I @f TU '-# E3 rTnf | Report No. SA -I la I II~nnUjaI~ UU - World ...

176

I TTR I CTED I @f TU '-# E3 rTnf | Report No. SA -I la I II~nnUjaI~ UU IPFP n rep(! [~~~~~~ ~ ~ ~ ~ ~ ~~ &PAWo' I" I This report was prepared tar Use w 11. li_1 n liated organizations. They do not accept responsibility for its accuracy or completeness. The report may not Ihe published nor may it be quoted as representing their views. INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION TW~rTT'% mCrr T A T T'7 A flTt-kTT fVC'L T7) A TTq ' 1INDUSTR J. XIiIZAT ION OFX PAY_IS A N THE RECORD, THE PROBLEMS AND THE PROSPECTS (in three volumes) VOLUME II SECTOR REPORTS March 10, 1970 South Asia Department Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

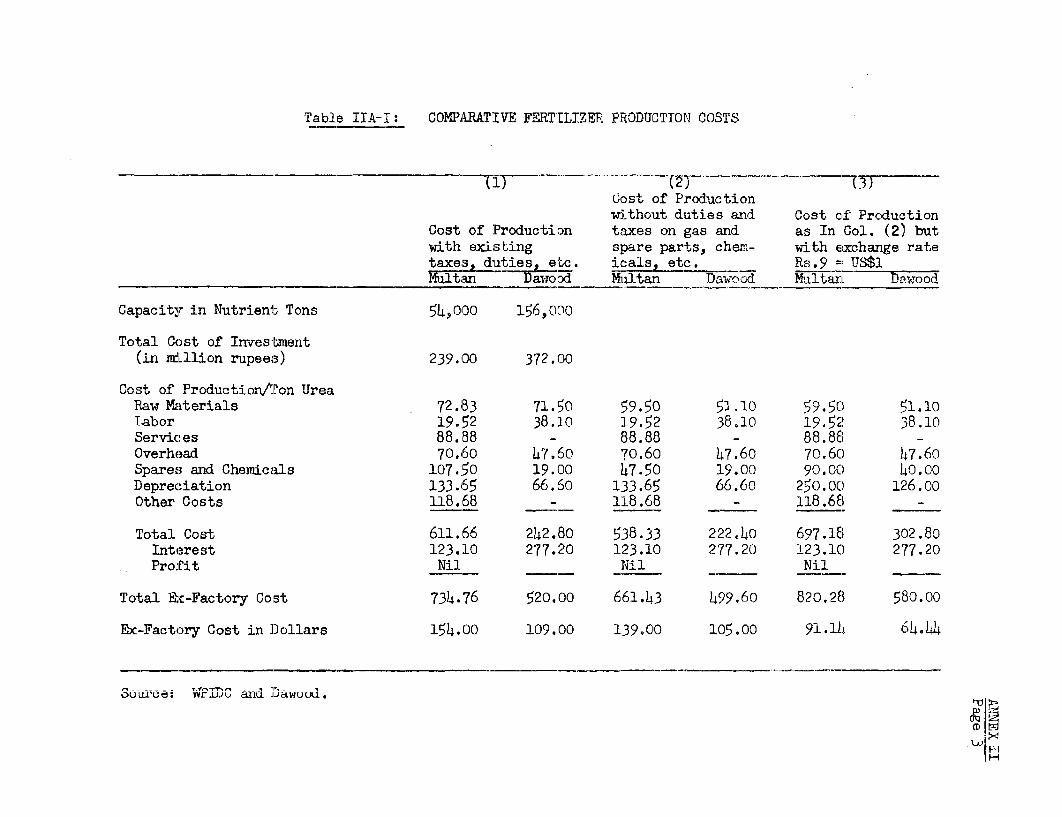

Category

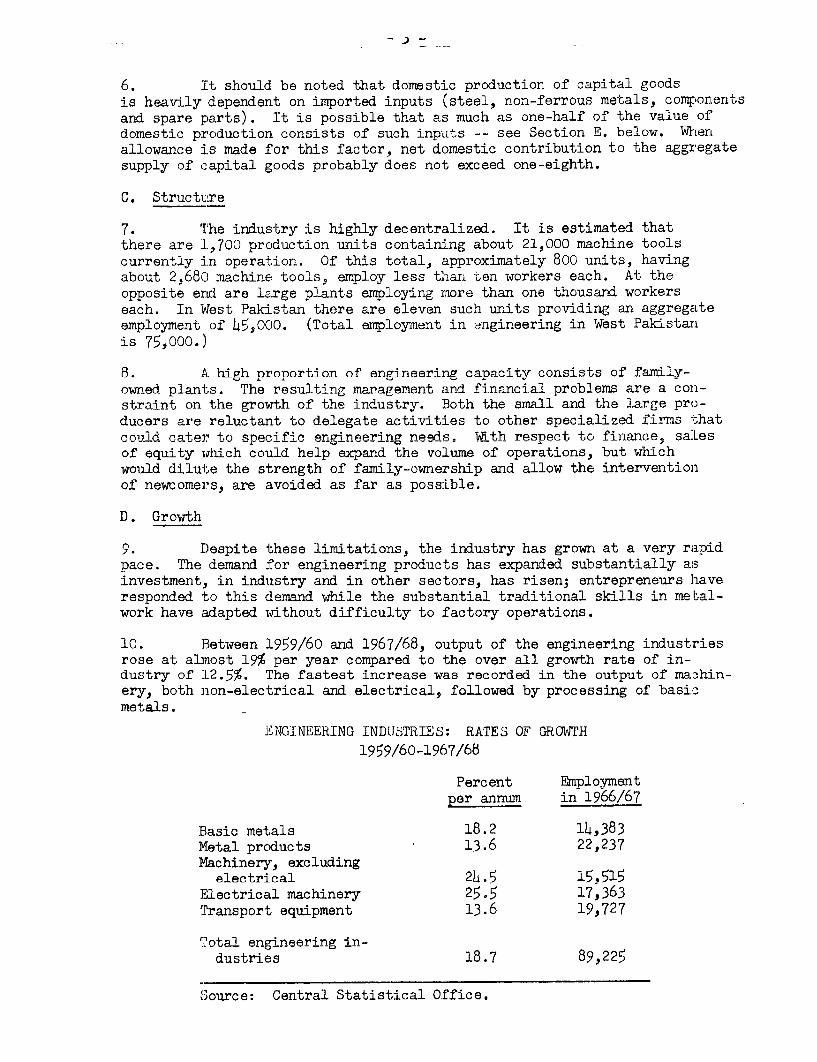

Documents

-

view

1 -

download

0

Transcript of I @f TU '-# E3 rTnf | Report No. SA -I la I II~nnUjaI~ UU - World ...

