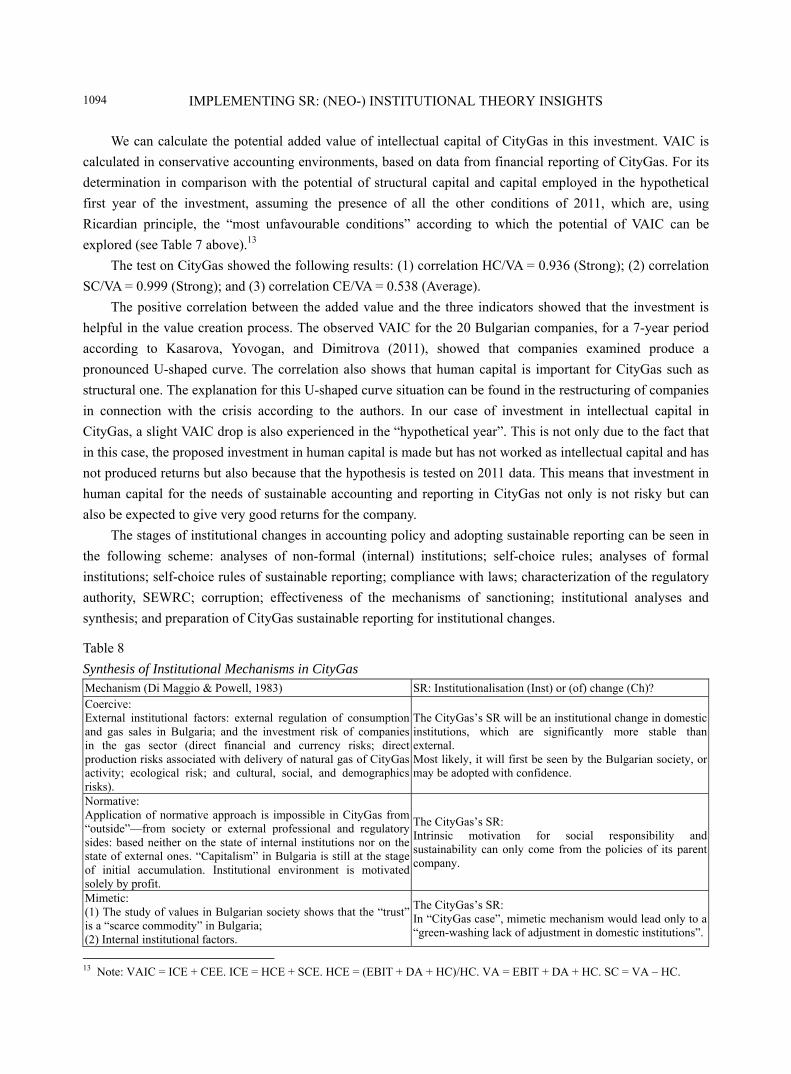

JMAA 2014.11

76

Volume 10, Number 11, November 2014 (Serial Number 114) Journal of Modern Accounting and Auditing David Publishing Company www.davidpublishing.com Publishing David

-

Upload

davidpublishing -

Category

Documents

-

view

0 -

download

0

Transcript of JMAA 2014.11

Volume 10, Number 11, November 2014 (Serial Number 114)

Journal ofModern Accounting and Auditing

David Publishing Company

www.davidpublishing.com

PublishingDavid

Publication Information: Journal of Modern Accounting and Auditing is published monthly in hard copy (ISSN1548-6583) and online (ISSN1935-9683) by David Publishing Company located at 240 Nagle Avenue #15C, New York, NY 10034, USA. Aims and Scope: Journal of Modern Accounting and Auditing, a monthly professional academic journal, covers all sorts of researches on accounting research, financial theory, capital market, audit theory and practice from experts and scholars. Editorial Board Members: Avis Andoni, Albania. Benedetta Siboni, Italy. Brad S. Trinkle, USA. Daniela Cretu, Romania. Drazen Koski, the Republic of Croatia. Elisabete Fátima Simões Vieira, Portugal. Emmanuel Attah, Ghana. Fabrizio Rossi, Italy. Haihong He, USA. Joanna Błach, Poland. João Paulo Torre Vieito, Portugal. Liang Song, USA. Lindita Rova, Albania. Mohammed Al-Omiri, Saudi Arabia. Mohamed Rochdi Keffala, Tunisia. Mohammad Talha, Saudi Arabia. Monika Wieczorek-Kosmala, Poland. Narumon Saardchom, Thailand.

Peter Harris, USA. Philip Harris Siegel, USA. Philip Yim Kwong Cheng, Australia. Rosa Lombardi, Italy. Sabina Hodzic, Croatia. Selim Mekdessi, Lebanon. Sheikh Abdur Rahim, Bangladesh. Thomas Gstraunthaler, South Africa. Tita Djuitaningsih, Indonesia. Tiziana Di Cimbrini, Italy. Tumellano Sebehela, United Kingdom. Valdir de Jesus Lameira, Brazil. Valerio Pesic, Italy. Vintilescu Belciug Adrian, Romania. Wan Mansor W. Mahmood, Malaysia. Yezdi H. Godiwalla, USA. Zeynep Özsoy, Turkey.

Manuscripts and correspondence are invited for publication. You can submit your papers via Web Submission, or E-mail to [email protected]. Submission guidelines and Web Submission system are available at http://www.davidpublishing.com. Copyright©2014 by David Publishing Company and individual contributors. All rights reserved. David Publishing Company holds the exclusive copyright of all the contents of this journal. In accordance with the international convention, no part of this journal may be reproduced or transmitted by any media or publishing organs (including various websites) without the written permission of the copyright holder. Otherwise, any conduct would be considered as the violation of the copyright. The contents of this journal are available for any citation, however, all the citations should be clearly indicated with the title of this journal, serial number, and the name of the author. Abstracted/Indexed in: Database of EBSCO, Massachusetts, USA Universe Digital Library Sdn Bhd, Malaysia Australian ERA ProQuest CSA-Natural Sciences, USA Chinese Database of CEPS, Airiti Inc. & OCLC Google Scholar Ulrich’s Periodicals Directory CiteFactor, USA Social Science Research Network (SSRN), USA

Polish Scholarly Bibliography Database of Summon Serials Solutions, USA Turkish Education Index Academic Keys Electronic Journals Library Chinese Scientific Journals Database, VIP Corporation, Chongqing, P.R. China Scholar Steer Scientific Indexing Services

Subscription Information: Price (per year): Print $640; Online $480; Print and Online $800 David Publishing Company 240 Nagle Avenue #15C, New York, NY 10034, USA Tel: 1-323-984-7526, 323-410-1082; Fax: 1-323-984-7374, 323-908-0457 E-mail: [email protected], [email protected]

David Publishing Company

www.davidpublishing.com

DAVID PUBLISHING

D

Journal of Modern Accounting and Auditing

Volume 10, Number 11, November 2014 (Serial Number 114)

Contents

Accounting

Implementing Sustainability Reporting (SR): (Neo-) Institutional Theory Insights in the Analysis of the SGR Group, Italy and CityGas, Bulgaria 1067

Maria-Gabriella Baldarelli, Mara Del Baldo, Ninel Nesheva-Kiosseva

Usefulness and Effectiveness of Related Party Transactions (RPTs) Disclosure: Empirical Evidence From Italy 1105

Amedeo De Cesari, Oscar Domenichelli, Martina Vallesi

Finance

Shadow Banking Credit Intermediation: Determinants of Default Risks in Securitization and Collateralization 1119

Mohd Yaziz Mohd Isa, Md. Zabid Haji Abdul Rashid

Organizational Management

Organizational Learning (OL) and Organizational Innovation (OI): The Case of Information and Communication Technology (ICT) Industry in Malaysia 1130

Gholamreza Zandi, Mohamed Sulaiman, Islam Mohamed Salim

Journal of Modern Accounting and Auditing, ISSN 1548-6583 November 2014, Vol. 10, No. 11, 1067-1104

Implementing Sustainability Reporting (SR): (Neo-) Institutional

Theory Insights in the Analysis of the SGR Group, Italy

and CityGas, Bulgaria∗

Maria-Gabriella Baldarelli University of Bologna, Bologna, Italy

Mara Del Baldo

University of Urbino “Carlo Bo”, Urbino, Italy

Ninel Nesheva-Kiosseva

New Bulgarian University, Sofia, Bulgaria

The aim of this paper1 is to investigate how the corporate characteristics and contextual factors influence the choice

of managers in initiating the sustainability report/reporting (SR) and to understand the role of organisational

dynamics. The research design develops through a deductive and inductive approach. The deductive approach is

based on an analysis of the Social and Environmental Accounting Research (SEAR) strands which use the theoretical

framework of (neo-) institutional theory to inquire the adoption and diffusion of SR. The inductive method is based

on a research case that focuses on the SGR Group. “How can the neo-institutional theory help explain the process of

SGR’s SR implementation in Italian and Bulgarian companies”? The study identifies both the internal and contextual

factors associated with the SR development and the regulative, normative, and cognitive dimensions/factors that

affect the implementation and institutionalisation of SR in Italy and Bulgaria, in accordance with the different

institutional environments in which the social and sustainability accounting projects are developed.

