IJGlobal SPRING 2019.pdf

104

Marching towards merchant European renewables march to the beat of a new drum Issue 374 Spring 2019 IJGLOBAL AWARDS 2018 – WINNERS INSIDE EUROPE Germany moves to cut coal MIDDLE EAST & AFRICA MBR Solar Park’s first CSP NORTH AMERICA Strong start to oil & gas LATIN AMERICA Peru gets connected ASIA PACIFIC Australia’s NSW Regional Rail Project Finance & Infrastructure Journal

-

Upload

khangminh22 -

Category

Documents

-

view

6 -

download

0

Transcript of IJGlobal SPRING 2019.pdf

Marching towards merchantEuropean renewables march to the beat of a new drum

Issue 374 Spring 2019

IJGLOBAL AWARDS 2018

– WINNERS INSIDE

EUROPE Germany moves to cut coal

MIDDLE EAST & AFRICA MBR Solar Park’s first CSP

NORTH AMERICA Strong start to oil & gas

LATIN AMERICA Peru gets connected

ASIA PACIFIC Australia’s NSW Regional Rail

Project Finance & Infrastructure Journal

Issue 374 Spring 2019

1ijglobal.com Spring 2019

19 IJGlobal Awards 2018 – the dealsPro�ling all of the winning deals at this year’s IJGlobal Awards. Discover the transactions from all of the world which moved the market forward.

63 IJGlobal Awards 2018 – the companiesAll of the outstanding companies of this year’s instalment of the prestigious IJGlobal Awards, including the four global award winners leading the pack.

82 Walking on cooling coalsGermany moves to cut coal, sending ripples through the country’s energy sector. By Lyudmila Zlateva & Sophia Radeva.

15 Cover story

Marching towards merchantBanks may have to start accepting merchant risk in order to �nance the next generation of European renewables. By Jon Whiteaker.

Contents

Contents

2ijglobal.com Spring 2019

Editorial DirectorAngus Leslie Melville+44 20 7779 [email protected]

EditorJon Whiteaker+44 20 7779 [email protected]

Assistant EditorEleonor Lundblad+44 20 7779 [email protected]

Funds EditorViola Caon+44 20 7779 [email protected]

Americas EditorIla Patel+44 02 7779 [email protected]

Senior Reporter, AmericasJuliana Ennes+1 212 224 [email protected]

Senior Reporter, Asia PacificMia Tahara-Stubbs+65 8117 [email protected]

Senior Reporter, M&AAlexandra Dockreay+44 20 7779 [email protected]

Reporter, EnergyElliot Hayes+44 02 7779 [email protected]

Reporter, Funds and M&AArran Brown+44 20 7779 [email protected]

Reporter, MEAJames Hebert+44 20 7779 [email protected]

Reporter, Asia PacificDavid Doré+852 2912 [email protected]

Reporter, EuropeEliza Punshi+44 20 7779 [email protected]

Senior Marketing ManagerAndrew Rolland+44 20 7779 [email protected]

Data ManagerNikola Yankulov+359 2 492 [email protected]

Data Analysts: Sophia Radeva, Lyudmila Zlateva, Daniela Todorova, Katerina Ilieva, Miroslav Hadzhiyski, Aleksandar Arsov

Business Development Manager, EMEADoug Roberts+44 207 779 [email protected]

Business Development Manager, AmericasAlexander Siegel+1 212 224 [email protected]

Business Development Manager, AmericasNicolas Cano+1 212 224 [email protected]

Senior Business Development ManagerTim Willmott+44 20 7779 [email protected]

Head of Sales, AmericasSusan Feigenbaum+1 212 224 [email protected]

Head of Subscription SalesNicholas Davies+44 20 7779 [email protected]

Production ManagerSteve Ashenden

Managing DirectorStuart Allen+44 20 7779 [email protected]

CEO, Specialist Information DivisionJeffrey Davies

IJGlobalEuromoney Institutional Investor PLC8 Bouverie StreetLondon, UK EC4Y 8AX +44 20 7779 8870© Euromoney Institutional Investor PLC 2019

ISSN 2055-4842

DirectorsDavid Pritchard (Chairman), Andrew Rashbass (CEO), Wendy Pallot (CFO), Sir Patrick Sergeant, Andrew Ballingal, Tristan Hillgarth, Imogen Joss, Tim Collier, Kevin Beatty, Lorna Tilbian, Jan Babiak

3 From the editor

Briefings6 Funds8 M&A10 Capital Markets12 Policy & Regulations14 People

Europe82 Power struggle

Uncertainty around conventional generation in

Bulgaria could open the door for renewables.

83 Veja Mate offshore wind, GermanyNew shareholders in one of Germany’s largest

offshore wind farms.

Middle East & Africa86 You queue and wait

Kuwait has once again restructured its PPP agency to

kick-start stalled projects.

87 DEWA solar IV, UAEThe MBR Solar Park’s fourth phase is the �rst to

feature CSP technology.

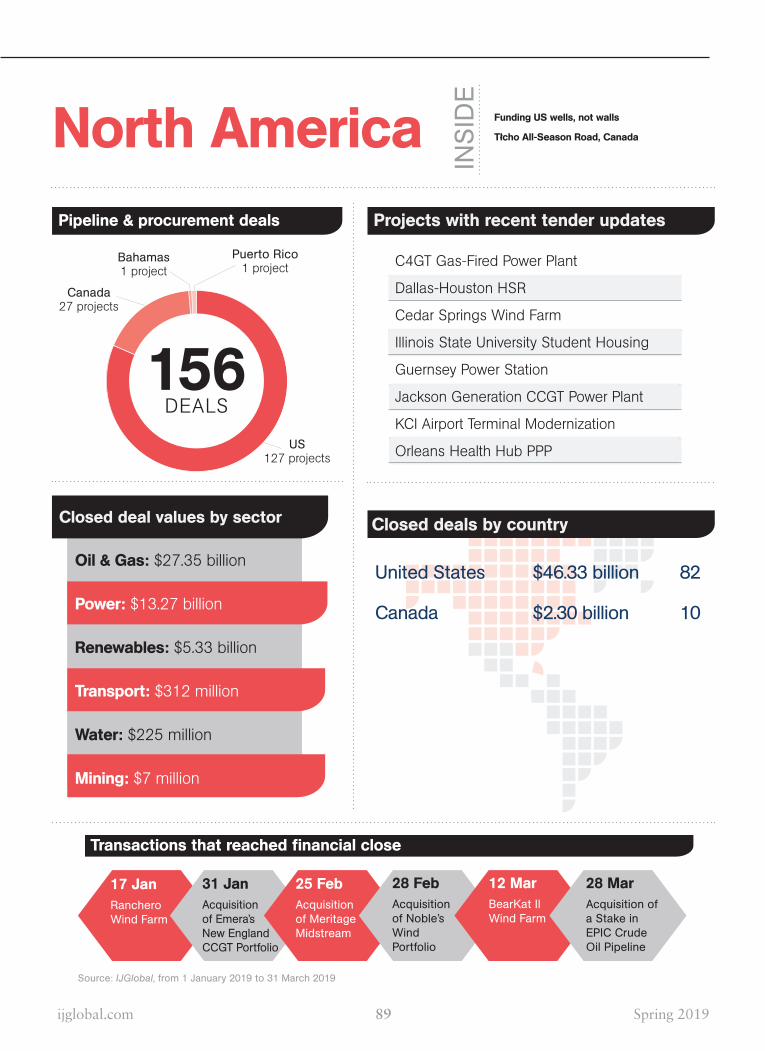

North America90 Funding US wells, not walls

The �rst couple of months of 2019 saw substantial

deals for the oil & gas industry in North America.

91 Tłıcho All-Season Road, CanadaThis P3 project uniquely features First Nations

involvement.

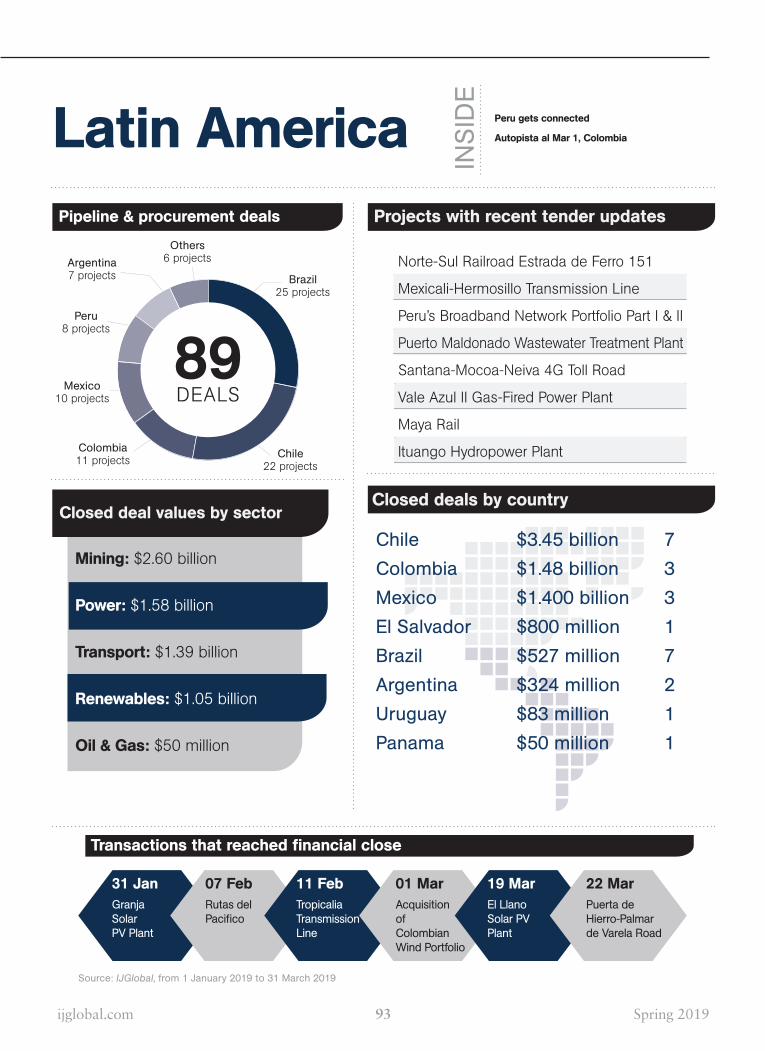

Latin America94 Get connected

Peru turns to project �nancing – and private

investors – to build out its �bre optic network.

