JOURNAL OF BUSINESS AND ACCOUNTING Corporate Crisis: An Examination of Merck's Communication...

150

JOURNAL OF BUSINESS AND ACCOUNTING Volume 5, Number 1 ISSN 2153-6252 Fall 2012 Corporate Crisis: An Examination of Merck’s Communication Strategies in the Vioxx Case .................................................................................. Mary Stone, Sheri L. Erickson, Marsha Weber Conflict Minerals Disclosures: A Mandate of the Dodd-Frank Act ............................................................................................ Deborah L. Lindbert and Khalid Razaki Hedging With Currency ETFS: The Implications of Return Dynamics ................................................................................................................................ Robert B. Burney Financial Statement Presentation: A Sneak Peak at the Proposed Format ........................................................................... Suzanne P. Ward, Dan R. Ward, and Alan B. Deck The Comparative Reporting Impact of the FASB and IASB Treatments of Research and Development Expenditures .................................................................................... Patricia G. Mynatt and Richard G. Schroeder IFRS Adoption in Japan: Road Map and Challenges ............................................................. Noriaki Yamaji, Joshua Hudson, and Douglas K. Schneider Issues With Mandatory Audit Firm Rotation ......................................... Homer L. Bates, Bobby E. Waldrup, David G. Jaeger, and Vincent Shea The Impact of Tax Incentives on the Location of Manufacturing Facilities ............................................................ Juan Luis Jay Ramirez, Anwar Y. Salimi, and Hassan Hefzi Tax Practitioners and Ordering Effects of Information in an Ethical Decision ........................................................... Scott Andrew Yetmar, Peter Poznanski, and Elizabeth Koran Anomalies of Tax Legislation: The First Time Homebuyer Credit ................................................................................................... Sheldon Smith and Amourae Riggs Accounting for Sustainability ............................................................................................................................... Mehenna Yakhou A Factor Analysis of the Skills Necessary In Accounting Graduates ......................................................................................... Suzanne N. Cory and Kimberly A. Pruske The Effect of Timing on Student Satisfaction Surveys ................................................................. Pierre L. Titard, James E. DeFranceschi, and Eric Knight Student Plagiarism and Economic Versus Moral Based Pedagogy .................................................................................................Tackett, Shaffer, Wolf and Claypool A REFEREED PUBLICATION OF THE AMERICAN SOCIETY OF BUSINESS AND BEHAVIORAL SCIENCES

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of JOURNAL OF BUSINESS AND ACCOUNTING Corporate Crisis: An Examination of Merck's Communication...

JOURNAL OF BUSINESS

AND ACCOUNTING Volume 5, Number 1 ISSN 2153-6252 Fall 2012

Corporate Crisis: An Examination of Merck’s Communication Strategies in the Vioxx Case .................................................................................. Mary Stone, Sheri L. Erickson, Marsha Weber

Conflict Minerals Disclosures: A Mandate of the Dodd-Frank Act ............................................................................................ Deborah L. Lindbert and Khalid Razaki

Hedging With Currency ETFS: The Implications of Return Dynamics ................................................................................................................................ Robert B. Burney

Financial Statement Presentation: A Sneak Peak at the Proposed Format ........................................................................... Suzanne P. Ward, Dan R. Ward, and Alan B. Deck

The Comparative Reporting Impact of the FASB and IASB Treatments of Research and

Development Expenditures .................................................................................... Patricia G. Mynatt and Richard G. Schroeder

IFRS Adoption in Japan: Road Map and Challenges ............................................................. Noriaki Yamaji, Joshua Hudson, and Douglas K. Schneider

Issues With Mandatory Audit Firm Rotation ......................................... Homer L. Bates, Bobby E. Waldrup, David G. Jaeger, and Vincent Shea

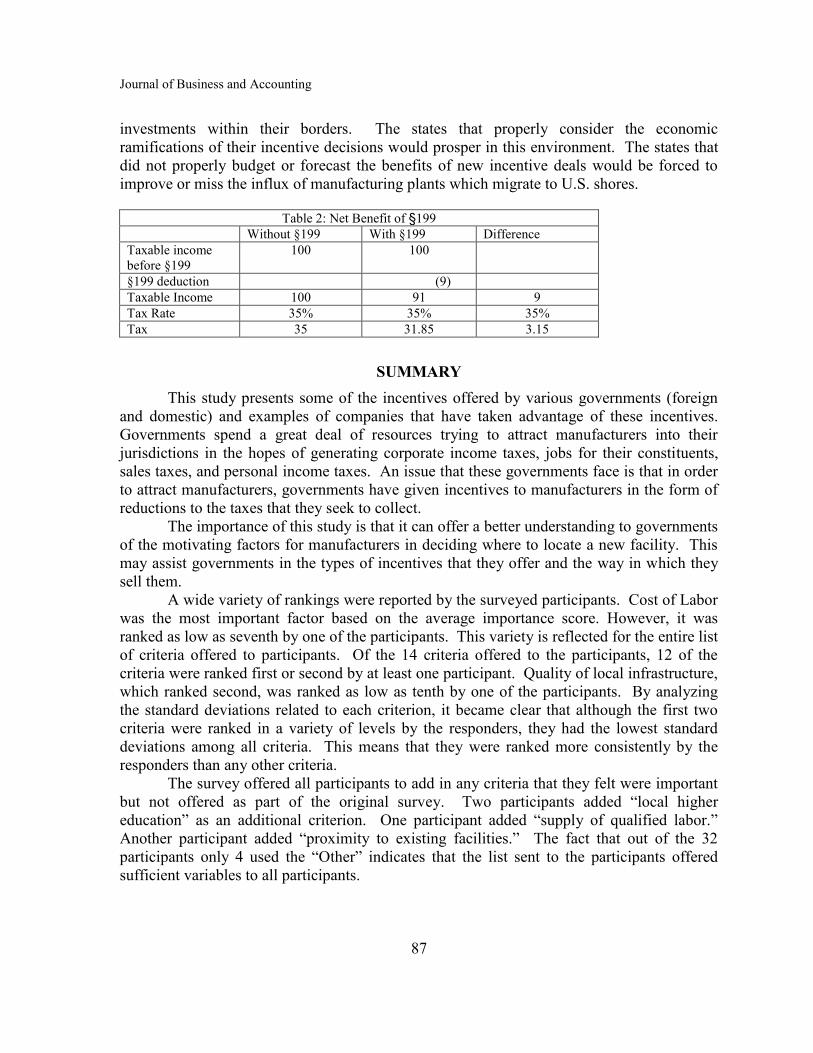

The Impact of Tax Incentives on the Location of Manufacturing Facilities ............................................................ Juan Luis Jay Ramirez, Anwar Y. Salimi, and Hassan Hefzi

Tax Practitioners and Ordering Effects of Information in an Ethical Decision ........................................................... Scott Andrew Yetmar, Peter Poznanski, and Elizabeth Koran

Anomalies of Tax Legislation: The First Time Homebuyer Credit ................................................................................................... Sheldon Smith and Amourae Riggs

Accounting for Sustainability ............................................................................................................................... Mehenna Yakhou

A Factor Analysis of the Skills Necessary In Accounting Graduates ......................................................................................... Suzanne N. Cory and Kimberly A. Pruske

The Effect of Timing on Student Satisfaction Surveys ................................................................. Pierre L. Titard, James E. DeFranceschi, and Eric Knight

Student Plagiarism and Economic Versus Moral Based Pedagogy

.................................................................................................Tackett, Shaffer, Wolf and Claypool

A REFEREED PUBLICATION OF THE AMERICAN SOCIETY

OF BUSINESS AND BEHAVIORAL SCIENCES

1

JOURNAL OF BUSINESS AND ACCOUNTING P.O. Box 502147, San Diego, CA 92150-2147: Tel 909-648-2120

Email: [email protected] http://www.asbbs.org

____________________ISSN 2153-6252_______________________

Editor-in-Chief

Wali I. Mondal

Managing Editors: Cheryl Prachyl, University of North Texas at Dallas

Carol Sullivan, University of St. Thomas

Editorial Board

Mark Aquilio

St. John’s University

MaryAnne Atkinson

Central Washington University

Douglas M. McCabe

Georgetown University

Michelle McEacharn

University of Louisiana-Monroe

Shamsul Chowdhury

Roosevelt University

Steve Dunphy

Indiana University – Northwest

Kingsley Olibe

Kansas State University

Darshan Sachdeva

California State University, Long Beach

Ramon Fernandez

University of St. Thomas

Saiful Huq

University of New Brunswick

William J. Kehoe

University of Virginia

Allen Schaeffer

Missouri State University

David Smith

National University

Sheldon Smith

Utah Valley State University

Robyn Lawrence

University of Scranton

Linda Whitten

Skyline College

The Journal of Business and Accounting is a publication of the American Society of

Business and Behavioral Sciences (ASBBS). Papers published in the Journal went through

a blind-refereed review process prior to acceptance for publication. The editors wish to

thank anonymous referees for their contributions.

The national annual meeting of ASBBS is held in Las Vegas in February of each year and

the international meeting is held in September of each year. Visit www.asbbs.org for

information regarding ASBBS.

