxx

Project Advance account (Asset) xxx

Description______________________________

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 21

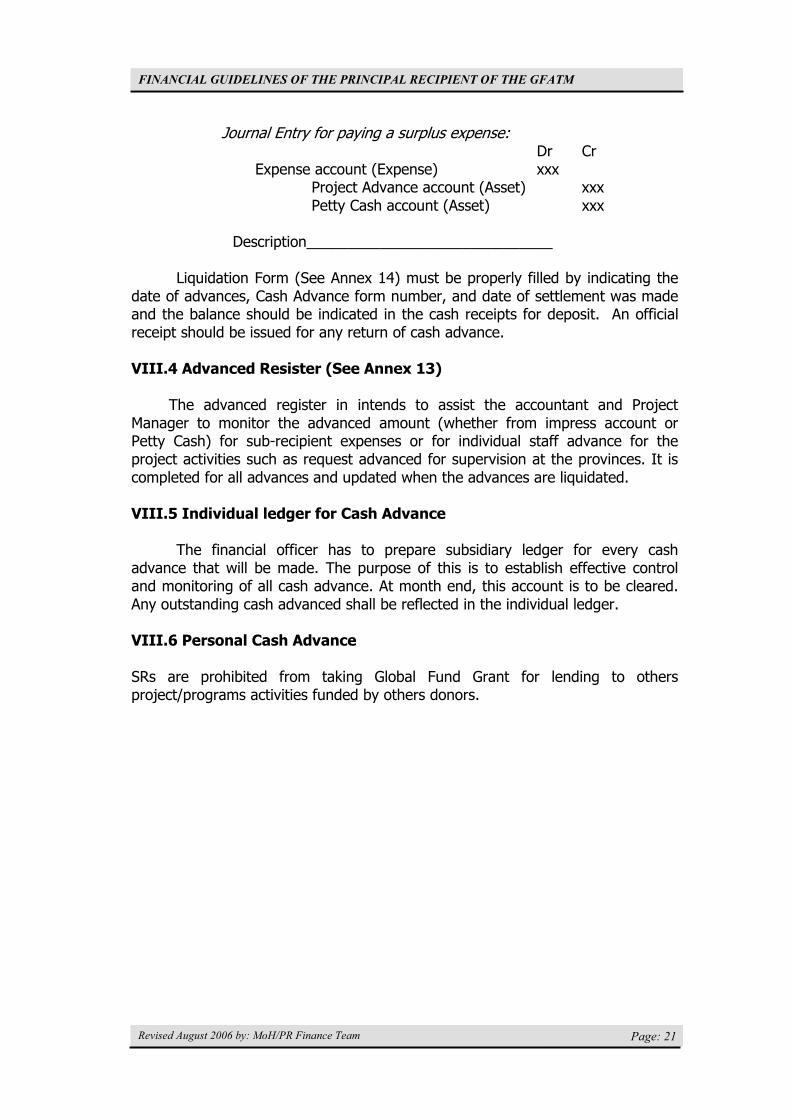

Journal Entry for paying a surplus expense: Dr Cr Expense account (Expense) xxx Project Advance account (Asset) xxx

Petty Cash account (Asset) xxx

Description______________________________

Liquidation Form (See Annex 14) must be properly filled by indicating the date of advances, Cash Advance form number, and date of settlement was made and the balance should be indicated in the cash receipts for deposit. An official receipt should be issued for any return of cash advance.

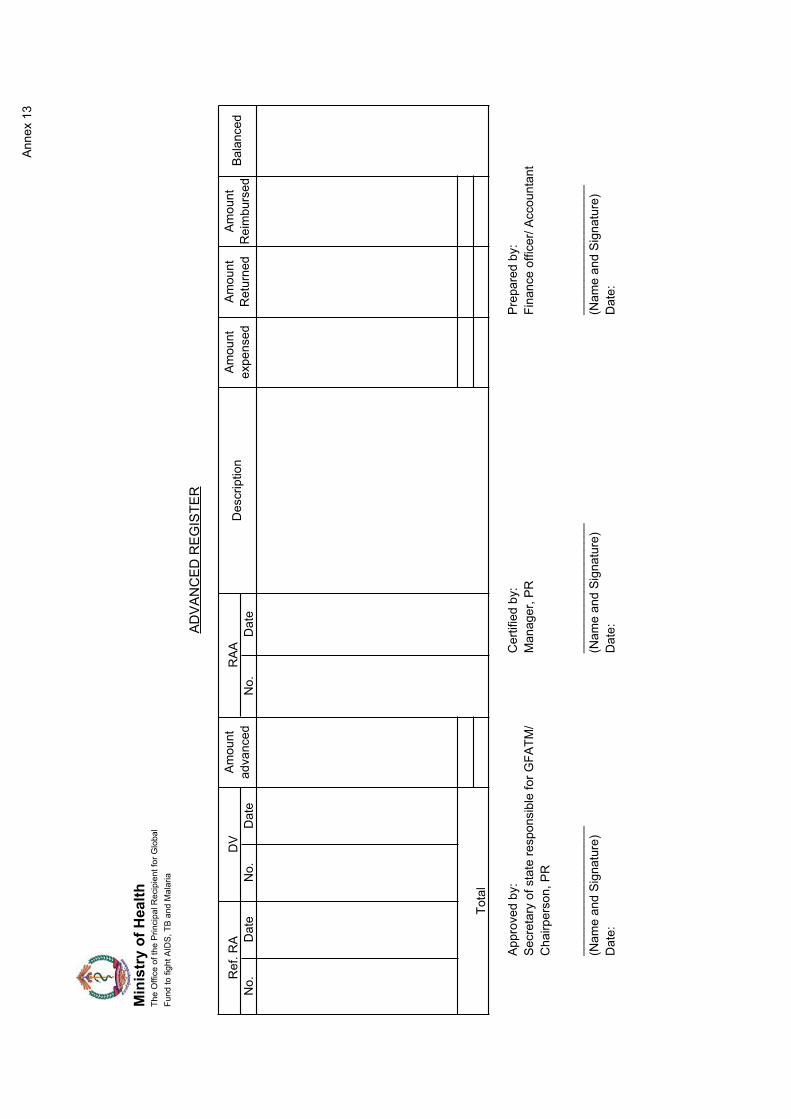

VIII.4 Advanced Resister (See Annex 13)

The advanced register in intends to assist the accountant and Project Manager to monitor the advanced amount (whether from impress account or Petty Cash) for sub-recipient expenses or for individual staff advance for the project activities such as request advanced for supervision at the provinces. It is completed for all advances and updated when the advances are liquidated.

VIII.5 Individual ledger for Cash Advance

The financial officer has to prepare subsidiary ledger for every cash advance that will be made. The purpose of this is to establish effective control and monitoring of all cash advance. At month end, this account is to be cleared. Any outstanding cash advanced shall be reflected in the individual ledger.

