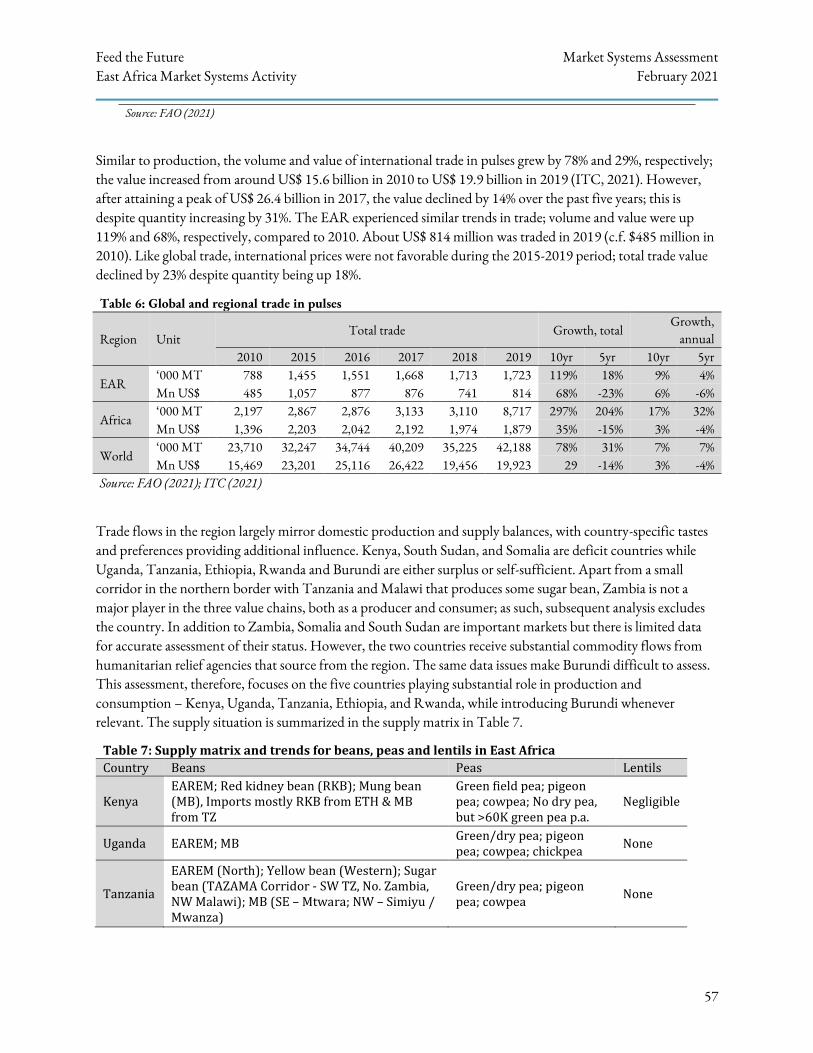

iTABLE OF CONTENTS - USAID Policy LINK Program

85

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021 1 i TABLE OF CONTENTS Cereals .......................................................................................................................................................... 3 1. Value Chain Overview and Market Segments ................................................................................ 3 1.1. Value Chain Actors ................................................................................................................................3 1.2. Target Cereal Crops ...............................................................................................................................5 2. Overview of Current Trade Flows .................................................................................................. 8 2.1. Cereal Trade Flows by Crop ..................................................................................................................9 2.2. Main Corridors for Cross-border Trade in Cereals ........................................................................... 11 2.3. Cereal Exports from East Africa ......................................................................................................... 13 3. Regional Growth Potential ........................................................................................................... 14 4. Constraints Analysis ...................................................................................................................... 17 4.1. Production Systems ............................................................................................................................. 17 4.2. Market Access and Market information ............................................................................................ 21 4.3. Technology and Inputs ....................................................................................................................... 25 4.4. Transport and Logistics ...................................................................................................................... 27 4.5. Access to Finance................................................................................................................................. 27 4.6. Processing and Value Addition........................................................................................................... 29 4.7. Policy Constraints ............................................................................................................................... 30 4.8. Political Economy Constraints ........................................................................................................... 35 4.9. Constraints on Women’s Participation in the VC ............................................................................ 36 4.10. Constraints on Youth Participation in the VC ............................................................................. 37 5. Opportunities ................................................................................................................................ 38 6. Appendix 1 ..................................................................................................................................... 45 Legumes...................................................................................................................................................... 48 1. Value Chain Overview and Market Segments .............................................................................. 48 1.1. Production Structure .......................................................................................................................... 48 1.2. Inputs Supply Structure ...................................................................................................................... 49 1.3. Marketing Structure ............................................................................................................................ 49

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of iTABLE OF CONTENTS - USAID Policy LINK Program

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

1

iTABLE OF CONTENTS

Cereals .......................................................................................................................................................... 3

1. Value Chain Overview and Market Segments ................................................................................ 3

1.1. Value Chain Actors ................................................................................................................................3

1.2. Target Cereal Crops ...............................................................................................................................5

2. Overview of Current Trade Flows .................................................................................................. 8

2.1. Cereal Trade Flows by Crop ..................................................................................................................9

2.2. Main Corridors for Cross-border Trade in Cereals ........................................................................... 11

2.3. Cereal Exports from East Africa ......................................................................................................... 13

3. Regional Growth Potential ........................................................................................................... 14

4. Constraints Analysis ...................................................................................................................... 17

4.1. Production Systems ............................................................................................................................. 17

4.2. Market Access and Market information ............................................................................................ 21

4.3. Technology and Inputs ....................................................................................................................... 25

4.4. Transport and Logistics ...................................................................................................................... 27

4.5. Access to Finance ................................................................................................................................. 27

4.6. Processing and Value Addition........................................................................................................... 29

4.7. Policy Constraints ............................................................................................................................... 30

4.8. Political Economy Constraints ........................................................................................................... 35

4.9. Constraints on Women’s Participation in the VC ............................................................................ 36

4.10. Constraints on Youth Participation in the VC ............................................................................. 37

5. Opportunities ................................................................................................................................ 38

6. Appendix 1 ..................................................................................................................................... 45

Legumes...................................................................................................................................................... 48

1. Value Chain Overview and Market Segments .............................................................................. 48

1.1. Production Structure .......................................................................................................................... 48

1.2. Inputs Supply Structure ...................................................................................................................... 49

1.3. Marketing Structure ............................................................................................................................ 49

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

2

1.4. Processing Structure ............................................................................................................................ 52

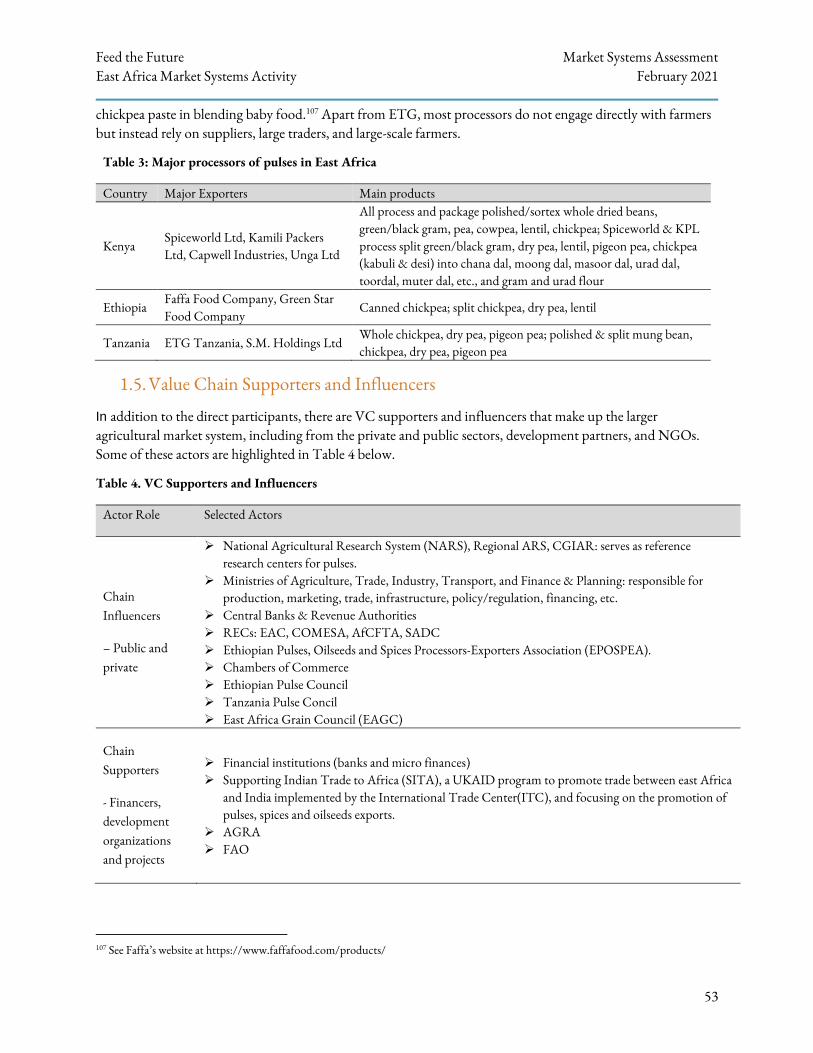

1.5. Value Chain Supporters and Influencers ........................................................................................... 53

2. Overview of cu©rrent trade flows ................................................................................................. 54

2.1. Sources of Supplies and Global Trade ................................................................................................ 54

2.2. Legumes Exports ................................................................................................................................. 58

2.3. Intraregional Trade in Grain Legumes ............................................................................................... 58

3. Regional Growth Potential ........................................................................................................... 61

4. Constraints Analysis ...................................................................................................................... 63

4.1. Production Systems ............................................................................................................................. 63

4.2. Prevalence of Pests and Diseases ......................................................................................................... 63

4.3. Market Access and Market Information ............................................................................................ 64

4.4. Market Infrastructure ......................................................................................................................... 65

4.5. Transport and Logistics ...................................................................................................................... 66

4.1. Access to Technology and Inputs....................................................................................................... 66

4.2. Access to Finance and Investment ...................................................................................................... 67

4.3. Policy Constraints to Cross-border Trade ......................................................................................... 69

4.4. Political Economy of Legumes Markets ............................................................................................. 72

4.5. Constraints to Participation of Women and Youth in the VC......................................................... 72

5. Opportunities ................................................................................................................................ 74

