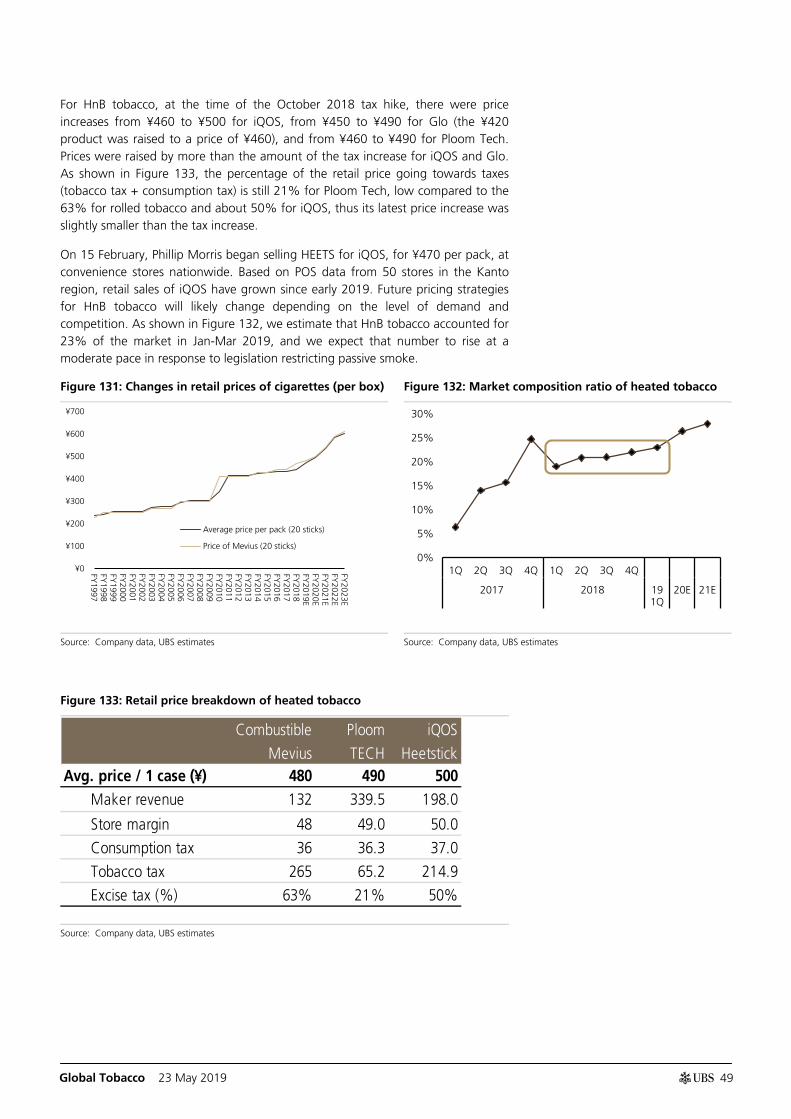

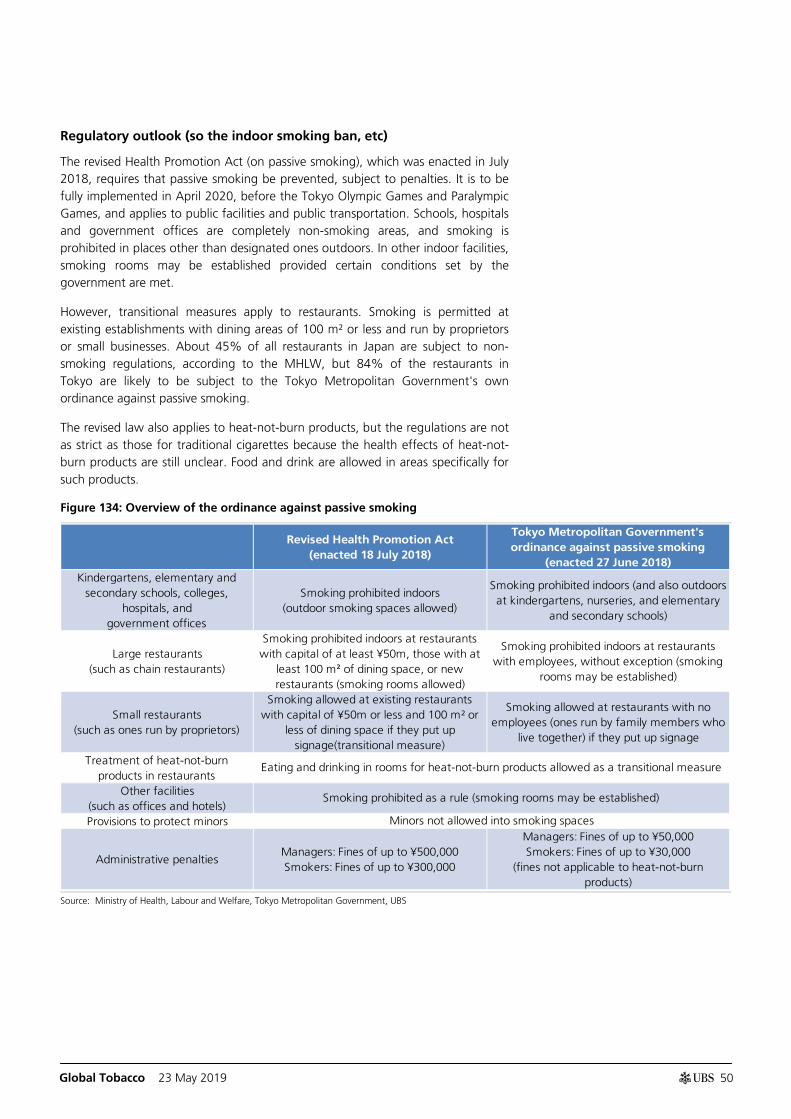

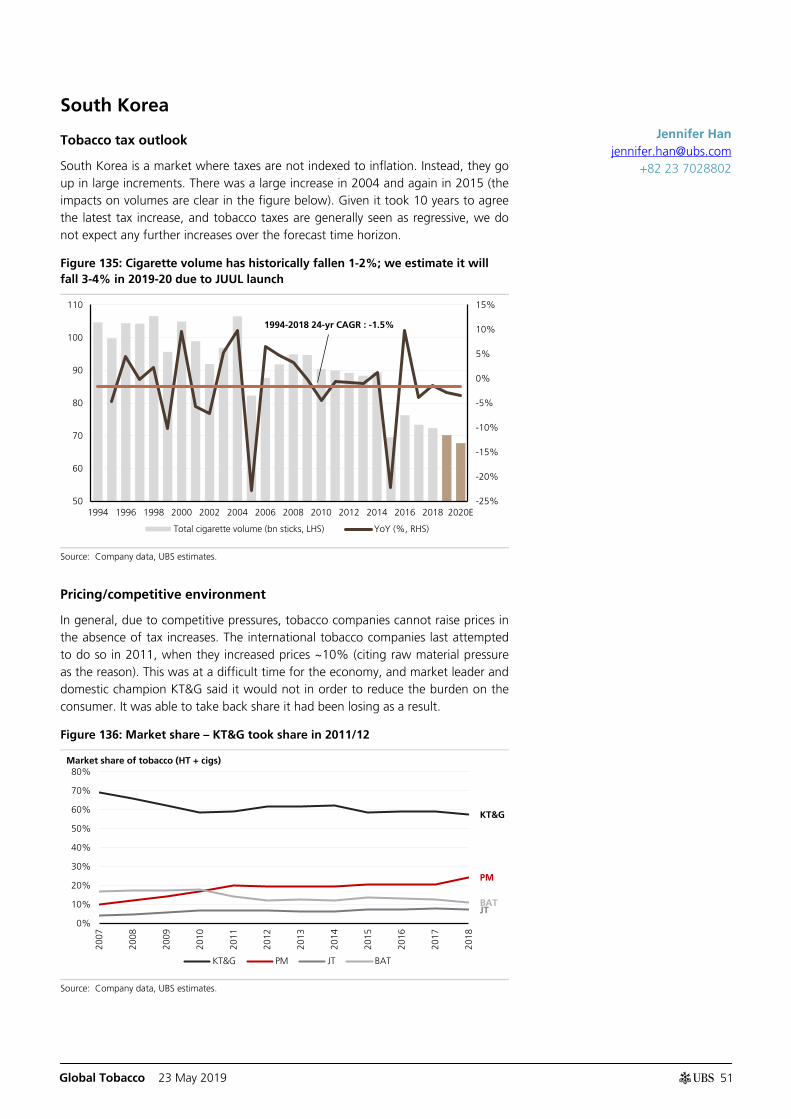

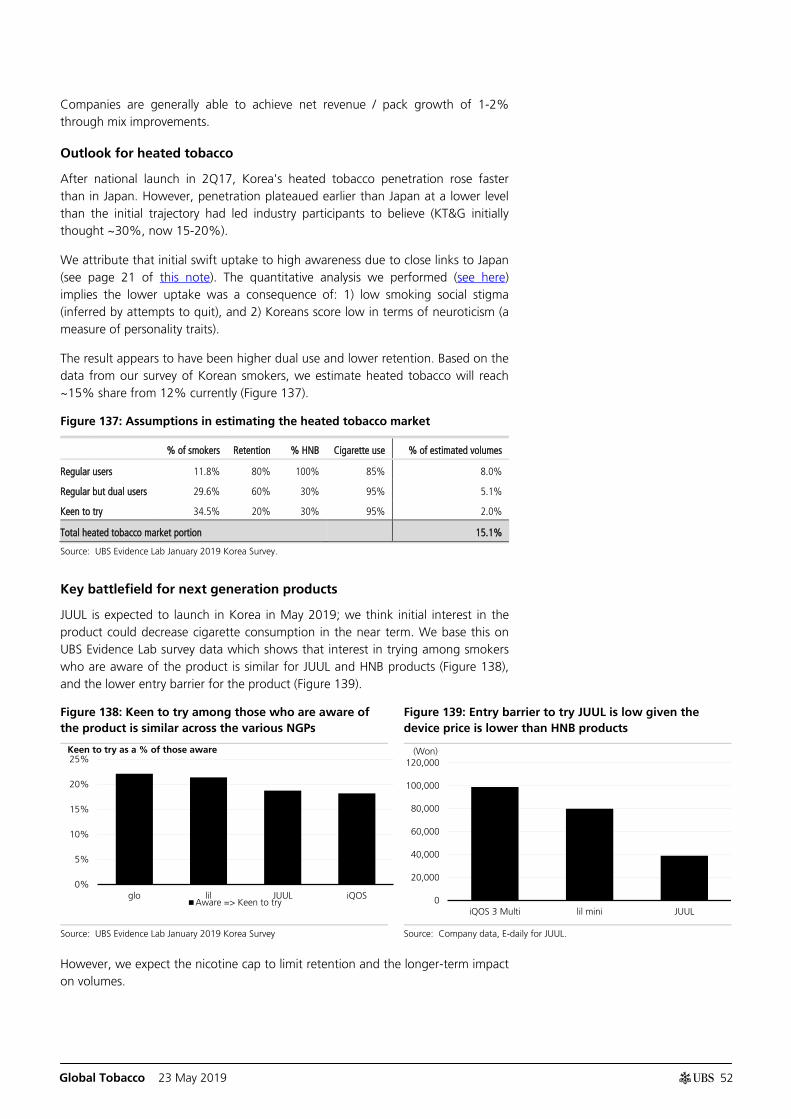

Global Tobacco

92

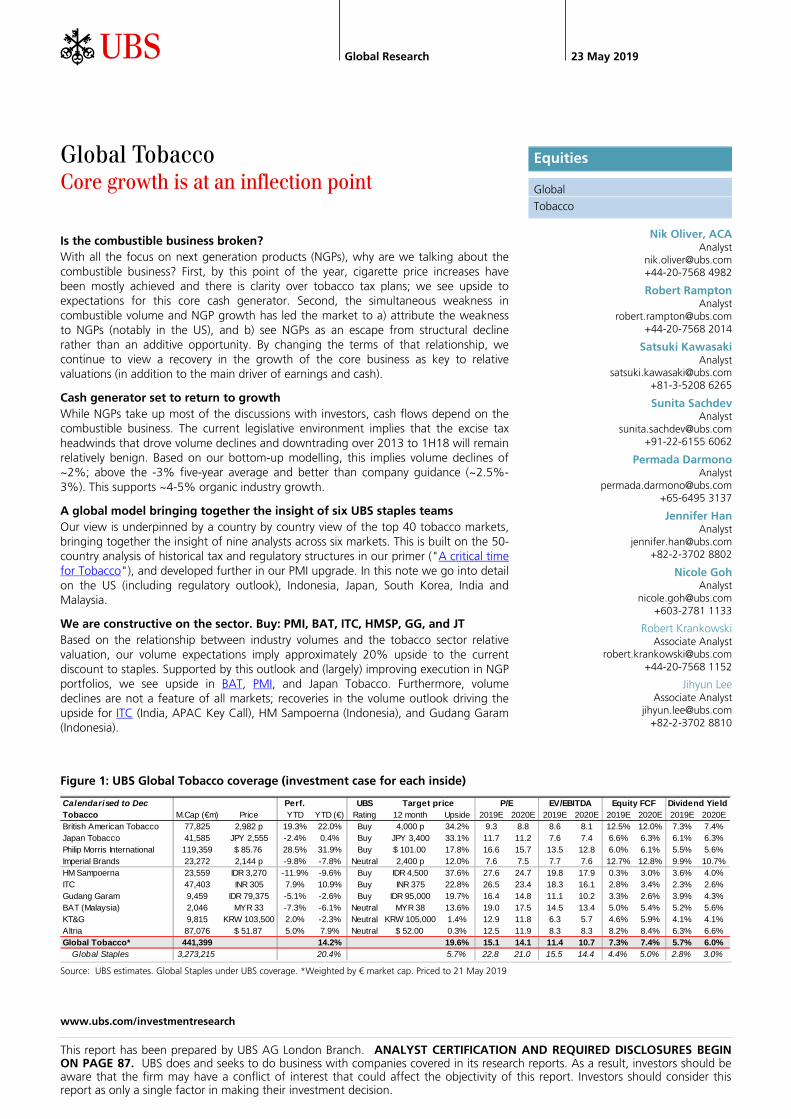

www.ubs.com/investmentresearch This report has been prepared by UBS AG London Branch. ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 87. UBS does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Global Research 23 May 2019 Global Tobacco Core growth is at an inflection point Is the combustible business broken? With all the focus on next generation products (NGPs), why are we talking about the combustible business? First, by this point of the year, cigarette price increases have been mostly achieved and there is clarity over tobacco tax plans; we see upside to expectations for this core cash generator. Second, the simultaneous weakness in combustible volume and NGP growth has led the market to a) attribute the weakness to NGPs (notably in the US), and b) see NGPs as an escape from structural decline rather than an additive opportunity. By changing the terms of that relationship, we continue to view a recovery in the growth of the core business as key to relative valuations (in addition to the main driver of earnings and cash). Cash generator set to return to growth While NGPs take up most of the discussions with investors, cash flows depend on the combustible business. The current legislative environment implies that the excise tax headwinds that drove volume declines and downtrading over 2013 to 1H18 will remain relatively benign. Based on our bottom-up modelling, this implies volume declines of ~2%; above the -3% five-year average and better than company guidance (~2.5%- 3%). This supports ~4-5% organic industry growth. A global model bringing together the insight of six UBS staples teams Our view is underpinned by a country by country view of the top 40 tobacco markets, bringing together the insight of nine analysts across six markets. This is built on the 50- country analysis of historical tax and regulatory structures in our primer ("A critical time for Tobacco"), and developed further in our PMI upgrade. In this note we go into detail on the US (including regulatory outlook), Indonesia, Japan, South Korea, India and Malaysia. We are constructive on the sector. Buy: PMI, BAT, ITC, HMSP, GG, and JT Based on the relationship between industry volumes and the tobacco sector relative valuation, our volume expectations imply approximately 20% upside to the current discount to staples. Supported by this outlook and (largely) improving execution in NGP portfolios, we see upside in BAT, PMI, and Japan Tobacco. Furthermore, volume declines are not a feature of all markets; recoveries in the volume outlook driving the upside for ITC (India, APAC Key Call), HM Sampoerna (Indonesia), and Gudang Garam (Indonesia). Figure 1: UBS Global Tobacco coverage (investment case for each inside) Source: UBS estimates. Global Staples under UBS coverage. *Weighted by € market cap. Priced to 21 May 2019 Calendarised to Dec Perf. UBS Target price P/E EV/EBITDA Equity FCF Dividend Yield Tobacco M.Cap (€m) Price YTD YTD (€) Rating 12 month Upside 2019E 2020E 2019E 2020E 2019E 2020E 2019E 2020E British American Tobacco 77,825 2,982 p 19.3% 22.0% Buy 4,000 p 34.2% 9.3 8.8 8.6 8.1 12.5% 12.0% 7.3% 7.4% Japan Tobacco 41,585 JPY 2,555 -2.4% 0.4% Buy JPY 3,400 33.1% 11.7 11.2 7.6 7.4 6.6% 6.3% 6.1% 6.3% Philip Morris International 119,359 $ 85.76 28.5% 31.9% Buy $ 101.00 17.8% 16.6 15.7 13.5 12.8 6.0% 6.1% 5.5% 5.6% Imperial Brands 23,272 2,144 p -9.8% -7.8% Neutral 2,400 p 12.0% 7.6 7.5 7.7 7.6 12.7% 12.8% 9.9% 10.7% HM Sampoerna 23,559 IDR 3,270 -11.9% -9.6% Buy IDR 4,500 37.6% 27.6 24.7 19.8 17.9 0.3% 3.0% 3.6% 4.0% ITC 47,403 INR 305 7.9% 10.9% Buy INR 375 22.8% 26.5 23.4 18.3 16.1 2.8% 3.4% 2.3% 2.6% Gudang Garam 9,459 IDR 79,375 -5.1% -2.6% Buy IDR 95,000 19.7% 16.4 14.8 11.1 10.2 3.3% 2.6% 3.9% 4.3% BAT (Malaysia) 2,046 MYR 33 -7.3% -6.1% Neutral MYR 38 13.6% 19.0 17.5 14.5 13.4 5.0% 5.4% 5.2% 5.6% KT&G 9,815 KRW 103,500 2.0% -2.3% Neutral KRW 105,000 1.4% 12.9 11.8 6.3 5.7 4.6% 5.9% 4.1% 4.1% Altria 87,076 $ 51.87 5.0% 7.9% Neutral $ 52.00 0.3% 12.5 11.9 8.3 8.3 8.2% 8.4% 6.3% 6.6% Global Tobacco* 441,399 14.2% 19.6% 15.1 14.1 11.4 10.7 7.3% 7.4% 5.7% 6.0% Global Staples 3,273,215 20.4% 5.7% 22.8 21.0 15.5 14.4 4.4% 5.0% 2.8% 3.0% Equities Global Tobacco Nik Oliver, ACA Analyst [email protected] +44-20-7568 4982 Robert Rampton Analyst [email protected] +44-20-7568 2014 Satsuki Kawasaki Analyst [email protected] +81-3-5208 6265 Sunita Sachdev Analyst [email protected] +91-22-6155 6062 Permada Darmono Analyst [email protected] +65-6495 3137 Jennifer Han Analyst [email protected] +82-2-3702 8802 Nicole Goh Analyst [email protected] +603-2781 1133 Robert Krankowski Associate Analyst [email protected] +44-20-7568 1152 Jihyun Lee Associate Analyst [email protected] +82-2-3702 8810

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Global Tobacco

www.ubs.com/investmentresearch

This report has been prepared by UBS AG London Branch. ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 87. UBS does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Global Research 23 May 2019

Global Tobacco Core growth is at an inflection point

Is the combustible business broken? With all the focus on next generation products (NGPs), why are we talking about the combustible business? First, by this point of the year, cigarette price increases have been mostly achieved and there is clarity over tobacco tax plans; we see upside to expectations for this core cash generator. Second, the simultaneous weakness in combustible volume and NGP growth has led the market to a) attribute the weakness to NGPs (notably in the US), and b) see NGPs as an escape from structural decline rather than an additive opportunity. By changing the terms of that relationship, we continue to view a recovery in the growth of the core business as key to relative valuations (in addition to the main driver of earnings and cash).

Cash generator set to return to growth While NGPs take up most of the discussions with investors, cash flows depend on the combustible business. The current legislative environment implies that the excise tax headwinds that drove volume declines and downtrading over 2013 to 1H18 will remain relatively benign. Based on our bottom-up modelling, this implies volume declines of ~2%; above the -3% five-year average and better than company guidance (~2.5%-3%). This supports ~4-5% organic industry growth.

A global model bringing together the insight of six UBS staples teams Our view is underpinned by a country by country view of the top 40 tobacco markets, bringing together the insight of nine analysts across six markets. This is built on the 50-country analysis of historical tax and regulatory structures in our primer ("A critical time for Tobacco"), and developed further in our PMI upgrade. In this note we go into detail on the US (including regulatory outlook), Indonesia, Japan, South Korea, India and Malaysia.

We are constructive on the sector. Buy: PMI, BAT, ITC, HMSP, GG, and JT Based on the relationship between industry volumes and the tobacco sector relative valuation, our volume expectations imply approximately 20% upside to the current discount to staples. Supported by this outlook and (largely) improving execution in NGP portfolios, we see upside in BAT, PMI, and Japan Tobacco. Furthermore, volume declines are not a feature of all markets; recoveries in the volume outlook driving the upside for ITC (India, APAC Key Call), HM Sampoerna (Indonesia), and Gudang Garam (Indonesia).

