impact of corruption on financial instability in pakistan

13

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan 1 , Norkhairul Hafiz Bajuri 2 , Saif-Ur-Rehman 3 , Lee Bee Yoke 4 , Faisal Khan 4 1 Corresponding Author, PhD Student at Department of Management, Faculty of Management, University Technology Malaysia [email protected]/ [email protected] 2 Senior Lecturer, Faculty of Management, University Technology Malaysia 3 Associate Professor, Faculty of Management, University Technology Malaysia 4 PhD Students, Faculty of Management, University Technology Malaysia Abstract This study attempts to examine the role of corruption, macroeconomic variables and market competitiveness on banking sector profitability. The study used unbalance panel data of 20 commercial banks for the period 2002 t0 2012. Moreover, banks are dividend to two categories i.e. government banks and private banks. The descriptive analysis indicates that the lagged profitability, equity to asset ratio, non-interest income, net-interest margin and loan growth are positively significant with banks profitability. In contrast, the loan loss provision contributes negatively to profitability. Real GDP growth and T-bill rates have positive significant effects on banks’ profitability. The descriptive results indicate that the banks with market strength in deposits, lending and high concentration ratio are performing better as compared to their counterpart. At the same time, the corruption index, government ownership and loan loss provisions negatively significant that indicate a major cause of concern to Pakistani banking sector. In comparative context, the government owned banks are exposed to corruption index and loan loss provisions more severely than privately owned banks. Overall, the private banks are better in managing their deposits, net-interest margin and non-interest income in Pakistani banking context. Keywords: Banking, profitability, panel data, generalized method of moments, ownership, and corruption index 1. Introduction Recently, market changing and varying policy environment has a substantial impact on world’s banking sector. After decades of globalization, deregulation and financial innovation, the banking sector began to flourish until the near fall down of the financial market a few years ago. Resultantly, a basic reassessment of the banking sector is demanded [47]. Current efforts to modify guideline and administration will lead to a new epoch of regulation and will be a likely determinant of dividend policy. In this line [1] argued that: “Basel III will force banks to shift their business model from liability management, in which business decisions are made about asset volumes, with the financing found in short term wholesale markets as necessary, to asset management, in which asset volumes are constrained by the availability of funding” The study mainly focuses to highlight the determinants of banks’ profitability by probing ownership structure, microeconomic variables and the balance sheet structure. In addition, the ownership structure is included to highlight any agency conflicts and its impact on bank performance. For the market concentration, the HHI index analyzed to check the monopolistic power of each bank in the banking sector. The balance sheet structure considers the daily business outcome and serves a proxy for prudent and sound risk management Along with this, ownership frequently focuses on the balance sheet makeup from end to end which it could influence banks’ profitability. In this framework, determinants of profitability mostly narrate to the balance sheet structure and macroeconomic variables due to the special nature of banks. Furthermore, the study takes into account the return on asset and return on equity to demonstrate a true version of banks’ profitability in Pakistani banking sector. The literature documents that restrictions on banking sector and capital requirements do not affect the banks’ profitability [11]. In this vein, [35] argued that risk influences the net profitability of banks. International Journal of Information Processing and Management(IJIPM) Volume 5, Number 3, August 2014 The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan 17

-

Upload

teknologimalaysia -

Category

Documents

-

view

3 -

download

0

Transcript of impact of corruption on financial instability in pakistan

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability

Hashim Khan1, Norkhairul Hafiz Bajuri2, Saif-Ur-Rehman3, Lee Bee Yoke4, Faisal

Khan4 1 Corresponding Author, PhD Student at Department of Management, Faculty of

Management, University Technology Malaysia [email protected]/ [email protected]

2 Senior Lecturer, Faculty of Management, University Technology Malaysia 3 Associate Professor, Faculty of Management, University Technology Malaysia

4 PhD Students, Faculty of Management, University Technology Malaysia

Abstract This study attempts to examine the role of corruption, macroeconomic variables and market competitiveness on banking sector profitability. The study used unbalance panel data of 20 commercial banks for the period 2002 t0 2012. Moreover, banks are dividend to two categories i.e. government banks and private banks. The descriptive analysis indicates that the lagged profitability, equity to asset ratio, non-interest income, net-interest margin and loan growth are positively significant with banks profitability. In contrast, the loan loss provision contributes negatively to profitability. Real GDP growth and T-bill rates have positive significant effects on banks’ profitability. The descriptive results indicate that the banks with market strength in deposits, lending and high concentration ratio are performing better as compared to their counterpart. At the same time, the corruption index, government ownership and loan loss provisions negatively significant that indicate a major cause of concern to Pakistani banking sector. In comparative context, the government owned banks are exposed to corruption index and loan loss provisions more severely than privately owned banks. Overall, the private banks are better in managing their deposits, net-interest margin and non-interest income in Pakistani banking context.

Keywords: Banking, profitability, panel data, generalized method of moments, ownership, and

corruption index 1. Introduction

Recently, market changing and varying policy environment has a substantial impact on world’s banking sector. After decades of globalization, deregulation and financial innovation, the banking sector began to flourish until the near fall down of the financial market a few years ago. Resultantly, a basic reassessment of the banking sector is demanded [47]. Current efforts to modify guideline and administration will lead to a new epoch of regulation and will be a likely determinant of dividend policy. In this line [1] argued that: “Basel III will force banks to shift their business model from liability management, in which business decisions are made about asset volumes, with the financing found in short term wholesale markets as necessary, to asset management, in which asset volumes are constrained by the availability of funding”

The study mainly focuses to highlight the determinants of banks’ profitability by probing ownership structure, microeconomic variables and the balance sheet structure. In addition, the ownership structure is included to highlight any agency conflicts and its impact on bank performance. For the market concentration, the HHI index analyzed to check the monopolistic power of each bank in the banking sector. The balance sheet structure considers the daily business outcome and serves a proxy for prudent and sound risk management Along with this, ownership frequently focuses on the balance sheet makeup from end to end which it could influence banks’ profitability. In this framework, determinants of profitability mostly narrate to the balance sheet structure and macroeconomic variables due to the special nature of banks. Furthermore, the study takes into account the return on asset and return on equity to demonstrate a true version of banks’ profitability in Pakistani banking sector.

The literature documents that restrictions on banking sector and capital requirements do not affect the banks’ profitability [11]. In this vein, [35] argued that risk influences the net profitability of banks.

International Journal of Information Processing and Management(IJIPM) Volume 5, Number 3, August 2014

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

17

Empirics provide mix results as far as the relationship between ownership structure and bank’s profitability is concerned [51, 3, 32, 37]. Some studies documented positive relationship between private ownership and bank’s profitability while the other argued insignificant or negative association. The agency theory of [33] has been able to provide a strong-bodied theoretical explanation for the relationship between ownership structure and banks’ profitability. Conclusively, earlier researches mainly focus bank-specific determinants of performance using balance sheet ratios [17, 22]. Recently, [24] examined the impact of global financial crises on profitability of banks for the Swiss banking sector and reported the significant results during the global financial crises. For instance, they stated a significance association between capital ratio and banks profitability in the pre-crisis sample and negative during the crisis.