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

3

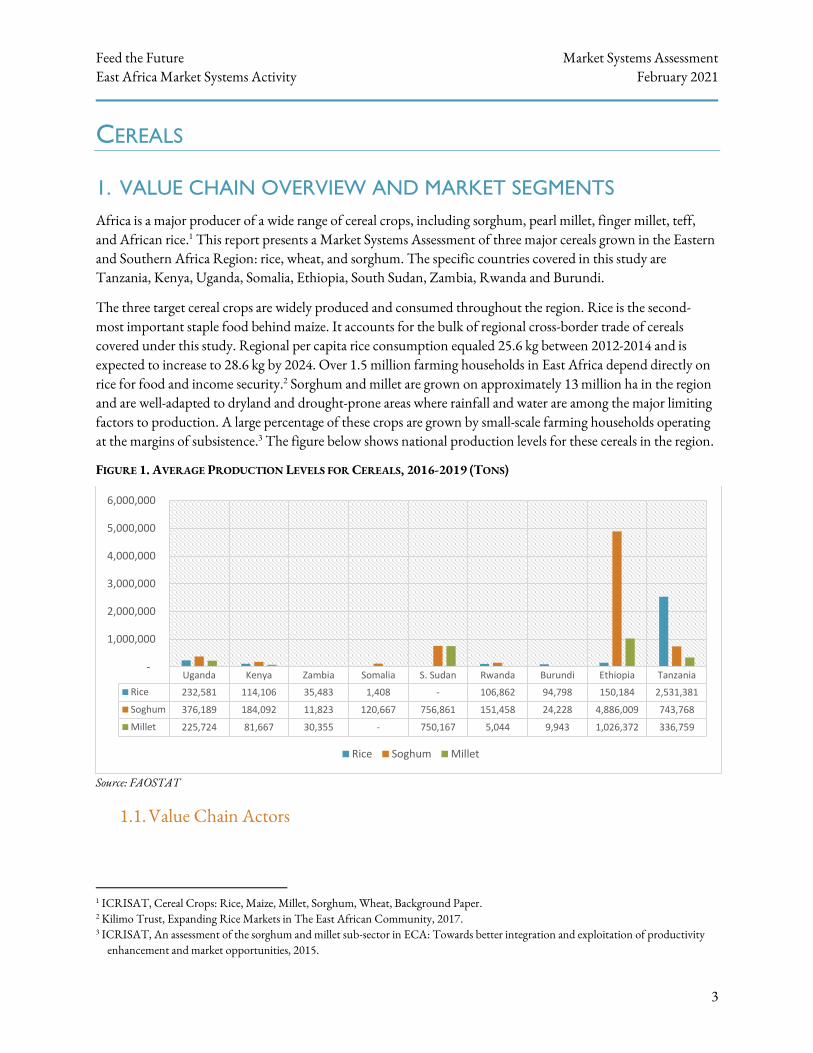

CEREALS

1. VALUE CHAIN OVERVIEW AND MARKET SEGMENTS

Africa is a major producer of a wide range of cereal crops, including sorghum, pearl millet, finger millet, teff, and African rice.1 This report presents a Market Systems Assessment of three major cereals grown in the Eastern and Southern Africa Region: rice, wheat, and sorghum. The specific countries covered in this study are Tanzania, Kenya, Uganda, Somalia, Ethiopia, South Sudan, Zambia, Rwanda and Burundi.

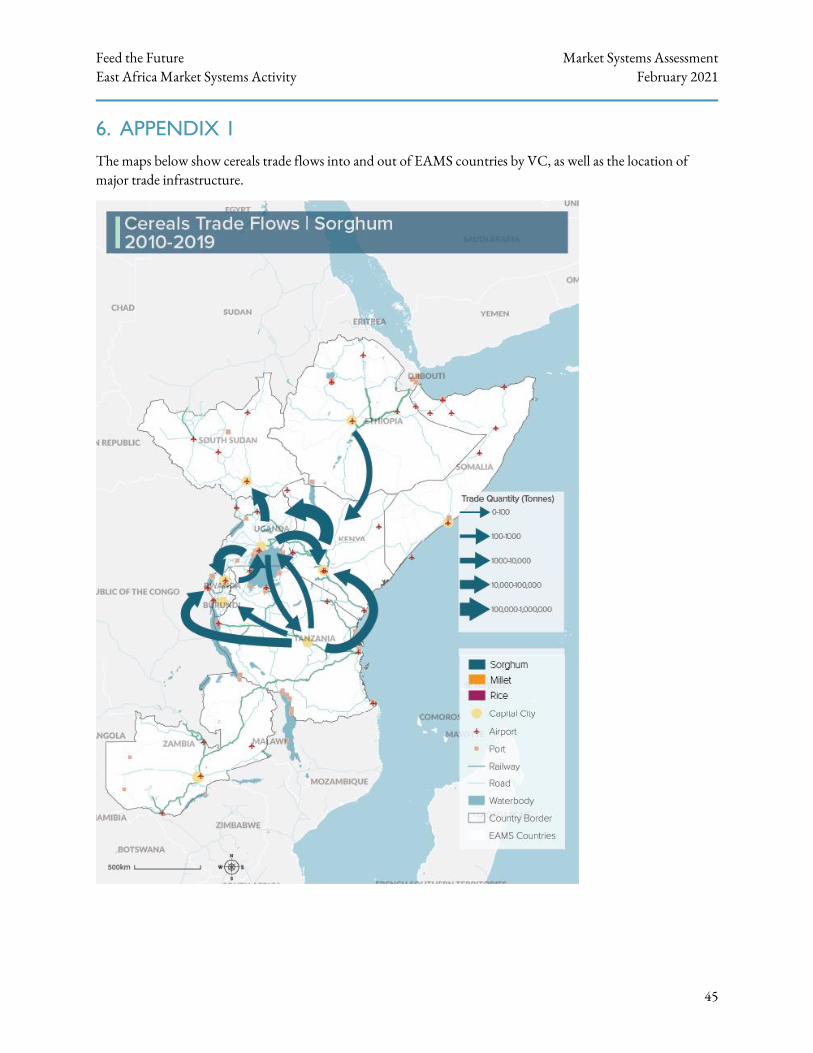

The three target cereal crops are widely produced and consumed throughout the region. Rice is the second-most important staple food behind maize. It accounts for the bulk of regional cross-border trade of cereals covered under this study. Regional per capita rice consumption equaled 25.6 kg between 2012-2014 and is expected to increase to 28.6 kg by 2024. Over 1.5 million farming households in East Africa depend directly on rice for food and income security.2 Sorghum and millet are grown on approximately 13 million ha in the region and are well-adapted to dryland and drought-prone areas where rainfall and water are among the major limiting factors to production. A large percentage of these crops are grown by small-scale farming households operating at the margins of subsistence.3 The figure below shows national production levels for these cereals in the region.

FIGURE 1. AVERAGE PRODUCTION LEVELS FOR CEREALS, 2016-2019 (TONS)

Source: FAOSTAT

1.1. Value Chain Actors

1 ICRISAT, Cereal Crops: Rice, Maize, Millet, Sorghum, Wheat, Background Paper. 2 Kilimo Trust, Expanding Rice Markets in The East African Community, 2017. 3 ICRISAT, An assessment of the sorghum and millet sub-sector in ECA: Towards better integration and exploitation of productivity

enhancement and market opportunities, 2015.

Uganda Kenya Zambia Somalia S. Sudan Rwanda Burundi Ethiopia Tanzania

Rice 232,581 114,106 35,483 1,408 - 106,862 94,798 150,184 2,531,381

Soghum 376,189 184,092 11,823 120,667 756,861 151,458 24,228 4,886,009 743,768

Millet 225,724 81,667 30,355 - 750,167 5,044 9,943 1,026,372 336,759

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Rice Soghum Millet

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

4

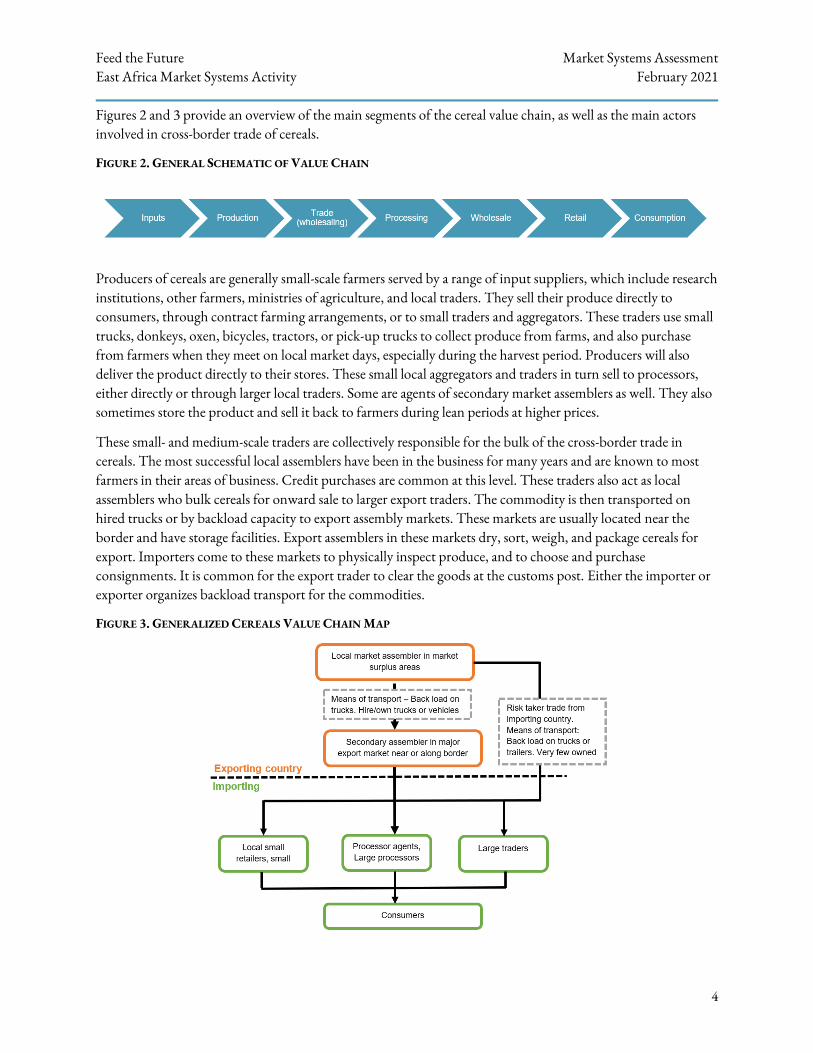

Figures 2 and 3 provide an overview of the main segments of the cereal value chain, as well as the main actors involved in cross-border trade of cereals.

FIGURE 2. GENERAL SCHEMATIC OF VALUE CHAIN

Producers of cereals are generally small-scale farmers served by a range of input suppliers, which include research institutions, other farmers, ministries of agriculture, and local traders. They sell their produce directly to consumers, through contract farming arrangements, or to small traders and aggregators. These traders use small trucks, donkeys, oxen, bicycles, tractors, or pick-up trucks to collect produce from farms, and also purchase from farmers when they meet on local market days, especially during the harvest period. Producers will also deliver the product directly to their stores. These small local aggregators and traders in turn sell to processors, either directly or through larger local traders. Some are agents of secondary market assemblers as well. They also sometimes store the product and sell it back to farmers during lean periods at higher prices.

These small- and medium-scale traders are collectively responsible for the bulk of the cross-border trade in cereals. The most successful local assemblers have been in the business for many years and are known to most farmers in their areas of business. Credit purchases are common at this level. These traders also act as local assemblers who bulk cereals for onward sale to larger export traders. The commodity is then transported on hired trucks or by backload capacity to export assembly markets. These markets are usually located near the border and have storage facilities. Export assemblers in these markets dry, sort, weigh, and package cereals for export. Importers come to these markets to physically inspect produce, and to choose and purchase consignments. It is common for the export trader to clear the goods at the customs post. Either the importer or exporter organizes backload transport for the commodities.

