I Report No. SA-6a - World Bank Document

100

| u,\|"W i I ' RESTRICTED u 1. I Report No. SA-6a This report was prepared tor use within the Bank and its affiliated organizations. They clo not accept responsibility for its accuracy or completeness. The report may not be published nor may it be quoted as representing their views. INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION u U nm r-I1N I.-L~ I IN %.I lVll. I ~r - I. %j XJIN AND PROSPECTS OF AFGHANISTAN May 27, 1969 South Asia Department Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

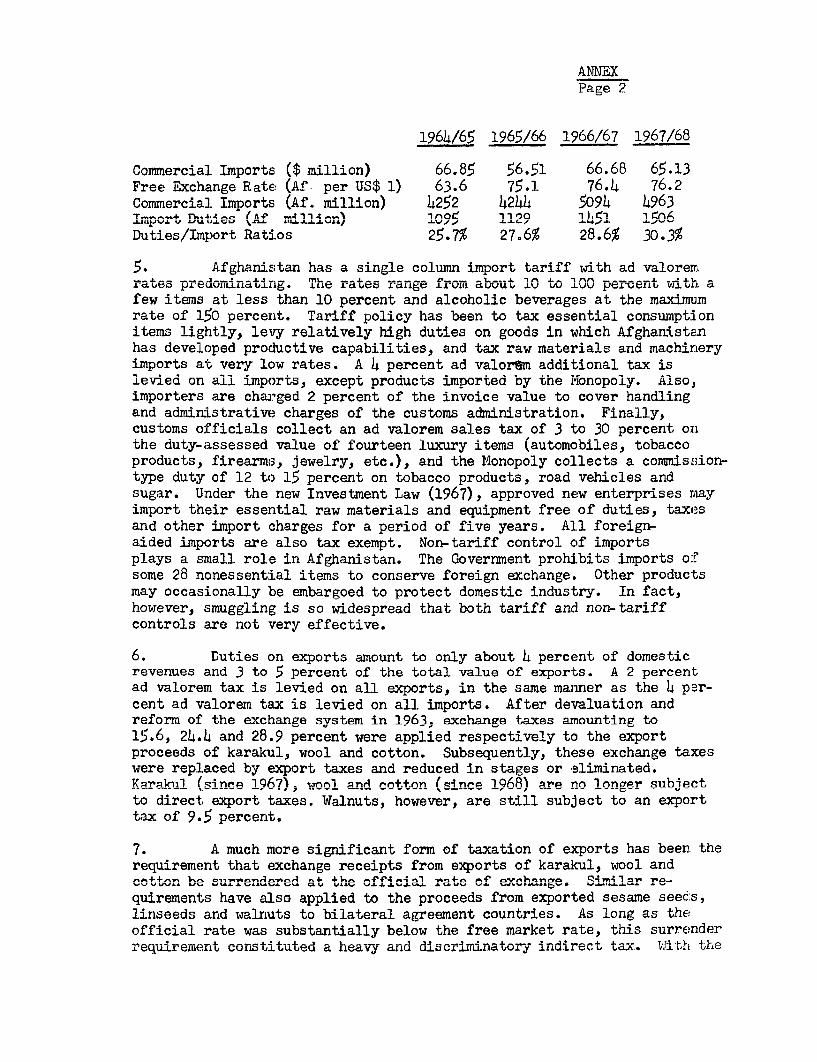

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of I Report No. SA-6a - World Bank Document

| u,\|"W i I ' RESTRICTED

u 1. I Report No. SA-6a

This report was prepared tor use within the Bank and its affiliated organizations.They clo not accept responsibility for its accuracy or completeness. The report maynot be published nor may it be quoted as representing their views.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATION

u U nm r-I1N I.-L~ I IN %.I lVll. I ~r - I. %j XJIN

AND PROSPECTS

OF

AFGHANISTAN

May 27, 1969

South Asia Department

Pub

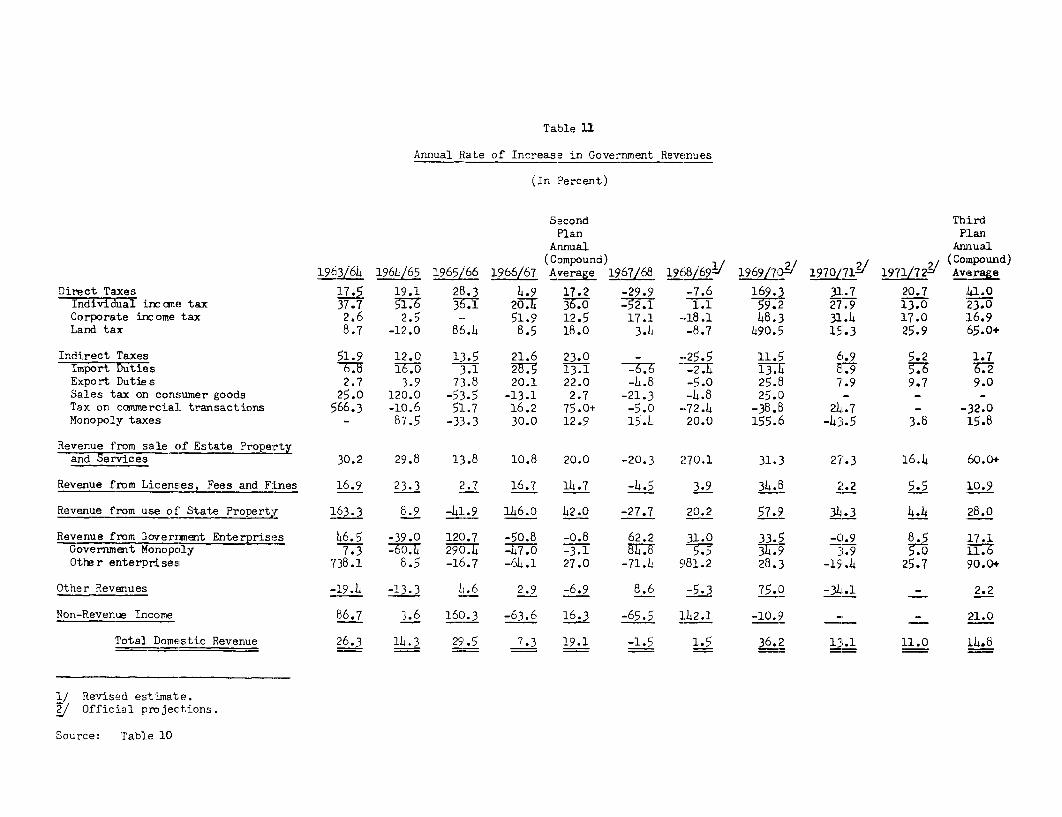

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

U.S. $1.00 Afghanis 45Afghanis 1, 000 = U.S. $22. 22Afghanis 1 million = U. S. $22. 222Afghanis 1 billion = U. S. $22. 2 million

Free Rate (Approximate)

U.S. $1.00 = Afghanis 76 (February 1969)Afghanis 1, 000 U. S. $13.16Afghariis 1 million = U.S. $13. 158Afghanis 1 billion U. S. $13.2 million

This report is based on the findings of an

Economic Mission which visited Afghanistan

from February 9-27, 1969. It was composed

of the following members:

Rudolf Hablutzel Chief of MissionAlfred S. Cleveland EconomistChristian G. A. Merat Fiscal EconomistPeter H. Oltmanns Tourism

TABLE OF CONTENTS

BASIC DATA - - -

siTThIARY ANnl rnAT'r!r.TI5qTnNq ---

(b) ProductioLn GOO. . ....................... 2

(c) Events in 1968,'69 .... . .... 8

TT mlut' mtYTof sT A~ ~MnU I;ImnV (1 n 7

*J1J.,JWJ L~'f. . .. . . . . . .. . . . . . . . . . ... . 7. .

TT FP *L rttTDl A'RT Qfnv DAMLY V n 1 '7

(b) Plan Priorities ... ................... 11

(c) Plan Flnancing .. ...... 13(d) Plan Revision ........... 13

(e) Overall Implementation .......... i

III. THE FINANC1'AL BJTTL.r ECK ....... 18 - 29

(a) Past Developments ....... ..... 18

(b) Domestic Revenues ..................... 19(c) Revenues for 196 9i70 .................. 21

(d) Ordinary Expenditures ................. 22

(e) Overall Budget Position and Outlook ... 24(f) Noney and Prices ...... ........... 26(g) Banking........ 27

IV. THE PRIVATE SECTOR ... ...................... 30 - 39

(a) Private Savings and Its Mobilization .. 31(b) New Industrial Activity .... ........... 33(c) Private Agricultural Investments ...... 35(d) Tourism .......... ......... ......... 38

V. BALANCE OF PAYMENTS .................. 0 - 44

ANNFJX Phe Rcvenue .ste, and Ne;J Rcvenue 'roposal S

-iJ SIoCAL APPE..DIX

Kk7 OF AFGA7 ',!.'1Ir,'t

Area: 245,000 square miles 12

LJp-Lat±±uio; J.:.)I Ui±L.± (u1icic-.laj

Rate of growth 1.9% (official)Population density per square mile '04Population density per square mile of cultivated land 1L,022

Gross Domestic Product at 1965/66 Market Prices:(Very rough estimate)

1967/68 19b3/b4 - _____d

$1,250 million $1,202 million

Real rate of growth 1962/63 - 1967/68 = 2% p.a. (compoumd rate)Per capita GNP in 1966/67 = about $80

Gross Domestic Product at Market Prices: (1967/68) $1,250 millionof which, in percent

Agriculture 53Industry 3Handicrafts 8Minerals. Fuel & Power 1Construction 1Transport & Communications 2Services 32

Percent c,f GDP at Markpt P,ri'Res

(Very rough estimate)1967/68 l96)h/65 - 1S67/68

Gross investment n.a. n.a.