2

JOURNAL OF BUSINESS AND ACCOUNTING

ISSN ISSN 2153-6252

Volume 5, Number 1 Fall 2012

TABLE OF CONTENTS

CORPORATE CRISIS: AN EXAMINATION OF MERCK’S COMMUNICATION

STRATEGIES IN THE VIOXX CASE

Mary Stone, Sheri L. Erickson, and Marsha Weber .................................................................. 3 CONFLICT MINERALS DISCLOSURES: A MANDATE OF THE DODD-FRANK ACT

Deborah L. Lindbert and Khalid Razaki ................................................................................. 15

HEDGING WITH CURRENCY ETFS: THE IMPLICATIONS OF RETURN DYNAMICS

Robert B. Burney ........................................................................................................................... 25 FINANCIAL STATEMENT PRESENTATION: A SNEAK PEAK AT THE PROPOSED

FORMAT

Suzanne P. Ward, Dan R. Ward, and Alan B. Deck ................................................................ 36 THE COMPARATIVE REPORTING IMPACT OF THE FASB AND IASB

TREATMENTS OF RESEARCH AND DEVELOPMENT EXPENDITURES

Patricia G. Mynatt and Richard G. Schroeder ......................................................................... 50 IFRS ADOPTION IN JAPAN: ROAD MAP AND CHALLENGES

Noriaki Yamaji, Joshua Hudson, and Douglas K. Schneider .................................................. 59 ISSUES WITH MANDATORY AUDIT FIRM ROTATION

Homer L. Bates, Bobby E. Waldrup, David G. Jaeger, and Vincent Shea .............................. 70 THE IMPACT OF TAX INCENTIVES ON THE LOCATION OF MANUFACTURING

FACILITIES

Juan Luis Jay Ramirez, Anwar Y. Salimi, and Hassan Hefzi ................................................. 76 TAX PRACTITIONERS AND ORDERING EFFECTS OF INFORMATION IN AN

ETHICAL DECISION

Scott Andrew Yetmar, Peter Poznanski, and Elizabeth Koran ................................................ 90 ANOMALIES OF TAX LEGISLATION: THE FIRST-TIME HOMEBUYER CREDIT

Sheldon Smith and Amourae Riggs ...................................................................................... 103 ACCOUNTING FOR SUSTAINABILITY

Mehenna Yakhou .................................................................................................................. 112 A FACTOR ANALYSIS OF THE SKILLS NECESSARY IN ACCOUNTING

GRADUATES

Suzanne N. Cory and Kimberly A. Pruske ............................................................................ 121 THE EFFECT OF TIMING ON STUDENT SATISFACTION SURVEYS

Pierre L. Titard, James E. DeFranceschi, and Eric Knight .................................................... 129

STUDENT PLAGIARISM AND ECONOMIC VERSUS MORAL BASED PEDAGOGY

James Tackett, Raymond Shaffer, Fran Wolf and Greg Claypool..........................................136

Journal of Business and Accounting

Vol. 5, No. 1; Fall 2012

3

CORPORATE CRISIS: AN EXAMINATION OF MERCK’S

COMMUNICATION STRATEGIES IN THE VIOXX CASE

Mary Stone

Sheri L. Erickson

Marsha Weber

Minnesota State University Moorhead

ABSTRACT

Image management is essential in crisis situations. This study uses critical analysis to

examine Merck’s communication strategies in the press when the drug Vioxx was removed

from the market. Benoit (1995) and Marcus and Goodman (1991) communication typologies

are used as a framework to determine whether Merck communicated in a way that enhanced

shareholder value. Marcus and Goodman find that when crises are classified as a scandal,

accommodating strategies provided more shareholder value, whereas in product recall type

crises, the results were unclear. Our research indicates that initial negative stock price

reaction could be the result of using defensive rather than accommodating strategies. In

addition, subsequent communication strategies result in mixed market reaction to

shareholders, which is in line with findings of Marcus and Goodman for product recall crises.

INTRODUCTION

Image management is essential to corporations and other organizations, particularly

in crisis situations. Numerous pharmaceutical drugs have been pulled from the market in

recent years, after information concerning product safety has come into question. A crisis of

this nature can deeply hurt an organization and affects many stakeholders. Seeger, Sellnow

and Ulmer (1998) define crisis as, “a specific, unexpected and non-routine organizationally-

based event or series of events which creates high levels of uncertainty and threat or

perceived threat to an organization’s high priority goals” (p. 233). One such crisis involved

Merck’s arthritis drug Vioxx, which was pulled from the market in September 2004 due to

evidence that the drug increased the risk of heart attack and stroke.

The purpose of this paper is to examine the image repair communication strategies

that Merck utilized in press releases during the Vioxx recall. We use Benoit’s (1995) Image

Restoration Typology to analyze Merck’s responses to the media following allegations that

Vioxx posed a health threat. We then compare the analysis using Benoit’s framework to the

framework used by Marcus and Goodman (1991) who found that different types of

communication strategies had varying levels of success in providing value to shareholders,

depending on the type of organizational crisis. As Rotthoff (2010) found, Merck lost $26.8

billion in stock value when Vioxx was pulled from the market.

Our motivation for this study stems from several prior studies. First, while Lyon and

Mirivel (2011) examined the communication strategies of Merck pharmaceutical

representatives with physicians, we examine communication strategies of Merck

representatives in the media. Lyon and Mirivel looked at the purpose and consequences of

communications. With the purpose of boosting sales of Vioxx, Merck’s sales representatives’

communications approach had the logical consequence of obscuring physicians’ ability to

Stone, Erickson, and Weber

4

make a significant choice and resulting in more patients’ lives being put at risk (Lyon &

Mirivel 2011). Our current study examines Merck’s communication strategies with the

overall market of consumers, physicians, and investors after the company pulled Vioxx off

the market. While the intended purpose of these communications is to repair Merck’s image

and maintain stock price for shareholders, our study will show that not all communication

strategies are beneficial.

Second, Chen, Ganesan, and Liu (2009) found that a firm’s strategy for dealing with a

product recall case has an effect on stock market reaction. They found that a proactive

communication strategy, as opposed to a reactive strategy, had a negative effect on firm

value. Marcus and Goodman (1991) discovered that the stock market reacts differently to

corporate communications that are accommodating compared to those that are defensive

during times of accident, scandal, and product safety crisis. Their study was conducted before

Benoit’s (1995) framework was developed, therefore a fresh look into this area, using

Benoit’s framework to categorize communication strategies, is warranted. Marcus and

Goodman (1991) conclude that their ambiguous results in the product safety crisis may be the

result of the latent nature of the effects of corporate communications, therefore suggesting a

replication with a different group of observations.

Our current research study will examine Merck’s corporate communications around

the time of their Vioxx product recall using Benoit’s (1995) framework. We will also

compare our findings to Marcus and Goodman (1991) to determine if their findings are

supported by our study.

MERCK AND COMPANY

Merck and Company, the world’s second largest pharmaceutical company, introduced

Vioxx in May 1999. Along with its competitor Celebrex, Vioxx was a pain relief medicine

used to treat arthritic inflammatory pain. These two medicines, categorized as Cox-2

inhibitors, were scientific breakthrough drugs because while their pain relieving attributes

were similar to aspirin and ibuprofen, they showed a lower risk of causing gastrointestinal

troubles, including ulcers. These drugs were hugely successful, earning more money in their

first year on the market than any other medicine before them (Petersen, 2000).

Research studies, which continued after Vioxx was on the market, revealed an

alarming result; Vioxx increased the risk of heart attacks and strokes by up to two to three

times (Weitz & Luxenberg, 2010). As a result, Merck & Co. voluntarily recalled Vioxx on

September 30, 2004. At the time of the recall, Vioxx was used by approximately 2 million

people and was the source of 11 percent of Merck’s revenue. Merck’s stock price plunged

and they quickly lost $26.8 billion in market capitalization (Rotthoff, 2010). Thousands of

lawsuits, brought by patients, their survivors, and shareholders have been filed against

Merck. In 2010, Merck agreed to a settlement which requires $4.85 billion in payments to

patients who were harmed or killed, $12.15 million payment for plaintiff’s attorney fees, and

many organizational restructuring activities which monitor product safety (The Associated

Press, 2010).

Journal of Business and Accounting

5

CORPORATE CRISIS AND REPUTATION MANAGEMENT

Corporate communication during a crisis reflects the firm’s strategic management of

the situation and is critical in determining how much, if any, damage is done to the firm’s

image. Because stakeholders attribute some responsibility to the organization or industry in

which the crisis exists, communications must explain the facts of the crisis and provide the

feeling that steps are being taken to ensure that the crisis won’t happen again (Fortunato,

2008). By strategically managing the crisis situation through reliable, credible, and

transparent communication, a corporation addresses stakeholders’ anxieties, manages its

corporate image, and restores its reputation (Geppert & Lawrence, 2008).

Communication is a goal-directed activity that involves a purpose. One of the central

goals of communication for the corporation is to maintain a positive public image (Benoit,

1995). A reputation may be damaged intentionally or unintentionally through word or deed.

When this happens the communicator is faced with the problem of negative public image.

According to Valentine (2007, p. 38), a damaged reputation can “translate into decreased

brand value; lowered share price; lost customers, partners, and strategic relationships; and

difficulty in recruiting and keeping top employees.”