VIII.6 Personal Cash Advance

SRs are prohibited from taking Global Fund Grant for lending to others project/programs activities funded by others donors.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 22

CHAPTER IX: CASH AND BANK MANAGEMENT

IX.1 CASH MANAGEMENT

a) Banking: The Secretary of State of the MoH responsible for GFATM program has established the Bank Account for the GFATM grant. These grant funds will provide available financial resources to the office of the Principal Recipient for the operating expenses activities of the PR and Sub-recipients for payments relating to the GF grant approved proposals.

b) Proceeding of Grant: The approved Sub-recipients will receive grant proceeds for their approved proposals through the Office of the Principal Recipient and upon submission of their respective disbursement requests based upon approved activities as reflected in the periodic reports submitted to the office of the Principal Recipient. The Bank accounts operated by Sub-recipients will be those reported to the office of the PR in compliance with the information provided in the Memorandum of Agreement (MoA) signed between the PR and the approved sub-recipient.

c) Type of Bank Accounts and Currency of Bank Account: The type of bank account opened by the Ministry of Health for the GFATM grant management is a U.S. Dollar based account held at the National Bank of Cambodia. As the disbursements from the Global Fund Headquarters are effected in U.S. Dollar currency, and that the majority of the disbursements are to the made in U.S. Dollars, Sub-recipient, will be required to open separate bank accounts, preferably at the Banks where they currently hold their accounts for other donor funds. However, SR shall operate and maintain a separate bank account for receipt and disbursement of fund under the Memorandum of Agreement with reputable and reliable bank in Cambodia. It is recommended to select National Bank of Cambodia for this purpose to ensure the reliability of banking system. If SR chooses to operate with other bank than this recommended one, it is the SR’s own responsibility to ensure the reliability of banking system for the entire operation of the Program.

c) Currency of the Bank Account: as explained above, and for practical operational purposes, it is highly recommended that all approved Sub-recipients of GF grants should open separate U.S. Dollar, non interest earning accounts, bank accounts. However, Sub-recipient is allowed to open bank account with an interest earning account unless there has been prior approved by the PR based upon case by case observation of SR’s financial and banking management system. Details of such accounts opened must be communicated to the office of the PR as required and stipulated in the Memorandum

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 23

of Agreement signed between the office of the Principal Recipient and all approved Sub-recipients.

IX.2 DESIGNATION OF BANK SIGNATORIES

a) Bank Signatory Panel: Bank signatories are designated by the Secretary of State of the MoH responsible for GFATM program for the operation of the GFATM grant special bank account by the office of the Principal Recipient (PR) of the MoH. For Sub-recipient, the designation of bank signatories for the operation of the special GFATM grant proceeds, received through the office of the PR, should be decided upon by the respective Directors of approved Sub-recipients. Existing Bank Signatories at SR levels can of course sign cheques and/or make other GF related approved transaction. It was agreed during the 7 may 2003 workshop conducted by the office of the PR at Sunway Hotel that two signatories of authorized authenticated specimen signature of the SRs will be joinly signed for any issuance of cheques or bank transferred under the Global Fund to fight AIDs, TB and Malaria (GFATM) Program Grant.

b) Responsibilities of Bank Signatories: The responsibilities of officially designated bank signatories include the following:

i. Ensure that GF grant funds are not deposited in personal bank accounts. Conversely, personal or other non-official funds must not be deposited in official bank accounts.

ii. Ensure that cheques and bank transfers have been properly prepared and are supported by adequate documentation.

IX.3 BANK TRANSFERS

a) Management of Bank Transfers: Bank transfer, where the local banking system can process bank transfers promptly and accurately, this method of payment can be used. When payments are made by means of a bank transfer, a Bank Transfer Request (BTR), should be prepared using the forms provided by the bank for this purpose.

b) Numbering Banks Transfers: The following information must be included in the BTR:

i. Date: Date of Transfer Request; ii. PV No.: Number of Payment Voucher (PV) for which the Bank

Transfer is being requested; iii. BTR No.: A sequential number is generated by the Concerned

Office’s Accounting System;

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 24

iv. The bank name, account number, title and currency of the Bank Account from which the transfers are requested to be made;

v. The name(s) of the payee(s), the name of the banks(s) and the bank account number(s) to which the transfers are requested to be made;

vi. The amounts to be transferred to each payee and the total amount of the transfer(s) being requested. The total amount of the BTR must be indicated both in words and in figures. The amount in words must indicate the currency of payment, in words; the amount in figures should be preceded by the currency symbol.

c) Signatories of Bank Transfers: The name(s) and signature(s) of the authorizing office(s) as designated bank signatories on the bank signatory appearing panel.

d) All other basic principals and controls regarding the issuance of cheques also apply to bank transfers regarding numbering, signatories and safe keeping, etc.

IX.4 USE OF CHEQUES

a) Only one cheque book must be used at any one time and spare cheque books must be kept in the safe of Principal Recipient, and Sub-recipients according to the already existing internal control arrangements.

b) Numbering of Cheques: The bank must be requested to provide serially numbered cheques. If no such serial numbering system exists, the concerned office must number the cheques serially, in ink, staring with No. 1, upon receipt of the cheques. The numbering sequence must be continued without interruption for cheques books received subsequently.

c & d) Control of Cheques: The stock of cheque books must be controlled by a register in which receipts and issues must be recorded. All cheques must be accounted for.

Cheques shall be made out to a payee who is the provider of goods and/or services as evidenced by supporting documentation. Cheques shall never be made out to third parties or to non-defined payees e.g., bearer, cash, etc.

e) Cheques shall not have erasures or corrections. If a mistake is made anywhere on a cheque it should be voided and a new cheque prepared. Authorized signatories shall ensure that this instruction is adhered to.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 25

f) i. Following issuance and signing, cheques which are not immediately mailed or delivered to payees must be kept in a secure location within the Finance Unit, and placed in the safe during non-working hours. During working hours, the cheques must also be kept in a secure manner in the custody of the responsible officer. When held for pickup, the responsible officer must compare cheques with the register before releasing them to payees. The payees must provide proof of identity which shall be recorded on the cheque register along with the signature of the recipient. In the event that the cheque(s) are not collected within 15 days of issuance, they must be cancelled and reissued when required again.

ii. A voided cheque is one that, owing to an error in preparation, is not actually used. Care must be exercised that such a cheque is properly "voided".

iii. In the Accounting System, the disbursement details including the cheque number would already have been recorded in the cash book. The PV will, therefore, have to be cancelled (using the 'cancel PV option'). Therefore, a new PV should be prepared and a new cheque assigned.

iv. If, for any reason, cheques are returned "uncashed" by the payees, such cheques must be "voided" and the original entry should be reversed as explained above.

g) Outstanding Cheques must be accounted for in the Cash Reconciliation form prepared at the end of each month when closing the monthly accounts.

