How do market reforms affect China's responsiveness to environmental policy

34

How do market reforms affect China’s responsiveness to environmental policy? B Karen Fisher-Vanden a, * , Mun S. Ho b a Dartmouth College, 6182 Fairchild Hall, Hanover, NH 03755, United States b Resources for the Future, United States Received 7 July 2004; received in revised form 21 April 2005; accepted 28 June 2005 Abstract A large percentage of total investment in China is allocated by the central government at below-market interest rates in pursuit of non-economic objectives. This has resulted in low rates of return and a high number of non-performing loans, threatening the future health of the Chinese economy. As a result, reform of capital markets is a high priority of the Chinese government. At the same time, the country is implementing various environmental policies to deal with serious pollution issues. In this paper we ask how reforms of the capital market will affect the functioning of a carbon tax. This allows us to assess how China’s willingness to join global efforts to reduce carbon emissions is influenced by China’s current efforts to reduce investment subsidies. We compare the costs of a carbon tax in a reformed economy with the costs of a carbon tax in the current subsidized economy. We find that in the subsidized economy the tax-interaction effect dampens the effect of a carbon tax resulting in smaller reductions in emissions than what would result in a reformed economy. Importantly, we also find that the effect on economic welfare from a carbon tax is lower in the subsidized economy; in fact, for lower levels of reductions, the carbon tax is actually welfare improving. These results have important implications for an economy undergoing economic transition. The carbon tax rate required to achieve a certain level of emission reductions will be higher in an economy with capital subsidies. However, the welfare implications 0304-3878/$ - see front matter D 2005 Elsevier B.V. All rights reserved. doi:10.1016/j.jdeveco.2005.06.004 B This work was supported by the Office of Science (BER), U.S. Department of Energy, Grant no. DE-FG02- 00ER63030. The authors would like to thank three anonymous referees for valuable comments on the original draft. * Corresponding author. Tel.: +1 603 646 0213; fax: +1 603 646 1682. E-mail address: [email protected] (K. Fisher-Vanden). Journal of Development Economics 82 (2007) 200 – 233 www.elsevier.com/locate/econbase

Transcript of How do market reforms affect China's responsiveness to environmental policy

Journal of Development Economics 82 (2007) 200–233

www.elsevier.com/locate/econbase

How do market reforms affect China’s

responsiveness to environmental policy?B

Karen Fisher-Vanden a,*, Mun S. Ho b

aDartmouth College, 6182 Fairchild Hall, Hanover, NH 03755, United StatesbResources for the Future, United States

Received 7 July 2004; received in revised form 21 April 2005; accepted 28 June 2005

Abstract

A large percentage of total investment in China is allocated by the central government at

below-market interest rates in pursuit of non-economic objectives. This has resulted in low rates of

return and a high number of non-performing loans, threatening the future health of the Chinese

economy. As a result, reform of capital markets is a high priority of the Chinese government. At

the same time, the country is implementing various environmental policies to deal with serious

pollution issues. In this paper we ask how reforms of the capital market will affect the functioning

of a carbon tax. This allows us to assess how China’s willingness to join global efforts to reduce

carbon emissions is influenced by China’s current efforts to reduce investment subsidies. We

compare the costs of a carbon tax in a reformed economy with the costs of a carbon tax in the

current subsidized economy. We find that in the subsidized economy the tax-interaction effect

dampens the effect of a carbon tax resulting in smaller reductions in emissions than what would

result in a reformed economy. Importantly, we also find that the effect on economic welfare from a

carbon tax is lower in the subsidized economy; in fact, for lower levels of reductions, the carbon

tax is actually welfare improving. These results have important implications for an economy

undergoing economic transition. The carbon tax rate required to achieve a certain level of emission

reductions will be higher in an economy with capital subsidies. However, the welfare implications

0304-3878/$ -

doi:10.1016/j.j

B This work

00ER63030. T

draft.

* Correspond

E-mail add

see front matter D 2005 Elsevier B.V. All rights reserved.

deveco.2005.06.004

was supported by the Office of Science (BER), U.S. Department of Energy, Grant no. DE-FG02-

he authors would like to thank three anonymous referees for valuable comments on the original

ing author. Tel.: +1 603 646 0213; fax: +1 603 646 1682.

ress: [email protected] (K. Fisher-Vanden).

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 201

of the tax indicate that the current system with capital subsidies is highly distorting implying that

there is a high efficiency cost for the non-economic objectives the government is pursuing by

maintaining this system of subsidies.

D 2005 Elsevier B.V. All rights reserved.

JEL classification: O10; P21; D58; Q00

Keywords: China; Environmental taxation; Capital subsidies; Carbon emissions; Global climate change;

Computable general equilibrium

1. Introduction

Are economic reforms in developing countries helping or hindering pollution

reduction and the implementation of environmental policies? Since the initiation of

market reforms in 1978, the fast-growing Chinese economy has become significantly

less energy- and carbon-intensive despite increases in household consumption of energy

as a result of increased vehicle ownership and household appliance use. There are two

factors contributing to these intensity declines. First, technological change has occurred

within Chinese industry that has led to improvements in energy and carbon efficiency.

Second, structural change, the shift from heavy to light industry and the closure of

small enterprises, has also contributed to the decline in China’s aggregate energy-

intensity. Recent studies point to technological change as an important factor behind the

past decline in China’s energy-intensity (e.g., Fisher-Vanden et al., 2004; Garbaccio et

al., 1999; Lin and Polenske, 1995). However, structural change is expected to be the

largest contributor to any future decline as China dismantles the state-directed

component of the economy through capital market reforms and privatization of state-

owned enterprises.

Although the carbon intensity of the Chinese economy is falling, total carbon emissions

are higher due to increased economic growth as a result of market reforms (Fisher-Vanden,

2003). That is, although the amount of carbon used to produce a unit of output has

decreased with the implementation of market reforms, market reforms have also led to

efficiency gains, resulting in much higher total output. The increase in carbon emissions

due to higher output levels has overwhelmed the decline in carbon intensity. This suggests

that future market reforms are likely to lead to a much higher accumulation of carbon in

the atmosphere. China is currently the second largest emitter of carbon emissions and is

projected to close in on the number one emitter (the U.S.) in the next few decades

(USDOE, 2004). Although this seems to be bad news for the environment, this previous

analysis ignored the effect market reforms may have on the economy’s responsiveness to

international climate policies.

The goal of this paper is to compare how the responsiveness to a climate policy is

affected by efforts to reform the capital markets. On the one hand, a nonreformed economy

which, as shown in previous studies, is much more carbon-intensive and may have greater

opportunities for reducing carbon emissions. On the other hand, a more efficient reformed

economy may be more responsive to an increase in the price of energy as a result of a

carbon tax policy.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233202

Although developing countries like China are unlikely to impose domestic carbon

reduction policies given their exemption from international climate treaties like the

Kyoto Protocol governing greenhouse gas emissions, they will face an opportunity cost

of emitting when an international emissions trading program is developed. Such a

program will likely allow countries facing a cap on emissions to purchase reductions

made in countries not facing a cap like China.1 If the Chinese government imposes this

opportunity cost in the form of a tax on carbon, then we should see reductions in

emissions through two channels. First, firms will attempt to substitute away from carbon-

intensive inputs, and second, consumers will substitute away from carbon-intensive

goods. Receipts from selling emission rights will raise income and consumption but

should shrink the size of carbon-intensive industries resulting in a change in the structure

of the economy.

In this paper we focus on only one market reform—capital market reform—due to its

important economic implications and likelihood of implementation in the near term.2 Prior

to 1978, China operated under a monobank system that passively collected household

savings and firms’ profits and distributed funds to enterprises based on priorities outlined

in the central plan. Since the initiation of market reforms in 1978, China has attempted to

move from a system of profit remittance to a system of taxes and retained profits. As

enterprises were able to retain more and more profits for investment purposes as a result of

these reforms, investment allocations from the state budget fell dramatically. However,

since the government controls the banks and routinely directs loans to be made based on

particular policy objectives or to keep money-losing state-owned enterprises afloat, the

majority of these domestic loans are not bmarketQ or bcommercialQ loans, but rather

government-directed bpolicyQ loans.Government-directed subsidized loans are financed by households who receive rates on

deposits that are lower than what would have prevailed if markets were allowed to operate.

Households continue to save despite these unfavorable terms due to the lack of other

available savings instruments in China, including capital controls on foreign exchange.

According to Lardy (1998), capital subsidies to loss-making state-owned enterprises are

large—since the late 1980s these subsidies amounted to at least 10% of GDP each year. As

a result of these nonmarket lending policies, a serious problem currently facing state-

owned commercial banks is the large and growing share of non-performing loans. Of total

loans outstanding in 1997, 27% were considered non-performing. Non-performing loans

have been rising 2% per year in recent years, threatening the financial health of state-

owned banks (Lardy, 1998). As a result, reform of the capital market has been a key focus

of the central government, with major reforms expected in the near future.

In this analysis we chose to focus on one environmental policy—carbon taxes—as an

illustrative example given China’s recent Environmental Tax Reform. We compare the

1 The Kyoto Protocol entered into force in February 2005. The European Union Emissions Trading System was

launched in January 2005, allowing member states to trade emission allowances and to purchases emission offsets

from countries outside of the EU. See Kruger and Pizer (2004).2 Price reform has almost completely been implemented for most commodities in China; however, privatization

has been slow in China due to issues such as the lack of government-provided social services that are currently

provided by state-owned enterprises.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 203

marginal cost of carbon emission reductions in a nonreformed economy with the marginal

cost of reductions in a reformed economy. We regard a nonreformed economy as one

where capital is subsidized in certain targeted industries and a reformed economy as one

where these subsidies do not exist. The nonreformed case represents the current situation

in China where government-supported industries and loss-making state-owned enterprises

receive loans at below-market interest rates.