Balance of paymentscurre.nt. aoun+. deficit+. .9 63

Investment income payments 0.3 0.3Government current revenue 7.4 7.1

Resource Gap as Percent of Public Sector Investment:

1967/68 74.L1UL46V. - L1U7I6Uu I78

Conversion - fficial rate: Af i5 U S$1Free market rate (February 1969): Af 76 = US$1

Percent change\,.L.ML ull± o UJ. of Aghl,I--s) ___7 _ fs±Ie 196L7U;-'

m " _ t I otal money supply i '/ 73. 9 OX* Time and Savings deposits 653 206.6Claims on private sector 2,349 37.0Claims on public sector (net) 4,49 8o.6Rate of change in prices 2J.4%7 z 169.3%

Public Sector Operations: (In millions of Afghanis)1967/68 1962/63 - 1966/6S7

Government revenue receipts 4L,109 16,075Government non-development

expenditures 3,444 13,116Revenue surplus 745 2,9959Government development expenditures 4,517 21,133External assistance to public

sector, of which:Commodity aid 705 2,754Project assistance 2,809 12,787

Deficit 258 2.,633

External Public Debt: (In millions of US$)

Total external public debt (as of December 31, 1968) 433.3net of undisbursed 495.7

Total estimated debt service 1968/69 13.9of which amortization 9.2interest L.7

Debt service ratio in 1968/69 = 19%

Balance of Payments: (In millions of US$)

Annual Average during 1969/70196L,/6<- 1968_/69 Proiected

Exports 69.080Im,ports 151.2 1DiC7

Aid 72.0Non-aid 65.8 75.0

Investment income (-) 3.5 () 6.')A-id disursmens 75. -M -In ' 7, 75 .

Debt repayment - 5.7 - 15.1)Res--rv Awd.,A.,.- (+A -A

Errors & Omissions + 6.o n.a.

1/ Including foreign currency deposits.V/ Vver 1966/ 967 . For the period April 1967/68 to Aprll 1968/769 prices

declined by over 60%.3 / Does~ riot= include -undilsb-k-sed portion of USR pr,ed r-i

Vh^nge P---re Position: (Tn mJ1. 'nof.*T T.J)

nr -I . A-.n . ,

A.,u-' Average during

1964/65 - 1967/68 January 1?69

Fore:ign assets 39.9 45-3r or eiLgi- lLau.:L L�.U 10.1 18.7

Net 29. 26.6

IMF Position: (DI millions of US$)

Quota 29.0Drawings outstanding 19.6

Annual Average duringl9oLi!o) - 196/6 (too lO (/0

Commodity concentration of exports(karakul, furs and skins,fruits, cotton) 73.3% 75.8%

SU1MMARY AND CONCLUSIONS

PAST ECONOMIC GROWTH

General

1. A decade or so ago, Afghanistan was one of the most primitivecountries in Asia. Since then, and although still poor and lacking innatural resources, the Country has, in certain respects, made impressiveprogress to-wards modernization. The principal production and populationcenters are now linked by modern Daved highways and international and domesticairlines are in operation. A large electric power system has been built, pro-duction and export of natural gas is inereasing ranidlv. h-igh-vielding wheatvarieties and fertilizer have been successfully introduced, and new privateindustrial investment has exceeded all PnePtntiqons- Schorol enrol l1 nnt hasmore than tripled and medical facilities and services have been significantlyimnroved PolitiJ nal It hility has been achievr iunder a onq+A i tutionnlmonarchy.

2. All this has been accomplished with relatively massive foreignassistance whilch. has finan.ced about three-fourthsoftheCoun+r4-1-'s d-+- l

ment expenditures over the past twelve years. Unfortunately, this has-notInat +-A 4v -rnvnn ,C ,.,an -, 4-4- ,-.nnnrr,w. ,..n.-lT, 1',nls -nare*s- ed in a.-vJ aFppreciable acceleration fV ecoc.L . L r + 'lWV l, bLecus

of almost exclusive application of foreign aid to infrastructure projects,w.icL haVe not always UbeU well conceiafved or o.f Llhgh p.rL.LUi.Lrty . On1LLy J.ctULL'y

has development strategy been shifted in favor of the produlctive sectors, butI -±eI 1.tuuI L.jLV±1 U±.L±±i-LLIL,irplpiementation is pro-V-ng dfLLL.LL -ul.

rro-u-u-vuion

3. I~~n 1 Ot67 /t68 a er.4anl 4-nw accontedn-n for about, 53 pecnt,nd of rr.no a

domestic prcduct. Services accounted for 32 percent and industry and handi-^n _ A + 11 ------- ^CP h .4 _ VAl tt A Q- ..f -+ . _ _ ¶ e 1 nl- - Wn A e A.VV. A4. Li. V'~ te * UV, 4 V. W ILa*..L 1L SJI.LJ A. lvJ. V -WG W aL *ILO.LU.. 4.4.4 t .V A 6

industry. Transport, electrical power, minerals and construction contributed-- 'rly I -.- -n-, 44

4-pec flTt t AC-..-4 4pe th be fact h4-.t - w i4rdAs of publ4ac i-nves-.ent

W."..J 44 jj~.4. 4. "JI UJ UJ.UJ.L , UVOIJ±Lt L. AC~ .4 O4L%..4,IJ.O 41AC WV LI UL".L 4. 4.4 4..4 "L4.4. S4f

over the past five years has been for power and roads.

4. In agriculture only about 3.5 million hectares are cropped out ofA4 total ofmAAAAP 11 mili. o1 n hec ares b.elie t be aOale. About 2 b1h ;- ecta +AC; U J VGAI- V ff A 94 II" L-L-Xj |VSX; CL ; ;UC Q VV A A VU -41V _VAV

are irrigated which could be doubled except for lack of water and poorly con-ur UL.O .LUIU o±n±1O 'LI. d41Uk ± ± 4L. OO es V-4a.I I - .- - - 41.LL.- --- .LLV.Vstr-uct-ed andu maint. ir.ire d irrigationl faclitiesJ. Fa.C1LLI,in Crctcs repiritv

and productivity is very low. The available information indicates that apartfrom changes in weather, production of food grains has remnained about the. saMeover the past 10 years. Wheat accounts for about 60 percent of grain production,of which only about 20 percent is marketed.

The most important development in agriculture in recent years has beenthe wheat program. After several years of experimental and pilot operations(which indicated possible increases in yields of 50 - 400 percent) improved seedand fertilizer were applied to about 5 percent of irrigated land in the 1.968planting season. Given favorable weather, this could result in a wheat crop15 - 20 percent larger than the past annual average. It is encouraging thatthis has occurred after a decline of some 30 - 40 percent in the price of wheat

uo a level lower than tne average in any oI the past three years. Thne Govern-ment's objective is self-sufficiency in wheat, the Country's principal staplefood, and it is nao predicted tnat this could occur within the next tw,,.o orthree years. An expanded system for distributing seed and fertilizer and amuch larger extension service will be required, however.

6. The most important cash crop in Afghanistan is cotton. From anaverage production of 85,o00 tons in 1962 - 65 output declined in the past twoyears to about 55,000 tons. This was due to the unfavorable price relationshipwith wheat and an unfavorable exchange surrender rate for cotton exports. IJiththe fall in the price of wheat the cotton/wheat price ratio improved substantial-ly and improved further with the Government's announcement last year of a muchhigher ex-farm price. This year the export tax on cotton was abolished and anexchange subsidy of Af 20 became effective in March to allow movement of exportswith the new ex-farm price. Consequently,for the 1969 spring planting, a sub-stantial increase in acreage is expected.

7. There has been a very substantial increase in production and process-ing of fruit for export, particularly raisins. Foreign demand has been increas-ing and several neaw raisin packing plants have been established.

8. Afghanistan's development strategy gives high priority to repair, im-provement and expansion of small-scale irrigation systems. Such projects offerhigh returns over short periods of time. Very few projects of this nature havebeen undertaken, however. They are generally too small for external financingand the financial and technical resources of the Ministry of Agriculture arelimited. A few medium-size projects are under construction and several largeirrigation schemes are in preparation, such as the Kundus-Khanabad and Har-L-Rudprojects, both of which are likely to attract foreign assistance.

9. A major bottleneck in agriculture is the lack of long and short-termcredit at reasonable rates. The Agricultural Development Bank has not beeneffective; however, and following a recent IBRD appraisal mission,steps are nowbeing taken to establish a sound basis for the Bankts future: onerations.

10. In Other sectors factorv sale industrv declined slightlv in 1967J68.Output of cement dropped by about 30 percent with completion of several largepower and road nrolects. Production of woolen fabrics; ginned cotton andcotton textiles declined and large inventories of cotton cloth accumulated.Surnrisinglyv nmeimr-ton of in trictv ihas hy 20 npercnt. Ht-igh fooi(prices resulted from the poor wheat harvest in 1966/67 which took purchasingpnwer away from- othAr 1 n-t AiimArn goods. Expnrts declined hv byhrnt 5 npercent anncommercial imports declined as wsell and aid-financed merchandise imports were1) percent low1er than in the previous year. All of this produced a minorrecession in :L967/68 which could not be offset by increased public spendingbecause of lack of projects, declining public revenues and the need to mair!tamonetary stability.

Events in 1968/69

11. The economy recovered partially in 1968/69. Wheat prices declinebd anda. ~LLLJ substantalO~L .,.nLaL'se in cottVon Vou-tlput Was UAJ9U toVU*. ManufL1acLUring.L1Ir UtpULt, .Lm-

creased somewhat as cotton textile inventories were reduced by half and export

- iii -

of cement to the USSR was begun. xnports may amoulnt to about ,71 millioncompared to $66 million the previous year, due to increased export of naturalgas to the U'SR and changes in t+he Pff'ective foreign nynhAnap su.frcE-d.r rntes.Demand is also increasing as a result of the private investment uooom, describeabelow. There is coaniderable uncerain-t as t whether +his up.^r' tren ^n11

be further supported by increased development expenditures by the Governmentin the coming .ear. The provisional budget for 1969/7- implies an *ncrease of23 percent, but slippage is likely because the funds are anything but assured.

12. Total money supply increased by about h percent in 1968/69 but thep- ce index fe' ;-1oug1.out-4 -h MUar Th free --- <,g rate- -,spoed,solr

.LU3 . ±J. e- iJ..UU LIUU I41IV yVt.i.A. ±LII L.L-U;V e 1.J4IU J&V .JJJIkJJ LJV~' I LL'-IU

ly.

Population and Family Planning

13. No overall census of population has ever been taken in Afghanistanand reliable demographic information is therefore alUm1ostU totally lacking. IIn1960 some small sample surveys were made which were used as a basis for thefirst estimatJe (3.o mil ion). From 190u to 1966 it was assumed tnat populutionincreased annually at a constant rate of 1.75 percent. For the period 1967 to1971 a rate Of 1.9 percent is assumed. In 1965 a cenaus was taken of the city ofKabul and its metropolitan area. The census indicated a population of about435,000 persons, or less than 3 percent of the estimated total population ofthe Country. The annual rate of increase was estimated at about 2.5 percent,but the basis for this estimate is not clear. The Revised Third Five Year Planincludes a nation-wide census to be completed in the year ending in March 1972.The Plan has not as yet been approved by the Parliament. Family planning inAfghanistan is at a very early stage. A Family Planning Council is in theprocess of being orgzmized with USAID assistance. Presumably the Council willdevelop and operate EL program in due course. Because of the Government's diffi-culties in mobilizing local resources for development, the assumed low rate ofpopulation increase, and other more urgent public health needs, it is unlikelythat family planning will have high priority over the next few years.

