Implementações do algoritmo de Fortune para variantes do ...

Upload

khangminh22Category

view

2download

0

Fortune Securities Limited |Equity Research

Indus Motor Company (INDU)

Repositioning to brace growth We re-initiate coverage on Indus Motor Company Ltd (INDU) with a BUY stance based on our DCF based Jun’21 Target Price of PKR 1,708/share. Our valuation implies an upside of 26.1% besides a forward dividend yield of 6.3% in FY21. This translates into a TSR of 32.4%. Theme of economic recovery is expected to play out in favour of the automobile sector, underpinned by low cost of consumer loans and a stable exchange rate. Pakistan, being a consumer economy, is slated to witness strong auto demand growth for long-term. INDU is poised to be a major beneficiary from an expected sharp recovery of 48% in auto demand, thereby continuing a 14.5% CAGR over FY21-25.We expect earnings to recover 86% in FY21 to PKR 120.42/share, gaining momentum over our investment case horizon and reaching of PKR 199.5/share in FY23 near to historical high. INDU trades at a forward PE of 11.2x/8.8x for FY21-22 offering DPS of PKR 85.0 & 110.0 over FY21-22. Our investment case relies on:

Repositioning: INDU has introduced Yaris to reposition its space in the 1.3L

and 1.5L category. Corolla, the star product, will stay in the product portfolio

and only compete in 1.6L and 1.8L category. Yaris is expected to solidify its

market share upto 39% as it takes on Corolla sales from lower cylinder

capacity category

Capacity expansion: In an anticipation of strong volumetric growth, INDU

has incurred a whopping capex during last two years to increase their

production capacity to 80,000 units on double shift basis

Cheap consumer financing: Volumetric growth from auto-financing is yet to

blossom as banks have just started rolling out attractive schemes;

outstanding auto loans stand at PKR 215bn (2% FY21TD) against Feb’20 peak

of PKR 219bn. INDU’s allocation of auto-financing cumulates to 30% of total

sales indicating strong recovery projections in the medium term

Strong cash generation: Pre-bookings are expected to sustain over

investment horizon rendering a cash rich balance sheet and healthy interest

income

Key Risks: Major downside risks to our investment thesis include: 1) lower than expected volumetric sales growth, 2) inability to pass on devaluation impact to end consumers, 3) intense competition from new players in sedan category, and 4) aggressive monetary tightening.

17th September’ 2020

tph June, 2015

REP-070

INDU FY18A FY19A FY20A FY21E FY22E FY23E

Net Sales (PKR mn) 139,715 157,996 86,167 138,194 171,419 211,570

Units sold (units) 63,068 65,399 28,378 47,006 55,264 64,777

Gross margin (%) 17.1% 12.1% 8.6% 10.7% 11.3% 12.0%

EBITDA margin (%) 15.1% 10.7% 8.1% 9.7% 10.0% 10.3%

PAT (PKR mn) 15,772 13,715 5,082 9,465 12,076 15,681

EPS (PKR) 200.7 174.5 64.7 120.4 153.6 199.5

DPS (PKR) 140.0 115.0 30.0 85.0 110.0 140.0

Dividend Yield (%) 8.1% 8.9% 2.9% 6.3% 8.1% 10.3%

PE (x) 8.6 7.4 15.8 11.2 8.8 6.8

ROA (%) 21.6% 18.7% 7.0% 12.1% 14.9% 17.2%

ROE (%) 46.4% 35.7% 12.5% 21.7% 25.1% 29.5%

EV/EBITDA (x) 3.7 4.5 5.5 4.8 3.5 2.5

Source: Company Accounts, Fortune Research

Investment Case

Target Price 1,708.0 Stance BUY

Performance (%) 1M 3M 12M

Absolute 1.4 41.1 35.8

Relative -5.8 12.0 1.3

52-week Performance

Key Stats

KATS Code INDU

Bloomberg Code INDU PA

Reuters Code INDM.KA

O/S shares (mn) 78.6

Market Cap (PKR'mn) 106,471

Market Cap (US$'mn) 641.4

Avg Daily Vol (000) 20.0

Free Float 17.0%

Current Price 1,354.6

Target Price 1,708.0

Upside to TP 26.1%

52 week range (PKR) 1,430.0-700.4

Rating BUY

Muqeet Naeem [email protected] (+92 21) 35309112

Fortune Securities Limited

Head Office 3rd Floor, Razi Tower, BC-13, Block No. 9, KDA Scheme No. 5 Clifton, Karachi Phone: (92 21) 35309101-09 Fax: (92 21)35309155