Benoit creates his theory based on the assumption that, due to this potential negative

image resulting from a damaged reputation, the communicator is motivated to restore its

image as one of the central goals of its communication to the public.

IMAGE RESTORATION THEORY

Researchers have developed several image restoration strategies based on social

legitimacy theory, which argues that an organization’s continued existence is contingent on

its ability to receive support or approval from stakeholder audiences. In addition to Benoit’s

theory, other image restoration typologies include Allen and Caillouet (1994); Hearit (1995),

Ware and Linkugel (1973), Scott and Lyman (1968), and Suchman (1995) ; however,

Benoit’s (1995, 1997) typology is used most often by communication researchers to analyze

strategic responses to legitimacy issues.

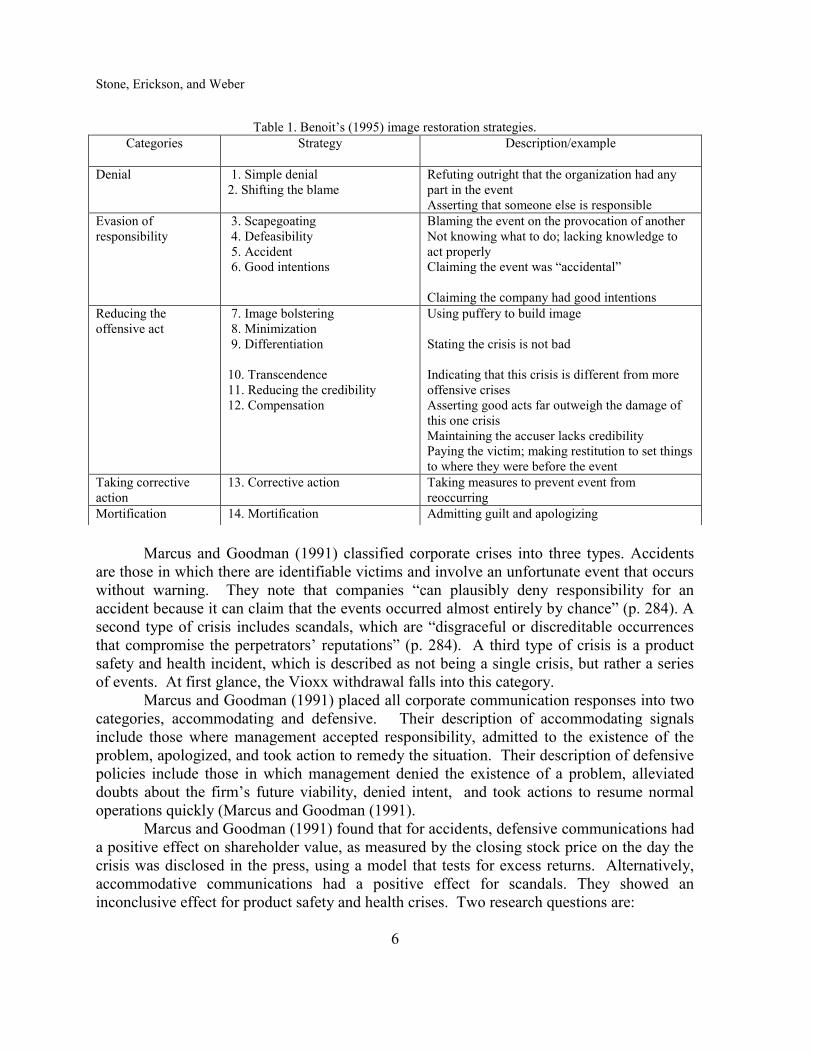

Benoit’s typology identifies five image restoration strategies: 1) denial, or refuting

that the company had any part in the crisis, 2) evasion of responsibility, where the firm

attributes the crisis to actions of another party, 3) reducing the offensiveness of the act, in

which the firm tries to make the crisis seem less threatening, 4) corrective action occurs when

the firm implements steps to solve the problem and prevent a repeat of the crisis, and

5) mortification, where the firm takes responsibility for the crisis and apologizes. The

communication classification categories are somewhat hierarchical in that denial is the best

strategy, if a company is truly blameless. Evasion of responsibility, blaming the crisis on the

provocation of another, claiming defeasibility or the accidental nature or good intentions of

the company becomes a good choice if the company is not able to convince the public that it

had no responsibility for the crisis. If it becomes clear that this strategy will not suffice, most

companies resort to attempting to reduce the offensiveness of the crisis. Very few companies

take immediate corrective action and even fewer use mortification by apologizing. Table 1

below provides a detailed summary of Benoit’s five categories which include 14 unique

communication strategies.

Stone, Erickson, and Weber

6

Table 1. Benoit’s (1995) image restoration strategies.

Marcus and Goodman (1991) classified corporate crises into three types. Accidents

are those in which there are identifiable victims and involve an unfortunate event that occurs

without warning. They note that companies “can plausibly deny responsibility for an

accident because it can claim that the events occurred almost entirely by chance” (p. 284). A

second type of crisis includes scandals, which are “disgraceful or discreditable occurrences

that compromise the perpetrators’ reputations” (p. 284). A third type of crisis is a product

safety and health incident, which is described as not being a single crisis, but rather a series

of events. At first glance, the Vioxx withdrawal falls into this category.

Marcus and Goodman (1991) placed all corporate communication responses into two

categories, accommodating and defensive. Their description of accommodating signals

include those where management accepted responsibility, admitted to the existence of the

problem, apologized, and took action to remedy the situation. Their description of defensive

policies include those in which management denied the existence of a problem, alleviated

doubts about the firm’s future viability, denied intent, and took actions to resume normal

operations quickly (Marcus and Goodman (1991).

Marcus and Goodman (1991) found that for accidents, defensive communications had

a positive effect on shareholder value, as measured by the closing stock price on the day the

crisis was disclosed in the press, using a model that tests for excess returns. Alternatively,

accommodative communications had a positive effect for scandals. They showed an

inconclusive effect for product safety and health crises. Two research questions are:

Categories

Strategy Description/example

Denial 1. Simple denial

2. Shifting the blame

Refuting outright that the organization had any

part in the event

Asserting that someone else is responsible

Evasion of

responsibility

3. Scapegoating

4. Defeasibility

5. Accident

6. Good intentions

Blaming the event on the provocation of another

Not knowing what to do; lacking knowledge to

act properly

Claiming the event was “accidental”

Claiming the company had good intentions

Reducing the

offensive act

7. Image bolstering

8. Minimization

9. Differentiation

10. Transcendence

11. Reducing the credibility

12. Compensation

Using puffery to build image

Stating the crisis is not bad

Indicating that this crisis is different from more

offensive crises

Asserting good acts far outweigh the damage of

this one crisis

Maintaining the accuser lacks credibility

Paying the victim; making restitution to set things

to where they were before the event

Taking corrective

action

13. Corrective action Taking measures to prevent event from

reoccurring

Mortification 14. Mortification Admitting guilt and apologizing

Journal of Business and Accounting

7

RQ1: What are the communication strategies, classified according to Benoit (1995), used by

Merck when Vioxx was pulled from the market?

RQ2: Do the strategies Merck used support the findings of Marcus and Goodman (1991)?

DATA AND METHODOLOGY

In the following section we analyze Merck’s responses to media questions on

September 30, 2004, when Vioxx was pulled from the market. We use a critical analysis

method to study communication strategies employed by Merck spokespeople to attempt to

repair its tarnished image. Critical analysis of strategic communication has been used by

many scholars, including Benoit (2006); Benoit and Czerwinski (1997); Benoit and Henson

(2009); Blaney, Benoit, and Brazeal (2002); Coombs (1995); Hearit (1995); Huang and Su

(2009); Erickson, Weber, Segovia, and Dudney (2010); Erickson, Weber, and Stone (2011);

and, Seeger, Sellnow, and Ulmer, (2003). A variety of texts have been evaluated using

critical analysis, including speeches, advertising, newspaper articles, and public relations

announcements.

Wall Street Journal, New York Times, and CNN Money excerpts from 2004, which

exemplify Merck’s responses to the crisis, were analyzed using Benoit (1995). Proquest was

used to find all articles regarding Vioxx and quotes from company employees and

spokespeople were used for analysis. Two researchers independently categorized the

excerpts and all categorizations were mutually agreed upon. Merck used a wide variety of

communication strategies to address questions that arose concerning this crisis. The

following section provides a summary of Merck’s responses and a brief analysis of

responses.

ANALYSIS OF COMMUNICATIONS

On September 30, 2004, Merck announced a worldwide withdrawal of Vioxx based

on results of trials indicating that individuals taking Vioxx were more likely to experience

cardiovascular problems than those not taking the medication. We analyzed 21 excerpts that

included 27 responses from October 1, 2004-December 21, 2004 and analyzed these

responses using Benoit’s (1995) Image Restoration Typology.