Our research finds that a carbon tax imposed on a subsidized economy results in a tax–

subsidy interaction effect that dampens the economy’s responsiveness to the carbon tax

and leads to lower reductions in overall carbon emissions in both levels and percentage

terms. However, when we measure the impacts of the carbon tax in terms of welfare, the

results are striking. The marginal welfare cost associated with a given percentage reduction

in emissions is lower in the subsidized economy; in fact, for emissions reductions less than

7%, imposing a carbon tax in a subsidized economy is actually welfare improving

(ignoring the non-economic reasons for the subsidies). This is due to the fact that the

burden of the carbon tax is heavily placed on industries receiving capital subsidies. Since

these subsidies cause output to be artificially high in industries receiving the subsidies,

imposing a carbon tax reduces the size of these industries to a level that is closer to optimal

in an economy without subsidies. This reduces the level of subsidies paid by households.

For lower levels of emission reductions, this raises household income, consumption and

welfare.

These results are consistent with results documented in the environmental tax-

interaction literature (e.g., de Mooij and Bovenberg, 1998; Bovenberg and Goulder, 1997)

which find that the possibility of welfare improvements from the imposition of a pollution

tax is higher, the greater the extent to which the imposition of a new tax shifts the tax

burden from the overtaxed input factor to the undertaxed input factor. In our case, capital

in industries receiving the subsidies is undertaxed while capital in industries not receiving

the subsidies is overtaxed. Since the industries receiving these capital subsidies are also the

more carbon-intensive, a carbon tax shifts the tax burden onto subsidized capital, which is

undertaxed.

These results have important implications for an economy undergoing economic

transition. The carbon tax rate required to achieve a certain level of emission reductions

will be higher in an economy with capital subsidies. However, the welfare implications of

the tax indicate that the current system with capital subsidies is highly distorting implying

that there is a high efficiency cost for the non-economic objectives the government is

pursuing by maintaining this system of subsidies.

This paper is organized as follows. Section 2 presents the theoretical implications of

reform in order to understand the channels by which these reforms affect China’s marginal

cost of carbon abatement. Section 3 describes the numerical model used in the analysis and

Section 4 presents the results. Lastly, Section 5 offers concluding remarks.

2. Theory

The existence of capital subsidies can influence the effectiveness of a carbon tax by

altering the composition of output and relative factor prices. First, the existence of capital

Table 1

Capital subsidies by industry

Agriculture 49%

Coal mining 77%

Crude petroleum 86%

Metal ore mining 66%

Other non-metallic ore mining 71%

Food manufacturing 58%

Textiles 44%

Apparel and leather products 28%

Lumber and furniture manufacturing 29%

Paper, cultural, and educational articles 36%

Electric power 65%

Petroleum refining 64%

Chemicals 53%

Building material 39%

Primary metals 66%

Metal products 15%

Machinery 47%

Transport equipment 55%

Electric machinery and instruments 37%

Electronic and communication equipment 42%

Instruments and meters 37%

Other industry 31%

Construction 22%

Transportation & communications 36%

Commerce 29%

Public utilities 21%

Culture, education, health and research 35%

Finance and insurance 5%

Public administration 22%

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233204

subsidies implies a composition of output that is different from the composition in an

economy without the subsidy. This is the result of a modification of the factor demand

equation for capital—derived from the firm’s profit maximization problem—when capital

subsidies are imposed:3

PQ;tBQi;t

BKi;t¼ 1� si;t� �

PK;t ð1Þ

where PQ,tuproducer price of good Q at time t; Qi,tuamount of good Q produced by

firm i at time t; si,tucapital subsidy received by firm i at time t; PK,tumarket price

of capital input at time t; and Ki,tuamount of capital input purchased by firm i at

time t.

All else equal, these factor demand equations imply that firms receiving capital

subsidies will demand more capital. Therefore, due to diminishing returns to capital, a

firm’s marginal product of capital, i.e., PQ;tBQi;t

BXi;t, will be lower with the subsidy. Whether

3 See Appendix A for derivation details.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 205

an industry produces more or less depends on consumer demand. Assuming constant

returns to scale and competitive markets for goods, in equilibrium, the price of a

consumption good is equal to the cost of producing the good, i.e.,

PQ;t ¼ Z 1� si;t� �

PK;t;PL;t;PE;t;PM ;t

� �ð2Þ

where Z(d ) is the cost function that is the dual of the production function, Q(K,L,E,M),

and Px,t is the market price of input X at time t, where X =K, L, E, M denotes the capital,

labor, energy and material inputs. Therefore, the price of goods produced in subsidized

industries is lower than what the price would be if these subsidies did not exist. Assuming

normal demand functions, the demand for the good is higher and industries receiving

subsidies, therefore, will be producing a larger share of aggregate output than what would

otherwise be the case without the subsidies.

Table 1 provides a list of capital subsidies by Chinese industry. Since the industries

receiving the largest share of capital subsidies are the energy- and carbon-intensive

industries such as electric power and primary metals, an economy with capital

subsidies will be more energy- and carbon-intensive than an economy without such

subsidies.

To capture the concept of state-owned banks as the main vehicle for household savings,

we assume a monopoly bank taking deposits from households, applying the structure of

subsidies set by the government and returning the capital income to households. The

existence of capital subsidies will alter the rate of interest on these deposits which, by

affecting the household consumption–investment tradeoff decision, will have an effect on

relative factor supplies and prices. This can be seen by examining the cost of capital

equation:4

ð1� s̄ÞPK;t þ PA;t�1 pt � d 1þ ptð Þð Þ ¼ rtPA;t�1 ð3Þ

where PA,t�1uprice of capital assets at time t�1;5 ducapital depreciation rate;

rtunominal rate of return on household deposits at time t;

s̄u1�Xi

1� si;t� � Ki;t�1

Kt�1

is the weighted average subsidy; and

ptuPA;t � PA;t�1

PA;t�1

is the rate of asset inflation.

5 It is important to distinguish between PK ,t and PA ,t. PK,t is the annual rental price of capital at time t whereas

PA ,t is the price of a unit of new investment goods. Given the assumption that new investment goods are perfectly

substitutable for existing capital, as implied by the capital accumulation Eq. (A.4) in Appendix A, the price of the

existing stock is also PA ,t.

4 The cost of capital equation is derived from the owners of market capital (i.e., households) maximizing the

discounted streams of net rental income for market capital subject to the market capital accumulation equation.

See Appendix A for further details.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233206

Eq. (3) is the familiar cost of capital equation which says that the return from holding a

physical asset is equal to the interest earned on bank deposits, ignoring uncertainty and

taxes. That is, the return from spending PA,t� 1 dollars to purchase one unit of capital

assets at time t�1—consisting of the marginal product of capital, (1� s̄)PK,t, plus capital

appreciation, less depreciation losses—is equal to the interest on the deposit of PA,t� 1.

Dividing through by PA,t� 1 and rearranging, we get

ð1� s̄Þ PK;t

PA;t�1þ 1� dð Þ PA;t

PA;t�1¼ 1þ rtð Þ: ð4Þ

This cost of capital equation tells us that the nominal rate of interest is lower, holding

the rental price of capital (PK,t) and price of capital assets (PA,t) constant, in an

economy where the monopoly bank chooses to charge some favored customers a lower

rental price.

For a given path of consumption prices, PC,t, a lower nominal rate of interest will affect

the household sector’s decision on how much to save and how much to consume as

represented by the following Euler equation:6

PC;tCt

� �¼ 1þ qð Þ

1þ rtþ1ð Þ PC;tþ1Ctþ1� �

: ð5Þ

This Euler equation tells us households choose levels of consumption and savings in

order to equate discounted marginal utility over time. Therefore, from Eq. (5), a lower real

rate of interest (i.e., (1+ rt +1)PC,t /PC,t +1) would imply higher consumption in period t—

and thus, lower investment in time t. As described in Appendix A, household savings

determines the pool of investment that accumulates in the aggregate capital stock. In the

steady state, the real rate of interest is determined by the rate of time preference which is

unaffected by the existence of subsidies. The steady state stock of capital is thus smaller in

the subsidized economy in order to generate the higher marginal product required to offset

the subsidy.

Whether or not an economy with capital subsidies is more energy intensive than an

economy without these subsidies will depend on two effects. First, a change in the price of

capital will have a cross-price effect on energy demand represented by

BXE

BPK

¼ B2PQ

BPEBPK

: ð6Þ

Therefore, the cross-price effect is positive if energy and capital are substitutes in

production; i.e., an increase in the price of capital will result in an increase in the factor

demand for energy.

A second effect of capital subsidies is caused by changes in the composition of

household consumption of goods with different energy intensities. Assume there are two

goods produced—an energy-intensive (CE) good and a non-energy-intensive (CN) good.

