GERMAN, EC AND U.S. MERGER CONTROL - CiteSeerX

111

COORDINATED EFFECTS AND COLLECTIVE DOMINANCE - A COMPARISON OF GERMAN, EC AND U.S. MERGER CONTROL Working Paper Thorsten Kaeseberg, M.A. (Economics) Humboldt-University Berlin email: [email protected] First draft: August 2002 Final version: January 2003

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of GERMAN, EC AND U.S. MERGER CONTROL - CiteSeerX

COORDINATED EFFECTS AND COLLECTIVE DOMINANCE -

A COMPARISON OF

GERMAN, EC AND U.S. MERGER CONTROL

Working Paper

Thorsten Kaeseberg, M.A. (Economics)

Humboldt-University Berlin

email: [email protected]

First draft: August 2002

Final version: January 2003

2

CONTENTS

1 INTRODUCTION ....................................................................................... 81.1 Focus of the paper ............................................................................................. 9

1.2 Reasons for the paper ........................................................................................ 10

2 STATIC OLIGOPOLY THEORIES, UNILATERAL EFFECTS

AND SINGLE DOMINANCE ....................................................................... 112.1 Cournot oligopoly model with homogeneous products

- Merger implications ....................................................................................... 11

2.1.1 Cournot-Nash equilibrium ...................................................................... 11

2.1.2 Consumer surplus ................................................................................... 12

2.1.3 Rationale for efficiency defence ............................................................ 12

2.1.4 Producer surplus and overall welfare ..................................................... 13

2.1.5 Rationale for using the HHI and �HHI .................................................. 13

2.1.6 Rationale for using market shares .......................................................... 14

2.1.7 Distortions in EC merger control? ......................................................... 14

2.1.8 The relationship between unilateral and coordinated effects -

an extension of the Cournot model ........................................................ 15

2.2 Bertrand oligopoly model with differentiated products

- Merger implications ...................................................................................... 16

2.2.1 Pre-merger equilibrium .......................................................................... 16

2.2.2 Post-merger equilibrium ......................................................................... 17

2.3 A two-step approach for assessing unilateral and coordinated effects ............. 17

2.4 Repeated interaction as necessary condition for collusion ............................... 18

3 DYNAMIC OLIGOPOLY THEORIES, COORDINATED EFFECTS AND

COLLECTIVE DOMINANCE ...................................................................... 193.1 The theory of repeated games ........................................................................... 20

3.1.1 Finitely repeated oligopoly games ......................................................... 20

3.1.2 Infinitely repeated oligopoly games (supergames)

3

with perfect information ........................................................................ 21

3.1.2.1 The basic model ........................................................................... 21

3.1.2.2 Equilibria ..................................................................................... 22

3.1.2.3 The Folk theorem ......................................................................... 22

3.1.2.4 The coordination problem ............................................................ 23

3.1.2.4.1 Explicit vs. tacit collusion ................................................. 23

3.1.2.4.2 Focal points and cheap talk ............................................... 23

3.1.3 Punishment strategies and renegotiation-proofness ............................... 24

3.2 Merger implications .......................................................................................... 25

3.2.1 Collusive effects of a merger ................................................................. 25

3.2.1.1 Reduction of number of firms ...................................................... 25

3.2.1.1.1 Coordination and monitoring - the "dinner party story" ... 26

3.2.1.1.2 Enforcement ...................................................................... 26

3.2.1.2 More symmetric distribution of assets ......................................... 27

3.2.1.2.1 Coordination and monitoring ............................................ 27

3.2.1.2.2 Enforcement ...................................................................... 28

3.2.1.2.3 A Trade-off ........................................................................ 28

3.2.1.2.4 The case of capacity constraints - the model of

Compte, Jenny and Rey .................................................... 29

3.2.1.2.4.1 The results of the model ......................................... 29

3.2.1.2.4.2 Application to Nestlé / Perrier ................................ 31

3.2.1.2.5 Policy implications ............................................................ 31

3.2.1.3 Loss of a maverick or reducing its incentive to compete ............ 32

3.2.1.3.1 Identifying a maverick ...................................................... 32

3.2.1.3.2 Merger scenarios ............................................................... 33

3.2.2 Comparative institutional analysis ......................................................... 34

3.2.2.1 Merger control and the prohibition of collusion as

(imperfect) substitutes ................................................................ 34

3.2.2.2 Comparative cost-benefit-analysis ............................................... 34

3.3 Other approaches to collusion ........................................................................... 35

3.3.1 Truly dynamic models ............................................................................ 36

3.3.1.1 Tangible industry conditions ....................................................... 37

3.3.1.2 Intangible industry conditions (beliefs) ....................................... 37

4

3.3.2 Evolutionary game theory ...................................................................... 38

3.3.2.1 Tit for tat as evolutionary stable strategy .................................... 38

3.3.2.2 Implications for merger policy .................................................... 39

3.4 Necessary conditions for collusion ................................................................... 40

3.4.1 "Few" firms - is there a "magic" number? ............................................. 40

3.4.1.1 Selten's "four are few and six are many" ..................................... 40

3.4.1.2 Renegotiation-proofness as binding constraint ............................ 42

3.4.2 Barriers to entry/exit and expansion ...................................................... 42

3.4.2.1 Barriers to entry/exit: prevention of hit-and-run competition ..... 43

3.4.2.2 Barriers to expansion: prevention of

competitive pressure by fringe firms ........................................... 43

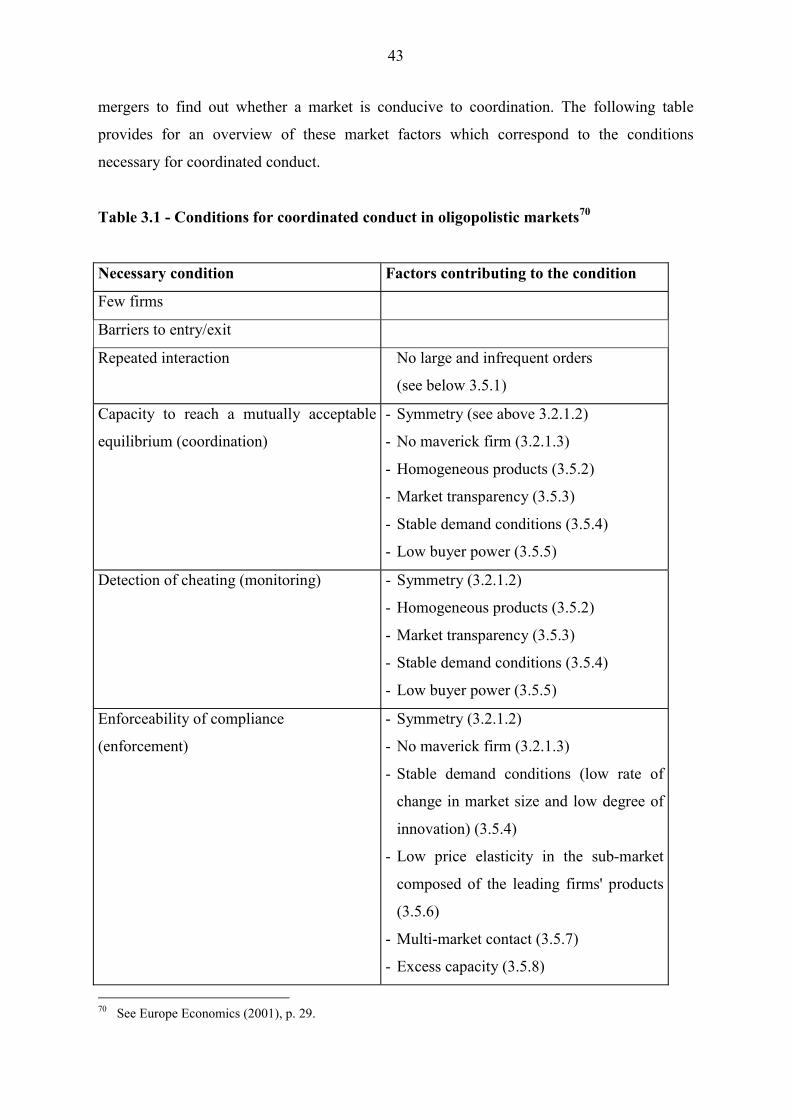

3.5 Market characteristics corresponding to the necessary conditions ................... 43

3.5.1 No large and lumpy orders ..................................................................... 45

3.5.2 Homogeneous products .......................................................................... 45

3.5.3 Market transparency ............................................................................... 46

3.5.3.1 Supergames with imperfect information ..................................... 46

3.5.3.2 Empiric evidence ......................................................................... 47

3.5.4 Stable demand conditions (low rate of change in market size

and low degree of innovation) ............................................................... 48