THE THIRD PLAN STRATEGY

Constraints to Development

114. The obstacles to effective development in Afghanistan are numerousand pervasive. Some are inherent or are deeply rooted in custom and tradition.Others, howerer, given adequate time and effort, are not insurmountable. Theyinclude the following:

(a) The Country has been unable to mobilize its own resourcesfor development. Agriculture contributes almost nothing topublic revenues, which have not increased over the past fouryears. Until recently, private investment has not beensupported by the Government. Total development expenditureshave barely amounted to 8 percent of GDP over the past sevenyears, of which public savings and central bank borrowing haveeach amounted to only 1 percent and the balance has beenfinanced from commodity and project assistance.

- iv -

(b) There is an acute shortage of competent managers, techniciansand slcilled manpower in both Government and industry. Theability to identify, prepare and implement projects is pari;icu-larly limited.

(c) Interaction of the executive branch of Government and theParliament is hampered by the fact that the idea of overridingnational needs is not widely appreciated in the Parliament whereinterests tend to be local and tribal. Thus essential develop-ment measures may be rejected or long delayed.

(d) Most of the data needed to plan and carry out development iseither lacking or is unreliable. For example, there are nonational accounts, no reliable population data and no means ofadjusting capital expenditure values to price changes. Much ofthe published data is essentially guesswork.

(e) Agricultural production is carried out mainly on small holdings.The rural population is largely illiterate and farmer associationand extension services are very inadequate. The lack of creditto farmers is particularly serious.

(f) As discussed below, the response of private investors to theInvestment Law has been encouraging, but obstacles to expansionof industry remain. Local markets are small and scattered andproduction costs tend to be high. Mutual suspicion of Govern-ment and nrivate businessmen seems to be lessening, but thereis still much uncertainty regarding the Government's own in-dustrial intentions= Pu'hli G sector enterprises, which comnrise

the bulk of manufacturing activities, are highly inefficieizt.S.mugg:i -n,g C cntiius nbae

Private industry badly needs short- and long-term credit, butthe Industrial Development Ba.I, la w1, proposed two years ag3o, hasnot besen enacted.

Plan Priorities

15. The Third 'Five Year Plan (1967/68 - 1971/72) visualized a marked shiftin prlorit from irerstrueture o th poucie sectors, ag cltr ad n

dustry. In both sectors, according to the Plan document, much greater reliance

for economic growth ra to be plce or. p4r; at er.terprise

16. During the Second Plan the agricultural sector as a w.4,le had shon

very little growth and staple foods probably did not keep pace with populationgrow WI. .4L4 Uthe mnird PLan eLj,IaJIL waJ.Q tWoi be LV o.L VILIneaseLd, prJouLcLtiviJ. V.I

from existing land by improving irrigation facilities and water management, and1 . 4. r - _ : - _ -- 4. L A- : -- 'I ..A: __ 1 _$ t4 .h *A 1 --- A___

- 1X -Vr AUU.LiLr ILO1XW LC%4_1ss11.L1 MUILVU09 SlUbU c.L..LL.Lr CLiv Lv- D_P1U%tDXXs-, s|U ,X Ot

fertilizer and pesticides. The credit gap in agriculture was to be remedied bya reorgan-ized arid revitalized Agricultural Development Bank; pasture ±i,ipfove,m,enrand livestock breeding programs were to be undertaken, and better price incentives-were to be offered to farmers, processors and exporters.

i7. A major objective 01 tne Tnird Plan woas to effect a sizeaUle lr,creasein private industrial investment. To this end the Plan called for provisionof tax and customs incentives under the new Foreign and Domestic Investment Law,establishment of an Industrial Development Bank to provide long- and short-termcredit and creation of a Development Center to channel foreign technicalassistance to entrepreneurs.

18. During the Second Plan period powver and transport absorbed about 63percent of total development outlays. This wras to be reduced to 22 percentin the Third Plan period and expenditures for development of agriculture andindustry were to be increased from 27 percent to 52 percent.

Plan Financing

19. During the Second Plan period about 75 percent of Afghanistan's devel-opment expenditures were financed from foreign loans, grants and commodity aid.About 11 percent and 12 percent respectively were financed from public domesticsavings and deficit financing.

20. Third Plan expenditures of hf 33 billion, 32 percent up from theSecond Plan, were to be covered by foreign assistance to the extent of about70 percent. declining from about 80 percent in the first year to 60 percentin the fifth year. Public savings, estimated at 20 percent of Total Planexpenditures, by contrast were to increase from 13 percent to 28 percent overthe Plan period through substantial new revenue measures.

Plan Revision

21. During the first two years of the Third Plan period (March 1967 - 69)the results were largelv disannointing. Total development outlavs declined andordinary expenditures increased at an annual rate of 13 percent. With thederGline of ennrnmir. nofivityf fnGvPern,menft revenues der1reaqed and npiblice savingsin the second year of the Plan were negligible. Deficit financing increasedS N fianr andr dnrl irments orf nr-veri±. qi1 ranndntinPre to Hdeline Olrff_icrial

reserves of convertible currency and gold dropped from $48.6 million to-$39 .llinuui 97/68.

22.T In July IQ9R a rvrevised plan was suhmitted to. the Parliament for thelast three years of the Third Plan period (1969/70 - 1971/72), but has not yetbeer. approved byr +the ParliarmentV. Fo r. +theri fi.l 1 fiv e -year eiri nnuhlir divt.elopr.-..

ment expenditures were reduced from Af 33 billion to Af 26 billion or by 21percent, which in real terms would be less than actual investment in the SecondPlan period. Over the next three years domestic revenues are expected to in-cnv.as e+ . Tn.,rll O-¶fr'fo nO nnO-Ifr -f -v.na"+ ha.i+ n_r;nev.r 0 yDnr,; +nr.oC r,'sJv2 . 'su~s c U vfl vU.,A.. V9 v.J t **'sJ. .. j i' s v9.* %'1 v v- s J M fl'.A 'J1

also expected to increase at an average rate of about 35 percent. Consequently,4the projected bu-dget s- 1 -l o Af 3.1 bi'o is11 - - ni -4d - . A-dpenentupo4neUL±W I..UJV %0U L3UU-rt;S O"P .LjJUO iJ.L nM.J _) . .J.. L-.LVL1I -.LO 011U.L.LK .LJV %AUZjJPU 'AJ1 UKW1 L4AJJVLA

revenue measures. The revised Third Plan document reaffirms the strategy ofemphasizing agriculture L-,u d 1 3 d-L -d A.LO is 1 ,,1ainly e wit

means of increasing public revenues by about Af 4 billion from new sources. Thebudget for tne year beginning March 21, 1969 incorporats mJost of the prEUoUeunew revenue measures. Enactment is very uncertain, due in part to the elEctionin September 1969.

- vi -

CN-erall' i mpnlem.entation

r --4nc-, Au,r;vi-. +11-, f'4 + 4- rM n~l-^C ,-f' +bIn M.)-; 1erq PI nn 11!5~

2- ,. Exv e.an. centt dAur4n the&1 frtJ~S two., .,asI~ ofl >->e al.i.^ pl. an r.ns. S0.t.

it is very difficult to shift investment away from large infrastructuare projectsand into relativly ojaallea. In.v j Ls in nhe 4 v, -F-, - - e.aors. -Fe- project

had been prepared in support of the new strategy and the investment actua:Llyachlieved in 4the -Li.VOU twoV JVarLI cVLons-sted a-eyo :br.vnsfrpo^

started during the Second Plan period. There was substantial slippage in other:&m.portant d' activities as well. The extremely low n saarewere not increased, the statistical system was not improved and the plannedexpansion Or II UCIIAe 1 Obanklng 1 W"O.s-a LIU,otUV11JLLDU acco,plihed ti th ecptono

wheat, little was done to improve the efficiency of irrigated agriculture andllVestock- production. The AgrlcultUral Developmenu BDanK Was not reorgdniLZUU,the Industrial Development Bank was not established, power rates were notrationalized, little of the proposed public industrial investment was accomplish-ed and reorganization of the State enterprises did not occur.

24. There were, however, several favorable developments as well. Projectassistance, althougn well short of hnird Plan targets, was not far below thepeak year 1966/67. Construction of schools and hospitals and communicationsprojects were on schedule. The wheat program was successfully launched, theresponse to the Private Investment Law was strong, large inventories of cementand textiles were reduced, the effective prices for cotton, wool and karakulwere increased and the sale of gas to the USSR was begun and increased rapidly.The economy showed d.efinite signs of recovery during the second half of 1968/69as food prices declined. Central Bank borrowing was held to prudent levelsand the free market rate of the Afghani fluctuated within narrow limits.

THE FITANCIAL BOTTLENECK

Past Developments

25. After excessive recourse in the first half of the sixties to the bank-ing system for development financing, a stabilization program was adopted inMay 1965 and the overall budget position was brought into surplus in each. ofthe last two years of the Second Five Year Plan (1965/66 and 1966/67). Sincethen, however, the fiscal situation has steadily deteriorated. As the economyentered the Third Plan period in Narch 1967 it was clear that additional localrevenues from new sources would be required. Proposals to this effect wereincluded in the Third Plan, but the Plan was not approved by the Parliament.Thus in the first two years of the Third Plan domestic revenues failed tcincrease as did commodity aid, while ordinary expenditures increased at a. rateof about 13 percent a year. In 1968/69 only 3 percent of total developmentexpenditures were financed from the current budget surplus compared to 2C per-cent three years ago. lJithout a significant increase in public revenues,public savings are likely to turn negative in 1969/70.

26. Reversal of this trend is the most urgent and central issue facingAfrhanistan at the nresent time. If nronosals now before the Parliament areapproved, total revenues would increase by about 20 percent annually over thenext three -mars The prospects, however, are veyry innre?rtain

i-orTles'U, c ReVE5nue

Domestic ravenues are duUUeLUb_L aboUU I percenlt pi u,pLuct

ihich is considerably less than in other developing countries. In recent years,import duties and export taxes have accounted for about 60 percent of totalrevenues, direct taxes for only 9 percent, and Monopoly operations and the saleof gas to the uSSR about 27 percent. The heavy reliance on export and importtaxes clearly inhibited foreign trade and private investment. The Governmentis now engaged in a major effort to remedy this situation including removalof most export taxes and rationalization of import tariffs.