2|P a g e

Fortune Securities Limited |Equity Research

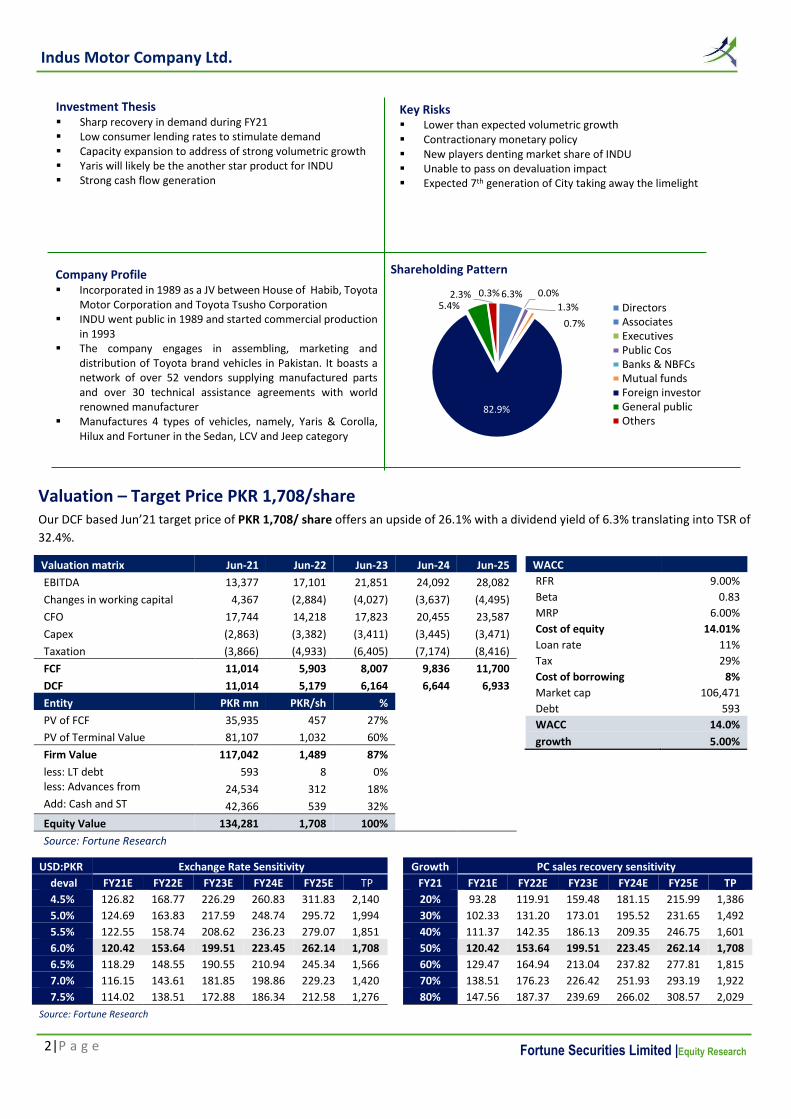

Indus Motor Company Ltd.

Valuation – Target Price PKR 1,708/share

Our DCF based Jun’21 target price of PKR 1,708/ share offers an upside of 26.1% with a dividend yield of 6.3% translating into TSR of

32.4%.

Valuation matrix Jun-21 Jun-22 Jun-23 Jun-24 Jun-25

EBITDA 13,377 17,101 21,851 24,092 28,082

Changes in working capital 4,367 (2,884) (4,027) (3,637) (4,495)

CFO 17,744 14,218 17,823 20,455 23,587

Capex (2,863) (3,382) (3,411) (3,445) (3,471)

Taxation (3,866) (4,933) (6,405) (7,174) (8,416)

FCF 11,014 5,903 8,007 9,836 11,700

DCF 11,014 5,179 6,164 6,644 6,933

Entity PKR mn PKR/sh %

PV of FCF 35,935 457 27%

PV of Terminal Value 81,107 1,032 60%

Firm Value 117,042 1,489 87%

less: LT debt 593 8 0% less: Advances from customers

24,534 312 18% Add: Cash and ST Investments

42,366 539 32%

Equity Value 134,281 1,708 100%

Source: Fortune Research

Shareholding Pattern

Key Risks Lower than expected volumetric growth Contractionary monetary policy New players denting market share of INDU Unable to pass on devaluation impact Expected 7th generation of City taking away the limelight

Investment Thesis Sharp recovery in demand during FY21 Low consumer lending rates to stimulate demand Capacity expansion to address of strong volumetric growth Yaris will likely be the another star product for INDU Strong cash flow generation

