Financial System of Bangladesh

44

ABSTRACT No economy can grow and improve the living standards of its population in the absence of a well functioning and efficient financial sector. The financial sector of Bangladesh is mainly composed of the Bangladesh Bank, scheduled banks, non-bank financial institutions, insurance companies, microfinance institutions and stock exchanges. Since the banking business is the most dominant aspect of the financial Sector, this paper basically deals with that. The capital market, insurance companies and other institutions have also been discussed here. At present there are several prudential norms, management guidelines and Advisory circulars given by the Bangladesh Bank for efficient, transparent and accountable banking business. However, in terms of several indicators like financial deepening, accounting and auditing Standards, risk management strategies, and financial reporting, Bangladesh financial sector is still lagging behind in comparison with many emerging economies. In a globalize and competitive environment, Bangladesh financial system must follow more effectively the accepted international norms and standards to become a middle income country within next few years. This is necessary to give a boost to the continuing good performance in various sectors of the economy. Kew word: NCBs, PCBs, NBFIs, DSE, CSE, Financial system of Bangladesh Page 1 of 44

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of Financial System of Bangladesh

ABSTRACT

No economy can grow and improve the living standards of its population in the absence of a well functioning and efficient financial sector. The financial sector of Bangladesh is mainly composed of theBangladesh Bank, scheduled banks, non-bank financial institutions, insurance companies, microfinance institutions and stock exchanges. Sincethe banking business is the most dominant aspect of the financialSector, this paper basically deals with that. The capital market, insurance companies and other institutions have also been discussed here. At presentthere are several prudential norms, management guidelines andAdvisory circulars given by the Bangladesh Bank for efficient, transparent and accountable banking business. However, in terms of several indicatorslike financial deepening, accounting and auditingStandards, risk management strategies, and financial reporting, Bangladesh financial sector is still lagging behind in comparison with many emerging economies. In a globalize and competitive environment,Bangladesh financial system must follow more effectively the accepted international norms and standards to become a middle income country within next few years. This is necessary to give a boost to the continuing good performance in various sectors of the economy.

Kew word: NCBs, PCBs, NBFIs, DSE, CSE,

Financial system of Bangladesh Page 1 of 44

Financial System of Bangladesh:

Introduction: Bangladesh has no alternatives but to set poverty reduction as its overarching development goal. Efforts to achieve this goal can greatly be facilitated by a higher growth rate. One has to agree that no economy can grow and improve the living standards of its population in the absence of awell functioning and efficient financial sector. Improvement of the financial sector can create a conducive environment to enable the poor and disadvantaged to get the benefits of accelerated growth.

The financial system of Bangladesh includes Bangladesh Bank (the Central Bank), scheduled banks, non-bank financial institutions, microfinance institutions (MFIs), insurance companies, co-operative banks, credit rating agencies and stock exchange. Amongscheduled banks there are 4 nationalized commercial banks (NCBs), 5 state-owned specialized banks (SBs), 30domestic private commercial banks (PCBs), 10 foreign commercial banks (FCBs) and 29 nonblank financial institutions (NBFIs) as of December 2006. However, Rupali Bank, an NCB is being sold to a foreign buyer,

Financial system of Bangladesh Page 2 of 44

(Loans & AdvancesShares,

Debentures)

(Deposit, Mutual fund, Unit

certificate, COD)

Money Market

Non-Security Market

Security Market

Capital Market

Organized Stock

Exchange

New Issue Market

Secondary Market

Over The Counter Market

(DSE, CSE)

Banking Non-Banking

Financial Supervisor/Regulator(Bangladesh Bank / Security Exchange

Commission)

Financial System Of Bangladesh

Financial Markets

Financial Institutions

BankingFinancial

Institutions

Non-BankingFinancial

Institutions

Financial Instruments

Primary/Direct

Secondary/Indirect

CommercialBanks

Specialized

Banks

InvestmentBanks

LeasingCompanies

OthersHousing

FinancialCompanies

and once this transaction is completed, the country will have only 3 NCBs. Which are being corporatized. Over and above the institutions cited above, three development financial institutions namely House Building Finance Corporation (HBFC), Ansar- VDP UnnayanBank and Karma Shangsthan Bank are operating in Bangladesh, all of which are state owned.

Financial system of Bangladesh Page 3 of 44

Financial system of Bangladesh Page 4 of 44

Central Bank and its Policies:

The objectives of the Bangladesh Bank (BB) is to formulate monetary policy which aims at supporting the highest sustainable output growth while maintaining price stability, adjusting smoothly to the internal andexternal shocks faced by the economy from time to time.Within this mandate, BB also supervises and regulates scheduled banks and non-bank financialinstitutions operating in Bangladesh. It maintains the traditional central banking roles of note issuance and the banker to the government and banks. Its prudential regulations include, among others, ensuring minimum capital requirements, applying limits on loan concentration and insider borrowing, and, providing guidelines for asset classification and income recognition.The Bangladesh Bank has the legal authority to impose penalties for non-compliance and also to intervene in the management of a bank if serious problems arise. It has the delegated authority of issuing policy directives regarding the foreign exchange regime.