Figure 1: UBS Global Tobacco coverage (investment case for each inside)

Source: UBS estimates. Global Staples under UBS coverage. *Weighted by € market cap. Priced to 21 May 2019

Calendarised to Dec Perf. UBS Target price P/E EV/EBITDA Equity FCF Dividend YieldTobacco M.Cap (€m) Price YTD YTD (€) Rating 12 month Upside 2019E 2020E 2019E 2020E 2019E 2020E 2019E 2020EBritish American Tobacco 77,825 2,982 p 19.3% 22.0% Buy 4,000 p 34.2% 9.3 8.8 8.6 8.1 12.5% 12.0% 7.3% 7.4%Japan Tobacco 41,585 JPY 2,555 -2.4% 0.4% Buy JPY 3,400 33.1% 11.7 11.2 7.6 7.4 6.6% 6.3% 6.1% 6.3%Philip Morris International 119,359 $ 85.76 28.5% 31.9% Buy $ 101.00 17.8% 16.6 15.7 13.5 12.8 6.0% 6.1% 5.5% 5.6%Imperial Brands 23,272 2,144 p -9.8% -7.8% Neutral 2,400 p 12.0% 7.6 7.5 7.7 7.6 12.7% 12.8% 9.9% 10.7%HM Sampoerna 23,559 IDR 3,270 -11.9% -9.6% Buy IDR 4,500 37.6% 27.6 24.7 19.8 17.9 0.3% 3.0% 3.6% 4.0%ITC 47,403 INR 305 7.9% 10.9% Buy INR 375 22.8% 26.5 23.4 18.3 16.1 2.8% 3.4% 2.3% 2.6%Gudang Garam 9,459 IDR 79,375 -5.1% -2.6% Buy IDR 95,000 19.7% 16.4 14.8 11.1 10.2 3.3% 2.6% 3.9% 4.3%BAT (Malaysia) 2,046 MYR 33 -7.3% -6.1% Neutral MYR 38 13.6% 19.0 17.5 14.5 13.4 5.0% 5.4% 5.2% 5.6%KT&G 9,815 KRW 103,500 2.0% -2.3% Neutral KRW 105,000 1.4% 12.9 11.8 6.3 5.7 4.6% 5.9% 4.1% 4.1%Altria 87,076 $ 51.87 5.0% 7.9% Neutral $ 52.00 0.3% 12.5 11.9 8.3 8.3 8.2% 8.4% 6.3% 6.6%Global Tobacco* 441,399 14.2% 19.6% 15.1 14.1 11.4 10.7 7.3% 7.4% 5.7% 6.0%

Global Staples 3,273,215 20.4% 5.7% 22.8 21.0 15.5 14.4 4.4% 5.0% 2.8% 3.0%

Equities

Global

Tobacco

Nik Oliver, ACA Analyst

[email protected] +44-20-7568 4982

Robert Rampton Analyst

[email protected] +44-20-7568 2014

Satsuki Kawasaki Analyst

[email protected] +81-3-5208 6265

Sunita Sachdev Analyst

[email protected] +91-22-6155 6062

Permada Darmono Analyst

[email protected] +65-6495 3137

Jennifer Han Analyst

[email protected] +82-2-3702 8802

Nicole Goh Analyst

[email protected] +603-2781 1133

Robert Krankowski Associate Analyst

[email protected] +44-20-7568 1152

Jihyun Lee Associate Analyst

[email protected] +82-2-3702 8810

Global Tobacco 23 May 2019

2

Contents

Executive summary .......................................................................... 4

Company investment cases ........................................................... 11

British American Tobacco (Buy, PT £40) ..................................................... 12

Japan Tobacco (Buy, PT JPY 3,400) ............................................................ 13

Philip Morris International (Buy, PT $101) ................................................... 14

Imperial Brands (Neutral, PT £24.00) .......................................................... 15

ITC (Buy, PT Rs375) .................................................................................... 16

Gudang Garam (Buy, PT Rp 95,000) .......................................................... 17

HM Sampoerna (Buy, PT Rp 4,500) ............................................................ 18

Altria (Neutral, PT $52) .............................................................................. 19

KT&G (Neutral, PT KRW 105,000) .............................................................. 20

BAT Malaysia (Neutral, PT RM 38.00) ......................................................... 21

Building a global tobacco model .................................................. 22

Global tobacco drivers ................................................................... 24

Volumes – record declines ......................................................................... 24

Revenue – struggling to offset declines ...................................................... 27

Tobacco industry outlook .............................................................. 28

Implications for organic growth – the model is fine .................................... 31

Volume upside – taking share from illicit? .................................................. 35

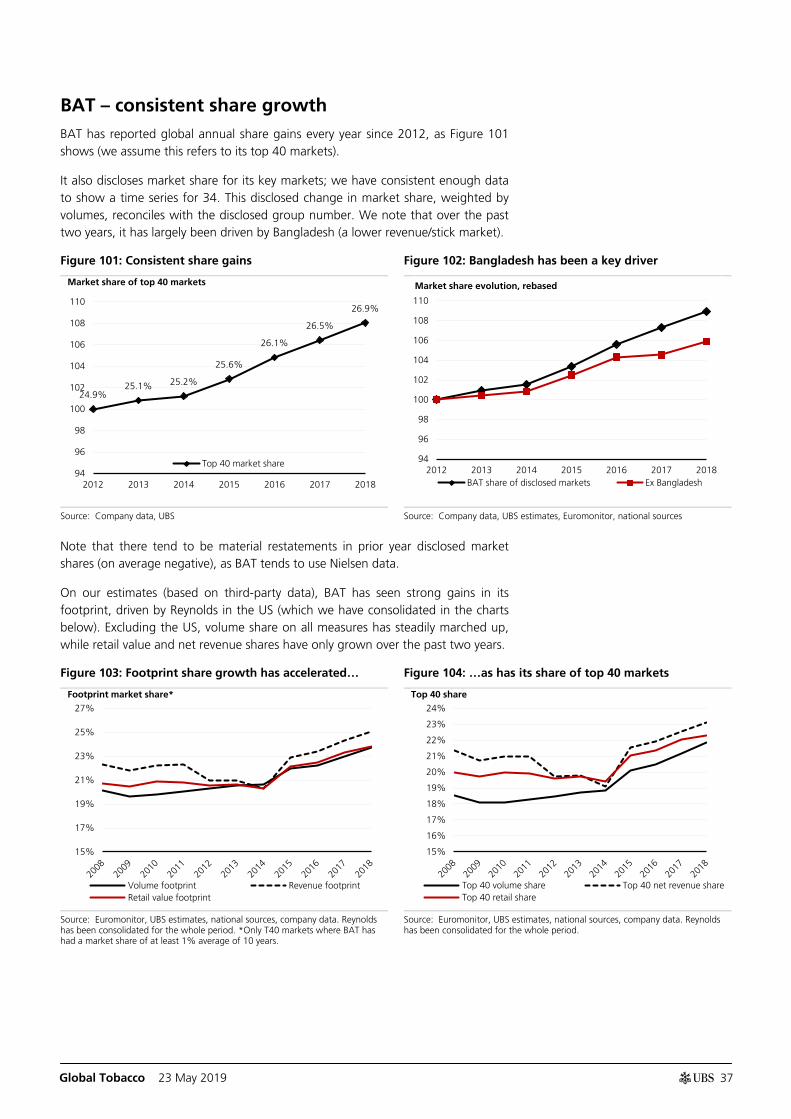

Who is gaining share? ................................................................... 36

PMI – iQOS is/will be the share driver ......................................................... 36

BAT – consistent share growth................................................................... 37

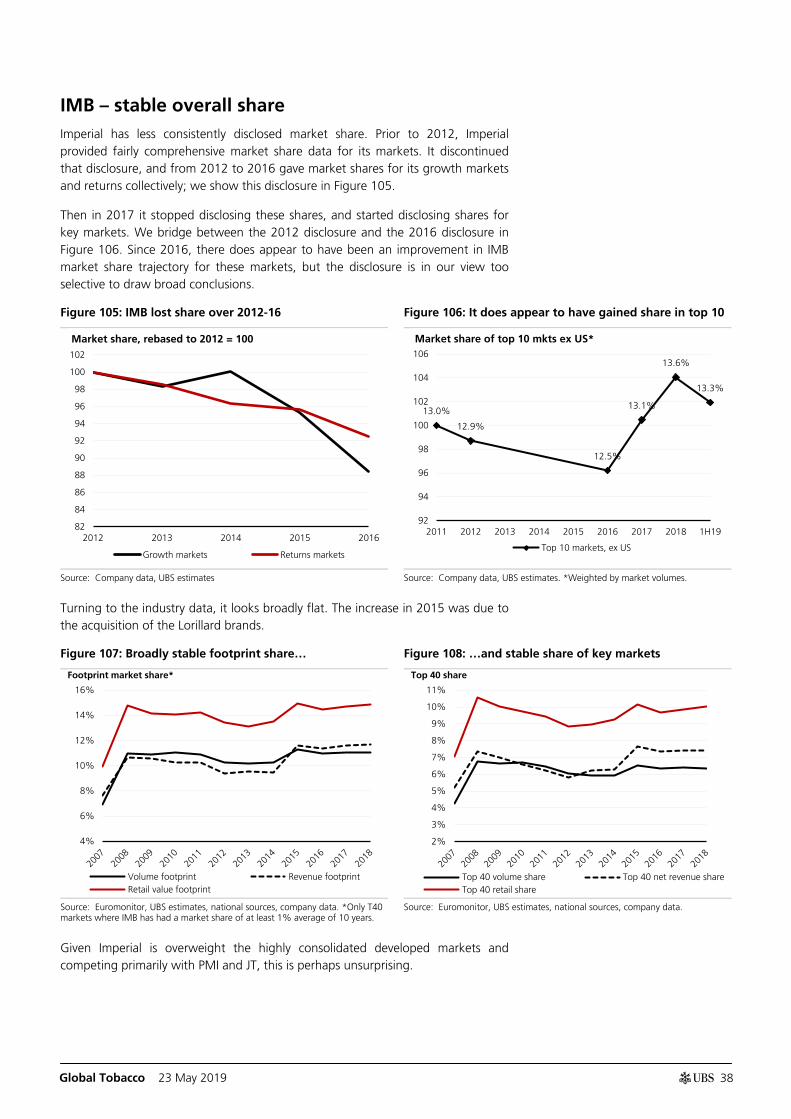

IMB – stable overall share .......................................................................... 38

JT – international business growing share .................................................. 39

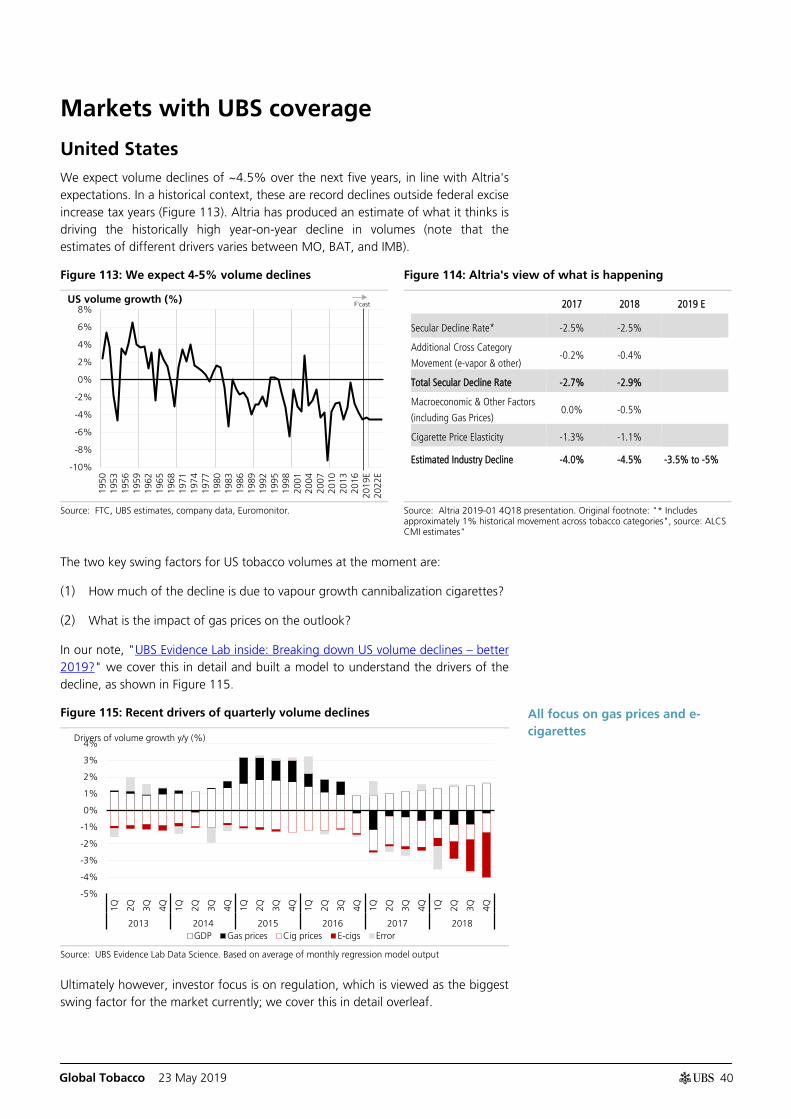

Markets with UBS coverage .......................................................... 40

United States ............................................................................................. 40

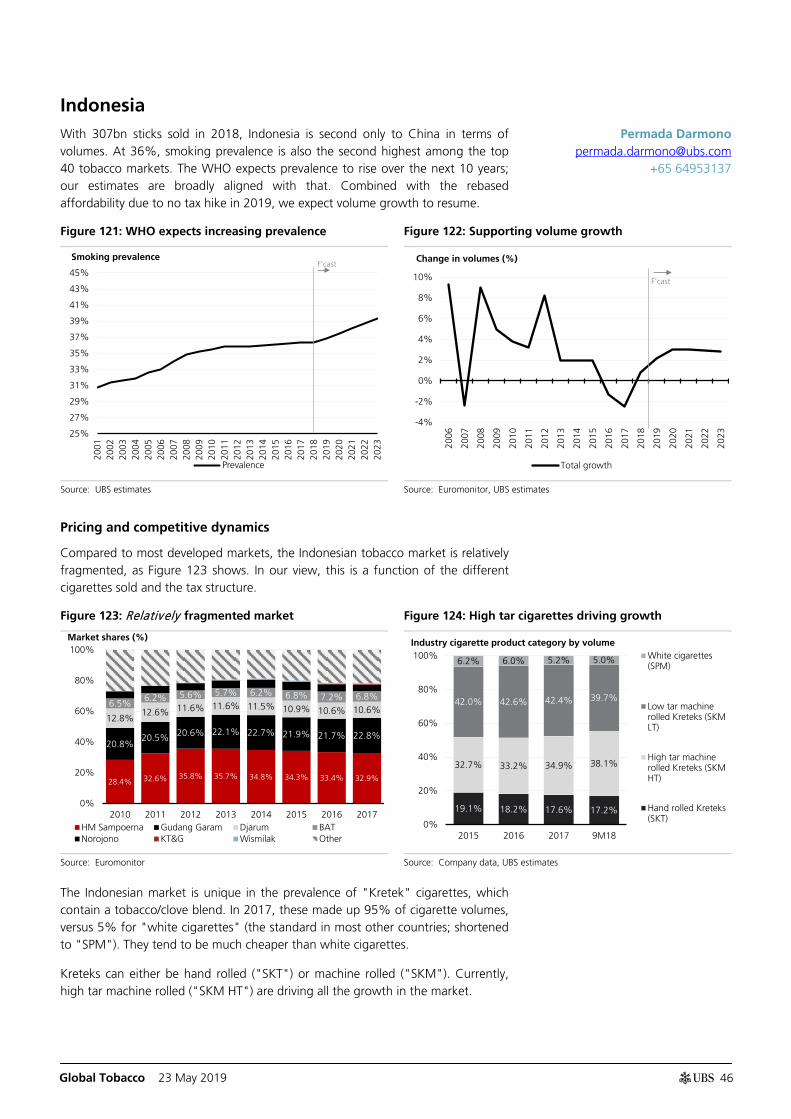

Indonesia ................................................................................................... 46

Japan ......................................................................................................... 48

South Korea............................................................................................... 51

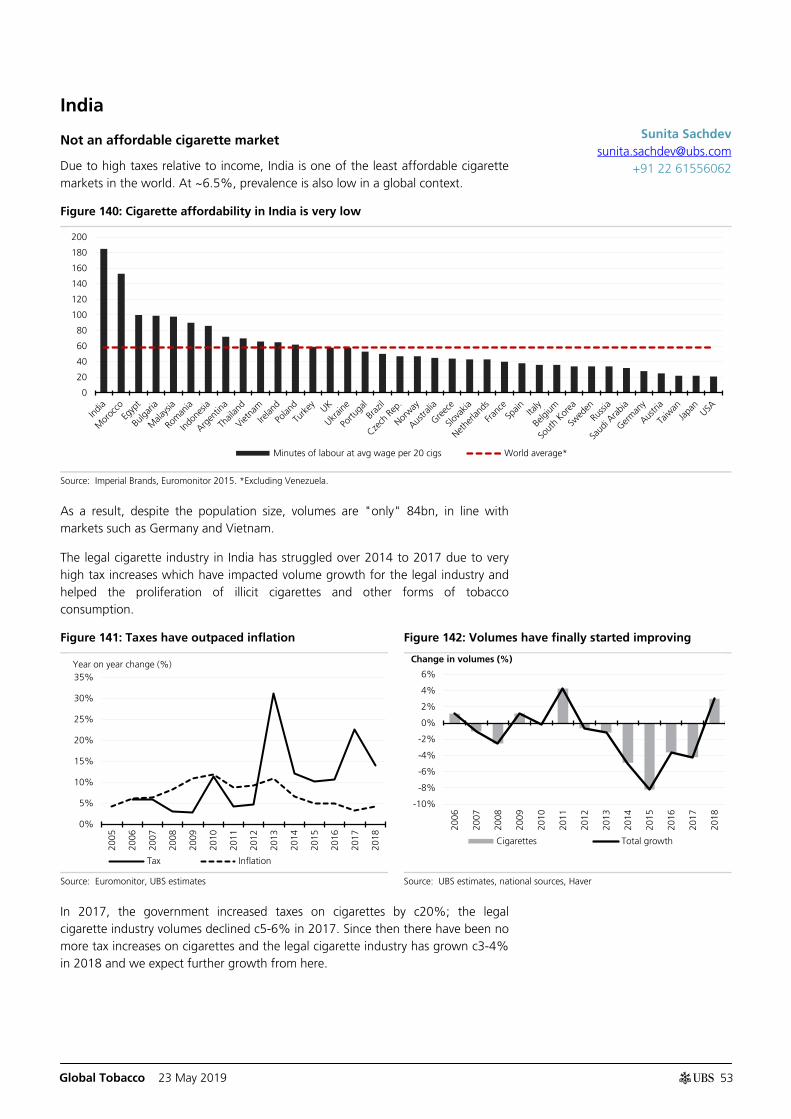

India .......................................................................................................... 53

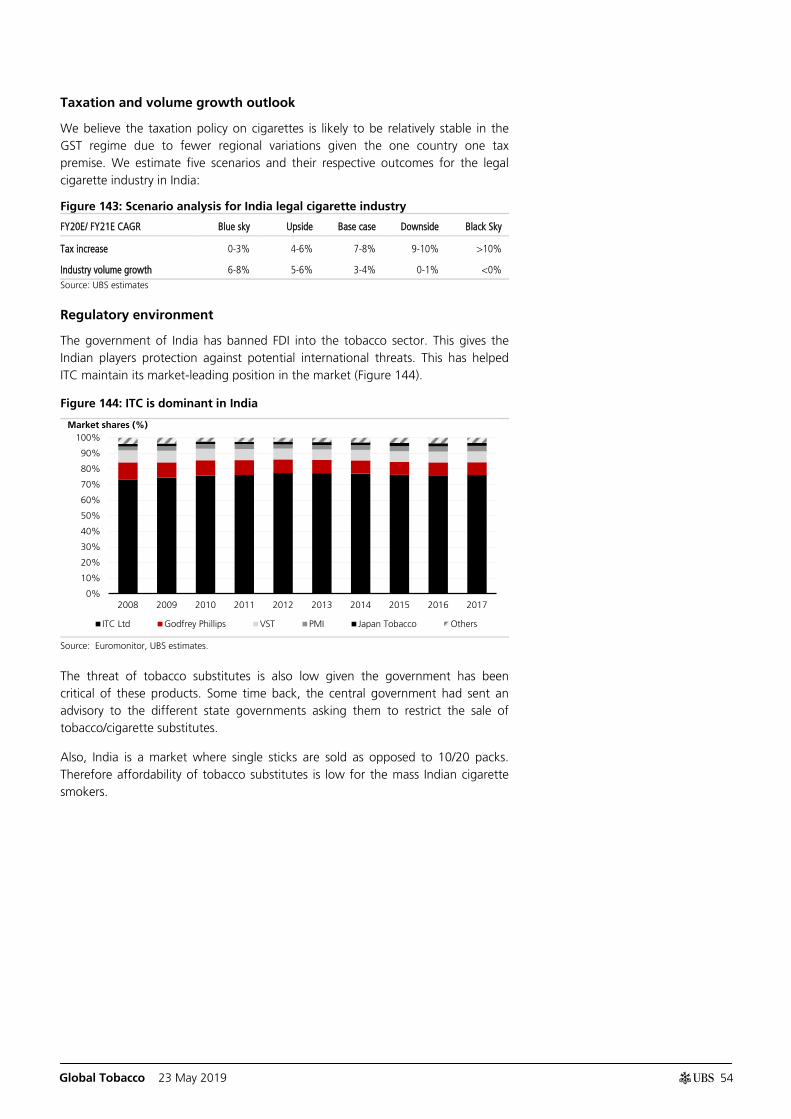

Malaysia .................................................................................................... 55

Global outlook detail ..................................................................... 57

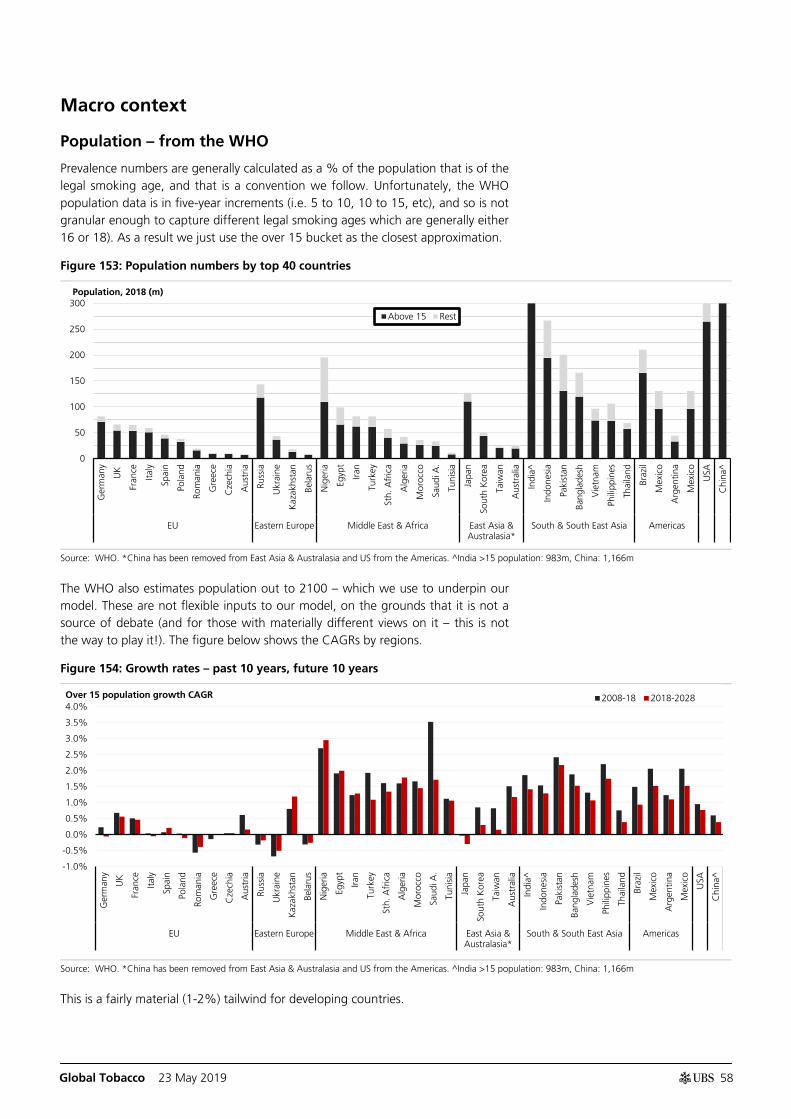

Macro context ........................................................................................... 58

Prevalence ................................................................................................. 64

Nik Oliver, ACA Analyst

[email protected] +44-20-7568 4982

Robert Rampton Analyst

[email protected] +44-20-7568 2014

Satsuki Kawasaki Analyst

[email protected] +81-3-5208 6265

Sunita Sachdev Analyst

[email protected] +91-22-6155 6062

Permada Darmono Analyst

[email protected] +65-6495 3137

Jennifer Han Analyst

[email protected] +82-2-3702 8802

Nicole Goh Analyst

[email protected] +603-2781 1133

Robert Krankowski Associate Analyst

[email protected] +44-20-7568 1152

Jihyun Lee Associate Analyst

[email protected] +82-2-3702 8810

Pinar Ergun, CFA Analyst

[email protected] +44-20-7568 6885

Charles Eden, ACA Analyst

[email protected] +44-20-7568 9622

Kate Rusanova Analyst

[email protected] +44-20 7568 9285

Global Tobacco 23 May 2019

3

Taxes ......................................................................................................... 69