0.3% 6.3% 0.0%

1.3%

0.7%

82.9%

5.4%2.3%

DirectorsAssociatesExecutivesPublic CosBanks & NBFCsMutual fundsForeign investorGeneral publicOthers

Company Profile Incorporated in 1989 as a JV between House of Habib, Toyota

Motor Corporation and Toyota Tsusho Corporation INDU went public in 1989 and started commercial production

in 1993 The company engages in assembling, marketing and

distribution of Toyota brand vehicles in Pakistan. It boasts a network of over 52 vendors supplying manufactured parts and over 30 technical assistance agreements with world renowned manufacturer

Manufactures 4 types of vehicles, namely, Yaris & Corolla, Hilux and Fortuner in the Sedan, LCV and Jeep category

WACC

RFR 9.00%

Beta 0.83

MRP 6.00%

Cost of equity 14.01%

Loan rate 11%

Tax 29%

Cost of borrowing 8%

Market cap 106,471

Debt 593

WACC 14.0%

growth 5.00%

USD:PKR Exchange Rate Sensitivity Growth PC sales recovery sensitivity

deval FY21E FY22E FY23E FY24E FY25E TP FY21 FY21E FY22E FY23E FY24E FY25E TP

4.5% 126.82 168.77 226.29 260.83 311.83 2,140 20% 93.28 119.91 159.48 181.15 215.99 1,386

5.0% 124.69 163.83 217.59 248.74 295.72 1,994 30% 102.33 131.20 173.01 195.52 231.65 1,492

5.5% 122.55 158.74 208.62 236.23 279.07 1,851 40% 111.37 142.35 186.13 209.35 246.75 1,601

6.0% 120.42 153.64 199.51 223.45 262.14 1,708 50% 120.42 153.64 199.51 223.45 262.14 1,708

6.5% 118.29 148.55 190.55 210.94 245.34 1,566 60% 129.47 164.94 213.04 237.82 277.81 1,815

7.0% 116.15 143.61 181.85 198.86 229.23 1,420 70% 138.51 176.23 226.42 251.93 293.19 1,922

7.5% 114.02 138.51 172.88 186.34 212.58 1,276 80% 147.56 187.37 239.69 266.02 308.57 2,029

Source: Fortune Research

3|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

Tied up with GDP growth

Cyclicality of the auto industry is underpinned by its strong correlation with GDP growth

and monetary policy environment. Upon a decade long analysis of automobile demand

against GDP growth for the period FY10-19, we witnessed a GDP growth multiplier of

1.5x for volumetric automobile sales growth. GDP growth slowed down during FY19-20

backed by aggressive monetary tightening causing a massive decline in auto demand,

which was exacerbated by the outbreak of novel Coronavirus during FY20. However,

with the economy moving back on recovery road along with expansionary monetary

policy, we expect industry demand to recover by 48% during FY21.

Monetary easing brings auto financing to the forefront

Despite policy rate cut of 625 bps since Mar’20, auto financing is yet to materialize as

lockdown restrictions resulted in slow recovery of economic activity. Outstanding auto

loans stand at PKR 215bn (end Jul’20) – which are 40% of total consumer financing.

Auto financing has grown at a 5yr-CAGR of 30% (PKR 64bn to PKR 198bn) during the

period of FY13-18, when policy rate contracted from 12% to 5.75%. With policy rate

reverting to demand conducive level, we believe auto demand will be revitalised from

here onwards. It is pertinent to note that roughly 30% of INDU sales are contributed

by auto financing as per the management.

Auto demand growth has

increased with a GDP growth

multiplier of 1.5x over the

last 10 years

Source: PBS, PAMA, Fortune Research

Total Sales PC’s, LCVs Jeeps (units) – Per capita income (USD)

Source: PBS, PAMA, Fortune Research

Total Sales PC’s, LCVs Jeeps (units) – GDP growth rate %

Source: SBP, Fortune Research

Auto loans outstanding – Policy rates

Soft monetary stance by SBP

has always provided a strong

stimulus to auto demand;

increasing auto financing by

leaps and bounds

4|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

Utilizations peaked during the last boom

There exists massive potential for automobile assemblers in Pakistan, nonetheless, it

is skewed towards middle to high income groups. Industry car sales demand peaked

in FY18 at 258k units, accomodated mainly by three OEMs having combined capacity

of 255k units. Since then, demand started dwindling and finally hit the rock bottom in

FY20 at 112k units. Current capacity of three OEMs stands at 266k units with other

new entrants i.e. Kia Lucky Motors (Kia) and Hyundai Nishat Motors (Hyundai) further

enhancing supply by another 65k units.