The effect of a capital subsidy on household demand for these two consumption goods

will depend on their relative capital intensities. If the energy-intensive good is more

6 See Eq. (A.13) in Appendix A for derivation details.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 207

capital-intensive than the non-energy-intensive good, and firms producing this good do

not receive subsidies, then the higher rental price of capital will lead to a substitution

away from CE towards CN. However, if the energy-intensive good is more capital-

intensive and the firms producing this good receive subsidies, then the rental price of

capital paid by these firms is lower and the effect on the composition of output is

ambiguous.

2.1. Effects of a carbon tax

The existence of a price of carbon brought about through the implementation of, say,

an international emissions trading program, results in an opportunity cost of emitting

carbon. The country as a whole may choose to emit the marginal ton, or not emit it and

sell the right at the international market price. The government may decide to impose a

carbon tax to force domestic producers to internalize this national opportunity cost. This

would be represented as a tax on the price of energy input; i.e.,

PE;t ¼ POE;t þ tc ð7Þ

where PE,tuprice of energy input; and POE,tu seller’s price of carbon-intensive energy

(e.g., coal).

Imposing such a carbon tax, tc, on the price of energy will have two broad impacts on

the economy. First, taxing energy will cause firms to substitute away from energy towards

other factors of production (factor substitution). Second, taxing energy will increase the

relative price of energy-intensive goods, causing consumers to shift consumption towards

less energy-intensive goods (output substitution).

The literature on the environmental tax-interaction effect has discussed how the

impact of an environmental tax depends on interactions with preexisting tax distortions

in factor markets. Earlier papers in this literature focused largely on the interactions

between environmental taxes and labor taxes, and have shown that environmental taxes

raise the price of goods relative to leisure, causing households to choose more leisure.7

This exacerbates the distortionary effects of the labor tax which leads to a decline in

welfare. This tax-interaction effect is offset to some extent through the recycling of

revenue generated by the environmental tax, i.e. the new tax revenue can be used to cut the

marginal rates of other distortionary taxes in the system. We should expect a similar

interaction effect to exist in an economy with a subsidy (or negative tax) that distorts the

capital factor market. As shown in these earlier papers focused on labor taxes, the labor–

leisure trade-off gives rise to a tax-interaction effect. Similarly, a negative capital tax

should affect the consumption–savings trade-off (driven by the rate of return on capital)

which will result in an interaction effect that has welfare implications. Other papers have

considered capital as a distinct factor of production. Goulder (1995) and Williams

(1999), in particular, have found the intertemporal effects on savings and investment

7 See, for example, Bovenberg and de Mooij (1994), Bovenberg and van der Ploeg (1994), and Parry (1995).

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233208

decisions to be important.8 We examine the implications of the environmental tax-

interaction literature below.

(1) Factor substitution

The extent of factor substitution resulting from the imposition of a carbon tax will

depend on changes in relative factor prices. Consider an ad valorem tax on the price

of energy in two economies—one with capital subsidies and one without. The direct

effect of the tax will cause a substitution to other factors of production such as

capital or non-energy materials. This also leads to an increase in the price of energy-

intensive goods relative to non-energy intensive goods. How does this affect the

supply of these factors?

From the cost of capital equation (Eq. (4)), we see that changes in the price of capital

9 The

is dete10 Sin

directly

substitu

quite li

carbon11 In a

from th

where

cost of

investm

the ste

8 See

assets and rental price of capital will change the rate of interest.9 If, after

incorporating general equilibrium effects, the short run rental price of capital

increases less than the price of capital assets with the carbon tax, then the short run

rate of interest will be lower.10 In an economy with subsidized capital (i.e., s N0),

however, this effect is dampened by the existence of the capital subsidy in the first

term of Eq. (4). Therefore, changes in the market rate of interest as a result of the

carbon tax will differ depending upon whether the economy includes a subsidy on

capital or not.

Differences in the impact of the carbon tax on the rate of interest between the two

economies means that the effect on savings and investment would be different. This

has implications for the future price of capital, and thus the future price of energy

relative to capital. Therefore, after incorporating general equilibrium effects, an

equal ad valorem carbon tax imposed in each economy—breformedQ and

bnonreformedQ—will have different effects on the substitution of non-energy factors

for energy.11

This factor substitution will have welfare implications as well. As discussed above in

relation to Eq. (1), the existence of a capital subsidy will result in a demand for

capital that is higher than what would be optimal if the subsidy did not exist. Factor

substitution away from energy towards capital could exacerbate this distortion in the

price of capital assets is determined by the market for investment goods whereas the rental price of capital

rmined by the factor market for capital.

ce investment goods are typically more energy intensive than consumption goods, a carbon tax would

affect the price of investment goods—i.e., the price of assets. The rental price of capital may rise due to

tion away from energy, but that depends on the relative intensities and other factor substitution. It is

kely that the price of assets would increase more than the rental price of capital with the imposition of a

tax.

model that includes intertemporal decision making, these short-run effects can be considered separately

e effects in the long run. As shown in Appendix A, imposing a carbon tax will result in a steady state

the stock of capital will adjust so that the real rate of return again equals the rate of time preference, q. Thecapital equation (4) must still hold in this new steady state, and thus changes in the long run price of

ent goods and rental price of capital would be different in the two economies. This results in differences in

ady state capital stocks, and differences in the substitution of other inputs for energy inputs.

also Bovenberg and Goulder (1997) and de Mooij and Bovenberg (1998).

12 Bov

zero or

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 209

capital market, leading to lower welfare. This is consistent with the findings of de

Mooij and Bovenberg (1998) and Bovenberg and Goulder (1997) who find that

welfare improvements from the imposition of an environmental tax are only possible

in a situation where the environmental tax alleviates inefficiencies in the tax system.

However, factor substitution is not the only effect. Output substitution, discussed

below, will also have an effect which could offset the factor substitution effects.

(2) Output substitution

A carbon tax will also change the composition of aggregate output differently in a

reformed economy versus a nonreformed one. This occurs in two ways. First, the

intertemporal effects of the tax—through the rate of interest—will change the

household’s consumption–savings decision. As discussed above, short run changes

in the interest rate resulting from the carbon tax will differ in the two economies.

This implies that changes in the savings rate as a result of the carbon tax will be

different in the two economies. Since household savings is used to purchase

investment goods, a higher savings rate implies a higher composition of investment

goods in aggregate output. Since investment goods tend to be more energy-intensive

than consumption goods, an economy with a greater composition of investment

goods tends to be more energy-intensive.

Second, the imposition of a carbon tax affects the consumption choice between CE

and CN within a given time period. A carbon tax increases the purchase price of CE

relative to CN, causing households to substitute away from the consumption of CE.

Relative factor prices will differ between an economy with subsidized capital and an

economy without subsidized capital, leading to differences in the cost of producing

CE relative to CN. Assuming zero profits, this implies that relative prices of output

will also differ between the two economies, leading to differences in the composition

of aggregate consumption.

As shown in Table 1, the energy-intensive industries are also the industries receiving

the highest capital subsidies. Therefore, a reduction in the consumption of CE will

imply a reduction in the amount of total subsidies paid. Since households pay for

these subsidies through a lower average return to capital, a reduction in CE implies

an increase in household capital income, all else equal. However, imposing a carbon

tax adds a distortion to the economy which, unless compensated by a reduction in

another distortionary tax, will lead to lower real incomes.12 Depending upon which

effect dominates, welfare could be higher or lower.

As even the simple analytical model presented in this section illustrates, the

difference in responsiveness of a nonreformed versus reformed economy to a carbon

tax depends largely on complex interactions. Thus, to fully assess the differences in

the impact of a carbon tax in a reformed versus nonreformed economy requires a

model that can account for general equilibrium effects, including intertemporal

equilibrium. Although the above discussion helps narrow our focus on the most

important interactions driving the difference in responsiveness between the two

enberg and Goulder (1997), de Mooij and Bovenberg (1998), and Goulder (1995) were unable to achieve

negative marginal welfare cost with any alternative revenue recycling scheme.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233210

economies, purely analytical methods cannot incorporate the necessary complexity

in a tractable manner, and thus a numerical approach is required. The next section

describes a numerical model of the Chinese economy developed to analyze the

effects of a carbon tax when capital is subsidized and when it is not.

3. Numerical model

The model used in this analysis is based on computable general equilibrium (CGE)

which means that the complex interactions between the four economic agents—producers,

households, government and the foreign sector—are explicitly modeled. The production

sector consists of 29 sectors consisting of agriculture, 21 bindustrialQ sectors (including fourenergy sectors and 17 non-energy sectors), construction, and six service sectors (see Table

1). Both direct and indirect effects of policy are captured. The household sector is modeled

in two stages. The first stage determines the household’s path of aggregate consumption and

savings by solving the intertemporal utility maximization problem described in Appendix

A. In the second stage, household demand of each of the 29 commodities is determined

given aggregate consumption from the first stage. The government sector collects taxes,

allocates subsidized capital, purchases goods and services and redistributes resources. The

foreign sector is modeled using the standard one-country Armington approach. Carbon

emissions are estimated in the model based on the amount and type of fossil fuel

consumed by each of the three domestic economic actors. Further details on the model

structure, features and base case assumptions are provided in Appendix B.

The primary source of data for model parameters is a social accounting matrix (SAM)

constructed using the official 1992 input–output tables for China, and supplemented by

data on government finances, trade, labor and energy.13 Projections of the Chinese labor

force are taken from World Bank (1990). Projections for the world price of oil are taken

from the U.S. Department of Energy/EIA (1999). Other future relative world prices are

assumed to be the same as in the base year.