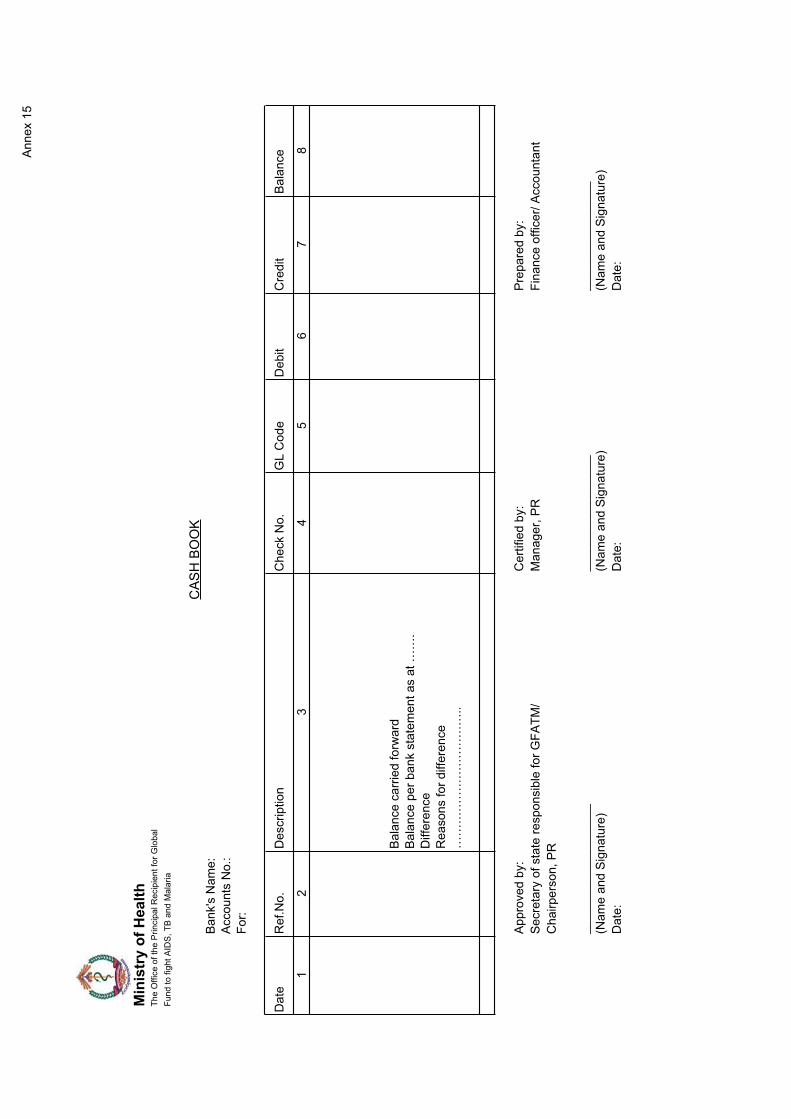

IX.5 CASH BOOK

a) Maintenance of the Cash Book:

i. A cash book must be maintained for the bank account and bank reconciliations must be prepared monthly for each account. The cash books and bank reconciliations are part of the monthly accounts.

ii. Disbursements shall be recorded in the accounts and the Cash Book as of the date they are made, that is, when the cheque is issued, the bank transfer is requested or cash is paid out.

b) The Cash Book must be reconciled at the end of each month and a new Cash Book maintained for the following month.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 26

XI.6 BANK STATEMENT

a) Timing of Receipt of Bank Statements from the Bank:

i. Bank Statements: Immediately after the end of each month, arrangements must be made with the bank to provide statements in duplicate, showing:

Opening balance at the beginning of the month; - Daily transactions (showing the cheque number or bank transfer number concerned for each payment by cheque or bank transfer respectively; and

Closing balance at the end of the month.

Where local regulations allow for paid cheques to be returned with the monthly bank statement, the cheques cashed during the month must be included with the original bank statement.

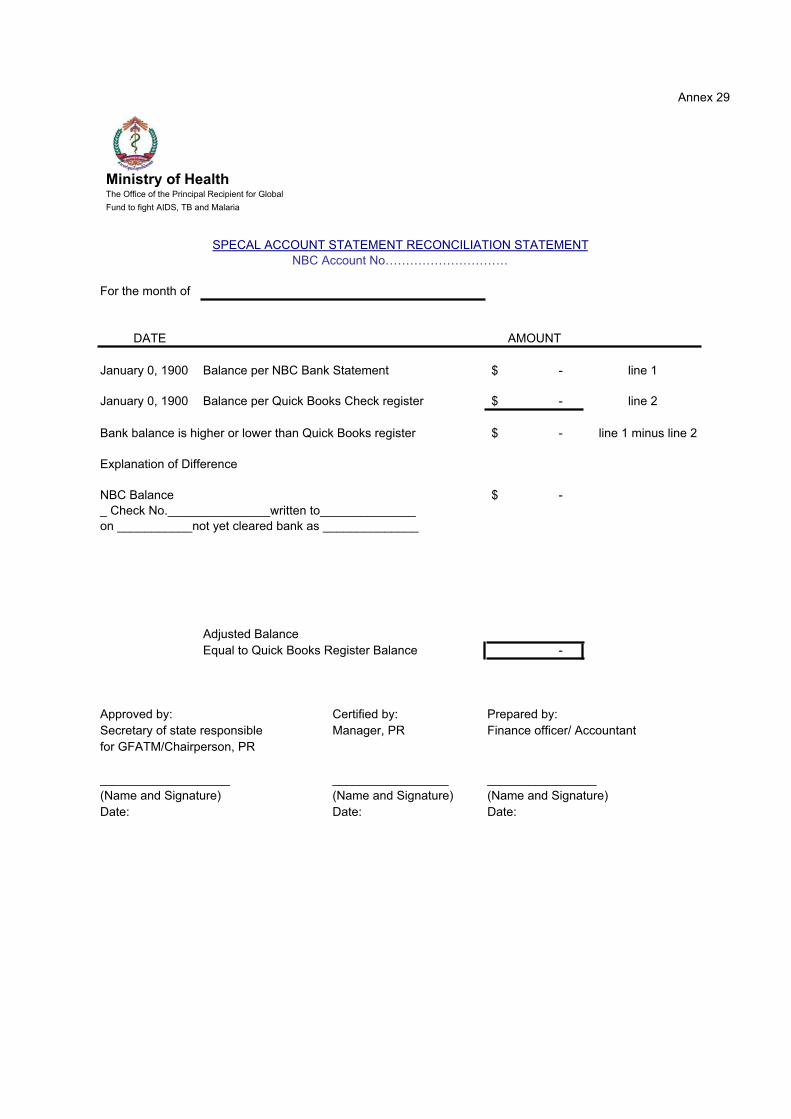

b) If any items appear on the bank statement that have not previously been incorporated in the office accounts (e.g., bank charges) they will form part of the bank reconciliation. Such items must be included in the accounts in order to ensure correct bank reconciliation.(Annex 29)