I TTR I CTED

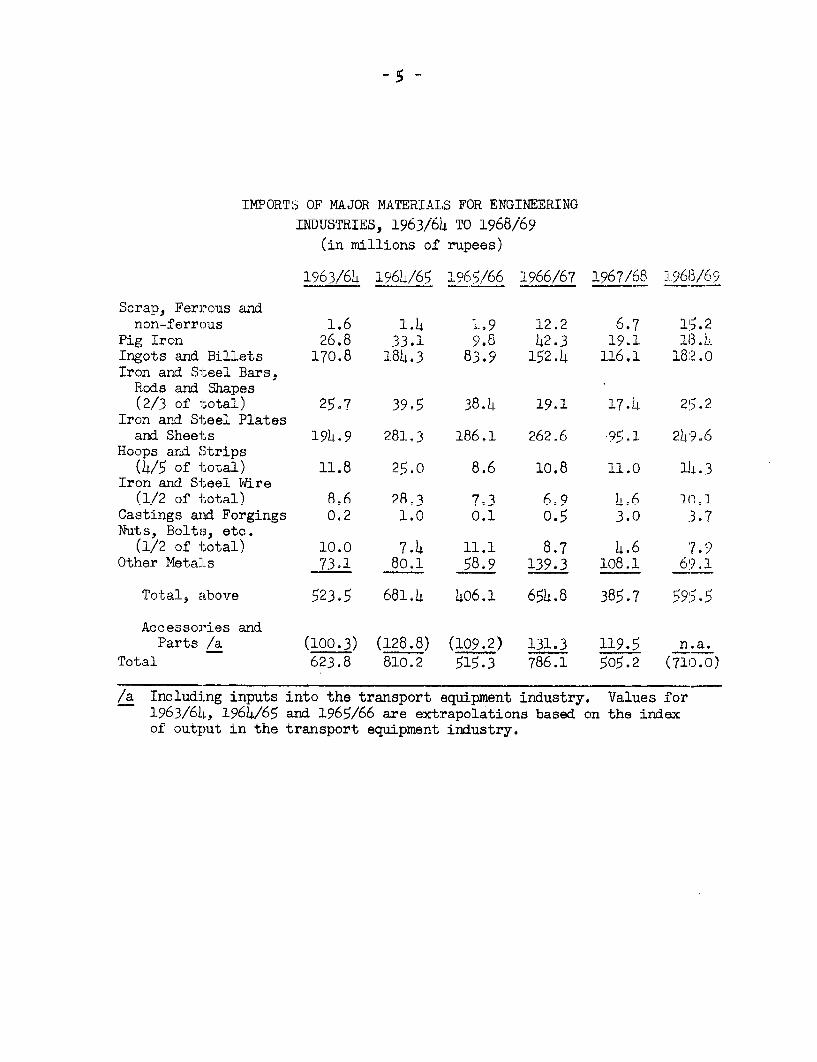

I @f TU '-# E3 rTnf | Report No. SA -I laI II~nnUjaI~ UU

IPFP n rep(

PART ONE: AGRO-BASED INDUSTRIES

PkRT I

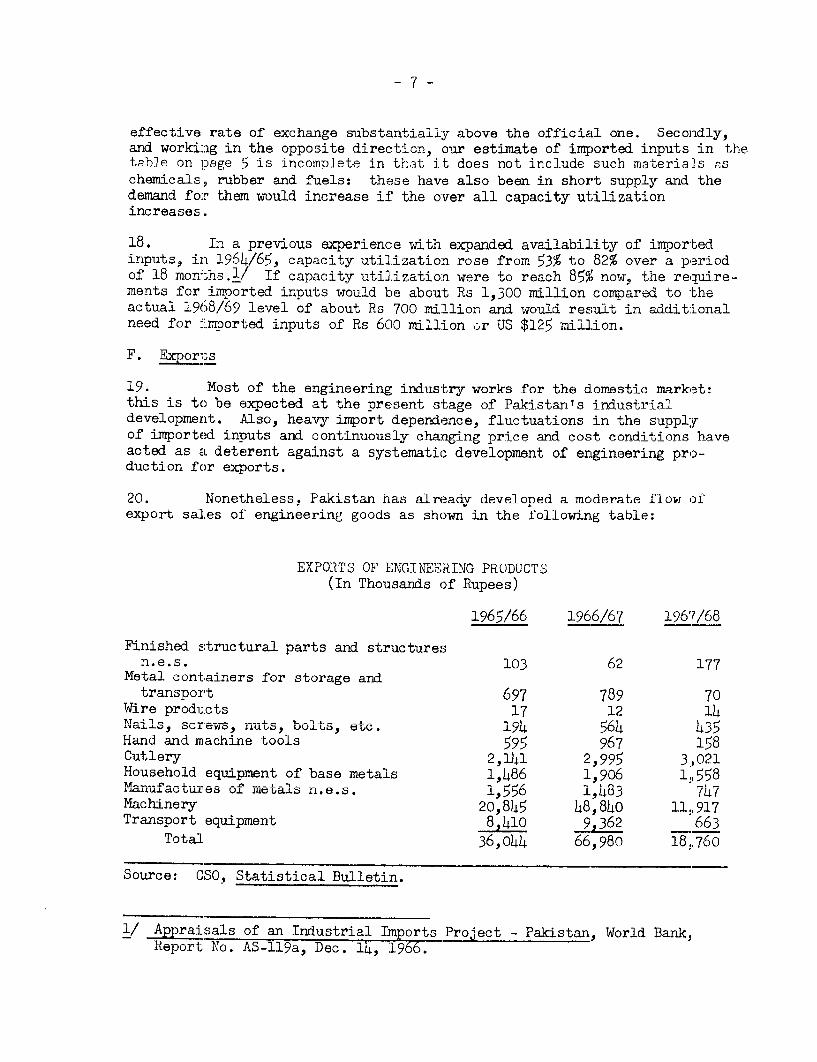

AGRO-BASED DDUSTRIES

TABLE OF CONTE\TTS

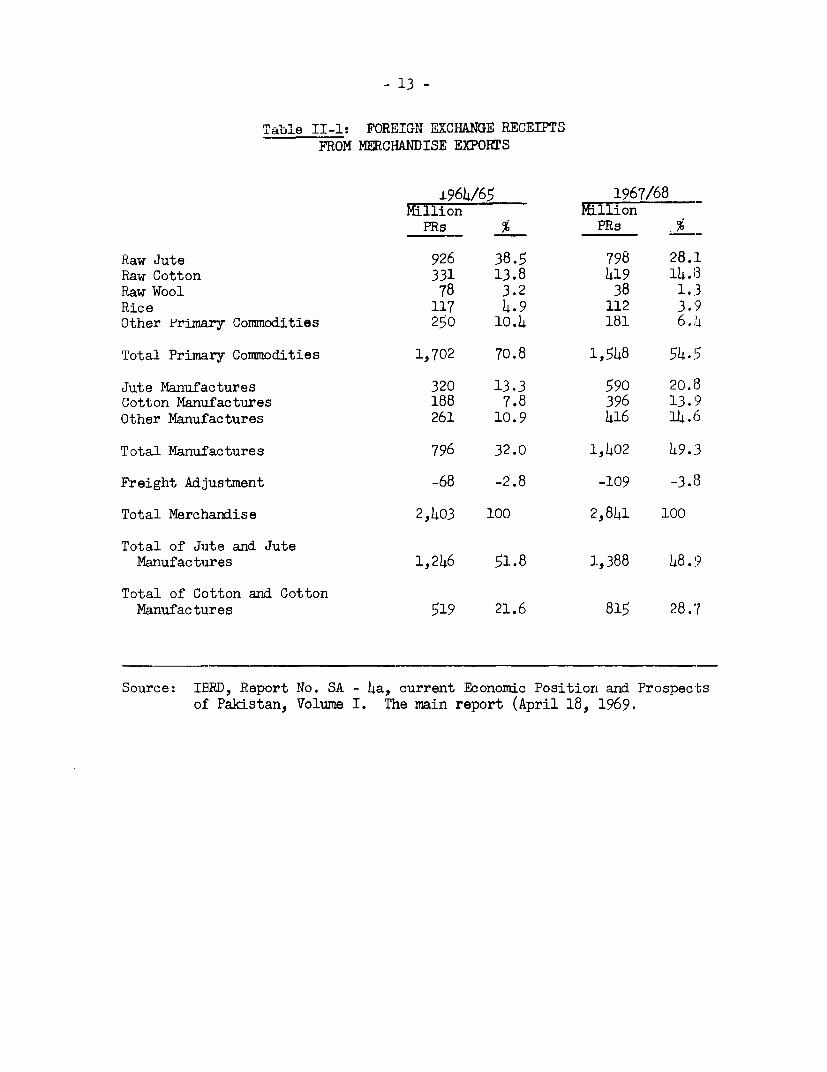

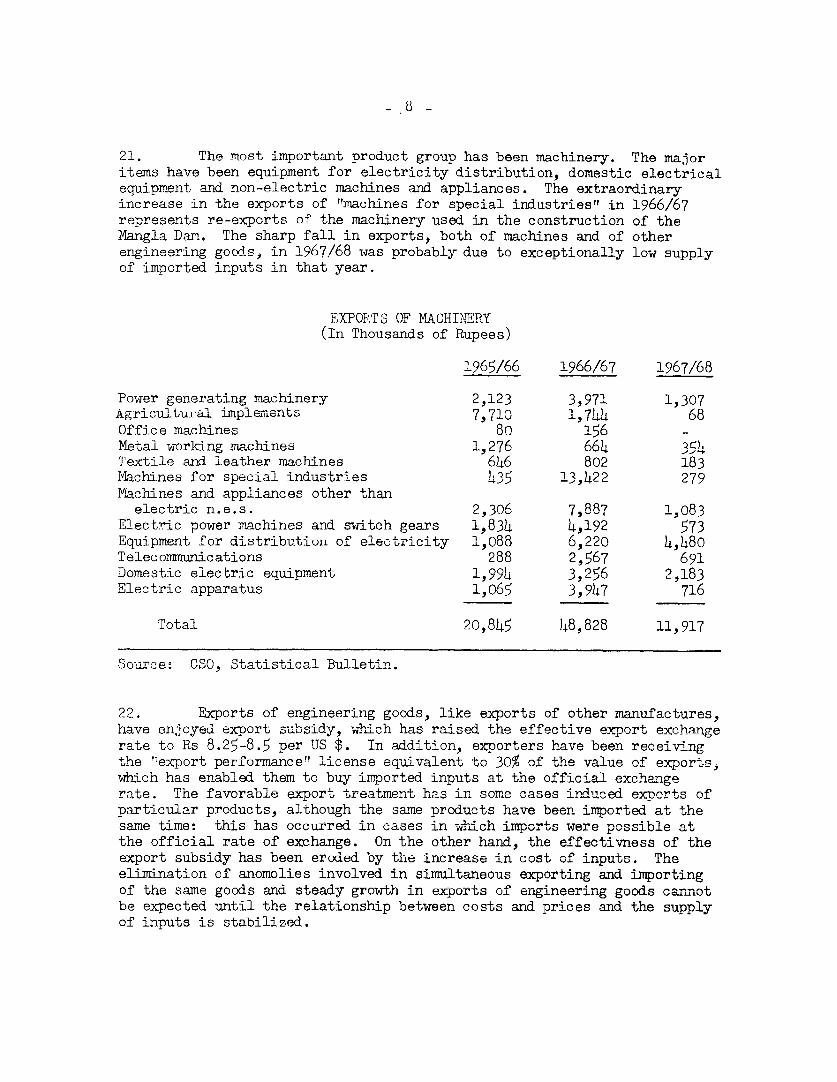

CIAPT7R T SUMMARYT

CWAPrV.- IT: TTTTr TF.YTTTF.S 7

A. Tr+.oduti+.o -n 7B. GrowthC. Pr ces, "osts and Profitaility 1.0D. Problems of the Industry l1

CHAPTER III COTTON TEXTILES r2

A. Introduction 22B1. GUrtVULh -

C. Prices, Costs and Profitability 25V. Problems oLf UiIndu.-

E. Conclusions 2

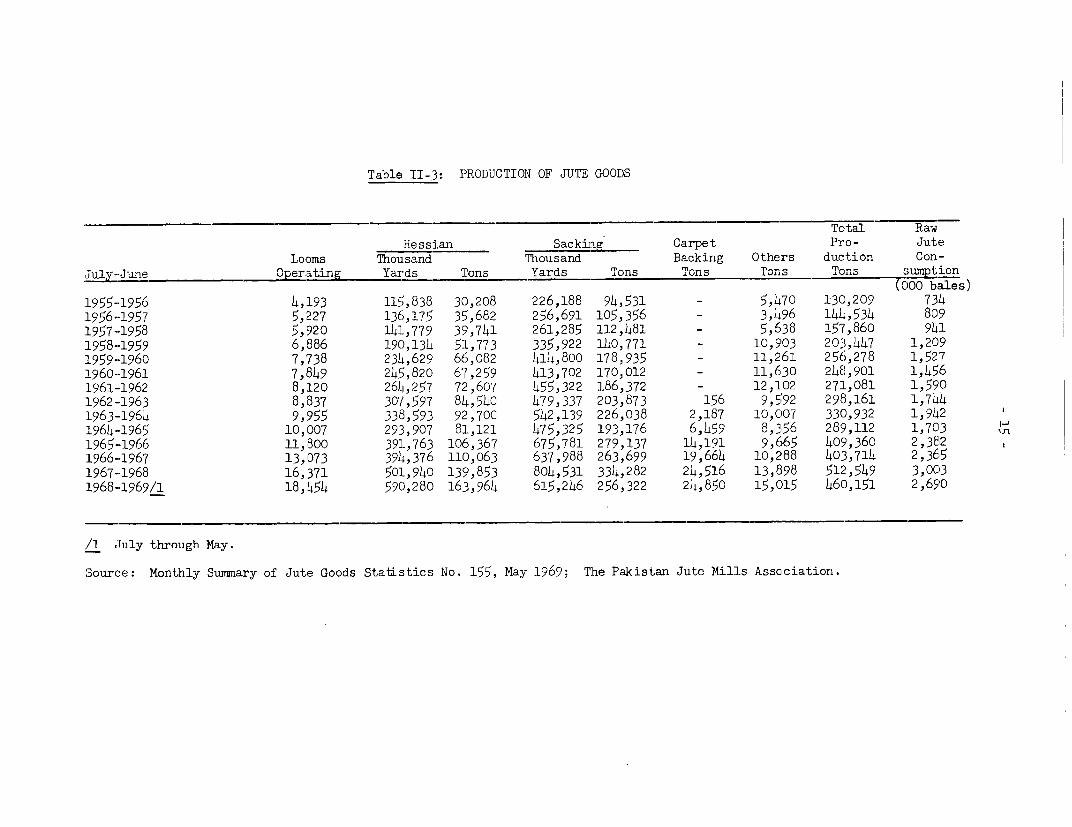

CHAPTER III COTTON GINNING 36

A. Introduction 6B.D Currernt SituationC. Problems of the Industry as They

Relate to the National Economy _'D. Recommendations ;37

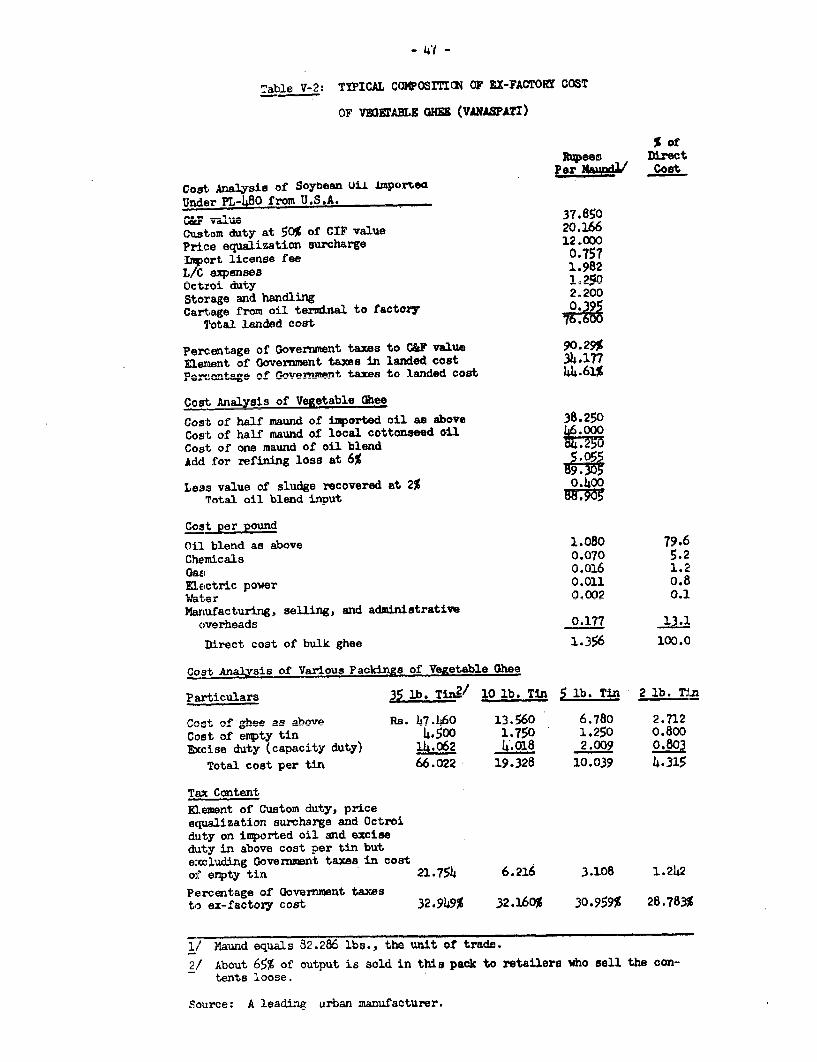

CHAPTER V VEGETABLE GHEE (VANASPATI) La

A. Introduction IlB. Past Growth LC. Prices, Costs and Profitability 142D. Investment 43E. Problems of the Industry 43F. Conclusions and Recommendations 4

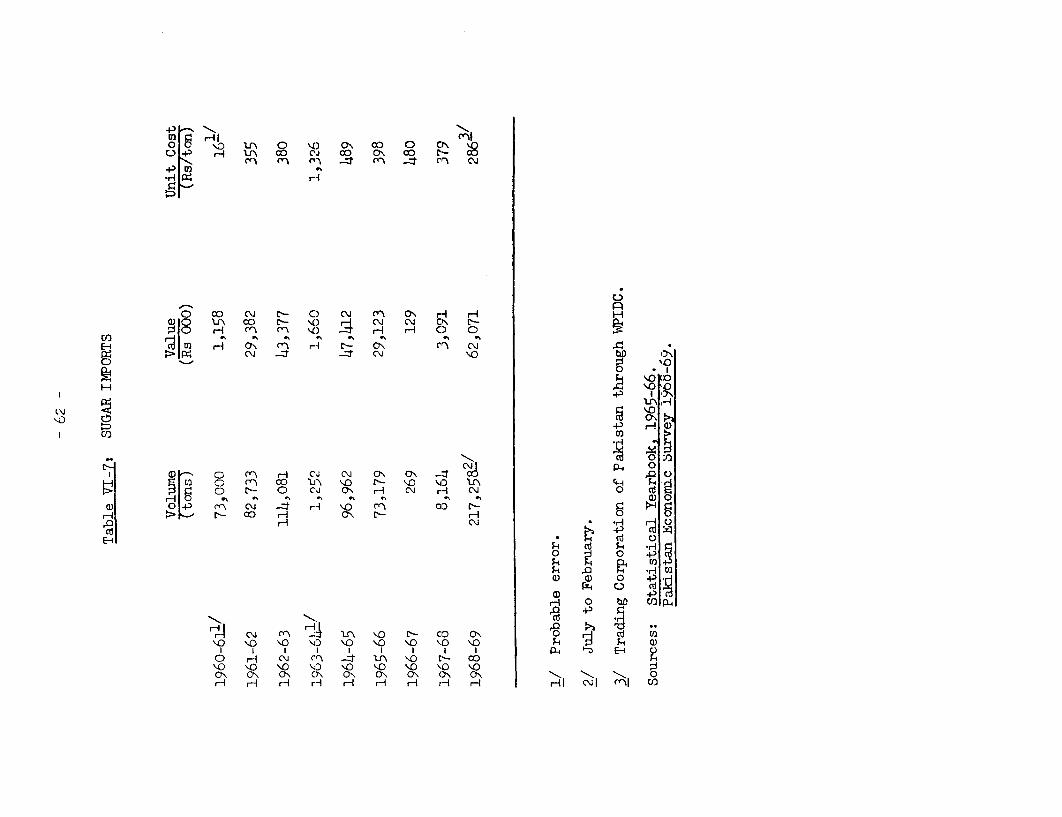

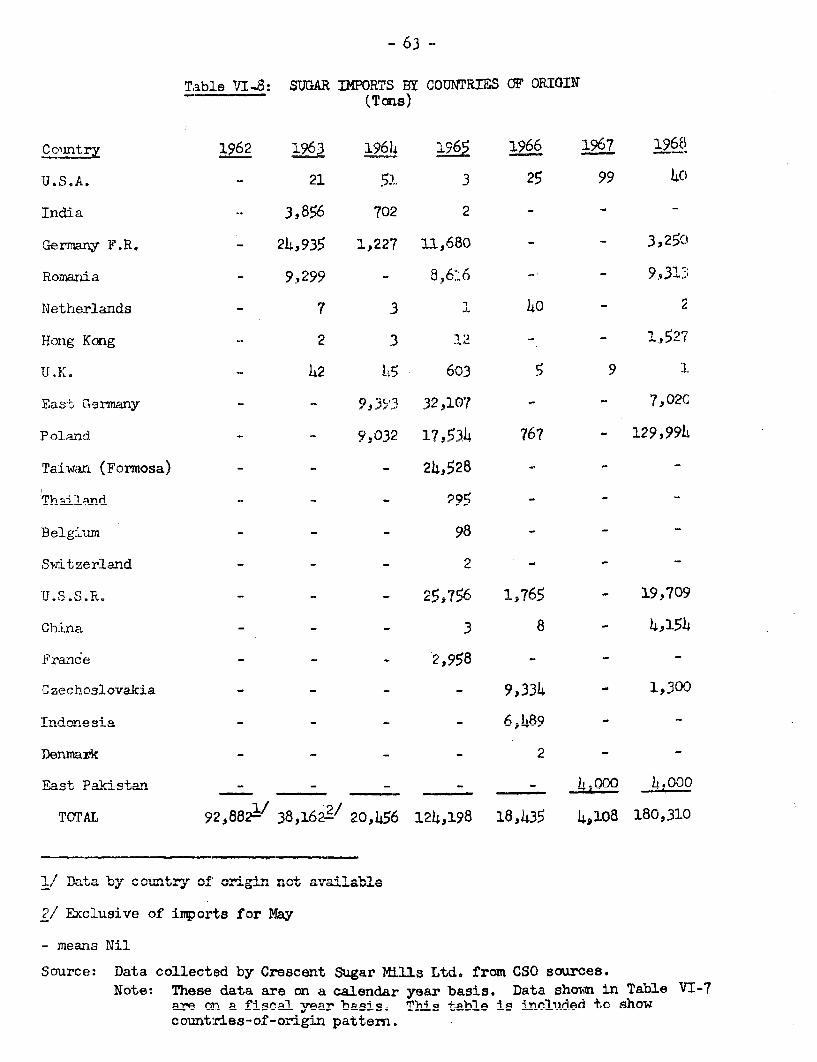

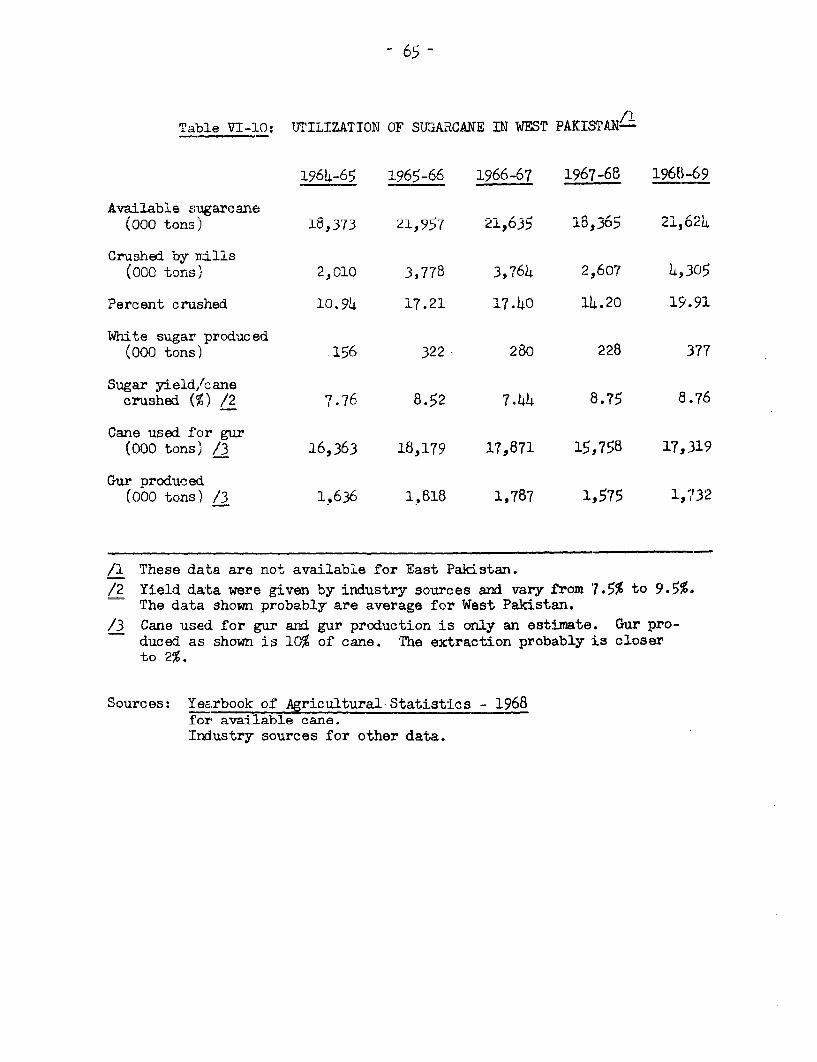

CHAPTEK VI SUGAR 4'