Earlier the demand was entertained by three players with PSMC leading market share,

with INDU and HCAR rounding off the podium places.

Currency risk has dissipated considerably

Pakistan’s Current Account Deficit (CAD) reached an alarming levels of USD 19.2bn

(6.1% of GDP) while PKR remained overvalued against the greenback. The government

took strong measures to tame the current account and SBP adopted market-based

exchange rate to provide stability to the local currency; which started to devalue from

a fixed exchange rate regime. Currently the CAD stands in a soft zone of USD 2.97bn

(1.1% of GDP), causing us to have a bearish stance over any near-term currency

shocks.

Presently, the real effective exchange rate (REER) of PKR is below 100, illustrating an

undervalued scenario against USD. We do not expect significant devaluation going

forward as forex reserves provide adequate import cover in short-medium term.

Source: SBP, Fortune Research

Real effective exchange rate (REER)

Source: SBP, Fortune Research

CAD – devaluation %

Source: PAMA, Fortune Research

Market Shares of OEMs

Source: PAMA, Fortune Research

Industry Capacity Utilization

The utilization levels peaked in

FY18 and have come down

significantly due to adverse

economic conditions

USD:PKR has stabilized, albeit to

a greater extent, from what it

used to be a few years back

when CAD stood at USD 19.2bn

(6.1% of GDP). PKR currently

stands undervalued against USD

5|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

Lagged price translation from devaluation

In Pakistan, automobile assemblers are exposed to exchange rate risks because

localization is insufficient. This convention is evident from surging import costs,

leaving assemblers with no choice but to transfer inflationary impact to end

consumers. However, gross margin is not completely shielded as assemblers are

unable to completely pass-on the exchange rate impact without compromising on

volumetric growth. Moreover, this impact is dealt by price hikes with a lag effect.

We have graphically explained this phenomena by plotting currency devaluation with

monthly prices of Toyota Corolla (flagship model of INDU) since July’17, portraying a

lagged price transfer.

INDU led margins in the past

Historically, INDU has posted relatively higher gross margin compared to it’s peers

primarily attributable to its high-end luxury vehicles, with Fortuner (high margin

automobile) contributing substantially in this regard. Both INDU and HCAR witnessed

high gross margin in FY17, with INDU peaking at 17.7%. FY19 had a sluggish industry

outlook amid PKR devaluation of 34%, this continued in FY20 which was also marred

by the pandemic in the latter half of the fiscal year. Understandably, INDU’s gross

margin lowered to 8.65% in FY20.

Based on our analysis, we do not anticipate INDU’s margin to reach their previous high

due to increased competition restricting them to incur price hikes while retaining its

market share.

Source: Company website, Pakwheels, Fortune Research

PKR/USD % vs Corolla price %

Lag Factor

Source: Company Accounts, Fortune Research

Gross margins %

Based upon the data that we

have populated; it can be

largely witnessed that INDU

was unable to pass on the

impact of rising costs from PKR

devaluation to the end

consumer instantaneously

INDU has posted relatively

higher gross margin compared

to its peers primarily from

Corolla which sells like hot

cakes and discovery of a market

for Fortuner

6|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

New entrants and expansions on board

The increase in competition is around the corner with new players making inroads to

dent the market share of existing OEMs. With monetary easing of 625bps by SBP and

declining COVID19 cases bringing positive tides, consumerism is likely to kick-start

once again as approximately 70% of Pakistan’s population belongs to less than 34

years old; a demographic print that can be a leading indicator. This demographic trait

was keenly observed by foreign players as well who took advantage of ADP Policy

2016-21 to set up auto assembly lines in hopes to capture the inevitable growth cycle.

On this premise, we expect a sharp industry recovery of 48% for FY21 which would

continue to grow at a CAGR of 14.5% over the remainder of our investment horizon.

Oligoplistic shackles have been broken

The Automotive Development Policy (ADP) 2016-21 has changed the landscape of the

sector by providing incentives to new players for setting up assembly lines, which have

potentially put a drastic end to the prevailing oligopolistic industry structure. The new

entrants, Kia and Hyundai, have commenced production in FY20 with other renowned

companies like Proton and Volkswagen in pipeline to commence operational activities

in FY21.

Kia and Hyundai have launched Sportage and Tucson, respectively, in a hybrid

segment of crossover SUV, providing consumers with a relatively superior drive in a

similar price point range. We believe that the crossover SUVs from new entrants is

unlikely to give direct competition to Toyota’s Fortuner as it operates in the main SUV

segment. Similarly, Hilux would also retain its prestige (over it’s main competitor Isuzu

D-max) due to its popularity in rural areas as well as being the favored choice of

military personnels.