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 27

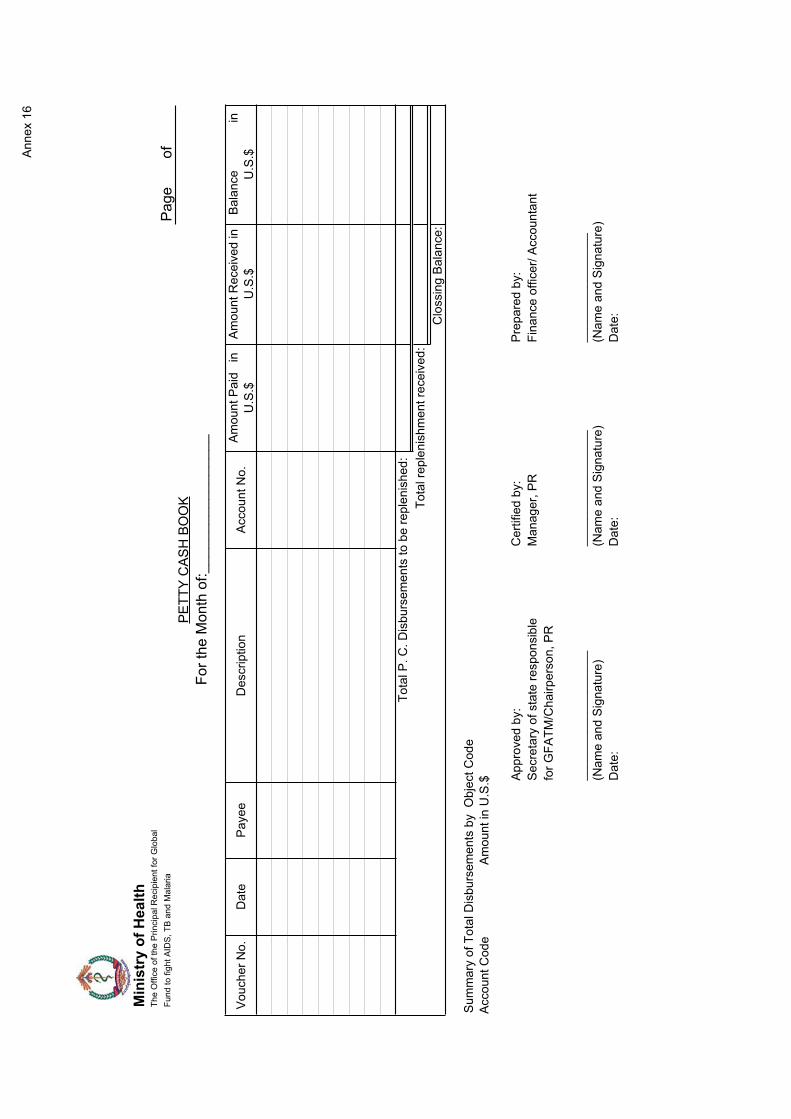

CHAPTER X: PETTY CASH BOOK

X.1 a) Maintenance of the Monthly Petty Cash Book: The maintenance of the Petty Cash Book is fairly simple in that this book is intended for the posting of payments made from cash available for the payment of amounts not exceeding U.S. $ 500.00 (Five Hundred U.S. Dollars) per payment.

b) The level of Petty Cash (for the office of the Principal Recipient (PR) has been decided to be the U.S. $5,000.00 (Five Thousand U.S. Dollars).

Petty Cash Limits In PR safe $5,000 In SRs safe should not exceed $5,000

Note: The SRs can decide on there own Petty Cash limits based on their exsisting procedure and guidelines, but in no case shall the Petty Cash limits exceed USD5,000.00.

c) Monthly Closing of the Petty Cash Book is recommended, however, the Petty Cash can be replenished more frequently, as the need may arise, during a particular month. Doing so shall require the closing of the Petty Cash Book by balancing it and preparing a Payment Voucher to which all Petty Cash Supporting documents are attached together with the reconciled Petty Cash Book. A cheque should be issue in the amount of the actual expenditures to bring back the Petty Cash to its original operating level.

d) To keep petty cash fund in separate locked cash box. Personal money should not be mixed with the the Petty Cash Fund.

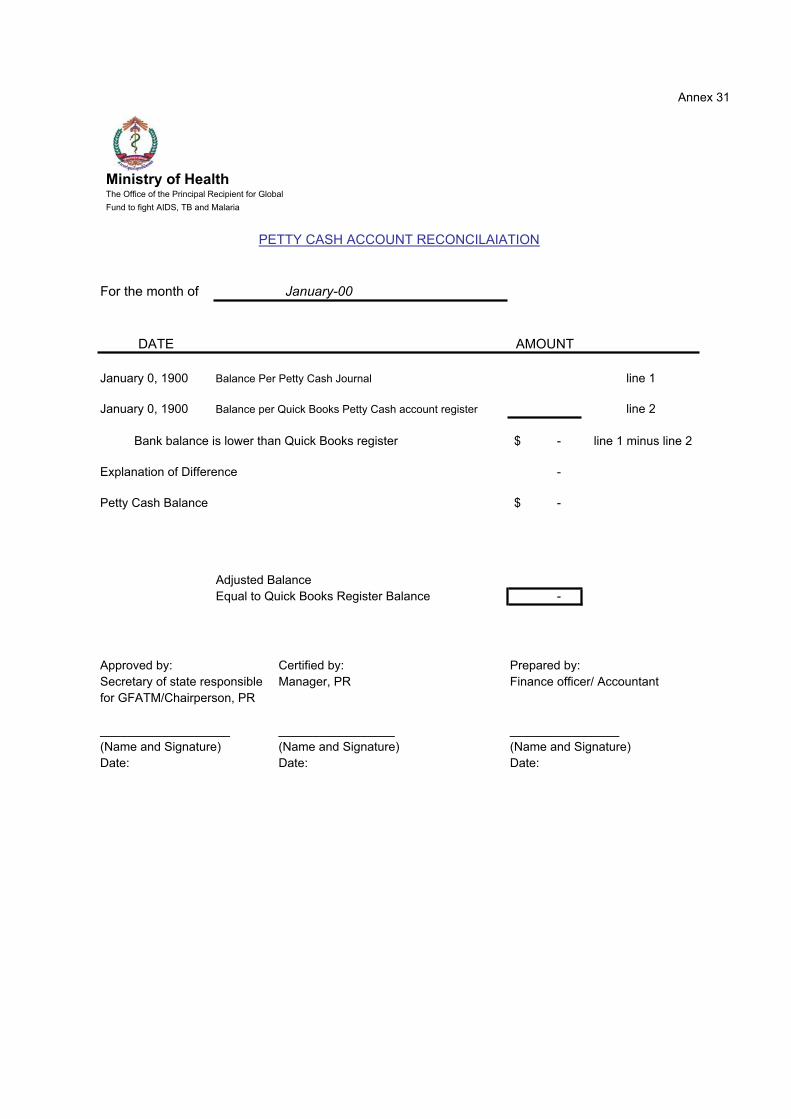

e) Cash Reconciliation Statement (Annex 30)