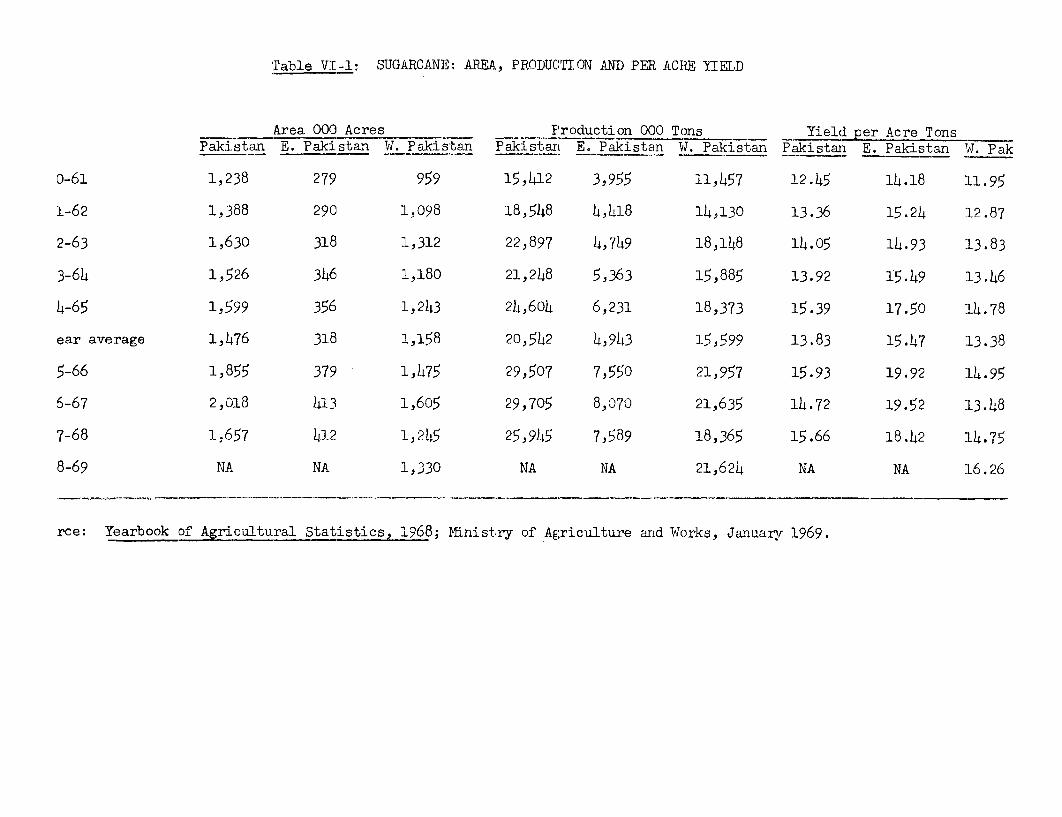

A. Introduction 9>B. Past Growth 50

(a) East Pakistan 5u(b) West Pakistan

C. Prices, Costs and ProfitabilityD. Problems of the Industry 52E. Conclusions and Recommendations 54

Page

CHAPTER VII SEAFOOD FREEZING 66

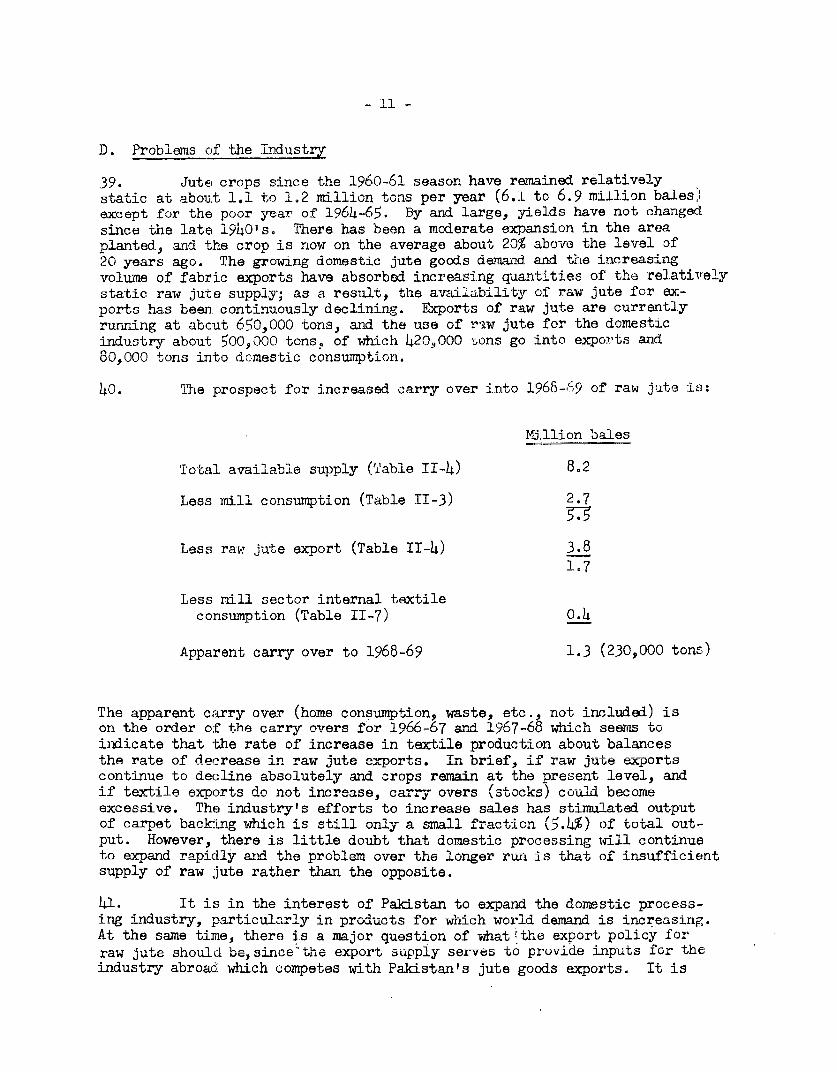

A. Introduction 66

B. Past Growth 66

C. Prices, Costs and Profitability 67

D. Problems of the Industry 67

E. Conclusions 69

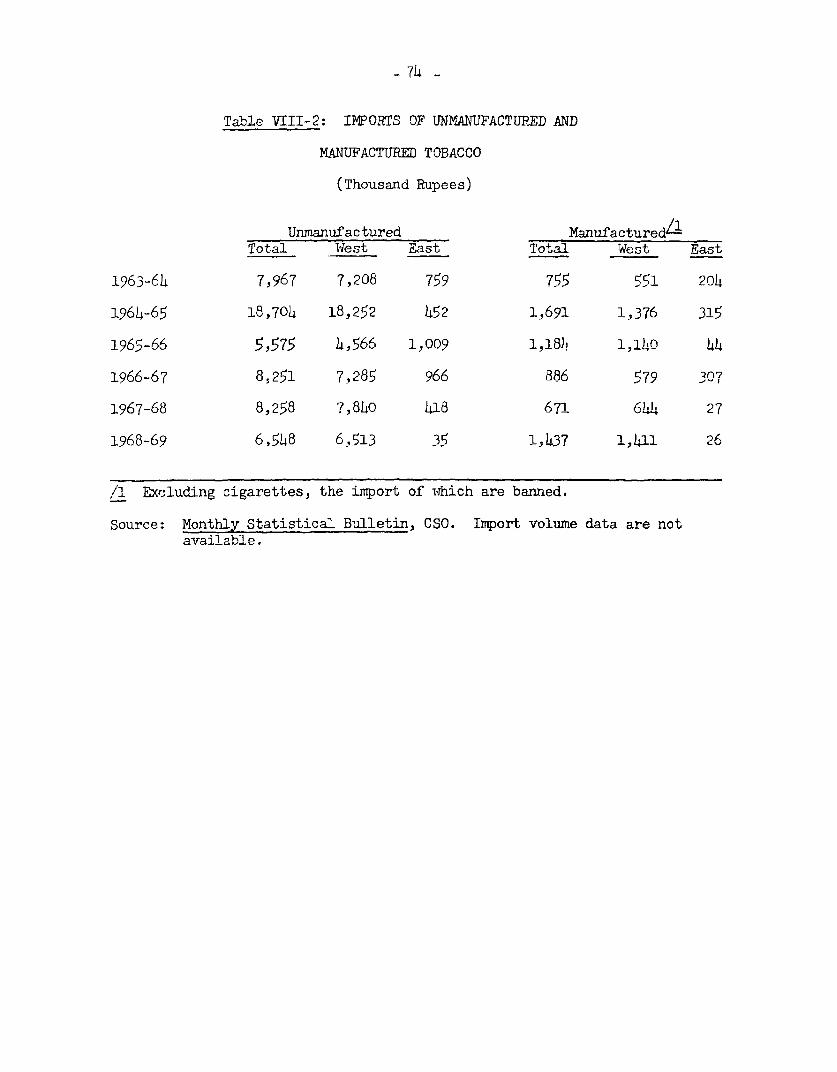

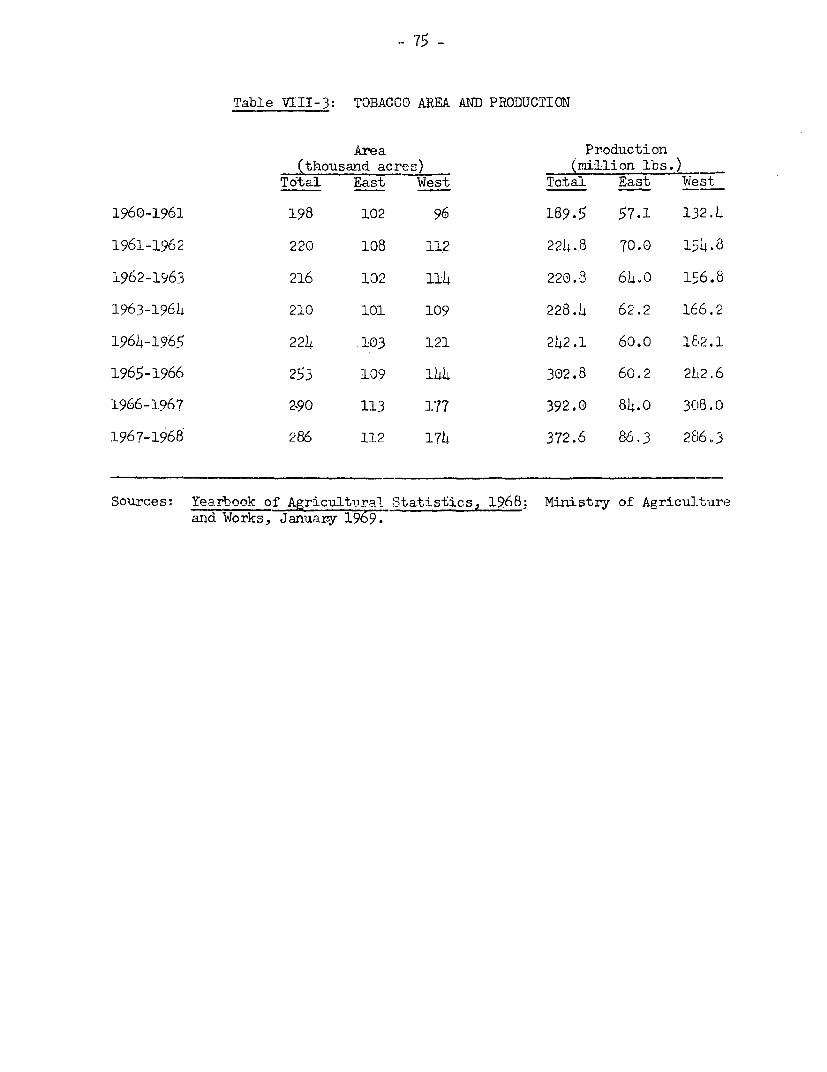

CHAPTER VIII TOBACCO 70

A. Introduction 70

B. Past Growth 70

C. Prices, Costs and Profitability 74

D. Problems of the Industry 74

E. Conclusions 75

ANNEX I ESTIMATE OF APPARENT USE OF COTTONSEED OIL, 1967/68

CHAPTER I

SUMT.rARY

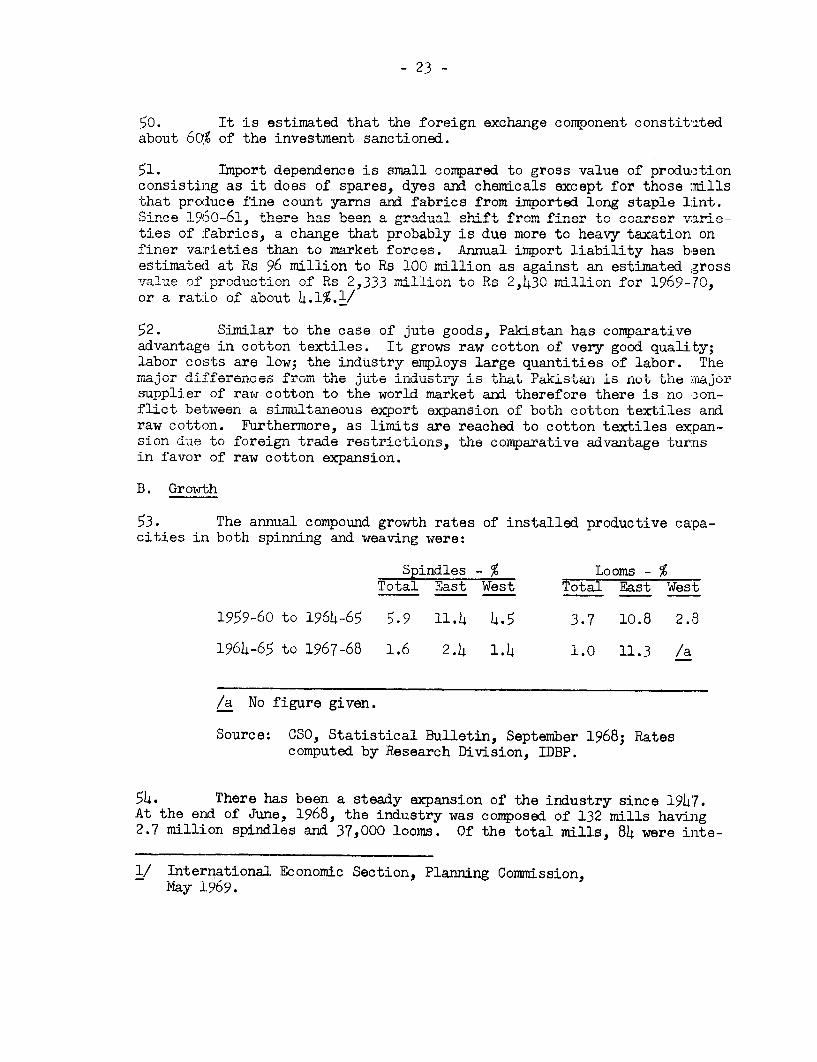

1. This section analyzes the problems and prospects of agriculturs-based indust.ries in Pakistan. It is essentially based on a sample surveyof some 40 plants of varying size and producing different products.

2. Th.e objective of the survey was to obtain within a limited timean understanding of the major problems in the agro-based industry sector. Theindustries considered important in this sectcr are:

Jute and jute manufacturesCotton and cotton textilesSugarVegetable aheeCotton ginningSeafood freezinzWool and wool manufacturesLeather tanning and manufacturesTobacco and manufactures

3. This is quite a formidable list and it has not been possiblewithin the time limit to deal with each in great detail. However, theindustries considered to be the most important in the agro-industry economyare di sc1sed in some detail in the chapters that follow.

4. Agro-bhasd industries dominate .the present industrial structureof Pakistan. They account for 64% of industrial employment and 63% of valueadded in industry (see Table I--1) -

The advantages of agro-based industries in Pakistan are avail-ability of domestic raw materials at prices comparable to those in otherprimarv producing coulntriA- labhor intensi veness when em.ployment atthe cultivation stageis included, low labor costs both in the production ofprimary inpu.ts and in processing anl, except fo- capiual plant, a small importdependence consisting largely of spare parts and secondary processingm.aterials. ValUe ad.(ed iS substantial since proces1ng 1s performed onlow-cost resource inputs of which some are by-products of other primaryproducts (motton seed bagasse, n qolasses, and lin+ers). Their produrtshave a large internal market. External markets are available, but under

constraints bo a certain poi- foxeign obs-cles Lo threatento become prohibitive.

- 2 -Table I-1

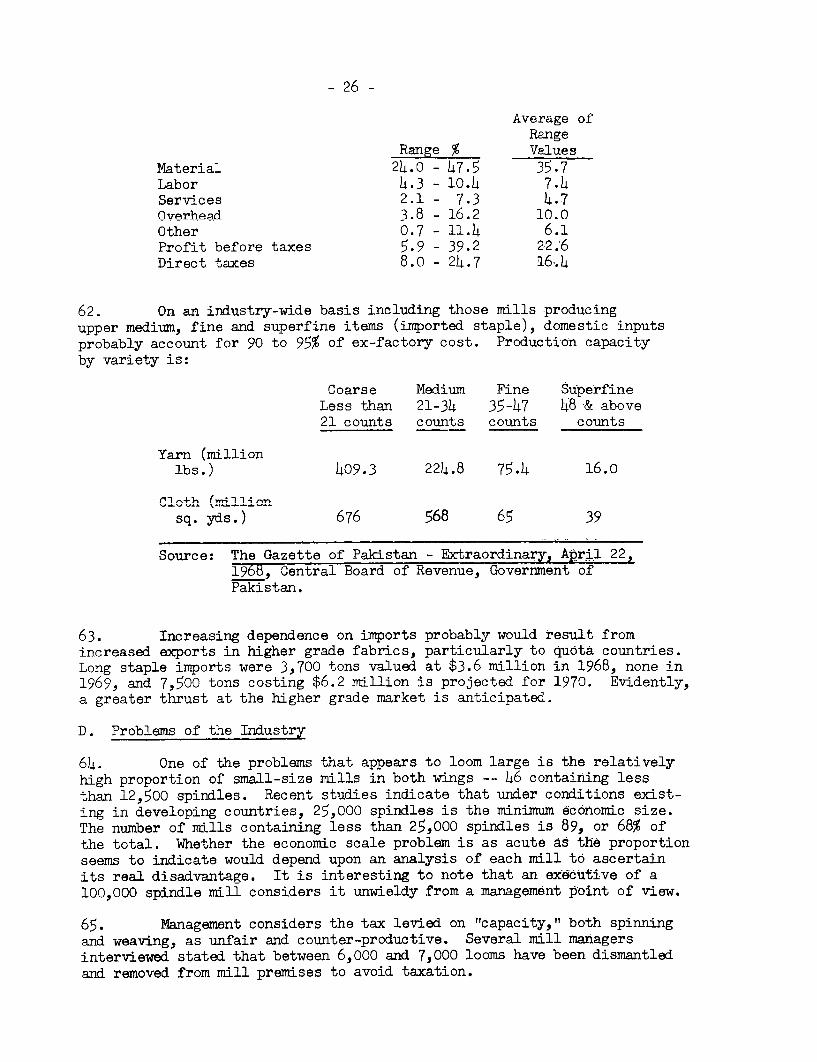

COMPARISON OF MAJOR AGRICULTURE-BASEDINWUSTRIES WITH ALL MAN-UFACTURING, 1966-67

(Million Rupees)

Employ- % of Total Gross Value % of Total Value % of Totalment Agro-Based of Agro-Based Added Agro-Based(to0o) Industry Production Industry Industry