Indigenous level of new players

Kia has injected USD 175mn to set up assembly plant with capacity of 50,000 units. Its

localization currently stands at 12% and is projected to stretch to 50% localization or

a similar level to existing OEMs in the next 5 years. On the other hand, Hyundai had

initially invested USD 150mn for a single-shift capacity of 15,000 units plant with

further plans of investing additional USD 80mn to enhance their production capacity

to 30,000 units p.a. by 2023. Currently, they are assembling with 20% localization

level, which they intent to increase to 45% in the next 5 years.

Source: PAMA, Fortune Research

Industry Sales

CAGR of 11.9% CAGR of 14.5%

Competition has been rising

over the last couple of years

owing to ADP Policy 2016-21

The rise of new players has put

an end to the oligopoly in the

automobile sector, which has

existed over the last few decades

Kia and Hyundai have been the

leading players in making inroads

in the local arena. It is pertinent

to note that they both,

internationally, belong to the

same auto-manufacturing group

7|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

New players such as Kia and Hyundai will enjoy cheap import tariffs for the first 5 years

of commissioning. They can import non-localized and localized part at customs duty

of 10% and 25% respectively, bolstering their competency in the OEM market.

However, during the tariff benefit window they will be planning to switch gears

towards localization to be more competitive with exisiting OEMs in upcoming years.

Ride sharing: Is it a threat?

Ride sharing in Pakistan has changed the overall transport system, with Careem and

Uber beginning operations in FY16. Mass transit providers like Airlift and Swvl have

provided working class, a cheap and scheduled alternative for daily commutation.

Both of these services being rendered for a separate segment of society, possessing

extraordinary capacity of revolutionizing conventional mode of traveling via hassle-

free services, proving popular especially in metropolitan cities suffering from

congested traffic and insufficient parking spaces. Cost-benefit analysis between self-

owned cars’ and ride-sharing services – Uber and Careem in this case – indicates

owning a car is relatively more expensive than the other. Successful operations of

these services combined with the change in perception amongst masses will

materialize into a relatively material threat for the automobile industry.

Electric Vehicle policy

Electric Vehicle (EV) policy has been approved by Economic Coordination (ECC) for the

next five years with the aim of cutting pollution and curbing climate change. The policy

is framed for only electric 2-3 wheelers and heavy commercial vehicles (buses and

trucks) in the initial phase, in which specific parts of 2-3 wheelers will be imported at

1% custom duty and 1% GST. The incentive for electric cars would be added to policy

at later stages, leaving room for current assemblers to fulfill the existing demand.

Ride-sharing can potentially

become a threat if used

extensively by the masses

Any near-term impact on auto

demand from EV policy seems

too far-fetched, in our view

Customs duty imposed on current

players for importing CKD parts

lies in the range of 55-75% based

on cylinder capacity

8|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

INDU expanded to cater growing demand

INDU has incurred whopping capex of c. PKR 15bn during FY19-20 to enhance capacity

to 80k units on double shift basis, potentially increasing to 90-100k units through

debottlenecking, from previous 66k units. Capacity expansion is currently in its final

stages with commissioning expected by 1HFY21. Sales culminated to 65k units in FY19

before bottoming out to remarkably low levels of 28k units in FY20. Aided by

recovering economic activity, we expect 65%YoY growth (c.47k units) during FY21,

likely attaining momentum in the medium term, going beyond the historic peak post

FY23.

At their highest levels, delivery time usually took 6-7 months due to capacity

restraints. Presently, this period has reduced to 2-3 months potentially sustaining due

to i) commencement of double shift from Sep’20 ii) expansion in latter half of CY20.

Yaris; likely star product of INDU

INDU’s popularity emanates from its competitive pricing and high resale value. They

have launched six variants of Toyota Yaris in Mar’20 in 1.3L and 1.5L segments, with

the intention of replacing/repositioning its star product Corolla while competing

Honda City’s in the same segment. Both variants are priced similarly, but Yaris is

equipped with additional features such as superior interior design and availability of

airbags (which are currently unavailable in Honda City).

Source: Company Accounts, Fortune

INDU’s utilization levels likely to improve

INDU has wisely expanded

capacity to c. 80k units to

cater growing demand of

automobiles in Pakistan

Introduction of Yaris will allow

it to position among price

points that are equivalent to

that of Honda City

Source: PAMA, Fortune Research

INDU Product mix

9|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

In our view, Toyota Yaris is expected to takeover some market share of Honda City

until it introduces 7th generation. It is pertinent to note that Honda has introduced

newer generations of Civic but continues to operate City’s 5th generation for more

than a decade. Historically, price difference between Corolla and City was

approximately 200k-300k (Corolla was more expensive) which has been reduced

substantially with the launch of new Yaris. Yaris replaced the basic variant of Corolla

XLI and GLI in 1.3L segments and added 1.5L in the product portfolio, with Corolla

retaining its existence in 1.6L and 1.8L segments.