28. The Budget request for 1969/70 proposes an increase in revenues ofAf 1,540 million or 36 percent over the level of the last three years. Over 60percent (Af 963 million) of the total increase would be from new revenue sourceswith principal reliance upon a land tax and reintroduction of the livestock tax.Even if the new taxes are approved shortly, it is very doubtful that more thanAf 400 million from new sources could be collected. Furthermore, the expectedincrease of about Af 580 million from existing sources cannot be supported onthe basis of past experience. Thus if Government revenues in 1969/70 are in-creased by Af 900 - 1,000 it will have been a creditable performance. FaiLureto broaden the tax base at this stage would raise serious questions about theCountry's abiLity to carry out a planned investment program.

Ordinary Expen.itures

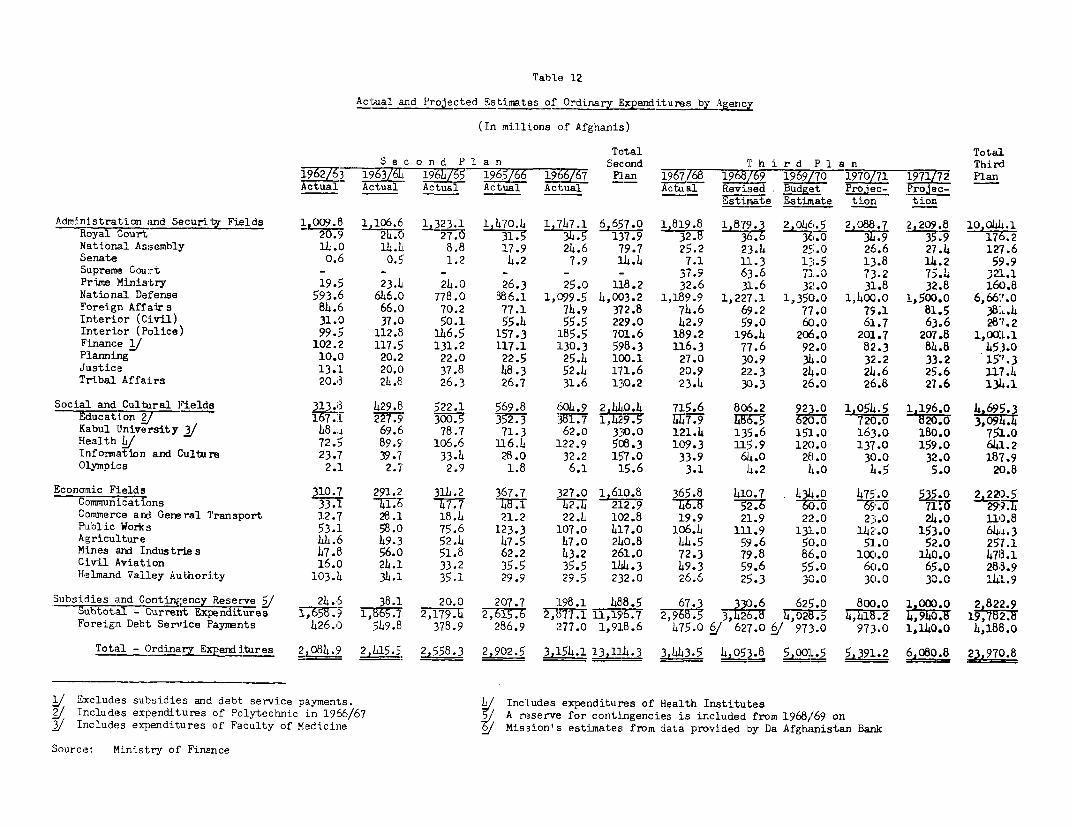

29. Ordinary expenditures are currently only about 5.5 percent of nationalproduct, reflecting exceedingly low Government salaries and minimum expend:ituresfor maintenance. Percentagewise. the structure of ordinary expenditures haschanged considerably in recent years. Civil administration costs have dec:Linedfrom 25 to 19 percent of the total while subsidies have increased from 8 to 15percent. The percentage of expenditures on education and economic administrationhas increased slightlv and national defense has maintained its share at 36 per-cent.

Overall Budget Position and Outlook

30. The Government estimates that development expenditures in 1968/659 willreonire riefirit finanrting on the nrdier of Af 880 million, an increase of Af (620million over 1967/68. However, the mission believes that disbursements for

rln.rnl onm n+.hnrp %cn tra"eQ+.n+.nor 1 +.v,_nc-rav r%4 -rinrlcz -n +h: arnTnw fc odevelopmenthave beenoverstated a transfe. of funds f the _a,,,, va_ .sn&been fully taken into account. The mission thus estimates that the deficit wTillnot exceed kf 700 r.illio-n ar.,ic an not appa to threan mone+ary sbi

31. ~Thle ris-zon is of thAe wopinilon that the G-verrn,ntfs est-i-.tes ofP

domestic revenues, current surplus and domestic development expenditures in1969/,70re ovryOt,lSi n lota riayepniures should be£5.'7/ I7 ~-'O. _ U V VP UkI.LJI1J.~ LJ.L .~ c"".. :6LU kiIALt. 5JUJLUL1C.L_,Y V.&PUL -L4.IU. 11 _5U± u

reduced, including the large incremental increase in expenditures for defense,±1 ~ UId.. ~ LJ'Le3~L ."A.otZiIUJ.' lLLures ar e0tZ_IiJ1CLUUU LJy LdJ.U JILLOO.LULI IUU.lf possibe Ttldevel opiment ex-pendiure r s:ntd yte-stnt

increase by about 14 percent over 1968/69, provided the Parliament passes thenew7 reveruae mJeasures in t[LUe.

- viii -

Money- andu Prices

32. S,-1-.ce 4the -taliatio prgr,, wa dpe n1965, *fghionfstan has

followed a very conservative fiscal and monetary policy. About half of theuvQ UOJ. Li Ls-U.L U Jher.LpasuI UVUL- I1- pc. I UU-L 1ID L1BLI UOLU±U J -U,-W

dowm of net foreign assets and money supply has increased at a rate of only about2 per^cent annually. iis a result of poor agricultural ou'puD and export pe.-formance in 1966/67, prices increased and the balance of payments remained underpressure. There was thus little latitude for further expansion of credit.

33. The situation eased considerably in 1968/69. In the first six monthsprices declined 24 percent from the level of the previous year and export per-formance improved considerably. Tnese trends are expected to continue in1969/70.

Banking

34. Afghanistan's banking system consists of the Government-owned DaAfghanistan Bank and two commercial banks. DAB performs some central bankingfunctions and is authorized to engage in commercial banking operations. How-ever, it is largely Government-oriented. It is not adequately equipped to re-gulate credit and money supply, nor does it service or regulate commercial banking.

35. Until 1964, the credit activities of the two commercial banks werequite limited and over half of their claims were in the form of equity invest-ments in industrial enterprises. Since then, deposits-have grown rapidly a;shave loans to the private sector. However, only short-term loans are availableand are made largely to finance foreign and domestic trade. Small and mediumsize enterprises have almost no commercial source of credit other than themoney lender in the bazaars at very high interest rates.

36. Afghanistan with increasing urgency wrill require a banking systemcapable of contributing more effectively to the development of its economy.The central banking functions of Da Afghanistan Bank need to cover the fieldlsof credit policy and leadership of financial institutions. Commercial bankingservices should reach the bulk of medium- and small-scale business firms andindividuals, instead of being restricted to only a small number of wealthy in-dividuals and large companies Lending policies of commercial banks shouldmore generally direct credit toward productive uses rather than tobusiness nfi familyr nonnP.ntnionq A new banking law was to he nrenared duririgthe Third Plan but has not materialized.

THE PRIVATE SECTOR

37. The Afghan Government has exercised extensive control over the economy.Several sectors, such as mining and electrical energy, have been reserved tothe Government which also owms and operates about 30 commercial-type enterprisesand holds substantial share capital in about 23 others. Many of the largerirrigation systems are owned and operated by the Government. Farm production islargely private but is subject to a variety of Government controls. Agriculturalmarketing is mixed. The Third Plan attempts to firmly commit the Government tomajor reliance upon private investment, Among other things, -the new Private

- ix-

In-vest,.wliu Ljcaw WsaJS U LJt; b t-U I g.L.JL.y- spUoVI-Ued, eU-tmJ, IpL iIr1Id d.L UUctioLrLUJ.L wvjUU_L 1Je

open to private participation and many of the Government enterprises would beU±.L~L.LU.ULuz ;)cJa-L U(J PzI.±VUU U1UL1Ubw'j.

fl.....J...(. - ¶- _ - I r - f t A*- -- , -rir1vate Javings and Its nouiiizat-ion

38. Information on private saving and investment in Afgnanistan is verylimited. The failure of agricultural output to grow appreciably indicates thatprivate investment in the sector has been small. In industry (excluding handi-crafts), and until very recently, private investment has been virtually non-existent. There is a general distrust of banks in Afghanistan and apparentlysubstantial amounts of savings are held in cash rather than being entrusted tothe banking system. The lack of credit at reasonable rates is particularlycrucial for Afghanistants future development. The Third Plan calls for estab-lishment of an Industrial Development Bank and reorganization of the AgriculturalDevelopment Bank.

39. The proposed Industrial Development Bank law has not been enactedover the past two years because of opposition in Parliament to the way in whichGovernment funds were to be involved. Amendments have been submitted and thereis some possibility that the law will be passed this year. The Bank was expectedto provide credit and technical assistance to new and expanding industries.Recently, the Cabinet decided to proceed with the technical assistance aspectof the Bank by establishing an Industrial Development Center, for which foreignadvisers are available. The proposed financing of the Bank includes Af 2L0million of equity capital of which ho Dercent would be foreign: and a 540 millionAf loan from the Government. During 1968 some 2,000 subscriptions were obtainedwhich oversubscribed domestic equity by 35 percent. It is reported that h1opercent of these subscriptions have been paid in.

40. In recent years, the Agricultural Development Bank has confined itsoperations to financng the sale of' trartors and shallow well numps. Afterconsiderable delay, initial steps are being taken to reorganize the Bank, in-cluding a reauest to the UNDP to nrnvide four exnerts for three years. It ishoped that these experts can begin their work by late summer. The reorganizationis aimed at securing more ef-npriAennc personnel, additional capital and variouslegal measures to permit the Bank to operate a comprehensive agricultural lend-io ng pgram. mfvr.m.enI of such a progran Twill take considerable time.