Merck used strategies intended to reduce the offensiveness of the crisis in 21 of its

responses. The most commonly used strategy was that of image bolstering (12 instances),

where Merck used phrases such as “serving the best interest of patients” (Merck yanks

arthritis drug Vioxx, 2004) and “putting patient safety first” (Mathews & Martinez, 2004) to

try to rebuild its reputation. Other examples of image bolstering included, “We were

financially strong before this and we will be financially strong after” (Martinez, et al, 2004)

and that Merck remains “very strong financially, with very strong cash flow” (Merck yanks

arthritis drug Vioxx, 2004). Another excerpt states, “…we concluded that a voluntary

withdrawal is the responsible course to take” (A Vioxx elegy, 2004, p. A.14). Perhaps the

most amusing example of bolstering was made by legal counsel for Merck: “Merck wasn’t

dragging its feet” and “It’s pretty hard for me to imagine that you could have done this more

quickly than we did” (Berenson, et al., 2004. p. 1.1).

Some of the above examples that mentioned that Merck was financially strong could

also be categorized as examples of minimization because Merck was attempting to show that

Stone, Erickson, and Weber

8

lost sales of Vioxx would not significantly harm the company financially. Another example

of the use of minimization included “we believe it would have been possible to continue to

market Vioxx with labeling that would incorporate these new data…” (A Vioxx elegy, 2004,

p. A.14). This example is an attempt by Merck to indicate that the only problem was

improper labeling, not the product itself.

Another way to reduce the offensiveness of the crisis is to reduce the credibility of the

accuser. Merck used this tactic three times after Vioxx was pulled off the market. One

comment, in response to an editorial, states that the editorial “is flawed in many important

respects” (Martinez & Hensley, 2004, p. B.8.) and “that the information was ‘taken out of

context’” (Mathews & Martinez, 2004). In response to a Congressional investigation, Merck

stated that documents “will be deliberately presented out of context to advance the interest”

of plaintiffs (Martinez, 2004).

Merck used evasion of responsibility strategies in 5 responses. Defeasibility was used

3 times, primarily when Vioxx was first pulled from the market and the company indicated

that, “What we saw was stunning. We certainly don’t understand the cause of this effect, but

it is statistically significant and it indicated there was an issue” (Berenson et al., 2004). Not

only does this imply that the company lacked the knowledge or ability to understand, but the

use of the word “issue” is an attempt to minimize the crisis. Another example of

defeasibility is, “I’m sorry that I didn’t know four years ago what I know now, but the data

didn’t lead us there four years ago” (Berensen, et al, 2004).

The company also used good intentions, another evasion strategy, twice when it

talked about the study of the effects of Vioxx and stated “we did our best to think of the most

comprehensive study we could have done” (Berenson et al., 2004). Finally, Merck stated that

it “acted responsibly and appropriately as it developed and marketed Vioxx” (E-mails

suggest Merck knew Vioxx’s dangers at early stages, 2004), an example of simple denial.

This strategy is only appropriate if the firm is truly blameless. If the firm uses a denial

strategy and later is found to have blame in the crisis, its reputation can be irreparably

damaged.

Journal of Business and Accounting

9

Table 2 provides a summary of our analysis of the responses made by Merck after

pulling Vioxx off the market.

Table 2. Categories of communication responses after pulling Vioxx.

Typology Number of

Times Used

Total for

Category

Denial:

Denial 1

Shifting the Blame

Total for Denial 1

Evasion of Responsibility

Scapegoating

Defeasibility 3

Accident

Good Intentions 2

Total for Evasion of Responsibility 5

Reducing the Offensiveness

Bolstering Image 12

Minimization 6

Differentiation

Transcendence

Reducing the Credibility 3

Compensation

Total for Reducing the Offensiveness 21

Taking Corrective Action

0

Mortification

0

TOTAL

27

In their research, Marcus and Goodman (1991) compared the stock market reaction of

accommodating communications to the reaction of defensive communications. Their

description of accommodating signals include those where management accepted

responsibility, admitted to the existence of the problem, apologized, and took action to

remedy the situation. Their description of defensive policies include those in which

management denied the existence of a problem, alleviated doubts about the firm’s future

viability, denied intent, and took actions to resume normal operations quickly. Mapping

Marcus and Goodman’s descriptions onto Benoit’s framework produces the following

comparison, as shown in Table 3. Accommodative communications are those which Benoit

titles Corrective Action, and Mortification; while Defensive policies are those categorized as

Denial, Evasion of Responsibility, and Reducing the Offensiveness.

Stone, Erickson, and Weber

10

Table 3. Comparison of Marcus and Goodman to Benoit.

Marcus and Goodman (1991) Corporate Policy signals Benoit’s Crisis Communication Framework

Accommodating Corrective Action

Mortification

Defensive Denial

Evasion of Responsibility

Reducing the Offensiveness

In effect, Merck used only defensive communication strategies for the crisis.

According to Marcus and Goodman’s (1991) study, this type of strategy only serves

shareholder interests effectively by providing significantly better returns to shareholders

when the cause of the crisis is an accident.

The crisis in this study involves a safety and product recall crisis, which, according to

Marcus and Goodman (1991), indicated no significant differences between accommodative

and defensive communication strategies. Although this crisis was that of the product recall

variety, it could be argued that because management had knowledge of the medical risks for

months, yet continued to market Vioxx, it could be considered a scandal. Prior knowledge of

the dangers of Vioxx was indicated on May 18, 2004 when the Wall Street Journal reported

that Merck had requested that their employee, Dr. Cannuscio, be removed from a study

which found harmful side effects for patients who used Vioxx. Merck, claimed, “Merck

disagreed with the conclusions and didn’t think it was appropriate to have a Merck author”

(Burton, 2004, p. B.1). Merck also stated, “You’re not able to control completely for the

differences between groups. There were serious limitations to the analysis” (Burton, 2004, p.

B.1). Also, on November 1, 2001, the Wall Street Journal reported that Merck executives

had been worried in the 1990s that Vioxx would show greater heart risk than cheaper pain

killers (Rotthoff 2010). Both of these communications with the public gave hints that the

product recall crisis was more of a scandal than an accident.

Regardless of whether this crisis is a scandal or a product recall, according to Marcus

and Goodman (1991), shareholders would have been better served by accommodating

strategies. Because Merck utilized defensive strategies, we would expect to see negative

stock market reactions, which is clearly the case on September 30, 2004. Merck withdrew

Vioxx after the market closed on 9/29/2004 and the stock price fell from $45.07 that day to

$33.00 at the close of the market on 9/30/2004, a loss of $26.8 billion in market value

(Rotthoff, 2010). Rotthoff shows the market acted quickly and efficiently to the news.

Marcus and Goodman suggest that Merck needed to handle the crisis, if classified as a

scandal, by using more accommodative strategies, such as corrective action and

mortification.

Corrective action could have included the offer to pay for medical exams for patients

taking Vioxx in order to access possible heart damage. Mortification requires an apology,

which legal counsel generally discourages. Merck researcher Dr. Reicin was the only

individual to say that she was “…sorry that I didn’t know four years ago what I know

now…” (Berenson, et al., 2004), but it isn’t clear what she was actually sorry about: Death

of patients who used Vioxx? Perhaps she was sorry about not withdrawing the drug sooner,

which Rotthoff (2010) contends would have resulted in a smaller total financial loss for

Journal of Business and Accounting

11

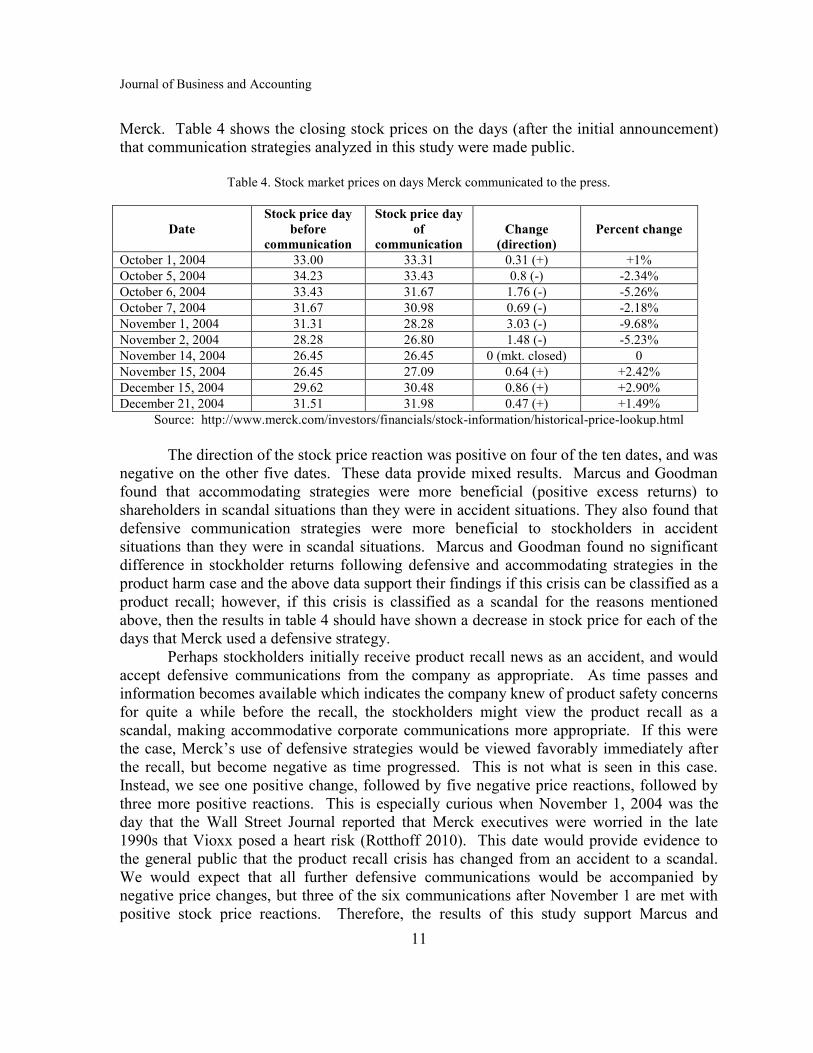

Merck. Table 4 shows the closing stock prices on the days (after the initial announcement)

that communication strategies analyzed in this study were made public.