igaF rfactori Rs

and refineries 23 6.1 773 11.0 437 14.9

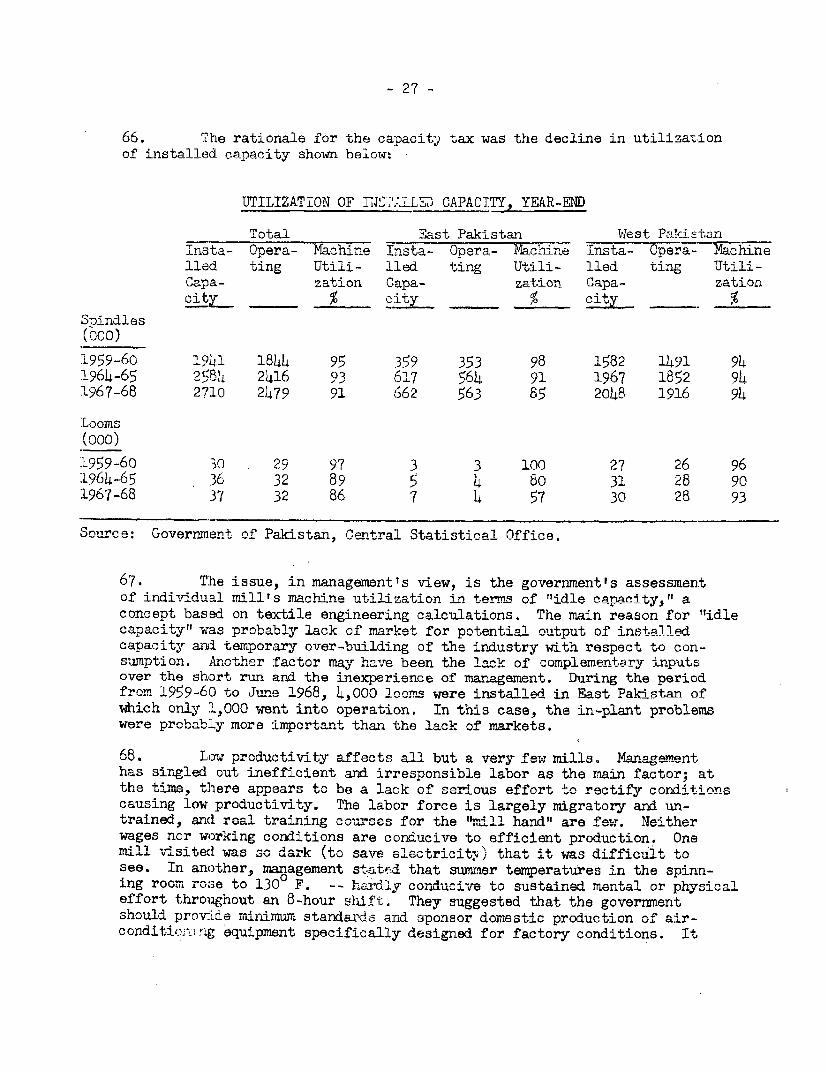

Edible oils and fats 6 1.6 599 8.5 146 5.0

Tea factories 10 2.6 445 6.3 198 6.7

Cigarettes 9 2.4 613 8.7 384 13.0

Cotton textiles 167 44.3 1,797 25.6 888 30.2

Woolen textiles 6 1.6 90 1.3 33 1.1

Jute textiles 82 21.8 768 10.9 339 11.5

Carpets and rugs 3 .8 20 .3 8 .3

Dyeing, printing andfinishing textiles 6 1.6 74 1.1 29 1.0

Footvwea~r, excep'trubber 3 .8 33 ,5 10 .3

Footwear, rubber 5 1.3 93 1.3 33 1.1

Pulp and paper board 8 2.1 181 2.6 89 3.0

Leather tanning andfinishing 7 1.9 171 2.h 43

Cotton ginning 1 4 4z 1-3.4 85 2

Jute pressing F 7 21 v '2

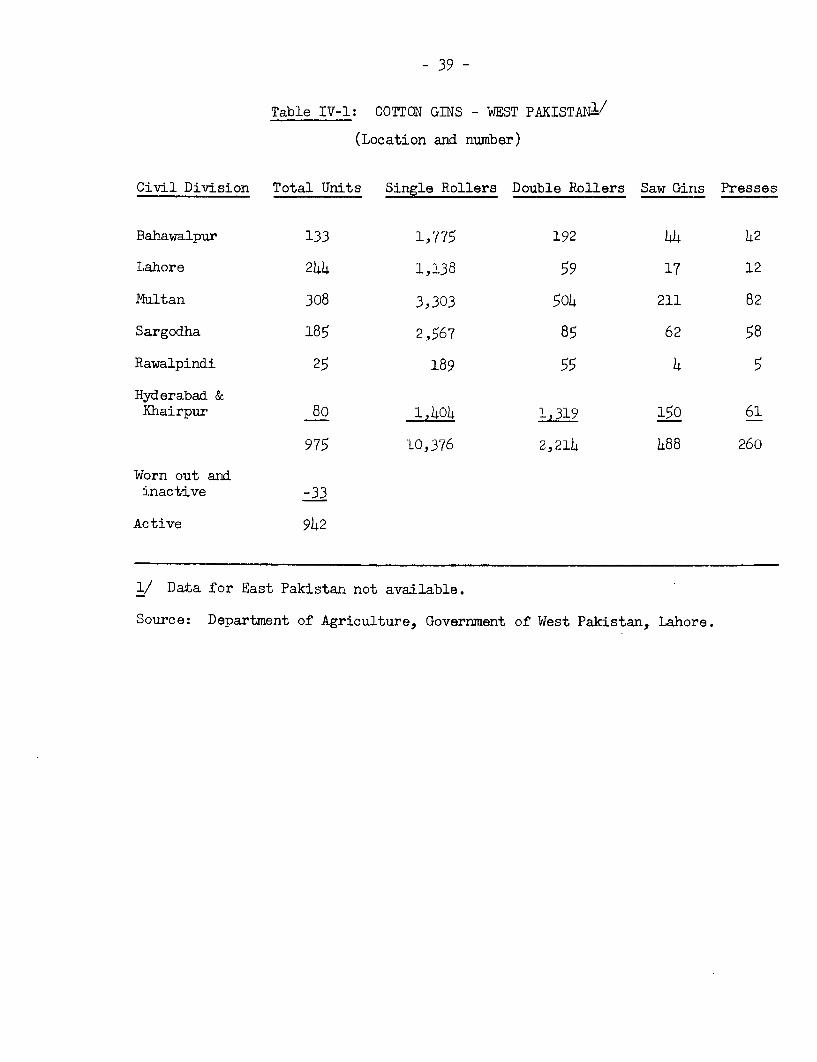

Total above 35O 92.8 6,17 97.0 ,791 94.8

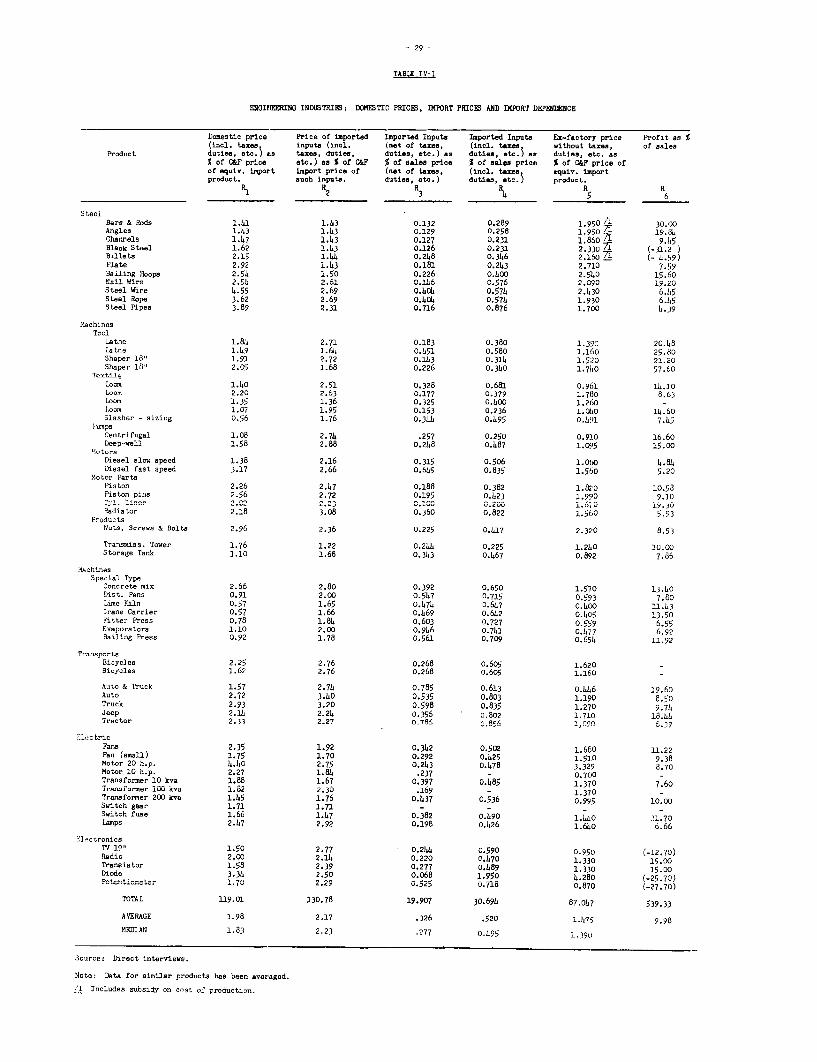

All Manufacturing 587 1l,352 4,664

Total AgricultureBased Industry: 377 7,028 2,944

as % of allmanufacturing 64.2 61.9 63.1

Soarce: GCensus of M--UP.factures International Econoindr Section,Planning Commission, y 17, 1969.

6. Investment in the industries is substantial, with foreign ex-change outlays accountin.b for abcut 50% of t-'Gotal- cos't. Tv-Lh recurringannual import requirements and annual external debt servicing constitutingsmall foreign exchange costs of production, the agro-based lndustries' out--put, appropriately priced, produces a benefit that ranks high in comparisonTr.rt;+h other rmanufacitaires notu based on iien-sprimu-n-y materlails.

7. The problems of particular interest tG the riassion were capaci1tyunder-utilization, costs and prices, impact of the bonus system and tariffs,raw materials supply, producti-v-.ty and labor efficiepcy. "Agro-basedindustries" is a conglomerate nomenclature covering widely disparate enter-prlses and in .ost of their problems there is, no inter-relation. Forexample, labor productivity in the cotton textile industry is a major

-mI:, Ls notL- so signtficant in the sugar, ghee and tanning indus-tries where -the mnajor problems are raw material quality, price and supply.

8. The country's agro-based industries fall into three categorieswith regard to output end -use: la) those that are largely export-oriented(jute goods., carpet wool and carpets, fine leathers); (b) nmixed domisticand export-oriented (cotton textiles); (c) totally domestic-oriented(sugar, ghee). Their finished product prices are only marginally highert-an unose of comparable imports if the prices of the latter are not dupn?,distress, or otherwise subsidized by country of origin and do not requirea high degree of protection. The major exception is sugar. Certaindomestically oriented agro-based industries sometimes compete with importsun-der special and peculiar conditions.

9. The principal objective of exchange policy (bonus exchange ratesystem) as it affects manufacturing was to raise the effective cost ofcompeting imports and to maintain the profitability of exports. Thepolicy, in general, has succeeded admirably and has contributed to thehandsome earnings of the export-oriented cotton and jute textile industries.Since the irnport content of production in these industries is low, theoperation oi the system has not affected them significantly on the importside even though the C.I.F. cost of imports is on the average about doublethat at the official rate of exchange.

10. The impact of the bonus system was perhaps more profound on thecotton textile industry than any other in the sector. Exports have beenextremely sensitive to fluctuations in the bonus rate. It can be arguedthat the boinus was the prime stimulant to the export orientation of theindustry ancl the basis for its high profits. The behavior of cottontextile exports in relation to fluctuations in the bonus rate raises somequestions: (a) does the industry depend solely on the export regime forits profit or nearly so; (b) is the industry excessively subsidized and canit actually meet competition in overseas markets at a reduced export sub-sidy rate; (c) is there a compelling need for continuing protectionand encouragement to an in(lustry now appi oaching middle age; (d) shoulclnot some of the benefits of the bonus system be extended to the producersof primawry inputs to the extent that their production needs encouragement?

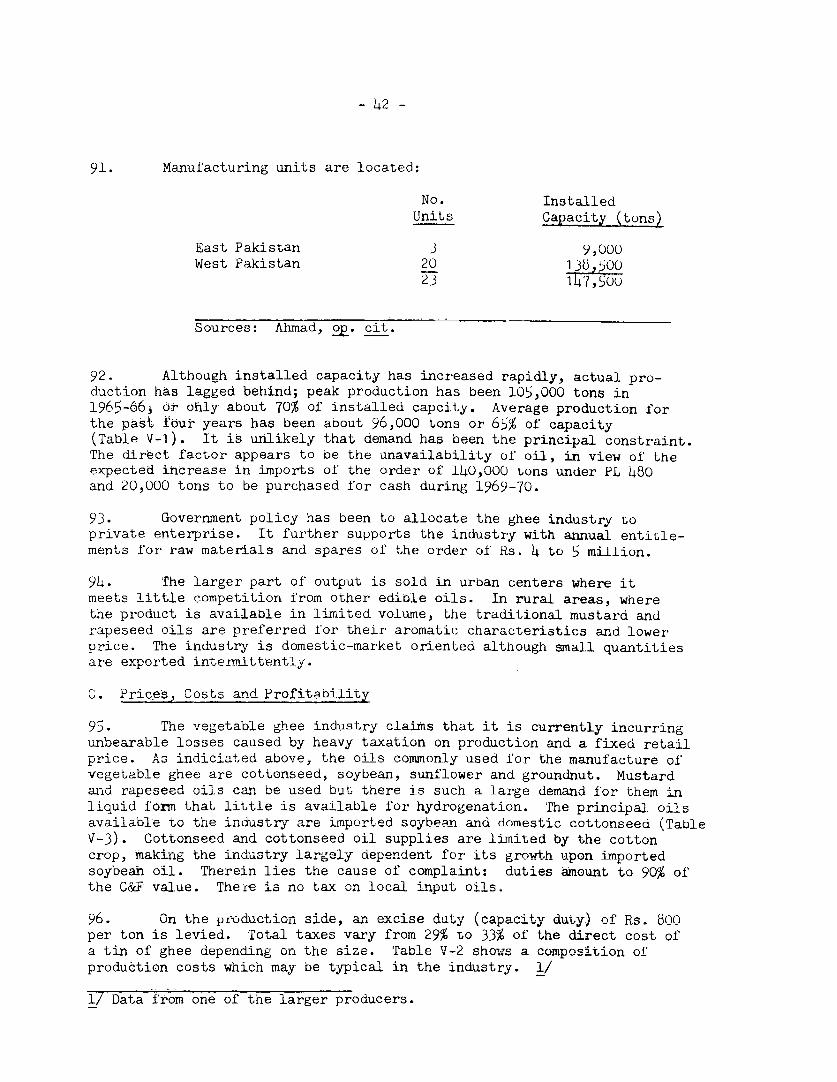

11. A special problem has arisen in the industry as a result of the

recent increase in Mwni;mm wages for uinskilled labor. The largest

employers in the sector, jute and cotton textiles, report that the labor

cost componer.t in the sales price averaged about 10% and 17% respectively.

In the jute textile industry, about 40d of the labor force is classified asuns1killed, axd in the cotton textile industry- about 30%. In the other

industries in the sector, the ratio is roughly 33% unskilled. On an industry--.ide basis, replies to the Mlssion qiuestionnaire suggested that about one-

third of the labor force would benefit from the wage increase in varyingamo-unrts. Although the quantitatiye bhasis for evaluatina the absoluite in-

crease in labor cost and its effect on production costs is not available

to the Mission, it would appear that it will be moderate.

12 * The question of price ntsrovflen for agricult1ral inputs

should be considered from several points of view, industry by industry.The sugar irndustry in both East and Wlest is disadvanta-eA b- low sucrosecontent in cane while at the same time enjoying the benefits of a ratherhigh government fixce selling price for the finished produc+. The obvious

means of raising prices to cane growers is by means of compensation related

to sucrose content. However, the schem.e was tried to the dissatisfactionof farmers who could not understand why they received higher prices at the

height of the season (w-hLen the sucrose content is at a maimwr.n) than theydid at the beginning when it was low. The only lasting solution to theproblem is a general up-grading of the crop through disse4iation of better

varieties, the extended use of fertilizer and other improved agronomicfactors -- all a long-term eflort. In the interim, it appears that theprice of sugar should be lowered for the benefit of the consumer, especially

in West Pakistan where profits in the industr-y are very large.

13. Prices paid to cotton growers could be related to the textile

industryts bonus exchange rate, while at the same time considering the

effect price changes would have on cotton textile productionr anu on ra-w

cotton exports. Since Pakistan will soon begin experiencing the restric-

tive effects of the International Cotton Textile Agreement, and sirnce raw

cotton exports are not subject to these restrictions, it would be desirable

to expanTd in the future exports of both cotton textiles (to the limit

possible) and raw cotton, and to adjust the producer prices and the bonus

exchange rate accordingly in favor of raw cotton. In the case of raw jute,

the need for price adjustment to the grower is determined primarily by the

need to increase the supply of raw jute to the domestic industry. Tne

optimum strategy in jute marketing and processing calls for a long-term

master plan in order to assure maximum benefits to East Pakistan, which in

jute processing has a unique comparative advantage.

l. Within the time available to the Mission, a reconnaissance of

the entire vegetable oil industry from farm to finished product was not

practicable. Effort and emphasis were put on the popular consumer items,

ghee or vanaspati. The principal problems of the industry are two: (a) an

increasing dependence on imported oil on which there are high import duties,

and (b) a high capacity tax. Ghee consumption in the country is in excess

of oil available to the industry. In order to minimize imports, a restruct-

uring of the cotton-ginning industry to include expanded production of

cotton seed oil is discussed in detail in Chapter V. Implementation of

the proposed scheme by concentrating cot-o..n seed crushiing facilities inthe cotton growing areas wouldserve to reduce the prevailing excessivewaste of po"ential cotton seed oil resulting from spoilage ard would alsoreduce transport costs.

15. Pulp and paper industries are located in both wings and arebased on different resources in each. In the East, the primary rawmaterials are wood and bamboo. In the West., primary inputs laroelv arewaste or by-product materials: wheat straw, liriters ard cotton mill was-,eThe demand f'or paper has been continuous-1r _., -l at rt cjrImo,oa-d rateof about l0,' annually. Projected demand for 1974-75 is about 190,000 tonswhich poses a problem of raw mater:al sunply. Wood soiirces in rite East cansupply only the existing newsprint mill; baxrC.oo in the northern area of "-theChittagong Hill tracts is comiitted to excisting mills, lea.ing the untapprclbamboo growths in the south as the so-urce of supply for the proposed newmill. In the West, wheat straw ard ntb r4rmiaterials are i n -lentifUl supplyfor the existing strawboard mills i-.- probably enough would be availablefor considerable future expansion.

16. An .Lho ugh the potenttial supply of bagasse for paper 4aing islarge, the material by itself makes an inferior quality, low strengtthpaper of limi ted usefulness nlless blended with long filore woo pulp jhj-c_would have to be imnorted. For future pulp requirements above local re-sources, consideration may be given to a joint ventuWre to tap the world! .most extens:ive bamsboo groves in Burma's Arakan region which is adjacent toEast Pakistan7s souther.n hborder.

17. The contrTs woolen iMclustry has been expanding ara recently iasentered the high-grade, machine-made carpet field. The industry, whichincludes wool scouring for export, textile production and carpet making,is import dependent for apparel wool, the local variety being too harsh intext.ure for -arment- Expor4s mad4e entirely of local woo' have a cost art-vantage over those made from imports (which are purchased against bonusvou h.es, +e p m onUq nh-r .eIr n 150 bo nLU0%) whlch places theindustry at a disadvantage relative to other exporting countries. However,receipts through the bonus market (Up to 7%4 of exchnge surrenderedoperate to permit exports.

18. The incentive policy for stimulating industrial growth appears tohave worked well in general. Ho-wever, it has resulted in some uneconomic.locations; cotton seed crushing plants nearly a hundred miles from growingcenters is nMre cri-L±±cal examirnaion of the external andinternal dis-economies engendered by unadvantageous locations appears tobe in order before grnting tax holidays as an incentive.

19. A seos problem confronting manufacturing inwustries which dcnot have the:ir own electric power generating facilities (most of them) isthe frequent and sometimes lengthy power outages. An estimate of produc-tion loss value is not available but it is safe to say that over a period.Of years it probably would be more than the cost of rehabilitating aninadequate distribution system.

20. Growth in the sector has been most impressive. The resultsfrom large expenditures for capital eqquipr±Ent ha-ve been most gratif-yiLngin terms of the industry's contribution to GNP. Some of the nation'smanufacturing plants installed unier previous rmulti-year plans are nowwell into their useful physical life span, and a few are outdated tech-nologically. The focus of development naturallyy is on new plants. Itis suggested that in the forthcoming Fourth Plan the necessary resourcesalso be directed toward replacement, rehabilitation and modernization ofexisting productive facilities which would raise productivity at a re-latively low cost.

CHirTER II

JUTE TEXTILES

A. Introduction

21. Jute and jute products are the country's leading foreignexchange earner accounting for receipts of Rs 1,388 million or 49% oftotal mercharndise exports in 1967-68 (Table II-I). In the same year,the crop was grown on 2.3 million acres ih the East (none in the V§st)pre-empting about 10% of the total cultivated area and yielded 6.7million bales or 1.2 million tons. For the period, the 56 mills (52in the East, 4 in the West) in the country nroduced 513,000 tons ofgoods (42% of raw f'ibre produced) valued at Rs 740 million. 1/ Theindustry consumed 535,000 tons of raw jute costing about Rs 470 million.,Value added. amounted to Rs 270 million. The industry employs 79,700 inthe East arnd possibly, 2,000 in th;e West_2/ or about 13% of aggregateindustrial employment.

22. T'he jute industry, and the associated production of its maininput, raw jute, is of critical importance for East Pakistan. Rawjute is its main cash crop, and jute manufacture the main industry, pro-viding 43% of industrial employment in the region.

23. East Pakistan commands outstanding comparative advantages injute manufacturing. The quality of raw jute is high. Labor costs, bothin production of raw jute and in jute manufacturing, are low and theproportion of labor costs in total cost is large. The dependence of theindustry on imported inputs is negligible -- 4-5% of the gross value ofproduction. Raw jute is a bulky, low value product and its cost oftransport to foreign manufacturing centers is high, thus putting themat a disadvantage compared to processing facilities located in Pakistan.,

24. East Pakistan accounts for about 45% of world production ofraw jute and about 33% of world production of raw jute and allied fiberscombined (raw jute, kenaf or mesta). At the present time, less than onehalf of itv domestic production of raw jute is processed into manufactureswhich are then exported: the share of Pakistan in world exDorts of jutemanufactures is now about 25%. In the exports of raw jute, East Pakistanhas a commanding position: it accounts for about 60 of world exnorts.Consequently, the trends in Pakistan's production of raw jute and manu-factures influence to a substantial extent the supplv nosition in theworld jute economy while the world demand trends directly affect theeconomy of East Pakistan.

25. The combination of a uniaue comraqrative advantage position inworld production of jute goods, scarcity of alternative employmentopportunities at the present time, and the very large share i-n u orld

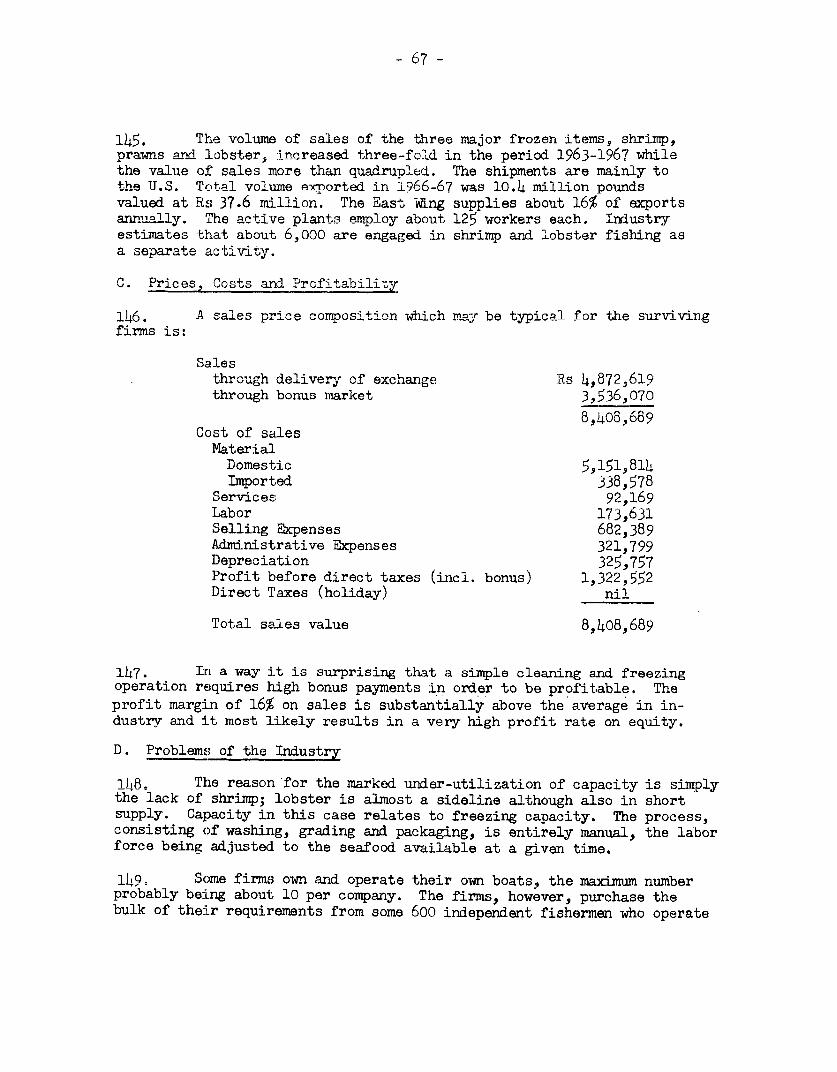

11 The value given is estimated on the basis of the average ex-factoryprice of product mix Rs 1,442 per ton given in Section C.