New Industrial Activjlt~T

) I 'N.ra ,rane ,na ninA ann,+ 4'.,an knr,A; n.v.n+c, .I-bnv. Tt, *'+iF1o

1!r

private industry in Afghanistan. Manufacturing was largely in the hands ofU-vtverra.r, + r.ad and A ; -e a._nte.4

at. Fa. of -a I I-tae hn s si fu.

The cotton textile industry is a prime example of excessive Government participa-tion andI control in I4.Ir IIULi.jJ1pUUUtU.Lon Jis ie'. U'beLwV cJapacity

yet large quantities of cotton textiles are imported and smuggling takes placeon a m.assive scale.

10 ' f)f L - tt …

L2. In i9'7 tne Foreign and Domest_ic rrivatLe InVetMe1ntl Law Was tenactd,

formally cormitting the Government to development of private industry and pro-viding a number of iaportant tax incentives. The response to tne new law wras

- x -

almost immediate and surprisingly strong. By the end of March 1969, 132 projectapplications had been received of which 79 had been approved and 18 others wereawaiting approval. l'otal investment of the 79 approved projects is estimated atabout Af 2.3 billion ($30.2 million). Thirteen of these include foreign partici-pation (largely Indian and Pakistani) estimated at about $5.1 million, If allof the 79 approved plants are established and operated as planned, new employ-ment wiould amount to about 14,000 jobs, largely unskilled. Twenty-seven cf theapproved projects are textile mills, mainly to produce rayon fabrics; twelve areraisin processing plants and four are metal fabrication enterprises. Theremainder are largely traditional agricultural processing operations, but alsoinclude pharmaceuticals and plastics. Twenty-nine plants are in operation ofwhich 10 were at full capacity and 7 at 50 percent of capacity or better inFebruary 1969. The total planned investment in the 29 Dlants is about $7.7million of which about half is in place. Export earnings at full output areestimated at about , million and total newi emDlovment at about 7.600 jobs.Actual and planned investment under the program is completely private.

43. Impressive as these results have been, the private investment programfaces a number nf serious problems including (a) timplv nrovision of technticalassistance in managernent, engineering and accounting, (b) a severe shortage ofsiiitable induistrial sites in Knhiul nndl (nr) lank of short-_ andi medi-nm-ternicredit to meet workirig capital and equipment needs. These are serious questionshut the apparent initial success of the program holds so.me promise for further

development of industries within the new policy environment.

Private Agricultural Investments

44. The success to date of the private industrial investment progranshows~ VthaV W.Lth1 adq.uateU cerUOJti.ves, pr1-J.-vte lfunds will be nvete in irdust-rialenterprises. For agriculture, no similar initiative has been taken but thereare sorJt- .L1u.LUUL.L1O U nLtdA W.LUA -,. )jUpproL.LCrat ±L.L1I1.LCLL a.LdU _LtitUW.Lt,ULV1Jio sUppor.,

such a program might succeed. The growing demand for tractors and shallow wellpum.ps, the currentl results of the wheat prograr,., the response of farm,ers to tadand price adjustments for cotton, wool and karakul, and the success of theprogram, or im.proved mU.arketing of karakul, give further encou,agement to -thosewho believe a "green revolution" can take place in Afghanistan.

45. Over the next few years the potential gains from new investment inagriculture lie primarily in rehabilitation and better operation of tradltionalirrigation systems; which could be accomplished quickly and the returns wouldbe high. Tne Agriculturai Development Bank could be a key element in sucJi aprogram but in addition to thorough reorganization of the Bank and improvementof operating procedures, several additional oDstacles would have to be overcome,including authorization of legal entities, such as cooperatives, with which theBank could negotiate, legal definition of water rignts and establishment Dfwater charges and procedures for system operation and maintenance, authorizationof chattel mortgages, and development of organizational and technical capabili-ties to prepare projects.

Tourism

46. In 1958 only about 400 persons visited Afghanistan. In 1968tourists numnbered nearly 45,000 and spent the equivalent of about $2.4million. At present the Country's ability to handle a larger number oftourists is limited because of lack of adequate accommodations in Kabul,and generally inacquate accommodations in the Provinces. With completion ofthe new Inter-Continental Hotel this year, first class accommodations Wi:Ll beavailable in Kabul and further hotel development at strategic locations out-side of Kabul, e.g., Bamyan, may be feasible. Another key tourism projectis improvement of Kabul Airport. Its present equipment permits only visuallandings and thus excludes all night traffic. The mission believes thatdefinite possibilities exist for development of tourism. The UNDP has beenrequested to provide an expert for 12 months to prepare a program. A favor-able response is expected shortly.

BALANCE OF PAIEENTS

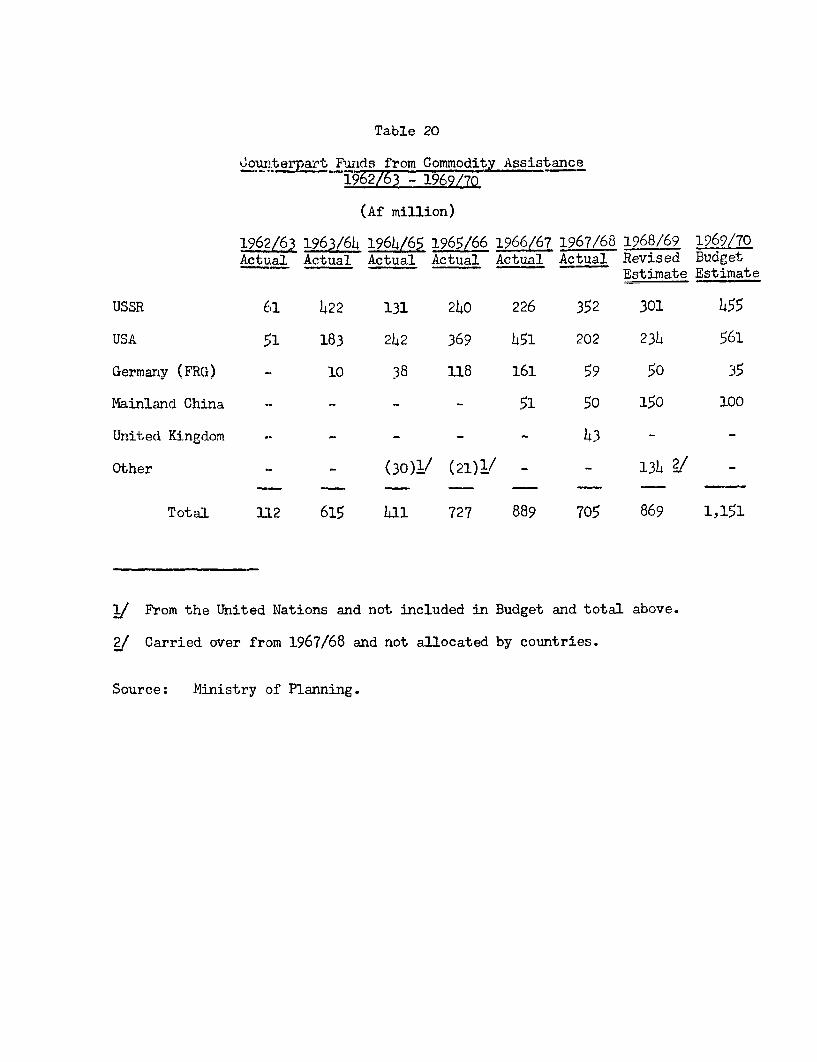

47. Over the past ten years Afghanistan's commercia:L exports andimports have shown a growth trend of about 3 percent a year, although theyhave been virtually stagnant since 1965/66. This trend is slightly inexcess of the real rate of growth of the economy. ExDorts. at $66 million,are about 8 percent of GNP. Merchandise imports amounted to $137 millionin 1967/68 (16 ngrrent of GNP! of *.^Thich 53 percent werp financed wi-th nroiectand commodity aid. Net capital inflow has declined recently because totalni shuremeri-s~ ha.re leveled off nnrd nm1-r.-tiz on n-a.rments havre increased.

t8. 6¢hmorts. Fr.-om an all=time high of $71 mllion in 1964/65 totalexports declined as a sharp spread developed between the free rate ofexchange and the ra a uat w-hich, thle proceeds from Afa prlnp 4 I -a'

exports hacd to be surrendered. Recently, the effective surrender ratewsIncreased by nearly 710, percent and exp,ort-s shou-lu therefLore recover

in the coming year. Exports of fruits and nuts have increased by 35percent- 4n +I-ree years. Exports of. carpet-C s have decl4ned and are not

k .,~ U .I I UIL 1:J0.. J £A&'J Iv 'J. '...jI L i 110 VO U,u.L1O 0.A i 0.1 0 JI

expected tc) recover- soon because of weak foreign demand and deteriorating.uaatL Ly. ]I:n I U.L 0.tr UdJitionl W...L U. Lucy L V%ecj Ver t.oU tlh e3706./ 566J le0vl

and shipments of natural gas to the USSR will add an additional $12 million,increas.lng10 I UV aboUUt; i6LL) 1iLLionL.LU11 ir. -971±/1rC. PuosUiLy UUtLo.L m&jjIJI.s col-lJ.U

reach $90 raillion in that year and increase at about 5 percent thereafter.

49. Exchange Rate System. The official exchange rate of Af 45 perTTC, d- __- _- '__ {_1 :_ \;_l nrtn__ __n:_ ___1.!__3 _US$1 Wasb est/a bU | L1tihU |i M1arlcUhl _7U) dSlU 1p96 and ap U p U lidt JUo -m Ur pol-r and GoVVEr-

ment imports. The free rate was then Af 51. Inflation caused the freera'e tuo increase 'a, Af & 14in 196± 5 and ex-ports,, (which were also subject toan export tax),suffered. In 1968 export taxes on cotton, wool and karakulwere eliminated and export subsidies were offered which substantially in-creased the effective exchange rates for these products. The official ratenow applies to fewer imported items; however, it does apply to externaldebt service which has expanded rapidly from $16 million in 1966/67 toabout $27 mlillion :Ln 1968/69.

