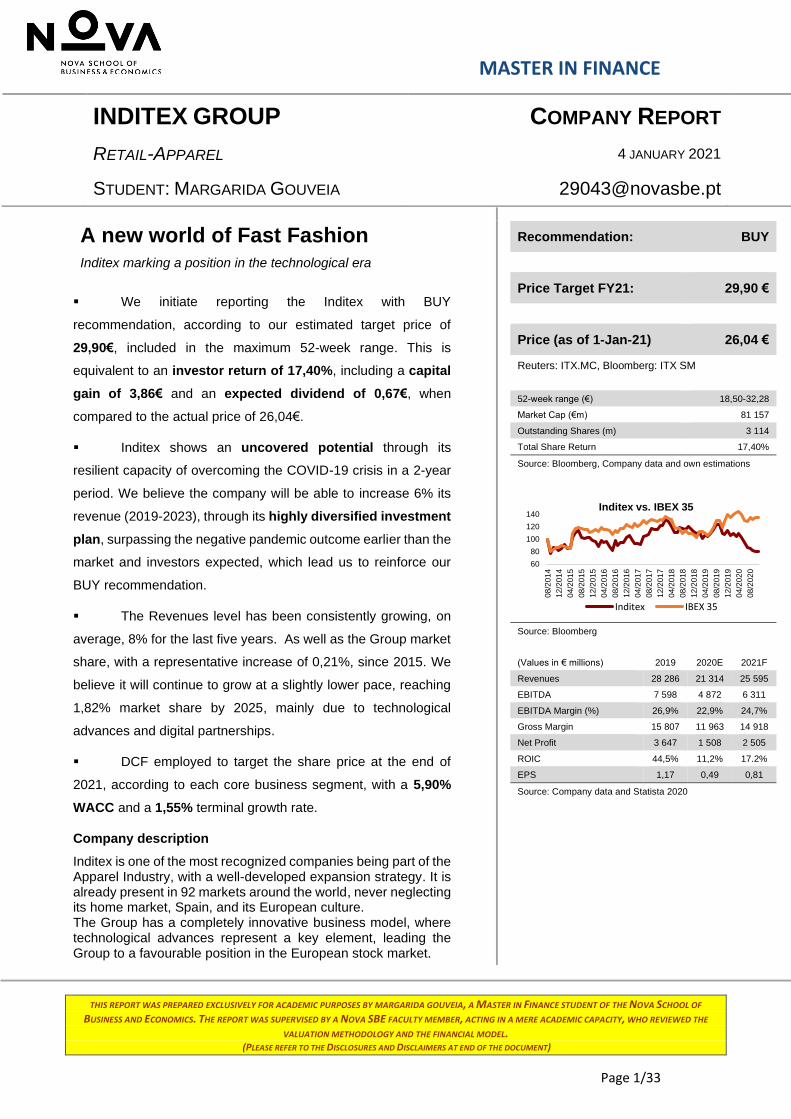

inditex group company report - retail-apparel - Nova SBE

33

MASTER IN FINANCE THIS REPORT WAS PREPARED EXCLUSIVELY FOR ACADEMIC PURPOSES BY MARGARIDA GOUVEIA, A MASTER IN FINANCE STUDENT OF THE NOVA SCHOOL OF BUSINESS AND ECONOMICS. THE REPORT WAS SUPERVISED BY A NOVA SBE FACULTY MEMBER, ACTING IN A MERE ACADEMIC CAPACITY, WHO REVIEWED THE VALUATION METHODOLOGY AND THE FINANCIAL MODEL. (PLEASE REFER TO THE DISCLOSURES AND DISCLAIMERS AT END OF THE DOCUMENT) Page 1/33 ▪ We initiate reporting the Inditex with BUY recommendation, according to our estimated target price of 29,90€, included in the maximum 52-week range. This is equivalent to an investor return of 17,40%, including a capital gain of 3,86€ and an expected dividend of 0,67€, when compared to the actual price of 26,04€. ▪ Inditex shows an uncovered potential through its resilient capacity of overcoming the COVID-19 crisis in a 2-year period. We believe the company will be able to increase 6% its revenue (2019-2023), through its highly diversified investment plan, surpassing the negative pandemic outcome earlier than the market and investors expected, which lead us to reinforce our BUY recommendation. ▪ The Revenues level has been consistently growing, on average, 8% for the last five years. As well as the Group market share, with a representative increase of 0,21%, since 2015. We believe it will continue to grow at a slightly lower pace, reaching 1,82% market share by 2025, mainly due to technological advances and digital partnerships. ▪ DCF employed to target the share price at the end of 2021, according to each core business segment, with a 5,90% WACC and a 1,55% terminal growth rate. Company description Inditex is one of the most recognized companies being part of the Apparel Industry, with a well-developed expansion strategy. It is already present in 92 markets around the world, never neglecting its home market, Spain, and its European culture. The Group has a completely innovative business model, where technological advances represent a key element, leading the Group to a favourable position in the European stock market. INDITEX GROUP COMPANY REPORT RETAIL-APPAREL 4 JANUARY 2021 STUDENT: MARGARIDA GOUVEIA [email protected] A new world of Fast Fashion Inditex marking a position in the technological era Recommendation: BUY Price Target FY21: 29,90 € Price (as of 1-Jan-21) 26,04 € Reuters: ITX.MC, Bloomberg: ITX SM 52-week range (€) 18,50-32,28 Market Cap (€m) 81 157 Outstanding Shares (m) 3 114 Total Share Return 17,40% Source: Bloomberg, Company data and own estimations Source: Bloomberg (Values in € millions) 2019 2020E 2021F Revenues 28 286 21 314 25 595 EBITDA 7 598 4 872 6 311 EBITDA Margin (%) 26,9% 22,9% 24,7% Gross Margin 15 807 11 963 14 918 Net Profit 3 647 1 508 2 505 ROIC 44,5% 11,2% 17.2% EPS 1,17 0,49 0,81 Source: Company data and Statista 2020 60 80 100 120 140 08/2014 12/2014 04/2015 08/2015 12/2015 04/2016 08/2016 12/2016 04/2017 08/2017 12/2017 04/2018 08/2018 12/2018 04/2019 08/2019 12/2019 04/2020 08/2020 Inditex vs. IBEX 35 Inditex IBEX 35

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of inditex group company report - retail-apparel - Nova SBE

MASTER IN FINANCE

THIS REPORT WAS PREPARED EXCLUSIVELY FOR ACADEMIC PURPOSES BY MARGARIDA GOUVEIA, A MASTER IN FINANCE STUDENT OF THE NOVA SCHOOL OF

BUSINESS AND ECONOMICS. THE REPORT WAS SUPERVISED BY A NOVA SBE FACULTY MEMBER, ACTING IN A MERE ACADEMIC CAPACITY, WHO REVIEWED THE

VALUATION METHODOLOGY AND THE FINANCIAL MODEL. (PLEASE REFER TO THE DISCLOSURES AND DISCLAIMERS AT END OF THE DOCUMENT)

Page 1/33

▪ We initiate reporting the Inditex with BUY

recommendation, according to our estimated target price of

29,90€, included in the maximum 52-week range. This is

equivalent to an investor return of 17,40%, including a capital

gain of 3,86€ and an expected dividend of 0,67€, when

compared to the actual price of 26,04€.

▪ Inditex shows an uncovered potential through its

resilient capacity of overcoming the COVID-19 crisis in a 2-year

period. We believe the company will be able to increase 6% its

revenue (2019-2023), through its highly diversified investment

plan, surpassing the negative pandemic outcome earlier than the

market and investors expected, which lead us to reinforce our

BUY recommendation.

▪ The Revenues level has been consistently growing, on

average, 8% for the last five years. As well as the Group market

share, with a representative increase of 0,21%, since 2015. We

believe it will continue to grow at a slightly lower pace, reaching

1,82% market share by 2025, mainly due to technological

advances and digital partnerships.

▪ DCF employed to target the share price at the end of

2021, according to each core business segment, with a 5,90%

WACC and a 1,55% terminal growth rate.

Company description

Inditex is one of the most recognized companies being part of the Apparel Industry, with a well-developed expansion strategy. It is already present in 92 markets around the world, never neglecting its home market, Spain, and its European culture. The Group has a completely innovative business model, where technological advances represent a key element, leading the Group to a favourable position in the European stock market.