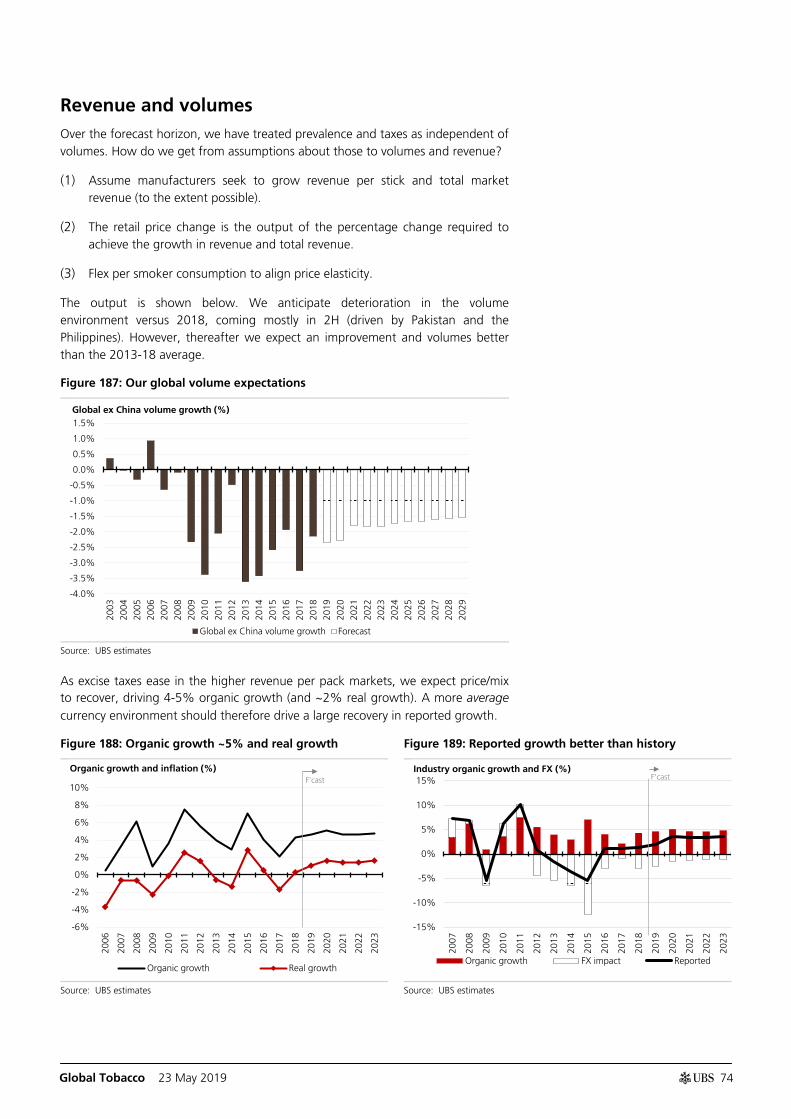

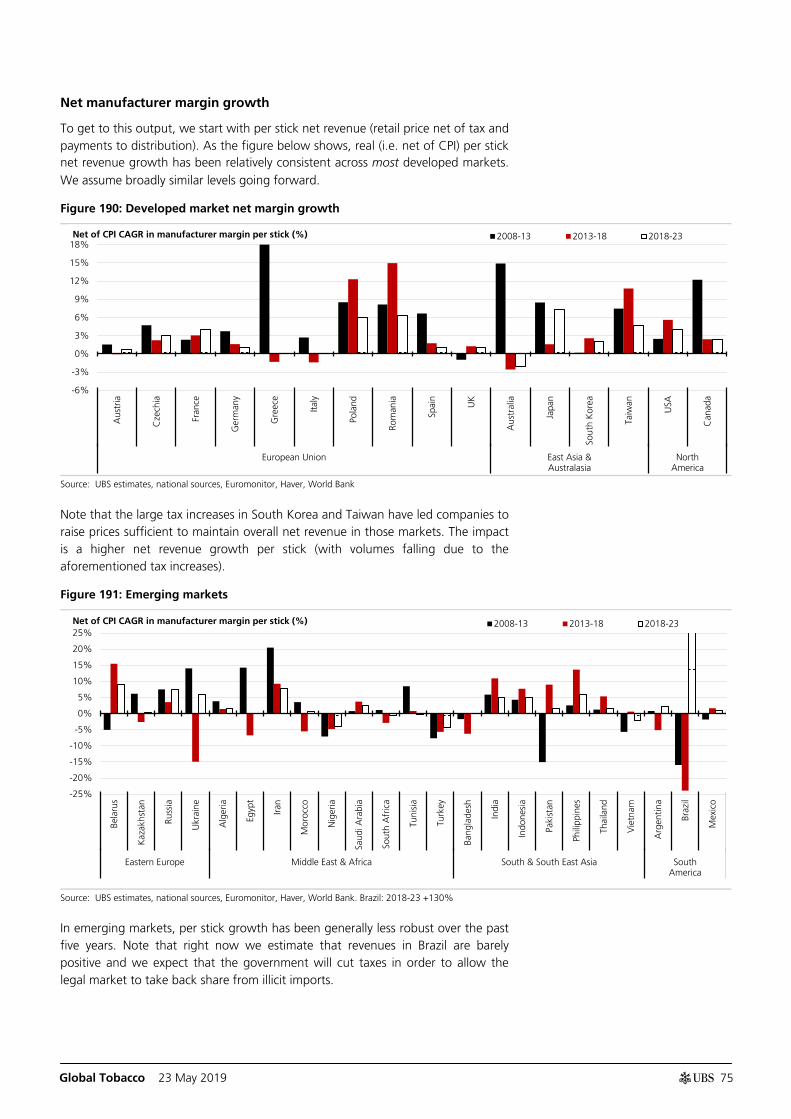

Revenue and volumes ................................................................................ 74

Reference sheets ............................................................................ 80

Combustible market summary ................................................................... 81

Global volume country drivers .................................................................... 82

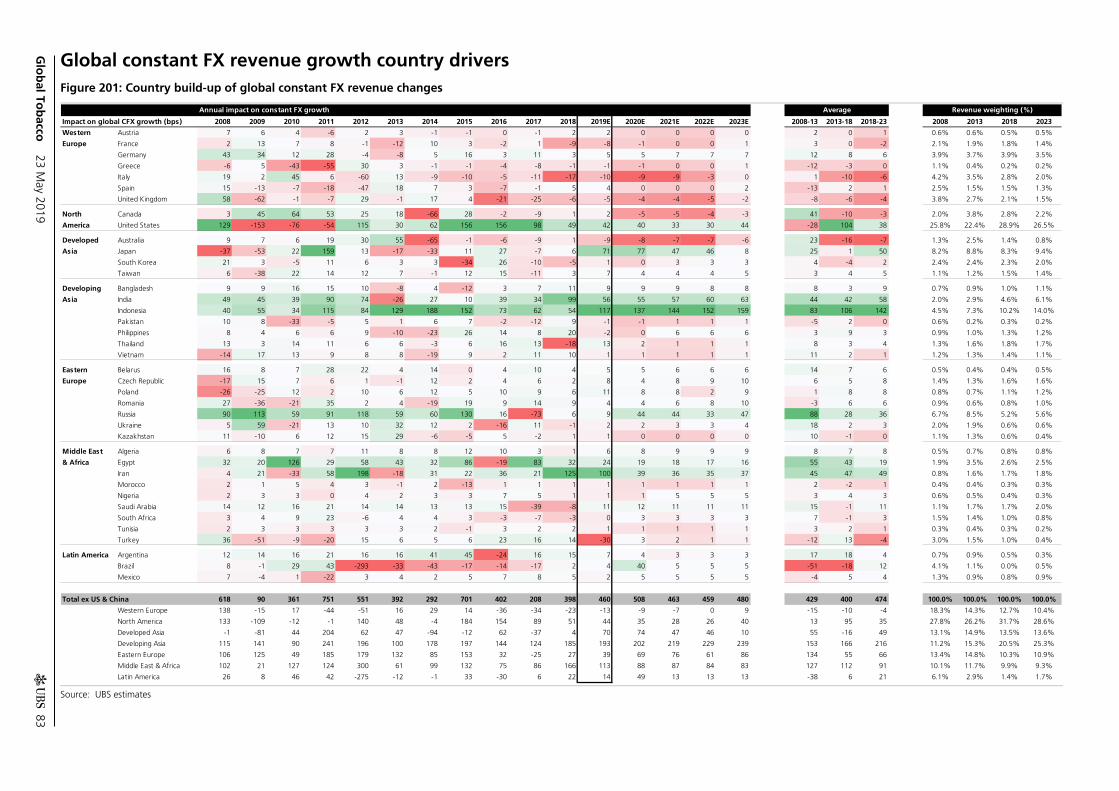

Global constant FX revenue growth country drivers ................................... 83

Global US$bn revenue growth drivers ........................................................ 84

Global Tobacco 23 May 2019

4

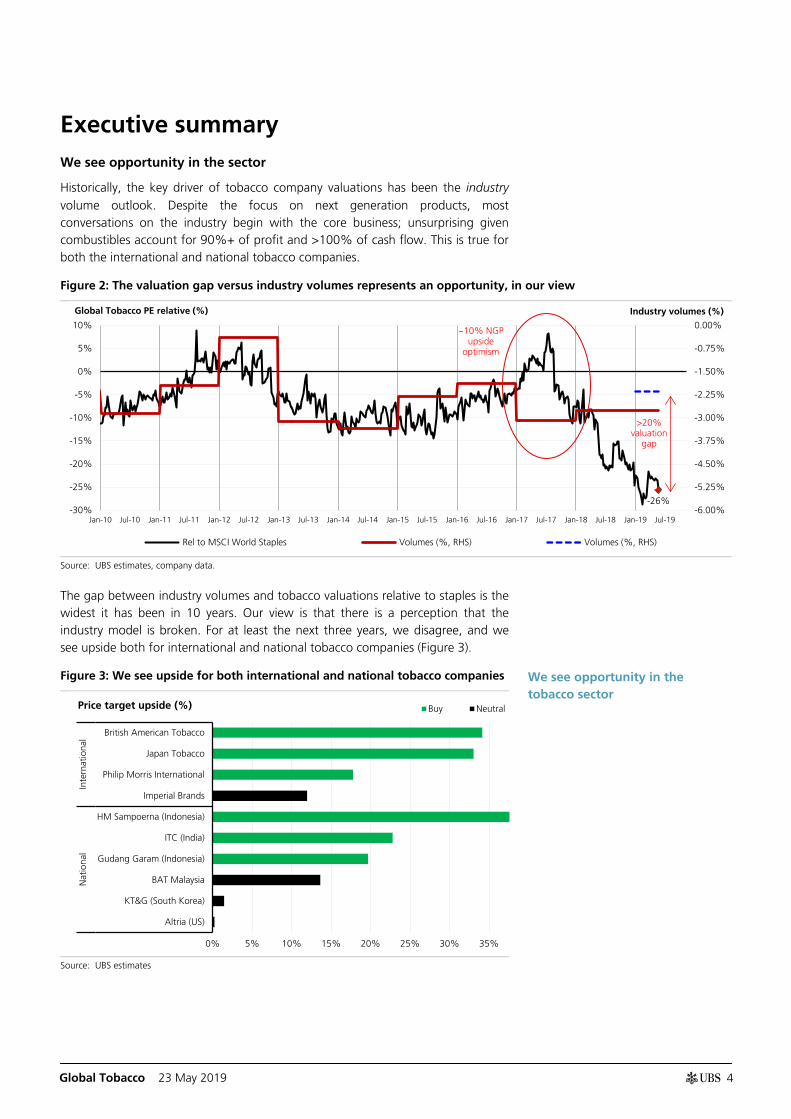

Executive summary We see opportunity in the sector

Historically, the key driver of tobacco company valuations has been the industry volume outlook. Despite the focus on next generation products, most conversations on the industry begin with the core business; unsurprising given combustibles account for 90%+ of profit and >100% of cash flow. This is true for both the international and national tobacco companies.

Figure 2: The valuation gap versus industry volumes represents an opportunity, in our view

Source: UBS estimates, company data.

The gap between industry volumes and tobacco valuations relative to staples is the widest it has been in 10 years. Our view is that there is a perception that the industry model is broken. For at least the next three years, we disagree, and we see upside both for international and national tobacco companies (Figure 3).

Figure 3: We see upside for both international and national tobacco companies

Source: UBS estimates

-26% -6.00%

-5.25%

-4.50%

-3.75%

-3.00%

-2.25%

-1.50%

-0.75%

0.00%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19

Rel to MSCI World Staples Volumes (%, RHS) Volumes (%, RHS)

Global Tobacco PE relative (%) Industry volumes (%)

~10% NGP upside

optimism

>20% valuation

gap

0% 5% 10% 15% 20% 25% 30% 35%

British American Tobacco

Japan Tobacco

Philip Morris International

Imperial Brands

HM Sampoerna (Indonesia)

ITC (India)

Gudang Garam (Indonesia)

BAT Malaysia

KT&G (South Korea)

Altria (US)

Inte

rnat

iona

lN

atio

nal

Buy NeutralPrice target upside (%)

We see opportunity in the tobacco sector

Global Tobacco 23 May 2019

5

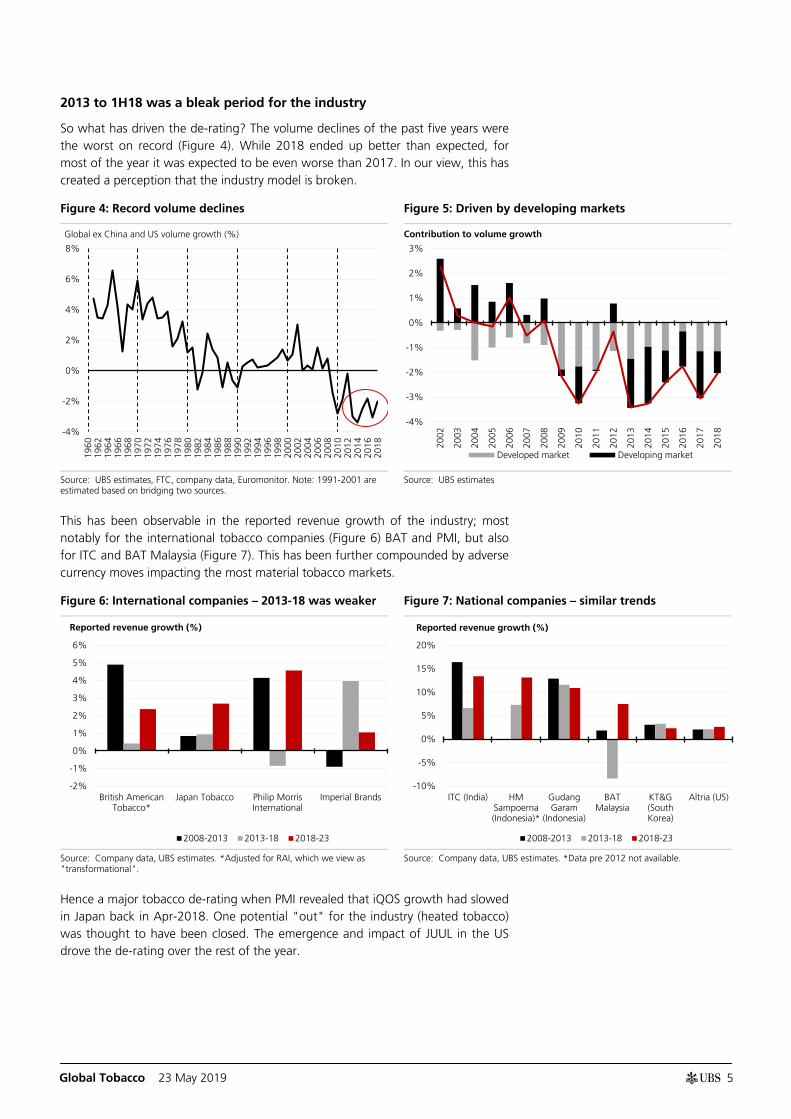

2013 to 1H18 was a bleak period for the industry

So what has driven the de-rating? The volume declines of the past five years were the worst on record (Figure 4). While 2018 ended up better than expected, for most of the year it was expected to be even worse than 2017. In our view, this has created a perception that the industry model is broken.

Figure 4: Record volume declines Figure 5: Driven by developing markets

Source: UBS estimates, FTC, company data, Euromonitor. Note: 1991-2001 are estimated based on bridging two sources.

Source: UBS estimates

This has been observable in the reported revenue growth of the industry; most notably for the international tobacco companies (Figure 6) BAT and PMI, but also for ITC and BAT Malaysia (Figure 7). This has been further compounded by adverse currency moves impacting the most material tobacco markets.

Figure 6: International companies – 2013-18 was weaker Figure 7: National companies – similar trends

Source: Company data, UBS estimates. *Adjusted for RAI, which we view as "transformational".

Source: Company data, UBS estimates. *Data pre 2012 not available.

Hence a major tobacco de-rating when PMI revealed that iQOS growth had slowed in Japan back in Apr-2018. One potential "out" for the industry (heated tobacco) was thought to have been closed. The emergence and impact of JUUL in the US drove the de-rating over the rest of the year.

-4%

-2%

0%

2%

4%

6%

8%

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Global ex China and US volume growth (%)

-4%

-3%

-2%

-1%

0%

1%

2%

3%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Developed market Developing market

Contribution to volume growth

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

British AmericanTobacco*

Japan Tobacco Philip MorrisInternational

Imperial Brands

2008-2013 2013-18 2018-23

Reported revenue growth (%)

-10%

-5%

0%

5%

10%

15%

20%

ITC (India) HMSampoerna(Indonesia)*

GudangGaram

(Indonesia)

BATMalaysia

KT&G(SouthKorea)

Altria (US)

2008-2013 2013-18 2018-23

Reported revenue growth (%)

Global Tobacco 23 May 2019

6

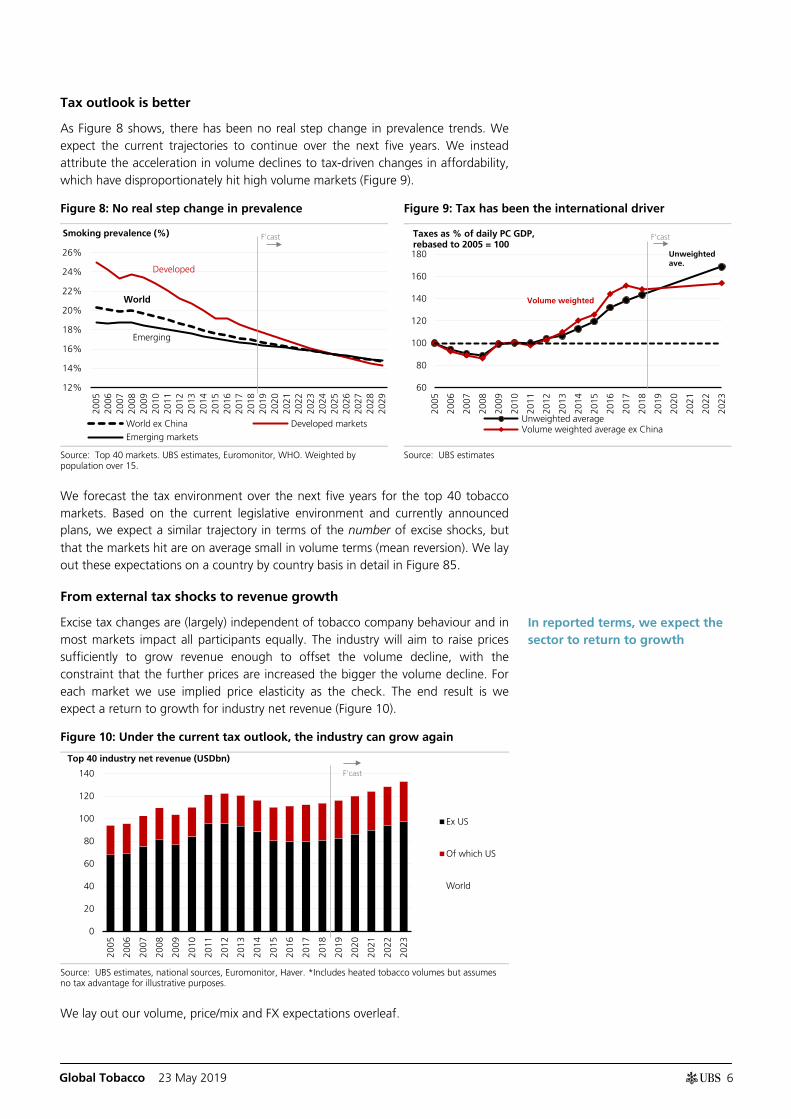

Tax outlook is better

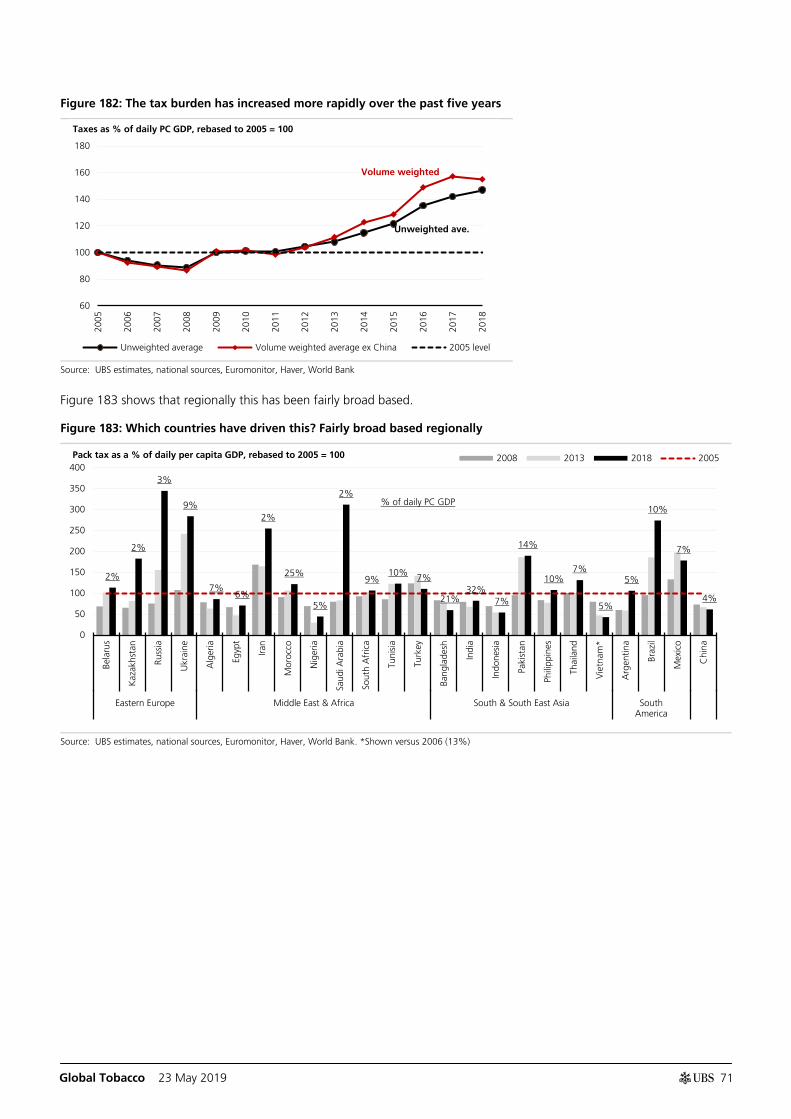

As Figure 8 shows, there has been no real step change in prevalence trends. We expect the current trajectories to continue over the next five years. We instead attribute the acceleration in volume declines to tax-driven changes in affordability, which have disproportionately hit high volume markets (Figure 9).

Figure 8: No real step change in prevalence Figure 9: Tax has been the international driver

Source: Top 40 markets. UBS estimates, Euromonitor, WHO. Weighted by population over 15.