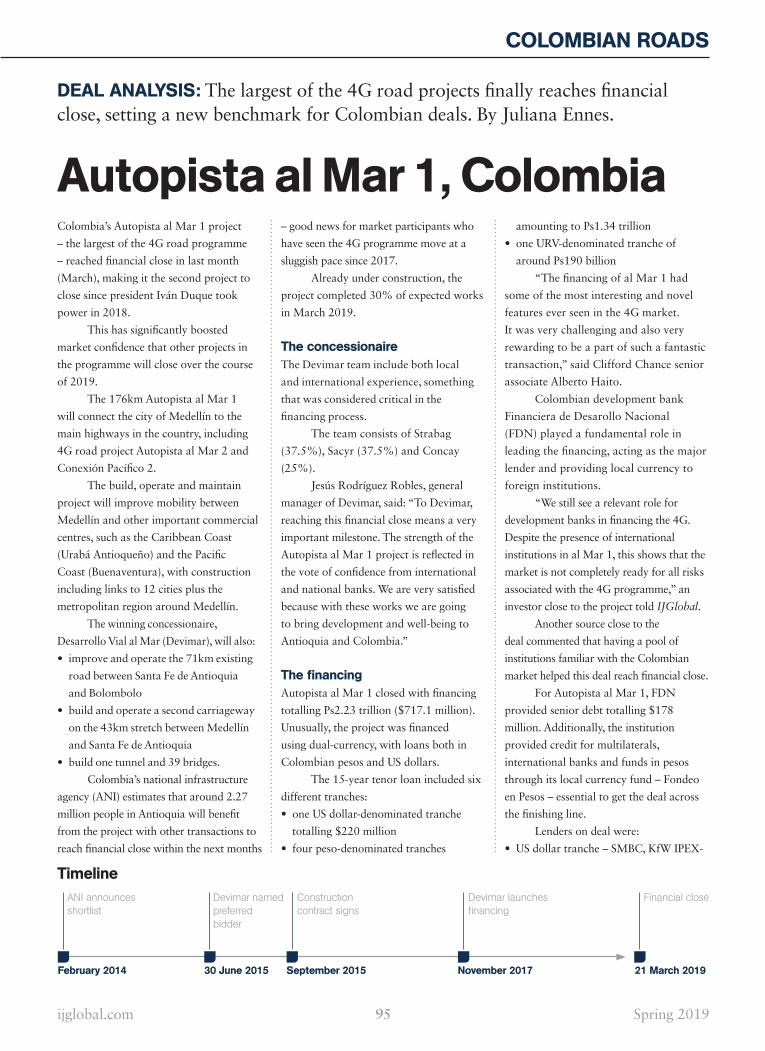

95 Autopista al Mar 1, ColombiaThe largest of the 4G road projects sets a new

benchmark for Colombian deals.

Asia Pacific98 Acquisition of Glow Energy, Thailand

Global Power Synergy had to forgo Glow Energy’s

trophy asset to �nally push through its deal with Engie.

99 NSW Regional Rail, AustraliaIts innovative debt structure makes this deal a

path�nder PPP in the Australian infrastructure market.

FROM THE EDITOR

3ijglobal.com Spring 2019

Athletes are keen on the tired sporting cliché of “taking one

game at a time”. As unedifying and uninspiring as this comment

is when spouted post-game by a player seemingly incapable of

original thought, you should grudgingly acknowledge that there

is logic behind it.

We know from our own experience that it helps to stay

focused on the task at hand. To not be deterred by a longer

series of tasks which subsequently need to be completed. Anyone

attempting a long-distance run knows that thinking too much

about the total distance can make your heart sink and your legs

heavy. Better to concentrate on one mile at a time.

This strategy for not being overwhelmed by a terrifyingly

daunting target came to my mind during IJGlobal’s recent

European renewable energy conference. Nestled in the picturesque

English countryside, delegates were fed a sobering state of play.

Some research, including that of the Global Carbon Project

initiative launched at the UN climate summit in Katowice, suggests

carbon emissions are rising not falling globally. This despite

tremendous investments in renewables energy over the last decade.

Various doom-inspiring statistics were bandied around at

the event. One panellist claimed the required capital investment for

keeping global average temperatures rising less than 2%, the target

of the Paris climate agreement, was the equivalent of �nancing the

$6 billion Hornsea II offshore wind project every day of the year.

Despite renewable energy capacity growing at an

exponential rate, power generated from renewables, even in

developed countries, is still less than thermal power.

And political risks are rising. Dieter Helm, a professor at

Oxford University who has written research papers for the UK

government, told conference attendees that no renewables are ever

fully subsidy free.

He argued that if power prices climb higher while the costs

of renewables development continue to fall, power supply will

become an even more political issue. Once renewables take the

energy market to zero marginal costs, it will be left to government

to decide who shoulders the remaining system costs connected to

power supply.

There is no easy answer to that. He notes that none of

the populist leaders to emerge around the work in recent years

support investment in renewables.

Meanwhile the demand for electricity is only set to rise, as

emergent technologies such as electric vehicles and AI, as well as a

move away from fossil fuel generated heat systems, will massively

increase the demand for electricity.

The countries with the highest carbon emission levels

also tend to be the fastest growing economically, with all the

implication for energy demand that implies. A number of

delegates acknowledged that the impact of policies and projects in

Europe is relatively small. What happens in China, India and Sub-

Saharan Africa will ultimately decide global temperatures.

Clearly there are enough bad headlines there to tempt someone

to lose hope but instead I came away from the conference inspired.

No matter what challenge there is facing the fast-changing

European renewables market, there were several delegates on

hand to suggest varying solutions.

The investors, fund managers and developers in the room

were well-aware of the formidable challenge at hand, but like a

long-distance runner they know that you have to stay focused on

the next mile.

The UK government may not be ready or willing to

implement the type of wholesale change Helm recommends. But

a representative from the Department of Business, Energy and

Industrial Strategy convincingly reassured delegates that it is

listening, and that a whitepaper due in July will contain details

on how it plans to address issues around managing the grid and

delivering new generation capacity.

Most agree that its CfD auctions have been a success and

should continue.

There was a consensus view on the inevitability of a

growing number of renewables assets in Europe needed to be

funded on a merchant basis. The structures needed to make

this happen are still up for debate but there is no shortage of

innovative structures being suggested.

Asset optimisation, through repowering or life extension, is

a growing challenge for the market, but assets owners seem willing

to accept that more carrot and less stick may be needed with O&M

providers when assessing how best to share these risks.

What struck me most from attendees was a widespread

willingness to be �exible to �nd solutions to problems.

The ultimate destination seems very far away right now

but that is not stopping those involved in renewables investment

making sure we get through the next few miles.

A formidable challenge

Despite the challenges facing European renewables, there is a willingness among market participants to be part of the solution.

Jon Whiteaker Editor

FUNDS

6ijglobal.com Spring 2019

BriefingsFUNDS

More funds news at ijglobal.com

BlackRock prepares new fundBlackRock is in a pre-marketing phase for

its latest fund.

IJGlobal has learnt that BlackRock

is in pre-marketing for its third global

renewable power fund which will target

assets in the US, Europe, Asia Paci�c and

Latin America.

The new fund will have a target of

$2.65 billion and the investment primary

term will be for 12 years. The fund is

targeting a return of 12%. It should have

a 65:35 split between green�eld assets and

operational assets.

The diversi�ed fund will target 80%

traditional renewable energy assets, while

the remaining 20% will be dedicated to

renewable infrastructure such as battery

storage and EV charging.

Prime Capital maiden fund plans Q3 first closeThe maiden infrastructure fund of

German alternative asset manager Prime

Capital plans to reach a �rst close in Q3,

according to a source.

Prime Green Energy Infrastructure

Fund aims to have raised €300 million

($336 million) at its �rst close in

September, with commitments from

between three and �ve investors.

Thereafter, a second close could

come in March 2020, with a �nal close

between June and September 2020.