Keywords: sustainability report (SR), organisational dynamics, neo-institutional theory, contextual factors, regulative,

normative, cognitive, and mimetic mechanisms, relational change, social and environmental accounting research (SEAR)

∗ Acknowledgements: We want to express our gratitude to Michaela Dionigi, the President of SGR Group, as well as to Demis Diotallevi (CEO), Elisa Tamagnini (CSR and Sustainability Officer), Emanuela Vespa (Marketing and Communication Department), and the CityGas staff for their precious and kindly collaboration in all steps of our research.

Maria-Gabriella Baldarelli, Ph.D., professor of Accounting, Department of Management, University of Bologna. Email: [email protected].

Mara Del Baldo, assistant professor of Small Business Management, Department of Economics, Society, and Politics, School of Economics, University of Urbino “Carlo Bo”.

Ninel Nesheva-Kiosseva, Ph.D., professor of Economics, Department of Economics and Business Administration, New Bulgarian University. 1 The first draft of this paper had been selected and presented at the 4th Italian Conference on Social and Environmental Accounting Research (Italian CSEAR 2012), September 20-21, Trento and at the Financial Reporting Workshop, June 13-14, 2013, Rome, Italy. In April 2013, this paper was awarded by a nomination assigned by the Department of Business Administration to participate in the competition for the prize Pythagora organised by the Bulgarian Ministry of Education and it was presented at the New Bulgarian University Conference of June 4, 2013, Social and Environmental Accounting: Experience and Research, Jubelee International Scientific and Practical Conference “Business Positive Force in Society. 20 Years MBA Business Administration”. This paper is the work of a common research project. However, Maria-Gabriella Baldarelli wrote Sections 3.1 (Methodology), 3.2 (SGR Group Profile), and 5 (Discussion); Mara Del Baldo wrote Sections 1 (Introduction), 2 (SR and Institutional Theory Relationships: Literature Review), 3.3 (The Process of Implementing the SR in SGR Group), and 6 (Conclusions); and Ninel Nesheva-Kiosseva wrote Section 4 (Sustainability Dimensions, Institutional Theory, and the Case Study of CityGas).

DAVID PUBLISHING

D

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1068

Introduction

Companies, and especially multinational corporations, are increasingly adopting sustainability

report/reporting (SR) practices (Cooper & Owen, 2007). At the same time, an increasing body of researchers

have sought to investigate the motives and drivers which lead organisations to initiate and undertake social and

environmental reporting (SER) (Adams, Hill, & Roberts, 1995; 1998; Young & Marais, 2012) and different

theoretical strands have been used to examine various aspects. These studies, which gave food to the

international academic Social and Environmental Accounting Research (SEAR) literature, have been primarily

focused on organisational processes and internal factors as well as on the content, nature, and extern of various

social and environmental reports.

In more recent years, the engagement research has been put forward as a strong approach in developing

theories to understand SER, enhance organisational practices and performances (Adams & Larrinaga-Gonzàlez,

2007; Contrafatto, 2010; 2011), and explore diverse issues, including change within organisations (Adams,

2002; Cooper, Taylor, Smith, & Catchpowle, 2005; Parker, 2005).

Our work is part of this field that is described by Bebbington, Higgins, and Frame (2009) who used an

institutional theory framework for an empirical research focused on reporting champions in New Zealand with

the aim of investigating how and why they initiated the SR.

The extent, to which organisations shape managerial decision-making to initiate the SR process (Gray,

Owen, & Adams, 2010; Bebbington, 2007; Bebbington & Contrafatto, 2006; Gray, Bebbington, & Walters,

1993), depends on a number of organisational dynamics and a variety of regulative, normative, and cognitive

drivers. Adams (2002) identified a multiplicity of corporate characteristics (size, industry, profit, or financial

performance) and contextual factors (country of origin and relative variety of social, political, and legal factors,

social and political change, economic cycles, cultural, specific events, media pressure, and stakeholders’ power)

which influence managers’ decisions to report.

Departing from these premises, the research question, which orients the analysis, can be summarised in

this term: “How can the neo-institutional theory help explain the process of SGR’s SR implementation in Italy

and Bulgaria?”.

Aiming to reply to this question, the research design develops through a deductive and inductive approach

(Denzin, 1978; Cox & Hassard, 2005).

The deductive approach is based on an analysis of the SEAR literature strands which use the theoretical

framework of (neo-) institutional theory to inquire the adoption and diffusion of SR. The inductive approach is

related to the analysis of an exemplary case study.

The inductive method is based on a research case (W. Naumes & M. J. Naumes, 2006) which focuses on

the enterprise SGR Group and the internal and external impact of implementing the SR in two different

countries.

The analysis carried out has enabled us to understand some features of the sustainability process started by

the company in Italy (SGR Group) and Bulgaria (CityGas) and to interpret them as the challenges launched by

the group to create, through its own activities, a civil economy (Bruni & Zamagni, 2004) which is typical of the

corporate culture of responsibility and sustainability.

We identify both the internal and contextual factors associated with the SR development and the

regulative, normative, and cognitive dimensions/factors, in order to understand the implementation and

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1069

institutionalisation of SR in Italy and Bulgaria, in accordance with the different institutional environments in

which the social and sustainability accounting projects are developed.

To reply to the research question, we focus on some points, the first of which is about the reaction of the

enterprise towards institutional pressure. The second one concerns the analysis of what happens inside and

outside the organisation involved in SR in Italy and Bulgaria. Thirdly, by studying institutionalisation at the

organisational level, the work provides a picture about the ways in which businesses outline the

institutionalisation process. Finally, it demonstrates the balanced nature of institutional change in the two

different countries.

Among the wide literature on SEAR, the study aims to add to the existing works which investigated the

spread of SR, using a neo-institutional lens. Different works have inquired this aspect but focus the analysis

mainly on large businesses and organisations (and never pay attention to small, medium, and family-owned

companies) belonging to North American and Australia or, more generally, located in English-speaking

countries (Contrafatto, 2011). There is, indeed, no empirical study focusing on Italian companies or on entities

belonging to Eastern European countries.

In our work, the attention has been addressed to an Italian medium-sized family group. The family

property and the strength of its roots within the local, surrounding fabric (Rimini) where it is located are

mirrored in the values system and in the objectives of the entrepreneurial and managerial heights, just as they

are in the motivations and the behaviours that have led to the introduction of SR.

Furthermore, the selected group has a branch in Bulgaria (Eastern countries) where SEAR is required,

thus contributing to developing the debate on this question which is still at the initial stage. Consequently, our

paper has the aim of contributing to filling some cognitive gaps in the SEAR literature by proposing

new/further lines of reflections that emphasises the relevance of internal and external contingent factors in SR

development and, as suggested by some scholars (Bebbington, 2007; Bebbington et al., 2009), the importance

of the empirical research to strive for the acknowledgment of the SR issue at the scientific, managerial, and

operational levels.

Moreover, the group belongs to a sector (multi-utility) to which only few studies addressed attention in

the past, while researches have mainly been developed on companies belonging to other sectors (Contrafatto,

2011). Finally, since the work is based on the engagement research approach, used to understand

organisational phenomena from the “inside”, thus favouring a more grounded and contextualized

comprehension of the rationale through which actors behave and individual/organisational action is being

constructed (Adams & Larrinaga-Gonzàlez, 2007), it aims to contribute to constructing the culture of

sustainability, which is particularly needed in still far-off contexts, like those of many Eastern European

countries.

