JMAA 2015.2

57

Volume 11, Number 2, February 2015 (Serial Number 117) Journal of Modern Accounting and Auditing David David Publishing Company www.davidpublisher.com Publishing David

-

Upload

davidpublishing -

Category

Documents

-

view

5 -

download

0

Transcript of JMAA 2015.2

Volume 11, Number 2, February 2015 (Serial Number 117)

Journal ofModern Accounting and Auditing

David

David Publishing Company

www.davidpublisher.com

PublishingDavid

Publication Information: Journal of Modern Accounting and Auditing is published monthly in hard copy (ISSN1548-6583) and online (ISSN1935-9683) by David Publishing Company located at 240 Nagle Avenue #15C, New York, NY 10034, USA. Aims and Scope: Journal of Modern Accounting and Auditing, a monthly professional academic journal, covers all sorts of researches on accounting research, financial theory, capital market, audit theory and practice from experts and scholars. Editorial Board Members: Avis Andoni, Albania. Benedetta Siboni, Italy. Brad S. Trinkle, USA. Daniela Cretu, Romania. Drazen Koski, the Republic of Croatia. Elisabete Fátima Simões Vieira, Portugal. Emmanuel Attah, Ghana. Fabrizio Rossi, Italy. Haihong He, USA. Joanna Błach, Poland. João Paulo Torre Vieito, Portugal. Liang Song, USA. Lindita Rova, Albania. Mohammed Al-Omiri, Saudi Arabia. Mohamed Rochdi Keffala, Tunisia. Mohammad Talha, Saudi Arabia. Monika Wieczorek-Kosmala, Poland. Narumon Saardchom, Thailand.

Peter Harris, USA. Philip Harris Siegel, USA. Philip Yim Kwong Cheng, Australia. Rosa Lombardi, Italy. Sabina Hodzic, Croatia. Selim Mekdessi, Lebanon. Sheikh Abdur Rahim, Bangladesh. Thomas Gstraunthaler, South Africa. Tita Djuitaningsih, Indonesia. Tiziana Di Cimbrini, Italy. Tumellano Sebehela, United Kingdom. Valdir de Jesus Lameira, Brazil. Valerio Pesic, Italy. Vintilescu Belciug Adrian, Romania. Wan Mansor W. Mahmood, Malaysia. Yezdi H. Godiwalla, USA. Zeynep Özsoy, Turkey.

Manuscripts and correspondence are invited for publication. You can submit your papers via Web Submission, or E-mail to [email protected]. Submission guidelines and Web Submission system are available at http://www.davidpublisher.com/. Copyright©2015 by David Publishing Company and individual contributors. All rights reserved. David Publishing Company holds the exclusive copyright of all the contents of this journal. In accordance with the international convention, no part of this journal may be reproduced or transmitted by any media or publishing organs (including various websites) without the written permission of the copyright holder. Otherwise, any conduct would be considered as the violation of the copyright. The contents of this journal are available for any citation, however, all the citations should be clearly indicated with the title of this journal, serial number, and the name of the author. Abstracted/Indexed in: Database of EBSCO, Massachusetts, USA Universe Digital Library Sdn Bhd, Malaysia Australian ERA ProQuest CSA-Natural Sciences, USA Chinese Database of CEPS, Airiti Inc. & OCLC Google Scholar Ulrich’s Periodicals Directory CiteFactor, USA Social Science Research Network (SSRN), USA

Polish Scholarly Bibliography Database of Summon Serials Solutions, USA Turkish Education Index CrossRef Electronic Journals Library Chinese Scientific Journals Database, VIP Corporation, Chongqing, P.R. China Scholar Steer Scientific Indexing Services

Subscription Information: Price (per year): Print $640; Online $480; Print and Online $800 David Publishing Company 240 Nagle Avenue #15C, New York, NY 10034, USA Tel: 1-323-984-7526, 323-410-1082; Fax: 1-323-984-7374, 323-908-0457 E-mail: [email protected], [email protected]

David Publishing Company www.davidpublisher.com

DAVID PUBLISHING

D

Journal of Modern Accounting and Auditing

Volume 11, Number 2, February 2015 (Serial Number 117)

Contents The Impact of Turnover Ratios on Jordanian Services Sectors’ Performance 77

Lina Warrad, Rania Al Omari

Information on Financial Statements for Loan Decision-Making of Commercial Banks in Vietnam 86

Mai Thi Hoang Minh

Growth and Inequality in Indonesia: Does Kuznets Curve Hold? 93

G. A. Diah Utari, Retni Cristina

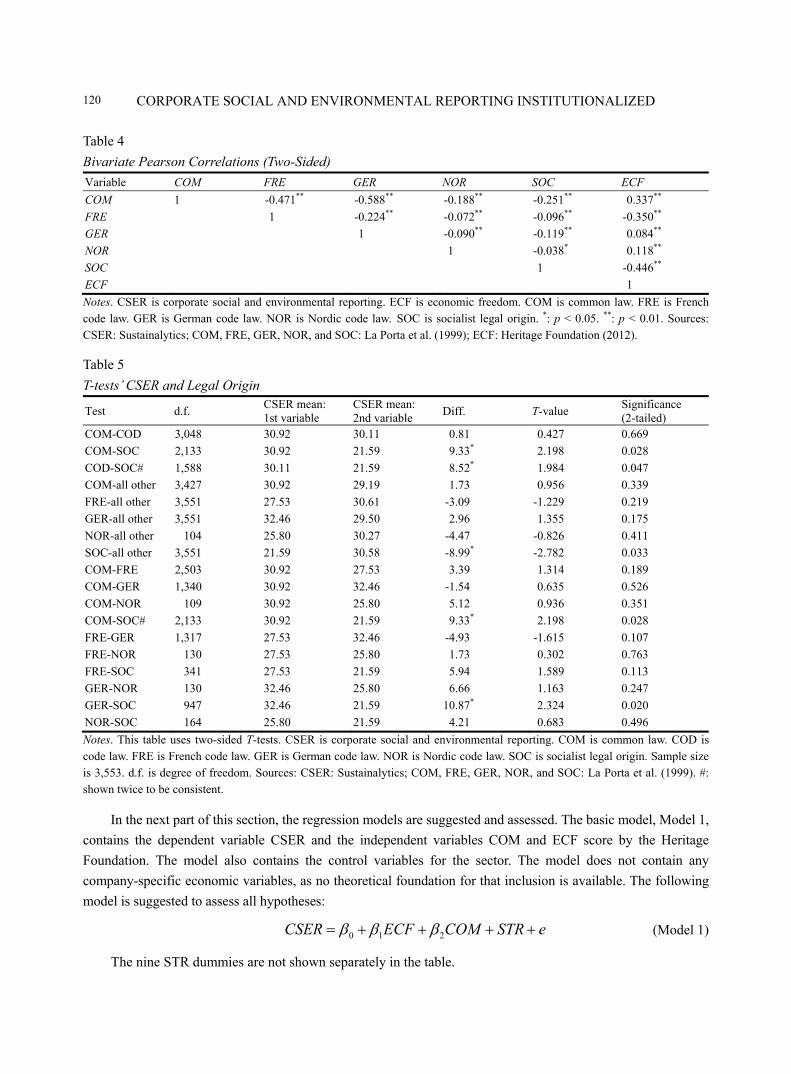

Corporate Social and Environmental Reporting Institutionalized 112

René P. Orij

Embedding Economic Excellence: A Transformational Definition of “Corporate Governance” for Malaysia 124

Zulkifflee Mohamed, Garry James Clayton, Mohd Yaziz Mohd Isa

Journal of Modern Accounting and Auditing, February 2015, Vol. 11, No. 2, 77-85 doi: 10.17265/1548-6583/2015.02.001

The Impact of Turnover Ratios on Jordanian

Services Sectors’ Performance

Lina Warrad Applied Science University, Amman, Jordan

Rania Al Omari Al-Asra University, Amman, Jordan

Profitability ratios are a group of financial ratios that indicate how much profit a business is earning within a

certain context, while asset utilization ratios indicate how efficient a business is in operating its assets to generate

cash. The difference between profitability ratios and turnover ratios is the fact that turnovers are more specific.

While profitability ratios measure overall performance in terms of profits, asset utilization ratios focus on specific

measurements within the business.1 We conduct this study to verify the impact of turnover ratios on Jordanian

services sectors’ performance during the period from 2009 to 2012. The study showed that there is no significant

impact of turnover ratios on Jordanian services sectors’ profitability, and by testing the main and sub hypotheses,

the study revealed that there is no significant impact of turnover ratios on Jordanian services sectors’ return on

assets (ROA), there is no significant impact of working capital turnover on Jordanian services sectors’ ROA,

there is no significant impact of total asset turnover on Jordanian services sectors’ ROA, and there is no

significant impact of fixed asset turnover on Jordanian services sectors’ ROA. Also, the study showed that there is

no significant impact of turnover ratios on Jordanian services sectors’ return on equity (ROE), there is no

significant impact of working capital turnover on Jordanian services sectors’ ROE, there is no significant

impact of total asset turnover on Jordanian services sectors’ ROE, and there is no significant impact of fixed

asset turnover on Jordanian services sectors’ ROE. Moreover, the study concluded that the educational services

sector has the lowest working capital turnover and healthcare services sector has the highest. In addition, we find

that the hotels and tourism sector has the lowest total asset turnover ratio, while the utilities and energy sector has

the highest and that the hotels and tourism sector has the lowest fixed asset turnover, while the utilities and energy

sector has the highest. The transportation sector has the lowest ROA and technology and communication sector

has the highest. Finally, we find that transportation sector has the lowest ROE and the technology and

communication sector has the highest.