3.5.4.1 Market size ........................................................................... 48

3.5.4.2 Innovation ............................................................................ 48

3.5.5 Low buyer power ................................................................................... 49

3.5.6 Low price elasticity in the sub-market composed of

the leading firms' products ..................................................................... 49

3.5.7 Multi-market contact .............................................................................. 50

3.5.8 Excess capacity ...................................................................................... 50

3.6 Facilitating practices and structural links ......................................................... 51

3.6.1 Facilitating practices .............................................................................. 51

3.6.2 Structural links ....................................................................................... 52

3.7 Evidence of current coordination ...................................................................... 52

3.8 Relative importance of the market characteristics ............................................ 54

3.9 Policy implications ........................................................................................... 54

5

4 COLLECTIVE DOMINANCE IN GERMAN MERGER CONTROL ...................... 564.1 GWB (Act against Restraints of Competition) ................................................. 56

4.1.1 The definition of collective dominance .................................................. 57

4.1.2 Legal constructions and economic meanings ......................................... 57

4.2 Guidelines for Merger Control Procedures ("Auslegungsgrundsätze")

4.2.1 Underlying economics ............................................................................ 58

4.2.2 Three-step approach ............................................................................... 59

4.2.2.1 Internal competition

("Wettbewerbsbedingungen - Binnenwettbewerb") .................... 59

4.2.2.2 External competition

("Wettbewerbsbedingungen - Aussenwettbewerb") .................... 59

4.2.2.3 Conduct ("Wettbewerbsgeschehen") ............................................ 60

4.2.3 Checklist and case law ........................................................................... 61

4.2.3.1 Concentration and market shares ................................................. 61

4.2.3.2 Symmetry ..................................................................................... 62

4.2.3.3 Ressources and vertical up- and downstream integration ............ 63

4.2.3.4 Structural links ............................................................................. 63

4.2.3.5 Barriers to entry ........................................................................... 64

4.2.3.6 Buyer power on the opposite side of the market ......................... 64

4.2.3.7 Market transparency and homogeneity ........................................ 65

4.2.3.8 Market phase ................................................................................ 65

4.2.4 Comparison with economic framework ................................................. 65

4.3 Cases ................................................................................................................. 66

4.3.1 RWE / VEW ........................................................................................... 66

4.3.1.1 Findings ....................................................................................... 66

4.3.1.2 Remedies ...................................................................................... 67

4.3.2 Shell / DEA ............................................................................................ 68

5 COLLECTIVE DOMINANCE IN EC MERGER CONTROL ............................. 705.1 Development - from Nestlé / Perrier to Airtours / First Choice ....................... 71

5.1.1 Nestlé / Perrier (1991) ............................................................................ 72

5.1.2 Kali&Salz / MdK (1993, 1998) .............................................................. 73

5.1.3 Gencor / Lonrho (1996, 1999) ................................................................ 73

6

5.1.4 Airtours / First Choice (1999, 2002) ...................................................... 74

5.1.4.1 The Commission's decision (1999) – shifting the goalposts ....... 74

5.1.4.2 Critique and interpretation - "collective confusion" .................... 76

5.1.4.2.1 Unilateral effects in a collective dominance case ............. 76

5.1.4.2.2 Interpretation: distortions in EC merger control ............... 77

5.1.4.2.3 Solutions to eliminate the distortions ................................ 78

5.1.4.3 The CFI's ruling (2002) - shifting back and

cementing the goalposts ............................................................ 79

5.1.4.3.1 Necessary conditions for coordination .............................. 79

5.1.4.3.2 Market characteristics ....................................................... 80

5.1.4.3.2.1 Product homogeneity .............................................. 80

5.1.4.3.2.2 Market transparency ............................................... 80

5.1.4.3.3 Implications for future policy ............................................ 81

5.1.5 UPM-Kymmene/Haindl and Norske Skog/Parenco/Walsum

(2001): coordination on other parameters than price or output? -

the case of capacity coordination ............................................................ 81

5.2 Approach to collective dominance ................................................................... 82

5.2.1 Identification of oligopolists and initial screening test .......................... 83

5.2.2 Structural market characteristics ............................................................ 83

5.2.2.1 Homogeneous goods .................................................................... 84

5.2.2.2 Market transparency .................................................................... 84

5.2.2.3 Mature market .............................................................................. 84

5.2.2.4 Low rate of product and/or process innovation ........................... 85

5.2.2.5 Symmetry of costs and market shares ......................................... 85

5.2.2.6 Structural links ............................................................................. 86

5.2.2.7 Other factors ................................................................................ 86

5.2.3 Impact of the merger .............................................................................. 87

5.2.3.1 Past level of competition ............................................................. 87

5.2.3.2 Impact of merger on competition between the oligopolists ......... 88

5.2.4 External competitive constraints on the oligopoly ................................. 88

5.2.4.1 Competitors ................................................................................. 88

5.2.4.1.1 Fringe firms and mavericks ............................................... 88

5.2.4.1.2 Potential competitors ......................................................... 88

7

5.2.4.2 Buyer power ................................................................................. 89

5.3 The future after Airtours: Merger Guidelines ................................................... 90

6 COORDINATED EFFECTS IN U.S. MERGER CONTROL .............................. 916.1 Difference in substance: the SLC test ............................................................... 91

6.2 Difference in procedure: ex-ante review .......................................................... 92

6.3 The role of concentration .................................................................................. 93

6.4 Coordinated effects under the 1992 Horizontal Merger Guidelines ................. 94

6.4.1 Market factors ........................................................................................ 94

6.4.2 Relating the market factors to the

necessary conditions of coordination ..................................................... 95

6.4.3 Evidence of prior or current coordination .............................................. 95

6.4.4 Analysis of entry .................................................................................... 96

6.4.5 The relationship between coordinated and unilateral effects ................. 96

6.5 Cases ................................................................................................................. 97

6.5.1 Union Pacific / Southern Pacific ............................................................ 97

6.5.2 Heinz / Beech-Nut .................................................................................. 98

7 COMPARISON, POLICY SUGGESTIONS AND

LOOK INTO THE FUTURE ......................................................................... 1007.1 'Soft' convergence ............................................................................................. 100

7.2 Differences and resulting suggestions for reform ............................................. 102

7.3 The European Commission's proposals for a reform of EC merger control ..... 103

7.3.1 Single dominance: one undertaking having market power

without coordinating .............................................................................. 103

7.3.2 Collective dominance: more undertakings having market power

with coordinating (collusive oligopolies) .................................................... 103

7.3.3 More undertakings having market power without coordinating

(non-collusive oligopolies) ..................................................................... 104

7.3.4 'Hard' convergence ................................................................................. 105

8

1 INTRODUCTION

"The ultimate issue in reviewing a merger under the antitrust laws ... is whether the challenged acquisition is

likely to hurt consumers, as by making it easier for the firms in the market to collude, expressly or tacitly, and

thereby force prices above or farther above the competitive level."

