IPO Note on Walton Hi Tech Industries Limited (WALTONHIL)

9

IPO Note on Walton Hi Tech Industries Limited (WALTONHIL) Date: September 22, 2020 Public Offer Price (BDT): 252.0 Cut off Price : 315.0 IPO Issue Size (BDT mn): 1,000.00 IPO Issue Size (No. of Shares) (mn): 2.93 1 EBL Securities Limited Research 2016- 17 2017-18 2018-19 2019- 20(9m An”) Financial Information (BDT mn): Net Sales 31,931 27,330 51,773 37,052 Gross Profit 11,346 8,007 20,968 16,196 Operating Profit 9,551 5,892 16,900 12,793 Financial Expenses 1,462 1,929 1,494 1,515 Profit After Tax 7,345 3,523 13,761 10,214 Assets 52,911 82,362 103,428 120,803 Debt 26,100 20,997 25,403 25,161 Equity 24,274 59,217 72,978 87,966 Retained Earnings 24,174 24,797 38,588 52,601 Cash & Cash Eqiv. 1,718 1,142 1,030 2,130 Margin: Gross Profit 35.5% 29.3% 40.5% 40.5% Operating Profit 29.9% 21.6% 32.6% 32.6% Pretax Profit 24.6% 13.9% 28.5% 28.5% Net Profit 23.0% 12.9% 26.6% 26.6% Growth (YoY): Sales 20.2% -14.4% 89.4% -28.4% Gross Profit 23.5% -29.4% 161.9% -22.8% Operating Profit 24.8% -38.3% 186.8% -24.3% Net Profit 18.2% -52.0% 290.6% -25.8% Profitability: ROA 13.9% 4.3% 13.3% 9.1% ROE 30.3% 5.9% 18.9% 12.7% Res. EPS (Post IPO) 24.5 11.7 45.9 33.7 NAVPS (Basic) 2,427.4 197.4 243.3 266.4 Leverage: Debt Ratio 53.0% 27.3% 27.7% 23.8% Debt-Equity 115.5% 38.0% 39.3% 32.7% Interest Coverage 6.53 3.05 11.31 8.28 *Income Statement figures are calculated by applying margins from Q1’20 based on Q3’20 net income. Balance sheet figures are from Q1’20. Post IPO Securities Holding: Shareholder Type No. of Shares (mn) % Holding Lock In Directors/Sponsors 300 99.03% 3 Years Mutual Funds (EIs) 0.29 0.10% Lock- in Free Other EIs 1.46 0.48% Public 0.29 0.10% NRBs 0.88 0.29% Total 302.93 100% Company Overview: Walton Hi Tech Industries Limited (WALTONHIL) manufactures and markets Refrigerator, Air Conditioner, Compressor, Television and Home & Electrical Appliances. It started off as a trading business but from 2008 Walton has started manufacturing business. Company Profile: Incorporation: April 17, 2006 Commercial Operation: April 02, 2008 Key Personnel: S M Nurul Alam Rezvi (Chariman), S M Shamsul Alam (Vice Chariman), S M Ashraful Alam (Managing Director), S M Mahbubul Alam (Director), S M Rezaul Alam (Director), Raisa Sigma Hima (Director). Number of Employees: 9,468 Plant Location: Chandra, Kaliakoir, Gazipur, Bangladesh. Business Profile: WALTONHIL distributes products throughout the country through its 13,000 Points of Sales (PoS). It has different from of distribution channels mainly Walton Plaza, Walton E-Plaza, Exclusive Distributors, Dealers, Sub-Dealers, Corporate Sales, International Business Unit (IBU), ODM (Original Design Manufacturer) and OEM (Original Equipment Manufacturer). Product Categories: Refrigerator, Air Conditioner, Compressor, Television and Home & Electrical Appliances. Revenue Composition (2018-19): Revenue Segments Domestic Sales (mn) Export (mn) Amount (mn) % Amount (mn) % Refrigerator 45,498 86.98% 34.5 57.78% Air Conditioner 2,251 4.30% 0.1 0.13% Television 3,699 7.07% 24.8 41.51% EAP 127 0.24% HAP 733 1.40% 0.3 0.58% Total 52,308 100.00% 60 100.00% Capacity Utilization Matrix: IPO Information Face Value 10.0 Cut off Price (Eligible Investors) 315.0 Offer Price (Public) (at 10% discount) 252.0 Authorized Capital (BDT mn) 6,000.0 Pre IPO Paid up Capital (BDT mn) 3,000.0 Post IPO Paid up Capital (BDT mn) 3,029.3 Retained Earnings as on 30 th Sep, 2019 (BDT mn) 52,600.7 IPO Issue Size (No. of shares) (mn) 2.93 IPO Issue Size (BDT mn) 1,000.0 1 st Day Free Float Shares (mn) 2.93 Issue managers AAA Finance & Investments Limited Auditor Mahfel Huq & Co Product Installed Capacity (In mn) Actual Production Capacity Utilization 2017: Refrigerator 1,500,000 1,416,445 94.43% Air Conditioner 50,000 22,532 45.07% 2018: Refrigerator 1,500,000 1,416,445 81.67% Air Conditioner 50,000 22,081 44.17% Compressor 1,000,000 200,000 20.00% 2019: Refrigerator 1,750,000 1,400,000 80.00% Air Conditioner 50,000 45,000 90.00% Compressor 1,000,000 900,000 90.00%