Investors are being offered a return of

between 8% and 10%.

The €500 million fund expects to

make seven to 12 investments in total.

It has secured exclusivity over its seed

portfolio comprising two Norwegian

projects and one Swedish.

Ardian reaches final close for Fund VFrench fund manager Ardian has held a

�nal close at €6.1 billion ($6.92 billion)

for Ardian Infrastructure Fund V, which is

the largest Europe-focused infrastructure

fund raised to date.

The fundraise attracted commitments

from 125 investors, from Europe, North

America, Asia and the Middle East. Former

investors re-upping their commitment

accounted for 70% of LPs, while 30% of

the LPs are new clients of Ardian.

Fund V will have a split

investment mandate of 80% allocated

to equity in operational assets and

the remainder allocated to equity in

green�eld development. The fund will

be especially interested in energy (gas,

electricity, renewables) and transportation

opportunities, as well as investing in other

public infrastructure assets including

health and environmental.

EQT IV fund holds €9bn final closeEQT has reached �nal close on its fourth

infrastructure vehicle at the €9 billion

($10.1 billion) hard cap, making it the

largest infrastructure fund so far.

The unlisted vehicle has a mandate

to invest in a number of geographies, but

will focus on operational assets in Europe

and North America – though investment

opportunities in Asia Paci�c will also be

considered – across energy, environmental

and social infrastructure, logistics,

telecoms and transport.

Ticket size will be between €100

million and €600 million, but has the

�exibility to consider larger opportunities

should they arise. Meanwhile, EQT is

planning an expansion in continental

Europe with the opening of two new

of�ces in France and Italy. EQT received

enough interest to have exceeded its hard

cap, but ultimately chose not to raise

the fund size in favour of raising a fund

consistent with what it sees as deal-

availability in the market.

Meridiam’s reopened Africa fund closes at €546m

Paris-headquartered investment �rm

Meridiam has closed its Africa fund at

€546 million ($614 million), having

reopened the vehicle in November (2018).

The reopened Meridiam Infrastructure

Africa Fund (MIAF) exceeded the €510

million target, dwar�ng its €207 million

�nal close in 2016.

MIAF’s initial commitment was fully

invested two years before the end of its

investment period, prompting Meridiam to

reopen the fund to allow MIAF to pursue

follow-on investment opportunities, further

diversify the portfolio, gain exposure to

larger assets, and bene�t from economies of

scale on �xed costs.

MIAF held �rst close in May 2015

with €150 million in commitments, and

reached a €207 million �nal close in July

2016. MAIF is now €350 million invested

with funds anticipated to be committed

in 2021.

First close for Marubeni-Mizuho-AM One fundThe specialist equity investment fund set

up by Marubeni, Mizuho Bank and Asset

Management One in Japan has reached

�rst close.

The fund, MM Capital Infrastructure

Fund I, raised ¥20 billion ($180 million)

Mizuho said it plans to reach out to

a number of investors over the next year

to take it to �nal close.

MM Capital Infrastructure Fund

I is targeting ¥50 billion, for equity

investments in operational assets in the

transportation and energy sectors.

The assets will be generating

steady cash �ows abroad, particularly

in OECD countries.

The fund is managed by MM

Capital Partners Company which is owned

by Marubeni (90%), Mizuho (5%) and

Asset Management One (5%).

M&A

8ijglobal.com Spring 2019

Latest German offshore wind sale launchesNorway’s Equinor is looking to sell its 50%

interest in the 385MW Arkona offshore

wind farm in the German Baltic Sea.

E.ON is the other shareholder in

the asset. The project entered commercial

operations in October 2018 and bene�ts

from a four-year PPA with ENGIE which

will buy the electricity on the German

day-ahead and intra-day market. Located

35km north east of Rugen Island, the

wind farm features 60x Siemens Gamesa

6.45MW turbines.

The Arkona sale process will be one

in a string of recent M&A transactions for

German offshore wind.

Highland Group and Copenhagen

Infrastructure Partners sold 80% of Veja

Mate in February (2019) to Commerz

Real, Ingka Group, Wpd Invest and KGAL

Group for around €600 million ($676

million). Meanwhile, the sale process for

Bard 1 has launched, GIP is in the process

of selling its 50% stake in Gode 1 and the

shareholders of Merkur Offshore Wind

are also seeking to sell their interests.

LS Power launches US CCGT sell-offLS Power has hired Barclays and Goldman

Sachs to run the auction of a pair of

operational, contracted combined-cycle

gas turbine (CCGT) plants in the US.

A teaser for the sale of the 516MW

Carville Energy Center near Baton Rouge,

Louisiana, and 1,127MW Oneta Energy

Center near Tulsa, Oklahoma, was issued

to market in March 2018.

The assets could be sold separately,

a source has said, as the plants were

individually project �nanced. Both CCGT

plants entered operations in 2003 and

feature General Electric 7FA turbines.

Carville has multiple offtakers,

including a utility and a steam customer,

under PPAs expiring in 2032. Most of

Carville’s output is contracted with Entergy

under a 485MW agreement signed in 2011.

Oneta’s offtakers, meanwhile, include a

utility, a municipality and two electric co-

operatives with contracts expiring in 2042.

IFM, PSA and Polish state fund sign DCT Gdansk purchaseA consortium of IFM Investors, Singapore-

based port operator PSA International and

state-owned Polish Development Fund

(PFR) signed a contract in March (2019)

to buy 100% of DCT Gdansk in Poland.

The sellers are Macquarie (64%) and three

Australian superannuation funds (36%).

The buyers valued DCT Gdansk

at between Z5 billion ($1.31 billion) and

Z6 billion. The 2018 EBITDA for DCT

Gdansk was €73.7 million ($83.3 million),

implying a multiple of between 16x and

19x EBITDA. The new owners are due to

re�nance the company’s €130 million debt

as part of the acquisition.

DCT Gdansk’ sale process

launched in Q3 2018, drawing interest

from bidders also including DP World,

Infracapital and QIC.

Japanese consortium invests in Taiwan offshore windGerman developer Wpd has selected a

Japanese consortium as preferred bidder in

the auction of a minority shareholding in

its Yunlin offshore wind farm in Taiwan.

The consortium will buy a collective

27% shareholding, after Wpd put up to

49% on sale. The buyers, led by Sojitz

Corporation, are Chugoku Electric Power

Company, Chudenko Corporation,

Shikoku Electric Power Company and

JXTG Nippon Oil & Energy Corporation.

Other bidders in the auction included

Japanese trading house Itochu Corporation

and Canadian pension fund CDPQ.

The sponsor is close to �nalising the

debt package for Yunlin, having run the

debt and equity processes concurrently.

A local and international bank club is in

place, with close to 20 lenders providing

around NT$80 billion ($2.6 billion) debt.

Ardian exits Indigo Group as it breaks into ChinaFrench fund manager Ardian has exited

its 49.2% shareholding in car parking and

mobility company Indigo Group, having

invested alongside Predica in May 2014.

The buyers are another French

fund manager Mirova, through the Core

Infrastructure Fund II, and German

insurance asset manager MEAG.

Ardian and Predica expanded

Indigo’s business into the Americas,

and then in March (2019) agreed to set

up a €30 million ($33.9 million) joint

venture platform with Chinese parking

management company Sunsea Parking, after

a competitive process to �nd a local partner.

Ardian and Predica ran an auction

back in 2017 to both exit Indigo, though

after �nding a Chinese buyer Shougang

the deal collapsed.

Marubeni exits Saudi power and water plantACWA Power has acquired Marubeni’s

shareholding in the captive power and

water plant that services the Rabigh re�nery

and petrochemicals facility in Saudi Arabia.

Marubeni has sold its 30% stake

in Rabigh Arabian Water & Electricity

Company (RAWEC), which owns the

plant, and its 34% stake in the O&M

company Rabigh Power Company (RPC).

ACWA Power now has a roughly 74%

stake in RAWEC, and an 85% stake in

RPC through its subsidiary NOMAC.

Additional shareholder JGC Corp

retains a 25% stake in RAWEC and a

15% in RPC.

The deal closed on 13 March

(2019), after ACWA Power exercised pre-

emption rights in May 2018.

BriefingsM&A

More M&A news at ijglobal.com

CAPITAL MARKETS

10ijglobal.com Spring 2019

Vinci issues Gatwick bondVinci has issued an £800 million ($1.04

billion) bond on behalf of Vinci Airports

to fund the purchase of a 50.01%

shareholding in London Gatwick Airport

it acquired at the end of last year.

The bond is arranged in two £400

million tranches, one maturing in March

2027 at an annual coupon of 2.25% and

one maturing in September 2034 at an

annual coupon of 2.75%.

The issue was 3x oversubscribed.

BNP Paribas, HSBC, NatWest Markets

and RBC Capital Markets were joint

bookrunners.

Vinci Airports acquired the majority

stake at the end of December 2018 in a

deal valued at £2.9 billion.

KKR’s Altice telecoms towers debt syndicatedFour underwriter banks – BNP Paribas,

Crédit Agricole CIB, DNB Bank and

Natixis – completed the syndication of

the €770 million ($872 million) senior

credit facilities backing KKR’s acquisition

of a stake in Altice’s French telecoms

towers business.