The study explores the existing literature in many ways. First, the Pakistani banking sector has considered for analysis for the period from 3002 to 2012 that makes the study unique due to data span over time period. As per author knowledge, no study has been conducted for the specific time and number of banks (20) whilst globalization, international convergence and increasing competition of banking directive and accounting standards perk up the compatibility of Pakistani banking sector. The study uses the data of 21st century when the world economy has exposed to different challenges [43, 6]. The study also focuses the individual economy, which has exposed to internal and external challenges like [32, 10]. 2. Role of Corruption in Pakistan

The root of corruption in Pakistan stemmed date back to the colonial period when the emperor gifted titles and land to their loyalists to corruption and nepotism [7]. In this context, two major crises are the basic cause of genesis of corruption in this part of the world; the spiral in arms and ammunition purchases due to the World War II and allocation of evacuee property after the partition of Indian subcontinent. Later on, industrial and trade licensing and patronage schemes like route permits and bonus voucher contributed in the earlier stem of corruption during 1950s and 1960s. In this vein, the nationalization policy of the 1970s opened the era of corruption and gives birth to a new breed of corrupt government employees. This temptation made us to witness the surge of corruption in business and religious circles in the decades of 1980. This malady causes are to be observed in the political matrix and socio-cultural of the society which presently burst into a gradual loss value system

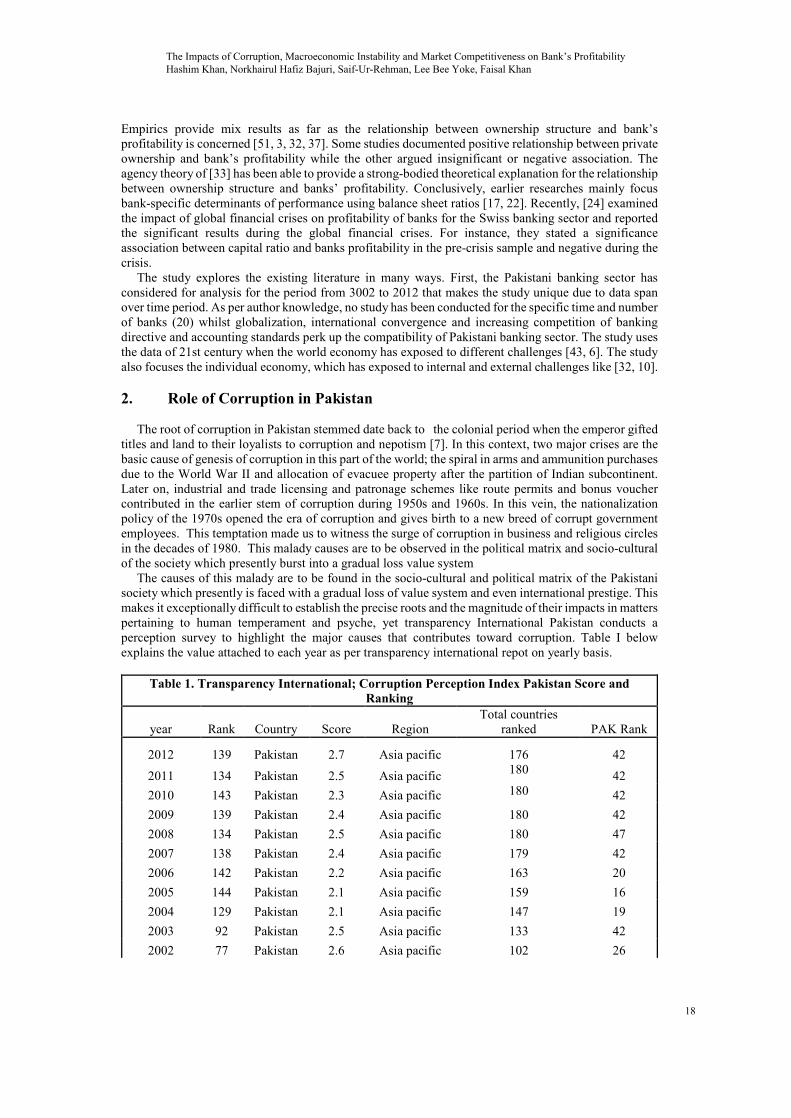

The causes of this malady are to be found in the socio-cultural and political matrix of the Pakistani society which presently is faced with a gradual loss of value system and even international prestige. This makes it exceptionally difficult to establish the precise roots and the magnitude of their impacts in matters pertaining to human temperament and psyche, yet transparency International Pakistan conducts a perception survey to highlight the major causes that contributes toward corruption. Table I below explains the value attached to each year as per transparency international repot on yearly basis.

Table 1. Transparency International; Corruption Perception Index Pakistan Score and Ranking

year Rank Country Score Region Total countries

ranked PAK Rank

2012 139 Pakistan 2.7 Asia pacific 176 42 2011 134 Pakistan 2.5 Asia pacific 180 42 2010 143 Pakistan 2.3 Asia pacific 180 42 2009 139 Pakistan 2.4 Asia pacific 180 42 2008 134 Pakistan 2.5 Asia pacific 180 47 2007 138 Pakistan 2.4 Asia pacific 179 42 2006 142 Pakistan 2.2 Asia pacific 163 20 2005 144 Pakistan 2.1 Asia pacific 159 16 2004 129 Pakistan 2.1 Asia pacific 147 19 2003 92 Pakistan 2.5 Asia pacific 133 42 2002 77 Pakistan 2.6 Asia pacific 102 26

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

18

2001 79 Pakistan 2.3 Asia pacific 91 13 2000 NA Pakistan NA Asia pacific 90 NA 1999 87 Pakistan 2.2 Asia pacific 99 13 1998 71 Pakistan 2.7 Asia pacific 85 15 1997 48 Pakistan 2.53 Asia pacific 52 5 1996 53 Pakistan 1.00 Asia pacific 54 2

http://www.transparency.org.pk/.../CPI2009/CPI20 Press Release November .doc. 3. Rational For Regulation and Supervision

The changes in behaviors refer to moral hazards when firms are insured or have limited liability to losses. In banking context, it means a changing attitude in term of risks since the downside losses for banks owners are inadequate to the sum of equity invested even as the potential of risk taking is unhindered. Based on fact that the downside losses are constrained by a put option value happening from the limited liability, banks could exploit shareholder value by captivating more risks than depositors are eager to admit. In this vein, [44] stated that the depositors and depositors’ insurance scheme burst into extreme risk taking and potential deficit (bankruptcies). In recent past, the government interventions have been able to avoid a collapse in banking sector. The banks are required to take measures to manage the risk and to prevent any disaster or even a systematic failure of banking industry [50].

Some researchers demonstrated moral hazard as less important than regulations and they stated that moral hazard has not fully been able to explain relationship between bank capital and risk taking. In this vein, [38] stated that one should take into account probable prospect streams of earnings and the truth that shareholders hardly ever haul out maximum payouts from banks. The effects pin down the ethical vulnerability problem. In spite of divergent elucidation, academician, researchers, supervisors and politician addressed the hazard problems in the recent past and found supervision mandatory. The regulations not only address the moral hazard issue but also regulate the other customer services, who are monetarily not conversant, that meet quite a few requirements.