FIGURE 3. GENERALIZED CEREALS VALUE CHAIN MAP

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

5

Source: FEWSNET

Although some exporters and importers develop lasting partnerships, the main determinant of trade is quality and price. Importing traders mostly sell their commodities at wholesale prices to large traders for onward sales to processors or small retailers, some of whom also act as small millers. Large processors are typically supplied with high quality commodities directly from importers, or indirectly through other large traders.

Brokers are also increasingly active along the Kenya, Tanzania, Uganda, and Rwanda borders as a result of customs harmonization processes. These brokers operate as intermediaries or commission agents in the exchange of grain between wholesalers. They are primarily engaged in setting daily spot prices and matching buyers and sellers in what would otherwise be a time-consuming search process. Because they have the trust of their clients, brokers act as inspectors and witnesses to each transaction and guarantee that the contract will be enforced. Several brokers are also providing services related to export-import trade such as drying, sorting, arranging transport services, loading, etc. Traders’ dependence on brokerage varies across regions, but relations between traders and brokers are generally long-term, with repeated interaction. More traders in surplus regions indicate regular use of brokerage and tend to work exclusively with a single broker.

End-buyers in the value chain include brewery companies, millers, stock feed manufacturing companies, biofuel manufacturers, and other processors. Recent contract farming opportunities presented by companies such as the East African Breweries (EABL) have triggered many stakeholders to invest in value chain development focusing on the production side of the value chain. However, there is a limited number of large players, and few stakeholders have invested in promotion of value-added products to date.

1.2. Target Cereal Crops

Cereals are consumer goods, and consumption levels vary significantly both between countries and rural and urban areas within countries, depending on population and corresponding purchasing power. The following three target crops were chosen based on their potential for value addition, contribution to food security, increased incomes, and expectations of increased demand due to urbanization and population growth. The following section describes regional consumption trends for each crop, and uses FAOSTAT and ICRISTAT data on current population levels, per capita consumption, and GDP growth to provide rough estimates of projected demand by 2024.

Rice

Regional demand for rice was an estimated 3.12M kgs in 2019 and is estimated to grow at an annual rate of 1.03%, reaching 3.6M kgs by 2024. Consumption levels are concentrated in less arid areas of the region, and are generally higher in urban centers compared to in rural areas. Though much rice is consumed in the traditional manner, there are also many opportunities for value addition. For example, rice bran is one of the most highly demanded rice by-products for manufacture of livestock, poultry, pig, and fish feed due to its high protein, oil, and digestible carbohydrates content.4 However, regional processors of animal feed are unable to procure the

4 Ruiz, B. (2016, June 15). Stabilized rice bran for poultry feeding. Retrieved March 25, 2018, from WATTAgNet.com:

https://www.wattagnet.com/articles/27289- stabilized-rice-bran-for-poultry-feeding

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

6

required volumes of rice bran due to limited supply of raw materials for manufacture of animal feed. In Kenya and Tanzania, the average supply deficit is 41% and 36%, respectively.5

Broken rice is also used in the regional brewery industry, both as a main ingredient (as with Congolese beer) or as an ‘adjunct’ grain to make beers lighter and produce a dry, clean taste.6,7 The EAC Customs Management Act allows the manufacturers to import broken rice for the brewery industry at a duty rate of 0% under the Duty Remissions Scheme, which has facilitated cross-border trade for this purpose.8 Broken rice is also used in the confectionary industry to make doughnut cakes (Vitumbua), rice cakes (Mkate wa Sinia), and as a substitute for wheat.

Finally, use of rice by-products such as rice husks, hulls, and straws is growing but is still largely unexploited in the EAC. Rice husks can be used to make briquettes for construction as well as domestic and industrial cooking and heating.9 In Rwanda, for example, the company STRAWTEC utilizes rice straws to make straw panels for the construction industry. And in Tanzania, Kilombero Plantations Limited (KPL) has a gasification plant that utilizes rice husks to generate electricity, while Mamboleo Farm Limited (MFL) has a locally built gasifier and is experimenting with production of stones from ash, as well as ash for cement substitution.10,11

Sorghum

In 2019, estimated regional demand for sorghum was 6.37M kgs. This is projected to grow to 8.2M kgs by 2024, an increase of 1.05% per year. In general, sorghum is more commonly consumed in rural areas, with urban demand mainly concentrated in areas close to production. It is grown primarily for food and consumed in a variety of forms that vary from region to region. In general, it is consumed as whole grain or processed into flour, from which traditional meals such as injera (Ethiopia) and ugali uji (Tanzania) are prepared.12

Additionally, new value-added/processed food products for human consumption are emerging such as popped sorghum, biscuits, simple cakes, cookies and instant soft porridge such as Morvite, a product of King Food in South Africa. Morvite is a pre-cooked sorghum dry powder with added vitamins that is prepared by adding either hot or cold water or milk to make a breakfast porridge or beverage.13

5 Kilimo Trust. (2017 B). Characteristics of markets for animal feeds raw materials in the East African community: Focus on maize bran

and sunflower seed cake. Kampala, Uganda: Kilimo Trust. 6 Eddings, B. (2018, March 5). Why some Brewers use rice or corn in their beer. 7 Rikolto VECO. (2017, June 7). Congolese rice farmers conquer the local market. Retrieved March 25, 2018, from Rikolto VECO:

https://www.rikolto.org/en/project/ Congolese-rice-farmers-conquer-local-market 8 EAC. (2006). Agriculture and rural development strategy for the East African Community. Arusha, Tanzania: EAC Secretariat. 9 Kabeja, B. B. (2016, January 2). STRAWTEC brings its green building technology to Rwanda. Retrieved March 25, 2018, from

CLEANLEAP: http://cleanleap.com/ strawtec-brings-its-green-building-technology-Rwanda 10 Klaus, T. (2017). Setting up value chains with rice husk and polish. 11 -ibid-.

12 Wambugu, S. M (2011). Increasing Sorghum Utilization and Marketability Through Food Products Diversification. Kenya industrial Research and Development Institute, Nairobi, Kenya. 31pp.

13 Taylor, J. R. N. (2003). Overview: Importance of sorghum in Africa. In: Proceedings of the Workshop on the Proteins of Sorghum and Millets: Enhancing Nutritional and functional properties for Africa. (Edited by Belton, P. S. and Taylor, J. R. N.), 2 – 4 April 2003, Pretoria, South Africa. 21pp

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

7

Sorghum is also processed into a variety of non-alcoholic drinks, such as Togwa in Tanzania, as well as alcoholic drinks such as various beer products produced throughout the region.14,15 Demand for traditional beers such as chibuku and Mwamba in Burundi, Zambia, Rwanda and Tanzania has increased in recent years, particularly in the rural areas. All countries in the region except for Ethiopia produce sorghum beer commercially.16 In addition, the Heineken Group recently increased the manufacturing of beer from locally sourced sorghum in Rwanda and Burundi.

Sorghum is also used for livestock feed. In East Africa, residual crop grazing is the major mode of utilization of sorghum straw to help maintain animal live weight, especially during dry seasons. Other methods of utilization of straw involve stalk feeding of supplemented treated or non-treated straw.17 With increased use of sorghum grains in breweries and milling industries, more by-products are becoming available for livestock use for poultry, rabbits, pigs, and ruminants. In poultry feed, sorghum cultivars with low tannins and that are less susceptible to molds have been used as alternative feeding material to maize.18 Poultry feed trials have shown that sorghum can replace maize completely in poultry feed especially in broilers in terms of growth rate, livability, egg production, and weight.19

Millet

Across the region, millet is widely recognized by consumers as a nutritious cereal. Its exceptionally high calcium content makes it an important food for pregnant women, nursing mothers and children. Demand for millet increasingly exceeds supply, and is expected to grow 1.06% per year from 1.88M kgs in 2019 to 2.49M kgs in 2024. As with sorghum, millet is consumed mainly in rural areas or urban centers close to production. It is a high-quality subsistence food crop: its small grains can be stored safely for many years without spoilage, and are an excellent dietary source of calcium, iron, manganese, and methionine, an amino acid lacking in the diets of hundreds of millions of the poor who live on starchy foods such as cassava, plantain, polished rice, and maize meal. Millet is also productive in a wide range of environments and growing conditions throughout the middle-elevation areas of the region.

There has been growing demand for millet from urban, middle class consumers, particularly for millet flour, for which demand is growing at 10% per year. A growing number of small, medium, and large commercial grain millers and processors in East Africa each mill 10–800 tons of millet per month, producing both pure millet flour or composite flour and porridge mixtures, mainly for the domestic market. It is primarily consumed as a thick porridge known as ugali, and as a thin porridge known as uji. It is estimated that potential utilization of millet flour will reach 169,000 t/year by 2025, fueled mainly by its status as a “smart food” desired by health-conscious consumers that have sufficient disposable income to afford processed and specialty food products. It

14 URT/PMO/RALG (2012). Kondoa District Social-Economic Profile, and Progress Report on Sorghum Production. United

Republic of Tanzania, Kondoa 15p 15 Dendy, D. V. N. (1995). Sorghum and Millet: Production and Importance. American Association of Cereal Chemistry, St. Paul, USA.

80pp 16 Mackintosh, I, and Higgins, B. 2004 The development of a sorghum-based lager beer in Uganda: A model of cooperation between

industry and government in the development of local ingredients for the production of a quality lager beer and consequential benefits for the parties involved, Aspects of Applied Biology 72: 235-245.

17 ICRISAT (2004). Sorghum. A Crop of Subsistence. International Crop Research Institute for Semi-Arid Tropics, Patencheru Andhra, India. 101pp.

18 Smith, S. E. (2010). What is sorghum? [http://www.wisegeek.com] site visited on 21/10/2013 19 Tulasi, S. L., Rajashekhe, A. R., Raghunadha, R. G., Prasad, V. L. K. Rao., P. P. and Ramachandraiah, D. (2004). Performance of

broilers on sorghum-based diets. International Sorghum and Millets 45: 37 – 40

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

8

also has excellent malting properties and is used to make local beers. Therefore, there is great potential for further product diversification. Furthermore, the high nutritional quality and gluten-free characteristics of millet flour offer potential for export to Europe, the United States, and other markets where the demand for gluten-free products is increasing.20

2. OVERVIEW OF CURRENT TRADE FLOWS

Cereals make up a substantial percentage of total regional exports and imports between East African nations. The magnitude of this cross-border trade differs by country and commodity type. To illustrate trade flow levels and trends, we have used four-year data series from the ITC-TRADEMAP Database to derive average annual estimates for cross border trade based on available trade data.21

The table below presents an overview of the magnitude (trade value in US$) and breakdown of regional trade in the targeted cereals by country. Overall, there is huge deficit of rice across the region except for Tanzania which has a positive trade balance. For the case of sorghum and millet, only Tanzania and Uganda have positive trade balance. It should be noted that this data only represents trade conducted within the region. Furthermore, the data does not capture informal trade, which may underrepresent the magnitude of the product flowing across regional borders. A significant proportion of cross‐border intra-EAC trade is conducted informally and equates to approximately 40% of GDP in African countries.