INDITEX GROUP COMPANY REPORT

RETAIL-APPAREL 4 JANUARY 2021

STUDENT: MARGARIDA GOUVEIA [email protected]

A new world of Fast Fashion

Inditex marking a position in the technological era

Recommendation: BUY

Price Target FY21: 29,90 €

Price (as of 1-Jan-21) 26,04 €

Reuters: ITX.MC, Bloomberg: ITX SM

52-week range (€) 18,50-32,28

Market Cap (€m) 81 157

Outstanding Shares (m) 3 114

Total Share Return 17,40%

Source: Bloomberg, Company data and own estimations

Source: Bloomberg

(Values in € millions) 2019 2020E 2021F

Revenues 28 286 21 314 25 595

EBITDA 7 598 4 872 6 311

EBITDA Margin (%) 26,9% 22,9% 24,7%

Gross Margin 15 807 11 963 14 918

Net Profit 3 647 1 508 2 505

ROIC 44,5% 11,2% 17.2%

EPS 1,17 0,49 0,81

Source: Company data and Statista 2020

60

80

100

120

140

08

/20

14

12

/20

14

04

/20

15

08

/20

15

12

/20

15

04

/20

16

08

/20

16

12

/20

16

04

/20

17

08

/20

17

12

/20

17

04

/20

18

08

/20

18

12

/20

18

04

/20

19

08

/20

19

12

/20

19

04

/20

20

08

/20

20

Inditex vs. IBEX 35

Inditex IBEX 35

INDITEX COMPANY REPORT

PAGE 2/33

Table of Contents

COMPANY OVERVIEW ........................................................................... 3

Indices .................................................................................................. 3 Shareholder Structure and Dividend Policy.................................... 4 Impact of Covid-19 ............................................................................. 5

THE SECTOR ........................................................................................... 6

Global economy .................................................................................. 6 Consumer Shifts ................................................................................. 7 ▪ Digitalisation .................................................................................. 7 ▪ Sustainability ................................................................................. 7 ▪ Innovation ...................................................................................... 7

COMPETITION ......................................................................................... 8

VALUE DRIVERS ..................................................................................... 9

SEGMENT ANALYSIS ............................................................................12

VALUATION ASSUMPTIONS .................................................................13

Revenues Forecast .......................................................................... 13 ▪ Spain ............................................................................................ 14 ▪ Europe (excluding Spain) .......................................................... 14 ▪ Americas ...................................................................................... 15 ▪ Asia and the rest of the world ................................................... 15 Costs .................................................................................................. 16 Depreciation & Amortisation ........................................................... 18 Capital Expenditures ........................................................................ 18 Net Working Capital ......................................................................... 19 Cost of Capital & Growth rate ......................................................... 20

VALUATION OUTCOME .........................................................................22

Discounted Cash-Flow Method ...................................................... 22 Multiples Valuation ........................................................................... 22

MAJOR RISKS ........................................................................................24

SENSITIVITY ANALYSIS ........................................................................25

FINAL RECOMMENDATION ...................................................................27

APPENDIX ..............................................................................................28

FINANCIAL STATEMENTS .....................................................................28

REPORT RECOMMENDATIONS ............................................................................ 31

INDITEX COMPANY REPORT

PAGE 3/33

Company Overview

Inditex is a global fashion retail group headquartered in Arteixo (A Coruña, Spain)

that designs, produces and commercializes fashion items, mainly apparel,

footwear and accessories. The company, initially denominated as Confecciones

GOA, was founded in 1963 by Amancio Ortega. In 1975, the founder opened the

first Zara store, and its success was followed by the successive launch of new

brands and international expansion. Ten years later, Inditex was founded to

incorporate all companies under one banner.

Nowadays, Inditex operates in 202 markets on five continents, selling products

through its over 7.300 stores across 96 markets and its online platform in an

integrated way. Revenues are segmented into four geographic areas: Spain,

Europe (excluding Spain), Americas and Asia and the rest of the world. As of the

first half of 2020, Europe accounted for the higher sales share (63,6%), 14,7%

coming from the Spanish market (Exhibit 1).

The company is made up of eight brands that serve distinct market segments. Zara

is the flagship brand of the Group and the one that generates the largest portion of

revenues (Exhibit 2). It aims to shrink the gap between customers’ needs and the

fashion industry’s offer at affordable prices. Still in the range of accessible brands

are Pull&Bear, Bershka and Stradivarius. On the other hand, Massimo Dutti

and Uterqüe are focused on high-end customers, producing high quality products.

Regarding Oysho, its product line includes lingerie, beachwear, home wear and

sport. Finally, Inditex also offers home furniture and decorative items under the

brand Zara Home, reaching a broad spectrum of consumers.

Today, Inditex is the world’s largest fashion group, with more than 176.000

employees from 172 different nationalities, who are responsible for the

anticipation of customers’ needs and consequent success of the Group’s strategy.

Indices

Inditex first went public during its Initial Public Offering in 2001. Currently, its shares

are listed on the four Spanish stock exchanges and the company integrates the

IBEX 35 Index and Euro STOXX 50 Index.

Inditex is the company with higher market capitalization of the IBEX 35 Index. By

observing the Exhibit 3, it is possible to note that the company’s stock price clearly

outperformed EURO Stoxx 50 from August 2017 until March 2020. In September

2019, analysts predicted that foreign exchange pressures were going to have a

Source: Company data

14,7%

48,9%

12,0%

24,4%

Exhibit 1: Revenues by geographic area in 1H2020

Spain

Europe (not Spain)

Americas

Asia and the rest of the world

Source: Company data

0,39% 6,10%

68,87%

6,25%

7,20%

8,61%2,59%

Exhibit 2: Revenues by brand in 1H2020 (in %)

Uterqüe

Massimo Dutti

Zara (Zara + Zara Home)

Stradivarius

Pull&Bear

Bershka

Oysho

INDITEX COMPANY REPORT

PAGE 4/33

negative impact on sales, and Inditex’s share prices fell as a consequence1. This

drop was accentuated by the Covid-19 crisis and the price reached a minimum of

21,19€ per share in October 2020.

Source: Bloomberg and own analysis

In addition, the Group is included in sustainability-based indices, reflecting the

strategy followed over the years to become more social and environmentally

friendly. In 2019, it obtained a score of 4,9 (out of 5) on FTSE4Good Index and a

score of 68 on Dow Jones Sustainability Index, 40 points higher than the industry

average, being considered as one of the most sustainable retail companies for the

nineteenth consecutive year by the latter Index.

Shareholder Structure and Dividend Policy

Inditex’s shareholder structure is dispersed (see Exhibit 4). The main shareholder

is Pontegadea Inversiones SL, that accounted for 50,01% of the shares by the end

of 2019. Institutional investors, who have the second highest stake, represented

33,87%. Additionally, Partler 2006 SL, Rosp Corunna Participaciones

Empresariales SL and Retail holds 9,28%, 5,05% and 1,71% of shares,

respectively. Lastly, Inditex owns 2.125.384 treasury shares that represents

0,068% of the share capital.

Since 2018, the ordinary dividend payout is 60% of the net profit generated in

the year. The dividend policy also includes the possibility of a bonus dividend.

Over the past few years, the dividend payout ratio has been growing, as well as

dividend per share (Exhibit 5). Despite the impact of the Covid-19 pandemic, the

Group plan to maintain its dividend policy (60% ordinary payout and bonus

dividends), which gives a positive sign to investors and indicates that, even facing

difficult times, the company is financial healthy.

1 https://www.retailgazette.co.uk/blog/2018/02/zaras-shares-fall-3-year-low-analysts-drop-full-year-estimates/

50

70

90

110

130

150

09/2

014

12/2

014

03/2

015

06/2

015

09/2

015

12/2

015

03/2

016

06/2

016

09/2

016

12/2

016

03/2

017

06/2

017

09/2

017

12/2

017

03/2

018

06/2

018

09/2

018

12/2

018

03/2

019

06/2

019

09/2

019

12/2

019

03/2

020

06/2

020

09/2

020

Exhibit 3: Relative Performance Inditex, IBEX35 and EURO Stoxx 50

Inditex IBEX 35 SX5E Index

50,01%33,87%

9,28%

5,05% 1,71%

0,07%

Exhibit 4: Inditex'sShareholding Structure 2019

Pontegadea Inversiones SL

Institutional

Partler 2006 SL

Rosp Corunna ParticipacionesEmpresariales SLRetail

Source: Company data

INDITEX COMPANY REPORT

PAGE 5/33

Exhibit 5: Inditex’s Historical Dividend Payout Ratio (2015-2019)

Impact of Covid-19

Until 2019, the Group grew steadily, having reached net sales of 28.2 billion euros

and net profits of 3.6 billion euros by the end of the year. This performance was

strongly impacted by the Covid-19 pandemic due to the temporary stores

closure. By end of April 2020, only 965 stores remained open in 27 countries, out

of a total of 7.469 (see Exhibit 6). At this time, the Group reported its first loss of

409M€. In the third quarter of 2020, Inditex registered a drop in net sales of 5.7bn€,

when compared to the same period of the previous year (Exhibit 7).

Inditex has been progressively recovering its performance, mainly due to the

strength of the business model and the online segment. However, it continues to

face a challenging and uncertain environment. One example is the new phase

of closures and restrictions established from 19 October in various markets. On

the other hand, it is not clear the impact that the pandemic will have on the

economy and, consequently, on consumers’ purchasing power. This makes it even

more difficult to predict sales for years to come. Nevertheless, based on forecasts

for the industry2, it is expected that the sector will recover the sales level of 2019

in 2022 and it will continue to grow in the following years, what will be discussed

in the Revenues Forecast Section.

2 Statista, 2020

2015 2016 2017 2018 2019

Dividend per share (in €) 0,52 0,60 0,68 0,75 0,88

Number of shares outstanding (in million) 3.113 3.114 3.113 3.114 3.114

Total dividends paid (in million €) 1.619 1.868 2.117 2.335 2.741

Net income available to shareholders 2.875 3.157 3.368 3.444 3.639

Dividend payout ratio 0,56 0,59 0,63 0,68 0,75

Source: Company data

-

10

20

30

2015 2016 2017 2018 2019 2020

Th

ousands

Exhibit 7: Revenue by quarter 2015-2020 (in million €)

1Q 2Q 3Q 4Q

Source: Company data and own calculations

Source: Company data

0

1

2

3

4

5

6

7

8

Jan

Jan

Fe

b

Mar

Ma

r

Ap

r

Ma

y

Ma

y

Jun

Jul

Jul

Th

ousands

Exhibit 6: Number of stores open (January-July 2020)

INDITEX COMPANY REPORT

PAGE 6/33

The Sector

The Apparel Industry is divided into three distinct segments as women, men, and

children’s apparel. Even though clothing is not a first order necessity good, it is a

key product to consumers, especially in the most advanced economies,

symbolizing the individual expression and social achievement.