2/ Director of Labor, Government of East Pakistan. No data are avail-able for the West. Figure given is an estimate.

production and trade in raw jute and jute goods, poses a special problemof policy planning for the government. The situation is conplicated furtherby four additional factors. World demand for jute goods is expandingrelatively slowly and is exposed to serious threat by synthetic substitutes.In the world supply of jute goods, Pakistan faces competition of the oldestablished European industry and of the large jute industry in East India.The supply of raw jute is highly variable partly because jute competes with ricefor land and labor; the introduction of IRRI rice, with rmuch larger yieldsper acre, may adversely affect the long-run attractiveness of jute growingunless larger yields are offset by lower rice prices or jute yields improvewithout a corresponding fall in the jute price. The world jute economyis characterized by extremely sharp fluctuations in price caused by out-put variations and by cyclical changes in demand for consumption and forinventories. These price fiuctuations, in turn, make production planningvncertain, discourage supply and stimulate the switch to syntheticsubstitutesi, thus ireducing demand.

26. In the past 10-15 years, the problem of planning in the juteindustry was simpler than it will be in the future although the problemslisted above have been present. East Pakistan was then only establishingits jute goods industry. By the mid-1960's, however, the first problemsemerged: there was excessive expansion in one key product line (sacking)which led to subsequent shut-down of capacity, while the most profitableline -- carpet backing -- was neglected. For the future, the problemswill increase in complexity. A master plan is needed for the developmentof the jute industry within the framework of an over-all strategy coveringalso production and marketing of raw jute. Such a plan could then hope-fully be integrated with a similar plan prepared by India and also byThailand. While the difficulties in preparing such master plans are greatin view of the complexity of the problem, and the difficulties of inte-grating the plans cannot be overestimated, there is little doubt that onlya systematic international approach to the jute problem can yield optimumresults. East Pakistan and West Bengal are probably the poorest among thedeveloping regions, with a severe imbalance between population and resources.A satisfactory solution of the jute problem will not solve their over-allproblem of growth and welfare, but its contribution to it may be significant.The alternative is a cut-throat competition between Pakistan and India dueto over-expansion, from wlhich both countries will suffer badly over theshort run: while over the long run, they may end up by having a mirch smallerjute sector than today, with a corresponding curtailment of employment andincome all around which neither country can afford.

B. Growth

27. Growth of the jute textile industry is a tribte to the deter-mination of a people to industrialize the country's most important non-foodcrop. yi Tnenienc-e left Pakihsta.n with a wrell established cash cr- ofsignificant volume and value and no means of conversion to textiles: thesole means of exchange realization was to export the crop to those withestablished mills or to those who were constructing facilities largelyfor their own internal needs.

-9-

28. The area cultivated and produc-.ion of raw fibre has remainedrelatively static. except 'or bad crop years; for the 20-year period1947-48 through 1967-68 (Table II-2). From the early rmills of the 1950 s,productive capacity has risen to 22;771 loomsn in 56 mnills FTr'om a totalof 130,209 tons of textiles in 1955-56, production in 1967-68 rose to512.549 tons, an annual compound growth of 12.2% Tn 1967-68, minlTIutilized 415% of prcduction of raw jute (Tables II-3 and II-4)¢ 1/

29. Jute textile exports amounted o Rs 600).1 million in foreignexchange earnings in 19671-68. The major b wers fere East Africa-) LUS.A,Australia, West Africa, Turkey ancd the U.K., in that order. These six,out of more, thcan 50 imPort-ing cou-intries, absorbed about 71< of totalexports in 1967-68.

30. Beginrnng in 1962, the industry entered the market for carpetbacking utili zd bvy the burgeonin- tufted carpet induSt~ry. The growth cfexports was phenomenal from 1'56 tons at the beginning to aoout 25,000 t.onsin 1968-69 (Table TT_I-. The prospect of capturing a sig-i.ficant share ofthe market promoted sanctions for the installation of 3,010 broad looms ofwhich 1,522 currently are eith- o-erating, installed but not operating, oron order (Table I-4). Assumning that the 685 now installed produced the2.8 thousand tons sho. n l T- uu.t per oom was 36 tonIs. Or.!that basis, t1he 1,522 looms that are intended to be operative in theirnmediate future would produce 54,500 tons, or 220p of 1968-69 exports.Total sanctioned looms would produce 108,000 tons or 436% of currentexports. Although the available raw jute supply level is sufficient toprovide for such production, there may be severe pressure on market pricesif this expansion. takes place over a very short period.

31. In addition to the 52 existing mills in the country, five newmills, each containing 250 looms, and two of 500 looms each are reported.to be ready for operation in 1970 bringing the total number of mills to59 having a loomage of 25,021.

32. Implausibly, four mills having a loomage of 1,421 have been con-st-Ucted in the sWest- wing. One of the mlills, at Jaranwala, was conceivedat the time when large areas of the surrounding countryside were waterloggedan'd it wvas believed that Jute -was the only crop that would thrive. Pilotplantings proved successful and the mill was constructed concurrently withthe success u lowering of gro-unrdwater through the tube well program.Local cultivators promptly put their lands to sugarcane with the resultentdei se of the m ll.

33. Transportation exrpenses for raw material from the fields andbaling houses of northern East Pakistan via Chittagong/Karachi to the Westwing mills andl the costs of finished product transport back to Karachi forexport wouldl seem to preclude the mills from Drofitable operation. It issuggest tuat consideration be given to relocating the mills to the East.

1/ Pakistan publishes two esti-mntes of rawT Jute production, an. rfoffici4crop estimate" by the Ministry of Agriculture (Table I-1) based onsample surveys and yields and a "trade estimnateA' anparently derivedfrom consumption, trade and stock statistics which differ markedly inmost years (Table I-3). Efforts to find a consistent or explainablebias in the two series have not been revealing. See Background Noteon Jute, No. 4, Economics Department, IBRD.

- 10 -

C. Prices, Costs and Profitability

34. The average price paid for raw jute as taken from the returnsto the Mission's questionnU-aire was Rs 875 per ton. The average ex-factoryselling price of the product mix was Rs 1,442 per ton. The wholesale(export) price was Rs 1,578 per ton iI.o.b. (L 138.75). Tne average con-version cost of Rs 567 in mid-1969 compares favorably with the conversioncost in India: the latter amounted to Rs 561 for sacking and Rs 871 forhessian in early 1968. 1/

35. Excise duty is Rs 200 per ton for hessian sacking, Rs 125 perton for other manufactures. in addition, for domestic sales, there is asales tax of 15% on duty paid value, a rehabilitation tax of 1% on dutypaid value and a defense surcharge of 25% of sales tax amount.

36. Except for capital costs, imported inputs are between 4% and 5%of gross value of production. Since jute textiles, unlike cotton, are not"finished"t , there is little consumption of dyes and chemicals. Again,unlike cotton, jute is very abrasive and the wear on machinery requiresreplacement of parts more frequently.

37. The composition of aggregate sales value as indicated bythe Mission sample is:

Rs (000) %

Raw jute 30,070 46.2Imported materials 945 1. 5/aServices 2,800 4.3Other domestic inputs 271 .4Labor 10,379 15.9Selling expense 4.,256 6.5Admin. expense 2,203 3.4Depreciation 954 1.5Profit after direct taxes 6,240 9.6Direct taxes 560 .9General expense 6,354 9.8

Aggregate sales price 65,032 100.0

/a The imported input in this particular sampleis below the industry average.

38. The after-tax profit of 9.6% on sales is comparable with that inthe rest of industry; and industry in Pakistan has generally been quite pro-fitable. The application of the bonus voucher rate of 30% to jute productsexports has helped profitability. The profit margin on sales of 9.6%compares to 5.7% in the Indian jute industry. 1/

1/ Bension Varon, Indian Exports of Jute Manufactures, Problems and Prospects,January 1969 (IBRD paper).

D. Problems of the Industry

39. Jutel crops since the 1960-61 season have remained relativelystatic at about 1.1 to 1.2 million tons per year (6.1 to 6.9 million bales)except for the, poor year of 1964-65. By and large, yields have not Changedsince the latei 19401s. Tnere has been a moderate expansion in the areaplanted, and the crop is now on the average about 20% above the level of20 years ago. The growing domestic jute goods demand and the increasingvolume of fabric exports have absorbed increasing quantities of the relativelystatic raw jute supply; as a result, tle avail.ability of raw jute for ex-ports has been. continuously declining. Exports of raw jute are currentlyrunning at abcut 650,000 tons, and the use of raw jute for the domesticindustry about 500,000 tons. of which 420000 t!ons go into exports and80,000 tons into domestic consumption.

Iho. The prospect for increased carry over into 1968-^9 of raw Jute -iS:

Mi.llion bales

lotal available supply (Table II-4) 8.2

Less mill consumption (Table [I-3) 2.7

Less raw jute export (Table II-4) 3.81 7

Less mill sector internal textileconsumption (Table II-7) 0.4

Apparent carry over to 1968-69 1.3 (230,000 tons)

The apparent carry over (home consumption, waste, etc. not included) ison the order of the carry overs for 1966=67 and 1967-68 which seea,s toindicate that the rate of increase in textile production about balancesthe rate of decrease in raw jute exports. iTn brief, if raw Jute exportscontinue to decline absolutely and crops remain at the present level, andif textile exrnrts do not in-crease, carry overs (stocks) co-aid becomaeexcessive. The industry's efforts to increase sales has stimulated outputof carpet backiing Lwhiich is still only a small fraction ().4p) Of total out-put. However, there is little doubt that domestic processing wfill continueto expand rapialy and the problem over the longer r-un is that of insufficientsupply of raw jute rather than the opposite.

41. It is in the interest of Pakistan to expand the domestic process-ing industry, particularly in products for which world demand is increasing.At the same time, there is a major question of whatVthe export policy forraw jute should be, since&`he export supply serves to provide inputs for theindustry abroad which competes with Pakistan's jute goods exports. It is

- 12 -

in Pakistan's interest to attract foreign manufacturers of jute goodsto invest in the development of Pakistan's lute goods industry, thusminimizing competition in jute products and benefitting to the maximumfrom foreipn experience in technioues of nrodur.tion; m, nmgm,ent n nrimarketing. At the same time, Pakistan cannot stop exporting raw jute aslong as other nroducing c-oiuntries are nrepared to supply jute or alliedfibers to European manufacturers. This is one reason why the jute prob-lem shouRld be apnroached in the internationnl context-ni if a. all psiAnother reason is that cut-throat competition between Pakistan and Indiasholllr he ' voidm d Tn 1967- the competition in sacking wTas so severethat its price was almost as low as that of raw jute. The third reason

+itha p;nrirc flucintuatinns shouild be rerifeld qndi t.he nri crp kpnt. t+ alevel which will discourage further large-scale inroads of syntheticsubstitutes into the Jute market. The new threat is the ne plastics --poly-propylene and polyethylene. Past attempts at price stabilization ona~, natior,.alr basis have notc been -cs .. J-

I, S TTv-,A oy. ,+- 1;- .,n+, nn nef' r. !Jflof +IT nnn.,vono-Fl -r; es 1 .

the East wing; it is unacceptably high in the West. Most mills operate12 s1ifts a wek +'ke-sf opraio is -deer.e 4..1ctcl y h.LL C Q1.L-LJ.UC ~L, i2. LILLI.U~ W iJ.LL _V - V4.'.-L Li. i..i)I _.. .L11JjJ± d.U UL'2±.; C LJL y UIle

larger mills. a principal reason being the difficulty of mustering thelarge labor Por.ce for the late hour shift. LTnder.=pm-ilo-..ent 4i the

industry is not viewed so much as a "problem" but as a way of life - acor.dition to be accepted. For example, ,any mills employ one weaver perone or two looms. MaLnagement states that attempts to change the patternIln Eastd Paita%.Ld.a couLIU adcase uphea-v aLs Uiithe LabUUr forUU W4LL(c WUrU

have unpleasant results.

43. A common complaint in the East was the price of power and thefrequent occurences o ooutages*. Those inter-v-ie-wed adva-nced no estimateof the cost of power failures in terms of lost production.

44. Another was the ever present one of inefficient and irresponsiblelabor. Tlere was no mention of imlpro-virg working conditions or wagescommensurate with improved productivity.

45. The processing industry in the country is not old consideringthe useful physical life of jute machinery and large scale replacementof machinery is not imminent. However, some equipment has proved to be notas eff'icient as it should be and replacement is desired. The cost of juteprocessing machinery has tripled since the earlier mills were constructedand replacements will be increasingly costly.

- 13 -

Table I-1: rOR$INE EsCIIV1n REEPTSFROM MERCHANDISE EXPORTS

1964/65 1967/68Million Mi.llion

PRs % PRs

Raw Jute 926 38.5 798 28.1Raw Cotton 331 13.8 419 14.8Raw Wool 78 3.2 38 1.3Rice 117 4.9 112 3.9Other Primary Commodities 250 10.4 181 6.4

Total Primary Commodities 1,702 70.8 1,548 54.5

Jute Manufactures 320 13.3 590 20.13Cotton Manufactures 188 7.8 396 13.9Other Manufactures 261 10.9 416 14.6

Total Manufactures 796 32.0 1,402 49.3

Freight Adjustment -68 -2.8 -109 -3.8

Total Merchandise 2,403 100 2,841 100

Total of Jute and JuteManufactures 1,246 51.8 1,388 48.9

Total of Cotton and CottonManufactures 519 21.6 815 28.7

Source: IBRD, Report No. SA - ha, current Economic Position and Prospectsof Pakistan, Volume I. The main report (April 18, 1969.

- 14 -

Table II-2: RAW JUTE - EAST PAKISTAN /

(Area, production and per acre yield)

Yield Pro- YieldArea Production Per Acre duction Per Acre

(000 acres) (000 baiesj'2 kbaies) _(00 ton32) (ton)

1,'7-1048 2X059 6,843 3.3 1 -

1948-1949 1,877 5,479 2.9 978 .5219L9-1950 1,561 3,333 2.1 595 .38

Three Years' Average 1,832 5,218 2.8 932 .51

1950-1951 1,711 6,007 3.5 1,073 .631951-1952 1,779 6,331 3.6 1,131 .641952-1953 1,907 6,823 3.6 1,218 .647953-L 754 95360 3.7 645 .671954-1955 1,243 4,662 3.8 833 .67

Five Years' Average 1,521 5,487 3.6 980 .64

1955-1956 1,634 6,500 4.0 1,161 .711956-1957 1,230 5,514 4.5 985 .801957-1958 1,563 6,200 4.0 1,107 .711958-1959 1,528 6,0oo 3.9 1,071 .70-959-1960 1,375 5,554 4.0 992 .72

Five vears' Average -,1,466 5',9 .11,63.7

1960-1961 1;518 5,62 3.7 1,00' .b61961-1962 2,061 6,969 3-4 1,244 .601962-1963 1,723 6,300 3.7 1,125 .651963-1964 1,700 5,875 3.5 1,049 .621964-1965 1,660 5,328 3.2 951 .57

Five Years' Average 1,732 6,019 3.5 1,075 .62

1965-1966 2,198 6,693 3.0 1,195 .541966-1967 2,165 6,40c 3. -1143 .531967-1968/3 2,400 6,850 2.9 1,223 .51

/1 No commercial jute is grown in the West Wing.

/2 1 bale = 400 lbs. 1 ton (2,240 lbs.) = 5.60 bales.

/3 Inclluding mesta.

Source: Yearbook of Agricultural Statistics, 1968; Ministry of Agriculture and Works,jarulJary 1°60, GoverSment of P.aki;stan.

Table_ II-3: PRODUCTION OF JUTE GOODS

Total RawHessian Sacking Carpet Pro- Jute

Looms Thousand Thousand Backing Others duction Con-JLLv--June Operqting Yards Tons Yards Tons Tons Tons Tons s lmption

t000 bales):1955--1956 4,193 115,838 3(,208 226,188 94,531 - 5,470 130,209 734:1956--1957 5,:227 136,175 35,682 256,691 105,356 - 3,496 144,534 809:1957--1958 5,920 141,779 39,741 261,285 112,481 - 5,638 157',860 941:1958--1959 6,886 190,134 51,773 335,922 140,771 - 10,903 203,447 1,209:1959-1960 7,738 234,629 66,082 414,800 178,935 - 11,261 256,278 1,527:1960-1961 7,849 245,820 67,259 413,702 170,012 - 11,630 248,901 1,4561961-1962 8,120 26L4,257 72,607 455,322 186,372 - 12,102 271,081 1,590:1962-1963 8,837 307',597 814,540 479,337 203,873 156 9,592 298,161 1,7W41963-1964 9,955 338,593 92,700 542,139 226,038 2,187 10, 007 33(,932 1,94.21964-1965 10,007 293,907 8:L,121 475,325 193,176 6,459 8,356 289,112 1,7031965--1966 11,800 391,763 106,367 675,781 279,137 L4,191 9,665 409',360 2,3821966--1967 13,073 394,376 110,063 637,988 263,699 :L9,664 10,288 403,714 2,3651967-1968 16,371 501,940 139,853 804,531 334,282 24,516 13,898 512,549 3,OC03:1968-1969/1 18,454 59(,280 16:3,964 615,246 256,322 24,850 15,C015 460,151 2,6590

/1 July through Nay.

Source: Monthly Summary of Jute Goods Statistics No. 155, May 1969; The PEkistan Jute Nills Association.