To simulate the effects of a reduction of capital subsidies on the structure of the Chinese

economy, we must include industry-specific subsidy rates. As described in detail in

Appendix B, these subsidy rates were estimated based on survey data from the Chinese

Academy of Social Sciences that provide data on investment by source (i.e., central budget

allocations, local budget allocations, domestic loans, retained earnings, foreign investment,

and other). These data allow us to estimate the portion of an industry’s capital stock

receiving favorable loan terms. The resulting subsidy rates are provided in Table 1.

4. Numerical results

When comparing the effects of a carbon tax in a nonreformed economy with the effects

of a carbon tax in a reformed economy, we are interested in two impacts. First, we are

13 Details on the construction of the SAM are provided in Garbaccio et al. (2000).

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 211

interested in the emission reductions generated by different carbon tax rates. This provides

us with a sense of the extent of the policy required to achieve a certain level of

environmental quality and a sense of the responsiveness of the economy (in terms of

reductions) to environmental policies. Second, we are also keenly interested in the welfare

implications of the tax since this would provide an indication of how willing the

government would be to implement such a policy. We examine both the carbon tax rates

required to achieve certain levels of emission reductions and associated welfare effects in

our analysis below. We begin with a brief description of the reference case and then

present results from the imposition of a carbon tax.

The literature on carbon taxes has been somewhat vague on the issue regarding the

precise measurement of the tax. We highlight this point by reporting two sets of results—

one using a unit carbon tax and one using an ad valorem carbon tax—in order to account

for differences in relative prices in the reformed and nonreformed economies.

4.1. Business-as-usual (BAU) scenario

Based on the model structure and assumptions outlined in the previous section, we

generate two bbusiness-as-usualQ (BAU) scenarios—one for an economy that includes

capital subsidies (the bNonreformQ case) and another for an economy that excludes these

subsidies (the bReformQ case). In the bNonreformQ scenario, the model includes industry-

specific capital subsidy rates (the s in Eqs. (1) and (4)) that are set based on the

information in Table 1. In the bReformQ scenario, on the other hand, the model assumes

these capital subsidy rates are zero. Therefore, the only difference in assumptions between

the two cases is the inclusion or exclusion of these capital subsidies; every other parameter

and exogenous variable is the same in both cases.14 These two BAU scenarios are used as

bases for comparison with simulations that include a carbon tax.

In the Reform case, the average annual growth rate of real GDP over the first 60 years is

5.3%, compared to an average annual growth rate of 4.5% in the Nonreform case. The

average annual growth of carbon emissions over this period is 3.4% in the Reform case

compared to 2.8% in the Nonreform case. Since the growth rate of GDP is larger than the

growth rate of carbon emissions in both cases, the carbon intensity of the Chinese

economy is falling over this time period. This fall in carbon intensity is larger in the

Reform case where the difference in growth rates between GDP and emissions is more

pronounced.15

4.2. Unit carbon tax

4.2.1. Effects on carbon emissions

To assess how the existence of a capital subsidy can affect the Chinese economy’s

responsiveness to environmental policy, we compare the schedule of carbon tax rates

14 It is important to note that revenues and government spending are endogenous and thus also differ in the two

cases.15 A detailed analysis of the effect of reforms on economic growth, energy use and carbon emissions in China

using a similar model is provided in Fisher-Vanden (2003).

$0

$5

$10

$15

$20

0 500 1000 1500 2000Reductions in Carbon Emissions in 2050

(Million tons carbon)

$/to

n c

arb

on

tax

No reform Reform

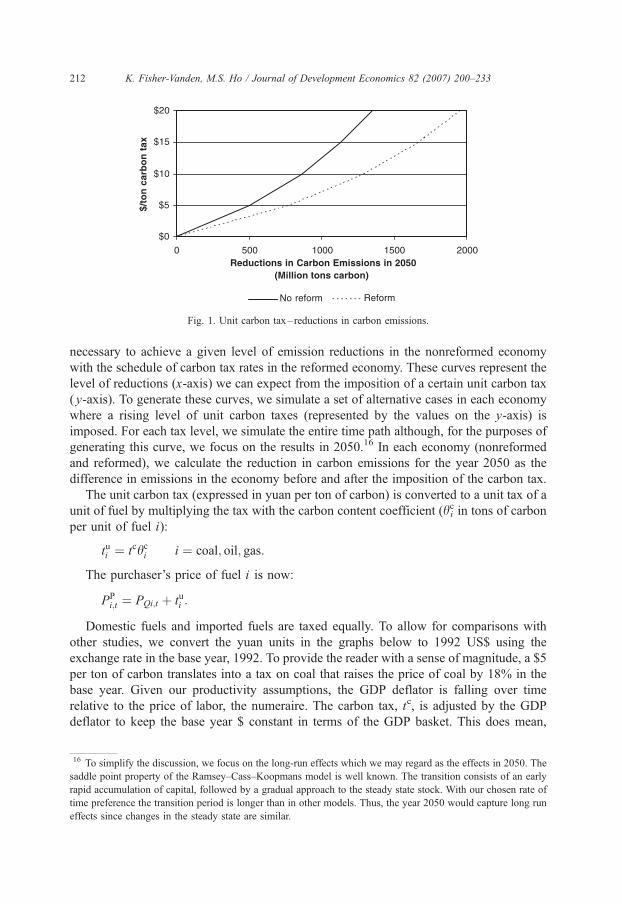

Fig. 1. Unit carbon tax–reductions in carbon emissions.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233212

necessary to achieve a given level of emission reductions in the nonreformed economy

with the schedule of carbon tax rates in the reformed economy. These curves represent the

level of reductions (x-axis) we can expect from the imposition of a certain unit carbon tax

( y-axis). To generate these curves, we simulate a set of alternative cases in each economy

where a rising level of unit carbon taxes (represented by the values on the y-axis) is

imposed. For each tax level, we simulate the entire time path although, for the purposes of

generating this curve, we focus on the results in 2050.16 In each economy (nonreformed

and reformed), we calculate the reduction in carbon emissions for the year 2050 as the

difference in emissions in the economy before and after the imposition of the carbon tax.

The unit carbon tax (expressed in yuan per ton of carbon) is converted to a unit tax of a

unit of fuel by multiplying the tax with the carbon content coefficient (hic in tons of carbon

per unit of fuel i):

tui ¼ tchci i ¼ coal; oil; gas:

The purchaser’s price of fuel i is now:

PPi;t ¼ PQi;t þ tui :

Domestic fuels and imported fuels are taxed equally. To allow for comparisons with

other studies, we convert the yuan units in the graphs below to 1992 US$ using the

exchange rate in the base year, 1992. To provide the reader with a sense of magnitude, a $5

per ton of carbon translates into a tax on coal that raises the price of coal by 18% in the

base year. Given our productivity assumptions, the GDP deflator is falling over time

relative to the price of labor, the numeraire. The carbon tax, tc, is adjusted by the GDP

deflator to keep the base year $ constant in terms of the GDP basket. This does mean,

16 To simplify the discussion, we focus on the long-run effects which we may regard as the effects in 2050. The

saddle point property of the Ramsey–Cass–Koopmans model is well known. The transition consists of an early

rapid accumulation of capital, followed by a gradual approach to the steady state stock. With our chosen rate of

time preference the transition period is longer than in other models. Thus, the year 2050 would capture long run

effects since changes in the steady state are similar.

$0

$5

$10

$15

$20

0% 10% 20% 30% 40%

Percentage Reduction in Carbon Emissions in 2050

$/T

on

Car

bo

n T

ax

Reform No Reform

Fig. 2. Unit carbon tax–% reductions in carbon emissions.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 213

however, that the $ per unit of coal or unit of oil is changing over time since the 29

commodity prices do not move in step.

The results are given in Fig. 1. We see that the reformed economy generates a much

lower schedule of carbon tax rates for reducing carbon than the nonreformed economy. Or,

put another way, at any given level of the tax, the reformed economy will generate more

emission reductions. These results, however, are partially the result of the fact that a

reformed economy (without a carbon tax) is a much larger economy than a nonreformed

economy. As discussed in Fisher-Vanden (2003), economic reforms lead to much higher

carbon emissions overall due to higher economic growth. Therefore, to control for the size

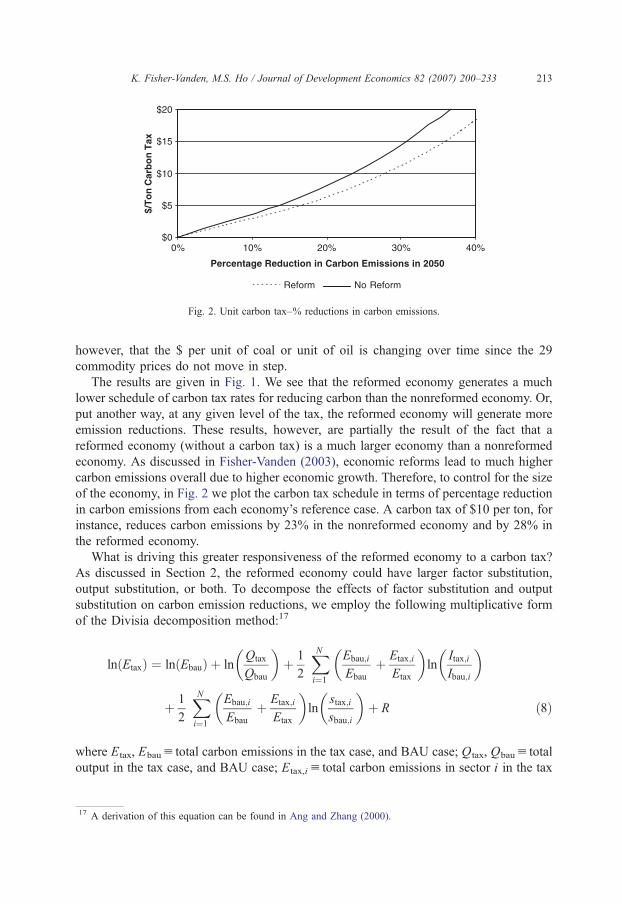

of the economy, in Fig. 2 we plot the carbon tax schedule in terms of percentage reduction

in carbon emissions from each economy’s reference case. A carbon tax of $10 per ton, for

instance, reduces carbon emissions by 23% in the nonreformed economy and by 28% in

the reformed economy.

