General report

37

NATIONAL ECONOMIC UNIVERSITY ADVANCED EDUCATIONAL PROGRAM --------------------------------- INTERSHIP REPORT LIENVIET POST BANK Student’s name : DINH DO VIET DUNG Student ID : CQ 520588 Class : High Quality Educational Program in Enterprise Intake : 52 Supervisior : DR TRUONG THI NAM THANG

Transcript of General report

NATIONAL ECONOMIC UNIVERSITY

ADVANCED EDUCATIONAL PROGRAM

---------------------------------

INTERSHIP REPORT

LIENVIET POST BANK

Student’s name : DINH DO VIET DUNG

Student ID : CQ 520588

Class : High Quality Educational Program in Enterprise

Intake : 52

Supervisior : DR TRUONG THI NAM THANG

Hanoi - 2014

INTRODUCTION

Vietnamese economy is facing a period of globalization,

competitiveness is raising increasingly, business

strategy planning is the one important part that every

company must take serious considerations and

implementations in order to make a better and sustain

business environment. Despite being one of the youngest

banks in Vietnam, LienVietPostBank (LVP) has overcome

many challenges and had some significant achievements

paving the way for future development. During the last 4

years, LVP continuously maintained its sustainable growth

and strengthened its position in the banking market. In

addition, LVP has a clearly defined business strategy,

which is to balance between profitability and sustainable

development, stay closer to farmers and focus more on

agriculture and rural development and afford to increase

their access to financial service. This proposal aims to

providing a good and basic idea of building a business

strategy for the company period 2014 to 2017. This is

only for reviewing purpose. Many thanks to bank's staffs

and directors, special to Mr. Trinh Ha Anh, and also

thanks to my instructor Ms. Truong Thi Nam Thang who

2

stick with me and help me to achieve the objectives.

This proposal is broken into three parts:

CHAPTER I: OVERVIEW OF LIENVIET POST JOINT-STOCK

COMERCIAL BANK

CHAPTER II: EVALUATION SITUATION AND BUSINESS PERFORMANCE

OF LIENVIET POSTBANK FROM 2010 TO 2013

CHAPTER III: PROBLEMS AND SOLUTION FOR DEVELOPMENT IN THE

FUTURE

3

ContentsINTRODUCTION......................................................2CHAPTER I: OVERVIEW OF LIENVIET POST JOINT-STOCK COMERCIAL BANK...4

1. General information..........................................4

2. Legal information.............................................7

3. Vision & Strategy.............................................7

4. Business scope................................................8

5. Product & services............................................9

6. Company Structure............................................10

7. Performance highlights.......................................12

CHAPTER II: EVALUATION SITUATION AND BUSINESS PERFORMANCE OF LIENVIET POSTBANK FROM 2010 TO 2013.............................131. Overview of business environment.............................13

2. Total assets.................................................14

3. Profit before tax............................................15

4. Capital mobilization.........................................16

5. Loans and advances...........................................17

6. Payment activities...........................................18

7. Other support................................................19

8. HR & Training activities.....................................20

9. Coporate social responsibility...............................21

CHAPTER III: PROBLEMS AND SOLUTION FOR DEVELOPMENT IN THE FUTURE.221. Profit in recent year is not achieved as expected............22

2. Other operating activities problems..........................23

3. Recommendation for developing in the future..................23

4

CHAPTER I: OVERVIEW OF LIENVIET POST JOINT-STOCKCOMERCIAL BANK

1. General informationLien Viet Post Joint Stock Commercial Bank

(LienVietPostBank), formerly known as LienVietBank(LBP),

was granted it Operation License No 91/GP-NHNN on March

28, 2008 by the Governor of the State Bank of Vietnam and

became the first newly established joint stock commercial

bank since 1993.

Established in Hau Giang Province – the heart of

Southwest Vietnam, LVP was one of the top ten commercial

banks in Vietnam in terms of chartered capital at that

time. Since its inception, the bank has paid attention to

applying modern technology, recruiting and retaining

talents and training staffs which have created solid

foundation for a fast and sustainable development.

Pursuing the strategy of sustainable development and

drastic management of the Board of Management and the

Board of Directors, after 5 years of operation, has

confirmed its solid position in the banking and financial

market in Vietnam by sizable total assets, healthy

profitability, modern technologies, wide branch network,

excellent quality of service, good human resource and

sound corporate governance with international standards.

5

In 2011, Vietnam Post Corporation (Vietnam Post), a

member of Vietnam Post and Telecommunication Group

(VNPT), became the Bank's biggest shareholder by

contributing capital to the Bank equal to the value of

the Vietnam Postal Savings Service Company (VPSC) and in

cash. Vietnam Post Saving Company (VPSC) is a subsidiary

of Vietnam Post Corporation (VNPost), which is a member

of Vietnam Post and Telecommunications Group (VNPT).

Since 1999, through VNPost’s network, VPSC has been

offering saving products and services such as remittance,

collectives to customers mainly in rural areas.

LVP and VNPost signed a 50-year-co-operation agreement

which allows LPB to be an exclusive bank in providing

postal saving services and other banking services through

out the network of more than 10,000 transaction points of

VNPost. On July 29th, 2011, LienVietBank declared the

merger and changed the name to LienVietPostBank. As of

December 31st 2012, VNPost increased their holding to

12.54% stakes in LPB. This gives LPB the opportunity to

be present in 63 cities and provinces with 90% coverage

at communal level around the country. Additionally, the

huge client base of more than 400,000 individual clients

and strong relationship with the World Saving Bank

Institution (WSBI) are great advantages that LPB acquired

through the merger.

6

In the next 10 years, it is expected that the Bank can

meet its goal of expanding full banking services to at

least 80% of more than 10,000 post offices throughout

Vietnam, including mobile wallets/cards, mobile micro-

finance services, banking transaction and other banking

products and services.

International relations: Since its establishment in 2008,

the Bank has approached and built relationships with

several international organizations and foreign financial

institutions such as:

IFC – International Finance Corporation: May 2011,

LVP’s initial trade line through IFC’s Global Trade

Finance Program (GTFP) reached USD 5 million. January

2012, the trade line is increased to USD 20 million to

help SMEs sustain import and export activities.

World Bank: In May 2012, the Bank participated in the

third Rural Finance Program III sponsored by the

International Development Association, a member of

World Bank, to support end-borrowers including

individuals, households and SMEs in rural areas.

WSBI – World Saving Bank Institute: In July 2011, LVP

officially became a member of WSBI, a global voice of

the world’s retail and saving banks. In November 2011,

WSBI with Bill & Melinda Gates Foundation began

assisting LVP in implementing the project of “Working

7

with saving banks to double the number of savings

accounts for the poor”.

JICA – Japan International Cooperation Agency:

September 2011, LVP participated in the third stage of

SMEs’ financing project of JICA.