This paper is divided into two main parts: The first one presents a literature review on SR and the

conceptual framework focused around (neo-) institutional theory, while the second one presents the

methodology and the main results of the empirical analysis, followed by the discussion and conclusions.

SR and Institutional Theory Relationships: Literature Review

As afore mentioned, the engagement research implies the adoption of a few specific interpretive research

methods and has the potential to provide valuable means to enhance the descriptive and theoretical

understanding of the processes and dynamics of SEAR.

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1070

An illustrative engagement research review provided by Contrafatto (2011) proposed a taxonomy of the

existing works. Using the criteria “issues and focus of analysis”, the author classified the body of SEAR

literature into four groups respectively focused on: motives/drivers, influencing factors, management

perception views, and impact/effects on organisations. The first group includes those studies which have mainly

examined motives and drivers for the initiation of SER (Buhr, 2002; O’Dwyer, 2002; Spence, 2007;

Bebbington et al., 2009; Farneti & Guthrie, 2009), while the second one relates to research exploring the

contextual and internal factors, including managerial attitudes, which influence the nature and extent of SER

and might contribute to or limit change in organisations (Adams, 1999; 2002; Adams & McNicholas, 2007;

Bebbington et al., 2009). The third class is formed by studies focusing on potential and actual possibilities of

SEAR to stimulate organisational change in practices, structures, performance, and/or values (Gray, Walters,

Bebbington, & Thomson, 1995; Larrinaga-Gonzàlez & Bebbington, 2001; Dey, 2007; Albelda-Perez,

Correa-Ruiz, & Carrasco-Fenech, 2007). Finally, the fourth group includes studies which have specifically

analysed the managerial perceptions and views about SEAR and related practices (Belal & Owen, 2007; Farneti

& Guthrie, 2009).

These studies were developed using different fieldwork methodologies (qualitative analysis, in-depth

ethnographic and action research studies) and research methods aimed to carry out the empirical investigation

and collect data and information (primarily interviews and, in addition, observations, visits and meeting

participations, documents analysis, and questionnaires).

Besides, several theoretical frameworks have been explicitly adopted. A prevalence of studies have drawn

on theories of organisational change to ascertain whether and to what degree social and environmental

accounting and reporting interventions produce any substantial organisational changes such as practice,

structures, performance, and value systems (Contrafatto, 2011). Particularly, Bebbington et al. (2009) and Dey

(2007) used institutional insights to investigate respectively the dynamics (drivers) leading to the initiation of

SER and the effects of social accounting intervention on existing organisational systems.

With respect to the subjects and themes, more attention has been addressed to the processes of

reporting/disclosing social and environmental information versus the theme related to the processes of social

and environmental accounting.

Other distinctive aspects are relative to the context of the analysis in terms of location (where the analysis

was conducted), the industry, and time period of the analysis. Firstly, a large number of studies were conducted

in English-speaking countries (especially in the United Kingdom (UK) and Australia/New Zealand). Secondly,

most of the studies considered large corporations that operated in the manufacturing and processing sectors

(i.e., chemical, pharmaceutical, extracting, etc.), while only few research works involved organisations

operating in other contexts, such as the public sector (Farneti & Guthrie, 2009), the public utility

(Larrinaga-Gonzàlez & Bebbington, 2001), and social economy (Dey, 2007). Thirdly, with regard to the time

period, the studies covered different decades, starting from the early 1990s (Gray et al., 1995) to the mid-2000s.

Finally, with regard to the level of analysis, most of the works have explored SEAR practices at the

organisational level of either individual or group of organisations and only a minority addressed the industrial

site or have attempted to explore the intra-organisational dynamics related to the process of initiation and

implementation of SEAR (Contrafatto, 2011).

One aspect which does emerge from the results and findings reported by the studies is that of

the heterogeneity, complexity, and contradictory nature of SEAR and related practices. In fact, a multitude of

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1071

organisational, contextual, and institutional factors influence both the decision-making about the initiation

of SEAR and its characteristics (nature and extent). Furthermore, they affect the nature and quality of

SEAR and impact on its relevance to promote change in the organisational realm. However, the way in which

these factors come together and influence the choice and process of SR (Gray, Owen, & Adams, 1996; Gray

et al., 2010; Bebbington, 2007; Bebbington & Contrafatto, 2006; Gray et al., 1993) remains unexplored and

unclear.

For this reason, the present work proposes filling this gap, on one hand, by extending the location in which

the research has been conducted to countries, other than the Anglo-Saxon or Australian ones, like Italy and

Bulgaria which are characterized by different conceptions of business and the role and nature of SEAR and SR;

and on the other hand, by expanding the analysis of internal contingent factors which are linked to family

ownership of the company and which mirror themselves in the mission and governance, and therefore, in the

choice of introducing SR and in the process of its implementation.

Among the strands of research outlined above, the present work, therefore, challenges issues treated in the

first three strands, proposing the enrichment of the knowledge of the multiple organisational, contextual, and

institutional factors that affect SR introduction and development.

In particular, with reference to the first group of studies, as mentioned above, a number of reasons have

been suggested as to why companies adopt SR. Through SR, companies have a chance to respond to stakeholder

expectations and, by doing so, contribute both to societal well-being (Morsing & Schultz, 2006; Deegan &

Samkin, 2006) and to managing their own legitimacy (Archel, Husillos, Larrinaga, & Spence, 2009) and

guarding a company’s reputation (Baldarelli & Gigli, 2012) and identity (Reynolds & Yuthas, 2008). Moreover,

companies adopt SR as they expect some instrumental payoff in terms of long-term profitability, which may

eventuate from improving their ability to attract labour, through reassuring shareholders of non-financial

risks, by reducing information asymmetries (Merkl-Davies & Brennan, 2007) or improving stakeholder

decision-making (Du, Bhattacharya, & Sen, 2010). Several researchers maintain that the reasons for SER are

primarily due to external “jolts” (Laughlin, 1991; Larrinaga-Gonzàlez & Bebbington, 2001; Mallin, Michelon, &

Raggi, 2012). Others hypothesize that not one, but several factors lead business firms to introduce and publish

SR (Duncan & Thomson, 1998).

The literature that falls into the second group of studies has mainly focused on the corporate organisational

factors (internal factors) which impact on the extent, nature, and sophistication of SER and, therefore, on its

potential to activate some forms of organisational change within organisations. Some scholars have gone

further in investigating the reasons why some organisations undertake SER and what drivers exist in both the

external (societal) and internal environments for reporting (Adams, 2002; Solomon & Lewis, 2002). In this

regard, the corporate governance literature provides interesting insights that assist in understanding the nature

of corporate social responsibility (CSR) reporting practices (Kolk, 2008; Young & Marais, 2012). The impact

of industry characteristics by adopting an industry risk perspective has also been considered (Bebbington,

Larrinaga, & Moneva, 2008; Unerman, 2008).

Furthermore, companies may also report because they are forced to do so by diverse institutional pressures.

Focusing on institutions, indeed, helps in understanding SR not only as a voluntary discourse but also as a

requirement imposed by the corporate environment. For instance, companies face coercive pressures to report on

specific environmental issues. These pressures arise from law and regulation and from other organisations, and

by pressures to conform to cultural expectations of society at large (Scott, 2008). Companies also face significant

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1072

normative pressures to engage in SR and CSR reports which arise traditionally from professionalization (Kolk &

Pinkse, 2010). Pressure to adopt SR may also be mimetic pressure as a response to uncertainty. In situations

where a clear course of action is unavailable, managers may imitate a peer organisation perceived to be

successful (Di Maggio & Powell, 1983). SR is thus a discretionary process reflecting managerial choice in the

midst of stakeholder and institutional pressures (Young & Marais, 2012).

These aspects have been considered especially by the literature of the second and third groups where in the

last decade, few contributions have been made to examining how and why SR practices become institutionalised

and reach an institutional status (Miller, 1994; Milne & Patten, 2002; Ball, 2005; 2007; Phillips, Lawrence, &

Hardy, 2004; Lounsbury & Crumley, 2007) and/or produce effects in terms of institutional change

(Larrinaga-Gonzàlez, 2007).