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of IPO Note on Walton Hi Tech Industries Limited (WALTONHIL)

IPO Note on Walton Hi Tech Industries Limited (WALTONHIL) Date: September 22, 2020

Public Offer Price (BDT): 252.0

Cut off Price : 315.0 IPO Issue Size (BDT mn): 1,000.00

IPO Issue Size (No. of Shares) (mn): 2.93

1

EBL Securities Limited Research

2016-

17 2017-18 2018-19

2019-20(9m An”)

Financial Information (BDT mn):

Net Sales 31,931 27,330 51,773 37,052

Gross Profit 11,346 8,007 20,968 16,196 Operating Profit 9,551 5,892 16,900 12,793

Financial Expenses 1,462 1,929 1,494 1,515

Profit After Tax 7,345 3,523 13,761 10,214

Assets 52,911 82,362 103,428 120,803

Debt 26,100 20,997 25,403 25,161

Equity 24,274 59,217 72,978 87,966

Retained Earnings 24,174 24,797 38,588 52,601

Cash & Cash Eqiv. 1,718 1,142 1,030 2,130

Margin:

Gross Profit 35.5% 29.3% 40.5% 40.5%

Operating Profit 29.9% 21.6% 32.6% 32.6%

Pretax Profit 24.6% 13.9% 28.5% 28.5%

Net Profit 23.0% 12.9% 26.6% 26.6%

Growth (YoY):

Sales 20.2% -14.4% 89.4% -28.4%

Gross Profit 23.5% -29.4% 161.9% -22.8%

Operating Profit 24.8% -38.3% 186.8% -24.3%

Net Profit 18.2% -52.0% 290.6% -25.8%

Profitability:

ROA 13.9% 4.3% 13.3% 9.1%

ROE 30.3% 5.9% 18.9% 12.7%

Res. EPS (Post IPO)

Restated

24.5 11.7 45.9 33.7

NAVPS (Basic) 2,427.4 197.4 243.3 266.4

Leverage:

Debt Ratio 53.0% 27.3% 27.7% 23.8%

Debt-Equity 115.5% 38.0% 39.3% 32.7%

Interest Coverage 6.53 3.05 11.31 8.28 *Income Statement figures are calculated by applying margins from Q1’20 based on Q3’20 net income. Balance sheet figures are from Q1’20.

Post IPO Securities Holding:

Shareholder Type No. of

Shares (mn) % Holding Lock In

Directors/Sponsors 300 99.03% 3 Years

Mutual Funds (EIs) 0.29 0.10%

Lock- in

Free

Other EIs 1.46 0.48%

Public 0.29 0.10%

NRBs 0.88 0.29%

Total 302.93 100%

Company Overview: Walton Hi Tech Industries Limited (WALTONHIL) manufactures and markets Refrigerator, Air Conditioner, Compressor, Television and Home & Electrical Appliances. It started off as a trading business but from 2008 Walton has started manufacturing business. Company Profile:

Incorporation: April 17, 2006

Commercial Operation: April 02, 2008

Key Personnel: S M Nurul Alam Rezvi (Chariman), S M Shamsul Alam (Vice Chariman), S M Ashraful Alam (Managing Director), S M Mahbubul Alam (Director), S M Rezaul Alam (Director), Raisa Sigma Hima (Director).

Number of Employees: 9,468

Plant Location: Chandra, Kaliakoir, Gazipur, Bangladesh. Business Profile: WALTONHIL distributes products throughout the country through its 13,000 Points of Sales (PoS). It has different from of distribution channels mainly Walton Plaza, Walton E-Plaza, Exclusive Distributors, Dealers, Sub-Dealers, Corporate Sales, International Business Unit (IBU), ODM (Original Design Manufacturer) and OEM (Original Equipment Manufacturer). Product Categories: Refrigerator, Air Conditioner, Compressor, Television and Home & Electrical Appliances.

Revenue Composition (2018-19):

Revenue Segments

Domestic Sales (mn) Export (mn)

Amount (mn) %

Amount (mn)

%

Refrigerator 45,498 86.98% 34.5 57.78%

Air Conditioner 2,251 4.30% 0.1 0.13%

Television 3,699 7.07% 24.8 41.51%

EAP 127 0.24%

HAP 733 1.40% 0.3 0.58%

Total 52,308 100.00% 60 100.00%

Capacity Utilization Matrix:

IPO Information

Face Value 10.0

Cut off Price (Eligible Investors) 315.0

Offer Price (Public) (at 10% discount) 252.0

Authorized Capital (BDT mn) 6,000.0

Pre IPO Paid up Capital (BDT mn) 3,000.0

Post IPO Paid up Capital (BDT mn) 3,029.3

Retained Earnings as on 30th Sep, 2019 (BDT mn)

52,600.7

IPO Issue Size (No. of shares) (mn) 2.93

IPO Issue Size (BDT mn)

1,000.0

1st Day Free Float Shares (mn) 2.93

Issue managers AAA Finance & Investments Limited

Auditor Mahfel Huq & Co

Product Installed Capacity

(In mn)

Actual Production

Capacity Utilization

2017:

Refrigerator 1,500,000 1,416,445 94.43%

Air Conditioner 50,000 22,532 45.07%

2018:

Refrigerator 1,500,000 1,416,445 81.67%

Air Conditioner 50,000 22,081 44.17%

Compressor 1,000,000 200,000 20.00%

2019:

Refrigerator 1,750,000 1,400,000 80.00%

Air Conditioner 50,000 45,000 90.00%

Compressor 1,000,000 900,000 90.00%

IPO Note on Walton Hi Tech Industries Limited (WALTONHIL) Date: September 22, 2020

Public Offer Price (BDT): 252.0

Cut off Price : 315.0 IPO Issue Size (BDT mn): 1,000.00

IPO Issue Size (No. of Shares) (mn): 2.93

2

EBL Securities Limited Research

Competitors: Listed Companies

1. Singer Bangladesh Limited 2. LG Buttefly 3. Samsung Bangladesh 4. Jamnua Group 5. Minister Hi-Tech Park Ltd

Raw Material Sources: WALTONHIL’s raw materials are Brass

Sheet, Aluminium Sheet, Filter Mesh & Baffle, Molecular Sieve,

Heat Shrink Tube, Plug Casing Assembly, Capacitor etc. Walton imports its raw materials from China, Hungary, Vietnam, Italy, India, Germany, South Korea. Belgium, Thailand, Singapore & Malaysia, Taiwan etc. IPO Fund Utilization Plan:

Particulars Amount (mn) %

Loan Repayment 330 33.00%

BMRE of Existing Projects 625 62.50%

Estimated IPO Expenses 45 4.50%

TOTAL 1,000 100%

BMRE of existing projects will be financed at a 50:50 debt equity ratio. The total project is expected to cost BDT 6.8 billion. BDT 2.775 billion of company’s own internal cash will be used alongside the IPO proceeds totaling BDT 3.4 billion equity contribution. Rest of the BDT 3.4 billion will be financed through a long term loan taken from DEG, a development finance institution in Germany.

BMRE of existing projects is expected to be completed within 12 month period from receiving the IPO fund/ proceeds.

WALTON has no Subsidiaries, Associates or any Joint Ventures.

Capital Raising History: Allotment Date of Allotment BDT

1st 17-04-2006 4,000

2nd 01-03-2007 9,996,000

3rd 02-09-2007 21,000,000

4th 14-09-2009 25,350,000

5th 14-09-2009 42,650,000

6th 27-06-2018 200,000

Total 2,850,548,200 * All the allotments were in Cash Consideration except 5th and 6th.

Lock-In Free Share (Trading Date: September 23, 2020):

Trading Day Lock-In Free

Shares (mn)

Tradable

Shares (mn)

Lock-In for

September 23, 2020 2.93 2.93 1st day

September 23, 2023 300.00 302.93 3 Years *As per BSEC directives, Directors/ Sponsors/Promoters will have to maintain at least 30% shareholding at any point in time. Distribution of IPO:

Eligible Investors General Public

Mutual Funds

(10%)

Other EIs

(50%)

NRB

(10%)

Others

(30%)

Amount (BDT mn) 101.0 508.6 96.8 293.6

Shares (mn) 0.29 1.46 0.29 0.88

1 https://www.thedailystar.net/business/news/made-bangladesh-

refrigerators-dominate-market-1808239 2 https://www.thedailystar.net/business/news/rural-demand-drives-

fridge-sales-1636753 3 https://www.dhakatribune.com/business/2019/04/05/ac-sellers-

brace-up-for-summer-sales

Industry Overview The Electrical & Electronics (E&E) industry has mainly dependent on imported products but that is changing as more local businesses have started manufacturing products locally. Currently, the market is growing at 20% which has encouraged both local and multinational manufacturers to enter into the market. E&E sector employs around 1 million people. Government has shown support to increase the sales in this industry by giving VAT exemption on the production of compressors, refrigerators and air conditioner till June 30, 2021. Online sales through Equal Monthly Installments (EMI) is becoming more prevalent in the E & E sector.

Freezer, frost & no-frost refrigerators are the main types of refrigerators that are sold in Bangladesh. Local manufacturing currently fulfils the 80% demand of the market. Some of the local manufacturers or assemblers are: Transcom, Minister, Vision, Jamuna, Singer Bangladesh and Samsung. Refrigerator industry has been growing at double digits over the last 5 years.1 The current market size of refrigerators is estimated to be at BDT 100 million2. Increase in purchasing power, availability of electricity in the rural areas, decrease in the price of the refrigerators and installment system are currently driving the refrigerator market’s growth.

Increased urbanization, increased global warming and increase in purchasing power are the factors driving the growth in AC industry in Bangladesh. In the summer season, the highest sales of AC is generally witnessed. Currently, there are 25 companies both local and foreign are selling ACs in Bangladesh3. In the last 5 years, AC demand has increased at the rate of 20%-25%. Current AC market size is BDT 65 billion and local companies have 40% market share.4 Middle income and lower middle income people’s demand for AC is increasing as local manufacturers are providing AC at a lower and more affordable price and as a result the current market size is expanding.

Bangladesh is the 15th in compressor manufacturing in the world and 2nd in the SAARC. Walton is the only compressor manufacturer in the country. Only 2% of the current BDT 10 billion market is fulfilled by local manufactures and there is a large opportunity for both local and foreign manufacturers to start manufacturing locally to fulfil the local demand.

COVID-19 had shut down the country for a 2 month period from March 25 to May 30. Summer season is generally the peak sales season for Refrigerators and AC. Almost 40% of the total sales are made in this period. 5Due to shutdown, this year’s E&E sales is forecasted to have downturn. Along with that, difficulty of import of raw materials that are used in manufacturing E&E will negatively impact the industry. COVID-19 can contract the per capita income and that would adversely impact the demand of the E&E product going forward as general population will be more inclined to not do large scale capital expenditure.