JP Morgan Chase, Wells Fargo and Industrial and

Commercial Bank of China (ICBC) are currently important

partners of LVP and play vital roles in assisting the

Bank to enhance trade finance for SMEs.

Table 1: Historical highlights

Mar

2008

Received operation license from the SBV

(formerly known as Lien Viet Joint-stock

Commercial Bank)Oct

2009

Increased chartered capital to USD 193 million

Jul

2010

Signed cooperation agreement with Wells Fargo

in Washington DCMay

2011

Officially formed relationship with IFC

through the GTFP with an initial trade line of

USD 5 millionJul

2011

Merged with Vietnam Postal Savings Company

(VPSC), and changed name to LienVietPostBank

Became a member of the World Savings Banks

Institute (WSBI).Sep Successfully participated in SMEs’ financing

8

2011 via Japan International Corporation Agency

(JICA) loans.Nov

2011

Successfully called for support from WSBI &

IFC in consulting microfinance development

strategy & competitiveness improvement. Jan

2012

On January 16th, 2012, the LPB’s GTFP trade

line was increased to US 20 million by IFC,

allowing LPB to further help SMEs sustain

import and export activities.May

2012

Successfully participated in the third Rural

Finance Program built by

The World Bank to support end-borrowers which

are individuals, households and SMEs in rural

areas.2013 Ranked 39th in the TOP 500 biggest private

enterprises in Vietnam according to VNR500.

9

2. Legal information

Abbreviation in English: LienVietPostBank

Headquarters: No. 32, Nguyen Cong Tru St, Ward 1, Vi

Thanh City, Hau Giang Province.

Business Registeration No.: 6300048638 (the banking

licence was issued by the State Bank of Vietnam and is

valid for 99 years from the issuing date).

Tax No: 6300048638

SWIFT Code: LVBKVNVXXXXChartered Capital: VND6,460 billion (around USD310 million as of June 30th , 2013).

Corporate Website: http://www.lienvietpostbank.com.vn/

Email [email protected]

Major Shareholders

Him Lam Joint Stock Company (10.44%)

Vietnam Post Corporation (Vietnam Post, 12.54%).

Strategic Partners

Vietnam Bank for Agriculture and Rural Development

(Agribank).

Wells Fargo Bank (The US).

Credit Suisse Bank (Switzerland).

Oracle Financial Services Software Limited.

10

3. Vision & StrategyMission: provide customers with diversified and

tailormade products which benefit the Bank and society at

large.

Vision: Become a leading retail & universal bank

targeting the mass market.

Strategy: pursue a retail customer-oriented strategy by

delivering excellent services

Expand network coverage to target the untapped rural

area and small and medium enterprise market segments.

Approach customers through advanced, user-friendly,

and cost effective technologies

such as Phone banking, Mobile banking, Internet

banking and Mobile money (Vi Viet)

Design products based on the needs of customers and

following standards of Simplicity, Comprehensibility,

Cost effectiveness.

Place transaction points at convenient locations and

in a simple and friendly arrangement manner.

Build corporate culture on 3 core values: Discipline,

Creativity and Humanity.

4. Business scopeLVP is providing various products and services as

follows:

11

(i) Mobilizing Capital from deposits, certificates of

deposits, bonds, and valuable papers, borrowings from

other credit institutions, short-term loans from the

State Bank of Vietnam, andother types of capital

mobilization if allowed;

(ii) Granting credit to individuals, enterprises in the

form of loans, discounting commercial papers, discounting

valuable papers, guarantee, financial lease and other

types of granting credit if allowed;

(iii) Payment and treasury services;

(iv) Others activities such as equity contribution,

shares investment, participation in money market,

subsidiaries establishment, fiduciary activities, agency

on banking and insurance services and so forth.

Besides the aforementioned business activities, LVP has

also obtained permissions from the State bank of Vietnam

to offer other services such as Foreign exchange services

(includes international payment services, foreign

exchange trading activities in global market, etc…);

International investments, etc.

12

5. Product & servicesCapital mobilization products:

LPB provides various term deposit products with

competitive interest rates. Some typical products are:

term saving deposits with flexible principle withdrawal,

floating rate deposits, step-up deposits, automatic

investment accounts, studying abroad saving deposits,

high interest-rate deposits.

Credit products:

Typical retail banking products: Flagship products, for

example, car loans, real-estate loans, consumer loans,

mortgage loans, study overseas loans, agricultural loans

and home loans.

Typical corporate banking products: Short-term credit

line, export financing, LienVietPostBank guarantee

product packages, foreign bill purchase and agricultural

loans.

Electronic banking products:

In 2012, LienVietPostBank launched two breakthrough

services including Green Banking (products and services

with environment-protecting covenants and non-cash

transaction services) and New Generation Banking (product

and services targeting at children and parents with

assistance in educating personal finance management).In

13

addition to traditional services in domestic payment,

international settlement, cash management and property

keeping services, LienVietPostBank was also eligible for

providing State budget collection and electricity bill

collection service in 2012. LVP is about to implement

telephone bill collection service for Viettel Telecom

Group and Vietnam Computerized Lottery Company.

Regarding electronic banking, in 2011, LVP launched Vi

Viet E-wallet, a mobile money and online payment

platform. LVP believes that one of the most efficient

ways to reach viral is to shift the majority of cash-

based financial transactions into digital form through a

mobile phone or any digital interfaces. LVP is now in the

process of improving Vi Viet E-wallet to transform it

into an effective tool to access its un-banked segment

and mass market coverage.

Services:

LPB provides full range of services from domestic

payment, international settlement and cash management to

financial consultancy and property keeping services.

In 2012, LPB has successfully developed and launched two

breakthrough services which are Green banking (including

products and services with environment-protecting

covenants and non-cash transaction services) and New

Generation Bank (including products and services

14

targeting at children and parents with assistance in

educating personal finance management). Besides, LPB is

also eligible for providing State budget collection

service, electricity bill collection service and

completing procedure to launch telephone bill collection

service for Viettel Telecom Group and Vietnam

computerized lottery company.