Assembling process ensures adequate liquidity

Automobile sector, around the world, operates under just-in-time manufacturing

process. This has enabled them to operate with low cash conversion cycles, in-fact

negative, ensuring pre-payments before delivery.

Cash and equivalents at Jun’20 for INDU stand at PKR 42bn (PKR 539/share) which is

c.40% of total market capitalization, portraying INDU as a cash rich company. The high

cash is a result of advances from customers on car booking which allows the company

to utilize excess cash to invest in PIBs & T-Bills and earn considerable return,

translating its impact in bottom-line, magnifying their profitability. However, if we net

off the impact of advances from cash and equivalents, company’s liquid position is still

satisfactory (PKR 18bn: PKR 227/share).

The just-in-time process of

assembling/manufacturing

allows auto players to keep

a cash rich position

Model Price/unit

Corolla

* Corolla Xli, 1.3L 2,519,000

* Corolla Xli 1.3L A/T 2,619,000

* Corolla Gli, 1.3L 2,769,000

* Corolla Gli, 1.3L A/T 2,869,000

Corolla Altis 1.6L M/T 3,159,000

Corolla Altis 1.6L A/T 3,309,000

Corolla Altis M/T 1.8L 3,479,000

Corolla Altis A/T 1.8L 3,679,000

Corolla Altis Grande MT 1.8L 3,679,000

Corolla Altis Grande AT 1.8L 3,899,000

Yaris

Toyota Yaris GLI MT 1.3 2,469,000

Toyota Yaris GLI CVT 1.3 2,649,000

Toyota Yaris ATIV X MT 1.5 2,789,000

Toyota Yaris ATIV X CVT 1.5 2,959,000

City

Honda City 1.3 i-VTEC 2,449,000

Honda City 1.3 i-VTEC Prosmatec 2,639,000

Honda City Aspire 1.5 i-VTEC 2,699,000

Honda City Aspire 1.5 i-VTEC Prosmatec 2,859,000

Source: Company Websites, PakWheels, Fortune Research, *Discontinued

10|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

Higher cash availability is translated into equity based expansion, keeping company

relatively debt free. Moreover, INDU is planning to launch Toyota Cross in the

crossover SUV segment during FY21, which will require additional capital expenditure

of PKR 10-13bn, potentially being financed from internal cash generation. It is

pertinent to mention that e have not incorporated the sales of Toyota Cross in our

investment case.

Corolla’s heritage

Toyota Corolla is undoubtedly the most popular Sedan in Pakistan, owing to its value

for money, availability of cheaper parts leading to lower maintenance costs, better

mileage and instant resale making it the preferred choice. Due to its built, it has also

proven to be extremely popular with for rural consumers and middle-income groups

by offering multiple variants ranging from 1.3L to 1.8L segments. All these factors have

contributed towards volumetric sales of more than 50,000 units p.a. for the past five

years (FY15-19) which no other car in Pakistan has ever managed.

Source: Company Accounts, Fortune Research

Other income generated from cash & ST investment

Toyota Corolla has an

unparalleled heritage

compared to peers

11|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

Key risks

Lower than expected volumetric growth

Our investment theme is based on recovery in volumetric sales amid improving

macroeconomic indicators. Lower than expected recovery in sales is a downside risk

to our investment case.

Impact of new players

INDU has kept a persistent share in Sedan segment due to its flagship model Corolla,

however, emergence of new players in this category can penetrate the market putting

our valuation at a downside risk.

Unable to pass on devaluation impact

Our base assumption implies that INDU will pass on any impact of currency

devaluation to end consumer. However, higher than expected currency devaluation

(6% is our base case) will compromise volumetric growth, exposing our investment

case to exchange rate risk. On the other hand, we have presented an exchange rate

sensitivity for investors assuming no annualized devaluation impact being passed

through to end consumers.

Interest rate risk

Monetary tightening of (200-300 bps) from current levels of 7% can disrupt auto

financing, hence, impeding recovery of volumes. As indicated by management, INDU

sales are roughly 30% from auto financing, therefore, changes in interest rates are a

downside risk to our volumetric estimates.

Ride sharing

Ride sharing gaining attraction in masses can be a potential threat to auto sales, as it

provides cheaper alternative to commute, putting our valuation at a downside risk.