The syndication was oversubscribed

with the following MLAs joining the deal:

Allied Irish Banks, Deutsche Bank, E.SUN

Commercial Bank, Edmond de Rothschild

AM’s BRIDGE funds, Generali Global

Infrastructure, Lloyds Bank, MUFG Bank,

Raiffeisen Bank International and Schroders.

The debt facilities comprise a €470

million acquisition facility to fund part

of the deal along with a €300 million

revolving credit facility to fund new

telecoms business Hivory’s growth.

KKR and Altice formed Hivory in

December 2018. It is the largest independent

telecoms tower company in France, and

third largest in France, with a portfolio of

over 10,000 of Altice’s French towers.

Altice agreed a sale of 49.99% of

SFR TowerCo, the holding company for

Altice’s French telecoms tower portfolio,

to KKR in June 2018. The deal had a

value of roughly €1.8 billion, which

represented 18x the 2017 EBITDA.

GHIAL prices bond for Hyderabad airport expansionGMR Hyderabad International Airport

(GHIAL) has priced a �ve-year senior

secured issuance of $300 million in the

international bond market at a coupon of

5.375%, to �nance the expansion of the

airport in Hyderabad.

The pricing took place on 3 April

(2019), after the bond launched the

week before.

GHIAL is a special purpose vehicle

for the design, �nancing, construction,

operation and maintenance of the Rajiv

Gandhi International Airport (RGIA).

The company will use the proceeds

toward capital expenditure on the master

plan for expanding RGIA. The expansion

will increase the airport’s capacity to 34

million passengers per year.

Mexico agrees to partially repay NAIM investorsThe Mexico City Airport Group (GACM)

and bondholders have reached an

agreement to liquidate bonds previously

issued to �nance the Nuevo Aeropuerto

Internacional de México (NAIM).

Under the agreement, GACM will

pay around Ps34 billion ($1.77 billion).

The payment does not cover the

entire debt of the project. The airport, which

was cancelled after construction reached

around 30%, had a total estimated cost of

$13.3 billion. The project had issued $6

billion in bonds to �nance the construction.

According to the minister of

communications and transport, Javier

Jimenez Espriu, the government will repay

$200 million yearly from the remaining

debt of $4.2 billion.

It is understood that this agreement

was reached so that GACM and the

Mexican government save pension fund

investments which provided a large part of

the bond �nancing for the airport.

Kenya to reissue mobile-based infra bondKenya’s National Treasury was due to

reissue the mobile-based infrastructure

bond M-Akiba in March (2019), after

the bond failed to meet its Sh1 billion

($10 million) target in 2017.

The new bond target is now pegged

at Sh250 million. The maturity is three years

with a �xed 10% interest rate. Proceeds

from the sale will support infrastructure

projects in the East African state.

Kenya’s government had looked to

raise Sh5 billion through M-Akiba, but

underperformed after �rst issue in June

2017 – Sh247.47 million – fell 75% short

of its target.

Airport Authority Hong Kong prices bonds for 3RSAirport Authority Hong Kong (AAHK)

has priced an offering of bonds due 2029

at 78bp above 10-year US Treasuries,

with proceeds going towards the

HK$141.5 billion ($18 billion) Three-

Runway System (3RS) project and

general corporate matters.

The $500 million, 3.45% bond sale

ended a hiatus of more than 15 years from

the dollar bond market for government-

backed AAHK – operator of Hong Kong

International Airport (HKIA).

Advisers to AAHK on the issue

included HSBC and Citigroup as joint lead

managers, and Linklaters.

HSBC and Citigroup guided the Reg

S bond at 105bp. However, strong demand

allowed them to settle on a price of 78bp.

The $3.6 billion �nal order book

had more than 160 accounts split among

investors from Asia (around 91%) and

Europe, Middle East and Africa.

BriefingsCAPITAL MARKETS

More capital markets news at ijglobal.com

12ijglobal.com Spring 2019

POLICY & REGULATION

Trump signs executive orders for energy infraUS president Donald Trump has signed two

executive orders speeding up the process for

energy infrastructure deals in the US and

making it harder for states to block projects

due to environmental concerns.

US secretary of energy Rick Perry

said that Trump took “sweeping action”

to ensure the US reaches it’s full “energy

potential and has the ability to deliver our

historic energy supply both around the

nation and the world.”

According to the president, the

executive orders will: “implement a

comprehensive whole-of-government

approach to streamline the development

of necessary energy infrastructure projects,

and reduce existing barriers to achieving

that goal.”

The Department of Energy will

be required to submit a report to the

president on the impact of limiting the

export of coal, oil, natural gas, and other

domestic energy resources through the

west coast of the US.

The second executive order calls for

streamlining the process for cross-border

international energy infrastructure projects.

Trump recently expressed his support

for TransCanada’s Keystone XL pipeline

project by issuing a new Presidential Permit

at the end of March (2019). The project

was halted in November 2018 after a US

judge in Montana blocked the project

on the grounds that a full environmental

analysis had not been completed.

Estonia halts offshore wind projectThe Estonian government has decided

not to proceed with an application for

a 600MW offshore wind farm, citing a

potential threat to national security.

A government spokesperson said

that the building permit �led by developer

Saare Wind Energy was refused on the basis

that, should it be granted, the applicant

may pose a risk to public order, social and

national security. The Ministry of Justice is

leading the challenge for the administration.

Saare Wind Energy has been working

on a plan to build an offshore wind farm

of 100x 6MW turbines off the island of

Saaremaa since 2015. Capex on the wind

farm is €1.7 billion ($1.91 billion).

The developer last sent a request

to the government at the end of 2017 for

the latter to make a decision regarding the

initiation of a building permit procedure.

The plan was for the wind farm

to have an annual output capacity of

2,800GWh, around 30.9% of Estonia’s

total electricity output in 2015.

Colombia rethinks power auctionsThe Colombian government has been

studying the possibility of making

participation in the long-term power

auction mandatory for the demand side.

The country’s �rst long-term

renewable power procurement process

ended earlier this year in February (2019)

and did not go to plan. No projects were

awarded, though it did attract interest

from international and local players.

The main problem according to

sources was a lack of interest from the

demand side. The government is currently

planning a new auction for either Q2 or

Q3 2019, with adjusted rules.

Among lessons learned from

the failed auction was the need for a

mechanism to create enough incentive

for the demand side to participate more

actively, or to including mandatory

participation in the auction.

Mandatory participation would

reduce the exposure of the demand side to

price volatility on the free market.

The Colombian government is also

looking over the possibility of creating

a guarantee scheme for the contracts

and launching an agenda for two power

auctions per year over the next two years.

Finland supports onshore windIn late March, the Finnish Energy Authority

awarded subsidies to support seven projects

in its �rst technology-neutral tender.

A total of 26 bids were received by

the authority – all for onshore wind – but

19 were rejected.

Average price for successful bids

was €2.49 ($2.81) per MWh. The lowest

accepted bid was for €1.27 per MWh

while the highest was €3.97 per MWh.

The price of accepted bids weighted

according to the yearly production of the

capacity on offer, was €2.58 per MWh

Meanwhile, the average price of the

declined bids was €8.52 per MWh. The

auction was open to projects generating

electricity from wind, solar, wave power,

biomass and biogas. The maximum annual

electricity generation for tenders was

1.4TWh. The combined annual production

of the accepted projects was 1.36TWh.

All awarded projects will receive a

premium based on its respective tender. A

full premium is paid when the average of

the three-month market price of electricity

is equal to or lower that the reference

price of €30 per MWh. If the market

exceeds the reference price, a sliding scale

will be used. No aid will be paid if the

market price is higher than the sum of the

reference price and the approved premium.

The subsidy will be paid for a period

of 12 years. This period will begin no later

than three years from the date on which the

approval decision was given. The maximum

annual cost incurred by the state from the

premium scheme total €3.5 million. This

is less than 5% of the costs incurred to

the state from the FiT system for the same

annual electricity production.

BriefingsPOLICY & REGULATION

More policy & regulation news at ijglobal.com

PEOPLE

14ijglobal.com Spring 2019

BanksFormer Natixis managing director Ranjan

Moulik has started a new role as MD

and head of �nancing at energy M&A

specialist IKAV. He started this new role

in March and will continue to be based

out of Paris, but will now focus his efforts

on equity opportunities in the renewable

energy space. Moulik stepped down from

his position as global head of power and

renewables at Natixis in late February,

having led the project �nance business for

nearly six years in Paris.

National Australia Bank has hired Barry

Dale at a director-level position in London.

Dale most recently served as energy and

infrastructure director at Scotiabank.

Also joining the swelling ranks at NAB’s

London of�ce is Camélia Chenaf, who

comes from SMBC where she has worked

since the summer of 2013, rising to vice-

president level in the Japanese bank’s

project and acquisition �nance team with

a primary focus on transport.

Canada Infrastructure Bank has hired

Sara Alvarado as head of risk, based in

Toronto. Alvarado has over 28 years

banking experience, and until last year

(2018) was a senior of�cer, infrastructure

new products and special transaction at

the EIB. She focused on the investment

plan for Europe to catalyse private sector

�nancing in policy priority sectors.