To fill such a cognitive gap, which requires more consistent research approaches (Gray, Javad, Power, &

Sinclair, 2001; Campbell, 2000), several innovative studies recently made (Larrinaga-Gonzàlez, 2007;

Bebbington et al., 2009) have adopted the institutional (Di Maggio & Powell, 1983; Scott, 1987; 1995)

and neo-institutional theories (Di Maggio & Powell, 1991; Powell, 1991) as a theoretical framework to

explain the standardisation or at least the procedures of SR/SER and to understand the drivers of institutional

change.

Table 1

Mechanisms/Structures of Institutionalisation Di Maggio and Powell (1983) Scott (1995) Example

Coercive mechanisms: The law or the market leads organisations to comply and align with the norms in order to gain legitimacy and survive. Consequently, behaviour becomes very similar in all of them.

Regulative structures: The law or the market involves thecapacity to establish rules, inspect conformity, and manage sanctions in order to influence future behaviour.

Consumer boycotts lead companies to change structures and practices. Environmental regulation makes companies adopt new technologies. In the context of SR, regulative structures and activities would include reporting regulations and their enforcement, aswell as the threat of regulation of reporting (i.e., European Commission recommendation).

Normative mechanisms: Diffused through professionalization, formal education, and professional networks, leading individuals to act according to shared social values and norms.

Normative structures: Based on social values and norms, leading individuals to act according to societal expectations of organisations: legitimate authority of norms and values; organisations genuinely think that, given their role in society, they have to acquire some structures or engage in some practices.

Deontological codes shape practices in many professions, such as accountants. In the context of SR, normative structures refer to rules that are followed on moral/ethical grounds or in order to conform to norms established by referential bodies (i.e., Eco Management and Audit Scheme (EMAS), Global Reporting Initiative (GRI), awards for best environmental, social, or sustainability reports, such as Association of Chartered Certified Accountants (ACCA) awards).

Mimetic mechanisms: Organisations imitate (mimetic process) those peer organisations that seem to be more successful and legitimate.

Cognitive structures: They are taken for granted symbols, meanings, and roles in social actions that support the legitimacy of organisations; The social construction of roles and organisations varies over time and space and contributes to stability; Cognitive structures form conceptually support of legitimacy. Their existence is very difficult to prove empirically.

The waves in the use of some concepts and techniques by organisations are associated with vogues (imitation) rather than rationality. In the context of SR, convergence is taking place in some organisational fields where reports are evolving rapidly (from environmental to CSR and SR).

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1073

Conceived in the social context in terms of institutions2, institutional literature focuses on institutional

stability and inertia on the process, which is called “isomorphism”, which arises from the need for organisations

to respond to environmental expectations, guarantee their survival, and increase their success possibilities in a

particular environment. Isomorphism emerges through three different mechanisms (also called as structures and

activities): coercive, normative, and mimetic (Di Maggio & Powell, 1983). In the same way, phrasing this

differently, Scott (1995) argued that legitimacy is based on three pillars of the institutional order: regulative,

normative, and cultural/cognitive (see Table 1).

Using the institutional theory framework, Bebbington et al. (2009) explored how institutional factors

combine with organisational dynamics to contribute to the initiations of the reporting activity.

Since the institutional theory has been blamed for its failure to address change (Greenwood & Hinings,

1996; Hoffman, 1999), neo-institutional theory has been used to develop emerging insights about how the social

context influences the choice of managers to initiate SR.3 Neo-institutional theory “asks questions about

how social choices are shaped, mediated, and channelled by the institutional environment” (Hopwood & Miller,

1974; Hoffman, 1999, p. 351), which is composed of organisations and organisational fields4. A neo-institutional

theory perspective has been adopted by Hoffman (1999), Jennings and Zandbergen (1995), and Bansal (2005) in

their studies of sustainable organisations (Larrinaga-Gonzàlez, 2007).

Hoffman studied how organisations and fields evolve as regards environmental concerns and demonstrated

how coercive, normative, and cognitive pressures have different importance over time and how the

organisational fields are changing.5 While one basic proposition of institutional theory is that different

pressures in one organisational field lead to convergence in organisational forms and practices; thus, the

frequency and quality of reporting would converge worldwide. Kolk (2005) observed that differences in

environmental reporting between United States (US) and European/Japanese multinational corporations were

increasing, suggesting that currently there is a variance of SR practices rather than a convergence in SR

internationally and hence global reporting could not be seen as being part of the same organisational field.

Concerning this, Jennings and Zandbergen (1995) proposed that, for a sustainable value or practice,

organisational fields tend to be local rather than non-local. This conclusion supports the different patterns

of SR.

Assuming as a possible explanation the existence of several organisational fields around the issue of SR,

Larrinaga-Gonzàlez pointed out the existence of locally based SR fields (i.e., EMAS, triple bottom line,

GRI, ISO 14001, etc.) and used the neo-institutional perspective in order to build an institutional explanation

of the development of SR and ascertain the consequences of the institutionalisation of SR. Facing the issue

of change and the institutionalisation of SR, Larrinaga-Gonzàlez (2007) identified specific research patterns:

2 “Institutions consist of cognitive, normative, and regulative structures and activities that provide stability and meaning to social behaviour” (Scott, 1995, p. 33). 3 Since organisations are immersed in a certain cultural and historical context, which is portrayed by the existence of systems of shared beliefs, symbols, and regulation requirements (Scott & Meyer, 1985), the basis of neo-institutional thinking is in the scepticism towards atomistic accounts of social processes and the conviction that institutional arrangements and social processes matter (Di Maggio & Powell, 1991). 4 An organisational field is formed by those organisations that collectively constitute a recognized area of institutional life (Di Maggio & Powell, 1983) “that partake of a common meaning system and whose participants interact more frequently and fatefully with one another than with actors outside the field” (Scott, 1995, p. 56). 5 Neo-institutional accounts of organisational activity downplay rational managerial action and focus on how the social context influences organisational participants to behave relatively unconsciously in ways that are “normal” to “fit in” and appear “appropriate” within the contexts in which they operate.

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1074

the initiating event that may alter the institutional arrangements; whether and how fields may evolve

(Bansal, 2005); what elements play a part in changes to coercive/normative/cognitive structures; and what

relationships exist between competitive forces and institutional structures in the process of institutionalisation.

With this respect, he illustrated how different events served to initiate SR in different contexts and

how the evolving composition of organisational fields allowed the redefinition of the institution, with the

emergence in recent years of social and ethical aspects of SR. He also explored the relationships between

institutionalisation and change and how this affects SR, and went further to examine the relationship between

institutional theory and the legitimacy theory (Deegan, 2002), which is more often adopted in accounting

research. He illustrated how the coercive, normative, and mimetic mechanisms of institutionalisation can

explain different processes of institutionalisation in SR: Coercion can account for SR as a response to

regulation or consumer pressure; normative mechanisms would explain SR as a response to voluntary

initiatives on the grounds of social responsibility; and mimicry could explain how SR could be the

consequence of some trends. SR is thus the result of a mixture of these three mechanisms, taking different

weights in different contexts.

From this theoretical premise, we can conclude this literature review stating that both: (1) the complexity

of the interplay among institutional, contextual, and organisational drivers that creates the conditions for the

“ignition” of the process of SER (Bebbington et al., 2009); and (2) the mixture of the mechanisms/structures of

institutionalisation imply that there is a need to conduct more empirical research to explore in a contextualized

way the conditions that stimulate or constrain SR and its possibilities to promote positive effects on

organisations and society at large (Contrafatto, 2011).

Consequently, after having analysed the literature, in the following sections, we will describe and discuss

the cases of SR implementation in SGR Group and the factors that affect its initiation in CityGas (the Bulgarian

subsidiary).

The Case Study of SGR Group

Methodology

The study of the case (Spence & Gray, 2008; Bebbington et al., 2009) follows the dynamics of the

research case (W. Naumes & M. J. Naumes, 2006).

The selected companies—SGR Group Rimini, Italy and the foreign subsidiary CityGas,

Bulgaria—represent an exemplary case (Yin, 1994) for three main reasons: Firstly, they belong to a sector

which has not been the subject of particular investigation on research questions on this topic; secondly, they are

located in different countries which are characterized for the presence of different external institutional factors

affecting the development of sustainability orientation and SR (Baldarelli & Nesheva-Kiosseva, 2011); thirdly,

because the process of the implementation of SR may be seen from its very first stages. The SGR Group

introduced its first SR in 2011, using internal human and technological resources and CityGas still finds itself

in a phase of primary development of the conditions for its adoption.