In contrast, [11] stated that neither official nor private firms are able to solve moral hazard. In addition to this, [19] stated that supervision could not authenticate banks’ risk assessments. Information asymmetries mostly root the above-mentioned inabilities of entities [11, 19]. Information asymmetries will guide to objectionable results on the fact that banks have inducement to play down their risk, as coverage-elevated risk will lead to elevated minimal capital ratios [19].

2.3. Recent Developments in International Bank Regulation

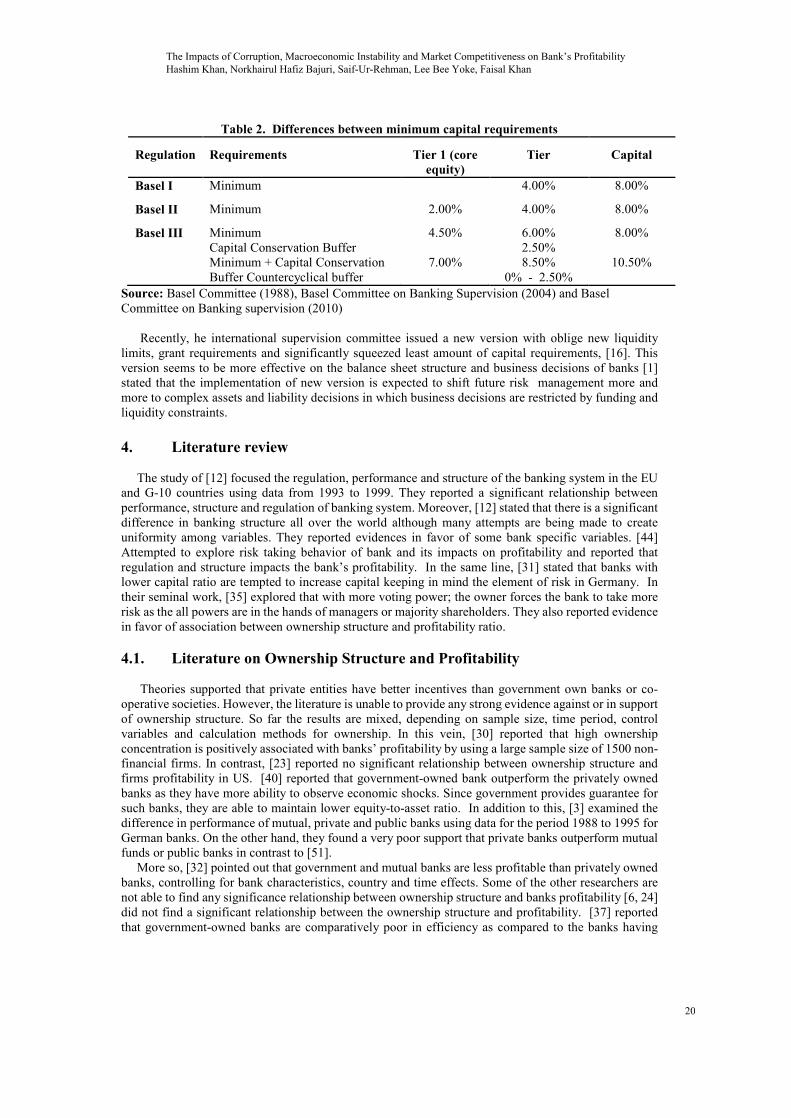

In 1988, the Basel Committee on Banking Supervision was able to issue the first normally established international treaty on banking supervision; the Basle Capital Accord (Basel 1). The credit risk was the main focus of the Basle Capital Accord [49] due to its intensity and importance for banking sector. This also focused the market risk (e.g. foreign exchange risk, interest risk, inflation etc) from the trading book in manipulative risk biased assets and capital requirements [11]. The Basel I also mentioned an adequate ratio between capital and risk weighted assets to maintain a sound position in the market. Table I below mentioned the minimum capital ratios under Basel I. Moreover, a new version of Basel I was initiated in the form of Basel II in 2004 based on moral hazard and regulatory arbitrage. It contains three pillars; first pillar deals with minimum capital requirement; second focuses the strategy for resonance risk management; and third sets out the supplies for market discipline and disclosures on risk management. The Basel II aims to strengthen the stability and soundness of financial indicators. Moreover, it also seems to be more risk-sensitive ad to make bank interior models and risk management rules to deals with these ratios. It also strengthens the disclosure and interaction to national management.

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

19

Table 2. Differences between minimum capital requirements

Regulation

Requirements

Tier 1 (core equity)

Tier

Capital

Basel I Minimum 4.00% 8.00%

Basel II Minimum 2.00% 4.00% 8.00%

Basel III Minimum Capital Conservation Buffer Minimum + Capital Conservation Buffer Countercyclical buffer

4.50%

7.00%

6.00% 2.50% 8.50%

0% - 2.50%

8.00%

10.50%

Source: Basel Committee (1988), Basel Committee on Banking Supervision (2004) and Basel Committee on Banking supervision (2010)

Recently, he international supervision committee issued a new version with oblige new liquidity limits, grant requirements and significantly squeezed least amount of capital requirements, [16]. This version seems to be more effective on the balance sheet structure and business decisions of banks [1] stated that the implementation of new version is expected to shift future risk management more and more to complex assets and liability decisions in which business decisions are restricted by funding and liquidity constraints. 4. Literature review

The study of [12] focused the regulation, performance and structure of the banking system in the EU and G-10 countries using data from 1993 to 1999. They reported a significant relationship between performance, structure and regulation of banking system. Moreover, [12] stated that there is a significant difference in banking structure all over the world although many attempts are being made to create uniformity among variables. They reported evidences in favor of some bank specific variables. [44] Attempted to explore risk taking behavior of bank and its impacts on profitability and reported that regulation and structure impacts the bank’s profitability. In the same line, [31] stated that banks with lower capital ratio are tempted to increase capital keeping in mind the element of risk in Germany. In their seminal work, [35] explored that with more voting power; the owner forces the bank to take more risk as the all powers are in the hands of managers or majority shareholders. They also reported evidence in favor of association between ownership structure and profitability ratio.

4.1. Literature on Ownership Structure and Profitability

Theories supported that private entities have better incentives than government own banks or co-operative societies. However, the literature is unable to provide any strong evidence against or in support of ownership structure. So far the results are mixed, depending on sample size, time period, control variables and calculation methods for ownership. In this vein, [30] reported that high ownership concentration is positively associated with banks’ profitability by using a large sample size of 1500 non-financial firms. In contrast, [23] reported no significant relationship between ownership structure and firms profitability in US. [40] reported that government-owned bank outperform the privately owned banks as they have more ability to observe economic shocks. Since government provides guarantee for such banks, they are able to maintain lower equity-to-asset ratio. In addition to this, [3] examined the difference in performance of mutual, private and public banks using data for the period 1988 to 1995 for German banks. On the other hand, they found a very poor support that private banks outperform mutual funds or public banks in contrast to [51].

More so, [32] pointed out that government and mutual banks are less profitable than privately owned banks, controlling for bank characteristics, country and time effects. Some of the other researchers are not able to find any significance relationship between ownership structure and banks profitability [6, 24] did not find a significant relationship between the ownership structure and profitability. [37] reported that government-owned banks are comparatively poor in efficiency as compared to the banks having

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

20

private ownership or mutual funds. In addition to this, [18] reported a moderate association between ownership structure and profitability for Argentinean banks for the period 1991-1999.