AdvisersSharlene Hay has joined BTY Group

as a director in its PPP advisory team

in London. Hay has over 10 years’

experience as an engineering and

infrastructure adviser. She joins from

Infrata where she was worked in the role

of principal consultant for over four years.

Clifford Chance

has appointed Toby

Parkinson as partner

in its infrastructure

division in London.

Parkinson returns

to the magic circle �rm from OMERS

Infrastructure, where he worked as

director of legal for three years and

provided legal advice to the transaction

teams in London. Parkinson �rst joined

Clifford Chance in 2006, where he worked

in the �rm’s infrastructure and private

equity team for 10 years.

Crowell & Moring

has appointed Robin

Baillie as a partner in

its energy practice in

London. Baillie joins

from Squire Patton

Boggs, where he headed its infrastructure

practice in the UK and Europe for over

four years. He has more than 20 years’

experience advising on energy and

infrastructure projects globally, with a

focus on the UK and North America.

Sponsors Dougie Sutherland

has stepped down

from Interserve’s

board of directors

following a dispute

with the group’s

shareholders over its rescue plan, which

was eventually rejected at another

shareholders’ meeting, causing Interserve

to go under administration. Sutherland

remains managing director of Interserve’s

developments division. He has been with

Interserve for over 12 years, having played

an important role in the Fit for Growth

business transformation programme.

UK �bre-to-the-premises network operator

Gigaclear has appointed Gareth Williams

as its chief executive. Williams, who

joins Gigaclear from Interoute, replaces

Matthew Hare who the company had

been trying to replace since last summer

following its acquisition by M&G

Prudential›s infrastructure investment

manager Infracapital, and after struggling

to deliver a number of new broadband

contracts under Hare’s watch.

Asset ManagersBrooks Kaufman has left IFM Investors

after spending nearly a decade with the

�rm, most recently as an investment

director of infrastructure based in New

York. Before joining IFM Investors in 2010,

Kaufman served on the board of directors

for the Duquesne Light for almost seven

years.

Meanwhile, IFM Investors has

appointed Lucie Mixeras as a director in

London. She joins from Crédit Agricole

where she was at vice-president level and

had worked for almost eight years. In her

new role, Mixeras will report into David

Cooper on the infra debt team.

Green Investment Group (GIG) managing

director Bill Rogers has resigned from

his role as head of distributed energy

and onshore wind, and is understood to

be on the verge of joining a Canadian

pension fund investor. Meanwhile,

Richard Braakenburg, who was senior

vice-president for distributed energy

and onshore renewables at GIG, has

also stepped down from his position

at the Macquarie-owned platform to

take on the role of CFO at Pivot Power

– an energy storage and electric vehicle

charging specialist.

Rogers spent more than six years at

GIG, having joined from Hudson Clean

Energy where he was managing director.

Braakenburg also spent a little more than

six years at GIG, having joined from the

UK Department of Energy and Climate

Change (DECC) where he was a senior

banking and �nance analyst.

BriefingsPEOPLE

More people news at ijglobal.com

15ijglobal.com Spring 2019

Given the slow growth of the corporate PPA market, some argue banks will have to start

accepting merchant risk in order to finance the next generation of

European renewables. By Jon Whiteaker.

Marching towards merchant

EUROPEAN POWER

16ijglobal.com Spring 2019

EUROPEAN POWER EUROPEAN POWER

Fundamental changes to the

European power market mean it is

marching in a new direction, though

arrival time (and ultimate destination) are

far from certain.

Unlike in North America, European

project �nance banks have not had to get

comfortable with full merchant risk for

conventional power, largely due to a lack of

new-build projects. Meanwhile renewable

energy assets the world over have until

recently been protected from variable

power prices by generous subsidies.

However, with governments

withdrawing subsidies for renewables and

a huge backlog of wind and solar plants

to be developed over the next decade, we

are going to see a profound change in how

European renewables are funded.

Countless con�dent market reports

and panellists at industry events have

been keen to promote corporate PPAs

as the solution to �nancing projects

in a post-subsidy world. Scepticism is

growing though.

In Chandra’s telling, most corporate

entities “do not have the incentive to

contract power over the long-term,

especially when you are in an environment

where prices are going to fall.”

The corporate PPA market has

certainly been growing in Europe, as it has

elsewhere, but Chandra is not the only one

to note a limit to corporate appetite.

“Clearly there’s a requirement for

more contracts. There is more demand

from generators for quality PPAs than

there are contracts available,” says Ricardo

Piñeiro, partner at Foresight Group.

New forms of state support or

regulation could provide extra comfort for

lenders and investors though there is little

certainty what this support would look

like even if it does emerge.

Which is why many now think

banks will have to start accepting

merchant risk on renewable power

transactions in Europe.

Anything but fully merchant“There is still a big resistance

from banks to do fully merchant

transactions,” according to Alejandro

Ciruelos, managing director, project &

infrastructure �nance at Santander.

He argues that lenders will only

accept some merchant risk if there is a

level of contracted revenue for the project

to anchor a debt �nancing off.

But will enough offtake agreements

emerge to meet demand?

Though the volume of corporate

PPAs is still low, some remain con�dent

that these contracts will provide the main

solution to the funding challenge.

“There is a lot of appetite from

corporates to enter into PPAs, not

least because they can use it towards

their sustainability goals,” said Sophie

Dingenham, corporate & projects partner

at law �rm Bird & Bird.

Dingenham says that many small

and medium sized companies are now

looking at longer-term power contracts

and she is con�dent “corporate PPAs can

support a large chunk of the renewable

energy generation in the coming years”.

Research from Bird & Bird shows

that corporate PPAs accounted for 7.2GW

of power purchased from generators

between January and July 2018, across 28

different markets globally. This is up from

just 5.4GW for the whole of 2017.

Bird & Bird estimates that 80% of

these corporate PPA deals were signed in

the US or in Nordic countries, however,

with activity in the rest of the world thin

on the ground.

Though there is interest on

the corporate side, there are no

standardised solutions and it is a slow

process for counterparties to fully

understand their obligations.

As Foresight’s Piñeiro says: “By

being available to discuss it doesn’t mean

corporates are prepared to sit down and

negotiate a contract”. He also notes that

there have actually been very few corporate

PPAs signed in most European markets.

Though sleeved and private wire

corporate PPAs may remain relatively

rare, Rob Dornton-Duff, managing

director at Riskbridge Associates, sees

a growing market for synthetic PPAs –

effectively a power hedge without a direct

physical offtake.

“There is an emerging market for

power hedging and it’s possible to hedge

UK and some European power out to 5

years in �xed rates, and as far as 10-15

years with caps, in reasonable quantity.”

“Clearly it is much better from

a bankability perspective to create a

synthetic PPA or hedge instead of running

merchant risk: merchant power is typically

a last resort. If there is any other option

people will take it.”

Dornton-Duff also thinks

governments will have to �nd a solution

if there is not enough contracted power

available to support their renewable

energy pipelines.

“The future of power in Europe is fundamentally going to be merchant”. That opinion may have seemed fanciful until

fairly recently, but Hari Chandra, managing director and global co-head of power, energy and infrastructure at Cantor Fitzgerald, is con�dent in his prediction.

Ricardo Piñeiro, Foresight Group

17ijglobal.com Spring 2019

EUROPEAN POWER EUROPEAN POWER

Falling project costs have fuelled the

march towards zero subsidies. If �nancing

gets more expensive, bidding will become

less aggressive.

“It’s a bit circular. If your debt

pricing goes up because it’s merchant,

then the subsidy bids will re�ect that.

You won’t have zero bids on subsidies,”

Dornton-Duff says.

Though this tension may force

governments in southern Europe to

provide some subsidy support, Piñeiro

does not expect to see other state-led

solutions emerge: “I don’t see any

indication that governments wish to

regulate or incentivise corporates to enter

PPAs directly with generators. This trend

will continue to be driven by corporate

sustainability targets.”

If sponsors must take merchant

exposure, some say this will just result in

renewables not being project �nanced.

“Equity capital may be willing to

take that merchant risk, with no leverage at

the project level,” Santander’s Ciruelos says.

Banks led by the noseIt is easy to make a case that if the

market moves towards merchant power

it will be sponsors rather than lenders

leading the way.

How quickly offshore wind moved

from a risky technology to a safe bet

for most PF banks shows lenders have

ultimately proved �exible in order to keep

doing deals.

Stewart Robinson, managing

director of power, energy and infrastructure

at Cantor Fitzgerald, says: “There are a

growing number of European investors

who are looking at deals with a merchant

tail, and increasingly pure merchant deals

that they recognise will play a part in how

the future pipeline gets �nanced.”

Robinson thinks there will still

be instances where a corporate PPA is

appropriate, and that there will be more

of these contracts than we see in the

market now, but says there is a price to

that certainty.

Renewable energy projects will

never again yield the high returns they

did under feed-in tariff schemes, which

makes it increasingly important to

maximise revenues.

“If PPAs were being offered at no

discount, everyone would be taking them

on. But everyone is either offering them

at a discount or signi�cant discount,”

according to Carlos Candil, MD for

power, energy and infrastructure at

Cantor Fitzgerald.

Sponsors may need to provide more

equity in this environment, but banks will

still play a role.