1. Financial Institutions:

The financial institution of Bangladesh consists of Banking Financial Institutions and Non-Banking Financial Institutions--

1.1.Banking Financial Institutions:

Financial system of Bangladesh Page 5 of 44

Banking financial institutions include the followings--

1.1.1.Commercial Banks:

The commercial banking system dominates Bangladesh'sfinancial sector with limited role of Non-BankFinancial Institutions and the capital market. TheBanking sector alone accounts for a substantial shareof assets of the financial system. The banking systemis dominated by the 4 Nationalized Commercial Banks ,which together controlled more than 54% of deposits andoperated 3388 branches (54% of the total).

1.1.2.Nationalised Commercial Banks:

The NCBs, which had major share of the total deposits and credit of the banking sector, were recently unable to compete with private sector banks and they accountedfor the major chunk of the classified loans. In this situation Sonali Bank, Janata Bank and Agrani Bank havebeen corporatized and incorporatized as public limited company. Sale of Rupali Bank to a foreign private entrepreneur is underway. The government will not interfere in these banks' day to day activities and instead these banks will be more accountable to the central bank.

Agrani Bank Janata Bank

Sonali Bank

Financial system of Bangladesh Page 6 of 44

1.1.3.Private Commercial Banks:

1. Al-Arafa Islami Bank Ltd.2. Al-Baraka Bank Bangladesh Ltd.

3. Arab Bangladesh Bank Ltd.

4. City Bank Ltd.

5. Dhaka Bank Ltd.

6. Eastern Bank Ltd.

7. IFIC Bank Ltd.

8. Islamic Bank (BD) Ltd.

9. National Bank Ltd.

10. National Credit & Commerce Bank Ltd.

11. Prime Bank Ltd.

12. Pubali Bank Ltd.

13. Rupali Bank Ltd.

14. Social Investment Bank Ltd.

15. Southeast Bank Ltd.

16. Standard Bank Ltd.

17. United Commercial Bank Ltd.

18. Uttara Bank Ltd.

Financial system of Bangladesh Page 7 of 44

1.1.4.Foreign Commercial Banks:

1. American Express Bank Ltd.2. ANZ Grindlays Bank PLc

3. Citibank N.A.

4. Credit Agricole Indo-Suez

5. Dutch-Bangla Bank

6. Faisal Islamic Bank of Bahrain

7. Habib Bank Ltd.

8. Hanil Bank

9. Hong Kong Bank

10. Muslim Commercial Bank Ltd.

11. National Bank of Pakistan

12. Societe General

13. Standard Chartered Bank

14. State Bank of India

15. The Bank of Tokyo-Mitsubishi

16. The Bank of Novaskosia

17. Hanvit Bank

Financial system of Bangladesh Page 8 of 44

18. The Hong Kong & Shanghai Banking Corp.Ltd.

1.1.5. Specialized Commercial Banks:

Public sector banks in charge of agricultural andindustrial term lending suffer from poor decisionmaking and low efficiency; and have never been run ascommercial enterprises, resulting in unsustainable NPLbehavior. Even though financial condition of theseinstitutions are weak, one cannot ignore there socialcommitment. In order to render them financially viable,restructuring of these institutions is necessary otherwise it will hinder the overall financial sectorstability and soundness.

1. Bangladesh Krishi Bank2. Bangladesh Shilpa Bank

3. Bangladesh Shilpa Rin Sangstha

4. Bank of Small Industries & Commerce

5. Rajshahi Krishi Unnayan Bank

Out of the 5 specialized banks, two (Bangladesh KrishiBank and Rajshahi Krishi Unnayan Bank) were created tomeet the credit needs of the agricultural sector whilethe other two ( Bangladesh Shilpa Bank (BSB) &Bangladesh Shilpa Rin Sangtha (BSRS) ) are forextending term loans to the industrial sector.

1.1.6.Other Banks :

Ansar and VDP Bank

Financial system of Bangladesh Page 9 of 44

BRAC Bank Ltd.

Karmasangsthan Bank

Grameen Bank

1.2. Non Banking Financial Institutions :

Non-Bank Financial Institutions are an important part of financial system in Bangladesh. NBFIs operations areregulated under the Financial Institutions Act, 1993. The NBFIs consist of investment/merchant banks, house finance companies, leasing companies etc. There were 29financial institutions operating in Bangladesh as of 31December 2006. Of these one is government owned, 15 arelocal (private) and the other 13 are established under joint venture with foreign participation. Bangladesh Bank has introduced a policy for loan and lease classification and provisioning for NBFIs from December2000 on a half-yearly basis. Among the 29 financial institutions, 12 have been listed in the stock exchanges up to 31 December 2006 to strengthen financial capability and the rest are under process to be listed in due course.

1.2.1.Leasing Companies:

1. Industrial Development Leasing Co. of Bangladesh Ltd.

2. Bangladesh Finance & Investment Co. Ltd.3. Bangladesh Industrial Finance Company Limited4. Delta Brac Housing Finance Corporation Ltd5. Bay Leasing & Investment Limited6. First Lease International Limited

Financial system of Bangladesh Page 10 of 44

7. Fareast Finance & Investment Limited8. Fidelity Assets & Securities Company Ltd.9. GSP Finance Company (Bangladesh) Limited10. Industrial and Infrastructure development

Finance Company limited

11. Infrastructure Development Company Limited12. Industrial Promotion and Development Company

(IPDC) of Bangladesh Limited

13. Islamic Finance & Investment Limited14. International Leasing & Financial Services

Ltd.15. LankaBangla Finance Ltd.16. Midas Financing Ltd.17. Oman Bangladesh Leasing & Finance Limited18. National Housing Finance and Investments

Limited

19. People's Leasing and Financial Services Ltd20. Phoenix Leasing Company Limited21. Prime Finance & Investment Ltd22. Saudi-Bangladesh Industrial & Agricultural

Investment Company Limited (SABINCO)23. Self Employment Finance Limited24. Union Capital Limited25. Vanik Bangladesh Limited26. United Leasing Company Ltd.27. Uttara Finance and Investments Limited28. The UAE-Bangladesh Investment Co. Ltd

Financial system of Bangladesh Page 11 of 44

1.2.2.Merchant Banks:

A Consultants and Financial Adviser Banco Trans World (BD) Ltd.