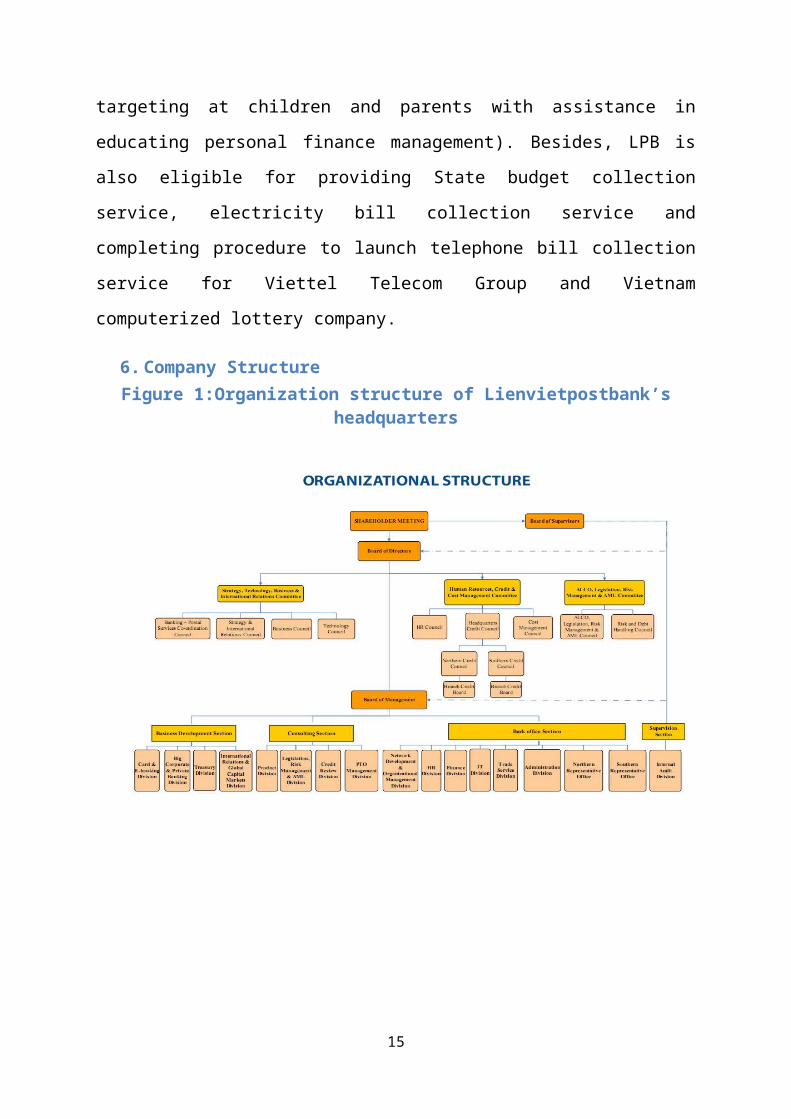

6. Company StructureFigure 1:Organization structure of Lienvietpostbank’s

headquarters

15

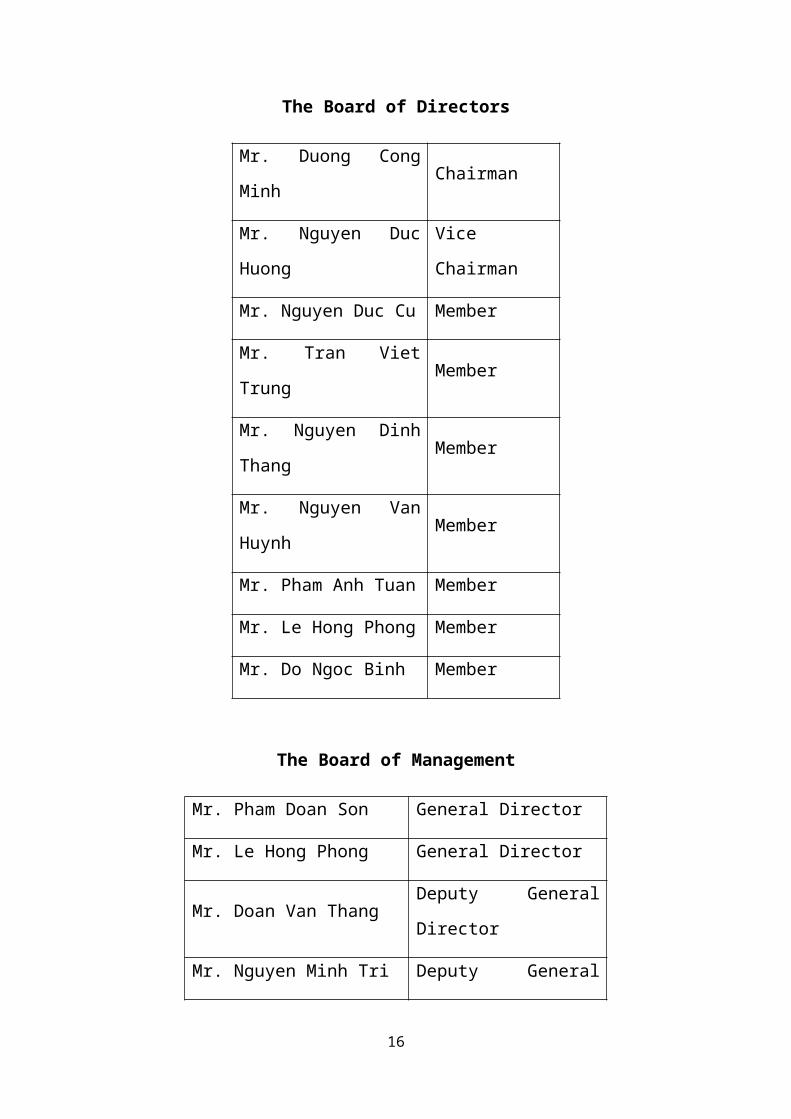

The Board of Directors

Mr. Duong Cong

MinhChairman

Mr. Nguyen Duc

Huong

Vice

Chairman

Mr. Nguyen Duc Cu Member

Mr. Tran Viet

TrungMember

Mr. Nguyen Dinh

ThangMember

Mr. Nguyen Van

HuynhMember

Mr. Pham Anh Tuan Member

Mr. Le Hong Phong Member

Mr. Do Ngoc Binh Member

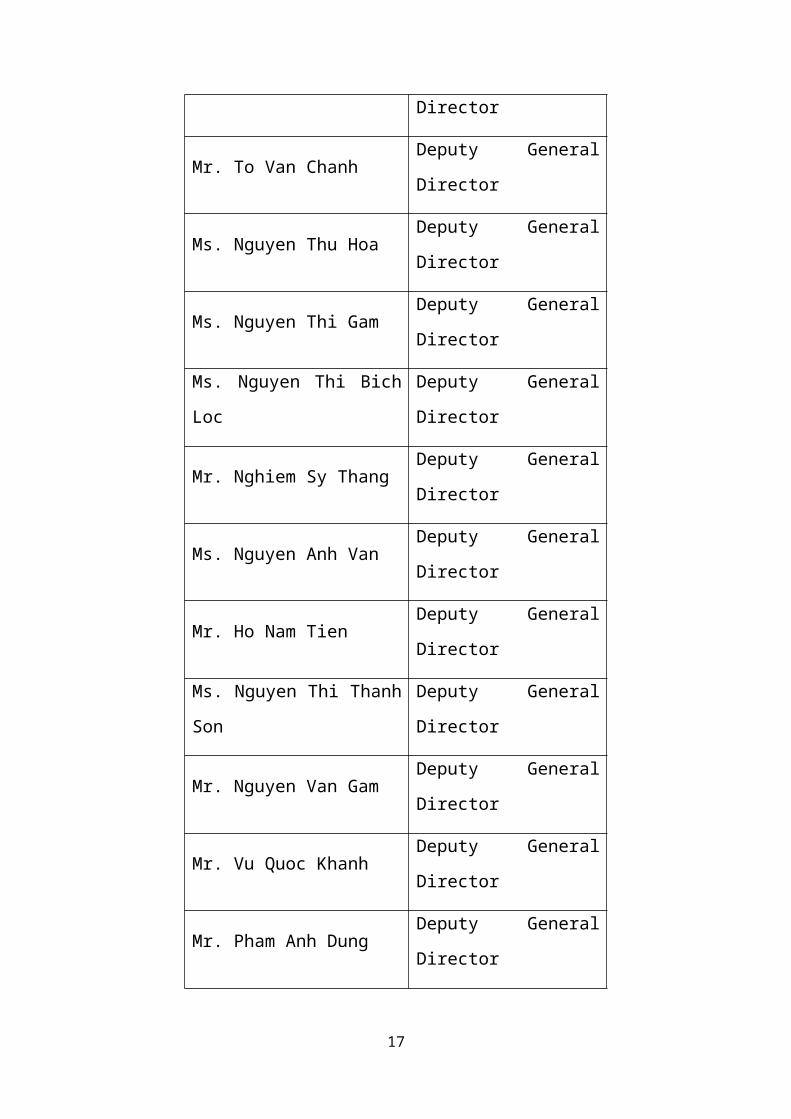

The Board of Management

Mr. Pham Doan Son General Director

Mr. Le Hong Phong General Director

Mr. Doan Van ThangDeputy General

Director

Mr. Nguyen Minh Tri Deputy General

16

Director

Mr. To Van ChanhDeputy General

Director

Ms. Nguyen Thu HoaDeputy General

Director

Ms. Nguyen Thi GamDeputy General

Director

Ms. Nguyen Thi Bich

Loc

Deputy General

Director

Mr. Nghiem Sy ThangDeputy General

Director

Ms. Nguyen Anh VanDeputy General

Director

Mr. Ho Nam TienDeputy General

Director

Ms. Nguyen Thi Thanh

Son

Deputy General

Director

Mr. Nguyen Van GamDeputy General

Director

Mr. Vu Quoc KhanhDeputy General

Director