“Gearing will be reduced as a

result of the lower level of contracted

revenues,” Foresight’s Piñeiro says. “This

will increase equity funding requirements

compared to subsidised assets in terms of

percentage of total funding.”

If the US market acts as a

model, sources suggest a Term Loan B

market may emerge. Forward purchase

agreements, power hedges, cash trapping

and cash sweeps could also all become

common transaction features.

Piñeiro thinks most lenders are

aware of the challenges in the market

and are considering solutions: “Most

of our relationship banks have showed

interest and willingness to engage

in �nancing unsubsidised projects,

especially in Spain and Portugal, as those

markets are more advanced.”

He says banks are analysing power

price sensitivity and the minimum price

they can accept. They have been looking

at power price forecasts anyway but now

must take a view.

Piñeiro can see shorter PPAs

matched with shorter-term debt: “I

would expect to see more mini-perm type

structures, with an element of re�nancing

risk that the sponsors will need to be

comfortable with. We are probably going

to see an increase in margins to re�ect the

merchant nature of the project, and the

gearing will decrease”.

The Spanish impositionThese types of merchant structure are

likely to appear in Spain �rst.

The country was badly bruised by

a generous subsidy scheme that led to

an unsustainable government debt pile.

The Spanish government announced a

moratorium on subsidies in 2012 and

retroactively cut feed-in tariffs a year

later. Since Spain’s renewables market

was revived in 2016, over 8GW of new

development rights have been awarded.

The projects awarded via auctions

bene�t from a pricing �oor but only

receive the market price for power.

Some developers are seeking

corporate PPAs but they have been hard to

come by to date.

Foresight signed on the �rst

corporate PPA for a solar asset in Spain,

a contract with Energya-VM for the

3.9MW Las Torres de Cotillas in Murcia,

in December 2017. It is understood they

are close to a second corporate PPA in the

country but clearly development of this

market has been slow.

Rob Dornton-Duff, Riskbridge AssociatesCarlos Candil, Cantor Fitzgerald

EUROPEAN POWER

18ijglobal.com Spring 2019

More recently, Nike signed a

PPA with Iberdrola and Caja Rural de

Navarra for 40MW of renewable power

earlier in February 2019 – the third such

deal between the sports company and

Iberdrola. The project that will supply the

power, Cavar Wind, however has a total

capacity of 111MW.

If large international corporates

are unwilling to take all the power

from a single wind farm, it shows how

dif�cult it is to eliminate all market risk

on these projects.

Cantor’s Candil says: “Spain is the

�rst market in Europe which has come

through with a large enough scheme of

assets which is being built. Some utilities

will build on balance sheet but others

will not.”

Cantor Fitzgerald has already

advised on one merchant power

transaction in Spain, though this was

a re�nancing of Arclight’s operational

Bizkaia gas-�red plant located in the

Basque region. As much as 66% of the

three-year debt is due to be repaid through

merchant cash�ows, and the private

placement was made to European, non-

Spanish, investors.

If established institutional investors

are taking merchant risk on debt for an

operational gas-�red power plant in Spain,

it doesn’t seem a huge stretch for banks to

lend to new-build merchant renewables in

the country.

“The new-build cost for solar in

Spain is now around €600,000 per MW,

down from €10 million per MW around

10 years ago,” Candil says. “At that price

it is very comparable to new gas-�red,

particularly when the stated load factors

for a modern-day CCGT are much higher

than they really are. So the power output

starts to be comparable”.

Lower project costs mean a lower

debt requirement. Banks look set to

provide at least some of the debt required

for these projects on a merchant risk basis.

The lack of subsidy support in

Spain and Portugal is forcing sponsors

to try to structure merchant �nancings.

Some expect projects in Eastern European

markets to follow suit and others think the

UK and German markets could be next if

proven structures emerge.

Sources suggest there are active

discussions happening on UK merchant

solar deals already.

The emergence of a merchant

power market in Europe now looks far

from fanciful.

Alejandro Ciruelos, Santander

IJGLOBAL AWARDS 2018

19ijglobal.com Spring 2019

It is that time of year again. IJGlobal is delighted to announce the winning deals and winning companies for the IJGlobal Awards 2018.

Gala awards ceremonies were held in London, New York, Dubai and Singapore during March to celebrate this year’s winners. The ceremonies were the end of a six-month process to identify the outstanding transactions and companies from 2018.

Each of the winning transactions and companies, across all regions and every sector category, are pro�led in the following pages.

Congratulations to all the winners!

EuropePage

22 European Offshore Wind SeaMade

23 European M&A Acquisition of John Laing Infrastructure Fund

23 European Telecoms Open Fibre Broadband

23 European Transmission & Distribution Idex Acquisition

24 European Water SAUR Acquisition

24 EuropeanPorts RotterdamWorldGatewayRefinancing

24 European Airports Belgrade Nikola Tesla Airport

25 European Rail Wales & Borders

25 EuropeanRefinancing TheM25Refinancing

25 EuropeanRoads 1915CanakkaleBridge&Motorway

26 European Social Infrastructure Haren Prison PPP

26 EuropeanBiomass GreenaliaBiomassPowerCurtis-Teixeiro

26 European Hydro Power Acquisition of Menzelet and Kilavuzlu HEPPs

27 EuropeanSolar RTRPortfolioAcquisitionandRefinancing

27 EuropeanWaste CoryRiverside

27 European Onshore Wind Tesla Wind: Dolovo Wind Farm

28 European Midstream Oil & Gas Gas to the West

28 European Upstream Oil & Gas Neptune Energy

28 European Power Bizkaia Energia

21ijglobal.com Spring 2019

22ijglobal.com Spring 2018

IJGLOBAL AWARDS 2018IJGLOBAL AWARDS 2018

European Offshore WindSeaMadeThe 487MW SeaMade offshore wind

farm in the North Sea was to an extent

an ef�cient and straightforward project

�nancing deal, with the sponsors bringing

the project across the line in less than

three months after launching the €1

billion ($1.1 billion) debt �nancing.

But make no mistake, SeaMade’s

journey from procurement to �nancial

close was not a simple one; it took a

fair share of political wrangling and the

merger of two separate projects (and

sponsor teams) to �nally achieve a deal

featuring one of the lowest interest rates

in 2018 for offshore wind debt.

SeaMade is the result of the

merger of two Belgian offshore wind

farms: the Otary consortium’s Seastar

project, and Otary and Engie Electrabel’s

Mermaid project.

Seastar and Mermaid were among

four offshore wind projects at the �nancing

stage that the Belgian government had

threatened to cancel in 2016, deeming the

subsidy packages too generous. With the

costs of developing offshore wind projects

in Europe having fallen dramatically in the

previous year, the government was keen to

achieve similar price reductions.

However, the Belgian government

had limited means and time to renegotiate

the subsidies. Under pressure to

decommission its two nuclear power

plants by 2025 (which account for 60% of

the country’s generating capacity) and to

increase its offshore wind capacity to 2GW

by 2020 meet EU emission targets, there

was no time to retender to the projects.

Instead, the government negotiated

a new tariff of €79 per MWh, allowing the

projects to proceed.

The sponsors of Seastar and

Mermaid ultimately decided to restructure

the projects’ ownership structures so

the full development could be �nanced

through one transaction.

The European Commission

approved the merger of the projects in

July 2018, resulting in Dutch utility Eneco

joining the equity consortium of the

SeaMade project. The new shareholding

structure comprised: Otary (70%);

Electrabel (17.5%); and Eneco (12.5%).

Otary is a consortium of eight

Belgian companies: investors Socofe, Rent-

A-Port Energy and SRIW, local authority

investment vehicle Z-kracht, dredging

company Deme, offshore developer

Aspiravi, and renewables developers Elicio

and Power at Sea. Each hold a 12.5%

stake in the consortium.

The Otary-led sponsor team reached

�nancial close on the €1.3 billion SeaMade

project in December 2018, with Eneco

signing a 15-year PPA to offtake all of the

power from the asset in the same month.

FinancingDebt �nancing for the project began in

March and featured a hedging strategy

with contingent hedge implemented prior

to �nancial close. The �nancing had to be

tailored to address SeaMade’s twin project

con�guration: it consists of two sites

with two concessions, resulting in two

cash �ow streams covered by one single

contractual set up.

The consortium of Otary,

Electrabel and Eneco closed on the €1

billion debt provided by a group of

�nancial institutions including the EIB,

Denmark’s EKF and a club of 15 banks.

This makes the gearing for Seamade

the highest yet in any offshore wind

jurisdiction, with only €300 million

equity being provided by the owners.

EKF covered €100 million of the

€804 commercial debt, with the remaining

€704 million being uncovered. All 15

banks participating in the project �nancing

provided roughly €50 million equal tickets

with pricing coming in at 135bp above

Euribor over the 1.5-year construction

period, and then 125bp for the remaining

16 years. The EIB provided €250 million

via the European Fund for Strategic

Investments. All lenders lent on the same

terms, including the EIB tranche.

ConstructionSeaMade is the last of the Belgian offshore

wind farms to be procured with subsidies.