Keywords: working capital turnover, total asset turnover, fixed asset turnover, return on assets (ROA), return on

equity (ROE), Amman Stock Exchange (ASE)

Lina Warrad, associate professor, Faculty of Economic and Administrative Science, Accounting Department, Applied Science

University. Email: [email protected]. Rania Al Omari, assistant professor, Faculty of Administrative and Financial Sciences, Accounting Department, Al-Asra

University. 1 Retrieved from http://smallbusiness.chron.com/difference-between-profitability-ratios-asset-utilization-ratios-37803.html.

DAVID PUBLISHING

D

IMPACT OF TURNOVER RATIOS ON JORDANIAN SERVICES SECTORS’ PERFORMANCE

78

Introduction Financial statements report on both a firm’s position at a point in time and its operations over some past

periods. However, the real value of financial statements lies in the fact that they can be used to help predict future earnings, dividends, and free cash flows. Profitability ratios and asset utilization ratios are considered to be the most common and simple to calculate. Each type of ratio reveals something different about a business, but they deal with some of the same measurements and issues (Schmidlin, 2014).

Working capital turnover ratio is a measure to determine how effectively a company is operating its assets to generate sales. The working capital turnover ratio is used to analyze the relationship between the money used to fund operations and the sales generated from these operations. The smaller the current capital compared to the sales in this ratio, the higher the capital turnover ratio.2 Moreover, the total asset turnover is similar to fixed asset turnover ratio, which measures a company’s effectiveness in generating sales from investments related to the company. Total asset turnover evaluates the efficiency of managing all the company’s assets.

The most active sector in the Jordanian economy is the service sector, which forms 67% of the GDP. Jordan has been a participant since December 2000 in the WTO General Agreement on Trade in services and one of the seven Mediterranean partners that officially opened negotiations on liberalization on services and the right of establishment at the Euro-Mediterranean Trade Ministerial Conference in Marrakech. Liberalization will provide Jordan with an access to the EU services market, the largest in the world, and provide benefits from EU service technologies, company links, and investments.3

This paper will try to investigate the previous relations mentioned above by studying the impact of turnover ratios on the performance of the Jordanian services sectors which are listed at Amman Stock Exchange (ASE) during the period from 2009 to 2012.

Previous Studies The impact of working capital turnover on chemical companies’ profitability measured by return on assets

(ROA) was presented by the study of Warrad (2014) which covered a period from 2009 to 2011, and a simple liner regression was applied. The study revealed a significant impact of independent variable working capital turnover on dependent variable ROA among chemical industries listed on ASE during the period from 2009 to 2011.

The working capital performance of Dabur India Ltd. during the period from 2003 to 2010 was investigated by Chakraborty’s (2013) study which used inventory turnover ratio, working capital turnover ratio, current asset turnover ratio, and debtor’s turnover ratio to achieve good performance of the company, while in terms of current ratio and the liquidity position of the company are not good.

Banks’ performance was investigated by Jahan’s (2012) study which used determinants of banks’ profitability, which are ROA, return on equity (ROE), and return on debt (ROD) as a criterion for the Bangladesh Bank to evaluate banks’ performance by evaluating the efficiency ratio, asset utilization ratio, asset size, and ROD as a determinant of banks’ profitability measured by ROA. The study was conducted on randomly selected six commercial banks of Bangladesh. The results showed that the Prime Bank is considered to be superior in terms of total assets, while the Arab Bangladesh Bank is showing high performance in terms of profitability. The explanatory variables operational efficiency, asset size, and ROD were found to be

2 Retrieved from http://www.finweb.com/investing/a-discussion-of-capital-turnover.html#axzz3CMBN0wvJ. 3 Retrieved from http://www.jedco.gov.jo/joomla/index.php?option=com_content&id=484&Itemid=266&lang=en.

IMPACT OF TURNOVER RATIOS ON JORDANIAN SERVICES SECTORS’ PERFORMANCE

79

positively related and asset utilization was found to be negatively related to ROA through the results of the regression analysis, but these associations are statistically insignificant.

The impact of working capital and liquidity on the profitability of Tata Motors during the period of 2002-2010 was presented by Raheja, Bhardwaj, and Priyanka (2012) who used Karl Pearson’s correlation, T-test, regression, rank correlation, average, and standard deviation to analyze the variables. The results revealed that there is no significant relationship between liquidity and profitability. Out of seven components of working capital, only two factors have a negative impact on profitability: working capital turnover ratio and cash turnover ratio. Also, the results showed that there was a positive correlation between working capital components and profitability.

The relationship between working capital management and profitability in firms belonging to information technology and telecommunication industry in India during the period from 1999 to 2010 was investigated by Singh’s (2012) study which used pooling cross section and time series data, and 11 firms were randomly selected, out of which, five belonged to the information technology industry and six were from the telecommunication industry. The study used the return on capital employed as a measure of profitability. Other variables for working capital management were working capital turnover, current ratio, days’ inventory outstanding, days’ sales outstanding, days’ payable outstanding, and cash conversion cycle. The study revealed a positive relationship among working capital turnover, current ratio, sales to total asset ratio, and profitability. Days’ inventory outstanding indicated a negative relationship with profitability. The relationship of current ratio with profitability was positive.

The confirmation of the existence of differences in retail firms’ strategy to the direction of accomplishing profitability targets was presented by Arnis, Kolias, and Filios (2008) who used ROE and ROA ratios as well as the average sales growth rate. The results did not differ statistically within the sub-sectors of the retail sector through the previous variables. However, significant differences not only among the sub-sectors but also among firms are noticed in the other elements which define the profitability, gross margin, asset turnover ratio, and the general expenses to sales ratio. We also find, by using econometric methods, that gross margin is positively correlated with general expenses to sales ratio and negatively correlated with asset turnover ratio. The study arrives at the conclusion that the retail firms use different strategies to achieve the same ROE and ROA. Finally, the results do not support the hypothesis that the rapid developing firms show less profitability as it is expressed by ROA.

A study of Fairfield and Yohn (2001) gave the evidence that disaggregating ROA into asset turnover and profit margin does not provide incremental information for forecasting the changes in ROA one year ahead, but that disaggregating the changes in ROA into the changes in asset turnover and the changes in profit margin is useful in forecasting the changes in ROA one year ahead.

The return on investment (ROI), ROE, and probable dividend action of J. C. Penney Company, Inc. in 1978 was analyzed by Weller (1977) who concluded that return on invested capital is not projected to return to a high level within the forecast period. The company attributed the deterioration of its fixed asset turnover to the poor performance of its soft line stores.

Hypotheses Main Hypotheses

For studying the effect of net working capital on net operating cash flow, we test the following hypotheses:

IMPACT OF TURNOVER RATIOS ON JORDANIAN SERVICES SECTORS’ PERFORMANCE

80

H1: There is no significant impact of turnover ratios on Jordanian services sectors’ ROA. H2: There is no significant impact of turnover ratios on Jordanian services sectors’ ROE.

Sub Hypotheses (Branched From the Main Hypotheses) H11: There is no significant impact of working capital turnover on Jordanian services sectors’ ROA. H12: There is no significant impact of total asset turnover on Jordanian services sectors’ ROA. H13: There is no significant impact of fixed asset turnover on Jordanian services sectors’ ROA. H21: There is no significant impact of working capital turnover on Jordanian services sectors’ ROE. H22: There is no significant impact of total asset turnover on Jordanian services sectors’ ROE. H23: There is no significant impact of fixed asset turnover on Jordanian services sectors’ ROE.

Research Methodology This section presents the research methodology adopted in this study. It explains sample selection criteria,

variables of the study, and research model and tests the hypotheses.

The Research Sample The study examines the financial reports of eight Jordanian services sectors listed on the ASE for the

period from 2009 to 2012.

Dependent Variables of the Study ROA. ROA provides the readers with a measure of the profitability of a concern and the effectiveness

with which the firm has used their assets. The ROA ratio may also be calculated on a pre-tax basis by using earnings before interest and tax (EBIT). Thus, the higher the ROA, the more profitable and effective the use of assets (Association of Chartered Certified Accountants [ACCA], 2008).

It can be calculated as follows (CFA, 2011):

Net ProfitROAAverage Total Assets

=

ROE. ROE shows the return on capital provided by shareholders. To calculate this important ratio, net profit is set in relation to the average shareholders’ equity over the business year. In the calculation, it is important to bring in net profit and shareholders’ equity after minority interest has been deducted in order to only consider figures that shareholders are actually entitled to. This ratio gives investors a figure that can be compared between different firms and investment opportunities (Brigham & Ehrhardt, 2005).

It can be calculated as follows (CFA, 2011):

’Net ProfitROE

Average Shareholders Equity

=

Independent Variables of the Study Working capital turnover. Working capital is known as current assets minus current liabilities. Working

capital turnover measures how efficiently the company generates sales on its working capital.4

4 Retrieved from http://www.investopedia.com/terms/w/workingcapitalturnover.asp.

IMPACT OF TURNOVER RATIOS ON JORDANIAN SERVICES SECTORS’ PERFORMANCE

81

It can be calculated as follows (CFA, 2011):

SalesWorking Capital TurnoverAverageWorking Capital

=

Total asset turnover. Total asset turnover measures overall investment efficiency by aggregating the joint impact of both short- and long-term assets. This comprehensive measure is a key component of the disaggregation of ROA.5

It can be calculated as follows (CFA, 2011):

SalesTotal Asset TurnoverAverage Total Assets

=

Fixed asset turnover. Fixed asset turnover measures the efficiency of long-term capital investment. The ratio reflects the level of sales generated by investments in productive capacity. The level and trend of this ratio are affected by characteristics of its components. First, sales growth is continuous, albeit at varying rates. Increase in capacity to meet that sales growth, however, is discrete, depending on the addition of new factories, warehouses, stores, and so forth. Compounding this issue is the fact that the management often has discretion over timing, form, and financial reporting of the acquisition of incremental capacity.