Bay Leasing and Investment Ltd.

Capital Market Services Ltd.

EC Securities Ltd.

Equity Valuation Research & Distribution Ltd.

Fidelity Assets and Securities Company Ltd.

Grameen Securities Management Ltd.

IDLC of Bangladesh

Millennium Investment Management Co. Ltd.

Pangaea Partners Bangladesh

Paramount Securities Limited

Prime Finance & Investment Ltd.

Prime Securities & Financial Services Ltd.

1.2.3.Insurance :

The insurance sector is regulated by the Insurance Act,1938 with regulatory oversight provided by the Controller of Insurance on authority under the Ministryof Commerce. A separate Insurance Regulatory Authority

Financial system of Bangladesh Page 12 of 44

is being established. A total of 62 insurance companieshave been operating in Bangladesh, of which 18 provide life insurance and 44 are in the general insurance field. Among the life insurance companies, except the state-owned Jiban Bima Corporation (GBC) foreign owned American Life Insurance Company (ALl CO), and the rest of the private. Among the general insurance companies, state-owned Shadharan Bima Corporation (SBC) is the most active in the insurance sector. A total of 31 insurance companies are listed in the capital market, of which 8 offer life insurances.

1.2.4.Board Of Investment in Bangladesh : The Board of Investment (BOI) was established by the Investment Board Act of 1989 to promote and facilitate investment in the private sector both from domestic andoverseas sources with a view to contribute to the socio-economic development of Bangladesh. It is headed by the Prime Minister and is a part of the Prime Minister's Office. Its membership includes representatives (at the highest level) of the relevant ministries - industry, finance, planning, textiles, et.al. - as well as others, such as the Governor of Bangladesh Bank, heads of some business associations. The Operation Head and CEO of BOI is the Executive Chairman. Click to open BOI Organogram.

Major Functions of BOI include: Providing necessary facilities and assistance in

the establishment of industries. Implementing investment related GOB policies.

Financial system of Bangladesh Page 13 of 44

Preparing investment schedule. Registering private sector industrial projects;

and identifying competitive investment sectors and facilitating investment by providing information and services.

The BOI also includes a Utility Service Cell that offers pre-investment counseling, facilitation of utility connections, and assistance with import clearance and warehousing licenses.

BOI offers Welcoming Service to the visiting foreign investors. The service includes reception at airport, hotel booking, transport arrangement and drawing up itinerary in accordance with the need of the foreign investors visiting Bangladesh.Click to contact BOI Welcome Service.

Composition of the Board : 1.The Board shall consist of the following members namely:

Chairman; Minister in charge of the Ministry of Division

dealing with industries who shall also be its Vice-Chairman, ex-officio;

Minister in charge of the Ministry or Division dealing with finance, ex-officio;

Minister in charge of the Ministry or Division dealing with power, fuel and mineral resources, ex-officio ;

Financial system of Bangladesh Page 14 of 44

Minister in charge of the Ministry or Division dealing with commerce, ex-officio;

Minister in charge of the Ministry or Division dealing with textiles, ex-officio;

Minister in charge of the Ministry or Division dealing with planning, ex-officio;

Governor of the Bangladesh Bank, ex-officio; Secretary of the Ministry or Division dealing with

industries, ex-officio; Secretary of the Ministry or Division dealing with

industries , ex-officio; Secretary of the Ministry of Division dealing with

with finance, ex-officio ; Secretary of the Ministry or Division dealing with

internal resources, ex-officio; President of the Federation of the Bangladesh

Chambers of Commerce and Industry, ex-officio; President of the Bangladesh Chamber of Industry,

ex-officio; Chairman of the Executive Council, who shall also

be its Secretary, ex-officio;2. The Chairman of the Board shall be the Prime Minister or a person nominated by him from amongst the Minister -members of the Board. 3. The Board may co-opt not exceeding four additional members. 4. No act or proceeding of the Board shall be invalid or called in question merely on the ground of existenceof any vacancy in, or any defect in the constitution of, the Board.

1.2.6.Investment Corp[oration of Bangladesh(ICB):

Financial system of Bangladesh Page 15 of 44

ICB first establish in 1976 through an ordinance with the following objectives-

To encourage and broaden the base of investment. To develop the capital market. To provide for matters ancillary thereto. To mobilize savings. To promote and establish subsidiaries for business

development. Operating investment account through buying and

selling of shares. Management of public issue. Advance against shares. Bridge finance. Management of mutual fund. Lease finance.

Basic Functions :

Underwriting of initial public offering of shares and debentures

Underwriting of right issue of shares Direct purchase of shares and debentures including

Pre-IPO placement and equity participation Providing lease finance to industrial machinery

and other equipments singly or by forming syndicate

Managing investors' Accounts Managing Open End and Closed End Mutual Funds Operating on the Stock Exchanges Providing investment counsel to issuers and

investors Participating in Government divestment Program

Financial system of Bangladesh Page 16 of 44

Participating in and financing of, joint-venture projects

Dealing in other matters related to capital marketoperations

Trusty, Custodian, Bank Guarantee Consumer Credit

Sources of funds :Deposit from sale of unit certificates is the main source of fund.