Richard Posner (1986)1

Horizontal mergers2 can have two distinct types of effects: The first type, called unilateral

effects both in economics and in U.S. merger control, arises from reduced mutual

interdependence in an oligopolistic market after the merger: Absent cost synergies due to the

merger and absent barriers to entry, the merged entity will raise prices (or suppress output)

because part of the cost of the price increase (or output decrease), from lost sales, is

internalised by the acquisition of the competitor. Moreover, the remaining competitors might

find it profitable in certain circumstances to respond by raising their price in turn. Hence,

even if all firms increase their prices following the merger, this is still strictly a unilateral

effect because it arises from inherently self-enforcing behaviour without any form of

coordination. Methodically, this outcome of mergers can be associated with non-cooperative

Nash equilibria in one-shot games (see section 2 below). In German and EC merger control,

concerns about price increases by the merged entity are captured under the concept of single

dominance if the merged firm's market power would allow it to "determine its policy [to a

certain degree] free from competitive restraint".3

Second, a horizontal merger might enable the remaining firms to do better than simply adapt

independently to the new environment, as hinted at by Posner's statement above: In

particular by leading to a more concentrated market, by making oligopolists more symmetric

or by removing a maverick firm, the merger might increase the scope for the remaining firms

to exercise market power collectively by coordinating their actions. Hence, due to the

merger, prices can increase above the one-shot Nash equilibrium level since firms are more

1 Case Hospital Corporation of America v. FTC, 807 F.2d 1381, 1386 (7th Cir. 1986).2 The other two types of mergers, vertical and conglomerate, have different effects, e. g. foreclosure and

portfolio effects.3 See the ECJ's definition of a dominant position in the Article 82 case 27/76, United Brands Company v.

Commission (1978) ECR 207. The Commission also applies this definition for the purpose of the MergerRegulation. The question whether there is a relevant difference between the economics of unilateral effectsand the legal definition of "single firm dominance" will be addressed below (2.1.7).

9

likely to attain - expressly or tacitly - a collusive outcome. This consequence of a merger

falls under the category of coordinated effects (or cooperative or pro-collusive effects) in the

U.S. and joint or collective or oligopolistic dominance4 respectively in Germany and the EC.

For collusion to work, there must be some mechanism in place to defeat its natural instability

arising from the incentive for each firm to undercut rivals and thus benefit privately from

their price increases, i. e. a mechanism to overcome the static non-cooperative Nash

equilibria in a prisoner's dilemma situation. In the context of dynamic competition in the

sense of repeated interaction of firms, this mechanism is provided for by (the possibility of)

punishment in the case of defection from the explicit or implicit agreement, and is

formalized by the theory of repeated games (see section 3).

1.1 Focus of the paper

From the above (non-Schumpeterian) welfare perspective, a complete merger framework

would have to balance unilateral and coordinated effects against efficiencies arising from the

merger. This is beyond the scope of this thesis. The focus will be on coordinated effects, in

particular on, first, the necessary conditions for coordination derived from the theory of

repeated games and, second, on the market factors which feed into these conditions. Both

conditions and market factors make up a normative framework for the assessment of

coordinated effects (see section 3 below). Before, unilateral effects will be explained shortly

to allow for a clear distinction of unilateral and coordinated effects and to determine their

relationship (section 2).

Moreover, to cope with the phenomenon "coordinated effects", there are several regulatory

instruments provided for in nearly every competition regime. They can be grouped into ex

ante regulation (merger control) and ex post regulation (in particular the prohibition of

horizontal restrictions of competition). Hence, defining a coherent policy towards

coordinated effects would require a comparative institutional5 cost-benefit-analysis of the

different instruments which would have to take into account, inter alia, different error costs.

This analysis is only alluded very briefly. The focus will be on merger control.

4 These terms are used synonymously.5 "Institution" in the sense of a set of rules and the instruments to implement them (see Richter/Furubotn

(1999), p. 7).

10

1.2 Reasons for the paper

Due to increasingly concentrated oligopolistic markets, the assessment of coordinated effects

by competition authorities within a merger control procedure becomes increasingly

important: For example half of the phase 2 (i. e. in-depth) investigations of the EC

Commission's Merger Task Force involve questions of collective dominance. In the U.S.,

preventing from coordinated effects has long been the main target of merger policy. Hence,

from a public policy perspective, it seems worth to compare the existing (i. e. positive)

merger control regimes with the normative framework derived from game theory. This

comparison, which will be carried out separately for German, EC and U.S. merger control

(sections 4-6), allows to criticize (and potentially improve) actual policy.

Aside from this reason for exploring merger policy towards coordinated effects for each of

the three merger regimes, there is an additional benefit from comparing different merger

control regimes with each other: Due to increasing communication between competition

authorities,6 there is a high probability of mutual learning and, consequently, convergence of

competition policies. Hence, the comparative approach allows to predict into which

directions the different merger control regimes will develop and where they will probably

converge to (section 7).

6 There are contacts between competition authorities, inter alia, on the level of global institutions (e. g. the

OECD or the International Competition Network) or in the context of global merger cases (these case-specific contacts are also to some extent institutionalised, see e. g. the respective EC-U.S. agreement).

11

2 STATIC OLIGOPOLY THEORIES, UNILATERAL EFFECTS AND

SINGLE DOMINANCE

"If I was Director-General of DG IV, I would be very happy if my policy induced the firms under investigation

to end up in a Cournot equilibrium."

L. Phlips, Applied Industrial Economics (1995)

In our context, static oligopoly theories (Cournot and Bertrand) serve four functions: First,

they give a rationale for merger control to target unilateral effects due to horizontal mergers.

Second, they explain why there might be a gap in those merger regimes which use

dominance tests (with a market share threshold). Third, as alluded by the introductory

quotation of Phlips (1995, p. 11), their equilibria serve as non-collusive benchmarks in the

sense of what would happen in a market without coordination. Fourth, they allow to

distinguish clearly and explain the relationship between unilateral and coordinated effects.

2.1 Cournot oligopoly model with homogeneous products - Merger implications

In static games, unilateral effects of a merger can be formalized by comparing the pre- and

the post-merger equilibrium.

2.1.1 Cournot-Nash equilibrium

The Nash equilibrium in a market with quantity-setting firms selling homogeneous goods

can be described by the Cournot oligopoly pricing formula. It shows the relationship

between the ratio between the profit margin and the price (Lerner index), the firm's market

share si�xi/X and the elasticity of demand �>0 at overall equilibrium demand X:

�

ii sXp

cXp�

�

)()(

. (1)

Apart from the basic Cournot oligopoly results (each firm recognizes that it possesses

(limited) market power and that the Cournot equilibrium is somewhere "in between" perfect

competition and the monopoly solution), the formula shows that the relative mark-up is

proportional to a firm's market share and inversely proportional to the elasticity of demand.

12

Moreover, the market share of the firms are directly related to their efficiencies (constant

marginal cost ci).

2.1.2 Consumer surplus

Incorporating the Herfindahl-Hirschman index of concentration (HHI)7

H � ��

n

iis

1

2

into the Cournot oligopoly pricing formula8 gives the following relationship:

p

scpn

iii )(

1��

�

= �

H . (2)

This suggests that with higher concentration due to a merger, mark-ups increase for a given

level of costs, and, hence, consumer surplus decreases. The explanation for this is that,

according to the Cournot model, the quantity produced by the merged firm following the

merger will be lower than the sum of the quantities produced by its parts before the merger

raising the market price. Stimulated by widened margins, the outsiders will - absent capacity

constraints - increase their outputs. However, this response by the non-merging firms will

always only partly offset the reduction in output by the merged entity, with the net effect that

all Cournot mergers in homogeneous goods markets - absent cost synergies - result in lower

total output, higher prices overall and, hence, lower consumer surplus.