4 https://www.dhakatribune.com/business/2019/04/05/ac-sellers-

brace-up-for-summer-sales i 5 https://www.dhakatribune.com/business/2020/04/29/coronavirus-

refrigerator-ac-sales-dip-in-peak-season

IPO Note on Walton Hi Tech Industries Limited (WALTONHIL) Date: September 22, 2020

Public Offer Price (BDT): 252.0

Cut off Price : 315.0 IPO Issue Size (BDT mn): 1,000.00

IPO Issue Size (No. of Shares) (mn): 2.93

3

EBL Securities Limited Research

Comparison among Recently listed Companies:

Scrips

Post IPO

Paid Up

(mn)

Issue

Size

(mn

Shares)

Re EPS

While

Listing

1st Day

Closing

Price

P/E

(listing

day)

Current

Price*

NAHEEACP 528 15 1.9 81.6 39.2 55.5

BPML 1,738 26 2.5 130.8 53.2 47.5

ACFL 1,008 21 2.7 55.0 20.7 29.5

VFSTDL 847 22 1.5 30.7 20.7 23.3

MLDYEING 1,604 20 1.4 24.2 17.5 50.0

SILVAPHL 1,300 30 0.8 29.0 36.7 20.3

IBP 930 20 1.1 32.4 41.4 22.1

KTL 890 34 1.2 24.4 12.5 12.1

SSSTEEL 2,450 25 1.3 50.1 39.1 12.6

GENEXIL 816 20 1.4 56.5 38.7 63.0

ESQUIRENIT 1,349 35 3.0 45.9 15.2 27.7

RUNNERAUTO 1,081 14 4.3 99.8 23.2 57.1

NEWLINE 699 30 1.1 19.8 17.7 13.4

SILCOPHL 944 30 1.1 25.1 22.6 26.1

SEAPEARL 1,150 15 0.7 36.4 54.3 79.1

COPPERTECH 600 20 0.8 44.8 56.0 23.2

RINGSHINE 4,351 150 1.60 15 9.4 7.6

ADNTEL 647 20 1.76 40.5 23.0 38.0

EIL 652 26.1 0.71 15 21.12 27.3

WALTONHIL 4,000 3 60.9 - - - *Current Prices are as on September 22, 2020.

Investment Insight

Investment Positive WALTONHIL is increasing its production capacity of

refrigerators from 1.75 million units to 2 million units, of air conditioner from 0.05 million units to 0.1 million units, of TV from 600,000 units to 1 million units. Also, production capacity of electricity appliances will be increased to 2 million units, home appliances to 1.5 million units and compressor to 1.5 million units. As a result, WALTONHIL is expecting a CAGR revenue increase of 12.42% and CAGR NPAT increase of 9.77% in the next 5 years.

WALTONHIL has established its own compressor manufacturing plant in 2017 which is expected to help WALTONHIL to reduce its manufacturing cost of refrigerators going forward. Gross profit margin of WALTONHIL in 2018-19 has increased by 11.20%.

WALTONHIL is eyeing export market to increase its revenue and significant growth can be expected in the export market in the coming years. In August 2019, WALTONHIL has announced that it is going to export 100,000 unit of refrigerators and 20,000 unit ACs to India through Hyundai Electronics. WALTONHIL has been exporting refrigerators to Yemen for last couple of years

and has started to export ACs from 2019. WALONHIL has also started exporting compressors in Iraq in 2019 and has a plan to export 100,000 units of LED TV by 2021 in Europe with Germany being the main market. WALTONHIL has set a target to export $1 billion of electronics and electrical appliances by 2028.

In last 5 years, Walton has witnessed 25.95% CAGR in its topline and 34.34% CAGR in its bottom line. Also, the profit margins of WALTONHIL has increased significantly in 2018-19.

Rapid urbanization and growing middle class will ensure the growth of the electronics and electrical appliances market in Bangladesh over the next decade.

99.03% of total post IPO shares are owned by WALTONHIL’s directors and sponsors and all of their shares have a 3 year lock in period. However, there will be lower liquidity as free float number of shares is relatively lower and that can lead to high buying pressure and unusual movement of share price.

In this year’s budget, government has extended all the concessionary duty benefit of the import and raw materials of the refrigerator and air conditioner compressor manufacturing industry. WALTONHIL will be able to manufacture refrigerator and air conditioner at a lower price as a result.

Investment Concern

WALTONHIL’s earning in the Q3 of 2019-20 has decreased by 53.59% YoY. Also, compared to Q1’20 EPS of BDT 15.22, total EPS in the next two quarters is only 10.31. This indicates slower business growth result and considering COVID-19 earnings may decrease even further in upcoming quarters.

WALTONHIL has suffered significant earnings loss in 2017-18 due to liquidity pressure in the money market. Due to high sensitivity of WALTONHIL’s total sales with macroeconomic and money market scenario, it has a higher business risk.

Due to COVID-19, WALTONHIL is going to face downturn in both its export and domestic sales. Economic contraction of Bangladesh can drag the downturn in sales over a prolonged period.

WALTONHIL has been taking a 3.4 Billion BDT long term loan to conclude its current BMRE project. This would increase its current long term loan by almost 50%.