At a worldwide level, the industry has been growing for the past five years,

achieving a market size of almost 1.6 trillion € in 2019, with an average CAGR of

3,58% from 2015 to 2019 (Exhibit 8). Regarding the future of the industry, Apparel

is expected to have a revenue decline of 19% (Exhibit 9). Nevertheless, it is

critical to highlight the exponentially higher forecasted CAGR for the period

between 2020 and 2025, of 5,50%.

Source: Statista, 2020

Fashion is facing major challenges, which are expected to shape the industry

growth for the upcoming years: Global economy and Consumer Shifts.

Global economy

Firstly, the macroeconomic context is challenging. The Covid-19 pandemic is

creating significant uncertainty, with a quantifiable impact on growth. Indicators of

recession will lead to consumers being increasingly cautions and, as a

consequence, a slowdown in the sector. As Exhibit 10 depicts, GDP will decrease

in 2020 as a result of the pressure that the global economy is facing, mainly due

to the lack of capacity of distinct markets to overcome the pandemic adversities

and the increase in public and private debt levels, exposing financial markets to

volatility. The impact will be more abrupt in the Group’s home market, Spain, where

it is predicted to achieve a negative value of 12,8%. Nevertheless, it is verified also

an enormous capacity to overcome the situation, in the following year. In addition,

it is also relevant to highlight the Asian smooth effect in the curve, leading to

assume a faster recovery from the crisis, comparing to the rest of the world, that is

-20%

-10%

0%

10%

20%

0

250

500

750

1 000

1 250

1 500

1 750

2 000

2017 2018 2019 2020F 2021F 2022F 2023F 2024F 2025F

Thousands

Exhibit 9: Expected Global Apparel Industry development, in terms of market size (million €) and growth

Source: IMF 2020, World Economic Outlook

-13%

-10%

-7%

-4%

-1%

2%

5%

8%

Exhibit 10: Real GDP Growth rate (%)

2019 2020F 2021F

Source: Statista, 2020 & Own calculations

5,50%

3,58%

2015-2019

2020-2025

INDITEX COMPANY REPORT

PAGE 7/33

expected to restore economically in 2022, with a forecasted real GDP growth of

4,2%.

Consumer Shifts

Secondly, the consumer behaviour has been impacting the way fashion companies

operate and their success on the market. The major opportunities for the industry

will come from three key pillars: digitalisation, sustainability, and innovation.

▪ Digitalisation

Over the years, consumers have made more purchases online, valuing the

convenience of not having to go to stores. This change in behaviour was largely

driven by the pandemic, given the closure of a large number of stores worldwide,

which resulted in an exponential increase in online sales. Fashion is the largest e-

commerce segment, and it is expected to grow 7,4% worldwide (CAGR 2020-

2025)3. Furthermore, the number of consumers who buys online worldwide is

expected continue to increase and reach 4.914 million in 2025, compared to 3.472

million in 20204 (Exhibit 11). Still regarding digitalisation, a study developed by

McKinsey5 states that fashion companies need to exploit social media platforms to

increase their sales. Social media is seen as a route to reach a large audience,

contributing to grab consumers’ attention and brand awareness.

▪ Sustainability

The fashion industry is extremely polluting and wasteful. It is responsible for 20%

to 35% of microplastic flows into the ocean and outweighs the carbon footprint of

shopping and international flights combined6. Consumers have been increasingly

aware of the environmental impacts of Apparel industry, putting players under

pressure. Thus, fashion companies will need to swap the way they operate to face

up the consumer demand for sustainable transformational changes, as well as

regulatory requirements.

▪ Innovation

The third major opportunity for the industry is innovation. Despite the increasing

importance of the digital segment, sales made in stores represents the higher stake

of total sales of fashion industry (80%7, approximately). Therefore, stores continue

to play an important role to customers, that are increasingly value the shopping

3 Statista, 2020 4 Statista, 2020 5 “The State of Fashion 2020 – Mckinsey & Company” 6 Chinasamy, Jasmine, “A monstrous disposable industry: Fast facts about fast fashion”, Unearthed, 12th September

2019 7 Statista, 2020

Source: Statista, 2020

2832 35 38 41 44 46 49

0

10

20

30

40

50

60

Hundre

ds

Exhibit 11: Number of users e-commerce worldwide (in

millions)

INDITEX COMPANY REPORT

PAGE 8/33

journey. To adapt to shift consumer behaviour, companies need to evolve, rethink

their store network, and focus on stores equipped with cutting edge tools. On the

other hand, stores will need to complement digital sales, creating an omnichannel

model. However, this will require a higher investment, which will keep a significant

number of companies away from this path. The ones capable of reduce the friction

in the customer experience will be a step ahead of their peers.

Competition

The Apparel Retail Industry is composed by a large number of small players, from

simple niches stores to entrepreneurial boutiques, exploiting opportunities side by

side with the world giants, like Inditex and H&M. As consequence, the market

assumes an extremely competitive and highly fragmented position, enhanced

through available market data, where the top 10 companies in the sector only

represent 10%8 of the global market share.

Inditex differentiates itself from its peers due to a business model that is strongly

customer oriented. Instead of allocating a high percentage of production to the next

season, the company allocates a small fraction and uses consumers’ feedback

and an efficient network to fill stores with new products. Through a close watch on

how the trends are evolving every day around the world, it creates new garments

and puts them into the market in a rapid manner. While most of the fashion

companies would take around six months to fill their stores with new products9,

Inditex takes only one or two weeks, what is one of the main competitive

advantages of the Group. This flexibility is possible by having 54% of the factories

close to the Group’s design facilities and 10 centralised logistic centres that

distribute stocks to online and physical warehouses all over the world with a

maximum delivery time of 48 hours (Exhibit 12).

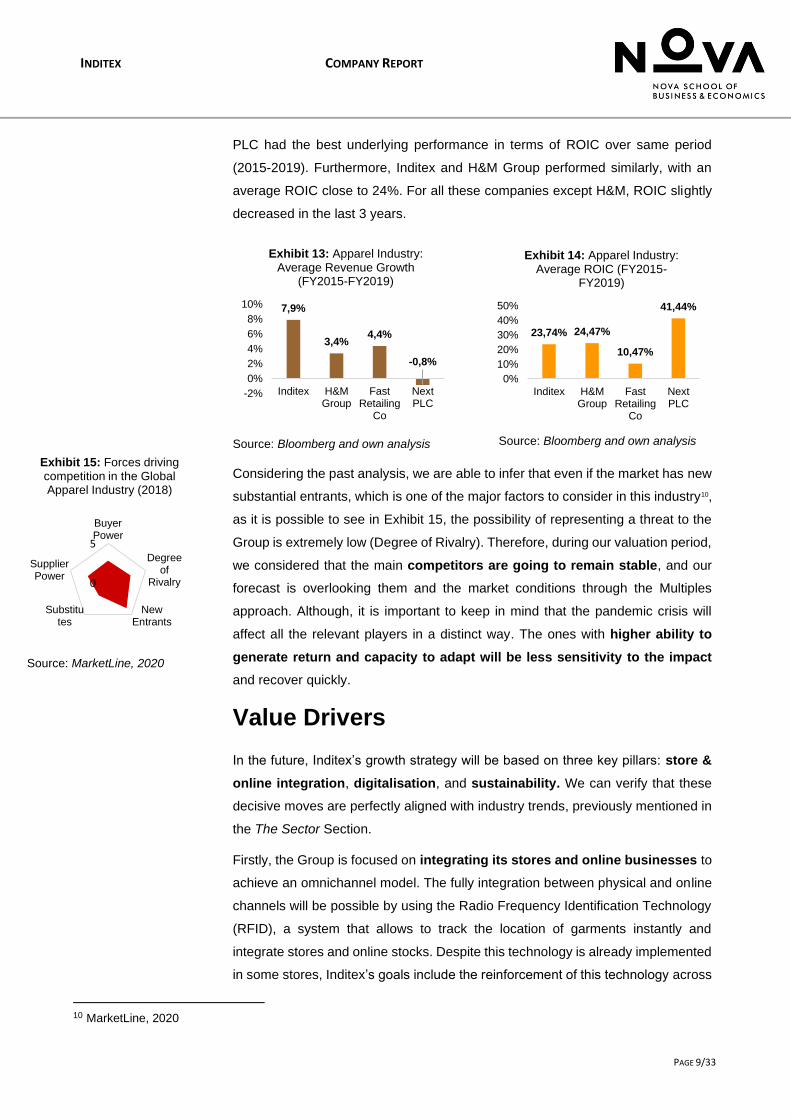

In order to understand how the Group is positioned in the market, we analysed

Inditex’s competitors and compared to the Group historical performance. From

2015 through 2019, Inditex’s revenues increased 7,9% on average. Based on

Exhibit 13, the company has been outperforming its main competitors. The

difference is quite noticeable comparing Inditex with Next PLC, with a negative

average growth (-0,8%) and H&M Group (3,4%). Since these values might not be

directly comparable, the Return on Invested Capital (ROIC) was analysed to

better evaluate the differences in value across these companies. Considering the

Exhibit 14, it is possible to see that, despite having the lower revenue growth, Next

8 https://www.themds.com/companies/the-winner-takes-it-all-top-10-fashion-companies-hold-10-of-the-global-market.html 9 https://martinroll.com/resources/articles/strategy/the-secret-of-zaras-success-a-culture-of-customer-co-creation/

Source: Own analysis

Exhibit 12: Inditex centralised distribution model

INDITEX COMPANY REPORT

PAGE 9/33

PLC had the best underlying performance in terms of ROIC over same period

(2015-2019). Furthermore, Inditex and H&M Group performed similarly, with an

average ROIC close to 24%. For all these companies except H&M, ROIC slightly

decreased in the last 3 years.