SGR Group is a multi-utility and family-owned company, unlisted, based in Italy, made up of several

companies, and with a long experience in gas distribution, that is, over 50 years, during which period it has

always been a one-family-owned enterprise, and this feature has been able to create a very strong connection

with the territory where the enterprise is operating.

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1075

As before mentioned, among the wide array of fieldwork methodologies applied to SEAR, we opted for

various methods to gather data and information (such as interviews, observations, visits and meeting

participations, documents analysis). The tools used are primarily semi-structured interviews, which are aimed at

the entrepreneurial team and corporate management. Such interviews have been carried out by the research

group during the company visits in Italy to the SGR Rimini and in Bulgaria to the CityGas Company, and took

place on a monthly basis, lasting about two hours each, during the years of: 2009-2011 and 2012. The

interviews have been conducted with 10 corporate members (nine Italians and one Bulgarian) considered

important for the purpose of the research investigation. Among these, interviews have been addressed to the

president of the group, the chief financial officer, and managers directly or indirectly involved in SR

(environmental affairs department, accounting department, marketing department, and sustainability manager).

All the interviews were transcribed and compared with the interviewed members of the company.

The second source of data collection derives from the consultation of corporate websites and the analysis

of corporate documentation: decisions of the board of directors, internal communications pertinent to

sustainability, drafts of SR, corporate books regarding company history, leaflets and pamphlets relating to

initiatives promoted about the theme, and corporate publications relevant to the 50th anniversary of its

constitution. Furthermore, we participated in focus groups and round tables in the planning of initiatives aimed

at raising awareness on the theme of sustainability in schools, social and civic groups, and local institutions

including the chamber of commerce. Finally, we were able to directly observe the behaviour of the committee

for sustainability during workshops, seminars, and thematic conventions, in which we participated at the

planning and execution stages.

Besides, we must make it clear that though not yet being in the position of having data/documentary

information relating to the Bulgarian subsidiary (CityGas), which does not draw up an independent SR, the case

(see Section 4) has been developed by way of analysis of micro- and macro-economic data relating to the

institutional environment (internal and external institutional factors) of which CityGas is part, with the end aim

of examining the possibilities of the CityGas Company (Bulgaria) creating SR, consistent with the sustainable

reporting of SGR Rimini (Italy) using an adopted institutional approach. The reflexions which emerged from

the analysis focused, therefore, on one hand, on the possibility of development of the direction towards

sustainability in such a context, and on the other hand, on the obstacles and opportunities derived from

implementation of the tool represented by SR. The analysis is based upon economic and interpretational

indicators of the reference context.

SGR Group Profile

SGR Rimini is an unlisted mixed holding company based in Rimini (Italy), made up of several companies,

all of which are still family-owned.

In 1956, Aldo Domeniconi founded Società Gas Rimini S.p.A., the first company in the area dedicated to

the management and distribution of gas for heating and household use that in 1959 begins the development of

the distribution network of methane gas from the city to the province of Rimini with the most innovative plants

in Europe; these plants in 1970 were connected to the national methane gas pipeline SNAM. Since 1998, the

company has adopted the 9001 system for quality certification (upgraded to Vision 2000 and ISO 9001

standard in the following years), and in 2010, it obtained the ISO 14001 (Environmental Management System)

and the BS OHSAS (Occupational Health and Safety Management System) 18001 certifications.

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1076

In over 50 years of business activity, SGR Rimini has left a significant mark on the history of the

distribution and sale of methane gas in two central Italian regions: the Marches and Emilia Romagna. It has

grown steadily through acquisitions, the winning of tenders, and strategies for sector diversification.

In 2005, SGR went to Bulgaria (through an international tender adjudication) to construct a gas network

for domestic and industrial use in the region of Trakia. During its first three years, the subsidiary company

CityGas Bulgaria won three prestigious awards: award for its contribution to the energy sector; as a major

investor of the year in the energy sector; and the annual award for the energy sector. In 2010, SGR acquired the

company Technoterm Bulgaria and the project finance for the Trakia Project with European Bank for

Reconstruction and Development (EBRD)/BERS and Banca Intesa San Paolo. In 2006, SGR Group won the

“Milano Finanza Creatori di Valore” award.

In 2011, the group reached a turnover of over 251 million Euro, had 328 employees, and obtained a return

on investment (ROI) rate of 11.60% and return on equity (ROE) rate of 12.13%.

The figures and table below illustrate an SGR organisation chart of the holding and group subsidiaries (see

Figure 1), the business areas (see Table 2), and the municipalities served in Italy and Bulgaria (see Figure 2).

Figure 1. SGR Group: organisation chart of the holding.

Table 2

SGR Group Business Areas Distribution of natural gas

Sale of natural gas and electric energy Planning, construction, management, and maintenance of heating plants in condominiums for which they carry out heat management Energy service and district heating

Assembly of solar power plants and sources of renewable energy

Assembly and maintenance of heating and conditioning plants (for families, businesses, and large plants)

Assistance and domestic or company emergencies intervention available 24 hours a day

Global service technicians specialized in the gas sector even for assistance abroad

Utilities technology

Congress centre

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1077

Figure 2. SGR municipalities served in Italy and Bulgaria (2012).

SGR Reti is the company which manages the gas distribution network plants and is the holder of natural

gas supply licences. SGR Servizi is the company which manages sales relations with clients. Utilia is

responsible for creating and developing software package management systems and application modules,

specialized for the energy and utilities sectors. As mentioned above, CityGas is a Bulgarian company controlled

by SGR which was joined by Technoterm in 2010. In 2004, SGR signed an agreement with Hera, to which the

group ceded 20% of SGR Servizi. Hera is an Italian listed company among the national leaders of the sector,

for the joint procurement of bulk gas and the direct sale of electric energy. It also represents the closest best

practice in the sector and has influenced the implantation of SGR Group’s SR, being the territorial corporate

leader (for 10/15 years) as well as one of the most important players in the sector at a national level. The Hera

Group is a huge produce of a process of concentration generated by laws and the rationalisation of operators in

the sector. In its hugeness, caused by the combination of several companies taken over in time, lies its

managerial, coordination, organisational homogeneity, cultural and structural weaknesses, unlike SGR Group.

Before describing the process of implementation of SR in SGR Group, it is necessary to draw attention to

its mission and governance in which internal contingent factors are reflected that have influenced the decision of

introducing SR. The SR represents, in fact, an accountability tool that should be coherent with both the mission

and the governance (Matacena, 2010) as verified in the first step of the study (Baldarelli & Del Baldo, 2013).

The mission of SGR Rimini is structured around the following “milestones”: (1) the values profile of the

founders and the top management team; and (2) an attention to CSR, taking care of the surrounding area, the

local community and the environment, as well as the development of human resources, service, transparency

and social relations, and the centrality of dialogue with the stakeholders. The mission states that: “We are

known as an innovative and dynamic multi-utilities company, respectful of the environment which is greatly

tied to the territory and the community”. The company slogan draws on some of the most important values that

the company embodies: “My energy is local, loyal, and social”. Embeddedness and sense of belonging to the

local community, transparency, solidarity, respect for people, and attention to social and environmental issues

are expressed in the ethical code and attributable to the so-called “system of perennial values” (Catturi, 2007),

to which every other corporate value is connected. In particular, coherence is seen as a commitment to the

transfer of the values into everyday actions.

As gathered from the interviews and meetings with various internal stakeholders (marketing manager;

organisational, quality, safety, and environment managers), SGR puts ideas, strategies, and actions before two

questions: “Are we dealing with an effective answer as regards the evident or latent expectations of one or more

categories of stakeholders?” and “Are we dealing with a choice/action capable of consolidating/fostering the

competitive advantage of the company?”. Similarly, from interviews conducted with company heads, it is

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1078

evident how these values are experienced by the owners and managers and spread throughout the entire

organisation. In other words, they reinforce the group’s corporate culture, implying the anthropological culture

which is reflected in accountability (Gray, Dey, Owen, Evans, & Zadek, 1997). The values therefore constitute

the first level in the orientation towards sustainability, foster social cohesion, and favour a pathway shared by

various stakeholders which is summed up in the code of ethics and the SR.

Another feature of sustainability in the group’s mission is the emphasis placed on reciprocal trust,

transparency, and corporate reputation which are included among the cornerstone principles (see Figure 3).