What is driving this greater responsiveness of the reformed economy to a carbon tax?

As discussed in Section 2, the reformed economy could have larger factor substitution,

output substitution, or both. To decompose the effects of factor substitution and output

substitution on carbon emission reductions, we employ the following multiplicative form

of the Divisia decomposition method:17

ln Etaxð Þ ¼ ln Ebauð Þ þ lnQtax

Qbau

� �þ 1

2

XNi¼1

Ebau;i

Ebau

þ Etax;i

Etax

� �ln

Itax;i

Ibau;i

� �

þ 1

2

XNi¼1

Ebau;i

Ebau

þ Etax;i

Etax

� �ln

stax;i

sbau;i

� �þ R ð8Þ

where Etax, Ebauu total carbon emissions in the tax case, and BAU case; Qtax, Qbauu total

output in the tax case, and BAU case; Etax,iu total carbon emissions in sector i in the tax

17 A derivation of this equation can be found in Ang and Zhang (2000).

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233214

case; Ebau,iu total carbon emissions in sector i in the BAU case; Itax, Ibauu total carbon

intensity (E /Q) in the tax case, and BAU case; Ii,tax, Ii,bauu total carbon intensity of

sector i in the tax case, and BAU case; stax,iu sector i’s share of total output in the tax

case; sbau,iu sector i’s share of total output in the BAU case; and Ruapproximation

residual.

The first two terms, which can be combined as ln�

Ebau

QbauQtax

�, represent carbon

emissions in the tax case, conditional on output in the tax case being produced at the

same carbon intensity as in the BAU case. The third term captures changes in carbon

emissions between the BAU and tax cases due to changes in industrial sector carbon

intensity. The fourth term represents changes in total carbon emissions due to changes

in the sectoral composition of total industrial output. Since this decomposition method

is an approximation, the last term captures the residual change.

The decompositions of the emission changes due to the imposition of a $10/ton

carbon tax for each economy are provided in Table 2. We see that in both cases,

within-industry reductions in carbon intensity is the primary factor driving the decline

in overall carbon emissions with the imposition of a carbon tax. In the Reform case,

the fall in output levels has a slightly larger contribution than in the Nonreform case,

although both are small—i.e., less than 4%. In addition, changes in the sectoral

composition of output plays a slightly larger role in the Nonreform case than in the

Reform case.

These results suggest that factor substitution plays a dominant role over structural

change and is more sensitive to increases in energy prices caused by the carbon tax.

Since the reduction in carbon emissions (in percentage terms) shown in Fig. 2 is much

larger for the Reform case, this would suggest that the change in the price of energy

relative to other inputs is much higher in the Reform case. As suggested in the

discussion of factor substitution in Section 2, the increase in the price of energy relative

to capital as a result of the carbon tax may be much lower in the Nonreform case due to the

interaction of the carbon tax with the capital subsidy that exists in the Nonreform case. To

Table 2

Unit carbon tax

Terms in Divisia equation Nonreform case Reform case

Level (billion

tons carbon)

Contribution to

decline in carbon

emissions

Level (billion

tons carbon)

Contribution to

decline in carbon

emissions

First term–BAU case carbon emissions 8.2122 8.4424

Second term—change in output levels �0.0082 3.09% �0.0128 3.91%

Third term—change in within industry

carbon intensity

�0.2424 90.88% �0.2959 90.32%

Fourth term— change in industry

composition of total output

�0.0161 6.03% �0.0189 5.77%

Sum 7.9454 8.1149

Compare 7.9455 8.1150

Residual 0.0001 0.0001

Divisia decomposition of steady state emissions (year 2050).

0%

2%

4%

6%

8%

10%

12%

2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Year

% D

iffe

ren

ce i

n P

rice

of

En

erg

y/P

rice

of

Cap

ital

Nonreform case Reform case

Fig. 3. Unit carbon tax–difference in relative prices.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 215

examine this closer, we compare the increase in the price of energy relative to capital in the

two cases.

In Fig. 3 we plot the change in the ratio of the price of energy to the price of capital

as a result of a $10/ton carbon tax for the entire transition path of the two economies.18

In both cases, the increase in the relative price of energy as a result of the carbon tax

declines over time.19 Comparing the two cases, the increase in the relative price of

energy is significantly higher in the Reform case for all periods. This is consistent

with the outcome that the reformed economy exhibits a larger percentage drop in

emissions as a result of the carbon tax. But, how much of this is due to the fact that

the overall price level relative to the price of labor numeraire differs between the two

economies?

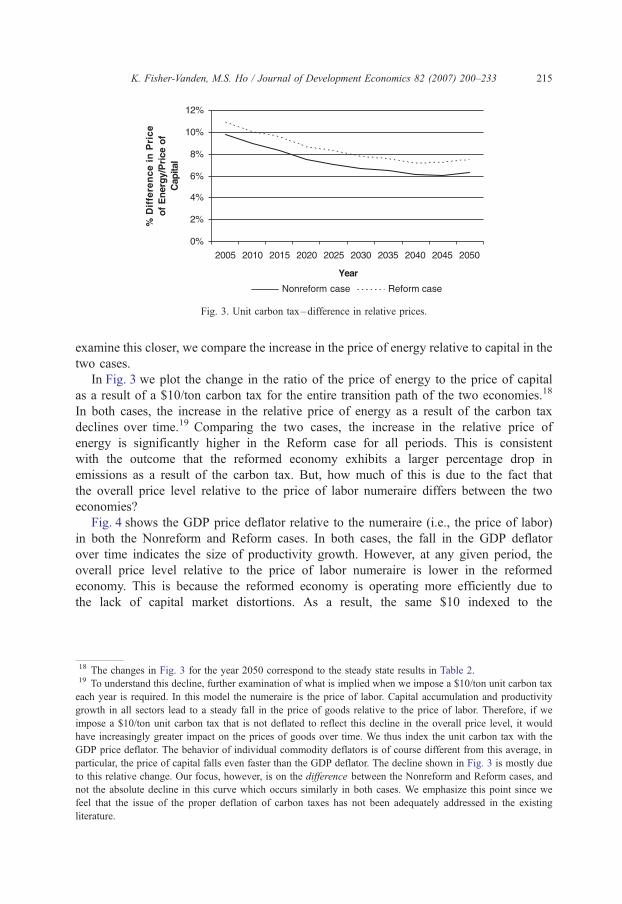

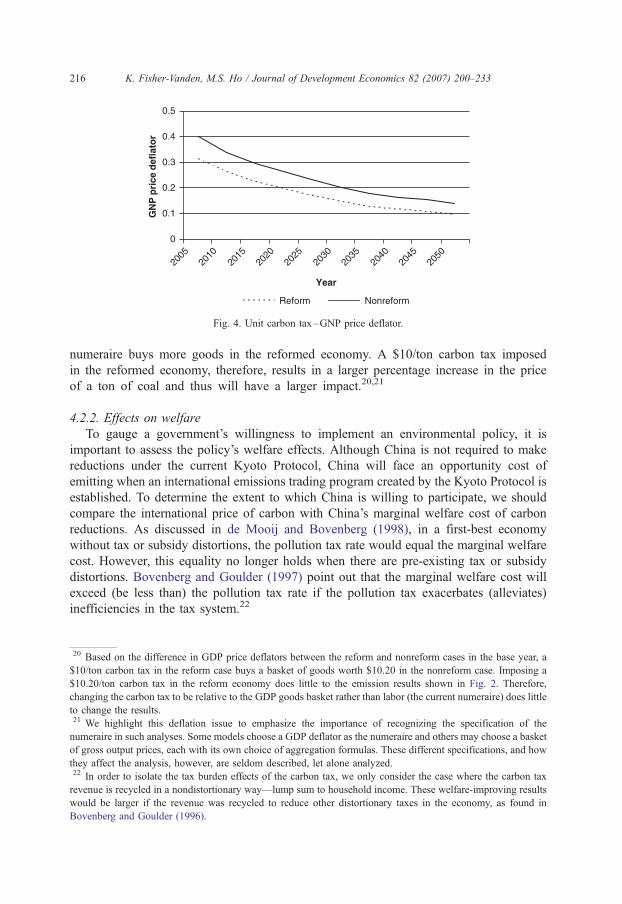

Fig. 4 shows the GDP price deflator relative to the numeraire (i.e., the price of labor)

in both the Nonreform and Reform cases. In both cases, the fall in the GDP deflator

over time indicates the size of productivity growth. However, at any given period, the

overall price level relative to the price of labor numeraire is lower in the reformed

economy. This is because the reformed economy is operating more efficiently due to

the lack of capital market distortions. As a result, the same $10 indexed to the

18 The changes in Fig. 3 for the year 2050 correspond to the steady state results in Table 2.19 To understand this decline, further examination of what is implied when we impose a $10/ton unit carbon tax

each year is required. In this model the numeraire is the price of labor. Capital accumulation and productivity

growth in all sectors lead to a steady fall in the price of goods relative to the price of labor. Therefore, if we

impose a $10/ton unit carbon tax that is not deflated to reflect this decline in the overall price level, it would

have increasingly greater impact on the prices of goods over time. We thus index the unit carbon tax with the

GDP price deflator. The behavior of individual commodity deflators is of course different from this average, in

particular, the price of capital falls even faster than the GDP deflator. The decline shown in Fig. 3 is mostly due

to this relative change. Our focus, however, is on the difference between the Nonreform and Reform cases, and

not the absolute decline in this curve which occurs similarly in both cases. We emphasize this point since we

feel that the issue of the proper deflation of carbon taxes has not been adequately addressed in the existing

literature.