Literature has focused on the importance of balance sheet structure on profitability as the main determinants. Most part of the literature has tested the association between equity to asset ratio and bank profitability. In corporate finance, the low risk is negatively associated with banks return. In contrast, [17] documented a positive Granger-causality relationship foe for banks in united state for the period 1984 to 1991. He investigated the association of expected bankruptcy costs and signaling and reported that the high value of equity-to-asset ratio has positive signal because it is assumed that market is performing better. Moreover, they found a little bit support for expected bankruptcy costs hypothesis. Moreover, the banks with low-interest un-insured debts have a temptation to adjust high level of equity due to exogenous shocks, which may cause bank’s failure in near future. The study of [18] conducted his research to test exogenous shift in breakdown probabilities due to worsening financial circumstance in the eighties. He compared the relationship between performance changes and equity-to-asset ratio in the period of 1990 t0 1992 compared to 1990-1992 compare to the period of 1983-1989.

5. Methodology 5.1. Econometric Model

The study follows the research design mentioned by [6, 24]. The research design is mentioned in equation 1 below. Equation i = + , +

+ +

+ , = + … ()

In equation 1, the dependent variable ( ) measures profitability, calculated by ROE and ROA, for bank at time, with = 1, … , and = 1, … , . N denotes the number of cross-sectional observations and T the length of the sample period. Moreover, the models also contain a constant term, calculated by the scalar, and of a vector of × 1 slope parameters () that estimate the sign of the explanatory variables. The explanatory variables are divided into 1 × vectors of bank-specific , industry-

specific and macroeconomic variables , where refers to the number of slope parameters for the different variables classes. Finally, the model includes a one-way error disturbance term u capturing a bank-specific or fixed effect (μ) and a remainder or idiosyncratic effect that vary over time and between banks(v )i. The study used dynamic model based on the assumption of persistence of banks’ profitability over time; hence the model includes one-period lagged dependent variable π, of bank i at time t [6, 24]

5.2 Generalized Method of Moments

In order to recover the problem of differences between the observations and estimations are minimized in terms of sum of squares in OLS model, the study sector applied generalized method of moments (GMM) techniques to trounce the problems of pooled ordinary least squares techniques. The GMM techniques do not make any assumptions surrounding the distribution of the data (i.e. normality or skewness); the potential non-normal distribution of the variables has no impacts on results. In addition to this, GMM also controls the problem of endogeneity of variables and serial correlation with the disturbance term [43, 6, and 24].

There are two widely accepted and applied GMM techniques; the Difference GMM estimator as described in Arellano and Bond (1991) and the System GMM estimator described in [5]. [8] and [46] stated that the Difference GMM technique first-differentiate equation (i) in time to remove the unobserved bank-specific effect in the error item(). This it is estimated by taking lags of potential predetermined and endogenous explanatory variables. The shortcoming of the Difference GMM is that it performs poorly when there is little correlation between the lagged values and current values of the

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

21

potential endogenous variables and provides biased results [46]. In contrast, the System GMM technique is equipped with the technique to overcome these problems by using an equation in levels in addition to the equation in first-differences. Moreover, the System GMM technique is able to incorporate time-invariant variables while the Difference GMM does not. The latter uses a differentiation technique in which the cross-dimension of the data as well as the time-invariant variables (without subscript t in equation (i), e.g. dummy for ownership) is removed. Hence, regressions are performed using the System GMM technique.

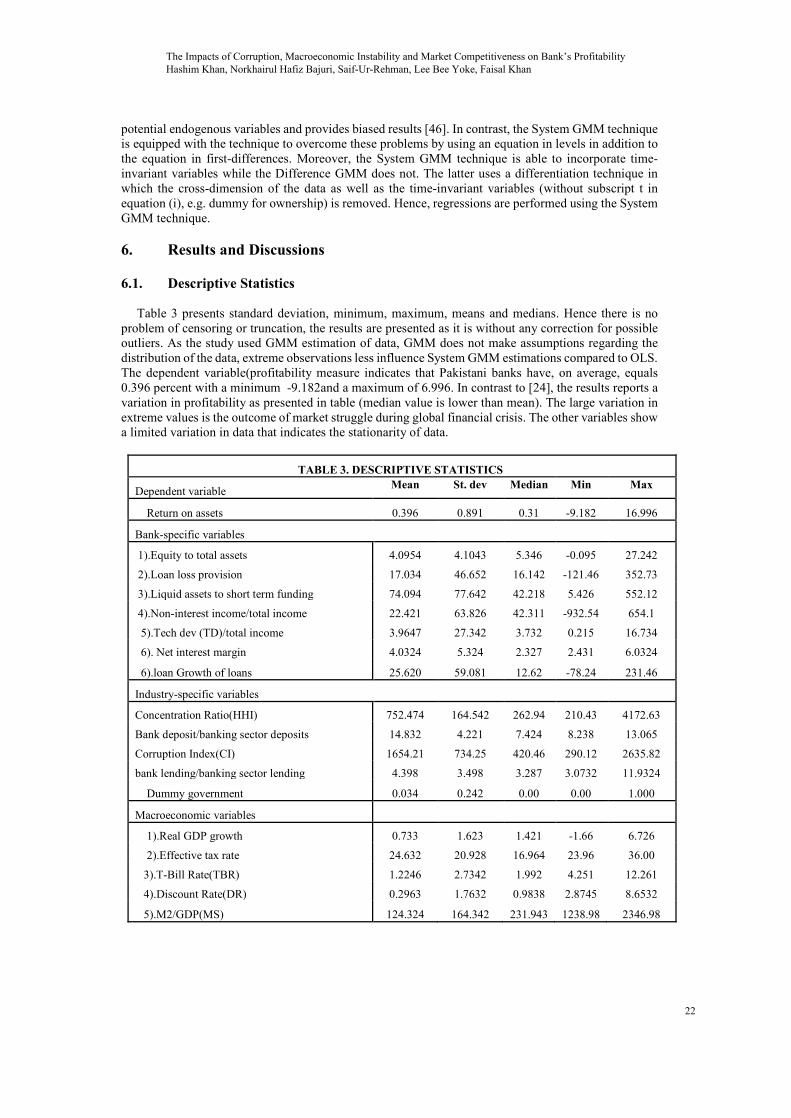

6. Results and Discussions 6.1. Descriptive Statistics

Table 3 presents standard deviation, minimum, maximum, means and medians. Hence there is no problem of censoring or truncation, the results are presented as it is without any correction for possible outliers. As the study used GMM estimation of data, GMM does not make assumptions regarding the distribution of the data, extreme observations less influence System GMM estimations compared to OLS. The dependent variable(profitability measure indicates that Pakistani banks have, on average, equals 0.396 percent with a minimum -9.182and a maximum of 6.996. In contrast to [24], the results reports a variation in profitability as presented in table (median value is lower than mean). The large variation in extreme values is the outcome of market struggle during global financial crisis. The other variables show a limited variation in data that indicates the stationarity of data.