SGR Group “wants to be the company of trust for its clients and the best place in which to work”.

Figure 3. SGR Group: cornerstone principles.

In an interview with the president of the group, Micaela Dionigi, values (humility, tenacity, determination,

spirit of sacrifice, and energy) emerge which have been inherited from the founders and interpreted by the

actual leader in coherence with the changed internal and external environmental context. Her relational

approach, founded upon a great capacity for listening and interacting, is translated into the principle of the

“door being open” to each collaborator. As she said during the interview: “From the beginning, I acted as a

friend”, and now “it is the company which acts as a friend”. “Before (but even now) we were and still are a

family”. The centrality of relations lies in the centrality of the person: “Over the years, the organization has

become less hierarchical and increasingly more orientated towards team work, aiming to seek a dynamic

balance between singular dimension and plural dimension” (Micaela Dionigi, SGR president).

From the interviews conducted with the sales manager of the group, it emerges that values contained in

the corporate mission are shared and embraced in the relationships among employees: professionalism,

dedication to work, simplicity in colleague relations, and reliability. The words of the chief financial officer

(CFO) testify that the example of the company owners is an authentic message which shapes action. Similarly,

interviews to other key figures in the company’s history have confirmed great entrepreneurial skills,

the solidity of the partners, the charisma and dynamism of the founder, Aldo Domeniconi, who laid down the

necessary conditions for the construction of a “personal” service, and the strong identification with the

surrounding territory. The importance of relationships comes from the past; going back 20-30 years into

the history of the group’s business activities, the supply of methane gas to the area and the country represents

a strong relationship with the territory. The centrality of relations is expressed in client orientation, as well

as in attention to the quality of service, safety, and orientation towards social responsibility and

eco-sustainability.

SGR has a “close” approach to the client, and this allows the company to “explain its business activity and

account for its profit” (CFO). When SGR developed the methane gas infrastructural network, potential clients

perceived the importance of its service, which marked an historic moment of change, like the one being

currently experienced in Bulgaria.

Transparency, integrity, efficiency, coherence, sustainability, personal responsibility, respecting and valuing

people, and quality of supplies and procurement

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1079

Due to the afore mentioned aspects (centrality of values and relationships, rootedness), the group can be

considered as a company “of the territory” (Del Baldo, 2010) which spreads the culture of sustainability

through a wide variety of initiatives and plays a central role (in collaboration with public and private operators

(universities, institutions, non-profit organisations, etc.)) which activates mechanisms of participation in the

socio-economic fabric and pathways to sustainable development aimed at the common good.

Following the description, we can potentially make some considerations that are involving all

mechanisms/structure of (neo-) institutional theory. We can find, in the liveliness and the need for closeness to

the surrounding area and the person, whether he be a customer or employee, a combination of the various

mechanisms which can be seen both in the external coercion due to competitiveness and in the presence of

sound values which orientate the same company thanks to the leadership (see Section 5). However, speaking of

the mission does not allow us to understand which directions such mechanisms take, so it is necessary to move

on to the analysis of the governance.

The SGR Group’s internal governance is composed by the board of directors, which involves five

members and has exclusive jurisdiction on defining the company and the group’s strategic lines and objectives,

including the policies of sustainability, and on the review and approval of the SR. The audit committee is a

collegial organ, nominated by the board of directors, and is made up of a president and two employees of the

group’s organisation and quality office. It was conceived as a listening channel and presides over the

functioning and observance of the organisation.

The decision-making process develops throughout the collegiate bodies within their established

competences. In the daily activity, on the contrary, the decision-making process is orientated by the president,

Michaela Dionigi, and the general director. The aspects relating to sustainability were included in the

duties of the communication and marketing office and of the quality, safety, environment, and sustainability

office.

The process of sustainability initiated by SGR influenced the micro-organisational processes and the

company structure. The CSR manager has existed for about three years. He collaborates and interacts, on a

daily basis, with other offices as well as with management, notwithstanding the direction of management which

does not establish rigid operational limits and which leaves room for individual initiative.

An SGR committee was intended at the design phase and has today been put into operation, subdivided

into areas, such as the coordination and dissemination of the culture of sustainability and social responsibility

organs. A specific “open letter” was inserted into the pay packet of every employee to spread and develop good

practices as well as to organise sustainable initiatives. Other initiatives are represented by the enhancement of

the weekly email to employees (“pills of sustainability”) through: messages of raising awareness throughout the

company; the creation of a database for the collection of data relating to economic, social, and environmental

dimensions; and the project for the study of stakeholder perception.

Since 2008, SGR has also adopted the code of ethics and the organisational model in accordance with the

Italian Legislative Decree 231/01. A company value charter is projected to be adopted.

The ethical code takes on a dual meaning: It represents the “constitutional charter” of the company; a

charter of moral rights and duties, which defines the ethical and social responsibilities of every participant of

the entrepreneurial organisation; and it constitutes a tool for governance and strategic management of the

company, identifying the duties of the company towards the stakeholders.

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1080

The adoption of the code of ethics has been based on a participative process, departing from its drafting

and constitution, reached via a fruitful and fair comparison, thus creating a codification process of the

behaviours of employees, managers, administrators, and collaborators based upon the will to cement the system

of legitimization of the company. In the comparison, the internal working group promoted a path of

stakeholders dialogue and stakeholders engagement that has permitted creating sharing around core values and

principles which constitute the essential traits of “SGR’s way of being”.

The fruits of this process can be “seen” in numerous tools and actions: the company notice board (“make

your voice heard”), the carrying on of dedicated relations events (for example, forums for technicians),

departmental meetings, meetings for those in charge of company operations (of an hour per day), interviews

with those responsible for the various, different areas (commercial area, technical area, and energy

savings/efficiency), annual meetings as well as a plenary one for the presentation of SR.

Stakeholders dialogue represents a means of comparison, negotiation, and acknowledgement of reciprocal

interests. Models of dialogue can be various: bilateral, multi-lateral (with every stakeholder individually, as is

now the case of SGR) or can assume the form of stakeholders network. The success of the stakeholder dialogue,

therefore, depends on both the wish of the company and the conviction of the stakeholders that it is not a matter

of pure rhetoric or manipulation. This model may be developed by the SGR Group in Bulgaria wherein a

network of relationships may be installed. Global strategies are often put to the test at a local level in the

convention the company wishes to transfer costs of competition nationwide.

The success of many companies continues to depend on their roots within the local area wherein they were

set up and developed thanks to positive stakeholder relationships which derive from the quality of human

capital (qualification of the manpower and specific work culture) as well as social capital (social cohesion,

institutional collaboration, informal networks among collective players, solidarity, and interpersonal trust).

In these cases, stakeholders dialogue represents a value-adding praxis of the social capital (Del Baldo, 2010).

Such a dialogue is linked to reciprocal trust.

To respond to and contemporise the stakeholders interests, SGR proceeded with their analysis, followed

by the stakeholders engagement plan, which includes diverse tools of consultation and communication.

Mention can be made of: intranet, accessible at all corporate levels; internet, accessible at several openings

levels; an internal blog; a newsletter; employee satisfaction questionnaires; informative brochures; company

notice boards; plenary meetings (once or twice a year); and company meetings for the offices with the

participation of management (monthly).

Democratic nature, trust, and a relational logic are aspects that have been put into motion in governing the

SGR Group, in that a participatory climate which spreads from the owners to every level of the company goes

together with the hierarchical structure of the various organs of the company organisation chart.

The decision-making process develops, combining participatory aspects to hierarchical decisions, though still

shared ones, which makes the leadership, close to the needs of everybody.

From an analysis of the minutes of the board of directors of Rimini Holding Spa, it is possible to identify

various phases which demonstrate how governance has developed the pathway towards sustainability. The most

important steps are listed in Table 3.

Therefore, the process of developing the SR finds a favourable environment in SGR, due to the attention

paid to social aspects (“open door” of the president, closeness to the needs of the employees in order to

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1081

reconcile working time with their families) and environmental aspects (attention paid to the saving of

non-renewable resources with the spreading of a culture for their preservation). The quality certifications,

which preceded the decision of implementing an SR, refined the business culture to the point of making a

document, in which this general “propensity” to sustainability is described, almost “necessary”.