It is set to feature 58x 8.0MW-167 DD

WTG Siemens Gamesa turbine mode

that will have a 167 meter diameter. The

turbines were still not certi�ed at the time

of �nancial close but will be erected on

monopile foundations.

Construction is due to start later this

year, and the sponsors are aiming to have

the project connected to the grid by 2020.

Once operational, SeaMade is

expected to be the largest offshore wind

project and infrastructure project to date

to be developed and �nanced in Belgium.

It will have signi�cant impact on Belgium’s

target of obtaining 13% of its energy from

renewable energy sources by 2020. Half

of this is due to be sourced from offshore

energy, and SeaMade is set to contribute

to almost 25% of the required offshore

energy production.

Each of the project’s twin wind

farms will each have its own offshore

substation which will collect the electricity

produced by the Mermaid and Seastar

sites, convert it from 33kV to 220kV and

export it to the offshore grid operated by

Elia System Operator.

Engie Fabricom, Tractebel, Smulders

and Geosea will be responsible for the full

EPCI of the substations.

Total value: €1.3 billion

Debt: €1 billion

Equity: €300 million

Sponsors: Otary, Electrabel, Eneco

Lenders: ASN Bank, Bank of

China, Bel�us Bank, BNP Paribas,

Commerzbank, EIB, ING Bank, KBC

Bank, KfW IPEX-Bank, MUFG Bank,

Rabobank, Santander, Siemens Bank,

Société Générale, Sumitomo Mitsui

Trust Bank, Triodos

ECA: EKF

Tenor: 17.5 years

Pricing: 135bp above Euribor over

the construction period, 125bp for the

remaining 16 years

Advisers: Société Générale, Allen &

Overy, Loyens & Loeff, Linklaters,

Kromann Reumert, Mott MacDonald

Financial close: 3 December 2018

23ijglobal.com Spring 2019

IJGLOBAL AWARDS 2018IJGLOBAL AWARDS 2018

European Transmission & DistributionIdex AcquisitionThis deal saw Antin Infrastructure Partners

acquire Idex, one of the largest energy

infrastructure and energy services companies

in France, from fellow investment �rm Cube

Infrastructure Managers.

Cube launched a competitive sale

process for the asset at the beginning of

the year, having bought the company from

IK Investment Partners in 2011 through

the Cube Infrastructure Fund.

Antin was named successful bidder

in May, and is understood to have defeated

Mirova and Partners Group in the �nal

round of the action with a valuation of

around €1.3 billion ($1.5 billion).

Antin provided equity from its third

fund Antin Infrastructure Partners III to

�nance the deal, while BNP Paribas, Crédit

Agricole, HSH Nordbank, Natixis and

NatWest Markets were the underwriters

on the roughly €673 million of debt

facilities. The debt consisted of a €453

million acquisition facility, a seven-year

€200 million capital expenditure facility

and a €20 million revolving credit facility.

Idex operates numerous French

district heating and cooling networks,

energy-from-waste facilities and biomass

boilers alongside a portfolio of energy

services contracts.

A key feature of the deal was selling

the business in such a way as to ensure

that the separate arms of the business

could be run as independently as possible,

ensuring greater attractiveness to private

equity players in light of a future sale date.

Total value: €1.3 billion

Debt: €673 million

Seller: Cube Infrastructure Fund

Buyer: Antin Infrastructure Partners III

Lenders: BNP Paribas, Crédit Agricole,

HSH Nordbank, Natixis, NatWest

Markets

Tenor: 7 years

Advisers: Clifford Chance, RBC Capital

Markets, Fresh�elds, Rothschild

Financial close date: 18 July 2018

European TelecomsOpen Fibre BroadbandOpen Fibre, owned by Italian utility

Enel and Cassa Depositi e Prestiti (CDP),

succeeded in securing a mammoth debt

�nancing worth €3.47 billion ($3.97

billion) to form part of a €6.5 billion

outlay of economy-boosting �bre

infrastructure across Italy.

The transaction constitutes the largest

project �nancing of broadband in Europe,

which will allow the rollout of broadband

grids in developed, highly populated areas,

as well as other, less developed, rural ones.

The national �ber-to-the-home (FttH) type

�bre optic network is expected to cover 18.8

million households across 271 cities and

over 7,000 municipalities.

The project represents a strategic

move for Italy in order to achieve the

targets set out by the 2020 Digital Agenda

to reach 85% of the population with at

least 100Mbps connection.

The €3.47 billion debt package

consisted of a seven-year €2.8 billion term

facility, a €370 million guarantee facility

and a €300 million revolving credit facility.

The deal was entirely underwritten

by BNP Paribas, Société Générale and

UniCredit, joined by CDP and the EIB as

initial mandated lead arrangers. The debt

facilities were syndicated to 10 Italian and

international banks: Banca IMI; Banco

BPM; MPS Capital Services; UBI Banca;

Crédit Agricole; ING; Caixa Bank; MUFG

Bank; NatWest; and Banco Santander.

Debt: €3.47 billion

Sponsors: Cassa Depositi e Prestiti

(CDP), Enel

Lenders: BNP Paribas, Société Générale,

UniCredit, CDP, EIB, Banca IMI,

Banco BPM, MPS Capital Services, UBI

Banca, Crédit Agricole, ING, Caixa

Bank, MUFG Bank, NatWest, Banco

Santander

Tenor: 7 years

Advisers: White & Case, Aon, Arthur

D. Little, Ashurst, EY, Gianni Origoni

Grippo & Partners

Financial close: 15 October 2018

European M&AAcquisition of John Laing Infrastructure FundThe acquisition of the John Laing

Infrastructure Fund (JLIF) was a seminal

deal of 2018, marking a number of

milestones, including the �rst ever take-

private of a FTSE 250 listed infrastructure

fund with a premium listing on the LSE.

JLIF had 67 investments spread

across six countries at the time of

the takeover, but its share price had

suffered owing to the collapse of UK

construction company Carillion and

political uncertainty surrounding PFI/PPPs,

resulting in a signi�cant discount to NAV.

Dalmore Capital identi�ed John

Laing Capital Management-managed

JLIF as a potential target in 2017,

later identifying Equitix Investment

Management as a co-sponsor to help

raise the roughly £1.6 billion ($2 billion)

required for the acquisition. Initially

rejected by the JLIF board, the consortium

eventually convinced it of the merits of

the deal and a scheme of arrangement was

put in place which garnered support from

the requisite number of shareholders in

September 2018.

Financial close on the deal was

reached the following month, concluding

a landmark transaction in the listed

infrastructure space.

Total value: £1.667 billion

Debt: £1 billion

Equity: £667 million

Buyer: Jura Acquisitions Limited

Seller: John Laing Infrastructure Fund

shareholders

Lenders: Lloyds, NatWest

Tenor: 12 months plus 12 months

extension

Pricing: �oating margins of 1.25%

in the �rst 12 months, 1.75% for

the subsequent 12 months, 2.25%

thereafter

Advisers: Allen & Overy, Aon, KPMG,

Lazard, Macquarie Capital, Stifel, WSP,

CMS, JP Morgan Cazenove, Rothschild

Financial close: 12 October 2018

IJGLOBAL AWARDS 2018 IJGLOBAL AWARDS 2018

24ijglobal.com Spring 2019

European AirportsBelgrade Nikola Tesla AirportVinci Airports reached �nancial close on the

concession to �nance, operate, maintain,

extend and upgrade Serbia’s Nikolas Tesla

Airport in December, less than one year

after it was selected as preferred bidder

following a competitive public tender.

Plans to privatise the airport

(which is 83.15% owned by the Serbian

government, while 16.85% of airport

company Aerodrom Nikola Tesla trades

on the Belgrade Stock Exchange) �rst

surfaced in late 2015, attracting 27

indicative offers by March 2017.

Vinci Airports was selected

as preferred bidder in early January

2018. The company signed the 25-year

concession agreement a few months later,

agreeing to a €501 million ($563 million)

upfront concession fee.

To complete the transaction, Vinci

Airports raised roughly €420 million

in loans from the IFC, EBRD, Proparco

and DEG, and six commercial lenders.

The IFC and EBRD each provided a

€72 million A loan and a €110 million

B loan. Banca IMI, UniCredit, Erste

Group, Kommunalkredit, CIC and

Société Générale joined the deal on the

B loan syndication.

The debt will cover part of the

concession fee as well as the extension

and upgrade works driving the airport’s

development.

Total debt: €420 million

Sponsor: Vinci Airports

DFI lenders: DEG, IFC, EBRD,

Proparco

Commercial banks: Banca

IMI, UniCredit, Erste Group,

Kommunalkredit, CIC, Société Générale

Tenor: 17 years (IFC and EBRD loan

A), 15 years (DEG, Proparco, and IFC

and EBRD loan B)

Advisers: Allen & Overy, Infrata, BDK

Advocati, Dentons, Lazard, Orrick,

Mott MacDonald

Financial close date: 17 December 2018

European PortsRotterdam World Gateway RefinancingRotterdam World Gateway (RWG), a

major container terminal opened in 2015

and owned by a consortium of APL,

MOL, HMM, CMA CGM and DP World,

achieved a signi�cant re�nancing in 2018

with Société Générale CIB acting as sole

�nancial adviser and placement agent

on €371 million ($415 million) of senior

bonds raised in the USPP market.