It can be calculated as follows (CFA, 2011):

SalesFixed Asset TurnoverAverage Fixed Assets

=

Research Model In order to test the study hypotheses, no research model can be designed, because we do not have an

effectible relation. Liner regressions. To test the research hypotheses, the Statistical Package for Social Sciences (SPSS)

program was used to prepare the table of analysis of variance (ANOVA) as shown in Table 1. H11: There is no significant impact of working capital turnover on Jordanian services sectors’ ROA.

Table 1 ANOVAa for H11 Model Sum of squares df Mean square F Sig. Regression 73.910 1 73.910 2.218 0.147b Residual 999.911 30 33.330 Total 1,073.821 31 Notes. a: Dependent variable: ROA. b: Predictors: (constant), working capital turnover.

By reviewing Table 1, we find that the P-value = 0.147 > 5%, which is not significant, and this supports the acceptance of main null hypothesis. There is no significant impact of working capital turnover on Jordanian services sectors’ ROA.

H12: There is no significant impact of total asset turnover on Jordanian services sectors’ ROA.

5 Retrieved from http://financialanalysishub.com/total-asset-turnover/.

IMPACT OF TURNOVER RATIOS ON JORDANIAN SERVICES SECTORS’ PERFORMANCE

82

Table 2 ANOVAa for H12 Model Sum of squares df Mean square F Sig. Regression 15.067 1 15.067 0.427 0.518b Residual 1,058.754 30 35.292 Total 1,073.821 31 Notes. a: Dependent variable: ROA. b: Predictors: (constant), total asset turnover.

By reviewing Table 2, we find that the P-value = 0.518 > 5%, which is not significant, and this supports the acceptance of main null hypothesis. There is no significant impact of total asset turnover on Jordanian services sectors’ ROA.

H13: There is no significant impact of fixed asset turnover on Jordanian services sectors’ ROA.

Table 3 ANOVAa for H13 Model Sum of squares df Mean square F Sig. Regression 0.338 1 0.338 0.009 0.923b Residual 1,073.483 30 35.783 Total 1,073.821 31 Notes. a: Dependent variable: ROA. b: Predictors: (constant), fixed asset turnover.

By reviewing Table 3, we find that the P-value = 0.923 > 5%, which is not significant, and this supports the acceptance of main null hypothesis. There is no significant impact of fixed asset turnover on Jordanian services sectors’ ROA.

H1: There is no significant impact of turnover ratios on Jordanian services sectors’ ROA.

Table 4 ANOVAa for H1 Model Sum of squares df Mean square F Sig. Regression 155.683 3 51.894 1.583 0.216b Residual 918.138 28 32.791 Total 1,073.821 31 Notes. a: Dependent variable: ROA. b: Predictors: (constant), fixed asset turnover, total asset turnover, and working capital turnover.

By reviewing Table 4, we find that the P-value = 0.216 > 5%, which is not significant, and this supports the acceptance of main null hypothesis. There is no significant impact of turnover ratios on Jordanian services sectors’ ROA.

H21: There is no significant impact of working capital turnover on Jordanian services sectors’ ROE.

Table 5 ANOVAa for H21 Model Sum of squares df Mean square F Sig. Regression 62.086 1 62.086 0.471 0.498b Residual 3,950.663 30 131.689 Total 4,012.749 31 Notes. a: Dependent variable: ROE. b: Predictors: (constant), working capital turnover.

IMPACT OF TURNOVER RATIOS ON JORDANIAN SERVICES SECTORS’ PERFORMANCE

83

By reviewing Table 5, we find that the P-value = 0.498 > 5%, which is not significant, and this supports the acceptance of main null hypothesis. There is no significant impact of working capital turnover on Jordanian services sectors’ ROE.

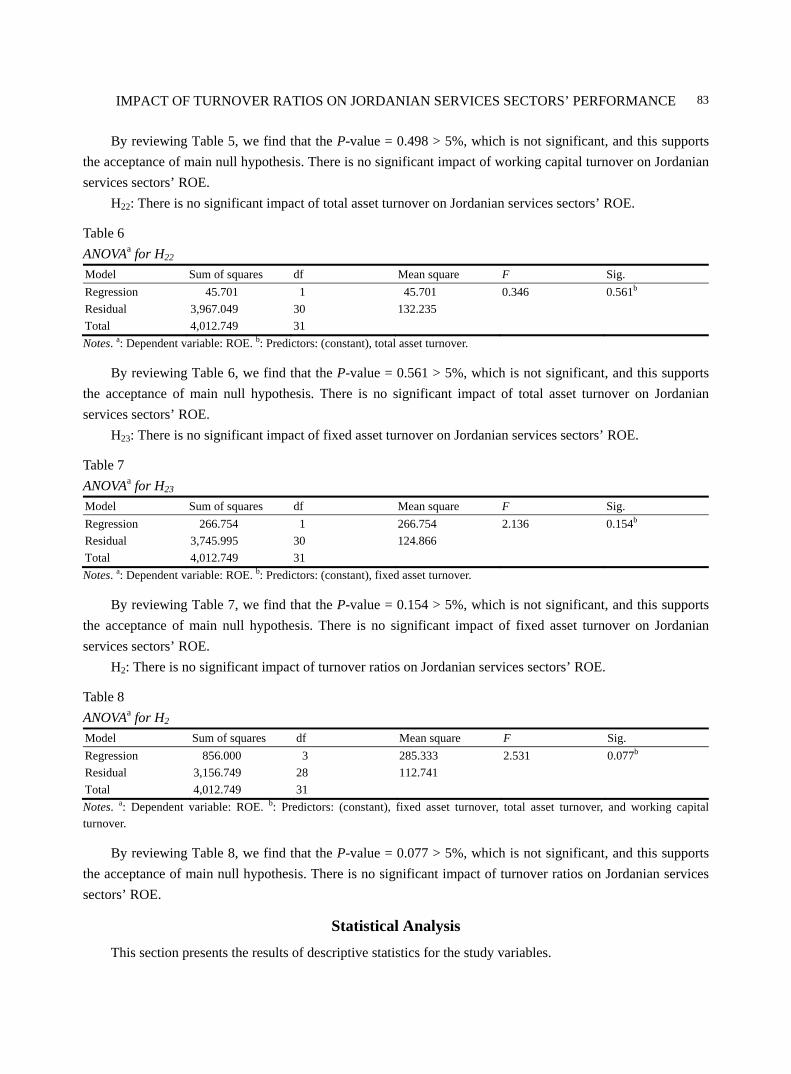

H22: There is no significant impact of total asset turnover on Jordanian services sectors’ ROE.

Table 6 ANOVAa for H22 Model Sum of squares df Mean square F Sig. Regression 45.701 1 45.701 0.346 0.561b Residual 3,967.049 30 132.235 Total 4,012.749 31 Notes. a: Dependent variable: ROE. b: Predictors: (constant), total asset turnover.

By reviewing Table 6, we find that the P-value = 0.561 > 5%, which is not significant, and this supports the acceptance of main null hypothesis. There is no significant impact of total asset turnover on Jordanian services sectors’ ROE.

H23: There is no significant impact of fixed asset turnover on Jordanian services sectors’ ROE.

Table 7 ANOVAa for H23 Model Sum of squares df Mean square F Sig. Regression 266.754 1 266.754 2.136 0.154b Residual 3,745.995 30 124.866 Total 4,012.749 31 Notes. a: Dependent variable: ROE. b: Predictors: (constant), fixed asset turnover.

By reviewing Table 7, we find that the P-value = 0.154 > 5%, which is not significant, and this supports the acceptance of main null hypothesis. There is no significant impact of fixed asset turnover on Jordanian services sectors’ ROE.

H2: There is no significant impact of turnover ratios on Jordanian services sectors’ ROE.

Table 8 ANOVAa for H2 Model Sum of squares df Mean square F Sig. Regression 856.000 3 285.333 2.531 0.077b Residual 3,156.749 28 112.741 Total 4,012.749 31 Notes. a: Dependent variable: ROE. b: Predictors: (constant), fixed asset turnover, total asset turnover, and working capital turnover.

By reviewing Table 8, we find that the P-value = 0.077 > 5%, which is not significant, and this supports the acceptance of main null hypothesis. There is no significant impact of turnover ratios on Jordanian services sectors’ ROE.

Statistical Analysis This section presents the results of descriptive statistics for the study variables.

IMPACT OF TURNOVER RATIOS ON JORDANIAN SERVICES SECTORS’ PERFORMANCE

84

Table 9 Independent Variables Ranking Among Jordanian Services Sectors

Sector Rank Working capital turnover Rank Total asset

turnover Rank Fixed asset turnover

Healthcare services 7 22.72691032 2 0.437600028 3 0.820361 Educational services 1 -341.5877909 3 0.485854432 2 0.725536 Hotels and tourism sector 2 -18.70213213 1 0.217584706 1 0.347901 Transportation sector 3 -9.023490437 7 1.232560347 6 2.336932 Technology and communication 4 3.348739266 5 0.638342112 5 2.108911 Media sector 6 8.266755908 4 0.615516328 4 1.394416 Utilities and energy 8 67.72690163 8 1.915349438 8 8.719408 Commercial services 5 6.2270192 6 0.818082456 7 2.373262

By reviewing Table 9, we found that the educational services sector has the lowest working capital turnover and utilities and energy sector has the highest. In addition, we find that the hotels and tourism sector has the lowest total asset turnover ratio and the utilities and energy sector has the highest. We also find that the hotels and tourism sector has the lowest fixed asset turnover and the utilities and energy sector has the highest.