- xii

50. Imports and Imort Policy. Merchandise imports, other thanthose finanGed linider fnreian aidrl hae remained essentially level over -hepast four years. During this period consumer goods declined and capitaLgoods were unchanged except in 1967/68 when they were about 60 percent ofthe previous 3-year average. The recession in the past two years accountsfor most of the decreases, and - ith partial recovery in 1968/69 and therecent growth of private investment, imports will very likely increase.Tmnrt+ An+ta uCndersates a+-Vl Ilvels becae - +f 1he Iarge -mruntr nof

.1,0 tC-- - ALtA~ Uw, UV , c.t uu. .V" . LI, w.i uc..c U,, -J f-fl - - -

smuggled goods. There are few quantitative restrictions on imports and ratesae genera LJ A4ly 'low and4 i n rneed4 of re-V JLon. iouver , sL1ha F U±ta lJLhet 1V

smuggling should accompany improvement of tariff policies. Othera vat X.L k U L.V.L L11r ±LII}.iUK I ± UI Ut 41i11)J.LL. 0'&J0 ± UU L1ULU.LJL DW11, U.6*

cotton textiles, sugar and wheat; and limiting consumer goods by permittingthe free exchlage rate to depreciate in resporse Do the expected increasein import demand, which will be met only partially by increased exchangeearnInly

51. Balance of Payment Outlook. Both commercial exports ana imipor Smay increase up to 10 percent in the current year (1969/70) and the balanceon goods and services (excluding aid imports) would therefore remain un-changed. However, the growth of amortization payments is likely to putsevere pressure on the availability of foreign exchange.

52. Afghanistan's gold and convertible currency reserves were reducedto about $141 million in 1967/68 from about $51 million the year before.With the recent decline of exports an IMF drawing of $4.8 million was madein June 15968 and another $7 million was provided for in the Stand-byAgreement of July 1968.

53. Debt Service. In 1968/69 foreign debt service payments are inthe neighborhood of 14 million or 19 percent of exports of goods and ser-v'ices. This ratic is likely to reach 25 percent in 1969/70 and stay at thatlevel for some ti22e. Afghanistan will continue to be heavily dependent onforeign aid for her future development program and it is imperative thatsuch aid be obtained at most favorable terms.

CHAP1TER I

PAST ECONOMIC GROWTH

(a) Gen(ral Background

1. Afghanistan is a large mountainous country, landlocked betweenIran, Pakistan and the Soviet Union. There is no railway in the country,but adequate road links exist with rail heads in West Pakistan at Peshawarand Chaman, and in the north to the Trans-Aral Railwav in the USSR. Recentl-the road was also extended to the Iranian border, but the connection toMeshed is still of inadenuate nunlitv- A long-standing nronosal to connectsouthern Afghanistan to Bander Abbas has not yet proved its economic feasi-hil it.v ThA nenrmV dend6 vryej larely on subsi vP npc,v.i P121±re. hut a

large part of the cultivated area requires irrigation. Only about 12 percentof the total area is believed to be cultvivable

2. wC Of cL av8 toa poulton of p;w|bbA,V 1 a_CA V :vrn>.++n7^1+^ erhaps 15 million, the, lags groupC+ be-7nzlongs to the Pushtu tribes, including up to 2 million nomads, but there area number of other etrhnic groups such as the Uzbekhs, the Turkomans, theTajiks, the Iranians, and the Hazarats - the latter being among the poorestgr oups, sliving in the central ,.umuctains. ThW UI±e lJWo Uo.fi.LLi-.L ag e are1rUdU d

Persian and Pushtu. During the past 30 years, which covers the rule of thepresent; v ng Muohammaud Zi Shll ahI U1ite unr LrLiUy hla rtJuy d a remakabl degreuc

of political stability. With the first constitution in 1923 the transitionbegan towards coristitutional monarchy, and with the new constit-utionL of 1964a parliament was established and members of the royal house excluded fromcabinet positions. Furthermore, it provided aii citizens with the right toa free education, and the right to own and dispose of private property.

3. In its foreign relations, Afghanistan has persistently pursued apolicy of non-alignment, but relations with Russia have been particularlygood ever since the military confrontation with British India in the courseof the Afghan Wars, at the end of which Afghanistan gained full nationalsovereignty in 1919. Relations with Pakistan have never been good becauseof territorial claims on the part of Afghanistan which on occasion resultedin a closing of the border, as for instance in the early sixties. Anattempt at mediation on the part of the Shah of Iran in 1964 helped to bringabout an improvement, and more recently, the issues arising with the inter-nal democratization process appear to have eased the Pushtunistan iSSUEf outof the poLitical limelight.

Afghanistan's geographical position has evidently been a factor inthe relatively higrh level of foreign economic assistance during the last 10years, when gross capital inflow reached about $5 per head per annum. Thishas not yet resulted in an appreciable acceleration of economic growth, andnational income is estimated to have remained nearly stagnant on a percapita basis. This is explained by two principal factors. One is connectedwith her traditionaL and custom-bound social structure, the extremely :Lowlevel of education in most areas, the absence of a modern code of law, andthe limited natbr.l renourres. The stennd faetror lies in the nature of theinvestments that were financed with foreign aid, which was almost exclusivelyin infr sruir-+iir nnr1 nro+. mlT.t(i. 'relate.dr +.to priority-v needs. On.l receently

was a change in the basic strategy attempted, and investment prioritiesshifted in favor of the productive sectors. As will be explained later inthis report, this change in strategy is only slowly beginning to become areality, and much of the expected increase in agricultural production in theimmediate future will be a result of the introduction of improved wheatvarieties rather than of any fixed investments. On the other hand, with theintroduction of a new Investment Incentives Law two years ago, private :in-vestment in manufacturing industry is presently showing signs of unprecedentedvigor, and if it actually expands to the scale believed to be possible, it

should usher in a new era of industrialization for Afghanistan.

5. A beginning has been made in Afghanistan in the field of economicplanning, but so far with little effectiveness, despite the availability oftechnical assistance on a sienificant scale. Consultations with, and coordi-nation of the activities carried out by expatriates is a major task of theMinist.ry of Planning. A Russian team did the groundwork for Afghanistan'sThird Five Year Plan. The Plan document was issued by the Planning Ministryin April 1967 just afte the beginn;ng of the Plan period; but It failed tobe approved by Parliament until it was time to substantially revise it inmid-1968. Planning consists mainly in the production of lists of orolects,and the implementation is very largely in the hands of the executing Minis-tries. The Pl~ anarg .M4- W stry, beain n on. eul- footing trth other Ministries.is not in a position, and for staffing reasons is not equipped, to assumeexecuttive or control functions, and serves mainly as liaison with foreign aidagencies and as secretariat for the High Economic Council. Project identifi-cation and preparation by the G-overnment is nadequate, eand is carried outmostly with the help of technical assistance. The Afghan contribution to the

implemlentation of the Five Year PlX in the form of finance for the dcmesticcurrency component of the program, has recently also diminished to the pointwhere in 1968/69 commodity aid counterpart financed four-fifths of locE1 de-velopment expenditures.

(b) Production

6. Statistical information on production in Afghanistan exists to someextent for crop output and production of factory-scale enterprises and elec-tricity, but not for other sectors. Even in agriculture, the basis is opento many questions; a substantial revision of crop data is presently in pro-gress, but unfortumately earlier years have not yet been covered, so that thecontinuity of the series is broken. On the basis of very rough estimates,GDP estimates have been made according to sectoral origin in Appendix Table 3.In 1967/68 agricuLture still accounted for about 53 percent of GDP, cornparedwith nearly 60 percent six years ago, of which perhaps EL quarter originatesfrom the livestock industry. The following table gives the approximateabreakdown of GDP by major sectors.

Af Million Percent

Agriculture 28,300 53Industry and Handicrafts 5,707 11Minerals, Fuel and Power 583 1Construction 860 1Transport and Communications 1,178 2Services 16,859 32

Net Domestic Product (1967/68) 53,487 100

- 3 -

7. A surprisingly small contribution annears to he made hv ut ii itiessuch as transport and electricity, and by construction, totalling less thanh nereent of' GDP. despite the fat. that. twothirds of total publio inVe.tmApentsin the last 5 years were made in powier and roads. This means of course thatthe capacity of these stors nater this relatiely massive inestrm.ent effort,has not only been geared up to meet current requireraents but future require-ments as well a i cler eg. * esen+ p capa-iy .- +he Kabalgrid which far exceeds any peak demand foreseeable in the near future.

8. The total value added in Transport and Communications today is stillsubstantially less than the average annual investment ex2nenditures in thatsector over the last six years. Even if the value of transport and communi-cation services had started TiAth zern i n I -A +-n r.nnh +.hez. nhn-vrp Af 1 178million in 1967/68 would have implied a capital/output ratio of nearly 10:1and in fact it w.s muTch higher t.han +.hat.- Th4 q does not of course mean t+hat-no new road construction will be required in the near future; quite the con-traryj since most of ns+. inm.ustm.ent was for major highwan.mys there is a needto build secondary and feeder roads to make it possible to reap the benefitsof +.hrp nPa. h; ahT.r:A|=rCZ T+ ; .c r-1a-nP n.rr+o .:n>w o=isc of the----, highways.er ho-a*-ever- thavt transpot. ser-v.rices_ h.r_.

grow,n at a pace considerably slower than in other countries at a similarst-nge of develo.J-ent.

9. In the case of manufacturing which contributes about 11 percent toGDP it must be noted immediately that factory-scale industries account foronly one-fi:Eth of the total, the balance being classified as "handicraft",i.e. small shops and home activities, including carpet-making. Factory-scaleindustries exist in such fields as cotton and woollen textiles, sugar, cement,flour milling, vegetable oils, cotton ginning, tanning, shoes, soap and ice.Fruit nrocessing including raisin eleaning and nackaging. as well as car)etwashing, are other fields of small-scale industries. There is clearly sulb-stantial senre for further inrb-strialization that noo_ld he undertaken in thefield of processing of agricultural and livestock products, even before anyother avenues are pursued=

10. Agriculture. Of the total land arc of 63 million hectares, abouit14 million hectares may be described as arable but only about 3.5 millionhectares are believed to be under crops, of which about 2.4 million hectares areuncr irrigation. Except for the lack of water and dilapidated structures, over5 million hectares could be irrigated, however. Cultivation practices areprimitive, and productivity very low. Livestock, principally sheep, accountsfor about one-sixth of totalagricultural income or about 7 percent of nationalincome. Production is essentially nomadic over Government-owned range landswhich have been severely damaged by overgrazing. Losses are heavv from disease.starvation, inadequate shelter and shortages of water. Rehabilitation of thisimportant element of Afghanistan's agriculture would be difficult but ex-perienced observers believe a progran of range improvement, selectivebreeding. disease control and greatly improved processing and marketing oflivestock products could, in time, yield high returns. The possibility ofexporting mTutton to other Moslem countries is narticularly interesting.