Table 4. Stock market prices on days Merck communicated to the press.

Date

Stock price day

before

communication

Stock price day

of

communication

Change

(direction)

Percent change

October 1, 2004 33.00 33.31 0.31 (+) +1%

October 5, 2004 34.23 33.43 0.8 (-) -2.34%

October 6, 2004 33.43 31.67 1.76 (-) -5.26%

October 7, 2004 31.67 30.98 0.69 (-) -2.18%

November 1, 2004 31.31 28.28 3.03 (-) -9.68%

November 2, 2004 28.28 26.80 1.48 (-) -5.23%

November 14, 2004 26.45 26.45 0 (mkt. closed) 0

November 15, 2004 26.45 27.09 0.64 (+) +2.42%

December 15, 2004 29.62 30.48 0.86 (+) +2.90%

December 21, 2004 31.51 31.98 0.47 (+) +1.49%

Source: http://www.merck.com/investors/financials/stock-information/historical-price-lookup.html

The direction of the stock price reaction was positive on four of the ten dates, and was

negative on the other five dates. These data provide mixed results. Marcus and Goodman

found that accommodating strategies were more beneficial (positive excess returns) to

shareholders in scandal situations than they were in accident situations. They also found that

defensive communication strategies were more beneficial to stockholders in accident

situations than they were in scandal situations. Marcus and Goodman found no significant

difference in stockholder returns following defensive and accommodating strategies in the

product harm case and the above data support their findings if this crisis can be classified as a

product recall; however, if this crisis is classified as a scandal for the reasons mentioned

above, then the results in table 4 should have shown a decrease in stock price for each of the

days that Merck used a defensive strategy.

Perhaps stockholders initially receive product recall news as an accident, and would

accept defensive communications from the company as appropriate. As time passes and

information becomes available which indicates the company knew of product safety concerns

for quite a while before the recall, the stockholders might view the product recall as a

scandal, making accommodative corporate communications more appropriate. If this were

the case, Merck’s use of defensive strategies would be viewed favorably immediately after

the recall, but become negative as time progressed. This is not what is seen in this case.

Instead, we see one positive change, followed by five negative price reactions, followed by

three more positive reactions. This is especially curious when November 1, 2004 was the

day that the Wall Street Journal reported that Merck executives were worried in the late

1990s that Vioxx posed a heart risk (Rotthoff 2010). This date would provide evidence to

the general public that the product recall crisis has changed from an accident to a scandal.

We would expect that all further defensive communications would be accompanied by

negative price changes, but three of the six communications after November 1 are met with

positive stock price reactions. Therefore, the results of this study support Marcus and

Stone, Erickson, and Weber

12

Goodman if the crisis is classified as a product recall, but do not support their study if the

crisis is classified as a scandal.

CONCLUSION

The current study examined stock price reaction to corporate communications

following crisis. Using Benoit (1995) and Marcus and Goodman (1991) as a framework,

authors mapped Merck Pharmaceutical’s image restoration communications around the time

of the Vioxx recall onto the former scholar’s outcomes. The communications were

categorized as “denial”, “evasion of responsibility”, and “reducing the offensiveness of the

act”, as per Benoit’s framework. These would all map to defensive strategies under Marcus

and Goodman’s typology.

Our results mirror Marcus and Goodman’s (1991) results if the Vioxx crisis can be

labeled as a product recall. However, if viewed as a scandal, our results do not support the

Marcus and Goodman study. We examined the direction of stock price change at the time of

corporate communication. All of the communications we analyzed were defensive, yet the

direction of stock price change was negative in over half of the observations, and was

positive in the remainder of the communications.

If corporate management believes that stockholders will view the product safety

crises more like an accident, management should use defensive strategies. If management

believes stockholders will view the crisis more like a scandal, accommodating strategies

should be used. In the early phases of a product recall crisis, management may want to make

stakeholders believe that this is an accident, not a scandal; therefore utilizing defensive

communication strategies. As the reality of the slow evolution of product recall cases

becomes known by the external stakeholders, the crisis begins to look more like a scandal

than an accident, making defensive communication strategies less appropriate. The mixed

pattern of results in the current study does not support this temporal view of product recall

crisis. Instead of the ambiguous results being a result of stakeholder attitudes differing over

time, perhaps attitudes differ between individual stakeholders. Some might view a product

recall crisis as an accident, while others view it as a scandal; leading to inconclusive results.

Crisis communication is important and management should be cautious when

selecting the proper communication strategy. More studies need to be conducted on product

recall crises in order to better understand which type of communication strategies provide

increased shareholder value. In addition, organizations need to determine if product recall

crises may actually fall into the accident category, like the Tylenol crisis, or into the scandal

category, which appears to be the case for the Vioxx crisis. When faced with a scandal,

companies should use accommodating communication strategies to provide increased

shareholder value.

REFERENCES

A Vioxx Elegy (2004, October 1). The Wall Street Journal. Retrieved March 4, 2010 from

http://proquest.umi.com

Allen, M. W., & Caillouet, R. H. (1994). Legitimation endeavors: Impression management

strategies used by an organization in crisis. Communication Monographs, 61(1), 44-62.

Journal of Business and Accounting

13

Benoit, W. (1995). Accounts, Excuses, and Apologies: A Theory of Image Restoration Strategies.

Albany, NY: State University of New York Press.

Benoit, W. (1997). Image repair discourse and crisis communication. Public Relations Review,

23(2), 177-186.

Benoit, W. (2006). President Bush’s image repair effort on Meet the Press: The complexities of

defeasibility. Journal of Applied Communication Research, 34(3), 285-306.

Benoit, W. & Czerwinski, A. (1997). A critical analysis of USAir’s image repair discourse. Business

Communication Quarterly, 60(3) 38-57.

Benoit, W. & Henson, J. (2009). President Bush’s image repair discourse on Hurricane Katrina.

Public Relations Review, 35, 40-46.

Berenson, A., Harris, G., Meier, B. & Pollack, A. (2004, November 14). Despite warnings, drug

giant took long path to Vioxx recall. The New York Times. Retrieved April 7, 2010 from

http://proquest.umi.com

Blaney, J., Benoit, W., & Brazeal, L. (2002). Blowout!: Firestone’s image restoration campaign.

Public Relations Review, 28, 379-392.

Burton, T.M. (2004, May 18). Merck takes authors name off Vioxx study. The Wall Street Journal.

Retrieved July 15, 2010 from http://proquest.umi.com

Chen, Y, Ganesan, S., & Liu, Y. (2009). Does a firm’s product-recall strategy affect its financial

value? An examination of strategic alternatives during product harm crises. Journal of

Marketing, 73, 214-226.

Coombs, W. (1995). Choosing the right words: The development of guidelines for the selection of

the “appropriate” crisis response strategies, Management Communication Quarterly, 8, 447-

476.

E-mails suggest Merck knew Vioxx’s dangers at early stage. (2004, November 1). WSJ.com.

http://online.wsj.com/articls/SB109926864290160719.html

Erickson, S., Weber, M., Segovia, J. & Dudney, D. (2010). Management use of image restoration

strategies to address SOX 404 material weaknesses. Academy of Accounting and Financial

Studies Journal, 14(2), 59-82.

Erickson, S., Weber, M., & Stone, M. (2011). Corporate reputation management: Citibank’s use of

image restoration strategies during the U.S. banking crisis. Journal of Organizational

Culture, Communications & Conflict, 15(2), 35-56.

Fortunato, J. (2008). Restoring a reputation: The Duke University lacrosse scandal, Public Relations

Review, 34, 116-123.

Hearit, K. M. (1995). From “we didn’t do it” to “it’s not our fault”: The use of apologia in public

relations crises. In W. N. Elwood (Ed.), Public Relations Inquiry as Rhetorical Criticism:

Case Studies of Corporate Discourse and Social Influence (p. 117-131). Praeger Series in

Political Communication. Westport, CT: Praeger.

Geppert, J. & Lawrence, J. (2008). Predicting firm reputation through content analysis of

shareholders’ letter. Corporate Reputation Review, 11(4), 285-307.

Huang, Y. & Su, S. (2009). Determinants of consistent, timely, and active responses in corporate

crises. Public Relations Review, 35(1), 7-17.

Lyon, A., & Mirivel J.C. (2011). Reconstruction Merck’s practical theory of communication: The

ethics of pharmaceutical sales representative-physician encounters. Communication

Monographs, 78(1), 53-72.

Marcus, A., & Goodman, R. (1991). Victims and Shareholders: The dilemmas of presenting

corporate policy during a crisis. Academy of Management Journal, 34(2), 281-305.