Table 10 Dependent Variables Ranking Among Jordanian Services Sectors Sector Rank ROA Rank ROE Healthcare services 4 2.45221 4 2.40506 Educational services 7 12.34124 7 16.08534 Hotels and tourism sector 3 2.347837 3 1.505846 Transportation sector 1 0.498605 1 -3.49581 Technology and communication 8 13.06871 8 21.74977 Media sector 2 2.167077 2 1.382623 Utilities and energy 6 4.083593 6 14.03826 Commercial services 5 3.065356 5 2.792097

By reviewing Table 10, we found that the transportation sector has the lowest ROA and the technology and communication sector has the highest. We also find that the transportation sector has the lowest ROE and the technology and communication sector has the highest.

Summary and Conclusion This study aims to approve if there is a significant impact of turnover ratios expressed by working capital

turnover, total asset turnover, and fixed asset turnover on Jordanian services sectors’ performance expressed by ROA and ROE.

The results showed that there is no significant impact of turnover ratios on Jordanian services sectors’ profitability, and by testing the main and sub hypotheses, the study revealed that there is no significant impact of turnover ratios on Jordanian services sectors’ ROA, there is no significant impact of working capital turnover on Jordanian services sectors’ ROA, there is no significant impact of total asset turnover on Jordanian services sectors’ ROA, and there is no significant impact of fixed asset turnover on Jordanian services sectors’ ROA.

IMPACT OF TURNOVER RATIOS ON JORDANIAN SERVICES SECTORS’ PERFORMANCE

85

Also, the study results showed that there is no significant impact of turnover ratios on Jordanian services sectors’ ROE, there is no significant impact of working capital turnover on Jordanian services sectors’ ROE, there is no significant impact of total asset turnover on Jordanian services sectors’ ROE, and there is no significant impact of fixed asset turnover on Jordanian services sectors’ ROE.

Moreover, the study concluded that the educational service sector has the lowest working capital turnover and the utilities and energy sector has the highest. We also find that the hotels and tourism sector has the lowest total asset turnover ratio and the utilities and energy sector has the highest and the hotels and tourism sector has the lowest fixed assets turnover while the utilities and energy sector has the highest. The transportation sector has the lowest ROA and the technology and communication sector has the highest. In addition, we find that the transportation sector has the lowest ROE and the technology and communication sector has the highest.

The findings of this study differ from studies investigating the same relations, and its results disagree with the results of most previous studies which found a significant effect of turnover ratios on profitability. This is what distinguishes this study from others, which can be explained by the distinct item between the sales as a numerator of the turnover ratios and the net income as a numerator of ROA and ROE which is cost of sales.

In order to maintain a significant effect of turnovers on profitability, the cost of sales should move in parallel with sales movements positively at the same percent or less.

This study mentioned that in order to intervene in market competition, the services sectors should follow the net profit deduction strategy, and the way to achieve that was to increase the cost of sales with a higher percent than the increase in sales. This revealed a distortion in the expected relationship between turnover ratios and profitability ratios, because of which, the study found no significant impact of turnover ratios on Jordanian services sectors’ profitability.

We will apply the study among Jordanian services sectors as a comparative study, in order to investigate different conclusions among different sectors within ASE sectors.

References Arnis, N. I., Kolias, G. D., & Filios, V. F. (2008). The profitability of the Greek retail firms and the relations among the

determinants (in Greek). Review of Economic Sciences, 14, 161-180. Association of Chartered Certified Accountants [ACCA]. (2008). Paper F7, financial reporting (International). Brigham, E. F., & Ehrhardt, M. C. (2005). Financial management, theory, and practice (11th ed.). Mason, OH: Thomson

Southwest. CFA. (2011). Financial reporting and analysis. Program Curriculum, Volume 3, Level 1. Chakraborty, N. (2013). Working capital performance: A case study on Dabur India Ltd.. International Journal of Research in

Commerce and Management, 4(10), 93-97. Fairfield, P. M., & Yohn, T. L. (2001). Using asset turnover and profit margin to forecast changes in profitability. Review of

Accounting Studies, 6(4), 371-385. Jahan, N. (2012). Determinants of bank’s profitability: Evidence from Bangladesh. Indian Journal of Finance, 6(2), 32-38. Raheja, R., Bhardwaj, R., & Priyanka. (2012). The impact of working capital management on profitability and liquidity.

International Journal of Research in Commerce and Management, 3(3), 99-102. Schmidlin, N. (2014). The art of company valuation and financial statement analysis: A value investor’s guide with real-life case

studies. John Wiley & Sons. Singh, D. P. (2012). Working capital management and profitability in the IT and telecom industry in India. Indian Journal of

Finance, 6(3), 54-61. Warrad, L. (2014). The impact of working capital turnover on Jordanian chemical industries’ profitability. American Journal of

Economics and Business Administration, 5(3), 116-119. Weller, E. A. (1977). Return on investment, return on equity, and probable dividend action (pp. 8-9). J.C. Penney Company.

Journal of Modern Accounting and Auditing, February 2015, Vol. 11, No. 2, 86-92 doi: 10.17265/1548-6583/2015.02.002

Information on Financial Statements for Loan Decision-Making

of Commercial Banks in Vietnam

Mai Thi Hoang Minh University of Economics, Ho Chi Minh City, Vietnam

Financial statements (FS) are tools which provide information to users for making business decisions. Among the

organizations, banks are the firms which conducted and did business with risks. In particular, commercial banks

continue to play a dominant role in the whole system, and local commercial banks still have an edge in its

widespread network across the country over foreign banks. This article is going to present the survey which clarifies

the role of FS in commercial banks’ loan decisions in Vietnam. Moreover, this paper also discusses FS’s quality

currently, thereby making suggestions for enterprises to enhance the usefulness of accounting information in

borrowing activities. This paper has taken performance with 74 official employees in commercial banks in Vietnam.

The results indicated the qualitative characteristics of banks when disclosing the financial statements. This article

also gave the six oriented solutions to improvement of the loan decision-making by banks.

Keywords: usefulness of financial statement (FS), accounting information quality, loan decisions, banking

Introduction The quality of accounting information is evaluated by its usefulness to users. At present, based on the

Ministry of Finance (2013) and the International Accounting Standards Board (IASB, 2010), criteria used to identify the usefulness of accounting information are displayed in the Conceptual Framework for Financial Reporting, and the requirements for accounting information in Vietnam are stated in Vietnamese Accounting Standards No. 1 (VAS 01). In fact, the usefulness of accounting information for users has been studied quite early. Recent researches have showed some issues related to quality of financial reporting in Vietnam which makes them less useful to loan decisions (Nichols, 1997). This study continues to learn more about financial reporting’s quality issues to make specific recommendations which help enhance their usefulness for business borrowing activities.

Results of Previous Researches About How Accounting Information Has Affected Loan Decisions

General Information Previous researches showed that accounting information plays an important role in banks in developed

economies. Since the 1970s, banks in USA have considered financial reporting as the most important source for loan decisions (Stanga & Benjamin, 1978). This information can change the decisions of commercial banks

Mai Thi Hoang Minh, associate professor, doctor of Accounting, vice dean of Principle Accounting Department, School of

Accounting and Auditing, University of Economics. Email: [email protected].

DAVID PUBLISHING

D

LOAN DECISION-MAKING OF COMMERCIAL BANKS IN VIETNAM

87

(Danos, Holt, & Imhoff, 1989). Operating cash flow was demonstrated to have a close relationship with credit risk at enterprises which have high long-term loan rates or less business risks (Independent Evaluation Group [IEG], 2010).

Information used for making loan decisions is plenty and its roles vary by country. In USA, credit history information, project’s financial reporting, financial operating cash flow, detail of fixed assets, and indirect cash flow statement are the most important (Catanach & Kemp, 1999). Meanwhile in Hong Kong, information from note in financial statements (FS) is the most exploited, while information on cash flow takes the next concern (Kwok, 2002; Marian, Lui, & Lew, 2002).

In Australia, each financial statement is exploited from a different angle, e.g., cash flow statement is used to evaluate the payment ability to make loan decisions. Balance sheet plays the assessment and monitoring roles and income statement is considered important when appraising the enterprise’s operation (Jones, 1998; Kitindi, Magembe, & Sethibe, 2007).

This role of accounting information to loan decisions in developing countries is less important. It is proved by individual country and showed that the quality of information on FS does not satisfy users in general and banks in particular.

Consequently, information on FS is not considered important when making decisions (Abu-Nassar & Rutherford, 1996; Dang, N. Marriott, & P. Marriott, 2006; 2008). The common issues of accounting information are delays, lack of reliability, and incomplete notes (Mirshekary & Saudagaran, 2005). However, FS is still used as a source of information. Income statement and balance sheet are most widely used. Especially, audited information will be more valuable.

Research Method This article summarized information from FS analysis process of 10 commercial banks in Vietnam and

surveyed 74 credit staffs to learn the role of information in the FS for making decisions for loans as well as for assessing their quality. Statistical inference methods and calibration techniques pair-sample t-test are used for data processing. Although the number of staffs surveyed in each bank was not large, the survey was distributed across multiple banks to ensure representativeness. Moreover, each bank applies loan process and FS analysis techniques consistent with all of their branches, hence, some branches can also be capable of representing the entire.

Criterion for Evaluating the Usefulness of Accounting Information in Accordance With International Accounting Standards

The quality of accounting information is evaluated by its usefulness to users. According to FS theory, properties affecting the usefulness of accounting information include two main quality indicators and four secondary quality indicators as follows.

The Main Quality Indicators The main quality indicators include “Relevant” and “True”. Relevant information is likely to create a difference or can change users’ decisions. This feature is

disclosed through the predicted value and asserted value. Value prediction means that information can be used as input data for a process which helps users predict future results. Value assertion is presented by the feedback from predicted value (Al-Razeen & Karbhari, 2004).

LOAN DECISION-MAKING OF COMMERCIAL BANKS IN VIETNAM

88

True information must have three properties: completeness, neutrality, and no errors. Completeness means presenting all necessary information so that users can understand what the phenomenon mentions about, including detailed descriptions and related explanations.