TABLE 3. DESCRIPTIVE STATISTICS

Dependent variable Mean St. dev Median Min Max

Return on assets 0.396 0.891 0.31 -9.182 16.996

Bank-specific variables

1).Equity to total assets 4.0954 4.1043 5.346 -0.095 27.242

2).Loan loss provision 17.034 46.652 16.142 -121.46 352.73

3).Liquid assets to short term funding 74.094 77.642 42.218 5.426 552.12

4).Non-interest income/total income 22.421 63.826 42.311 -932.54 654.1

5).Tech dev (TD)/total income 3.9647 27.342 3.732 0.215 16.734

6). Net interest margin 4.0324 5.324 2.327 2.431 6.0324

6).loan Growth of loans 25.620 59.081 12.62 -78.24 231.46

Industry-specific variables

Concentration Ratio(HHI) 752.474 164.542 262.94 210.43 4172.63

Bank deposit/banking sector deposits 14.832 4.221 7.424 8.238 13.065

Corruption Index(CI) 1654.21 734.25 420.46 290.12 2635.82

bank lending/banking sector lending 4.398 3.498 3.287 3.0732 11.9324

Dummy government 0.034 0.242 0.00 0.00 1.000

Macroeconomic variables

1).Real GDP growth 0.733 1.623 1.421 -1.66 6.726

2).Effective tax rate 24.632 20.928 16.964 23.96 36.00

3).T-Bill Rate(TBR) 1.2246 2.7342 1.992 4.251 12.261

4).Discount Rate(DR) 0.2963 1.7632 0.9838 2.8745 8.6532

5).M2/GDP(MS) 124.324 164.342 231.943 1238.98 2346.98

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

22

6.3. Correlation between the Variables

The results of correlations between the explanatory variables and the dependent variable are presented in table 4. The correlation matrix explains the issue of multicollinearity among the variables because high correlation with ROAA could also reflect the problem of endogeneity. If the correlation among the variables is above 0.80, there may be an issue of multicollinearity. The results clearly indicate that the data is not exposed to any of the above mentioned issues. Some of the variables are negatively correlated with ROA indicating a rise in loan loss provisions, liquid asset, corruption index, money supply and tax causes a decline in ROA. The other variables are positively correlated that indicate a positive contribution in bank’s profitability ratio. Resultantly, the correlation matrix detects no multicollinearity issue among the potential variables.

Table 4. CORRELATION

VARIABLE

S

ROA

EQ/AS

LLP

LA/ST

NII

NIM

TDEV

LG

HHI

BD/BS

CI

BL/BS

TB

DR

RGD

ETAX

MS

ROA 1.

00

EQ/ASST

0.543

1.00

LLP

-0.

16

-0.173

1.00

LA/ST

-0.

51

-0.322

-0.

35 1

NII 0.

28 0.242

-0.

30

-0.0

3 1

NIM 0.

09 0.032

0.06

0.07 0.06

1

TDEV 0.

03 0.143

-0.

08 0.023 0.54

0.09

1

LG

0.214

0.062

-0.

29

-0.3

6 0.19

O.12

0.09 1

HH-INDEX

0.356

0.432

0.09

0.18 0.13

0.09

0.09

0.16 1

BD/BSD

0.184

0.272

0.26

0.091 0.14

0.05

0.09

0.11

0.48

1.00

CI

-0.

34

-0.267

0.25

-0.0

2 -0.09

0.10

-0.13

0.38

-0.

15

-0.2

4

1.00

BL/BSL

0.26

0.28

0.41

0.13 0.18

0.03 0.

04

0.31

0.27

0.21

-0.14

1.00

TB 0.

07 0.0

9 0.

02 0.1

5 0.21

-0.0

8

0.05

0.19

0.20

0.32

0.27

0.20

1.00

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

23

DR

0.091

0.12

-0.

01 0.062 0.19

-0.0

5 0.16

-0.05

0.05

0.05

0.17

0.13

0.31 1

RGDPG

0.212

0.234

0.03

0.11 0.04

0.07 0.

21

0.13

0.15

0.11

-0.14

0.01

-0.08

0.02 1

ETAXR

-0.

06

-0.052

0.31

0.12 -0.02

0.15 0.

14

-0.17

-0.

15

-0.0

9

-0.18

-0.2

1

-0.10

0.02

-0.

05 1

MS

-0.

10

-0.0

1.

-0.

04 0.007 0.02

0.19

-0.19

0.02

-0.

04

-0.137

-0.02 -0

-0.02

-0.01

-0.

12 0.022 1

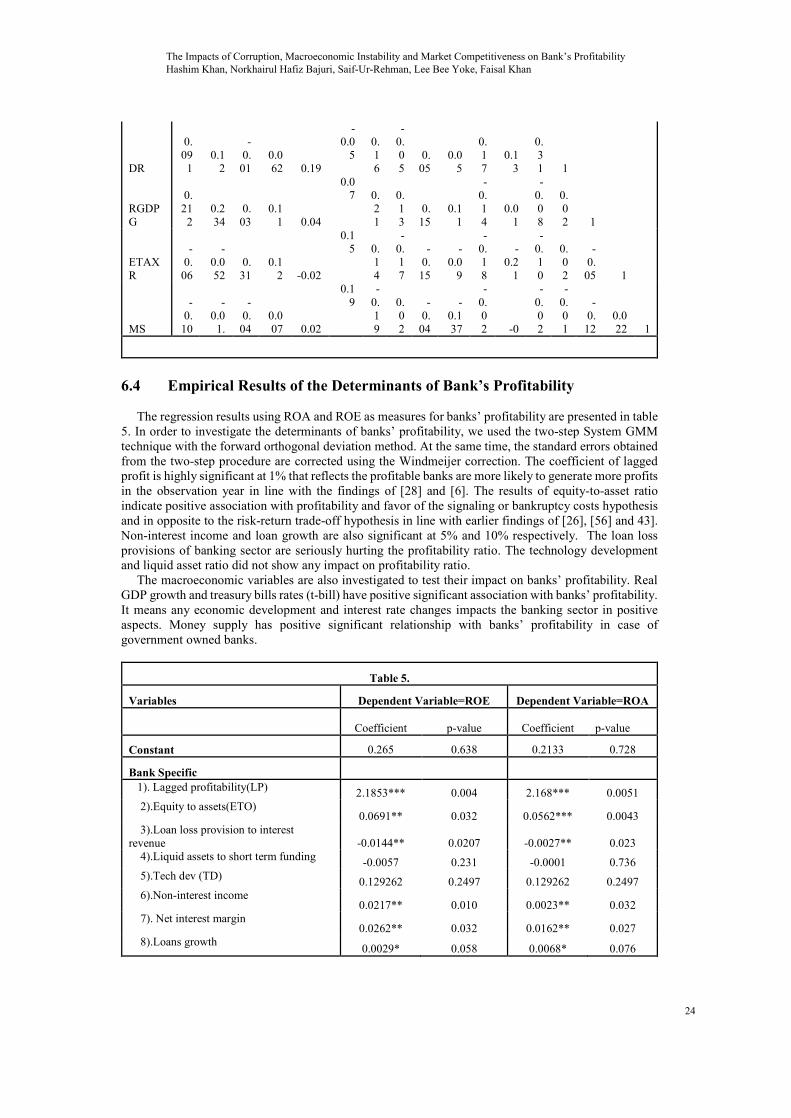

6.4 Empirical Results of the Determinants of Bank’s Profitability

The regression results using ROA and ROE as measures for banks’ profitability are presented in table 5. In order to investigate the determinants of banks’ profitability, we used the two-step System GMM technique with the forward orthogonal deviation method. At the same time, the standard errors obtained from the two-step procedure are corrected using the Windmeijer correction. The coefficient of lagged profit is highly significant at 1% that reflects the profitable banks are more likely to generate more profits in the observation year in line with the findings of [28] and [6]. The results of equity-to-asset ratio indicate positive association with profitability and favor of the signaling or bankruptcy costs hypothesis and in opposite to the risk-return trade-off hypothesis in line with earlier findings of [26], [56] and 43]. Non-interest income and loan growth are also significant at 5% and 10% respectively. The loan loss provisions of banking sector are seriously hurting the profitability ratio. The technology development and liquid asset ratio did not show any impact on profitability ratio.