Source: Bloomberg and own analysis

Considering the past analysis, we are able to infer that even if the market has new

substantial entrants, which is one of the major factors to consider in this industry10,

as it is possible to see in Exhibit 15, the possibility of representing a threat to the

Group is extremely low (Degree of Rivalry). Therefore, during our valuation period,

we considered that the main competitors are going to remain stable, and our

forecast is overlooking them and the market conditions through the Multiples

approach. Although, it is important to keep in mind that the pandemic crisis will

affect all the relevant players in a distinct way. The ones with higher ability to

generate return and capacity to adapt will be less sensitivity to the impact

and recover quickly.

Value Drivers

In the future, Inditex’s growth strategy will be based on three key pillars: store &

online integration, digitalisation, and sustainability. We can verify that these

decisive moves are perfectly aligned with industry trends, previously mentioned in

the The Sector Section.

Firstly, the Group is focused on integrating its stores and online businesses to

achieve an omnichannel model. The fully integration between physical and online

channels will be possible by using the Radio Frequency Identification Technology

(RFID), a system that allows to track the location of garments instantly and

integrate stores and online stocks. Despite this technology is already implemented

in some stores, Inditex’s goals include the reinforcement of this technology across

10 MarketLine, 2020

7,9%

3,4%4,4%

-0,8%

-2%

0%

2%

4%

6%

8%

10%

Inditex H&MGroup

FastRetailing

Co

NextPLC

Exhibit 13: Apparel Industry: Average Revenue Growth

(FY2015-FY2019)

Source: Bloomberg and own analysis

Source: MarketLine, 2020

0

5

BuyerPower

Degreeof

Rivalry

NewEntrants

Substitutes

SupplierPower

Exhibit 15: Forces driving competition in the Global Apparel Industry (2018)

23,74% 24,47%

10,47%

41,44%

0%

10%

20%

30%

40%

50%

Inditex H&MGroup

FastRetailing

Co

NextPLC

Exhibit 14: Apparel Industry: Average ROIC (FY2015-

FY2019)

INDITEX COMPANY REPORT

PAGE 10/33

all eight of its brands over the next two years. By the end of 2022, it is expected to

be fully implemented and operational. As it happened in the past, we believe that

this technology will contribute to a lower inventory on sales in the future, with a

consequent decrease in the average holding period (AHP).

In addition, the Group differentiates itself from the competition by understanding

that customers want to experience shopping, not just buy products. Therefore, to

strengthen its position in the market, the company intends to capitalize on the store

experience by focusing on high quality stores: all integrated, digital, and eco-

efficient. Inditex is committed to upgrade the integrated store platform by rolling

out new advanced technology solutions. Between 2020 and 2021, its plan also

includes the “absorption” of 1.000-1.200 small stores (500-600 annually),

especially of brands other than Zara, and the staff to be re-deployed to tasks such

as dispatching online purchases. Lastly, the Group has announced the opening of

450 new larger stores, that will be acting as distribution hubs for online sales. In

the future, stores area is expected to grow 2.5% per year (Exhibit 16). According

to the company, the total investment allocated to the integrated store platform plan

will be around 1.7 billion euros (900 million euros a year). These investments are

incorporated in the forecasts in “Property, Plant and Equipment”. Despite the

current challenging times, Inditex is highly committed to the store optimisation

program, having registered a provision at the end of the first quarter to accomplish

this strategic goal. These efforts lead us to believe that, by the end of 2022, all

stores will be upgraded and fully integrated, as planned by the Group.

The second pillar, digitalisation, relates to Inditex’s efforts to scaling up its online

sales and it is directly connected with the store optimization program, described

before. The company expects the online segment to constitute at least 25% of the

total sales by 2022 (Exhibit 17), compared to 14% in FY2019. We believe that

Inditex will reach this goal, since it is planning to invest a significant amount (1

billion euros between 2020 and 2022) to boost its online capabilities and leverage

the online network. Digital investments will include the development of “Inditex

Open Platform”, the Group’s proprietary digital operating system, over which all

of the integrated digital operations related to the e-commerce will run. This

investment was included in “Other intangible assets”. Investments also include

new online studios with 64.000 m2 for Zara in Arteixo, Spain.

On the other hand, our belief that e-commerce will keep on being the fastest

growing revenue channel is supported by the ongoing trend worldwide towards

online shopping, as described in The Sector Section. Moreover, Inditex has a

strong presence on social media, in platforms such as Instagram, Facebook,

Twitter and Weitao, having reached 178 million followers around the world by 2019

0%

1%

2%

3%

4%

5%

4000

4500

5000

5500

6000

2018

2019

2020F

2021F

2022F

2023F

2024F

2025F

Exhibit 16: Stores area growth - Historical and

forecast

Total area (000m2)

Growth

Source: Company data and own estimates

Source: Own estimates

14%

30%

28%

27%

26%

26%

26%

0% 100%

2017

2018

2019

2020F

2021F

2022F

2023F

2024F

2025F

Exhibit 17: Expected Online Sales development

Online Offline

INDITEX COMPANY REPORT

PAGE 11/33

(Exhibit 18). As described before, the social media is playing an increasingly

important role in the fashion industry. We believe that the Group’s position in these

platforms will continue to increase in the coming years, contributing positively to

an increase in revenues.

In what concerns the last pillar, sustainability, it is a key part of the strategy. The

Group coordinates its economic growth with environmental goals to move closer

to a circular economy. Seeking to reduce its environmental footprint, it is searching

for more sustainable processes and raw materials. The goal for 2025 is that

100% of cotton, polyester and linen used to produce its products will be recycled

or will come from sustainable sources. Taking into account that cotton is the most

common raw material used to produce Inditex’s products, we expect that a change

in its consumption will result in a change in the company’s costs, more specifically

in the cost of goods sold (COGS).

The production of sustainable cotton implies extra costs because the ecological

procedures are costly. A common practice consists of avoiding chemical products,

namely pesticides. While reducing the dependency of these produts, producers

have to hire more employees to perform activities such as cleanence and repair of

damages caused by pragues, which leads to an increase in production costs and,

consequently, to an increase of raw materials’ prices. On the other hand, these

materials can be hard to find and to produce, increasing even more the final

products’ prices. As a consequence, we believe that COGS as a percentage of

sales will continue to increase until 2025, following the same trend of the past. At

this point, we expect that 100% of raw materials will come from organic sources

(Exhibit 19), leading the company to achieve a steady-state in what regards to its

costs.

However, in terms of gross margin (Exhibit 20), we believe that this strategic point

will not have a huge impact despite the increase of costs because sustainable

clothes are sold at higher prices, reflecting their high quality, which will contribute

positively to the increase of the value of revenues expected for the coming years.

Some people are willing to pay more for products that are produced with less

negative impact.

There are other initiatives that reflect some of the efforts intended by the Group to

become a more sustainable business in the future and preserve the planet: have

used-clothing containers in all stores by the end of 2020; reduce the surplus at the

end of the fashion season, mainly due to the implementation of the RFID

technology, contributing to zero waste; eliminate single-use plastic from customer

interfaces and recycle all waste generated in its facilities by 2023.

55,0%

56,0%

57,0%

58,0%

59,0%

60,0%

0

5

10

15

20

25

2017

2018

2019

2020

2021F

2022F

2023F

2024F

2025F

Th

ousands

Exhibit 20: Inditex's Gross Margin Evolution

Gross Margin

Gross Margin (%)

Source: Company data and own analysis

Source: Company data

85 86

121 144

178

0

50

100

150

200

2015 2016 2017 2018 2019

Mill

ions

Exhibit 18: Followers of Inditex on Social Media

Platforms

105%

183%

581%

111%

0%

200%

400%

600%

2018 2019

Exhibit 19: Use of sustainable & recycled materials growth (2018-

2019)

Sustainable cottonRecycled polyesterSutainable linenSustainable viscose

Source: Company data

INDITEX COMPANY REPORT

PAGE 12/33

Segment Analysis

In connection with the industry and competition analysis, the geographic

segmentation unlocks the relevance of each region and the potential growing

opportunities the leading Apparel Corporations should pursue, in the short-term.

According to Exhibit 21, the Americas together with Asia and the rest of world

account for more than 72% of the industry. Having into account that Asia &

RoW includes Middle East and African markets. Furthermore, the Asia-Pacific

region conquers over 38%, representing the area with higher potential for future

development, mostly China and India.

Deeply analysing, the Asia-Pacific region shows a remarkable CAGR of 4,1%,

for the period between 2015 and 2019. In addition, the region has been less

affected by the pandemic, and thereby the fastest to recover. As result, it has been

a visible growth in the investment, around this area, where most of the international

apparel companies, like Inditex, have placed their manufacturing centres,

increasing their dependence on foreign developing markets.