Neutrality means that information contained in the FS must be free from bias. It should reflect a balanced view of the affairs of the company without attempting to present them in a favored light. Information may be deliberately biased or systematically biased. Neutral or reliable accounting information does not target interests of specific users of accounting information (i.e., does not favor certain users of accounting information over the others) and presents the actual position of banking. No error does not mean absolutely having no error, and the information on the report must be generated from fairly chosen processes. Besides, no error is found when applying those processes.

Additional Quality Indicators

Additional quality indicators include comparability, verifiability, timeliness, and understandability. These indicators enhance the usefulness of information which is identified as relevant and true.

Comparability helps users to indicate the similarity and difference among items, normally related to two items or more.

Verifiability means that independent observers who have knowledge in various fields can still agree that the information is presented truly. The verification can be done first through observation (direct) or checking the input of the calculation method and then by recalculating the result using the same method (indirect).

Timeliness means that information must be transferred to users to make decisions at the point time and can affect their decisions.

Understandability means that information should be classified, described, and presented in a clear and concise way.

Information on FS for Loan Decisions of Commercial Banks in Vietnam and Quality Assessment

Role of FS in Loan Processes

In comparison with other elements affecting loan decisions in Vietnam, FS just plays an average role, much lower than information provided by independent organizations. It has five levels of information in banking statements as illustrated in Table 1. This partly reflects low trustfulness of banks on information provided by enterprises compared with other sources.

Table 1 Units for Magnetic Properties No. Content 1 The information from credit center, assurance assets, customer’s business plan, and direct check 2 Intuition of decision-maker 3 FS and tax reports 4 The information from internal chart

5 Industry statistical information and macroeconomic indicators, the information from the press, the introduction of bank’s leaders/other clients, and the third party guarantee

Information from checking customers directly and assurance asset value are also much more important than that from FS. It indicates that most banks do not rely on the information provided by enterprises but apply other strategies to minimize credit risks. Customers’ business plans are highly considerable.

LOAN DECISION-MAKING OF COMMERCIAL BANKS IN VIETNAM

89

It means that there is a great need for information helping predict future events. Intuition in decision processes plays a rather important role which reinforces the judgment that banks in Vietnam make decisions by emotional orientation model rather than by rational model.

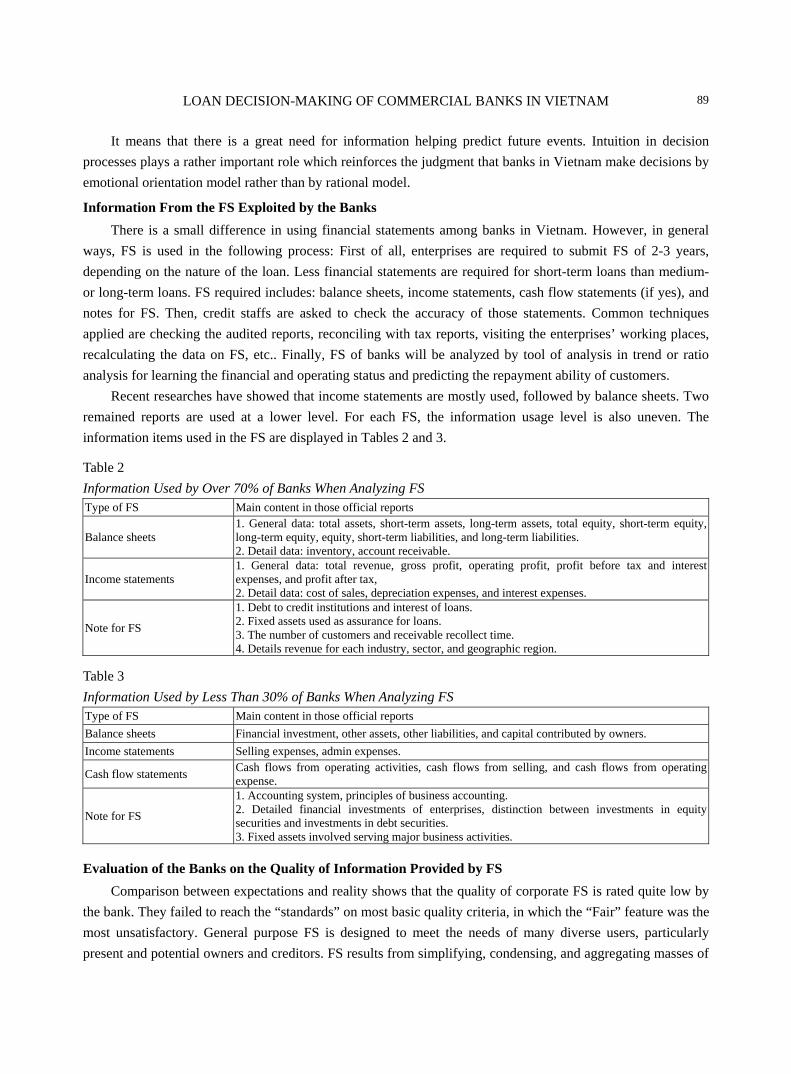

Information From the FS Exploited by the Banks There is a small difference in using financial statements among banks in Vietnam. However, in general

ways, FS is used in the following process: First of all, enterprises are required to submit FS of 2-3 years, depending on the nature of the loan. Less financial statements are required for short-term loans than medium- or long-term loans. FS required includes: balance sheets, income statements, cash flow statements (if yes), and notes for FS. Then, credit staffs are asked to check the accuracy of those statements. Common techniques applied are checking the audited reports, reconciling with tax reports, visiting the enterprises’ working places, recalculating the data on FS, etc.. Finally, FS of banks will be analyzed by tool of analysis in trend or ratio analysis for learning the financial and operating status and predicting the repayment ability of customers.

Recent researches have showed that income statements are mostly used, followed by balance sheets. Two remained reports are used at a lower level. For each FS, the information usage level is also uneven. The information items used in the FS are displayed in Tables 2 and 3.

Table 2 Information Used by Over 70% of Banks When Analyzing FS Type of FS Main content in those official reports

Balance sheets 1. General data: total assets, short-term assets, long-term assets, total equity, short-term equity, long-term equity, equity, short-term liabilities, and long-term liabilities. 2. Detail data: inventory, account receivable.

Income statements 1. General data: total revenue, gross profit, operating profit, profit before tax and interest expenses, and profit after tax, 2. Detail data: cost of sales, depreciation expenses, and interest expenses.

Note for FS

1. Debt to credit institutions and interest of loans. 2. Fixed assets used as assurance for loans. 3. The number of customers and receivable recollect time. 4. Details revenue for each industry, sector, and geographic region.

Table 3 Information Used by Less Than 30% of Banks When Analyzing FS Type of FS Main content in those official reports Balance sheets Financial investment, other assets, other liabilities, and capital contributed by owners. Income statements Selling expenses, admin expenses.

Cash flow statements Cash flows from operating activities, cash flows from selling, and cash flows from operating expense.

Note for FS

1. Accounting system, principles of business accounting. 2. Detailed financial investments of enterprises, distinction between investments in equity securities and investments in debt securities. 3. Fixed assets involved serving major business activities.

Evaluation of the Banks on the Quality of Information Provided by FS Comparison between expectations and reality shows that the quality of corporate FS is rated quite low by

the bank. They failed to reach the “standards” on most basic quality criteria, in which the “Fair” feature was the most unsatisfactory. General purpose FS is designed to meet the needs of many diverse users, particularly present and potential owners and creditors. FS results from simplifying, condensing, and aggregating masses of

LOAN DECISION-MAKING OF COMMERCIAL BANKS IN VIETNAM

90

data obtained primarily from a company’s accounting system. They sometimes are unable to reflect the real situation of that firm at that time for presented FS.

The accounting estimates are not clearly explained and the method of estimate is unreasonable. These reasons make the FS reduce its relevance for decision-making and partly explain the reason why the FS failed to play the important role in lending decisions (Nguyen, 2008).

Besides the above unappreciated factors, FS now achieved some certain requirements of the banks. Specifically, banks do not require changing the method of evaluating the value of assets or current liabilities. At the same time, they are also satisfied with the classification and presentation of current information.

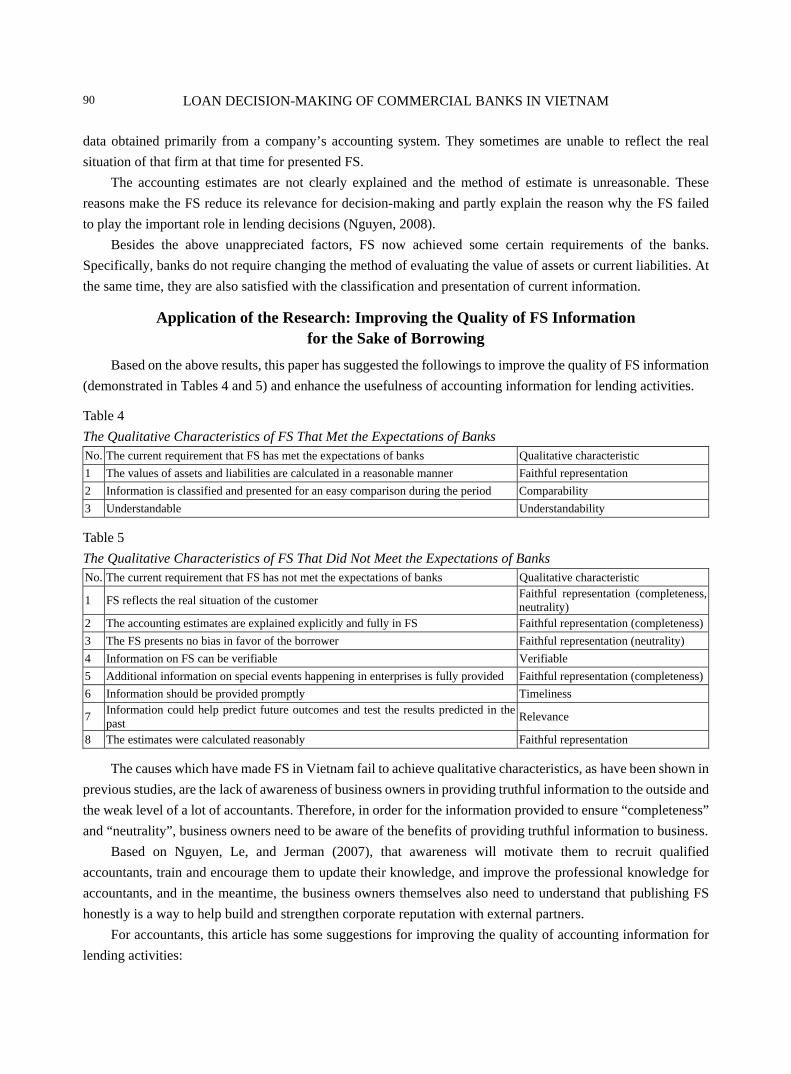

Application of the Research: Improving the Quality of FS Information for the Sake of Borrowing

Based on the above results, this paper has suggested the followings to improve the quality of FS information (demonstrated in Tables 4 and 5) and enhance the usefulness of accounting information for lending activities.