Martinez, B. (2004). Merck’s woes grow as credit rating is put on watch. The Wall Street Journal.

November 2. Retrieved from Proquest databases March 4, 2010.

Stone, Erickson, and Weber

14

Martinez, B., & Hensley, S. (2004). Cardiologist calls for inquiry into FDA’s Handling of Vioxx.

The Wall Street Journal. October 7, p. B.8. Retrieved from Proquest databases March 4,

2010.

Martinez, B., Mathews, A., Lubline, J. & Winslow, R. (2004). Expiration date: Merck pulls Vioxx

from market after link to heart problems. The Wall Street Journal. October 1, p. A1.

Retrieved from Proquest databases March 4, 2010.

Mathews, A.W. & Martinez, B. (2004). E-mails suggest Merck knew Vioxx’s dangers at early

Stage. Retrieved from WSJ.com on March 5, 2010.

Merck yanks arthritis drug Vioxx (2004). CNNMoney.com, October 6, 2004. Retrieved March 4,

2010 from http://money.cnn/com/2004/09/30/news/fortune500/merck/

Petersen, M. (2000). Pushing pills with piles of money; Merck and Pharmacia in arthritis-drug

battle, The New York Times. October 5, 2000.

http://www.nytimes.com/2000/10/05/business/pushing-pills-with-piles-of-money-merck-

and-pharmacia-in-arthritis-drug-battle.html

Rotthoff, K.W. (2010). Product liability litigation: An issue of Merck and lawsuits over Vioxx.

Applied Financial Economics, 20(24), 1867-1878.

Scott, M. H., & Lyman, S. M. (1968). Accounts. American Sociological Review, 33(1), 46-62.

Seeger, M., Sellnow, T., & Ulmer, R. (2003). Communication and Organizational Crisis. Westport,

CT: Praeger.

Seeger, M. W., Sellnow, T. L., & Ulmer, R. R. (1998). Communication , organization and crisis. In

M. E. Roloff (Ed.), Communication Yearbook, (Vol. 21, pp. 231-275). Thousand Oaks,

CA: Sage.

Suchman, M. C. (1995). Managing legitimacy: Strategic and institutional approaches. The

Academy of Management Review, 20(3), 571-610.

Table 4, http://www.merck.com/investors/financials/stock-information/historical-price-lookup.html

The Associated Press (2010). Merck’s Vioxx settlement requires committee, medical officer to

monitor drug development. February 10, 2010.

http://www.nj.com/business/index.ssf/2010/02/mercks_vioxx_settlement_requir.html

Valentine, L. (2007) Talk is not cheap. ABA Banking Journal December, 38-41.

Ware, B. L., & Linkugel, W. A. (1973). They spoke in defense of themselves: On the generic

criticism of apologia. Quarterly Journal of Speech, 59(3), 273-283.

Weitz & Luxenberg, P.C. (2010) Vioxx – get the history of the major drug recall.

http://www.weitzlux.com/vioxx/recallhistory_94.html

Journal of Business and Accounting

Vol. 5, No. 1; Fall 2012

15

CONFLICT MINERALS DISCLOSURES:

A MANDATE OF THE DODD-FRANK ACT

Deborah L. Lindberg

Illinois State University

Khalid Razaki

Dominican University

ABSTRACT

For certain humanitarian reasons, such as deprivation of financial resources to

militant groups that seek arms for nefarious purposes, the civilized world is seeking to

eliminate or significantly diminish the trade in “conflict minerals”. The United States is

trying help in this effort by various means, including (a) forcing the publicly traded user

companies of these minerals to establish their supply sources, and (b) after a proper audit,

reporting the results in annual financial statements and official websites.

Section 1502 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of

2010 (Dodd-Frank Act) requires a new reporting requirement for publicly traded companies

that manufacture products for which “conflict minerals” are necessary for their functionality

or production. The conflict minerals included in this provision of are cassiterite, columbite-

tantalite, gold, wolframite, or their derivatives. The supply source of concern is the

Democratic Republic of the Congo or countries adjoining the Congo. The requirements apply

to both domestic and foreign issuers of publicly traded equities (issuers), including smaller

companies that must report to the Securities and Exchange Commission.

Industries that may be subject to these new reporting requirements include aerospace,

automotive, electronics, communication, jewelry, and manufacturers of healthcare machines.

However, while it could be argued that the U.S. Congress' attempts to curb violence in the

Congo and adjoining countries is commendable, there are several issues regarding the

disclosure requirements for conflict minerals.

INTRODUCTION

For certain humanitarian reasons, such as deprivation of financial resources to

illegitimate groups that seek arms for nefarious purposes, the civilized world is seeking to

eliminate or significantly diminish the trade in “conflict minerals”. The United States is

trying help in this effort by various means, including (a) forcing the publicly traded user

companies of these minerals to establish their supply sources, and (b) after a proper audit,

reporting the results in annual financial statements and official websites.

Though there are no specified penalties for the use of conflict minerals (McDermott

Will & Emery, 2010), the U.S. Congress hoped that mandating public disclosure might

shame [the “name and shame” incentive, according to Ayogu and Lewis, 2011] user

companies to curb or eliminate such trade, resulting in the denial of funds to abusers of

human rights (Zweig, 2011).

Section 1502 of the Dodd-Frank Wall Street Reform and Consumer Protection Act of

2010 (Dodd-Frank Act) requires a new reporting requirement for publicly traded companies

that manufacture products for which “conflict minerals” are necessary for their functionality

Lindberg and Razaki

16

or production (McDermott Will & Emery, 2010). The conflict minerals included in this

provision of the Dodd-Frank Act are cassiterite, columbite-tantalite, gold, wolframite, or

their derivatives (SEC, 2010). By passing this section of the Dodd-Frank Act, Congress in

effect ordered the U.S. Securities and Exchange Commission (SEC) to require publicly

traded companies to disclose whether raw materials essential to their products originated

from the Democratic Republic of the Congo or countries adjoining the Congo (DRC

countries) (SEC, 2010; Zweig, 2011). Countries contiguous to the Democratic Republic of

the Congo included in this legislation are South Sudan, Uganda, Rwanda, Burundi, Tanzania,

Malawi, Zambia, Angola, Congo, and the Central African Republic (Ayogu and Lewis,

2011).

The disclosure requirements apply to both domestic and foreign issuers of publicly

traded equities (issuers), including smaller companies that must report to the Securities and

Exchange Commission (SEC, 2010). Industries that may be subject to these new reporting

requirements include aerospace, automotive, electronics, communication, jewelry, and

manufacturers of healthcare machines (Ayogu and Lewis, 2011).

BACKGROUND

Warring factions in the Democratic (sic) Republic of Congo have financed the acts of

murder, mutilation, kidnapping, rape, child labor, pillaging by mining and selling “conflict”

minerals (described below). The Congolese supply amounts to about 20% of the total global

supply (Zweig, 2011).

Congress adopted Section 1502 of the Dodd-Frank Act in the hopes that reporting

requirements about conflict minerals will help curb the violence in the Congo (SEC, 2010).

Disclosures related to the so-called “conflict” minerals are aimed at stemming the brutal

militia groups that often take over the mining and sale of these minerals to finance their

military actions (Wyatt, 2012). While the conflict mineral disclosures mandated by the Dodd-

Frank Act do not impose any penalties on companies that are using such minerals in their

products, the intention of the disclosures is to allow the investing public the opportunity to

judge such companies (McDermott Will & Emery, 2010).

Zweig (2011) expected that about 1200 companies would eventually fall under this

reporting provision. The number of companies meeting this reporting requirement is

increasing (from 2 companies in 2010 to over 40 in 2011 (Ibid). There are significant

monetary and non-monetary costs of adopting this requirement. Zweig (2011) cites the case

of a small company with a market value of $11 million and net income of $228,000 that

estimated its cost of compliance to be around $1 million. Such costs are obviously

prohibitive and untenable for smaller companies.

CONFLICT MINERALS

The conflict minerals specified in the Dodd-Frank Act, for which disclosure by

publicly traded companies will be required, are cassiterite, columbite-tantalite, gold, and

wolframite, or their derivatives (SEC, 2010). Each mineral will be discussed in the following

sections.

Cassiterite: Cassiterite is an important source of the type of tin used in coffee cans

and circuit boards (Wyatt, 2012). It is also used in cell phones, DVD players, and computers.

Journal of Business and Accounting

17

Columbite-tantalite: “Coltan” is short for columbite-tantalite (Epstein & Yuthas,

2011). In industrial uses this mineral is known as “tantalite” or “tantalum.” After columbite-

tantalite is refined it is used in products ranging from small cell phones to giant turbines

(Wyatt, 2012). It is also used in such consumer electronic products as DVD players, video

games, and computers. In Intel’s 2011 annual report, the corporation notes that its goal for

2012 is to verify that the tantalum used in it microprocessors is conflict free (Intel

Corporation, 2012).

Gold: Gold is of course extensively used in jewelry. In addition, gold is often used in

electronic products as a conductor (Wyatt, 2012). This precious metal also has a myriad of

other uses, ranging from dentistry to coins to electric wiring.