Source: UBS estimates

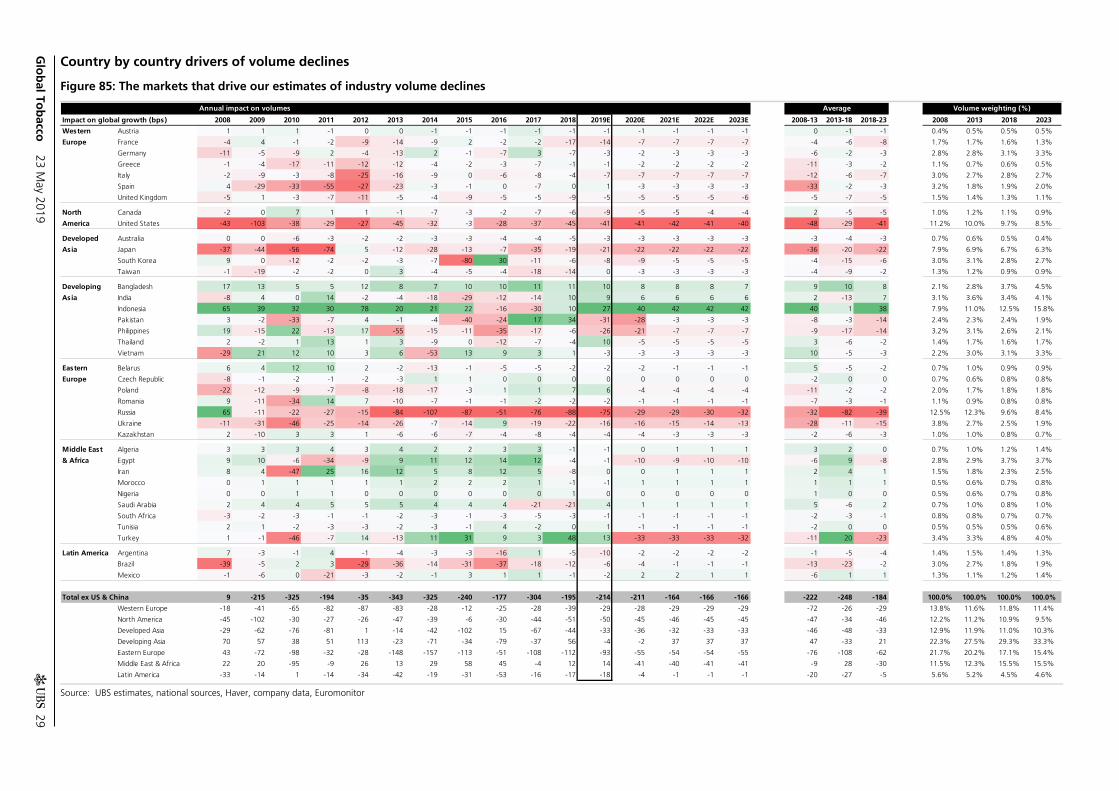

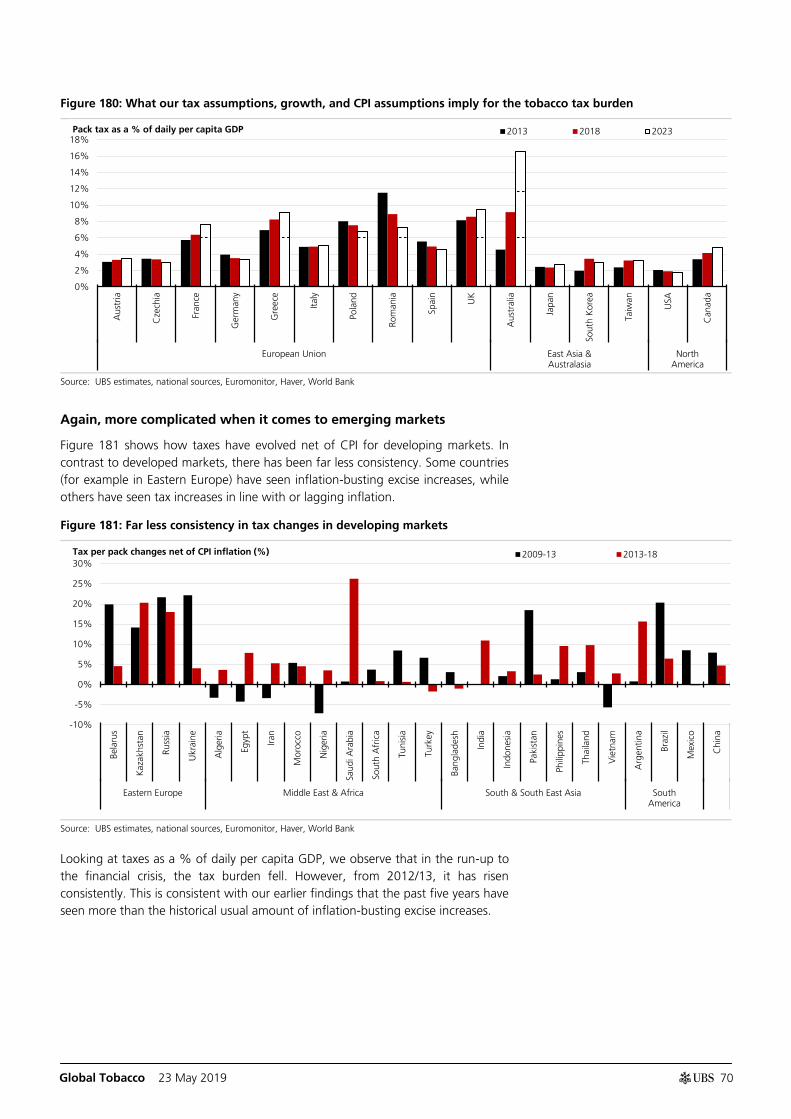

We forecast the tax environment over the next five years for the top 40 tobacco markets. Based on the current legislative environment and currently announced plans, we expect a similar trajectory in terms of the number of excise shocks, but that the markets hit are on average small in volume terms (mean reversion). We lay out these expectations on a country by country basis in detail in Figure 85.

From external tax shocks to revenue growth

Excise tax changes are (largely) independent of tobacco company behaviour and in most markets impact all participants equally. The industry will aim to raise prices sufficiently to grow revenue enough to offset the volume decline, with the constraint that the further prices are increased the bigger the volume decline. For each market we use implied price elasticity as the check. The end result is we expect a return to growth for industry net revenue (Figure 10).

Figure 10: Under the current tax outlook, the industry can grow again

Source: UBS estimates, national sources, Euromonitor, Haver. *Includes heated tobacco volumes but assumes no tax advantage for illustrative purposes.

We lay out our volume, price/mix and FX expectations overleaf.

12%

14%

16%

18%

20%

22%

24%

26%

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

World ex China Developed markets

Emerging markets

Smoking prevalence (%) F'cast

Developed

Emerging

World

60

80

100

120

140

160

180

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Unweighted averageVolume weighted average ex China

Taxes as % of daily PC GDP, rebased to 2005 = 100

Unweighted ave.

Volume weighted

F'cast

0

20

40

60

80

100

120

140

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Ex US

Of which US

World

Top 40 industry net revenue (USDbn) F'cast

In reported terms, we expect the sector to return to growth

Global Tobacco 23 May 2019

7

The consumer can absorb improved price/mix

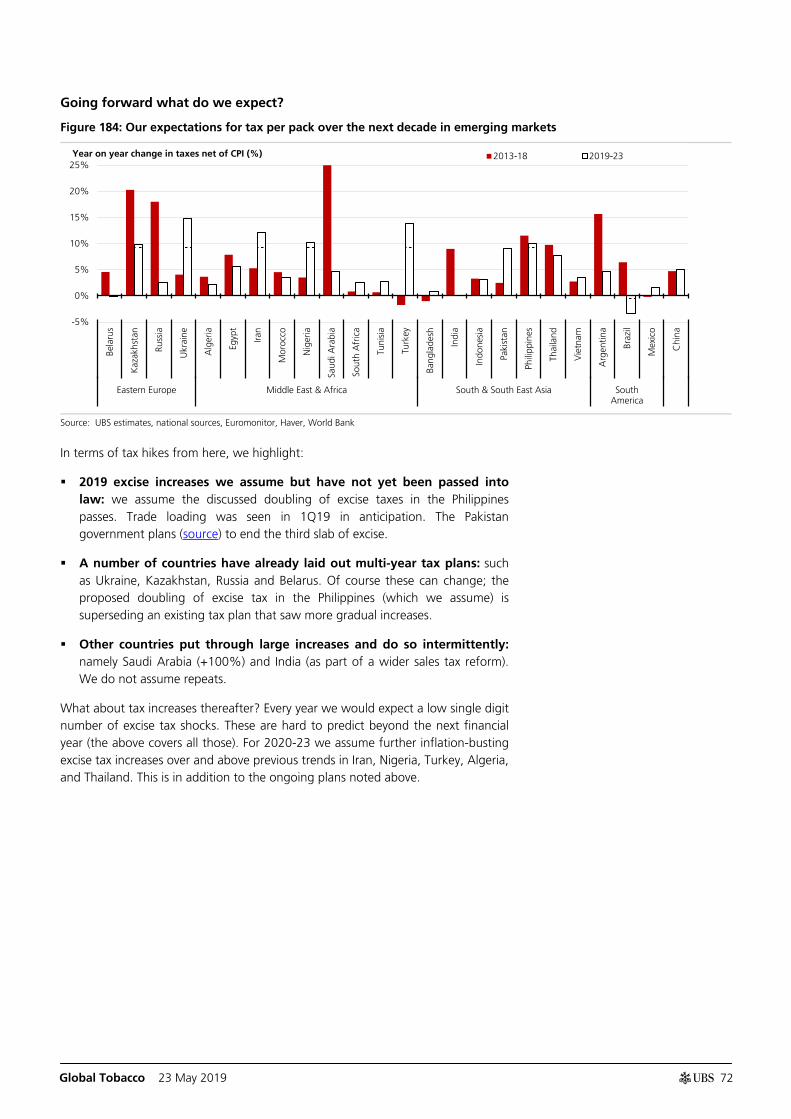

Based on our market by market analysis, we anticipate a recovery as shown in Figure 11. In addition to price increases tolerable by each market, this takes into account positive geographic mix (for example falling Pakistan volumes), price increases in response to excise increases (such as the Philippines), and recoveries in market revenue (most notably Brazil).

Figure 11: We expect a recovery in price/mix

Source: Top 40 markets, company data, UBS estimates

On the one hand, excise tax increases hit all industry participants and demand for cigarettes is inelastic. On the other, consumers respond to price increases with downtrading and illicit cigarettes, there are competitive pressures, and tobacco companies may aim to absorb some of the change.

We expect an improvement in the volume outlook

The volume outcome is that we expect declines of 2.1% for 2019/20, behind the 1.9% for 2018 but better than the average since 2013 (and better than expectations for most of 2018).

Figure 12: Our volume expectations compare favorably to past five years

Source: UBS estimates

PMI expects -2.5% to -3.0% for 2019, and acknowledged 1Q was better than expectations. Meanwhile, BAT expects a 3% decline for 2019.

0%

2%

4%

6%

8%

10%

12%

14%

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

World

Ex US

5yr ave(ex US)

Constant currency price/mix

F'cast

Inc US

Ex US

-4.0%

-3.5%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Global ex China volume growth Forecast

Global ex China volume growth (%) Global ex China volume growth (%)

F'cast

Sector price/mix has proved robust

Current legislative landscape implies volume declines ~2%

Global Tobacco 23 May 2019

8

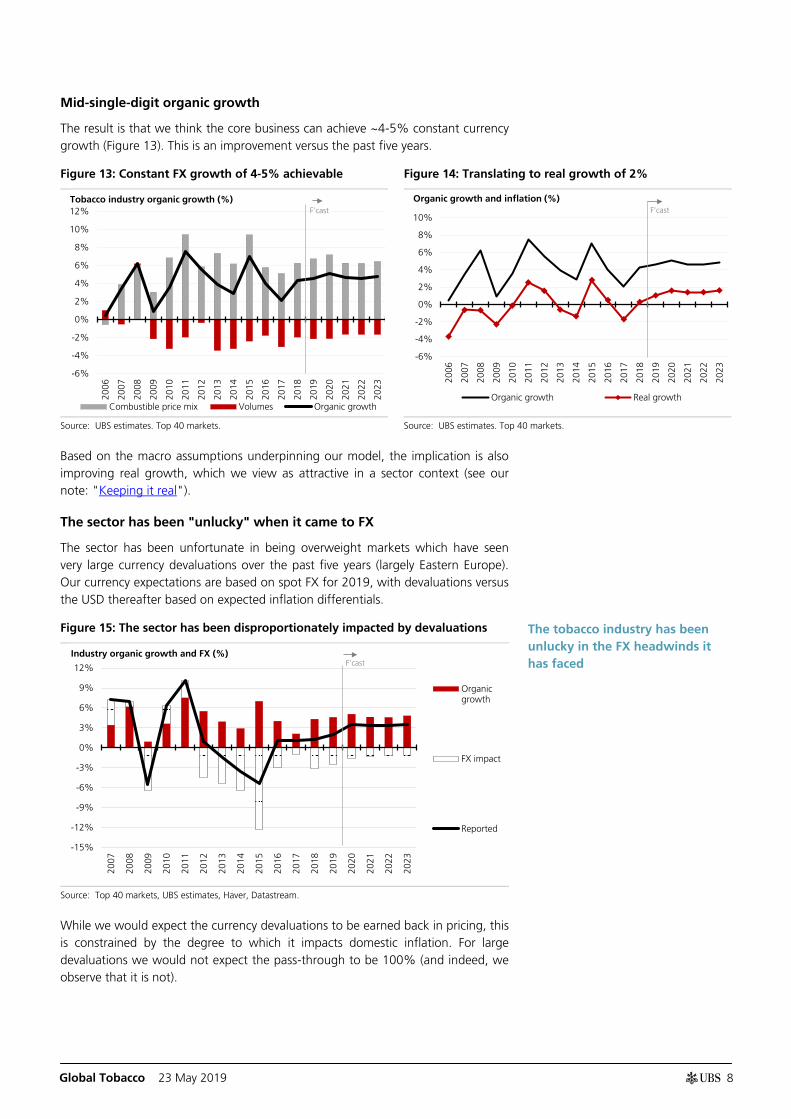

Mid-single-digit organic growth

The result is that we think the core business can achieve ~4-5% constant currency growth (Figure 13). This is an improvement versus the past five years.

Figure 13: Constant FX growth of 4-5% achievable Figure 14: Translating to real growth of 2%

Source: UBS estimates. Top 40 markets. Source: UBS estimates. Top 40 markets.

Based on the macro assumptions underpinning our model, the implication is also improving real growth, which we view as attractive in a sector context (see our note: "Keeping it real").

The sector has been "unlucky" when it came to FX

The sector has been unfortunate in being overweight markets which have seen very large currency devaluations over the past five years (largely Eastern Europe). Our currency expectations are based on spot FX for 2019, with devaluations versus the USD thereafter based on expected inflation differentials.

Figure 15: The sector has been disproportionately impacted by devaluations

Source: Top 40 markets, UBS estimates, Haver, Datastream.

While we would expect the currency devaluations to be earned back in pricing, this is constrained by the degree to which it impacts domestic inflation. For large devaluations we would not expect the pass-through to be 100% (and indeed, we observe that it is not).

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Combustible price mix Volumes Organic growth

Tobacco industry organic growth (%) F'cast

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Organic growth Real growth

Organic growth and inflation (%) F'cast

-15%

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Organicgrowth

FX impact

Reported

Industry organic growth and FX (%) F'cast

The tobacco industry has been unlucky in the FX headwinds it has faced

Global Tobacco 23 May 2019

9

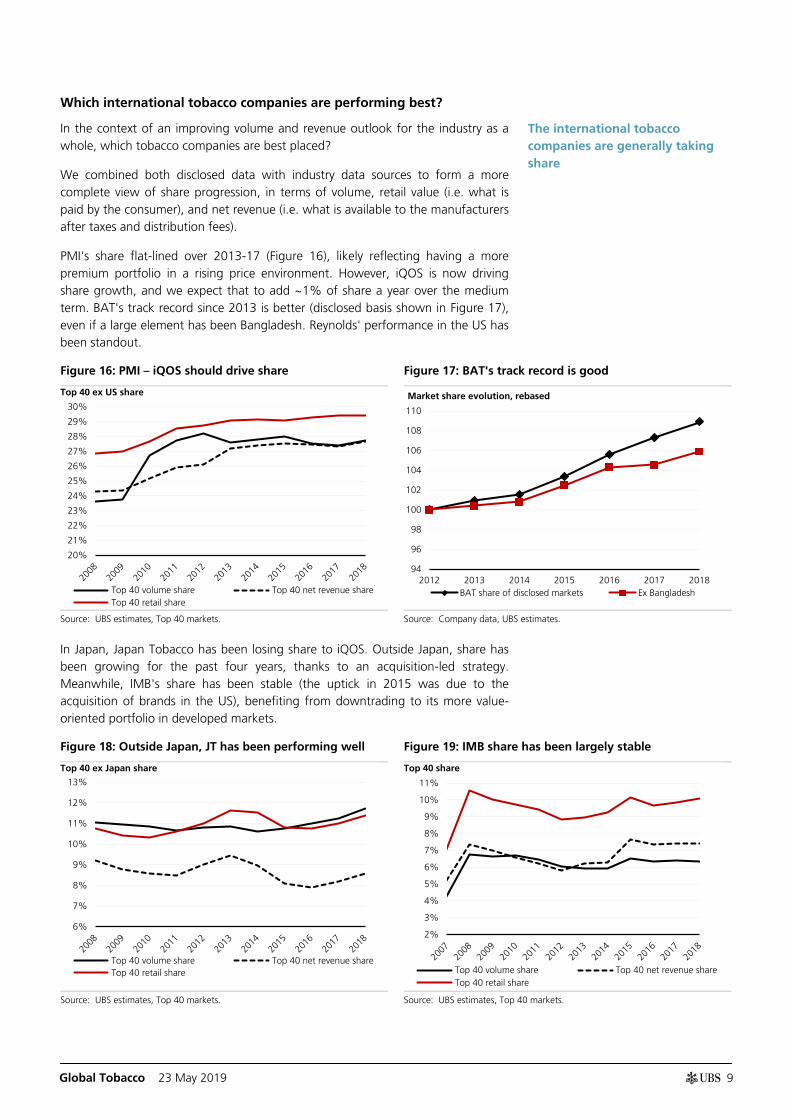

Which international tobacco companies are performing best?

In the context of an improving volume and revenue outlook for the industry as a whole, which tobacco companies are best placed?

We combined both disclosed data with industry data sources to form a more complete view of share progression, in terms of volume, retail value (i.e. what is paid by the consumer), and net revenue (i.e. what is available to the manufacturers after taxes and distribution fees).

PMI's share flat-lined over 2013-17 (Figure 16), likely reflecting having a more premium portfolio in a rising price environment. However, iQOS is now driving share growth, and we expect that to add ~1% of share a year over the medium term. BAT's track record since 2013 is better (disclosed basis shown in Figure 17), even if a large element has been Bangladesh. Reynolds' performance in the US has been standout.

Figure 16: PMI – iQOS should drive share Figure 17: BAT's track record is good

Source: UBS estimates, Top 40 markets. Source: Company data, UBS estimates.

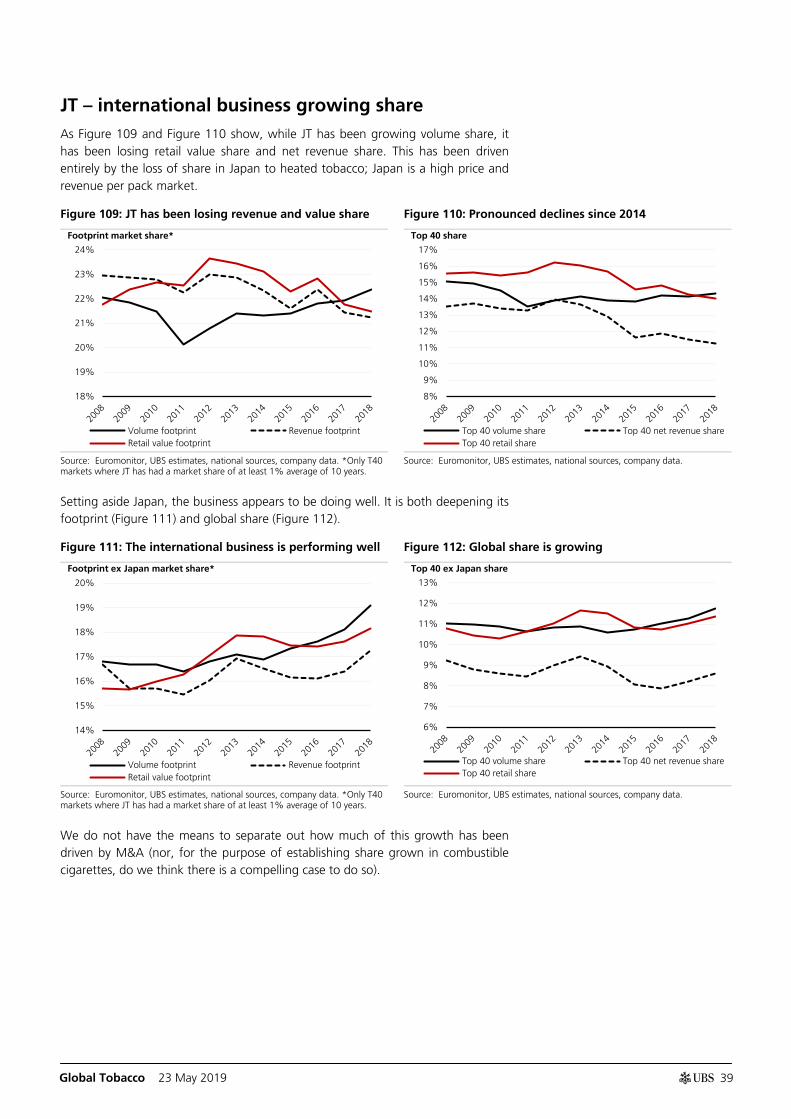

In Japan, Japan Tobacco has been losing share to iQOS. Outside Japan, share has been growing for the past four years, thanks to an acquisition-led strategy. Meanwhile, IMB's share has been stable (the uptick in 2015 was due to the acquisition of brands in the US), benefiting from downtrading to its more value-oriented portfolio in developed markets.

Figure 18: Outside Japan, JT has been performing well Figure 19: IMB share has been largely stable

Source: UBS estimates, Top 40 markets. Source: UBS estimates, Top 40 markets.

20%

21%

22%

23%

24%

25%

26%

27%

28%

29%

30%

Top 40 volume share Top 40 net revenue shareTop 40 retail share

Top 40 ex US share

94

96

98

100

102

104

106

108

110

2012 2013 2014 2015 2016 2017 2018BAT share of disclosed markets Ex Bangladesh

Market share evolution, rebased

6%

7%

8%

9%

10%

11%

12%

13%

Top 40 volume share Top 40 net revenue shareTop 40 retail share

Top 40 ex Japan share

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

Top 40 volume share Top 40 net revenue shareTop 40 retail share

Top 40 share

The international tobacco companies are generally taking share

Global Tobacco 23 May 2019

10

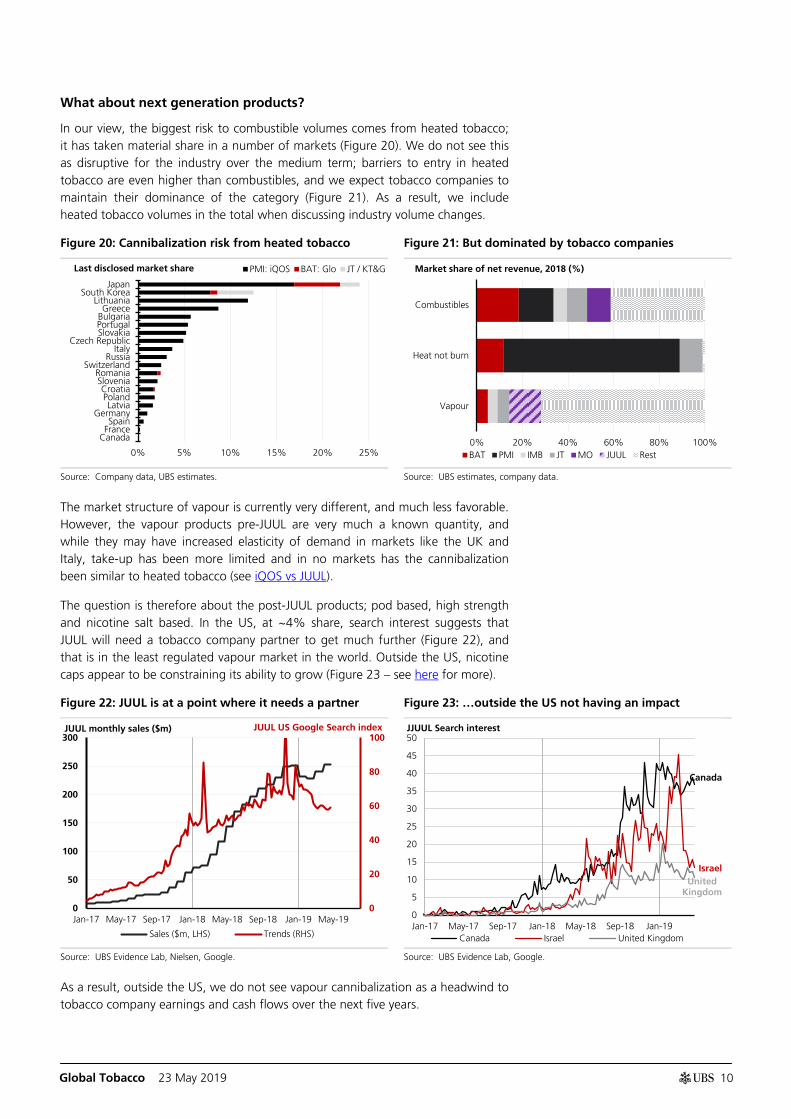

What about next generation products?