WALTONHIL’s receivable turnover ratio has decreased to 2.11 in 2018-19 from 6.10 in 2019-20. The decrease in turnover ratio means suboptimal working capital management and would led to increase in more short term loans.

IPO Note on Walton Hi Tech Industries Limited (WALTONHIL) Date: September 22, 2020

Public Offer Price (BDT): 252.0

Cut off Price : 315.0 IPO Issue Size (BDT mn): 1,000.00

IPO Issue Size (No. of Shares) (mn): 2.93

4

EBL Securities Limited Research

Relative Valuation and Pricing:

*EPS is 2019-20’s 9M Annualized EPS. NAVPS is as on 31Ss March, 2020.

Probable Price Ceiling in the first 3 trading days:

Pricing Based on Relative Valuation

Particulars EPS* Multiple Value

Market Forward P/E 33.72 15.03 506.81

Sector Forward 33.72 19.94 672.38

Sensitivity Analysis

Price @10(x)PE 33.72 10.00 337.20

Price @12(x)PE 33.72 12.00 404.64

Price @14(x)PE 33.72 14.00 472.08

Price @16(x)PE 33.72 16.00 539.52

Price @18(x)PE 33.72 18.00 606.96

NAV Based Pricing

NAVPS Multiple Value

NAVPS (Market) 266.38 1.51 402.23

NAVPS (Sector) 266.38 1.10 293.02

DAY Opening Price Highest Limit (%) Closing Price P/E

1st 252.0 50.0% 378.0 11.21

2nd 378.0 50.0% 567.0 16.81

3rd 567.0 7.5% 610.0 18.09

20.72

24.48

11.74

45.87

33.73

0.50

5.50

10.50

15.50

20.50

25.50

30.50

35.50

40.50

45.50

50.50

2015-16 2016-17 2017-18 2018-19 2019-20 9m An'

Five Year's Restated Post IPO EPS (BDT)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2015-16 2016-17 2017-18 2018-19 2019-20 Q1

Profitability Margins of WALTONHIL

GP Margin OP Margin NPAT Margin Pre Tax Profit Margin

IPO Note on Walton Hi Tech Industries Limited (WALTONHIL) Date: September 22, 2020

Public Offer Price (BDT): 252.0

Cut off Price : 315.0

IPO Issue Size (BDT mn): 1,000.00

IPO Issue Size (No. of Shares) (mn): 2.76

5

EBL Securities Limited Research

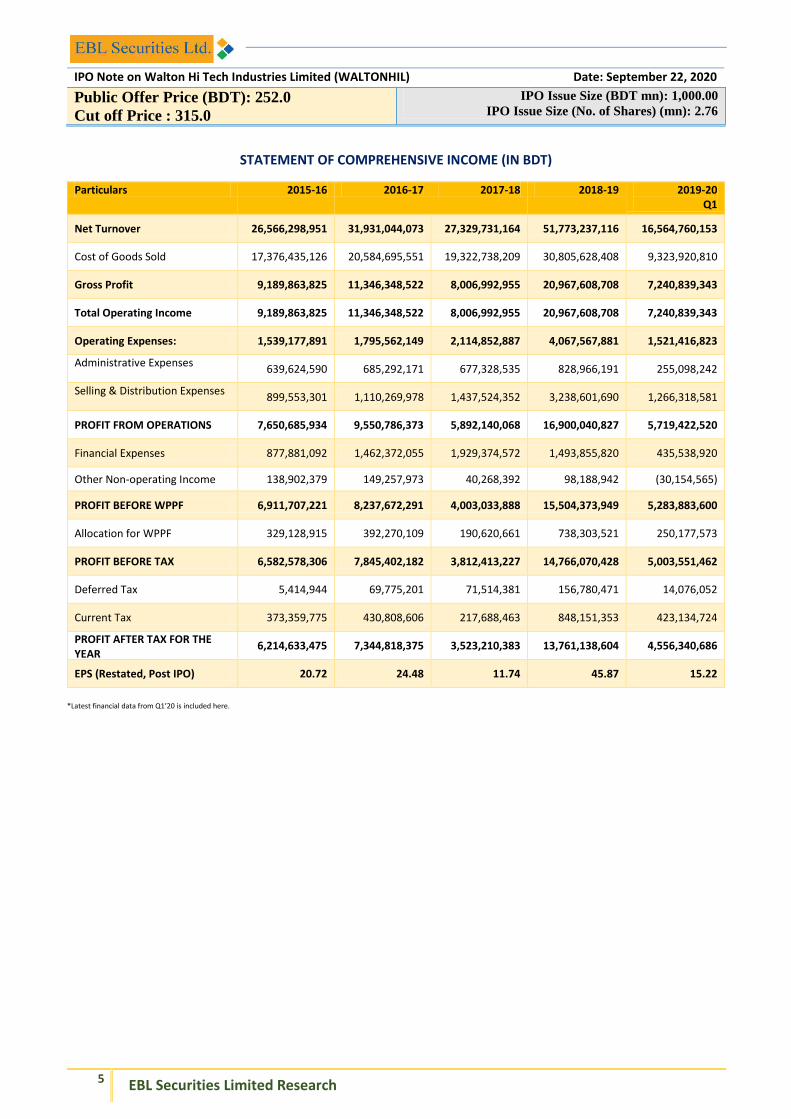

STATEMENT OF COMPREHENSIVE INCOME (IN BDT)