America is the most affected area of the Apparel Industry, due to COVID-19 crisis,

reaching a decrease in their revenues of almost 22%. Nevertheless, as observable

in Exhibit 23, close to 2022 is expected to surpass the crisis and being in an

ascending position.

Looking at Europe in 2020, there is a more concentrated impact in the Apparel

value. The virus caused a 17,1% decrease in revenues, possible to overcome in

the beginning of 2022.

Nevertheless, it is possible to verify in Exhibit 22 that Inditex was always above the

industry CAGR, in all regions, except in Spain. At a worldwide level, the difference

represents almost 1,6%, leading us to conclude that the Group should recover its

sales value at a higher pace than the industry, in general.

CAGR Apparel (2015-2019)

CAGR Inditex (2015-2019)

Americas 3,44% 6,72%

Europe (not Spain) 2,93% 5,91%

Asia & RoW 4,11% 4,29%

Spain 3,26% 2,95%

World 3,58% 5,17%

Exhibit 22: Apparel Industry CAGR, for each segmented region (%)

Source: Statista, 2020 and own calculations

29,9%

26,0%

42,7%

1,4%

Exhibit 21: Geographic segmentation of the Global

Apparel market (2019)

Americas

Europe (not Spain)

Asia & RoW

Spain

Source: Statista, 2020

-25,8%-17,1%

-15,4%

-18,0%

21,8%16,2% 14,1% 15,9%

12,3% 9,4% 9,9% 9,4%9,1%

5,4% 8,2% 6,3%

Americas Europe Asia & RoW Spain

Exhibit 23: Projected Regional growth, for the Apparel Industry (2020-2023)

2020F 2021F 2022F 2023F

Source: Statista, 2020

INDITEX COMPANY REPORT

PAGE 13/33

Besides the region segregation relevance, there is an industry category

segmentation impacting Inditex attitude in the market, predominantly the target

category womenswear, conquering 51% share of the Apparel industry value,

while menswear only represents 33%, and childrenswear, 16%.

Valuation Assumptions

To determine the Inditex’s value, we will start by identifying of what drives the

company’s business. In this section, we will discuss and explain a set of inputs

fundamental to the DCF analysis.

Revenues Forecast

As previously mentioned in the Value Drivers Section, Inditex is planning to follow

a strategy based on the same growth drivers as the Apparel Industry. In this way,

we considered that by applying the industry growth11 in our projections for Inditex

revenue development up until 2025, we will incorporate the impact of these value

drivers (innovation, digitalisation, and sustainability) into the forecast.

On the other hand, it is possible to observe that Inditex has been growing

according to the industry trend in each of the segmented regions, however showing

some disparities. These disparities were counted as a marginal error, estimated

through an average of the prior four years, excluding 2020 from our considerations.

We considered it reasonable not to count with the year 2020 for the average

estimation, in the succeeding years, since this atypical pandemic period does not

reflect the usual marginal difference between the Group and the industry. Thus, in

order to project Revenues as accurately as possible, we consider the industry

forecasts for the upcoming years in each of the Group operating segments,

together with the percentage of growth discrepancy expected.

In this way, we consider that the usually positive marginal difference, in terms of

growth, between Inditex and the industry places the company in a favourable

position. In order to get a deeper understanding of what drives the company’s

performance, we analysed each one of the core business segments: Spain,

Europe (excluding Spain), Americas and Asia and the rest of the world (Asia &

RoW).

11 Statista, 2020

INDITEX COMPANY REPORT

PAGE 14/33

▪ Spain

Starting with the Group home market, Spain, has the highest market share, with

21% of the Apparel Industry sales in this area being captured by Inditex. Moreover,

this country is responsible for 17% of the Group’s total revenues by 2019, a

percentage that has been decreasing for the past four years (Exhibit 24), not as a

consequence of a reduction in sales, but rather due to the Inditex expansion plan,

where other regions are gaining more space. Although, the company’s strategy for

the future does not place Spain aside, with a considerable investment projecting a

studio for online productions, to be placed in the north of the country. Even though,

it is forecasted that this area, as all the others, will reach a negative peak in 2020,

reflected through a decrease of 1,6 billion euros in revenues, 16,3% below the

industry results, that already anticipated a negative outcome of 34,2%. This is a

result of Spain being one of the most affected countries in Europe. For Inditex,

Spain will be the region taking more time to fully recover from this situation.

At a revenue level, it will take approximately five to six years. Nevertheless, it is

predicted to continue generating revenues that will follow a positive trend (Exhibit

25), which lead us to believe that the Group will be able to maintain its competitive

advantage in this business segment, in the long-term, where almost half of the

European stores are located.

▪ Europe (excluding Spain)

Looking at Europe (excluding Spain), it is possible to understand that is one of

the main focus of the company, since in 2019 this area represented 48% of the

Inditex sales, enhancing the importance in the Group’s performance.

Therefore, the company has been trying to diversify the distribution of its stores

along this area, in order to have larger stores able to arrive to the most part of the

population. However, the region felt the pandemic impact, projected to be severe

in 2020, counting for a decrease in value of 17%. Industry’s projections states that

the recovery process will be quicker that in the Group home market, Spain. Still,

the Group reached results below the industry projections by 6,75%. For the future,

we expect Inditex to demonstrate an exponential growth above the industry

average of 3%, by approximately 5% in 2025. Thus, we expect that the area

growth will be 8%, corresponding to 18,6 billion euros in revenues, at this date

(Exhibit 26). Hence, the projections will be grounded on the propensity to maintain

this favourable growth trend, exceeding the apparel market, in the next five years,

mainly due the brand awareness and the consumer willingness to follow the

Group’s fashion trends.

Source: Company data

4,766

3 133

3 642

3 978

4 225

4 393

4 487

0

1 000

2 000

3 000

4 000

5 000

Exhibit 25: Revenues in Spain, from 2019 to 2025, in

million €

Source: Company data, Statista & Own analysis

13 682

10 422

12 674

14 485

15 885

17 253

18 603

0

4 000

8 000

12 000

16 000

20 000

Exhibit 26: Revenues in Europe (ex. Spain), from 2019 to 2025, in million €

Source: Company data, Statista & Own analysis

INDITEX COMPANY REPORT

PAGE 15/33

▪ Americas

Concerning Americas, we are estimating the sales to increase from 2020

onwards, as illustrated in Exhibit 27. By 2023, we expect the economic impact of

the virus to start to be surpassed. Even knowing that Inditex did not conquer a

considerable position in the American market, the Group is trying to gain market

share for the last five years, reaching almost 1% in 2019. In the long-term, this

position is expected to be enhanced, with a stable growth rate of 9%, almost

4,8% beyond the market expectations, in 2025. In an area where

competitiveness (in terms of variety) and cultural issues are huge obstacles to

consider when approaching the market, even considering the increment in the

number of stores, it might be extremely difficult for Inditex to achieve a dominant

position there.

▪ Asia and the rest of the world

Regarding Asia and the rest of the world, Inditex is far away from gaining a

significant position in the Asian market, having into account its dimension,

cultural dynamics, and intrinsic price competitiveness effects. Despite the

positive trend followed in the forecast, where the revenues are projected to

increase more than 2,7 billion euros by 2025 (see Exhibit 28), at a stable growth

rate of 6%, Inditex is expected to grow less 1,25% than the industry, estimated to

2023. On the other hand, this region is the one less affected by the Covid-19 crisis,

registering a loss of just 200 million euros, recovered in the following year. This

occurs mostly due to the capacity of the Asian market to manage and surpass the

crisis, more rapidly than in Europe.

Analysing at a worldwide level, the online integrated platform, the global advanced

radio frequency identification technology, the stock control system, and the

integration with the physical stores, will allow Inditex to recover from COVID-19

crisis in a two-years range. Despite a 0,12% decrease in market share for 2020, it

is expected a significantly quick recovery, exceeding the industry results in most

of the regions, together with a gradual improvement of the company’s performance

comparatively to the market. Afterwards, Inditex is forecasted to reach around

36,2 billion euros in revenues by 2025, with an annual growth around 7% and a

tendency to accomplish the steady state. In these projections, there are two

important notes to retain. Firstly, almost 23,1 billion euros (65%) occur in Europe

(Exhibit 29). Secondly, more than 9,4 billion euros are obtained through their online

platform, taking us to the last analysis relatively to the revenue’s generation, the

sales channel.

Source: Company data

17%48%

16%

19%65%

Exhibit 29: Sales by Geographic area, as

percentage of Inditex total sales

SpainEurope (not Spain)AmericasAsia & RoW

4 434

2 558

3 269

3 815

4 304

4 768

5 181

0

1 500

3 000

4 500

6 000

Exhibit 27: Revenues in Americas, from 2019 to

2025, in million €

Source: Company data, Statista & Own analysis

5 403

5 200

6 010

6 554

7 008

7 477

7 935

0

2 000

4 000

6 000

8 000

Exhibit 28: Revenues value in Asia & RoW, from 2019 to

2025, in million €

Source: Company data, Statista & Own analysis

INDITEX COMPANY REPORT

PAGE 16/33

Source: Statista 2020, Company data and own analysis

The channel customers choose or have the opportunity to use define a firm’s

development, if the corporation has an upgraded system ready to face this change,

as Inditex has. This allowed the Group to avoid an extremely difficult situation in

2020, when consumers do not have a possible alternative and end up buying more

than 30% of the items online. This historical propensity forced the company to have

their online platform and logistic system ready, to correspond to the consumer

needs, which was an advantage for Inditex considering the capital investments the

Group has been doing. Thus, we expect the online platform to represent 26%

of the total revenues by 2025, where this value reaches a stable point above the

company’s target of 25%.