Performance of ICB:The company has recently setup there subsidiaries for its specialized areas of operation:

Asset management . Mutual fund management. Management of securities trading.

ICB is profitable organization, every year they declareattractive dividend against there mutual fund and unitcertifactes.

Existing Board :

CHAIRMAN OF THE BOARD :Mr. Feroz AhmedSecretary, Ministry of CommerceGovt. of the people's republic of Bangladesh.

MANAGING DIRECTOR AND DIRECTORS : Mr. Habibullah Bahar

Economic Adviser Bangladesh Bank

Mr. Hussain Jamil

Financial system of Bangladesh Page 17 of 44

Commissioner Chittagong Division, Chittagong

Brigadier General Md. Ahsan Habib Director Bangladesh National Cadet Corps

Mr. Md. Ziaul Haque Khondker Managing Director

Md. Kazi Sanaul Hoq Deputy General Manager

Mr. Elias Ahmed Managing Director, Sadharan Bima Corporation

Mr. Mukter Hussain Managing Director, Janata Bank

Mr. S. M. Aminur Rahman Managing Director, Sonali Bank

Mr.Syed Abu Naser Bukhtear Ahmed Managing Director & CEO, Agrani Bank

Mr. Md. Amanullah Managing Director Bangladesh Shilpa Bank

Mr. F R M Hafiz ul Islam Managing Director Bangladesh Shilpa Rin Sangstha

Financial system of Bangladesh Page 18 of 44

Share Capital Ownership Pattern :Classification of Shareholders as on 30 June, 2007

Shareholder No. ofShareholder

s

No. ofShares

Percentage

Government of Bangladesh 1 1350000

27.00

Nationalised Commercial Banks 4 1137220

22.74

Development Financial Institutions 2 1281550

25.63

Insurance Corporations 2 617781 12.35 Denationalised Private Commercial Banks 2 454263 9.09 Private Commercial Banks 3 28286 0.57 Foreign Commercial Banks 2 450 0.01 First BSRS Mutual Fund 1 7500 0.15 Other Institutions 12 29454 0.59 General Public 1121 93496 1.87 Total 1150 5000000

100.00

2.Financial Instruments:

Financial system of Bangladesh Page 19 of 44

Financial instruments/assets is acclaim against theincome or wealth of business firm, house hold or unitof Government, represent usually by a certificate,receipt, computer recorded file, or other legaldocuments and usually created by o r related to thelending of money. Example includes—stock, bonds,insurance polices, future contracts, and deposit heldin a bank or credit union. It’s an asset from the viewpoint of investor and it’s a liability from the viewpoint of issuers.

Although there are thousand of different financialinstruments, they are generally fall into fourcategories—

Money Equities/Stock

Debt securities

Derivatives

2.1.Money:

Money is one of the most important inventories of thehistory of human civilization. Any financial assetthat is generally accepted in payment for purchase ofgoods and services is money. In most simple way moneyis defined as “money is what money does” that isanything that performs the function of money iscalled money. Examples—currency, coin and checkingaccounts.

2.2.Stock/Equities:

Financial system of Bangladesh Page 20 of 44

Stock represents ownership shares in a business firmand, as such, are claim against the firm’s profit andagainst proceeds from the sale of its assets. Weusually further subdivided equities into-

Common stock :Which entitles its holders tovote for the members of a firmes board ofdirectors and, therefore, determine companypolicy.

Preferred stock: Which normally carries novoting privileges but does entitle its holderto a fixed share of the firms net earningsahead of its common stockholders

2.3.Debt securities:

Debt securities includes such familiar instrumentsas bonds, notes, accounts payable, and savingsdeposits. These financial instruments entitle itsholders to a priority claim over the holders ofequities to the assets and income of an individual,business firm, or unit of Government. Usually thatclaim is fixed in amount andtime(maturity)and ,depending on the terms of theindenture that accompanies most debt securities.Financial analysts usually divide debt securitiesinto two broad class :(a)Negotiable, which can easilybe transferred from holder to holder as a marketablesecurity, and (b)Nonnegotiable, which can not legallybe transferred to another party.

Financial system of Bangladesh Page 21 of 44

2.4.Derivatives:

Derivatives are among the news kinds of financialinstruments that are closely linked to financialassets .These unique financial clams have a marketvalue and that is return on a financial assets, suchas stocks, bonds, notes, future contracts, optionetc. Financial derivatives are consists of a range ofproducts for hedging risk. Derivatives productsincludes--

Future Forward

Option

Cap’s Ce Collar

SWAP

Financial system of Bangladesh Page 22 of 44

3.Financial Market

Financial market is a market where financialsecurities are traded. Financial market are the heartof financial system, attracting savings and settinginterest rates and the prices of financial assets(stock,bond, etc).The basic role of financial market is tostabilized savings into investment. The domesticfinancial market broadly categorized into two class-

Money Market Capital Market

3.1.Money market:

The money market is designed for short term loans. Itis the institution through which individual andinstitutions with temporary surpluses of funds meet theneeds of borrowers who have temporary funds shortages.One of the principal function of money market is tofinance the working capital needs of corporations andto provide the Governments with short-term funds in luewith tax collections. The securities traded in themoney market are—Reserve funds, Commercial paper,Treasury bills, Bankers acceptance, Certificate ofdeposits(CDs),and other short term debt securities.