In our view, the biggest risk to combustible volumes comes from heated tobacco; it has taken material share in a number of markets (Figure 20). We do not see this as disruptive for the industry over the medium term; barriers to entry in heated tobacco are even higher than combustibles, and we expect tobacco companies to maintain their dominance of the category (Figure 21). As a result, we include heated tobacco volumes in the total when discussing industry volume changes.

Figure 20: Cannibalization risk from heated tobacco Figure 21: But dominated by tobacco companies

Source: Company data, UBS estimates. Source: UBS estimates, company data.

The market structure of vapour is currently very different, and much less favorable. However, the vapour products pre-JUUL are very much a known quantity, and while they may have increased elasticity of demand in markets like the UK and Italy, take-up has been more limited and in no markets has the cannibalization been similar to heated tobacco (see iQOS vs JUUL).

The question is therefore about the post-JUUL products; pod based, high strength and nicotine salt based. In the US, at ~4% share, search interest suggests that JUUL will need a tobacco company partner to get much further (Figure 22), and that is in the least regulated vapour market in the world. Outside the US, nicotine caps appear to be constraining its ability to grow (Figure 23 – see here for more).

Figure 22: JUUL is at a point where it needs a partner Figure 23: …outside the US not having an impact

Source: UBS Evidence Lab, Nielsen, Google. Source: UBS Evidence Lab, Google.

As a result, outside the US, we do not see vapour cannibalization as a headwind to tobacco company earnings and cash flows over the next five years.

0% 5% 10% 15% 20% 25%

JapanSouth Korea

LithuaniaGreece

BulgariaPortugalSlovakia

Czech RepublicItaly

RussiaSwitzerland

RomaniaSloveniaCroatiaPolandLatvia

GermanySpain

FranceCanada

PMI: iQOS BAT: Glo JT / KT&G Last disclosed market share

0% 20% 40% 60% 80% 100%

Combustibles

Heat not burn

Vapour

BAT PMI IMB JT MO JUUL Rest

Market share of net revenue, 2018 (%)

0

20

40

60

80

100

0

50

100

150

200

250

300

Jan-17 May-17 Sep-17 Jan-18 May-18 Sep-18 Jan-19 May-19

Sales ($m, LHS) Trends (RHS)

JUUL monthly sales ($m) JUUL US Google Search index

Canada

Israel United

Kingdom

0

5

10

15

20

25

30

35

40

45

50

Jan-17 May-17 Sep-17 Jan-18 May-18 Sep-18 Jan-19Canada Israel United Kingdom

JJUUL Search interest

Global Tobacco 23 May 2019

11

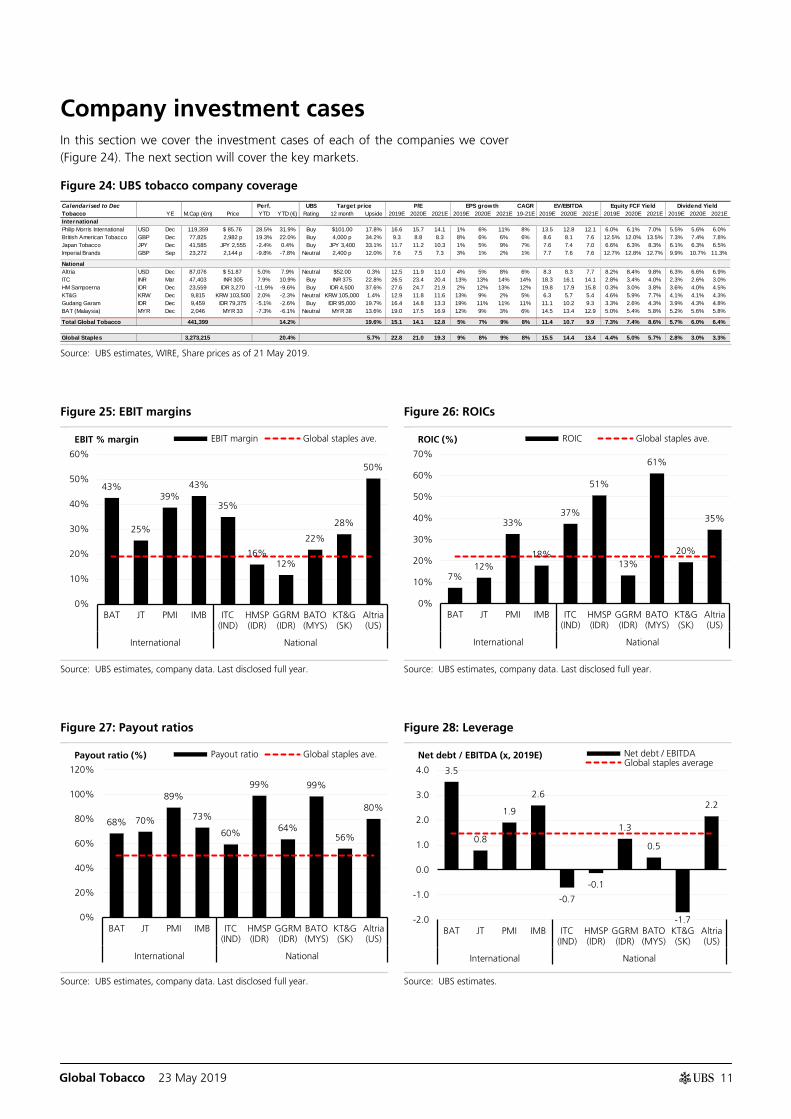

Company investment cases In this section we cover the investment cases of each of the companies we cover (Figure 24). The next section will cover the key markets.

Figure 24: UBS tobacco company coverage

Source: UBS estimates, WIRE, Share prices as of 21 May 2019.

Figure 25: EBIT margins Figure 26: ROICs

Source: UBS estimates, company data. Last disclosed full year. Source: UBS estimates, company data. Last disclosed full year.

Figure 27: Payout ratios Figure 28: Leverage

Source: UBS estimates, company data. Last disclosed full year. Source: UBS estimates.

Calendarised to Dec Perf. UBS Target price P/E EPS growth CAGR EV/EBITDA Equity FCF Yield Dividend Yield Tobacco YE M.Cap (€m) Price YTD YTD (€) Rating 12 month Upside 2019E 2020E 2021E 2019E 2020E 2021E 19-21E 2019E 2020E 2021E 2019E 2020E 2021E 2019E 2020E 2021EInternationalPhilip Morris International USD Dec 119,359 $ 85.76 28.5% 31.9% Buy $101.00 17.8% 16.6 15.7 14.1 1% 6% 11% 8% 13.5 12.8 12.1 6.0% 6.1% 7.0% 5.5% 5.6% 6.0%British American Tobacco GBP Dec 77,825 2,982 p 19.3% 22.0% Buy 4,000 p 34.2% 9.3 8.8 8.3 8% 6% 6% 6% 8.6 8.1 7.6 12.5% 12.0% 13.5% 7.3% 7.4% 7.8%Japan Tobacco JPY Dec 41,585 JPY 2,555 -2.4% 0.4% Buy JPY 3,400 33.1% 11.7 11.2 10.3 1% 5% 9% 7% 7.6 7.4 7.0 6.6% 6.3% 8.3% 6.1% 6.3% 6.5%Imperial Brands GBP Sep 23,272 2,144 p -9.8% -7.8% Neutral 2,400 p 12.0% 7.6 7.5 7.3 3% 1% 2% 1% 7.7 7.6 7.6 12.7% 12.8% 12.7% 9.9% 10.7% 11.3%

NationalAltria USD Dec 87,076 $ 51.87 5.0% 7.9% Neutral $52.00 0.3% 12.5 11.9 11.0 4% 5% 8% 6% 8.3 8.3 7.7 8.2% 8.4% 9.8% 6.3% 6.6% 6.9%ITC INR Mar 47,403 INR 305 7.9% 10.9% Buy INR 375 22.8% 26.5 23.4 20.4 13% 13% 14% 14% 18.3 16.1 14.1 2.8% 3.4% 4.0% 2.3% 2.6% 3.0%HM Sampoerna IDR Dec 23,559 IDR 3,270 -11.9% -9.6% Buy IDR 4,500 37.6% 27.6 24.7 21.9 2% 12% 13% 12% 19.8 17.9 15.8 0.3% 3.0% 3.8% 3.6% 4.0% 4.5%KT&G KRW Dec 9,815 KRW 103,500 2.0% -2.3% Neutral KRW 105,000 1.4% 12.9 11.8 11.6 13% 9% 2% 5% 6.3 5.7 5.4 4.6% 5.9% 7.7% 4.1% 4.1% 4.3%Gudang Garam IDR Dec 9,459 IDR 79,375 -5.1% -2.6% Buy IDR 95,000 19.7% 16.4 14.8 13.3 19% 11% 11% 11% 11.1 10.2 9.3 3.3% 2.6% 4.3% 3.9% 4.3% 4.8%BAT (Malaysia) MYR Dec 2,046 MYR 33 -7.3% -6.1% Neutral MYR 38 13.6% 19.0 17.5 16.9 12% 9% 3% 6% 14.5 13.4 12.9 5.0% 5.4% 5.8% 5.2% 5.6% 5.8%

Total Global Tobacco 441,399 14.2% 19.6% 15.1 14.1 12.8 5% 7% 9% 8% 11.4 10.7 9.9 7.3% 7.4% 8.6% 5.7% 6.0% 6.4%

Global Staples 3,273,215 20.4% 5.7% 22.8 21.0 19.3 9% 8% 9% 8% 15.5 14.4 13.4 4.4% 5.0% 5.7% 2.8% 3.0% 3.3%

43%

25%

39% 43%

35%

16% 12%

22%

28%

50%

0%

10%

20%

30%

40%

50%

60%

BAT JT PMI IMB ITC(IND)

HMSP(IDR)

GGRM(IDR)

BATO(MYS)

KT&G(SK)

Altria(US)

International National

EBIT margin Global staples ave.EBIT % margin

7% 12%

33%

18%

37%

51%

13%

61%

20%

35%

0%

10%

20%

30%

40%

50%

60%

70%

BAT JT PMI IMB ITC(IND)

HMSP(IDR)

GGRM(IDR)

BATO(MYS)

KT&G(SK)

Altria(US)

International National

ROIC Global staples ave.ROIC (%)

68% 70%

89%

73%

60%

99%

64%

99%

56%

80%

0%

20%

40%

60%

80%

100%

120%

BAT JT PMI IMB ITC(IND)

HMSP(IDR)

GGRM(IDR)

BATO(MYS)

KT&G(SK)

Altria(US)

International National

Payout ratio Global staples ave.Payout ratio (%)

3.5

0.8

1.9

2.6

-0.7

-0.1

1.3

0.5

-1.7

2.2

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

BAT JT PMI IMB ITC(IND)

HMSP(IDR)

GGRM(IDR)

BATO(MYS)

KT&G(SK)

Altria(US)

International National

Net debt / EBITDAGlobal staples average

Net debt / EBITDA (x, 2019E)

Global Tobacco 23 May 2019

12

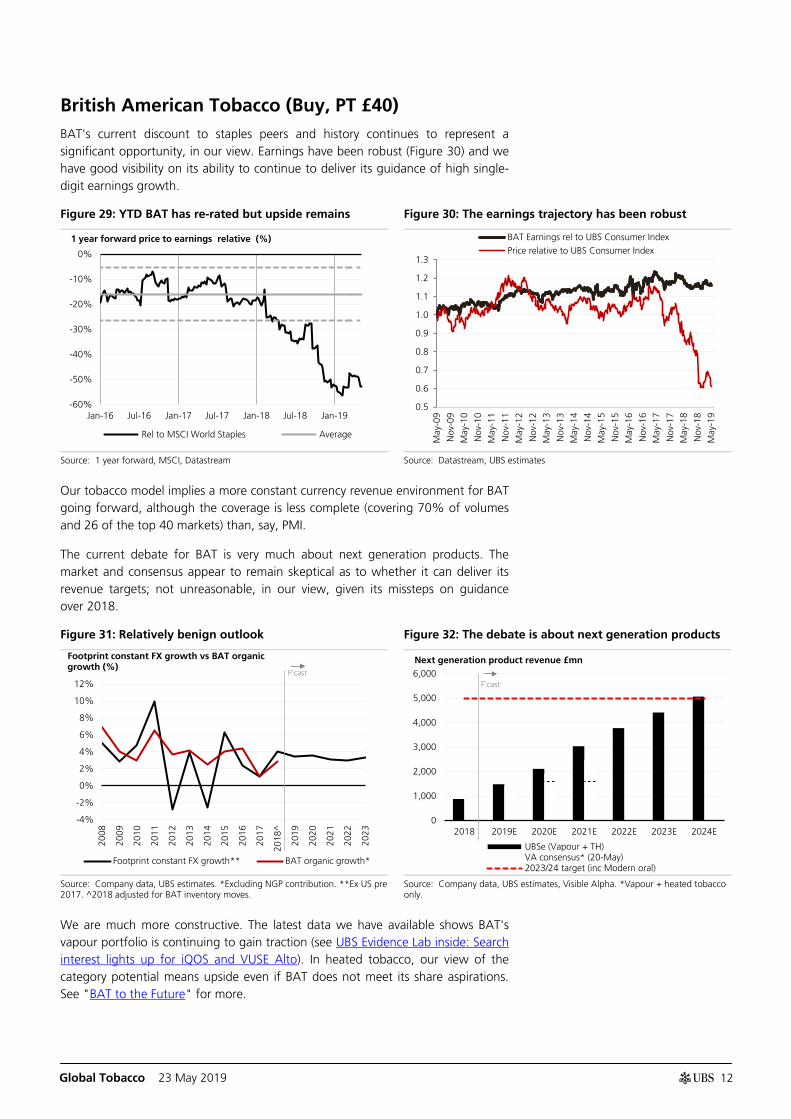

British American Tobacco (Buy, PT £40) BAT's current discount to staples peers and history continues to represent a significant opportunity, in our view. Earnings have been robust (Figure 30) and we have good visibility on its ability to continue to deliver its guidance of high single-digit earnings growth.

Figure 29: YTD BAT has re-rated but upside remains Figure 30: The earnings trajectory has been robust

Source: 1 year forward, MSCI, Datastream Source: Datastream, UBS estimates

Our tobacco model implies a more constant currency revenue environment for BAT going forward, although the coverage is less complete (covering 70% of volumes and 26 of the top 40 markets) than, say, PMI.

The current debate for BAT is very much about next generation products. The market and consensus appear to remain skeptical as to whether it can deliver its revenue targets; not unreasonable, in our view, given its missteps on guidance over 2018.

Figure 31: Relatively benign outlook Figure 32: The debate is about next generation products

Source: Company data, UBS estimates. *Excluding NGP contribution. **Ex US pre 2017. ^2018 adjusted for BAT inventory moves.

Source: Company data, UBS estimates, Visible Alpha. *Vapour + heated tobacco only.

We are much more constructive. The latest data we have available shows BAT's vapour portfolio is continuing to gain traction (see UBS Evidence Lab inside: Search interest lights up for iQOS and VUSE Alto). In heated tobacco, our view of the category potential means upside even if BAT does not meet its share aspirations. See "BAT to the Future" for more.

-60%

-50%

-40%

-30%

-20%

-10%

0%

Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19

Rel to MSCI World Staples Average

1 year forward price to earnings relative (%)

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

May

-09

Nov

-09

May

-10

Nov

-10

May

-11

Nov

-11

May

-12

Nov

-12

May

-13

Nov

-13

May

-14

Nov

-14

May

-15

Nov

-15

May

-16

Nov

-16

May

-17

Nov

-17

May

-18

Nov

-18

May

-19

BAT Earnings rel to UBS Consumer Index

Price relative to UBS Consumer Index

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

^

2019

2020

2021

2022

2023

Footprint constant FX growth** BAT organic growth*

Footprint constant FX growth vs BAT organic growth (%) F'cast

0

1,000

2,000

3,000

4,000

5,000

6,000

2018 2019E 2020E 2021E 2022E 2023E 2024E

UBSe (Vapour + TH)VA consensus* (20-May)2023/24 target (inc Modern oral)

F'cast

Next generation product revenue £mn

Global Tobacco 23 May 2019

13

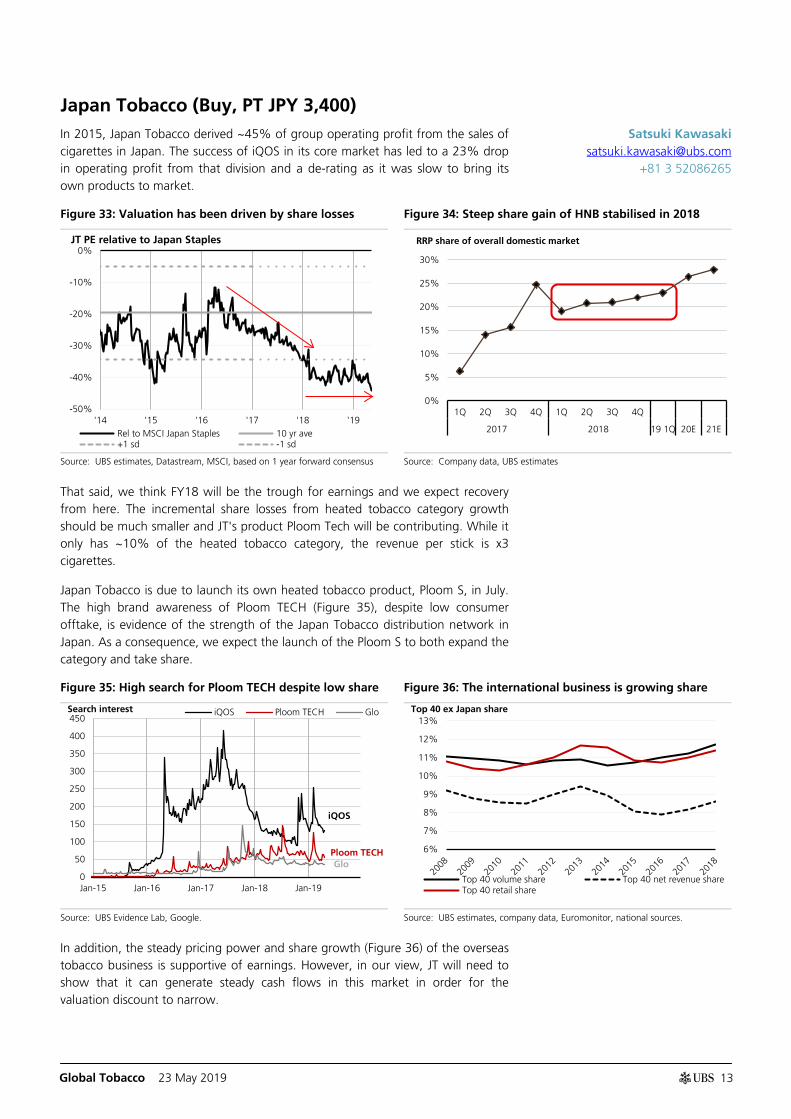

Japan Tobacco (Buy, PT JPY 3,400) In 2015, Japan Tobacco derived ~45% of group operating profit from the sales of cigarettes in Japan. The success of iQOS in its core market has led to a 23% drop in operating profit from that division and a de-rating as it was slow to bring its own products to market.

Figure 33: Valuation has been driven by share losses Figure 34: Steep share gain of HNB stabilised in 2018

Source: UBS estimates, Datastream, MSCI, based on 1 year forward consensus Source: Company data, UBS estimates

That said, we think FY18 will be the trough for earnings and we expect recovery from here. The incremental share losses from heated tobacco category growth should be much smaller and JT's product Ploom Tech will be contributing. While it only has ~10% of the heated tobacco category, the revenue per stick is x3 cigarettes.

Japan Tobacco is due to launch its own heated tobacco product, Ploom S, in July. The high brand awareness of Ploom TECH (Figure 35), despite low consumer offtake, is evidence of the strength of the Japan Tobacco distribution network in Japan. As a consequence, we expect the launch of the Ploom S to both expand the category and take share.

Figure 35: High search for Ploom TECH despite low share Figure 36: The international business is growing share

Source: UBS Evidence Lab, Google. Source: UBS estimates, company data, Euromonitor, national sources.

In addition, the steady pricing power and share growth (Figure 36) of the overseas tobacco business is supportive of earnings. However, in our view, JT will need to show that it can generate steady cash flows in this market in order for the valuation discount to narrow.

-50%

-40%

-30%

-20%

-10%

0%

'14 '15 '16 '17 '18 '19Rel to MSCI Japan Staples 10 yr ave+1 sd -1 sd

JT PE relative to Japan Staples

0%

5%

10%

15%

20%

25%

30%

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2017 2018 19 1Q 20E 21E

RRP share of overall domestic market

iQOS

Ploom TECH Glo

0

50

100

150

200

250

300

350

400

450

Jan-15 Jan-16 Jan-17 Jan-18 Jan-19

iQOS Ploom TECH GloSearch interest

6%

7%

8%

9%

10%

11%

12%

13%

Top 40 volume share Top 40 net revenue shareTop 40 retail share

Top 40 ex Japan share

Satsuki Kawasaki [email protected]

+81 3 52086265

Global Tobacco 23 May 2019

14

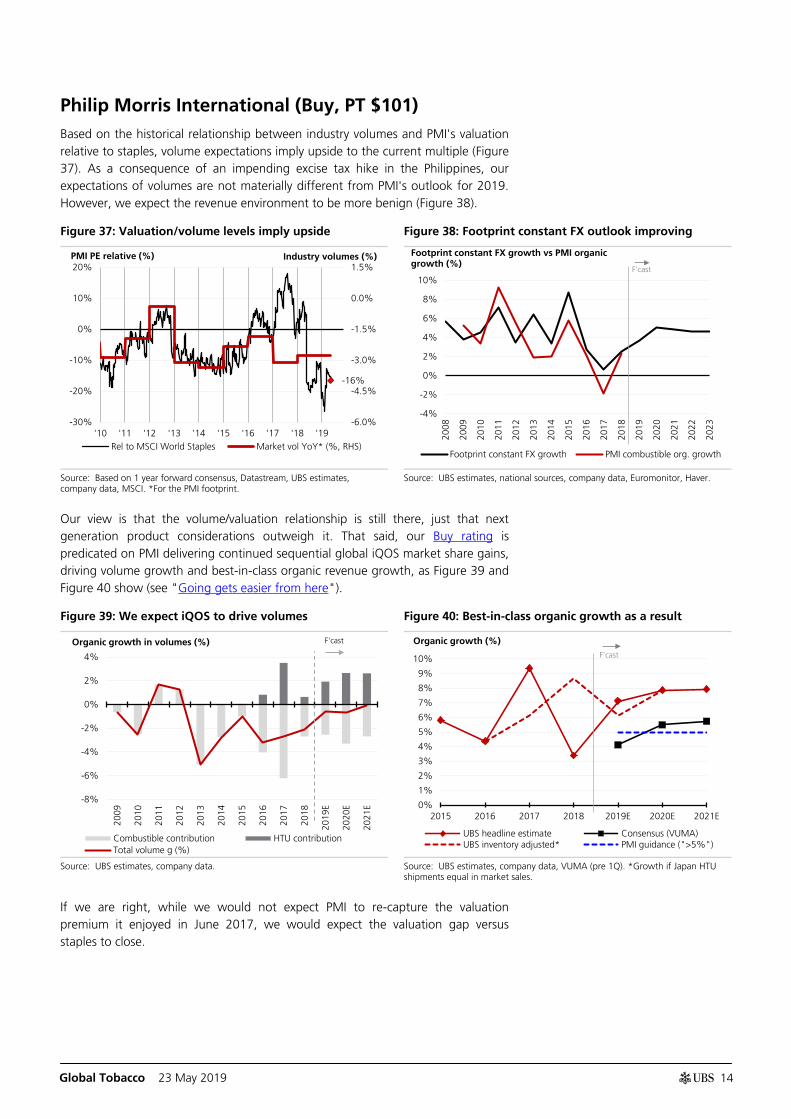

Philip Morris International (Buy, PT $101) Based on the historical relationship between industry volumes and PMI's valuation relative to staples, volume expectations imply upside to the current multiple (Figure 37). As a consequence of an impending excise tax hike in the Philippines, our expectations of volumes are not materially different from PMI's outlook for 2019. However, we expect the revenue environment to be more benign (Figure 38).