0

0.1

0.2

0.3

0.4

0.5

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

Year

GN

P p

rice

def

lato

r

Reform Nonreform

Fig. 4. Unit carbon tax–GNP price deflator.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233216

numeraire buys more goods in the reformed economy. A $10/ton carbon tax imposed

in the reformed economy, therefore, results in a larger percentage increase in the price

of a ton of coal and thus will have a larger impact.20,21

4.2.2. Effects on welfare

To gauge a government’s willingness to implement an environmental policy, it is

important to assess the policy’s welfare effects. Although China is not required to make

reductions under the current Kyoto Protocol, China will face an opportunity cost of

emitting when an international emissions trading program created by the Kyoto Protocol is

established. To determine the extent to which China is willing to participate, we should

compare the international price of carbon with China’s marginal welfare cost of carbon

reductions. As discussed in de Mooij and Bovenberg (1998), in a first-best economy

without tax or subsidy distortions, the pollution tax rate would equal the marginal welfare

cost. However, this equality no longer holds when there are pre-existing tax or subsidy

distortions. Bovenberg and Goulder (1997) point out that the marginal welfare cost will

exceed (be less than) the pollution tax rate if the pollution tax exacerbates (alleviates)

inefficiencies in the tax system.22

20 Based on the difference in GDP price deflators between the reform and nonreform cases in the base year, a

$10/ton carbon tax in the reform case buys a basket of goods worth $10.20 in the nonreform case. Imposing a

$10.20/ton carbon tax in the reform economy does little to the emission results shown in Fig. 2. Therefore,

changing the carbon tax to be relative to the GDP goods basket rather than labor (the current numeraire) does little

to change the results.21 We highlight this deflation issue to emphasize the importance of recognizing the specification of the

numeraire in such analyses. Some models choose a GDP deflator as the numeraire and others may choose a basket

of gross output prices, each with its own choice of aggregation formulas. These different specifications, and how

they affect the analysis, however, are seldom described, let alone analyzed.22 In order to isolate the tax burden effects of the carbon tax, we only consider the case where the carbon tax

revenue is recycled in a nondistortionary way—lump sum to household income. These welfare-improving results

would be larger if the revenue was recycled to reduce other distortionary taxes in the economy, as found in

Bovenberg and Goulder (1996).

-$5

$0

$5

$10

$15

$20

$25

0% 10% 20% 30% 40%

Percentage Reduction in Carbon Emissions in 2050

Mar

gin

al w

elfa

re c

ost

($/

ton

)

Reform Nonreform

Fig. 5. Unit carbon tax–marginal welfare cost.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 217

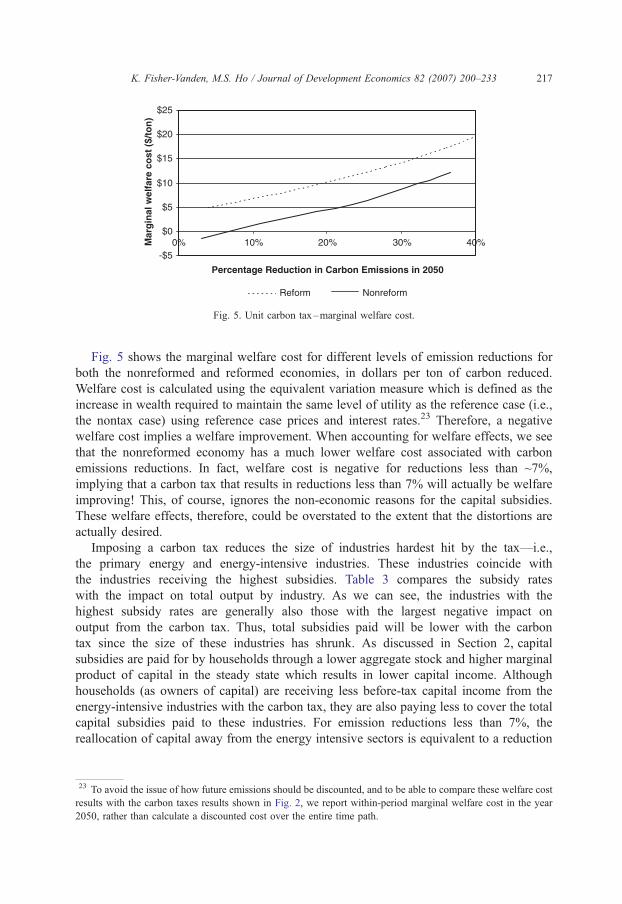

Fig. 5 shows the marginal welfare cost for different levels of emission reductions for

both the nonreformed and reformed economies, in dollars per ton of carbon reduced.

Welfare cost is calculated using the equivalent variation measure which is defined as the

increase in wealth required to maintain the same level of utility as the reference case (i.e.,

the nontax case) using reference case prices and interest rates.23 Therefore, a negative

welfare cost implies a welfare improvement. When accounting for welfare effects, we see

that the nonreformed economy has a much lower welfare cost associated with carbon

emissions reductions. In fact, welfare cost is negative for reductions less than ~7%,

implying that a carbon tax that results in reductions less than 7% will actually be welfare

improving! This, of course, ignores the non-economic reasons for the capital subsidies.

These welfare effects, therefore, could be overstated to the extent that the distortions are

actually desired.

Imposing a carbon tax reduces the size of industries hardest hit by the tax—i.e.,

the primary energy and energy-intensive industries. These industries coincide with

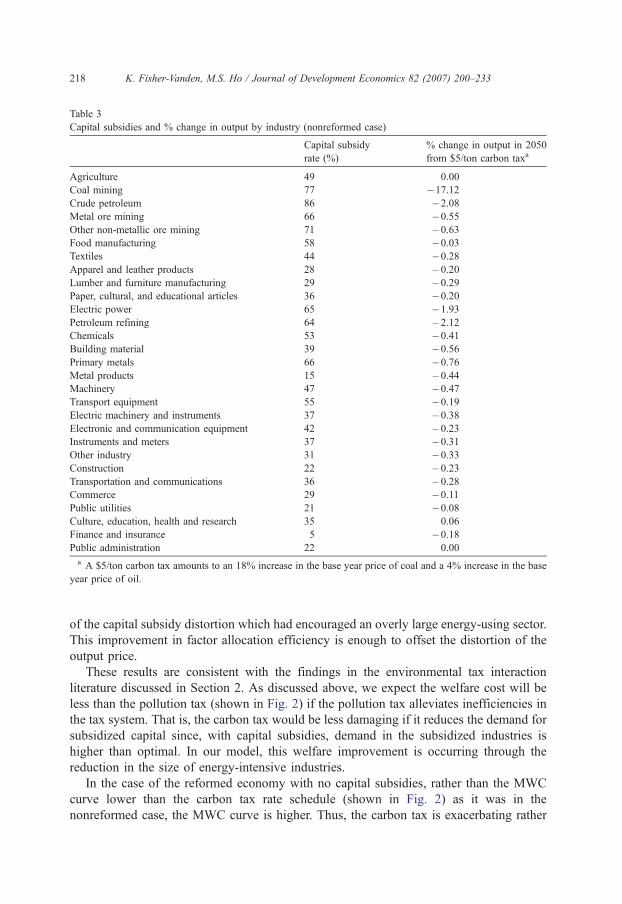

the industries receiving the highest subsidies. Table 3 compares the subsidy rates

with the impact on total output by industry. As we can see, the industries with the

highest subsidy rates are generally also those with the largest negative impact on

output from the carbon tax. Thus, total subsidies paid will be lower with the carbon

tax since the size of these industries has shrunk. As discussed in Section 2, capital

subsidies are paid for by households through a lower aggregate stock and higher marginal

product of capital in the steady state which results in lower capital income. Although

households (as owners of capital) are receiving less before-tax capital income from the

energy-intensive industries with the carbon tax, they are also paying less to cover the total

capital subsidies paid to these industries. For emission reductions less than 7%, the

reallocation of capital away from the energy intensive sectors is equivalent to a reduction

23 To avoid the issue of how future emissions should be discounted, and to be able to compare these welfare cost

results with the carbon taxes results shown in Fig. 2, we report within-period marginal welfare cost in the year

2050, rather than calculate a discounted cost over the entire time path.