- h -

ii. Reiiable information on foodgrain production i s wuavaiiaui e, buuwhat has been compiled shows that in the last 10 years, if adjustments aremade for the weather, output has remained the same. Ifneat accounts for 60percent of all grains and the balance consists of corn, barley, and rice.Only about 20 percent of wheat production is marketed. Experiments havebeen made over a number of years with new wheat varieties, mostly in USAID-sponsored stations. At the present stage some optimism seems justified asto the results that can be expected in coming years, after a difficult startduring wihich some problems peculiar to Afghanistan appear to have held up thefarmers' response to new varieties. For one thing, the use of chemical fer-tilizers was reported to depress yields of some local varieties of wheat, andthis was obviously unhelpful for the propagation of fertilizer use; in thecase of Mexican varieties - in contrast to the experience found elsewhere -their yield response to fertilizer in most parts of the country was unnotice-able or nil if nitrogen alone was applied. At the same time the yield poten-tial of Mexican wheat under conditions of low fertilization and traditionalcultivaticin practices has been shown to be somewhat less than that of thenative wheats. These were formidable problems for the initiation of a Mexicanwheat program, quite apart from the need, difficult to meet, of providing in-creased Quantities of water, and the administrative problems for the Govern-ment to distribute the required quantity of fertilizer in the appropriate mixto the farmers in a country with over 90 nercent illiteracy. Yet it was wortitrying since experiments had shown that with appropriate inputs the yieldcould be imnroved bv between 50 and ))o0n prrPnt, ; rpenndrin on the soil. Itis now reported that in the 1968/69 wheat campaign some 5 percent of theirrigAtedi wheat. nlrea wasq~ plnted- wi+th imnrnoed vanrietiesz (comnarPed TAithN1 I nper

cent last year). In combination with very favorable snowfall reports, thisod rde +Sult. in a wheat crop as .muca 1 i5-20 perfcent hig,hesr thmn t.hp rpst

average, which had been subject to a maximum output deviation factor of' lessthnn 7 percent. This me-ns that for the first time production would havegone appreciably beyond the historic stagnation level. Government officialshblieve +tha- in +hen 1069 O nO season as much as 10=15 E rf ------- r he' +

irrigated area will be under Mexican wheat. What is most encouraging inthisc- developnment -Ls , tha i occurred i"n -spite of a substantla decl"-e JnI~.a -a..~1---af -_L UI) .5 J.L 'J.A AJ 5 U 44U o L VUC 'Si a O uL UdSi ~JCL. ~AO'....L, J4

the price of wheat, which during the 1968/69 planting season was more thana +hird lower +ha,n a Tyea be-,A I mer 4h1 4h-e -v-rg- --- p in -TI no

the last 3 years.

12. The Government has supported the wheat campaign with a substamtial; v _~~~~~~~~~~~~~~~L l Et n:~U I:. L _au _ _J -L _.. 12eL e .increas sexivs .L.± ±| CU D _L LE Ul- JLI[IUJUl L WliLIUl are U;U Wso LIAI ra ;:UL idy Ialdl, W- .JI '

tiaUy 55 percent but has now been reduced to 30 percent. A total of :L6,O0Otons was reported.ly Lm.lported -I 1968 Uand the target has been raised to about33,000 tons for 1969. Urea is imported together with superphosphate, mostlyfrom the uSSR, but also under U.S. commodity aid, and the u.S. also suppliesdi-ammonium phosphate. Administrative bottlenecks will make it difficult toexpand fertilizer distribution at the proposed rate, particularly since thereare few private traders and distributors with any experience in fertilizer,and sinlce past poLicies have been toward discouraging private enterprise insuch fields.

- 5 -

13. The most important cash crop is cotton, which is traditionall;ygrowm on 2 percent of the irrigated land. From the average 1962-65 produc-tion level of 85,000 tons, output has declined in the last 2 years to around55,000 tons. This has been the result of a combination of factors, the mostimportant of which was the unfavorable price relationship with wheat, whichcame down from a ratio of about 1.7 in 1962 to about 0.9 last year, as aconsequence of wheat shortages on the one hand and an unfavorable exchangerate for cotton exports on the other. Somewhat belatedly, some action hasbeen taken finally in 1968 to correct the exchange rate structure and tobring the cotton price up to Af 72 per seer from a level of Af 52 in 196$7.As a result, the cotton/wheat price ratio is now more favorable than it hasbeen for manv vears. and during the current Tlantinp season some acreage ex-pansion can reasonably be expected. Even though cotton does compete withwheat on the land- evivn a i nprnent increase wouild amolunt to only I percentof the wheat acreage, and should not noticeably affect the wheat program. Inthe long run such competition could well become aproblemn but the obviousanswer will be the vigorous promotion of irrigation improvement and expansionfror which +.here isc morer sonpen +.hnn wThat+. +.ho novernentr+. has at.+.Pmnt.ed tnachieve.

14. As already pointed out, the main problem in recent years for cottonhas . .beer. i --- -r n- e..Jarm price. Prior +o bunt+ 1906. r4 n-ninacapacity had been inadequate, but this is no longer a bottleneck since capac-it.J is now forL 1.60,000 tons of see d. Ucot1to c,mpared..L wit lVas yLe.a. U -r' -pou

tion of 55,000 tons. Almost four-fifths of Afghanistan's cotton exports goUo th ULSQRA UAU-.Ld b.ilatra Lrd UlaUt eme: d41 UIhe bJdLLV "c 0 toc0nvertib_l_e

currency areas. Exchange earnings had to be surrendered at the official rateof Af 45 to tne dollar. Even after the export tax was abolished this was -I

effect still an indirect way of taxing these exports as -bhe free exchangerate has been around Af 75-80 for some time. As of March 1969 an exchangesubsidy of Af 20 per U.S. dollar is becoming effective, to allow the move-ment of exports with the new announced ex-farm price of Af 72 per seer. Thisshould prove adequate, and it might in fact promote exports at the cost ofdomestic mill consumption, so long as government-fixed textile prices con-tinue to be kept low. We shall come back to this question in the context ofmanufacturing industries.

15. A favorable development is the increasing attention given byprivate business to fruit growing and processing for export, particularlyraisins. This has in recent years been a highly successful export item.Afghanistan has an extremely large selection of outstanding quality grapes.Vineyards are the only place in the country where chemicals are used forplant protection. The establishment of new raisin cleaning and packagingplants continues and gives hope for even larger expansion of exports, whichhave so far been mainly to Pakistan and India. Owing to mildew, the raisincrop last year was reduced but exchange earnings increased as foreign demandmoved prices up.

16. Irrigation. It has now been recognized for some time that newlarge-scale foreign financed water engineering works did not provide theanswer to Afghanistan's problem of agricultural development. Two-thirds of

- 6 -

the cropped area are already irrigated but many structures are regularlycrumbling under the impact of water flows, and need redesigning and buildingto better standards. Much of the current repair work is done b the . rnerethemselves along traditional methods.

17. Small new irrigation schemes involving improvements to already ex-isting irrigation systems have been accorded top priority by the Governr2entbecause of their very favorable cost/benefit ratio, as well as very shortgestation periods. Very few projects of this nature have been undertaken,however, partlv because they are unsuitable in size for external financjng,and the Ministry of Agriculture and Irrigation has only limited resourcesboth in personnel and in investment fuiinds. Ex-penditure is rn the order ofAf 3 million ($4,o000) a year and is spent mostly on design and training.Tn some cases, the cost of projects is to be shared between the farmers andthe Government.

18. A few medium-size projects are under construction, and severaLlarge=scale irrigation schemes are under preparat-ion, such as the K ,-,ndu-,-Khanabad and the Hari Rud projects, both of which are likely to attractforeign assiLstar.ce. In fact., a IUgoslav cred'it' hlas 'a"ready lbeern offered4 forHari Rud but the project is not ready for implementation.

19. Agricultural Credit. The availability of both long- and short-termcredit for agriculture is highly inadequate, and the importance of overcormingthis bottleneck can hardly be overstated. As in other parts of the sub-continent the small farmers are often indebted to local moneylenders -whocharge 40-100 percent interest and have control over the price of the debtor'scrop at harvest time. Rural cooperatives do not exist, except that in veryrecent years farmers have themselves organized into groups in certain areas,e.g. in Nangarhar, under the leadership of '"bondholders" or treasurers,usually the richest man in the village, who collects con-tributions from thefarmers and is able to provide collateral for loans to be obtained from theAgricultural Bank. This development deserves encouragement and should be ofhelp in the future, development of agricultural credit.

20. The Agricultural Bank has been in existence for a number of yearsbut has so far been relatively ineffective in providing credit to farmersexcept by financing the sale of a number of pumps and of 400 tractors overthe last 3 years on the basis of 200 percent land collateral, 25 percent down-payment and five-year terms for the balance at 6 percent interest. Demandfor tractors is reportedly adequate for about 100 a year but arrangementshave not been made yet for continued imports of tractors. The Bank ha, beentoo much infvolved in providing finance for government-sponsored schemes andthere is not enough information about its present assets. Following a recentIBRD appraisal mission, various steps are presently to be undertaken towardsestablishing a soumd basis for the Bank's future operations, e.g. the audit-ing of accounts, the strengthening of the staff, investigations into theeconomics of farm mechanization and pump irrigation, and arrangements fortechnical assistance for its future management,

- 7 -

21. Other Sectors. Although factory-scale industries contribute only2 percent to GNP, production data, to the extent that they are available,give some indication of trends in the economy as a whole. Total industrialoutput declined during 1967/68 by 1 or 2 percent after having shown signsof growth in the preceding years. Output of cement dropped by almost athird because of a reduction in construction activities, mainly in the publicsector where several large projects were completed and total development ex-penditures declined. Production of ginned cotton declined by 23 percent, andof cotton textiles by 3 percent. At the same time large inventories of fin-ished cotton cloth were built up. Output of woollen fabrics declined by 27percent. Declines occurred also in lapis lazuli, coal, soap, and salt,against increases in the case of shoes, flour, and vegetable oils.

22. Not much is known about production of handicrafts, the value ofwhich is estimated at four times the value added in factory-scale industries,except that the production of carpets and rugs for export declined by morethan a third. This is partly attributed to continued weakness in foreigndemand, but difficulties related to the quantity and quality of productionare also reported.