Figure 37: Valuation/volume levels imply upside Figure 38: Footprint constant FX outlook improving

Source: Based on 1 year forward consensus, Datastream, UBS estimates, company data, MSCI. *For the PMI footprint.

Source: UBS estimates, national sources, company data, Euromonitor, Haver.

Our view is that the volume/valuation relationship is still there, just that next generation product considerations outweigh it. That said, our Buy rating is predicated on PMI delivering continued sequential global iQOS market share gains, driving volume growth and best-in-class organic revenue growth, as Figure 39 and Figure 40 show (see "Going gets easier from here").

Figure 39: We expect iQOS to drive volumes Figure 40: Best-in-class organic growth as a result

Source: UBS estimates, company data. Source: UBS estimates, company data, VUMA (pre 1Q). *Growth if Japan HTU

shipments equal in market sales.

If we are right, while we would not expect PMI to re-capture the valuation premium it enjoyed in June 2017, we would expect the valuation gap versus staples to close.

-16%

-6.0%

-4.5%

-3.0%

-1.5%

0.0%

1.5%

-30%

-20%

-10%

0%

10%

20%

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19Rel to MSCI World Staples Market vol YoY* (%, RHS)

PMI PE relative (%) Industry volumes (%)

-4%

-2%

0%

2%

4%

6%

8%

10%

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Footprint constant FX growth PMI combustible org. growth

Footprint constant FX growth vs PMI organic growth (%) F'cast

-8%

-6%

-4%

-2%

0%

2%

4%

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

E

2020

E

2021

E

Combustible contribution HTU contributionTotal volume g (%)

Organic growth in volumes (%) F'cast

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2015 2016 2017 2018 2019E 2020E 2021E

UBS headline estimate Consensus (VUMA)UBS inventory adjusted* PMI guidance (">5%")

Organic growth (%) F'cast

Global Tobacco 23 May 2019

15

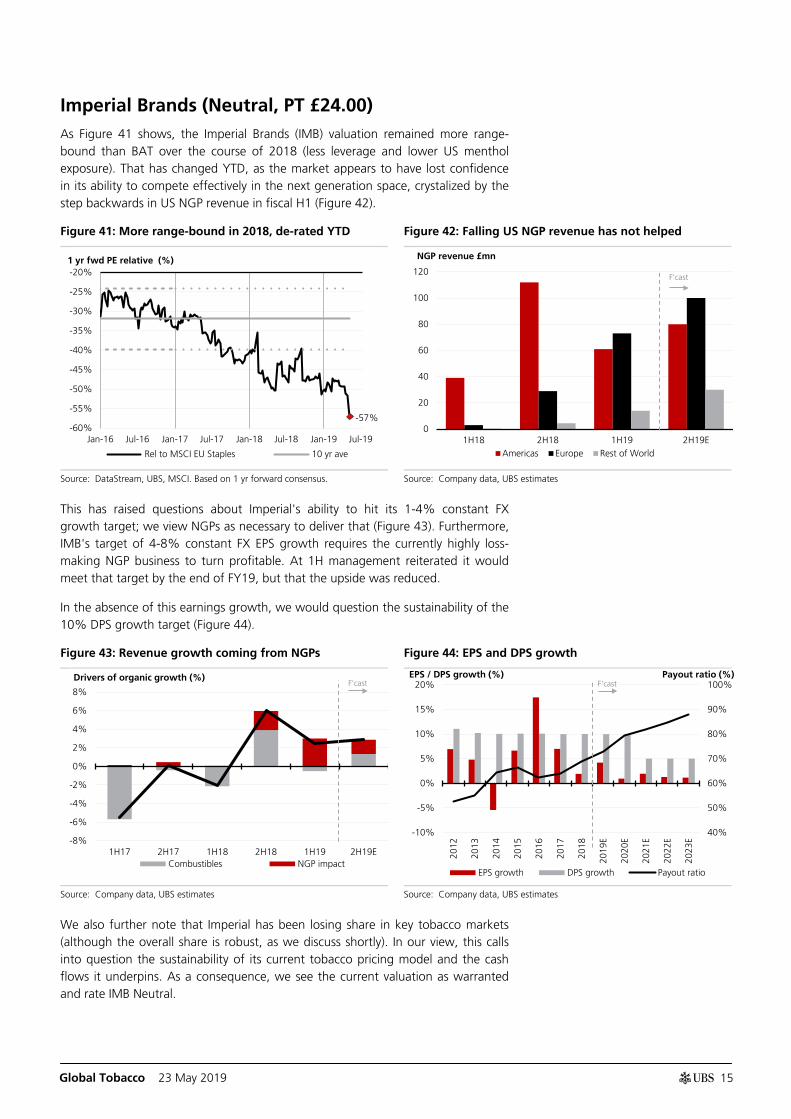

Imperial Brands (Neutral, PT £24.00) As Figure 41 shows, the Imperial Brands (IMB) valuation remained more range-bound than BAT over the course of 2018 (less leverage and lower US menthol exposure). That has changed YTD, as the market appears to have lost confidence in its ability to compete effectively in the next generation space, crystalized by the step backwards in US NGP revenue in fiscal H1 (Figure 42).

Figure 41: More range-bound in 2018, de-rated YTD Figure 42: Falling US NGP revenue has not helped

Source: DataStream, UBS, MSCI. Based on 1 yr forward consensus. Source: Company data, UBS estimates

This has raised questions about Imperial's ability to hit its 1-4% constant FX growth target; we view NGPs as necessary to deliver that (Figure 43). Furthermore, IMB's target of 4-8% constant FX EPS growth requires the currently highly loss-making NGP business to turn profitable. At 1H management reiterated it would meet that target by the end of FY19, but that the upside was reduced.

In the absence of this earnings growth, we would question the sustainability of the 10% DPS growth target (Figure 44).

Figure 43: Revenue growth coming from NGPs Figure 44: EPS and DPS growth

Source: Company data, UBS estimates Source: Company data, UBS estimates

We also further note that Imperial has been losing share in key tobacco markets (although the overall share is robust, as we discuss shortly). In our view, this calls into question the sustainability of its current tobacco pricing model and the cash flows it underpins. As a consequence, we see the current valuation as warranted and rate IMB Neutral.

-57% -60%

-55%

-50%

-45%

-40%

-35%

-30%

-25%

-20%

Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19

Rel to MSCI EU Staples 10 yr ave

1 yr fwd PE relative (%)

0

20

40

60

80

100

120

1H18 2H18 1H19 2H19EAmericas Europe Rest of World

NGP revenue £mn

F'cast

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

1H17 2H17 1H18 2H18 1H19 2H19ECombustibles NGP impact

Drivers of organic growth (%) F'cast

40%

50%

60%

70%

80%

90%

100%

-10%

-5%

0%

5%

10%

15%

20%

2012

2013

2014

2015

2016

2017

2018

2019

E

2020

E

2021

E

2022

E

2023

E

EPS growth DPS growth Payout ratio

F'cast EPS / DPS growth (%) Payout ratio (%)

Global Tobacco 23 May 2019

16

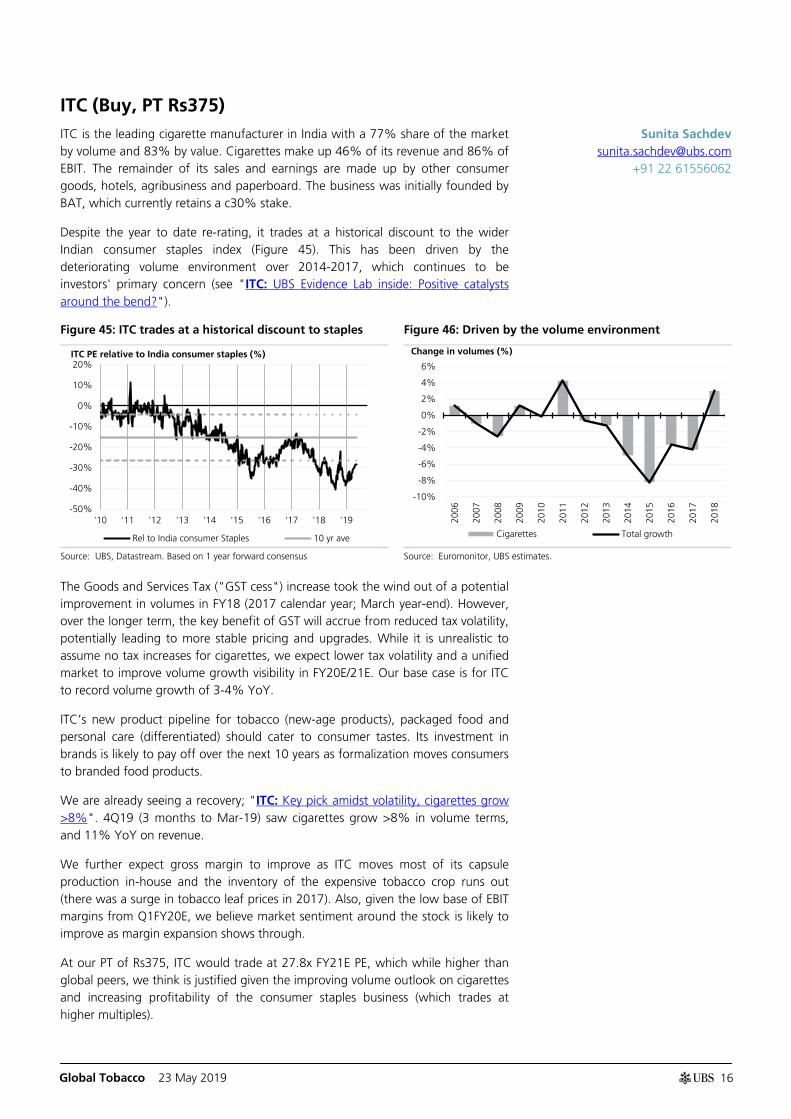

ITC (Buy, PT Rs375) ITC is the leading cigarette manufacturer in India with a 77% share of the market by volume and 83% by value. Cigarettes make up 46% of its revenue and 86% of EBIT. The remainder of its sales and earnings are made up by other consumer goods, hotels, agribusiness and paperboard. The business was initially founded by BAT, which currently retains a c30% stake.

Despite the year to date re-rating, it trades at a historical discount to the wider Indian consumer staples index (Figure 45). This has been driven by the deteriorating volume environment over 2014-2017, which continues to be investors' primary concern (see "ITC: UBS Evidence Lab inside: Positive catalysts around the bend?").

Figure 45: ITC trades at a historical discount to staples Figure 46: Driven by the volume environment

Source: UBS, Datastream. Based on 1 year forward consensus Source: Euromonitor, UBS estimates.

The Goods and Services Tax ("GST cess") increase took the wind out of a potential improvement in volumes in FY18 (2017 calendar year; March year-end). However, over the longer term, the key benefit of GST will accrue from reduced tax volatility, potentially leading to more stable pricing and upgrades. While it is unrealistic to assume no tax increases for cigarettes, we expect lower tax volatility and a unified market to improve volume growth visibility in FY20E/21E. Our base case is for ITC to record volume growth of 3-4% YoY.

ITC’s new product pipeline for tobacco (new-age products), packaged food and personal care (differentiated) should cater to consumer tastes. Its investment in brands is likely to pay off over the next 10 years as formalization moves consumers to branded food products.

We are already seeing a recovery; "ITC: Key pick amidst volatility, cigarettes grow >8%". 4Q19 (3 months to Mar-19) saw cigarettes grow >8% in volume terms, and 11% YoY on revenue.

We further expect gross margin to improve as ITC moves most of its capsule production in-house and the inventory of the expensive tobacco crop runs out (there was a surge in tobacco leaf prices in 2017). Also, given the low base of EBIT margins from Q1FY20E, we believe market sentiment around the stock is likely to improve as margin expansion shows through.

At our PT of Rs375, ITC would trade at 27.8x FY21E PE, which while higher than global peers, we think is justified given the improving volume outlook on cigarettes and increasing profitability of the consumer staples business (which trades at higher multiples).

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Rel to India consumer Staples 10 yr ave

ITC PE relative to India consumer staples (%)

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Cigarettes Total growth

Change in volumes (%)

Sunita Sachdev [email protected]

+91 22 61556062

Global Tobacco 23 May 2019

17

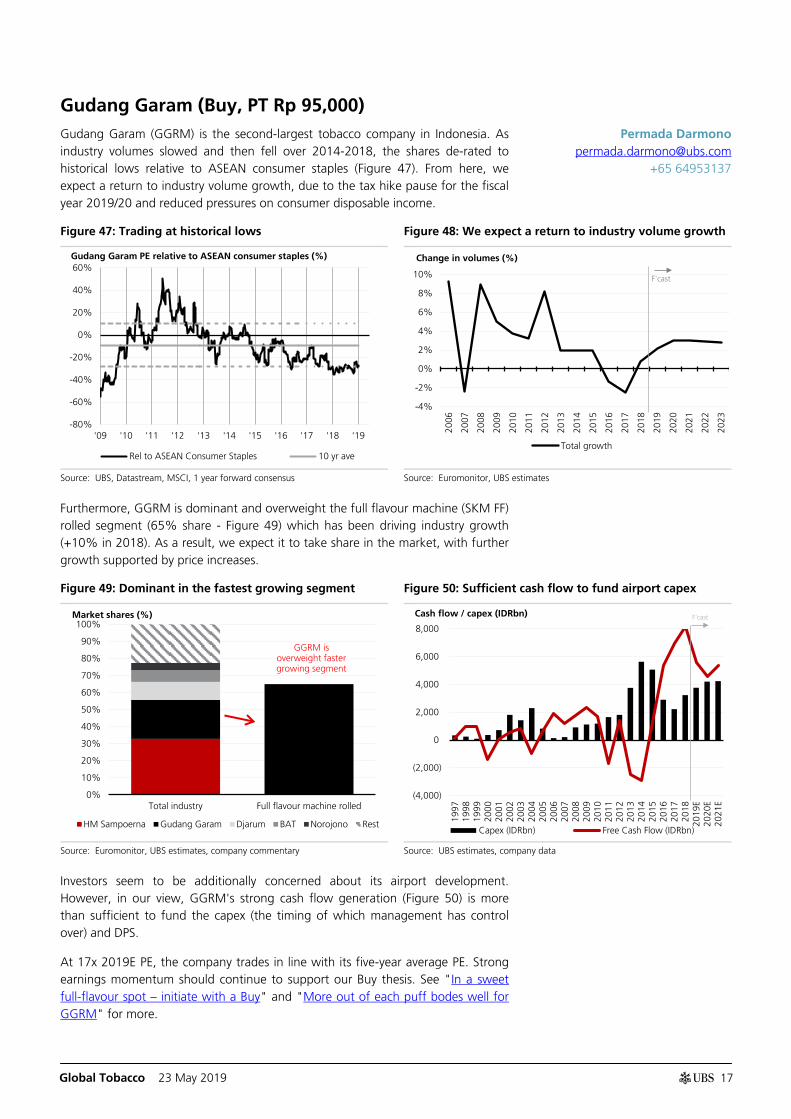

Gudang Garam (Buy, PT Rp 95,000) Gudang Garam (GGRM) is the second-largest tobacco company in Indonesia. As industry volumes slowed and then fell over 2014-2018, the shares de-rated to historical lows relative to ASEAN consumer staples (Figure 47). From here, we expect a return to industry volume growth, due to the tax hike pause for the fiscal year 2019/20 and reduced pressures on consumer disposable income.

Figure 47: Trading at historical lows Figure 48: We expect a return to industry volume growth

Source: UBS, Datastream, MSCI, 1 year forward consensus Source: Euromonitor, UBS estimates

Furthermore, GGRM is dominant and overweight the full flavour machine (SKM FF) rolled segment (65% share - Figure 49) which has been driving industry growth (+10% in 2018). As a result, we expect it to take share in the market, with further growth supported by price increases.

Figure 49: Dominant in the fastest growing segment Figure 50: Sufficient cash flow to fund airport capex

Source: Euromonitor, UBS estimates, company commentary Source: UBS estimates, company data

Investors seem to be additionally concerned about its airport development. However, in our view, GGRM's strong cash flow generation (Figure 50) is more than sufficient to fund the capex (the timing of which management has control over) and DPS.

At 17x 2019E PE, the company trades in line with its five-year average PE. Strong earnings momentum should continue to support our Buy thesis. See "In a sweet full-flavour spot – initiate with a Buy" and "More out of each puff bodes well for GGRM" for more.

-80%

-60%

-40%

-20%

0%

20%

40%

60%

'09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19

Rel to ASEAN Consumer Staples 10 yr ave

Gudang Garam PE relative to ASEAN consumer staples (%)

-4%

-2%

0%

2%

4%

6%

8%

10%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Total growth

F'cast

Change in volumes (%)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Total industry Full flavour machine rolled

HM Sampoerna Gudang Garam Djarum BAT Norojono Rest

Market shares (%)

GGRM is overweight faster growing segment

(4,000)

(2,000)

0

2,000

4,000

6,000

8,000

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

E20

20E

2021

E

Capex (IDRbn) Free Cash Flow (IDRbn)

F'cast Cash flow / capex (IDRbn)

Permada Darmono [email protected]

+65 64953137

Global Tobacco 23 May 2019

18

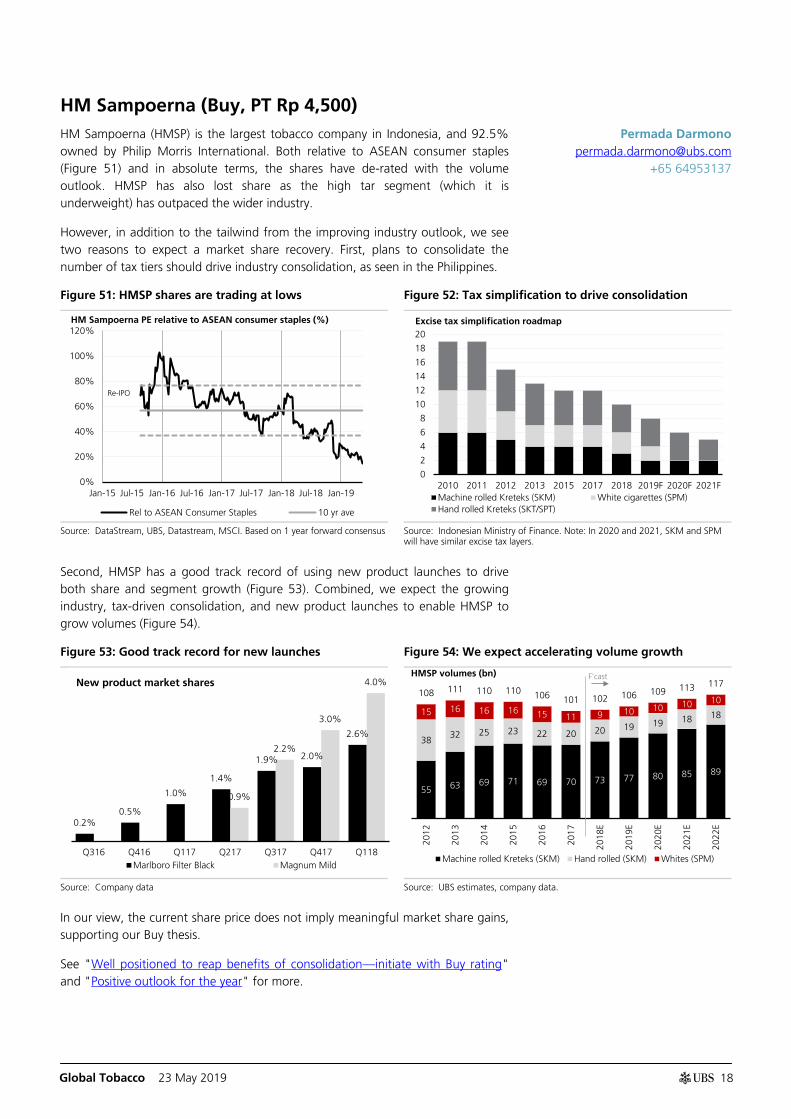

HM Sampoerna (Buy, PT Rp 4,500) HM Sampoerna (HMSP) is the largest tobacco company in Indonesia, and 92.5% owned by Philip Morris International. Both relative to ASEAN consumer staples (Figure 51) and in absolute terms, the shares have de-rated with the volume outlook. HMSP has also lost share as the high tar segment (which it is underweight) has outpaced the wider industry.

However, in addition to the tailwind from the improving industry outlook, we see two reasons to expect a market share recovery. First, plans to consolidate the number of tax tiers should drive industry consolidation, as seen in the Philippines.

Figure 51: HMSP shares are trading at lows Figure 52: Tax simplification to drive consolidation

Source: DataStream, UBS, Datastream, MSCI. Based on 1 year forward consensus Source: Indonesian Ministry of Finance. Note: In 2020 and 2021, SKM and SPM

will have similar excise tax layers.

Second, HMSP has a good track record of using new product launches to drive both share and segment growth (Figure 53). Combined, we expect the growing industry, tax-driven consolidation, and new product launches to enable HMSP to grow volumes (Figure 54).

Figure 53: Good track record for new launches Figure 54: We expect accelerating volume growth

Source: Company data Source: UBS estimates, company data.

In our view, the current share price does not imply meaningful market share gains, supporting our Buy thesis.

See "Well positioned to reap benefits of consolidation—initiate with Buy rating" and "Positive outlook for the year" for more.

0%

20%

40%

60%

80%

100%

120%

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19

Rel to ASEAN Consumer Staples 10 yr ave

HM Sampoerna PE relative to ASEAN consumer staples (%)

Re-IPO

0

2

4

6

8

10

12

14

16

18

20

2010 2011 2012 2013 2015 2017 2018 2019F 2020F 2021FMachine rolled Kreteks (SKM) White cigarettes (SPM)Hand rolled Kreteks (SKT/SPT)

Excise tax simplification roadmap

0.2% 0.5%

1.0%

1.4%

1.9% 2.0%

2.6%

0.9%

2.2%

3.0%

4.0%

Q316 Q416 Q117 Q217 Q317 Q417 Q118Marlboro Filter Black Magnum Mild

New product market shares

55 63 69 71 69 70 73 77 80 85 89

38 32 25 23 22 20 20 19 19 18 18 15 16 16 16 15 11 9 10 10 10 10

108 111 110 110 106 101 102 106 109 113 117

2012

2013

2014

2015

2016

2017

2018

E

2019

E

2020

E

2021

E

2022

E

Machine rolled Kreteks (SKM) Hand rolled (SKM) Whites (SPM)

HMSP volumes (bn) F'cast

Permada Darmono [email protected]

+65 64953137

Global Tobacco 23 May 2019

19

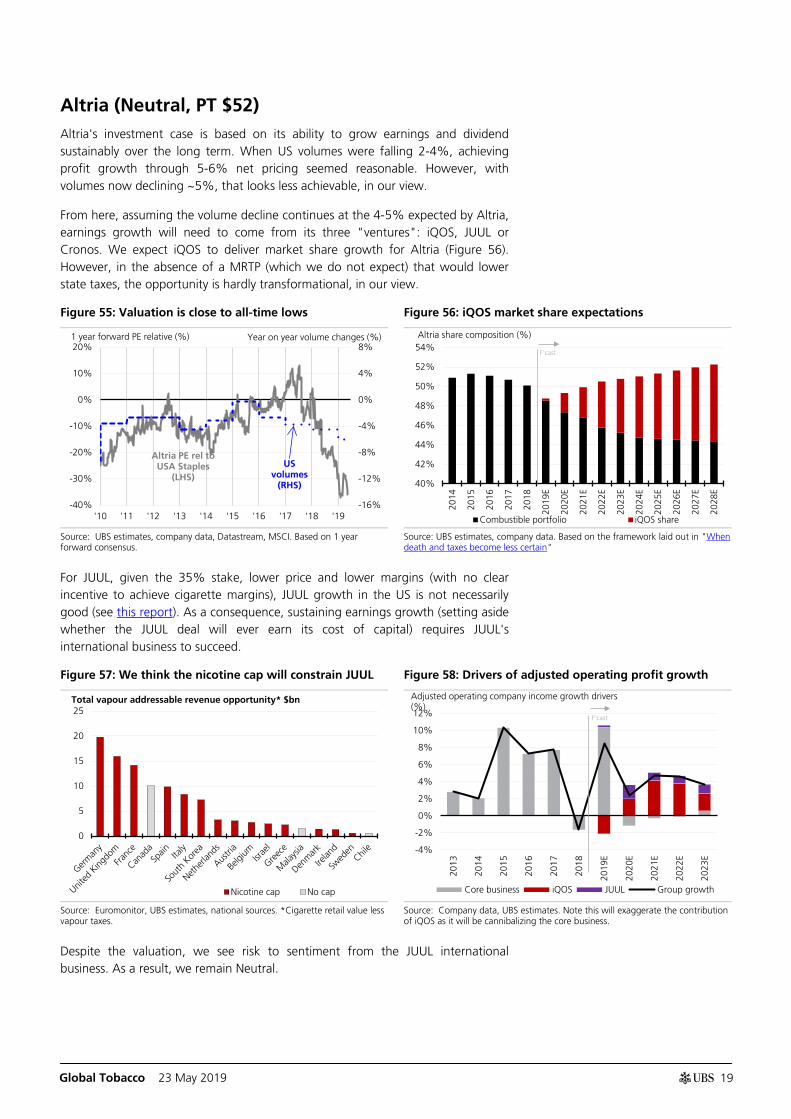

Altria (Neutral, PT $52) Altria's investment case is based on its ability to grow earnings and dividend sustainably over the long term. When US volumes were falling 2-4%, achieving profit growth through 5-6% net pricing seemed reasonable. However, with volumes now declining ~5%, that looks less achievable, in our view.