Mr. Pham Anh DungDeputy General

Director

17

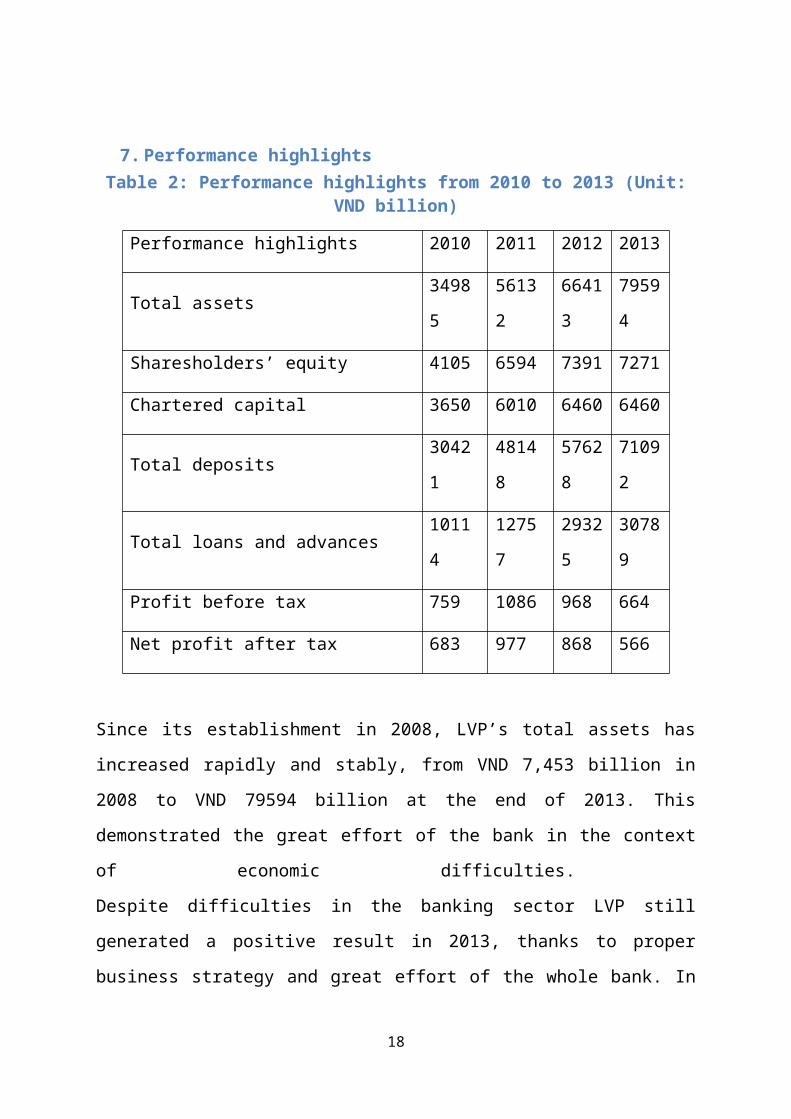

7. Performance highlights Table 2: Performance highlights from 2010 to 2013 (Unit:

VND billion)

Performance highlights 2010 2011 2012 2013

Total assets3498

5

5613

2

6641

3

7959

4

Sharesholders’ equity 4105 6594 7391 7271

Chartered capital 3650 6010 6460 6460

Total deposits3042

1

4814

8

5762

8

7109

2

Total loans and advances1011

4

1275

7

2932

5

3078

9

Profit before tax 759 1086 968 664

Net profit after tax 683 977 868 566

Since its establishment in 2008, LVP’s total assets has

increased rapidly and stably, from VND 7,453 billion in

2008 to VND 79594 billion at the end of 2013. This

demonstrated the great effort of the bank in the context

of economic difficulties.

Despite difficulties in the banking sector LVP still

generated a positive result in 2013, thanks to proper

business strategy and great effort of the whole bank. In

18

2013, the bank’s profit before tax was VND 664 billion,

the dividend payout ratio was 8%, and the provision were

sufficiently allocated in compliance with the State Bank

of Vietnam’s regulations.