0 -r4 r- C) 0 C) co IU\ r-l r- (n C C) O -1I P I 1 1 .I I . . . . . . . .,. . .

bQ c> Y\4) 9oD No\ o9c) - r-- o co c\ 0:: a) in' Hr C\r1 H r-i OJ r-i NIJ C\J CHNJ CD .

m -_OJ ONl > C\OJ IA r1 r-i CO (\I U r-l 1 V\t :Ws . ............... - D1t

IY) E) eH * *H* **r- CC o n O. H rH OJ OJC 'J c 1( odU1 E-4 4-' @ s r1 H r- OJ C'J OJ C\J (n z J r-

HO C\r J r-H O r'-'0 CO 9t) -I O-O C) O ') 0 r rI yH- O r- r . . . . . . . 0 9 0 . * MD r

.q ^ O C))0 r-H CM ---C r-i C\J r1 44 (\ X 00 C) 9) \rMl Ft PZ as ~~~~~~~~~o:\ r- \D r-- co cc 7 - c^- \.o r-- sD0 1E\ UN 9) 9D - -u chj

| Z~~~~~~~~~~~D CG r-i r- Ll C) OlJ 9D UX 0-\gD 04 V\ CO E- r) V% L- 4Cq vL\: -4 C)0 r-r- H H -r- ONAACo 1 0 C' rE\O) U'C\ C) C\ J r Lr\

Cti 0 cl $0 Oc) oca) Q c O I r- r- r O-s ID ) \0 I rdt | -I r--IHHH r-CO

3 .H *--I) .-- | l ) C0 V\ ' CO ICC) ACO 0a C) aC H 0 Cct; t.3 - rtI Id sD oJinna xOu2r-U JnJ )O -.=~~~~~~~~~~ 91 --- -7-F rn J 1tt CMt CM rif r-1 Ot r- ZX Jr 't_ ) I

~ri E- Eq K' i r-I rQrI ri rI r- l - 1.- r- I 1 -- ri r-1i ri r- 1, rI ri, '{i

H -4-' ,t4O Inx c' ON oX ' t- C\i 'L - D o ,C ->:. -.t G, rl -- °\ -J ON °> C) 't 4 tJFz Cli r II _1 _ (J I C\r C) _J rrIC C) C\ OJ \r C\ 4 CJ UN J C O *r4w 0 @4 tt 0 CJ irr J 0 0\ CIN rHI H4 H oi ONCM (NJ H ONJ N OJ CHti) , <

0 g4 ''-% Q. .. .. Ut ) eW A * tnE-i $-P -HH H; g r rI-i rH H r-l r4 r-i rH rHi ri CD

(DU) 4

P. to -4-- ON L-zt 'U-, r\ O C .7tr' .L \ -- -.4") -4 OC 0 C) :J 0o O a V\ C\o. c r- Cr\ CC) O04J t (tn -J rHl O'NC\ -i J r- :it *r4

43> CMt P C \ (NJ H CNI C\ I rH l rH C\ (J \Jd

oo EH

43'

H

;.. rc

Is~

Hr- C\Ol cLA :Nt) D X) O. rCi OJ In _JU\ V\ t-aD 'r4ii- f U IUUU\lJ\ V\in -r\V\lrN ) \D 'NO 1ID \0 \9D \0 I'D \0 r- >

O ONO\ ON N\ ON, ON. N. \ N\ ON OX C\ NO CN ION CP\ .-.~~a r4 r 4 r4 r~~~ r 4 r4 r1 ~ r1 r- r r-l r1i r4A r-4 r-i r4 r4 r-l 1_ 4 Fr aOI I I I I I II I i t I I I I I I I I -s C)

D) 0 rH (NJ Z A-C 1\'\\0 ('-CO ON O r-0 HJ ".)fN't -\ [-lj-\ UI b-\ Ill UE UL' U-r UE UE IJ' NO N) 'D \j) \,O N4D NO tD ,ON ON ON ON 0', ON , ON ON \ CO ON C' C ON CN Cr'. ONr ON C' O

H r4 -r1 r4H r1H rHl 'j rl- rj r- r r- r-A r- r- r1 -t r1 f--f J >s, C8

n rw- 17 -

Table II-5: BROAD LOOMS POSITICN AS OF JUNE 30, 1969

Installed bhut Sanctioned butName of' Mill (45) Operating not Operating On Order not, Ordered

Adamjee 128 95Amin loh 125Chittagong 100 20Ca,rpeting 50 25People 79Dl atn A r,, TVle1 AA h8 LR

Crescen.t 85 15Bawa30Latif EBawany 39 60

Nishat 23 2Tac_ 10 - -

Hafiz 60Qaumi 25Victory- - 65Gul Ahiried - 65Jessore - 50Anwara - 5Janata - 65Noapara - -( -

Easteni -- 65Pak - - -65Sonali - - - 65National - - -65Delta - - - 65Star Alkaid - - -50Monawar - - - 50Hossain - - - 50Banani - - - 25East Bengal - - -25Osmania - _ - 25Rubi General - _ - 25Karnaphuli - 200'R.R. - 65 - -

M.M. - - 65Bengal - - - 65Mashriqui _ _ 50Taj 50Allied - - 5Broad Burlap - _ - 65Purbachal - - 65 -Sultana - - - 65Chand - -- 65Mahsin - -- 65S.K.J. - - - 6$

Total (3,010) 685 247 590 1,4 8 8

Source: EPIDC

Table II46: JUITE LOOKAGE POSIT ON AS OF JUNE 30, 1969

Sanctioried Iris talled % of OperaLtirg % of

Flat Looms (Hessian ard Sackirg) Hess- - 7aE =a F ress- Sac k- 0tr Sanctiomid s-StaTot IxtaAl.diaj ing ian ing ian ing

EPIDC Mills (7) 1,825 1,151 2,976 1,P280 8146 2,126 71.14 ,091 ,789 1,880 88.84

EPL)C/Associate t4ills (22) 4,029 3,044 7,073 3,,279 3,0144 6,323 89.3 2,772 2,-59 5,531 137.5

Private! Mills (23) 7,226 6,260 13747 1 6160 901 95.7 4 5,860 12,2714 95.1

East Pakistan (52) 13,070 10,455 23,,525 11,300 10,050 21,350 90.8 10,277 9,408 19,6135 92.2

Weist Pakistan (W4)I li5 971 1,1 _ 1650 971 1A42L LOO.0 88 4131 519 36.5

Total (56) 13,5,20 11,416 21&,9146 11,750 11,021 22,77L 91.3 10,365 9,1339 20,2014 8138.7

Other E;quipn*nt -- E. Pakisan OperalSE

Broad looms (Sanctioned 3,t)10) 68,

Cot ton baggi rC looms 112

Carpet looms5

TaLpe locons 5:3

Tvistirg spindles (twine) 7,1400

Source: East Pakistan Industrmal 3evelowient t orooraticn.

Table II-7: SHIPMENTS FROM 1{ILLS(Tons)

= or Exor For Internal Cons-uxmtion =TotalCarpet Ship -

ulyr-June Hessi.an Sackinig B Lcking Others Total Hessian Sacking Cthers Total rrients_

1955-1956 24,221 60,7'15 Nil 7 84,943 5,496 29,694 5,130 40,320 125,2631956-1957 26,198 5'a1393 ll; 80,706 7, 647 45,738 3,605 57,:L90 137,89,61957-1958 32,510 70,7 67 " 384 103,661 8,288 42, 964 5,688 56,940 160,6011958-1959 44,299 91,33.12 "I 1L,666 137,277 5,296 42,293 7,684 55,273 192,5501959-1960 59,1 87 132,L16 " i,19c) 196,793 6,708 38,0o61 6,OhO 50, 309 247,6021960-1961 61,784 135,506 5,301 202,591 6, 091 35,894 6,061 48,o46 250,6371961-196:2 65, 396 146,437 " '3,891 215,774 8,4L58 40,730 7,663 56,,351 272,62,51962-1963 71,2'94 1&5,2:13 81 2,16L 218,752 9, 327 480,543 7,61L4 65,484 284,23F61963-196 | 78, j789 168,238 1,264 2,431 250,722 10, 031 50,287 8,491 68,309 31-9,531iQ64-1965 73,5,79 138,956 6,482 2,61i2 221,629 9,L44 51,6;26 7,660 68,730 290,3591S65-1966 91, 370 208,378 13,188 :3, 542. 316,478 16,568 4u,126 6,469 71,163 387,611966-196-7 90,373 232,5164 15,071 24,22C) 346,628 13,5993 49,103 4,8 05 67,901 414,52 9 11967-1968 1i30,0)35 260,3:11 25,,090! 6j,996 422,432 13,6L8 58,179 6,228 78,055 5(0,487 H1968-196'9/1 143,503 230,0OL5 24,336 7,808 405,692 12, 317 48,438 6,318 67,123 4'72,81.5 \

/1 July through May.

Source: Monthly Sumnary of Jute Goods Statistics No. 1.55, May 1969The Pakistan Jute Mi'L1s Association.

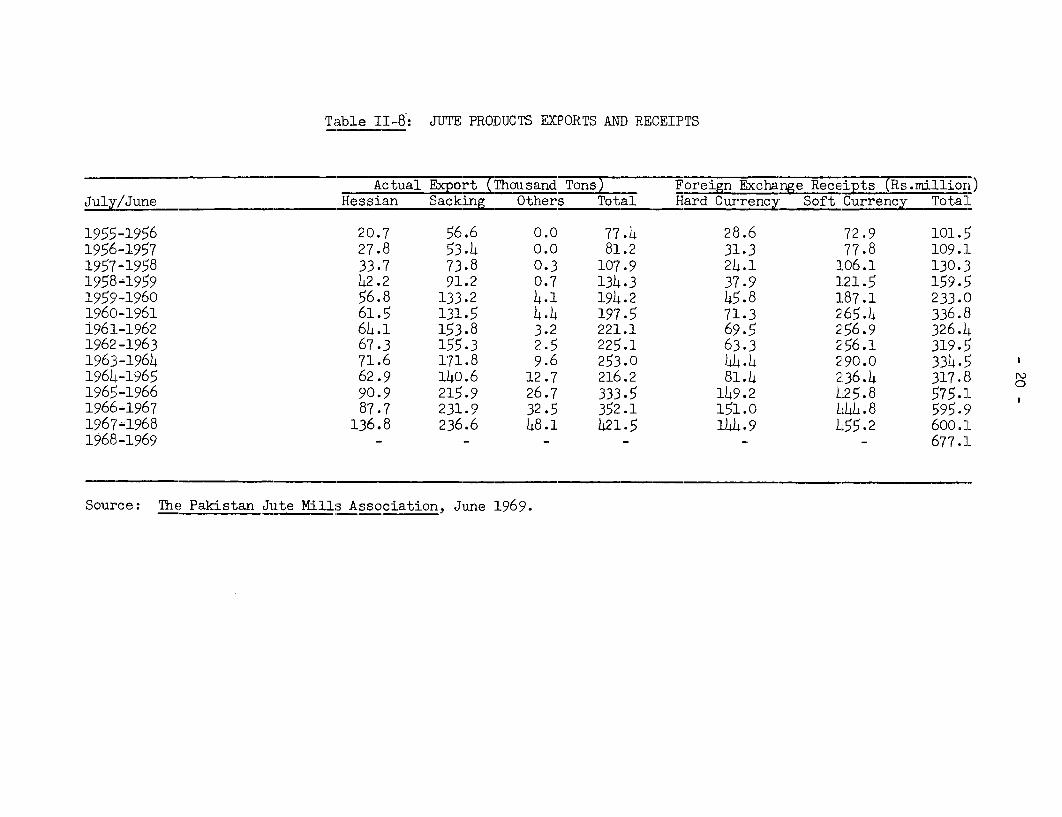

Table II-8: JUTE PRODUCTS EXPORTS AND RECEIPTS

Actia1 E7a= Thou sand Ton s7 _ Foreign Excchnge Receipt 7Rs .miJliorl)July/June Hessian Sacking Others Total Hard Currency Soft Currency 1'otaIL

1955-1956 20 .7 56.6 0.0 77.4 28.6 72.c9 ]01.',1956-1957 2'7.8 53.4 0.0 81.2 31.3 77.8 1-09.11957-1958 33.7 73.8 0.3 107.9 24.1 106.1 130.319584-959 4X2.2 91.2 0.7 134.3 37.9 121.5; 1-59.-51959-1960 56.8 133.2 4.1 194.2 45.8 187.1 2 33.0(1960-1961 6:1.5 131.5 4.4 197.5 71.3 265.4 336.81961-1962 64.1 153.8 3.2 221.1 69.5 2'56.c9 326.41962-1963 67.3 155.3 2.5 225.1 63.3 2'56.1 -319.51963-1964 71.6 171.8 9.6 253.0 44.4 2'90.C) 334.5 a1964-1965 62.9 140.6 12.7 216.2 81.4 2'36. 4 317.8 o1965-1966 90.9 215.9 26.7 333.5 149.2 425.8 5'75.11966-1967 87.7 231.9 32.5 352.1 151.0 444.8 8 595-91967T1968 136.8 236.6 48.1 421.5 144.9 455.2 600 . 119681-1969 - - - -- 67 7 77. 1

Source: The Pakistan Jute Mills Association, June 1969.

_ 21 -

Table II-9: EORTS SSIA, SACKIN.G OTHER JUTE MANUFACTURES BY DESTINATION

(Tons)

1965-66 1967-680Hess- Sacking Others Total Hess- Sacking Other&,Total

Destination ian _ianr

E. Arica 1J 4,136 32,166 321 46i623 32,059 67,9)49 11j3() 1()1;138U. S. A. 29,335 - 21,539 50,874 37,455 63 37,96'; 75,483Australia 1,616 37,740 107 39,463 2,018 39,084 14', 41,247W. Africa 660 53,873 494 55,027 6,240 34,533 473 41,246Tarkev 4,833 1,128 86 6,047 15,744 5,615 46 21,405United Kingdom 10,077 3,812 228 14117 13,484 4,399 366 18,249Chile - 8,363 - 8,363 - 10,203 75 10,278Netherlands 215 3,655 - 3,870 1,022 8,295 78:l 10,098New Zealirmi - 672 152 824 - 8,762 158 8,920Cambodia - 4,503 176 4,679 - 8,525 - 8,52'Japan _ _ - - 5,216 - 2,0993 7,315Italy - A427 _ 1,1427 442 6,7 1:1 7 917

Peru 16 4,13)4 _ 4,150 21 6,922 - 6,9)43R om~ri a - - )421 6,223 _ - ,Iran 965 365 423 1,753 1,259 4,689 3441 6,289Argenti rii 1)1;162 - - 1L4.162 5,646 104 1L 5,751Canada 5,524 - - 5,524 4,004 _ 589 4,593Belgium 136 1,393 - 1,529 1,123 2,433 56)4 4,120W. Indies 226 19,701 - 19,927 88 3,837 62 3,987Burma - 16,744 336 17,080 1,309 1,45o 716 3,475Uruguay 2,801 - - 2,801 3,)41)4 - '. 3,)41Iraq - 208 562 770 915 2,297 - 3,212Germany 230 584 - 814 1,1)45 1,371 43 2,559Brit. Guiana - 2,132 - 2,132 - 1,959 - 1,959Ei r e 34() - - 34 1 , 654 - 14

Hongkong 198 1,145 65 3 1,996 288 119 1,1810 1,587New Guin!-a - )481 - 1 -)]6(5 T 14 7)Nicaragua 275 6l44 - 91'9 32 1,400 - 1,432Denmark 5 75' 156 - 728 618 249 35:2 1,219Sudan - 3,073 - 3,073 - 1,178 23 1,201Greece 51 1,19)4 - 1,245 139 1,046 - 1,185Ceylon - - 44 6 1,1)40 1)4 1,160Albania - - - - 915 - 915Singapora - - 587 587 106 258 505 869Hungary - - - - 28 464 - 492

M o r,-),- 1~~~~ ~~~~~~~~~~.00 IPAMoro^c: tJt.,UtJ - - - 4uu -Kuwait - _ _ 6' 321 - 386Phii LpinT.s - = 22 359 381Cyprus 36 717 - 753 22 323 - 345Malaya -- 55 550 - - 2 327AfghanLst'an 123 - _ 123 76 184 h'7 307Yugoslavia 21 162 - 183 195 105 - 300France - - - - 284 - 28)4Lebanon - 209 - 209 - 283 - 283Norway 123 - - 123 228 8 - 236IJ. S. S. R. - 502 - 502 - - - -

Bulgaria - 155 - 155 _- -China 2,877 3,904 - 6,781 _ 104 - 1.04Indonesia, I0. ,,727 376 i,5(8 _ _ _

Other Coumtries 982 5,213 61 6f,2'5 172 566i 93 836TOTA t. 9°,93. 215,882 26,655 333 ,)j72 136,84() '36,623 o8 , (13, )421',l58

_ ~~~~~ ~ ~~~ ~ ~ ~ ~~~~~~~~~~~~~~~~.9 9 _1 1 ,8 6 .3 48 ,

Sour(:e: Monthly Sunmnary of Jute Goods Statistji(s, No. 15', May 1969,

The Pakistan Jute Mills Association.

CHAPTER III

COTTON TEXTILES

A. Introduction

46. Originally established for import substitution, the industry

has grown to a leading position in the industrial structure of thecoLintrv in terms of the value of fixed assets and inventories, employ-ment provided, value of products and by-products manufactured. Afterju_te nroduicts, cotton goodrs are the nation's second largest manufacturedexports, accounting for Rs. 396 million or 28.3% of total receipts fromexport f- manufactures and 13.9% of total merchandise exports. Exports

of cotton goods have now almost reached the value of exports of raw

cotton; toether5 thev account for 28.7% of total exports. (Table II-1).

h7. %he indllstry nrovides employment for about 1h3.000 in the West.24,OQo i t,e East, a total of 167,000 or about 28.4% of employment inmaiaf-p'+.ctng induistri RS.l/

48. Total value of' production was Rs 1,797 million, Rs 208 millionin the E,as, and Rs 1,595 in the West. Gross value added was Rs 888 million,Rs 89 m-llion in ti-he East and Rs 799 million in the West.

49. Actual investment in the industrv was not obtainable. However.a possible measure may be obtained from sanctioned investment :-/

Sanctioned Investment in Cotton Textiles(TS mi. 1 in

1960/61-1964/65

Tota East West

New mills 391.,6 176.6 215.0

Balancing, modernization,replacement 593.n .7

902.2 269.6 7 2.6

1965 through 1960

New mills 897.0 215.4 681.6

Balancing, modernization,replacement 159.,6 15.5 ;44.;l

1,056.6 230.9 82g;.7Grand Total 203db. ,500.5 j,38.3

1/ Censu,s of Manufactu,ri,ng Industries 1966/67. Bureaus o,f Statistics -

Governments of East and West Pakistan.

2/ CQtton Textile Industry, Growth Prospects over Fourth Five-YearPlan (1970-75).

- 23 -

50. It is estimntAd that the fore-ign echange compnonnt constitutedabout 6Q9 of the investment sanctioned.

51. Import dependence is small compared to gross value of productionconsistinic1 -g- as it r1oes rof' spares, dyes:b mr n hrn m 2+ cmmcl ic t for thsc lthat produce fine count yarns and fabrics from imported long staple lint.Since 196 0-62, there has been a graual shift from. finer to coarser varie-ties of fabrics, a change that probably is due more to heavy taxation onfinn rr- +

40 +Hn- +- m..rn4"-+ fnmCe. A--n,.1 - ,flrv4l 14A n1,414

4.-. InS 'kaenvine. uarie_ies *han to ._ Ic forces. -L.ua -Jl ipr liablit. y .has bsen

estimated at Rs 96 million to Rs 100 million as against an estimated grossvalue of poutLnof Ps 2,3 rLllo 4to Rs 240 rlllon for14- 1969IA-70,

or a ratiLo of about 4.1%._/

52. Similar to the case of jute goods, Pakistan has comparativeadvaLtage In cotton textiles. It gro-ws raw cotton of ve,-y good quality;labor costs are low; the industry employs large quantities of labor. Themlajor du:.ferences fro, the jute iduusury is tU;zb rak±taii ls niot ithe -irlajorsupplier of raw cotton to the world market and therefore there is no ,-on-flict belween a simultaneous export expnLsion of both cotton textiles andraw cotton. Furthermore, as limits are reached to cotton textiles expan-sion d-ue to foreignL traue restrictionLs, the comparative advantage turnsin favor of raw cotton expansion.

B. Growth

53. The annual compound growth rates of installed productive ca:pa-cities in both spinning and weaving were:

Spindles - % Looms-%Total East West Total East West

1959-60 to 1964-65 5.9 11.4 4.5 3.7 10.8 2.3

1964-65 to 1967-68 1.6 2.4 1.4 1.0 11.3 /a

/a No figure given.