TABLE 1. CROSS BORDER TRADE (FIVE-YEAR AVERAGE 2016-2019) – US$ 000”

Tanzania Kenya Uganda Rwanda Burundi Zambia Ethiopia Somalia S. Sudan Rice

Imports

2.4

1,359.0

17,821.0

6,997.2

1,653.8

23.0 - - -

Exports

27,663.6

27.8

139.8

1.8

0.4 NA - - - Trade Balance

27,661.2

(1,331.2)

(17,681.2)

(6,995.4)

(1,653.4) - - - -

Sorghum

Imports

529 1,615 1,247 4,906

92 0 NA 316 4,000

Exports

3,463

123

4,772

0

31 - NA - - Trade Balance

2,934

(1,492)

3,525

(4,906)

(61) - -

(316)

(4,000)

Millet

Imports

8

9,317

15

73

142 - - 7 147

Exports

809

153

8,587

-

7 - - - - Trade Balance

801

(9,164)

8,572

(73)

(135) - -

(7)

(147)

20 Integrated sorghum and millet sector for increased economic growth and improved livelihoods in Eastern and Central Africa

Proceedings of the ECARSAM Stakeholders Conference 20–22 November 2006, Dar es Salaam, Tanzania, 2012. 21 The linear correlation between trade volume and value is a justification for using trade value information (data) as a proxy for traded

volume.

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

9

Source: Computed from ITC-TRADEMAP Database

Analysis from FAOSTAT to compare total volume of trade (including intraregional trade) shows that, overall, the region is a net importer for cereals.

TABLE 2. TOTAL TRADE VOLUME (FIVE-YEAR AVERAGE 2016-2019) – IN TONS

Tanzania Kenya Uganda Rwanda Burundi Zambia Ethiopia Somalia S. Sudan

Rice

Imports

43,111.20 581,653 36,676 80,206 154 10,105 292,610 377,506 12,836

Exports

6,518.20 202 9,673 31,829 - 2,528 15 - 5 Surplus/ deficit (36,593.00) (581,451.20) (27,002.60) (48,376.80) (154.20) (7,577.00) (292,594.80) (377,505.80)

(12,831.20)

Sorghum

Imports 634 133,261 17,011 27,973 633 828 634.2 70,539 92,281

Exports 7,859 65,845 79,789 1,437 22 231 7,859 7 - Surplus/ deficit 7,224.60

(67,416.00) 62,777.80 (26,535.60) (611.40) (597.40) 7,224.40 (70,532.20)

(92,281.00)

Millet

Imports 55 27,899 45 224 32 6 1 - 103

Exports 1,704 58 7,651 - - 17 - 14 4 Surplus/ deficit 1,648.80

(27,840.40) 7,605.80 (223.60) (31.80) 11.20 (1.20) 14.40 (99.40)

Source: FAOSTAT

2.1. Cereal Trade Flows by Crop

Rice

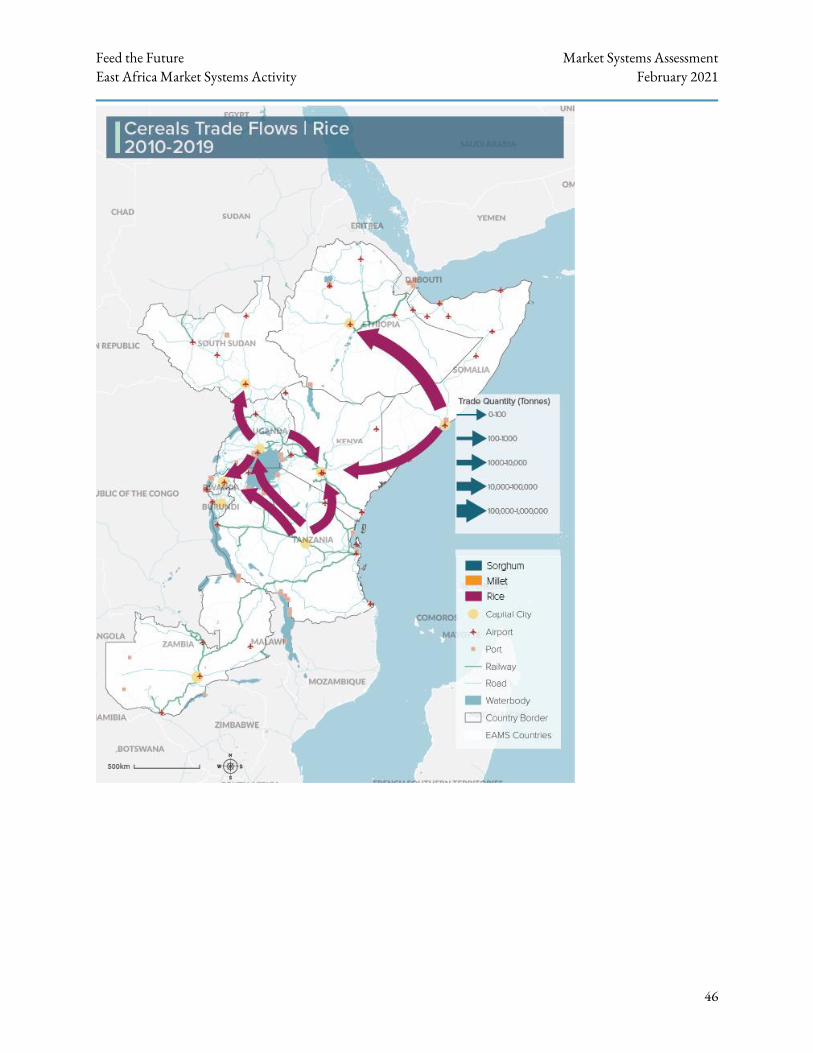

Rice accounts for the bulk of regional cross-border trade for cereals covered under this study. Total value of imports from within the EAMS countries is estimated at around US$ 32 million per annum. Tanzania is the region’s biggest producer of rice– total production is estimated at 2,531,381 tons per annum, providing over 90% of the rice traded in the region. Uganda is the second largest producer at 2,531,381 tons per annum. Uganda is also the largest importer at US$ 20 million, followed by Rwanda at US$ 8 million.

FIGURE 4. MAIN IMPORTERS OF (BUYERS) FOR RICE IMPORTED WITHIN THE REGION (US000’)

Computed from TRADEMAP Data

FIGURE 5. MAIN EXPORTERS (SUPPLIERS) FOR RICE EXPORTED WITHIN THE REGION (US000’)

2,067 1,482

8,234

20

20,813

1 6 -

5,000

10,000

15,000

20,000

25,000

Burundi Kenya Rwanda Somalia Uganda Tanzania, Zambia

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

10

Sorghum

Around US$ 18.4 million worth of sorghum per year is traded within the region. Ethiopia is the main regional producer of sorghum at 4,886,009 tons per year, followed by South Sudan (756,861 tons), Tanzania (743,768 tons) and Uganda (376,189 tons). Kenya is the largest regional exporter of sorghum, exporting an average value of US$ 9.3 million per annum. This equates to over 50 percent of the value traded within the region. The second largest exporter is Uganda at US$ 5.4 million per year. The major importers are South Sudan and Rwanda with average annual imports estimated at US$ 8.5 million and US$ 4.9 million, respectively. In recent years, Burundi has begun to import increasing volumes of sorghum to fuel domestic beer production and consumption. The value of sorghum imports from the geographic focus region into Burundi have therefore soared by a CAGR of 509%, significantly higher compared to other countries in the region, though they are from a lower base, and relatively low aggregate levels.

FIGURE 6. MAIN IMPORTERS (BUYERS) OF SORGHUM TRADED WITHIN THE REGION (US000’)

Computed from TRADEMAP Data

FIGURE 7. MAIN EXPORTERS (SUPPLIERS) OF SORGHUM EXPORTED WITHIN THE REGION (US000’)