2.1.3 Rationale for efficiency defence

If the merger allows for cost synergies, e. g. - statically - due the exploitation of economies

of scale and/or the amalgamation of overhead functions or - dynamically - due to learning

effects or increased potential for innovation, prices do not necessarily rise. This is the

rationale for an efficiency defence like the one explicitly provided for in the U.S. Merger

Guidelines which in particular recognize efficiencies which flow from the attainment of

scale economies, better integration of production facilities, plant specialisation and lower

transport costs. Under the Guidelines, efficiencies are cognizable if they are verified, merger

specific, and not a disguised anticompetitive effect.9

7 The HHI varies between 0, when the market is entirely fragmented (each firm has a market share close to

0), and 10.000, when there is only one firm in the industry with 100% of the market.8 By multiplying both sides of equation (1) by si and summing over all i.

13

2.1.4 Producer surplus and overall welfare

The effect on producer surplus and, hence, on overall welfare is more difficult to determine:

For symmetric firms (i.e. firms with equal cost functions), Bergstrom and Varian (1985)

show a positive relationship between the number of firms in the market and overall welfare.

However, this does not hold for firms with different cost functions.

Farrell and Shapiro (1990, p. 342), for instance, show that - with costs unchanged - the

overall welfare effect depends on the relative cost structures of the merging and non-merging

parts, and hence on the reallocation of output between these firms: in Cournot equilibrium,

larger firms have lower marginal costs, thus overall welfare is enhanced despite increased

concentration if a fixed total output X is shifted towards them away from smaller, less

efficient firms. Thus, although Cournot mergers, absent cost synergies, necessarily raise

prices and reduce consumer surplus, they may enhance total welfare nonetheless.

However, transferring production from a high-cost plant to a low-cost plant is not a

convincing efficiency since such a transfer can be achieved without a merger. Thus, such a

welfare gain is not merger specific in the sense of the U.S. Guidelines.

2.1.5 Rationale for using the HHI and �HHI

Equation (2) provides a direct link between concentration measured by the HHI and

unilateral effects: Mergers in already highly concentrated markets and/or which substantially

increase concentration should cause more concern with respect to a reduction in consumer

surplus than in the case of fragmented markets and/or a negligible changes in concentration.

Hence, the Cournot framework gives a rationale for using the HHI and a change in HHI as

screening devices for unilateral effects of mergers as they are used under the U.S. Merger

Guidelines.10

9 1992 Horizontal Merger Guidelines, Section 4 (revised 1997).10 However, in markets in which products are differentiated either by virtue of their characteristics or by

strong branding, market shares can provide an unreliable guide to the possible extent of any unilateraleffects. In such cases it is often more informative to directly assess the proportion of each of the mergingfirms' customers who would have switched to the other merging firm's products following a price rise('diversion ratios').

14

Table 1.1:

Safe harbours for mergers under the 1992 U.S. Horizontal Merger Guidelines11

safe unsafe unsafe

safe safe unsafePost- 1800merger

HHI 1000safe safe safe

0 50 100

Increase in HHI

However, in the case of coordinated effects, the HHI has to be used with caution: First, the

HHI "punishes" asymmetry. This has to be kept in mind when discussing the role of

symmetry of firms for coordinated effects. Second, the link between concentration and

coordinated effects is a more indirect one than between concentration and unilateral effects

(see below 3.2.1.1).

2.1.6 Rationale for using market shares

Similarly, equation (1) rationalises the use of market shares as indicator of the likely market

power created by the merger. In single dominance cases, the European Commission regards

40% as critical threshold for the market share of the merged firm.

2.1.7 Distortions in EC merger control?

Comparing the European single dominance test with the economic framework set out so far,

Motta (1999, 2000) concludes that the European approach has two distortions which have

repercussions on the application of the concept of a collective dominant position by the

Commission and, hence, have to be analysed in our context:

First, Motta criticizes that all mergers which allow firms to unilaterally raise prices but do

not create or reinforce dominant positions cannot be prohibited.12 This critique relies on the

11 See Section 1.51: a market with a post-merger HHI below 1000 is regarded as "unconcentrated", a market

with a post-merger HHI between 1000 and 1800 as "moderately concentrated" and a market with a post-merger HHI above 1800 as "highly concentrated". The table is taken from Viscusi et al. (1995), p. 214.

15

assumption that the legal definition of "single firm dominance" as the potential for the

merged firm to "behave independently of competitors" requires more than the prognosis of a

price increase by the merged entity (i. e. unilateral effects). Second, so far, EC merger

control does not provide an efficiency defence.

With regard to the first alleged distortion, Motta's critique has to be relativized: Significant

unilateral effects can arise only if actual competitors are not able to offset the merged

entity's suppress of output (i. e. in particular, if they face capacity constraints or barriers to

expansion respectively) and if there are barriers to entry such that there is no constraint by

potential competition.13 Qualitatively, this is (already in theory) not different from the

dominance test which requires that the merged firm is not significantly constrained by its

competitors and thus can behave independently.

However, Motta's critique can also be interpreted quantitatively: The 40%-threshold creates

a gap for those cases in which, due to barriers to expansion and entry, relevant unilateral

effects arise, but in which the threshold is not met. Whether such unilateral effects are

"significant enough" and, hence, should be captured by merger control, is a normative

question outside the scope of this thesis. However, the Commission might want to capture

those cases (positive analysis). Hence, Motta's critique might provide an explanation for the

Commission's attempt to stretch the concept of collective dominance in order to capture such

unilateral effects. This will be further explored when discussing the Commission's Airtours

decision in the context of EC merger control (see below 5.1.4.2.1 and 5.1.4.2.2).

2.1.8 The relationship between unilateral and coordinated effects - an extension of the

Cournot model

Willig (1991) extends the Cournot model by integrating coordinated effects (exogenous

paramter �) and assuming the following relationship between the Lerner index and the mode

of behaviour among firms in the market:

pcp � =

�

�H ,

12 This critique is shared by Caffarra and Neven (2000).13 This is recognised by all competition authorities. Aside from rivals' ability to expand output (i. e. their cost

functions) and the likelihood of entry, the size of unilateral effects depends particularly on the elasticity ofdemand and the degree of countervailing buyer power.

16

where �=0 represents price taking behaviour, �=1 represents Cournot behaviour and �=1/H

pure cartel behaviour. With � rising from 1 to 1/H, mark-ups are generated which are higher

than the Cournot value. Hence, although the mode of conduct is determined exogenously and

not much can be said about the actual effects of a merger, the model highlights that unilateral

and coordinated effects are conceptually different: Assuming that pre-merger firms are not

colluding, the post-merger equilibrium is either another Cournot equilibrium if the mode of

conduct parameter (�=1) does not change, or a collusive equilibrium, characterised by �>1.

2.2 Bertrand oligopoly model with differentiated products - Merger implications

In the case of symmetric price-setting firms which produce a homogeneous product and

which are able to supply the entire market, prices converge to marginal cost ("Bertrand

paradox").14 There are two main approaches to solve the paradox which both make the

Bertrand model more realistic: First, firms can have capacity constraints or sufficiently

increasing marginal cost so that they cannot serve the entire market demand. Second, firms

can produce products that are differentiated in product or geographical space.

Both assumptions are reflected in the U.S. Horizontal Merger Guidelines which distinguish

between the setting where firms are distinguished primarily by differentiated products

(Section 2.21 of the Guidelines) and firms distinguished primarily by their capacities

(Section 2.22). Here, the focus will be on product differentiation as suggested by the practice

of the U.S. competition authorities.

2.2.1 Pre-merger equilibrium

Whereas in the Cournot model with homogeneous goods the "reaction curves" are

downwards sloping, in the Bertrand model an increase in the price charged by one firm also

induces the other firms to increase their prices, such that the price of all products in the

market are likely to rise. In this case, the reaction curves are upwards sloping.