The macroeconomic variables are also investigated to test their impact on banks’ profitability. Real GDP growth and treasury bills rates (t-bill) have positive significant association with banks’ profitability. It means any economic development and interest rate changes impacts the banking sector in positive aspects. Money supply has positive significant relationship with banks’ profitability in case of government owned banks.

Table 5.

Variables Dependent Variable=ROE Dependent Variable=ROA

Coefficient p-value Coefficient p-value

Constant 0.265 0.638 0.2133 0.728

Bank Specific 1). Lagged profitability(LP) 2.1853*** 0.004 2.168*** 0.0051

2).Equity to assets(ETO) 0.0691** 0.032 0.0562*** 0.0043

3).Loan loss provision to interest revenue -0.0144** 0.0207 -0.0027** 0.023

4).Liquid assets to short term funding -0.0057 0.231 -0.0001 0.736 5).Tech dev (TD) 0.129262 0.2497 0.129262 0.2497 6).Non-interest income

0.0217** 0.010 0.0023** 0.032 7). Net interest margin

0.0262** 0.032 0.0162** 0.027 8).Loans growth 0.0029* 0.058 0.0068* 0.076

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

24

Macro-Economic

1) Real GDP growth 0.0222* 0.0561 0.0193** 0.011

2).Effective tax rate 0.00779 0.218 0.0082 0.439

3).T-Bill Rate(TBR) 1.815309* 0.0595 0.0061** 0.015

4).Discount Rate(DR) 0.00431 0.915 0.0042 0.391

5).M2/GDP(MS) 0.00046 0.542 0.0002 0.481

Market specific

1).Bank deposit/banking sector deposits 0.0144** 0.01743 0.01871** 0.04215

2).bank lending/banking sector lending 0.0388** 0.02059 0.0039** 0.04010

3).Concentration Ratio(HHI) 6.09E-06** 0.041831 0.000014*** 0.001831

4).Corruption Index(CI) -0.087892** 0.043112 -0.094215** 0.045622

5). Government dummy -0.10404* 0.06752 -0.06255* 0.05431

F-test 24.61 31.8

Arrelano-Bond test for AR(1) Z = -0.04*** 0.002 Z = -2.33*** 0.02 Arrelano-Bond test for AR(2) Z = -0.64 0.42 Z = -0.73 0.504

Hansen-test over identification Χ2 = 132.47 0.407 Χ2 = 162.89 0.436

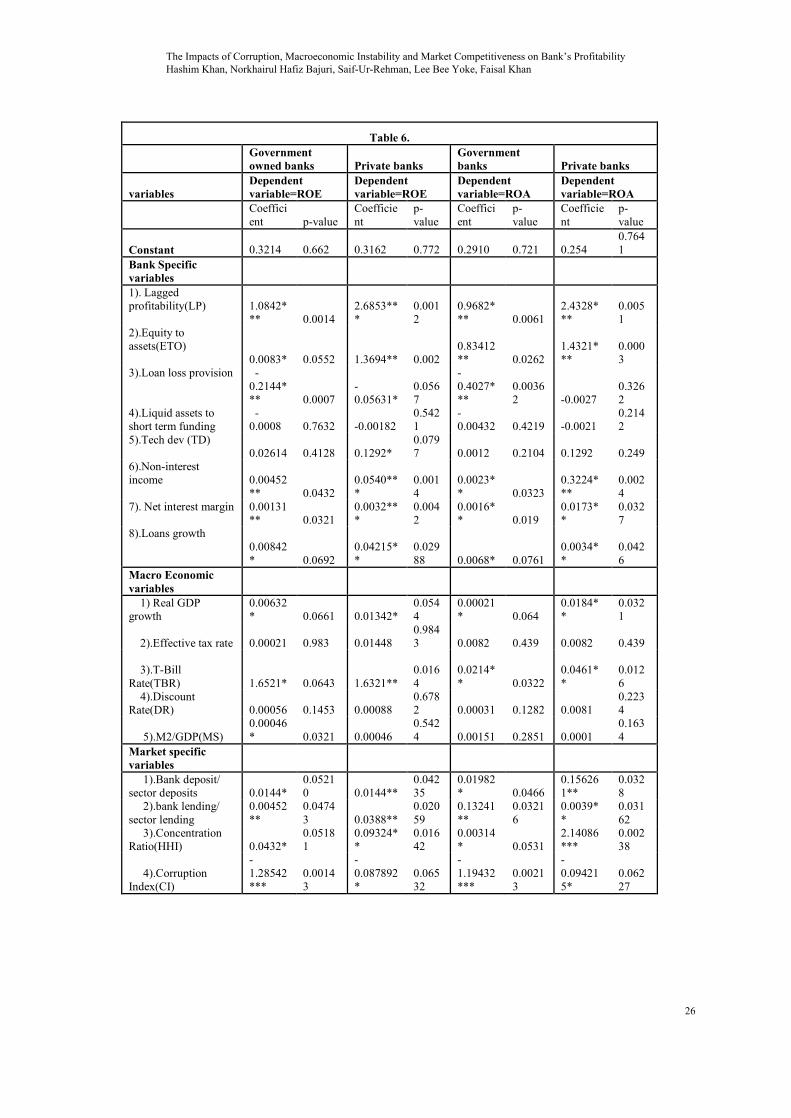

6.5 Comparison of Government and Private Banks

When we compare the government and private banks in Pakistan, the interesting results appeared in the analysis. The results are presented in table 5 below. Firstly, the government banks are highly exposed to corruption and provisions for bad loans. Similarly, the private banks are better in managing their loan growth as the results indicate positive association between loan growth and private banks profitability. Net interest margin and non-interest income also have higher significant impacts on private banks as compared to their counterpart. Moreover, the macrocosmic conditions influence both categories of banks almost in same way. On the other side, the private banks perform well in market competitive segment as the bank’s deposits to total banking sector deposits and bank’s lending to banking sector lending is concerned. At the same time, t-bill rates and net-interest margin are more prominent source of income for private banks.

6.6 Conclusion

As far as the results are concerned, the last year profitability, equity to asset and loan loss provision, net interest margin and net interest income are the main determinants of banks profitability as far as the bank specific variables are concerned. In case of macroeconomic variables, the GDP growth and market rate of interest also determine the bank profitability in Pakistani banking sector. However, the macro-economic variable show a weak association with banks profitability and the investors need not to consider seriously as compared to banks specific variables. In the meanwhile, the GDP return on asset in a significant way. While in case of market specific variables, the bank’s deposits also play a significant role in determining banks profitability in Pakistan. The banks having higher lending ratio in market are also efficient in generating profit. The banks with higher market concentration are also efficient in generating more profit as compared to their counterpart. The banks are exposed to corruption in Pakistan, the higher the corruption rate, the lower the banks profitability ratio. The reason may that the banking sector is the most sensitive and attached to all sectors in economy. The government owned banks are inefficient as compared to their counterpart in managing the profitability in Pakistan.