19

CHAPTER II: EVALUATION SITUATION AND BUSINESS PERFORMANCEOF LIENVIET POSTBANK FROM 2010 TO 2013

1. Overview of business environmentVietnam, like the rest of Asia, has entered a period of

slower growth. The main reason was the difficulties in

both domestic and global economies. Many companies faced

with declining business activities and even with

bankruptcy risks. Beside the manufacturing and

agricultural sector, other industry sectors are being

adversely by slower growth and the Banking sector is no

exception. With lower credit growth, tighter margins and

high levels of non - performing loans, it is evident that

banks are operating in a challenging environment.

However, there are still positive signs. The national

economy has shown signs of gradual recovery which will

bring in more investment opportunities and business

improvement. What’s more important is that LienVietBank

has reinforced its brand awareness, reputation and

influence among clients and on the financial market. This

is not only due to its effective business operation but

also the commitment to sustainable development by

fulfilling the social responsibility as a corporate

citizen, specifically the credit program for agriculture

and rural development.

20

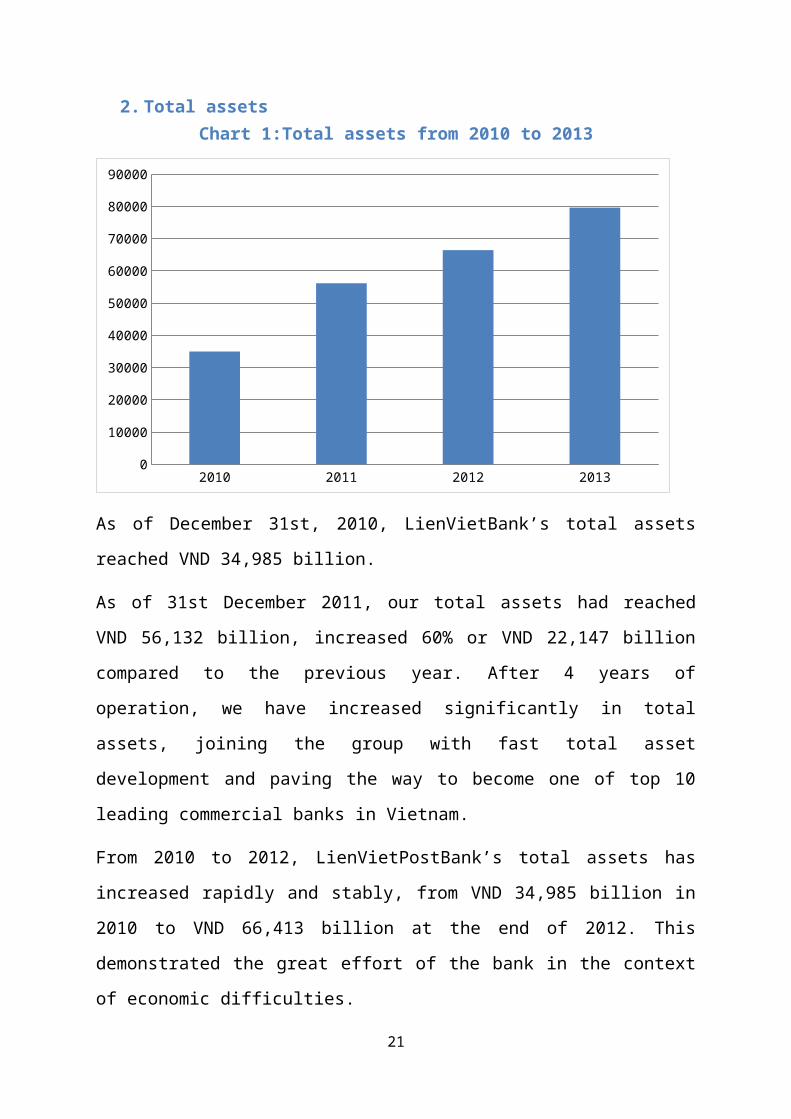

2. Total assets Chart 1:Total assets from 2010 to 2013

2010 2011 2012 20130

10000

20000

30000

40000

50000

60000

70000

80000

90000

As of December 31st, 2010, LienVietBank’s total assets

reached VND 34,985 billion.

As of 31st December 2011, our total assets had reached

VND 56,132 billion, increased 60% or VND 22,147 billion

compared to the previous year. After 4 years of

operation, we have increased significantly in total

assets, joining the group with fast total asset

development and paving the way to become one of top 10

leading commercial banks in Vietnam.

From 2010 to 2012, LienVietPostBank’s total assets has

increased rapidly and stably, from VND 34,985 billion in

2010 to VND 66,413 billion at the end of 2012. This

demonstrated the great effort of the bank in the context

of economic difficulties.

21

As of December 31st, 2013, LienVietBank’s total assets

reached VND 79,594 billion.

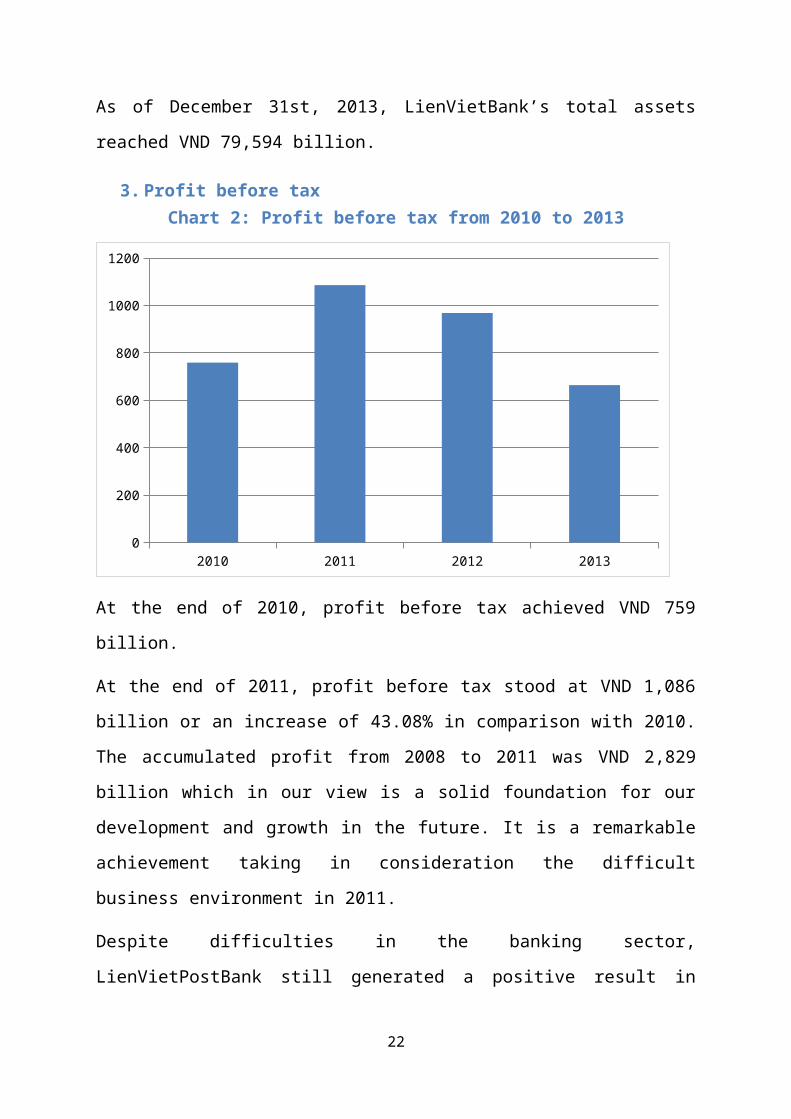

3. Profit before taxChart 2: Profit before tax from 2010 to 2013

2010 2011 2012 20130

200

400

600

800

1000

1200

At the end of 2010, profit before tax achieved VND 759

billion.