If one of two firms which produce each other's closest substitutes in a differentiated products

market tries to raise its price, it may gain extra revenue per product sold, but it will loose

more revenue in total from the sales that are diverted to the other firm if it was originally

selling at the profit maximising price. Hence, neither firm has an incentive to raise prices

and/or reduce output.

14 See Shapiro (1989), pp. 343-348.

17

2.2.2 Post-merger equilibrium

However, if these two firms merge, the two competing products will be under common

ownership. As a result, the lost sales caused by increasing the price of one of the products

are likely to be recaptured by the merged firm, even if only partially, in the sales of the other

product. Thus, there is an incentive for the merged firm to unilaterally raise the prices of

both products. Moreover, since the reaction curves are upwards sloping, non-merging firms

may also be able to raise their prices. For competition authorities, it is very difficult to

distinguish this unilateral effect arising from oligopolistic interdependence from parallelism

due to coordination, i. e. coordinated effects, although both are theoretically clear separable.

2.3 A two-step approach for assessing unilateral and coordinated effects

Comparing pre- and post-merger equilibrium without and with collusion, builds upon the

idea that firms at one point in time face the strategic choice of either competing (in a

Cournot or Bertrand style depending on the setting) or colluding. Hence, due to this

assumption, a merger which changes the market structure, either leads to unilateral or

coordinated effects (so far, the latter are exogenously given) suggesting that competition

authorities have to deal only with one effect when assessing a merger.

However, there might be a non-static real world sequence in which the firms initially adapt

to the new environment, i. e. the immediate post-merger equilibrium is non-collusive and

there are only unilateral effects, but, particularly with subsequent learning, this may be

displaced by collusion. This sequence is not unrealistic since the non-cooperative gains from

realising increased unilateral market power as such are "certain" (only the size of the

additional profit depends on the market structure). In contrast, gains from cooperation are

uncertain since they, by definition, depend on the other oligopolists or the stability of the

(implicit) agreement respectively. Hence, a merger might possibly lead to both unilateral and

coordinated effects.

This suggests a two-step-approach:

1. An analysis of unilateral effects will show the likelihood of a significant increase in prices

even without any collusion (or of the creation or strengthening of a single dominant

position respectively).

2. If unilateral effects are negligible or unlikely, but the structure and other characteristics of

the market suggest a likelihood of collusive conduct between the remaining firms (or the

18

creation or strengthening of a collective dominant position), then an analysis of

coordinated effects should also be carried out.

2.4 Repeated interaction as necessary condition for collusion

Static oligopoly theory allowed for three main conclusions: First, one shot games provide for

a non-collusive benchmark for oligopolistic markets. Or as the introductory quote of Phlips

makes clear: The competitive Nash equilibrium of a single shot game is the best result

antitrust policy against collusion can hope for in oligopolistic markets. Second, coordinated

effects or collective dominance respectively is "more" than just oligopolistic

interdependence. Third, the collusive outcome is not a Nash equilibrium of a single-period

game since an individual firm can increase its profit by producing more output or charging a

lower price given that all other firms adhere to the collusive strategies. Hence, without

repeated interaction, there cannot be collusion.

19

3 DYNAMIC OLIGOPOLY THEORIES, COORDINATED EFFECTS AND

COLLECTIVE DOMINANCE

"Successful coordinated interaction entails reaching terms of coordination that are profitable to the firms

involved and an ability to detect and punish deviations that would undermine the coordinated interaction.

Detection and punishment of deviations ensure that coordinating firms will find it more profitable to adhere to

the terms of coordination than to pursue short-term profits from deviating, given the costs of reprisal."

1992 U.S. Horizontal Merger Guidelines15

As demonstrated in section 2, static oligopoly theories cannot explain collusion due to the

lack of dynamics, i. e. repeated interaction of firms over time. However, in reality, inter alia

durable investments and barriers to entry promote long-run interactions among a relatively

stable set of firms.16 Assuming repeated interaction of a small number of identical firms

which produce a homogeneous product, Chamberlin (1933) introduced the concept of tacit

collusion:"If each seeks his maximum profit rationally and intelligently, he will realize that when there are

only two or a few sellers his own move has a considerable effect upon his competitors, and that

this makes it idle to suppose that they will accept without retaliation the losses he forces upon

them. Since the result of a cut by any one is inevitably to decrease his own profit, no one will cut,

and although the sellers are entirely independent, the equilibrium result is the same as though

there were a monopolistic agreement." (emphasis added)17

The main contribution of this statement is that it identifies the threat of retaliation as

mechanism which allows firms to gain profits above the static Nash outcome without legally

enforceable cartel agreements and even without communication. This idea has been

formalized by the theory of repeated games (see below 3.1).

However, Chamberlin's conjecture is far too optimistic about the success of collusion since it

assumes costless coordination on the monopoly outcome and perfect information, i. e.

costless monitoring of this outcome. In particular Stigler (1964) worked out factors that

hinder collusion such as unobservable price, demand shocks and buyer power as they relate

to the ability of firms to find, monitor and enforce a collusive equilibrium. Given these

15 Section 2.1 ("Lessening of Competition Through Coordinated Interaction").16 Tirole (1998), p. 239.17 Chamberlin (1933), p. 48.

20

necessary conditions of collusion, coordination is potentially more sinister than unilateral

exercise of market power (it results in welfare losses in terms of lower output, higher prices,

X-inefficiency, slower innovation, and reduced product variety), but also less frequent.

In order to design a merger policy which shall prevent coordination that would arise due to a

merger (coordinated effects), it is necessary to understand how a merger alters firms'

incentives to collude (3.2). These incentives depend, as the introductory quotation from the

U.S. Merger Guidelines suggests, on the relative gains of coordination which, in turn,

depend on market factors like those already identified by Stigler. Hence, a normative merger

framework has to derive the conditions for collusion from firms' incentives (3.4) and to

relate these conditions to those factors which render a market conducive to coordination

(3.5).

3.1 The theory of repeated games

Since the 1980s, the theory of repeated games has become the main tool for modelling the

mechanism of collusion. The various models differ in several dimensions:

- the number of periods in the game (finitely/infinitely; see 3.1.1 and 3.3.1.2),

- the punishment strategies (3.1.3),

- the information available to players (perfect/imperfect; infra 3.5.3.1), and

- the way in which players form beliefs about each other and each other's strategies

(3.3.1.2).

Generally, collusion is the more difficult to sustain the more realistic assumptions the model

makes (e. g. imperfect information).

3.1.1 Finitely repeated oligopoly games

Selten (1978) shows that, given the logic of game theory, no cooperation is possible as soon

as the game is finite. If the game has a final period, firms will cheat, as there cannot be

retaliation in the future. Knowing this, firms will also cheat in the period before the last and

so on until the first period. With this backward induction argument, the game unravels from

the back, and firms will never cooperate. Hence, the unique subgame perfect equilibrium18 of

a finitely repeated game with a unique Nash equilibrium in the stage game is a simple

repetition of the stage-game equilibrium. Thus, the dynamic element contributes nothing to

18 In general, the equilibrium concept of subgame perfection requires that future strategies out of the

equilibrium must themselves constitute an equilibrium in the future (sub)game (see e. g. Shapiro (1989), pp.357-360).

21

the model.19 This so-called "chain-store paradox" can be overcome by permitting the length

of the game, T, to be infinite or at least possibly infinite (see below 3.1.2) or by giving up the

assumption of perfect rationality (see below 3.3).

3.1.2 Infinitely repeated oligopoly games (supergames) with perfect information

The above inability of the firms to collude in a credible fashion rests on the exogenously

given terminal date of the game. However, in reality, competition continues indefinitely, or

at least firms cannot be sure when it will end. Indefinitely repeated games are fundamentally

different from finitely repeated ones in that there is always the possibility of retaliation and

punishment in the future.