Table 3

Rimini Holding Spa: Board of Directors’ Deliberations Date of summoning of the board of directors

Subject of deliberation

July 14, 2004 Participation in a tender for a licence of natural gas distribution and sale relative to the gas region of Thrace, in Bulgaria.

July 1, 2008 Approval of the Ethical Code and Organization, Management and Control Model formulated by the work group and appointed members of the relative Supervisory Committee (ex D.Lgs.231/01).

November 17, 2009 Confirmation of the Supervisory Committee for three years of 2009-2011.

March 30, 2010 Analysis of the project of the energy efficiency. Energy Efficiency Project relative to the conversion of the internal plants of national clients and potential Bulgarian clients of CityGas Bulgaria.

September 29, 2011 The company’s board of directors assesses the offers of assurance in the SR for the 3-year period of 2012-2014.

This determined the attribution of the duty to a new staff unit which was hired with a temporary contract

within the office which dealt with “quality and sustainability” with the primary duty of developing the SR

following the G3 lines. Afterwards, the contract was made permanent with the aim of spreading the culture of

sustainability within and outside the company. Moreover, during the introduction of the SR surfaced an amount

of work concerning the finding of data and information which leads the new employee to interact with all the

members of the business.

The figure of the CSR manager has been originated from 2010 and represents a “corporate presidium” of

sustainability, who collaborates and interacts on a daily basis with other offices and the management,

notwithstanding their tendency not to set rigid boundaries of activities and to allow the freedom of individual

initiative. The offices providing reference points are those of marketing and communication, quality, safety, and

sustainability. A committee is being set up for sustainable development, divided into areas and conceived as an

organ of coordination aimed at the diffusion of the culture of sustainability and social responsibility.

The new organisational function, which is separated from the previous one within which it was included

and which plays its very own role of autonomy, has become, in its turn, an area where training people can be

included in order to develop internal and external learning and synergies and introduce those innovations that

the company needs. In such a way, it becomes a “relational engine” for the stakeholders engagement, to which

it is operatively delegated in the company trying firstly to create those relational goods (based on internal and

external stakeholders dialogue) which should be at the basis of SR in a virtuous bi-directional circuit of

accountability-governance, which allows for some reflections also in terms of neo-institutional theory.

Once the characteristics of the company are defined, we can examine the process of sustainability

development in more detail.

The Process of Implementing the SR in SGR Group

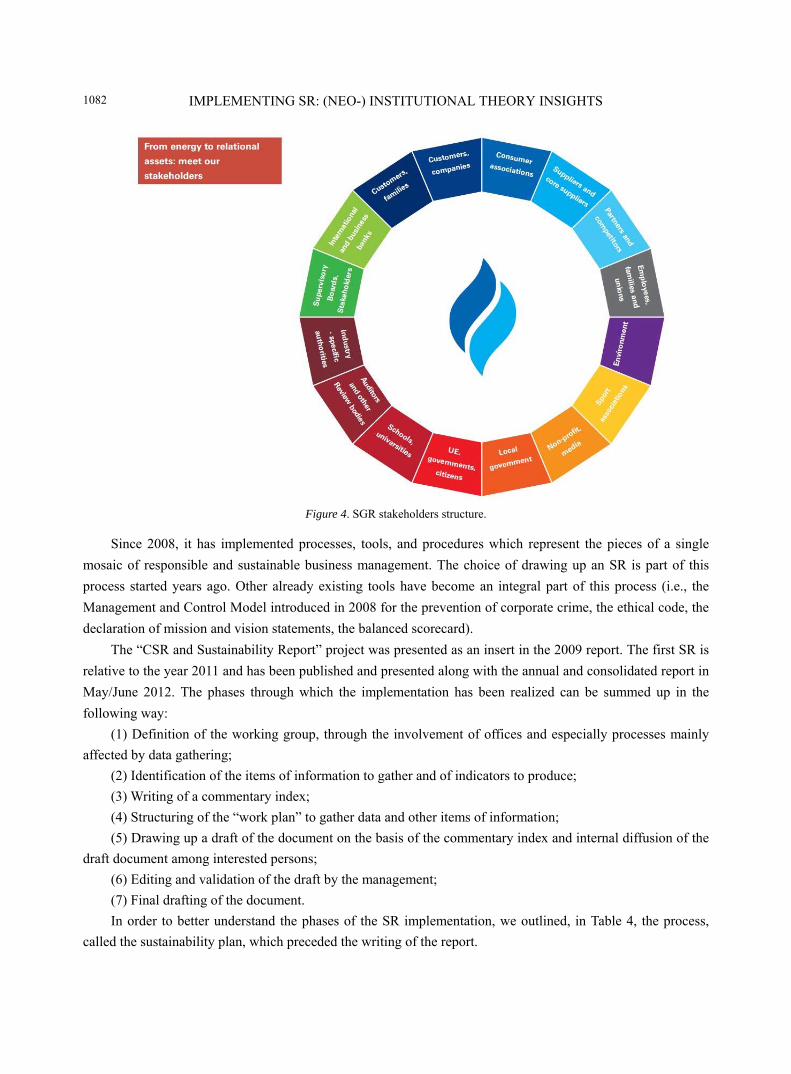

SGR Rimini has always considered CSR and sustainability an integral part of its mission, values, and

strategies and as the basis on which to build solid relations with its stakeholders (see Figure 4).

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1082

Figure 4. SGR stakeholders structure.

Since 2008, it has implemented processes, tools, and procedures which represent the pieces of a single

mosaic of responsible and sustainable business management. The choice of drawing up an SR is part of this

process started years ago. Other already existing tools have become an integral part of this process (i.e., the

Management and Control Model introduced in 2008 for the prevention of corporate crime, the ethical code, the

declaration of mission and vision statements, the balanced scorecard).

The “CSR and Sustainability Report” project was presented as an insert in the 2009 report. The first SR is

relative to the year 2011 and has been published and presented along with the annual and consolidated report in

May/June 2012. The phases through which the implementation has been realized can be summed up in the

following way:

(1) Definition of the working group, through the involvement of offices and especially processes mainly

affected by data gathering;

(2) Identification of the items of information to gather and of indicators to produce;

(3) Writing of a commentary index;

(4) Structuring of the “work plan” to gather data and other items of information;

(5) Drawing up a draft of the document on the basis of the commentary index and internal diffusion of the

draft document among interested persons;

(6) Editing and validation of the draft by the management;

(7) Final drafting of the document.

In order to better understand the phases of the SR implementation, we outlined, in Table 4, the process,

called the sustainability plan, which preceded the writing of the report.

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1083

Table 4

The Sustainability Plan of SGR Rimini Governance sustainability tools

Commitment Action

Promote the Management and Control Model (ex D.Lgs. No. 231), adopted in 2008

A Supervisory Committee was set up in every company of the group, in order to supervise and control the effectiveness, functioning, and observance of the model. Continuous training inherent to D.Lgs. 231/01 and the model. Publication of the Model 231 on the internet website (http://www.sgrservizi.it/2158/1/Home.html) and the company intranet.

Promote the group’s Ethical Code, adopted in 2008

Sharing the code: The SGR Group requested all those collaborating in company activities to bring their conduct in line with the practices outlined in the current code. Publication of the Ethical Code on the internet website (http://www.sgrservizi.it/2158/1/Home.html) and the company intranet.

Publish a single SR for the whole group in coherence with the initiatives of GRI

2011. Adoption of the SR covering all the dimensions: economic sustainability, social sustainability, and environmental sustainability.

Promote the SR and the culture of sustainability

2011. Numerous internal and external initiatives to promote the culture of sustainability: (1) Periodic meetings with the non-profit association “Children of the World” on the theme of CSR; (2) Collaboration with the University of Bologna, seat of Rimini, and the University of Urbino to deepen the theme of CSR and sustainability; (3) Support and external consultants to start up the process of the accountability of sustainability; (4) Creation of a CSR committee to monitor and stimulate sustainable practices within the company. By 2012. Presentation of the SR at the general assembly along with the presentation of the financial report. Inclusion of the SR, Ethical Code,and the Management and Control Model in the Welcome Kit handed out to new employees. By 2012. Promotion of the SR on the internet website (http://www.sgrservizi.it/2158/1/Home.html).

Note. Source: SGR Rimini Sustainability Report 2011 (http://www.sgrservizi.it/2158/1/Home.html).

What follows (see Table 5) is a summary of commitments, with reference to the diverse stakeholders’

categories.