Table 4 The Qualitative Characteristics of FS That Met the Expectations of Banks No. The current requirement that FS has met the expectations of banks Qualitative characteristic 1 The values of assets and liabilities are calculated in a reasonable manner Faithful representation 2 Information is classified and presented for an easy comparison during the period Comparability 3 Understandable Understandability

Table 5 The Qualitative Characteristics of FS That Did Not Meet the Expectations of Banks No. The current requirement that FS has not met the expectations of banks Qualitative characteristic

1 FS reflects the real situation of the customer Faithful representation (completeness, neutrality)

2 The accounting estimates are explained explicitly and fully in FS Faithful representation (completeness)3 The FS presents no bias in favor of the borrower Faithful representation (neutrality) 4 Information on FS can be verifiable Verifiable 5 Additional information on special events happening in enterprises is fully provided Faithful representation (completeness)6 Information should be provided promptly Timeliness

7 Information could help predict future outcomes and test the results predicted in the past Relevance

8 The estimates were calculated reasonably Faithful representation

The causes which have made FS in Vietnam fail to achieve qualitative characteristics, as have been shown in previous studies, are the lack of awareness of business owners in providing truthful information to the outside and the weak level of a lot of accountants. Therefore, in order for the information provided to ensure “completeness” and “neutrality”, business owners need to be aware of the benefits of providing truthful information to business.

Based on Nguyen, Le, and Jerman (2007), that awareness will motivate them to recruit qualified accountants, train and encourage them to update their knowledge, and improve the professional knowledge for accountants, and in the meantime, the business owners themselves also need to understand that publishing FS honestly is a way to help build and strengthen corporate reputation with external partners.

For accountants, this article has some suggestions for improving the quality of accounting information for lending activities:

LOAN DECISION-MAKING OF COMMERCIAL BANKS IN VIETNAM

91

(1) In terms of accounting estimates (estimates of doubtful receivables, obsolete inventory value, product warranty obligations, etc.): They need to be reviewed for developing, implementing, and disclosing information. Vietnam has had some legal documents which show the method for calculating the accounting estimates. This is required by VAS; however, the current study showed that the borrowers do not perform well. The documents guiding the implementation of the current accounting estimates are Circular 228/2009/TT-BTC and Circular 89/2013/TT-BTC. Businesses can refer to these documents but we should note that the above guidelines are documents which serve for calculating deductible expenses when calculating corporate income tax. Therefore, there are some points which might not fit in the actual business activities. Businesses should develop written procedures for estimates of their own instead of just copying the instructions of tax authorities. The process should also be reviewed over time, and should also be assessed if old processes and estimation methods are still reasonable and make appropriate adjustments when necessary. Presentation of details of the estimate method not only enhances the completeness of the FS, but also helps increase the verifiability;

(2) Complete presentation of loans and fixed assets used as collateral for business loans. This information is important which once disclosed can help FS users make some predictions about future obligations as well as financial risk assessment of the business. The discloser of this information helps increase the relevance of FS and give a true and fair view of FS. For banks, this information can be found through their own information systems, however, complete disclosure of information will help increase the timeliness of the information, and the verification investigation will take place more smoothly and help shorten the time to consider the loan application;

(3) For fixed assets, in addition to sorting out in the current form, businesses should consider the track record of fixed assets, classified as fixed assets for main operations of business and fixed assets not serving the main business activity;

(4) Although it is not financial information but survey shows information about the board of directors, the history of the company is also interested in finding out more in the lending process. Enterprises should prepare this information and may consider disclosure in the notes to FS or other statements included;

(5) With business operating in many sectors or many regions, it is necessary for information systems management, account details, etc., to record accounting information effectively and efficiently, so that business is able to track revenues and expenses separately according to sectors and geographical areas. This will provide useful information for the evaluation of performance of the business. Those unlisted enterprises are also advised to disclose segment information in FS under the guidance of the VAS No. 28, “Segment Reporting”;

(6) Disclosure of information on important current events is also evaluated as unsatisfactory, reducing the relevance of FS information. Therefore, prior to publication of the FS, the organizations should review all information and events which are not mentioned on FS but are significant, such as contingent liabilities, commitments, events of related parties, etc..

Conclusion The quality of FS is always cared by both business and other users. Under the gaze of the commercial

banks, based on the quality of financial information, Vietnamese FS of banking has faced many issues together with problems, in which faithful representation is most underrated. This article gives some suggestions for enterprises to improve the faithful representation, relevance, and timeliness of FS, thereby making them more useful to borrowing activities of business.

LOAN DECISION-MAKING OF COMMERCIAL BANKS IN VIETNAM

92

References Abu-Nassar, M., & Rutherford, B. A. (1996). External users of financial reports in less developed countries: The case of Jordan.

The British Accounting Review, 28(1), 73-87. Al-Razeen, A., & Karbhari, Y. (2004). Annual corporate information: Importance and use in Saudi Arabia. Managerial Auditing

Journal, 19(1), 117-133. Catanach, A. H., & Kemp, R. S. (1999). The information needs of bank lending officers. Commercial Lending Review, 14(3),

76-78. Dang, D. S., Marriott, N., & Marriott, P. (2006). Users’ perceptions and uses of financial reports of small and medium companies

(SMCs) in transitional economies: Qualitative evidence from Vietnam. Qualitative Research in Accounting and Management, 3(3), 218-235.

Dang, D. S., Marriott, N., & Marriott, P. (2008). The banks’ uses of smaller companies’ financial information in the emerging economy of Vietnam: A user’s oriented model. In M. Tsamenyi, & S. Uddin (Eds.), Corporate governance in less developed and emerging economies (Vol. 8, pp. 519-548). Emerald Group Publishing Limited.

Danos, P., Holt, D., & Imhoff, E. (1989). The use of accounting information in bank lending decisions. Accounting, Organizations, and Society, 14(3), 235-247.

Independent Evaluation Group [IEG]. (2010). An evaluation of World Bank support, 2002-08: Gender and development. World Bank, IFC, MIGA. Retrieved from http://ieg.worldbank.org/Data/reports/gender_eval.pdf

International Accounting Standards Board [IASB]. (2010). Conceptual framework for financial reporting. Jones, S. (1998). An evaluation of user ratings of cash vs. accrual based financial reports in Australia. Managerial Finance, 24(11),

16-28. Kitindi, E. G., Magembe, B. A. S., & Sethibe, A. (2007). Lending decision making and financial information: The usefulness of

corporate annual reports to lenders in Botswana. The International Journal of Applied Economics and Finance, 1(2), 55-66. Kwok, H. (2002). The effect of cash flow statement format on lenders’ decisions. The International Journal of Accounting, 37(3),

347-362. Marian, Y. J. W. T., Lui, G., & Lew, A. Y. (2002). The expectations-performance gap in financial reporting from the perspective of

Hong Kong bank loan officers. Pacific Accounting Review, 14(1), 1-22. Ministry of Finance. (2013). Vietnamese Accounting Standard No. 21-24-28 (based on the Decision of Minister, Hanoi, Vietnam). Mirshekary, S., & Saudagaran, S. M. (2005). Perceptions and characteristics of financial statement users in developing countries:

Evidence from Iran. Journal of International Accounting, Auditing, and Taxation, 14(1), 33-54. Nguyen, P. S. (2008). Enhancing the usefulness of financial statements of Vietnamese enterprise at current period (The Ph.D.

dissertation). Nguyen, V. T., Le, T. B. N., & Jerman, R. (2007). Institutional impact to the process of making decision: Case study for banking of

SMEs in US and Vietnam. Retrieved from http://www.apim.edu.vn/ Nichols, L. M. (1997). An investigation of the effect of reporting changes proposed by the AICPA on lending decisions. Journal of

Applied Business Research, 13(2), 47-53. Stanga, K. G., & Benjamin, J. J. (1978). Information needs of bankers. Management Accounting, 59, 17-21.

Journal of Modern Accounting and Auditing, February 2015, Vol. 11, No. 2, 93-111 doi: 10.17265/1548-6583/2015.02.003

Growth and Inequality in Indonesia: Does Kuznets Curve Hold?