3.1.2.1 The basic model

Assume that player i's overall payoff in the game is given by

�i = ��

�0tit

t�� (5)

where � is the discount factor.20

The game beginning at date t is assumed to look the same for all t in the sense that the

feasible strategies and the prospective payoffs that they induce are always the same.21 Each

firm produces its share of the collusive output in each period, as long as the others continue

to do so. If, however, any firm produces more than its "quota" under this arrangement, this

defection signals a collapse of the tacitly collusive arrangement, and each firm plays its static

noncooperative strategy thereafter ("Nash forever"). In the case of a quantity-setting

supergame, each firm plays its static Cournot output following any deviation ("trigger

strategy" or "grim strategy").

19 Considering the example of a two-fold repetition of Cournot oligopoly with i firms, each firm's strategy

consists of its first- and its second-period output conditional on its rivals' first-period outputs. Anyequilibrium must involve static Cournot behaviour in the second period because otherwise some firm wouldhave an incentive to change its second-period behaviour. Hence, e. g. to flood the market in the secondperiod if one deviates during the initial period is not credible. Since no credible punishment for defectors ispossible here, it is not possible to support any first-period outcome other than the standard Cournotequilibrium, i. e. there are no linkages in behaviour between the two periods.

20� = e-r�, where r is the instantaneous rate of interest and � is the real time between "periods". � close to 1represents high patience or rapid changes of price or quantity.

21 Investments by the firms or changes in the competitive environment will be addressed below (3.3.1.1).

22

3.1.2.2 Equilibria

To show that these strategies form a subgame perfect equilibrium two conditions have to be

verified: First, no firm wants to defect from the collusive scheme. Second, the punishment

strategies are themselves credible.

Starting with the second condition, credibility requires that the punishment itself forms a

perfect equilibrium. A punishment involving repetition of an equilibrium in the stage game

is credible, since it is always a perfect equilibrium to simply repeat any equilibrium in the

stage game indefinitely.

By cooperating, firm i earns �i*/(1-�). Hence, there is an equilibrium as long as the no-

defection condition

�i*/(1-�) � �i

d + ��ip/(1-�) (6)

<=> �i* � �i

d - ��id + ��i

p

<=> � � pi

di

idi

��

��

�

�

*

(7)

holds (where �id is firm i's profit from deviating from the collusive scheme and �i

p the profits

during the infinitely long punishment phase). That means that only mild punishments (�ip <

�i*) and bounded profits from defection (�i

d < �) are sufficient for collusion to succeed if � is

close enough to 1. Moreover, stronger, swifter, or more certain punishments allow the firms

to support a more collusive equilibrium outcome.22

3.1.2.3 The Folk theorem

Using such a framework, Friedman (1971) first showed formally that any Pareto optimal

outcome - in particular, many outcomes involving joint monopoly pricing - can arise as the

subgame-perfect equilibrium path of a repeated game, provided only that there is sufficiently

little discounting (i. e. � close to 1), as there will be if the market participants can respond

rapidly to each other (so-called folk theorem). Because of this multiplicity of equilibria,

supergame theory is "too successful" in explaining tacit collusion.23 On the other hand, any

attempts to theoretically limit the number of equilibria, are, so far, based on ad hoc

assumptions. Kreps (1990, p. 529) calls this the "twin problems of too many equilibria and

the selection of one of them".

22 Hence, anything (e. g. unlimited capacities) that makes more competitive behaviour as threat feasible or

credible actually promotes collusion. Shapiro calls this the "topsy-turvy principle of tacit collusion" (1989,p. 357).

23 Tirole (1998), p. 529.

23

Hence, game theory cannot predict whether firms will indeed coordinate on a particular

collusive equilibrium. It is possible, however, to derive necessary conditions for collusion

from game theory (see below 3.2 and 3.4).

3.1.2.4 The coordination problem

As a consequence of the folk theorem, firms that want to collude face the problem that -

given a mutually acceptable collusive equilibrium exists - they have to coordinate on it.

3.1.2.4.1 Explicit vs. tacit collusion

Cartels are forbidden and, therefore, void and unenforceable under most of the competition

laws. Hence, if in the case of explicit collusion, firms establish an equilibrium as described

above, it, nevertheless, has to be sustainable. There is, thus, no difference between explicit

and tacit collusion with regard to the stages of monitoring and enforcement.

However, in the initial stage of coordination, communication (i. e. explicit collusion) would

reduce the costs of finding equilibrium. Hence, with regard to their "behavioural"

instruments (in contrast to the "structural" approach of merger control; e. g., in the EC,

especially Article 81 EC), the task of competition authorities is (at least) to force firms into a

trade-off: Communication reduces the costs of finding equilibrium, but increases the

likelihood that collusion is detected and that the firms are fined.

3.1.2.4.2 Focal points and cheap talk

With direct communication being impossible or too costly due to expected fines, firms have

to solve the coordination problem tacitly, i. e. by a trial-and-error method.

Given this highly imperfect process of selecting a particular outcome only through market

interactions, "focal points"24 can be helpful: These are outcomes, or at least behavioural

rules, which are self evident. Firms may want to try to affect the perception of particular

outcomes, or particular rules, as self-evident. Hence, focal points may be created, inter alia,

by price leadership or by cheap talk25, i. e. costless, non-binding and non-verifiable messages

which are likely to affect the listener's beliefs (e. g. a public speech in which a well-defined

price increase is announced). In the case of tacit collusion, such practices are the only

"evidence" that competition authorities might find.

24 The theory of focal points was proposed by Schelling (1960).25 See Farrell and Rabin (1996). Cheap talk is one example of so-called "facilitating practices" which will be

addressed below (3.6.1).

24

3.1.3 Punishment strategies and renegotiation-proofness

Punishment strategies that have been used as threat in collusion models include, among

others,

- reversion to the noncooperative Cournot or Bertrand outcome ("trigger" or "grim

strategy" or "Nash forever" respectively),

- a phase of expanded outputs which optimally punishes the defector and a progressive

reversion to the low output level ("stick-and-carrot") (Abreu et al. (1986)),

- an output level which minimizes the profit of the firm that has deviated, given the

anticipated best reply of this deviator to the strategy of the punishing firm (minimax

strategy).

However, the minimax strategy lacks credibility because it is not in the best interest of the

punishing firm to use it and, therefore, no mutual best reply. Thus, this strategy infringes the

concept of subgame-perfection which demands that equilibrium strategies should be mutual

best replies not only for the whole game, but also in particular contingencies, which

correspond to particular truncations of the game.

Moreover, if the pre-specified punishment hurts the "innocent" firms as well as the defector,

firms would have an incentive not to implement it, but to renegotiate in order to achieve an

equilibrium in which all firms are better off. The expectation of renegotiation undermines the

strength of the punishment. This suggests that standard subgame-perfection is not generally

the binding constraint on collusion, but instead the more restricting concept of renegotiation

proofness (see Farrell and Maskin (1987) and below 3.4.1.2). The effect of renegotiation on

the credibility of punishment strategies depends on the cost of renegotiation: The higher the

cost, the less the credibility problem.26

3.2 Merger implications

So far, the theory of repeated games suggests that there are four necessary criteria for

collusion:

1. repeated interaction,

26 With respect to renegotiation, the same statement holds as for "negotiation" (i. e. the initial coordination on

an equilibrium): It does not necessarily imply that the firms actually get together and communicate, but thepossibility to communicate might make it easier. This also implies that the standard policy suggestion thatcompetition authorities should raise the cost of communication between firms is only partially correct withrespect to negotiation. Raising the cost of renegotiation, in contrast, makes collusion easier to sustain (see

25

2. the capacity to reach a mutually acceptable equilibrium (coordination),

3. the possibility of detection of cheating (monitoring),

4. enforceability of compliance (enforcement), i. e. firms find it rational to comply with the

collusive scheme since the profit from collusion is higher than the sum of the profit from

deviating and the profit during the punishment phase (see equation (6)).