Cash count should be performed by Accountant or a person who is not involve of handling the petty cash, on a regular basis in order to reconcile the actual cash against the cash book/petty cash book. The result of the weekly cash count should be reconciled with the balance per Cash book/Petty Cash Book. This is to be continued and completed until end of the month. Any discrepancies between the cash balance counted and balance per cash book should be investigated immediately and has to report to top management on the form where indicated. Cash Count Sheet (Annex IV.31) must be prepared showing the actual date, time of count and signed by the Accountant who has counted the cash and properly acknowledged, and verified by

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 28

Project Manager. Then, This Cash Reconciliation Statement has to be approved by Chairperson, and/or Secretary of State of the MoH responsible for GFATM program. But for SRs This Cash Reconciliation Statement is submitted to Director for approval.

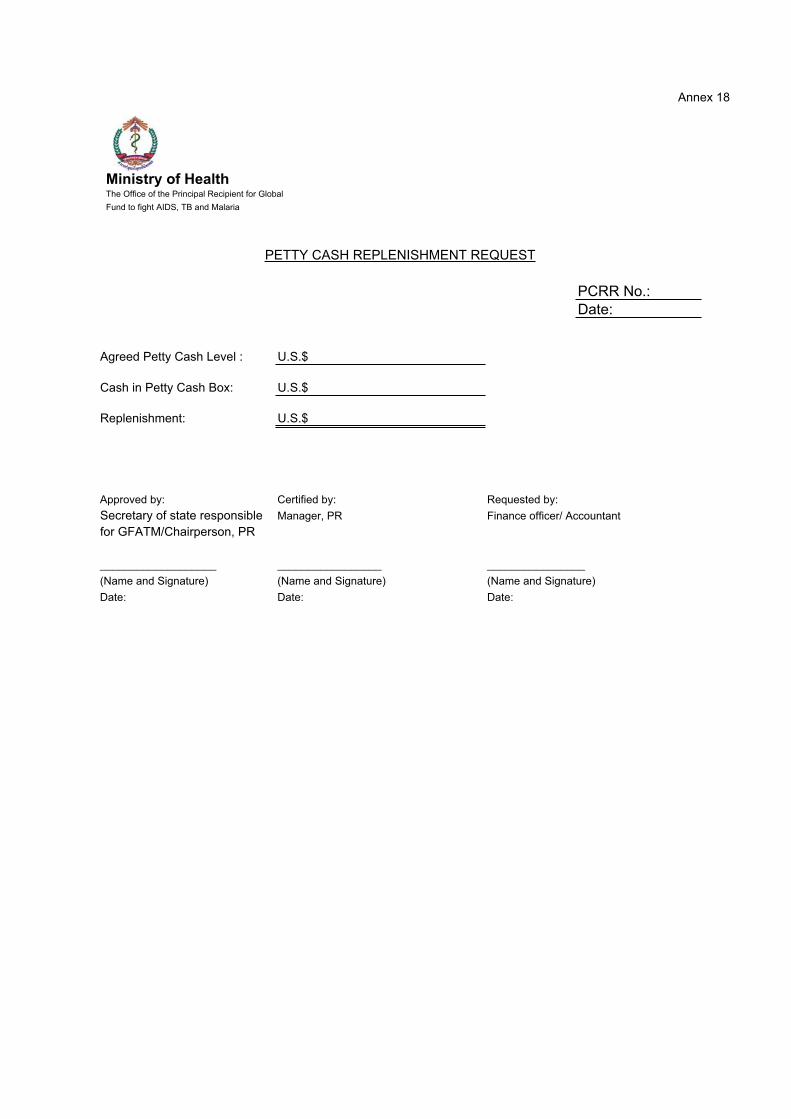

f) Petty Cash replenishment Imprested Fund Method of International Accounting Standards should be used in the replenishment of fund. When Petty Cash fund is at low level equivalent to 10% of the limit amount is allowed for replenishment. The amount of replenishment should be the amount of total expenditures incurred for the period. The form for Petty Cash Replenishment sees Annex 18.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 29

CHAPTER XI: ACCOUNTING

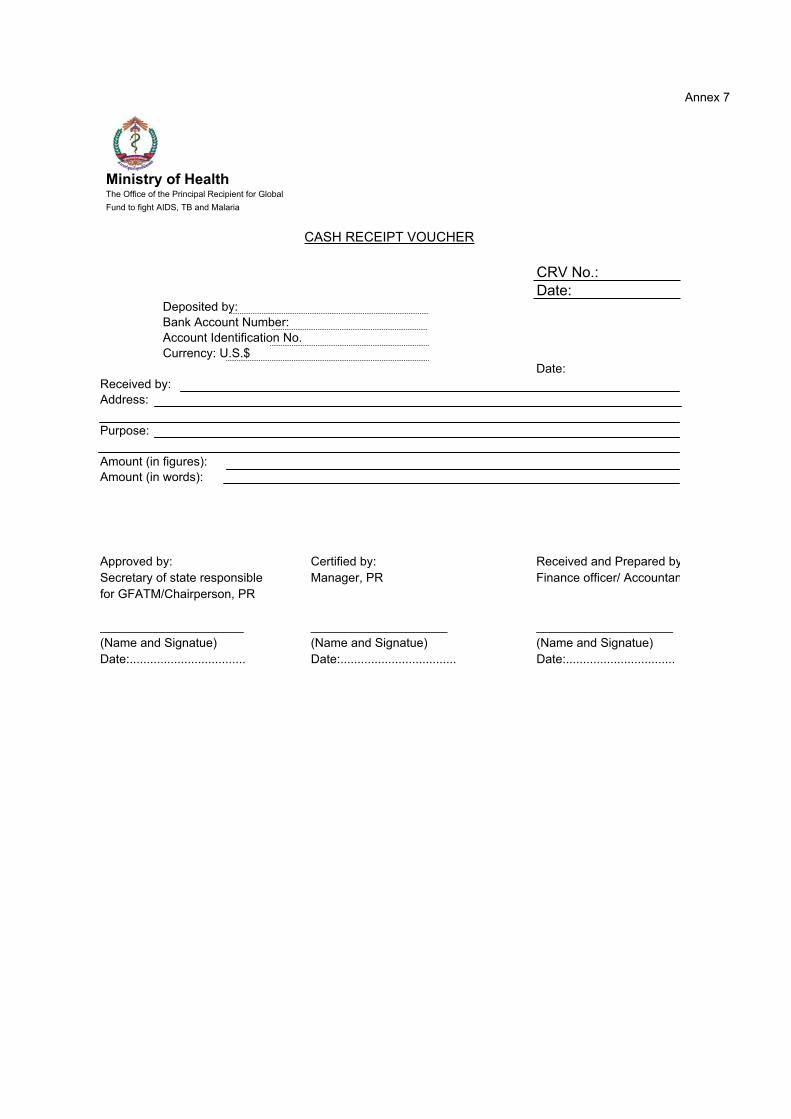

XI.1 Receipt Vouchers:

i. General: Receipt Vouchers must indicate the date of receipt, purpose of receipt and account code to be credited. Receipt Vouchers issued for funds received in repayment of advances must show the number(s) of the Payment Voucher(s) under which the advances were originally made.