Particulars 2015-16 2016-17 2017-18 2018-19 2019-20 Q1

Net Turnover 26,566,298,951 31,931,044,073 27,329,731,164 51,773,237,116 16,564,760,153

Cost of Goods Sold 17,376,435,126 20,584,695,551 19,322,738,209 30,805,628,408 9,323,920,810

Gross Profit 9,189,863,825 11,346,348,522 8,006,992,955 20,967,608,708 7,240,839,343

Total Operating Income 9,189,863,825 11,346,348,522 8,006,992,955 20,967,608,708 7,240,839,343

Operating Expenses: 1,539,177,891 1,795,562,149 2,114,852,887 4,067,567,881 1,521,416,823

Administrative Expenses 639,624,590 685,292,171 677,328,535 828,966,191 255,098,242

Selling & Distribution Expenses 899,553,301 1,110,269,978 1,437,524,352 3,238,601,690 1,266,318,581

PROFIT FROM OPERATIONS 7,650,685,934 9,550,786,373 5,892,140,068 16,900,040,827 5,719,422,520

Financial Expenses 877,881,092 1,462,372,055 1,929,374,572 1,493,855,820 435,538,920

Other Non-operating Income 138,902,379 149,257,973 40,268,392 98,188,942 (30,154,565)

PROFIT BEFORE WPPF 6,911,707,221 8,237,672,291 4,003,033,888 15,504,373,949 5,283,883,600

Allocation for WPPF 329,128,915 392,270,109 190,620,661 738,303,521 250,177,573

PROFIT BEFORE TAX 6,582,578,306 7,845,402,182 3,812,413,227 14,766,070,428 5,003,551,462

Deferred Tax 5,414,944 69,775,201 71,514,381 156,780,471 14,076,052

Current Tax 373,359,775 430,808,606 217,688,463 848,151,353 423,134,724

PROFIT AFTER TAX FOR THE YEAR

6,214,633,475 7,344,818,375 3,523,210,383 13,761,138,604 4,556,340,686

EPS (Restated, Post IPO) 20.72 24.48 11.74 45.87 15.22

*Latest financial data from Q1’20 is included here.

IPO Note on Walton Hi Tech Industries Limited (WALTONHIL) Date: September 22, 2020

Public Offer Price (BDT): 252.0

Cut off Price : 315.0

IPO Issue Size (BDT mn): 1,000.00

IPO Issue Size (No. of Shares) (mn): 2.76

6

EBL Securities Limited Research

STATEMENT OF FINANCIAL POSITION (IN BDT)

Particulars 2015-16 2016-17 2017-18 2018-19 2019-20 Q1

Non-Current Assets: 14,211,488,479 23,273,823,672 58,696,298,063 60,230,346,433 63,073,710,790

PPE-Carrying Value 9,464,360,715 18,623,423,060 54,862,816,863 57,575,574,816 60,293,533,788

Intangible Assets, net 23,464,087 44016640 39,844,314 29,332,788 23,466,231

Investment - Long Term (at Cost)

100,000,000 280,000,000 793,862,675 494,171,979 518,880,578

Other Non-current Assets 4,618,248,733 4,326,383,972 2,999,774,211 2,131,266,850 2,237,830,193

Deferred tax 5,414,944

Current Assets: 19,061,475,692 29,637,013,951 23,665,691,884 43,197,763,333 58,340,908,342

Inventories 9,184,915,305 16,075,153,633 12,304,993,861 13,530,290,768 18,715,865,117

Accounts Receivable 4,358,471,782 8,913,997,928 8,376,550,686 24,479,836,553 33,129,520,306

Advances, Deposits and Prepayments

3,911,688,926 1,611,833,003 940,843,187 3,574,831,967 3,753,636,424

Short Term Investment 827,294,811 1,318,307,645 901,717,714 582,901,194 612,046,253

Cash and Cash Equiv. 779,104,868 1,717,721,742 1,141,586,436 1,029,902,851 2,129,840,242

TOTAL ASSETS 33,272,964,171 52,910,837,623 82,361,989,947 103,428,109,766 120,802,572,879

SHAREHOLDERS' EQUITY AND LIABILITIES:

Shareholders' Equity: 100,000,000 100,000,000 3,000,000,000 3,000,000,000 3,000,000,000

IPO Fund 1,000,000,000

Revaluation Reserve 31,419,620,702 31,390,563,206 31,365,271,196

Retained Earnings 16,829,279,305 24,174,097,681 24,797,308,063 38,587,504,162 52,600,683,502

Non-Current Liabilities: 2,396,208,315 4,865,799,177 10,024,196,097 7,078,903,507 7,076,489,027

LT Loans - Secured 2,345,832,800 4,756,626,163 9,732,083,072 6,194,630,678 6,278,099,322

UNDP Fund 50,375,515 44,812,757 19,625,000 95,004,333 85,503,900

Deferred Tax Liability 64,360,257 272,488,025 789,268,496 712,885,805

Current Liabilities: 13,947,476,551 23,770,940,765 13,120,865,085 23,371,138,891 25,760,129,154

Short Term Bank Loans 11,084,895,809 20,015,287,276 8,220,973,654 16,370,583,014 16,370,583,014

LT Loans – Cur. Portion 709,678,396 1,328,461,436 3,043,923,730 2,837,393,300 2,512,325,917

Trade Creditors 528,479,787 481,141,872 361,418,639 876,557,103 3,280,249,955

Others 2,743,332 154,800

Liabilities for Expenses and Provision

1,621,679,227 1,945,895,381 1,494,549,062 3,286,605,474 3,596,970,268

TOTAL SHAREHOLDERS' EQUITY AND LIABILITIES

33,272,964,171 52,910,837,623 82,361,989,947 103,428,109,766 120,802,572,879

NAV per share (Basic) 1,692.93 2,427.41 197.39 243.26 293.22

No. of Share Outstanding 10,000,000 10,000,000 300,000,000 300,000,000 300,000,000

*2019-20 data are as on 30th September, 2019.