Costs

Cost of Sales

The cost of sales includes mainly raw materials and consumables. These costs

vary with some factors, such as the price of goods and the volume of sales. Starting

with the price of goods, we analyzed the price of cotton, since it is the most

common raw material used to produce Inditex’s garments. As shown in Exhibit 31,

prices have been highly volatile over the years. However, COGS did not follow the

same pattern, as shown in Exhibit 32, making cotton prices bad inputs to forecast

this caption.

Despite the efforts made by Inditex to manage costs in a very strict way, the

average of the COGS as a percentage of sales increased in the past. Furthermore,

the company is committed to become more sustainable, which implies the use of

non-processed materials, such as organic cotton. This raw material is

approximately 20% to 30% more expensive than “ordinary” cotton, mainly because

-30%

-20%

-10%

0%

10%

20%

30%

-

6 000

12 000

18 000

24 000

30 000

36 000

2019 2020F 2021F 2022F 2023F 2024F 2025F

Exhibit 30: Inditex Expected Revenues from 2019 to 2025 by geographic area (in million €)

Total Spain Total Europe (not Spain)

Total Americas Total Asia & RoW

Growth rate

0

5

10

15

2015 2016 2017 2018 2019

Th

ousands

Exhibit 32: Cost of sales in million € (2015-2019)

Source: Company data

Source: Index Mundi, 2020

1,1

1,3

1,5

1,7

1,9

jan/1

5

ago/1

5

ma

r/16

out/16

ma

i/17

dez/1

7

jul/18

fev/1

9

set/

19

abr/

20

Exhibit 31: Cotton prices in U.S. cents per pound (2015-

2020)

INDITEX COMPANY REPORT

PAGE 17/33

the extra costs implied in its production and the relatively lower supply, as

discussed in the Value Drivers Section. Since Inditex is planning to continue to

increase the percentage of organic cotton until 2025, we expect that costs as a

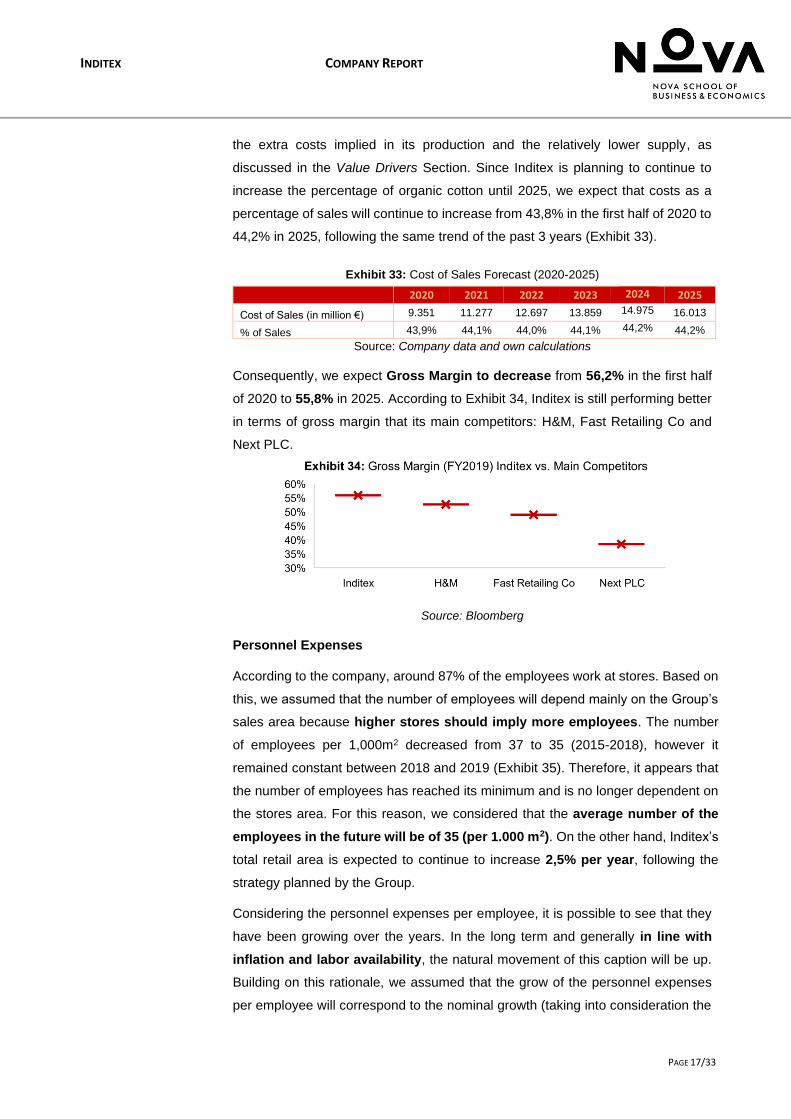

percentage of sales will continue to increase from 43,8% in the first half of 2020 to

44,2% in 2025, following the same trend of the past 3 years (Exhibit 33).

Exhibit 33: Cost of Sales Forecast (2020-2025)

Source: Company data and own calculations

Consequently, we expect Gross Margin to decrease from 56,2% in the first half

of 2020 to 55,8% in 2025. According to Exhibit 34, Inditex is still performing better

in terms of gross margin that its main competitors: H&M, Fast Retailing Co and

Next PLC.

Source: Bloomberg

Personnel Expenses

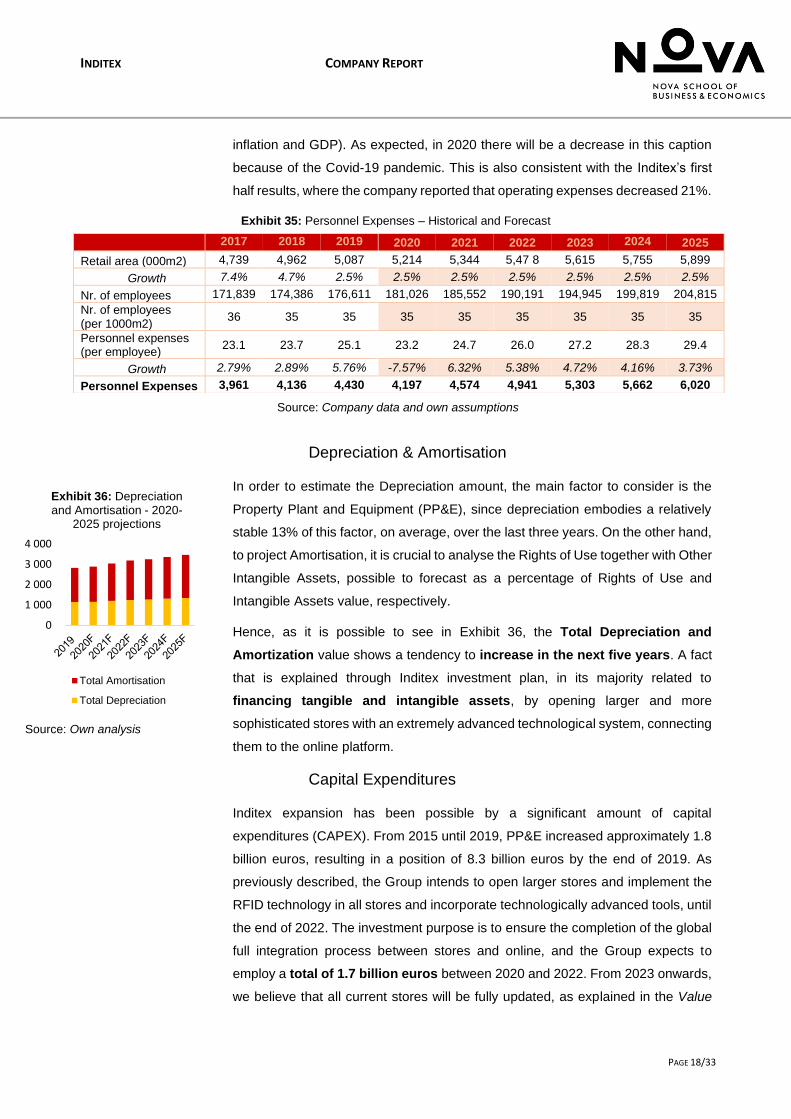

According to the company, around 87% of the employees work at stores. Based on

this, we assumed that the number of employees will depend mainly on the Group’s

sales area because higher stores should imply more employees. The number

of employees per 1,000m2 decreased from 37 to 35 (2015-2018), however it

remained constant between 2018 and 2019 (Exhibit 35). Therefore, it appears that

the number of employees has reached its minimum and is no longer dependent on

the stores area. For this reason, we considered that the average number of the

employees in the future will be of 35 (per 1.000 m2). On the other hand, Inditex’s

total retail area is expected to continue to increase 2,5% per year, following the

strategy planned by the Group.

Considering the personnel expenses per employee, it is possible to see that they

have been growing over the years. In the long term and generally in line with

inflation and labor availability, the natural movement of this caption will be up.

Building on this rationale, we assumed that the grow of the personnel expenses

per employee will correspond to the nominal growth (taking into consideration the

2020 2021 2022 2023 2024 2025

Cost of Sales (in million €) 9.351 11.277 12.697 13.859 14.975 16.013

% of Sales 43,9% 44,1% 44,0% 44,1% 44,2% 44,2%

INDITEX COMPANY REPORT

PAGE 18/33

inflation and GDP). As expected, in 2020 there will be a decrease in this caption

because of the Covid-19 pandemic. This is also consistent with the Inditex’s first

half results, where the company reported that operating expenses decreased 21%.