Reserve funds: Reserve fund are simply thesedeposit that can be bought and sold in the moneymarket. Depository financial institutions offeringchecking accounts are required to have reserve asa percentage of the amount of these account.

Treasury bills: Treasury bills are the short-termdebt instruments for the government. Treasurybills always sold less than its par value. The

Financial system of Bangladesh Page 23 of 44

difference between the par value of the bills andthe price the investor pays for them is thediscount on the bills.

Commercial paper: Commercial paper is a short termdebt of a business firm or financial institution,which has been sold in the market. It is alsoissued at a discount from its face value. interestrates on commercial paper usually are well abovethe rates of treasury bills.

Bankers acceptance: A bankers acceptance is ashort term debt issued by a business firm on whicha large commercial bank has guaranteed payment tothe investors. So the purchasers o f anacceptance does not have to worry about the riskof borrowers.

Certificate of deposits(CDs): Certificate ofdeposits are large interest bearing deposits in abank. They have fixed maturities normally one yeaand they have pay interest at maturity.

3. 2 .Capital market:

The capital markets, is distinction from other parts ofthe financial market ie, the money markets, are thosefor long-term government securities, corporate bonds,stocks, municipal bonds issued by state and localgovernment units, and mortgages. Industry and commerceas well as government and local authorities raisecapital from the capital market which performs severalimportant functions in the process of economicdevelopment. Most important among them are thepromotion of savings and investment and efficient

Financial system of Bangladesh Page 24 of 44

allocation of funds among competing uses. Participantsin the capital markets are many. They include thecommercial banks, saving and loan associations, creditunions, mutual saving banks, finance houses, financecompanies, merchant bankers, discount houses, venturecapital companies, leasing companies, investment banks,investment companies, investment clubs, pension funds,stock exchanges, security companies, underwriters,portfolio-managers, and insurance companies. Financialinstruments in the Capital market have originalmaturities of more than one year. Capital market issubdivided into three parts—

Bond Market Stock Market

Mortgage Market

3.2.1.Bond Market:

Bond market is a long terms debt instruments issued bya corporation and the market where the long-term debtinstruments are traded is called bond market. Thematurity of bond at least ten years and have a fixedinterest payment made semiannually. Bond is a securedloan. Different types of bond are--

Zero coupon bond Municipal bond

Corporate bond

Financial system of Bangladesh Page 25 of 44

Interest bond

Junk bond

3.2.2. Stock Market:

Stock market is a market for the sale and purchase ofsecurities, in which the prices are controlled by thelaws of supply and demand. The basic function of stockmarket is to allow public companies, Governments, localauthorities and other incorporated bodies to raisecapital by selling securities to investors. Stockholders are the owners of the company. There are twotypes of stock market--

Organized stock exchange Over-The-Counter(OTC)

3.2.2.1.Organised Stock exchange:

Organized stock exchange is a formal organization,where listed companies stock are traded. Two organizedstock exchange of Bangladesh are—Dhaka Stock Exchange(DSE) and Chittagong Stock Exchange(CSE) and isregulated by Securities and Exchange Commission (SEC)

Securities and Exchange Commission (SEC) :

Financial system of Bangladesh Page 26 of 44

The Securities and Exchange Commission (SEC) was established on 8th June, 1993 under the Securities and Exchange Commission Act, 1993. The Chairman and Membersof the Commission are appointed by the government and have overall responsibility to administer securities legislation. The Commission, at present has three full time members, excluding the Chairman. The Commission isa statutory body and attached to the Ministry of Finance.

Mission of the SEC is to: Protect the interests of securities investors. Develop and maintain fair, transparent and

efficient securities markets. Ensure proper issuance of securities and

compliance with securities laws

Commissions main functions are:

1. Regulating the business of the Stock Exchanges or any other securities market.

2. Registering and regulating the business of stock-brokers, sub-brokers, share transfer agents, merchant bankers and managers of issues, trustee of trust deeds, registrar of an issue, underwriters, portfolio managers, investment advisers and other intermediaries in the securities market.

Financial system of Bangladesh Page 27 of 44

3. Registering, monitoring and regulating of collective investment scheme including all forms of mutual funds. 4. Monitoring and regulating all authorized selfregulatory organizations in the securities market. 5. Prohibiting fraudulent and unfair trade practices relating to securities trading in any securities market. 6. Promoting investors’ education and providing training for intermediaries of the securities market. 7. Prohibiting insider trading in securities. 8. Regulating the substantial acquisition of shares and take-over of companies. 9. Undertaking investigation and inspection, inquiries and audit of any issuer or dealer of securities, the Stock Exchanges and intermediaries and any self regulatory organization in the securities market. 10. Conducting research and publishing information.