- 692 24 3 - 884

13,778

- -

5,000

10,000

15,000

Burundi Kenya Rwanda Somalia SouthSudan

Uganda Tanzania Zambia

115 -

1,781

4,906

1,094

8,521

1,356 661

-

2,000

4,000

6,000

8,000

10,000

Burundi Ethiopia Kenya Rwanda Somalia SouthSudan

Uganda Tanzania

2 156

9,310

617 - -

5,421

1,987

-

2,000

4,000

6,000

8,000

10,000

Burundi Ethiopia Kenya Rwanda Somalia SouthSudan

Uganda Tanzania,

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

11

Computed from TRADEMAP Data

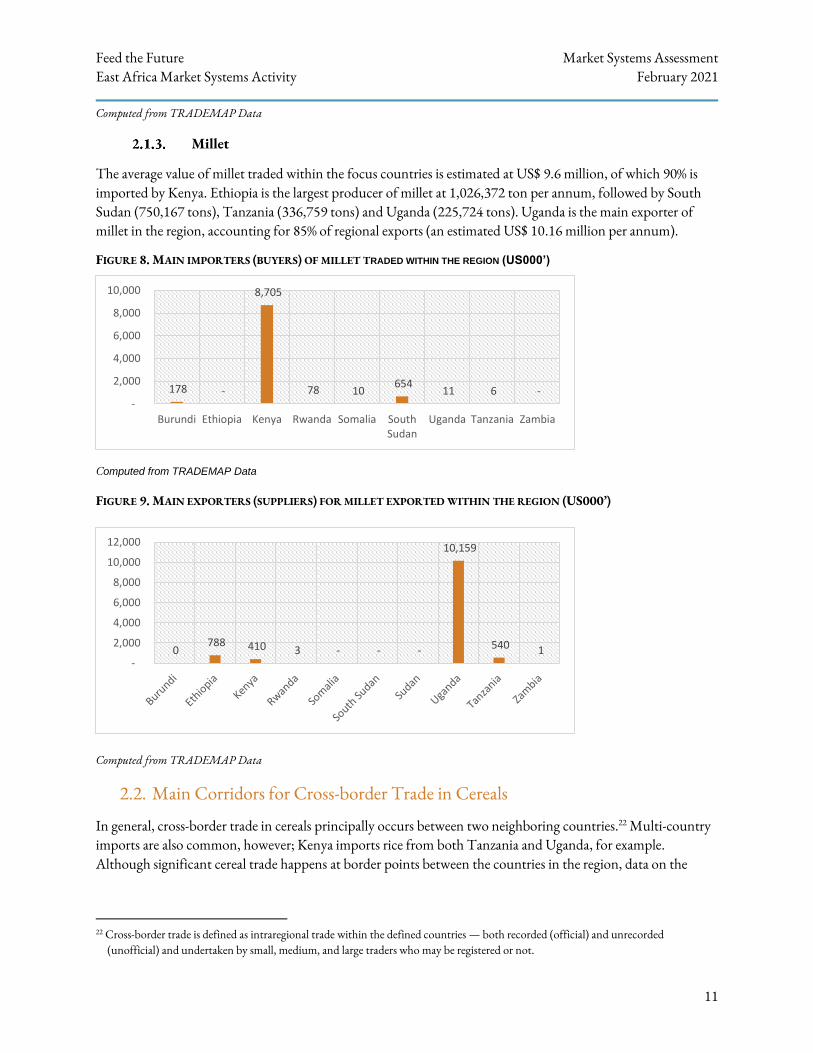

Millet

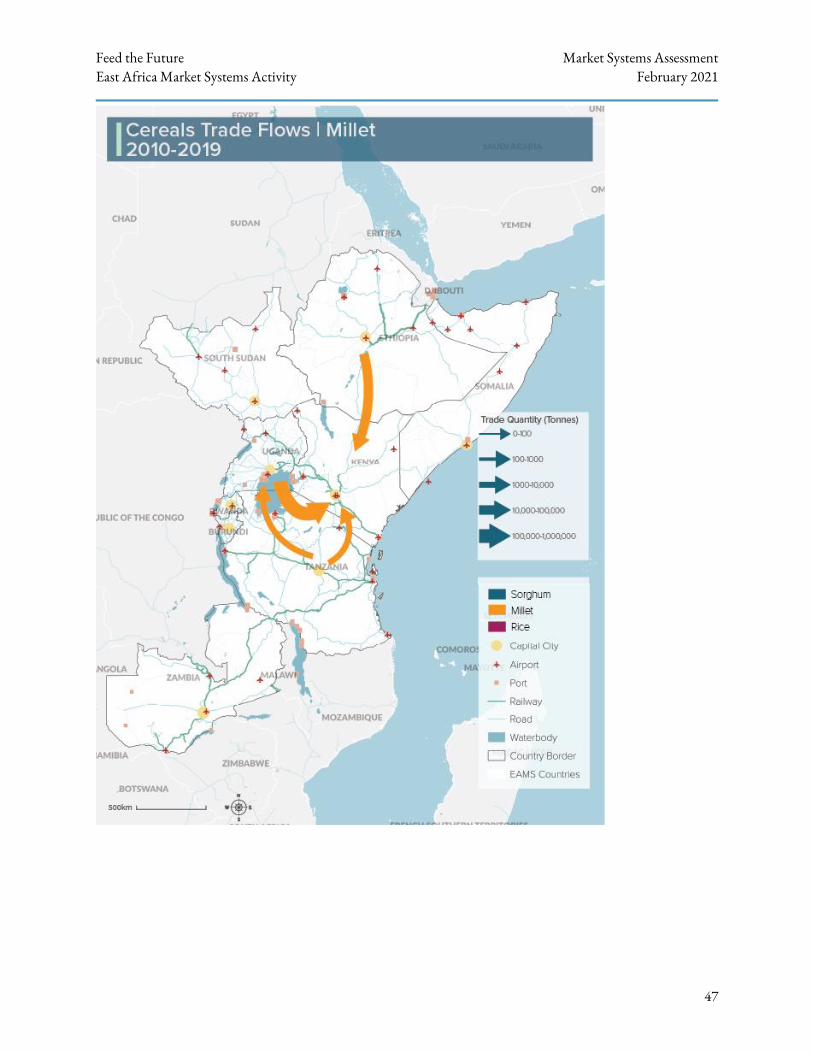

The average value of millet traded within the focus countries is estimated at US$ 9.6 million, of which 90% is imported by Kenya. Ethiopia is the largest producer of millet at 1,026,372 ton per annum, followed by South Sudan (750,167 tons), Tanzania (336,759 tons) and Uganda (225,724 tons). Uganda is the main exporter of millet in the region, accounting for 85% of regional exports (an estimated US$ 10.16 million per annum).

FIGURE 8. MAIN IMPORTERS (BUYERS) OF MILLET TRADED WITHIN THE REGION (US000’)

Computed from TRADEMAP Data

FIGURE 9. MAIN EXPORTERS (SUPPLIERS) FOR MILLET EXPORTED WITHIN THE REGION (US000’)

Computed from TRADEMAP Data

2.2. Main Corridors for Cross-border Trade in Cereals

In general, cross-border trade in cereals principally occurs between two neighboring countries.22 Multi-country imports are also common, however; Kenya imports rice from both Tanzania and Uganda, for example. Although significant cereal trade happens at border points between the countries in the region, data on the

22 Cross-border trade is defined as intraregional trade within the defined countries — both recorded (official) and unrecorded

(unofficial) and undertaken by small, medium, and large traders who may be registered or not.

178 -

8,705

78 10 654

11 6 - -

2,000

4,000

6,000

8,000

10,000

Burundi Ethiopia Kenya Rwanda Somalia SouthSudan

Uganda Tanzania Zambia

0 788 410 3 - - -

10,159

540 1 -

2,000

4,000

6,000

8,000

10,000

12,000

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

12

actual volumes traded between these points is scarce. The main trade corridors for cereals in the region are as follows:

Uganda – South Sudan Trade

Uganda is considered South Sudan’s main trading partner compared with other countries in the region. Virtually all cereals (rice, sorghum, and millet) are traded at these border points.23 Trade between South Sudan and Uganda has grown rapidly, albeit unevenly, over the past six years. The restoration of peace in South Sudan, coupled with improved security in northern Uganda, has led to significant increases in the amount of trade between the two countries. However, significant volumes of transactions are informal and cross the borders unrecorded. The trade is also highly asymmetric with the volume of exports from Uganda to South Sudan being disproportionately larger than the volume of exports from South Sudan to Uganda. Ugandan cereal exports to South Sudan totaled US$74.4 million during 2018.24

Uganda – Kenya Trade

The food security linkages between Kenya and Uganda are among the strongest in the region. Primary agricultural commodities (millet and sorghum) usually flow from Uganda to Kenya.25 Four major border points handle cross border trade in cereal commodities between Kenya and Uganda: Busia, Malaba, Suam, and Lwakhakha. A number of small ports along Lake Victoria also move foodstuffs in both directions. Food also moves across the northern sections of the border, although volumes are limited due to the sparse populations in these predominantly pastoral zones.

Tanzania – Kenya Trade

Agricultural trade between Kenya and Tanzania has historically been very strong. In recent years, Tanzania has made much progress in its infrastructure, which has widened the food sources available for the Kenyan market. The main border points between Kenya and Tanzania include Horohoro, Taveta, Rombo, Namanga, and Sirari. Foodstuffs move through each of these points, as well as across Lake Victoria. Out of the three target cereal crops, rice is the main product traded between these two countries.

Tanzania – Uganda Trade

Both sides of the border between Uganda and Tanzania have similar and favorable agro-climatic conditions, conducive for ample food production with surpluses exported to Kenya and Rwanda. There is limited trade within the border areas. Agricultural trade between Uganda and Tanzania is low compared to trade between Tanzania and Kenya, Zambia, Rwanda, Burundi, DRC, and Malawi. The main border point between Tanzania and Uganda is at Mutukula, but goods are also shipped across Lake Victoria from Bukoba in Tanzania. Rice is the primary cereal product traded between Tanzania and Uganda. Rice imported from Tanzania remains the largest commodity traded between the two countries, mostly informally. It should be noted that most of the Tanzanian rice imported to Uganda is re-exported to South Sudan where demand continues to grow as result of relative calm.

23 African Development Bank: South Sudan: A Study on Competitiveness and Cross Border Trade with Neighbouring Countries, 2013.

24 UN-COMTRADE database 25 Kenya’s major agricultural exports to Uganda are not primary commodities, but value-added processed goods, such as wheat flour,

cooking oil and sugar.

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

13

Tanzania – Zambia Trade

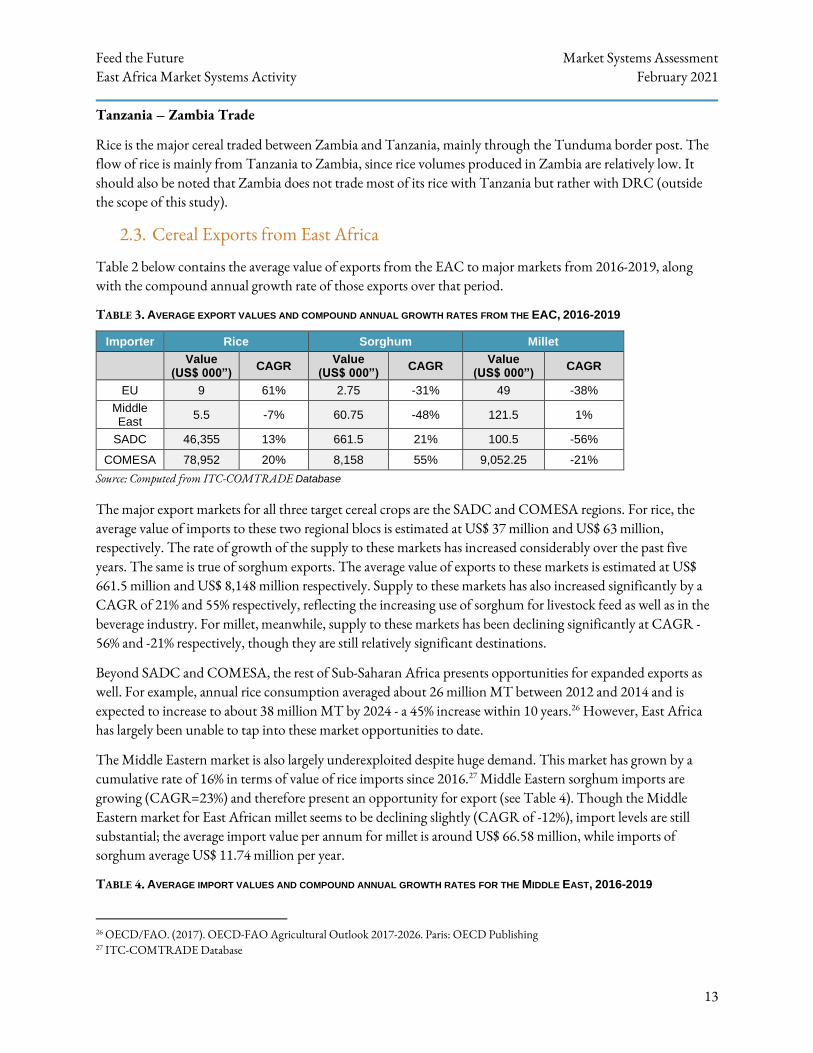

Rice is the major cereal traded between Zambia and Tanzania, mainly through the Tunduma border post. The flow of rice is mainly from Tanzania to Zambia, since rice volumes produced in Zambia are relatively low. It should also be noted that Zambia does not trade most of its rice with Tanzania but rather with DRC (outside the scope of this study).

2.3. Cereal Exports from East Africa

Table 2 below contains the average value of exports from the EAC to major markets from 2016-2019, along with the compound annual growth rate of those exports over that period.

TABLE 3. AVERAGE EXPORT VALUES AND COMPOUND ANNUAL GROWTH RATES FROM THE EAC, 2016-2019

Importer Rice Sorghum Millet

Value

(US$ 000”) CAGR

Value (US$ 000”)

CAGR Value

(US$ 000”) CAGR

EU 9 61% 2.75 -31% 49 -38%

Middle East

5.5 -7% 60.75 -48% 121.5 1%

SADC 46,355 13% 661.5 21% 100.5 -56%

COMESA 78,952 20% 8,158 55% 9,052.25 -21%

Source: Computed from ITC-COMTRADE Database

The major export markets for all three target cereal crops are the SADC and COMESA regions. For rice, the average value of imports to these two regional blocs is estimated at US$ 37 million and US$ 63 million, respectively. The rate of growth of the supply to these markets has increased considerably over the past five years. The same is true of sorghum exports. The average value of exports to these markets is estimated at US$ 661.5 million and US$ 8,148 million respectively. Supply to these markets has also increased significantly by a CAGR of 21% and 55% respectively, reflecting the increasing use of sorghum for livestock feed as well as in the beverage industry. For millet, meanwhile, supply to these markets has been declining significantly at CAGR -56% and -21% respectively, though they are still relatively significant destinations.