Exhibit 35: Personnel Expenses – Historical and Forecast

Depreciation & Amortisation

In order to estimate the Depreciation amount, the main factor to consider is the

Property Plant and Equipment (PP&E), since depreciation embodies a relatively

stable 13% of this factor, on average, over the last three years. On the other hand,

to project Amortisation, it is crucial to analyse the Rights of Use together with Other

Intangible Assets, possible to forecast as a percentage of Rights of Use and

Intangible Assets value, respectively.

Hence, as it is possible to see in Exhibit 36, the Total Depreciation and

Amortization value shows a tendency to increase in the next five years. A fact

that is explained through Inditex investment plan, in its majority related to

financing tangible and intangible assets, by opening larger and more

sophisticated stores with an extremely advanced technological system, connecting

them to the online platform.

Capital Expenditures

Inditex expansion has been possible by a significant amount of capital

expenditures (CAPEX). From 2015 until 2019, PP&E increased approximately 1.8

billion euros, resulting in a position of 8.3 billion euros by the end of 2019. As

previously described, the Group intends to open larger stores and implement the

RFID technology in all stores and incorporate technologically advanced tools, until

the end of 2022. The investment purpose is to ensure the completion of the global

full integration process between stores and online, and the Group expects to

employ a total of 1.7 billion euros between 2020 and 2022. From 2023 onwards,

we believe that all current stores will be fully updated, as explained in the Value

2017 2018 2019 2020 2021 2022 2023 2024 2025

Retail area (000m2) 4,739 4,962 5,087 5,214 5,344 5,47 8 5,615 5,755 5,899

Growth 7.4% 4.7% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5%

Nr. of employees 171,839 174,386 176,611 181,026 185,552 190,191 194,945 199,819 204,815

Nr. of employees (per 1000m2)

36 35 35 35 35 35 35 35 35

Personnel expenses (per employee)

23.1 23.7 25.1 23.2 24.7 26.0 27.2 28.3 29.4

Growth 2.79% 2.89% 5.76% -7.57% 6.32% 5.38% 4.72% 4.16% 3.73%

Personnel Expenses 3,961 4,136 4,430 4,197 4,574 4,941 5,303 5,662 6,020

Source: Company data and own assumptions

0

1 000

2 000

3 000

4 000

Exhibit 36: Depreciation and Amortisation - 2020-

2025 projections

Total Amortisation

Total Depreciation

Source: Own analysis

INDITEX COMPANY REPORT

PAGE 19/33

Drivers Section, and the amount invested in PP&E is meant to grow at the same

pace as the new stores’ area. According to Inditex’s projections, it is estimated a

gross space growth of 2,5% per year going forward. By the end of 2025, PP&E is

expected to reach 10,454 million euros (see Exhibit 37).

On the other hand, one of the Group’s key strategic pillars is digitalisation. It plans

to invest around 1 billion euros between 2020 and 2022 to develop the “Inditex

Open Platform”, where the digital transactions will take place. This amount was

incorporated into the forecasts as being an investment in Intangible Assets. For

the future, it is expected the online channel to continue to be responsible for an

increase in Inditex’s sales. Consequently, it is rational to continue to invest in this

segment, contributing to the increase in future cash flows. Thus, we estimate

intangible assets as a percentage of sales, considering the last 3 years. This

rationale was built on the fact that in the past, intangible assets represented a

relatively constant percentage of sales (2% per year). It seemed reasonable to

consider that this relation will be maintained in the future, however with higher

growth of 5% to keep up with the increasing trend of becoming even more digital.

Net Working Capital

An important determinant of value creation lies in the Group’s capacity to optimize

its working capital management. The changes in this input vary according to

Inventories, Trade and Other Receivables in addition to Payables, as well as

Income Tax Receivables and Payables, without disregarding Other Current

Assets, and Working Cash.

Over the past few years, the average holding period (AHP), determined as

inventories as a percentage of COGS, has been decreasing. Thus, the time

inventory stands in the warehouse has been lower, reflecting a sign of good

inventory management. More efficiency in manage the inventory level is in

accordance with Inditex’s investment in building a global stock integration system

and a single inventory position. As a matter of fact, when presenting the 1H2020

results, Pablo Isla stated that running the business with less inventory is an effort

that is being developed by the Group, leading us to consider that the AHP will

continue to decrease in the future at the same pace of the past. This measure

was used as an approximation to forecast inventory levels.

Regarding Trade and Other Receivables, in Exhibit 38 it is also possible to observe

coherence in the average collecting period (ACP) during the last three years.

Therefore, an estimation using an average of the ACP is a reasonable inference,

assuming the company will maintain its trade terms management conditions.

Source: Company data and own assumptions

88 8866 66 64 63 62

11 11 10 11 11 11 11

162 164 159 162 162 161 161

Exhibit 38: AHP, APP and ACP using the past 3 years

to forecast 2020-2023 period

Average Holding Period

Average Collecting Period

Average Payable Period

-40%

-20%

0%

20%

40%

60%

0

500

1000

1500

2000

Exhibit 37: CAPEX Forecast in million €

CAPEX Growth

Source: Own estimates

INDITEX COMPANY REPORT

PAGE 20/33

Looking at Trade and Other Payables, Inditex has been persistently increasing the

value, since 2017. While the average payable period had a small variation between

159 and 164 days. This means Inditex takes on average 162 days to fulfill their

accounts payable requirements.

With respect to Income Tax Receivable and Payables, it varies according to the

sales and cost of sales value, respectively, and consequently influence the core

taxes amount. These parameters vary according to the taxation of each country.

Not neglecting the Other Current Assets, which have been showing an increasing

trend, in the last five years, except for 2019, representing an average 0.5% of

revenues and just exhibiting a maximum of 0.2% variation. Considering the

working cash, it was assumed that represents 2% of the total revenues.

It is possible to observe that Inditex formulates a negative working capital value

in every financial year (Exhibit 39), meaning the Group receives money faster

than it pays to creditors. Not such a differentiation factor from the industry that also

follows this operation tactic to finance its current activity, since it receives from

customers at the moment they acquire the item, although hold the payments to

suppliers.

Source: Company data and own calculations

Cost of Capital & Growth rate

Inditex is a company with a low level of leverage, translated into a debt-to-value

ratio of 0,01. Therefore, it is almost a debt free company, that uses excess cash to

finance its activity and investments. Given the low amount of debt, the weighted

average cost of capital is very close to the cost of equity.

-923 -1 718 -1 871 -2 088

-2 309 -2 514

-817 -1 301

-1 638

-7 000

-2 000

3 000

2017 2018 2019 2020F 2021F 2022F 2023F 2024F 2025F

Exhibit 39: Operating Working Capital components: relevance and evolution along the years

Inventories Working Cash Trade and other receivables

Other current assets Income tax receivable Trade and other payables

Income tax payable

INDITEX COMPANY REPORT

PAGE 21/33

To determine the cost of equity, the Capital Asset Pricing Model (CAPM) was

applied. The current yield on the German’s 10-year Treasury Bond was considered

as the risk-free rate, thus resulting in a rate of -0,58%12. Regarding the Market

Risk Premium, it was considered to be 6,75%13, based on a recommendation from

KPMG. In order to determine the levered beta, we regressed Inditex’ stock returns

against market returns, using data from the last 5 years. The MSCI World in EUR

index, composed by a considerable number of industries and companies and

consequently, well-diversified, was chosen as a market proxy. In order to avoid

biases associated with shorter periods of time, monthly returns were considered

instead of weekly or daily returns. We arrived at a raw beta of 1,18. However, the

standard error of this regression is 0,19, meaning that the true beta may lie in the

interval between 0,81 and 1,55 (95% confidence interval)14. A widespread of the

confidence interval makes this method very imprecise and has a huge impact on

the company value, as we will discuss in the Sensitivity Analysis Section. In

addition, the regression’s R-squared is only 39,69%.

To improve the beta estimation and cross-check the result achieved, we analysed

6 industry peers: H&M, Fast Retailing Co, Next PLC, Hugo Boss, JD Sports

Fashion and American Eagle Outfitters, thus decreasing the effect of

idiosyncratic shocks. Unleveraging the betas of these similar companies in terms

of operating performance and capital structure led to an industry unlevered beta of

0,96. A beta of 0,96 implies that these securities’ prices tend to be slightly less

volatile than the overall market. By analysing the Apparel Industry’s fundamental

characteristics, it makes sense as the demand for fashion items is somehow linked

to the state of the economy. Taking as an example the current situation due to the

Covid-19 pandemic, there is much focus on purchasing essential items and fashion

becomes an after-thought for consumers with less purchasing power.

Nevertheless, this impact is felt mainly in the luxury segment. Since we are

primarily considering fast fashion players, this may explain a beta below one.

Lastly, the unlevered beta was re-levered by applying the Inditex’s market debt-to-

equity ratio of 0,01, yielding a levered beta of 0,96, as expected given the low

amount of debt. Based on the computed parameters, Inditex’s cost of equity is

5,94% and the weighted average cost of capital is 5,90% (Exhibit 40), both

parameters very close as previously stated.