3.2.1 Collusive effects of a merger

There are three main mechanisms by which mergers can directly change each of the above

conditions 2-4 such that the the likelihood of coordinated effects is increased:

1. By definition and most obviously, a merger reduces the number of firms in the market

(see below 3.2.1.1).

2. A merger can lead to a more symmetric distribution of assets (3.2.1.2).

3. A merger might decrease the incentives of a maverick firm to compete, or, more

obviously, might lead to the loss of a maverick firm (3.2.1.3).

Furthermore, a "concentration"27 notified by oligopolists which falls short of a full merger,

but is still captured by merger control (i. e. in particular a joint venture) creates a structural

link and, thus, an element of joint welfare maximization. Existing structural links are

analysed below (3.6.2) as factor which facilitates collusion. The statements made there also

hold with regard to the creation of such a link.

3.2.1.1 Reduction of number of firms

The reduction of the number of firms in the market facilitates coordination on a collusive

equilibrium as well as monitoring and enforcement of this equilibrium:

3.2.1.1.1 Coordination and monitoring - the "dinner party story"28

In the case of explicit collusion, costs due to communication increase with the number of

firms. In the case of tacit collusion, coordination on a specific equilibrium becomes more

McCutcheon (1997)). Hence, the first-best solution for competition authorities would be to distinguishbetween negotiation and renegotiation.

27 See § 37 GWB and Article 1 Merger Regulation.28 Baker (2002, p. 139) calls this reasoning the "dinner party story" since fewer firms make coordination more

likely or more effective for the same reason that "friends arranging a restaurant get-together likely will findit easier to coordinate the calendars of four people than five and more likely will notice if one personaccepts but does not show up".

26

difficult as the number of firms increases due to higher learning costs.29 In both cases, with

more firms, the probability of differing costs and other characteristics, i. e. asymmetry, and,

hence, of more divergent preferences increases.

With respect to monitoring, the argument is similar: The more firms there are in the market,

the harder it will be to determine the identity of the deviator once it becomes clear that

cheating has occured. Punishment strategies that specifically target the deviator (e. g. the

carrot-and-stick method of Abreu) become harder to apply. Moreover, an increase in the

number of firms decreases the impact of an individual firm's action on the aggregate market

parameters. Thus, if a firm believes that its actions cannot be monitored, it will more likely

deviate from the collusive equilibrium.

3.2.1.1.2 Enforcement30

Moreover, the gains from collusion are higher the less firms there are in the market because

the individual firm receives a higher share of the collusive profit (with symmetric firms and

constant marginal costs in the case of perfect collusion: �m/n per period). The gains from

cheating are lower since the firm can capture a smaller share of the market by undercutting

the other firms relative to the situation with more smaller firms in the market (in a repeated

Bertrand oligopoly framework the additional profit from cheating is: �m(1-1/n)-�).

Together, this implies that a higher concentration of the market increases the incentive to

collude. Formally (with "Bertrand forever" as punishment and, hence, zero profit), this can

be expressed by the condition under which the fully collusive outcome is sustainable:

n

m�

��11 > �m (8)

<=> � > 1-n1 . (9)

The required discount factor is larger for larger n. In that sense, collusion is more likely with

less firms.

29 In general, the number of bilateral relations is given by

)!2(2!�N

N .

27

3.2.1.2 More symmetric distribution of assets

In general, symmetry of firms refers to similarity of their cost structures. However,

symmetry can also concern other dimensions such as market shares, number of varieties in

the product portfolio, technological knowledge, capacities and degree of vertical integration.

The most general result of most of the models addressing this issue is that asymmetries make

collusion more difficult, in particular without any facilitating practices like cheap talk.31 Like

market concentration, asymmetry feeds into the three necessary criteria of coordination,

monitoring and enforcement:

3.2.1.2.1 Coordination and monitoring

Coordination on a particular equilibrium becomes difficult when firms' costs differ

significantly since low cost firms prefer a lower price and a higher output than high cost

firms.32 Moreover, if firms' cost structures differ significantly, their incentives to cheat differ

accordingly. Hence, if any company within an oligopoly shows persistent cost advantages,

this particularly disrupts a harmony of interests and creates an incentive for aggressive

competitive behaviour.33

A similar argument can be made for monitoring: Kreps (1990) points out that firms need to

have an implicit "rule" to follow. In a situation with symmetric firms, they can check that all

firms behave similarly. This "relative" comparison is easier than an "absolute" monitoring.

3.2.1.2.2 Enforcement

Finally, firm homogeneity facilitates the enforcement of compliance. For instance

Vasconcelos (2001), using a quantity setting supergame-framework with stick and carrot

punishment schemes in the style of Abreu and firms with linearly increasing marginal costs,

shows the following:

The smallest firm in an implicit agreement, being the one which is allotted the lowest share

in the collusive aggregate output34, represents the main obstacle for collusion to be enforced

30 See Tirole (1998), pp. 247-248.31 E. g. Rothschild (1999). It should be noted, however, that the presence of one highly efficient firm (or a

small group of similar and efficient firms) along with several less efficient firms could contribute to thestability of an agreement. In that case, the low cost firm(s) could take on the role of the leader(s) with theremaining firms as followers (Ross and Baziliauskas, 2000).

32 In theory, the low cost firm could pay the high cost firm to shut down its production. However, these sidepayments are not practical (there is, inter alia, an asymmetric information problem).

33 Kantzenbach et al. (1995), p. 61.34 Since, as output increases, marginal cost rises more rapidly for a small firm than for a large firm, joint profit

maximization implies that the smaller (and, hence, the more inefficient) a member firm is, the lower its

28

because its share may be too low with regard to its optimal deviation output. If it is not too

low, then its incentive constraint is binding on the collusive path. On the other hand, if the

punishment is started, then the largest firm (i. e. the one with the highest market share) is the

one which is proportionally more penalized by the price cut. Therefore, this firm faces the

greatest incentives to deviate from the first period of the punishment strategy, making its

incentive constraint binding on the punishment path. In that sense, asymmetry makes the

enforcement of collusion more difficult.

3.2.1.2.3 A trade-off

Extending the above result by comparative statics, Vasconcelos (2001) shows that a merger

can induce two distinct effects:

1. If collusion is not feasible before the merger, then a merger might make collusion

possible afterwards. This will happen when the merger involves very small and inefficient

firms that are not able to credibly participate in a collusive scheme before the merger

takes place, because their share in the aggregate output is too low in the above sense.

2. If firms in the market are already colluding before the merger, then a merger either has no

effect on the possibility of collusion or it hurts that possibility. The latter case will happen

when the merger increases the size of the largest firm in the market, because this will

induce an increase in the minimal threshold on the discount factor above which an

industry-wide collusive agreement is sustainable.35 The intuition which underlies this

result is the same as above: The larger the largest firm, the higher will be its share on the

one period losses due to the first phase of the punishment strategy. Therefore, increasing

weight has to be attached to the future stream of payoffs in order for this firm to comply

with the punishment strategy.

Hence, there is an important trade-off: Although collusion is facilitated due to an increase in

the number of competitors, this effect can be countervailed by a more asymmetric post-

merger industry configuration. In Vasconcelos' model, the effect of market concentration is

share in the aggregate output is. Banning side payments, this implies a correspondingly smaller share in thejoint profit.

35 See equation (31) in Vasconcelos (2001, p. 24): 1k�

�� > 0, where k1 is the fraction of the - fixed (!) -

industry capital stock owned by the the largest firm. ki is a parameter of the cost function which is Ci(qi, ki)

= cqi+i

i

kq2

2

, i. e. asymmetry is dealt with by assuming that firms have a different share of industry capital

which affects marginal costs.