Table 3

Capital subsidies and % change in output by industry (nonreformed case)

Capital subsidy

rate (%)

% change in output in 2050

from $5/ton carbon taxa

Agriculture 49 0.00

Coal mining 77 �17.12Crude petroleum 86 �2.08Metal ore mining 66 �0.55Other non-metallic ore mining 71 �0.63Food manufacturing 58 �0.03Textiles 44 �0.28Apparel and leather products 28 �0.20Lumber and furniture manufacturing 29 �0.29Paper, cultural, and educational articles 36 �0.20Electric power 65 �1.93Petroleum refining 64 �2.12Chemicals 53 �0.41Building material 39 �0.56Primary metals 66 �0.76Metal products 15 �0.44Machinery 47 �0.47Transport equipment 55 �0.19Electric machinery and instruments 37 �0.38Electronic and communication equipment 42 �0.23Instruments and meters 37 �0.31Other industry 31 �0.33Construction 22 �0.23Transportation and communications 36 �0.28Commerce 29 �0.11Public utilities 21 �0.08Culture, education, health and research 35 0.06

Finance and insurance 5 �0.18Public administration 22 0.00

a A $5/ton carbon tax amounts to an 18% increase in the base year price of coal and a 4% increase in the base

year price of oil.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233218

of the capital subsidy distortion which had encouraged an overly large energy-using sector.

This improvement in factor allocation efficiency is enough to offset the distortion of the

output price.

These results are consistent with the findings in the environmental tax interaction

literature discussed in Section 2. As discussed above, we expect the welfare cost will be

less than the pollution tax (shown in Fig. 2) if the pollution tax alleviates inefficiencies in

the tax system. That is, the carbon tax would be less damaging if it reduces the demand for

subsidized capital since, with capital subsidies, demand in the subsidized industries is

higher than optimal. In our model, this welfare improvement is occurring through the

reduction in the size of energy-intensive industries.

In the case of the reformed economy with no capital subsidies, rather than the MWC

curve lower than the carbon tax rate schedule (shown in Fig. 2) as it was in the

nonreformed case, the MWC curve is higher. Thus, the carbon tax is exacerbating rather

Table 4

Ad valorem tax rates (1992 US$)

Coal (%) Oil (%)

$5/ton 18 4

$10/ton 36 8

$15/ton 54 12

$20/ton 73 16

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 219

than alleviating distortions in the Chinese economy. The carbon tax results in lower

welfare since the tax causes a reduction in demand for capital that is less than optimal. The

carbon tax increases the price of capital intensive goods since the production of these

goods is also energy intensive. This leads to lower demand for these goods and thus lower

overall demand for capital.

4.3. Ad valorem carbon tax

As discussed in the previous section, due to differences in the price level between the

reformed and nonreformed economy, a $/ton tax will have a larger impact on the reformed

economy. To avoid these price level issues associated with the unit tax, another set of

simulations were generated where an ad valorem carbon tax (rather than a unit carbon tax)

is imposed.24 That is, instead of Eq. (7) we have:

PE;t ¼ POE;t 1þ tcð Þ:

The ad valorem tax rate was chosen to replicate the unit tax in the base year—i.e., the

year when prices are the same in both economies. Therefore, the carbon tax has the same

percentage impact on both economies. This allows us to distinguish between the tax–

subsidy interaction effect and the effects due to differences in price levels. Table 4

provides the actual ad valorem tax on coal and oil implied by each of these $/ton levels.

The new simulation results are provided in Fig. 6. For comparisons with the unit tax

results, the y-axis in Fig. 6 pertains to the $/ton unit tax replicated by the ad valorem tax in

the base year.

4.3.1. Effects on carbon emissions

The difference in the impacts on carbon emissions of an ad valorem tax between the

two economies is not as large as in the unit tax case shown in Fig. 2. However, we still see

carbon taxes having a larger impact on emissions in the reformed economy compared to

the nonreformed economy. This percentage difference between the two cases is picking up

the tax–subsidy interaction effect that exists in the nonreformed economy but not in the

reformed economy. As discussed earlier, the carbon tax is less effective in terms of

emission reductions in the nonreformed economy because the existence of a subsidy on

24 In terms of indexing, we can describe an ad valorem tax, say, on coal as a tax that is indexed by changes in the

price of coal over time. This is in contrast to the unit tax which was indexed by changes in the overall price level

(captured by the GDP deflator).

$10

$20

$30

$40

$50

20% 30% 40% 50%

Percentage reduction in carbon emissions in 2050

$/to

n c

arb

on

tax

No Reform Reform

Fig. 6. Ad valorem tax–% reductions in carbon emissions.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233220

capital dampens the effect of the carbon tax on households’ intertemporal trade-off

between savings and consumption. The carbon tax in the reformed economy causes a

much larger drop in the savings rate than in the nonreformed economy, leading to a higher

price of capital which, once general equilibrium effects are incorporated, further raises the

relative price of energy goods. In equilibrium, the increase in the price of energy relative to

other factors as a result of the carbon tax is higher in the reform economy, causing a greater

substitution away from the use of energy in production.

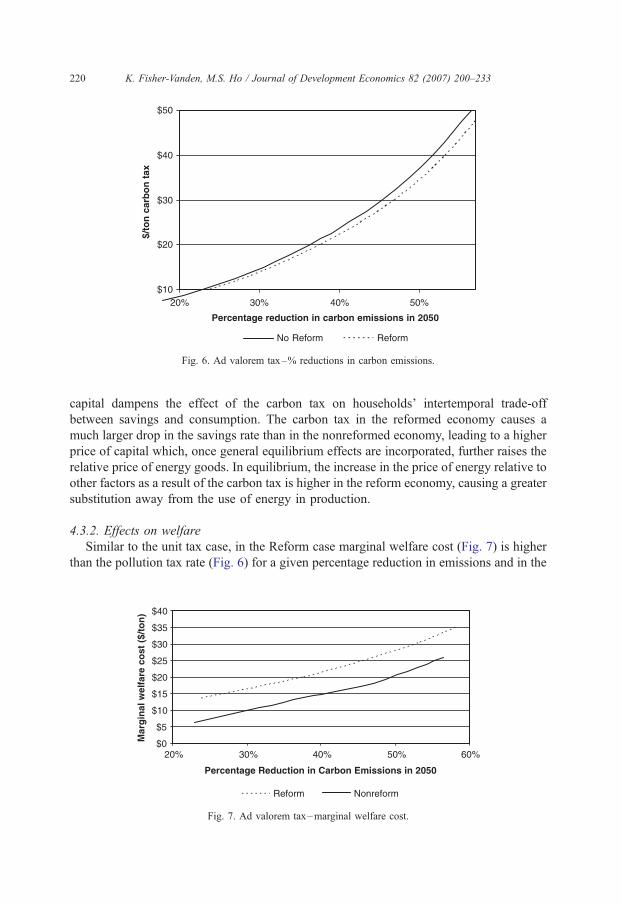

4.3.2. Effects on welfare

Similar to the unit tax case, in the Reform case marginal welfare cost (Fig. 7) is higher

than the pollution tax rate (Fig. 6) for a given percentage reduction in emissions and in the

$0

$5

$10

$15

$20

$25

$30

$35

$40

20% 30% 40% 50% 60%

Percentage Reduction in Carbon Emissions in 2050

Mar

gin

al w

elfa

re c

ost

($/

ton

)

Reform Nonreform

Fig. 7. Ad valorem tax–marginal welfare cost.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 221

Nonreform case, MWC is lower than the pollution tax rate. As explained previously, this is

because the carbon tax exacerbates distortions in the Chinese economy in the Reform case,

but alleviates distortions in the Nonreform case.

5. Conclusions

China has experienced phenomenal economic growth since the initiation of market

reforms in the late 1970s which focused on product markets. Reform of the capital

markets is far more complex and has received attention only recently. A large

percentage of total investment in China is allocated by the central government based on

development priorities. Firms receiving government-directed investment are typically

charged below-market interest rates with little attention given to project risk. This has

resulted in low rates of return and a high percentage of non-performing loans.

Reform of China’s capital market is critical to the future health of the Chinese

economy in a number of ways (see, e.g., Fisher-Vanden, 2003). In this paper, we

focused on the impact a regulated capital market has on an economy’s responsiveness to

environmental policies. In particular, we compare the carbon tax schedule associated

with carbon emission reductions in an economy with government-directed subsidized

capital with the carbon tax schedule in an economy without these subsidies. The

subsidized capital case resembles the current situation in China where government-

supported industries and loss-making state-owned enterprises receive loans at below-

market interest rates. Our results show that a carbon tax imposed on the subsidized

economy results in a tax–subsidy interaction effect that dampens the economy’s

responsiveness to the carbon tax, leading to lower reductions in overall carbon

emissions. However, for lower levels of emission reductions, imposing a carbon tax can

achieve welfare improvements in a subsidized economy, ignoring the non-economic

reasons for the subsidies. This is the result of the carbon tax reducing the size of

industries receiving the majority of capital subsidies, thus reducing the total subsidies

paid by a tax on household capital income.

Although, as shown in our analysis, capital market reforms are important for an

economy’s responsiveness to policy, we have left out other distortions such as

imperfectly competitive markets and other important areas of reform that could have

even greater implications for an economy’s responsiveness—for example, the

privatization of state-owned enterprises. Whereas capital market reforms affect the

allocation of investment flows each year, privatization affects the allocation of capital

stock or the accumulation of investment flows over time. Future research requires

the analysis of the effects of privatization on the responsiveness of the Chinese

economy.