12|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

Company financials

Income Statement (PKR mn) FY18A FY19A FY20A FY21E FY22E FY23E

Net Sales 139,715 157,996 86,167 138,194 171,419 211,570

Cost of Sales 115,831 138,805 78,716 123,446 152,026 186,277

Gross Profit 23,885 19,192 7,451 14,748 19,393 25,292

Distribution cost 1,284 1,404 1,469 1,749 2,100 2,518

Admin cost 1,524 1,410 1,385 1,575 1,841 2,156

Other Expenses 194 235 197 316 391 483

WPPF and WFF 1,705 1,406 232 933 1,191 1,546

Other Income 3,901 4,307 3,205 3,241 3,226 3,581

EBIT 19,179 14,737 4,168 10,175 13,870 18,589

D&A 1,924 2,121 2,839 3,202 3,232 3,261

EBITDA 21,103 16,858 7,007 13,377 17,101 21,851

Finance Cost 80 67 86 85 87 84

EBT 22,999 18,976 7,287 13,331 17,009 22,087

Taxation 7,227 5,261 2,205 3,866 4,933 6,405

PAT 15,772 13,715 5,082 9,465 12,076 15,681

EPS (PKR) 200.7 174.5 64.7 120.4 153.6 199.5

DPS (PKR) 140.0 115.0 30.0 85.0 110.0 140.0

Balance Sheet (PKR mn) FY18A FY19A FY20A FY21E FY22E FY23E

Fixed assets 7,311 13,898 16,574 16,236 16,386 16,535

Long-Term Loans and Advances 49 16 13 13 13 13

Other non-current assets 24 11 75 10 10 10

Total non-current assets 7,384 13,925 16,661 16,258 16,409 16,558

Current assets (ex-cash & STI) 17,311 24,174 21,251 17,682 22,375 28,076

Cash & equivalents 57,232 26,684 42,366 42,171 46,816 52,547

Total current assets 74,543 50,858 63,617 59,853 69,192 80,623

TOTAL ASSETS 81,927 64,783 80,279 76,111 85,600 97,181

Share capital 786 786 786 786 786 786

Reserves 35,958 39,259 40,383 45,290 49,506 55,126

Total shareholder's equity 36,744 40,045 41,169 46,076 50,292 55,912

Long Term Loan - 81 479 285 176 157

Other non-current liabilities 23 478 4 - - -

Total non-currrent liabilities 23 559 483 285 176 157

Current portion of long term loan - - 113 194 110 20

Trade and other payables 15,731 15,950 13,593 14,776 16,590 18,263

Advances from customers 27,491 7,930 24,534 14,776 18,433 22,829

Other current liabilities 1,938 299 385 4 - -

Total current liabilities 45,160 24,179 38,626 29,750 35,133 41,112

TOTAL LIABILITIES & EQUITY 81,927 64,783 80,279 76,111 85,600 97,181

Cash Flow Statement (PKR mn) FY18A FY19A FY20A FY21E FY22E FY23E

Net cash from operating activities 25,617 (11,552) 24,703 7,276 16,081 19,311

Net cash from investing activities (2,869) (8,662) (5,575) (2,799) (3,382) (3,411)

Net cash from financing activities (10,224) (10,333) (3,446) (4,672) (8,054) (10,170)

Net increase/(decrease) in cash flow 12,523 (30,548) 15,682 (195) 4,646 5,731

Source: Company Accounts, Fortune Research

13|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

Analyst Certification The research analyst on the cover of this report certifies that: 1) all of the views expressed in this report accurately reflect his or her personal views about any and all of the subject securities or issuers; 2) no part of any of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) expressed by the research analyst(s) in this report; 3) he/she does not have a financial interest in any and all of the subject securities or issuers aggregating more than 1% of the value of the company(s); 4) he/she or its close relative has not served as a director/officer/associate in the past three years in any and all of the subject securities or issuers; 5) he/she or its close relative has received any compensation from any and all of the subject securities or issuers in the previous 12 months; and 6) he/she has not traded in the subject security(ies) or issuer(s) in the past 7 trading days and will not trade in the next 5 trading days of issuing a coverage initiation or a material Target Price revision report.