Table 5

Summary of Stakeholders’ Commitments People (employees)

Commitment Action

Increase interviews with people

2005. Introduction of a survey on the internal climate and a questionnaire to assess satisfaction. The survey is carried out every year in the month of July. These are fundamental tools in the processes of continuous improvement and the involvement and development of employees. 2010. Area meetings to discuss the results of the survey and plan actions for improvement.

Increase the training and awareness of employees regarding the themes of safety, to reduce the frequency and gravity of industrial accidents

2010. Courses on safety for a total of 973 hours concluded.

Implement the training scheme and apply it to all members of the companies

2010. Training activities become increasingly important. The total number of training hours amounted to 10,441 taking into consideration both internal and external training (refresher courses, training, conventions, etc.).

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1084

(Table 5 continued) People (employees)

Commitment Action

Develop activities to reconcile life and work

2010. Two questionnaires were attached to employees’ paychecks to assess the feasibility of extra courses beyond working hours and verify the degree of interest expressed in the project of life and work reconciliation promoted by legislation number 53/00.

Increase internal communication

By 2011. Restyling company intranet and provision of an area dedicated to sustainability, which allows members to send suggestions and advice about improving corporate sustainability. 2011. The Mia Voce Project: setting-up of a wall at the Rimini seat dedicated to employees’ messages. Each month, in agreement with the management, a theme is proposed and employees can express their opinions about it. Plenary meetings, which generally take place once or twice a year.

Diffusion of the culture of sustainability and a corporate atmosphere based on shared values

2011. Initiatives regarding information and awareness about sustainability aimed at internal and external members of the group.

Clients and suppliers

Commitment Action

Define systems of periodic surveys to assess the degree of client satisfaction

Half-yearly interviews conducted by the authorities for electric energy and gas. A project to develop internal interviews has been launched and carried out to clients who have had recent dealings with the companies of the SGR Group.

Maintain and develop the activity of information aimed at saving energy and protecting the environment and safety

2010. Distribution of Water Conservation Kits to clients made up of hydraulic dampers and low-energy fluorescent light bulbs.

Promotion of energy efficiency in the final uses 2010. Making end-users aware of responsible energy consumption. Promoting respect from suppliers for the principles which have inspired the organisational model of the SGR Group

2011. Requested adhesion to the same principles which inspired the group’s Management and Control Model.

Support where possible the development of purchasing processes with features of eco-sustainability

The diffusion of electronic negotiation tools to replace, where possible, traditional paper-based processes.

Define and promote supplier assessment systems 2011. The launch of the development of a project for supplier assessment.

The environment

Commitment Action

Adopt new guidelines and procedures of the group relative to environmental management

2010. The start of work procedures from the attainment of the following certifications: (1) ISO 14001 Environmental Management System; (2) BS OHSAS 18001 Health and Safety Management Systems.

Increase the activity of awareness about energy saving use

2011. “M'illumino di meno”. National initiative aimed at making people aware of an intelligent use of electric energy in which the SGR Group participated through a symbolic action: with a gift token of onelow-energy consumption light bulb + a handbook of good daily habits. Raising awareness about the use of alternative energy sources. 2011. Relations with schools were strengthened through the organisation and promotion of the theme of energy efficiency. Progetto ERRE, which stands for renewable energy and emission reduction, was promoted by the Council of Rimini.

Rationalize energy consumption in Bulgaria by developing a project of energy efficiency

2011. CityGas Bulgaria becomes the official representative in the country in raising awareness on the theme of energy saving and energy efficiency through a communication campaign. The message is the development of a culture of respect for the environment through the reduction of current polluting heating systems.

Institutions and communities of reference

Commitment Action Make channels of communication coherent and transparent, drawing inspiration from the values of sustainable development and the participation demands of all interlocutors (clients, suppliers, employees, and territory)

2011. “La mia energia è…” institutional publicity campaign:(1) new SGR services website; (2) creation of sales leaflets, 2011 calendar and 2011 diary; (3) creation of company profile; (4) new layout of clients’ offices; and (5) sales letters. Creation of information areas within the bill.

IMPLEMENTING SR: (NEO-) INSTITUTIONAL THEORY INSIGHTS

1085

(Table 5 continued) Institutions and communities of reference

Commitment Action

Promotion of a dialogue with local, national, and international institutions

2011. Collaborative relations with public institutions on a national and international scale. Proactive role in the sector and multi-sector to promote themes of sustainability. Energy Efficiency Project in Bulgaria with the EBRD and the Ministry of Bulgaria. CityGas Bulgaria becomes the spokesbody for raising awareness in the country on the theme of energy saving and efficiency through a widespread campaign of communication aimed at developing a culture of respect for the environment by means of reducing current polluting heating systems. The average natural gas consumption per capita in Bulgaria is 2.5 times lower than the European Union (EU)average.

Management of plants in the territory and protection of the biodiversity of the landscape

Improvement and conservation of the natural heritage in areas in which there are plants or green areas near plants (Progetto Natura 2000,http://www.natura.org/).

Support to the community Commitment to the growth and development of territories through the support of initiatives, social, cultural, and sports events (Some examples are given in the right-hand column)

2010. Special recognition given to Micaela Dionigi, chairman of the SGR Group: for the quality of the hosted internships, from Uni Rimini(company consortium for the university in the Rimini area) and for the sensitivity shown in the support of better healthcare for everyone, from Ausl Rimini. 2011. Economic contribution towards the acquisition of two buses to transport the disabled and elderly and schoolchildren. Economic contribution towards the acquisition of garden games for the nursery school. Economic contribution in favour of the health authority of Rimini for the purchase of a multi-layer CT scanner and van for mammogram screenings. Economic contribution to the Istituto Oncologico Romagnolo. Purchase of a defibrillator placed inside the congress structure. Economic contribution to numerous cultural initiatives including “International Study Day” of Pio Manzù and the painting exhibition “Paris. The marvellous years. Impressionists against the Salon as well as Caravaggio and other 17th century painters” and the Plautine feasts. Economic contribution in favour of Crabs, the basketball team of Rimini and numerous other sports associations. Economic support of events promoted and organised by the towns of Rimini, Sarsina, San Leo, Gabicce, Coriano, Talamello, and Pietrarubbia.Other initiatives: Rimini Onlus Solidale, Progetti Tanzania e Bangladesh, and Noi e l’arte.

Collaborations with the university

2011. Inauguration at the SGR congress centre of the new Rimini seat of Bocconi Alumni Association (BAA), to promote initiatives forvalues gained to benefit various professional families operating in our area. Dialogue with all the institutions operating in the territory (confederation of industry, universities, the Council of Rimini, the province of Rimini, foundations and other cultural associations, high schools, local and non-local banks, other sector associations, etc.) with the aim of bringing, even to the province, events and informative debates which give rise to comparison and stimulation and which are usually more common in city areas. Collaboration with the University of Bologna, the seat of Rimini, and the University of Urbino to deepen the themes of sustainability. Collaboration with the junior schools, the University of Bologna, the seat of Rimini, and other educational bodies in work-related learning projects.

1086

The d

Italian Stud

analysis of

expectation

The applica

Partic

and 6), as

contributed

1.1

200

201

201

IMPL

document con

dy Group for

f the relation

ns, is singled

ation level of

cular attention

a standard of

d either direct

17%0.69%

0.99%

Collectivity

09

10

11

To

LEMENTING

nsists of six se

r Social Repo

ns with stake

d out in the a

f the guidelin

n has been gi

f measuring t

tly or indirect

F

Figure 6

39.20%40.99%

31.6

Company

otal Value Adde

G SR: (NEO-

ections drawn

orting (GBS,

eholders and

ccountability

es has been v

ven to the de

the wealth pr

tly to its activ

Figure 5. SGR G

6. SGR Group: a

6.48% 6.62

61%

Shareho

2

€ 32,

ed to the territo

-) INSTITUT

n up in confo

2007). The

for directing

y standard AA

verified by a c

etermination a

roduced and d

vity.

Group: added-v

added value dis

1.61%

2%8.63%

lders B

2009 2010 2

€ 41,553,0

,271,968

€ 40,287,87

€ 38,735,218

TT

ory

TIONAL THE

ormity with th

reference mo

g the compan

A1000 Accou

consultancy f

and distributi

distributed by

value distributio