At the end of 2011, profit before tax stood at VND 1,086

billion or an increase of 43.08% in comparison with 2010.

The accumulated profit from 2008 to 2011 was VND 2,829

billion which in our view is a solid foundation for our

development and growth in the future. It is a remarkable

achievement taking in consideration the difficult

business environment in 2011.

Despite difficulties in the banking sector,

LienVietPostBank still generated a positive result in

22

2012, thanks to proper business strategy and great effort

of the whole bank. In 2012, the bank’s profit before tax

was VND 968 billion, the dividend payout ratio was 10%,

and the provision were sufficiently allocated in

compliance with the State Bank of Vietnam’s regulations.

At the end of 2013, profit before tax achieved VND 664

billion, an decrease of 31.40% versus 2012.

4. Capital mobilizationChart 3: Capital mobilization from 2010 to 2013

0

10000

20000

30000

40000

50000

60000

70000

80000

Deposits from customers

Deposits fromcredit institutions

As of December 31st 2010, total capital mobilization of

the bank reached VND 30,421 billion. In which, deposits

from customer (corporate and individuals) were VND 15,439

billion, accounting for 50.75% of total capital

mobilization. Deposits from credit institutions (borrowed

from the State Bank and other financial institutions)

23

were VND 14,982 billion, accounting for 49.25% of total

capital mobilization.

As of 31st December 2011, total mobilized capital reached

VND 48,148 billion or an increase of 58% from 2010, which

is an equivalent of VND 17,727 billion. Deposits from

corporate and individual customers were VND 26,663

billion accounting for 55.38% of total mobilized capital

and deposits from credit institutions were VND 21,485

billion, or approximately 44.62%.

In 2012, the State Bank of Vietnam cut the interest rate

six times, from 14% to 8%, which made the mobilization

market sharply fluctuated. To deal with this situation,

the bank diversified its products, improved service

quality and issued various customer service policies. The

actions have helped the bank not only retain the existing

customers, but also reach new customers. Besides, the

capital mobilized through the Postal savings system has

been stable and grown steadily with the total amount of

VND 10,201 billion at 31st December 2012, accounting for

24.68% of total bank deposits. The total bank deposits

grew by 19.69%, to end the year at VND 57,628 billion.

As of 31st December 2013, total mobilized capital reached

over VND 71000 billion or an increase of 23% from 2012.

Deposits from corporate and individual customers were VND

55,558 billion accounting for 78.12% of total mobilized

24

capital and deposits from credit institutions were VND

15,558 billion, or approximately 21.87%.

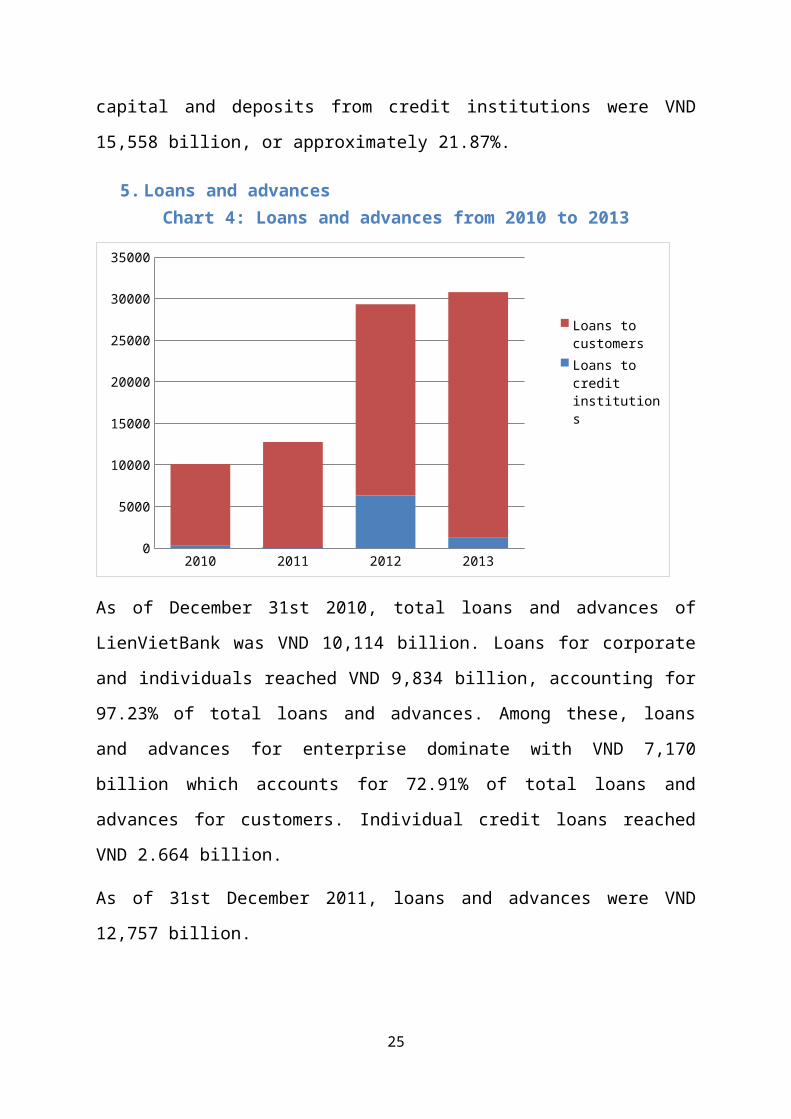

5. Loans and advancesChart 4: Loans and advances from 2010 to 2013

2010 2011 2012 20130

5000

10000

15000

20000

25000

30000

35000

Loans to customersLoans to credit institutions

As of December 31st 2010, total loans and advances of

LienVietBank was VND 10,114 billion. Loans for corporate

and individuals reached VND 9,834 billion, accounting for

97.23% of total loans and advances. Among these, loans

and advances for enterprise dominate with VND 7,170

billion which accounts for 72.91% of total loans and

advances for customers. Individual credit loans reached

VND 2.664 billion.