IPO Note on Walton Hi Tech Industries Limited (WALTONHIL) Date: September 22, 2020

Public Offer Price (BDT): 252.0

Cut off Price : 315.0

IPO Issue Size (BDT mn): 1,000.00

IPO Issue Size (No. of Shares) (mn): 2.76

7

EBL Securities Limited Research

RATIO ANALYSIS

Particulars 2015-16 2016-17 2017-18 2018-19 2019-20 Q1

Liquidity Ratios

Current Ratio 1.37 1.25 1.80 1.85 2.26

Quick Ratio 0.71 0.57 0.87 1.27 1.54

Cash Ratio 0.12 0.13 0.16 0.07 0.11

Operating Efficiency Ratios

Inventory Turnover Ratio 2.89 1.99 2.22 3.83 3.54

Receivable Turnover Ratio 6.10 3.58 3.26 2.11 2.00

Avg. Collection Period (Days) 59.06 100.50 110.34 170.22 180.00

Inventory Conversion Period(Days)

124.46 181.24 162.09 94.08 101.69

Operating Cycle (Days) 183.53 281.74 272.43 264.30 281.69

A/C Payable Turnover Ratio 32.88 42.78 53.46 35.14 11.37

Payables Pay. Period (Days) 10.95 8.41 6.73 10.24 31.66

Cash Conversion Cycle 172.58 273.32 265.69 254.06 250.02

Total Asset Turnover 79.84% 60.35% 33.18% 50.06% 54.85%

Fixed Asset Turnover 280.70% 171.46% 49.81% 89.92% 109.89%

Operating Profitability Ratios

Gross Profit Margin (GPM) 34.59% 35.53% 29.30% 40.50% 43.71%

Op. Profit Margin (OPM) 28.80% 29.91% 21.56% 32.64% 34.53%

Pre Tax Profit Margin 24.78% 24.57% 13.95% 28.52% 30.21%

Net Profit Margin (NPM) 23.39% 23.00% 12.89% 26.58% 27.57%

Leverage Ratios:

Total Debt to Equity 0.93 1.16 0.38 0.39 0.33

Debt to Total Assets 47.4% 53.0% 27.3% 27.7% 23.8%

Coverage Ratios:

Times Interest Earned (TIE) 8.71 6.53 3.05 11.31 13.13

Valuation Ratios:

NAVPS (Basic) 281.14 331.59 23.17 24.88 25.53

EPS (Restated, Post IPO) 1.09 1.17 1.27 0.98 1.60

Growth Rates:

EPS Growth Rate 23.66% 18.19% -52.03% 290.59% 32.73%

Sales Growth Rate 26.53% 20.19% -14.41% 89.44% 27.98%

Gross Profit Growth Rate 33.10% 23.47% -29.43% 161.87% 38.13%

EBIT Growth Rate 29.39% 24.84% -38.31% 186.82% 35.37%

Net Income Growth Rate 23.66% 18.19% -52.03% 290.59% 32.73%

Other Data:

Number of shares outstanding 10,000,000 10,000,000 300,000,000 300,000,000 300,000,000

DUPONT ANALYSIS:

Net Profit AT/Sales 23.39% 23.00% 12.89% 26.58% 27.57%

Sales/Total Assets 79.84% 60.35% 33.18% 50.06% 54.85%

ROA 18.68% 13.88% 4.28% 13.31% 15.12%

Net Profit AT/Total Assets 18.68% 13.88% 4.28% 13.31% 15.12%

Total Asset/ Total Equity 1.97 2.18 1.39 1.42 1.37

ROE 36.71% 30.26% 5.95% 18.86% 20.76%

Extended DUPONT ANALYSIS:

Net Profit/Pretax Profit 94.41% 93.62% 92.41% 93.19% 91.26%

Pretax Profit/EBIT 86.04% 82.14% 64.70% 87.37% 87.48%

EBIT/Sales 28.80% 29.91% 21.56% 32.64% 34.53%

Sales/Assets 79.84% 60.35% 33.18% 50.06% 54.85%

Assets/Equity 1.97 2.18 1.39 1.42 1.37

ROE 36.71% 30.26% 5.95% 18.86% 20.76%

IMPORTANT DISCLOSURES

Disclaimer: This document has been prepared by the Research Team of EBL Securities Limited (EBLSL) for information purpose only of its clients residing both in Bangladesh and abroad, on the basis of the publicly available information in the market and own research. This document does not solicit any action based on the material contained herein and should not be taken as an offer or solicitation to buy or sell or subscribe to any security. Neither EBLSL nor any of its directors, shareholders, member of the management or employee represents or warrants expressly or impliedly that the information or data or the sources used in the documents are genuine, accurate, complete, authentic and correct. However all reasonable care has been taken to ensure the accuracy of the contents of this document. Being a broker, EBLSL may have a business relationship with the public companies from time to time. EBLSL and its affiliates, directors, management personnel and employees may have positions in, and buy or sell the securities, if any, referred to in this document. EBLSL disclaims liability for any direct, indirect, punitive, special, consequential, or incidental damages related to the report or the use of the report.