ii. Provisional Receipts: Provisional receipts must be issued if, on occasion, cash must be accepted by a staff member other than an authorized officer. Such a provisional receipt must be replaced as soon as possible by an official receipt signed by an authorizing officer.

XI.2 Payment Vouchers:

A Payment Voucher (PV) must be issued for ALL payments and supporting documentation must always be attached. The original PV with supporting documentation must be retained by the office.

Completion of Payment Vouchers/Disbursement Voucher:Payment Vouchers must indicate:

i. The Payment Voucher number, (serial number of the Payment Voucher)

ii. The amount of payment;

iii. The payee staff or vendor number;

iv. A description of the goods received or services rendered. Payments to vendors must indicate the invoice number and, if applicable, payments to staff or consultants must indicate period covered.

v. The automated accounting system assigns sequential numbers automatically to Disbursement Voucher (DV), cheques, bank transfers and demand drafts.

vi. The signature of the payee or a receipt or other valid document replacing the signature. In cases where the signature of the payee has not been obtained, adequate

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 30

documentation must be attached to the DV indicating, in some way, that the payee did receive the payment (e.g., bank debit advice, etc.);

vii. The signatures of the Certifying (Committing) and Approving (Verifying).

viii. Supporting documentation requirements are that: Payment Vouchers must be supported by appropriate and complete documentation: original invoices, payee’s receipts/cancelled cheques, and other relevant documentation supporting the transaction.

ix. Disbursements to vendors must be supported by the original invoice and must include verification that the goods have been received.

x. Disbursements to consultants must be supported by the original invoice or receipt and must include verification that services have been rendered.

xi. Disbursements for local salaries must be supported by a payroll.

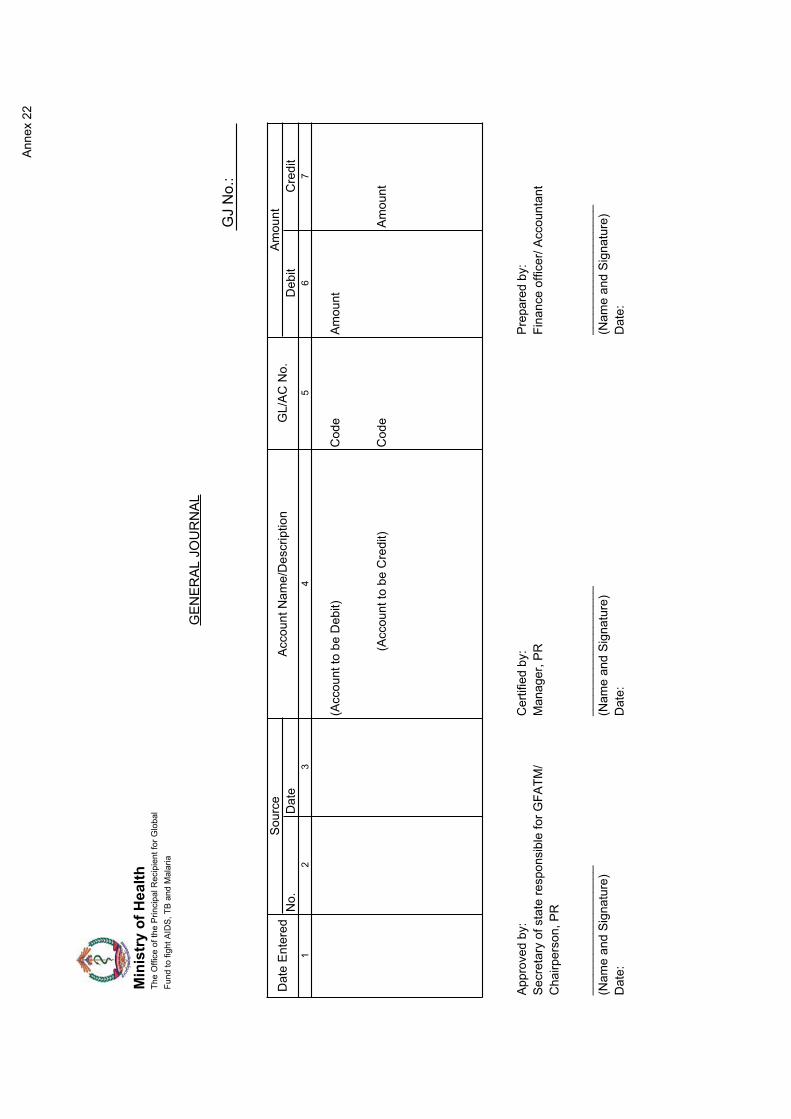

XI.3 Journal Vouchers:

A Journal Voucher must be prepared and posted in the office accounting system as is the case with Payment Vouchers and Receipt Vouchers. The purpose of the Journal Voucher is to adjust accounts, i.e., when a Payment or Receipt Voucher has been issued containing erroneous account codes Debited or Credited.

The account code entries in the Journal Voucher are to re-credit the account originally erroneously debited and vis-versa.