Appendix A. Theory derivations

In China coal, oil and gas consumption comprises 93% of total primary

energy consumption, with hydroelectricity consumption making up the remaining

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233222

7%.25 As a result, and for the purpose of illustration, we therefore assume that carbon

emissions are the direct result of the amount of total energy consumed. In this theoretical

model, four factors of production—capital (K), energy (E), labor (L) and non-energy

materials (M)—are employed to produce two goods: an energy-intensive good (QE) and a

non-energy-intensive good (QN).26 In a nonreformed economy, certain protected

industries and firms receive capital at a lower than market rate of interest. These capital

subsidies are industry and firm specific, resulting in the following profit maximization

problem for firm i:

maxPi;t ¼ PQ;tQi;t � 1� si;t� �

PK;tKi;t � PL;tLi;t � PE;tEi;t � PM ;tMi;t ðA:1Þ

where Pi,tuprofit of firm i at time t; PQ,tuproducer price of good Q at time t;

Qi,tuamount of good Q (either QE or QN) produced by firm i at time t and of the form,

Qi,t=Q(Ki,t,Li,t,Ei,t,Mi,t); si,tucapital subsidy received by firm i at time t; Px,tumarket

price of input X at time t, X =K, L, E, M; Xi,tuamount of input X purchased by firm i at

time t, X =K, L, E, M.

Firm i’s demand for inputs other than capital are obtained from the following first-order

conditions for profit maximization:

PQ;tBQi;t

BXi;t¼ PX ;t where X ¼ L; E; M : ðA:2Þ

The existence of a capital subsidy modifies the firm’s demand for capital as follows:

PQ;tBQi;t

BKi;t¼ 1� si;t� �

PK;t: ðA:3Þ

The subsidy on capital is paid for by captive savings. As a result, households receive a

lower overall rate of return on capital compared to a deregulated capital market. In period

t, households save St and deposit this amount in the state bank, receiving a rate of return of

rt. The state bank collects these deposits and uses the funds to purchase investment goods

It that are accumulated into a stock of total capital assets; i.e.,

Kt ¼ 1� dð ÞKt�1 þ It: ðA:4Þ

The state bank rents these capital assets out to firms so no capital stock is wasted;

i.e.,

Kt�1 ¼Xi¼1...n

Ki;t�1: ðA:5Þ

25 Nuclear energy is a very recent addition, and biomass energy is not marketed and therefore not in the GDP

data, although separate data show a large contribution to total energy use.26 Capital and labor are supplied by households, and E and M are intermediate goods.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 223

In each period, the state bank receives a stream of income equal to the sum of the

subsidized rental income collected from each firm; i.e.,

P¯K;tKt�1 ¼Xi¼1...n

1� si;t� �

PK;tKi;t�1 ðA:6Þ

where PK,tu the non-subsidized (i.e., market) rental price of capital paid by firms at time t;

and P̄̄K,tu the average rental price of capital received by the state bank at time t.

The total value of capital assets held by the state bank at the end of t is the current value

of last period’s stock less depreciation plus investment:

PA;tKt ¼ 1� dð ÞPA;tKt�1 þ PA;tIt

PA,tuprice of capital assets at time t; ducapital depreciation rate.

The above wealth accumulation equation may also be written to make the capital gains

explicit:

PA;tKt ¼ PA;t�1Kt�1 þ PA;t � PA;t�1� �

Kt�1 � dPA;tKt�1 þ PA;tIt:

The value of new investment is the household saving deposits at time t, plus capital

income collected at time t (Eq. (A.6)), minus interest payments to households; i.e.,

PA;tIt ¼ St þ P¯K;tKt�1 � rtPA;t�1Kt�1 ðA:7Þ

where rtu rate of return on household deposits at time t.

The return on savings made at time t�1 is equal to the capital income generated plus

net capital appreciation; i.e.,

rtPA;t�1Kt�1 ¼ P¯K;tKt�1 þ PA;t � PA;t�1� �

Kt�1 � dPA;tKt�1: ðA:8Þ

Since the state bank controlled stock of capital assets is the only assumed vehicle for

household savings,27 households face rt in their decision of how much to consume and

save in each period. Dividing through by Kt� 1, we obtain the following cost-of-capital

equation:

ð1� s̄ÞPK;t þ PA;t�1 pt � d 1þ ptð Þð Þ ¼ rtPA;t�1 ðA:9Þ

27 This assumption is consistent with the situation in China where the only savings option available to

households historically has been to hold deposits in state banks. In 1994, the household savings rate was

estimated at 31% (World Bank, 1997). Factors contributing to the high rate of household savings include the lack

of consumer credit requiring households to save for big ticket items; uncertainty with respect to the future

availability of retirement, medical, and educational benefits; and firms requiring workers to invest a portion of

their earnings in the firm—a form of forced savings.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233224

where

s̄u1�Xi

1� si;t� � Ki;t�1

Kt�1is the weighted average subsidy; and

ptuPA;t � PA;t�1

PA;t�1is the rate of asset inflation:

Dividing through by PA,t� 1 and rearranging, we get

ð1� s̄Þ PK;t

PA;t�1þ 1� dð Þ PA;t

PA;t�1¼ 1þ rtð Þ: ðA:10Þ

The household sector determines how much of the two goods to consume and how

much to save in each period by solving an intertemporal utility maximization problem.

We apply the Ramsey–Cass–Koopmans formulation (see, e.g. Barro and Sala-I-Martin,

1998) where households maximize the discounted sum of the log of aggregate

consumption:

MaxCt

Xlt¼1

1

1þ qð Þtlog Ctð Þ ðA:11Þ

subject to an intertemporal budget constraint:

Xlt¼1

1

Pts¼0 1þ rsð Þ Yt ¼

Xlt¼1

1

Pts¼0 1þ rsð Þ PC;tCt

� �ðA:12Þ

where Ctuaggregate consumption at time t; qu rate of time preference; Ytuhousehold

income at time t; rtumarket rate of interest at time t from Eq. (A.10); and PC,tuprice

of aggregate consumption at time t.

Maximizing Eq. (A.11) subject to Eq. (A.12) gives the familiar Euler equation:

PC;tCt

� �¼ 1þ qð Þ

1þ rtþ1ð Þ PC;tþ1Ctþ1� �

: ðA:13Þ

Household savings (St) is the residual of subtracting the value of aggregate

consumption in period t from after-tax household income in period t:

St ¼ Yt � PC;tCt: ðA:14ÞWe assume that the utility function is separable so that aggregate consumption is

divided between the two goods (energy-intensive and non-energy intensive) independent

of the rate of interest.28 Household consumption of the two goods is derived by

maximizing the intra-period utility function, U(CE,CN), subject to the following budget

constraint:

PC;tCt ¼ PCE;tCE;t þ PCN;t

CN;t ðA:15Þwhere CE,tuhousehold consumption of the energy-intensive good; and CN,tuhousehold

consumption of the non-energy-intensive good.

28 The inclusion of leisure in the utility function to allow for labor–leisure trade-offs may not be appropriate for

China, and therefore was not included in this formulation.

K. Fisher-Vanden, M.S. Ho / Journal of Development Economics 82 (2007) 200–233 225

The steady state of this economy is reached when all real quantities are constant relative

to effective labor supply. Consider, for simplicity, the case with no technical change and no

population growth. The steady state is then defined by:

Ct ¼ Ct�1 ¼ CSS and Kt ¼ Kt�1 ¼ KSS ðA:16Þ

where the SS subscript denotes steady state values. These imply that

ISS ¼ dKSS

rSS ¼ q: ðA:17Þ

Appendix B. Numerical model description

B.1 Model structure

B.1.1. Production sector

To simulate the effects of policy on structural change—e.g., the shift from heavy

industrial production to light—and thus on energy use and carbon emissions, the

producing sector is split into 29 sectors consisting of agriculture, 21 bindustrialQ sectors,construction, and six service sectors as listed in Table 1. The term industrial in the Chinese

data refers to mining, manufacturing and utilities. These 21 sectors include four energy

sectors (coal mining, crude oil/natural gas, refined oil and electricity) and 17 non-energy

sectors. Each sector chooses an input mix that maximizes profit in a manner similar to that

described in Appendix A. Instead of a simple production function like that given in Eq.

(A.1), output is produced from capital, labor, land and 19 intermediate inputs using a

nested production structure:

Qi;t ¼ f Ki;t; Li;t; Ti;t;E dð Þ;M dð Þ; t� �

ðB:1Þ

where Ti,tu land input; Ki,tucapital input; Li,tu labor input; Ei,tu intermediate energy

inputs; and Mi,tu intermediate non-energy materials inputs.

The nested structure of production in industry i at time t is depicted in Fig. B.1.

The zero profit condition of the producers is given by:

PQ;tQi;t ¼ 1� si;t� �

PK;tKi;t � PL;tLi;t � PE;tEi;t � PM ;tMi;t: ðB:2Þ

B.1.2. Household sector

The household sector is modeled in two stages. In the first stage, the household

determines its path of aggregate consumption and savings as described in Appendix A

(Eqs. A.11–A.14). Household income is defined as:

Yt ¼ 1� tlð Þ PL;tLt� �

þ 1� tk 1� dð Þð ÞYK;t þ Govt transferst

þ ROW transferst � FEESt ðB:3Þ

Qi,t

Ti,t Ki,t Li,t Ei,t Mi,t

--coal --agriculture --transport equip