Wolframite: Wolframite is used to produce the tungsten that is used in such products

as light bulbs and machine tools (Wyatt, 2012). It is also used in armor-piercing ammunition.

These conflict minerals are sometimes referred to as “3TG” minerals (tin, tantalum,

tungsten, and gold (Ayogu and Lewis, 2011). Refer to Table 1 for a summary of conflict

minerals and their uses in products.

Table 1: Conflict Minerals and Their Use in Products

Conflict Mineral Other Names for

These Minerals Consumer Products

Cassiterite Tin

Coffee cans;

Computers;

Cell phones;

DVD players

Columbite-tantalite

Coltan;

Tantalite;

Tantalum

Cell phones;

DVD players;

Video games:

Computers;

Turbines

Gold Gold Jewelry;

Electronic products

Wolframite Tungsten

Light Bulbs;

Machine Tools;

Armor-piercing ammunition

CONFLICT MINERALS DISCLOSURES

The rules issued by the SEC require a reporting issuer (publicly traded company) to

disclose whether its conflict minerals originated in one of the DRC countries after conducting

a reasonable country of origin inquiry process. Thus, the burden of proof shifts from

corporations relying on their suppliers’ assurances that they don’t have conflict minerals to

the publicly traded company determining the source of the minerals. If the company

concludes its conflict minerals did not originate in any of the DRC countries, it would

describe this determination and the reasonable country of origin process it used to make it. If

Lindberg and Razaki

18

the reporting company concludes that its conflict minerals did originate in one or more of the

DRC countries, it would disclose this conclusion and be required to provide a “Conflict

Minerals Report” and a certified private sector audit of the Conflict Minerals Report (SEC,

2010). Each of these requirements will be discussed in the following sections.

REQUIRED DISCLOSURES - NO CONFLICT MINERALS FROM DRC

COUNTRIES

If after a reasonable country of origin inquiry process a reporting company concludes

its conflict minerals did not originate in any of the DRC countries, it would describe this

determination and the inquiry process it used to make it. Similarly, if after a reasonable

inquiry of the country of origin a company is unable to determine the origin of its minerals, it

must disclose that fact (Ayogu and Lewis, 2011). More specifically, the issuer will be

required to:

Make the disclosure available on its Internet website

Provide the Internet address of this website

Maintain records demonstrating that its conflict minerals did not originate in any

of the DRC countries (SEC, 2010).

CONFLICT MINERALS REPORT - REQUIRED FOR CONFLICT MINERALS

FROM DRC COUNTRIES

If the reporting company concludes that its conflict minerals did originate in one or

more of the DRC countries, the company must disclose this conclusion and issue a Conflict

Minerals Report as an exhibit to the annual report. Specific disclosures would require the

issuer to:

Describe its products manufactured or contracted to be manufactured containing

conflict minerals originating in any of the DRC countries

Disclose the facilities used to process such conflict minerals

Disclose conflict minerals’ country of origin

Describe the efforts used to determine the mine or location of origin with the

“greatest possible specificity”

Note that the Conflict Minerals Report is included as an exhibit to the annual

report

Furnish the Conflict Minerals Report

Make the Conflict Minerals Report available on its Internet website

Disclose that the Conflict Minerals Report is posted on its Internet website

Provide the Internet address of this website (SEC, 2010).

Reporting companies would describe the measures taken by the company to exercise

due diligence regarding the source and chain of custody of conflict minerals that are

necessary to the functionality or production of its products (SEC, 2010).

CERTIFIED INDEPENDENT PRIVATE SECTOR AUDIT

There must be a certified private sector audit of the Conflict Minerals Report (SEC,

2010). However, many constituencies expressed significant reservations regarding several

Journal of Business and Accounting

19

aspects of the audit requirement. For example, in a letter to the SEC sent by Grant Thornton

LLP during the comment period, the CPA firm expressed the following concerns:

It appears that either an attestation engagement or a performance audit would

meet the audit requirement. However the two engagements differ significantly in

nature, scope, and reporting requirements, potentially causing confusion and

misunderstanding among users of the audit report.

The objective of the audit, including the opinion or conclusion to be expressed on

the issuer's Conflict Minerals Report is not described.

The criteria to be used to evaluate the subject matter in the Conflict Minerals

Report are not described (Grant Thornton LLP, 2011).

The American Institute of Certified Public Accountants (AICPA) expressed similar

reservations and concerns in a letter that the organization sent to the SEC (Coffee, 2011).

Moreover, both Grant Thornton and the AICPA expressed concerns regarding

independence issues surrounding the private sector audit of the Conflict Minerals Report.

Grant Thornton noted that the SEC proposal, while consistent with terminology used in the

Dodd-Frank Act, indicates that the independent audit is a “critical component of due

diligence” on the part of the reporting company (Grant Thornton LLP, 2011). However, this

statement is contrary to the concept of an independent audit opinion (Grant Thornton LLP,

2011), since the auditor should not be part of the process regarding the assertion by

management that the audit firm is attesting to. The AICPA noted that since the rules

regarding private sector audit is silent as to independence issues, the SEC needed to clarify

which independence standards apply to the audits of Conflict Mineral Reports. Independence

requirements under Attestation Engagements issued by the AICPA, Performance Audits

within Government Auditing Standards (GAGAS), and audits following SEC independence

standards have differing requirements regarding the independence of the audit firm from its

client (Coffee, 2011).

Several of these concerns were addressed in the final rules issued by the SEC on

August 22, 2012 (Ernst & Young, 2012). For example, regarding auditor independence, the

final rules indicate that the independent private sector audit of the Conflict Minerals Report

must comply with independence standards issued by the Governmental Accounting Office

(GAO). Further, the SEC stated that an audit firm could perform both the audit of the

Conflict Minerals Report and the audit of the financial statements of the issuer and still be

considered independent (SEC, 2012). In the final rules the SEC also indicated what the

objective of an audit of a Conflict Minerals Report it, noting that “the audit’s objective is to

express an opinion or conclusion as to whether the design of the issuer’s due diligence

framework as set forth in the Conflict Minerals Report, with respect to the period covered by the

report, is in conformity with, in all material respects, the criteria set forth in the nationally or

internationally recognized due diligence framework used by the issuer, and whether the issuer’s

description of the due diligence measures it performed as set forth in the Conflict Minerals

Report, with respect to the period covered by the report, is consistent with the due diligence

process that the issuer undertook” (SEC, 2012, p. 217). However, there is still ambiguity in terms of the auditing standards to employ for an

audit of a Conflict Minerals Report. In its final report, the SEC notes that either the standards

Lindberg and Razaki

20

for Attestation Engagements or the standards for Performance Audits will be applicable

(SEC, 2012).

EFFECT OF THE DISCLOSURES ON CORPORATE BEHAVIOR

Even though the disclosure requirements for conflict minerals are not yet in place,

companies such as Intel, Motorola and Hewlett-Packard have already taken significant steps

to inspect and adjust their supply lines to avoid obtaining conflict minerals from DRC

countries (e.g., Wyatt, 2012). For example, in its 2011 annual report disclosures, Intel noted

that it has developed programs to allow for tracking of its source materials, in particular those

sourced from the Democratic Republic of the Congo. Further, Intel states that it will continue

to work to establish a conflict-free supply chain for the company and its industry (Intel

Corporation, 2012).

Several other corporations have already expressed concern about the “reputational

effect” their association with conflict minerals may have. To illustrate, in its 2011 annual

report disclosures, Sprint notes that because their supply chain is complex, the company may

face reputational challenges with its customers and other stakeholders if they are unable to

verify the origins of all the metals used in its products (Sprint Nextel Corporation, 2012).

Dell, Inc. makes a similar statement in its annual report for the fiscal year ended February 3,

2012, noting that the corporation may face reputational harm if its customers or other

stakeholders conclude that Dell is unable to verify sufficiently the origin of the minerals used

in its products (Dell, Inc., 2012). These and other examples of corporate disclosures

associated with the SEC’s disclosure requirements for conflict minerals are provided in Table

2.

Table 2: Conflict Minerals Disclosure Examples

Company FY Ended p. # Excerpts of Disclosures Related to “Conflict Minerals”

Advanced

Micro Devices,

Inc.

12/31/11

26,27

These new requirements could affect the sourcing and availability of

minerals used in the manufacture of semiconductor devices. Also, there

will be additional costs of compliance such as costs related to determining

the source of any conflicting minerals used in our products.

Cabot

Corporation

9/30/11

5

“An independent audit conducted by a third party auditor assigned by the

Electronics Industry Citizenship Coalition and Global e-Sustainability

Initiative (as part of the Conflict-Free Smelter Validation Program)

confirmed that our tantalum supply chain is free of conflict minerals.”

Dell, Inc.

2/3/12

35

“We will incur costs to comply with the new disclosure requirements of

this law and may realize other costs relating to the sourcing an availability

of minerals used in our products. Further, since our supply chain is

complex, we may face reputational harm if our customers or other

stakeholders conclude that we are unable to verify sufficiently the origins

of the minerals used in the products we sell.”

Helen of Troy

Limited

2/29/12

25 If rules are not modified before becoming effective, they will increase the

cost of our sourcing compliance operations.