29

more than compensated by post-merger asymmetry if firms have already been colluding

before the merger.

3.2.1.2.4 The case of capacity constraints - the model of Compte, Jenny and Rey

Using a similar method as Vasconcelos, but a Bertrand supergame, Compte, Jenny and Rey

(2002), instead of asymmetric capital share affecting marginal cost, assume asymmetric

capacity constraints. ki denotes firm i's limited capacity with k1...kn. M is the market size.

K-i � ��ij jk is the total capacity of firm i's rivals.

3.2.1.2.4.1 The results of the model

The first important result relates to mergers involving the largest firm such that capacity is

transferred from a small firm to the largest. The following table shows the effect of a

decrease in the "small"36 firm's capacity ki, of an increase in the large firm's capacity kn and -

as their sum - the overall impact of the transfer ki kn on collusion, i. e. either an increase

(+) in the lowest discount factor �(k) for which collusion is sustainable, no change of the

factor (=) or a decrease (-):

Table 3.1 - Impact of changes in capacity

case 1

K-n < M

kn < M

case 2

K-n < M

kn > M

case 3

K-n > M

kn < M

case 4

K-n > M

kn > M

ki � + + - - / =

kn � + = + =

ki kn + + = - / =

Source: Compte / Jenny / Rey (2002), p. 14

In the cases 1 and 2, when small firms cannot serve the entire market, transferring capacity

from a small firm to the largest one decreases the scope for collusion (� increases) because

the transfer reduces small firms' punishment ability. If additionally kn<M (case 1), such a

transfer increases the large firm's incentive to deviate. In contrast, if small firms can cover

the whole market (cases 3 and 4), such a transfer is either neutral or it facilitates collusion.

30

The result of cases 1 and 2 is very similar to that of Vasconcelos: Although the merger leads

to higher concentration, increased asymmetry decreases the scope for collusion.

Based on this result, Compte et. al. (2002, pp. 14-16) derive their second important result,

the distribution of capacity that most facilitates collusion: To facilitate collusion, first, the

retaliation possibilities of the smallest firms should be increased (up to M if possible).

Second, among the distributions which maximize punishment possibilites, the gains from

deviating should be minimized. If total capacity K<1�n

n M, i. e. the smallest (n-1) firms

cannot cover the market, the main problem is the deviation concern, i. e. the largest firm's

incentive to deviate. Starting from any asymmetric situation, transferring capacity from the

largest firm to a small one both enhances the small firm's retaliation power and limits the

large firm's incentive to deviate. Hence, the distribution of capacities that most facilitates

collusion in this case is the symmetric.37

3.2.1.2.4.2 Application to Nestlé / Perrier

In the light of these results, Compte et al. evaluate the Commission's decision in

Nestlé/Perrier, a merger on the French bottled water market which the Commission used to

introduce the concept of oligopolistic dominance into EC competition law (see below 5.1.1).

Before the merger, Nestlé had a market share of 17.1 % in terms of sold water, Perrier 35.9

% and BSN 23 %. The merger was cleared only after Nestlé accepted to sell Volvic, a major

still mineral source of Perrier, to BSN. Moreover, Nestlé commited itself to sell various

brands and some capacity to a third party so that this third party could become an active

player in the market.38

Estimating the ratios of capacity over market size for the four different scenarios (1.) pre-

merger, (2.) after the merger with the resale of Volvic to BSN, (3.) without the resale of

Volvic and (4.) with the resale and the divestiture to create a new third player, Compte et al.

(pp. 20-21) compute the minimum discount factor � that allows a collusive equilibrium in

each of the scenarios with the following result: �2<�1<�4<�3. That means, contradicting the

Commission's opinion, the scenario that minimises the scope for collusion is the solution in

36 "Small" in this context just means "not the largest".37 Compte et. al. first derive this result for "collusive �-equilibria", i. e. equilibria, where firms follow the

same strategy and maintain constant market shares �i with 0��i�ki (2002, p. 5). However, the above resultstill holds for general collusive equilibria (2002, p. 15).

31

which Nestlé and Perrier merge, but do not transfer Volvic to BSN. Hence, according to the

model, it would have been best to clear the merger without conditions or, as second best

solution, to block it completely.

3.2.1.2.5 Policy implications

Both the results of Vasconcelos and Compte et al. have several policy implications: First, the

instruments used to assess unilateral effects and single dominance respectively do not reflect

the possible adverse effects of increased asymmetry on collusion. As both Vasconcelos and

Compte et. al. hint at, the HHI even punishes asymmetry (see above 2.1.5). Second, in

addition to the common wisdom that asymmetry hurts collusion, competition authorities

have to take into account which firms (in particular the largest and the smallest) are involved

in a merger. Third, if asymmetry decreases the likelihood of collusion in the above sense, in

theory, this effect might outweigh unilateral effects due to a merger with the consequence

that a single dominant position should be tolerated. Fourth, the models at least cast doubt on

the standard remedy of divesting capacity of the merged firm and transferring it to

competitors.39

However, it has to be kept in mind that models which concentrate on the effects of symmetry

necessarily abstract from other factors which might be prevailing.

3.2.1.3 Loss of a maverick or reducing its incentive to compete

The concept of a maverick appears in the U.S. Merger Guidelines, where a maverick firm is

described as one with "a greater economic incentive to deviate from the terms of

coordination than do most of [its] rivals" (Section 2.12). As an example, the Guidelines

describe a firm that has an "unusually disruptive and competitive" influence in the market.

Mavericks can be seen as an extreme case of dissimilarity of firms in which one firm is so

different from the other firms that it is unwilling to accept the terms of coordination. Hence,

aside from increasing concentration and making firms more symmetric, the loss of a

maverick or relaxing its constraint on collusion can be a third consequence of a merger that

increases the likelihood of coordinated effects.

38 After the decision, the Commission was criticized for having "constructed" a market structure. Especially

from a Hayekian perspective, this seems questionable since a market structure 'designed on the drawingboard' is based on less information than a structure which evolves evolutionary in a selection process.

39 See Motta, Polo and Vasconcelos (2002), pp. 8-10; aside from increasing symmetry, the divestiture of assetsto strenghten an existing competitor might also allow for multimarket contacts which also increase the riskof collusion (see below 3.5.7).

32

3.2.1.3.1 Identifying a maverick

According to Baker (2002, pp. 173-177), mavericks can be identified in three ways:

1. The first way is to observe that the firm actually constrains industry pricing, i. e. by

revealed preference.

2. Some factors likely affecting the market price preferred by the maverick are firm specific.

For example, a firm's marginal costs may rise or fall for reasons related to the nature or

location of its production processes, and in consequence may not be paralleled by cost

changes affecting its rivals. If that firm is a maverick, the market price will change due to

the "natural experiment" because the maverick constrains collusion. If another firm is the

maverick, the market price will remain unchanged.

3. The third approach relies on a priori factors, i. e. the reasons for a firm's preference for a

high or low price in the particular market under investigation. The U.S. Merger

Guidelines provide for two examples of a priori factors tending to identify a likely

maverick. First,"in a market where capacity constraints are significant for many competitors, a firm is more

likely to be a maverick the greater is its excess or divertible capacity in relation to its sales or its

total capacity, and the lower are its direct and opportunity costs of expanding sales in the relevant

market. This is so because a firm's incentive to deviate from price-elevating and output-limiting

terms of coordination is greater the more the firm is able profitably to expand its output as a

proportion of the sales it would obtain if it adhered to the terms of coordination and the smaller

is the base of sales on which it enjoys elevated profits prior to the price cutting deviation."

(Section 2.12)

Second,"[a] firm also may be a maverick if it has an unusual ability secretly to expand its sales in relation