23. It seems surprising that with all these downward indicators theproduction of electricity increased by 20 percent in 1967/68. While somethinglike a third of production probably goes into losses and thefts and this mayhave increased more than regular consurnntion; it is also plausible that do-mestic use has continued to increase rapidly, considering that electricity is

r1 .ih.-tant.i b:et v llow costh+ a t. abou+it. TTSl penTr k-Tqh _

2)i Besides -t.mhe 4vdlrm ;n +.,,i ̂+- n actiies u.hich alco resulted

in a reduction in wage increases and increased unemployment, another factort' + recessionist trend .n the vecoromly Lhas been 'the hnig2h pjrce o- 'W-e

following the bad harvest of 1966/67, which continued to prevail through1967,X6 Ld has 11only co,me1 UdoWII UULJrin Ulit LastL 0LV r,onths. I nLUdJ.Ly, CAjJPUL UL

declined in 1967/68 by about 5 percent to a point lower than in any of thelast 5 years, with bhi1 CoinSe-qurL-Ce of1 some ueclin Iln cOmImrnvClal ±uimjput,i aswell. Independently of this, aid-financed merchandise imports declined by1L4 perer. Vfrll,ih 11966 L /7V Jle-vel. All unese factors,ver ' ogether, ;lCCO'E - ;tfor what can be described as a minor recession. To combat it, more vigorousactivity on the part of the public sector would have been called for, butfor one thing there happened to be a dearth of projects which might have beeniXitiated with foreign aid so that no impulse could be imparted tnroughgreater public investments. For another, public revenues started to declinein 1967/68 and the Government was firmly pledged to the monetary stabilizationprogram which had been initiated in 1964/65 so that the scope for deficitfinancing was relatively small. In fact, an overall budget surplus had beenachieved in 1966/67. Money supply contracted in that year, as well as inthe following, and the bazaar rate of exchange has remained extraordinarilystable at Af 75-76 until July 1968 when it even began to improve.

(c) Events in 1968/69

25. As already noted, the price of wheat started to decline in micd-1965and the current crop is expected to be an all-time record in the neighborhoodof 2.5 million tons compared with the past average of just under 2.2 milliontons. Simultaneously, a recovery of the cotton crop by 15 percent is expect-ed. The fruit and raisin crop has suffered from mildew and will be less thanlast year. Total foodgrain production would be up by about 8 percent butgains in cotton would be more than offset by the decline in fruits.

26. There are indications also that manufacturing production has entereda phase of moderate upswing since last summer. By the end of the calendaryear accumulated inventories in cotton textiles were reduced by half to about25 percent of annual production and with the import quota obtained also lastyear from the USSR, mill offtake should be able to expand considerably. Thesame is true with cement which also now is exported to the USSR.

27. Expcorts other than natural gas should receive a moderate boostfrom the changes in effective exchange rates and recover at least by 5 percerntto the 1966/67 level. An-other gann will result from the innreased natural gassales to the USSR by $4 million to $7 million, so that total exports would gomn frnm AOfA m; I1; nn +.n nhrm+. S;71 mi 11i nn

28. Demand for goods an.d services is also increasing through what canbe described as the beginning of a private investment boom which will beevaluated 4- Chapter TIV of- 4U --i report. Yn.-4. U_ -or r.o thi upar trn -will--A4 -A- . -- 4 V ~ L J.-4 V 'J± ULWI.&O I 1= UW . VVULU WdSIVI J UA L 11V AL4.0J Lk.JVVVC.± U..L U$.4kA VVLA

be further supported, and unemployment reduced, by expansion of the Govern-..er.ts' develop,ment.t prgrL' ULhIo,n er,ssiloe o oeqeto.

ProvisionaI budget figures for next year imply an increase by 23 percent indoMestic development expenditures but this is subject to substantial sl.ippageas the additional resources are anything but assured. Nevertheless it issafe to assume that development expenditures will further increase. If theIndustrial Development Bank is established, some of that increase would bechanneled into the private sector.

29. Finally, private credit expansion which during the first 10 monthsof 1968/69 amounted to Af 194 million compared with Af 60 million during thewhole of 1967/608 is another indication that the economy is picking up somestrength although, as will be noted later on, actual credit is not a truereflection of demand for private credit because of the severe institutionallimitationls of Afghanistan's banking system.

30. Total money supply expanded in 1968/69 up to January by 4 percentbut the price index has followed a downward trend, mainly of course throughincreased supplies of wheat, but non-food prices also declined moderately.The free exchange rate has improved from an average of Af 76.h in 1967,(68to an average of Af 74.8 per U.S. dollar.

TIM Tv-RD PLAN STrATEGY

(a) Constraints to Development

31. The obstacles to effective development programming and implermenta-tion in Afghanistan are numerous and pervasive. Some are inherent, such aslimited natural resources, geographic isolation and uncertain weather con-ditions. Others aLre deeply rooted in customs and traditions. There are manyothers, however, for which practical solutions are possible over varying periodsof time, provided the necessary measures are taken, including strengtheningexisting institutions or creating new ones. They include the following:

(i) The country has been unable to effectively mobilize its own re-sources for development. Afghanistan is poor, but public savingshave been far below the potential, and until recently the poE:si-bilities of channeling private savinas into productive investmenthave failed to receive adequate Government support. Agriculture,which accounts for more thnn 5O percennt of GnDP. nontrihutes iervlittle to public revenues, which have not increased appreciablyin the- lt fnor years= As a rensult tntal resl npm.enit expemrii-tures have amounted to barely 8 percent of gross domestic productover the past sevren years, anrd the Governent t s surplus of reve-nues over ordinary expenditures has amounted to only about 1 per-cent of C-DP. C entr- - bar,k b1. - 1h I. - - - g.a. s IV,be e nJ - an.other 1 per, c-"- ee nt,

and the balance (6 percent of GDP) has been financed from commod--ty &.d prjecj assiLstar.ce.

m; o _ 1_u _ __ v" __v __4. _r _ - -- _4

technicians and skilled manpower in both Government and industry.TLhe, ab-.LLUy to ±tider>y, prepare aUnd ±IUJ,±Lpemenut UdVeUJlopJImen pr9u-

grams and projects is particularly limited. There is a largenumber of experienced traders in Afghanistan but an industrialmanagerial group has not emerged, primarily because there is so"lite private manufacturing. in agriculture, Tne snurtage ofLextension workers and small irrigation design engineers is l-ikelyto be a serious obstacle to the planned expansion of output.Some training programs in these areas do exist and more areplanned; but heavy reliance upon foreign personnel may be expect-ed to continue.

(iii) The interaction of the executive branch of Government and theParliament is hampered by the fact that the idea of overridingnational needs is not widely appreciated in the Parliament whereinterests tend to be tribal and local. Thus reaction to legis-lative propo6al's frequently takes the form of negative criticism.Measures essential to development, including annual budgets, aswell as laws establishing new institutions. may therefore be re-jected or long delayed.

- 10 -

(iv) Most of the statistical information required to plan and carrrout deveLopment is either lacking or is quite unreliable. Thereare no national accounts and no means of determining the realvalue of capital expenditures. Virtually no data exists on thesize, composition and growth of population. The amount, clas,i-fication and use of arable land is unknown. The country's agiri-culture :is predominantly for subsistence but reliable informationon investment and output of the non-monetized part of the sectoris lacking. The 31 State and mixed State enterprises are eitherfar behind in reportina the results of their operations or do notreport at all. There is no central planning, control or coordi-natinn of S tiAq+An_r. Thln npannr+.mernt nf Stnti5.tics in the Minis-try of Planning receives whatever information is available fromministries and other maoncrios uhlicoh a y , .relativrely auitnnomous in

deciding what data to generate and release. M2ch of the pub-lishvhed informe sieon iis s cr.tatez bsmlhodns.

{1rl~ ~ ~ ~~~~~~~~~~)- 'Pt t-t1z1t tn+z; htnt;t8h mnll hlnrincrq nnd

low yields. The rural population is largely illiterate and pro-duction rl.d .arketi. ;=g Cooperati te tS±x+ .- ion setrvrices i .nre

very inadequate. The weather is extremely variable and in irri-gated agricv.1ture a large partL of 'Vile avrai.able aeri lsdue to badly maintained facilities, poor water control and high-Jly uncertaIin w-vatLer iLghts. A maJor constlra-.ItJ iL tLhe LacL o

agricultural credit. Reorganization of the Agricultural Devel-opweuut E,anK wi.Ll he:.Lp out, 1U W1I.t w ake uucid.uerabule tLi for the

Bank to make an impact. In the meantime farmers are at themercy of money lenders, ginneries, traders and other intermediaries.

(vi) As will be discussed in more detail, the response of private n1-vestors to the Investment Law has been encouraging, but majorproblems to expansion of industry remain. Among Afghan business-men there is a traditional preference for trading and money lend-ing, in which turnover of capital is rapid and risks are short-term. Relatives and close friends are also greatly preferrecd ascustomers. Local markets for manufactured goods are sma-l.This, together with the countryt s land-locked position and thehigh cost of transportation for imported materials means thatproduction costs tend to be high. The mutual suspicion of Gov-ernment and private business seems to be lessening somewhat, butthere is still much uncertainty regarding the Government's ownintentions in respect to industrial investment and the threat ofnationalization of successful private industries remains. Tileindustrial sector badly needs short- and long-.term credit whichthe banking system is unable or unwilling to provide. TheIndustrial Development Bank Law was proposed 12 years ago buthas not been passed yet. Little or nothing is being done aboutthe extensive smuggling of competitive goods. Public sector indus-trial enterprises which comprise the bulk of the country's manu-facturing activities, lacking incentives and competent manages-ment, are highly inefficient.

(b) Plan Priorities

32. Development planning in Afghanistan is in large part a matter ofthe nature And lev-el of foreign. pronect assisance and i coordinationwith domestic capital required to support and complement it. Not only isa lar,g a..,.~.,t,o of.A +ec>-cl4O. assit,.L U1.* a prreu-st.~.ite for dSL'4 the prepa,av

of Five Year Plans as well as individual projects, but foreign donors haveiucL ~.' i±AUL%t 441 P 'J I_,kJUJt- LJ0 d4LU UtJ%J1iLL.L V .AL10 U±U' U.Ln~ wJA.

funding schedules. The past preference of donors for relatively large pro-jts$'L,0 an te U lic seuuor has± als:o uiewlv t4±IL~ LIU UUL'u Vd..LLva Ue. o .LU JtL.Ls

carried ovrer from year to year and from one plan period to another has beenlarge. For example, about 57 percent of pUDLiC investment during the ThirdPlan period was estimated to be for completion of projects carried overfrom the ,Second rlan. This factor has limited the effective scope of devel-opment planning, as well as the flexibility for annual budgeting.

33. Both the First and Second Five Year Plan documents stated thatpriority would be given to increasing agricultural output. However, partlyas a result of the project selection process as described, actual emphasisin both plan periods was on roads, electric power and large irrigationfacilities. Development investment during the First Plan is estimated atAf 10.6 billion and Af 25 billion during the Second, a ltotal of Af 35.6billion of the 10 year period. Of this amount, nearly 75 percent was allo-cated to transport, communications and State enterprises, largely electricpower.