Beyond SADC and COMESA, the rest of Sub-Saharan Africa presents opportunities for expanded exports as well. For example, annual rice consumption averaged about 26 million MT between 2012 and 2014 and is expected to increase to about 38 million MT by 2024 - a 45% increase within 10 years.26 However, East Africa has largely been unable to tap into these market opportunities to date.

The Middle Eastern market is also largely underexploited despite huge demand. This market has grown by a cumulative rate of 16% in terms of value of rice imports since 2016.27 Middle Eastern sorghum imports are growing (CAGR=23%) and therefore present an opportunity for export (see Table 4). Though the Middle Eastern market for East African millet seems to be declining slightly (CAGR of -12%), import levels are still substantial; the average import value per annum for millet is around US$ 66.58 million, while imports of sorghum average US$ 11.74 million per year.

TABLE 4. AVERAGE IMPORT VALUES AND COMPOUND ANNUAL GROWTH RATES FOR THE MIDDLE EAST, 2016-2019

26 OECD/FAO. (2017). OECD-FAO Agricultural Outlook 2017-2026. Paris: OECD Publishing 27 ITC-COMTRADE Database

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

14

Crop Import Value (US$ 000”)

CAGR

Sorghum 11,738 23%

Millet 66,577 -12%

3. REGIONAL GROWTH POTENTIAL

Demand for cereals and cereal-derived products from processors and consumers will continue to grow across the region over the coming years due to a variety of factors, presenting a substantial opportunity for increased trade flows within the region. Increasing the availability of cereals and cereal products to meet this demand will be key to boosting regional trade and integration. Several of the key drivers of regional growth potential are outlined below.

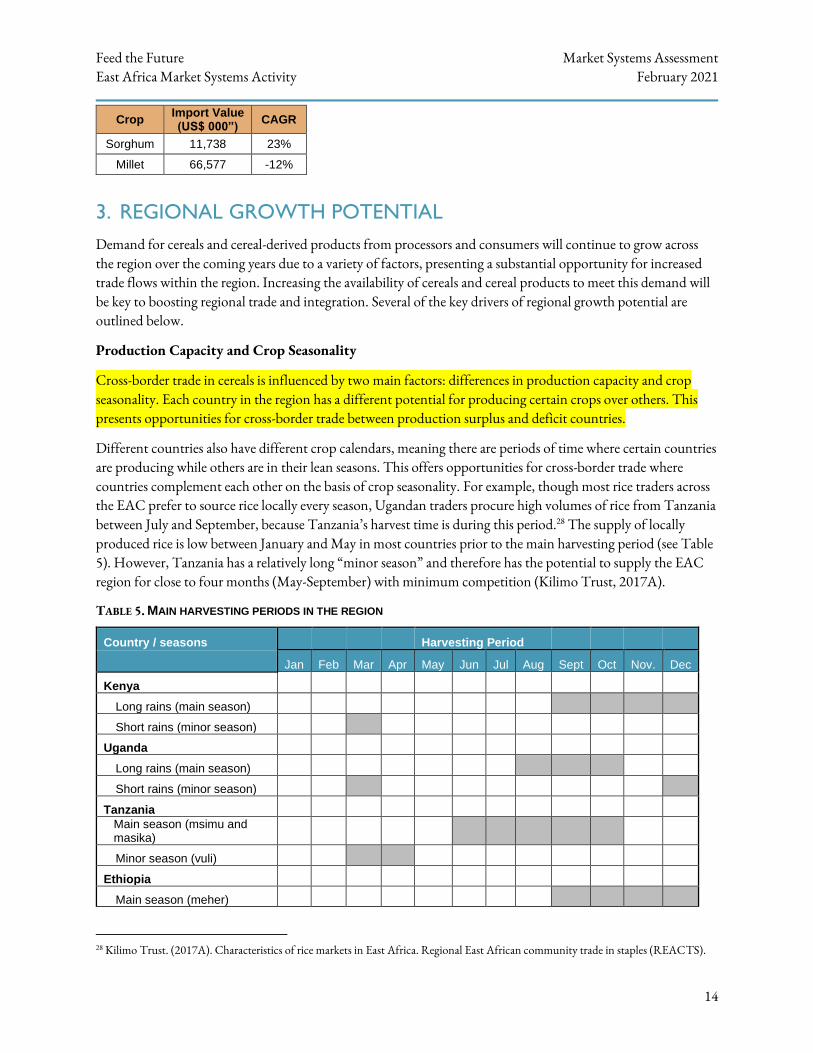

Production Capacity and Crop Seasonality

Cross-border trade in cereals is influenced by two main factors: differences in production capacity and crop seasonality. Each country in the region has a different potential for producing certain crops over others. This presents opportunities for cross-border trade between production surplus and deficit countries.

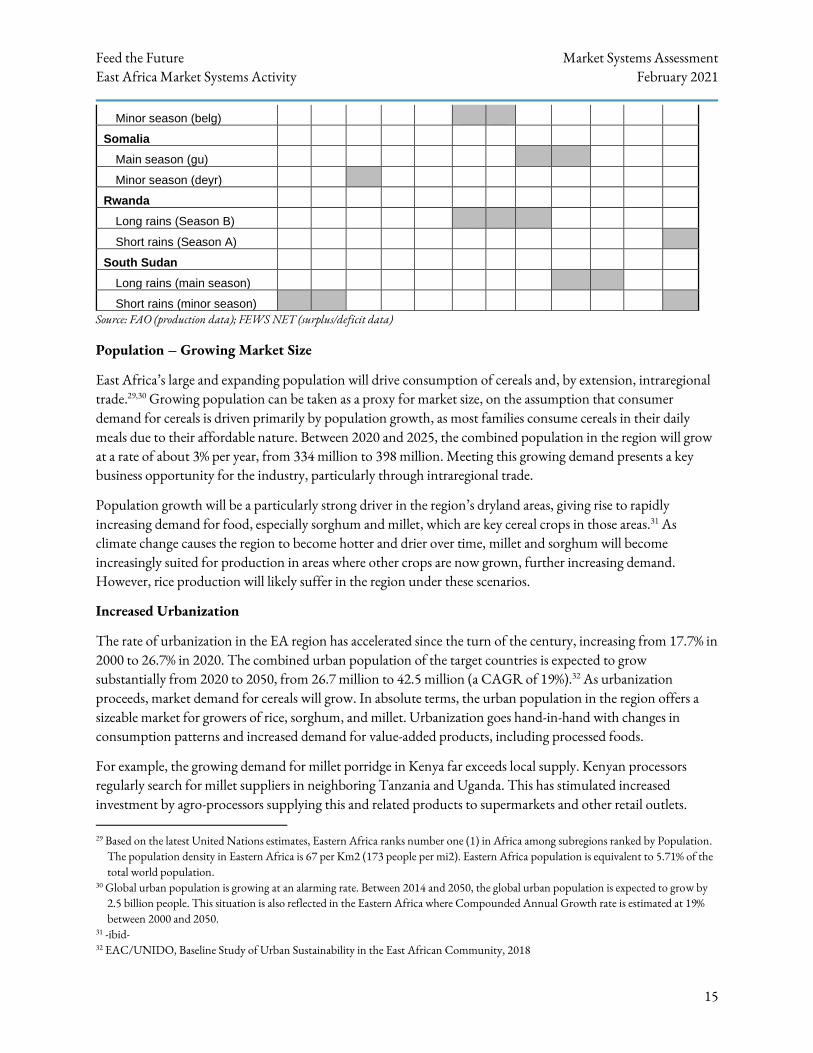

Different countries also have different crop calendars, meaning there are periods of time where certain countries are producing while others are in their lean seasons. This offers opportunities for cross-border trade where countries complement each other on the basis of crop seasonality. For example, though most rice traders across the EAC prefer to source rice locally every season, Ugandan traders procure high volumes of rice from Tanzania between July and September, because Tanzania’s harvest time is during this period.28 The supply of locally produced rice is low between January and May in most countries prior to the main harvesting period (see Table 5). However, Tanzania has a relatively long “minor season” and therefore has the potential to supply the EAC region for close to four months (May-September) with minimum competition (Kilimo Trust, 2017A).

TABLE 5. MAIN HARVESTING PERIODS IN THE REGION

Country / seasons Harvesting Period

Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov. Dec

Kenya

Long rains (main season)

Short rains (minor season)

Uganda

Long rains (main season)

Short rains (minor season)

Tanzania

Main season (msimu and masika)

Minor season (vuli)

Ethiopia

Main season (meher)

28 Kilimo Trust. (2017A). Characteristics of rice markets in East Africa. Regional East African community trade in staples (REACTS).

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

15

Minor season (belg)

Somalia

Main season (gu)

Minor season (deyr)

Rwanda

Long rains (Season B)

Short rains (Season A)

South Sudan

Long rains (main season)

Short rains (minor season)

Source: FAO (production data); FEWS NET (surplus/deficit data)

Population – Growing Market Size

East Africa’s large and expanding population will drive consumption of cereals and, by extension, intraregional trade.29,30 Growing population can be taken as a proxy for market size, on the assumption that consumer demand for cereals is driven primarily by population growth, as most families consume cereals in their daily meals due to their affordable nature. Between 2020 and 2025, the combined population in the region will grow at a rate of about 3% per year, from 334 million to 398 million. Meeting this growing demand presents a key business opportunity for the industry, particularly through intraregional trade.

Population growth will be a particularly strong driver in the region’s dryland areas, giving rise to rapidly increasing demand for food, especially sorghum and millet, which are key cereal crops in those areas.31 As climate change causes the region to become hotter and drier over time, millet and sorghum will become increasingly suited for production in areas where other crops are now grown, further increasing demand. However, rice production will likely suffer in the region under these scenarios.

Increased Urbanization

The rate of urbanization in the EA region has accelerated since the turn of the century, increasing from 17.7% in 2000 to 26.7% in 2020. The combined urban population of the target countries is expected to grow substantially from 2020 to 2050, from 26.7 million to 42.5 million (a CAGR of 19%).32 As urbanization proceeds, market demand for cereals will grow. In absolute terms, the urban population in the region offers a sizeable market for growers of rice, sorghum, and millet. Urbanization goes hand-in-hand with changes in consumption patterns and increased demand for value-added products, including processed foods.

For example, the growing demand for millet porridge in Kenya far exceeds local supply. Kenyan processors regularly search for millet suppliers in neighboring Tanzania and Uganda. This has stimulated increased investment by agro-processors supplying this and related products to supermarkets and other retail outlets.

29 Based on the latest United Nations estimates, Eastern Africa ranks number one (1) in Africa among subregions ranked by Population.

The population density in Eastern Africa is 67 per Km2 (173 people per mi2). Eastern Africa population is equivalent to 5.71% of the total world population.

30 Global urban population is growing at an alarming rate. Between 2014 and 2050, the global urban population is expected to grow by 2.5 billion people. This situation is also reflected in the Eastern Africa where Compounded Annual Growth rate is estimated at 19% between 2000 and 2050.

31 -ibid- 32 EAC/UNIDO, Baseline Study of Urban Sustainability in the East African Community, 2018

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

16

Similarly, increasing demand for cereals from brewing companies, particularly for sorghum, has strong potential to boost cross-border trade between production surplus and production deficit countries.