From here, assuming the volume decline continues at the 4-5% expected by Altria, earnings growth will need to come from its three "ventures": iQOS, JUUL or Cronos. We expect iQOS to deliver market share growth for Altria (Figure 56). However, in the absence of a MRTP (which we do not expect) that would lower state taxes, the opportunity is hardly transformational, in our view.

Figure 55: Valuation is close to all-time lows Figure 56: iQOS market share expectations

Source: UBS estimates, company data, Datastream, MSCI. Based on 1 year forward consensus.

Source: UBS estimates, company data. Based on the framework laid out in "When death and taxes become less certain"

For JUUL, given the 35% stake, lower price and lower margins (with no clear incentive to achieve cigarette margins), JUUL growth in the US is not necessarily good (see this report). As a consequence, sustaining earnings growth (setting aside whether the JUUL deal will ever earn its cost of capital) requires JUUL's international business to succeed.

Figure 57: We think the nicotine cap will constrain JUUL Figure 58: Drivers of adjusted operating profit growth

Source: Euromonitor, UBS estimates, national sources. *Cigarette retail value less vapour taxes.

Source: Company data, UBS estimates. Note this will exaggerate the contribution of iQOS as it will be cannibalizing the core business.

Despite the valuation, we see risk to sentiment from the JUUL international business. As a result, we remain Neutral.

-16%

-12%

-8%

-4%

0%

4%

8%

-40%

-30%

-20%

-10%

0%

10%

20%

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19

1 year forward PE relative (%) Year on year volume changes (%)

Altria PE rel to USA Staples

(LHS) US

volumes (RHS) 40%

42%

44%

46%

48%

50%

52%

54%

2014

2015

2016

2017

2018

2019

E

2020

E

2021

E

2022

E

2023

E

2024

E

2025

E

2026

E

2027

E

2028

E

Combustible portfolio iQOS share

Altria share composition (%)

F'cast

0

5

10

15

20

25

Nicotine cap No cap

Total vapour addressable revenue opportunity* $bn

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2013

2014

2015

2016

2017

2018

2019

E

2020

E

2021

E

2022

E

2023

E

Core business iQOS JUUL Group growth

Adjusted operating company income growth drivers (%)

F'cast

Global Tobacco 23 May 2019

20

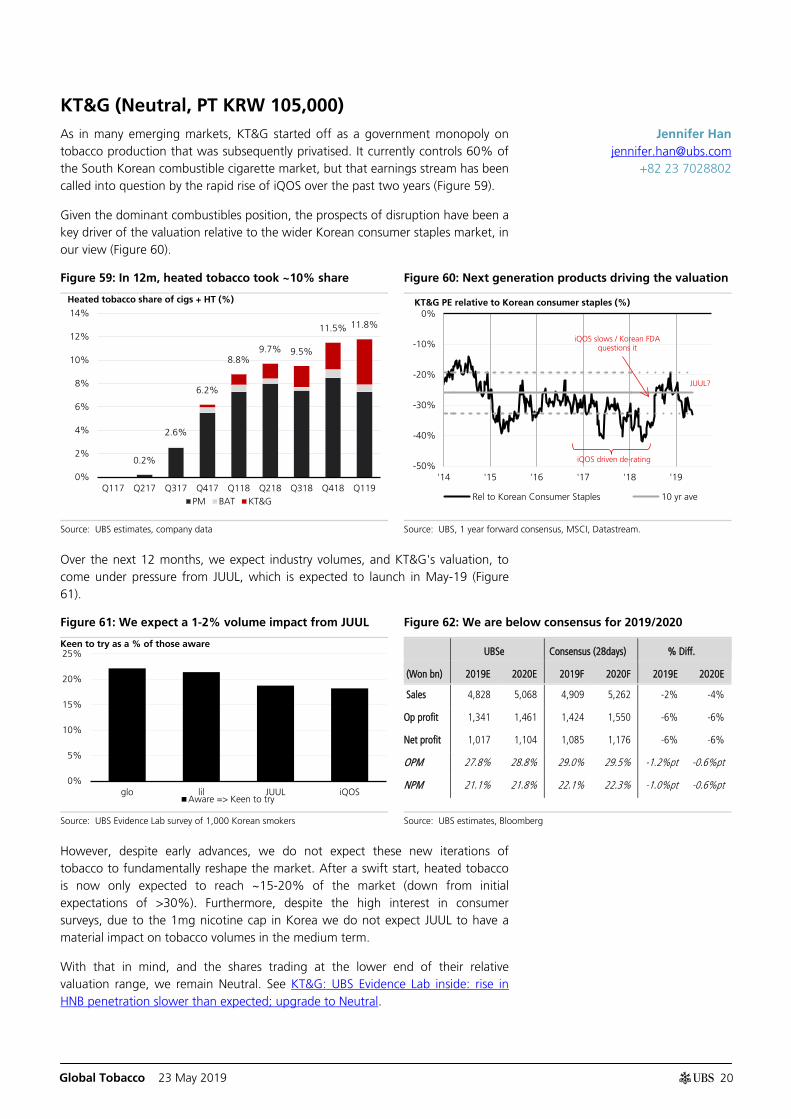

KT&G (Neutral, PT KRW 105,000) As in many emerging markets, KT&G started off as a government monopoly on tobacco production that was subsequently privatised. It currently controls 60% of the South Korean combustible cigarette market, but that earnings stream has been called into question by the rapid rise of iQOS over the past two years (Figure 59).

Given the dominant combustibles position, the prospects of disruption have been a key driver of the valuation relative to the wider Korean consumer staples market, in our view (Figure 60).

Figure 59: In 12m, heated tobacco took ~10% share Figure 60: Next generation products driving the valuation

Source: UBS estimates, company data Source: UBS, 1 year forward consensus, MSCI, Datastream.

Over the next 12 months, we expect industry volumes, and KT&G's valuation, to come under pressure from JUUL, which is expected to launch in May-19 (Figure 61).

Figure 61: We expect a 1-2% volume impact from JUUL Figure 62: We are below consensus for 2019/2020

UBSe Consensus (28days) % Diff.

(Won bn) 2019E 2020E 2019F 2020F 2019E 2020E

Sales 4,828 5,068 4,909 5,262 -2% -4%

Op profit 1,341 1,461 1,424 1,550 -6% -6%

Net profit 1,017 1,104 1,085 1,176 -6% -6%

OPM 27.8% 28.8% 29.0% 29.5% -1.2%pt -0.6%pt

NPM 21.1% 21.8% 22.1% 22.3% -1.0%pt -0.6%pt

Source: UBS Evidence Lab survey of 1,000 Korean smokers Source: UBS estimates, Bloomberg

However, despite early advances, we do not expect these new iterations of tobacco to fundamentally reshape the market. After a swift start, heated tobacco is now only expected to reach ~15-20% of the market (down from initial expectations of >30%). Furthermore, despite the high interest in consumer surveys, due to the 1mg nicotine cap in Korea we do not expect JUUL to have a material impact on tobacco volumes in the medium term.

With that in mind, and the shares trading at the lower end of their relative valuation range, we remain Neutral. See KT&G: UBS Evidence Lab inside: rise in HNB penetration slower than expected; upgrade to Neutral.

0.2%

2.6%

6.2%

8.8% 9.7% 9.5%

11.5% 11.8%

0%

2%

4%

6%

8%

10%

12%

14%

Q117 Q217 Q317 Q417 Q118 Q218 Q318 Q418 Q119PM BAT KT&G

Heated tobacco share of cigs + HT (%)

-50%

-40%

-30%

-20%

-10%

0%

'14 '15 '16 '17 '18 '19

Rel to Korean Consumer Staples 10 yr ave

KT&G PE relative to Korean consumer staples (%)

iQOS driven de-rating

iQOS slows / Korean FDA questions it

JUUL?

0%

5%

10%

15%

20%

25%

glo lil JUUL iQOSAware => Keen to try

Keen to try as a % of those aware

Jennifer Han [email protected]

+82 23 7028802

Global Tobacco 23 May 2019

21

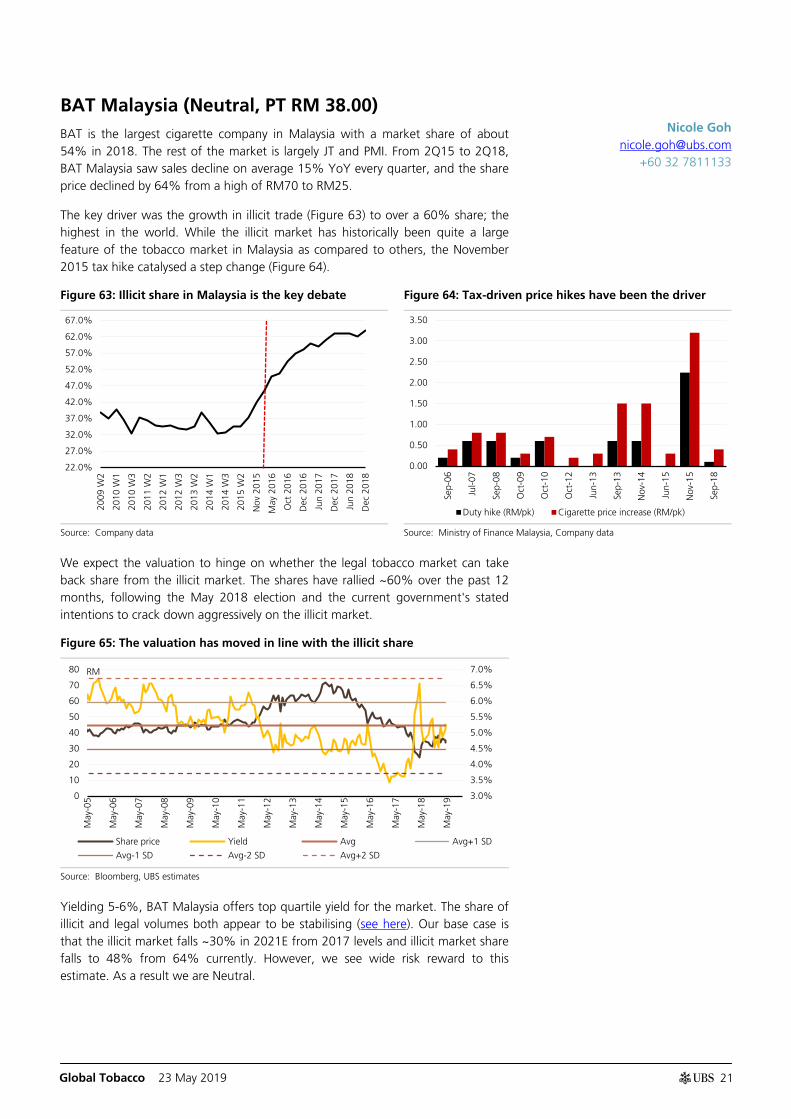

BAT Malaysia (Neutral, PT RM 38.00) BAT is the largest cigarette company in Malaysia with a market share of about 54% in 2018. The rest of the market is largely JT and PMI. From 2Q15 to 2Q18, BAT Malaysia saw sales decline on average 15% YoY every quarter, and the share price declined by 64% from a high of RM70 to RM25.

The key driver was the growth in illicit trade (Figure 63) to over a 60% share; the highest in the world. While the illicit market has historically been quite a large feature of the tobacco market in Malaysia as compared to others, the November 2015 tax hike catalysed a step change (Figure 64).

Figure 63: Illicit share in Malaysia is the key debate Figure 64: Tax-driven price hikes have been the driver

Source: Company data Source: Ministry of Finance Malaysia, Company data

We expect the valuation to hinge on whether the legal tobacco market can take back share from the illicit market. The shares have rallied ~60% over the past 12 months, following the May 2018 election and the current government's stated intentions to crack down aggressively on the illicit market.

Figure 65: The valuation has moved in line with the illicit share

Source: Bloomberg, UBS estimates

Yielding 5-6%, BAT Malaysia offers top quartile yield for the market. The share of illicit and legal volumes both appear to be stabilising (see here). Our base case is that the illicit market falls ~30% in 2021E from 2017 levels and illicit market share falls to 48% from 64% currently. However, we see wide risk reward to this estimate. As a result we are Neutral.

22.0%

27.0%

32.0%

37.0%

42.0%

47.0%

52.0%

57.0%

62.0%

67.0%

2009

W2

2010

W1

2010

W3

2011

W2

2012

W1

2012

W3

2013

W2

2014

W1

2014

W3

2015

W2

Nov

201

5

May

201

6

Oct

201

6

Dec

201

6

Jun

2017

Dec

201

7

Jun

2018

Dec

201

8

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Sep-

06

Jul-0

7

Sep-

08

Oct

-09

Oct

-10

Oct

-12

Jun-

13

Sep-

13

Nov

-14

Jun-

15

Nov

-15

Sep-

18

Duty hike (RM/pk) Cigarette price increase (RM/pk)

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

0

10

20

30

40

50

60

70

80

May

-05

May

-06

May

-07

May

-08

May

-09

May

-10

May

-11

May

-12

May

-13

May

-14

May

-15

May

-16

May

-17

May

-18

May

-19

Share price Yield Avg Avg+1 SD

Avg-1 SD Avg-2 SD Avg+2 SD

RM

Nicole Goh [email protected]

+60 32 7811133

Global Tobacco 23 May 2019

22

Building a global tobacco model How to approach the globally diversified tobacco companies?

The tobacco majors (BAT, IMB, PMI, and JT) are all highly diversified. With the exception of the US (which we cover in detail later in this note), no single market is sufficient to materially move the needle over time.

Furthermore, while there have been efforts to internationalise anti-smoking efforts, the legislative and tax context remain highly fragmented. Finally, the large changes in excise tax (which can lead to doubling of pack prices) can inject volatility into the core business on a year on year basis.

Estimate each of the key markets

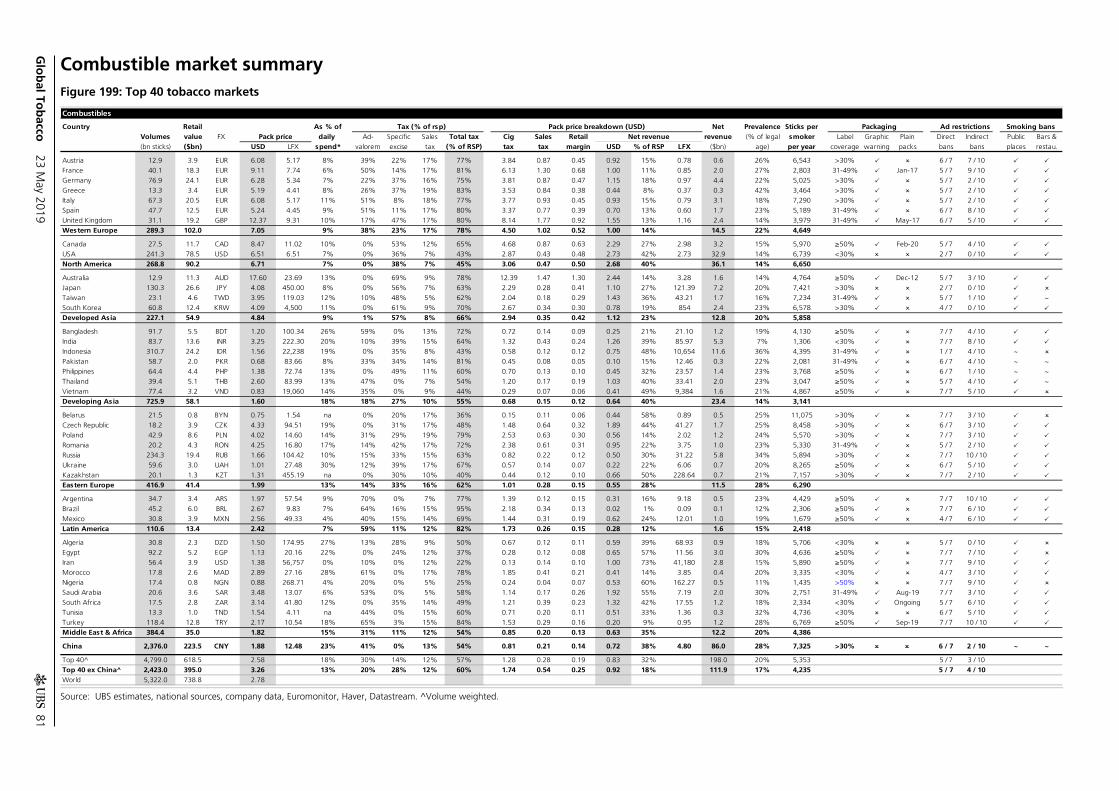

We have built an explicit model for cigarette (and heated tobacco) consumption for the top 40 tobacco markets (shown overleaf). We cover each element in detail in the "Global Outlook Detail" section. The key inputs (which we forecast) are:

(1) Macro variables: factors such as population, GDP growth, inflation and currency depreciation. In our model we generally use UBS estimates and consensus views out to 2023.

(2) Prevalence: taken as a % of population over 15.

(3) Sticks per smoker: Our volume numbers are based on industry and company data. Where there are discrepancies, we defer to company data.

(4) Taxes per pack: our estimate of average tax per pack. This is based on industry data, as well as national sources (for instance, government websites).

(5) Distribution margin: unless we have information to indicate otherwise (for example Japan), we assume ~8% distribution take.

(6) Cigarette pack prices: based on a mixture of industry data, surveys, and tobacco inflation indexes.

The output of the above is a revenue number for a given market. There is also a heated tobacco overlay.

Important caveats

(1) Market shares: we use third-party industry data for market shares. We observe that it on average understates the market share of the tobacco companies when compared to national sources of disclosed shares.

(2) Company coverage: the top 40 (39 ex China) markets we cover represent ~60-80% of the international tobacco company volumes.

(3) Prices are market averages: our revenue estimates are based on market averages, but shares are based on volumes.

(4) Net revenue is an estimate: at a group level, we can square our estimates with company data (and divisionally for PMI), allowing for volume differences.

We have taken a view on the 40 largest tobacco markets globally

Glo

bal To

bacco

23 May 2019

23

Markets in our model

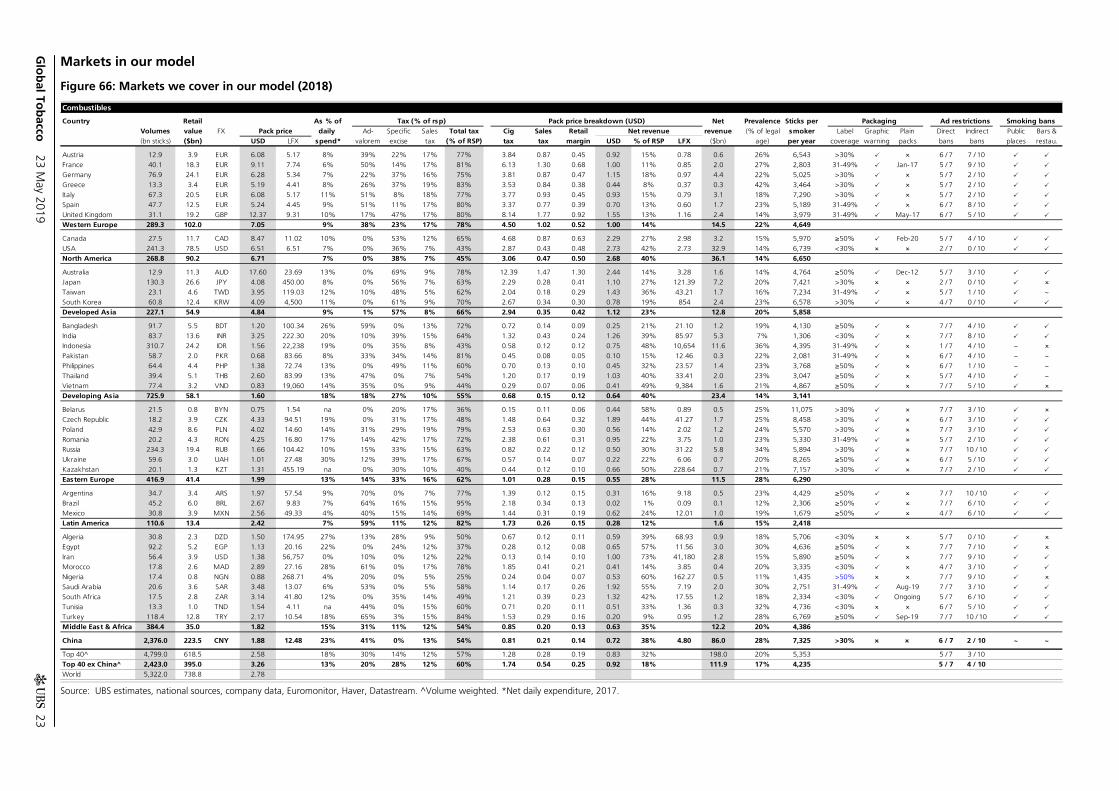

Figure 66: Markets we cover in our model (2018)

Source: UBS estimates, national sources, company data, Euromonitor, Haver, Datastream. ^Volume weighted. *Net daily expenditure, 2017.

Combustibles

Country Retail As % of Tax (% of rsp) Pack price breakdown (USD) Net Prevalence Sticks per Packaging Ad restrictions Smoking bansVolumes value FX Pack price daily Ad- Specific Sales Total tax Cig Sales Retail Net revenue revenue (% of legal smoker Label Graphic Plain Direct Indirect Public Bars &

(bn sticks) ($bn) USD LFX spend* valorem excise tax (% of RSP) tax tax margin USD % of RSP LFX ($bn) age) per year coverage warning packs bans bans places restau.