G. A. Diah Utari, Retni Cristina Central Bank of Indonesia, Jakarta, Indonesia

Sustainable economic growth has put Indonesia as a middle-income country (MIC) and currently, the level of per

capita income has already exceeded US$3,000. The increase in income per capita is followed by the increasing

number of middle-class population and the reduction in poverty. However, it has not been accompanied by

declining inequality that reflects the quality of economic growth. According to Kuznets theory, an increase in

inequality is a common problem in the process of economic growth. Inequality will further decline after the country

has reached a certain threshold level of income. This study aims to analyze the trend and nature of income

inequality in Indonesia and to test whether the Kuznets Curve holds. This paper used dynamic panel method with

26 provincial panel data from 2000 to 2011. The empirical result proves the existence of inverted U-shaped

Kuznets Curve in Indonesia and it may have the turning points when the real GDP per capita in each province

reached Rp. 179.41 million/year or around US$17.000. For the determinant of inequality in Indonesia, this study

found that the percentage of urban population, inflation, and share of agricultural sector contributed to the increase

of inequality, while high-level education and share of industrial sector are associated with the lower level of

inequality.

Keywords: growth, middle class, poverty, inequality, Kuznets Curve, dynamic panel

Introduction The Indonesian economy has regained the status of lower middle-income countries (MICs) since 2003 and

currently, the level of per capita income has already exceeded US$3,000. The increase in per capita income is followed by the increasing number of people who are in the middle class and the declining number of people who are in poor or near poor category (see Figure 1). With its robust recent growth performance, which has been growing at 5.7% on average over the last decade and endurance throughout the global financial crises, Indonesia is gaining prominence as an emerging market economy with global influence. It is also considered as one of the largest MICs in the world.

An increasing number of middle-class categories have positive sides, but at the same time, there are also challenges. On the positive side, it will create potential demand for goods and services and thus will boost investment opportunity. The increasing number of middle-income people benefited the government, because it raised potential tax payers and can gradually reduce the amount of government’s subsidy. However, we also have to be aware of the fact that this social transformation can lead to a middle-income trap.

G. A. Diah Utari, senior researcher, Centre for Central Banking Research and Educations, Central Bank of Indonesia. Email:

[email protected]. Retni Cristina, researcher, Centre for Central Banking Research and Educations, Central Bank of Indonesia.

DAVID PUBLISHING

D

94

As incproducts thBoston Coand high-tehigh-tech preflecting tdomestic instill dominthose that acannot satisustainable(middle-inc

Figure 1. G

come rises anhat previouslnsulting Grouech products products are the dependenndustries to p

nated by enerare able to suisfy the incree growth pathcome trap).

GROW

GDP/capita and

Figure 2. W

nd living staly address juup (2012) share the mostmostly fulfil

nce on goodproduce high-rgy/resource cupply goods aeasing need oh in the futu

WTH AND I

percentage of m

Wealth and spen

andards improst their basic

hows that thert popular onelled from abrs of high ad-tech productcommodities and services of the middleure, which c

INEQUALITY

middle-class pe

nding. Source:

ove, consumec needs to thre is a big jume for the midroad. This ca

dded value (ss is still limit(see Figure

of high addee-income groould lead In

Y IN INDON

ople. Source: P

Boston Consult

ers’ needs alshose that offemp in the purddle class (sean be seen insee Figure 3)ted. The struc4). Therefored value and a

oup, this woudonesia to s

NESIA

Povcal Net and W

ting Group.

so follow a ner greater conrchase of con

ee Figure 2). n the structur). On the othcture of Indone, economic are innovativuld be a risk tuck in the c

World Bank.

natural progrenvenience. Snsumer durabThe domestire of Indoneher hand, thnesian exportactors that ca

ve. If domestik for the achicurrent level

ession from Survey from ble products ic needs for sian import e ability of t products is an exist are ic industries ievement of l of income

GROWTH AND INEQUALITY IN INDONESIA

95

Figure 3. Indonesia’s import structure. Source: United Nations Conference on Trade and Development (UNCTAD).

Figure 4. Indonesia’s export structure. Source: United Nations Economic and Social Commission

for Asia and the Pacific (UNESCAP).

Another challenge that we also have to face is the increasing inequality which is represented by the Gini ratio1. For almost three decades, GDP per capita has increased by five times, but Gini ratio has also increased from 0.30 in 1984 to 0.41 in 2012 (see Figure 5).

Figure 5. GDP/capita and inequality. Source: Statistics Indonesia BPS.

1 The Gini coefficient is derived from the ratio of the share of income going to the lowest quintile of the income distribution and the share going to the highest quintile. The Gini coefficient can be viewed as an average of deviations of quintile shares from 0.2, the value that holds under full equality (Barro, 2008).

0

0.2

0.4

0.6

0.8

1

1996 1999 2002 2005 2008 2012% R&D-Intensive % Energy/Resource-Intensive % Labor-Intensive

0

0.2

0.4

0.6

0.8

1

1996 1999 2002 2005 2008 2009 2012% R&D-Intensive Commodities % Energy/Resource-Intensive % Labor-Intensive

05001000150020002500300035004000

0.2

0.25

0.3

0.35

0.4

0.45

Gini Ratio GDP/capita (in USD-PPP 2005 contant)

GROWTH AND INEQUALITY IN INDONESIA

96

Based on the abovementioned background, it is necessary to analyze how the quality of economic development in Indonesia could support the long-term goal of achieving a sustainable and equitable growth. Therefore, the aim of this paper is:

(1) To analyze the trend of income inequality in Indonesia and how it evolves as the income level rises; (2) To test whether the Kuznets Curve holds and if it is proven to hold, then we would like to find the

turning point of the income level.

Growth and Inequality in Indonesia

Indonesia had successfully maintained quite high economic growth and reduced poverty (see Figure 6) during the period from the 1980s to the mid-1990s. In line with the increase of GDP per capita (see Figure 7), the number of poor people2 decreased from 35 million in 1984 (21.6% of total population) to 22.5 million in 1996 (11.3% of total population). In 1996, the methodology was revised and the percentage of poverty with the new definition was estimated at 17.5%. In 1998, poverty jumped significantly due to the impact of the Asian financial crises before it started to decrease in 2000. Afterwards, poverty kept going down except in 2006, which was due to rising domestic oil price that drove up the price of staple food. As a result, people who were not classified as poor but whose income was around the poverty line shifted to the poor category. Even though the average growth rate after the crises3 (5.6%) is smaller than that before the crisis4 (6.7%), the declining rate of the number of poor people is higher. After the crises, the number of poor people was reduced over 1.45 million each year (or about 0.88% a year), while before the crises, the declining rate was 1.04 million people a year (or about 0.85% a year). This indicates an improvement in the government poverty alleviation program after the crises.

Figure 6. GDP growth and poverty. Source: BPS.

2 According to BPS, people are classified as poor people if their monthly income per capita is below the poverty line. 3 Period before the crisis is calculated between 1984 and 1996. 4 Period after the crisis is calculated between 1999 and 2012.

0

10

20

30

40

50

60

1984 1987 1990 1993 1996 1996 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 20120

1

2

3

4

5

6

7

8

9

No. of poor people (million - RHS) GDP Growth (LHS) (%) of Poor People (LHS)

Revised Method

GROWTH AND INEQUALITY IN INDONESIA

97

Figure 7. GDP per capita and poverty. Source: UNESCAP and BPS.

Although both the GDP per capita and the number of poor people have gradually increased and decreased respectively after the crises, the inequality as indicated by Gini ratio tends to increase (see Figure 8). The inequality decreases during the period of 1984-1987 in line with the decrease of GDP growth. After 1987, Gini coefficient was relatively stable and began to increase from 1993 to 1996. During this period, the economic growth was relatively high, which stood between 6% and 8% (see Figures 3-12). The Gini ratio then declined as a result of the 1997 Asian Financial Crisis (AFC). Comparing to the period before the crises, the inequality tends to increase for the last decade. There was a relative constancy of the overall Gini index before the crises. It changed very slightly, which was only 0.01 over 12 years (1984-1996). After the crises (1999-2012), the Gini index increases to 0.12 point, 10 times higher than the period before.

Figure 8. GDP growth and Gini ratio.

Figure 9 shows the share of national income that is proxied by expenditure of three income groups, namely, the 20% richest households, the 40% middle-income households, and the 40% poorest households. The 20% richest households enjoy, on average, 44% of income while the middle-income households and the poorest households enjoy 37% and 20% of income respectively. For the last three years, it seems that there is a significant increase in the share of income enjoyed by the 20% richest households, which is accompanied by the decline in income share of the 40% poorest households and the 40% middle-income households. By the end of 2012, the share of income enjoyed by the richest group was 49%, increased from 41% in 1999. During the period of 1999-2012, the 20% highest income group has gained 20% additional share, while the 40% poorest and the middle-income households have loosed income share by 22% and 9.5% respectively.

05001000150020002500300035004000

0

10

20

30

40

50

60

1984 1987 1990 1993 1996 1996 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012No. of Poor People (Million-RHS) (%) of Poor People (LHS) GDP/capita (in USD-PPP 2005 contant)

0

2

4

6

8

10

0.00

0.10

0.20

0.30

0.40

0.50

1984 1987 1990 1993 1996 1999 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Gini Ratio (LHS) g-GDP (LHS)

Revised Method

GROWTH AND INEQUALITY IN INDONESIA

98

Figure 9. Share of national income. Source: BPS.

Figure 10. Gini ratio (urban-rural-national). Source: BPS.

After the AFC, the domestic economy had been exposed to the volatility of global economic conditions which contributed to the increase of inequality. In late 2005, the hike of world oil prices forced the government to raise domestic oil prices that pushed inflation higher. Inflation reduces the real income and the impact is worse to low-income people compared to the high-income one. As a result, we see the increase of inequality in 2006. Later in the period after 2008, the impact of the subprime mortgage crisis also spread to financial markets in developing countries. Subprime mortgage crisis has triggered a reversal of capital flows in developing countries so that the exchange rate and asset prices fall. In addition, the impact of the subprime mortgage crisis is also accompanied by soaring oil prices, followed by a rise in prices of many other commodities. The combination of all these events caused considerable inflationary pressures to domestic economy which contributed to the increase of inequality after 2008.