As of 31st December 2011, loans and advances were VND

12,757 billion.

25

In compliance with the State Bank of Vietnam’s

orientation and the Government’s policies, in 2012,

LienVietPostBank focused on lending to prioritize sectors

such as manufacturing, agriculture and rural areas.

Lending to those sectors such as real-estate, finance was

tightened to ensure loan quality and increase capital

efficiency. As of 31st December 2012, the total loans and

advances to customers was VND 22,992 billion, in which

41.02% of its outstanding loan was to finance agriculture

and rural areas in Vietnam.

As of December 31st 2013, total loans and advances of

LienVietBank was VND 30,789 billion. Loans for corporate

and individuals reached VND 29,548 billion, accounting

for 95.96% of total loans and advances. Loans and

advances credit institutions dominate with VND 1,241

billion which accounts for 4.03% of total loans.

6. Payment activitiesAfter 3 years of operation, LienVietBank has built and

improved the domestic payment system via the channels:

the interbank electronic payment channel of SBV (CITAD),

the payment system of Vietnam Bank for Agricultural and

Rural Development (VBA) and the payment system of

Vietcombank (VBC-Money). The Bank has also completed the

implementation of the Western Union payment application

with the Bank for Investment and Development of Vietnam

26

(BIDV). LienVietBank always pays attention to carry out

and develop the centralized international payment

activities, processing transactions at the Payment

Center, to reduce risk and enhance prestige and service

quality. Together with developing the existing

relationships the Bank also has continued searching and

expanding new relationships with local and foreign banks,

representative offices of foreign banks in Vietnam.

Result:

2011 was a year of dramatic economic turbulence causing

the decrease in trade flows both domestically and

globally. Vietnam was not an exception, with the

country’s export and import activities suffering from

international financial crisis and economic downturn.

Nevertheless, LienVietPostBank witnessed the significant

increases in international payments with import revenue

at USD 551.84 million, a 146% increase from 2010 and

export revenue at USD 120.62 million, a growth of 43% in

comparison to the previous year. International payment

activities contributed a large portion of revenue coming

from services.

In 2012 International payment volume through

LienVietPostBank increased 30.62% to nearly USD 598

million in comparison to that of 2011. Especially, the

volume of export payment by L/C through LienVietPostBank

27

reached USD 63 million, an impressive growth of 207% in

comparison to that of the previous year. International

payment activities of LienVietPostBank were made in the

U.S, Taiwan, Hong Kong, Singapore, Japan, South Korea,

China and the Europe.

In 2013 International payment volume through

LienVietPostBank reached over USD 500 million in,

decreased 19.6% comparison to that of 2012.

7. Other supportNetwork expansion

LienVietBank is constantly pursuing the network

development strategy. By December 31st, 2010,

LienVietBank had established a network of 45 transaction

points throughout the country, including 01 Head Office,

01 Transaction Center placed in Hau Giang Province, 15

branches and 29 transaction offices.

Since 1st July 2011, LienVietPostBank has officially

utilized the system of more than 10,000 transaction

points , after Vietnam Post Corporation has contributed

capital to the bank through the corporate value of its

affiliate, the Vietnam Postal Savings Services Company

(VPSC) and through cash. With the wide network spreading

over 63 provinces/ cities and more than 10,000 wards

nationwide, LienVietPostBank would be able to bring

28

modern banking products and services to all customers,

including those who are living in remote areas.

As of 3/2014, the number of branches amounted to 82

across the country. LienVietPostBank is expected to be

present in 56 provinces across the country by the end of

2014.

Technology

Oracle Form – LPB’s Core Banking system utilizes Oracle

Form & Report to support the full spectrum of banking

operations.

GPS - To provide higher safety and security,

LienVietPostBank‘s IT system uses the Global Positioning

System

(GPS) which monitors the network operations, enhances

cashflow management and onsite collection services.

Daily reports & Post Office Transactions – LPB’s IT team

has developed its own core system for the Postal

Transaction Office System which fully serve the needs of

more than 10,000 transaction points of VNPost to connect

and integrate with the current core banking system of

LPB, allowing efficient network management of more

than10,000 postal transaction offices across 63 provinces

nationwide.

29

Recognitions - IT Head of LienVietPostBank received the

CSO award which reflects the Bank’s remarkable effort in

providing a more secured information technology system.

8. HR & Training activitiesIn the past 5 years, the number of employees at

LienVietPostBank increased rapidly in line with the

network development of branches. Compared to the time the

Bank was set-up, the current number of employees

increased more than fourfold to nearly 2,500. Besides,

20,000 additional employees of Vietnam Post Corporation

(VNPost) are also involved in providing the bank’s

services at over 10,000 postal transaction offices after

the stake contribution of VNPost to LienVietPostBank

through the corporate value of one of its subsidiaries –

the Vietnam Postal Savings Service Company.

In addition to the growth in the number of employees,

LienVietPostBank has also paid great attention to the

quality of human resources. This could be seen by

qualified applicants and training programs for their

employees. The majority of LVP employees graduated from

leading domestic universities such as National Economics

University, Academy of Finance, Banking Academy, Foreign

Trade University and other prestigious universities in

the UK, United States, France, Australia, and Germany...

Currently, the ratio of employees who hold Master degrees

30

is 7% and Bachelordegrees is over 85%. After the

recruitment of a competent staff, the training is the

next step to build a team of qualified employees.

9. Coporate social responsibility“Integrating business and society” is LienVietPostBank’s

long-term operational orientation. Along with effective

business development, LienVietPostBank has committed to

contribute to the development of the community and

society through direct social charitable activities.

LienVietPostBank has focused on the following social

activities: financing the construction of education,

healthcare and culture premises; supporting the

sustainable development of agriculture and rural areas;

sponsoring for sport events and assistance for disaster

victims.

Currently, LienVietPostBank has built itself to be “The

best bank on Corporate Social Responsibility” in which it

pursues sustainable development and commits to operate in

accordance with its core values.

In 2013, LPB committed to contribute nearly USD 5 billion

donation in the following areas: Education & Culture

- Sponsor for construction of schools, bridges, public

healthcare stations, historical and cultural memorials,

granting education and training equipment. LPB has funded

various schools in over 20 provinces in Vietnam.

31

- Fund for Intellectual Talent Encouragement via

scholarship programs and education promotion funds in

coordination with universities and localities.