Strong and Growing Economies

Continuous economic growth in East African countries and rising per capita incomes will raise the spending capabilities of individuals and increase demand for consumer products including cereals.33 With an average economic growth rate of 6.7% between 2013 and 2017 – double the African average – East Africa is one of the fastest growing regions in the world. This strong performance is underpinned by notable improvements in agricultural production and sustained infrastructure investment.34 Rising disposable income levels will drive individuals to purchase more cereals and cereal-derived products, which in turn, will positively influence the local market and intraregional trade growth for these products.

As incomes rise, diets change and the demand for livestock products (i.e., meat, milk) increases. This growing demand is increasing the market value of both rice by-products and sorghum and millet residues. Crop residues (stover) from sorghum and millet as well as grains are vital feed stocks for cattle, goats and chickens, and rice bran is a sought-after component of livestock, poultry, pig, and fish feed. Pearl millet grain is also a valuable animal feed, comparable to maize for poultry, but with a higher protein content and a better-balanced amino acid profile, so that less protein concentrate is required in a pearl millet-based feed ration.

Rising incomes will also drive demand for specialty products such as health foods made from cereals. There has been a growing realization of the health benefits of sorghum and millet. For example, several small (and to some extent medium) processors have formulated blending recipes for composite flour from sorghum and millet as well as wheat, to take advantage of the high nutritional content of millet. As awareness and importance of healthy diets increases among the growing middle class, it will trigger increased demand and promote cross-border trade.

High Degree of Specialization for Actors

There is a significant degree of specialization among actors involved in the trading of cereals. For example, sorghum buyers for brewing purposes require only the “white” variety, while the “red” variety is more demanded for school feeding programs, particularly in Kenya. Traders will be increasingly looking for specialized varieties instead of the “generic” product. This is expected to drive future investments in the value chain, particularly in terms of service provision support, marketing strategies, technology, and innovation. This means that cross-border trade in these value chains will increasingly be of both a more varied and more specialized nature.

Services Opportunities

As the value chain continues to mature towards sophisticated commercial level operations, there will be increased prospects for linking the cereal sector to the service industry. Industry stakeholders should begin to factor this into their investment decisions and operations and make necessary adjustments. Relatively little attention has been paid to the role of services in value chains, and the barriers that exist to accessing or

33 For example, following a strong growth that lifted the average income of the people to the levels of the group, Tanzania has joined the

ranks of Middle-Income Countries (MIC) eight years ahead of schedule. The GDP per Capita in Tanzania is equivalent to 8 percent of the world's average.

34 UNECA, 2018.

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

17

importing these services despite emphasis on industrialization as an engine to drive national economies. Likewise, the increasing contribution of knowledge services, such as research and development, in industrial value chains is often neglected.

Access to service inputs in the cereal sector in the region is therefore critical to promote future growth and competitiveness. Services such as information and communications technology (ICT), transport and logistics will become increasingly important. Companies that are unable to access well-priced and good quality services domestically, or imported from abroad, will find it difficult to participate in regional or global value chains. Any barriers to services trade could pose a significant constraint on the emergence of a robust cereal value chain in the region.

Establishment of One-Stop Border Post (OSBP) system

With the establishment of One-Stop Border Posts (OSBP) between EAC partner states, there will be greater prospects for improved formal cross-border EAC trade for cereal products. As part of ongoing efforts to promote free trade, the EAC has made significant efforts to provide guidance on the rules and regulations for conducting cross-border trade. For example, the EAC and the ILO have developed a comprehensive information pack (Simplified Guide/Tool) containing up-to-date and relevant information on the existing policies, procedures, requirements, rules of origin, taxes, tariffs, exemptions, and facilities available to cross-border traders, to facilitate trade within the region. This guide provides information on key EAC trade rules, regulations and procedures related to trade within the EAC (intra-EAC trade) in a simplified and user-friendly manner.

Further prospects for improvement of cross-border trade are expected to derive from recent changes to EAC export regimes. For example, in June 2018, the EAC rolled out a new export regime that seeks to establish a Single Customs Territory (SCT). As a result, exporters in the EAC have started to enjoy faster transit times because these commodities are being cleared under the SCT.35 The new regime seeks to minimize delays and costs for goods moving across borders to export markets by having them cleared at the point of origin. This helps avoid further customs checks at border points and during loading for overseas shipping.

4. CONSTRAINTS ANALYSIS

This section examines the major constraints causing continued inefficiencies for intraregional trade in cereals, highlighting common constraints across EAMS countries where cross-border trade in cereals products is relatively significant.

4.1. Production Systems

The risks and vulnerabilities of climate change are now noticeable in many countries in EA; for example, in Uganda there was a recorded 40 -55% reduction in cumulative rains for the October-December 2016 rainy season, which had a significant effect on crop yields.36 It has been argued that potential gains for sorghum and millet are as large as those derived from the Green Revolution in rice and wheat, and realizing even a modest portion of that potential would be transformative in the impoverished areas that are traditionally reserved for

35 This is part of the implementation of a directive of the 19th East African Community Summit in February 2018, which requires the

Single Customs Territory regime to cover all products. 36 -ibid-

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

18

sorghum and millet production.37 This would require increased access to productive resources such as land, improved infrastructure (e.g., irrigation systems relevant for small scale agriculture, seeds, fertilizers and agrochemicals) and other supportive services such as extension services, finance, etc.

Low Yields

Sorghum and millet remain low-yielding food grains due to low and irregular rainfalls, high temperatures, poor soils, and inappropriate agronomic practices.38 Even in favorable seasons, average yields are lower than the average yield for maize. Average productivity estimates for sorghum and millet in the region are about 800 kg/ha compared to those found in other parts of the world (1200 kg/ha in Asia, 4000 kg/ha in America, and 5000 kg/ha in Europe).39 Although sorghum and millet are more tolerant to drought, their productivity is low when they do not receive enough water. Additionally, the rice ecologies are prone to drought, especially upland rice farming areas, where the poorest rice farmers are located. The lowland rice ecologies also have challenges of water control and weed management.40

None of the EAC countries is self-sufficient in rice production and deficits are covered through imports. Rice imports mainly from Asia (Thailand, India, Pakistan, and Vietnam) have tripled over the last ten years to meet rice demands in the EAC. This clearly shows a gap in the local production of rice which can be attributed to: (1) small scale of operations by the majority of producers who cultivate farms of less than a hectare, (2) inadequate access to inputs and improved varieties, and (3) limited access to markets which reduces smallholders’ appetite for “farming as a business” (i.e., taking risks with productivity-enhancing inputs and other good agricultural practices).

Post-Harvest Loss

One of key challenges that exacerbates food insecurity and stifles efforts for commercialisation of sorghum and millet in the region is postharvest losses (PHL). According to estimates by the African Postharvest Losses Information System (APHLIS), the average percentage of PHL losses for rice, sorghum and millet are estimated at around 12.6%, 12%, and 9% respectively. The major causes of post-harvest losses are high crop perishability; mechanical damage; excessive exposure to high ambient temperature, relative humidity and rain; contamination by spoilage fungal and bacteria; invasion by birds, rodents, insects and other pests; and inappropriate handling, storage and processing techniques. Losses may be aggravated by poor infrastructure, harvesting methods, post-harvest handling procedures, distribution, sales and marketing policies. The economic importance of the factors leading to high post-harvest losses varies from commodity to commodity, season to season, and the enormous diversity of circumstances under which commodities are grown, harvested, stored, processed and marketed.

There are a number of other “indirect” factors which contributes to high incidences of PHL for cereals in the region. For example, information is not readily available on post-harvest grain quality management. Potential low-cost technologies and interventions for post-harvest losses have not been adequately identified. Weak linkages between farmers and processors also exacerbate the challenge of post-harvest loss. The combination of

37 -ibid- 38 ICRISAT 2015, 39 FAO, 1994 40 Seck, P. A., Tollens, E., Wopereis, M. C., Diagne, A., & Bamba, I. (2010). Rising trends and variability of prices: Threats and

opportunities for Sub-Saharan Africa. Food Policy, 403-411.

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

19

these constraints leads to reduced productivity; as a result, farmers are not interested in expanding or commercializing millet cultivation, preferring to grow the crop on small plots for household consumption.

Prevalence of Pests and Diseases

Cereal VCs are impacted by a variety of biological threats that affect plant health and harvest that vary across VCs and along the stages of each VC (from production to post-harvest). These biological threats include:

• Pests. The prevalence of pests in the region is a major constraint to cross-border trade in cereals. Pests in the field threaten quantities of raw commodities harvested, while pests in storage damage quality and increase postharvest losses. Insect pest infestations also spread across borders, devastating harvest seasons if not dealt with swiftly through cross-border coordination. Specific pests impacting each cereal VC are summarized below:

o Sorghum: The main insect pests for sorghum in order of economic importance are midge, shoot fly, stem borers, and the cotton bollworm.41

o Millet: About a hundred insect pests attack millet in the field and during storage, some of which are common throughout the millet growing areas. Stem borers and grain midge are of regular occurrence. Sporadic attacks of blister beetles, armyworms, grasshoppers, chinch bugs, leaf beetles, head caterpillars and head bugs result in severe yield losses in certain seasons. There are higher incidences of storage pests during the rainy season.

o Rice: Though rice is not as susceptible to insect pests as other crops, snails and worms can impact plant health. Crop damage by quelaquela birds is a constant, serious threat to the crop, and rodents are a notable pest particularly in Uganda.

o Desert locust: Swarms of desert locusts, which can emerge in periods of heavy rains, devasted cereal crops (including rice, millet, and sorghum) across East Africa and the Horn of Africa in 2020. Locust swarms cover vast grounds in short periods of time and are difficult to control, making them a formidable transboundary pest. Effects of climate change and extreme weather will continue to increase the frequency of locust plagues (i.e., infestations that affect multiple countries simultaneously), making multilateral coordination critical for swift action. In early 2021, locusts have already damaged significant crops in Ethiopia, Somalia, and Kenya, though quick action seems to have quelled breeding, heavy rains in February could lead to new hatchings in late March.

• Diseases. The most common diseases for sorghum are caused by fungus: anthracnose (colletotrichum graminicola);42 charcoal rot (macrophomina phaseolina);43 gray leaf spot (cercospora sorghi); and rough

41 ICRISAT, Pests of African Sorghum. 42 Small, circular red lesions with a distinct margin develop on leaves and stems; lesions may enlarge during humid weather conditions;

plant becomes defoliated; tan spots with red margins may appear on upper parts of stems; plants may die before reaching maturity 43 Lower stalk appears shredded and dark gray; small, black fungal structures on internal parts of the stalk giving tissues a dark gray color;

pith decomposes leaving only the outer stem tissue; infected plants will usually lodge

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

20

spot (ascochyta sorghi).44 Other fungi diseases include covered kernel smut (sporisorium sorghi)45 and zonate leaf spot (gloeocercospora sorghi).