XI.4 Supporting document

i Attachments, (supporting documentation), to Payment Vouchers/Receipt Vouchers and Journal Vouchers:

Supporting documentation is a vital accounting control requirement and designated staff handling finance related activities must at all times ensure that supporting documentation are stamped ‘PAID with the Logo of the PR or SR’ and kept under lock to ensure that no one tampers with such official original supporting documents.

ii The loss and/or misplacements of such valuable documents can cause great financial damage to the office concerned. Supervisors must ensure that adequate safeguarding measures are implemented to avoid loss and/or misplacement of supporting documents.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 31

CHAPTER XII: PAYROLL PROCEDURES

XII.1 Payroll Procedures (General): For the office of the Principal Recipient (PR) of the MoH the procedures to

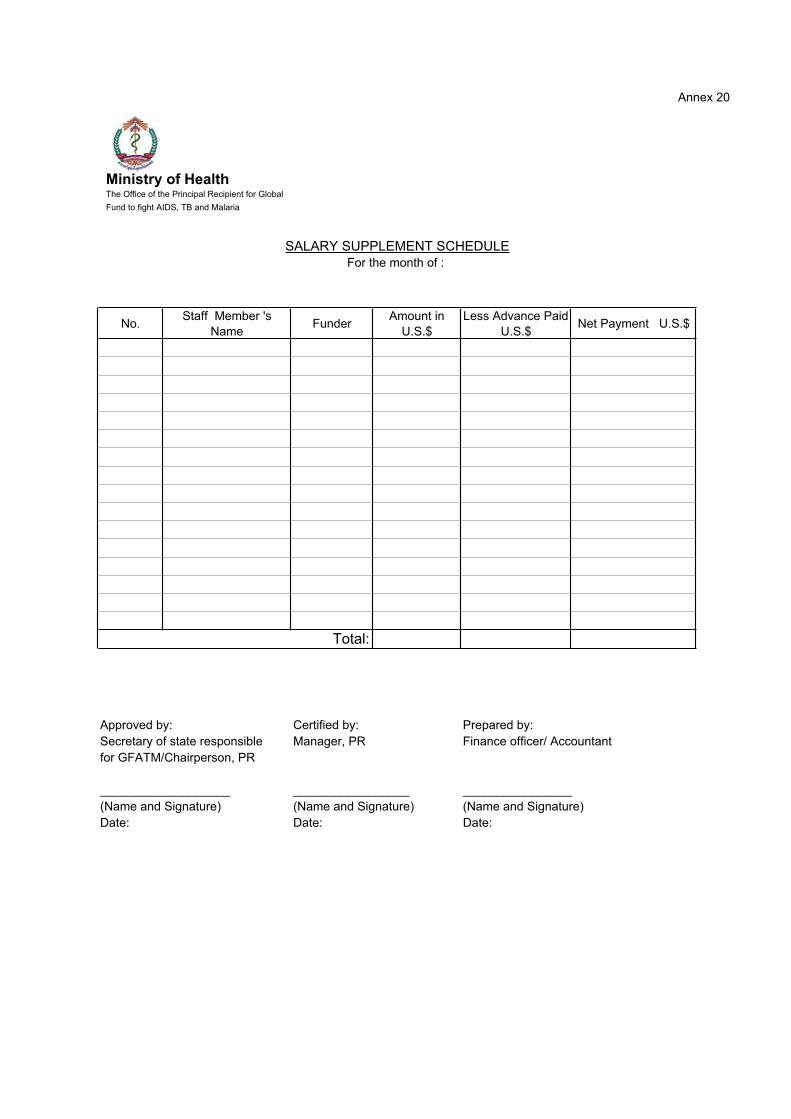

be implemented is through the use of form (See Annex 20), included in these Financial Guidelines issued by the office of the PR. For the approved Sub-recipients the applicable payroll procedures will be that already existing at each Sub-recipient’s office.

XII.2 Calculation for Payroll: When payment of salaries are being processed the designated Finance Officer of the PR or the SR should ensure that any outstanding advance made to the staff member is deducted from the month-end salary payment after the deadline for liquidation as stated in chapter IX, paragraph d), page 18. The procedure applicable to staff of Sub-recipients should be that already existing and practiced at the Sub-recipients level.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 32

CHAPTER XIII: RETENTION/PROTECTION OF FINANCIAL RECORDS AND DOCUMENTS

XIII.1 Period of Retention of Financial Records: As financial records pertaining to activities relating to the GFATM grants

will be subject to periodic internal audits as well as external independent audits, in compliance with the GF conditionality the office of the Principal Recipient (PR), MoH, as well as all approved Sub-recipient in receipt of GF grants are required to retain all original financial documents and records throughout the cycle of the GFATM program and at least five years beyond the date of final completion of the GFATM related activities.

XIII.2 Routine Measure for Safekeeping Financial Documents and Records: Original financial documents and records must not be disposed of prior to the period referred to in paragraph a) above. Measures to safeguard and protect PR and SR financial records include the following:

When offices are closed, cheque books, all payment, petty cash and office accounting forms must be safeguarded; The office computerized accounting system must be backed-up and CDs or diskettes placed in the office safe; Pre-numbered Receipt Vouchers, if any, must be placed in the office safe; Pre-paid gasoline coupons must also be placed in the office safe.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 33

CHAPTER XIV: HAND OVER INSTRUCTIONS FOR FINANCIAL MATTERS

General Requirements for Hand-over of Financial Matters: The generally accepted accounting requirements for the hand-over of

financial matters by the designated officer to other designated official due to foreseen prolonged absences, either on annual or sick leave, or due to termination of employment, are:

A written statement providing the status of the accounts and budgets; A written hand-over note listing the contents of the office safe, i.e., blank cheques books and lose cheques and gasoline coupons; A petty cash book reconciliation, together with supporting document justifying the expense paid-out by P.C., and a cash count sheet (see Annex 31) to these Financial Guidelines) signed by both person acting as receiver and provider.

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 34

CHAPTER XV: REPORTING REQUIREMENTS

XV.1 Year End Report requirement

a) General Requirements:The general requirements for the year-end reporting consist of a number of

measures aimed at ensuring a smooth transition to the following fiscal year.

b. Outstanding payment before the Year-End: Offices should make every effort to clear all unpaid items before the end of