- Fund for the 5th Quang Nam Heritage Festival 2013

- Sponsor for Elderly Association in Phu Tho Province

- Other programs to reduce poverty

32

CHAPTER III: PROBLEMS AND SOLUTION FOR DEVELOPMENT IN THEFUTURE

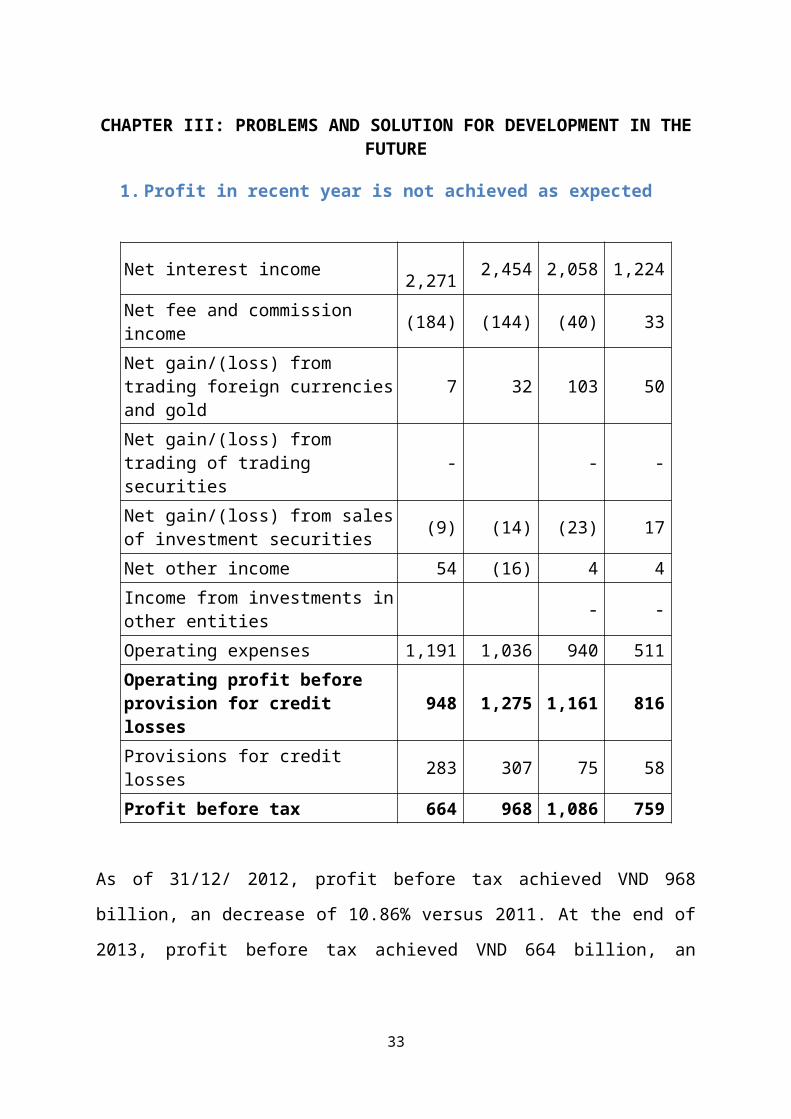

1. Profit in recent year is not achieved as expected

Net interest income 2,271 2,454 2,058 1,224

Net fee and commission income (184) (144) (40) 33

Net gain/(loss) from trading foreign currenciesand gold

7 32 103 50

Net gain/(loss) from trading of trading securities

- - -

Net gain/(loss) from salesof investment securities (9) (14) (23) 17

Net other income 54 (16) 4 4Income from investments inother entities - -

Operating expenses 1,191 1,036 940 511Operating profit before provision for credit losses

948 1,275 1,161 816

Provisions for credit losses 283 307 75 58

Profit before tax 664 968 1,086 759

As of 31/12/ 2012, profit before tax achieved VND 968

billion, an decrease of 10.86% versus 2011. At the end of

2013, profit before tax achieved VND 664 billion, an

33

decrease of 31.40% versus 2012 and an decrease of 38.85 %

compare with 2010.

Causes:

Vietnam, like the rest of Asia, has entered a period

of slower growth. The main reason was the

difficulties in both domestic and global economies.

Many companies faced with declining business

activities and even with bankruptcy risks. Beside the

manufacturing and agricultural sector, other industry

sectors are being adversely by slower growth and the

Banking sector is no exception.

In 2012, the State Bank of Vietnam (SBV) cut the

interest rate six times, from 14% to 8%, which made

the mobilization market sharply fluctuated. In 2013,

the interest rate remaining around 7%, many banks

face with the excess of capital. The bank is facing

with the excess of capital. With tighter margins,

profit before tax also reduce despite of both loans

and redits is higher.

Because of the high levels of non - performing loans,

the bank have to increase the provision for credit

losses amount. It‘s strong impact on profit result.

Network expansion cost in recent year increase

rapidly, so the operating expenses also increasing.

34

2. Other operating activities problems Although they have been oriented to become a leading

retail bank, a specific marketing strategy has yet to

be made. The structure of individual customers

accounted low ration on both mobilization and

lending.

Risk management need improve: LienVietPostBank

doesn’t have early debt warning system.

The information technology system needs upgrade after

6 years woking.

3. Recommendation for developing in the futureGeneral targets

Continue to restructure the bank’s system;

Capture the new market share and new opportunities;

Expand the joint venture, link and proceed towards

standardize the rules, regulations, and procedures

according to the international standards and especially

focus on customer services and attracting new customers,

promote the bank’s brand;

Detect and solve the problem loans and non-performing

loans;

Train and re-train the human resources of the whole bank,

focus on qualification and occupational ethics.

Solution

35

Maintaining the existing funding and mobilizing lower

cost funds to get low input average interest rate, to be

ready for financing in accordance with the regulations of

low ceiling interest rates and finding appropriate

products of bond investment when it’s hard for financing

(in 2013 and 2014, even when the inflation and interest

rates increase then)

Focusing on handling non-performing loans and problem

loans as well as collecting existing loans in order to

reduce capital losses and to increase income and fund for

new loans.

Despite the challenges of global financial crisis, there

still have many opportunities. Accordingly, the funded

loan will be used effectively only when there are new

suitable products. For now, LienVietPostBank should focus

on developing retail products, finding suitable market

segment which is to cooperate with strategic partners,

promoting China cross border payments, and tightening the

wholesale lending conditions, engaging in

financingnational projects which have guarantees from the

Government.

Analyzing the efficiency of the investment products in

order to provide solutions of “taking profit” or

“stopping loss” the derivative products invested in

global capital markets in the last few years in order to

36

reclaim capital in 2013 and to search for effective

products for the next few years.

Launching a movement to facilitate economic analysis

activities widely, deeply and systematically in order to:

promptly detect the strengths and weaknesses of the whole

LienVietPostBank system, of each branch, of each

department; attach special importance to quality of

audit, maintain control before, during, after each

operation to avoid unexpected results.

37