Journal of Business and Accounting

21

Intel

Corporation

12/31/11

19 “In 2012, Intel will continue to work to establish a conflict-free supply

chain … Intel’s goal for 2012 is to verify that the tantalum we use in our

microprocessors is conflict free, and our goal for 2013 is to manufacture

the world’s first verified, conflict-free microprocessor.”

Motorola

Solutions, Inc.

12/31/11

27

The implementation may limit the pool of suppliers who can provide us

verifiable DRC Conflict Free components and parts, and we are not certain

that we will be able to obtain products in sufficient quantities that meet the

requirements.

RF

Monolithics

Inc.

8/31/11

15 It is unclear whether we will be affected materially.

Sprint Nextel

Corporation

12/31/11

23

The proposed regulation may leave only a limited pool of suppliers who

provide conflict free metals, and we not be able to obtain products in

sufficient quantities or at competitive prices. Also, because our supply

chain is complex, we may face reputational if we are unable to sufficiently

verify the origins for all metals used in the products we sell.

Tiffany & Co.

1/31/12

13

Once polished, it is not considered possible to distinguish conflict

diamonds from diamonds produced in other regions. Tiffany seek(s) to

exclude such diamonds, which represent a small fraction of the world’s

supply, from legitimate trade using an international system of certification

and legislation known as the Kimberley Process Certification Scheme.

*A Supermetals Business listed under Discontinued Operations in Cabot’s 10-K for the fiscal year

ended September 30, 2011 (Cabot Corporation, 2012).

Source: Recent 10-K reports of the corporations listed in this table were the source of the conflict

minerals disclosures included above (Advanced Micro Devices, Inc., 2012; Cabot Corporation, 2012; Dell Inc.,

2012; Helen of Troy Limited, 2012; Intel Corporation, 2012; Motorola Solutions, Inc., 2012; RF Monolithics,

Inc., 2012; Sprint Nextel Corporation, 2012; Tiffany & Co., 2012). The page numbers indicated are from the

SEC’s “Edgar” database of Form 10-K’s for each respective company.

ANTICIPATED COSTS

There are significant costs associated with the compliance by SEC reporting

companies regarding the conflict minerals disclosure mandate in the Dodd-Frank Act of

2009. The National Association of Manufactures has estimated national compliance costs

between $9 billion and $16 billion, whereas the SEC estimate is $71 million (Ayogu and

Lewis, 2011). The extreme variation between the two estimates results from the speculative

nature of the estimation process, the verification process, and the underlying assumptions.

Plausible cost estimates will be available only after the SEC has finalized all the requisite

rules for verification and reporting. An enumeration of possible costs to companies using

conflict minerals is presented below:

Verification Cost: This cost component may be the most significant monetary

cost. Under the new requirements, the cost of establishing source of supply is

shifted from supplier to user (reporting issuer). It should be noted that there is

an “escape clause” for companies experiencing problems with verification. If

a company cannot determine the origins of its conflict minerals, it can just

disclose that fact without any further consequences (Ayogu and Lewis, 2011).

Increased audit costs due to greater testing by auditors. The SEC can help

significantly reduce the overall cost of compliance by providing specific

definitions and audit standards (Ayogu and Lewis, 2011).

Lindberg and Razaki

22

Cost of recording and reporting: A company must file three different forms of

paperwork and publish a “Conflict Minerals Report” in both its audited annual

financial statements and website (Ayogu and Lewis 2011).

If current supply of conflict minerals is tainted, its replacement from

legitimate sources might constrict the remaining global supply, resulting in

higher raw materials cost (Zweig, 2011).

Reputational Cost (Zweig 2011, Ayogu and Lewis 2011): cost of potential

harmful public aversion and bad publicity if a legitimate source of supply

cannot be found. This cost may be difficult to measure or estimate.

Opportunity costs of lost business if customers avoid or boycott products

containing conflict minerals (Zweig, 2011).

Opportunity cost related to increased cost of capital if major investors

(pension plans, religious and other human rights activist investors, social

values investment funds, etc.) disinvest or refuse to invest in involved

companies. On the other hand, there seems to be no effect on the stock prices

of companies that did report using conflict minerals (Zweig, 2010).

FILING REQUIREMENTS

Issuers are required to file a newly created specialized disclosure report (Form SD)

annually by May 31 for the prior calendar year (Ernst & Young, 2012.) The first required

filings of form SD will be on May 31, 2014 for calendar year 2013 (SEC, 2012). The SEC

finalized rules allow issuers to describe their products as “DRC conflict undeterminable” for

the first two years if the issuers cannot determine the source and/or chain of custody of the

minerals they use; during this “transition” period, any such issuers must file the Form SDs,

but they don’t have to have them audited (Ernst & Young, 2012.)

CONCLUSION

While it could be argued that the U.S. Congress' attempts to curb violence in the

Congo and adjoining countries is commendable, there are still several unresolved issues

regarding the disclosure requirements for conflict minerals. For instance, since disclosures

are based on a “reasonable” country of origin inquiry process, the term reasonable is subject

to interpretation by companies, and likely will not be interpreted in a consistent manner

among companies. The “due diligence” required regarding the source and chain of custody of

conflict minerals is also subject to wide interpretation. In addition, the specific requirements

of the certified independent private sector audit that is to be furnished as part of the Conflict

Minerals Report has many unanswered questions (Ayogu and Lewis, 2011; Coffee, 2011;

Grant Thornton LLP, 2011).

The costs of compliance with this mandate are expected to be very significant. In the

case of smaller companies, they may be prohibitive. At present, these costs cannot be fairly

estimated due to the non-specificity by the SEC regarding definitions and standards. Without

making any value judgments, this is another case of increased regulation for the

accomplishment of the government’s socio-political goals that places a financial burden on

businesses. Perhaps most importantly, however, the only consequences of a publicly traded

company continuing to use conflict minerals are the reputational effects of using these

Journal of Business and Accounting

23

minerals. However, if nothing else, disclosures regarding conflict minerals will heighten

awareness of the humanitarian issues in the DRC and their relationship to U.S. trade (Ayogu

and Lewis, 2011).

REFERENCES

Advanced Micro Devices, Inc. (2012). Form 10-K (Annual Report Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934). For the fiscal year ended December 31, 2011,

www.sec.gov/Archives/edgar/data/2488/000119312512075837/d257108d10k.htm.

Ayogu, M. and Lewis, Z. (2011). “Conflict Minerals: An Assessment of the Dodd-Frank Act.” The

Brookings Institute, October 3, http://www.brookings.edu/research/opinions/ 2011/10/03-

conflict-minerals-ayogu.

Cabot Corporation (2012). Form 10-K (Annual Report Pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934). For the fiscal year ended September 30, 2011,

www.sec.gov/Archives/edgar/data/16040/000119312511324512/d230919d10k.htm.

Coffee, S.S. (2011). Letter to U.S. Securities and Exchange Commission. (American Institute of

Certified Public Accountants, New York, NY), March 1, http://www.sec.gov/comments/s7-

40-10/s74010-123.pdf.

Dell, Inc. (2012). Form 10-K (Annual Report Pursuant to Section 13 or 15(d) of the Securities

Exchange Act of 1934). For the fiscal year ended February 3, 2012,

www.sec.gov/Archives/edgar/data/826083/000082608312000006/dell10k020312.htm.

Epstein, M.J. and Yuthas, K. (2011). “Conflict Minerals: Managing an Emerging Supply-Chain

Problem.” Environmental Quality Management, Volume 21, Issue 2, 13-25.

Ernst & Young (2012). “Final Conflict Minerals Rule Addresses Many Stakeholder Concerns.”

August 24. http://www.ey.com/UL/en/AccountingLink/Current-topics-SEC-Other-

regulators.

Grant Thornton LLP. (2011). Letter to U.S. Securities and Exchange Commission. (Grant Thornton

LLP, Chicago, IL). March 2, http://www.sec.gov/comments/s7-40-10/s74010-127.pdf.

Helen of Troy Limited (2012). Form 10-K (Annual Report Pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934). For the fiscal year ended February 29, 2012.

www.sec.gov/Archives/edgar/data/916789/000110465912030645/a12-2513110k.htm.

Intel Corporation (2012). Form 10-K (Annual Report Pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934). For the fiscal year ended December 31, 2011,

www.sec.gov/Archives/edgar/data/50863/ 000119312512075534/d302695d10k.htm.

McDermott Will & Emery (2010). “The ‘Conflict Minerals’ Provision in the Dodd-Frank Act

Imposes New Disclosure Requirements on Manufacturers.” July 22,

http://www.mwe.com/publications/uniEntity.aspx?xpST=PublicationDetail&pub= 5870.

Motorola Solutions, Inc. (2012). Form 10-K (Annual Report Pursuant to Section 13 or 15(d) of the

Securities Exchange Act of 1934). For the fiscal year ended December 31, 2011.

www.sec.gov/Archives/edgar/data/68505/000119312512063569/d280303d10k.htm.

RF Monolithics (2012). Form 10-K (Annual Report Pursuant to Section 13 or 15(d) of the Securities

Exchange Act of 1934). For the fiscal year ended August 31, 2011.

www.sec.gov/Archives/edgar/data/922204/000119312511318374/d257460d10k.htm.

Securities and Exchange Commission (SEC) (2010). “SEC Proposes Specialized Disclosure of Use