This document is not directed to, or intended for distribution to or use by, any person or entity that is citizen or resident of or located in any locality, state, country, or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The information and data presented herein are the exclusive property of EBLSL and any unauthorized reproduction or redistribution of the same is strictly prohibited. No part of this report should be copied or used in any other report or publication or anything of that sort without proper credit given or prior written permission taken from the authorized publisher of this report. This disclaimer applies to the report irrespective of being used in whole or in part.

Analyst Certification: The person or persons named as the author(s) of this report hereby certify that the recommendations and opinions expressed in the research report accurately reflect their personal views about the subject matter(s) discussed. The views of the author(s) do not necessarily reflect the views of the EBL Securities Limited (EBLSL) and/or any of its salespeople, traders and other professionals and are subject to change without any prior notice. All reasonable care has been taken to ensure the accuracy of the contents of this document and the author(s) will not take any responsibility for any decision made by investors based on the information herein.

Compensation of Analyst(s): The compensation of research analyst(s) is intended to reflect the value of the services they provide to the clients of EBLSL. The compensation of the analysts is impacted by the overall profitability of the firm. However, EBLSL and its analyst(s) confirms that no part of the analyst’s compensation was, is, or will be, directly or indirectly, related to the specific recommendations, opinions or views expressed in the research reports.

General Risk Factors: The information provided in the report may be impacted by market data system outages or errors, both internal and external, and affected by frequent movement of market events. The report may contain some forward looking statements, projections, estimates and forecasts which are based on assumptions made and information available to us that we believe to be reasonable and are subject to certain risks and uncertainties. There may be many uncontrollable or unknown factors and uncertainties which may cause actual results to materially differ from the results, performance or expectations expressed or implied by such forward-looking statements. EBLSL cautions all investors that such forward-looking statements in this report are not guarantees of future performance. Investors should exercise good judgment and perform adequate due-diligence prior to making any investment. All opinions and estimates contained in this report are subject to change without any notice due to changed circumstances and without legal liability. However, EBLSL disclaims any obligation to update or revise any such forward looking statements to reflect new information, events or circumstances after the publication of this report to reflect the occurrences and results of unanticipated events.

For U.S. persons only: This research report is a product of EBL Securities Ltd., which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker-dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

This report is intended for distribution by EBL Securities Ltd. only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor.

EBLSL Rating Interpretation

Overweight : Stock is expected to provide positive returns at a rate greater than its required rate of return Accumulate : Stock is expected to provide positive inflation adjusted returns at a rate less than its required rate of return Market weight : Current market price of the stock reasonably reflect its fundamental value Underweight : Stock expected to fall by more than 10% in one year Not Rated : Currently the analyst does not have adequate conviction about the stock's expected total return

About EBL Securities Ltd.: EBL Securities Ltd. (EBLSL) is one of the fastest growing full-service brokerage companies in Bangladesh and a fully owned subsidiary of Eastern Bank Limited. EBLSL is also one of the top five leading stock brokerage houses of the country. EBL Securities Limited is the TREC-holder of both exchanges of the country; DSE (TREC# 026) and CSE (TREC# 021). EBLSL takes pride in its strong commitment towards excellent client services and the development of the Bangladesh capital markets. EBLSL has developed a disciplined approach towards providing capital market services, including securities trading, margin loan facilities, depository services, foreign trading facilities, Bloomberg Terminal, online trading facilities, research services, panel brokerage services, trading through NITA for foreign investors & NRBs etc.

EBLSL Key Management

Md. Sayadur Rahman Managing Director [email protected] Md. Humayan Kabir SVP & Chief Operating Officer (COO) [email protected]

EBLSL Research Team

M. Shahryar Faiz SAVP & Head of Research [email protected] Mohammad Asrarul Haque Research Analyst [email protected] Mohammad Rehan Kabir Senior Research Associate [email protected] Arif Abdullah Research Associate [email protected] Farzana Hossain Laizu Junior Research Associate [email protected] Md Rashadur Rahman Ratul Junior Research Associate [email protected]

EBLSL Institutional & Foreign Trade Team

Asif Islam Associate Manager [email protected]

For any queries regarding this report: [email protected]

EBLSL Research Reports are also available on www.eblsecurities.com > Research

Our Global Research Distribution Partners

To access EBLSL research through Bloomberg use <EBLS>

Our Locations

Head Office:

Jiban Bima Bhaban,

10 Dilkusha C/A, 1st Floor,

Dhaka-1000

+8802 9553247, 9556845

+8802 47111935 FAX: +8802 47112944 [email protected]

HO Extension-1:

Modhumita Building 160 Motijheel C/A, 2nd Floor, Dhaka-1000. +88 02 9569480, 9564393, +88 02 8825236

HO Extension-2:

Bangladesh Sipping Corporation (BSC) Tower 2-3, Rajuk Avenue (4th floor), Motijheel, Dhaka-1000 +880257160801-4

Chattogram Branch:

Suraiya Mansion (6th Floor); 30, Agrabad C/A Chattogram-4100 +031 2522041-43

Dhanmondi Branch:

Sima Blossom, House # 390 (Old), 3 (New), Road # 27 (Old), 16 (New),Dhanmondi R/A, Dhaka-1209. +8802-9130268, +8802-9130294