Austria 12.9 3.9 EUR 6.08 5.17 8% 39% 22% 17% 77% 3.84 0.87 0.45 0.92 15% 0.78 0.6 26% 6,543 >30% 6 / 7 7 / 10

France 40.1 18.3 EUR 9.11 7.74 6% 50% 14% 17% 81% 6.13 1.30 0.68 1.00 11% 0.85 2.0 27% 2,803 31-49% Jan-17 5 / 7 9 / 10

Germany 76.9 24.1 EUR 6.28 5.34 7% 22% 37% 16% 75% 3.81 0.87 0.47 1.15 18% 0.97 4.4 22% 5,025 >30% 5 / 7 2 / 10

Greece 13.3 3.4 EUR 5.19 4.41 8% 26% 37% 19% 83% 3.53 0.84 0.38 0.44 8% 0.37 0.3 42% 3,464 >30% 5 / 7 2 / 10

Italy 67.3 20.5 EUR 6.08 5.17 11% 51% 8% 18% 77% 3.77 0.93 0.45 0.93 15% 0.79 3.1 18% 7,290 >30% 5 / 7 2 / 10

Spain 47.7 12.5 EUR 5.24 4.45 9% 51% 11% 17% 80% 3.37 0.77 0.39 0.70 13% 0.60 1.7 23% 5,189 31-49% 6 / 7 8 / 10

United Kingdom 31.1 19.2 GBP 12.37 9.31 10% 17% 47% 17% 80% 8.14 1.77 0.92 1.55 13% 1.16 2.4 14% 3,979 31-49% May-17 6 / 7 5 / 10

Western Europe 289.3 102.0 7.05 9% 38% 23% 17% 78% 4.50 1.02 0.52 1.00 14% 14.5 22% 4,649

Canada 27.5 11.7 CAD 8.47 11.02 10% 0% 53% 12% 65% 4.68 0.87 0.63 2.29 27% 2.98 3.2 15% 5,970 ≥50% Feb-20 5 / 7 4 / 10

USA 241.3 78.5 USD 6.51 6.51 7% 0% 36% 7% 43% 2.87 0.43 0.48 2.73 42% 2.73 32.9 14% 6,739 <30% 2 / 7 0 / 10

North America 268.8 90.2 6.71 7% 0% 38% 7% 45% 3.06 0.47 0.50 2.68 40% 36.1 14% 6,650

Australia 12.9 11.3 AUD 17.60 23.69 13% 0% 69% 9% 78% 12.39 1.47 1.30 2.44 14% 3.28 1.6 14% 4,764 ≥50% Dec-12 5 / 7 3 / 10

Japan 130.3 26.6 JPY 4.08 450.00 8% 0% 56% 7% 63% 2.29 0.28 0.41 1.10 27% 121.39 7.2 20% 7,421 >30% 2 / 7 0 / 10

Taiwan 23.1 4.6 TWD 3.95 119.03 12% 10% 48% 5% 62% 2.04 0.18 0.29 1.43 36% 43.21 1.7 16% 7,234 31-49% 5 / 7 1 / 10 ~

South Korea 60.8 12.4 KRW 4.09 4,500 11% 0% 61% 9% 70% 2.67 0.34 0.30 0.78 19% 854 2.4 23% 6,578 >30% 4 / 7 0 / 10

Developed Asia 227.1 54.9 4.84 9% 1% 57% 8% 66% 2.94 0.35 0.42 1.12 23% 12.8 20% 5,858

Bangladesh 91.7 5.5 BDT 1.20 100.34 26% 59% 0% 13% 72% 0.72 0.14 0.09 0.25 21% 21.10 1.2 19% 4,130 ≥50% 7 / 7 4 / 10

India 83.7 13.6 INR 3.25 222.30 20% 10% 39% 15% 64% 1.32 0.43 0.24 1.26 39% 85.97 5.3 7% 1,306 <30% 7 / 7 8 / 10

Indonesia 310.7 24.2 IDR 1.56 22,238 19% 0% 35% 8% 43% 0.58 0.12 0.12 0.75 48% 10,654 11.6 36% 4,395 31-49% 1 / 7 4 / 10 ~

Pakistan 58.7 2.0 PKR 0.68 83.66 8% 33% 34% 14% 81% 0.45 0.08 0.05 0.10 15% 12.46 0.3 22% 2,081 31-49% 6 / 7 4 / 10 ~ ~

Philippines 64.4 4.4 PHP 1.38 72.74 13% 0% 49% 11% 60% 0.70 0.13 0.10 0.45 32% 23.57 1.4 23% 3,768 ≥50% 6 / 7 1 / 10 ~ ~

Thailand 39.4 5.1 THB 2.60 83.99 13% 47% 0% 7% 54% 1.20 0.17 0.19 1.03 40% 33.41 2.0 23% 3,047 ≥50% 5 / 7 4 / 10 ~

Vietnam 77.4 3.2 VND 0.83 19,060 14% 35% 0% 9% 44% 0.29 0.07 0.06 0.41 49% 9,384 1.6 21% 4,867 ≥50% 7 / 7 5 / 10

Developing Asia 725.9 58.1 1.60 18% 18% 27% 10% 55% 0.68 0.15 0.12 0.64 40% 23.4 14% 3,141

Belarus 21.5 0.8 BYN 0.75 1.54 na 0% 20% 17% 36% 0.15 0.11 0.06 0.44 58% 0.89 0.5 25% 11,075 >30% 7 / 7 3 / 10

Czech Republic 18.2 3.9 CZK 4.33 94.51 19% 0% 31% 17% 48% 1.48 0.64 0.32 1.89 44% 41.27 1.7 25% 8,458 >30% 6 / 7 3 / 10

Poland 42.9 8.6 PLN 4.02 14.60 14% 31% 29% 19% 79% 2.53 0.63 0.30 0.56 14% 2.02 1.2 24% 5,570 >30% 7 / 7 3 / 10

Romania 20.2 4.3 RON 4.25 16.80 17% 14% 42% 17% 72% 2.38 0.61 0.31 0.95 22% 3.75 1.0 23% 5,330 31-49% 5 / 7 2 / 10

Russia 234.3 19.4 RUB 1.66 104.42 10% 15% 33% 15% 63% 0.82 0.22 0.12 0.50 30% 31.22 5.8 34% 5,894 >30% 7 / 7 10 / 10

Ukraine 59.6 3.0 UAH 1.01 27.48 30% 12% 39% 17% 67% 0.57 0.14 0.07 0.22 22% 6.06 0.7 20% 8,265 ≥50% 6 / 7 5 / 10

Kazakhstan 20.1 1.3 KZT 1.31 455.19 na 0% 30% 10% 40% 0.44 0.12 0.10 0.66 50% 228.64 0.7 21% 7,157 >30% 7 / 7 2 / 10

Eastern Europe 416.9 41.4 1.99 13% 14% 33% 16% 62% 1.01 0.28 0.15 0.55 28% 11.5 28% 6,290

Argentina 34.7 3.4 ARS 1.97 57.54 9% 70% 0% 7% 77% 1.39 0.12 0.15 0.31 16% 9.18 0.5 23% 4,429 ≥50% 7 / 7 10 / 10

Brazil 45.2 6.0 BRL 2.67 9.83 7% 64% 16% 15% 95% 2.18 0.34 0.13 0.02 1% 0.09 0.1 12% 2,306 ≥50% 7 / 7 6 / 10

Mexico 30.8 3.9 MXN 2.56 49.33 4% 40% 15% 14% 69% 1.44 0.31 0.19 0.62 24% 12.01 1.0 19% 1,679 ≥50% 4 / 7 6 / 10

Latin America 110.6 13.4 2.42 7% 59% 11% 12% 82% 1.73 0.26 0.15 0.28 12% 1.6 15% 2,418

Algeria 30.8 2.3 DZD 1.50 174.95 27% 13% 28% 9% 50% 0.67 0.12 0.11 0.59 39% 68.93 0.9 18% 5,706 <30% 5 / 7 0 / 10

Egypt 92.2 5.2 EGP 1.13 20.16 22% 0% 24% 12% 37% 0.28 0.12 0.08 0.65 57% 11.56 3.0 30% 4,636 ≥50% 7 / 7 7 / 10

Iran 56.4 3.9 USD 1.38 56,757 0% 10% 0% 12% 22% 0.13 0.14 0.10 1.00 73% 41,180 2.8 15% 5,890 ≥50% 7 / 7 9 / 10

Morocco 17.8 2.6 MAD 2.89 27.16 28% 61% 0% 17% 78% 1.85 0.41 0.21 0.41 14% 3.85 0.4 20% 3,335 <30% 4 / 7 3 / 10

Nigeria 17.4 0.8 NGN 0.88 268.71 4% 20% 0% 5% 25% 0.24 0.04 0.07 0.53 60% 162.27 0.5 11% 1,435 >50% 7 / 7 9 / 10

Saudi Arabia 20.6 3.6 SAR 3.48 13.07 6% 53% 0% 5% 58% 1.14 0.17 0.26 1.92 55% 7.19 2.0 30% 2,751 31-49% Aug-19 7 / 7 3 / 10

South Africa 17.5 2.8 ZAR 3.14 41.80 12% 0% 35% 14% 49% 1.21 0.39 0.23 1.32 42% 17.55 1.2 18% 2,334 <30% Ongoing 5 / 7 6 / 10

Tunisia 13.3 1.0 TND 1.54 4.11 na 44% 0% 15% 60% 0.71 0.20 0.11 0.51 33% 1.36 0.3 32% 4,736 <30% 6 / 7 5 / 10

Turkey 118.4 12.8 TRY 2.17 10.54 18% 65% 3% 15% 84% 1.53 0.29 0.16 0.20 9% 0.95 1.2 28% 6,769 ≥50% Sep-19 7 / 7 10 / 10

Middle East & Africa 384.4 35.0 1.82 15% 31% 11% 12% 54% 0.85 0.20 0.13 0.63 35% 12.2 20% 4,386

China 2,376.0 223.5 CNY 1.88 12.48 23% 41% 0% 13% 54% 0.81 0.21 0.14 0.72 38% 4.80 86.0 28% 7,325 >30% 6 / 7 2 / 10 ~ ~

Top 40^ 4,799.0 618.5 2.58 18% 30% 14% 12% 57% 1.28 0.28 0.19 0.83 32% 198.0 20% 5,353 5 / 7 3 / 10

Top 40 ex China^ 2,423.0 395.0 3.26 13% 20% 28% 12% 60% 1.74 0.54 0.25 0.92 18% 111.9 17% 4,235 5 / 7 4 / 10 World 5,322.0 738.8 2.78

Global Tobacco 23 May 2019

24

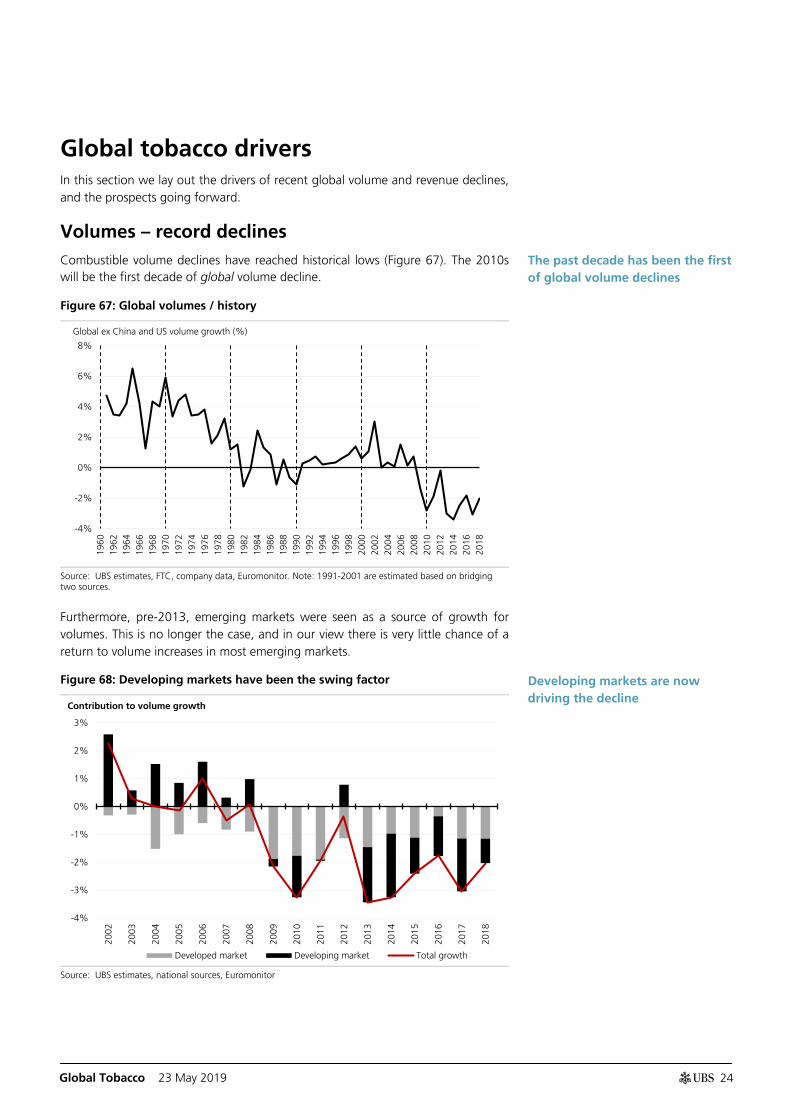

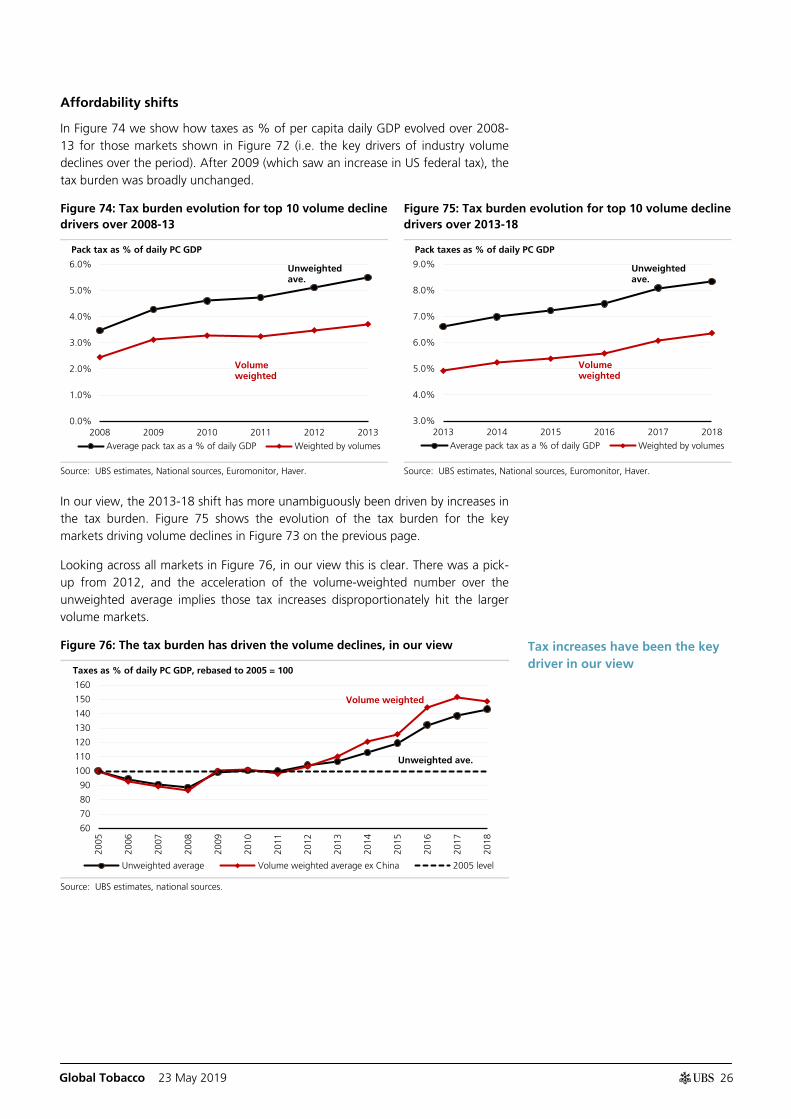

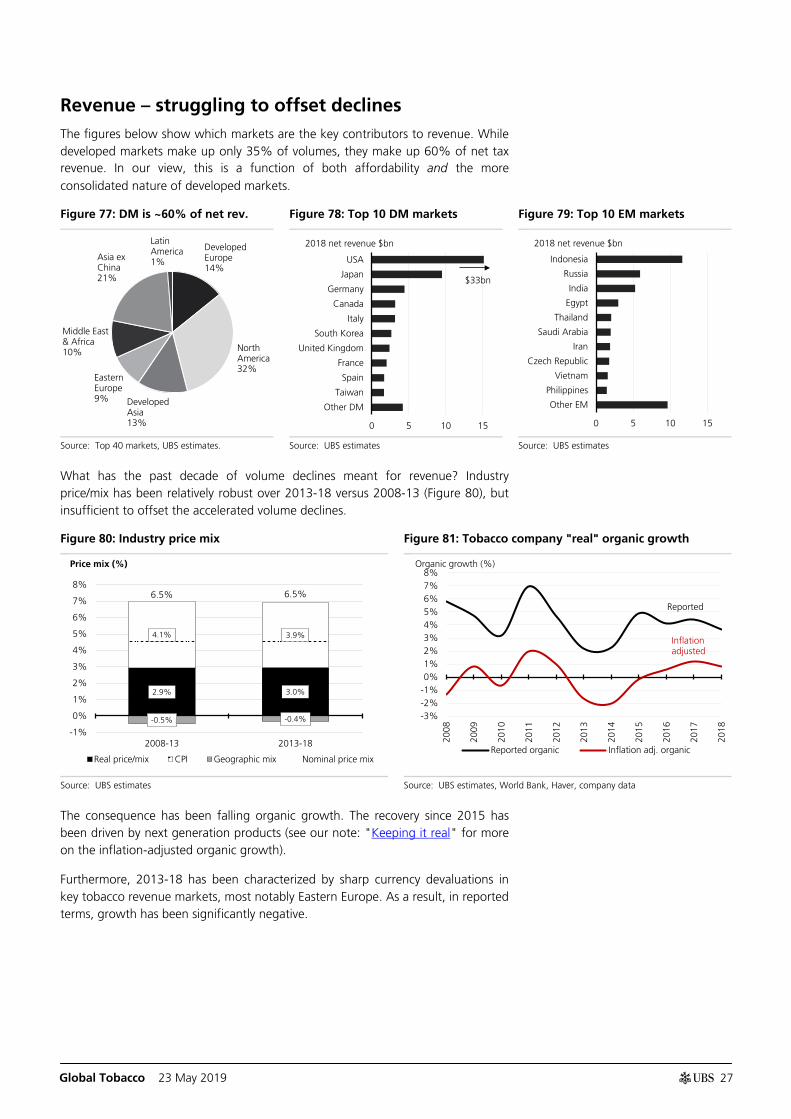

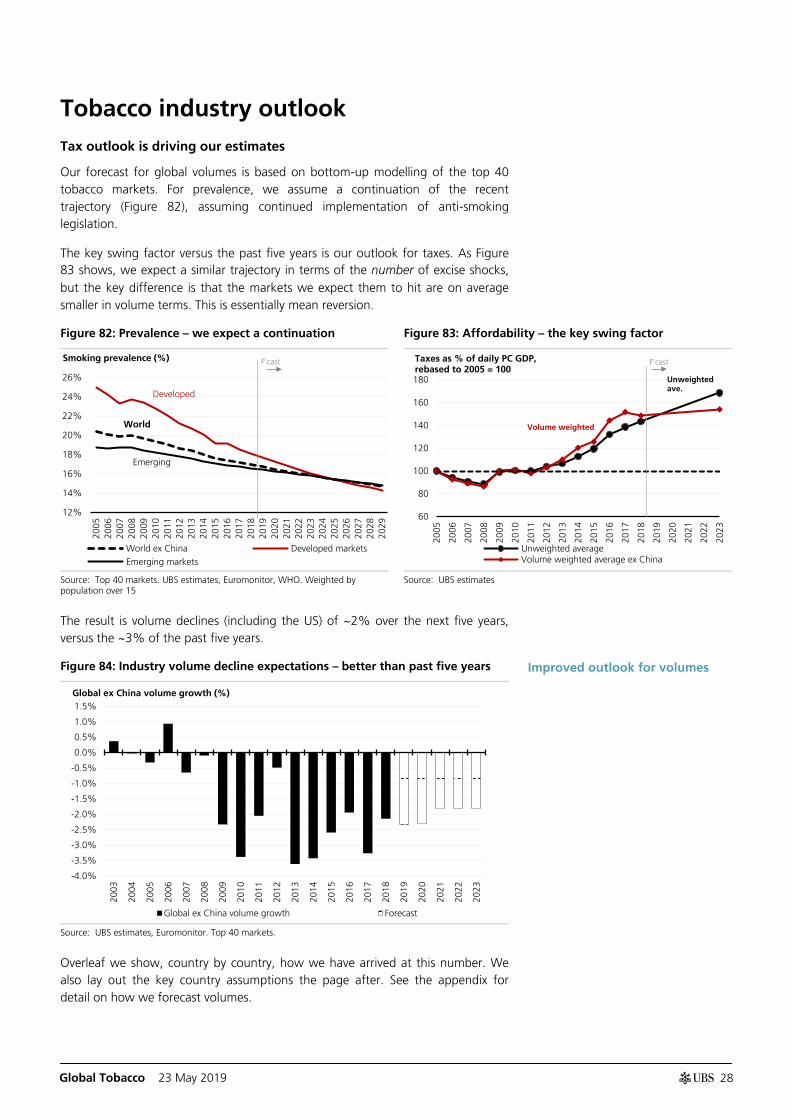

Global tobacco drivers In this section we lay out the drivers of recent global volume and revenue declines, and the prospects going forward.

Volumes – record declines Combustible volume declines have reached historical lows (Figure 67). The 2010s will be the first decade of global volume decline.

Figure 67: Global volumes / history

Source: UBS estimates, FTC, company data, Euromonitor. Note: 1991-2001 are estimated based on bridging two sources.

Furthermore, pre-2013, emerging markets were seen as a source of growth for volumes. This is no longer the case, and in our view there is very little chance of a return to volume increases in most emerging markets.

Figure 68: Developing markets have been the swing factor

Source: UBS estimates, national sources, Euromonitor

-4%

-2%

0%

2%

4%

6%

8%

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Global ex China and US volume growth (%)

-4%

-3%

-2%

-1%

0%

1%

2%

3%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Developed market Developing market Total growth

Contribution to volume growth

The past decade has been the first of global volume declines

Developing markets are now driving the decline

Global Tobacco 23 May 2019

25

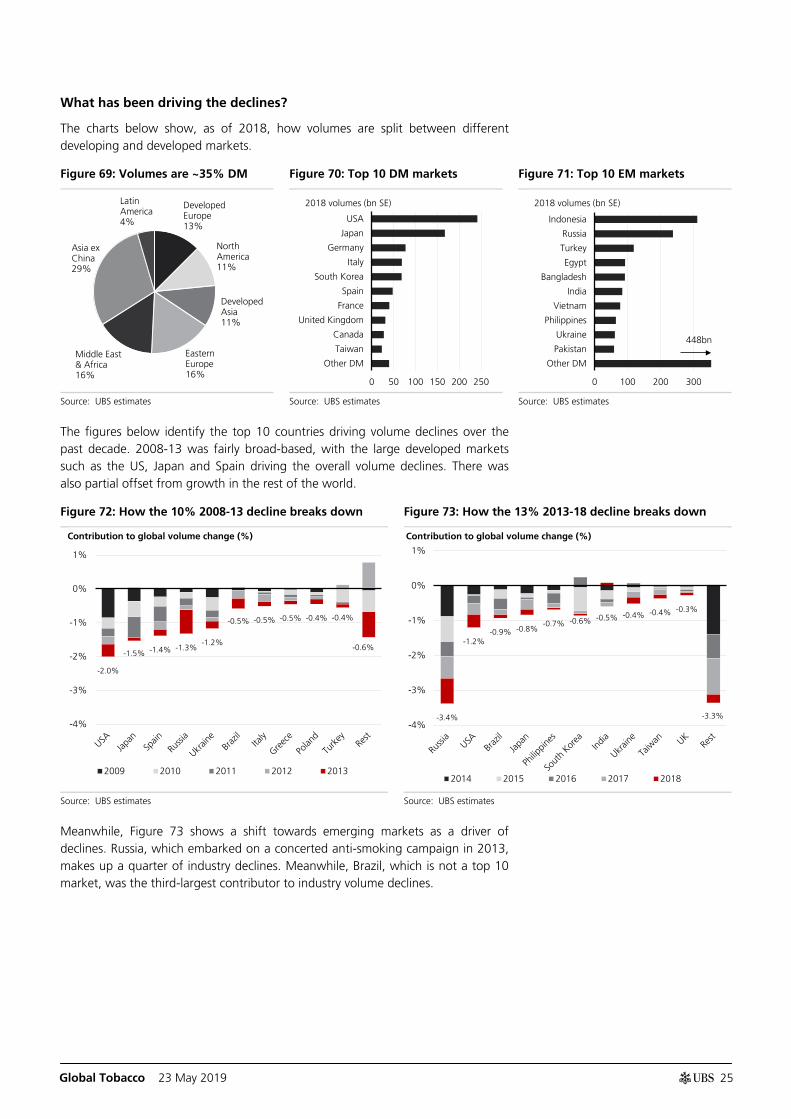

What has been driving the declines?

The charts below show, as of 2018, how volumes are split between different developing and developed markets.

Figure 69: Volumes are ~35% DM Figure 70: Top 10 DM markets Figure 71: Top 10 EM markets

Source: UBS estimates Source: UBS estimates Source: UBS estimates