Source: CSO, Statistical Bulletin, September 1968; Ratescomputed by Research Division, IDBP.

54. There has been a steady expansion of the industry since 1947.At the erLd of June, 1968, the industry was composo:i of' 132 mnilTs hbaing2.7 million spindles and 37,000 looms. Of the total mills, 84 were inte-

l/ International Economic Section, Planning Commission,May 1.969.

- 24 -

grated spinning and weaving, 45 were spinning only, and 3 had onlyweaving facilities.l/ This remarkable growth was engendered by severalfactors: at Independence, virtually all of the larger mills were inIndia. and the effort toward self-sufficiency stimulated both millconstruction and cotton growing; existence of a large hand loom industrythat was dependent upon machine-spun yarns accounts, even today, for therelatively large number of mills producing yarn only; there was a size-able overseas market: and the bonus system made production for exportshighly profitable.

55. The industry is broad in structure. It is linked backward toainning (a few mills own their own ginning facilities), and is integratedforward through the finished product. Mills are located in both wings,the West having 751 of the spindles and 81% of the looms. Soinnablecotton is grown exclusively in the West.

56. Exports of cloth and yarn have been extremely responsive toinereasAs nr decreases in the bonus rate. In January 1959, a bonus of 20%was instituted on yarn which resulted in a sharp rise of its export fromPR 12 A million in 1958 to Rs 102.9 million in 1959. The large exp-ortcreated a domestic shortage, causing a consequent reduction in bonus to10% in Febhrary 1960. and its complete withdrawal in January 1961. Exportsdropped sharply until the 10% bonus was reinstated in February 1963 whicharrested the romwnward trend. To reverse the trend. the bonus rate wasraised to 15 in January 1964 and exports rose to Rs 86.7 million. Therate was magin rnisi to 2?Q in Novemher 1960)4. which resulted in a steadvrise in exports to Rs 104.5 million by 1966-67. Subsequent to devalua-tion of +he porin sterling in November 196?7v the bhons was raised to 30%in the same month, and exports during 1967-68 rose to Rs. 200 million. 2 !

57. Cloth exports behaved in much the same manner. A bonus of 20%was promulgated in Jon Jnuar 1959, sedring expnorts up from Ts 4.1 m-nllionin 1958 to Rs 58.2 million in 1960. In July, 1963, the rate on finishedcloth was raise to 30% increasing ex-pnorts to Rs 74.4 million. The ratewas raised to 40% in January 1964 and exports rose to Rs 155.8 million in' cn4 47 Q48- , .1,4-.A 7-, +k- m-PfPer,-.+i wrn f-"rnm Tnv%rmhir 1 QA7A7UU %j fv * Li U . IUv,> U-- .A. v; -*Y w - .. . i _ | . .. .' _ ... _ .w.. _ -, v

of 40% on finished and 30% on grey cloth, exports for 1967-68 totaledas 200O LL.u1' onl.3!~

1/ The number of finishing facilities is not available. All of thelarger mills visited by the Mission and some of the smaller oneshad their own plants.

?/ EPB: Commmodity Notes, Cotton Yarn and Piece Goods (1968-69).3/ Ibid.; The industry is not entitled to an Export Performance

Li cen.se since it is based on indiigeno raw material.

58. Of cloth exports, 40% are shipped to quota countries, 20% tothe Socialist Blc)n and 40% to other countries. Historically, exportvalues of cloth generally have exceeded that of yarn. The latest excep.-tion to the general trend was in 1907-68 when yarn value exceeded cloth.In conformity with the policy to export a maximum of finished instead ofsern -Y-rocessed goods, cloth e.xports are A,Pected to axceed yarn in 1968-

69.- " (Table III-1).

C. Prices, Costs and Profitability

59. Domestic mills are the major buyers of local cotton - theyabsorbed in 1965/66 thr4ough 1067/68, about 6J% of domestic spinnable nLnt(Table IV-2). Apparently it is not the custom of the industry to car:rya large inventory of raw material, a procedure at some issue with cottonexporters who suggest that mills should carry a stock equivalent to threem,on'ths requirem,ent- to prevent th--ie price st-r uCt-re fror. being dlisturbed by

scarcity buying. Apparently exporters can buy cotton at a lower prica (so-called "export parity") than mills, the rationle belng that textileproduct-e.xporters who receive a generous bonus exchange rate can afford ahi-Lgher price thUa cotton shippers -wo must- surrender hei4r procees at theofficial rate with no bonus. The differential must be small; it was mnen-tionued only b-y sormLe of the mill maragemrents intervievwed" by the Mission todiscuss industry problems. It was capacity taxes and an inefficient laborforce t'nat headued thie 11±sU 0.1. Ullelr co-I1plaints.

60 l*Iore time than was available to tlh1e r Ussion wouulU be rt

obtain cost data on even a few specific items, if, indeed they could beacquired,, since these data are among the most jealously guarded of corporatesecrets. Returns from the Mission's Industrial Study Questionnaire covereda variety of cotton textile operations. Those that produced orny yarns(the majority of returns), those that produced coarse to medium yarns andcloth and those that made a fairly wide range of coarse, medlum an-d ineyarns andl fabrics.

61. The segment that produces fine items has a larger import inputcontent cdue to the use of American and Egyptian long-staple cottor tharnthe sector which produces yarns only or fabrics of average and lowerquality. Import inputs for this latter segment consist entirely of spareparts, dyes and processing chemicals and probably accounts for less than5% of total sales value. Unfortunately, the firms, in answering thequestionnaire, misconstrued the question concerning imports believing itto refer to raw materials only and failed to give volumes and values ofspare parts, dyes, chemicals and other miscellaneous secondary materials.A limitecd number of replies that were complete enough to be usable gaveimport data. They are shown in Table III-2. The range of factor inputsand other cost items as a percent of the sales price are shown below.

1/ Export data for the full year 1968-69 is not available.

- 26 -

Average ofRange

Range % ValuesMaterial 24.0 - 47.5 35.7Tbhor 4.3 - 10.h 7.hServices 2.1 - 7.3 4.7Overhead 3.8 - 16.2 10.0Other 0.7 - 11.4 6.1Profit before taxes 5.9 - 39.2 2,2.6Direct taxes 8.0 - 24.7 16.4

629 nn an industrv-wide basis including those mills producingupper medium, fine and superfine items (imported staple), domestic inputsprobablyt mr-rmini f 90 nt 95% of ex-faetory cost. Production eapacityby variety is:

Coarse Medium Fine SuperfineLess thnn 21 -34 35-4r7 hR &, above

21 counts counts counts counts

Yarn (millionlbs.) 409.3 224=8 75.4 16.0l

sq. yds.) 676 568 65 39

Source: The Gazette of Pakistan - Extraordinary, Api'jl 22,1968, Central Board of Revenue, Government ofPakistan.

63. Increasing dependence on imports probably would result fromincreased exports in higher grade fabrics, particularly to quota countries.Long staple imports were 3,700 tons valued at $3.6 million in 1968, none in1969, and 7,500 tons costing $6.2 million is projected for 1970. Evidently,a greater thrust at the higher grade market is anticipated.

D. Problems of the Industry

64. One of the problems that appears to loom large is the relativelyhigh proportion of small-size mills in both wings -- 46 containing lessthan 12,500 spindles. Recent studies indicate that under conditions exist-ing in developing countries, 25,000 spindles is the minimum economic size.The number of mills containing less than 25,000 spindles is 89, or 68% ofthe total. Whether the economic scale problem is as acute as the proportionseems to indicate would depend upon an analysis of each mill to ascertainits real disadvantage. It is interesting to note that an executive of a100,000 spindle mill considers it unwieldy from a management point of view.

65. Management considers the tax levied on "capacity," both spinningand weaving. as unfair and counter-productive. Several mill managersinterviewed stated that between 6,000 and 7,000 looms have been dismantledAind removed from mill premises to avoid taxation.

- 27 -

66. The rationale for the capacity/ tax was the decline in utilizationof installed capacity shown below:

UTILIZATION OF ITN-Y7LLSD CAPACITY, YEAR-END

Total East Pakistan W0est Palkistan±nsta- Opera- Machine Insta- O-pra- Machine Insta- nTeia- hinelled ting Utili- lied ting Utili- lled ting Utili-Capa- zation Gapa- zat.ion Cana- zationcity __ city % city %

Spindles(000)

1959-60 1941 1844 95 359 353 98 1582 1491 94194-65 258)4 2)16 93 617 56)Q 91 1967 1852 9):1967-68 2710 2479 91 6,62 563 85 2048 1916 94

Loomsf onrl )(ooo)1959-60 30 29 97 3 3 100 27 26 96.1964-65 36 32 89 5 4 80 31 28 901967-68 37 32 86 7 4 57 30 28 93

Sonlrce: Goverrn'nment of Pakistan, Central Statistica1 Office.

67. The issue, in managementts view, is the government's assessmentof individua.l m.ill's mwacjhine utilization in term.q of "idle cnapaity;" aconcept based on textile engineering calculations. The main reason for "idlecapacitY aS- nrobably lack of r.rke for potential outpniut of installedcapacity ani temporary over-building of the industry with respect to con-Sump ion. Another fa+nor may hava e been the rlock of nmplermrentary -nputs

over the short run and the inexperience of management. During the periodfrom 19910-60 to JTne 1968, )4,000 looms were inst lhd in ERst Pakistan of

which only :1,000 went into operation. In this case, the in-plant problemswere probablr y ro.ore i-Morvant thn - the lack of ,m, * rkets.

68. Tow productivity affects all but a very few mills. Managementhas singled out inefficient and irresponsible labor as the main factor; att-Lh e- tima, +lthere appna¶' 4-to bo a 1 ala_ of se rno effort to rec+ifyr wo.nditionscausing low productivity. The labor force is largely migratory and un-trained, and real trainiing cou ses for the "mill ha-d" are few. Neitherwages nor working conditions are conducive to efficient production. Onemill visitecd was so dark (to save e'l" that it was difficlt tosee. In another, management statP4d that suwwmer temperatures in the spinn-

nrLg room rose to 13)0° F. -- h2.d1.-y conaducive to sustained mental or p1hysicaleffort throughout an 8-hour sit. They suggested that the governmentshould pro-v-ide miLnimu-i;m standa&-, anld sponsor domestic production of air-conditic.r&ng equipment specifically designed for factory conditions. It

- 28

has been said that the most difficult segment of industrial personnel totrain is management. Attracted by the protection given, it is possible thatsome entrepreneurs entered the industry from the general business communityand have not developed industrial management skills to the required degree.

69. Utilization of quotas in 1967/68 was unsatisfactory in the E.C.MJcountries except for the Federal Republic of Germany where it was fulfilled.Of the fabric quota of 2,270 tons in E.C.M. anid Austria, 917 tons were sold,

leaving a deficit of 1,353 tons (Table III-3). Wider widths of fabric werein large demand in E.C.M. countries, but only a few mrLills -were equipped withbroad looms. The situation is changing now as broad looms are being in-

stalled. There was also a quota of 530 tons for made-up articles in the E.C.M.,

none of which was utilized. Thus, of the total quota for fabrics and made-up

articles in E.C.M. of 2,800 tons (about 25 million square yards), under-

utilization in 1967/68 was 1,883 tons (16.8 million square yards). Lack of

timely communication between exporters and buyers in the sophisticated overseas

markets contributed to quota shortfalls. Quota utilization was considerably

better in the U.S. and U.K. In the U.S., of the fabrics quota of 59.7 millionsquare yards, 41.4 million or 69.5% was used in 1967/68. Pakistan has met her

fairly small "cowutry quota" of the U.K. (22.53 million square yards) and has

been successful in getting a large share in the "global quota" available to

all exporters (43.37 million square yards), which has resulted in aggregateexports of 66 million square yards in 1967.

70. Altogether, the available export quotas for cotton fabrics and made-

up articles in 1967/68 were about 150 million square yards, of which 117 million

or 78% were utilized. The percentage of utilization is expected to increase

in 1968/69, as strenuous efforts were made, under the leadership of the Export

Promotion Bureau, to expand the export flow. Aggregate exports of Pakistanicotton fabrics and made-up articles are now running at Rs. 220 million p.a.

($46 million), of which exports to the quota countries may reach as much asone-half. The room for further expansion within the present quotas is quite

limited. Thus, the future trade policies of the quota countries will exer-

cise a substantial impact on the development of Pakistan's cotton textile

industry.

71. The little-known domestic market, while not an industry problem,

should be mentioned, Virtually all domestic yarn sales are to small machine-

weaving enterprises (some comprise as little as 4 power looms) and to thehand loom industry. This non-mill sector produced an estimated 820 million

yards of fabric in 1967-68 against 767 million for the recognized industry.Assuming the mill sector supply to domestic consumption was the differencebetween cloth production and export, the domestic availability was about

1,300 million square yards representing an apparent per capita consumptionof 10.8 yards.l/ Hand loom production is traditional, a facet of the over-

all economic pattern-and will remain so for a considerable period. The "mill

sector" accepts the competition and continues to supply it with yarn -- its

basic raw material.

l/ IDBP, Cotton Textile Industry, Growth Prospects over Fourth Five-YearPlan 1970-75.

29 -

Ex ort of Cotton_Fabrics and Made-up 2Articles to C=ta C(_utrjes

(in Millions of Square Yards)

Export Quota Expected Exports Actual Exports1968/69 1968/69 1967/68

United States /Cotton 'abrics 62.7 U0. a 4i.4Made-up Articles 8.9 8.9 rL.a.

Total 71 .o St' n.a.

united nidomCountry ZQota 23.1 2 3 . 1 /Z 22.8Global Quota 43.7 43.7/D

Total 66.8

ECM Countries andAustria

Cotton Fabrics 20. 4 14.4e 8.3Made-up Articles 4.7u 0.6 -

Total 24.7 15.0 8.3

GRAND TOTAL 163.1 150.7 (115.9)

/a Actual exports in the first nine months of the quota year were 42 millionsqulare yards.

A Actual exports in 1968.

/c Approximate. The quota is expressed in tons (2,270 tons) and has beenonverte-Ad into yardals using t h1-e converslion fLacuor of one squaare yard

0.245 lbs.

/d Approximate. The quota is expressed in tons (530 tons) and has beenconverted into yards using the conversion factor of one square yard =0.245 lbs.

/e rull utilization of the quotas in Germany (450 tons) and Italy (990 tons),one-fourth in France (113 tons) and 22% in Benelux countries (83 tons).

Source: Export Promotion Bureau.

E. Conclusions

72. The profitability of the industry appears quite satisfactory and isheav-ily dependent on the bonus exchange rate.

73. The lack of real training given lower level persomnel, low wagesand unsatisfactory working conditions are a contributing factor to the lowrate of productivity. -Whether, and to what degree, low-output machinery is

a substantial obstacle to increasing productivity should be determined by aGoverrerimet- industly survey. An extension of the investigation that was madeto determine "capacity tax" could provide a starting point.

74. A large number of spinning mills are under-sized, with a capacityof about one-half of the desirable level. it is suggested that over the nextseveral years priority be given to balancing of capacity rather than toestablishment of new mills.

75. Export sales are transacted by mill management which is also in-volved in day-to-day operations. It is probable that sales could be increasedif professional representatives could be commissioned to promote Pakistanicotton goods and handle transactions overseas. A more direct channel ofmarket intelligence would thus be established.

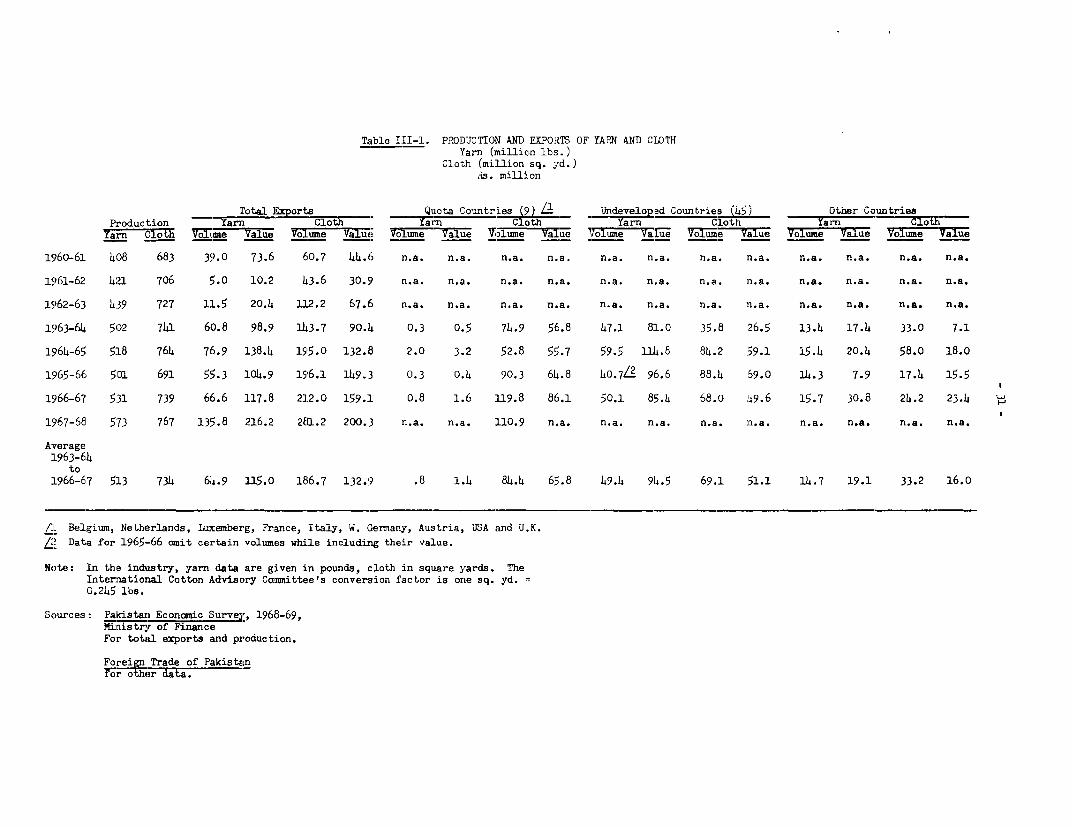

Tzible III-1. PRODUCTION AND EXPORTS OF YARN AND CLOTHYarn (milLion lbs. )

Cloth (million sq. ydi.)Rs. million

Total Exports Quota Countries (5) Undeved Countries (45) Other Countries

Production Yarn1 Co ta Yarn oI-Mth Yarn Cloth Ya_r_n -l

in Co Voi Value e V Valu V Value Ioume Va ulue V lume Value VolvuxIiel =aue roiiie Ta=ue

15'60-61 408 683 39 .0 73.6 60.7 44.6 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

15161-62 4_L 706 ;.0 10.2 t3.6 30.9 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

1962-63 4.39 727 LL.5 20.4 L12.2 67.6 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

1963-64 502 741 60).8 98.9 )L3.7 90.l1 0.3 0.5 74.9 56.8 47.1 81.0 35.8 26.5 13.4 17.4 33.0 7.1

1'64-65 518 764 76.9 138.4 1955.0 132.13 2.0 3.2 52.8 55.7 59.5 11LA.8 84.2 59.1 15.4 20.4 58.0 18.0

1965-66 5D1 691 55-3 104.9 156.1 149.3 0.3 o.4 90.3 64.8 oL0.7L2 96.6 88.4 59.0 L4.3 7.9 17.4 15.5

1966-67 531 739 66.6 117.8 212.0 159.1 o.8 1.6 L119.8 86.1 50.1 85.41 68.o 49.6 15.7 30.8 24.2 23.4

1967-68 573 767 135.8 216.2 2cL.2 200.3 n.a. n.a.. :110.9 n.a. n.a. n.a. n.a. m.a. n.a. n.a. n.a. n.a.