The Information Required in an SEC Registration Statement:

Copy of the issuer’s articles of incorporation Purpose for which the proceeds of the issue will

be spent. Offering price to the public Offering price for special groups, if any Free promised to developers and or promoters Underwriter’s fees Net proceeds to the issuer

Financial system of Bangladesh Page 28 of 44

Information on the issuer’s products, history, andlocation

Copies of any indentures affecting the new issue Names and remuneration of offers in the issuing

firm Details about any unusual contracts, such as a

managerial profit-sharing plan Detailed statement of capitalization Details balance sheet Detailed income and expenses statements for 3

preceding years Names and addresses of the issuer’s officers and

directors and of the underwriters Names and addresses of any investors owning more

than 10 percent of the class of stock

Copy of the underwriting agreement Copies of legal opinions on matters related to the

issue Details about any pending litigation

The Commission :

Mr. Faruq Ahmad Siddiqi, ChairmanMr. Saleh Ahmed Chowdhury, MemberMr. Mohammad Ali Khan, Member Mr. Mansur Alam, Member

Principal Officers:

Capital Market Regulatory Reforms & Compliance:

Financial system of Bangladesh Page 29 of 44

Mr. Mohammad Abdul Hannan Zoarder, Executive Director

Mr. A.K.M. Ziaul Hasan Khan, Director.

Administration:

Mr. Md. Saifur Rahman, Director Mr. Mohammad Abul Hasan, Deputy Director Mr. M.A. Maleque, Accounts Officer

Corporate Finance: Mr. Md. Hasan Mahmud, Director Mr. Mir Mosharraf Hossain, Deputy Director Mr. Md. Abul Kalam, Deputy Director

Chairman’s Office:

Ms. Farhana Faruqi, Assistant Director

CDS: Mr. Farhad Ahmed, Executive Director

Enforcement:

Mr. M. Mizanur Rahman, Director Mr. Mohammad Jahangir Alam, Deputy Director Mr. Prodip Kumar Basak, Deputy Director Mr. Md. Monsur Rahman, Deputy Director

Capital Issue (Initial Public Offering has been

renamed): Mr. Farhad Ahmed, Executive Director Mr. M. Mahbubul Alam, Director. Mr. Kamrul Anam Khan, Deputy Director

Law:

Financial system of Bangladesh Page 30 of 44

Mr. M. Mizanur Rahman, Director

Mr. Mahbubur Rahman Chowdhury, Deputy Director

Management Information Systems: Mr. Md. Ashraful Islam, Director Mr. Rajib Ahmed, Deputy Director

Registration & Licensing: Ms. Ruksana Chowdhury, Executive Director Mr. Md. Anowarul Islam, Director Mr. Md. Mahmoodul Hoque, Deputy Director

Finance:

Mr. Md. Saifur Rahman, Director Mr. Mohammad Rezaul Karim, Deputy Director

Research & Development: Mr. Mohammad Abdul Hannan Zoarder, Executive

Director Mr. Shafiul Azam, Deputy Director

Supervision & Regulation of Markets and Intermediaries:

Mr. Mohammad Abdul Hannan Zoarder, Executive Director

Mr. Md. Ashraful Islam, Director Mr. Ripan Kumar Debnath, Deputy Director Mr. Sheikh Mahbub Ur Rahman, Deputy Director Ms Farhana Faruqi, Assistant Director

Financial system of Bangladesh Page 31 of 44

Surveillance : Mr. Md. Anwarul Kabir Bhuiyan, Executive

Director Mr. Mohammad Rezaul Karim, Deputy Director

World Bank Project :

Mr. Mohammad Abdul Hannan Zoarder, Executive Director

ADB Project : Mr. Md. Anwarul Kabir Bhuiyan, Executive

Director On Education Leave :

Mr. ATM Tariquzzaman, Executive Director

Dhaka Stock Exchange(DSE):

The Dhaka Stock Exchange (DSE) is registered as aPublic Limited Company and its activities are regulatedby its Articles of Association rules & regulations andbye-laws along with the Securities and ExchangeOrdinance, 1969, Companies Act 1994 & Securities &Exchange Commission Act, 1993.

Function of DSE :

The major functions are:

Listing of Companies.(As per Listing Regulations). Providing the screen based automated trading of

listed Securities.

Financial system of Bangladesh Page 32 of 44

Settlement of trading.(As per Settlement ofTransaction Regulations)

Gifting of share / granting approval to thetransaction/transfer of share outside the tradingsystem of the exchange (As per Listing Regulations42)

Market Administration & Control.

Market Surveillance.

Publication of Monthly Review.

Monitoring the activities of listed companies.(As per Listing Regulations).

Investors grievance Cell (Disposal of complaintbye laws 1997).

Investors Protection Fund (As per investorprotection fund Regulations 1999)

Announcement of Price sensitive or otherinformation about listed companies through online.

MARKETS:

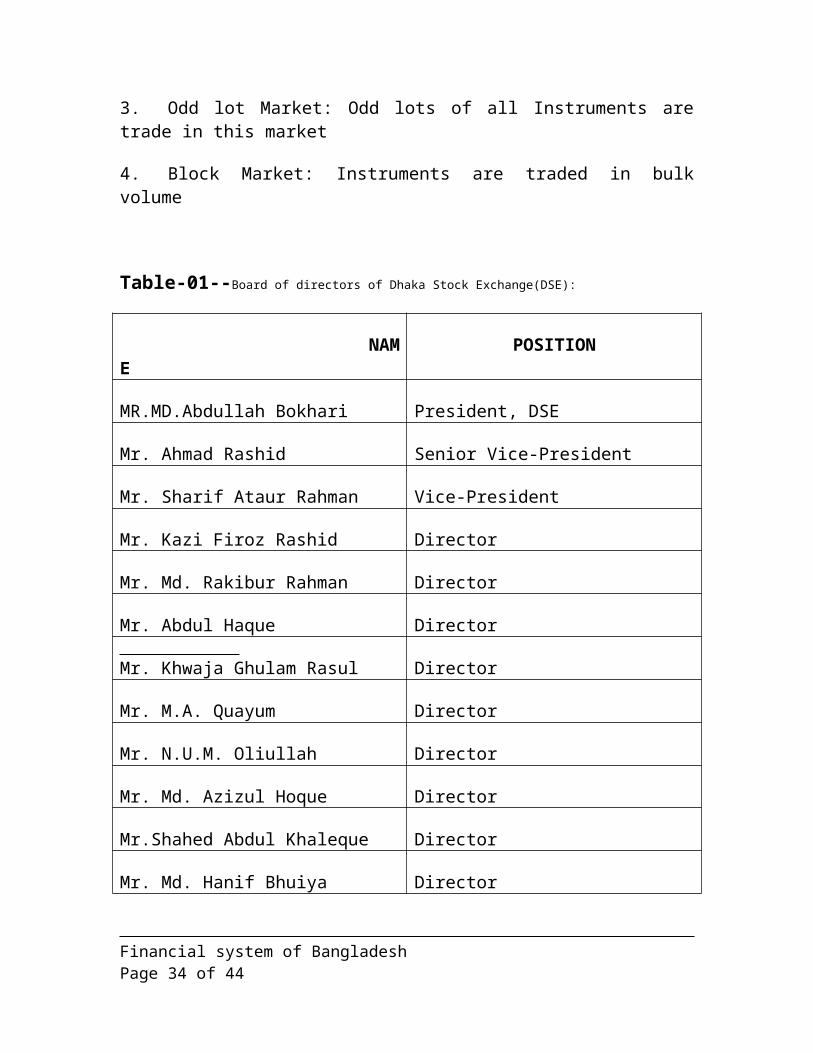

Four types of market at DSE:

1. Public Market: In this market instruments aretraded in normal volume

2. Spot Market: Instruments are traded in normalvolumes under corporate action if any

Financial system of Bangladesh Page 33 of 44

3. Odd lot Market: Odd lots of all Instruments aretrade in this market

4. Block Market: Instruments are traded in bulkvolume

Table-01--Board of directors of Dhaka Stock Exchange(DSE):

NAME

POSITION

MR.MD.Abdullah Bokhari President, DSE

Mr. Ahmad Rashid Senior Vice-President

Mr. Sharif Ataur Rahman Vice-President

Mr. Kazi Firoz Rashid Director

Mr. Md. Rakibur Rahman Director

Mr. Abdul Haque Director

Mr. Khwaja Ghulam Rasul Director

Mr. M.A. Quayum Director

Mr. N.U.M. Oliullah Director

Mr. Md. Azizul Hoque Director

Mr.Shahed Abdul Khaleque Director

Mr. Md. Hanif Bhuiya Director

Financial system of Bangladesh Page 34 of 44

Salahuddin Ahmed Khan Chief Executive Officer

Shaikh Mohammadullah, MBA(IBA), FCS

General Manager & Secretary

Satipati Moitra, M.Com,FCMA

Chief Financial Officer

A.S.M. Khairuzzaman General Manager & Head ofICT

INFORMATION AND COMMUNICATION TECHNOLOGY DIVISION:

System & Market Administration Department Network Department

Web Development Department

MIS & Development Department

Back Office Software Development Department

Application Support Department

Hardware Support Department

ADMINISTRATION DIVISION:

Board & Membership Affairs Department HRM, Administration & Training Affairs Department

Logistics, Maintenance, Protocol Department

Financial system of Bangladesh Page 35 of 44

Research, Development & Information Department

Publication & Public Relation Department

Security Department

Dse Training Academy

Personal Officer to CEO

OPERATION DIVISION:

Surveillance Department Monitoring, Investigation & Compliance Department

Listing Affairs & Market Operation Department

Internal Audit & Compliance Department

FINANCE DIVISION:

General Accounts Department DSE FSDP Department

Clearing Accounts Department

Chittagong Stock Exchange(CSE) :

Board of Directors:

Chittagong Stock Exchange Ltd. (CSE) has a policymakingBody of 25 members, of whom 12 are elected and 13 are

Financial system of Bangladesh Page 36 of 44

non elected. This Board comprises of one President, three Vice Presidents and 20 Directors. There is an independent secretariat headed by a Chief Executive Officer (CEO).

Table-02-- Board of Directors of Chittagong Stock Exchange Ltd.

1. Mr. M.K.M. Mohiuddin President

2. Mr. Nasiruddin Ahmed Chowdhury

Vice-President

3. Mr. Fakhor Uddin Ali Ahmed Vice-President

4. Mr. A.Q.I. Chowdhury Vice-President

5. Mr. Abu Sayed Md. Shahidullah

Director

6. Mr. Al Maruf Khan Director

7. Mr. ASM Nayeem Director

8. Mr. Bijan Chakroborty Director

9. Mr. Mirza Salman Ispahani Director

10.

Mr. Morshed Murad Ibrahim Director

11.

Mr. Syed Mahmudul Huq Director

12.

Mr. Tareq Kamal Director

Financial system of Bangladesh Page 37 of 44

13.

Dr. A. Majeed Khan Director

14. Prof. Abu Ahmed

Director

15. Engr. Ali Ahmed

Director

16.