Millet is also affected by fungal diseases including leaf spot (cercospora penniseti);46 downy mildew (sclerospora graminicola);47 rust (puccinia substriata);48 and seedling and leaf blight (helminthosporium nodulosum).49 Millet blast disease is by far the most devastating, causing over 50% yield loss.50

Rice is also susceptible to diseases, particularly the rice yellow mottle virus and rice blast fungus. Rice blast is the most significant, sometimes causing more than 30% yield reductions; it affects 54% of the cultivated rice area in Uganda with severities recorded in the main rice-producing districts of Bugiri, Butaleja, Mbale and Lira.51

• Parasitic weeds. There are various types of parasitic weeds that affect cereal VCs, ultimately feeding on and strangling host plants for nutrients and water. They pose a significant threat to rain-fed production, and given their genetic and biochemical characteristics, they are difficult to control or eradicate as they are resistant to traditional weed control practices. The most common weeds are striga asiatica, s. aspera, and s. hermonthica in rain-fed uplands, and rhamphicarpa fistulosa in rain-fed lowlands. The known hot spots for parasitic weed infestation in rice are in southern Tanzania (i.e., all three types of common weeds), eastern Uganda (striga asiatica), and western Kenya. Parasitic weeds have been reported to have cause up to 59% and 61% rice yield losses in Kenya and Tanzania, and yet the locations of highest frequency of these occurrences have been in areas populated by some of the most vulnerable rice farmers. The physical losses caused by parasitic weeds in 2016 were estimated at 20,000 MT (8.1 million USD) and 17,000 MT (6.81 million USD) in Tanzania and Uganda respectively.52

• Aflatoxins are common challenges for cereals in East Africa, though the levels of aflatoxins and their significance as a constraint to cross-border trade varies by cereal VC.53 Aflatoxin-contaminated food is

44 Small, oval or elongated red spots on leaves; lesions coalesce and develop hard black fungal fruiting bodies, giving the leaves a

sandpaper-like texture; rough areas may become large enough to kill entire leaf 45 Head replaced by brown, powdery mass of fungal spores covered by gray to brown membrane; entire head may be affected or fungus

may be localized at the top, bottom or sides of the head; plants are usually or normal height 46 Small dark lesions on leaves which are usually oval in shape but may be oblong to rectangular; centers of lesions are gray to tan in color

with visible black dots; lesions may be covered in spores during wet weather; lesions may also be present on the stems and are slightly longer than those on the leaves

47 Chlorosis of leaves beginning at base of the infected leaf beginning lower down on the plant and progressing upwards; downy white to gray fungal growth on undersides of leaves; brown, necrotic leaves; distinct margin between diseased leaf tissue at base of leaf and healthy tissue towards tip

48 Small yellow or white raised spots on upper and lower leaf surfaces; spots tend to be more numerous on lower leaf surface; spots enlarge and develop into red-brown pustules which may be surrounded by a yellow halo

49 Disease occurs in India, Japan and Africa; fungus attacks other millet species; disease spread through infected seed 50 Esele JP. 1989. Cropping systems, production technology, pests and diseases of millet in Uganda in Small Millets in Global Agriculture

(Seetharam A, Riley KW and Harinarayana G, eds.). Ottawa, Canada: IDRC. 51 Onaga, G., & Asea, G. (2016). Occurance of rice blast (Magnaporthe oryzae) and identification of potential resistance sources in

Uganda. Crop protection, 65-72. 52 Rodenburg, J., Demont, M., Zwart, S. J., & Bastiaans, L. (2016). Parasitic weed incidence and related economic losses in rice in Africa.

Agriculture, Ecosystems and Environment, 235, 306-317. 53 Aflatoxin is a toxic metabolite of certain molds in the genus Aspergillus. Aflatoxins are highly resistant to processing. In animal feed

aflatoxins have a significant effect on livestock productivity and contamination can be transferred up the food chain to humans particularly through milk.

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

21

a public health concern. For example, contamination of staple foods in Kenya has in the past led to loss of human lives as well as condemnation of large quantities of food, contributing to food insecurity. Aflatoxin-related cases have been reported in several countries in the region. For example, a study conducted in four (4) agro-ecological zones in Kenya concluded that overall, 76% of maize, 64% of millet and 60% of sorghum samples tested positive for aflatoxin B1. Of these, the proportion of samples with aflatoxin B1 levels above the Kenya Bureau of Standards limit of five parts per billion was 26% for maize, 10% for millet, and 11% for sorghum.54

4.2. Market Access and Market information

Low, Irregular Supply and Poor Grain Quality

Despite growing demand from agro-processors, traders, and other end buyers, many producers are unable to meet the necessary market standards and production targets to enter into structured supplier contracts with such buyers. Low and variable production and the lack of an efficient marketing chain increases processors’ cost of production, thus reducing profits. There are also cases where grain delivered to processors is usually of poor quality. There are number of instances where grain is contaminated by foreign matter (stones, dust, sand, husk etc). High moisture content caused by poor drying and or poor storage results in high moisture content and spoilage. Quality is also affected by immature grain because the crop is sometimes harvested too early.

A small number of medium and large-scale mills have been built over the last 5-10 years that operate higher quality processing machines –with de-stoners, polishers, and graders – and brand their output. To ensure the quantities and quality of supply, the millers have increasingly vertically integrated trading operations, proactively purchasing paddy directly from farmers or small traders and selling milled rice to traders. A few millers own their distribution networks with transporters, wholesalers, and retail operations in urban centers. The density of commercial processors is greatest where there are more commercially orientated smallholders. These schemes are not widespread yet, and tend to be unsophisticated, save a few exceptions, and the number of smallholders engaged in this way per scheme is low, ranging from under 100 to 1,500.55

Market Infrastructure

Market infrastructure is critical to enhance market access, reduce post-harvest losses, and promote integration between growers, wholesalers, and retailers. Access to adequate storage facilities is the most important market infrastructure for cereals to prevent quality deterioration and to make calculated marketing decisions. Without access to appropriate storage and fumigation, both farmers and traders are unable to store cereals until the pries in markets have improved. Inadequate storage leads to high physical losses due to pests and rodents, while quality deterioration is caused by humidity.

Market infrastructure (storage warehouses, collection and aggregation points) can also facilitate mass marketing and provision of other supply chain services. While lacking in East Africa, these kinds of infrastructure could provide “embedded” services: product distribution; storage; grading, sorting, and proper integration of post-harvest technology into marketing supply-chain. Furthermore, the infrastructure arrangement does not promote a transparent and efficient platform for sale and purchase of produce by connecting growers through

54 African Journal for Food and Agriculture, Nutrition and Development, Vol. 20 No. 4 (2020) 55 Kilimo Trust, Expanding Rice Markets in the EAC, 2017

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

22

growers’ associations with wholesale buyers in various markets across the countries and the region. As such, they do not provide incentives for improved quality and productivity, thereby improving farmers’ income.

Additionally, the success of warehouse financing is dependent on the availability of infrastructure to facilitate the storage of grain for use as collateral. However, across East Africa, there is a need for increased certified warehouses equipped with the monitoring systems needed to guarantee minimum quality requirements. The high costs incurred in establishing and operating warehouses, coupled with low volumes from small-scale traders, makes it difficult to attain the economies of scale needed to make warehouse operations commercially viable, and thus attract private investment.56

To improve structured cereals trade in the region and market access, commodity exchanges have been set up in Ethiopia, Rwanda, Tanzania, and Zambia. However, challenges for cereals trade on these exchanges include: (i) existence of registered and licensed warehouses able to effectively manage warehouse receipt systems, certify and guarantee commodity quantity and quality, and with oversight by Warehouse Regulatory Authorities, (ii) policies that enable enforcement and compliance with national and regional standards for agricultural commodities across value chains, (iii) existence of an enabling legal and regulatory framework governing these commodity exchanges (with regulatory oversight and supervision being done mainly through Capital Markets Authorities in the different countries), (iv) effective engagement of the financial services industry to support the clearing of payment systems and providing different financing solutions to those engaged in trade on the exchange, (vi) acquisition of the right technology systems for trade platform management, and (v) availability of willing buyers (off-takers), with enough financial resources and wider off-take opportunities. For example, the Uganda Commodity Exchange has struggled with generating sufficient commodity volumes to sustain its operational costs, forcing it to function only as a regulator on behalf of the Ugandan government.57

Marketing Coordination

The marketing of cereals is characterized by long and inefficient marketing chains that lack formal, organized market structures and have numerous middlemen. Producers lack market information and market access - simultaneously, buyers lack information on crop availability, quality and price. Additionally, the growing sophistication of consumers means that cereal buyers are increasingly becoming more specific on the products they purchase. In most cases, producers are not necessarily aware of these standards, and even if they are, it is difficult to meet the volumes and quality required. Also, smallholder farmers find it difficult to implement standards because cost of compliance can be prohibitive. Furthermore, institutions responsible for quality control are not sufficiently equipped in terms of personnel, technical and even financial resources, which brings inefficiencies in the marketing system.

Marketing through rural producer organizations (POs) capitalizes on economies of scale and can be a means to overcome constraints faced by individual small-scale farmers. Through POs, higher food-quality and safety standards can be better met if farmers make joint investments and are willing to exercise mutual control and ban free-rider behavior. Bargaining power vis-à-vis input suppliers, traders and retailers can be more effective and POs are also the basis for gradually improving the share of the farmers in value addition.58 POs can also be used a vehicle for channeling essential services needed by small scale farmers. Contract farming could also give

56 ATPAF. 2016. "Towards Creating an Enabling Environment for Grain Trade in Africa: Technology, Investment, Information, Policy

and Services." link 57 IACO. 2015. An Overview of Commodity Exchanges in Africa. link 58 SNV-Netherlands Development Organisation: Producer Organisations: Going into Business with Formal Markets, 2016.

Feed the Future Market Systems Assessment East Africa Market Systems Activity February 2021

23

processors the leverage for quality products and timely supply especially if processors undertake regular inspection of producers’ facility and field level performance of the crops.

Despite the prevalence of POs in staple crops throughout the region, sorghum and millet producers are not well organized, which constrains their integration into more commercial supply chains. At present, the rice VC has multi-layered marketing channels without any significant vertical coordination between key actors. This makes it difficult to bring together farmers either through cooperatives, contract farming systems and retail chains and ultimately facilitate better delivery of output; reduce market risks; attract more investment; and/ or acquire better extension services. Without stronger linkages between markets and producers, farmers are not incentivized to invest in upgrading their production and post-harvest techniques.

One of the major challenges in the millet value chain is that actors work independently without deliberate attempts to form strategic partnerships. Where they do, they are short term—temporary and not binding. In such circumstances, there are losses in efficient information exchange, economies of scale and decreased competitiveness. Usually, partnerships across the market participants—farmer and trader, trader and transporter and wholesaler and retailer listed above—are weak, largely informal, and do not create sustainable market access. One also finds that these partnerships tend to be firmer as one climbs the marketing chain: very weak at the farm level and stronger as one climbs higher up the marketing chain. Partnerships help create market links that are necessary and key to increasing production because they provide a powerful incentive for smallholder farmers to invest in productivity-enhancing technologies.

Price Competitiveness

A major constraint to sorghum and millet grain marketing is the low and variable producer price, which fluctuates between and within markets depending on progression of the marketing season and in reaction to lower yields. Prices are lowest immediately after harvesting and can peak during lean season periods. Lower yields for sorghum and millet translate into higher prices (particularly for millet) compared to maize and imported wheat, which makes them uncompetitive as a source of animal feed and meal. These prices do not support production of these commodities as a reliable source of income. The lower price of maize and the preference for imported wheat among higher-income consumers mean that the growth in urban markets has not resulted in a proportionate growth in demand for sorghum and millet.59