Average:L963-64

to1L966-67 513 734 6i4 .9 LL5.0 186.7 132.9 .8 1.4 8 4.4 65.8 49.L 94.5 69.1 51.1 14.7 19.1 33.2 16.0

/:L Belgium, Netherlands, luxcemberg, France, Italy, W. (Germany, Austria, USA and U.K.

/2 Data for 1965--66 azit certain volumes while includinlg their value.

Note: In the industry, yarn data are given in pounds, cloth in sqlaare yards. TheInternational Cotton Advisory Camiittee 's conver3ion factor is one sq. yd. =O.245 lbs.

Sources: Palcistan Economic Survey, 1968-69,Ministry of FinancieFor totalI exports and production.

Forel Trade of Pakistan;r -'hr data .

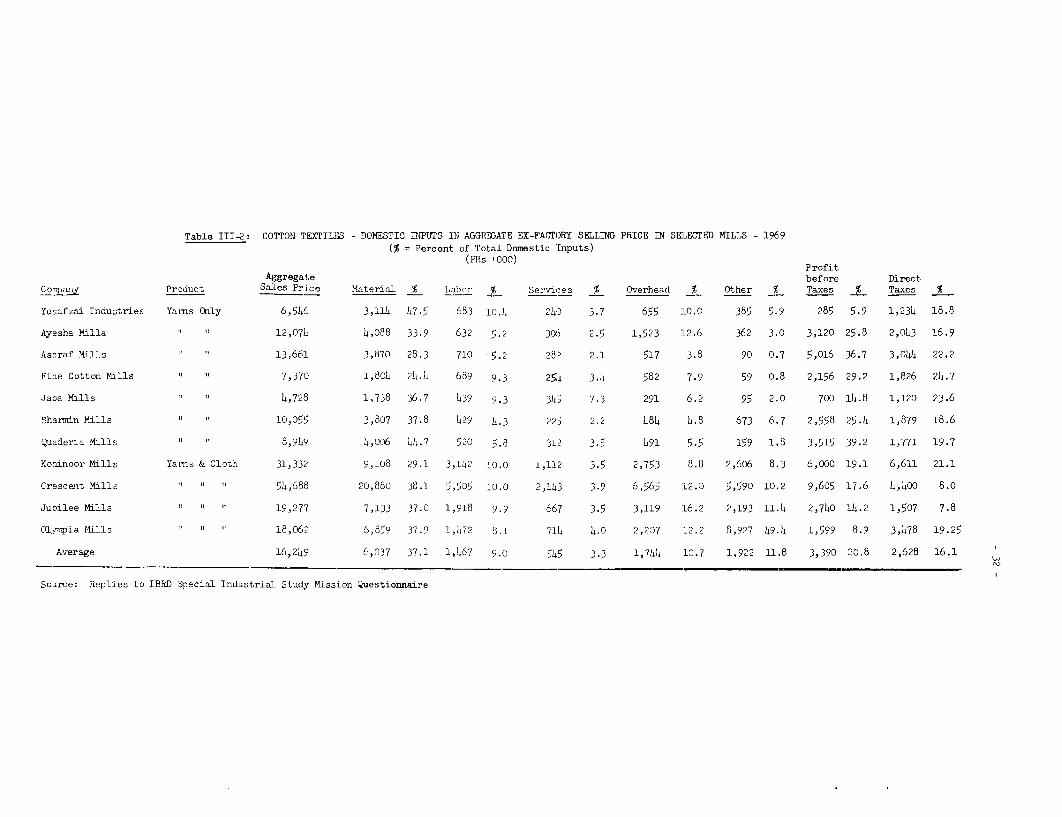

Table III4: COTTON IEXTILES - DOMESTIC INPTlTS IN ACGR3GATE EX-FACTORY SELLING PRICE IN SELECTED MILLS - 1969(% = Percent of Total Donmestic Inputs)

(ERs 000) Profit

Aggregate before DirectCO__an Product Sales Price Material % Lobkr .2 Services % Overhead % Other % T'axes % Taxes %

Yusafzai Industries Yarns Only 6,5146 3,114 47.5 683 10., 240 3.7 655 10.0 385 5.9 285 5.9 1,234 18.8

Ayesha Milla i 12,071 4 ,088 33.9 632 5.2 306 2.5 1,523 12.6 362 3.0 3,120 25.8 2,043 16.9

Ashraf Mills 13,661 3,870 28.3 710 '5.2 282 2.1 517 3.8 90 0.7 ;,016 36.7 3,044 22.2

Fine Cotton M lls 7,370 1,804 21.4 659 9.3 251 3.4 582 7.9 59 o.8 2,156 29.2 1,826 24.7

Jaba Mills 4,728 1,738 36.7 439 9.3 345 7.3 25'1 6.2 95 2.0 700 14.8 1,120 23.6

Sharmin Mills " 10,055 3,807 37.8 429 1l.3 225 2.2 4184 .8 673 6.7 2,558 25.4 1,879 18.6

Quaderia Mills 8,919 1,006 11.7 520 ,.8 312 3.5 491 5.5 159 1.8 3,515 39.2 1,771 19.7

Kohinoor Mills Yarns & Cloth 31,332 9,108 29.1 3,1.L2 10.0 1,112 3.5 2,753 8.8 2,606 8.3 6,oo0 19.1 6,611 21.1

Crescent Mills 54,688 2C,880 38.1 5,5D5 10.0 2,143 3.9 6,565 12.0 5,590 10.2 9,605 17.6 4,10oo 8.0

Jubilee Mills 19,277 7,133 37.0 1,918 9.9 667 3.5 3,119 16.2 2,193 11.4 2,740 14.2 1,507 7.8

OlysTia Mills 18,062 6,859 37.9 1,472 8.1 714 4.0 2,207 12.2 8,927 49.4 1,599 8.9 3,478 L9.25

Average 16,249 6,037 37.1 1,457 9.0 545 3.3 1,744 10.7 1,922 11.8 3,390 20.8 2,628 16.1

Saurce: Replies to IBRD Special Industrial Study Mission Questionnaire

Table III-3: EXPORTS OF COTTON TEXTILESTO QUCTA COUNTRIES, 1967-68

E.C.M. and ArUSTdA(metric tons) QUOTA

% of - --Fabrics Available Utilized Available Shortfall

Benelux /1 370 224 60.5 - 146France 450 27 6.0 - 423Italy 900 216 24.0 - 684W. Germarny 450 450 100.0 0Austria 100 1il 0.0 - 100

2,270 917 -1,353

Madeups /2

Benelux -30 nil 0.0 - 130France 10 0.0 - 150Italy 200 0.0 - 200W. Germanv 5n fn o. r-

530 - 530

Total for E.C.M. 2,700 917 34.0 -1,783

Total for Austria 100 nil 0.0 - 100

Total 2,800 917 32.8 -1,883

U.S.A. (million sq. yd.) /2

Fabrics 59.745 41.405 69.5 - 18.:340Madeiins n.a.f) n.a.,)

U.K. (million sRn-. )

QuotaFabrics Total

Country Global ExportsA

1966 22.32 35.00 57.321967 22.83 43.37 66.201968 23.06 43.73 66.79

/1 Belgium, Netherlands and Luxembourg/2 Apparel and other items, e.g., T shirts, shop towels, etc./3 The rnota for 1968/69 ji 8,930 million sq. yds., ail of which Is ex-

pected to be utilized.

/4 Exclusive of exports for re-export.

Source: Export Promotion Bureau, July, 1969.

- 3L -

Table III-4; COTTON SPOT PRICES -KARACHT - SEPT. 16; 1 969) /1

Rs/maund Rs/lb. $/lb.

Desi Sind 90.00 1.09 .23

Desi Punjab 88.oo 1.07 .22

Desi Bahawalpur 89.00 1.08 .23

4-F Roller 101.00 1.23 .26

4-F Sawgin 106.50 1.29 .27

LSS Roller 101.50 1.23 .26

LSS Sawgin 106.50 1.29 .27

NT Roller (new) 114.00 1.39 .29

NT Sawgin (new) 118.00 1.43 .30

289-F Roller 111.00 1.35 .28

289-F Sawgin 117.00 1.42 .30

AC-134 Roller 112.00 1.36 .29

AC-134 Sawgin 118.50 1.44 .30

/1 The Pakistan Times - September 17, 1969.so Rs L.75 = $1

Table III-5: PERCENT DISTRIBUTION OF EXPORTS OF COTTON CLOTH AND YARN

4-Year

1963-64 1964-65 1965-66 1966-67 Average

Quota Countries (9)Larn

Volume 0.5 2.6 0.5 1.2 1.2

Value 0.5 2.3 0.4 1.4 1.2

ClothVolume 52.1 27.1 46. 56.5 45 .2

Value 62.8 41.9 43.4 54.1 49.5

Undeveloped Countries (45)Yarn

Volume 77.5 77.4 73.6 75.2 76.1

Value 81.9 83.0 92.1 72.5 82.2

ClothVolume 24.9 43.2 45.1 32.1 37.0

Value 29.3 44.5 46.2 31.2 38.5

Other CountriesYarnVolume 22.0 20.0 25.9 23.6 22.7

Value 17.6 14.7 7.5 26.1 15.6

ClothVolume 23.0 29.7 8.9 11.4 17.8

Value 7.9 13.6 10.4 14.7 12.0

Total Exports as % ofTotal Production

Yarn 12,1 14.8 11.0 12.5 12.7

Cloth 19.4 25.5 28.4 28.7 25.4

Source: Table III-1.

CHAPTER IV

COnTTON G.TNN'TNG

A. Introduction

76. The total area under cotton during 1968-69 was 4.36 million acres,

of which orly 34,000 acres were in the East Wing and h.33 million acres in

the West. Of the total, 3.8 million acres are under medium-staple American

varieties and 0.4 mIllion are ulnder short-staple (non-spinnable) indigenous

varieties known as "Desi". The crop during the same year is estimated to

be 2.99 million bales of 392 lbs. each, of whirh 2.79 million are medium-

staple (nominally 1 1/16 in.) and 0.20 million are Desi. No medium-staple

varieties are grown in East Pakistan.

77. Raw cotton is purchased from the farmer by the ginner according to

established grades. The ginner processes the material and bales it for mar-

ket. It is in the gin that the lint is separated from the seed, The ginner

returns from 13 to 15% of the seed contained in the purchased raw cotton to

the farmer, who uses lt for sowei-ng, stock feeding and other pu-roses. The

baled cotton is disposed of through established channels, where it is ulti-

mately utilized either by the domestic textile industry or exported.

B. Current Situation

78. Over the past 12 years, cotton crops have about doubled from approX -

mately 1.5 million bales to the nearly 3 million bales estimated for the

1969-70 season. The increase was largely the result of better cultivation

practices such as row sowing (instead of broadcast), use of fertilizers and

additional irrigation pro-vided by the tubewell program wvhich augmented canal

water supply. For the same period, domestic mill consumption also about

doubled to approximately 2 million bales.

79. Estimated 1969-70 exports ar;e 50,000 bl 'es of spinnable cotton

and 150,000 bales of non-spinnable Desi cotton. The latter is used princi-

pally in Japan for matting and surgical cottorn, anLd in Europe and the U.S.

for stuffing and surgical cotton.l/

80. Currently, there are 942 active ginning facilities in West Pakistan

of which 450 are said to be "large'". There are 33 establisIhIMents containing

worn-out equipment which are closed down. Only 260 of the 942 units contain

baling presses; it is assumed that the smaller operators tranisport their

cotton to the presses. Distribution of ginning plants is shown in Table IV-1.

81. In the past, virtually all of the plants were owned by Indian na-

tionals. After their departure from Pakistan, the properties were takeni o-ver

by Pakistani authorities who, over a period of time, allocated them to Pakistan

citizens and eventually awarded them legal title. It is said that most of

the machinery in the plants was from 20 to 40 years old at the time of allo-

cation. The new owners, during the period in which they did not have legal

1/ Purists refer to Desi as "little more than a weed".

title, understandably did little or nothing to renew or rehabilitateepnp, m1r,-n . 1T-rr±hpr_ f-rom +.hp bhpai-nninci nnperatio)n orf +the fn+ilitips I.TnQ

contracted out to local people, a procedure which added to the lack o:-inte~rest -inr efetivr prain

C.ProiLems: of} t-he Industry as They

Relate to the National Econory

82. Current capacity of the ginning industry is estimated at 3 mi:Llionb-a7es, wh-X}ch quantitati4vel is adqut 4for--,-.- P_---- prcssn _urren crops XIfu~u V~ y L10~U:;JU~ 10.U Uu.1rueIG L;LU * .Lcotton cultivation is expanded to areas where it is not now grown, more

gitning 44 iailtes wilbe elrd

83. The roller ginsa rg o d are laglyU outmoded and are in an advalced stageof physical obsolescence. Roller gins, both single and double, const:itute96% of equippment a,nd many sho-uld be retired and repiaced with modern sawgins.

84. The girming process not only separates lint from seed, but also issupposed to remove dust and other field trash through cleaning prior go actualginning. Some existing gins have precleaning equipment. Ginners are reluc-tait to install new or operate existing precleaning equipment, since -Lt re-duces the weight of ginned cotton by the amount of trash removed, therebyreducing revenue. Domestic textile mill operators report that domestic balesas received from saw gins contain 5% trash, from roller gins, 8%. Im)ortedAnerican long-staple contains about 1.5%. As a result of high trash content,some text;ile mill operators report blow room losses of up to 13%, a f-gureconsidered intolerable in the world cotton textile industry. The effect ofhigh trash content on export prices could not be determined in the timeavailable for investigation. Waste loss is related to income taxation, theallowable loss being 3.5%. The Cotton Ginners Association is lobbyinge foran increase to 6% for roller girns and 5% for saw gins in the southern zone,and 5% and 7% in the central zones, the saving purportedly to be invested incleaning equipment.

D. Recommendations

85. It is recommended that a comprehensive study of the ginning industrybe made and should include the following salient points:

(a) Establish the state of obsolescense of ginning facilities,area by area, with the objective of replacing over-agefacilities with new plants containing modern saw gins andprecleaning equipment.

(b) Where feasible, consider concentrating larger ginning fa-cilities to replace scattered small gins.

(c) Establish seed crushing facilities at the larger gins of acapacity large enough to process seed from nearby smallergins also. The refined oil and ghee industry could par-ticipate in the establishment of a logical move in the

effort to disperse industries into rural areas. Thepresent trade in cottonseed, with its inherent waste,would be eliminated if seed were crushed promptly andstored as oil, a far less expensive form for storage,handling, and transport than bulk, low-density seed.

(d) Consider promulgation of a law or regulation that all seedmust be crushed within 210 days of harvest, the objec-tive being to eliminate the present waste caused by over-long and bad storage with consequent deterioration of oilcontent. Certain countries have such a law, the purposeof which is to minimize insect infestation.

- 39 -

Table IV-1: COTTON GINS - WEST PAKISTAN-/

(Location and number)

Civil , Dlsion Toal Uris ingle P.Lol'lers I---"le Rlers Saw Gir Pess'IL VJ4.J.L . '.-.'L ± LiLid,L ULJJ.. Ij. 1j i%.VJL .L.~ L%L LU.).L 1LU-L.A.O± I U±±LLO I. IJ V0 V

Bahawalpur 133 1,775 192 44 42

Lahore 244 1,138 59 17 12

Multan 308 3,303 504 211 82

Sargodha 185 2,567 85 62 58

Rawalpind.i 25 189 55 4 5

Hyderabad &Knairpuir ou 1,404 1,319 15U 6,1

975 10,376 2,214 h88 260

worn out andinactive -33

Active 942

1/ Data for East Pakistan not available.

Source: Department of Agriculture, Government of West Pakistan, Lahore.

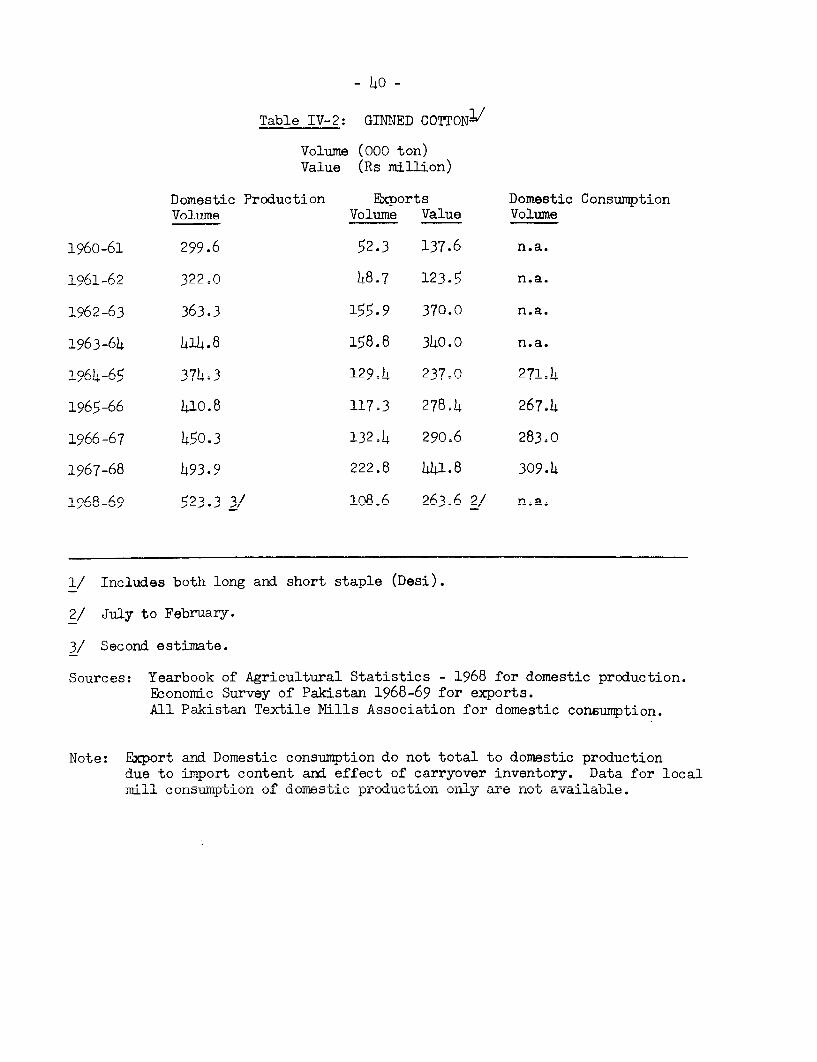

- ho -

Table IV-2: GINNED COTTONI/

Volume (000 ton)Value (Rs million)

Domestic Production Exports Domestic ConsumptionVolume Volume Value Volume

1960-61 299.6 52.3 137.6 n.a.

1961-62 322' 0 h8.7 123.5 n.a.

196-63 - 1J$.9 370.0 n.a.

1963-6) )I8), 158. 3),0.0 n.a.

1964-65 37). 3 129Ah 237.0 271 A

1 A[)_AA i n R 117 - 27R-), 2(7-),

l966=67 450, *3 132.4 290Q.6 283,0

1967-68 493.9 222.8 )W11.8 309.4

1968-69 523.3 3/ lo8-6 263.6 2/ n..

1/ Includes both long and short staple (Desi).