Mr. Amir Humayun Mahmud Chowdhury

Director

17.

Mr. Anis A. Khan Director

18.

Mr. Farooq Sobhan Director

19.

Mr. Mamun Rashid Director

20.

Mr. Md. Sarwar-E-Alam Director

21.

Prof. Rabiul Husain Director

22.

Mr. Mohd. Safwan Choudhury Director

23.

Mr. Waliur Rahman Bhuiyan Director

24.

Mrs. Yasmeen Murshed Director

25.

Mr. A. B. Siddique CEO

Listing requirements of CSE :

1. The Company shall apply to the Chittagong StockExchange (the Exchange) with an application fee ofTk. 10,000/-(ten thousand), and shall

Financial system of Bangladesh Page 38 of 44

simultaneously furnish a copy thereof, along withthe copies of documents mentioned under subregulation (ii), to the Securities and ExchangeCommission (SEC).i) The Company shall, among others, submit the

following documents along with the application:(a) Memorandum of Association and Articles of

Association;(b) A brief profile of the company, including

brief particulars of existing sponsor-directors of the company;

(c) Certificate of incorporation andcertificate of commencement of business;

(d) Audited financial statements for the lastfive years;

(e) Members/ shareholders list together withshareholding position;

(f) Return of allotment(s) filled with theRegistrar of Joint Stock Companies andFirms;

(g) Existing material agreements includingdeed of mortgage (if any);

(h) Status of loan including informationconcerning loan default, if any, of thecompany;

(i) VAT and Tax identification numbers;(j) Due diligence certificate from the

directors as per format prescribed by theExchange;

(k) No objection certificate from the lendingbank(s) /financial institutions of thecompany, if any, where applicable;

Financial system of Bangladesh Page 39 of 44

(l) Undertaking in the prescribed form aslaid down in the listing regulations ofthe Exchange to the effect that thecompany shall comply with the securitieslaws including requirements of the saidlisting regulations upon listing with theExchange;

(m) Relevant resolution(s) of theshareholders in the general meeting ofthe company and the Board’s resolution,if so authorised, for the purpose oflisting with the Exchange;

(n) Credit rating report issued by the creditrating company registered with theCommission with minimum investment gradeof “BBB”;

(o) Information Document as per formatprescribed by the Exchange;

(p) The shareholders resolution in respect ofdisposal of shares in accordance with theregulation 5.

ii) Upon receipt of the application, the Exchangeshall examine and inform the company within 15(fifteen) days from the receipt of theapplication, with a copy to the Commission ,to remove the deficiencies, if any, within 30(thirty) days from the date of receipt fromthe Exchange.

iii) The Exchange shall furnish to the Commissionthe copies of all information and documentsreceived from the company pursuant to the

Financial system of Bangladesh Page 40 of 44

Exchange’s letter mentioned under the sub-regulation (iii) within the following workingday of receipt.

iv) After fulfillment of all requirements by thecompany, the Exchange shall list the company’sshares within three weeks from the date ofpublication of the Information Document, asmentioned in regulation 4, under intimation tothe Commission, provided there is no contraryopinion of the Commission in this respect.

v) In case of failure to fulfil the requirementsby the company, the Exchange shall reject theapplication for listing showing reasonsthereof, under intimation to the Commission,within 60(sixty) days from the date ofapplication.

3.2.2.2.Over The Counter :

An over-the-counter contract is a bilateral contract inwhich two parties agree on how a particular trade or agreement is to be settled in the future. It is usuallyfrom an investment bank to its clients directly. It is mostly done via the computer or the telephone. For derivatives, these agreements are usually governed by an International Swaps and Derivatives Association agreement.

An over-the-counter is not an organization but an intengable market for purchase and sale of securities not listed by the organised stock exchange.There are

Financial system of Bangladesh Page 41 of 44

basically small and new organization who can not full fil the criteria of organised stock exchange to become the membership of the securities and exhange commission.The World largest OTC market is the US-National Association of Securities Dealers Automated Quotation System(NASDAQ).

3.2.3.Mortage Market:

Mortage is pledge of specific property given by a borrowers as a security on loan.two types mortage are—

Physical mortage—physical property like houes, automobile, bulding, land etc.

Chattel mortage—Chattel mortage are personal values as an individual.

Other types of mortage are—

Blanket mortage--It covers manyloan ata time.

Closed-end mortage—it forvides to takean additional loan unles the additional is of lower priority than existing loan.

Open-end mortaage—It allows the scencity provided by the mortage to beused as a collateral or additional loan.

Financial system of Bangladesh Page 42 of 44

Reference:

Ahmed ,Dr. Salehuddin , “The Road Map to FinancialSystem Standards for Middle Income Bangladesh"

Ahmed, Md. Nehal., Chowdhury, Mainul Islam, “Non-Bank Financial Institutions in Bangladesh”an analytical review, March 2007

Chowdhury,Dr.Toufic Ahmed , “financial system of Bangladesh”

Dhaka Stock exchange Ltd,available via internet: http://www.dsebd.org/

Chittagong stock exchange Ltd, available via internet, http:// www.csebd.org/

Financial system of Bangladesh Page 43 of 44

Investment Corporation of Bangladsh,available via Internet:www.icb.gov.bd.

Board of Investment of Bangladsh: Available via internet;www.boi.gov.bd.

securities and Exchange Commission ;Available via internet;wwwSecbd.org.

Financial system of Bangladesh Page 44 of 44