12 As of 31 December 2020 13 Equity Market Risk Premium – Research Summary, 31 March 2020 14 True raw beta = Raw beta +/- 1.96 SE

Inputs

Target D/EV 0,01

Risk-free rate -0,58%

Tax rate 25%

MRP 6,75%

ΒU (industry) 0,96

ΒL 0,96

Cost of Equity 5,94%

Cost of Debt 0,05%

WACC 5,90%

Exhibit 40: Cost of Capital inputs

Source: Own assumptions and calculations

INDITEX COMPANY REPORT

PAGE 22/33

The perpetual growth rate is the rate at which we expect Inditex to grow throughout

the years, until perpetuity. Therefore, this rate was computed considering the

combination of the terminal ROIC of 26,51% with the terminal Reinvestment

Rate (RR) of 5,84%, forecasted as an average of the last three years, since it is

the period where the company starts presenting more stability and Inditex will not

be able to maintain its cash flows growing at the same rate for eternity. As result,

the rate at which the terminal value is expected to grow is approximately

1,55%. Given the relevance of this parameter, it will be challenged further through

a sensitivity analysis, discussed later in this analysis.

Valuation Outcome

Discounted Cash-Flow Method

The final firm value was determined through the DCF method, by discounting the

forecasted free cash flows at the WACC, which in the case of Inditex is close to

the cost of equity since the company presents almost no debt in its capital

structure. We assumed that Inditex will manage its capital structure to a target

level, which makes DCF the most suitable method to determine its value. As

depicts in Exhibit 41, for the forecasted period ending in 2025, the free cash flow

presents an upward trend, reflecting mainly the revenues increase, a strong

working capital management, and the investment in CAPEX. Another crucial

estimation is the terminal value, that reflects a steady-state performance. We

arrived at a terminal value of 4.439 million euros and an enterprise value of

93.989 million euros. Subtracting net debt and non-controlling interests, the

equity value amounted to 93.567 million euros. In what concerns shares

outstanding, we considered that its number will remain constant in the future

(3.114.38 million shares, not considering treasury shares). Finally, we arrived at

YE2021 target price of 29,90€ per share, what corresponds to a capital gain of

3,86€, given the current share price of 26,04€ per share. Furthermore, it is

expected the payment of a dividend of 0,67€ per share. This corresponds to a

total return of 17,40% and, consequently, our model discloses a BUY

recommendation.

Multiples Valuation

With the intention of better understand the Inditex’s fair value when compared to

its peers, we applied a Multiples valuation approach. Firstly, it was identified the

range of companies, within the industry, facing similar risks associated to

economic issues, positioned in identical market segments, and having a structured

expansion plan.

Source: Own assumptions and calculations

0

1000

2000

3000

4000

5000

Exhibit 41: Inditex's Expected Unlevered FCF

INDITEX COMPANY REPORT

PAGE 23/33

When deciding the most appropriate multiples to use, we start by a broader

analysis of Price to Earnings ratio (P/E), Price to Sales ratio (P/Sales), Enterprise

Value to Sales, EBIT and EBITDA. Considering that sales are a really volatile

parameter to ground our analysis on and both Inditex and its comparables have

a high investment level, EV/EBIT is more appropriate than EV/EBITDA. Since

EBITDA does not take into consideration the investments made by the company

may possibly lead to an overvalued estimation. EV/EBIT multiple discounts the

cash required for investments, turning out to be a better proxy of the cash available

to pay financial debt. As a result, we concluded that P/E and EV/EBIT are the most

reasonable multiples to follow our approach, combining the equity level with firm

structure, even though earnings value could be affected by one-time events.

Companies’ choice was elaborated keeping in mind Inditex’s strategic position

within the industry, as referred before, and three other criteria as the EBITDA

Margin, the Revenue growth, and the Debt-to-Equity (D/E). We attributed the

same weight deviation factor to each criteria (33%). These parameters allow us to

consider growth, profitability, and capital structure position of the other firms, when

compared to Inditex. The final rank was composed by a group of six firms that

presents the lowest deviation from Inditex’s situation. Nevertheless, the variation

range of both parameters is quite large and higher than the estimated final share

price, as visible in Exhibit 42, which is mostly due to the Inditex completely

differentiated business model and the current situation.

Deeply looking to the Inditex peers, it is imperative to recognize that Hennes &

Mauritz (H&M) is the most genuinely comparable company (Exhibit 44), with

only 10% EBITDA margin deviation, 2% D/E deviation, and a revenue growth

deviation near 0%. With a vast presence around the globe, both H&M and Inditex

are European firms, having a similar expansion plan and target audience, behind

its strategic operational situation. Followed by a Japanese growing company, Fast

Retailing Co, whose main strategy grounds on the intension to expand its already

large operational area, supported by continuous investment and the concept of

selling worthy products at low cost. After, Next PLC has a similar cultural origin

and variety of products, although does not have such a broader international

action. Hugo Boss distances itself from Inditex through its less global activity

network and the distinct strategic growth drivers, with a higher connection to brand

positioning. JD and American Eagle Outfitters have both, a different and more

specific target customer when compared to Inditex. These firms are located in a

more sportive fashion category, and even considering their widespread stores

locations, the brand development is fair behind.

P/E EV/EBIT

Inditex 26,00x 19,96x

H&M 22,76x 17,99x

Fast Retailing 91,07x 40,16x

Next PLC 15,23x 14,19x

Hugo Boss 14,57x 11,59x

JD 32,50x 23,50x

American E. Outfitters

14,11x 15,50x

Average 31.71x 20.49x

Share Price 15,01€ 17,72€

Exhibit 42: P/E and EV/EBIT multiples of Inditex and its

comparables

Source: Bloomberg and https://craft.co/inditex/competitors

INDITEX COMPANY REPORT

PAGE 24/33

In sum, it is reasonable to affirm that both, P/E and EV EBITDA, have presented a

highly diversified range of results. Following the Exhibit 43 and focusing our

analysis on the middle quartiles, share price is likely to vary from 11,59€ to 23,88€,

according to the P/E multiple, and to reach values between 15,33€ and 23,48€,

looking at the EV/EBIT multiple. This led us to conclude that, using the median, as

recommended, Inditex would achieve a share price of 15,01€ through the P/E, and

of 17,72€ in line with the EV/EBIT, which are values slightly below the minimum

ever reached by the Group. A fact that takes us to confirm a reality, where there

is the need to confirm the quality of the comparables representing the Apparel

industry and how properly can the peers estimate the firm’s future conditions

(Exhibit 44), as well as to analyse the time reference we are grounding our

estimations on. As a matter of fact, one period is not completely illustrative of the

future lucrativeness of the company and four out of the six comparables present

lower EV/EBIT and P/E multiples than the company, which may take us to

undervalue Inditex. Even more, considering the virus drastic temporarily effect on

multiples.

Major Risks

In this section, we will identify some risks that we consider to be underlying the

company’s business and that could jeopardize Inditex’s future performance.

Covid-19 pandemic: The pandemic has had a significant impact on sales, mainly

due to the closing of stores and restrictions on the number of customers. Our

revenue forecast is based on the assumption that the full recovery of the Covid-

19’s impact will happen in 2022 and will increase at a relatively high pace going

forward. However, if the depth and length of the pandemic were greater than

expected, this recovery could be delayed and, as a result, sales would be lower

than we anticipated for the coming years. The case where 2019 sales level is only

reached in 2023 will be further analysed in the Sensitivity Analysis Section.

Source: Bloomberg, Company data and own calculations

Inditex

H&M

Fast Retailing

Next PLC

Hugo Boss

JD

American Eagle

Outfitters0x

18x

36x

54x

72x

90x

0x 10x 20x 30x 40x

P/E

EV/EBIT

Exhibit 44: P/E and EV/EBIT multiples for Inditex and its comparables

10 15 20 25

P/E

EV/EBIT

Exhibit 43: Share Price variation for EV/BITDA and

P/E, in €

INDITEX COMPANY REPORT

PAGE 25/33

Delay of an effective Vaccine: In line with the last year and observing the

pandemic effect in each quarter of the year, it was possible to conclude that the

effect was softening along the time, since the companies are more prepared to

deal with the situation and the consumer is more opened and adapt to the

alternative consumption methods. Although, it is critical to account for the time it

can take for the vaccine to start making the difference and to be achieved

the group immunity, allowing the physical stores restrictions to be erased and

the population of each region to gain trust in a real recovery, incentivizing

consumption and, if still on time, avoiding an irreversible economic crisis.

Increased COGS: Inditex is focused on cost efficiencies, which requires great

control in terms of management of different lines of costs. Despite these efforts,

the ability to reduce costs not only depends on the company, but also on the market

conditions. We are already considering that COGS as a percentage of sales will

increase due to the higher prices of organic cotton, mostly related to production

costs. However, there are additional risks that can lead costs to increase even

more, as production disruption of certain raw materials due to extreme events,

such as weather events and diseases (e.g., Covid-19). This could lead to

significant pressure on Inditex’s activity if demand is lower, as well as reputational

risks related to brand perception. We will analyse the impact on the share price of

an increase in costs in the Sensitivity Analysis Section.

Sensitivity Analysis

Inditex, like other companies on the market, is facing an uncertain environment

and small changes in certain inputs can have a significant impact on the estimated

value. Given that, this section aims to test the company’s share price, when

faced with changes in some key drivers.

Firstly, we considered a sensitivity analysis of the share price, stressing the

terminal growth rate and the WACC. Concerning the first input, we assumed a

terminal growth rate of 1,55%. Since Inditex is a mature company, we do not

expect a high level of growth rate in the future. For instance, instead of 1,55%, it