The deal attracted strong investor

interest from Europe and North America.

The quality of the asset, its shareholders

and its customer offering resulted in an

oversubscription by 3.8 times the funding

requirement, enabling Société Générale CIB

to tighten the pricing prior to allocation to

nine major accounts.

The new debt will be used to

re�nance RWG’s existing debt facilities,

close out existing swaps and pay other

costs, including signi�cant savings in

interest costs.

The new �nancing structure

will also provide a �exible platform to

facilitate the expansion of the terminal.

RWG can accommodate ultra

large container vessels and has an annual

capacity of 2.35 million TEU. It has

eleven deep-sea cranes, three barge/feeder

cranes, two rail cranes and 50 automatic

stacking cranes.

Total value: €371 million

Total debt: €371 million

Borrower: Rotterdam World Gateway

Sponsors: DP World, APL, CMA CGM,

Hyundai Merchant Marine, Mitsui

OSK Lines

Bond arranger: Société Générale

Bond investors: Aegon, Allianz, Aviva,

Macquarie, Metlife, Nationwide,

Northwestern, Nuveen, Sun Life

Tenor: 17 years and 11 months

Advisers: Allen & Overy, BDO, Clifford

Chance, Marsh, Royal Haskoning

DHV, Société Générale CIB, WSP,

Norton Rose Fulbright

Financial close date: 6 April 2018

European WaterSAUR AcquisitionEQT’s maiden infrastructure investment

in France saw two of its funds

successfully acquire and re�nance French

water utility SAUR Group.

EQT acquired a majority stake in

the Saur holdco Holding d’Infrastructures

de Metiers de l’Environnement (HIME)

via the EQT Infrastructure III and the

EQT Infrastructure IV funds, alongside

BNP Paribas, SWEN Capital partners

and two more co-investors that took a

combined 25% of the enterprise. The

enterprise valuation was close to €1.6

billion ($1.8 billion).

The sellers, a group of former

creditors led by BNP Paribas and

Groupe BPCE, took over HIME in 2013

following the holdco’s close encounter

with bankruptcy.

The business was an attractive one,

considering not only SAUR’s domestic

operations but also its global presence

with engineering operations in Poland,

Saudi Arabia, Scotland and Spain.

BNP Paribas and Natixis were the

underwriters on the €1.04 billion debt

package, which consisted of three facilities:

a seven-year €786 million term loan with

the purpose of re�nancing existing debt; a

seven year €160 million capital expenditure

facility to fund the capex programme and

permitted acquisitions; and a seven-year

€100 million revolver for �nancing general

purposes and debt service payment.

Total value: €1.6 billion

Total debt: €1.04 billion

Total equity: €560 million

Buyers: EQT Infrastructure with BNP

Paribas, SWEN Capital Partners and

two more co-investors

Sellers: BNP Paribas, Groupe BPCE and

other shareholders

MLAs: BNP Paribas, Natixis

Tenor: 7 years

Pricing: low-200s over Euribor

Advisers: Clifford Chance, DNV GL,

McKinsey, Rothschild, BNP Paribas,

Fresh�elds, Morgan Stanley, Natixis

IJGLOBAL AWARDS 2018 IJGLOBAL AWARDS 2018

25ijglobal.com Spring 2019

European Roads1915 Canakkale Bridge & MotorwayThis deal saw a Turkish-Korean sponsor

team assemble a group of over 20 banks

and �nancial institutions to bring one

of the most ambitious of Turkey’s recent

transport projects across the �nishing line.

A consortium of Yapi Merkezi,

Limak, SK and Daelim was awarded the

BOT project in January 2017, outbidding

Japan’s IHI, China’s CRBC, and Turkey’s

Cengiz and Kolin.

The winning team signed a 16-

year concession with Turkey’s General

Directorate of Highways in March of

that year.

The sponsors brought together 23

banks and institutions on the impressive

€2.265 billion ($2.54 billion) debt

package which featured ECA-covered

commercial debt, ECA direct lend, Islamic

and uncovered local tranches.

Total value: €3.1 billion

Total debt: €2.265 billion

Sponsors: Yapi Merkezi (25%), Limak

(25%), SK (25%), Daelim (25%)

Lenders: Standard Chartered,

Natixis, ING, Deutsche Bank, Bank

of China, DZ Bank, ICBC, Intesa

Sanpaolo, Siemens Bank, ICIEC

(Islamic Development Bank), Korea

Development Bank, Kuwait Finance

House, KEB Hana Bank, Shinhan Bank,

EKF, Korea Eximbank, Finansbank,

Garanti, Akbank, Isbank, Vakifbank,

Yapi ve Kredi Bankasi, Kuveyt Turk

ECAs: KSure, Korea Eximbank

Tenor: 15 years with a 5-year grace

period

Pricing: all-in pricing around 2.6-2.7%,

around 500bp above Libor (uncovered

commercial tranche), around 150bp

with a 10-15% ECA premium (covered

commercial tranche)

Advisers: Standard Chartered,

Shearman & Sterling, Lake Fisher,

Clifford Chance, Verdi , Arup , Mott

MacDonald , Marsh, Finansbank ,

Garanti, EY

European RefinancingThe M25 Refinancing The largest infrastructure re�nancing in

the UK since the Intercity Express deal of

2015, this deal saw sponsor consortium

Connect Plus greatly improve on the

original �nancing which featured cash

sweeps and debt pricing re�ecting the

drying up of credit in the middle of the

�nancial crisis.

Primary �nancing for the project

reached �nancial close in May 2009 with

£698.58 million ($896 million) senior debt

and roughly £390 million of EIB debt.

The pricing margin on the commercial

term loan started at 250bp above Libor for

years 1-7, stepping up to 300bp for years

8-10 and 350bp for years 11-27.

Debt was due to mature in 2036;

but cash sweeps of 50% from years 7-19,

and 100% onwards, were clearly an

incentive to re�nance, though signi�cant

swap breakage costs meant replacing the

debt package would be challenging.

The sponsors opted to re�nance

the £698.58 million bank debt through

a public bond �nancing, bringing in

HSBC, Lloyds and Barclays to structure

the transaction. The £893 million public,

A+ rated bond priced on 24 July 2018,

revealing the magnitude of the swap

breakage costs.

The Connect Plus closed on the

deal to deliver the M25 upgrade work in

2009 with Balfour Beatty and Skanska

playing lead roles along with Atkins and

Egis Projects.

Bond value: £893 million

Maturity: 31 March 2039

Pricing: 115bp above Libor, 2.607%

coupon

Sponsors: Dalmore Capital, Equitix,

GCM Grosvenor, Balfour Beatty, Egis,

DIF

Joint bookrunners: HSBC, Lloyds,

Barclays

Known investor: Legal & General

Investment Management

Advisers: EY, HSBC, Ashurst, DLA

Piper, Linklaters, Arup, Hogan Lovells

European RailWales & BordersSMBC and Equitix’s contract to lease the

rolling stock for KeolisAmey’s Wales &

Borders franchise dealt a fresh blow to

traditional rolling stock leasing companies

(ROSCOs) who in recent years have seen

their dominance in the market challenged

by new rolling stock funders.

Unlike ROSCOs, who have large

�eets of often amortised trains, these new

funders lease rolling stock under a single-

�eet �nancing model.

Contracts to build the trains were

awarded to rolling stock manufacturers

CAF and Stadler Rail. CAF was

awarded a contract worth around £700

million ($918.8 million), while Stadler

took three contracts worth roughly

£500 million.

Debt to support the rolling stock

procurement was structured in bank and

institutional investor tranches.

SMBC and Equitix reached

�nancial close on the deal with CAF in

December, supported by a £552 million

debt package comprising: £68.73 million

�oating rate term loan due 5 December

2048; £341 million �xed rate private

placement tranche with that matures on

30 September 2024; £34.36 million �xed

rate term loan due 30 December 2033;

and £108 million equity bridge loan due

13 December 2023.

Total value: £700 million

Debt: £552 million

Sponsors: SMBC, Equitix

Train manufacturer: CAF

Lenders: Crédit Agricole, NatWest,

SMBC Nikko Securities, CaixaBank

Tenor: £68.73 million (due December

2048), £341 million (due September

2024), £34.36 million (due December

2033), £108 million (due December

2023)

Advisers: Ashurst, Addleshaw Goddard,

Clifford Chance, Goldman Sachs, IPEX

Consulting, Stephenson Harwood,

Quasar Associates

Financial close date: 17 December 2018

IJGLOBAL AWARDS 2018 IJGLOBAL AWARDS 2018

26ijglobal.com Spring 2019

European Hydro PowerAcquisition of Menzelet and Kilavuzlu HEPPsOne of the largest acquisition �nancings

in the Turkish electricity market to date,

this deal saw Entek Elektrik acquire

two operational assets in the south east

of the country from the Privatisation

Administration of Turkey (PA) following a

competitive tender.

Entek Elektrik won the privatisation

of the 124MW Menzelet and 54MW

Kılavuzlu hydropower plants in

Kahramanmaras province in 2017 and set

up a SPV, Menzelet Kılavuzlu Elektrik, to

own and operate the assets for 49 years.

The buyer opted to pay 35% of the