Acronyms bps basis points LCY Local Currency BVPS Book Value per share MRP Market risk premium CAGR Compounded Annual Growth Rate NAV Net Asset Value CAPM Capital Asset Pricing Model NPV Net Present Value DCF Discounted Cash Flow PB Price-to-Book Value DDM Discounted Dividend Model PCF Price-to-cash flow DE Debt-to-Equity PE Price-to-Earnings DPS Dividend per share PKR Pakistani Rupee DY Dividend yield ppt percentage point EPS Earnings per share PS Price-to-Sales EUR Euro PV Present Value EV Enterprise Value RFR Risk-free rate EVA Economic Value Added RI Residual Income FCF Free Cash Flow ROA Return on Assets FCFE Free Cash Flow to Equity ROE Return on Equity FCFF Free Cash Flow to Firm SOTP Sum Of The Parts FCY Foreign Currency TP Target Price g Growth TSR Total Stock Return IRR Internal Rate of Return USD US Dollars JPBV Justified Price-to-Book Value WACC Weighted average cost of capital

Disclosure The investment recommendation(s) take into account both risk and expected return. FSL based the long-term Target Price estimate on fundamental analysis of the subject security(ies)’s future prospects, after having taken perceived risks into consideration. FSL have conducted extensive research to arrive at the investment recommendation(s) and target price(s) for the subject security (ies). Readers should understand that financial projection(s), target price estimate(s) and statement(s) regarding future prospects may or may not be realized. Forward looking statement(s), opinion(s) and estimate(s) included in this report constitute FSL’s judgment as of this date and are subject to change without prior notice. The target price(s) stated in reports on company update(s), initiation(s) and corporate action adjustment(s) of stocks listed on the PSX are on a 12-month basis. All other reports on PSX-listed securities, such as scoops, sector or company commentaries, do not include, denote, or imply any changes to target price(s). Disclaimer The research report prepared by Fortune Securities Limited (hereinafter referred as FSL) are based on public information and the report is for information purposes only and does not constitute nor it is intended as an offer or solicitation for the purchase or sale of security(ies) or other financial instruments. FSL makes every effort to use reliable, comprehensive information, but it makes no representation that the information contained herein is accurate or complete. Facts and views presented in this report have not been reviewed by and may not reflect information known to professionals in other business areas of FSL or any of its associated entities. FSL has established information barriers between business groups and associations maintaining complete independence of this research report. This report is not intended to provide personal investment advice nor does it provide individually tailored investment advice. This report does not take into account the specific investment objectives, financial situation/financial circumstances and the particular needs of any specific person. Investors should seek financial advice regarding the appropriateness of investing in financial instruments and implementing investment strategies discussed or recommended in this report and should understand that statements regarding future prospects may not be realized. FSL recommends that investors independently evaluate particular investments and strategies and it encourages investors to seek the advice of a financial advisor. FSL has taken all reasonable care to ensure that the information contained herein is accurate, up to date, and complies with all Pakistani legislations. However, no liability can be accepted for any errors or omissions, or for any loss resulting from the use of the information provided as any data and research material provided ahead of an investment decision are for information purposes only. We shall not be liable for any errors in the provision of this information, or for any actions taken in reliance thereon. Copyright and confidentiality No part of this document may be reproduced without the written permission of FSL. The information within this research report must not be disclosed to any other person if and until FSL has made the information publicly available.

Key risks ‒ Lower than expected volumetric growth ‒ Contractionary monetary policy ‒ New players denting market share of INDU ‒ Unable to pass on devaluation impact ‒ Expected 7th generation of City can shrink the sales of Yaris ‒

Valuation Methodology To arrive at period-end Target Price(s), FSL uses different valuation methodologies: ‒ Discounted Cash Flow (DCF, DDM) ‒ Relative Valuation (PE, PB, PS, PCF) ‒ Equity and Asset return based methodologies (EVA, RI, etc.)

Rating

BUY TSR > 15% HOLD -10% > TSR > 15% SELL TSR < -10% NR Not Rated

TSR = Capital gain + DY Old Rating Overweight TSR > 15% Marketweight 0% > TSR > 15% Underweight TSR < 0%

14|P a g e

Fortune Securities Limited |Equity Research

Indus Motor Company Ltd.

Research Team

Chief Executive

Anis ur Rahman, CFA [email protected] ( +92 21) 35309111

Institutional Sales

Irfan Surya [email protected] ( +92 21) 35309131

Director Research

Syed Arif ur Rehman [email protected] ( +92 21) 35309113

Retail Sales

Taha Aslam [email protected] ( +92 21) 35309124

Equity Research

Wajid Rizvi [email protected] (+ 92 21) 35309086

Arvind Anand

(+ 92 21) 35309119

Hasnain Murtaza [email protected] (+ 92 21) 35309119

Muqeet Naeem

(+ 92 21) 35309119

Mahnoor Shafqat

(+ 92 21) 35309119

Kishan Sidi Solanki [email protected] (+ 92 21) 35309112

Copyright © 2022 FDOKUMEN