In comparing the private and government banks, the results indicate that government banks are exposed to high level of corruption risk, the results in table 6 below also points out the overall efficiency of private banks as compared to government banks. The results clearly indicates the performance and efficiency of private banks in all aspects in on the higher side and they efficient in managing the net interest income, coping the corruption risk and market concentration efficiently.

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

25

Table 6.

Government owned banks Private banks

Government banks Private banks

variables Dependent variable=ROE

Dependent variable=ROE

Dependent variable=ROA

Dependent variable=ROA

Coefficient p-value

Coefficient

p-value

Coefficient

p-value

Coefficient

p-value

Constant 0.3214 0.662 0.3162 0.772 0.2910 0.721 0.254 0.7641

Bank Specific variables 1). Lagged profitability(LP)

1.0842*** 0.0014

2.6853***

0.0012

0.9682*** 0.0061

2.4328***

0.0051

2).Equity to assets(ETO)

0.0083* 0.0552 1.3694** 0.002

0.83412** 0.0262

1.4321***

0.0003

3).Loan loss provision -0.2144*** 0.0007

-0.05631*

0.0567

-0.4027***

0.00362 -0.0027

0.3262

4).Liquid assets to short term funding

-0.0008 0.7632 -0.00182

0.5421

-0.00432 0.4219 -0.0021

0.2142

5).Tech dev (TD) 0.02614 0.4128 0.1292*

0.0797 0.0012 0.2104 0.1292 0.249

6).Non-interest income

0.00452** 0.0432

0.0540***

0.0014

0.0023** 0.0323

0.3224***

0.0024

7). Net interest margin 0.00131** 0.0321

0.0032***

0.0042

0.0016** 0.019

0.0173**

0.0327

8).Loans growth 0.00842* 0.0692

0.04215**

0.02988

0.0068* 0.0761

0.0034**

0.0426

Macro Economic variables 1) Real GDP growth

0.00632* 0.0661 0.01342*

0.0544

0.00021* 0.064

0.0184**

0.0321

2).Effective tax rate 0.00021 0.983 0.01448 0.9843 0.0082 0.439 0.0082 0.439

3).T-Bill Rate(TBR) 1.6521* 0.0643 1.6321**

0.0164

0.0214** 0.0322

0.0461**

0.0126

4).Discount Rate(DR) 0.00056 0.1453 0.00088

0.6782 0.00031 0.1282 0.0081

0.2234

5).M2/GDP(MS) 0.00046* 0.0321 0.00046

0.5424 0.00151 0.2851 0.0001

0.1634

Market specific variables 1).Bank deposit/ sector deposits 0.0144*

0.05210 0.0144**

0.04235

0.01982* 0.0466

0.156261**

0.0328

2).bank lending/ sector lending

0.00452**

0.04743 0.0388**

0.02059

0.13241**

0.03216

0.0039**

0.03162

3).Concentration Ratio(HHI) 0.0432*

0.05181

0.09324**

0.01642

0.00314* 0.0531

2.14086***

0.00238

4).Corruption Index(CI)

-1.28542***

0.00143

-0.087892*

0.06532

-1.19432***

0.00213

-0.094215*

0.06227

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

26

7. Limitations

The study uses the unconsolidated statements of banks and drops the consolidated statements because the selection procedure enables us to avoid the double counting. It can be argued that Pakistani banks manage their ownership structure, profitability ratio and balance sheet structure on consolidated basis in order to comply with prudential regulations. Secondly, the study only classify banks into two ownership categories i.e. government and private banks, while there are many studies that used different threshold to classify ownership into different categories like institution ownership, family ownership etc. since it is difficult to obtain data, thus it falls as a basic limitation of the study. References: 1. Allen, W., Chan, K. K., Milne, A., & Thomas, S. “Basel III: Is the Cure Worse than the Disease”,

Retrieved from http://ssrn.com/abstract=1688594, 2010, September 30. 2. Allison, P. D.” Missing data “(Sage University Paper Series on Quantitative Applications in the

Social Sciences series no. 07-136). Thousand Oaks, CA: Sage, 2001. 3. Altunbas, Y., Evans, L., & Molyneux, P,” Bank Ownership and Efficiency. Journal of Money”,

Credit and Banking, 33(4), 926-954, 2001. 4. Arellano, M., & Bond, S,” Some Tests of Specification for Panel Data”, Monte Carlo Evidence and

an Application to Employment Equations. The Review of Economic Studies, 58(2), 277-297, 1991. 5. Arellano, M., & Bover, O. “Another look at the instrumental variable estimation of error-

components models”. Journal of Econometrics, 68(1), 29-51., 1995. 6. Athanasoglou, P. P., Sophocles, N. B., & Delis, M. D, “Bank-specific, industry-specific and

macroeconomic determinants of bank profitability”. International Financial Markets, Institutions and Money, 18(2), 121-136, 2008.

7. Ayadi, R., Llewellyn, D. T., Schmidt, R. H., Arbak, E., & De Groen, W. P. “Investigating Diversity in the Banking Sector in Europe: Key Developments”, Performance and Role of Cooperative Banks. Brussels: Centre for European Policy Studies, 2010.

8. Baltagi, B. “Econometric Analysis of Panel Data (3th ed.)”, West Sussex: John Wiley & Sons Ltd, 2005.

9. Baltagi, B. H. Econometrics (4th Ed.). London: Springer. 2008. 10. Barry, T. A., Lepetit, L., & Tarazi, A. “Ownership structure and risk in publicly held and privately

owned banks”. Journal of Banking & Finance, 35(5), 1327-1340, 2011. 11. Barth, J. R., Caprio Jr., G., & Levine, R, “Bank regulation and supervision: what works best? “,

Journal of Financial Intermediation, 13(2), 205-248, 2004. 12. Barth, J. R., Nolle, D. E., & Rice, T. N. Commercial Banking Structure, Regulation and

Performance: An International Comparison. Managerial Finance, 23(11), 1-39, 1997. 13. Basel Committee, “International convergence of capital measurement and capital standards”, Basel:

Bank for International Settlements, 1988. 14. Basel Committee on Banking Supervision, “Amendment to the Capital Accord to incorporate market

risks”. Basel: Bank for International Settlements, 1997. 15. Basel Committee on Banking Supervision. “International Convergence of Capital Measurement and

Capital Standards”, a Revised Framework. Basel: Bank for International Settlements, 2004. 16. Basel Committee on Banking Supervision. Basel III: “A Global regulatory framework for more

resilient banks and banking systems”. Basel: Bank for International Settlements, 2010. 17. Berger, A. N,”The Relationship between Capital and Earnings in Banking”. Journal of Money,

Credit and Banking, 27(2), 432-456, 1995. 18. Berger, A. N., Clarke, G. R., Cull, R., Klapper, L., & Udell, G. F.” Corporate governance and bank

performance”: A joint analysis of the static, selection, and dynamic effects of domestic, foreign, and state ownership. Journal of Banking & Finance, 29(8-9), 2179-2221, 2005.