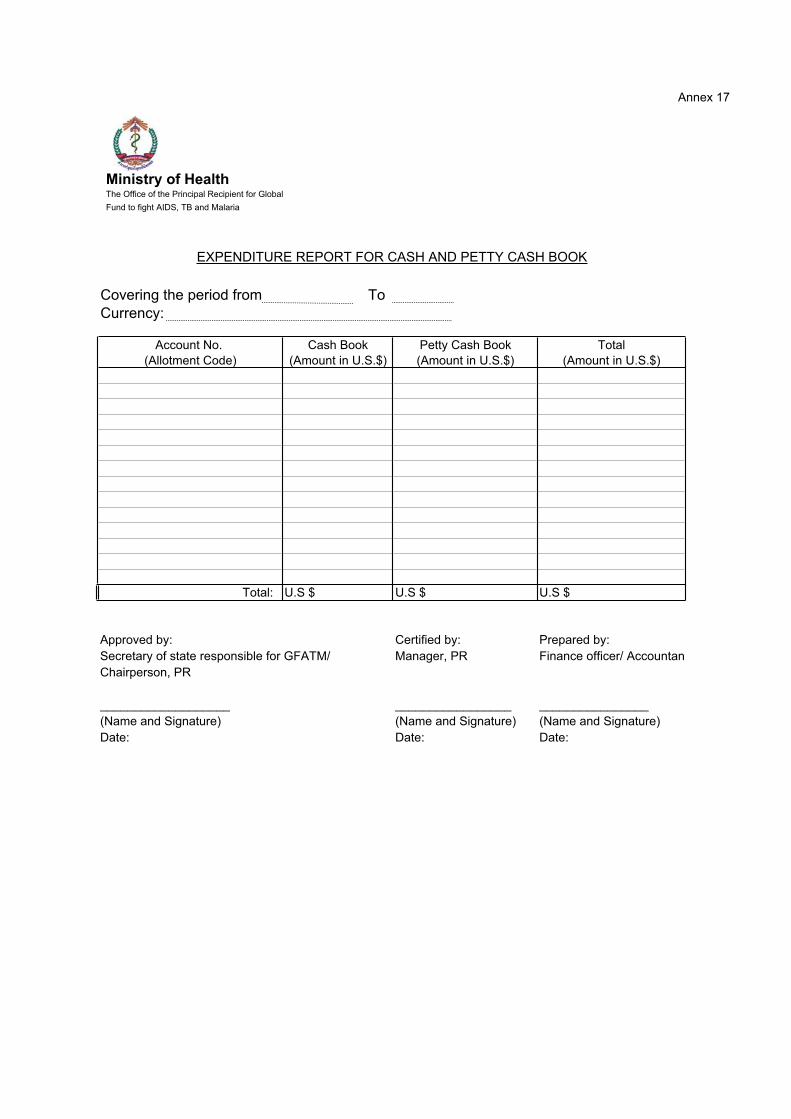

the year although some items may still have to be paid during the following year, such as: Purchase Orders not yet honored; rent, utilities, telephone bills, freight and transportation charges, cost of repairs and/or services, etc. Closing of the accounts for the last month of the fiscal year and preparing the “Yearly Budget Control Statement” (Annex 4 ), as well as (Annex 3), that are part of these Financial Guidelines.

XV.2 Financial Report

a) Month end Procedure

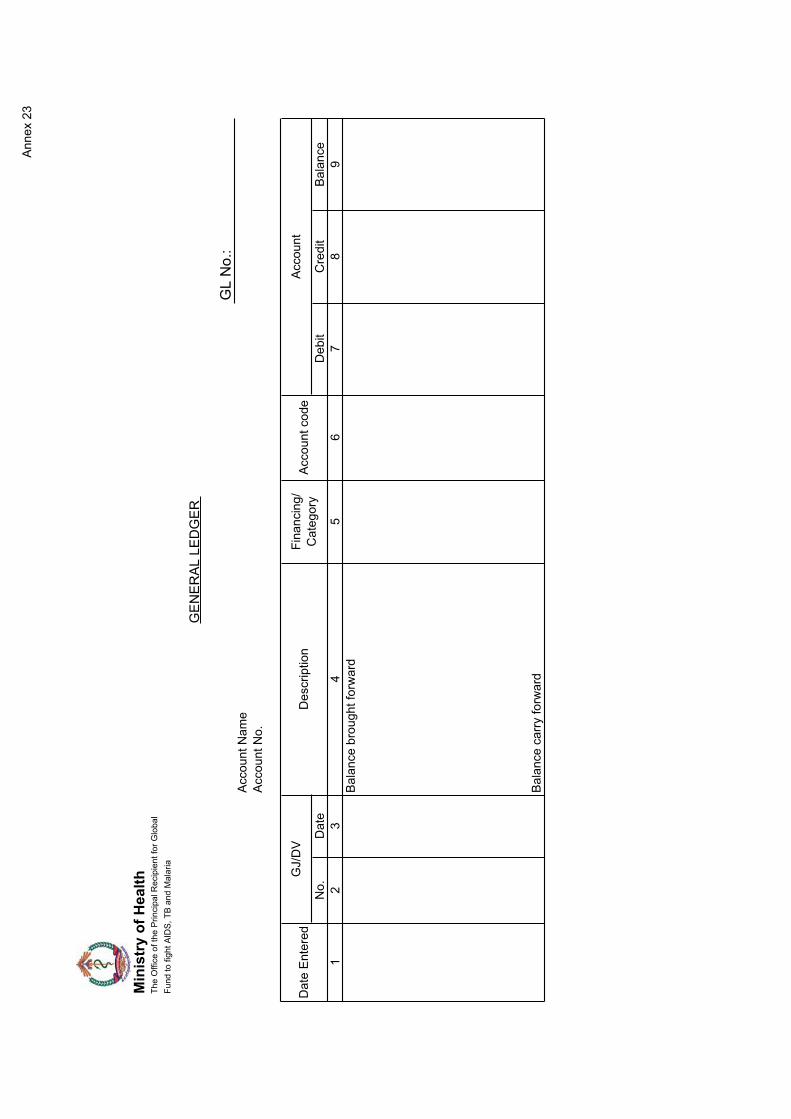

The Principal Recipient Project’s monthly consolidated financial statements and other related reports must be printed out from Quick Book Accounting Software or any other accounting software, and need to be reviewed first by the Finance Officer or/and Senior Finance Officer before submission to the Secretary of State of the MoH responsible for GFATM program/ Manager. This is to be done before closing the accounting period. To ensure that the financial data for each month is complete and accurate, the General Ledger accounts should be reconciled to the supporting accounting records below. Any differences arising should be investigated immediately and adjusting entries should be recorded, this is applicable for each account of SRs.

From the Bank Accounts- Cash in bank accounts from the General Ledger account should be equal to the Bank Reconciliation Statement per bank account of project outlets (Sub-Recipient and PR office). Bank reconciliation should also be equal to Daily Cash Position Book. If it is not equal to the balance in the manual Daily Cash Position Book, these differences maybe due to the following;

Posting error to incorrect account code Some transactions of the bank are not yet posted in the general ledger

FINANCIAL GUIDELINES OF THE PRINCIPAL RECIPIENT OF THE GFATM

Revised August 2006 by: MoH/PR Finance Team Page: 35

Petty Cash Balance-The balance in the General Ledger accounts should be reconciled against the amount in cashbook and amount in Cash Reconciliation Statement.

Advance Account-The balance in the Advance account in the general ledger should be tallied as per Advance Control Book and to the total balances per Individual Advance Card.

Payroll Account-The balance in the general ledger account should be tallied against total salaries as per Payroll register. Any errors should be investigated immediately.

Expenditures Account- the balance in the general ledger accounts specially those major expenditures should be tallied with relevant accounting records such as subsidiary ledgers or Contract Registers/Purchase Register .Make sure that all respective disbursements vouchers were checked by the respective Finance Officers.

After review and confirmation of general ledger accounts against accounting books and registers. The detailed General Ledger and Final Financial Statements reports will be finally printed out from the General Ledger and Reports Window of Accounting Software respectively, and kept in the General Ledger Binder and Financial Report Binder as a comprehensive records for the audit trail and bank confirmation.