10

15

20

25

30

35

40

45

50

55

1999 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

% o

f GD

P

40% residents with lowest income 40% residents with middle income

20% residents with highest income

0.20

0.25

0.30

0.35

0.40

0.45

1984 1987 1990 1993 1996 1999 2002 2003 2004 2005 2006 2007 2008 2009 2010 2012

Urban Rural National Average

Inequcompared tincreasing average. Thincreased rthan 50% (2010), Inddata, the upopulation Asian averassociated have a high

0

10

20

30

40

50

60

70

80

90

0

10

20

30

40

50

60

70

80

90

ality seemed to rural areastrend. Inequhe influence rapidly over tof the increa

donesia has gurban populat

in Indonesiarage since 19with econom

h level of urb

Figure

Indonesia

Indonesia

UP

GROW

to be more s with a leveluality in urban

of urban Ginthe last decadase in inequarown to becotion in 2012

a is relatively995. Accordi

mic growth. Fban population

11. Indonesian

Figure 12. U

a Malay

Malays

1995-2000

WTH AND I

apparent in ul of 0.33 (seen areas was

ni on the natiodes. As statedality in Indonome one of th

was 44.9%.y higher (see Fing to the stu

For some richn (see Figure

urban populati

Urban populati

ysia K

UP 20

sia Kor

UP 200

INEQUALITY

urban Indone Figure 10). higher than i

onal aggregatd in Kanbur anesia at the n

he most urban Comparing Figure 11). Tudy of Lewi

her countries 12).

ion and South E

on of some cou

Korea

005-2010

rea J

00-2005

Y IN INDON

esia, reachingInequality in in rural areaste grew over and Zhuang (2national leve

nized countriewith average

The urban popis (2013), thein Asia like

East Asia averag

untries. Source:

Jepan

UP 2012

Jepan

UP 2005-2

NESIA

g a level of 0both urban a

s and was vetime as Indon2013), urbanil. According

es in the regioe South Eastpulation has ee level of urKorea, Japan

ge. Source: UN

UNESCAP.

China

China

2010

0.43 in Septeand rural areaery close to tnesia’s urbanization contri

g to World Bon. Based on t Asian counexceeded therbanization isn, and Malay

NESCAP.

Philippines

Philippines

UP 2012

99

mber 2012, as shows an the national n population ibuted more

Bank Report UNESCAP

ntries, urban e South East s positively sia, they do

s

GROWTH AND INEQUALITY IN INDONESIA

100

The pattern of rising inequality also occurred in provinces. From Table 1, we can see that almost all provinces experienced worsening inequality in 2012 compared to 1984, almost two decades before. The provincial average of inequality increased from 0.29 in 1984 to 0.31 in 1996 and then to 0.32 in 2008, and became 0.38 in 2012. There is a significant increase in the provincial average Gini ratio from 2008 to 2012 (17.9%), compared to the increase from 1984 to 1996 (4.5%) and from 1996 to 2008 (4.7%). In 1984, the number of provinces that have inequality above national average is 13 and in 1996, it declined to 10 provinces.

Table 1 Inequality in Provinces No. Province 1984 1996 2008 2012 1 Papua 0.37 0.39 0.40 0.44 2 Gorontalo 0.34 0.44 3 DIY 0.34 0.38 0.36 0.43 4 West Papua 0.31 0.43 5 Bali 0.29 0.31 0.30 0.43 6 North Sul 0.35 0.34 0.28 0.43 7 DKI 0.29 0.36 0.33 0.42 8 South Sul 0.35 0.32 0.36 0.41 9 West Java 0.30 0.36 0.35 0.41 10 Central Sul 0.30 0.30 0.33 0.40 11 South East Sul 0.32 0.31 0.33 0.40 12 Riau 0.26 0.30 0.31 0.40 13 South Sum 0.27 0.30 0.30 0.40 14 Banten 0.34 0.39 15 South Kal 0.26 0.29 0.33 0.38 16 Central Java 0.31 0.29 0.31 0.38 17 West Kal 0.25 0.30 0.31 0.38 18 Maluku 0.30 0.27 0.31 0.38 19 Lampung 0.29 0.28 0.35 0.36 20 NTT 0.31 0.30 0.34 0.36 21 East Kal 0.36 0.32 0.34 0.36 22 East Java 0.31 0.31 0.33 0.36 23 West Sum 0.26 0.28 0.29 0.36 24 Bengkulu 0.21 0.27 0.33 0.35 25 NTB 0.30 0.29 0.33 0.35 26 Kepri 0.30 0.35 27 North Mal 0.33 0.34 28 Jambi 0.20 0.25 0.28 0.34 29 North Sum 0.26 0.30 0.31 0.33 30 Central Kal 0.29 0.27 0.29 0.33 31 Aceh 0.26 0.26 0.27 0.32 32 West Sul 0.31 0.31 33 Babel 0.26 0.29 Above average 13 10 17 18 Below average 13 16 16 15 Provincial average 0.29 0.31 0.32 0.38 Note. Source: BPS and the authors’ calculation.

GROWTH AND INEQUALITY IN INDONESIA

101

After the crises, if we take a look at more recent periods of 2008 and 2012, in 2012, there are 18 provinces that have inequalities above national average, increased from 17 provinces in 2008. For the period of 2008-2012, Bali, West Papua, and North Sulawesi experienced the highest increase in Gini coefficient. Among 18 provinces with inequality above national average in 2012, some of them are provinces with urban population or GDP per capita above provincial average. Provinces with urban population above national average are DKI, DIY, Banten, West Java, East Kal, Bali, Riau, East Java, Central Java, North Sumatra, North Sulawesi, and NTB (see Figure 13). Provinces with GDP per capita above provincial average are DKI, Riau, West Papua, Papua, and West Sulawesi (see Figure 14). The high inequality in urban areas occurs because these places can attract large numbers of less-skilled people who think that there are more economic opportunities in urban areas than in rural areas. Meanwhile, there are also high inequalities in provinces with high GDP per capita. Except for DKI, those provinces with high GDP per capita have abundance of natural resources. Using national average for GDP per capita and inequality (see Figure 15), we can see that there are four provinces that have both GDP per capita and inequality above average. Meanwhile, there are only three provinces (Babel, Riau, and West Sulawesi) with GDP per capita above average and inequality below average.

Figure 13. Urban population provinces. Source: http://www.datastatistik-indonesia.com.

Figure 14. GDP/capita by provinces. Source: BPS.

0102030405060708090

100

DK

ID

IYB

ante

n W

est J

ava

East

Kal

Bal

iR

iau

East

Java

Cen

tral J

ava

Nor

th S

umN

orth

Sul

NTB

Sout

h K

alSo

uth

Sum

Ben

gkul

uC

entra

l Kal

Wes

t Sum

Gor

onta

loJa

mbi

Sout

h Su

lA

ceh

Lam

pung

Wes

t Kal

Nor

th M

alM

aluk

uSo

uth

East

Sul

Papu

aC

entra

l Sul

NTT

% Urban Population in 2010 National Average

05000

100001500020000250003000035000400004500050000

DK

IEa

st K

alB

abel

Ria

uW

est P

apua

Papu

aW

est S

ulEa

st Ja

vaC

entra

l Sul

Cen

tral K

alSo

uth

Sum

Nor

th S

umSo

uth

Kal

Bal

iW

est S

umW

est J

ava

Ace

hW

est K

alN

orth

Sul

Jam

biD

IYSo

uth

Sul

Cen

tral J

ava

Sout

heas

t Sul

Lam

pung

NTB

Ben

gkul

uM

aluk

uN

TT

GDP Per Capita in 2011 (Rp) National Average of GDP Per Capita

102

We alDuncan, 2Figure 16, level in 20persistencecompared t

5 This methdeviation fro(average – stdeviation); a

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

-

L

MM

H

Fig

lso adopt the013)5 to seewe see that

01 and 2012.e. Jambi and to other prov

od was mentio

om the averagetandard deviati

and (3) High = p

- 5,000

Jambi, Aceh,South Sum, N

Low-Low

Medium-Medium

Low-Medium

Medium-Low

High-Medium

GROW

gure 15. Inequa

e approach ue the persiste

Papua and D. Lampung, NCentral Kali

vinces.

Figu

oned in OECD e. Persistence oion); (2) Mediupoverty or inequ

10,000 1

Pap

West S

Gorontalo

West Sum, KepNorth Sum, NTB

m Me

WTH AND I

ality and GDP/c

used in the pence in inequDIY are provNTT, South Simantan have

ure 16. Persiste

working paperf poverty or in

um = (average –uality rate ≥ (av

15,000 20,00

West Papupua

Sul

pri, North Mal,B, South Kal, E

edium-High & Hi

INEQUALITY

capita. Source:

aper by OECuality betweevinces with aSulawesi, ande the less inc

ence of inequali

r by Miranti etnequality is clas– standard deviverage + standa

00 25,000

Riau

ua

Central Kal,East Java

igh-High

Y IN INDON

BPS and the au

CD (Miranti,en two pointa degree of ind South East Screment of G

ity (2001 and 20

t al. (2013). Thssified as followiation) ≤ pover

ard deviation).

30,000 35

Babel

NESIA

uthors’ calculati

Vidyattamats in time innequality perSulawesi mov

Gini during th

012).

he classificatiows: (1) Low = rty or inequality

5,000 40,00

East Kal

Maluku, CenBali, West KNorth Sul, D

ion.

a, Hansnata, Cn 2001 and 2rsisted at theve from medhe period of

on is divided upoverty or ineq

y rate ≤ (averag

00 45,000

DKI

ntral Sul,Kal,DIY

Cassells, & 2012. From e same high ium to high 2001-2012,

using standard quality rate < ge + standard

50,000

GROWTH AND INEQUALITY IN INDONESIA

103