19. Blum, J. M. Why 'Basel II' “may need a leverage ratio restriction”. Journal of Banking & Finance, 32(8), 1699-1707, 2008.

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

27

20. Bourke, P.,” Concentration and other determinants of bank profitability in Europe”, North America and Australia. Journal of Banking and Finance, 13(1), 65-79, 1989.

21. Brooks, C.,” Introductory Econometrics for Finance (2nd Ed.)”. New York: Cambridge University Press, 2008.

22. Demirgüç-Kunt, A., & Huizinga, H. “Determinants of Commercial Bank Interest Margins and Profitability”: Some International Evidence. The World Bank Economic Review, 13(2), 379-408, 1999.

23. Demsetz, H., & Villalonga, B. “Ownership structure and corporate performance”. Journal of Corporate Finance, 7(3), 209-233, 2001.

24. Dietrich, A., & Wanzenried, G, “Determinants of bank profitability before and during the crisis: Evidence from Switzerland”. Journal of International Financial Markets, Institutions and Money, 21(3), 307-327, 2011.

25. European Central Bank.. Beyond ROE – “How to measure bank performance”: Appendix to the report on EU banking structures. Frankfurtam Main: ECB, 2010.

26. García-Herrero, A., Gavilá, S., & Santabárbara, D. What explains the low profitability of Chinese banks? Journal of Banking & Finance, 33(11), 2080-2092, 2009.

27. Gillan, S. L. Recent Developments in Corporate Governance: An Overview. Journal of Corporate Finance, 12(3), 381-402, 2006.

28. Goddard, J., Molyneux, P., & Wilson, J.” The profitability of European Banks”: A cross-sectional and dynamic panel analysis. The Manchester School, 72(3), 363-381, 2004.

29. Goddard, J., Molyneux, P., Wilson, J. O., & Tavakoli, M. “European banking”: An overview. Journal of Banking & Finance, 31(7), 1911-1935, 2007.

30. Gompers, P., Ishi, J., & Metrick, A.” Corporate Governance and Equity Prices”. The Quaterly Journal of Economics, 118(1), 107-155, 2003.

31. Heid, F., Porath, D., & Stolz, S., “Does capital regulation matter for bank behavior?”. Evidence for German savings banks. Frankfurt am Main: Deutsche Bundes bank, 2004.

32. Iannotta, G., Nocera, G., & Sironi, A. “Ownership structure, risk and performance in the European bank industry”. Journal of Banking & Finance, 31(7), 2127-2149, 2007.

33. Jensen, M. C., & Meckling, W. H. “Theory of the firm: managerial behavior, agency costs and ownership structure”. Journal of Financial Economics, 3(4), 305-360, 1976.

34. Kimball, R. C. “Economic Profit and Performance Measurement in Banking”. New England Economic Review, 9(July/Augusts), 35-53, 1998.

35. Laeven, L., & Levine, R. “Bank governance, regulation and risk taking”. Journal of Financial Economics, 93(2), 259-275, 2009.

36. Matthews, K., & Thompson, J. “The Economics of Banking (2nd ed.)”. West Sussex: John Wiley & Sons Ltd, 2008.

37. Micco, A., Panizza, U., & Yaňez, M. “Bank ownership and performance. Does politics matter”? Journal of Banking & Finance, 31(1), 219-241, 2007.

38. Milne, A., & Whalley, A. E. Bank Capital Regulation and Incentives for Risk-Taking. Retrieved from http://ssrn.com/abstract=299319, 2001.

39. Modigliani, F., & Miller, M. H.,” The Cost of Capital, Corporation Finance and the Theory of Investment”. The American Review, 48(3), 261-297, 1958.

40. Molyneux, P., & Thornton, J.,” Determinants of European bank profitability”: A note. Journal of Banking and Finance, 16(6), 1173-1178, 1992.

41. Moore, D. S., McCabe, G. P., Duckworth, W. M., & Sclove, S. L. “The Practice of Business Statistics”. New York: W.H. Freeman and Company, 2003.

42. Oesterreichische, “Nationalbank (OeNB) Financial Market Authority (FMA). Guidelines on”: Managing Interest Rate Risk in the Banking Book. Vienna: OeNB Printing Office, 2008.

43. Pasiouras, F., & Kosmidou, K. “Factors influencing the profitability of domestic and foreign commercial banks in the European Union”. Research in International Business and Finance, 21(2), 222-237, 2007.

44. Rime, B.,” Capital requirements and bank behavior: Empirical evidence for Switzerland”. Journal of Banking & Finance, 25(4), 789-805, 2001.

45. Roodman, D. A,”Note on the Theme of Too Many Instruments”. Oxford Bulletin of Economics and Statistics, 71(1), 135-158, 2008.

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

28

46. Roodman, D.,”How to do xtabond2: An introduction to difference and system GMM in Stata”. Stata Journal, 9(1), 86-136, (2009).

47. Rosenthal, J. “Chained but untamed”. The Economist, (2011, May 12). 48. Ruxton, G. D,”The unequal variance t-test is an underused alternative to Student's t-test and the

Mann–Whitney U test”. Behavioral Ecology, 17(4), 688-690, 2006. 49. Santos, J. A,”Bank Capital Regulation in Contemporary Banking Theory: A Review of the

Literature”. Financial Markets, Institutions & Instruments, 10(2), 41-84, 2001. 50. Saunders, A., & Cornett, M. M,”Financial Institutions Management: A Risk Management

Approach”. New York: McGraw-Hill, 2008. 51. Saunders, A., Strock, E., & Travlos, N. G.,” Ownership Structure, Deregulation, and Bank Risk

Taking”. The Journal of Finance, 45(2), 643-654, 1990. 52. Schildbach, J,”Home, sweet home? International banking after the crisis”. Frankfurt am Main:

Deutsche Bank Research, 2011. 53. Schooner, H. M., & Talyor, M. W, ”Bank insolvency. In Global Bank Regulation: Principles and

Policies” (pp. 241-258). San Diego: Academic Press, 2010. 54. Short, B. K.” The relation between commercial bank profit rates and banking concentration in

Canada, Western Europe, and Japan”. Journal of Banking and Finance, 3(3), 209-219, 1979. 55. Stiroh, K. J, “Diversification in Banking: Is Non-Interest Income the Answer?” Journal of Money,

Credit, and Banking, 36(5), 853-882, 2004. 56. Trujillo-Ponce, A. European Financial Management Association 2011 Annual Conference. “Why

are (or were) Spanish banks so profitable (pp. 1-33)”. Sevilla: Pablo de Olavide University, 2011. 57. Valverde, S., & Fernández, F. “The determinants of bank margins in European banking”. Journal of

Banking & Finance, 31(7), 2043-2063, 2007. 58. Van Greuning, H., & Bratanovic, S. B, “Analyzing Banking Risk: A Framework for Assessing

Corporate Governance and Risk Management (3th Ed.)”. Washington, D.C.: The World Bank, (2009).

The Impacts of Corruption, Macroeconomic Instability and Market Competitiveness on Bank’s Profitability Hashim Khan, Norkhairul Hafiz Bajuri, Saif-Ur-Rehman, Lee Bee Yoke, Faisal Khan

29